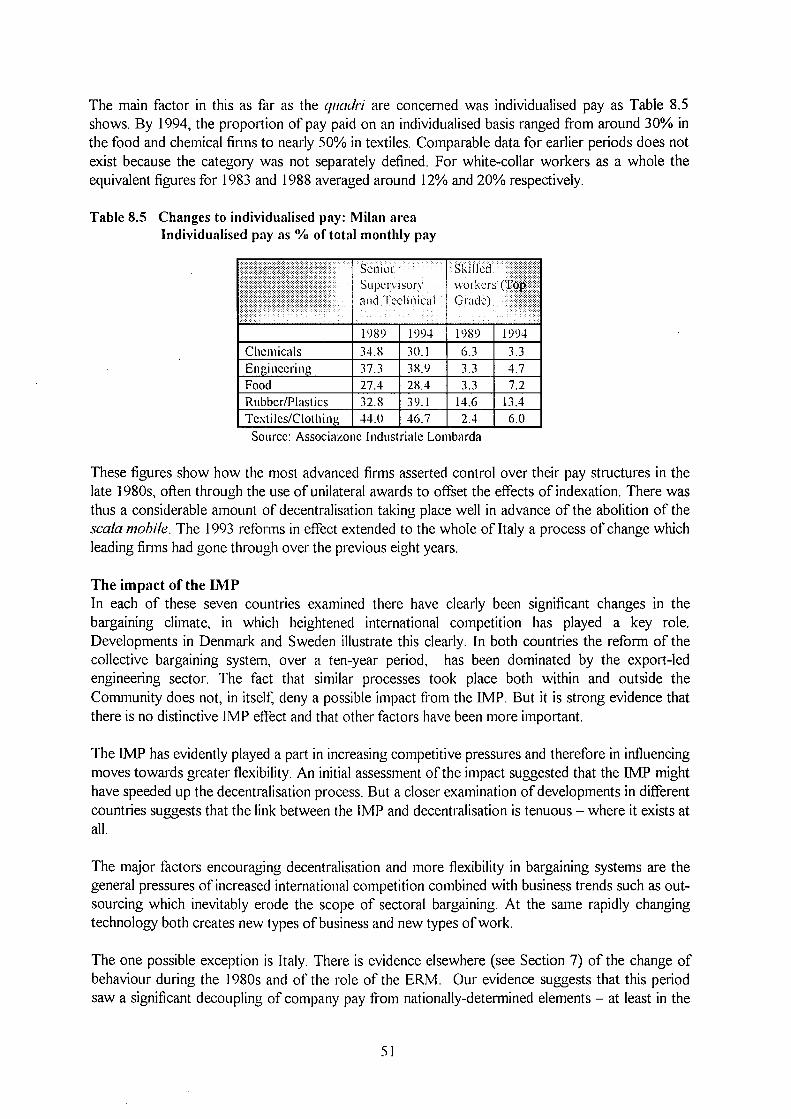

The Impact of the Single European Market on Pay and Collective Bargaining

124

The impact of the internal market on pay and collective bargaining Employment & social affairs * * * * . * * * * * European Commission

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of The Impact of the Single European Market on Pay and Collective Bargaining

The impact of the internal market on pay and collective bargaining

Employment & social affairs

* * * * . * * * * *

European Commission

The impact of the internal market on pay and collective bargaining

IDS Incomes Data Services Ltd

Employment Sc social affairs Employment and labour market

European Commission Directorate-General for Employment, Industrial Relations

and Social Affairs Unit V/A.2

Manuscript completed in August 1996

This report was prepared by David Shonfield in collaboration with Pete Burgess, Ken Mulkearn, Tony Morgan, Kevin Doogan, School for Policy Studies, University of Bristol.

This report was financed by and prepared for the use of the European Commission, Directorate-General for Employment, Industrial Relations and Social Affairs. It does not necessarily represent the Commission's official position.

A great deal of additional information on the European Union is available on the Internet. It can be accessed through the Europa server (http://europa.eu.int).

Cataloguing data can be found at the end of this publication.

Luxembourg: Office for Official Publications of the European Communities, 1997

ISBN 92-828-1802-0

© European Communities, 1997 Reproduction is authorised provided the source is acknowledged.

Printed in Belgium

Contents

1. Introduction 1

2. Methodological approach 4

3. Summary of the main findings 8

4. Company views: the IMP and corporate personnel policies 11

5. Survey of employers' organisations and trade unions 15

6. The impact of the IMP: an inter-sectoral analysis of pay statistics 20

7. Indexation, inflation and pay: the impact of the ERM 33

8. The IMP and pressures for decentralisation 37

9. 'Marketisation' and the growth of variable pay 55

10. The impact of foreign direct investment 67

11. The impact of the IMP on small and medium enterprises 77

Appendix I: Location 85

Appendix II: The impact of liberalisation in air transport and 99 telecommunications

References and additional sources 109

1. Introduction

This report examines the development of nominal wages and the collective bargaining process in the EU Member States. It is based on a review of changes in pay and bargaining over the ten-year period 1985 to 1995 and an assessment of the extent to which these changes have been influenced by the Internal Market Programme (IMP).

There is, by definition, no direct impact from the IMP on pay and bargaining. Specific IMP measures have had a substantial impact on individual sectors, two of which - air transport and telecommunications - are the subject of case studies appended to this report. But in general this report is about the indirect impacts of the IMP as a whole on pay and bargaining developments. From an early stage it has been clear that analysis of quantitative data would produce only limited results. This report therefore relies to a large extent on a qualitative analysis of change in bargaining, supported by our own and other surveys of companies and representatives of employers' organisations and trade unions.

Structure of this report We begin with a review of the main literature which has helped in identifying the themes of this report. We then outline a number of hypotheses about the possible impacts of economic integration on pay and collective bargaining and set out the four key hypotheses we have used to test for the impact of the IMP. We follow this with a summary of our conclusions, before going on to review our findings in detail.

The impact of economic integration The starting point for our research is the work carried out by two study groups set up by the Commission in 1989 and 1991. These exercises reached a number of conclusions about the possible impact of economic integration on European labour markets. We have drawn on these to arrive at a series of hypotheses from which we have selected four main theses to be tested.

This earlier research (Marsden et al 1992, 1992a) concluded that pressures on labour markets from increasing integration came from four main directions: the easing of trade restrictions; increased possibilities for labour mobility; greater capital integration; and progress towards monetary union.

Five main sets of problems of pay adaptation were identified: the imbalances in direct labour costs and social charges; inflationary expectations and their embodiment in bargaining practices; wage structure pressures of economic integration; rigidities in public sector pay; and pressures caused by the introduction of new systems of management and work organisation.

The findings suggested that a number of developments were necessary for the successful transition to the Single Market.

1. There was a need to change the 'speed of adaptation of wage expectations', specifically to move away from indexation and quasi-indexation towards pay increases based on productivity.

2. There was a need to change the pay 'linkage' between sectors, to avoid the damaging effects of comparability - particularly in the low-wage economies.

3. Greater decentralisation of the bargaining process would both aid in weakening existing sectoral and occupational linkages and encourage pay arrangements linked to performance.

4. The development of different types of performance pay would blur the edges of distributional conflicts, giving the parties involved a greater number of registers on which compromise could be negotiated.

5. In the public sector, systems building automaticity into the evolution of pay - such as implied indexation and increments related to age or seniority - would require revision.

Some of these developments were already partly in place, some were anticipated and others required policy changes from governments, employers and trade unions. In general, the conclusion was that 'the scope that governments and employers have to buy change from employees' was being constrained by the move to the Single Market - particularly the economic and financial convergence criteria agreed at Maastricht. However, the effect was at least partially offset by the reduced bargaining power of employees and hence the lower price employers have to pay for changes in working practices (Marsden 1992a).

There was thus some optimism that the increased competitive pressures from the move to the Single Market could be contained without a severe rupture in industrial relations.

Other themes The literature on the possible impacts of economic integration is copious on the question of monetary convergence and union, but virtually silent on the question of the IMP. The other themes of relevance to this report are outlined below.

Pay and inflation As far as monetary union is concerned, the issue examined in this report is whether the disciplines of the ERM (and subsequently the EMU convergence criteria) have changed the attitudes of pay bargainers to inflation. The hypothesis (Giavazzi et al 1988; Barreli 1990) is that the previous lack of credibility of government policies on exchange rates and inflation was replaced by an ERM-induced credibility, and that this in turn caused a change in inflationary expectations. We examine this issue in Section 7.

The impact of EMU Boyer (1993) argues that the move from 'National Labour Standards' to a 'European Monetary Standard' means that pay-setting will become a key variable in determining the competitiveness of different regions. He postulates a number of alternative wage-setting systems which might be compatible with EMU, ranging from the complete decentralisation of pay negotiations to sectoral agreements at European level. However, despite some evidence of convergence of nominal wages in the 1980s, under the discipline of the ERM, there is no evidence of general transition to pay regimes suitable for full monetary union. Reviewing the literature on pay and the possible effects of economic integration, Boyer's realistic, if somewhat downbeat, conclusion is that 'The acceleration of European integration ... shows starkly that economists do not yet have theories and models at their disposal which allow them to be sufficiently clear about the stakes involved in changing an economic and financial regime.'

Flexibility and decentralisation A more flexible and decentralised regime of pay determination at company level (Weitzman 1984) is seen by Boyer as one possible development. And this is a key element in the evolution of a 'European Model' of wage bargain outlined by Vaughan-Whitehead (1990). On this view there is a broad convergence of pay structures on systems characterised by four main components: a basic

wage fixed at sectoral level; an element to reward individual performance; a share in company profits; other benefits accentuating the diversification of benefits. We look in more detail at these issues in Sections 8 and 9.

Social dumping One persistent theme of discussions on the impact of economic integration is the variation in labour costs and labour regulation in Member States and the spectre of'social dumping'. Social dumping has been used to describe a variety of phenomena. As defined by Buigues et al (1990) social dumping is 'the recourse to working conditions and social standards which are below the levels which the productivity of the economy could normally justify, with the purpose of increasing market shares and improving competitiveness. Member States with better working conditions could be forced to reduce or, at the very least, to halt the process of improvement, for fear of activities relocating to countries with inferior conditions'.

Such a process is almost impossible to measure objectively and thus, not surprisingly, social dumping has become more a term of political abuse than a description of actual economic effects. For this reason we have essentially excluded the question of social dumping from this report.

Occasionally, however, the issue has become a matter of the public policy of Member States. In 1993, for example, the UK government placed advertisements in the German business press arguing that German firms could 'profit from making Great Britain your place of business' because of significantly lower wages and social charges. The advertisements coincided with the political controversy over the decision by Hoover to relocate production from France to the UK, closing its factory in Dijon and negotiating reduced terms and conditions of employment in Glasgow. This event was seen as a portent of competitive undercutting of pay and conditions as international firms took advantage of the need for jobs in depressed areas. A case study of the Hoover relocation has therefore been included as an appendix to this report.

Another, more important, aspect of the debate is the way some companies have used differences in labour costs and, especially, in working practices as a bargaining counter in negotiations involving new investment. This is not a new phenomenon, but it has been of particular important in recent years in one country - Germany - and one sector, the motor industry. A further case study therefore examines the most important example of this approach to collective bargaining, at Mercedes-Benz.

2. Methodological Approach

The central aim of this report is to determine whether the Internal Market has had particular effects on pay and bargaining developments which can be distinguished from the other pressures which have operated during the period. This task is particularly hard because of the slippery and subjective nature of many of the issues involved - above all changes in the attitudes of employers and unions -and the overwhelming importance of the general pressures of increased international and national competition and technical change. In addition one has to bear in mind the specific impact of German unification and the general effects of the recession of the early 1990s.

To disentangle these factors - or at least to clarify the areas where an IMP effect might be identifiable - we constructed a diagram of possible effects on European integration on pay and collective bargaining (see Chart). The different elements in this flow-chart are derived partly from earlier research carried out for the Commission (Marsden 1992; 1992a) and partly from some of the sectoral studies carried out during the general review of the impact of the ΓΜΡ. The sectoral studies on air transport, telecommunications services and equipment and the automotive industry proved especially useful in focusing research. In addition, we have benefited from the experiences of the companies consulted for this research and in previous assessments of trends in pay and bargaining (IDS 1988; Shonfield 1992).

In establishing the possible linkages between the IMP and changes in pay and bargaining, the chief difficulty is that the effects noted in the diagram can be attributed to the general increase in competitive pressures during the period. Those directly involved in the bargaining process are adamant that it is these general pressures which are responsible and not the IMP. Employers and unions agree that increased integration has altered the 'mindset' of negotiators in various ways, but point out that the IMP was itself the result of the general world-wide increase in competition during the 1980s and the awareness of the danger of'Eurosclerosis'.

The dynamics of change involved a combination of political, economic and technological factors.

Political factors included the 'backlash' against regulation and union power, which began in the United States and the UK at the end of the 1970s but exerted a powerful general influence on policy makers throughout the 1980s. In addition there were more specific political priorities to be addressed such as the transition to democracy in Spain; the 'crisis of institutions' in Italy; and, most notably, the consequences of German unification. Al of these have had a substantial continuing impact on the social and industrial relations climate.

For many large companies there was a crisis of management. Established structures failed to respond adequately to the recession of the 1980s and to the challenges of new technology. Speed and flexible response to market signals became crucial competitive attributes for a large number of businesses. The result was a massive and sometimes continuous overhaul of management systems, together with the introduction of new techniques (and the re-invention of old ones). This was an uneven process, most notable in the Anglo-Saxon economies, but also increasingly important in countries such as France and Italy.

Al of this meant that flexibility was the buzz word of the 1980s, well before the IMP. Disentangling cause and effect is a largely fruitless exercise. To some extent, therefore, the methodology employed here has consisted in working backwards from a number of observed effects to draw out the possible linkages which connect to the IMP measures.

The diagram is largely based on trends in larger finns and in high-technology manufacturing industry. This was necessary to avoid blurring a picture that was already complicated. We have distinguished in the diagram between IMP measures and the impact of the ERM (and the anticipatory effects of EMU) by the use of rounded boxes to define the latter process.

Inevitably a diagram of this type involves some shorthand. The main argument is that the increased competition, investment flows, merger and acquisition activity and concentration of production which accompanied the IMP have led to new pressures on national systems. This one might term a 'large firm' effect. At the same time the IMP presented smaller enterprises both with increased opportunities for expansion and trade and with a sharp increase in competitive pressure. The effects do not all point in the same direction, indeed a number of them have been contradictory. The combination of competitive pressures, accompanied by the disciplining effects of the ERM, led to something of a 'pincer effect', with both upward and downward pressures on pay.

Four hypotheses From the possible effects outlined in the diagram we defined three initial hypotheses: on the decentralisation of bargaining, the 'marketisation' of pay, and the linkage between pay and inflation. During the course of the research we decided to include a fürther hypothesis on the impact of increased foreign direct investment (FDI). The four hypotheses are as follows:

1. The IMP has encouraged the decentralisation of wage-setting and bargaining processes.

2. The IMP has encouraged the 'marketisation' of pay, above all the development of pay systems linked more closely to the performance of the enterprise.

3. The IMP has encouraged FDI, producing pay pressures in 'host' countries and a spread of'new' personnel policies and reward practices

4. The disciplines of the ERM/EMS and the Maastricht convergence criteria have severed the automatic linkage between pay and inflation.

These four hypotheses form the core of our assessment of the impact of the IMP and form the subjects of Sections 7 to 10 of this report.

The evidence The earnings data used in this report come from Eurostat and officiai national sources, and details are as noted in the text. Data from Italy are provided by surveys conducted by two employers' associations: Confindustria and the Associazone Industriale Lombarda. Additional material on France was provided by the Union des Industries Métallurgiques et Minières.

To test our hypotheses we also gathered evidence from the following sources:

1. An EDS survey of international companies operating in Europe. This survey focused on whether the IMP had in any way affected personnel and pay policies, either directly or indirectly, and on the use of labour cost comparisons in pay negotiations. Details of the responses and results are set out in Section 4.

2. An IDS survey of the main employers and trade union organisations in EU Member States. This survey focused on the main factors influencing bargaining, the linkages between different sectors and between company and sectoral bargaining and the main trends in pay and bargaining during the period of IMP. Details of the responses and results are set out in Section 5.

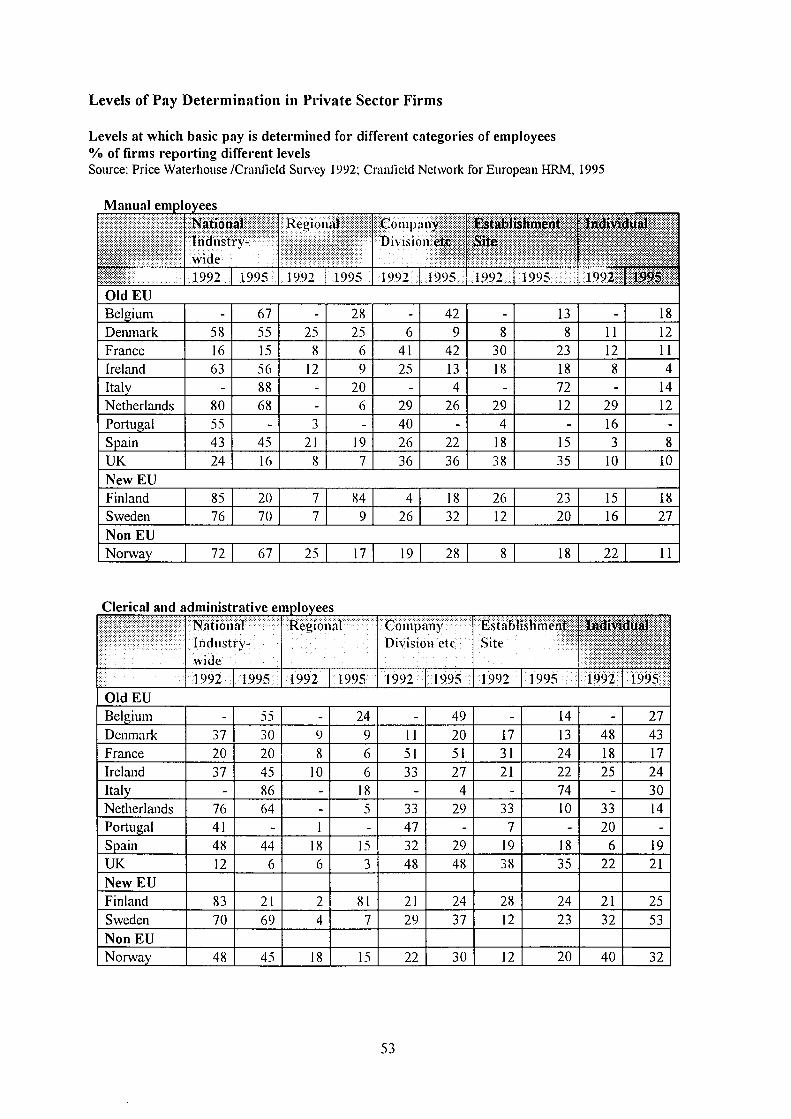

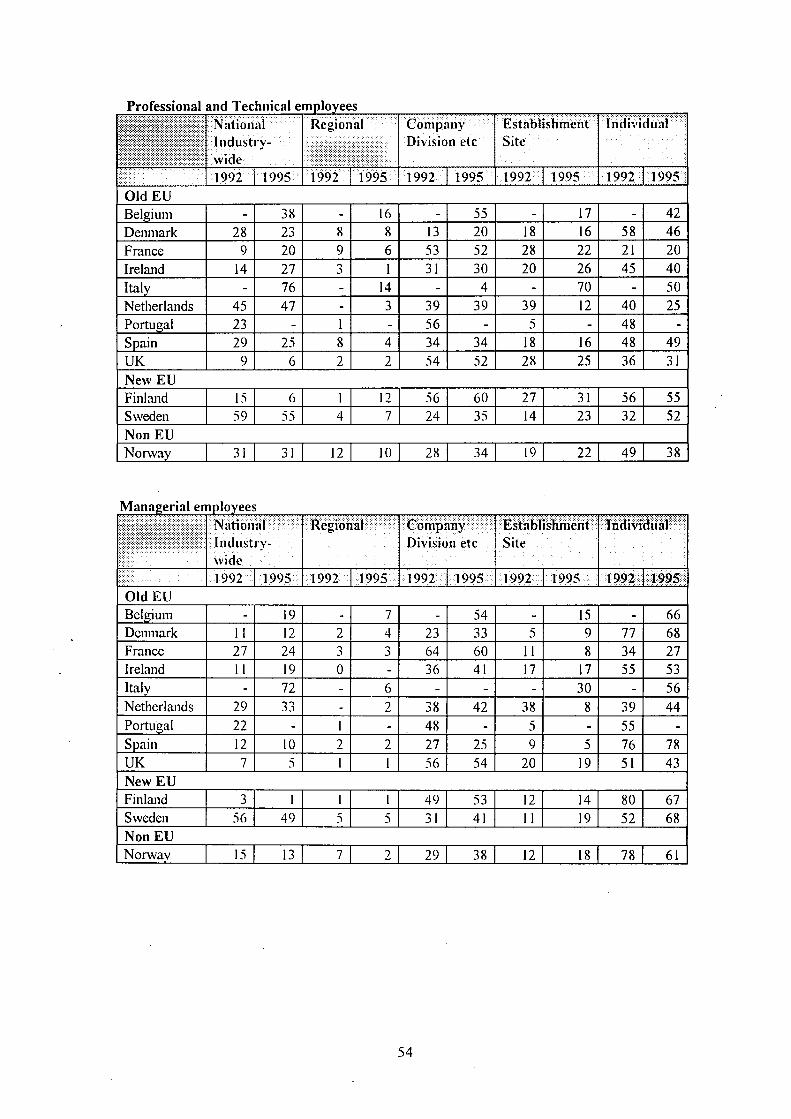

3. The 1992 and 1995 surveys of company bargaining conducted by Cranfield School of Management in association with a number of leading business research establishments. The surveys cover both private and public sector organisations employing 200 or more people. The data we use here are for the private sector only, unless otherwise stated. The 1992 survey (in association with Price Waterhouse) covered some 4,700 organisations in 12 countries. The results were published two years later (Brewster and Hegewisch 1994). The results of the 1995 survey, covering some 4,800 organisations in 13 countries, have not yet been published and are due to appear later in 1996. We have been given access to the data by the Cranfield researchers for the purposes of this report. The 1992 survey has provided some evidence for corporate attitudes to the IMP, in Section 4. Data for both 1992 and 1995 have been used extensively in Sections 8 and 9.

Note The period covered by this report includes the unification of Germany. To enable consistent comparisons all earnings and survey data for Germany relates to the former West Germany only.

DIAGRAM OF POSSIBLE EFFECTS OF EUROPEAN INTEGRATION ON PAY AND COLLECTIVE BARGAINING

Removal of barriers

Technical harmonisation

\

Increase in FDI

and reinvestment

Increased possibility of

relocation and shins in

investment Increasing pressure

for flexibility on

pay and. work

Increased trade

Economies of scale

M&A activity

MNC rationalisation

Liberalisation

measures

Concentration of

production

Public procurement

measures

ERM/EMS:;

Convergence criteria

post1992

Increasing competition

Higher productivity

Rationalisation of

supply chains

Single sourcing

Outsourcing

Increased

specialisation and

potential for

rentsharing

Increased scope for

national firms

Spread of "best

practice"

Competition in

sectors previously

protected. Services

more international

Opportunities and

competitive

pressures for SMEs

Potential for transfers

of lessskilled low

paid workers.

Upward pressures

on pay in advanced

firms. Downward

pressures on

suppliers.

Downward pressures on

pay and especially fixed

labour costs in SMEs

Enhanced credibility for national

monetary and fiscal policies

Potential for greater consensus on

national policies to control inflation

M ...EFFECTS

Companylevel

♦ variable pay

• more labour cost awareness

♦ sensitivity to nonwage :COStS. ;'.

• MNCs intracompany

mobility more compatible

svstems

Sectoral level

• pressure on skill

differentials

• divergences between SMEs

and MNCs

• greater divergence within

sectors

• divergences between

dynamic and sluggish

sectors

• emphasis on subsidiarily

decentralisation

Public policy

pressure to control NWLCs

pressure to hold down

e sector pay

links between pay and

inflation broken or modified

• segmented pay round

3. Summary of the main findings

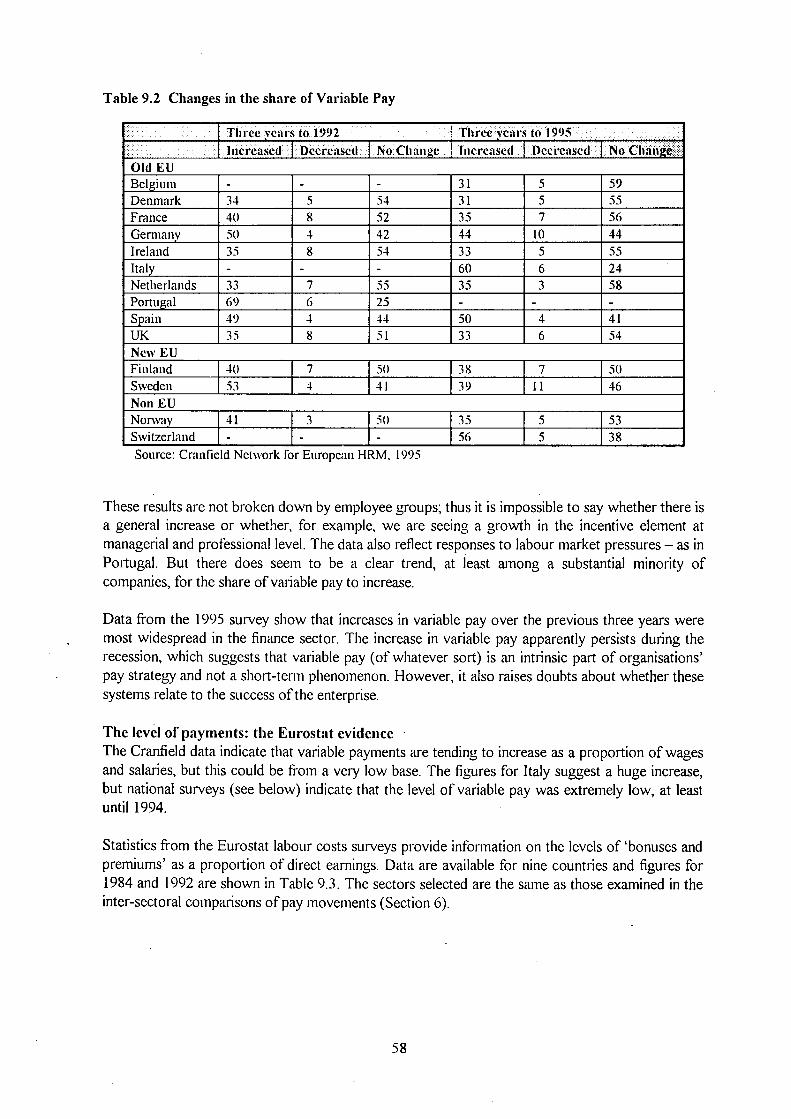

There were several major changes to pay determination and the pattern of collective bargaining between 1985 and 1995. These reflected a variety of international and domestic pressures in the different countries. There is no identifiable general Internal Market Programme effect. Responses from a survey of employers and trade unions across Europe point to some impact from the IMP and the ERM in smaller countries: Belgium, Ireland, Portugal and Austria.

The impact of the Single Market on corporate personnel and pay policies has generally been limited. The numbers of staff* being transferred between countries has increased and company remuneration systems are tending slowly to converge for this reason. The main indirect effects of European integration at company level are: an increased concern to control labour costs; changes to grading or classification of employees; and links between pay and performance. Some companies are concerned that European Works Councils will inevitably lead to increased pressure for pay comparability and upward harmonisation.

There has been a significant change in attitudes to pay and inflation in a number of countries. With the outstanding exception of the UK, there has been a distinct shift in the reference point. Inflation forecasts have become more important as a point of reference in pay negotiations than backward-looking informal indexation. The increased credibility of national economic policies and institutions because of the disciplining effect of the ERM and economic convergence criteria appears to have played an important part in this. There are some indications of a more fundamental change, namely the signs of a breakdown of'national autonomy' in wage-setting in countries such as Belgium and Ireland.

Against this there do not appear to be any major changes in the linkages between different sectors. A survey of trade unions and employers and analysis of sectoral pay movements both indicate there is considerable continuity in bargaining and there are no general signs of any segmentation in the bargaining process. Public sector pay has, however, declined as an influence on the private sector. Sectors such as textiles and construction are less influential. The survey evidence suggests that economic factors, such as growth, employment levels and productivity, are a more significant influence on pay bargaining than they were before the IMP.

Major reforms of collective bargaining have taken place in two countries, in Italy in 1992/93 and in Spain in 1994. Both of these reforms were partly influenced by the European integration process.

The Italian reforms - principally the abolition of indexation and the allocation of separate roles for industry-wide and company bargaining - were the result of a long process of change in which the ERM played a significant role in modifying inflationary expectations. The reforms also reflect a period which saw a significant decoupling of pay from nationally-determined elements, at least in the more advanced sectors of manufacturing. The Single Market seems to have played a part in this, at least to the extent that reform would have been more arduous had the IMP not existed.

The reform of the Workers' Statute in Spain liberalised and deregulated industrial relations in a number of ways, mainly promoting collective bargaining as a replacement for the courts and labour ordinances. The new Statute recognised the importance of reform as a consequence of European integration. The subsequent period of collective bargaining saw major new agreements concluded at the start of 1996 in the banking and telecommunications sectors. In both sectors there is explicit

recognition that increased competition stemming from IMP measures was a decisive element in forcing changes to working practices.

The coverage of collective bargaining has not altered in the IMP period. Union density has declined but is generally high by world standards. Sectoral bargaining continues to be of great importance in most countries. The direct intervention of government in collective bargaining has declined, although it continues to be quite active in about half the Member States.

There has been significant decentralisation of bargaining in many EU countries, in which heightened international competition has played a key role. Great diversity remains but there has been some degree of convergence. Most countries do appear to be evolving their own particular solutions in order to achieve greater scope for local negotiations. There is no single common strand to this process, although in general there seems to be a greater degree of 'subsidiarity' in the bargaining process: the content of central and sectoral agreements is changing even where the form remains the same. The IMP has evidently had some influence in this, but decentralisation began several years before the Single Market process and was by no means an 'EC phenomenon'. It took place elsewhere in Europe (notably Sweden) and in other parts of the world. Decentralisation was in some cases driven by domestic factors - as in the UK and France - and there were other cases, Ireland and Spain, where European integration had an opposite effect, reinforcing the need for a more co-ordinated approach.

Variable pay seems in general to be on the increase, but this is not a development peculiar to EU countries. The same tendency can be seen elsewhere. Companies are introducing these systems for various reasons, above all to motivate employees but also to relate pay more closely to productivity. It appears that variable pay may have developed earlier in the older EU Member States, but this is not an IMP effect.

Payment systems related to company performance are becoming more widespread in some countries, including France, the UK, the Netherlands and Italy. However, there is nothing to suggest that finns are favouring this form of remuneration over other systems, such as individual or group incentives. There is very little sign that a European Model of remuneration is developing. There are nominal profit-sharing arrangements in some countries which do not seem to be related to company performance: examples are Spain and, to a degree, the Netherlands. Finally, there are two countries where profit-sharing has become widespread during the period under review, the UK and France. In both cases, fiscal incentives, introduced or extended in the mid-1980s, have proved to be the decisive factor. Thus these developments are, by definition, based on national factors and not European integration.

At a sectoral level, the liberalisation measures in the air transport and telecommunications sectors have increased competitive pressures. In air transport, low cost competition has emerged on some routes (mainly domestic) but with the exception of Ireland this had very little direct impact on bargaining in established airlines. The general need to reduce labour costs to compete internationally has been more important. In telecommunications, the impact of liberalisation measures has still to be felt in most countries. The exceptions are the UK, where liberalisation began independently of the IMP, and Spain, where important changes to working practices (not pay) have just been agreed. In France, Germany and Italy a two-tier approach to employment conditions either has been adopted or is being prepared. This will mean future employees will not enjoy the same job guarantees and pension rights as existing staff.

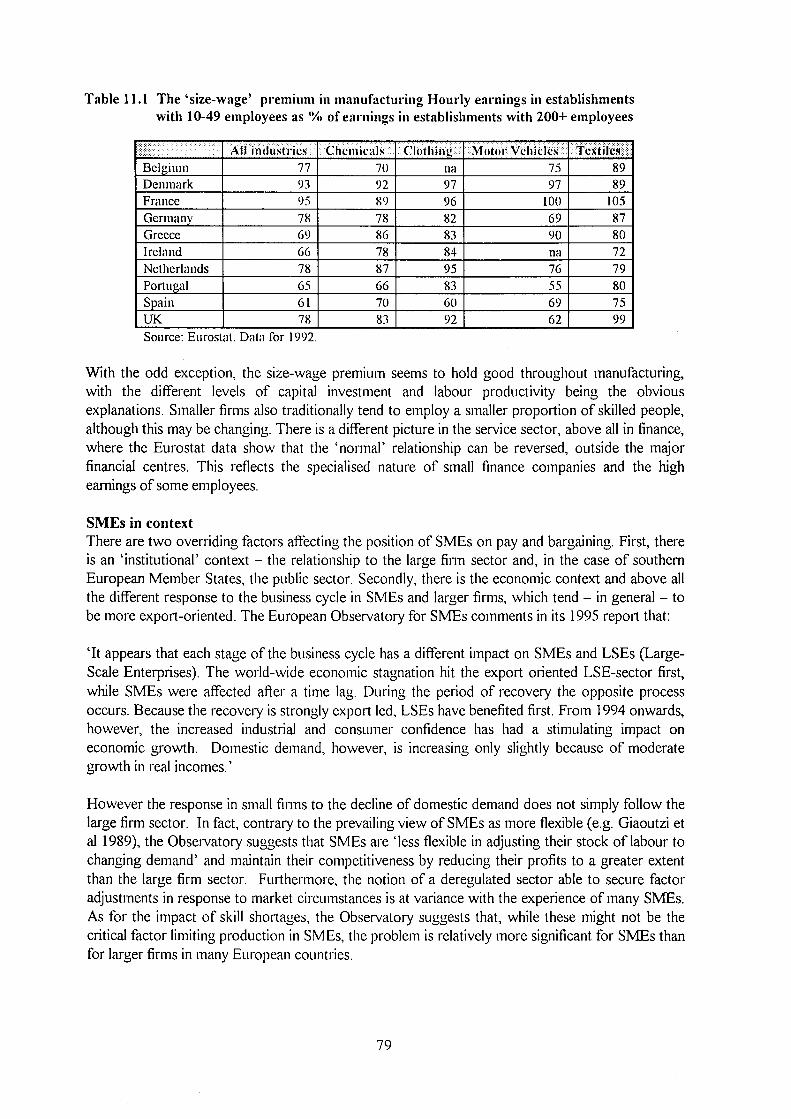

As regards the impact on Small and Medium Enterprises, only in Germany does there appear to be a distinctive 'Single Market effect', and this is confined to the problem of the employment of foreign workers in the construction industry. There is broad agreement that the situation needs to be regulated, but there has been some disagreement about the measures to be adopted. This issue clearly has implications for the EU, in that some of the workers involved are from Member States with much lower wage levels - the UK, Ireland and Portugal. However, the great majority of the workers concerned are from countries outside the EU, such as Poland and Russia.

There are some signs of increased friction between SMEs and larger firms in countries such as Ireland and Italy, but existing collective bargaining arrangements have been sufficiently adaptable. Overall, there may have been some easing of wage pressures because of restructuring in large firms.

In general, some of the fears about the impact of the IMP appear to have been unfounded. The widespread view that the economic 'core' would be enriched at the expense of the peripheral countries or regions has not so far proved correct. Foreign Direct Investment appears to have pushed up pay in Spain and in the UK. The opening up of the Spanish market resulted in severe competition for qualified staff and managers, widening pay differentials in domestic firms. The pay effect of FDI in the UK is less than in previous periods because of the shift in inward investment patterns away from the US towards Europe and Japan. Japanese investment has had a major impact on working practices and productivity in parts of UK manufacturing. The evidence of new pay pressures in Ireland is inconclusive: an increasing proportion of manufacturing employment is in non-union electronics firms which are outside the scope of collective bargaining. Across the EU as a whole, the impact of increased FDI on pay and bargaining has been very small.

The dangers of 'social dumping' have been exaggerated. There are only isolated examples of competitive undercutting of pay and conditions by firms exploiting labour cost differences between countries. On the other hand, there is evidence from Germany that firms are increasingly using the possibility of relocation as a bargaining counter to achieve changes in working practices at home.

10

4. Company views: the IMP and corporate personnel policies

The evidence on corporate behaviour suggests that the IMP has had little impact on personnel

policies. The 1992 survey conducted by the Cranfield School of Management, covering nearly

4,700 organisations in 12 countries, found that only a small minority of private sector employers -

on average some 6.5% in the eight Member States in the survey - had developed a formal (i.e.

written) personnel strategy in relation to the Single Market (Table 4.1). A somewhat larger

minority stated they had an 'unwritten' strategy. These overall figures lead to the conclusion that

the large majority of firms regarded the Single Market as essentially irrelevant to personnel issues.

Table 4.1 The impact of 1992 on corporate personnel policy 'Has your organisation developed a human resources strategy in response to the Single European Market?'

% of organisations, private sector only

EU members

Denmark

France

Germany

Ireland

Netherlands

Portugal

Spain

UK

Non EU members

Finland

Norway

Sweden

Yes:

Written

■Yes:

Unwritten

No

7

8 - 1

5

7

6

8

9

12

14

12

15

9

30

20

17

77

72

79

70

79

55

65

70

6

6

.1

14

8

10

79

81

86

Source: Price Watcrhouse/Cranfield Survey, 1992

This pattern was not entirely the same across all Member States. A wider strategic response was

most commonly reported from employers in Spain and Portugal, particularly from the major private

sector employers. This seems, however, to have been more the effect of entry into the Community

than a specific response to the IMP.

Changes to corporate personnel policies in the mn up to 1992 (IDS 1988; Marsden et al 1992)

were essentially focused on transfers of professional and managerial staff between countries. There

were two broad aims. One was to facilitate the creation of teams of professionals and executives

from different countries. The other aim was the development of a European management cadre,

capable of switching from country to country. This was particularly evident in US-owned firms and

in those sectors, such as chemicals, which already treated Europe as a Single Market, or which

were adopting a pan-European product strategy.

Two changes were identified as important in this process. The first was to bring systems such as job

evaluation more into line in different countries - making them more compatible, if not identical. The

second was to change the approach to transfers between different countries, moving away from an

'expatriate' package, with staff paid their home country salary plus extra elements to compensate

for the transfer, housing costs etc. Staff transferred between European operations would henceforth

be paid in line with local practice.

However, there was no evidence at all of any change in policies below managerial and professional level. The vast majority of companies continued to take the.view that pay and collective bargaining were a responsibility of management in local countries and business units. Some firms stated they were monitoring the outcome of collective bargaining more closely, but in almost all cases central controls were applied to only a small minority of key positions. Labour cost comparisons between different countries were seen as having very limited relevance to pay negotiations.

Research carried out in 1993/94 on the personnel policies of the largest international companies in Europe (Lester 1994) broadly confirmed the picture of a gradual move to a more 'European' approach. However, this later research argued that companies were tending to keep expatriates on the home country payroll 'in spite of the Single Market'. This finding probably reflects the response of companies (especially in the UK) to the sudden movement in exchange rates following the ERM crisis in 1992.

Results of company survey To assess the current position we surveyed a small number of international companies to identify:

a. whether any specific Single Market measures had a direct impact on personnel policy

b. whether there were indirect effects on personnel policy from the Single Market or moves towards monetary union

c. whether there had been changes in the use of labour cost comparisons.

A short questionnaire was sent to 50 companies, producing 19 responses. These were combined with the results of three in-depth interviews. The companies which responded are based in 10 different countries, are mainly involved in manufacturing, and employ a total of around 280,000 people in the EU.

Main findings Bearing in mind the limited number of companies, the main points to emerge from this research are as follows:

1. Very few companies thought the Single Market had a significant impact on industrial relations, although a majority believed it had been a factor influencing change. Most companies said that there had been no direct impact on personnel policies.

2. The number of transfers between different EU countries has increased, in some cases dramatically. Companies have installed comparable management pay structures and performance schemes in response, as well as moving away from the traditional approach to rewarding expatriates.

3. The main indirect impacts of the European integration process, identified by a minority of companies, were: increased control of labour costs, changes to the grading or classification of employees, and links between pay and performance.

4. Use of labour cost comparisons in pay negotiations had increased a little since 1990, but only one company stated that such comparisons were used 'always or often'. Unions tend to focus

12

exclusively on labour costs in different EU countries. Companies are more concerned with relative costs in North America and South East Asia.

5. In several cases the Single Market had led to the relocation of indirect functions, such as customer service and order processing, although it was pointed out that these decisions were not necessarily made on purely economic grounds.

6. The issues of greatest current concern were the costs and possible impact on collective bargaining of European Works Councils.

Observations by individual companies Comments were invited on the subjects covered in the questionnaire. Some of these are reproduced below:

Direct effects 'There has been no direct impact on personnel policies. The Single Market programme is still so far from any practical personnel changes that we do not see any impact before social systems, taxation, pensions etc are uniform' (Petrochemicals company).

'The failure to totally free up pensions, their transfer, elimination of taxation on private or corporate plans remains a serious barrier to the mobility of skilled people' (Paper company).

'Directives on telecommunications and the deregulation of this sector have had and have a major influence on personnel policies: mainly on productivity, re-engineering processes, reducing redundancies and flexibility. These are already areas of improvement in human resources policies but we have had to speed our measures' (Telephone company)

Indirect effects 'It is now even more important to divorce pay discussions from central union/EWC negotiations or there is a threat that all countries will end up paying the maximum level of salaries and benefits. It is not easy to see remuneration being harmonised at the lowest common denominator! Therefore central unions are banned from our EWC and we are approaching wage and salary negotiations on a more decentralised basis' (Paper company)

'Grade restructuring to give greater flexibility. Management by objectives to provide a link between pay and performance. Discussion groups on labour costs' (Tobacco company)

'Productivity improvement programmes. Widened population eligible for variable pay' (Food company) 'A reorganisation of sales and logistics took place in the last 214 years leading to a single warehouse for Europe and major changes in business procedures; this leads to different notions of profitability in the remaining structure with direct consequences on remuneration which we are still evaluating' (Electronics company)

13

General comments 'Our business is multinational, not European specific. Within Europe, national characteristics tend to dominate (legal and cultural considerations) despite an international approach by our company to sales and marketing, distribution and production rationalisation. Labour costs are a major factor in business decisions, but all bargaining is at national level. The Works Council Directive could herald the start of a major change. Unions and many politicians will wish to go beyond 'Information and Consultation' and enter into international negotiations. We would resist such temptations!' (Tyre company)

'Where the possibility exists for reducing labour costs on activities which do not directly impact on our customers, consideration is being given to the most suitable EU country, or wider Europe (this is a difficult subject)' (Automotive components company)

'We are moving to a more consistent approach. Where subsidiaries make changes in the personnel field we seek to ensure that these are convergent rather than divergent. The increasing number of international teams in our business has led us to organise a programme to make systems and allowances simpler and more consistent to avoid friction caused by companies treating staff differently. We are also progressively extending a common job evaluation system throughout the company. The main force for change is globalisation of the markets for our equipment, rather than developments in Europe. However, Europe is more implicated because there is a greater number of European teams and the number of transfers of staff runs into thousands (Telecommunications company).

14

5. Survey of employers' organisations and trade unions

The aims of this survey were to gain the views of the major representatives of employers and employees on recent changes in pay and industrial relations and, specifically, on the following issues:

1. The relative importance of inflation, pay comparability and general economic factors in pay bargaining and how these influences had changed since the mid-1980s.

2. The relative importance of particular sectors in the bargaining process and how sectoral influences had changed since the mid-1980s.

3. The role of company-level bargaining and the influence of prominent firms.

4. The pattern and length of the pay round.

A questionnaire was sent to 63 organisations: the central employers' and trade union confederations in each country plus the organisations responsible for collective bargaining in several key business sectors, mainly engineering/metalworking, chemicals, textiles/clothing and banking/finance. Questionnaires were also sent to tripartite organisations where appropriate.

Al EU countries were included in the survey, with the exceptions of Finland, Luxembourg and the UK. The UK was excluded both because of its uniquely fragmented bargaining arrangements and because an extensive survey of UK companies had already been carried out in July 1995. A summary of the findings for the UK is reproduced at the end (see Box).

There were 33 responses, with replies from all the countries surveyed except Greece. The number of responses was divided roughly equally between employers and unions, with the largest number coming from Denmark, Sweden and Spain.

Analysis of the main results (see Tables 5.1-5.4) produces several conclusions. The overall impression is there has been considerable continuity in bargaining during the IMP period, but that certain significant changes have taken place. In particular, there has been a modification of the relationship between pay and inflation, and associated with this a greater impact from general economic factors, such as employment and productivity. There also seem to have been changes in the pay 'linkages' between different sectors.

The areas of continuity 1. Inflation, along with economic growth, remains the strongest factor influencing pay increases. Nearly all respondents (with some exceptions in Denmark and Sweden) saw inflation - either past, present or future - as an 'important' influence.

2. Pay increases agreed at sectoral level continue to exert considerable influence. There are no general signs of greater segmentation in the bargaining process. Opinion is divided equally between those who think that pay comparability has become more important and those seeing it as less important. The consensus view is 'no change'.

3. Company pay agreements are still a relatively insignificant influence in most EU bargaining systems, the outstanding exception being the UK (see below).

15

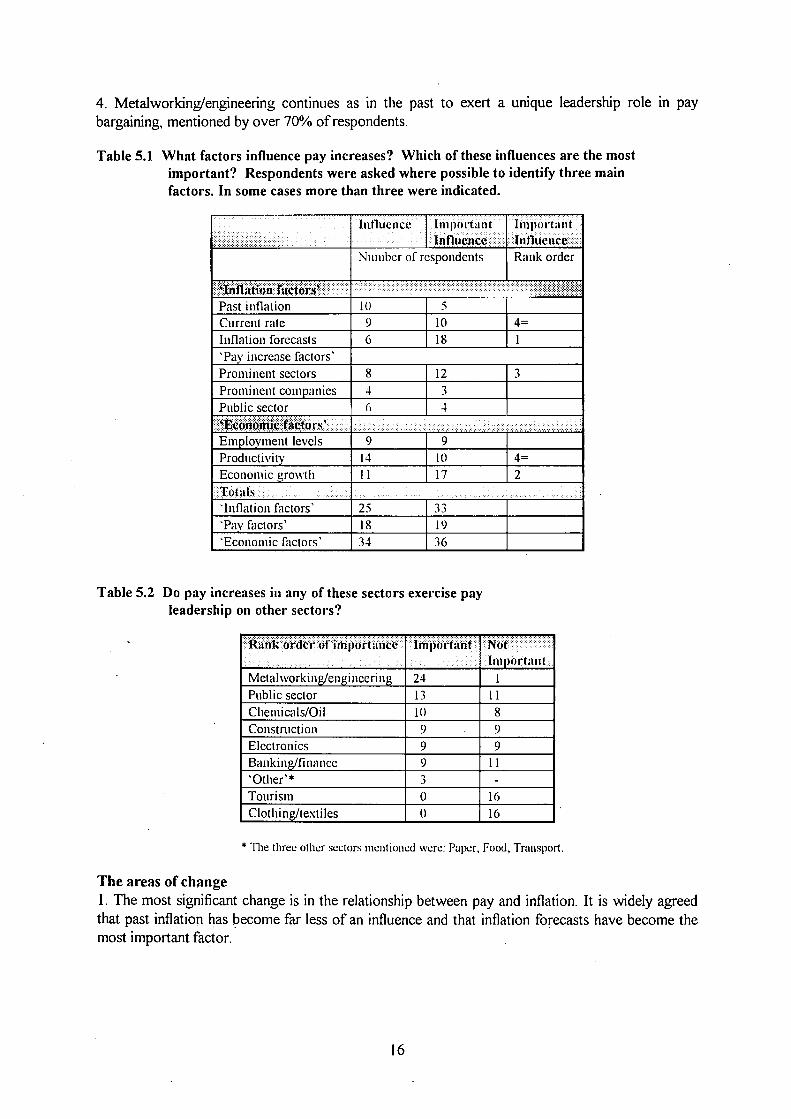

4. Metalworking/engineering continues as in the past to exert a unique leadership role in pay

bargaining, mentioned by over 70% of respondents.

Table 5.1 What factors influence pay increases? Which of these influences are the most important? Respondents were asked where possible to identify three main factors. In some cases more than three were indicated.

'Inflation factors'

Past inflation

Current rate

Inflation forecasts

'Pay increase factors'

Prominent sectors

Prominent companies

Public sector

'Economic factors'

Employment levels

Productivity

Economic growth

Totals

'Inflation factors'

'Pay factors'

'Economic factors'

Influence Impo liant

Influence

Number of respondents

Important

Influence

Rank order

'■ ' : - i ' - . " . .

10

9

6

5

10

18

4=

1

8

4

6

12

3

4

3

9

14

11

9

10

17

4=

2

25

18

34

33

19

36

Table 5.2 Do pay increases in any of these sectors exercise pay leadership on other sectors?

Rank order of importance

Metalworking/engineering

Public sector

Chemicals/Oil

Conslmction

Electronics

Banking/finance

'Other'*

Tourism

Clothing/textiles

Importiini

24

13

10

9

9

9

3

0

0

Not

Important

1

11

8

9

9

11

-

16

16

* The three other sectors mentioned were: Puper, Food, Transport.

The areas of change

1. The most significant change is in the relationship between pay and inflation. It is widely agreed

that past inflation has become far less of an influence and that inflation forecasts have become the

most important factor.

16

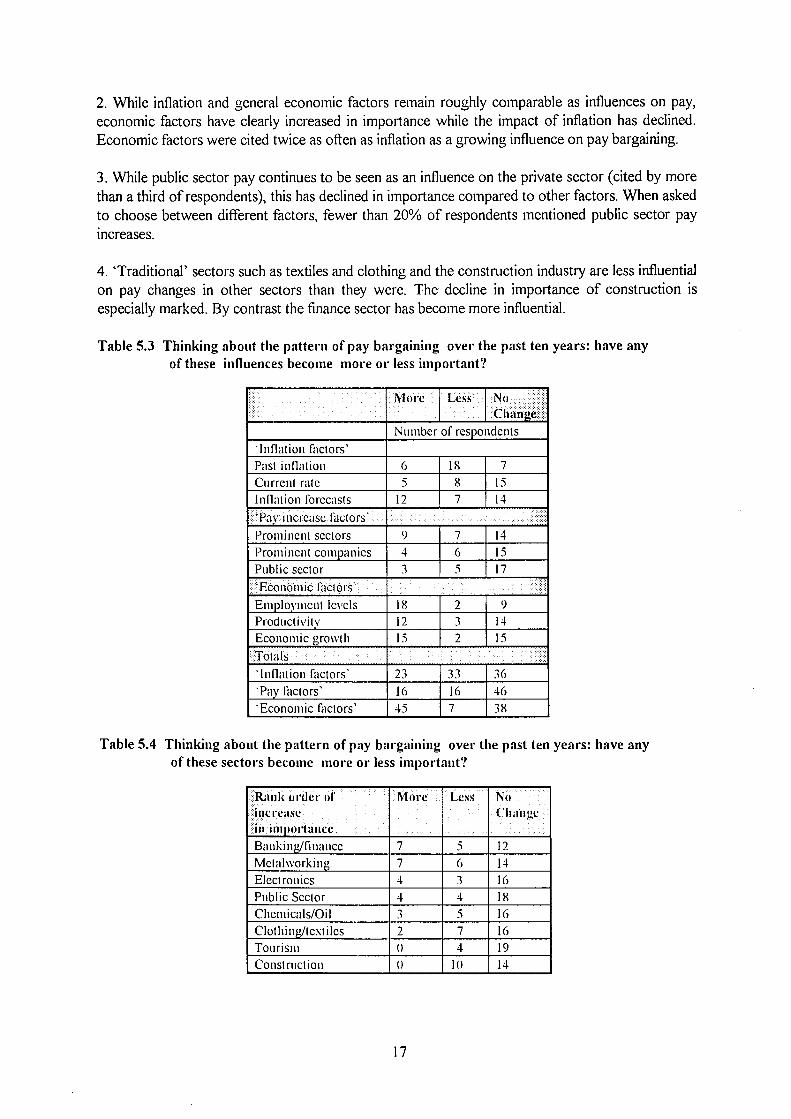

2. While inflation and general economic factors remain roughly comparable as influences on pay, economic factors have clearly increased in importance while the impact of inflation has declined. Economic factors were cited twice as often as inflation as a growing influence on pay bargaining.

3. While public sector pay continues to be seen as an influence on the private sector (cited by more than a third of respondents), this has declined in importance compared to other factors. When asked to choose between different factors, fewer than 20% of respondents mentioned public sector pay increases.

4. 'Traditional' sectors such as textiles and clothing and the construction industry are less influential on pay changes in other sectors than they were. The decline in importance of construction is especially marked. By contrast the finance sector has become more influential.

Table 5.3 Thinking about the pattern of pay bargaining over the past ten years: have any of these influences become more or less important?

'Inflation factors' Past inflation Current rale Inflation forecasts ' Pa v i ncrease facto rs ' Prominent sectors Prominent companies Public sector "Economic factors' Employment levels Productivity Economic growth Totals 'Inflation factors' 'Pay factors' 'Economic factors'

.Moret·:: Less No Change

Number of respondents

6 5

12

18 8 7

7 15 14

9 4 3

7 6 5

14 15 17

18 12 15

2 3 2

9 14 15

23 16 45

33 16 7

36 46 38

Table 5.4 Thinking about the pattern of pay bargaining over the past ten years: have any of these sectors become more or less important?

Rank order of increase in importarne Banking/finance Mclalworking Electronics Public Sector Chemicals/Oil Clothing/textiles Tourism Construction

More

7 7 4 4 3 2 0 0

Less

5 6 3 4 5 7 4

10

. No :'. Change

12 14 16 18 16 16 19 14

17

Inflation forecasts: the role of government The modification of the link between inflation and pay reflects a number of factors, among them the general decline in inflation. We look at this subject in more depth in Section 7. One significant point to emerge from the survey is the importance of government forecasts. Where inflation forecasts were used, government figures were almost universally seen as important. The exceptions were Belgium (where there is still partial indexation) and France. Much less weight was given to Central Bank or independent forecasts and even less to 'in-house' forecasts.

There was, however, far less unanimity on whether such forecasts act as the basis for consensus between the social partners. The responses from Spain, Austria and Italy indicated that this was the case. Elsewhere - for example Denmark and Ireland - there were differences of opinion.

Company bargaining When asked whether company bargaining has a general influence on pay increases, a substantial minority (around a third) said that it did. This is a higher proportion than might have been expected, given the traditional low profile of company bargaining. However, when asked whether pay increases in prominent companies were an important influence, fewer than 10% of respondents agreed.

The clearest signs of the increasing influence of company bargaining came from Denmark, Sweden and the Netherlands - reflecting some significant decentralisation of the bargaining process in the last few years. In each case, large exporters and internationally-oriented firms are seen as setting the pace: Philips and Unilever in the Netherlands; Volvo and Ericsson in Sweden; Novo and Danfoss in Denmark. In general the most influential companies are concentrated in three main sectors: cars, telecommunications and petrochemicals. The car industry has traditionally played a leading role in the pay round and this was much in evidence in responses from France, Germany, Italy and Sweden. There were some indications that the role of the car industry has become weaker in recent years in France, as it has done in the UK. In the case of Italy, Fiat continues to exert a great influence - on industrial relations rather than pay.

The pay round Nearly three-quarters of respondents stated that there was a recognised order of pay bargaining - a 'pay round' - with the normal cycle of bargaining being either annual or every two years. There seems to be no clear pattern of one sector 'leading' the pay round, despite the acknowledged importance of the engineering sector. In most countries the pattern seems to vary from year to year.

Bargaining reforms and the impact of European integration The survey did not reveal any general bargaining trends which can be related to the IMP. However, respondents did point to some relevant developments in particular countries:

1. In Belgium, a trade union commented there was a tendency towards decentralisation to company level but the 'social partners resisted together the push for decentralisation that was attempted by the Government with the Plan Global' - the programme of wage restraint introduced in November 1993 following the breakdown of negotiations between employers and unions.

2. In Denmark, an employers' organisation observed that the long-term trend towards decentralisation needed to be seen in the context of the 'general economic climate with more international competition (which) has more influence on the overall level of pay-rise expectations in all sectors'. However, 'the pattern and structure of bargaining are unchanged by the internal

market, whose effects are only marginal in the process. International competition sets the level of expectations and national structures determine the distribution of wage increases'.

3. In Spain, the newly-agreed reform of job classification in the engineering industry - replacing 142 job categories with seven grades - was noted as an example of a new type of agreement which would probably make it easier to remove fixed elements, such as seniority, and put greater emphasis on variable pay, linked to productivity.

4. In Ireland, it was emphasised that bargaining over the tenns of national agreements now takes place within the parameters set up by European-wide inflation, in particular the rates of inflation and pay growth set by 'competitor countries'. Competitive labour cost pressures in both metalworking and textiles have exerted a downward pressure on central negotiations.

5. In Austria pay increases in the public sector and in textiles and banking were seen as more influential than before - an effect associated with 'the opening of markets during the integration process'.

6. In Portugal, a union pointed to the way that the convergence criteria for EMU had been used by the government to justify a policy of income restriction and to call for wage moderation in the name of controlling inflation and improving competitiveness. Unions had felt their power to protest reduced by rising unemployment in 1993 and 1994, with some sectors, such as public administration, suffering a decline in real pay. However, the tripartite accord agreed in January 1996 between the government and the social partners was seen as a promising sign.

Pay benchmarking in the UK The fragmented nature of pay arrangements in the UK means that the issues of inflation and pay linkages require separate analysis. IDS research on pay benchmarking in the UK (IDS 1995) shows that:

1. The current rate of retail price inflation remains the principal influence on pay increases. This applies both to settlements determined by collective bargaining and to those which are based on perfonnance. An analysis of over 2,000 salary reviews for executives since 1990 shows that the average increase tracks movements in the current inflation very closely. This applies bolli to 'general' and 'all-merit' increases.

2. Although inflation forecasts are used by employers in setting pay budgets, the influence of such forecasts on collective bargaining is very limited compared to elsewhere in Europe.

3. Surveys by the Confederation of British Industry show that pay comparability pressures have declined significantly since the late 1980s. Sectoral pressures are consistently stronger in the service sector than in manufacturing.

4. The fragmentation of wage-setting and the abolition of minimum wage legislation has been accompanied by a huge growth in the number of pay clubs and surveys, especially in sectors with weak collective bargaining.

5. An IDS survey of companies in July 1995 found thai the main influences on bargaining apart from the current rate of inflation were, first, pay increases within the relevant business sector and. secondly, the 'going rate' in large finns. Pay settlements in the public sector were also seen as an important general influence.

19

6. The impact of the EVIP: an inter-sectoral analysis of pay statistics

A number of possible sectoral pay effects might be expected from the ΓΜΡ. If the ΓΜΡ has required labour market adjustments then one would expect to see changes in the dispersion of earnings in different sectors over the period. Such effects might include:

• greater divergence between dynamic and sluggish sectors; • relative depression of earnings in sectors most exposed to international competition; • relative increases in earnings in capital-intensive industry.

In individual countries one might expect to see evidence of change where the Single Market stimulated growth in certain industries or where relatively small industries expanded because of access to new markets or because of new investment.

In order to test for such effects, and for possible variations in different countries, we conducted a review of pay trends since 1985 in eight sectors. The sectors chosen for an analysis were as follows:

Manufacturing

Ceramics Chemicals Clothing Footwear Motor Vehicles/parts Textiles

Services Finance Retailing

Industrial Classification (NACE)

248 25 435/4 451/2 35 43

812/3 64/653-6

Data were collected for the period 1984/85 to 1993/94. In most cases the data were provided by Eurostat sources, supplemented by national statistics and ILO data where necessary. In addition data from some industry sources (for footwear, primary textiles and motor vehicle assembly) were analysed to provide a cross-check on earnings movements and relativities.

The sectors provide data for nearly every EU country, although in some cases comparable information is not available for particular years. The major omission is Italy, where there are no comparable data available. We have included comments where there is relevant information available from industry sources. Data for Sweden have been included for selected years to provide a benchmark for the three Member States which were not members of the Community during the period.

Characteristics of the sectors The aim in choosing these eight sectors was to look at pay developments in a cross-section of industry and commerce, with a range of different and contrasting characteristics. These characteristics are summarised in the Chart, which also identifies particular national factors of relevance.

20

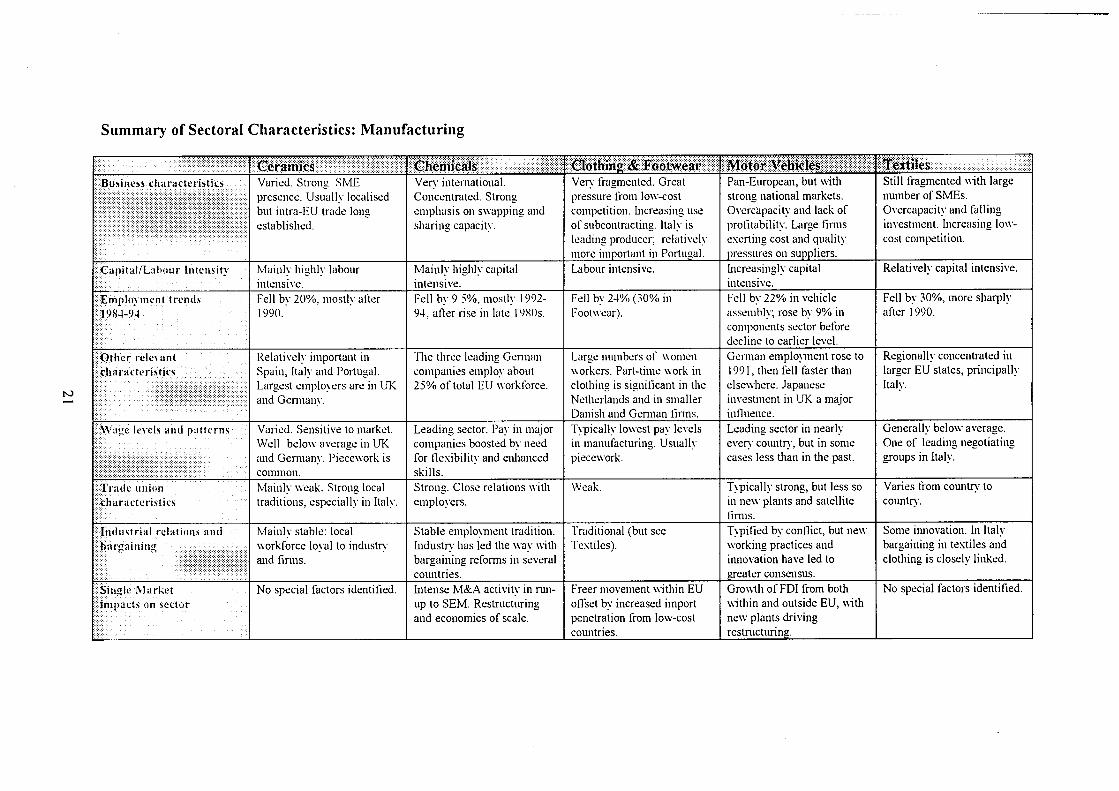

Summary of Sectoral Characteristics: Manufacturing

to

Business characteristics

Capital/Labour Intensity

Employment trends 1984-9-1

Other relevant characteristics

Wage levels and patterns

Trade union characteristics :

Industrial relations and bargaining

Single Market impacts on sector

Ceramics Varied. Strong SMI: presence. Usually localised but intra-EU trade long established.

Mainly highly labour intensive. Fell by 20%, mostly after 1990.

Relatively important in Spain, Italy and Portugal. Largest employers are in UK and Germany.

Varied. Sensitive to market. Well below average in UK and Germany. Piecework is common. Mainly weak. Strong local traditions, especially in Italy.

Mainly stable: local workforce loyal to industry and firms.

No special factors identified.

Chemicals Very international. Concentrated. Strong emphasis on swapping and sharing capacity.

Mainly highly capital intensive. Fell by 9.5%, mostly 1992-94, after rise in late 1980s.

The three leading German companies employ about 25% of total EU workforce.

Leading sector. Pay in major companies boosted by need for flexibility and enhanced skills. Strong. Close relations with employers.

Stable employment tradition. Industry has led the way with bargaining reforms in several countries. Intense M&A activity in runup to SEM. Restructuring and economies of scale.

Clothing & '.Footwear Very fragmented. Great pressure from low-cost competition. Increasing use of subcontracting. Italy is leading producer; relatively more important in Portugal. Labour intensive.

Fell by 24% (30% in Footwear).

Large numbers of women workers. Part-time work in clothing is significant in the Netherlands and in smaller Danish and German linns. Typically lowest pay levels in manufacturing. Usually piecework.

Weak.

Traditional (but see Textiles).

Freer movement within EU offset by increased import penetration from low-cost countries.

Motor Vehicles Pan-European, but with strong national markets. Overcapacity and lack of profitability. Large firms exerting cost and quality pressures on suppliers. Increasingly capital intensive. Fell by 22% in vehicle assembly; rose by 9% in components sector before decline to earlier level. Gemían employment rose to 1991, then fell faster than elsewhere. Japanese investment in UK a major influence. Leading sector in nearly even' country, but in some cases less than in the past.

Typically strong, but less so in new plants and satellite finns. Typified by conflict, but new-working practices and innovation have led to greater consensus. Growth of FDI from both within and outside EU, with new plants driving restnicturina.

Textiles Still fragmented with large number of SMEs. Overcapacity and falling investment. Increasing low-cost competition.

Relatively capital intensive.

Fell by 30%, more sharply after 1990.

Regionally concentrated in larger EU states, principally Italy.

Generally below average. One of leading negotiating groups in Italy.

Varies from country to country.

Some innovation, hi Italy bargaining in textiles and clothing is closely linked.

No special factors identified.

IO ι J

Sources: Panorama of EU Industry; industry and company sources.

Summary of Sectoral Characteristics: Services

Business characteristics

Capital/Labour Intensity Employment trends 1984-94 Other relevant characteristics

Wage levels and patterns

Trade union characteristics

Industrial relations and bargaining Single Market impacts ori sector

Finance Both global and national. Rapidly changing markets with integration of different segments driven by liberalisation and technical chanae.

Labour intensive, although with increasing automation. Rose by around 15%. After rapid rises during the 1980s, employment stablised in the earlv 1990s. Focus of late 1980s boom in the UK following deregulation in 1986. Major employer of women workers, especially in northern EU stales. Significant proportion of part-time workers in Denmark. Leading sector, especially in Italy, Belgium , Spain and Portugal. Outside the major countries pay levels in smaller finns are often above average for the sector. Varies from country to country. Tendency to act independently of "mainstream". Traditionally conservative and stable in most countries. Some breakdown of consensus with rapid changes in the sector and declining job security. Restructuring and M&A activity, usually with the aim of reinforcing positions in national markets.

Sources: Panorama of EU Industry: industry and company sources. Note: Employment trends for these two sectors are estimates because of changed definitions.

Retailing Great variations between fragmentation and concentration. Large numbers of self-employed in southern states. Increasing control of suppliers by large retail chains. Labour intensive. Rising employment in late 1980s (nolablv in France) partly offset bv falls in 1990s. Big supennarket chains concentrated in France, Germany and UK. Large numbers of women workers. High proportion of part-time workers in Netherlands, Denmark and UK. Usually low. UK.

Pay in larger linns a little higher, but not in France and the

Weak with execeptions such as Sweden and Ireland.

fraditionally conservative. High labour turnover.

No special factors identified.

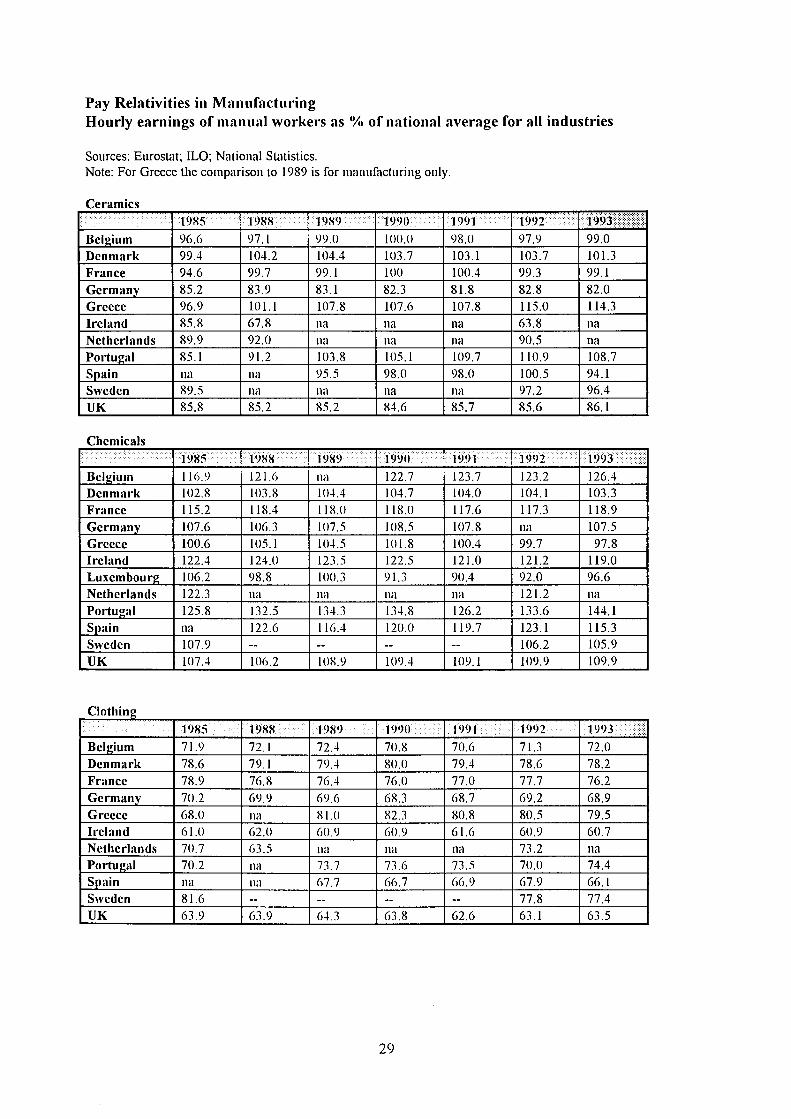

Manufacturing sectors The main statistical evidence for the six manufacturing sectors is presented in the Tables at the end of this section. In each case the figures show the average hourly earnings of manual workers as a percentage of the national average for all industries (NACE 1-5). The general picture is of broad stability over the period, but there are some significant exceptions to this pattern. As Marsden and Silvestre point out (Marsden et al 1992) normally 'the structure of relative wages between industries displays a great deal of stability both in the short-run and over longer periods'. The main reasons for this are that differences in skill-mix and working patterns are more or less fixed. Given that this is the normal pattern - and one which holds good not only for the EU but for other industrialised economies such as the United States - any degree of variation which is sustained for more than one or two years is likely to be of significance.

As a general observation it should be noted that earnings rose in real terms over the period in all countries except Greece. Elsewhere, increases were well above inflation in most sectors, the exceptions being clothing and footwear in France and footwear in Belgium.

An analysis of the individual sectors produces the following observations:

Ceramics 1. Against a pattern of broad stability in most countries (the data for Ireland are probably unreliable). Both Greece and Portugal, have increases in relative earnings over the 1988-1993 period. There seems to be a similar development in Spain, cut short by the recession in 1993.

2. The absence of data for Italy prevents a comparison with Spain and Portugal, the two other countries where the industry is most important, but reports from industry sources in Italy (// Sole 1996) indicate a virtual absence of unemployment in recent years, accompanied by high earnings from piecework.

3. Other data (for monthly earnings) show relative pay in Germany and France is lower than these figures suggest. German pay levels, unusually, show some decline: over the last few years parts of the industry have been hit by severe job loss because of low-cost competition from eastern Europe.

Chemicals 1. In general relative pay is fairly stable, with the industry predictably ahead of the average and in some cases moving further ahead. Stability is especially marked in Germany, the dominant force in the European chemical industry.

2. The relative importance of the chemical industry as a wage leader in smaller countries is seen in the figures for Portugal and Ireland. In Ireland the industry is highly unionised and it is the one sector where pay rises have tended to breach the terms of national agreements.

3. The figures for Belgium show a significant increase at the end of the 1980s and again in 1993. The chemical industry is the one sector in Belgium where company-level bargaining predominates. The sectoral agreement for chemicals only sets a minimum rate.

4. There have been huge changes in employment and skill-mix during the period (and major increases in productivity levels) which are not reflected in these figures. For example, pay per head in the UK chemical industry increased by 30% between 1990 and 1992.

23

Clothing 1. The general picture is of almost total stability, with the industry consistently at the foot of the (industrial) earnings league year after year. The exception is Greece, but the figure for 1985 is taken from a different source. Other data (for monthly earnings) show earnings in Greece are relatively lower than these figures suggest.

2. A striking feature of this set of data is the way that completely different bargaining arrangements - for example Belgium, Denmark, Germany and France - produce the same pattern of consistency. Earnings in the UK were relatively lower than in any country other than Ireland. Ironically, clothing was the only significant manufacturing sector covered by minimum wage legislation in the UK until the abolition of the Wages Councils in 1993.

3. Data on monthly earnings from the late 1980s suggest that earnings in Italy are relatively high.

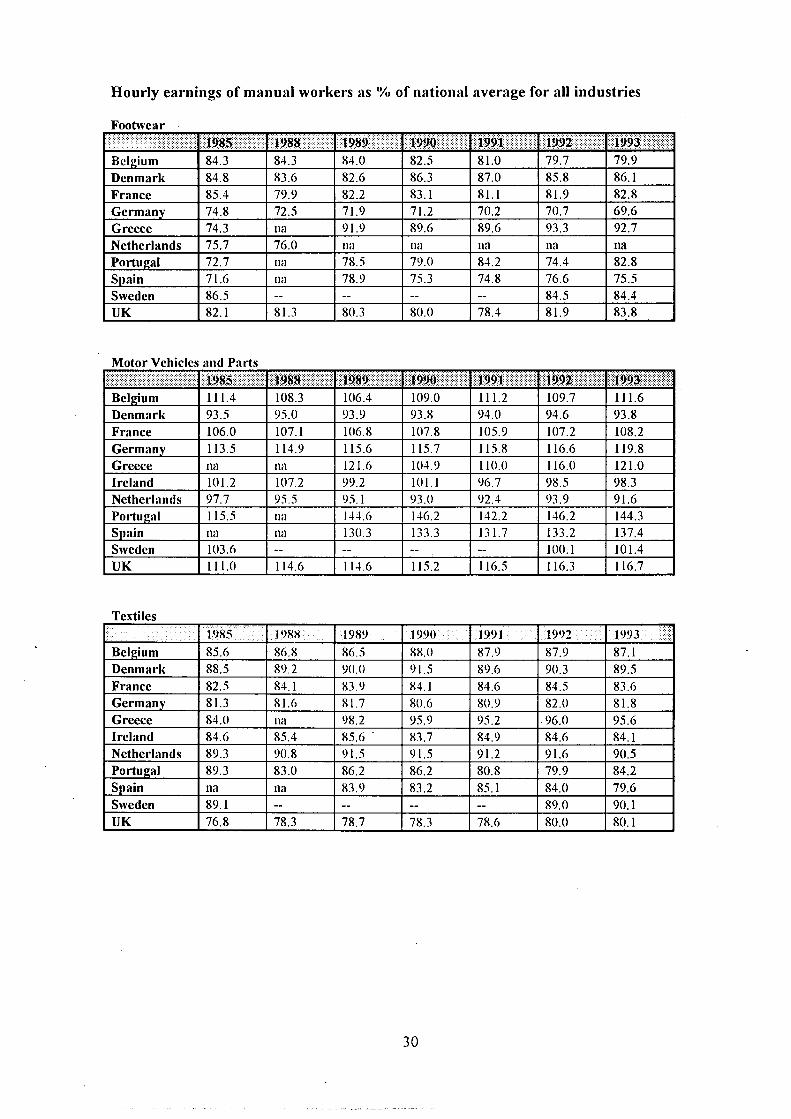

Footwear 1. The overall pattern is less stable than in the clothing industry.

2. There are clear signs of a relative decline in earnings in Belgium and in Germany, where the industry rivals clothing at the foot of the earnings league.

3. There is some evidence of a North/South division, with relative earnings rising in southern Europe. However, in Spain relative earnings fell back sharply in 1994, from 75% to 71% of the average.

Motor Vehicles and Parts 1. Unlike the other sectors there are different tendencies at work in different countries.

2. Relative earnings in the UK and Germany show a clear upward movement since the mid-1980s. By comparison France and Belgium are stable, although relative earnings rose to a ten-year high in France in 1994. In the Netherlands there is evidence of some decline and the industry is, unusually, below the average.

3. Relative pay in Germany continued to rise despite the reversal of employment trends in 1991. Cuts in pay and hours were agreed at Volkswagen in 1994, but the signs are that changes in working practices have continued to sustain the relative earning position of workers in the motor industry.

4. Earnings in Spain and Portugal are well above the average, reflecting the pay levels in foreign multinationals. In Portugal the figures for monthly earnings from the labour costs survey confirm an upward movement between 1984 and 1988.

5. In Ireland, the decline reflects the insignificance of this sector compared to other parts of manufacturing.

Textiles 1. Overall the picture is very stable, with some convergence of relative earnings in the different countries.

24

2. There is some evidence of relative decline in Portugal from these figures (until 1992) but other sources suggest this may not have been the case.

3. The lack of data for Italy, the most important country, means that important changes are concealed. Recent years have seen relocation of companies outside Italy (and Europe), increasing capital intensity, serious job loss and the fragmentation of production units, with increasing employment in the 'submerged economy'. The 1995-99 industry agreement attempts to tackle these problems in several ways, exerting greater control over sub-contracting but allowing dispensations on minimum pay rates so that finns operating illegally can gradually bring their pay into line with industry rates.

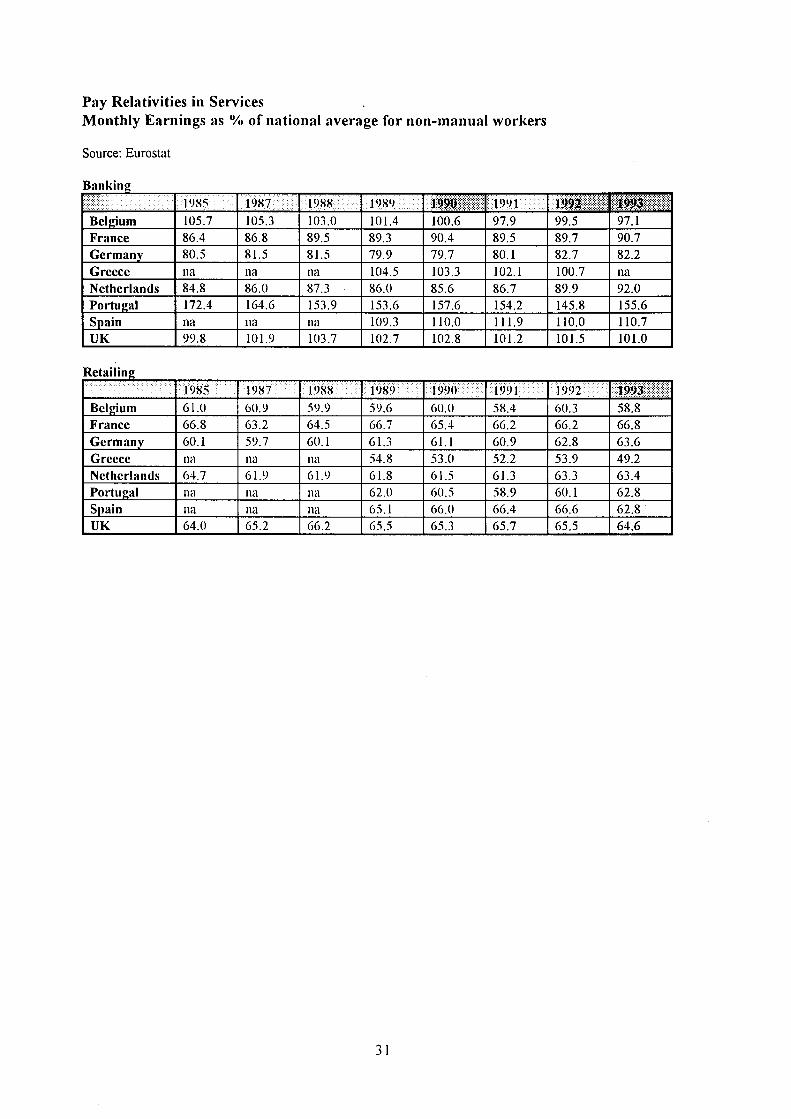

Service sectors The main statistical evidence for the two service sectors is presented in Tables at the end of Section, which show monthly earnings as a percentage of the average for national industrial average for non-manual workers. Unfortunately comparative data are only available for eight EU countries, and for Portugal and Spain only from 1989 onwards. In making our assessment of trend, we have also drawn on data from other sources (national statistics and the labour costs survey).

Retailing 1. Earnings relativities are very stable over time and, with the exception of Greece, very similar in the different countries. Data from the labour costs survey confirm this stability for several countries (France, Germany, Greece, Italy, Portugal and the UK). This survey also suggests that retail earnings in Italy are comparatively high at around the average for manual workers. In Sweden retail employees seem to have fared rather better than average during the 1980s. In 1993, average pay was around 94% of the average for white-collar workers in production industries - a long way ahead of the EU average.

•Ό"·

2. The stable pattern is surprising in view of the significant increases in the part-time workforce between 1984 and 1992. The most notable increase was in Ireland (from 22% to 40% of the workforce) and here relative monthly earnings did decline sharply. In Germany and France the proportion of part-timers also rose, although the total remained quite low in France (21%) compared to Germany, Belgium and Denmark (around 40%), the UK (50%) and the Netherlands (60%). The 1992 figures also show an increase in part-time work in southern European countries, although from a very low base.

Finance 1. Unlike the other sectors discussed here, a substantial proportion of employment is in the public sector and has therefore been subject to pay restraint over the period.

2. The figures show some fluctuations, with relative pay rising in France and the Netherlands and falling in Belgium; and rising slightly in Germany and the UK (after deregulation).

3. There seems to be a major difference between northern and southern countries. Pay levels in Spain and, especially, Portugal are well above the white-collar average. Other data (from the labour costs survey and industry sources) suggest the same is true of Italy.

4. Greece seems to be an exception to this rule. This is surprising in view of the decisive role that the banks play in the economy. A peculiarity about collective bargaining in the Greek banks is that

25

there is no employers' federation and the agreement reached between individual banks and the union federation is legally binding on all employers in the sector.

5. In the northern countries, pay levels are around average or, in the case of Germany, rather lower. The German private banking sector is well-known for its relatively low pay levels. Earnings levels are set by the industry agreement; there is little or no supplementary pay. A similar situation exists in the French private banking sector.

6. There is some evidence of convergence to a northern European norm in the banking sector. The one exception to this pattern is Sweden, where pay in banking moved well ahead of other sectors in the 1980s and in 1993 was nearly 10% above average white-collar pay in production industries.

The dispersion of earnings To aid interpretation of these trends and to check for any changes in the pattern we examined the overall dispersion of earnings in industry during the period. The Chart at the end of the Section gives the results for 13 countries and shows the industries with the highest and lowest earnings levels for manual workers and the degree of earnings dispersion.

In terms of the industries involved the overall impression is of stability. The differences between sectors such as clothing and footwear at the foot of the earnings league are often marginal. However, the clothing industry generally appears at the bottom and oil refining at the top. This pattern is very much as expected.

There are significant differences in the degree of dispersion. Sweden, Denmark and Finland have a relatively narrow dispersion throughout the period (widening somewhat in Finland in the early 1990s). At the other end of the spectrum are the UK, Spain and Portugal.

Compared to the mid-1980s the dispersion widens in Belgium, Finland, France, Greece, Ireland, Spain and the UK. Dispersion is unchanged in Germany, the Netherlands and Sweden. Austria and Denmark have a narrower dispersion.

There is little evidence of new low-pay sectors other than in Greece.

There are some differences in the pattern of dispersion between the 'old' EU members and the three newcomers. Different industries are involved in Finland. The dispersion narrows in Austria. The dispersion in Sweden is narrower than elsewhere.

The changing earnings pattern and the impact of the IMP The picture presented so far indicates broad stability when macro earnings figures and relativities are looked at in isolation. But in other respects this impression of stability is wholly misleading. A quite different impression is gained when one examines the make-up of the workforce and the impact of technical change and new working methods on skill mix. Such changes are impossible to quantify from year to year, but over the past ten years there have been dramatic shifts. Jobs have disappeared but at the same time there has been continuous grade drift and consequent changes in earnings. Normal earnings data rarely reveal this. However, surveys conducted by some employers' associations provide the evidence.

26

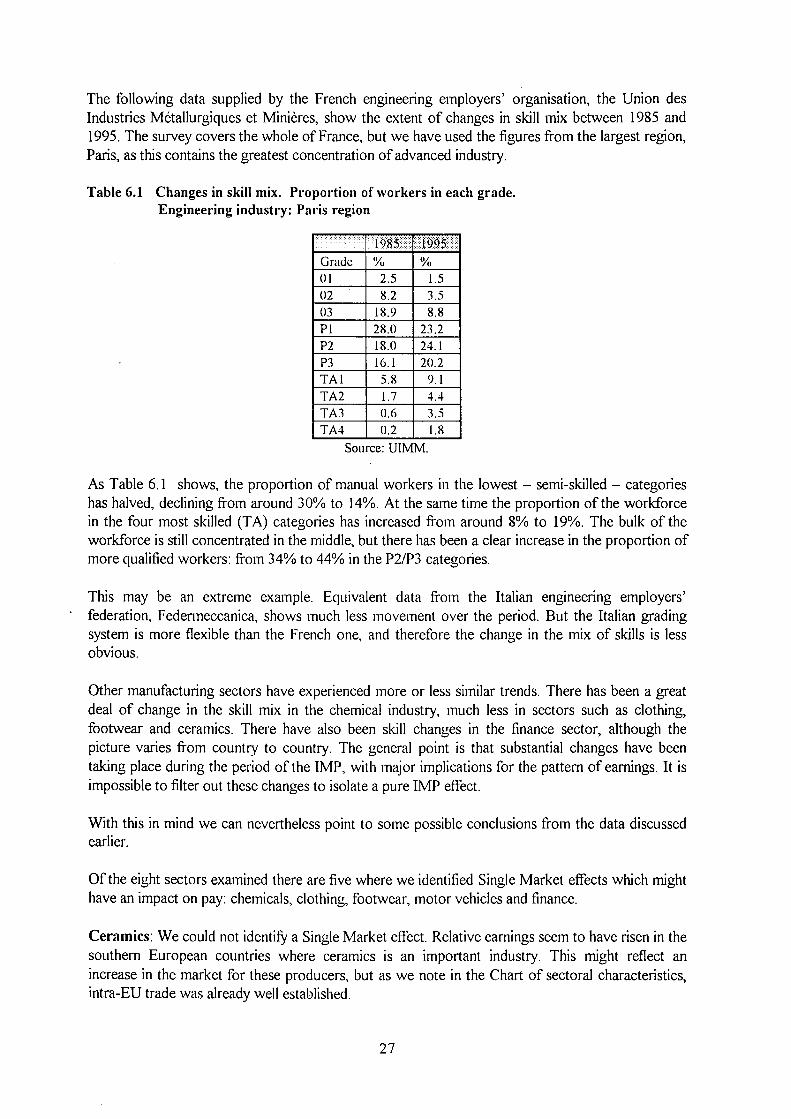

The following data supplied by the French engineering employers' organisation, the Union des Industries Métallurgiques et Minières, show the extent of changes in skill mix between 1985 and 1995. The survey covers the whole of France, but we have used the figures from the largest region, Paris, as this contains the greatest concentration of advanced industry.

Table 6.1 Changes in skill mix. Proportion of workers in each grade. Engineering industry: Paris region

Grade 01 02 03 PI P2 P3 TAI TA2 TA3 TA4

1985 %

2.5 8.2

18.9 28.0 18.0 16.1 5.8 1.7 0.6 0.2

1995 ¡ %

1.5 3.5 8.8

23.2 24.1 20.2

9.1 4.4 3.5 1.8

Source: UIMM.

As Table 6.1 shows, the proportion of manual workers in the lowest - semi-skilled - categories has halved, declining from around 30% to 14%. At the same time the proportion of the workforce in the four most skilled (TA) categories has increased from around 8% to 19%. The bulk of the workforce is still concentrated in the middle, but there has been a clear increase in the proportion of more qualified workers: from 34% to 44% in the P2/P3 categories.

This may be an extreme example. Equivalent data from the Italian engineering employers' federation, Federmeccanica, shows much less movement over the period. But the Italian grading system is more flexible than the French one, and therefore the change in the mix of skills is less obvious.

Other manufacturing sectors have experienced more or less similar trends. There has been a great deal of change in the skill mix in the chemical industry, much less in sectors such as clothing, footwear and ceramics. There have also been skill changes in the finance sector, although the picture varies from country to country. The general point is that substantial changes have been taking place during the period of the IMP, with major implications for the pattern of earnings. It is impossible to filter out these changes to isolate a pure IMP effect.

With this in mind we can nevertheless point to some possible conclusions from the data discussed earlier.

Of the eight sectors examined there are five where we identified Single Market effects which might have an impact on pay: chemicals, clothing, footwear, motor vehicles and finance.

Ceramics: We could not identify a Single Market effect. Relative earnings seem to have risen in the southern European countries where ceramics is an important industry. This might reflect an increase in the market for these producers, but as we note in the Chart of sectoral characteristics, intra-EU trade was already well established.

27

Chemicals: Restructuring in the industry has helped keep pay buoyant because of changes in staffing levels, working practices and the skill mix. These developments were already taking place, but the Single Market has accelerated the process of concentration.