The New York Cotton Exchange and the Development of the Cotton Futures Market

24

The President and Fellows of Harvard College The New York Cotton Exchange and the Development of the Cotton Futures Market Author(s): Kenneth J. Lipartito Source: The Business History Review, Vol. 57, No. 1 (Spring, 1983), pp. 50-72 Published by: The President and Fellows of Harvard College Stable URL: http://www.jstor.org/stable/3114394 . Accessed: 13/06/2011 12:44 Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at . http://www.jstor.org/action/showPublisher?publisherCode=pfhc. . Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. The President and Fellows of Harvard College is collaborating with JSTOR to digitize, preserve and extend access to The Business History Review. http://www.jstor.org

Transcript of The New York Cotton Exchange and the Development of the Cotton Futures Market

The President and Fellows of Harvard College

The New York Cotton Exchange and the Development of the Cotton Futures MarketAuthor(s): Kenneth J. LipartitoSource: The Business History Review, Vol. 57, No. 1 (Spring, 1983), pp. 50-72Published by: The President and Fellows of Harvard CollegeStable URL: http://www.jstor.org/stable/3114394 .Accessed: 13/06/2011 12:44

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unlessyou have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and youmay use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at .http://www.jstor.org/action/showPublisher?publisherCode=pfhc. .

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printedpage of such transmission.

JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

The President and Fellows of Harvard College is collaborating with JSTOR to digitize, preserve and extendaccess to The Business History Review.

http://www.jstor.org

By Kenneth J. Lipartito DOCTORAL CANDIDATE

THE JOHNS HOPKINS UNIVERSITY

The New York Cotton Exchange and the Development of the Cotton Futures Market

?The development of a national market was one of the key features of the

nineteenth-century economy. In this process, innumerable institutions played a role, some large and well-known, others neither so large, nor quite so well- known, at least to the public at large. One such organization was the New York Cotton Exchange. It evolved in the aftermath of the Civil War, and over the years grew from an informal, even ad hoc organization into a formalized institution that served both public and private functions. This article by Mr. Lipartito explores the development of the Exchange and its place in the shifting national market for cotton.

The large national market of the United States has played a crucial role in this nation's economic history. Its well-organized and bustling nature engendered capital formation and regional specialization, both essential for economic growth. Once in place, the national market encouraged the integration of production and distribution in a manner making for even greater efficiency, typical of corporate planning in modern economies. How such a market was created and organized remains unclear, however. Most economic historians who have studied the process have pointed to technology, and to innovations in transpor- tation and communication. But if the story could be told by economic forces alone, there would be little left to say after 1890. By then the canal era had passed, most of the nation's railroad track had been laid, and the

telegraph pole had become a permanent feature of the landscape. Yet even at that late date, the extension of the market was far from over. It continued to grow in the late nineteenth century and with it a variety of new institutions took shape.1

THE NEW YORK COTTON EXCHANGE

The place of economic organizations in this process has been long neglected. In the cotton market of the post-bellum South, for example,

Business History Review, Vol. LVII, No. 1 (Spring 1983). Copyright @ The President and Fellows of Harvard College.

1Stuart Bruchey, The Roots of American Economic Growth, (New York, 1965); Alfred D. Chandler Jr., The Visible Hand, (Cambridge, Mass., 1977); George Rogers Taylor, The Transportation Revolution, (New York, 1951).

50

cotton exchanges played a crucial role in market formation. One institu- tion in particular deserves note - the New York Cotton Exchange. Though just one of several cotton exchanges operating in the late nineteenth century, the New York Cotton Exchange was a leader in the development and refinement of cotton futures trading. In the cotton market no large production or distribution firms rose to play a leading role in market integration. Instead, it was the Cotton Exchange that

helped to clear pockets of localism, reduce high marketing costs, reform the South's archaic marketing system, and pave the way for the integra- tion of cotton production and distribution in the twentieth century.2

The Exchange effected these important changes through its control over cotton futures trading. For decades futures trading had been slowly evolving in the major commodity markets. In the antebellum South large New York commercial and financial houses used a form of futures or "too arrive" contracts to regulate the movement of the cotton crop. These

precursors of the modern futures contract protected the merchant by guaranteeing him a specified future price for specific quantities of cot- ton. In the volatile post-bellum years such protection became crucial. With prices fluctuating wildly due to unusual post-war conditions and with finance capital at a premium, southern merchants, shippers, and planters needed some way to shield themselves from undue speculative risk. The modern futures contract developed to fulfill this need. By the 1860s the firm of Leverich and Sons, established New York merchants and later members of the Cotton Exchange, was using a crude but effective form of futures contract to allow its correspondents in the South to hedge against risk. By doing so they lowered their marketing costs, and improved their financial stability and credit worthiness.3

After the war, hedging became crucial to all aspects ofcrop marketing. The old cotton factorage system of the South, which had collapsed with slavery's demise, was replaced by more specialized, functional market- ing. Smaller shippers and merchants (independent of the huge, diver- sified mercantile houses) relied on hedging to protect themselves from risk, thereby lowering the cost of marketing the South's crop. With prepacked, presold bales moving overland directly from farm to factory [see Table 1] mills and merchants were vulnerable to price fluctuations.

2Charles McCurdy, "American Law and the Marketing Structure of the Large Corporation," Journal of Economic History, 38 (September 1978), 631-650; Chandler, The Visible Hand, 224-35, 240-81.

3Stanley Dumbell, "The Origins of Cotton Futures," Economic History, 1 (May 1927), 259-67; Leverich and Sons, Wastebook, New York Historical Society, 1864-68 passim. The Leverich records in these years cite several innovative futures-type contracts. These years were unusual for the cotton trade, however; so it is difficult to generalize from these records. The attempts to use a futures-type contract to protect against price fluctuations does reveal the needs of the post-war cotton market and the attempts at an innovative response which were taking place. For those unfamiliar, hedging is the offsetting of risks. A cotton merchant would buy a futures contract if he had cotton to sell at a future date. Because the contract was for a set price, he would be protected against unexpected changes in the market. Thus if the price of cotton fell, his losses on his inventories would be offset by his gains in the futures market.

THE NEW YORK COTTON EXCHANGE 51

They needed futures contracts to manage the high risk of holding cotton inventories bought months in advance of their use.4

Similarly, in finance, the personal relations which had linked north- ern capital and southern agriculture were replaced by indirect market contacts such as the futures contract. Because safely hedged cotton was worth up to 90 percent of its value as collateral, even small merchants and shippers who used futures could secure credit. Banks began to depend less on word of mouth and more on the security implied in the hedge when they made loans. In this new financial system, futures contracts provided the security and insurance needed to move cotton in more efficient ways.5

But the proliferation of futures contracts created a need for a new type of organization, a formal futures market. To meet this need, the major New York cotton merchants incorporated the New York Cotton Ex- change in 1871. The founding of this institution had two important consequences. First, the Exchange (along with similar ones which evolved later in the South) ordered and regulated the trade in futures contracts. It established standards for the contract and rules for trading. It gradually eliminated the worst abuses of speculation. In doing so, the Exchange also instilled public confidence in the futures market. This helped to increase the volume of trading and make the futures contract an integral part of cotton marketing at all levels [see Table 2].6

Organization under institutions like the Cotton Exchange and the expanding volume of futures trading brought a second major change in the futures market. By the 1880s futures trading had evolved into a tool for organizing and rationalizing the cotton market itself. By buying and selling futures contracts in anticipation of market swings, speculators decreased otherwise violent price shifts and softened the disruptive effects of unforeseen changes. Moreover, sharp speculators kept markets joined across space. They traded in contracts in markets where prices were below or above normal, forcing them to approach the

4Harold Woodman, King Cotton and his Retainers: Financing and Marketing the Cotton Crop of the South, (Lexington, Ky., 1968), chapter 6; Chandler, The Visible Hand, 211-212; Woodman, King Cotton and his Retainers, 273-75; Julius Baer and George Woodruff, Commodity Exchanges, (New York, 1929), 83-122; United States House of Representatives, Report on the Internal Trade of the United States, (Washington, D.C., 1881). 46th Congress, 3rd session, 187. The telegraph and transcontinental cable linked Liverpool, New York, and New Orleans in a financial chain. Much hedging and futures trading was done on the Liverpool Exchange, since the majority of the United States' cotton crop was exported to Europe. In America, the New York Cotton Exchange became the center of domestic futures trading, though it initially borrowed some of the basic techniques from Great Britain. For more on the international side of the cotton futures trade, see Robert Bouilly, The Develop- ment of American Cotton Exchanges, 1870-1916, unpublished doctoral dissertation, (University of Missouri, 1975), 369-72.

5Chandler, The Visible Hand, 211-12; Rodger Ransome and Richard Sutch, One Kind of Freedom, (Cam- bridge, Mass., 1977), 106-125.

6Robert Bouilly notes that financial instability and disputes over margins may have been initial reasons for organizing the New York Cotton Exchange. See Bouilly, The Development of American Cotton Exchanges, 49. More generally, the institutionalization of futures trading was one more step in the long process of separating futures trading from the actual exchange of cotton. Under the Exchange the futures price became a readily identifiable entity, distinct from the spot price of cotton. It reflected guesses about future market conditions, not current market conditions, as the spot price did.

52 BUSINESS HISTORY REVIEW

TABLE 1 OVERLAND COTTON MOVEMENT (BALES) (000 OMITTED)

Year Gross number Direct (5 Year Intervals) of bales manufacturers

1874 378,813 237,572 1877 636,885 300,282 1882 1,134,788 477,480 1887 1,292,167 795,070 1892 1,800,480 1,199,694 1897 1,282,211 873,005 1902 1,675,040 1,186,985 1907 1,705,151 1,328,505 1912 1,931,416 1,528,263 1915 2,146,152 1,517,200

Source: Overland: 1874, 1877, Commercial and Financial Chronicle, Sept. 11, 1879, 271; 1882, 1887, 1892, 1897, Ibid., suppl. Sept. 7, 1899, 12; 1902, 1907, 1912, 1915, Ibid., August 25, 1917, 790.

Direct to Manufacturers: 1874, 1877, Dana, Cotton From Seed to Loom; 1882, 1887, 1892, Commer- cial and Financial Chronicle, Sept. 13, 1884, 281; Sept. 13, 1890, 323; Sept. 13, 1889, 458; 1902, 1907, 1912, 1915, Ibid., Sept. 6, 1902, suppl. 13.

TABLE 2 VOLUME OF FUTURES TRADING (BALES)

Year New York New Orleans Year New York New Orleans (000 omitted) (000 omitted) (000 omitted) (000 omitted)

1871-72 4,933 1883-84 24,334 9,588 1872-73 5,299 1884-85 20,058 8,037 1873-74 6,187 1885-86 22,683 7,475 1874-75 8,357 1886-87 26,186 11,227 1875-76 7,233 1887-88 24,759 9,049 1876-77 10,908 1888-89 19,155 6,570 1877-78 13,009 1889-90 21,107 6,782 1878-79 25,416 1890-91 24,433 8,555 1879-80 33,976 2,033 1891-92 34,359 12,131 1880-81 28,124 10,115 1892-93 53,273 16,516 1881-82 32,200 16,171 1893-94 37,858 12,570 1882-83 26,542 13,054 1894-95 39,368 14,723

1895-96 56,469 15,498 1896-97 34,066 9,273 1897-98 29,587 5,662

Source: New York, 1871-1894: United States Congress, Senate, Committee on Agriculture and Forestry, Conditions of Cotton Growers in the United States, Senate Report 986, 53rd Congress, 3rd session, 1895, pt. 2, 545. New York and New Orleans, 1895-98:Robert Bouilly, The Development of American Cotton Exchanges, unpublished doctoral dissertation, (University of Missouri, 1975) 556. According to Bouilly, no more figures are available on futures trading until 1918.

THE NEW YORK COTTON EXCHANGE 53

national average. By moderating the effects of changing conditions and linking remote markets, speculation in futures helped to impose worldwide supply and demand conditions on local markets, thus moving the entire cotton trade towards the ideal of a single market with a single, internationally determined price for each grade of cotton.7

METHODS OF THE EXCHANGE

The means the New York Cotton Exchange used to help achieve these results were unspectacular but effective. Initially intended to serve only its members, the Exchange had no legal authority to control or regulate the futures trade. Its original corporate charter merely authorized it to provide suitable space and accommodations for its members to use in trading. The charter also allowed the organization to adopt appropriate rules for smooth and efficient trading. The motives of the founders were simple self-interest. Organized trading in a single room under standard- ized rules was simpler and cheaper than trading on one's own. Moreover, the club-like atmosphere of the Exchange provided a secure, relaxed setting for picking up the latest gossip about the market. But these modest goals were soon turned into more ambitious objectives. In its attempt to fulfill these purely private aims the Exchange acquired powers which brought it into the public sphere as the unsanctioned but recognized regulator of futures trading.8

To understand how private intent produced public effects, we must look at some of the Exchange's early actions. Through its administrative body, the twelve-member Board of Managers, the Exchange provided such services as an arbitration panel to hear member disputes over contracts and a grading and inspecting system to classify cotton. The panel and the grading system both operated to prevent manipulation of member by member, but by establishing a system of fair dealing, they made speculation a reaction to and an anticipation of market conditions, not private schemes. If futures trading was to assist in the organization of the cotton market, then traders had to have accurate information and a secure atmosphere to make rational decisions. The early policies of the Board of Managers provided such an environment.

It might seem that in a free market such an institutional structure would be unnecessary. But organization was needed because, as already noted, rational decisions required accurate, unbiased information.

7 Baer and Woodruff, Commodity Exchanges, see chapters VII, XII; The numerous uses of futures trading are also discussed in Arthur Peterson, "Futures trading with Particular Reference to Agricultural Commodities," and S.S. Heubner, "The Functions of Produce Exchanges," The Annals of the American Academy of Political and Social Science, 38 (September 1911), 68: 319-353.

8New York Cotton Exchange, Charter bylaws and rules [hereinafter cited as NYBR] (New York, 1906), Act of Incorporation, sect. 3. (Reprint of original Charter of 1871). The role of such economic motivations is discussed in Lance Davis and Douglass North, Institutional Change in American Economic Development (New York, 1971).

54 BUSINESS HISTORY REVIEW

Speculation based on false rumors or deceptive contracts did little to bring markets together or provide merchants with safe hedges. Moreover, the futures market needed public approval. Not all shippers, spinners, and cotton factors recognized the value of futures trading, and more than a few of them considered it immoral, unfair, and manipula- tive. To be won over, they had to be convinced the practice took place in a fair and honest manner. The Exchange had to clean up futures trading to legitimize it and broaden the use of futures contracts. In doing so it made futures an even more useful tool in organizing the cotton market.

The process by which the Exchange legitimized the futures trade was guided by the organization's private intentions. All changes had to show private benefit before they could be accepted. This policy produced serious disagreements only when the general interests of the majority were at odds with the specific interests of a minority. The Board of Managers had to deal with this sort of conflict in the early years of the Exchange. All agreed the Exchange was intended for private benefit. But the members' private interests were varied and conflicting. The Board, however, saw itself as the spokesman for the general private interests. It believed that this view was in accord with the corporate spirit of the Exchange. In the end the Managers won out. By promoting the general member interest they were able to serve the needs of both their members and the cotton market.

Through leadership such as this, the Board of Mangers played a key role in setting the course of the Exchange. But its influence rested on rather limited powers granted to it in the original corporate charter. The Board had the authority to appoint committees to study problems as they arose, vote on changes in the bylaws, pass on recommendations for amendments, and make and enforce all regulations on futures trading. To back up its decrees, it could impose fines and suspend or expel recalcitrant members. Significantly, fines never exceeded $100 per year and usually averaged between $30 and $45. Moreover, members were rarely expelled unless they did something which "discredited" the Exchange or its members. The Board's credibility and its closeness to its membership seem to have been more important than penalties in maintaining order.9

The closeness which existed between members and managers miti- gated potential conflict within the Exchange and gave the managers the power to shape the development of the institution. Wisely, the mana- gers cultivated this intimacy by allowing members themselves to pre- sent petitions and grievances. They also encouraged participation in the rule-making process. In 1874, for example, the Board declared "that the

9The New York Cotton Exchange, Annual Reports, 1871-1914; NYBR, 1900, section 30, title III; Jonathan Lurie, The Chicago Board of Trade (Urbana, 1978), 31-35. Lurie tells a similar story for the Chicago Board of Trade.

THE NEW YORK COTTON EXCHANGE 55

members are generally invited to confer with the Committee on Bylaws and are requested to send in writing any changes they may desire." More importantly, a two-thirds majority of a quorum of the membership was required to pass any amendment to the bylaws. Access to the Exchange's legal machinery was open. Its administration was fluid; most managers did not serve for long stretches. All the evidence suggests an institution which saw itself as a servant of its members. 10

Nevertheless, the Board of Managers did not allow its intimacy with the membership to obscure its mission to serve the general interests of the Exchange and to promote "just and fair" trading practices. The Board also sought an authority apart from member goodwill to enable it to stand above individual interests. Beginning in 1872, the Board set out to acquire this power by taking command of the valuable property rights embodied in memberships.

In this effort the managers faced an uphill struggle. In 1874 John Elliot and Charles Ketchum obtained a New York State Supreme Court injunction against the Exchange's arbitration panel, preventing it from disposing of the memberships of failed members Samuel Weeks and John Valentine. Elliot and Ketchum contended that Weeks and Valen- tine had turned this property over to them before their bankruptcy and that, therefore, their claim superseded the Board's. In a rare display of swift, unified action, the Managers moved to expel Elliot and Ketchum for contesting a justly heard claim, and worse, for dragging the state into an in-house dispute. The Board thus affirmed its control over mem- bership property and took the bold step of severing its authority from the goodwill of the members. It strengthened its position in the ensuing years by passing a rule which called for public notice ten days in advance and a $100 fee for membership transfers.11

By gaining exclusive control over the right to create and sell mem- berships, the Board built for itself a base independent of member favor. It envisioned memberships as a form of collateral which could be re- tracted from or assigned against those who refused to pay fines, dis- obeyed rules, or defaulted in their dealings. It could act like a court in a bankruptcy case, selling off the memberships of failed traders. The Board's decisions in these matters were, after appeal, final. By achieving control of memberships in this way, the Board acquired a second source of authority to back up its decrees and shape Exchange policy - com- mand over real property.12

Having established an independent base of power, the Board sought further reforms in the futures trade. It passed rules which required that

10 New York Cotton Exchange, Minutes of the Board of Managers, [hereafter cited as BMM], 1874, 247-48; Lurie, Chicago Board of Trade, 51.

I"BMM (1874), 121; BMM (1874), 86-88; BMM (1874), 164. 12Lurie, Chicago Board of Trade, 66-72.

56 BUSINESS HISTORY REVIEW

:::op

:%40

:.iA

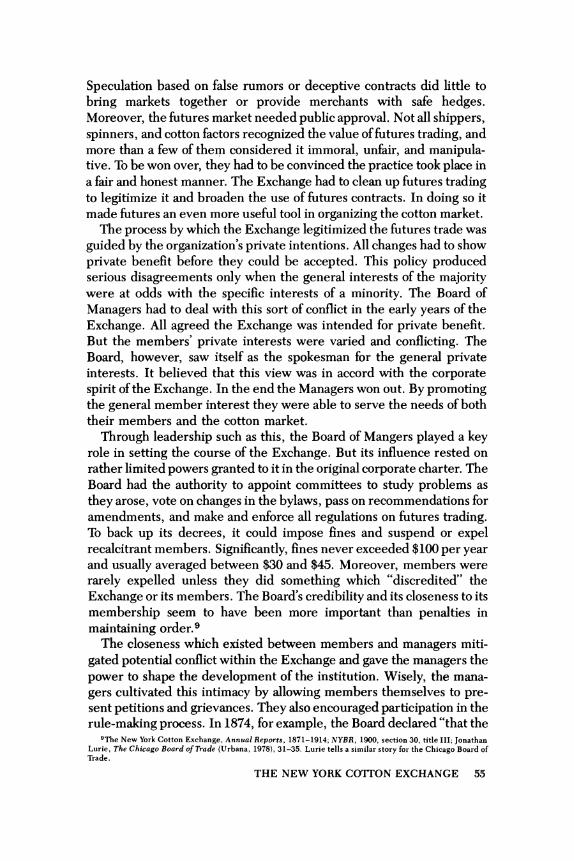

:;:aiL .::??i:1:::: :::::IV ::::AOL

"Trading in the Ring." Dealers bought and sold cotton futures contracts on the floor of the New York Cotton Exchange. Such spirited trading made New York the center of the American futures market.

all trading take place between 10 a.m. and 3 p.m. and that no member use fictitious names in his dealings. It allowed only one standard contract form and banned "unethical, uncommercial and unbusiness-like activi- ties." To maintain a safe and secure environment for all of its members, the Board empowered a committee to investigate the "doubtful and spurious transactions made either verbally or in writing by members of the Exchange," and recommended that a fine of $250 be levied against all who continued to make agreements in violation of accepted practices. Similarly, it passed a rule requiring all members to report their transac- tions to the Exchange Superintendent or face a fine. The Board enforced such decrees in a way that was neither punitive nor directly coercive; it simply refused to arbitrate any agreements made otherwise, thus de- priving them of the valuable protection of the Exchange bylaws.13

13BMM (1874), 111; BMM (1873), 385; BMM (1876), 216; BMM (1881), 275. In 1876 and 1881 two other rulings tightened control. The first offered a reward to members who reported rule violations; the second proclaimed that no notice be taken publicly of sales made contrary to rules, thus preventing them from affecting the futures market. The fight over these and other such rules indicates that there were probably splits between members over policy. But I have little evidence on them and I am more interested in the institution's actions as a whole.

THE NEW YORK COTTON EXCHANGE 57

By enforcing a standard form of the futures contract, prohibiting spurious sales, and refusing to recognize illegal or manipulative agreements, the Board enhanced the social utility of futures trading while cultivating the futures market for its own members. Private machinations were banned because they resulted in the unjust gain of one member at the expense of another. At the same time such practices distorted the allocative functions of futures trading by creating a gap between the futures market and commercial conditions. For speculation to be useful, it had to follow and anticipate the economy's prevailing winds, not the lies and schemes of some unscrupulous operator. By building a stable trading structure for its own members, the Exchange benefited the whole economy.

This pattern of private action and public gain continued throughout the nineteenth century as the Exchange gradually extended its power to protect its members' businesses. In 1885, G.E. Staeglen of the Stuttgart Cotton Company brought suit against certain members who had de- famed him publicly during the hours of trading. Subjected to the humili- ation of unfounded rumors about his and his firm's integrity, Staeglen wrote to the Board exclaiming that as a member of the organization he was entitled to protection and fair treatment. As a result the Managers voted to expel Charles Crosby and John Bower for "false and misleading statements" they had made against Staeglen. With this action the Board acknowledged the importance of all information, however casual, ex- changed under its roof. Unfounded rumors could be telegraphed quickly to all parts of the world. That they should destroy a member's reputation was unconscionable. But a member could only be hurt by rumors or heedless speculation because they influenced the futures market itself. By banning irresponsible gossip for its members' sake, the Exchange also squelched its effect on the market.14

There were of course limits on the Exchange's ability to promote the public interest. The organization could not engage in activities which did not promise a direct and substantial benefit to its members. In 1896, for instance, when some Board executives tried to amend the bylaws to provide more money for the Cotton Exchange Inspection Fund, the general membership stubbornly refused to comply. The Inspection Fund had been set up to pay for mistakes that the Exchange's inspectors made in grading cotton. When a series of errors led to a rapid drain on the Fund, the Board tried to bolster it with general Exchange resources. Although the Board considered this action "essential and absolutely necessary to the fulfillment of the contracts traded upon the Exchange," its efforts were thwarted by members who did not find the situation serious enough to warrant extending their organization's liabilities. Only

14BMM (1885), 227; BMM (1885), 313.

58 BUSINESS HISTORY REVIEW

a small percentage of the contracts were settled by delivery of cotton; thus the benefits of the Fund were marginal to most traders. The Board wanted to increase the Exchange's responsibilities without offering the members adequate compensation; such altruistic behavior violated the spirit of the organization.15

BALANCING PRIVATE AND PUBLIC NEEDS

The initial success of the Exchange depended on its ability to balance private and public needs. So long as the important outside interests -

merchants, farmers and manufacturers - were content that the actions of the Exchange were not detrimental to their businesses, things pro- ceeded smoothly. Early on, failure to achieve this balance might have stunted the growth of futures trading and the demand for futures con- tracts. But as time passed and the Exchange won over skeptics, it gained confidence and began to look beyond its limited origins. The organiza- tion's success in establishing control over its members encouraged it to embark on a quest for more private power. This venture disrupted the private-public balance so carefully forged in early decades.

The first violation of the Exchange's accord with the cotton trade came with the passage and enforcement of the Commission Laws. The Com- mission Laws were a complex code which limited memberships, raised brokerage rates, and increased membership values. In essence these laws were designed to give the Exchange market power, though of a limited sort as the organization was not a monopoly.16

The Commission Laws were enacted over the wishes of some mem- bers, who saw them as a violation of the Exchange's private purposes. The battle was fought mainly between 1875 and 1889. The Board of Managers, after overcoming some initial reluctance, supported the new laws and helped to get them passed. In 1882 the Board proposed that the Exchange create 65 new memberships to be sold at $6,000 apiece and raise the cost of joining to $12,000. It also recommended that the Exchange set a floor on member brokerage rates and that it ban secret repayments and rebates. These recommendations became the basis of Article X of the bylaws, the modern Commission Law statutes of the Exchange. 17

15BMM (1896), 181. Both graders and inspectors salaries and the Inspection Fund were paid out of revenues collected from the inspection service charges to members. NYBR, 1906, section 87. This rule prohibited the Exchange from committing its resources to a liability which had no definite limit or termination.

16BMM (1871), 28-29; BMM (1873), 342. Before the actual battle over the Commission Laws, the Exchange fought for control in a different way. It attempted to limit access to the trading pit by designating the men who could and could not act as a member's clerk or representative. The managers feared if they did not retain the right to make this choice unwanted speculators and non-members might gain access to futures trading. This

might have diluted the Exchange's authority. 17The laws followed a serpentine course to enactment. Proposals to limit competition and institute minimum

rates were countered by conservative opposition which tried to keep the institution on its original, restricted course. BMM (1871), 172; BMM (1882), 12.

THE NEW YORK COTTON EXCHANGE 59

The enforcement of these rules generated serious opposition. Those members who had voted against the original Commission Law proposals tried (unsuccessfully) to reestablish rebates and to allow non-resident members equal status with resident members. Moreover, they suc- ceeded in rescinding Rule 17, which had allowed the Board to expel violators of the Commission Laws. Controversy raged between those who wanted open trading at competitive prices and those who preferred minimum prices and limited competition. Higher profits and more valuable memberships pleased supporters of the law. Its detractors complained of its cost and inconvenience, especially the unnecessary interference it provoked in private affairs. The issue was not settled until 1893 when Board President James Bloss wrote a letter to the Board of Managers calling for the reinstatement of the expulsion clause and stricter enforcement of the existing Commission Laws. After Bloss's letter, opinion began to swing in favor of the Laws, and in 1896 the Board was able to make them more exacting by specifying differential rates of brokerage for members, non-members, joint accounts, agents of mem- bers and non-members, With these new rules the Commission Laws became standard procedure for trading in the New York futures

market.18 The Commission Laws were significant because they constrained

price competition between members (who nonetheless found other ways to compete) and because they firmly established the power of the Exchange over the futures market. Rules which discriminated against non-members, limited the power of members to designate clerks and operatives, and restricted the extension of trading privileges to the partners and employers of members acted to close off the trading ring. In this way the Commission Laws forced the public to rely on a specific group of brokers for futures contracts. This meant more than higher prices. It meant the formation of a professional body of speculators responsible for serving the cotton trade. These professionals dominated the important day-to-day trading which was so crucial to the integration of the cotton market. They alone acted as arbitragers or "pit-scalpers," speculators who trade on minute price swings or on small differentials between markets (and thus keep the cotton market united under a single price regime). Larger speculative ventures were still open to all, but the less spectacular trading came under the exclusive control of the Ex- change members.19

18BMM (1884), 286; BMM (1893), 68; BMM (1896), 60; BMM (1896), 105. Non-resident members, those not having permanent offices within New York City, had to pay slightly higher rates than resident members.

19Holbrook Working, "Futures Trading and Hedging," American Economic Review 43 (September 1953), 314-343. Pit scalpers were small-time dealers who traded on minute price variations between markets. Because they did not attempt to hold contracts for more than one trading period, they made hundreds of transactions each day. Paying non-member rates would have wiped out the small profit margins on which their business rested. Robert Bouilly notes that the Commission Laws battle may have involved an attempt to extend memberships

60 BUSINESS HISTORY REVIEW

vgo :g AA?:

Alf:'

Apr:- IIMIL-.~i~ii::.~:-

r. *Www WRI-ass _: :-aa~-~a, a:

im - 21k. . n? mi

mmii i

:;i ~ gsgg*' ~ Al~l~l ~ I~ is~gg~ ~ s~Z~i-:--~-: :: :-_:_1::-1:1 IMM:WI YA-LS-::

W4.

Courtesy Library of Congress

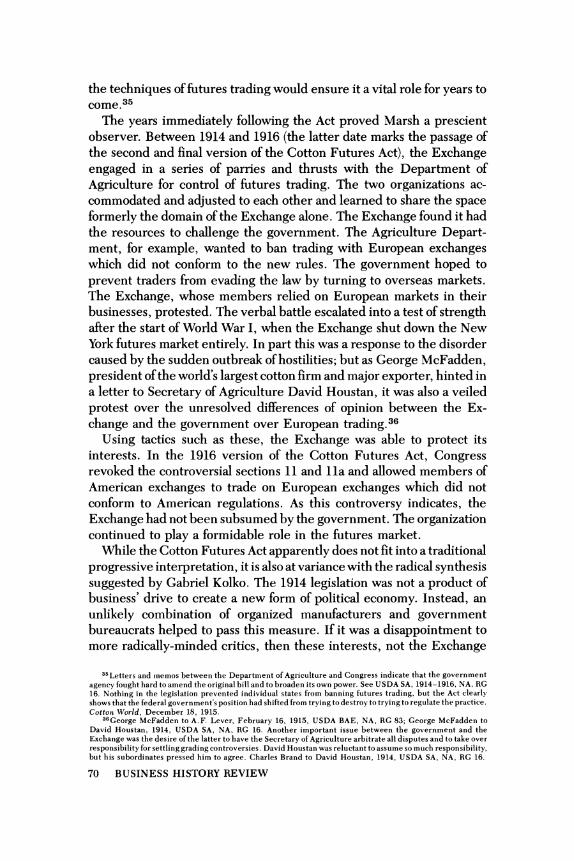

The New York Cotton Exchange.

This photograph depicts the building originally used by the Exchange. The organization later moved into a nineteen-story structure that housed the trading floor along with the offices of the Exchange and its member firms.

THE NEW YORK COTTON EXCHANGE 61

On balance, the effect of the Commission Laws on the cotton economy was ambiguous. On the one hand, minimum rates, reduced price com- petition, and restricted memberships certainly increased members' profits at the public's expense. When the difference between hedged and unhedged cotton was either a small profit or bankruptcy, the Ex- change could force non-members to pay more for a contract without seriously reducing its volume of trade. On the other hand, the Commis- sion Laws opened up new avenues for the professional broker. By pushing up rates and raising broker profits, the Exchange enabled individual members to serve the public full time and encouraged firms to employ staffs exclusively to satisfy the growing public demand for futures contracts. In this way the Laws may have helped spread the use and acceptance of futures contracts faster than would have otherwise been possible.20

The most important result of the Commission Laws was, however, political and not economic. By making futures trading dependent on the 400 or so men who were members of the New York Cotton Exchange, the institution took on a heavy social burden - a burden it was not prepared to shoulder. It had made itself a highly visible symbol of the art of futures trading, and it had ensured that the public would focus its wariness of speculation on the Exchange. The organization had left itself vulnerable to the charge of monopoly. By extending its reach through the new laws, the Exchange broke its tacit agreement with the public which had kept the organization officially within the private sphere. Now its actions had an obvious public effect. Few internal checks existed within the Exchange to stop it from exercising its power in an irresponsi- ble manner. In the eyes of some participants in the cotton market, the private-public allegiance forged between 1870 and 1890 had been destroyed.

Public attitudes towards futures trading began to change in the 1890s. New critics appeared to attack the role the Exchange played in the cotton market. Congressional committees began to take a hard look at futures trading, and some congressmen turned sympathetic ears to- wards the populists and other agrarians who believed futures trading depressed cotton prices. Even those who used futures contracts were unsure how ethical or useful they were. As Rufus Hatch, himself a dealer in futures, testified before Congress: "Short selling, long buying is [sic]

and open up the trade. He is correct in that the Laws allowed non-New York residents to join the Exchange and created new memberships for purchase. But as the battle over discrimination against non-resident members indicates, the attempt to open up the Exchange faced strong opposition from a majority with opposite inten- tions. Overall, the thrust of the Laws was to raise rates, limit membership sales, and close off access. See Bouilly, The Development of American Cotton Exchanges, 370-72.

20The Exchange wrote to A. Brittin, president of the New Orleans Cotton Exchange, asking that he go along with New York's attempt to raise brokerage rates. Brittin happily complied. The Commission Laws, in creating a new professional class, may have also opened up new tensions and conflicts within the Exchange.

62 BUSINESS HISTORY REVIEW

pure gambling and harmful to the economy." But he added ambiva-

lently, "I do it whenever it looks profitable and safe. We are a nation of gamblers and sometimes the lambs get fleeced."21

Attacks on the futures trade swelled between 1892 and 1896, when several bills to proscribe the suspect practice were introduced in Con- gress. Some critics, populists in particular, began to cite the Exchange and other organized Northern financial interests as a major cause of the South's economic woes. They questioned the right of an unsanctioned private body to build and control a market so vital to the farmers interests.22

When populism faded and the economy recovered from its long depression after 1896, this wave of criticism ebbed. No national and little state legislation remained on the books, and the Exchange ap- peared to have ridden out the storm in good shape. Indeed, the populist protest actually seemed to have revealed the strength and resiliency of the Exchange. Critics had failed to halt the organization's expansion and the growth of futures trading because they had not considered how important futures had become to the entire cotton market. In small interior towns southern merchants relied on the New York futures price to make rational buying and selling decisions and to plan for market changes. Manufacturers, attempting to gain a firmer hold over their sources of supply, ventured South to procure needed fiber themselves, using the New York futures price as a guide. Even the majority of the mills which still relied on merchants hedged with futures to protect against fluctuations in the value of their inventories. The futures price had thus become crucial to those who planned for the production and distribution of cotton and its products.23

The growing importance of futures trading made it virtually impossi- ble for critics to destroy either the futures market or the New York Cotton Exchange. But these developments also brought new political interests into the picture. The cotton manufacturers, unlike the farmers and the ambivalent southern merchants, were quite content to let the futures trade proceed under the guidance of institutions like the Ex- change. Convinced that futures trading was essential to their long-term plans, the manufacturers did not even balk at the power the Exchange

21United States Congress, Committee on Agriculture and Forestry, Conditions of Cotton Growers, 53rd Congress, 3rd session, (Washington, D.C. 1895); New York Times, December 20, 1880, p. 4.

22The Southern Mercury, April 28, 1895; April 28, 1898; March 12, 1892; United States Senate, Bills and Resolutions, 52nd Congress, 1st session, H.R. 969 (Washington, D.C., 1892), 2, 6.

23The Populists failed to make common cause with the socialist movement, depite the agrarian party's ignominious defeat in 1896 and its subsequent repudiation of Democratic fusion. See David Montgomery, "On Goodwyn's Populists," Marxist Perspectives, I (Spring 1978), 162-78. The Populists also had a conservative streak, as their dedication to capitalism and private property indicates. The farmers were not very effective political agitators. Only South Carolina passed an anti-futures bill. For an account of the cotton exchanges' political fight against their critics, see Bouilly, The Development of American Cotton Exchanges, 375-80; United States Congress, Committee on Agriculture and Forestry, Conditions of Cotton Growers, 50; Report of the Commissioner of Corporations on Cotton Exchanges, Part I (Washington, D.C., 1908), 14, United States Congress, Conditions of Cotton Growers, 441, 452.

THE NEW YORK COTTON EXCHANGE 63

held over the important New York futures market. They were content not to stir up any bitter feelings among the more vociferous critics of the Exchange by challenging the status quo. But these new manufacturing interests were also prepared to fight the Exchange if it embarked on what they perceived as an ill-conceived course. The futures market had become too valuable to them to remain the exclusive terrain of one institution.

PUBLIC PRESSURE

As the recognized leader of American futures trading, the Exchange was under considerable pressure to act responsibly. Every measure, even those seemingly private, was carefully scrutinized by the cotton economy's business interests. When, early in the 1900s, the Exchange seemed again to violate the public-private accord, even the most con- servative sectors of the cotton trade reacted.

The trouble arose after the Exchange adopted a system of fixed differentials or fixed differences. Essentially, the fixed differences sys- tem meant that the Exchange chose to set the ratios of value between different grades of cotton in the futures market, rather than letting them fluctuate with economic conditions as they would in the spot market. As a result, the price of cotton futures diverged from the price of spot market cotton, to the consternation of spinners, shippers, and merchants.24

The problem of fixed differences became especially acute in 1904-05 when late summer storms hit the Gulf states, destroying a large percent- age of the cotton crop and lowering its average grade. Low quality cotton abounded in the world's spot markets, but the differentials in the New York futures market did not reflect these new conditions. The differen- tials remained fixed, as they were changed only at infrequent intervals by the Exchange's Committee on Revisions. The oversupply of low- quality fiber thus went unnoticed in the New York futures market, and futures dealers who held contracts there received overvalued poor- quality cotton when settlement time came. Like good businessmen, they began to buy new futures contracts at reduced prices, discounting the futures market's failure to account for the new commercial condi-

24A difference is the price ratio between the basis grade, middling cotton, and all other grades of cotton. Thus, good ordinary quality cotton might be %/ middling, or worth 7/8 the price of middling cotton when delivered in fulfillment of a futures contract. A hedge is only safe when the ratio between the spot and futures price is stable. See Working, "Futures Trading and Hedging." The origins of the fixed differences system remain somewhat obscure. According to Bouilly, it evolved in the 1870s when the Exchange established a Committee on Quotations to set the official daily futures market price quotations for each grade of cotton. This was necessary because of the low volume of trade in some grades in New York. A committee system was used because it allowed less manipulation by individual members who wanted to set higher or lower ratios to suit their own needs. Toward the end of the nineteenth century the Exchange confronted the limits of its administrative power as the fixed differences, set at more and more distant intervals to prevent manipulation, undermined the market. See Bouilly, The Development of American Cotton Exchanges, 357-63.

64 BUSINESS HISTORY REVIEW

tions. In doing so they artificially depressed the New York futures price, until it was out of touch with the rest of the cotton trade.

Both the cotton industry and, in a different way, the government stood to lose if the Exchange maintained the system that had produced these results. The depression in the futures prices undermined the immediate economic benefits that the cotton trade had enjoyed from futures trading and endangered the long-term plans of New England spinners and government agriculturalists for improving the quality of the nation's cotton crop. The fixed differentials encouraged an artificial depression and unsystematic perturbations in the futures price; this made it impossible for merchants to hedge safely against price changes. Buyers who depended on the futures price as the basis for their bids to farmers also suffered as the price no longer served as an adequate reflector of commercial conditions.

At the same time, by arbitrarily setting the price of low quality cotton above that prevailing in the spot market, the Exchange encouraged farmers to grow a lower quality crop (even while New England spinners were trying to convince them to grow better quality cotton). In a letter to Secretary of Agriculture David Houstan, Theophious Parsons, chairman of the Long Staple Committee of Boston's Awkwright Club, set forth the textile trade's major needs. Prominent on Parsons' list was a plan to increase cotton quality so that mills could produce the finer fabrics then in demand. The manufacturers had actually sent men to the South to show farmers how to cultivate higher quality, long-staple cotton.25

The Department of Agriculture concurred with Parsons and agreed that the country needed better quality fiber. It too had sent experts to the South to encourage farmers to plant new strains of long-staple cotton. But as both the agriculturalists and spinners were coming to realize, they could do nothing without first changing the conditions in the futures market. So long as the differentials were out of touch with economic reality, farmers were encouraged to grow low-quality fiber to sell in the overvalued New York futures market. More generally, the important role of futures prices in cotton marketing meant that any unanticipated price shifts (such as those the fixed differentials produced) subverted the normal market forces adjusting supply to demand. Thus inadvertently the Exchange had adopted a policy which was in conflict with the needs of two very important interests.26

25Members of this organization included Amoskeage, Lyman, Parkhill and Wampanoag Mills. Theophious Parsons to David Houstan, October 27, 1913, National Archives, Washington, D.C. [hereafter cited as NA], Record group 16 [hereafter RG], United States Department of Agriculture, Office of the Secretary of Agricul- ture [hereafter cited as USDA SA].

26United States Department of Agriculture, Bureau of Agricultural Economics [hereafter USDA BAE], Project Files, January 1, 1908, April 12, 1912, NA, RG 83; Charles Brand to the Executive Committee of the American Thread Company, 1914, NA, RG 83, USDA BAE. It is also important to realize that the long secular decline in cotton prices and the difficult times southern cotton farmers had experienced raised cries of overproduction in the South. Anything which shifted supply and demand conditions unfavorably for the

THE NEW YORK COITON EXCHANGE 65

The Exchange could not ignore the swelling outcry against its prac- tices. In 1908 the Bureau of Corporations conducted a lengthy investiga- tion of cotton exchanges and concluded by admonishing the New York Exchange to abandon its questionable fixed differences system. Earlier, the organization's own members had debated the merits of fixed differ- entials. In 1904 George McFadden had expressed his doubts about their fairness and utility. Endorsing the sentiments of fellow member George Brennecke, McFadden wrote to the Board of Managers that "no mea- sure should be entertained for individual interests" and that uncommer- cial or fixed differences could be construed "as favoring a special against a general interest." Similar misgivings were echoed in a minority report of the Revision Committee, which noted with alarm the Exchange's practice of setting the ratios between grades of cotton without regard to market conditions. Such strong protests from within and from without forces one to ask why the Exchange held on so stubbornly to the fixed differences system.27

I believe that the Exchange needed and maintained the fixed differ- ences system because it was facing two closely related problems it could not handle with its private status. First, speculation was becoming wild and untamed. Bucket shops - private gambling dens where men and women literally bet on stock and commodity prices - had proliferated, challenging the "legitimate" speculation of the futures market. Worse, speculation in the futures market itself had developed an unsavory flavor. The Exchange had originally tried to eliminate what it perceived as unethical speculation and manipulation of the market. But in 1904 Daniel Sully disrupted the futures trade with an attempt to corner the cotton market. In a brazen attempt to push up cotton prices for his own ends he tried to buy up the available supply of cotton fiber in New York City. He hoped that when his contracts fell due those who owed him cotton would have to come to him for the commodity and pay exorbitant prices.28

While corners like this were rarely successful (Sully's failed in 1905 and he was wiped out), they certainly disrupted the futures market. Neither grizzled traders nor cautious professional brokers had any de- sire to see their businesses disturbed by either untutored amateurs or scurrilous operators. Moreover, such manipulations discredited futures

farmers, as the price depressions brought on by the fixed differences might, could only increase farmers' frustration. See Gavin Wright, The Political Economy of the Cotton South, (New York, 1978), 181-182; Report of the Commissioner of Corporations on Cotton Exchanges, Part I, 336-357; BMM (1903), 167.; BMM, "Report of the minority .. ," 1903, 390.

27BMM, James Bloss to the Board of Managers, 1896, 68; Report of the Commissioner of Corporations, Part I, 283-285.

28For an overview of the bucket shop wars, see Lurie, The Chicago Board of Trade, 75-105; BMM (1903), 338. Bouilly points out that corners were frequent problems for exchanges in the nineteenth and twentieth centuries. The organizations fought to control them, but they were expected. That the Sully episode stands out is an indication of the magnitude of the problem and the Exchange's sense of a loss of control. Bouilly, The Development of American Cotton Exchanges, 33.

66 BUSINESS HISTORY REVIEW

trading and associated it with the disreputable bucket shops. Members of the Exchange openly acknowledged that "the disastrous Sully episode has compelled many to admit that something must be done to put our contracts on a more secure basis and to make it more difficult to corner the market."29

Yet the Exchange could do little to remove this difficulty. It was handcuffed by a second problem - its declining spot market. As the cotton trade rerouted its shipments around New York, the city's avail- able supplies dwindled, making it easier to corner the market [see Table 3]. One effective way to fight the corners was to maintain a bountiful cotton supply, but conditions in the spot market made this an unlikely solution.

In addition to the growth of corners and the decline in spot sales, the

Exchange was facing a legal challenge in this period. In 1905, after a three-year battle in the lower courts, futures contracts were declared legal and enforceable by the United States Supreme Court. Writing the majority opinion in the Chicago Board of Trade v. Christie Grain and Stock Company, Oliver Wendell Holmes hailed speculation as "society's adjustment to the probable" and held that because futures contracts implied actual delivery of a physical commodity, they were a form of legal speculation. The delivery clause of the futures contract thus be- came the linchpin which made the contract legal, but the New York spot market's decline threatened to knock out that linchpin. The option of delivery became rather hollow when the city had no cotton for dealers to deliver.30

TABLE 3 % SPOT SALES, NEW YORK - BALE SOLD/TOTAL CROP

1870 16.9 1882 3.5 1895 2.4 1871 17.6 1883 5.2 1896 2.9 1872 12.8 1884 3.1 1897 1.4 1873 11.1 1885 3.1 1898 0.9 1874 11.5 1886 3.8 1899 1.5 1875 8.1 1887 1.8 1900 0.9 1876 8.7 1888 2.3 1901 0.2 1877 6.9 1889 1.3 1902 1.1 1878 5.4 1890 1.1 1903 2.4 1879 5.6 1891 1.8 1904 0.8 1880 4.8 1892 2.9 1905 2.1 1881 6.7 1893 2.7 1906 0.9

1894 1.1 Source: Report of the Commissioner of Corporations on Cotton Exchanges (Washington, D.C., 1909),

248-49.

29BMM (1893),398; BMM (1893), 388. 30Lurie, The Chicago Board of Trade, 193-197.

THE NEW YORK COTTON EXCHANGE 67

Holmes' ruling had made the preservation of the New York spot market imperative, but it had also blocked another avenue of escape from the problem of corners. One simple way to bring this undesirable

speculation under control would have been to allow traders to refuse to make delivery of cotton when contracts came due. Futures contracts were frequently fulfilled without cotton when both parties agreed to settle on the change in price alone. But mutual assent could hardly be secured if one party was trying to corner the market. He would insist on

delivery to increase the demand for his carefully hoarded stocks of cotton. Had the Exchange modified the futures contract so that either

party might decline to make or take delivery of cotton when the contract fell due, it would have eliminated the corners; but it would have also

endangered its precarious legal sanction by weakening the delivery clause. Members admitted as much when in fear of the Court's reaction

they struck down a proposal which would have allowed sellers to post- pone cotton delivery.3'

Hemmed in by its declining spot trade, its vulnerable legal position, and its faltering control over speculation, the Exchange turned to the fixed differences as a temporary solution to its problems. By raising the

price of cotton in New York, the organization encouraged shipment to the city's warehouses. Though it is true the total effect was small (see Table 3), the members believed eliminating the system would make matters worse. Moreover, the fixed differences had provided some help. As statements by contemporaries indicate, the New York spot market had become a repository for low-grade cotton, the very kind overvalued

by the fixed differences. The system was not a long-term solution, as even its most ardent supporters admitted. But it did provide immediate

help. Unwilling to abandon the system, the Exchange drew the enmity of the greater part of the cotton trade, as well as needed fiber to its door.

It might seem curious that members of the Exchange would settle for such a limited solution. But in all fairness to their talent and creativity, they could do little else. The managers did try to institute a plan which would have licensed southern warehouses to supply certificates of own-

ership for traders to tender in fulfillment of contracts. but this sensible solution ran up against conservative opposition. Turning over control of the spot market to southern warehouses would have set a dangerous precedent, sharply reversing the trend towards the accumulation of

power and authority in New York. Members were not interested in so

31BMM (1903), 387-398. The southern warehouse plan did not cause a conflict between the managers and members. As already noted, control was fluid and open in the Exchange. Some managers opposed the plan, and even its supporters appreciated their opponents' argument. The conflict was between those who feared a violation of tradition and those who feared government reprisal. Bouilly agrees that the declining spot market was crucial in this. He also agrees that the fixed differences attracted low-quality cotton to New York, supporting the spot market. My information indicates that the fixed differences were a part of a deliberate and conscious

policy which resulted from the squeeze of a legal threat and unrestrained cornering. See Bouilly, The Develop- ment of American Cotton Exchanges, 357-363.

68 BUSINESS HISTORY REVIEW

drastic a reform. As they had demonstrated earlier in the Inspection Fund conflict, they did not consider broadly defined self-interest suffi- cent reason for tampering with tradition. Thus they voted down the plan and stuck with the politically dangerous fixed differences system.32

Unwilling to tolerate this situation, the Department of Agriculture and cotton manufacturers joined hands and appealed to Congress for the power to reform the Exchange. In part because of their vigorous lobby- ing efforts, the legislature passed the Cotton Futures Act of 1914. This law required all exchanges to conform to specific rules and regulations set by the government or face a destructive tax of 10 per pound of cotton traded on contract.33

The fixed differences system was not the sole reason for the legisla- tion. But the Exchange's recalcitrance over this issue acted as a catalyst, spurring the government and private industry to action. The act gave the Department of Agriculture powers to set standards for cotton grad- ing and enact a system of commercial differences (differentials based on

spot market conditions) for futures exchanges. The law was a combina- tion of reforms which among other things was aimed at upgrading the American cotton crop as the government agriculturalists and the spin- ners wished.34

This legislation was not, however, a product of crusading, anti- business progressivism. If anything it preserved the powers of the Exchange by solving problems - the declining spot market for example - which were beyond the private institution's reach. More importantly, the Cotton Futures Act provided futures trading with a needed legisla- tive sanction to replace the shaky judicial sanction of earlier years. In this way the Act protected the market from more radical critics who believed futures trading had no legal basis. While the Department of Agriculture gained certain regulatory powers, it in no way replaced the still private Cotton Exchange. Indeed, as one of the institution's enthusiastic sup- porters, Arthur Marsh, optimistically noted, the government would have to rely on the Exchange for vital information about the futures market. The organization's control over information and expertise about

32BMM (1903), 387-398. 33Other interests were important in bringing about the law. Farmers who feared futures trading were of

course in favor of the Act. But so were southern cotton exchanges. Because they lacked the problem of a declining spot market, they did not need a fixed differences system. Moreover, they were jealous of New York's preeminent position. This allowed them to be more "socially responsible" and to support the law. Bouilly, The Development of American Cotton Exchanges, 448-451.

34United States Cotton Futures Act, Statutes at Large, (Washington, D.C., 1916); United States Depart- ment of Agriculture, Rules and Regulations of the Secretary of Agriculture under the Cotton Futures Act, (Washington, D.C., 1914), Agriculture Department Circular 46. The role of fixed differences in bringing about this legislation is actually somewhat complicated. The system was of course abhorrent to the Department of Agriculture and the cotton spinners. And it did disrupt the futures market to the detriment of all who used it. But it also confirmed the worst fears of farmers who claimed that the futures market depressed prices and was controlled by men, not the laws of supply and demand. As R. Bouilly notes, the Exchange only exacerbated the problem by responding to public outcry with the haughty claim that it had no public or semi-public obligations to fulfill. Bouilly also recognizes the cotton spinners as an important voice in the call for reform, but he fails to appreciate how they allied with the Department of Agriculture in this. See Bouilly, The Development of American Cotton Exchanges, 424-426.

THE NEW YORK COTTON EXCHANGE 69

the techniques of futures trading would ensure it a vital role for years to come.35

The years immediately following the Act proved Marsh a prescient observer. Between 1914 and 1916 (the latter date marks the passage of the second and final version of the Cotton Futures Act), the Exchange engaged in a series of parries and thrusts with the Department of Agriculture for control of futures trading. The two organizations ac- commodated and adjusted to each other and learned to share the space formerly the domain of the Exchange alone. The Exchange found it had the resources to challenge the government. The Agriculture Depart- ment, for example, wanted to ban trading with European exchanges which did not conform to the new rules. The government hoped to

prevent traders from evading the law by turning to overseas markets. The Exchange, whose members relied on European markets in their businesses, protested. The verbal battle escalated into a test of strength after the start of World War I, when the Exchange shut down the New York futures market entirely. In part this was a response to the disorder caused by the sudden outbreak of hostilities; but as George McFadden, president of the world's largest cotton firm and major exporter, hinted in a letter to Secretary of Agriculture David Houstan, it was also a veiled protest over the unresolved differences of opinion between the Ex- change and the government over European trading.36

Using tactics such as these, the Exchange was able to protect its interests. In the 1916 version of the Cotton Futures Act, Congress revoked the controversial sections 11 and 11a and allowed members of American exchanges to trade on European exchanges which did not conform to American regulations. As this controversy indicates, the Exchange had not been subsumed by the government. The organization continued to play a formidable role in the futures market.

While the Cotton Futures Act apparently does not fit into a traditional progressive interpretation, it is also at variance with the radical synthesis suggested by Gabriel Kolko. The 1914 legislation was not a product of business' drive to create a new form of political economy. Instead, an unlikely combination of organized manufacturers and government bureaucrats helped to pass this measure. If it was a disappointment to more radically-minded critics, then these interests, not the Exchange

35Letters and memos between the Department of Agriculture and Congress indicate that the government agency fought hard to amend the original bill and to broaden its own power. See USDA SA, 1914-1916, NA, RG 16. Nothing in the legislation prevented individual states from banning futures trading, but the Act clearly shows that the federal government's position had shifted from trying to destroy to trying to regulate the practice. Cotton World, December 18, 1915.

36George McFadden to A.F. Lever, February 16, 1915, USDA BAE, NA, RG 83; George McFadden to David Houstan, 1914, USDA SA, NA, RG 16. Another important issue between the government and the Exchange was the desire of the latter to have the Secretary of Agriculture arbitrate all disputes and to take over responsibility for settling grading controversies. David Houstan was reluctant to assume so much responsibility, but his subordinates pressed him to agree. Charles Brand to David Houstan, 1914, USDA SA, NA, RG 16.

70 BUSINESS HISTORY REVIEW

itself, were to blame. Indeed, they went so far as to exaggerate the institution's strong points to stave off more thorough-going reform. They stressed the stability and rationality of futures trading under the Ex- change and claimed the trade's problems were amenable to a very moderate brand of legislation.37

CONCLUSION

As these episodes in the Exchange's history show, private institutions and private power played a crucial role in the economy, helping to build an integrated national market. But this history also points out a basic problem in American economic development. To effect needed changes, the Exchange had to build up a stock of private power which could exert formidable influence on a major part of the economy. This power could be used for good or ill, but it was always directed by private intentions, regardless of its public consequences. Because this process initially provided both public and private benefits, it worked well early on. But it soon led to conflicts. The Exchange continued to add to its private power even as its success in moulding the futures market made it invaluable as a public, or semi-public, institution. And the Exchange's private status entailed cumbersome traditions and a limited vision which restricted the organization's ability to grow and change with the economy, as the fixed differences problem indicated.38

The reform of the Exchange underscored the incomplete though inev- itable role of private power in making economic policy. Farmers, mer- chants, futures dealers themselves, and, most importantly, organized cotton spinners led the fight for reform. They forced the Exchange to respond to their needs, but to do so they had to appeal to public authority - Congress and the Department of Agriculture. This appeal preserved private power in the futures market. It redirected it without breaking it up. The Cotton Futures Act was well within a tradition which held that private and public interests could best be served once private power was balanced by public authority. Given the success that the Exchange had realized in regulating futures trading, it is hard to imagine the government taking any other course. Nothing short of large-scale

37Herman, Wolfe & Company to David Houstan, Dec. 5, 1915, USDA BAE, NA, RG 83. Charles Brand pointed out to the Cotton Futures Act's sponsor A.F. Lever that "there had arisen a public demand for the abolition of all cotton exchanges." Members of the Exchange must have been aware of this threat also; Charles Brand to A.F. Lever, May 25, 1914, USDA BAE, NA, RG 83. The reformers tried to make it seem as though the spot and futures prices could be made to move in perfect harmony. This would only be possible in a world of perfect information and perfect foreknowledge. David Houstan to A.F. Lever, March 28, 1914, USDA BAE, NA, RG 83.

38The terms "private" and "public" are perhaps not precise enough to express what I mean. Intentions were private in that they were aimed at either personal or corporate gain. The Exchange's reduction of "private" manipulation was not a public action; it was a change from personal private gain to general or corporate private gain, in accord with business ethics, not political principle.

THE NEW YORK COTTON EXCHANGE 71

economic planning could have served as well, and not even the most radical critic or the most committed agrarian wanted that.39

Yet nagging questions remained. Private power was still incomplete because it could not avoid conflicts on its own. Public power was limited and followed the lead of private groups. Questions of monopoly, dis- tribution of economic benefits, concentration of private power, and the direction of economic development fell outside of this type of reform. These were not questions which asked how to adjust the private power- public benefits mechanism, but questions which challenged it. While the Cotton Futures Act reestablished the old private-public accord, it did not solve the deeper problem of where the balance should fall. The question of how much authority useful, efficient, but still private institu- tions should exercise over economic growth was left to be answered in the future.

39According to Robert Bouilly, the New York Cotton Exchange was unwilling to reform. This is too harsh. It tried to reform but failed because it could not overcome its traditional private conception of its role. It was, however, under very real pressures from the courts, the decline of the spot trade, and the growth of unchecked manipulative speculation. Its failure to solve these problems did not stem so much from its lack of a social conscience as from the limits of its purely private power in the state of the American economy at that time. See Bouilly, The Development of American Cotton Exchanges.

72 BUSINESS HISTORY REVIEW