“Shale gas revolution and what it means for international energy geopolitics and new world order?"

27

Transcript of “Shale gas revolution and what it means for international energy geopolitics and new world order?"

tuncay babali

https://www.ipsa.org/my-ipsa/events/paper-room?title=&field_profile_name_last_value=Babali&title_1=&field_eventpan_code_value=&field_eventpan_session_nid=All

1"

"

Shale gas revolution and what it means for international energy geopolitics and new world order?

By Dr. Tuncay BABALI1

Paper presented on July 24th, 2014 at the RC41 Geopolitics Panel: Great Powers and Geopolitics during XXIIIrd World Congress of Political Science, IPSA/AISP

Montreal, Quebec, Canada 19–24 July, 2014 (Work in progress. Please do not cite without author´s permission. Comments are welcome)

Congress Theme: Challenges of Contemporary Governance Abstract: The future of energy and it's geopolitics can be discussed from many angles; exciting innovation and technology based advances, renewable energy and environmentally friendly applications, climate change's impact, arctic and Eurasian promises are to name a few. However, a closer and deeper analysis reveals the fact that in reality there is only one that has the real potential and promise that emerges above the rest: Shale gas revolution.

However, that promise very much depends on North America (namely US and Canada foremost) becoming a single and transparent energy market for all as the new supply hub of the world. This can only be realized if the actors (companies, leaders of NAFTA and stakeholders) could believe in it and act accordingly. This might very well be one of the decisive elements on the new world order as it has never been before. Like the US once was the prime supplier of the world’s oil until the 1960s now through valuable cooperation and strategic vision to be created among the US and Canada primarily has the potential to create the world’s biggest and most reliable supply chain on hydro-carbon resources. However, this will depend on how the new market is structured and rules of the new game in town to be clear to all producers, consumers and transit countries alike. Not only that but it also requires successful address of the real environmental dangers of the shale gas production. Despite its undoubtedly revolutionary and here to stay nature of the shale gas, it has yet to reach out to emerging markets. Signs of failure of the promises with wrong early practices in countries like Poland and Ukraine have the potential to lead more geopolitical and geoeconomical rivalries and shift of alliances in classical hydrocarbon energy geopolitics. So without declaring the winners and losers, what will be the choice of energy for the future and why questions will continue to dominate the energy geopolitics debate beyond its traditional scope? KEYWORDS: Energy geopolitics, shale gas revolution, new world order, future of OPEC, Hydraulic fracturing, horizontal fracturing, Environmental aspects, Renewable energy sources, oil & gas law & legislation & regulation, climate change

Introduction: The future of energy and it's geopolitics can be discussed from many angles; exciting innovation and technology based advances, renewable energy and environmentally friendly applications, climate change's impact, arctic and Eurasian promises are to name a few.2 However, a closer and

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""1 Tuncay BABALI, Ph.D (Houston), MA (London), Ambassador of Turkey to Canada. Former fellow at Harvard WCFIA (2009-2010). 2 This fast increasing demand has forced the developed world to seek new reserves (in the Arctic, in the Caspian basin etc.) … and new sources (shale).This is changing the energy geopolitcs in the world dramatically. "

2"

"

deeper analysis reveals the fact that in reality there is only one that has the real potential and promise that emerges above the rest: Shale gas revolution.3 However, that promise, as will be discussed in this paper, very much depends on North America (namely US and Canada foremost) becoming a single, transparent and well regulated energy market for all, as the new supply hub of the world. 1/3 of all the oil that the US imports is supplied by Canada. One in seven cars in the US is fuelled by Canadian resources.4 Canada and US hold an estimated 1,238 TCF + 59 billion barrels of recoverable shale resources. And only the US and Canada have currently added significant volumes to their national production from shale reservoirs. These statistics alone should give an idea about the energy integration potential between these two countries. With strategic planning this could turn into a bigger hope and source of inspiration not just for North America but to the whole world.

For instance Canada’s gigantic Duvernay shale gas deposit (4Bbbl) already attracts huge investments from China, Japan and latest from Malaysia with the declaration of $36 billion investment in shale gas production and LNG sector.5 The US production increase is immense. Yet faltering and not coming fast enough regulation is hindering the potential and emerging markets and the rest of the world cannot yet see the price drop over oil. This keeps some countries to be able to play around the classical hydrocarbon dependency of the world on geopolitical grounds. This new energy powerhouse and supply hub can only be realized if the actors (companies, leaders of NAFTA and stakeholders) could believe in it and act accordingly in a visionary way. This might very well strengthen the unipolarity of the new world order as it has never been before. Like the US once was the prime supplier of the world’s oil until the 1960s now through valuable cooperation and strategic vision to be created among the US and Canada primarily has the potential to create the world’s biggest and most reliable supply chain on hydro-carbon resources.

However, this will depend on how much cooperation and strategic vision will be put forward and how fast the projects like Keystone XL6 to create extra connectivity between East-West and North-South in North America through new pipelines are able to be created. Another aspect that would be vital is how the new market is structured and rules of ``the new game in town`` to be clear to all producers, consumers and transit countries alike. Not only that but it also requires successful address of the real environmental dangers of the shale gas production.

Despite its undoubtedly revolutionary and here to stay nature of the shale gas, it has yet to reach out to emerging markets like G20 member countries such as Turkey, South Korea. This is extremely important also from the perspective of reaching out to sustainable robust growth patterns after the world economic and Euro crisis as well as reaching out to UN millennium

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""3 Vast amounts of hydrocarbons have moved from their original source rock formations and become trapped in shale and tight rock, and the extent of these formations is huge; containing 1.5 trillion barrels of total global conventional proven oil reserves. Source: International Energy Agency (IEA) 4 Canada and the United States: Energy Partners, video by Connect2Canada , published on June2, 2014 on http://www.youtube.com/watch?v=m9UjtnFPdZk 5 “Petronas Moves Ahead With Canada LNG Project Hailed by Najib,” Bloomberg, http://www.bloomberg.com/news/2013-10-06/petronas-plans-35-billion-lng-project-in-canada-najib-says.html 6 A pipeline project aiming to bring Canadian crude oil (from Alberta oil sands) to Gulf of Mexico through US.

3"

"

sustainable development goals. Reviews for both are going to be underway during this year’s G20 Summit at Brisbane, Australia and next year in Turkey.7 Signs of failure of the promises with wrong early practices in countries like Poland and Ukraine have the potential to lead more geopolitical and geoeconomical rivalries and shift of alliances in classical hydrocarbon energy geopolitics. World must be vigilant about such developments which might have direct bearings on the shape and direction of the new world order. In the final analysis what will be the choice of energy for the future and why questions will continue to dominate the energy geopolitics debate beyond its traditional scope. Course and outcome of this debate will have an immense impact on the new world order.

Future of energy geopolitics and the new world order debate after shale gas revolution: Shale gas revolution may be the biggest energy story today, but it is real. It is here. It is very much the fact of life now in North America. Edward Morse, Citi Bank`s foremost global energy expert8, explains in his Foreign Policy article how much U.S. hydrocarbon (oil and gas) production from shale has grown in recent years, why it will continue, and how that will drive a fundamental change in global energy geopolitics.9

A decade ago, the future of American hydrocarbon production looked bleak. Domestic production was declining and big U.S. energy companies, believing their fortunes lay offshore and abroad turned their attention to these areas. However, then something unexpected happened: “a surge of innovation allowed companies to extract vast quantities of natural gas trapped in once-inaccessible deposits of shale. The resulting abundance drove down U.S. gas prices to about one-third of the global average.”10 Since the technology involved in extracting these resources is now transferable outside the U.S., so that its spread and geopolitical impacts to the rest of the world is inevitable.

How it happened? Beginning in the 1970s, also with the impact of the OPEC crisis, production from onshore U.S. hydrocarbon fields declined as those fields became "mature." So the major oil companies were forced to abandon the development of new resources on mainland U.S. In order to find new lucrative fields, they shifted their attention to foreign new frontier lands and deep offshore waters. “Such investments were enormously expensive and often required decades to negotiate and develop. In order to build the capital resources and global reach necessary to deal with national governments and complete mammoth projects, the major oil companies began to acquire or merge with their peers.”11 Over the 1980s and 90s, however, these International Oil Companies (IOCs) became excessively bureaucratic and clumsy. In a hasty manner they focused on replacing their declining reserves and invested in gigantic and daunting foreign reserves, such as the Kashagan field, in

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""7"Turkey's economy has transformed very fast over the past few decades. 50 years ago according to the World Bank

and IMF figures, the country's GDP per capita was just over $250 - roughly the level of the least developed countries of today. Now the average per capita GDP in real terms is over $11000, and the country, by many standards, a developed nation has three times higher annual energy demand than the world average (around 4,5%). "8 Edward L. Morse is Global Head of Commodities Research at Citi. 9 Morse, Edward, L., Welcome to the Revolution, Foreign Affairs. May 2014, Vol. 93 Issue 3, p3-7. 5p. 10 Morse, Edward, L., ibid. 11 Hefner III, Robert A. The United States of Gas, Foreign Affairs. May2014, Vol. 93 Issue 3, p9-14. 6p

4"

"

Kazakhstan, which has an estimated 13 billion barrels of recoverable oil; its first phase of development alone cost $50 billion.12 In the late 1990s and early 2000s, natural gas prices were going up, and the industry has just discovered about the vast shale gas and tight oil deposits in rock formations. So companies attempted to crack open the shale in vertical wells and release the gas by injecting sand, water, and chemicals into the rock, a process known as “hydraulic fracturing,” or "fracking." However it was not cost effective.

The advent of large-scale shale gas production did not occur until Mitchell Energy and Development Corporation owned by George Mitchell, an independent oil man wildcatting in the Barnett formation, experimented during the 1980s and 1990s to make deep shale gas production a commercial reality in North-Central Texas. As the success of Mitchell Energy and Development became apparent, other companies aggressively entered this play13 so that by 2005, the Barnett Shale alone was producing almost half a trillion cubic feet per year of natural gas.

Table 1: U.S. Gas Production (1900-2013)

As recently as 2007, shale gas accounted for just five percent of U.S. natural gas production; by 2012, it accounted for thirty-five percent of U.S. gas production, and that figure certainly will rise further. Some experts argue that a further 30 percent increase in U.S. natural gas production is

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""12 Hefner III, Robert A., ibid. 13“His innovation was to drill horizontally into the shale, exposing thousands of feet of gas-bearing rock, rather than the 100 feet or so (or often just ten or 20 feet) encountered in a vertical well. In short order, gas prices got even higher and Mitchell's techniques got even better, and he started achieving some commercial success. In 2002, Devon Energy, sensing the coming revolution, bought Mitchell's company and ramped up the innovation necessary to develop the Barnett formation. Chesapeake Energy and other independent companies soon joined in, thus kicking off the U.S. shale boom. Within the decade, Chesapeake surpassed ExxonMobil as the largest U.S. natural gas supplier, and not long after, the United States surpassed Russia as the world's largest natural gas producer.” Hefner III, Robert A., ibid.

5"

"

plausible before 2020, and from then on, it should be possible to maintain a constant or even higher level of production for decades to come. For the past three years, according to the IEA figures the U.S. has been the world's fastest-growing hydrocarbon producer. Having already outstripped Russia as the world's largest gas producer, by the end of the decade, the U.S. is expected to become one of the world's largest gas exporters.14

U.S. oil production, meanwhile, has grown by 60 percent since 2008, climbing by three million barrels a day to more than eight million barrels a day. Given the research and development now under way, it is likely that U.S. production could rise to 12 million barrels per day or more in a few years and be sustained there for a long time.15

Table 2: U.S. Oil Production (1900-2013)

This stunning shift has been very impressive. Conventional oil production in the United States (production from conventional reservoirs without fracking) peaked in 1970 at 9.7 million barrels per day (bpd) and then declined, reaching a low of 5 million bpd in 2008. In 2008, the United States was a net importer of petroleum products, taking in about two million barrels per day; by the end of 2013, it was a net exporter, with an outflow of more than 2 million barrels per day. With output up 56% since 2008 – an increase that, in absolute terms, is larger than the total

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""14 Morse, Edward, L., “The Dynamic Duo: Another Year of Volatile Change,” Citi Research paper, January 2014 ; Morse, Edward L., presentation and discussion at the workshop co-organized by the Atlantic Council Canada and Ottawa University Collaboratory on Energy, Research and Policy session at the University of Ottawa, January 29, 2014. 15 Morse, Edward, L., ibid.; Leverett, Flynt & Leverett, Hillary Mann, “America’s Shale Revolution and the Dangerous Myth of Energy Independence,” The World Financial Review, May 28, 2014. http://www.worldfinancialreview.com/?p=1820

6"

"

output of each of eight of the 12 OPEC countries.16 With shale coming on line, the United States rose to 7.5 million bpd of crude oil in 2013, making it the world’s third-largest producer (after Saudi Arabia and Russia). New drilling techniques extract oil and gas from US shale rock formations, putting the country's output at astonishingly 25m barrels per day.17

In short, shale / tight oil and shale gas resources have revolutionized U.S. oil and natural gas production, providing 29 percent of total U.S. crude oil production and 40 percent of total U.S. natural gas production in 2012.18

In addition, on natural gas liquids and condensates, U.S. liquid fuel production has reached 11 million bpd. That is reducing U.S. demand for imported oil (in 2005, imports amounted to 60 percent of U.S. liquid fuel demand; by 2011, this figure had dropped to 45 percent; preliminary data for 2013 suggest it may now be down to 35 percent).19

With this trajectory, as the U.S. Energy Information Administration (EIA) estimates, US surpasses Russia as world's top oil and natural gas producer in 2013. Within a couple of years, it will exceed 10m barrels a day as overtaking not only Russia but also Saudi Arabia and becomes the world's largest oil producer. As the EIA figures indicate that U.S. crude oil production rose to an average of 7.6m barrels a day in August 2013, the highest monthly totals since 1989. Oil production is rising to 8.4m barrels a day in 2014. "Total petroleum and natural gas hydrocarbon production estimates for the U.S. and Russia for 2011 and 2012 were roughly equivalent (within 1 quadrillion Btu of one another). In 2013, however, the production estimates widen out, with the U.S. expected to outproduce Russia by five quadrillion Btu," the agency announced. 20

U.S. pipeline exports to Mexico and eastern Canada are likely to grow by 400 percent, to eight billion cubic feet per day, by 2018, and perhaps to ten billion by 2020. U.S. exports of liquefied natural gas (LNG) look likely to reach nine billion cubic feet per day by 2020.21

By the end of 2014, the U.S. should overtake Russia also as the largest exporter of diesel, jet fuel, and other energy products, and by 2015, it should overtake Saudi Arabia as the largest exporter of petrochemical feedstocks.

Table 3: Canadian Gas and Oil Production

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""16 Yergin, Daniel, “The Global Impact of US Shale,” Project Syndicate, January 8, 2014. http://www.project-syndicate.org/commentary/daniel-yergin-traces-the-effects-of-america-s-shale-energy-revolution-on-the-balance-of-global-economic-and-political-power 17 Leverett, Flynt & Leverett, Hillary Mann, ibid. 18"http://www.eia.gov/todayinenergy/detail.cfm?id=11611 "

19 EIA; Leverett, Flynt & Leverett, Hillary Mann, ibid 20 Goldenberg, Suzanne, US surpasses Russia as world's top oil and natural gas producer, theguardian.com, October 4, 2013. http://www.theguardian.com/business/2013/oct/04/us-oil-natural-gas-production-russia-saudi-arabia 21 EIA, IEA figures; Morse, Edward, L.,ibid.

7"

"

Not only the U.S. but Canadian production has also greatly benefited from improvements in hydraulic fracturing technology. Increase in gas production from artificially fractured horizontals is primarily driven by the Montney field in British Columbia and Alberta, and the various Cretaceous plays of the Alberta basin center gas accumulations. Increases in oil production from artificially fractured horizontals are primarily driven by the Bakken and Cardium fields.

The application of fractured horizontal wells in Western Canada is at an earlier state than in the US, where most of the activity has been concentrated on tight sand and hybrid fields, rather than pure shale areas. Significant and sustainable growth is expected as this technology is applied to shale fields like the Duvernay and Muskwa. Dramatic rise in production and immense potential for the future will also fundamentally change the global energy industry and calls for new mechanisms to address the new realities which will definitely include new pricing mechanism (for further discussion see p.13), trade, regulation and export patterns. This revolutionary nature of the change in shale oil and gas production has reversed the earlier conventional global view that hydrocarbon production would inevitably decline and after certain period of time they would be extinct. It is very clear by now that it is not going to happen and because of the shale gas revolution the industry will benefit first and foremost the U.S. and Canada is economy and also the global economy.

This revolution, however is not immune from concerns, including environmental problems associated with hydraulic fracturing and adverse potential effects on climate change and water safety. Equally the potential geopolitical consequences - which this article will also discuss, of rising U.S. and Canada hydrocarbon production, and declining role and the power of the Organization of Petroleum Exporting Countries (OPEC) and of countries such as Saudi Arabia, Qatar and Russia, through now available U.S. liquefied natural gas (LNG) and oil exports to Europe and east Asia.

Good for global economy: Global economy will benefit immensely from the shale revolution taking place in the world. Positive effects are expected to disseminate and grow beginning from the producer countries.

8"

"

Thanks to the new dynamism through shale development, the U.S. trade balance for oil, which in 2011 was -$354 billion, should flip to +$5 billion by 2020. Long after the WWII and 1960s period, for the first time by the start of 2013, oil, natural gas, and petrochemicals had become the single largest category of U.S. exports, surpassing agricultural products, transportation equipment, and capital goods. The U.S. gas trade balance is ecpected to shift from -$8 billion in 2013 to +$14 billion by 2020.22

Shale gas revolution will also have a critical impact on producer countries’ current account balances (CAD) This is a very significant factor for the emerging economies since the energy imports constitutes the largest items –in many cases, such as in Turkey close to half in the CAD. The impact of energy prices to imports was $60.1 billion in 2012 whereas the total imports in the same year was $236 billion. The same number for the year 2013 was $55.9 billion while total imports were standing at $245 billion.23 For the U.S. over the last decade or so, energy imports have accounted for roughly half of America’s massive trade deficit. To the extent that America has to import less oil and gas, it is clearly positive for the U.S. balance of payments. There are also measures of GDP and job growth associated with shale production.24

""

Moreover, because natural gas currently supplies about 25 percent of the total energy consumed in the U.S., the boom is saving U.S. consumers hundreds of billions of dollars a year. Combined with other benefits, those savings have given the U.S. a long-term economic advantage over its competitors and helped the country recover from the Great Recession.25 It is estimated that the shale revolution supports overall around two million jobs in energy and related sectors in the U.S. More than one million Americans alone work in the oil and gas industry, an increase of roughly 40 percent between 2007 and 2012. Also, now the US is not importing any LNG – thereby saving $100 billion on its annual import bill. At current prices, the increase in US oil production has been cutting another $100 billion from that bill.26

""

Americans pay a fraction of the price for natural gas that the rest of the world's consumers do, saving as much as $300 billion annually compared with consumers in China and Europe. Already, the development of the United States' enormous shale oil and gas reserves has boosted U.S. GDP by as much as one percent. In addition, these trends will provide a significant boost to the U.S. economy. Households could save close to $30 billion annually in electricity costs by 2020, compared to the U.S. Energy Information Administration's current forecast. Gasoline costs could fall from an average of five percent to three percent of real disposable personal income. The price of gasoline could drop by 30 percent, increasing annual disposable income by $750, on average, per driving household. The oil and gas boom could add about 2.8 percent in cumulative GDP growth by 2020 and bolster employment by some three million jobs.27 Shale-energy development has also generated royalty payments to a variety of provincial, state and local governments as well as many individuals.

Shale gas revolution has already started to change the balance of the world economy. Competitiveness indexes of the large producers such as the U.S. and Canada are improving """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""22"EIA, IEA figures; Morse, Edward, L.,ibid."

23"http://www.treasury.gov.tr/default.aspx?nsw=QQl5h+br0ZErvDuyH2bTyg==-SgKWD+pQItw=&nm=853""

24 Morse, Edward, L.,Citi Resarch paper, ibid. 25 Morse, Edward, L., Foreign Affairs, ibid. 26 Yergin, Daniel, ibid. 27 Morse, Edward, L., Foreign Affairs, ibid.

9"

"

dramatically. Especially it gives the U.S. a huge advantage. Less expensive natural gas is fueling manufacturing boom in these countries as entrepreneurs are less concerned about the energy prices to make or expand their investments on new facilities such as chemical, steel, and aluminum plants.

The costs of finding and producing oil and gas in shale and tight rock formations are steadily going down and will drop even more in the future. The future price of natural gas will be determined by the cost of extraction, not by the size of the supplies of gas found, as was the case with conventional natural gas. Prices, in the long run will further fall as the new innovation and experience continues to lower upfront investment costs and improve productivity at the wellhead. Additional future technological advances and new perfected techniques not yet applied to downstream activities such as in the transportation and distribution sectors as well as consumer markets, implementation and efficiency improvements will generate billions of dollars more in savings which will further feedback and sustain the growth in the industry. Therefore positive spillover effects over economic growth in emerging and new producing countries will be more evident than ever.

Geopolitical impacts; Winners-Loosers and beyond What is unfolding after the shale gas revolution in North America, is a paradigm shift in thinking about energy geopolitics and hydrocarbon industry. Not many years ago, there was almost a consensus among the experts that U.S. hydrocarbon production was in decline, OPEC production was on the rise and non-OPEC increase was not living up to the earlier promises. Today, it is crystal clear that the U.S. and Canadian production will only rise for decades to come and will be sustainable.

Mostly secure and diversified supply-driven myth of energy independence now perceived as more a reachable goal than ever. The shale boom will not only enhance America’s energy security particularly, but will render a potential to strengthen its unipolar primacy by increasing supplies and lowering energy prices, in return boosting a U.S. economic recovery while liberating the U.S. from the obligation to work and do business with uncooperative hydrocarbon powers by taking market share and significant volumes from them and cutting their vital hydrocarbon export revenues.

For instance, by 2020, the U.S. will be a net exporter of natural gas, on a scale potentially rivaling both Qatar and Russia, and the consequences will be enormous. Not long ago Russia was consulting with Iran and Qatar other two largest gas producers of the world for securing and controlling the high enough prices for gas and hopefully establishing Organization of Gas Exporting Countries (OGEC) in a similar fashion like OPEC. Now that is no more feasible. Furthermore Russia’s other attempt to form an” international energy club” under Shanghai Cooperation Organization (SCO)28 mechanism motivated by coordinating energy cooperation, """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""28On 26 October 2005, during the Moscow Summit of the SCO, the Secretary General of the Organisation said that the SCO will prioritise joint energy projects; such will include the oil and gas sector, the exploration of new hydrocarbon reserves, On 30 November 2006, at The SCO: Results and Perspectives, an international conference held in Almaty, the representative of the Russian Foreign Ministry announced that Russia is developing plans for an SCO "Energy Club. "The need for this "club" was reiterated by Moscow at an SCO summit in November 2007. Blagov, Sergei, “Russia Urges Formation of Central Asian Energy Club,” Eurasianet.org, November 6, 2007. http://www.eurasianet.org/departments/insight/articles/eav110707a.shtml";"

http://en.wikipedia.org/wiki/Shanghai_Cooperation_Organisation""

10"

"

enlarging domestic market opportunities and financing these projects along with national, mutual and regional interests. The shale gas revolution forces strategists and proponents of both initiatives to think twice.

Therefore, beyond the U.S. and Canada, the spread of shale gas revolution and tight oil exploitation will have geopolitically immense implications. There is no longer any debate about the proportions of the new resource potential and its clear multifaceted benefits, and that reality is motivating many governments to expedite the capacity building to develop commercially available resources. In the geopolitics of energy, there are always winners and losers. This time though shale revolution will create its own winners and loosers. !

Chart!1:!!World!Shale!Resources29!

Many countries are already trying to duplicate the North American success in the sector. Depending on many factors though, perhaps many will succeed. “U.S. recoverable shale resources constitute only about 15 percent of the global total. That means the same shale promise, even more so, applies for the rest of the world.”30 Several nations have begun to evaluate and test the production potential of shale formations located in their countries. Poland, for example, has leased prospective shale acreage and drilled 43 test wells as of April 2013. Argentina, Australia, China, England, Mexico, Russia, Saudi Arabia, and Turkey have begun exploration or expressed interest in their shale formations.31 It is highly likely that these countries will see meaningful production before the end of this decade or so."As a result, global energy trade and supply chain will be dramatically changed and redistributed.

The market impact of shale resources outside the United States will depend on their own production costs and volumes. In many cases, even significantly smaller differences in costs, well

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""29"These shale oil and shale gas resource estimates are highly uncertain and will remain so until they are extensively

tested with production wells."30 Morse, Edward, L.,ibid. 31 http://www.eia.gov/todayinenergy/detail.cfm?id=11611""

11"

"

productivity, or both can make the difference between a resource that is a market game changer and one that is economically irrelevant at current market prices.32 In addition, to help projecting the impact of shale gas and unconventional gas for the rest of the world, it requires addressing a series of fundamental questions; How large is the shale gas resource base?; Where are the high quality (“hot spot”) shale gas plays? And will the shale gas resource be developed in an environmentally sound way?33 Map 1: World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the U.S.34

Potential impact on the Middle East:

It is no secret that there is a rising anxiety in the Middle East that a shale revolution and sudden jump in US oil and gas production will result in U.S. disengagement from the Middle East. But this overstatement overlooks the real impact of the oil imports from the Middle East on the U.S. policy. This amount is for a long time insignificant compared to other sources (such as Venezuela). Even before the revolution, the Middle East provided only about 10% of total U.S. supply. In other words direct oil imports do not shape U.S. policy toward the region. In addition drive for fuel efficient car industry will further reduce these imports anyway. It is obvious that the U.S. will still import oil from foreign suppliers for foreseeable future, however more of it, no matter the lively environmentalist debate over Keystone XL or safety of rail shipments, will come from Canada.

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""32"http://geology.com/energy/world-shale-gas/ "

33"“Economic and Market Impacts of Abundant International Shale Gas Resources,” a presentation by Vello A.

Kuuskraa, President of Advanced Resources International, Inc. prepared for and presented at CSIS, Washington, DC, May 5, 2011.""34"US Energy Information Administration (EIA), "World Shale Gas Resources: An Initial Assessment of 14 Regions

Outside the United States" US Department of Energy, April 2011 ; http://geology.com/energy/world-shale-gas/ "

12"

"

In other words it was not the oil imports from the region that helped define US strategic interests in the Middle East, but rather geopolitical turmoil in the Middle East would have direct impact on price of oil (impact of NATO’s recent Libya operation over the price of oil is case in point) and that would ultimately effect the global economic performance and world politics in general. Put differently, America’s interest in stabilising energy interdependence has been embodied in its commitment to defend the free flow of Persian Gulf hydrocarbons to global markets. But the U.S. interest in Persian Gulf oil, has never been primarily about its own energy demand.

It was very costly too: keeping substantial military forces on the ground in the region after the first and second Gulf Wars; Occupying Iraq for years and maintaining international sanctions on Iraq (both wars and sanctions killed over a million Iraqis), and Iran, imposing them on third-country entities transacting with these countries.

Therefore any conclusion that shale revolution will grant the U.S. energy independence is misguided. Even if the most optimistic projections of shale gas and oil production are realized, U.S. energy companies will and should engage in global energy markets. Responsibility of a great power requires and serves the world energy security better by engaging in visionary and strategic diplomacy with other important global and regional actors and allies.

The Middle East will continue to be an arena of great geopolitical importance, and its oil will be essential to the functioning of the global economy. If for nothing else the U.S. the world’s only super power will be engaged in the Middle East for basically two reasons:

a) Security of Israel and b) not to let anyone else to control the politics of the wells in the region. It is about the ability to control who gets access to the Middle East oil.

This clearly shows that the region will remain as one of the vital strategic interest for the U.S.

The other argument that is also being used for the continuing importance of the Middle East for the U.S. is that: There are skeptics about America’s shale oil increase. The IEA projects that U.S shale oil production will peak by 2020, plateau for a few years, then decline.35 Since U.S. conventional oil production continues declining, as does Gulf of Mexico production. After a decade or so, shale oil won’t keep overall U.S. oil production from ultimately declining. Thus, the world will continue seeking the Middle East oil over the long term. Only time will show the validity of this argument.

For specific countries shale revolution will have mixed impacts:

For Saudi Arabia, developing power plants using domestic shale resources and the exploitation of its shale resources means freeing up more oil for exports, sustaining if not increasing revenues which is crucial for functioning overall economy of the country. However, how much the impact of the shale revolution over the price of oil will be absolutely important for the future of Saudi Arabia. Oil below $80-90 dollars range could have serious negative impact over the functioning of the Kingdom. """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""35http://www.eia.gov ; http://www.eia.gov/todayinenergy/detail.cfm?id=13251

13"

"

One positive impact can also be seen by the increase in U.S. oil production over the last couple of years is that this trend is tempering down the maximalist demands of Iran in nuclear talks. Argument can be made that sanctions forced and created more positive incentives for Iran to return to the negotiating table seriously which it was unwilling to do until recently. Russia: Russia is believed to hold one of the world's largest oil-bearing shale formations: with an estimated 75 billion barrels of recoverable tight oil (50 percent more than the United States), production growth spells more government revenue. And for a host of other countries, the motivations range from reducing dependence on imports to increasing export earnings to enabling domestic economic development. But the industry has lagged behind America in its embrace of horizontal drilling and hydraulic fracturing to get at the oil and gas.36 The pricing basis and the amount of natural gas that can be sold in a spot market will be two key factors that will effect countries like Russia. Most LNG trade links the price of natural gas to the price of oil. Which many countries and potential producers and more importantly oil companies started to challenge. Many argue that they should be calculated separately and the trajectory of the shale revolution supports this idea. “The shale gas revolution has already delinked these two prices in the U.S., where the traditional 7:1 ratio between oil and gas prices has exploded to more than 20:1. That makes LNG exports from the United States competitive with LNG exports from Qatar or Russia, eroding the oil link in LNG pricing.”37

In addition, spot market potential is immense with shale gas development. Traditional LNG contracts are tied to specific destinations and cannot be traded to third parties. LNG that is quickly being developed with huge investments mainly in Canada and Australia and elsewhere will quickly boost the spot market. Even it affects the established LNG exporters very quickly. For instance, for Japan, the eroding US demand for LNG from Qatar proved fortunate in the aftermath of the disaster at the Fukushima nuclear-power plant in 2011. Much of that LNG now goes to Japan to generate power. New LNG exports available to Europe and East Asia from the U.S. and Canada will ultimately diminish the Gazprom's grip on markets and pricing. This spot market supply will ultimately bring down prices of natural gas around the world.

Currently, European countries overwhelmingly depended on Russian gas supplies. 6 out of 28 member countries of the EU depend on these supplies 100%. Dependence rate in key transit countries such as Turkey and Ukraine is well over 50%. And many worry about the use of gas supplies as a political weapon. So developing shale potential is also considered a national security issue for these countries.

Caspian frontier: Shale revolution will also have an impact on new hydrocarbon frontiers such as the Caspian basin. Before the change started, many IOCs focused primarily on finding new oil reserves, invested their capital in mega projects and challenging fields such as the Kashagan field, in Kazakhstan, which is the largest oil find in the world for the last 40 years. However, its phased development and immense magnitude of challenges to develop, already scared of some major consortium leader companies. Besides, resource nationalism, mainly inspired by the Russian """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""36 Morse, Edward, L., ibid. 37Ibid.

14"

"

practices over BP-TNK and Shell, shaken the legal contractual basis of the project many times causing years of delay to start even the first phase. Now, IOCs having abundance of alternative shale resources, countries like Kazakhstan which tried to abuse the host country’s position, are now less powerful in terms of negotiation positions vis-à-vis IOCs. Resource countries in need of exploration and development investment, should better observe the contractual commitments previously made or risk losing the development potential all together. China:

Desperate in energy supplies to keep up high growth rates for its economy China with the world's largest recoverable shale gas reserves, over 1,200 tcf, more than the U.S. and Canada combined, also gives a high priority on developing its abundant shale gas potential.38 China sees an essential opportunity to mitigate growing public discontent, health and image problems vis-à-vis bad record on carbon emissions and climate change, stemming from the heavy urban air pollution, by replacing environmentally hazardous coal with natural gas in power generation. However lack of technology and innovation to make significant contribution yet keeps the country vulnerable to classical hydrocarbon geopolitics. Therefore the country still seeks opportunities to seize, like talks of over $400 billion deal with Russia after Ukraine crisis and makes investments in nearby gas reach countries of Central Asia such as Turkmenistan. OPEC: Following the shale revolution OPEC will be among the loosers in the new geopolitics of global energy. As the U.S. moves from having had a net hydrocarbon trade deficit of some 9 m barrels per day in 2007, to having one of under 6 m barrels today, to enjoying a net positive position by 2020.39 Loosing market share and incrementally lower prices could pose a big challenge to oil producers heavily dependent on exports for easy revenue. Growing populations and declining per capita incomes because of oil curse or dutch disease are already playing a central role in triggering domestic upheaval in Iraq, Libya, Nigeria, and Venezuela. Therefore the future does not look bright for those countries. So, the shale revolution will likely lead an end to OPEC's decades long dominance over price well above the production costs since 1970s. This vicious circle and maneuvering ability to arrange desired prices with adverse consequences to the world economy could not be broken until now. World energy geopolitics tied to a vision of a single North American energy market

Shale gas revolution can only reach to the rest of the world if North America creates successful single energy market and shares its experiences and know-how with the rest of the world. The North American energy trade is $65 billion annually between the U.S. and Mexico and over $100 billion annually between the U.S. and Canada.40 Canada and US hold an estimated 1,238 Tcf +

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""38 http://geology.com/energy/world-shale-gas/ 39 Morse, Edward, L., Foreign Affairs, ibid. 40 Beyong energy the NAFTA countries economic and trade scale is immense:“the three countries constitute around one-fourth of global GDP, and they have become each other's largest trading partners. Particularly notable is the integration of trade. A 2010 NBER study shows that 24.7% of imports from Canada were U.S. value-added, and 39.8% of U.S. imports from Mexico were U.S. value-added. (By contrast, the U.S. value-added in imports from China was only 4.2%.) This phenomenon of tight integration of trade stands apart from other major trading blocks including theEuropean Union or East Asian economies… The three Nafta countries together account for $6.63

15"

"

59 billion barrels of recoverable shale resources.41 And only the US and Canada have currently added significant volumes to their national production from shale reservoirs.

The above picture and shale-energy revolution necessitates all three countries, but more urgently the U.S. and Canada should lay down foundations of creating single energy market in North America. However, this vision remained illusional and national energy policies have proven to be dysfunctional in both countries. Part of the problem in Canada stems from the provincial-federal debate and political peculiarities of the state structure which apparently works against producing policies to develop and implement new pipeline connectivities and completion of the existing ones. A unified energy policy could materialize export of 4-5 bcm gas to the U.S. from Canada in a couple of years.42

Key drivers in realizing shale revolution in the U.S. and Canada include some peculiar elements that only exist in these countries. The rest of the world must better analyze these peculiar conditions should they wish to emulate the same positive experience. This is also partly the reason why, despite the early promises in countries like Poland (Poland, with 187 tcf, has the largest shale gas reserves in Europe and France isn't far behind with 180 tcf43) and Ukraine could not live up to their potential so far.44 Those are:

- A legal system that ensures the private control of both surface and subsurface land use - open capital markets and sufficient investments - availability of services, materials and consumables - sufficient infrastructure, - favorable regulatory environment, - stable political regime

Although other places, such as China and Europe, have substantial shale resources, they don't have the entrepreneur-friendly system and elements of it mentioned above needed to develop those resources quickly and productively.

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""

trillion in total exports and imports.” Shultz, George P., The North American Global Powerhouse, The WSJ, July 11,2013, http://online.wsj.com/news/articles/SB10001424127887324637504578566192239796864 41 IEA and EIA figures: Major Canadian liquids reservoirs include the Duvernay (4 Bbbl) and Muskwa (2 Bbbl). Major US liquids reservoirs include the Eagle Ford (14 Bbbl), Bakken (15 Bbbl), and Permian basin (10 Bbbl) The application of fractured horizontal wells in Western Canada is at an earlier state than in the U.S., where most increase in gas production from artificially fractured horizontals is primarily driven by the Montney in B.C. & Alberta, and the various cretaceous plays of the Alberta basin center gas accumulations. Increases in oil production from artificially fractured horizontals are primarily driven by the Bakken and Cardium plays. More significant growth is expected as this technology is applied to shale plays like the Duvernay and Muskwa 42"Morse, Edward, L., “The Dynamic Duo: Another Year of Volatile Change,” ibid. ; Morse, Edward L., presentation

and discussion, ibid. "43 http://geology.com/energy/world-shale-gas/, US Energy Information Administration, "World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States" US Department of Energy, April 2011. 44 The other reason for early disappointments for look like promising early success stories is that: Companies have perfected their techniques in producing U.S. shale gas, and also, in the process, were able to dampen gas prices so low as to discourage more investment in new production. Some IOCs companies that followed smaller innovative independents who started the revolution in shale production are now losing money on their own abroad and mainland fields. This is the negative element into the play in many of the promising countries.

16"

"

Furthermore, the promise of the shale-energy revolution can be realized from the R&D under way at institutes, universities, laboratories and companies in North America. “Much of this research is funded by a combination of government and industry money. When good ideas do emerge, the system means that organizations are on hand that know how to scale and commercialize them. Through this R&D, North America can lead the way to a more environment-friendly outlook for the production and use of energy.”45

Canada and the U.S. elites must be very careful about their policy goals with the new revolution. The energy elites especially in the U.S. have talked about “energy independence” 1970s, around the time of the first major oil crisis. Proponents of this view portray shale revolution as a geopolitical game changer, which they say will ultimately free the U.S. from a dependence to politically hostile regions of the world for oil supplies and will be able to use its future excessive gas and oil resources to weaken unpredictable and unreliable hydrocarbon powers.

Even if more and more oil rail tankers and gas supplies come on line from Canada to the U.S. enabling the latter to sell its own resources more in LNG form to Europe, the production will still be a fraction of Russia’s oil and mainly gas exports to Europe. And since European gas prices are lower than lucrative East Asian market prices, it is virtually certain that most U.S. and Canadian LNG will go to Asia. The U.S. and Canada therefore has to devise a strategic vision to keep the balance between the market forces and geopolitical goals that they want to achieve with these abundant resources. Otherwise these uncooperative hydrocarbon forces could be much more destabilizing factor than the potential of shale resources in their respective regions.

The presumption that the U.S. demand for oil and gas imports would drop to levels satisfiable with supplies from “friendly” neighbors, rather than countries geopolitically at odds with Washington is dangerously unnecessary one. It is dangerous because it ignores the realities of today’s energy markets; it is unnecessary because it requires wrong and provocative foreign policy choices aiming at creating more adversaries and rivals than potential partners.46 Political leaders from both countries need to recognize that today North America (including Mexico through NAFTA) has an unprecedented opportunity for long-term sustainable economic growth if it is disseminated with like minded pluralistic democratic partners and allies that share the """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""45"Shultz, George P., ibid."

46 Flynt and Hillary Mann Leverett argue that about how the “shale revolution” will let the U.S. achieve “energy independence” is fundamentally detached from physical and economic reality. According to them “the proposition that attaining a mythical-yet-still-enthusiastically-sought condition of energy independence will let the United States become even more assertive toward countries determined to preserve and enhance their strategic independence—whether they are major energy exporters like Russia and Iran or major energy consumers like China—is dangerously delusional. The idea that the United States will ever export enough shale gas in the form of liquefied natural gas (LNG) at sufficiently low prices to undercut the enormous built-in advantages that an established major gas producer like Russia enjoys in gas export markets in Eurasia seems highly fanciful.” They also claim that “Pursuing energy independence, in defiance of reality in today’s oil and gas markets is counterproductive for America’s standing and influence. It is counterproductive most immediately because it reinforces official Washington’s longstanding conviction that the United States doesn’t have to engage in real diplomacy with strategic rivals—that is, diplomacy which recognises and accommodates their legitimate national interests (e.g., Russia’s interest in not having the West turn other post-Soviet states into anti-Russian platforms, or Iran’s interest in developing safeguarded but indigenously managed nuclear fuel cycle capabilities).” Leverett, Flynt & Leverett, Hillary Mann, ibid.

17"

"

same values. This potential can create further incentives to transform semi or pseudo pluralistic societies and regimes to better democratic countries. This global policy can only be achieved through the North American vision that is shared and believed first and foremost by the leaders of these countries. Interconnectedness of the national grids of the NAFTA countries through pipelines such as KeystoneXL and creating available gas and LNG ports, sustainably supplied from the west via pipelines on Atlantic seaboard of Canada are must elements of this policy. Therefore, it is a must to unleash the true potential further cross-border infrastructure and markets for crude oil, refined products, natural gas and electricity to enable the integration of both conventional and unconventional forms of energy across the region.

Also the new regulations respectful of environment being devised in the U.S. and Canada will set the standards well beyond North America. Working to reduce the emissions that accelerate climate change should be the goal that politicians, energy business leaders and environmentalists should be able to agree upon. By tirelessly seeking this kind of unlikely alliances based on common risks, stakeholders can create strong, sensible standards that reduce the risks of shale development with unconventional techniques.

North American market should adopt a balance between the price of gas and new investment costs in order to continue reap the benefits of the revolution. Otherwise costs could very well end up being higher than the declining price of gas available which will ultimately hinder the new investments. New licenses should be issued cognizant of this balance. Otherwise those who think the U.S. and Canada could be new supply base to Europe and Asia in very short period of time can be disappointed. High upfront costs mean that investors only finance projects for which there are customers committed to buying contracts for decades, at least 20 years. Therefore most of the new LNG projects with export licenses, originating from North America may never be built.

North American political and energy policy elites should adopt energy interdependence approach rather than energy independence. Working globally with key producer, consumer and transit countries to create energy interdependencies will serve better to all countries national interests. In other words will be a win-win situation for all.

The United States came out of World War II self-sufficient. It would not become a net oil importer more than a quarter century after the war’s end. Shale promise gives a second and more robust chance to North America to take advantage of this situation and strenghten their allies and than use it also towards the new frontiers such as Eurasia and the Arctic in a balanced way not to create new alienated hydrocarbon rich countries but to create more interdependencies and incentives to cooperate.

As coming out of World War II, America wanted to guarantee Middle East oil flows to Western Europe and Japan, because it was absolutely essential to their post-war recovery, now again vibrant, cheap, secure and diversified supply through shale abundance to emerging economies of the world will also prove critical to the U.S. and Canada’s own long-term economic and trade diversification and prospects. In a broader context, should the U.S. and Canada act together as single energy market and provide energy security to allies and like minded countries around the shared values or committed countries to reach these standards would secure economic and political stability in wider geographies through creating new long-term economic and security partnerships and interdependencies. For nearly seventy years this is the most real chance to

18"

"

bolster North American (and in a broader sense Trans-Atlantic-NATO’s strategic standing in other newly important parts of the world. This chance is too real and too big to be missed. Unfulfilled promise, skeptics and concerns by the emerging markets:

Skeptics mainly point out to three problems that could lead the downgrade of the effects of the revolution: environmental regulation, declining rates of production, and drilling economics.

Fredd Krupp outlines environmental damages to both air and water from shale oil and gas production, noting that hydraulic fracturing, or “fracking”47, is not the only element of the process that has raised environmental concerns. He also notes that shale gas production can release the greenhouse gas methane in significant quantities including through leaks, contributing to climate change. He discusses technologies for reducing methane emissions from gas wells. Topics include Colorado's oil and gas production regulations and the impact of the surge in U.S. petroleum production on the development of renewable energy sources.48 Hydraulic fracturing poses potential environmental risks, such as the polluting of underground and surface water resources, the spilling of oil or gas or hazardous material into the nature during the transportation phase and triggering of seismic activity. All these risks must be mitigated more effectively should we live up to true potential of the revolution. More effective mechanisms to share the best practices are needed. More importantly the industry should be more vocal in this message and should lead the way itself. Otherwise local restrictions and excessive regulations (as in the case of New York and Pennsylvania, France and Germany) would slow the revolution even has the potential to halt it.49 As for declining rates of production, the accumulation of fracked wells with a long tail of production is building up a durable base of flows that will continue over time, and the economics of drilling work in favor of drilling at a high and sustained rate of production. Finally, some questions the economics of hydraulic fracking, but these concerns have been unproven. It is true that through 2012-13, the upstream sector of the U.S. oil and gas industry has been massively spending more than it earned. But the costs were driven by the need to acquire new land for exploration and to pursue unproductive drilling in order to hold the acreage until the later development. Now as some argue that markets at least in North America becoming “mature,” the industry's cash flow should be increasingly positive in coming years.50

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""47 Hydraulic fracturing, or "fracking"- the process of injecting sand, water, and chemicals into shale rocks to unlock them open and release the hydrocarbons trapped inside. 48 Krupp, Fred, Don't Just Drill, Baby--Drill Carefully. Foreign Affairs, May2014, Vol. 93 Issue 3, p15-20. 6p. 49 “Such is the case in Europe, where the problem is magnified by a hyperactive green movement determined to block the development of shale gas. France has banned fracking entirely, and Germany has put a de facto moratorium in place. Without a massive change in attitude, Europe will take even longer than China to develop its shale gas resources. Even if it does develop them, the results will be less robust and very slow in coming.”; “New York State, which sits atop the Marcellus Shale, a rock formation that extends through Pennsylvania to West Virginia and holds an estimated 141 tcf of recoverable natural gas, imposed a statewide moratorium on fracking in 2010. Last year, in Colorado, the cities of Boulder and Fort Collins voted to ban fracking for at least five years, and nearby Lafayette prohibited all new oil and gas wells. Similar efforts are under way in other states, including California. In 2011, France declared its own moratorium on fracking; after its 2013 election, the German government did the same, pending an environmental risk assessment.” Krupp, Fred. Ibid. 50 Krupp, Fred, ibid.

19"

"

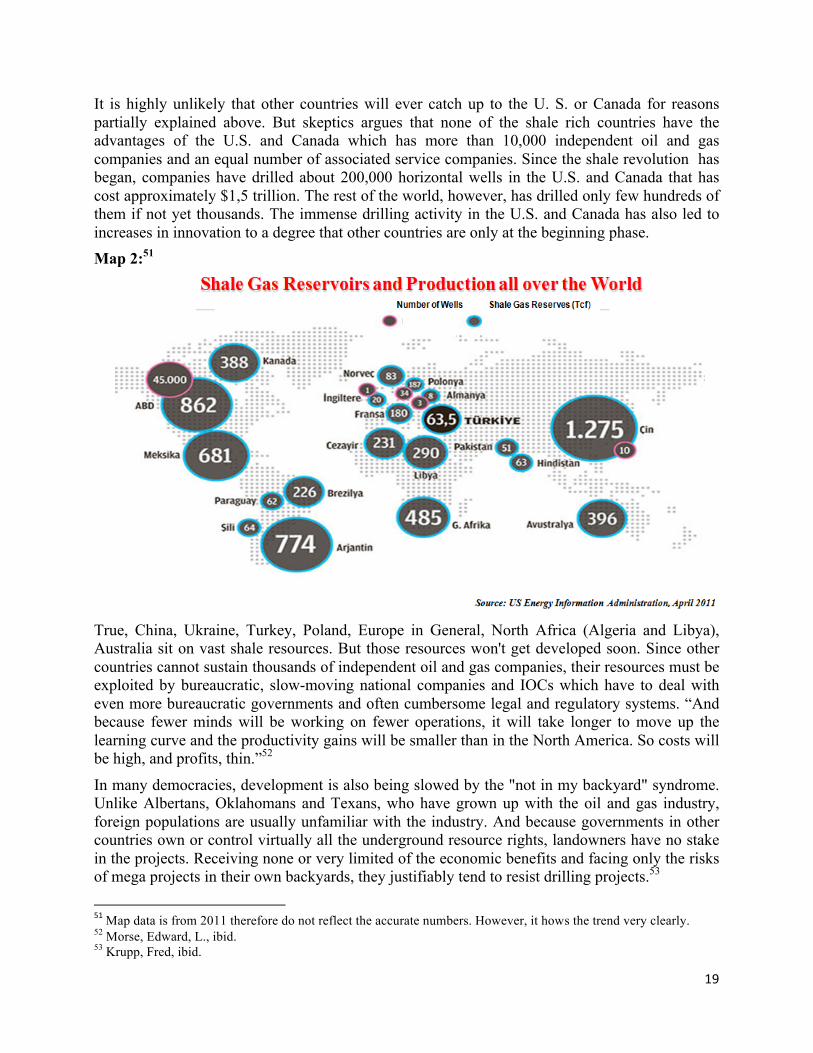

It is highly unlikely that other countries will ever catch up to the U. S. or Canada for reasons partially explained above. But skeptics argues that none of the shale rich countries have the advantages of the U.S. and Canada which has more than 10,000 independent oil and gas companies and an equal number of associated service companies. Since the shale revolution has began, companies have drilled about 200,000 horizontal wells in the U.S. and Canada that has cost approximately $1,5 trillion. The rest of the world, however, has drilled only few hundreds of them if not yet thousands. The immense drilling activity in the U.S. and Canada has also led to increases in innovation to a degree that other countries are only at the beginning phase. Map 2:51

True, China, Ukraine, Turkey, Poland, Europe in General, North Africa (Algeria and Libya), Australia sit on vast shale resources. But those resources won't get developed soon. Since other countries cannot sustain thousands of independent oil and gas companies, their resources must be exploited by bureaucratic, slow-moving national companies and IOCs which have to deal with even more bureaucratic governments and often cumbersome legal and regulatory systems. “And because fewer minds will be working on fewer operations, it will take longer to move up the learning curve and the productivity gains will be smaller than in the North America. So costs will be high, and profits, thin.”52

In many democracies, development is also being slowed by the "not in my backyard" syndrome. Unlike Albertans, Oklahomans and Texans, who have grown up with the oil and gas industry, foreign populations are usually unfamiliar with the industry. And because governments in other countries own or control virtually all the underground resource rights, landowners have no stake in the projects. Receiving none or very limited of the economic benefits and facing only the risks of mega projects in their own backyards, they justifiably tend to resist drilling projects.53

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""51"Map data is from 2011 therefore do not reflect the accurate numbers. However, it hows the trend very clearly."

52 Morse, Edward, L., ibid. 53 Krupp, Fred, ibid.

20"

"

Shale gas revolution has yet to reach emerging markets

Why shale gas revolution did not affected so far the emerging markets? One of the reason for that is hydrocarbons themselves are cheap: a barrel of oil (even priced over $100) is cheaper than equal volumes of any other liquid on the planet—milk, Diet Coke, shampoo, even water. This makes it very hard to displace crude oil and other hydrocarbons—and explains why demand-based visions of energy independence have had no strategically meaningful impact on the global energy balance.54

In the second half of this decade, however, the revolution is likely to spread globally more quickly than most think.

Edward Morse indicates that traditional finding and development costs indicate that natural gas prices need to be above $4 per thousand cubic feet and oil prices above $70 per barrel for the economics of drilling to work -- which suggests that abundant production might drive prices down below what is profitable. But as demand grows for natural gas -- for industry, residential and commercial space heating, the export market, power generation, and transportation -- prices should rise to a level that can sustain increased drilling: the $5-$6 range, which is about where prices were this past winter. Efficiency gains stemming from new technology, meanwhile, are driving down break-even drilling costs. In the oil sector, most drilling now brings an adequate return on investment at prices below $50 per barrel, and within a few years, that level could be under $40 per barrel.55

The U.S. government has so far approved five applications for LNG export projects, with another nineteen pending. But it is far from clear how much U.S. gas will actually be available for export in coming years. Companies are much more keen to supply domestically and near by markets such as Mexico rather than emerging markets such as to some G20 countries poor of energy. Countries like Turkey, 16th largest economy in the world according to IMF figures was unable to secure just 2bcm contract to be operational 7 years from now. Besides unknowns about the regulatory regime is also hindering the potential to reach out to emerging markets for the global economic prosperity. Also not decreasing prices of oil and gas as would have been expected increases the frustration. Probably oil base pricing and geopolitical upheavals in the so called “Arab Spring countries,” and readily available customers such as Japan to soak all the excessive LNG otherwise would have been floating in the spot markets such as from Qatar, are the factors that also contributes to this frustration.

Another key factor for emerging economies is that the regulatory regime must fulfill certain criteria and should be applicable and transparent to all such as:

- Tariff regime: Principles of the tariff-regime must be global & shared by all. - Transparency: All criteria and procedures should be made public. - Stability: Concerned parties should face the least possible regulatory uncertainty. - Simplicity: In both methodology and tariffs, in so far as possible - Non-discrimination: Non-discrimination among equal parties secured through Third Party

Access (TPA). - Cost-reflectiveness: Costs not directly related to market operations should not included.

Cross-subsidies should not be allowed. """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""54 Krupp, Fred, ibid. Morse, Edward, L., ibid. 55 Hefner III, Robert A. The United States of Gas, Foreign Affairs. May2014, Vol. 93 Issue 3, p9-14. 6p ; Morse, Edward, L., ibid.

21"

"

Enironmental concerns must be addressed:

With the scale of the shale production boom more and more people are expressing concern about the environmental problems associated with the shale gas and oil production with new techniques. These concerns ranging from the contamination of drinking and natural (underground and surface) water reservoir from the spills, local air pollution from drilling sites, noise and dirt/waste/dust from sites of development. Until recently, many people assumed that natural gas would be good for the environment. The assumption holds that unlike coal-fired power plants, natural-gas-fired ones would unleash negligible amount of hazardous air pollutants such as mercury and sulfur dioxide. However recent studies show that producing natural gas can negatively impact the environment in a multiple ways: by releasing methane56, by contaminating water resources especially with poor implementation of the well techniques.57 Not only that there is a danger that if cheap natural gas hype continues that might discourage investments in zero-carbon renewable sources of energies such as solar, wind and geothermal. Therefore, renaissance in the gas industry by shale development must not cast doubt on the transition to much needed mix of renewable energy resources. Despite all the direct and indirect benefits for the economy, the public opinion is far from convinced about the environmental risks of shale development. The Pew poll conducted in September 2013, shows that public opinion is divided and more on the negative side of the debate. In that study about 50 percent of respondents opposed fracking technique, whereas about 45 percent favored it.

No one can say with certainty how much methane is actually leaking from wellheads, processing plants, pipelines, and other natural gas facilities.58 One thing is certain this issue must be addressed. The new emissions controls and measures such as shift to lower-emitting equipment in wells and valves and strict mandate to monitoring and repairing the equipment could reduce unintended methane leaks. Industry must take the lead and invest in those measures before even mandatory regulations. A collaboration and cooperation on voluntary basis among the companies, environmental groups, and local communities, governments and various stake holder organizations can inspire regulators to impose effective environmental auditing standards/certificates to improve climate, water and waste management techniques by environmentally friendly ways.

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""56"A greenhouse gas that has high negative impacts on climate change. Unburned methane is a particularly powerful.

It is dozens of times as potent a greenhouse gas as carbon dioxide. "57"In a 2011 study, the Ground Water Protection Council, an association of state regulators, concluded that the gas

industry, through poor well construction and surface spills, had directly caused groundwater contamination in Ohio and Texas. Krupp, Fred, ibid."58"One third of the methane leakes in the U.S. in to the atmosphere comes from the oil and gas development sites.

The U.S. Environmental Protection Agency estimated in 2012 that total methane emissions in the United States from the natural gas supply chain represented 1.5 percent of all U.S. natural gas produced, meaning that 1.5 percent of the gas was lost through emissions. But that number may understate the true level: a 2013 Harvard study found that total U.S. methane emissions could be 50 percent higher than the EPA'S estimate. Krupp, Fred, ibid.

22"

"

Although these voluntary efforts by industry leaders can help improve the situation, ultimately only strong regulatory regime enforced by a legal system can fully address the wider public confidence issue in new techniques and shale promise.

To summarize, such regimes should ensure at least standards to: - reduce land use impacts - reduce water use and disposal59 - limit and capture methane emissions - assure environmentally safe wells and hydraulic fractures

On the other hand, make no mistake that shale gas will never be the solution to global climate change. But it can be part of the solution in a number of ways:

- by helping to reduce the use of high-carbon poor quality coal like lignite in the U.S., Canada, and perhaps in China, Europe, and other places that have similar dilemma. - by reducing emissions of climate pollutants with best practices it could earn valuable time to allow indigenous communities and wildlife biodiversity a chance to adapt.

If these serious problems associated with shale development can be resolved and improvements on environmental ground are made, the future of the shale revolution can grove healthier for all stake holders. And this responsibility falls upon mostly to the U.S. and Canada since the other countries with large shale gas reserves are likely to follow the lead in developing them, so the regulations in the U.S. and elsewhere in Canada (especially in Alberta and British Columbia) will set the bar well beyond North American borders.

Conclusion:

In this paper, the aim was not to identify exactly what will be the geopolitical consequences of the shale revolution in the U.S. and Canada in a wider global context, neither the goal was to declare the winners or losers. The people and the market that the industry is operating is making those decisions as we discuss. Rather, by attempting to touch on some broader issues associated around these grand topics, the idea is to stimulate more research and debate among scientists, politicians, leaders, policy makers and implementers to think more thoroughly on what will be the future choice of energy and related security issues, how and why.

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""59"“Development of the shale gas includes many unique challenges, including water availability and water disposal.

For developers to be successful, they must create innovate solutions to developmental challenges associated with supplying the necessary volumes of water for hydraulic fracturing. For example, Chesapeake Energy is constructing a 500 acreHfoot reservoir to hold water from the Little Red River for Fayetteville development. Currently, hydraulic fracturing flowHback water is being transported to a permitted land disposal facility, a disposal well or recycled for other hydraulic fracturing treatments. As more wells are drilled and development increases, it is anticipated that companies will continue designing leading edge technological solutions to water availability and disposal including expanding the volume of water that is reHused.” For further discussion: Arthur, J. Daniel & Bohm, Brian, “Evaluating the Environmental Implications of Hydraulic Fracturing in Shale Gas Reservoirs,” http://www.all-llc.com/publicdownloads/ArthurHydrFracPaperFINAL.pdf "

23"

"

The unconventional energy trend has already impacted energy, geopolitics, and national security. Energy futures and new energy geopolitics will be affected, raising the question: what might the geopolitical security implications be?

In short, it now looks as if shale-energy revolution is the biggest reality of the twenty-first century energy trends that has just translated the quest for plentiful, sustainable, cost effective environmentally friendly energy to fuel sustainable global economic growth to shape up the new world order.

Overall, however, the shale-energy revolution does provide a new source of power and resilience to the U.S. and to lesser extent Canada and gives unique chance to enhance America’s position and ideals in the world. That would very much depend on how transparent and willingly the U.S. and Canada would be able to create interdependent energy market first among themselves and later with broader global partners such as emerging economies who would be more willing to act around the shared values of the humanity. On another point, the shale-energy revolution, once again shows how technology and innovation can change the balance of global economic and political power and reshape the new world order. References:

- Arthur, J. Daniel & Bohm, Brian, “Evaluating the Environmental Implications of Hydraulic Fracturing in Shale Gas Reservoirs,” http://www.all-llc.com/publicdownloads/ArthurHydrFracPaperFINAL.pdf

- Canada and the United States: Energy Partners, video by Connect2Canada , published on June2, 2014 on http://www.youtube.com/watch?v=m9UjtnFPdZk

- Blagov, Sergei, “Russia Urges Formation of Central Asian Energy Club,” Eurasianet.org, November 6, 2007. http://www.eurasianet.org/departments/insight/articles/eav110707a.shtml;"

- “Economic and Market Impacts of Abundant International Shale Gas Resources,” a presentation by Vello A. Kuuskraa, President of Advanced Resources International, Inc. prepared for and presented at CSIS, Washington, DC, May 5, 2011.

- Goldenberg, Suzanne, US surpasses Russia as world's top oil and natural gas producer, theguardian.com, October 4, 2013. http://www.theguardian.com/business/2013/oct/04/us-oil-natural-gas-production-russia-saudi-arabia

- Hefner III, Robert A. The United States of Gas, Foreign Affairs. May2014, Vol. 93 Issue 3, p9-14. 6p - http://geology.com/energy/world-shale-gas/ - http://www.eia.gov/todayinenergy/detail.cfm?id=11611 - http://www.eia.gov/todayinenergy/detail.cfm?id=13251 - Krupp, Fred, Don't Just Drill, Baby--Drill Carefully.Foreign Affairs, May2014, Vol. 93 Issue 3, p15-20. 6p. - Leverett, Flynt & Leverett, Hillary Mann, America’s Shale Revolution and the Dangerous Myth of Energy

Independence, The World Financial Review,May 28, 2014. http://www.worldfinancialreview.com/?p=1820

- Morse, Edward, L., Welcome to the Revolution, Foreign Affairs. May 2014, Vol. 93 Issue 3, p3-7. 5p. - ----------------------, “The Dynamic Duo: Another Year of Volatile Change,” Citi Research paper, January

2014. - ----------------------, presentation and discussion at the workshop co-organized by the Atlantic Council

Canada and Ottawa University Collaboratory on Energy, Research and Policy session at the University of Ottawa, January 29, 2014.

- Pastor, Robert A., Beyond the Continental Divide, The American Interest, Vacation (July/August) 2012. Published on June 6, 2012 at http://www.the-american-interest.com/articles/2012/06/06/beyond-the-continental-divide/

- Rose, Gideon;Tepperman, Jonathan, Power to the People, Foreign Affairs. May 2014, Vol. 93 Issue 3, p2-2. 1p.

24"

"

- Shultz, George P., The North American Global Powerhouse, The WSJ, July 11,2013, http://online.wsj.com/news/articles/SB10001424127887324637504578566192239796864

- The Impact of U.S. Liquefied Natural Gas (Agenda), Stratforvideo Published on Apr 20, 2012 http://www.youtube.com/watch?v=F4f14Hm1aVI

- http://www.treasury.gov.tr/default.aspx?nsw=QQl5h+br0ZErvDuyH2bTyg==-SgKWD+pQItw=&nm=853

- US Energy Information Administration, "World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States" US Department of Energy, April 2011.

- http://en.wikipedia.org/wiki/Shanghai_Cooperation_Organisation - Yergin, Daniel, “The Global Impact of US Shale,” Project Syndicate, January 8, 2014. http://www.project-

syndicate.org/commentary/daniel-yergin-traces-the-effects-of-america-s-shale-energy-revolution-on-the-balance-of-global-economic-and-political-power