THE IMPACT OF BANK DISTRESS ON COMMERCIAL BANKS IN NIGERIA (A CASE STUDY OF FIRST BANK OF NIGERIA...

72

CHAPTER ONE 1.0 INTRODUCTION 1.1 BACKGROUND OF THE STUDY In any modern economy, the efficient production and exchange of goods and services requires money and bank is the instrument for affecting it. The last few years have been both traumatic and revolutionary for the banking industry. The industry produced the largest number of technically insolvent and under capitalized banks. The magnitude of distress in the nation’s banking industry reached on unprecedented level making it an issue of concern to the government, the regulatory authority, the bankers and the general public. The Nigeria banking scene was characterized by changes designed to promote banking in the country. The changes may be categorized into phases, but due to the nature of work, we will consider tow phase 1

-

Upload

polyibadan -

Category

Documents

-

view

2 -

download

0

Transcript of THE IMPACT OF BANK DISTRESS ON COMMERCIAL BANKS IN NIGERIA (A CASE STUDY OF FIRST BANK OF NIGERIA...

CHAPTER ONE

1.0 INTRODUCTION

1.1 BACKGROUND OF THE STUDY

In any modern economy, the efficient production

and exchange of goods and services requires money and

bank is the instrument for affecting it. The last few

years have been both traumatic and revolutionary for

the banking industry. The industry produced the

largest number of technically insolvent and under

capitalized banks. The magnitude of distress in the

nation’s banking industry reached on unprecedented

level making it an issue of concern to the

government, the regulatory authority, the bankers and

the general public.

The Nigeria banking scene was characterized by

changes designed to promote banking in the country.

The changes may be categorized into phases, but due

to the nature of work, we will consider tow phase

1

namely; the era of laissez – fair banking (1834 –

1952), the era of limited was monopolized by foreign

banks, principally the African banking corporation

which was the precursor of the (BBWA) British bank

for West African the present First Bank of Nigeria,

the Barclays bank DCO (Dominion Colonial and

Overseas) the present day Union Banks, and the

British and French Bank, the for – runner of present

United Bank of Africa. Although, discrimination

against Nigerians by these banks led to the

establishment of some indigenous banks which

unfortunately offers litter or no competition to the

foreign banks essentially because of their weak

capital base or poor managerial capacity.

Consequently, all but three to the indigenous banks

failed. The survived includes the National Bank of

Nigeria established in 1933, the Agbonmagbe Bank (now

2

Wema Bank) established 1945 and the African

Continental Bank 1947.

A commission of inquiry headed by G.D. patron set

up in 1948 to investigate the business of banking in

Nigeria. Their report led to the enactment of the

first banking legislation in Nigeria, the banking

ordinance of 1952. The 1952 ordinance laid down the

standard and procedure for the conduct of banking

business by prescribing the mandatory minimum capital

requirement for the banks both expatiates and

indigenous regulations to Ʃ100, 000 and Ʃ12,500

respectively and it is also introduced regulations to

check bank failure. However, the entire indigenous

bank established in the country during this period

also all failed. The bank failures of this era were

attributed largely to the monopolistic structure of

the banking industry, which allowed the foreign banks

to enjoy exclusive patronage form British firms. The

3

indigenous banks that survived were able to make it

because of the support they got from their state

government.

The distress phenomenon in Nigeria banking

industry is of recent origin. The manifestation

became discernable with some policy shocks staring

1988 with Central bank of Nigeria (CBN) directive to

banks that naira backing for foreign exchange

application be lodged with CBN. This was followed in

1989 by another directive requiring public sector

deposits to be transferred to CBN. These two

directives exposed the precious liquidity position of

some banks and the distress they have subterraneous

harbored. What was thought to be a temporary

liquidity problem for few banks soon catches up with

a lot more banks.

It is important to stress in this work that

banking system was already in distress by the time

4

NDIC was established. By them, 7 (seven) banks were

known to be technically insolvent. The government at

that time, did not embark upon a clearing exercise

that would have removed from the system that

distressed institutions because it was feared that

such an action would lead to loss of public

confidence and flight of foreign capital more so

there was no deposit insurance institution to

expeditiously manage such bank closures. The NDIC was

nevertheless required to insure all banks. That means

that the corporation has been involved in managing

distressed banks even before it could settle down and

minister enough resources for this important task.

The intermediating role of banks and their

relevance both in the transmission of monetary

policies and in the payment system underscore their

importance as well as the problem that bank distress

at the prevailing dimension in our economy could

5

precipitate. Arising from their intermediation, banks

generate financial resources and put these at the

disposal of deficit economic growth in the form of

increased output. Therefore, an industry wide

insolvency of banks, such as the one experienced in

Nigeria, should be expected to retard the economy’s

rate of capital formation, reduce its level of

employment and output and ultimately the pace of

economic growth.

1.2 STATEMENT OF THE PROBLEM

A serious problem posed by widespread distress

among banks is the threat to banking habit and the

development of an inefficient payment mechanism. The

loss of confidence, the after math of the distress

that hit the banking sector forced several businesses

to take fewer risks by taking back their fund to well

established safe havens dominated by older generation

banks.

6

This research work is therefore concerned with

“Evaluating the impact of bank distress on the profit

growth of commercial banks”, using (A vase of

selected commercial banks).

1.3 PURPOSE/OBJECTIVES OF THE STUDY

The main purpose/objective of this study is to

have an overview of the effect of bank distress on

the profit growth of commercial banks. Investigate

into the reasons for bank failure in Nigeria.

Other objectives include:

1. To evaluate the cause of bank distress in

Nigeria. To find out the impact.

2. To find out the possible prevention strategies or

failure resolution options of bank distress.

1.4 RESEARCH QUESTIONS

1. What are the causes of bank distress?

2. What is the impact of bank distress?

7

3. What is the profit growth rate of commercial bank

during distress?

4. What are the effects of bank distress?

5. What are the possible solution options to this

phenomenon in the banking scene?

1.5 RESEARCH HYPOTHESES

H1: Distress has no effect on the average profit of

commercial banks.

H0: Distress has effect on the average profit of

commercial banks.

1.6 SIGNIFICANCE OF THE STUDY

This research project will be of importance of

the following persons:

i. New generation banks, which may wish to know the

implication of banks distress in the banking

industry and how to restore the confidence of the

customers and uphold efficient payment mechanism.

8

ii. Nigeria Deposit Insurance Corporation: The work

could be of immense help to NDIC in the area of

distress management and prevention strategies.

And also, in the area of failure resolution

option in banking industry.

iii. Students who may wish to know the extent of

distress in the banking industry and the trend of

distress as it affect the modern banking will

also benefit from this bank.

1.7 SCOPE, LIMITATIONS AND DELIMITATIONS

While the banking impact distress in Nigeria will

theoretically serve as the population of study. The

project is designed to appraise the impact of bank

distress on the profit growth of First Bank of

Nigeria. It will also analyze the trend of this bank

profit within a period of 3 years (2011 – 2013).

9

1.8 DEFINITION OF TERMS

DISTRESS: It can be defined as an extreme suffering

caused by lack of money or a state of danger,

calamity and misfortunate acute poverty.

EVALUATION: This can also be defined as form of idea

or judgment of something and also to work out

something in numerical value.

IMPACT: This can be defined as a strong effect or

impression to bank. It is also a situation whereby

something will be to be press closely or firmly

together.

COMMERCIAL BANK: Commercial bank or business bank is

a type of bank that provides services, such as

accepting deposits, giving business loans and basic

investment products. Commercial bank can also refer

to a bank or a division of a bank that mostly deals

with deposit and loans from corporations or large

10

businesses, as opposed to individual members of the

public (retail banking).

11

CHAPTER TWO

2.0 REVIEW OF RELATED LITERATURE

2.1 DEFINITIONS OF DISTRESS IN BANKING INDUSTRY

In ordinary parlance, the word “distress”

connotes “unhealthy situation” or a state of

inability or weakness, which prevents the achievement

of set and goals aspiration (Smith and Wall, 2009;

Ologun, 2007). Benson et al (2008) defined distress

as “a situation of complete or near loss of

stakeholders funds”. According to Alashi (2005),

distress is “a cessation of independent operation or

continuance without the assistance of relevant

authorities such as a deposit insurance institution”.

Thus, the traditional quantifiable measures of

failure (loss figures presented in standard financial

statement) are not very helpful in assessing the

degree or severity of distress of such a financial

institution (Alashi, 2005).

12

To evolve a working definition of distress, it is

desirable to synthesize those factors that will be

the unhealthy as well as state some broad set

obligations and aspiration of a typical financial

institution. A financial institution is described as

unhealthy, if it is unable to meet its obligation to

customers, owners and the economy occasioned by

severe financial, operational and managerial weakness

(Ologun, 2007).

Elebuta (2009), distress in banking when a fairly

reasonable proportion banks in the banking sector is

unable to meet their obligation to customers, owners

and the economy as a result of weakness in the

financial, operational and managerial capabilities

which renders them earlier illiquid or insolvent.

2.2 SYMPTOMS OF DISTRESSED BANKS IN NIGERIA

In recent times, bank failure has been an issue

of major concern to government, depositors, bankers

13

and promoters and indeed the public at large. This

concern stems from the crucial role banks plays in

the economy. The concern for the healthy and survival

of banks underscore the importance government

attached to close supervisions of banks, with the

primary objectives of identifying early warning signs

of distress in order to minimize the incidence of

failure. Regulators and researcher in response to

this concern have over the years been engaged in the

attempt to evolve reliable set of determinants for

the banks’ failure. The office of United States

controller of currency carried one of such analysis

out in 1988. The composite CAMEL rating emerged from

the studies.

The categorization of a financial organization as

a “problem” or “distressed” institution is usually

based on CAMEL rating system (Sinkey 1980; Ebibodaghe

1993 and Nyong 1994). Under this system, the

14

regulatory supervisory authorities assess a bank’s

performance in five area namely;

C – Capital Adequacy

A – Asset Quality

M – Management Competence

E – Earning Strength and

L – Liquidity Sufficiency.

Based on these parameters, appropriate financial

ratio has been developed to assess the condition of

banks to determine their health status, as well as

extent of distress. Under these parameters a banks’

capital adequacy ratio and ratio of non – performing

credit to shareholders funds among others are used to

make statements about the health status of the banks.

When these ratios deviate negatively from the

predetermined critical level by relevant authorities

the bank is described as haven – exhibited symptoms

of distress.

15

According to Ebhodaghe (2005), a distressed bank

is usually one where the evaluation depicts poor

condition in all or most of the five performance

factors as follows:

i. Gross under capitalization in relation to the

level of operation.

ii. High level of classified loan and advances.

iii. Liquidity reflected in the inability to meet

customers’ cash withdrawals.

iv. Low earnings resulting from huge operational

losses and

v. Weak management as reflected by poor credit

quality, inadequate internal controls, high rate

of frauds and forgeries, labour turnover e.t.c.

Egbojikwe (2005) identifies the following as the

common feature of a distressed bank:

Large volume of non – performing assets.

Persistent liquidity deficiency.

16

Accumulated losses which erodes shareholder’s

base.

The bank will in most cases require financing

assistance from regulatory authorities.

The interplay of these features as exposed above,

mostly lead to possible distress. Comparative

analysis has revealed that all the failed banks are

associated with one or more of these characteristics.

2.3 CAUSES OF DISTRESS IN BANKS

According to Ojo (2003), distress in banking is

connected to the prevailing economic recession, macro

– economic instability, poor asset quality,

mismatching of assets and liabilities, bad management

and insider abuse. Similarly, Ologun (2004) also

pointed out that inadequate legal framework and

structure, ownership, inadequate capital, poor

management, political instability, upsurge in number

of banks, illiquidity and insider abuse are the

17

contributing factors to bank distress. We shall

therefore x – ray some of these factors that account

for the precarious situation in the banks as follows:

a. The Inhibitive Policy Environment

Prior to the adoption of a comprehensive economic

programme under SAP, Nigeria’s banking system could

be described simply as highly regulated. Some of

these regulations had sometimes been counter –

productive and had contributed to the strains in the

system.

b. Macro – Economic Instability

The performance of any economy has a direct

impact on the financial sector. In recent years in

Nigeria, we have had a level of macro – economic

instability that has adversely affected the

performance of banking sector. Since the introduction

of SAP in 1985, the nation has witnessed a lot of

18

inconsistent and frequent changes in macro – economic

policies.

c. Unfavourable Policies of Government

The economic policies (monetary and fiscal) of

Nigeria have always charged at such a pace that both

players and spectators were at a time confused. Some

have been apportioned more than a fair share of the

blame for our economic woes. Looking at most of our

policies, one can point five levels of deficiency in

them. These levels are:

i. Wrong timing in policy changes.

ii. Bad choices on policy targets.

iii. Lack of internal linkage for the existing

economic base.

iv. Improper coordination of policy initiatives.

v. The human factor in policy implementation.

19

With all these, some harsh policies have

inflicted many damages on the especially the

sensitivity banking sector.

d. Political Instability and Interference

The political instability in our country

especially the June 1993 and 1994 political crisis

contributed in no small way to the worsening of the

financial situation our banks and other financial

institutions. The crisis nailed the coffin of about

80 of our finance houses and savings and local

companies to the liquidators’ grave. Since many banks

either had investment or their subsidiaries among

those finance companies they faced the same problem.

During this period, there were massive panic

withdrawals from banks, economic activities were at

their lowest ebb people fleeing en – mass to the

village and there was a general sense of insecurity.

20

Many banks especially the commercial banks have not

recovered from the economic setbacks of the period.

e. Indiscipline and Corruption in the Society

A society produces its type. There is no point

telling a child to be honest when all he sees around

him is but dishonesty. Since the late 70s the level

of discipline and integrity in Nigerian society has

gone drastically down: the quest for materialism has

become the order of the day. As a result, money no

matter its source has come to be worshipped as a

result of a status symbol. The end justifies the

means. With level of materialization and consequent

corruption pervading the society bankers have joined

the bandwagon. To them, their last resort is the

depositor’s fund kept in their trust. This accounts

for this high incidence of banks fraud and forgeries.

f. Lack of Experienced and Adequate Personnel

21

As the rapid expansion of the banking industry

began in the mid 80s there were no adequate

experienced personnel to cope with it. The few

experiences hands went for the high pecked job

thereby creating opportunities for both inexperienced

and those who had no business being in banking to

flood the industry. This was followed by rapid

promotion for these inexperienced hands due to the

polarization of the system. This led to the dilution

of standards and professionalism was thrown to the

wind. Honesty and integrity, which are hallmark of

banking, took secondary position. Materialism and

inordinate ambition to a mass wealth have become the

order of the day.

g. Fraud, Forgery and Insider Abuse

Fraud, forgeries and insider Abuse have become

very rampant in the banking sector, because the

staggering volume of money involved, they have

22

contributed in no small way in rendering the banks

insolvent. In the year 2001, 732 cases of fraud and

forgeries were reported out of which 388 were

successfully executed representing 53.7%. The amount

involved was N2.185 billion, while actual losses

totaled N1.07 billion, mainly through defalcation of

customers’ cash lodgment by bank employees,

substitution and depression of clearing cheques and

manipulation of customers’ accounts.

h. Poor Loan Administration

This has created the greatest internal problem

for Nigerian banks. The staggering volume of non –

performing assets or bad debts resulting from poor

laon administrations has left many banks in

precarious financial situations. Many loans grated

are not properly appraised. Others are not secured.

Many directors and management staff have used their

positions lend to their private companies, friends

23

and relatives without going through the due process

of appraisals. Some loans are grated on speculative

criteria.

i. Poor Internal Control

Despite the lofty objectives of a good internal

control, most of the banks and financial institutions

do have neither the financial nor the administrative

internal control unit. Where an internal control unit

exists, it is made very porous, powerless and

toothless bulldogs.

j. High Overhead Cost

Most of our banks are in the habit of incurring

huge capital expenses in setting up their branch and

corporate offices. Sometimes these exotic

architectural designs gulp a lot of money. These

expenses are smacks of immodesty and extravagance. In

their interior – décor, these banks exhibit signs if

imprudence. All these, tends to erode the capital

24

base if the banks and accumulate a lot of overhead

for the banks.

2.4 CLASSES OF DISTRESS

There are many classification of distress but for

the purpose of this paper and analytical convenience,

we shall use the following classifications:

i. Illiquid but solvent: This is a situation whereby

a bank cannot meet its customer’s obligation e.g.

withdrawal demand. However, the bank has

realizable assets more than its liabilities.

ii. Insolvent but liquid: This occurs when the

realizable assets of a bank are less than its

liabilities.

iii. Illiquid and insolvent: This is a situation

whereby a bank cannot meet its customer’s

obligations and the bank liabilities have far

exceeded its realizable assets. This is referred

25

to as absolute bank failure or terminal distress

(Gashinbaki, 2000).

2.5 PREDICTING POTENTIAL OF FAILURE IN NIGERIA

BANKING SECTOR

Manifestations and features of ill – heath were

given by the Central Bank of Nigeria Economic Review

(2005) to include: liquidity problems, distress

borrowing and resort to risky and speculative as well

as technical insolvency among banks. However,

Theodossior (2002) was of the opinion that the

determination of solvency of banks is an obstacle to

prompt action since financial distress may not be

apparent in the first instance. They asserted that:

ordinarily as long as a bank can meet all of its

obligations over the long run, it is considered

viable. Measuring such stream of income involves

calculating the Net Present Value of the expected

cash flows and it provides the economic measure of

26

solvency. However, such estimation can be very

difficult to undertake and subjective at best. On the

other hand, the reliance on the book value solvency

or the market value of the bank as a proxy for Net

Present is a very imperfect measure of its arbitrary

nature and the possibility that the bank can

manipulate the manner in which such activities are

presented.

The deficiency promoted the CBN and NDIC to

develop a standard rating system for revealing the

extent of distress in any bank in a consumption

measure categorized into sound, satisfactory,

marginally distressed and distressed. The parameters

that enabled this categorization is called CAMEL

(Capital Adequacy, Asset Quality, Management

Competence, Earning Strength and Liquidity).

Banks adjusted to be distressed by this system

are placed on strict supervision or liquidated, but

27

no sooner than banks rated as sound by this system

enters the distress region. This however, translates

to mean that distress classification is equally a

medicine after death. This therefore calls for

preventive rather than creative measures in terms of

predicting probability of failure for effective

decision making capable of jumpstarting the

deteriorating performance of the banking sector.

2.6 EMERGENCE OF DISTRESS BANKS IN NIGERIA

The health Nigerian banks cannot be divorced from

their antecedents. As could be recalled, when modern

banking business commenced in Nigeria by 1892, it was

solely a business for foreigners. The skewness in the

ownership structure in favour of foreigner largely

contributed to the observed lack of access to banks’

credit to by indigenous Nigerian entrepreneurship

during that period. Nigerian entrepreneurs who came

into banking from late 1920s to early 1950s did so

28

with the principal aim of redressing the situation

and meeting the financial requirements of Nigerian

businesses. Due to problems such as inadequate

capital, mismanagement, overtrading, lack of

regulation and unfair competition from the foreign –

owned banks, 21 of the 25 indigenous banks that were

established up to 1954 failed. The failures were

resolved mainly through self liquidation. The mass

bank failure was a bitter experience for the economy

as it brought untold hardship to depositors who lost

their money and lost confidence in the ability of

Nigerians to manage a banking business.

It was not until government started to regulate

banking through the Banking Ordinance of 1952 and the

establishment of the Central Bank in 1959, which was

followed by the promulgation of the Banking Degree of

1969, which the bank started to stabilize in the

century. The oil boom, which commenced in 1973, and

29

the economic growth, which ensured, made banking to

thrive and to be very lucrative. The economic

downturn, noticeable from mid – 1981, brought strains

to the Nigerian economy that soon became depressed.

As economic agents were able to moderate their boom

consumption habits in line with the realities of the

depressed economy, the financial condition of

individuals, firms and governments worsened and they

were unable to honour their contractual obligations

of loan repayment to banks thus impairing banks’

portfolio quality. This economic predicament,

combined with other factors such as mismanagement,

adversely affected the health of many banks.

These factors examined here led some banks into

financial distress characterized by poor asset

quality, illiquidity, under – capitalization and

insolvency. By 1989, seven banks, mostly owned by

state governments were technically insolvent. The

30

situation has since deteriorated as a second

generation of distressed banks emerged. With the

exception of the slight decline from nine in 1990 to

eight in 1991, the number of distressed banks

increased from seven (7) in 1989 to twenty – eight

(28) in 1993, representing an increase of 300%. The

number peaked at alarming 60 as at end of 1995 out of

which 31 were not only insolvent but also terminally

depressed. The total number of distressed banks

however declined to 52 at the end of 1996.

Happily however, by the year 2000, the number had

substantially dropped to only 11, out of which three

were technically distressed and their licenses

revoked, while the remaining eight were recapitalized

and the broads/managements reconstituted.

2.7 THE ROLE OF BANKS IN ECONOMIC DEVELOPMENT

It is widely acclaimed that banking system in

particular and the financial system in general, play

31

crucial role in economic development. By mobilizing

savings and channeling them for investments

especially in the real sectors, the banking system,

increases the quantum of goods and services produced

in the economy thus, national output increases and

the level of employment improves. At a broad levels

of generalization, empirical studies have established

strong evidence of a positive correlation between

real growth of output and bank assets (Adelman and

Morris, 1967; Goldsmith, 1969; Cameron, 1972;

McKinnon, 1973; Gurley and Shaw, 1976; Geffen and

Rose, 1991; Levine, 1992 among others).

Needless to say that the banking system is able

to play the positive role only if it is functioning

efficiently. However, if it is repressed or

distressed, in efficient and incapable o providing

timely and quality services, the banking system could

become a major hindrance to economic growth and

32

development as observed by Cameron (1972) and

McKinnon (1973). It is for this reason that

governments the world over take keen interest in the

performance of their financial system and would like

to see the system being “supply – leading” and

therefore catalystic for industrialization and

development. This was particularly the case in

Germany and Japan as reported by Patrick and Cameron

(1967).

Government’s interest in the banking sector is

usually aimed at ensuring a safe and sound system

were depositors and consumers are protected so as to

ensure monetary stability (Spong, 2009). Also,

government through in laws, policies and regulatory

institution exclusively regulates banks in order to

minimize bank and cost of failure (Dale, 1984).

33

However, in spite of government’s efforts to

protect the financial system, especially the banking

sub – sector, failures do occur.

The failures have had serious implications for

the financial system and by extension, the economy

(NDIC, 1998). A generalized state of banking distress

is expected to retard the economy’s rate of capital

formation, reduce the level of employment and lower

output, largely because banks will be unable to

excess financial resources and put them at the

disposal of the deficit economic units for increased

consumption and output.

Recent macroeconomic statistics in Nigeria

support these claims: real GDP growth was 2.3% in

1993, 1.3% in 1994 and 2.17% in 1995. Similarly,

manufacturing capability utilization fell from 37.2%

in 1993 to 30.4% in 1994 and 27.9% in 1995. While the

number of distressed banks for the corresponding

34

period was 38 in 1993; 45 in 1994 and 60 for 1996

(NDIC, 1998). Also, securities issued by banks to

fund owners become less attractive in the event of

widespread insolvency, thereby increasing the

holders’ risk exposure and also making them lose

confidence in banking system. This clearly undermines

the development of a good banking culture.

Another serious danger posed by generalized

distress among banks is the threat to the development

of an efficient payment mechanism. Settlement of

transaction becomes predominantly cash – based with

its associated risk. Also, the effectiveness of

monetary policy is reduced in direct proportion to

the extent of loss of confidence in the banking

system as reflected in the instability that would

characterize the demand for money and the proportion

of money in circulation that would be outside the

banking system as banks are no longer seen as safe

35

depositories. In Nigeria today, more than 50% of

money supply is estimated to be outside the banking

system (NDIC, 2008).

According to Utomi (2002), 80% of the country’s

money never passes through a bank. Until the 1990s,

the figure was 90%. Many Nigerians prefer it that

way.

Ede (2002) said, “in an age when electronic

commerce drives the world’s economies, Nigerian banks

remain “inhospitable” behemoths whose customers spend

hours or days to get the simplest transactions

completed”. As a result, many Nigerians squirrel away

naira notes at home, preferring to risk armed break –

in rather than face exorbitant transaction fees.

In Nigeria, one of the Africa’s most prosperous

yet economically dysfunctional nations, the simple

task of depositing your salary or taking it our again

can require hours of patience and a lifetime of

36

negotiating savvy. The result is that today, Africa’s

most populous country runs on cash.

“Everybody is getting ripped off and nobody wants

to rock the boat. So they either keep quiet or just

avoid banks altogether” Ede (2002).

2.8 CONSEQUENCES OF BANK DISTRESS

While the genesis of the crisis is traceable to

the deregulation and liberation of entry

requirements, the question has frequently been asked:

why did the government not into the necessary

guidelines to regulate the sub – sector right from

the beginning of deregulation? Moreover, why did the

government wait to react only as the problems arose?

(Ekpenyong, 1994:18). The weakness in government

policies in regulating the banking sub – sector in a

free market economy, which it experimented with and

the concomitant bank distress had far – reaching

37

consequences not only on the economy but also

virtually on every Nigerian.

Banks are intermediary institutions, which

collect deposits from the surplus spending unit and

efficiency channel and allocate them to deficit

spending units to accelerate economic growth and

development. By this role, banks also generate

employment. They find the it difficult fulfilling

their roles as engines of growth in the economy,

which they may not be able to do efficiently under

the present crisis situation because of the

difficulties in mobilizing deposits from the surplus

sector (Molokwu, 1994:51). Ebhodaghe (1994:30)

concurs the bank distress retards economy’s rate of

capital formation; reduce its level of employment and

ultimately the pace of economic growth.

Bank distress also engenders crisis of confidence

in the entire industry. This clearly paralyses the

38

development of a good banking culture. Several

circumstances in Nigeria contributed to the crisis of

confidence: withdrawal of public sector deposits;

June 12 crisis; and even the promulgation of Failed

Bank Degree. These sent an alarming signal to the

public who made huge withdrawals and made it was

impossible for even the healthy banks since investors

do not know which of the banks are actually

distressed.

Hence, the development of an enduring banking

culture, which has been at the forefront of banking

policy in the last three (3) decades, became

disrupted (Molokwu, 1994:17). More importantly as

Ebhodaghe (1996:20) argues, this development

increases the banks’ cost of intermediation, as banks

need to pay higher returns to attract and retain

deposits. Many banks at the height if tension offer

interest rates on deposits higher than the prevailing

39

market rates to boast their deposits and lure

customers and this further complicated the situation.

Coupled with the high cost of intermediation, there

will be great and pervasive uncertainty such that the

perceived real return on financial assets will be

lowered. Frequent government intervention through the

regulatory authorities adds to other indirect cost.

Finally, depositors’ fund in the event of liquidation

will be lost at least recoverable to the extent of

N50, 000 where there is explicit/implicit provision

for protection depositors.

Gilbert and Kochin (1994) and Ebhodaghe (1996)

concur that expenditure of economic agents are

constrained by the quality of credits made available

to them. Developments that reduce the total quantity

of bank credit or disrupt the operations of banks as

intermediaries will reduce spending and consequently

will affect aggregate economic performance adversely.

40

The extent that bank failures disrupt the process of

financial intermediation, inducing credit – granting

activities of banks, aggregate economic activities

may be adversely affected.

Ebhodaghe (1996) observes the trend of net

domestic credit to the economy and them compared it

with the trend of key economic parameters such as

rate of growth of real Gross Domestic Product (GDP),

the rate of manufacturing capacity utilization and

per capita income in Nigeria and compared the

variables with the level of distress in the system.

Appendix A presents the selected macroeconomic

indicators and the level of distress in the banking

system. In the analysis Ebhodaghe (1996) confirms

that assertion that developments, which disrupt the

operations of banks, as financial intermediaries will

adversely affect total quantity of bank credit. He

41

equally shows that performance in the real sector is

related to the stability in the banking industry.

Apart from the threats posed by bank distress to

the economy which affect everybody directly or

indirectly, it is worth discussing the other

stakeholders that suffer when a bank is in distress

or when it is liquidated.

Owners

In Nigeria, the inability or refusal of owners to

recapitalize distressed banks culminated into their

liquidation and total loss investment by owners of

such banks. This exposes them to risk and indirectly

discourage their feature participation in banking

business or even other productive activities within

the economy and therefore promotes investment abroad.

Employees

The employees of distress banks also suffer.

Rehabilitation and turnaround measures involve re –

42

sizing of banks and consequently certain jobs may be

eliminated or contracted. The loss of jobs leads to

economic disenfranchisement of many families thus

confounding the challenges of the trying environment

(Udezue: 1997). The attendant substantial increase in

the unemployment level negates government’s current

efforts at addressing the unemployment problem and

partly explains the current social unrest

particularly amongst the youth.

Depositors

Depositors also suffer when a bank is in distress

and incur some costs. In the event of liquidation,

they lose everything except if there is

implicit/explicit insurance cover. They also incur

additional cost of re – establishing relationship and

good rapport with other banks, which they have for

long developed with the failed banks.

43

Despite the preceding arguments that see distress

as negative and dysfunctional, there exist arguments

too that distress could indeed be functional, albeit

to some limited extent. Oboh (1999: 05) observes that

bank distress experience increase awareness of the

ethics and demands of the banking profession. Thus,

the regulatory authorities, banks and the public are

red – alert on the legal and professional banking

practice. It is also a fact that it has helped to

expunge the “bad eggs” and prepare the grounds for

importing the industry and restoring stability.

From the foregoing, it is clear that adequate

measures must be put in place to forestall future

occurrences. This is more important as bank distress

has many spills – over consequences.

CONCLUSION

44

This paper examines causes and consequences of

bank distress in Nigeria. The central idea is to

sensitize all the stakeholders on this all important

area within the hope that careful and systematic

monitoring of the affairs of banks would receive

complementary (in addition to the supervisory and

regulatory authorities) attention from several

quarters. With this, the life of banks could be

prolonged and all the negative consequences of

failure minimized. This is reinforced by the time –

honoured dictum that knowledge of causes and

consequences of failure in organizations energizes

the desire for organizations to survive.

45

CHAPTER THREE

3.0 RESEARCH DESIGN AND METHODOLOGY

3.1 RESEARCH METHODOLOGY

In this chapter, research is connected with the

procedures for gathering or processing information

for the accomplishment of the research objectives. In

order to effectively and satisfactory conduct the

study, the researcher has done in mind, the method of

the research, the approach to research work upon

which the study will exhaustively conducted

(Creswell, J.W., 2008). View research as a process of

steps used to collect and analyze information to

increase our understanding of a topic or issue. It

consists of three steps: pose a question, collect

data to answer the question and present an answer to

the question.

The methodology of this research work is

theoretical and analytical in approach. Both primary

46

data and secondary for the purpose with the use of

questionnaire and the secondary data were collected

form record publications and commercial banks

journals. The study shall employ the survey research

method in the process of data collection. The method

entails identifying collection of data through

questionnaire administration.

3.2 RESEARCH DESIGN

According to Kumer (2005), “a research design is

the plan which guides the data collection and

analysis phases of a research project”. It is the

frame work which specifies the type of information to

be collected and source of data collection procedure.

3.3 SAMPLE AND SAMPLING TECHNIQUES

Sample is a four representation of the population

since it is impossible to study the whole population;

47

a sample is drawn from the population to make

generalization.

In obtaining the sample, the researcher took

cognizance of two of the features of scientific

research to which is the representation and

unbalances. To ensure that these features are present

in the sample strategies and simple random sampling

techniques were used. This asks the question on how

many are to be surveyed. The researcher used the

sample size of 25.

3.4 METHOD OF DATA COLLECTION

Data are unprocessed information that is

systematically collected to support facts earlier

gathered for the research work. The researcher makes

use of necessary techniques in ensuring the

successful completion of this work; the questionnaire

was used as the major instrument of data collection.

It was administered on a total of 25 respondents,

48

made of banks’ staffs. Some basic historic documents

were also relied upon for the purpose of data

collection. While the researcher contracted journals,

magazines and commercial publications,

3.5 DATA ANALYSIS TECHNIQUE

Data analysis is the application of logic to the

understanding of data that have been gathered about a

subject matter.

The analytical tools that may be involved or used

in this research analysis includes simple percentage

and Chi – square (X2) method will be used to calculate

the extent, the research variable answer to the

questionnaires and the research hypothesis

respectively.

Chi – square formula:

X2 = Ʃ(O – E) 2 E

DF (Degree of freedom) = N – 1

49

Where;

X2 = Chi square calculated value

O = Observed frequency

E = Expected frequency which is delivered by

While;

Df = Degree of freedom

N = Number of observation

∞ = Level of significant (5%).

50

CHAPTER FOUR

4.0 DATA PRESENTATION AND ANALYSIS

4.1 INTRODUCTION

This chapter deals with the presentation,

analysis of data collected through the administration

of the questionnaire for analytical purpose, the

results and findings are put under two-sub-headed

based on the research questionnaire. Therefore, the

tools of data analysis were essentially statistical

in nature. These are the simple percentage method and

the application of the chi-square to test the

hypothesis.

4.2 PRESENTATION OF DATA

Thirty (30) questionnaires were distributed out

of which twenty five (25) were returned, and analyses

were based on (25).

4.3 RESPONSE TO THE QUESTIONNAIRE

51

As early mentioned, twenty-five (25) of the

questionnaire issued where well represented by 83% of

the total number of the questionnaire distributed.

This resources rate was seen to be satisfactory to

the researcher given the way Nigerians responds to

such research project. The questionnaire was designed

to obtain information from respondent on age, sex

marital states etc.

Table 4.3 (1) Sex sample or differentiation of

respondent

Response Frequency Percentage (%)Male 9 36Female 16 64Total 25 100

52

The analysis show that 64% of the respondents are

female this could be interpreted that majority of the

bank staff are female.

Table 4.3 (2) Sample response on respondent’s “age”

Age Frequency Percentage (%)Under 21yrs - 021-30yrs 19 7631-40 4 1641-50 2 850 and above -Total 25 100

The analysis on the table shows that the

substantial number of respondents fails into the

active between 21 yrs – 30 years.

Table 4.3 (3): Marital status of the respondent.

Marital Status

Qualification

Frequency Percentage

(%)SSEC/GCE - 0ND/NCE 19 76HND/BSC 6 42MSc/PhD - 0

53

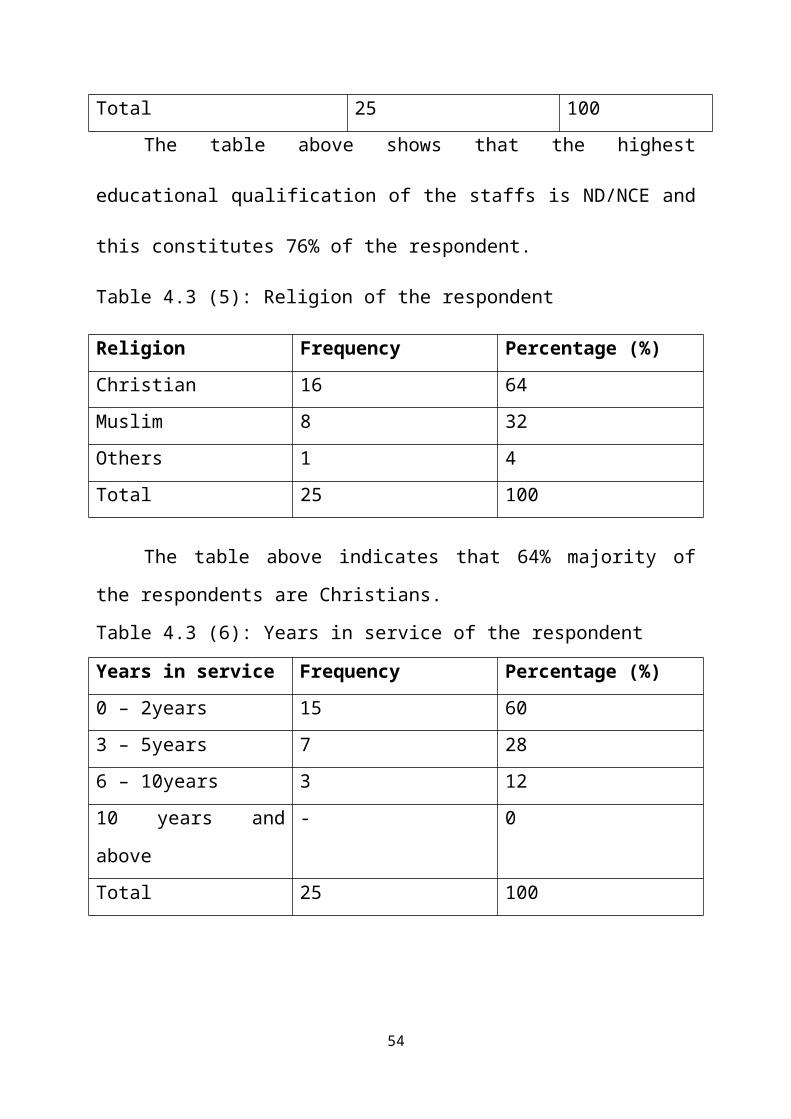

Total 25 100The table above shows that the highest

educational qualification of the staffs is ND/NCE and

this constitutes 76% of the respondent.

Table 4.3 (5): Religion of the respondent

Religion Frequency Percentage (%)Christian 16 64Muslim 8 32Others 1 4Total 25 100

The table above indicates that 64% majority of

the respondents are Christians.

Table 4.3 (6): Years in service of the respondent

Years in service Frequency Percentage (%)0 – 2years 15 603 – 5years 7 286 – 10years 3 1210 years and

above

- 0

Total 25 100

54

From the table above it can be seen that 60%

majority of the staffs spend 0 to 3years in the in

the system.

Table 4.3 (7 – 12): Economic factors as causes of

bank distress are

S/

N

Response Agreed Disagre

e

Percenta

ge (%)

agreed

Percenta

ge (%)

disagree

d7 Poor credit

policy

administratio

n

20 5 80 20

8 Poor recovery

method

22 3 88 12

9 Insider

dealing/abuse

6 19 24 76

55

10 Inadequacies

of

professionall

y trained

manpower

13 12 52 48

11 Poor

management

10 15 40 60

12 Fraud in

banks

7 18 28 72

The table above indicates that majority of the

respondents agrees that economic factors of bank

distress are: poor credit policy administration, poor

recovery method, inadequacies of professionally

trained manpower which constitutes 80%, 88% and 52%

respectively, while those that disagreed on insider

dealings/Abuse, poor management and fraud in banks

which also constitutes 76%, 60% and 72% of the

respondents respectively.

Table 4.3 (13): Political instability is part of the

cause of bank distress

Response Frequency Percentage (%)56

Agreed 25 100Disagreed - 0Total 25 100

The above table indicates that political

instability is a part of the cause of bak distress

and this constitutes 100% i.e. all the total

respondents agree.

Table 4.3 (14): The major causes of bank distress is

economic instability.

Response Frequency Percentage (%)Agreed 25 100Disagreed 0 0Total 25 100

The above indicates that the major cause of bank

distress is economic instabiligy with 100% agree

respondents.

Table 4.3 (15): Distress has no effect on the average

profit of commercial banks

Response Frequency Percentage (%)Agree 6 24Disagree 19 76

57

Total 25 100

The above table shows that distress has effect on

the average profit of commercial banks in Nigeria by

76% of the respondent, while, 24% of the respondents

agrees that distress has no effect on the average

profit of commercial banks in Nigeria.

Table 4.3 (16): Fraudulent practices among the

practioners contributes to the causes of bank

distress.

Response Frequency Percentage (%)Agree 9 36Disagree 16 64Total 25 100

58

The above table shows that fraudulent practices

among the practioners does not contributes to the

causes of bank distress, supported by 64% of the

respondent.

Table 4.3 (17): Bank distress is as a result of lack

of adequate banking supervision.

Response Frequency Percentage (%)Agree 12 48Disagree 13 52Total 25 100

The table above review that 13 respondent

equivalent to 52% disagree that bank distress is as a

result of lack of adequate banking supervision

Table 4.3 (18): Under – capitalization of the

industry also contributes to the causes of the

distress.

Response Frequency Percentage (%)Agree 21 84%Disagree 4 16Total 25 100

59

The table above indicate that 21 of the

respondent equate 84% agree with the statement while

4 of the respondent of 16% disagree.

Table 4.3 (19): Under reliance on Forex trading

causes the bank distress.

Response Frequency Percentage (%)Agree 10 40Disagree 15 60Total 25 100

The table above review that 15 respondent

constituting 60% disagree to the statement while 10

respondents of 40% agree.

Table 4.3 (20): Bank distress was as a result of

rapid changes in government policies.

Response Frequency Percentage (%)Agreed 25 100Disagreed - -Total 25 100Source: Field survey 2012

60

The table shows that majority of the people agree

that bank distress was as a result of rapid change in

government policies.

Table 4.3 (21): Undue interference by shareholders

also contributes to the distress.

Response Frequency Percentage (%)Agreed 11 44Disagreed 14 56Total 25 100

The table above indicates that 14 respondent

consisting 56% disagree that undue interference by

shareholders also contributes to the distress while

11 respondent equivalent 44% agree.

4.3.1 TEST OF HYPOTHESIS

In order to test the hypothesis, the chi-square

method is made of the formula for chi-square shown

below:

X2 = Σ(O−E)2

E

61

Where, X2 = chi – square

O = Observed Frequency

E = Expected Frequency

Σ = Summation

H0: Distress has no effect on the average profit of

commercial banks.

H1: Distress has effect on the average profit of

commercial banks.

Respon

se

F0 Fe F0 – Fe (F0 –

Fe)2

(F0 –Fe)2

Fe

X2 cal

Agreed 6 12.5 -4.5 42.25 3.38Disagr

eed

19 12.5 4.5 42.25 3.38

Total 25 25 6.6

Significant = 0.05

Degree of freedom = (r – 1) (c – 1)

= (2 – 1) (2 – 1)

= 1

Critical value = 1, 0.05

X2 tabulated = 3.84

X2 calculated = 0.36

62

DECISION RULE

Since my X2 tabulated value is (3.84) is less

than my X2 calculated value (6.66) then H1 will be

accepted. Therefore, Distress has effect on the

average profit of commercial banks.

63

CHAPTER FIVE

5.0 SUMMARY, CONCLUSION AND RECOMMENDATION

5.1 SUMMARY OF FINDINGS

This research work is concerned with the distress

of profit growth in commercial banks in Nigeria

banking industries.

The review of 104 years of banking experience in

Nigeria has been characterized by significant growth

in the number, structure and the spread of the

financial institutions. In other words, the Nigerian

bankng sector had over the years undergone a series

of structural and institutional changes. The system

has moved from an under-developed state with few

banks in the 1960s to a more diversified and

competitive industry with an avalanche of commercial

and Merchant banks, as well as specialized banks.

However, this positive impact of the reforms was

undermined by the advent of distress in the banking

64

system, even though generally modest until 1989. The

distress in the industry had become generalized,

spreading to virtually all the system’s sub-sectors.

5.2 CONCLUSION

The main thrust of this study was an

investigation into the nature, extent and causes of

distress in the Nigeria financial industry,

particularly the banking sub-sector.

The study confirmed the presence of distress in

the banking industry, but generalized that the

distress could not be described as systematic since a

good number of banks remain healthy to which many

customers “flown for safety”. On the whole, 80.9% of

the banks are believed to be healthy, 11.1% believed

to the mildly distressed, and 8.09% confirmed to be

severely distressed. All the major factors causing

distress namely institutional, economic, and

political etc contributed in varying degrees to the

65

distress, rating institutional factors (in terms of

poor management, credit policy, ineffective machinery

for debt recovery, insider dealings, abuses, fraud

and poor credit administration) highest thus,

significant to the distress.

The findings of this study as shown above,

revealed that various distress resolution option were

used by the regulatory/supervisory authorities in

trying to address the problems of distress in Nigeria

banking system without any success. The resolution

framework appears to have some inadequacies

associated with it. Some of the inadequacies include

the lack of sufficient resources to handle failure

resolution and the ineffectiveness of holding actons

to handle distress.

Based on the above, we can conclude that the

ineffectiveness of the existing distress resolution

framework that resulted in a continuous increase in

66

the depth of distress and number of distress banks in

the system, can be attribute to the

inadequacies/lapses inherent in the operational

framework. This therefore, calls for reform of the

operational aspect of the existing distress

resolution framework for it to be effective in

addressing distress problems in the Nigeria banking

system.

5.3 RECOMMENDATIONS

In order to minimize the effect distress on banks

clientele and the economy as a whole and also avoid

the encroachment of the factors responsible for

distress into the banking system, the regulatory

authorities may have to use better measures of

evaluating the feature of distress at an early stage.

This will no doubt create sufficient lead-time to

apply remediable solution before serious damage is

done.

67

It can also be seen that the relative

ineffectiveness of the existing distress resolution

options can be traced to a great extent on the

inadequacies in the operational framework. This

therefore, calls for substantive reforms as they

affect banks distress resolution options.

Accordingly, the following recommendations are being

proposed:

a) Measures to minimize the undesirable effects of

holding actions

i. To the extent that banks on which holding actions

are imposed are not bidding for their own

account, they should be allowed to participate in

the foreign exchange transaction on behalf of

their customers since foreign exchange is sold on

cash and carry to the customers through their

banks. Thsis could minimize the loss of good

business and high network customers.

68

ii. Banks could allow lending to “first class

customers” beyond the level of preceding month’s

recoveries, with the prior approval of the

relevant supervisory agency as long as the bank’s

account with the CBN is not overdrawn. Indeed,

banks should no longer be allowed to overdrawn

their accounts with the CBN.

b) Need to Set aside financial resources to handle

bank distress

Since the government is so much concerned with

the need to deal with widespread bank insolvency in

the system, there is the need for an explicit

financial provision in the national budget to deal

with defaults and distress in the nation’s financial

sector. Such commitments on the part of the

government will go a long way in restoring public

confidence in the banking system.

c) Increased supervisory capacity.

69

There is need for increased bank supervisory

capacity especially in the off- site surveillance,

where emphasis should be on development of an early

warning model for early indemnification of distress,

and on – site inspection.

70

REFERENCE

Alashi, S.O (2005) “bank failure resolution: the main

option” NDIC quarterly vol. 3 (2)

Central bank of Nigeria/Nigerian deposit Insurance

Corporation (2006), a study of distress in the

Nigerian financial services industry, Lagos.

Doguwa, S.I (2004) “an early warning model for

identification of problem banks in Nigeria”

Abuja, CBN: economic and financial review vol.

34.

Donli, J.G. (2004): causes of bank distress and

resolution options. Nigerian tribune 10th

February. 2. Ibrahim, u. (2011): NDIC pays n3.36

to failed banks’ depositors. The nation August 3,

pg. 11.

Ebhodagbe, J.U. (2007), “deposit insurance: the

Nigerian experience and future perspectives. A

paper presented at a seminar on issues in central

71

banking and bank distress in sub Saharan African

countries, at CBN training centre, Lagos.

Ede, (2002), bank rehabilitation: the Nigerian

experience” at a seminar of World Bank/Federal

Reserve System, Washington D.C.

Gashinbaki, I.B. (2000) Bank Failure: The Worst

Corporate Crisis of the Millennium in Nigeria,

Lagos, Frankad Publishers Ltd.

Olugun, S.O. (2004). “Bank Failures in Nigeria:

Genesis, Effects and Remedies” CBN Economic and

Financial Review.

Utomi, (2002). “Implications of Failed Banks on the

Nigerian Economy” NDIC Quarterly, Volume 6 No 2.

72