The Fidelity Master Trust Trustees' Report and Financial ...

247

The Fidelity Master Trust Trustees’ Report and Financial Statements For the year ended 30 June 2021 Scheme Registration No. 12008988

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of The Fidelity Master Trust Trustees' Report and Financial ...

The Fidelity Master Trust

Trustees’ Report and Financial Statements For the year ended 30 June 2021

Scheme Registration No. 12008988

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

Contents Page

Trustees’ Report 1 - 14

Investment Report 15 - 20

Independent Auditor’s Report 21 - 23

Fund Account 24

Statement of Net Assets Available for Benefits 25

Notes to the Financial Statements 26 - 34

Independent Auditor’s Statement about Contributions 35

Summary of Contributions 36

Chair’s Statement 37 - 60

Appendix 1 – Statement of Investment Principles 61 - 123 (Full version all sections)

Appendix 2 - Fund charges summary 124 - 131

Appendix 3 - Example cost and charges illustrations 132 - 206

Appendix 4 – Implementaton Report 207 - 245

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

1

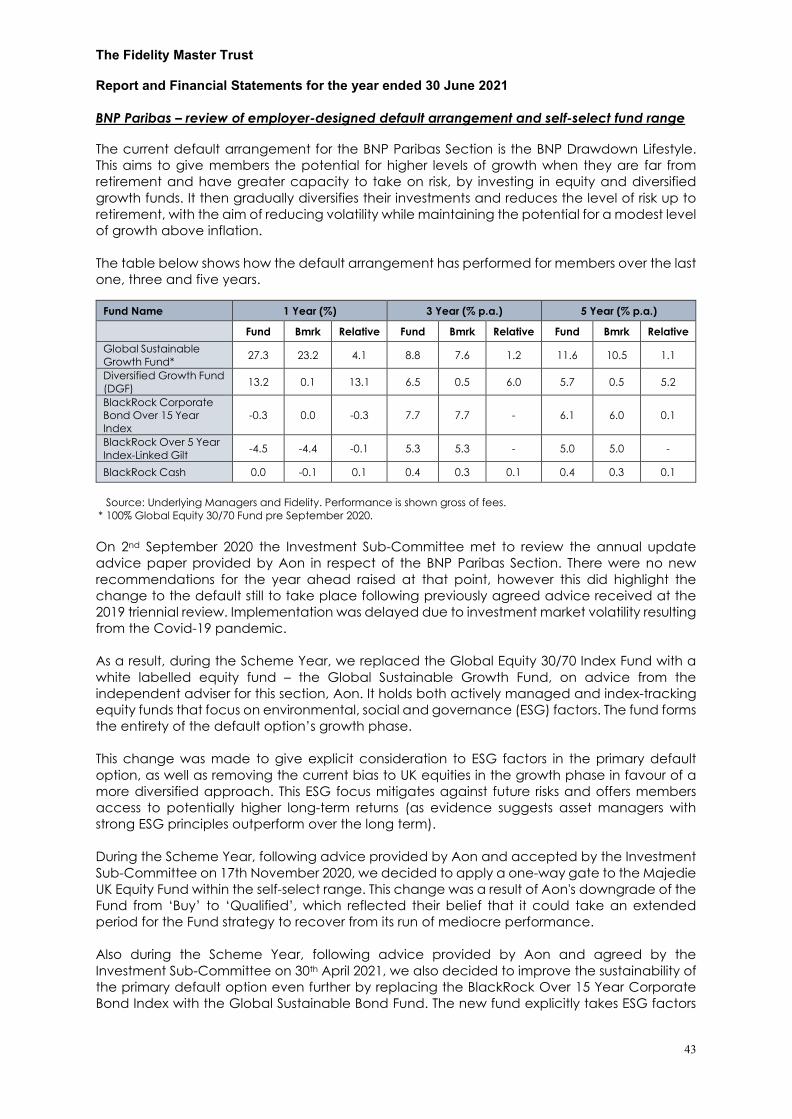

Trustees’ Report 1 Constitution of the Scheme The Scheme was set up on 13 December 2013 to provide defined contribution benefits to the current and former employees of the Participating Employers, a list of which can be found on pages 5 to 9. It may also provide benefits to members who have been transferred to the Scheme by the trustees of another pension scheme. The Scheme is a registered pension scheme for tax purposes under the Finance Act 2004 (Registered Pension Scheme number 0081028RS). The Scheme is governed by a Master Trust Board which meets the independence requirements as defined by the Department for Work and Pensions (DWP). The Board is responsible for ensuring the Scheme is operating in accordance with the Scheme Trust Deed and Rules dated 13 December 2013 and Deed of Amendment dated 24 June 2016, together with the Deeds of Participation for each Participating Employer and the Statement of Investment Principles. Participating Employers are able to vary the rules in certain areas and these are set out in the relevant Deed of Participation. The Scheme’s Trust Deed and Rules were updated to incorporate the new Master Trust Requirements introduced under the Pension Schemes Act 2017 via a Deed of Amendment dated 7 February 2019. The Fidelity Master Trust received authorisation from the Pensions Regulator (TPR) with effect from 28 June 2019. The Scheme is now subject to TPR’s ongoing supervision to ensure the Scheme continues to meet the authorisation criteria set out in the Pension Schemes Act 2017. FIL Life Insurance Ltd, ‘(Fidelity)’, is the Scheme Sponsor and is responsible for setting up the Master Trust and appointing the Trustees. The Trustees are responsible for the administration and investment policy of the Scheme. The Trustees meet formally four times a year, and more frequently as required. Under the terms of the Trust Deed, resolutions are passed on a simple majority of those voting, with the Chair having a casting vote when necessary. The Trustees have established three joint Sub-Committees with the Independent Governance Committee (IGC) of Fidelity which is responsible for oversight of Fidelity’s contract based workplace pension schemes. Each Committee comprises of at least two independent Trustees including the independent Chair:

• The joint Communications Sub-Committee, which allows the Trustees to better understand and influence Fidelity’s communication strategy, and to set the strategy for the Trust;

• The joint Investment Sub-Committee, which allows the Trustees to better understand and influence Fidelity’s investment strategy, and to set the strategy for the Trust; and

• The joint Administration Sub-Committee, set up during the year, which allows the Trustees to better understand, influence and monitor Fidelity’s administration proposition. The first Administration Sub-Committee meeting was held on 23 June 2020.

The Trustees have a delegation policy covering the payment of retirement benefits, transfers and certain discretionary benefit payments including the authority to make decisions on death, ill health and serious ill health cases. The delegation policy is reviewed on a regular basis and delegated decisions are reported at each Trustee meeting.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

2

The Trustees appointed Fidelity as Scheme Administrator (‘the Administrator’) on 1 April 2014. The Administrator is responsible for the day-to-day operation of the Scheme including member communications, member and Participating Employer websites, record keeping, allocation of contributions to member funds and payment of benefits. The Administrator is remunerated through the Annual Management Charges (AMCs) deducted from members’ pension accounts. In some cases, fees may be payable by a Participating Employer. All other fees are paid by Fidelity except for bespoke investment adviser fees which are met by the Participating Employer. 2 The Trustees As Scheme Sponsor, Fidelity is responsible for the appointment and removal of the Trustees. Trustees are appointed for a fixed term of office of up to 5 years, subject to a 10 year cumulative maximum. Details of the current Trustees may be found on pages 58 and 59, in the Chair’s Statement. The Trustees have a Trustee Action Plan which is used to help ensure the Scheme is run efficiently. The Trustees have responsibility for controls and risk management and have identified and logged risks in a risk register. The risk register is used to document the risks to which the Scheme is exposed and to record the likelihood and impact of those risks and the mitigating actions required. The risk register consists of six key areas covering operational, investment, governance, strategic, communication and regulatory and compliance risks, and is updated at least annually or as and when risks are identified or the assessment changes. Details of any changes to the risk register are formally recorded and shared with TPR as part of the annual supervisory return. The Trustees are now subject to TPR’s ongoing supervision to ensure the Scheme continues to meet the authorisation criteria set out in the Pension Schemes Act 2017. TPR has published its supervision and enforcement policy which sets out how it will supervise master trusts and use its enforcement powers. All master trusts will be supervised and required to submit an annual supervisory return. The Regulator expects those responsible for running master trusts to:

• be open, honest and transparent in their interactions with TPR, responding promptly to information requests;

• proactively liaise with TPR and volunteer information about material developments, risks and issues in their scheme, which may affect the scheme’s ability to continue to meet the authorisation criteria and other obligations;

• satisfy TPR that they continue to meet their obligations and that there is a low risk of them failing to meet their obligations going forward, including providing relevant evidence; and

• be proactive in identifying and monitoring risks, and proactive in rectifying any issues that may arise and affect the scheme’s ability to continue to meet the authorisation criteria or other obligations.

In addition to the supervisory requirements, the Trustees continue to commission an independent reporting accountant to assess the design and operating effectiveness of the control procedures of the Scheme on an annual basis. The AAF 05/20 assurance report on internal controls covers the control procedures in place to meet the control objectives described in the Institute of Chartered Accountants in England and Wales (‘ICAEW’) Assurance reporting on Master Trusts (TECH 05/20 AAF).

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

3

3 Conflicts of Interest A conflicts of interest policy is in place to assist the Trustees in identifying, managing and monitoring any actual or potential conflicts of interest which may arise in relation to the Scheme. This policy is reviewed annually. The Trustees keep a register of interests which is reviewed at the start of each Trustees’ meeting and any additional conflicts noted at that time. 4 Statement of Trustees’ Responsibilities The financial statements, which are prepared in accordance with United Kingdom Generally Accepted Accounting Practice, including the Financial Reporting Standard applicable in the UK (FRS 102) are the responsibility of the Trustees. Pension scheme regulations require, and the Trustees are responsible for ensuring, that those financial statements:

• show a true and fair view of the financial transactions of the Scheme during the Scheme year and of the amount and disposition at the end of that year of the assets and liabilities, other than liabilities to pay pensions and benefits after the end of the Scheme year; and

• contain the information specified in Regulation 3A of The Occupational Pension

Schemes (Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations 1996, including making a statement whether the financial statements have been prepared in accordance with the relevant financial reporting framework applicable to occupational pension schemes.

In discharging the above responsibilities, the Trustees are responsible for selecting suitable accounting policies, to be applied consistently, making any estimates and judgments on a prudent and reasonable basis, and for the preparation of the financial statements on a going concern basis unless it is inappropriate to presume that the Scheme will not be wound up. The Trustees are also responsible for making available certain other information about the Scheme in the form of an Annual Report (called Trustees’ Report and Financial Statements). The Trustees have a general responsibility for ensuring that adequate accounting records are kept and for taking such steps as are reasonably open to them to safeguard the assets of the Scheme and to prevent and detect fraud and other irregularities, including the maintenance of an appropriate system of internal control. The Trustees are responsible under pensions legislation for ensuring that payment schedules are prepared, maintained and from time to time revised showing the rates of contributions payable to the Scheme by or on behalf of the employers and the active members of the Scheme and the dates on or before which such contributions are to be paid. The Trustees are also responsible for keeping records of contributions received in respect of any active member of the Scheme and for adopting risk-based processes to monitor whether contributions are made to the Scheme by the employer in accordance with the payment schedules. Where breaches of the schedules occur, the Trustees are required by the Pensions Acts 1995 and 2004 to consider making reports to TPR and affected members.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

4

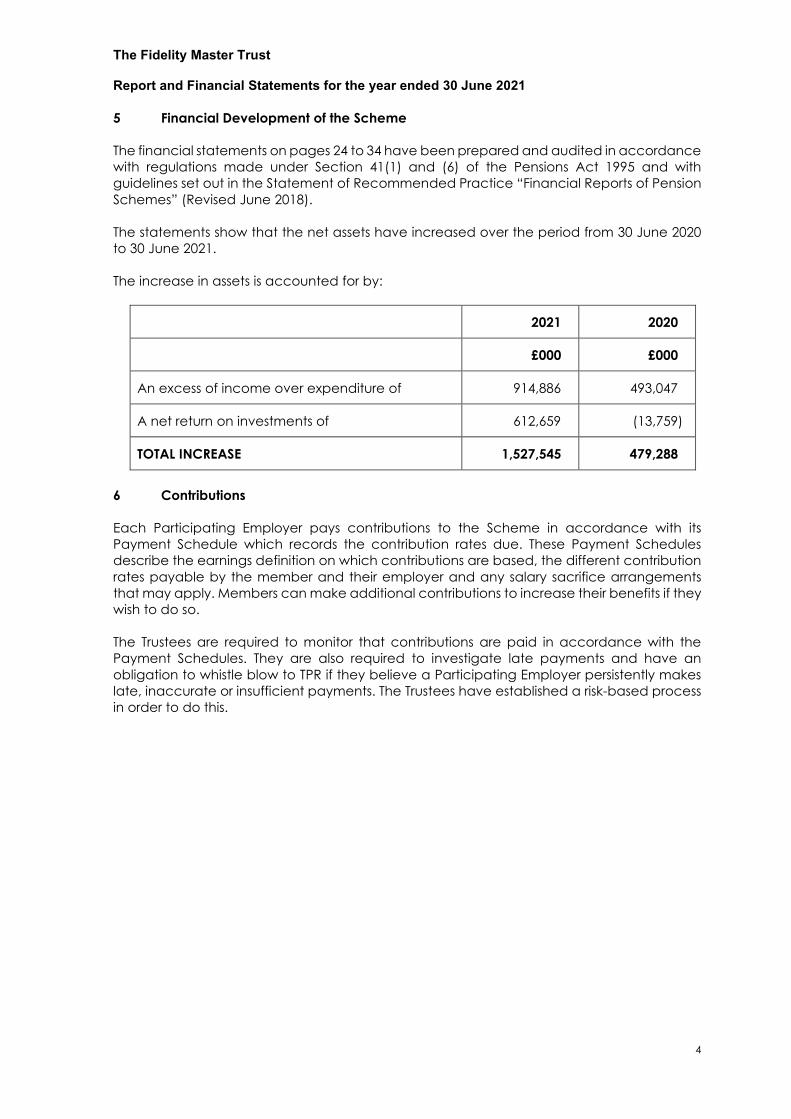

5 Financial Development of the Scheme The financial statements on pages 24 to 34 have been prepared and audited in accordance with regulations made under Section 41(1) and (6) of the Pensions Act 1995 and with guidelines set out in the Statement of Recommended Practice “Financial Reports of Pension Schemes” (Revised June 2018). The statements show that the net assets have increased over the period from 30 June 2020 to 30 June 2021. The increase in assets is accounted for by:

2021 2020

£000 £000

An excess of income over expenditure of 914,886 493,047

A net return on investments of 612,659 (13,759)

TOTAL INCREASE 1,527,545 479,288

6 Contributions Each Participating Employer pays contributions to the Scheme in accordance with its Payment Schedule which records the contribution rates due. These Payment Schedules describe the earnings definition on which contributions are based, the different contribution rates payable by the member and their employer and any salary sacrifice arrangements that may apply. Members can make additional contributions to increase their benefits if they wish to do so. The Trustees are required to monitor that contributions are paid in accordance with the Payment Schedules. They are also required to investigate late payments and have an obligation to whistle blow to TPR if they believe a Participating Employer persistently makes late, inaccurate or insufficient payments. The Trustees have established a risk-based process in order to do this.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

5

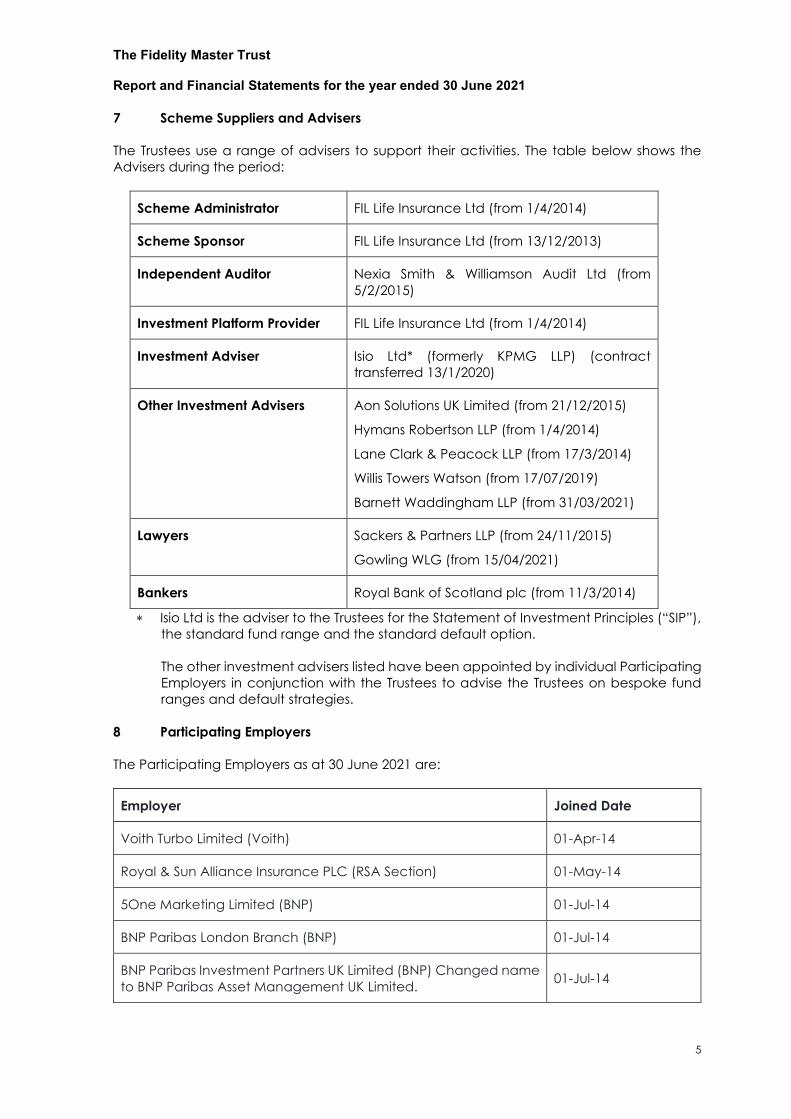

7 Scheme Suppliers and Advisers The Trustees use a range of advisers to support their activities. The table below shows the Advisers during the period:

Scheme Administrator FIL Life Insurance Ltd (from 1/4/2014)

Scheme Sponsor FIL Life Insurance Ltd (from 13/12/2013)

Independent Auditor Nexia Smith & Williamson Audit Ltd (from 5/2/2015)

Investment Platform Provider FIL Life Insurance Ltd (from 1/4/2014)

Investment Adviser Isio Ltd* (formerly KPMG LLP) (contract transferred 13/1/2020)

Other Investment Advisers Aon Solutions UK Limited (from 21/12/2015)

Hymans Robertson LLP (from 1/4/2014)

Lane Clark & Peacock LLP (from 17/3/2014)

Willis Towers Watson (from 17/07/2019)

Barnett Waddingham LLP (from 31/03/2021)

Lawyers Sackers & Partners LLP (from 24/11/2015)

Gowling WLG (from 15/04/2021)

Bankers Royal Bank of Scotland plc (from 11/3/2014)

∗ Isio Ltd is the adviser to the Trustees for the Statement of Investment Principles (“SIP”), the standard fund range and the standard default option. The other investment advisers listed have been appointed by individual Participating Employers in conjunction with the Trustees to advise the Trustees on bespoke fund ranges and default strategies.

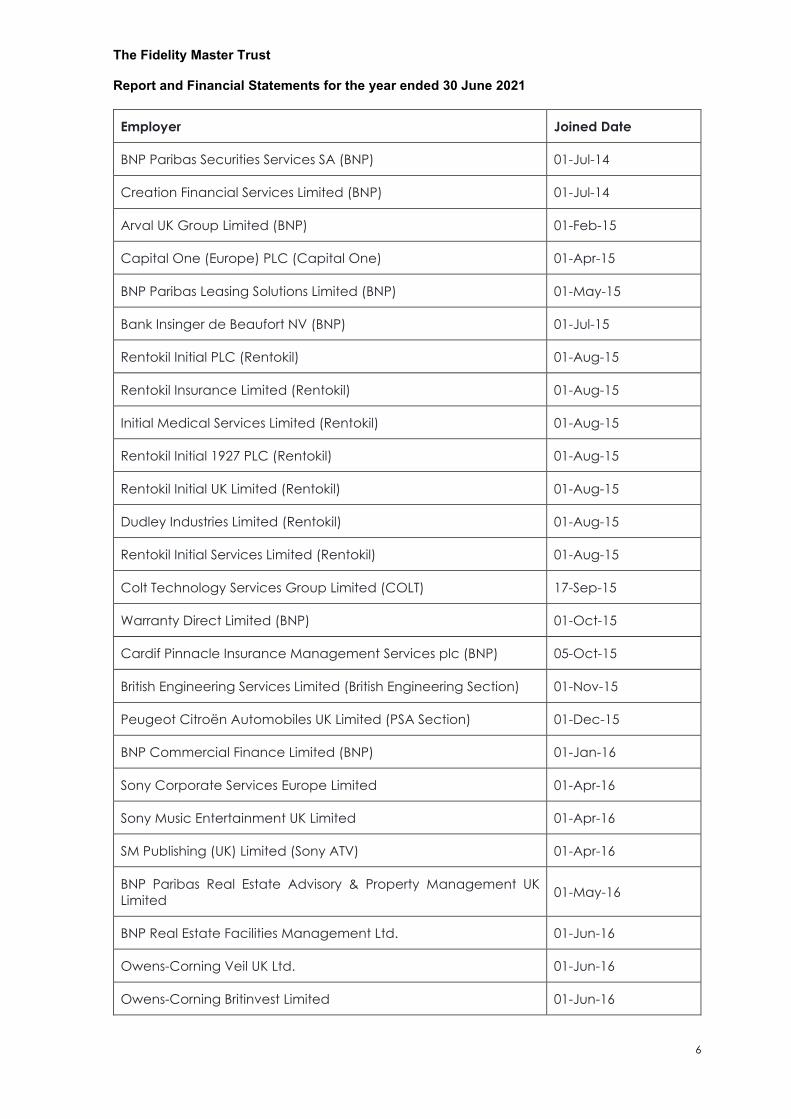

8 Participating Employers The Participating Employers as at 30 June 2021 are:

Employer Joined Date

Voith Turbo Limited (Voith) 01-Apr-14

Royal & Sun Alliance Insurance PLC (RSA Section) 01-May-14

5One Marketing Limited (BNP) 01-Jul-14

BNP Paribas London Branch (BNP) 01-Jul-14

BNP Paribas Investment Partners UK Limited (BNP) Changed name to BNP Paribas Asset Management UK Limited. 01-Jul-14

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

6

Employer Joined Date

BNP Paribas Securities Services SA (BNP) 01-Jul-14

Creation Financial Services Limited (BNP) 01-Jul-14

Arval UK Group Limited (BNP) 01-Feb-15

Capital One (Europe) PLC (Capital One) 01-Apr-15

BNP Paribas Leasing Solutions Limited (BNP) 01-May-15

Bank Insinger de Beaufort NV (BNP) 01-Jul-15

Rentokil Initial PLC (Rentokil) 01-Aug-15

Rentokil Insurance Limited (Rentokil) 01-Aug-15

Initial Medical Services Limited (Rentokil) 01-Aug-15

Rentokil Initial 1927 PLC (Rentokil) 01-Aug-15

Rentokil Initial UK Limited (Rentokil) 01-Aug-15

Dudley Industries Limited (Rentokil) 01-Aug-15

Rentokil Initial Services Limited (Rentokil) 01-Aug-15

Colt Technology Services Group Limited (COLT) 17-Sep-15

Warranty Direct Limited (BNP) 01-Oct-15

Cardif Pinnacle Insurance Management Services plc (BNP) 05-Oct-15

British Engineering Services Limited (British Engineering Section) 01-Nov-15

Peugeot Citroën Automobiles UK Limited (PSA Section) 01-Dec-15

BNP Commercial Finance Limited (BNP) 01-Jan-16

Sony Corporate Services Europe Limited 01-Apr-16

Sony Music Entertainment UK Limited 01-Apr-16

SM Publishing (UK) Limited (Sony ATV) 01-Apr-16

BNP Paribas Real Estate Advisory & Property Management UK Limited 01-May-16

BNP Real Estate Facilities Management Ltd. 01-Jun-16

Owens-Corning Veil UK Ltd. 01-Jun-16

Owens-Corning Britinvest Limited 01-Jun-16

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

7

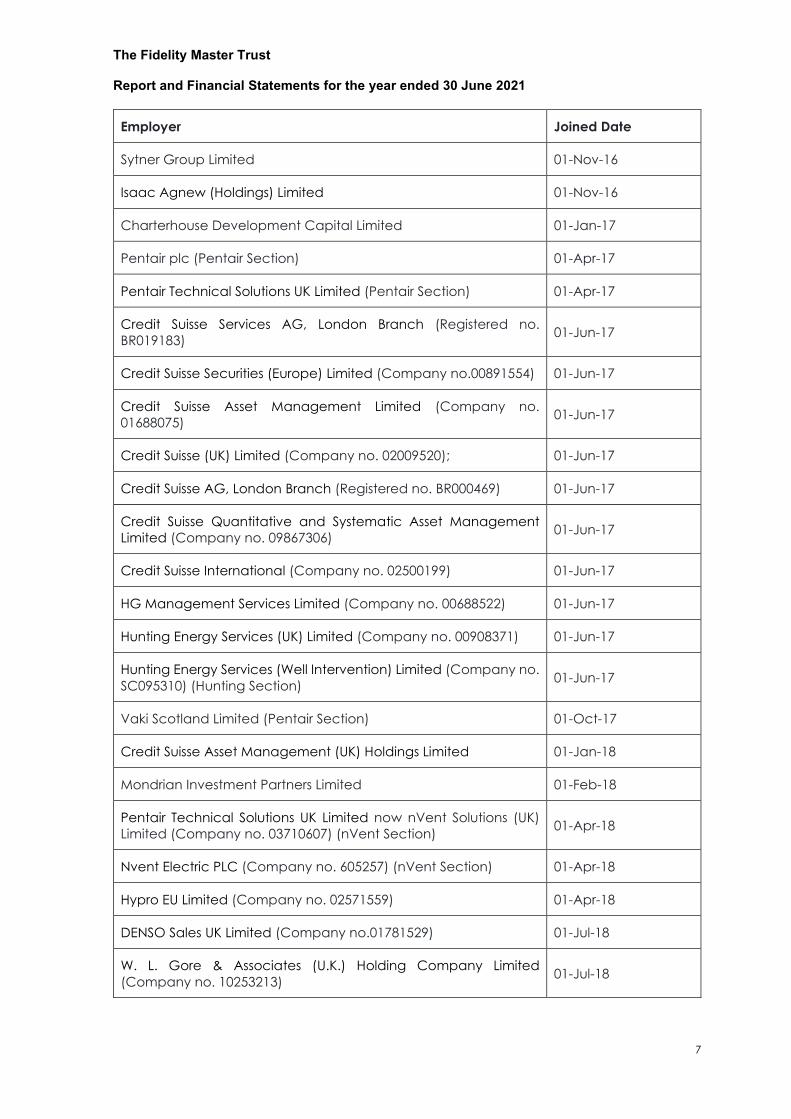

Employer Joined Date

Sytner Group Limited 01-Nov-16

Isaac Agnew (Holdings) Limited 01-Nov-16

Charterhouse Development Capital Limited 01-Jan-17

Pentair plc (Pentair Section) 01-Apr-17

Pentair Technical Solutions UK Limited (Pentair Section) 01-Apr-17

Credit Suisse Services AG, London Branch (Registered no. BR019183) 01-Jun-17

Credit Suisse Securities (Europe) Limited (Company no.00891554) 01-Jun-17

Credit Suisse Asset Management Limited (Company no. 01688075) 01-Jun-17

Credit Suisse (UK) Limited (Company no. 02009520); 01-Jun-17

Credit Suisse AG, London Branch (Registered no. BR000469) 01-Jun-17

Credit Suisse Quantitative and Systematic Asset Management Limited (Company no. 09867306) 01-Jun-17

Credit Suisse International (Company no. 02500199) 01-Jun-17

HG Management Services Limited (Company no. 00688522) 01-Jun-17

Hunting Energy Services (UK) Limited (Company no. 00908371) 01-Jun-17

Hunting Energy Services (Well Intervention) Limited (Company no. SC095310) (Hunting Section) 01-Jun-17

Vaki Scotland Limited (Pentair Section) 01-Oct-17

Credit Suisse Asset Management (UK) Holdings Limited 01-Jan-18

Mondrian Investment Partners Limited 01-Feb-18

Pentair Technical Solutions UK Limited now nVent Solutions (UK) Limited (Company no. 03710607) (nVent Section) 01-Apr-18

Nvent Electric PLC (Company no. 605257) (nVent Section) 01-Apr-18

Hypro EU Limited (Company no. 02571559) 01-Apr-18

DENSO Sales UK Limited (Company no.01781529) 01-Jul-18

W. L. Gore & Associates (U.K.) Holding Company Limited (Company no. 10253213) 01-Jul-18

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

8

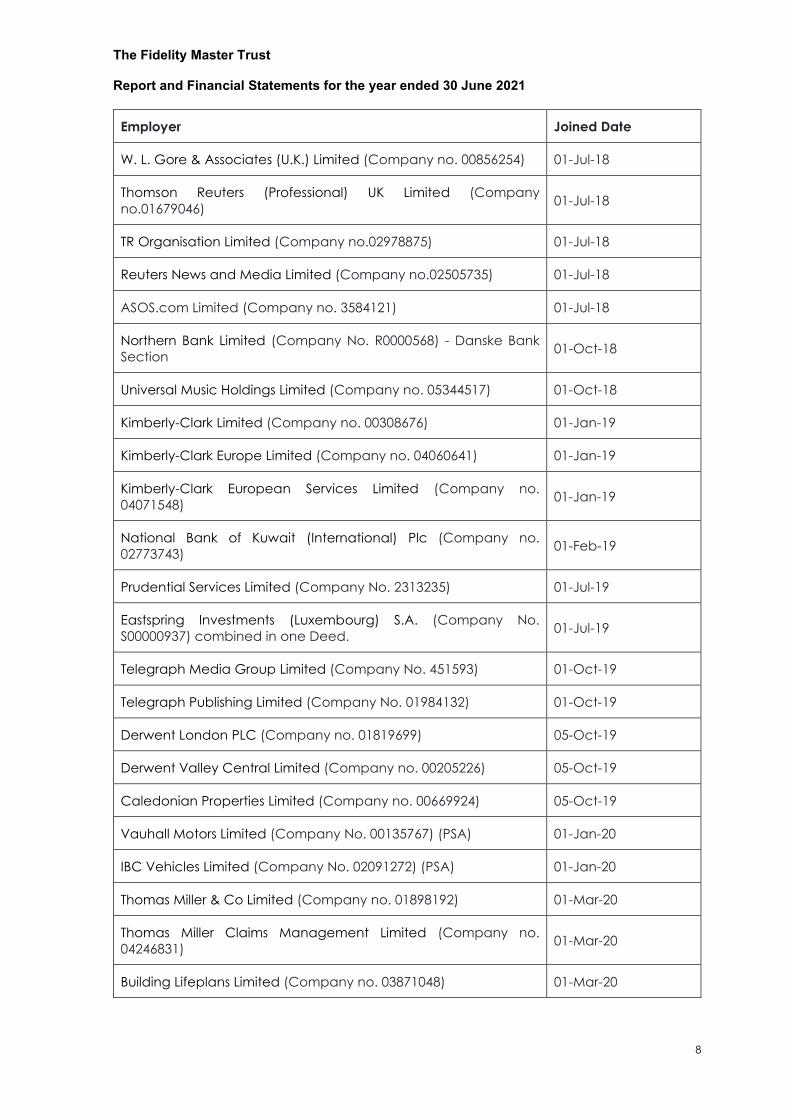

Employer Joined Date

W. L. Gore & Associates (U.K.) Limited (Company no. 00856254) 01-Jul-18

Thomson Reuters (Professional) UK Limited (Company no.01679046) 01-Jul-18

TR Organisation Limited (Company no.02978875) 01-Jul-18

Reuters News and Media Limited (Company no.02505735) 01-Jul-18

ASOS.com Limited (Company no. 3584121) 01-Jul-18

Northern Bank Limited (Company No. R0000568) - Danske Bank Section 01-Oct-18

Universal Music Holdings Limited (Company no. 05344517) 01-Oct-18

Kimberly-Clark Limited (Company no. 00308676) 01-Jan-19

Kimberly-Clark Europe Limited (Company no. 04060641) 01-Jan-19

Kimberly-Clark European Services Limited (Company no. 04071548) 01-Jan-19

National Bank of Kuwait (International) Plc (Company no. 02773743) 01-Feb-19

Prudential Services Limited (Company No. 2313235) 01-Jul-19

Eastspring Investments (Luxembourg) S.A. (Company No. S00000937) combined in one Deed. 01-Jul-19

Telegraph Media Group Limited (Company No. 451593) 01-Oct-19

Telegraph Publishing Limited (Company No. 01984132) 01-Oct-19

Derwent London PLC (Company no. 01819699) 05-Oct-19

Derwent Valley Central Limited (Company no. 00205226) 05-Oct-19

Caledonian Properties Limited (Company no. 00669924) 05-Oct-19

Vauhall Motors Limited (Company No. 00135767) (PSA) 01-Jan-20

IBC Vehicles Limited (Company No. 02091272) (PSA) 01-Jan-20

Thomas Miller & Co Limited (Company no. 01898192) 01-Mar-20

Thomas Miller Claims Management Limited (Company no. 04246831) 01-Mar-20

Building Lifeplans Limited (Company no. 03871048) 01-Mar-20

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

9

Employer Joined Date

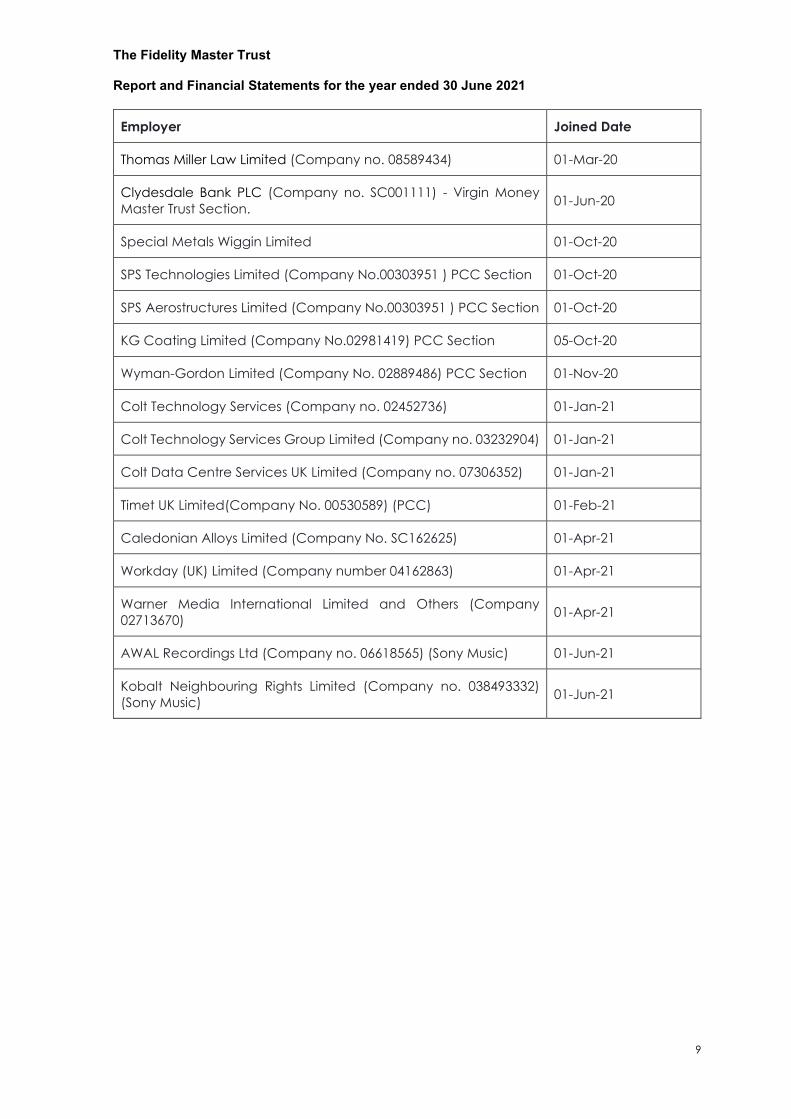

Thomas Miller Law Limited (Company no. 08589434) 01-Mar-20

Clydesdale Bank PLC (Company no. SC001111) - Virgin Money Master Trust Section. 01-Jun-20

Special Metals Wiggin Limited 01-Oct-20

SPS Technologies Limited (Company No.00303951 ) PCC Section 01-Oct-20

SPS Aerostructures Limited (Company No.00303951 ) PCC Section 01-Oct-20

KG Coating Limited (Company No.02981419) PCC Section 05-Oct-20

Wyman-Gordon Limited (Company No. 02889486) PCC Section 01-Nov-20

Colt Technology Services (Company no. 02452736) 01-Jan-21

Colt Technology Services Group Limited (Company no. 03232904) 01-Jan-21

Colt Data Centre Services UK Limited (Company no. 07306352) 01-Jan-21

Timet UK Limited(Company No. 00530589) (PCC) 01-Feb-21

Caledonian Alloys Limited (Company No. SC162625) 01-Apr-21

Workday (UK) Limited (Company number 04162863) 01-Apr-21

Warner Media International Limited and Others (Company 02713670) 01-Apr-21

AWAL Recordings Ltd (Company no. 06618565) (Sony Music) 01-Jun-21

Kobalt Neighbouring Rights Limited (Company no. 038493332) (Sony Music) 01-Jun-21

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

10

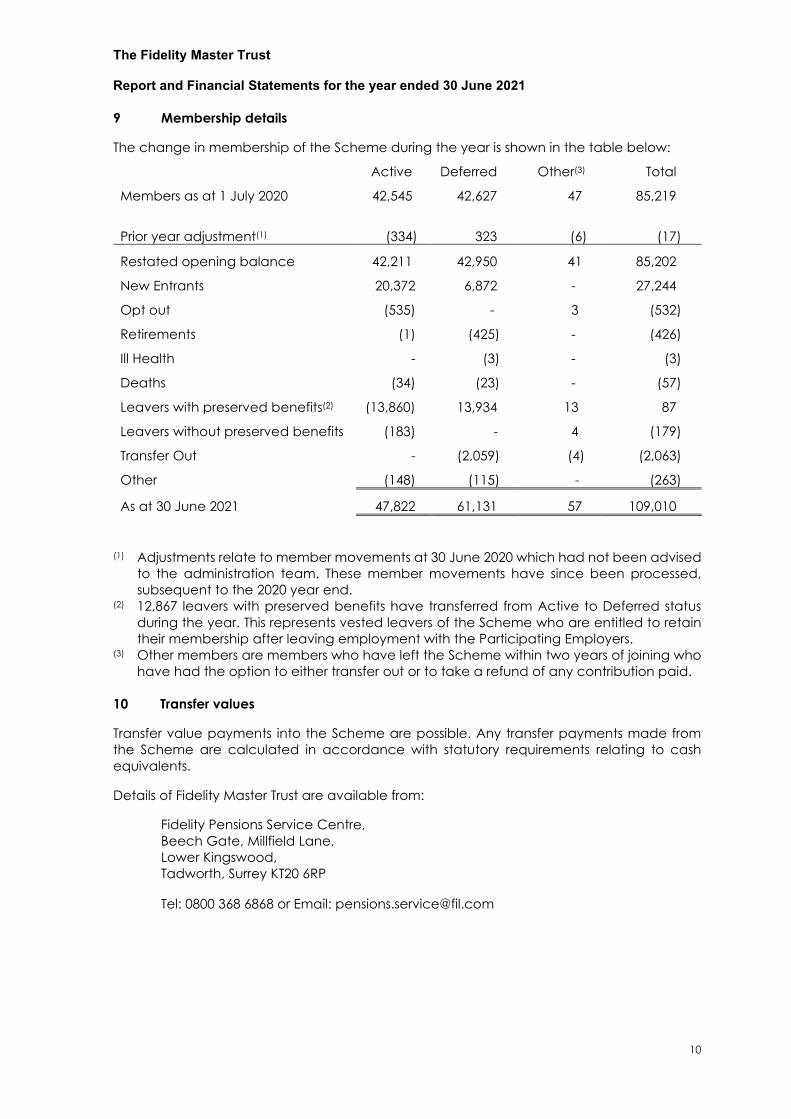

9 Membership details The change in membership of the Scheme during the year is shown in the table below:

Active Deferred Other(3) Total

Members as at 1 July 2020 42,545

42,627 47 85,219

Prior year adjustment(1) (334) 323 (6) (17)

Restated opening balance 42,211 42,950 41 85,202

New Entrants 20,372 6,872 - 27,244

Opt out (535) - 3 (532)

Retirements (1) (425) - (426)

Ill Health - (3) - (3)

Deaths (34) (23) - (57)

Leavers with preserved benefits(2) (13,860) 13,934 13 87

Leavers without preserved benefits (183) - 4 (179)

Transfer Out - (2,059) (4) (2,063)

Other (148) (115) - (263)

As at 30 June 2021 47,822 61,131 57 109,010

(1) Adjustments relate to member movements at 30 June 2020 which had not been advised

to the administration team. These member movements have since been processed, subsequent to the 2020 year end.

(2) 12,867 leavers with preserved benefits have transferred from Active to Deferred status during the year. This represents vested leavers of the Scheme who are entitled to retain their membership after leaving employment with the Participating Employers.

(3) Other members are members who have left the Scheme within two years of joining who have had the option to either transfer out or to take a refund of any contribution paid.

10 Transfer values Transfer value payments into the Scheme are possible. Any transfer payments made from the Scheme are calculated in accordance with statutory requirements relating to cash equivalents. Details of Fidelity Master Trust are available from:

Fidelity Pensions Service Centre, Beech Gate, Millfield Lane, Lower Kingswood, Tadworth, Surrey KT20 6RP Tel: 0800 368 6868 or Email: [email protected]

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

11

11 Disclosure of information This report has been prepared in accordance with the Occupational Pension Schemes (Disclosure of Information) Regulations 1996. 12 Statement of Investment Principles The Trustees have produced a Statement of Investment Principles detailing decisions about investments for the purposes of the Plan in accordance with section 35 of the Pensions Act 1995. A copy of the statement is included in Appendix 1. 13 Sustainable Investing and Investor Engagement The primary objective of the fund managers of the underlying investments is to produce financial returns for investors in line with their investment objective. The Trustees believe that investing sustainably can help reduce specific risks and therefore increase the potential to achieve better investment returns over the long-term. Consequently, the Trustees expect fund managers’ investment processes to take social, environmental and governance issues into account when, in its view, these may have a material impact on either investment risk or return. One of the most effective ways to bring about change is to encourage fund managers to engage actively with the companies they invest in. That is why the Trustees actively monitor the fund managers’ level of engagement, voting activities and the investment processes they apply. The goal of the Trustees is to see whether their engagement has resulted in a positive outcome for members.

The Trustees review voting and engagement activities on a quantitative and qualitative basis. The Trustees also meet directly with fund managers to understand how they have exercised their voting rights and what key issues the managers have engaged on. This is done on an annual basis. The Trustees will also strive to ensure all managers of funds available in the core range apply the UK Stewardship Code and are signed up to the UN Principles for Responsible Investment (UNPRI) which works to incorporate ESG factors into investment and ownership decisions. Fund managers are also assessed against the Trustee’s sustainability beliefs, and this information is available to the members of the Master Trust once a year via the Implementation Statement (Appendix 4).

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

12

14 Internal Dispute Resolution Procedure The Trustees have put in place a two stage dispute procedure to resolve any disputes raised by beneficiaries or potential beneficiaries of the Scheme. Details of the dispute procedure can be obtained by writing to:

The Fidelity Master Trust, Fidelity Pensions Service Centre, Beech Gate, Millfield Lane, Lower Kingswood, Tadworth, Surrey KT20 6RP

Alternatively, copies can be obtained by calling the Pensions Service Centre on 0800 368 6868 (calls are recorded) or by email to [email protected]. 15 The Pensions Ombudsman – Early Resolution Service The role of the Pension Ombudsman’s Early Resolution Service is to help members or their beneficiaries at any time with any questions they may have about the Plan or with any difficulty they failed to resolve with the Trustees or administrator.

The address to contact is:

The Office of the Pensions Ombudsman 10 South Colonnade Canary Wharf E14 4PU

Tel: 0800 917 4487 and select the option to discuss a potential complaint Email: [email protected] www.pensions-ombudsman.org.uk

16 Pensions Ombudsman The Pensions Ombudsman may be able to investigate any complaint or dispute that the early resolution service is unable to resolve for you. The address is:

The Office of the Pensions Ombudsman 10 South Colonnade Canary Wharf E14 4PU

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

13

17 The Pensions Regulator The Pensions Regulator can intervene if it considers that a scheme’s trustees, advisers or the employer are not carrying out their duties correctly. The address for the Regulator is:

The Pensions Regulator, Napier House, Trafalgar Place, Brighton, BN1 4DW. Tel 0845 600 0707 Email: [email protected]

18 The Department for Work and Pensions (DWP) Pension Tracing Service The Pensions Tracing Service is able to help members trace benefits which they may have from previous employers. The contact details are:

Tel: 0800 731 0193 Website: www.gov.uk/find-lost-pension

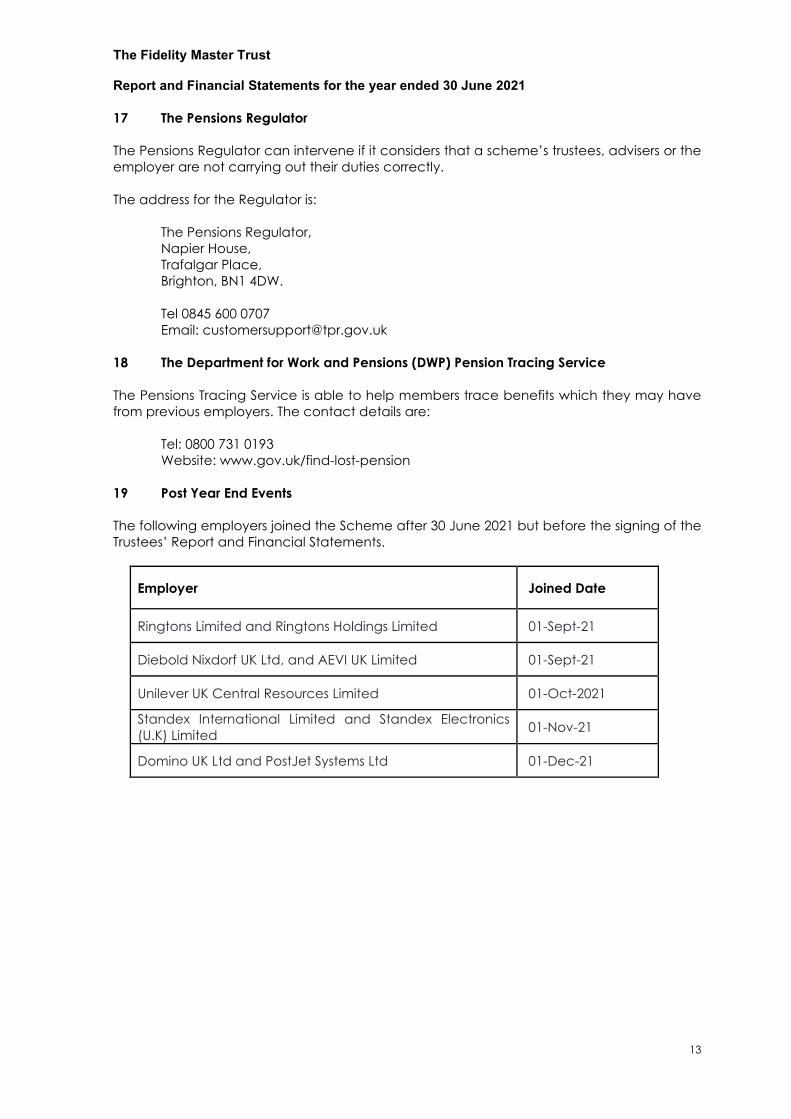

19 Post Year End Events The following employers joined the Scheme after 30 June 2021 but before the signing of the Trustees’ Report and Financial Statements.

Employer Joined Date

Ringtons Limited and Ringtons Holdings Limited 01-Sept-21

Diebold Nixdorf UK Ltd, and AEVI UK Limited 01-Sept-21

Unilever UK Central Resources Limited 01-Oct-2021

Standex International Limited and Standex Electronics (U.K) Limited 01-Nov-21

Domino UK Ltd and PostJet Systems Ltd 01-Dec-21

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

14

20 COVID-19 Pandemic The Trustees have assessed, and continue to monitor, the consequences of the COVID-19 pandemic for the Scheme and have considered the following areas in particular:

• The administration of benefits by the Scheme’s Administrator, FIL Life Insurance Ltd, including their business continuity planning, operational resilience, cyber/IT security measures and the maintenance of their control environment;

• The financial position of the Participating Employers and the payment of contributions due;

• The effect on the Trustees‘ investment strategy, the value of the Scheme’s assets and the ability to provide sufficient cashflow to support benefit and other payments.

• The communication to members in relation to the impact of volatility in markets as a result of COVID-19 and the long-term nature of pension benefits, and other educational materials.

The Trustees are satisfied having assessed these areas that the risks posed to the operation and management of the Scheme and its investments as a result of the COVID-19 pandemic have been sufficiently understood and mitigated where appropriate. Signed on behalf of the Trustees: ____________________________

Dianne Day

Chair of the Board of Trustees

Date:

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

15

Investment Report The Trustees are required to develop and maintain a Statement of Investment Principles (‘SIP’), obtaining advice from a regulated investment adviser to ensure that the investments and default arrangements proposed are appropriate, consistent with the Pensions Regulator’s framework and likely to achieve optimum outcomes for members. The SIP has been prepared in accordance with Section 35 of the Pensions Act 1995 and outlines the Scheme’s investment objectives and strategy. The Trustees monitor compliance with the SIP. During the period under review all investments were in accordance with the SIP. The SIP is included as Appendix 1 and is also available on the following publicly accessible webpage: www.fidelitypensions.co.uk/costs-charges Investments under the sole governance of the Trustees The Fidelity Master Trust offers a standard fund range and a default strategy available to employers who do not wish to establish a bespoke default and fund range. Members who are automatically enrolled are invested in the default until such a time that they make an alternative investment choice. The risk profiles and investment objectives for both the default investment strategy and all other investment funds can be found on the fund factsheets. The investment objectives of the default fund can also be found in the Scheme literature. The Trustees receive advice from their investment adviser regarding the appropriateness of funds for the membership. The membership profile is considered when producing this advice. The appropriateness for active and deferred members is considered together with the risk and maturity profile. The investment advice received also ensures that a suitable range of investments is provided for those members who wish to make an active investment choice. This advice is reviewed at least every three years or in the event of a significant change to the member demographic profile or investment policy to ensure it remains appropriate.

Investments with shared governance by the Trustees and Employers

In addition to the standard fund range, the Scheme can accommodate bespoke investment strategies which can be created from the full range of funds available via Fidelity’s Workplace Investing Platform or blended funds which invest in a combination of funds. Some Participating Employers have introduced employer-designed fund ranges and default strategies for their section of membership but the Trustees are ultimately responsible for the investment selection. Where an employer-designed range is required, the Trustees take investment advice from an adviser jointly appointed by the Participating Employer and the Trustees to ensure that the proposals are suitable and in accordance with the Scheme’s SIP. Fidelity will also carry out due diligence to ensure that the proposals are deliverable. Assuming both the Trustees and Fidelity are comfortable, the employer-designed fund range can be adopted on a shared governance basis. The investment advice is reviewed at least every three years or in the event of a significant change to ensure it remains appropriate. Fidelity reports quarterly to the Master Trust Board on investment performance. The Trustees can access details of all funds and holdings online at any time. Participating Employers can access details for their section of the Scheme. If necessary (in conjunction with their investment advisers) the Trustees can remove any investment options that are no longer deemed suitable for Scheme investment, for example where a fund is underperforming or is no longer appropriate for the Scheme’s objectives.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

16

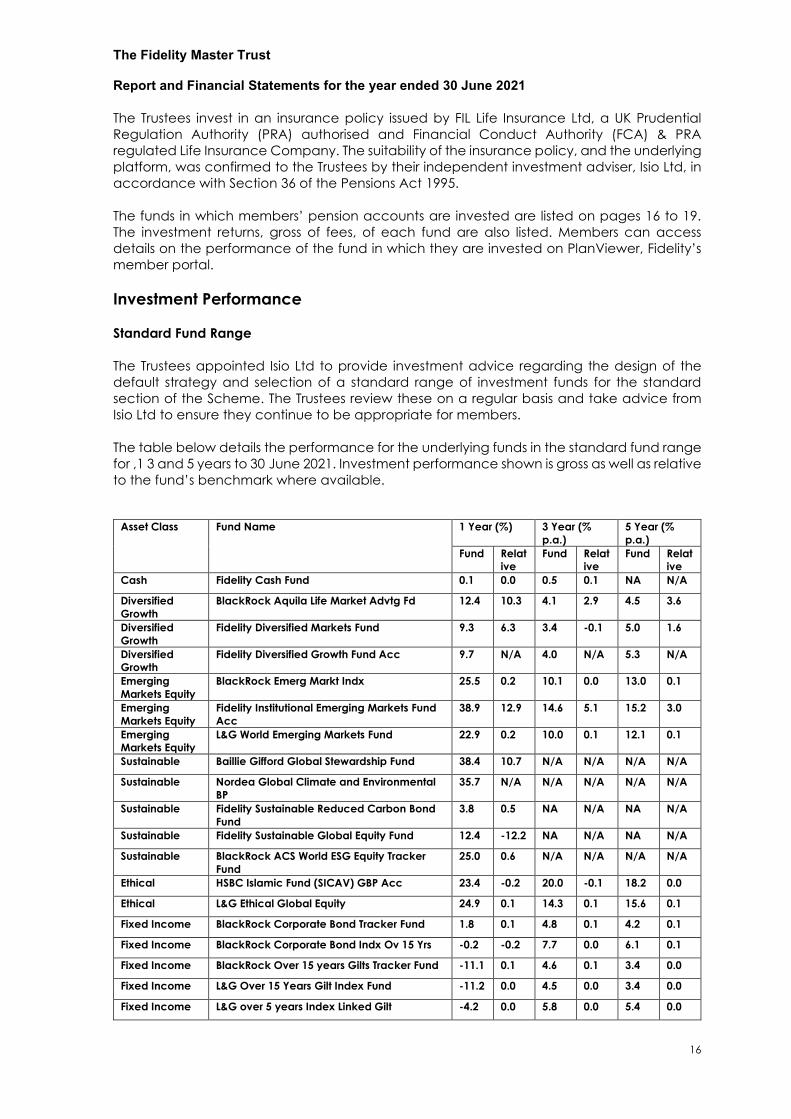

The Trustees invest in an insurance policy issued by FIL Life Insurance Ltd, a UK Prudential Regulation Authority (PRA) authorised and Financial Conduct Authority (FCA) & PRA regulated Life Insurance Company. The suitability of the insurance policy, and the underlying platform, was confirmed to the Trustees by their independent investment adviser, Isio Ltd, in accordance with Section 36 of the Pensions Act 1995. The funds in which members’ pension accounts are invested are listed on pages 16 to 19. The investment returns, gross of fees, of each fund are also listed. Members can access details on the performance of the fund in which they are invested on PlanViewer, Fidelity’s member portal. Investment Performance Standard Fund Range The Trustees appointed Isio Ltd to provide investment advice regarding the design of the default strategy and selection of a standard range of investment funds for the standard section of the Scheme. The Trustees review these on a regular basis and take advice from Isio Ltd to ensure they continue to be appropriate for members. The table below details the performance for the underlying funds in the standard fund range for ,1 3 and 5 years to 30 June 2021. Investment performance shown is gross as well as relative to the fund’s benchmark where available.

Asset Class Fund Name 1 Year (%) 3 Year (% p.a.)

5 Year (% p.a.)

Fund Relative

Fund Relative

Fund Relative

Cash Fidelity Cash Fund 0.1 0.0 0.5 0.1 NA N/A

Diversified Growth

BlackRock Aquila Life Market Advtg Fd 12.4 10.3 4.1 2.9 4.5 3.6

Diversified Growth

Fidelity Diversified Markets Fund 9.3 6.3 3.4 -0.1 5.0 1.6

Diversified Growth

Fidelity Diversified Growth Fund Acc 9.7 N/A 4.0 N/A 5.3 N/A

Emerging Markets Equity

BlackRock Emerg Markt Indx 25.5 0.2 10.1 0.0 13.0 0.1

Emerging Markets Equity

Fidelity Institutional Emerging Markets Fund Acc

38.9 12.9 14.6 5.1 15.2 3.0

Emerging Markets Equity

L&G World Emerging Markets Fund 22.9 0.2 10.0 0.1 12.1 0.1

Sustainable Baillie Gifford Global Stewardship Fund 38.4 10.7 N/A N/A N/A N/A

Sustainable Nordea Global Climate and Environmental BP

35.7 N/A N/A N/A N/A N/A

Sustainable Fidelity Sustainable Reduced Carbon Bond Fund

3.8 0.5 NA N/A NA N/A

Sustainable Fidelity Sustainable Global Equity Fund 12.4 -12.2 NA N/A NA N/A

Sustainable BlackRock ACS World ESG Equity Tracker Fund

25.0 0.6 N/A N/A N/A N/A

Ethical HSBC Islamic Fund (SICAV) GBP Acc 23.4 -0.2 20.0 -0.1 18.2 0.0

Ethical L&G Ethical Global Equity 24.9 0.1 14.3 0.1 15.6 0.1

Fixed Income BlackRock Corporate Bond Tracker Fund 1.8 0.1 4.8 0.1 4.2 0.1

Fixed Income BlackRock Corporate Bond Indx Ov 15 Yrs -0.2 -0.2 7.7 0.0 6.1 0.1

Fixed Income BlackRock Over 15 years Gilts Tracker Fund -11.1 0.1 4.6 0.1 3.4 0.0

Fixed Income L&G Over 15 Years Gilt Index Fund -11.2 0.0 4.5 0.0 3.4 0.0

Fixed Income L&G over 5 years Index Linked Gilt -4.2 0.0 5.8 0.0 5.4 0.0

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

17

Asset Class Fund Name 1 Year (%) 3 Year (% p.a.)

5 Year (% p.a.)

Fund Relative

Fund Relative

Fund Relative

Fixed Income L&G Corporate Bond All Stocks Fund -0.6 -0.2 3.9 0.1 3.3 0.1

Fixed Income Fidelity Institutional Sterling Corporate Bond Fund Acc

3.6 1.8 6.0 1.2 5.3 1.3

Fixed Income Fidelity Pre-Retirement Bond Fund F Accumulation Shares

-2.0 1.3 5.6 1.3 4.8 1.3

Fixed Income Fidelity Institutional UK Aggregate Bond Fund Acc

-0.7 1.7 5.2 1.2 4.5 1.4

Global Equity BlackRock Aquila MSCI World Global Equity Index Fund

24.9 0.6 13.9 0.6 14.8 0.7

Global Equity BlackRock ACS 30:70 Global Equity Curr Hedged Fund

31.5 0.5 10.3 -0.1 12.1 -0.2

Global Equity L&G Global Equity Market Weights 30:70 Index Fund GBP Hedged

30.0 0.0 10.3 0.0 12.5 0.0

Global Equity (UK Biased)

BlackRock ACS 50:50 Global Equity Fund 22.2 -0.1 6.7 -0.1 9.9 -0.1

Global Equity (UK Biased)

L&G Global Equity 50/50 22.3 0.1 7.0 0.1 10.6 0.1

International Equity (ex UK)

BlackRock ACS World ex UK Fund 25.5 0.1 14.1 0.2 15.0 0.3

International Equity (ex UK)

L&G World ex-UK Developed World Equity Index Fund

25.5 0.0 14.2 0.0 15.6 0.0

Multi Asset Schroder Dynamic Multi Asset Fund 16.4 13.9 5.6 3.9 5.5 3.5

Property L&G 70:30 Hybrid Property Fund 079 11.4 -0.6 3.9 -0.2 5.5 0.1

UK Equity BlackRock ACS UK Equity Fund 20.9 -0.1 1.9 0.0 6.4 0.0

UK Equity L&G UK Equity Index Fund 21.2 0.1 2.0 0.1 7.1 0.1

Note: N/A denotes that performance for the fund/benchmark is not available Past performance is not a reliable indicator of future results. The value of investments and the level of income from them may go down as well as up and a member may not get back the amount invested. Source: Fidelity Employer-Designed Fund Range The Scheme provides Participating Employers with the flexibility to create their own investment strategy from the Workplace Investing platform to suit their requirements. Blended funds which combine funds from different managers can also be accommodated. These “tailored” funds can be modified, with underlying funds being added or removed over time. Employer-designed funds and default arrangements operate on a shared governance basis as described above. The table below shows the investment performance (gross of fees) for the additional underlying funds used by bespoke sections available for 1, 3 and 5 years (where available) to 30 June 2021 and performance relative to the funds’ benchmark.

Asset Class Fund Name 1 Year (%) 3 Year (% p.a.) 5 Year (% p.a.)

Fund Relative

Fund Relative

Fund Relative

Alternatives TM Fulcrum Diversified Liquid Alternatives Fund

15.6 N/A N/A N/A N/A N/A

Cash BlackRock Cash Fund 0.1 0.2 0.5 0.2 0.4 0.2

Cash L&G Cash Fund 0.0 0.1 0.4 0.1 0.4 0.1

Diversified Growth

Baillie Gifford Diversified Growth Fund 14.7 11.1 5.1 1.2 5.9 3.3

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

18

Asset Class Fund Name 1 Year (%) 3 Year (% p.a.) 5 Year (% p.a.)

Fund Relative

Fund Relative

Fund Relative

Diversified Growth

L&G Diversified Fund 13.7 -4.5 7.4 -2.3 8.2 -4.2

Diversified Growth

BNY Mellon Real Return Fund (Exempt Class 2)

13.6 9.5 8.4 4.0 4.8 0.4

Diversified Growth

SSGA As of Priced Dynamic Diversified sub-Fund

18.0 17.9 5.9 5.5 6.4 6.0

Diversified Growth

Nordea 1 - GBP Diversified Return Fund 10.9 6.9 6.4 1.9 N/A N/A

Diversified Growth

Invesco Global Targeted Returns (UK) Fund

-0.7 -0.7 -0.1 -0.7 N/A N/A

Diversified Growth

BlackRock Dynamic Allocation Fund 10.6 10.5 6.1 5.7 N/A N/A

Diversified Growth

Schroder Diversified Growth Series 2 18.4 11.2 7.0 0.3 6.8 -0.3

Emerging Markets Equity

JPM Life All-Emerging Market Equity Fund 31.6 5.6 17.7 8.1 18.2 5.9

Emerging Markets Equity

State Street Emerging Markets Equity Index Fund

23.1 0.1 9.8 0.1 N/A N/A

Sustainable BlackRock ACS World Multifactor ESG Equity Tracker Fund

25.9 0.4 N/A N/A N/A N/A

Sustainable Impax Environmental Leaders (Ireland) Sterling 'S'

32.6 8.0 N/A N/A N/A N/A

Sustainable Schroder Sustainable Global Multi Factor Equity

26.8 2.2 N/A N/A N/A N/A

Ethical BMO Responsible UK Equity B Acc 26.1 4.6 6.3 4.2 10.8 4.4

Ethical L&G UK Ethical Equity Index 19.3 0.0 2.2 0.0 7.1 0.1

European Equity

BlackRock ACS Continental European Equity Fund

22.0 -0.4 9.9 -0.2 11.7 -0.1

Fixed Income BlackRock Index Linked Gilt Tracker Fund -4.4 0.0 5.5 0.0 5.3 0.0

Fixed Income Fidelity Global High Yield W-Accumulation

14.8 1.7 5.6 -0.1 6.5 1.1

Fixed Income Fidelity Institutional Long Dated Sterling Corporate Bond Fund Acc

2.4 1.5 7.7 0.7 6.5 0.9

Fixed Income L&G Overseas Bond Index Fund 085 -11.8

0.0 1.8 0.0 0.9 0.0

Fixed Income L&G Pre-Retirement Fund -2.5 -0.2 5.4 0.0 4.3 0.0

Fixed Income L&G Emerging Markets Passive Local Currency Bond

-6.0 -0.4 2.1 -0.3 N/A N/A

Fixed Income Fidelity Institutional Index Linked Bond Fund Acc

-4.3 0.2 5.4 0.2 5.1 0.1

Fixed Income BNY Mellon Global Dynamic Bond Fund 3.4 1.4 3.4 1.0 2.7 0.3

Fixed Income SSGA As of Priced UK Index Linked Gilts All Stocks Index sub-Fund

-4.0 -0.1 4.6 -0.2 4.5 -0.1

Fixed Income SSGA As of Priced Sterling Non-Gilts Bond All Stocks Index sub-Fund

1.5 -0.2 5.0 0.3 4.2 0.2

Fixed Income L&G Inflation Sensitive Pre-Retirement Fund

-1.3 -0.2 5.2 0.1 4.6 0.1

Fixed Income M&G Total Return Credit Fund 9.2 9.2 5.2 4.8 5.0 4.6

Fixed Income State Street As of Price (Net) UK conventional Gilts All Stock Index Sub-Fund

-6.1 0.1 N/A N/A N/A N/A

Global Equity Global Developed Small Cap Index Fund 36.6 0.0 N/A N/A N/A N/A

Global Equity L&G All World Equity Index Fund GBP Hgd 35.9 -0.1 N/A N/A N/A N/A

Global Equity AQR Sustainable Style Premia Global Equity UCITS Fund

20.4 -4.0 N/A N/A N/A N/A

Global Equity Unconstrained

BNY Mellon Global Equity Fund 22.6 -1.9 14.4 1.5 13.5 -0.3

Global Equity Unconstrained

Schroder QEP Global Active Value Fund 29.8 5.2 9.0 -3.9 10.9 -2.9

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

19

Asset Class Fund Name 1 Year (%) 3 Year (% p.a.) 5 Year (% p.a.)

Fund Relative

Fund Relative

Fund Relative

International Equity (ex UK)

BlackRock Overseas Cons Indx 24.2 0.1 12.9 0.5 14.1 0.4

International Equity (ex UK)

BlackRock Aquila Currency Hedged World ex UK Equity

36.7 -0.1 14.2 -0.3 14.4 -0.2

International Equity (ex UK)

State Street As of Price (Net) International Equity Index Sub-fund

25.5 0.2 N/A N/A N/A N/A

Japanese Equity

BlackRock ACS Japanese Equity Fund 11.2 0.4 5.6 0.3 10.1 0.3

Multi Asset Baillie Gifford Multi Asset Growth 15.2 11.6 5.5 1.5 N/A N/A

Multi Asset Fidelity Multi Asset Allocator Strategic Fund W-Accumulation

9.7 N/A 7.1 N/A 5.8 N/A

Multi Asset Fidelity Multi Asset Allocator Defensive Fund W-Accumulation

4.8 N/A 5.6 N/A 3.8 N/A

Multi Asset Fidelity Multi Asset Allocator Growth Fund W-Accumulation

14.8 N/A 8.8 N/A 7.5 N/A

Multi Asset Fidelity Multi Asset Balanced Income Fund W Accumulation Shares

10.4 N/A N/A N/A N/A N/A

Multi Asset L&G Retirement Income Multi Asset Fund 10.4 6.8 N/A N/A N/A N/A

Pacific Equity BlackRock Pacific Rim Equity Index Fund 29.1 0.3 9.3 0.3 12.0 0.0

Property L&G Managed Property Fund 7.7 -0.8 2.9 -0.1 5.2 0.8

Property Threadneedle Pensions Property Fund 9.1 0.6 3.6 0.7 5.2 0.3

TDF Timewise Target Retirement 2020 Sub-Fund

9.1 3.4 6.2 0.8 6.8 0.6

TDF Timewise Target Retirement 2025 Sub-Fund

15.0 4.1 7.0 0.5 8.1 0.3

TDF Timewise Target Retirement 2030 Sub-Fund

21.5 6.0 8.3 0.8 9.5 0.6

TDF Timewise Target Retirement 2035 Sub-Fund

25.1 4.6 9.5 0.4 10.7 0.5

TDF Timewise Target Retirement 2040 Sub-Fund

27.1 3.7 10.7 0.8 11.5 0.7

TDF Timewise Target Retirement 2045 Sub-Fund

27.3 3.7 10.9 0.8 11.6 0.8

TDF Timewise Target Retirement 2050 Sub-Fund

27.3 3.7 10.9 0.8 11.6 0.8

TDF Timewise Target Retirement 2055 Sub-Fund

27.2 3.7 10.9 0.9 11.6 0.8

TDF State Street Timewise Target Retirement 2065 Sub-Fund

27.4 3.9 10.9 0.9 N/A N/A

TDF Timewise Target Retirement Choice Sub-Fund

8.1 3.7 6.1 1.0 6.0 0.7

TDF Timewise Target Retirement 2060 Sub-Fund

27.2 3.7 11.0 1.0 11.7 0.8

Traditional Balanced

BlackRock Consensus 85 Fund 13.8 0.1 7.0 0.3 8.4 0.3

Traditional Balanced

Standard Life Managed Fund FA 14.2 -0.8 6.1 0.5 8.4 1.0

UK Equity Baillie Gifford UK Equity Focus Fund 27.1 4.0 9.0 6.0 13.5 6.4

UK Equity LF Majedie UK Equity Fund X Share Class 26.2 4.8 1.7 -0.3 6.8 0.4

UK Equity MPF As Of Priced (Net) UK Equity Index Sub-Fund

20.3 0.7 N/A N/A N/A N/A

US Equity BlackRock ACS US Equity Fund 27.7 0.2 17.1 0.3 17.0 0.1

Note: N/A denotes that performance for the fund/benchmark is not available Past performance is not a reliable indicator of future results. The value of investments and the level of income from them may go down as well as up and a member may not get back the amount invested. Source: Fidelity

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

20

12 Month Investment Market Review to 30 June 2021 Global equity markets added value over the quarter to 30 September 2020, despite some regional divergence. Overseas markets, in particular the US, were supported by increased optimism surrounding an economic recovery as well as continued signs of long term loose monetary policy. However, UK equities underperformed the wider market, with key headwinds being sector composition (such as high relative exposure to oil and gas) and continued uncertainty surrounding the potential for a UK/EU trade deal. Q4 2020 saw the announcements of a COVID-19 vaccine having a positive impact as markets rallied, boosting the global economic outlook. Markets were further aided by additional support measures announced by governments and central banks. UK equities performed well over the quarter due to their higher weighting towards more economically sensitive sectors which rebounded on the news of effective vaccines for COVID-19. Gilt yields decreased modestly over the quarter as the Bank of England announced an increase to its asset purchase program to support the economy as another national lockdown was announced in the UK. Global markets performed positively during Q1 2021 following further US fiscal stimulus and the successful rollout of the COVID-19 vaccination programmes in the UK and US. This positive sentiment led to sharp rises in gilt yields, as investors rotated portfolios into higher risk asset classes. While global equities performed positively over Q1, Emerging Markets delivered relatively weak returns as their vaccination programme lagged developed markets. UK equities performed well over the quarter as the reduction in people being hospitalised with COVID-19 increased investor optimism for a sustainable reopening of the economy. As gilt yields increased markedly over the quarter, government bonds delivered negative returns. Investor optimism strengthened during the quarter to 30 June 2021 as vaccinations continued to be successfully rolled out and businesses re-opened, leading to positive global equity returns. The continued monetary stimulus measures from central banks further enhanced these returns. Credit markets delivered positive performance as they benefited from narrowing credit spreads and strong fundamentals, including low expected default rates and supportive monetary policy. Gilt yields declined over the quarter following a significant rally in Q1, as investors weighed the impact of the COVID-19 delta variant on the promise of an economic reopening. Additionally, consideration was given to what extent the recent inflationary pressures would be transitory in nature. Signed on behalf of the Trustees: ____________________________

Dianne Day

Chair of the Board of Trustees

Date:

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

21

INDEPENDENT AUDITOR’S REPORT TO THE TRUSTEES OF THE FIDELITY MASTER TRUST Opinion We have audited the financial statements of the Fidelity Master Trust for the year ended 30 June 2021 which comprise the Fund Account, the Net Assets Statement and the notes to the financial statements, including significant accounting policies. The financial reporting framework that has been applied in their preparation is applicable law and United Kingdom Accounting Standards, including FRS 102 “The Financial Reporting Standard applicable in the UK and Republic of Ireland” (United Kingdom Generally Accepted Accounting Practice). In our opinion the financial statements:

• show a true and fair view of the financial transactions of the scheme during the year ended 30 June 2021, and of the amount and disposition at that date of its assets and liabilities, other than the liabilities to pay pensions and benefits after the end of the year;

• have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice; and

• contain the information specified in Regulation 3A of the Occupational Pension Schemes (Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations 1996, made under the Pensions Act 1995.

Basis for opinion We conducted our audit in accordance with International Standards on Auditing (UK) (ISAs (UK)) and applicable law. Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the financial statements section of our report. We are independent of the scheme in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, including the FRC’s Ethical Standard and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Conclusions relating to going concern In auditing the financial statements, we have concluded that the trustees’ use of the going concern basis of accounting in the preparation of the financial statements is appropriate. Based on the work we have performed, we have not identified any material uncertainties relating to events or conditions that, individually or collectively, may cast significant doubt on the scheme’s ability to continue as a going concern for a period of at least twelve months from when the financial statements are authorised for issue. Our responsibilities and the responsibilities of the trustees with respect to going concern are described in the relevant sections of this report.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

22

Other information The other information comprises the information included in the Trustees’ Report and Financial Statements, other than the financial statements and our auditor’s report thereon. The trustees are responsible for the other information contained within the Trustees’ Report and Financial Statements. Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon. Our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the course of the audit, or otherwise appears to be materially misstated. If we identify such material inconsistencies or apparent material misstatements, we are required to determine whether this gives rise to a material misstatement in the financial statements themselves. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard. Responsibilities of trustees As explained more fully in the Statement of Trustees’ Responsibilities set out on page 3, the trustees are responsible for the preparation of financial statements and for being satisfied that they give a true and fair view, and for such internal control as the trustees determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. In preparing the financial statements, the trustees are responsible for assessing the scheme’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the trustees either intend to wind up the scheme or have no realistic alternative but to do so. Auditor’s responsibilities for the audit of the financial statements Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

23

Irregularities, including fraud, are instances of non-compliance with laws and regulations. We design procedures in line with our responsibilities, outlined above, to detect material misstatements in respect of irregularities, including fraud. The extent to which our procedures are capable of detecting irregularities, including fraud, is detailed below: Based on our understanding of the scheme and industry, we identified that the principal risks of non-compliance with laws and regulations related to breaches of UK pensions legislation such as the Pensions Acts 1995, 2004, 2008 and 2014 and we considered the extent to which non-compliance might have a material effect on the financial statements. We also considered those laws and regulations that have a direct impact on the financial statements such as the Occupational Pension Schemes (Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations 1996, made under the Pensions Act 1995. We evaluated trustees’ opportunities for fraudulent manipulation of the financial statements (including the risk of override of controls) and determined that the principal risks were related to misappropriation of assets, particularly cash and investments and posting inappropriate journal entries. Audit procedures performed included:

• enquiry of the trustees to identify the existence of any correspondence with the Pensions Regulator or any instances of non-compliance with applicable laws and regulations

• review of minutes of trustee meetings • obtaining independent confirmation of, and testing of a risk-based sample of

investment balances at the year end • testing of a risk-based sample of journal entries to supporting documentation • designing audit procedures to incorporate unpredictability around the nature, timing

or extent of our testing A further description of our responsibilities is available on the Financial Reporting Council’s website at: www.frc.org.uk/auditorsresponsibilities. This description forms part of our auditor’s report. Use of our report This report is made solely to the scheme’s trustees, as a body, in accordance with Regulation 3 of the Occupational Pension Schemes (Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations 1996, made under the Pensions Act 1995. Our audit work has been undertaken so that we might state to the scheme’s trustees those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the scheme’s trustees as a body, for our audit work, for this report, or for the opinions we have formed. Nexia Smith & Williamson Statutory Auditor Chartered Accountants Bristol Date:

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

24

FUND ACCOUNT Notes Year to

30/06/2021 £’000s

Year to 30/06/2020

£’000s Contributions and Benefits Employer contributions 316,158 268,722 Employee contributions 12,036 8,058 Total contributions 4 328,194 276,780 Transfers in 5 732,980 298,351 Other income 6 1,639 3,941 1,062,813 579,072 Benefits paid or payable 7 (25,056) (20,382) Payments to and on account of leavers 8 (122,871) (65,643) (147,927) (86,025) Net additions from dealings with members 914,886 493,047 Return on investments Change in market value of investments 9 612,659 (13,759) Net returns on investments 612,659 (13,759) Net increase in the fund during the period 1,527,545 479,288 Net assets of the Scheme at beginning of period 2,944,157 2,464,869

Net assets at the end of period 4,471,702 2,944,157 The notes on pages 26 to 34 form part of these financial statements.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

25

STATEMENT OF NET ASSETS AVAILABLE FOR BENEFITS AS AT 30 JUNE 2021 Note 30/06/2021

£’000s 30/06/2020

£’000s Investment assets Pooled investment vehicles 4,388,025 2,908,604 AVC investments 65,078 21,694 Total investments 9 4,453,103 2,930,298 Current assets 12 18,838 17,021 Current liabilities 13 (239) (3,162) Net assets of the Scheme 4,471,702 2,944,157

The financial statements summarise the transactions and net assets of the Scheme. They do not take account of obligations to pay benefits which fall due after the end of the Scheme year. The notes on pages 26 to 34 form part of these financial statements. These financial statements were approved by the Trustees on _____________________

____________________________

Dianne Day

Chair of the Board of Trustees

Date:

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

26

NOTES TO THE FINANCIAL STATEMENTS 1 Basis of preparation

These Financial Statements have been prepared as at 30 June 2021 in accordance with the Occupational Pension Schemes (Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations 1996, Financial Reporting Standard 102 – The Financial Reporting Standard applicable in the UK and Republic of Ireland (FRS 102) issued by the Financial Reporting Council and the guidance set out in the Statement of Recommended Practice “Financial Reports of Pension Schemes” (Revised June 2018) (“the SORP”).

2 Identification of the financial statements The Scheme is a registered pension scheme under Chapter 2, Part 4 of the Finance Act 2004. This means that contributions by the Employers are normally eligible for tax relief, and income and capital gains earned by the Scheme are generally tax exempt. The address for enquiries to the Scheme is The Fidelity Master Trust, Fidelity Pensions Service Centre, Beech Gate, Millfield Lane, Lower Kingswood, Tadworth, Surrey, KT20 6RP.

3 Accounting policies

The principal accounting policies are set out below. 3.1 Functional currency The functional currency used in these financial statements is Sterling (GBP).

3.2 Valuation of investments The market value of pooled investment vehicles is taken as the net asset value price determined in accordance with fair value principles, as advised by the investment manager.

3.3 Contributions and benefits Contributions and benefits are accounted for in the period in which they fall due. When there is a choice of benefits, these are accounted for on the later of the date of retirement/death and the date at which the option is communicated to the Trustees.

3.4 Transfer Values

Individual transfers are accounted for when the transfer has been agreed by both parties and the receiving scheme has accepted liability for the transfer. Bulk transfers are accounted for on the accruals basis where the Trustees have agreed to accept the liability for members’ benefits.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

27

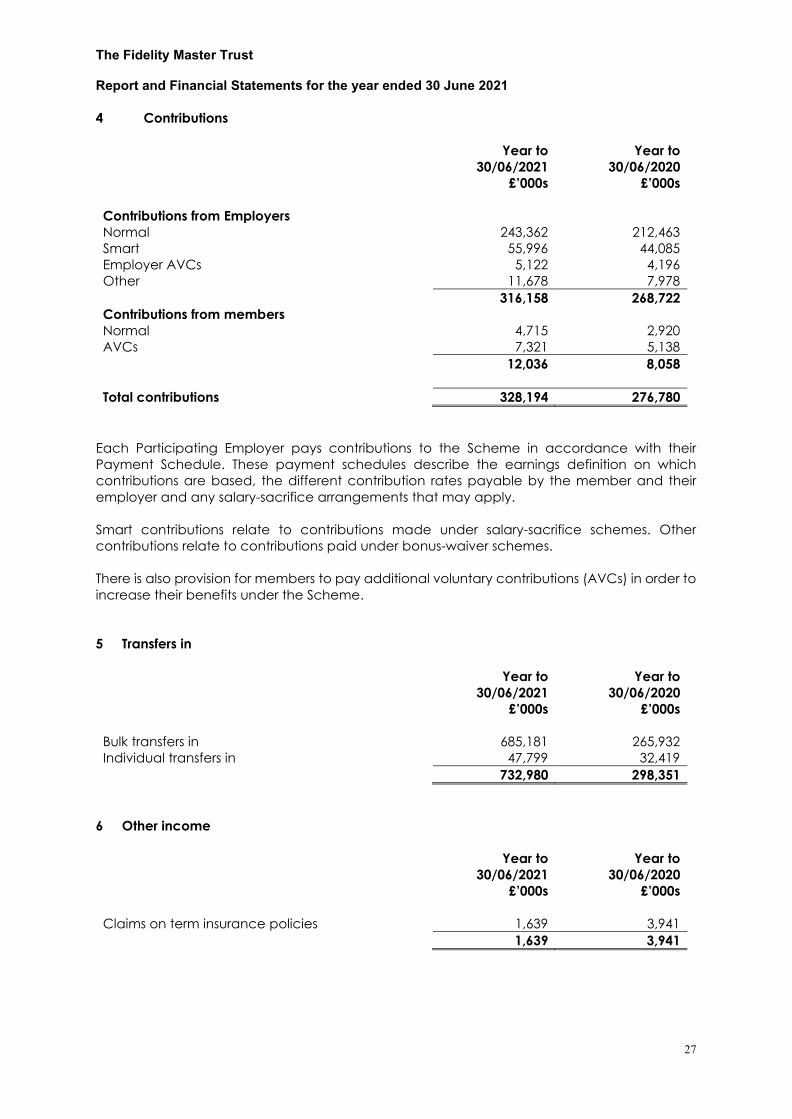

4 Contributions Year to

30/06/2021 £’000s

Year to 30/06/2020

£’000s Contributions from Employers Normal 243,362 212,463 Smart 55,996 44,085 Employer AVCs 5,122 4,196 Other 11,678 7,978 316,158 268,722 Contributions from members Normal 4,715 2,920 AVCs 7,321 5,138 12,036 8,058 Total contributions 328,194 276,780

Each Participating Employer pays contributions to the Scheme in accordance with their Payment Schedule. These payment schedules describe the earnings definition on which contributions are based, the different contribution rates payable by the member and their employer and any salary-sacrifice arrangements that may apply. Smart contributions relate to contributions made under salary-sacrifice schemes. Other contributions relate to contributions paid under bonus-waiver schemes. There is also provision for members to pay additional voluntary contributions (AVCs) in order to increase their benefits under the Scheme. 5 Transfers in Year to

30/06/2021 £’000s

Year to 30/06/2020

£’000s Bulk transfers in 685,181 265,932 Individual transfers in 47,799 32,419 732,980 298,351

6 Other income Year to

30/06/2021 £’000s

Year to 30/06/2020

£’000s Claims on term insurance policies 1,639 3,941 1,639 3,941

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

28

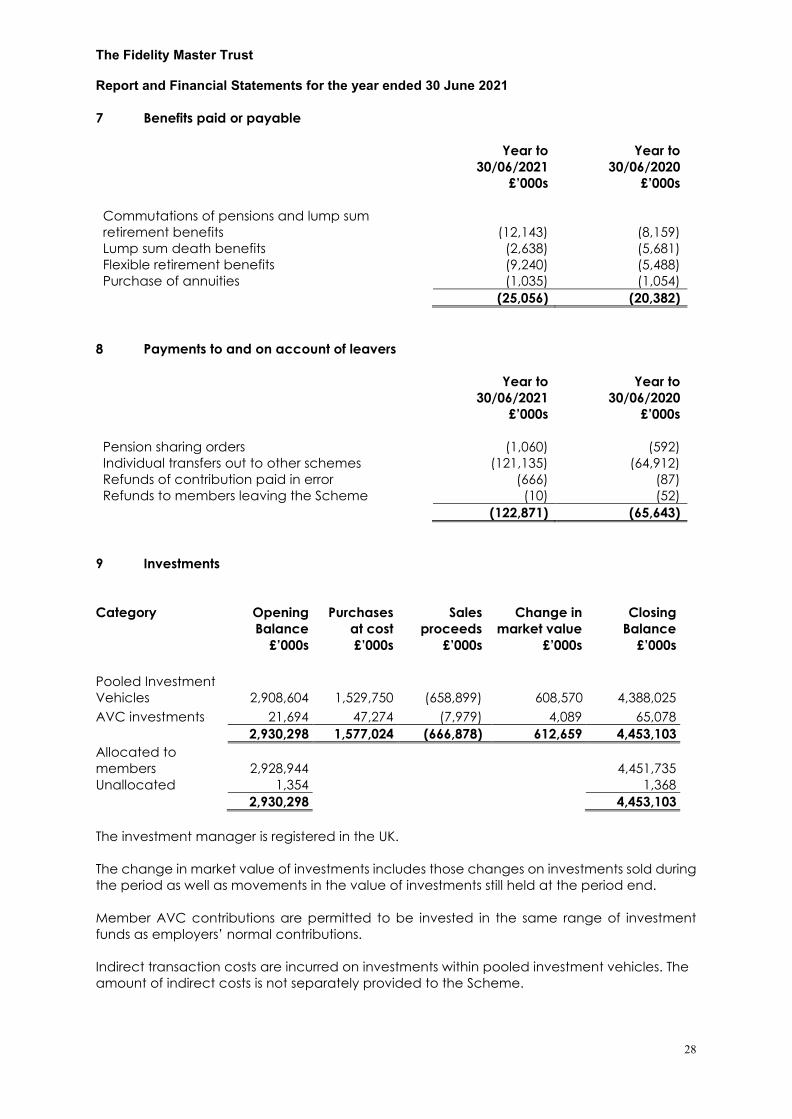

7 Benefits paid or payable

Year to 30/06/2021

£’000s

Year to 30/06/2020

£’000s Commutations of pensions and lump sum retirement benefits (12,143) (8,159) Lump sum death benefits (2,638) (5,681) Flexible retirement benefits (9,240) (5,488) Purchase of annuities (1,035) (1,054) (25,056) (20,382)

8 Payments to and on account of leavers Year to

30/06/2021 £’000s

Year to 30/06/2020

£’000s Pension sharing orders (1,060) (592) Individual transfers out to other schemes (121,135) (64,912) Refunds of contribution paid in error (666) (87) Refunds to members leaving the Scheme (10) (52) (122,871) (65,643)

9 Investments Category Opening

Balance Purchases

at cost Sales

proceeds Change in

market value Closing

Balance £’000s £’000s £’000s £’000s £’000s Pooled Investment Vehicles 2,908,604 1,529,750 (658,899) 608,570 4,388,025 AVC investments 21,694 47,274 (7,979) 4,089 65,078 2,930,298 1,577,024 (666,878) 612,659 4,453,103 Allocated to members 2,928,944

4,451,735

Unallocated 1,354 1,368 2,930,298 4,453,103

The investment manager is registered in the UK. The change in market value of investments includes those changes on investments sold during the period as well as movements in the value of investments still held at the period end. Member AVC contributions are permitted to be invested in the same range of investment funds as employers’ normal contributions. Indirect transaction costs are incurred on investments within pooled investment vehicles. The amount of indirect costs is not separately provided to the Scheme.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

29

9.1 Pooled investment vehicles (including AVC investments) 30/06/2021

£’000s 30/06/2020

£’000s Equity funds 2,449,173 1,675,117 Bond funds 258,061 178,819 Diversified growth funds 1,381,153 762,417 Multi asset funds 243,832 205,291 Property funds 6,505 6,516 Cash funds 114,379 102,138 4,453,103 2,930,298

10 Investment Fair Value Hierarchy The fair value of financial instruments has been determined using the following fair value hierarchy: Level 1 - The unadjusted quoted price in an active market for identical assets or liabilities that the entity can access at the measurement date.

Level 2 - Inputs other than quoted prices included within Level 1 that are observable (ie developed using market data) for the asset or liability, either directly or indirectly. Level 3 - Inputs are unobservable (i.e. for which market data is unavailable) for the asset or liability. The Fund’s investments have been analysed using the above hierarchy categories as follows: 30/06/2021 Level 1 Level 2 Level 3 Total £’000s £’000s £’000s £’000s Pooled investment vehicles - 4,388,025 - 4,388,025 AVC investments - 65,078 - 65,078 - 4,453,103 - 4,453,103

Analysis for the prior period end is as follows: 30/06/2020 Level 1 Level 2 Level 3 Total £’000s £’000s £’000s £’000s Pooled investment vehicles - 2,901,136 7,468 2,908,604 AVC investments - 21,694 - 21,694 - 2,922,830 7,468 2,930,298

In the prior year, all funds are categorised as Fair Value Hierarchy Level 2 funds, apart from the L&G and Threadneedle Property funds which, due to the impact of COVID-19, were changed from Level 2 to Level 3 due to a temporary suspension of the Property funds. Dealing in the Threadneedle Pensions Property fund recommenced from 17 September 2020 and dealing in the L&G 70:30 Hybrid Property Fund and L&G Managed Property Fund recommenced from 1 October 2020.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

30

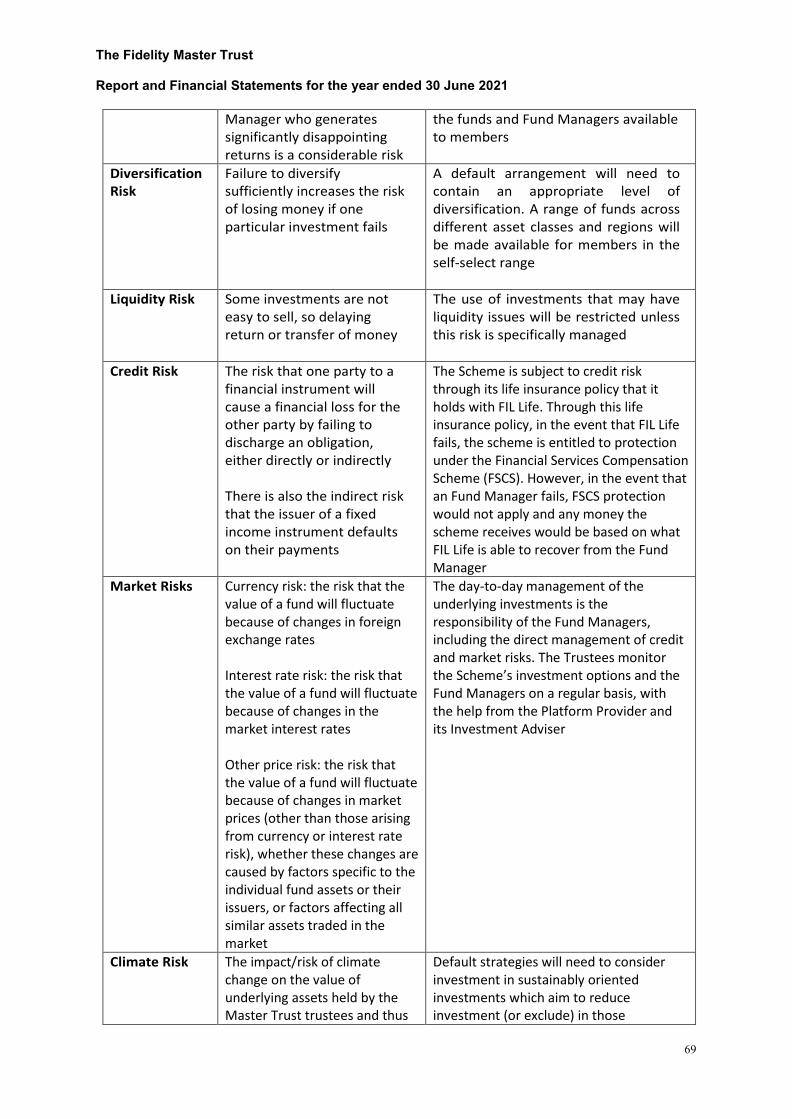

11 Investment Risks FRS 102 requires the disclosure of information in relation to certain investment risks. Credit risk is the risk that one party to a financial instrument will cause a financial loss for the other party by failing to discharge an obligation, either directly or indirectly. In response to the above the Scheme is subject to credit risk in relation to:

i. Fidelity through its holding in unit linked insurance funds provided to the Scheme by Fidelity.

ii. The Scheme is also subject to indirect credit and market risk arising from the underlying investments held in the underlying funds.

Market risk comprises currency risk, interest rate risk and other price risk, defined as follows:

• Currency risk is the risk that the fair value or future cash flows of a financial asset will fluctuate because of changes in foreign exchange rates.

• Interest rate risk is the risk that the fair value or future cash flows of a financial asset will

fluctuate because of changes in market interest rates.

• Other price risk is the risk that the fair value or future cash flows of a financial asset will fluctuate because of changes in market prices (other than those arising from interest rate risk or currency risk), whether those changes are caused by factors specific to the individual financial instrument or its issuer, or factors affecting all similar financial instruments traded in the market.

Market risks are inherent to certain asset classes and securities and as such, funds that invest in, or have economic exposure to, these asset classes and securities will be subject to these market risks. The Master Trust’s participating employers access their DC investments through the Master Trust’s life policy issued by Fidelity. Fidelity offers the Trustees a range of unit linked funds that in turn are invested with a range of underlying fund managers. The day to day management of the underlying investments within these funds is the responsibility of the respective managers, including the direct management of credit and market risks. Before offering a unit linked insurance fund via the FIL Life Platform, Fidelity carries out due diligence on the credit risk of funds as well as fund managers or insurance companies that manage the funds and that contract with FIL Life. Once a fund is brought onto the FIL Life platform this due diligence is carried out and refreshed on a regular basis. Credit risk arises through reinsurance agreements between FIL Life and third party insurance companies. If a third party insurance company were in a position where they were unable to honour a reinsurance agreement with FIL Life then there would be financial loss for FIL Life and the schemes that contract with FIL Life.

The Trustees determined the Scheme’s investment strategy after taking advice from its investment adviser. The Fund has exposure to the aforementioned risks via the investments held to implement the investment strategy.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

31

11 Investment Risks (continued) Within each investment portfolio, investment objectives and restrictions to manage risk are implemented through the legal agreements in place with the Scheme’s investment managers. The Trustees monitor the performance of the strategy and associated risks, and each investment manager against its objectives and restrictions, on a regular basis. Please note the default strategy used by the Scheme and the range of underlying funds and their collective blends are either part of the standard fund range or have been agreed by the Trustees of the Scheme on the advice of their investment advisers. The risk categorisation table on the next page for each of the funds is based purely on information supplied by Fidelity on behalf of the managers of the underlying funds. It should not be relied upon to make any decisions relating to the funds provided to the Scheme. Member level risk disclosure will depend on the funds invested in by members.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

32

11 Investment Risks (continued)

Risk Categorisation

Value

Direct and Indirect Credit

Risk Indirect Market Risk

30/06/2021

£000’s 30/06/2020

£000’s Credit Risk Currency Interest Rate Other Price

Risk Global equity index 1,217,112 796,041 × Diversified Markets Fund 780,109 485,430 Ethical global equity 775,261 624,536 × Diversified Growth Fund 558,896 246,756 Multi asset Fund 230,742 193,841 UK Aggregate Bond 160,615 101,612 × × Cash 114,676 102,351 × Global 30/70 95,195 14,750 × US Equity 68,879 47,452 × World emerging markets 68,137 41,895 × UK Equity 53,529 34,490 × × Pre retirement Bond 52,477 30,606 × World ex UK Developed equity 47,272 25,566 × Over 5 year Gilts 35,191 30,905 × × European equity 32,347 25,557 × Corporate Bonds 31,273 25,794 × Global 50/50 29,401 21,501 × Pacific Rim Equity 26,663 19,056 × Islamic Fund 16,469 9,063 × Standard Life Managed Fund 12,098 10,949 Japanese equity 11,064 8,915 × Over 15 years Gilts 7,990 9,536 × × Total return credit 5,044 4,649 × Dynamic Allocation Fund 4,707 3,663 Index linked bond Fund 4,150 1,524 × × Property Fund 4,005 12 × 70/30 property 3,044 2,750 × Overseas Equity 2,806 1,683 × Market Advantage Fund 2,182 1,910 Annuity Targeting Fund 932 978 × × Managed Property 482 4,706 × Fixed Interest Gilts 180 577 × × UK Corporate Bond 133 98 × × Global high yield Fund 42 23 × Low Volatility Fund - 837 × Consensus equity - 257 × Select Global equity - 29 × 4,453,103 2,930,298

= risk applies × = risk does not apply In the table above, similar funds are grouped together as they share the same risk profile.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

33

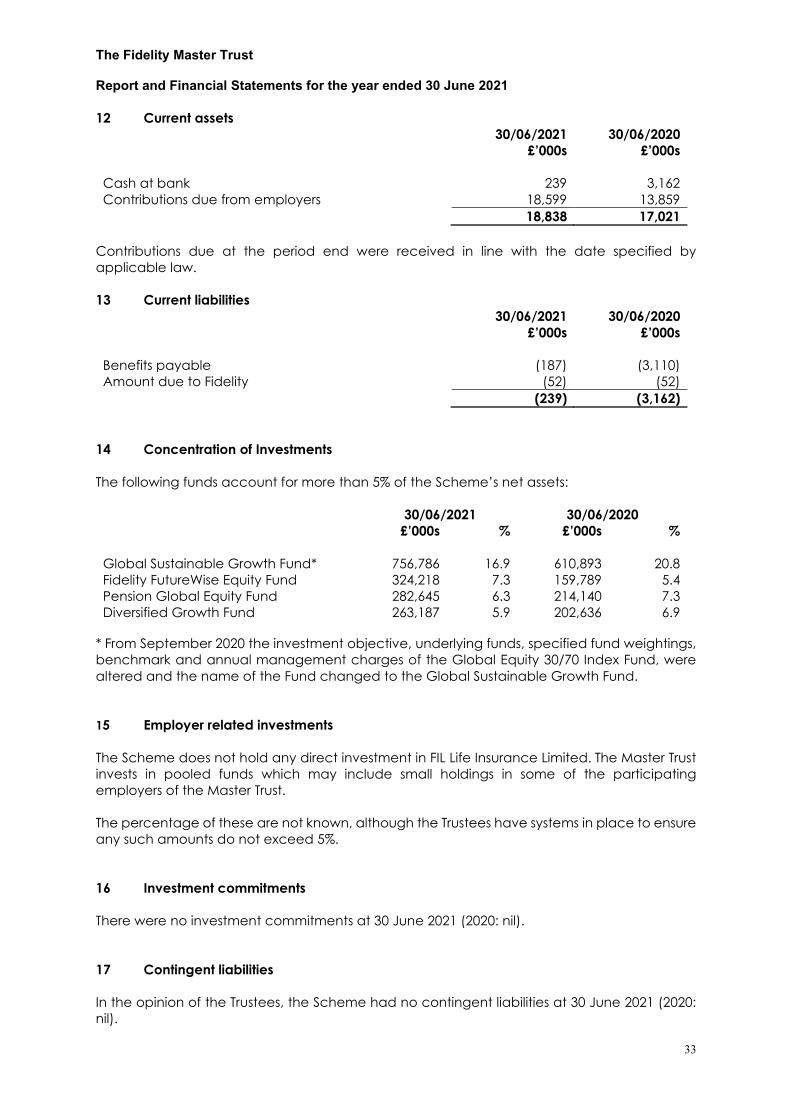

12 Current assets 30/06/2021

£’000s 30/06/2020

£’000s Cash at bank 239 3,162 Contributions due from employers 18,599 13,859 18,838 17,021

Contributions due at the period end were received in line with the date specified by applicable law. 13 Current liabilities 30/06/2021

£’000s 30/06/2020

£’000s Benefits payable (187) (3,110) Amount due to Fidelity (52) (52) (239) (3,162)

14 Concentration of Investments The following funds account for more than 5% of the Scheme’s net assets: 30/06/2021 30/06/2020 £’000s % £’000s % Global Sustainable Growth Fund* 756,786 16.9 610,893 20.8 Fidelity FutureWise Equity Fund 324,218 7.3 159,789 5.4 Pension Global Equity Fund 282,645 6.3 214,140 7.3 Diversified Growth Fund 263,187 5.9 202,636 6.9

* From September 2020 the investment objective, underlying funds, specified fund weightings, benchmark and annual management charges of the Global Equity 30/70 Index Fund, were altered and the name of the Fund changed to the Global Sustainable Growth Fund. 15 Employer related investments The Scheme does not hold any direct investment in FIL Life Insurance Limited. The Master Trust invests in pooled funds which may include small holdings in some of the participating employers of the Master Trust. The percentage of these are not known, although the Trustees have systems in place to ensure any such amounts do not exceed 5%. 16 Investment commitments There were no investment commitments at 30 June 2021 (2020: nil). 17 Contingent liabilities In the opinion of the Trustees, the Scheme had no contingent liabilities at 30 June 2021 (2020: nil).

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

34

18 Related parties The unit trusts, OEICs and SICAV’s in which the Scheme’s assets are invested incur management fees which are charged to each fund concerned and received by FIL Investment Services (UK) Limited (FISL) or FIL Fund Management (Bermuda) Limited in their capacity as managers of these funds. In addition, FISL and FIL Investment Management (Luxembourg) S.A. receive fees for administration services from each fund concerned. These fees are incurred but are not separately identifiable. All professional fees in respect of services provided to the Trustees together with the fees for the independent trustees (PTL Governance Limited, ITS Limited and Punter Southall Governance Services Limited) were paid by Fidelity. 19 Subsequent events There are no subsequent events requiring disclosure in the Financial Statements.

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

35

INDEPENDENT AUDITORS STATEMENT ABOUT CONTRIBUTIONS Independent Auditor’s Statement about Contributions to the Trustees of the Fidelity Master Trust. We have examined the summary of contributions payable to the Fidelity Master Trust (“the Scheme”) for the year ended 30 June 2021 which is set out on page 36. In our opinion contributions for the Scheme year ended 30 June 2021 as reported in the summary of contributions and payable under the payment schedules have in all material respects been paid at least in accordance with the payment schedules. Scope of work on Statement about Contributions Our examination involves obtaining evidence sufficient to give reasonable assurance that contributions reported in the attached summary of contributions have in all material respects been paid at least in accordance with the payment schedules. This includes an examination, on a test basis, of evidence relevant to the amounts of contributions payable to the scheme and the timing of those payments under the payment schedules. Respective responsibilities of Trustees and the Auditor As explained more fully in the Statement of Trustees’ Responsibilities, the Trustees are responsible for securing that payment schedules are prepared, maintained and, from time-to-time, revised and for monitoring whether contributions are made to the scheme by the employers in accordance with the payment schedules. It is our responsibility to provide a Statement about Contributions payable under the payment schedules and to report our opinion to you. Use of our report This statement is made solely to the Trustees, as a body, in accordance with our engagement letter dated 11 June 2019. Our work has been undertaken so that we might state to the Trustees those matters we are required to state to them in an auditor’s statement and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Trustees, as a body, for our work, for this statement or for the opinions we have formed. Nexia Smith & Williamson Chartered Accountants Statutory Auditor Bristol Date:

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

36

SUMMARY OF CONTRIBUTIONS PAYABLE IN THE PERIOD During the year from 1 July 2020 to 30 June 2021, the contributions payable to the Scheme by the employers were as follows:

Employee Employers £’000s £’000s Required by the payment schedules Normal and Smart contributions 4,715 299,358 Total (as reported on by the independent auditor) 4,715 299,358 Other contributions payable AVCs 7,321 5,122 Other employer additional – Bonus Waiver - 11,678 Total (as per Fund Account) 12,036 316,158

Signed on behalf of the Trustees: ____________________________

Dianne Day

Chair of the Board of Trustees

Date:

The Fidelity Master Trust Report and Financial Statements for the year ended 30 June 2021

37