Strategic alliances in Mexico : effects on the value of the firms

195

INSTITUTO TECNOLÓGICO Y DE ESTUDIOS SUPERIORES DE MONTERREY in collaboration with I. T. E. S. 1\L . (:, c. :\f. nrnT.T()TF.CA COLtCCION Dt NEGOCIOS Y ALTA úl?.[CCION THE COLLEGE AND GRADUATE SCHOOL OF BUSINESS THE UNIVERSITY OF TEXAS AT AUSTIN February, 1997

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Strategic alliances in Mexico : effects on the value of the firms

INSTITUTO TECNOLÓGICO Y DE ESTUDIOS SUPERIORES DE MONTERREY

in collaboration with

I. T. E. S. 1\L . (:, c. :\f. nrnT.T()TF.CA

COLtCCION Dt NEGOCIOS Y ALTA úl?.[CCION

THE COLLEGE AND GRADUATE SCHOOL OF BUSINESS

THE UNIVERSITY OF TEXAS AT AUSTIN

February, 1997

STRATEGIC ALLIANCES IN MEXICO.

EFFECTS ON THE VALUE OF THE FIRMS

by

Jesus Esteban Macías, MAE

DOCTORAL RESEARCH REPORT

Presented to the Instituto Tecnologico y de

Estudios Superiores de Monterrey

in Partial Fulfillment

of the Requirements

for the Degree of

Doctor of Philosophy

THE UNIVERSITY OF TEXAS AT AUSTIN

February, 1997

ABSTRACT

STRATEGIC ALLIANCES IN MEXICO. EFFECTS

ON THE VALUE OF THE FIRMS

This research lists the most important Mexican strategic alliances during the 1989-1996

period, principally the ones who issue at the Mexican Stock Exchange. The study looks for

consistency with other studies regarding causes and effects of strategic alliances on firm

value. It is based on an event study on stock retums of the acquiring firms ·finding a

significant jump close to the merging announcement, called day zero. The first test using

the event study method was done by Fama, Fisher, Jensen, and Roll in the lnternational

Economic Review, February 1969. This method, either (explicitly or implicitly) assume

that markets are informationally efficient or they explicitly test for the informational

efficiency (Starks, Laura 1993).The study proved that stockholders of Mexican merging

companies experienced on average 4.5% increase in abnormal returns around the

announcement day established at -4+8 days period consistent with other studies in

empirical evidences. The Mexican market was found to react efficiently to alliance

announcements. Reasons for the abnormal retum effect were looked to come from previous

undervaluation of stocks, financia! performance, and synergy coming from assets and

organizational restructuring. The event study was complemented by a Discriminant Model

finding that debt burden, cash flow, and missvaluation of assets and debt were found to be

significant in explaining differences among abnormal retums of the allying firms. The

economic envirorunent prevalent during 1989-1994 period was found to be acting as a

mood variable stimulating number of alliances and abnormal retums. This was related to

financia! globalization and emergent markets where alliance events have increasingly

occurred.

Aknowledgements

Abstract

STRATEGIC ALLIANCES IN MEXICO

EFFECTS ON THE VALUE OF THE FIRMS

TABLE OF CONTENTS

Introduction .......................................................................................................................... 1

Chapter I Overview of Strategic Alliances ............................................................................ 6

I. l Intemational strategic alliances : key to success ora new failure ............................. 6

l. 2: Theoretica1 background ...................................................................................... 13

Financia! restructuring and organizational restructuring ................................ 14

Value creation in strategic alliances ?-----------------------------------------------14

Where does va1ue creation come from ?.. ................................. ...... ... ....... ..... 15

Diffcrcntial efficiency ...................................... ... .......................................... 17

Inefficient management. ......................................... ....................................... 17

Operating synergy ........................... ............................................................ 18

Purc diYasification ..................................................................................... 18

Financial syncrgy ..... . .............. ..... .......... ................. .. .................................. 18

Stratcgic rcalignment ......... ..... .... ........... .. ................. .................................. 18

Undcrvaluation ........................................................................................... 19

Agcncy Prob1cms and Managerialism ........................................ .................... 20

Winncr's cursc-hubris ................................................................................. 20

Thc free cash flow hypothesis .......... ....................... .. .................................... 20

Markct Powcr. ........ . ....... .... ........ .. ........ ...................................................... 21

Tax shiclds ............. . .. .. ................................... .. ...... .... ...................... 21

Rcdistribution of Wcalth ................................................ .. ............................ 22

Cultural and organizational compatibility ...................................................... 22

Mcrgcrs undcr agcncy thcory .... ... ............ .. ........... ...................................... 23

Financia! Globalization... . ················································· ............. 23

Chapter 11 : Mexican Strategic Allianccs. 1989 - 1996 ....................................................... 26

Conccntrations.. . . . . . . . . . . . ... ... ..... ...... ......... .. .. .. .. ... .. .... .. .. . . .. 36

Privatizations of formcr public firms ....... . ............................... . ······ ... 39

Chapter 111 : Methodology ....................... .... ...... ." ................................................................ 43

H~-pothcscs ..... .. .............................. .. .......... ....... ................... ..... ................ .43

Methodology explanation ..... .. ......................................... . . ·· ··· ······ ... 51

Definition of synergy ......... .. ...................................................... .

Model for calculating abnorrnal returns ............ .............. ... ..... ....... .

. .. 51

. ... 52

Justification of thc model. ..... .. .. ........... .. .................................................... 53

Assumptions ............................. ............................... ................. ..... ... ....... . .5 5

Discrimination between high versus medium and low performers .................. .56

Short run performance .................... .. ................ .... .... ....... .... ........ ... .. .......... .56

Thintrading .......................... ........ .. ......... .. .... ....... ... ............ ... ....... .. ........... .5 8

Statistical tests on the market model... .......... .. .. ... ....... ... .. ................ ...... ..... 62

Testing significance in abnonnal retums ............................... ............. ... ....... 62

Test on sizc effect. .... ... .... ... .................. ...... ... ............ ....... .. ..... ...... .. .... ........ 64

lndustry effccts......... .......... .... .......... .. .............. ........ .. ........ ..... .. ... ... ....... . .65

lndustry and finn conccntration. .. . .. .... ........................... .. ............... 66

Data: firms alliances sample...... ... ............. .. ... ............. .................. .67

Holdout sample .................. ....... ...... ......... ... ... .... ... ......... .. ... ....... .... . . .. . 68

Chapter IV : Empirical Evidence Review ........................................................................... 70

Financia! Postmerger performance ........................................................ ....... 76

Opportunism explainning gains ..... .. ...... .......... . ············ .................. 78

Leveragcd rccapitalizations.. .. .. .. . . . ..... ..... ........ . . . . . . . . . . .. . . . . . . .............. 80

Lcveragcd buyouts and put bonds : thc cntrecluncnt hypothcsis .......... ... ........ 81

Markct sharc cffcct, pricc cffect and cost cffecL ....... ........... .. ..... ... .. .. ... ...... 83

Forcclosurc mcrgers ...... .............. ............... ... .................. .... .. .... ........ .... ... .. 85

Rclatcd and unrclatcd mcrgers. ..................... ........ ....... ..... . ..... ... .... ..... 85

Forward and backward integration. Toe use of modcrators .................. ...... 86

Acquiring firms gains and owncrship concentration .......... ....... .......... .......... 87

Joint ven tu res ..... .... .............. ........... ..... .. ............ . ........... ...... ..... .. . ............. 88

Mcrgcrs cfficiency versus markct powcr: valuation cffccts ....... . .. ...... .. ... ... 89

Conccntration po,vcr . . . . . .. . . . . . . . . . . ..... ................ . . ........... 89

T;:irgct opposition and sizc dTcct. 90

Takcovcr rcgulation cffccts on multinational mcrgcrs 91

Rol of Taxation and mcrgcr succcss ...................... ..... .... ..... ..... .. ................... 92

Contagious mcrgers ............................................................... ..... ... ..... .. ....... 9 5

Merger cffect of accounting practiccs ........................................................... 98

Prcdicting mergers..... ... .. .. . . . . ................... ......... .......... .. . . .. . . . ... .... . . ........ 99

Morale for predicting merger success .......................................................... 100

The endogeneity problem in predicting the outcome of tender offers ............. 102

Chapter V : Results ........................................................................................................... 105

Conclusions ........................................................................................................................ 140

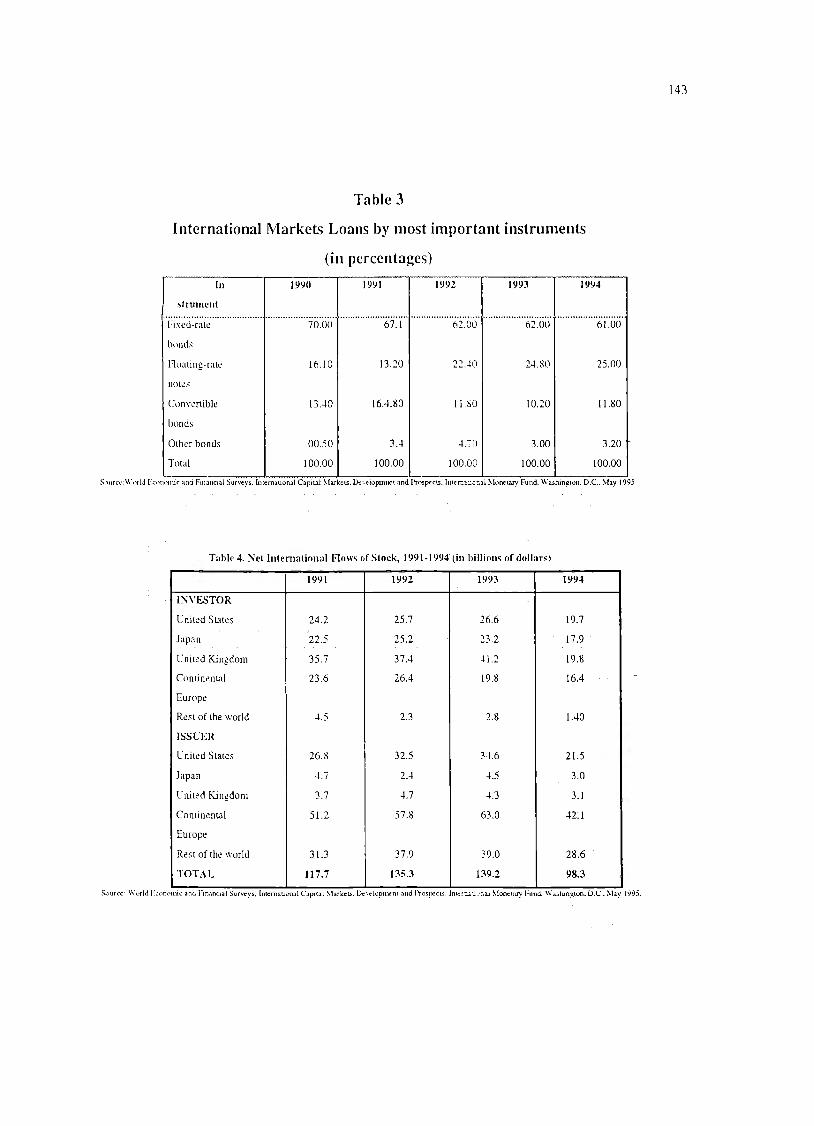

Tables ................................................................................................................................. 142

Table 1. World flow of resources ................ ..... ........ ............................................................ 142

Table 2. International Bond Issues ....................................................................................... 142

Table 3. International market loans by most important instruments ..... .. ... ............................. 143

Table 4. Net international fk,·,,s 0fstock, 1991-1994 ............................... ..... ... .................... 143

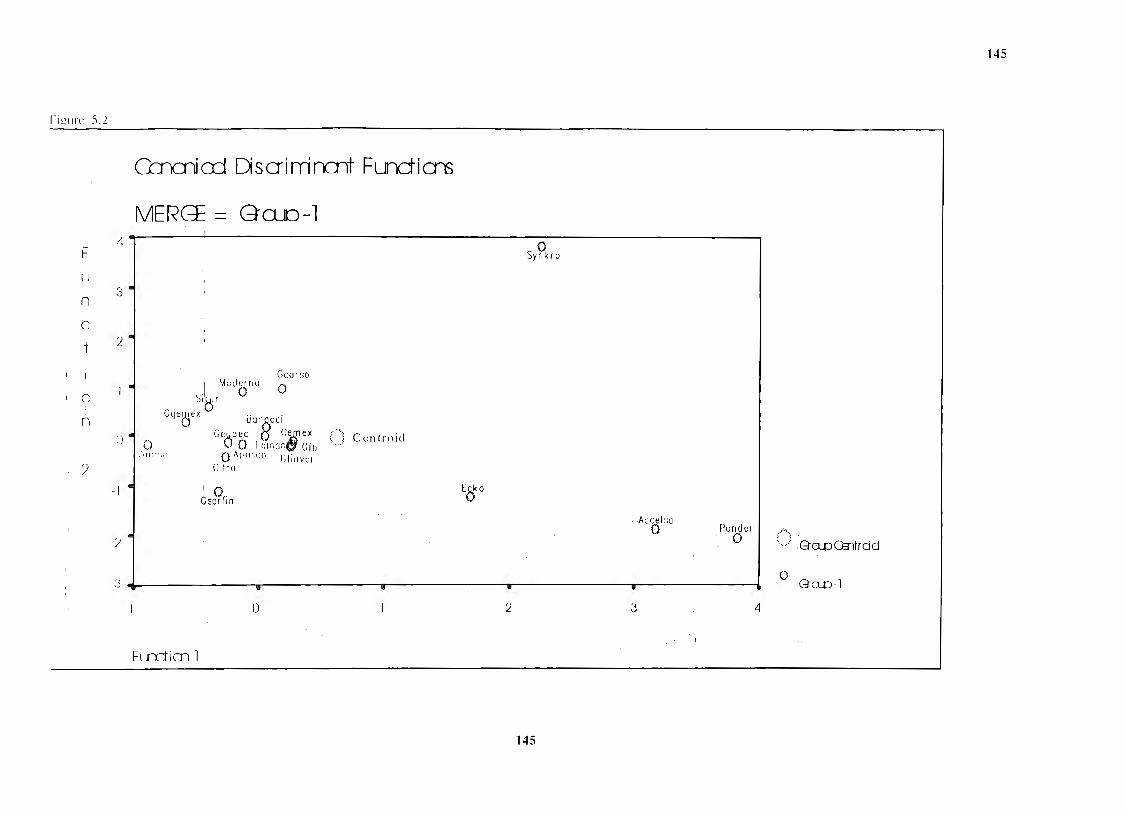

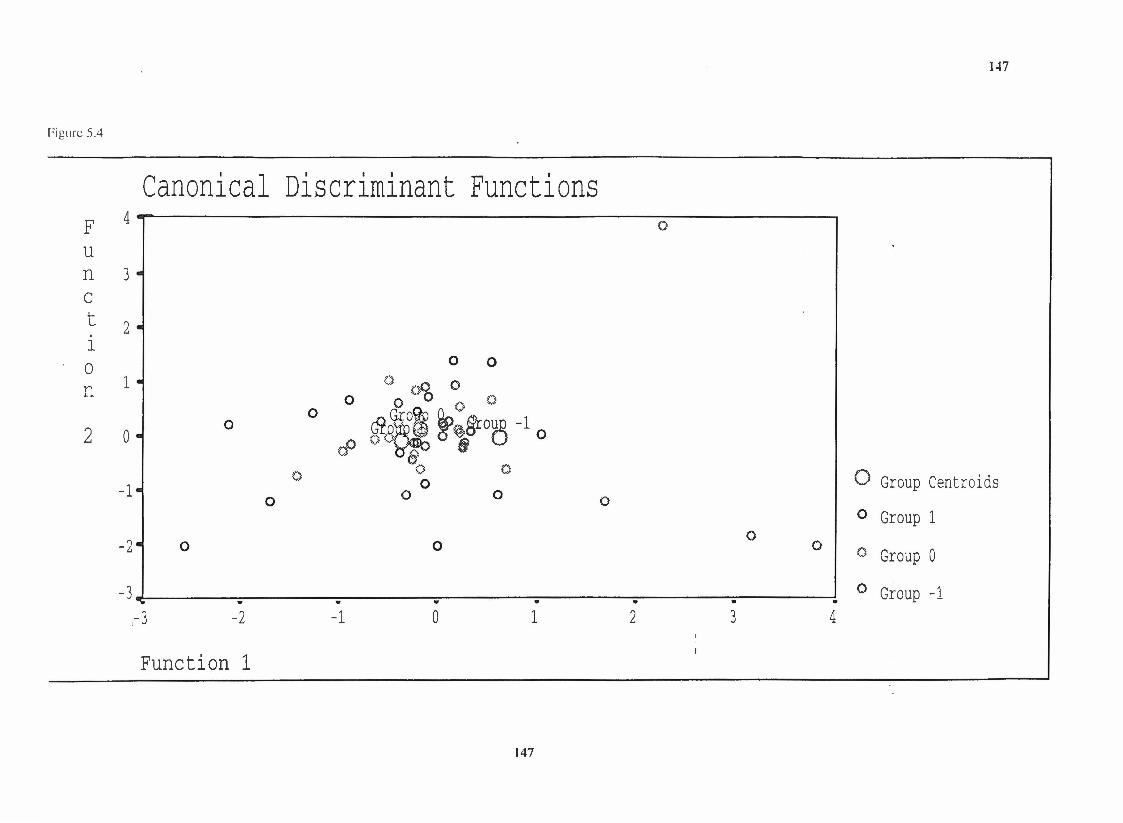

Table 5. Canonical discriminant functions ...................................................... ... .. ........... ...... 144

Refcrenccs ...................................................................................................... .... ................ 149

Main currículum data on Mexican merging finns. 1989-1997 ............................................. 166

Vita .................................................................................................................................... 173

INTRODUCTION

In the last twenty years important economic changes were applied in Mexico.

This was thought to respond the higher international competition accelerated with the

telccommunications recent revolution.Trade and investment went into liberalization

policies that accelerated the need for rnodernization. Firms took shorter positions to

investment oppo1iunities in a Iack of capital market. Orthodox and heterodox

measures tried to stop capital outflows, mainly through increasing rates of interest,

privatizing econornic activity, adjusting for foreign exchange, and restructuring

externa! debt.

Strategic alliances were observed to increase, particularly during the 1982.

1987, and 1994 debt crises. Each of these unstable periods were followed by periods

of hyperinflation, deep recession, and Iack of externa! capital to support grov..1h.

Privatization and rnerger expansion contributed very much to the

consolidation of new huge industrial and financia! groups in México, many of them

coming from higher foreign participation in the new path of internationalization of

Mexican firms.

Consistently, monopoly regulation changed rapidly clairning social welfare

(Oficial Newspaper Dec-28-1992). However, this antitrust government behavior did

not irnped mergers and other kind of alliances, to be able to compete with foreigners.

Mergers in Mexico do not concentrate in specific areas. They cover a wide

range of activities forming huge industrial and financia! groups. As an example, the

Telmex reprivatization, on December 20, 1989, stirnulated mergers between the

strong Mexican financia! group -Inbursa- and sorne domestic and foreign companies.

Carso group merged with France Cable&Radio, and with South Western Bell, with

20.4% of controlling stock. Carso - lnbursa group covers a wide range of econornic

activities restaurants, communications, construction, industry, and sorne others.

2

How the financia[ community has interpreted these merging events is the main

question in this study. Far instance, during the Telmex privatization - mer.ger event, a

71.4% increase in total revenues was reported in 1990 and 21.3%; 17.5%; and 14.5%

respectively in 1991-1993. In consequence, the stock value rose steady 32.2% in real

terms, from 1989 to 1993 (Grubman, J. 1993).

In a recent date Telmex announced a new alliance with the strong mass media

private group Televisa, to share its cable net far integral communication -phone,

electronic data interchange, fund transmissions, etc. After this announcement, Telmex

registered a 3% increase in stock price over the 3 days following the anriouncement,

an amount approximately 2.2% higher than the market retum over that period,

Simply stated, mergers mean the formation of one or more economic units

from two or more previous ones. They can be horizontal, vertical, conglomerate,

financia!, managerial, concentric, etc. Sorne estimations have been provided regarding

the rate of increase in merging events, worldwide, and for instance Gobbelies (1995)

faund that this rate has almost doubled in the nineties as compared to the eighties.

Severa! theories have been proposed to explain the merger strategy, an old

business practice, dating from 1895 in the US.

Mergers seem to vary consistently with sorne econorruc, managerial and

financia! processes, far instance the product life cycle (Porter, Michael 1985).

F ollowing this theory, in incipient industries, merging beco mes attractive to share

growth opportunities far financia! or distributional fulfillment. On maturity, vertical

and concentric merging may appear attractive to increase economies of scale in

research, marketing, production, and financia! opportunities. This is especially

important when profitability growth begins to slow down as competition increases. At

the decline stage, horizontal merging may seem attractive far conglomerates to protect

market positions and to create new entry barriers.

.)

Depending on the specific circumstances and processes in which a merger

occurs, a "win to win" situation mayor may not emerge. Sorne research has.shown -

though not conclusively- that mergers benefit stockholders of both the acquiring and

the target firms (Dodd and Ruback, 1977), emphasizing a bigger effect on target firms,

measured as stock prices increase as well as better accounting performance. Far

example, Franks, Harns and Tirman (1991) in an examination of 399 acquisitions show

that stockholders of the target firms have larger gains around the announcement.

Possible explanations of this "value creation" have been grouped into three

majar explanations: First, sorne synergy emerges from the union, as firmsL resources

are better allocated. Also these firms tend to reduce costs and/or to increase future

income. Second, previous undervaluation of assets existed prior to the merger, and

this situation is recognized and corrected far the market. Third, a redistribution of

benefits arises from stakeholders to target stockholders and from these to acquiring

stockholders through control processes.

Whatever the explanation, what seems important is that new stake-stock holder

relationships emerge creating interesting agency considerations. The mechanisms

through which this value creation or distribution occurs possibly distort asset pricing

practices, as well as formal or informal leasing contracts or direct and indirect asset

transfers. This may increase stock retum abnormally.

Previous research has indicated that the size of the stock gains at the merger

announcement depends on severa! factors. These factors are: the form in which the

merger occurs, the amount of leverage, the merging mechanism u sed, the financia! and

contracting cost process announced far accomplishing the merger, the characteristics

of the management teams and the board of directors, and the specific bargaining power

the firms have. This signaled through the financia! and organizational mechanisms

employed, principally those related to financia! complementary assets valuation

(accountability), and press news.

4

The task of this research is to look for consistent evidence in the Mexican

experience, to look for robust increases in the acquiring firms' stock returns and in the

financia! situation of these companies. Evidence will be examined befare and/or after

the merger announcement.

The first step in this research is to examine the stock returns reaction for value

creation or distribution in the Mexican merger experience. After statistical tests the

second step is to determine what financia! situations may be explaining synergy, if any,

i.e. value creation, distribution, signaling, etc.

Another question in this work is to rev1ew if the Mexican expenence m

mergers has been primarily the case of combining of assets bringing revaluaticm or the

case of a tax-treatment. Also of interest is whether these mergers may have been a

transfer of benefits from combined stakeholders to merging stockholders. lf so, sorne

tests will be performed looking for evidence regarding how the tax system and

Monopoly regulation in Mexico encourages or discourages firm concentration and/or

restructuring.

Also important m this work, is whether there exists prívate information

asymmetry creating hubris expectations, sentiment biases and/or noise reactions, as

well as other expectations.

Another question that leads this research is to estimate the bargaining power

effect in the abnormal retums merger event. For instance, the effect of a new kind of

government protection to the merger firms creating monopoly eamings, overvalued

prices or better leverage. Thus a Discrirninant model is specified to look for this

bargaining power as in Telmex, Fertimex, petrochernichal plants, and banks.

Besides employing the event study methodology to test for abnormal retums,

financia! ratios are utilized to look for market undervaluation due to rapid inflationary

periods and -or- former public ownership. Similarly, a Discriminant model is

performed to control for size and financia! performance as well as to look for

monopoly considerations or greater market control in the merging firms. Thus, the

5

research employs a combination of statistical event study method with financia! models

based on Discriminant analysis that gives us a way to account for qualitative

differences in the merging firms as well as to estímate their importance in explaining

the Mexican merging process.

Summarizing the description of this work, I considered important to resume

the main theories that explain causes and effects of establishing strategic alliances such

as mergers, acquisitions, joint ventures, etc. This was done in chapter 1. From this

theory review the main hypotheses were obtained. Also important was to review what

has been happening in other countries regarding strategic alliances, to infer sorne

specific circumstances, methodology and data collection and processing. - This was

done on chapter 2. On chapter 3, the methodology was explained and justified,

marking its limitations and possibilities. In chapter 4 a review what has been happening

in Mexico regarding strategic alliances while in chapter 5 the results were presented.

On the overall development of the work two things were followed, mainly if there was

a satisfactory response in the Mexican stock market to strategic alliance

announcements and what were the circumstances that can help to explain high

abnormal effect comparing to low abnormal effect. This obviously would have

implications for financia! restructuring schemas as well as portfolio selection and

financia! regulation based on perfect market behavior in Mexico.

6

CHAPTER I

OVERVIEW OF STRATEGIC ALLIANCES

1.1 Intemational strategic alliances: key to success or a new failure.

Some researchers affirm to have found enough empirical evidence in

interpreting different kinds of corporate restructuring as a value creation process.

Most studies base their conclusions studying how stock retums increase significantly

after a corporate restructuring is announced. These reasonings and evidences

contributed to the idea that value creation is realized in the stock market. and it is

interpreted as a successful event if, in the short run, stock prices increase by more

than the market index or whatever benchmark is employed.

Not only mergers and acquisitions fall within the concept of corporate

restructuring. Also included are spinning off divisions into independent status,

repurchasing shares or arranging le\'eraged buyouts, forming out new firms to

partially owned subsidiaries, and some other. Empírica! evidence indicates that these

restructurings create value because they are contributing to a better resource

allocation among firms.

However, other researchers doubt this value creation process always take place

because sorne of the restructurings may be followed by value destruction processes

instead of value creation processes. For instance, sorne restructurings are proceeded

by high interest debt issuance and/or sales of assets that destroy value and reduce

employment opportunities. In the US " ... during the 1980s, 557 publicly held firms of

ali sizes went private through leveraged buyouts or buybacks. The total amount that

changed hands was nearly $170 billion. much of it raised through the issuing of high

interest debt, or junk bonds. The outcome is often similar to the outcome of a hostile

takeover -in order to pay down the debt, substantial sales of assets occur-" (Martin,

John. 1993).

7

Succcss in corporate restructuring is thus notan easy question to answer. In this

work success is interpreted in the short run as val ue creation proccsses real ized by the

stock market performance or 69 operating performance. More recently a greater focus

is given to the long run effects of these restructurings and not only to the short run

effects (see for instance Kothari, Wamer. 1995).

Sorne researchers affirm that alliance success depends on the reasons to why the

firms ally, the circumstances in which the alliances occur, and the managers· skills

dealing with economic and regulatory risks as well as the characteristics of the

merging firms.

Guidelines for successful alliances in empirical studies have concluded that

corporate restructurings have to increase competitive advantage of firms as a si ne

quct non condition for a successful restructuring. F ocusing more on unique strengths

than correcting weaknesses, financia!, manufacturing or technological transfer may

spread to both engaged firms. Very general conditions have been formulated to

forecast when an alliance can be successful or non successful.

This lack of predictability may be overcome by the market in sorne way. If not,

the question is why the stock market reacts to thc:;e announcements. Reasons may be.

sentiment, speculative behavior, managers' maniqueism, portfolio selection bias

(market imperfections), and/or information signaling plus rational behavior.

One key issue is to know how the alliance will impro\·e the allocation of the

resources as well as to how the alliance could make managers to perform to greater

competitiveness orto reinforce bargaining power.

It is accepted that management ski lis explain much of the success of the firms.

detecting opportunities and managing risks. Most of the empirical evidence and

theory agrees to conclude that success of most alliances derives frorn managerial

skills.

8

For instance, Mexico is seen internationally as an investrnent opportunity for

devcloping successful strategic alliances principally in supplying technology and

investment capital. "Companies can sell to Mexico by licensing technology,

exporting, forming a joint venture or acquiring a company. As companies will

become more vertically integrated in the Mexican market, their involvement and

control will increase, but so may their business risk. (Fraser, Dave 1992 p: 86-93).

However, management skills are not easily transferable from one business to

another. Could we believe that in an alliance, this management transfer occurs more

evenly? But, is this true? Is it necessarily true? So why stocks anticípate v~ry: much to

a possible value creation process if this process besides their difficulties.

Gundlach, Gregory T. and Mohr, Jakki J. 1992, found that competitors are

increasingly relying on collaborative relationships guided by intermediate forms of

govemance (strategic alliances, hybrids, networks) to find and maintain competitive

advantages. Such alliances contrast with what governrnent antitrust legislation

intends.

Malott, R. H. 1992 found that in any business relationship, it is important to

understand one another objectives and to adhere to one's own. Malott gives evidence

for FMC Corp. He calculated that over the past 2 decades, the proportion of FMC's

revenues generated overseas has risen from 14%-43%. Alliances have helped FMC

create worldwide scale in production, marketing, or distribution.

Among the causes of alliance failure are the absence of common or

complementary objectives, overestimated synergies, and organizations that have

incompatible philosophies and values.

Roberts, Roger F. (1992) concluded that if a business is subject to intemational

competition, it cannot afford to take a go-it-alone strategy. Managers often get

involved in a technology sharing situation that is accompanied financia! risk. Roberts

9

says that combining managers and other firm capabilities accclerates firm · s

devclopment, principally in thc international operations.

Savona, Dave ( 1992) pro vides evidence on alliance failure. He recommends a

study prior to mergc and to have prepared a contingency plan in case of failure.

Managers capability on managing corporate styles and cultures is also stated to be a

key to success for international alliances.

Bronder, Christopher and PritzL Rudolf (1992) affirm that understanding the

development process of the alliance is critica! to predicting success. A "structured

procedure" for developing strategic alliances is presented in 4 critica! ph_a~s. First: it

is a strategic decision which includes situation analysis, identification of strategic

cooperation potential, and evaluation of shareholder value potential. Second,

configuration of a strategic alliance, includes deciding on the field of the cooperation

and the intensity of the cooperation as well as an analysis of opportunities for

multiplication. Third: partner selection, includes fundamental. strategic, and cultural

fit. Fourth: managing a strategic alliance, includes contract negotiations, coordination

interface, and leaming, adaptation, and review.

Lorange, Roos, Johan, and Bro11i1, ( 1992) found that answenng questions

regarding the broad benefits of the alliance, how the two parties can complement each

other, and the managerial capacity of the firms is key for success. In the more

intensive phase of the formation process, the prospective partners should address

questions concerning market potential, key competitors, worst-case scenarios, and

cornpetitive advantages of the alliance. Additionally, they mention to also look at

political considerations in forming strategic alliances. The support of interna! and

externa! stakeholders must be lined up early on. In the intensiYe phase, managers and

others who might be active in the alliance are the key people to consider.

These findings are becoming highly mentioned in similar studies on

forecasting the effects of a corporate or organizational restructuring. Most of the

10

empirical studies agree that selection of thc right partner is fundamental. Senior

management commitment and clear communication between partners are critical

paths to success. Overly optimistic expectations, poor communications, arÍd lack of

shared benefits are among the reasons for alliance disintegration.

Magee, John F. (1992) found that while there are a number of risks involved in

formulating an strategic alliance, technology gains overcomes very much the risks

absorbed with technology improvement can cut costs, increase the bottom line, forge

synergies, and secure a competitive advantage. Alliances may be the fastest and most

cost-effective way to gain technological competence. Also he remark~d._ that the

problems rose among partners involves control, the shifting balance of power and the

fear of losing competitive advantage. Among the major causes why sorne US

alliances did not succeed were a lack of careful management and not extracting all the

advantages from the agreement.

Levinthal, Martinez, Quelch, and Ganitsky, (1993) found key to success for

Latin American company mergers the external causes around it. They mentioned the

recent política! events, the economic policies, true reforms, regional integration,

geopolitical forces, and Latín American firm' s characteristics. They also subs•.:rib~

that the mode of entry will anticípate success or failure. Sorne ways to enter the Latin

American market they mentioned are: exporting, doing strategic alliances, creating

in-bond assembly plants, acquisitions, and green-field investments.

Flanagan, Patrick (1993) concluded from an interview with Jose A. Collazo,

chairman and CEO of Infonet Services Corp., that a strategic alliance should not be a

quick-fix to a problem; the strategy should be based on the benefits that the alliance

brings to both parties. Therefore during the alliance negotiations, the most important

aspect is to retain the ability to walk away from the deal.

Collazo distinguished many reasons for establishing strategic alliances:

• fil! in gaps in the current market and in the technological availability of each firm. • turn excess manufacturing capacity into profits.

11

• reduce risk and cntry costs into ncw rnarkets. • accclcrate product introductions. • overcome legal and trade barriers. • extend the scope of existing operatíons. • cut exit costs when divesting operation. • cconomies of scale.

Valigra, Lori (1993), also interviewed Mobuo Mii, general manager of IBM's

Entry Systems Technology business unit. They talked about the future of PC

development. He believed that Japanese companies are not that loyal to

stockholders. New technology needs more than a one-company investment, and

therefore this faster technology diffusion means that strategic alliances and joint

ventures will become more frequent. For example, IBM is in an alliance with

Toshiba for small, flash memories and flat displays and with Toshiba and Siemens for

dynamic RAM chips. Based on this interview Valigra concluded that technology

transfer could be a good predictor for alliance success.

Wood, Freddie ( 1993), studied the textile industry and concluded that over the

. past 4 decades, the textile industry has had a revolutionary change. In the l 990s, 2

trends forced change: globalization and consolidation.

Globalization entails free trade with Canada and Mexico, anticipating that

succeeding textile firms will have 4 characteristics in common in which strategic

alliances have predominance: appropriate strategies, world-class manufacturing,

flexibility and speed, and information as a competitive weapon.

Silverman, Susann (1993), analyzed the strategy for The Continuum Co., a

$124-million software maker, which has become the largest international provider of

software for insurance companies. Silverman concluded that taking market

opportunities is the key to predicting merger success, though the investment could be

or not related to the main source of business. The Continuum most recent acquisition

was in August 1993, when it paid $63 million in stock for the world's number three

insurance software company, Paxus Corp. of Sydney, Australia. The purchase of

12

Paxus nearly doubles Continuum's size to $246 million. Continuum now gets sorne

$200 million, or 81 % of its sales, from foreign markets. Just two years befare

Continuum had rnade another key Australian acquisition, sorne $30 million with that

38% of sales, carne from abroad.

Fahim-Nader and Vargas, (1993) provide evidence of how to improve

diversified mergers within large firms foreign direct investrnent. Managing

intercultural differences seemed to be the cue for success, as well as market

opportunities.

Hunter, David (1993) g1ves empirical evidence of market shar.e as an

explanatory variable for merger success. He refers to manager Bolduc plan to expand

Grace's water treatment business with Aquatec. According to Ian PriestnelL President

of Grace Dearbom, the acquisition gave Grace just over 29% share in South America

(excluding Mexico and Central America) and nearly 50% in Brazil.

Newell G. Roberto (1992), concluded that privatizations are a good source of

strategic alliances, most of them successful in terms of abnormal retums.

Opportunities for large profits were observed in the bidders of the telephone

companies of countries moving to privatize their govemment-owned telephon-=

companies. In 1990 Ameritech and Bel! Atlantic bought Telecom New Zealand for

$2.46 billion. In July 1991, they offered 725 million shares to the public, which

brought the companies a profit of $150 million befare underwriting costs. The

investment gave 22% retum in the first year.

Mirchandani, Dilip K ( 1 992), cites adequate diversification as the main reason

to succeed in generating stock profits. This is done by combining product lines and

consolidating physical facilities as well as expanding the intemational market. For

instance in the last 6 months, there has been a major push into the Caribbean as

countries, Mexico, and Eastem Europe expanding intemational operations ..

13

Morris, Gregory (1992) studies related mergers to explain and to predict

merger success. He studied The Westlake Group (Houston) which is the kcystone of

Chao Group Intemational, This firm was founded in 1957 by Taiwanese enfrepreneur

T. Chao. Beyond its established regions, Westlake is investing in Mexico and wants

to take part in the growing Asian markets as well. Currently, it operates businesses in

conjunction with Himont, Mitsubishi Corp., for the petrochemical division.

According with the author, the key seemed to be diversification, thus taking what the

firm identifies as market or technological opportunity which has to be taken fast.

I.2 Theoretical background

Strategic alliances are different kinds of agreements, formal and/or informal that

can be simple collaborative agreements to more formalized joint ventures, i.e. a

merger1 or an acquisition, where two or more firms join partially or completely, to

accomplish sorne general or specific goals generally to increase competitiveness and

create value.

Mergers and acquisitions, manufacturing contracts, distribution channel

contracts, collaborative agreements, network agreements, international management

contracts, and others, such as franchises and supplier agreements are different kinds

of strategic alliances that integrate businesses processes to foster firms' financia!,

manufacturing, and/or marketing objectives.

I l\lcrgers and Acquisitions. Thc most common financia! proccdures used in mergcrs and acquisitions, are: - l'ublicly lraded limitcd partnershirs - Employec stock oplions plans - Lcvcraged buyouts, named as U)O's - Public offcring ofstocks which can be acquired. liquidatcd, and bankruptcy. - Lcvcraged management buyouis - Lcvcragcd rccaritalizations - Scllolls and SrinolTs

14

Financia! restructuring and organizational restructuring.

Financia! restructuring alters the cornposition of the firm' s asset portfolio or the

claims against those assets. It takes a variety of forms, which fall i"nto broad·

categories: rnergers or reverse rnergers, the latter including divestitures, spinoffs,

splitups, stock repurchases, partial public offerings, and leveraged buyouts.

Organizational restructuring includes chariges that are not only related to cost

reductions but to a better use of available resources. Arnong the important

organizational ch,mges rnost repeated are the change in the board of directors, the

change in the CEO, the change in the managers compensation policie~, :.ª relative

downsizinrr ;ind optirnization of the firm operations, and so on.

Sorne other difficulties regarding the characterization of strategic alliances anse

the new with complexity of the financia! instrurnents. F or instance, a swap agreernent

can establish a future interchange of assets or liabilities between two firms; This

agreement could not be accounted in the financia! statements and thus, not realized by

the investor community as an alliance.

After the financia! restructuring takes place in a swap agreement, the firm can

take advantage of tax allowances, cash flow stabilization, and assets expansion. The

firm is not longer the sarne because we ignore the future compromises the firm has to

fulfill in sorne sense they have allowed their financia! statements.

For instance, when doing off-balance agreements, like a swap contract, we said

that financia! information is no longer valid. It lacks of consistency in showing

profitability and risk in the valuation. This situation may arise rneasurement errors

and create sorne irnportant biases principally if the off balance practices becorne a

comrnon practice without an adequate rule for disclosure.

Value creation in strategic alliances?

15

There is controversy about how of value creation takes place in a restructuring

process. Sorne people argue that value creation is a si ne qua non condition in a

strategic alliance, insisting that value creation is the primary objeciive when

undergoing a restructuring. Others, however, insist that accounting and tax practices

that make value creation tacit and thus a problem in the long run. This value created is

not casy to sustain often the alliance

For the U.S. financia! market one study has estimated a total of $400 billion in

mergers and acquisitions from 1977 to 1986 (Jensen, 1991 ). The author concluded

that this big wealth effect resulted in more efficient utilization of corporate a,ssets.

However, sorne mergers such as those that occurred in forceable or hostile

circumstances, could result in value destruction rather than value creation. Peter

Drucker (1986), for example, contends: "There can be absolutely not doubt that

hostile takeovers are exceedingly bad for the economy". Acquired companies, he

says, are so burdened with debt as to severely impair the company · s potential for

economic performance. He states that takeovers precipitate the sell off of the most

Yaluable parts of the acquired businesses, destroying synergies that previously

existed.

Further, "The Business Roundable", comprised of the chief executives of

America · s 200 largest corporations, has agreed with Drucker, contending that hostil e

takeovers "create no new wealth, but merely shift ownership and replace equity with

large amounts of debt". The concem is that short-sighted institutional investors

undervalue companies whose current eamings have been temporarily depressed by

eff011s to invest for the long run. (Martin, John 1993).

\Vhere does value creation come from?

Research has shown that mergers can benefit stockholders of both, the acquiring

and target firms (Dodd and Ruback, 1977). In fact, rnergers were known during the

16

sixties and seventies as "the 2 + 2 = 5" effect, a form of synergy creation.

Explanations about where this value comes from are related to different theories

(Weston, Fred. 1990).

The possible explanations can be grouped into three major explanations:

1.-some synergy emerges from the union, because firms' resources are better allocated.

II.- previous undervaluation of assets existed prior to the merger

III.- there is sorne redistribution of benefits from stakeholders to target stockholders

and from these to acquiring firms through control processes.

The reasons why value creation takes place with the alliance among. the most

mentioned are undervaluation, leveraging, and signaling.

Undervaluation in target stocks occurs as a result of large inflationary periods

and long public ownership. This makes mergers a very profitable business for target

firms, however the increased value is now shared with the acquirers.

Leveraging is referred to be explaining why target stocks increase the most.

Leverage reduces dividend disbursements so favoring cash and increasing after tax

retum. Also, it stimulates managers performance.

Favorable signaling is referred to be present in explaining higher variation in

the target stocks, because a low price is interpreted by investors befare the merger

process. Different reasons explain motives and results for mergers.

Combining assets and creating moriopoly power in sorne restructuring countries

has explained merger gains. Tests for market concentration have been performed to

account for socially unfair distribution of benefits resulted in merger processes.

Protection from government in mergers is an additional source of value

redistribution for its impact on monopoly creation, tariff protection, over regulation,

and overpricing.

17

Tax advantages Cor mergers is other variable that has becn spcciiicd to cxplain

higher stock variations. However. as it will be seen in the next chapter, most studies

have found this variable to be of low reliability and low significance.

In many countries the "noisc" or sentiment theories hold that mergers create

hubris expectations that exceeds value creation so a lower postevent stock

performance would be observed correcting the announcement stock variation.

Downsizing is also in the '"name of the game ., for man y mergers: spinning off

divisions into independent status, repurchasing shares or establishing leveraged

buyouts, forming out new owned subsidiaries and so on are part of the same .process.

Sorne other important remaining theories for why mergers occur and they are

said to create value are:

Efficiency theory: Agency theory; Managerialism theory; Winner's Curse -

Hubris theory; Free Cash Flow theory; Market Power theory; Taxes theory;

Redistribution of Wealth theory: Govemment Privatization theory, Cultural and

Organizational Compatibility theory, and Financia! Globalization theory,.

Efficiency theory2 has severa! expressions. Among the most mentioned are:

Differential Managerial: Inefficient ivfan2.gement; Operating Synergy; Financia!

Synergy; Pure Diversification; Strategic Realignment and Undervaluation theory.

Differential efficiency

This theory presumes that the acquiring fim1 is more efficient than the target

one -or viceversa - in terms of management or operations, so there is an increase in

social value from the merger that makes investors to raise their price expectations.

Inefficient management

: A capital market is efficient ( 1) if it does not negleciany infomiation relevant to the determination of sccurily priccs. and (2) if it has rational e\pcciaiions (Fama. 1976)

18

According to this theory, Mergers result from the idea that some other

management group can run the business 111 a better way, due to cultural or

geographical advantages. This theory proposed the idea of mergers· between

companies that are not distinctly related, but led by efficient managers temporarily

will perform much better. This argument has been used to describe the period of

government enterprises during the thirty years after the 1929 crisis.

Operating synergy

Economies of scale result as a consequence of indivisibility, complementary, and

better utilization of capacities after merger. This theory applies to vertical and

horizontal integration that increases communication and coordination while reducing

bargaining costs and other wastes. The accepted Financia! Wisdom (Doctrine) from

Jensen (1984), refers to the company's increased productivity in achieving positive

stock price changes, rather than from market power.

Pure di versification

Mergers increase value due to investor preferences for diversification,

reputation, and tax advantages. Risk is said to be reduced, as a result of tumover and

reorganization. So, it is expected that the overall measure of returns increases.

Financia! synergy

In this theory, the cost of capital is reduced as a result of lower bankruptcy

risks. This theory assumes that the cash flows between the two firms are not perfectly

correlated, so the merger will benefit debt holders at the expense of shareholders

(Higgins and Schall, 1975). Financia! synergy, also describes the idea of excess cash

flow in bidders and good gro\v1h potential in targets. Many successful mergers

19

appcar to be related to this theory. For examplc, the merger between Phillip Morris

and General f oods in 1987, allowed Phillip Morris to combine their cash flow (but

low growth potential) with the high growth potentiai (low cash flow) of General

Foods.

Strategic realignment

From a strategic point of view, changes in the environment call for rapid

adjustments among firms to gain competitive advantages, or simply to survive.

Merging suggests the idea that long run strategy is taking place and so!'Tle other

favorable announcements will be given. As a result the the market will create

unexpected synergies. This long-run view contrasts greatly with the short run excess

cash flow theories, where rapid adjustments occur in the market.

Undervaluation

Because of agency considerations, long term investments are undervalued by

investors (prohibiting short term earnings), so they become attractive for raiders and

when merged, result in stock increases. Also, as a resHlt of long periods of inflation,

replacement costs increase more rapidly than stock value, making it more profitable

to merge than to build a new company. This theory may be highly valid in Mexico,

where merging increased after short periods of three digit hyperinflation.

Information and signaling

An alliance conveys information to the market that it had not realized befare.

For instance that the merger will strength both companies. Thus, brands multiply for

both companies, so the market anticipates value creation through brand synergy.

Recent theoretical research on market efficiency 11 links expectations with

information, saying that the investors are able to gain sorne information from prices.

20

Therefore, rational cxpectations are csscntial to markct erticicncv so mcrgcr

information is csscntial.

Agcncy problems and managerialism

When managers own a portian of the firm's equity, they may become more

interested in merger possibilities than otherwise because of the potential increase in

their stockholdings . Very often this theory anticipates low success from a merger

due to inefficient alliance investments. Additionally, managers seek to protect their

privileges, or even more to increase them, and they find mergers a good \\.'.ª):'. of doing

so; their salaries become adjusted to the size of the firm. Therefore, expenses grow

and dividends may fall.

Winner's curse - hubris

Managers of sorne bidding firms may assess the target value higher than the true

value for presumptuousness or hubris (Roll 1986), therefore, the bidders firm

reputation increases due to a combination of psychological and informative

imperfections. Market may react to to.is overestimation increasing hubris

expectations. No value is created so it expects in the long run it will adjust downward.

The free cash flow hypothesis

Excess cash flow would usually be paid to the shareholders as dividends, but

this would reduce the amount of resources that managers can control. Managers tend

to prefer short term retums rather than long term retums.

Thus, managers tend to invest the free cash flow in mergers or to increase debt

in exchange for stock (Jensen, Michael 1988) which conflicts principals in the short

run. while it promises higher long term returns. Thus, the mechanism utilized to ally

will anticípate higher stock returns.

21

Markct powcr

Alliances rnay increases market share for the acquiring firm, whether or not

this be necessarily good. If the new cornbined companies'market share is higher than

the eme allowed by the government, there may be more problems than advantages

(antitrust regulation). Economies of scale and power considerations are more

important to stimulate mergers if cartels are allowed or tolerated. lf this is not the

case. too concentrated market power may discourage consumers in buying in such a

market. Competition means to consumers an attraction regarding quality_ and fair

price; this may increase international demand and the perspectives of the firm become

favored.

Tax shields

Theory affirms that mergers may be tax induced only if there are no other

forrns of obtaining the tax deductions. Mexican legislation <loes not allow the transfer

of tax credits between separate firms, although managers can find sorne other ways

for transferring legal allowances. According to this theory, taxes niay affect mergers

rate to take advantage of tax allowances (Smirlock. Beatty, and Majd. H. 1986). This

theory indicates that target stockholders will be taxed higher because of capital gains.

Nevertheless although tax allowances may influence the decision to merge, they are

not the important factor.

A legitimate business must exist apart from the tax advantage. Otherwise the

merger is undesirable. regardless the availability of tax credit. For instance recapture

of depreciation allowances due to mergers mitigates the incentives. Similarly, good

will. which is not tax deductible. stimulates mergers, and can be much more

important than tax shields in the long run.

22

.Iones and Taggart ( 1984) combined !he !ax thcory with the theory of the life

cyck ancl rcach intercsting conclusions. Thcy say that young iirms lind merger with

high taxed firms, favorable because the formcr has more expenses than income. When

thc younger finr. grows, it becomes more attractivc to sell it to a corporation.

Afterwards the organization will be better off in the hands of low tax firms such as a

royalty trust or another younger firm.

This theory seerns appropriate for small and medium cnterprises

technologically advanced, such as computer components, software, specialized

sen·ices and so on, where economies of scale exists.

Redistribution of wealth

In a merger sorne redistribution occurs among stakeholders. Value may shift

from bondholders to stockholders and from labor to stockholders or consumers

(Asquith and Kim 1982: Dennis and McConnell 1986). For instance, when

leveraging, the firm cash flow increases, managers compensations increase and

possibly consumers' welfare reduce as prices go up.

Cultural and organizational compatibility

One of the most important new paradigms that are leading the expansion and

development of alliances worldwide is that cooperation has to be combined

appropriately with competition in arder to compete successfully. Speed and pace in

strategy implementation orients critica! decisions in a world of superior products and

internationalization. Today's decision maker needs not only to function m a

competitive and hostile environment but also to be able to cooperate with other

companies. perhaps even with one that. in other respects. is his competitor.

For many multinational firms. strategic alliances have become increasingly

important tools for cnsuring specd and tlcxibility ll1 carrymg out thcir businesses

strategics. Firms engaging in allianccs. it was recognizcd save rcsourccs. time. and

energy by combining projccts, resources. clicnts. etc.

For instance, Fiat-Geotech saw the need to changc its strategy to onc of

cooperation with others. To avoid an anticipated increase in European protectionism

and to attempt to enlarge its markct share, HCM began to search actively for a joint

venturc partner in Europe. This resulted in 1987 in Fiat-Hitachi Excavators SPA with

in a 51/49% joint venture to manufacture and thc market a new Iine of hvdraulic

excavators in Europe.

Mergers under agency theory.

Severa! explanations regarding reasons to ally are derived from agency theory.

According to these explanations tax shields, managers bonus-oriented behavior, of the

lack of adequate monitoring of managers create a tendency for sorne firms to establish

strategic alliances. These explanations are based on the belief that managers

controlling more companies should earn more. This stimulates alliances and if

managers are owners there will be a tendency to look for underYalued companies, to

buy them and to take advantage of stock appreciation as weli as tax shields increasing

debt/equity ratios.

Financia! globalization.

Among the theories that explain the causes and circumstances under which

alliances occur, the one related with the internationalization of capital has particular

relevance for this study. Lower international entry regulations, trade liberalization, as

well as the expansion of information systems sho11ened the intemational product life

cycle so creating the need to rapidly cover wider markets ..

Changes in the international financia! market accelerated the intemational

capital mobility with that volatility went up. This. ho\,·ever, has permitted developing

24

economies to reccivc big inflows of capital, not only to the bond markct but also to

the stock market. Alliances in this process, increased consistently with the higher

international sharc in stock trading -and issuance- by foreign institutional investors.

Financia! globalization is defined as the generation of a market structure

characterized by the flows of capital at world leve! by international and national

agents who induce a greater diversification and expansion of the sources and uses of

financia! funds (Mexican Stock Warehouse, 1994).

Financia! globalization has changed portfolio management looking for higher

returns. This stimulated higher volatility interest rate during the eigh_ties. Thus

im·estors found in alliances high expected retums.

In this context. Mexico went into the world economic integration. Its inclusion

in the General Agreement on Tariffs and Trade (GATT) and the recent decision to

form part of the trilateral Free Trade Agreement with the United States and Canada,

accelerated Mexico s is financia! and trading globalization process.

Different sources of funds emerged altogether with LDC21 debt problem. The

greater mobilization of international funds shrank world interest rates, exchange rates

~md inflation rates. This changed the ways firrns used to make businesses. Finance

oriented corporations looked for a reduction in their financia! costs from traditional

banking to other self-financing methods such as mergers.

The intemationalization of Mexican sources of funds increased the issuance of

convertible bonds, options, and ADR 'son Mexican shares in other countries.

There new financia! instruments enabled alliances principally the ones related

to the securitization of assets. The sale and trading of bank loans with securitized

stock as collateral and the issuance of securities that act as substitutes for loans (such

as commercial paper, floating rate promissory notes and europromissory notes) as

\vell as their sale in thc secondary market helped foreign firms to approach each other

signalling thc market to stirnulate allianccs.

25

The devclopment or financia! markets supported the idea or firms risk sharing.

This stimulated the expansion of international capital flows, specially since 1985.

This flow went from $444 billion dollars in 1985 to $5.1 trillion dollars in 1995. The

decline in financing for developing countries was offset by a higher leveraging of

banks and prívate firms from emergent bond markets

lssuance of bonds from emergent markets grew considerably. Total issues rose

from $38 billion dollars in 1980 to $256 billion dollars in 1989, and $800 billion in

1994, an increase of more than 1000% in the period.

Sorne money carne to developing countries as investrnents but most on

securities bascd collaterized loans. In the 1983-94 period there was a net reduction of

funds for LDC countries increasing capital expansion through banking, directly to

company, and through the rnarket system, which opened an increasing process of

international strategic alliances, principally mergers and acquisitions.

The greater foreign participation in developing countries' stock rnarkets was

concentrated principally by institutions such as pension funds, insurance companies,

investment funds, and for big companies and big investors. These assets grew at an

annual rate of 18% frorn 1987/1994. The argentine rnarket grew 250%, Mexico

260%, South Korea 85% and Taiwan 310%, while the developed markets grew only

13%.

Price/eamings and price/book value ratios were lower on average in LDC

countries relative to developed countries. This financia! expansion accelerated

mergers, acquisitions, and other strategic alliances in Mexico.

26

CIIAPTER II

MEXICAN STRATEGIC ALLIANCES: 1989-1996

In the last few years there have been a number of impor1ant stratcgic allianccs

in Mexico. A review of few most recent ones is presented here.

According to a study from The First Boston Corporation. mergers and

acquisitions, including privatization in Mexico, totaled $7.2 billion in 1992. In

addition and Mexican companies issued $4.3 billion in equity on New York stock

exchanges. This feature was similar throughout the early 1990' s. For_ ~\'.ample

Telefonos de Mexico alone amounted to $1. 76 billion from the privatization in

1990 and the subsequent equity offerings.

On September 1992, there was announced a $520 million investment of Bel!

Atlantic in Grupo Iusacell, the national cellular carrier in Mexico that competes with

Telmex. This merger opened a strong competition in a previously monopolized

market.

Rodrigo Calderón, from Siemens- AlcateL announced the acquisition of

Teletra Industrial SA de CV with presence in Italy, Spain, Brazil and México.

Another strengthening in Alcatel operations was the merger with Rotwell Inc.

Besides it is targeting Italcable and Stet, with operations in Italy.

Northern Telecom initiated joint ventures with Matra from France and STC

from England, to build submarine cable for Mexican-European communication.

Also important is its association with Motorola to forro the firm Motorola Norte! to

expand the production and service through networks. Also importan! was the

agreement with Nippon Telegraph and Telephone Corporation. With these alliances,

competition in telecommunication services has been growing in México.

McCarthy, Joscph (1993) studied the most important cement company m

Mexico, Cementos Mexicanos, (Cemex). This company shelled out SSOO million in

27

1989 to acquirc cemcnt companics in Mexico, Texas, and California and another

$1.9 billion last year far majority holdings in 2 Spanish cement companics. as well

as investments in Nicaragua and Venezuela. The acquisitions made Cemcx the

largest cement company in North America and the 4th-largest in the world.

Howevcr, McCarthy says Cemex disappointed shareholders, who worried that

the company was no longer the monopoly in the Mexican construction market.

Investors, particularly U.S. investors, have questioned the amount of debt needed to

finance Cemex the transactions and has expressed doubts regarding whether If the

company has sufficient international management expertise.

Moody's Investors Service placed Cemex's senior debt rating on re\'Íew after

the Spanish purchases, although the company rnaintained its Ba-2 designation. For

the year ended December 31, 1992, Cemex sales jumped 29% to $2.2 billion while

net incorne rose 24% to $548 million, including $8.5 million from the Spanish

compames.

Is the telecommunication industry, Telecommunications Inc. agreed to acquire

Grupo Televisa while Grupo Azteca (Channel 13 on Television), his competitor,

formed an alliance with NDC.

Peagam, Norman; Marray, Michael (May 1993 p: 133-134) studied \1exico's

Grupo Televisa which grew as the dominant media empire in the Spanish-speaking

world, involved in network and cable television, radio, the music business, and

magazme publishing throughout its home markets - Spain, the US, and Latín

America.

Televisa dominates the Mexican television market, with an estimated 93% of

the audience. In 1992, sales grew by 33 .5% to N$4.23 l billion ($1. l 08 billion),

65% accounted from television revenues. Operating profits grew 57% to N$643

million.

28

Nafta incrcased the potcntial far advcrtising in Spanish so Televisa increased

value evenly since 1990. Besides television high market share. in July 1992,

Televisa became the biggest publisher of Spanish-language magazines in the world

as a result of its $130-million acquisition of the Latín American and US businesses

of America Publishing Group. The high speed of expansion is being matched in

Latin America, with sorne other joint ventures or acquisitions in Peru, Chile,

Venezuela, Argentina. and Mexico itself.

Hartshom, David, (1993) reviewed the joint venture of PanAmSat with

Televisa in 1994. Grupo Televisa SA agreed to invest an aggregate amou~1L_of $200

million for a 50% senior equity position in PanAmSat's global satellite

communications system. The backing equips Anselmo has to compete more

extensively against Intelsat; The alliance also enables Grupo Televisa to establish a

stronger presence intemationally linking key Latín American markets with the

world.

The researcher said that Grupo Televisa's investment, along with other

financing obtained from PanAmSat, will be used to build, launch, and insure 3

additional satellites that PanAmSat has contracted to purchase frorn Hughes Aircrdt

Co. With the existing PAS-1 satellite, the new satellites will cover the Atlantic,

Pacific, and Indian ocean regions, creating the world's only privately-owned global

satellite communications network.

Conger, Lucy (1993) rated the privatization of the Mexican financia! system

as one of the world's most successful privatization programs where the more salient

feature was the overvalue paid to the govemment. as well as the formation of

corporate financia! groups within the Mexican financia! system. Of the 18 banks that

the govenunent sold off, 12 were bought by brokerages, having paid 2.5 to 5 .3

times book value for their banks

29

Thc main characteristic in thc privatization of thc banking systcm was the

clash bctwcen the brokerages and the banks to form these Financia! Uroups.

Santillan, Roberto ( i 995) also studied the privatization process of the Mexican

Banks, concluding that significant value creation took place.

Concentration of financia! power has been supported by the Mcxican

Governmcnt (recall from 60 to 19 institutions). Mexico's 1990 Financia! Groups

Law provides the legal framework for a universal banking system. The government

hopes that a few dominant institutions will be both easier to regulate and more

internationally competitive.

Profits in the financia! groups have been huge, but in the 1995 debt crisis

these institutions claimed higher government support via Fobaproa, a former trust

from Central Bank, Banxico. Fobaproa banking capitalization objective is giving

rapid results. The capitalization process increased bankers resources and at the same

time more government support. However, the magnitude of the crisis woke mergers

and strategic alliances to be formed to exchange new capital -mostly foreign- for

debt, overcoming capitalization problems in the short run. Within the most recent

strategic a.lliances and mergers regarding the banking system have been the

following:

In February 1995, Banamex entered into a joint venture with American

Express to issue Gold Cards to Mexican consumers. With deposits of $25 billion,

Banamex controls almost 25% of the country's deposit base, including 50% of

Mexico City.

Banoro and Bancreser merged to position number 8 in the financia! system.

Banco Union (who had restructured BCH bank) merged with Cremi, a former mine

specialized bank. Months Iater, Banca Cremi and Banco del Centro joined together

and formed an alliance with Banco Santander (Spain) in 1996.

30

Grupo Invcrlat-Comermex mcrged with Bank of Montrcal in 1995 whilc

Grupo Financiero Bancomcr (thc second largest bank in México) formcd alliancc

with I3ank of Toronto in 1996.

Other institutions are looking for partners as well as sorne foreigners are

targeting other Mexican financia! survivors, as Banco Internacional who formed an

alliance with Portuguese institutions as well as Banco Central Hispano in 1995.

Following its globalization objectives, and after expanding operations to UK.

Spain, Taiwan and South Korea, Metropolitan Life has acquired 24.5% interest in

Seguro Genesis, a Mexican carrier. Madrid-based Banco Santander joined Met with

a matching 24.5% holding. The remaining 51 % is held by Mexican investors.

Seguro Genesis began issuing life and pension products August 14, 1992. with Met

providing administrative support and advice.

The insurance broker Johnson & Higgins (J&H) is forging ahead with plans

for increased trade between the US and Mexico by acquiring 25% of the largest

broker in Mexico, Brockman y Schuh.

Besides the financia! institution, Wood Andrew detected information

regarding the 1993 acquisition of ABS by General Electric Pbstics Mexico. GE

acquired the commercial acrylonitrile butadiene styrene (ABS) operation of

Industries Resisto! SA (IRSA), part of the Mexican conglomerate DESC. This

conglomerare issues in the Mexican brokerage house as well as it has issued debt

paper and ADR s in USA.

Humder and Alperwicz (1993) provides inforrnation regarding the red iron

oxide pigments business. New entrant Laporte, bought Silo, the 3rd largest producer

worldwide in January 1993 for $9 million. With this acquisition, Laporte is

competing with Bayer, the leader and the number 2 worldwide producer Harcros.

This latter bought Pfizer's iron oxide business in 1990 and Northem Pigments, the

solc Canadian producer. in 1991.

31

Laportc entercd the business 111 early 1992 with its USO $60 million

acquisition of formulator Rockwood. In Mcxico, the numbcr 2 produccr, Hako, a

subsidiary of holding company Gerlo, bought the number one producer De Mato

from Fero in 1992.

A very mentioned Mexican mcrger has been the $477 million acquisition of

Grupo Modelo by Anheuser-Busch Cos. Inc. who agreed to acquire approximately

18% of Grupo Modelo SA de CV. The investment agreement, gives Anheuser

Busch an option to purchase up to 49% of Grupo Modelo over the next 4 years.

However, the investment agreement does not include new distribution arrangements.

Grupo Modelo will invest half of the proceeds from the sale in expansion,

including a brewery in the state of Zacatecas. The remainder will be divided among

the existing partners, who have continued controlling the company.

Hidrosina S.A.de C.V., a group of prívate Mexican investors led by 3

entrepreneurs, purchased 30 gasoline stations in Mexico City from Petroleas

Mexicanos (Pemex), the state-run monopoly. The historie move could signal future

joint ventures with foreign marketers.

The Pemex divestiture could create sorne important companies as well as

stimulates sorne interesting mergers. For instance, distribution of liquid gas for

domestic use was privatized in the State of Mexico and Querétaro. Also , Pemex had

announced the creation of two new firms that will merge to Grupo PMI Comercio

Internacional (PMI Holdings North América, Inc. and PMI Norteamérica, SA de

CV).

Currently other firms that are subsidiaries of PMI outside the country are PMI

Holdings NV, in Curazao, Antillas Holandesas; PMI Holdings BV, in Amsterdan,

Holland, and PMI Services B V, also in Holland. Also, PMI Services North America

INC. with a branch in Houston, PMI Services Europe, L TO, in London. England;

32

Pemex Internacional Espaí'ía, SA. in Madrid, Spain, and J>MI Trading LTD, in

Dublin, Republic of Ireland.

Alperowicz, Natasha (Nov. 1992), studies new trends in thc cngineering and

construction industry. She mentions two important new paths: the acquisition of

proprietary technology and the drive to get more international business, usually

through an acquisition or alliance with a regional partner. Another trend is achieving

preferred contractor status. Researcher Alperowicz found in The North American

Free Trade Agreement an upper interest in Canada · and Mexico for strategic

alliances. Therefore, in November 1992, Fluor Daniel Inc., (lrvine, C::<!lifornia)

a1U1ounced an exclusive association with ICA Industrial (Mexico City).

Other interesting recent alliances in Mexico have been the one of Empresas La

Moderna with Asgrow Seed Co (USA) on November 7, 1994, Banacci ( Mex) with

MCI (US) on October 17, 1994; Wall-Mart and Cifra and Dillard Department Stores

(US) on October 14, 1994; GF Bancomer and VISA (Mex) with-GTE Corp (US) on

September 27, 1994; Refmex of Industrias Penoles (Mex) with Indresco (US) on

August 16, 1994.

Also interesting have been the alliances bdween Baja Celular of Grupo

Protexa (Mex) with Motorola (US) on June 23, 1994, joint venture; Parker Lafarge

(US) with Cementos Mexicanos (CEMEX) on May 18, 1994 to sell a cement plant

in New Braunfels, Texas; Consorcio G. Grupo Dina S.A. de C.V (Mex) with Motor

Coach Industries International, Inc. on January 28, 1994, merger agreement.

Kayser-Roth Corp (US) allied with Grupo Synkro (Mex) on November 23,

1993; Grupo Mexico (MEX) with ASARCO (USA) on November 13, 1993;

Rodman & Renshaw Capital (US) with Abaco Casa de Bolsa (Mex) on November

1993; Compañia Industrial de Parras (Mex) with Cone Milis Corp. (US) on March,

1993.

33

Fomento Economico Mexicano (Femsa) with Coca-Cola Co (US) on March

25. 1993; Fomento Economico Mexicano (Femsa) with Philip Morris (US) on

December 3, 1992; Geo New York Life (Mex) with New York Life Worldwide

Developments on September 23, 1994.

Valves and Pipe Fittings, NEC (Mex) with Kitz Corp of America on July 14,

1994 "plan joint venture"(in negotiation); Del Monte Foods Corp (US) with Group

of Investors on June 27, 1994; Mobilon with Nextel Communications June 6, 1994;

AXA's ( Mex) subsidiary Alimentos with Lee (Sara) Corp/ AXA on March 2, 1994.

A Group Led by Carlos Cabal Had Agreed to Buy PPI Del Mont~ Fresh

Produce. Backed by the Mexican government, the Cabal group will purchase PPI

Del Monte from Polly Peck International PLC for $500 million. The move by

Grupo Cabal represented a bid by Mexican agribusiness interests to become bigger

players in the world fruit market by acquiring one of the big names. Unfortunately,

this alliance had problems to succeed for judicial problems of Mr. Cabal.

Technology Corp (USA) on November 20, 1993 established a "Joint-Yenture"

Grupo Azteca (Mex) with National Broadcasting Co (NBC) November 16, 1993,

"plans to acquire interest in". Ford Motor Company's Favesa S.A. de C.V. with

Lear Seating Corporation, a subsidiary of Lear Holdings, on November 1993

completed the previously announced purchase of most of shares. Electroforjados

Nacionales SA de CV with Harsco Corp. on November, 1993. Tapetes Automotrices

Mexicanos SA de CV Tamex with Collins & Aikman Corp (Doblin Textiles) on

November 1, 1993.

Yirmar Telecomunicaciones SA de CV with American Telephone &

Telegraph Co ATT on September 23 1993. Pacific Star de Occident (Mex) with

Pillsbury Co (The) on September 3, 1993 "agrees to acquire interest in". Aceros

Fortuna, S.A. de C.V (Mex) with Carpenter Technology Corporation on July 29,

34

1993 ·'agrced to acqu,re equity". Kennedy Agentes de Seguros (Me:-.:) with

Alexander & Alexander Services July 26, 1993 "acquired majority".

Novaquirn S.A. de C.V. (Mex) with Uniroyal Chernical Co on· July 26.

1993, joint venture. Brockman & Schuh (Mex) with Johnson & Higgins on J\fay 24.

1993 "agreed to acquire interest in". Arancia SA (Mex) with CPC International on

October 31, 1994 "joint venture". Altos Hornos de Mexico SA with Inland Steel

Industries Inc. October 17, 1994 joint venture. Auto Todo of Mexico with Genuine

Parts Co September 8, 1994 joint venture.

Grupo Iusacell SA (Mex) with Sprint Corp on July 26, 1994 "joint venture''.

Ispat Mexicana with Wheeling Pittsburgh Corp's steel, July 6, 1994 joint \·enture.

Grupo Video Visa (Mex) with Handleman Co on .Tune 2, 1994, "joint venture''.

Grupo Industrial Alfa SA de CV with Shaw Industries Inc. on May 31, 1994 "joint

venture".

Grupo Financiero Bancomer SA with NationsBank Corp.on April 15. 1994

"joint venture". FINSA Grupo Arguelles of Mexico with Morrison Knudsen Corp.

on March 1, 1994 "joint venture". Transportes de Nuevo Laredo, Mexico with

Roadway Services Inc June 1, 1993, "joint venture''.

Consorcio Larmo (Mex) with Durakon Industries Inc on March 23, 199 ··joint

venture". Grupo Industrial Durango with Temple-Inland Inc on January 6. 1993

"joint venture". El Puerto de Liverpool (Mex) with Kmart Corp on January 4. l 993

"joint venture" Compute with Acer on Jun 14, 1994 "joint venture".

Also important is the 50/50 merger between Holiday Inn Worldwide and