Stock-picking in defensive sectors will be key to ... - Davy

86

January 4, 2012 Research Report: Outlook for the year ahead Davy on 2012 Stock-picking in defensive sectors will be key to outperforming market in uncertain environment www.davy.ie Bloomberg: DAVY<GO> Research: +353 1 6148997 Institutional Equity Sales: +353 1 6792816 Davy Research Davy Research [email protected] / +353 1 6148997 Uncertain economic outlook for Europe in 2012 • The euro area sovereign debt crisis has led to a collapse in consumer and business confidence. • It is now likely that the euro area will experience a double-dip recession in 2012. • The combination of weak domestic demand and slowing exports will likely slow 2012 UK and Irish GDP growth forecasts to below those experienced in 2011. Equity markets will find it difficult to make progress • Consensus is forecasting mid-single-digit percent top-line growth and double-digit profit growth. We believe that this will be difficult to achieve in this economic environment • 2012 therefore could be another year of earnings downgrades. • In this environment, careful stock picking in defensive sectors is likely to be the key to outperforming the market. Top picks characterised by growth and balance sheets • Our top picks by sector, outlined in Table 2, are characterised by companies that can grow the top line in any environment combined with strong balance sheets and cash flow. • Our short recommendations are based on those companies with stretched balance sheets where the risk to earnings is firmly to the downside. • In absolute terms we like Kerry, Glanbia and Südzucker but we believe that Holcim, ArcelorMittal and Air France KLM will struggle in 2012. Please refer to important disclosures at the end of this report. J&E Davy, trading as Davy is regulated by the Central Bank of Ireland. Davy is a member of the Irish Stock Exchange, the London Stock Exchange and Euronext. For branches in the UK, Davy is authorised by the Central Bank of Ireland and subject to limited regulation by the Financial Services Authority. Details about the extent of our regulation by the Financial Services Authority are available from us on request. All prices are as of close of December 30th. All authors are Research Analysts unless otherwise stated. For the attention of US clients of Davy Securities, this third-party research report has been produced by our affiliate, J & E Davy. Highlighted content Equity markets – stock picking will remain a critical skill in terms of generating positive absolute and relative returns Economy – combination of weak domestic demand and slowing export growth paints grim picture for Irish economy in 2012 Construction and building materials – our top picks are Wolseley, HeidelbergCement, CRH and Geberit Steel – declining steel production in China is driving down iron ore prices Paper and packaging – a key milestone for Smurfit Kappa Group in 2012 will be refinancing its 2013 and 2014 loan maturities Food and beverage – Kerry Group should navigate the food sector headwinds and maintain growth momentum; C&C and the spirits players are our top beverage picks Pharmaceuticals and healthcare – biotechs provide exposure to organic growth potential and the prospect of ultimate partnering/acquisition by the cash-rich, legacy pharma sector Transport and logistics – low-cost carriers remain our preferred plays; Deutsche Post DHL favoured name among logistics stocks Gaming – our top picks are Paddy Power and William Hill Resources – oil price strength will help Dragon Oil, Tullow Oil and Premier Oil Financials – deleveraging remains the key to 'rightsizing' the sector Media – focus on cash generation continues for Independent News & Media Support services – DCC will continue to acquire niche, higher margin businesses

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Stock-picking in defensive sectors will be key to ... - Davy

January 4, 2012

Research Report: Outlook for the year ahead

Davy on 2012

Stock-picking in defensive sectors will be key to outperforming market in uncertain environment

www.davy.ie Bloomberg: DAVY<GO> Research: +353 1 6148997 Institutional Equity Sales: +353 1 6792816 Davy Research

Davy Research [email protected] / +353 1 6148997

Uncertain economic outlook for Europe in 2012

• The euro area sovereign debt crisis has led to a collapse in consumer and business confidence.

• It is now likely that the euro area will experience a double-dip recession in 2012.

• The combination of weak domestic demand and slowing exports will likely slow 2012 UK and Irish GDP growth forecasts to below those experienced in 2011. Equity markets will find it difficult to make progress

• Consensus is forecasting mid-single-digit percent top-line growth and double-digit profit growth. We believe that this will be difficult to achieve in this economic environment

• 2012 therefore could be another year of earnings downgrades. • In this environment, careful stock picking in defensive sectors

is likely to be the key to outperforming the market. Top picks characterised by growth and balance sheets

• Our top picks by sector, outlined in Table 2, are characterised by companies that can grow the top line in any environment combined with strong balance sheets and cash flow.

• Our short recommendations are based on those companies with stretched balance sheets where the risk to earnings is firmly to the downside.

• In absolute terms we like Kerry, Glanbia and Südzucker but we believe that Holcim, ArcelorMittal and Air France KLM will struggle in 2012.

Please refer to important disclosures at the end of this report.

J&E Davy, trading as Davy is regulated by the Central Bank of Ireland. Davy is a member of the Irish Stock Exchange, the London Stock Exchange and Euronext. For branches in the UK, Davy is authorised by the Central Bank of Ireland and subject to limited regulation by the Financial Services Authority. Details about the extent of our regulation by the Financial Services Authority are available from us on request. All prices are as of close of December 30th. All authors are Research Analysts unless otherwise stated. For the attention of US clients of Davy Securities, this third-party research report has been produced by our affiliate, J & E Davy.

Highlighted content

Equity markets – stock picking will remain a critical skill in terms of generating positive absolute and relative returns

Economy – combination of weak domestic demand and slowing export growth paints grim picture for Irish economy in 2012

Construction and building materials – our top picks are Wolseley, HeidelbergCement, CRH and Geberit

Steel – declining steel production in China is driving down iron ore prices

Paper and packaging – a key milestone for Smurfit Kappa Group in 2012 will be refinancing its 2013 and 2014 loan maturities

Food and beverage – Kerry Group should navigate the food sector headwinds and maintain growth momentum; C&C and the spirits players are our top beverage picks

Pharmaceuticals and healthcare – biotechs provide exposure to organic growth potential and the prospect of ultimate partnering/acquisition by the cash-rich, legacy pharma sector

Transport and logistics – low-cost carriers remain our preferred plays; Deutsche Post DHL favoured name among logistics stocks

Gaming – our top picks are Paddy Power and William Hill

Resources – oil price strength will help Dragon Oil, Tullow Oil and Premier Oil

Financials – deleveraging remains the key to 'rightsizing' the sector

Media – focus on cash generation continues for Independent News & Media

Support services – DCC will continue to acquire niche, higher margin businesses

Research Report: Davy on 2012 January 4, 2012

2 Davy Research

Contents

Stock ratings 4

Outlook for equity markets 6 Top picks for 2012 6

Euro area slowdown poses clear downside risks to economic outlook for 2012 10 Outlook for the Irish economy 12 UK struggling with the fiscal adjustment 15

Market summary 16

Irish market summary 16 European market summary 18

Construction and building materials 20 Sector performance in 2011 20 Key themes for 2012 21 How key stocks are positioned for 2012 23

Steel 28 Sector performance in 2011 28 Key themes for 2012 28 How key stocks are positioned for 2012 29

Paper and packaging 32 Sector performance in 2011 32 Key themes for 2012 32

Food and beverage 34 Food sector performance in 2011 34 Key themes for 2012 34 How key stocks are positioned for 2012 35 Beverage sector performance in 2011 38 Key themes for 2012 39 How key stocks are positioned for 2012 42

Pharmaceuticals and healthcare 46 Sector performance in 2011 46 Key themes for 2012 46 How key stocks are positioned for 2012 47

Transport and logistics 51 Sector performance in 2011 51 Key themes for 2012 51 How key stocks are positioned for 2012 52

Gaming 56 Sector performance in 2011 56 Review of 2011's key events 56 Key themes for 2012 60 How key stocks are positioned for 2012 61

Research Report: Davy on 2012 January 4, 2012

3 Davy Research

Resources 63 Sector performance in 2011 63 Key themes for 2012 63 How key stocks are positioned for 2012 64

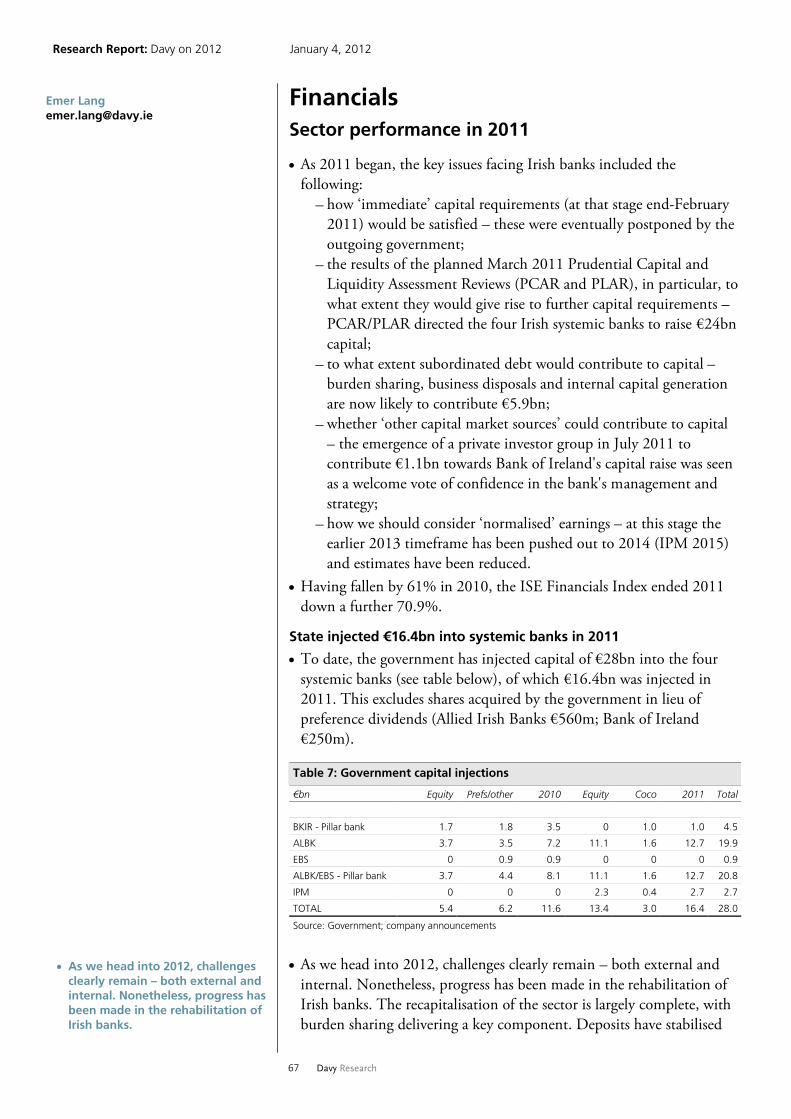

Financials 67 Sector performance in 2011 67 Key themes for 2012 68 How key stocks are positioned for 2012 69

Media 76 Sector performance in 2011 76 Key themes for 2012 76 How key stocks are positioned for 2012 77

Support services 79 Sector performance in 2011 and outlook for 2012 79 DCC – Performance in 2011 79 DCC – Key themes for 2012 79 CPL – Performance in 2011 80 CPL – Key themes for 2012 80

Important disclosures 84

Contacts 86

Research Report: Davy on 2012 January 4, 2012

4 Davy Research

Stock ratings

Table 1: Stock ratings

Sector Current rating Date of issue Previous rating Date of issue

Financials

Allied Irish Banks Under review 04/01/2011 Neutral 07/09/2010

Bank of Ireland Outperform 04/11/2011 Under review 04/01/2011

FBD Holdings Outperform 08/03/2010 Neutral 30/06/2009

IFG Group Neutral 16/09/2011 Restricted 04/05/2011

Irish Life & Permanent Neutral 04/01/2011 Outperform 30/06/2009

Airlines and other transport

Aer Lingus Outperform 23/04/2010 Neutral 30/06/2009

Air France KLM Neutral 09/09/2011 Underperform 13/01/2011

Amadeus IT Holding Outperform 08/11/2011

Deutsche Post DHL Outperform 26/01/2011

easyJet Outperform 22/07/2011 Neutral 19/04/2011

IAG Neutral 09/09/2011 Outperform 05/08/2011

Irish Continental Group Outperform 30/06/2009

Lufthansa Neutral 09/09/2011 Outperform 21/03/2011

PostNL Neutral 16/06/2011

Ryanair Holdings Outperform 07/12/2009 Neutral 02/11/2009

TNT Express Neutral 07/10/2011 Outperform 16/06/2011

Betfair Neutral 11/11/2011 Outperform 14/09/2011

bwin.party Under review 18/04/2011 Underperform 02/11/2010

Ladbrokes Outperform 14/08/2009 Underperform 30/06/2009

Paddy Power Outperform 30/06/2009

William Hill Outperform 16/02/2011 Neutral 03/09/2010

Construction and build mats

Buzzi Unicem Neutral 12/09/2011 Outperform 23/03/2011

CRH Outperform 12/09/2011 Neutral 13/06/2011

Geberit Outperform 12/09/2011 Underperform 14/01/2011

Grafton Group Underperform 12/09/2011 Neutral 03/03/2011

HeidelbergCement Outperform 04/09/2009 Underperform 30/06/2009

Holcim Neutral 22/08/2011 Outperform 19/03/2010

Italcementi Underperform 05/02/2010 Neutral 04/09/2009

Kingspan Group Outperform 12/05/2011 Neutral 30/06/2009

Lafarge Underperform 19/03/2010 Outperform 04/09/2009

Readymix Outperform 29/03/2011 Restricted 13/10/2010

Saint-Gobain Neutral 12/09/2011 Outperform 23/04/2010

SIG Neutral 12/07/2010 Outperform 30/06/2009

Siteserv Neutral 30/06/2009

Travis Perkins Neutral 03/08/2011 Underperform 16/05/2011

Wienerberger Neutral 12/09/2011 Outperform 22/02/2011

Wolseley Outperform 12/09/2011 Neutral 14/05/2010

Housebuilders

Abbey Outperform 30/06/2009

Barratt Developments Underperform 08/04/2011 Outperform 30/06/2009

Bellway Neutral 08/04/2011 Outperform 30/06/2009

Berkeley Outperform 08/04/2011 Neutral 30/06/2009

Bovis Homes Underperform 08/04/2011 Outperform 30/06/2009

Persimmon Outperform 30/06/2009

Redrow Underperform 08/04/2011 Neutral 10/09/2010

Taylor Wimpey Neutral 08/04/2011 Outperform 30/06/2009

Research Report: Davy on 2012 January 4, 2012

5 Davy Research

Ratings table continued

Steel

ArcelorMittal Underperform 10/11/2011

ThyssenKrupp Underperform 10/11/2011

Salzgitter Underperform 10/11/2011

Voestalpine Outperform 10/11/2011

Beverage

Britvic Neutral 25/02/2011 Outperform 27/09/2010

C&C Outperform 30/06/2009

Carlsberg Neutral 06/01/2010 Outperform 30/06/2009

Diageo Outperform 11/01/2010

Heineken Underperform 08/06/2010 Neutral 14/08/2009

Pernod Ricard Outperform 22/03/2011 Neutral 27/04/2010

Food

ARYZTA Outperform 14/06/2010 Neutral 30/06/2009

Associated British Foods Outperform 05/07/2011 Neutral 03/11/2010

Continental Farmers Group Outperform 05/08/2011

CSM Neutral 29/04/2011 Outperform 01/09/2010

Donegal Creameries Outperform 17/09/2010 Underperform 30/06/2009

Fyffes Outperform 27/01/2011 Neutral 18/02/2010

Glanbia Outperform 11/05/2010 Restricted 10/03/2010

Greencore Group Neutral 05/12/2011 Restricted 25/10/2011

Kerry Group Outperform 30/06/2009

Origin Enterprises Outperform 30/06/2009

Südzucker Outperform 12/02/2010

Tate & Lyle Neutral 04/04/2011 Underperform 13/08/2010

Total Produce Outperform 14/05/2010 Neutral 30/06/2009

Pharmaceuticals and healthcare

AGI Therapeutics Neutral 14/04/2010 Under Review 30/06/2009

Elan Corp Outperform 30/06/2009

ICON Neutral 27/10/2011 Outperform 05/08/2011

Merrion Pharmaceuticals Restricted 20/10/2011 Outperform 13/05/2011

Trinity Biotech Outperform 06/05/2011 Neutral 30/06/2009

United Drug Outperform 30/06/2009

Resources

Aminex Outperform 30/06/2009

Cairn Energy Underperform 25/11/2011 Outperform 25/05/2011

Dragon Oil Outperform 21/04/2011 Neutral 14/12/2009

Kenmare Outperform 06/04/2010 Restricted 12/03/2010

Ormonde Outperform 04/05/2011 Neutral 30/06/2009

Petroceltic Outperform 30/06/2009

Petroneft Outperform 18/12/2009 Neutral 30/06/2009

Premier Oil Neutral 25/03/2011 Outperform 14/07/2010

Providence Resources Outperform 09/06/11

Tullow Oil Outperform 30/06/2009

Other industrials/misc

Balmoral Intl. Land Neutral 08/03/2010 Outperform 30/06/2009

CPL Resources Outperform 30/06/2009

Datalex Outperform 13/12/2011 Neutral 30/06/2009

DCC Outperform 30/06/2009

NTR Under Review 12/11/2010 Outperform 16/10/2009

Smurfit Kappa Group Outperform 30/06/2009

TVC Holdings Outperform 30/06/2009

Independent News & Media Outperform 29/03/2010 Under Review 09/03/2010

UTV Media Neutral 30/06/2009

Source: Davy

Research Report: Davy on 2012 January 4, 2012

6 Davy Research

Outlook for equity markets Top picks for 2012

As we enter a New Year, it is difficult to see how companies can achieve top-line growth that will drive improvements in profitability. While we have become more positive on the outlook for the US relative to Europe, growth rates are likely to remain close to zero; in emerging markets, we believe that growth rates will continue to slow. Yet consensus estimates for equity markets in both the US and Europe are assuming mid-single-digit revenue growth and over 10% earnings growth in 2012. This also assumes that operating margins reach cycle-high levels. We believe these forecasts are too optimistic and will likely decline during the year. In this environment, it will be difficult for the overall market to make progress, and stock picking will remain a critical skill in terms of generating positive absolute and relative returns. In a slow/no growth environment, we look for stocks with a number of distinct characteristics:

strong cash flow and balance sheets, which will allow companies to pursue shareholder returns-enhancing activities such as acquisitions, share buybacks or more progressive dividend policies;

potential to generate positive returns over their cost of capital – in an environment of little or no growth for the foreseeable future, companies that are generating negative returns will find it difficult to restore returns and therefore will continue to destroy economic value;

ability to grow despite the macro environment – we are looking for companies providing innovation/technological solutions that will help other businesses or consumers to save money/reduce costs;

exposure to relatively more attractive end-markets – either sectorally or geographically – this may result in positive earnings revisions or at least limit negative revisions;

attractive valuation in absolute, relative and historical terms; decent income in terms of dividend yield. We have screened all of the stocks in our universe across all sectors under these criteria. We have identified the stocks we think will outperform and underperform the relevant sectors. These ideas, provided in Table 2, will help investors to generate positive relative returns in 2012. It is important to note that this analysis is based on our macro assumption of limited recovery in developed markets in 2012 and the likely slowdown in growth in most emerging markets. Of the names emerging from this analysis, on an absolute basis we like Kerry, Glanbia and Südzucker; on the short side, we think that Holcim, ArcelorMittal and Air France will struggle in 2012.

Barry Dixon, Head of Research [email protected]

Stock picking will remain a critical skill in terms of generating positive absolute and relative returns

Key stock characteristics in a slow/no growth environment

Strong cash flow and balance sheet

Potential to generate positive returns over the cost of capital

Ability to grow despite the macro environment

Exposure to relatively more attractive end-markets

Attractive valuation in absolute, relative and historical terms

Decent income in terms of dividend yield

Research Report: Davy on 2012 January 4, 2012 Table 2: Most and least preferred stocks by sector – 2012

Sector relative outperformers Sector relative underperformers

Industrials Construction and building materials

Wolseley US non-residential construction markets looking more positive. This represents almost 50% of trading profit.

Holcim Slower volume growth in India (20% of Holcim's profits), combined with excess capacity, makes for a difficult pricing and margin environment.

Substantial restructuring programme has resulted in disposal of underperforming/low-return businesses, improving profitability and returns and eliminating debt.

Low capacity utilisation levels will limit potential for cement price increases. This, combined with high input costs, will continue to put pressure on Holcim's margins in 2012 and likely result in further earnings downgrades.

Wolseley now has one of the strongest balance sheets in the sector, which will allow it to pursue returns-enhancing activities including acquisitions, share buybacks and a more progressive dividend policy.

The relatively high rating is based on its perceived low debt levels. With net debt/EBITDA of close to 3.0 times in 2012, it is not the safe haven it is perceived to be.

Lafarge With net debt of almost €12bn at end-2011 and net debt/ EBITDA of 3.6 times, Lafarge has one of the most indebted balance sheets in the sector.

Free cash flow of less than €900m will increase the pressure to continue to sell assets/businesses. We think it could struggle with execution of these deals.

Many of Lafarge's end-markets will continue to struggle, particularly in Africa-Middle East. A sluggish top-line, combined with ongoing margin pressure, could result in further downgrades to earnings forecasts.

ArcelorMittal We expect Chinese steel demand to slow from an estimated 11% in 2011 to 5% or below in 2012 as domestic demand weakens across a range of sectors.

Steel producers in Europe and North America continue to operate at c.70% capacity utilisation. Weaker domestic demand, combined with increased pressure from Chinese imports, will continue to put pressure on steel prices.

While raw material costs (mainly iron ore) will likely fall, the decline will not be sufficient to offset the impact of falling steel prices – causing margins to further contract.

With net debt of over $25bn and negative free cash flow in 2011, ArcelorMital can ill-afford any further deterioration in its earnings forecasts. However, we think that this is inevitable.

Resources

Dragon Oil Adjusted for cash set aside for abandonment, Dragon had $1.35bn in net cash at end-September. It is also producing over 62,000 barrels of oil per day with cost at the lower end of the curve. This production profile is set to grow to 100,000 barrels per day by 2015 using capital and reserves within the scope of the existing asset base.

Cairn Energy Cairn Energy’s transition from developer and producer back to a rewarding explorer is taking more time and money than originally envisaged. Instead of finding itself in a sweet-spot, Cairn has fallen between two stools.

EV per barrel is low at 2.7x if gas is included in reserves and it is trading at a material discount to our current NAV per share of 632p (which itself is built out on an $85 per barrel oil price).

Management’s focus for value creation is now on its exploration portfolio, which is narrow and dominated by Greenland. The market is suffering from Greenland fatigue, which may only be surmounted by a discovery.

New management is solid and has put in place the asset base to maximise the output potential of its Turkmen assets. While this growth trajectory produces material top-line growth in itself, we think management attention will increasingly shift to additional growth vectors. To this end, value-enhancing deals are a real possibility – especially in a market favouring cash-rich buyers.

However, drilling activity in 2012 is not guaranteed. This means the market may wait another 12 months for a drilling event to unlock substantial value.

Transport and logistics

easyJet easyJet generates £400m in free cash flow (pre-capex). As capex slows, we believe that this will be returned to shareholders in the form of special dividends similar to the £150m being paid in March 2012.

Air France KLM Air France is the most highly indebted company in the sector with net debt of over €6.5bn at end-2011 and free cash flow in 2011 estimated at just €75m. The decline in underlying profitability in 2012 will likely result in negative free cash flow.

Slower capacity growth has the added benefit of allowing more active management of fares. This will help to offset increasing costs, enhancing margins and returns.

The company is highly exposed to the premium traffic market, which we believe will continue to suffer in terms of both loads and yields in 2012. This could result in further margin and earnings pressure.

Well placed to attract business and consumer traffic down-trading from flag carriers in a difficult environment. Business offering enhanced by the launch of its 'Flexi-fare' product.

Management has few levers to pull apart from a dilutive rights issue in order to repair its balance sheet.

Research Report: Davy on 2012 January 4, 2012 Table 2 continued

Sector relative outperformers Sector relative underperformers

Ryanair Ryanair generates c.€1bn in free cash flow annually pre-capex. In the absence of a new aircraft deal and little or no debt on the balance sheet, a significant portion of this could be returned to shareholders in the form of special dividends similar to the €500m returned in 2011.

IAG IAG as a whole has c.10% premium traffic (c.45% of passenger revenue). This is clearly exposed to any downturn. Premium traffic tends to lag business confidence (PMIs) by three to six months. Of its corporate revenue, banking, professional and other services (e.g. telcos) represents 63%.

Slower growth in capacity will result in greater ability to actively manage yields upwards, which will help to offset cost increases and enhance margins.

Further earnings pressure could come from industrial relations problems in Iberia, while potential acquisitions such as BMI will take time to embed and enhance value.

Ryanair will continue to grow high-margin ancillary revenues, harvesting its 80m passenger base.

While net debt to capital is relatively low (c.31.1%), a high level of capital expenditure to renew the long-haul fleet should see this rise and we expect IAG to be free cash flow negative in 2012 and 2013. While the recovery plan is on track, the pension deficit remains at c.£2.5bn with a review due in March 2012.

Amadeus Amadeus' GDS business will benefit from growth in travel in emerging markets and from its IT Services business.

Lufthansa Representing some 25% of operating income, Lufthansa cargo is exposed to declining air cargo. The night-time flying ban at its hub at Frankfurt Main will also suppress profits.

Its transaction-based model offers exposure to the long-term growth in the global travel industry without the traditional volatility associated with the airline sector. This is reflected in its returns, which are 4x its cost of capital.

With almost 50% of long-haul passengers exposed to the premium end of the business, Lufthansa is exposed to a potential decline in this high yielding traffic.

Amadeus generates €500m in free cash flow annually, which will be used to pay down debt and enhance shareholder value.

The proposed investment of a 29.2% stake by Etihad in Air Berlin highlights the potential for increased competition by the Gulf carriers over time.

Consumer Food & Beverages

Südzucker Positive pricing environment for sugar is likely to continue as demand grows, inventories remain at low levels and the structure of EU market stays favourable for large processors.

Heineken Heineken, the most exposed of the brewers to difficult European markets (c.40% of EBIT), is likely to see little profit growth in 2012.

Supported by the cash flow of its quota sugar business, SZU's outward expansion could gather momentum. The significance of the imminent ED&F Man acquisition is under-appreciated by the market in our view. Ex-sugar additional investments may also be considered in the likes of its CropEnergies (ethanol) and Beneo (ingredients) units.

The company has flagged 2012 as a year of investment (primarily on its Global Business Services project and the funding of a needed step-up in marketing investment); combined with higher input cost pressures, potentially negative operating leverage due to declining volumes in Europe, less incremental benefit from its cost savings programme and increasing competitive threats in key emerging markets, this leads us to keep our cautious stance on Heineken's prospects for 2012.

The strength of the balance sheet (net debt/EBITDA well below 1x) will also allow SZU to fund a large increase in dividend in 2012.

Kerry Leading player in the global food ingredients market that will continue to develop and acquire ingredients technologies to drive top-line growth.

One-Kerry strategy will continue to deliver margin enhancements, helping to offset the impact of higher input costs.

The company generates €250m in free cash flow; with €1bn of debt and over €600m in EBITDA, it is well positioned to fund continued organic and acquisition-led growth.

Glanbia The company has established a leading position in whey-based global nutritionals, a sector where underlying volume growth remains strong. Product line reformulation, international expansion and further acquisitions all remain on the agenda.

There is a prospective growth opportunity for Glanbia in Irish milk processing which will arise from quota removal.

An anticipated step-up in free cash flow will provide more scope to invest for organic and acquisition-led growth.

Gaming

Paddy Power Paddy Power has by far the best earnings track record in the sector. Betfair We have concerns that when the new CEO takes over in August, he may make difficult strategic decisions that impact earnings in the short term.

This, combined with significant scope for earnings upgrades and arguably the best strategic positioning of any European gaming company, makes the stock a lock-away for portfolios.

It continues to face regulatory risk with some countries, including Spain, not allowing exchanges to operate.

Paddy Power has the least regulatory risk of all of the companies in our gaming universe. The stock trades close to our fair value of 825p.

Source: Davy estimates

Research Report: Davy on 2012 January 4, 2012

9 Davy Research

We have also identified a number of small-cap names that we think will provide significant upside in 2012.

Table 3: Small-cap opportunities in 2012

Stock Sector Comment

FBD Financials - Insurance A joint venture with its 25.6% shareholder, Farmer Business Developments, reduces FBD's exposure to property assets – a notable impediment for potential shareholders up to now – and puts the focus firmly back on the core insurance business with its dominant farming market position.

The insurance business is supported by a strong balance sheet (60% cash/bonds), a product of FBD's strategy of de-risking. 2011 looks set to be a very strong year, driven by benign claims; two upgrades (by c.19% in aggregate) since August put operating EPS guidance in a 155-165c range.

FBD has got no credit for its property JV or earnings upgrades, continuing to trade at a modest single-digit P/E. In addition, the prospect of improved returns from the core insurance business (ROE>20%) strengthens the case for a progressive dividend policy, enhancing the share’s attractiveness.

Origin Enterprises Agribusiness Management has done a great job in re-strategising the business over recent years. It is now firmly focused on agronomy and agri inputs, both of which continue to benefit from increasing farm incomes and an inexorable rise in global food demand.

With net debt/EBITDA of circa 1.2 times, it has the financial clout to invest to maintain growth around core activities (non-core activities are a potential source of cash on sale).

The share price is behaving as though activities are more strongly calibrated to commodity food prices than is in fact the case.

The shares are outstanding value.

Ormonde Mining Metals & Mining Ormonde is set to develop an important source of non-Chinese tungsten within the next 18 months. The project is located in western Spain and when fully commissioned will account for 12% of non-Chinese tungsten supply. Ormonde controls 100% of the project.

The project is technically very robust with at least ten years of mine life which can easily be extended. The price of tungsten is stable and has very solid supply demand fundamentals. The metal has strategic status.

The project will be financed over the next six months with numerous options open to management. On a pre-funding basis, the stock is worth more than twice its current value even applying a near-50% discount to current tungsten prices.

Source: Davy estimates

Research Report: Davy on 2012 January 4, 2012

10 Davy Research

Euro area slowdown poses clear downside risks to economic outlook for 2012 European recession now likely The key development since we published our last forecasts for the Ireland and UK economies has been the deteriorating outlook in Europe. The intensification of the sovereign debt crisis has led to a renewed collapse in consumer and business confidence. That deterioration in confidence appears to have led households and companies to postpone spending. Hence, purchasing manager indices (PMIs) for the European manufacturing and services sectors have fallen sharply. The PMIs have now fallen to levels that suggest eurozone GDP will contract in Q4 following a marginal 0.2% rise in Q3. With the latest EU summit agreement failing to address investors' concerns, no rebound in confidence appears likely in the near term. It is now likely that the euro area economy will experience a double-dip recession through Q4 2011 and Q1 2012.

European debt crisis will affect activity through three main channels

Funding costs As yields on sovereign debt have increased, they have passed through into bank funding costs within the euro area. This channel is likely to be less important for Ireland given that the sovereign is already reliant on official EU/IMF funding support. Similarly, Irish banks were already reliant on ESCB support and focused on aggressive deleveraging targets. So renewed tensions in European wholesale funding markets will have little direct impact on Ireland, where both banks and sovereign are already shut out of those markets.

Conall Mac Coille, Chief Economist [email protected]

A recession in the euro area now seems likely following the intensification of the European debt crisis

Figure 1: Eurozone PMIs

30

35

40

45

50

55

60

65

2007 2008 2009 2010 2011

Services Manufacturing

50 = no change

Source: Datastream

There are three key channels through which the debt crisis will affect the Irish economy, with export demand the most important

Research Report: Davy on 2012 January 4, 2012

11 Davy Research

In the case of the UK, gilt yields have remained close to historic lows as expectations for the Bank of England rate have been pushed out and the Monetary Policy Committee voted to expand its quantitative easing programme to £275bn, with expectations of additional asset purchases from February. That said, as in Europe, UK banks have seen pressure on their funding costs. In Q3, respondent to the Bank of England's Credit Conditions survey, lenders indicated that they planned to pass on higher funding costs to households and companies.

Confidence The intensification of the European debt crisis will mean that a restoration of depressed consumer confidence is less likely in the near term. Households are unlikely to reduce precautionary saving given uncertainty about employment and income growth. Similarly, uncertainty about euro area economic prospects has led firms to postpone investment plans. This trend is clearly evident in surveys of investment intentions, which have trended sharply downwards since September. In Ireland, levels of household and investor confidence were already low before the intensification of the debt crisis. Hence, household savings rates have remained about 10%, holding back consumer spending. Similarly, investment spending remains exceptionally weak in Ireland, around 25% of its peak level. While these factors have held back economic growth in Ireland, they could suggest that a sharp downward adjustment in savings behaviour is less likely in 2012. In contrast, there has been relatively little adjustment in the UK economy by households. The household savings ratio was 7.4% in Q2 2011, up from 5.9% the previous quarter. These levels are well below those in the early 1990s recession when the UK household savings rate reached a peak of 12.0%. In part, the lack of upward pressure on the UK household savings rate must reflect the historic low Bank of England rate. But if economic prospects deteriorate, a key risk for the UK is that households will respond in a more similar fashion to their counterparts in Ireland. Indeed, the GfK and Nationwide surveys of consumer confidence point to a renewed deterioration in the final quarter of 2011. Up to the third quarter, the prospects for UK investment appeared relatively promising. Respondents to the Deloitte survey of Chief Financial Officers indicated that on balance they did not plan to continue deleveraging their balance sheets or reduce their exposure to risk. Furthermore, companies felt that the cost of external finance was attractive. However, a clear trend in the UK investment intentions surveys is that uncertainty concerning economic prospects in the euro area has led companies to postpone investment spending.

Export demand Clearly weaker euro area growth will depress demand for both Irish and UK exports. Irish GDP growth in 2011 has been completely dependent on the export sector. That said, Ireland's exports are concentrated in niche sectors, some of which are defensive in nature and may fare relatively well in a recession. Nonetheless, Irish export growth is likely to slow in 2012, depressing a key platform for GDP growth.

Household savings rates have remained about 10%, holding back consumer spending. Similarly, investment spending remains exceptionally weak in Ireland, around 25% of its peak level.

Weaker euro area growth will depress demand for both Irish and UK exports

Research Report: Davy on 2012 January 4, 2012

12 Davy Research

In the UK, it had been hoped that the large depreciation in the sterling exchange rate in 2007 was finally being felt in a reallocation of resources towards the export sector. But UK export growth has clearly disappointed expectations in 2011, failing to compensate for the weakness of domestic demand and the fiscal adjustment that the coalition government has implemented. The weaker outlook for euro area demand will make it harder for the UK economy to rebalance towards the export sector as the coalition continues the planned fiscal consolidation.

But the outlook remains especially uncertain with both upside and downside risks emanating from policy responses to the debt crisis Our central view is that the ECB/EU/IMF will continue to meet the funding needs of European sovereigns and banks so that a calamitous chain of sovereign defaults and bank runs is avoided. But those funding needs are likely to be met on an ad-hoc basis so that they remain a key factor undermining confidence both in markets and the wider economy. That said, a more activist policy response that alleviated market concerns could lead to an improvement in economic prospects. EU agreements may eventually be sufficient to restore the risk-free status of European sovereign debt despite the haircuts applied to Greek sovereign debt in 2011. If so, the ECB could still expand its existing securities markets programme, in a similar fashion to the Bank of England's asset purchase facility, leading to sharp reductions in sovereign bond yields and rebounding confidence. However, such a rosy scenario seems unlikely in the near term as the adequate policy responses remain elusive. Outlook for the Irish economy

Growth slowing in the second half of 2011 Irish GDP expanded at a brisk pace in the first half of 2011 before contracting in the third quarter. Overall, the average level of GDP in 2011 is 1.0% higher than in 2010. So our current forecast for calendar year GDP growth in 2011 to equal 1.1% is broadly on track, ahead of the out-turn for the final quarter of the year. If so, 2011 will be the first year of positive GDP growth for the Irish economy since 2007. However, GDP growth has been sharply split between the buoyant export sector and weak domestic demand. In the year to Q3, consumer spending had fallen by 4.0%. Investment spending had declined by 21.9% in the year to Q3,

although this largely reflected volatile aircraft orders and may rebound in Q4.

Government consumption contracted by 3.7% in the year to Q3. Weak domestic demand pushed down on imports, which fell by 3.2%

in the year to Q3. Exports were up 2.2% on the year, and the annual rate of growth is

likely to pick up in Q4 2011 as the 2.7% quarterly fall in Q4 2010 falls out of the annual comparison.

Our central view is that the ECB/EU/IMF will continue to meet the funding needs of European sovereigns and banks so that a calamitous chain of sovereign defaults and bank runs is avoided

More aggressive policy responses

could see a rebound in growth, but this seems unlikely in the near term

2011 will be the first year of positive GDP growth since 2007

Growth was split between a buoyant export sector and weak domestic demand

Research Report: Davy on 2012 January 4, 2012

13 Davy Research

GDP growth was also split between a strong performance in the first half, with quarterly growth of 1.8% and 1.4% respectively in Q1 and Q2, and a sharp 1.9% contraction in Q3. However, the fall in Q3 may be largely erratic as it was mainly related to volatile shifts in investment spending, specifically aircraft orders. Investment could easily rebound in Q4. Nevertheless, the exceptionally strong growth in the first half will not be repeated in H2.

Combination of weak domestic demand and slowing export growth paints grim picture for Irish GDP growth in 2012 Overall we expect that Irish GDP growth will slow in 2012 below the 1.1% we are currently forecasting for GDP growth in 2011. We plan to review our forecasts for the Irish economy in the near future. Uncertainty and weakening confidence following the intensification of the European debt crisis are likely to delay investment plans by Irish companies. That said, with nominal investment spending now just 22% of its peak level at €3.1bn in Q3 2011 and down from €5bn at the beginning of 2010, there is limited room for further large downward adjustments. Similarly, Irish households are less likely to reduce their high levels of savings given concerns about economic and employment prospects. Savings rates are likely to remain depressed despite the squeeze on real incomes from the fiscal adjustment, which this year will be implemented through higher value added taxes. That said, underlying inflationary pressures are likely to fall back through 2012, helping to alleviate the squeeze on real incomes.

Figure 2: Ireland real GDP (seasonally adjusted)

38

39

40

41

42

43

44

45

46

2008 2009 2010 2011

GDP

Billions, constant prices

Source: Davy; CSO

The rate of expansion is set to slow heading into the final quarter, ahead of a challenging 2012

Irish GDP growth is likely to slow in 2012 below the 1.1% expected for this year

Household savings are likely to remain high as concerns about economic prospects remain and despite the squeeze on real incomes from the fiscal adjustment

Research Report: Davy on 2012 January 4, 2012

14 Davy Research

Figure 3: European and Irish consumer confidence

-40

-35

-30

-25

-20

-15

-10

-5

0

2007 2008 2009 2010 2011

20

40

60

80

100

120

140

European Consumer Confidence Irish Consumer Confidence

IndexIndex

Source: Datastream

However, the most worrying impact of the European debt crisis on the Irish economy will be through reduced export demand. Thus far, Irish trade in goods data up to October do not indicate any marked impact from the euro area slowdown on exports. Also, Figures 4 and 5 illustrate that Irish exports are concentrated in pharmaceuticals, food and beverages, and computer and IT services. So export prospects will in part depend on how these sectors perform in addition to aggregate global demand.

Nonetheless, reduced demand is likely to have a significant impact on Irish exports in 2012. As export growth slows, Irish GDP is likely to fall back from the rates of expansion seen in 2011 as domestic demand remains weak and as private spending growth fails to offset the ongoing fiscal adjustment.

Reduced demand is likely to have a significant impact on Irish exports in 2012

Figure 4: BOP data on services exports

Transport Tourism and Travel Communications

Insurance Financial Services Computer Services

Royalties Business Services Other Services n.e.s.

Source: Datastream

Figure 5: Disaggregated goods data by SITC

Food, Beverages and Tobacco Crude Materials, Semi-Manufactured Goods ,Fuels & Misc

Chemicals and Pharmaceutical Products Machinery and Transport Equipment

Other Finished Manufactured Articles

Source: Datastream

Research Report: Davy on 2012 January 4, 2012

15 Davy Research

UK struggling with the fiscal adjustment

Unlike Ireland, growth in the UK economy had already slowed sharply at the start of 2011. The level of GDP in the UK was broadly flat between Q4 2010 and Q2 2011 before a 0.5% increase in Q3. However, the rebound in Q3 is not expected to be sustained, with PMIs for both the manufacturing and services sectors falling back in Q4. Consumer confidence had fallen back sharply towards the end of 2010 as households realised the new coalition government's fiscal austerity plans were about to hit real incomes. Consumer spending has now contracted for the five consecutive quarters to Q3 2011.

Figure 6: UK GfK and Nationwide measures of consumer confidence

-50

-40

-30

-20

-10

0

10

2005 2006 2007 2008 2009 2010 2011

20

30

40

50

60

70

80

90

100

110

120

GfK Nationwide

BalanceIndex

Source: Datastream

Optimistic expectations for UK growth had focused on the gradual positive impact of the sterling depreciation on exports. But exports contracted in Q2 2011 and Q3 2011, and this poor performance precedes the weakening in euro area demand in Q4. In part, the weak UK export growth has reflected the specialisation of the UK in financial services exports which have been adversely affected by the global crisis. In the Autumn Budget Statement, Chancellor George Osborne was forced to dramatically revise up his projections for the UK deficit and debt over the medium term. UK general government debt is now expected to peak at 94% of nominal GDP, higher than in many of the UK's triple AAA rated peers. Hence, a key danger to the outlook for the UK is that a more severe fiscal adjustment may be required in Budget 2012 for the UK to maintain its top credit rating and hit the targets outlined in the budget statement. In our last UK economic forecast (mid-October), we expected GDP to contract in the fourth quarter, flatten off in Q1 and recover gradually thereafter. This implies calendar year GDP growth of 0.7% in 2011 and 1.0% in 2012. Since that time, however, conditions in the euro area have continued to weaken markedly and the revisions to our next UK projections are therefore likely to be to the downside.

Consumer spending has now contracted for the five consecutive quarters to Q3 2011

Measures of consumer confidence indicate that there may have been some small deterioration in the final quarter of 2011

Since our forecast in mid-October, conditions in the euro area have continued to weaken markedly so the revisions to our next UK projections our likely to be to the downside

16 Davy Research

Research Report: Davy on 2012 January 4, 2012

Irish market summary

S U M M A R Y Price Change % No. (m) Mkt Wght 11 Yr End 2011 Debt/(Cash)/EBITDA EBITDA €m* Company (c) Wk YTD Shrs Cap €m % Pr/Bk 11 12F 11 12F 13F

CRH 1536 2.7 -0.9 719 11043 25.8 Dec2011 E 1.04 2.0 1.6 1617.8 1714.7 1750.6 Ryanair Holdings 363 -3.5 -3.8 1479 5363 12.0 Mar2012 E 1.58 0.2 -0.5 881.8 878.4 955.1 Elan Corp (USc) 1374 6.6 147.4 587 6228 11.9 Dec2011 E 9.37 1.2 0.7 185.5 182.2 256.0Kerry Group 2829 2.3 13.3 176 4968 9.6 Dec2011 E 2.62 1.6 1.1 620.9 665.5 707.9 ARYZTA 3749 2.5 7.1 86 3235 7.5 Jul 2011 P 1.68 2.2 1.9 485.1 500.3 519.6 Paddy Power 4452 2.0 45.0 49 2168 4.4 Dec2011 E 6.99 -0.6 -0.9 139.5 155.7 164.0 DCC 1828 -1.2 -22.5 84 1527 3.6 Mar2012 E 1.51 0.8 0.5 268.6 289.6 298.9 Dragon Oil (USc) 548 -1.8 -12.6 511 2802 3.2 Dec2011 E 1.39 -1.4 -1.6 1100.5 1200.9 1031.4 Bank of Ireland 8 -5.8 -78.0 30133 2471 2.9 Dec2011 E 0.32 490.0 590.0 910.0 Glanbia 463 -0.5 25.7 295 1362 1.4 Dec2011 E 2.66 2.4 1.8 205.5 215.7 219.7 Top Ten Companies 1608.3 1.4 5.7 41167 82.3 1.36

Tullow Oil (USc) 1402 4.9 14.2 904 15198 Dec2011 E 4.11 1.3 1.3 2037.0 2221.0 2042.3 Kenmare (USc) 54 5.4 49.2 2410 1296 3.0 Dec2011 E 3.66 4.5 0.6 62.6 255.2 435.6 C&C 287 -0.2 -15.2 337 968 2.2 Feb 2012 E 1.36 -0.6 -1.1 133.3 139.3 145.0 Kingspan Group 636 -2.2 -15.1 167 1062 1.9 Dec2011 E 1.55 1.5 1.1 130.0 141.5 165.6 ICON (USc) 1711 2.3 -19.4 59 779 1.8 Dec2011 E 1.47 -2.4 -1.6 76.9 106.3 139.4 Smurfit Kappa Group 467 -0.2 -36.0 222 1036 1.6 Dec2011 E 0.53 2.9 2.8 1004.8 919.1 848.7 Grafton Group 239 -3.4 -30.8 231 552 1.2 Dec2011 E 0.57 2.5 2.2 95.9 97.2 110.1 United Drug 205 2.5 -2.4 239 489 1.1 Sep 2011 P 1.30 1.5 1.2 90.5 91.1 93.0 Irish Continental Grp 1517 1.1 -2.2 25 377 0.6 Dec2011 E 2.21 0.2 -0.1 49.0 55.0 58.4 Greencore Group (Stg) 62 -0.1 -38.5 385 242 0.6 Sep 2011 P 0.76 3.7 2.9 68.6 92.9 100.2 Trinity Biotech (USc) 1018 0.1 19.2 21 167 Dec2011 E 1.42 -3.6 -4.3 20.4 21.7 21.0 Aer Lingus 64 -1.4 -41.2 534 339 0.3 Dec2011 E 0.39 -2.0 -2.4 135.1 151.8 164.2 FBD Holdings 650 2.4 4.8 33 216 0.3 Dec2011 E 1.03 Total Produce 37 -2.6 -1.3 330 122 0.3 Dec2011 E 0.69 1.2 0.9 57.1 59.3 61.0 Origin Enterprises 305 1.7 -4.7 133 406 0.2 Jul 2011 E 1.86 1.3 0.9 71.2 70.4 71.0 Fyffes 36 0.6 -2.6 297 107 0.2 Dec2011 E 0.74 0.3 0.1 23.6 22.9 23.1 IFG Group (Stg) 84 0.1 -18.7 126 126 0.2 Dec2011 E 1.05 0.0 -0.5 24.9 25.7 26.0 Petroneft (USc) 18 -2.2 -74.0 412 88 0.2 Dec2011 E 1.06 1.2 0.6 20.9 42.2 68.9 Independent News & Media 21 0.0 -59.2 550 113 0.2 Dec2011 E 1.72 5.1 4.9 85.0 80.7 76.4 Allied Irish Banks 7 15.0 -77.0 513008 35398 0.2 Dec2011 E 3.11 -4.0 50.0 175.0 UTV Media (Stg) 93 -4.0 -30.5 96 106 0.2 Dec2011 E 0.68 2.0 1.4 28.7 30.9 31.4 Abbey 520 0.0 2.0 22 114 0.1 Apr2012 E 0.72 -5.2 -3.9 14.5 17.1 18.2 CPL Resources 255 0.0 0.8 37 95 0.1 Jun 2012 E 1.43 -3.6 -3.8 8.8 9.7 10.6 TVC Holdings plc 76 4.1 16.9 101 77 0.1 Mar2012 E 0.70 -23.8 -737.9 3.1 0.1 0.1 Donegal Creameries 310 -7.4 -22.4 10 31 0.1 Dec2011 E 0.49 2.2 1.7 10.0 11.8 12.0 Continental Farmers Group 28 0.0 N/A 163 46 Dec2011 E 0.65 -0.5 0.3 6.8 8.9 11.1 Datalex (USc) 35 0.1 74.7 72 25 0.0 Dec2011 E 0.99 -2.9 -2.2 4.4 7.5 8.1 Irish Life & Permanent 2 20.0 -97.8 36526 877 0.0 Dec2011 E 0.19 AGI Therapeutics (USc) 6 0.5 111.4 67 4 0.0 Dec2011 E 0.69 N/A N/A -3.3 -3.5 -3.5 Siteserv plc 2 0.0 -60.0 124 2 0.0 Apr2012 E 0.28 7.5 6.7 19.1 20.7 21.3 Readymix 4 0.0 -81.0 110 4 0.0 Dec2011 E 0.07 N/A 1.4 -6.5 6.9 8.3 Merrion Pharmaceuticals 21 13.9 -92.4 17 4 0.0 Dec2011 Total Market (ISEQ) 2901.8 1.3 0.6 86803 100.0 1.29

D A V Y S E C T O R I N D I C E S

Index Change % Mkt Wght Hist Hist

Wk YTD Cap €m % Pr/Bk ROE %

Banks 51.2 -4.8 -75.9 37868 3.1 0.32 N/A Other Financials 54.5 2.0 -57.1 1219 0.6 1.04 24.0 Total Financials 62.6 -3.8 -70.8 39087 3.6 0.34 N/A Mid-Caps 2428.9 0.9 -18.7 45636 17.7 1.02 9.2 Non-Financials 2930.4 1.6 5.1 47716 96.4 1.54 10.9 Construction 1672.2 2.1 -3.7 12778 29.0 1.02 5.3 Food & Beverage 4571.3 1.8 5.7 11443 22.0 1.91 15.8 Resource 250.8 4.1 10.2 19884 Extractive 53.6 4.0 22.2 1611

*Operating profit before provisions in place of EBITDA for Banks

17 Davy Research

Research Report: Davy on 2012 January 4, 2012

S U M M A R Y ( C O N T I N U E D ) Yield (%) Ent Value / EBITDA Dil. Adj. EPS (c) EPS Growth (%) P/E Ratio Company 11 12F 13F 11 12F 13F 11 12F 13F 11 12F 13F 11 12F 13F

CRH 4.1 4.1 4.1 8.3 7.4 6.9 83.9 93.1 96.2 1.2 11.0 3.4 18.3 16.5 16.0 Ryanair Holdings 0.0 0.0 0.0 6.3 5.6 4.2 29.9 30.2 35.5 11.3 1.0 17.3 12.1 12.0 10.2 Elan Corp (USc) 0.0 0.0 0.0 41.2 41.5 28.8 6.0 12.1 27.0 N/A 103.2 122.9 230.3 113.3 50.8 Kerry Group 1.1 1.2 1.3 9.6 8.5 7.6 211.9 228.0 243.9 10.3 7.6 7.0 13.4 12.4 11.6 ARYZTA 0.8 0.9 0.9 9.2 8.8 8.1 310.1 338.4 364.3 27.1 9.1 7.6 12.1 11.1 10.3 Paddy Power 2.2 2.7 2.8 14.9 13.0 12.0 201.9 231.6 243.0 16.5 14.7 4.9 22.0 19.2 18.3 DCC 4.1 4.3 4.5 6.5 5.8 5.2 187.9 207.6 221.0 -7.2 10.5 6.4 9.7 8.8 8.3 Dragon Oil (USc) 2.8 2.8 2.8 1.9 1.4 1.5 134.5 144.2 117.3 80.1 7.2 -18.7 5.3 4.9 6.1 Bank of Ireland 0.0 0.0 0.0 -8.6 -2.2 -0.5 N/A N/A N/A N/A N/A N/AGlanbia 1.6 1.7 1.8 8.7 7.8 7.2 43.3 45.6 46.9 13.7 5.3 2.9 10.7 10.1 9.9 Top Ten Companies 1.8 1.8 1.9 N/A N/A 28.9 N/A 18.7 14.5

Tullow Oil (USc) 0.5 0.9 1.0 11.0 10.2 11.2 94.4 106.6 91.9 N/A 12.9 -13.9 23.1 20.4 23.7 Kenmare (USc) 0.0 0.0 0.0 31.3 7.2 3.3 0.2 8.3 15.4 N/A N/A 85.0 452.3 8.4 4.5 C&C 2.7 3.0 3.0 6.5 5.6 4.7 28.4 31.1 33.2 17.1 9.5 6.9 10.1 9.2 8.6 Kingspan Group 1.9 2.3 2.7 9.7 8.6 7.0 37.0 42.5 55.2 17.4 14.7 29.9 17.2 15.0 11.5 ICON (USc) 0.0 0.0 0.0 10.8 7.9 5.8 54.1 93.3 139.7 -62.3 72.5 49.7 31.6 18.3 12.2 Smurfit Kappa Group 0.0 0.0 0.0 4.0 4.1 4.2 102.8 84.0 72.1 27.9 -18.3 -14.2 4.5 5.6 6.5 Grafton Group 3.1 3.4 3.8 8.3 7.9 6.8 15.0 16.0 21.0 -18.5 6.5 31.1 15.9 14.9 11.4 United Drug 4.2 4.4 4.5 6.7 6.3 5.8 22.8 23.9 24.8 0.0 4.9 3.5 9.0 8.6 8.3 Irish Continental Grp 8.8 6.6 6.6 7.3 6.2 5.5 110.2 136.6 152.1 -8.3 23.9 11.4 13.8 11.1 10.0 Greencore Group (Stg) 10.3 8.1 9.4 6.7 5.1 4.5 10.4 10.6 12.4 -7.4 1.9 16.2 5.0 4.9 4.3 Trinity Biotech (USc) 0.0 0.0 0.0 7.0 5.7 5.5 77.1 82.2 86.9 20.1 6.7 5.7 13.2 12.4 11.7 Aer Lingus 0.0 0.0 0.0 N/A N/A N/A 8.3 10.7 12.7 -45.7 30.2 18.3 7.7 5.9 5.0 FBD Holdings 5.1 5.4 5.7 151.4 149.3 153.7 54.7 -1.4 3.0 4.3 4.4 4.2 Total Produce 4.8 5.0 5.2 3.7 3.3 3.0 7.1 7.5 7.8 4.2 5.4 3.7 5.2 4.9 4.8 Origin Enterprises 3.1 3.3 3.4 5.1 4.7 4.3 40.2 44.4 46.8 7.7 10.6 5.4 7.6 6.9 6.5 Fyffes 5.2 5.8 5.9 2.9 2.8 2.5 5.9 6.0 6.1 7.4 1.4 1.9 6.1 6.0 5.9 IFG Group (Stg) 4.6 4.9 5.2 4.2 3.6 3.0 14.6 14.8 15.1 -3.6 1.6 2.2 5.7 5.6 5.5 Petroneft (USc) 0.0 0.0 0.0 6.7 3.4 1.7 2.1 4.7 9.1 N/A 130.6 91.3 13.5 5.9 3.1 Independent News & Media 0.0 0.0 0.0 3.0 2.7 2.3 9.0 9.4 9.2 -12.2 4.9 -2.1 2.3 2.2 2.2 Allied Irish Banks 0.0 0.0 0.0 -0.2 -0.6 -0.4 N/A N/A N/A N/A N/A N/AUTV Media (Stg) 5.4 8.6 8.6 5.1 4.3 3.7 18.3 20.3 20.9 9.7 10.8 3.0 5.0 4.6 4.4 Abbey 1.6 1.7 1.7 2.5 2.6 1.7 38.4 47.6 50.4 12.4 24.1 6.0 13.6 10.9 10.3 CPL Resources 2.4 2.7 2.7 7.2 5.9 4.9 25.4 27.5 30.2 17.6 8.5 9.6 10.0 9.3 8.5 TVC Holdings plc 0.0 0.0 0.0 N/A N/A N/A 3.9 0.9 0.9 -66.1 -77.4 -1.1 19.5 86.3 87.3 Donegal Creameries 5.2 5.2 5.2 0.5 N/A N/A 58.9 72.8 74.4 87.0 23.5 2.3 5.3 4.3 4.2 Continental Farmers Group 0.0 0.0 0.0 6.5 5.5 4.9 2.2 3.1 4.1 -31.4 38.2 34.4 12.6 9.1 6.8 Datalex (USc) 0.0 0.0 0.0 4.5 2.1 1.4 5.4 9.0 9.8 45.6 66.3 8.6 8.4 5.0 4.6 Irish Life & Permanent 0.0 0.0 0.0 -4.0 -0.7 -0.3 N/A N/A N/A N/A N/A N/AAGI Therapeutics (USc) 0.0 0.0 0.0 0.7 N/A N/A -5.0 -5.3 -5.3 N/A N/A N/A N/A N/A N/ASiteserv plc 0.0 0.0 0.0 7.7 6.8 6.5 2.3 3.6 4.5 330.6 54.6 27.7 0.9 0.6 0.4 Readymix 0.0 0.0 0.0 N/A 1.9 1.0 -11.4 0.1 1.0 N/A N/A N/A N/A 57.7 4.2 Merrion Pharmaceuticals Total Market (ISEQ) 1.9 1.9 2.0 N/A N/A N/A N/A 15.2 12.1

D A V Y S E C T O R I N D I C E S ( C O N T I N U E D ) Yield(%) 5 Year CAGR (%) EPS Growth (%) P/E Ratio 11 12F 13F EPS Dividend 11 12F 13F 11 12F 13F

Banks 0.0 0.0 0.0 N/A N/A N/A N/A N/A N/A N/A N/AOther Financials 4.9 5.2 5.5 27.7 8.9 32.2 -0.5 2.7 4.7 4.8 4.6 Total Financials 0.6 0.6 0.7 N/A N/A N/A N/A N/A N/A N/A N/AMid-Caps 2.2 2.2 2.4 -12.2 -19.3 4.0 23.9 19.8 10.0 8.1 6.7 Non-Financials 1.9 2.0 2.0 -2.0 -0.7 16.0 12.8 8.9 13.7 12.2 11.2 Construction 3.8 3.9 3.9 -17.6 2.7 2.0 13.4 7.4 18.3 16.1 15.0 Food & Beverage 1.6 1.6 1.7 7.8 0.5 14.4 7.7 6.8 11.3 10.5 9.8 Total Market (ISEQ) 1.9 1.9 2.0 -50.7 -40.5 N/A N/A N/A N/A 15.2 12.1

18 Davy Research

Research Report: Davy on 2012 January 4, 2012

European market summary S U M M A R Y

Price Change % (local) Change % (euro) Relative to E300 Mkt Cap Mkt Cap 11 Yr End EBITDA (c) Wk YTD Wk YTD Wk YTD (local m) (€m) 11 12F 13FA I R L I N E S Aer Lingus (AERL ID) 64 -1.4 -41.2 -1.4 -41.2 -2.5 -34.1 339 339 Dec 2011 E 135.1 151.8 164.2 Air France KLM (AF FP) 397 0.4 -70.9 0.4 -70.9 -0.8 -67.4 1193 1193 Dec 2011 E 1302.6 1176.5 1759.0 easyJet (EZJ LN) 393 1.8 -10.7 1.9 -8.3 0.8 2.8 1691 2027 Sep 2011 P 359.0 343.0 365.0 IAG (IAG SM) 174 -3.2 -45.3 -3.2 -45.3 -4.3 -38.7 3228 3228 Dec 2011 E 1478.5 1345.5 1529.5 Lufthansa (LHA GY) 919 0.1 -43.8 0.1 -43.8 -1.1 -37.1 4206 4206 Dec 2011 E 2483.0 2483.0 2797.0 Ryanair Holdings (RYA ID) 363 -3.5 -3.8 -3.5 -3.8 -4.6 7.8 5363 5363 Mar 2012 E 881.8 878.4 955.1

T R A N S P O R T L O G I S T I C S Amadeus IT Holding (AMS SM) 1254 3.2 -20.1 3.2 -20.1 2.0 -10.5 5610 5610 Dec 2011 E 1035.0 1148.0 1247.0 Deutsche Post DHL (DPW GY) 1188 1.9 -6.5 1.9 -6.5 0.8 4.8 14363 14363 Dec 2011 E 3782.6 3790.6 4032.4 PostNL (PNL NA) 246 5.2 -73.2 5.2 -73.2 4.0 -69.9 965 965 Dec 2011 E 533.0 551.0 595.0 TNT Express (TNTE NA) 577 1.5 7.9 1.5 7.9 0.3 5.8 3136 3136 Dec 2011 E 258.8 525.0 649.4

G A M I N G Betfair (BET LN) 753 -6.8 -21.9 -6.6 -19.8 -7.7 -10.2 787 943 Apr 2012 E 74.7 89.8 91.7 bwin.party (BPTY LN) 164 25.9 -20.2 25.9 -20.2 24.4 -10.6 1367 1638 Dec 2011 E 185.2 216.4 216.4 Ladbrokes plc (LAD LN) 130 5.9 6.0 6.0 8.9 4.8 22.0 1180 1415 Dec 2011 E 237.2 254.8 262.6 Paddy Power (PWL ID) 4452 2.0 45.0 2.0 45.0 0.9 62.4 2168 2168 Dec 2011 E 139.5 155.7 164.0 William Hill plc (WMH LN) 203 7.5 18.8 7.6 22.1 6.4 36.8 1423 1706 Dec 2011 E 296.2 301.8 307.4

C O N S T R U C T I O N Buzzi Unicem (BZU IM) 676 2.3 -20.8 2.3 -20.8 1.1 -11.3 1256 1118 Dec 2011 E 409.9 444.4 506.6 CRH (CRH ID) 1536 2.7 -0.9 2.7 -0.9 1.5 11.0 11043 11043 Dec 2011 E 1617.8 1714.7 1750.6 Geberit (GEBN VX) 18100 0.3 -16.3 1.0 -14.0 -0.2 -3.6 7212 5938 Dec 2011 E 550.0 589.0 632.5 Grafton Group (GN5 ID) 239 -3.4 -30.8 -3.4 -30.8 -4.5 -22.5 552 552 Dec 2011 E 95.9 97.2 110.1 HeidelbergCement AG (HEI GY) 3279 1.3 -30.1 1.3 -30.1 0.2 -21.7 6148 6148 Dec 2011 E 2306.0 2473.0 2631.0 Holcim (HOLN VX) 5025 0.4 -28.9 1.0 -26.9 -0.1 -18.1 16436 13532 Dec 2011 E 3856.0 4109.0 4393.0 Italcementi (IT IM) 456 -2.9 -27.9 -2.9 -27.9 -4.0 -19.3 1013 807 Dec 2011 E 751.2 784.7 870.4 Kingspan Group (KSP ID) 636 -2.2 -15.1 -2.2 -15.1 -3.3 -4.9 1062 1062 Dec 2011 E 130.0 141.5 165.6 Lafarge (LG FP) 2716 2.9 -42.1 2.9 -42.1 1.7 -35.2 7802 7802 Dec 2011 E 3299.0 3384.0 3488.0 Saint-Gobain Group (SGO FP) 2967 2.6 -23.0 2.6 -23.0 1.5 -13.7 15887 15887 Dec 2011 E 5006.0 5157.0 5557.0 SIG plc (SHI LN) 84 2.9 -34.7 3.0 -32.9 1.8 -24.9 496 595 Dec 2011 E 127.2 130.3 144.3 Travis Perkins plc (TPK LN) 796 -0.2 -24.8 -0.1 -22.7 -1.2 -13.5 1937 2322 Dec 2011 E 376.7 392.0 418.6 Wienerberger (WIE AV) 697 -0.2 -51.2 -0.2 -51.2 -1.4 -45.4 819 819 Dec 2011 E 256.7 263.5 291.5 Wolseley plc (WOS LN) 2132 2.5 4.2 2.6 7.1 1.4 19.9 6075 7282 Jul 2011 P 761.0 807.0 875.0

S T E E L ArcelorMittal (USc) (MT NA) 1413 0.9 -47.5 1.6 -45.9 0.5 -39.4 22056 22056 Dec 2011 E 9865.0 9560.0 10185.0 Salzgitter (SZG GY) 3863 -0.3 -33.1 -0.3 -33.1 -1.4 -25.1 2322 2322 Dec 2011 E 605.4 602.1 620.8 Thyssenkrupp (TKA GY) 1773 0.1 -42.8 0.1 -42.8 -1.0 -35.9 9119 9119 Sep 2011 P 3385.0 2946.0 3600.0 Voestalpine (VOE AV) 2167 1.0 -39.2 1.0 -39.2 -0.2 -31.9 3663 3663 Mar 2012 E 1662.0 1603.0 1661.0

H O U S E B U I L D I N G Abbey (ABBY ID) 520 0.0 2.0 0.0 2.0 -1.1 14.2 114 114 Apr 2012 E 14.5 17.1 18.2 Barratt Developments plc (BDEV LN) 93 2.0 4.8 2.1 7.7 1.0 20.6 897 1075 Jun 2012 E 206.1 249.4 253.8 Bellway plc (BWY LN) 713 2.5 6.3 2.7 9.3 1.5 22.4 861 1032 Jul 2011 E 76.3 89.3 96.3 Berkeley Group (BKG LN) 1276 -0.2 43.4 -0.1 47.3 -1.2 65.0 1675 2008 Apr 2012 E 131.3 151.3 177.7 Bovis Homes plc (BVS LN) 439 1.3 6.1 1.5 9.0 0.3 22.1 587 704 Dec 2011 E 31.6 47.6 64.7 Persimmon plc (PSN LN) 470 1.9 12.8 2.0 15.9 0.9 29.8 1420 1702 Dec 2011 E 173.7 229.3 234.1 Redrow plc (RDW LN) 113 -0.2 -16.5 -0.1 -14.1 -1.2 -3.8 350 419 Jun 2012 E 39.6 46.7 47.1 Taylor Wimpey plc (TW/ LN) 38 2.0 19.0 2.1 22.3 1.0 37.0 1201 1439 Dec 2011 E 153.2 172.6 190.9

F O O D ARYZTA (YZA ID) 3749 2.5 7.1 2.5 7.1 1.3 20.0 3235 3235 Jul 2011 P 485.1 500.3 519.6 Associated British Foods (ABF LN) 1107 0.3 -6.3 0.4 -3.7 -0.7 7.9 8764 10505 Sep 2011 P 1213.0 1351.0 1384.0 Continental Farmers Group (CFGP ID) 28 0.0 0.0 0.0 0.0 -1.1 -1.9 46 46 Dec 2011 E 6.8 8.9 11.1 CSM NV (CSM NA) 1208 1.2 -53.9 1.2 -53.9 0.1 -48.4 853 853 Dec 2011 E 209.5 226.5 268.3 Donegal Creameries (DCP ID) 310 -7.4 -22.4 -7.4 -22.4 -8.4 -13.1 31 31 Dec 2011 E 10.0 11.8 12.0 Fyffes (FFY ID) 36 0.6 -2.6 0.6 -2.6 -0.5 9.1 107 107 Dec 2011 E 23.6 22.9 23.1 Glanbia (GLB ID) 463 -0.5 25.7 -0.5 25.7 -1.7 40.7 1362 1362 Dec 2011 E 205.5 215.7 219.7 Greencore Group (Stg) (GNC LN) 62 -0.3 -38.7 -0.2 -37.0 -1.3 -29.4 239 242 Sep 2011 P 68.6 92.9 100.2 Kerry Group (KYG ID) 2829 2.3 13.3 2.3 13.3 1.2 26.9 4968 4968 Dec 2011 E 620.9 665.5 707.9 Origin Enterprises (OGN ID) 305 1.7 -4.7 1.7 -4.7 0.5 6.8 406 406 Jul 2011 E 71.2 70.4 71.0 Südzucker (SZU GY) 2465 0.1 23.7 0.1 23.7 -1.1 38.6 4668 4668 Feb 2012 E 1007.1 956.7 928.4 Tate & Lyle (TATE LN) 705 2.1 36.0 2.2 39.8 1.1 56.6 3287 3940 Mar 2012 E 451.0 458.0 472.0

B E V E R A G E Britvic plc (BVIC LN) 322 4.7 -32.0 4.8 -30.2 3.6 -21.8 777 931 Sep 2011 P 185.7 192.5 199.1 C&C (GCC ID) 287 -0.2 -15.2 -0.2 -15.2 -1.3 -5.0 968 968 Feb 2012 E 133.3 139.3 145.0 Carlsberg (CARLB DC) 40500 1.0 -27.5 1.1 -27.4 0.0 -18.7 61785 8316 Dec 2011 E 14167.0 15067.4 15994.6 Diageo (DGE LN) 1407 2.1 18.7 2.2 22.0 1.0 36.6 35162 42149 Jun 2012 E 3522.5 3746.2 4018.2 Heineken (HEIA NA) 3577 1.8 -2.5 1.8 -2.5 0.6 9.2 20604 20604 Dec 2011 E 3565.8 3689.0 3834.0 Pernod Ricard (RI FP) 7166 2.8 1.9 2.8 1.9 1.6 14.1 18982 18982 Jun 2012 E 2226.0 2376.0 2536.4

19 Davy Research

Research Report: Davy on 2012 Janaury 4, 2012

S U M M A R Y ( C O N T I N U E D )

2011 Debt/(Cash)/EBITDA Yield (%) Ent Value / EBITDA EPS Growth (%) P/E Ratio Pr/Bk 11 12F 11 12F 13F 11 12F 13F 11 12F 13F 11 12F 13FA I R L I N E S Aer Lingus (AERL ID) 0.39 -2.0 -2.4 0.0 0.0 0.0 N/A N/A N/A -45.7 30.2 18.3 7.7 5.9 5.0 Air France KLM (AF FP) 0.18 3.6 3.6 0.0 0.0 0.0 2.5 2.9 1.8 N/A N/A N/A N/A N/A N/AeasyJet (EZJ LN) 0.99 -0.2 0.3 11.6 1.9 2.1 4.4 5.3 4.8 75.2 -27.6 10.4 7.6 10.4 9.4 IAG (IAG SM) 0.68 1.1 1.4 0.0 0.0 0.7 1.9 2.4 2.5 265.2 -57.1 50.5 9.7 22.7 15.1 Lufthansa (LHA GY) 0.48 0.5 0.6 5.7 5.7 7.9 1.5 1.6 1.4 -57.3 -14.7 57.4 8.7 10.2 6.5 Ryanair Holdings (RYA ID) 1.58 0.2 -0.5 0.0 0.0 0.0 6.3 5.6 4.2 11.3 1.0 17.3 12.1 12.0 10.2

T R A N S P O R T L O G I S T I C S Amadeus IT Holding (AMS SM) 4.01 1.8 1.3 3.0 3.7 4.1 7.2 6.1 5.3 11.5 14.9 10.8 11.0 9.6 8.7 Deutsche Post DHL (DPW GY) 1.30 -0.4 -0.4 5.8 6.0 6.6 2.9 2.9 2.6 4.8 18.2 11.5 10.2 8.6 7.7 PostNL (PNL NA) 3.36 1.9 2.0 8.5 0.0 0.0 3.7 3.7 3.4 -46.9 4.1 13.9 4.6 4.4 3.9 TNT Express (TNTE NA) 1.47 0.2 0.1 1.1 2.0 3.0 12.4 6.1 4.8 -61.0 82.1 49.2 35.9 19.7 13.2

G A M I N G Betfair (BET LN) 4.54 -1.4 -1.5 1.9 2.1 2.1 9.2 7.3 6.8 -50.8 78.8 14.1 32.5 18.2 15.9 bwin.party (BPTY LN) 2.44 -2.9 -3.1 0.0 0.0 0.0 6.0 4.4 3.7 -3.3 24.8 0.0 13.7 11.0 11.0 Ladbrokes plc (LAD LN) 3.40 1.8 1.5 5.9 6.5 6.9 6.8 6.1 5.6 -16.6 11.2 9.4 9.0 8.1 7.4 Paddy Power (PWL ID) 6.99 -0.6 -0.9 2.2 2.7 2.8 14.9 13.0 12.0 16.5 14.7 4.9 22.0 19.2 18.3 William Hill plc (WMH LN) 1.49 1.3 1.1 3.5 5.2 5.5 6.1 5.8 5.4 -2.2 4.6 4.7 8.9 8.6 8.2

C O N S T R U C T I O N Buzzi Unicem (BZU IM) 0.54 2.8 2.4 0.0 0.7 0.9 5.8 5.2 4.4 -62.0 33.4 47.6 36.0 26.9 18.3 CRH (CRH ID) 1.04 2.0 1.6 4.1 4.1 4.1 8.3 7.4 6.9 1.2 11.0 3.4 18.3 16.5 16.0 Geberit (GEBN VX) 4.67 -0.9 -1.1 3.4 3.7 3.9 12.2 11.2 10.2 -2.1 6.5 8.8 17.7 16.6 15.3 Grafton Group (GN5 ID) 0.57 2.5 2.2 3.1 3.4 3.8 8.3 7.9 6.8 -18.5 6.5 31.1 15.9 14.9 11.4 HeidelbergCement AG (HEI GY) 0.48 3.4 3.0 1.5 3.0 3.0 6.0 5.5 5.0 -0.3 48.5 15.9 12.6 8.5 7.3 Holcim (HOLN VX) 0.90 2.8 2.4 3.0 3.0 3.0 7.4 6.8 6.0 -26.9 30.5 11.2 18.7 14.4 12.9 Italcementi (IT IM) 0.37 2.9 2.7 2.6 2.7 2.9 5.5 5.2 4.6 -5.5 7.2 18.7 29.7 27.8 23.4 Kingspan Group (KSP ID) 1.55 1.5 1.1 1.9 2.3 2.7 9.7 8.6 7.0 17.4 14.7 29.9 17.2 15.0 11.5 Lafarge (LG FP) 0.46 3.6 3.3 3.7 3.7 3.7 6.3 6.0 5.6 -24.1 8.0 12.8 9.8 9.1 8.1 Saint-Gobain Group (SGO FP) 0.84 1.4 1.3 4.2 4.7 5.6 4.6 4.4 4.0 31.1 12.1 15.1 9.0 8.0 7.0 SIG plc (SHI LN) 0.66 1.0 0.8 2.4 3.3 4.5 4.9 4.6 4.0 28.8 8.0 15.0 9.1 8.4 7.3 Travis Perkins plc (TPK LN) 0.89 1.6 1.2 2.5 2.8 3.1 6.6 6.0 5.4 16.5 4.7 9.3 9.1 8.7 8.0 Wienerberger (WIE AV) 0.26 1.9 1.8 1.7 2.0 2.3 6.5 6.4 5.7 N/A 167.4 75.1 56.9 21.3 12.1 Wolseley plc (WOS LN) 1.78 0.7 -0.1 2.1 2.8 3.3 8.6 7.5 6.6 91.4 12.9 13.1 15.0 13.3 11.8

S T E E L ArcelorMittal (USc) (MT NA) 0.42 2.6 2.5 4.1 4.1 4.1 3.8 3.7 3.5 -4.3 7.0 18.5 10.5 9.8 8.3 Salzgitter (SZG GY) 0.53 -1.0 -0.7 1.9 2.1 2.4 2.0 2.4 2.7 350.8 11.4 10.2 15.6 14.0 12.7 Thyssenkrupp (TKA GY) 0.82 1.1 1.2 2.5 1.4 2.3 3.8 4.5 3.6 N/A N/A 59.1 N/A 17.8 11.2 Voestalpine (VOE AV) 0.72 1.7 1.5 3.7 4.6 4.6 3.9 3.7 3.4 -2.6 3.8 8.3 7.3 7.0 6.5

H O U S E B U I L D I N G Abbey (ABBY ID) 0.72 -5.2 -3.9 1.6 1.7 1.7 2.5 2.6 1.7 12.4 24.1 6.0 13.6 10.9 10.3 Barratt Developments plc (BDEV LN) 0.30 2.1 1.8 0.0 0.0 0.0 6.1 5.1 5.4 265.5 49.1 3.9 11.5 7.7 7.4 Bellway plc (BWY LN) 0.81 1.7 1.6 1.5 1.7 1.8 12.9 11.1 10.1 42.7 13.2 8.9 16.9 14.9 13.7 Berkeley Group (BKG LN) 1.74 -2.4 -1.7 1.4 1.5 1.6 10.2 9.2 7.4 17.3 14.0 17.3 17.5 15.3 13.1 Bovis Homes plc (BVS LN) 0.80 0.2 1.1 1.4 1.8 1.8 18.6 13.3 12.1 43.7 59.5 39.7 28.8 18.1 12.9Persimmon plc (PSN LN) 0.78 -0.4 -0.0 1.9 2.2 2.2 7.7 6.2 6.4 47.0 39.2 2.4 13.1 9.4 9.2 Redrow plc (RDW LN) 0.74 2.6 2.1 0.0 0.0 0.0 11.4 9.6 9.0 83.2 23.6 2.5 15.6 12.6 12.3 Taylor Wimpey plc (TW/ LN) 0.66 0.7 1.1 0.0 0.0 0.0 8.5 8.1 7.3 114.7 115.3 40.2 29.1 13.5 9.6

F O O D ARYZTA (YZA ID) 1.68 2.2 1.9 0.8 0.9 0.9 9.2 8.8 8.1 27.1 9.1 7.6 12.1 11.1 10.3 Associated British Foods (ABF LN) 1.52 1.1 0.9 2.2 2.3 2.5 8.4 7.6 7.4 2.5 16.6 3.3 15.0 12.8 12.4 Continental Farmers Group (CFGP ID) 0.65 -0.5 0.3 0.0 0.0 0.0 6.5 5.5 4.9 -31.4 38.2 34.4 12.6 9.1 6.8 CSM NV (CSM NA) 0.74 3.1 2.8 7.6 8.0 8.4 7.2 6.6 5.4 -42.6 14.7 33.2 11.6 10.1 7.6 Donegal Creameries (DCP ID) 0.49 2.2 1.7 5.2 5.2 5.2 0.5 N/A N/A 87.0 23.5 2.3 5.3 4.3 4.2 Fyffes (FFY ID) 0.74 0.3 0.1 5.2 5.8 5.9 2.9 2.8 2.5 7.4 1.4 1.9 6.1 6.0 5.9 Glanbia (GLB ID) 2.66 2.4 1.8 1.6 1.7 1.8 8.7 7.8 7.2 13.7 5.3 2.9 10.7 10.1 9.9 Greencore Group (Stg) (GNC LN) 0.76 3.7 2.9 10.3 8.1 9.4 6.7 5.1 4.5 -7.4 1.9 16.2 5.0 4.9 4.3 Kerry Group (KYG ID) 2.62 1.6 1.1 1.1 1.2 1.3 9.6 8.5 7.6 10.3 7.6 7.0 13.4 12.4 11.6 Origin Enterprises (OGN ID) 1.86 1.3 0.9 3.1 3.3 3.4 5.1 4.7 4.3 7.7 10.6 5.4 7.6 6.9 6.5 Südzucker (SZU GY) 1.38 0.8 0.7 2.8 3.0 3.1 6.7 7.0 7.2 47.8 -3.5 -5.4 12.9 13.4 14.2 Tate & Lyle (TATE LN) 2.94 1.1 0.7 3.5 3.6 3.8 8.4 7.9 7.3 40.1 2.5 5.4 13.0 12.7 12.0

B E V E R A G E Britvic plc (BVIC LN) 35.23 2.4 2.3 5.5 5.8 6.1 6.7 6.3 6.1 -15.2 6.1 6.5 9.8 9.2 8.7 C&C (GCC ID) 1.36 -0.6 -1.1 2.7 3.0 3.0 6.5 5.6 4.7 17.1 9.5 6.9 10.1 9.2 8.6 Carlsberg (CARLB DC) 0.88 2.0 1.5 1.4 1.6 1.8 6.7 6.0 5.3 -1.9 14.2 12.3 11.8 10.3 9.2 Diageo (DGE LN) 5.25 2.0 1.5 3.0 3.2 3.4 11.4 10.4 9.2 8.4 9.5 8.5 15.5 14.2 13.1 Heineken (HEIA NA) 1.98 2.2 1.8 2.2 2.4 2.7 7.3 6.7 6.0 0.5 11.0 10.1 14.1 12.7 11.5 Pernod Ricard (RI FP) 1.88 3.8 3.2 2.1 2.4 2.7 12.4 11.3 10.2 13.0 12.2 10.1 15.4 13.7 12.4

Research Report: Davy on 2012 January 4, 2012

20 Davy Research

Construction and building materials Sector performance in 2011

European construction sector fell 20% in 2011

European construction stocks fell for a second year running. The E300 Construction & Building Materials Index fell 20% in 2011, which followed a 1% decline the previous year. The index has now fallen in four of the last five years and closed 2011 53% off its all-time high.

While the index gained 8% in Q4, its decline of 26% in Q3 proved decisive. The sector actually started 2011 reasonably well, gaining 2.8% in Q1, although this was given back in the second quarter.

Amongst the European construction stocks we cover, there were two discernible themes during 2011. First, the UK housebuilders outperformed. Berkeley was the clear winner last year, rising over 40%. However, all of the other UK housebuilders also gained, with the exception of Redrow (-16%). Second, the worst underperformers were typically those stocks with meaningful exposure to Continental Europe: Rockwool (-34%), SIG (-35%), Lafarge (-41%) and Wienerberger (-50%) all fell sharply.

Earnings in 2011 fell short of expectations

At the beginning of 2011, we identified what we considered would be the main themes for the European building materials sector for the year. These included: limited volume growth potential; rising energy costs; improving residential markets but a weak infrastructure sector; and the expectation that emerging markets would continue to outperform. We also suggested that if volume growth was achieved, there would a disproportionate increase in operating profits due to positive incremental margin effects.

As it turned out, 2011 operationally was another challenging year for the sector. We estimate that the sector's revenues (excluding the UK housebuilders) were up circa 3% last year; this was broadly in line with our start-of-year forecast of 3-4% growth. However, even though 2011 started well (helped by more benign weather compared to Q1 2010), there was a tangible slowdown in many markets towards year-end.

Limited revenue growth (when achieved, it was often more a function of price increases rather than volume expansion) along with the impact of higher input costs constrained the scope for margin improvement. EBITDA in 2011 was more or less unchanged year-on-year (yoy), well behind our expectation at the start of the year of circa 9% growth.

After a reasonable start to the year, evidence that tepid recovery had begun to stall by year-end

Construction markets and sectors generally performed as expected in 2011, although it became clear as the year progressed that what appeared to be the early stages of a recovery had stalled (even though activity levels in many end-markets remain well below pre-2008 levels).

Tim Cahill [email protected] Barry Dixon [email protected] Florence O'Donoghue [email protected] Robert Gardiner [email protected] Killian Murphy [email protected]

There were two discernible themes during 2011: UK housebuilders outperformed, and the worst underperformers were those with meaningful exposure to Continental Europe

Limited revenue growth along with the impact of higher input costs constrained the scope for margin improvement

Research Report: Davy on 2012 January 4, 2012

21 Davy Research

By country and region, Germany – albeit coming off a very depressed level – stood out. Residential activity in France was strong, while many Nordic end-markets did reasonably well. It was a disappointing year for the UK, with new residential and residential RMI at best remaining stable at a depressed level. Eastern European construction markets were patchy, although activity levels were healthy in Poland ahead of this year's UEFA football championships. But, overall, much of the early year momentum had long since evaporated by the end of 2011 as worries about austerity measures and the impact of the European sovereign debt crisis took centre-stage.

In contrast, there were very tentative signs of improvement in some US construction end-markets by the close of the year. Private construction volumes looked to have finally bottomed out in 2011, although concerns about infrastructure spending levels remain.

Focus on debt reduction continued

Corporate activity was, once again, extremely muted. If anything, many European building materials companies continue to be net sellers of businesses as efforts continued to lower debt levels and streamline operating structures. Lafarge, SIG, Wolseley and Italcementi all sold businesses during the year, while those that undertook significant deals in 2010 (Travis Perkins and Kingspan) focused on integration. CRH continued to undertake a number of relatively modest bolt-on transactions. Wienerberger and Saint-Gobain also acquired on a limited scale, with the latter agreeing to pay Wolseley over £310m for Brossette and Build Center.

With further disposals and no acquisitions of significance, most companies in the sector continued to lower net debt. Reflecting this, we estimate the sector closed 2011 with net debt/EBITDA of under 2x. This, however, is a weighted average; within the sector, there are some lingering potential balance sheet risks (noticeably amongst the cement companies).

Key themes for 2012

Another challenging year ahead with limited potential for volume growth

We expect that, operationally, 2012 will be another challenging year for our European construction stocks. With economic headwinds amplifying in many parts of the developed world, volume growth once again will be difficult to achieve. While demand in many end-markets remains substantially below pre-2008 levels, any real evidence of a cyclical recovery has halted – at least for now.

Entering 2012, the European building materials sector has to deal with both a fragile private sector and the effects of government austerity programmes.

For the sector overall, we are forecasting revenue growth of less than 1% in 2012. Margins, aided by a more benign input cost

There were very tentative signs of improvement in some US construction end-markets by the close of the year

Key themes for 2012

Another challenging year ahead with limited potential for volume growth

US construction market currently more attractive than Europe; we prefer Latin America over other emerging markets

Management teams to remain cautious about deployment of balance sheets

Research Report: Davy on 2012 January 4, 2012

22 Davy Research

environment, may improve – but only slightly. Our current sector forecast is for EBITDA growth of under 5% in 2012. Even if this is achieved, it will still leave EBITDA for the sector over 25% below peak levels, with margins remaining much lower than the long-term average.

US construction market currently more attractive than Europe; we prefer Latin America over other emerging markets

As noted, there was increasing evidence towards the end of the year that US construction activity had begun to stabilise and even exhibit some initial signs of modest improvement. Our view for 2012 is that modest growth, albeit off a very depressed base (circa 60% from peak), is plausible for the residential market. We expect non-residential activity to be flat to marginally higher. Even infrastructure investment, where significant declines were a possibility at one point, may only decline relatively marginally in 2012.

In contrast, there is ample reason to be worried about Europe, especially as austerity looms and the real economy effects of the lingering European sovereign debt crisis kick-in. Overall, we think it is possible that European construction volumes could contract a further 2-3% in 2012.

But within Europe, performance between countries and regions will vary significantly. We think the best-performing construction markets will be Germany, Switzerland, Austria, the Nordic region and Poland, with modest growth a realistic possibility. We expect construction activity in France, the UK, the Netherlands and Belgium to contract this year. But even worse affected will be Spain, Italy, Ireland, Portugal, the Czech Republic and much of south-east Europe (for example Romania and Bulgaria).

Emerging markets delivered reasonable top-line growth in 2011, with both volumes and prices rising. However, price increases were not enough to offset inflation and margins fell by over 400 basis points yoy on average. Looking ahead, we remain concerned about inflation, particularly in Asia, and on a relative basis would have a preference for Latin America in 2012.

Management teams to remain cautious about deployment of balance sheets

As noted, many building materials companies were net sellers of businesses during 2011. Further disposals and possible distressed sales by private companies may well create some interesting opportunities for those companies with strong balance sheets. That said, our view is that management teams will generally remain risk averse in relation to leverage.

Those that are likely to sell assets in 2012 include Lafarge, HeidelbergCement and Italcementi. Best positioned and most likely to acquire are CRH and Saint-Gobain, while Wolseley may look externally at opportunities now that its restructuring has been successfully completed. Kingspan also may look to bolster its presence

We think it is possible that European construction volumes could contract a further 2-3% in 2012

The best-performing construction markets in Europe will be Germany, Switzerland, Austria, the Nordic region and Poland, with modest growth a realistic possibility

Research Report: Davy on 2012 January 4, 2012

23 Davy Research

in markets where it has ambitious medium-term expansion plans (for example, North America).

How key stocks are positioned for 2012

Sector looks cheap but re-rating will be a struggle as long as earnings downside risk persists

The E300 Construction & Building Materials Index enters 2012 trading on a forward earnings multiple of under 11x. This compares with its long-term average of almost 13x.

The sector does not look expensive, but we are conscious of the downside risk to earnings. As long as this downside risk persists, we believe the sector will struggle to re-rate.

In this environment, stock picking is ever more important. Our stock picking criteria within the building materials sector for 2012 is weighted towards two criteria: (i) end-market and segment exposure; and (ii) financial health, including the ability to generate free cash.

Using these parameters, our favoured stocks at the present are Wolseley, HeidelbergCement, CRH and Geberit. While 'neutral' for now, we think it is likely we will upgrade our rating on Travis Perkins at some point this year. Our least preferred companies are Lafarge, Holcim, Grafton, Saint-Gobain and Italcementi.

Top picks entering year: Wolseley, HeidelbergCement, CRH and Geberit

Wolseley was the best-performing stock in the sector in Q4 2011. Despite this, we still believe that it can continue to outperform. Our investment thesis is framed on the following: improving returns; little debt; spare operating capacity; and its greater proportionate exposure to the US at present. Circa 50% of Wolseley's trading profits are now generated in the US, well above that of any of its peers.