Managing Debt, Creditors, and Collectors

23

Managing Debt, Creditors, and Collectors FIRST STEPS TO DEBT FREEDOM

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Managing Debt, Creditors, and Collectors

Managing Debt, Creditors, and Collectors

FIRST STEPS TO DEBT

FREEDOM

Why is Managing Debt Important?Staying on top of your debt is important because it affects your credit. Having bad credit will narrow your options when it comes building your wealth in the future.

Example: Because of poor debt management in the past, the bank no longer feels comfortable offering you a loan to remodel your house, which would increase it’s value in the long run.

First Steps to Debt Freedom

STEP ONE Check Your Credit

History

STEP TWO Create a Budget

STEP THREE Negotiate with

Creditors

STEP FOUR Contact Debt

Collectors

STEP FIVE Stick to the Plan

Step One:Check Your Credit HistoryChecking your Credit History Report is the first step to lowering your debt as it contains an overview of all of your current debt and information you will need when creating your budget.

*Special Note: All links from this lesson will be in the video’s description or on our website under this video.

Credit History

Simplified

You can go to AnnualCreditReport.com to download or print out your credit report for free once a year. If you need any help with this step, we have created a lesson all about how to check your credit report.

Visit the link in the description of this video or if you are on our website scroll up to Credit History Simplified.

For the purposes of this lesson you will need to focus on the number of debts you have, how much of each debt is left, and what the minimum payments are for each debt. This includes any collections reported on your credit history.

If you had problems managing your debt in the past, your credit history will show you how that has affected your credit. You can use this information to help plan your future mangement.

If you have already used up your free yearly credit report earlier this year that’s okay! Even though some information might be out-of-date, the old report will still be helpful.

Step Two:Create a BudgetBuilding a budget is the most important step to managing your debt. Once you have built a proper budget you will have a better understanding of what you can and can’t afford. It will strengthen your positions when negotiating with Debt Collectors and Creditors. At least once a year, you should revaluate your budget to adjust it and your spending.

Budgetingfor Beginners

Create a Budget that prioritizes paying off your debt.

Go through all of your loan and credit card agreements. Make a list of your debt by monthly payments lowest to

highest.

Spend a particular amount of time on going over the interest for each loan. How much does it add to your debt? Will the interest percent increase in the future? How much of your monthly payment goes toward the interest cost?

First, build your budget around making all of your minimum payments.

Then, use any extra money left over to pay towards your debts. It is almost impossible to pay off debt if you just pay the minimum balance every month.

For step-by-step instructions on how to create a budget watch our lesson on it! The link will be the video’s description.

If you are on our website look for Budgeting for Beginners

Methods For Paying Down Debt

When using your extra money to pay off your debts consider the following options:

Avalanche Method-Pay off the debt with the highest interest rate first.

Snowball Method-Pay off the smallest debt first.

Each of these options has their own merit. Which one you should use will depend on your type of debt and your personality.

Mortgages do not work with these options as they have fixed payment plans.

Step Three:Negotiate with CreditorsCreditors are companies or individuals who have given you loans/credit cards. They have the ability to change your loan agreement, especially if you have a sudden change’s to income. If you lost your job or have been unable to work do to illness or injury immediately contact your creditors to inform them of the situation.

Negotiating 101 Try to talk to your creditors if you believe that your debt

may be sent to a debt collector. It is a myth that making any payment, no matter how small, will stop a debt from going to a collector.

Once a debt is sent to a collector it will lower your credit score.

When negotiating with creditors remember these simple rules:

Keep calm, cool, and collected while negotiating.

Take notes about the conversation.

Be honest about your situation.

If you come to an agreement about a new repayment plan, get the new plan in writing.

Negotiating 101 Write down some simple true sentences that you can

repeat to reinforce your position. Some examples: My wife was laid off

The interest rates have doubled

I can no longer keep up

I am considering bankruptcy

Once an agreement has been worked out keep your promises. If you fail to stick to the new payment plan, creditors will be

less likely to help you in the future.

If you are having trouble get a credit counselor to negotiate on your behalf. You can find free credit counselors here: www.nfcc.org

Step Four:Contacting Debt CollectorsIf you have debts that have gone to collections, but you have not made contact with the debt collector yet, now is the time to do so. Don’t worry we will go over the best way to interact with debt collectors.

Who are Debt

Collectors?

If sufficient payments have not been made on a debt for some time that debt will be considered “defaulted”. Defaulted debt is sent to a debt collectors. Most loans and credit cards will list the requirements for defaulting on them.

A Debt Collectors job is to get back the money owed. Most debt collectors follow a process in order to accomplish this. The process is as follows:

Step 1: Attempting to contact the debtor (person who owes the money).

Step 2: If unable to contact the debtor, attempting to contact friends and family of the debtor.

Step 3: Attempting to sue the debtor for the debt.

If the debtor does not show up to court, they will loose the ability to dispute the debt.

The court may take part of the debtors wages to pay back the debt. This is called garnishing.

The court may force the debtor to sell their assets in order to repay their debts.

Two Types of Debt Collectors

In-House Debt Collectors These debt collectors work for the same company or

corporation that offered you the loan or credit card.

3rd Party Debt Collectors These debt collectors work for a separate company.

Sometimes they are hired by the creditor to collect the debt or sometimes they buy the loan at a discount and collect on it.

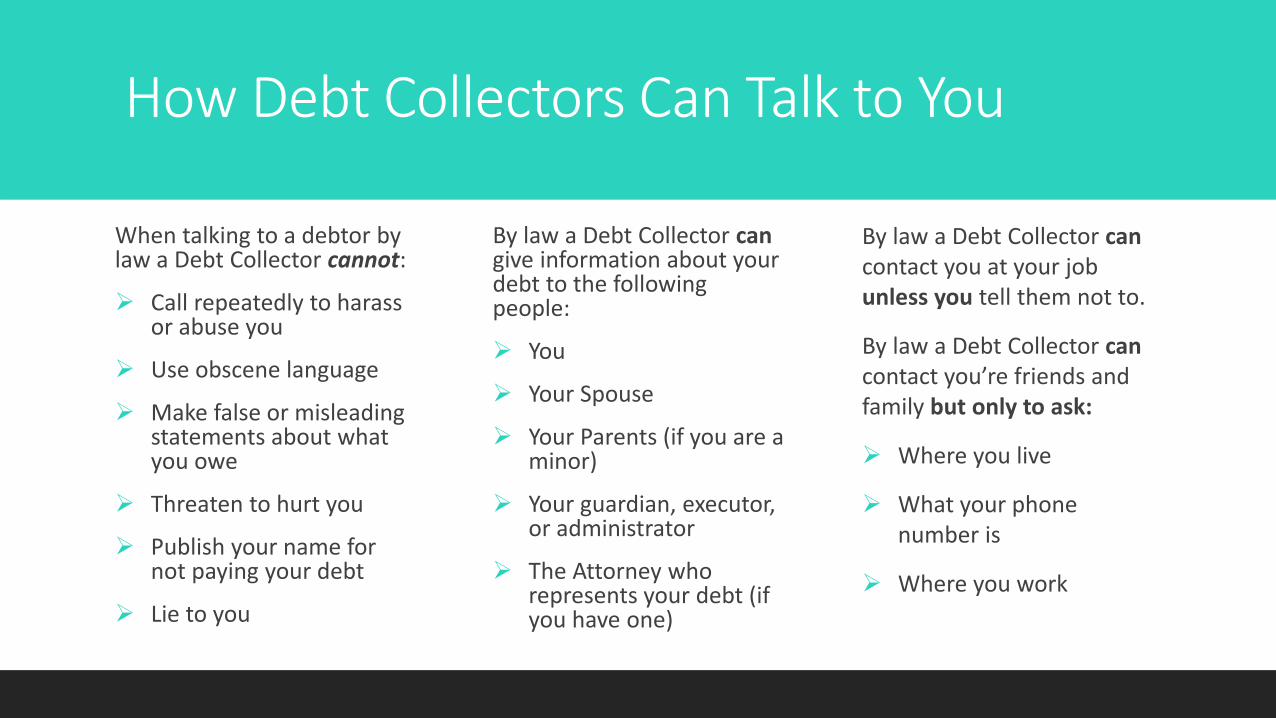

How Debt Collectors Can Talk to You

When talking to a debtor by law a Debt Collector cannot:

Call repeatedly to harass or abuse you

Use obscene language

Make false or misleading statements about what you owe

Threaten to hurt you

Publish your name for not paying your debt

Lie to you

By law a Debt Collector cangive information about your debt to the following people:

You

Your Spouse

Your Parents (if you are a minor)

Your guardian, executor, or administrator

The Attorney who represents your debt (if you have one)

By law a Debt Collector cancontact you at your job unless you tell them not to.

By law a Debt Collector cancontact you’re friends and family but only to ask:

Where you live

What your phone number is

Where you work

How to Talk to Debt CollectorsVerify the Debt Information

Ask for:

The debt collectors name and business address

Original creditor’s name and business address

The account number

The amount owed

When the collector obtained the debt and what amount the debt was at that time.

More Questions to Ask

If you are unsure about the debts legitimacy ask for:

When the account became delinquent

Whether the debt’s statue of limitations has expired

Documentation proving you’re required to pay

A copy of the last bill

If the statue of limitations has expired on the debt or if the debt is not yours, dispute the debt immediately.

How to Talk to Debt CollectorsBe Wary of Scams

Do not share sensitive information with anyone on the phone.

A debt collector does not need your social security, bank account, or credit card information. They likely all ready have access to that information.

If you feel pressured to reveal sensitive information or if they cannot provide answers to the previous questions they are probably a scam.

Communication is Key

If the debt is legitimate and you cannot pay it back in full, ask to set up a payment plan.

Be open and honest about your financial situation. Most Debt Collectors will be willing to work around the difficulties in your life.

Do not lie about your job situation. Debt collectors have tools which they can use to verify information you give. Lying will destroy any trust between you.

Tips for Unreasonable Debt Collectors Or Scams

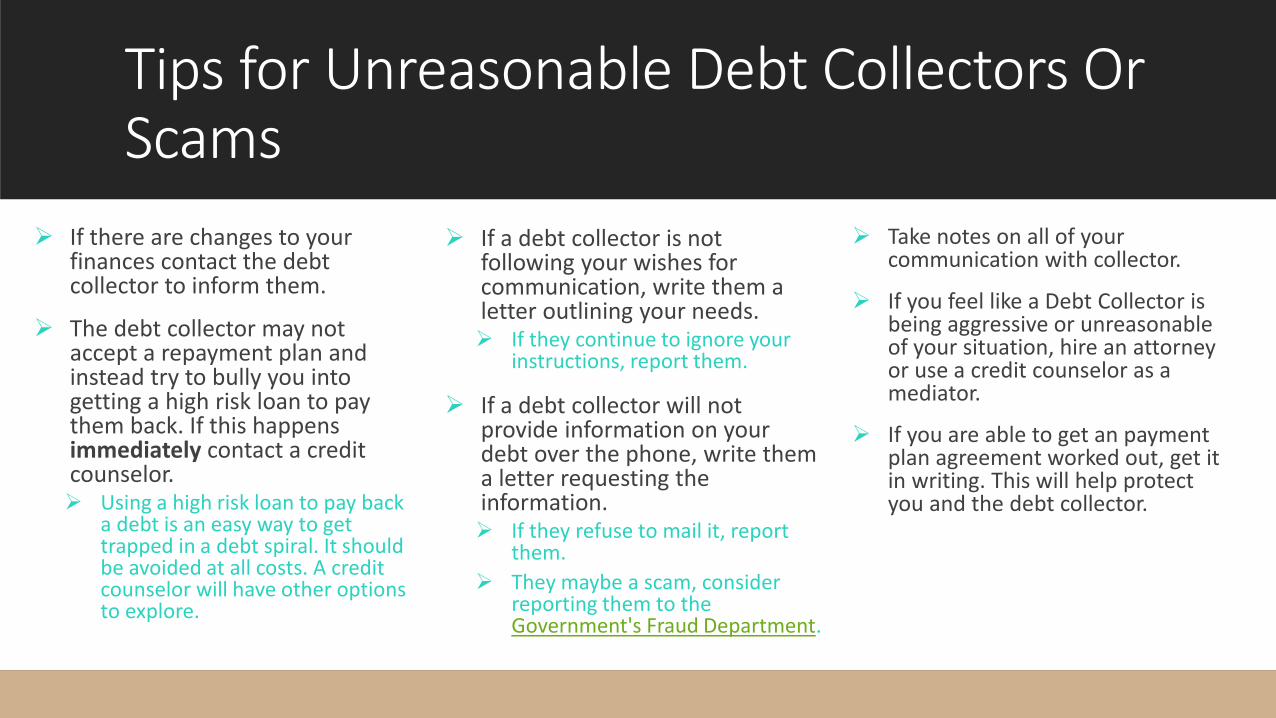

If a debt collector is not following your wishes for communication, write them a letter outlining your needs. If they continue to ignore your

instructions, report them.

If a debt collector will not provide information on your debt over the phone, write them a letter requesting the information. If they refuse to mail it, report

them.

They maybe a scam, consider reporting them to the Government's Fraud Department.

If there are changes to your finances contact the debt collector to inform them.

The debt collector may not accept a repayment plan and instead try to bully you into getting a high risk loan to pay them back. If this happens immediately contact a credit counselor. Using a high risk loan to pay back

a debt is an easy way to get trapped in a debt spiral. It should be avoided at all costs. A credit counselor will have other options to explore.

Take notes on all of your communication with collector.

If you feel like a Debt Collector is being aggressive or unreasonable of your situation, hire an attorney or use a credit counselor as a mediator.

If you are able to get an payment plan agreement worked out, get it in writing. This will help protect you and the debt collector.

Final Notes for Debt Collectors

Every state has special laws for debt collectors. For more information about Washington State’s laws visit: www.atg.wa.gov/collection-agencies.

If a debt collector is trying to get a hold of you don’t ignore them. If you don’t make contact quickly, you will be sued for the debt. The court might garnish your wages They can force you to sell your assets

We highly suggest visiting the CBFP’s website about debt collection. They have a ton of resources including: Letter outlines to send collectors How to report Debt Collectors How to dispute a debt How to find a credit lawyer

For further rules and laws you can also visit: www.washingtonlawhelp.org

Step Five:Stick to the PlanOnce you have created a budget and worked through managing your current debt, you now have to follow the plan to the letter. Depending on the type and amount of debt that you owe, this step can take years. We have provided some tips that can help you stay on track.

Simple Tips to Remember

Go through your credit cards. If you are trapped in debt the best policy is to only have one credit card active for emergencies. Call the banks and ask to deactivate your extra cards so you won’t

be tempted to use them.

Cancel credit cards once you pay them off. This is a very important. Canceling cards makes it impossible to slip up and use them. You can always apply for more cards once you get out of debt.

Inform your friends and family of what you are doing. Many people view debt as shameful and will not talk about it.

This can actually make the whole process more stressful and painful.

Having someone to confide in can be a great relief. They can help encourage you, plus give you advice from their own experience.

Keep track of your progress, mark important milestones on your calendar and celebrate when you accomplish them. Example: After paying off a fourth of your debt have a special dinner with

friends and family to celebrate.

Will Consolidation Loans and Credit Cards help?

Many people believe that using consolidation loan’s is an easy way to get out of debt. This is not true.

Consolidation loans are a good tool to help manage your debt if your credit is good, your finances are stable, and you have no trouble paying your minimum payments. However, if your debt is stacking up, you are starting to fall behind, or you are having trouble controlling your spending, they will do more harm then good.

Always be cautious when getting into more debt in order to pay off old debt. It is a slippery slope which can lead to a debt spiral.

The End

But Wait! There’s More!Test Your New Knowledge and Sign Up for More Free Finance Information!

Click the Link Below Or Scan The QR Code:https://www.surveymonkey.com/r/8GWJGMW