The Regulation of Hedge Funds, Private Equity, and Sovereign Wealth Funds

24

Electronic copy available at: http://ssrn.com/abstract=1620822 Electronic copy available at: http://ssrn.com/abstract=1620822 Electronic copy available at: http://ssrn.com/abstract=1620822 Electronic copy available at: http://ssrn.com/abstract=1620822 HEDGE FUNDS, PRIVATE EQUITY AND SOVEREIGN FUNDS 135 Myriam Senn * The Regulation of Hedge Funds, Private Equity and Sovereign Wealth Funds 1. Introduction The issue of regulating hedge funds (HF), private equity (PE) and sovereign wealth funds (SWF) is lively debated. The activities developed by these invest- ments vehicles on the financial markets are regularly linked to the 2007-2009 financial crisis. Indeed, it is recognized that they did not cause it. However, during the G20-meeting held in April 2009 it was agreed that all systemically important financial institutions, instruments, and markets should be subject to an appropri- ate degree of regulation and oversight. Only systemic important hedge funds were named expressly. 1 As “unregulated” financial entities, there is a feeling of unease towards the activities of these investment vehicles, which is due to the perception of their clout, a sense of lack of transparency regarding their operations and their apparently unlimited possibilities to influence market developments. They raise challenges for investor protection and financial stability. As pools of private capi- tal, they play an important role in the financial landscape and indeed, their devel- opment and operations should not be hindered by misplaced regulatory measures. The report concentrates on an analysis of the situation in Switzerland. The first part focuses on the legal issues in relation to hedge funds and private equity as private investment vehicles. The second part concentrates on their behavior as shareholders. Finally, the third part deals with the sovereign wealth funds as gov- ernmental investment vehicles. The characteristics of these pools of capital, their role, and the regulatory framework are discussed. 2. Legal Issues Relating to Hedge Funds and Private Equity 2.1 Preliminary Remark When approaching hedge funds and private equity as “unregulated” financial entities from a regulatory point of view, definitional challenges arise. Are they financial entities or products? 2 As the efforts of international bodies working on * Private docent, University of St.Gallen. The focus of the article is placed on comparative aspects as proposed by the General Reporter, Professor Eddy Wymeersch. 1 G20, The Global Plan for Recovery and Reform, London, April 2, 2009. 2 Hedge Funds Oversight, Final Report, IOSCO, June 4, 2009.

Transcript of The Regulation of Hedge Funds, Private Equity, and Sovereign Wealth Funds

Electronic copy available at: http://ssrn.com/abstract=1620822 Electronic copy available at: http://ssrn.com/abstract=1620822 Electronic copy available at: http://ssrn.com/abstract=1620822Electronic copy available at: http://ssrn.com/abstract=1620822

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

135

Myriam Senn*

The Regulation of Hedge Funds, Private Equity and Sovereign Wealth Funds

1. Introduction

The issue of regulating hedge funds (HF), private equity (PE) and sovereign wealth funds (SWF) is lively debated. The activities developed by these invest-ments vehicles on the financial markets are regularly linked to the 2007-2009 financial crisis. Indeed, it is recognized that they did not cause it. However, during the G20-meeting held in April 2009 it was agreed that all systemically important financial institutions, instruments, and markets should be subject to an appropri-ate degree of regulation and oversight. Only systemic important hedge funds were named expressly.1 As “unregulated” financial entities, there is a feeling of unease towards the activities of these investment vehicles, which is due to the perception of their clout, a sense of lack of transparency regarding their operations and their apparently unlimited possibilities to influence market developments. They raise challenges for investor protection and financial stability. As pools of private capi-tal, they play an important role in the financial landscape and indeed, their devel-opment and operations should not be hindered by misplaced regulatory measures.

The report concentrates on an analysis of the situation in Switzerland. The first part focuses on the legal issues in relation to hedge funds and private equity as private investment vehicles. The second part concentrates on their behavior as shareholders. Finally, the third part deals with the sovereign wealth funds as gov-ernmental investment vehicles. The characteristics of these pools of capital, their role, and the regulatory framework are discussed.

2. Legal Issues Relating to Hedge Funds and Private Equity

2.1 Preliminary Remark

When approaching hedge funds and private equity as “unregulated” financial entities from a regulatory point of view, definitional challenges arise. Are they financial entities or products?2 As the efforts of international bodies working on

* Private docent, University of St.Gallen. The focus of the article is placed on comparative

aspects as proposed by the General Reporter, Professor Eddy Wymeersch. 1 G20, The Global Plan for Recovery and Reform, London, April 2, 2009. 2 Hedge Funds Oversight, Final Report, IOSCO, June 4, 2009.

Electronic copy available at: http://ssrn.com/abstract=1620822 Electronic copy available at: http://ssrn.com/abstract=1620822 Electronic copy available at: http://ssrn.com/abstract=1620822Electronic copy available at: http://ssrn.com/abstract=1620822

M Y R I A M S E N N

136

the issue show, it has proved to be notoriously difficult to define them. Any attempt appears to be unsatisfactory and no general consensus on a definition could be reached up to now. Thus, it is not tried to draw up a definition at this place.

2.2 Current Situation in Switzerland

In Switzerland, no specific legal regime applies to hedge funds and private equity. Alfred Winslow Jones is considered to be the father of the first hedge fund, which was in 1949. His strategy consisted in combining long-positions in undervalued securities with short-positions in overvalued securities to minimize the effects of movements on the exchange. To increase the rate of return of the portfolios, he worked with the leverage effect.3 Indeed, hedge funds are investment vehicles which appear to be elusive and can adapt to market circumstances at any time. In the more recent terminology, it appears that there is a consensus on the fact that hedge funds are commonly referred to as “private pools of capital”.4 Basically, they correspond to a special form of collective investment.

Switzerland has only played a minor role as a domicile for hedge funds and a loca-tion for hedge fund managers up to now. No hedge fund is registered in Switzer-land and there is no urgent need to regulate these funds, although the Swiss mar-ket is an important market for placing shares of funds of hedge funds. More than 5 percent of the assets invested in Switzerland are invested in hedge fund products. In part, it may be due to the fact that hedge funds are submitted to fewer restric-tions than other investment vehicles regarding the types of investments they can make.5

On their side, private equity funds as an alternative form of investment follow another strategy. They represent an expanding branch in Switzerland. They are characterized by private and institutional investors or so-called financial sponsors investing in venture capital, start-up and small and medium-sized companies. Most of these companies are not listed on an exchange and the investments rationales are not only financial, but also strategic and long-term participations are considered.6 In addition, banks can give credit to private equity funds which

3 P. M. HILDEBRAND, Jüngste Entwicklungen in der Hedge-Fonds-Branche, Swiss National

Bank, Quartalsheft 1/2005 (23), 42-57; F.-S. L’HABITANT, Hedge Funds: Myths and Limits, London: John Wiley & Sons 2002.

4 HILDEBRAND (n. 3), 42-57; US PRESIDENT’S WORKING GROUP, Principles and Guidelines Regard-ing Private Pools of Capital, 2007.

5 DIE EIDG. BANKENKOMMISSION, Hedge-Fonds, Marktentwicklung, Risiken und Regulierung, Positionspapier der Eidg. Bankenkommission, 2007, 12; P. BUSCHOR, Rechtliche Rahmen-bedingungen für Hedge Funds in der Schweiz, Zurich: Dike Verlag AG 2010, 3 et seq.

6 DIE EIDG. BANKENKOMMISSION (n. 5), 12; R. GRONER, Private Equity-Recht, Bern: Stämpfli Verlag AG 2007, 1 et seq.; J. FRICK, Private Equity im Schweizer Recht, Schweizer Schriften zum Handels- und Wirtschaftsrecht Band 272, Zurich: Dike Verlag 2009, 3 et seq.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

137

corresponds to a leverage of equity capital and they can support them when struc-tured products are used. Indeed, similarly to hedge funds, liquidity is a core fea-ture of their operations.

The Federal Act on Collective Investment Schemes7 offers a workable and flexible legal framework for investment funds. Accordingly, hedge funds or also private equity funds can choose among different corporate forms to register and develop their activities as alternative investments:

– They can constitute themselves as open-ended hedge funds or collective invest-ment schemes, which means that they can either be constituted based on an agreement or adopt the form of an investment company with a variable capital basis, the so-called SICAV.

– They can also constitute themselves as closed-ended funds or collective invest-ment schemes under the form of a Limited Liability Partnership (LLP or Kom-manditgesellschaft) or the form of investment schemes with fixed capital or a limited number of shares, the so-called SICAF. In this case, the investor cannot require the restitution of the participation at the net asset value.8

However, as stated, no hedge fund is registered in Switzerland. It is well-known that these funds select their domicile based on tax-incentives considerations and are registered in some tax heaven. In comparison to these foreign locations, the Swiss tax regime is not favorable to the establishment of these funds and hedge funds managers and it would have to be changed. However, the developments abroad have to be taken into account too. For instance, after Great Britain increased its top rate of tax for high earners, large numbers of hedge funds are considering moving away from the country, and some speculate to move to Swit-zerland.9

As far as asset managers are concerned, there is no general authorization require-ment and supervision in Switzerland. They do not have to be licensed when they manage their clients’ assets based on a private agreement and their clients’ funds are placed on accounts in their client’s name and not on the asset manager’s name. However, managers of investment funds or who manage Swiss collective invest-ment schemes must be granted an authorization,10 albeit the supervisory authority

7 Federal Act on Collective Investment Schemes (Collective Investment Schemes Act, CISA) of

June 23, 2006, SR 951.31. 8 Article 70 CISA; DIE EIDG. BANKENKOMMISSION (n. 5), 51. 9 Switzerland as a financial centre, Alpine ambitions, in The Economist, December 19, 2009,

118; Finanzplatz Schweiz gewinnt auf Kosten von London, in Neue Zürcher Zeitung, Febru-ary 28, 2010.

10 Article 13 paragraph 2 letter f CISA. Article 13 CISA, Obligation to be granted an authorization, reads as: 1 Any person or entity managing a collective investment scheme or safekeeping its assets

must be granted an authorization from the supervisory authority.

M Y R I A M S E N N

138

can grant exemptions.11 Asset managers managing foreign collective investment schemes can submit themselves voluntarily to the supervision of the responsible authority. This will apply when they are domiciled in Switzerland, supervision is required by the foreign regulation, and the foreign regulatory regime is considered equivalent to the Swiss one.12 In practice however, hedge funds are often domi-ciled in off-shore places which regulatory regime is not considered equivalent to the Swiss one. Thus, voluntarily submission is then denied to the hedge funds managers.

To be licensed, a fund manager must have a fit and proper character and be pro-fessionally qualified. Other, qualified participants too must have a good reputation and be in a position to conduct their business with circumspection (e.g. in relation to conflict of interest) and solidly. The internal organization and internal rules governing the operations, such as rules on risk management and compliance, must be adequate, the financial situation must be satisfactory and they must fulfill the other duties as laid down in the CISA. There is an internal and an external audit and the conditions applying to be granted a license must be fulfilled at any time. Reviews are conducted at least once a year by an audit company reporting to the supervisory authority.13

For investors, hedge funds investments represent risky investments. Participations in hedge funds are reserved to sophisticated or qualified investors in the sense of the CISA, that is supervised finance intermediaries such as banks, securities deal- 2 The following are submitted to an authorization requirement: a. fund management companies, b. SICAVs, c. limited partnerships for collective investments, d. SICAFs, e. custodian banks, f. investment managers of Swiss collective investment schemes, g. distributors, h. representatives of foreign collective investment schemes. 3. The Federal Council may exempt investment managers, distributors and representatives

that are already subject to a supervision by an official supervisory authority from the obliga-tion to be granted an authorization according to this Act.

4. Investment managers of foreign collective investment schemes (article 119 et seq.) may apply for an authorization to the supervisory authority provided that:

a. their registered office or place of residence is in Switzerland, b. they need to be subject to a supervision in accordance with a foreign legislation, c. the foreign collective investment scheme managed by them is subject to a supervision

considered of an equivalent standard to that applying in Switzerland. 5. Persons or entities listed in paragraph 2 letters a to d will only be allowed to register in

the Commercial Register once an authorization has been granted by the supervisory authority.

11 Article 10 paragraph 5 and article 31 paragraph 3 CISA. 12 Article 13 paragraph 4 CISA. 13 Article 14 CISA.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

139

ers, or investment funds managers, supervised insurance companies, public corpo-rations or pension funds with professional asset management, wealthy private persons, or investors working together with a supervised finance intermediary based on a written asset management agreement. Further categories can be designed.14 The funds are not distributed to a broader public. However, participa-tions in funds of hedge funds (FoHF) can be distributed both to qualified investors as well as to a broader public. Participations in private equity funds on their side can be offered to qualified investors only.

Indeed, investor’s protection is not secured with a general ban on sales to small and private investors. However, these investors will not be motivated to invest in these funds. Although there are transparency requirements,15 a sense of intransparency regarding hedge funds dominates. These investors could invest through their securities dealers who are obliged to observe the rules of conduct. In particular they have to act in accordance with the knowledge of their clients who have to be aware of the risks of their investments and understand them.16

2.3 International Developments

Basically, any regulation of hedge funds and private equity funds should master two main challenges: ensuring investor protection and minimizing systemic risks. Thus, efforts made at the international level to regulate hedge funds focus on regulating their asset managers with regard to investor protection on the one side. On the other side, transparency requirements regarding information on potential systemic risks constitute the second pillar and must be defined. In its report on Hedge Funds Oversight, IOSCO, for instance, recommends six high level principles to regulate hedge funds:

1. Hedge funds and/or hedge fund managers/advisers should be subject to man-datory registration,

2. Hedge fund managers/advisers which are required to register should also be subject to appropriate ongoing regulatory requirements relating to:

– organisational and operational standards,

– conflicts of interest and other conduct of business rules,

– disclosure to investors, and

– prudential regulation,

14 Article 10 paragraph 3 CISA. 15 DIE EIDG. BANKENKOMMISSION (n. 5), 12-13. 16 Article 11 Federal Act on Securities Exchanges and Securities Trading of March 24, 1995

(Securities Exchange Act, SESTA), SR 954.1.

M Y R I A M S E N N

140

3. Prime brokers and banks which provide funding to hedge funds should be sub-ject to mandatory registration/regulation and supervision. They should have in place appropriate risk management systems and controls to monitor their coun-terparty credit risk exposures to hedge funds,

4. Hedge fund managers/advisers and prime brokers should provide to the rele-vant regulator information for systemic risk purposes (including the identification, analysis and mitigation of systemic risks),

5. Regulators should encourage and take account of the development, implemen-tation and convergence of industry good practices, where appropriate,

6. Regulators should have the authority to co-operate and share information, where appropriate, with each other, in order to facilitate efficient and effective oversight of globally active managers/advisers and/or funds and to help identify systemic risks, market integrity and other risks arising from the activities or expo-sures of hedge funds with a view to mitigating such risks across borders.17

The publication of these recommendations has been welcome. The focus is placed on hedge funds managers and not on the product, the hedge funds. Authorization requirements should depend on determined threshold levels of managed funds.

According to the IMF, alternative investment funds should not be regulated in the same way as banks or securities dealers. They do not exercise any custody func-tion, their structure is different as far as their liabilities are concerned and they are not involved in payment transactions similarly to banks.18 The European Union also published a Proposal for a Directive on Alternative Investment Fund Manag-ers in April 2009. It has been largely criticized and a review is under way. The aim is to create a comprehensive and effective regulatory and supervisory framework for AIFMs at the European level. It should contribute to overcome gaps and incon-sistencies in existing regulatory frameworks at the national level.19 In addition, it should be mentioned, that some market participants consider extending the MiFID20 rules of conduct to all investment products.

17 IOSCO, Hedge Funds Oversight, Final Report, June 3, 2009, 9-16. 18 IMF Global Financial Stability Report, Responding to the Financial Crisis and Measuring

Systemic Risks, Executive Summary, April 2009; BUSCHOR (n. 5), 162; in the same sense: P. JACQUEMOUD & G. BARAZZONE, Proposed Regulatory Framework For Hedge Funds, in Juslet-ter dated June 22, 2009, para 8.

19 Proposal for a Directive on Alternative Investment Funds Managers (AIFM) of April 2009; K. LANNOO, Bringing hedge funds into the regulatory mainstream, in ECMI Commentary No. 24/23, June 2009; Hedge funds and private equity, Off target, in The Economist, January 30, 2010, 82.

20 Directive 2004/39/EC of the European Parliament and of the Council of April 21, 2004 on markets in financial instruments amending Council Directives 85/611/EEC and 93/6/EEC and Directive 2000/12/EC of the European Parliament and of the Council and repealing Council Directive 93/22/EEC.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

141

2.4 Possible Future Regulatory Measures

With regard to these developments and in case an adaptation of the rules would be considered in Switzerland, the following measures would possibly have to be considered:

– First, due to the fact that there is a mandatory requirement to authorize Swiss asset managers of collective investment funds, exemptions should be granted by the supervisory authority in accordance with the then generally recognized threshold levels.

– Second, there is the issue of access to the EU market. Authorizations require-ments would have to be recognized as equivalent to the EU ones.

– Third, international proposals to regulate these funds plan the introduction of a duty to disclose all information potentially relevant with regard to systemic risks to the responsible supervisory authority. Although hedge funds are more moderate in their volume than investment funds, the collapse of a large fund could have a systemic impact and influence market liquidity. There is a concern that the leverage effect of their operations and the build-up of significant posi-tions in certain assets could trigger significant price movements upon a certain liquidity level. Thus, central banks and supervisory authorities should obtain data about the portfolios of large hedge funds and information on their behav-ior on the financial market. In Switzerland, these funds are not submitted to any such duty as of today. However, large international investment banks, including both Swiss large banks, extend credit to finance the investments of these funds, which expose them as counterparties to their credit risks. They also offer services to manage the securities and handle their trading activities, the so-called prime brokerage. As a result, they are in a position to furnish informa-tion about the activities of hedge funds to the responsible authorities. This information can be used to supervise systemic risks.21 However, disclosure rules should apply directly to hedge funds. They should not be mandatory for private equity, because its volume is not systemically relevant. At this point, hedge funds and private equity funds, similarly to other investors and shareholders, are submitted to duties of disclosure when their stakes in listed companies reach, exceed, or fall under the statutory thresholds laid down in article 20 SESTA.22

This issue remains theoretical, because, as mentioned, no hedge fund is regis-tered in Switzerland as of today, but only asset managers of foreign hedge funds not submitted to regulation and whose prime brokers are located abroad.

21 DIE EIDG. BANKENKOMMISSION (n. 5), 12-13; BUSCHOR (n. 5), 184; P.M. HILDEBRAND, Hedge

Funds and Prime Broker Dealers: Steps towards a “best practice proposal”, in Banque de France, Financial Stability Review – Special issue on Hedge Funds, April 10, 2007.

22 For a regulatory proposal see: JACQUEMOUD & BARAZZONE (n. 18).

M Y R I A M S E N N

142

– Fourth, regulation should focus on funds managers and not on prime brokers’ regulation. In relation to the activities of funds of hedge funds and private equity funds, the deposit banks should be regulated specifically.

– Fifth, there is no direct debate regarding extending the protection of investors to a wider public than to qualified investors. Additional, specific regulation does not appear to be necessary at this point.

As far as compensation issues are concerned, there is not a public debate focusing specifically on hedge funds and private equity funds managers in Switzerland. The issue regards the whole financial market. A FINMA-Circular entered into force on January 1, 2010.23 It is intended to apply to banks, securities dealers, financial groups and conglomerates, insurance companies, and insurance groups and conglomerates subject to supervision. It should also apply to persons and firms authorized under the CISA.24 Its implementation is mandatory for large banks and insurance providers, which means seven banks and five insurance companies cur-rently. These firms have at least CHF 2 billion in equity capital or as solvency. Thus the scope of application is determined by threshold values based on equity capital requirements for banks and solvency margin requirements for insurance providers.

Finally, as far as the rules on market conduct are concerned, they apply to hedge funds as well.25 In practice, as of today, no case of market abuse by hedge funds or misselling of hedge funds or funds of hedge funds has been reported. Hedge funds are not more inclined to market abuses than other investors. However, situations may arise where opposing interests among investors, lenders and managers of hedge funds could create incentives for inadequate or misleading valuations of complex financial instruments or positions. Thus, the FINMA supports efforts at the international level to introduce more concrete requirements for transparency and independence in the valuation of hedge fund portfolios.26

3. Role of Hedge Funds and Private Equity as Shareholders

3.1 Behavior as Investors

In Switzerland, investments by hedge funds and also private equity funds are often considered with suspicion. Hedge funds have to face allegations of destroying the

23 FINMA-Circular 2010/1, Remuneration Schemes, Minimum standards for remuneration

schemes of financial institutions. 24 Article 13 paragraphs 2-4 CISA. 25 Market behaviour rules for the securities market, FINMA-Circular 08/38 of November 20,

2008. 26 DIE EIDG. BANKENKOMMISSION (n. 5), 12-13.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

143

financial substance of the companies they invest in or intend to take over. They operate through excessive leverage and their transactions are accompanied by diverse fears regarding employment, domination by foreign investors, or the uncertain strategic future of the companies they invest in, to cite a few. However, the attitude towards hedge funds is not comparable to the so-called “locust” phe-nomenon or “Heuschrecke” in Germany. It designs a pronounced negative attitude towards investments by private equity funds, banks, and hedge funds, and at the same time towards some capitalist practices. That metaphor has not been adopted in Switzerland.

In Switzerland, private equity funds are important investors. They usually operate alone and can invest in various types of both listed and non-listed companies. Their investments will often result in the takeover through leverage buyouts. These companies are then deslisted and the “going private” is followed by a medium- or long-term restructuration. Then, the companies may be sold again either in the course of a private transaction or through a “going public”. Although these funds offer management services, the goal of their transactions remains to maximize their return.27

In comparison, hedge funds adopt a more activist attitude than private equity funds as shareholders, although they are less interested than these funds to take over and control the companies they invest in. They first aim at realizing short-term benefits. They usually build a position in companies which in their view should adopt another strategy to produce a reevaluation of the shares. These activities or greenmail raise takeover fears. The hedge fund then, for instance, will request the payout of dividends or reserve of equity capital, the splitting of the company or its separation from business units, or they can try to prevent deter-mined acquisitions. Thus, they use their shareholding position to influence the management. In case their advices are implemented and the situation of the com-pany actually improves, they can realize their gains. Hedge funds do not always operate alone. They often try to gain supporters to put the board of directors under pressure to adopt a different strategy. However, this attitude has come under severe criticism.28

A comparison of the investment strategies of hedge funds and private equity funds shows that it is difficult to draw a line between them. Hedge funds also pursue strategies leading to take overs and private equity funds may operate in the same way as hedge funds on exchanges.

27 GRONER (n. 6), 1 et seq.; FRICK (n. 6), 3 et seq. 28 DIE EIDG. BANKENKOMMISSION (n. 5), 15 et seq.; see also J. ARMOUR & B. CHEFFINS, The Rise and

Fall (?) of Shareholder Activism by Hedge Funds, ECGI Working Paper Series in Law, 136/2009.

M Y R I A M S E N N

144

In Switzerland, shareholders’ activism by these funds has been the focus of mediatic and public interest in a range of cases. They used techniques to pursue their investment goals disclosing only minor stakes in listed Swiss industrial com-panies (such as Sulzer, Saurer, or Implenia), while they had actually acquired large stakes. They used structured products and cooperated with financial insti-tutes to acquire shares indirectly and, thus, evade the disclosure rules. They could build “clandestine” positions and confuse other market participants. In addition, the rule on disclosure of shareholdings, a core transparency rule, may itself not always have provided satisfactory information regarding the exercise of voting rights of stakes in companies. A shareholding could be feigned for example through a securities lending operation, where the economic owner can remain unknown. In other cases, hedge funds and private equity funds may have operated in concerted actions, although they would not declare any alliance, voting agree-ment, or acquisition strategy applied jointly with other, often institutional inves-tors. Some cases have led to lengthy legal complaints, such as the “Sulzer” case which is still pending before court.29 In a first phase, presumptions are discussed in the media. The investors concerned use media alerts to explain their point of view and justify their operations, denying any “bad” intentions, hidden transactions to build positions, or cooperation with other investors.

3.2 Laxey versus Implenia

To illustrate the situation and the role of an activist hedge fund, a concrete case is briefly discussed: Laxey versus Implenia. Laxey Partners Limited (LPL, Laxey) is a regulated investment manager incorporated in the Isle of Man. It has a wholly owned subsidiary, Laxey Partners (UK) Limited, a private limited company incor-porated in England. Laxey is a globally active value investor. It operates as a hedge fund. Its investment philosophy is to invest in undervalued companies. After researching them, it declares supporting them, enhancing their shareholder value. It invests basically in three areas: in European value investments in listed operat-ing companies, in global discount arbitrage strategies, and in general global spe-cial and arbitrage situations. It manages various investment vehicles, the majority are private ones.30

Implenia is a shareholding company incorporated under Swiss law. It is Switzer-land’s largest construction and building services provider. The company is listed on the SIX Swiss Exchange and the SESTA-rules regarding the mandatory offer 29 See for instance: Fall Sulzer kostet Neuer Zürcher Bank die Selbständigkeit, Bank Sarasin

will nach Finma Bericht die Mehrheit übernehmen, in Neue Zürcher Zeitung Online, November 3, 2009.

30 With some exceptions: The Value Catalyst Fund (VCF), a closed-end fund, Terra Catalyst Fund (Terra CF), also a closed-end fund, and Douglas Bay Capital a holding company for investments in quoted and unquoted small to medium sized businesses; see: http://www. laxeypartners.com/default.aspx?Content=welcome.html (20.12.2009).

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

145

apply.31 Its share capital is composed of registered shares. Registered owners of these shares have the right to vote upon request if:

a. they can prove that they acquired and hold the shares in their own name and for their own account. Persons who do not provide such evidence shall only be regis-tered as nominees with the right to vote if they undertake in writing to disclose the names, addresses and number of shares of the persons for whose account they hold the shares. The board of directors is empowered to enter into agreements with the nominees regarding their notification duties;

b. the recognition of an acquirer as a shareholder does not hinder or risk hindering the corporation and/or its subsidiaries, according to the information available to the corporation, from providing the legally required evidence about the composi-tion of its shareholder body and/or beneficial owners. In connection with the pro-ject development and real estate business run through the corporation’s subsidi-aries, the corporation is specifically entitled to refuse to register persons abroad pursuant to the statute, if such registration could raise any doubt about the Swiss control of the corporation and/or its subsidiaries.32

In June 2007, Implenia announced that Laxey had emerged as a new major share-holder pursuing the goal to force Implenia into a strategic change and thereby pushing through an own agenda. However, the Board of Directors did not enter Laxey as a major foreign shareholder in its shareholders’ register, because it would jeopardize Implenia’s real estate business owing to the provision of the “Lex Koller”, a Swiss statute limiting foreign ownership of real estate in Switzerland.33 In addition, the board of directors would only accept to register such a shareholder if the price offered to the other shareholders in the case of a takeover offer would be adequate. At the same time, Implenia’s management opined that the company was already best placed to generate added value. Following the preliminary notifi-cation of a public takeover offer by Laxey in November 2007, the Board declared that the offer price was unfair and rejected it. At that point, the price was signifi-cantly below the market price of the shares. Then, in December 2007, the supervi-sory authority stated that Laxey had operated with Contracts for Difference (CFDs) to build its position and it required their disclosure as an indirect acquisi-tion of Implenia shares as underlying value. In the course of an extraordinary gen-eral meeting of Implenia it was confirmed that the statutory restrictions on share registration applied to Laxey shareholding. Laxey could only register voting shares amounting to 4.9 % of Implenia’s total share capital, although its effective stake was much higher.

31 Article 32 SESTA. 32 Article 7 paragraph 4 of the Articles of Association of Implenia AG, Zurich, April 16, 2009. 33 Federal Act on the Acquisition of Real Estates by Persons Abroad of December 16, 1983, SR

211.412.41.

M Y R I A M S E N N

146

Both the Takeover Board and the former Federal Banking Commission had to rule on the case requiring transparency from Laxey and the respect of the best price rule with regard to the takeover offer. In March 2008, after an investigation, the supervisory authority concluded that Laxey had infringed its disclosure obliga-tions34 when building its Implenia’s stake. De facto, Laxey had placed Implenia shares with counterparties, parking them and was in a position to redeem them at any time. Thus, Laxey could retain potential control over the voting rights of the shares, which indeed represented an indirect acquisition of shares. At that time, Laxey’s shareholding represented 22.89 %. Laxey submitted the case to the Federal Administrative Court and to the Federal Supreme Court, but its claims were rejected. The Supreme Court stated that Laxey had purchased Implenia shares on the open market from December 2006 onward, and transferred them to various banks. In return, these banks issued Laxey CFDs at a 1:1 ratio. It was an indirect acquisition of shares which was subject to a notification obligation.35

The takeover fight lasted approximately one year. Finally, Laxey informed the market that its takeover bid had failed. Only 2.79 % (according to Implenia) or 4.23 % (according to Laxey) of the Implenia shares had been tendered. Laxey’s overall shareholding was estimated to have reached 38.1 % of the share capital (including the non-disclosed shares), while 4.9 % were registered shares. Follow-ing Laxey’s announcement, the price of Implenia shares dropped. Then, in April 2009, Implenia’s board declared that it would be sticking to the statutory registra-tion restrictions and reject any application for registration that would run counter to these restrictions. With regard to the stake hold by Laxey, it informed the share-holders that talks had been initiated with Laxey to work out a solution. In the meantime Laxey hold more than 50 % of the voting rights of Implenia. Its goal was to build a large shareholding, to make it easier to offload at a profit. A placement of the shares would have to fulfil three conditions: First it would have to align the interests of both parties. Second, attractive investment fundamentals had to be found. Third, a broad pool of mainly domestic capital had to be found. Negotia-tions first failed. Finally, in November 2009, it was announced that all Implenia shares hold by Laxey had been placed with various investors. Laxey claimed that it did not incur any loss.

Other cases could be cited where financial investors, in particular hedge funds, have used their non-controlling interests to influence the strategy of companies to achieve short-term profits when they are eligible to exercise their voting rights. 34 Article 20 SESTA. 35 Federal Supreme Court, Judgements 2C_77/2009, 2C_78/2009 of March 11, 2010 and of

June 2, 2009; Federal Administrative Court, Judgement B-2775/2008 of December 18, 2008; Implenia’s Press release of December 22, 2008. Concurrent cases were brought by the Federal Department of Finance regarding the disclosure obligations and the Canton Zurich Public Prosecution Office regarding a charge of criminal offence of price manipulation. Implenia’s Press release of June 22, 2009.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

147

Indeed, shareholder’s activism does not mean that the influence is negative. Short-term investment strategies need not contradict a company’s long-term interests.36

3.3 Regulatory Consequences

The companies must be in a position to deal with such developments. In case there are doubts regarding the effective number of shares hold by these investors, they can – as far as it is foreseen in their statutes – refuse to register them.37 The hedge funds, private equity funds, or investors concerned will have only a very limited number of voting rights, which restricts their potential influence.

In case the disclosure rules38 have not been complied with or there is a suspicion that they have not been complied with, the supervisory authority will carry out an investigation. However, possible breaches of the duty of disclosure are not typi-cally related to hedge funds, but regard any investor. The enforcement of these rules is very challenging and experience has shown that it is very difficult to impose the drastic statutory fine. Its amount can represent the double of the pur-chase price or the sale proceeds of the shareholding which has not been declared (article 41 SESTA). This situation was dissatisfying and the practice developed made a revision of these rules necessary. Furthermore, in relation to several raids on Swiss companies conducted by hedge funds, the companies also intervened through contacting politicians and required the review the existing disclosure rules. Circumventive transactions would have to be seized more easily. Thus, the focus of the revision was placed on increasing the transparency of the sharehold-ings, ensuring the effective enforcement of the rules, and providing proper instruments to the authority to ensure their implementation. The new provisions introduced aim at ensuring the respect of the rules and the correct information of the companies regarding the evolution of their shareholdings. In detail, the revi-sion focused on the following points:39 The threshold percentages of shareholdings

36 DIE EIDG. BANKENKOMMISSION (n. 5), 12-13. 37 Article 658d Swiss Federal Code of Obligations of March 30, 1911 (CO), SR 220. 38 Article 20-21 SESTA. 39 Article 20 SESTA now reads as: 1 Whosoever directly, indirectly or in concert with third parties acquires or sells for their

own account shares or purchase or sale rights relating to shares in a company incorporated in Switzerland whose equity securities are listed in whole or in part in Switzerland and thereby attains, falls below or exceeds the threshold percentages of 3, 5, 10, 15, 20, 25, 33⅓, 50 or 66⅔ of voting rights, whether or not such rights may be exercised, must notify the company and the stock exchanges on which the equity securities in question are listed.

2 The conversion of participation or bonus certificates into shares and the exercise of conversion or share acquisition rights shall be considered equivalent to an acquisition for the purposes of this Act. Similarly, the exercise of sale rights shall be considered equivalent to a sale for the purposes of this Act.

M Y R I A M S E N N

148

to be declared now begin at 3 instead of 5 % and further thresholds have been introduced. There are now detailed rules regarding the disclosure of derivative products. While the original rule stated that the direct and indirect holding of shares had to be disclosed, the new rules lay down that all operations with finan-cial instruments, which may potentially lead to the acquisition of shares, have to be disclosed.40 In addition, urgent measures have been adopted at the ordinance level. It has been adapted and now applies to derivatives products without taking into account whether they give rise to a specific performance (Realerfüllung). By this way, it is possible to seize cash-settlement options. Every operation now has to be declared.41 The statute stipulates that the voting rights can be suspended up to five years in case there is the suspicion that a shareholding has not been disclosed. These new rules have entered into force on December 1st, 2007.

3.4 Responses by Companies

From the point of view of the companies, the issue is to determine how far they can resist unwanted influence and pressure from activist shareholders. Which defenses can boards use? When transfer restrictions are laid down in the statutes,

2bis Especially transactions involving financial instruments which economically enable the

acquisition of equity securities in view of a public takeover offer shall constitute an indirect acquisition.

3 A group organized pursuant to an agreement or otherwise shall comply with the obliga-tion to notify laid down in para. 1 as a group and shall disclose:

a. its total holdings, b. the identity of its members, c. the nature of the agreement, d. the representation. 4 If a company or stock exchange has reason to believe that a shareholder is in breach of

the obligation to notify, it shall inform FINMA of such fact. 4bis At the request of FINMA, the company or one of its shareholders, the judge may sus-

pend for a period of up to five years the exercise of the voting rights by the person who has breached the obligation to notify when buying or selling their holding. If the person has breached the obligation to notify when acquiring a holding in view of a public takeover offer (Chapter 5), the Takeover Board (Art. 23), the offeree company or its shareholders may request from the judge the suspension of the voting rights.

5 FINMA shall issue rules relating to the scope of the obligation to notify, the treatment of share acquisition and sale rights, the calculation of voting rights and the time limits within which the obligation to notify must be fulfilled and a company must publish changes in its ownership structure pursuant to para. 1. The Takeover Board shall have the right to put for-ward proposals. Taking into account internationally recognised standards, FINMA may pro-vide for exceptions to reporting or publication obligations for banks and securities dealers.

6 Whosoever intends to acquire securities may obtain a ruling from FINMA as to whether or not they will be subject to the obligation to notify.

40 See point 3.2, Laxey versus Implenia. 41 Ordinance of the Swiss Financial Market Supervisory Authority of 25 October on Stock

Exchanges and Securities Trading (FINMA Stock Exchange Ordinance, SESTO-FINMA), SR 954.193.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

149

the board will be able refuse to register shareholders, limiting the exercise of their voting rights. Other measures regard the takeover offers. Article 32 SESTA states that any shareholder acquiring and exceeding a shareholding of 33.3 % of the voting rights of a company must submit a takeover offer. It is assumed that the shareholder will then be in a position to control the company. However, listed companies can choose to submit themselves to these rules, opt out, or opt up. The regime they opt for must be introduced in their articles of association and the information must be accessible to the public. The exchange too shall ensure that the listed companies disclose the regime they have opted for.42 These provisions apply to companies incorporated in Switzerland and listed in whole or in part on an exchange in Switzerland.43 The mandatory offer rules shall ensure equal treat-ment of shareholders. They represent an exit strategy for minority shareholders who must be offered a fair opportunity to sell their shares. As a result, a control shareholder has a fiduciary duty to act in the interest of the company and other shareholders. In a takeover case, the board has to behave neutrally, although in a case of unfriendly takeovers, a possible defense will be to present concurrent offer(s) which will result in an auction. The board will take position and inform the market with regard to a raider or undesired shareholders, in which case it will try to gain support of the other shareholders.

According to company law, one or several shareholders (including hedge funds and private equity funds) can request the organization of a general meeting when they represent at least 10 % of the shareholding capital of a company.44 Shareholders can submit agenda items to be dealt with at a general meeting pro-vided they hold shares for a nominal value of CHF 1 million.45 Thus, hedge funds and private equity funds, depending on their shareholding and intentions, will be in a position to submit a motion to dismiss the board of directors, to split-up a company, to merge it with another one, or to submit a motion to close down cer-tain, such as less beneficial parts of the business, or to sell it off to third parties (major disposals). These decisions belong to the competence of the general meet-ing. The submission of such motions will put a great pressure on the company and force the board of directors and management to present alternative or opposite measures.

42 According to article 5 paragraph 3 SESTA in connection with the SIX Swiss Exchange Circu-

lar No. 1, annex 1, point 3.05. See for instance the information provided by the SIX Swiss Exchange, http://www.six-exchange-regulation.com/obligations/reporting/opting/search_ de.html (20.12.2009). Furthermore, every amendment of the articles of association regarding the already reported opting-out or opting-up provisions must be notified to SIX Exchange Regulation.

43 Article 22 SESTA. 44 Article 699 paragraph 3 CO. 45 Article 699 paragraph 3 CO.

M Y R I A M S E N N

150

The Swiss legal system knows both registered and bearer shares. Companies are free to choose between them. In case of registered shares, shareholders’ identity is known and when limits to the registration of the number of voting rights a share-holder can exercise are set,46 the company disposes of an effective control instru-ment. In case of bearer shares, it will not be possible to know the identity of the shareholders as long as the SESTA disclosure rules are not fulfilled. Moreover, investors trying to build a position in a company may operate with indirect share-holdings. They may use structured or derivatives products or complex financial constructions such as entering into equity swaps, CDSs and similar transactions to hide their ownership, although this is not compatible with the new rules. A further technique or approach is to create undisclosed or secret alliances with other shareholders, thus denying that they really exist or that there are connections among these investors.

In addition, it should also be mentioned that in Switzerland, similarly to other countries, there is a debate about “empty voting”. The developments in relation to the use of derivative financial instruments, the increased use of securities lending transactions and the active role played by hedge funds have led to an effective decoupling of the economic risk taken from the voting right. In fact, they reveal the antagonism between the short-term investment strategies and the long-term interests of a company when hedge funds minimize economic risks linked to a shareholding with the help of derivative products or through a securities lending transaction and, as a result, are in a position to pursue their strategic interests without financial risk. In particular,

– it is possible to exercise voting rights based on securities lending transactions, but the person exercising that right does not actually bear the risk of the shares on which the operation is based, i.e. “empty voting”.

– with the use of derivative financial instruments it is possible for a person to secure its position as a shareholder in a way that it is economically profitable to vote against the interests of the other shareholders in order to benefit from a loss on stock market prices (“empty voting”).

– with the constitution of large positions in derivative products, cash settled financial products with a bank or banks, it is possible to create hidden, callable or “parked” positions of voting rights (“hidden [morphable] ownership”). Even in cases where no fulfillment or settlement in the form of a share transfer has been arranged, it is not excluded, that in some cases the interests of both the bank or banks and of the person acquiring the financial instruments are very similar and the bank may agree to transfer its hedge position to the acquirer of the financial instruments.47

46 Article 685 CO. 47 Disclosure Office of the SWX (SIX) Swiss Exchange, Annual Report 2006, 3.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

151

Indeed, these developments are opposed to the classical understanding of a share-holder carrying a risk and at the same time being in a position to exercise the vot-ing rights. The Swiss legislator has already dealt with the issue and refined the transparency rules, as stated. Company law too could be sharpened. In particular, securities lending transactions executed solely to influence issues at general meetings represent malpractices and should be forbidden. These short-term dis-placements of voting rights can be countered by the use of nominal shares and the bylaws rules regarding their registration. In the course of summer 2009, the debate focused on the opportunity to unambiguously separate the financial aspects of owning shares from their voting rights. Proponents of that solution praise its positive influence on the corporate governance of companies. However, critics consider it to reinforce the negative aspects of “neo-capitalism”, because investors can take only small financial risks and at the same time make use of dis-proportionate voting rights. On the other hand, investments by hedge funds or private equity funds often also result in the recapitalization of companies in diffi-cult both financial and strategical situations. These funds may provide liquidity in cases where banks or other credit institutes would refuse to provide any financing.

Finally, there is no rule comparable to the Regulation FD in the US48 in Switzer-land. However, companies have to inform the market on a regular basis on the development of their operations. In case of information regarding changes of strategy or other important events, article 53 of the Listing Rules on ad-hoc pub-licity of the SIX Swiss Exchange will apply.49 Any information which could influ-ence the price of shares has to be communicated according to that rule to avoid sudden distortions of the share prices or other disproportionate reactions as well as insider dealing operations. Other duties to publish information regard for instance the notice in advance of a planned takeover.50

48 Regulation FD (Fair Disclosure) addresses the selective disclosure by issuers of material

nonpublic information and clarify issues under the law of insider trading, i.e. when insider trading liability arises in connection with a trader’s “use” or “knowing possession” of mate-rial nonpublic information; and when the breach of a family or other non-business relation-ship may give rise to liability under the misappropriation theory of insider trading. 17 CFR Parts 243.100-243.103, Release Nos. 33-7881, 34-4314.

49 Article 53 Listing Rules, Obligation to disclose potentially price-sensitive facts. 1. The issuer must inform the market of any price-sensitive facts which have arisen in its

sphere of activity. Price-sensitive facts are facts which are capable of triggering a signifi-cant change in market prices.

2. The issuer must provide notification as soon as it becomes aware of the main points of the price-sensitive fact.

3. Disclosure must be made so as to ensure the equal treatment of all market participants. See also: Directive Ad hoc Publicity (DAH); http://www.six-exchange-regulation.com/admission_

manual/03_01-LR/en/9007199333477771.html#9007199333490571 (20.12. 2009). 50 Articles 5-8 of the Ordinance of the Takeover Board on Takeovers, SR 954.195.1.

M Y R I A M S E N N

152

4. Sovereign Wealth Funds

During the 2007-2009 financial crisis, financial market participants and states have seen a rise of investments by SWFs. These investments have been welcome and SWFs have become important financial market participants in terms of size and as a source of capital. However, in the past they repeatedly provoked defen-sive actions by governments. They raise security and economic sovereignty issues. Economic studies assert that SWFs will continue to grow disproportionately for some time and attempt to diversify their holdings through cross-border invest-ments. Their rise is closely linked to global macroeconomic imbalances.51 Due to their lack of transparency it is difficult to understand their investment rationales and calls for protectionism against their influence are widespread, which is accen-tuated by the fact that the donor countries often are autocratic regimes.

4.1 Definition

The notion of SWF52 has long been ambiguous. They form a heterogeneous group of financial market participants and represent countries with various political backgrounds and economic development. They are based on diverse institutional arrangements and can pursue a range of objectives. Their practices and operations are not standardized. With the adoption of the Santiago Principles,53 the Interna-tional Working Group of Sovereign Wealth Funds (IWG-SWF)54 has provided the following definition:

SWFs are defined as special purpose investment funds or arrangements, owned by the general government. Created by the general government for macroeconomic purposes, SWFs hold, manage, or administer assets to achieve financial objectives, and employ a set of investment strategies which include investing in foreign financial assets. The SWFs are commonly estab-lished out of balance of payments surpluses, official foreign currency operations, the proceeds of privatizations, fiscal surpluses, and/or receipts resulting from commodity exports.

This definition relies only on what SWFs say they are. They define themselves as government-owned investment companies and there is agreement among them about the following key criteria:

a. SWFs are owned by sovereign governments and are investment vehicles usually managed separately from central bank reserves.

51 P. M. HILDEBRAND, The challenge of sovereign wealth funds (Central Bank Articles and

Speeches), BIS Review 2007 (150), http://www.bis.org/review/r071219d.pdf, 1 (25.10.2009). 52 The term was introduced by A. ROZANOV in 2005: Who holds the wealth of nations?, in Cen-

tral Banking, Volume 15/4, 52-57. 53 Generally Accepted Principles and Practices “Santiago Principles” (October 2008),

http://www.iwg-swf.org/pubs/gapplist.htm (30.12.2009). 54 The IWG was established at a meeting of countries with SWFs on April 30–May 1, 2008, in

Washington, D.C. It comprises 26 IMF member countries with SWFs.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

153

b. SWFs pursue diversified investment strategies including investments in foreign financial assets. Funds investing solely in domestic assets are not considered to be SWFs.

c. SWFs are established by governments for macroeconomic purposes and pursue financial objectives, the maximization of their investments. They can be classified as conservative investors with a medium- to long-term timescale.

d. SWFs are not hold inter alia for traditional balance of payments or monetary policy purposes, foreign currency reserve assets, or operations of state-owned enterprises.55

The goal of these statements made by SWFs is to appease the fears of recipient countries that they could use their investments for speculative matters or to desta-bilize the economies they are investing in.

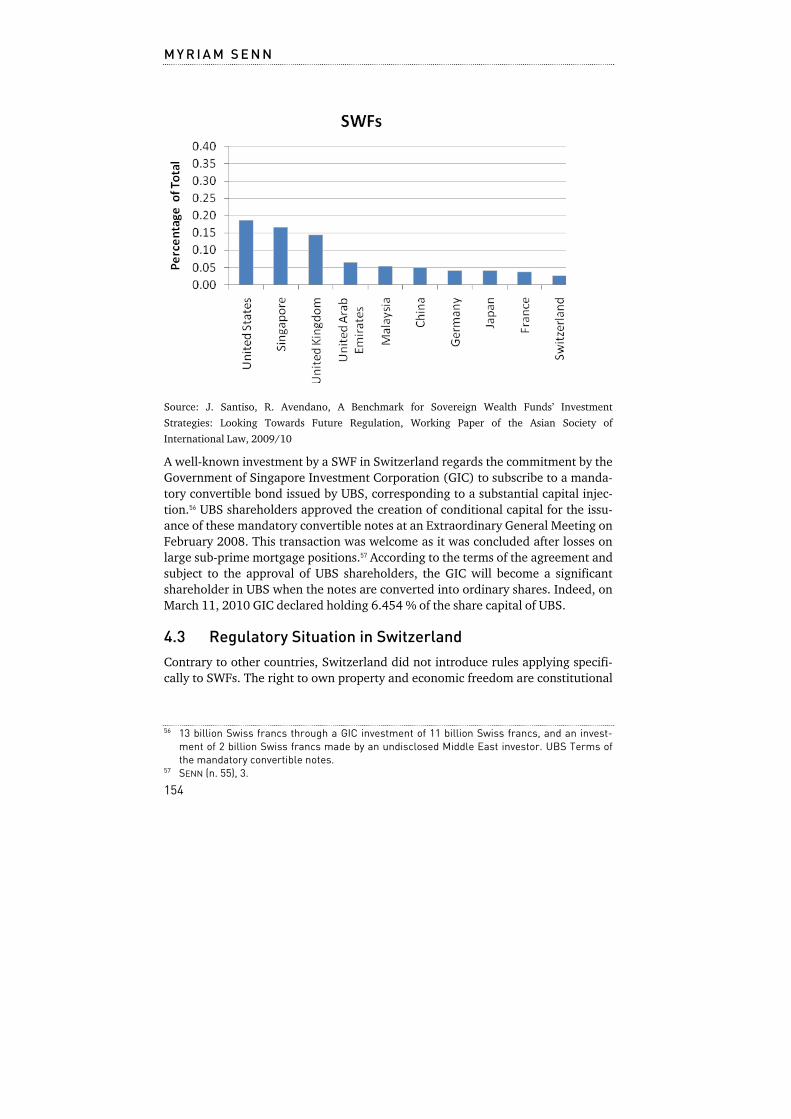

4.2 Country Distribution

According to figures established by the OECD, Switzerland belongs to the ten countries which have received most inflow of capital coming from SWFs. The numbers reproduced hereinafter reflect the situation at the mid of 2009:

Country SWFs

United States 0.19

Singapore 0.17

United Kingdom 0.14

United Arab Emirates 0.06

Malaysia 0.05

China 0.05

Germany 0.04

Japan 0.04

France 0.04

Switzerland 0.03

55 M. SENN, Sovereign Wealth Funds – A Challenge for Institutional Governance, Jusletter,

Special issue on Economic Law, April 19, 2010, 3.

M Y R I A M S E N N

154

Source: J. Santiso, R. Avendano, A Benchmark for Sovereign Wealth Funds’ Investment Strategies: Looking Towards Future Regulation, Working Paper of the Asian Society of International Law, 2009/10

A well-known investment by a SWF in Switzerland regards the commitment by the Government of Singapore Investment Corporation (GIC) to subscribe to a manda-tory convertible bond issued by UBS, corresponding to a substantial capital injec-tion.56 UBS shareholders approved the creation of conditional capital for the issu-ance of these mandatory convertible notes at an Extraordinary General Meeting on February 2008. This transaction was welcome as it was concluded after losses on large sub-prime mortgage positions.57 According to the terms of the agreement and subject to the approval of UBS shareholders, the GIC will become a significant shareholder in UBS when the notes are converted into ordinary shares. Indeed, on March 11, 2010 GIC declared holding 6.454 % of the share capital of UBS.

4.3 Regulatory Situation in Switzerland

Contrary to other countries, Switzerland did not introduce rules applying specifi-cally to SWFs. The right to own property and economic freedom are constitutional

56 13 billion Swiss francs through a GIC investment of 11 billion Swiss francs, and an invest-

ment of 2 billion Swiss francs made by an undisclosed Middle East investor. UBS Terms of the mandatory convertible notes.

57 SENN (n. 55), 3.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

155

rights.58 SWFs are treated like other foreign investors. However, investments by SWFs can be controlled or limited indirectly in relation to the application of diverse, specific rules. Organizations responsible for infrastructure provision for instance, such as energy and transport, are controlled by the state based on statu-tory regulation. With regard to private companies, company law offers a suitable instrument to avoid the acquisition of important participations by undesired inves-tors. The transferability of the voting rights can be restricted and the exercise of these rights curtailed. It is possible to fix the number of voting rights to be held by individual shareholders in the by-laws. However, when the registration of a share-holder is declined, it must occur for good reasons.59

In addition, special rules apply to regulated industries, such as the financial sector. Banking and securities market regulations, for example, require the disclosure of the beneficial owners of the regulated financial institutions, such as banks, securi-ties dealers, or exchanges. The goal of the rules is to protect financial institutions and markets from criminal, politically-motivated, or irresponsible actors. The owners or shareholders of these institutions must fulfill the requirement of ensur-ing an irreproachable business conduct. As a rule, any acquisition of large share or capital holdings, that is, in excess of 10 % must be submitted to the responsible supervisory authority before the acquisition. The authority will have to approve or decline the deal. Transactions by shareholders must also be submitted to the authority for approval when a holding is increased or falls below the statutory thresholds. In addition, all authorized financial institutions must inform the supervisory authority once a year of their shareholdings. In case of a new foreign shareholder assuming control, a supplementary license must be obtained and the institution would qualify as a foreign institution according to Swiss law. Hence, the supervisory authority can grant authorizations and accept or decline share-holders in application of the rule of guarantee of irreproachable business conduct.60 Thus, these rules would also apply to SWFs acquiring stakes in author-ized financial institutions of 10 % or more of the shareholding capital.

As of today, no case of refusal of an investment by a SWF has been made public. However, it cannot be ignored that investments by SWFs result in a form of cross-border nationalization in recipient countries.61 In fact, their investments may destabilize economic sectors in the countries they invest in and represent a threat to a free market economy. As a result, some states like the US and Germany for

58 Article 26 Guarantee of ownership and article 27 Economic Freedom, Federal Constitution

of the Swiss Confederation of April 18, 1999, SR 101. 59 Articles 685-685g CO. 60 Articles 3, 3bis and 3ter of the Federal Act on Banking of November 8, 1934, for instance.

SwissBanking, Sovereign Wealth Funds – A Position Paper by the Swiss Bankers Associa-tion (May 2008), 12-14; SENN (n. 55), 11-12.

61 A term coined by L. Summers, Davos Annual Meeting 2008 and L. SUMMERS, Funds that shake capitalist logic, in Financial Times, July 29, 2007.

M Y R I A M S E N N

156

instance have introduced specific statutes to control and limit these investments.62 This has not been the case of Switzerland. SWFs are submitted to generally appli-cable rules, such as the transparency rules of the Securities Exchange Act, regard-ing the disclosure of shareholdings. These rules apply to any investor acquiring or selling shares or purchasing or selling rights relating to shares.63 Although there is no legal investors’ duty to declare their voting attitude, as far as the GIC invest-ment in UBS was concerned, for example, GIC gave a clear statement of its inten-tions when the investment was done. GIC then declared:

GIC’s preferred practice in respect of our public equity investments is to take relatively small stakes in companies for portfolio diversification. However, we made this significant invest-ment in UBS because we have confidence in the long-term growth potential of the bank’s businesses, particularly its global wealth management business.64

SWFs have made a number of similar transactions during the crisis. Their invest-ment activities have led to the formation of large exposures, often in the financial sector. However, they are frequently confronted with allegations of non-transpar-ency regarding their policies.65 Moreover, the technical complexity of the funds enhances the challenge to understand them. Are they solely passive long-term investors? They could not strive for financial benefits and thus have to face the allegations of recipient countries for pursuing strategic and political interests in their transacted investments. Such interests may lead to a tendency to invest in distressed industries where they can counter political or public opposition as wel-come investors. To this day however, it has remained almost unnoticed that SWFs have lost billions from their initial investments, mainly in the financial sector. In the future, they will most probably be seeking to invest increasingly in equity mar-kets.66

62 In the US, the Committee on Foreign Investment in the United States (CFIUS) reviews

transactions that could result in a foreign national assuming control of a US business with regard to potential impact on national security; all transactions must be approved by the CFIUS. In Germany, a statute requiring interministerial approval of foreign investments, which could pose a threat to national interests, was passed in 2008. Acquisitions of stakes of more than 25 % of voting shares in German companies by investors outside the European Union come under scrutiny. Section 721 of the Defense Production Act, U.S.C. (1950) c. 50 App., s. 2170, as amended by the Foreign Investment and National Security Act of 2007 (FINSA), and as implemented by Executive Order 11858, and regulations at 31 C.F.R. Part 800; H. WILLIAMSON, Germans agree sovereign funds law, in Financial Times, April 10, 2008; SENN (n. 55), 8.

63 Article 20 SESTA. 64 Statement by T. Tan Keng Yam, Deputy Chairman and Executive Director, GIC (GIC Media

Conference on December 10, 2007). 65 HILDEBRAND (n. 3), 3; R. BECK & M. FIDORA, The Impact of Sovereign Wealth Funds on Global

Financial Markets, in European Central Bank, Occasional Paper Series, July 2008 (91), 14-23.

66 W. MIRACKY & B. BORTOLOTTI (eds.), Weathering the Storm, Sovereign Wealth Funds in the Global Economic Crisis of 2008, Monitor, SWF Annual Report 2008, 3-5; V. FOTAK & B.

H E D G E F U N D S , P R I V A T E E Q U I T Y A N D S O V E R E I G N F U N D S

157

At this point, it cannot be stated, whether SWFs usually delegate a member to the board of the companies they are investing in. However, in practice, it is regularly the case in Switzerland that members can be delegated to the board depending on the stake they or their company hold in a company. This is usual in case of take-overs. The bidder will nominate new board’s members. As far as SWFs are concerned, there has been no case of delegation of a member to the board as of today. In case a SWF would delegate board members proportionally to the stake hold in a company, there would be no specific rules applying to that member only. It could then not be excluded, that a SWF could try to displace some activities of the company in another country or organize a know-how transfer to their country of origin.

As far as the annual reports of the investee companies are concerned, the compa-nies have to provide information on their significant shareholders:

– Companies whose shares are listed on a stock exchange shall include in the attachment to the balance sheet important shareholders and their participa-tions insofar as these are known or should be known to them.

– Important shareholders are deemed to be shareholders and groups of shareholders with restricted shareholding rights whose participation exceeds five percent of all shareholdings rights. If the articles of incorporation provide for a lower percentage limit for registered shares,67 such limit shall be applicable to the duty to publish.

– In addition, any participation in the company and derivates products hold by each member of the board of directors, the executive board and the advisory board and the participations hold by their family and closed relationships must be disclosed, with the exact designation of the name and function of the mem-ber concerned.68

Thus, the threshold percentage hold by a SWF will be disclosed in the annual report when it reaches or exceeds five percent and is known or should be known to the company. In addition, an investee company may well include a passage in its annual reports about the presence of a SWF and its potential influence of the development, strategy and future of the company. However, there is no duty to disclose information on the way a SWF exercised its voting rights at general meetings. SWFs are treated similarly to other investors and no mechanisms have been introduced to review or supervise the activities deployed by SWFs in investee

MEGGINSON & H. LI, Sovereign Wealth Funds losses in listed firm stock investments, in W. MIRACKY & B. BORTOLOTTI (eds.), Weathering the Storm, Sovereign Wealth Funds in the Global Economic Crisis of 2008, Monitor, SWF Annual Report 2008, 53-58.

67 Article 685d paragraph 1 CO, Registered shares listed on a securities exchange, a. Prerequisites for refusal.

68 Article 663c CO, Participation in public companies.

M Y R I A M S E N N

158

companies. In case of companies limiting the percentage of shares to be hold by each shareholder, the influence of a SWF may be very limited.69

5. Conclusion

The report has described the regulatory situation with regard to three different investment vehicles: hedge funds, private equity, and sovereign wealth funds in Switzerland. Three aspects have been discussed. The first one has concerned the organization of these funds, the second has regarded their operations and role as shareholders and the third has concentrated on the sovereign wealth funds. The report shows that both the concrete situation and the regulatory situation and approach vary largely depending on the type of investment vehicle considered and the goal pursued. They are influenced by a range of factors such as fiscal, regula-tory, investment opportunities, or also trading market. While the overall regula-tory objectives regard investors’ protection and the control of systemic risks, the specificities of each vehicle require different regulatory approaches.

69 See n. 67.