The Presence of Non..;Ec Multinationals in European Industry

36

ONDERZOEKSRAPPORT NR 9328 The Presence of Non..;Ec Multinationals in European Industry by Reinhilde VEUGELERS D/1993/2376/28

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of The Presence of Non..;Ec Multinationals in European Industry

ONDERZOEKSRAPPORT NR 9328

The Presence of Non..;Ec Multinationals in

European Industry

by

Reinhilde VEUGELERS

D/1993/2376/28

THE PRESENCE OF NON-EC MULTINATIONALS IN EUROPEAN INDUSTRY

BY

REINHILDE VEUGELERS 0

September 1993

Abstract After a sketch of FDI flows in general and towards the EC in specific, the implications of foreign presence in the EC industries are analyzed through a study of non-EC affiliates . After a first overview of the size of this foreign presence in terms of sales and entries, according to the various home countries and within various industries, the different characteristics of foreign affiliates relative to EC companies are studied. Diversification, average size, size distribution and concentration are sketched for the non-EC versus the EC sample. Next, the industry distribution of (sales by) non-EC divisions is explained by relating this distribution to industry characteristics capable of generating the MNE phenomenon such as the presence of intangible assets, strategic motives, requirement of local presence and availability of other modes of serving foreign markets. The existence of comparative advantages of the various home markets are then related to the foreign penetration of these nationalities within EC industries. By including the comparative advantages of EC industries into the analysis, the impact of foreign presence by nationality and by industry on the EC's economy is considered.

o This work is part of the SPES project on "The Europeanisation of Industry" (SPES-0028-UK). The author would like to thank Rita Sepelie and Kris Frooninckx for the computational assistance as well as Leo Sleuwaegen for the interesting discussions. Financial support from the FKFO (2.0052.92) and the DPWB (SS/Dl/007) is gratefully acknowledged.

1

1. THE EC POSITION IN FDI FLOWS

Investments by foreign companies into the European Market has

traditionally attracted a lot of academic and professional attention

if only because of the ambiguous consequences of such investment for

the EC's economic, political and social objectives. The lifecycle of

papers dealing with this critical issue have correlated intensively

with the various stages of integration within the EC. In the fifties

and sixties, US companies rushed into Europe. Although econometric

tests of American FDI in Europe yielded inconclusive results

pertaining to the effects of integration on inward investment flows

and the impact of such investment on economic growth, a fear of

economic and political dependence was created on the continent.

Nowadays, a different structure of FDI flows creates a more subtle

athmosphere. The following table details the position of EC, Japan

and the US as host as well as home country to FDI in 1987 .

Table 1

Share in 1987 flows Average yearly growth 84-87

EC (12) us JAPAN

OUT

54.7% 15.3 % 30.0 %

Source: Eurostat, 1990

14.5% 5.7%

18.4%

IN

23.8 % 74.3 % 1. 9 %

17.0% 9.2%

Whereas the US has clearly lost its position as major home country of

foreign investment flows -most of the US outward FDI flows are

reinvested earning into the EC- and despite the fast growing

2

investment flows originating from Japan, the main geographical source

of outward investment are the 12 EC countries. Most of these

investment flows end in the US, which has become a major host

country. All this leaves for 1987 the EC to be the major net

exporter of FDI and the US the major net importer. But as the growth

figures shows, the expansion of inward FDI in the US which was one of

the hallmarks of the eighties has given way to substantial growth in

inward investment from the US as well as from Japan in a EC

rejunenated by the the 1992 integration project.

The following table details the position of the EC in in- and

outward FDI in terms of the individual member states as well as the

industries in which these flows occur (Year=l987). The UK emerges as

the most important source as well as destination of investment flows.

The German economy displays an important outward FDI activity, but

its capital market structure generates negligeable inward FDI flows.

The industry distribution clearly awaits more detailed breakdowns,

but apparent are the European MNEs in refining and chemicals, whereas

most incoming FDI flows originate in the finance and banking sector.

OUTWARD FDI INWARD FDI OUTWARD FDI INWARD FDI --------------------- --- --------- ---- --------------------------------

BY MEMBER STATES BY INDUSTRY ---------------------------------------------------------------------UK 54% UK 40% ENERGY 18% CHEMICALS 13% GER 17% FRA 16% CHEMICALS 10% AGRI&FOOD 10% NETH 12% ITA 14% ELECT 9% ELECT

5% FRA 11% SPA 11% AGRI&FOOD 8% FIN &BANK 39% ITA 2% NETH 7% TRADE&HOTEL 16% REAL ESTATE 12% BLEU 2% BLEU 6%

Source: Eurostat, European Communities Direct Investment, 1984-1989, 1992.

3

When focusing on the EC as destination of FDI flows, about half of

these flows are intra-EC leaving half of the flows to be "foreign".

As a% of total non-EC inflows, the EFTA countries account for 30%,

whereas the US and Japan account for resp 15% and 12% (Year=l987).

The intense economic linkages between the neighbouring EFTA and

EC blocks is reflected in the strong position of the latter among the

non-EC investors. The EFTA countries, led by Sweden and Switzerland

have been traditionally very outward oriented, especially into the EC

and in manufacturing. Recent FDI patterns strengthen this

orientation towards the EC and in manufacturing.

US MNEs have traditionally been the most active investors in the

EC, with a preference for the UK. Although manufacturing takes up

the majority of US flows, banking, finance and insurance are also

important sectors.

Japanese direct investment into the Community is increasing

rapidly but still remains at negligible levels compared to the US.

Again the UK is the main beneficiary of the Japanse inflows. Total

flows are dominated by finance and insurance representing almost one

half of the total. In manufacturing, the electronics sector is the

most important, followed by chemicals, machinery and transport

equipment. (Source: Panorama of EC Industry, 1991)

The statistical picture of foreign involvement on the basis of FDI

flow statistics clearly shows some global trends at play such as the

strong position of the EC as home country, Japanese FDI into the US

and the EC and the pull exerted by the EC single market. Within this

setting, foreign investment flows into the European industry are

evaluated more on the grounds of their competitive results, then in

terms of economic and political dependency, as in the fifties and

4

sixties. However, in order to asses the impact of foreign companies

on the competitiveness and long-term performance of the EC, a more

indepth study of the geographical and industry origin of this foreign

presence, in all of its aspects, is required. (Cumulated) flow data

on foreign direct investment, although they give a clear picture of

the recent trends in multinational operations are a poor indication

of the relative importance of various home countries certainly at a

more disaggregated industry level. The distribution of foreign

affiliates across industries, supplemented with information on trade

flows and alliances as alternative forms of foreign involvement can

serve as a more useful proxy to measure the impact of a foreign

presence on the structure of EC industries. This paper is an attempt

to tackle this study.

2. THE PRESENCE OF NON-EC COMPANIES IN THE EC MATRIX

The analysis of foreign penetration through affiliates draws on an

elaborate micro database, the EC market share matrix, constructed

specifically for the SPES project on "The Europeanisation of

Industry". Appendix 1 contains a short description of the

methodology of the data collection. Within this EC matrix the

leading firms that have foreign, i.e. non-EC, parentage are singled

out and analyzed along country of origin and industry distribution.

2.1. The share of non-EC companies in the EC matrix

In contrast to data on FDI flows, focusing on the share in numbers of

and sales by subsidiaries as a measure of market penetration will

give more weight to the US as home country, given its long

5

established presence and despite the recent declines in FDI flow

shares.

/1 CIES

Table 2

SALES (MIO ECU)

AVERAGE SIZE

________ ... __ __________________________________________________________

TOTAL 407 797639.24 1959.8

EC 362 89% 681056.29 85% 1881.37

NON-EC 45 11% 116582.95 15% 2590.73 CAN 3 7% 4360.06 4% 1453.35 JAP 2 4% 730.32 1% 365.16 EFTA (SWE/SUI) 8 18% 25976.15 22% 3247.02 us 32 71% 85516.42 73% 2758.59

About 11% of all matrix companies originate from outside the EC, with

the overwhelming majority indeed from the US with the EFTA, i.e.

Sweden and Switzerland, coming in second. The recent nature of

Japanese investment is reflected in the low share of this country in

terms of number of companies in the matrix. These 11 % of foreign

companies account for 15% of the matrix sales, which already

indicates that the average size of foreign companies is higher than

their EC counterparts. The last column reveals that this larger

average size prevails especially for the Swiss, Swedish and US

companies, whereas the freshly established Japanese are clearly

smaller in size.

In order to check whether this larger size is due to the

concentration of foreign companies in large-scale industries or

whether they are indeed larger than EC companies within industries, a

closer look at the industry distribution of foreign involvement is

called for.

6

2.2. The industry distribution of non-EC firms

Given the limited number of foreign observations, an industry

classification, more aggregated than the NACE 3 digit is used, unless

otherwise stated. Figure 1 shows the foreign penetration in terms of

sales and numbers for each of these industries. The operations of

firms within industries are used as unit of analysis.

Insert Figure 1 here

The industry in which the non-EC presence is particularly pervasive

is computer and office equipment where they take up 54% of total

matrix sales. With only 16% of total matrix entries, non-EC

activities are substantially larger than the EC activities within

this industry.

Other industries in which non-EC companies hold an above average

share in industry sales are tobacco (34%), soap & cosmetics (31%),

scientific and photographic equipment (28%), toys and sporting goods

(27%), food (20%), motor vehicles (19%) and industrial & farm

equipment (18%). In all these industries, non-EC operations are

larger in size than the EC operations active in these industries, as

a comparison with their share in entries reveals. With the exeption

of the tobacco, motor vehicles and soap & cosmetics industry, all of

these industries are characterized by a below average average size

Industries in which non-EC companies hold a negligible share are

iron & steel (5%) non-metallic mineral products (3%), metal products

(7%), other transportation equipment (2%), aerospace (1%), textiles

(4.5%), apparel (1%) and wood (0.5%). Also in electrics and

electronics, non-EC firms hold a modest 8%, in telecommunications

7

this is only 4%. With the exeption of iron & steel and aerospace,

these are again all industries that are smaller in average size than

on average.

Before relating the industry distribution of non-EC presence to

industry characteristics as well as host and horne countries

competitive advantages, a profile of non-EC companies relative to

their EC counterparts across all industries is sketched .

2 .3. Differential characteristics of non-EC firms

If only because of different strategic avenues out of different

competitive capabilities, foreign companies are often characterized

as constituting a different strategic group within an industry. This

section will study to which extent foreign companies differ in terms

of diversification, scale, size distribution and concentration. The

implications of any differences for European industry are indicated.

(i) Diversification

On the basis of their sales realized in different industries (as

defined on the NACE 3 digit level), non-EC companies are less

diversified than their EC counterparts . The reciprocal of the Berry

index for non-EC companies, RNEC• is higher than the equivalent for

the EC companies .

8

Table 3

+

.503 .480 .85

with RNEc= ~ Ri * Si/SNEC i€NEC

REc= ~ Ri * Si/SEc i€EC

.636 .15

with Ri = ~sij 2;si2 j

However, a more crude measure of diversification, i.e. the average

number of matrix entries per company for which the non-EC and the EC

firms account for, reveals the opposite tendency. Non-Ec companies

have more activities in various NACE3 sectors than their EC

companies.

Table 4

+

4.69 4.67 .85 4.82 .15

AE=average number of matrix entries

The intangible assets given rise to multinational operations nurture

at the same time diversification strategies. The drive for economies

of scope can be organised along geographical as well product avenues,

where both alternatives are not necessarily exclusive . As such ,

multinationals firms are more likely to be diversified. The

diversification strategy of a subsidiary however is determined by the

parent company which considers each subsidiary within its global

sourcing system. When these activities are mere screw drivers for

products imported from within the company, the diversified activities

of affiliates within a global network can be of smaller size,

reconciling tables 3 and 4.

The columnwise information provided by the matrix allows to

assess the influence of differences in diversification strategies on

9

the share of foreign involvement within industries. Whereas

traditional information on foreign involvement ignores

diversification strategies, the matrix allows to establish the true

share of foreign involvement, taking into account diversification.

To check to which extent this diversification influences the pattern

of foreign involvement, the traditional approach was performed for

the non-EC and EC companies, classifying their total sales in the

industry in which their largest sales are based. Before comparing

the "classical" penetration figures·with the matrix approach, the

diversification strategies of non-EC companies are discussed.

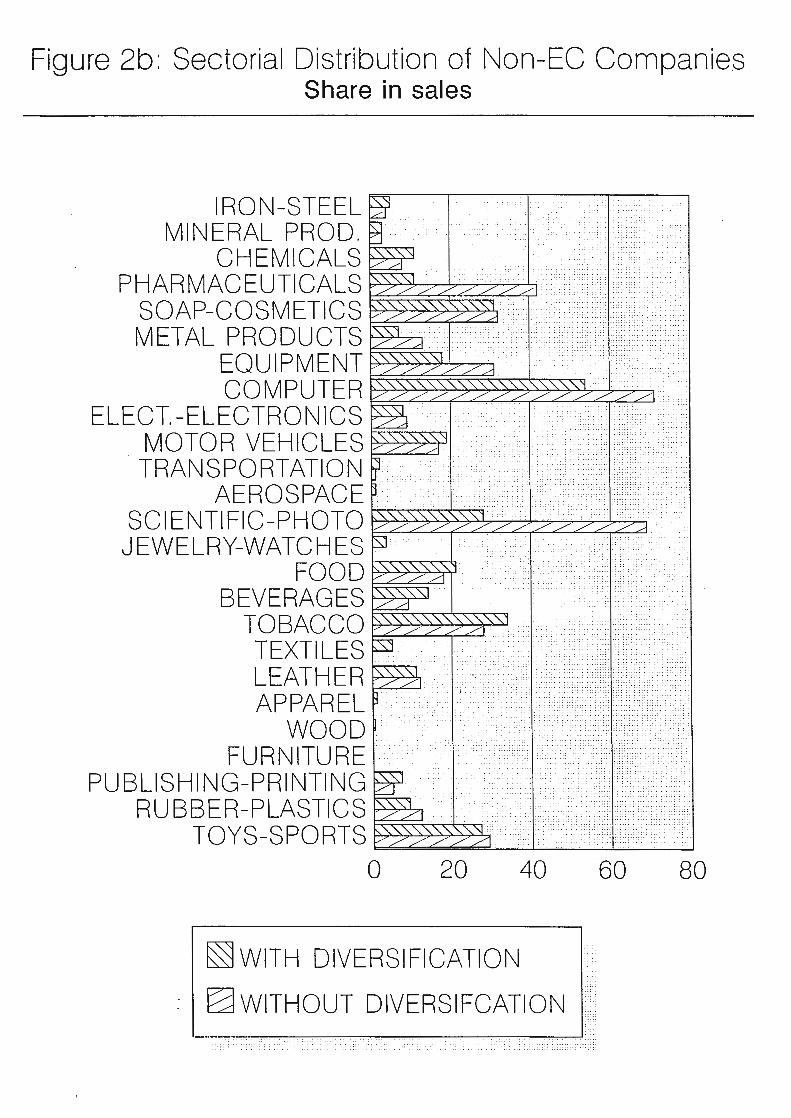

Figure 2a details the comparison between this traditional and

the matrix approach, plotting the ratio of non-EC industry sales when

total firm sales are classified to the major industry to non-EC

industry sales on the basis of the matrix. A value larger (smaller)

than 1 implies that ignoring diversification under(over-)estimates

the size of non-EC sales within this industry, reflecting an industry

where inward (outward) diversification is most pervasive.

Insert figure 2a here

In industries like chemicals (1.10), metal products (1.27),

industrial equipment (1.17), beverages (1.19), publishing and

printing (1.32), rubber & plastics (1.10) and toys and sporting goods

(1.12) taking into account diversification strategies substantially

increases non-EC sales in these industries, reflecting that there is

considerable inward diversification from non-EC companies based in

other industries. On the other side of the spectrum, iron & steel

(.83), pharmaceuticals (.62), electronics (.84), scientific &

photographic equipment (.74) are industries where taking into account

10

diversification lowers non-EC sales. All these industries can hence

be characterized by important outward diversification flows by non-EC

companies.

For a number of industries, foreign sales in Europe are only

composed of sales by MNES that have their major activity in other

industries. The list includes aerospace, jewelry and watches,

textiles, apparel, wood and furniture.

The impact of diversification on foreign involvement involves a

comparison of diversification strategies of EC versus non-EC

companies. Figure 2b presents the foreign share in total matrix

sales when diversification is ignored. For easy comparison, the

matrix penetration figure is plotted as well.

Insert figure 2b here

The "classical" approach, ignoring diversification overestimates the

foreign presence in industries like pharmaceuticals, metal products,

industrial and farm equipment, computers and scientific equipment.

In pharmaceuticals, scientific equipment and to a lesser extent

computer, this overestimation is due to the more intense outward

diversifying activities of non-EC companies relative to their EC

partners. As figure 2a revealed, non-EC companies display an inward

diversification policy in metal products and equipment, but this

inward diversification is less intensive than the EC inward

diversification, resulting in the overestimation of non-EC presence

despite inward diversification.

In industries like drink, tobacco, textiles and jewelry &

watches, and to a lesser extent in chemicals, food and motor

vehicles, the classical approach underestimates the "true" foreign

11

presence. A more intense inward diversification pattern from non-EC

companies explains this underestimation in drink, food, chemicals,

jewelry & watches and textiles. In tobacco and motor vehicles, this

underestimation is due to the less intense outward diversifying

activities of non-EC companies as compared to their EC counterparts.

In a number of industries the diversification patterns are not

pervasiness or different enough to yield a significant impact on the

non-EC penetration. In soaps & cosmetics, EC and non-EC companies

display modest inward diversification activities, whereas electrics &

electronics witnesses an equally intensive outward diversification

for EC and non-EC companies.

(ii) Average divisional size

As already indicated supra, non-EC firms and operations are on

average larger in size than EC firms and operations. The following

table details the average division size. With their 15% share in

sales, non-EC multinationals contribute 19% to total average size,

which indeed reflects their larger average division size.

AS TOT

417.9

Table 5

401.5 . 85 81%

549.2 .15 19%

The following decomposition exercise allows to trace the difference

in average division size between EC and non-EC companies into a

proportional effect - the difference in average size due to sector

composition- and a differential effect -the difference in average

size within industries.

12

13

i i

lh S NEG S EC

(ASiNEC - ASEci) ASNEC - ASEC 2:: (---- - + -----) i SNEC SEC

differential effect

+

i i

lh S NEG S EC

(ASiNEC ASEci) 2:: (--- - - ------) + i SNEC SEC

proportional effect

AS= average size (sales/entries) S= sales i= industry

The following results were obtained:

Table 6

Diff + Prop

549.2 401.5 147.7 61.8 85 . 9

Non-EC operations are on average larger than EC operations both

because they are more present in large scale sectors (prop>O) as well

as because they are within sectors larger than their EC counterparts

(diff>O). All this is not surprising. The intangible asset

advantage on which MNEs are building their international expansion,

makes them less sensitive to the classical barriers to entry that

characterize large scale sectors, explaining the proportional effect.

The differential effect can be explained by the fact that, given the

alternatives of exports when MOS plants are not (yet) feasible, MNEs

do not have to operate with below MOS plants when targetting the EC

market. In addition, foreign companies may easier decide to

disinvest when sales no l onger guarentee MOS operations and may be

more able to expand production capacity out of their advantages.

The decomposition reveals that the proportional effect is more

important in explaining the differences in scale than the

differential effect, which implies that after correcting for sectoral

distribution, EC companies are less at a disadvantage in terms of

scale relative to non-EC companies.

(iii) Size distribution and Concentration

A much debated issue is the relation between foreign companies and

concentration in the host economy. The often empirically documented

positive correlation between the two phenomena is not surprising.

Again the intangible assets given rise to multinational operations,

are at the same time typical barriers to entry establishing high

concentration within the industry. However, this positive

correlation does not help to disentangle the causal relationship in a

dynamic setting: does high concentration attract foreign companies

(see strategic incentives to become MNE) or do multinationals, out of

their specific advantages, increase concentration. This causal

issue, which is clearly important to asses the impact of foreign

presence on the EC industry structure, cannot be pursued here given a

lack of dynamic data. Having to restrict the focus on a static

setting, and in order to avoid the simultaneity issue that typically

creeps up in static analysis, a direct way to measure the

contribution of affiliates of non-EC companies to industrial

concentration in the EC is attempted. Three concentration measures

are studied: the entropy, the relative entropy and the Herfindahl

index, to capture various aspect of the concentration phenomenon,

i.e. inequality in size, number of firms and market shares.

14

All of these measure will be disaggregated into a non-EC and EC

component . Again the unit of analysis is the division.

E

5 . 104

Table 7: The Entropy Decomposition

ENEC * MNEC + EEC * MEG Ew

3 . 19 . 15 4.94 .85 4.678

+ logl/MNEC*MNEC + logl/MEc*MEc EB

. 285 . 138 . 422

Table 8 : The Relative Entropy Decomposition

15

R R R R E = E NEG * MNEc*logNNEc/logN + E EC * MEc*logNEc/logN + E B * log2/logN ERw ERB

.85 . 84 .095 . 84 .83 . 61 . 115 . 777 .07

Non-EC firms have a lower entropy measure than EC firms . This could

be due to more inequality of sizes or simply becuase there are fewer

non- EC firms in the matrix. The relative entropy figures reveal that

it is indeed the latter case that prevails . The equal relative

entropy figures for both groups indicates that there is no

distinction in size distribution within both groups.

The low between-entropy figure might reflect an important

inequality in size between both groups, as also suggested by the

previous analysis. After correcting for the number of groups , the

relative between-entropy indeed remains lower than the within- group-

entropy. The high relative entropy, indicating low inequalities in

size in European industry, reflects mainly the low inequalities

within the non-EC and EC companies and prevails despite the larger

inequality in size between both groups .

A second measure of concentration is the Herfindahl index that

can similarly be decomposed in different subsegments. The

contribution of non-EC firms to the total concentration within the EC

is considerable, despite their small share in sales. This large

contribution is due to the higher level of the H-index within the

non-EC groups as compared to the EC group. But nevertheless the low

index numbers in all categories reveal low concentration.

Table 9: The Herfindahl decomposition

H

.021 .013 .85 53%

. 065 .15 47%

Whereas this exercise gives an overall picture of the contribution on

non-EC firms to total EC concentration, such an analysis should

clearly be supplemented with a similar exercise at the industry

level. Given the limited number of non-EC companies in the sample,

such an attempt is not pursued here.

2.3. A characterization of non-EC intensive industries

The foreign presence and penetration within European industries can

be typified through characteristics of these industries that favor

multinational production. Whereas this section concentrates on

industry characteristics in general and within the EC, the next

section will include industry specific horne market characteristics to

explain the industry distribution.

Although industry characteristics that can explain the intensity

of multinational operations should be considered simultaneously in

explaining the industry distribution of non-EC sales in the matrix,

such an attempt will not be made here given the limited size of the

16

sample. Attention is restricted to a one-by-one analysis of these

characteristics.

As already frequently pointed out, intangible assets, such as

(technological) know-how and/or brandname give rise to the MNE

phenomenon. Hence, MNEs are often characterised by high R&D,

advertising or phyical capital in which these assets are embodied.

As such industries, intensive in these intangible assets are

projected to have more multinational companies. As table 10 points

out, R&D and ADV intensive industries witness a deeper penetration of

foreign companies, in sales as well as in number of companies.

Physical capital that gives rise to scale economies exploitable

through other means of foreign operations does not create more

intensive foreign presence.

Besides of exploiting advantages on the basis of intangible

assets, strategic motives may equally drive the international

expansion of MNEs. Follow-.the-leader, preemption, footholds in

rivals'home markets are all examples of strategic incentives for

multinational operations. Mutual forbearance on the other hand is a

strategic motive that restricts international operations. These

strategic incentives are more likely to prevail in industries where

concentration on a global scale is high. Table 10 confirms that

indeed in these industries, non-EC presence is higher in sales. The

presence of important EC rivals on whose ownership specific

advantanges foreign firms may want to tap or in whose home markets

foreign firms may want to establish a foothold, seems to restrict

foreign penetration, which might reflect a.o . mutual forbearance.

'1992', as measured by the vulnerability index, is too recent a

phenomenon to explain the presence of non-EC companies in the matrix .

17

Irrespective of intangible assets or strategic considerations, a

physical presence in the market may be necessary to serve this

market. Government intervention may be one such reason . Industries

in which procurement , regulation or other non-tariff barriers prevail

are indeed more intensively penetrated by non-EC affiliates .

Transportation costs need to be considered in conjunction with other

industry characteristics before its positive impact on foreign

penetration will prevail.

Companies wanting to serve foreign markets may have other

alternatives available besides direct investment . Simple exports

allow foreign sales without considerable investment in the host

economy. Alliances with local companies may be another mode of

foreign operations that allows to tap on the specific advantages of

local partners and generates access to local distribution networks.

Industries in which exports are a viable foreign sales strategy as

reflected by the total trade flows that occur within these

industries, are less penetrated by foreign affiliates. More

specifically, industries in which there is an intense trade flow

between EC and non-EC countries are less characterized by the

presence of non-EC companies . Alliance intensive industries are

typically more inhabited by multinat i onal companies , a difference

that is even significant in terms of number of companies, indicating

that alliances complement rather than substitute multinational

operations. When concentrating on industries characterized by

important a l liances between EC and non- EC companies as a direct

alternative for non- EC affiliates , non- EC companies have a larger

share in terms of entries but not in terms of sales, in which a

substitute character seems to prevail.

18

Table 10

Non-Ec share in sales numbers

in HIGH/LOW in HIGH/LOW /1 HIGH sectors sectors

INTANGIBLE ASSET INTENSIVE

R&D 11 15.0 11 . 9 13.6 10.0 Advertising 13 17.8 8.4 13 . 6 9.0 Physical capital 12 10.4 15 . 8 10.9 11.9

STRATEGIC

Global concentration 22 14.1 6.4 11.5 10.7 Strong EC Rivals 8 11.6 14.0 11.2 11.5 1992 12 12.8 13.6 10.8 11.9

LOCAL PRESENCE REQUIRED

Procurement/regulation 7 16.9 11.8 12.7 10.9 Non-tariff barriers 16 14.5 11.0 12.2 10.0 Transportation costs 12 11.4 14.9 10.8 11.9

ALTERNATIVES FOR FOREIGN OPERATIONS

Trade General 16 12.7 14.2 11 . 0 12.1 EC-nonEc 13 12.6 13 . 9 10.2 12.7

Alliances General 21 14.6 6 . 0 12.4 6.0 EC-nonEc 13 12.8 15 . 6 13.3 10.5

Note: All of the industry characteristics are represented by dummies for either high (above average) or low(below average). Source: Lyons & Davies (1992) except Global Concentration, Strong EC Rivals and Alliances (Veugelers (1992)) Note: In bold are the signficantly different means (a=.05). The limited number of sectors in the sample (25), prohibits in most cases the reaching of adequate levels of statistical significant differences.

The following figure details for each industry in which foreign

companies are intensively engaged in (i.e. non-EC share above

average) which of the aforementioned industry characteristics prevail

in explaining this foreign penetration.

Insert figure 3 here

19

All of the non-EC intensive industries are characterized by high or

medium R&D intensive technologies, with the exeption of soap &

cosmetics, food, tobacco and toys & sporting goods. The MNEs present

in these industries build more on brandname as intangible asset as

reflected by their high advertising intensity.

Given that for all of these industries (exept chemicals) the

concentration on a world scale is medium to high (i.e. C4>.3)

strategic incentives cannot be ignored. Strategic considerations

vis-A-vis EC rivals are more likely in chemicals, machinery,

automobiles, food and rubber & plastics in which the EC global

companies hold a comparative advantage, cf. infra.

Only in pharmaceuticals, computers, electrical and electronic

equipment, exogeneous factors like government regulation, procurement

and other tariff barriers are pervasive enough to contribute to

explaining the non-EC affiliative presence.

Trade is no viable alternative for non-EC companies looking

towards the EC market in industries like pharmacuticals, soap &

cosmetics, food, tobacco and rubber & plastics. Only in

pharmaceuticals government intervention can be pinpointed as cause

for this low export orientedness. In all other industries, local

presence is more driven by the need for customer responsiveness.

The lack of alliances with EC companies as alternative to get

access to European markets may explain why in industries like soap &

cosmetics, computers, food and toys & sporting goods more affiliative

presence can be indicated.

For the industries in which non-EC penetration is negligeable, i.e.

below average, the same exercise can be performed to analyse the

reasons for this non-presence.

20

Insert figure 4 here

With the exeption of transportation equipment, aerospace and watches,

all of these industries score low in R&D intensity. Brandnarne as

possible source of intangible asset is only pervasive in watches and

drink and medium in apparel, furniture and printing & publishing.

The reason why there is so little non-EC presence in these industries

despite the presence of intangible assets can be related to presence

of trade as a viable substitute for transportation equipment,

aeropsace, watches, and (to a lesser degree) apparel . Alliances

between EC and non-EC companies are actively being used, possibly as

alternative to local production, in drink, furniture and printing &

publishing. Also a lack of comparative advantage from large EC

companies prevails in all of these industries, except in printing &

publishing.

2.4. Foreign presence and host and home market comparative advantages

Countries that on the basis of entrepreneurial advantages related to

technological knowhow or brandnarne, have build a strong competitive

position in an industry, are more likely to be a home country to

multinational corporations. Likewise, does the competitive position

of the host market have an influence on multinational activities.

When the horne market's competitive position originates from

locational advantages, this attracts foreign companies.

Entrepreneurial advantages may stimulate, through expected

spillovers, or distract, through mutual forbearance, foreign

penetration.

21

A profile of comparative advantages of the major home markets as

well as the EC host market is therefore needed to further explain the

industry distribution on non-EC multinationals. Such a profile is

also important when assessing the positive or negative impact of non-

EC firms on the EC economy. The EC economy stands to gain more when

foreign companies originate from strong countries, whereas if strong

EC companies prevail within an industry, foreign presence tapping on

this advantage may endager the EC's competitive position, unless such

competitive position is built through the presence of non-EC

companies .

The following tables relate the foreign penetration per industry

(on the basis of sales) to the comparative advantages of the various

home markets as well as the host market. The comparative advantage

of the home market is on the basis of share of sales by its companies

in total world sales (source: Fortune). The comparative advantage of

the European industry is on the basis of share in global sales as

well as share in exports, to disentangle resp entrepreneurial versus

locational advantages. The US which is the main home market to non-

EC companies is tackled first.

Gji/Gi GRCAj i= - - - - - -

Gj/G

Ej·/E· . ~ ~

ERCAJi= --:---EJ/E

sj i/Si FPji=

sj ;s

j=country (USA, EFTA, EC) i=industry G=Global sales (Source:Fortune) E=Exports (Source: OECD), 1991 S=Matrix sales, 1987

22

LOW MNE PRESENCE DESPITE COMPETITIVE ADVANTAGE

PHARMACEUTICALS Aerospace Wood

FOOD DRINK Apparel Furniture

FPUS·<l l.

Table 11

GRCAUS·>l l.

STRONG MNE PRESENCE ON BASIS COMPETITIVE ADVANTAGE

SOAP & COSMETICS Computers Scientific & Photograp Equipment Tobacco

FPUS·>l l.

~----------------------------------·--------------------------------~

LOW MNE PRESENCE BECAUSE NO COMPETITIVE ADVANTAGE

CHEMICALS MACHINERY Electrics & Electronics Jewelry & Watches

IRON & STEEL MINERALS METALS TEXTILES LEATHER Wood RUBBER & PLASTICS

STRONG MNE PRESENCE DESPITE NO COMPETITIVE ADVANTAGE

AUTOMOBILES

GRCAUS ·<l l.

Note: Industries are indicated in bold when GRCAEC>l and in capital when ERCAEC>l .

US companies hold a strong position in EC-industries like soap &

cosmetics, computers, scientific & photographic equipment and tobacco,

built on their strong competitive position . In all of these industries,

the EC has no global entrepreneurial advantage and only in soap &

23

cosmetics has the EC a revealed comparative advantage in exports,

reflecting locational advantages.

24

Automobiles is a sector in which the US holds an above average share

despite the current lack of a global competitive advantage (Note however

GRCAUSA=.93). However most of the US companies have been established

since decades when the US still enjoyed a dominant position in this

industry. The EC capitalizes on a strong competitive position in this

industry in terms of global sales as well as exports. The long

established US companies, like Ford and General Motors, certainly have

contributed to this competitive position, while currently trying to

rebuild their comparative advantage using a.o. the EC entrepreneurial and

locational advantages.

In a number of industries, the US holds a strong global comparative

advantage, which is however not reflected in a strong foreign presence

within the EC. The presence of alternative strategies, like exports or

alliances, as well as host market characteristics are called for to

explain this low presence. In pharmaceuticals, aerospace and wood,

companies exploit their global comparative advantages through exports and

alliances for these industries. For food, drink, apparel and furniture,

neither exports nor alliances are intensively being used. The fact the

the EC market offers no entrepreneurial nor locational advantages on which

to tap may contribute to the low US penetration in industries like wood,

apparel and furniture, whereas the locational advantages that the EC

offers in pharmaceuticals and drink are not strong enough to compensate

for the lack of entrepreneurial advantages. In food, the strong

comparative advantage of the EC in terms of global production as well as

exports may create mutual forbearance type of arguments for a rawboned EC

presence.

The second most important home economy is the EFTA (i.e. Sweden

and Switzerland). Whereas the analysis should ideally be on the

level of each country separately, both countries are grouped together

in a rest category, which may contaminate the results once in a

while.

LOW MNE PRESENCE DESPITE COMPETITIVE ADVANTAGE

MINERALS METAL PRODUCTS Wood

Other transport

FPEFTA·<l ~

Table 12

GRCAEFTA·>l ~

STRONG MNE PRESENCE ON BASIS COMPETITIVE ADVANTAGE

PHARMACEUTICALS MACHINERY

Elec&Electronics Food

FPEFTA·>l ~

~----------------------------------·--------------------------------~

LOW MNE PRESENCE BECAUSE NO COMPETITIVE ADVANTAGE

IRON & STEEL CHEMICALS SOAP & COSMETICS Scientif & Photographic Equip Jewelry & Watches FURNITURE

Computers AUTOMOBILES Aerospace Tobacco LEATHER Apparel RUBBER & PLASTICS

STRONG MNE PRESENCE DESPITE NO COMPETITIVE ADVANTAGE

GRCAEFTA;<l

Note: Industries are indicated in bold when GRCAEC>l and in capital when ERCAEC>l.

25

Building on a strong competitive position, EFTA companies are

overrepresented in industries like pharmaceuticals, machinery,

electrical & electronic equipment and food. The EFTA presence in

pharmaceuticals may explain the superior export performance of this

industry in Europe despite the lack of global comparative advantage

from EC companies .

The industries in which the EFTA holds a competitive advantage

but lacks sales by affiliates within the EC are minerals, metal

products, wood and other transportation equipment . The low

locational advantages of the EC within wood and other transportation

equipment may contribute to this low presence. In minerals, EFTA

companies may be refrained from establishing within the EC to tap on

locational advantages by the presence of strong EC rivals. In metal

products, EFTA companies are more intensily engaged in exports and

alliances as alternative modes to tap locational advantages.

The Japanese presence in the EC matrix is too small to be

subject to thorough analysis. A quick overview of the sectors in

which Japanese companies are present, mineral products (glass),

machinery, automobiles and other transportation equipment, reveals

that only in machinery and automobiles the Japanese have a

comparative advantage -on the basis of share in global production as

well as exports- but that more importantly in all of these

industries, the EC has a comparative advantage on the basis of share

in global production as well as exports, indicating that an apparent

motive for Japanese foreign presence is to tap on specific advantages

of the host market, locational - as well as entrepreneurial

advantages.

26

CONCLUSIONS

The presence of leading non-EC companies within the EC is a

phenomenon that is restricted in numbers and size, although these

companies, mostly from US origin, are larger in terms of average

company and divisional size, mostly due to their presence in large

scale sectors. These non-EC companies display more activities, but

this diversification is of smaller average size. In industries like

pharmaceuticals, industrial equipment , computers, scientific

equipment, a differential diversification strategy of non-EC

companies versus their EC counterpart, results in a upwardly biased

presentation of the foreign penetration if diversification would be

ignored.

Despite their limited presence on average within the EC, non-EC

companies can be pervasive within specific industries, notably in

computer & office equipment, food & tobacco, soap & cosmetics,

scientific & photographic equipment, toys and sporting goods . All of

these industries display an intangible asset intensity but also

global competitive considerations and in a few instances government

intervention may drive this foreign penetration . Where non-EC

presence is pervasive in industries where the home country enjoys a

comparative advantage but where the EC scores mostly low on

entrepreneurial as well as locational advantages, the EC is likely to

win from this foreign presence. In a number of other instances, this

beneficial impact may be less obvious. The presence of strong EC

rivals may attract their non- EC rivals, establishing footholds in

industries like machinery, food and automobiles. But a full

assessment of the impact of foreign affiliates on the comparative

27

advantage profiles of the EC awaits a longitudinal study of both

variables .

28

APPENDIX: METHODOLOGY OF DATA COLLECTION

This appendix provides a methodological explanation of a unique new

micro data source, the EC market share matrix. For each NACE

industry (the EC industry classification scheme) at the 3 digit level

of aggregation, the 5 leaders are identified from information on

company reports, business and trade directories, industry case

studies and other sources. The data collection exercise is confined

to manufacturing industries only (NACE 2-4) where 1987 is the only

chosen year. The first figure located is the company's worldwide

sales by origin (production in ECU million) in 1987. Wherever

possible, sales by both destination and sales by origin were

collected. Intra-company sales are noted but not netted out.

Secondly, the geographical breakdown of the production of each firm

is recorded from the company reports. Thirdly, the company reports

are again used to assess the product breakdown, i.e. the range of

products manufactured by each firm on the basis of which production

figures are allocated to NACE codes. Forthly, ownership is checked

in each case in the company report. If the parentage remained

unclear "Who owns whom" is consulted. In those cases where a firm

has foreign parentage, the country of origin is recorded.

Subsidiaries are consolidated where there are consolidated accounts

or where the firm holds 50% or more of equity. Associate companies

with less then 50% held, are also consolidated if there is evidence

of control by a minority shareholding. The end result is a market

share matrix, where the rows represents firms, in total 315, and the

columns are all Nace 3 digit industries (NACE 2-4). Each entry ij in

the matrix represents firm i's production in industry j ..

29

The market share matrix is a unique database in the following

respects:

1. The matrix is confined to the 'leading' firms where 'leading'

means that the firms should be one of the 5 largest producers within

a NACE 3-digit manufacturing industry.

2. Since many market leaders are diversified across industries, we

collected information on their market shares in all the industries in

which they operate, not just in those where they are leading.

3 . At the aggregate level, virtually all EC firms of any significiant

size will have been included because the vast majority of the big

firms will be in a leading position in at least one of the industries

in which they operate. The matrix also includes a number of quite

small firms who have qualified as either a 'leader' of a small

industry or as one of the smallest 'leaders'. A weakness of the

market share matrix is that it will have excluded numerous middle

sized firms, who although they may be diversified, do not quite

attain a leading position in any industry. It may also have excluded

the occasional large firm who comes 6th or 7th in a large scale

industry.

30

Figure 1 : Sectorial Distribution of Non-EC Companies

IRON-STEEL MINERAL PROD.

CHEMICALS~~ PHARMACEUTICALS~~ SOAP-COSMETICS~~~~ METAL PRODUCTS~

EQUIPMENT~~~ COMPUTER~~~~~~~~

ELECT.-ELECTRONICS ~...........,. MOTOR VEHICLES~~,........ TRANSPORTATION

AEROSPACE~ SCIENTIFIC-PHOTO~~~~·

JEWELRY-WATCHES FOOD~~~

8 EVERAGE S ;;;;;;c:_::~~~ TOBACCO ~~~~..>......>.J TEXTILES LEATHER~~·

APPAREL WOOD

FURNITURE PUBLISHING-PRINTING~···

RUBBER-PLASTICS ~::7'--, TOYS-SPORTS~~~~·

AVERAGE SHARE~~ ~~~~~~~~~

0 1 0 20 30 40 50 60

~SHARE IN SALES EJ SHARE IN ENTRIES "' ~~--------------------------~~

Figure 2 : With or Without Diversification

IRON-STEEL ·

MINERAL PROD. ·

CHEMICALS ~~~~~

PHARMACEUTICALS .~~~~

SOAP-COSMETICS

METAL PRODUCTS

EQUIPMENT

COMPUTER

ELECT.-ELECTRONICS

MOTOR VEHICLES

TRANSPORTATION

SCIENTIFIC-PHOTO •·•

FOOD

BEVERAGES .·

TOBACCO

LEATHER ··••

PUBLISHING-PRINTING

RUBBER-PLASTICS

TOYS-SPORTS

~ 1 - RATIO ~ RATIO

~~--------------~~

Figure 2b: Sectorial Distribution of Non-EC Companies Share in sales

IRON-STEEL MINERAL PROD.

CHEMICALS~ PHARMACEUTICALS~~~~

SOAP-COSMETICS ·'" '''''''"'""''' METAL PRODUCTS~

EQUIPMENT~~~· COMPUTER~~~~~~~~

ELECT.-ELECTRONICS MOTOR VEHICLES~~ TRANSPORTATION

AEROSPACE SCIENTIFIC-PHOTO~~~~~~~~~~ JEWELRY-WATCHES

FOOD~~

BEVERAGES~~ TOBACCO ~~~"" TEXTILES LEATHER~ APPAREL

wooD .·• FURNITURE ·.

PUBLISHING-PRINTING RUBBER-PLASTICS~*~~

TOYS-SPORTS ~~;:::;::;::;::~·~~~~....;,;;.J 0 20 40 60 80

~WITH DIVERSIFICATION

~WITHOUT DIVERSIFCATION

INTANGIBLE ASSET INTENSIVE

R&D

ADV

STRATEGIC

GLOBAL CONCENTRATION

STRONG EC RIVALS

Figure 3

CHEMICALS ' 1\

PHARMACEUTICALS

SOAP & COSMETICS

MACHINERY

COMPUTERS

ELEC. & ELECTRONICS

AUTOMOBILES

SCIENT. PHOTO EQUIP.

FOOD

TOBACCO

RUBBER & PLASTICS I

TOYS & SPORT GOODS e

LOCAL PRESENCE REQUIRED

PROCUREMENT REGULATIONS

NON TARIFF BARRIERS

TRADEABILITY EC-NON EC

ALLIANCES EC-NON EC

INTANGIBLE ASSET INTENSIVE

Figure 4

IRON- STEEL

LOCAL PRESENCE REQUIRED

MINERALS R&D

"~' ' ...... ...... ' ......

' I

It• METAL PRODUCTS

' I

' ~~ -e TRANSPORTATION EQ. ",I? '

AEROSPACE . .\ t"JL \ """"" '

ADV JEWELRY & WATCHES~ ,, \ //1 I

Ill DRINK \ ' II I

STRATEGIC \\ ' 111 /

\\ /1.1 / • TEXTILES \\Ill . '

WI

'J ' . LEATHER GLOBAL .///', ' -/~rv~~· ' CONCENTRATION , '' • APPAREL

~- !_ \ \/

\ \ \

\ \

\ \ \ . WOOD \ \

\ \ \ FURNITURE \\ .

STRONG EC RIVALS e ,, ~\' ,, -

- PRINT & PUBLISHING • - -j--

PROCUREMENT REGULATIONS

NON TARIFF BARRIERS

TRADEABILITY EC-NON EC

ALLIANCES

EC-NON EC