Telecommunications - Trefis

54

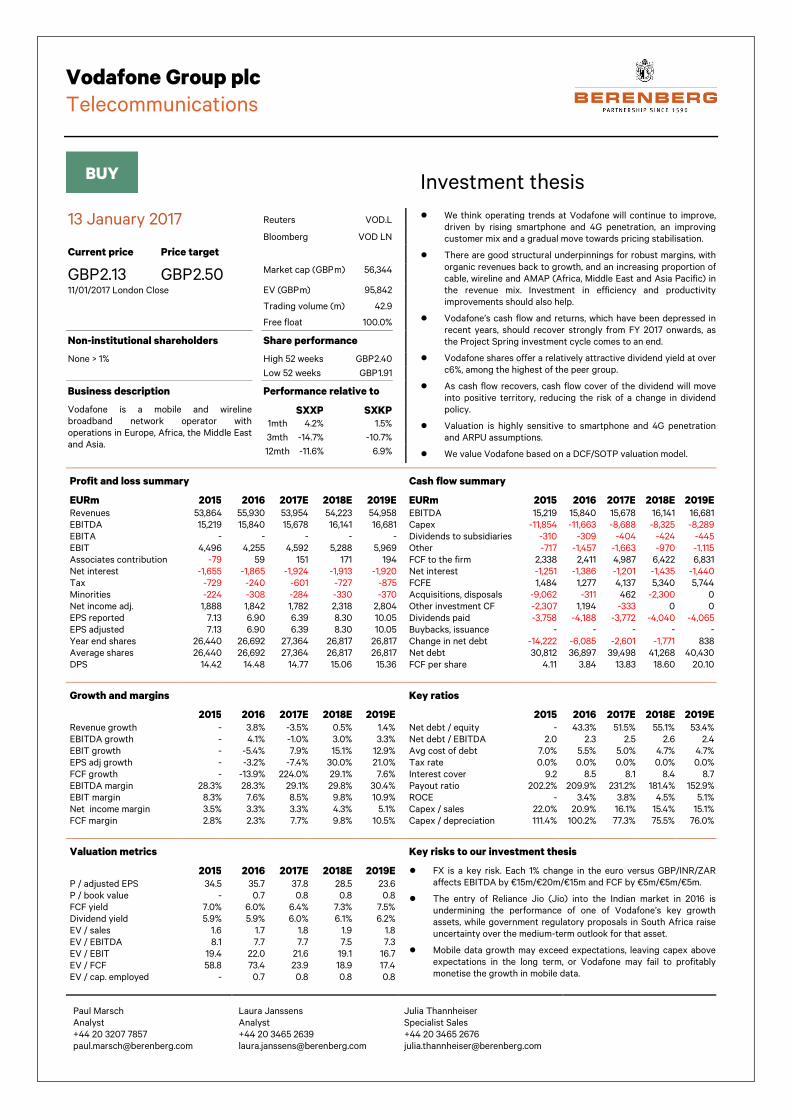

ATLAS ALPHA • THOUGHT LEADERSHIP • ACCESS • SERVICE 13 January 2017 Vodafone Group plc BUY Telecommunications Trimming estimates, reiterating Buy Paul Marsch Analyst +44 20 3207 7857 [email protected] Laura Janssens Analyst +44 20 3465 2639 [email protected] Julia Thannheiser Specialist Sales +44 20 3465 2676 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Telecommunications - Trefis

ATLAS ALPHA • THOUGHT LEADERSHIP • ACCESS • SERVICE

13 January 2017

Vodafone Group plc

BUY

Telecommunications

Trimming estimates,

reiterating Buy

Paul Marsch Analyst

+44 20 3207 7857 [email protected]

Laura Janssens Analyst

+44 20 3465 2639 [email protected]

Julia Thannheiser Specialist Sales

+44 20 3465 2676 [email protected]

Vodafone Group plc

Telecommunications

THE TEAM

Paul Marsch has been with Berenberg since 2009. He was previously head of telecoms

research at Morgan Stanley, where he was consistently very highly ranked. Paul has 20

years’ experience in telecoms research, as well as having worked for five years in the

telecoms industry for Cable & Wireless.

Laura Janssens joined Berenberg in September 2011 and was previously head of global

telecoms research at UBS and head of European telecoms research at Merrill Lynch. She

has also worked at telecoms consultancy Analysys, and at BT. She has 17 years of

telecommunications experience. Laura has been a top-ranked individual analyst in the Extel

survey on several occasions.

Julia Thannheiser joined the Berenberg specialist sales desk in May 2013. Prior to this, she

spent over three years as a telecoms analyst at UBS. Julia holds a BSc from the University

of Maastricht and an MSc from Cass Business School.

For our disclosures in respect of Article 20 of Regulation (EU) No. 596/2014 of the

European Parliament and of the Council of 16 April 2014 on market abuse (market abuse

regulation - MAR) and our disclaimer please see the end of this document.

Please note that the use of this research report is subject to the conditions and restrictions

set forth in the disclosures and the disclaimer at the end of this document.

Vodafone Group plc

Telecommunications

3

Table of contents

Trimming estimates, reiterating Buy 4

Investment thesis 5

Vodafone Group plc – investment thesis in pictures 6

Swings and roundabouts, but we will still own it 7

Dividend drives valuation appeal 13

Estimate changes 21

Appendix: Operating KPIs and background data 33

Financials 43

Vodafone Group plc

Telecommunications

Trimming estimates, reiterating Buy

● Trimming estimates, reiterating Buy: We trim our estimates but reiterate our Buy case, as we still believe that the market will come to value Vodafone’s relatively attractive dividend yield as cash flow cover continues to rebuild. A 1% reduction to our FY 2017-19E “organic” group revenue and EBITDA estimates plus a 1-3ppt drag from adverse currency movements in Egypt and Turkey results in 2-4% reductions to our reported group revenue and EBITDA estimates. We reduce our estimates for Vodafone India on increased uncertainty (competition and demonetisation), while our Italy estimates are trimmed to reflect caution ahead of Iliad’s (ILD) entry, which we expect in H2 2017. These reductions are largely offset by higher estimates for almost all Vodafone’s other business units, reflecting strong trends in Q3, and encouraging signs in Germany and Spain into Q4 (eg competitor price increases). Our 250p price target is unchanged with reduced estimates offset by the extension of our price target date to end-March 2018.

● Dividend yield of 6.1% is 33% higher than peers: Vodafone’s dividend yield is among the most attractive of its large cap peer group. Among peers there are few we would own at present (BT Group, KPN, Telefónica Deutschland), so Vodafone, trading in line with peers on EV/EBITDA, EV/OpFCF and FCF yields, stands out with its 6.1% dividend yield, 33% above peers, with falling risk as FCF cover rebuilds after Project Spring.

● H2 revenues to slow, but medium-term growth unaffected: We expect Q3 group organic service revenue growth to slow to +1.6% yoy from +2.4% in Q2, as pressure in India builds, with a further modest slowdown to +0.8% yoy in Q4 as German cuts to mobile termination rates (MTR) bite and the “comp” gets tougher after last year’s leap year. Beyond that, we believe that Vodafone can sustain a medium-term revenue CAGR of 1.5% pa, with good structural and self-help drivers for margin expansion, against a backdrop of falling capex/sales. Hence dividend cover should rebuild to 1.5x/1.2x (pre/post-spectrum) by FY 2020E.

● Upside case to 336p: Revenue growth and margins +1ppt above our respective estimates, combined with upside from potential in-market consolidation deals in India (Vodafone + Idea), Germany and the UK (Vodafone + Liberty Global), would raise our price target to 336p per share.

● Downside case to 182p: Revenue growth and margins 1ppt below our expectations, combined with capex/sales 1ppt above our expectations would see our price target fall to 182p. The risks are skewed to the upside.

13 January 2017

BUY

Current price

Price target

GBP 2.14

GBP 2.50

12/01/2017 London Close

Market cap (GBP m) 56,674 Reuters VOD.L Bloomberg VOD LN

Changes made in this note

Rating: Buy (no change) Price target: GBP 2.50 (no change)

Estimates changes 2017E 2018E 2019E

old ∆ % old ∆ % old ∆ %

Sales 43,406 -1.8 44,289 -3.3 45,076 -3.7

Ebitda 12,629 -1.9 13,088 -2.6 13,683 -3.7

EPS 5.03 0.0 5.93 10.3 7.83 1.1 Source: Berenberg estimates

Share data

Shares outstanding (m) 27,364 Enterprise value (GBP m) 96,172 Daily trading volume 42,900,000

Interactive model click here to explore

* there may be a delay for the new estimates to be

updated on the interactive model

View all interactive models in Telecoms

Y/E 31/3., EUR m 2016 2017E 2018E 2019E 2020E 2021E

Sales 55,930 53,954 54,223 54,958 55,805 56,661 EBITDA 15,840 15,678 16,141 16,681 17,222 17,820

Operating Profit (adj.) 4,255 4,592 5,288 5,969 6,702 7,474

Net Income (adj.) 1,842 1,782 2,318 2,804 3,465 4,059 EPS (recurring) 6.90 6.39 8.30 10.05 12.41 14.54

DPS 14.48 14.77 15.06 15.36 15.67 15.98

DPS (GBPp) 11.45 12.44 13.03 13.29 13.55 13.83

Capex (accrued) 11,663 8,688 8,325 8,289 8,290 8,252

Spectrum Investment 4,057 3,095 770 841 1,500 1,500

FCF (company defined) 1,277 4,137 5,340 5,744 6,310 6,749 Net Debt 36,897 39,498 41,268 40,430 39,740 38,693

PE (Adj.) 35.9 38.0 28.7 23.7 19.2 16.4 Dividend Yield 5.8% 6.0% 6.1% 6.2% 6.3% 6.5%

EV/EBITDA (Berenberg adj.) 7.7 7.8 7.6 7.3 7.1 6.9

EV/OpFCF (Berenberg adj.) 16.2 15.9 13.9 13.2 12.7 12.0

FCFE Yield (normalised) 6.0% 6.4% 7.2% 7.5% 7.7% 8.1% FCF Yield (Berenberg adj.) 4.9% 5.1% 5.8% 6.0% 6.1% 6.4%

Capex/Sales 20.9% 16.1% 15.4% 15.1% 14.9% 14.6% Source: Company data, Berenberg

Paul Marsch

Analyst

+44 20 3207 7857

Laura Janssens

Analyst

+44 20 3465 2639

Julia Thannheiser

Specialist Sales

+44 20 3465 2676

Vodafone Group plc

Telecommunications

BUY

Investment thesis

13 January 2017 Reuters VOD.L

● We think operating trends at Vodafone will continue to improve,

driven by rising smartphone and 4G penetration, an improving

customer mix and a gradual move towards pricing stabilisation.

● There are good structural underpinnings for robust margins, with

organic revenues back to growth, and an increasing proportion of

cable, wireline and AMAP (Africa, Middle East and Asia Pacific) in

the revenue mix. Investment in efficiency and productivity

improvements should also help.

● Vodafone’s cash flow and returns, which have been depressed in

recent years, should recover strongly from FY 2017 onwards, as

the Project Spring investment cycle comes to an end.

● Vodafone shares offer a relatively attractive dividend yield at over

c6%, among the highest of the peer group.

● As cash flow recovers, cash flow cover of the dividend will move

into positive territory, reducing the risk of a change in dividend

policy.

● Valuation is highly sensitive to smartphone and 4G penetration

and ARPU assumptions.

● We value Vodafone based on a DCF/SOTP valuation model.

Bloomberg VOD LN

Current price Price target

GBP 2.13 GBP 2.50 Market cap (GBP m) 56,344

11/01/2017 London Close EV (GBP m) 95,842

Trading volume (m) 42.9

Free float 100.0%

Non-institutional shareholders Share performance

None > 1% High 52 weeks GBP 2.40

Low 52 weeks GBP 1.91

Business description Performance relative to

Vodafone is a mobile and wireline

broadband network operator with

operations in Europe, Africa, the Middle East

and Asia.

SXXP SXKP

1mth 4.2% 1.5%

3mth -14.7% -10.7%

12mth -11.6% 6.9%

Profit and loss summary

EURm 2015 2016 2017E 2018E 2019E

Revenues 53,864 55,930 53,954 54,223 54,958

EBITDA 15,219 15,840 15,678 16,141 16,681

EBITA - - - - -

EBIT 4,496 4,255 4,592 5,288 5,969

Associates contribution -79 59 151 171 194

Net interest -1,655 -1,865 -1,924 -1,913 -1,920

Tax -729 -240 -601 -727 -875

Minorities -224 -308 -284 -330 -370

Net income adj. 1,888 1,842 1,782 2,318 2,804

EPS reported 7.13 6.90 6.39 8.30 10.05

EPS adjusted 7.13 6.90 6.39 8.30 10.05

Year end shares 26,440 26,692 27,364 26,817 26,817

Average shares 26,440 26,692 27,364 26,817 26,817

DPS 14.42 14.48 14.77 15.06 15.36

Cash flow summary

EURm 2015 2016 2017E 2018E 2019E

EBITDA 15,219 15,840 15,678 16,141 16,681

Capex -11,854 -11,663 -8,688 -8,325 -8,289

Dividends to subsidiaries -310 -309 -404 -424 -445

Other -717 -1,457 -1,663 -970 -1,115

FCF to the firm 2,338 2,411 4,987 6,422 6,831

Net interest -1,251 -1,386 -1,201 -1,435 -1,440

FCFE 1,484 1,277 4,137 5,340 5,744

Acquisitions, disposals -9,062 -311 462 -2,300 0

Other investment CF -2,307 1,194 -333 0 0

Dividends paid -3,758 -4,188 -3,772 -4,040 -4,065

Buybacks, issuance - - - - -

Change in net debt -14,222 -6,085 -2,601 -1,771 838

Net debt 30,812 36,897 39,498 41,268 40,430

FCF per share 4.11 3.84 13.83 18.60 20.10

Growth and margins

2015 2016 2017E 2018E 2019E

Revenue growth - 3.8% -3.5% 0.5% 1.4%

EBITDA growth - 4.1% -1.0% 3.0% 3.3%

EBIT growth - -5.4% 7.9% 15.1% 12.9%

EPS adj growth - -3.2% -7.4% 30.0% 21.0%

FCF growth - -13.9% 224.0% 29.1% 7.6%

EBITDA margin 28.3% 28.3% 29.1% 29.8% 30.4%

EBIT margin 8.3% 7.6% 8.5% 9.8% 10.9%

Net income margin 3.5% 3.3% 3.3% 4.3% 5.1%

FCF margin 2.8% 2.3% 7.7% 9.8% 10.5%

Key ratios

2015 2016 2017E 2018E 2019E

Net debt / equity - 43.3% 51.5% 55.1% 53.4%

Net debt / EBITDA 2.0 2.3 2.5 2.6 2.4

Avg cost of debt 7.0% 5.5% 5.0% 4.7% 4.7%

Tax rate 0.0% 0.0% 0.0% 0.0% 0.0%

Interest cover 9.2 8.5 8.1 8.4 8.7

Payout ratio 202.2% 209.9% 231.2% 181.4% 152.9%

ROCE - 3.4% 3.8% 4.5% 5.1%

Capex / sales 22.0% 20.9% 16.1% 15.4% 15.1%

Capex / depreciation 111.4% 100.2% 77.3% 75.5% 76.0%

Valuation metrics

2015 2016 2017E 2018E 2019E

P / adjusted EPS 34.5 35.7 37.8 28.5 23.6

P / book value - 0.7 0.8 0.8 0.8

FCF yield 7.0% 6.0% 6.4% 7.3% 7.5%

Dividend yield 5.9% 5.9% 6.0% 6.1% 6.2%

EV / sales 1.6 1.7 1.8 1.9 1.8

EV / EBITDA 8.1 7.7 7.7 7.5 7.3

EV / EBIT 19.4 22.0 21.6 19.1 16.7

EV / FCF 58.8 73.4 23.9 18.9 17.4

EV / cap. employed - 0.7 0.8 0.8 0.8

Key risks to our investment thesis

● FX is a key risk. Each 1% change in the euro versus GBP/INR/ZAR

affects EBITDA by €15m/€20m/€15m and FCF by €5m/€5m/€5m.

● The entry of Reliance Jio (Jio) into the Indian market in 2016 is

undermining the performance of one of Vodafone’s key growth

assets, while government regulatory proposals in South Africa raise

uncertainty over the medium-term outlook for that asset.

● Mobile data growth may exceed expectations, leaving capex above

expectations in the long term, or Vodafone may fail to profitably

monetise the growth in mobile data.

Paul Marsch

Analyst

+44 20 3207 7857

Laura Janssens

Analyst

+44 20 3465 2639

Julia Thannheiser

Specialist Sales

+44 20 3465 2676

Vodafone Group plc

Telecommunications

Vodafone Group plc – investment thesis in pictures

Vodafone offers among the most attractive dividend yields;

Vodafone’s dividend yield, declared in euros, now exceeds

6.1%and is among the most attractive in the sector, we believe.

Dividend cover Dividend cover Dividend cover Dividend cover –––– we forecast it to rise we forecast it to rise we forecast it to rise we forecast it to rise furtherfurtherfurtherfurther

Dividends are covered by recurring FCF from FY17; group Dividends are covered by recurring FCF from FY17; group Dividends are covered by recurring FCF from FY17; group Dividends are covered by recurring FCF from FY17; group

dividend policy is to pay a rising dividenddividend policy is to pay a rising dividenddividend policy is to pay a rising dividenddividend policy is to pay a rising dividend

Source: Berenberg estimates. Note: * Telefónica dividend includes is based

on EUR0.40 cash

Source: Company data, Berenberg estimates

Organic financial trends have improved

Recovery in revenue trends has been followed by EBITDA and adjusted operating profit.

Source: Berenberg estimates

Capital intensity should fall further

The high capex of Project Spring is in the rear-view mirror, and

capital intensity should fall further in coming years.

Upside to GBP3.36, downside to GBP1.82

With faster revenue growth, higher margins, and deal potential

could see upside to GBP3.36. If revenues and margins are weaker,

and capex higher than we expect, downside to GBP1.82 exists.

Source: Company data Source: Berenberg estimates

0.0

%

3.0

% 3.6

%

3.7

% 4.4

%

4.4

%

4.5

%

4.5

%

4.6

%

4.8

% 5.4

%

5.5

%

5.8

%

6.1

%

6.4

% 6.9

%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

TI

(Ord

s)

TD

C

KP

N

DT

E

BT

TE

F*

OR

A

TI

(sa

vs)

Av

g.

SC

MN

TLS

N

PR

OX

TN

OR

VO

D

TE

FD

Te

le2

Dividend yield (2017E)

-2.3% -3.0% -2.8%-0.4%

1.0% 2.0% 2.3%

-2.7%

-11.0% -10.0%

-3.6%

1.9%3.6% 4.3%

2.0%

-28.2% -29.9%

-16.4%

-5.9%-1.6%

11.4%

-35.0%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

H1/14 H2/14 H1/15 H2/15 H1/16 H2/16 H1/17

Vodafone group organic revenue and EBITDA trends (HY yoy %)Group service revenues Adj. EBITDA Adj. Op Profit

11854 11663

8688 8325 8289 8290 8252

22.0%20.9%

16.1%15.4% 15.1% 14.9% 14.6%

0.0%

5.0%

10.0%

15.0%

20.0%

2000

4000

6000

8000

10000

12000

14000

FY15 FY16 FY17E FY18E FY19E FY20E FY21E

Ca

pe

x/s

ale

s %

Ca

pe

x £

m

Vodafone capex (€m) and capital intensity (%)

Project Spring capex

Vodafone Group plc

Telecommunications

7

Swings and roundabouts, but we will still own it

60-second summary

We update our estimates and reiterate the buy case, citing the attractive peer group-leading dividend yield. Our estimates are revised down modestly, primarily reflecting increased uncertainty in India (Jio entry and demonetisation), our cautious medium-term view on Italy (Iliad entry), and adverse FX movements in Egypt and Turkey. The organic impact is largely compensated by increased estimates across most of Vodafone’s other business units.

Our price target is unchanged at 250p as we roll forward our price target date to March 2018. We cite an upside case of GBP3.36 in the event of better than expected revenue growth and margins, and synergies from potential deals in India (Idea), Germany and UK (both with Liberty Global). We cite a downside case to GBP1.82 in the event that revenue growth and margins fall short of our expectations, and capex/sales ends up higher than we expect.

The basic Vodafone story of low-single-digit revenue growth, expanding margins, and falling capital intensity remains intact, allowing recovery in FCF to cover the dividend. The shares trade in line with peers on most metrics, but the 6.1% dividend yield stands out at a full 33% higher than the peer group average.

Still worth owning

We think the case for owning Vodafone shares remains intact following a second half of 2016 which saw them underperform both the UK index and the SXKP peer group (once adjusted for currency). There have been some developments over that period that have marginally eroded the bull case on the shares, but on balance we think the positives for the equity case still outweigh the negatives.

When we laid out our investment case for Vodafone shares in mid-2016, we highlighted:

● the appeal and reducing risk of the Vodafone dividend;

● the appealing diversified and stabilising revenue base;

● the clear structural support for medium-term margin expansion;

● the likelihood of capital intensity declining; and

● the strong medium-term growth in FCF.

We think the investment case for Vodafone shares remains largely intact. Although there are clear challenges to some elements of the story (eg competitive tensions in India, currency devaluation in Egypt, new entrant risk in Italy), there have also been positive surprises such as the strong near-term performance in both Italy and Spain, the robust financial performance in Germany, and the strong EBITDA contributions from many of the smaller business units in both Europe (Portugal, Greece, Netherlands, Other Europe) and AMAP (Turkey, Egypt, Other AMAP).

Figure 1: Vodafone’s dividend yield is 33% above the peer group average

Source: Berenberg estimates

0.0

%

3.0

%

3.6

%

3.7

% 4.4

%

4.4

%

4.5

%

4.5

%

4.6

%

4.8

% 5.4

%

5.5

%

5.8

%

6.1

%

6.4

%

6.9

%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

TI…

TD

C

KP

N

DT

E

BT

TE

F*

OR

A TI…

Avg

.

SC

MN

TLS

N

PR

OX

TN

OR

VO

D

TE

FD

Te

le2

Dividend yield (2017E)

Vodafone Group plc

Telecommunications

8

Figure 2: Vodafone FCF dividend cover should recover to 1.5x/1.2x

(pre/post average spectrum costs) by FY 2020E

Source: Berenberg estimates

Our latest views on the above list are as follows.

● The appeal and reducing risk of the Vodafone dividend: We think this remains the case. We wonder whether the market is missing the natural currency hedge built in to Vodafone’s dividend since it switched to reporting (and declaring dividends) in euros. On FY 2018 estimates, Vodafone now offers a dividend yield of 6.1%, with at least low-single-digit growth possible. There are higher-yielding stocks in the sector, but among the liquid large caps, we would prefer to own Vodafone than alternatives. The dividend appeal itself reflects what we expect to be continued robust financial performance.

● Diversification and stabilisation of the revenue base: In local-currency terms Vodafone has been back in revenue growth territory for several quarters now. The big news of the last quarter was the return to organic service revenue growth in the Europe region, underpinned by a solid performance in Germany, strong growth in Italy and a strong bounce in Spain.

● Clear structural support for margin expansion: Our basic case on Vodafone margins was that they would benefit from: faster growth of higher-margin cable, and higher-margin AMAP revenues; the ongoing migration by Vodafone to own-network in the wireline broadband segment (transferring opex to capex and benefiting EBITDA margins in the process); falling churn (usually accompanied by better margins); Project Spring operating leverage (as Spring opex stopped growing); and investment in productivity projects. We still think this case is intact, with competitive tension in India and incremental caution on Italy partially offset by better margin trends in several other business units (eg Spain, Netherlands, Portugal, Greece, Turkey, Egypt).

● The likelihood of capital intensity declining: If anything, we have increased confidence that Vodafone Group’s capital intensity will decline in the medium term. Guidance at the half-year stage seemed to spook some observers. CFO Nick Read’s guidance for capex/sales to be in the “mid-teens” range for the next few years has typically been taken to imply something in the range 14-16%, with the near term at the higher end of that range, and the medium term towards the lower end. Given the H1/FY 2017 capex/sales of 14.7%, the market seemed spooked by the reiteration of guidance, as it implied H2 capex/sales of c17%. Management has since clarified that there is no change to capex guidance. Furthermore, CEO Vittorio Colao has been increasingly vocal on his cautious view of the near/mid-term potential of 5G, suggesting that 5G capex is some way off having an impact on Vodafone’s financials. Overall then, we remain comfortable with the idea that capital intensity at Vodafone can decline in the medium term.

Vodafone Group plc

Telecommunications

9

Figure 3: EBITDA margins expanding, EBITDA growing faster than service revenues into H1/FY 2017

Source: Berenberg estimates

Figure 4: Declining capex/sales post-Project Spring

Source: Berenberg estimates

● The strong medium-term growth in FCF: Again, we think this aspect of the Vodafone equity story remains intact, with stable low-single-digit revenue growth potential, expanding margins, and falling capital intensity, FCF, pre-spectrum, should be able to grow strongly from last year’s c€1.3bn to our estimated c€3.9bn this year, and on to €4.7bn in FY 2018E and €5.4bn in FY 2019E. That means that Vodafone’s dividend cover should progress from 0.3x in FY 2016E, to 1.03x in FY 2017E, and on to 1.35x by FY 2019E. If we incorporate spectrum on the basis of our expectations for FY 2017 and FY 2018, and our assumption that spectrum costs will average €1.5bn pa in the medium term, then Vodafone’s dividend cover reaches 1.0x by next year (FY 2018), and continues to gradually improve in the medium term.

As with most telcos in our coverage list, there are threats and risks to challenge the equity story. We would specifically highlight the following four risks.

● India – competition/regulation/demonetisation threat: Competitive tensions in the Indian mobile market continued to ratchet through the year-end, with Jio extending its aggressive offers beyond 3 December 2016 to end-March 2017, and Bharti Airtel and Vodafone responding. The TRAI, the regulator, sided with Jio, in an interconnect dispute

-2.3% -3.0% -2.8%-0.4%

1.0%2.0% 2.3%

-2.7%

-11.0% -10.0%

-3.6%

1.9%3.6% 4.3%

2.0%

-28.2%-29.9%

-16.4%

-5.9%

-1.6%

11.4%

-35.0%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

H1/14 H2/14 H1/15 H2/15 H1/16 H2/16 H1/17

Vodafone group organic revenue and EBITDA trends (HY yoy %)

Group service revenues Adj. EBITDA Adj. Op Profit

11854 11663

8688 8325 8289 8290 8252

22.0%20.9%

16.1%15.4% 15.1% 14.9% 14.6%

0.0%

5.0%

10.0%

15.0%

20.0%

2000

4000

6000

8000

10000

12000

14000

FY15 FY16 FY17E FY18E FY19E FY20E FY21E

Ca

pe

x/s

ale

s %

Ca

pe

x £

m

Vodafone capex (€m) and capital intensity (%)

Project Spring capex

Vodafone Group plc

Telecommunications

10

and raised a potential fine of INR30bn against the big three incumbents, including INR10.5bn (€140m) against Vodafone. The Indian government’s demonetisation of INR500 and INR1000 notes has also created uncertainty, particularly for the pre-paid market.

Competitively, Vodafone has responded to Jio through accelerating 4G deployment, with new 4G offers, and by strengthening its voice offers. Vodafone also introduced in Mid-December its M-Pesa “Pay” service allowing merchants and retailers to receive e-payments from their customers without exchanging cash, looking to counter the effects of demonetisation.

We reduced our Vodafone India estimates back in June 2016 ahead of the launch of Jio, and in this report we further reduce our India expectations, forecasting Vodafone India (local currency) service revenue growth to slow from +5.4% yoy in Q2 to +1.5%, -1.7%, -1.9% and -1.3% yoy over the next four quarters. We had previously expected Indian service revenue growth to slow to low-single digits at the trough. Our 2022 local-currency India revenues and EBITDA are reduced by 4% and 7% respectively.

Looking forward, there could be a positive catalyst if and when Jio removes its free offers from the market (expected end-March 2017), and if we see further signs of consolidation in India (in this report, we estimate that synergies arising from a Vodafone+Idea combination could be worth at least 10p/share to Vodafone investors).

● Italy – new entrant risk: We are also lowering our medium-term expectations for Vodafone in India, in anticipation of Iliad’s entry into that market late in 2017. In our Telecom Italia report, Not the bargain it seems, dated 30 September 2016, we wrote in detail about our concerns for the long-term impact of Iliad in the Italian market. Italy is a high churning mostly pre-paid mobile market, with spend per pop broadly in line with European peer markets following two years of price increases, and clear scope for a price discounter to make an impact.

In short, we expect Iliad to gain over 10% share of the Italian mobile market in the long term, with 37% of its gains coming from 3/Wind, 29% from Vodafone and 27% from Telecom Italia. Vodafone has a partial offset through its wireline broadband agreement with Enel Open Fibre, which should enable to extend its successful broadband strategy in Italy. While we suspect Vodafone is inclined to make room for Iliad in the mobile market, we believe there is a risk that Telecom Italia might pre-empt Iliad’s entry with the launch of a second brand aimed at the low end of the market. Our 2020 Vodafone Italy revenue and EBITDA estimates are reduced by 7% and 8% to reflect our caution.

● Emerging markets – currency risk: In the last few months Vodafone has seen currency volatility in two of its second-tier markets, Egypt and Turkey. Egypt devalued its currency by two-thirds, and Turkey has seen its currency devalue by 20% since mid-2016, including a 7% weakening so far in 2017. Egypt and Turkey together account for c8% of Vodafone Group EBITDA and about 22% of Vodafone’s AMAP regional EBITDA.

Both had been delivering strong local-currency revenue growth, and Egypt in particular has shown very good margins in recent periods. Even together they are a relatively small part of the pie for Vodafone, and the effect of adverse FX movements in those markets has been partially offset by continued strengthening of the South Africa rand against the euro (ZAR up 15% since mid-2016), and modest strengthening of the Indian rupee (INR up 3.5% since mid 2016). Back in Europe, the UK pound has bounced off its lows since October 2016, and certain of Vodafone’s other trading currencies have moved favourably (HUF, QAR, KES, AUD, NZD).

● South Africa – medium-term risk from government proposals: One risk we think worth flagging now, although we need to do more work on it as the situation develops, relates to South Africa, where the government has issued a white paper containing quite radical proposals for the reform of the mobile industry. In summary, this white paper on ICT seems to suggest that: 1) the government will create a new national mobile wholesale infrastructure for access by new competitors, MVNOs, etc; and 2) there will be no more spectrum auctions or allocations to private companies – all future high-demand spectrum will be owned by the government wholesale mobile network. Although the detailed meaning of the whitepaper is unclear at this time, the CEO of Vodafone’s competitor MTN suggested that the white paper implies that operators must sell their existing spectrum back to the government for use in the wholesale mobile network. It is not clear what the white paper means for pending allocation and auction of the 700, 800 and 2600Mhz spectrum that was recently cancelled following a dispute between the regulator and the government. Vodafone’s response to the white paper came from

Vodafone Group plc

Telecommunications

11

Vodacom CEO Shameel Jossub at the Q2 results conference call, when he said the following.

“I would like to say that Vodacom is committed to the objectives of the white paper, which is to make broadband more accessible and affordable for all South Africans. The white paper as we currently understand is basically an intent of how government would like to achieve these objectives. For this to take effect, a number of laws and regulations will first need to be changed to give this a legally binding effect. The process could take anything from 18 to 24 months. As it stands, there’s currently a number of grey areas within the policy paper and these are still open for debate. As part of the process, we will have the opportunity to engage. But just to be clear on our stance, we feel that the white paper will not achieve the objectives that are set out, so we have a problem in the how it gets implemented. What we would recommend is a hybrid model and the hybrid model being basically to say let the current networks and the investment that needs to be put in continue to happen, but let's set some spectrum aside for open access so that we don't become the guinea pig for the world, but at least we can give smaller players access to spectrum whilst allowing the bigger networks to continue to flourish and to basically cover rural areas.”

This is one to watch, in our opinion.

Thoughts ahead of Q3/Q4

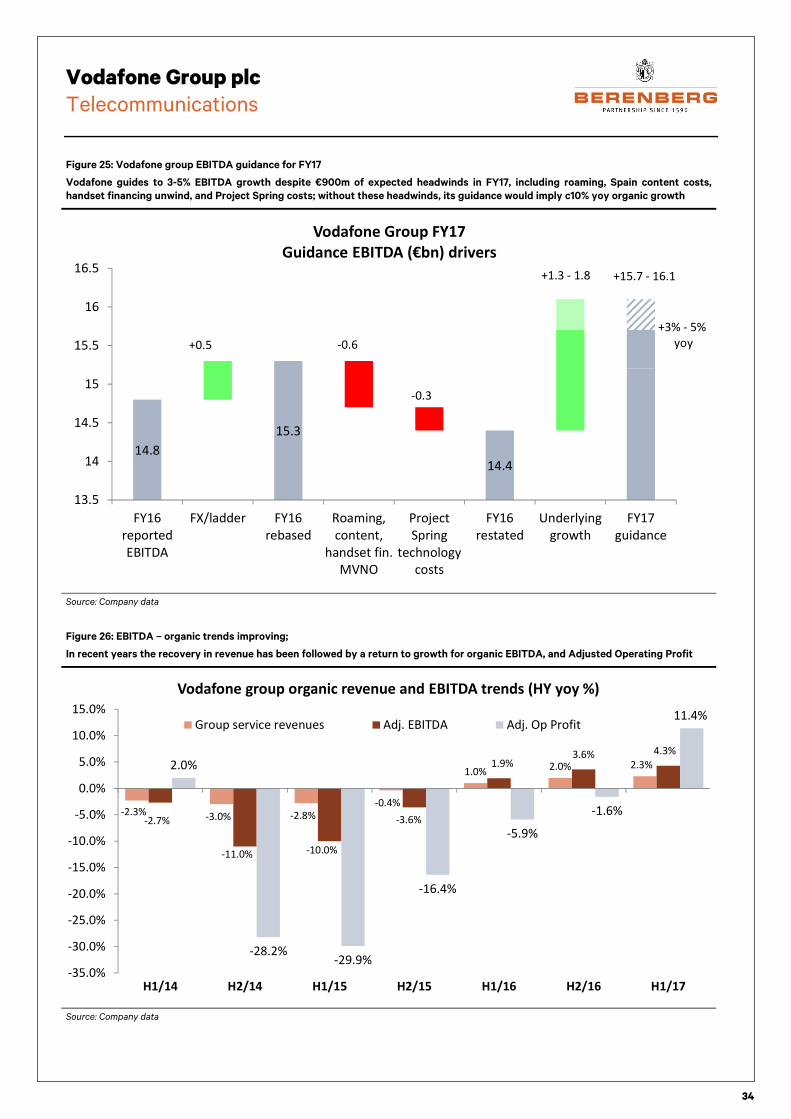

Group organic service revenue trends are likely to slow through Q3 and Q4. We expect Q3 service revenue growth of 1.6% yoy, and Q4 service revenue growth of 0.8% yoy. There are several factors at play.

● German MTR cuts: These will have an impact from Q4, with the 40% cumulative reduction in MTRs over two years equating to a c1.2ppt drag on German service revenues. Vodafone had guided that a 50% cut would drag on German service revenues by 1.5%. The actual cut imposed at 1 December 2016 was 36%, with a further 6% cut in December 2017. We estimate that the 2016 cut will drag by c1ppt on German service revenues, but we have to factor in that the cut only happened at the start of December, so we will see just one month’s impact in Q3, implying a drag of c33bp on German service revenues, and c7bp incremental drag on group organic service revenues. Q4 should see the full 1ppt impact in Germany, but the incremental impact versus Q3 will be only 67bp, translating into 13bp of drag at group level.

● Leap year creates tougher comp: Pre-paid markets in particular will face a tougher comp in Q4 since Q4 FY 2016 benefited from an extra leap-year day. A leap year has the potential to boost growth by c1ppt, so lapping such a boost can potentially also cause c1ppt of drag. However, the leap year would have different effects across the Vodafone revenue base, primarily affecting mostly pre-paid markets like Italy, Egypt, Portugal and Greece. If we weight the theoretical 1ppt drag by the weight of Vodafone’s pre-paid markets in the revenue pie, then the leap year could equate to an incremental drag of around 25bp.

● India slowdown: Indian service revenue growth is likely to slow to reflect continued tough competitive conditions in that market. Since the Q2 stage, there has been incremental bad news, with the extension by Jio of its free offers. While this will have only one month’s impact in Q3, we will see a full quarter’s impact in Q4. We forecast Indian service revenues to slow to 1.5% growth from 5.4% yoy in Q2. That constitutes a 47bp incremental drag on group service revenues in Q3. In Q4 we expect a further slowdown to -1.7% yoy, constituting a further 35bp drag at group level.

In aggregate then, we can identify a total 54bp of incremental service revenue drags in Q3 and a further 73bp of drags in Q4. We believe there may be a number of other small drags which together would have an impact of c30bp as we progress through the next two quarters. On the other hand, there should also be some positive factors at play to partially offset new drags.

● UK: lapping the 08XX drag, easier “comp” in UK enterprise, and in UK carrier;

● Spain: easier “comp” as “out-of-bundle” effects that dragged in recent quarters are lapped, plus the continued unwind of device leasing drag;

● Vodacom: first benefits from new government contract, plus reducing drag from new customer identification rules in Vodacom’s international markets.

Vodafone Group plc

Telecommunications

12

In aggregate then, we think Q3 service revenues could slow to 1.56% yoy, while Q4 revenues could slow to 0.8% yoy.

Slowing growth could raise concern for investors, but we think the growth trend will stabilise into next year with Vodafone capable of generating a medium-term revenue CAGR of c1.5% pa. Figure 15, in a later section of this report, details some of the factors we incorporate into our medium-term estimates.

Figure 5: We expect group organic service revenues to slow into Q3 and Q4 in the face of tougher

comps, India pressure and new regulatory drags (Germany)

Source: Berenberg estimates

-3.8%

-5.2% -5.1%

-4.0% -4.2%

-1.5%

-0.4%

0.1%

0.8%1.2% 1.4%

2.5%2.2% 2.4%

1.6%

0.8%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3

17E

Q4

17E

Group organic service revenue growth (% yoy)

Vodafone Group plc

Telecommunications

13

Dividend drives valuation appeal

Vodafone’s dividend stands out versus peers

The shares really stand out on the dividend, where the valuation relative to the peers has benefited due to GBPEUR currency fluctuations. Given that Vodafone is declaring the dividend in euros, yet the share price is quoted in GBP, the weakening of sterling against the euro has had a beneficial effect on the dividend yield, which has increased to over 6% (6.1% in 2017E rising to 6.4% in 2019E).

This runs counter to our mid-2016 thesis that dividend risk at Vodafone would decline as capex fell after Project Spring, and FCF recovered to cover the dividend both before and after average spectrum costs.

Of course, euro-based investors may feel that they are taking on more currency risk owning a GBP-listed stock in the aftermath of the Brexit vote, but with Vodafone, given that the majority of its earnings, and all of its dividend, are denominated in euros, there should be an inherent hedge built in to the share.

Figure 6 shows how the dividend on Vodafone shares compares with its peer group: we think Vodafone’s dividend has relative appeal compared with most of the names shown.

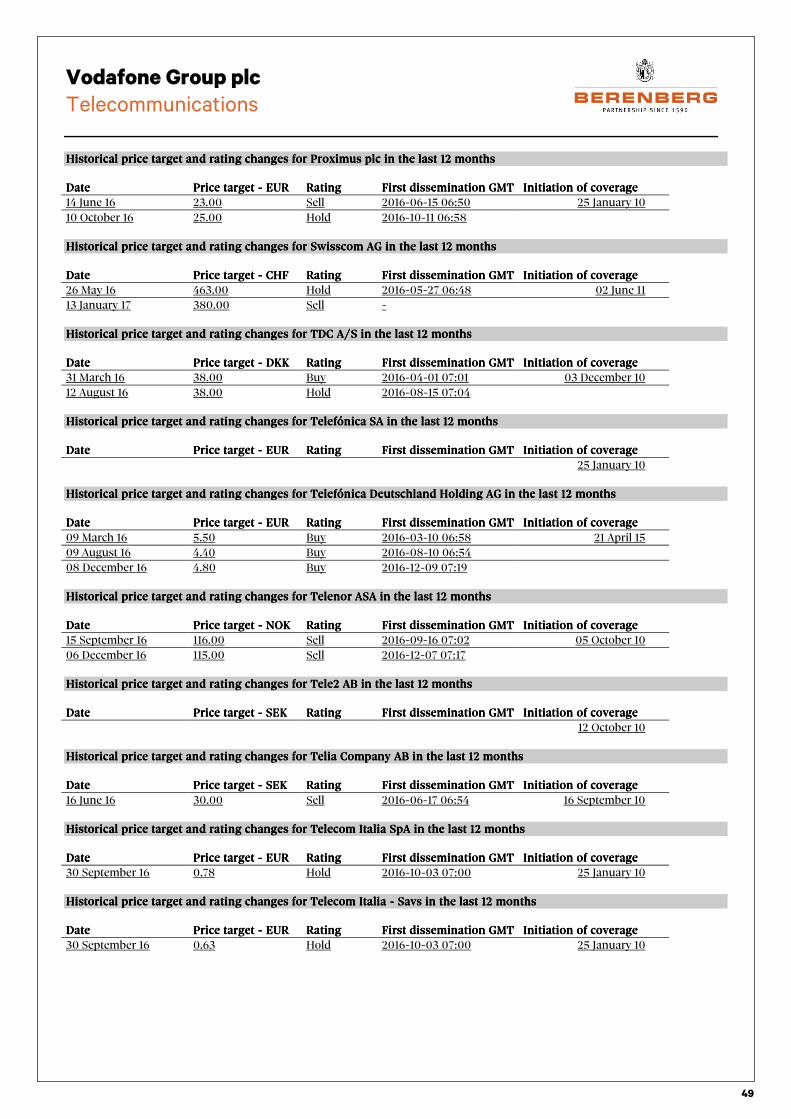

There are higher dividend yields available among the peer group, from Tele2, and from Telefónica Deutschland for example. We like the latter, and have a Buy rating and €4.80 price target: with its limited free float it is relatively small, but we would nevertheless own the shares. We do not like Telenor (Sell, price target NOK115), or Proximus (Hold, price target €25.0, below the current price), and Telia is also a Sell (price target SEK30). Swisscom is now a Sell, with a price target of CHF380. Telecom Italia currently pays a dividend only on its savings shares, and although this is close to the peer group average we have concerns about the challenges it faces in the medium term.

As yet we have no rating on Orange, and Telefónica SA is a Hold, trading close to our price target of €9.6. We like BT shares (Buy), believing there is significant upside to our price target of 506p, but the dividend is well below Vodafone’s, and significant regulatory uncertainty hangs over the shares for now.

Figure 6: Vodafone’s dividend yield is 33% higher than the peer average

Source: Berenberg estimates * TEF dividend based on 40c cash for 2017

Vodafone Group plc

Telecommunications

14

Deutsche Telekom has a lower dividend and less of an upside case than Vodafone, in our view. KPN shares we rate a Buy, with a price target of €3.55, offering significant upside for a relatively cheap stock, but again the dividend yield is well below that offered by Vodafone. Finally, TDC’s dividend yield is the lowest of the incumbent peers (excluding Telecom Italia ordinaries, which do not pay a dividend), and our TDC price target of DK38 is close to the current price.

So, working down the list, and ruling out the names that we either do not like, or that have limited upside, Vodafone stands out as having upside to our price target, significant upside in a “blue-sky scenario” that we discuss later, and pays one of the highest “safe” dividend yields in the sector.

VOD trades in line with peers on EBITDA, OpFCF, and FCF yields

On other valuation metrics, Vodafone trades broadly in line with its peer group on most of the metrics we use (see Figure 7).

● The 7.5x EBITDA multiple for 2017E falls to 7.1x by 2019E, with the shares at a 3-4% premium to the sector over the next three years.

● On EV/OpFCF the shares trade at a 3-5% premium to peers for 2017-19E, with the multiple falling from 13.9x to 12.6x.

● On normalised FCFF yield the shares trade at a 2-3% premium over 2017-19E, as the FCFF yield rises from 5.8% to 6.1%. by 2019E, while on normalised FCFE yield they trade at a more interesting 2.4% discount in 2017E, but this moves to 3% premium by 2019E.

● P/E makes no sense for this stock, given the high proportion of legacy spectrum amortisation and PPA in the numbers.

Price target unchanged

We have left our price target unchanged at £2.50, as illustrated in Figure 12, which sums up the following key components of the valuation:

● €119bn aggregate value of the consolidated business units;

● €6.4bn value of associates Safaricom, Indus Towers, and Vodafone Australia Holdings (note the negative equity value);

● €8.1bn value of tax assets based on the discounted value of savings to cash taxes derived from Vodafone’s tax management (note that our business unit DCFs use normalised cash taxes);

● €39.3bn of net debt adjusted for the outstanding €1.6bn convertible, the remaining €2.4bn Verizon loan note asset, and €1.2bn of minority net debt adjustments;

Figure 7: Vodafone versus peer valuation comparables

Vodafone trades broadly in line with peers on EV/EBITDA, and FCF yields, and offers a relatively attractive dividend yield

Source: Berenberg estimates. “Normalised” figures reflect the effect of cash flow “leakage” (eg spectrum expense, abnormal capex cycles,

headcount reduction costs, and unfunded pension liabilities) by adding the NPV of such leakage to EV, and excluding annual cash outflows from

FCF. In this way the numerator and denominator are consistent and reconciled.

Vodafone

Relative Valuation Comparables 2017 2018 2019 2017 2018 2019 2017 2018 2019

Vodafone 7.5 7.3 7.1 13.9 13.2 12.6 5.8% 6.0% 6.1%

Sector (average) 7.3 7.0 6.8 13.5 12.7 12.0 6.0% 6.1% 6.2%

Premium/(discount) vs simple 3.2% 4.2% 3.9% 2.9% 3.9% 5.2% 2.7% 1.7% 1.0%

Vodafone

Relative Valuation Comparables 2017 2018 2019 2017 2018 2019 2017 2018 2019

Vodafone 7.3% 7.5% 7.8% 28.5 23.6 19.1 6.1% 6.2% 6.4%

Sector (average) 7.1% 7.6% 8.0% 15.9 14.1 14.2 5.3% 5.2% 5.5%

Premium/(discount) vs simple -2.4% 1.3% 3.0% 79.3% 67.1% 34.3% -13.3% -16.6% -13.5%

Div Yield

Adjusted EV/EBITDA

Normalised FCFE Yield

Adjusted EV/OpFCF Normalised FCFF Yield

Adjusted PE

Vodafone Group plc

Telecommunications

15

DCF/SOTP valuation

Figure 8: DCP/SOTP valuation

Source: Berenberg estimates

Revenue EBITDA EV/EBITD OpFCF EV/OpFCF EV

Valuation by Segment €m Code Method FY18 FY18 Multiple FY18 Multiple €m Stake Vodafone % of AV Minority

Germany GE DCF 10,604 3,685 8.2 1,988 15.3 30,344 100.0% 30,344 22.7% 0

o/w KDG GEK DCF 2,440 1,171 11.1 683 19.1 13,028 76.0% 9,901 7.4% (3,127)

Italy IT DCF 5,992 2,172 8.0 1,273 13.6 17,381 100.0% 17,381 13.0% 0

UK UK DCF 6,787 1,357 8.9 407 29.8 12,135 100.0% 12,135 9.1% 0

Spain SP DCF 5,185 1,478 9.6 700 20.2 14,122 100.0% 14,122 10.6% 0

Netherlands NL DCF 1,783 624 7.3 365 12.4 4,545 100.0% 4,545 3.4% 0

Portugal PO DCF 998 359 8.8 210 15.1 3,159 100.0% 3,159 2.4% 0

Greece GR DCF 881 282 5.6 150 10.5 1,578 100.0% 1,578 1.2% 0

Other Europe OE DCF 3,009 903 9.3 451 18.6 8,412 100.0% 8,412 6.3% 0

India IN DCF 6,340 1,680 5.8 729 13.3 9,731 100.0% 9,731 7.3% 0

Vodacom VO DCF 5,848 2,369 8.6 1,550 13.2 20,430 65.0% 13,280 9.9% (7,151)

Turkey TK DCF 2,822 607 5.3 198 16.3 3,216 100.0% 3,216 2.4% 0

Egypt EG DCF 836 383 4.3 257 6.5 1,662 54.9% 912 0.7% (749)

Other AMAP OA DCF 1,967 492 8.3 206 19.9 4,102 100.0% 4,102 3.1% 0

Common function CF DCF 1,400 (250) 15.2 (670) 5.7 (3,796) 94.7% (3,595) (2.7%) 201

Segment totals 54,453 16,141 7.9 7,816 16.3 127,021 93.9% 119,322 96.5% (10,826)

Associates (proportionate value)

Metho

d

EBITDA

FY18 Multiple EV €m

Net (Debt)

€m

Ownershi

p %

Equity

Value

Safaricom Multiple 986 7.0 6,902 259 40.0% 2,864

Indus Towers Multiple 407 10.2 4,147 (170) 42.0% 3,977

Vodafone Australia Holdings Multiple 193 6.5 1,253 (1,660) 50.0% (407)

Total Associate Investments 6,435

Value of tax asset

BV of

DTA €m

% that

benefits

tax Years

Capitalise

at €m

Tax asset 29,121 60.0% 30 7.2% 8,096

Total proportionate asset value

Segments + associates + investments + tax assets 133,853

Adjustments For Group Net Debt and Other Liabilities €m

Group Net debt (@ p/t date) (41,268)

Add mandatory convertible (issued with a view to being covered by VZ loan note proceeds) (1,588)

Offset with Verizon loan note US$ 2,500 FX 1.05 2,376

Adjust for Minorities Share of Net Debt Net debt % Stake Value €m

KDG 3,091 76.0% 742

Vodacom 1,040 65.0% 364

Voda Egypt 0 54.9% 0

Vodafone Qatar 143 38.3% 88

Total Minorities Debt Adjustments to Group EV 4,274 27.9% 1,194

Other Obligations & Liabilities Per 20F Probability €m

Vod Esar (Hutch Cap Gain Tax) $2bn (1,295) 30.0% (389)

Vod Essar (Hutch Cap Gain - Fine) $2bn? (1,295) 30.0% (389) Include?Other 0 0.0% 0

Total Other Obligations & Liabilities (777) Y

Adjustments to EV for leakage Cashflows €m

Spectrum payments (21,587)

Other FCF not captured in segment EV 1,969

Disposals of PP&E 2,368 Include?

Total EV Adjustments (17,251) Y

Total Net Debt & other liabilities (57,313)

Equity Value €m 76,539

FX (GBPEUR =) 1.153

Equity value £m 66,383

Equity Value per share €

Number of shares 000's 27,912

Adjust for mandatory convert share repuchased £m 2,800 @price £: 2.000 Shares: 1,400 26,512

Equity Value Per Share 2.50

Proportionate adjustment

Vodafone Group plc

Telecommunications

16

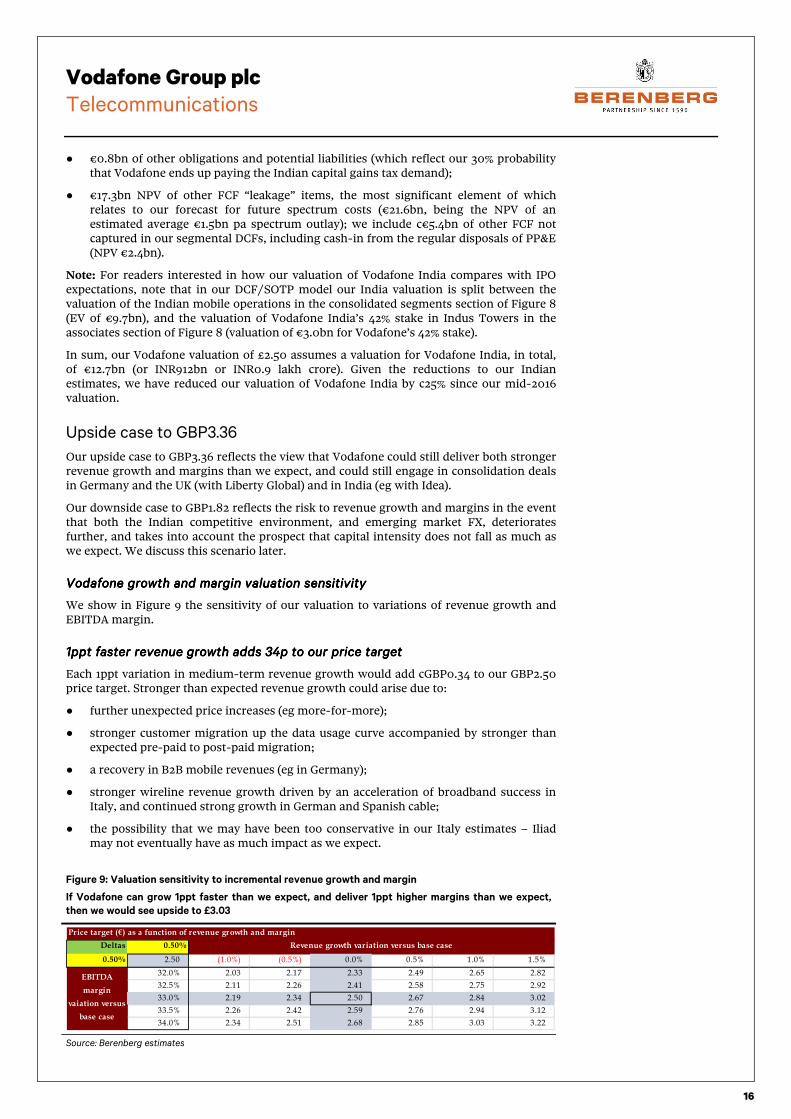

● €0.8bn of other obligations and potential liabilities (which reflect our 30% probability that Vodafone ends up paying the Indian capital gains tax demand);

● €17.3bn NPV of other FCF “leakage” items, the most significant element of which relates to our forecast for future spectrum costs (€21.6bn, being the NPV of an estimated average €1.5bn pa spectrum outlay); we include c€5.4bn of other FCF not captured in our segmental DCFs, including cash-in from the regular disposals of PP&E (NPV €2.4bn).

Note: For readers interested in how our valuation of Vodafone India compares with IPO expectations, note that in our DCF/SOTP model our India valuation is split between the valuation of the Indian mobile operations in the consolidated segments section of Figure 8 (EV of €9.7bn), and the valuation of Vodafone India’s 42% stake in Indus Towers in the associates section of Figure 8 (valuation of €3.0bn for Vodafone’s 42% stake).

In sum, our Vodafone valuation of £2.50 assumes a valuation for Vodafone India, in total, of €12.7bn (or INR912bn or INR0.9 lakh crore). Given the reductions to our Indian estimates, we have reduced our valuation of Vodafone India by c25% since our mid-2016 valuation.

Upside case to GBP3.36

Our upside case to GBP3.36 reflects the view that Vodafone could still deliver both stronger revenue growth and margins than we expect, and could still engage in consolidation deals in Germany and the UK (with Liberty Global) and in India (eg with Idea).

Our downside case to GBP1.82 reflects the risk to revenue growth and margins in the event that both the Indian competitive environment, and emerging market FX, deteriorates further, and takes into account the prospect that capital intensity does not fall as much as we expect. We discuss this scenario later.

VodafoVodafoVodafoVodafone growth and margin valuation sensitivityne growth and margin valuation sensitivityne growth and margin valuation sensitivityne growth and margin valuation sensitivity

We show in Figure 9 the sensitivity of our valuation to variations of revenue growth and EBITDA margin.

1ppt faster revenue growth adds 34p to our price target1ppt faster revenue growth adds 34p to our price target1ppt faster revenue growth adds 34p to our price target1ppt faster revenue growth adds 34p to our price target

Each 1ppt variation in medium-term revenue growth would add cGBP0.34 to our GBP2.50 price target. Stronger than expected revenue growth could arise due to:

● further unexpected price increases (eg more-for-more);

● stronger customer migration up the data usage curve accompanied by stronger than expected pre-paid to post-paid migration;

● a recovery in B2B mobile revenues (eg in Germany);

● stronger wireline revenue growth driven by an acceleration of broadband success in Italy, and continued strong growth in German and Spanish cable;

● the possibility that we may have been too conservative in our Italy estimates – Iliad may not eventually have as much impact as we expect.

Figure 9: Valuation sensitivity to incremental revenue growth and margin

If Vodafone can grow 1ppt faster than we expect, and deliver 1ppt higher margins than we expect,

then we would see upside to £3.03

Source: Berenberg estimates

Price target (€) as a function of revenue growth and margin

Deltas 0.50%

0.50% 2.50 (1.0%) (0.5%) 0.0% 0.5% 1.0% 1.5%

32.0% 2.03 2.17 2.33 2.49 2.65 2.82

32.5% 2.11 2.26 2.41 2.58 2.75 2.92

33.0% 2.19 2.34 2.50 2.67 2.84 3.02

33.5% 2.26 2.42 2.59 2.76 2.94 3.12

34.0% 2.34 2.51 2.68 2.85 3.03 3.22

Revenue growth variation versus base case

EBITDA

margin

vaiation versus

base case

Vodafone Group plc

Telecommunications

17

In our estimate changes today, we have increased our local-currency revenue estimates in Spain, Portugal, Greece, Turkey, Egypt, Other EU and Other AMAP – ie in segments accounting for one-third of Vodafone Group revenues. Where we have reduced revenues estimates, excluding India and Italy, our reductions are driven predominantly by lower equipment estimates.

1ppt higher margins would add 18p tour price target1ppt higher margins would add 18p tour price target1ppt higher margins would add 18p tour price target1ppt higher margins would add 18p tour price target

Each 1ppt variation in medium-term margin would add 18p to our price target (see Figure 10). In our estimate changes today, we have raised EBITDA expectations for Germany, Spain, Netherlands, Portugal, Greece, Turkey, Egypt, Other EU and Other AMAP (ie segments accounting for 55% of group EBITDA).

We note that Vodafone has a target to increase EBITDA margins in all of its business units in the medium term, and it is clear from the plans laid out by CFO Nick Read that it has good self-help options available to it at the business unit level to do so.

In addition, as we have noted in this report, and in prior research, there are structural factors at play that could boost margins more than we expect (eg growth in revenues, improving revenue mix due to faster AMAP and cable top-line growth, the general downward trend in churn rates, operating leverage from Project Spring).

A combination of 1ppt faster revenue growth, with 1ppt higher margin outcome in the medium term, would therefore add c53p to our valuation.

A synergistic India consolidation deal could add at least 10p to our price targetA synergistic India consolidation deal could add at least 10p to our price targetA synergistic India consolidation deal could add at least 10p to our price targetA synergistic India consolidation deal could add at least 10p to our price target

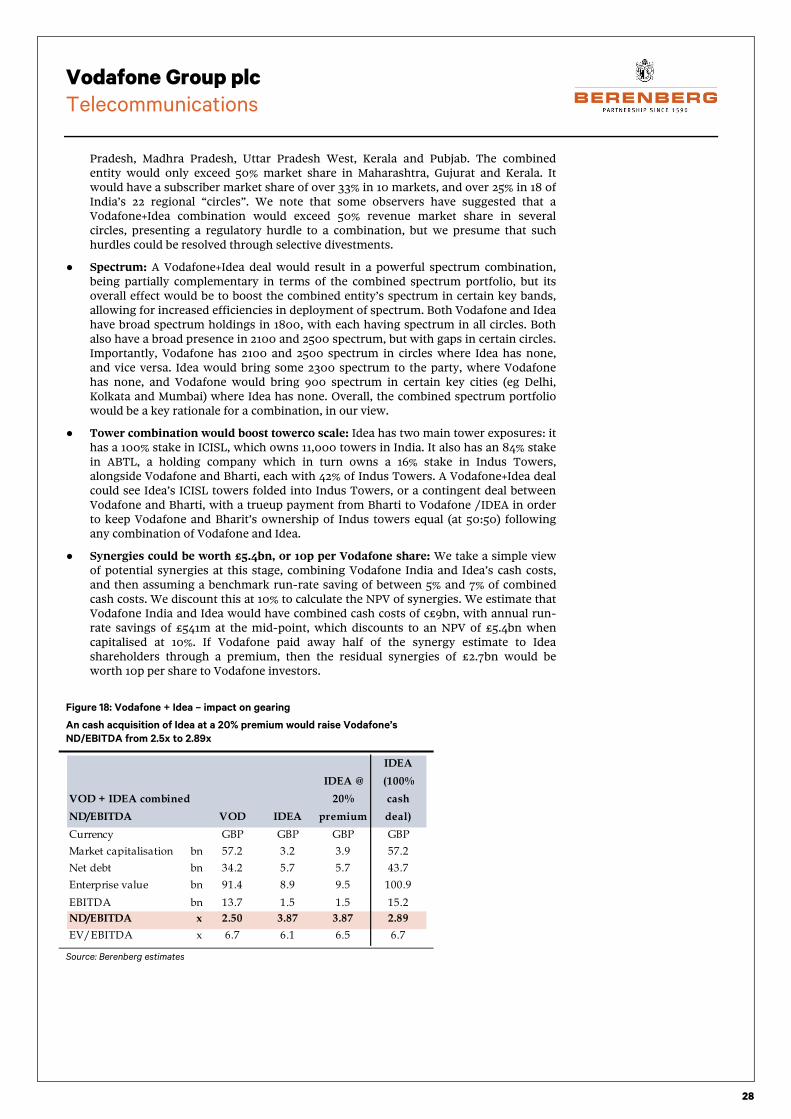

Most observers seem to agree that the Indian market now needs to see consolidation. Idea would make an ideal partner for Vodafone, and a deal on the right terms could release synergies with an NPV of GBP5.4bn, worth 10p per share for Vodafone investors if split equitably with Idea shareholders. We attach a high probability to “something” happening in the Indian market in the near-to-medium term.

Figure 10: Price target risks skewed to the upside

An upside case of 335p exits in the event of 1ppt faster revenue growth, higher margins, a synergistic

India consolidation deal, and further synergistic deals with Liberty Global. A downside case to 180p

could occur if revenue growth and margins are 1ppt lower than we expect, and capex/sales is 1ppt

higher than we expect.

Source: Berenberg estimates

Vodafone Group plc

Telecommunications

18

Further deals with Further deals with Further deals with Further deals with Liberty could release c24p per share of synergiesLiberty could release c24p per share of synergiesLiberty could release c24p per share of synergiesLiberty could release c24p per share of synergies

We continue to believe that further deals between Vodafone and Liberty Global remain possible. On our calculations (see our Vodafone report Upgrading to buy on operating momentum, dated 28 April 2015), we believe that synergies with an NPV of €12.7bn remain to be extracted across Germany and the UK business units of Vodafone and Liberty Global. Again, if split equitably between Vodafone and Liberty Global shareholders, such deals would add 24p to our Vodafone price target. While we still believe in the compelling strategic logic for further deals with Liberty Global, for now we have a higher conviction that “something” will happen in the Indian market than we do in the European arena.

Downside case to GBP1.82

1ppt lower revenue growth and margins 1ppt lower revenue growth and margins 1ppt lower revenue growth and margins 1ppt lower revenue growth and margins would reducewould reducewould reducewould reduce our price target by 47pour price target by 47pour price target by 47pour price target by 47p

What if things turn out the other way around, and revenues and margins are 1ppt lower than we expect? The impact is broadly the same in terms of pence per share, reducing our price target by a combined 47p.

In today’s report we have again reduced our estimates for India, and we have also factored in our concerns about the Italian market pending the entry of Iliad, which we expect in late 2017. Areas where our assumptions may be too optimistic include the following.

● Indian competition effect could turn out to be even worse than we expect: However, we have tried to reflect the likely prospect that Jio will, at some point, have to start charging for its currently “free” services. Not only is Jio’s offer subject to legal challenge by Bharti Airtel, which is also pressuring the regulator (TRAI) to step in and force Jio to start charging, but presumably Mukesh Ambani wants to make some money out of mobile at some point. At present Jio intends to run its free offers through to the end of March 2017.

● Visibility on the effect of demonetisation is very low: Demonetisation is the other big uncertainty in India (the removal of INR500 and INR1000 notes, accounting for c80% of all notes, from circulation, and replacement by new INR500 and INR2000 notes). We have very limited visibility on the impact on mobile consumers and their ability to recharge their mobiles.

● Adverse currency movements: Vodafone has seen two major adverse FX impacts in recent months – in Egypt and Turkey – together accounting for c8% of group revenue and EBITDA. However, the South African ZAR and Indian INR have both strengthened against the euro compared with a year ago, and that has provided a buffer to the drag from Egypt and Turkey. More currency volatility could occur, especially as US President-elect Trump starts to implement his economic policies.

● Further out, South Africa uncertainty could increase: The South African government has made some radical proposals to reform the mobile telecom market, with a white paper currently being debated in the country. The proposals seek to develop better mobile coverage of rural South Africa by creating an industry structure more suited to supporting MVNOs and smaller players. The aim is to renationalise spectrum for use by a government-owned network wholesale business, which will rent access to spectrum to mobile network operators and MVNOs. It is still early days, and the proposals have provoked considerable debate in South Africa, and may be subject to significant changes before being implemented. South Africa constitutes c6% of Vodafone Group revenues and c7% of Vodafone Group EBITDA.

1ppt higher1ppt higher1ppt higher1ppt higher capex/sales capex/sales capex/sales capex/sales would reducewould reducewould reducewould reduce our price target by 20p/shareour price target by 20p/shareour price target by 20p/shareour price target by 20p/share

For all the focus on capex across the sector, telecom valuations are not that sensitive to assumptions about capex/sales. A 1ppt increase in capex sales, which over ten years would mean Vodafone spending an additional €5.3bn cumulative, would take just 20p from our price target once discounted by our WACC of 7.2%. Note that this sensitivity does not change any of our assumptions about revenues or margins, only capex.

On the contrary, we believe that if capex does turn out materially higher than we currently expect it will be accompanied by a higher revenue trajectory than we currently expect, and the impact on value would therefore be less than in our downside case.

Vodafone Group plc

Telecommunications

19

Finally, while we have laid out our upside and downside cases in Figure 10, there is one omission that is worth thinking about. In the event that Vodafone did embark on in-market consolidation deals in India, Germany and the UK, these would be accompanied by a high probability of market repair, which would likely result in higher value for Vodafone, beyond the synergies that we include in our calculations.

The internet of things (IoT): too soon to get excited

We have received a couple of enquiries about the potential upside from the rapid development of demand for IoT applications, following publicity on IoT at the Consumer Electronics Show (CES) in Las Vegas earlier this month. We include more detail on our thoughts below, but at this stage it does not really move the needle enough for us to factor it in to our upside/downside cases.

Huge IoT SIM growth is forecast over the next four to six yearsHuge IoT SIM growth is forecast over the next four to six yearsHuge IoT SIM growth is forecast over the next four to six yearsHuge IoT SIM growth is forecast over the next four to six years

Investors may have noted the growing industry and media excitement about IoT. This year’s CES in Las Vegas was accompanied by numerous IoT product announcements (eg network connected smart hairbrushes!). Vodafone’s German business unit CEO, Hannes Ametsreiter, was recently quoted in the Süddeutsche Zeitung suggesting that global network connected devices could reach up to 500bn units in 2020 from 7bn today – representing a CAGR of 191%.

Other industry observers are certainly predicting very healthy growth for IoT connections over the next four to five years, but estimates vary very widely, and it is very difficult to find estimates on a comparable basis. To illustrate, we summarise two such forecasts in Figures 11 and 12, from Ericsson and IHS.

So why should telecom investors not get So why should telecom investors not get So why should telecom investors not get So why should telecom investors not get carried awaycarried awaycarried awaycarried away by IoT? by IoT? by IoT? by IoT?

At this stage, the revenue and profit upside, albeit large in absolute terms, does not quite move the needle in terms of the size of the global mobile market. For example, the GSMA (an industry association) estimates that global mobile operator revenues in 2015 amounted to $1.1trn.

This revenue base was generated by 7.6bn SIMs and 4.7bn unique customers. From that, we can calculate global ARPS (average revenue per SIM) of c$16.6pcm and ARPU (average revenue per unique user) of $10.25pcm. Embedded within these estimates is existing revenues derived from IoT via from what must be around 300m IoT device SIMs at the end of 2015.

Figure 11: Ericcson IoT estimates

Ericcson provides one of the few estimates we could find that actually breaks down IoT growth into

cellular and non-cellular.

(Billions of units)

ApplicationApplicationApplicationApplication 2016201620162016 2022202220222022 CAGRCAGRCAGRCAGR

Wide-area IoT* 0.4 2.1 30%

o/w cellular IoT 0.4 1.5 25%

Short-range IoT** 5.2 16.0 20%

PC/Laptop/tablet 1.6 1.7 0%

Mobile phones 7.3 8.6 3%

Fixed phones 1.4 1.3 0%

TotalTotalTotalTotal 16.016.016.016.0 29.029.029.029.0 10%10%10%10%

Source: Ericcson Mobility Report, November 2016

* Wide-area IoT relates to devices connected via cellular networks and other forms of radio network (eg LoRa, Sigfoc,

Ingenu)

** Short-range IoT relates to devices connected via non-cellular radio conenctss, (eg near-field, wifi, bluetooth)

Vodafone Group plc

Telecommunications

20

Figure 12: IHS estimates for IoT installed base growth

IHS’s estimates are very different to Ericcson’s, although they predict similarly

impressive growth in the IoT installed base. It is not clear whether IHS estimates

incorporate mobile phones, tablets, etc, or just relate to other types of IoT devices.

Source: IHS

IoTIoTIoTIoT SIM ARPUs are likely to be well below mobile phone ARPUsSIM ARPUs are likely to be well below mobile phone ARPUsSIM ARPUs are likely to be well below mobile phone ARPUsSIM ARPUs are likely to be well below mobile phone ARPUs

Looking forward to 2022, the global mobile industry revenue uplift from IoT is noticeable, but not sufficient, on its own, to materially move the needle. While we do not have any reference point for IoT SIM APRUs, what most industry commentators seem to agree on is that IoT ARPUs will be significantly below mobile phone user ARPUs. This reflects the scale economics of IoT. Industrial scale machine-to-machine (M2M) applications should account for a large proportion of IoT SIMs, while in the consumer market IoT is likely to be characterised by a wide range of applications, covering both narrowband low-speed uses (eg fridge monitoring) and high-speed broadband uses (video security systems). Overall, the expectation is that IoT ARPUs will be significantly lower than typical current mobile phone ARPUs.

IoT growth could boost global mobile industry revenues by 1.2% by 2022IoT growth could boost global mobile industry revenues by 1.2% by 2022IoT growth could boost global mobile industry revenues by 1.2% by 2022IoT growth could boost global mobile industry revenues by 1.2% by 2022

If we assume, just for the sake of illustration, that IoT SIMs generate monthly ARPUs of $1, then we can use Ericcson’s cellular IoT forecast to estimate the revenue uplift from IoT growth to 2022. Ericcson forecasts cellular IoT SIMs to grow from 0.4bn units in 2016 to 1.5bn in 2022, ie growth of 1.1bn SIMs. The revenue uplift, at $1pcm per SIM, would be $13.2bn. In the context of current global mobile industry revenues of $1.1trn (per GSMA estimates), cellular IoT would account for 1.2ppt of growth over the 2016-22 period – in other words, a tiny portion.

At this stage then, assessing the IoT opportunity is a work in progress, but worth flagging given some of the astonishing estimates industry participants are starting to make about IoT SIM growth.

15.417.7

20.423.1

26.730.7

35.8

42.6

51.1

62.1

75.4

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

IoT installed base, global market, (blns)

Vodafone Group plc

Telecommunications

21

Estimate changes

● We cut local-currency revenues on lower equipment sales.

● We cut local-currency EBITDA estimates for India, Vodacom, Italy and the UK.

● We raise local-currency EBITDA estimates for most other business units.

● The net result is modest reductions for organic revenues and EBITDA estimates…

● …compounded by adverse FX in Egypt and Turkey

Changes to revenue and EBITDA estimates presented in this report reflect changes to most of Vodafone’s key business units – these are summarised in Figure 13.

On a currency-neutral basis, our group revenue and EBITDA estimates are not changing very much (see Figure 14). In fact, our revenue estimates are very modestly reduced mostly on account of lower expectations for equipment sales.

Regionally, revenues are trimmed in Europe, and unchanged in AMAP (pre-FX), while EBITDA is raised in Europe and trimmed in AMAP (pre FX), with AMAP reductions just outweighing EU increases.

At EBITDA level, our changes reflect primarily the increased FX pressure from Egypt and Turkey. Beyond FX, our changes to EBITDA reflect the expected variations across Vodafone’s diverse portfolio.

We have adopted a more cautious stance for India (revenues and EBITDA), Italy (revenues and EBITDA, reflecting medium-term caution ahead of Iliad’s entry), Vodacom (EBITDA), and the UK (revenues and EBITDA).

However, we have also adopted a more positive view of developments in most of Vodafone’s other markets, including important ones such as Spain, the Netherlands, Turkey, Egypt, and other smaller business units in both Europe and AMAP.

The net impact of changes to organic estimates is fairly minor downgrades to revenues and EBITDA, amplified by the adverse FX movements in Egypt and Turkey.

Our group FCF estimates would be looking at upgrades for FY 2017-19E were it not for adverse FX, with EBITDA pressure (India), offset by corrections to our overly cautious working capital assumptions. Our FY 2017 net debt figure reflects proceeds from the first tranche of the Verizon loan note maturity.

Figure 13: Revenue and EBITDA estimate revisions(FY 2017-19E), organic (pre-FX)

Source: Berenberg estimates

Business unit/segment

% of group Up/Down? % of group Up/down?

Germany 19.6% ���� 22.8% ����

UK 12.5% � 8.4% ����

Italy 11.1% � 13.5% ����

Spain 9.6% � 9.2% ����

Netherlands 3.3% � 3.9% ����

Other Europe 9.0% � 9.6% ����

Europe 64.8% ���� 67.3% ����

India 11.7% ���� 10.4% ����

Vodacom 10.8% � 14.7% ����

Turkey 5.2% � 3.8% ����

Egypt 1.5% � 2.4% ����

Other AMAP 3.6% � 3.0% ����

AMAP 32.8% �������� 34.3% ����

Reported Revenues 100.2% ���� 100.0% ����

Revenue estimates FY17-19 EBITDA estimates FY17-18

Vodafone Group plc

Telecommunications

22

Figure 14: Estimate changes

Changes reflect mostly adverse FX arising from Egypt and Turkey. In organic terms, we are adopting a more cautious stance on Indian,

UK and South African margins, and in the medium term on Italy. On the other hand we are more positive on EBITDA trends in

Vodafone’s other business units.

Source: Berenberg estimates

Estimate Changes FY17 FY18 FY19 Rationale

Group Revenues €mln

New €mln 53,954 54,223 54,958

Old 54,943 56,061 57,057

Change % (ex FX) (0.7%) (0.8%) (1.2%)

Change % (1.8%) (3.3%) (3.7%)

Consensus 54,206 55,202 55,821

We are above (below) consensus by.. (0.5%) (1.8%) (1.5%)

Group EBITDA €mln

New €mln 15,678 16,141 16,681

Old 15,986 16,567 17,320

Change % (ex FX) (1.1%) (0.3%) (1.4%)

Change % (1.9%) (2.6%) (3.7%)

Consensus 15,721 16,253 16,798

We are above (below) consensus by.. (0.3%) (0.7%) (0.7%)

Group Operating Profit €mln

New €mln 4,592 5,288 5,969

Old 4,680 5,257 6,124

Change % (ex FX) (1.6%) 2.4% (0.8%)

Change % (1.9%) 0.6% (2.5%)

Consensus 4,479 5,150 5,703

We are above (below) consensus by.. 2.5% 2.7% 4.7%

Group Capex €mln

New €mln 8,688 8,325 8,289

Old 8,726 8,650 8,780

Change % (0.4%) (3.8%) (5.6%)

Consensus 8,787 8,604 8,686

We are above (below) consensus by.. (1.1%) (3.2%) (4.6%)

Group FCF

New €mln 4,137 5,340 5,744

Old 3,935 5,453 5,843

Change % (ex FX) 5.6% 1.1% 1.5%

Change % 5.1% (2.1%) (1.7%)

Consensus 4,110 5,243 5,717

We are above (below) consensus by.. 0.7% 1.8% 0.5%

Group Net Debt (reported) €mln

New €mln 39,498 41,268 40,430

Old 41,455 41,011 39,965

Change % (ex FX) (4.8%) 0.2% 0.2%

Change % (4.7%) 0.6% 1.2%

Consensus 39,711 39,712 39,434

We are above (below) consensus by.. (0.5%) 3.9% 2.5%

Reductions to IT, UK, IN, SA partially offset by increases in

GE, SP, NDL, PT, GR, Other EU, TKY, EWG, Other AMAP.

EGP and TKL devalutions are partially offset by other FX

movements.

Near-term uplift in Operating Profit results from IFRS

treatment of NDL D&A as an asset held for sale. BY 2018,

the reduced EBITDA expectations drag on Operating Profit

too.

FCF revisions reflect tougher India and adverse FX, offset by

revised working capital assumptions.

Modest tweaks to capex expectations reflect lower revenues.

Capital intensity assumptions are almost unchanged.

EU revenues reduced by c2% (cuts to GE, IT, NDL, UK,

offset by increases to SP, PO, GR, Other EU). AMAP

revenues increased (SA, TK, EG, Other AMAP, offset by

reductions in IN, SA). Note that estimate reductions relate

primarily to equipment sale assumptions, except in India,

which reflects competition.

FY17 revisions reflects proceeds from Verizon loan note,

while FY18 and FY19 reflect assumption loan note proceeds

will be used to repuchase shares.

Vodafone Group plc

Telecommunications

23

Capturing the moving parts

The Vodafone modelling task these days is about capturing a whole array of moving parts. We summarise our medium-term expectations for Vodafone’s six key business units in Figure 15 below. In short, this suggests a medium-term outlook for Vodafone characterised by the following.

● A robust European performance: This should be underpinned by a solid stable outlook in Germany, revenue and profit growth in Spain, and a medium-term recovery in the UK. We note that price increases occurred over recent weeks in Germany (United Internet) and Spain (Telefónica), and Vodafone’s vigorous marketing and advertising in the UK suggests that problems with its IT systems are starting to fade (even though the financial impacts are likely to drag on numbers for some time).

● Italy challenges: Growing challenges in Italy arise from the entry of Iliad in late 2017, with the potential for pre-emptive moves by Telecom Italia ahead of that. On our Italy mobile market assumptions, Iliad should gain over 10% market share in the long term, with most of that gain sourced from 3/Wind, but with 28.9% of ILDs gain sourced from Vodafone. Vodafone management clearly have a more optimistic view of their ability to accommodate Iliad’s entry to the market, and we may well turn out to be too pessimistic in our assumptions. History is on our side though, and Telecom Italia has already made worrying comments about launching a second low-end brand ahead of Iliad’s launch, so we believe it makes sense to adopt a cautious approach. We discuss our revised expectations for Italy in more detail later in this section.

● India pressure from Jio and demonetisation: Pressure on Vodafone in India, with continued competitive actions by new entrant Jio, and the hard-to-predict effects of demonetisation, means that one of Vodafone’s key AMAP growth assets is struggling to get much above low-single-digit revenue and EBITDA growth in the medium term. We discuss developments in India in more detail later in this section. Our more cautious stance could be challenged if Jio is forced to lift its “free” offers before the end of March 2017, although we do not expect this to happen. In the medium term, our estimates may prove too conservative if we see material in-market consolidation in India, and in this respect we note the combination of Reliance Communications and Aircel, recent press comments on the prospects for Bharti Airtel to acquire Telenor’s Indian operations, and the ongoing “noise” about Vodafone and Idea combining.

● Solid Vodacom: The company is achieving low-single-digit revenue growth and mid-single-digit EBITDA growth. Drags from its international operations should start to fade in the coming quarters, lifting the contribution from those operations (Tanzania, DRC, Mozambique, Lesotho). Data use and 4G adoption should continue to support revenues and the combination of continued South African revenue growth, recovery of growth in Vodacom’s international markets, and a focus on cost efficiencies should allow EBITDA to grow faster than revenues.

● Robust local currency performance across smaller assets: Strong local-currency revenue and EBITDA trends are apparent for the main second-tier assets in Egypt, Turkey and the Netherlands. We note that at the Q2 stage many of Vodafone’s smaller assets surprised positively at either the revenue or EBITDA level, trends that we have reflected in our estimate revisions today.

Therefore, the overall picture for Vodafone’s group revenue and EBITDA outlook continues to feel robust. There are, however, a few areas where we need to be more cautious, and we discuss the two main ones, India and Italy, in more detail now.

India and Italy India and Italy India and Italy India and Italy –––– caution revisited.caution revisited.caution revisited.caution revisited.

In our revised estimates, we have tried to reflect an assessment of the threats and risks facing Vodafone, particularly with respect to two key areas:

● India – competition/regulation/demonetisation threat;

● Italy – new entrant risk.

Vodafone Group plc

Telecommunications

24

Figure 15: Key business unit assumptions

Source: Berenberg estimates

Business Unit

FY16-19

CAGR Comment/Key assumptions: We expect…:

Germany Our estimates take account of:

Service revenues 1.5% - MTR reductions from 1 December 2016 (34%), and again on 1 December 2017 (6%), amount to a cumulative drag of 1.2ppt on revenues

Mobile 0.5% - Unwind of the benefit to revenue growth arising from the reclassification of CPE into service revenues; will drag on FY18 financials

Wireline 2.9% - Likely gradual loss of MVNO revenues from UTDI as it migrates 4G service over to TEFD/E+ in the mid-term

Total revenues 1.0% - Customer mix could see more prepaid offsetting slower postpaid additions

EBITDA 2.1% + Continued more-for-more tariff traction, combined with increasing smartphone penetration and 4G adoption

OpFCF 3.8% + On-going easing of tension with DT in the B2B segment

+ Robust, albeit slowing, underlying cable growth (ex CPE reclassification effect)

+ Easing pressure on the low end mobile segment from DRI/UTDI, and gradual unwind of roaming drag

+ scope for mid-term margin improvement due to full year benefit from synergies, mix and efficiencies

Italy Our estimates take account of:

Service revenues (1.3%) - A slowing pace of recovery in mobile ARPU as the uplift from the price increases of the last two years starts to fade

Mobile (2.1%) - An expect impact from Iliad's entry from end-calendar 2017

Wireline 2.2% - Pre-emptive moves by Telecom Italia ahead of Iliad's entry, eg the introduction of a low-end brand, which may provoke a response

Total revenues (1.1%) + Continued growth in fixed broadband subscribers

EBITDA (1.6%) + A growing benefit as Enel gradually deploys its full fibre footprint to up to 9.5mln premises

OpFCF (3.6%) + Continued, albeit lessening, cost efficiencies

+ Continued benefits from migration of customers off TI wholesale broadband offers, to own sub-loop network, or Enel network

UK Our estimates take account of:

Service revenues 0.3% - A modest threat from SKY's MVNO launch

Mobile (0.2%) - Modest pressure from migration of TALK MVNO to O2 UK

Wireline 2.0% - On-going mix-shift towards sim-only contracts in the market, which impacts service revenues, but aids margin

Total revenues 0.4% + Fading roaming drag

EBITDA 5.5% + Easier 'comp' due to lapping 08XX effect

OpFCF 11.8% + Easier 'comp' in enterprise segment through rest of FY17

+ Fading headwinds from low-margin carrier voice

+ Fading IT cost drags, and on-going efficiency improvements

Spain Our estimates take account of:

Service revenues 2.6% - Modest pricing threat, with VOD to respond on front-book pricing only

Mobile 2.9% - Another rise in content costs in H2

Wireline 1.8% + Easier 'comp' into Q3 arising as out-of-bundle' factors lap

Total revenues 2.5% + Good postpaid adds and rising TV and FBB base

EBITDA 4.7% + Regained commercial momentum after April price increases

OpFCF 7.4% + Continued unwind of the drag from device financing

+ Margin benefit from rising revenues

+ Margin benefit from Ono synergies

India Our estimates take account of:

Service revenues 1.4% - Continuing R Jio pressure arising from extension of 'free' offer to end March 2017, aggressive responses from incumbents

Mobile 1.4% - Data pricing pressure, and flattening of the data user base growth for Vodafone, with incremental data demand going to R Jio

Wireline 2.2% - potential for further MTR reductions (from 14p/min) as suggested by R Jio

Total revenues 1.4% - Demonetisation impacting users ability to recharge prepaid phones with INR 500 and INR1000 notes

EBITDA 2.7% + Robust Q2 voice trends, and some signs of SIM growth recovery in to Q3

OpFCF 13.5% + Postpaid additions remained robust, and we assume prepaid additions start to recover into FY18

+ Lapping drag (2.5ppt) from change to dealer commissions as of Q1 FY17 (note this is excluded from VOD 'organic' figures anyway)

+ Improving economics from secondary circles after roaming terms were recently renegotiated

+ scale benefits to margins as revenues recover in mid-term

Vodacom Our estimates take account of:

Service revenues 3.2% + Reacceleration of subscriber growth

Mobile 3.1% + Particularly in international markets, as drag from new registration procedures eases

Wireline 4.0% + Data users and volumes continue to grow

Total revenues 2.7% + Migration from 3G to 4G drives ARPU uplift (c19%)

EBITDA 5.6% + New government contract comes in to P&L in H2 Fy17

OpFCF 10.9% + Margin uplift as International resumes good growth (only 26% margins)

+ Focus on cost efficiencies, particularly in network

- Mozambique and DRC economic weakness

- Uncertainty created by government telecom's White Paper

Others

Turkey - Growth expected to start slowing in coming quarters from mid-high teens rate in recent years

Egypt - Leap year effect will drag into H2, as will new service revenue VAT. Strong Q2 seasonality effects will also unwind

Netherlands - should see benefits from improved profitability post-divestments, and revenue and opex synergies going forward

Vodafone Group plc

Telecommunications

25