Left Ventricular Rotational Mechanics in Tanzanian Children with Sickle Cell Disease

Supply Constraints in the Tanzanian Economy: Simulation Results from a Macroeconometric Model

Susan Horton, University of Toronto John McLaren, Princeton University

Economic events of the 1970s and early 1980s (world recession and disruption of international trade and finance) hit sub-Saharan Africa particularly badly. There has been heated debate as to the role o f additional external resources and domestic ad- justment measures in economic recovery. This paper uses a supply constrained ma- croeconometric model of the Tanzanian economy to simulate the effects of several alternative strategies. The results highlight the problems of either a strategy of de- valuation or of more external aid alone. One inexpensive policy advocated is that of freeing project aid for general balance of payments support.

1. INTRODUCTION

The severe external shocks of the 1970s and 1980s fell pa_~ticularly heavily on countries in sub-Saharan Africa. Real gross domestic prod- uct (GDP) growth was negative for a number of these countries in the period 1980-1985 (World Bank 1987), and for a larger number, in- eluding Tar~zania, real per capita GDP fell during that period. There has been considerable debate as to the role of external versus domestic factors in the poor performance of sub-Saharan African countries. Equally, there has been substantial disagreement about the role of external finance, as compared to domestic policy reform, in future recovery.

Address correspondence to Susan Horton, Department of Economics, University of Toronto, 150 St. George Street, Toronto MSS IAI, Canada.

This paper uses an econometric model built by Nguyuru Lipumba, Benno Ndulu, and various others in the Department of Economics, University of Dares Salaam, with the assistance of Susan Horton, University of Toronto, and Andre PIourde, University of Ottawa. The authors are indebted to a number of people in the three universities for their assistance. Jeffrey Fine, Gerry Helleiner and Sam Wangwe were particularly important for their support and encourage- ment of the overall project. The project was made possible by a collaborative research grant from IDRC (International Development Research Centre of Canada). The authors would like to thank Jeffrey Fine, Gerry Helleiner, and Andre Plourde for helpful comments on an earlier draft, and Monica Neitzert for excellent research assistance.

Received May 1988; accepted February 1989.

Journal of Policy Modeling I !(2):297-313 (I 989) © Society for Policy Modeling, 1989

297 0161-8938/89/$3.50

298 S. Horton and J. Mcl.aren

The conventional wisdom is that external shocks such as those ex- perienced recently in sub-Saharan Africa require the usual expenditure switching policies: devaluation to shift production toward tradables, declines in domestic absorption to allow for resources to switch, and changes in institutions and incentives to favor exporters (in the case of sub-Saharan Africa, the latter frequently implies an increase in agricultural producer prices). In fact, these policies are being imple- mented to varying degrees by a number of countries in the region.

The alternate view is that such policies involve unnecessarily large costs and may be ultimately counterproductive. It is argued that the sub-Saharan African countries are so dependent on imports for crucial intermediate inputs that short-run balance of payments adjustment measures cause "external strangulation," whereby capital utilization falls and investment suffers. According to this view, external finance is crucial in the adjustment process.

This paper empirically examines alternate strategies to deal wi th external shocks in a supply-constrained economy. It uses a macro- econometric model of Tanzania, built to reflect the crucial role of foreign inputs in domestic production and the importance of supply constraints. The model and the role of supply constraints are discussed in section 2.

Six different simulations are presented, ranging from devaluation, (both one-shot and crawling peg), increases in export crop producer prices, and a reduction in the government deficit (to represent the "conventional wisdom" approach to adjustment), to increases in e×- ternal finance (the "alternate" approach to adjustment) and to a low- cost policy of untying project aid, allowing it to be used for general balance of payments support (an approach which some donors have followed in Tanzania). The simulations are compared to a base case and are described in section 3.

The results (section 4) suggest that in most circumstances, the short- run prospects for Tanzania are relatively bleak: Real GDP growth is likely to be sluggish, declines in real per capita GDP will persist over the immediate future, and there is little prospect for improvement in thc balance of payments. Conventional adjustment policies work rel- atively badly in an open economy such as Tanzania: There is very rapid transmission of higher import prices into domestic inflation, which quickly eats up nominal devaluations. Injections of foreign re- sources lead to once-and-for-all gains but, in the absence of changes in domestic policy, do not generate enough structural change to sustain the economy's tuture path. Freeing of aid (in paxticular, reallocating

SUPPLY CONSIRAINTS IN THE TANZANIAN ECONOMY 299

aid from capital good imports to intermediates) can have a beneficial (and low-cost) impact on growth and development.

The results obtained are specific to one country and dependent on the specification of the particular model used. Nevertheless, the results may be arguably of broader applicability in illustrating the contentions about external strangulation and supply-constrained economies. Al- though there are now a large number of case studies of shocks and adjustment (see, e.g., studies synthesized by Balassa 1983, 1984; Helleiner 1986; Taylor 1987), these tend to use accounting frameworks rather than explicit macro models. Moreover, working macro models of low-income, sub-Saharan countries are rather few in number (for a survey of such models, see Harris 1985). Therefore, the present paper is of some interest in that it is frequently argued that these countries merit special treatment in debt forgiveness, etc. The concluding section (5) examines the broader implications of the paper's findings.

2. LITERATURE SURVEY: DESCRIPTION OF THE MODEL

There is substantial disagreement as to the appropriate form of ad- justment in developing countries in the face of external shocks such as those of the 1970s and 1980s. There is disagreement on the appro- priate model to be used to examine response to shocks, the empirical results from actual studies, and the policy prescriptions as to the relative role of domestic policy reform and external financing.

The IMF orthodoxy is based on a model termed the "monetary approach to the balance of payments" (Khan et al. 1986). In this model, exchange rate changes and ceilings on domestic credit expan- sion (including subceilings on government credit) are of paramount importance and are supplemented by other reforms such as trade lib- eralization, interest rate changes, and price changes for export crops. The role of financing is to smooth the adjustment process. Sub-Saharan Africa is not qualitatively different from other countries in this model, except that "The Fund has recognized that the deep-seated structural problems require longer periods of adjustment" (Zulu and Nsouli 1985). "Longer" means longer than those associated with 1- or 2- year standby arrangements, m the context of the Fund's 1979 cend~- tionality rules.

Empirical studies supporting this viewpoint include those of Balassa (1983, 1984). In a decomposition exercise for 12 developing countries (Balassa 1984), he finds that growth was correlated with domestic policy variables but not with reliance on additional external finance.

300 S. Horton and J. McLaren

He argues that similar conclusions emerge from a study of 19 oil- importing, sub-Saharan African countries (Balassa 1983).

Critics of this viewpoint use alternate models emphasizing structural problems. A starting point is the two-gap model literature (Chenery and Bruno 1962; McKinnon 1964), in which the lack of substitutability between traded and nontraded goods makes foreign exchange partic- ularly important in easing supply constraints and helping growth. The World Bank relies on Revised Minimum Standard Models (RMSM) based on similar principles (Khan et al. 1986). Taylor (1987) develops a model of "externally strangled" small, open economies for whom conventional adjustment is painful and unnecessarily costly.

Empirical studies have also been done to exemplify this alternate view. Taylor (1987) summarizes results of 18 studies of developing countries, of which six fall into the "externally strangled" category. Heheiner (1986) similarly synthesizes seven decomposition studies and argues that " . . . conventional macroeconomic accounting may seri- ously understate the degree to which recent austerity.., reduces future output, welfare and growth."

One recent debate among opponents of devaluation has focused on whether or not devaluation is necessarily contractionary. This hypoth- esis was popularized by Cooper (1969), who offered both theoretical arguments and empirical evidence to support the view. The theory was formalized by Krugman and Taylor (1978), who used a Keynesian model in which there were four contractionary effects (income distri- bution toward those with a higher propensity to save, presumably capitalists; an increase in the trade deficit in domestic currency, as- suming inelastic export supply and import demand; automatic increases in tax collection from ad valorem trade taxes; and a reduction in real money balances, if the money supply is not fully adjusted for the increase in prices). Econometric results using panel data (Edwards 1986) give some support to the h,opothesis that devaluation is con- tractionary in the short run.

The present study uses a full-scale macro model of one sub-Saharan African country to examine empirically these opposing viewpoints. It incorporates supply constraints of the kinds postulated by the alternate view and examines whether (as is argued) the openness of the economy leads to nominal devaluations being rapidly nullified by subsequent inflation, and if external finance is as expansionary as claimed. A number of simulations are performed to compare the different policies advocated by the two views.

The simulations use a 90-equation macroeconometric model of the Tanzanian economy built as a collaborative research effort between

SUPPLY CONSTRAINTS IN THE TANZANIAN ECONOMY 301

the Departments of Economics of the Universities of Dares Salaam and Toronto (of the 90 equations, 37 are behavioral). The model is described in detail in Lipumba et al. (1988), and only the salient features are discussed here.

The model disaggregates GDP into eight sectors (agriculture, man- ufacturing, construction, commerce, transport, utilities, public admin- istration, and miningmthe latter being exogenous). Employment is determined exogenously for six sectors; for the othc~" two (manufac- turing and construction), it is determined simultaneously with sectoral output. Real absorption is divided into real private consumption (mod- eled using a consumption function), real fixed capital formation (an accelerator, with supply constraints), and real government expenditure (exogenous). The government sector determines the nominal govern- ment deficit, depending on (endogenous) government revenues and (exogenous) government expenditures. The nominal government def- icit then feeds into the money supply, which in turn affects prices. The monetary sector is a very simple one in which money demand adjusts to money supply, and there is no role for the rate of interest. (The unimportance of the interest rate is due to the absence of well- developed financial markets.) In the price sector, there are estimated equations for six sectoral deflators (the seventh is exogenous, and the eighth is determined endogenously) and three economywide deflators (for GDP and fixed capital formation, plus the consumer price index [CPI]). Sectoral deflators depend on sectoral wages and productivities, and an import price index. Economywide deflators depend on import prices, overall productivity, and the money supply.

The external sector is modeled in the greatest detail, since it is argued that this is the main route by which supply constrairits operate. It occupies 32 of the 90 equations. Five different export craps are dis- tinguished (coffee, tea, cotton, tobacco, and sisal), as well as imports of three types (consumer, intermediate, and capital goods).

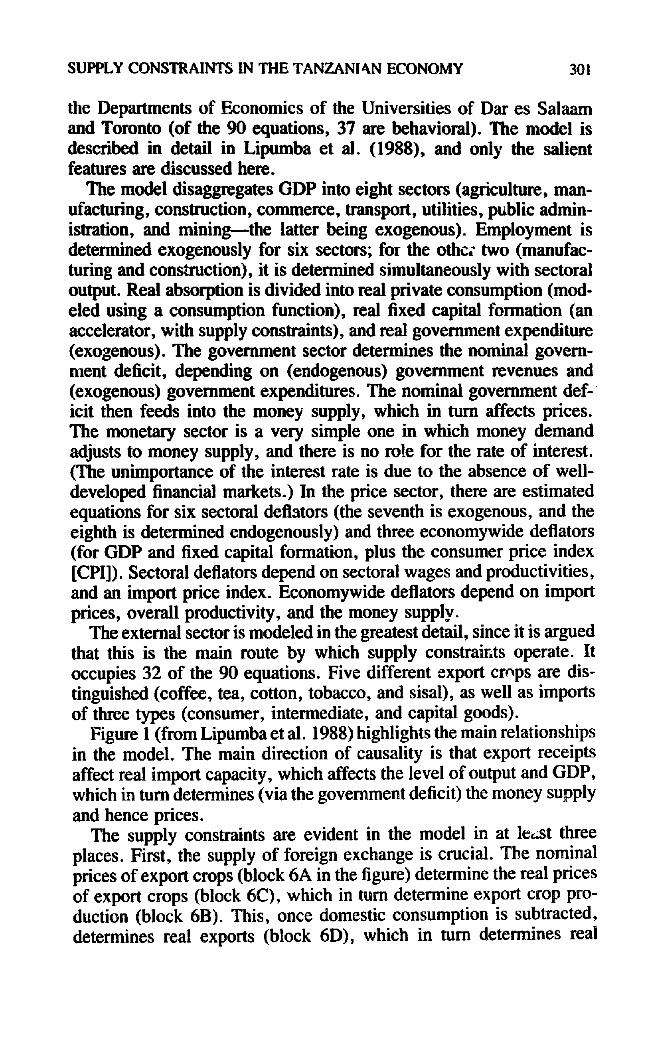

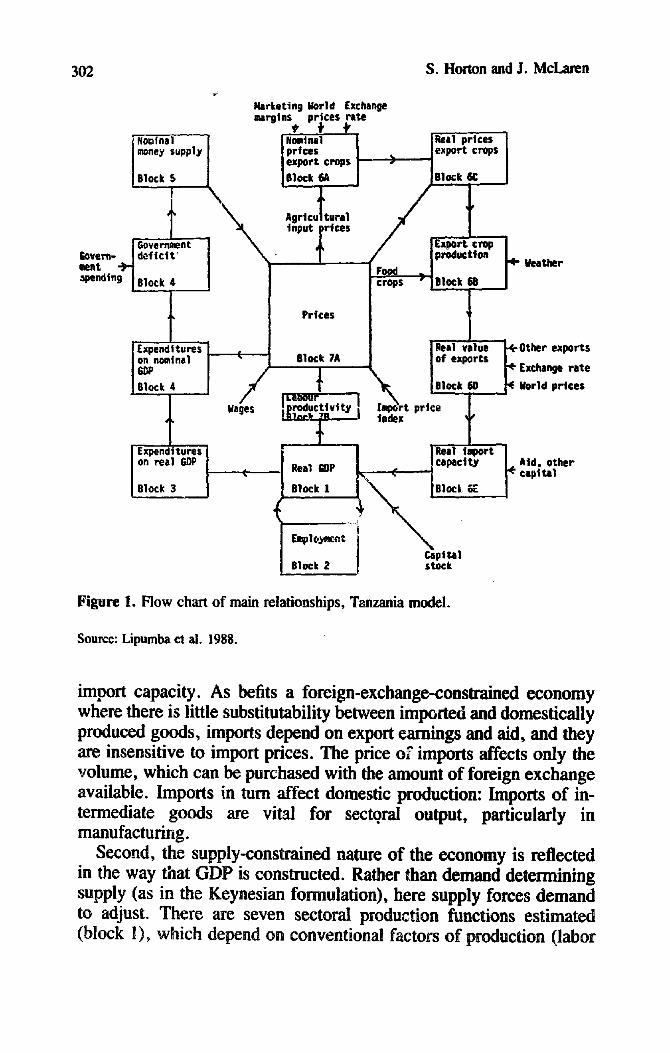

Figure 1 (from Lipumba et al. 1988) highlights the main relationships in the model. The main direction of causality is that export receipts affect real import capacity, which affects the level of output and GDP, which in turn determines (via the government deficit) the money supply and hence prices.

The supply constraints are evident in the model in at least three places. First, the supply of foreign exchange is crucial. The nominal prices of export crops (block 6A in the figure) determine the real prices of export crops (block 6C), which in turn determine export crop pro- duction (block 6B). This, once domestic consumption is subtracted, determines real exports (block 6D), which in turn determines real

3 0 2

Harketin 9 gorld Exchange mrglns prices rate

i Nomtnal I prices I export, crops J Block 5A i

No~tnal .... J money supply

lock S

[Government ~velf~l- _ ~ doftclt' merit ")'1 ~e"dt'g leloc ~ 4

i Expendtturo'i I I ) B l ~ k 4

E "~ Wages

S. Horton and J. McLaren

Agricultural input Irtces

Real prices ] export crops

i810~k 6C

crops - lelock 6S

geather

Prices

[Real value 81ock 7A [of exports

1L ~r lio,~k ~0

t price i index

i~,1 t . . r t Real GOP _ ~ capacity

c i Block I \ ie:oc~ ~E

Emplo~at Capital

Block 2 stock

t ~ Other exports Exchange rate World prices

~ Ald, other capital

Figure 1. Flow chart of main relationships, Tanzania model.

Source: Lipumba et ai. 1988.

import capacity. As befits a foreign-exchange-constrained economy where there is little substitutability between imported and domestically produced goods, imports depend on export earnings and aid, and they are insensitive to import prices. The price of' imports affects only the volume, which can be purchased with the amount of foreign exchange available. Imports in turn affect domestic production: Imports of in- termediate goods are vital for sectoral output, particularly in manufacturing.

Second, the supply-constrained nature of the economy is reflected in the way that GDP is constructed. Rather than demand determining supply (as in the Keynesian formulation), here supply forces demand to adjust. There are seven sectoral production functions estimated (block 1), which depend on conventional factors of production (labor

SUPPLY CONSTRAINTS IN THE TANZANIAN ECONOMY 303

and capital), and additionally on measures of imt, arted intermediate inputs. The situation in Tanzania's manufactunng sector, where ca- pacity utilization is estimated to have fallen to 27 percent in 1984, exemplifies the "'external strangulation" argument.

A third supply constraint exists in the agricultural sector, where food production and export crop production are substituted on a one-for- one basis. This latter constraint is perhaps unnecessarily rigid, and a better approach might be to allow some limited substitutability between food and export crops. Future work with the model will include efforts to improve the modeling of food crop production (not an easy task, in view of the data limitations).

One supply constraint that is not incorporated in the model at present because of a lack of data is the constraint on agricultural output because of a lack of availability of consumer goods (as postulated by Berthe- lemy and Morrisson 1987; Bevan et al. 1987).

The model has been estimated for the years 1966-1984 and is main- tained at the University of Dar es Salaam, where it is run on a personal computer using the Bank of Canada's Time Series Simulator (TSS) software (Bank of Canada 1986). Model equations were estimated by Ordinary Least Squares (OLS), two stage least squares, and single equation maximum ILkelihood methods, and, hence, are subject to possible simultaneous equations bias. However, the relatively short time series did not permit the use of more sophisticated techniques of model estimation. Thus, the results should be treated with some caution.

3. SIMULATIONS

The simulations presented here are for the first 5 years following the end of the estimation period (i.e., 1985-1989 inclusive). The base case does not incorporate the policy changes that occurred in the Tan- zanian economy after 1984 (devaluation, changes in crGp marketing practices, changes in government spending). It simulates what would have happened had the economy continued with pre-1984 policies. The alternate policy simulations allow an individual examination of some of the policy changes that actually occurred, as well as some that did not.

Table 1 lists the assumptions both for the base case and the alternate policy simulations. In general, the assumption is that values of ex- ogenous variables are at their 1984 levels or follow their historic trends. There are two exceptions. One is that public-sector employment is frozen at its 1984 level, rather than growing at 7 ~rcent (the historical

304 S. Horton and J. McLaren

Table 1: Simulation Assumptions

Base case (BASERUN) 1.1 Nominal wages (treated as policy variables in the model) rise at their

historical rate of change, as determined by autoregression results. These range from 3.5 to 7 percent, depending on the sector.

!.2 The U.S. dollar price of imports rises at its historical rate of 7.9 percent per annum.

1.3 In six of the seven sectors for which labor is exogenous, labor grows at its historical rate. These rates range between 2.0 and 6.1 percent, depending on the sector. In the seventh sector (public administration), labol force is held constant at the 1984 level.

! .4 The terms of trade for export crops remain at their 1984 level, (i.e., export prices in U.S. dollars rise at the same rate as import prices).

1.5 Real government consumption expenditures and real development expenditures are constant at their 1984 levels.

1.6 The weather is good for each crop for each year (i.e., all weather dummies are held equal to zero).

! .7 The real value of exports other than the five principal export crops is constant at its 1984 U.S. dollar value.

1.8 Net capital inflows are constant at their 1984 level in U.S. dollar terms.

Devalue (DEVALUE) 2.1 The exchange rate changes from 15.292 Tanzanian shillings per U.S. dollar

to 22.937 Tazanian shillings per U.S. dollar (a 50 percent nominal devaluation).

Crawling-peg exchange rate (CRAWLPEG) 3.1 The exchange rate changes from 15.292 Tanzanian shillings per U.S. dollar,

to 22.937 in 1985, to 25.230 in 1986, to 27.753 in 1987, to 30.529 in 1988, and to 33.579 in 1989 (i.e., a 50 percent nominal devaluation in the first year, followed by 10 percent nominal devaluations in each successive year).

Raise aid (AIDRISE) 4.1 The level of net foreign transfers rises by 50 percent in U.S. dollar terms

over its 1984 value.

Raise producer prices (PRODUCER) 5.1 The time path of nominal export crop producer prices is exogenized and set

equal to the base case time path times 1.5. Thus, each year's producer price for each crop is 50 percent greater than it was in the base case. (In the base case, producer prices are determined in the small country manner, i.e., as a function of world prices, the exchange rate, marketing margins, and domestic inflation).

5.2 Real government consumption and development expenditure are held constant as in the base case. "Other government expenJitures," held constant in real terms in the base case, are increased by the rise in the cost to the marketing board of buying the export crops from the farmers.

SUPPLY CONSTRAINTS IN THE TANZANIAN ECONOMY 305

Table 1 (continued)

Change in composition of imports (IMPCH) 6.1 The demand schedule for intermediate imports is shifted up by I billion

1976 Tanzanian shillings. 6.2 The demand schedule for capital imports is shifted down by ! billion 1976

Tanzanian shillings (i.e., foreign exchange allocation policy is assumed to have changed).

6.3 The fixed capital formation function is shifted down by 2.7 billion 1976 Tanzanian shillings. (This is meant to capture the effect of the decrease in capital imports on domestic investment)

Cut in government deficit 0DEFCUT) 7.1 Government expenditures in 1985-1989 are 82.65 percent of the real value

in 1984 (i.e., t~ese are cut by the amount that would result in a "'balanced budget" or z~ ~ment budget deficit in 1984).

trend), on tHCorrespondingly, governmen~ expenditure is also frozen at its 1984 level in real terms, for the same reason.

4. RESULTS

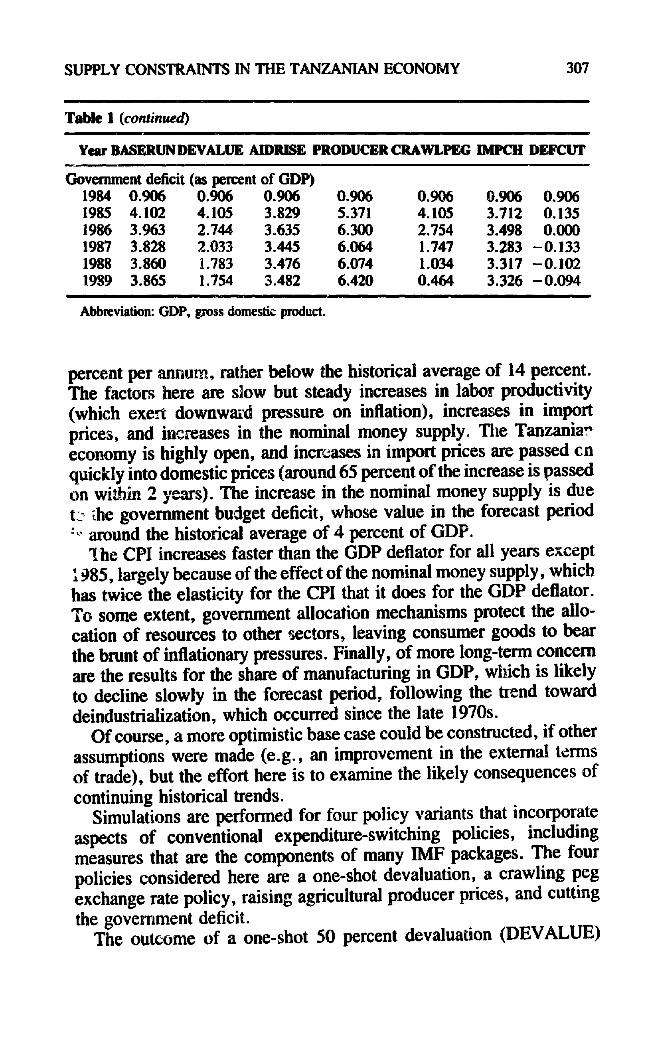

This section discusses the base case in some detail, and then high- lights the main features of the six alternate policy variants. Table 1 provides a summary of the most salient outcomes of the policy sim- ulations: The variables tabulated :=clude the conventional indicator of economic growth (real GDP) and the two main constraints, i.e., the balance of paymeat~ basic balance (deficit, in current U.S. dollars) and the GDP deflator. Other variables are real imports, the consumer price index, the share of the government deficit in GDP, and the share of manufacturing in GDP, an important indicator of structural change and development.

The base case (BASERUN) itself is not particularly optimistic. Real GDP growth is very low after the first year and is largely attributable to the assumed increase in employment in all sectors other than public administration. Per capita growth continues to be negative, as it has been since the late 1970s. The balance of payments deficit also con- tinues to worsen, which suggests that far from repaying accumulated arrears on the foreign account, Tanzania is likely to accumulate further external debts. This increasing deficit is a result of roughly constant real imports and real exports. The real deficit stays approximately constant, and the nominal deficit rises. Inflation (as measured by the GDP deflator) is likely to continue at a rather modest rate of about 6

306 S. Horton and J. McLaren

Table 1: Simulation Results, Selected Variables

Year BASERUNDEVALUE AIDRISE PRODUCERCRAWLCqgG IMPCH DEFClYr

Real GDP (1976 prices, nun TzeazaniaH s~iiiin~;) 1984 24365 2 4 3 6 5 24365 24365 24365 24365 24365 1985 25157 25242 25468 25157 25242 25635 25103 1986 25385 26712 25700 25390 26737 25854 25316 1987 25538 27168 25858 25671 27532 26004 25455 1988 25650 2 7 3 2 8 25972 25795 28134 26115 25554 1989 25768 2 7 4 5 1 26093 25918 28715 26232 25661

Balance of p~yments deficit (current prices, U.S. $) 1984 283.7 283.7 283.7 283.7 283.7 283.7 283.7 1985 333.4 335.8 443.2 332.8 335.8 348.4 330.6 1986 355.1 385.1 468.9 293. ! 385.9 369.9 351.7 1987 388.9 446.5 507.4 394.8 455.5 403.8 383.9 1988 406.9 463.5 530.7 417.1 488.7 423.6 401.2 1989 440.0 485.5 568.4 427.9 527.7 456.4 433.8

GDP deflator (1976 = 100) 1984 306.2 306.2 306.2 306.2 306.2 306.2 306.2 1985 326~5 368.0 322.7 326.5 368.0 321.4 327.3 1986 347.0 434.3 342.5 349.0 446.5 341.1 341.3 1987 369.4 456.9 364.5 373.4 495.5 362.5 356.6 1988 393.5 483.2 387.2 400.9 550.2 385.3 373.0 1989 419.1 511.0 411.7 430.0 609.1 409.5 390.2

Real ";mports (1976 prices, .,nrn Tank'-Jan shillings) 1984 6732.4 6732.4 6732.4 6732.4 6732.4 6732.4 6732.4 1985 4322.3 4335.3 4848.8 4332.3 4335.3 4394.3 4308.7 1986 4303.7 4503.6 4831.2 4307.2 4507.4 4375.3 4288.0 1987 4306.0 4618.3 4838.3 4625.5 4673.4 4381.2 4287.9 1988 4269.4 4585.1 4804.3 4597.3 4723.5 4349.7 4254.1 1989 4271.4 4607.8 4807.7 4592.7 4833.9 4351.8 4259.4

Consumer prices (1976 = 100) ! 984 543.7 543.7 543.7 543.7 543.7 543.7 543.7 1985 556.4 637.9 546.0 556.4 637.9 542.6 558.4 1986 593.2 713.4 564.8 599.9 736.7 556.0 576.2 1987 673.6 724.0 639.3 689.2 781.1 629.6 631.0 1988 770.5 797.8 728.7 792.2 874.1 717.3 696.4 1989 884.2 899.0 833.5 921.3 987.6 819.8 771.5

Share of manufacturing in GDP (percent) 1984 8.976 8.976 8.976 8.976 8.976 8.976 8.976 1985 8.858 9.108 9.438 8.858 9.108 10.982 8.875 1986 8.792 9.708 9.361 8.807 9.778 10 .901 8.766 1987 8.747 9.626 9.312 9.000 9.921 10.844 8.680 1988 8.671 9.511 9.229 8.949 10.018 10.758 8.568 1989 8.617 9.453 9.168 8.903 10.166 10.685 8.479

SUPPLY CONSTRAINTS IN THE TANZANIAN ECONOMY 307

,, , , | ,,,

Table 1 (continued) ii i i

Year BASERUNDEVALUE AIDRISE PRODUCER CRAWLPEG IMPCH DEFCUr

Government deficit (as percent of GDP) 1984 0.906 0.906 0.906 0.906 0.906 0.906 0.906 1985 4.102 4.105 3.829 5.371 4.105 3.712 0.135 1986 3.963 2.744 3.635 6.300 2.754 3.498 0.000 1987 3.828 2.033 3.445 6.064 1.747 3.283 -0.133 1988 3.860 |.783 3.476 6.074 1.034 3.317 -0 .102 1989 3.865 1.754 3.482 6.420 0.464 3.326 -0 .094

i , H

Abbreviation: GDP, gross domestic product.

percent per annum, rather below the historical average of 14 percent. The facton here are slow but steady increases in labor productivity (which exert downwa~'d pressure on inflation), increases in import prices, and increases in the nominal money supply. The Tanzania~ economy is highly open, and increases in import prices are passed cn quickly into domestic prices (around 65 percent of the increase is passed on wi~in 2 years). The increase in the nominal money supply is due t~- ;.he government budget deficit, whose value in the forecast period "~- around the historical average of 4 percent of GDP.

the CPI increases faster than the GDP deflator for all years except 985, largely because of the effect of the nominal money supply, which

has twice the elasticity for the CPI that it does for the GDP deflator. To some extent, government allocation mechanisms protect the allo- cation of resources to other ~ectors, leaving consumer goods to bear the brunt of inflationary pressures. Finally, of more long-term concern are the results for the share of manufacturing in GDP, which is likely to decline slowly in the forecast period, following the trend toward deindustrialization, which occurred since the late 1970s.

Of course, a more optimistic base case could be constructed, if other assumptions were made (e.g., an improvement in the external terms of trade), but the effort here is to examine the likely consequences of continuing historical trends.

Simulations are performed for four policy variants that incorporate aspects of conventional expenditure-switching policies, including measures that are the components of many IMF packages. The four policies considered here are a one-shot devaluation, a crawling peg exchange rate policy, raising agricultural producer prices, and cutting the government deficit.

The outcome of a one-shot 50 percent devaluation (DEVALUE)

308 S. Horton and J. McLaren

(where the Tanzanian shilling goes from 15.292 to the U.S. dollar to 22.937) involves some rather unpleasant trade-offs. Although growth of real GDP is higher (notably in 1986, where growth is 5.8 percent versus 0~9 percent in the base case; over 5 years growth is 10.1 percent, versus 5.8 percent in the base ease), this is accompanied by higher inflation. In a very open economy such as Tanzania's, the higher prices of imports are transmitted rapidly into domestic prices. Between 1984 and 1986, there is 41.8 percent inflation versus a 15.8 percent increase in import prices, implying that after 2 years the real devaluation is only 24 percent. The only saving factor in the model is that goverm,~ent revenue is buoyant with respect to nominal GDP, such that the gov- ernment budget deficit falls steadily and, hence, dampens any further inflationary spiral. However, this factor does not operate s;xongly enough for very large devaluations (the model does not converge for devaluations for 100 percent or more).

Tb.erefore, in this simulation devaluation is expansionary, the op- posite of what was predicted in the Krugman-Taylor (1978) model, a model that has much in common with the Tanzanian one. One reason for the difference is straightforward: In the former model, all the contractionary effects work through a fall in aggregate demand. Since the Tanzanian model is supply constrained, these effects are inhibited. The second reason for the difference is more subtle. In both models the nominal wage is fixed, and in both models the devaluation raises domestic prices. However, in the Krugman-Taylor model, with its Leontief technology, price signals do not affect production decisions; the only effect of the falling real wage on output is indirect, through the distribution of income. By contrast, the present model employs a technology in manufacturing that is Cobb-Douglas in labor and utilized capital stock. Thus, a fall in real wage increases labor demand, the labor intensity of capital use, and, hence, output. Clearly, the presence or absence of wage indexation and the substitutability of labor for other factors of production are key issues in the question of whether or not a devaluation will be contraetionary.

Devaluations do not necessarily cause the balance of trade to im- prove, or even the monetary balance (Cooper [1969] presents some empirical findings). However, if neither balance improves, the ease in favor of devaluation is somewhat weaker. In the simulation results for Tanzania, the balance of payments basic balance does not improve. Although there are improvements in exports (via the effect of the exchange rate on producer prices and, hence, on export crop produc- tion), imports also increase. This is because the model assumes that all foreign exchange receipts are spent on imports, and that because

SUPPLY CONSTRAINTS IN THE TANZANIAN ECONOMY 309

of supply constraints, import demand is insensitive to import prices. The extra imports allowed in in the first 2 years do, however, enable the supply-constrained manufacturing sector to increase its share of GDP relative to the base case. Thus, although devaluation improves growth and industrialization (as its proponents argue), it also increases inflation rapidly in an open economy (as its opponents argue) and has little effect on improving the balance of payments.

The crawling peg simulation (CRAWLPEG) examines the effect of a continually falling nominal exchange rate, a policy advocated by some external obse~ers. The aim is to crawl toward a better real exchange rate. In the simulation, there is a nominal devaluation of 90 percent over 5 years (a nominal devaluation of 50 percent in the first year followed by tour successive annual devaluations of 10 percent). The results of this policy are similar to those of the one-shot deval- uation, but more pronounced. Growth performance is better than all the other simulations. The devaluation causes modest increases in real exports, which, in turn, cause increased real imports. These then loosen the supply constraints in manufacturing, which modestly increases its share of GDP. However, the balance of payments is substantially worse than in the base case. The most unfavorable outcome is the effect on inflation. The GDP deflator increases by almost 100 percent over 5 years, which casts doubt on the su~tainability of the crawling peg strategy, given that nominal wages are rising by only 3.5 percent to 7 percent per annum (depending on the sector). Inflation also means that the real devaluation is only about a half of the nominal one (after 5 years, the nominal devaluation is 90 percent, but the real devaluation is only 52.7 percent).

Increases in producer prices of export crops financed by government deficits has been one policy used by African countries averse to de- valuation. The simulation here (PRODUCER) :~s of a policy where nominal producer prices are 50 percent higher than in the base case for each of the 5 years 1985-1989. As might be expected, the ex- penditure switching benefits of this policy are weaker than those for a corresponding devaluation. The growth of GDP improves mildly over the base case (6.4 percent versus 5.8 percent in the base case by 1989), the share of manufacturing rises modestly (8.9 percent versus 8.6 percent by 1989) and the balance of payments also improves slightly in 1986 (after crop exports have improved but imports have not yet responded to the increased foreign exchange availability). The cost is higher inflation than in the base case (40.4 percent versus 36.9 percent over the 5-year period), and a substantially higher government deficit (about 6 percent of GDP, versus 4 percent in the base case).

310 S. Horton and J. McLaren

Thus, the producer price policy outcomes are a weaker version of the devaluation ones, with the exception of the government deficit outcome.

Cutting the government deficit (DEFCUT) is a policy frequently employed in conjunction with expenditure switching. The deficit cut modeled here is rather severe: Real government expenditure is cut by 17.35 percent of the base case level in each year, an amount that would balance the government budget in 1984. The policy has relatively little to recommend it when considered alone: Inflation falls mildly (over 5 years inflation, as measured by the GDP deflator, is 27.4 percent versus 36.9 percent in the base case), and the balance of payments improves very marginally relative to the base case. However, GDP grows more slowly, real imports are slightly lower, and the process of deindus- trialization is slightly more pronounced than in the base case. The long- run effects of a lower government deficit (lower expenditures on health, education, extension, roads, etc.) are not modeled, but they are likely

• to be adverse. The simulation results suggest that cutting the deficit on its own is not a highly desirable policy.

Two other simulations consider alternatives to the conventional ex- penditure switching policies, i.e., higher aid and freer aid. The set of trade-offs here is rather different. An increase in nominal aid inflows by 50 percent of the 1984 amount (AIDRISE) causes GDP to grow faster (7.1 percent over 1984-1989 versus 5.7 percent for the base case). Higher aid also enables higher imports and causes the share of manufacturing to increase (9.2 percent versus 8.6 percent in the base case by 1989). There is also a beneficial effect on inflation. The gains dwindle over time as the higher nominal aid is eroded somewhat by increases in the price of imports. One rather paradoxical result is that the balance of payments is actually worse than in the base case. The model embodies the spendthrift propensity of Tanzania, in that the elasticities of capital and intermediate imports, with respect to foreign capital inflows, are high. The beneficial effects of higher aid are un- surprising: This is a standard result of two-gap (and other) models. However, in the absence of any expenditure-switching policies, there are few benefits for exports and the balance of payments.

The final simulation examines the effects of freeing aid from project- specific aid to general balance of payments support (IMPCH). Oper- ationally, this implies reducing capital imports and increasing inter- mediate imports correspondingly. Several donors have already done this for Tanzania, since building new capacity makes little sense when existing capacity is not operating because of the lack of spare parts or other intermediate inputs. However, it should be pointed out that this

SUPPLY CONSTRAINTS IN THE TANZANIAN ECONOMY 311

policy is not necessarily zero cost to individual donors, if the capital imports were previously tied aid and if the intermediate goods are not tied aid. This simulation is one of the most attractive, in terms of its outcomes, of the six considered in this paper. The share of manufac- turing in GDP increases more than in all the other simulations, as in Ndulu's (1986) results for a similar experiment a p p l ~ only to the manufacturing sector. Here, the aggregate results are also encouraging: Overall GDP growth is superior to all but the devaluation scenario, while the inflation outcome is better than all but the stagnation deficit cut. The only drawback of the policy is a negative accelerator effect on fixed capital investment: The loss of I billion Tanzanian shillings in capital imports causes a fall in fixed capital formation of around 2.7 billion Tanzanian shillings (much as in McKinnon's 1964 model). Obviously, there are limits to the use of this policy, since it relies on capital being underutilized because of a lack of intermediate imports. However, this policy could be a very useful strategy for the short run.

5. CONCLUSIONS

The article describes a number of policy simulations using a supply- constrained model of Tanzania. There are three chief supply con- straints. One is that foreign exchange availability constrains imports, which in turn affects sectoral production. Another is that in the agri- cultural sector, there is one-for-one substitution between export and food crops. The thh,~ is that GDP is supply-constrained, rather than demand-constrained as in the more usual Keynesian formulation. The model is also one of a very open economy.

Such a model bears out some of the criticisms of conventional IMF- type policies. Devaluation (whether one-shot or crawling peg) initially causes growth, both because of the incentives to export (which in turn enable increased imports and, hence, higher domestic production), and lower real wages (which given an incentive to increased sectoral output). Thus, devaluation in this model, unlike others, is not coa- tractionary. However, devaluation does not improve ::he balance of payments because of the high elasticity of demand for imports and their insensitivity to price. Inflation also rapidly erodes the gains to nominal devaluation, such that after 2 years a nominal devaluation of 50 percent results in a real devaluation of only 24.0 percent. That the inflationary results are not worse is due to the buoyancy of government revenue with respect to nominal GDP. The inflation can also be given a structuralist interpretation: that the shift to export crops causes in- flation via the one-for-one su~,stitution of export for food crops.

312 S. Horton and J. McLaren

Increasing producer prices and paying for this by a government subsidy is a policy sometimes adopted by countries unwilling to de- value. The outcomes of this latter policy are similar to those of a devaluation, but all the outcomes (both good and bad) are weaker.

Another component of many stabilization packages, decreasing the government deficit, is found to have little to recommend it other than the fact that it dampens inflation. There are losses in terms of slower growth of real GDP, and lower real imports, which cause the manu- facturing share in GDP to fall.

At the same time, exclusive reliance on foreign aid is not a panacea: It does enhance import capacity and increases GDP. However, it does not lead to structural shifts to favor exports, and, therefore, it does not permanently enhance the domestic capability to generate foreign exchange.

Finally, a low (although not zero) cost policy is to encourage donors to free up project aid for general balance of payments support. In an economy with considerable underutilized capacity, this is a very at- tractive short-run strategy.

Although the results are specific to a model of one particular country, one might expect other low-income, supply-constrained economies in sub-Saharan Africa to behave similarly. Ongoing work with the model includes an explicit investigation of the supply-constrained properties (comparing the behavier with an otherwise identic~ model that is demand driven: Plourde) and further policy simulations.

REFERENCES

P~aia.~sa, B. (! 984) External Shocks and Adjustment Policies in Twelve Less Developed Countries: 1974-76 and 1979-81. World Bank Development Research Department Discussion Paper no. DRD80, Washington, D.C. (! 983) Policy Responses to External Shocks in sub-Saharan African Countries, Journal

of Policy Modeling 5: 75-105. Bank of Canada (1986) Micro Time Series Simulator (TSS). Bank of Canada, Ottawa. Berthelemy, J.C., and Mor:isson, C. (1987) Manufactured Goods Supply and Cash Crops in

sub-Saharan Africa, World Development 15: 1353-1367. Bevan, D.L., Bigsten, A., Collier, P., and Gunning, J.W. (1987) Peasant Supply Response in

Rationed Economies, World Development 15:431-439. Chenery, H., and Bruno, M. (1962) Development Alternatives in an Open Economy: The Case

of Israel, Economic Journal 72: 79-102. Cooper, R.N. (1969) Currency Devaluation in Developing Countries: A Cross-sectional As-

sessment. Yale Economic Growth Center Discussion Paper no. 72, New Haven, CT. Edwards, S. (1986) Are Devaluations Contractionary? Review of Economics and Statistics 68:

501-508. Harris, J.R. (! 98~) A Survey of Macroeconomic Modelling in Africa. Paper presented at Eastern

and S~u:hern Af:ica Macroeconomic Research Network meetings, Nairobi, December.

SUPPLY CONSTRAINTS 1N THE TANZANIAN ECONOMY 313

Helleiner, G.K. (1986) Balance-of-Payments Experience and Growth Prospects of Developing countries: A synthesis, World Development 14: 877-908.

Khan, MS., Montiel, P., and Haque, N.U. (1986) Adjustment with Growth: Relating the Analytical Approaches of the World Bank and the IMF. World Bank Development Policy lssues Series no. VPERSS, Washington DC.

Krugman, P., and Taylor, L. (1978) Contractionary Effects of Devaluation, Journal of Inter- national Economics 8: 445-456.

Lipumba, N., Ndulu, B., Horton, S., and Plourde, A. 0988) A Supply Constrained Macro- econometric Model of Tanzania, Economic Modelling 5: 354-376.

McKinnon, R. (1964)Foreign Exchange Constraints in Economic Development and Efficient Aid Allocation, Economic Journal 74: 388-405.

Ndulu, B.J. (1986) Investment, Output Growth and Capital Utilization in an African Economy: The Case of Manufacturing Sector in Tanzania, Eastern African Economic Review 2: 14- 30.

Taylor, L. (1987) Varieties of Stabilization Experience: Towards a Sensible Macroeconomics in the Third World. Cambridge, MA: MIT (mimeo).

World Bank (1987) World Development Report 1987. Washington, D.C.: World Bank, 1987 Zulu, J.B., and Nsouli, S.M. (i 985) Adjustment programs in Africa: the recent experience. IMF

Occasional Paper no. 34, Washington D.C.

Copyright © 2022 FDOKUMEN