STRATEGIC MANAGEMENT - ZARA

24

Olympe LEU Ombeline MANCEAU Leila BENNOUNA Romy GAESSLER Biqi HU Sandra KAMSU STRATEGIC MANAGEMENT BBA

-

Upload

parisbusinesscollege -

Category

Documents

-

view

3 -

download

0

Transcript of STRATEGIC MANAGEMENT - ZARA

Olympe LEU Ombeline MANCEAU

Leila BENNOUNA Romy GAESSLER

Biqi HU Sandra KAMSU

STRATEGIC MANAGEMENT -‐ BBA

Executive Summary I/ Introduction ........................................................................................... 3 II/ Situation Assessment: .......................................................................... 4 III/ Market Size of ZARA and Competition ............................................. 6 IV/ China, an opportunity : Overview of the fast fashion market and its consumers. .............................................................................................. 10

1) The opportunity. .............................................................................. 11 2) Three alternatives for the establishment of Zara stores ................... 12

a- Department Stores ........................................................................ 12 b- Shopping Mall .............................................................................. 13 c- Business Street .............................................................................. 13

3) The importance of e-commerce and social medias. ........................ 15 a- ‘e-commerce’ and its two chinese dominante platforms. ............. 15 b- Media platforms and ‘m-commerce’. ........................................... 16

4) The chinese consumers. ................................................................... 17 a- The different groups. .................................................................... 17 b- Factors of success. ........................................................................ 19 c- The styling. ................................................................................... 19

V/ Strategy for doubling nb of stores + increasing sales ........................ 21 1) Distribution ...................................................................................... 21 2) Strategy ............................................................................................ 21

VI/ Value of chain .................................................................................. 23 VII/ Conclusion ...................................................................................... 24

Ombeline MANCEAU

I/ Introduction Today, Zara is a brand which is present all over the world. But it is more present in Europe,

because it is a Spanish brand.

We have been interested by the Zara case, and we have noted that the brand was not really

present in China. China is very different than other countries in Europe. In fact, the Fashion is

absolutely not the same in China than in France.

We would like Zara brand more known by Chinese people.

So what is the strategy to adopt to double number of stores and increasing our

sales in China?

Leila BENNOUNA

II/ Situation Assessment:

Zara is a Spanish clothing and accessories retailer. Zara was founded in 1975 by Armencio

Ortega Agona and his wife, in La Corogne in Spain. In 1985, a holding company named, Inditex

was formed over Zara.

Inditex is a Spanish multinational clothing company, it is the biggest fashion group in the world

and operates over 6,200 stores worldwide and owns brands like Zara, Massimo Dutti, Bershka,

Oysho, Pull and Bear, Stradivarius and Uterqüe.

Since 2011, the Chairman and CEO of the Inditex group is Mr Pablo Isla Alvarez, he has been

working for the Inditex group since 2005 as the Deputy Chairman and CEO and is the one in

charge of all of the important decisions with Mr Armencio Ortega Agona who is the founder and

member of the board.

Zara exists in 87 countries and has 1991 stores around the world with 450 in Asia including 121

in China. Zara has 22 online stores in the world including China. Zara’s net sales is 10 804

millions of euros in 2013.

Zara practices fast fashion, with values that are to provide fast, affordable and fashionable items,

Zara holds 6 days worth of inventory, comparing to other competitors that holds 52 days

minimum.

Inside Inditex Group, Zara is the brand that produces the greatest benefits of all and

possesses something, which attracts attention: the complete absence of advertising. In

comparison with other clothing retailers, who spent 3 to 4% of sales on advertising, Zara spent

just 0.3%. The little they spend goes to reinforce its identity as a clothing retailer; low-cost but

high fashion.

Failure rates of Zara's new products were reported have been said to be just 1%, considerably

lower than the industry average of 10%.

Organizitional Chart :

Mr. Pablo Isla Álvarez de Tejera

PRESIDENT/CEO

Mr. Amancio Ortega Gaona

DIRECTOR

Gartler S.L

COMPANY SECRETARY

Mr. José Arnau Sierra

GENERAL MANAGER

Mrs. Irene R. Miller

ACCOUNTS, FINANCE & HR EXECUTIVE

Mr. Nils S. Andersen

MARKETING EXECUTIVE

Mr. Emilio Saracho

OPERATIONEL EXECUTIVE

Sandra KAMSU

III/ Market Size of ZARA and Competition At least half of Zara’s companies’ factories are in Europe There are over 6500 Zara stores located across 88 countries. There are exactly 2041 Zara stores in the word 1324 Stores in Europe representing half of their total stores. And 152 in China which has the largest number of stores in Asia since Asia has 460 stores therefore China alone represents approximately 33%

• We have identified three brands standing out from the retail clothing industry: in addition to Zara, Gap and H&M embody the most serious competitors. But we will focus on H&M

• Zara walks at the pace of society dressing ideas, trends and tastes that society has matured. Latest fashion

• H&M offers fashion and quality at a low price. Fashion and quality at best price while Zara benefits from a very strong style identity strengthen by one of its main touch points, its stores, so that it easily gathers a community on an emotional level.

• Customer’s relation with H&M is much more functional, since it is known that, for quite a good price, it is almost sure to find something appealing, given the wide offer provided by the brand, in terms of length and depth of the collection.

• According to Tiplady (2006), Zara reported a 21% sales growth of $8.15 billion in 2005, which put it just ahead of H&M who reported $7.87 billion in sales in 2005.

• Zara’s parent company, Inditex, opened 448 new stores in 2005; while H&M only opened 190 new stores. Their expansion plans included adding as many as 490 stores in 2006. By 2010, their global total was expected to be almost 5,000 stores. So far in 2006, Zara has expanded cautiously in the United States, with only 19 stores. Meanwhile, their biggest competitor, H&M, has 91 stores in the US, which is still cautious.

• With a brand value of 13 billion euros, H&M is currently the highest valued fashion brand in Europe. Close on its heels is the equally ambitious Zara, valued at 7.8 billion euros

• H&M and Zara have very different strategies when it comes to the weighting their offer. The bulk of H&M’s offering is women’s wear and this focus is communicated in their advertising. Menswear at H&M takes a backseat. Zara’s apparel split is much more even – considering the retailer gets so much coverage for its women’s wear offering, the breakdown is in fact very balanced.

• These weightings suggest that Zara and H&M are competing for and pitching at different consumer types. The Zara customer could be more mature, and shop across the breadth of the retailer’s offering for his or her partner and children, while the predominant H&M consumer is shopping for women’s wear. Strategically, Zara are splitting their focus across all three channels – a sign of confidence and clarity or perhaps too broad a vision?

• H&M have the larger online offering, with currently just under two thousand more options than Zara. The pricing strategy at the two retailers varies dramatically, despite having similar entry and exit points.

• H&M’s apparel pricing spans $1-$291 and Zara’s is $5-$322, however average price point at H&M is $21.40 and at Zara is $48. Even more telling is the price point which each invests in most heavily.

• H&M’s most optioned price bracket in tops is $20-$30, whereas Zara’s is $40-50. • If we catch a glance further on the retail clothing market, these brands are facing

difficulties on their home market: Sweden (H&M), Spain (Zara). Each of them, from the base that the expansion is never over, sets out to conquest promising developing countries. China, in this framework, looks like the new Eldorado, but other areas, like South America, South Africa, south East Asia or Australia are equally at stake. The main dilemma for the brands is therefore to keep spreading worldwide without ignoring their home market, at the risk of seeing their competitors step into the breach

http://www.businessweek.com/stories/2006-04-04/zara-taking-the-lead-in-fast-fashionbusinessweek-business-news-stock-market-and-financial-advice http://en.wikipedia.org/wiki/Zara_%28retailer%29#Stores https://fastfashiontrend.wordpress.com/2012/12/07/competition/ https://fastfashiontrend.wordpress.com/2012/11/24/89/ http://fr.slideshare.net/rainajhamb/case-study-zara http://editd.com/blog/2014/04/zara-vs-hm-whos-in-the-global-lead/ http://retail.economictimes.indiatimes.com/re-tales/Uniqlo-vs-Zara-vs-H-M-vs-the-world-of-fashion-retailing/91

Olympe LEU

IV/ China, an opportunity : Overview of the fast fashion market and its consumers. Fashion is one of the fastest moving and dynamic sectors around the world. Combine that Fashion is one of the fastest moving and dynamic sectors of retailing around the world. Combine that with a retail market that offers enormous growth potential, a rapidly expanding modern retail sector and millions of new consumers and you then have something exciting. And that is China. The Chinese fashion market is currently worth a huge £98billion, and by being accountable for 30% of the global fashion markets growth over the next five years, it is the world’s fastest growing fashion market. With a complex way of working compared to the UK and other European countries, the Chinese retail structure can be a challenge. The key differences from other markets: - China is a very youthful market. - Consumers want to dress up rather than dress down. - What is considered “cool and edgy” in many global markets may not be understood by the

majority of Chinese consumers. - Extreme styling does not work, but “lifestyle images” that help people aspire to a “better

lifestyle” can, whether it be a more European look - For womenswear: feminine usually works.

1) The opportunity.

It is a very exciting time for retailing in China. The landscape is going through an incredible transition with forecasts for 3,000 new shopping malls opening in the next 2 to 3 years. This is unprecedented and we have never seen any country in the world open such a volume of commercial space. This will mean that international brands looking at China will never again see such an opportunity to deliver rapid expansion, whether through their own stores or with domestic fashion retailers stocking multiple brands. Driving this expansion of retail space is the Government’s focus on accelerating domestic consumption in order to reduce the reliance on manufacturing exports. This is a highlevel strategic policy that will take years for its effect to be fully felt, but it is critically important to the development of a consumer economy in China. Consumers are already becoming more sophisticated and international in their outlook and experience as huge numbers of people travel overseas for holidays now. We are also seeing younger consumers embracing new fashion brands particularly in tier 1 and 2 cities. They are going beyond luxury brands and want to stand out from the crowd by finding and wearing new labels which very often they find by searching online. Ecommerce in China should not be overlooked or underestimated by anyone looking at the market. Growth has been explosive. China is already the second biggest ecommerce market in the world behind America. This is because of the sheer size of the Chines e market, but the penetration of ecommerce as a percentage of total retail sales is still in single digits. But this will quickly move above 10% and make China the biggest ecommerce market in the world. The key challenge for international brands looking to open in China is in how to set up the appropriate distribution strategy. Multi-brand domestic fashion retailers are beginning to develop but department stores remain very important. Primarily they operate a concession model and there is no doubt that the interest in international brands is growing. But retailers will want to know that new brands can be established quickly and help capture shopper interest and traffic. The challenge for brands is therefore in how to build this presence and a following on marketing budgets that are far smaller than luxury houses. This can be very difficult in a country the size of China, but this is where online and mobile provide a powerful route to consumers.

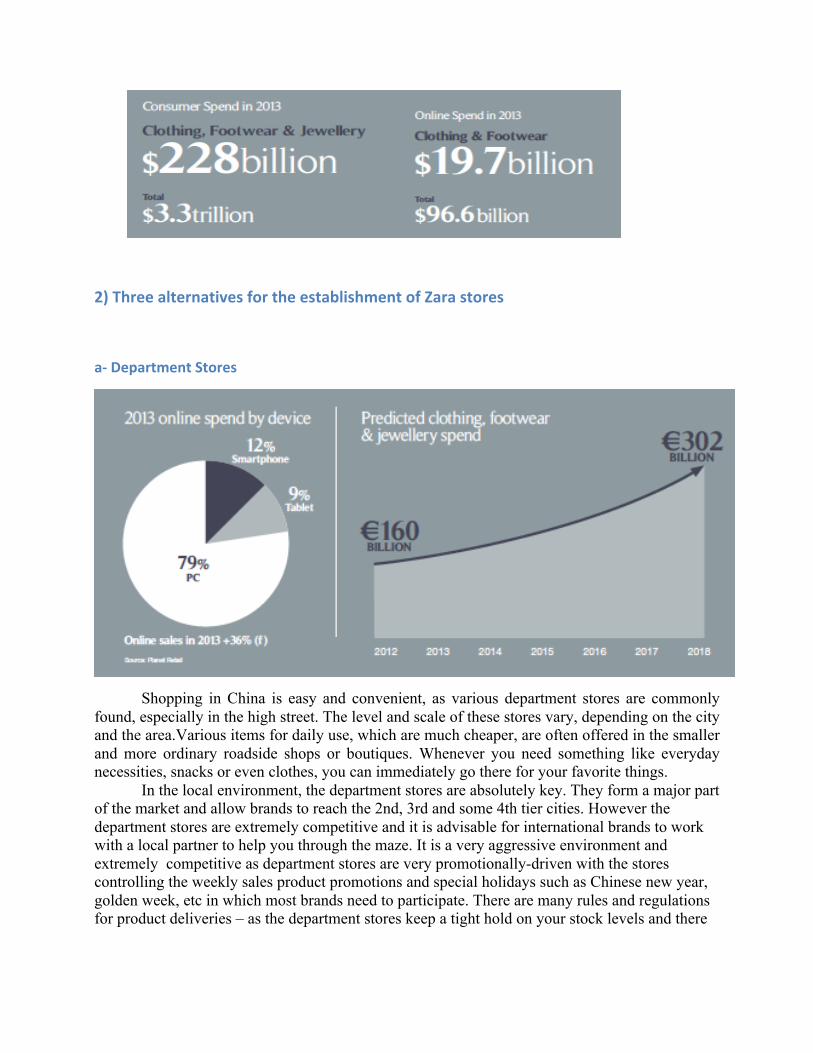

2) Three alternatives for the establishment of Zara stores

a-‐ Department Stores

Shopping in China is easy and convenient, as various department stores are commonly found, especially in the high street. The level and scale of these stores vary, depending on the city and the area.Various items for daily use, which are much cheaper, are often offered in the smaller and more ordinary roadside shops or boutiques. Whenever you need something like everyday necessities, snacks or even clothes, you can immediately go there for your favorite things. In the local environment, the department stores are absolutely key. They form a major part of the market and allow brands to reach the 2nd, 3rd and some 4th tier cities. However the department stores are extremely competitive and it is advisable for international brands to work with a local partner to help you through the maze. It is a very aggressive environment and extremely competitive as department stores are very promotionally-driven with the stores controlling the weekly sales product promotions and special holidays such as Chinese new year, golden week, etc in which most brands need to participate. There are many rules and regulations for product deliveries – as the department stores keep a tight hold on your stock levels and there

is very limited stockroom space. It is better to have frequent drops rather than hold stock in the store.

b-‐ Shopping Mall In the busy streets of the downtown area, usually in the shopping center of a city, there are large-scale and high-class emporiums, in which not only the domestic brands but also many well-known international brands are all sold. Everyday items, cosmetics, household appliances, bedding, clothes, and everything up-market that you wish for can be found easily to satisfy your every need. Bargaining is seldom acceptable, but there are often special promotions or end-of-season sales with an attractive price.

c-‐ Business Street Most large and distinctive Chinese cities, like Beijing, Shanghai, Xian, Hangzhou, Guangzhou, feature special business streets, where local products are on sale. Merchandise of the same kind is usually sold in the same street, which makes shopping easy and saves you time. For example, the Hongqiao Market in Beijing, also known as the 'Pearl Market', especially attracts female overseas tourists and mainly sells pearl jewellery, while Silver Street, where many boutiques are located, always tempt the youth by its modern fashion. You may also find various characteristic streets selling the four treasured tools of studying (writing brush, ink, inkstone and paper), painting and calligraphy, handicraft, silk and embroidery, jade articles, crockery, furnishings, musical instruments, boutiques, even flowers, as well as grocery streets or food streets. Some of the business streets are pedestrian malls, where tourists can relax and shop at their leisure.

3) The importance of e-‐commerce and social medias.

a-‐ ‘e-‐commerce’ and its two chinese dominante platforms. With 568 million Internet users in China, retailers are also recognising the importance of having an online presence as part of their marketing, to target younger shoppers.

“in other countries, e-commerce is a way to shop, in China it is a lifestyle”. A little over a decade ago, China’s path to e-commerce leadership would have been difficult to foresee, even as the tech boom in the US and other markets saw the development of e-commerce as an important B2C and C2C channel. In 2000, China had yet to develop any e-commerce applications, and had only 2.1 million total internet users. Payment systems and physical delivery mechanisms to facilitate the development of e-commerce transactions were well-developed in other markets, but were simply lacking in China. Fast forward to the end of 2013: with Chinese internet users quickly approaching 600 million, and e-commerce revenue growth (from 2009-2012) topping 70 percent compounded annually, China is on pace to pass the US and become the largest e-commerce market in the world

By 2015, e-commerce transactions in China are projected to hit USD 540 billion, or approximately 10 percent of total retail transactions, and by 2020, China’s e-commerce market is forecasted to be larger than those of the US, Britain, Japan, Germany, and France combined. Essentially, China’s large and growing middle-class have become accustomed to making frequent e-commerce purchases. Furthermore, as in many longer-standing e-commerce markets, they are also developing brand awareness, an increasing proclivity to purchase high quality and/or individually satisfying products, and showing a commitment to brand loyalty and repeat business The future development of China’s e-commerce channel is closely linked to technology developments and also the behaviors of Chinese consumers, including the way they research and order products online, and their preference for speed and convenience. Two purchase platforms dominate the e-commerce landscape : - Alibaba’s Taobao (淘宝网) – Taobao is a C2C site analogous to Ebay, and was created by Alibaba in 2003. Sellers are able to post new and used goods for sale or resale on the Taobao Marketplace, either at a fixed price or by auction. Taobao claims over 500 million registered consumer accounts, 800 million product listings, and holds a staggering 80 percent share of China’s C2C market.11 Like Ebay, Taobao’s market is a place where many merchants sell their products directly to customers; however Taobao doesn’t charge any commission fees on transactions: its main revenue stream is from advertising on the site. - Alibaba’s Tmall (天猫) – In 2008, Tmall was created as a B2C site (similar segment as Amazon), to compliment Taobao’s C2C marketplace. Tmall is able to provide a unique ‘mall experience’ for brands to set up their own mall website. Sellers pay a deposit to list on the site, and Tmall earns a commission on each transaction.12 Popular domestic and foreign brands occupy ‘mall space’. Each brand can have its own virtual store in the mall, and for foreign sellers, a Tmall store avoids the requirement of obtaining an ICP license needed to sell on-line in China. The Tmall model has proven tremendously successful: in 2012, Tmall accounted for around 51 percent of China’s B2C online sales, up from 35 percent in 2010. Comparably, Amazon’s share of the market in the US is closer to 20 percent. Together, these two giants dominate China’s market, selling everything from Lamborghinis to shoe laces. However, despite Alibaba’s market position, the e-commerce market in China is large enough for other competitors and niche players to thrive, including some regional platforms, such as Daminwang (大闽网) in Fuzhou, and Jingdong (京东) 360buy.com.

b-‐ Media platforms and ‘m-‐commerce’. China’s social media platforms have become an important additional driver or facilitator of e-commerce activity. These platforms, such as Tencent’s We Chat or Sina Weibo (China’s leading Twitter-style microblogging platoform) have been growing rapidly: Tencent’s We Chat reported over 600 million subscribers, up from 300 million in January 2013. With almost instantaneous feedback and easy-to-use interfaces, social media platforms have become a staple in the life of Chinese e-consumers. Consumers in China use these platforms for immediate ‘buy/don’t buy’ advice from friends, to post product reviews, and to seek product knowledge/advice from key opinion leaders. According to recent e-commerce statistics in China,

40 percent of China’s online shoppers read and post reviews about products – more than double the number in the US. These social media platforms are stepping up their integration into the e-commerce chain. Retailers are developing a more sophisticated social media presence, and some social media platforms – We Chat is a recent example – have added payment functionality, so users can make purchases directly from the application. These trends are fostering an environment whereby mobile devices are an increasingly crucial element in China’s e-commerce arena. Accompanying the rise of e-commerce in China is a clear trend towards mobile devices. In the space of a few years, China has emerged as the country with the largest number of mobile-based e-commerce transactions. In 2012, mobile transactions totaled USD7.8 billion,19 representing 3.7 percent of all e-commerce transactions in China. However, by 2015 mobile commerce in China is forecasted to more than quintuple, to USD41.4 billion,20 representing 8 percent of all e-commerce transactions. Mobile purchasing aligns with the Chinese consumer’s desire for speed, and the convenience of ‘any time’ shopping. The trend towards ‘smarter’ and more functional phones and tablets, coupled with the rising use of social media platforms to inform and connect consumers, is likely to fuel the continued rise in the number and proportion of so-called ‘m-commerce’ transactions in the Chinese e-commerce market. Roughly 40 percent of all e-commerce transactions are fashion and accessories, purchased by younger, white-collar, urban female shoppers.

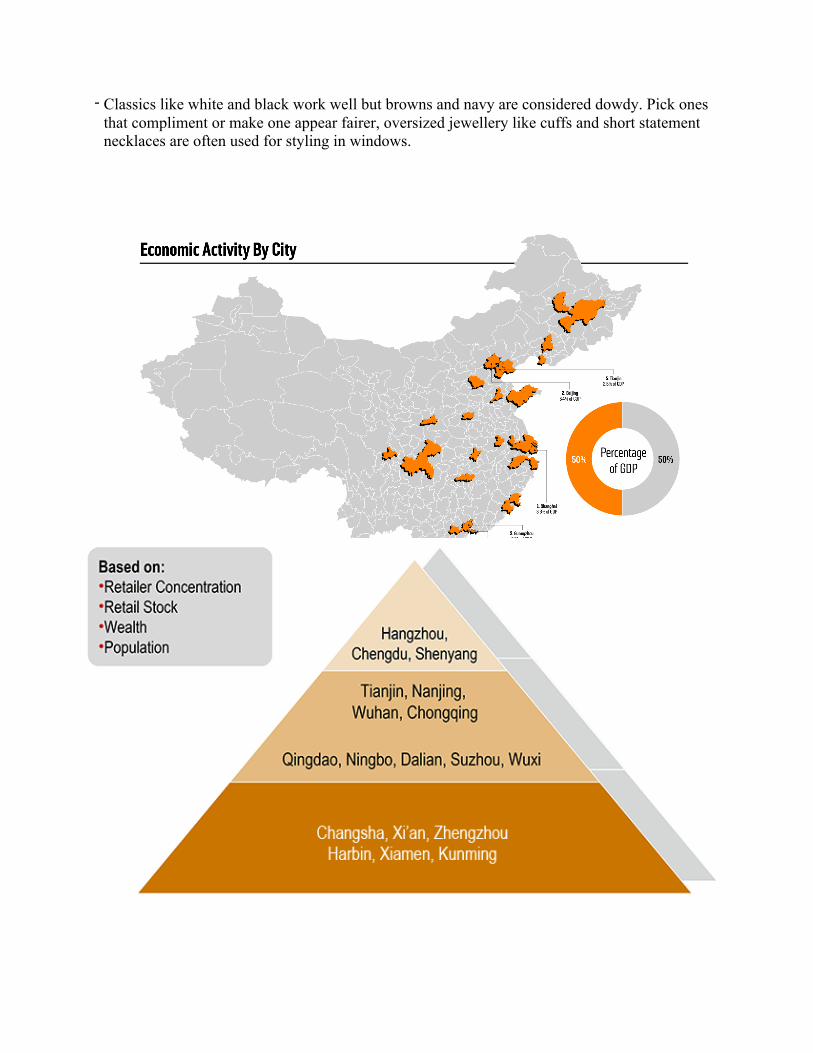

4) The chinese consumers.

a-‐ The different groups. Some foreign companies are hesitant to enter the market, however, because they do not understand Chinese consumers and their shopping habits. Despite the country’s rapid economic rise, China’s regions have developed at different rates, and consumer trends vary greatly among different groups and regions. Understanding the preferences and mindset of consumer groups is the key to successfully expanding a retail business in China. In the past three decades, Chinese consumers’ shopping habits have changed dramatically as incomes have risen and new products and concepts have entered the China market. Consumer habits continue to evolve today, and examining generations of consumers can reveal certain shopping trends. The older generation generally maintains “traditional” spending habits, middle-aged Chinese oscillate between tradition and new trends, and the younger generation is becoming more Westernized and quality conscious. The current Chinese consumer population can be separated into several groups with distinguishing characteristics : - Frugal retired : Born before 1960, most of these Chinese consumers grew up in tough political

and economic times, did not receive systematic education, and worked at state-owned enterprises. The difficult environment during their early lives made these individuals frugal and sensitive toward changes in consumer goods prices.

- Wealthy retired : This group experienced difficulties similar to the frugal retired consumers, but wealthy retired individuals primarily worked in government and government-funded

enterprises that provided higher wages and better retirement benefits. Though many of these consumers are frugal, they are less price-sensitive and often value quality more than cost. In the next 5-10 years, spending habits of Chinese consumers who are older than 50 will change slightly. These consumers will increase spending on groceries as the government raises retirement pensions in line with inflation rates. Though they will consume healthcare and entertainment products, their children will likely buy these products for them.

- Frugal forties : These consumers, who grew up during the Cultural Revolution (1966-76) and early stage of the reform era, swing between tradition and new trends. They work in various companies—state-owned, private, and foreign-invested—and earn modest incomes. These consumers generally save a large proportion of their earnings to take care of their children and parents.

- Wealthy forties : These consumers share the same background as the frugal forties, but they work for the government or large state-owned enterprises and have slightly higher incomes. Though they must also raise children and look after their parents, they are willing to pay premiums for quality products. In the next decade, consumers in their forties will have fewer childcare responsibilities and expenses. These consumers will thus increase spending on entertainment, groceries, travel, and high-quality and healthcare products.

- Thirties : Many consumers in this group are well-educated and grew up in a more open environment than their parents. Compared with older generations, Chinese in their thirties save less, spend more on entertainment, and often shop online. They also pursue value and quality rather than low prices. These individuals will become the most important consumers in the next decade, buying for their parents, children, and themselves.

- Twenties : Consumers in the first generation of the one-child policy have opposite shopping habits from their parents. These consumers barely save and spend most of their income on entertainment, advanced electronics, and other trendy products. They often shop online and look for products that help distinguish their personalities. They can also be impulse buyers. As consumers in their twenties age and start new families, their shopping habits may become slightly more conservative, though they will still favor high-quality and convenient products and spend more on groceries than previous generations.

- New generation : The new generation of consumers (under the age of 20) is the most Westernized and open to new products. These consumers pursue individualism and often use the Internet to follow global trends. Though most in this group do not yet earn an income, they significantly influence their parents’ decisions on food, clothing, electronics, and other purchases. Social media is an effective marketing tool to reach this group of consumers (see the CBR, January-March 2011, Social Media in China: The Same, but Different).

- Migrant workers : Migrant workers (generally 25-45 years old) are rural residents who moved to the cities for jobs starting in the 1990s. They can be even more frugal than elderly consumers, buying only the necessities and saving money to send remittances to their families in rural areas. Many migrant workers are expected to see a big increase in incomes and move their families to the cities in the future. They will significantly increase spending on groceries once they receive city household registration, or hukou, status and fully integrate into city life. Migrant workers’ consumption levels are unlikely to match that of their urban peers, however.

- The rich : There are more than 1 million Chinese with assets over $1.5 million, and the number is increasing rapidly. Rich consumers (generally 20-60 years old) are fairly concentrated in large urban areas, with Beijing, Guangdong, and Shanghai housing about half of this group. These individuals are successful entrepreneurs, top managers, and business owners. They

pursue the best products available, particularly imports, and are the perfect candidates for marketing new products. Premium supermarkets have already emerged in China to provide high-quality products to wealthy consumers (see Choosing the Right Retail Format).

As incomes increase and the young generation becomes the main body of consumers, the Chinese will gradually turn from buying only basic necessities to leading comfortable, high-quality lifestyles.

b-‐ Factors of success. Foreign companies must understand certain factors to successfully sell to Chinese consumers : - Some consumer habits can change - Small discounts are better than none - Product safety mistakes can be devastating - “Face” matters Chinese greatly value “face”—a quality associated with dignity, honor, and

pride—and will pay more to save face. For example, when purchasing gifts for important friends and family during Chinese New Year, consumers generally buy gifts that are of the appropriate value for the receiver and pay particular attention to product packaging. Consumers that cannot afford a higher-quality gift will buy the product with the nicest packaging within their price range. In addition, consumers will pay more for gifts with fancier packaging, even if the product is of equal quality to a less expensive item.

- Chinese consumers generally favor foreign brands - Pricing is a sensitive issue Pricing a foreign brand in China can be tricky. On one hand,

Chinese shoppers believe the higher the price, the better the quality or the higher the status. If a foreign brand is priced lower than a local one, shoppers may suspect that it has defects. On the other hand, the premium Chinese consumers are willing to pay varies by product category and by consumer groups. For example, young shoppers are willing to pay double for foreign-branded infant formula or five to seven times more for foreign bottled mineral water, but older consumers are not. Most modern retailers in China implement a high-low pricing policy.

c-‐ The styling. - Clothes need to be easy to wear. For example, as soon as you put on the garment, the customer

should be able to see the look. If the garment gets complicated – too much draping etc it is not so sellable. Outfits are key, suggesting to the consumer “how to wear” that look

- People tend to want to look “neat and tidy” - Clean, neutral colours are ok but not muddy unclear colours. Colours that can help flatter the

Asian skin tone. China loves colour. Mid colours that are popular in Europe are a hard sell in China.

- Colours that can make you look “poor” are not good. - China’s women want to look more youthful and love details. This does not mean over

accessorizing. It can be details in the cut, trim etc.

- Classics like white and black work well but browns and navy are considered dowdy. Pick ones that compliment or make one appear fairer, oversized jewellery like cuffs and short statement necklaces are often used for styling in windows.

Biqi HU

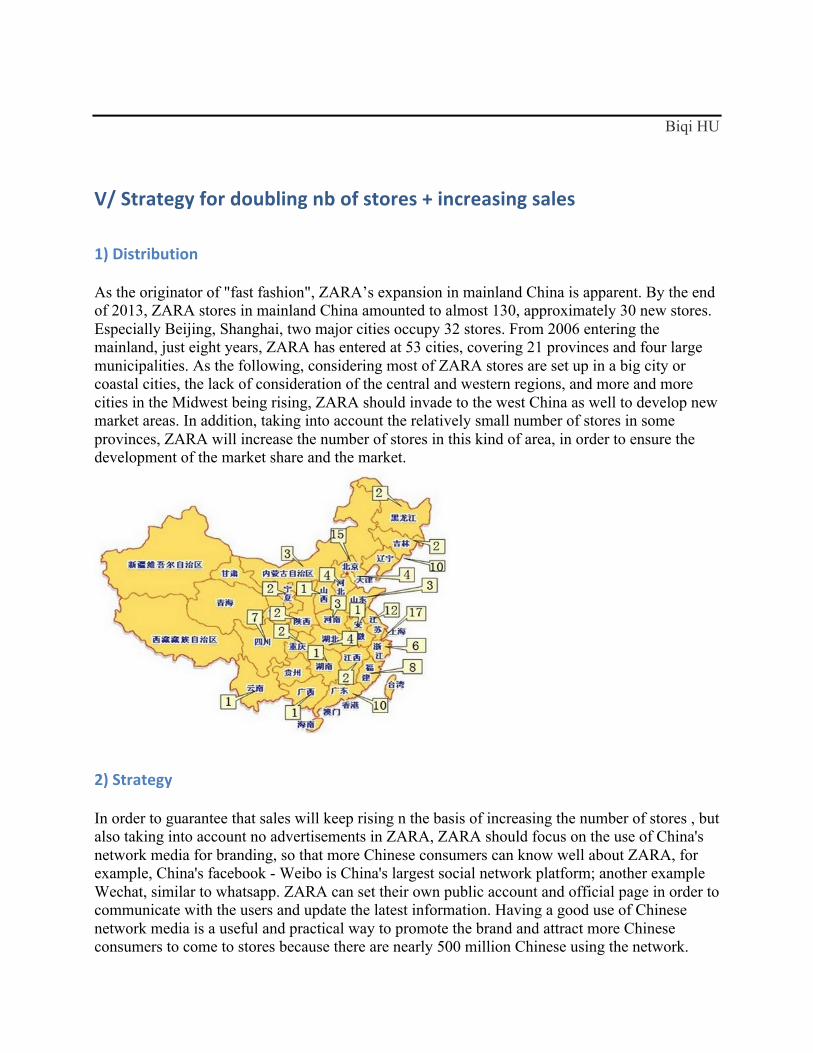

V/ Strategy for doubling nb of stores + increasing sales

1) Distribution

As the originator of "fast fashion", ZARA’s expansion in mainland China is apparent. By the end of 2013, ZARA stores in mainland China amounted to almost 130, approximately 30 new stores. Especially Beijing, Shanghai, two major cities occupy 32 stores. From 2006 entering the mainland, just eight years, ZARA has entered at 53 cities, covering 21 provinces and four large municipalities. As the following, considering most of ZARA stores are set up in a big city or coastal cities, the lack of consideration of the central and western regions, and more and more cities in the Midwest being rising, ZARA should invade to the west China as well to develop new market areas. In addition, taking into account the relatively small number of stores in some provinces, ZARA will increase the number of stores in this kind of area, in order to ensure the development of the market share and the market.

2) Strategy

In order to guarantee that sales will keep rising n the basis of increasing the number of stores , but also taking into account no advertisements in ZARA, ZARA should focus on the use of China's network media for branding, so that more Chinese consumers can know well about ZARA, for example, China's facebook - Weibo is China's largest social network platform; another example Wechat, similar to whatsapp. ZARA can set their own public account and official page in order to communicate with the users and update the latest information. Having a good use of Chinese network media is a useful and practical way to promote the brand and attract more Chinese consumers to come to stores because there are nearly 500 million Chinese using the network.

Romy GAESSLER

VI/ Value of chain Model Day -15 of Zara: . D-15: creation: Model drawn by being inspired clothes of luxuries and customer expectations . D-13: Cup: Manage by computer in a factory belonging to the group of a Coruna. . D-5: Preparation: By a subcontractor finish in a factory of the parent company . D- 3: Expedition: Truck or plane . D Putting on sale: Labelling and on shelf putting As we can see, Zara has a deadline of 15 days of manufacturing for a product. Per months or per days, Zara created a lot of clothes and to be profitable it must find tissues have a low price. It is necessary to know that Zara takes its tissues in other countries, because that returns to it cheaper. China is a country where there are the most factories, with a low price. We also noticed that jackets at Zara for example are making in china, because it’s cheaper. Factory exists just in Spain, and they must send the products in stores in time in the world. If there is a delay in the shipping, they may be a problem and sales and less. For stores in China, Zara makes in Spain and then she exports products in China. If the sales of products Zara climb on the Chinese market, between the time of the manufacturing of the product and the time of the export, Zara wastes time. If the company want to have a factory in China, it must respect laws in this country, respect the environment, and pay correctly employees… Required the company keep customers and to have always a good image of brand. We should open a factory in China to not problem in the time of products. It is very important for a big company, to make the right choice.

Indeed, it must be careful, if there is a problem with the export in the world (strike..), in the factory in Spain… We conclude that from Zara could have it own factory in China to lose fewer time and could be more profitable in the years, which follow.

Ombeline MANCEAU

VII/ Conclusion