Talent + Leadership - Korn Ferry

76

PLUS: A.G. LAFLEY ON WINNING | LIFE’S BETTER AT THE TOP LOCAL IS THE NEW GLOBAL STRATEGY | GROWING FAST IN SLOW TIMES QUARTER TWO VOLUME FOUR N O . $14.95 US / CAN 1 4 Talent + Leadership Cheap Energy Forever Boone Pickens’s Newest Plan

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Talent + Leadership - Korn Ferry

PLUS:

A.G. LAFLEY ON WINNING | LIFE’S BETTER AT THE TOP

LOCAL IS THE NEW GLOBAL STRATEGY | GROWING FAST IN SLOW TIMES

Q U A R T E R T W O

V O L U M E F O U R

NO.

$14.95 US / CAN

14

Talent + Leadership

Cheap EnergyForever

Boone Pickens’s Newest Plan

The aim for Korn/Ferry Briefings

is audacious, to provide great insights to help

leaders lead.

Not by telling them what to

think — but what to think about.

Cover: Dan Bryant

Printed in the USA

Briefings is produced with solar power, FSC®-certified paper, and soy-based inks, in a fully sustain-able and environmentally respon-sible manner.

Chief exeCutive offiCer Gary Burnison

Chief marketing offiCer Michael Distefano

editor-in-Chief Joel Kurtzman

Creative direCtor Joannah Ralston

CirCulation direCtor Jaye Cullen

marketing manager Stacy Levyn

ProJeCt manager Tiffany Sledzianowski

web CommuniCations sPeCialist Edward McLaurin

board of advisors Sergio Averbach Stephen Bruyant-Langer Cheryl Buxton Dennis Carey Bob Damon Ana Dutra Joe Griesedieck

Contributing editors Chris Bergonzi David Berreby Lawrence M. Fisher Victoria Griffith Dana Landis

Robert Hallagan Katie LaheyRobert McNabbByrne MulrooneyIndranil RoyJane StevensonAnthony Vardy

Stephanie Mitchell P.J. O’RourkeGlenn RifkinStephen J. TrachtenbergAdrian Wooldridge

ISSN 1949-8365 Copyright 2013, Korn/Ferry International

Requests for additional copies should be sent directly to: Briefings Magazine1900 Avenue of the Stars, Suite 2600 Los Angeles, CA [email protected]

Advertising Sales Representatives:Jack MillerOffice: 972-985-4023 Mobile: 214-707-1334 Fax: 972-985-4047Email: [email protected] Preston Park Blvd., Suite 785, Plano, TX 75093

Circulation customer service phone: +1(310) 556-8585

For reprints, contact Tiffany Sledzianowski at +1(310) 226-6336.

Jeff MillerOffice: 972-985-4024 Mobile: 214-632-1549 Fax: 972-985-4047Email: [email protected]

Client: Jackson Family Wines

Product: Cardinale Wine

Creative: F.Verite_SevenPerfectScores_BriefingsQ2No14_2013 FINALAttention: Tiffany Sledzianowski / [email protected] +1 (310) 226-6336

Publication: Korn/Ferry Briefings Color: 4C

Publication Date: Q2 #14 Trim size: 8.25” x 10.75”

Creative designed and serviced by For questions, concerns or inquiries: Studio +1.818.932.0499 / [email protected] 6732 Eton Ave., Woodland Hills CA 91364 USA

La Muse

T h e W i n e A d v o c A T e

2008 vintage ~ 100 points2007 vintage ~ 100 points 2001 vintage ~ 100 points

La Joie

T h e W i n e A d v o c A T e

2007 vintage ~ 100 points2005 vintage ~ 100 points

R o B B R e P o R T

2007 vintage ~ Best of the Best2001 vintage ~ Best of the Best

Le Désir

T h e W i n e A d v o c A T e

2008 vintage ~ 100 points2007 vintage ~ 100 points

© 2013 Vérité. All rights reserVed.

Seven perfect scores.

One extraordinary achievement.Three perfect expressions.

Pierre Seillan—the celebrated French vigneron at Vérité who today makes Sonoma his home—

blushes with gratification when reflecting on an historic and unprecedented accomplishment.

Awarded seven 100-point scores by Robert Parker, Jr. of The Wine Advocate, these accolades

recognize Pierre’s philosophy on farming, winemaking and blending that make Vérité wines unique.

www.VeriteWines.comTo join our mailing list, please write to us at [email protected]

Client: Jackson Family Wines

Product: Cardinale Wine

Creative: F.Verite_SevenPerfectScores_BriefingsQ2No14_2013 FINALAttention: Tiffany Sledzianowski / [email protected] +1 (310) 226-6336

Publication: Korn/Ferry Briefings Color: 4C

Publication Date: Q2 #14 Trim size: 8.25” x 10.75”

Creative designed and serviced by For questions, concerns or inquiries: Studio +1.818.932.0499 / [email protected] 6732 Eton Ave., Woodland Hills CA 91364 USA

La Muse

T h e W i n e A d v o c A T e

2008 vintage ~ 100 points2007 vintage ~ 100 points 2001 vintage ~ 100 points

La Joie

T h e W i n e A d v o c A T e

2007 vintage ~ 100 points2005 vintage ~ 100 points

R o B B R e P o R T

2007 vintage ~ Best of the Best2001 vintage ~ Best of the Best

Le Désir

T h e W i n e A d v o c A T e

2008 vintage ~ 100 points2007 vintage ~ 100 points

© 2013 Vérité. All rights reserVed.

Seven perfect scores.

One extraordinary achievement.Three perfect expressions.

Pierre Seillan—the celebrated French vigneron at Vérité who today makes Sonoma his home—

blushes with gratification when reflecting on an historic and unprecedented accomplishment.

Awarded seven 100-point scores by Robert Parker, Jr. of The Wine Advocate, these accolades

recognize Pierre’s philosophy on farming, winemaking and blending that make Vérité wines unique.

www.VeriteWines.comTo join our mailing list, please write to us at [email protected]

24

65

54

38

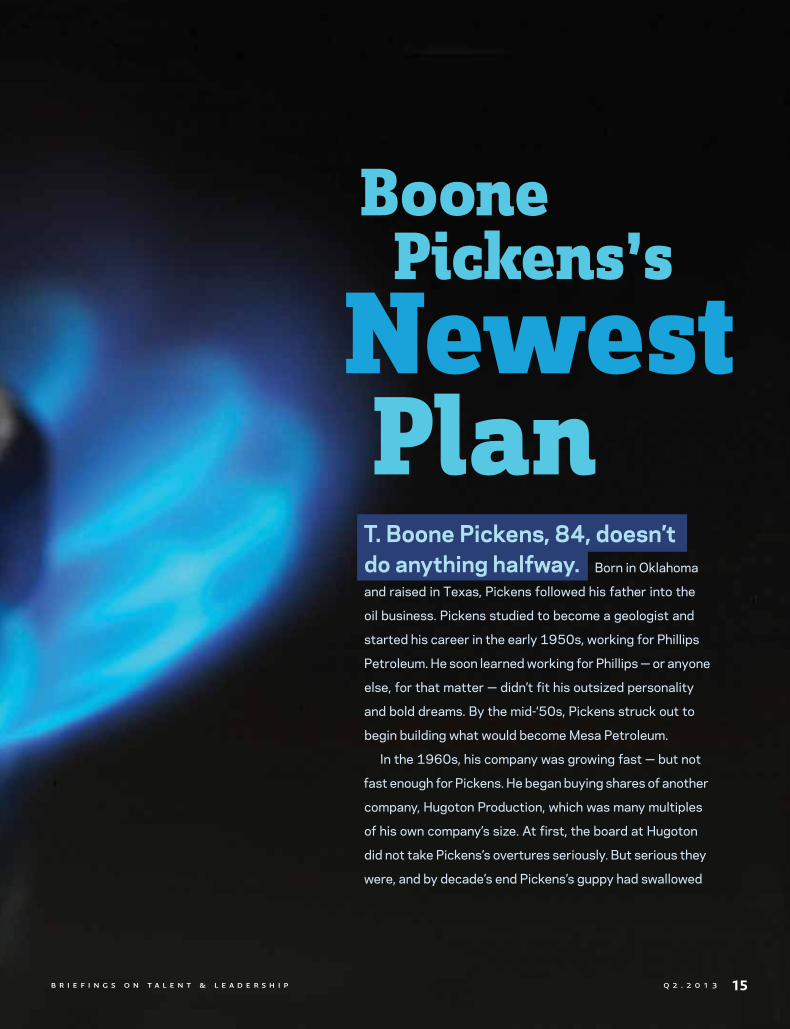

14 boone pickens’s newest plan At 84, Pickens has one goal: change the world. BY joel kurtzman

24 it’s better at the top The more senior your job, the less stress you have. BY glenn rifkin

32 total recall Memory is malleable and depends on mood. BY david BerreBY

38 the purpose of strategy is to win Some executives just want to play, when their goal should be winning. BY michael distefano and joel kurtzman

46 joichi ito — a renegade in the lab To stay at the cutting edge, MIT went out of its academic comfort zone and hired a leader for its Media Lab who never finished college. BY lawrence m. fisher

54 calling on a steady hand Franco Bernabè is leading Telecom Italia at a time of globalization and rapid change. BY timothY hindle

Governance

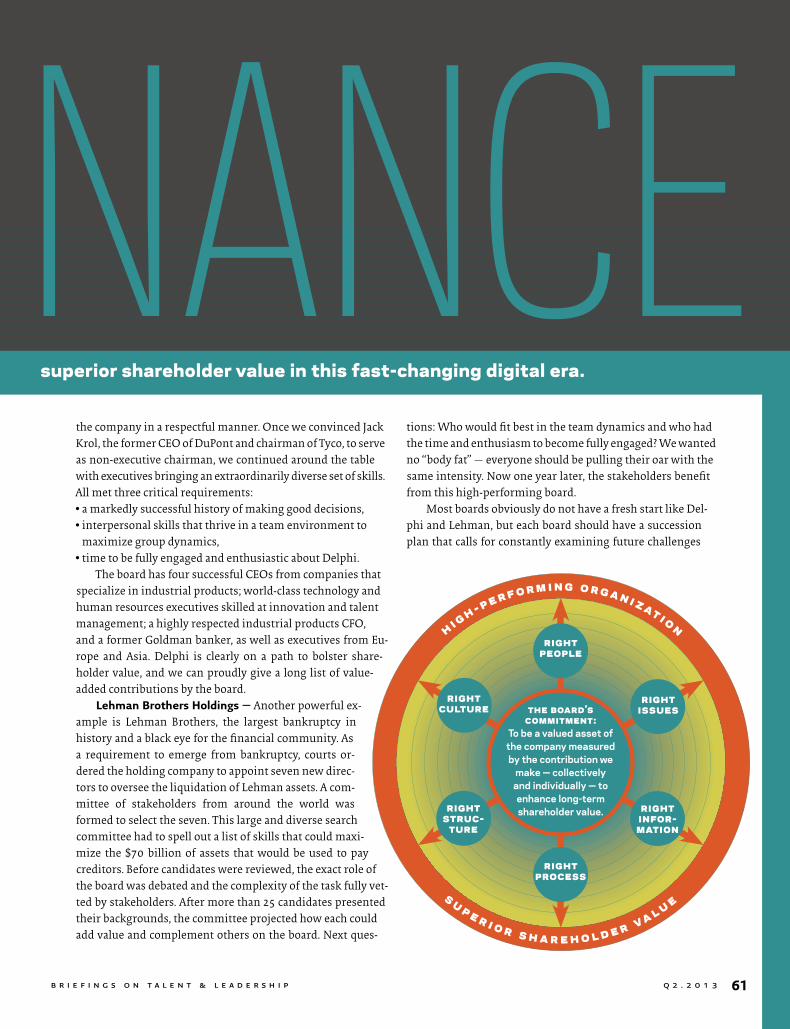

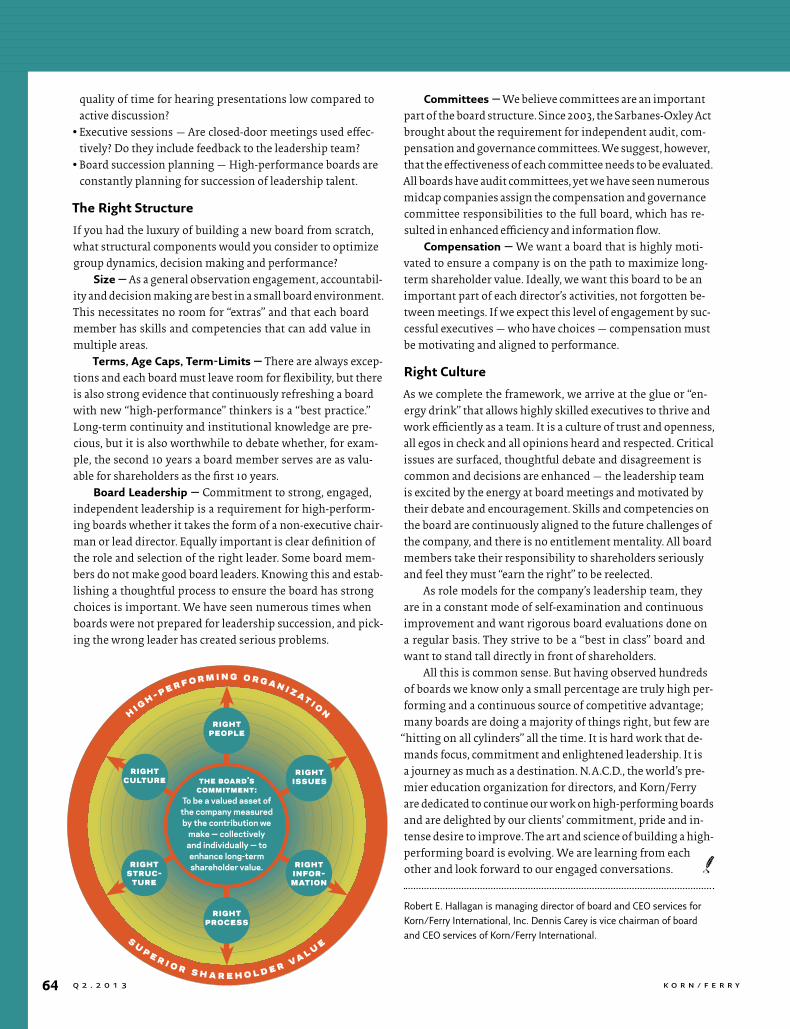

60 building boards that perform Best practices in the boardroom start with real independence. BY roBert e. hallagan and dennis careY

65 the boardroom collides with the digital age The world has gone digital; governance must too. BY mina gouran

4 letter from the ceo

latest thinkinG

6 to be or not to be strategic The role of H.R. is evolving.

8 growth now: focus on minds, not markets Talent is the real engine of growth.

11 overplaying your strengths Hidden weaknesses derail leaders.

in review

70 “the pause principle”

PartinG thouGhts

72 we’ve seen it all before Bad behavior in government is nothing new. BY joel kurtzman

Q2.2013

A. W. Faber-Castell Vertrieb GmbH • 90546 Stein • Germany • www.Graf-von-Faber-Castell.com

A fascinating encounterThe tenth Pen of the Year features a combination of two materials that could hardly be more

complete opposites: The deep structure of ancient wetland oak, whose beauty has been naturally wrought over thousands of years together with gold that lends a supernatural sheen to the most beautiful

works of art created by mankind. All metal fittings are 24-carat gold-plated.

4 Q 2 . 2 0 1 3

From the CEOby gary burnison

With hundreds of employees in the audience, the CEO be-gan speaking. Suddenly, he noticed a man in the corner of the room leaning against the wall, not paying attention to the presentation. Furthermore, the man wasn’t dressed like the rest of the audience; he was in jeans and a ragged T-shirt, with a baseball cap on sideways. Here was a perfect example, the CEO thought, to show employees that such laxity was no longer going to be permitted.

“You in the corner,” the CEO yelled out. “How much do you make a week?”

Looking up in surprise, the guy replied that he made about $400 a week. With a smirk, the CEO reached into his pocket and pulled out $1,000 in cash. “You’re fired!” he said. As the man in the baseball cap took the money, the CEO noticed a funny grin on his face, but he ignored it.

After his speech, the CEO called one of his lieutenants over. “So, how do you think I did?” he asked. “I sure made an example of that guy. By the way, who was he?”

“That was Johnny, the pizza delivery guy.”Moral of the story and cardinal rule No. 1 in communi-

cating: Before you speak, know your audience. At its best, communication does more than inform. It

inspires and moves us to consider what we might become if we, too, were “more” — more determined, more prepared, more confident and more empowered.

During the recent holiday season, I had the joy of en-tertaining five of my teenagers over a 10-day period. My role: provider of transportation, purveyor of snacks and procurer of incidentals. On the condition that they had to

“check” their “i-Gadgets” in the car, I took my motley crew and their friends to see “The Hobbit.” At the end of this

nearly three-hour film, everyone in the theater immedi-ately began clapping — viewers were cheering at a blank screen. Why? Because they connected emotionally with the story.

Think of the movie “Rocky,” a fictional rags-to-riches tale of an unknown boxer who suddenly gets a shot at the world heavyweight championship. Even though Rocky loses the fight in a split decision by the judges after 15 punishing rounds, he is the champion for whom the au-dience always cheers. (The movie went on to win three Oscars, including Best Picture.) Even today, the iconic image of Rocky running up the steps of the Philadelphia Museum of Art and pumping his fists in the air evokes the heart-pumping determination of a character who was incapable of empowerment until he believed in himself.

To connect with others, to inspire others through communication, you don’t have to be Rocky or, for that matter, Ernest Hemingway or George Clooney. You don’t have to spin tales of how others accomplished the seem-ingly impossible. But you must be authentic, particularly in times like these.

Returning from the holidays, it is always refreshing to sense the overwhelming renewed hope at the start of a new year — employees return to work optimistic, even when there’s no rational reason for it. When we walked through the doors in the first week of January 2013, soci-ety faced the same issues it did in December 2012.

The world’s central banks continue to dole out money as if it were candy, unemployment rates in most of the world remain high, and companies continue to ask fewer workers to do more for less. With the exception of the

The MessageIs the Messenger

Consider a new CEO, tasked with turning around an industry laggard, who took to the podium at his first town hall meeting, with a command-and-control style that showed that there was a new sheriff in town and things were going to change.

K o r n / F e r r y

Q 2 . 2 0 1 3 5

Dav

id S

tric

k

recent silver lining in China — where growth is hopefully accelerating — most workers probably feel as if they have been riding a stationary bike for the past four years, ped-aling faster and faster, yet not advancing.

No matter. We arrive at our workplaces in the first week of January filled with more enthusiasm than we had 10 days before. Why? Hope and human nature have en-tered the picture. We want to be inspired. We want to be optimistic. We want to grow, learn and be developed. And we want to be part of something bigger than ourselves.

Leadership is all about creating this once-a-year feel-ing every day — regardless of whether the team is winning or losing.

Leaders listen, learn and then lead. They anticipate, navigate and communicate. In good times, team mem-bers look to the leader for guidance and praise, and in difficult times they turn to the leader for assurance. Communication informs, persuades, guides and assures, as well as inspires. Leaders communicate frequently, with passion, through stories that connect emotionally with others.

Leaders listen, rather than simply hearing; they speak, rather than just talking. Leaders inquire, not question; before they speak, they observe. Leaders reveal more of themselves, allowing others to see their soul.

The actions of leaders are ultimately more lasting than their words. In fact, more important than what they say is how they say it. The role of the leader is much more than merely relaying information contained in tables, charts and slides; it’s about being the message.

There are no better examples of “being the message” than T. Boone Pickens, the legendary oilman, corporate raider, alternative energy pioneer and hedge fund man-ager, or A.G. Lafley, former chairman and chief executive of Procter & Gamble. Both are highlighted in this issue of Korn/Ferry Briefings on Talent & Leadership. As you will read, Pickens is a man who can tell a good story and, at a vibrant and fit 84, he’s done it more than once. Lafley discusses strategy — during his 10 years leading P&G, the company added $100 billion in shareholder value.

In Briefings, Korn/Ferry shows how companies can grow faster by focusing on developing executives first, markets second. Because stress is inextricably linked to these times, we decided to tackle it. Whether it comes from sprinting for a plane or from running in place in this listless economy, staffers are fatigued, which drags down morale. Research not only shows there are ways to cope with stress, but also indicates that leaders at the top

of an organization are often far less stressed than the workers reporting to them. This insight sheds light on better ways to lead, and it illustrates why it is important for bosses to listen and to empathize with those they lead.

Also, one of our regular contributors, David Berreby, takes a look at the way humans remember events and discusses what researchers are now coming to realize — while our brains do compute, we are not computers. Our memories tend to be changeable, and how we feel today determines to a certain extent the way we recall what happened yesterday. Finally, Briefings takes a look at MIT’s Media Lab, one of the most creative places on earth. In choosing its new leader, MIT went beyond its academic comfort zone and hired Joichi Ito, a brilliant, iconoclastic, venture capital investor and technologist who never fin-ished college. Ito is a global citizen. He was born in Japan, grew up in Detroit and worked in Tokyo, Silicon Valley, Boston and Dubai.

We hope you enjoy this issue of Briefings, finding rea-sons to be hopeful and inspired — and bring that opti-mism and enthusiasm into the movie you’re living every day, so that 12 months from now you can say it was, indeed, a very good show.

B r i e f i n g s o n T a l e n T & l e a d e r s h i p

Q 2 . 2 0 1 36

T in ing

Hal

May

fort

h

SAY WHAT? Smart Growth (n.) : The ability to grow the top and bottom line of a business in an extremely challenging business environment where demand conditions are weak and disruptive change is high. Source: The Korn/Ferry InSTITuTe

ting more pressure on the function. Boards are spending a lot more time embedded in H.R. They are more heavily involved in talent, going one, two and sometimes three levels down in the organization.”

While the demand for a more mission-oriented approach to staff-ing and recruiting has grown, the supply seems to have lagged. In a recently published survey conducted by the University of Southern Cali-fornia’s Center for Effective Organi-zations, today’s human resources professionals reported spending no more time being a strategic partner than did the respondents to the ini-tial survey in 1995. Edward Lawler, a USC professor and founder and di-rector of the center, said the survey results “clearly show [that] being a strategic contributor demands high levels of business knowledge, infor-mation systems that have the right metrics and analytics, [and] organi-zation designs and practices that link H.R. managers to business units. The results also show that H.R. is not do-ing what needs to be done.”

The generally accepted model for

how personnel departments could help shape corporate strategy was proposed by David Ulrich, a profes-sor at the University of Michigan, in 1997. In the Ulrich model, human re-sources would operate on three lev-els: as a corporate-level partner that helps define strategy, as a consultant that helps line managers implement strategy, and as a skilled administra-tor that stewards company-wide ser-vices to support strategy. In theory, this would allow personnel depart-ments to spend less time on admin-istrative duties — perhaps outsourc-ing them entirely — and more time helping to steer the organization.

In practice, many organizations are falling short of that ideal, in large part because human resources pro-fessionals historically have not been required to possess the competencies and background necessary to have a say in corporate strategy. “It is still difficult to find the right kind of H.R. leadership — people who think about organizational capability in the ag-gregate,” said Emilie Petrone, senior client partner in human resources practice for Korn/Ferry International.

For at least 15 years, it has been considered axiomatic that the management of human re-

sources must be integrated into an organization’s overall strategy in or-der to meet the demands of a rapidly changing business environment. In their 2001 book, “The H.R. Scorecard: Linking People, Strategy, and Perfor-mance,” Brian Becker, Mark Huselid and David Ulrich encapsulated the rationale: “The evidence is unmis-takable: H.R.’s emerging strategic potential hinges on the increasingly central role of intangible assets and intellectual capital in today’s econ-omy.” Since then, changes in technol-ogy, demographics and globalization have only intensified the need for the human resources profession to raise its game.

“The expectations of the H.R. role have grown tremendously,” said Kim Shanahan, North American human resources practice leader for Korn/Ferry International. “CEOs are put-

The Latest

Is H.R. evolving as it needs to, or is it time for a new model?

To Be or Not To Be Strategic

K o r n / F e r r y

Q 2 . 2 0 1 3 7

Stev

en G

uarn

acci

a

“The challenge for H.R. is to develop a critical mass of people who are up to the task.”

Ulrich thinks that personnel di-rectors haven’t been quick enough to grasp the essentials of business man-agement and that they compound that error by focusing on activity rather than outcomes. “You’re not measured by what you do but by what you deliver,” Ulrich has said.

Despite extensive efforts to mea-sure what it delivers, the human re-sources profession has had some dif-ficulty doing so. To be sure, it has no shortage of yardsticks — cost per hire, revenue per employee, turnover rates, compensation value added, among others. However, implicit in the track-ing of these metrics is an assump-tion that they indicate a personnel-related contribution to bottom-line outcomes like growth, competitive-

ness and profitability. While that as-sumption is intuitively reasonable, it is not dispositive, and it is met with skepticism by some non- H.R. execu-tives. Many studies have examined this issue, but the results have been inconclusive.

“The bottom-line effects of strate-gic H.R. issues — such as CEO readi-ness, depth of bench and diversity of workforce — are real, but difficult to quantify,” said Petrone. “For instance, you can definitely correlate employee satisfaction to customer satisfaction, but how do you parse what part of that is due directly to H.R.?”

Some obstacles to strategic in-volvement lie outside a personnel department’s purview. Peter Cappelli, a professor at Wharton and the di-rector of its Center for Human Re-sources, pointed to the changing fo-cus of corporate strategy: “At least

[among] U.S. publicly held compa-nies, most now have a financial strat-egy that drives the business. There is nothing like an overall business strategy, [so] the idea that the func-tion of H.R. should be to help exe-cute strategy has little meaning.”

Akiko Takahashi, executive vice president and chief personnel officer of Melco Crown Entertainment in Hong Kong, suggested that human resources departments can only be as important as the CEO allows: “For H.R. to be a strategic partner, it needs to report to a CEO who innately be-lieves in human capital. [Human re-sources’] ability to influence has to come from the CEO’s authority.”

Perhaps the biggest obstacle to achieving “strategic H.R.,” however, is that no one inside or outside of human resources seems to agree on exactly what it means. Although no

B r i e f i n g s o n T a l e n T & l e a d e r s h i p

Q 2 . 2 0 1 38

an almost intrinsic binding force in an increasingly specialized, far-flung and self-managed world.

Paul Buller, professor of manage-ment at Gonzaga University in Spo-kane, Wash., sees it this way: “H.R. needs to become an internal consul-tant and change agent to facilitate vertical and horizontal integration, so that everyone in the organization sees how what they are doing is con-nected to the big picture — a ‘line of sight’ that allows for continual adap-tation. This would provide a unique source of competitive advantage that would be hard to imitate.”

Some predict that were human resources to become a more widely integrated competency, it would en-gender an osmotic permeability be-tween H.R. and line management. Eventually, the distinction between the two would vanish. Laurie Ruet-timann, a recruiter, trainer and founder of HRM Today, a social net-work for human resources profes-sionals, put it succinctly: “H.R. [will be] fixed when it ceases to be H.R. and starts to be a core and critical management responsibility. [H.R.] shouldn’t serve the business. We should be the business.”

one disputes that talent manage-ment, workforce productivity, lead-ership development and a high- performance culture are crucial to corporate performance, few agree about how, or even whether, person-nel departments influence those fac-tors. As a practical matter, some are suggesting that it’s time to back off the demand for strategy with a capi-tal “S” and seek a more straightfor-ward, results-oriented model.

“The way to become a business partner is to quit agonizing over be-ing a business partner and trying to force unnecessary activity on the rest of the enterprise,” said Dan Bowling, former global head of human re-sources at Coca-Cola Enterprises.

“Focus instead on what is important.”One alternative model that has

gained some traction envisions hu-man resources not as a single de-partment trying to morph itself in multiple directions, but rather as competencies embedded company-wide, sometimes as discrete job functions, but more often as distrib-uted responsibilities in which every employee has a human resources component to their job. This model, in short, casts human resources as

K o r n / F e r r y

HAPPY ENTREPRENEUR, HAPPY COMPANY

A recent survey of 3,000 high-impact entrepreneurs in 34 countries suggests that those in China, India, Kenya, New Zealand and the United States have the most positive overall opinions of the policies in place to promote their growth. The five countries surveyed with the most nega-tive overall perceptions are Greece, Venezuela, Ukraine, Andorra and Poland. Source: MonITor Group

The Latest Thinking

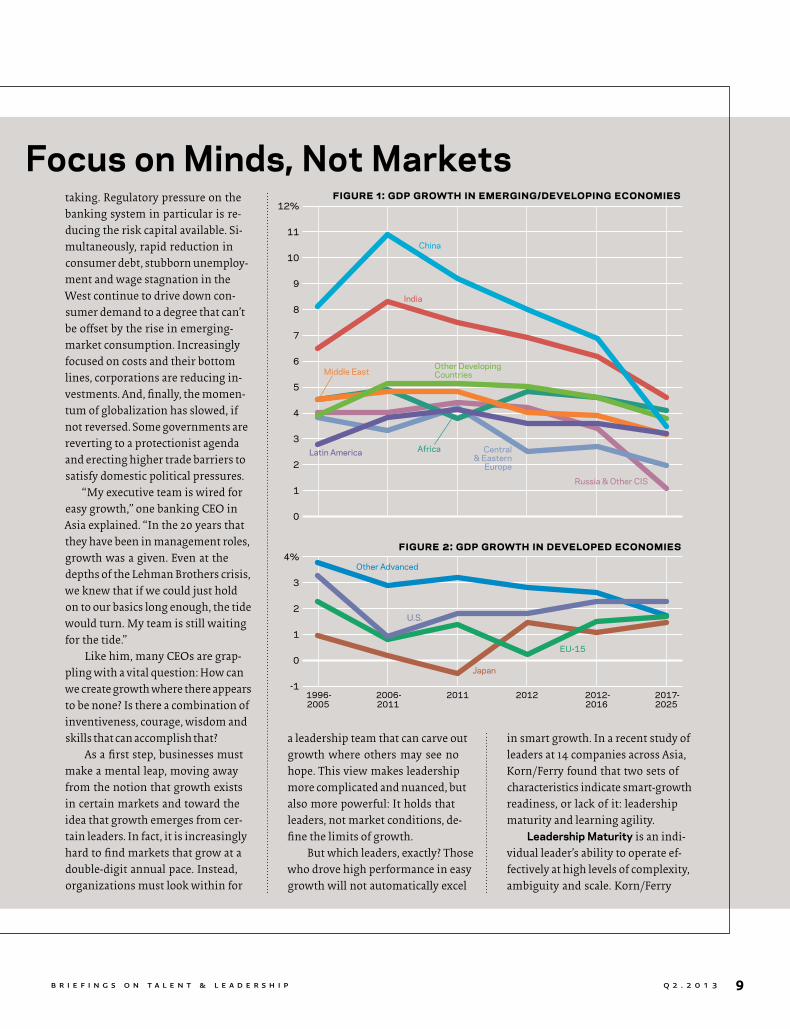

The nature of economic growth has changed. From the mid-1990s to 2007, developing

economies — especially those in Asia — experienced a period of growth un-matched in scale, optimism or speed. This era can be characterized as one of “easy growth.” During this time, it became easier and cheaper to gain access to capital than in any other pe-riod in history, globalization created unprecedented admittance to new markets and consumers, and house-hold consumer borrowing drove spending around the world. A gen-eration of corporate leaders was shaped by this period, when growth was there for the taking; all they had to do was show up.

And now, suddenly, that era is over (see Figures 1 and 2), and we have entered the era of “smart growth,” in which growth is slow but change is fast. In his recent report, Smart Growth: Is Asia Ready?, Korn/Ferry leadership and talent consulting managing director Indronil Roy ex-plained how this period of complex-ity and uncertainty — in markets, finance and currency — will require leaders to think and act differently to unearth growth where none is evident. Leaders’ shrewdness about growth will make a difference in corporate performance.

How long will smart-growth con-ditions persist? A resounding num-ber of CEOs believe these conditions will last for the rest of the decade, if not longer, for myriad reasons. The global financial crisis led to a stricter regulatory regime that is (some-times justifiably) constraining risk

Growth Now: Focus on Minds, Not Markets

9b r i e F i n g s o n T a l e n T & l e a d e r s h i p

12%

11

10

9

8

7

6

5

4

3

2

1

0

4%

3

2

1

0

-11996- 2005

2006- 2011

2012- 2016

2017- 2025

2011 2012

China

India

Other Developing CountriesMiddle East

Other Advanced

Japan

EU-15

U.S.

Latin America Africa Central & Eastern

Europe

Russia & Other CIS

FiGure 2: GDP Growth in DeveloPeD economies

FiGure 1: GDP Growth in emerGinG/DeveloPinG economies

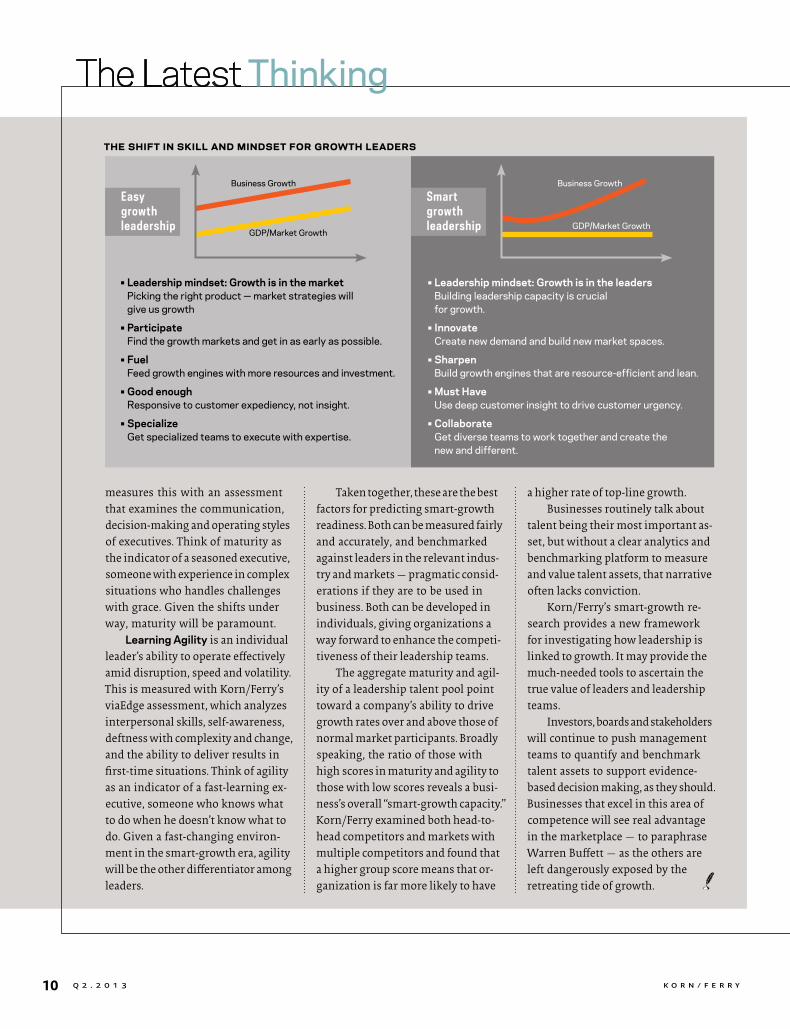

in smart growth. In a recent study of leaders at 14 companies across Asia, Korn/Ferry found that two sets of characteristics indicate smart-growth readiness, or lack of it: leadership maturity and learning agility.

Leadership Maturity is an indi-vidual leader’s ability to operate ef-fectively at high levels of complexity, ambiguity and scale. Korn/Ferry

a leadership team that can carve out growth where others may see no hope. This view makes leadership more complicated and nuanced, but also more powerful: It holds that leaders, not market conditions, de-fine the limits of growth.

But which leaders, exactly? Those who drove high performance in easy growth will not automatically excel

taking. Regulatory pressure on the banking system in particular is re-ducing the risk capital available. Si-multaneously, rapid reduction in consumer debt, stubborn unemploy-ment and wage stagnation in the West continue to drive down con-sumer demand to a degree that can’t be offset by the rise in emerging-market consumption. Increasingly focused on costs and their bottom lines, corporations are reducing in-vestments. And, finally, the momen-tum of globalization has slowed, if not reversed. Some governments are reverting to a protectionist agenda and erecting higher trade barriers to satisfy domestic political pressures.

“My executive team is wired for easy growth,” one banking CEO in Asia explained. “In the 20 years that they have been in management roles, growth was a given. Even at the depths of the Lehman Brothers crisis, we knew that if we could just hold on to our basics long enough, the tide would turn. My team is still waiting for the tide.”

Like him, many CEOs are grap-pling with a vital question: How can we create growth where there appears to be none? Is there a combination of inventiveness, courage, wisdom and skills that can accomplish that?

As a first step, businesses must make a mental leap, moving away from the notion that growth exists in certain markets and toward the idea that growth emerges from cer-tain leaders. In fact, it is increasingly hard to find markets that grow at a double-digit annual pace. Instead, organizations must look within for

Growth Now: Focus on Minds, Not Markets

Q 2 . 2 0 1 3

Q 2 . 2 0 1 310 K o r n / F e r r y

The Latest Thinking

the shiFt in skill anD minDset For Growth leaDers

Business Growth Business Growth

GDP/Market GrowthGDP/Market Growth

•Leadershipmindset:Growthisinthemarket •Leadershipmindset:Growthisintheleaders Picking the right product — market strategies will Building leadership capacity is crucial give us growth for growth.

•Participate •Innovate Find the growth markets and get in as early as possible. Create new demand and build new market spaces.

•Fuel •Sharpen Feed growth engines with more resources and investment. Build growth engines that are resource-efficient and lean.

•Goodenough •MustHave Responsive to customer expediency, not insight. Use deep customer insight to drive customer urgency.

•Specialize •Collaborate Get specialized teams to execute with expertise. Get diverse teams to work together and create the new and different.

Easygrowthleadership

Smartgrowthleadership

a higher rate of top-line growth. Businesses routinely talk about

talent being their most important as-set, but without a clear analytics and benchmarking platform to measure and value talent assets, that narrative often lacks conviction.

Korn/Ferry’s smart-growth re-search provides a new framework for investigating how leadership is linked to growth. It may provide the much-needed tools to ascertain the true value of leaders and leadership teams.

Investors, boards and stakeholders will continue to push management teams to quantify and benchmark talent assets to support evidence-based decision making, as they should. Businesses that excel in this area of competence will see real advantage in the marketplace — to paraphrase Warren Buffett — as the others are left dangerously exposed by the retreating tide of growth.

Taken together, these are the best factors for predicting smart-growth readiness. Both can be measured fairly and accurately, and benchmarked against leaders in the relevant indus-try and markets — pragmatic consid-erations if they are to be used in business. Both can be developed in individuals, giving organizations a way forward to enhance the competi-tiveness of their leadership teams.

The aggregate maturity and agil-ity of a leadership talent pool point toward a company’s ability to drive growth rates over and above those of normal market participants. Broadly speaking, the ratio of those with high scores in maturity and agility to those with low scores reveals a busi-ness’s overall “smart-growth capacity.” Korn/Ferry examined both head-to-head competitors and markets with multiple competitors and found that a higher group score means that or-ganization is far more likely to have

measures this with an assessment that examines the communication, decision-making and operating styles of executives. Think of maturity as the indicator of a seasoned executive, someone with experience in complex situations who handles challenges with grace. Given the shifts under way, maturity will be paramount.

Learning Agility is an individual leader’s ability to operate effectively amid disruption, speed and volatility. This is measured with Korn/Ferry’s viaEdge assessment, which analyzes interpersonal skills, self-awareness, deftness with complexity and change, and the ability to deliver results in first-time situations. Think of agility as an indicator of a fast-learning ex-ecutive, someone who knows what to do when he doesn’t know what to do. Given a fast-changing environ-ment in the smart-growth era, agility will be the other differentiator among leaders.

Ever

ett P

eck

weaknesses. Research shows that high performers in all fields, espe-cially when under stress, instinctively double down on the core attributes that made them high performers in the first place. Michael M. Lombardo and Robert W. Eichinger, cofounders of the talent management consul-tancy Lominger, were among the first to link this phenomenon to executive dysfunction in their book

“Preventing Derailment: What to Do Before It’s Too Late.” They pointed out that poor executive performance is often not due to a weakness, but rather to a strength in overdrive: ex-treme confidence careening toward

I n a recent interview with The New York Times, James P. Hackett, the president and CEO of Steelcase,

recalled a meeting in 1994 with J.W. “Bill” Marriott Jr., Marriott Corp.’s chairman of the board. Hackett was a young chief executive, 39 years old, seeking wisdom and guidance from the seasoned Marriott.

“I had been struggling with this notion of identity,” said Hackett.

“What does a CEO look like and feel like? As we were talking, I remember being struck by the look in [Marri-ott’s] eyes. I understood in that mo-ment that he knew who he was. I remember this like it was yesterday. Since then, the [CEOs] I’m most im-pressed with have [that same] sense of peace and self-awareness.”

Hackett’s intuitive observation is borne out by research. A multitude of studies have pointed to executive self-awareness as the bedrock of per-sonal and corporate performance. The work of influential psychologist Albert Bandura links self-awareness to self-efficacy, which he defines as a person’s perception of his or her own ability to succeed in specific situa-tions. In general, Bandura contended, the more you know about yourself, the more likely you are to feel confi-dent in taking things on and seeing them through.

According to Anthony K. Tjan, co-author of “Heart, Smarts, Guts, and Luck”: “In my experience and in the research my coauthors and I did for our book, there is one quality that trumps all, evident in virtually every great entrepreneur, manager and

The hidden weakness that derails leaders

Overplaying Your Strengths

b r i e F i n g s o n T a l e n T & l e a d e r s h i p Q 2 . 2 0 1 3 11

leader. That is self-awareness. The conviction — and yes, often the ego — that founders and CEOs need for their vision makes them less than optimally wired for embracing vulnera-bilities or leading with humil-ity. This makes self-awareness that much more essential.”

In a recent Korn/Ferry Interna-tional report, “Survival of the Most Self-aware,” author J. Evelyn Orr, director of intellectual property re-search and development, concluded that “when all things are equal, self-awareness is a key trait that explains why some business leaders succeed when others derail. Self-awareness is knowing your strengths and limi-tations, the willingness to seek and act on feedback, the ability to admit mistakes, and the tendency to re-flect and apply personal insights.”

Unfortunately, most leaders fall short of that ideal. They have a distorted perception of themselves that can manifest itself in a num-ber of ways: a tendency to overesti-mate skills or underestimate short-comings (known as “blind spots”), or an inability to recognize an un-tapped capacity (known as a “hidden strength”). Based on feedback from more than 2,700 professionals, Orr’s report indicated that 79 percent had at least one blind spot and 40 percent had at least one hidden strength.

Lack of self-awareness takes its most insidious form, however, when leaders have an accurate sense of their talents, but routinely overuse or misapply them, turning them into

Q 2 . 2 0 1 312

Hal

May

fort

h

leader’s mindset and behavior are ex-plored in concert, he will not become aware of the self-defeating assump-tions, impulses and emotional reac-tions that drive his excesses and will therefore not have the tools to mod-ulate his behavior.

“Modulate” is the operative word. Indeed, some in the field of leader-ship development are gravitating away from thinking in terms of ab-solute strengths and weaknesses.

“There is no such thing as an unqual-ified strength,” wrote Morgan W. McCall Jr., a professor at the Univer-sity of Southern California’s Mar-shall School of Business and an expert on the topics of executive development and derailment. “Any effective development strategy will have to acknowledge that what mat-ters are combinations of strengths and weaknesses as they manifest themselves in specific situations.”

All behaviors, then, are seen ob-jectively as competencies that have a wide spectrum of application — they are only potential strengths or potential weaknesses, depending upon the degree to which and the circumstances in which they are brought to bear. In other words, said author Kaplan, “There is no fixed setting on the dial for the proper use of a virtue.”

sult is lopsided leadership: too much of one thing, made worse by too little of its complement. Versatile leader-ship arises only from acknowledging that each approach is a half-truth and from embracing both.”

Many leaders know this on an intuitive level, but they tend not to accept it in practice. In their careers, they have seen the efficacy of their strengths and have come to rely upon them heavily as a source of security. When faced with the prospect that the very intensity that fueled their rise to the top can be sabotaging their effectiveness, they are often panic-stricken at the thought of needing to ease up. Not surprisingly, then, development efforts that focus solely on prescribing behavioral changes or counterbalances to over-use have limited success because they do not address the leader’s un-derlying mindset — the cognitive, emotional and motivational roots of the imbalance.

“A leader’s mindset will throw off his form just as an athlete’s does,” said Robert B. Kaiser, who coau-thored “Fear Your Strengths” with Kaplan. “Correcting it is far more challenging than simply shoring up a deficiency. It requires intellectual honesty and the courage to rummage in the attic of your mind.” Unless the

arrogance, detail orientation deteri-orating into micro-management, forcefulness sliding into abusiveness, consensus-building degenerating into indecision.

This leader’s compulsion to over-rely on strengths is more than just an occasional phenomenon. For many, it becomes habitual and ingrained — a default position. In fact, according to Drs. Robert and Joyce Hogan, lead-ing thinkers in the area of personal-ity assessment and organizational leadership, overused strengths con-stitute leaders’ most common flaw, and the most dangerous. The research, they say, draws a consistent conclu-sion: When leaders collapse, it is almost invariably the result of over-playing the characteristics that ini-tially contributed to their success.

“Not only does overusing one’s strength corrupt and degrade its value,” said Robert E. Kaplan, coau-thor of the new book, “Fear Your Strengths,” “but it begets weakness in yet another way. By embracing their strength as the only truth, these executives consequently ignore an equal and opposing strength. For instance, a leader who adopts an automatic and uncompromisingly forceful stance in all circumstances will be unlikely to be tuned in to en-abling the efforts of others. The re-

1. Tape recorders (79%) 2. Fax machines (71%) 3. The Rolodex (58%) 4. Standard working hours (57%) 5. Desk phones (35%)

6. Desktop computers (34%) 7. Formal business attire like suits, ties, pantyhose, etc. (27%) 8. The corner office for managers/executives (21%) 9. Cubicles (19%) 10. USB thumb drives (17%)

THE ENDANGERED SPECIES LIST: OFFICE EDITIONAccording to professionals, the top 10 items and office trends that are becoming rare and could even disappear in the next five years are:

Globally, professionals selected tablets (55%), cloud storage (54%), flexible working hours and smartphones (which tied at 52%) as office tools that are becoming more ubiquitous. Source: LInKedIn

The Latest Thinking

K o r n / F e r r y

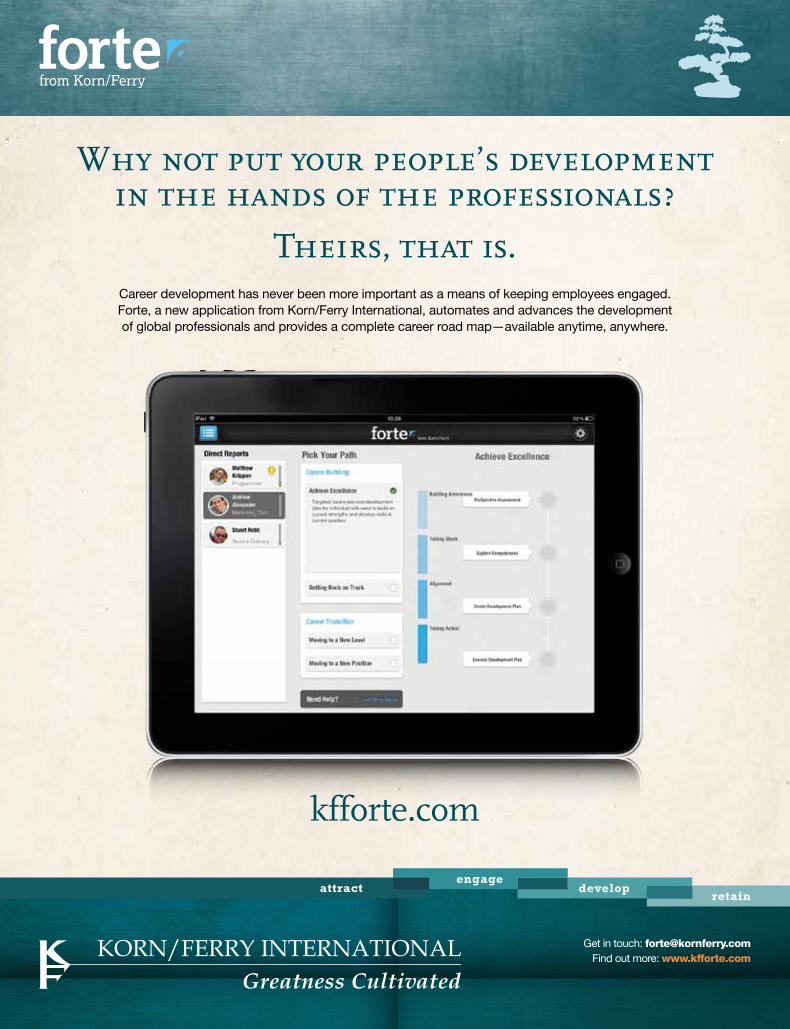

Why not put your people’s development in the hands of the professionals?

Theirs, that is.Career development has never been more important as a means of keeping employees engaged. Forte, a new application from Korn/Ferry International, automates and advances the development of global professionals and provides a complete career road map—available anytime, anywhere.

Get in touch: [email protected] Find out more: www.kfforte.com

kfforte.com

K o r n / F e r r y

15Q 2 . 2 0 1 3

Newest Plan

do anything halfway. Born in Oklahoma

and raised in Texas, Pickens followed his father into the

oil business. Pickens studied to become a geologist and

started his career in the early 1950s, working for Phillips

Petroleum. He soon learned working for Phillips — or anyone

else, for that matter — didn’t fit his outsized personality

and bold dreams. By the mid-‘50s, Pickens struck out to

begin building what would become Mesa Petroleum.

In the 1960s, his company was growing fast — but not

fast enough for Pickens. He began buying shares of another

company, Hugoton Production, which was many multiples

of his own company’s size. At first, the board at Hugoton

did not take Pickens’s overtures seriously. But serious they

were, and by decade’s end Pickens’s guppy had swallowed

T. Boone Pickens, 84, doesn’t

Boone Pickens’s

b r i e F i n g s o n T a l e n T & l e a d e r s h i p

Q 2 . 2 0 1 316

Prev

ious

pag

e: ©

Zoon

ar/i

gor t

erek

hov/

AGE.

Thi

s pa

ge: A

ssoc

iate

d Pr

ess.

Opp

osite

pag

e: R

EUTE

RS/T

im S

haffe

r

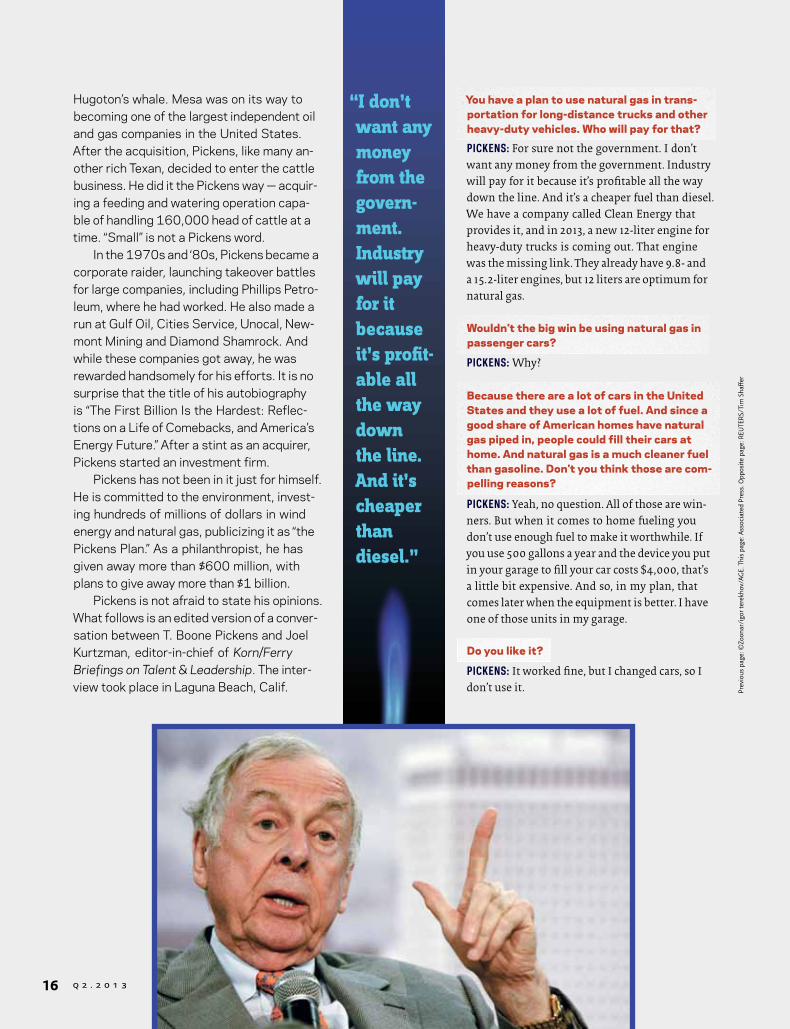

You have a plan to use natural gas in trans-portation for long-distance trucks and other heavy-duty vehicles. Who will pay for that?

PICKENS: For sure not the government. I don’t want any money from the government. Industry will pay for it because it’s profitable all the way down the line. And it’s a cheaper fuel than diesel. We have a company called Clean Energy that provides it, and in 2013, a new 12-liter engine for heavy-duty trucks is coming out. That engine was the missing link. They already have 9.8- and a 15.2-liter engines, but 12 liters are optimum for natural gas.

Wouldn’t the big win be using natural gas in passenger cars?

PICKENS: Why?

Because there are a lot of cars in the United States and they use a lot of fuel. And since a good share of American homes have natural gas piped in, people could fill their cars at home. And natural gas is a much cleaner fuel than gasoline. Don’t you think those are com-pelling reasons?

PICKENS: Yeah, no question. All of those are win-ners. But when it comes to home fueling you don’t use enough fuel to make it worthwhile. If you use 500 gallons a year and the device you put in your garage to fill your car costs $4,000, that’s a little bit expensive. And so, in my plan, that comes later when the equipment is better. I have one of those units in my garage.

Do you like it?

PICKENS: It worked fine, but I changed cars, so I don’t use it.

Hugoton’s whale. Mesa was on its way to becoming one of the largest independent oil and gas companies in the United States. After the acquisition, Pickens, like many an-other rich Texan, decided to enter the cattle business. He did it the Pickens way — acquir-ing a feeding and watering operation capa-ble of handling 160,000 head of cattle at a time. “Small” is not a Pickens word.

In the 1970s and ‘80s, Pickens became a corporate raider, launching takeover battles for large companies, including Phillips Petro-leum, where he had worked. He also made a run at Gulf Oil, Cities Service, Unocal, New-mont Mining and Diamond Shamrock. And while these companies got away, he was rewarded handsomely for his efforts. It is no surprise that the title of his autobiography is “The First Billion Is the Hardest: Reflec-tions on a Life of Comebacks, and America’s Energy Future.” After a stint as an acquirer, Pickens started an investment firm.

Pickens has not been in it just for himself. He is committed to the environment, invest-ing hundreds of millions of dollars in wind energy and natural gas, publicizing it as “the Pickens Plan.” As a philanthropist, he has given away more than $600 million, with plans to give away more than $1 billion.

Pickens is not afraid to state his opinions. What follows is an edited version of a conver-sation between T. Boone Pickens and Joel Kurtzman, editor-in-chief of Korn/Ferry Briefings on Talent & Leadership. The inter-view took place in Laguna Beach, Calif.

“I don’t want any money from the government. Industry will pay for it because it’s profitable all the way down the line. And it’s cheaper than diesel.”

Q 2 . 2 0 1 3 17

Q 2 . 2 0 1 318

Asso

ciat

ed P

ress

lion vehicles, it’d take you 10 years or longer. And you don’t do it by converting existing passenger vehicles to start with. You do it with new cars — when you sell your car and buy a new one, you get one that uses natural gas.

What are the other steps?PICKENS: My pitch to Obama was first, you announce that all federal government vehicles would run on domestic re-sources. They told me this point would be in the State of the Union speech. That way you leave it open to natural gas, electricity and batteries, and so on. I mean, we’re not trying to pick winners, but we are trying to use our own resources. That’s what my pitch is. So the federal vehicles start us on the

learning curve about what’s the best fuel for our fleet. And that’s how you figure out how to do it. Then I said six months after that, you go back to the American people and say, “Look, the federal fleet mandate worked.” You might want to give some kind of tax credit for people to do it, but the idea is to keep it simple. So, the speech is, “We need to get on our own resources in this country, and as president of the United States, I’m going to come to you individually and hopefully

What about filling stations? PICKENS: There are already 1,500 stations in the United States where you can get natural gas fuel.

Isn’t that a small percentage of filling stations?PICKENS: That’s why I say, you press first to do heavy-duty trucks. Once that’s accomplished, then you’ll start to see the whole thing come together.

Given how much natural gas we have in the U.S., why hasn’t it moved faster? PICKENS: Because I’ve been a crummy salesman, and I’m the only one trying to sell it right now.

You certainly put it into people’s consciousness with your speeches, ads and editorials for the Pickens Plan. Do you think people are paying attention now?

PICKENS: Yeah. But look, the only reason it’d happen and peo-ple would be using natural gas in their cars is if people made money off of it. Somebody’s got to make money or they don’t fill in their link in the chain, and it all breaks down. So my view is, if you’re going to do the whole country, all 250 mil-

K o r n / F e r r y

Q 2 . 2 0 1 3 19

Shut

ters

tock

Why is that?PICKENS: Only one reason. It’s oversupplied.

Why is there an oversupply now? Is it because of hydraulic fracturing technology, fracking? PICKENS: Well, when it comes to fracking completions, the cost of wells is higher everywhere else in the world than the United States. It’s cheaper here than any place else, so you get more supply. We should take our hats off and thank the oil and gas industry in America. They’ve gotten us the cheapest energy in the world. But no one in government has the guts to say this industry’s done a pretty damn good job.

Do you subscribe to the idea that because of fracking there’s an energy revolution under way in the United States? PICKENS: The simple answer is no. And, by the way, I saw fracking going on in Texas in the ‘50s. Look, the United States has always had natural gas. It’s always been there and it’s al-ways been oversupplied. That’s why it’s never sold at parity with crude oil on a price basis. Parity would be a price of 6 to 1 against oil, given the energy it possesses for a given volume. But I’ve never seen it better than 10 to 1, and today it’s 20 to 1.

Do you anticipate natural gas prices in the U.S. falling further? PICKENS: Again no.

Why is that? PICKENS: Simple. In the U.S., we’ve gone from 1,600 rigs drill-ing for natural gas down to 400. Natural gas production is in decline again in the United States — for a while, because of oversupply.

So the rig count is down because of low prices resulting from oversupply?PICKENS: You got it. Like I said, when there’s that 6-to-1 parity with crude oil on a price basis there’s a lot of reason to drill. Right now, at 20 to 1, there’s no reason to drill more wells. I’ve seen the ratio as close as 10 to 1, when we had $100 oil and $10 natural gas. But there isn’t anybody today who’s predict-ing $10 natural gas. There’s nobody today even predicting $8 natural gas. They quit drilling because, at $3 a MCF for natural gas, nobody can make any money.

you’ll follow my lead, so the next car you buy would be one that uses domestic resources.” That’s my pitch. And you could get families around the table and have them all talk about which kind of vehicle they think is best — batteries, natural gas, ethanol, all of them — and have each family member re-search it so when they went out to buy their next car, they’d be doing it together. It’d draw people together around this issue. But the bottom line is this: If you don’t pick a domestic energy source, it means you’re picking OPEC, because those are the only two choices.

You’ve been called a legend in the energy industry... PICKENS: You know what the definition of a legend is, don’t you? It’s somebody who’s 75 years old and still has a job.

Point taken. But you really are a legend. You started one of the most successful independent oil companies, led some well-publicized takeovers, began a corporate gov-ernance movement, started a successful hedge fund, were a pioneer in wind energy, and now you’re focusing on natural gas. Sounds like a legend to me. PICKENS: I even did some offshoots from wind. That cost me $150 million.

Is it correct to say you don’t think wind energy is an opportunity right now?PICKENS: That’s right. And do you know why wind doesn’t work?

Why? PICKENS: Because it’s priced off the margin, and the margin is natural gas. So, if in the U.S., natural gas is trading at $6 a thousand cubic feet (MCF), that makes wind work. But if natural gas is at $4 a MCF, it kills wind. It’s that simple.

Natural gas in the U.S. has been trading at very low levels — as low as between $2 and $3 a MCF, recently. PICKENS: Well, right now, we’re back up to $3.75 a MCF. And, when you look at what natural gas really is, it gets interest - ing. See, natural gas happens to be the superior end of the hydrocarbon chain for environmental and energy reasons. It’s a pretty clean fuel, compared to all the others. So what we’ve got is a situation in the U.S. where the superior end of the chain sells at a discount to the competition, which is crude oil. Isn’t that something?

B r i e f i n g s o n T a l e n T & l e a d e r s h i p

“What we’ve got is a situation in the U.S. where the superior end of the chain sells at a discount to the competition, which is crude oil. Isn’t that something?”

Q 2 . 2 0 1 320

two-thirds out of our trade deficit, which goes to purchasing foreign oil. And if you look at Australia and Canada — they’re both living off their own resources, producing their own oil and gas. And they’re doing just fine. But that’s not what the administration is doing.

There’s a lot of volatility in natural gas prices. Is that normal?PICKENS: Sure. If you go back and look at natural gas prices, they’ve never been smoothed out or stable. They’re volatile. You get into critical weather, draw down your storage for nat-ural gas, and prices go up. You fill up your storage in the fill season, which starts in March and goes through October. When you get your storage filled, prices come down. Natural gas is volatile. On the other hand, look at oil. Oil’s been pretty stable for the last two, three years, around $100.

Companies are planning roughly 85 new job-creating manufacturing projects in the U.S. worth at least $60 billion, due to low natural gas prices. Do you think that level of investment will continue if natural gas rises to, say, $5 a MCF? PICKENS: Oh yeah. Even at $5, natural gas in the U.S. is the cheapest fuel in the world. If you look at natural gas prices today in Japan, they’re $16 to $18. In Beijing, they’re $15. In the Middle East, they’re $14, in Europe, $13, and in the U.K., they’re $10. Here, they’re under $4. Because of those prices, you’re going to have industries moving back to the United States because the fuel’s so cheap here. And it’s a better place to do business.

These new plants are expected to create tens of thousands of new jobs. PICKENS: That’s why I say, you’d think that this administra-tion would look at some of these things and say, “Gosh, we should hug up this industry, because the oil and gas indus-try is putting us back on our feet.”

What should the Obama administration do?PICKENS: Get up and say we have the cheapest energy in the world and we’re going to support the industry because we want manufacturing to come back to the United States. It’s just good business. I’ve said it before, this administration, and almost all previous administrations, don’t understand our energy portfolio.

At what price point will they roll out the rigs again?PICKENS: When you have $5 natural gas, you’ll see activity. When you have $6 natural gas, you will see full action. You know why all this is happening?

No, tell me.PICKENS: O.K. I will. You know what mineral rights are?

The right to own what’s under the ground.PICKENS: Exactly. But did you know there’s only one place in the world that has freehold mineral rights? It’s the United States. In the rest of the world, the government owns all the mineral rights. So ask yourself, what impact does the right to own mineral rights have? Because these rights are freehold and you and I can buy them, half of the 4 or 5 million wells drilled in the world have been drilled in the United States. That’s because of our freehold mineral rights.

The International Energy Agency recently projected that the United States would become the world’s largest oil producer sometime around 2030, as a result of fracking shale oil. Do you see that happening?

PICKENS: No.

Why is that?PICKENS: I just don’t know where all that oil — more than 10 million barrels a day — is going to come from. I don’t see enough oil reservoirs available to us for that to happen. Now, to be honest, did I foresee what has taken place in the last 10 years with regard to production from oil source rock and shale? The answer is, no, I didn’t see that. And I don’t want to tell you I saw something coming if I didn’t. But I have seen a lot of things coming — and I’ve seen a lot of things going, too. And regarding oil, I just don’t see the U.S. becoming the world’s No. 1 producer. But, if you take all of North America together — Canada, the United States and Mexico — that’s a different story. If that group of countries works together, then yes, we can become energy and oil independent on a North American basis. But here’s the deal. If you were presi-dent, and you saw the United States had this kind of resource potential, and you looked around the world and saw how good countries look financially if they’re operating on their own energy resources, you just might think, “Hey, this is a real simple way to solve our country’s problems.” Right? Let’s just use our own energy resources. Just doing that would cut

“I just don’t see the U.S. becoming the world’s No. 1 producer. But, if you take all of North America together — Canada, the United States and Mexico — that’s a different story.”

K o r n / F e r r y

Q 2 . 2 0 1 3 21

Cour

tesy

of C

hoic

e En

viro

nmen

tal o

f Flo

rida

East.” Well, since we’re only getting 2.25 million barrels a day from the Middle East anyway, we can cover that with our domestic resources right now. That will give us the option to move the Fifth Fleet out, and our people out of the area. We spent $1.5 trillion on the Iraqi and Afghan wars, and lost 7,000 of our people with 40,000 injured — and we use very little oil from the Middle East. So if I were running for presi-dent of the United States and you elected me, I would stop using oil from the Middle East. Completely.

What about OPEC?PICKENS: Well, we’re importing 4.5 million barrels a day from OPEC. The part of OPEC we’re importing from includes Nigeria, Venezuela and Angola. If I were president, I’d move to get out of that, too. But I’d make getting out of the Middle East my first move so we can get our people out of the harm’s way. Like I said, we can do North American energy indepen-dence. Between Canada and Mexico, we’re getting about 5 million barrels a day of the roughly 9 million barrels a day we’re importing.

Some people are suggesting the U.S. should begin exporting natural gas. Is that wise? PICKENS: I’m not big on exporting natural gas, but you have to give producers of natural gas an opportunity to sell their

You’re a proponent of using natural gas for transporta-tion. What happens if prices for natural gas rise?PICKENS: Let’s say you use natural gas as a transportation fuel in trucks, and let’s say it is $4 a MCF. Now, if you compare diesel to natural gas on a gallon basis, if natural gas is selling at $4 a MCF, it would be the same as $2-a-gallon diesel fuel. But diesel fuel sells for over $4 a gallon, so natural gas is a lot cheaper than diesel — about half the cost. Now, if natural gas went to $8 a MCF, it would be the same as diesel fuel selling for $2.50 a gallon. But since diesel is selling at $4 a gallon, natural gas is still $1.50 a gallon cheaper even at $8 a MCF.

You’ve been outspoken about the true cost in blood and treasury of defending Middle East oil. How dependent on the Middle East is the U.S.? PICKENS: Do you know how many barrels a day come through the Straits of Hormuz?

No. PICKENS: Then I’ll tell you — 17 million barrels a day. You know how much of that comes to the United States? Only 2.25 mil-lion barrels a day. During the elections the president said, “I can tell you this. We’re going to get off of oil from the Middle

B r i e f i n g s o n T a l e n T & l e a d e r s h i p

Q 2 . 2 0 1 322

Asso

ciat

ed P

ress

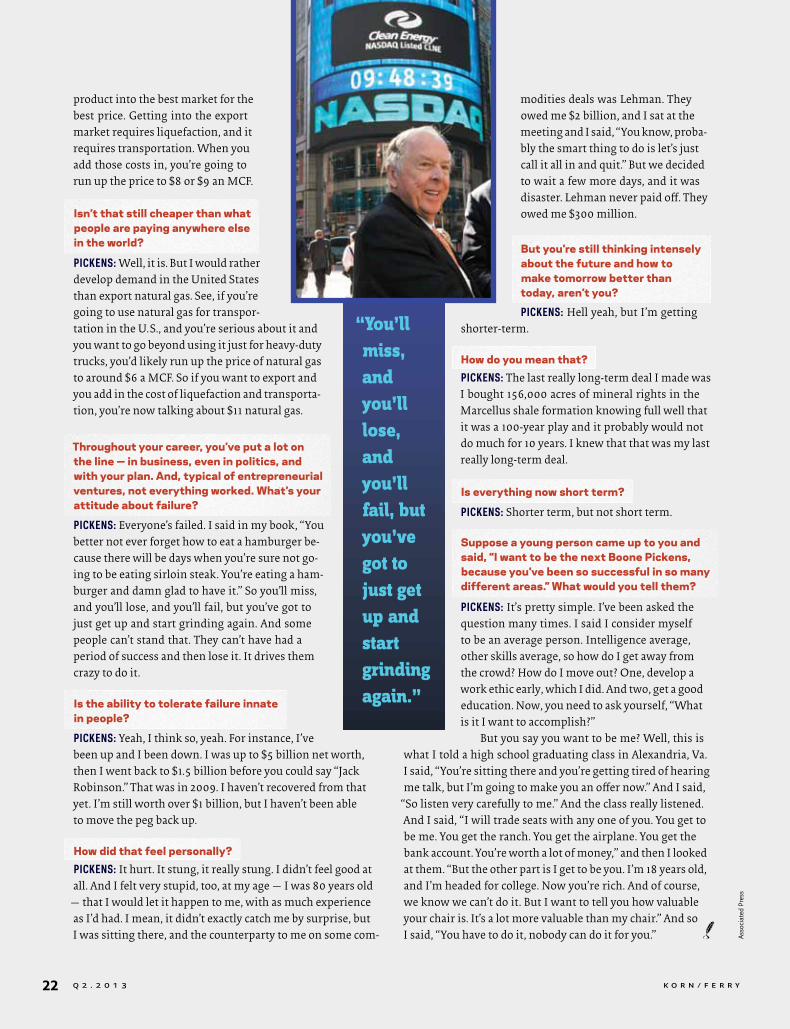

modities deals was Lehman. They owed me $2 billion, and I sat at the meeting and I said, “You know, proba-bly the smart thing to do is let’s just call it all in and quit.” But we decided to wait a few more days, and it was disaster. Lehman never paid off. They owed me $300 million.

But you’re still thinking intensely about the future and how to make tomorrow better than today, aren’t you?

PICKENS: Hell yeah, but I’m getting shorter-term.

How do you mean that?PICKENS: The last really long-term deal I made was I bought 156,000 acres of mineral rights in the Marcellus shale formation knowing full well that it was a 100-year play and it probably would not do much for 10 years. I knew that that was my last really long-term deal.

Is everything now short term?

PICKENS: Shorter term, but not short term.

Suppose a young person came up to you and said, “I want to be the next Boone Pickens, because you’ve been so successful in so many different areas.” What would you tell them?

PICKENS: It’s pretty simple. I’ve been asked the question many times. I said I consider myself to be an average person. Intelligence average, other skills average, so how do I get away from the crowd? How do I move out? One, develop a work ethic early, which I did. And two, get a good education. Now, you need to ask yourself, “What is it I want to accomplish?”

But you say you want to be me? Well, this is what I told a high school graduating class in Alexandria, Va. I said, “You’re sitting there and you’re getting tired of hearing me talk, but I’m going to make you an offer now.” And I said,

“So listen very carefully to me.” And the class really listened. And I said, “I will trade seats with any one of you. You get to be me. You get the ranch. You get the airplane. You get the bank account. You’re worth a lot of money,” and then I looked at them. “But the other part is I get to be you. I’m 18 years old, and I’m headed for college. Now you’re rich. And of course, we know we can’t do it. But I want to tell you how valuable your chair is. It’s a lot more valuable than my chair.” And so I said, “You have to do it, nobody can do it for you.”

product into the best market for the best price. Getting into the export market requires liquefaction, and it requires transportation. When you add those costs in, you’re going to run up the price to $8 or $9 an MCF.

Isn’t that still cheaper than what people are paying anywhere else in the world?

PICKENS: Well, it is. But I would rather develop demand in the United States than export natural gas. See, if you’re going to use natural gas for transpor-tation in the U.S., and you’re serious about it and you want to go beyond using it just for heavy-duty trucks, you’d likely run up the price of natural gas to around $6 a MCF. So if you want to export and you add in the cost of liquefaction and transporta-tion, you’re now talking about $11 natural gas.

Throughout your career, you’ve put a lot on the line — in business, even in politics, and with your plan. And, typical of entrepreneurial ventures, not everything worked. What’s your attitude about failure?

PICKENS: Everyone’s failed. I said in my book, “You better not ever forget how to eat a hamburger be-cause there will be days when you’re sure not go-ing to be eating sirloin steak. You’re eating a ham-burger and damn glad to have it.” So you’ll miss, and you’ll lose, and you’ll fail, but you’ve got to just get up and start grinding again. And some people can’t stand that. They can’t have had a period of success and then lose it. It drives them crazy to do it.

Is the ability to tolerate failure innate in people?

PICKENS: Yeah, I think so, yeah. For instance, I’ve been up and I been down. I was up to $5 billion net worth, then I went back to $1.5 billion before you could say “Jack Robinson.” That was in 2009. I haven’t recovered from that yet. I’m still worth over $1 billion, but I haven’t been able to move the peg back up.

How did that feel personally?PICKENS: It hurt. It stung, it really stung. I didn’t feel good at all. And I felt very stupid, too, at my age — I was 80 years old

— that I would let it happen to me, with as much experience as I’d had. I mean, it didn’t exactly catch me by surprise, but I was sitting there, and the counterparty to me on some com-

“You’ll miss, and you’ll lose, and you’ll fail, but you’ve got to just get up and start grinding again.”

K o r n / F e r r y

Advice you can trust starts with a conversation.

V3 Wealth ManagementUBS Financial Services Inc.

2029 Century Park East, Suite 3000Century City, CA 90067

ubs.com/team/v3

UBS Financial Services Inc. is a subsidiary of UBS AG. ©2012 UBS Financial Services Inc. All rights reserved. Member SIPC. 7.00_Ad_8x10.5_JP0405_AmaJ

Performance. As important on the track as it is for lasting success.

We will not rest

Q 2 . 2 0 1 324

Jam

es B

enne

tt

It’s Better at the Top

When the renowned Stanford neuroscientist Robert Sapolsky began to measure the impact of stress in baboon society in Africa — research that has continued more than three decades — he made an unexpected discovery. Baboons, which live in large, closely knit social groups, exhibited very clear hierarchical behaviors. Large dominant males sat at the top of the hierarchy, and those lower in the pecking order were constantly harassed and abused by those higher up. By measuring the cortisol, or stress hormone, levels in these baboons, Sapolsky determined that the higher the social rank in the group, the lower the stress levels in the baboon. Life at the top, it seemed, was pretty darn cushy for the top-banana baboon.

The Higher You Go, the Less Stress You Feel By Glenn Rifkin

K o r n / F e r r y

Q 2 . 2 0 1 326

Jam

es B

enne

tt

That’s all well and good if you live on a savanna and spend much of your day foraging for fruit, having sex with willing females and snoozing while your mate picks the nits out of your fur. But how does this relate to stress levels in human primates? From the earliest days of organizational behavior research, conventional wisdom presumed that the highest-ranking leaders like chief executives, generals and political leaders carried far more stress — that unwelcome byproduct of leadership. The higher you rose in an organization, the greater the demands, and with that came peptic ulcers and long, sleepless nights. Or so it was assumed.

But recently, a study released jointly by researchers at Harvard, Stanford and the University of California, San Diego, revealed that high-ranking leaders displayed lower levels of stress than nonleaders. The study, conducted at the Kennedy

School of Government at Harvard, included military officers and government officials. In testing these high-level leaders, it was discovered that, as with baboons, their cortisol levels decreased as they rose through the ranks.

As such studies are wont to do, these drew a widespread but fleeting media response. It made for a good raised-eye-brow moment but seemed to promise little response in cor-porate boardrooms. For aspiring leaders, however, the study set off a spark of interest and debate. If achieving the highest levels of leadership brings not only untold riches, vast power and influence, and in some cases, fame, could attaining a lofty perch bring less stress as well?

For members of the research team, the findings were pro-vocative. James Gross, a Stanford psychology professor who specializes in research on regulating emotions, said that the

K o r n / F e r r y

Q 2 . 2 0 1 3 27

researchers were as surprised as anyone by the results. “We took a close look at leaders versus nonleaders and wondered if we not only asked them how stressed they were but looked at the physiology through salivary testing that measured cor-tisol levels, would we see differences?” Gross explained. “There was a very clear difference between the two groups. Leaders reported less stress than nonleaders.”

The results triggered a second study of 100 more leaders in an attempt to quantify the parameters. All leaders, after all,

are not the same, and expected levels of stress would certainly vary between a leader with one direct report versus someone with 1,000 people reporting to him or her.

In fact, despite such varied parameters, the trigger for stress came down to one crucial element. “The critical ingre-dient to having lower stress seems to be a perceived sense of control,” Gross said. “We found that the greater your level of leadership responsibility, the more control you have, the less stressed you are.”

Acknowledging that with global political and economic uncertainty rampant, stress levels are rising for everyone, the researchers asked, “If you are a leader in uncertain times, does that make you more stressed than everybody else?” The con-clusion: No, because these leaders are able to assert more con-trol over their world and have additional resources at their disposal to address the challenges.

The study said: “Occupying a position marked by a large number of subordinates and possessing substantial author-ity over one’s subordinates are two aspects of leadership that confer such benefits. That these positions elevate one’s psy-chological experience of control is not surprising; they are likely to be marked by prestige as well as objective power and influence.”

This level of social control, a personal sense of power and the ability to get people to listen to what you say are more likely to lead to lower stress levels than, say, high levels of compensation. Certainly, an executive making $30 million a year in salary, bonuses and stock options will fly a private jet, which reduces the stress of air travel. But “the critical ingre-dient, the kind of control that seems to affect stress, is social control,” Gross said. “This is good news for aspiring leaders. As they develop more and more leadership skills and accept more responsibility, they can look for opportunities to de-velop more social ties to those in their organizations, and this sense of personal power is really stress-buffering. As they move through the ranks and if they can work to develop

this social intelligence, it is not only good for their careers but also for their health.”

The Whitehall Study

In fact, the Harvard-Stanford-San Diego study may not be all that groundbreaking. It is not, for example, the first of its kind. The famous Whitehall Study in Britain, which began in 1967, measured health issues and the impact of organiza-tional rank. The Whitehall Study did not focus specifically on

stress, but the parameters were strikingly close. And its con-clusions were startlingly similar to those of the recent leader-ship study here.

The two-part Whitehall Study tracked more than 28,000 British civil servants of every rank, from top to bottom, over several decades. Despite conventional wisdom and the expec-tations of Sir Michael Marmot, the study‘s director, the high-est-ranking workers did not have higher levels of disease-inducing stress. Indeed, Marmot‘s efforts demonstrated that between the ages of 40 and 64, civil servants at the bottom of the Whitehall hierarchy had a mortality rate four times higher than those at the top.

“The remarkable finding, which ran counter both to my expectations at the time and, I think, most other people’s, was, firstly, just looking at heart disease; it was not the case that people in high-stress jobs had a higher risk of heart attacks,” said Marmot in an interview at the University of California, Berkeley. “Rather, it went exactly the other way: people at the bottom had a higher risk of heart attacks.

“Secondly, it was a social gradient. The lower you were in the hierarchy, the higher the risk. So it wasn’t top versus bottom, but it was graded. And, thirdly, the social gradient applied to all the major causes of death.”

Instead of looking specifically at cholesterol levels or blood pressure, obesity and diabetes, the study illuminated the onset of all the major causes of death: heart disease, gas-trointestinal disease, renal disease, stroke, cancers unrelated to smoking, as well as accidental and violent deaths.

What stands out about the Whitehall Study is that inter-views with civil servants over the years pointed to the same outcomes as Sapolsky’s baboon research and Gross’s new stress study. It isn’t as much about the sheer amount of stress but rather the perceived and real absence of control by non-leaders at lower-level positions. Quoted in a Wired magazine article, Marmot noted: “Researchers call it the ‘demand-

It isn’t as much about the sheer amount of stress but rather the perceived and real absence of control by nonleaders at lower-level positions.

B r i e f i n g s o n T a l e n T & l e a d e r s h i p

(continued on page 29)

Rye Barcott, a special adviser to the CEO at Duke Energy in Charlotte, N.C., and a former Marine captain, brings a radi-

cally different perspective to the issue of leadership and stress. Having com-manded Marine units in Bosnia and the Horn of Africa, Barcott, now 33, found himself leading a human intelligence unit in the volatile city of Fallujah in Iraq in 2006. There, Barcott encountered a type of stress that most organizational leaders will never experience.

On one memorable day, Barcott got word that a local sheik had been assas-sinated. What is more, the assassins were two boys, ages 11 and 15. The trig-german was the 11-year-old.

Responsible for “human operations,” as the effort to win the hearts and minds of the local population was euphemisti-cally labeled, Barcott knew this was a dangerous situation. After the killing, Barcott and his team spread out across

the city. Barcott himself joined the Iraqi police at the crime scene and eventually found himself seated across from the boys in the interrogation room. What-ever was going to happen, it was time sensitive. Decisions would have to be

made quickly before the situation esca-lated into an ugly and dangerous scene.

“I needed to go out with the Iraqi police unit so we could acquire informa-tion to keep our unit safe from attacks that were already in motion,” Barcott recalled. “I realized there were a number of possible bad outcomes and I had to make the best out of a situation that only had negative outcomes.”

From his work with the Iraqi police, Barcott was able to learn that an I.E.D. had been planted in another part of the city specifically for his troops. The two boys were sent to Abu Ghraib prison, and the bomb was neutralized before it could kill any troops or civilians.

For Barcott, who also founded and ran an aid organization in the Kibera slum in Nairobi, Kenya, while serving in the Marines, dealing with intense levels of stress is not about having control. In fact, for Marines and other military lead-ers, the moments of highest stress in

combat are moments of the greatest un-certainty. There are a number of differ-ent outcomes, and “the fog of war is high.”

“I challenge the thesis about less stress due to more control,” he said. “The reason we experience stress differently

in combat has less to do with the amount of control and more to do with being in the service of others. When you are thinking about how your team is going to be affected, it puts you in a different frame of mind than if you are an individ-ual actor. The best leaders I worked with were always putting the welfare of the men and women who served under them ahead of themselves.”

The Marines, in fact, have a decision-making cycle called an “Ooda Loop.” Ooda is an acronym that stands for “observe, orient, decide and act.” The theory is that the faster a leader can execute these four actions, the more effective the team will be, especially in a time of war when the stress is high.

“When you go into a high-stress en-vironment, the mind switches from fo-cusing on the consequences of all that can go wrong to ‘what are the best de-cisions I can make with the least amount of damage with the information I have?’ ” Barcott explains.

If great leaders experience less stress, Barcott believes, it is because of an accumulated body of experience coupled with a framework for translat-ing that experience into knowledge. “In the military, you wear a set of ribbons, which are there for a number of reasons — personal achievements, unit achieve-ments, experiences you’ve had,” he said. “The accumulation of experience is often valued as wisdom; and in some cases, that is bona fide. But experience doesn’t translate into knowledge unless you have the framework for reflection and making sense of that experience.”

In other words, whether or not a leader is feeling great stress is not the primary concern. “A leader casts a long shadow over an organization,” Barcott continued. “It’s always important to con-tain the anxiety you feel, which doesn’t mean you aren’t true to your emotions. But when the stakes are very high, the organization will feel that leader’s stress. A leader needs to be in a position of demonstrated grace under pressure. It has an amazing effect.”

The Ooda Loop

K o r n / F e r r y

Asso

ciat

ed P

ress

Q 2 . 2 0 1 328

Q 2 . 2 0 1 3 29

Jam

es B

enne

tt

control’ model of stress, in which damage caused by chronic stress depends not just on the demands of the job but on the extent to which we can control our response to those de-mands.” If a man or woman has “a high degree of control over work, it is less stressful and will have less impact on health.”

Far-reaching Implications

Before today’s leaders lean back in their Aeron chairs and contentedly put their feet up on their desks, they must be aware that the generalizations spawned by such studies are replete with gaping plausibility holes.

For many leaders, this smacks of a chicken-and-egg situa-tion that pushes the theoretical up against the individual realities of life at the top. For example, Rick Goings, CEO of Tupperware since 1992 and a former Navy officer, is skeptical about the Harvard-Stanford-San Diego study. “I ask myself this question, Does it mean that leadership leads to lower stress or that people who are predisposed to lower stress are better leaders?”

If you believe that leaders tend to self-select and those who successfully maneuver their way to the top do so be-cause they handle stress far better, then the study may be lit-tle more than a self-fulfilling prophecy, according to Goings.

A Buddhist who has been practicing transcendental medi-tation for 35 years, Goings doesn’t believe a leader can exert enough control over his or her environment to eliminate stress-inducing challenges.

“This is what I try to teach my direct reports,” he said. “I can’t control all of these economic circumstances. I can’t con-trol what Chavez is doing in South America or what happened in Egypt. But I can control how I react to it. I’m not saying

you don’t occasionally go into stress survival mode, but I don’t live there.”

For Goings, the absence of control is the more familiar territory but not a place that guarantees a negative experience.

“I push back on that theory,” he said. “The way my people thrive here is by building one-on-one relationships of trust. If you do that, you don’t need control. I believe that all a com-pany is is a collection of people and the company that has the ability to recruit, develop, empower and reward the best peo-ple wins in the end.”

Goings’s theory resonates with small-business owners as well. Tom Tremblay, owner and president of the Guardair Corporation, based in Chicopee, Mass., a manufacturer of pneumatic powered tools used for industrial cleaning and maintenance, is convinced his stress levels are impacted more by his company’s profit margins than by his own sense of control.