TARIFFS AND TRADE

199

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED MDF/W/52 15 August 1986 Special Distribution PROBLEMS OF INTERNATIONAL TRADE IN FORESTRY PRODUCTS Background Note by the Secretariat Revision1 1Problems of International Trade in Forestry Products was first circulated under the document symbol Spec(84)13. That document was considered by the Working Party on Trade in Certain Natural Resource Products and is herewith re-issued, revised, in follow-up of the Working Party's report (MDF/23), adopted by the CONTRACTING PARTIES on 26 November 1985 (L/5933). 86-1290

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of TARIFFS AND TRADE

GENERAL AGREEMENT ONTARIFFS AND TRADE

RESTRICTED

MDF/W/5215 August 1986

Special Distribution

PROBLEMS OF INTERNATIONAL TRADE IN

FORESTRY PRODUCTS

Background Note by the Secretariat

Revision1

1Problems of International Trade in Forestry Products was firstcirculated under the document symbol Spec(84)13. That document wasconsidered by the Working Party on Trade in Certain Natural ResourceProducts and is herewith re-issued, revised, in follow-up of the WorkingParty's report (MDF/23), adopted by the CONTRACTING PARTIES on 26November 1985 (L/5933).

86-1290

MDF/W/52Page 2

Foreword

(i) The present note is a revised and partly up-dated version ofdocument Spec(84)13 and Add.1, both of March 1984, and of Corr.1 andCorr.1/Suppl.1 thereto. These documents were considered by the WorkingParty on Trade in Certain Natural Resource Products and comments andsuggestions made by the Group, as well as corrections submitted inwriting, are taken up and reflected in the present document. To theextent possible, the note also reflects some recent trade and trade-policy developments of relevance to international trade in forestryproducts.

(ii) For procedural and practical reasons, the product coverage of thesecretariat's note had to be limited, in essence, to the productsclassifiable in CCCN Chapters 44, 45 and 47, e.g. wood and cork andmanufactures thereof (other than furniture) and wood-pulp and cellulose.The limited product coverage notwithstanding, the secretariat did bearin mind the interest manifested by a number of contracting parties instudying also problems of trade for products covered by CCCN Chapter 48,e.g. paper, paperboard and products thereof. One of the countriesinterested in identifying problems of international trade in thatproduct area did present several position papers dealing, in part orwholly (MDF/W/1, MDF/W/3 and Add.1 and NDF/W/49), with forestryproducts' trade-related issues, including also paper and paper products.

(iii) In relation to forestry products trade problems, the WorkingParty, under its Chairman Mr. M. Cartland (Hong Kong), met formally inJune and September 1984 and again in September 1985. In addition, themainly interested delegations met informally, in bilateral orplurilateral consultations, with the Group's Chairman, on a number ofoccasions in the spring and autumn of 1985. Notes on the proceedings ofthe formal meetings are contained in documents MDF/W/2, MDF/W/16 andMDF/W/53. A summary of the Group's main findings, together withsuggestions on possible follow-up, is contained in documents MDF/3 andMDF/23, the Chairman's reports submitted to the GATT Council ofRepresentatives. The report contained in document MDF/23 was forwardedby the Council to the Forty-First Session of the CONTRACTING PARTIES(C/M/194). As noted in document L/5933 and in the Summary RecordSR.41(2, page 15, CONTRACTING PARTIES adopted the report on 26 November1985.

(iv) In the revision of Spec(84)13 - Problems of International Trade inForestry Products - the originally used paragraph numbers have been keptthroughout, if for no better reason than to facilitate reference tocomments made by delegations in relation to specific paragraphs. Somewider ranging comments and certain additional information that has cometo the fore since Spec(84)13 was issued are accommodated in footnotes.

IFor views expressed on dealing with problems of internationaltrade in natural resource products attention is invited to the record ofdiscussions in the Senior Official Group in November 1985, notablydocuments SR.SOG/2 (page 9), SR.SOG/8 (pages 2 and 3) and SR.SOG/11(page 17) and also to PREP.COM(86)SR/3, pages 35-42 and SR/6 - pages 34to 37.

MDF/W/52Page 3

(v) It is realized that a virtually world-wide survey of forestryindustry related activities and of trade and trade problems, as has beenattempted in this note, can never be more than a sketch or overview, andcan never be fully up-to-date. Nevertheless, it is hoped that the dataelaborated and presented in this document will be of some use tocontracting parties, as discussion background material, for theirfurther work. Suggestions by contracting parties for corrections oramendments that may be required would be appreciated.

MDF/W/52Page 4

TABLE OF CONTENTS Page

Foreword 2

INTRODUCTION AND OVERVIEW

Area and product coverage 7Methodology and statistics used 9Recent production and trade developments 10Developments in forestry-industries' technologies 11Forest-policy measures and developments in international

trade of forestry products 13Tariffs and non-tariff measures affecting forestry

products' trade 14Sources and acknowledgement 16

A. FOREST RESOURCES, THEIR USE AND POTENTIAL

General 17Forest resources, by major countries and areas 18Forest land ownership structure and use patterns 20Forest-use policies and objectives 23Protected forest lands, reforestation 24Forest resource appraisals 25Age and species composition of forests, forest management,

forest yields 27Forest die-back problems 29Timber yields as related to tree species and site

conditions 29"Softwood" and "hardwood", definitions 31Climatic factors influencing tree species - composition

of forests 32Major forest tree species of Japan 34Forest-fire data 34Plantation forests and comparative advantage 35Species composition of North-American forests 36Little-known or "secondary" wood species 37

Forest Resources Survey

General 39ECE/FAO/UNEP: Forest Resource Surveys 39Explanatory notes to Table I 40Canada - forestry care and production objectives 41Chile - forestry - industry achievements and targets 42SUMMARY TABLE I (Forest Resources, Wood Production,

Imports, Exports, Trade Balance) 43EC - Forestry policy objectives, wood-industry production

levels and developments 46US forestry products production, trade and requirements 50Japan - forest resources, production, requirements and

trade 51China, Republic of - forest resources and policy measures

and objectives, imports 55Korea, Republic of - afforestation 56Nordic countries - forest resources 56USSR and CMEA countries - forest resources, resource- and

trade developments 57Other countries' and developing countries' forest resource

situation and trade 60

MDF/W/52Page 5

TABLE OF CONTENTS (cont'd) Page

B. PRODUCTION OF MAJOR CATEGORIES OF FOREST PRODUCTS

General 65Explanatory notes to Summary Table II 66Forest products-resource and -industry development,

South Africa Rep. 67New Zealand forest industries' development and targets 67Prerequisites for developing primary forest-products

production, logging and forest-care operations 68Resource accessibility - road infrastructure 70"Floating" 73Wood and cellulose yields in various processing operations 74Disposition of total industrial roundwood production 76Factors contributing to cyclical fluctuation in wood

production and trade 78SUMMARY TABLE II (Per Caput and Total Production of Wood,

Semi-Manufactures and Woodpulp, Net Trade andAvailabilities) 80

ECE and FAO forest products statistics and publications 82Developments in various countries' saw-mill, ply-mill and

pulp production and trade 84

C. INTERNATIONAL TRADE FLOWS IN FORESTRY PRODUCTS

General 88SUMMARY TABLE III-A (Imports and Exports of Wood-, Cork-,

Products thereof and Woodpulp) 89World production and world exports of industrial roundwood 92World production and world exports of sawnwood, plywood,

particle board and woodpulp 93Major importers of roundwood, sawnwood, woodpulp, plywood

and particle board 95SUMMARY TABLE IV-A (Percentage Shares of Different Importers

in Total, in respect of product categoriesreferred to above) 97

IV-B (as above, in respect of exports) 98Major exporters of roundwood, sawnwood, plywood, particle

board, woodpulp 99Technical and marketing characteristics influencing trade-

flows in wood products 100Factors influencing demand for construction grades of wood

in the United States 102Summary data on wood-use in house construction 103House construction, wood-industry activity and -trade in

North America 106House construction and demand for wood products in Europe 107Other factors (including transport, tariff treatment, regional

cooperation, etc.) influencing trade developments forforest-industry products 108

MDF/W/52Page 6

TABLE OF CONTENTS (cont'd) Page

D. TARIFFS AND NON-TARIFF MEASURES AFFECTING TRADE

General 111Private and public ownership patterns 111Pre-Tokyo Round import tariff treatment for various forestry products 112Average duty rates, pre- and post-Tokyo Round, by broad product

categories 114SUMMARY TABLE V-A (Pre- and post-Tokyo Round Tariff Rates, at the

4-digit CCCN position level) 118V-B (Value of Imports from World, at the same level of

detail, and m.f.n. and GSP origin shares in imports) 119Notes on data in the preceding Tables 121Import and/or export duties on forestry products in developing country

areas 122Nominal and effective rates of protection 124Tariff escalation 125Classification criteria 127Distinctions made in tariff schedules for different wood products 128Technical standards, building codes and traditions 131Drawing up technical specifications for little-known woods 133Phyto-sanitary regulations 134Import licensing, controls, restraints, prohibitions 135Other policy measures and action affecting production, prices and trade 135

E. ADDITIONAL NOTES RELATING TO CORK

General 137

ANNEX I-A

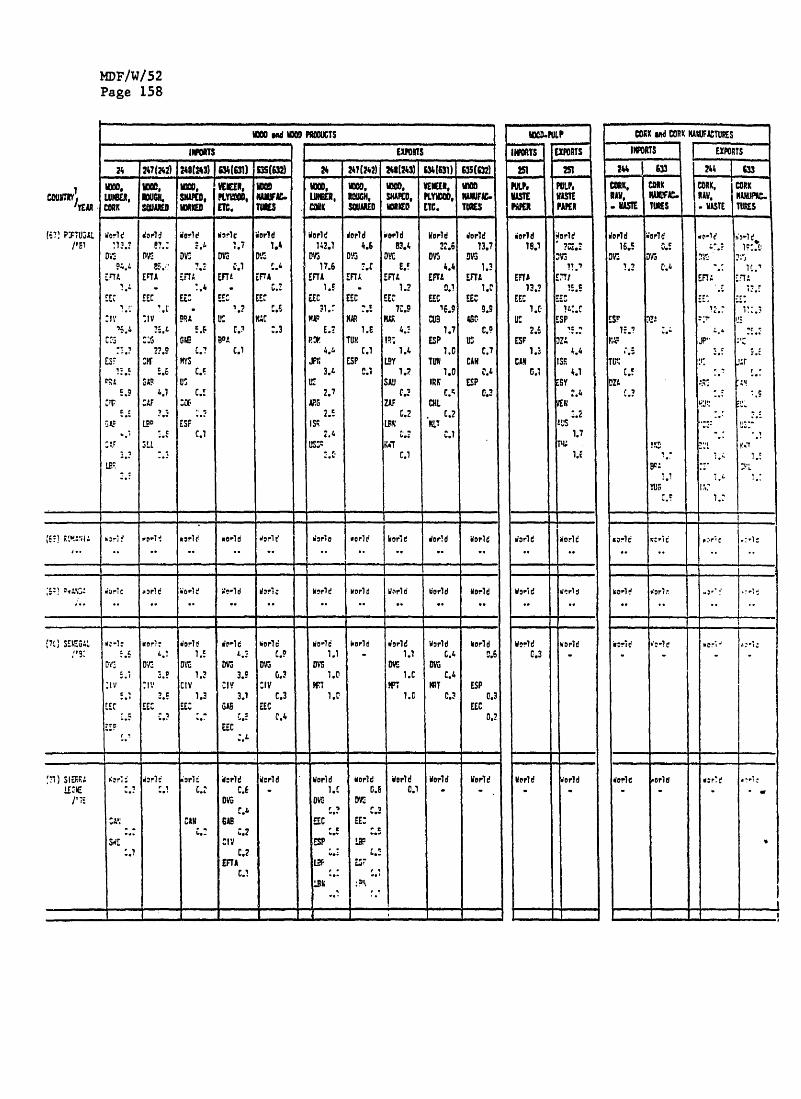

SUMMARY TABLE III-B (Imports and Exports of individual GATT membercountries of wood, cork and products thereof, andof woodpulp, by origins and destinations) 139

- abbreviations used in Table III-B 164

ANNEX I-B

Volume of Production, Exports and Imports of GATT member countries in1963, 1973, 1979 and 1981 of: 165

- Industrial roundwood 166- Pulpwood 167- Sawnwood 168- Plywood 169- Particle-board 170- Fibre-board 171- Woodpulp 172

ANNEX II

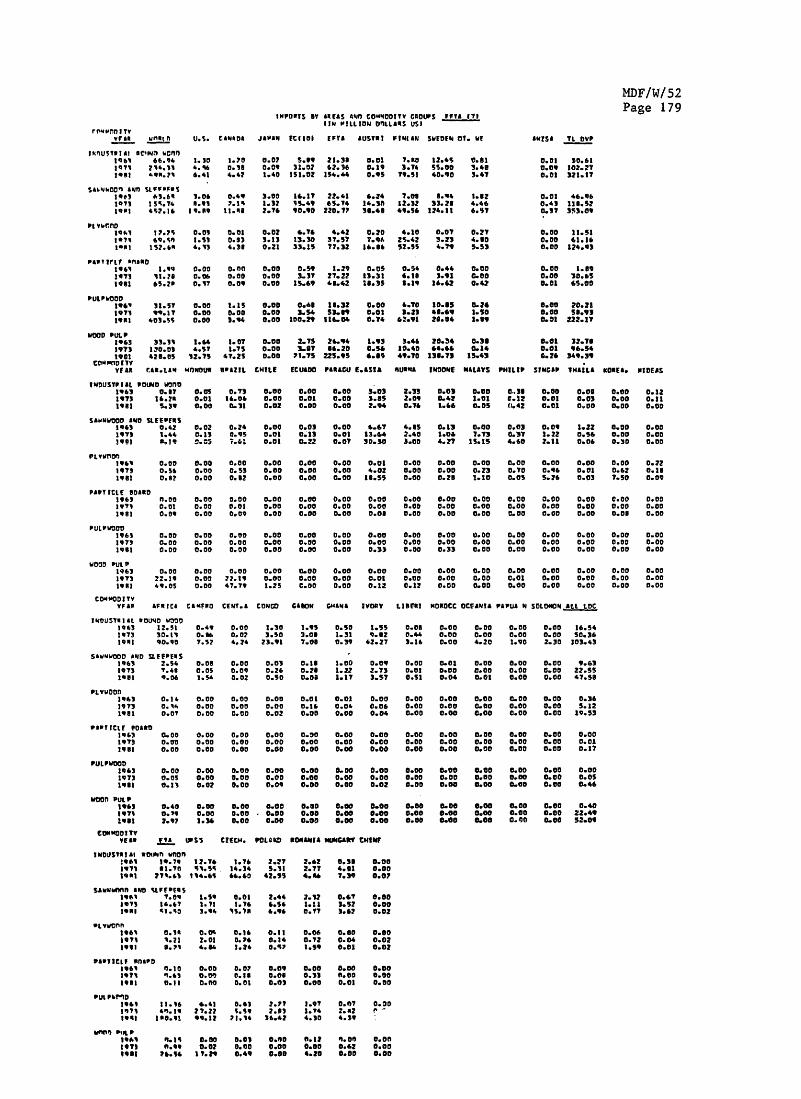

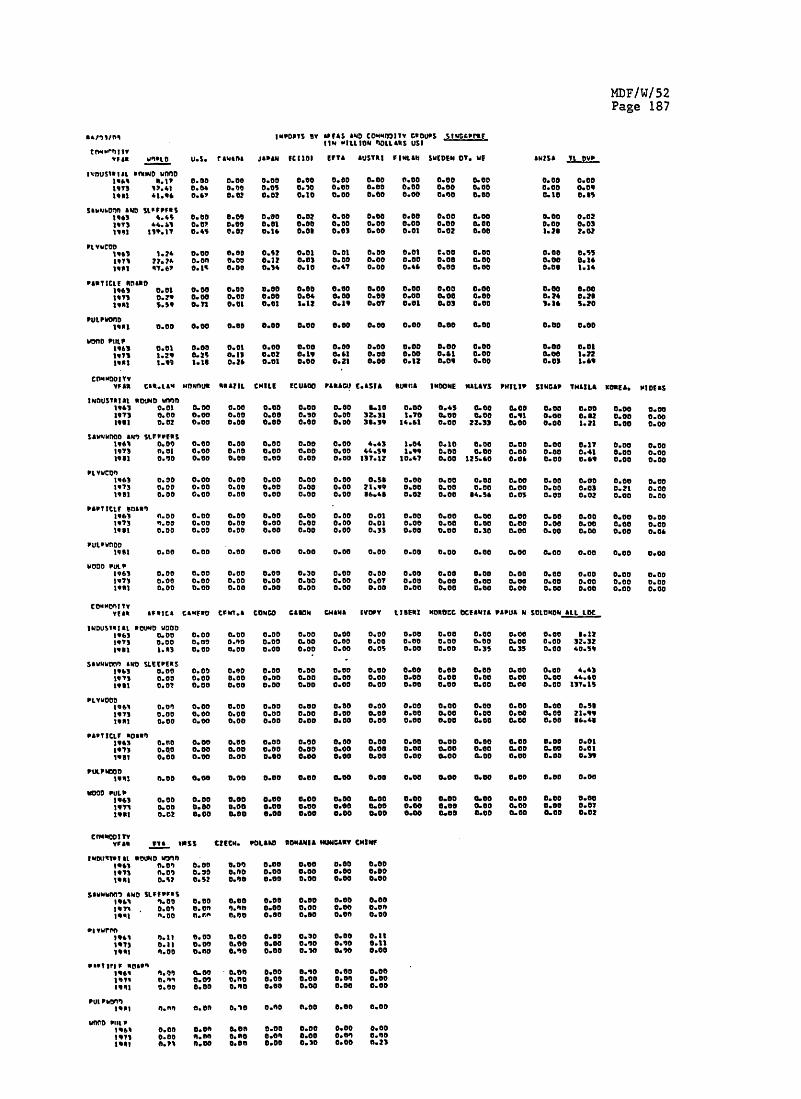

Trade Matrix for Imports of Wood and Wood Semi-Manufacturesand Woodpulp for Major Import Markets - 1963, 1973, 1981 - 173

- Reproduction of headnote texts for several of the text summarytables 196

MDF/W/52Page 7

Introduction and Overview

1. The present information note is one of several background papersthe secretariat was requested to prepare, in follow-up of the November1982 GATT Ministerial Meeting, with a view to addressing problems ininternational trade in various natural resource products, in theirprimary form and as semi-manufactures and manufactured products.

2. Natural and/or managed forests of differing size and tree-speciescomposition are found around the globe and are absent only from theclimatically most inhospitable regions. An attempt is being made inthis note to provide some relevant data for all GATT contractingparties. Summary data relating to resources, production and trade inforestry products are, to the extent possible, also provided in respectof the Republic of China and the USSR.

3. Forests, both the virgin natural forests and forests planted andmanaged in various ways by man, are a planetary resource of greatimportance in maintaining and equilibrating the atmospheric-,terrestrial- and oceanic-carbon cycle, as a source of atmosphericoxygen, as wildlife habitat, floristic gene-bank, for watershedprotection, for recreational purposes and as a source of construction-and fuel-wood, and of vari2us herbs, medicinal plants, - gums, resinsand of several tree fruits and oils, of fibres and of various dyeing-,tanning materials and certain other products for specific industrialuses. Forests are also of importance, in some cases essential,in operating certain agro-forestry activities and, if propery managed,can provide specialized pasture for game-farming operations.

4. Given the many uses to which forest products can be put, thesubject3is potentially a vast one. For practical and proceduralreasons , the present note concentrates on the subject of internationaltrade issues as they relate to wood and cork, and to manufacturesthereof, and to one of the main wood derivatives - pulp. Morespecifically, the products covered in this note are those classified

1There are a number of other countries in Latin America, Africa,Asia and Oceania which are significant producers and exporters offorestry products (including, in the latter region, Papua and NewGuinea), and there are certain other countries, though not among majorproducers, for which forestry exports are actually or potentially ofimportance, but for which, for lack of space, data could not be providedin the Summary Tabulations. Statistics on forestry-production and-trade for these countries are, however, generally available from therelevant FAO forestry statistics and are, to some extent, also providedin footnotes to text-passages and in Annex II.

2There are 20 four-digit headings in CCCN Chapters 1-24 allocatedexclusively or predominantly to various tree-fruits.

3cf: MDF/23, MDF/3; MDF/W/2, 16, 53; C/W/467 and Add.1, MDF/W/49and Corr.1; C/M/183, 187, 188, 190, 191 and 192.

MDF/W/52Page 8

in the Customs Cooperation Council Nomenclature (CCCN) in Chapter 44(wood and wood products), in Chapter 45 (cork and cork products) and inCCCN Chapter 47 (woodpulp). Details of the product coverage in relationto specific tariff headings and positions in these three CCCN Chaptersare shown in Table V.

5. Slightly more than 30 per cent of the earth's land surface iscovered by forests or woodlands. Man has exploited forests whereverforest resources were easily accessible, and where uses and markets forforest products could be found, and has changed, in the process, thenatural vegetation cover. In the more densely populated areas, forestscompete not only with agriculture but also with land-use for urbansettlements, industrial establishments and road networks. In otherareas of the world forests have been thinned out by use for fuelwood,for pasture, and expanding agriculture, shifting cultivation, in somecases to the point of virtual destruction. In many parts of arid andsemi-arid Africa, Asia, South America and certain insular locations thedestruction of forests is of crisis proportions.

6. Given the great diversity of forests in the different areas of theworld, and the way local populations experience their respective forest,there exists no really adequate way of conveying verbally, in a fewsuccinct paragraphs, a picture of the world's forest-cover and-characteristics. In the circumstances, it was thought that, forpurposes of this note, a tabular presentation of some quantitative datawould, perhaps, best convey the extent of possible forest resources.This approach does have some limitations as regards possibilities forexact inter-country comparisons and attention is therefore invited tothe many caveats in the text preceding Table I in Section A.

7. One of the difficulties in dealing with the subject ofinternational trade in wood and wood semi-manufacturers is the profusionof commercially used names for given species of wood and the largenumber of tree species. In the 'Sixties it was considered (Elseviers)that there existed more than 2,500 botanical tree species, and hencespecies of wood. Recent reference books list even more species. Formany of the main species there may exist several sub-species and alsolocal variants of names and designations. Considerable time and effort

1CCCN Chapter 46 covers plaiting materials and products madethereof. These materials and products are not covered in this note, norare bamboo poles or rattan, both of which are classifiable inChapter 14. To the extent that bamboo or rattan has been processed intoa product covered in Chapter 44, the tariff information provided inSection D might be relevant.

2For a development of the question of forest classification andnomenclature see "Tropical Forests Ecosystem - a state of knowledgereport", prepared by UNESCO/UNEP/FAO, 1978. For a short survey of theworld's major forest regions, in terms of wood resources, with a summarydescription of forest characteristics, see "Wood Resources and Their Useas Raw Material", UNIDO/1S.399, Aug. 83 (based on FAO's comprehensiveforest documentation) and, for a short descriptive commentary, a specialissue of the publication "Co-Evolution", No. 15 (83/84).

MDF/W/52Page 9

has been invested by many individuals, research institutions andcommittees in arriving at a uniform international nomenclature for theidentification of the main species used and traded. Even so, thereremain today at least some five hundred different wood species-varietieswhich are of actual or potential significance in international trade.It is clearly beyond the possibilities of a note like this one to dealin any detail with all the possible variants. The approach adopted wastherefore, to examine, first, the existing import tariff schedules ofGATT member countries and, then, to note the kind of distinctions made,by species or otherwise, and, finally, to examine these distinctions andthe effect they may have on trade. On the basis of this examination, itcan be said that the species-distinctions in the tariff schedules ofGATT member countries are, on the whole, quite limited. Nevertheless,such species-distinctions as do exist in the tariff schedules could, insome cases, be a source of uncertainty as to what tariff treatment isapplicable to a given wood variety, or to the products made thereof.

8. As regards statistical tabulations, two approaches have beenadopted. One, as in Table I - Section A, attempts to provide a"snapshot", as it were, of the situation at a given moment, bringingtogether various elements which, it is hoped, will permit an overallimpression to be gained of forest resources, current forestry productionand use and the Interaction of resources and needs on trade flows.Similarly, in Table II - Section B, it is attempted to providefollow-through data on timber availabilities, the primary manufacturingstages which the available timber undergoes in given countries (takingaccount also of net imports or exports) and, finally, an account of thetype and approximate volume of wood semi-manufactures and of woodpulpavailable for further processing. The juxtaposition of the various datais not without risk and in order to avoid, to the extent possible,misleading conclusions to be drawn from these summary tabulations,relating to one year only, attention is invited to the variousqualifying remarks in the text of this note. The second approach is ofthe more customary nature, setting out statistical data on trends inproduction and trade by means of time-series tabulations; these areshown in Annex I-B and Annex II.

9. Given the vast amount of forestry data which are compiledworldwide and the practical difficulties not only in presenting these,but also in reading tightly packed statistical tables, this note optsfor selectivity, limiting the data presented for forest resources andproduction in the summary tabulations to 1979. For import and exportdata in Table III (which also gives origins of import and exportdestinations) and in Table IV, the data shown were the latest available(up to 1982) when Spec(84)13 was issued. Data in Section D (Table V)are, again, the latest available or, for MTN trade concessions, thefinal MTN tariff rates (i.e. those applied as of 1.1.1986, or1.1.1987). As regards Annex I-B, production and trada data are shownfor 1963, 1973, 1979 and 1981. Data covered in the trade matrix in

1Among these, dealing with a wide range of forestry-researchrelated topics, the International Union of Forestry ResearchOrganizations (IUFRO), founded in 1891-92, might be cited. Today, IUFROhas a membership of about ten thousand scientists, and 500 institutesfrom 85 countries - united in promoting international co-operation inforestry research activities.

2An indication is also provided of import duty reductions to bephased in by Japan over the period 1986 to 1988.

MDF/W/52Page 10

Annex II cover 1963, 1973 and 1981, unless otherwise indicated. Theyear 1963 was chosen as a point of departure, because UN statisticsavailable for that year are more readily comparable with statistics forsubsequent years than the pre-1963 data. 1973 seemed a logicalinterval, was a year of high-level wood industry activity in NorthAmerica, but is also the year in which the post-war housing constructionboom in Europe came to an end; 1979 was chosen because much of theresource/cum/production statistics available from different sourcescould be related to 1979/80 and, finally, 1981 was chosen as the yearfor which data for a considerable number of countries were available atthe time of writing. Several of the developed countries in 1984 and1985, saw a recovery in forestry industry product:Lon and trade, oftenfalling short, however, of the peak levels reached in the mid 1970's, orin 1979. Nevertheless, the data for these earlier years do provide anindication of most countries'forestry related activities and interests.Certain recent trade developments are, to the extent possible,identified separately in later parts of this note.

10. While only a relatively small part of the world's total forestryproducts production moves into international trade (say, around 10 percent, in terms of the volume of industrial roundwood productionequivalent) exports of wood-, cork- and semi-manufactures thereof and of

IThe trade situation, which, for practical purposes, in Spec(84)13had to be frozen in 1981/82, has, of course, further evolved. While theperiod 1981 through the first half of 1983 can, in general, becharacterized as recessionary, for both production and trade in forestryproducts, an improvement in trade opportunities and in the actual volumeof trade flows, particularly those destined to the United States, can benoted as from the second half of 1983, when - in some cases - the highpoints reached in the 1970s were again attained, or even surpassed, withsome exceptions, notably a stagnation or even decline in the volume ofshipments of tropical wood semi-manufactures from Africa to Europe, areflection of the recession in housebuilding and construction activityin Europe (Imports of tropical sawnwood into Europe peaked in 1979).The upturn in demand for forestry products in certain markets over thelast two years notwithstanding, the profitability record of the forestproduct industries was rather mixed, depending not only on past andpresent management results of the enterprises concerned, but dependentalso on the structure of firms, with those firms that could benefit fromthe earlier and more significant upturn in demand for such downstreamproducts as pulp, paper and paper products experiencing generally betterreturns than firms dependent on wood products only. Like prices formany other commodities, export prices for logs and lumber ininternational markets in the mid-Eighties were, on the whole, belowthose of earlier years (but are now expected to firm). Early 1986returns point to a slowdown of export growth for several major forestryproducts exports and possibly a weakening of export prices for woodpulp.It should, however, also be recalled in this context that, since thetrade data for 1979, 1981 and 1982 were recorded, the world's majortrading currencies have undergone repeated - and sometimes major -

adjustments which have, of course, not been without repercussion ontrading opportunities and the direction of trade-flows. Recent changesin petroleum prices will also not be without repercussions on productionand trade-flow possibilities.

MDF/W/52Page 11

woodpulp, from all sources, are important in international trade,amounting to somewhat more than 31 thousand million bS dollars annually,on average, in 1979 and 1980 (not including certain finished woodmanufactures or furniture), or about 1.7 per cent of world exports ofall commodities.

11. It is important to bear in mind that the wood-processing industrieshave undergone major technical and structural changes since internationaltrading opportunities opened up again, in a significant way, in themid-1950s, when the combined effect of the ravages of war and, as aresult thereof, currency restrictions, had started to be overcome inmany countries, and when efforts and institutional arrangements forregional and global co-operation, including those arising from the earlyGATT multilateral trade negotiation rounds, started to take effect.

12. On the technical side there have been remarkable changes in forestcultivation, -harvesting and -logging practices and facilities.Silviculture, as a science, and in actual practice, has made greatprogress. At the level of the wood-processing industries,machine-shaping and -joinery has become increasingly widespread, while,unfortunately, artisanal skills have been on the decline, at leastrelatively so. Increasing reliance on machine processing has favouredthe use of uniform, homogeneous inputs. This, in turn, favouredincreasing use of the technically more homogeneous coniferous woods (interms of processing characteristics), then increased use of blackboard,plywood and fibre- and particle-board, of varying characteristics andspecifications, and of certain varieties of tropical woods.

13. The increasing availability of these items and particularly so the,by now, widespread use of particle-board and fibre-board (at least inthe developed areas), has considerably enlarged the raw material base ofthe industry. "Wood-waste" (both processing-waste and waste-wood, i.e.wood from species previously considered unfit for joinery, panel-boards,and pulpnrs) has become a very relative term, indeed. Newwood-lar.,nating, wood-preservation and wood-colouring techniques havestif "jrther enlarged the resource-base for the industry by opening upuse-possibilities for less durable and less decorative woods (of whichone demand-enhancing variant is a partly transparent overprint processfor otherwise non-decorative veneers). As regards pulpwoodrequirements, the recycling of paper, increased use-possibilities forshort-fibre hardwood pulps and of wood chips, including those fromrubber trees and mangrove tree varieties, have still further enlargedthe raw material base. Moreover, pulping processes which produce largerusable quantities of pulp for a given quantity of wood input, ascompared with conventional, chemical, pulp-manufacturing processes, arecoming more widely into use. Nor are developments at their end. Greatstrides are being made in developing production and markets for greater

IMore than 2.0 per cent if paper were also be included. The1.7 per cent figure also does not cover the not inconsiderable value ofwooden crates and packings, used in exports of non- wood products.

MDF/W/52Page 12

strength "oriented-flakeboard". The increasing availability and use ofmedium-density fibreboard - more recently also in Europe - increasescompetition for natural wood in furniture making. Greater use ofexterior-grade flakeboard for construction will increase competitivepressure on construction-grade plywood. Fighting back, the plywoodindustry has now under development processes and center-less veneerlathes for producing technically acceptable peeled plywood veneer fromsmall-diameter logs. The particle-board industry's response is afurther speed-up in panel-forming and pressing processes. Computercontrol or sorting, sawing and milling operations is starting to spreadfor producing sawn and milled wood products. Milling machines withmicrochip-sensors and precise, motor- or hydraulically-controlled,operations, and even high pressure water-jet cutting and lasercontrolled finishing and cutting techniques are starting to make theirappearance. Certain production processes, such as door manufacture(sometimes wafer-thin veneers over a honeycomb cardboard core) and eventhe fabrication of wall-size panels for pre-fabricated houses (inparticular2European modular prefabs), are starting to be fullyautomated.

14. The whole of the forest products trade has been impacted in a majorway by the rapid development of the export trade in tropical timber,estimated by FAO to have grown, in log equivalents, from about 7 millioncubic metres in the 1950's to approximately 70 million cubic metres in arecent year. While in the early 1950s only a few dozen tropical woodspecies were of some significance in international trade, the number of

'This is primarily a North American development and is only nowstarting to spread to Europe where it is also known as structureboard,or waferboard ("Stirlingboard", in the UK). Outer - and inner - layersof thin woodflakes are put down in different directions, rather than atrandom. This orientation gives more strength (two- or three-foldincrease in bending strength). (Because of their matted appearance suchboards require veneer or plastic overlays, if intended for furnituresurface materials.) As regards medium density fibre (MDF) board it isprobably correct to say that (once it becomes more widely available) itcould have a wider range of uses than any other manufactured boardmaterial. MDF board has high strength, smooth surfaces, excellentmachining characteristics (like good, solid wood) good edge quality andgood finishing properties.

2An interesting summary description of modern manufacturingprocesses in the wood processing industry and the characteristics anduses of many types of wood semi-manufactures was recently published in"A Review of Technology and Technological Development in the Wood andWood Processing Industry and its Implications for Developing Countries",document: UNIDO/IS. 413, of Nov. 1983. For somewhat broader aspects ofwood industry production and trade developments, with particularemphasis on tropical wood varieties, attention is invited to (FAO) UNIDOdocument "Wood Resources and their Use as Raw Material", UNIDO/IS. 339,and "First World-Wide Study of the Wood and Wood-Processing Industries",UNIDO/IS. 398. Another, recent, study to be mentioned is "MechanicalProcessing of Tropical Hardwood in Developing Countries: Issues andProspects for the Plywood Industry's Development in the Asia - PacificRegion" in: Case Studies on Industrial Processing of Primary Products,Commonwealth Secretariat and IBRD.

MDF/W/52Page 13

tropical species traded now is figured in hundreds. Originally, exportsfrom tropical suppliers consisted mainly of logs. Many of thesecountries now restrict or prohibit, or otherwise discourage, logexports, while encouraging exports of sawnwood and plywood, exports ofboth of which have expanded manifold, as have exports of other productsmade of tropical wood varieties.

15. Problems of log restrictions have, in some cases, been overcomethrough joint ventures for forest-resource exploitation, accompanied bythe establishment of transformation industries and internationalmarketing support measures. Many of the forestry enterprises which havesprung up over the last two decades have been geared expressly tosupplying export markets and most of these ventures have been quitesuccessful in this respect. Joint ventures and transnational investmenthave not been limited to developed and developing country co-operation,but are also a feature of developed-cum-developed and developing-cum-developing country co-operation. As joint ventures spread, trade flowswere affected, and so were production developments in various locations.

16. Large-scale increases in exports of semi-finished wood productsto distant markets have been made possible by standardizing grading,performance specifications, shipping documentation, contract conditions,transport and also improved customs clearance facilities, assisted,inter alia, by the work of international standardizing bodies.Container transport is becoming increasingly important for shipments ofwood semi-manufactures and is also widely used for shipping waste paperto be recycled into paper and paperboard manufactures. After the spreadof shipping bundled lots, sometimes palletized, the development ofspecialized ocean transport and of special port terminal-facilities havebeen key elements in the development of that trade. Part of the tradein woodpulp is conducted on the basis of long-term supply contracts;for transport to Japan some 70 special purpose wood-chip bulktransporters ply the Seas. In some cases the interested industries -particularly in respect of pulp and products made thereof - havediversified both their sources of raw material supplies and their marketoutlets through international investment in the form of new foreigninvestment, by acquisitions, or joint ventures, all spurred byincreasing demand for wood, pulp and paper, in the face of expandingconsumer markets and explosive growth in the needs of the print -,publishing and communications-media, for data-processing uses (so farthe paperless office is a myth, but work on many fronts (including byECE) for standardizing intra- and inter-industry and transport-documentation electronic data interchanges (EDI), aiming at anincreasingly paperless office-environment) is accelerating, and in usesfor sanitary purposes and by the packaging industries.

IFor a recent bibliographical listing of ISO standards for wood,wood semi-manufactures, cork and for paper pulp, see ISO document"1 Bibliography", 4th edition, Geneva, March 1984. Among internationalbodies involved in wood-industry products' standardization work, theUN/ECE should be mentioned. For ECE-recommended standards forconstruction sawn-wood, cf. Timber Bulletin, Volume XXXIV, supplement 16,November 1982. Work on shipping policies, standardization of freighttariff rules, multi-modal (door to door) container traffic, etc., hasbeen, and continues to be, undertaken by UNCTAD and OECD.

MDF/W/52Page 14

17. Certain forest resources, hitherto largely inaccessible, are seenas becoming exploitable, for instance additional timber and wood-chipsfrom the USSR could become available for export in the wake of ongoingexploration and development of resources in Siberia and the expansionand improvement of the USSR's transport system. In the Amazon Basin,considerable progress has been made for operating, on a sustained-yieldbasis, several large woodpulp complexes, the output of which is destinedpredominantly for export, and, overall, the accessibility of the Amazonregion's forest resources is improving, as transport infrastructure-development (including rail) proceeds. In other regions of the world(for instance in New Zealand, South Africa, in several EEC countries andin parts of the United States) output from timber and pulpwoodplantations, established in earlier decades, is starting to becomeavailable for harvesting and is already a factor in the market.Pulpwood plantations are also being created in several locations inAfrica, in Asia and in Oceania. Reforestation efforts are beingintensified almost everywhere.

18. While it will be seen from Section A that different regions andcountries are differently endowed with forest resources, either in termsof forest per total land-area, or forest resources per caput, and whileforestry policy objectives are, by necessity, accorded different levelsof importance within different countries' socio-economic policyobjectives, it can be said, generally, that the governments of all ofthe countries covered by this note are keenly aware of the need toprotect forest resources and all of them have on their statute bookspolicies for maintaining forests at desirable levels and, wheneverpossible, to manage this resource so as to obtain sustained yields andto balance short-, medium- and long-term interests. This is trueregardless of whether forest-ownership is public, provincial, communalor private. There exists considerable concern and international supportfor the adoption of appropriate forest management policies and someinternational financial and technical assistance has been directed tofinance efforts for halting desertification and for promotingreforestation, including schemes financed by the EEC, by individualgovernments and by the IBRD and by regional development-banks anddevelopment-associations.

19. As regards trade, it will be noted that, as a result of variousregional-integration schemes and -preferential arrangements, thesuccessive Lom6-Conventions and the GSP, a large part of internationaltrade in wood and wood products has been moving free of import dutiesfor some time, at least as far as imports into many developedmarket-economy countries are concerned. Undoubtedly, the differentregional arrangements are of considerable importance in promotingregional economic development and trade expansion. This is the verypurpose of these arrangements. Yet, for the group of products coveredby this note, an examination of the data in Table III-B, on import-sourcing and export-destinations, shows (North America, perhaps, excepted)that resource- and trade-complementarity is often more important betweendifferent regions than within a given region or preference-area.

20. Trade liberalization and duty-reduction or elimination in variouscontexts notwithstanding, some wood products and wood-derivative productsare considered "sensitive" in several developed countries and continueto be (or are now [temporarily]) subject to positive m.f.n. importduties, which may be relatively high, in some instances. M.f.n. importduties on wood and wood products in many of the developing countries arevery often high, though, perhaps, not higher than import duties for manyother classes of goods.

MDF/W/52Page 15

21. Since virtually all countries have some forests or woodlands and,associated therewith, some wood production and -processing, imports ofwood and wood products are quite often considered as being not amongessential import needs and are thus likely to be among restricted itemswhen balance-of-payments import restrictions, currently widespread inthe developing areas, are imposed.

22. Less favourable tariff treatment for wood and wood products,depending on origin, is a matter of serious concern to a number ofcountries, including some of the major forestry products producers andexporters. In past discussions, these countries have pointed out thatfor many types of forestry products the market is highly competitive andprice sensitive, with the result that even relatively low nominal ratesof duty can have disproportionate effects on export marketingpossibilities, particularly when tariff protectionism on top of suchnatural protection as significant transport costs. Another area ofconcern as regards wood products is the existence of differentiation intariff treatment for given products having the same use, but made fromdifferent woods. Another question that arises is the level of effectivetariff protection, as compared with nominal tariff levels.

23. From such documentation on non-tariff measures as has been examinedfor this note, it is evident that certain non-tariff measure obstaclesto trade in forestry products exist. Some of these measures areintended to deal with temporary problems (mitigating storm damage, ormeasures for protecting the balance-of-payments) or with measuresdesigned to protect the flora, or health (formaldehyde emissions, etc.).Other measures may be designed to serve forest-resource maintenance or-development, or social policy objectives. The picture of the manypossible and varied government support activities, actual or onlyperceived, gets blurred, and sometimes very complicated, by the factthat the State is, ..in many instances, the owner of part, perhaps eventhe major part, of the forest resource. Forest resource disposition- ordevelopment-measures thus become merged with general economic objectivesand policies.

24. Like other sectors of trade, international trade in wood andwood-products is affected by numerous technical standards andregulations. A reading of the relevant documentation suggests that someof the existing technical barriers to trade are, perhaps, due toinsufficient familiarity of importers, exporters and administrationswith the technical characteristics of wood and wood-products availablefrom, and being offered for export by, suppliers in other countries.There is some indication that problems in this area, notwithstanding thefact that standards are sometimes set and enforced by national- orregional professional or industry associations, can often be, and havein the past been, resolved through bilateral consultations betweeninterested countries.

If recently published data on international transportation costfor US imports in 1981 are generally representative, the freight factor(ratio of international transportation cost to the free-alongside valueof the product being shipped) for lumber (and even more so for paper andpaperboard) is particularly high, when compared with freight factors for18 other broad import categories. Ref: H. McFarland "TransportationCost for US Imports from Developed and Developing Countries" in TheJournal of Development Studies, London, Vol. 21, No. 4, July 1985.

MDF/W/52Page 16

25. Special thanks are due to the Geneva-based Timber Section of theECE/FAO Agriculture and Timber Division for the generous access providedto their reference library facilities. Without this facility thepreparation of the overview note (within a relatively short span oftime, when Spec(84)13 was first presented) would not have been possible.The findings arrived at in this note are, of course, the soleresponsibility of the author. Suggestions for any corrections oramendments that might be required will be appreciated.

1Since Spec(84)13 was circulated, 1985 having been designated"International Year of the Forest", much further research by manyindividuals and institutes has gone into the investigation of theworld's varied forest resources, their protection, and their proper usefor social and economic development. Some of the research results,findings and conclusions, for instance those published in connectionwith the IX World Forestry Congress (Mexico, July 1985) and consideredto be relevant for this note, have - to the extent possible - beenreflected in this revision and partial up-date. Last, but not least, itshould be mentionned that ECE/FAO in September/October 1985 published anup-dated and much expanded survey of "The forest resources of the ECEregion (Europe, the USSR, North America)". The wealth of informationprovided by that survey (some 200 pages, including notes on methodology)goes well beyond the summary information, based to some extent onearlier ECE/FAO survey data, attempted in this note. Other material,such as papers prepared for UNIDO's recent "First World-Wide Study ofthe Wood and Wood Processing Industries" did become available in time tobe reflected, as appropriate, in this note and account has also beentaken of some of the major conclusions of the first meeting of ILO's,recently established, Forestry and Wood Industries Committee (cf. ILO,document IC/FWI/1/17 - 1986).

MDF/W/52Page 17

A. FOREST RESOURCES, THEIR USE AND POTENTIAL

26. The main thrust of this overview note is aimed at trade-relatedtopics. However, as primary production and, thereafter, exports of wood(and some of the products derived therefrom) depend on the existence ofan adequate natural resource base, namely forests of various types andspecies-composition, it seems relevant to consider briefly that resourcebase, first globally, then by regions and, in tabular form, bycountries.

27. On a global basis, were it not for the competition in land-use byagriculture, pasture, fuelwood collection, timber offtake, urbansettlement, road networks, and, in some regions, an expanding desert,more than 60 per cent of the world's land surface might be, andpresumably once was, covered by forests, nature's way of providing aprotective cover for the soil. As it is, the original natural forestshave been much thinned out, in some areas to the point of virtualdisappearance. Overall, only slightly mor? than 30 per cent of theearth's land surface, or 4,100 million ha. , is now covered with closedforests or other wooded land, wherein the latter designation,standardizing efforts for common definitions notwithstanding, allows aconsiderable range of interpretations as to the nature and density oftree-stands. It is estimated that about three-fourths of the world'sforest/wo2dland area would qualify for the designation "closedforests".

28. As regards types of natural forests, one finds pine, spruce, birch,aspens, alders and larch in the boreal forests in the North, then,proceeding southward, vast stretches of increasingly more varied standsof conifers, mixed conifer-broadleaved forests in the temperate regions,sparse tree coverage in most of the Mediterranean regions, some scrubsand woodland in the savanna, then, increasingly dense, humid forests andthe wet, evergreen tropical forests of Latin America, Africa and Southand South-East Asia and parts of Oceania. Tree coverage decreases againas one moves still farther south, except where a maritime, humid climatefavours forest growth, such as in parts of southern Chile. In allregions, elevation above sea level makes a considerable difference as tothe type of forests one finds, with, as a rule, coniferous tree-standson the flanks of the great mountain ranges. Australia and such insularlocations as Madagascar are different again as regards flora and forestcharacteristics. More than one half of all tropical shores are fringedwith mangroves and the great river systems on earth have their owncharacteristic forests. Different tree species have, over the ages,found the particular ecological niche most suited to their needs, or oneto which they could adapt. This has led to a bewildering variety oftree species, most of all in the tropical forests.

IOne hectar (ha.)2= 100 x lOOmetres = 10,000 square metres = 2.47acres; 100 ha. = 1 km2 1 million ha. = 10,000 km , cf. alsofootnote 2 on page 13.

2"Closed forest" is a forest which has a closed tree canopy."Other wooded land" designates, in general, areas where treespredominate, but without constituting a full tree canopy. (Closed

.1/.

MDF/W/52Page 18

Footnote (cont'd)

forests - as defined by FAO - are those which, by their different strataand their undergrowth, cover a large part of, or all, the ground andwhich, in general, do not have a continuous herbaceus stratum (except incertain coniferous forests.) Other wooded land - also "open treeformations" - are those in which the canopy is generally less closed.These are essentially mixed broadleaved forest-grassland formations,such as the South-Amercian "cerrado" and "chaco", the African woodlandsand wooded and tree savannas. - FAO Forestry Paper 37). About 1,600million ha. of closed forests are in the temperate zone and about 1,200million ha. in the tropical regions. The volume of standing timber perhectar in the closed forest averages 80 to 100 cubic metres in thetemperate regions and 100 to more than 200 cubic metres (on account ofthe more active bioclimatic conditions) in the tropics. The estimatedtotal volume of growing stock of closed forests is 145,000 million inthe temperate regions and about 185,000 million in the tropical forest.About 75 per cent of the forest area in the temperate and northernregions is covered with coniferous stands. Coniferous forests accountfor 2.5 per cent of total forest area in the tropical regions. The term"other wooded land" applies to about 400 million ha. in the temperatezone and 750 million ha. in the tropical area. Total growing stock inthese "other" woodlands is estimated at 20,000 million cubic metres,two-thirds of which is in the tropical regions (as defined by FAQ, thearea occuring between the Tropics of Cancer and Capricorn). Less thanone-half of the forest area is considered "operable" - the remainder isnot operational for a variety of reasons, such as physical or economicinaccessability, or legal constraints designed to preserve the forestfor its protection potential. The operable volume of growing stock inthe developed areas is estimated at 96,000 million cubic metres (ofwhich 72,500 million coniferous). The figures for total (figures forconiferous in parentheses) volume of operable growing stock, in1000 million cubic metres, are: North America - 36.4 (26.6); Europe -14.1 (8.8); USSR - 40.0 (33.2) - other developed - 5.5 (3.9). Theestimated volume of total growing stock in the developing areas (much ofit not operable, however) is of the order, in 1000 million cubic metres,of close to 80.0 for South, -Central America and Caricom, 38.8 forAfrica and 43 for Asia (including insular). Ref: "Wood Resources andTheir Use as Raw Material"; op.cit.

MDF/W/52Page 19

29. Broadly speaking, the USSR accounts for about 22 per cent of theworld's forest area (about 29 per cent of world closed forest area). Ofthe world's coniferous forests, the share of the USSR, in terms of area,is about 60 per cent. Total growing stock (in 1975) was estimated at74,700 million cubic metres. Growing stock of "operable" forests(i.e. physically accessible and with logging plans) is of the order ofclose to 50,000 million cubic metres (including stands newly accessiblevia the BAM railroad and feeder lines). Coniferous specie representmore than four-fifths of the USSR's operable forest stock. Thecorresponding percentages for other regions, as regards total forestarea (and closed forests respectively), are: about 19 per cent (7 percent) for the African continent; about 19 per cent (22.5 per cent) forSouth- and Central-America; 15.4 per cent (17.6 per cent) for NorthAmerica; about 13 per cent (15 per cent) for Asia; 4.6 per cent (3 percent) for the Oceania Pacific region; 4.1 per cent (5.2 per cent) forthe European region. For the world as a whole, somewhat more than onehalf of the forest and woodland area is located in developing countries.Forest resources in terms of ha. of closed forest/per caput (plus ha. ofopen forest/per caput) in the early 1970s were estimated to be of thefollowing orders of magnitude: North America 2.0 (0.7); CentralAmerica 0.5 (0.02); South America 2.4 (0.7); Africa 0.4 (1.3);Europe 0.3 (0.1); USSR 3.0 (0.4); Asia 0.2 (9.3); Oceania and Pacificregions 3.6 (4.8). World average: 0.7 (0.3).

30. In terms of total area under forests, it can be said that in mostof the developed countries the forest area is either stable, orincreasing slowly. In the developed countries most lumber companies andState forest administrations act on the principle that they are not inthe tree-cutting business but in the tree-growing business; theobjective is not only to preserve the area under forests but also tomake each hectar of forest produce annually more timber than is cut(until final harvest and/or replanting at a given site). In most of thedeveloping countries, despite recent attention and ongoing efforts forreforestation, or afforestation, the total area under forests is stilldecreasing. As population growth in most developing countries is high(absolutely, or in relative terms), average per caput availabilities offorest land in the developing countries have probably declined since theabove estimates were published.

31. Not only is the forest-resource endowment different from region toregion, but there are also great differences in the way this resource isused. In the developed countries the overwhelming part of the forestresource, if harvested, is nowadays, it was not always so, destined forthe market. In order to be profitable, it is marketed largely forindustrial uses. In most of the developing countries, however,conditions are such that most of the wood removals are for firewood, forcooking and heating.

North America's coniferous forests account for more than onefourth of the world total.

2Data based on, and adapted from, "The Global 2000 Report to thePresident" - US Council on Environmental Quality and US Dept. of State,Washington D.C., 1980. Summary data on land suitable as arable/cum/cropland and of forest land potential in different regions of the worldare given in the GAIA Atlas of Planet Management, Pan Books Ltd,London 1985, pages 24-32. Data on total forest and woodland areas ofGATT countries are given in Table I of this note.

MDF/W/52Page 20

32. While in Latin America, except for unexplored and unsettled areas(such as the vast 'terras devolutas' in Brazil, which are owned by theFederal Government), much of the land, including the forest, isprivately owned, in Africa and Asia, and partly in developing Oceania,the forests are administered and exploited on the basis of communal-,rather than individual- or State-ownership, although the State oftenholds ownership-title. The communal rights and uses include thegathering of forest-fruits and -fibres, the collection of wooden polesetc. for construction, and of firewood, as well as certain grazing andhunting rights. This system works well as long as sufficient forest-space in relation to population and its needs is available. Oncepopulation increases significantly, strains on the system develop rapidly,starting normally either from the fuelwood- or the food-shortage end.Once food starts to be in short supply, pressure arises for bringingadditional land under cultivation. As easily cultivable land is normallyalready being exploited, this means recourse to nearby forest land. Theforest is cleared, often by burning, and food crops are then planted.Within two to three years, tree-undergrowth and weeds (which are difficultto eliminate from the imperfectly cleared ex-forest plot) take overagain, making agricultural pursuits toilsome and unproductive. Thisprovides an incentive to repeat the clearing/cum planting operation on anew plot - i.e. shifting cultivation, which leaves behind a degradedforest and is at present-, probably, the main source of overall forestdestruction in the developing areas. In the forests of some of thedeveloped countries, wildlife populations (both small and big game) arerising rapidly, the result both of recent restrictive regulations andreduced forest-care operations. There is some reason to fear long-termdegradation and damage to the rejuvenation of existing natural forests(a matter which is particularly serious in respect of protectivemountain forests), due to excessive forest resource use (including forsports and leisure), or destruction by wildlife or, in some cases, feralanimals.

33. Collection of wood for fuel needs places a heavy toll on theforest. First, deadwood is collected. When deadwood is gone, branchesare chopped off. Finally, the trees go. With fuelwood lacking,agricultural waste materials and dried animal dung are used for fuel.With less natural. fertilizer thus available, soil fertility and foodproduction-capacity declines. This produces pressure for more land tobe brought under cultivation, which manifests itself in increased pressureon remaining forest lands. When combined pressure for fuelwood andcultivable land leads to increased hillside-farming and fuelwoodcollection, soil erosion makes rapid headway, followed by silting ofwater-courses and flooding, creating new and additional problems overwider and wider areas. In the arid and semi-arid zones of the world,wind, rather than' water, is the main agent of erosion. Once theprotective cover of trees and shrubs is removed, most often for firewoodand animal fodder, the destructive force of the wind is unrestrained.The fine fertile soil particles are swept away, leaving the heavier,sandy ones behind. The soil becomes progressively less fertile and lessproductive. Once wind erosion has started, the moving soil particlesadd to the process, in sand-blasting fashion, scouring everything intheir path.

IThe question of forest ownership - very relevant in the context ofassessing resource potential - is a very complex one. Some of thesecomplexities, starting with the very definition of what constitutes a

./.

MDF/W/52Page 21

Footnote (cont'd)

forest (with considerable differences between different countries), arehighlighted in a "unasylva" review article (in Vol. 37, No. 148 (85/2))of "Forêt et environnement en droit compare et international",M. Prieur ed., Presses universitaires de France, 1983.

2J. Westoby, in a book review article, published in "unasylva",Vol. 37, No. 148/85-2, makes the point that it is a misconception toassume that tropical deforestation is necessarily the result ofoverpopulation, recalling that vast areas of tropical forest weredestroyed in centuries past, in places and at times "when there waslittle if any population; indeed, populations - slaves and laterindented labour - had to be brought in to accomplish the deforestation... Brazil's northeast, and most of the Caribbean were deforested in thesixteenth and seventeenth centuries ... in all three tropical regionsdeforestation accelerated in the nineteenth century ... Throughout thetropics it was export-oriented agriculture that pushed the forest back".Even now, the problem is seen as being caused by shifted cultivators(their lands having been absorbed by other users and, perhaps, uses)rather than by shifting cultivation, which, as previously practised, inaccordance with tribal traditions, was ecologically sustainable. Allthis argues for appropriate reforms in many of the areas where tropicalforests are now under assault. More generally it can be said that theterm "shifting cultivation" is variously used by different authors, andthe practice of shifting cultivation may produce widely differingresults. An interesting summary of work conducted by FAO onalternatives to shifting cultivation (in collaboration with researchinstitutes in the UK, Netherlands, France, Tanzania and Ghana) is givenin an article by J.P. Lauly, in "unasylva", Vol. 37,No. 147 (85/1).

3Cf. FAO, WFD/1/1985.

MDF/W/52Page 22

34. In the tropical forests, where fuelwood is not generally in shortsupply, forest clearing for agricultural uses also has its problems; anestimated 11 million ha. of tropical forest and woodland (of which7.5 million ha. in the "closed forest" category) are "cleared", ordegraded each year. Tropical forest soils are generally poor innutrients, so much so that no single tree species can establish itselfas truly predominant. The great species variety Tf the tropical forestis a reflection of the poor soil nutrient levels. The bulk of thenutrients is in the living phytomass, e.g. the trees, shrubs and theunderbrush. Leaves are shed and new leaf growth occurs round the year,and, apart from a shallow layer of surface soil, there is consequentlylittle humus formation, as everything is recycled very rapidly,especially so as most tropical trees - once fallen or felled - are notvery rot-resistant, in the hct and humid environment. When the treesare removed, only few nutrients remain in the so-J. The shallow surfacelayer, even if enriched by ashes - as in slash burning - is quicklydestroyed by weathering and leaching. The forest-to-atmosphere, andback again, water-cycle (forests create their own micro-climate) isinterrupted, the soils dry out, get parched and become unproductive, asnutrient elements needed for plant growth (nitrogen, phosphorus,potassium, calcium, magnesium) are often in short supply - while levelsof aluminium and iron, in a way toxic for plants, are frequently high.Thus, after one or two relatively satisfactory harvests, there is anincentive to shift cultivation to other plots oa virgin forest lands,with all the longer-term problems this entails.

35. These are not imagined scenarios. Even though some of theunderlying statistics on fuelwood-use and -needs, and on the extent ofshifting cultivation, are only estimates, the problems cited are realand widespread. Fortunately, policies and measures for halting thedestruction or degradation of forest resources are being adopted almosteverywhere. Among measures being introduced are the establishment offuelwood-plantations, promotion of better coppice practices, the

IThe fact that most tropical tree varieties (unlike the temperatezone forest-tree varieties, which are mainly fertilized by wind-bornepollens) depend on very specific pollinators (a specific insect varietyor a specific animal) for effective pollination, is another reason.

A concise summary of the status of the world's rain forests, theiruse and protective measures, country-by-country, is contained in "RainForests", National Geographic Magazine, Vol. 163, No. 1, January 1983.

3According to recent FAO estimates, 100 million people indeveloping countries already have insufficient fuelwood for cooking andheating. Another 1,000 million people can only meet these needs bydepleting fuelwood resources. Asia experiences the most acute fuelwoodshortages. Almost all of India and Pakistan are affected by fuelwoodshortages, as are the more heavily populated plains and islands of SouthEast Asia. The Himalayas are particularly badly stricken. In Africathe most severe shortages are in East Africa and Madagascar, but all ofthe arid zones are in danger. In Latin America, the Andean plateau andthe Eastern plains of Brazil are the most critical areas. Ref. FAO,document WFD/1/1985. A detailed map of the fuelwood situation in thedeveloping areas, country-by-country, was published in 1981 by FAO, as a"unasylv" supplement.

MDF/W/52Page 23

introduction of cooking stoves, stricter land-use regulations andimproved agro-silvicullure practices and, to halt desertification, theplanting of windbreaks , hopefully to be complemented by better(holistic!) range-management. With few exceptions, progress in allthese endeavours is slow, however.

36. Reduced, and perhaps declining, as the earth's forest cover..ge maybe, the world's forests continue to be so large as to be defined andappraised only with great difficulty. What is even more difficult is anassessment of the way it can be seen as a resource, since forest-policyobjectives and -uses overlap with many other sectoral and general policyobjectives, to which different importance is attributed in differentsocio-political contexts, depending also on changing environmentalobjectives. In some areas of the world, where forest coverage is nowmuch reduced, because of intensive agricultural uses, the increasedagricultural land-use option was probably mainly prompted by economicconsiderations. For many governments, forest-policy considerationscarry less importance than agricultural policy objectives. Forests thatare being converted to agriculture provide food already in the shortterm, while the forest itself is seen more as a capital asset, often anot very productive one, or productive only in the longer term. It is,of course, realized that forestry activities, including reforestationwork, do provide employment opportunities, an aspect accorded very highimportance in some developing and developed countries. It is alsorecognized that income generated by forestry related employment is fedback into the overall economy. Yet, wherever agricultural land isscarce in relation to food needs, the forests normally lose out toagriculture.

37. While in terms of purely economic returns forestry use objectivesmay now be determined mainly by medium-term considerations, long-termpolicy objectives are not absent. Contrary to a widely-held belief, theimportance of protecting the environment and preserving, orre-establishing, a proper balance between forestry and other land-usesis not something that has been recognized only recently. In fact,governments of most countries, and earlier on some colonialadministrations, have since long attached great importance to properforest management and the maintenance of a balanced ecosystem generally.In some countries forestry legislation goes back well over a hundredyears (in some instances to the late Middle Ages) and in other instances

'Partly under bilateral aid schemes, as in Senegal, where - withCanadian assistance - a 300 km. eucalyptus belt has been built to haltthe acivance of the desert. Other large-scale windbreak plantations,benefiting from international technical and financial assistancemeasures, include a project on the high plateaus of Ethiopia, a projectin Niger, started some time ago with assistance from the US and certainEC sponsored initiatives in some African countries, etc.; Algeria, onits part, has also made great efforts in combating desertification.

2Acceptance of wood-burning stoves, or hearths, which permit10-15 per cent wood-fuel thermal energy content to be recovered (insteadof 2-5 per cent in the typical, three-stone, open-pit fire which is,moreover, through high pollutant emissions, very detrimental to thehealth of users) by local populations is often difficult to achieve.FAO, among others, is doing considerable work for the adoption indeveloping countries of better technologies for the conversion of woodenergy into heat energy and/or mechanical energy. This is only a smallpart of a much wider, integrated, FAO "Tropical Forestry Action Plan",outlined in FAO document M-30 ('85/'86), bearing that title.

MDF/W/52Page 24

at least to the beginning of this century. In some cases (for instance,Switzerland, India) forest-policy objectives and prescriptions arewritten into the Constitution. In many cases forest use and forestryobjectives are regulated by national or federal and provincial laws.While the policy objectives are not always the same, virtually allprovide for maintaining a balance between silvicultural and agriculturaluses, and many of the implementing regulations insist on, and providefor, measures of, at least limited, reforestation. In the case ofprofessionally managed private forest lands reforestation measures areundertaken as a matter of course, even in the absence of Stateregulations. This is so also in the main tropical wood-producing and-exporting countries, notably those of South and South-East Asia and inWest Africa. As a result of these policies and measures, and, ofcourse, also the availability of substitute fuels and industrial rawmaterials other than wood (formerly based on wood, wood ash, etc.), andthe emergence of new sources of wood supplies through trade development,the area under forest in Western Europe and in the United States hasbeer growing, slowly but steadily, with some war-time exceptions,through most of this century. The provisions made for preservingforests for watershed protection purposes, for recreation, and aswildlife and botanical sanctuaries, are also of some significance. Inthe United States, national parks and federal forest lands, the formerfully protected and the latter protected in various ways, wereestablished as from the turn of the century, comprising a very largearea, indeed, and total f rest area in the US is now larger than at thebeginning of the century. Canada, with a total of some 340 million ha.

1The Cote d'Ivoire, for instance, is currently intensifyingreforestation efforts under a programme envisaging outlays equivalent toclose to US$60 million, somewhat more than one-half to be derived fromIBRD financing. More generally, in an IBRD, UNDP and World ResourcesInstitute (the latter a private, Washington-based research institute)study it is proposed to spend US$8 billion over a five-year period(beginning in 1987) to begin reversing the trend of tropicaldeforestation. Many tropical countries are to be covered in thisproposed project, with $1.2 billion earmarked for India and $785 millionfor Brazil. Several countries, including France and FR Germany(FF500 million and DM150 million, respectively, over five years),announced at the February 1986 Silva Conference in Paris large-scalefinancial assistance for protecting and building up again Africa'sforest resources.

2The federal US Government owns about one third (= 290 millionhectares) of all US land; 100 million hectares have been set aside asnational parks, wilderness and primitive areas and other similarreserves. No logging is permitted in these areas, so they are notconsidered commercial forests. Consequently, a large part of trees inthese reserves are over-aged, and thus vulnerable to insect attack anddamage (currently a major problem, also for adjoining private timberlands in Texas and Louisiana). Total commercial forest area, includingprivate and other publicly owned forest land, is of the order of200 million ha., of which about 120 million ha. is owned by privateindividuals, and about 21 million ha. by forest industry companies. Theremaining forests are publicly held in national and state forests, ofwhich 37 million ha. national forests, in which controlled logging ispermitted, but sometimes contested (even violently, nail-spiking,"ecotage") by environmentalists.

MDF/W/52Page 25

of forests, has set aside 9 million ha. as protected parks. In theBrazilian Amazon Basin about 17 million ha. is protected forest andforest reserves in other parts of the country have also been, or arebeing, created. Some of the countries in East Africa have very largeprotected areas of savanna woodland. Protected natural parks are alsoof importance in most of the countries of Western Europe, certain otherdeveloped Countries, and are also found in a number of developingcountries. This has to be taken into account in respect of data on3total forest areas, recorded in Table I for the different countries.

38. Any attempt to appraise the economic value of a given forest areamust evidently take into account such factors as forest composition bytree species, -age, growing stock, growth potential, cost of harvesting,transport, nearness to markets, market demand for the wood and otherforest products concerned, value and importance attached to other thaneconomic considerations, and, last but not least, alternatives andpreferences for either present or future resource use. In other words,the appraisal must take into account, inter alia, both current andfuture revenue and capital appreciation potential. Options available,and exercised, will depend not only on current market conditions forforest products, and on expectations as to future supply/demandrelationships and prices for forestry products, but also on the generaleconomic and fiscal policies prevailing in countries concerned and onthe ownership structure of the forests. That this is not idle

While the latter figure may seem small in relation to the overalllevel of the resource, the park area nevertheless covers an area largerthan the total area under forests in F.R. Germany, the three Beneluxcountries and Denmark combined. The Canadian forest resource proper,namely "stocked, productive, non-reserved forest land" is of the orderof 190 million hectares, of which 36 per cent is mature forest,3 per cent is over-mature, 45 per cent is immature forest and 8 per centconsists of regenerating areas. The degree of private ownership variessomewhat across Canada, but about 80 per cent of total forest lands areowned and administered by provincial governments and about 11 per centby the federal government. Private holdings account for over90 per cent of Prince Edward Islands' (the smallest province) 225,000hectares of forest land and almost 75 per cent of Nova Scotia's4.4 million hectares. Public agencies own about 90 per cent of the120 million hectares located in Ontario and Quebec and over 95 per centof the 116.5 million hectares found in British Columbia, Alberta,Saskatchewan and Manitoba. Source: Government of Canada - ForestryService, "Canada's Forests ... Fibre for the World".

2In Indonesia steps are being taken to require each of thecountry's 27 provinces to convert 10 per cent of the land to forestpreserves. Once these measures are implemented, the country will haveforest preserves totalling about 18 million hectares.

3For details in respect of ECE countries, see "The forest resourcesof the ECE etc.", 1985, op.cit.

4That there may be differences of view as to the true value oftimberland and other forest industry corporate assets has recently beendemonstrated in the context of a number of contested take-overinitiatives of some major forest product companies headquartered inNorth America.

MDF/W/52Page 26

speculation is demonstrated by the considerable difficulties whichwood-processing industries have in some countries, though possessinglarge forest resources, in persuading private owners to offer timber tothe market for industry or for pulping. The disposition to do so, aswell as to engage in forest-care activities, will depend, inter alia, onthe extent to which forest owners are dependent on forest-resourceincome, on the marginal tax rate to which such income may be subject(which under a system of progressive income taxes would be differentfrom case to case and, perhaps, year to year), special forestry- andland-tax provisions, inheritance taxes, etc. State aids to forestmanagement and/or forest harvesting, as in the case of some assistancecurrently provided in the fight against forest die-back, could also makea difference in the way forests are cared for ayd the level of stocksthat are removed and which then come to market.

39. One other important element in regard to forestry resource uses isthe fact that, apart from import duties, and from natural protectionprovided by transport costs (abstracting for the time being fromnon-tariff measures which could affect supplies and hence marketprices), timber prices in many markets are closely related to pricedevelopments in the international market. While, in principle, thisshould be considered desirable, certain problems may arise for properforest management and -use where such integration into the world marketof the forestry resource, and as a consequence fluctuating and often lowprices for timber, coincides with forestry activity being carried outjointly with agricultural activities which, through import protection,are less integrated into the international economy, the forest ownersbeing also farmers. In such cases, agriculture, benefiting perhaps froma variety of support measures, while forestry does not, or much less so,proper forest management may become a problem, with forestry activities

IWith the possible exception of Switzerland (mainly windbreakdamage removals so far) and of some of the countries in Eastern Europe,there was no evidence, at the end of 1985, of significant additionalquantities of industrial roundwood coming to market as a consequence offorest die-back problems in certain areas of Europe. This may, ofcourse, not hold in the future, but an attempt is being made by theindustry to accommodate die-back sanitation fellings (not yet a problemin most areas) through reduced fellings of healthy trees. It shouldalso be pointed out that, apart from some temporary pre-processingstorage problems, wood from die-back trees is normally just as strongand useful as that from the, presumably, healthy trees. In the UnitedStates South and South-East exceptionally large sanitation fellings in1985, to combat insect infections, have, however, led to a largeimbalance in supply and demand of roundwood, with offer prices fallingin some geographic areas to about one-fourth of the national average.(Cf. also footnote 2 on page 24). Developments in European andNorth-American forest die-back sanitation feelings, which may have aneffect on the market, are to be monitored by ECE under a project decidedupon in the autumn of 1985.

MDF/W/52Page 27

being neglected, as compared to agriculture. While, in terms ofregulatory policies and -measures for purposes of environmentalprotection most governments, have, by now, fairly wide authority andintervention possibilities (regardless of the type of forest ownership),possibilities for directing the use of forest resources in the non-Statesector are much more limited. Another important element to consider isthe degree of vertical integration, namely common ownership of theforest resources and of the downstream forest products industries. Inmost of the EEC countries, and certain other European countries, thereexists very little of such integration, while in the United States, andto some extent in Canada, and also in one or two countries in northernEurope and in countries such as Brazil, vertical integration, in termsof privately-controlled forest-resources and forest product-processingindustries, is fairly common. (The integration is not necessarily oneof ownership of the primary resources, but may take the form oflong-term leases or use-contracts in respect of forest land.)Evidently, vertical integration does provide an additional degree offreedom to management, as far as planning of resource-use and-disposition is concerned.

40. In considering forestry resource-potential in relation to areaunder forests, it is relevant to bear in mind that forests havedifferent growth rates, varying with the age of the tree population, byspecies and by site-conditions. Apart from the far North and certaininhospitable mountain climates, where growth is slow, throughout, it canbe said that forests composed of young trees grow quickly. Quick growthnotwithstanding, a certain growth-result has to be attained to makeharvesting worthwhile. During the growth process forests have to becared for, including repeated thinning out, to permit the more promisingportion of the trce-population to develop to the fullest extent thosemarketing- and uss-acharacteristics which are most desired for woodindustry urposes.- Through proper forestry techniques, foresters caninfluence usable trunk length, or diameter growth, or both, to mentionorly some of the intervention possibilities. With good management,various production objectives can be achieved and overall forest growthcan be favourably influenced. This is one of the reasons why productionfrom well-managed forests may often contribute a disproportionally largeshare of a country's overall wood-production volume and -value, and whyforest plantations may well hold the answer to meeting the world'sincreasing requirements for wood and the many products derived therefrom.