The Import Menace The Slide Continues - Magazinos.com

124

www.businesstoday.in January 31, 2016 `60 STEEL INDUSTRY The Import Menace BT BUSINESS CONFIDENCE INDEX The Slide Continues HBR EXCLUSIVE BUILDING A DIGITAL PLATFORM Online grocery is hot. Hundreds of players have jumped in. Several hundred million dollars were invested in 2015 alone. But it has also been a graveyard for start-ups

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of The Import Menace The Slide Continues - Magazinos.com

www.businesstoday.in January 31, 2016 `60

STEEL INDUSTRYThe Import Menace

BT BUSINESS CONFIDENCE INDEXThe Slide Continues

HBR EXCLUSIVE

BUILDING A

DIGITAL PLATFORM

Online grocery is hot. Hundreds of players have jumped in. Several hundred million dollars were invested in 2015 alone. But it has also been a graveyard for start-ups

Grocery (31jan2016).indd 1 01/08/2016 10:47:21 PM

One of the biggest casualties of the first dotcom crash of 2000/01 in the US was a company called Webvan. It was founded in 1997, and headquar-tered in Silicon Valley. It was envisaged as an online grocery business,

taking orders and delivering on-demand fresh produce. It had a raft of big venture capitalists’ backing, and was considered a business that would revolutionise groceries much the same way that Amazon was trying to revolutionise the book sales business. It raised almost $400 million from venture capitalists and then another $345 million in an IPO in 1999. At its peak, it was valued at over $5 billion. In 2000, it bought out a smaller rival called HomeGrocer.com, which had started operations one year before it did. Webvan spent millions on infrastructure and publicity and branding, but ran out of cash in 2001.

A number of reasons were put forward for the crash of Webvan by analysts in the aftermath of the dotcom bust. Most agreed it was an idea before its time. The Internet was still in the narrowband and at the dial-up connection stage, the technology platforms were buggy, the company was trying an inventory-led model, which was not very cost-effective, and an inexperienced team ended up burning too much cash while earning too little revenues.

Around the time Webvan shut shop, a few offline grocers, including Safeway, started grocery delivery to homes. This was roughly the time when a few super-market chains in India, like Subhiksha, also tried to systematise grocery delivery. Safeway, while not unsuccessful, did not go on to become a big player in the

online grocery or grocery delivery business. Walmart in the US has a vastly bigger online grocery business, while Amazon.com has also got into the grocery delivery game.

The history of Webvan is instructive, because grocery delivery and online grocery ordering are becoming a hot area for new entrepreneurs as well as big retail chains once again. In India, more than a hundred players are in the business. Some of them are considered veteran players – having survived for five or more years. Others are brash newcomers. A few have all-India aspirations while others are trying to service extremely local markets. The business

models all these players are trying out also vary widely. Some see themselves primarily as specialised order takers and delivery businesses. They work with other offline stores to pick up goods once an order has been placed, and then drop them off to the customer. Others see themselves as true grocers, keeping a fair amount of inventory at all times. Still others essentially aggregate orders every day till a certain time, then go to the main mandis for shopping, and deliver to the customers in the evening. There are others who run big retail stores and are get-ting into the online order and delivery game to compete with new-age rivals.

While some players have managed to raise substantial funds, a few dozen start-ups, offering to deliver groceries, have also shut shop in the country. The mortality rate is probably higher than in other online businesses, because of the margins, non-standardisation of goods, and the fact that a big chunk of the orders involves perishables.

The grocery delivery business in India is somewhat more complicated than it is in the US because of one factor – in India, neighbourhood kiranas have always offered delivery options to regular customers, and the new businesses have to compete with them as well.

So, how will the new grocery delivery business play out? Our cover story on page 58 looks at all the issues in detail.

[email protected]@ProsaicView

From the EditorThat Grocer Online

For reprint rights and syndication enquiries, contact [email protected] or call +91-120-4078000

www.syndicationstoday.in

http://www.businesstoday.in

Editor-in-Chief: Aroon Purie Group Chief Executive Officer: Ashish BaggaGroup Editorial Director: Raj ChengappaIEditor: Prosenjit DattaManaging Editor: Rajeev Dubey Deputy Editors: Alokesh Bhattacharyya, Venkatesha Babu, Anand AdhikariICORRESPONDENTSSenior Editors: P.B. Jayakumar, Nevin John, Goutam Das Senior Associate Editors: Mahesh Nayak, Ajita Shashidhar, Joe C. MathewAssociate Editors: E. Kumar Sharma, Dipak Mondal, Manu Kaushik, Taslima Khan, Anilesh MahajanSenior Assistant Editors: Sarika Malhotra, Chanchal Pal Chauhan, Sumant BanerjeeAssistant Editor: Nidhi SingalIRESEARCHPrincipal Research Analyst: Niti Kiran

ICOPY DESK

Senior Editors: Rishi Joshi, Mahesh JagotaAssociate Editor: Samarpan DuttaChief Copy Editors: Gadadhar Padhy, Sapna Nair PurohitSenior Sub Editor: Devika Singh

IPHOTOGRAPHYPhoto Editor: Vivan MehraDeputy Chief Photographer: Shekhar GhoshPrincipal Photographer: Rachit Goswami Senior Photographer: Nilotpal BaruahSenior Photo Researcher: Nikhil VermaIARTArt Editor: Safia ZahidDeputy Art Director : Anand SinhaAssistant Art Directors : Amit Sharma, Ajay ThakuriChief Visualiser: Vikas Gupta Senior Visualiser: Raj Verma Senior Designer: Devender Singh Rawat

IPRODUCTION

Chief of Production: Harish AggarwalSenior Production Coordinators: Narendra Singh, Rajesh VermaAssistant Manager: Rajkumar WahiSenior DTP Designer: Mohammed ShahidILIBRARYAssistant Librarian: Satbir Singh

IGroup Business Head: Manoj SharmaAssociate Publisher (Impact): Anil FernandesIIMPACT TEAM

Senior General Manager: Jitendra Lad (West)General Managers: Upendra Singh (Bangalore),Velu Balasubramaniam (Chennai)Deputy General Manager: Kaushiky Chakraborty (East)IMarketing: Vipul Hoon, General Manager; Reynold Robert, Brand ManagerINewsstand Sales: D.V.S. Rama Rao, Chief General Manager; Deepak Bhatt, General Manager (National Sales); Vipin Bagga, Deputy General Manager (Operations); Manish Kumar Srivastava, Regional Sales Manager (North); Joydeep Roy, Regional Sales Manager (East); Rajeev Gandhi, Regional Sales Manager (West); Arokia Raj L, Regional Sales Manager (South)

Vol. 25, No. 2, for the fortnight January 18-31, 2016. Released on January 18, 2016.

Editorial Office: India Today Mediaplex, FC 8, Sector 16/A, Film City, Noida-201301; Tel.: 0120-4807100; Fax: 0120-4807150 Advertising Office (Gurgaon): A1-A2, Enkay Centre, Ground Floor, V.N. Commercial Complex, Udyog Vihar, Phase 5, Gurgaon-122001; Tel.: 0124-4948400; Fax: 0124-4030919; Mumbai: 1201, 12th Floor, Tower 2 A, One Indiabulls Centre (Jupiter Mills), S.B. Marg, Lower Parel (West), Mumbai-400013; Tel.: 022-66063355; Fax: 022-66063226; Chennai: 5th Floor, Main Building No. 443, Guna Complex, Anna Salai, Teynampet, Chennai-600018; Tel.: 044-28478525; Fax: 044-24361942; Bangalore: 202-204 Richmond Towers, 2nd Floor, 12, Richmond Road, Bangalore-560025; Tel.: 080-22212448, 080-30374106; Fax: 080-22218335; Kolkata: 52, J.L. Road, 4th floor, Kolkata-700071; Tel.: 033-22825398, 033-22827726, 033-22821922; Fax: 033-22827254; Hyderabad: 6-3-885/7/B, Raj Bhawan Road, Somajiguda, Hyderabad-500082; Tel.: 040-23401657, 040-23400479; Ahmedabad: 2nd Floor, 2C, Surya Rath Building, Behind White House, Panchwati, Off: C.G. Road, Ahmedabad-380006; Tel.: 079-6560393, 079-6560929; Fax: 079-6565293; Kochi: Karakkatt Road, Kochi-682016; Tel.: 0484-2377057, 0484-2377058; Fax: 0484-370962 Subscriptions: For assistance contact Customer Care, India Today Group, A-61, Sector-57, Noida (U.P.) - 201301; Tel.: 0120-2479900 from Delhi & Faridabad; 0120-2479900 (Monday-Friday, 10 am-6 pm) from Rest of India; Toll free no:1800 1800 100 (from BSNL/ MTNL lines); Fax: 0120-4078080; E-mail: [email protected]

Sales: General Manager Sales, Living Media India Ltd, B-45, 3rd Floor, Sector-57, Noida (U.P.) - 201301; Tel.: 0120-4019500; Fax: 0120-4019664 © 1998 Living Media India Ltd. All rights reserved througout the world. Reproduction in any manner is prohibited.

Printed & published by Ashish Kumar Bagga on behalf of Living Media India Limited. Printed at Thomson Press India Limited, 18-35, Milestone, Delhi-Mathura Road, Faridabad-121007, (Haryana). Published at K-9, Connaught Circus, New Delhi-110 001. Editor: Prosenjit Datta

Business Today does not take responsibility for returning unsolicited publication material.All disputes are subject to the exclusive jurisdiction of competent courts and forums in Delhi/New Delhi only

Editor's letter.indd 2 01/08/2016 10:39:32 PM

Re: Letters to the Editor

WRITE TO: The Editor, Business Today, India Today Mediaplex, FC-8, Sector 16/A, Film City, Noida-201301. Email: [email protected]/[email protected] Website: www.businesstoday.in Unsolicited articles will not be returned or acknowledged.Business Today reserves the right to edit letters for brevity and clarity before publication.

FOR SUBSCRIPTION ASSISTANCE WRITE TO:Customer Care, India Today Group, A-61, Sector-57, Noida (U.P.) — 201 301Phone: (0120) 2479900 from Delhi & Faridabad; (0120) 2479900 (Monday-Friday; 10 am-6 pm) from Rest of India; Toll free no. 1800 1800 100 (from BSNL/ MTNL lines); Fax: (0120) 4078080 E-mail: [email protected]

HOW TO CONTACT

BTBT SCRAPBOOK� React to articles in BT�Suggest story ideas�Share your experience as consumer or SME�See what others have to say on our storieson scrapbook at www.businesstoday.in

6 BUSINESS TODAY January 31 2016

Best Wishes for BT’s Majestic MarchThis refers to Business Today’s 24th Anniversary Issue (January 17, 2016). First of all, kudos to BT for successfully completing 24 years in the turbulent media industry. It is a remarkable feat. The excellent sug-gestions by experts in the last edi-tion have depicted innovative means to speed up the progress of the Indian economy. With abun-dant resources at our disposal and a vast talent pool, the policymakers must accelerate reforms and disin-vestment, attract huge investments, bolster governance, ensure timely execution of the revamped plans, and make India a global economic and military giant along with the US and China. Many of the mea-sures and weapons that are recom-mended by Admiral Arun Prakash (Retd.) in the defence policy arena are yet to be brought into our de-fence quiver. Keeping in mind the recent terrorist attack in Pathankot, the Centre has to take up these mat-ters seriously on a war-footing for

creating a conducive investment climate at the earliest. Also, BT’s tie-up with Harvard Business Review and publication of lead articles in its issues is a significant journalistic service at an affordable price. It de-serves mentioning as global prac-tices are well illustrated, enhancing Indian managerial outlook and effi-cacy. May the unfolding years add to the feathers of glory in BT’s crowded cap. I offer my best wishes for its majestic march into the fu-ture with flying colours. B. Rajasekaran, Bangalore

It’s Important to Make Ideas HappenThis refers to your 24th Anniversary Issue. Contributions from stalwarts and experts, suggest-ing innovative ideas, are indeed worthy of sharing with BT readers. But it is not enough to just have ideas, it is also important to make them happen. The value of an idea lies in using it. Nelson Mandela is of-ten quoted as saying: “It always seems impossible until it is done.” (And if we split this word it can read as: I M Possible.) Every new idea looks crazy at first. John S. Herrington had once said: “There are no dreams too large, no innova-

tions unimaginable and no frontiers beyond our reach.” So let’s have a crack at them. Hope BT continues its long journey ahead for bringing out a Golden Jubilee Issue! J.S. Broca, New Delhi

Odd-Even Formula:A Futile AttemptThis refers to a piece by environ-mentalist and activist Sunita Narain (Air Pollution Is Slow Murder; Must be Stopped (January 17). The only solution for mini-mising pollution caused by vehi-cles is to ban sale and purchase of cars in metros and other big cities where the level of pollution is high. All other measures are a fu-tile attempt. When the roads are not equipped to handle the grow-ing number of cars in a city, how can their sale be allowed? There is logic in stopping the sale of motor vehicles. When shows are house-ful, ticket sales are stopped. Same is the case for trains and flight tickets, so why not in the case of vehicles? The odd-even formula will not solve any pollution prob-lem Delhiites are facing. So, the formula should be dropped. Mahesh Kapasi, New Delhi

Government decides to shut three HMT units, offer VRS. Vijay scooter, Ambassador car and now HMT watches... Is it development, modernisation or sab ka vikas sab ka saath?.– Afaq Mehmood, @iamafaque

Twitter is considering 10,000-character limit for tweets.It will be boring to read such long tweets. Moreover, it’s fun to write your thoughts in few words. – Chhavi Sinha, @ChhaviSinha24

Both cars and two-wheelers need to be brought under odd-even, says CSE. Shut this nonsense. It has made Delhi into a poor capital of India.– Vick Mederata, @VickraMederata

www.twitter.com/bt_india

Send all your comments to: [email protected]

Letters to Editor.indd 2 01/08/2016 11:41:51 PM

C O V E R B Y A J A Y T H A K U R I J A N U A R Y / 3 1 / 2 0 1 6 V O L U M E 2 5 / N U M B E R 2

COVER STORY

58

CONTENTSFOCUS

26 I Where Angels Fear to Trade2016 starts on an uncertain note for the Indian equity markets amid global concerns

20 I Drowning in LossesChennai’s industry has suffered grievously from the floods in December

14 I Quick takes on major events

UPFRONT

38 I Keep the Buzz GoingUse social media to promote an event and then retain the buzz around it

46 I Oiling the Economy’s WheelsSteep slump in global oil prices has come to govern-ment’s rescue. But it has not helped the economy

74 I Fighting the Import MenaceA dramatic surge in import of steel has undermined the profitability of domestic industry and increased distressed assets

84 I Sun’s Eclipse2015 was a forgetful year for Sun Pharma, but can it bounce back in the new year?

88 I The Final BetReliance Communications’ plan to become India’s second-largest telecom player looks promising, but is difficult to put into practice

FEATURES

32 I Waiting for the BudgetCorporate sentiment has taken a beating for the fourth straight quarter, reveals the Business Today-C fore Survey

52 I Venezuela: A New Beginning?India needs to watch the political developments in Venezuela closely and enhance its engagement with the eventual dispensation, says Deepak Bhojwani

30 I Graphiti on stock market: Bears on the Prowl

24 I There Are No Free LunchesFacebook is projecting its Free Basics service as a purely altruistic exercise. It is anything but...

18 I Cess Pool MysteryA CAG report, noting that the cesses collected for various noble initiatives often remain either unutilised or unaccounted for, points to the need for transparency in fund utilisation

18

24 54 I Requiem for a CodeWhile some proposals of the abandoned Direct Taxes Code are already in force, its wider objectives seem to have been abandoned

40

“Need to Inject demand into the

economy”Arvind Subramanian

54

January 31 2016 BUSINESS TODAY 9

Online grocery is hot. Hundreds of players have jumped in. Several hundred million dollars were invested in 2015 alone. But it has also been a graveyard for start-ups

The Perishable Business

PH

OT

OG

RA

PH

BY

VIV

AN

ME

HR

A &

SH

EK

HA

R G

HO

SH

;IM

AG

ING

BY

AN

AN

D S

INH

A

Content.indd 2-3 09-01-2016 1:28:54 PM

C O V E R B Y A J A Y T H A K U R I J A N U A R Y / 3 1 / 2 0 1 6 V O L U M E 2 5 / N U M B E R 2

COVER STORY

58

CONTENTSFOCUS

26 I Where Angels Fear to Trade2016 starts on an uncertain note for the Indian equity markets amid global concerns

20 I Drowning in LossesChennai’s industry has suffered grievously from the floods in December

14 I Quick takes on major events

UPFRONT

38 I Keep the Buzz GoingUse social media to promote an event and then retain the buzz around it

46 I Oiling the Economy’s WheelsSteep slump in global oil prices has come to govern-ment’s rescue. But it has not helped the economy

74 I Fighting the Import MenaceA dramatic surge in import of steel has undermined the profitability of domestic industry and increased distressed assets

84 I Sun’s Eclipse2015 was a forgetful year for Sun Pharma, but can it bounce back in the new year?

88 I The Final BetReliance Communications’ plan to become India’s second-largest telecom player looks promising, but is difficult to put into practice

FEATURES

32 I Waiting for the BudgetCorporate sentiment has taken a beating for the fourth straight quarter, reveals the Business Today-C fore Survey

52 I Venezuela: A New Beginning?India needs to watch the political developments in Venezuela closely and enhance its engagement with the eventual dispensation, says Deepak Bhojwani

30 I Graphiti on stock market: Bears on the Prowl

24 I There Are No Free LunchesFacebook is projecting its Free Basics service as a purely altruistic exercise. It is anything but...

18 I Cess Pool MysteryA CAG report, noting that the cesses collected for various noble initiatives often remain either unutilised or unaccounted for, points to the need for transparency in fund utilisation

18

24 54 I Requiem for a CodeWhile some proposals of the abandoned Direct Taxes Code are already in force, its wider objectives seem to have been abandoned

40

“Need to Inject demand into the

economy”Arvind Subramanian

54

January 31 2016 BUSINESS TODAY 9

Online grocery is hot. Hundreds of players have jumped in. Several hundred million dollars were invested in 2015 alone. But it has also been a graveyard for start-ups

The Perishable Business

PH

OT

OG

RA

PH

BY

VIV

AN

ME

HR

A &

SH

EK

HA

R G

HO

SH

;IM

AG

ING

BY

AN

AN

D S

INH

A

Content.indd 2-3 09-01-2016 1:28:54 PM

Page: 116-119From time to

time, you will see pages titled “An Impact

Feature” or “Advertorial” in

Business Today. This is no different from an

advertisement and the magazine’s editorial staff

is not involved in its creation in any way.

An Feature

www.facebook.com/BusinessToday@BT_India

businesstoday.inCONTENTS

LEADERSPEAK122 I R.S. SodhiMD, Amul

120 I PEOPLEBUSINESS

EX-LIBRIS112 I The Real-Life MBA: Corporate Wisdom on Tap; Indian Family Business Mantras: Lessons in Managing Family Businesses

122The New CEO of WiproAbid Ali Neemuchwala’s elevation was speculated right from the time he joined the company after a 23-year stint at TCS. He was considered very close to TCS CEO N. Chandrasekaran, and Wipro bagging him was considered a coup, finds out Venkatesha Babubusinesstoday.in/wipro-neemuchwala

The Transformation of Narendra ModiHe is pushing for more consensus building, talking to opposition leaders at tea, offering water to protesting leaders, attending their birthday parties, and moving away from the reputation of being an adamant politician, says Anilesh Mahajanbusinesstoday.in/Modi-transform

BT COLUMNS

PERSPECTIVES

Foodpanda's Job Cuts Signal Increasing Impact of AutomationFood-tech company foodpanda eliminated 15 per cent of its workforce – that translates to between 250 and 300 employees. The company links the job cuts to automationbusinesstoday.in/foodpanda-tech

GM Eyes Big in India Under Mary BarraThe American carmaker has operated in India for almost two decades, but it hasn’t been able to succeed in a market dominated by Japanese and Korean companiesbusinesstoday.in/GeneralMotors-india

PERSONAL TECH

108 I Tech Trends 2016If 2015 was the year of innovations in the hardware space, with fancy gadgets hitting the stores every other day, this New Year will be more about the awakening of the virtual mind

92 I Luxury Banned in DelhiThe ban on new registrations of 2,000-cc (and above) cars may be a precursor to harsher times for diesel

96 I Pet ProjectThe pet products market may still be small, but DogSpot.in is gearing up to make a splash with fresh infusion of funds from Ratan Tata

HBR EXCLUSIVE100 I How to Launch Your Digital PlatformA playbook for strategists

NEWS

Brick-and-mortar Retail Makes a Comeback in 2015The year saw the beginning of the e-commerce euphoria dying out... because profitability didn’t seem to be anywhere in sightbusinesstoday.in/ecommerce-retail

INTERVIEW

“Both cars and two-wheelers need to be brought under odd-even”Vivek Chattopadhyaya, Programme Manager (Air Pollution Control Unit), Centre for Science and Environment, talks to Sarika Malhotra about Delhi’s odd-even drive to combat pollution businesstoday.in/oddeven-pollution

Content.indd 6 01/09/2016 2:28:39 AM

Subscribe NowWWW.BUSINESSTODAY.IN/DIGITALMAGAZINE

Tap to download & subscribe

STAY AHEADOF THE CURVEBusiness Today now available on iPad, iPhone,

Android, Kindle Fire, PC & Mac

UPFRONT

12 BUSINESS TODAY January 31 2016

AJA

Y T

HA

KU

RI

THE H-BOMBNorth Korea leader Kim Jong Un claims his country has successfully tested a hydrogen bomb. Scientists in many countries though doubt his claims.

NO MORE INCREDIBLE The government drops Aamir Khan as brand ambassador of Incredible India campaign. His supporters perceive this as the backlash to his intolerance comments in an interview a month ago.

THE SELFIE COPYWRONGA Federal Judge in the US says that the monkey whose selfie went viral on the net does not own the copyright.

THE SCIENCE & THE CIRCUSIndian born Nobel Laureate Venkataraman Ramakrishnan calls the Indian Science Congress a “circus” in a newspaper interview after hearing some of the topics discussed in it, including Homoeopathy and Astrology.

SHIA-SUNNI OR OIL RIVALRY?After Sunni-dominated Saudi Arabia executed 47, including Shia cleric Nimr al-Nimr, its Embassy in Shia-dominated Iran was attacked and ransacked by an irate mob in Tehran. Saudi Arabia announced breaking off diplomatic ties with Iran and its allies Bahrain, Sudan and UAE also either broke off ties or downgraded their relationship. But more than the Shia-Sunni rivalry, analysts see the event as the after-effect of oil rivalry. Both sides have refused to curtail production to steady global oil prices.

UPFRONT.indd 2 01/08/2016 10:43:53 PM

CALENDAR

14 15REACHING OUT TO KOREAWHAT: India-Korea Business SummitWHEN: January 14-15, Le Meridien, New Delhi

WHAT TO LOOK FOR: More than 100 top executives representing the largest Korean companies, South Korean government officials, besides Indian CEOs. The summit will focus on emerging business opportunities in India in infrastructure, ICT, power, smart cities and manufacturing.

REALITY CHECKWHAT: National Real Estate Summit 2016WHEN: January 21, PHD House, New Delhi

TECH-ENABLING INDIAWHAT: i-Bharat 2016WHEN: January 11, Federation House, New Delhi

WHAT TO LOOK FOR: The second edition of the FICCI-Department of Electronics & IT event is titled ‘Embracing Technology: Transforming India’. It aims to discuss the various technologies and government policies that could enable smart cities, implement Digital India and e-governance.

14 BUSINESS TODAY January 31 2016

THE FUTURE OF RETAIL WHAT: CII National Retail Summit 2016WHEN: January 15, Taj Mahal Hotel, New Delhi

WHAT TO LOOK FOR: CEOs of some of India’s largest retail companies will deliberate on the future of retail, new trends, including omni-channel. The Summit aims to create a roadmap for the retail sector in the current policy environment. Expect sharing of new ideas and innovative practices and the impact of disruptive technologies on the retail sector.

15

11

13 18

21

SHOWCASING INDIAWHAT: Make In India WeekWHEN: February 13-18, NSCI Worli, Mumbai

WHAT TO LOOK FOR: Showcase of innovative products and manufacturing processes developed in India. Commerce Ministry’s Department of Industrial Promotion and Policy is organising the Make in India Week between February 14 and 18 under the aegis of the Maharashtra government. Expect representatives from nearly 1,000 companies from 60-odd countries to participate in the week-long celebrations to commemorate Prime Minister Narendra Modi’s ‘Make In India’ initiative. The Delhi Road Show of the Make in India week is being organised at the India Habitat Centre on January 8.

WHAT TO LOOK FOR: In the wake of the new and stringent Real Estate Bill to be tabled before the Parliament shortly, the event assumes significance to discuss the new challenges to the real estate sector and the impact of the government policies.

UPFRONT1-Calender.indd 2 09-01-2016 1:29:27 PM

and higher education as envisaged in the Finance Act was not transparently ascertainable from the Union account.”

It also points out that only part of the funds obtained through a number of other cesses are accounted for. Of the `5,784 crore collected as cess for research and devel-opment since 1996, only `550 crore – or less than 10 per cent – has been utilised. In 2014/15 alone, the govern-ment collected `907 crore through this cess, but the only outgo recorded is a transfer of `7 crore to a fund adminis-tered by the Technology Development Board. Again, of the primary education cess in force since 2004, which had mopped up `1,54,818 crore, `13,298 crore remains unused or unaccounted for. Of the clean energy cess in force since 2010/11, over 40 per cent – `6,258 crore out of `15,174 crore col-lected – is unuti l ised (see No Accountability). There is no separate fund in which cesses are deposited – they go into the Consolidated Fund of India, alongside all revenue and loans obtained by the Central government.

The latest cess, imposed since last November 15, is the Swachh Bharat Cess of 0.5 per cent on all services, to fund the clean-up campaign of Prime Minister Narendra Modi. But there is no clarity on how much has been collected or how it is being spent, if at all. Service tax was raised last year from 12.37 per cent to 14 per cent, while cess was in-creased to 14.5 per cent.

“It is the government’s right to levy cess to raise money for a specific pur-pose,” says K.V. Thomas, Congress MP from Ernakulam, Kerala, and Chairperson of the Public Accounts Committee (PAC). “But government must be more transparent about the way it uses money. The PAC, under its former chairman, Murli Manohar Joshi, had raised this issue on several occasions. We will also look into it when we take stock of the accounts.”

Have these funds been diverted for other purposes? No one knows.

“If the money collected through a particular cess is not used for the purpose it was intended, it must have been used for something else,” says a CAG official involved in the preparation of the December report, who does not want to be named. “There are many departments and ministries which spend more than the money allotted to them. Unused funds could have been diverted.” In 2014/15, for example, defence pension cost the government `9,436 crore – more than what had been budgeted for it.

The difference between a cess and general funds sanctioned for different ministries and departments is that the former does not need to be annually passed by Parliament as long as it is used for the purpose it was collected. “There are situations where a government needs an uninterrupted flow of funds, where the com-mitment is long term, and which thus warrant imposing

a cess,” says Sen. “Or else, fund utilisation will have to be voted upon every time, which is cumbersome.” But he stresses that it is important to earmark the funds properly, which is not being done. “Ideally, cess funds should be escrowed,” he adds.

But the government remains reluctant to part with details. There are just two references to cesses, for instance, in the plan outlay for 2015/16. At one point it says: “An estimated receipt of `27,575 crore by way of proceeds from the (Primary) Education Cess will be credited to Prarambhik Shiksha Kosh.” The second mention says the government will spend `1,645 crore of the cess on diesel (part of the road cess) on railways. ~

@dipak_journo

Cess Pool MysteryThe CAG report, noting that the cesses collected for various noble initiatives often remain either unutilised or unaccounted for, points to the need for transparency in fund utilisation. By DIPAK MONDAL

FOCUS20 Drowning in Losses

24 No Free Lunches

26 Where Angels

Fear to Trade

January 31 2016 BUSINESS TODAY 1918 BUSINESS TODAY January 31 2016

The report of the Comptroller and Auditor General (CAG) in late December, raising questions about the utilisation of funds col-

lected by the government under various cesses, has jolted taxpayers. “The problem is lack of transparency,” says Pronab Sen, Chairman, National Statistical Commission. “The finance ministry should regularly reveal how much it col-lects and how much it disburses. But it does not.”

The CAG report notes that `64,000 crore was collected as cess on secondary and higher educa-tion between 2005/06 and 2014/15. “Neither was a fund designated to deposit the proceeds of the cess nor were schemes identified on which the cess proceeds were to be spent,” it says. “Conse- quently, the commitment of furthering secondary

Major Cesses Period Total collection

Unutilised/unaccounted for

Primary Education

2004-2015 1,54,818 13,298

Secondary & Higher Ed

2006-2015 64,288 64,288

Clean Energy 2010-2015 15,174 6,258

Roads 2010-2015 1,01,141 1,219

R&D 1996-2015 5,784 5,234

NO ACCOUNTABILITYNo one knows what has been done with the cess on secondary and higher education collected over a decade.

Figures in `crore, Source: CAG

OTHER CESSESAdministered by Revenue Department

Administered by Revenue Department

National Calamity Contingent Duty Swachh Bharat Cess

Coal and Coke Rubber Mica Iron Ore, Manganese Ore & Chrome Ore

Lime Stone and Dolomite Cine Workers

Prevention & Control of (Air & Water) Pollution

Research and Development Beedi Fund Cess Collection on Textiles & Textile Machinery

RA

J V

ER

MA

Focus Lead Cess Tax.indd Custom V 01/08/2016 10:42:42 PM

and higher education as envisaged in the Finance Act was not transparently ascertainable from the Union account.”

It also points out that only part of the funds obtained through a number of other cesses are accounted for. Of the `5,784 crore collected as cess for research and devel-opment since 1996, only `550 crore – or less than 10 per cent – has been utilised. In 2014/15 alone, the govern-ment collected `907 crore through this cess, but the only outgo recorded is a transfer of `7 crore to a fund adminis-tered by the Technology Development Board. Again, of the primary education cess in force since 2004, which had mopped up `1,54,818 crore, `13,298 crore remains unused or unaccounted for. Of the clean energy cess in force since 2010/11, over 40 per cent – `6,258 crore out of `15,174 crore col-lected – is unuti l ised (see No Accountability). There is no separate fund in which cesses are deposited – they go into the Consolidated Fund of India, alongside all revenue and loans obtained by the Central government.

The latest cess, imposed since last November 15, is the Swachh Bharat Cess of 0.5 per cent on all services, to fund the clean-up campaign of Prime Minister Narendra Modi. But there is no clarity on how much has been collected or how it is being spent, if at all. Service tax was raised last year from 12.37 per cent to 14 per cent, while cess was in-creased to 14.5 per cent.

“It is the government’s right to levy cess to raise money for a specific pur-pose,” says K.V. Thomas, Congress MP from Ernakulam, Kerala, and Chairperson of the Public Accounts Committee (PAC). “But government must be more transparent about the way it uses money. The PAC, under its former chairman, Murli Manohar Joshi, had raised this issue on several occasions. We will also look into it when we take stock of the accounts.”

Have these funds been diverted for other purposes? No one knows.

“If the money collected through a particular cess is not used for the purpose it was intended, it must have been used for something else,” says a CAG official involved in the preparation of the December report, who does not want to be named. “There are many departments and ministries which spend more than the money allotted to them. Unused funds could have been diverted.” In 2014/15, for example, defence pension cost the government `9,436 crore – more than what had been budgeted for it.

The difference between a cess and general funds sanctioned for different ministries and departments is that the former does not need to be annually passed by Parliament as long as it is used for the purpose it was collected. “There are situations where a government needs an uninterrupted flow of funds, where the com-mitment is long term, and which thus warrant imposing

a cess,” says Sen. “Or else, fund utilisation will have to be voted upon every time, which is cumbersome.” But he stresses that it is important to earmark the funds properly, which is not being done. “Ideally, cess funds should be escrowed,” he adds.

But the government remains reluctant to part with details. There are just two references to cesses, for instance, in the plan outlay for 2015/16. At one point it says: “An estimated receipt of `27,575 crore by way of proceeds from the (Primary) Education Cess will be credited to Prarambhik Shiksha Kosh.” The second mention says the government will spend `1,645 crore of the cess on diesel (part of the road cess) on railways. ~

@dipak_journo

Cess Pool MysteryThe CAG report, noting that the cesses collected for various noble initiatives often remain either unutilised or unaccounted for, points to the need for transparency in fund utilisation. By DIPAK MONDAL

FOCUS20 Drowning in Losses

24 No Free Lunches

26 Where Angels

Fear to Trade

January 31 2016 BUSINESS TODAY 1918 BUSINESS TODAY January 31 2016

The report of the Comptroller and Auditor General (CAG) in late December, raising questions about the utilisation of funds col-

lected by the government under various cesses, has jolted taxpayers. “The problem is lack of transparency,” says Pronab Sen, Chairman, National Statistical Commission. “The finance ministry should regularly reveal how much it col-lects and how much it disburses. But it does not.”

The CAG report notes that `64,000 crore was collected as cess on secondary and higher educa-tion between 2005/06 and 2014/15. “Neither was a fund designated to deposit the proceeds of the cess nor were schemes identified on which the cess proceeds were to be spent,” it says. “Conse- quently, the commitment of furthering secondary

Major Cesses Period Total collection

Unutilised/unaccounted for

Primary Education

2004-2015 1,54,818 13,298

Secondary & Higher Ed

2006-2015 64,288 64,288

Clean Energy 2010-2015 15,174 6,258

Roads 2010-2015 1,01,141 1,219

R&D 1996-2015 5,784 5,234

NO ACCOUNTABILITYNo one knows what has been done with the cess on secondary and higher education collected over a decade.

Figures in `crore, Source: CAG

OTHER CESSESAdministered by Revenue Department

Administered by Revenue Department

National Calamity Contingent Duty Swachh Bharat Cess

Coal and Coke Rubber Mica Iron Ore, Manganese Ore & Chrome Ore

Lime Stone and Dolomite Cine Workers

Prevention & Control of (Air & Water) Pollution

Research and Development Beedi Fund Cess Collection on Textiles & Textile Machinery

RA

J V

ER

MA

Focus Lead Cess Tax.indd Custom V 01/08/2016 10:42:42 PM

20 BUSINESS TODAY January 31 2016

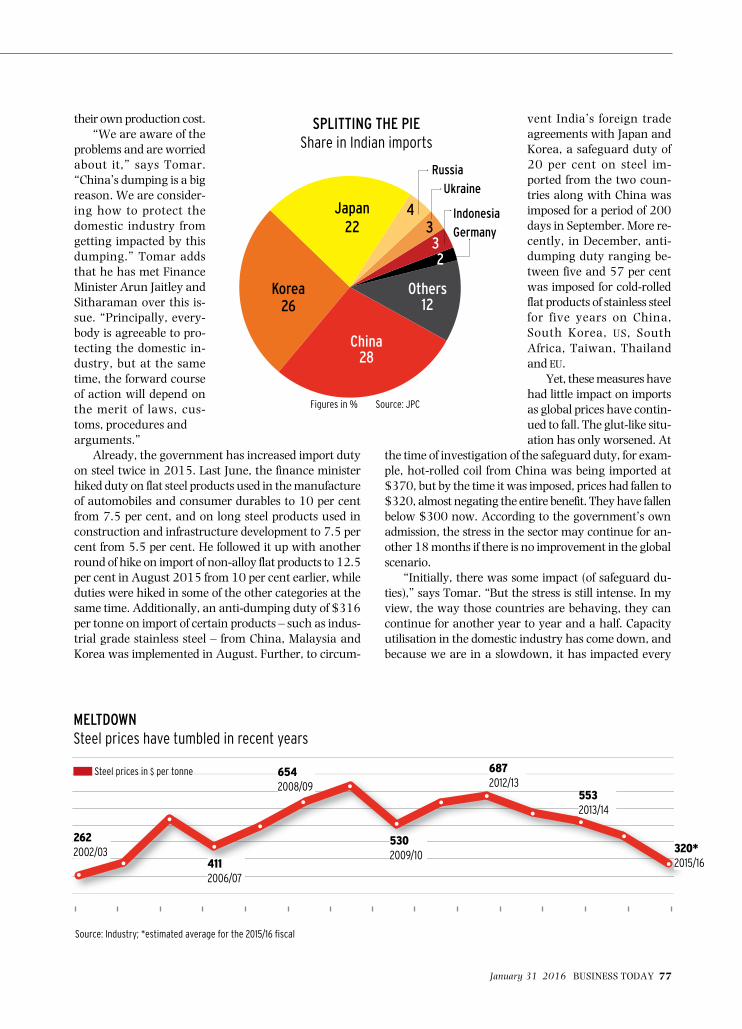

The devastating floods in Tamil Nadu in early December, especially in and around Chennai, have dragged down

Indian manufacturing. Though manufactur-ing has been sluggish in recent years, the Nikkei India Manufacturing Purchasing Managers Index (PMI), a measure of manu-facturing output released every month, had been rising, however slowly, continuously for the past 25 months. In December, however, it dipped, and that too to a 28-month low, from 50.3 in November to 49.1 – its sharpest fall since the early months of the downturn of 2008/09. Why? “India's manufacturing sector took a turn for the worse at the year

end, with already gloomy internal demand further hampered by floods in the South of the country,” Pollyanna De Lima, author of the PMI report and economist with global fi-nancial services firm Markit, wrote.

How much is the damage? Estimates vary. N.K. Ranganath, CEO and Managing Director of leading pump manufacturer Grundfos and former president of the CII’s Tamil Nadu chapter, maintains it could be anything between `20,000 and `50,000 crore. “It was an unprecedented calamity,” he says. “The scale of damage inflicted on industry is only now coming to light and be-ing tabulated.” The Associated Chambers of

FOCUS Chennai FloodsJ

AI

SO

N G

Drowning in LossesChennai’s industry has suffered grievously from the fl oods in December By VENKATESHA BABU

In dire straits: People being evacuated from fl ood-hit regions of Chennai

ONE OF THE WORST AFFECTED

IS THE AUTOMOTIVE INDUSTRY ON

CHENNAI’S OUTSKIRTS,

WHERE FACTORIES OF

TOP COMPANIES ARE LOCATED

Focus-Chennai Flood.indd 2 01/09/2016 12:53:09 AM

22 BUSINESS TODAY January 31 2016

Commerce and Industry of India (ASSOCHAM) in its pre-liminary estimate pegged the losses at more than may Rs 15,000 crore, while Aon Benfield, UK-based reinsur-ance broker, has put them at $3 billion (`20,000 crore). A senior government official claims it is too early to say. “It will take many more weeks to arrive at a comprehensive number for the scale of loss suffered by industry,” he says. “But it is apparent that the damage has been higher than initially estimated.”

One of the worst affected is the automotive industry on Chennai’s outskirts, where factories of top companies such as Hyundai, Ford, BMW, Renault-Nissan, Daimler, Royal Enfield and Apollo Tyres are located. Indeed, every third car in the country is manufactured in this area. All of them had to shut down for three days to a week. Some, led by Hyundai, have sought to make up by work-ing extra shifts since then, including on Sundays. Again, Tamil Nadu accounts for close to 20 per cent of the turnover of the country’s auto components industry, em-ploying over 600,000 people. “In the wake of this unforeseen calamity, there is an ur-gent need to announce a relief and rehabili-tation package for the industry and its em-ployees, especially for the SME segment,” says Arvind Balaji, President, Automotive Component Manufacturers Association.

More than the automobile makers, it is this segment that is affected, because many units neither have the deep pockets nor in many cases the expertise, to quickly set things right. Some of them are not even prop-erly insured. “After so much destruction, the General Insurance Corporation (GIC) has re-ported insurance claims of merely $300 mil-

lion,” says a senior function-ary of the Federation of I n d i a n C o m m e r c e a n d Industry (FICCI), who does not want to be named.

Indeed, the state is home to the highest number of small and medium enter-prises (SMES) in the country (which includes the auto an-cillary makers). “There is an urgent need to announce a relief and rehabilitation pack-age for the Tamil Nadu indus-try, especially for the SME seg-ment,” says Balaji. Even big players like Grundfos India have been unable to meet some of their export dead-lines, because some of the components are sourced from vendors and suppliers in the SME sector. “The Centre and the state should work to-gether to provide help to these small companies by giv-ing tax breaks, asking banks to extend loans and so forth,” says Ashok R. Thakkar, Convenor of FICCI’s infra-structure panel.

Most IT majors have large units in Chennai and these too have also suffered.

Already, a number of them have announced that their 2015/16 third quarter results would be impacted because of the floods. Some have also announced setting aside a fund to aid the relief and rehabilitation. TCS has earmarked Rs 1,100 crore for affected employees, while Cognizant has committed $40 million (Rs 260 crore) for the city’s reha-bilitation. Some outside this sector have also responded similarly. “But the state needs to help industry,” says Ranganath.

The floods may have receded but it will take many months – if not years – for the industries that have suffered to bounce back. ~

@venkateshababu

FOCUS Chennai Floods

A NUMBER OF IT MAJORS HAVE

ALREADY ANNOUNCED THAT THEIR

2015/16 THIRD QUARTER

RESULTS WOULD BE IMPACTED

HARD HITEstimates of the

damage to industry caused by the

Chennai deluge

CII’s Tamil Nadu chapter:

Aon Benfield (re-insurance

brokers):

TCS:

HELPING HAND PROVIDED BY COMPANIES:

` 20,000-50,000 crore

$3 billion(Rs 20,000 crore)

` 1,100 crore(For their employees)

`260 crore(For general

rehabilitation)

Focus-Chennai Flood.indd 4 01/09/2016 12:53:34 AM

24 BUSINESS TODAY January 31 2016

Rarely has any company spent so much money to promote an ostensibly

“free” service. Facebook took full- page cover ads in most major newspapers to tout the benefits of Free Basics, a supposedly free Internet service. Facebook is try-ing very hard to make the Indian telecom regulator, TRAI, give an approval for the Free Basics ser-vice. Under the Free Basics scheme, users won’t have to pay data charges for accessing Facebook and certain other sites that it approves, through a mo-bile device using a Reliance Communication connection in India. (Free Basics is being of-fered in 38 poor countries in partnership with a different telco in each country). Mark Zuckerberg pitches it as a purely altruistic service, which would benefit millions of poor people access the Internet.

That is, of course, only half the truth. The service might be free but Facebook gets to col-lect user data. More importantly, Facebook controls and directs which sites the user can access easily. It is, what is dubbed, the Walled Garden strategy. In essence, users get to access only those sites for free which Facebook ap-proves. To access others, he or she pays the full data usage charges. Also, in all probability, sites that are not approved by Facebook will not be as easy to access as the ones it approves, even if one is paying the data charges. Facebook can use all sorts of technology to promote some sites against others. It can also use the data and its control over access to make money in many ways.

Facebook had earlier tried to offer much the same through its Internet.org programme. An outcry forced it to change the name. Facebook is not alone in trying such offerings. Earlier, Airtel, the country’s largest mobile services company, had tried to offer something

similar before backing out be-cause of stiff resistance from Net Neutrality activists. The propo-nents of Net Neutrality say that users should be able to access all legal content and applications, regardless of source, and Internet service providers cannot offer preferential treatment to certain sites while blocking oth-ers. Net Neutrality is important because it puts all content sites on an equal footing and lets the user decide which it will prefer.

Though Net Neutrality activ-ists like to see the Free Basics is-

sue in black and white, the truth is that even if TRAI does allow Facebook to offer it in India, it is unlikely to be as much of a threat as they think it will be. For one, Reliance Communications is not a monopoly – far from it, it is now the fifth largest player with 118 million subscribers, and even if it gains in size after its proposed merger (see story on page 88), it will still not be the sole gateway to the internet for a country as vast as India. It would not even be the sole gateway for mobile users, forget those accessing the Net through other means. More importantly, few users are under the illusion that anything really comes for free – they know that if they want to access impor-tant sites, they will have to pay anyway, and are prepared to do so. And few users on the Net would prefer to be stuck to a few sites approved by Facebook. Finally, people who may opt for free services of the nature of Free Basics may not be the kind of customers who generate much revenues and profits for sites.

In all likelihood, Free Basics is unlikely to be allowed by TRAI given the amount of op-position it is facing from the activists. But even if it is, the fear that it will stifle Net Neutrality is vastly overblown. ~

@ProsaicView

FOCUS Net Neutrality

There Are No Free LunchesFacebook is projecting its Free Basics service as a purely altruistic exercise. It is anything but... By PROSENJIT DATTA

IN ESSENCE, USERS GET TO ACCESS ONLY

THOSE SITES FOR FREE WHICH FACEBOOK

APPROVES. TO ACCESS OTHERS, HE OR SHE PAYS THE FULL DATA

USAGE CHARGES

Focus-Facebook.indd 2 01/08/2016 11:13:20 PM

26 BUSINESS TODAY January 31 2016

The first shock of the year has already registered. On January 7, the BSE Sensex fell 554.50 points – or 2.2 per cent – to

touch 24,851.83, its steepest drop in the past three months. Indeed, stock markets around the world followed suit, all due to China de-valuing its currency by 0.51 per cent to 6.5646 against the US dollar earlier in the day – its lowest levels since March 2011. But to many market watchers, it came as no surprise. “Equity markets in India are expected to be volatile for global reasons,” says Sankaran Naren, Chief Investment Officer, ICICI Prudential Mutual Fund. “For investors, hybrid funds would be the best way to tackle the situ-ation for the next six months.”

The Chinese Yuan appreciated significantly in the past four years relative to many of its trading partners’ currencies, rendering Chinese exports less competitive than before in an economy much focused on exports. To beat

this trend, the Yuan was devalued in August last year and has now been devalued again. There is every chance of further devaluation in coming months. This could impact several segments of domestic industry in India – tyres, tiles, steel and more – if Chinese offerings be-come cheaper than local goods. “What China does will have a huge bearing on India, putting pressure on the current account deficit and the rupee,” says Saurabh Mukherjea, CEO-Institutional Equities, Ambit Capital. China is making structural changes to its economy to shift focus and become a domestic consump-tion-led economy. However, until that process is complete, to keep its exports competitive, its currency is likely to be forcibly depreciated.

The difficulties of the Chinese economy, however, are not the only global threats. “There is need for caution not just because of China, but also due to the likelihood of oil ex-porting countries selling off their investments, as well as concerns of war in West Asia,” says Naren. The drop in crude oil prices, beginning roughly around the time the National Democratic Alliance (NDA) government took charge, has been a very lucky break for India, saving it around $70-80 billion, but it has also shaken the economies of the oil producing countries, some of which have gone from healthy surpluses to staring at deficits. They could well sell off part of their global equity holdings to reduce debt, which in turn would put pressure on Indian equities. As for war, the depredations of the Islamic State (ISIS) and the growing standoff between Saudi Arabia and Iran make it a distinct possibility.

“In the first half of 2016, there are known (unknowns) and unknown unknowns,” says

FOCUS Stock Market

THE FIRST MONTHS OF 2016 TOO ARE LIKELY

TO BE UNCERTAIN BUT MANY

EXPERTS FEEL THE DANGERS ARE FOR THE SHORT TERM

Where Angels Fear to Trade 2016 starts on an uncertain note for the Indian equity markets amid global concerns. By MAHESH NAYAK

AJ

AY

TH

AK

UR

I

Focus-Market.indd 2 01/09/2016 12:49:54 AM

28 BUSINESS TODAY January 31 2016

Uday Kotak, Executive Vice Chairman and Managing Director, Kotak Mahindra Bank. “I’ve entered 2016 with a conservative mind-set.” Kotak feels a combination of things could go wrong in the first half of 2016 due to de-velopments in the US, China and oil producing nations. For instance, with US corporate bond spreads increasing, he feels there could be a credit accident globally or in large companies.

Domestic Issues2015 was not a particularly happy year for the bourses in India. The euphoria of 2014, with the swearing in of the new NDA government, having faded, the Chinese devaluation, a sub-normal monsoon and indifferent corporate earnings took their toll. On December 31, the Sensex closed at 26,117 points, 5 per cent be-low its level exactly a year ago. The first months of 2016, too, are likely to be uncertain, but many experts feel the dangers are only for the short term. “Looking forward five years, it is a great time to be in India and build busi-nesses,” says Kotak. “The countries I would really bet on are US and India.”

Prateek Agrawal, Head of Business and CIO, ASK Investment Managers, agrees about India. “December 2015 quarter results are likely to be the worst, after which corporate performance will improve. I expect the sec-ond quarter of 2016/17 to be a bumper one. All this will give a fillip to the mar-ket. Global developments will not matter all that much if there is strong do-mestic corporate growth.”

A m b i t C a p i t a l ’ s Mukherjea, however, re-mains sceptical. “The earn-ings growth of large-cap companies is likely to re-main weak over the next

couple of years,” he says. “The benchmark indices are likely to remain under pressure. Our Sensex estimate by the end of 2016/17 is around 29,000.” Much will depend on the policies pursued by the government and the Reserve Bank of India, as well as the adoption of advanced technology. “We like companies which have consistently expanded whilst maintaining balance sheet discipline,” he adds. Kotak too worries about the balance sheet discipline. “The high debt of many Indian companies is a concern,” he says. “They have to bring down debt. In an envi-ronment where wholesale price index (WPI) is negative, high leverage is dangerous.”

One important silver lining for the equity markets is the growth of mutual funds, espe-cially the rise in the number of retail investors using systematic investment plans (SIPS). The average monthly inflow into mutual funds through the SIP route in recent months has been around `2,500 crore. Mutual funds were the unsung heroes of the equity market in 2015 and the same is expected this year.

As is the case every year, the forthcoming Budget will impact the market, with the ex-tent of government spending playing a key

role in reviving sectors such as infrastructure. The implementation (or other-wise) of further reforms, especially the passing of key reform bills including the Goods and Services Tax bill, will also make a big difference. The mon-soon too will be crucial – after two consecutive years of below average rains that badly affected rural spending, it is hoped that the Gods will be be-nevolent in 2016. ~

@maheshnayak

FOCUS Stock Market

ONE IMPORTANT SILVER LINING

FOR THE EQUITY MARKETS IS THE

GROWTH OF MUTUAL FUNDS, ESPECIALLY THE

RISE IN THE NUMBER OF

RETAIL INVESTORS USING SIP

“THERE ARE MANY KNOWN (UNKNOWNS) AND UNKNOWN UNKNOWNS AT PLAY. I’VE ENTERED 2016 WITH A CONSERVATIVE MINDSET”

Uday Kotak, Executive Vice Chairman & Managing Director, Kotak Mahindra Bank

WAIT AND WATCHFactors that will impact the Indian equity market in 2016

• Global developments, especially in China, US and West Asia

• Government decisions on spending to revive growth

• The year’s monsoon

• Corporate earnings recovery

• Money flows from FIIs and domestic institutions

Focus-Market.indd 4 09-01-2016 1:45:43 PM

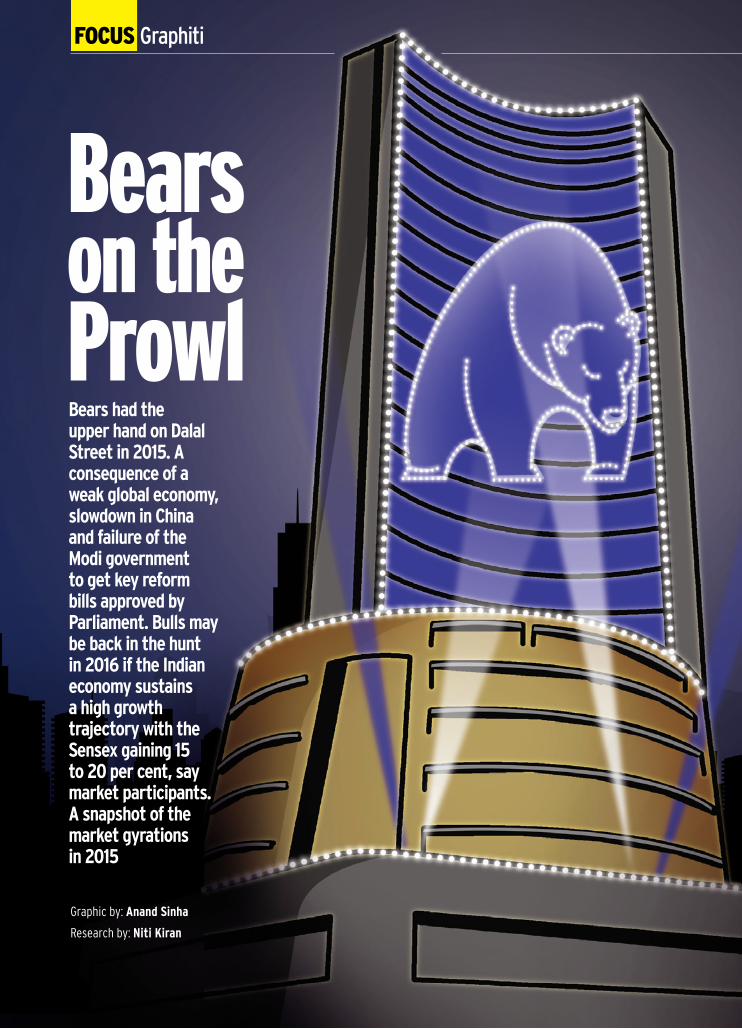

FOCUS Graphiti

Research by: Niti Kiran

Graphic by: Anand Sinha

Bears on the ProwlBears had the upper hand on Dalal Street in 2015. A consequence of a weak global economy, slowdown in China and failure of the Modi government to get key reform bills approved by Parliament. Bulls may be back in the hunt in 2016 if the Indian economy sustains a high growth trajectory with the Sensex gaining 15 to 20 per cent, say market participants. A snapshot of the market gyrations in 2015

160

140

120

100

80

60

40

20

0

Bovespa Hang Seng

PE Sensex Market Cap

NASDAQComposite

Sensex

The Sensex traded at a price-to-earnings ratio of around 19 in 2015, only marginally higher than the fi ve-year average. It indicates that the market was not expecting corporates to surprise with better-than-expected earnings

Indeed, the year was a mixed bag for the global equity markets. Emerging markets remained volatile through the year. The Sensex shed 5 per cent in 2015

A lacklustre market did not deter Indian companies from tapping the primary market. India Inc. raised ` 68,608 crore, a

76 % jump over the previous year

FIIs exited India with net outfl ows of Rs 20,585 crore in the fi rst nine months of 2015/16 but mutual funds came to the rescue with investments of over

`59,000 cr. in the same period

50,00,000

48,00,000

46,00,000

44,00,000

42,00,000

40,00,000

38,00,000

36,00,000

25

20

15

10

5

01 Jan., 2015

2 Jan. 2015 2 Dec. 2015

31 Dec., 2015

45,11,847

19.818.8

44,38,824

But long term investments in equities are still giving good returns. On average, a 10-year holding period since April 1979 has given a return of 17 per cent

31 Mar. 1989 31 Mar. 2015

10 Year CAGR return30.0%

20.0%

10.0%

0.0%

-10.0%

PE: price-to earnings ratio; Market Cap in ` crore

Data rebased to 100

These are rolling returns. For instance, if somebody invested on April 03, 1979, he would have exited the market after 10 years (on March 31, 1989) with annualised returns of over 19 per cent. This process was repeated for each trading day since April 03, 1979 and 10 year annualised returns were calculated – it yields an average of 17 per cent .

Source: CMIE, ACE Equity

FOCUS GRAPHITI Market.indd All Pages 01/09/2016 12:54:35 AM

FOCUS Graphiti

Research by: Niti Kiran

Graphic by: Anand Sinha

Bears on the ProwlBears had the upper hand on Dalal Street in 2015. A consequence of a weak global economy, slowdown in China and failure of the Modi government to get key reform bills approved by Parliament. Bulls may be back in the hunt in 2016 if the Indian economy sustains a high growth trajectory with the Sensex gaining 15 to 20 per cent, say market participants. A snapshot of the market gyrations in 2015

160

140

120

100

80

60

40

20

0

Bovespa Hang Seng

PE Sensex Market Cap

NASDAQComposite

Sensex

The Sensex traded at a price-to-earnings ratio of around 19 in 2015, only marginally higher than the fi ve-year average. It indicates that the market was not expecting corporates to surprise with better-than-expected earnings

Indeed, the year was a mixed bag for the global equity markets. Emerging markets remained volatile through the year. The Sensex shed 5 per cent in 2015

A lacklustre market did not deter Indian companies from tapping the primary market. India Inc. raised ` 68,608 crore, a

76 % jump over the previous year

FIIs exited India with net outfl ows of Rs 20,585 crore in the fi rst nine months of 2015/16 but mutual funds came to the rescue with investments of over

`59,000 cr. in the same period

50,00,000

48,00,000

46,00,000

44,00,000

42,00,000

40,00,000

38,00,000

36,00,000

25

20

15

10

5

01 Jan., 2015

2 Jan. 2015 2 Dec. 2015

31 Dec., 2015

45,11,847

19.818.8

44,38,824

But long term investments in equities are still giving good returns. On average, a 10-year holding period since April 1979 has given a return of 17 per cent

31 Mar. 1989 31 Mar. 2015

10 Year CAGR return30.0%

20.0%

10.0%

0.0%

-10.0%

PE: price-to earnings ratio; Market Cap in ` crore

Data rebased to 100

These are rolling returns. For instance, if somebody invested on April 03, 1979, he would have exited the market after 10 years (on March 31, 1989) with annualised returns of over 19 per cent. This process was repeated for each trading day since April 03, 1979 and 10 year annualised returns were calculated – it yields an average of 17 per cent .

Source: CMIE, ACE Equity

FOCUS GRAPHITI Market.indd All Pages 01/09/2016 12:54:35 AM

Apr-Jun 2015 Jul-Sep 2015 Oct-Dec 2015

Apr-Jun 2015 Jul-Sep 2015 Oct-Dec 2015

Business Confi dence Index

THE SLIDE CONTINUES

Business sentiment hits another low

On January 6, a group of industry captains, including Ajay Piramal, R. Seshasayee, Harshavardhan Neotia and Sunil Kanoria, met Finance Minister Arun Jaitley at North Block to apprise him of industry expecta-tions from the upcoming Budget. While pre-budget meetings with the FM happen every year, industry lead-ers were never so anxious to put out a list of things that they wanted to see in Budget 2016.

The macro, consumer and invest-ment indicators have remained sub-dued for the longest time and the ap-petite for fresh investments in the private sector has been down for sev-eral quarters. The confidence levels have also been dipping with every quarter. This was reflected in the re-cent Business Today-C fore Business Confidence Survey. “Sharp degree of volatility in the global markets, recent

political outcome in local and Bihar elections, and the government’s ina-bility to get big-ticket reforms under-way may have led to a dip in confi-dence levels,” says Shubhada Rao, Chief Economist of Yes Bank.

The confidence levels, on a scale of 100, have dipped for the fourth consecutive quarter to 53.2 between October and December, down from 55.4 in the July-September quarter. The dip in sentiments shows that businesses are losing hope in the re-vival of the Indian economy. The business confidence index has been moving up and down in the past two years. It began to improve during January-March 2014, just before the general elections, and had reached 62.2 in October-December 2014. The survey was launched in the January-to-March quarter of 2011. Market research agency C fore quizzed 500

Corporate sentiment has taken a beating for the fourth straight quarter, reveals the BusinessToday-C fore Business

Confi dence Survey. The Union Budget is an opportunity for the government to get the economy on track. By MANU KAUSHIK

Waiting for the Budget

*Big businesses: Turnover `500 crore Medium businesses: Turnover `100-500 crore Small businesses: Turnover `5-100 crore Micro businesses: Turnover `5 crore

Apr-Jun 2014

Jul-Sep 2014

Oct-Dec 2014

Jan-Mar 2015

Apr-Jun 2015

Jul-Sep 2015

Oct-Dec 2015

BCI by SizeConfi dence levels fell across businesses of all sizes.

56.8

60.5

62.2

60.4

57.4

55.4

53.2

Big businesses

Medium businesses

Small businesses

Micro businesses

59.5

57.8

57.1

56.3

58.1

56.2

54.8

53.7

53.7

54.6

53.1

52.2

BCI by SectorSentiment has dipped across sectors

THE BIG PICTUREWhat the macroeconomic indicators reveal

Services Light Industry Heavy Engineering

56.9 57.3 58.754.4 55.6 57.253.1 54.3 52.4

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15

4.2 4.3

6.3

3.8

9.8

There is little change in exports...

... and CPI infl ation in recent months...

... but the spike in the Index of Industrial Production augurs well for the economy

Exports Imports

Jun-1522,274

33,068

Jul-15 23,14335,794

Aug-15 21,27233,676

Sep-15 21,72032,209

Oct-15 21,40830,937

Nov-15 20,01329,795

In $ million

(Y-o-Y % change )

Jun-15 Nov-15

5.4

3.7 3.74.4

5.05.4

Consumer Price Indices : Base Year 2012

IIP growth (%)

BCI.indd 2-3 01/09/2016 1:58:34 AM

Apr-Jun 2015 Jul-Sep 2015 Oct-Dec 2015

Apr-Jun 2015 Jul-Sep 2015 Oct-Dec 2015

Business Confi dence Index

THE SLIDE CONTINUES

Business sentiment hits another low

On January 6, a group of industry captains, including Ajay Piramal, R. Seshasayee, Harshavardhan Neotia and Sunil Kanoria, met Finance Minister Arun Jaitley at North Block to apprise him of industry expecta-tions from the upcoming Budget. While pre-budget meetings with the FM happen every year, industry lead-ers were never so anxious to put out a list of things that they wanted to see in Budget 2016.

The macro, consumer and invest-ment indicators have remained sub-dued for the longest time and the ap-petite for fresh investments in the private sector has been down for sev-eral quarters. The confidence levels have also been dipping with every quarter. This was reflected in the re-cent Business Today-C fore Business Confidence Survey. “Sharp degree of volatility in the global markets, recent

political outcome in local and Bihar elections, and the government’s ina-bility to get big-ticket reforms under-way may have led to a dip in confi-dence levels,” says Shubhada Rao, Chief Economist of Yes Bank.

The confidence levels, on a scale of 100, have dipped for the fourth consecutive quarter to 53.2 between October and December, down from 55.4 in the July-September quarter. The dip in sentiments shows that businesses are losing hope in the re-vival of the Indian economy. The business confidence index has been moving up and down in the past two years. It began to improve during January-March 2014, just before the general elections, and had reached 62.2 in October-December 2014. The survey was launched in the January-to-March quarter of 2011. Market research agency C fore quizzed 500

Corporate sentiment has taken a beating for the fourth straight quarter, reveals the BusinessToday-C fore Business

Confi dence Survey. The Union Budget is an opportunity for the government to get the economy on track. By MANU KAUSHIK

Waiting for the Budget

*Big businesses: Turnover `500 crore Medium businesses: Turnover `100-500 crore Small businesses: Turnover `5-100 crore Micro businesses: Turnover `5 crore

Apr-Jun 2014

Jul-Sep 2014

Oct-Dec 2014

Jan-Mar 2015

Apr-Jun 2015

Jul-Sep 2015

Oct-Dec 2015

BCI by SizeConfi dence levels fell across businesses of all sizes.

56.8

60.5

62.2

60.4

57.4

55.4

53.2

Big businesses

Medium businesses

Small businesses

Micro businesses

59.5

57.8

57.1

56.3

58.1

56.2

54.8

53.7

53.7

54.6

53.1

52.2

BCI by SectorSentiment has dipped across sectors

THE BIG PICTUREWhat the macroeconomic indicators reveal

Services Light Industry Heavy Engineering

56.9 57.3 58.754.4 55.6 57.253.1 54.3 52.4

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15

4.2 4.3

6.3

3.8

9.8

There is little change in exports...

... and CPI infl ation in recent months...

... but the spike in the Index of Industrial Production augurs well for the economy

Exports Imports

Jun-1522,274

33,068

Jul-15 23,14335,794

Aug-15 21,27233,676

Sep-15 21,72032,209

Oct-15 21,40830,937

Nov-15 20,01329,795

In $ million

(Y-o-Y % change )

Jun-15 Nov-15

5.4

3.7 3.74.4

5.05.4

Consumer Price Indices : Base Year 2012

IIP growth (%)

BCI.indd 2-3 01/09/2016 1:58:34 AM

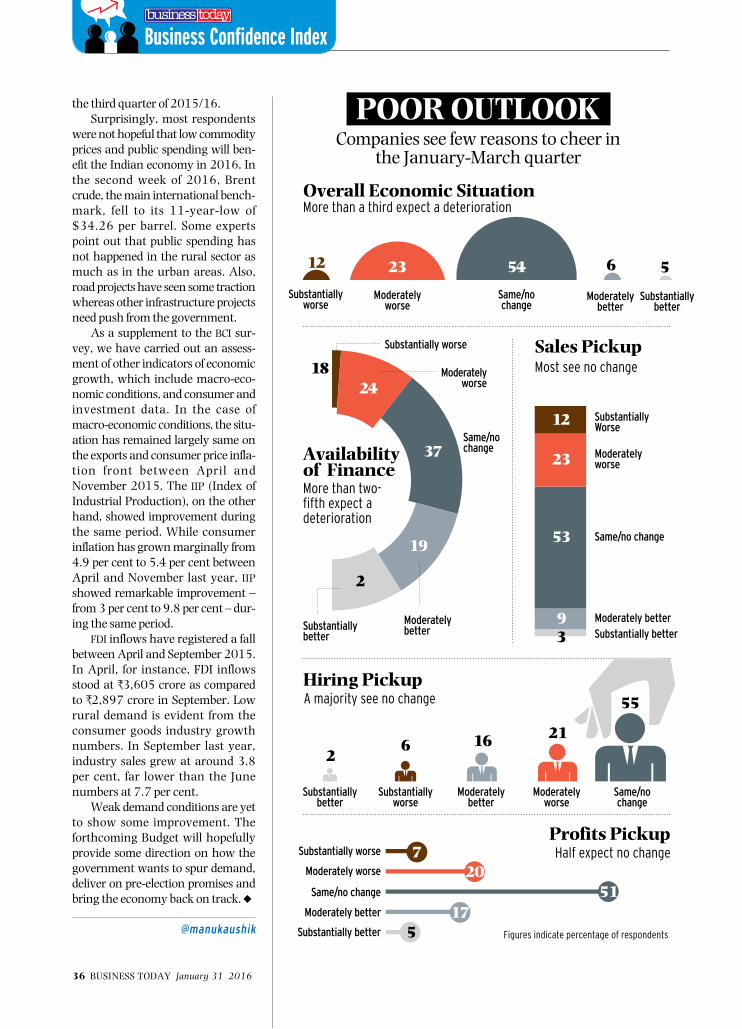

CEOs and chief financial officers across 12 cities for the survey.

Besides the broad index which has declined, there were various other parameters that have regis-tered a downswing, including the overall economic situation, the sur-vey noted. In the previous survey, just 18 per cent of respondents had expected the economic situation to deteriorate compared to 35 per cent saying the economic situation will worsen in the January-March 2016 period, this time.

Similarly, other parameters, such as the overall business situa-tion, cost of external finance, pro-duction level, order book and sales pick-up have also fallen. In the case of cost of external finance, the swing is most remarkable. In the previous survey, 66 per cent respondents had expected that the cost of finance will go down in the October-December 2015 period, whereas in the current survey, just 10 per cent foresee cost of finance to improve between January and March.

The response on cost of finance is surprising given that interest rates in India have come down consider-ably over the past one year. Last September, the Reserve Bank of India (RBI) had cut the repo rate by 50 basis points to 6.75 per cent, which was a 4.5-year low.

Respondents were, however, gung-ho about certain other param-eters such as profits pick-up and hir-ing pick-up. In the previous survey, 46 per cent respondents had said that the hiring situation would get worse in the October-December quarter. In comparison, just 27 per cent say that it will get worse in the January-March quarter.

More respondents are optimistic about private sector investments. For instance, 34 per cent respondents expect the private investment cycle to improve in the last quarter of 2015/16. In the previous survey, only 19 per cent respondents had expected an uptick in private sector investments and industrial activity in

34 BUSINESS TODAY January 31 2016

Business Confi dence Index

LOSING THE PLOTBusiness environment remained largely unchanged on key parameters in the October-December quarter

Profit MarginsTwo-fi fth saw no change

Hiring Conditions Almost half saw no change

Sam

e/no

ch

ange

Subs

tant

ially

w

orse

Mod

erat

ely

bett

er

Subs

tant

ially

be

tter

Mod

erat

ely

wor

se

4

29

3

16

48

Overall Economic Conditions

Same/no change

Substantially worse

Moderately better

Almost half saw no change

9

21

6Substantially better

47

Moderately worse 17

Demand ConditionsTwo-fi fth felt that the situation

had improved

Sam

e/no

ch

ange

Subs

tant

ially

w

orse

Mod

erat

ely

bett

er

Subs

tant

ially

be

tter

Mod

erat

ely

wor

se

18

35

7

33

7

1927

5

Moderately worse

41

Same/no change

Substantially worse

Moderately better

Substantially better

8

(All fi gures are in %)

BCI.indd 4 01/09/2016 1:59:00 AM

the third quarter of 2015/16.Surprisingly, most respondents

were not hopeful that low commodity prices and public spending will ben-efit the Indian economy in 2016. In the second week of 2016, Brent crude, the main international bench-mark, fell to its 11-year-low of $34.26 per barrel. Some experts point out that public spending has not happened in the rural sector as much as in the urban areas. Also, road projects have seen some traction whereas other infrastructure projects need push from the government.

As a supplement to the BCI sur-vey, we have carried out an assess-ment of other indicators of economic growth, which include macro-eco-nomic conditions, and consumer and investment data. In the case of macro-economic conditions, the situ-ation has remained largely same on the exports and consumer price infla-tion front between April and November 2015. The IIP (Index of Industrial Production), on the other hand, showed improvement during the same period. While consumer inflation has grown marginally from 4.9 per cent to 5.4 per cent between April and November last year, IIP showed remarkable improvement – from 3 per cent to 9.8 per cent – dur-ing the same period.

FDI inflows have registered a fall between April and September 2015. In April, for instance, FDI inflows stood at `3,605 crore as compared to `2,897 crore in September. Low rural demand is evident from the consumer goods industry growth numbers. In September last year, industry sales grew at around 3.8 per cent, far lower than the June numbers at 7.7 per cent.

Weak demand conditions are yet to show some improvement. The forthcoming Budget will hopefully provide some direction on how the government wants to spur demand, deliver on pre-election promises and bring the economy back on track. ~

@manukaushik

Business Confi dence Index

36 BUSINESS TODAY January 31 2016

23 54 6 5

Companies see few reasons to cheer in the January-March quarter

Overall Economic Situation

Sales Pickup

More than a third expect a deterioration

Most see no change

POOR OUTLOOK

Moderately worse

Moderately worse

Same/no change

Same/no change

Substantially worse

Substantially worse

Moderately better

Moderately better

Substantially better

Substantially better

Availabilityof FinanceMore than two-fi fth expect a deterioration

Figures indicate percentage of respondents

12

18

12

23

53

93

24

37

19

2

Moderately worse

Substantially better

Substantially Worse

Same/no change

Moderately better

5655

211662

Hiring Pickup

Substantially better

Substantially worse

Same/no change

Moderately better

A majority see no change

Moderately worse

Profits PickupHalf expect no change

Same/no change

Substantially better

Substantially worse

Moderately better

Moderately worse

720

5117

5

BCI.indd 5 01/09/2016 1:59:15 AM

I t is a no-brainer when you think about it really. Any event you plan, whether it is a global confer-ence or a small networking mixer, is social by design, right? Hence,

it is certain that social media would be key to every aspect of event planning. Yet, strangely enough, for many compa-nies, hosting an event means throwing together a Facebook page to tell people when the event is happening, along with a few tweets or LinkedIn posts. Shouldn't you instead use social to start a nuanced, long-term conversation with your at-tendees? If you are involved with plan-ning an event, consider these tips for weaving social into your event’s fabric, so that the buzz prevails long after the last cheque is cleared.

SOCIAL UNIVERSE

At the beginning, you would want to decide your mix of social networks to get the word out about the event and connect with prospec-tive attendees. Facebook has the most on offer – most attendees are already on it and are familiar with interacting with brand pages; you can host all sorts of content like photos, videos, surveys and dedicated event pages. Facebook also offers targeted ads that let you pick geographic or demo-graphic segments to boost visibility. Head to LinkedIn if you are organis-ing an industry event – LinkedIn Groups, in particular, where you are likely to find key influencers and po-tential attendees. Save Twitter for the actual event experience, to leverage the event hashtag, which is vital to marketing your event – it is used to track everything from promotions, campaigns, conversations and high-lights. Ensure that the hashtag is unique and short, and include it in invites, tickets, blog posts, traditional advertisements and posters.

As you inch closer to the event and significant speakers confirm their presence, start promoting it by in-cluding their social accounts (Facebook, Twitter) in the communi-cation announcing your event – this makes the event instantly shareable to your speakers’ own social media followers – and remember to include subtle calls to action to register for your event. If ticket sales need a pick-

me-up, consider putting an affiliate/ referral program in place that allows influencers to attend your event for free, if they popularise your event on their social channels and drive ticket sales. Giveaways via Twitter contests work well too, but please avoid spam-ming Twitter. You don’t want your event hashtag to end up in power users’ Twitter mute lists.

During the event, it is a good idea to share live quotes, photos, short videos, or have the team walk around the venue, sharing interesting photos of attendees and conversations hap-pening along the sidelines. Either way, dedicate at least a couple of people to monitor your social feed when the event is on, to track conver-sations about the event and also to address questions or complaints com-ing up on the event hashtag. It may be worth grabbing a spare projector and setting up a ‘social wall’ that displays tweets and posts in real time, encouraging attendees to participate in the conversation.

As the curtain comes down on the event, don’t let the buzz dissipate. You can retell the story of the event in your attendees’ words with tweets and posts shared, and video snippets of their takeaways from the sessions. This gives people who could not attend a peek into what happened, luring them to be a part of it next time! ~

@2shar

LISTENING POST

Multi-lingual TextingInstant messaging platform Hike has launched its app in Hindi, Marathi, Tamil,

Gujarati, Bengali, Malayalam, Kannada and Telugu languages. “This launch means that people and communities across the length and breadth of India can now be in touch with their families, friends and contacts in their own native languages, defying the English language barrier erstwhile felt in messaging apps,” the company said in a press release. The app, available for Android phones, features a multi-lingual keyboard that allows the user to type in nine languages including English. The multi-lingual interface helps users choose a language as soon as they download the app. Users can also use the glide functionality at the bottom of the chat panel to swap languages.

Drone Selfi esTwitter has attained a patent from the United States Patent and Trademark Offi ce

for an unmanned aerial vehicle (UAV) that can be controlled by tweets, and can share images and videos on the platform. As per the patent fi led by Twitter in June, “Account holders of the messaging platform may control the UAV with commands embed-ded in messages and directed towards an account associated with the UAV”. The patent also states that the UAV may include a display screen and/ or a micro-phone to facilitate telepresence or interview functionality. When asked to describe the device by CNBC, all that the Twitter spokes-person said was – “Two words: Drone Selfi es”. – DEVIKA SINGH

Keep the Buzz Going

WHAT’S TRENDING

Use social media to promote an event and then retain the buzz around it. By TUSHAR KANWAR

38 BUSINESS TODAY January 31 2016 January 31 2016 BUSINESS TODAY 39

Surging Popularity Expanding FootprintGlobal social networks ranked by number of users (in millions)

Average monthly social media user engagement in select global regions as of June 2015 (in hours)

DIGITAL DASHBOARD

AJ

AY

TH

AK

UR

I

Facebook WhatsApp QQ Facebook Messenger

1,550

6.1 6.1

5.2

3.8

2.1

900 860700 653 650

400316 300 300 249 230 212 211 200

105 100 100 100 97

QZone WeChat Instagram Twitter Baidu Tieba

Skype Viber Tumblr Sina Weibo

BBM LinkedIn* Latin America

Europe North America

Middle East and Africa

Asia Pacifi c

PinterestVKontakteYYSnapchatLINE

Source: Statista Source: comScore

Social Media.indd All Pages 08-01-2016 5:20:55 PM

I t is a no-brainer when you think about it really. Any event you plan, whether it is a global confer-ence or a small networking mixer, is social by design, right? Hence,

it is certain that social media would be key to every aspect of event planning. Yet, strangely enough, for many compa-nies, hosting an event means throwing together a Facebook page to tell people when the event is happening, along with a few tweets or LinkedIn posts. Shouldn't you instead use social to start a nuanced, long-term conversation with your at-tendees? If you are involved with plan-ning an event, consider these tips for weaving social into your event’s fabric, so that the buzz prevails long after the last cheque is cleared.

SOCIAL UNIVERSE