THE ROLE OF DAILY CONTRIBUTION COLLECTORS IN THE GROWTH OF MICRO, SMALL AND MEDIUM ENTERPRISES IN...

29

THE ROLE OF DAILY CONTRIBUTION COLLECTORS IN THE GROWTH OF MICRO, SMALL AND MEDIUM ENTERPRISES IN ZARIA METROPOLIS By SAYEDI, Shuaib Ndagi DEPARTMENT OF BUSINESS ADMINISTRATION, FACULTY OF MANAGEMENT AND SOCIAL SCIENCES IBRAHIM BADAMASI BABANGIDA UNIVERSITY, LAPAI.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of THE ROLE OF DAILY CONTRIBUTION COLLECTORS IN THE GROWTH OF MICRO, SMALL AND MEDIUM ENTERPRISES IN...

THE ROLE OF DAILY CONTRIBUTION COLLECTORS IN THE

GROWTH OF MICRO, SMALL AND MEDIUM ENTERPRISES IN

ZARIA METROPOLIS

By

SAYEDI, Shuaib Ndagi

DEPARTMENT OF BUSINESS ADMINISTRATION,

FACULTY OF MANAGEMENT AND SOCIAL SCIENCES

IBRAHIM BADAMASI BABANGIDA UNIVERSITY, LAPAI.

ABSTRACT

Daily Contribution Collectors (DCCs) or Mobile Collectors (MC) are one of theinformal sources of financing. Informal financial sources have contributedsignificantly to the growth of Micro, Small and Medium Enterprises (MSMEs) inmany developing countries, such as Nigeria. However, they are often faced withproblems of regulation; cost of operations and arbitrary charges onsavings/credits which are unsecured. Therefore, the study examined the roles ofDCCs on the growth of MSMEs in terms of number of employees and annual salesturnover. The study was conducted in Zaria metropolis comprising Zaria andSabon Gari Local Government Areas with population of 17,532 MSMEs operators.Random samples of 391 MSMEs operators who were customers of DCCs areselected from the population using YaroYomens’ formula of determining thesample size. The questionnaire instrument was used to source information fromthe respondents. A set of questionnaires was administered to samples of MSMEsoperators who patronize DCCs. Another set of 13 questionnaires was alsoadministered to DCCs for validity and reliability. Subsequently, the data collectedwere analyzed using descriptive statistics, Pearson product moment correlationcoefficient and t - test statistics to test the hypotheses. The study found that dailyvisits for savings collection is main reason why MSMEs operators saved moneywith DCCs. The correlation coefficient results show that DCCs contributed to thegrowth of MSMEs in terms of increase in number of employees and annual salesturnover. T – test statistic affirms the result by stating that there is significantrelationship between DCCs and MSMEs in terms of number of employees while therelationship was undefined in terms of annual sales turnover. The study therefore,recommended that daily visits for savings collection be encouraged andstrengthened. Moreover, government (at all levels) should search and come outwith sustainable financing ways of assisting MSMEs financing. This is becauseMSMEs have contributed to employment generation and annual sales turnover,therefore, alleviating poverty among the teaming population of Nigeria.Keywords: DCCs, MSMEs, informal sector, Employees and Annual Sales Turnover

1

1.0 Introduction

The rapid growth of informal financial institutions

in recent years in most developing countries is due to

strict conditions attached to loan by formal financial

institutions and inadequate funds made available by

these institutions (Banks and other formal lending

institutions). However, the need to provide funding to

the poor segments of the populations who are

economically active increased the relevance of informal

financial institutions which include Rotational Saving

and Credit Associations (RSCAs), Daily Contribution

Collectors (DCCs) and money lenders, etc.

Daily Contribution scheme which DCCs are the funds

custodian started approximately 50 years ago (1940s)

because of the weaknesses of RSCAs (Seibel, 2001). The

scheme has different names among the three major ethnic

groups in Nigeria. It is called “Ajo” or “susu” among

Yorubas in the West, “Otu” for Igbos in the East and

“Asusu” for Hausas in the North. The DCCs come round on

a daily basis to collect funds from their customers at

home or business premises. The savings collected are

returned at the end of the month (30 days) or as agreed

after deduction of the initial saving or deposit as

commission, translating to 3.33 percent (Ahiawadzi and

Alabi(s), 2007). The financial services provided by the

DCCs have assisted Micro, Small and Medium Enterprises

(MSMEs) to improve their operational efficiency.

2

MSMEs mean different things to different people

because of varying definitions from country to

countries. Even within a country, definitions vary

within different organizational bodies. Srivastava

(2010) states that the definition of MSMEs is based on

five main parameters namely labour, capital, loan size,

fixed assets and annual sales turnover. Ayyagari, Beck

and Demirgue – Kunt (2005) state that the World Bank SME

Department defines micro enterprises as employing up to

10 workers, assets of $10,000 (N1, 500, 000) and annual

sales turnover of $100,000. Small enterprises employ up

to 50 workers, assets and annual sales turnover up to $3

million; and medium enterprises employ up to 300

workers, total assets and annual sales turnover up to

$15 million. Osalor (2010) opines that micro

enterprises employ up to 5 workers, small enterprises

employ from 5 to 19 workers, medium enterprises employ

from 20 to 99 workers, and large enterprises employ 100

workers above.

The definition of MSMEs and Small and Medium

Enterprises (SMES) are similar but different in terms of

broadness. MSMEs are broader in definition relative to

SMEs which shall be used interchangeably in subsequent

discussions. This is because many countries such as

Nigeria and United States of American (U.S.A) etc, do

not create distinction between MSMEs and SMEs sometimes.

In Nigeria, Small and Medium Industries and Equality

3

Investment Scheme (SMIEIS) defines SMEs as any

enterprise with a maximum assets base of N 200m

excluding land and working capital with number of staff

employed not less than 10 or more than 300 (Gunu, 2009).

Irrespective of the nature and composition of MSMEs

and SMEs, informal financial sector which includes DCCs

provides significant percent of informal financial

services to them. CBN (2005) affirms that formal

financial system provided services to about 35 percent

of the economically active population while, the

remaining 65 percent is served by informal financial

sector. The problem of unserved populations by formal

financial system in Nigeria has made Central Bank of

Nigeria (CBN) to come out with microfinance policy. This

policy encourages the establishment of new microfinance

banks and conversion of existing community banks to

microfinance banks after increasing the capitalization

from 5 to 20 million Naira. Consequently, the structures

and services provided by formal financial sector were

increased by decreasing the services of informal

financial sector.

However on 24 September, 2010, CBN recommended

revocation of 224 microfinance banks out of 820 (CBN,

2010). Subsequently, Nigerian Deposit Insurance

Corporation (NDIC) closed 223 microfinance banks (NDIC,

2010). These set backs have increased the activities and

services provided by DCCs and other members of informal

4

financial sector to increase. Oloyede (2008) observes

that “Alajo” or “Ajo” (mobile collectors) appear

prominent among the family members of informal financial

sector. Although, they have problems of regulations,

cost of operation, arbitrary charges on savings and

credits. In spite of that, DCCs and other members of

informal financial sector still contribute to the growth

of MSMEs in terms of number employees and annual sales

turnover in many developing countries which this study

eventually found out.

The main objective of the study is to examine the

role of DCCs to the growth of MSMEs in Nigeria.

Specifically, the study intend to:

i. Examine the role of DCCs on employment generation.

ii. Examine the role of DCCs on the growth of annual

sales turnover of MSMEs.

In line with the above objectives, the

following null hypotheses are stated for testing:

H01: DCCs play no significant role on the growth of

MSMEs’ number of employees.

H02: DCCs play no significant role on the growth of

MSMEs’ annual sales turnover.

2.1 Review of Related Literature

It has been observed over years that MSMEs are

vehicle for poverty alleviation, employment generation

and wealth creation. Nkange (2007) notes that in most

5

developing countries, MSMEs have been used as strategy

for employment generation, food security, poverty

alleviation, rapid industrialization and reversing

rural-urban migration. However, they are faced with

problems of financing, financing sources to choose from

and management capabilities. Aina (2007) identifies that

the rising poverty in Nigeria is due to poorly executed

government programmes toward SMEs to alleviate poverty.

The study suggested more effective and fully funded SMEs

programmes and policies which attract grass root

participation to eradicate poverty. A study conducted by

Onugu (2005) on randomly selected 300 SMEs using

regression as an analytical tool, identified 10 problems

confronting SMEs in Nigeria. These problems are arranged

in order of their magnitude as management, access to

finance, infrastructure, government policy inconsistency

and bureaucracy, environmental factors, multiple taxes

and levies, access to modern technology, unfair

competition, marketing problems and non-availability of

raw materials. The study suggested that promoters of

SMEs should ensure the availability or possession of

management capacity and acumen before pursuing financial

resources for the development of the respective

enterprises.

In addition to the above studies, Gunu (2009)

conducted a study in Ilorin on 50 randomly selected SMEs

using descriptive statistics to present the survey

6

findings. The study found that the major constraint in

sourcing for found from Nigeria Stock Exchange (NSE) is

listing constraint. He suggested that government should

encourage listed SMEs by the way of providing necessary

incentives such as reduction of quotation fee, listing

fee and years of required trading record, etc. A recent

study by Abdullahi, Zakari and Muhammed (2010) in Minna

on randomly selected 540 SMEs using t-test statistic,

identified SMEs have limited credits to use. The limited

credits to SMEs are due to lack of supply as a result of

rationing behaviours of formal and informal financial

institutions. The study concluded that established

formal lending institutions should improve lending terms

and favourable conditions to enable SMEs get access to

credits. So, access to finance is major constrain

confronting MSMEs in Nigeria and financing sources can

be through formal or informal financial institutions.

Formal and informal financial sectors

(institutions) represent interface between demand of

individuals, households and enterprises for financial

services. However, formal financial sector attaches

strict conditions for financial services such as minimum

cash requirement on certain customers’ accounts and

collateral for credits. These make informal financial

sector to be relevance in providing financial services

to MSMEs. Alabi, Alabi and Akorobo (2007) conducted a

study in Ghana on 5 “Susu” clubs and associations; 10

7

mobile collectors; and 5 cooperative using paired

observation test. The study revealed that there is a

relationship between informal financial institutions and

development of MSMEs in terms of turnover on investment

and employment generation. Self regulation was also

identified to be a major set back and recommended a

system of regulating them. In a related study, Oloyede

(2008) investigated Informal Financial Sector, Savings

Mobilization and Rural Development in 16 Local

Government Areas of Ekiti state in Nigeria. The study

sampled 1,100 entrepreneurs and civil servants residing

in rural areas using descriptive statistics as tool for

the analysis. The study found Ajo (Daily Contribution

Scheme) to appear prominent among the family of informal

financial sector, mobilizing savings and channeling

credits to productive investment. It further identified

myriad of problems such as self regulation that still

beset their effective performance. The study suggested

appropriate policy reform by government, harnessing the

much needed rural financing for sustainable economic

development.

Iganiga and Asemotal (2008) also conducted a

similar study in Benin and Ekpoma on 20 informal

financial institutions’ operators, their modus operandi

and the extent of financial intermediation in different

social settings, using descriptive analysis and simple

percentages. The study found mobile collectors and money

8

lenders to be prevalent in semi-urban and urban areas

among entrepreneurs (MSMEs) such as artisans, traders

and skilled workers providing financial services. The

study recommended development of the sector to guarantee

credits and provision of insurance against risks. Yusuf,

Gafar, and Ajaiya (2009) conducted a study in Offa town-

Kwara state on 550 informal sectors (MSMEs and others)

who were members of Rotational Savings and Credits

Associations (RSCAs). The study used p-alpha class

poverty measure and multiple regression analysis. And

found informal financial institutions playing important

role in reducing poverty among people in terms of wealth

creation and employment generation. In a recent related

study by Daniel (2010) on 3,000 SMEs operated by women

using descriptive statistic. The study found informal

financial sector keeping savings and lending to SMEs. It

also identified the sector of lacking strong capital

base and Ajo or susu operators (mobile collectors or

DCCs) are found of absconding with customers’ money. The

study recommended expansion programmes by formal

financial sector to carter for SMEs financing.

From aforementioned studies, many investigations

are conducted on RSCAs and how they affect MSMEs. A

thorough and extensive research conducted has revealed

that the study has never been carried out on the roles

of Daily Contribution Collectors (DCCs) or mobile

collectors to the growth of MSMEs. The DCCs appear

9

prominent among family members of informal financial

sector. This is a gap in the field of academic

discourse. Thus, this study intends to fill the existing

vacuum in order to advance the frontier of knowledge.

3.1 Research Methodology

This study adopts a survey research method using

primary data. The Primary data are unstructured

interviews conducted and two sets of questionnaires

administered to MSMEs operators and DCCs.

The study was conducted in Zaria metropolis of

Kaduna State, Nigeria. The populations of MSMEs in Zaria

metropolis consisting Zaria and Sabon Gari Local

Government Areas (LGAs) are 5,578 and 11,954

respectively (Revenue Office, 2011a and Revenue Office,

2011b). The populations consist of both permanent and

temporary shops of MSMEs operators situated in these

Local Government territories.

The total population of MSMEs in both LGAs is

17,532. Random Samples of 391 MSMEs operators were

selected from the population. The sampled population is

customers who patronize DCCs. This sample size was

determined using Yaro Yamen’s formula as shown below

(Kelechi, 2008 in Ogbadu, 2009).

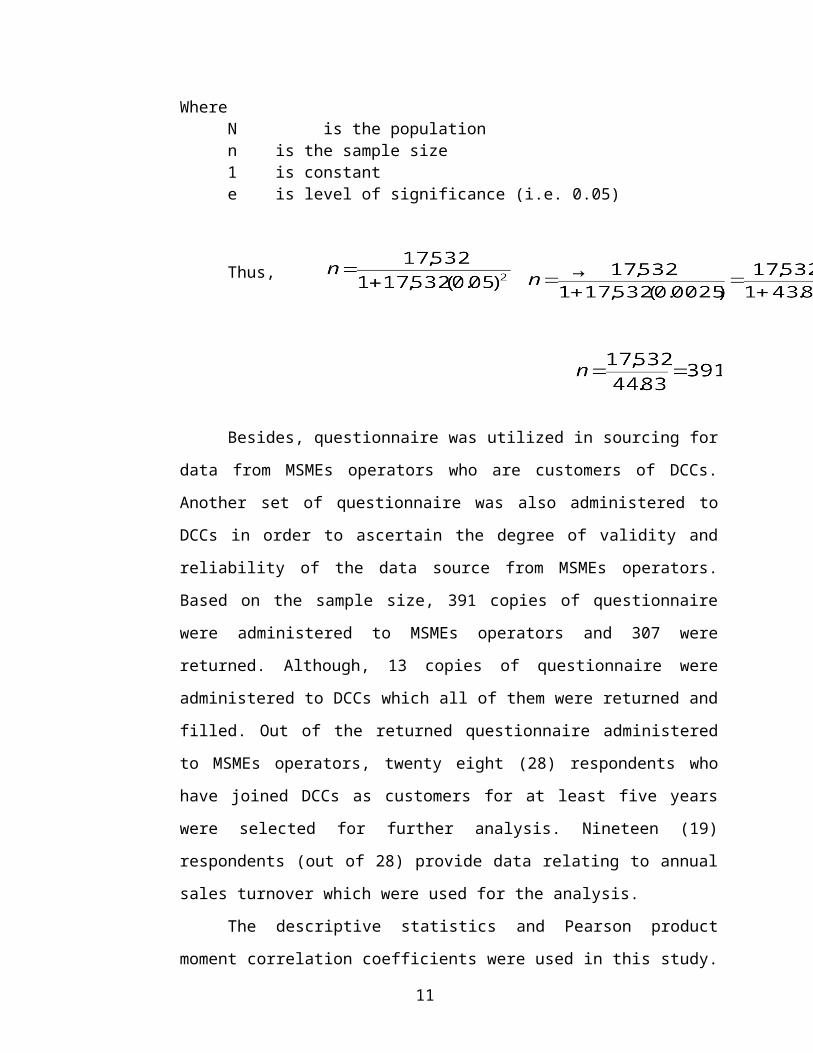

Therefore,

10

WhereN is the populationn is the sample size 1 is constante is level of significance (i.e. 0.05)

Thus, →

Besides, questionnaire was utilized in sourcing for

data from MSMEs operators who are customers of DCCs.

Another set of questionnaire was also administered to

DCCs in order to ascertain the degree of validity and

reliability of the data source from MSMEs operators.

Based on the sample size, 391 copies of questionnaire

were administered to MSMEs operators and 307 were

returned. Although, 13 copies of questionnaire were

administered to DCCs which all of them were returned and

filled. Out of the returned questionnaire administered

to MSMEs operators, twenty eight (28) respondents who

have joined DCCs as customers for at least five years

were selected for further analysis. Nineteen (19)

respondents (out of 28) provide data relating to annual

sales turnover which were used for the analysis.

The descriptive statistics and Pearson product

moment correlation coefficients were used in this study.

11

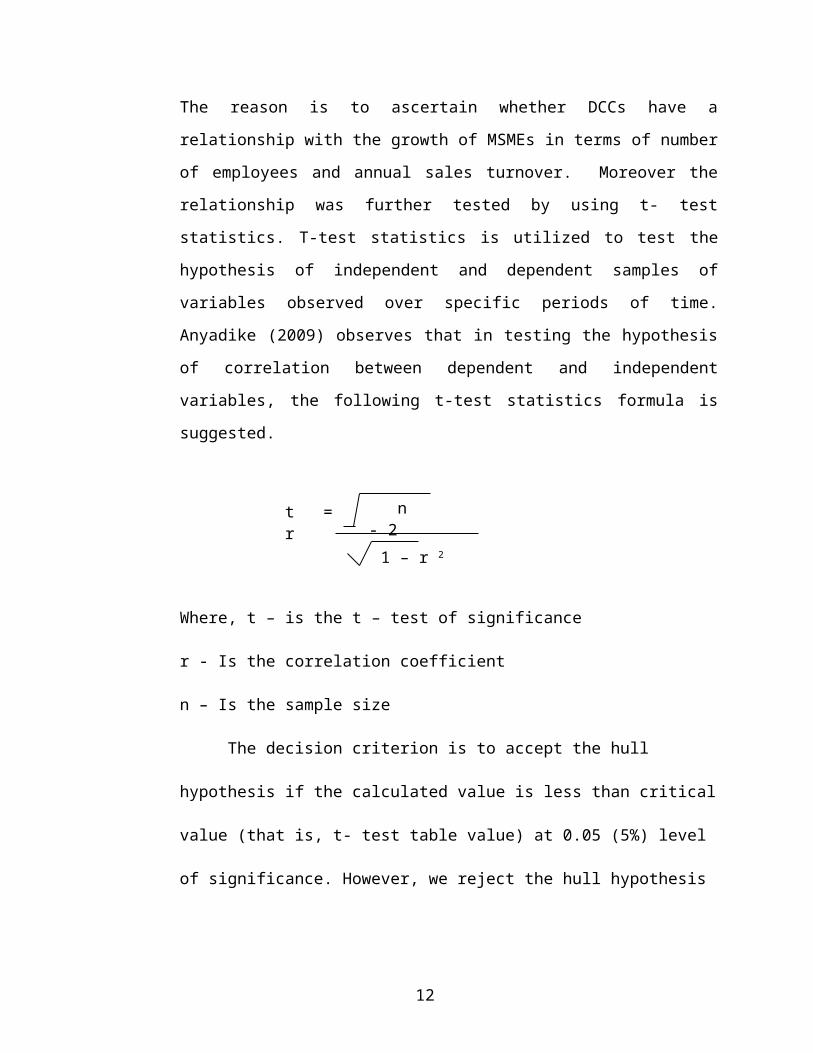

The reason is to ascertain whether DCCs have a

relationship with the growth of MSMEs in terms of number

of employees and annual sales turnover. Moreover the

relationship was further tested by using t- test

statistics. T-test statistics is utilized to test the

hypothesis of independent and dependent samples of

variables observed over specific periods of time.

Anyadike (2009) observes that in testing the hypothesis

of correlation between dependent and independent

variables, the following t-test statistics formula is

suggested.

Where, t – is the t – test of significance

r - Is the correlation coefficient

n – Is the sample size

The decision criterion is to accept the hull

hypothesis if the calculated value is less than critical

value (that is, t- test table value) at 0.05 (5%) level

of significance. However, we reject the hull hypothesis

12

n - 21 – r 2

t = r

if the calculated value is more than critical value at

0.05 level of significance.

4.1 Data Presentation and Analysis

Data are presented and analysed in

sections. Section A deals with responses received from

DCCs while section B deals with responses received from

MSMEs.

4.2 Section A : Analysis Relating to DCCs

In this section, data relating to responses

received from DCCs are presented and analyzed below.

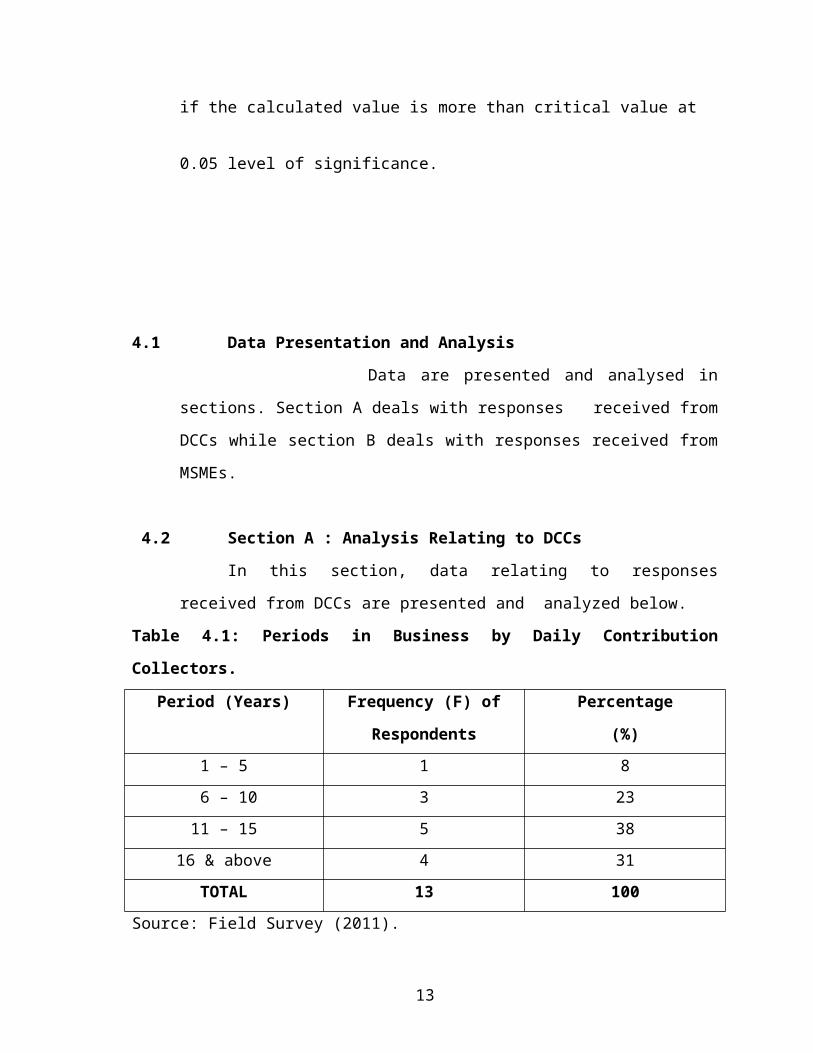

Table 4.1: Periods in Business by Daily Contribution

Collectors.

Period (Years) Frequency (F) of

Respondents

Percentage

(%)1 – 5 1 8 6 – 10 3 2311 – 15 5 38

16 & above 4 31TOTAL 13 100

Source: Field Survey (2011).

13

Table 4.1 shows that majority of Daily contribution

collectors have spent more than 10 years in operating

informal financial scheme and carrying depositors or

savers’ risk (MSMEs). Five respondents have spent more

than 10 years in the business representing 38 percent

while four respondents have more than 15 years in the

business representing 31 percent. In addition, three

respondents have spent between six and 10 years in the

business representing 23 percent. The least is one

respondent representing eight percent spending between

one and five years in the business.

Hence, it implies people who are experienced embark

of this business. This is because more than 60 percent

of sampled DCCs have more than 5 years in the business

sustaining informal sector to grow.

Table 4.2: Deposits Constituting Large Accounts of Daily

Contribution Collectors (DCCs)

Amount (N) Frequency (F) of

Respondents

Percentage (%)

50 – 200 4 31210 – 500 4 31510 – 1000 3 231000 and 2 15

14

aboveTOTAL 13 100

Source: Field survey (2011).

Table 4.2 shows that amount of money collected by

DCCs that constitute larger accounts of deposits to them

range from 50 to 500 Naira. Four collectors representing

31 percent respond that 50 to200 Naira are larger

accounts of collections, while another four collectors

representing 31 percent also respond that 210 to 500

Naira are larger account of collections. Three

collectors representing 23 percent respond that 510 to

1000 Naira are the larger accounts, white two (2)

respondents indicate 1000 Naira and above.

Besides the analysis of responses received from

administered questinionaires, interviews were conducted.

A question was asked while interviewing the managing

director of PAT Azeez services on the amount of money

his company charges monthly as commission on daily

savings or deposits. The director replied that the

commission collectable / chargeable is the initial

saving or deposit of the customer. However, if the

customer decided to stop further contributions, the same

initial saving is taken and remainder returned to the

owner. On the question of amount of money charged on a

loan, he replied that 50 Naira is charged for every 1000

Naira per month and no collateral. The loan scheme is

15

designed for customers who have spent three years

contributing money on daily basis.

From the analysis of table 4.3, the sum of 62

percent of DCCs customers contribute between 50 and 500

Naira. This means majority of the customers of DCCs are

low income earners that need financial support to

improve their operational efficiency.

4.3 Section B: Analysis Relating to MSMEs.

In this section, data relating to responses coming

from MSMEs are presented. and analysed .

Table 4.3: Amounts of Money MSMEs Contribute on DailyBasis to DCCs.

Amount (N) Frequency (F) ofRespondents

Percentage (%)

50 – 200 91 30210 – 500 102 33.0510 – 1000 76 25Above 1000 38 12

TOTAL 307 100 Source: Field Survey (2011).

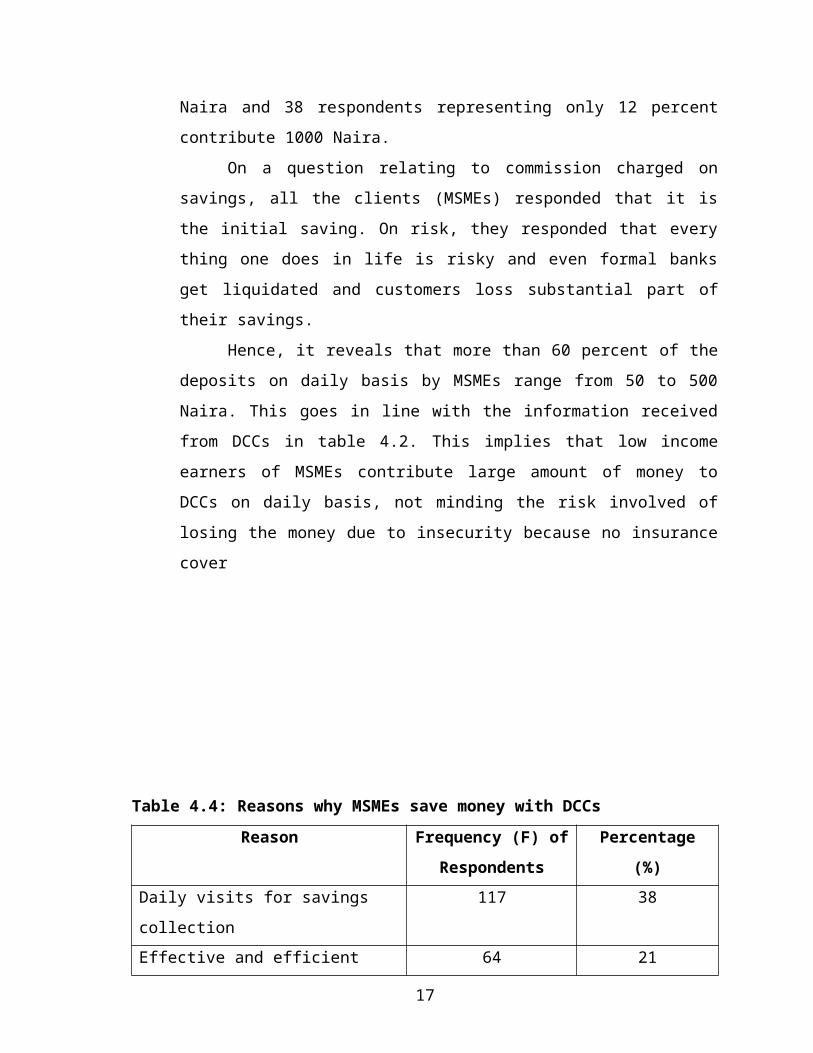

Table 4.3 shows that 102 respondents representing33 percent contribute between 210 and 500 Naira, while91 respondents representing 30 percent contributionranges from 50 to 200 Naira. Seventy Six respondentsrepresenting 25 percent contribute between 510 and 100

16

Naira and 38 respondents representing only 12 percentcontribute 1000 Naira.

On a question relating to commission charged onsavings, all the clients (MSMEs) responded that it isthe initial saving. On risk, they responded that everything one does in life is risky and even formal banksget liquidated and customers loss substantial part oftheir savings.

Hence, it reveals that more than 60 percent of thedeposits on daily basis by MSMEs range from 50 to 500Naira. This goes in line with the information receivedfrom DCCs in table 4.2. This implies that low incomeearners of MSMEs contribute large amount of money toDCCs on daily basis, not minding the risk involved oflosing the money due to insecurity because no insurancecover

Table 4.4: Reasons why MSMEs save money with DCCsReason Frequency (F) of

RespondentsPercentage

(%)Daily visits for savings collection

117 38

Effective and efficient 64 21

17

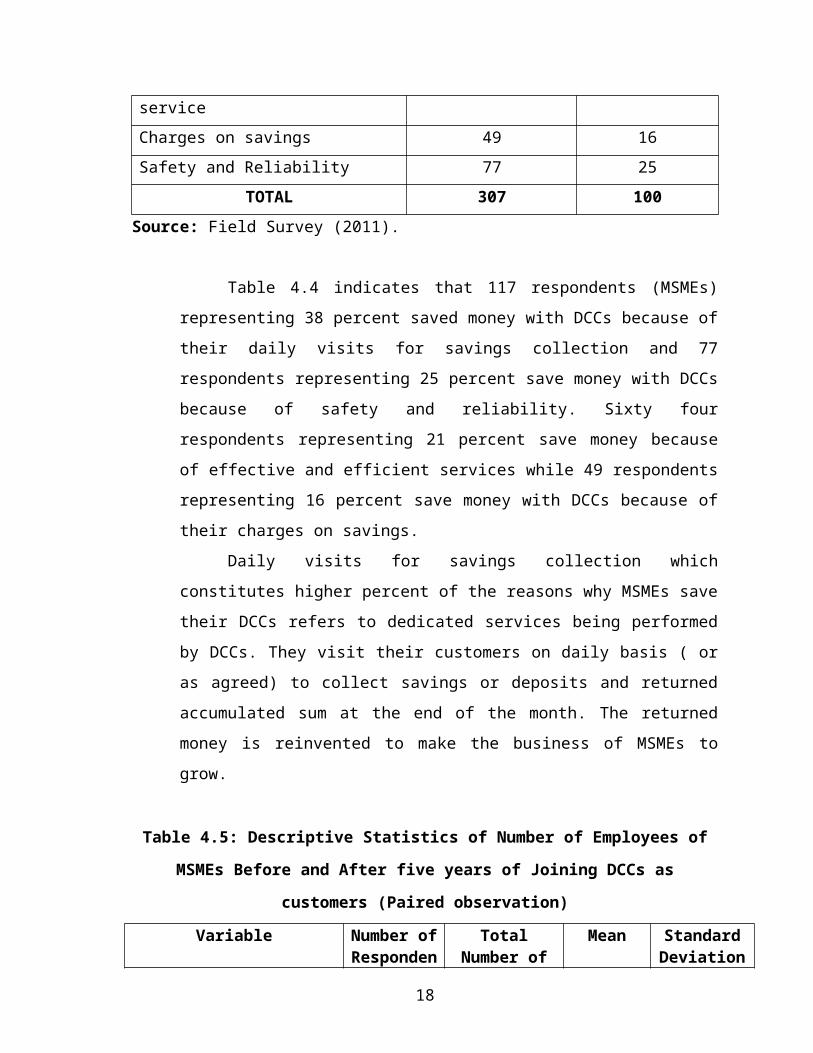

serviceCharges on savings 49 16Safety and Reliability 77 25

TOTAL 307 100Source: Field Survey (2011).

Table 4.4 indicates that 117 respondents (MSMEs)representing 38 percent saved money with DCCs because oftheir daily visits for savings collection and 77respondents representing 25 percent save money with DCCsbecause of safety and reliability. Sixty fourrespondents representing 21 percent save money becauseof effective and efficient services while 49 respondentsrepresenting 16 percent save money with DCCs because oftheir charges on savings.

Daily visits for savings collection whichconstitutes higher percent of the reasons why MSMEs savetheir DCCs refers to dedicated services being performedby DCCs. They visit their customers on daily basis ( oras agreed) to collect savings or deposits and returnedaccumulated sum at the end of the month. The returnedmoney is reinvented to make the business of MSMEs togrow.

Table 4.5: Descriptive Statistics of Number of Employees of

MSMEs Before and After five years of Joining DCCs as

customers (Paired observation)

Variable Number ofResponden

TotalNumber of

Mean StandardDeviation

18

ts(MSMEs)

Employees

Number of Employees

Before Joining DCCs

28 69 2.4643 1.7420

Number of Employees

After 5 years of

Joining

28 101 3.6071 2.8074

Source: Field Survey (2011).

Table 4.5 indicates an increment in number of

employees, mean and standard deviation after five years

of joining DCCs. This means that DCCs contribute to

employment generation of MSMEs.

Table 4.6: Descriptive Statistics of Annual Sales Turnover of

MSMEs Before and After 5 years of Joining DCCs as Customers

(paired observation)

Variable Number ofRespondents(MSMEs)

Annualsales

TurnoverN

Mean StandardDeviation

Sales Turnover

Before Joining DCCs

19 34,873,00

0

1,835,0

00

53853

Sales Turnover After

5 years of joining

19 46,580,00

0

2,452,0

00

68722

Source: Field Survey (2011).

Table 4.6 shows an increment in annual sales

turnover, mean and standard deviation after five years

19

of Joining DCCs. It means DCCs contribute to sales

growth of MSMEs.

Table 4.7: Results of Pearson Correlation Coefficient and T –

Test of MSMEs

Number Of Employees Before And After 5 Years of

Joining DCCs as

Customers (Paired Observation)

Variable Number of Respondents(MSMEs)

Total Number of Employees

Correlation Result

T-test Result

Number of Employees Before Joining DDCs

28 69 - -

Number of Employees After 5 Years of Joining DDCs

28 101 -1 ≤ r ≤

+ 1

r = 0.70

t0.05(26) = 1.71

t = 5.00

Source: Field Survey (2011).Correlation results can be -1≤ r ≤ +1. If the r =

-1 (Negative Correlation), r= 0 (No relationship

exists) and r= 1(Strong positive relationship). Table

4.7 shows the result of correlation coefficient and

there is relative strong positive correlation between

number of employees before and after five years of MSMES

joining DCCs as customers

20

Furthermore, the t – test statistic shows that

there is significant relationship between number of

employees before and after five years of MSMES joining

DDCs as customers. This is because the t – test

calculated value (5.00) is more than the t – test

critical value (t0.05 = 1.70). So, we reject hull

hypothesis and accept the alternative hypothesis. Type I

error is committed because we reject what ought to be

accepted.

Table 4.8: Results of Pearson Correlation Coefficient and T –

Test of MSMEs Annual

Sales turnover before and after 5 Years of

Joining DCCs as Customers (Paired Observation)

Variable Number ofRespondents(MSMEs)

Annual saleTurnover

N

Correlation

Result

T-test Result

Annual sale

Turnover

Before

Joining DDCs

19 34,873,000 - -

Annual sale

Turnover

After 5

Years of

Joining DDCs

19 46,580,000 -1≤ r ≤

+ 1

r = 1.00

t0.05(17) = 1.74

t =

Source: Field Survey (2011).

21

∞

Table 4.8 shows that there is strong positive

correlation between annual sales turnover before and

after five (5) years of joining DCCs as customers.

The t- test statistic indicates that the relationship is

undefined between annual sales turnover before and after

five (5) years of MSMEs joining DCCs as customers. The

reason is that the t – test statistic (calculated value)

indicates undefined value (∞).

4.3 Findings of the study.

Small amount of deposits or small savings

constitute larger accounts to DCCs. Therefore, majority

of customers are micro and small enterprises. Secondly,

the amount charged as commission on savings is the

initial savings contributed by MSMEs operators. Even, if

the customer seized to continue with the contributions.

Secondly, the amount charged as interest on loan is 50

Naira for every 1,000 Naira borrowed per month without

collateral. Thirdly, DCCs contribute to employment

generation and annual sales turnover of MSMEs. This is

because statistical results show an increment in means

and standard deviations after five years of joining

DCCs. Lastly, correlation results reveal that there is a

positive correlation between DCCs and MSMEs in terms of

number of employees but not annual sales turnover. The t

– test statistic affirms the result that the hull

22

hypothesis should be rejected. This is because there is

a significant relationship between DCCs and MSMEs in

terms of numbers of employees while the relationship is

undefined between DCCs and MSMEs in terms of annual

sales turnover.

5.1 Conclusion and Recommendation

Micro, Small and Medium Enterprises (MSMEs) growth

and survival depend on number of competent employees and

capital. This is because the resources are used to boost

sales which have relationship with profit making of the

organization. To achieve these objectives, MSMEs saved

part of their daily earnings with DCCs. The savings

collected by DCCs is risky because their activities are

not regulated. The amount charged as commission on

savings is significant relative to formal banking

system, because initial saving or deposit is taken as

commission. That is 50 Naira is charged for every 1,000

Naira loan per month.

In addition, there is a positive relationship

between DCCs and MSMEs in terms of number of employees

but not annual sales turnover. T – test statistic

indicates that there is significant relationship between

DCCs and MSMEs in terms of number of employees while the

relationship is undefined in terms of annual sales

turnover.

23

Based on the finding and conclusion, the following

recommendations are made. Firstly, policy makers (CBN

and others) should enact appropriate laws to regulate

the activities of the collectors. Secondly, formal banks

that are regulated and insured by CBN and NDIC

respectively should endeavour to use DCCs as their

agencies in loan disbursement. The reason is that, DCCs

are more familiar and closer to MSMEs operators.

Thirdly, the amount charged as commission on savings

should be reviewed down ward to half of the initial

savings. The reason is that, the present charges are

higher relative to formal bank system charges on savings

or deposits. Daily visits for savings collection should

be encouraged and strengthened. This is because the main

reason why MSMEs save money with DCCs is daily visiting.

Fifthly, government (federal, state and local) should

search for sustainable financing ways to assist MSMEs

financing. The reason is that, they contribute to

employment generation and economic growth, thereby

reducing poverty in Nigeria.

24

References

Abdullahi, H., Zakari, Y.A. and Mohammed, Y. (2010). Formaland Informal Institution

Lending Policies and Access to Credit by Small ScaleEnterprises In Minna: An

empirical assessment. The Lapai journal of Management Science,Volume1 (1):

84-94.

Alabi, G., Alabi, J. and Akorobo, S.T. (2007). The Role of“susu”, A Traditional Informal

Banking System in the Development of Micro and SmallScale Enterprises (MSEs) in Ghana, Journal of InternationalBusiness and Economic Research, volume 6(12): 99 – 116.Retrieved November 15, 2010 from www.cluteinstitute-onlinejournals.com/PDFS/2007222.pdf.

Ahiawadzi, A, Alabi, G. and Alabi, J. (2007). Effects of“susu” – A Traditional Micro-

Finance Mechanism: An Organized and Unorganized Microand Small Enterprise (MSEs) in Ghana, Africa Journal ofBusiness Management, Volume 1(8): 201 – 208. RetrievedNovember 27, 2010, fromwww.academicjournals/PDF/pdf/Nove/Alabi%2001.pdf.

25

Aina, O. (2007). The Role of SMEs in poverty Alleviation inNigeria, Journal of land used

and Development Studies, volume 13(1):124 – 139. RetrievedMarch 20, 2011,

from Journalanduse.org/…/JOURNAL10.pdf.

Anyadike, R.N.C. (2009) Statistical Methods for the Social and EnvironmentalSciences.

Spectrum Book Limited, Ibadan – Oyo State, Nigeria,PP.149

CBN (2005). Microfinance Policy, Regulator and SupervisoryFramework for Nigeria.

Retrieved Dec. 20, 2010, fromwww.cenbank.org/out/publications/gu....

CBN (2010). Two Hundred and Twenty Four (224) Micro FinanceBanks licences are Recommended for Revocation. Sunday Trust,September 26, P. 11 – 12.

Daniel, M. (2010). Enhancing the Capacities of SMEs forPoverty Reduction. Retrieved

March 20, 2010, fromwww.docstoc.com/docs/46146169/there...

Gunu, U. (2009). An Investigation into Small and Medium ScaleEnterprises Funding

and the Nigerian Stock Market: A Study of IlorinMetropolis. Lapai International Journal of Management and SocialScience (LIJOMASS), Volume 2(1): 33 – 45.

Iganiga and Asemotal (2008). The Nigeria Unorganized RuralFinancial Institutions

and Operations. A Frame Work for Improved Rural CreditSchemes in a Fragil Environment, Journal of Social Sciences,Volume 17 (1): 63-71. Retrieved December 10, 2010, fromwww.Krepub;ishers.com/.../jss-17-063-08-531-iganiga-B.o-ab.pdf.

26

NDIC (2010). List of 223 Closed Microfinance Banks as at 24September, 2010.

Sunday Trust, Sept. 26, p. 53 – 55.

Nkanga, E. (2007). Promoting SMEs Via Technology. RetrievedOctober 6, 2010,

from www.thisdayonline.com/nview.php.

Oloyede J.A. (2008). Informal Financial Sector, SavingsMobilization and Rural

Development in Nigeria, Journal of Africa Economic and BusinessReview. Volume 6 (1):44: Retrieved November 30,2010, fromwww.theaebr.com.vol.6No1spring2008Oloyede.pdf.

Ogbadu,E.E.(2009).Profitabilty Through Effective Managementof Material. Journal of

Economics and International Finance, Volume 1(4),pp. 099 –1055.Retrived April 14, 2012, from www.academicjournal.org/jeif/pdf/pdf 2009/sep/ogbadu.pdf,

Onugu, A.N. (2005). Small and Medium Enterprises in Nigeria(SMEs). Unpublished

dissertation, St. clement University, Swiss. RetrievedMarch 20, 2011, fromwww.stclements.edu/grad/gradonug.pdf.

Revenue Office (2011a). Zaria Local Government Area, Kaduna -State, Nigeria.

Revenue Office (2011b). Sabon Gari Local Government Area,Kaduna-State

Nigeria.

Seibel, H.D. (2001). Mainstreaming Informal FinancialInstitutions, Journal of

27

Development Entrepreneurship, volume 6 (1): 83-95. RetrievedDecember 2, 2010, fromwww.microfinancegatewayorg/gm/document-1.9.../250.pdf.

Srivastava, R. (2010). Status of Micro, Small and Medium Enterprises inAfrica.

Retrieved March 20, 2011, fromwww.140online/net/articles/current.

Yusuf N., Gafar, T. and Ajaiya, M.A. (2009). InformalFinancial Institutions and

Poverty Reduction in the Informal Sector of Offa Town,Kwara State: A Case Study of Rotational Saving andCredit Associations (RSCAs), Journal of Social Science, Volume20(1): 71-81. Retrieved November 30, 2010, fromwww.krepublishers.com/.../jss-20-01-071-09-605-Yusuf-N-Tt.pdf.

28