TARGET MARKET: CHINA - European Commission

99

TARGET MARKET: CHINA MARKETING STRATEGIES FOR TOURISM DESTINATIONS A COMPETITIVE ANALYSIS

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of TARGET MARKET: CHINA - European Commission

Marketing Strategies for Tourism Destinations. Target market: CHINA

TARGET MARKET: CHINA

MARKETING STRATEGIES FOR TOURISM DESTINATIONS

A COMPETITIVE ANALYSIS

Marketing StrategiesFor Tourism Destinations

A Competitive Analysis

Target Market - China

A report produced for European Travel Commission (ETC)by Tourism Development International

Brussels, 2014

Marketing Strategies for Tourism Destinations. Target market: CHINA

Published and printed by:European Travel CommissionRue du Marché aux Herbes, 611000 Brussels, BelgiumWebsite: www.etc-corporate.orgEmail: [email protected]

This report was compiled and edited by:Tourism Development Internationalon behalf of the European Travel Commission.

The designations employed and the presentation of material in this publication do not imply the expression of any opinion whatsoever on the part of the European Travel Commission concerning the legal status of any country, territory, city or area, or of its authorities or concerning the delimitations of its frontiers or bound-aries.

Cover photo: Nanchang scenery, view from the Tengwang pavilion, China; Copy-right: chungking.

Marketing Strategies for Tourism Destinations. Target market: CHINA

ContentsForeword i

Introduction 1a. DefiningtheCompetitiveEnvironmentforDestinationEurope 2b. Destinations in the Global Market Place: a Comparative Analysis 2

Summary of China Market Study 10

1. The Chinese Outbound Travel Market 151.1. A Large and Fast Growing Market 151.2. Chinese Tourism to Europe 171.3. Characteristics of the Chinese Traveller 181.4. Drivers of Growth 221.5. Successful Destination Strategies 25

2. Travel Destinations in the Chinese Market 262.1. Visa Regimes 262.2. Air Connections 282.3. Political, Economic and Socio-Cultural Links 312.4. Consumer Assessment (TripAdvisor) 33

3. ProfileofEurope’sMainCompetitorsinChina 353.1. Destination Marketing Organisations 353.2. The Australian Tourism Sector 363.3. The Republic of Korea Tourism Sector 423.4. The Malaysia Tourism Sector 463.5. The New Zealand Tourism Sector 493.6. The Russian Federation Tourism Sector 533.7. The Thailand Tourism Sector 573.8. The United States of America Tourism Sector 61 3.9. Conclusions 66

4. Marketing Strategy and Activities of Tourism Australia and Brand USA in China 674.1. Tourism Australia Marketing Strategy and Activities in China 674.2. Brand USA Marketing Strategy and Activities in China 73

5. Key Factors in Destination Marketing in China 785.1. Market Perceptions 785.2. Marketing Performance and Opportunities 79

Appendices

Appendix 1 European and Competing Destinations WET TTCI and 84 Bloom Country Brand Rankings

Appendix 2 Weekly City-to-City Flights from Main Chinese Centres 87Appendix 3 TripAdvisor Ratings 89Appendix 4 Bibliography and References 91

Marketing Strategies for Tourism Destinations. Target market: CHINA

AcknowledgmentsThis report was prepared by Peter Mac Nulty and Robert Cleverdon of Tourism Development International on commission to the European Travel Commission (ETC), and was carried out under the supervision of Ms Valeria Croce, Head, Research and Development Department at ETC.

Thereportispartofaseriesoffact-findingreportsonthetourismstrategyde-veloped by destinations competing with Europe in select long-haul markets. The project was realised as part of the European Commission and ETC joint initiative “Destination Europe 2020”.

We would like to acknowledge the support and contributions of the many ETC members, marketing organisations and tour operators associations who contrib-uted to the realisation of this report.

We also gratefully acknowledge the support of ETC partners, who committedly contributed to the realisation of this project. A special note of thanks to Mr Charlie Ballard, Director of Advertising Research at TripAdvisor, Mr Xu Jing, Regional DirectorforAsiaandthePacificatUNWTO,andMrDanielVelasco,Consultantat Amadeus Travel Intelligence Unit, for their contributions.

Marketing Strategies for Tourism Destinations. Target market: CHINA

i

ForewordIn an increasingly vibrant landscape, marked by new players, technological inno-vation and rapidly changing consumers, the need arises for European destina-tionstocloselymonitorothers’efforttowinmarketsharesintheglobaltourismmarket.

This compilation of best practice examples in tourism and promotion strategies is meant to provide insights relevant to ETC and its member countries through a better understanding of the environment in which they operate.

This series of reports provides insights into the strategic vision and the operation-al actions tourism destinations worldwide are developing to attract an increas-ingnumberofvisitorsfromthemostpromisingsourcemarkets.Thisfact-findingresearchoffersabird’s-eyeviewofthecompetitiveenvironment,andaportraitof the tourism strategy and marketing activities of competing destinations. Ref-erencestoofficialdocumentsandpubliclyavailablereportsfacilitateaccesstodetailed information, for those interested in achieving a higher level of knowl-edge.ForEurope’sstrongestcompetitors,portraitsareenrichedwithfirst-handinformation gathered through personal interviews with NTOs marketing directors, representatives of the travel trade and experts.

The common structure of reports facilitates cross-market comparisons. Key re-sults are synthesised in a highly visual executive summary, conceived for dis-semination to the public at large.

We trust these reports will become for ETC and its members an important tool to identify key opportunities and challenges, and to strengthen their comparative advantage in the global tourism market.

Executive UnitEuropean Travel Commission

Marketing Strategies for Tourism Destinations. Target market: CHINA

IntroductionThisreport’saimistocollectmeaningfulknowledgeaboutthetourismstrategyofdestinations competing with destinations in Europe in select long-haul markets. This study is part of a series of publications, which offer an overview of the en-vironment,inwhichEuropeantourismdestinationsoperate,andaprofileofthetourism strategy and marketing activities of competing destinations. A listing of officialdocuments,publiclyavailablereportsandmediafeaturesisprovidedinanappendix and through the footnotes to permit more detailed examination of the informationpresentedandissuesraised.Eachreportalsoprovidesfirst-handin-formation on a selection of competing destinations, gathered through interviews withNTOs’marketingdirectors,traveltradeandexperts.

This project focuses on countries competing with European destinations in high potential long-haul markets, namely Brazil, Canada, China, Japan, Russia and theUnitedStates.Inthisanalysis,Europeisdefinedasthe33countrieswhichare members of the European Travel Commission plus France, the Netherlands and the United Kingdom.

The analysis followed a three step approach.

ThefirststepwastoidentifythekeymarketsforEuropeandtheprimarydesti-nations competing with Europe in those markets. These markets are presented in Figure 1.

The second step consisted of assessing strengths and weaknesses of destina-tions,whicharesignificantcompetitorstoEuropeinthesixtargetmarkets.Theassessment has been based on the following indicators:

• the World Economic Forum Travel and Tourism Competitive Index (WEF TTCI),

• travel trade interviews and expert opinion,• visa regimes and other visitor entry requirements,• air connectivity and capacity,• price competitiveness,• political, economic and socio-cultural links,• destination tourism development policy, • destination tourism marketing strategy.

The third step consisted of identifying those destinations which are the strongest competitorsforEuropeineachmarket,i.e.destinationswhichattractsignificantvolumes of travellers and are actively investing in increasing their share in the market.Adetailedprofileof theorganisations inchargeofpromoting inboundtourism to these destinations has been compiled. Information about the strongest competitors has been collected by the means of personal interviews as well as from secondary sources.

Definingthecompetitive environment for Destination Europe

1

Marketing Strategies for Tourism Destinations. Target market: CHINA

a. Defining the Competitive Environment For Destination Europe Experts from the European Travel Commission (ETC) Executive Unit, Market Intelligence Committee and Operation Groups, as well as experts from Tourism DevelopmentInternational(TDI),wereinvolvedinatwo-stageprocesstodefinethe competitive environment, in which European destinations operate.

In the initial stage, those long-haul markets which show the best prospects for Europeasatourismdestinationwereidentified.Basedonacompoundanalysisof the relative importance of, and growth prospects for a large number of mar-kets,sixwereidentifiedasprioritiesforDestinationEurope. The experts were then asked to list countries which are actively targeting those marketsas tourismdestinations.Thesecompetingdestinationsaredefinedascountries which are currently investing in tourism promotion and which already receive considerable volumes of tourists from the selected markets. The outcome ofexperts’evaluationofthecompetitiveenvironmentisreportedinFigure1.

Figure 1: Market: Destination Pairings

MarketsCompetitor

1 2 3 4 5 6 7

Brazil USA Mexico Australia Russian Federation

Canada USA /USA large cities

Mexico China South Africa

China USA Australia Russian Federation

Rep of Korea

Thailand Malaysia New Zealand

Japan USA Rep of Korea

Thailand Malaysia

Russia Egypt China Dubai United States

Thailand

United States

China Brazil Australia USA large cities

South Africa

b. Destinations in the Tourism Global Market Place: a Comparative AnalysisAn overall assessment of the comparative resources and capabilities of the se-lected destinations was undertaken based on publicly available international indi-cators, which monitor aspects crucial to determine their strength and weakness-es as tourism destinations.

The World Economic Forum Travel and Tourism Competitiveness Index (WEF TTCI) provides a broad assessment of a large number of characteristics and fea-tures that facilitate the development and functioning of tourism in a country. The survey assembles results for 79 pillars under three main “sub-indexes”:

1. Travel & Tourism Regulatory Framework,2. Business Environment & Infrastructure, 3. Travel & Tourism Human, Cultural and Natural Resources.

Factors and policies conducive of

travel and tourism development

2

Marketing Strategies for Tourism Destinations. Target market: CHINA

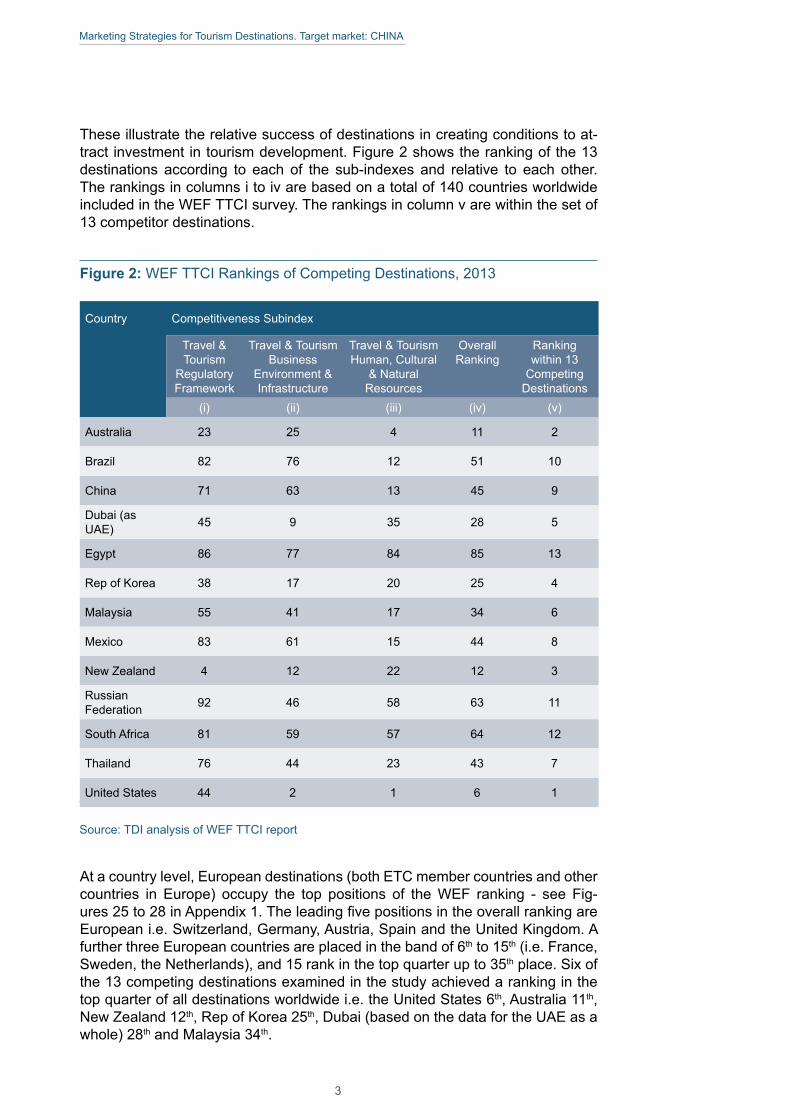

These illustrate the relative success of destinations in creating conditions to at-tract investment in tourism development. Figure 2 shows the ranking of the 13 destinations according to each of the sub-indexes and relative to each other. The rankings in columns i to iv are based on a total of 140 countries worldwide included in the WEF TTCI survey. The rankings in column v are within the set of 13 competitor destinations.

Figure 2: WEF TTCI Rankings of Competing Destinations, 2013

Country Competitiveness Subindex

Travel & Tourism

Regulatory Framework

Travel & Tourism Business

Environment & Infrastructure

Travel & Tourism Human, Cultural

& Natural Resources

Overall Ranking

Ranking within 13

Competing Destinations

(i) (ii) (iii) (iv) (v)

Australia 23 25 4 11 2

Brazil 82 76 12 51 10

China 71 63 13 45 9

Dubai (as UAE) 45 9 35 28 5

Egypt 86 77 84 85 13

Rep of Korea 38 17 20 25 4

Malaysia 55 41 17 34 6

Mexico 83 61 15 44 8

New Zealand 4 12 22 12 3

Russian Federation 92 46 58 63 11

South Africa 81 59 57 64 12

Thailand 76 44 23 43 7

United States 44 2 1 6 1

Source: TDI analysis of WEF TTCI report

At a country level, European destinations (both ETC member countries and other countries in Europe) occupy the top positions of the WEF ranking - see Fig-ures25to28inAppendix1.TheleadingfivepositionsintheoverallrankingareEuropean i.e. Switzerland, Germany, Austria, Spain and the United Kingdom. A further three European countries are placed in the band of 6th to 15th (i.e. France, Sweden, the Netherlands), and 15 rank in the top quarter up to 35th place. Six of the 13 competing destinations examined in the study achieved a ranking in the top quarter of all destinations worldwide i.e. the United States 6th, Australia 11th, New Zealand 12th, Rep of Korea 25th, Dubai (based on the data for the UAE as a whole) 28th and Malaysia 34th.

3

Marketing Strategies for Tourism Destinations. Target market: CHINA

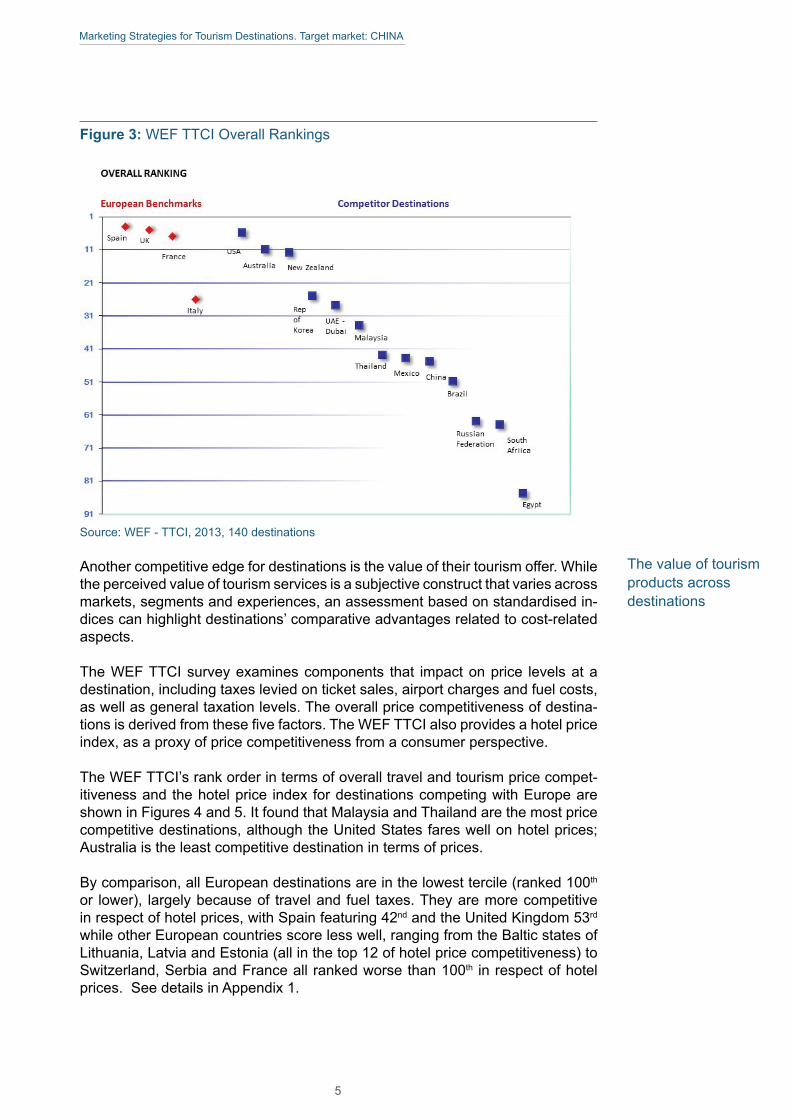

Figure 3 shows the overall ranking position for four European countries (France, Italy, Spain and the United Kingdom), selected as benchmarks, and the 13 com-peting destinations.

The comparative analysis of the resources and capabilities of the 13 destinations identifiedascompetitorsatsub-indexlevel(seeAppendix1)suggestswhatfol-lows:High ranking: United States, Australia and New Zealand. These countries show strengths in the following areas:

• New Zealand in respect of its travel and tourism regulatory framework,• the United States for the travel and tourism business environment and

infrastructure, and for travel and tourism human, cultural and natural resources,

• Australia for travel and tourism human, cultural and natural resources.

The United States fares less well in respect of the travel and tourism regulatory framework, and lower rankings (though still in the top 25 globally) are recorded by Australia in respect of the business environment and infrastructure, and the regu-latory framework, and by New Zealand for human, cultural and natural resources.

Mid ranking: Republic of Korea, Dubai (UAE), Malaysia, Thailand, Mexico, China, Brazil. Six of these seven destinations, the exception being Dubai, score more highly than their overall ranking in respect of human, cultural and natural resources. The weaknesses for this group of destinations are in the regulatory framework (i.e. Mexico, Brazil, Thailand, China) and the business environment and infrastructure (i.e. Brazil, China, Mexico).

Mid-to-low ranking: Russian Federation, South Africa. Bothcountries’rank-ings are pulled down by their low assessment in respect of travel and tourism regulatory framework. In the case of South Africa, this is due to low performance on safety and security, and health and hygiene; while for the Russian Federation, theweaknessesaremorewidespreadacrossfourofthefivepillarsinthesub-in-dex.

Low ranking: Egypt. Its weak positioning reveals in each of the three sub-in-dexessuggests that thisdestinationsdoesn’thaveanoverallcomparativead-vantage in respect todestinations inEurope,butmaybeattractive inspecificmarkets and segments.

4

Marketing Strategies for Tourism Destinations. Target market: CHINA

Figure 3: WEF TTCI Overall Rankings

Source: WEF - TTCI, 2013, 140 destinations

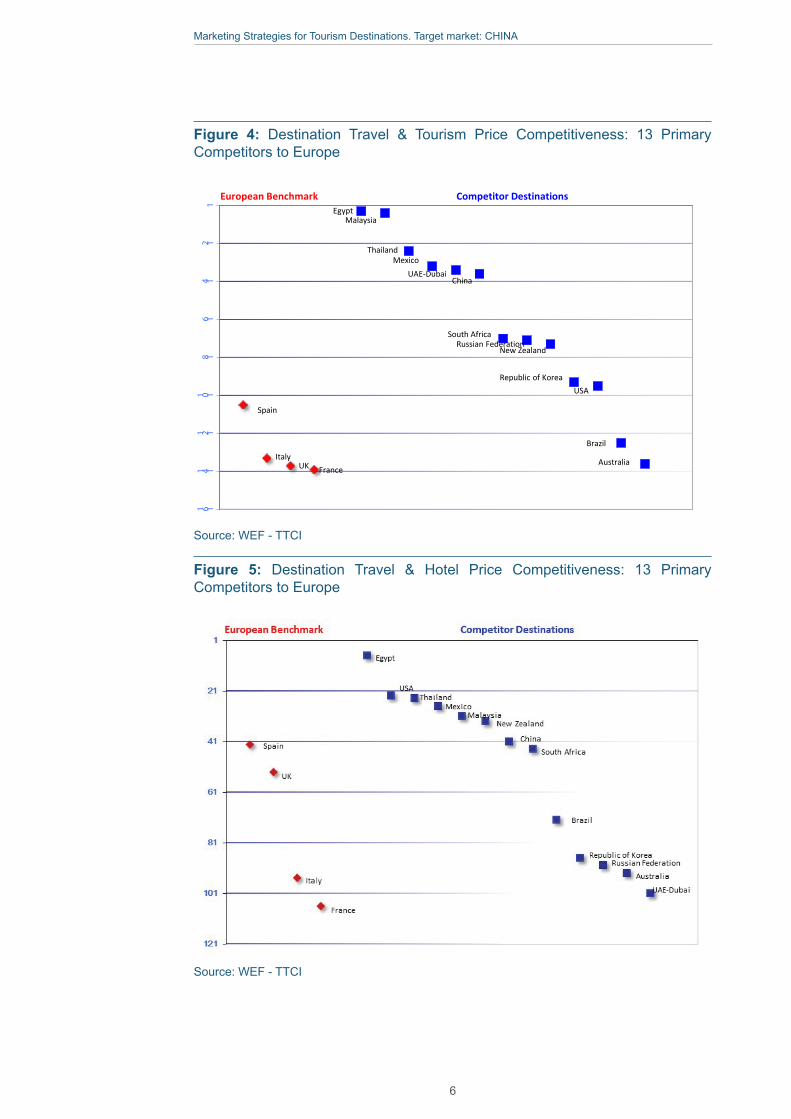

Another competitive edge for destinations is the value of their tourism offer. While the perceived value of tourism services is a subjective construct that varies across markets, segments and experiences, an assessment based on standardised in-dicescanhighlightdestinations’comparativeadvantagesrelatedtocost-relatedaspects.

The WEF TTCI survey examines components that impact on price levels at a destination, including taxes levied on ticket sales, airport charges and fuel costs, as well as general taxation levels. The overall price competitiveness of destina-tionsisderivedfromthesefivefactors.TheWEFTTCIalsoprovidesahotelpriceindex, as a proxy of price competitiveness from a consumer perspective.

TheWEFTTCI’srankorderintermsofoveralltravelandtourismpricecompet-itiveness and the hotel price index for destinations competing with Europe are shown in Figures 4 and 5. It found that Malaysia and Thailand are the most price competitive destinations, although the United States fares well on hotel prices; Australia is the least competitive destination in terms of prices.

By comparison, all European destinations are in the lowest tercile (ranked 100th or lower), largely because of travel and fuel taxes. They are more competitive in respect of hotel prices, with Spain featuring 42nd and the United Kingdom 53rd while other European countries score less well, ranging from the Baltic states of Lithuania, Latvia and Estonia (all in the top 12 of hotel price competitiveness) to Switzerland, Serbia and France all ranked worse than 100th in respect of hotel prices. See details in Appendix 1.

The value of tourism products across destinations

5

Marketing Strategies for Tourism Destinations. Target market: CHINA

Figure 4: Destination Travel & Tourism Price Competitiveness: 13 Primary Competitors to Europe

12 1

4 16 1

8 11 0 1

1 2 11 4 1

1 6 1

UK

Russian Federation

Malaysia

Thailand

New Zealand

European Benchmark Competitor Destinations

Source: WEF - TTCI

USARepublic of Korea

Australia

Egypt

South Africa

China

MexicoUAE-Dubai

Spain

France

BrazilItaly

Source: WEF - TTCI

Figure 5: Destination Travel & Hotel Price Competitiveness: 13 Primary Competitors to Europe

Source: WEF - TTCI

6

Marketing Strategies for Tourism Destinations. Target market: CHINA

The rating of a country as a brand in the perception of prospective visitors is an important travel decision making criterion in respect of choice of destination. The impressions created in the minds of consumers in travel markets around the worldarecreatedthroughalargenumberofinfluences.TheBloomConsultingGroup in its annual Country Brand Ranking1identifiesfourvariablesascontribut-ingtoadestination’simageandtherebyestablishingitstourismbrandrankingsi.e.

1. Tourismeconomicreceiptsandgrowth(afirstindicatorofacountry’sappeal),

2. The destination products and experiences researched online (meas-uring its online appeal),

3. Thecountry’sbrandstrategy(assessingtheaccuracyandeffective-ness of its communication efforts),

4. Officialwebsiteandsocialmediaperformance.The results of the 2013 Country Brand Ranking of 187 countries and territories are outlined in Figure 6. It shows that the United States has the strongest tourism brand followed by Thailand, Australia, China, Malaysia, the Republic of Korea and Mexico which all feature in the top 20 destinations. None of the 13 primary competitors to Europe across the six selected markets is ranked lower than 42nd (Brazil). Nine European countries are ranked in the leading 20 destinations, led by Spain, France, the United Kingdom and Italy. Full details for all European countries are presented in Appendix 1.

Figure 6: Country Tourism Brand Ranking: Primary Competitors to Europe

Source: Bloom Country Brand Ranking Tourism Edition 2013

1 Bloom Country Brand Ranking Tourism Edition 2013 http://bloom-consulting.com/sites/default/files/files/Bloom_Consulting_Country_Brand_Ranking_Tourism_2013.pdf

Country Brand Rankings

7

Marketing Strategies for Tourism Destinations. Target market: CHINA

The competitive strength of any country as a tourism destination is a combination ofmanyfactors,someofwhicharefixedorotherwisefactualwhileothersaresubjecttotheinfluenceofbothproductdevelopmentsandmarketingandpromo-tional activities. No destination is outstandingly strong or weak across all parame-ters. The strongest individual destination is the United States, rated as having the leading tourism brand and achieving 6th place in the global WEF TTCI survey of alltourismdevelopmentfactors(behindfiveEuropeancountries).

The power of strong tourism industries combined with market-driven tourism product/experience development and well-targeted marketing is illustrated by comparing rankings on the WEF TTCI broad tourism development and facilitation survey (that does not take account of destination marketing) and the Bloom Con-sulting Group destination brand ranking (which features destination marketing el-ements as a key criterion). This is borne out particularly in the cases of Thailand, China, Malaysia, Mexico, Egypt, South Africa and the Russian Federation where weaknesses in either or both of the regulatory framework, and business environ-ment and infrastructure, may be compensated for by price advantages and the appealofthecountries’tourismproductoffering.

Figure 7: Country Tourism Rankings

Country Bloom Country Brand Ranking

Overall WEF TTCI Ranking

Europe’sCompetitorsUnited States 1 6Thailand 6 43Australia 8 11China 10 45Malaysia 15 34Rep of Korea 18 25Mexico 19 44Egypt 22 85UAE - Dubai 25 28South Africa 28 64Russian Federation 30 63New Zealand 38 12Brazil 42 51European Benchmarks Spain 2 4Germany 3 2France 4 7United Kingdom 5 5Italy 7 26Austria 11 3Switzerland 14 1

Sources: WEF TTCI survey, and Bloom Country Brand Ranking Tourism Edition 2013

8

Marketing Strategies for Tourism Destinations. Target market: CHINA

Information Note - Exchange Rates The monetary values quoted in the report are taken from the sources referenced, including amounts stated in the source document in US dollars. In all cases, conversion has been made to Euros. The conversion rates used are the average rates across the year between the local currency (or US dollar where that is the currency stated in the source document) and the Euro for the year of the data. For future forecasts/targets, the rate between the local currency and the Euro as at June 2014 have been used.

9

Marketing Strategies for Tourism Destinations. Target market: CHINA

KEY DEMOGRAPHIC AND ECONOMIC DATA 2013

CHINA’S PERFORMANCE IN INTERNATIONAL TOURISM

OUTBOUND DESTINATIONS VISITED BY CHINESE

International arrivals generated

2012: 82mn2013 : 97.3mnup 18 to 19%

Expenditure

Population

1,351mn

$9,828 €7,280

GDP PPP per capita

Average annual GDP growth over past decade

1. Hong Kong

2. Thailand

3. South Korea

4. Macau

5. Taiwan

6,752,781

4,997,216

3,440,969

3,132,728

2,815,741

6. Singapore

7. Malaysia

8. Japan

9. Vietnam

10. France

1,563,044

1,476,636

889,847

682,053

648,376

Summary of China Market StudyOUTBOUND TRAVEL AND COMPETITIVE ENVIRONMENT

10

14 5

9

6

8

7

3

Leading outbound tourism country in terms of EXPENDITURE

CNY42,026 €5,075

GDP PPP per capita current prices2

Second largest outbound market in terms of OVERNIGHT STAYS in 20133

2012: $102bn (€78 bn)

2013: $120 – 130bn (€89 – 96 bn)

up 18 to 27% in dollar terms but slightly less in Euros (14 to 23%) as a result of the depreciation of the dollar against the Euro since 2012

2World Economic Outlook Database, October 2013, IMF. Euro values converted at average exchange rate for 2013. 3 World Travel Monitor 2013, IPK International

TOP destinations are Asian

Total trips to Europe:

3 million (first stop) with aggregate arrivals circa 5 million

10

Marketing Strategies for Tourism Destinations. Target market: CHINA

STRONG NON ASIAN GROWTH MARKETS GROWTH PER ANNUM 2005 - 2012

PURPOSE OF VISIT

30 29 29 20

United ArabEmirates

2000 2010

United States of America

Switzerland France

90

46

54

Private (leisure)Public (business, official)

Private (leisure)Public (business, official)

POSITIVE INFLUENCES ON GROWTH

Steadily developing economy

Easing of visa policies of foreign countries/regions

Increasing international flights

Expanding tourism consumption demand

Appreciation of Chinese currency

OUTBOUND TRAVEL AND COMPETITIVE ENVIRONMENT

Destination success in the Chinese tourism market from:

1. Understanding and catering for cultural needs, 2. Innovating, investing and working across sectors to deliver the right products/experiences, 3. Catering for increased FIT travel, 4. Focusing destination marketing on authentic features and offerings, 5. Incorporating China-friendly elements in the experiences offered, 6. Accurate product: market matching in line with the preferences and trends of the Chinese market, 7. Facilitating Chinese travellers to enter, travel around and obtain Chinese-oriented service.

Europe’s primary competitors across all aspects of tourism according to the WEF TTCI are other industrial-ised nations e.g. United States, Australia, New Zealand, Republic of Korea,

In terms of overall price competitiveness in travel and tourism, European destinations are among the world’s most costly,

The 2013 Bloom Consulting Country Brand Ranking rates the United States as the leading tourism destina-tion brand with Australia also in the top ten, while nine of the leading 20 tourism destination brands are European.

p.a. p.a. p.a. p.a.

11

Marketing Strategies for Tourism Destinations. Target market: CHINA

Seven destinations are shortlisted as significant competing destina-tions to Europe in the Chinese market: Australia, Malaysia, New Zealand, Republic of Korea, Russian Federation, Thailand and the USA,

All seven are making major efforts to support and increase the com-petitiveness of their travel and tourism industries by:

Australia and the USA are the most active and effective long haul competitors to Europe for the Chinese tourist,

Australia’s success in the Chinese markets is a result of:

PRINCIPAL COMPETING DESTINATIONS

COMPETING DESTINATION ORGANISATIONS

Europe’s primary competitors across all aspects of tourism according to the WEF TTCI are other industrialised nations e.g.

USA, Australia, New Zealand, Republic of Korea

In terms of overall price competitiveness in travel and tourism,

European destinations are among the world’s most costly

The seven countries competing with Europe for the Chinese tourist are pursuing marketing strategies that:

1. Seeking to develop new and improved infrastructure and tourism products/experiences across a broad range of visitor interests,

2. Focusing on delivering a high standard of tourism service,

3. Paying special attention to facilitating entry into their countries and targeting the Chinese tourist.

1. Stress the authenticity of their natural and cultural heritage in developing brand images and positioning,

2. Pay equal attention to established source markets and newly emerging ones to achieve a balanced set of markets,

3. Seek a market: product “matching” approach that provides high quality experiences based of detailed research into the needs and expectations of different market segment, with China a primary target market target,

4. Focus on a number of common segments across competitors e.g. MICE, medical tourism, shopping, festivals and events,

5. Pay special attention to attracting high value/affluent tourists,

6. Show a significant and continuing switch away from traditional advertising and promotional methods to electronic digital marketing.

1. Early awareness of China’s potential and the need to understand the Chinese traveller,

2. The necessity for a partnership approach to developing the Chinese market,

3. Substantive and sustained marketing campaigns targeted at affluent, urban Chinese who are experienced travellers,

4. Deploying marketing and promotional tools tailored to the needs and expectations of the Chinese traveller.

Brand USA’s achievement in only its third year of operation has been to translate interest and desire to visit the country into firm travel intentions – close to 60% of respondents intending to visit in the coming year,

The partnership approach is central to Brand USA’s marketing strategy and campaign components, giving a wide range of destination, travel trade and media partners the opportunity to piggyback on the digital and traditional marketing tools, public relations and promotional efforts developed and conducted by Brand USA,

In any destination marketing strategy based on partnerships, accountability to its partners is vital. Brand USA has a rigorous system of monitoring, assessing and evaluating its activities.

2World Economic Outlook Database, October 2013, IMF. Euro values converted at average exchange rate for 2013. 3 World Travel Monitor 2013, IPK International

Total trips to Europe:

3 million (first stop) with aggregate arrivals circa 5 million

12

Marketing Strategies for Tourism Destinations. Target market: CHINA

Traditionally-held perceptions of Europe, the United States and Australia in China are that Europe is rich in cultural heritage, tradition and luxury, The United States represents wealth, modernity and popular culture, and Australia offers a natural environment and a relaxed lifestyle,

Europe and the United States are top of the list in terms of choice as first time overseas destinations, while all three destinations can offer the range of attractions and activities to cater for the more experienced traveller seeking places to visit and things to do outside the normal tourist circuits,

All the three destinations have extensive Chinese language programmes – both in marketing campaigns in China, and in the delivery of tourism products and services in the destination. The United States has an advan-tage in that it is seen by the Chinese as being more attuned to Chinese tourists’ needs,

All have invested heavily and effectively in studies and surveys to better understand the attitudes, motivations, behaviour and characteristics of Chinese travellers in order to be able to design marketing and promotional strategies and campaigns to achieve the highest possible penetration of the China market,

The ETC is disadvantaged against Tourism Australia and Brand USA through a far smaller marketing budget in China,

The disparate and limited marketing activities of European countries, without a strong, financially-empowered coordinating mechanism, lead to the prevailing market perception of Europe of a collection of countries without a central theme. Competition can be fostered – indeed market competition is the essence of business in both Australia and the United States – by linking together on certain marketing activities, generating benefit to all, in the spirit of co-opetition (i.e. cooperation AND competi-tion) whereby the overall market is increased through working together enabling the destination’s individual marketing activities to compete for a larger total market. The strength of both Tourism Australia and Brand USA is their focus on the partnership approach to destination marketing,

Historical culture and heritage are Europe’s key assets in the current (unmanaged) positioning of Europe; but the challenge of any future marketing campaign will to shift this positioning to highlight Europe’s contemporary vibrancy, enterprise and innovation within tourism, and in particular to create knowledge about the rich and diverse tourism experi-ences that Europe can offer beyond the introductory tour of iconic sites and features.

COMPARATIVE ASSESSMENT: EUROPE, THE UNITED STATES, AUSTRALIA

The 2013 Bloom Country Brand Ranking rates the

USA as the leading tourism destination brand with Australia also in the top ten, while nine of the leading 20 tourism destination brands are European

13

Marketing Strategies for Tourism Destinations. Target market: CHINA

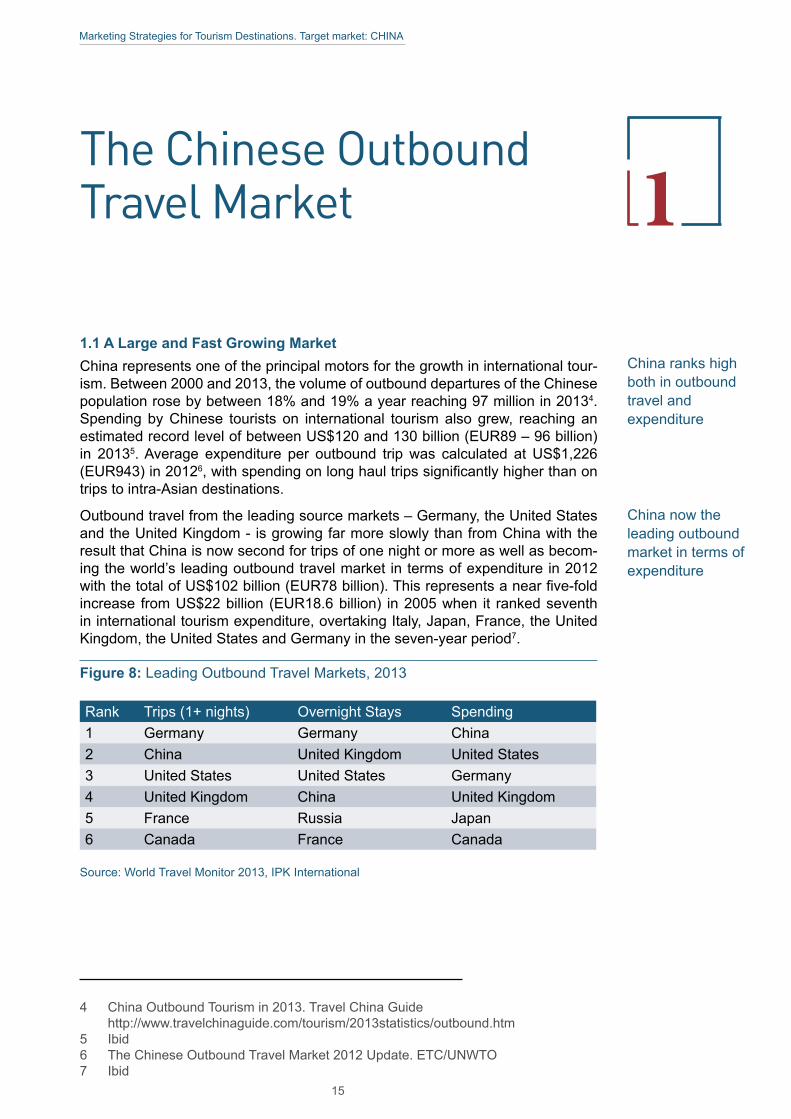

The Chinese Outbound Travel Market 11.1 A Large and Fast Growing Market China represents one of the principal motors for the growth in international tour-ism. Between 2000 and 2013, the volume of outbound departures of the Chinese population rose by between 18% and 19% a year reaching 97 million in 20134. Spending by Chinese tourists on international tourism also grew, reaching an estimated record level of between US$120 and 130 billion (EUR89 – 96 billion) in 20135. Average expenditure per outbound trip was calculated at US$1,226 (EUR943) in 20126,withspendingonlonghaultripssignificantlyhigherthanontrips to intra-Asian destinations.

Outbound travel from the leading source markets – Germany, the United States and the United Kingdom - is growing far more slowly than from China with the result that China is now second for trips of one night or more as well as becom-ingtheworld’sleadingoutboundtravelmarketintermsofexpenditurein2012withthetotalofUS$102billion(EUR78billion).Thisrepresentsanearfive-foldincrease from US$22 billion (EUR18.6 billion) in 2005 when it ranked seventh in international tourism expenditure, overtaking Italy, Japan, France, the United Kingdom, the United States and Germany in the seven-year period7.

Figure 8: Leading Outbound Travel Markets, 2013

Rank Trips (1+ nights) Overnight Stays Spending1 Germany Germany China2 China United Kingdom United States 3 United States United States Germany4 United Kingdom China United Kingdom5 France Russia Japan6 Canada France Canada

Source: World Travel Monitor 2013, IPK International

4 China Outbound Tourism in 2013. Travel China Guide http://www.travelchinaguide.com/tourism/2013statistics/outbound.htm

5 Ibid6 The Chinese Outbound Travel Market 2012 Update. ETC/UNWTO7 Ibid

China now the leading outbound market in terms of expenditure

China ranks high both in outbound travel and expenditure

15

Marketing Strategies for Tourism Destinations. Target market: CHINA

The main destinations for Chinese tourists are in Asia, with the Special Admin-istrative Regions (SAR) of Hong Kong and Macao attracting over 2/3 of total departures from China. In terms of arrivals of Chinese tourists, the top ten des-tinations are (2012 data): Hong Kong & Macau (China) 23 million, Rep of Korea 3.4 million, Thailand 2.8 million, Taiwan 2.6 million, Singapore 2.1 million, United States 1.6 million, Japan 1.5 million, Vietnam and Malaysia both 1.4 million. The trend towards intraregional travelwithinAsia reflects the continuedexpansionof the Chinese population able to travel abroad and who choose a nearby des-tination for their initial trip. In 2013, while total outbound trips rose 25%, Asian destinations recorded a rise of 31% while long haul trips grew by a lower 11%.

Intra-Asian destinations also dominate for Chinese outbound trip destinations organised through travel agencies, as illustrated in Figure 9.

Figure 9: Top 10 Outbound Destinations Visited by Chinese Tourists in 2013

1. Hong Kong

2. Thailand

6,752,781

4,997,216

3,440,969

3,132,728

2,815,7419. Vietnam

10. France

1,563,044

1,476,636

889,847

682,053

648,376

3. South Korea

4. Macau

5. Taiwan

6. Singapore

7. Malaysia

8. Japan

Source: China National Tourism Administration

Outside Asia, the strongest growth has been recorded to the United Arab Emir-ates (30% p.a. 2005-2012), the United States and Switzerland (both 29% p.a.), and France (20% p.a.). In the last two years Australia (+16% in 2012 to 0.6 mil-lion arrivals), and New Zealand (+48% to over 0.2 million) have been especially strong destinations for the Chinese. The United States, Europe, Australia and New Zealand have grown substantially in recent years, in response to easier travel regulations and increased promotional targeting.

Figure 10: Strong Non-Asian Growth Markets (% Growth Per Annum 2005-2012)

30

United ArabEmirates

29

United States of America

29

Switzerland

20

France

Source: Euromonitor International

Most travel from China remains

within Asia

Easing of travel regulations

contributing to growth outside of Asia

16

Marketing Strategies for Tourism Destinations. Target market: CHINA

Lookingahead,UNWTO forecasts thatAsiaand thePacificwill generate358million tourist arrivals in 2020 and 541 million tourist arrivals in 2030. Of these, nearly 20% will travel to destinations outside the region8. China will be the prime generator of Asian outbound travel. The forecast of 100 million Chinese trips abroad by 2020 made by UNWTO in the late 1990s9 will be achieved in 2014. While faster growth will remain for intraregional travel, demand for long haul trips willremainstrong,growingbybetween6.5%and7%ayearoverthenextfiveyears to exceed 35 million by 201910.

In terms of individual long haul destinations, Euromonitor International’s fore-casts for the period 2012 – 201711 see the strongest growth in Chinese visitors in Switzerland, Spain, the UAE, the United States (all more than doubling the level of arrivals), Italy, Austria, New Zealand and Australia.

1.2 Chinese Tourism to Europe Chinese tourism to Europe has grown at the rate of 18% a year between 2008 and 2013, reaching a level of 7,475,00012, following an annual rise of 11% in the previousfiveyears,illustratingthatChineseoutboundtravelgrowthwaslargelyunaffected by the global recession13. Despite this rapid growth, Chinese tourists comprised just 1.3% of total arrivals in Europe in 201314. As a proportion of all Chineselonghaultrips(definedasoutsideNortheastAsia),Europe’ssharehasfallen by over 9% between 2004 and 2014, now accounting for one-in-three such trips15.

The average expenditure of a Chinese visitor on a trip to European Union states was US$3,734 (EUR2,835) in 201116.

China was the 15th most important source market for European destinations in terms of international tourist arrivals in 2013, but the 2nd market from outside the region, after the United States.

The leading European destinations visited by the Chinese in 2012 were the Rus-sian Federation 0.8 million, France 1.3 million, Germany 0.8 million, Switzerland 0.7 million, Austria 0.4 million, Italy 0.3 million, United Kingdom 0.2 million17. In terms of regions within Europe, Chinese travellers primarily visit Western Europe-an and Central/Eastern European destinations, these two regions accounting for 55% and 20% respectively of Chinese arrivals in Europe in 201318.

8 Ibid9 Tourism 2020 Vision. 1997. UNWTO10 European Tourism in 2014: Trends and Prospects (Q1 2014). ETC.11 Euromonitor International

http://skift.com/2013/09/03/top-25-most-popular-destinations-for-chinese-tourists/12 ETC Dashboard13 European Tourism Portfolio Analysis: Market Share and Origin Market Growth.

ETC14 Ibid15 European Tourism in 2014: Trends and Prospects (Q1 2014). ETC.16 MarketProfileChina.December2013.ETC17 Euromonitor International

http://skift.com/2013/09/03/top-25-most-popular-destinations-for-chinese-tourists/18 European Tourism Portfolio Analysis: Market Share and Origin Market Growth.

ETC

China will be the prime generator of Asian outbound travel to 2020

China is the 2nd market for Europe from outside the region, after the United States

Western Europe accounts for over half of Chinese arrivals in Europe18

17

Marketing Strategies for Tourism Destinations. Target market: CHINA

Chinese trips to Europe are forecast to grow at an average annual rate of be-tween7.5%and8%overthenextfiveyears,resultinginareversalofthede-clineofEurope’smarketshareofChinese longhaul travel19. Total arrivals will approach 12 million by 2019.

1.3 Characteristics of the Chinese Traveller Population: 1,351 million population, forecast to grow at 0.23% to 2025, but declining thereafter as deaths outnumber births20.

Gross Domestic Product (2013): US$8,939 billion (EUR6,900 billion), with growth of between 6 and 7% a year forecast to 201921.

GDP Per Capita (2013): US$6,569 (EUR5,075), rising to a forecast level of US$9,300 (EUR6,890) by 201722. Wide variation in the distribution of income, with 120 million Chinese having a disposable household income of over US$6,000 (EUR4,330) in 2010, while the lowest quintile of 151 million people had just over US$1,100 (EUR795)23, as converted from Chinese yuan at the average 2010 exchange rate of 6.77 yuan to the dollar.

Figure 11: Demographic and Economic Facts

Population

1,351mn

$7,958 GDP per capita

Average annual 3 GDP growth over past decade

1

2

The major urban centres of Beijing, Shanghai, Guangzhou and Shenzhen ac-count for most of the outbound travel demand among Chinese, but demand from smaller cities and towns is also growing fast. Shanghai is the primary source of outbound business travel24.

Chinese travel is traditionally concentrated in the May and October holiday periods, but it is becoming increasingly spread across the year. A continuation of this trend is anticipated as holiday entitlements increase and longer duration trips are taken25.

Air transport dominates. China has a target of 244 airports by 2020, with a total of over 300 million passengers a year at present and a forecast growth rate in domestic air demand of 8% a year to 2028, fuelled by strong economic growth, market liberalisation and fast urbanisation with rising household travel expendi-tures26.

19 European Tourism in 2014: Trends and Prospects (Q1 2014). ETC.20 China Population 2013. World Population Statistics. 18 September 2013. http://www.worldpopulationstatistics.com/china-population-2013/21 IMF World Economic Outlook China22 Ibid 23 The Chinese Outbound Travel Market 2012 Update. ETC/UNWTO24 Ibid25 Ibid26 Ibid

China GDP forecast to grow to US$9,300

by 2017

Total Chinese arrivals to Europe forecast

to reach 12 million by 2019

Chinese travel is traditionally

concentrated from May to October

18

Marketing Strategies for Tourism Destinations. Target market: CHINA

AsofSeptember2010,23airlinesoperated471weeklyflightsbetweenChineseand European airports, with a capacity of 140,000 seats27.

Thesplitbetweenpublic(i.e.business,official)andprivate(leisure)changeddra-matically between 2000 and 2010, from 46:54 to 10:90, as holiday travel surged. Holiday travel – particularly group travel – expanded throughout the decade in line with the liberalisation of outbound travel.

Information is readily absorbed by Chinese people though there remains heavy reliance on peer group information from other Chinese. Electronic technology combines these two characteristics to fuel outbound travel growth, and to in-crease the proportion of trips – or trip components – booked online.

There are 591 million Chinese internet users with 464 million citizens accessing the net via smartphones or other wireless device28.Already,one-in-fiveChinesetravellersbooksonline,aproportion thatwill risesignificantlyas independent-ly-arranged–orFIT(flexibleindependenttravel)-travelexpands.

Theincidenceoffirsttimeoverseastravellersstillaccountsforthemajoritybutthe proportion is declining (65% to 59% between 2011 and 2012) as regular over-seas trip taking grows29.

One third of all trips are through travel agents – 33.6 million in 201330. The Chi-nese Government regulation requires leisure travel to long haul destinations to be booked via licensed travel agencies but this condition has been eased recent-lyresultingintravelagencies’shareoftripstodestinationsexceptHongKongand Macau falling from 89% in 200931 to between 70 and 75% in 201332

Given the size of the Chinese population and the severe restrictions on overseas traveluntil1988,themajorityofoutboundtravellersarestillontheirfirsttripout-side the country. Highly structured package tours are the medium for such travel-lers, largely unaware of what to expect or do when in a foreign country.

However, informed and stimulated by digital media, Chinese travel tastes are broadeningoutand themain trendnow is fordiversification,withnicheprod-ucts and destinations gaining ground, and more self-organised trips being taken. More experience and language skills lead to different forms of “semi” or “partly” – organised trips with tour operators providing visa, air trip and, in some cases, hotel bookings.

Just under half - 47% - of Chinese outbound tourists are travelling with members of their family, and another 24% with friends. Only 7% travel entirely without com-panions. 3% of travellers are participants in groups organised by their work units or companies - mostly for technical tours, incentives, and study33.

27 Ibid28 17 July 2013. http://www.bbc.co.uk/news/technology-23343058 29 http://www.travelchinaguide.com/tourism/2012statistics/outbound.htm 30 ibid31 The Chinese Outbound Travel Market, 2012 Update, ETC/UNWTO32 Author’sestimatebasedondatain http://www.travelchinaguide.com/tourism/2013statistics/outbound.htm 33 Annual Report of China Outbound Tourism Development 2010 cited in The Chinese

Outbound Travel Market, 2012 Update, ETC/UNWTO

Private travel accounts for 90% of outbound travel

One-in-fiveChinesetravellers books online

First time overseas travellers still account for the majority but the proportion is declining

Just under half of Chinese outbound tourists are travelling with members of their family

Trend towards more self-organised trips

19

Marketing Strategies for Tourism Destinations. Target market: CHINA

The Chinese leisure market divides between the first time traveller attracted by:• doing lots of things in a short timeframe,• shopping for international brands,• good value-for-money,• findingfamiliarfoodsandinteractingwithChinesecommunities,• the prestige of visiting – and having photos taken in front of – iconic

sites, • a safe environment.

the more experienced traveller, still attracted by many of these features but also looking to travel as a means of:

• expressingincreasingself-confidenceandindividualism,• seeking an emotional connection with the destination, through authen-

ticity, clean air/blue skies, access to arts and culture etc.

The non-traditionalist Chinese tourists are fragmented into a range of sub-seg-ments or niches but even niche products have relatively large volume demand given the scale of the Chinese market34. Nonetheless, the greater segmentation ofthemarketmakesitmoredifficulttoachieveeconomiesofscaleintermsofcosts. This needs to be compensated for by using new online booking and sales concepts,making itpossible tospecificallyaddresscustomergroupseven forvery special interests and destinations.

Figure 12: Sophistication and Status for the Chinese Traveller

Source: Understanding Chinese Outbound Tourism: What the Chinese blogosphere is saying about Europe. UNWTO/ETC. 2012.

34 DestinationInvestment.NewNetworksforServingAffluentChineseVisitors.DrWolfgang Georg Arlt, COTRI – Chinese Outbound Travel Research Institute, IRB, March 2013.

Greater segmentation of the market will

require more effective online marketing

20

Marketing Strategies for Tourism Destinations. Target market: CHINA

The characteristics of the different “tribes” are summarised in Figure 13. Tra-ditionalists, estimated to still account for 70% of demand, travel predominantly for reasons of prestige and are in tour groups. The Wenyi youth and Experi-ence-centered tribes each account for 10%, with the remaining estimated 10% split between Connoisseurs (7%) and Hedonists (3%).

Figure 13: Characteristics of the Chinese Travel Tribes

Tribe Why They Travel

Mode of Travelling

With Whome

Brings on the Trip

Traditionalists Prestige Tour Groups Tour Groups Camera

Wenyi Youth Freedom, Uniqueness

Backpacking Alone or with Friends

Notebook, favourite book, mp-3 player, internet device

Experience – centered

Togetherness, curiosity

Backpacking or independent driving

Alone, with family or in ‘in-depth travel’tourgroups

Guidebook, phrasebook, electronic dictionary

Hedonists Pleasure City travel, shopping

With friends Their parents’credit card

Connoisseurs Aesthetics, knowledge

Independent driving

With partner or family

Camera with equipment, specialised guidebook, laptop

Source: Understanding Chinese Outbound Tourism: What the Chinese blogosphere is saying about Europe. UNWTO/ETC. 2012

ForthefirsttimeChineseoverseastraveller,thefocusisondoingasmuchaspossible. Trip durations are short – typically 4 days, each day packed with activi-ties, and duty free shopping is given the highest priority.

The more experienced Chinese traveller is increasingly seeking out sites and attractions away from the honeypot areas, seeking a more depth experience of the destinations visited. There is a trend towards “deep tours” focused on a single country, or two countries35.

35 The Chinese Outbound Travel Market, 2012 Update, ETC/UNWTO

ForthefirsttimeChinese overseas traveller, the focus is on doing as much as possible

21

Marketing Strategies for Tourism Destinations. Target market: CHINA

1.4 Drivers of GrowthIdealised as means to greater self-realisation, travel has become integral to the Chinese middle-class lifestyle36

There seems little doubt that outbound travel for both business and leisure pur-poses will continue to expand over the present decade and beyond given:

• the dynamics of the socio-demographic trends in China,• theChinesepopulation’srisingawarenessof,andinterestin,engag-

ing in foreign travel,• the greater ease of making foreign outbound travel arrangements aris-

ingfromtheChineseGovernment’scommitment tosupport tourism,improved connectivity and changes to visa regimes.

Though the Chinese population is forecast to grow at a low rate of 0.23% a year, thiswillstillrepresentanincreaseinthecountry’spopulationinexcessof3mil-lion people a year. By 2030, the Chinese will make up just under 20% of the world population37.

Key demographic trends with implications for travel and tourism are: the levelling out of fertility rates, large-scale urbanisation and the rapidly ageing population38. By 2030, the largest group in the Chinese population will be aged 60-64. An age-ingpopulationwithretireeshavingfinancialmeanstotravelwillboostoverseastravel. Increased and diversified leisure time, outside the prescribed “GoldenWeeks” will also serve to increase travel.

China’seconomicgrowth ratewill slowdownover thenextfiveyears,edgingdown from the 7.7% recorded in 2012 and forecast in 2013 to an annual rate of expansion of 6.5% by 201939. This is still above the rate of economic growth achieved elsewhere in the world. Income levels will continue to rise both in the medium and longer terms and will lead to growing numbers of middle class Chi-neseconsumerswithsufficientdisposableincometotravel.

At the centre of the growth of all forms of consumer spending and activity – in-cluding overseas travel and tourism - is the Chinese urban middle-class popula-tion. In 2000, only 4% of urban households in China were middle class; by 2012, that share had soared to over two-thirds; and by 2022, China’smiddle classshould number 630 million – that is, three-quarters of urban Chinese households and 45% of the entire population.40ThenumbersofaffluentmiddleclassChineseis forecast to rise from 175 million in 2011 to 1.4 billion by 203041.

36 The Chinese Outbound Travel Market 2012 Update. ETC/UNWTO.37 Demographic Change and Tourism. 2010. ETC & UNWTO.38 Ibid39 IMF World Economic Outlook China40 HalfaBillion:China’sMiddleClass-ClassConsumers.DBarton,McKinseyand

Company in The Diplomat, 30 May 2013 41 China Digital Times, 2011. Chinese Middle Class four times larger than America.

http://chinadigitaltimes.net/2011/09/within-a-generation-china-middle-class-four- times-larger-than-americas/

Travel has become integral to the

Chinese middle-class lifestyle

Ageing Chinese population will boost

overseas travel

22

Marketing Strategies for Tourism Destinations. Target market: CHINA

At present only about 7% of the Chinese have an annual income above US$15,000 (EUR11,000)andthecountry’stotalconsumptionexpenditureperhousehold–atUS$13,428 (EUR9,950) a year – is relatively low compared to other Asian coun-tries such as Japan and the Republic of Korea. The relatively small number of af-fluentChineseconsumerswillgrowandwillfollowthesamepatternofspendingon property, Western branded goods and luxury items, as well as travel. Given theyoungprofileoftheseconsumers,thisspendingtrendispredictedtocontinuefor the foreseeable future42.

The increasing urbanisation of the Chinese population will also be an important factorinstimulatingtravelandtourism.AlreadyhalfofChina’spopulationliveinCities, a proportion that will grow to two-thirds by 2030. Major cities like Beijing, Shanghai, Guangzhou and Shenzen will get bigger but the approximately 170 “second tier” cities, many of which were boosted through the Chinese stimulus package providing better transport infrastructure and services, will also represent large travel markets e.g. Chongqing (29 million population), Chengdu (14 mil-lion), Wuhan (8.3 million).

The increased rapid, recent and continuing urbanisation of the Chinese popu-lation has led to environmental problems of pollution in many cities leading to a desire to go to places without such issues. Worsening pollution and overcrowding will increasingly act as “push” factors for outbound tourism43. The impact of digital technology on Chinese travellers continues to be immense. The Chinese have over 600 million smartphone users, the largest in the world, with sales of 283 million smartphones (to 216 million new users) forecast in 201444. Two-thirds of Chinese blog/have a personal space, almost half use social networking sites and email and 83% use instant messaging45. More extensive uses of digital technology will be made both by destinations and travel organisa-tionssothat,combinedwiththeChinesepublic’sheighteneduseofsocialmedia,awareness of, interest in, and demand for travel will continue to grow.

This heightened understanding of tourist destinations around the world is giving rise to a growing sense of prestige among the Chinese about the type of trip – with package tours regarded as inferior to independently-organised travel – and destinations that have been little visited by the Chinese and/or which create a strong desire among the Chinese to visit through their marketing campaigns hav-ing a high prestige. The Chinese outbound market will increasingly fragment, with package tours gradually losing relative importance towards growing semi-pack-aged and fully independent travel arrangements.

42 ITB World Travel Trends Report 2013/2014. March 2014. IPK International reporting presentation of Chandrashekhar Singh Khangjrakpam, Centaur Research.

43 NineImportantDevelopmentsinChina’sOutboundTourism2013.WolfgangArlt,COTRI – China Outbound Tourism Research Institute http://www.forbes.com/sites/profdrwolfgangarlt/2014/01/01/nine-important-developments-in-chinas-outbound-tourism-2013/

44 Smartphone explosion in 2014 will see usership in India pass US. The Guardian – Global Development. 13 January 2014.

45 China Internet Network Information Center, 2013 cited in Chinese & Brazilian Outbound Tourism Markets and Netnography, Eduardo Santander, ETC. 7th UNWTO/PATA Forum on Tourism Trends and Outlook, October 2013

Increasing urbanisation of population will stimulate outbound travel from China

Environmental problems of pollution will stimulate desire to go to places without such issues

Digital technology crucial for Chinese travellers

23

Marketing Strategies for Tourism Destinations. Target market: CHINA

Two recent initiatives of the Chinese Government have served to increase travel and tourism by the Chinese population.

The first dates back to the early 1990swhen theChineseGovernment’sAp-proved Destination Status (ADS), a bilateral tourism agreement with – to date – 148 countries, was introduced to guarantee safe and reliable tourism services to Chinese travellers. It only concerns tour groups handled by assigned Chinese local travel agents who are allowed to promote and organise tourist groups to approved destinations, including visa application and payment of foreign curren-cy top foreign parties. Having ADS permits countries to undertake marketing in China. Chinese travellers wishing to travel independently can do so making their own visa and other arrangements. In October 2013, the China National Tourism Law was passed, making it illegal to sell tours below cost and to engage in the practice of “forced shopping”. This entails the operator taking the tourists only to those shops that provide the operator with concessions, thereby making up the shortfall on the low price of the tour that attracted the tourist to purchase it.

The second initiative is the introduction by the Communist Party General Sec-retary Xi Jinping in 2013 of the concept of the Chinese Dream. He describes it as “a national rejuvenation, improvement of people’s livelihoods, prosperity,construction of a better society and military strengthening.” He exhorts young people“todaretodream,workassiduouslytofulfilthedreamsandcontributetothe revitalisation of the nation”46

In consequence of these and other Chinese Government initiatives, trade has been increasingly liberalised and air routes increased, leading to large growth of: 1. international operations in China (many of which generate interest in visita-tion by the Chinese e.g. Swiss companies), 2. Chinese enterprises abroad, and 3. overseas travel and tourism by the Chinese.

The Chinese Government is actively supporting outbound tourism. In a January 2013 meeting with UNWTO Secretary General, Taleb Rifai, the Chairman of the ChinaNationalTourismAdministration(CNTA),ShaoQiwei,confirmedthattour-ismremainedoneoftheChineseGovernment’skeystrategicpillarsforeconomicgrowth,and thatoutbound tourismwill alsoboostChina’sdevelopment in thelongterm.Thepromotionofoutboundtourismisvaluedbecauseofthebenefitsofmutualcollaboration,thebenefitsofwhichwilleventuallyflowbacktoChina47.

The increase in air service connectivity between China and trading partners and tourism destinations in Asia and interregionally has been very strong and will con-tinuetoexertamajorinfluenceonChineseoutboundtouristflowsanddirections.Between2008/9and2013/4,scheduledservicecapacityfromChina’stwomaincities of Beijing and Shanghai grew by more than double to Thailand and the United States cities of Los Angeles and New York, and by close to double in the peak tourist season on the routes to Sydney (Australia) and Moscow (Russian Federation). The leading European destinations saw capacity increases over the period of up to a quarter, though new European routes were developed. Capaci-ties will continue to increase in line with demand.

46 ChineseDream.en.wikipedia.org/wiki/Chinese_Dream47 COTTM – China Outbound Travel and Tourism Market – April 2013. COTRI –

ChinaOutboundTourismResearchInstitute.www.slideshare.net/COTRI_Outbound/cotm-china-outbound-travel-and-tourism-market-presentation-april-2013

Liberalisation has led to expansion of air

routes

Chinese Government is actively supporting

outbound tourism

Recent policy initiatives contributed to increased travel by

Chinese

24

Marketing Strategies for Tourism Destinations. Target market: CHINA

Visa formalities are being eased across the world. While visas are still required for Chinese tourists to major destinations like the United States and Australia, the speeding up of processing is likely to serve to increase the numbers of Chinese FIT travellers.

Figure 14: NineImportantDevelopmentsinChina’sOutboundTourism2013

1Quantitative Growth

2New Push Factor

Pollution

3New Push Factor

Overcrowding

4Encouragement by new

Chinese Government

5Visa Policy Dominos

Starting to Fall

6Move Towards More Self

Organised Trips

7Move Towards New

Destinations

8Chinese Investors

Shopping Spree

9Major Players Enter the

Scene

1.5 Successful Destination Strategies Destination regions face increasing competition for the Chinese tourist. There are severalfactorsthatwilldeterminetheabilityofadestinationtoattractsignificantflowsofChinesetourists:

1. ExtenttowhichtheculturalinfluencesandspecificneedsofChinesetourists are understood and catered for,

2. The provision of the right combinations of travel offer to the groups of Chinese tourists being targeted48,

3. Recognition of the increased share of Chinese FIT travel,4. Developing tourist products and experiences in line with the needs

and expectations of the different Chinese market segments,5. Designing destination marketing to appeal to the Chinese desire for

authentic features and offerings,6. Degree to which China-friendly elements are built into the experienc-

es offered, 7. Facilitation of travel to and around the destination.

48 NewChineseTouristsinEuropefrom2017.TrendSurveybyZ_punktTheForesight Company in cooperation with the TUI Think Tank at TUI AG, 2012

25

Marketing Strategies for Tourism Destinations. Target market: CHINA

2Travel Destinations in the Chinese Market

Based on the investigations and research conducted into recent trends in Chi-nesevisitorflowsandthecomparativeassessmentthatintroducesthisreport,ashort list of seven destinations was selected for further examination in respect of the Chinese market. The seven – in alphabetical order - are:

1. ASEAN countries (Republic of Korea, Thailand, Malaysia),2. Australia,3. New Zealand,4. Russian Federation, 5. United States.

The remainder of this chapter illustrates the positioning of these countries in the Chinese market as compared to Europe. The positioning is assessed on factors thatfacilitatetourismflows,suchasvisaregimes,transportroutes,andthepo-litical, socio economic and cultural links existing between the market and each destination.

This section is enriched by an analysis of TripAdvisor ratings on accommodation, attractions and eateries, presented in Appendix 3. While not representative of Chinesetravellers,TripAdvisorratingsareusedasaproxyforconsumers’ap-preciation of key aspects of a holiday experience across competing destinations.

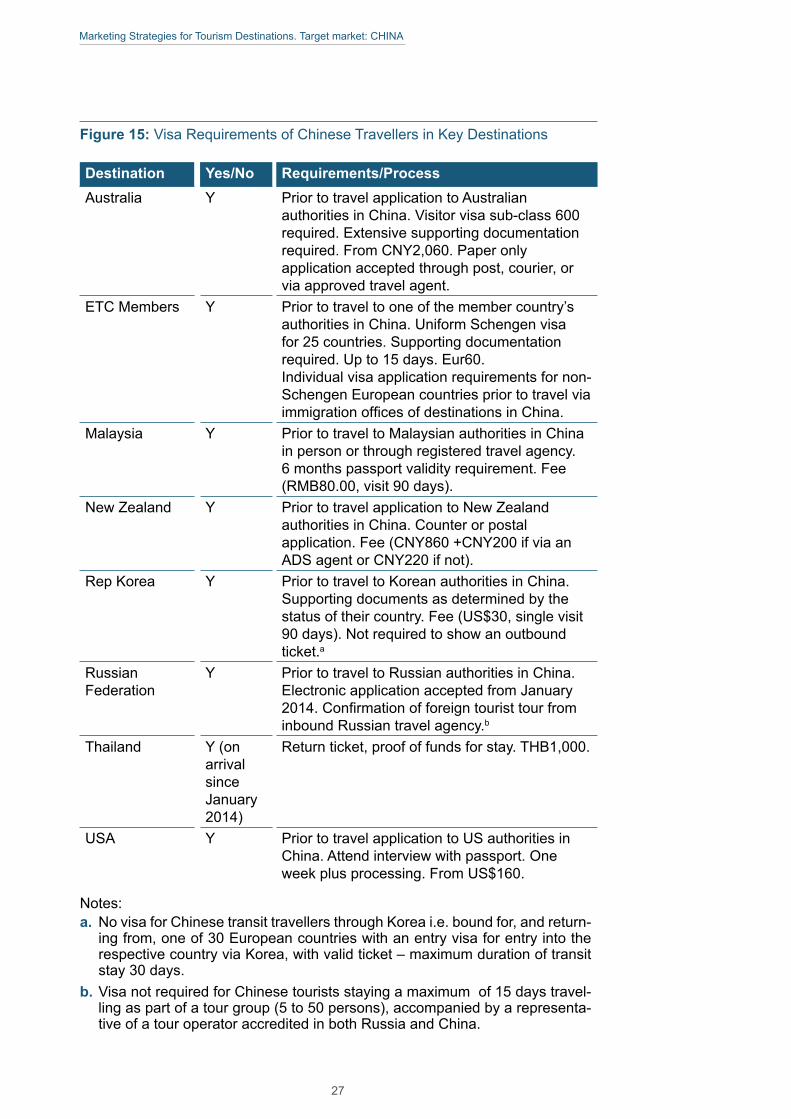

2.1 Visa Regimes The detailed comparison of visitor entry requirements for the selected 13 destina-tions competing with Europe considered three elements:

1. Whether the destination imposes a visa requirement for entry to the country,

2. The documentation and other details demanded for issuance of a visa,

3. A qualitative assessment of the “hassle” factor involved in obtaining the visa.

Among the seven countries selected as prime competitors to Europe in the Chi-nese market, all destinations (including ETC member countries) - with the single exception of Thailand, where visas are granted on arrival – require Chinese trav-ellers to obtain a visa ahead of travel.

26

Marketing Strategies for Tourism Destinations. Target market: CHINA

Figure 15: Visa Requirements of Chinese Travellers in Key Destinations

Destination Yes/No Requirements/ProcessAustralia Y Prior to travel application to Australian

authorities in China. Visitor visa sub-class 600 required. Extensive supporting documentation required. From CNY2,060. Paper only application accepted through post, courier, or via approved travel agent.

ETC Members Y Priortotraveltooneofthemembercountry’sauthorities in China. Uniform Schengen visa for 25 countries. Supporting documentation required. Up to 15 days. Eur60.Individual visa application requirements for non-Schengen European countries prior to travel via immigrationofficesofdestinationsinChina.

Malaysia Y Prior to travel to Malaysian authorities in China in person or through registered travel agency. 6 months passport validity requirement. Fee (RMB80.00, visit 90 days).

New Zealand Y Prior to travel application to New Zealand authorities in China. Counter or postal application. Fee (CNY860 +CNY200 if via an ADS agent or CNY220 if not).

Rep Korea Y Prior to travel to Korean authorities in China. Supporting documents as determined by the status of their country. Fee (US$30, single visit 90 days). Not required to show an outbound ticket.a

Russian Federation

Y Prior to travel to Russian authorities in China. Electronic application accepted from January 2014.Confirmationofforeigntouristtourfrominbound Russian travel agency.b

Thailand Y (on arrival since January 2014)

Return ticket, proof of funds for stay. THB1,000.

USA Y Prior to travel application to US authorities in China. Attend interview with passport. One week plus processing. From US$160.

Notes:a. No visa for Chinese transit travellers through Korea i.e. bound for, and return-

ing from, one of 30 European countries with an entry visa for entry into the respective country via Korea, with valid ticket – maximum duration of transit stay 30 days.

b. Visa not required for Chinese tourists staying a maximum of 15 days travel-ling as part of a tour group (5 to 50 persons), accompanied by a representa-tive of a tour operator accredited in both Russia and China.

27

Marketing Strategies for Tourism Destinations. Target market: CHINA

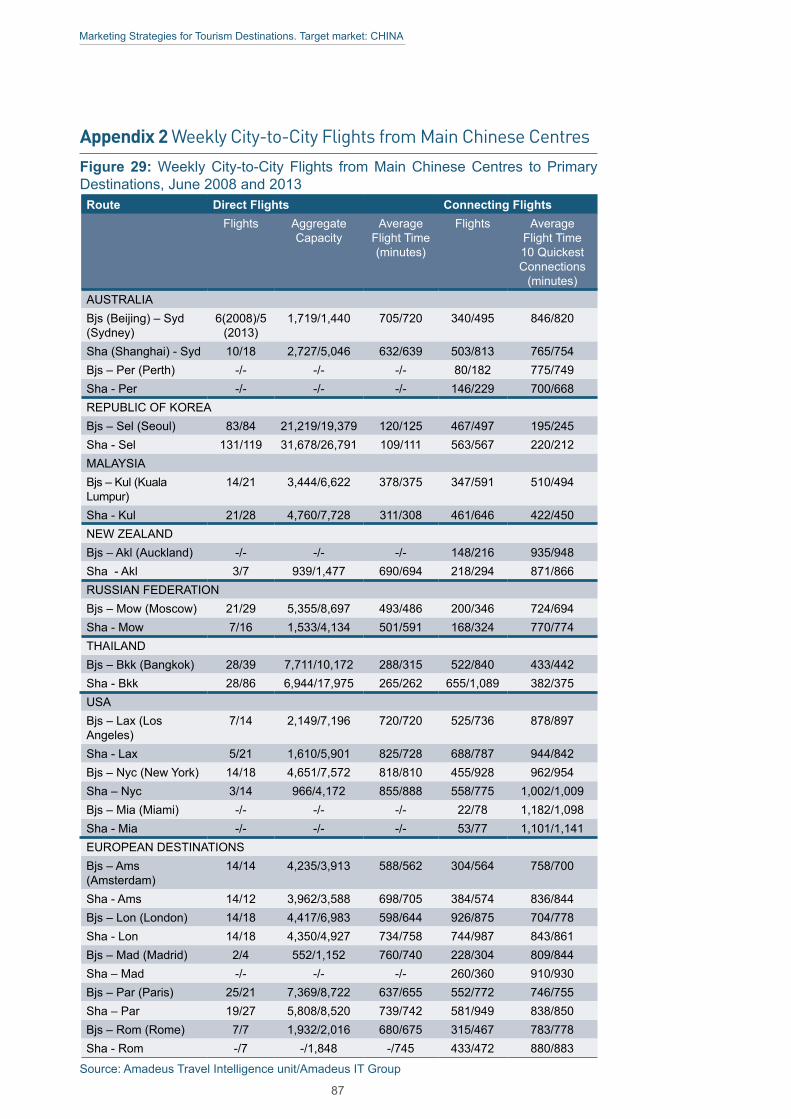

2.2 Air ConnectionsThescheduledaircapacityfromChina’stwoprincipalinternationalairgatewaystotheshortlisteddestinationscompetingwithEuropewasmonitoredonETC’sbehalf by Amadeus. Two points in the year were examined – week 24 in 2013 (broadly corresponding to high season) and week 6 in 2014 (low season), though this can only be taken as an approximate measure given the difference in north-ern and southern hemisphere climates at the different times of the year. Data for two years were considered in order to provide an indication of the trend in capacity on the various routes i.e. June 2008/June 2013, and February 2009/February 2014.

Thedestinationswith thegreatest frequencies fordirect flightsandcapacitiesare,astobeexpected,AsiandestinationsinvolvingshorterflighttimesthantoAustralia, New Zealand, the United States or Europe. The weekly capacity of directflightsfromthetwomainChineseairportstoSeoulisbetween46and47thousandonjustover200flights,withajourneytimeofaroundtwohours.ForBankgok, therearebetween28 thousand seats (on125 flights) and33 thou-sandseats(on140flights),dependingonseason,withjourneytimesofbetweenfour-and-a-halfandfive-and-a-halfhours.However,whereasdirectflightcapacityoverthefiveyearperiodtoBangkokrosebybetweenoneandone-and-a-halftimes, seats to Seoul showed little change. Capacity of direct air services from China’stwoprincipalairportstoKualaLumpuralmostdoubledovertheperiod.

JourneytimesondirectflightstotheRussianFederation–takingthecapitalcity,Moscow – range between 8 and over 10 hours. There is considerable seasonal variationinthevolumeofflightswithmorecapacityinJune(nearly13,000seatson45flightsinaggregatefromBeijingandShanghai)thaninFebruary(lessthan7,500seatson25flights).CapacityroseslightlyinthewinterperiodbutgrewbyoverahalfinJune2013comparedwiththesameweekfiveyearsearlier.

Flights from China to Australia also show considerable seasonal variation but in the reverse order with more seats in the southern hemisphere summer period (32flightswithcapacityofover10,000)thaninJune(23flightswith6,500seats).TherearenodirectflightsbetweenmainChineseairports to thewesternAus-traliancityofPerth.Directflightseatcapacityalmostdoubledoverthefiveyearperiod during the summer hemisphere months but by just under a half in June 2013 compared with the same month in 2008. Direct air capacity to New Zealand islimitedtoflightsbetweenShanghaiandAucklandwithadoublingofcapacityin the peak period, though this increase partly offset the withdrawal of direct air services from Beijing two years ago.

The three United States airports included in the present study are Los Angeles, New York and Miami. There are no direct scheduled air services from China to Miami.LosAngelesreceives35flightsaweekfromBeijingandShanghaiwith13,000seats.NewYorkhas32directflightsprovidingacapacityofover11,500.Directflightjourneytimesarearound12hourstoLosAngelesandbetween13.5and nearly 15 hours for New York.

Considerable seasonal variation in thevolumeofflights

from China

28

Marketing Strategies for Tourism Destinations. Target market: CHINA

Capacity increases to the United States airports have been extremely high: in the case of Los Angeles, the rise was three-and-a-half times in the week being stud-ied between June 2008 and 2013 and by almost double between February 2009 andthesameweek in2014.ForNewYork,directflightseatcapacitydoubledJune to June and one-and-a-half-times from February 2009 and February 2014.

The pattern for China-Europe direct air services is for modest growth except for those cities with low base volume in the initial year being examined. This pro-duces a high growth rate even though the number of seats is relatively small e.g. capacity to Madrid rose 88% between February 2009 and 2014 but still amounts to just over 1,000 seats a week.

The discrepancy between Europe and its competitors is less marked when con-nectingflightsareconsidered.ApartfromthefastestgrowthdestinationssuchasBangkok and New York, and newly emerging destinations with low base volumes ofconnectingflightsinthefirstofthetwoyearsexaminede.g.PerthandMiami,theincreaseinconnectingflightservicesisbroadlysimilarbetweentheEurope-an benchmark destinations and competitors. Figure 16: Changes in Weekly Direct Flight Seat Capacity from China (Beijing and Shanghai Aggregated) to Selected Destinations, June 2008-June 2013 and February 2009-February 2014

Source: TDI calculations based on data supplied by Amadeus

The analysis points to a comparative advantage of competing destinations in terms of air connections with China. Over the past five years, direct air capacity from China both to major short haul destinations (e.g. Thailand and Malaysia) and to long haul destination competing with Europe (i.e. Australia, Russian Fed-eration and, most significantly, the United States) has expanded more significant-ly than to Europe.

Fulldetailsofflights,capacitiesandflighttimefordirectandconnectingflightsfor a week in June 2008 and 2013, and a week in February 2009 and 2014 are shown in Appendix 1.

NOTE:figures infrontofbreak(/)relatetothefirstyear inthetimeseries i.e.June 2008, while those after the break are for the later year i.e. June 2013.

Significantcapacityincreases to the United States airports

More modest growth in China-Europe direct air services

Europe's competitors have a comparative advantage in terms of air connections with China

29

Marketing Strategies for Tourism Destinations. Target market: CHINA

Figure 17: Direct Flights CapacityTo

urism Strategy of Europ

e’s Main Co

mpe

titors – China

Rep

ort

0 5,

000

10,0

00

15,0

00

20,0

00

25,0

00

Beijing

–

Bang

kok

Beijing

– K

uala

Lu

mpu

r Be

ijing

– Seo

ul

Beijing

–

Sydn

ey

Beijing

–

Auc

klan

d

Beijing

-‐ Asia

Pacific

Feb-‐

09

Feb-‐

14

Jun-‐

08

Jun-‐

13

0 10

,000

20

,000

30

,000

40

,000

Shan

ghai

-‐ Ba

ngko

k Sh

angh

ai -‐

Kual

a Lu

mpu

r

Shan

ghai

-‐ Se

oul

Shan

ghai

-‐ Sy

dney

Sh

angh

ai -‐

Auc

klan

d

Shan

ghai

-‐ Asia

Pacific

Feb-‐

09

Feb-‐

14

Jun-‐

08

Jun-‐

13

0 2,

000

4,00

0 6,

000

8,00

0

Beijing

–

New

Yor

k Be

ijing

–

Los

Ang

eles

Beiji

ng -‐

USA

Feb-‐

09

Feb-‐

14

Jun-‐

08

Jun-‐

13

0 20

00

4000

60

00

8000

Shan

ghai

–

New

Yo

rk

Shan

ghai

-‐ Lo

s Ang

eles

Shan

ghai

-‐ USA

Feb-‐

09

Feb-‐

14

Jun-‐

08

Jun-‐

13

Figu

re 1

6 Di

rect

Flig

hts

Cap

acity

0 1,

000

2,00

0 3,

000

4,00

0 5,

000

6,00

0 7,

000

8,00

0 9,

000

10,0

00

Beijing

–

Am

ster

dam

Be

ijing

–

Lond

on

Beijing

–

Paris

Beijing

–

Rom

e Be

ijing

–

Mos

cow

Be

ijing

–

Mad

rid

Beiji

ng -‐

Euro

pe

Feb-‐

09

Feb-‐

14

Jun-‐

08

Jun-‐

13

0 1,

000

2,00

0 3,

000

4,00

0 5,

000

6,00

0 7,

000

8,00

0 9,

000

Shan

ghai

-‐ Am

este

rdam

Sh

angh

ai -‐

Lond

on

Shan

ghai

–

Paris

Shan

ghai

-‐ Ro

me

Shan

ghai

-‐ M

osco

w

Shan

ghai

-‐ Eu

rope

Feb-‐

09

Feb-‐

14

Jun-‐

08

Jun-‐

13

Beijing

Shan

ghai

Source: TDI calculations based on data supplied by Amadeus30

Marketing Strategies for Tourism Destinations. Target market: CHINA

2.3 Political, Economic and Socio-Cultural Links China has developed and maintains strong relations with each of the seven coun-tries under study, there remaining few barriers to the encouragement and facilita-tion of tourism to and from China.

4% of the Australian population – 0.9 million - are of Chinese ancestry49, with 319,000 having been born in Mainland China. Chinese Australians are now one of the most well-established immigrant ethnic groups in Australia. Chinese news-papers are published in Australia and three shortwave and longwave radio chan-nels broadcast in Mandarin and Cantonese while the Australian public broad-caster SBS also provides television and radio on weekends. Chinese Australian social websites like Xīn Zújì (新足迹, www.oursteps.com.au) and FREEOZ (www.freeoz.org) are popular.

The relationship between China and Australia has grown closer in recent years, both countries being actively engaged economically, culturally and politically through a number of regional bodies e.g. APEC, East Asia Summit, G20. China isnowAustralia’slargesttradingpartnerandhaslargeinvestmentsinAustralianmining companies. Diplomatic relations between China and the Republic of Korea were only estab-lished in 1992, following the latter’swithdrawal of recognition of theRepublicof China (Taiwan). Since then, their political, economic, diplomatic, and cultural relations have advanced with unprecedented speed and scope. Currently, China istheRepublicofKorea’slargesttradingpartnerwhileitisChina’sthirdlargest.Though there remain apprehensions on both sides – among the Koreans about China’srapidemergenceasaglobalpoweranditssupportfortheDemocraticPeople’sRepublicofKorea (NorthKorea),andamong theChineseabout theRepublicofKorea’sstrongalliancewiththeUnitedStates–thishasnotdeterredcontinued expansion of all aspects of trade (including tourism).

The Korean and Chinese people are knowledgeable about each other’s cul-ture and customs. Just over 1% of the Korean population is from China, though three-quarters of the 624,994 recorded in the 2009 census are ethnic Koreans50.

China and Malaysia have close and strong diplomatic relations. Chinese people are the second largest ethnic group in Malaysia making up 24.6% of the popula-tion51. They have been dominant in trade and business since the early 20th centu-ry.MalaysiahasbeenChina’stoptradingpartnerwithinASEAN(AssociationofSoutheast Asian Nations – ten member countries) since 2008.

China and New Zealand have maintained strong diplomatic relations since 1972, leadingin2008toNewZealandbeingthefirstdevelopedwesterncountrytoen-ter into a free trade agreement with China. In the six years since the arrangement came into place, which enabled New Zealand to secure a greater share of the rapidly expanding Chinese market as well as the potential for deeper bilateral relations, China has become an increasingly important trade partner of New Zea-land.In2013,NewZealand’sexportstoBeijingexceededNZD7billion(EUR4.3billion)and,inthefirstquarterofthatyear,ChinaovertookAustraliaasNewZea-land’stopexportmarket52.

49 2011 Census. Australian Bureau of Statistics50 More than 1 million foreigners line in Korea. The Chosunilbo. August 6 2009.51 Malaysian Population and Housing Census 2010.52 New Zealand between two great powers. Robert Patman, Fair Observer.

Relationship between China and Australia has grown closer in recent years

China is the RepublicofKorea’slargest trading partner

Chinese people are the second largest ethnic group in Malaysia

China is New Zealand’stopexportmarket

31

Marketing Strategies for Tourism Destinations. Target market: CHINA

The 171,000 strong Chinese community makes up 4% of the New Zealand popu-lation in 201353, having grown by 16% since the previous census in 2006.