TEMITOPE PROJECT

169

THE EFFECT OF INTERNAL CONTROL ON ORGANIZATIONAL PERFORMANCE (A CASE STUDY OF ECOBANK NIGERIA PLC) BY AMOO TEMITOPE GRACE ACT/2009/0036 ADEYIGA ADEBAYO ECN/2009/0005 BEING A RESEARCH PROJECT CARRIED OUT AND SUBMITTED TO THE DEPARTMENT OF ACCOUNTING, FACULTY OF MANAGEMENT SCIENCES OSUN STATE UNIVERSITY, OSOGBO NIGERIA IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OF BACHELOR OF SCIENCES (B.Sc) DEGREE IN ACCOUNTING 1

-

Upload

osunstateuniversity -

Category

Documents

-

view

0 -

download

0

Transcript of TEMITOPE PROJECT

THE EFFECT OF INTERNAL CONTROL ON ORGANIZATIONAL PERFORMANCE

(A CASE STUDY OF ECOBANK NIGERIA PLC)

BY

AMOO TEMITOPE GRACE

ACT/2009/0036

ADEYIGA ADEBAYO

ECN/2009/0005

BEING A RESEARCH PROJECT CARRIED OUT AND SUBMITTED TO

THE DEPARTMENT OF ACCOUNTING,

FACULTY OF MANAGEMENT SCIENCES

OSUN STATE UNIVERSITY, OSOGBO

NIGERIA

IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OFBACHELOR OF SCIENCES (B.Sc) DEGREE IN ACCOUNTING

1

JULY 2013

CERTIFICATION

It is certified that this research project, written by Amoo

Temitope Grace with matriculation number ACT/2009/0036 was

supervised by me and submitted to the Department of Accounting,

Faculty of management sciences. Osun State University Osogbo,

Okuku Campus.

Mr J.O Oyewole Date

Project supervisor

2

PROF. Temi Ologunorisa Date

Head of Department

DEDICATION

This research work is specially dedicated to Almighty God in

Heaven, the one who loves me dearly, unconditionally and

eternally, the source and the strength with which I have been

able to pull through the challenges that came with this work, for

his protection and guidance over my life right from the inception

and towards successful completion of this academic programme.

Also, to my beloved parents; Mr and Mrs AMOO for their supports

both financially and morally to accomplish the great task of

passing through this practical project. My prayer to you is that

you will eat the fruits of your labor in Jesus name (Amen).

3

ACKNOWLEDGEMENT

Nothing can man receive except it is given from above. I thank

God for sparing my life till today and being my help in the times

of need, and for giving me the strength and courage to complete

this programme. May his holy name be praised.

I also thank God for his faithfulness and love towards me,

for his mercy endures forever. Through him I went, I saw and I

conquered.

4

My heartfelt gratitude goes to my supervisor Mr J.O Oyewole for

his support during the course of this project work may the

Almighty God bless him in Jesus name (Amen).I cannot thank you

enough for the personal advice that you gave me concerning my

career. May the Lord Almighty grant you all your heart desires in

Jesus name (Amen).

My profound gratitude also goes to my parents; Mr & Mrs Amoo for

their financial and moral support towards my education and

achievement. They have been there for me. May you live long and

enjoy the fruit of their labor in Jesus name (Amen).

I want to say a big thank you to my Head of Department Prof.

Temi Ologunorisa who gave all the necessary advice, co-operation,

assistance and correction through this research work, I will

forever be grateful. Special thanks to all the lecturers within

the department such as Mr Lere Adebayo, Mr Feyi Oluwaremi, Mr

Lanre Fatoki, Mr Adedire Odelabu, Mr Babatunde lawal, Mr Sunday

Sasona and Mr Gbadebo.

My profound gratitude goes to my siblings, Amoo Juwon, Tobi,

Adura, Gbenga, Esther, Abayomi, Segun for their support and

prayer towards the completion of this research work. May the Lord

Almighty bless them all.

I cannot but appreciate my special boy friend Adebayo Yinka

Adeyiga for his love, support and encouragement towards the

completion of this project. May the Almighty God greatly reward

him.

5

I am grateful to the management of Ecobank for their great

assistance and cooperation in making this research work possible

and also I wish to acknowledge the various authors whose

literature I have used.

Finally, my appreciation goes to all my colleagues and

friends, Folarin Olamide, Ajayi Damilola, Olugbose Arinola,

Bisola Oyelade, Adegbenle Abisola, Ajiboye Abiola, Yemi Coker,

Olayide, Majekiodunmi Olabode, Sanni, to mention but a few. I

cannot forget you all, I love you all, I am so grateful.

6

TABLE OF CONTENT

Pages

Title Page i

Certification ii

Dedication iii

Acknowledgement iv

Abstract xi

CHAPTER ONE 1-10

INTRODUCTION 1

1.0 Background to the study 1

7

1.0.1 Historical Background 4

1.1 Statement of the problem 5

1.2 Research questions 6

1.3 Objective of the study 6

1.4 Hypothesis of the study 7

1.5 Significance of the study 7

1.6 Scope of the study 8

1.7 Limitations of the study 8

1.8 Organization of the study 9

1.9 Operational definition of terms 10

CHAPTER TWO 11-49

8

Literature Review 11

2.0 Introduction 11

2.1 Theoretical framework 11

2.1.2 Theoretical concept 13

2.2 Empirical Review 18

2.3 The Concept of Internal Control 19

2.3.1The Objectives and roles of internal control framework 22

2.3.2 The major elements of an internal control process 23

2.3.3 Evaluation of internal control systems by supervisory authorities 35

2.4 Roles and responsibilities of external auditors 38

2.5 The concept of fraud 39

2.5.1 Classification of fraud 40

2.5.2 Type of bank’s common fraudulent practices 41

9

2.5.3 Causes of bank frauds 42

2.5.4 Factors influencing the existence of fraud in banks 42

2.5.5 Internal control and fraud prevention 43

CHAPTER THREE 50-57

3.0 Introduction 50

3.1 Research Design 50

3.2 Population of study 51

3.3 Sample and sampling techniques 51

3.4 Sources of data collection 51

3.5 Research instrument 52

3.5.1 Procedure for administration of research instrument 52

3.5.2 Validity of the instrument 53

3.5.3 Reliability of the instrument 53

10

3.6 Method of data analysis 54

3.7 Limitation of methodology 55

3.8 Model specification 55

CHAPTER FOUR 58-80

4.1 Introduction 58

4.2 Data Analysis, presentation and interpretation 58

4.3 Test of Hypotheses and discussion 74

4.4 Test of Hypotheses and discussion 75

CHAPTER FIVE 81-86

5.1 Introduction 81

5.2 Summary of major findings 81

5.3 Conclusion 82

5.4 Recommendations 83

11

5.5 Areas for further research 86

Bibliography

Appendix I

Appendix II

LIST OF TABLES

4.1.1Introducton

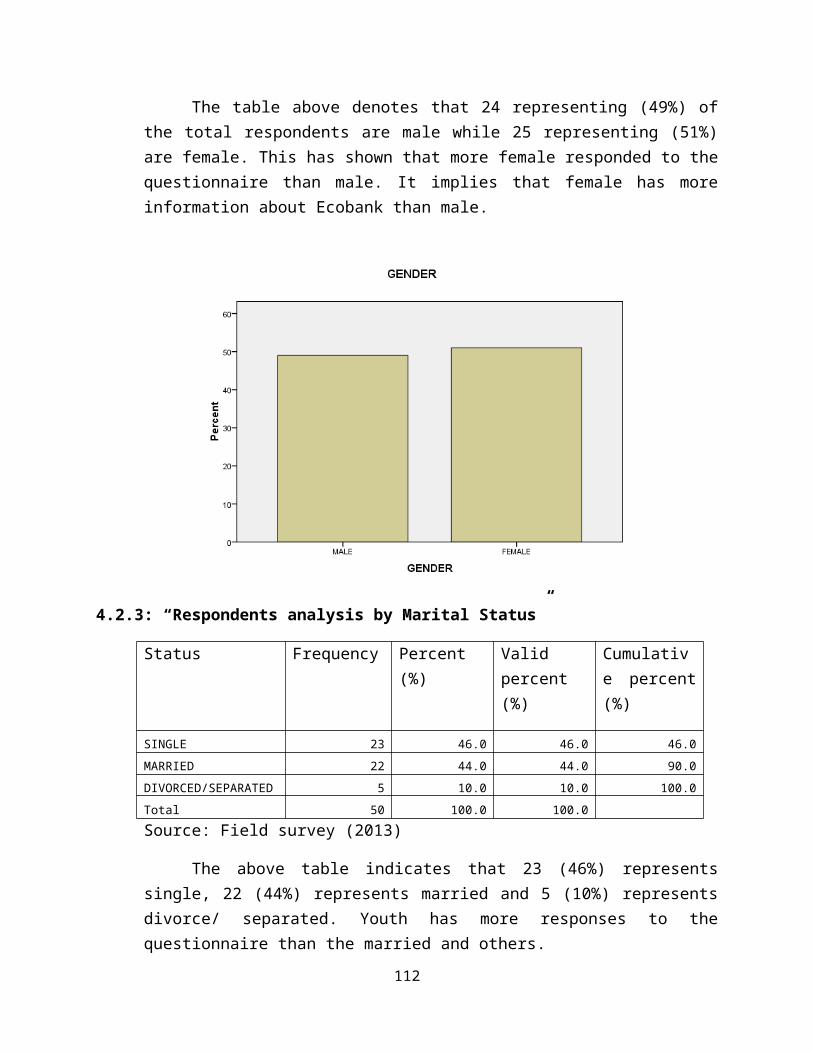

4.2.1 Respondents analysis by age

4.2.2 Respondents analysis by sex

4.2.3 Respondents analysis by marital status

4.2.4 Respondents analysis by education

4.2.5 Respondents analysis by length of service

4.2.6 Respondents analysis by position held

4.2.7 There are adequate assets listing done by the management

4.2.8 Positions in place ensure assets additions, disposal, replacement and transfers for proper accountability

12

4.2.9 Capital assets purchased are approved by appropriate level of management

4.2.10 Assets numbering is done to show location and protection of the assets

4.2.11 There is free access to cheque books and organization assets

4.2.12 A person responsible from inventory management is different from the book-keeper.

4.2.13 Stock taken is done following the procedures and in the presence of the internal auditor.

4.2.14 The petty cashier is different from the main cashier.

4.2.15 There are adequate policies to ensure effective collectionand follow up of due accounts.

4.2.16 Cost of production as been reducing dramatically for the past two years

4.2.17 The Company is now in a better position to serve clients more effectively and efficiently.

4.2.18 Effectiveness is measured through quality service and product.

4.2.19 The Company is able to build customers satisfaction through quality product and services.

4.2.20 Performance of the company result from asset financing, employee skils and processes involved in production.

4.2.21 There is evaluation and discussion of organization performance periodically by management.

4.2.22 Stock out increases the cost of production.

13

4.3.1 Weaknesses in internal control system in Nigeria banks do not lead to fraud.

4.3.2 Analysis showing the weaknesses in the internal control system and fraud.

4.4.1 There is no significant relationship between internal control system and organizational performance.

4.4.2 Analysis showing the internal control system and organizational performance

14

ABSTRACT

This project work takes a look at the effect of internal control

on organizational performance using a case study of Ecobank

Nigeria Plc. The main purpose of this study is to examine the

effect of internal control on organizational performance i.e how

as internal control aid organizational performance in Ecobank

Nigeria Plc.

The research design used during the course of this study was the

descriptive survey research design in which a population of 50

staff of Ecobank Nigeria Plc was look into. The researcher made

use of stratified sampling technique and the research instrument

used during the course of this research was questionnaire.

Statistical package for social sciences (SPSS) was being employed

to analyze data in form of frequency tables in knowing the effect

of internal control on organizational performance.

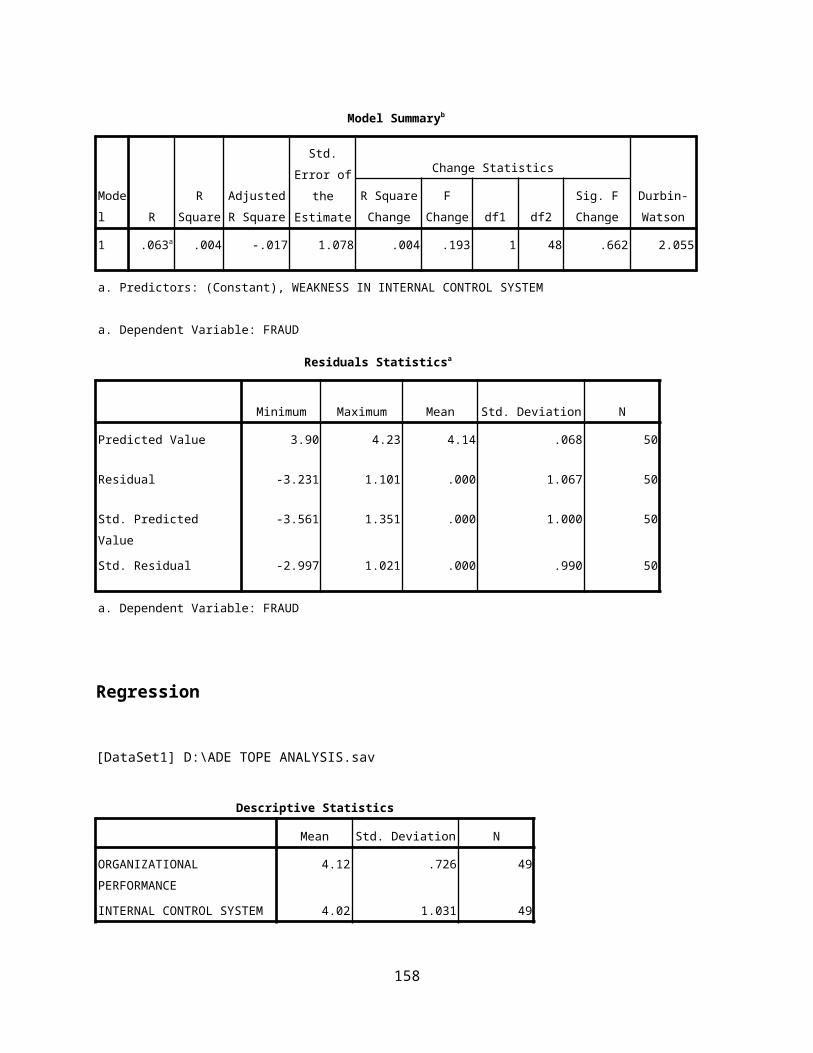

Findings reveals that the calculated t-statistics for the

parameter estimates was (t = 3.653), P < 0.01 which is greater

than tabulated t statistics (1.9960) at 0.01 level of

significance. Therefore, the Null hypothesis is rejected and

Alternative hypothesis is accepted, that is there is significant

relationship between internal control system and organizational

performance of Ecobank Nigeria Plc.

15

Furthermore findings also reveals that the calculated t-

statistics for the parameter estimates was (t = 0.439), P < 0.01

is less than tabulated t statistics (1.9960) at 0.01 level of

significance. Therefore, the Null hypothesis is accepted and

Alternative hypothesis is rejected, that is, Weakness in the

internal control system in Ecobank Nigerian Plc does not lead to

frauds.

Based on the findings of the study, it is recommended that the

management of Ecobank Nigeria Plc should design more effective

internal control systems by ensuring that adequate asset listings

is done by management, capital assets purchased are approved by

appropriate level of management and asset numbering is done to

show location and protection of the assets. Also Management

should encourage staff to participate in decision making.

Employees feel encouraged and motivated in accomplishing the

goals of the company in which they have taken part in

formulating.

CHAPTER ONE

INTRODUCTION

1.0 BACKGROUND TO THE STUDY

Banking institutions occupy a central position in the nations’

financial system and are essential agents in the development

process of the economy. By intermediating between the surplus and

16

deficit spending units, banks increase the quantum of National

savings and investments and hence national output. By granting

credits, banks create money thus influencing the level of money

supply which is an essential item in the growth of national

income as it determines the level of economic activities in the

country.

Banks are central to the payments system by facilitating economic

transactions between various national and international economic

units and by so doing encourage and promote trade, commerce and

industry.

For banks to be able to function effectively and contribute

meaningfully to the development of a country, the industry must

be stable, safe and sound. And for these conditions to be

obtained there must be a sound accounting system, which is

occasioned by an internal control system.

In view of the economic growth in companies’ size and

complexities, proper management of modern business undertakings

are not possible unless they have an effective system of internal

control.

A system of effective internal controls is a critical component

of bank management and a foundation for the safe and sound

operation of banking organizations. A system of strong internal

controls can help to ensure that the goals and objectives of a

banking organization will be met, that the bank will achieve

long-term profitability targets and maintain reliable financial

17

and managerial reporting. Such a system can also help to ensure

that the bank will comply with laws and regulations as well as

policies, plans, internal rules and procedures, and decrease the

risk of unexpected losses or damage to the Bank’s reputation.

Internal control, the strength of every organization, has become

of paramount importance today in Nigerian banks. The reason being

that the control systems in any organization is a pillar for an

efficient accounting system.

The need for the internal control systems in organizations,

especially banks, cannot be undermined, due to the fact that the

banking sector, which has a crucial role to play in the economic

development of a nation, is now being characterized by macro

economic instability, slow growth in real economic activities,

corruption and the risk of fraud.

Fraud, which is the major reason for setting up an internal

control system, has become a great pain in the neck of many

Nigerian bank managers. It has also become an unfortunate staple

in Nigeria’s international reputation. Fraud is really eating

deep into the Nigerian banking system and that any bank with a

weak internal control system, is dangerously exposed to bank

fraud.

The CBN reported that cases of attempted fraud and forgery in

banks, as at half-year 2007 have surpassed what was recorded for

the whole year 2006. The CBN half-year report for 2007, revealed

a total of 741 cases of attempted fraud and forgery, involving

18

5.4 billion, $35,406.1, 150 Euros were reported as at June, 2007.

In 2006, 1,193 cases were reported involving 4.6 billion, $1.8

million and 14,389.7 pound sterling. The CBN also reported that

the backward development was attributable to weaknesses in the

internal control systems of the banks. This has clearly painted

the picture of how fraud has penetrated in the financial strength

of Nigerian Banks.

In a nut-shell, the damage which this menace, called fraud has

done to the banks is innumerable and needs urgent attention.

Therefore, the attempt to put an end to this economic

degradation, gave rise to the topic of this research study the

effect of internal control on organizational performance in the

banking sector with Eco bank Nigeria PLC as a case study.

However, this study is aimed at verifying the conception that an

effective and efficient internal control system is the best

control measure for preventing and detecting fraud, especially in

the banking sector.

Internal control is the methods employed to help to ensure the

achievement of an objective. Internal controls are policies,

procedures, practices and organizational structures implemented

to provide reasonable assurance that an organization’s business

objectives will be achieved and undesired risk events will be

prevented or detected and corrected, based on either compliance

or management initiated concerns (Awe, 2005). The Institute of

Chartered Accountants of England and Wales (ICAEW), defined

19

internal control as the whole system of controls, financial or

otherwise, established by management in order to carry on the

business of an enterprise in an orderly and efficient manner, to

ensure adherence to management policies, safeguard the assets and

secure as far as possible, the completeness and accuracy of the

records. They are tools used by management everyday for the

smooth running of their organization or businesses. Internal

controls also refer to the measures instituted by an organization

so as to ensure attainment of the entity’s objectives, goals and

missions. They are a set of policies and procedures adopted by an

entity in ensuring that an organization’s transactions are

processed in the appropriate manner to avoid waste, theft and

misuse of organization resources. Internal Controls are processes

designed and effected by those charged with governance,

management, and other personnel to provide reasonable assurance

about the achievement of an entity’s objectives with regard to

reliability of the financial reporting, effectiveness and

efficiency of operations and compliance with applicable laws and

regulations (Mwindi, 2008). Enforcement of internal controls

should be designed to promote operational efficiency and

effectiveness, provide reliable financial information, safeguard

assets and records, encourage adherence to prescribed policies,

and comply with regulatory agencies. A sound internal control

will ensure that transactions are: valid, properly authorized,

recorded, properly valued, properly classified, reconciled to

20

subsidiary records and not carried through by a single employee

(i.e. ensure separation of duties) ( Adeyemo Kingsley A,2012).

Organizations establish systems of internal control to help them

achieve performance and organizational goals, prevent loss of

resources, enable production of reliable reports and ensure

compliance with laws and regulations. In the words of ETUK IFIOK

CHARLES (1999) et al “Internal Control is the whole system of

controls, financial and otherwise, established by the management

in order to carry on the business of the enterprise in an orderly

and efficient manner, ensure adherence to management policies,

safeguard the assets and secure as far possible the completeness

and accuracy of the records”. All managers in an organizational

department operate according to stated plans, objectives and the

methods they use. The policies, procedures, organizational design

and physical barriers constitute the internal controls structure

of an institution. Managers should realize that a strong internal

control structure is fundamental to the success of an

organization in term of its purpose, operations and resources.

Responsibility for providing an adequate and effective internal

control structure rests with an organization’s management.

Control is important because it single-handedly links with the

effectiveness of other managerial functions such as planning.

When it comes to planning, it determines whether activities are

on going toward the achievement of goals and accomplishment of

objectives. Control mechanisms keep the plans running smoothly

21

and up to date. Control is also important in employee empowerment

wherein performance of the employees could be properly managed.

Performance is controlled in terms of appraisal, lessening

haphazard decisions on allocation of positions/job titles.

Nonetheless, control mechanisms are also important in keeping a

balance within the workplace especially since controlling means

to minimize unethical decisions of the employees and the

organization as a whole.

The questions are: what can be said to be the cause or causes of

the increasing rate of fraud in banks? What is the impact of

internal control in the prevention and detection of fraud in

banks, what is the impact of internal control on the

organizational performance of the Eco bank Nigeria plc?

1.0.1 HISTORICAL BACKGROUND OF ECO BANK NIGERIA PLC

Eco bank Nigeria is a member of Eco bank, the leading independent

pan-African bank, with headquarters in Lome and East Africa. Eco

bank, which was established in 1985, has grown to network of over

1000 branches, employing over 10,000 people, with offices in 32

countries.

The bank began operation in 1986, it operates as a universal

bank, providing wholesale, retail, corporate, investment and

transaction banking services to its customers in the Nigeria

market. The bank divides its operations into three major

divisions; retail banking, wholesale banking and treasury and

financial institution.

22

The bank also offers capital market and investment banking

services. During the fourth quarter of 2011, Eco bank Nigeria

acquires 100% of the shareholding in oceanic bank, creating the

expanded Eco bank plc. At December 2011, the expanded Eco bank

Nigeria controlled total assets value at approximately US$8.1

billion (NGN 1.3trillion) making it one of the five largest bank

in Nigeria. At that time the bank had 610 free-standing branches

making it the second largest bank in the country by branch

network. Internal control has been a way of evaluating the

performance of the management in Eco bank Nigeria plc.

1.1 STATEMENT OF THE PROBLEM

The series of business failures and corporate scandals have been

identified by KPMG to be as a result of weak internal control

system. The failure of Enron in 2001 caused a precipitous decline

in investor confidence in the capital markets. The federal

government through the regulatory authorities has responded to

this, by passing guidelines using SAS2 under information which is

to be disclosed in financial statements. The guidelines codified

the responsibilities of corporate executives, corporate

directors, lawyers, accountants and created a board oversight

regime for auditors of public companies. In seeking to enhance

accountability and restore investor’s confidence, the guidelines

emphasizes the critical role of internal control over financial

reporting. This gave rise to the need for corporate governance

especially in public institutions.

23

International Auditing Guidelines (IAG) deals with the auditor’s

responsibility for detection of material misstatement resulting

from error when carrying out an audit of financial statements.

The guidelines in conjunction with the related SEC rules and

auditing standard No 2, established by the public company

Accounting Oversight Board (PCAOB), requires management of a

public accounting and the company’s independent auditor to issue

two new reports at the end of every fiscal year. These reports

must be included in the company’s annual report filed with the

Securities and Exchange Commission (SEC). In the past, a

company’s internal controls were considered in the context of

planning the audit, but were not required to be reported publicly

except in response to the SEC’s form requirements when related to

a change in auditor. The new audit and reporting requirements

have drastically changed the situation and have brought the

concept of internal control over financial reporting to the

forefront for audit committees, management, auditors, and users

of financial statements. The new requirements also highlight the

concept of a material weakness in internal control over financial

reporting, and mandate that both management and the independent

auditor must publicly report any material weakness in internal

controls over financial reporting that exists as a result of

physical year, at the end of assessment dates. Under both PCAOB

auditing standard NO 2 and the SEC rules implementing the

guidelines, the existence of a single material weakness requires

24

management and the independent auditors to conclude that internal

control over financial reporting is not effective.

Against this background this study investigated the purpose of

ascertaining the effect of internal control system on

organizational performance.

1.2 RESEARCH QUESTIONS

This study seeks to tackle among others questions such as:

1) What is the relationship between internal control and

organizational performance?

2) What are the implication, consequence and benefit of internal

control on organizational performance?

3) What are those challenges which a weak internal control can pose

on organizational performance?

4) What are those things that must be done and put in shape by the

company to ensure an effective internal control system?

5) What are the limitations of internal control?

6) What are the various component of internal control?

1.3 OBJECTIVE OF THE STUDY

The main objective of this research study is to examine the

effect of internal control system on organizational performance

in the Nigerian banking industry using Eco Bank of Nigeria PLC as

a case study. Apart from the main objective, the research also

sets out to achieve some specific objectives which are;

1) To examine the various component of internal control system.

25

2) To determine the effects of internal control on the

organizational performance of the financial institution.

3) To know the effect of the internal control in monitoring

compliance.

4) To critically examine how effective the internal control has been

used to reduce the level of risks.

5) To ascertain how useful is internal control to organizational

performance.

6) To recommend ways by which internal control can be used

effectively so as to achieve the organizational goal.

1.4 HYPOTHESIS OF THE STUDY

The following research hypotheses were generated for the study:

HO: Weakness in the internal control system in Nigerian banks

does not lead to frauds.

H1: Weakness in internal control system in Nigerian banks leads

to frauds.

HO: There is no significant relationship between internal control

system and organizational performance.

H1: There is significant relationship between internal control

system and organizational performance.26

1.5 SIGNIFICANCE OF THE STUDY

This study shall be of great benefits to the management of the

organization in order to deal extensively with effect of internal

control on organizational performance and this will eventually

lead to high productivity in the organization and also prevent

risks within the organization. This study will help organization

to have better understanding on how to install a good internal

control system for the effective running of their organization.

To managers of organizations and individuals, this study would

assist them in the area of identifying the effect of internal

control on organizational performance and its consequences. As

for managers in all organization within the country the result of

this research will help them to reduce the level of risk and

fraud within their organization so as to increase the confident

level of their shareholders. Managers ensure that as goods and

services are produced, machines or other equipment are properly

used so any malfunctions can be avoided. Improper usage of

company assets can create downtime if goods have to be re-

produced because of product defects.

Moreover, the study will be more relevant to management and

social science students because they will be exposed to the

effect of internal control on organizational performance and not

only that it would also serve as an eye opener to the fact that

as managers, there are lots of issue relating to internal control

27

within the organization which if left unattended to will

jeopardized organizational goal of the company.

The study will also attempt to contribute to the available

literature or researches that will serve as a guide for

organizational staff in order to prevent fraud and risks within

the organization.

Policy makers would also benefit from this study in formulating

policies relating to the effect of internal control on

organizational performance.

The study of the effect of internal control on organizational

performance is another area of study that is wide for researchers

to tap into. So, this study would benefit researchers in looking

beyond the scope of the present study and impacting to the

knowledge already acquired.

The effect of internal control on organizational performance will

also help practitioners such as Auditor, tax practitioners, etc

in increasing their credibility.

1.6 SCOPE OF THE STUDY

This research by the grace of God is expected to go in-depth.

Meanwhile the scope of the study is to determine the effect of

internal control on organizational performance (Using a case

study of Eco Bank), The research focuses on Eco bank Nigeria plc.

This research work will cover the period between 2000 - 2012. The

entire organization’s staff of this bank will be concern in this

28

research, as their view will be collected through detailed

questionnaire.

As Eco Bank Plc are located virtually throughout the geographical

area in Nigeria, this research work cover two major part of

geographical location in Nigeria southern part Osun State

(Osogbo) and West Central part Kwara State (Offa).

Lastly, the research laid emphasis on banking sector as one of

the main determinant of economic growth and development in the

country.

1.7 LIMITATIONS OF THE STUDY

In the course of this study, the researcher would encounter a

lot of hindrances among these, the most salient one include

finance which the researcher is faced with. Insufficient funds

required for expenses like transportation, acquisition of

research instruments, sourcing for both primary and secondary

data etc. Also information on the secondary source of data

available to the researcher was either outdated or incomplete and

the one available on the internet requires some form of

subscription before access is allowed.

Time also posed a constraint on this research work such as time

to study and time to attend lecture etc.

29

Attitude of respondent is also another limiting factor to this

research work. Most respondent are often reluctant to part with

information even after being assured confidentiality they still

prefer to be secretive.

Despite the limitations of this study I still hope to do better

work on this field.

1.8 ORGANIZATION OF THE STUDY

This research work is divided into five chapters.

Chapter one contains introduction to the research work which

summarizes background to the study as well as the main feature of

the effect of internal control on the organizational performance

of the Eco bank plc. In this chapter, statement of the problem,

objective of the study, significance of the study, research

hypothesis, research questions, scope of the study, limitation of

the study, and organization of the study are discussed

extensively.

Chapter two of this research work is known as the review of

related literature otherwise known as the literature review and

the theoretical frame work, which reviews previous research work

in the field of study and analysis of various principles relating

to the research topic.

Chapter three is concerned with the research methodology. This

discusses research design, the population size to be studied,

sample size determination, sampling techniques applied , method

30

of data analysis and interpretation, the statistical tools used

in the analyzing the formulated hypothesis .

Chapter four of this research work is the data presentation,

analysis and interpretation.

Chapter five summarizes the whole research project stating the

findings useful conclusion and the recommendation and this

constitute the concluding part of the research work.

1.9 OPERATIONAL DEFINITION OF TERMS

Internal Controls: The Institute of Chartered Accountants of

England and Wales (ICAEW), defined internal control as the whole

system of controls, financial or otherwise, established by

management in order to carry on the business of an enterprise in

an orderly and efficient manner, ensure adherence to management

policies, safeguard the assets and secure as far as possible, the

completeness and accuracy of the records.

Internal Audit: It is an independent appraisal activity

established within an organization as a service to it. It is a

control which functions by examining and evaluating the adequacy

and effectiveness of other controls; a management tool which

analyses the effectiveness of all parts of an entity’s operations

and management.’ (CIMA’s Management Accounting Official

Terminology)

31

Monitoring: According to CIMA, it is a process that assesses the

quality of the system’s performance over time.

According to Sunny, New Palta and Root. It can be defined as the

final internal control standards, which assess the quality of

performance.

Control Environment: According to the first internal control

standard, it relates to the departments that set a positive and

supportive attitude towards internal control and conscientious

management.

Reasonable Assurance Concept: It refers to the fact that internal

controls even when they are appropriately designed and operating

effectively cannot provide absolute assurance of achieving

control objectives.

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION

32

Fundamental to the success of any organization is the achievement

of its objectives. The objectives could be profit maximization,

shareholders’ wealth maximization, cost minimization, and

customer’s satisfaction (to mention but a few).

However, the achievement of organizational objectives is one

thing; the process of achieving such objectives is another. This

is more so in that the achievement of stated goals and objectives

rest mainly on having an effective internal control system that

ensures the organizational performance is according to plan.

Incidentally, corporate planning and control are independent

management functions especially in ascertaining performance and

assessing the future direction of an organization. In addition,

corporate planning and control are important in determining the

performance of any organization. Planning is concerned primarily

with the setting of goals and control is a mechanism that ensures

that an organization achieves its predetermined corporate goals

and objectives. It is important to note that no manager can

successfully accomplish his/her task unless he/ she performs

necessary functions. It is nevertheless true that control is

peculiarly dependent upon a well organized system.

2.1 Theoretical framework of the term “Internal Control” and

“Internal Control System”

In the modern business world, the term “ Internal Control “ is

being used to refer to two basic concepts; the internal control

system and the internal control itself.

33

Internal Control System

The internal control system refers to an organized

amalgamation of functions and procedures, within a complete

system of controls established by the management and whose

purpose is the successful function of the business (Cheung,

1997). The internal control system encompasses all the methods

and procedures followed by the management in order to ensure, to

a great extent, as much successful cooperation as possible with

the director of the company, the insurance of the capital, the

prevention and the detection of fraud, as well as the early

preparation of all the useful financial information ( Meigs,

1984; Papadatou, 2005 ). According to Cook and Wincle (1976), the

internal control system resembles the human nervous system which

is spread throughout the business carrying out orders and

reactions to and from the management. It is directly linked to

the organizational structure and the general rules of the

business ( Cai, 1997 ).

Internal Control

The term was adopted by the Anglo- Saxons ( “ Internal

Auditing “ ) and it refers to the unit of internal control which

aims at the evaluation of the sufficient functioning of the

internal control system, that is the secondary functions

( Controls ) and suggests that there is room for improvements in

cases where weaknesses are being discovered ( Financial Postman

Magazine, 2004 ). What is indicative of the importance of

internal control is the sum of the definitions that have been

34

given for this term. According to the AICPA (American institute

of certified public accountants), (1963) a system of internal

control extends beyond those matters which relate directly to the

functions of accounting and the financial statements. In

addition, based on the ASOBAC (Committee on Basic Auditing

Concepts, 1973), internal control is a systematic procedure which

will lead to evaluate the degree of correlation between those

established criteria and the real results of the business.

Internal control, as defined by the APC (Auditing Practices

Committee, 1980), is an independent examination and certification

from an inspector appointed by the business to control the

finances according to the legal framework established each time.

Furthermore, according to Miller and Bailley (1989), internal

control is a systematic review and a subjective investigation of

one element and encompasses the verification of the specific

information as these are determined from the general practice.

The internal control helps the company to achieve its goals using

a systematic approach of assessing the effectiveness of handling

dangers (IIA, 1999). Internal control, as defined by the Hellenic

Institute of Internal Auditors (H.I.I.A., 2004) is an

independent, objective, adequately designed and organized

procedure, which through the technical and the scientific

approaches; assess how adequately the system of internal control

functions. From the above definitions, it is clear that the

internal control is not just a one-sided tool for controlling the

order and rightness of certain situations, but it is a method of

35

detecting the value added up to a company, achieving the index of

effectiveness and profitability of the company (Nagy and Cenker ,

2002) (Godwin, 2004). Besides, the purpose of this control that

is internal control is to detect the problem of risk and fraud

within the organization to be reformed in the future and anyone

that ought to exist (Mcnamee and Mcnamee, 1995). The deviation

between the already achieved and the programmed situation can

also become possible through controlling the parameter of correct

handling of danger situations.

Bounton and Kellerwalter (1996) claimed that the objective

purpose of internal control is, on the one hand, the allowance of

specific and high level of services offered towards the

management, and on the other hand, the allowance of assistance

towards the members of the organization for the most effective

practicing of their duties. The internal control systems are

being implemented in businesses as tools that add up value to the

company. In this way, we can achieve a systematic approach

towards the most effective operation of the organization, as a

unity (Schleifer and Greenwalt, 1996). Finally, as mentioned by

the COSO report (Committee of Sponsoring Organizations of the

Treadway Commission, 1992), internal control is defined as a

procedure which offers fundamental security to the business

concerning the credibility of financial affairs. The report

defines internal control and describes a framework for internal

control, but the difference of this report is that it also

36

provides criteria for the management to utilize so as to evaluate

controls. (Aldridge and Colbert, 1994).

2.1.2 Theoretical Concept of Fraud as Related to Internal Control

Fraud is an intentional strategy to achieve a personal or

organizational goal or human needs by deceit. A layman definition

of fraud includes dishonesty in the form of an intentional

deception or a willful misrepresentation of a material fact,

lying, the willful telling of an untruth, and cheating, the

gaining of an unfair or unjust advantage over another. Fraud

involves coercing people to act against their own best interest.

In order to explain why fraud is conceived in the society, the

following theories have been advanced by scholars.

1. Sociological theory of Crime/Fraud:

2. Culture Transmission Theory.

3. Psychological/physiological theory of crime:

4. The Fraud Triangle.

5. Fraud Deterrence Cycle.

Sociological theory of crime/fraud: According to this theory,

Fraud is a crime and it is important to remember that the concept

of what constitutes a crime is constantly being adapted to meet

the particular needs of any society. That most people are capable

of committing a crime in sudden anger, drunkenness or as a result

of stress and there may be little that we can do to prevent these

37

isolated acts by individuals. O’ Donnell, (1974) stated that we

may be able to reduce the amount of crimes by removing the

factors which predispose these individuals or groups towards

criminal acts and motivation. He thus suggests that there are

predisposing factors of crimes and there are the precipitating

factors which trigger off tendencies for frauds and criminal

motives in groups or individuals concerned. The theory states

that crime and criminal motives are a part of a ‘normal’ social

order in that it can be an expression of the same motivations

that give rise to accepted behavior. Oluwadare,(1993) stated that

the embezzler, the fraudster and the law abiding storekeeper are

concerned with making money. One makes money into his private

pocket (egoism) and the other making the money for the

organization (altruism). Durkheim, one of the founders of

sociology argued that crime is an integral part of all healthy

societies.

Psychological/Physiological theory: Oluwadare, (1993) posited

that there are explanations by some scholars that crime is a

personal rather than a social problem. That this approach varies

from those who believe that some people are innately wicked to

those who hold the view that there is a genetic cause for

criminality connected with the endocrine glands. Lombrose, (1876)

believed that criminality is inborn because after he examined the

skull of a notorious bandit and found characteristics which he

believed to be result of a “throw back” to an earlier

evolutionary type. He concluded that there was a criminal type

38

which resulted in “insensitivity to pain, extremely acute sight,

love of orgies, irresistible caring for evil for its own sake

etc” Rosenthal (1972) in his support for this theory suggested a

possible link with crime while quoting studies of twins made in

three continents over a period of forty years in which he claimed

identical twins shared crime traits at a rate more than double of

that of non identical twins. Culture transmission theory: This

theory views crime as the end product of a process of social

living. Tarde (1886) suggested that criminal behavior or criminal

motives is learned in the family and the community in areas where

this behavior is the ‘norm’ (i.e. a standard behavior shared by a

group and accepted within it).

The fraud triangle: The fraud triangle theory propounded by

Donald Cressey states that every fraud has three things in

common: (1) Pressure sometimes referred to as motivation and

usually an “un-shareable need”; (2) Rationalization of personal

ethics; and (3) Knowledge and opportunity to commit the crime.

Singleton et al in their work on the fraud triangle theory stated

that pressure or incentive or motivation refers to something that

has happened in the fraudster’s personal life that creates a

stressful need for funds and thus motivates him to steal. This

motivation may be some financial strain but it could be the

symptoms of other types of pressures. According to Kenyon and

Tilton (2006), Management or other employees may find themselves

offered incentives or placed under pressure to commit fraud. They

cited as an example that when remuneration or advancement is

39

significantly affected by individual, divisional or company

performance, individuals may have an incentive to manipulate

results or to put pressure on others to do so. Similarly,

pressure may come from the unrealistic expectations from

investors, banks or other sources of finance. They therefore

stated that incentives or pressures may take a variety of forms

within an organization. These include; bonuses or incentive pay

representing a large portion of an employee or group’s

compensation, triggers built into debt covenants tied to share

price targets and levels, significant stock option awards

throughout the organization but particularly to top management,

and aggressive earnings-per-share and revenue targets set by top

management and communicated to analysts, investment bankers, and

other market participants, with resultant pressure from these

groups. Rationalization and attitude according to Kenyon and

Tilton, (2006) in their write up on Potential Red Flags and Fraud

Detection Techniques stated that some individuals are more prone

than others to commit fraud. That the propensity to commit fraud

depends on people ethical values as well as on their personal

circumstances. The authors asserted that ethical behavior is

motivated both by a person’s character and by external factors.

External factors which include job insecurity such as during a

downsizing or redundancy or a work environment that inspires

resentment such as being passed over for promotion. Likewise,

external environment includes the tone at the top i.e. the

attitude of management toward fraud risk and management’s

40

response to actual instances of fraud. They posited that when

fraud has occurred in the past and management has not responded

appropriately, others may conclude that the issue is not taken

seriously and they can get away with it. Where instances exist

that create opportunities for management or other staff to commit

fraud, according to Kenyon and Tilton, (2006), those who might

not otherwise be inclined to behave dishonestly may be tempted to

do so. They therefore stated that absence or ineffective

controls, lack of supervision or inadequate segregation of duties

may provide such opportunities. Tommie W Singleton et al stated

that the ‘Report to the Nation (RTTN) (2004) research carried out

by Association of Certified Fraud Examiners showed that most

employees and managers who commit fraud tend to have a long

tenure with a company. A simple explanation deduced by the

scholars is that employees and managers who have been around for

years know quite well where the weaknesses are in the internal

controls and have gained sufficient knowledge of how to commit

the crime successfully.

The Fraud Deterrence Cycle: The Fraud Deterrence Cycle is an

interactive process which include establishment of corporate

governance, implementation of transaction-level control

processes often referred to as the system of internal accounting

controls, retrospective examination of governance and control

processes through audit examinations and investigation and

remediation of suspected or alleged problems. Fraud may be

categorized into Corporate, management Fraud and fraud as a tort.

41

Corporate fraud on the other hand is any fraud perpetrated by,

for or against a business corporation Singleton, Bologna,

Lindquist (2006). Management Fraud is the intentional

misrepresentation of corporate or unit performance levels

perpetrated by employees serving in management roles who seek to

benefit from such frauds in terms of promotions, bonuses or other

economic incentives and status symbols. Colbert, and Meany,

reiterated that an essential component of any entity’s internal

control system including fraud prevention and detection is the

‘tone at the top’. The actions and attitudes of management and

the board of directors set the tone at the top. Their views

towards controls and enforcement of established policies and

procedures permeate the organization and are an important factor

in the success of fraud related policies. In recent years, there

has been great concern on the management of banks’ assets and

liabilities because of large scale financial distress Adam,

(2009). The banking sector has been singled out for the special

protection because of the vital role banks play in an economy.

Bank supervision entails not only the enforcement of rules and

regulations, but also judgments concerning the soundness of bank

assets, its capital adequacy and management Volcker, (1992). In

Nigeria, the rising cases of bank distress have also become a

major source of concern for policy makers. McNamara, C (2009)

stated that performance management is a relatively new concept to

the field of management. That performance management reminds us

that being busy is not the same as producing results. It reminds

42

us that training, strong commitment and lots of hard works alone

are not results. That the major contribution of performance

management is its focus on achieving results -- useful products

and services for customers inside and outside the organization.

Despite the recent attention to achieving maximum performance,

McNamara (2009) stated that there is no standard interpretation

of what that means or what it takes to get it. However having

stated what people are suggesting that it takes for organizations

to achieve maximum performance he stated that, we should be aware

of the various views and be able to choose our own. Recent report

from the Nigerian Deposit Insurance Corporation (NDIC) stated

that Nigerian banks recorded 2007 cases of fraud involving over

=N=53 billion naira in 2008 compared to 1,533 cases involving

=N=10 billion in 2007. The report stated that =N=17.5 billion was

lost to fraud in 2008 as against =N=2.9 billion in 2007.

43

2.2 EMPIRICAL REVIEW

The Nigerian banking industry which is regulated by the Central

Bank of Nigeria is made up of; deposit money banks referred to as

commercial banks, development finance institutions and other

financial institutions which include; micro-finance banks,

finance companies, bureau de changes, discount houses and primary

mortgage institutions. The development in Nigeria banking sector

dated back to 1892 when the first commercial bank (The African

Banking Corporation) was established in Lagos. According to

Adekanye (1986) “the bank experienced some difficulties which led

to the establishment of British Bank of West Africa”.

According to Jigyasu Prani (2006) no banking legislation existed

until 1952, at which point Nigeria had three foreign banks (the

Bank of British West Africa, Barclays Bank, and the British and

French Bank) and two indigenous banks (the National Bank of

Nigeria and the African Continental Bank) with a collective total

of forty branches. The 1952 ordinance set standards, required

44

reserve funds, established bank examinations, and provided for

assistance to indigenous banks. Yet for decades after 1952, the

growth of demand deposits was slowed by the Nigerian propensity

to prefer cash and to distrust cheques for debt settlements.

British colonial officials established the West African Currency

Board in 1952 to help finance the export trade of foreign firms

in West African and to issue a West African currency convertible

to British pounds sterling, but colonial policies barred local

investment of reserves, discouraged deposit expansion, precluded

discretion for monetary management, and did nothing to train

Africans in developing indigenous financial institutions. In 1952

several Nigerian members of the Federal House of Assembly called

for the establishment of a central bank to facilitate economic

development. Although, the motion was defeated, the colonial

administration appointed Bank of England officials to study the

issue. He advised against a central bank questioning such a

bank’s effectiveness in an undeveloped capital market. In 1957,

the colonial office sponsored another study that resulted in the

establishment of a Nigerian central bank and the introduction of

a Nigerian currency. The Nigerian pound on a par with the pound

sterling until the British currency’s devaluation in 1967, was

converted in 1973 to decimal currency, the naira (=N=),

equivalent to two old Nigerian pounds. The smallest unit of the

new currency was the kobo, 100 of which equaled 1 naira. The

naira, which exchanged for US$1.52 in January 1973 and again in

march 1982 (or #0.67 = US$1), despite the floating exchange rate,

45

depreciated relative to the United State dollar in the 1980s. The

average exchange rate in 1990 was #8.004 =US$1. Depreciation

accelerated after the creation of a second-tier foreign exchange

market under World Bank structural adjustment in September 1986.

The Central Bank of Nigeria, which was statutorily independent of

the federal government until 1968, began operations on July 1,

1959. Following a decade of struggle over the relationship

between the government and the Central Bank, a 1968 military

decree granted authority over banking and monetary policy to the

Federal Executive Council. The role of the Central Bank, similar

to that of central banks in North America and Western Europe, was

to establish the Nigerian currency, control and regulate the

banking system, serve as banker to other banks in Nigeria, and

carry out the government’s economic policy in the monetary field.

This policy included control of bank credit growth, credit

distribution by sector, cash reserve requirements for commercial

banks, discount rates-interest rates the Central Bank charged

commercial and merchant banks-and the ratio of banks’ long-term

assets to deposits. Changes in Central Bank restrictions on

credit and monetary expansion affected total demand and income.

2.3 THE CONCEPT OF INTERNAL CONTROL

The structure of modern banking system and the high expectation

from the investors and the society at large has called for a more

tightened internal control system. Internal control has been

variously defined.

46

According to Princeton (2008) internal control is a process

effected by an organization’s structure, work and authority

flows, people and management information system, designed to help

the organization accomplish specific goals or objectives. From

the definition, the objective of any internal control should be

directed towards the attainment of the organizational objectives.

In the words of Okozie (1999)” internal control is the whole

system of controls, financial and otherwise, established by the

management in other to carry on the business of the enterprise in

an orderly and efficient manner, ensure adherence to management

policies, safeguard the assets and secure as far as possible the

completeness and accuracy of the records”. A sound internal

control system should provide the platform for recording and

processing transactions in such a way that it forms adequate

basis for the preparation of the financial statement. An

efficient internal control system involves a clear definition and

segregation of duties for various employees or groups within a

company. The intent of separating the duties is to protect

against fraud, waste, abuse and mismanagement of resources.

Effective internal control helps to assure the accuracy of

reports to management and the various supervising bodies (in the

case of banks).

According to Asuquo (2005) “Internal control is made up of

internal checks, internal audit, accounting controls and other

forms of control such as budgetary and physical control”. Okozie

47

(1999) posited that “the primary responsibility for the

maintenance of the effective internal control rest with the

management of any enterprise”. Management responsibilities are

normally discharged by:

Installation of an effective accounting system;

Ensuring that employees understand relevant codes of

conduct.

Monitoring relevant legal requirements and ensuring that

operating procedures and conditions meet these requirements.

The establishment of an independent Internal audit function.

The appointment of an audit committee where appropriate.

According to Van Creveld (2005), internal control has further

been defined as a process effected by an organization’s

structure, work and authority flows, people and management

information systems, designed to help the organization accomplish

specific goals and objectives. It is a means by which the

organization’s resources are directed, monitored and measured, it

plays an important role in preventing and detecting fraud and

protecting the organization’s resources both physical machinery

and property and intangible (e.g. reputation, intellectual

property such as trademarks and patents). At the organizational

level, internal control objectives relate to reliability of

financial reporting, timely feedback on the achievement of

operational or strategic goals and compliance with laws and

regulations. At the specific transaction level, internal control

refers to the action taking to achieve a specific objectives e.g.

48

how to ensure the organization’s payment to third parties are for

valid services rendered. A system of effective internal control

is a critical component of bank management and a foundation for

the safe and sound operation of banking organizations. A system

of strong internal control can help to ensure that the goals and

objectives of a banking organization will be met, that the bank

will achieve long term profitability targets and maintain

reliable financial and managerial reporting. Such a system can

also help to ensure that the bank will comply with laws and

regulations as well as policies, plans, internal rules,

procedures, and decrease the risks of unexpected losses or damage

to the bank’s reputation.

Internal control are policies, procedures, practices and

organizational structures implemented to provide reasonable

assurance that an organization’s business objectives will be

achieved and undesired risk events will be prevented or detected

and corrected, based on either compliance or management

initiated concerns (Awe,2005).

The institute of Chartered Accountants of England and

Wales (ICAEW), defines internal control as the whole system of

controls, financial or otherwise, established by management in

order to carry on the business of an enterprise in an orderly and

efficient manner, ensure adherence to management policies,

safeguard the assets and secure as far as possible, the

completeness and accuracy of the records. Mayo and BPP (1988)

defined it as a measure taken by an organization for the purpose

49

of protecting its resources against wastes, fraud, inefficiency;

ensuring accuracy and reliability in accounting and operating

data; securing compliance with organization policies and

evaluating the level of performance in all the divisions of the

organizations. From these definitions, it can be deduced that

internal control comprises the plan of an organization and all of

the coordinate methods and measures adopted within it, to

safeguard its assets, check the accuracy and reliability of its

accounting data, promote operational efficiency and encourage

adherence to prescribed managerial policies. Internal control

objectives are channeled towards ensuring adherence to managerial

policies and achieving organizational goals in general.

ICAN (2006a, b) categorized controls into three major

classifications:

Preventive controls: These are controls that predict

potential problems before they occur and make

adjustments. They also prevent an error, omission or

malicious act from occurring. Examples of preventive

controls includes: using well-designed documents to

prevent errors. Establishing suitable procedures for

authorization of transactions. Employing only qualified

personnel. E.g segregates duties.

Detective controls: These controls are designed to

detect and report the occurrence of an omission, an error or a

malicious act. Examples of detective controls include: duplicate

checking of calculations, Periodic performance reporting with

50

variance error message over tape labels and Hash totals counter

cheques post-due account reports.

Corrective controls: These controls help to minimize

the impact of a threat, identify the cause of a problem, correct

errors arising from the problem. They also correct problems

discovered by detective controls and modify the processing

system(s) to minimize future occurrence of the problem. Examples

of corrective controls are: contingency planning back up

procedures rerun procedures.

2.3.1 The Objectives and Roles of Internal Control Framework

Internal control is a process effected by the board of

directors, senior management and all levels of personnel. It is

not solely a procedure or policy that is performed at a certain

point in time, but rather it is continually operating at all

levels within the bank. The board of directors and senior

management are responsible for establishing the appropriate

culture to facilitate an effective internal control process and

for monitoring its effectiveness on an ongoing basis; however,

each individual within an organization must participate in the

process. The main objectives of the internal control process can

be categorized as follows:

1. Efficiency and effectiveness of activities (performance

objectives);

2. Reliability, completeness and timeliness of financial and

management information (information objectives); and

51

3. Compliance with applicable laws and regulations (compliance

objectives).

Performance objectives for internal controls pertain

to the effectiveness and efficiency of the bank in using its

assets and other resources and protecting the bank from loss.

The internal control process seeks to ensure that personnel

throughout the organization are working to achieve its goals

with efficiency and integrity, without unintended or excessive

cost or placing other interests (such as an employee’s, vendor’s

or customer’s interest) before those of the bank.

Information objectives address the preparation of

timely, reliable, relevant reports needed for decision-making

within the banking organization. They also address the need for

reliable annual accounts, other financial statements and other

financial –related disclosures and reports to shareholders,

supervisors, and other external parties. The information received

by management, the board of directors, shareholders and

supervisors should be of sufficient quality and integrity that

recipients can rely on the information in making decisions. The

term reliable, as it relates to financial statements, refers to

the preparation of statements that are presented fairly and based

on comprehensive and well-defined accounting principles and

rules.

Compliance objectives ensure that all banking business

complies with applicable laws and regulations, supervisory

requirements, and the organization’s policies and procedures.

52

This objective must be met in order to protect the bank’s

franchise and reputation.

2.3.2 The Major Elements of an Internal Control Process

The internal control process, which historically has

been a mechanism for reducing instances of fraud,

misappropriation and errors, has become more extensive,

addressing all the various risks faced by banking organizations.

It is now recognized that a sound internal control process is

critical to a bank’s ability to meet its established goals, and

to maintain its financial viability.

Internal control consists of five interrelated

elements: and these elements are explained with it and of

suitable principle to be followed by concern people in an

organization.

1. Management oversight and the control culture;

2. Risk recognition and assessment;

3. Control activities and segregation of duties;

4. Information and communication; and

5. Monitoring activities and correcting deficiencies.

The problems observed in recent large losses at banks can be

aligned and with these five elements. The effective

functioning of these elements is essential to achieving a bank’s

performance, information, and compliance objectives.

A. Management oversight and the Control Culture

1. Board of directors

53

Principle 1: The board of directors should have responsibility

for approving and periodically reviewing the overall business

strategies and significant policies of the bank; understanding

major risks run by the bank, setting acceptable levels for these

risks and ensuring that senior management takes the steps

necessary to identify, measure, monitor and control these

risks; approving the organizational structure and ensuring that

senior management is monitoring the effectiveness of the

internal control system. The board of directors is ultimately

responsible for ensuring that an adequate and effective system

of internal control is established and maintained.

The board of directors provides governance,

guidance and oversight to senior management. It is

responsible for approving and reviewing the overall business

strategies and significant policies of the organization as well

as the organizational structure. The board of directors has the

ultimate responsibility for ensuring that an adequate and

effective system of internal control is established and

maintained. Board members should be objectives, capable, and

inquisitive, with a knowledge or expertise of the activities of

and risks run by the bank. In those countries where it is an

option, the board should consist of some members who are

independent from the daily management of the bank. A strong,

active board, particularly when coupled with effective upward

communication channels and capable financial, legal and internal

audit functions, provides an important mechanism to ensure the

54

correction of problems that may diminish the effectiveness of

the internal control system.

One option used by banks in many countries is the

establishment of an independent audit committee to assist the

board in carrying out its responsibilities. The establishment of

an audit committee allows for detailed examination of

information and reports without the need to take up the time of

all directors. The audit committee is typically responsible for

overseeing the financial reporting process and the internal

control system. As part of this responsibility, the audit

committee typically oversees the activities of, and serves as a

direct contact for, the bank’s internal audit department and

engages and serves as the primary contact for the external

auditors. In those countries where it is an option, the

committee should be composed mainly or entirely of outside

directors (i.e., members of the board that are not employed by

the bank or any of its affiliates) who have knowledge of

financial reporting and internal controls. It should be noted

that in no case should the creation of an audit committee amount

to a transfer of duties away from the full board, which alone is

legally empowered to take decisions.

2. Senior management

Principle 2: Senior management should have responsibility for

implementing strategies and policies approved by the board:

developing processes that identify, measure, monitor and control

55

risks incurred by the bank: maintaining an organizational

structure that clearly assigns responsibility, authority and

reporting relationships; ensuring that delegated

responsibilities are effectively carried out; setting

appropriate internal control policies; and monitoring the

adequacy and effectiveness of the internal control system.

Senior management is responsible for carrying out

the directives of the board of directors, including the

implementation of strategies and policies and the establishment

of an effective system of internal control. Members of senior

management typically delegate responsibility for establishing

more specific internal control policies and procedures to those

responsible for a particular business unit. Delegation is an

essential part of management; however, it is important for

senior management to oversee the managers to whom they have

delegated these responsibilities to ensure that they develop and

enforce appropriate policies and procedures.

Compliance with an established internal control

system is heavily dependent on a well documented and

communicated organizational structure that clearly shows lines

of reporting responsibility and authority and provides for

effective communication throughout the organization. The

allocation of duties and responsibilities should ensure that

there are no gaps in reporting lines and that an effective level

56

of management control is extended to all levels of the bank and

its various activities.

3. Control culture

Principle 3: The board of directors and senior management are

responsible for promoting high ethical and integrity standards,

and for establishing a culture within the organization that

emphasizes and demonstrates to all levels of personnel the

importance of internal controls. All personnel banking

organization need to understand their role in the internal

controls process and be fully engaged in the process.

An essential element of an effective system of

internal control is a strong control culture. It is the

responsibility of the board of directors and senior management

to emphasize the importance of internal control through their

actions and words this includes the ethical values that

management displays in their business dealings, both inside and

outside the organization. The words, attitudes and actions of

the board of directors and senior management affect the

integrity, ethics and other aspects of the bank’s control

culture.

In varying degrees, internal control is the

responsibility of everyone in a bank. Almost all employees

produce information used in the internal control system or take

other action needed to effect control. An essential element of a

strong internal control system is the recognition by all

57

employees of the need to carry out their responsibilities

effectively and to communicate to the appropriate level of

management any problems in operations, instances of non-

compliance with the code of conduct, or other policy violations

or illegal actions that are noticed. This can best be achieved

when operational procedures are contained in clearly written

documentation that is made available to all relevant personnel.

It is essential that all personnel within the bank understand

the importance of internal control and are actively engaged in

the process.

In reinforcing ethical values, banking organizations

should avoid policies and practices that may inadvertently

provide temptations for inappropriate activities. Examples of

such policies and practices include undue emphasis on

performance targets or other operational results, particularly

short-term ones that ignore longer-term risks; compensation

schemes that overly depend on short performance; ineffective

segregation of duties or other controls that could allow the

misuse of resources or concealment of poor performance; and

insignificant or overly onerous penalties for improper

behaviours.

While having a strong internal control culture does

not guarantee that an organization will reach its goals, the

lack of such a culture provides greater opportunities for errors

to go undetected or for improprieties to occur.

58

B. Risk Recognition and Assessment

Principle 4: An effective internal control system requires that

the material risks that could adversely affect the achievement

of the bank’s goals are being recognized and continually

assessed. This assessment should cover all risks facing the bank

and the consolidated banking organization (that is, credit risk,

country and transfer risk, market risk, interest rate risk,

liquidity risk, operational risk, legal risk, and reputational

risk). Internal controls may need to be revised to appropriately

address any new or previously uncontrolled risks.

Banks are in the business of risk-taking. Consequently it is

imperative that, as part of an internal control system these

risks are being recognized and continually assessed. From an

internal control perspective, a risk assessment should identify

and evaluate the internal and external factors that could

adversely affect the achievement of the banking organization’s

performance, information and compliance objectives. This process

should cover all risks faced by the bank and operate at all

levels within the bank. It differs from the risk management

process which typically focuses more on the review of business

strategies developed to maximize the risk/reward trade-off

within the different areas of the bank. Effective risk

assessment identifies and considers internal factors (such as

the complexity of the organization’s structure, the nature of

the bank’s activities, the quality of the personnel,

organizational changes and employee turnover) as well as

59

external factors (such as fluctuating economic conditions,

changes in the industry and technological advances) that could

adversely affect the achievement of the bank’s goals. This risk

assessment should be conducted at the level of individual

businesses and across the wide spectrum of activities and

subsidiaries of the consolidated banking organization. This can

be accomplished through various methods. Effective risk

assessment addresses both measurable and non-measurable aspects

of risks and weighs costs of controls against the benefits they