Size effect in Indian Stock Market

14

Size Effect in Indian Stock Market An Empirical Study in National Stock Exchange Mishra Radhakrishna 1 , Sahoo Rashmita 2 1 Dept. of Finance, Bijupatnaik Institute of IT and Management Studies, Bhubaneswar, [email protected], #9437287858 2 Dr. Rashmita Sahoo, Dept. of Business Administration, Utkal University, Bhubaneswar, [email protected], #9937034547

Transcript of Size effect in Indian Stock Market

Size Effect in Indian Stock Market

An Empirical Study in National Stock Exchange

Mishra Radhakrishna1, Sahoo Rashmita

2

1Dept. of Finance, Bijupatnaik Institute of IT and Management Studies, Bhubaneswar,

[email protected], #9437287858

2Dr. Rashmita Sahoo, Dept. of Business Administration, Utkal University, Bhubaneswar,

[email protected], #9937034547

Abstract

The present study is based on the study of one of the anomalies of the stock market. It aims to

find out the presence of size effect on stock returns in the Indian stock market. The research is

carried on to study the impact of the size of the company on the returns from its stock in the

stock market (viz. National Stock Exchange). To conduct the study the market capitalization of

the stocks are taken as the size of the company (i.e. Large Cap, Mid Cap and Small Cap).

Returns from the stocks of 50 companies each from all the three sizes of the companies has been

compared to prove the hypothesis. To study the impact of the size effect the daily returns from

the stocks has been compared and further the respective abnormal returns have also been

compared for an elaborate analysis. Moreover the study focuses on finding answer to the

question, “Can anybody outperform the market by designing size based investment strategies?”

The present study is of immense use for the portfolio managers, asset management companies as

well as individual investors. Stock prices of last five years have been taken for the study.

Key words: Anomaly, Abnormal return, Efficient Market Hypothesis, Size effect

Introduction:

The size effect in the stock market is one of the most studied topics in finance theory. Since

some of the researchers like Banz (1981) had found that the small firms had given higher returns

than big firms, a large number of researchers have contributed a lot to this theory with empirical

evidences. However many studies have also proved that, now-a-days the size effect in the stock

market is losing its existence. The size of the firm measured by the market capitalization which

is arrived at by multiplying the market price of the share with the number of shares outstanding

in the market. The different sizes of the firms are categorized as Large Cap, Small cap and Mid

Cap. Post 1990s the Indian stock market has shown enormous changes. The opening up of the

Indian economy has fascinated the foreign institutional investors and the Indian stock market has

shown spectacular growth during this period. With the introduction of modern financial

instruments like derivatives the market is becoming more and more efficient and attractive to the

investors. This also has necessitated the increase in the role of the market regulators. It also has

enforced the modern institutional as well as individual investors to search for strategies which

can give them better return. In such an environment the current study is based on an argument

which has been in lime light since long. It attempts to find out the presence of size premium in

the stock market. In simple terms it attempts to answer a question whether one can make

abnormal return by designing portfolio based on size of the firm. Empirical studies have shown

the availability of extra normal returns by using active investment strategies based on a number

of firm variables such as size (Banz, 1981), leverage (Bhandari, 1988), price earnings ratio

(Basu, 1977), book to market ratio (Stattman, 1980); Rosenberg, Reid and Lanstein, (1985), etc.

These evidences, since inconsistent with the CAPM, are popularly known as CAPM anomalies.

Literature Review:

The presence of size effect is first documented by Banz (1981). He proved with empirical

evidences that the small size firms have outperformed the large size firms. Again the same is

confirmed by Reinganum (1981) and reported that a strong firm size still emerged. Roll (1981)

found that the small size firms are less frequently traded than the large firms; resulting a lower

systematic risk in the daily returns and shown higher returns. Christie and Hertzel (1981) argued

that as the risk measures are non-stationary which causes the size effect. Cook and Rozeff (1984)

studied the universal presence of size effect.

Arbel and Strebel (1983) found out that the size effect is may be due to the neglected firm effect.

According to James and Edmister (1983) the firm size and trading activity are highly correlated,

but differences in trading activity are not the major reason for the firm size anomaly. Keim

(1983) argued that there exists a relationship between the size effect and the seasonality effect or

January effect. He said that nearly fifty percent of the size effect is due to abnormally large

returns on the small size firms in January during the period 1963-1979. Brown, Kleidon and

Marsh (1983) verified that the magnitude of the size effect were not constant during 1967-1979.

Barry and Brown (1984) evidenced that differential information hypothesis is related to the size

effect and can explain a large part of it. Chan, Chen and Hsieh (1985) concluded that small firms

are more sensitive to changes in economic conditions (and hence more prone to risk) than large

firms and therefore carry higher risk. Amihud and Mendelson (1986) argued that a part of size

effect may, in fact, be the liquidity premium. Reinganum (1990) argued that the market

microstructure may have an important influence on the measured size effect. Therefore,

international evidence on size effect with different market organisation and structures should

reveal differences in magnitude of the size premiums across markets.

Rathinasamy and Mantripragda (1996) examined size effect and January effect using risk

adjusted Treynor and Sharpe portfolio performance measures and concluded that while the return

increased along with risk for small firms in January, the extra return was more than what was

warranted by the extra risk. Patel (2000) reported the presence of a strong size effect in 9 out of

22 emerging markets including India over the period 1988 to 1998. In a comprehensive study

regarding firm size and cyclical variations in stock returns, Timmermann and Quiros (2000)

documented that the behaviour of common stock returns for small and large firms varies

significantly over different phases of business cycles; expansion and recession. Annaert,

Crombez, Spinel and Holle (2002) studied size effect for a cross-section of European stocks over

15 European countries and found a large size premium but reported that this premium existed

only in the cross-section of the whole European market. If small and big stocks were selected

relative to the market size of the country, the strategy was no longer profitable. Xu (2002)

reported a strong size effect in China using market capitalization as the size measure. Mohanty

(2001) documented the presence of a strong size effect in Indian stock market over the period

1991.2000 using market capitalization as the measure of firm size. In a survey of mutual fund

managers, investment analysts and stock brokers, Sehgal (2002) found a greater support for size

effect in India, as 60% of the respondents believed that stocks of small companies provide higher

returns than stocks of bigger companies. Sehgal et al (2003) reported the presence of a strong

size effect and a weak and conditional value effect for the Indian stock market over the period

July 1989 to March 1999 using three different measures of size, viz., enterprise value, total assets

and market capitalisation. Contrary to the findings of Berk (1996) Muneesh and Sehgal (2003)

reported the presence of a strong size effect in India even with the use of some non- market

based size measures, i.e., total assets and net sales.

RESEARCH METHODOLOGY:

To study the presence of size effect the data of last 5 years has been taken from the stock market

(National Stock Exchange). Fifty companies each from large cap, mid cap and small cap has

been selected and their daily returns are calculated. The daily prices from the date 1st April 2009

to 31st March 2014 has been taken for research. 1247 prices have been collected and their

respective 1246 returns are compared to prove the hypothesis.

Data Collection

All Large Cap Mid Cap Small Cap

Time Period 1-Apr-2009 to

31-Mar-2014

1-Apr-2009 to

31-Mar-2014

1-Apr-2009 to

31-Mar-2014

1-Apr-2009 to

31-Mar-2014

No. of

Observations 3741 1247 1247 1247

No. of

companies 150 50 50 50

The Daily Returns:

The daily returns from the stocks are calculated by finding out the log value of the daily price

differences.

Rt = [ln (Pt/Pt-1)]*100

The lognormal returns follow the normal distribution more closely than returns. (Lauterbach and

Ungar (1995).

The abnormal return (Error Term):

To find out the abnormal return the theoretical return is calculated for each and every stock on a

daily basis. Then the theoretical return is deducted from the real return, the difference between

them is known as the abnormal return or error term. The theoretical return is calculated by

applying the CAPM model.

Theoretical return Rj= Rf + (Rm-Rf)βj

Here Rj = Expected return from the stock

Rf = Risk free return

Rm = Return from the market

βj = Beta of the stock ‘j’

The abnormal return or the error term is arrived at by deducting the above mentioned theoretical

return from the actual return from the stock.

Ej = Rj – Rj

Descriptive Statistics:

The descriptive statistics such as Mean and Standard deviation is of the actual returns and the

abnormal returns are calculated. The standard deviation is calculated to prove the consistency in

return.

Testable Hypothesis:

The null hypothesis Ho: a1 = a2 = a3

Alternative hypothesis H1: a1 ≠ a2 ≠ a3

Where, a1, a2 and a3, represents the average of the returns from the stocks of different sizes (i.e.

Large Cap, Mid Cap and Small Cap) of firms. To test the hypothesis first the correlation among

the returns is found out. Its significance level will prove that whether the correlation between the

returns is only a matter of chance or permanent. If the correlation is a matter of chance then there

exists the size effect in the stock market.

To test this null hypothesis first ANOVA is applied to find out whether the daily returns and the

abnormal returns are dependent on each other or different.

DATA ANALYSIS:

Analysis of Daily Returns:

Table 1. Descriptives – Daily Return

N Mean Std. Deviation Std. Error

Large Cap 1246 .03816387042531 1.310908162369949 .037137549736836

Mid Cap 1246 .07061040671595 1.247025625404414 .035327780782782

Small Cap 1246 -.81320413364151 16.822684785396845 .476580519412833

Total 3738 -.23480995216675 9.774550889072641 .159873750588057

The table 1 above displays the descriptive statistics of the daily returns from the stocks for the

period of 2004 to 2014. The stock returns are calculated based on the size of the company. The

mean return from the mid cap is maximum i.e. 0.07 with a standard deviation of1.24. The return

from the large cap is lower than mid cap i.e. 0.0381 with bit high standard deviation of 1.31. But

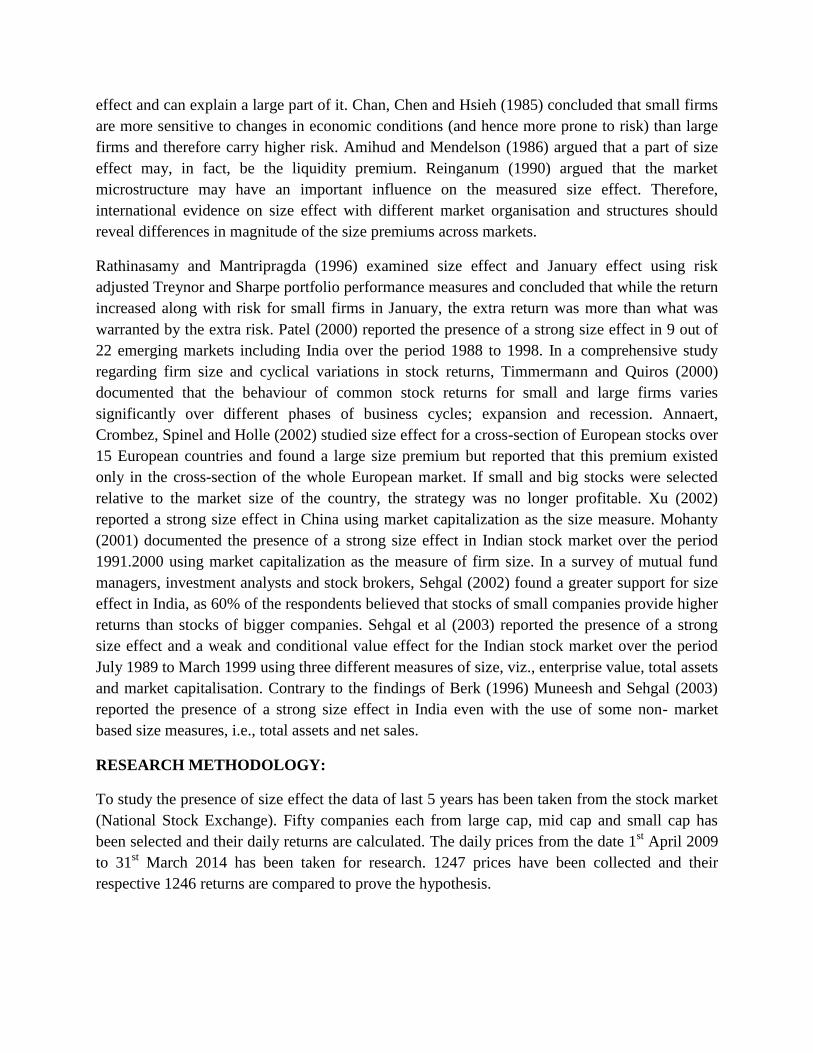

the mean return from the small cap is negative i.e. -0.813 with a very high standard deviation of

16.8226. From this we can infer that the return from the mid cap is higher and also more

consistence with a lower standard deviation. The small cap has performed the worst in this

period of research. In this period of 10 years the performance of the mid cap has outshined all the

other categories of stocks based on size.

The figure below (Fig1) is the graphical presentation the returns. From this figure it can be

inferred that the mean return from the mid cap is higher than any other types of stocks. This

shows the performance of the mid cap has outshined all the type of stocks.

Fig-1

Table-2 Correlations- Daily Return

Large_Cap Mid_cap Small_Cap

Large_Cap Pearson Correlation 1 .831** -.924

**

Sig. (2-tailed) .000 .000

N 1246 1246 1246

Mid_cap Pearson Correlation .831** 1 -.819

**

Sig. (2-tailed) .000 .000

N 1246 1246 1246

Small_Cap Pearson Correlation -.924** -.819

** 1

Sig. (2-tailed) .000 .000

N 1246 1246 1246

**. Correlation is significant at the 0.01 level (2-tailed).

The Table – 2 shows the correlation among the different types of stocks. It shows a strong

positive correlation between the large cap and mid cap i.e. 0.831. But the correlation among the

small cap and large cap is highly negative (i.e. -0.924) and mid cap and small cap (-0.819) is also

highly negative. This increases the chances of earning abnormal return by designing a portfolio

taking different stocks from large cap and small cap or Mid cap and Small Cap.

Though the coefficient of correlations among the large cap and mid cap is very high and positive

but it is highly significant rejecting the null hypothesis. This implies that the correlation is just a

matter of chance and it is not permanent. In case of the coefficient of correlation among large cap

and small cap is also highly hence it proves that this correlation is also a matter of chance. So far

as the level of significance of the coefficient of correlation among the mid cap and small cap is

concerned it is also highly significant, and shows that it is also a matter of chance and not

permanent.

ANOVA:

Table – 3 ANOVA – Daily Return

Sum of Squares df Mean Square F Sig.

Between Groups 625.911 2 312.955 3.280 .038

Within Groups 356413.964 3735 95.425

Total 357039.875 3737

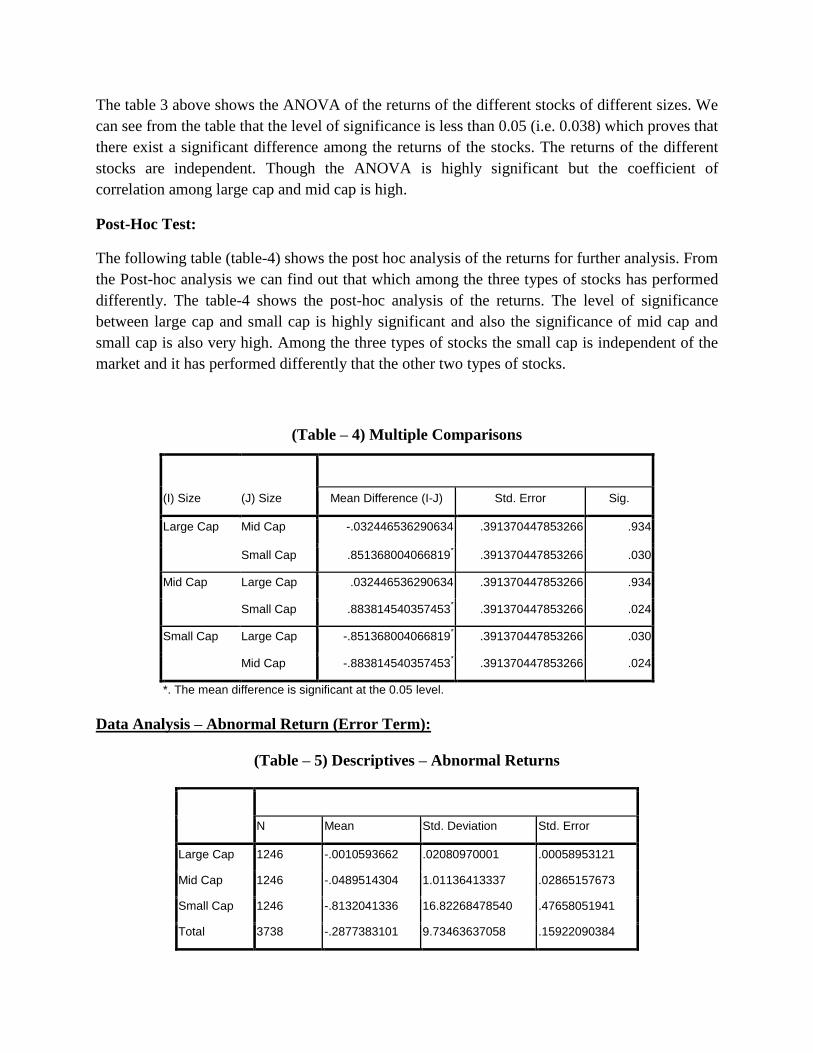

The table 3 above shows the ANOVA of the returns of the different stocks of different sizes. We

can see from the table that the level of significance is less than 0.05 (i.e. 0.038) which proves that

there exist a significant difference among the returns of the stocks. The returns of the different

stocks are independent. Though the ANOVA is highly significant but the coefficient of

correlation among large cap and mid cap is high.

Post-Hoc Test:

The following table (table-4) shows the post hoc analysis of the returns for further analysis. From

the Post-hoc analysis we can find out that which among the three types of stocks has performed

differently. The table-4 shows the post-hoc analysis of the returns. The level of significance

between large cap and small cap is highly significant and also the significance of mid cap and

small cap is also very high. Among the three types of stocks the small cap is independent of the

market and it has performed differently that the other two types of stocks.

(Table – 4) Multiple Comparisons

(I) Size (J) Size

Mean Difference (I-J) Std. Error Sig.

Large Cap Mid Cap -.032446536290634 .391370447853266 .934

Small Cap .851368004066819* .391370447853266 .030

Mid Cap Large Cap .032446536290634 .391370447853266 .934

Small Cap .883814540357453* .391370447853266 .024

Small Cap Large Cap -.851368004066819* .391370447853266 .030

Mid Cap -.883814540357453* .391370447853266 .024

*. The mean difference is significant at the 0.05 level.

Data Analysis – Abnormal Return (Error Term):

(Table – 5) Descriptives – Abnormal Returns

N Mean Std. Deviation Std. Error

Large Cap 1246 -.0010593662 .02080970001 .00058953121

Mid Cap 1246 -.0489514304 1.01136413337 .02865157673

Small Cap 1246 -.8132041336 16.82268478540 .47658051941

Total 3738 -.2877383101 9.73463637058 .15922090384

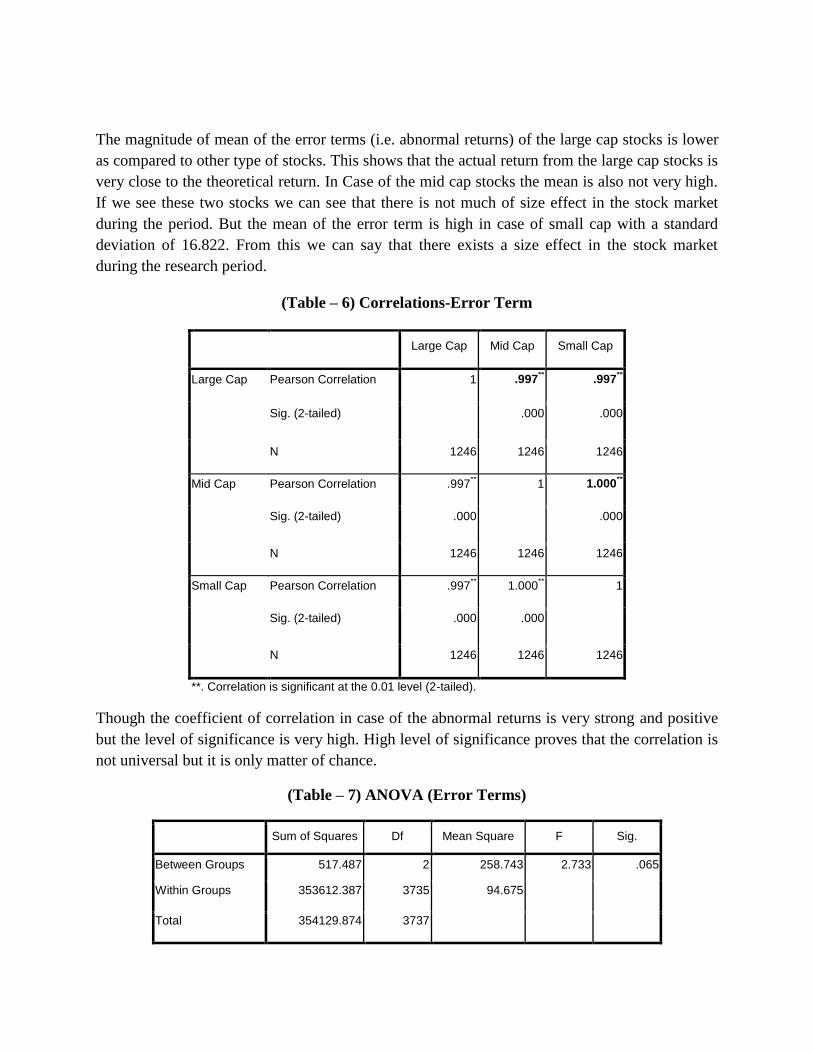

The magnitude of mean of the error terms (i.e. abnormal returns) of the large cap stocks is lower

as compared to other type of stocks. This shows that the actual return from the large cap stocks is

very close to the theoretical return. In Case of the mid cap stocks the mean is also not very high.

If we see these two stocks we can see that there is not much of size effect in the stock market

during the period. But the mean of the error term is high in case of small cap with a standard

deviation of 16.822. From this we can say that there exists a size effect in the stock market

during the research period.

(Table – 6) Correlations-Error Term

Large Cap Mid Cap Small Cap

Large Cap Pearson Correlation 1 .997** .997

**

Sig. (2-tailed) .000 .000

N 1246 1246 1246

Mid Cap Pearson Correlation .997** 1 1.000

**

Sig. (2-tailed) .000 .000

N 1246 1246 1246

Small Cap Pearson Correlation .997** 1.000

** 1

Sig. (2-tailed) .000 .000

N 1246 1246 1246

**. Correlation is significant at the 0.01 level (2-tailed).

Though the coefficient of correlation in case of the abnormal returns is very strong and positive

but the level of significance is very high. High level of significance proves that the correlation is

not universal but it is only matter of chance.

(Table – 7) ANOVA (Error Terms)

Sum of Squares Df Mean Square F Sig.

Between Groups 517.487 2 258.743 2.733 .065

Within Groups 353612.387 3735 94.675

Total 354129.874 3737

The table – 7 above shows the ANOVA of the abnormal returns. The ANOVA is insignificant

proving that there is no significant difference among the mean of the error terms. From this we

can say that all the three types of firms have shown similar performance so far as abnormal

return or error term is concerned.

Conclusion:

The size effect is one of the most discussed issues of the stock market. From the last ten years

data we can say that there exist a size effect in the Indian stock market. This means that an

investor can achieve better return by designing a portfolio based on the size of the firm. The

coefficient of correlation among the large cap and mid cap is high and positive but the coefficient

of correlation among the large cap and small cap is negative and very strong. Same is in the case

of mid cap and small cap stocks. So here we can conclude that one can make better return from

the stock market by designing portfolios based on size based strategies. If we see the post hoc

test of the actual returns we can see that there exist a size effect in the stock market and the small

cap stocks are the drivers of the size effect. We can see that during this period the mid cap stock

has performed better that the other two types of the stocks. But so far as the abnormal returns are

concerned as the ANOVA is insignificant; we can say that the presence of the size effect in the

Indian stock market is due to the systematic risk component of the stocks.

Bibliography:

Amihud, Y. and Mendelson H., “Liquidity and Stock Returns”, Financial Analysts Journal, May-

June 1986, pp.43-48.

Annaert J., Crombez J., Spinel B., and Holle F.V. "Value and Size Effect: Now You See it, Now

You Don't", 2002 (May), Working Paper, Ghent University, Belgium.

Arbel, Avner, Steven Carvell and Strebel, Paul, “Giraffes, Institutions and Neglected Firms”,

Financial Analysts Journal, May-June, 1983, pp.57-63.

Banz, Rolf W. “The Relationship between Return and Market Value of Common Stock”, Journal

of Financial Economics, March 1981, pp.3-18.

Barry, Christopher B. and Brown, Stepehen J. “Differential Information and the Small Firm

Effect”, Journal of Financial Economics, 1984, 13, pp.283-294.

Basu, Sanjoy, “Investment Performance of Common Stocks in Relation to their Price-Earnings

Ratios: A Test of Efficient Market Hypothesis”, Journal of Finance, 1977, vol.32, pp.663-682.

Berges, A. McConnel J. and Schlabraum G., “The Turn-of-the Year Effect in Canada”, Journal

of Finance, 1984, vol.39, pp.182-192.

Berk, J., "A Critique of Size Related Anomalies", Review of Financial Studies, 1995, 8, pp.275-

286.

Berk, J., "An Empirical Re-examination of the Relation Between Firm Size and Return", Revised

Working Paper, School of Business Administration, University of Washington, October 1996.

Bhandari, L.C., "Debt-Equity Ratio and Expected Common Stock Returns: Empirical Evidence",

Journal of Finance, 1988, 43, pp.507-528.

Black, F., "Capital Market Equilibrium with Restricted Borrowing", Journal of Business, 1972,

45, pp.444-455.

Blume, Marshall E. and Stambaugh R.F., “Biases in Computed Returns: An Application to the

Size Effect”, Journal of Financial Economics, November 1983, pp.387-404.

Brown, Phillip, Keim, Donald B., Kleidon Allan W., and Marsh Terry A., “Stock Return

Seasonalities and `Tax-Loss Selling’ Hypothesis: Analysis of the Arguments and Australian

Evidence”, Journal of Financial Economics, June 1983, 12, pp.105-127.

Brown, Phillip, Kleidon Allan W. and Marsh, Tarry A., “New Evidence on the Nature of Size

Related Anomalies in Stock Prices”, Journal of Financial Economics, June 1983, 12, pp.33-56.

Calvet, A., and Lefoll, J., "Risk and Return on Canadian Capital Markets: Seasonality and Size

Effect", Journal of the French Finance Association, 1989, 10, pp.21-39.

Chan, K.C. and Chen, Nai-Fu, “Structural and Return Characteristics of Small and Large Firms”,

Journal of Finance, September 1991, 56, 4, pp.1467-1484.

Chan, K.C., Chen Nai Fu and Hsieh, David A. :”An Exploratory Investigation of the Firm Size

Effect”, Journal of Financial Economics, 1985, 14, pp.451-471.

Chan, L., Hamalo, Y., and Lakonishok, J., "Fundamentals and Stock Returns in Japan", Journal

of Finance, 1991, 46, pp.1739-1764.

Christie, Andrew A. and Michael Hertzel, 1981, “Capital Asset Pricing ANOMALIES’: Size and

Other Correlations”, Manuscript (University of Rochester, Rochester, NY).

Cook, Thomas J. and Rozeff Michael, “Size and Earnings/Price Ratio Anomalies: One Effect or

Two?” Journal of Financial and Quantitative Analysis, December 1984, pp.449-466.

Corhay, A., Hawawini, G., and Michel, P., "The Pricing of Equity on the London Stock

Exchange: Seasonality and Size Premium", in Stock Market Anomalies, E. Dimson (ed.),

Cambridge University Press, 1988, pp.197-212.

Cornoilay, C. and Pasquier, J., "CAPM, Risk Premium Seasonality and the Size Anomaly: The

Swiss Case", Journal of the French Finance Association, 1991, 21, pp.23-44.

Fama, E., and French, K., "The Cross Section of Expected Stock Returns", Journal of Finance,

1992, 47, pp.427-466.

Fama, E., and French, K., "Common Risk Factors in the Returns of Stocks and Bonds", Journal

of Financial Ecoomics, 1993, 33, pp.3-56.

Fama, E. and French K. "Size and Book to Market Factors in Earnings and Returns", Journal of

Finance, 1995, 50, pp.131-155.

Fama, E., and French, K., "Multifactor Explanations of Asset Pricing Anomalies", Journal of

Finance, 1996, 51, pp.55-84.

Fama, E., and MacBeth, J., "Risk, Return and Equilibrium: Empirical Tests", Journal of Political

Economy, 1973, 71, pp.607-636.

Gupta, L.C., "Return on Indian Equity Shares", reviewed in ICFAI Journal of Applied Finance,

Volume 6, No.4, October 2000.

Hawawini, G., "Stock Market Anomalies and the Pricing on the Tokyo Stock Exchange", in

Japanese Financial Market Research, W. Ziemba, W. Bailey and Y. Hamao (eds.), North -

Holland, 1991, pp.231-250.

Hawawini, G., and Keim, D.B., "The Cross Section of Common Stock Returns: A Review of the

Evidence and Some New Findings”, In Security Market Imperfections in Worldwide Equity

Markets, Keim, D.B. and Ziemba (eds) 2000, Cambridge University Press, pp.3-43.

Hawawini, G., and Viallet, C., "Seasonality, Size Premium and the Relationship Between the

Risk and Return of French Common Stocks", working paper, INSEAD, Fontainebleau, France,

1987.

Herrera, M. and Lockwood, L., "The Size Effect in the Mexican Stock Market", Journal of

Banking and Finance, 1994, 18, pp.621-632.

Ho, Y.K., "Stock Return Seasonalities in Asia Specific Markets", Journal of International

Financial Management and Accounting, 1990, 2, pp.47-77.

James, Christopher and Edmister, Robert O., “The Relation between Common Stock Return,

Trading Activity and Market Value, Journal of Finance, September 1983, 38, pp.1075-1086.

Keim, Donald B., “Size-related Anomalies and Stock Return Seasonality: Further Empirical

Evidence”, Journal of Financial Economics, June 1983, 12, pp.13-32.

Kim, Y.G., Chugh K.H. and Pyun C.S., "Size, Price Earnings Ratio and Seasonal Anomalies in

the Korean Stock Market". In Pacific Basin Capital Market Research, S.G.Rhee and R.P. Chang

(eds.), North-Holland, 1992.

Ma, T., and Shaw, T.Y., "The Relationship between Market Value, P/E Ratio, Trading Volume

and the Stock Return of Taiwan Stock Exchange", in Pacific Basin Capital

Markets Reearch, S.G. Rhee and R.P. Chang (eds.), North-Holland, 1990, pp.313-335.

Mohanty, P., "Efficiency of the Market for Small Stocks", 2001, NSE Research Paper Series

(nseindia.com).

Muneesh K. and Sehgal S., “Company Characteristics and Common Stock Returns: The Indian

Experience”, Working Paper, Department of Financial Studies, University of Delhi, 2003.

Patel, S.A., "Characteristics-based premia in Emerging Markets: Sector Neutrality, Cycles and

Cross Market Correlations" in Security Market Imperfections in Worldwide Equity Markets,

2000, D.B. Keim, W.T. Ziemba (eds.) Cambridge University Press, pp.416-432.

Rathinasany R.S., and Mantripragada, K.G., "The January Size Effect Revisited: Is it a case of

Risk Mismeasurement?". Journal of Financial and Strategic Decisions, 1996, Vol.9, No.3, pp.9-

14.

Reinganum, Marc R., “Misspecifications of Capital Market Pricing: Empirical Anomalies based

on Earnings Yields and Market Values”, Journal of Financial Economics, 1981, 9, pp.19-46.

Reinganum, Marc R., "Market Microstructure and Asset Pricing: An Empirical Investigation of

NYSE and NASADQ Securities", Journal of Financial Economics, 1990, 28, pp.127-148.

Roll, Richard, “A Possible Explanation of the Small Firm Effect”, Journal of Finance, September

1981, 36, pp.879-888.

Rosenberg, B., Reid, K., and Lanstein, R., "Persuasive Evidence of Market Efficiency", Journal

of Portfolio Management, 1985, 11, pp.9-17.

Sehgal S., “Investor Behaviour in the Indian Capital Market”, Review of Commerce Studies,

Jan-June 2002, 20-21, pp.123-152.

Sehgal, S., "Common Factors in Stock Returns: The Indian Evidence", The ICFAI Journal of

Applied Finance, Vol.9, No.1, January 2003, pp.5-16.

Stattman, D., "Book Values and Stock Returns", The Chicago MBA - A Journal of Selected

Papers, 1980, 4, pp.25-45.

Timmermann, Allan and Quiros, P.G., "Firm Size and Cyclical Variations in Stock Returns",

The Journal of Finance, June 2000, pp.1229-1262.

Wong, K.A., and M.S. Lye, "Market Values, Earnings Yields and Stock Returns", Journal of

Banking and Finance, 1990, 14, pp.311-326.

Xu, J., "The Size Effect of the Stock Returns in the Chinese Market", 2002 (March), Working

Paper, Peking University, China.

-----xxxx----