Study on Regulatory Regimes in Selected Professional ...

399

0 Study on Regulatory Regimes in Selected Professional Services in EU Member States Final Report August 2009 CARIBBEAN REGIONAL NEGOTIATING MACHINERY

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Study on Regulatory Regimes in Selected Professional ...

0

Study on Regulatory Regimes in Selected Professional

Services in EU Member States

Final Report

August 2009

CARIBBEAN

REGIONAL NEGOTIATING MACHINERY

Study on Regulatory Regimes in Selected Professional Services in

EU Member States

Contract/Project No AOR 026/2009/WP2/no. 28.1-1.040

Caribbean Region

By

Noel Watson John J. Downes

Submitted by

The Views expressed in this report do not necessarily reflect the views of the European Commission

7

TABLE OF CONTENTS

I. Executive Summary and Recommendations .................................. 2

II. Introduction ............................................................................ 10 1. Brief Guide to the EPA ...................................................... 11 2. Mutual Recognition of Professional Qualifications in the EU .... 15

III. Methodology ............................................................................ 17 1. Introduction .................................................................... 17 2. Business Environment/Market Related Issues ...................... 19

2.1. Overview of the specific domestic market for each of the selected countries .............................................................................. 19

2.2. Trade related issues in the selected industries in the selected

countries .............................................................................. 21 2.3. General Framework for Setting up in Business or Supplying

Services ............................................................................... 21 2.4. Regulatory and Administrative Issues for the Listed Professions ......

..................................................................................... 22

IV. Opportunities for TRADE IN SERVICES ........................................ 26 1. Estonia: Opportunities for Cariforum Service Providers ......... 28

1.1. Size and structure of domestic market for each service .............. 28 1.2. Trade in Services ................................................................... 30 1.3. Steps for Establishing a Business in Estonia .............................. 34 1.4. Industry Specific Opportunities in Estonia ................................. 35

2. France: Opportunities for Cariforum Service Providers .......... 41 2.1. Size of each selected industry ................................................. 42 2.2. Trade in Services ................................................................... 43 2.3. Steps for Setting up a Business in France ................................. 48 2.4. Industry Specific Opportunities in France .................................. 49

3. Germany: Opportunities for Cariforum Service Providers....... 55 3.1. Size of each selected industry ................................................. 55 3.2. Trade in Services ................................................................... 56 3.3. Steps for Setting up a Business in Germany .............................. 60 3.4 Industry Specific Opportunities in Germany .............................. 61

4. Italy: Opportunities for Cariforum Service Providers ............. 67 4.1. Size of each selected industry ................................................. 68 4.2. Trade in Services ................................................................... 69 4.3. Steps for Setting up a Business in Italy .................................... 73 4.4 Industry Specific Opportunities in Italy .................................... 74

5. Malta: Opportunities for Cariforum Service Providers ............ 79 5.1. Size of each selected industry ................................................. 79 5.2. Trade in Services ................................................................... 80 5.3. Steps for Setting up a Business in Malta ................................... 84 5.4. Industry Specific Opportunities in Malta.................................... 85

6. Netherlands: Opportunities for Cariforum Service Providers .. 93 6.1. Size of each selected industry ................................................. 93

6.2. Trade in Services ................................................................... 94 6.3. Steps in Setting up a Business in The Netherlands ..................... 98 6.4. Industry Specific Opportunities in the Netherlands ..................... 99

7. Spain: Opportunities for Cariforum Service Providers ......... 102 7.1. Size and structure of domestic market for each service ............ 102 7.2. Trade in Services ................................................................. 103 7.3. Steps in Setting up a Business in Spain .................................. 107 7.4. Industry Specific Opportunities in Spain ................................. 108

8. UK: Opportunities for Cariforum Service Providers ............. 113 8.1. Size of each selected industry ............................................... 113 8.2. Trade in Services ................................................................. 114 8.3. Steps in Setting Up a Business in the United Kingdom .............. 118 8.4. Industry Specific Opportunities in the U.K. .............................. 119

V. General Regulatory and Administrative Framework for Supplying Services .................................................................................. 129

1. Estonia ......................................................................... 129 1.1. General Regulatory Environment ........................................... 129 1.2. Setting up a Business........................................................... 129 1.3. Estonian Chamber of Commerce and Industry ......................... 130 1.4. Types of Business Undertaking .............................................. 131 1.5. Foreign Enterprise Entities Operating in Estonia....................... 137 1.6. Business Accounting Principles .............................................. 137 1.7. Auditing Standards .............................................................. 138 1.8. Taxation ............................................................................. 138 1.9. Visas, Work and Residence Permits etc .................................. 141 1.10. General Restrictions Tabled by Estonia under the EPA .............. 145

2. France .......................................................................... 145 2.1. General Regulatory Environment ........................................... 145 2.2. Setting up a Business........................................................... 146 2.3. Types of Business Undertakings. ........................................... 147 2.4. Other Legal Requirements .................................................... 149 2.5. Foreign Professionals wishing to Provide Professional Services in

France ............................................................................... 150 2.6. Visas, Work and Residence Permits Etc. ................................. 151 2.7. Taxation ............................................................................. 152 2.8. E-commerce ....................................................................... 152 2.9. Contacts ............................................................................. 153 2.10. General Restrictions Tabled by France under the EPA ............... 153

3. Germany ...................................................................... 153 3.1. General Regulatory Environment ........................................... 153 3.2. Setting up a Business........................................................... 154 3.3. Types of Business Undertakings ............................................ 154 3.4. Taxation ............................................................................. 156 3.5. Business Premises Law ......................................................... 156 3.6. Employment Law Provisions .................................................. 156 3.7. Other Legal Requirements .................................................... 157 3.8. Visas, Work and Residence Permits ........................................ 158 3.9. E-commerce ....................................................................... 161 3.10. Bank Accounts .................................................................... 161 3.11. General Restrictions Tabled by Germany under the EPA............ 161 3.12. Contacts ............................................................................. 161

4. Italy ............................................................................. 163 4.1. General Regulatory Environment ........................................... 163 4.2. Setting Up in Business ......................................................... 163

4.3. Types of Business Undertakings. ........................................... 163 4.4. Visas, Work and Residence Permits etc .................................. 165 4.5. Bank Accounts .................................................................... 167 4.6. Taxation ............................................................................. 167 4.7. General Restrictions Tabled by Italy under the EPA .................. 167

5. Malta. ........................................................................... 167 5.1. General Regulatory Environment ........................................... 167 5.2. Types of Business Undertaking .............................................. 167 5.3. Taxation ............................................................................. 169 5.4. Visas, Work and Residence Permits etc. ................................. 169 5.5. Accounts ............................................................................ 172 5.6. General Restrictions Tabled by Malta under the EPA ................. 172

6. Netherlands. ................................................................. 172 6.1. General Regulatory Environment ........................................... 172 6.2. Setting Up as Business ......................................................... 172 6.3. Types of Business Undertakings ............................................ 173 6.4. Recognition of Foreign Qualifications ...................................... 174 6.5. Taxation ............................................................................. 175 6.6. Visas, Work and Residence Permits Etc .................................. 176 6.7. General Restrictions Tabled by the Netherlands under the EPA ........

................................................................................... 181 7. Spain ........................................................................... 182

7.1. General Regulatory Environment ........................................... 182 7.2. Types of Business Undertakings. ........................................... 182 7.3. Setting up a Business........................................................... 183 7.4. Taxation ............................................................................. 184 7.5. Employment Issues ............................................................. 185 7.6. Business Premises ............................................................... 185 7.7. Visas and Work Permits ........................................................ 185 7.8. Bank Accounts. ................................................................... 187 7.9. General Restrictions Tabled by Spain under the EPA ................ 188

8. United Kingdom. ............................................................ 188 8.1. General Regulatory Environment ........................................... 188 8.2. Types of Business Undertakings ............................................ 189 8.3. Business Premises ............................................................... 196 8.4. Taxation ............................................................................. 197 8.5. Business Licenses ................................................................ 199 8.6. Employment Issues ............................................................. 200 8.7. Visas, Work Permits etc ........................................................ 201 8.8. Bank Accounts .................................................................... 204 8.9. General Restrictions Tabled by Spain under the EPA ................ 204

VI. Regulatory Framework for Trade IN SPECIFIC Services ............... 205 1. Introduction .................................................................. 205 2. Accountancy Services and Auditing .................................. 206

2.1. Estonia ............................................................................... 206 2.2. France ............................................................................... 209 2.3. Germany ............................................................................ 212 2.4. Italy. ................................................................................. 218 2.5. Malta ................................................................................. 222 2.6. Netherlands ........................................................................ 226 2.7. Spain ................................................................................. 230 2.8. United Kingdom .................................................................. 235

3. Architects ..................................................................... 261 3.1. Estonia ............................................................................... 261

3.2. France ............................................................................... 265 3.3. Germany ............................................................................ 268 3.4. Italy. ................................................................................. 274 3.5. Malta ................................................................................. 276 3.6. Netherlands ........................................................................ 278 3.7. Spain ................................................................................. 279 3.8. United Kingdom .................................................................. 281

4. Engineers...................................................................... 285 4.1. Estonia ............................................................................... 285 4.2. France ............................................................................... 285 4.3. Germany ............................................................................ 286 4.4. Italy .................................................................................. 292 4.5. Malta ................................................................................. 295 4.6. Netherlands ........................................................................ 297 4.7. Spain ................................................................................. 298 4.8. United Kingdom .................................................................. 300

5. Management Consultants ................................................ 304 5.1. Estonia ............................................................................... 304 5.2. France ............................................................................... 305 5.3. Germany ............................................................................ 305 5.4. Italy .................................................................................. 309 5.5. Malta ................................................................................. 310 5.6. Netherlands ........................................................................ 310 5.7. Spain ................................................................................. 311 5.8. United Kingdom .................................................................. 312

6. Tourist Guide Services .................................................... 314 6.1. Introduction ........................................................................ 314 6.2. Estonia ............................................................................... 314 6.3. France ............................................................................... 315 6.4. Germany ............................................................................ 316 6.5. Italy .................................................................................. 319 6.6. Malta ................................................................................. 320 6.7. Netherlands ........................................................................ 321 6.8. Spain ................................................................................. 321 6.9. United Kingdom .................................................................. 322

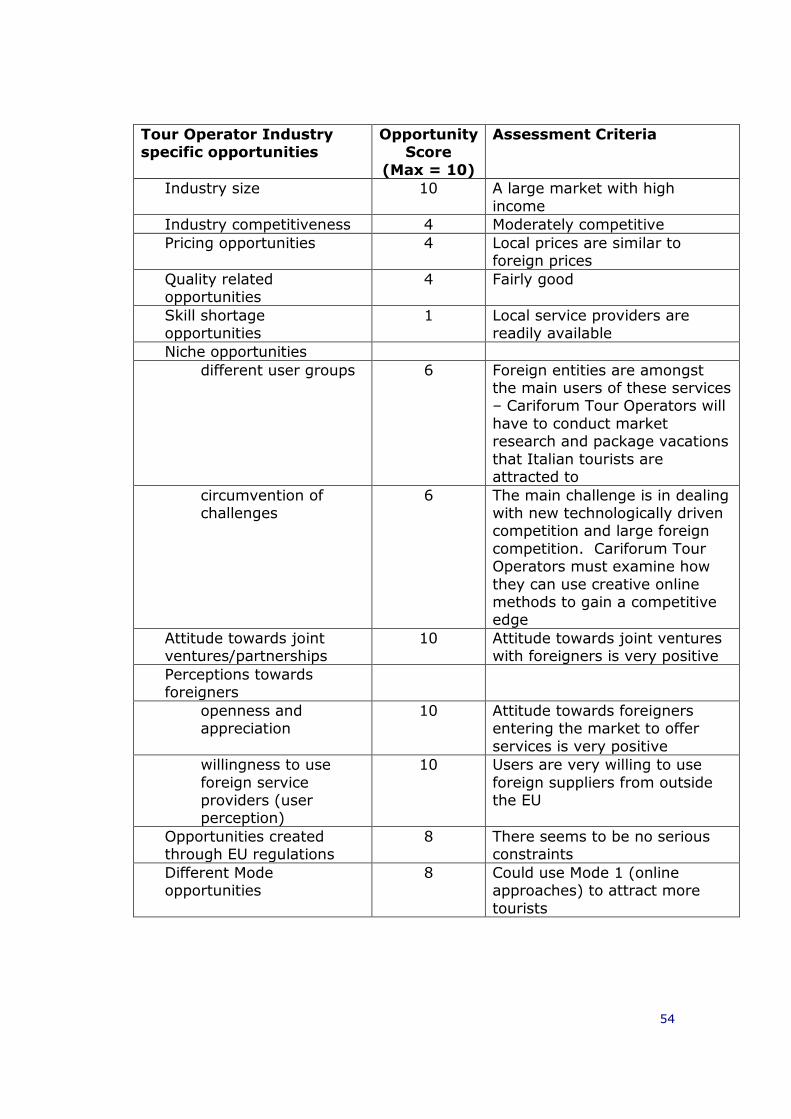

7. Tour Operators .............................................................. 328 7.1. Estonia ............................................................................... 328 7.2. France ............................................................................... 331 7.3. Germany ............................................................................ 332 7.4. Italy .................................................................................. 339 7.5. Malta ................................................................................. 341 7.6. Netherlands ........................................................................ 342 7.7. Spain ................................................................................. 342 7.8. United Kingdom .................................................................. 343

VII. Appendices ............................................................................ 346 1: General Considerations and Macroeconomic Comparisons ............. 346 2: Opportunities at the country level: ............................................. 353 3. General Framework for Supplying Services: ................................. 358 4. Summary of Regulatory Framework for the Professions in The 8 EU Member States .............................................................................. 364 5: Questionnaire on the business environment ................................ 378 6. Contacts and Interviewees in EU Member States.......................... 383

1

Abbreviations and Explanations

ACP African Caribbean Pacific

Cariforum

Caribbean Forum of States : Antigua and Barbuda, the Bahamas, Barbados, Belize, Dominica, the Dominican Republic, Grenada, Guyana, Haiti, Jamaica, Saint Lucia, Saint Vincent and the Grenadines, Saint Kitts and Nevis, Surinam, and Trinidad and Tobago. Cuba is a member but was not involved in this EPA.

CRNM Caribbean Regional Negotiating Machinery

CSS Contractual Services Suppliers

EEA European Economic Area: Iceland, Liechtenstein, Norway.

EPA Economic Partnership Agreement

EU

European Union : Austria, Belgium, Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania,

Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden. United

Kingdom

IP Independent Professionals

OECD

Organisation for Economic Cooperation and Development

comprises 30 countries including France, Germany, Italy, the Netherlands, Spain and the UK.

Schengen Countries

Austria, Belgium, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands,

Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden.

UNCPC United Nations Central Product Classification

2

I. EXECUTIVE SUMMARY AND RECOMMENDATIONS

The project arises from the European Partnership Agreement (EPA)

between the EU and the Cariforum countries regarding trade relations 2008-2028.

Amongst the aims of the EPA are to:

Improve Cariforum countries global competitiveness. Enable them to take advantage of key opportunities in the export

of services. Liberalise investment and trade in services.

The EPA will require adjustments in EU legislation, regulations and administrative procedures.

It will be necessary to develop mutual recognition procedures for

professional and other qualifications.

The objectives of this report are to:

Set out the opportunities that arise for certain key professions. Provide trade data.

Outline the existing legal, regulatory and administrative framework for these professions in 8 EU Member States.

The professions concerned are:

Accountancy, auditorship and book-keeping. Architecture.

Engineering. Management Consultancy. Tourist Guiding.

Tour Operations.

In defining those professions this report uses the UNPC Classification System.

The 8 EU Member States covered are: Estonia, France, Germany, Italy, Malta, Netherlands, Spain and the United Kingdom.

Opportunities for trade in the selected countries are presented in the

table set out in Part VII: Appendix 2 of this report. In summary

The most open markets for Cariforum suppliers appear to be in

Estonia, Italy, Netherlands and the UK. Less open are those in France, Germany, Malta and Spain but that

does not mean that there no opportunities in those countries as the report indicates below.

Cariforum professionals may take the opportunities afforded by

their capacity to provide services at a lower cost, using modes 1

3

and 4, to markets where costs are substantially higher e.g. France,

Germany, Italy, Netherlands, Spain and the UK. The proximity of Estonia to Scandinavia and its links with the

former Soviet countries may provide Cariforum professionals working with Estonian counterparts with opportunities to penetrate

those larger markets. The proximity of Malta and its linkages with North Africa likewise

provides opportunities to tap into those larger markets.

In addition to the UK, Anglophone Cariforum professionals may find it easier to engage in business in markets where English is

widely understood such as Estonia, Germany, Malta and the Netherlands.

Surinamese professionals have an advantage in penetrating the

Dutch market based on historical relationships, common language and the Surinamese diaspora in the Netherlands. The same is true

for professionals from the Commonwealth countries in respect of the UK.

The study finds that due to the general level of maturity of markets in the EU, in all of the selected markets there are minimal or no

competitive edges to be gained from the following factors:

Industry competitiveness

- Nearly all industries are very competitive so very few

opportunities could be found based on monopoly or some other market structure.

- There are a few exceptions for tour guides in niche areas or

certain geographical regions.

Quality of service

- In all industries the quality of services provided were rated as

―fairly good‖ or international standard.

Availability of service providers

- There were no industries where there was a declared shortage of service providers, in fact, with the global recession and the use of offshoring, the converse was usually true.

The main opportunities are due to the following factors:

The sheer size and income of the EU market

- This gives the relatively tiny Cariforum service providers a vast array of opportunities to skim off minute pieces of the EU

market. This activity will have no significant impact on the EU market but could have a relatively substantial impact on Cariforum exports and foreign exchange earnings.

4

Price-related opportunities.

- Due to the fact that in all industries Cariforum prices (fees & charges) are generally lower than those in the EU. As long as EU

users of services can verify that the quality of services provided by Cariforum services providers is of ―international standard‖ then the price advantage should result in an increased demand.

Positive attitude towards joint ventures

- The survey found that in all of the selected industries across the

eight countries, there was a positive attitude towards joint

ventures. Joint ventures typically represent a win-win situation that can increase earnings and minimize risks and costs for both

parties while not posing major threats to either. A table setting out the general framework for Cariforum citizens wishing

to supply professional services in the 8 EU countries is set out in Part VII: Appendix 3 of this report.

The report provides details on:

The system, rules and procedures governing trade under all four modes of delivery and, where relevant, entry, residence and

setting up in business or taking up employment opportunities in the 8 Member States.

The nature of the legal system in each of the 8 states

The rules and procedures governing the various types of business entities, their registration and liabilities.

Any compulsory membership provisions for business entities.

Tax provisions applicable to individuals and business entities.

There are detailed descriptions of the regulations governing each of the professions in each Member State set out in this report. A summary is provided in Part VII: Appendix 4

Exploitation of the opportunities identified in this report will require aggressive and proactive initiatives by:

Caribbean service providers themselves, Association representing service providers e.g. Coalitions of Service

Providers, Caribbean policymakers and negotiators, and Caribbean High Commissions and Diplomatic Attaches in the

various EU countries.

5

These players will have to engage in activities such as the following: view the large EU market as part of their day to day opportunity set;

operate using all the modes of trading services; and exploit all of the potential opportunities.

Cariforum diplomatic representatives need to pressure their EU

counterparts (e.g. at the British Home Office) to ensure that simple fast

track processes for acquiring business visas, as envisaged by the EPA, are put in place.

A survey of Cariforum interest in exporting selected services to the EU

should be conducted in order to target more closely those who are

interested. It cannot be taken for granted that most Cariforum services providers want or need to penetrate EU markets.

Funded service trade missions should be arranged to selected EU

Member States for serious export oriented professionals. Criteria for

seriousness should be developed such as:

A one-page outline of export history and capacity Contribution to the cost of the mission, which is reimbursable on

presenting a report on opportunities and making at least one

presentation to an industry grouping

A small and efficient Regional Unit, such as the Caribbean Coalition of Services Providers, should be supported and given a mandate to seek export opportunities in professional services. This would include:

Searching all major global databases for Request for Proposals and

bid documents; Circulating information to relevant national associations; Helping to put Regional teams together;

Arranging joint ventures with EU and other non-Cariforum service providers;

Having a constantly updated website with links to sites where bids are advertised.

Branches of this Unit should be established/strengthened in each Cariforum Member State.

A more aggressive outward looking approach by Cariforum services

providers. This may require some training or stimulus for them to think global; remember size of the global market; use the Internet to find sites where requests for proposals are advertised; look for partners and

pull teams together to submit large bids.

Cariforum service providers should aggressively look for Requests for Proposals and bid documents and be the senior partners in putting teams together. This approach will tend to yield to higher earnings

(including finder‘s fees) than playing the subsidiary partner.

6

Regional services providers should be oriented to seek opportunities to trade by all four modes. They should not be afraid of setting up a

business in the EU if it is the best way to supply the diaspora market. However, they should be reminded that they do not have to set up in

EU to export services if they use the other three modes of supply. Cariforum service providers should be encouraged to make corporate

visits to key EU organizations including EC funded organizations, private sector associations and private sector companies to submit business

profiles, request to be put on any list that they send out to seek bidders and enter and stay in their hearts and minds.

Professional associations in the Cariforum countries need to prepare for mutual recognition of professional qualifications by:

Preparing a document setting out the qualifications required to

practice the profession and, in particular, addressing the following,

even if the answer is ―not applicable‖:

- Academic qualifications: what is needed; what are the essential entrance requirements; what are the syllabus requirements; are their rules governing the nature, amount and grading of

assessments; whether there are rules governing where these qualifications are acquired; rules governing how long or how

many attempts may be made to acquire these qualifications. - Professional experience: is this a pre- or post-qualification

requirement; what type of experience is needed; where must it be acquired; who, if anyone, is qualified to supervise the

experience; how is the experience tested or reviewed; what is its duration; can it be part-time or interrupted for time off.

- Professional associations: is membership compulsory; are their categories of membership; are there services which can only be

legally provided by a member of that association; are there services which members are prohibited from providing; is there

corporate membership and if so are there rules governing it (e.g. more than 50% of the shares or control of the company must be in the hands of chartered accountants); is there a disciplinary

system; is there a system of quality assurance/peer review; is the association linked with others abroad.

- Professional cards, certificates, diplomas etc.: are there rules

requiring a professional to carry, hold, display a card, badge,

certificate, diploma etc.; is there a system of practising certificates; how might these be suspended or revoked.

- Negotiations: associations should elect a negotiating team.

Preferably it should include a person with international

experience and a person with academic training experience.

7

- Contact points for recognition procedures: an administrator(s)

that may be contacted by individual professionals enquiring whether their qualifications are recognised in an EU Member

State and who also might be contacted by a person qualified in the EU and is seeking recognition of their qualification in the

Cariforum country. - Lifelong learning provisions: whether there are continuing

professional development requirements.

- The effects of recognition of foreign qualifications in the Cariforum country: whether the person whose qualification is recognised is required to undertake a professional examination

(e.g. a foreign accountant might be required to take a course in Trinidadian and Tobago Business Law and Taxation) or other

requirement; are there restrictions on what they might and might not do.

- Fees: are the fees that may be charged regulated by law/ by the professional association; can a client challenge the fees charged

and, if so, how; are their rules governing anti-competitive practices and unfair trading.

- Complaints procedures: is there a system in the country/provided by the association for dealing with complaints

against a member; do foreign clients resident within/outside of the jurisdiction have access to this system.

- Exemptions: are there exemptions granted to any of the professional requirements.

- Use of professional titles: are these protected in law.

Preparing a gap analysis between the professional requirements in the Cariforum country and those of the EU Member States.

Identify best practice that already exists between professional

associations in the Cariforum countries and those in EU Member States.

Give consideration to harmonising professional qualifications in the Cariforum states in order to strengthen their bargaining power in

negotiating with EU counterparts.

Conduct a review of the existing qualifications and training

requirements with a view to matching international best practice and harmonisation with that in the EU states.

Tour operators, travel agents, destination management companies,

ground handlers, tourist transportation providers, tourist

accommodation providers, tourist guides and other tourist service

8

providers should form professional associations on a Cariforum wide

basis and have an umbrella organisation to promote their common interests.

There is a need for the Cariforum countries to take advantage of the

assistance provided under the EPA to develop strong and efficient institutional and regulatory frameworks for tourism. These should replace out of date laws and regulations that tend to solely focus on

industry regulation. There is a need to develop a modern legal framework that enshrines the principles of sustainability in the law

itself; that promotes tourism development; that facilitates investment; encourages and facilitates SMEs to take advantage of niche markets; that ensures that tourism resources are identified, classified, protected,

enhanced and utilised sustainably; that furthers the Millennium Development Goals through tourism development.

The tourism sector needs to find support for developing direct sell-

mechanisms to the EU market through e-commerce. They will require

to build consumer confidence in the EU by harmonising legal provisions in the Cariforum countries with those in the EU dealing with package

travel; ―unpackaged travel‖; distance selling; e-commerce (e.g. electronic signatures); credit cards; data protection; financial insolvency. This is more achievable on a Cariforum-wide basis than in

individual countries. Many countries outside of the EU have harmonised with these provisions.

Professional and trade associations need to be improved and become

more outward-looking. They should not merely be accreditation bodies

or professional guilds but should provide members with business services. Business associations play a major role in economic change.

Thus, they need to be strengthened in the Cariforum countries by a review of their operations, identification of best practice, a gap analysis and a plan for implementing change. Specialized training programmes

for the professional associations should be developed. A Professional Associations Executive Management course should be developed.

Strategic and business plans should be produced for each association. Associations might share some common administrative and business

facilities. New methods of consultation with members and meetings should be developed to ensure active participation e.g. through virtual meetings, association websites, professional blogs etc.

Languages: The lack of sufficient foreign language skills, particularly in

the Anglophone countries means that it may be difficult for professionals from those countries to fully avail themselves of the opportunities afforded in continental Europe by this EPA. A review of

language teaching in schools needs to be undertaken, particularly in Anglophone countries. Universities and colleges should devise intensive

business language and culture courses for undergraduates on vocational courses and for qualified professionals.

9

Hidden cultural barriers: it is important to understand the cultural

norms, business ethos and the nuances of inter-personal dealings in the business community of the host country in order to successfully

network and obtain business there. Familiarisation events might be put on for business professionals in cooperation with foreign embassies,

consulates and cultural associations.

Access, Distance and Costs: obtaining visas, long-distance travel and the costs of transport and accommodation may be prohibitive for many

SMEs. There is a need for cooperation to share costs to send fact-finding and networking groups to the EU. Support funding might be

sought together with sponsorship arrangements with airlines, tour operators and hotel chains.

Protectionism: though outwardly open to business, EU counterparts

may in practice rely on well-established networks and contractual partners and may be reluctant to welcome Cariforum competitors. The

EPA sets out commitments of EU Member States and a system for complaints and dispute settlement.

Difficulty of obtaining and disseminating information: it is difficult for SMEs to obtain up to date information on business opportunities in the

EU. Also, those that do obtain such information are not always efficient in disseminating it. In many countries Business Schools gather, assess, review and disseminate this information to businesses and

professionals, often for a small charge. Arrangements should be made between professional associations and the higher educational

institutions to cooperate on these matters. This may be a mutual benefit/no cost arrangement, a commercial one, one sponsored from public or private funds or a combination thereof.

Where EU regulations require a professional to have professional indemnity insurance the costs may prove prohibitive for the Cariforum

professional. However, for the most part, they type of contractual agreement that the Cariforum professional will have with an EU

counterpart will require the latter to have professional liability insurance not the former. Where it is a requirement, Cariforum professional associations should cooperate to seek a common policy. This will

strengthen their negotiating power with the relevant financial institutions. The latter will lower premiums for members of well-run,

properly policed and quality assured professional associations.

The cost of exchange transactions is very expensive. Title 3 deals with current payments and capital movement. The aim is to ease the

process through which payments for commercial transactions can be made and the process by which capital related to investment is moved

between the two sides.

There needs to be greater cooperation on a regional level both at the professional level and the state level. Regional and international

regulatory harmonisation is taking place elsewhere in order to facilitate trade and competitiveness. The Cariforum countries need to address

this.

10

II. INTRODUCTION

This project arises from the Economic Partnership Agreement (EPA)

between the Caribbean ACP (Cariforum) and the EU governing trade relations 2008-2028. A key aim of that agreement is to improve the

Cariforum countries‘ global competitiveness and promote export diversification. It is expected that the main gain will be in services as these countries already have market access for their goods. The World Bank has

observed that the key opportunities for market growth in the Cariforum countries are in the export of services.

Title II of the EPA provides arrangements for a progressive two-way liberalisation of investment and trade in services. It is acknowledged that this will require adjustments to legislation, regulations and administrative

provisions in the EU. Article 82 para. 2 provides:

“the Parties shall encourage the relevant professional bodies in the

respective territories to jointly develop and provide recommendations on mutual recognition to the Cariforum/EU Trade and Development Committee…for the authorisation, licensing,

operation and certification of investors and service suppliers and, in particular, in the professional services sector”.

Thus, it is envisaged that there will be subsidiary agreements on mutual recognition.

In addition to helping professional associations to prepare for mutual

recognition negotiations with EU counterpart associations under Articles 82 and 85 of the EPA, this report will provide information on the regulatory

frameworks and provide market intelligence to assist small and medium professional services businesses on supplying services in 8 EU Member States.

The objective of this report is to set out the opportunities that arise from this Agreement; to provide trade data; and outline the regulatory

framework for providing selected professional services in 8 Member States of the EU and to assist the Cariforum countries and the relevant professional associations within them in making the necessary adjustments

and informing negotiations so as to maximize the benefits envisaged by the EPA.

11

1. Brief Guide to the EPA

The parties negotiated provisions on market access, mutual recognition

and cooperation in the provision of professional services. The UN Central Product Classification System was used for the purposes of this

negotiation. The negotiations focussed on, amongst other things, the removal of barriers to providing services in respect of;

Market access. National treatment: the extent to which foreign service suppliers are

treated like domestic service suppliers.

There are also provisions on cooperation and mutual recognition of

qualifications in respect of professional services and technical assistance for the tourism sector.1

There are provisions in the EPA to facilitate trade in services by making it

easier for Cariforum nationals to visit EU Member States for brief periods for business purposes. Those purposes must relate to research and design,

marketing, training, trade fairs, sales, purchasing and tourism. However, this does not compel EU Member States to issue any Cariforum national with a visa.

Article 60(5) expressly provides that Member States can retain or amend their rules governing, for example, visas, residence permits and work

permits ―….provided that such measures are not applied in such a manner as to nullify or impair the benefits accruing to any Party under the terms of a specific commitment‖.

Each state is entitled to retain its domestic regulations governing the professions in respect of such matters as qualifications, certification,

registration and licensing etc.

The EPA deals with the standard 4 modes of trade in services:

Mode 1: Cross-Border Supply

Services flow from the territory of one Member State to that of another e.g. by internet, telephone or other telecommunications. The commitments given in this regard are rather conservative. Auditing

services are limited in 21 states and architecture in 13.

1 The authors are greatful to CRNM for their briefing guides and, in particular, CRNM’s “Brief

Treatment of Professional Services in the WPA”, 3200 3/EPA-8(08).

12

Mode 2: Consumption Abroad

The consumer moves into another Member‘s territory to obtain

services. The commitments for this mode of delivery are more liberal than those given in respect of mode 1. Most countries made no

reservations in respect of this mode of delivery.

Mode 3: Commercial Presence

A service supplier from one Member State establishes a territorial

presence in another Member State, including through ownership or lease of premises there, in order to provide a service. The system is based on reservations rather than permissions i.e. if the EU Member

State has not stated a reservation or limitation in the List of Commitments on Commercial Presence; it is presumed that there is

none other than the usual restrictions in relation to visas etc. There are some limitations in respect of certain professional services

and these are indicated below in the relevant parts of this report. Of those relevant to this study are those in respect of accountancy,

auditing and book-keeping.

Mode 4: Presence of Natural Persons

Persons from one state enter the territory of another in order to

provide a service. This enables the temporary entry and stay of key personnel and graduate trainees for periods of up to 3 years for intra-corporate transfers: 90 days in any 12 month period for business

persons; 12 months for graduate trainees (Article 82). Article 84 requires Member States to endeavour to facilitate the entry and stay of

short term visitors for business purposes. Article 60(1) makes plain that the EPA does not affect measures in respect

of citizenship, residence or employment on a permanent basis. Member States are entitled to maintain or adopt measures regulating temporary

stays in their territory, for example, provided that these ―…are not applied in such a manner as to nullify or impair the benefits accruing to any Party

under the terms of a specific commitment‖. Chapter 4 deals with the temporary presence of natural persons for

business purposes. Article 80(1) provides that this covers:

Key personnel – business visitors responsible for setting up a commercial presence and those involved in intra-corporate transfers;

Graduate trainees;

Business services sellers; Short term visitors for business purposes;

Contract services suppliers (CSS) ; Independent professionals (IP).

13

Those entering for business purposes do so in order to:

Engage in research and design. Undertake marketing research.

Attend or provide training seminars. Attend trade fairs and exhibitions. Negotiation of sales of services.

Negotiation of the purchase of services. Tourism personnel visiting to make arrangements for tours.

Those visiting for business purposes cannot sell services directly to the general public whilst in the Member State or acquire remuneration for the

provision of services during their visit.

The following table sums up the general provisions on entry requirements

under the 4 modes. It is important, however, to look at the detailed provisions for each country set out in Section V.

Road Map for Entry into the EU - Entry Requirements for Different Modes

and Categories

Mode Entry requirements Relevant requirements

Mode 1 Not relevant because there is no movement

of natural persons

Ability to meet required standards

Mode 2 Not relevant because

the service provider does not move

Qualifications and ability

to meet required standards (of the local

market)

Mode 3 Visa, residence

permit and work permit

Establishment of

company or other business entity.

Taxation compliance, etc

Mode 4

Contract Service Suppliers

Business Visa Proof that the person is

entering only for ―business purposes‖ e.g.

market research, seminars, fairs,

exhibitions, negotiate sales etc.

14

Independent

Professional

Business Visa Proof of membership of profession/qualification. Proof that the person is

entering only for ―business purposes‖ e.g.

market research, seminars, fairs,

exhibitions, negotiate sales etc.

Intra-corporate transferees

Business Visa,

residence permit and work permit

Proof of membership of

company; reason for transfer; remuneration

and subsistence provisions; undertaking

to return on completion of period.

Independent/self-employed professionals have access to the EU in respect of 11 sectors including:

Accounting and book-keeping services.

Taxation advisory services. Architectural services. Urban planning and landscape architectural services.

Engineering. Integrated engineering.

EU Member States may still apply Economic Needs Tests (ENTS) but there are no restrictions on the number of service suppliers that may enter a

market.

Currently, EC Directives on Mutual Recognition of Professional Qualifications only apply to EU nationals. The EPA provides for negotiations between professional associations from the Cariforum and EU states on the

development of mutual recognition agreements. These will then be submitted to the Joint Committee established under the EPA in order to

assess the agreements‘ compatibility with the provisions of the EPA and World Trade Organization commitments.

Article 24 of the Cotonou Agreement provides for cooperation in the field of tourism and for the liberalisation of tourism services. The Tourism Section

of the EPA safeguards the interests of SMEs in the tourism sector in the Cariforum countries. It does so by an article on the prevention of anti-competitive practices through tourism distribution networks. Provision is

made for consultation and dialogue through the Cariforum-EC Trade and Development Committee. In addition to provisions for assistance and

15

training to the service suppliers and support for training institutions, there

are also provisions for mutual recognition of qualifications in the tourism sector.

Title 2 of the EPA contains provisions for the development of common rules

for e-commerce e.g. on electronic signatures and consumer protection. Title 3 deals with current payments and capital movement. The aim is to ease the process through which payments for commercial transactions can

be made and the process by which capital related to investment is moved between the two sides.

2. Mutual Recognition of Professional Qualifications in the EU

European Union citizens have a right to establish themselves and/or their business and to provide services anywhere in the EU. These are fundamental freedoms established under the Single Market. There are EU

rules guaranteeing mutual recognition of professional qualifications (MRQs) between Member States. These cover, amongst other things:

Harmonisation of training requirements in specific sectors which give automatic recognition of professional qualifications. These are mainly to be found in the health professions.

Mutual recognition which applies to all professions for which Member States require a qualification (―the general system‖), with the exception

of the specific sectors mentioned above. Coordination of the laws of Member States on self-employment,

commercial agents, harmonising the civil law on the relationship

between agent and principal.

The EU system was recently reformed to: Make labour markets more flexible.

Further liberalise the provision of services. Encourage more automatic recognition of professional qualifications.

Simplify administrative procedures. Directive 2005/36/EC consolidates and modernises 15 existing directives

covering the whole range of MRQs except those relating to lawyers, commercial agents and activities relating to toxic substances. The 20

October 2007 was the end of the transposition period. The preamble to this Directive on the Recognition of Professional qualifications states:

“(4)…there should be specific rules aimed at extending the possibility of pursuing professional activities under the original professional title”.

“(8)…The services provided should be subject to the application of the

disciplinary rules of the host Member State having a direct and specific link with the professional qualifications, such as the definition of the profession; the scope of activities covered by a profession or reserved

to it; the use of titles; and serious professional malpractice which is specifically linked to consumer protection and safety”.

16

“(10)…The Directive does not create an obstacle to the possibility of

Member States recognising, in accordance with their rules, the professional qualifications acquired outside the territory of the European

Union by third country nationals. All recognition should respect in any case minimum training conditions for certain professions. “.

The Directive contains provisions on the following, amongst other things:

Professional experience. Professional associations.

Professional cards, certificates, diplomas, etc. Contact points for recognition procedures. Lifelong learning provisions.

The effects of recognition. The principles of free provision of professional services.

Exemptions. Administrative cooperation. Information to be given to the recipient of the service.

A general system for recognising evidence of training. Levels of qualifications.

Equal treatment of qualifications. Conditions for recognition. Knowledge of languages.

Use of academic titles. Use of professional titles.

The Directive applies to EU citizens wishing to pursue their profession in another Member State, whether on a self-employed or employed basis. It

applies to natural persons not to juridical persons (e.g. companies). It also applies to a person who acquires a professional qualification in another

Member State but wants to practice in his/her own state.

17

III. METHODOLOGY

1. Introduction

In addition to researching the trade in services and the opportunities that

might arise from the liberalisation under the EU-Cariforum agreements, the consultants researched the regulatory regimes currently in force in Estonia, France, Germany, Italy, Malta, Netherlands, Spain and the United

Kingdom. In respect of the following professions and trades:

Accountancy, Auditing and Book-keeping.

Architecture. Engineering

Management Consultancy Tour Operations. Tourist Guide Services.

Our approach to the level of disaggregation in the selected service industries was based on UNCPC classifications. An important point to note

is that the selected services in this assignment are typically defined at the UNCPC 3 or 4-digit level (UNCPC classification is the international classification usually used when categorizing services - see

http://unstats.un.org/unsd/statcom/doc02/cpc.pdf).

This means that the selected service industries are broadly defined and

could be disaggregated further. For example, under the UNCPC, Management Consulting Services is classified as 8311 which is the 4-digit level; however this is broken down in six 5-digit categories as follows:

1. General Management Consulting Services. 2. Financial Management Consulting Services.

3. Human Resources Management Consulting Services. 4. Marketing Management Consulting Services. 5. Production Management Consulting Services.

6. Other Management Consulting Services.

On the other hand, Engineering Services is defined as 833, which is the 3-

digit level. However, this is broken down into six 4-digit categories which are each, in turn, broken down into four 5-digit categories (which means that there are 24 sub-categories of engineers). There are similar sub-

classifications of architectural and accounting &auditing services.

In this assignment we will treat the selected service industries under the

broad UNCPC 3 or 4-digit categories but if any exceptions or significant differences are identified, they will be included.

18

The consultants researched the regulatory regimes currently in force in

Estonia, France, Germany, Italy, Malta, Netherlands, Spain and the United Kingdom in respect of the specified professions and trades. All of these

states, with the exception of the UK have a legal system based on the Roman Law and are described as Civil Law systems.2

It should be noted that the United Kingdom has three separate legal jurisdictions; England and Wales, Scotland and Northern Ireland. England, Wales and Northern Ireland are part of the Common Law tradition found in

the Anglophone Caribbean countries. So too is the Republic of Ireland. Scots Law has its roots in the Civil Law tradition of continental Europe but

with substantial Common Law influences. Both are covered in this report. Some of the professional bodies for Northern Ireland are arranged on an all-Ireland basis and these are also covered.

Some countries (UK, Germany, Italy and Spain) have considerable decentralization and whilst differences are pointed out in the report, we

have given a general national overview.

The review was based on:

Legislation 3.

Regulations. Administrative procedures.

Industry practices.

The consultants have identified and referred to the specific laws and

regulations and provide a database of contacts of all relevant professional organisations and regulatory bodies. In particular, the consultants

gathered information on the following: Academic qualifications. Accreditation bodies.

Professional training. Professional affiliations(s).

Professional curriculae and examinations. Licensing, certification, registration, permits and fees. Language requirements.

Citizenship, visas etc. Administrative processes.

Professional standards. Processes for incorporating new companies.

Processes for establishing joint ventures or other alliances. Capitalization requirements.

2 They are based on the Roman Law “ius civilis”, hence Civil law. The Dominican Republic, Haiti and

Surinam also have Civil Law systems. 3 Where possible, the title of the legislative provision is given in the original language and according to

the official legal formulary. This varies considerably across the Member States and particularly between

Common Law countries (e.g. England and Wales) and Civil Law countries (e.g. Germany).

19

The methodology included the following:

Internet research - to obtain information on the business environment and relevant regulatory framework issues

Telephone interviews to collect information from relevant officials and industry players

Field research by consultants to collect information not available on the internet and to hold face to face discussions with critical industry players

Visits to relevant staff at DG Trade, DG Dev, DG Enterprise and Industry, Internal Market and Competition to obtain information on EU

policies and requirements. Visit to France, Belgium, The Netherlands, The U.K., Estonia and Malta

to a) develop a feel for cultural aspects of the countries, b) establish

business relationships, and c) collect any outstanding data. Conduct a two day workshop in Barbados with relevant persons from

the Cariforum countries to outline the main findings and to obtain their feedback and input.

In some countries information was more readily available than others and

this will be evident in this report. This may be an important indicator of how open to business under the EPA they are.

We have referred to titles being ―protected in law‖. This means that there is legislation or regulations laid down by the State as to who may use this title. Even where a title is not directly protected in law it will usually be

criminal offence to pass oneself off as being a member of a professional association or holder of professional qualifications when that is not the

case.

2. Business Environment/Market Related Issues

The analysis of the business environment/market related issues includes the following:

2.1. Overview of the specific domestic market for each of the selected countries

(a) Size of overall market and growth trends

i. Population

ii. GDP

iii. GDP per capita

iv. GDP growth

(b) Other factors important to trade

i. Extent to which English is spoken – is language a barrier

ii. Quality of the ICT infrastructure

iii. Availability of air and ground transportation

20

(c) Size and structure of domestic market for each service

i. Contribution of selected industries to GDP

ii. Size of firms in each selected industry

1. number of firms in each selected industry

2. average turnover

3. number of employees

iii. Survey of associations (or a sample of service providers) in each of the selected industries to determine

1. number of service providers in each of the selected industries

2. size of local versus foreign services providers

3. attitude towards foreigners entering the market

4. attitude towards joint ventures and collaboration

5. competitiveness of service providers in each industry

6. main challenges

7. main users of particular service

a. public sector

b. multinationals

c. large local private entities,

d. small local private sector entities

e. NGOs

f. foreign governments,

g. foreign private sector

iv. Survey of (a sample of) services users to determine

1. the ease with which these services are available

domestically

2. the quality of services provided

3. the price competitiveness of local versus foreign

service providers

4. preparedness to use foreign suppliers within the EU

5. preparedness to use foreign suppliers from outside of the EU

(d) Overview of the EU policies and requirements and, to do so,

will visit relevant staff at DG Trade, DG Dev, DG Enterprise and Industry, Internal Market and Competition.

(e) Indicate to what extent there is currently cross-border trade in these service sectors

21

2.2. Trade related issues in the selected industries in the selected countries

(a) To the extent possible, provide data on trade in the mentioned services in the target countries (imports and

exports)

(b) To the extent possible, identify if there is there outsourcing of

these services (off-shoring) to firms overseas by large firms in Europe.

(c) What are relevant EU policies and requirements with respect

to trade in these services

(d) To what extent there is currently cross-border trade in these

service sectors

i. Within the EU (intra-European supply of services).

ii. With countries outside of the EU

(e) To what extent does trade take place in all four modes

i. Mode 1: Cross border – where only the service moves e.g. by internet, courier, telephone, etc

ii. Mode 2: Consumption abroad - Consumer comes to service provider

iii. Mode 3: Establishment of a commercial presence in the foreign country

iv. Mode 4: Movement of natural persons – where there is

temporary movement of service providers.

A questionnaire was prepared and was used by the experts and local

resources in the EU target markets to elicit the above information (see Part VII: Appendix 5).

2.3. General Framework for Setting up in Business or Supplying Services

For each country we sought to address the following:

The Consultant is considering going to country X to look for work – Can

he/she actually go to look for work or must they have a contract before they can go.

Do you need a visa to enter that country? How long does it take to

obtain it? How much does it cost? Who do you have to apply to? What

are the likely hitches?

The basic rules (e.g. registration, administrative, fees, permits, licences) governing setting up in business as:

A sole trader.

22

A partnership.

A company (different types).

Are these rules different for non-EU persons or businesses?

What are the rules re registration for national and local taxes? Also, does one have to register with the Customs Department?

Are there geographical restrictions on where they can and cannot do business?

Are there local taxes and restrictions?

What are the provisions governing e-commerce?

If qualified with a professional body in the Cariforum countries, does one have to register with the equivalent in the relevant EU country in order to provide those services there (e.g. accountancy)? If so, what

does this entail time-wise, fees, etc.

Are there restrictions on bringing staff to that country to engage in the business and, if so, what are they? Is there any limitation on the length of their stay? Do they need visas and work permits?

What are the rules on repatriating profits?

Are there restrictions on a non-EU citizen opening a bank account?

What are they? What does he/she need to do to open an account?

Are there rules governing the charges that can be made for supplying

professional services?

2.4. Regulatory and Administrative Issues for the Listed Professions

The following matters were addressed for each profession and each state. We looked at how each profession is regulated, the rules governing access

and rules on establishing a business/professional presence in that EU Member State:

Designation/ Title:

Whether the designation or title of the profession is protected?

If so, whether that is that by law, regulation, professional

association, educational establishment?

How it is protected and what are the consequences for a person providing those services without that official designation?

Are there specialist sub-designations? E.g. Management Accountant, Public Sector Accountant, Domestic Tour Operator,

Trekking Tourist Guide?

23

If there are specialist designations, how are these

regulated/protected? What proof of specialist qualifications/training/experience is needed? Are there specialist

professional associations?

Can a corporate body be designated a member of the professions or become a member of the professional association?

Is there associate membership or quasi-membership e.g. paralegals?

Qualifications:

What are the qualifications that are needed to become a member of/practice that profession or to provide those professional

services?

How does a person become a member:

Registration procedure, entry qualifications, fees, examinations and other

assessments etc.

Are there rules about where those qualifications were acquired?

What are the rules governing mutual recognition of foreign

qualifications?

Must the qualification be acquired at an accredited institution and,

if so, who does the accreditation? Are any of these in the Caribbean?

Does the professional association provide courses that lead to the

attainment of the qualification? Do they also offer courses to

external candidates i.e. those overseas?

Are there rules governing the length of time it took to acquire those qualifications? The number of attempts made? Expiry of

qualifications? Transitional arrangements whereby those who acquired qualifications under an old regime/system can gain recognition under the new system?

Is there a ―fast track‖ system for acquiring the qualifications e.g.

intensive training courses or exemptions from some parts of the course for those that are qualified in other professions or disciplines?

Training/ Experience

Is there a special training requirement to qualify for membership of

the profession?

24

Is there a geographical requirement laid down as to where that

training or experience took place or was acquired e.g. ―in France‖, ―in an urban environment‖, ― in both an urban environment and in

at least one project of 12 months duration in a rural setting‖, ―with at least 6 months experience overseas‖ ?

Are there accredited institutes, firms or professionals that provide

training or work experience?

Is there a system of Accreditation for Prior Experience (APE) which

exempts candidates from some or all of the requirements for formal qualifications?

Are there rules governing the content of the training course?

Are there Continuing Professional Development (CPD) requirements?

Regulatory Authority

What is the name of the Ministry or State body responsible for

regulating the profession?

What is/are the name(s) of the professional association(s)? What is

their status e.g. State professional associations, private associations, quasi-public bodies?

Is membership of a particular/any professional association

compulsory? If not, does it provide privileges?

Which body issues the certificate/diploma etc of membership of the

profession? Are there rules about the display of the certificate/logo etc at business premises, in business stationery, online etc?

Is a special licence needed for the provision of all/some of the professional services?

Are there rules governing the type of business that a member of

the profession can provide services through (sole trader, partner, limited liability company, unlimited liability company etc.)?

Are there legal requirements that make it compulsory for individuals, corporate bodies, public institutions to engage the

services of particular professions (e.g. company accounts must be audited by a chartered accountant, tour operators must use the services of a licensed tourist guide etc)?

Can a person be a member of more than one profession? Can the

firm be multi-disciplinary e.g. a firm combining lawyers, architects, engineers and accountants?

25

Are there special rules governing conflict of interest? Activities in

which members of the profession are prohibited from engaging in?

Are there special rules on disclosure of information; on fees and other charges?

What is the disciplinary body for the profession? What are the rules

governing disciplinary matters?

26

IV. OPPORTUNITIES FOR TRADE IN SERVICES

In this section of the report, each of the eight selected countries will be

examined in turn. In each case the following format will be followed:

The business environment will be initially outlined (subject to the

availability of data) with the presentation of industry GDP data, trade data4

and other data on industry size and structure.

A flow Chart will be presented outlining the process of setting up a business in each of the selected countries.

An assessment will be made of opportunities in each of the selected

industries for each country using a scoring system based on

responses to questions asked to industry associations and users of the selected services. The assessment will be made using the

following template:

Industry specific opportunities

Measurement Criteria

Industry size 1= up to 5000 Firms or up to 25000 employees; 4=>5000-15000 Firms or >25000-50000 employees; 7=>15000-25000 Firms or >50000-100000 employees;

10=>25000 Firms or >100000 employees Very large is a sign of more opportunity

Industry competitiveness

Very competitive=1, Moderately competitive=4, Not competitive=10

Very competitive is a sign of less opportunity

Pricing opportunities

Local prices cheaper =1, Prices same as foreign = 4, Local more expensive = 10

Local prices cheaper is a sign of less opportunity

Quality related

opportunities

International Standard =1, Fairly Good =4, Poor=10,

If the country has international standards there is less opportunity for Cariforum service providers

4 It should be noted that the Euro was introduced in 12 EU countries on January 1, 1999, at an exchange

rate of 1:1 with the ECU, which was the unit of currency used for official transactions up to that point.

Many transactions in the EU were therefore measured in EUC/Euro. In this document, wherever one

observes “in 1000 million ECU/EUR”, it is equivalent to “in € billions”.

It should also be noted that in most cases, industry specific trade data were unavailable in the eight (8)

selected countries. However, in all cases trade in “Other Business Services” was available. “Other

Business Services" is a relatively broad category which includes: merchanting and other trade related

services, operational leasing services, legal, accounting, auditing, tax consulting, book-keeping,

management consulting, public relations, advertising, market research, public opinion polling, research

and development, architectural, engineering, other technical services, agricultural, mining, on-site

processing, waste treatment depollution and services between affiliated enterprises).

27

Cont………

Industry specific based opportunities

Measurement Criteria

Skill shortage opportunities Services readily available=1, Moderately available =4, Not easily available = 10 If services are readily available then there is less opportunity for Cariforum service providers

Niche opportunities

different user groups 1=Multinationals and foreign private sector

are not main users; 4= local private sector are main users; 10= Main users are multinationals and foreign private sector

When multinationals and foreign private sector are not main user groups there is less opportunity

circumvention of

challenges

10= Challenges faced by the local industry

can be capitalized upon by Caribbean service provider, 1=where there are no

challenges faced by the industry or they cannot be capitalized on

Attitudes towards joint ventures/partnerships

1=Negative; 10 =positive

Perceptions towards foreigners

openness and appreciation

1=Negative attitude towards foreign service providers entering the market; 10= Positive attitude towards foreign service

providers entering the market

willingness to use

foreign service providers (user

perception)

1=Not willing; 4=Somewhat willing but

skeptical; 10=Very willing

Opportunities created through

EU regulations

10= If there are no EU restrictions that

discriminate against foreign services providers

Different Mode opportunities 10=Price and skill shortage opportunities can be exploited using certain modes

28

1. Estonia: Opportunities for Cariforum Service Providers

Country specific opportunities

Score Assessments

Country specific opportunities

a. Positively disposed to diversity

8 A quite diverse history – Baltic, Scandinavian, Soviet

b. Language 7 Most business people speak English

c. Proximity to other regions 10 A natural gateway to the former

Soviet, Baltic and Scandinavian States

d. Persons willing and prepared to coordinate and cooperate

10 Consultants made linkages with Chamber of Commerce which is favorably disposed to coordinating

trade missions and conducting matchmaking

1.1. Size and structure of domestic market for each service

Contribution of selected industries to GDP (in Euros Millions)

Industry 2003 2004 2005 2006 2007 2008

Accountancy services & auditing 95.62 115.83 122.00 144.15 167.97 190.32

Architecture and engineering

(only consolidated information is

available) 286.86 328.15 388.17 458.65 534.46 570.95

Management

Consultancy 52.16 57.91 66.54 91.73 122.16 111.02

Tourist Guide

Services and Tour Operators (only consolidated

information is available) 669.33 772.11 865.07 1009.03 1145.27 1189.47

Source: Statistics Estonia and calculations by Chamber of Commerce.

29

Size of each selected industry

Industry Number

of firms

Average

Turnover/Sales (million/€)

Number of

Employees (average)

Largest two firms

(by relevant business

organization)

Accountancy

services & auditing

2500 0.35 10 1. KPMG Baltics AS,

2. Pricewaterhouse

Coopers AS

Architecture 950 0.13 5-9 1. EA Reng AS,

2. SWECO Projekt AS

Engineering 2550 0.29 7-12 1. K-Projekt AS,

2. Nord Projekt AS

Management Consultancy

540 0.26 1-5 1. BDA Consulting OÜ,

2. Christiansen

Consulting OÜ

Tourist Guide Services

200 0.09 1-5 1. Gotravel OÜ,

2. Risiekspert OÜ

Tour Operators 250 0.64 10 1. Estravel AS,

2. Kalevatravel AS

Source: Industry Associations in Estonia, 2009

Number of Local and Foreign Firms in Each Industry

Industry Total #

firms

%

foreign firms

Number

of local firms

Number of

foreign firms

Accountancy services & auditing

2500 20% 2000 500

Architecture 950 15% 808 143

Engineering 2550 20% 2040 510

Management Consultancy 525 35% 341 184

Tourist Guide Services 200 15% 170 30

Tour Operators 250 35% 163 88 Source: Compiled from Data provided by Industry Associations in Estonia, 2009

Distribution of Local Firms by Size Based on Number of Employees (% in each category)

Firm Size (No. employees) 1-10 11-20 21-50 Over 50

Accountancy services & auditing

60% 25% 10% 5%

Architecture 75% 15% 7% 3%

Engineering 75% 10% 8% 7%

Management Consultancy 50% 35% 10% 5%

Tourist Guide Services 85% 10% 5% 0%

Tour Operators 50% 30% 15% 5%

Source: Industry Associations in Estonia, 2009

30

Distribution of Foreign Firms by Size Based on Number of Employees

(% in each category)

Firm Size (number of

employees)

1-10 11-20 21-50 Over 50

Accountancy services &

auditing

15% 15% 20% 50%

Architecture 45% 50% 3% 2%

Engineering 45% 50% 3% 2%

Management Consultancy 40% 45% 10% 5%

Tourist Guide Services 75% 10% 15% 0%

Tour Operators 40% 40% 15% 5%

1.2. Trade in Services

Overall Export of services5

Chart 1 shows the steady growth of Estonia‘s export of services

between 2000 and 2007. The country saw steady growth in exports rising from €1.6 billion in 2000 to €3.2 billion in 2007.