STRATEGIC PLANNING FOR THE INDIAN CIVIL AVIATION ...

24

STRATEGIC PLANNING FOR THE INDIAN CIVIL AVIATION INDUSTRY B.R. Someshekar and S. Chandra National Aerospace Laboratories Bangalore Abstract A strategic planning exercise was undertaken by the authors fond the Indian civil aviation industry on behalf of Technology, Information, Forecasting and Assessment Council (TIFAC) of the Department of Science and Technology, which has developed a technology plan to enable India to become a major global player economically by 2020. Called Technology Vision 2020, the exercise was initiated by TIFAC and Confederation of Indian Industry (CH). In continuation of the above work we now present an overview of a technology and business strategy for the industry. It is suggested that a comphrensive strategic plan is now essential to address the development of all components of the industry. The need to develop strategic plans and monitor its implementation has become common in most corporate offices of large industries in the world today. Strategic planning involves the addressing of complex issues which involves both technology and business. The rationale for establishing such think tanks is that it is essential to carry out a systematic analysis of all forces shaping the business environment in order to establish where opportunities and threats might arise. In developing a broad strategy for an industry as a whole in a country which presently holds only about 0.14% of the world's production, there are even more difficult issues to consider. These include politics, strategic defense policies of foreign governments, economic conditions, technology strategies by nations who already have a well established industry and finally competitive strategy of compares and countries elsewhere. The aviation industry which includes military and civil aviation has been regarded as strategic by an expert panel constituted to identify industries to be developed by 2020. This term is used broadly and need not necessarily be associated with defense, where indigenous technologies will have to be, developed especially when unavailable from other countries. Technologies can be strategic from an economic sense as well, given its ability to create wealth and have export and employment potential for any country or company. Many developed countries regard the civil aviation sector as very important because of its influence on the national economy, technical capability and strategic influence. Spin offs into a broad and varied range of industrial sectors has also been possible. It is an industry that involves one of the largest varieties of technologies and number of components/assemblies and equipment. Countries in the Asia-Pacific region, which entered the industry much later have emerged as important players in the past decade. In comparison, the Indian civil aviation industry which is much older, still operates from a small base even though its domestic market potential and skilled man power should have given it intrinsic advantages to emerge as a globally important player in the civil aviation industry by now.

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of STRATEGIC PLANNING FOR THE INDIAN CIVIL AVIATION ...

STRATEGIC PLANNING FOR THE INDIAN CIVIL AVIATION INDUSTRY

B.R. Someshekar and S. Chandra National Aerospace Laboratories

Bangalore

Abstract

A strategic planning exercise was undertaken by the authors fond the Indian civil aviation industry on behalf of Technology, Information, Forecasting and Assessment Council (TIFAC) of the Department of Science and Technology, which has developed a technology plan to enable India to become a major global player economically by 2020. Called Technology Vision 2020, the exercise was initiated by TIFAC and Confederation of Indian Industry (CH). In continuation of the above work we now present an overview of a technology and business strategy for the industry. It is suggested that a comphrensive strategic plan is now essential to address the development of all components of the industry.

The need to develop strategic plans and monitor its implementation has become common in most corporate offices of large industries in the world today. Strategic planning involves the addressing of complex issues which involves both technology and business. The rationale for establishing such think tanks is that it is essential to carry out a systematic analysis of all forces shaping the business environment in order to establish where opportunities and threats might arise. In developing a broad strategy for an industry as a whole in a country which presently holds only about 0.14% of the world's production, there are even more difficult issues to consider. These include politics, strategic defense policies of foreign governments, economic conditions, technology strategies by nations who already have a well established industry and finally competitive strategy of compares and countries elsewhere.

The aviation industry which includes military and civil aviation has been regarded as strategic by an expert panel constituted to identify industries to be developed by 2020. This term is used broadly and need not necessarily be associated with defense, where indigenous technologies will have to be, developed especially when unavailable from other countries. Technologies can be strategic from an economic sense as well, given its ability to create wealth and have export and employment potential for any country or company. Many developed countries regard the civil aviation sector as very important because of its influence on the national economy, technical capability and strategic influence. Spin offs into a broad and varied range of industrial sectors has also been possible. It is an industry that involves one of the largest varieties of technologies and number of components/assemblies and equipment. Countries in the Asia-Pacific region, which entered the industry much later have emerged as important players in the past decade. In comparison, the Indian civil aviation industry which is much older, still operates from a small base even though its domestic market potential and skilled man power should have given it intrinsic advantages to emerge as a globally important player in the civil aviation industry by now.

Market potential studies carried out for TIFAC -NAL Joint Board list a number of opportunities that should be utilised. To develop these opportunities, the design of strategic plans are very important. Elsewhere, we can see the, scale of economic activity associated with this industry. Specially, United States exports close to $40 Billion worth of commercial aircraft, engines and parts every year accounting for the largest share of its net trade surplus. By 1992, the industry employed an estimated 300,000 workers for civil aviation manufacture in the US These workers are well paid, highly skilled and enjoy a good quality of living. Indirect benefits also percolates to a number of manufacturing and service industries in nearly every state of United States of America. Boeing for example relies on more than 5000 domestic suppliers and spends an average $10 billion a year on goods and services produced by U.S. firm. These amounts are not small and can influence the state of the economy in any country.

The civil aviation industry is dominated by the United States of America in the manufacture and export of aircraft and remains the world's largest market for the industry. Ale size of the domestic market alone makes it attractive for aircraft design, manufacture and maintenance of aircraft in that country. Recent mergers and acquisitions in the manufacturing sector and airline operations have created corporations with the wherewithal to survive the capital intensive and long gestation nature of the industry. Europe is the next major player now undergoing radical changes in the form of collaboration and mergers, for manufacture, export and airline operations. However, Asia-pacific including China is the most promising region, with maximum growth predicted in nearly all sectors of the civil aviation market. The main reason for this development has been the growth in the, liberalized economies in the region. In the North American and European region, the industry is recovering from the effects of a major recession and the industry's growth is more sedate. The civil aviation industry is highly sensitive to economic conditions prevailing globally and historically has been very closely related to GDP growth. The business cycle in the industry is in fact an indicator of the world economic conditions.

The close relationship of the civil aviation manufacturing industry with the defence industry nearly in a, all major manufacturing Countries (Boeing, McDonald Douglas and Lockheed in USA; British Aerospace in UK, Aerospatiale in France) makes it important for policy planners to note that technologies that are considered important from the defence viewpoint may not be available for the civil aviation industry of a foreign country. Economic realities have however forced major corporations to collaborate on a number of aircraft programs. It is fist becoming a tradition for risk sharing partnerships between companies from different companies. With government subsidies and funding shrinking, these organisations eschew nationalistic tendencies and allow market forces to prevail when starting new ventures.

In this article, we review the state of the industry around the world and in India. From our reach we present the technologies and aircraft that are expected in twenty years and an overview of a strategic plan, India will need to emerge as a important player in the civil aviation industry.

The world economic scenario is now improving with most of the OECD countries coming out of recession. An annual average of about 3% GDP growth has taken place over the last 20 yeas. However, this growth has been interrupted by recessions, which were sometimes triggered or further aggravated by political crises, trade conflicts, speculation or even bad economic management. The latest recession which began in the middle to late eighties enveloped nearly all OECD countries and was further aggravated by the Gulf War. United States recovered in 1993 and recovery is now under way in Europe. Japan also now shows promise of recovery.

A striking has been the performance of the 'Asian Tigers', economies in the South East Asian region which have not paused even during this troubled period This is all the more creditable as the growth in these regions is export led. China which liberalised its economy in a phased manner from the early eighties is the engine of growth in the region. However, the Chinese economy has been subjected to high rates of inflation in the recent past and the Government has been forced to adopt strict monetary policies to control inflation.

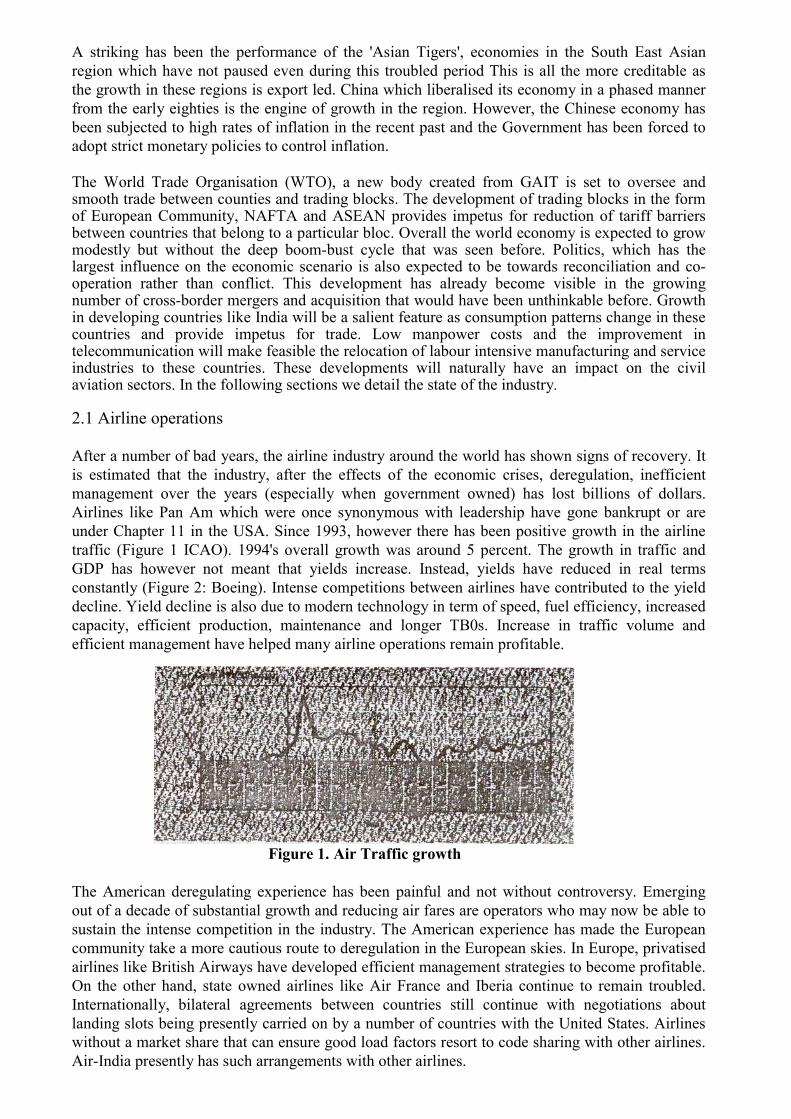

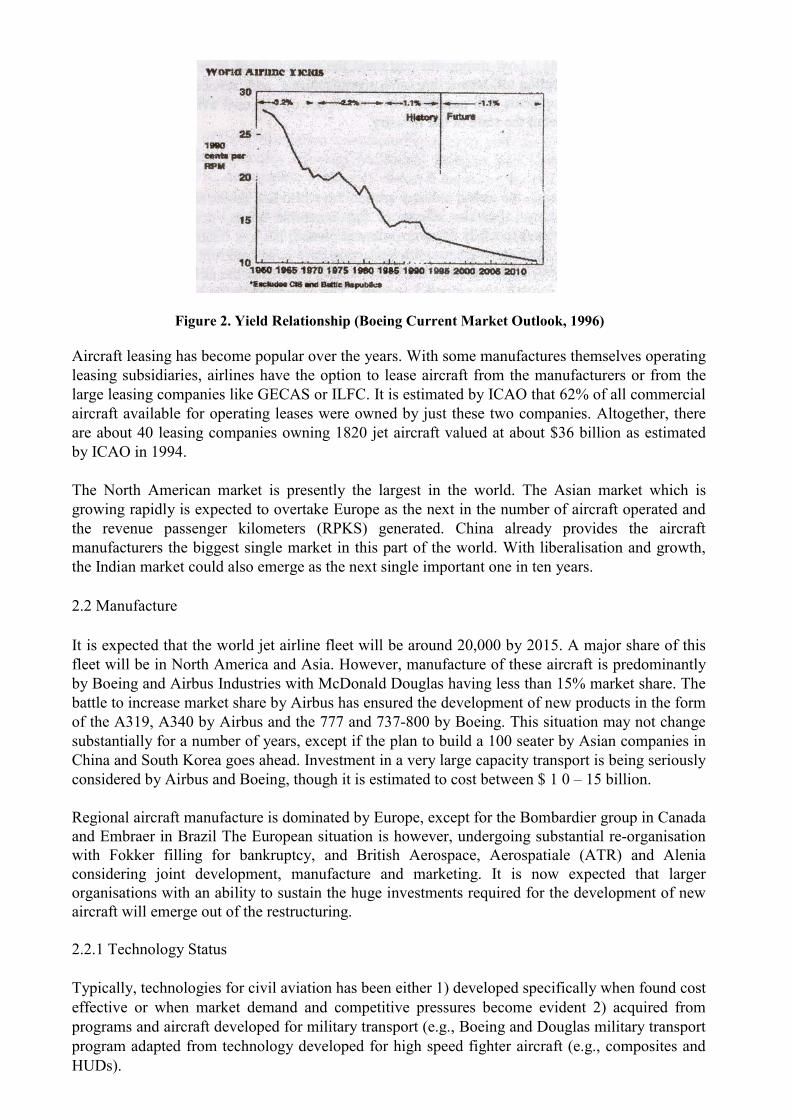

The World Trade Organisation (WTO), a new body created from GAIT is set to oversee and smooth trade between counties and trading blocks. The development of trading blocks in the form of European Community, NAFTA and ASEAN provides impetus for reduction of tariff barriers between countries that belong to a particular bloc. Overall the world economy is expected to grow modestly but without the deep boom-bust cycle that was seen before. Politics, which has the largest influence on the economic scenario is also expected to be towards reconciliation and co-operation rather than conflict. This development has already become visible in the growing number of cross-border mergers and acquisition that would have been unthinkable before. Growth in developing countries like India will be a salient feature as consumption patterns change in these countries and provide impetus for trade. Low manpower costs and the improvement in telecommunication will make feasible the relocation of labour intensive manufacturing and service industries to these countries. These developments will naturally have an impact on the civil aviation sectors. In the following sections we detail the state of the industry. 2.1 Airline operations After a number of bad years, the airline industry around the world has shown signs of recovery. It is estimated that the industry, after the effects of the economic crises, deregulation, inefficient management over the years (especially when government owned) has lost billions of dollars. Airlines like Pan Am which were once synonymous with leadership have gone bankrupt or are under Chapter 11 in the USA. Since 1993, however there has been positive growth in the airline traffic (Figure 1 ICAO). 1994's overall growth was around 5 percent. The growth in traffic and GDP has however not meant that yields increase. Instead, yields have reduced in real terms constantly (Figure 2: Boeing). Intense competitions between airlines have contributed to the yield decline. Yield decline is also due to modern technology in term of speed, fuel efficiency, increased capacity, efficient production, maintenance and longer TB0s. Increase in traffic volume and efficient management have helped many airline operations remain profitable.

Figure 1. Air Traffic growth

The American deregulating experience has been painful and not without controversy. Emerging out of a decade of substantial growth and reducing air fares are operators who may now be able to sustain the intense competition in the industry. The American experience has made the European community take a more cautious route to deregulation in the European skies. In Europe, privatised airlines like British Airways have developed efficient management strategies to become profitable. On the other hand, state owned airlines like Air France and Iberia continue to remain troubled. Internationally, bilateral agreements between countries still continue with negotiations about landing slots being presently carried on by a number of countries with the United States. Airlines without a market share that can ensure good load factors resort to code sharing with other airlines. Air-India presently has such arrangements with other airlines.

Figure 2. Yield Relationship (Boeing Current Market Outlook, 1996) Aircraft leasing has become popular over the years. With some manufactures themselves operating leasing subsidiaries, airlines have the option to lease aircraft from the manufacturers or from the large leasing companies like GECAS or ILFC. It is estimated by ICAO that 62% of all commercial aircraft available for operating leases were owned by just these two companies. Altogether, there are about 40 leasing companies owning 1820 jet aircraft valued at about $36 billion as estimated by ICAO in 1994.

The North American market is presently the largest in the world. The Asian market which is growing rapidly is expected to overtake Europe as the next in the number of aircraft operated and the revenue passenger kilometers (RPKS) generated. China already provides the aircraft manufacturers the biggest single market in this part of the world. With liberalisation and growth, the Indian market could also emerge as the next single important one in ten years. 2.2 Manufacture

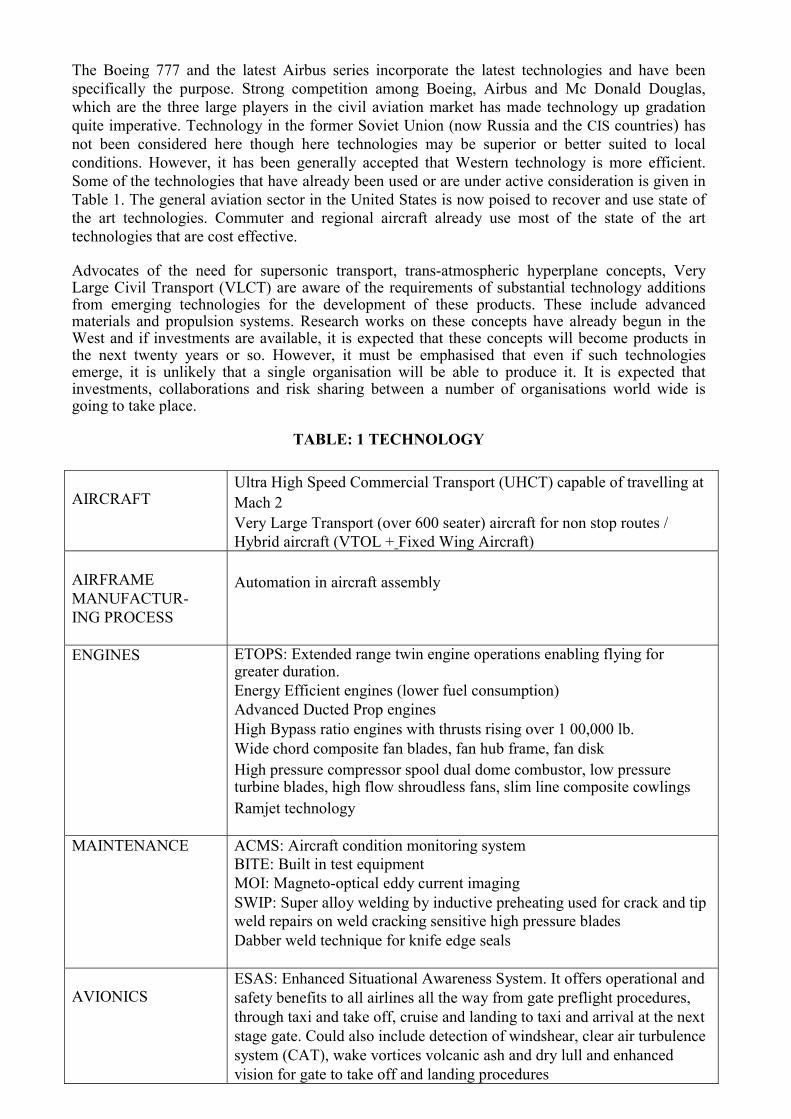

It is expected that the world jet airline fleet will be around 20,000 by 2015. A major share of this fleet will be in North America and Asia. However, manufacture of these aircraft is predominantly by Boeing and Airbus Industries with McDonald Douglas having less than 15% market share. The battle to increase market share by Airbus has ensured the development of new products in the form of the A319, A340 by Airbus and the 777 and 737-800 by Boeing. This situation may not change substantially for a number of years, except if the plan to build a 100 seater by Asian companies in China and South Korea goes ahead. Investment in a very large capacity transport is being seriously considered by Airbus and Boeing, though it is estimated to cost between $ 1 0 – 15 billion. Regional aircraft manufacture is dominated by Europe, except for the Bombardier group in Canada and Embraer in Brazil The European situation is however, undergoing substantial re-organisation with Fokker filling for bankruptcy, and British Aerospace, Aerospatiale (ATR) and Alenia considering joint development, manufacture and marketing. It is now expected that larger organisations with an ability to sustain the huge investments required for the development of new aircraft will emerge out of the restructuring. 2.2.1 Technology Status Typically, technologies for civil aviation has been either 1) developed specifically when found cost effective or when market demand and competitive pressures become evident 2) acquired from programs and aircraft developed for military transport (e.g., Boeing and Douglas military transport program adapted from technology developed for high speed fighter aircraft (e.g., composites and HUDs).

he Boeing 777 and the latest Airbus series incorporate the latest technologies and have been

dvocates of the need for supersonic transport, trans-atmospheric hyperplane concepts, Very

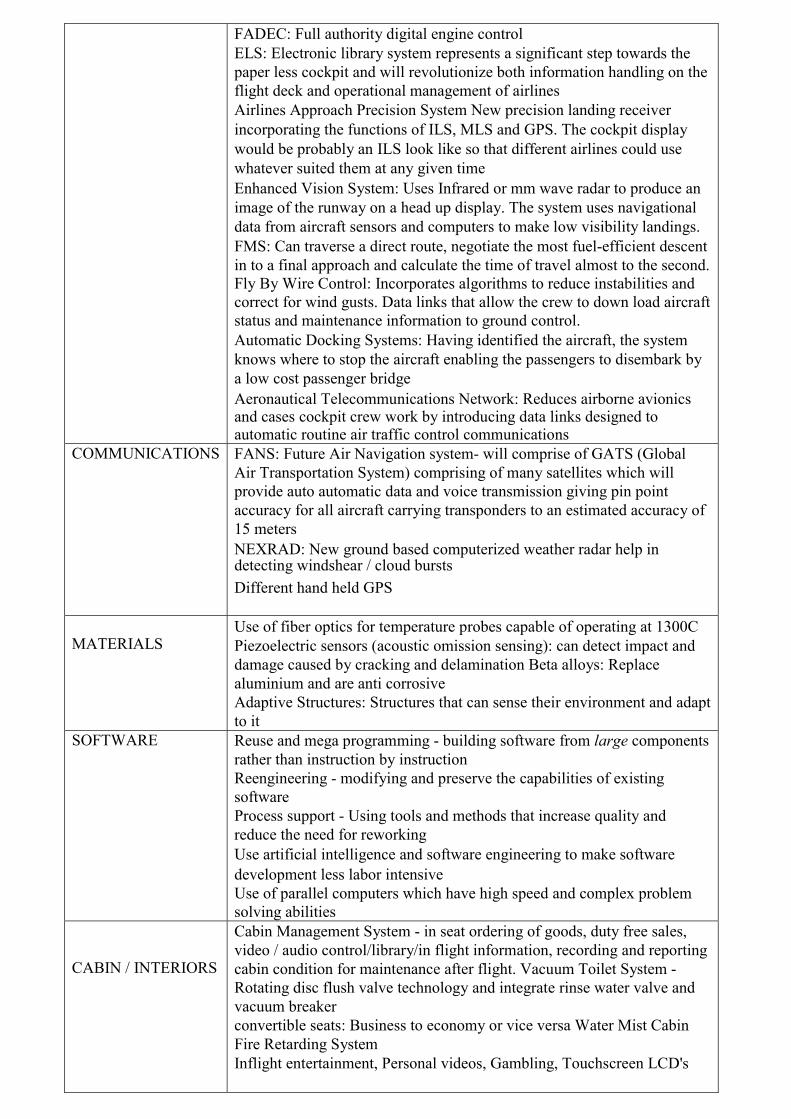

TABLE: 1 TECHNOLOGY

IRCRAFT

Ultra High Speed Commercial Transport (UHCT) capable of travelling at

e Transport (over 600 seater) aircraft for non stop routes /

Tspecifically the purpose. Strong competition among Boeing, Airbus and Mc Donald Douglas, which are the three large players in the civil aviation market has made technology up gradation quite imperative. Technology in the former Soviet Union (now Russia and the CIS countries) has not been considered here though here technologies may be superior or better suited to local conditions. However, it has been generally accepted that Western technology is more efficient. Some of the technologies that have already been used or are under active consideration is given in Table 1. The general aviation sector in the United States is now poised to recover and use state of the art technologies. Commuter and regional aircraft already use most of the state of the art technologies that are cost effective. ALarge Civil Transport (VLCT) are aware of the requirements of substantial technology additions from emerging technologies for the development of these products. These include advanced materials and propulsion systems. Research works on these concepts have already begun in the West and if investments are available, it is expected that these concepts will become products in the next twenty years or so. However, it must be emphasised that even if such technologies emerge, it is unlikely that a single organisation will be able to produce it. It is expected that investments, collaborations and risk sharing between a number of organisations world wide is going to take place.

A

Mach 2 Very LargHybrid aircraft (VTOL + Fixed Wing Aircraft)

IRFRAME

UR- utomation in aircraft assembly A

MANUFACTING PROCESS

A

ENGINES ETOPS: Extended range twin engine operations enabling flying for

ngines (lower fuel consumption)

rusts rising over 1 00,000 lb.

pressure s

greater duration. Energy Efficient eAdvanced Ducted Prop engines High Bypass ratio engines with thWide chord composite fan blades, fan hub frame, fan disk High pressure compressor spool dual dome combustor, low turbine blades, high flow shroudless fans, slim line composite cowlingRamjet technology

MAINTENANCE CMS: Aircraft condition monitoring system

ging ating used for crack and tip

ABITE: Built in test equipment MOI: Magneto-optical eddy current imaSWIP: Super alloy welding by inductive preheweld repairs on weld cracking sensitive high pressure blades Dabber weld technique for knife edge seals

VIONICS

SAS: Enhanced Situational Awareness System. It offers operational and

t A

Esafety benefits to all airlines all the way from gate preflight procedures, through taxi and take off, cruise and landing to taxi and arrival at the nexstage gate. Could also include detection of windshear, clear air turbulence system (CAT), wake vortices volcanic ash and dry lull and enhanced vision for gate to take off and landing procedures

FADEC: Full authority digital engine control ELS: Electronic library system represents a significant step towards the

e

anding receiver y

or mm wave radar to produce an

aft, the system y

tions Network: Reduces airborne avionics

paper less cockpit and will revolutionize both information handling on thflight deck and operational management of airlines Airlines Approach Precision System New precision lincorporating the functions of ILS, MLS and GPS. The cockpit displawould be probably an ILS look like so that different airlines could use whatever suited them at any given time Enhanced Vision System: Uses Infrared image of the runway on a head up display. The system uses navigational data from aircraft sensors and computers to make low visibility landings. FMS: Can traverse a direct route, negotiate the most fuel-efficient descent in to a final approach and calculate the time of travel almost to the second. Fly By Wire Control: Incorporates algorithms to reduce instabilities and correct for wind gusts. Data links that allow the crew to down load aircraftstatus and maintenance information to ground control. Automatic Docking Systems: Having identified the aircrknows where to stop the aircraft enabling the passengers to disembark ba low cost passenger bridge Aeronautical Telecommunicaand cases cockpit crew work by introducing data links designed to automatic routine air traffic control communications

COMMUNICATIONS f GATS (Global

y of

New ground based computerized weather radar help in

FANS: Future Air Navigation system- will comprise oAir Transportation System) comprising of many satellites which will provide auto automatic data and voice transmission giving pin point accuracy for all aircraft carrying transponders to an estimated accurac15 meters NEXRAD: detecting windshear / cloud bursts Different hand held GPS

ATERIALS

se of fiber optics for temperature probes capable of operating at 1300C

can sense their environment and adapt

M

UPiezoelectric sensors (acoustic omission sensing): can detect impact and damage caused by cracking and delamination Beta alloys: Replace aluminium and are anti corrosive Adaptive Structures: Structures thatto it

SOFTWARE and mega programming - building software from large components

the capabilities of existing

pport - Using tools and methods that increase quality and

ftware engineering to make software

ave high speed and complex problem

Reuserather than instruction by instruction Reengineering - modifying and preservesoftware Process sureduce the need for reworking Use artificial intelligence and sodevelopment less labor intensive Use of parallel computers which hsolving abilities

ABIN / INTERIORS

nt System - in seat ordering of goods, duty free sales, g

d

Business to economy or vice versa Water Mist Cabin

ersonal videos, Gambling, Touchscreen LCD's

C

Cabin Managemevideo / audio control/library/in flight information, recording and reportincabin condition for maintenance after flight. Vacuum Toilet System - Rotating disc flush valve technology and integrate rinse water valve anvacuum breaker convertible seats: Fire Retarding System Inflight entertainment, P

ngine manufacture has been limited to a few companies in the West. American manufacturers,

Maintenance facilities have normally been in the form of large self-owned facilities by airlines

s for third party engine overhaul have been established by companies around the world and

.4 Pilot Training

ost developed countries have well established training facilities. These facilities cater for local as

The use of simulators to aid and sometimes replace actual flight training is increasing. Various

2.5 Airports and ATC

estion and air space crowding in many of the countries that are

EGE and Pratt & Whitney, and Rolls Royce in Britain are the primary engine suppliers for civil aircraft. LAE and CFM International both consortiums involving the above engine manufacturers and other smaller companies have developed the V2500 and CFM-56 engines. The primary aim of these consortiums is to share resources, spread risk and consolidate technical and marketing abilities. Russian engine bureaus also have the capability to manufacture engines for civil aircraft, though trials of Western engines on Russian aircraft are presently on, since the Western engines are regarded as more efficient.

until recently. However, there has been a trend to sell these facilities and concentrate on the core activity of running the airline. This has encouraged a number of third party operators to undertake maintenance of the aircraft A number of third party airframe maintenance operators are now established around the world, with certification from local certification agencies and FAA and JAA. It is estimated that a set-up for airframe maintenance and modification for Boeing 737 to Boeing 747 including major modification ~y require over $30 million. Facilitiewould be about $100 million for a four-engine type set-up with thrusts of 100,000 lbs. It appears that a number of such facilities have either been commissioned or are being planned in China to cater to the expansion in air traffic that is expected in South East Asia and China. Both airframe and engine maintenance facilities are labour intensive and it is expected that countries with cheaper man- hour rates will benefit in the longer term. 2 Mwell as overseas students for pilot training and can include training from the ab-initio stage till ATPL. There is a chronic shortage of pilots in the countries that are growing rapidly at present. These include notably China, India and sonic South East Asian countries. To offset these shortages, China for example has considered short-term measures in the form of hiring overseas pilots and sending a large number of students abroad for training. Long term measures include collaborations with reputed airlines, aircraft manufacturers and foreign training academics to cater for the growth.

levels of simulator training exists from full scale flight simulators for particular aircraft to cockpit training devices that are cheap but useful for early training. Most countries are keen to establish these facilities locally. It is expected however, that small countries without the required volume for the establishment of such facilities will continue to use overseas facilities.

There is considerable congpresently undergoing rapid growth. Available airport capacity can limit increases in frequencies. Increases in aircraft movements are already significantly restricted at such airports as London Heathrow, Gatwick, Chicago O'Hare, Tokyo and Hong Kong. It is expected that this growth will lead to creation of more city airports, expansion of the present airports and creation of new airport centres. Environment concerns, especially noise pollution from airports is being resolved through new concepts in airport design, re-engine programs for old aircraft and noise control regulations.

Automation and optimal use of airports and air traffic control is expected to provide some relief

Aircraft manufactures are now seriously considering the development of bigger aircraft, the Very

d

he airport market consists of terminals, runways, ATC equipment, automation and ground

2.6 Management Trends

he nature of the industry has undergone radical change over the past decade. The American de-

Many airlines have settled to running airline operations, and have sold off maintenance operations

Collaborations risk sharing, and the employment of subcontractors (Boeing has over 500 sub-

Internationalisation of development financing, purchase and operation of aircraft has led to global

2.7 Government policies

all the, aircraft manufacturing countries, governments are aware of the strategic nature of their

owned by the Governments themselves.

over the next few years. New concepts and designs in air traffic control principal among them being the use of FANS-Future Air Navigation System and the Global Positioning Systems (GPS) is expected to add to the optimal use of air space.

Large Commercial Transport (VLCT) for use by 2005. It is expected that such aircraft may in fact be required between cities that have particularly crowded airspace. Regional aircraft with seats over 30 are now tending to become popular on feeder-hub routes, where frequencies are curtailedue to congestion. Tsupport equipment. The share of equipment is around 30% of the total airport infrastructure market. The international market for airport infrastructure development is projected to be at $300-350 billion up to the year 2010. Asia-Pacific region is expected to continue having one of the biggest activities in airport construction and modernization projects, accounting for more than 35% of the world total. Recent reports describe a $150 Billion plan by China to modernise existing airports and develop new ones and is regarded as one of the largest investment plans by the industry in many years.

Tregulation process has now stabilised resulting in a number of mega carriers. Managements are continuously focussed on providing the most cost effective operations possible resulting in better value for shareholders. Airlines routinely use code-sharing, share maintenance and training facilities with other airlines and have arrangements with region& and commuter operators for feeding traffic between them.

to third party operators around the world. This trend is expected to continue and a number of such centres are expected to develop in the Asian region. These maintenance operations are certified by overseas agencies and sometimes have been developed as part of offset arrangements.

contractors abroad) in other countries for economic reasons, technology superiority or based on an offset management is now in vogue. Such internationalisation of the industry has also resulted in market penetration in various countries which had protectionist measures. It has now become certain that no single manufacture or even a single country (except probably the United States) will be able to afford the development costs unless they seek partnerships with other countries and be reasonably certain of export markets.

lease/finance corporations dedicated to the aircraft industry". Banks and finance institutions now lend to customers in different countries via syndicates and consortiums to spread risk.

Inaerospace industries. In recent years, developing nations like Brazil, Indonesia and Malaysia have regarded the industry as strategically important. The Malaysian government, for example plans to concentrate on composite technology development. Indonesia is building commuter and regional aircraft for export, Brazil has the Embraer group that has successfully flown a very cost-effective regional jet recently and is serious competition for aircraft made by Western manufacturers. In all these countries, Governments have played active facilitator roles even if the industry was not

w accepted that subsidies, government funds and

tion in management may not be efficient and could lead to macro-economic problems,

ntries, governments play active roles in the marketing of the ountry's aerospace products, invest in aerospace R&D, provide tax shelters for plants in areas

aircraft for airworthiness and air safety issues are generally handled by

Government agencies. There is increasing interest in evolving common regulatory policies to

3 Indian Scenario

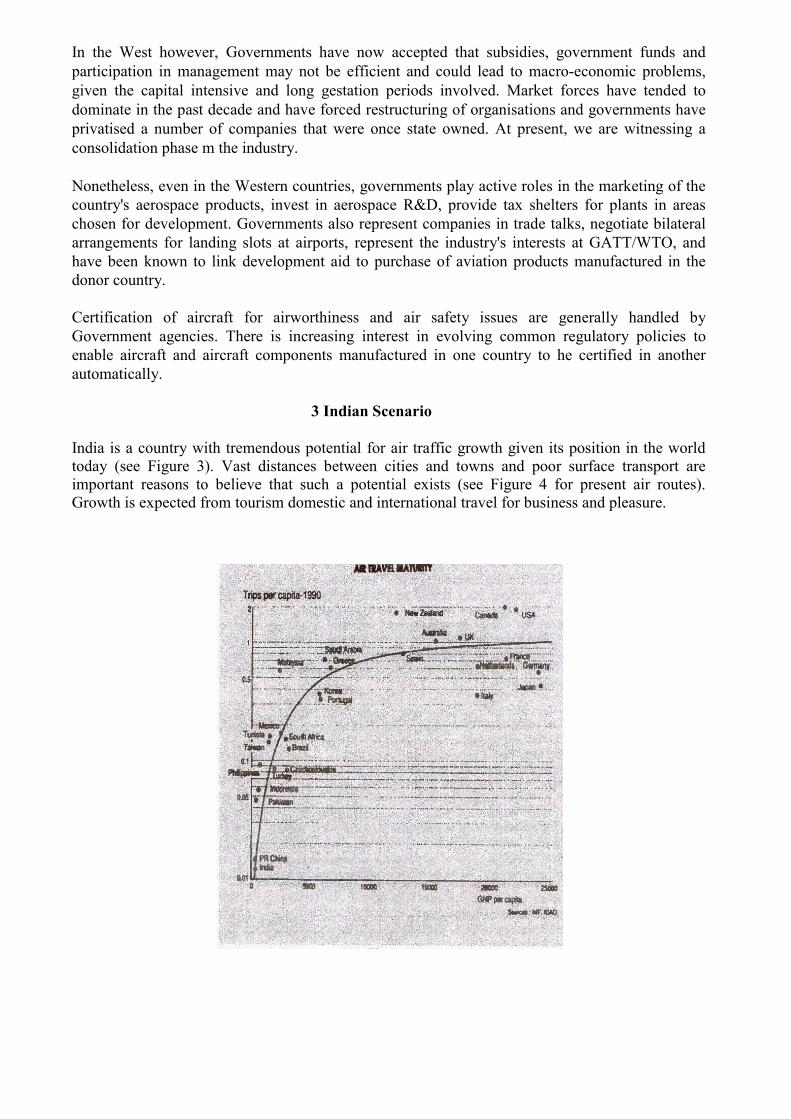

India is a country with tremendous p c growth given its position in the world today (see Figure 3). Vast distances between cities and towns and poor surface transport are

In the West however, Governments have noparticipagiven the capital intensive and long gestation periods involved. Market forces have tended to dominate in the past decade and have forced restructuring of organisations and governments have privatised a number of companies that were once state owned. At present, we are witnessing a consolidation phase m the industry. Nonetheless, even in the Western coucchosen for development. Governments also represent companies in trade talks, negotiate bilateral arrangements for landing slots at airports, represent the industry's interests at GATT/WTO, and have been known to link development aid to purchase of aviation products manufactured in the donor country.

Certification of

enable aircraft and aircraft components manufactured in one country to he certified in another automatically.

otential for air traffi

important reasons to believe that such a potential exists (see Figure 4 for present air routes). Growth is expected from tourism domestic and international travel for business and pleasure.

About 12 million passengers used domestic airlines in 1995 and about 2 million tourists arrived in

e country in the same year. A Ministry of Civil aviation estimate projects about 22 million

Until recently, there was no condition t erator, Indian Airlines. Though, about 40% market share is now held by private airlines, yields have not shown any decline, but have

thdomestic passengers and about 5 million tourists by 2000. In comparison to other countries, this figure is still considerably small. Air traffic growth is closely linked to economic activity. Econometric models developed in the country to predict traffic growth considered economic indicators like GDP, Industrial production (IIP), foreign tourist arrivals (FTA) as main parameters. There is a view that growth may not he sensitive to yields unlike other countries. There are primarily two factors for this view: lack of adequate competition and the nature of the traveller, the majority of whom travel on business.

FIG 4. Air Routes

o the public sector op

risen constantly in rupee terms. Fares have risen about 2.3 times from December 1990. This is due to fuel costs and capital costs in purchase and leasing. This is in sharp contrast to the constant decline in yields around the world allowing vast majority of people to travel and is primarily responsible for the growth in air traffic since 1960. Yet in dollar terms, air travel is cheaper in India. Air travel in India is cheaper than Indonesia or Pakistan and presently works out to be about 9 cents per kilometer against 17 cents in Pakistan. However, when we consider the average Indian’s purchasing power, it is beyond his reach. In a population close to a billion, only 12 million trips were made showing 0.013 trips per capita. It is possible that among the 12 million, a number of persons made more than a single trip. When we compare this to the status of countries which boast of about 0. 1 trips per capita (Figure 3), India will require about 100 million passengers and over 500 aircraft compared to the 70 aircraft operating on trunk routes today. An average growth of about 12% in travel would lead to 100 million passengers only by 201 5. A target of about 1 00 million passengers and about 500 aircraft would lead to a healthy domestic industry.

The trunk routes may only contribute to sedate growth in air traffic as there is congestion already

n these routes and development of new airports and runways is not easy in the metropolitan cities.

replacement market as many aircraft will be over 25 years old by 2010. As the economy grows

ploy skilled labour ranks next only to the automobile industry.

Development of aircraft production facilities, runways and airports present enormous potential

king in the aerospace production league table is 17th and holds about 0. 14% market share. To visualise the sector's development and position by 2020, one should plan

ppropriate technology. India presents the need for the most advanced technology for trunk routes and international travel

oThe real addition will come from feeder routes, feeder to hubs and new city pairs which have potential to provide traffic because of economic activity or tourism. This will require considerable investment in appropriate commuter and regional aircraft and airport infrastructure at district headquarters, tourist spots and locations where industrial activity can be identified. States like Maharashtra, Karnataka Gujarat, UP and have considered investment and incentives for this sector.

NAL's market research shows that there exists demand in the corporate sector from the

further, many new organisations will be interested in acquiring corporate aircraft. It is expected that charter for aircraft of corporate travel will grow considerably. TAAL for example recently announced a scheme to hire its rugged aircraft to corporate travelling into remote parts of the country where aircraft have to use semi-prepared runways. A helicopter charter industry has become evident in recent years

The industry’s potential to em

markets for construction and service industries. It is expected that India will modernise all its airports including the ones that exist in smaller towns and cities. Air cargo for internal transportation of essential and fragile goods and air cargo for export of perishable commodities, expensive and fragile products will continue to increase. This sector also will make a large contribution to the export trade of the country.

3.1 Indian requirements

Recent surveys show ~s ran

strategies for the next 25 years based on what the industry situation is presently. It is expected that India will buy over 50,000 crores of commercial jet aircraft by 2010. Extrapolating rather conservatively India may spend another 15,000 crores for new aircraft. This is assuming that growth will stabilize at around 5% after 2010 after a certain standard of living has been reached as it has happened in the West (see Figure 3). These figures by themselves, even if one does not assume export potential shows the need to pursue the development of local aviation industries before 2020. One can safely assume that the market, industry and the Government are already fully aware of this and expect to minimise the cost of the purchases. Strategies include offset production, collaboration to make components, manufacture of small to medium size aircraft. It is expected that if strategic planning is done, the country would have absorbed the technology completely by 2020, by collaboration and joint ventures. It is expected that the present liberalised regime will remain in place and there will be increasing collaboration between countries and companies. However, since the spin-offs between countries and companies aviation sectors will continue, there may be cases where countries will be reluctant to part with technologies. As, a result, crucial areas in the sector will have to be identified and research and development will need to commence. These may include engines and propulsion systems including advanced technology engines for aerospace planes, smart structures and the use of active control, composite structures, strategic materials, sensors, advanced avionics and flight simulation. Indian requirements for civil aviation can be summarised as follows: arewhich will be cost elective and reliable. However, it will also need technology aircraft and ground infrastructure in many towns and small cities that is rugged, less capital intensive, and requires less maintenance. Choosing this combination will require continuous technology assessment.

Table 2: Aircraft Demand Forecast

AICRAFT TYPE 01-2010

1993-2000 20

NUMBERS Value in lion $

Numbers Value in Million $ Mil

Commercial 400+ 7 12 1560 910 300+ 14 1400 26 2600 250+ 6 420 11 770 200+ 12 470 12 470 150+ 6 180 60 1800

100+(civil) 33 825 32 800 78 4080 153 8000

Re r gional/Feede 40+ 40 360 60 540

B usiness/Commuter 20+ 45 225 45 225 10+ 1 330 66 200 10

195 715 171 965 G l

Aviation/Trainer enera

<10 1 270 165 330 35Helicopters

5+ 10 10 10 10 10+ 5 166.5 30 99.9 030+ 10 90 15 135

70 266.5 55 244.9

As the economy grows further and living stand s improve, advanced technology that is more

use will be "required (e.g.9 pressurized cabins) in certain cases. The ability of the

able to recognise the potential size of the market available to local and

foreign manufacturers. The most obvious point that is raised when shown this data is whether local

w players in product development for the civil aviation sector.

Apart from the National Aerospace Laboratories (NAL's plans to develop a Light Transport

ardcomfortable to industry to change from one type of technology to another or upgrade will be crucial. Table 2 shows the forecast till 2010. This data is based on TIFAC-NAL market research surveys and data collected elsewhere (CII, Boeing, Aeronautical Society of India, Airbus and forecasts by regional aircraft manufacture)

From Table 2, we are

manufacture of all these aircraft is not possible. It has been the experience of most manufacturers that domestic markets tend to be insufficient to make projects viable at present. It has also been noted that all the technologies to make these products are not normally available in a single country. Venture capital is also not easily available unless it can be seen clearly that the project is viable. As a result, the trend is to seek partners, collaborations, risk sharing or co-production and license production arrangements.

The Indian scenario consists of fe

Aircraft (SARAS) and the design and development of two seater trainers: HANSA), HAL's plans to produce a civilian version of the Advanced Light Helicopter (ALH) there is no other active program for the design, development or manufacture of civil aviation aircraft (Figure 5). TAAL, a private sector company has begun producing small aircraft: Viator (six seater) and Observer (eleven seater) in

SARAS A ALH HANS

ollaboration with Partanevia of Italy. Air India and Indian Airlines maintain their aircraft which involves considerable technological capabi AL has begun third party maintenance of

chases. iven the investments required for developing wide-bodied aircraft from scratch, we assume that

include trainer and general aviation aircraft (< 10 seats), commuter and regional aircraft (10-70

sengers are made by just three manufacturers in

the West, GE, P&W and BMW-Rolls Royce. Investment for a research and development facility

the industry and Government can

develop a comphrensive strategy. Airline operations have not been profitable even with increase in

Figure 5 c

lity and Haircraft. HAL has been recognised as a sub-contractor for aircraft components by Boeing, Fokker, Airbus and other agencies and has been manufacturing components for aircraft being made by them. Aircraft purchases made by India has not been tied to any offset arrangement so far. An important opportunity for the industry is getting offset arrangements for aircraft purGIndia will not venture into such a project alone. This implies that India will be involved in large aircraft purchase deals in the next twenty years. From market forecasts, we see that a sum of Rs.40,000 crores - Rs.65,000 crores will be spent by 2020. Even if 20% of this amount (Rs. 8000 crores) can be generated as offsets to Indian companies by 2020, a substantial amount of money can be saved. Getting offset will also be beneficial as Indian companies will get certification by American (FAR) and European (JAR) certification agencies and can attract work from overseas.

In Table 2, we can see that India requires substantial number of various types of aircraft. These

seats) and large passenger aircraft (over 70 seats). These present real opportunities for local manufacture / assembly and offset arrangements.

Jet engines for aircraft carrying more than 100 pas

for a completely new jet engine manufacturing facility is impractical. The cost of development of a new engine for the 777 has been about $4 billion and the three manufacturers are competing ferociously for =ket share and do not expect fair returns in a short time. Engine technology is strategic however, and should be absorbed gradually by the country by encouraging manufacture of components and the use of design facilities in the country.

The demand projected in Table 2 will materialise" only if

yields. The high cost of fuel (ATF) which accounts for close to 40% of the operating costs and the high capital costs of purchasing/leasing aircraft from abroad appears to be responsible. Both these costs are also dependent on the stability of the currency. Any devaluation adversely affects these costs. The Government and the industry need to address these issues in the longer term if air traffic is expected to grow substantially. These include 1) tax incentives for manufacture of smaller aircraft (< 20 seats) than can be operated on the feeder routes 2) reduction in taxes on ATF for feeder routes as that would consequently reduce operating costs and ticket prices 3) Infrastructure finance funds for airport and route development infrastructure.

India will require additional maintenance and training facilities for civil aviation aircraft.

stablishment of additional airframe maintenance and engine overhaul facilities have already been

ilots. A number of private airlines have sent

pilots abroad for training Additional simulator facilities are also required in the country. It is

00 for airport

infrastructure. A new airport proposed in Mumbai is expected to cost over $2.8 Billion. Private

trategic Planning

The purpose of strategic planning

Eidentified as a priority by TIFAC-NAL market surveys. Most private airlines are sending their aircraft abroad for maintenance. It is expected that a few facilities for air frame maintenance and engine overhaul will come up before 2010. Export markets that have been identified in the TIFAC- NAL market surveys can also be tapped if these facilities acquire a good reputation. Recent reports indicate that Indian Airlines plans to convert its advanced engine maintenance center to a third party set up in collaboration with a foreign partner.

Currently there exists a serious shortfall of trained p

expected that if pilot training schools are set up in the country before 2000, and develop a reputation for quality, they will be able to attract overseas students for training here.

Based on TIFAC-NAL market research, India will require over $1 Billion by 20

sector participation is expected for the Bangalore International Airport, Kochi and other airports. A number of airports will become international airports before 2020, and smaller towns and cities will upgrade before 2020. As a result, opportunities for equipment and infrastructure facilities required for airports will become available.

4 S

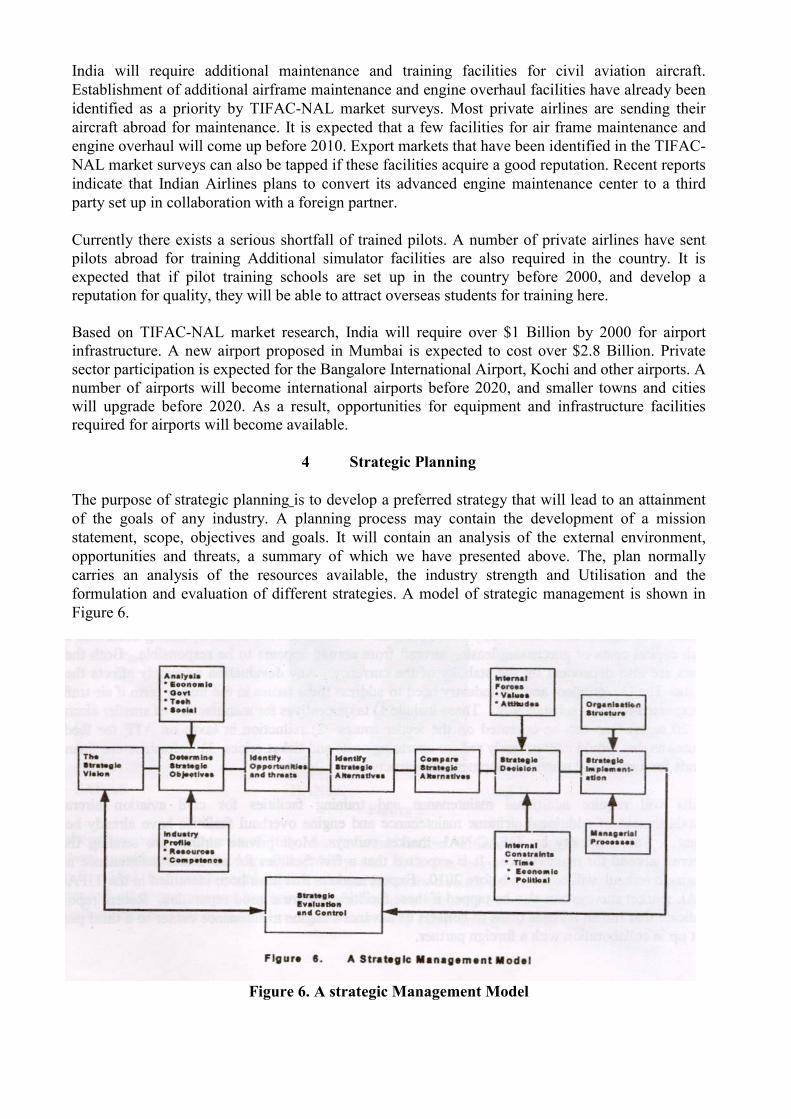

is to dev egy that will lead to an attainment of the goals of any industry. A planning proc y contain the development of a mission

elop a preferred stratess ma

statement, scope, objectives and goals. It will contain an analysis of the external environment, opportunities and threats, a summary of which we have presented above. The, plan normally carries an analysis of the resources available, the industry strength and Utilisation and the formulation and evaluation of different strategies. A model of strategic management is shown in Figure 6.

Figure 6. A strategic Management Model

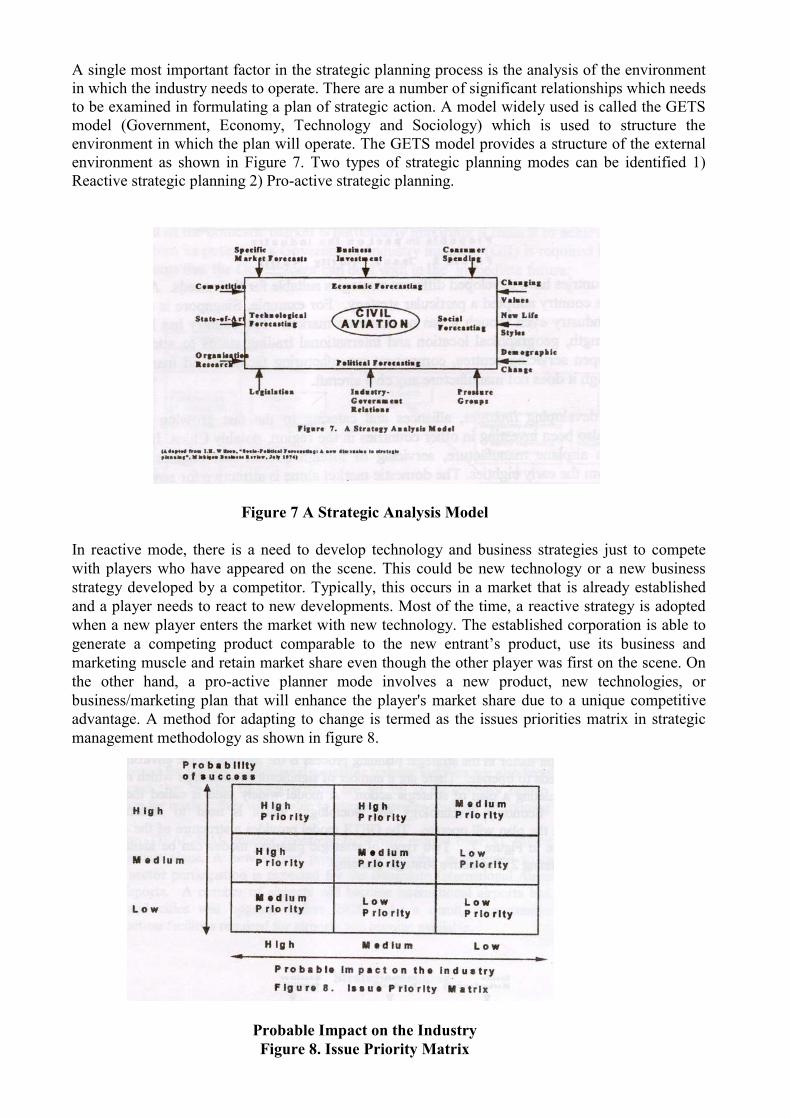

A single most important factor in the strategic planning process is the analysis of the environment

which the industry needs to operate. There are a number of significant relationships which needs be examined in formulating a plan of strategic action. A model widely used is called the GETS

In reactive mode, there is a need to develop technology and business strategies just to compete with players who have appeared on the scene. This could be new technology or a new business strategy developed by a c arket that is already established and a player needs to react to new developments. Most of the time, a reactive strategy is adopted

intomodel (Government, Economy, Technology and Sociology) which is used to structure the environment in which the plan will operate. The GETS model provides a structure of the external environment as shown in Figure 7. Two types of strategic planning modes can be identified 1) Reactive strategic planning 2) Pro-active strategic planning.

Figure 7 A Strategic Analysis Model

ompetitor. Typically, this occurs in a m

when a new player enters the market with new technology. The established corporation is able to generate a competing product comparable to the new entrant’s product, use its business and marketing muscle and retain market share even though the other player was first on the scene. On the other hand, a pro-active planner mode involves a new product, new technologies, or business/marketing plan that will enhance the player's market share due to a unique competitive advantage. A method for adapting to change is termed as the issues priorities matrix in strategic management methodology as shown in figure 8.

Probable Impact on the Industry Figure 8. Issue Priority Matrix

A number of countries hav uitable for their needs. A SWOT nalysis can show why a country adopted a particular strategy. For example, Singapore is a major layer in the aerospace industry even though it has no domestic market. The country has however sed its technology strength, geographical location and international trading status to attract a

d engines and component manufacture from the early eighties. The domestic market alone is attractive for any manufacturer

ion with CASA of Spain and more recently has developed a 50-seater aircraft called N-250. Brazil has also a big

erospace Companies (SBAC) to focus on the development of aerospace activities in the country. All the major manufacturers and suppliers to the industry are actively

.1 Domestic market development

is to achieve the status of

a global player. Given its potential a Government-Industry initiative (GII) is required here. There ent can deal with in the immediate future:

e developed different strategies sapunumber of companies to open servicing centres, component manufacturing facilities and marketing offices in Singapore, though it does not manufacture any civil aircraft.

Its strategy is developing linkages, alliances and catering to the fast growing ASEAN region. Singapore has also been investing in other countries in the region, notably China. In contrast, embarked upon airplane manufacture, servicing of foreign aircraft an

to look at China seriously. The Government is a major player in market development, negotiations for foreign investment and has been successful in employing political strategies in extracting offsets and lower prices from foreign manufacturers. Investment in China has been driven always by the expected future volumes. Thus, the domestic market potential of China, its low cost manpower and a Government committed to the development of civil aviation in the country for technology and economic purposes are the reasons for the spectacular growth.

Indonesia and Brazil also present interesting case studies. A domestic market is available in Indonesia as it is a country composed of a number of islands. Government initiatives have resulted in the establishment of IPTN which manufactures the CN-235 in collaborat

domestic market and its airplane manufacture; Embraer has developed a commuter and regional aircraft, notably Banderainte and the new EMB-145. The Banderainte has been exported to a number of countries and the EMB-145 is expected to capture a substantial market share among aircraft of its class.

Japan and Korea have in contrast concentrated on third party supply of components to a variety of manufacturers in the West. In UK, the Department of Trade and Industry (DTI) has established Society of British A

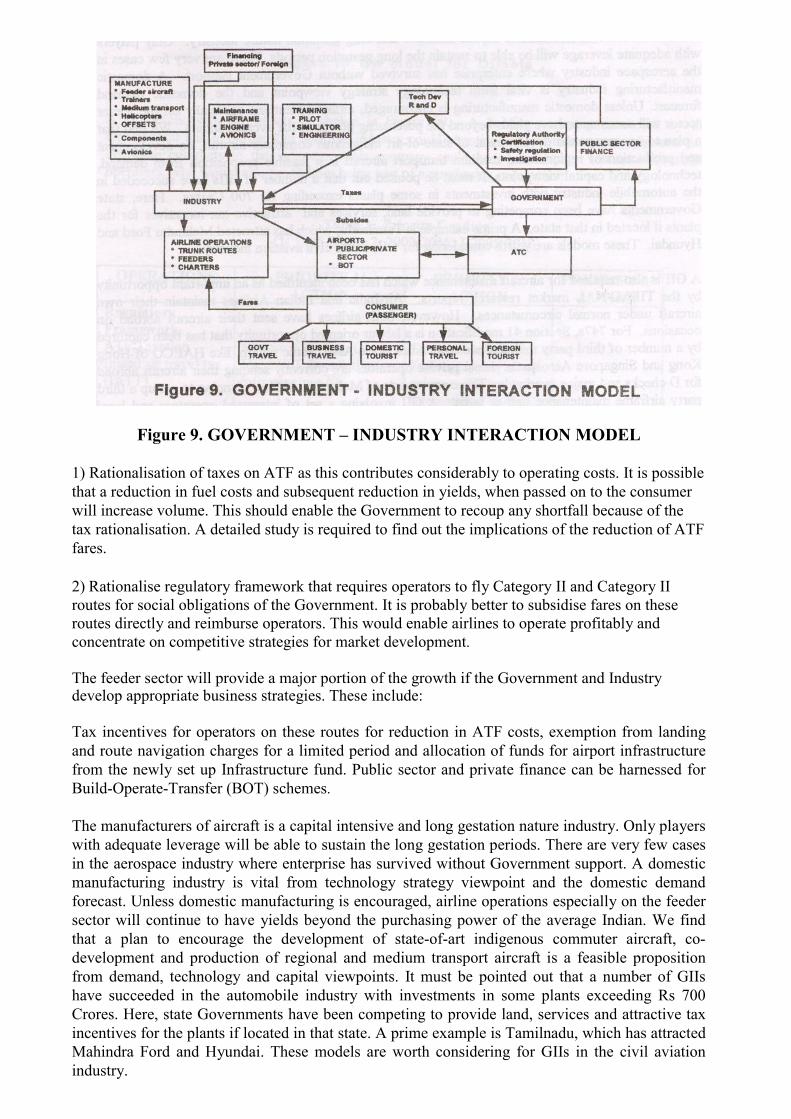

involved in SBAC. In all these cases, there is strong evidence of support and strategic planning by both Government and industry. A strategic plan for civil aviation in India can be formulated based on three important components using a Government-Industry interaction structure as shown in Figure 9.

4

The development of the domestic market is particularly important if India

are two major problems that the Governm

at a reduction in fuel costs and subsequent reduction in yields, when passed on to the consumer will incre of the

x rationalisation. A detailed study is required to find out the implications of the reduction of ATF

irectly and reimburse operators. This would enable airlines to operate profitably and concentrate on competitive strategies for market development.

Tax incentives for operators on these routes for reduction in ATF costs, exemption from landing

cture and private finance can be harnessed for

Build-Operate-Transfer (BOT) schemes.

has survived without Government support. A domestic manufacturing industry is vital from technology strategy viewpoint and the domestic demand

Figure 9. GOVERNMENT – INDUSTRY INTERACTION MODEL

1) Rationalisation of taxes on ATF as this contributes considerably to operating costs. It is possible th

ase volume. This should enable the Government to recoup any shortfall because tafares.

2) Rationalise regulatory framework that requires operators to fly Category II and Category II routes for social obligations of the Government. It is probably better to subsidise fares on these routes d

The feeder sector will provide a major portion of the growth if the Government and Industry develop appropriate business strategies. These include:

and route navigation charges for a limited period and allocation of funds for airport infrastrufrom the newly set up Infrastructure fund. Public sector

The manufacturers of aircraft is a capital intensive and long gestation nature industry. Only players with adequate leverage will be able to sustain the long gestation periods. There are very few cases in the aerospace industry where enterprise

forecast. Unless domestic manufacturing is encouraged, airline operations especially on the feeder sector will continue to have yields beyond the purchasing power of the average Indian. We find that a plan to encourage the development of state-of-art indigenous commuter aircraft, co-development and production of regional and medium transport aircraft is a feasible proposition from demand, technology and capital viewpoints. It must be pointed out that a number of GIIs have succeeded in the automobile industry with investments in some plants exceeding Rs 700 Crores. Here, state Governments have been competing to provide land, services and attractive tax incentives for the plants if located in that state. A prime example is Tamilnadu, which has attracted Mahindra Ford and Hyundai. These models are worth considering for GIIs in the civil aviation industry.

A GII is also required for aircraft maintenance which has been identified as an important opportunity by the TIFAC-NAL market research reports. Air-India and Indian Airlines maintain

eir own aircraft under normal circumstances. However, both airlines have sent their aircraft broad on occasions. For 747s, Section 41 modifications is a labour oriented opportunity that has

A GII e

d

operators, who would also profit from being part of a purchasing consortium.

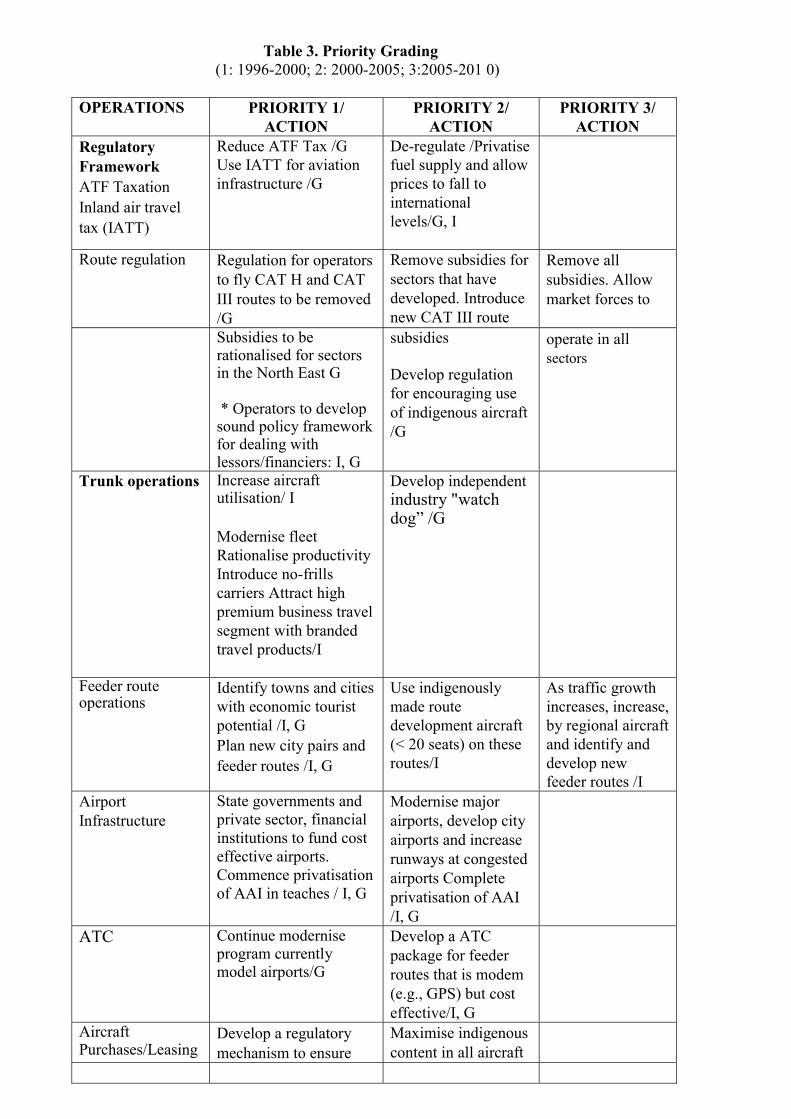

thabeen captured by a number of third party maintenance companies in the Asia-Pacific region, like HAECO of Hong Kong and Singapore Aerospace. Most private operators are currently sending their aircraft abroad for checks and major overhauls. There are reports of Malaysian Airlines planning to set up a third party airframe maintenance unit in India. A GII involving a set of interested operators and local financial institutions could be considered with a foreign partner. This linkage may enable export prospects. A set of GII’s is shown in Table 3.

exclusively for offsets is shown in Figure 10. A holding company promoted by thGovernment and in partnership with the industry could negotiate offsets from a manufacturer andistribute contracts to the industry. This company could be a joint-equity venture with airline

Table 3. Priority Grading

(1: 1996-2000; 2: 2000-2005; 3:2005-201 0)

OPERATIONS PRIORITY 1/ ACTION

PRIORITY 2/ ACT

PRIORITY 3/ ACTION ION

Regulatory Framework ATF Taxation Inland air travel tax (IATT)

Reduce ATF Tax /G Use IATT for aviation infrastructure /G

De-regulat /Privatise fuel supply and allow prices to fall to international levels/G, I

e

Route regulation to fly CAT H and CAT

III ro ed /G

for sectors that have dev e new C e

Remove all subsidies. Allow m

Regulation for operators Remove subsidies

utes to be remov eloped. IntroducAT III rout

arket forces to

Subsidies to be rationalised for sectors in the North East G * Operators to develop sound policy framework

g use us aircraft

perate in all sectors

for dealing with lessors/financiers: I, G

subsidies

Develop regulation for encouraginof indigeno/G

o

Trunk operations sation/ I

ity troduce no-frills

nded

Increase aircraft utili

Modernise fleet Rationalise productivIncarriers Attract high premium business travel segment with bratravel products/I

Develop independent industry "watch dog” /G

Feeder route operations

and cities with economic tourist e

development aircraft (< 20 seats) on these routes/I

As traffic growth increases, increase, by regional aircraft and identify and develop new feeder routes /I

Identify towns

potential /I, G Plan new city pairs and feeder routes /I, G

Use indigenously made rout

Airport Infrastructure

d cost ffective airports.

Modernise major airports, develop city airports and increase runways at congested

of AAI

State governments and private sector, financialinstitutions to funeCommence privatisation of AAI in teaches / I, G

airports Complete privatisation/I, G

ATC

model airports/G for feeder

routes that is modem

Continue modernise program currently

Develop a ATC package

(e.g., GPS) but cost effective/I, G

Aircraft Purchases/Leasing

ry Develop a regulatomechanism to ensure

Maximise indigenous content in all aircraft

offsets purchase aircraft s.

e y Air-

India can generate offsets /I, G

ontent in all aircraft

from foreign countrieFor example, ensurMCLR purchase b

Ensure indigenous cpurchases. Ensure that there is no dumping of old aircraft in the country

purchases /G

MANUFACTURE Trainers locally

developed trainer Market aircraft widely in the country. Upgrade technology with flying clubs. Government can consider soft loans for purchase of locally built trainers I/G

Set up marketing network in other countries and export aircraft /I

Manufacture

aircraft. /I, G

10-20 Seaters trate r

orator for manufacturing the aircraft /I, G

ide

s /I

eveloped countries /I

Develop and demonsa modem commuteaircraft. Identify anindustry collab

Build aircraft. Introduce the aircraft as ideal for route development. Provincentives for operators to buy theaircraft for feeder operation

Explore marketing of aircraft abroad in emerging markets and in the replacements market in d

ft

Ensure offset for Explore if a ircraft

.

rcraft India.

/I

Regional aircra

purchase of short haul aircraft 11

Become a major component manufacture for regional aircraft produced by companies abroad 11

regional acan be produced based on the commuter aircraftIntroduce a family concept of aiproduced in

Medium transport tudies Conduct detailed s Use component for the development of

the medium transport aircraft. Identify collaborators and undertake design and development /I

ng base sub-

lop an

manufacturing base that can be sourced by foreign

, G

manufacturito develop major assemblies for theaircraft. Deveengine components

manufacturers. /I

MAINTENANCE

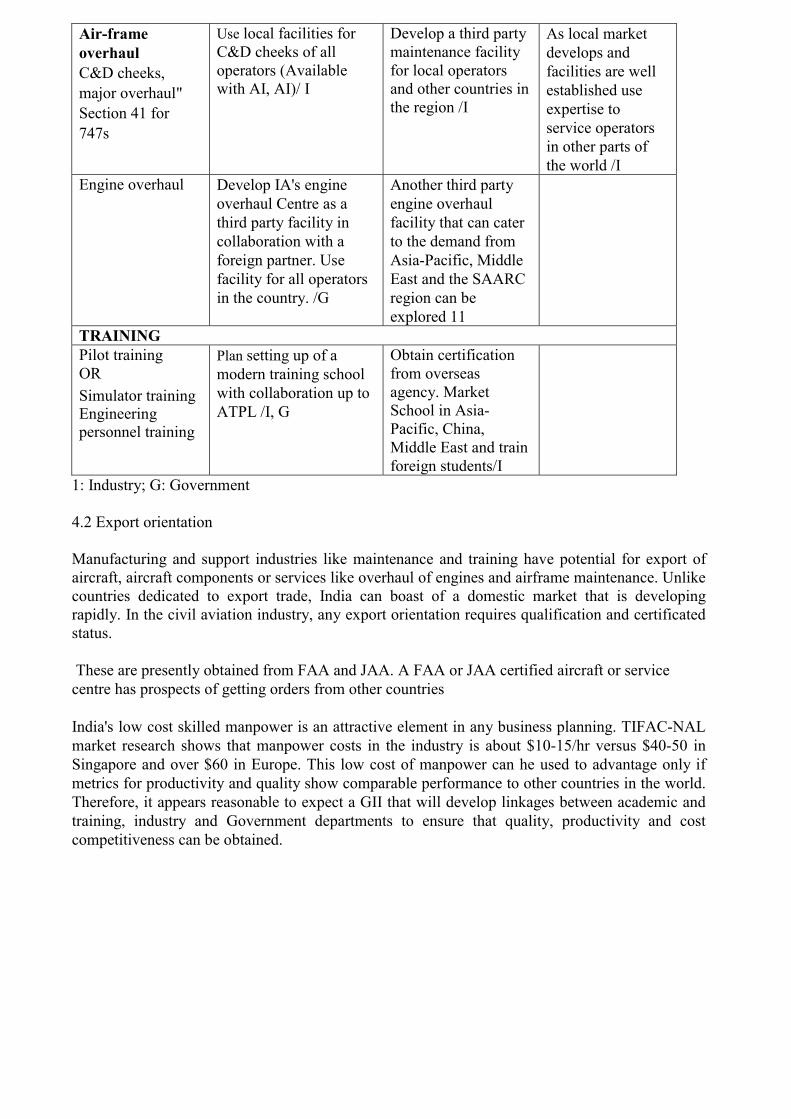

Air-frame overhaul C&D cheeks,

ection 41 for 47s

Use local facilities for C&D cheeks of all operators (Available with AI, AI)/ I

facility

and other countries in e region /I

As local market develops and facilities are well established use xpertise to ervice operators other parts of e world /I

major overhaul" S7

Develop a third partymaintenancefor local operators

th esinth

Engine overhaul evelop IA's engine

Use cility for all operators

in the country. /G

nother third party

AARC region can be explored 11

Doverhaul Centre as a third party facility incollaboration with a foreign partner. fa

Aengine overhaul facility that can cater to the demand fromAsia-Pacific, Middle East and the S

TRAINING Pilot training OR Simulator training Engineering personnel training

l to

ts/I

Plan setting up of a modern training schoowith collaboration up ATPL /I, G

Obtain certification from overseas agency. Market School in Asia-Pacific, China, Middle East and train foreign studen

1: Industry; G: Government 4 tation M u nt ing have potential for export of a ft comp ices like over rame maintenance. Unlike countries dedicated to export trade, India can estic market that is developing rapidly. In the civil aviation industry, any export alification and certificated status.

e presently obtained from FAA and JAA. A FAA or JAA certified aircraft or service

orders from other countries

e, it appears reasonable to expect a GII that will develop linkages between academic and y and Government departments to ensure that quality, productivity and cost

c

.2 Export orien

pport industries like maionents or serv

anufacturing and sircraft, aircra

enance and trainhaul of engines and airfboast of a dom orientation requires qu

These arcentre has prospects of getting India's low cost skilled manpower is an attractive element in any business planning. TIFAC-NAL market research shows that manpower costs in the industry is about $10-15/hr versus $40-50 in Singapore and over $60 in Europe. This low cost of manpower can he used to advantage only if metrics for productivity and quality show comparable performance to other countries in the world. Therefortraining, industrompetitiveness can be obtained.

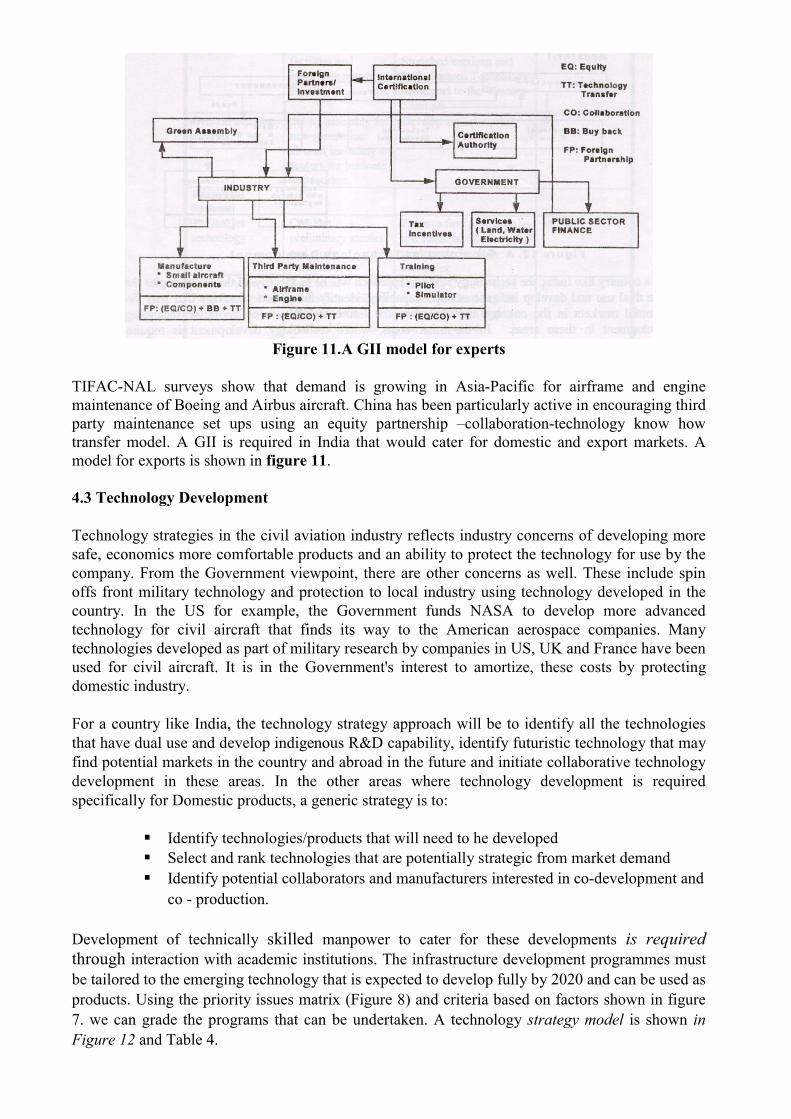

Figure 11.A GII model for experts

NAL surveys show that demand is growing in Asia-Pacific for airframe and enance of Boeing and Airbus aircraft. China has been particularly active in encourag

aintenance set ups using an equity partnership –collaboration-technology kno model. A GII is required in India that would cater for domestic and export markets. A

ports is shown in figure 11.

4.3 Technology Development

TIFAC- ngine mainte ing third party m w how transfer model for ex

Technology strategies in the civil aviation indust reflects industry concerns of developing more

ts way to the American aerospace companies. Many gies developed as part of military research by companies in US, UK and France have been

Government's interest to amortize, these costs by protecting omestic industry.

t and rank technologies that are potentially strategic from market demand � Identify potential collaborators and manufacturers interested in co-development and

elop fully by 2020 and can be used as . U n tors shown in figure

7. we can g d in Figure 12 an

rysafe, economics more comfortable products and an ability to protect the technology for use by the company. From the Government viewpoint, there are other concerns as well. These include spin offs front military technology and protection to local industry using technology developed in the country. In the US for example, the Government funds NASA to develop more advanced technology for civil aircraft that finds itechnoloused for civil aircraft. It is in thed For a country like India, the technology strategy approach will be to identify all the technologies that have dual use and develop indigenous R&D capability, identify futuristic technology that may find potential markets in the country and abroad in the future and initiate collaborative technology development in these areas. In the other areas where technology development is required specifically for Domestic products, a generic strategy is to:

� Identify technologies/products that will need to he developed � Selec

co - production. Development of technically skilled manpower to cater for these developments is required through interaction with academic institutions. The infrastructure development programmes must

ed to the emerging technology that is expected to devbe tailorproducts si g the priority issues matrix (Figure 8) and criteria based on fac

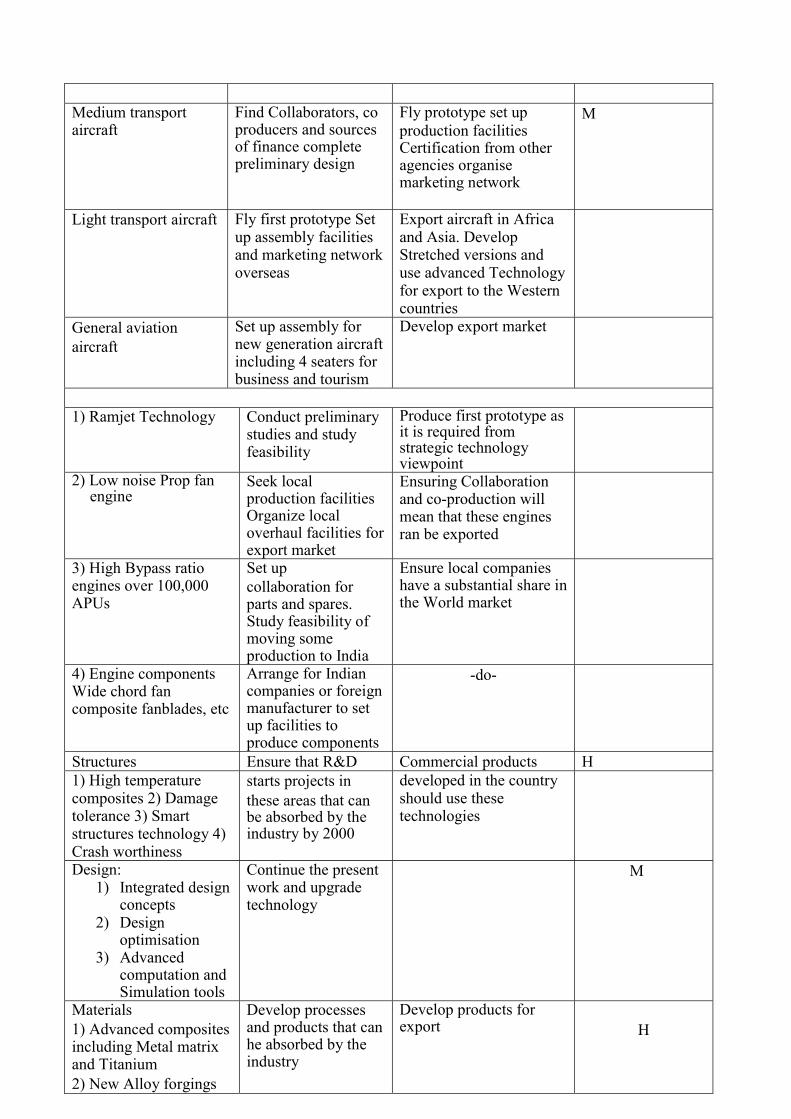

ra e the programs that can be undertaken. A technology strategy model is shownd Table 4.

Medium transport aircraft

Find Collaborators, co producers and sources

Fly prototype set up production facilities

M

of finance complete preliminary design

Certification from other agencies organise marketing network

Light transport aircraft Fly first prototype Set up assembly facilities and marketing network verseas

Export aircraft in Africa and Asia. Develop Stretched versions and se advanced Technology

ern

o ufor export to the Westcountries

General aviation aircraft raft

cluding 4 seaters for business and tourism

Set up assembly for new generation aircin

Develop export market

1) Ramjet Technology

y

pe as Conduct preliminary studies and study feasibilit

Produce first prototyit is required from strategic technology viewpoint

2) Low noise Prop fan engine

Seek local s

n be exported

production facilitieOrganize local overhaul facilities for export market

Ensuring Collaboration and co-production will

ean that these engines mra

3e) High Bypass ratio ngines over 100,000

f e

to India

Ensure local companies

APUs

Set up collaboration for parts and spares. Study feasibility omoving somproduction

have a substantial share in the World market

4) omponents Wide chord fan composite fanblades, etc

reign

components

Engine c Arrange for Indian companies or fomanufacturer to set up facilities to produce

-do-

Structures Ensure that R&D Commercial products H 1) High temperature composites 2) Damage tolerance 3) Smart structures technology 4)

the

untry hould use these

technologies

Crash worthiness

starts projects in these areas that can be absorbed byindustry by 2000

developed in the cos

Design: 1) Integrated design

concepts 2) Design

misation

ools

M

opti3) Advanced

computation andSimulation t

Continue the present work and upgrade technology

Materials 1) Advanced composites

Metal matrix and2) New ings

and products that can

evelop products for export

H

including Titanium

Alloy forg

Develop processes

he absorbed by the industry

D

3) A ramics 4) Fibreprobes above 1300C 5) Adapsmart st

dvanced Ce optics for

tive structures ructures material

AVIONICS. . FADEC ELS Approach Precision Systems FMS GPS and DGPS FLW control

evelop processes and products that can he absorbed by the industry

Develop products for export

High order faulttolerance

D H

Communication FANS ETIPS

Differential GPS

ents cts for export

nd local use

Upgrade technology for domestic use and export

H NEXRAD OPS and

Produce componand produa

SOFTWARE Reuse and ogramming Use of

ed software el

ftware

Use the software strengths of the country to develop market share in these areas

Continue, upgradation of technology and develop products for export

M mega prAI and advancengineering parallcomputing so

5 Conclusions

This article has dealt with a number of aspects of the industry to develop a broad idea of the

uire dust tant yer in the next y

ec resou etition and their interactions he large ents and the export opportunities, there is a need for

mphrensive planning process.

Narasimha, R., A Civil Aviation indus ikram Sarabhai Lecture, 1991 (Also NAL TM DU 9101).

n, Vol I, II,III,1994

advantage, Pitman, 1989.

different strategies reqtwenty years. The task ofconsidering the market, tis complex. Given tdeveloping such a co

d to enable the in ry to become an imporlans for the various components of the industrrces required, comp

pladeveloping individual phnology, financial domestic requirem

6 References

Allo, R.J. The Practical Strategist, Cambridge, Ballinger, 1988. C handrashekar S, Technology Priorities for India's development: Need for restructuring, EPW, Oct 8,1995. Harvey, D.F., Strategic Management and Business Policy, Merill 1988 Miller, D., Configuration of strategy and structure: Towards a synthesis, Strategic Management Journal, 9, 55-76, 1987.

try" for India, V

TIFAC, TIFAC-NAL Market -Research Reports on Civil Aviatio TIFAC, Civil Aviation: Technology Vision: 2020, V:04:ES, 1996. TIFAC, Strategic industries: Technology Vision: 2020, V:08, VH: ESDR, 1996 Twiss, B.C, and Goodridge, M.C., Managing technology for competitiveWilliams, I.H., Socio Political Forecasting: A new dimension in strategic planning, Michigan Business Review, July 1974