SLatin America and the Caribbean, - Technical Departnlent

174

SLatin America and the Caribbean, - Technical Departnlent Regional Studies Program. Report No. 18 Private Financing of Higher Education in Latin America and the Caribbean by Sam Carison Human Resources Division July 1992 Papers in this series are not formal publications of the World Bank. They present preliminary and unpolished results of country analysis or research that is circulated to encourage discussion and comment; any citation and the use of this paper should take vecount of its provisional character. The .iodings, interpretations, and conclusions expressed in this paper are entirely those of the author(s) and should not be attributed in any manner to the World Bank, its affiliated organizations, members of its Board of Executive Directors or the countries they represent. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

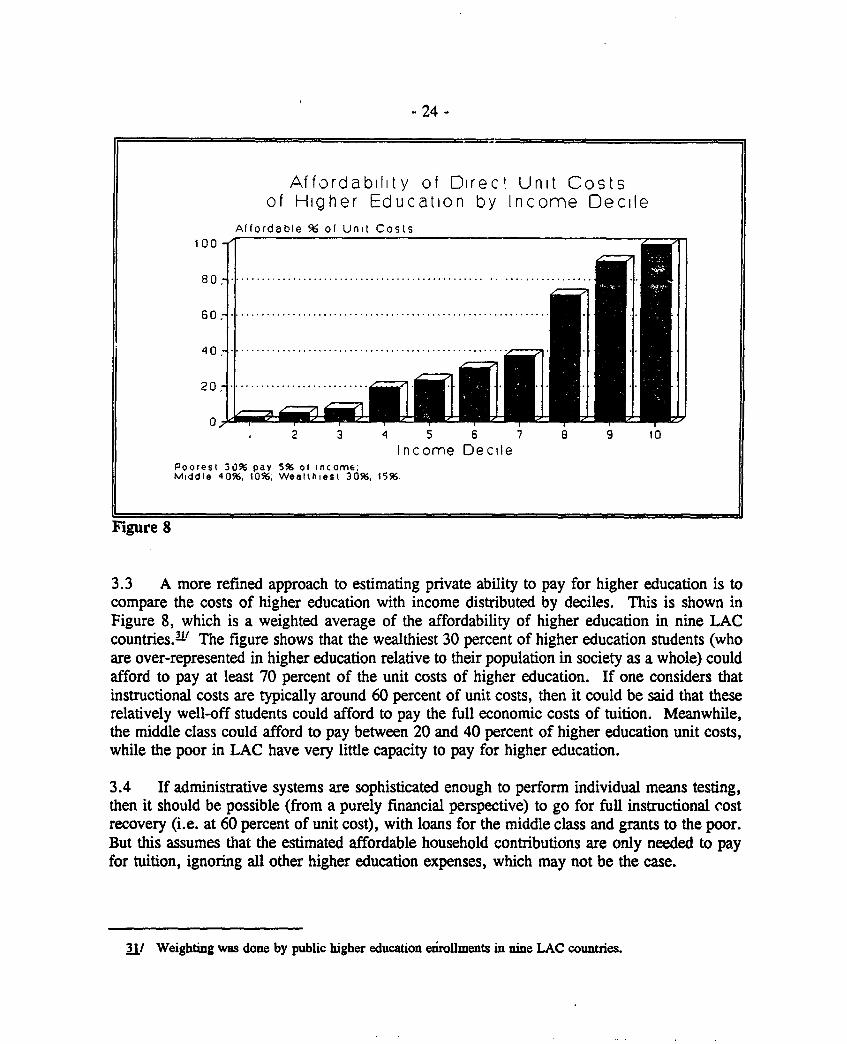

-

Upload

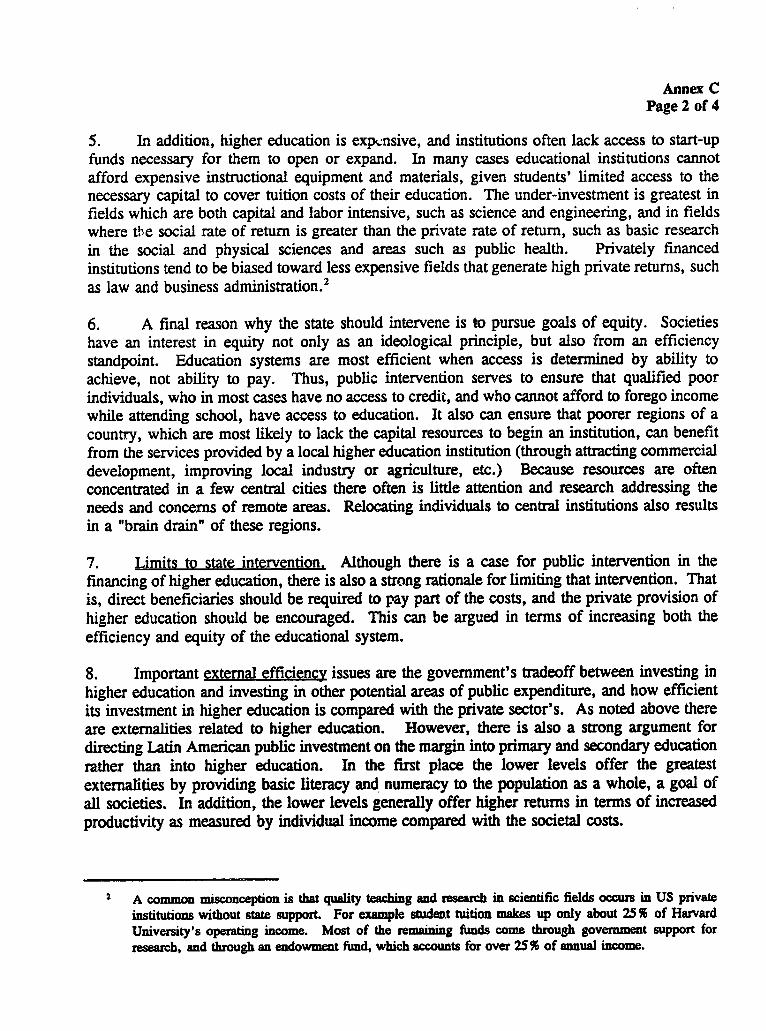

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of SLatin America and the Caribbean, - Technical Departnlent

SLatin America and the Caribbean,- Technical Departnlent

Regional Studies Program.

Report No. 18

Private Financing of Higher Educationin Latin America and the Caribbean

by

Sam Carison

Human Resources Division

July 1992

Papers in this series are not formal publications of the World Bank. They present preliminary and unpolished results of country analysis or research

that is circulated to encourage discussion and comment; any citation and the use of this paper should take vecount of its provisional character. The

.iodings, interpretations, and conclusions expressed in this paper are entirely those of the author(s) and should not be attributed in any manner to

the World Bank, its affiliated organizations, members of its Board of Executive Directors or the countries they represent.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

This report was prepared by Sam Carlson (LATHR). It has benefitted greatly from the guidance and comments of peerreviewers Jee-Peng Tan (SASVP), Douglas Albrecht (PHREE), Nicholas Barr (EC2HR) and William Saint (AFTED).Additional comments from George Psacharopoulos, David Hughart (LATDR), Laurence Wolff and Julian Schweitzer (LATHR)were extremely helpful in making revisions. Guozhong Xie (EA3IE), Hongyu Yang, Haeduck Lee and Judy Baker (LATHR)assisted with the statistical analysis of hcusehold survey data, while Barbara Diallo (LATHR) provided professional computing4nd formatting support. Douglas Albrecht (PHREE) designed several of the student loan financial models used in this report,and the research of Mr. Albrecht and Adrian Ziderman (PHREE) was particularly important for setting this regional study ina global context.

ABSTRACT

The purpose of this study is to contribute directly t he current debate on highereducation finance reform in Latin America and the Caribbean kLAC), on both practical andtheoretical levels. Given macroeconomic constraints, increasing demand for higher educationand the need to improve the efficiency and equity of public expenditures, the objective is toanaly:,e the potential for increased stulent fees, expanded student loan schemes and effectivescholarship programs. These private sources of finance may be among the most importzntelements of public higher education reform in Latin America.

By mobilizing affordable private financing LAC governments could increase the totalresources going into public higher education by about 35 percent in real terms. This is basedon tuition fees equal to 30 percent of higher education unit costs. These fees would beaffordable by about 40 percent of LAC households. Student loan programs would be requiredfor another 40 percent of students, while the remaining 20 percent of the student body wouldneed scholarships (which could be financed by tuition revenue). Tuition fees set between 25 to35 percent of higher education unit costs appear to reflect the optimum balance of all financial,institutional and political factors.

Student loan programs in Latin America and the Caribbean recover an average of 40percent of the money disbursed (in net present value terms), and cover less than 8 percent, onaverage, of the higher education student body in each country. Adopting reforms suggested inthis report, it should be possible to increase this recovery to at least 50 percent, while at thesame time expanding loan programs to cover up to 60 percent of the student body. Privatizationof some or all loan program services, so as to max-mize administrative and financial efficiency,should be considered as an alternative or complement to existing public programs.

CONTENTS

Chapter Page

Executive Summary ....................................... i

1 Introduction ........................................... 1

2 Trends in Higher Eiucation Finance in Latin America and the Caribbean ..... 6Public Expenditures ................................... 6Private Expenditures .................................. 10Equity ........................................... 12

3 The Ability to Pay for Higher Education ......................... 23Student Fees ....................................... 23Willingness to Pay for Higher Education ...................... 34Student Loan Repayments ............................... 38

4 Student Loan Programs in Latin America and the Caribbean ............. 41Background ........................................ 41Financial Analysis of Student Loan Programs ................... 47Administration of Student Loan Programs ..................... 59Options for Reform of Student Loan Programs .................. 62Loan Program Privatization .............................. 73Alternative Lending Scenarios ............................ 75

5 Scholarships for HigherEducation ............................. 79Loans Versus Scholarships .............................. 84

6 Political Feasibility of Higher Education Finance Reform ............... 86Political Strategy forReform ............................. 93

7 Synthesis: Fees, Loans and Scholarships ........................ 100

Bibliography/Sources .................................... 103

Annex A: Trends in Higher Education Enrollments and Expenditures

Annex B: Selected Tables and Graphs from Household Survey Data andStudent Loan Program Simulations

Annex C: The Economics of Higher Education and Implications for Reform

Annex D: Summary of APJCE Student Loan Questionnaire Responses

Annex E: Checklist for Designing Student Loan Programs

Annex F: Feasibility of Using Social Security Institutes for Student LoanCollection

Annex G: Household Survey Data Description

Annex H: Sources for Determination of Higher Education Unit Costs

ExEcUTIVE -AORY

1. The purpose of this study is to contribute directly to tne current debate on highereducation finance reform in Latin America and the Caribbean (LAC), on both practicaland theoretical levels. Given macroeconomic constraints, increasing demand for highereducation and the need to improve the efficiency and equity of public expenditures, theobjective is to analyze the potential for increased student fees, expanded student loanschemes and effective scholarship programs. These private sources of finance may beamong the most important elements of public higher education reform in Latin America.

POTENTIAL NEW PRIVATE FINANCING FOR H.E.RELATIVE TO CURRENT PUBLIC H.E. SPENDING

INDEX * 100140

130*

120-

110

100 ,

1 2 3 4 6 6 7 8 9 10 11 12 13 14 16 16 17 18 19 20

YEARS

- PUBLIC SPENDING - NEW PRIVATE FUNDS

Base tlne Index Includes 1% annualgrowth In real public expenditures.

Figure 1

2. Figure 1 shows that by mobilizing affordable private financing LAC governmentscould increase the total resources going into public higher education by 35 percent in realterms.1' This is based on tuition fees equal to 25-35 percent of unit costs, which would

1/ This is based on computer models which simulate the net effects of tuition fees, student loan schemesand scholarship programs. The index shown reflects weighted average composite indices for Mexico,Brazil, Argentina, Venezuela and Colombia (each country is shown individually in Annex B).

- ii -

be equivalent to about one-half of estimated urit instructional costs. These fees wouldbe affordable by about 40 percent of LAC households. Student loan programs would berequired for another 40 percent of students. It is estimated these programs would recoverabout 50 percent of the money disbursed in net present value. The remaining 20 percentof the student body would need scholarships, which could be financed from tuitionrevenue. While higher fee levels might result in greater cost recovery, especially ifstudent loan programs become more efficient, the political and financial start-up costs ofsuch a policy are likely to be prohibitive. Lower fee levels would clearly mean lesspolitical pressure and lower start-up costs, but the improvements in cost recovery,efficiency and equity would be so limited as to question whether the reforms wereworthwhile. Tuition fees set at 25 to 35 percent of higher education unit costs appearto reflect the optimum balance of all financial, institutional and political factors."

3. Trends in Higher Education Finance in LNC Compared to most other regions ofthe world, Latin America spends a larger share of the government budget on educationand a greater proportion of the education budget is allocated to higher education. In1989 more than 25 percent of LAC government education spending went to highereducation, up from 16 percent in 1970 and 23 percent in 1980. In large part, this isbecause total higher education enrollment in Latin America increased twelve-fold between1960 and 1985 and the enrollment rate (weighted average) increased from 6 to 22percent. Since publicly-funded institutions accounted for much of the growth in highereducation enrollments, government expenditures on higher education increased, as well.

4. Over the next 20 years the demand for higher education in LAC will rise even more,due to population growth and increasing enrollment ratios at lower levels. Unfortunately,adverse macroeconomic conditions and intersectoral competition for public funds havereduced most governments' ability to finance education (at all levels), such that even noweducation is underfunded in most LAC countries. For efficiency, equity and scarcityreasons alternative financial resources for higher education must be found; the currentsystem is unsustainable. The logical solution is to tap the ability and willingness ofprivate households to invest in higher education.

5. Private Financinp LAC countries currently charge public higher education tuitionfees equal to just 7 percent, on average, of total unit costs (with a range from 0 to 26percent). However, students pay for other incremental, non-tuition higher educationcosts (such as food, rent, books, transportation, etc.), which together with tuition

2/ Unit costs include all public higher education expenditures (instruction, research, extension, etc.),whereas unit instructional costs include only those costs directly related to providing instruction. Thelatter are estimated to be about 60 percent of total unit costs.

3/ Obviously, tuition fees will and should be determined on a country-by-country basis; this suggestedtuition fee level reflects averages for the LAC region as a whole.

- iii -

constitute total financial costs.!' To these financial costs should be added theopportunity cost of foregone earnings, to calculate total private economic costs of highereducation. In all LA.C countries, these non-tuition expenses are greater than publictuition fees currently .. iarged, and greater than the unit costs of public higher education(except Brazil). This suggests that non-tuition expenses are the greatest financial oustacleto higher education, not tuition fees.

6. Equity Free (or low charge) public higher education has not meant equal accessto higher education. In fact, because most Latin American public higher education is free(or very low charge), it has resulted in rationing. Those who are admitted into publichigher education institutions are generally those who score highest on entrance exams,which in most cases requires access to quality (often private) primary and secondaryeducation.Y The poor have restricted access to quality lower education and are the leastable to afford the private costs of higher education, especially foregone earnings' Infact, a 1987 study showed that students from families in the upper two income quintilesre( ve about 75 percent of LAC higher education subsidies, while those from familiesn .e ower twe mcome quintiles receive just 13 percent of LAC higher education

subsidie,.-' Finally, tecause much of the public revenues needed to finance free publichi gher education in LAC come from non-progressive commodity taxes rather than incometaxes, it is -ften society at large, including the poor, which subsidizes higher educationfor the we'-off, a truly perverse equity impact.

Ability to Pay For Higher Education

7. Ability to Pay Tuition Fees Recent household survey data suggests that theaverage Latin American household could afford to pay an estimated 28 percent of thetotal financial costs of higher education, by contributing 10 percent of annual income.'Meanwhile, students from the wealthiest 30 percent of LAC households could afford topay 70 percent of the total financial costs of higher education, which would be equivaient

I/ These incremental costs are those which higher education students would not incur if they were notenrolled in school, and are particularly relevant for students who must relocate to attend highereducation.

J/ In the case of higher education systems with open admissions in LAC, testing at the end of the firstyear typically selects those who will continue on to the second year, so that in effect *admissions* takesplace after the first year rather than before it - the rationing effect is the same. If there is no selection,then it is quality rather than access which is rationed.

§/ This argues for increased student loans to the most disadvantaged students to finance this lost income.

2/ Petrei, 1987.

8/ Note that this examines finan.ial costs (which include total unit costs, plus all non-tuition expenses),and does not include the foregone earnings of students.

- iv -

to more than 100 percent of public higher education unit costs. At the other end of thespectrum, students from the poorest 30 percent of Latin American households couldafford to pay just 15 percent of total costs, mainly through loans.2' Obviously, thesecalculations are based on averages and are therefore only indicative. Nevertheless, itprovides strong evidence of the ability to pay tuition fees at LAC public higher educationinstitutions, which has been a contentious issue in the debate on higher education finance.

8. Willinness to Pay Tuition Fees The tuition fees which students should be willingto pay for higher education can be estimated by discounting into net present value acertain percentage of higher education graduate income over 20 years, and then breakingthis down into yearly tuition payments.L' For the region as a whole, "worthwhile"tuition fees range from 13 percent of higher education unit costs in Argentina, to 88percent of unit costs in Guatemala, with a weighted average (by enrollment) of about 30percent of unit co5ts. Note that this 3C per-ent weighted average corresponds closely tothe 4bility of LAC households to pay for higher education.

Student Loan Programs

9. Description and General Characteristics Student loan programs exist in at least20 LAC countries. About half of the programs are private, although almost all areheavily financed by national governments. Few students actually receive student loans,however, from less than 1 percent (Guatemala) to 21 percent (Chile). Low coverage isnot a function of student demand, but rather of loan prngram resources. Because allprograms are subsidized they are far from self-sufficient and require annual infusions ofadditional public funds, the size of which determine the number and amount of loansavailable each year. While internal sources of funds have grown over time (e.g. fromloan repayments), they remain relatively small because of high interest rate subsidies,default rates and administrative costs.

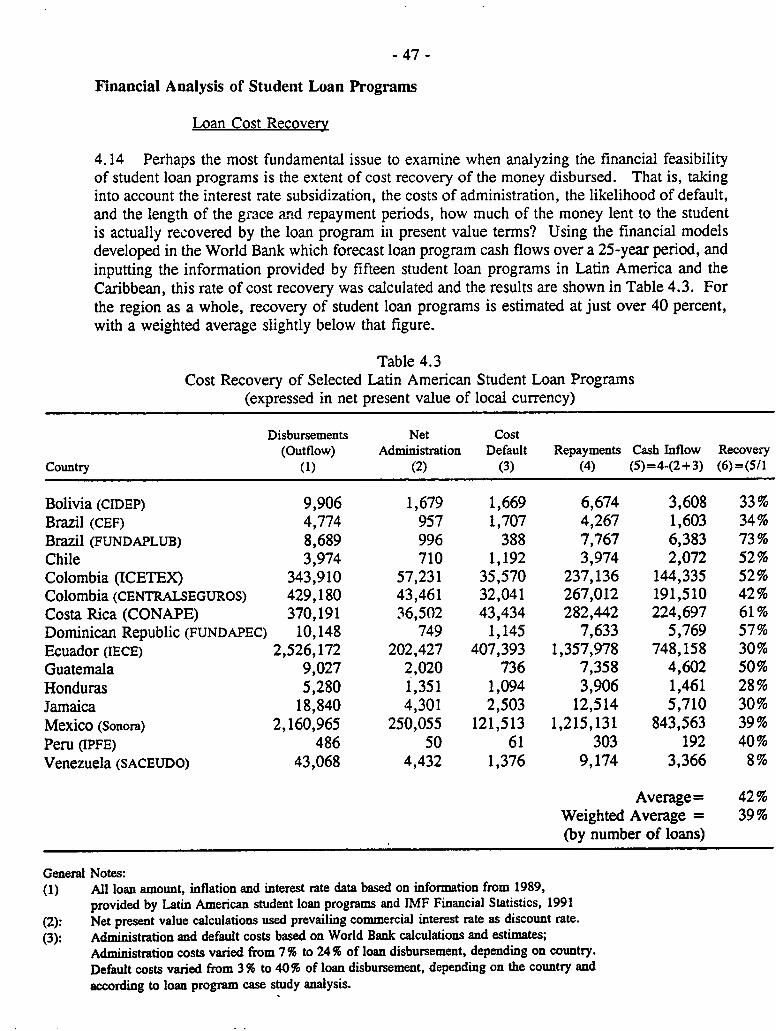

10. Loan Recovery LAC student loan recovery averages about 40 percent in netpresent value terms. This is based on financial models developed in the World Bankwhich forecast loan program cash flows over a 25-year period, and information providedby fifteen LAC student loan programs. The models incorporate interest rate subsidies,administrative costs, default rates, and grace and repayment periods, to estimate howmuch of the money lent to the student is actually recovered by the loan program in netpresent value terms.

2/ For the average LAC household, 10 percent of annual income was used to calculate affordable privatefinancing. For the wealthiest 30 percent of LAC households, 15 percent of annual income was used,while for the poorest 30 percent of LAC households, just 5 percent of annual income was used.

)0/ The analysis used 5 percent of higher education graduate income over 20 years, discounted at 5percent, to determine the 'value' of higher education.

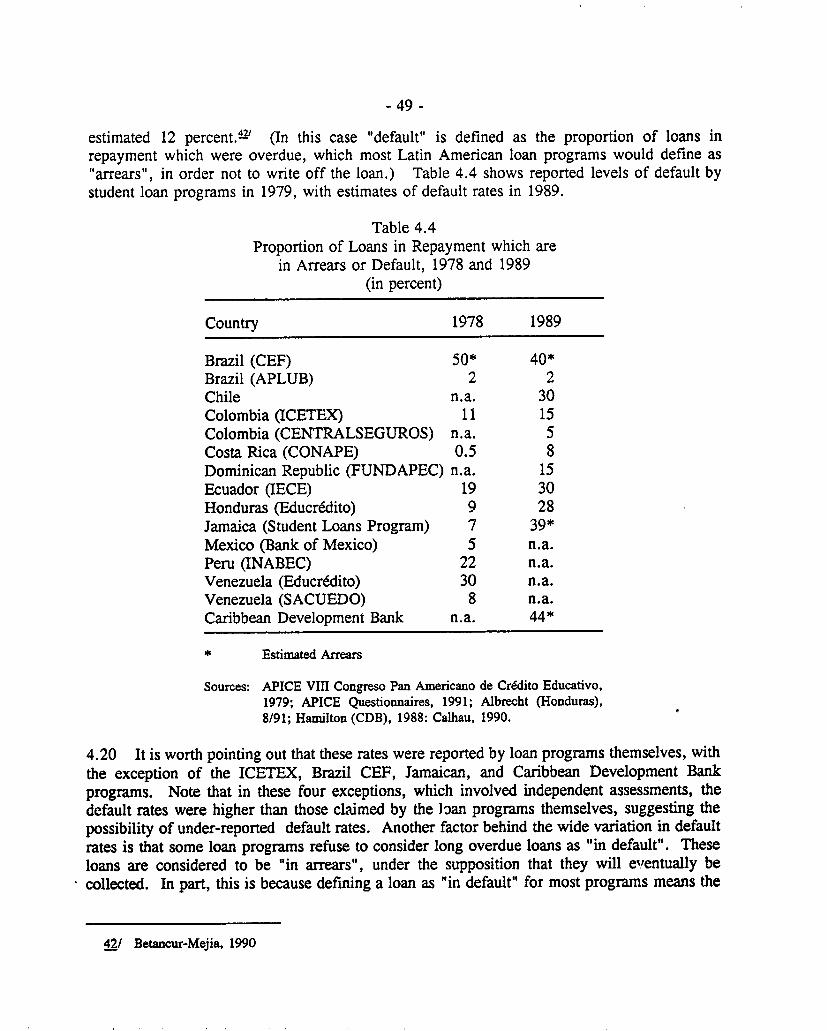

11. Default Rates Default rates were difficult to determine, but are estimated atbetween 2 and 40 percent, with the average around 15 percent. One important factorbehind high default rates is that repayment burdens are unreasonably high in the firstyears after graduation, because rzpayment periods are too short (meaning payments arehigh), and many graduates do not find fully productive employment immediately aftergraduation.

12. Impact Loan programs in LAC ha, not yet been used as a means of costrecovery of public higher education expenditures because of low coverage and heavyinterest rate subsidization, not to mention high inflation. Rather, student loans have beenprimarily a means 'o help students finance the living and maintenance costs (i.e. non-tuition expenses) of higher education.

13. Administrative Analysis Many loan programs in Latin America lack qualified,trained personnel, in part because salaries are low relative to what could be earned in theprivate sector. Another problem is the scarcity of information technology hardware andsoftware, which is necessary for financial and statistical projections. Thirdly, financialconstraints prevent expansion of programs which could generate administrative economiesof scale. Interestingly, nearly all loan programs surveyed mentioned political favoritismas a major source of administrative inefficiency. In general, the analysis indicates thatprivate loan schemes function more efficiently than public loan programs, although theyoffer loans to far fewer students.

Options for Reform of Student Loan Programs

(1) Positive (though subsidized) Interest Rates

14. Loan programs should charge positive real interest rates, although it is recognizedthat student loan interest rates are likely to remain somewhat subsidized because ofpoitical pressures and capital market failure. These rates should be variable, indexedto inflation and/or commercial interest rates. Furthermore, continued subsidizationrequires improved targeting (see Option 5).

- vi -

(2) Longer Loan Repayment Periods

15. Loan programs should lengthen their reoayment periods, in order to reducemonthly payments and the likelihood of default. A 10-year repayment would beaffordable for most higher education graduates, yet would avoid the excessive interestsubsidy losses of longer repayment plans. By contrast, most LAC programs requirerepayments in less than 5 years, a response to hyperinflation in the 1980s. Now thatinflation has slowed in most countries, the repayment pcriod should be extended, whilemaintaining positive real interest rates.

(3) Repayment Schedules Which Corre! 'd ., Graduate Earnings

16. 10 percent of higher education graduate earnings is w.,ely accepted as themaximum reasonable level of repayment. This calls for a modified repayment streamwhich more closely parallels higher education graduate age-earning profi! , That is,instead of making loan repayments of equal amounts every month, repayments should bebased on a percentage of the graduate's income. In general, this means repaymentswould be low at first, but would increase in value as the earnings of graduates increaseover time.

(4) Default Reduction Measures

17. Student loan programs should increase their loan collection efforts, because manygraduates can afford to repay loans, yet choose not to. Collection efforts include: (a)authorization of loan programs to pass along defaulters' names to other institutions (e.g.credit agencies, social security institutes, the internal revenue service, banks, employers,etc.), which could deduct required amounts from borrowers, or withhold services; (b)simplification of payment procedures through automatic employer or bank accountdeduction; (c) requiring borrowers to take out default insurance; (d) publishing the namesof defaulters in newspapers; (e) seizure and sale of guarantor collateral; and (f) the useof private collection agencies, whose fee would paid by the borrower as a penalty.

(5) Increased Targeting of Student Loans

18. Tuition fee in. ases will increase the demand for student loans, which meansimproved targeting criteria are required. The targeting criteria most often cited aremeans testing (i.e. analysis of household income) and academic performance. Based onmeans testing, a "sliding scale" can be applied such that the loan is calculated to bridgethe gap between expected parental contributions and higher education cost s. For familiesin the greatest need, care should be taken not to propose loans whic ., will result inunbearable repayments, meaning that average higher education graduate earnings shouldbe considered in calculating the level of an affordable loan. Particularly for poorstudents, financial aid should not be restricted to covering the direct tuition costs ofhigher education, but should cover tuition, books, living costs and even opportunity

- vii -

costs, so that stud.nts may attend school full-time. A recent study esimated the cost ofthis targeting procedure in Jamaica at US$40 per loan which, given the relatively highvalue of the loans disbursed, is quite reasonable.L'

(6) Personnel Incentives and Technology Upgrading

19. Revised incentive structures (both positive and punitive) for loan program staffare essential. For example, payment of loan collection sta:f should be at least partiallycommission-based, and loan application reviewers could receive bonuses for meetingtargeting criteria. In addition, loan programs should allocate more resources to stafftraining, and to the acquisition of simple computer hardware ant software, for improvedfinancial management of loan funds.

(7) Counseling and Follow-Up

20. All loan programs need to increase their counseling of loan beneficiaries,explaining repayment procedures and default sanctions to both loan applicants ana newgraduates. Secondly, experience has shown that the first year after school is the mcstcritical; during this time patterns for repayment are developed and graduates are ingreatest flux. Loan programs should make special efforts to track students during thisfirst year, and only universities which assist loan programs in following students aftergraduation should be eligible for loans.

- (8) Private Loan Schemes

21. An alternative or complement to a reformed public sector loan program is aprivate loan scheme. This may be particularly appropriate if a country is considering amajor expansion in lending coverage and volume, because in many LAC countriesprivate financial institutions are relatively well developed and could handle the technical,administrative and financial responsibilities of an expanded loan program more efficientlythan public institutions. In this case, governments could provide partial (not total)coverage of the default and interest rate risks, in order to stimulate private financialsector participation.

JJ/ Grosh, 1992.

-viii -

Costs and Benefits of Expanded Student Loan Programs

22. Start-Up Costs For the first 5-8 years, public higher education expenditures mightactualiy be greater with a loan program than without it, because of administrative costs(which are particularly high during the start-up period), and the time it takes borrowersto enter the repayment period. Simulations indicate "start-up costs" of about US$30 perborrower, for a program to f-aance tuition fees equal to 25 percent of unit costs. Thesecosts could be further reduced if lending was contracted out to commercial banks, inexchange for contributions tc the loan program's initial capital fund. Furthermore,international development agenzies could play an important role in financing these start-up costs if the private sector does not.

23. Benefits If (a) the average level of loan recovery for the region's student loanprograms could be increased to 50 percent, (b) loan programs were expanded to cover60 percent of the student population, and (c) public higher education institutionsestablished fees equal to 25 percent of their unit costs, then over a 25-year period LACgovernments could reduce their expenditures on higher education by some 20 percent.12

Over time these savings could go to improving the quality of higher education and/or toincreasing primary education expenditures. Compared to current levels of primaryeducation spending in LAC, these savings on higher education could result in increasesin public primary education spending on the order of 30 percent once loan programswere fully established.

Scholarships for Higher Education

24. Some students' household incomes are so low that the loans required to attendhigher education would be so great as to make their loan repayments unbearable, mostlikely leading to default. Al,rnatively, high loan amounts and the uncertainty ofinvesting in higher education might lead some qualified students to avoid borrowingaltogether ("risk aversion"), resulting in a socially inefficient and inequitable exclusionof talented higher education candidates. In both cases, scholarships are preferred.

25. This report assumes that funding for scholarships would come from earmarkingone-half of tuition revenue. Analysis suggests that as tuition fees rise beyond 35 percentof unit costs, the percentage of students who could be offered scholarships actuallydeclines. This is because as fees increase, the percentage of students who can afford topay decreases, and the size of the scholarship increases. The optimum fee level for the

12/ The additional savings which might be generated through the payment of school fees by moreprivileged students (who would not need loans) are not considered here, on the assumption that thesesavings would go to finance scholarships andlor be turned over to the universities for their ownpurposes. That is, this estimate of savings is rather conservative because fee revenue from non-borrowers is not factored in.

- ix -

purposes of scholarship coverage appears to be around 30 percent of public highereducation unit costs.

Political Strategy for Increased Private Financing of Higher Education

26. The first step in a political strategy for reform is to establish the facts concerninghigher education financing, enrollment, demograpnics, efficiency and equity. This is atask best undertaken by an independent research institution (internal or external), so asto maximize public acceptance of the analysis. The second step is to initiate aneducational campaign and national debate in the media concerning higher educationfinance reform. This would increase the sense of the people's "ownership" of thedebate's conclusions, and the accountability of public higher education students to societyat large.

27. Thirdly, through negotiation, mechanisms need to be developed for distributingthe net additional resources mobilized by public higher education finance reform in sucha way as to maximize political support for the reform process. One such mechanismwould be to earmark additional resources for three education funds, corresponding tomajor stakeholders in the reform: one for university professors; another forunderprivileged and/or academically gifted students; and a third for basic education(grades 1-9) teachers. The funds would play an important role in building politicalsupport for finance reforms and would demonstrate that any fiscal savings would remainwithin the education sector. The key point here is to focus the resources on people whocan be mobilized to support the reforms.

28. To further reduce opposition it is recommended that fee increases and loanprogram strengthening be "grandfathered", so that presently enrolled students retainbenefits and the reforms are enacted incrementally with each incoming class. Feeincreases could be introduced on a small scale, with yearly increases which keep up withinflation. Over time, if public expenditures on higher education are held constant innominal terms, inflation will gradually shift the balance from public to private financing.

Synthesis: Fees, Loans and Scholarships

29. The ovekall conclusion of this report is that tuition fees could reasonably be raisedto between 25 and 35 percent of higher education unit costs. This is based on analysisof: the ability and willingness to pay for higher education; the feasibility of student loanprograms; and the need to offer scholarships to the disadvantaged and/or academicallygifted. In other words, there is analytical convergence of these three components ofprivate higher education finance.

30. At this tuition level, (a) most LAC households could afford to pay fees and/ortake out student loans, (b) public higher education expenditures could be lower than they

are now, (c) the start-up costs of a loan program would be affordable, and (d) politicalopposition should be manageable. By raising fees to 30 percent of unit costs,governments could argue that fees would not unreasonably reduce access to highereducation for the middle class (recall that the real factors to access are quality basiceducation and the ability to forego earnings), while they would tap the resources of thosewho could afford to pay and finance targeted scholarships for the poor out of tuitionrevenue. This would improve the equity, efficiency and qualit of higher education.

31. Fee levels exceeding 35 percent of unit costs might result in greater resourcemobilization, but only if (a) political resistance can be overcome, anj (b) loans programscan be expanded to cover almost the entire student body, and their efficiency can begreatly improved. Moreover, higher tuition fees might induce unproductive rent-seekingbehavior on the part of higher education students, who attempt to conceal their householdincomes and use political connections in order to government subsidies and/or grants.

32. By implementing these reforms LAC governments could increase the totalresources going into public higher education by an average of 35 percent in real terms.This would provide funds for improvements in higher education access and quality, andfree up public resources which could then be allocated to lower educational levels. Bothmeasures would improve the supply of trained and trainable manpower in Latin Americanand the Caribbean, which is increasingly necessary for the region to compete successfullyin today's global economy.

CHAPTER 1

INTRODUCTION

1.1 The purpose of this study is to contribute directly to the current debate on highereducation finance reform in Latin America, on both practical and theoretical levels.Given macroeconomic constraints, increasing demand for higher education and the needto increase the efficiency and equity of. government expenditures, the objective is toanalyze the potential for increased student fees, expanded student loan schemes andeffective scholarship programs.

1.2 While a wide range of options exist for expanding higher education financing,such as voucher systems, tax credits, sale of university services, etc., this study focuseson student financing through tuition fees and loan programs. Student loan programs area particularly attractive option in Latin America because they already exist in manycountries, and because administrative systems are sophisticated enough to operate loanprograms effectively.

1.3 More specifically, the study analyzes (a) student willingness and capacity to payschool fees and repay student loans, and (b) the balance between targeted scholarshipsand student loans. In addition, this report aims to improve the feasibility, organizationand implementation of student loan schemes. Used here, the term "feasibility"encompasses financial, administrative and political dimensions.

The Problem and Issues to be Addressed

1.4 Between 1960 and 1989 total higher education enrollments in Latin Americaincreased twelve-fold, and enrollment rates (weighted average) increased from 6 to 22percent. In fact, enrollnent ratios in the region are now ten Limes those in AnglophoneAfrica and more than double those in South Asia.0' Since publicly-funded institutionshave accounted for much of the growth in higher education enrollments, governmentexpenditure3 on higher education have increased as well. In 1989 25 percent ofgovernment education spending went to higher education, up from 16 percent in 1970and 23 percent in 1980 (see Table 1.1). Over the next 20 yexs the demand for highereducation Latin America will rise still more, due to population growth and increasingenrollment ratios at the secondary level. Because unit costs for higher education arerelatively high and rising (compared with basic education), the demand for expenditures(public and private) on higher education will increase even more.

I3/ Winlder, 1990.

-2-

Table 1.1Latin America

Allocation of Public Recurrent Expenditureon Education, by Level, 1965 - 1987

(percentages)

1965 1970 1975 1980 1989

Primary 62.4 57.4 51.6 50.9 45.8

Secondary 23.3 26.7 25.0 25.6 28.8

Higher 14.3 15.9 23.4 23.5 25.4

Source: World Bank, 1986; UNESCO Statistical Yearbook, 1991

1.5 In recent years, however, adverse macroeconomic conditions and keen intersectoralcompetition for public funds have reduced most governments' ability to continue expandingeducation, such that even now education is underfinanced. In view of Latin America's relativelylow projected economic growth rates and rising higher education demand, financing difficultieswill only intensify.1 4' Alternative financial resources must be found; the current system isunsustainable.

1.6 The logical solution is to tap the ability and willingness of private households to investin higher education. That is, the high public cost of higher education can be partially recovered

by introducing (or increasing) fees for higher education, at the same time as student loanprograms are established (or expanded), so that students who need to can borrow to pay these

fees and repay their loans out of their future income. Selective scholarships, some based on

need and others on merit, would be maintained to preserve equity and encourage academicperformance. Lastly, in view of the fact that many of the benefits of higher education are

enjoyed by the individual as opposed to society (as evidenced by higher private than social rates

of return to higher education), it is reasonable for governments to ask for increased privatecontributions.

Rationale for Student Loan Programs

1.7 Student loan programs have the potential to improve the efficiency, equity and stabilityof higher education spending, while reducing the fiscal cost to the public sector. Demandefficiency (getting students with the greatest potential social productivity into school) may

increase because student quality, performance and finishing times (input-output ratios) should

14/ In essence, LAC governments have attempted to massify what was designed to be an elite system,

leading predictably to financial unsustainability.

-3-

improve, as the applicait pool expands via loan programs and students perceive a greaterfinancial stake in their studies. Supply efficiency may increase as students behave more likeinvestors (comparing marginal costs and benefits), choosing schools which offer education andtraining with the maximum economic value.

1.8 With regard to equity, if loans are extended to cover living expenses (and even foregoneearnings) of students from poor families, a fairer distribution of higher education opportunitieswould result. Secondly, given that (a) a high percentage of government revenues used to financepublic education come from non-progressive commodity taxes (about 40% for Latin America andthe Caribbean) and (b) most students in higher education come from middle- and upper- classfamilies, reducing public expenditures on higher education via tuition fees and student loanswould reduce the extent to which the poor now subsidize the rich. In addition, future equitywould be enhanced by a loan program if such a program expanded higher education access andenrollment, as higher education graduates typically earn more than those with lower educations.Finally, while every effort must be made to ensure that no competent student is excluded fromhigher education because s/he cannot afford it, some poorer students may be forced todiscontinue their studies if fees are introduced. But such an equity loss must be weighed againstthe equity gains resulting from a potential shift in education expenditures towards basic educationwhich higher education fees and loan programs might eventually permit.

1.9 By diversifying sources of funds (away from the public sector), a student loan programwould also provide greater long-term stability to education financing. That is, public highereducation expenditures often fluctuate considerably from year to year (depending on overallmacroeconomic conditions), making efficient multi-year educational investmnrts and programsdifficult to implement. By mobilizing private sources of financing, a student loan programwould lessen the impact of these public financing swings.

1.10 Perhaps most importantly, student loan programs would address one of the central issuesin higher education today: financial constraints. By tapping the willingness of private householdsto invest in education, additional resources would be mobilized.

1.11 Admittedly, the experience to date of student loan programs in Latin America (andaround in the world, in both developed and developing countries) has not been terriblyencouraging. The problems are numerous and can be categorized under the headings offinancial, administrative and political constraints. On the financial side, heavily subsidizedinterest rates, poorly conceived payment streams, high inflation and inappropriate lendingprocedures have prevented even theoretical self-sustainability. Higher than expectedadministrative costs, low repayment rates, and inadequate incentives (positive and negative) tocollect and repay loans, have further impaired the financial health of loan schemes. Finally,political resistance to loan programs in combination with increased tuition fees has been well-organized, articulate and effective in preventing their implementation. Overcoming these threecategories of problems is one of the objectives of this study.

Methodology

1.12 For the preparation of this report this study analyzed and synthesized information fromfive sources:

a. existing literature on student loans;b. 1989 household survey data from 13 LAC countries;c. a questionnaire distributed to 20 Latin American student loan programs;d. six commissioned case studies of student loan programs in Latin America

and the Caribbean (Colombia, Chile, Brazil, Venezuela, Mexico andJamaica);

e. student loan simulation models developed in the World BankL".

1.13 Each source targeted a different aspect of private finance analysis. The review ofexisting literature was the most general, providing background information and helping to focusthe report. The household survey tapes provided invaluable information for the calculation ofhousehold and higher education graduate incomes, used to determine ability to pay. Thequestionnaire gathered information from administrators of student loan programs concerning (a)the financial, administrative and political problems they face implementing such programs, and(b) their suggestions for minimizing or resolving these problems. Supplementing thesequestionnaires, the commissioned case studies provided in-depth information concerning theactual functioning of several student loan schemes and the prospects for establishing newprograms. Finally, the student loan simulation models permitted the financial analysis ofexisting LAC student loan programs and the effects of implementing suggested reforms. Thatis, existing LAC loan programs were compared to computer-simulated programs to assess theirrelative impacts on repayment burdens, the probability of default, and overall loan recovery.

Enrolhment Forecasts

1.14 A sound estimate of higher educatio. enrollments over the next 25 years, under bothstatus quo and reform scenarios, is obviously important in making financial projections. Withrespect to the status quo scenario, it is highly unlikely the high-growth trend in publicenrollments through the 1970s and 1980s can be sustained under current financing patterns (inpart this report is intended to address that problem); growth will have to slow down. As for theimpact of finance reforms on enrollments, several effects are possible: raising tuition fees mightreduce demand, and a portion of official enrollments (based on "professional" and "ghost"students) might disappear; on the other hand, expanding student loan and scholarship programs

ji/ The author especially wishes to thank Doug Albrecht (PHREE) and Guozhong Xie (AS1CO) whodeveloped the financial models. Without them this study would not have been possible.

-5-

might make higher education more accessible, thereby raising demandA' Uncertainty leadsto the following assumption: population growth, enhanced financing mechanisms, risingsecondary enrollments, and the increased importance of higher education will more thancompensate for enrollment cuts due to tuition increases. For this report a 1 percent annualincrease in public higher education enrollments was used in making financial projections.

Organization of Report

1.15 This report flows from description to analysis and then synthesis. In Chapter 2background information and financial trends are described in order to provide a context for theprivate financing of higher education in Latin America and the Caribbean. Next, in Chapters3, 4 and 5 the three elements of private higher education finance are analyzed as follows: tuitionfees and the ability to pay (Chapter 3); student loan schemes and their performance in LAC(Chapter 4); and then scholarship programs and their financial sources (Chapter 5). Followingthe financial chapters is a discussion of the political factors behind Latin American highereducation finance reform (Chapter 6), which analyzes probable winners and losers and proposesa strategy for a political coalition supporting reform. This allows the reader to choose whichaspects of private finance are the most relevant, rather than reading the entire report. Finally,Chapter 7 is a synthesis chapter, which attempts to tie together in a meaningful way the analysispresented in Chapters 3-6. At the risk of over-generalization it tries to arrive at normativestatements as to the optimal ranges of tuition fees, student loans and scholarships. But first, itis important to discuss more global trends in higher education finance in Latin America and theCaribbean, a subject to which we now turn.

16/ In the case of Chile, the reforms led to a slight decline in public enrollments of less than one-half apercent per year between 1980 and 1990, while private enrollments grew from zero to levels roughlyequal to public enrollments.

CHAPTER 2

TRENDS IN HIGHER EDUCATION FINANCE IN LATIN AMERICA AND THE CARIBBEAN

Public Exnenditures

2.1 As shown in Figure 2, government expenditures in Latin America and the Caribbean onhigher education increased from 23 percent of total education expenditures in 1980 to more than25 percent in 1989. Not surprisingly, there is considerable range in this expenditure category,from 14 percent in Ecuador to 40 percent in Costa Rica (see Annex A, p. 3).' At the sametime primary eGucation spending as a percentage of total education spending has steadilydecreased. Given estimated social and private rates of return to different levels of education,and the fact that tertiary enrollments in LAC constitute just one-tenth of primary enrollments,such high public expenditures for higher education do not appear justifiable. (See Annex A, p.7. for rat- of return estimates.)

Public Recurrent Education Spendingin LAC by Level, 1965 - 1989

Percent70 -

so -

40-

30-

20 -

1965 1970 1975 1980 1989

Year

Primary Secondary 1 Higher

Figure 2

2.2 Compared to other regions of the world (whether developing or developed), LatinAmerica spends a higher share of the government budget on education and a higher proportionof the education budget is allocated to higher education.!' Obviously, this is closely related

17/ UNESCO Statistical Yearbook, 1991 and 1989.

18/ Winkler, 1990

-7-

to the fact that higher education enrollments in Latin America are higher than in any otherdeveloping region, although below those in most developed countries. On the other hand,compared to East Asian countries with similar levels of GDP/capita (e.g. Korea, Philippines,Indonesia), Latin America places much greater emphasis on public, as opposed to private,financing of higher education.

2.3 In fairness, it must be pointed out that viewed independently of other educational levels,higher education spending in Latin America has declined considerably in real terms. Because

of enrollment increases real spending per student has particularly suffered. A study completed

in 1990 (for Argentina, Brazil, Mexico, Chile and Venezuela) showed that between 1980 and

1985 higher education expenditures per student decreased by an average of 43 percent in real

terms. Thus, while conclusions regarding the privileged status of public higher education

spending are valid, it must be kept in mind that from the perspective of higher education

administrators, professors and students, higher education experienced dramatic funding cuts over

the last decade. This is particularly important when considering questions of political economyand higher education finance reform.

Higher Education Finance Problems in the U.L

Lest Latin American and Caribbean governments believe their region is unique in facingfinancial constraints and pressures for reform, a recent article on university financing in the UnitedStates illustrates that financial problems are widespread. For the first time in 30 years, stategovernments around the nation are spending less .n their public higher education institutions thisacademic year than they did in the year before, according to the Illinois State University's Centerfor Higher Education.

In the State of Virginia, the government recently cut operating subsidies to its 15 publiccolleges, universities and community colleges by US$ 300 million, with another US$ 300 million

cut from building projects. Public per student spending was cut by 11 percent, while tuition fees

were raised 40 percent (to US$3,304), and another 15 percent hike in tuition is planned for 1992.

In the State of Massachusetts, public higher education spending has been cut 30 percentsince 1990, while tuition fees increased 121 percent (to US$8,400) between 1988 and 1992. InCalifornia, public university tuition fees were raised 40 percent for the 1991/92 academic year, withanother 24 percent increase planned for next year. In Maryland, the government recently cut US$160 million from public higher education funding.

The American Association of State Colleges and Universities has described the cuts in publichigher education spending over the last two years as "record breaking", as higher educationinstitutions have been forced not only to raise tuition but also to reduce the number of classes

offered, eliminate some teaching positions and increase class sizes. (Washington Post, 1/29/92)

Box 1

-8-

2.4 Unit Expenditures: Relative to unit expenditures at the primary and secondary level,higher education continues to be much more costly. For the Latin America and Caribbeanregion as a whole, higher education unit costs for 1989 were approximately seven times greaterthan those for primary education (US$1,512 compared to US$220).-9, With respect to thecomparison of higher education unit costs to GDP per capita, a rough 1:1 average ratio emerges(excluding Argentina), albeit with considerable variation. Table 2.1 below shows these public

expenditure ratios for higher and primary education in nine Latin American countries, as wellas a comparison of higher education unit costs to GDP per capita.

Table 2.1Ratio of Public Higher Education Unit Costs to

Primary Unit Costs and GDP/Capita, 1989

Higher UC: Higher UC:Country Primary UC GDP/Capita

Argentina 1.2 0.15Brazil 6.8 1.9Chile 11.7 0.6Colombia 8.3 1.6Ecuador 8.0 1.0Jamaica 16.0 1.45Guatemala 6.2 0.7Mexico 10.5 0.5Venezuela 16.7 .95

Source: UNESCO Statistical Yearbook, 1991; World Development Report 1991

2.5 Higher education unit expenditures include more than simple instructional costs.

Unfortunately, it is difficult to differentiate between these instructional costs and other highereducation expenditures, for example research. While it is a fair estimate that most of the unit

expenditures at the primary level reaches primary students (if only in the form of a teacher infront of them), the same cannot be said of higher education, where funding for research and

other public services is included in the urAit cost calculation (see Text Box 2). Thus, the unit

cost is a kind of index on which tuition fees and student loans can be based; it should not be

interpreted as the target measure under a full cost recovery policy via school fees (in which case

the appropriate measure would be unit instructional costs).

19/ On the other hand, because of rapid enrollment growth in higher education, unit expenditures have

declined considerably in real terms over the last 10 years (from an estimated US$1,580 to US$1,005,in constant 1980 US dollars).

-9-

Unit Costs versus Instructional Costs: Ideally, instructional costs for higher education could beneatly separated from the costs of research, extension, administration and the host of other non-teachingactivities many higher education institutions engage in. This would strengthen a university's (or agovernment's) ability to determine tuition levels, as it is only reasonable to ask students to pay for what theyreceive. Students should not be asked to pay for research (which is a form of public good), extension or othernon-teaching programs (e.g. in Brazil the unit cost figures include some US$2,000 per year spent on operatingpublic teaching hospitals!). This way students (and parents) would know what they were getting for theirmoney and universities could more easily justify tuition fees.

Unfortunately, it is not easy to separate undergraduate, graduate, and research costs, as well as thosefor administration, extension and other activities. Data collection and disaggregation, methodologicaldifferences over expenditure allocation, and the difficulty of estimating costs over time (e.g. publicexpenditures for a subsidized student loan program) make this exercise problematic. Researchers who haveattempted to do this have concluded that the most practical approach is to use a proxy for differentiatinginstructional from research costs: i.e., the weekly teaching load (James, 1977).

Using this proxy, a full-time professor working 40 hours per week but teaching just 24 hours perweek, would result in instructional costs equivalent to 60 percent of the professor's salary; the other 16 hoursthe professor is presumably conducting research. (Note that in most Latin America higher educationinstitutions, for every hour of instruction one hour is allocated for class preparation, so actual teaching timewould be just 12 hours.) As teacher salaries are the main expenditure item for most higher educationinstitutions, the convention is to extend that 60 percent figure to all expenditures, so that one could estimateunit instructional costs to be 60 percent of total unit costs. This figure could then be used to determineappropriate tuition fees for students.

However, this hypothetical proxy simply assumes that when a professor is not teaching s/he is doingresearch. There is little information available regarding the actual use of time by professors in Latin America;in public universities with few or no incentives for scholarship, many professors may simply use that time forclass preparation, another job, or even leisure. In this case, the only higher education activity during the weekis teaching; the professor is simply paid 40 hours for 24 hours of work, and the full cost of the professor (andby extension the total unit cost) should be allocated to instructional expenditures. Furthermore, this proxyignores the significant laboratory and eqipment costs of certain academic specializations (e.g. physics,chemistry, medicine), because it only considers personnel costs. It would be an illuminating exercise forMinistries of Education and higher education systems in Latin America to analyze more closely their highereducation expenditures, especially the use of professors' time, and attempt to disaggregate instructional fromnon-instructional costs. Obviously, this would be different for each. institution as the emphases on research,extension and teaching would be distinct. Tuition fees (in part based on estimates of ability to pay theseinstructional costs) could then be set on this basis.

For the purposes of this report, however, overall unit cost calculations are used. This is largely forthe sake of expediency, as the problems of collecting, analyzing and comparing information across countriesconcerning instructional versus non-instructional expenditureE go beyond the scope of this. study.Furthermore, unit cost calculations have been generalized at the country level (not by institution or field ofstudy), for the purposes of comparison to household income. In other words, institutions with lowinstructional to unit cost ratios are balanced by those with high ratios of instructional to unit costs. Thisallows for generalizations about overall household ability to pay for higher education, while recognizing thatin practice this exercise should be done on the micro-level (e.g., a student's household income, compared toinstructional costs for the particular higher education institution attended).

Box 2

- 10 -

Private Expenditures

2.6 Tuition Fees: While many Latin American and Caribbean countries do not charge tuitionat public higher education institutions, some countries do collect fees. Table 2.2 shows recentdata concerning student fees as a percentage of unit costs in public higher education institutionsin Latin America and the Caribbean. On average (unweighted), LAC countries recover just 7percent of unit costs through school fees. In no case do fees exceed 26 percent of unit costs(C'ile). Relative to other regions, this is below cost recovery levels in Asia and North America,although well above recovery rates in Africa and the Middle East..' However, it should bepointed out that LAC governments are increasingly aware of the need to increase cost recoveryat the higher education level; it is expected that public higher education tuition charges willincrease significantly during the 1990s.

Table 2.2Student Fees as a Percentage of Unit Cost in Public Higher Education Institutions

Country Percentage Year

Argentina 0 1990Barbados 15 1990Bolivia 3 1991Brazil 0 1991Chile 26 1987Colombia 10 1991Costa Rica 16 1991Ecuador 2 1991Guatemala 2 1991Honduras 3 1991Jamaica 25 1991Mexico 0 1991Peru 0 1991Uruguay 0 1991Venezuela 0 1991

Source: APICE Questionnaires; Higher Education Reform in Brazil;Reimers, 1990; Albrecht/Ziderman, 1991b; Hinchcliffe, 1991.

20/ A recent study of 43 countries showed that on average U.S. public higher education institutions recoverabout 25 percent of unit costs through tuition fees, while Indonesia and South Korea collect 25 percentand 24 percent, respectively. It is interesting that among public higher education systems surveyed,Chile recovers the greatest percentage (26 percent). (Albrecht/Ziderman, 1992)

- 11 -

2.7 Non-Tuition Expenditures: Private expenditures include fees paid at both public andprivate higher education institutions, as well as other incremental expenses such as food, rent,books, transportation, exam fees, etc. To these direct costs should be added the opportunity costof foregone earnings. Table 2.3 provides estimates by country of average fees, living expensesand foregone earnings, and compares these costs to GDP per capita. In all cases, total expenseswell exceed GDP per capita.

Table 2.3Private Costs for Public Higher Education, 1989

(US$1989)

Non-Tuition Foregone Total GDP/Country Fees Expenses Earnings Expenses Capita Ratio of

(1) (2) (3) (4) = 1 +2+3 (5) (4):(5)

Brazil 0 2,574 4,477 7,051 2,540 2.8Colombia 190 2,174 1,356 4,561 1,200 3.8Costa Rica 284 1,778 2,197 4,259 1,780 2.4Ecuador 22 2,054 1,376 3,452 1,020 3.4Guatemala 12 2,574 1,440 4,026 910 4.4Honduras 17 2,374 2,958 5,349 900 5.9Mexico 0 1,661 2,284 3,945 2,010 2.0Uruguay 0 1,574 2,034 3,608 2,620 1.4Venezuela 0 2,650 1,916 4,566 2,450 1.9

Source: APICE Questionnaires; Wolff, 1991; Reimers, 1990; Albrecht/Ziderman, 1991b; Hinchcliffe, 1991; Chen-Young, 1990; Household Surveys (see Annex 6).

History of Higher Education Finance: Recent research at the World Bank into the history ofhigher education around the world revealed two interesting facts: (1) until the early 19th centurythe private sector (including the Church) funded most of the development of universities, as opposedto governments, making these institutions wore responsive to student needs; and (2) the rationalefor heavy government funding and provision of higher education (which began in the Europe in themid-1800s) was the preparation of selected individuals for administrative and technical careers inthe civil service, a form of employer-based training. This structure was adopted by manydeveloping countries at independence but then expanded rapidly, in essence a massification of anelite system which has led to financial crisis.

Source:. Albrecht and Ziderman, 1992.

Box 3

- 12 -

2.8 Non-tuition expenses are clearly much greater than tuition fees currently charged. Evenmore striking, however, is the comparison of estimated non-tuition expenses to unit costs, shownin Table 2.4 In all countries surveyed (with the exception of Brazil) non-tuition studentexpenditures exceeded unit costs, suggesting that even if fees are increased to 100 percent of unitcosts, non-tuition expenses will remain the greatest financial obstacle to higher education.

Table 2.4Non-Tuition Student Expenses as a Ratio of Unit Costs

Ratio ofExpenses/Costs

Brazil .5Colombia 1.3Costa Rica 1.1Ecuador 1.8Guatemala 4.2Honduras 2.8Jamaica 1.8Mexico 1.7Peru 1.1Uruguay 1.2Venezuela 1.2

Sources: APICE Questionnaires; Wolff, 1991; Reimers,1990; Albrecht/Ziderman, 199 1b; Chen-Young,1990.

Equity

2.9 The equity dilemma of higher education is acute: if higher education is not subsidizedmany people cannot afford it (a demand-side constraint); if it is heavily subsidized then its sizeis limited by the need to contain costs, or its quality declines, or both (a supply-sideconstraint).' The goal is to find the optimal level of subsidy which minimizes both of theseconstraints.

2.10 Advocates of free public higher education argue that forcing students to pay tuition fees,in addition to already costly living expenses and opportunity costs, reduces the poor's access tohigher education and preserves the privileged status of the wealthy. Similarly, raising studentloan interest rates, requiring loan guarantors (or some form of collateral), and other measuresto increase student loan repayments are also said to hurt the poor in particular, as they are leastable to put up collateral and typically manifest greater "risk-aversion". On the other hand,

21/ Barr, 1992.

- 13 -

proponents of public higher education fees and student loan programs claim they improve socialequity, insofar as they can maintain the educational opportunities of poor students, whileredistributing the costs of higher education for a more equitable sharing of costs and benefits.L

2.11 While each of these statements is partially true they must be examined in a broadercontext, which includes analysis of issues such as: (a) the socioeconomic makeup of highereducation students (within the current environment of heavily subsidized tuition fees); (b) thequality of basic education for the poor; and (c) the -vailability of scholarships and loan programsbased on economic need. It is argued here that access to higher education among low incomestudents is more a function of the latter two issues than of general subsidies for higher education.That is, higher education equity can be improved through better quality primary and secondaryschooling, and targeted financial aid for the poor, accompanied by greater cost recovery amongthe middle and upper classes.

Share of LAC Higher Education SubsidiesReceived by Income Group, 1987

Quintile 54 9%

Ouintile 15%

Quintile 2

2%6%Quintile 3

13%

Figure 3

2.12 Because higher education students throughout Latin America and the Caribbeanoverwhelmingly come from upper- and upper-middle class backgrounds, free (or low tuition)higher education primarily benefits those who can afford to pay (see Chapter 3). A study donein 1987 (Figure 3) shows that students in the highest income group (Quintile 5) receive almost50 percent of all higher education subsidies. By contrast, students from the lowest income group

22/ Woodhall, 1987, p. 72.

- 14 -

(Quintile 1) receive just 5 percent of such subsidies. In other words, the rich benefitted fromfree higher education ten times more than the poor. Interestingly, the over-representation of

youth with high socioeconomic status in higher education (as measured by higher education

enrollment compared to population) is larger in I atin America than it is in Asia, the Middle East

or OECD countries.L'

2.13 This finding is supported by several more recent studies which analyze higher education

enrollments and income distribution. In Venezuela, it was found that the likelihood of a child

in the top two income quintiles attending higher education (80 percent of which is public and

free) is about twenty times greater than that of a child in the lowest two income quintiles. In

Brazil, it was found that 44 percent of all public higher education students come from families

earnings at least ten times the minimum wage per month (roughly US$6,600 per year). Finally,

in Colombia, 66 percent of all higher education students come from families in the top three

income deciles, while just 12 percent come from households in the lowest three income

deciles.'

2.14 In some countries public higher education finance is not only inequitable but also

regressive. For example, in Brazil, elite, high-quality public higher education is offered at no

charge to students (many of who attended expensive private secondary schools to gain admittance

into public higher education), while low-quality private higher education must be paid for by

tower income groups. Moreover, because much of the public revenues needed to finance free

public higher education in Latin America and the Caribbean come from non-progressive

commodity taxes (about 40 percent), it could be said that it is in large part the poor who

subsidize higher education for the rich, a most perverse equity impact.

2.15 Because Latin American public higher education is free (in most cases) it results in

rationing of access and/or quality. This means that those who attend higher education

institutions are those most able to afford the non-tuition expenses and costs of lost wages, and

those who score highest on entrance exams. [The former requires either parental support,

financial aid or night-time study opportunities, all of which are in short supply for poor students.

The latter requires access to high quality (often private) primary and secondary education, rarely

available to low income students.]J& Indeed, the lack of access to secondary education, in

particular, may be the greatest barrier to higher education for children of low socioeconomic

status.' The result of inequitable access is that many higher education students receive

23/ Winkler, 1990

24/ Brazil: Wolff, 1991; Venezuela: Wolff/Brunner, 1992; Colombia: Betancur-Mejia, 1990

25/ In countries with open admission, access becomes function of successful completion of the first year of

study so that lower educational opportunities still determine in large part access to higher education.

If no selection occurs, rationing takes the form of limiting educational quality.

26/ Winkler, 1990.

- 15 -

government subsidies they do not really need, while those individuals who need the subsidiesmost are excluded.

2.16 In short, what was said with respect to the U.K. system of higher education subsidizationapplies also to Latin America: "...to defend grants in higher education on grounds of socialequity is a monstrous perversion of the truth."' Free (or low charge) higher education hasnot meant equal access to higher education opportunities.

2.17 Female Participation in Higher Education: Related to the issue of income equity is genderequity: do females have the same access as males to higher education? In LAC the answer isyes, as seen in Table 2.5. In fact, for the region as a whole female enrollments in highereducation are slightly higher than those of males. The fields of specialization do tend to besomewhat gender-specific, however - women are heavily represented in the teacher training andsocial science programs, while the majority of engineering and the physical sciences students aremen. But so long as tuition fees are not greatly differentiated by area of specialization, currentpatterns and future changes in the private financing of higher education raise few serious genderissues.

Table 2.5Enrollment in Higher Education by Gender, 1990

(percent)

Females Males

Argentina 53 47Brazil 52 48Chile 44 56Colombia 52 48Costa Rica 58 42Jamaica 60 40Mexico 42 58Paraguay 46 54Uruguay 58 42Venezuela 47 53

Average 51 49

Source: UNESCO 1992 Statistical Yearbook

27/ Mark Blaug, 1972, quoted in Woodhall, Student Loans as a Means of Financing Higher Education,World Bank Staff Working Paper, No. 599.

- 16 -

2.18 Case Study for Higher Education EAuity: Chile - Chile provides an excellent test case ofthe impact of higher education reform on equity (see Text Box 4 for a brief description of thatreform). In 1980 tuition fees were raised at public higher education institutions, theestablishment of private institutions was encouraged, and student loan programs were expanded.A recent study on the impact of these reforms (including equity) suggested that raising highereducation fees did not have an adverse impact on equity, in large part because they wereaccompanied by student loan programs targeted on lower income students. Furthermore, thereforms allowed the expansion of higher education to twice its size without increasing publicexpenditures, so that public expenditure increases could be directed to primary education wherethe positive equity effects are greatest.

Chile: Student Socio-Economic StatusBy Father's Education, 1976 - 1984

Percent

60

197619 198Year s

Milliterate I OPrimary IS Secondary University

Figure 4

2.19 Figure 4 shows the socio-economic status of Chilean university students, as indicated bytheir father's education, at three different points in time: 1976, 1981 and 1984 (recall that thereform began in 1980). Comparing the socio-economic background of students over timereveals very little difference before and after the reform; the Chilean higher education remainedskewed towards the upper socio-economic levels, but was no more so after tuition fees wereraised. However, comparing public and private enrollments, more than 40 percent of publicstudents in 1990 came from households in which the father had less than a complete secondaryeducation, whereas less than 15 percent of students in private universities came from such

- 17 -

households' This suggests that the public institutions do offer lower income groups moreeducational opportunities than private institutions, in large part through student loan programswhich are only available to public higher education students.

Chilean Higher Education EnrollmentBy Income Quintile, 1990

Quintile 3

Quintile 2I13%

Quintille 1

Quintile 425%

Quintile 536%

Source: Brunnef and Briones, 1992

Figure 5

2.20 Figure 5 shows higher education enrollment in Chile in 1990 by income quintile. Therecan be little doubt that enrollment patterns remain inequitable. On the other hand, comparingFigure 5 to Figure 3, it would appear that access to higher education in Chile is more equitablethan it is for Latin America as a whole. The lower three income quintiles have higherrepresentation in Chilean higher education than they do for Latin America as a whole, while thehighest quintile has a lower representation. ' Unfortunately, this information is not availablefor Chile from before 1980 so the impact of the reform cannot be determined from this graph.

28/ Brunner and Briones, "Higher Education in Chile: Effects of the 1980 Reform" (draft), prepared forthe World Bank, January 1991.

29/ Note that the figures illustrate slightly different information: Figure 3 shows the share of highereducation subsidies received by each income quintile, while Figure 5 shows higher education enrollmentby income quintile. In this sense the two figures are not directly comparable, but if enrollment is usedas a proxy for public subsidy they can be compared.

- 18 -

2.21 The expansion of student loan programs under the Chilean reform has clearly benefittedthe lower classes. A study done in 1985 on the redistributive impact of public educationalexpenditures indicated that more than 50 percent of public funds allocated to student loanprograms benefitted the poorest 60 percent of society, whereas only 25 percent of direct publicspending on higher education did so (see Table 2.6 below).

Table 2.6Chile: Redistributive Impact of Public Expenditure

Among Different Educational Levels, 1985(percent)

Level Poorest 30% Middle 30% Richest 40%

Preschool 45 35 20

Primary 47 31 22

SecondaryGeneral 37 35 29Vocational 37 37 26

HigherDirect 10 15 75Student Loans 22 29 49

Source: Universidad de Chile/ODEPLAN, Encuesta CASEN, 1985; inCasteneda, Para Combatir la Pobreza: Politica Social yDecentralizaci6n en Chile Durante los '80, CEP, Santiago de Chile,1990.

- 19 -

2.22 This 1985 study was reinforced by a more recent review of the student loan program in1990, shown in Figure 6 below. Here we see that the vast majority of lower income studentswere receiving student loans in 1990, compared to a minority of upper income students. Almost80 percent of the lowest income students obtained student loans in 1990, versus less than 25percent among the wealthiest students. This indicates that higher education reforms have shiftedpublic expenditures from upper- to lower- income groups.

Chile: Percent of Students With LoansBy Income Quintile, 1990

Percent

100 -

601.. . . . . . .. . . . .

40 - . . .. . . . .

20, -. -

I23 4 5

Income GuintileSource: Brunner and Briones, 1992

Figure 6

2.23 Piecing together this analysis, one can say that higher education reform in Chile has hada favorable or neutral impact on equity within higher education, insofar as expanded student loanprograms have directed more public resources to less advantaged Chilean higher educationstudents, while the socioeconomic composition of the public higher education student body hasnot become more skewed towards the upper classes (and in fact appears slightly more equitablethan that of Latin American public higher education students as a whole). In fairness, however,because almost all of the growth in higher education enrollments has occurred in urban areas,it could be said that the reforms have had a negative geographic equity impact. On balance,while it is difficult to make a definitive statement about the positive equity impact of Chile'shigher education reform, the analysis suggests that such a reform in other countries is unlikelyto have a negative impact.

- 20 -

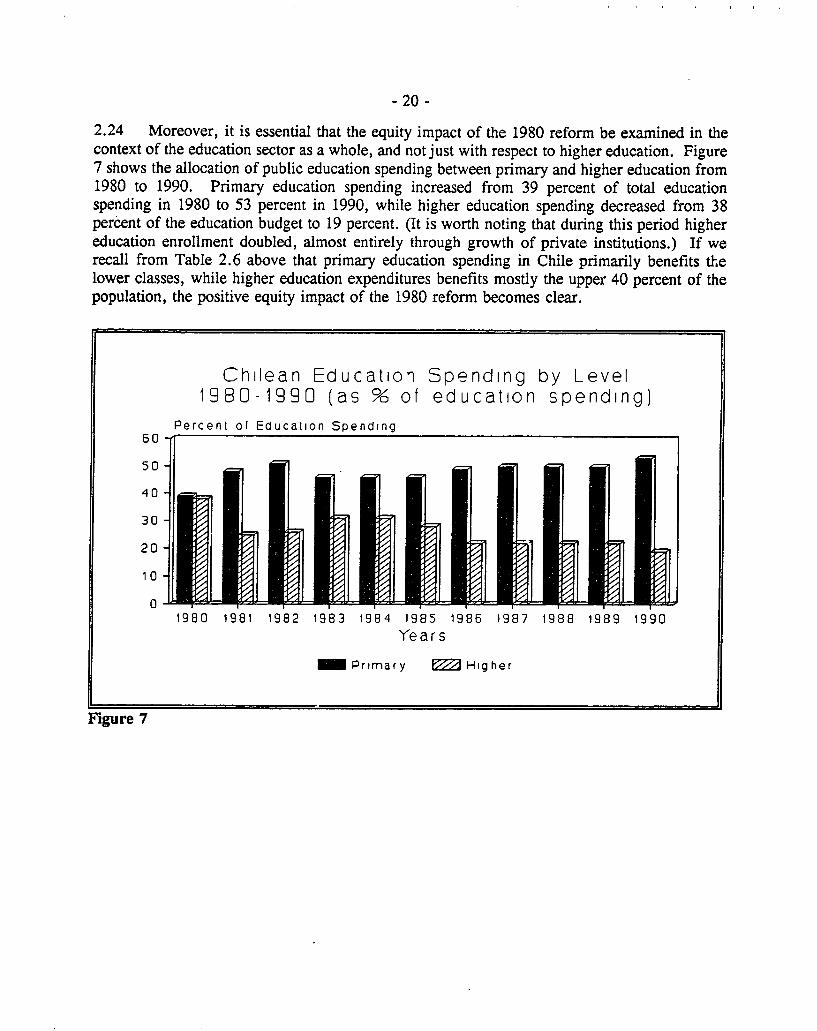

2.24 Moreover, it is essential that the equity impact of the 1980 reform be examined in thecontext of the education sector as a whole, and not just with respect to higher education. Figure7 shows the allocation of public education spending between primary and higher education from1980 to 1990. Primary education spending increased from 39 percent of total educationspending in 1980 to 53 percent in 1990, while higher education spending decreased from 38percent of the education budget to 19 percent. (It is worth noting that during this period highereducation enrollment doubled, almost entirely through growth of private institutions.) If werecall from Table 2.6 above that primary education spending in Chile primarily benefits thelower classes, while higher education expenditures benefits mostly the upper 40 percent of thepopulation, the positive equity impact of the 1980 reform becomes clear.

Chilean Educatioi Spending by Level1980-1990 (as % of education spending)

Percent of Education Spending60-

50 -

40 -

30-

201

10

01980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990

Ye ars

M Prtmary E Higher

Figure 7

- 21 -

Chile: Case Study of Reform: Before 1980 Chile's higher education system resembled those in many otherLatin American countries. There were 8 autonomous, "free of charge", highly selective universities, entirelyfunded by the public treasury. The 1980 higher education reform changed all that. It deregulated the system;opened up higher education to private initiative; diversified the system to include 4-year professional institutes(PIs) and 2-year technical training centers (17Cs); divided up the 2 national universities into 12 newuniversities and 2 PIs; increased cost recovery through tuition fees; expanded the student loan program; anddiversified funding sources.

The reforms produced the following effects: (1) total higher education enrollment more than doubled,with expansion provided entirely by mushrooming private institutions; (2) Chilean higher education is nowmainly private at non-university levels (PIs and TrCs) and has a dual public/private nature at the universitylevel (85% public); (3) higher education institutions have been established throughout the country, increasingaccess for students in all regions; (4) most higher education is provided by a large number of small privateinstitutions, plus a few medium-sized schools; and (5) the supply of higher education places now exceeds totaldemand.

Finance: The new private institutions are solely dependent on tuition fees for their resources andreceive no public funds. Meanwhile, public institution funding changed from a single source to a diversifiedsystem based on: public institutional core funding; a government-subsidized student loan program; privately-financed tuition fees; the number of highly qualified students each institution enrolls; and competitively-selected research projects. In 1981, 68 percent of public higher education institution funding came from thestate, with 15 percent derived from paid (or deferred) tuition fees, and 17 percent from other sources. Bycontrast, in 1990 public allocations constituted about 34 percent of total income for public institutions, withtuition fees providing about 22 percent, and the remaining 44 percent coming from targeted public allocations,sale of services, research grants and private donations.

Quality: On the whole, the 1980 Reform does not appear to have negatively affected the quality ofthe public institutions, although quality does not seem to have improved either. Lack of reliable informationand limited time-frames make it difficult to offer qualitative assessments about the new private institutions,of which there are 40 universities, 82 PIs and 168 TTCs. With respect to the private universities, they engageonly in teaching (no research), and offer mostly low-cost specializations using part-time teachers. Criticismsof their quality led to the introoction in 1990 of a public accreditation system for private universities.