Futures & Options Segment - NSE

24

Futures & Options Segment 6

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Futures & Options Segment - NSE

Futures & OptionsSegment 6

88

89

Futures & Options Segment

The derivatives trading on NSE commenced on June 12, 2000 with futures trading on S&P

CNX Nifty Index. Subsequently, the product base has been increased to include trading in

futures and options on S&P CNX Nifty Index, CNX IT Index, Bank Nifty Index and Single

securities (188 stocks as stipulated by SEBI) and futures on interest rate. Futures and options

contracts were introduced on CNX Nifty Junior and CNX 100 indices for trading in F&O

segment on June 1, 2007.The turnover in the derivatives segment has witnessed considerable

growth since inception. In the global market, NSE ranks first (1st) in the world in terms of

number of contracts traded in the Single Stock Futures, second (2nd) in Asia in terms of

number of contracts traded in equity derivatives instrument. Since inception, NSE established

itself as the sole market leader in this segment in the country with more than 98 % market

share.

Trading Mechanism

The derivatives trading system at NSE is called NEAT-F&O trading system. It provides a

fully automated screen-based trading for all kind of derivative products available on NSE on

a nationwide basis. It supports an anonymous order driven market, which operates on a

strict price/time priority. It provides tremendous flexibility to users in terms of kinds of

orders that can be placed on the system. Various time and price related conditions like

Immediate or Cancel, Limit/Market Price, Stop Loss, etc. can be built into an order. Trading

in derivatives is essentially similar to that of trading of securities in the CM segment.

The NEAT-F&O trading system distinctly identifies two groups of users. The trading user more

popularly known as trading member has access to functions such as, order entry, order matching

and order & trade management. The clearing user (clearing member) uses the trader workstation

for the purpose of monitoring the trading member(s) for whom he clears the trades. Additionally,

he can enter and set limits on positions, which a trading member can take.

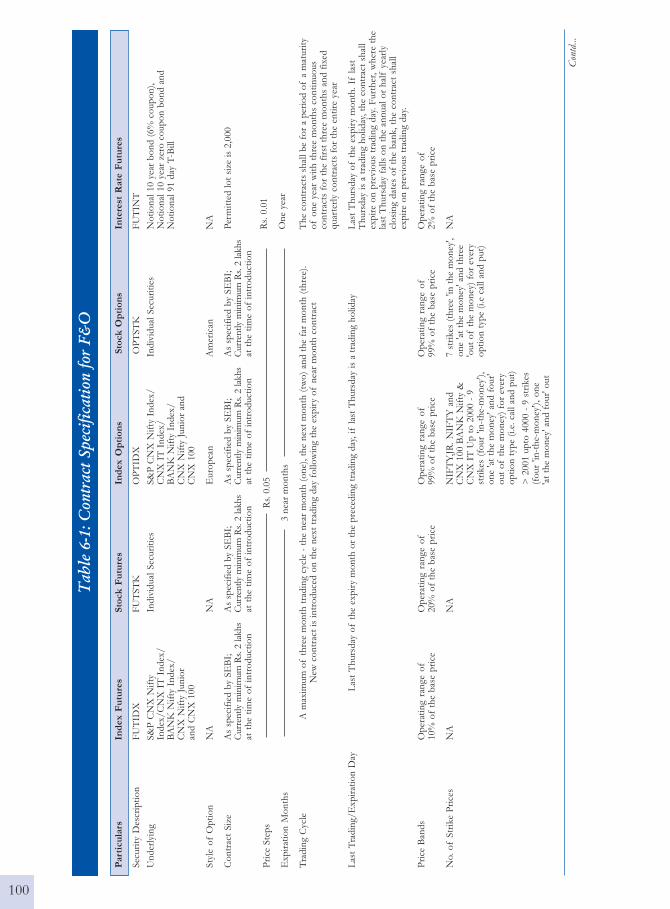

Contract Specification

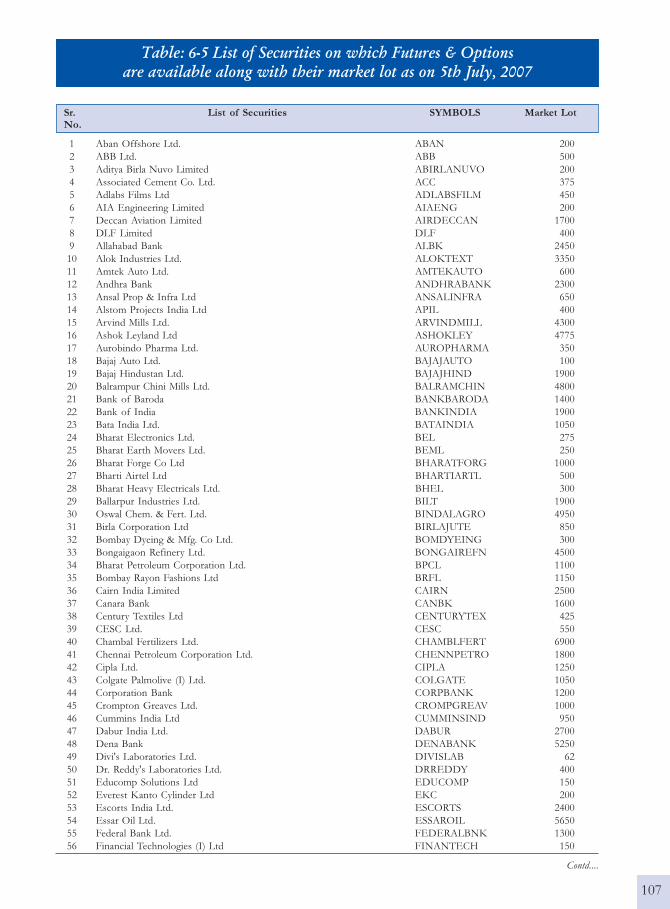

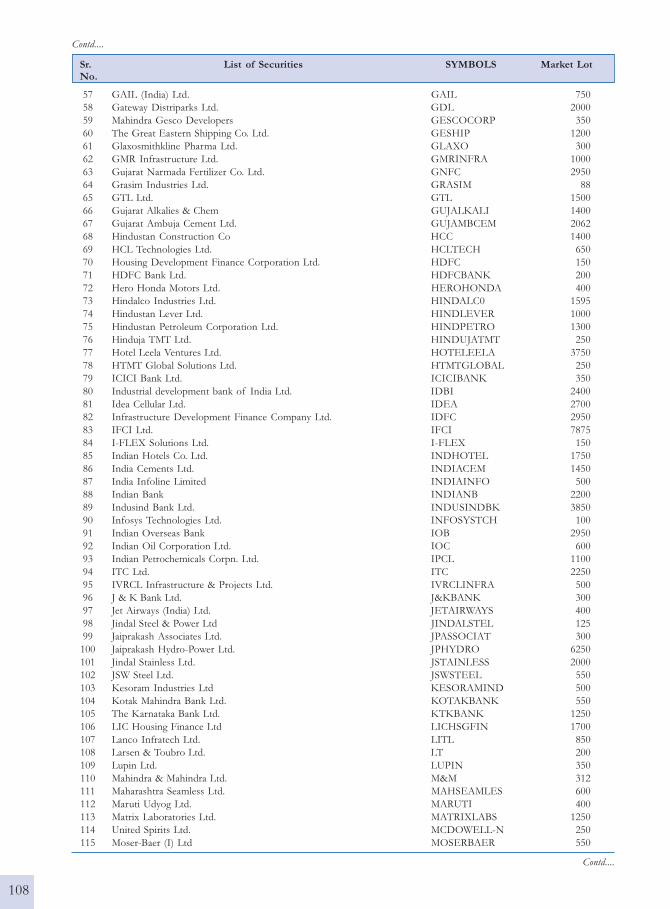

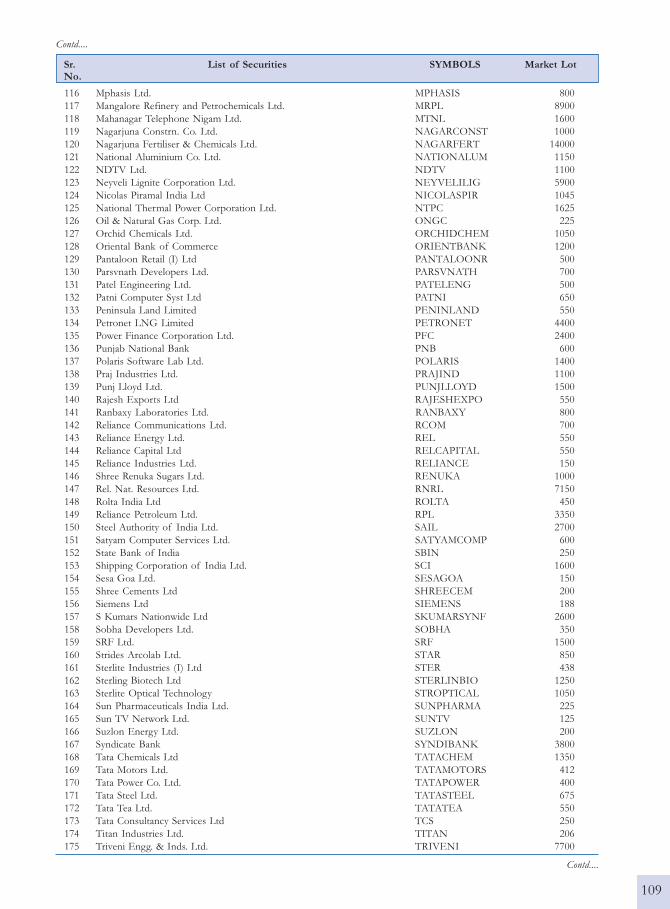

The contract specification for derivatives traded on NSE are summarised in Table 6-1.

The index futures and index options contracts traded on NSE are based on S&P CNX Nifty

Index, CNX IT Index, Bank Nifty, CNX Nifty Junior and CNX 100 while stock futures and

options are based on individual securities. Stock futures and options were available on 188

securities. Interest rate future contracts are available on Notional 91 day T-bill and Notional

10 year bonds (6% coupon bearing and zero coupon bond). While the index options are

European style, stock options are American style.

At any point of time there are only three contract months available for trading, with 1

month, 2 months and 3 months to expiry. These contracts expire on last Thursday of the

expiry month and have a maximum of 3-month expiration cycle. If the last Thursday is a

trading holiday, the contracts expire on previous trading day. A new contract is introduced

on the next trading day following the expiry of the near month contract. All the derivatives

contracts are presently cash settled.

66666

90

Introduction of strike prices for option contracts

NSE introduces option strikes on a daily basis based on the price of the underlying. With

regard to options on stocks the Exchange provides a minimum of seven stick prices for

every option type (i.e call & Put) during the trading month. At any time, there are at least

three strikes in-the-money (ITM), three strikes out-of-the-money (OTM) and one strike

at-the-money (ATM).

The number of strikes provided in options on Nifty, Nifty Junior, CNX 100, CNX IT and

Bank Nifty are related to the range in which previous day's closing value of the respective

indices falls as per the following table:

Nifty Index Level Strike Interval Scheme of strikes to be introduced

(ITM-ATM-OTM)

Upto 2000 25 4-1-4

>2001 upto 4000 50 4-1-4

>4001 upto 6000 50 5-1-5

>6000 50 6-1-6

Selection Criteria for Stocks and Indices

Eligibility Criteria of Stocks

• The stock shall be chosen from amongst the top 500 stocks in terms of average daily

market capitalisation and average daily traded value in the previous six months on a

rolling basis.

• The stock's median quarter-sigma order size over the last six months shall be not less

than Rs.1 lakh. For this purpose, a stock's quarter-sigma order size shall mean the

order size (in value terms) required to cause a change in the stock price equal to one-

quarter of a standard deviation.

• The market wide position limit in the stock shall not be less than Rs. 50 crore. The

market wide position limit (number of shares) shall be valued taking the closing prices

of stocks in the underlying cash market on the date of expiry of contract in the month.

The market wide position limit of open position (in terms of the number of underlying

stock) on futures and option contracts on a particular underlying stock shall be 20% of

the number of shares held by non-promoters in the relevant underlying security i.e.

free-float holding.

Continued Eligibility

• For an existing stock to become ineligible, the criteria for market wide position limit

shall be relaxed upto 10% of the criteria applicable for the stock to become eligible for

derivatives trading. To be dropped out of Derivatives segment, the stock will have to

fail the relaxed criteria for 3 consecutive months.

• If an existing security fails to meet the eligibility criteria for three months consecutively,

then no fresh month contract shall be issued on that security.

• Further, the members may also refer to circular no. NSCC/F&O/C&S/365 dated

91

August 26, 2004, issued by NSCCL regarding Market Wide Position Limit, wherein it is

clarified that a stock which has remained subject to a ban on new position for a significant

part of the month consistently for three months, shall be phased out from trading in

the F&O segment.

However, the existing unexpired contracts may be permitted to trade till expiry and new

strikes may also be introduced in the existing contract months.

Re-introduction of dropped stocks

A stock which is dropped from derivatives trading may become eligible once again. In such

instances, the stock is required to fulfill the eligibility criteria for three consecutive months

to be re-introduced for derivatives trading.

Eligibility Criteria of Indices

• The Exchange may consider introducing derivative contracts on an index if the stocks

contributing to 80% weightage of the index are individually eligible for derivative

trading. However, no single ineligible stocks in the index shall have a weightage of

more than 5% in the index.

• The above criteria is applied every month, if the index fails to meet the eligibility

criteria for three months consecutively, then no fresh month contract shall be issued

on that index, However, the existing unexpired contacts shall be permitted to trade

till expiry and new strikes may also be introduced in the existing contracts.

Selection criteria for unlisted companies

For unlisted companies coming out with initial public offering, if the net public offer is Rs.

500 crore or more, then the Exchange may consider introducing stock options and stock

futures on such stocks at the time of its' listing in the cash market.

Internet Trading

As on March 30 2007, 68 members on the F&O segment provided internet based trading

facility to the investors. About 167 lakh trades amounting to Rs. 922,887.03 crore ( US $

211, 719.90 million) constituting about 12.55 % of the total trading volume in this segment

were routed and executed through the internet. The following table gives the growth of

internet trading in the F&O segment.

Year Enabled Trading Volume Trading Volume % of total

Members* ( Rs. crore) (US $ million) Trading Volume

2002-03 13 5,148.96 1,083.99** 1.42

2003-04 14 42,990.50 9,907.93 2.02

2004-05 63 105,333.96 24,076.33 4.14

2005-06 127 428,569.48 96,070.27 8.88

2006-07 68 922,887.03 211,719.90 12.55

* At the end of financial year.

** Trading volume is compiled from June 24, 2002.

92

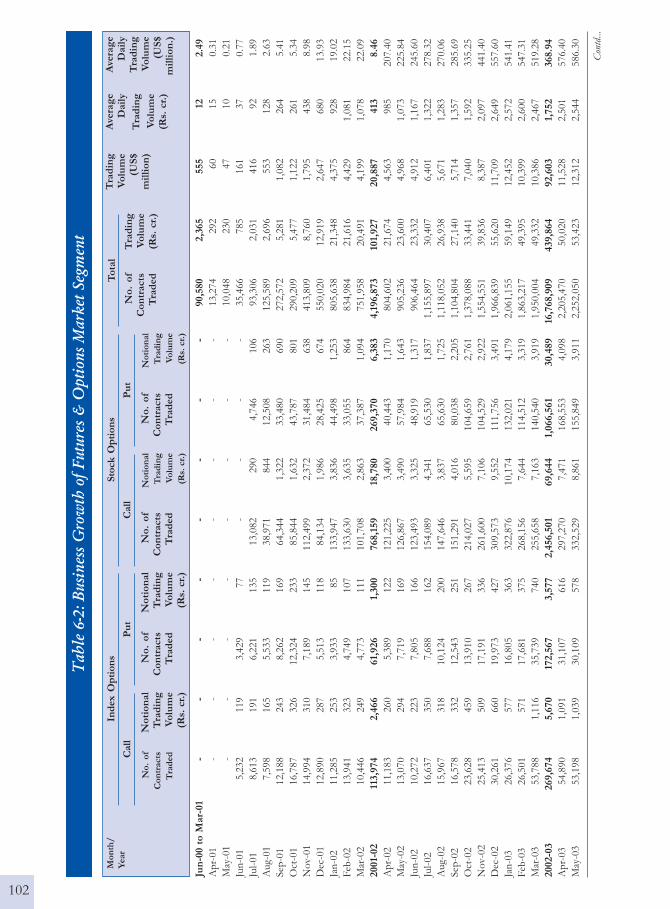

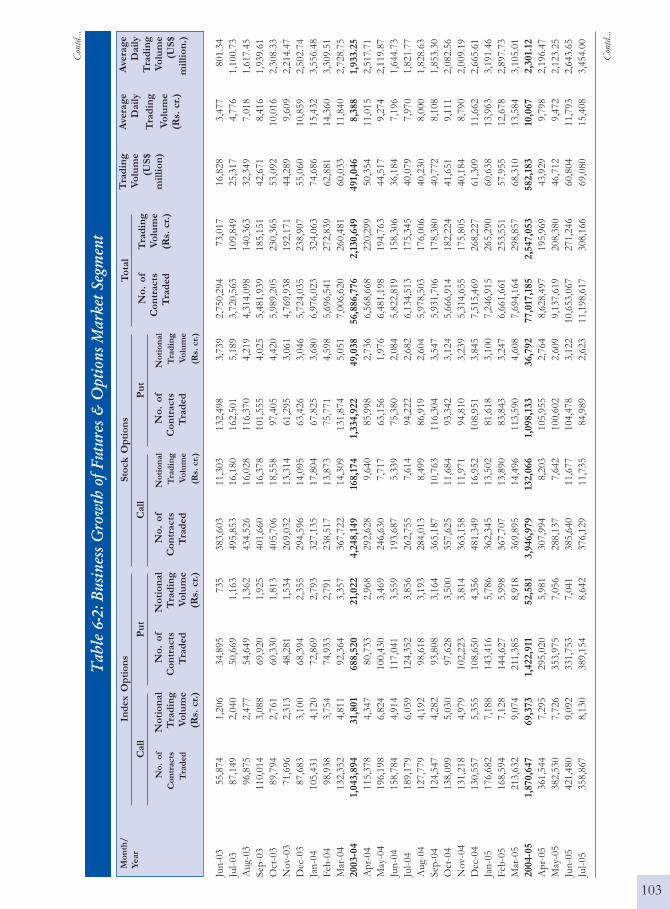

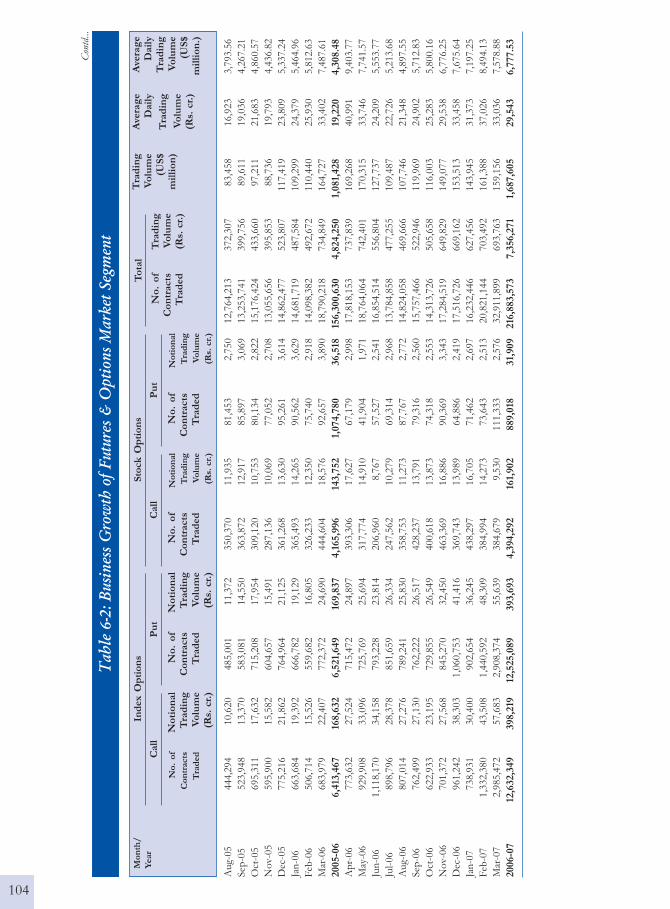

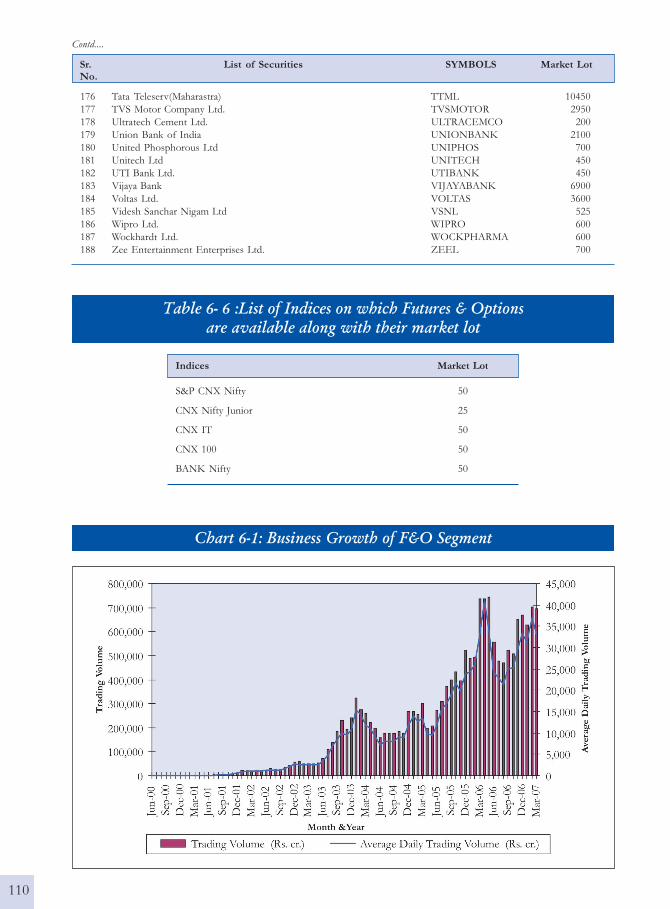

Trading Value

The F&O segment reported a total trading value (notional) of Rs.7,356,271 crore (US $

1,687,605 million) during 2006-07 as against Rs. 4,824,250 crore (US $ 1,687,605 million), a

rise of more than 52.49 % in the past one year. The business growth of F&O segment is

presented in Table 6-2 and Chart 6-1. The F&O segment provides a nationwide market. The

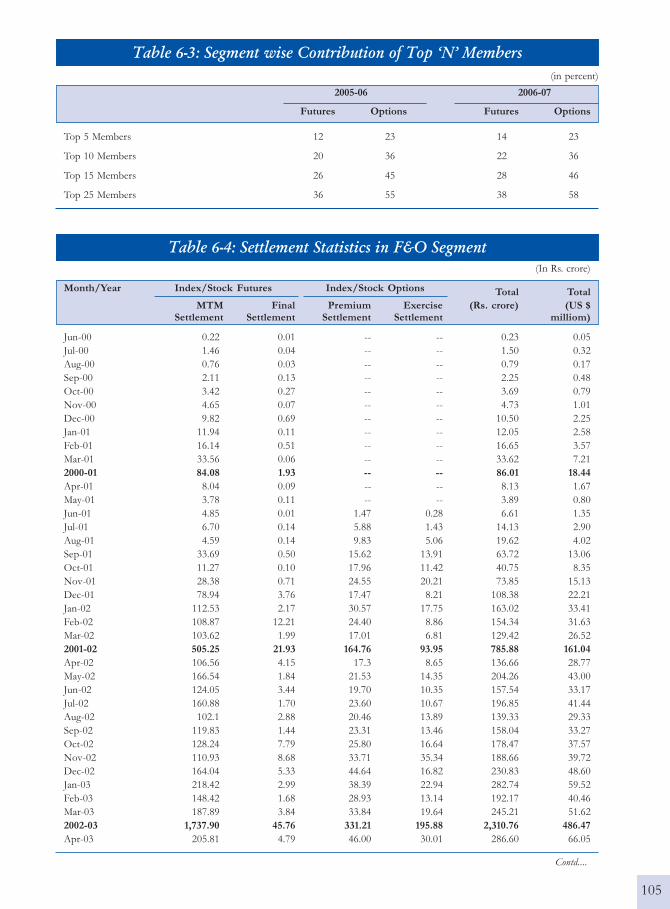

turnover of the top '5' and '10' members accounted to Rs. 1,805,717.55 crore ( US $ 414,250.41

million) and Rs. 2,813,590.61 crore (US $ 645,466.99 million) respectively in 2006-07 in the

Futures segment. However, the turnover of the top '5' and '10' members in the options

segment accounted to Rs. 450,639.73 crore (US $ 103,381.45 million) and Rs. 713,617.56

crore (US $ 163,711.30 million) respectively in the same period. The value contribution of

Top 'N' members is presented in Table 6-3.

Transaction Charges

The maximum brokerage chargeable by a trading member in relation to trades effected in

the contracts admitted to dealing on the F&O segment of NSE is fixed at 2.5% of the

contract value in case of index futures and stock futures. In case of index options and stock

options it is 2.5% of notional value of the contract [(Strike Price + Premium) × Quantity)],

exclusive of statutory levies.

The transaction charges payable to the exchange by the trading member for the trades executed

by him on the F&O segment are fixed at the rate of Rs. 2 per lakh of turnover (0.002%)

subject to a minimum of Rs. 1,00,000 per year. However, for the transactions in the options

sub-segment the transaction charges will be levied on the premium value at the rate of

0.05% (each side) instead of on the strike price as levied earlier.

The trading members contribute to Investor Protection Fund of F&O segment at the rate

of Re.1/- per Rs. 100 crore of the traded value (each side) in case of Futures segment and

Rs.1/- per Rs. 100 crore of the premium amount (each side) in case of Options segment.

The trading members are also required to pay securities transaction tax (STT) on non-delivery

transactions at the rate of 0.017% (payable by the seller) for derivatives w. e. f June 1, 2006.

No transaction charges will be payable in respect of trades done in Interest Rate Futures in

the Futures and Options Segment of the Exchange with effect from 1st April 2007 till 31st

March 2008. Every Trading Member participating in trading in such Interest Rate Futures at

any time during the year 2007-08 shall be required to make a lump sum contribution of

Rs.500/- for the whole year as a contribution to Investor Protection Fund.

There would be no transaction charges levied on turnover above Rs.10 crores per trading

member per day for trades done in NIFTY Junior and CNX 100 in the Futures sub-segment

till September 30, 2007. Further, no transactions charge will be levied on trades done in

NIFTY Junior and CNX 100 in the Options sub-segment till September 30, 2007.

93

Clearing and Settlement

NSCCL undertakes clearing and settlement of all trades executed on the F&O segment of the

Exchange. It also acts as legal counterparty to all trades on this segment and guarantees their

financial settlement. The Clearing and Settlement process comprises of three main activities,

viz., Clearing, Settlement and Risk Management.

Clearing Mechanism

The first step in clearing process is working out open positions and obligations of clearing

(self-clearing/trading-cum-clearing/professional clearing) members (CMs). The open

positions of a CM is arrived at by aggregating the open positions of all the trading members

(TMs) and all custodial participants (CPs) clearing though him, in the contracts which they

have traded. The open position of a TM is arrived at by summing up his proprietary open

position and clients' open positions, in the contracts which they have traded. While entering

orders on the trading system, TMs identify orders as either proprietary or client. Proprietary

positions are calculated on net basis for each contract and that of clients are arrived at by

summing together net positions of each individual client. A TM's open position is the sum

of proprietary open position, client open long position and client open short position.

Settlement Mechanism

All futures and options contracts are cash settled i.e. through exchange of cash. The underlying

for index futures/options of the Nifty index cannot be delivered. The settlement amount

for a CM is netted across all their TMs/clients, across various settlements. For the purpose

of settlement, all CMs are required to open a separate bank account with NSCCL designated

clearing banks for F&O segment.

Settlement of Futures Contracts on Index or Individual Securities

Futures contracts have two types of settlements, the MTM settlement which happens on a

continuous basis at the end of each day, and the final settlement which happens on the last

trading day of the futures contract.

� MTM Settlement for Futures: The positions in futures contracts for each

member are marked-to-market to the daily settlement price of the relevant futures

contract at the end of each day. The CMs who have suffered a loss are required to

pay the mark-to-market (MTM) loss amount in cash which is in turn passed on to

the CMs who have made a MTM profit. This is known as daily mark-to-market

settlement. CMs are responsible to collect and settle the daily MTM profits/losses

incurred by the TMs and their clients clearing and settling through them. Similarly,

TMs are responsible to collect/pay losses/ profits from/to their clients by the

next day. The pay-in and pay-out of the mark-to-market settlement are effected

on the day following the trade day (T+1).

After completion of daily settlement computation, all the open positions are reset to

the daily settlement price. Such positions become the open positions for the next day.

94

� Final Settlement for Futures: On the expiry day of the futures contracts, after the

close of trading hours, NSCCL marks all positions of a CM to the final settlement

price and the resulting profit/loss is settled in cash. Final settlement loss/profit amount

is debited/credited to the relevant CM's clearing bank account on the day following

expiry day of the contract.

� Settlement Prices for Futures: Daily settlement price on a trading day is the

closing price of the respective futures contracts on such day. The closing price

for a futures contract is currently calculated as the last half an hour weighted

average price of the contract in the F&O Segment of NSE. Final settlement

price is the closing price of the relevant underlying index/security in the Capital

Market segment of NSE, on the last trading day of the Contract. The closing

price of the underlying Index/security is currently its last half an hour weighted

average value in the Capital Market Segment of NSE.

Settlement of Options Contracts on Index or Individual Securities

Options contracts have three types of settlements, daily premium settlement, interim

exercise settlement in the case of option contracts on securities and final settlement.

� Daily Premium Settlement for Options: Buyer of an option is obligated to pay the

premium towards the options purchased by him. Similarly, the seller of an option is

entitled to receive the premium for the option sold by him. The premium payable

position and the premium receivable position are netted to compute the net premium

payable or receivable amount for each client for each option contract. The CMs who

have a premium payable position are required to pay the premium amount to NSCCL

which in turn passed on to the members who have a premium receivable position.

This is known as daily premium settlement. CMs are also responsible to collect and

settle for the premium amounts from the TMs and their clients clearing and settling

through them. The pay-in and pay-out of the premium settlement is on T+1 day

(T=Trade day). The premium payable amount and premium receivable amount are

directly credited/debited to the CMs clearing bank account.

� Interim Exercise Settlement: Interim exercise settlement takes place only for option

contracts on individual securities. An investor can exercise his in-the-money options

at any time during trading hours, through his trading member. Interim exercise

settlement is effected for such options at the close of the trading hours, on the day of

exercise. Valid exercised option contracts are assigned to short positions in the option

contract with the same series (i.e. having the same underlying, same expiry date and

same strike price), on a random basis, at the client level. The CM who has exercised

the option receives the exercise settlement value per unit of the option from the CM

who has been assigned the option contract.

Exercise settlement value is debited/credited to the relevant CMs clearing bank account

on T+1 day (T=exercise date).

95

� Final Exercise Settlement: Final Exercise settlement is effected for option positions

at in-the-money strike prices existing at the close of trading hours, on the expiration

day of an option contract. All long positions at in-the-money strike prices are

automatically assigned to short positions in option contracts with the same series, on

a random basis.

For index options contracts, exercise style is European style, while for options contracts

on individual securities, exercise style is American style. Final Exercise is Automatic

on expiry of the option contracts.

Final settlement loss/profit amount for option contracts on Index is debited/credited to

the relevant CMs clearing bank account on T+1 day (T=expiry day). Final settlement loss/

profit amount for option contracts on Individual Securities is debited/credited to the relevant

CMs clearing bank account on T+2 day. Open positions, in option contracts, cease to exist

after their expiration day.

The pay-in / pay-out of funds for a CM on a day is the net amount across settlements and

all TMs/clients, in F&O Segment.

Settlement of Interest Rate Futures Contracts

Daily Mark to Market settlement and Final Mark to Market settlement in respect of admitted

deals in Interest Rate Futures Contracts shall be cash settled by debiting/crediting of the

clearing accounts of Clearing Members with the respective Clearing Bank. All positions

(brought forward, created during the day, closed out during the day) of a F&O CM in Futures

Contracts, at the close of trading hours on a day, shall be marked to market at the Daily

Settlement Price (for Daily Mark to Market Settlement) and settled. All positions (brought

forward, created during the day, closed out during the day) of a F&O Clearing Member in

Futures Contracts, at the close of trading hours on the last trading day, shall be marked to

market at Final Settlement Price (for Final Settlement) and settled. Daily settlement price

shall be the closing price of the relevant futures contract for the trading day. Final settlement

price for an interest rate futures contract shall be based on the value of the notional bond

determined using the ZCYC computed by the Exchange or by any other agency as may be

nominated in this regard. Open positions in Futures contract shall cease to exist after its

expiration day.

� Daily Settlement Price: Daily Settlement price for an interest rate future contract is

the closing price of such interest rate futures contract on the trading day. The closing

price for an interest rate futures contract is calculated on the basis of the last half and

hour weighted average price of such interest rate futures contract. In absence of

trading in the last half an hour, the theoretical price is taken or such other price as

may be decided by the relevant authority from time to time. Theoretical daily settlement

price for unexpired futures contracts shall be the futures prices computed using the

(price of the notional bond) spot prices arrived at from the applicable ZCYC Curve.

The ZCYC shall be computed by the Exchange or by any other agency as may be

96

nominated in this regard from the prices of Government securities traded on the

Exchange or reported on the Negotiated Dealing System of RBI or both taking trades

of same day settlement (i.e. t = 0).

In respect of zero coupon notional bond, the price of the bond shall be the present

value of the principal payment discounted using discrete discounting for the specified

period at the respective zero coupon yield. In respect of the notional T-bill, the

settlement price shall be 100 minus the annualized yield for the specified period

computed using the zero coupon yield curve. In respect of coupon bearing notional

bond, the present value shall be obtained as the sum of present value of the principal

payment discounted at the relevant zero coupon yield and the present values of the

coupons obtained by discounting each notional coupon payment at the relevant zero

coupon yield for that maturity. For this purpose the notional coupon payment date

shall be half yearly and commencing from the date of expiry of the relevant futures

contract. For computation of futures prices from the price of the notional bond

(spot prices) thus arrived, the rate of interest may be the relevant MIBOR rate or

such other rate as may be specified from time to time.

� Final Settlement Price: Final settlement price for an interest rate futures contracts on

zero coupon notional bond and coupon bearing bond shall be based on the price of

the notional bond determined using the zero coupon yield curve. In respect of notional

T-bill it shall be 100 minus the annualized yield for the specified period computed

using the zero coupon yield curve.

Settlement of Custodial Participant (CP) Deals

NSCCL provides a facility to entities like institutions to execute trades through any TM, which

may be cleared and settled by their own CM. Such entities are called Custodial Participants (CP).

To avail of this facility, a CP is required to register with NSCCL through this CM, which allots

them a unique CP code. The CP and the CM are required to enter into an agreement as per

specified format. Thereafter, all trades executed by such CP through any TM are required to have

the CP code in the relevant field on the F&O trading system at the time of order entry. Such

trades executed on behalf of a CP are required to be confirmed by their CM (and not the CM of

the TM through whom the trade was executed), within the time specified by NSE, using the

confirmation facility provided by NSCCL to the CMs in the F&O segment. Till such time the

trade is confirmed by the CM of the CP, the same is considered as a trade of the TM and the

responsibility of settlement of such trade vests with the CM of the TM. Once the trades have

been confirmed by the CM of the CP, they form part of the obligations of the CM of the CP

and they shall be responsible for all obligations arising out of such trades including the payment

of margins and settlement of obligations.

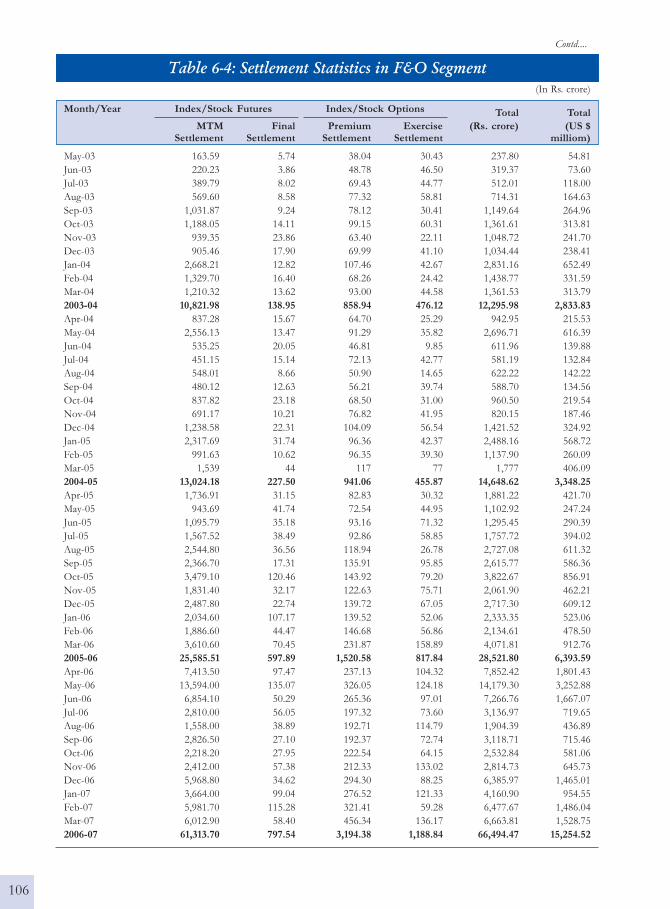

Settlement Statistics

All derivative contracts are currently cash settled. The participants discharge their obligations

through payment/receipt of cash. During the year, 2006-07, such cash settlement amounted

97

to Rs.66,494.47 crore. The details of settlement are presented in Table 6-4. The settlement

of futures and of options involved Rs. 62,111.24 crore and Rs. 4,383.22 crore respectively.

Risk Management System

NSCCL has developed a comprehensive risk containment mechanism for the F&O segment.

The salient features of risk containment measures on the F&O segment are:

• The financial soundness of the members is the key to risk management. Therefore, the

requirements for membership in terms of capital adequacy (net worth, security deposits)

are quite stringent. These requirements have already been explained in Table 2-1 in

Section 2 of this publication.

• NSCCL charges an upfront initial margin for all the open positions of a Clearing Member

(CM). It specifies the initial margin requirements for each futures/options contract on a

daily basis. It follows VaR-based margining computed through SPAN. The CM in turn

collects the initial margin from the trading members (TMs) and their respective clients.

• The open positions of the members are marked to market based on contract settlement

price for each contract at the end of the day. The difference is settled in cash on a T+1

basis.

• NSCCL's on-line position monitoring system monitors a CM's open position on a real-

time basis. Limits are set for each CM based on his effective deposits. The on-line

position monitoring system generates alert messages whenever a CM reaches 70 %, 80

%, 90 % and a disablement message at 100 % of the limit. NSCCL monitors the CMs

for Initial Margin violation, Exposure margin violation, while TMs are monitored for

Initial Margin violation and position limit violation.

• CMs are provided a trading terminal for the purpose of monitoring the open positions

of all the TMs clearing and settling through him. A CM may set limits for a TM clearing

and settling through him. NSCCL assists the CM to monitor the intra-day limits set up

by a CM and whenever a TM exceed the limits, it stops that particular TM from further

trading.

• A member is alerted of his position to enable him to adjust his exposure or bring in

additional capital. Margin violations result in disablement of trading facility for all

TMs of a CM in case of a violation by the CM.

• A separate Settlement Guarantee Fund for this segment has been created out of deposits

of members.

The most critical component of risk containment mechanism for F&O segment is the

margining system and on-line position monitoring. The actual position monitoring and

margining is carried out on-line through Parallel Risk Management System (PRISM) using

SPAN(R)* Standard Portfolio Analysis of Risk) system for the purpose of computation of

on-line margins, based on the parameters defined by SEBI.

* SPAN ® is a registered trademark of the Chicago Mercantile Exchange (CME) used here under license.

98

NSE - SPAN

The objective of NSE-SPAN is to identify overall risk in a portfolio of all futures and

options contracts for each member. The system treats futures and options contracts uniformly,

while at the same time recognising the unique exposures associated with options portfolios,

like extremely deep out-of-the-money short positions and inter-month risk.

Its over-riding objective is to determine the largest loss that a portfolio might reasonably be

expected to suffer from one day to the next day based on 99% VaR methodology.

SPAN considers uniqueness of option portfolios. The following factors affect the value of

an option:

i. Underlying market price

ii. Volatility (variability) of underlying instrument

iii. Time to expiration

iv. Interest rate

v. Strike price

As these factors change, the value of options maintained within a portfolio also changes.

Thus, SPAN constructs scenarios of probable changes in underlying prices and volatilites in

order to identify the largest loss a portfolio might suffer from one day to the next. It then

sets the margin requirement to cover this one-day loss.

The complex calculations (e.g. the pricing of options) in SPAN are executed by NSCCL.

The results of these calculations are called risk arrays. Risk arrays, and other necessary data

inputs for margin calculation are provided to members daily in a file called the SPAN Risk

Parameter file. Members can apply the data contained in the Risk Parameter files, to their

specific portfolios of futures and options contracts, to determine their SPAN margin

requirements.

Hence, members need not execute a complex option pricing calculations, which is performed

by NSCCL. SPAN has the ability to estimate risk for combined futures and options portfolios,

and also re-value the same under various scenarios of changing market conditions.

NSCCL generates six risk parameters file for a day taking into account price and volatilities

at various time intervals and are provided on the website of the Exchange.

Margins

The margining system for F&O segment is as below:

� Initial margin: Margin in the F&O segment is computed by NSCCL upto client level for

open positions of CMs/TMs. These are required to be paid up-front on gross basis at

individual client level for client positions and on net basis for proprietary positions.

99

NSCCL collects initial margin for all the open positions of a CM based on the margins

computed by NSE-SPAN. A CM is required to ensure collection of adequate initial

margin from his TMs up-front. The TM is required to collect adequate initial margins

up-front from his clients.

� Premium Margin: In addition to Initial Margin, Premium Margin is charged at client

level. This margin is required to be paid by a buyer of an option till the premium

settlement is complete.

� Assignment Margin for Options on Securities: Assignment margin is levied in addition to

initial margin and premium margin. It is required to be paid on assigned positions of

CMs towards interim and final exercise settlement obligations for option contracts on

individual securities, till such obligations are fulfilled. The margin is charged on the net

exercise settlement value payable by a CM towards interim and final exercise settlement.

� Exposure Margins: Clearing members are subject to exposure margins in addition to

initial margins.

� Client Margins: NSCCL intimates all members of the margin liability of each of their

client. Additionally members are also required to report details of margins collected

from clients to NSCCL, which holds in trust client margin monies to the extent reported

by the member as having been collected form their respective clients.

100

Tab

le 6

-1:

Con

trac

t Sp

ecif

icat

ion

for

F&

O

Part

icu

lars

Ind

ex

Fu

ture

sS

tock

Fu

ture

sIn

dex

Op

tio

ns

Sto

ck

Op

tio

ns

Inte

rest

Rate

Fu

ture

s

Sec

uri

ty D

escr

ipti

on

FU

TID

XF

UT

ST

KO

PT

IDX

OP

TST

KF

UT

INT

Un

der

lyin

gS&

P C

NX

Nif

tyIn

div

idual

Sec

uri

ties

S&

P C

NX

Nif

ty I

nd

ex/

Ind

ivid

ual

Sec

uri

ties

No

tio

nal

10

year

bo

nd

(6%

co

up

on

),In

dex

/C

NX

IT

In

dex

/C

NX

IT

In

dex

/N

oti

on

al 1

0 ye

ar z

ero

co

up

on

bo

nd

an

dB

AN

K N

ifty

In

dex

/B

AN

K N

ifty

In

dex

/N

oti

on

al 9

1 d

ay T

-Bill

CN

X N

ifty

Jun

ior

CN

X N

ifty

Jun

ior

and

and

CN

X 1

00C

NX

100

Sty

le o

f O

pti

on

NA

NA

Euro

pea

nA

mer

ican

NA

Co

ntr

act

Siz

eA

s sp

ecif

ied

by

SE

BI;

As

spec

ifie

d b

y SE

BI;

As

spec

ifie

d b

y SE

BI;

As

spec

ifie

d b

y SE

BI;

Per

mit

ted

lo

t si

ze i

s 2,

000

Cur

rentl

y m

inim

um R

s. 2

lak

hs

Cur

rentl

y m

inim

um R

s. 2

lak

hs

Cur

rentl

y m

inim

um R

s. 2

lak

hs

Cur

rently

min

imum

Rs.

2 lak

hs

at t

he

tim

e o

f in

tro

duct

ion

at t

he

tim

e o

f in

tro

duct

ion

at t

he

tim

e o

f in

tro

duct

ion

at t

he

tim

e o

f in

tro

duct

ion

Pri

ce S

tep

s

Rs.

0.0

5

Rs.

0.0

1

Exp

irat

ion

Mo

nth

s

3 n

ear

mo

nth

s

On

e ye

ar

Tra

din

g C

ycle

A m

axim

um

of

thre

e m

on

th t

rad

ing

cycl

e -

the

nea

r m

on

th (

on

e),

the

nex

t m

on

th (

two

) an

d t

he

far

mo

nth

(th

ree)

.T

he

con

trac

ts s

hal

l b

e fo

r a

per

iod

of

a m

aturi

tyN

ew c

on

trac

t is

in

tro

duce

d o

n t

he

nex

t tr

adin

g d

ay f

ollo

win

g th

e ex

pir

y o

f n

ear

mo

nth

co

ntr

act

of

on

e ye

ar w

ith

th

ree

mo

nth

s co

nti

nuo

us

con

trac

ts f

or

the

firs

t th

ree

mo

nth

s an

d f

ixed

quar

terl

y co

ntr

acts

fo

r th

e en

tire

yea

r

Las

t T

rad

ing/

Exp

irat

ion

Day

Las

t T

hurs

day

of

the

exp

iry

mo

nth

or

the

pre

ced

ing

trad

ing

day

, if

las

t T

hurs

day

is

a tr

adin

g h

olid

ayL

ast

Th

urs

day

of

the

exp

iry

mo

nth

. If

las

tT

hurs

day

is

a tr

adin

g h

olid

ay,

the

con

trac

t sh

all

exp

ire

on

pre

vio

us

trad

ing

day

. F

urt

her

, w

her

e th

ela

st T

hurs

day

fal

ls o

n t

he

ann

ual

or

hal

f ye

arly

clo

sin

g d

ates

of

the

ban

k, t

he

con

trac

t sh

all

exp

ire

on

pre

vio

us

trad

ing

day

.

Pri

ce B

and

sO

per

atin

g ra

nge

of

Op

erat

ing

ran

ge o

fO

per

atin

g ra

nge

of

Op

erat

ing

ran

ge o

fO

per

atin

g ra

nge

of

10%

of

the

bas

e p

rice

20%

of

the

bas

e p

rice

99%

of

the

bas

e p

rice

99%

of

the

bas

e p

rice

2% o

f th

e b

ase

pri

ce

No.

of

Str

ike

Pri

ces

NA

NA

NIF

TY

,JR

. N

IFT

Y a

nd

7 st

rike

s (t

hre

e 'in

th

e m

on

ey',

NA

CN

X 1

00 B

AN

K N

ifty

&o

ne

'at

the

mo

ney

' an

d t

hre

eC

NX

IT

Up

to

200

0 -

9'o

ut

of

the

mo

ney

) fo

r ev

ery

stri

kes

(fo

ur

'in-t

he-

mo

ney

'),

op

tio

n t

ype

(i.e

cal

l an

d p

ut)

on

e 'a

t th

e m

on

ey' a

nd

fo

ur'

out

of

the

mo

ney

) fo

r ev

ery

op

tio

n t

ype

(i.e

. ca

ll an

d p

ut)

> 2

001

up

to 4

000

- 9

stri

kes

(fo

ur

'in-t

he-

mo

ney

'),

on

e'a

t th

e m

on

ey' a

nd

fo

ur'

out

Contd...

101

Tab

le 6

-1:

Con

trac

t Sp

ecif

icat

ion

for

F&

O

Part

icu

lars

Ind

ex

Fu

ture

sS

tock

Fu

ture

sIn

dex

Op

tio

ns

Sto

ck

Op

tio

ns

Inte

rest

Rate

Fu

ture

s

of

the

mo

ney

) fo

r ev

ery

op

tio

n t

ype

(i.e

. ca

ll an

d p

ut)

> 4

001

up

to 6

000

- 11

str

ikes

(fiv

e 'in

th

e m

on

ey',

on

e'a

t th

e m

on

ey' a

nd

fiv

e' o

ut

of

the

mo

ney

') f

or

ever

yo

pti

on

typ

e (i

.e c

all

and

put)

> 6

000

-13

stri

kes

(six

'in

th

em

on

ey',

on

e 'a

t th

e m

on

ey'

and

six

'o

ut

of

the

mo

ney

')fo

r ev

ery

op

tio

n t

ype

(i.e

cal

l an

d p

ut)

Str

ike

Pri

ce I

nte

rval

(in

Rs.

)N

AN

AU

p t

o 2

000

25

Bet

wee

n 2

.5 a

nd

50

NA

2001

-400

0

50

dep

end

ing

on

th

e p

rice

4001

-600

0

50

of

un

der

lyin

g>

600

0

50

Set

tlem

ent

In c

ash

on

T+

1 b

asis

In c

ash

on

T+

1 b

asis

In c

ash

on

T+

1 b

asis

Dai

ly s

ettl

emen

t o

n T

+1

Dai

ly M

ark-

to-M

arke

t se

ttle

men

tb

asis

an

d f

inal

set

tlem

ent

and

Fin

al S

ettl

emen

t w

ill b

eo

n T

+1

bas

iso

n T

+1

bas

is

Dai

ly S

ettl

emen

t P

rice

Clo

sin

g p

rice

of

futu

res

Clo

sin

g p

rice

of

futu

res

Pre

miu

m V

alue

(net

)P

rem

ium

Val

ue

(net

)A

s m

ay b

e st

ipula

ted

by

NSC

CL

con

trac

t o

n t

he

trad

ing

day

con

trac

t o

n t

he

trad

ing

day

in t

his

reg

ard

fro

m t

ime

to t

ime

Fin

al S

ettl

emen

t P

rice

Clo

sin

g va

lue

un

der

lyin

gC

losi

ng

valu

e un

der

lyin

gC

losi

ng

valu

e o

f su

chC

losi

ng

valu

e o

f su

chA

s m

ay b

e st

ipula

ted

by

NSC

CL

ind

ex/

secu

rity

on

th

e la

stin

dex

/se

curi

ty o

n t

he

last

un

der

lyin

g se

curi

ty (

ind

ex)

un

der

lyin

g se

curi

ty (

ind

ex)

in t

his

reg

ard

fro

m t

ime

to t

ime

trad

ing

day

of

the

futu

res

trad

ing

day

of

the

futu

res

on

th

e la

st t

rad

ing

day

of

the

on

th

e la

st t

rad

ing

day

of

the

con

trac

t.co

ntr

act.

op

tio

ns

con

trac

t.o

pti

on

s co

ntr

act.

Set

tlem

ent

Day

Las

t tr

adin

g d

ay

Mar

gin

s U

p-f

ron

t in

itia

l m

argi

n o

n d

aily

bas

is

NA

: N

ot

app

licab

le

Contd...

102

Contd...

Tab

le 6

-2:

Bu

sin

ess

Gro

wth

of

Fu

ture

s &

Op

tion

s M

ark

et S

egm

ent

Ind

ex O

pti

on

s

Call

Pu

t

No

. o

f

Co

ntr

acts

Tra

ded

No

tio

nal

Tra

din

gV

olu

me

(Rs.

cr.

)

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

gV

olu

me

(Rs.

cr.

)

To

tal

No

. o

fC

on

tracts

Tra

ded

Jun

-00 t

o M

ar-

01

--

--

--

--

90,5

80

2,3

65

555

122.4

9

Ap

r-01

--

--

--

--

13,2

74

292

6015

0.3

1

May

-01

--

--

--

--

10,0

48

230

4710

0.2

1

Jun

-01

5,2

32

119

3,4

29

77-

--

-35,4

66

785

161

370.7

7

Jul-

01

8,6

13

191

6,2

21

135

13,0

82

290

4,7

46

106

93,3

06

2,0

31

416

921.8

9

Aug-

01

7,5

98

165

5,5

33

119

38,9

71

844

12,5

08

263

125,5

89

2,6

96

553

128

2.6

3

Sep

-01

12,1

88

243

8,2

62

169

64,3

44

1,3

22

33,4

80

690

272,5

72

5,2

81

1,0

82

264

5.4

1

Oct

-01

16,7

87

326

12,3

24

233

85,8

44

1,6

32

43,7

87

801

290,2

09

5,4

77

1,1

22

261

5.3

4

No

v-0

114,9

94

310

7,1

89

145

112,4

99

2,3

72

31,4

84

638

413,8

09

8,7

60

1,7

95

438

8.9

8

Dec

-01

12,8

90

287

5,5

13

118

84,1

34

1,9

86

28,4

25

674

550,0

20

12,9

19

2,6

47

680

13.9

3

Jan

-02

11,2

85

253

3,9

33

85133,9

47

3,8

36

44,4

98

1,2

53

805,6

38

21,3

48

4,3

75

928

19.0

2

Feb

-02

13,9

41

323

4,7

49

107

133,6

30

3,6

35

33,0

55

864

834,9

84

21,6

16

4,4

29

1,0

81

22.1

5

Mar

-02

10,4

46

249

4,7

73

111

101,7

08

2,8

63

37,3

87

1,0

94

751,9

58

20,4

91

4,1

99

1,0

78

22.0

9

2001-

02

113,9

74

2,4

66

61,

926

1,300

768,1

59

18,7

80

269,3

70

6,3

83

4,1

96,8

73

101,

927

20,8

87

413

8.4

6

Ap

r-02

11,1

83

260

5,3

89

122

121,2

25

3,4

00

40,4

43

1,1

70

804,6

02

21,6

74

4,5

63

985

207.4

0

May

-02

13,0

70

294

7,7

19

169

126,8

67

3,4

90

57,9

84

1,6

43

905,2

36

23,6

00

4,9

68

1,0

73

225.8

4

Jun

-02

10,2

72

223

7,8

05

166

123,4

93

3,3

25

48,9

19

1,3

17

906,4

64

23,3

32

4,9

12

1,1

67

245.6

0

Jul-

02

16,6

37

350

7,6

88

162

154,0

89

4,3

41

65,5

30

1,8

37

1,1

55,8

97

30,4

07

6,4

01

1,3

22

278.3

2

Aug-

02

15,9

67

318

10,1

24

200

147,6

46

3,8

37

65,6

30

1,7

25

1,1

18,0

52

26,9

38

5,6

71

1,2

83

270.0

6

Sep

-02

16,5

78

332

12,5

43

251

151,2

91

4,0

16

80,0

38

2,2

05

1,1

04,8

04

27,1

40

5,7

14

1,3

57

285.6

9

Oct

-02

23,6

28

459

13,9

10

267

214,0

27

5,5

95

104,6

59

2,7

61

1,3

78,0

88

33,4

41

7,0

40

1,5

92

335.2

5

No

v-0

225,4

13

509

17,1

91

336

261,6

00

7,1

06

104,5

29

2,9

22

1,5

54,5

51

39,8

36

8,3

87

2,0

97

441.4

0

Dec

-02

30,2

61

660

19,9

73

427

309,5

73

9,5

52

111,7

56

3,4

91

1,9

66,8

39

55,6

20

11,7

09

2,6

49

557.6

0

Jan

-03

26,3

76

577

16,8

05

363

322,8

76

10,1

74

132,0

21

4,1

79

2,0

61,1

55

59,1

49

12,4

52

2,5

72

541.4

1

Feb

-03

26,5

01

571

17,6

81

375

268,1

56

7,6

44

114,5

12

3,3

19

1,8

63,2

17

49,3

95

10,3

99

2,6

00

547.3

1

Mar

-03

53,7

88

1,1

16

35,7

39

740

255,6

58

7,1

63

140,5

40

3,9

19

1,9

50,0

04

49,3

32

10,3

86

2,4

67

519.2

8

2002-0

3269,6

74

5,6

70

172,5

67

3,5

77

2,4

56,5

01

69,6

44

1,066,5

61

30,4

89

16,7

68,9

09

439,8

64

92,6

03

1,752

368.9

4

Ap

r-03

54,8

90

1,0

91

31,1

07

616

297,2

70

7,4

71

168,5

53

4,0

98

2,2

05,4

70

50,0

20

11,5

28

2,5

01

576.4

0

May

-03

53,1

98

1,0

39

30,1

09

578

332,5

29

8,8

61

155,8

49

3,9

11

2,2

52,0

50

53,4

23

12,3

12

2,5

44

586.3

0

Ave

rag

eD

ail

yT

rad

ing

Vo

lum

e(U

S$

mil

lio

n.)

Tra

din

gV

olu

me

(Rs.

cr.

)

Mo

nth

/

Year

Sto

ck

Op

tio

ns

Call

Pu

t

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

g

Vo

lum

e

(Rs.

cr.

)

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

g

Vo

lum

e

(Rs.

cr.

)

Ave

rag

eD

ail

y

Tra

din

g

Vo

lum

e(R

s. c

r.)

Tra

din

gV

olu

me

(US

$m

illi

on

)

103

Contd...

Tab

le 6

-2:

Bu

sin

ess

Gro

wth

of

Fu

ture

s &

Op

tion

s M

ark

et S

egm

ent

Jun

-03

55,8

74

1,2

06

34,8

95

735

383,6

03

11,3

03

132,4

98

3,7

39

2,7

50,2

94

73,0

17

16,8

28

3,4

77

801.3

4

Jul-

03

87,1

49

2,0

40

50,6

69

1,1

63

495,8

53

16,1

80

162,5

01

5,1

89

3,7

20,5

63

109,8

49

25,3

17

4,7

76

1,1

00.7

3

Aug-

03

96,8

75

2,4

77

54,6

49

1,3

62

434,5

26

16,0

28

116,3

70

4,2

19

4,3

14,0

98

140,3

63

32,3

49

7,0

18

1,6

17.4

5

Sep

-03

110,0

14

3,0

88

69,9

20

1,9

25

401,6

60

16,3

78

101,5

55

4,0

25

5,4

81,9

39

185,1

51

42,6

71

8,4

16

1,9

39.6

1

Oct

-03

89,7

94

2,7

61

60,3

30

1,8

13

405,7

06

18,5

58

97,4

05

4,4

20

5,9

89,2

05

230,3

65

53,0

92

10,0

16

2,3

08.3

3

No

v-0

371,6

96

2,3

13

48,2

81

1,5

34

269,0

32

13,3

14

61,2

95

3,0

61

4,7

69,9

38

192,1

71

44,2

89

9,6

09

2,2

14.4

7

Dec

-03

87,6

83

3,1

00

68,3

94

2,3

55

294,5

96

14,0

95

63,4

26

3,0

46

5,7

24,0

35

238,9

07

55,0

60

10,8

59

2,5

02.7

4

Jan

-04

105,4

31

4,1

20

72,8

69

2,7

93

327,1

35

17,8

04

67,8

25

3,6

80

6,9

76,0

23

324,0

63

74,6

86

15,4

32

3,5

56.4

8

Feb

-04

98,9

38

3,7

54

74,9

33

2,7

91

238,5

17

13,8

73

75,7

71

4,5

98

5,6

96,5

41

272,8

39

62,8

81

14,3

60

3,3

09.5

1

Mar

-04

132,3

52

4,8

11

92,3

64

3,3

57

367,7

22

14,3

09

131,8

74

5,0

51

7,0

06,6

20

260,4

81

60,0

33

11,8

40

2,7

28.7

5

2003-0

41,

043,8

94

31,

801

688,5

20

21,

022

4,2

48,1

49

168,1

74

1,334,9

22

49,0

38

56,8

86,7

76

2,1

30,6

49

491,

046

8,3

88

1,933.2

5

Ap

r-04

115,3

78

4,3

47

80,7

33

2,9

68

292,6

28

9,6

40

85,9

98

2,7

36

6,5

68,6

68

220,2

99

50,3

54

11,0

15

2,5

17.7

1

May

-04

196,1

98

6,8

24

100,4

30

3,4

69

246,6

30

7,7

17

63,1

56

1,9

76

6,4

81,1

98

194,7

63

44,5

17

9,2

74

2,1

19.8

7

Jun

-04

158,7

84

4,9

14

117,0

41

3,5

59

193,6

87

5,3

39

75,3

80

2,0

84

5,8

22,8

19

158,3

06

36,1

84

7,1

96

1,6

44.7

3

Jul-

04

189,1

79

6,0

59

124,3

52

3,8

56

262,7

55

7,6

14

94,2

22

2,6

82

6,1

34,5

13

175,3

45

40,0

79

7,9

70

1,8

21.7

7

Aug-

04

127,7

79

4,1

92

98,6

18

3,1

93

284,0

13

8,4

99

86,9

19

2,6

04

5,9

78,5

03

176,0

06

40,2

30

8,0

00

1,8

28.6

3

Sep

-04

124,5

47

4,2

82

93,8

08

3,1

64

365,1

87

10,7

63

116,3

04

3,5

47

5,9

31,7

06

178,3

80

40,7

72

8,1

08

1,8

53.3

0

Oct

-04

138,0

99

5,0

30

97,6

28

3,5

00

357,6

25

11,6

84

93,3

42

3,1

24

5,6

66,9

14

182,2

24

41,6

51

9,1

11

2,0

82.5

6

No

v-0

4131,2

18

4,9

79

102,2

23

3,8

14

363,1

58

11,9

71

94,8

10

3,2

39

5,3

14,6

55

175,8

05

40,1

84

8,7

90

2,0

09.1

9

Dec

-04

130,5

57

5,3

55

108,6

50

4,3

56

481,3

49

16,9

52

108,9

51

3,8

45

7,5

15,4

69

268,2

27

61,3

09

11,6

62

2,6

65.6

1

Jan

-05

176,6

82

7,1

88

143,4

16

5,7

86

362,3

45

13,5

02

81,6

18

3,1

00

7,2

46,9

15

265,2

90

60,6

38

13,9

63

3,1

91.4

6

Feb

-05

168,5

94

7,1

28

144,6

27

5,9

98

367,7

07

13,8

90

83,8

43

3,2

47

6,6

61,6

61

253,5

51

57,9

55

12,6

78

2,8

97.7

3

Mar

-05

213,6

32

9,0

74

211,3

85

8,9

18

369,8

95

14,4

96

113,5

90

4,6

08

7,6

94,1

64

298,8

57

68,3

10

13,5

84

3,1

05.0

1

2004-0

51,

870,6

47

69,3

73

1,422,9

1152,5

81

3,9

46,9

79

132,0

66

1,098,1

33

36,7

92

77,0

17,1

85

2,5

47,0

53

582,1

83

10,0

67

2,3

01.

12

Ap

r-05

361,5

44

7,2

95

295,0

20

5,9

81

307,9

94

8,2

03

105,9

55

2,7

64

8,6

28,4

97

195,9

69

43,9

29

9,7

98

2,1

96.4

7

May

-05

382,5

30

7,7

26

353,9

75

7,0

56

288,1

37

7,6

42

100,6

02

2,6

09

9,1

37,6

19

208,3

80

46,7

12

9,4

72

2,1

23.2

5

Jun

-05

421,4

80

9,0

92

331,7

53

7,0

41

385,6

40

11,6

77

104,4

78

3,1

22

10,6

53,0

67

271,2

46

60,8

04

11,7

93

2,6

43.6

5

Jul-

05

358,8

67

8,1

30

389,1

54

8,6

42

376,1

29

11,7

35

84,9

89

2,6

23

11,1

98,6

17

308,1

66

69,0

80

15,4

08

3,4

54.0

0

Contd...

Ind

ex O

pti

on

s

Call

Pu

t

No

. o

f

Co

ntr

acts

Tra

ded

No

tio

nal

Tra

din

gV

olu

me

(Rs.

cr.

)

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

gV

olu

me

(Rs.

cr.

)

To

tal

No

. o

fC

on

tracts

Tra

ded

Ave

rag

eD

ail

yT

rad

ing

Vo

lum

e(U

S$

mil

lio

n.)

Tra

din

gV

olu

me

(Rs.

cr.

)

Mo

nth

/

Year

Sto

ck

Op

tio

ns

Call

Pu

t

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

g

Vo

lum

e

(Rs.

cr.

)

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

g

Vo

lum

e

(Rs.

cr.

)

Ave

rag

eD

ail

y

Tra

din

g

Vo

lum

e(R

s. c

r.)

Tra

din

gV

olu

me

(US

$m

illi

on

)

104

Contd...

Tab

le 6

-2:

Bu

sin

ess

Gro

wth

of

Fu

ture

s &

Op

tion

s M

ark

et S

egm

ent

Aug-

05

444,2

94

10,6

20

485,0

01

11,3

72

350,3

70

11,9

35

81,4

53

2,7

50

12,7

64,2

13

372,3

07

83,4

58

16,9

23

3,7

93.5

6

Sep

-05

523,9

48

13,3

70

583,0

81

14,5

50

363,8

72

12,9

17

85,8

97

3,0

69

13,2

53,7

41

399,7

56

89,6

11

19,0

36

4,2

67.2

1

Oct

-05

695,3

11

17,6

32

715,2

08

17,9

54

309,1

20

10,7

53

80,1

34

2,8

22

15,1

76,4

24

433,6

60

97,2

11

21,6

83

4,8

60.5

7

No

v-0

5 5

95,9

00

15,5

82

604,6

57

15,4

91

287,1

36

10,0

69

77,0

52

2,7

08

13,0

55,6

56

395,8

53

88,7

36

19,7

93

4,4

36.8

2

Dec

-05

775,2

16

21,8

62

764,9

64

21,1

25

361,2

68

13,6

30

95,2

61

3,6

14

14,8

62,4

77

523,8

07

117,4

19

23,8

09

5,3

37.2

4

Jan

-06

663,6

84

19,3

92

666,7

82

19,1

29

365,4

93

14,2

65

90,5

62

3,6

29

14,6

81,7

19

487,5

84

109,2

99

24,3

79

5,4

64.9

6

Feb

-06

506,7

14

15,5

26

559,6

82

16,8

05

326,2

33

12,3

50

75,7

40

2,9

18

14,0

98,3

82

492,6

72

110,4

40

25,9

30

5,8

12.6

3

Mar

-06

683,9

79

22,4

07

772,3

72

24,6

90

444,6

04

18,5

76

92,6

57

3,8

90

18,7

90,2

18

734,8

49

164,7

27

33,4

02

7,4

87.6

1

2005-0

6 6

,413

,467

168,6

32

6,5

21,

649

169,8

37

4,1

65,9

96

143,7

52

1,0

74,7

80

36,5

18 1

56,3

00,6

30

4,8

24,2

50

1,0

81,

428

19,2

20

4,3

08.4

8

Ap

r-06

773,6

32

27,5

24

715,4

72

24,8

97

393,3

06

17,6

27

67,1

79

2,9

98

17,8

18,1

53

737,8

39

169,2

68

40,9

91

9,4

03.7

7

May

-06

929,9

08

33,0

96

725,7

69

25,6

94

317,7

74

14,9

10

41,9

04

1,9

71

18,7

64,0

64

742,4

01

170,3

15

33,7

46

7,7

41.5

7

Jun

-06

1,1

18,1

70

34,1

58

793,2

28

23,8

14

206,9

60

8,7

67

57,5

27

2,5

41

16,8

54,5

14

556,8

04

127,7

37

24,2

09

5,5

53.7

7

Jul-

06

898,7

96

28,3

78

851,6

59

26,3

34

247,5

62

10,2

79

69,3

14

2,9

68

13,7

84,8

58

477,2

55

109,4

87

22,7

26

5,2

13.6

8

Aug-

06

807,0

14

27,2

76

789,2

41

25,8

30

358,7

53

11,2

73

87,7

67

2,7

72

14,8

24,0

58

469,6

66

107,7

46

21,3

48

4,8

97.5

5

Sep

-06

762,4

99

27,1

30

762,2

22

26,5

17

428,2

37

13,7

91

79,3

16

2,5

60

15,7

57,4

66

522,9

46

119,9

69

24,9

02

5,7

12.8

3

Oct

-06

622,9

33

23,1

95

729,8

55

26,5

49

400,6

18

13,8

73

74,3

18

2,5

53

14,3

13,7

26

505,6

58

116,0

03

25,2

83

5,8

00.1

6

No

v-0

6 7

01,3

72

27,5

68

845,2

70

32,4

50

463,3

69

16,8

86

90,3

69

3,3

43

17,2

84,5

19

649,8

29

149,0

77

29,5

38

6,7

76.2

5

Dec

-06

961,2

42

38,3

03

1,0

60,7

53

41,4

16

369,7

43

13,9

89

64,8

86

2,4

19

17,5

16,7

26

669,1

62

153,5

13

33,4

58

7,6

75.6

4

Jan

-07

738,9

31

30,4

00

902,6

54

36,2

45

438,2

97

16,7

05

71,4

62

2,6

97

16,2

32,4

46

627,4

56

143,9

45

31,3

73

7,1

97.2

5

Feb

-07

1,3

32,3

80

43,5

08

1,4

40,5

92

48,3

09

384,9

94

14,2

73

73,6

43

2,5

13

20,8

21,1

44

703,4

92

161,3

88

37,0

26

8,4

94.1

3

Mar

-07

2,9

85,4

72

57,6

83

2,9

08,3

74

55,6

39

384,6

79

9,5

30

111,3

33

2,5

76

32,9

11,8

99

693,7

63

159,1

56

33,0

36

7,5

78.8

8

2006-0

7 1

2,6

32,3

49

398,2

19 1

2,5

25,0

89

393,6

93

4,3

94,2

92

161,

902

889,0

18 3

1,909

216

,883,5

73

7,3

56,2

71

1,6

87,6

05

29,5

43

6,7

77.5

3

Ind

ex O

pti

on

s

Call

Pu

t

No

. o

f

Co

ntr

acts

Tra

ded

No

tio

nal

Tra

din

gV

olu

me

(Rs.

cr.

)

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

gV

olu

me

(Rs.

cr.

)

To

tal

No

. o

fC

on

tracts

Tra

ded

Ave

rag

eD

ail

yT

rad

ing

Vo

lum

e(U

S$

mil

lio

n.)

Tra

din

gV

olu

me

(Rs.

cr.

)

Mo

nth

/

Year

Sto

ck

Op

tio

ns

Call

Pu

t

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

g

Vo

lum

e

(Rs.

cr.

)

No

. o

fC

on

tracts

Tra

ded

No

tio

nal

Tra

din

g

Vo

lum

e

(Rs.

cr.

)

Ave

rag

eD

ail

y

Tra

din

g

Vo

lum

e(R

s. c

r.)

Tra

din

gV

olu

me

(US

$m

illi

on

)

105

Table 6-3: Segment wise Contribution of Top ‘N’ Members

Table 6-4: Settlement Statistics in F&O Segment(In Rs. crore)

Month/Year Index/Stock Futures Index/Stock Options Total Total

MTM Final Premium Exercise (Rs. crore) (US $Settlement Settlement Settlement Settlement milliom)

Jun-00 0.22 0.01 -- -- 0.23 0.05

Jul-00 1.46 0.04 -- -- 1.50 0.32

Aug-00 0.76 0.03 -- -- 0.79 0.17

Sep-00 2.11 0.13 -- -- 2.25 0.48

Oct-00 3.42 0.27 -- -- 3.69 0.79

Nov-00 4.65 0.07 -- -- 4.73 1.01

Dec-00 9.82 0.69 -- -- 10.50 2.25

Jan-01 11.94 0.11 -- -- 12.05 2.58

Feb-01 16.14 0.51 -- -- 16.65 3.57

Mar-01 33.56 0.06 -- -- 33.62 7.21

2000-01 84.08 1.93 -- -- 86.01 18.44

Apr-01 8.04 0.09 -- -- 8.13 1.67

May-01 3.78 0.11 -- -- 3.89 0.80

Jun-01 4.85 0.01 1.47 0.28 6.61 1.35

Jul-01 6.70 0.14 5.88 1.43 14.13 2.90

Aug-01 4.59 0.14 9.83 5.06 19.62 4.02

Sep-01 33.69 0.50 15.62 13.91 63.72 13.06

Oct-01 11.27 0.10 17.96 11.42 40.75 8.35

Nov-01 28.38 0.71 24.55 20.21 73.85 15.13

Dec-01 78.94 3.76 17.47 8.21 108.38 22.21

Jan-02 112.53 2.17 30.57 17.75 163.02 33.41

Feb-02 108.87 12.21 24.40 8.86 154.34 31.63

Mar-02 103.62 1.99 17.01 6.81 129.42 26.52

2001-02 505.25 21.93 164.76 93.95 785.88 161.04

Apr-02 106.56 4.15 17.3 8.65 136.66 28.77

May-02 166.54 1.84 21.53 14.35 204.26 43.00

Jun-02 124.05 3.44 19.70 10.35 157.54 33.17

Jul-02 160.88 1.70 23.60 10.67 196.85 41.44

Aug-02 102.1 2.88 20.46 13.89 139.33 29.33

Sep-02 119.83 1.44 23.31 13.46 158.04 33.27

Oct-02 128.24 7.79 25.80 16.64 178.47 37.57

Nov-02 110.93 8.68 33.71 35.34 188.66 39.72

Dec-02 164.04 5.33 44.64 16.82 230.83 48.60

Jan-03 218.42 2.99 38.39 22.94 282.74 59.52

Feb-03 148.42 1.68 28.93 13.14 192.17 40.46

Mar-03 187.89 3.84 33.84 19.64 245.21 51.62

2002-03 1,737.90 45.76 331.21 195.88 2,310.76 486.47

Apr-03 205.81 4.79 46.00 30.01 286.60 66.05

Contd....

2005-06 2006-07

Futures Options Futures Options

Top 5 Members 12 23 14 23

Top 10 Members 20 36 22 36

Top 15 Members 26 45 28 46

Top 25 Members 36 55 38 58

(in percent)

106

Table 6-4: Settlement Statistics in F&O Segment(In Rs. crore)

Month/Year Index/Stock Futures Index/Stock Options Total Total

MTM Final Premium Exercise (Rs. crore) (US $Settlement Settlement Settlement Settlement milliom)

May-03 163.59 5.74 38.04 30.43 237.80 54.81

Jun-03 220.23 3.86 48.78 46.50 319.37 73.60

Jul-03 389.79 8.02 69.43 44.77 512.01 118.00

Aug-03 569.60 8.58 77.32 58.81 714.31 164.63

Sep-03 1,031.87 9.24 78.12 30.41 1,149.64 264.96

Oct-03 1,188.05 14.11 99.15 60.31 1,361.61 313.81

Nov-03 939.35 23.86 63.40 22.11 1,048.72 241.70

Dec-03 905.46 17.90 69.99 41.10 1,034.44 238.41

Jan-04 2,668.21 12.82 107.46 42.67 2,831.16 652.49

Feb-04 1,329.70 16.40 68.26 24.42 1,438.77 331.59

Mar-04 1,210.32 13.62 93.00 44.58 1,361.53 313.79

2003-04 10,821.98 138.95 858.94 476.12 12,295.98 2,833.83

Apr-04 837.28 15.67 64.70 25.29 942.95 215.53

May-04 2,556.13 13.47 91.29 35.82 2,696.71 616.39

Jun-04 535.25 20.05 46.81 9.85 611.96 139.88

Jul-04 451.15 15.14 72.13 42.77 581.19 132.84

Aug-04 548.01 8.66 50.90 14.65 622.22 142.22

Sep-04 480.12 12.63 56.21 39.74 588.70 134.56

Oct-04 837.82 23.18 68.50 31.00 960.50 219.54

Nov-04 691.17 10.21 76.82 41.95 820.15 187.46

Dec-04 1,238.58 22.31 104.09 56.54 1,421.52 324.92

Jan-05 2,317.69 31.74 96.36 42.37 2,488.16 568.72

Feb-05 991.63 10.62 96.35 39.30 1,137.90 260.09

Mar-05 1,539 44 117 77 1,777 406.09

2004-05 13,024.18 227.50 941.06 455.87 14,648.62 3,348.25

Apr-05 1,736.91 31.15 82.83 30.32 1,881.22 421.70

May-05 943.69 41.74 72.54 44.95 1,102.92 247.24

Jun-05 1,095.79 35.18 93.16 71.32 1,295.45 290.39

Jul-05 1,567.52 38.49 92.86 58.85 1,757.72 394.02

Aug-05 2,544.80 36.56 118.94 26.78 2,727.08 611.32

Sep-05 2,366.70 17.31 135.91 95.85 2,615.77 586.36

Oct-05 3,479.10 120.46 143.92 79.20 3,822.67 856.91

Nov-05 1,831.40 32.17 122.63 75.71 2,061.90 462.21

Dec-05 2,487.80 22.74 139.72 67.05 2,717.30 609.12

Jan-06 2,034.60 107.17 139.52 52.06 2,333.35 523.06

Feb-06 1,886.60 44.47 146.68 56.86 2,134.61 478.50

Mar-06 3,610.60 70.45 231.87 158.89 4,071.81 912.76

2005-06 25,585.51 597.89 1,520.58 817.84 28,521.80 6,393.59

Apr-06 7,413.50 97.47 237.13 104.32 7,852.42 1,801.43

May-06 13,594.00 135.07 326.05 124.18 14,179.30 3,252.88

Jun-06 6,854.10 50.29 265.36 97.01 7,266.76 1,667.07

Jul-06 2,810.00 56.05 197.32 73.60 3,136.97 719.65

Aug-06 1,558.00 38.89 192.71 114.79 1,904.39 436.89

Sep-06 2,826.50 27.10 192.37 72.74 3,118.71 715.46

Oct-06 2,218.20 27.95 222.54 64.15 2,532.84 581.06

Nov-06 2,412.00 57.38 212.33 133.02 2,814.73 645.73

Dec-06 5,968.80 34.62 294.30 88.25 6,385.97 1,465.01

Jan-07 3,664.00 99.04 276.52 121.33 4,160.90 954.55