Stock Market Reactions to SFAS No. 96: Evidence from Early Bank Adopters

23

THE FINANCIAL REVIEW VOL. 28 No. 4 NOVEMBER 1993 PP. 469-491 Stock Market Reactions to SFAS No. 96: Evidence from Early Bank Adopters Insup Lee” and Frederic M. Stiner, Jr.”” Abstract Statement of Financial Accounting Standards (SFAS) No. 96, “Accounting for Income Taxes,” issued by the Financial Accounting Standards Board (FASB) in De- cember 1987 changed accounting for income tax recog- nition and accrual. The original deadline for implemen- tation of SFAS No. 96 was December 15, 1988, and earlier adoption was encouraged. This study examines empirically the stock price impact of four pertinent an- nouncement dates regarding SFAS No. 96 for 19 banks that adopted the statement in late 1987 and early 1988. Our results suggest that these early bank adopters have different characteristics from other banks that cause them to benefit from the changes in accounting for de- ferred taxes and explain their voluntary adoption of the standard. Introduction Financial accounting for income taxes has never been a simple matter because of the complexities of cal- culating domestic and international taxes and reporting the effects of these taxes in financial statements. The American standard for many years has been Accounting Principles Board Opinion (APBO) No. 11, “Accounting for Income Taxes” [l], issued in December 1967. This standard has met with harsh criticism over the years because assumptions about tax rates often permitted Acknowledgement: The authors thank George C. Philippatos, Harold A. Black, Robert L. Schweitzer, Janet Todd, M. Andrew Fields, and an anony- mous referee for their helpful comments. Financial support from the Univer- sity of Delaware Financial Institution Research and Education (FIRE) Center and the Department of Accounting Research Fund is gratefully acknowl- edged. *University of Delaware, Newark, DE 19716 and Korea Securities Research Institute, Seoul, Korea **University of Delaware, Newark, DE 19716 469

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Stock Market Reactions to SFAS No. 96: Evidence from Early Bank Adopters

THE FINANCIAL REVIEW VOL. 28 No. 4 NOVEMBER 1993 PP. 469-491

Stock Market Reactions to SFAS No. 96: Evidence from Early

Bank Adopters

Insup Lee” and Frederic M . Stiner, Jr.””

Abstract

Statement of Financial Accounting Standards (SFAS) No. 96, “Accounting for Income Taxes,” issued by the Financial Accounting Standards Board (FASB) in De- cember 1987 changed accounting for income tax recog- nition and accrual. The original deadline for implemen- tation of SFAS No. 96 was December 15, 1988, and earlier adoption was encouraged. This study examines empirically the stock price impact of four pertinent an- nouncement dates regarding SFAS No. 96 for 19 banks that adopted the statement in late 1987 and early 1988. Our results suggest that these early bank adopters have different characteristics from other banks that cause them to benefit from the changes in accounting for de- ferred taxes and explain their voluntary adoption of the standard.

Introduction Financial accounting for income taxes has never

been a simple matter because of the complexities of cal- culating domestic and international taxes and reporting the effects of these taxes in financial statements. The American standard for many years has been Accounting Principles Board Opinion (APBO) No. 11 , “Accounting for Income Taxes” [l], issued in December 1967. This standard has met with harsh criticism over the years because assumptions about tax rates often permitted

Acknowledgement: The authors thank George C. Philippatos, Harold A. Black, Robert L. Schweitzer, Janet Todd, M. Andrew Fields, and an anony- mous referee for their helpful comments. Financial support from the Univer- sity of Delaware Financial Institution Research and Education (FIRE) Center and the Department of Accounting Research Fund is gratefully acknowl- edged. *University of Delaware, Newark, DE 19716 and Korea Securities Research Institute, Seoul, Korea **University of Delaware, Newark, DE 19716

469

470 Lee and Stiner

corporations to have large deferred tax accounts which would never be paid.’

A new standard, Statement of Financial Accounting Standards (SFAS) No. 96, “Accounting for Income Taxes” [ 111, was issued by the Financial Accounting Standards Board (FASB) in December 1987 after a long discussion (Beresford, et al. 153). SFAS No. 96 is very complex, with a number of consequences for how a com- bination might be recorded, and for recognition of net operating losses and tax credit carryforwards. The orig- inal deadline for implementation of SFAS No. 96 was December 15, 1988, and companies that were covered were encouraged to adopt the standard early. However, the furor over the statement led to another pronounce- ment, SFAS No. 100, “Accounting for Income Taxes-De- ferral of the Effective Date of FASB Statement No. 96 [12], which was issued in December 1988. Because of continuing controversy, SFAS No. 103 C131 further post- poned implementation to December 15, 1991. Further postponement and changes were proposed 1261, and im- plementation was again formally postponed in SFAS No. 108 [14]. In 1992, SFAS No. 109 [151 superseded SFAS No. 96.

There are many studies indicating that firms adopt- ing a new accounting principle before the required date of adoption are motivated by circumstances different from those of firms that wait until the deadline for adop- tion.’ Early adoption is a management choice, and man- agers may be signalling information to investors by the early adoption of an accounting principle.

While there are many studies of early adoption by industrial firms (see Holthausen and Leftwich [l?], Liebtag [20], and Trombley [291, among others), there is little literature on early adoption by banks. Banks pose special problems in research because of government reg- ulation of capital adequacy ratios3 When capital ade- quacy falls below regulatory standards, there are sub- stantial regulatory costs due to increased supervision, Moyer 1201, for example, provides evidence that bank managers choose between accounting principles to meet capital adequacy guidelines. If this is true, then man- ages may use early adoption of SFAS No. 96 t o adjust capital ratios in a desirable manner.

Stock Market Reactions to SFAS 471

The purpose of this study is twofold. The first is to examine the shareholder wealth impact of adoption of SFAS No. 96 on four pertinent announcement dates for banks that adopted the statement in late 1987 or early 1988. Specifically, this study examines the stock price behavior of these banks for an eleven-day period sur- rounding (1) the first day of the first Wall Street Journal (WSJ) report on SFAS No. 96, (2) the date of the report that banks may be exempt from the statement, (3) the date of the US. Securities and Exchange Commission (SEC) decision that there were no exceptions for any in- dustry, and (4) the date on which each early adopter filed with the SEC. The second purpose is to investigate relationships between the characteristics of these early adopters and the impact of these announcements on the banks’ stock prices. If adoption of SFAS No. 96 should result in an increase in reported capital, then the capital as a percentage of assets would increase. Higher capital to asset ratios in turn decrease regulatory costs and per- haps allow an increase in dividend payments. In addi- tion, banks with low equity ratios might benefit from an early adoption of such a statement.

APBO No. 11 us. SFAS No. 96

The issue in accounting for income taxes is the de- cision of when to recognize income tax liability and how this liability should be measured. Because of the timing differences of revenue and expense recognition that arise between income tax accounting and financial ac- counting, the actual tax paid in one period may not be the tax expense recognized for financial accounting pur- poses. The solution to this problem in APBO No. 11 (paragraph 19) was the “deferred method,” which was:

. . . . a procedure whereby the tax effects of current timing differences are deferred currently and allo- cated to income tax expense of future periods when the timing differences reverse. The deferred method emphasizes the tax effects of timing differences on income of the period in which the differences orig- inate. The deferred taxes are determined on the basis of the tax rates in effect at the time the timing differences originate and are not adjusted for sub-

472 Lee and Stiner

sequent changes in tax rates or to reflect the im- position of new taxes. The tax effects of transactions which reduce taxes currently payable are treated as deferred credits; the tax effects of transactions which increase taxes currently payable are treated as deferred charges.

Recognition of tax expense occurred in the time period that the taxable event was recognized, and the mea- surement had to be at the tax rates in effect at that time. Taxes were to be allocated among operating income, ex- traordinary items, and prior period adjustments. If the tax was not paid in the year when the expense was rec- ognized, a deferred credit (a payable) was recorded. A financial statement presentation problem arose because the tax rate originally used to record the deferred credit never changed. Because corporate income tax rates gen- erally declined in the 15 years subsequent to APBO No. 11, many corporations built enormous deferred tax pay- able accounts reflecting taxes accrued a t high rates. These credits were not reduced when rates were reduced and might never be expected to reverse, provided the corporation continued to replace equipment as the cor- poration grew. The question arose that if these deferred credits were not liabilities and not to be placed in stock- holders’ equity, what were they?

The resolution of this problem was SFAS No. 96. While APBO No. 11 emphasized reporting the current expenses on the income statement, SFAS No. 96 em- phasizes having a correct deferred tax liability on the balance sheet. A tax liability is still recognized when the transaction giving rise to the liability is re~ognized.~ However, SFAS No. 96 requires that reporting entities state the accrual of taxes payable at the prevailing tax rates when the transaction giving rise to the tax is rec- ognized. The new method is called “the liability method.”

Under SFAS No. 96, a reporting entity must first determine its tax liability in accordance with generally accepted accounting principles (GAAP). The company then calculates its tax payable according to the tax code. Differences between GAAP and tax return income tax expense can arise either from differences between GAAP

Stock Market Reactions to SFAS 473

and the tax basis of assets and liabilities, or from per- manent income differences. Only a difference in assets and liabilities will be used to create a deferred tax pay- able account. Temporary differences will create a change in the deferred tax account. For example, if equipment is depreciated on an accelerated basis for taxes, and de- preciated on a straight-line basis for financial reporting, the accumulated depreciation accounts will not be equal until the equipment is fully depreciated.

For those corporations that have deferred tax cred- its, the new standard requires that existing deferred tax credits be recalculated using current rates. Any result- ing reduction in deferred taxes must be taken through the income statement. When the new standard is imple- mented, a corporation has a choice of either making a cumulative adjustment to the current period's income or restating previous financial statements. If the firm chooses to show a cumulative adjustment in the current year, then the effect on income must be disclosed. Ap- plying this to banks, any such adjustment that increases income will increase both retained earnings and total reported capital.

Early Adoptions and Accounting Issues Bennington and Davis [3] suggest reasons that a

bank would become early adopters of SFAS No. 96. The first step for the bank is to compare current year's in- come (or loss) to the deferred tax position. Bennington and Davis [3] present a decision matrix based upon whether the deferred tax position is a debit or credit. Under each criterion, they show the consequences of early compliance or deferring compliance. Prior to the Tax Reform Act of 1986, banks had large credit balances in their deferred tax accounts. This reflected the provi- sions for bad debts being taken earlier for book purposes rather than for tax purposes. After 1986, banks can write off loans only in the year in which the loan be- comes worthless. Assuming a credit deferred tax posi- tion (taxes payable), Bennington and Davis [31 show that an early adoption would increase capital. Moyer [21] has shown that bank managers have an incentive to make changes n capital adequacy ratios. Banks fail-

474 Lee and Stiner

ing to meet federal capital minimums must present reg- ulators with written reports on how the minimums will be met. We suggest that this is the incentive to be an early adopter of SFAS No. 96.

The Tax Reform Act of 1986 also eliminated a bank’s ability to carryback net operating losses [NOLs] ten years, and instead it forced banks to comply with the requirement for other corporations to carryback losses only three years. A number of banks have NOL carryforwards. These NOL carryforwards cannot be ac- counted for as an asset. Therefore, a bank may recognize these by either adjusting the deferred tax liability or by recognizing the NOL as an asset only when the tax ef- fect is seen (Nurnberg [241). Previously, an NOL could be accounted for as an extraordinary item in the income statement. SFAS No. 96 could have an effect on banks involved in acquisitions because the NOL must be used to reduce deferred tax credit. Under the new standard, an NOL must be associated on one’s financial statement with the item which gave rise to the NOL. (See Stewart and Ripepi [28] also.)

When adopting SFAS No. 96, a bank has the choice of either restating prior periods or showing the effect of the change in the current period as a cumulative effect for a change in accounting principles. In either case, a bank will increase stated capital by early adoption. If a bank used the change to decrease unprofitability, rather than increase earnings, this means that the banks may return to profitability and increasing surplus sooner. A bank might apply the benefit of the change to the NOL carryforwards for tax purposes. Again, this does not in- crease current income, but may mean that the bank re- turns to reporting profits sooner.

Hypotheses Tested Current thinking about market behavior indicates

that investors will change their expectations only in re- sponse to changes in expected cash flow. Therefore, a change in accounting methods that changes earnings without a change in cash consequences should have no impact on the market valuation of a bank. On the other hand, if investors perceive that the new standard will

Stock Market Reactions to SFAS 475

have an impact on equity return, then there should be a market r e a c t i ~ n . ~

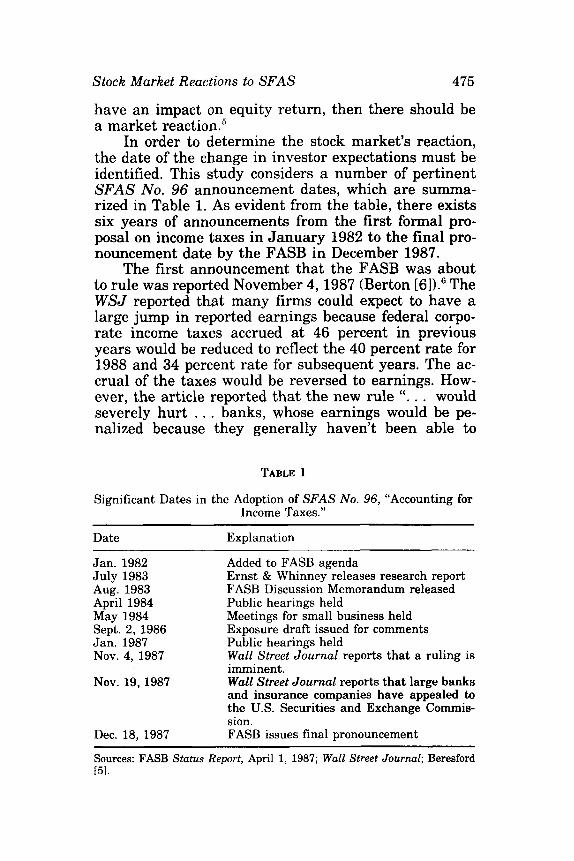

In order to determine the stock market’s reaction, the date of the change in investor expectations must be identified. This study considers a number of pertinent SFAS No. 96 announcement dates, which are summa- rized in Table 1. As evident from the table, there exists six years of announcements from the first formal pro- posal on income taxes in January 1982 to the final pro- nouncement date by the FASB in December 1987.

The first announcement that the FASB was about to rule was reported November 4, 1987 (Berton [6]).6 The WSJ reported that many firms could expect to have a large jump in reported earnings because federal corpo- rate income taxes accrued at 46 percent in previous years would be reduced to reflect the 40 percent rate for 1988 and 34 percent rate for subsequent years. The ac- crual of the taxes would be reversed to earnings. How- ever, the article reported that the new rule “. . . would severely hurt . . . banks, whose earnings would be pe- nalized because they generally haven’t been able to

TABLE 1

Significant Dates in the Adoption of SFAS No. 96, “Accounting for Income Taxes.”

Date Explanation

Jan. 1982 July 1983 Aug. 1983 April 1984 May 1984 Sept. 2, 1986 Jan. 1987 Nov. 4, 1987

Nov. 19, 1987

Dec. 18, 1987

Added to FASB agenda Ernst & Whinney releases research report FASB Discussion Memorandum released Public hearings held Meetings for small business held Exposure draft issued for comments Public hearings held Wall Street Journal reports that a ruling is imminent. Wall Street Journal reports that large banks and insurance companies have appealed to the U.S. Securities and Exchange Commis- sion. FASB issues final pronouncement

Sources: FASB Status Report, April 1, 1987; Wall Street Journal; Beresford I51.

476 Lee and Stiner

build up such reserves.” This report indicates that in general bank stocks would be hurt due to most banks’ tendency not to build up large deferred tax payable ac- counts subsequent to the Tax Reform Act of 1986. With- out large deferred tax payable accounts, banks in gen- eral would not increase reported earnings. However, the authors hypothesize that the market is aware of the type of banks that would benefit from the early adoption of SFAS No. 96. Consequently, the authors expect a posi- tive stock price impact for these early adopters.

A subsequent WSJ article (November 19, 1987) in- dicated that some large banks and insurance companies had appealed to the SEC to exempt them from the law (Berton and Slater [71>.7 The authors’ hypothesis is that an appeal would result in either a negative impact or have no effect on these early adopters’ stock prices. If such an appeal were expected to succeed, there would be a negative price impact on these potential beneficiaries. However, if the market anticipates that such an appeal would not succeed, there would be no significant impact on stock prices of these potential early adopters.

On December 8, 1987, the FASB announced that there were no exceptions for any industry [271.* The au- thors hypothesis is that the SEC’s decision not to grant any exemption for banks would have a positive impact on stock prices of these potential early adopters. Finally, the authors assess the stock price impact of banks that actually filed their decision with the SEC to adopt SFAS No. 96. Stock price impact should be minimal because the market has already taken the SEC filing into con- sideration for these early adopters.

In relating the characteristics of the early adopters to the stock price impact for these banks, the authors use two ratios: (1) return on equity measuring profita- bility and (2) equity ratio indicating capital structure as independent variables. Applying the eleven-day cumu- lative abnormal returns as a dependent variable for each of nineteen early adopters reveals how a bank’s profitability and capital structure are related to each bank’s stock market response.

The hypothesis is that the stronger the pre-adoption profitability, the lower the positive stock market reac-

Stock Market Reactions to SFAS 477

tion. Because gains from recalculation of a deferred tax payable account may be shown on the income statement as a cumulative adjustment, or as a restatement of prior years financial statements, the lower-profit banks will experience the most positive price impact. For the equity ratio, the hypothesis is that the banks with the strongest capital-to-asset ratios will have the least positive price impact. Given two banks with the same dollar amount of income to add to retained earnings, the bank with the lowest capital will have the highest percentage increase in capital, and therefore the largest stock price impact.

Data and Methodology The August 1989 edition of Disclosure's CD-ROM

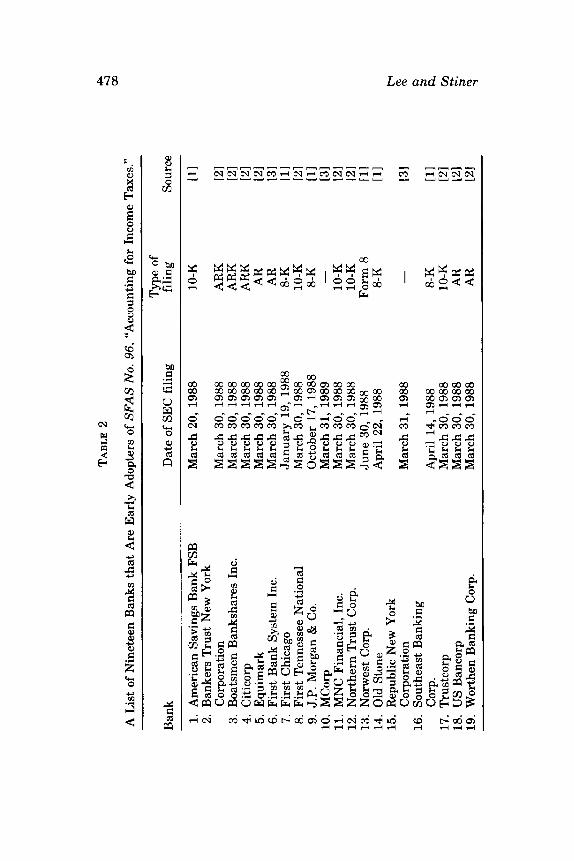

[lo] was searched for all companies for reference of SFAS No. 96. There were 1,307 companies identified as a result of this first screening. This population was fur- ther screened for those companies in SIC 602, Banking. There were 67 banks in this category. In this population, there were 24 banks that described an early adoption of SFAS No. 96. From these, 19 banks were selected as the final sample of 24 because no price information was found for the other five banks.g Table 2 contains the list of these banks along with their respective SEC filing dates. The remainder of the population mentioned the statement, but said that they were either studying the matter or that the consequences were believed to be im- material. An early adoption must be disclosed initially in a filing with the SEC. These filings may be done using one of three forms: 8K, 10-Q, or 10-K.1° For the 19 early bank adopters, all three forms were retrieved. The date of filing with the SEC is used as the event date."

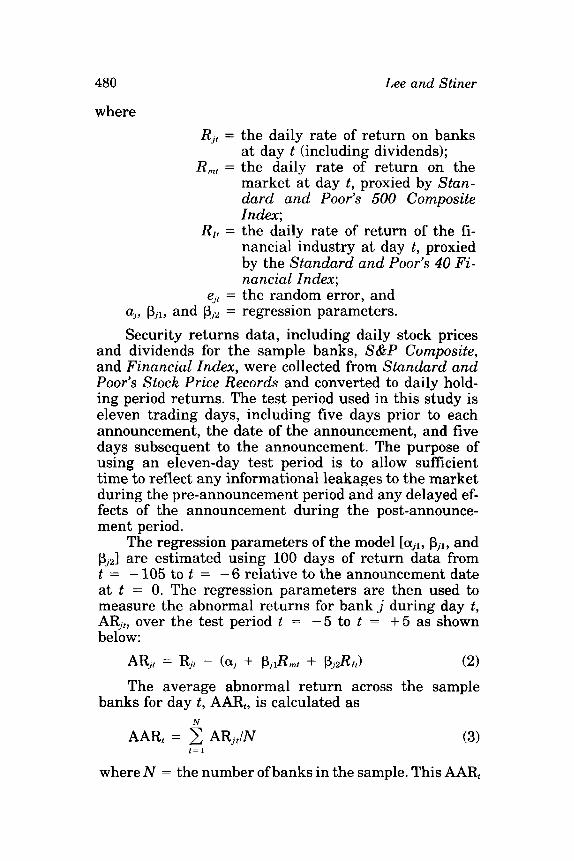

To test the market's reaction to each announcement, abnormal returns are computed using a two-factor mode1.12 This model is selected to control for the possible effect of the different interest rate trends during the sample period. The model used in this study to generate normal returns is:

TAB

LE 2

A L

ist o

f N

inet

een

Ban

ks t

hat

Are

Ear

ly A

dopt

ers

of S

FA

S N

o. 9

6, “

Acc

ount

ing

for

Inco

me

Taxe

s.”

Ban

k T

ype

of

Sour

ce

Dat

e of

SE

C fi

ling

fili

ng

1. A

mer

ican

Sav

ings

Ban

k FS

B

2. B

anke

rs T

rust

New

Yor

k

3. B

oats

men

Ban

ksha

res

Inc.

4.

Citi

corp

5. E

quim

ark

6. F

irst

Ban

k Sy

stem

Inc.

7.

Fir

st C

hica

go

8. F

irst

Ten

ness

ee N

atio

nal

9. J

.P. M

orga

n &

Co.

10

. MC

orp

11. M

NC

Fin

anci

al, I

nc.

12.

Nor

ther

n T

rust

Cor

p.

13. N

onve

st C

orp.

14

. Old

Sto

ne

15.

Rep

ublic

New

Yor

k C

orpo

ratio

n 16

. Sou

thea

st B

anki

ng

Cor

p.

17. T

rust

corp

18

. U

S B

anco

rp

19. W

orth

en B

anki

ng C

orp.

Cor

pora

tion

Mar

ch 2

0, 1

988

Mar

ch 3

0, 1

988

Mar

ch 3

0, 1

988

Mar

ch 3

0, 1

988

Mar

ch 3

0, 1

988

Mar

ch 3

0, 1

988

Janu

ary

19, 1

988

Mar

ch 3

0, 1

988

Oct

ober

17,

198

8 M

arch

31,

198

9 M

arch

30,

198

8 M

arch

30,

198

8 Ju

ne 3

0, 1

988

Apr

il 22

, 19

88

Mar

ch 3

1, 1

988

Apr

il 14

, 198

8 M

arch

30,

198

8 M

arch

30,

198

8 M

arch

30,

198

8

10-K

AR

K

AR

K

AR

K

AR

A

R

8-K

10

-K

8-K

-

10-K

10

-K

Form

8

8-K

8-K

10

-K

AR

A

R

key:

AR

= a

nnua

l re

port

file

d w

ith

the

SEC

. AR

K =

com

bine

d 10

-K a

nd a

nnua

l re

port

file

d w

ith

the

SEC

. 8-

K =

not

ifia

ble

even

t rep

orts

. 10

-K =

ann

ual

fili

ng w

ith

the

SEC

. 10

-Q =

qua

rter

ly f

ilin

g w

ith

the

SEC

. Fo

rm 8

= a

men

ded

10-K

. K

ey t

o so

urce

s:

[l] O

btai

ned

from

the

sta

mpe

d fi

ling

at th

e SE

C, a

s sh

own

in t

he Q

-file

. [2

1 R

epor

t fo

und

at t

he S

EC, b

ut t

he s

tam

ped

filin

g at

the

SEC

ille

gibl

e or

om

itted

by

Q-f

ile. T

he e

xact

dat

e is

[31

Fili

ng d

ate

unkn

own

and

repo

rt c

over

pho

toco

py n

ot f

ound

. M

arch

31,

198

8 as

sum

ed,

sinc

e th

at w

as t

he

assu

med

to

be t

he d

eadl

ine

for

the

10-K

repo

rt.

dead

line

for

the

10-K

.

b 2

480

where

Lee and Stiner

R,, = the daily rate of return on banks at day t (including dividends);

Rmt = the daily rate of return on the market at day t , proxied by Stan- dard and Poor’s 500 Composite Index;

R,, = the daily rate of return of the fi- nancial industry at day t, proxied by the Standard and Poor’s 40 Fi- nancial Index;

e,, = the random error, and a,, pJ1, and p,2 = regression parameters. Security returns data, including daily stock prices

and dividends for the sample banks, S&P Composite, and Financial Index, were collected from Standard and Poor’s Stock Price Records and converted to daily hold- ing period returns. The test period used in this study is eleven trading days, including five days prior to each announcement, the date of the announcement, and five days subsequent to the announcement. The purpose of using an eleven-day test period is to allow sufficient time to reflect any informational leakages to the market during the pre-announcement period and any delayed ef- fects of the announcement during the post-announce- ment period.

The regression parameters of the model [aJ1, p,l, and are estimated using 100 days of return data from

t = - 105 to t = -6 relative to the announcement date at t = 0. The regression parameters are then used to measure the abnormal returns for bank j during day t, AR,,, over the test period t = -5 to t = +5 as shown below:

(2)

The average abnormal return across the sample AR,t = R,, - (a] + P l 8 m t + P&/t)

banks for day t , AARt, is calculated as N

AAR, = 2 ARj,IN t = l

(3)

where N = the number of banks in the sample. This AAR,

Stock Market Reactions to SFAS 48 1

indicates the market's reaction to the event a t a partic- ular date t .

The cumulative average abnormal return over the eleven-day period from day - 5 to + 5 , the CAAR [ - 5,51, is computed as:

CAAR[-5,5] = 2 GAR, I = -5

(4)

To test whether AAR, is significantly different from zero, the statistic, TAAR,, is calculated following the crude dependence adjustment of Brown and Warner 191 as follows:

TAAR, = AAR, (5) where cr = the standard deviation of AARt, measured over the 100-day period from t = - 105 to t = - 6.

The statistical significance of CAAR accumulated from day W to day T is calculated as follows:

T

TCAAR, = 2 TAARJSQRTLT- W + 11 t = W

which has an approximately normal standard distribu- tion.

In order to measure the possible relationship be- tween a bank's characteristics and the stock market re- sponse, the authors apply two regression equations using return on equity (ROE) and equity ratio (ER) as inde- pendent variables and eleven-day CAAR, [-5,51 as the dependent variable as follows:

(7) (8)

where a = the intercept term, p = the slope coefficient, and e, = random error term.

CAAR,[ -5,5] = a + p ROE, + e, CAAR,[-5,5] = a + p ER, + e,

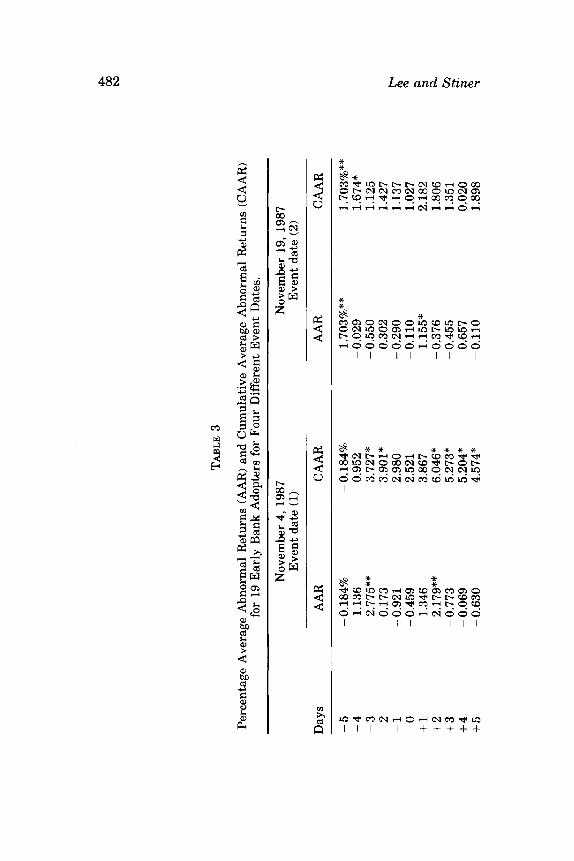

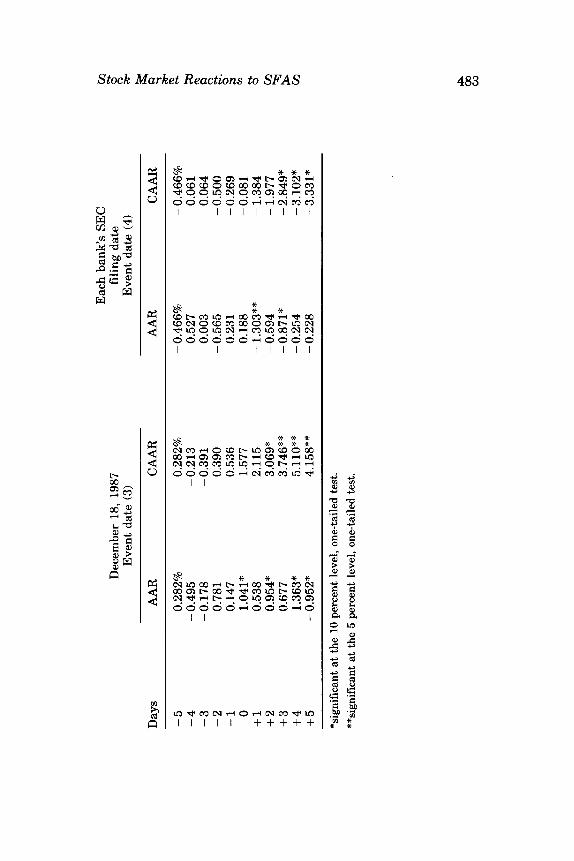

Empirical Results Table 3 presents percentage average abnormal re-

turns (AAR) and cumulative average abnormal returns (CAAR) for nineteen banks for the four FASB announce- ment dates that we in~estigated. '~ For the first event

TABL

E 3

Perc

enta

ge A

vera

ge A

bnor

mal

Ret

urns

(A

AR

) and

Cum

ulat

ive

Ave

rage

Abn

orm

al R

etur

ns (

CA

AR

) fo

r 19

Ear

ly B

ank

Ado

pter

s fo

r Fo

ur D

iffe

rent

Eve

nt D

ates

.

Nov

embe

r 4,

198

7 E

vent

dat

e (1

) N

ovem

ber

19, 1

987

Eve

nt d

ate

(2)

Day

s A

AR

CA

AR

A

AR

C

AA

R

-5

-4

-3

-2

-1 0

+1

+

2

+3

+

4

+5

- 0

.184

%

1.13

6 2.

775*

* 0.

173

- 0

.921

- 0

.459

1.

346

2.17

9**

- 0

.773

- 0

.069

- 0

.630

- 0.

184%

0.

952

3.72

7*

3.90

1*

2.98

0 2.

521

3.86

7 6.

046*

5.

273*

5.

204*

4.

574*

1.70

3%**

- 0

.029

- 0

.550

0.

302

- 0.

290

-0.1

10

- 0.

376

- 0

.455

0.

657

-0.1

10

1.15

5*

1.70

3%**

1.

674*

1.

125

1.42

7 1.

137

1.02

7 2.

182

1.80

6 1.

351

0.02

0 1.

898

R is.

9

% ?

-4

- 0

.495

- 0

.213

0.

527

0.06

1 3Y

-3

- 0

.178

- 0

.391

0.

003

0.06

4 $ E

+1

0.

538

2.11

5 - 1

.303

**

- 1

.384

0"

+2

0.

954"

3.

069*

- 0.

594

- 1

.977

to

+4

1.

363*

5.

110*

* - 0.

254

-3.1

02*

&I

+5

- 0.

952*

4.

158*

* - 0.

228

-3.3

31*

Eac

h ba

nk's

SEC

Eve

nt d

ate

(4)

E -5

0.

282%

0.

282%

- 0.

466%

- 0.

466%

iY

-2

0.78

1 0.

390

- 0.

565

- 0.

500

g.

+3

0.

677

3.74

6**

-0.8

71*

- 2.

849*

2

Dec

embe

r 18

, 198

7 fi

ling

date

E

vent

dat

e (3

)

Day

s A

AR

C

AA

R

AA

R

CA

AR

-1

0.14

7 0.

536

0.23

1 - 0.

269

0 1.

041*

1.

577

0.18

8 - 0.

081

*sig

nifi

cant

at t

he 1

0 pe

rcen

t le

vel,

one-

taile

d te

st.

**si

gnif

ican

t at t

he 5 p

erce

nt l

evel

, one

-tai

led

test

.

484 Lee and Stiner

date analyzed (November 4, 1987) in which the WSJ re- ported that an FASB ruling was imminent, the AAR on the announcement date is -0.459 percent and statisti- cally insignificant. This indicates that there was no sig- nificant market reaction to the report in the WSJ. The statistically significant AARs occurred on days - 3 and +2 , but the cause of such results is not clear. The CAARs of days - 3 and + 2 are also statistically signif- icant and are the result of the significant reactions ob- served on these days. The CAAR for the eleven-day in- vestigation period, CAAR[ - 5,51, is approximately 4.6 percent and is statistically significant at the 10 percent level using a one-tailed test. This eleven-day CAAR re- sult indicates that the WSJ report had a positive wealth impact, which supports our hypothesis.

For the second event date (November 19, 1987) in which the WSJ reported that large banks and insurance companies appealed to the SEC to exempt them from the new FASB ruling, no statistically significant reaction to any conventional level is observed for any trading day except for days - 5 and + 1. The AAR on the announce- ment date is - 0.11 percent, which is statistically insig- nificant. Thus, the appeal by lobbyists did not appear to draw any significant market reaction to stock prices for these early adopters. The hypothesis was that such ap- peal may cause negative or no impact on these banks’ stock price in general, and the results are consistent with the hypothesis.

For the third event date (December 18, 1987), when the FASB issued the final statement that there were no exceptions for any industry, there exists a statistically significant market reaction to this announcement, as evidenced by a significant AAR of 1.041 percent. In ad- dition, the CAAR [ - 5,51 is approximately 4.16 percent, which is statistically significant at the 5 percent level. These results indicate that there was a significant pos- itive market reaction to this announcement by the FASB. These findings support the hypothesis that the early adopters benefit from such a statement because they differ from other banks in general.

Finally, the fourth event date occurred on the filing of financial statements with the SEC, revealing that the bank was an early adopter of SFAS No. 96. The mar-

Stock Market Reactions to SFAS 485

ket’s reaction on the filing date appears to be statisti- cally insignificant, as evidenced by the AAR of 0.188 percent. This indicates that the market had already in- corporated the impact of such a statement on these banks’ stock price, and hence actual filing with the SEC has no valuation impact for these early adopters. This is again consistent with the hypothesis of no significant price impact. However, the AAR on day + 1 is signifi- cantly negative ( - 1.303 percent), and the CAAR [ - 5,5] shows significant negative reactions ( - 3.331 percent). These negative abnormal returns are statistically sig- nificant at the 10 percent level.

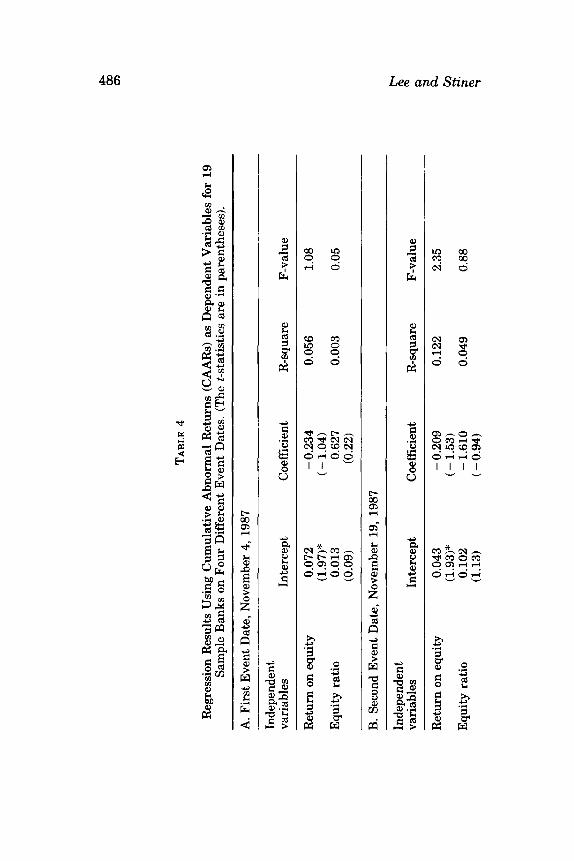

Table 4 presents regression results using CAARs as dependent variables for 19 early bank adopters for four different event dates. The negative coefficients for all of the four event dates indicate an inverse relationship be- tween the profitability (measured by the return on eq- uity) and stock price reaction. This is consistent with our hypothesis that banks with higher profitability will have lower positive stock price reactions to SFAS No. 96. However, none of the coefficients is statistically sig- nificant. For the equity ratio, the results are mixed. The first WSJ report date and the SEC filing date are as- sociated with positive coefficients, while the second and third event dates show negative coefficients. None of the t-statistics is significant. These findings are not entirely consistent with the hypothesis that higher bank equity ratios are universally related to stock price reaction.

Conclusions The first WSJ report that SFAS No. 96 was immi-

nent caused a positive stock price impact over the eleven-day period for those banks that would later be early adopters of the standard. The second announce- ment, that banks might be exempt, had no significant effect on the stock prices of these banks. This may in- dicate that the initial market evaluation was that these banks would benefit from SFAS No. 96, or at least not be worse off than their present condition if banks were exempt. The third announcement, that the FASB de- cided not to grant an exemption to the financial indus- try, resulted in a statistically significant positive impact

TA

BL

E 4

Reg

ress

ion

Res

ults

Usi

ng C

umul

ativ

e A

bnor

mal

Ret

urns

(C

AA

Rs)

as

Dep

ende

nt V

aria

bles

for

19

Sam

ple

Ban

ks o

n Fo

ur D

iffe

rent

Eve

nt D

ates

. (T

he t-

stat

istic

s ar

e in

par

enth

eses

).

A. F

irst

Eve

nt D

ate,

Nov

embe

r 4, 1

987

Inde

pend

ent

vari

able

s In

terc

ept

Coe

ffic

ient

R

-squ

are

F-va

lue

Ret

urn

on e

quity

0.

072

- 0.

234

0.05

6 1.

08

Equ

ity r

atio

0.

013

0.62

7 0.

003

0.05

(1

.97)

* (-

1.0

4)

(0.09)

(0.2

2)

B. S

econ

d E

vent

Dat

e, N

ovem

ber

19, 1

987

Inde

pend

ent

vari

able

s In

terc

ept

Coe

ffic

ient

R

-squ

are

F-va

lue

Ret

urn

on e

quity

0.

043

- 0

.209

0.

122

2.35

Equ

ity r

atio

0.

102

- 1

.610

0.

049

0.88

(1

.93)

* ( - 1

.53)

(1.1

3)

( - 0.

94)

c m Q

J

R

b g. m 7

C. T

hird

Eve

nt D

ate,

Dec

embe

r 18

, 198

7

Inde

pend

ent

vari

able

s In

terc

ept

Coe

fici

ent

R-s

quar

e F

-val

ue

;F e ?

Ret

urn

on e

quity

0.

055

-0.1

13

0.05

46

0.98

E 5 F:

(1.6

8)

(- 1

.13)

g. 8 3

(2.9

1)**

( -

0.9

9)

Equ

ity r

atio

0.

122

- 1

.549

0.

0695

1.

27

3

D. F

ourt

h E

vent

, Uni

que

for

Eac

h Sa

mpl

e B

ank

Inde

pend

ent

b

(0

vari

able

s In

terc

ept

Coe

ffic

ient

R

-squ

are

F-v

alue

Ret

urn

on e

quity

0.

033

- 0

.038

0.

009

0.17

Equ

ity r

atio

- 0

.076

0.

856

0.03

5 0.

61

to

( - 2.

70)*

* ( - 0

.41)

( - 1

.35)

(0

.78)

*sig

nific

ant a

t the

10

perc

ent l

evel

, tw

o-ta

iled

test

. **

sign

ifica

nt a

t th

e 5

perc

ent l

evel

, tw

o-ta

iled

test

.

488 Lee and Stiner

on both the announcement date and the eleven-day pe- riod. For each banks’ SEC filing date, there was no sig- nificant stock price reaction on the announcement date. The authors’ interpretation of results on the fourth event date is that each individual bank’s filing had no implications for shareholders’ wealth because the mar- ket had already considered the impact of the statement on a bank that was an early adopter. These results sup- port the hypothesis that these early adopters have char- acteristics different from those of other banking firms, and hence they benefit from the changes in accounting for deferred taxes.

Bennington and Davis [31 state that early adoption would increase capital and show a stronger financial po- sition. The authors’ regression results using CAAR and return on equity suggest that banks with lower profit- ability benefit from the early adoption. This adds fur- ther support to Moyer’s findings [21] that bank man- agers use accounting principles to adjust their capital adequacy ratios. For banks that have accumulated de- ferred taxes, early adoption of SFAS No. 96 could be one way of increasing capital and reducing or avoiding reg- ulatory costs. On the other hand, the relationship be- tween the equity ratio and stock price impact is not clear. This may suggest that capital ratios are not an important criterion for the early adoption decision.

Notes

1. For example, these criticisms came from industry [221, public accounting [4], and financial analysts [231.

2. For example, Ayres [2] and Trombley [29]. See also a study by Lamy, Marr and Thompson [18], which uses a similar approach to examine the effect of the announcement of the Mexican debt prob- lem on U.S. banks’ share prices.

3. Moyer [21] summarizes changes in the definition of primary capital adequacy during the period 1981-1986.

4. SFAS No. 96 also modified recognition slightly where there are differences in tax and financial asset records.

5. Ou and Penman [25] cite evidence that fundamental analysis can provide excess returns.

6. Although the FASB issues many discussion memoranda and draft opinions, the actual date for a final opinion cannot be antici- pated very well. Often, years pass between issuance of a Discussion Memorandum and a final opinion.

7. The political nature of the decision is shown by the Congres-

Stock Market Reactions to SFAS 489

sional interest in the topic. Senator Robert Dole (R., Kan.) also pleaded with the SEC for an exemption (Wall Street Journal, No- vember 20, 1987, p. 11). We suggest that since most banks were not early adopters, they were the source of the pressure. The sample banks would therefore not be lobbyists.

8. Actual report date is December 21. 9. The price data were collected by hand for the 19 banks ana-

lyzed. 10. These three filings are required under authority provided by

the 1934 Securities Exchange Act. The 8-K report must be filed within 10 days of a notifiable incident, such as a merger proposal or change of auditors. The 10-Q is the quarterly report to the SEC re- quired to be filed with 45 days of the close of a quarter. The 10-K is the annual report to the SEC, required to be filed within 90 days of the close of the fiscal year.

11. While a sample of 19 seems small, there were only 24 banks describing an early adoption. Moreover, a 2-factor model should overcome a small sample bias.

12. See Flannery and James [16], Booth and Officer [81, and Lee and Schweitzer [19] for the same approach. There may exist an iden- tification problem because some of our sample banks are also in- cluded in the S & P 40 Financial Index.

13. Earlier announcement dates could have been used. However, due to mergers, this would have reduced the sample size.

References

[ 11 Accounting Principles Board. Opinion No. 1 1 , “Accounting for Income Taxes.” December 1967.

[2] Ayres, F. L. “Characteristics of Firms Electing Early Adoption of SFAS 52.” Journal of Accounting and Economics NMay

[3] Bennington, Debbie, and Debra Davis. “SFAS No. 96: Should Your Bank Implement Early?” Bank Accounting and Finance l(Summer 1988):50-57.

[4] Beresford, Dennis R. “Deferred Tax Accounting Should Be Changed.” CPA Journal 52(June 1982):16-23.

[5] Beresford, Dennis R., Lawrence C. Best, Paul W. Craig, and Joseph V. Weber. Accounting for Income Taxes: A Review of Alternatiues. Stamford, CT: FASB, 1983.

[6] Berton, Lee. “FASB Is Expected to Issue Rule Allowing Many Firms to Post Big, One-Time Gains.” Wall Street Journal, No- vember 4, 1987, p. 4, col. 2.

[7] Berton, Lee, and Karen Slater. “Large Insurance Firms, Banks Seeking Relief from Costly Accounting Proposal.” Wall Street Journal, November 20, 1987, p. 11, col. 1.

[8] Booth, James R., and Dennis T. Officer. “Expectations, Interest Rates, and Commercial Bank Stocks.” Journal of Financial Re- search 8(Spring 1985):51-58.

1986): 143-58.

490 Lee and Stiner

[9] Brown, S. J., and J. B. Warner. “Using Daily Stock Returns.” Journal of Financial Economics 14(March 1985):3-31.

[lo] Compact Disclosure 11, 1989. (Disclosure, Inc., 5161 River Rd., Bethesda, Md., 20816).

[ 113 Financial Accounting Standards Board. Statement of Financial Accounting Standards No. 96. “Accounting for Income Taxes.” Stamford, CT: FASB, 1987.

[ 121 Financial Accounting Standards Board. Statement of Financial Accounting Standards No. 100. “Accounting for Income Taxes- Deferral of the Effective Date of FASB Statement No. 96.” Stamford, CT: FASB, 1988.

[ 131 Financial Accounting Standards Board. Statement of Financial Accounting Standards No. 103. “Accounting for Income Taxes- Deferral of the Effective Date of FASB Statement No. 96.” Stamford, C T FASB, 1989.

[ 141 Financial Accounting Standards Board. Statement of Financial Accounting Standards No. 108. “Accounting for Income Taxes- Deferral of the Effective Date of FASB Statement No. 96.” Stamford, CT: FASB, 1992.

[ 151 Financial Accounting Standards Board. Statement of Financial Accounting Standards No. 109. “Accounting for Income Taxes.” Stamford, CT: FASB, 1992.

[16] Flannery, Mark J. and Christopher M. James. “The Effect of Interest Rate Changes on the Common Stock Returns of Finan- cial Institutions.” Journal of Finance 39(September 1984):1141- 53.

[17] Holthausen, R. W., and R. W. Leftwich. “The Economic Con- sequences of Accounting Choice.” Journal of Accounting and Economics 5(August 1983):75-117.

[18] Lamy, Robert E., M. Wayne Marr, and G. Rodney Thompson. “The Mexican Debt Crisis, the IMF, and the Efficiency of Bank Share Prices.” Studies in Banking and Finance 3(1986):203-17.

[ 191 Lee, Insup, and Robert Schweitzer. “Shareholder Wealth Effects of Interstate Banking: The Case of Delaware’s Financial Center Development Act.” Journal of Financial Services Research 2(June 1989):65-72.

[20] Liebtag, B. “FASB on Income Taxes.” Journal of Accountancy 163(March 1987):80-84.

[211 Moyer, Susan E. “Capital Adequacy Ratio Regulations and Ac- counting Choices in Commercial Banks.” Journal ofAccounting and Economics 13(July 1990):123-54.

[22] National Accounting Association. “Association Urges Action on Deferred Income Tax Accounting.” Managrnent Accounting 63(February 1982):66-71.

[23] Norby, William C. “Obsolescence of Deferred Tax Accounting.” Financial Analysts Journal 38(February 1982):75-76.

Stock Market Reactions to SFAS 491

1241 Nurnberg, Hugo. “Income Tax Allocation Under SFAS 96.” CPA Journal 58(July 1988):34-47.

1251 Ou, Jane A., and Stephen H. Penman. “Financial Statement Analysis and the Prediction of Stock Returns.” Journal of Ac- counting and Economics ll(November 1989):295-329.

[26] Read, William J., and Robert A. J. Bartsch. “The FASB Pro- posed Rules for Deferred Taxes.” Journal of Accountancy

1271 Slater, Karen. “FASB Adopts Rule That Will Boost Companies’ Profits.” Wall Street Journal, December 21, 1987, p. 6, col. 4.

1281 Stewart, John E., and Amy A. Ripepi. “Financial Reporting of Income Taxes Is Altered by a New FASB Statement.” Taxation for Accountants 41(September 1988):182-87.

[29] Trombley, Mark A. “Accounting Method Choice in the Software Industry: Characteristics of Firms Electing Early Adoption of SFAS No. 86.” Accounting Review 64(July 1989):529-38.

172( August 199 1 ):44-53.