SOLID FOUNDATION FOR FUTURE VALUE - BIDV

32

SOLID FOUNDATION FOR FUTURE VALUE November 2021

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of SOLID FOUNDATION FOR FUTURE VALUE - BIDV

SOLID FOUNDATION FOR FUTURE VALUE

November 2021

Contents

2

SECTION 1 – VIETNAM MACRO ECONOMY

• Macroeconomic Highlights ……………….…………………………….….... p.3

• Banking Industry Review ……………………….………………………….... p.6

SECTION 2 – BIDV OVERVIEW

• BIDV Profile ……………………………………………………………......... p.9

• BIDV Performance in 2016 – Q3.2021 ……..………………………………. p.19

SECTION 3 – CAPITAL RAISING PLAN

• Overall Plan ………………………………………………………………… p.30

VIETNAM MACRO ECONOMY1

Macroeconomic Highlights

4

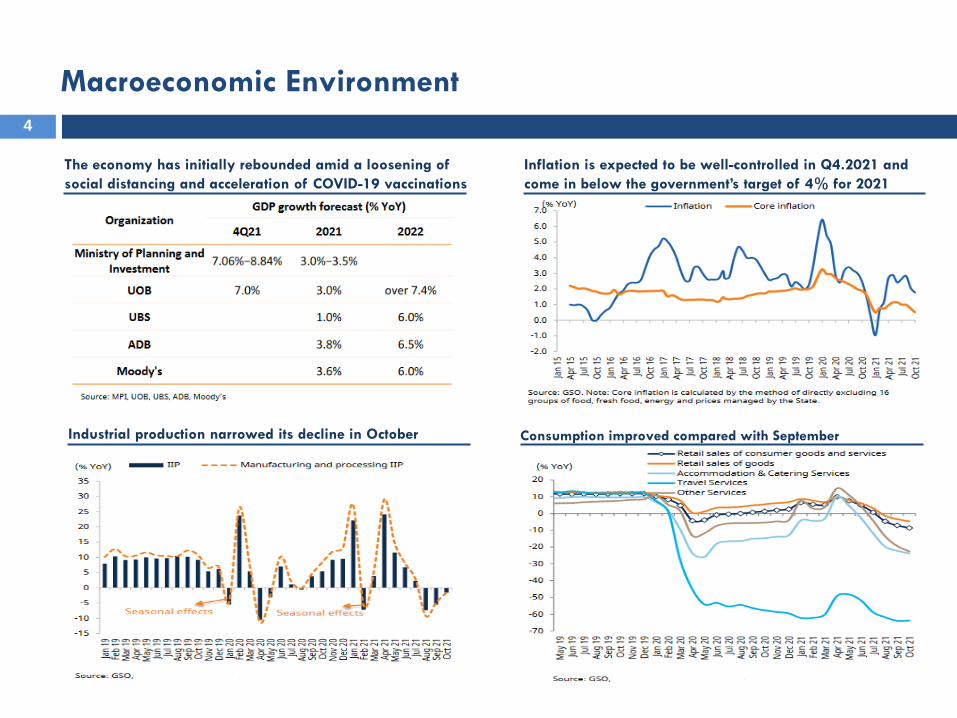

Macroeconomic Environment

The economy has initially rebounded amid a loosening of

social distancing and acceleration of COVID-19 vaccinations

Inflation is expected to be well-controlled in Q4.2021 and

come in below the government’s target of 4% for 2021

Industrial production narrowed its decline in October Consumption improved compared with September

5

Macroeconomic Environment

Exports expected to regain growth momentum when

production and business activities recover Registered FDI maintained double-digit growth rate

Public investment is expected to recover in 2022−2024Vietnam’s market is expected to enjoy high EPS growth,

fair 2021 forward P/E

VIETNAM MACRO ECONOMY1

Banking Industry Review

7

Supportive monetary and fiscal policies

Supportive monetary policy Headroom for fiscal policy remains comfortable

Lower financing cost to encourage investment VND appreciates relative to US$ in 10M2021

Banking industry8

2012 2021

42%

42%

33%

50%

40%

52%

46%

33%44%

41%

Market share in 2020

Credit growth is expected to accelerate for financing the recovery Pandemic-driven bad debt concerns

16% 12% 11%

29%15%

41%40% 42%

47%

45%

43% 48% 48%

24%

40%

State-owned Commercial Banks Joint Stock Commercial Banks Other

Total Assets Lending Deposits Charter Captial Profit after Tax

BIDV OVERVIEW2

BIDV Profile

Differentiating BIDV

BIDVPayment system Network

Customer base Financial Capacity

Credit Rating Information Technology

# 1 by Total Assets

# 1 by PPOP

# 2 by National Network Coverage

(190 Branches, 895 Transaction Offices, over

1,900 ATMs and 33,000 POS)

# 1 by Customer Loans

# 1 by Customer Deposits

• Settlement bank for Vietnam stock market

• The only settlement bank for domestic transactions

of Master Card in Vietnam

• The Vietnam Domestic Technology and

Operations Bank of the Year awarded by

Asian Banking & Finance (ABF)

• Ranking first for Readiness for IT

application to business for 10 years

A leading bank in Vietnam market10

Moody’s

(March 2021)

Rating Ba3

Outlook Positive

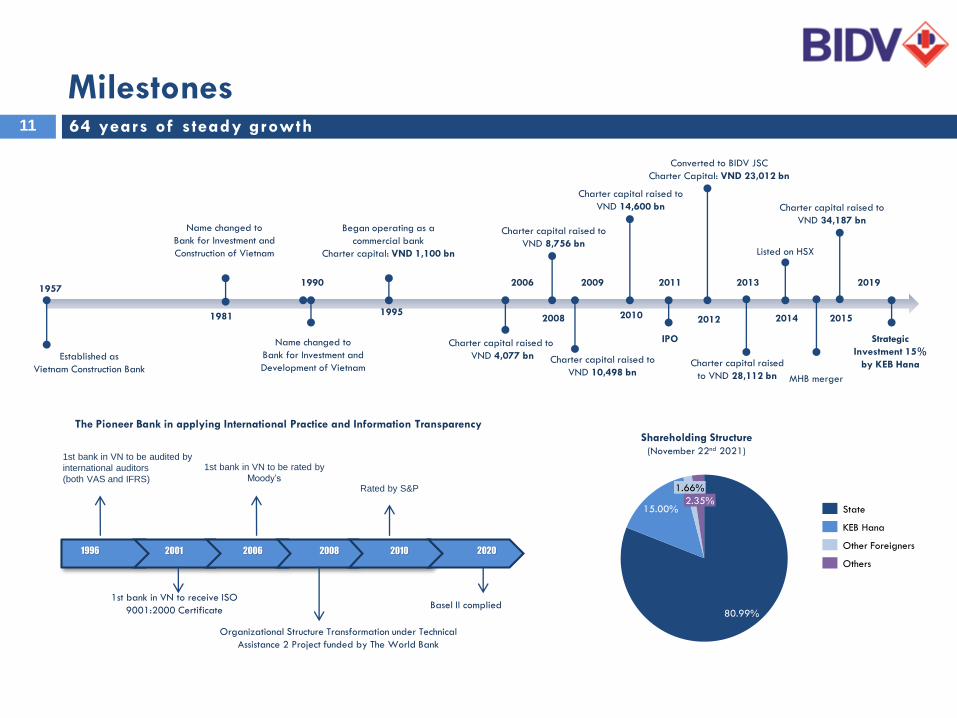

Milestones

1957

Established as

Vietnam Construction Bank

1990

Name changed to

Bank for Investment and

Development of Vietnam

1995

Began operating as a

commercial bank

Charter capital: VND 1,100 bn

Charter capital raised to

VND 4,077 bn

2006

1981

Name changed to

Bank for Investment and

Construction of Vietnam

2008

Charter capital raised to

VND 8,756 bn

2009

Charter capital raised to

VND 10,498 bn

2010

Charter capital raised to

VND 14,600 bn

2011

IPO

2012

2013

Charter capital raised

to VND 28,112 bn

Converted to BIDV JSC

Charter Capital: VND 23,012 bn

Listed on HSX

2014

MHB merger

2015

Charter capital raised to

VND 34,187 bn

2019

64 years of steady growth11

Shareholding Structure (November 22nd 2021)

1st bank in VN to be audited by

international auditors

(both VAS and IFRS)

1st bank in VN to receive ISO

9001:2000 Certificate

1st bank in VN to be rated by

Moody’s

Organizational Structure Transformation under Technical

Assistance 2 Project funded by The World Bank

Rated by S&P

1996 2001 2006 2008 2010 2020

Basel II complied

The Pioneer Bank in applying International Practice and Information Transparency

Strategic

Investment 15%

by KEB Hana

80.99%

15.00%

1.66%

2.35%State

Others

KEB Hana

Other Foreigners

Mission, Vision & Core Value

Mission

Vision

• Best services for customers

• Best value to shareholders

• Professional working environment for employees

• Pioneer in community development activities

Being a leading financial institutions in Southeast Asia

with the best digital platform in Vietnam, striving to be in

Top 100 largest banks in Asia.

Commit ted to del ivering the best value12

cCore

values

Customer

OrientationInnovation

Quality and

Trustworthiness

Social

Responsibility

2021 – 2025 Strategy

13

Scale

Asset Quality

Profitability

•Total Assets: 9 - 13% pa

•Lending: 9.5-12.5% pa.

•Deposits: 10.5-15% pa.

•NPL: ≤ 1.6%

•ROA: 1%

•ROE: 17%

1

• Sound financial capacity as a basis for growingoperational scale, increasing market share andmaintaining a leading position in the banking market

2

• Sustainable performance, improving the quality ofassets, increasing the proportion of non-interest income.providing the best banking - finance - insuranceproducts and services to customers.

3

• Customer structure has shifted positively, becoming theleading bank in Vietnam in terms of market share in thesegment of retail & SMEs.

4• Managing and operating transparently, effectively as

international practices.

5• As a leading bank in information technology and digital

banking applications in Vietnam.

6

• High quality human resources ensure in the trend ofintegration and technology 4.0; Professional, modern,learning and creative working environment.

Organization Chart

14

ORGANIZATIONAL STRUCTUREAs of June 30th 2021

GOVERNANCE CHARTAs of June 30th 2021

Diversified Business

189 Domestic Branches

01 Oversea Branch

895 Transaction Offices

1,900 ATMs

33,000 POS

Internet Banking

Mobile Banking

Extensive Domestic Network Coverage for both Traditional and Modern

Distribution Channels*

International Expansion

• RMA with 1,100 banks and 50 Nostro accounts with large banks all

over the world

• Joint-ventures with international partners Russia, Singapore,

Malaysia, Cambodia, Laos

• Representative Offices in Cambodia, Laos, Myanmar, Russia, Taiwan

• Branch in Myanmar

* As of September 30th 2021

15

16

BIDV’s Market Position (as of 30/09/2021)

Achievements

Top 10 Vietnam companies

Outstanding Retail Bank in Vietnam

2016-2020, Best Digital Business

Transformation 2020

Best Payment Bank in Vietnam

Best SME 2018-2020

Best Cash Management Bank in Vietnam

Best Transaction Bank in VietnamTop 300 Global Banking Brand

Top 4 most valued brands in Vietnam

Top 10 sustainable companies

2018-2020

Best SME Bank 2018-2020

Best FX Provider 2018-2020

Top 2000 World’s Biggest Public

Companies, Top 50 Vietnam

Companies

17

Leadership in Contactless active

terminals penetration 2019,2020

Best SME Bank Vietnam

2018, 2019,2020

6 excellent high technology applied products: BIDV-Ezone; BIDV Paygate; Automatic

deposit investment system and bilateral payment for Vietnam Social Security; BIDV’s

bank statement system; Cross-selling management system - BIDV Sale Power; Sales

support mobile application for corporate customers named B.Sales.

BIDV Shares

18

Ticker BID

Listed on Ho Chi Minh Stock Exchange

Listing Date 24th January 2014

Outstanding Volume (shares) 4,022,018,040

Free-floating ratio 4.01%

Foreign ownership 16.66% (15% by Hana)

Market Cap (VND tn)VND 180 trillion (USD 7.9 billion)

Rank the 9th in Vietnam Stock Market

Last closed price

(November 22nd 2021)45,750 VND

52-week high/low 49,000 / 37,900 VND

EPS 2,449 VND

P/B (November 22nd 2021) 2.17x

P/E (November 22nd 2021) 18.3x

Share Price Performance

Peer ComparisonNovember 22nd, 2021

0

2

4

6

8

10

12

14

16

18

20

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

BID CTG VCB VPB TCB MBB ACB STB HDB

Market Cap P/E P/B

BIDV OVERVIEW2

BIDV Performance

Steady balance sheet growth20

Total Assets(VND billion)

Customer Deposits(VND billion)

Customer Loans(VND billion)

1.006.635

2016

1.312.8861.202.283

2017 2018

1.489.957

2019

1.516.686

2020

1.685.678

3Q2021

+11,1%10,8%

723,697

866,885

988,739

1,116,998

1,214,296

1,328,680

2017 20192016 2018 2020 3Q2021

9.4%+14%

726,022

859,985

989,671

1,114,163

1,226,6741,309,953

202020172016 2018 3Q20212019

+6.8%+14%

Profit Before Tax (VND billion)

10,733

3Q202120172016 20202018

7,709

2019

13,000

8,6659,473

10,876

9,214+41%

+11%

Loan portfolio focusing on retail and SME components21

• Market share: 13.4%

• The Bank’s lending increased by 9.4% from end of 2020 to VND 1,328,680 billion as of September 30th 2021

• Loan portfolio:

• Focusing on retail and SME components (37.7% and 22.5% respectively as of 2020).

• Short term loans increased proportion and accounted for 64.7% of the portfolio.

Trend in Gross Customer Loans(VND billion)

58.0%

11.9%

1,328,680

2017

33.2%

2016

32.6%

61.8%

7.2%

31.4%30.9%

2018

1,214,296

62.6%

6.6%

30.8%

54.8%

2019

62.9%

5.8%

723,697

64.7%

2020

5.4%

29.8%

3Q2021

866,885

988,739

1,116,998

9.4%

9.4%14%

Short-term Long-termMedium-term

Loan portfolio by customers

40,2%Corporate

22,5%

Retail

SME

37,3%

Q3.2021

Diversified focusing on high-growth sector and good credit quality22

Loan portfolio by group (%)

4,4%

Agriculture, forestry & seafood

1,1%

Mining

16,1%

8,9%

Electricity, petroleum & water5,6%

Manufacturing & processing

Construction

30,8%

Wholesale & retail trade

3,9%Transport & warehousing

11,8%Services

2,5%

Real estate14,8%

Others

Loan portfolio by industry

• Credit quality was improved with NPL ratio according to Circular

No.11 was at 1.39% (The ratio of 2020 was 1.54%) .

• Loan portfolio by industry improved positively by increasing

loans for high-growth industries (such as services, wholesale &

retail) and decreasing loans for high-risk industries (such as real

estate, mining, manufacturing).

2016

1,99%

3,75%

94,26%

3,52%

1,62%

94,86% 95,77%

2017 2020

1,90%

2,33%

2018 2019

1,74%

1,10%2,23%

96,03%

1,76%

1,12%

97,12%

1,61%

97,29%

3Q2021

NPL Special Mentioned Current

2020

5,4%

Agriculture & forestry

12,1%

7,5%

3,0%

7,1%

Electricity, petroleum & water

Manufacturing & processing

Mining

19,1%

15,8%

Others

Wholesale & retail trade

Construction

23,1%

2,2%Transport & warehousing

4,6%Services

Real estate

2016

Deposits23

82.1%

17.2%

Specific Purpose Term Deposit Demand Deposit

• Market share: 11.0%

• Customer deposits grew by 14% p.a. in the period of 2016-2020 thanks to nationwide network and strong brand name.

• Deposit structure: Individuals deposit accounted for 48% of total mobilized funds, ensuring the stable deposit growth.

Customer Deposits by Term(VND billion)

0.7% 0.5%

82.1%

17.2%

2017

18.6%

80.7%

0.7%

16.4%

726,022

82.9%

2016

1,226,674

2018

1.1%

16.0%

82.9%

18.0%

81.4%

2020

18.5%

81.0%

0.4%

3Q2021

1,114,231

2019

859,985

989,671

1,309,953

0.8%

+6.8%

+14%

Deposit Breakdown

48%

45%

7%

FI

Corporate

Individuals

Q3.2021

Financial Performance24

Total Operating Income

(VND billion)

Net Interest Income

(VND billion)Non-Interest Income

(VND billion)

2017 20202018

50.035

20192016 3Q2021

44.483

30.434

39.017

48.165 47.144

13,2%

2016 2017 1H20212018 2019 2020

35.964

23.435

30.955

35.99534.956

11,2%

20172016 2018 2019

11.179

2020 3Q2021

6.999

8.062

9.527

12.171

14.238

+19,4%

17.280

2016 20192017

16.167

2018 2020 3Q2021

13.527

15.504

17.696

13.216

6,9%

Total Operating Expense

(VND billion)

2,528

25

Financial Performance

89%

6%

From deposits

From loans to customers

From debt securities

0%

2%

From guarantee

From finance leases

1%

Others

2%

74%

10%

13%

Interest income

0%

Investment income

Fee & commission

2%

Other income

Gold and FX

0%

Securities income

Non-interest income accounted for bigger proportion in TOI Interest income from loans to customers is driven factor in NII

24%

20%

24%

12%

7%

13%

Insurance activities

Payment services

Other service

Card

Digital banking

Trade finance

Leading banking service focusing on settlement and insurance

58%

17%

19%

6%

0%

Taxes and fees

Administration Expense

Staff Cost

Rental & Fixed Assets

Provision expense

0%

Insurance for customer deposits

Well-managed operating expense

Q3.2021

Q3.2021 Q3.2021

Q3.2021

Key Ratios26

Source: BIDV Financial Reports

Asset quality 2016 2017 2018 2019 2020 3Q2021

Loans to deposits 100% 101% 99.9% 100.0% 99.0% 101.4%

Loan loss reserve coverage (Provision/NPL) 69.7% 80.7% 66.0% 74.2% 88.4% 140.2%

NPL ratio 1.99% 1.62% 1.90% 1.74% 1.76% 1.61%

Credit Cost 1.39% 1.87% 2.04% 1.90% 1.98% 2.36%

Profitability 2016 2017 2018 2019 2020 3Q2021

Net interest margin 2.72% 2.98% 2.94% 2.82% 2,61% 2.36%

Non-interest income/Operating Income 23.0% 20.7% 21.4% 25.3% 28.5% 23.7%

ROAA 0.67% 0.63% 0.60% 0.62% 0.49% 0.64%

ROAE 14.4% 14.9% 14.6% 13.1% 9.4% 12.3%

CIR 44.4% 39.7% 36.2% 35.9% 35.4% 28.9%

Retail Banking 27

Retail Deposits (VND billion )

308,337

374,526

425,879

488,761

2016 20182017 2019 2020 3Q2021

185,216

238,527

14.8%

23.1%

Retail Loans (VND billion)

8,802

10,040

11,340

12,786

14,24115,331

2016 2017 20202018 2019 3Q2021

7.7%12.8%

Customer Base (thousand people) Retail Loans Breakdown (VND billion)

32,3%

Mortgages

Consumers

22,2%

Commercial & Production 45,0%

0,5%

OthersQ3.2021

435,283

523,643571,204

625,666 634,127672,843

20202016 2017 3Q202120192018

6.11%

9.9%

28

Digital Banking

BIDV’s digital banking vision 2030 - Become the leading financial

institution in Southeast Asia with the best digital platform in Vietnam,

and strive to be among the 100 largest banks in Asia.

Digital Channels: Internet banking, Mobile banking, Web Chat,

Messenger, Facebook Fan Page, YouTube Channel, 3rd party

app/web, Online Application for Internet & mobile banking…

Innovation products: Apple Watch, Interactive game, Smart

Keyboard for fund transfer, Chatbot, Notification for transaction (OTT

messages) in Smart Banking; Virtual Account, Swift GPI in iBank

Number of E-banking users: (Update September 2021): 8.5 million,

include Smartbanking: 6.0 million (70%).

Transaction Value (the 9 months of 2021): ~120 billion USD,

increased 38% compare with 2020.

Update 1H202129

Source: BIDV Financial Reports

Income Statement (VND billion) 2016 2017 2018 2019 2020 3Q2021CAGR

2016-2020

Net interest income 23,435 30,955 34,956 35,995 35,797 35,964 13.1%

Net fee & commission income 2,509 2,966 3,551 4,283 4,266 4,770 12.8%

Total operating income 30,434 39,017 44,483 48,165 50,035 47,143 15.2%

Operating expense 13,527 15,504 16,117 17,280 17,696 13,216 9.8%

Profit before provision 16,907 23,513 28,366 30,885 32,339 33,928 18.9%

Provision expenses 9,199 14,847 18,894 20,009 23,125 23,195 32.4%

Profit before tax 7,709 8,665 9,473 10,876 9,214 10,733 3.0%

Taxation charge 1.48 1.72 1,931 2,211 1,851 2,150 3.3%

Net profit 6,229 6,946 7,542 8,665 7,363 8,583 2.9%

Balance Sheet (VND billion) 2016 2017 2018 2019 2020 3Q2021CAGR

2016-2020

Total assets 1,006,404 1,202,284 1,313,038 1,490,105 1,516,870 1,685,678 12.3%

Customer loans 723,697 866,885 988,739 1,116,925 1,214,296 1,328,680 15.2%

Customer deposits 726,022 859,985 989,671 1,114,231 1,226,674 1,309,953 16.8%

CAPITAL RAISING PLAN3

Overall Plan

Projected Shareholding Structure

STAGE 1: 2019 STAGE 3: From 2022

• Issuing shares to foreign investors

(total up to 30%):

- Strategic Investor (KEB Hana): 15%

- Financial investor: up to 12%

• State ownership ≥ 65%

• Additional public offering

• Issuing additional shares to foreign

• Foreign Investors (may hold >30% in

total)

• State ownership decrease to ≥ 51%

• IPO finished on December, 2011

• Transforming to Joint Stock

Commercial Bank in April 2012

• State ownership: 80.99%

• KEB Hana: 15%

• Other Foreigner ownership: 3%

STAGE 2: To 2022

31

KEB Hana

Foreigners

80,99%

3,00%

15,00%1,01%

Others

State

5%

65%Sate ownership

30%Foreign ownership

Others

5%5%

OthersEmployees

39%

Foreign ownership

51%

Sate ownership

(*) According to “The Development Strategy of the Vietnam Banking Sector to 2025, vision to 2030” approved by the Prime Minister in Decision No.986/QD-TTg dated 8th Aug 2018

This Presentation (the Presentation) has been prepared by IR Team - BIDV for the purpose of setting out certain

confidential information in respect of BIDV’s business activities and strategy. This Presentation is for the exclusive use of

the recipients to whom it is addressed.

This presentation is to provide general information and analysis on BIDV for those who qualify as a “professional

securities investor” as defined in the Securities Law. Such investors should use information, analysis, comment in this

presentation as a reference source only. This presentation and any meeting where this presentation is made are for the

purpose of providing information and do not intend to advertise BIDV or BID stock or to advice readers to buy or sell BID

stock or any other securities. No representation or warranty, express or implied, is made concerning, and no reliance

should be placed on, the accuracy, fairness, or completeness of this Presentation. BIDV takes no responsibility with regard

to the accuracy or completeness of any information contained here. Viewpoint and analysis in the report can be changed

without notification.

The presentation is a property of BIDV and under copyright protection. Infringement of copy, change and reprint of the

report without permission of BIDV is illegal. BIDV owns the copyright on this documentation.

IR Team:

Ms. Tran Nguyet Quynh Hoa - Tel: +84 937 050 282 - Email: [email protected]

Mr. Nguyen Xuan Thieu - Tel: +84 899 568 688 - Email: [email protected]

Mr. Nguyen Phi Long - Tel: +84 936 337 717 - Email: [email protected]

Ms. Hoang Ngoc Anh - Tel: +84 947 653919 - Email: [email protected]

Important Notice32