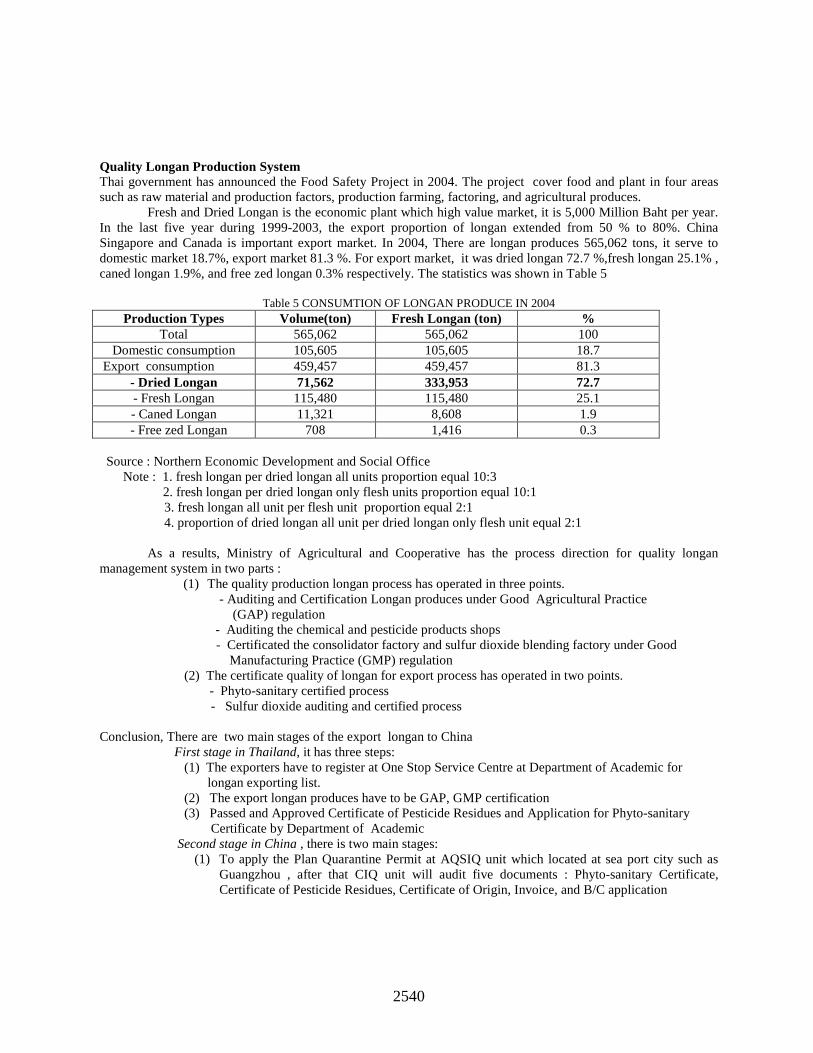

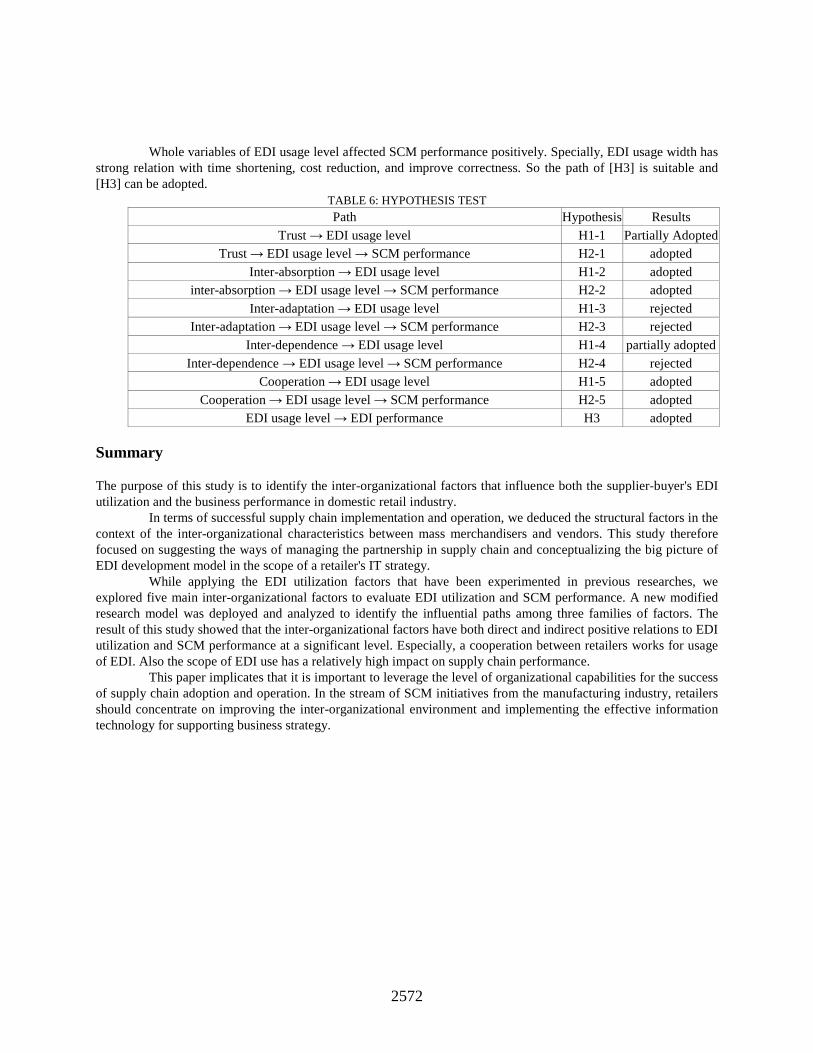

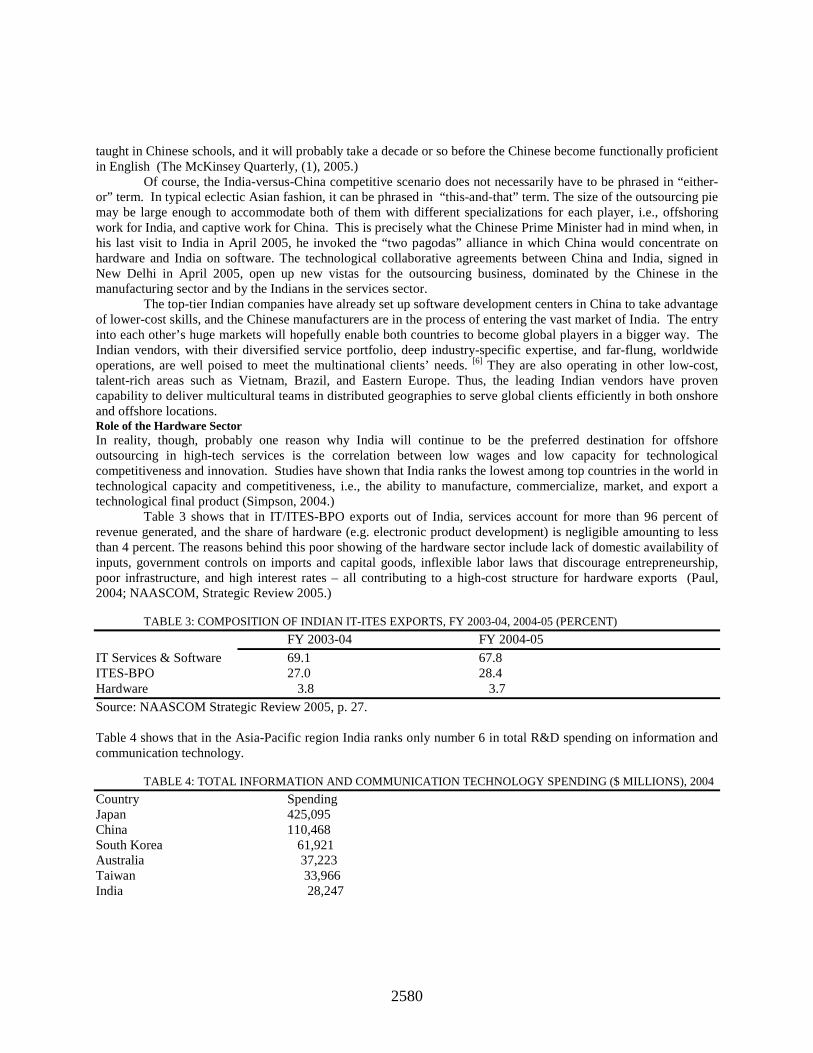

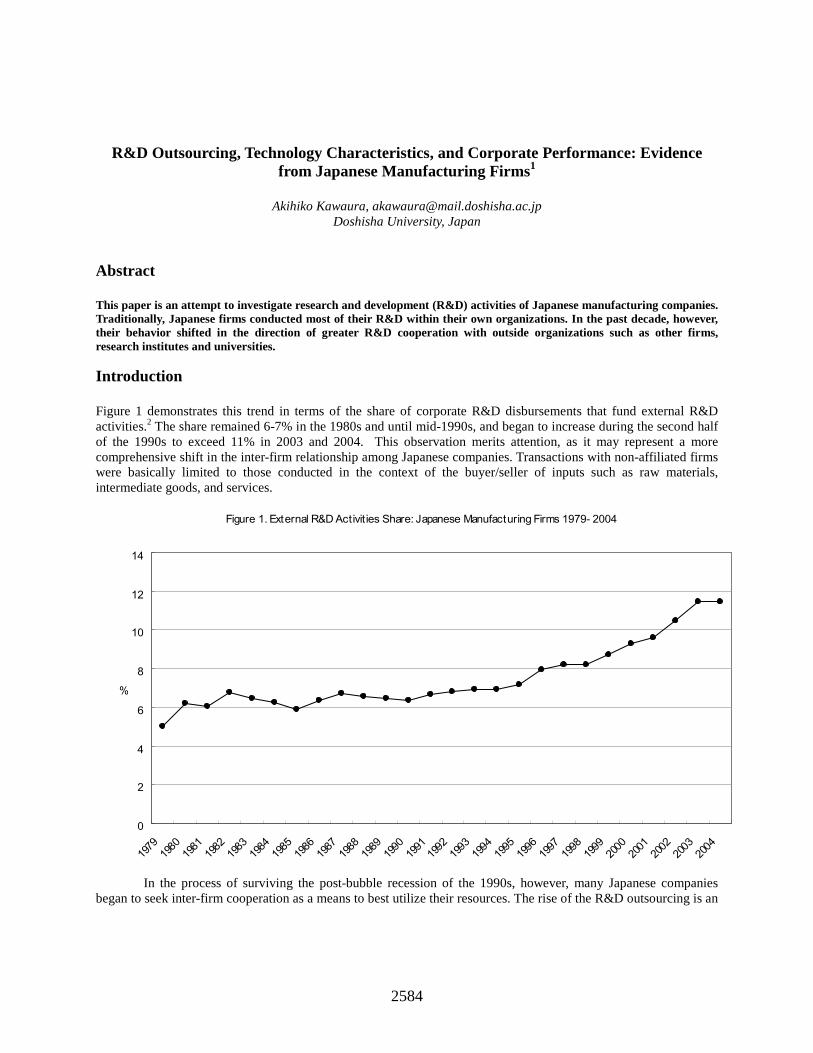

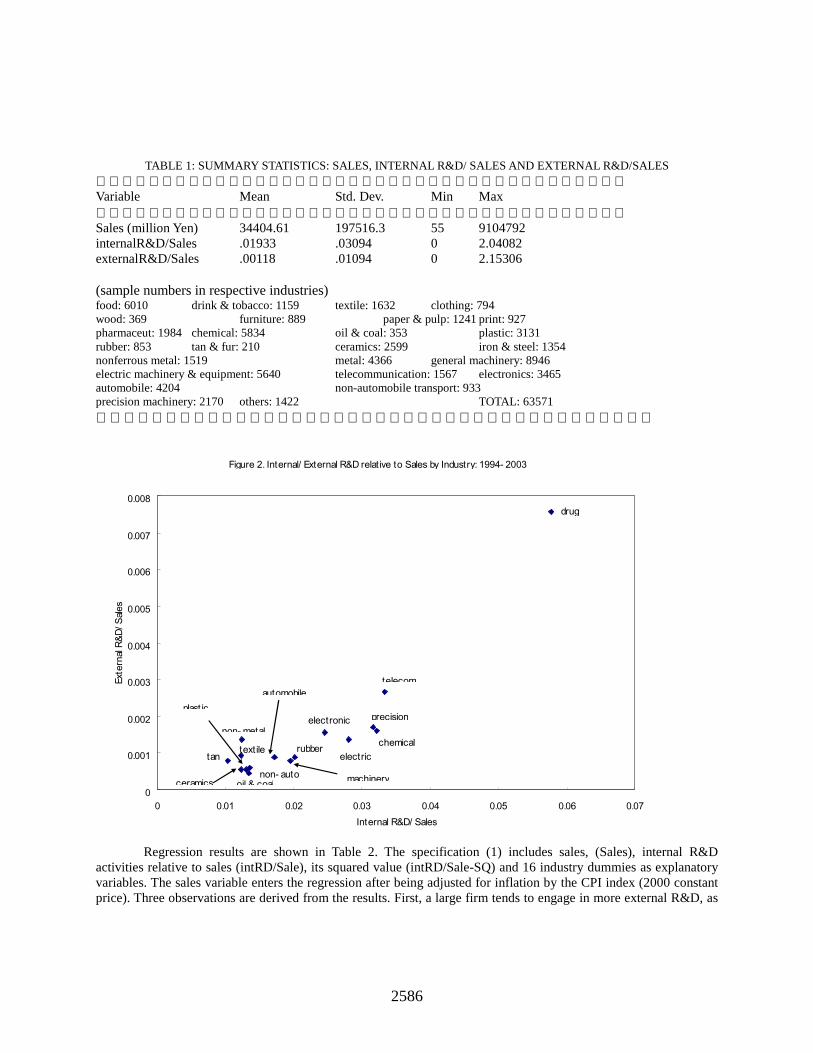

Section 10 for CD - CiteSeerX

156

2440 Criteria for Performance Evaluation of Offshore Projects – The Changing Dimensions Vasanthi Srinivasan, [email protected] Vishnuprasad Nagadevara, [email protected] Indian Institute of Management Bangalore, India Abstract As the outsourcing industry matures, there is a growing recognition that a more holistic evaluation of outsourcing performance is required. The parameters and the criteria for evaluation would change in a long-term strategic oriented outsourcing partnership. This paper attempts to examine how performance measures used by customers change during a long-term partnership. It is an exploratory study to understand the evolution of metrics in a long-term partnership from a vendor perspective. In-depth interviews were conducted with key managers from vendor organizations in India who have been in the business of outsourcing for over 20 years. The findings indicate that there has been a change in the performance metrics and evaluation criteria over the period. While these changes in criteria have evolved over time in mature partnerships, many new partners are attempting to introduce the metrics into projects at an early stage resulting in a more holistic evaluation of outsourcing. Introduction Much has been written about the phenomenal growth of the software services sector in India and its contribution to the national and the international economy. A Nasscom-Mckinsey study cites a 34% increase in software and services export from 2004-05 from $12.8 billion to $17.2 billion (Nasscom Mckinsey, 2005). This study also predicts that by 2010, the US IT and BPO off shoring market will be $ 110 billion. It is also being recognized that Offshoring and outsourcing have been a source of competitive advantage for organizations (DiRomaualdo and Gurbaxani, 1998). The theoretical justification for outsourcing initially has been the transaction cost theory. The goal of an organization is to reduce cost and achieve efficiency. In the initial stages of outsourcing, labour cost arbitrage appears to have played a significant role to propel the growth of outsourcing (Arora and Athreya, 2002). It was also found that organizations would outsource non-core, low value, routine and highly modularized activities in the initial stages. These have typically been “lift and drop” processes—simple tasks with defined interfaces that can easily be taken from one location to another. However as firms look to extract more value from outsourcing, they will need to outsource more complex processes. These processes are more likely to be more deeply embedded in organizations and may be touching up on many other internal processes and relying on multiple IT systems (Chevalier and Robertson, 2005). Evidence from research studies suggests that it is often more profitable from the client perspective to outsource projects that are more complex and strategic in nature (Gopal, Sivaramakrishnan et al, 2003). Some authors have posited through simulations that, a significant value can be gained by off shoring tasks with an “optimal level of complexity that maximizes the return from off shoring at any given time period or experience level under given situation (Gupta, Seshasai and Mukherji, 2007). This will mean that outsourcing will need to be more strategic in nature and will have to build value drivers. Given the time differences, the concept of a 24-hour knowledge factory that attempts to establish a virtually seamless relationship between the vendor and the client is a growing reality. This would necessitate high interdependencies in processes and would require fostering a climate of long-term partnership between the client and the vendor instead of maintaining an arm’s length contractual relationship between them. The relationship between the client and vendor is going beyond simple contractual obligations and deliverables. Both parties have started to invest in time, efforts and money in managing and maintaining relationships. In a study on managing outsourcing relationships dealing with essential practices for buyers and sellers, a survey of both buyers and providers of outsourcing services was done in April 2006 to better analyze the

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Section 10 for CD - CiteSeerX

2440

Criteria for Performance Evaluation of Offshore Projects – The Changing Dimensions

Vasanthi Srinivasan, [email protected] Vishnuprasad Nagadevara, [email protected] Indian Institute of Management Bangalore, India

Abstract As the outsourcing industry matures, there is a growing recognition that a more holistic evaluation of outsourcing performance is required. The parameters and the criteria for evaluation would change in a long-term strategic oriented outsourcing partnership. This paper attempts to examine how performance measures used by customers change during a long-term partnership. It is an exploratory study to understand the evolution of metrics in a long-term partnership from a vendor perspective. In-depth interviews were conducted with key managers from vendor organizations in India who have been in the business of outsourcing for over 20 years. The findings indicate that there has been a change in the performance metrics and evaluation criteria over the period. While these changes in criteria have evolved over time in mature partnerships, many new partners are attempting to introduce the metrics into projects at an early stage resulting in a more holistic evaluation of outsourcing. Introduction Much has been written about the phenomenal growth of the software services sector in India and its contribution to the national and the international economy. A Nasscom-Mckinsey study cites a 34% increase in software and services export from 2004-05 from $12.8 billion to $17.2 billion (Nasscom Mckinsey, 2005). This study also predicts that by 2010, the US IT and BPO off shoring market will be $ 110 billion. It is also being recognized that Offshoring and outsourcing have been a source of competitive advantage for organizations (DiRomaualdo and Gurbaxani, 1998).

The theoretical justification for outsourcing initially has been the transaction cost theory. The goal of an organization is to reduce cost and achieve efficiency. In the initial stages of outsourcing, labour cost arbitrage appears to have played a significant role to propel the growth of outsourcing (Arora and Athreya, 2002). It was also found that organizations would outsource non-core, low value, routine and highly modularized activities in the initial stages. These have typically been “lift and drop” processes—simple tasks with defined interfaces that can easily be taken from one location to another. However as firms look to extract more value from outsourcing, they will need to outsource more complex processes. These processes are more likely to be more deeply embedded in organizations and may be touching up on many other internal processes and relying on multiple IT systems (Chevalier and Robertson, 2005). Evidence from research studies suggests that it is often more profitable from the client perspective to outsource projects that are more complex and strategic in nature (Gopal, Sivaramakrishnan et al, 2003). Some authors have posited through simulations that, a significant value can be gained by off shoring tasks with an “optimal level of complexity that maximizes the return from off shoring at any given time period or experience level under given situation (Gupta, Seshasai and Mukherji, 2007). This will mean that outsourcing will need to be more strategic in nature and will have to build value drivers. Given the time differences, the concept of a 24-hour knowledge factory that attempts to establish a virtually seamless relationship between the vendor and the client is a growing reality. This would necessitate high interdependencies in processes and would require fostering a climate of long-term partnership between the client and the vendor instead of maintaining an arm’s length contractual relationship between them.

The relationship between the client and vendor is going beyond simple contractual obligations and deliverables. Both parties have started to invest in time, efforts and money in managing and maintaining relationships. In a study on managing outsourcing relationships dealing with essential practices for buyers and sellers, a survey of both buyers and providers of outsourcing services was done in April 2006 to better analyze the

2441

link between the value achieved through outsourcing and the effective management of the outsourcing relationship. Out of surveys of nearly 200 experienced buyers, providers and influencers of outsourcing, nearly all of them agreed that at least 10% of the annual contract value of outsourcing deals is at stake when it comes to effective relationship management. 80% of buyers and 60% of providers said that relationship management can account for 30% or more of annual contract value. Effective relationship management creates increased customer satisfaction, delivery of value added projects on time and on budget, quick response time to requests, greater innovation and thought leadership and resources freed internally to do other work. The study quotes "In fact, our study found that buyers and providers alike realized that managing complex outsourcing relationships effectively - both between the buyer and the provider, and among myriad internal stakeholders on both sides - enhances the value to both organizations. But perhaps most importantly, good relationships don't happen by goodwill alone: they require good governance structures, effective relationship management processes, skilled individuals, and more." Some authors (Goles, 2001) propose that a high vendor-client alignment, teamwork, balance of control and process agility in the relationship will lead to more successful outcomes.

The outsourcing activities, which started out of labour cost arbitrage and cost reduction, have slowly started to mature into informal strategic alliances. Drawing on the body of existing literature on outsourcing, conceptualizing it as a strategic alliance between two or more partners would provide scope for examining the nature and role of performance objectives, parameters, criteria and metrics differently. Field of Performance Management Performance management as an area of serious academic study at the firm level has gained recognition. It is often described as the “process of quantifying the efficiency and effectiveness of past actions through acquisition, collation, sorting, analysis, interpretation and dissemination of appropriate data” (Neely, 1998). Over time, the field of performance management has evolved from a measurement focus to a management focus (Otley, 1999). With the shift towards management focus, performance measurement systems based primarily on financial performance measures lack the focus and robustness needed for internal management and control (Atkinson, Waterhouse & Wells, 1997). With this changed emphasis, organizations are looking at measures that “effect positive change in organizational culture, systems and processes, by helping to set agreed upon performance goals, allocating and prioritizing resources, informing managers to either confirm or change current policy or programme directions to meet those goals and sharing results of performance in pursuing those goals “ (Amaratunga & Baldry, 2002). In the context of manufacturing outsourcing, Lee et al (2003) point out that “unlike the past the performance of an enterprise now depends much on the performance of its partners in the value chain”. We believe this comment is relevant in the context of outsourced environment, be it in manufacturing or services.

Some authors therefore propose that collaborative performance management may be the right direction in the realm of performance management (Busi and Bititchi, 2006). The outsourced environment is a “complex web of contracts, both explicit and implicit between two organizations”. The explicit contracts are often market based, short term and financial in nature, but the implicit contracts tend to rely on trust, motivation and a learning relationship to deliver intangibles such as service, flexibility and innovation (Atkinson, Waterhouse &Wells, 1997). The contracts are executed through a plethora of relationships across two organizations. These relationships are at multiple hierarchical levels and often call for planning, designing, implementing and operating structures and process which would allow for effective managing. Performance measurement in such a context is therefore not only a function of evaluation of outputs (financial and material) but also the process of collaboration. Collaborative performance according to the authors (Busi & Bititchi, 2006) would consist of the use of the following measures:

a. Extended process measures: How is the extended process performing? b. Collaborating measures: Are the enterprises able to work as a single unit? c. Collaboration management measures: Is the management of the companies providing and creating an

environment to allow collaboration to flourish?

2442

Such set of measures pose fundamental challenges for organizations: they require a deeper understanding of each other’s future strategies and plans, greater and open sharing of information and finally an understanding of the range of qualitative and quantitative measurements that would be required. Objectives of the Study As has been discussed earlier, conceptualizing outsourcing from a “strategic value adding alliance perspective”, allows an opportunity to look at collaborative performance measures to assess the efficiency and effectiveness of an outsourcing partnership. The recent literature on outsourcing has greatly hyped the role of “strategic long term value added outsourcing “. If this is the reality, then there is a need to examine whether the performance metrics have changed over time. Prior literature on control of outsourced projects (Choudhury and Sabherwal, 2003) suggests that in the initial stages of outsourcing, outcome controls and in particular output and scheduling of outputs are adopted. As the project progressed, behavior controls were introduced. Very few organizations use the self-control or clan control in the project performance assessment. While this is already happening at the level of the project, one would expect a similar trend to continue at the level of the strategic alliance.

To explore this relationship, it was decided to do in-depth interviews with heads of Quality and Customer Relationship Management in a vendor organization in India. The organization is one of the oldest IT services organizations in India and has experience of managing projects, which were as recent as a few months and also project relationships for over 20 years. The interviews focused on the following aspects:

a. What is the nature of the kinds of outsourcing relationships? What have been the dynamics? How has the relationship between the vendor and the client changed?

b. How did the projects evolve over a period in time with the long-term clients? c. What kind of metrics was being used to evaluate the effectiveness of the organization, in the initial stages

of outsourcing and now? Each interview conducted was for two hours and the above-mentioned themes were explored in an unstructured manner. The key aspects that emerged from the interviews are given below: Characteristics of the Industry Have Changed Since the early days of outsourcing, five significant shifts have happened in the industry: The shifts collectively can be described as three generations1

Characteristics First generation Second generation Third generation Period 1980’s Early 1990’s Early 2000 onwards Key decision maker Chief Information

officer Chief Technology officer

Chief Executive officer

Role of the Vendor Code delivery Project manager Business value creator Expectation from outsourcing

Cost, quality, delivery Cost, quality, delivery and functionality

Cost, quality, delivery, functionality and value add

Key influencer IT and technology personnel in house

Internal IT and line managers, IT consultants

Management consultants

In the early days of the outsourcing industry, the key decision makers in the client organizations were usually the IT departments or the Chief Information Officer.

When multiple projects with differing technologies and platforms began to be offshored, the Chief Technology officers began to play a critical role in influencing decisions, which were based on compatibility and functionality. In the last few years, it appears that the CEO’s have become the drivers of outsourcing since IT has increasingly become a driver of strategic performance and a tool for effective management reporting and control.

2443

The vendors have had to move from a functionality driven orientation to a performance driven orientation to a Value creating orientation. As one our respondents mentioned, “Most clients today outsource different modules to different vendors. The challenge for all of us is to understand inter-operability. It is inter-operability that you can bring value. It is not about being good at what you can bring to the table, but it is about being able to integrate what some one else is bringing to the table with what you have to offer”. The challenges of the transition include viewing IT as an enabler of business rather than a technology tool. This calls for a significant mind set change in the vendor organizations.

There is a need for capabilities, which are not just in the realm of technology; there is a need for increasing domain specialists who can bring value to the client beyond technology. One of the outsourcing vendor organizations started to maintain a team of experts who regularly study the client’s operations and business opportunities and advise the client on possible business strategies. In the case of the large third party vendors, there is also an expectation that since they work for multiple clients, they would be able to bring in the industry best practices in their offering. Thus, client-vendor relationship is evolving from providing service into an advisory or even a consultant’s role. The Role of Changing Metrics in the Evaluation of Outsourcing Success Given the context, the first generation outsourcing metrics broadly consisted of the number of deliverables, like design specifications, test plans, software modules, functional requirements etc), time schedules, work effort, number of service requests handled, number of defects per line of code and broad overarching customer measures related to customer satisfaction.

The second generation outsourcing metrics consisted of usability of the software by non IT users, maintainability which focused on the level of difficulty in the maintenance and support of the software and availability or uptime of the system. The perceptible shift in measures is reflective of the phase when IT was seen as a tool to increase efficiency.

The third generation metrics include all the above metrics, which have become a part of the contractual obligation of a vendor. No vendor today can be happy at having delivered on these metrics and most mature clients treat these metrics as “Business As Usual’ metrics. These metrics are taken for granted by the clients. Some of the emerging metrics in this space include:

a. Interoperability of solutions: Most large complex outsourced projects have multiple vendors. Since most vendors have acquired capabilities in niche areas, it is in the interest of the client to bring in those vendors. In this context, most clients expect the vendors to not just understand their software delivery but also the requirements of the entire software and thereby incorporate features of compatibility with other vendor software. b. Understanding the client’s customers: In recent times, a number of clients have been investing in educating their vendors on the end customer. It has led the vendor to realize that what is of utmost importance is not the client’s immediate requirement but the needs of the end customer. This has provided opportunities for many vendors to build domain expertise in certain functional areas, which are relevant to the client. The belief is that a sound understanding of the customers of the client would enable the vendor to make innovations in service delivery. The increasing domain expertise of the vendors is enabling the client organizations to invite them in to strategic conversations, which otherwise would have been internal to the client. This is one of the key indicators of a collaborative performance c. Repository of best practices: The third party software vendors are increasingly being viewed as a repository of best practice. Their domain expertise, with an understanding of the client business has meant that they are often seen as possessing greater experience on an application than the client. It is believed that the knowledge and prior experience of the vendor will result in solutions that are state of the art and are best practices in the industry. There is also a belief that the vendors would bring in solutions that would allow productivity gains and mitigate both technical and managerial risks on projects. Increasingly, contracts with incentives for “gain sharing” have been entered into between vendors and clients. d. Influencers:

2444

Mature partnerships appear to have reached a stage where the client organization in its strategic planning process invites the vendor organization to act as a sounding board for its future policies. The vendor provides information related to their own partnership and also the possible opportunities for pilot testing, research and development. The percentage of investment on new areas for exploration is gradually increasing. This is believed to be the new wave in outsourcing management.

Summary and Conclusions This exploratory study indicates that the changes in the context have impacted the outsourcing relationships and this has resulted in differing shades of engagement between the vendor organization and the client. It also appears that increasingly vendor relationships are seen as platforms for collaboration and are viewed as strategic. This has resulted in changing metrics from delivery focus to functionality focus and finally business interest focus. The move to include many process metrics beyond output metrics appears It is expected that more sophisticated metrics will evolve for measuring collaborations. In mature relationships, the trend seems to be around more holistic measurements of the partnership. Some authors (Misra, 2004) have suggested a life cycle approach to the use of metrics in an outsourcing engagement. This is consistent with our understanding of the current phenomenon. Appropriate metrics allow the parties to create conditions for successful performance.

The dominant role of IT consultants who appear to push these collaborative measurements in to early stage projects requires further exploration. Most of the third generation collaboration measures are measures of trust and a growing recognition and respect for the distinctive competencies that each party brings to the relationship. There is a need for further research on this dimension

References [1] Amaratunga, D & Baldry, D. (2002) Moving from Performance Measurement to Performance Management

Facilities, Vol. 20(5/6) 217-223 as cited in Busi M and Bititchi, Umit S., Collaborative performance Management: present gaps and future research. International Journal of Productivity and Performance Management, Vol 55(1/2) 7-26 Umit S (2006): Collaborative performance Management: present gaps and future research. International Journal of Productivity and Performance Management. Vol 55(1/2) 7-26

[2] Arora, A. and S. Athreye (2002): The software industry and India’s economic development. Information Economics and Policy, Vol. 14(2): 253-273.

[3] Atkinson, A.A, Waterhouse, J H, Wells, R. B. (1997) A Stakeholder’s approach to strategic Performance Management. Sloan Management Review, Spring, 25-37

[4] Busi, M & Bititchi, Umit S (2006): Collaborative performance Management: present gaps and future research. International Journal of Productivity and Performance Management, Vol 55(1/2) 7-26

[5] Chevalier, J & Robertson, H (2005) Offshore business process outsourcing: strategies to minimize failure in Technology and Offshore Outsourcing strategies by Brudenall, P. Palgrave London

[6] Choudhury, V& Sabherwal, R (2003): Portfolios of Control in Outsourced Software Development Projects. Information Systems Research, Vol. 14(3):291-314

[7] CMA News Hamilton (2006) Relationships everything in outsourcing: A study, Vol 80 (2): 11 [8] DiRomaualdo, A & Gurbaxani, V (1998), Strategic Intent for IT outsourcing, Sloan Management Review

Summer Vol 39(4) [9] Goles, T (2001) The impact of client vendor relationship on outsourcing success, Unpublished dissertation

University of Houston as cited in Levina, N & Ross J W (2003) From the Vendor’s perspective: Exploring the value proposition in the Information Technology outsourcing, MIS Quarterly, Vol 27 (3) 331-354

[10] Gopal, A., Sivaramakrishnan, K., Krishnan, M.S. & Mukhopadhyay, T. (2003) Contracts in offshore software development: An empirical analysis, Management Science, Vol 49(12)

2445

[11] Gupta, A, Seshasai, S, Mukherji, S (2007) Offshoring: The Transition from Economic Drivers Toward Strategic Global Partnership and 24-Hour knowledge Factory. Journal of Electronic commerce in Organizations, Vol 5(2),1-23

[12] Misra, Ram B (2004) Global IT outsourcing: Metrics for Success of all parties. Journal of Information Technology Cases and applications, Vol 6(3) 21-35

[13] Nasscom Mckinsey Report (2005): Extending India’s leadership of the IT and BPO industries [14] Neely, A D (1998) Performance Measurement: Why, what and how, Economics Books, London [15] Otley, D (1999) Performance Management: A framework for management control systems research.

Management Accounting Research, Vol 10(4) 363-82

End Notes

1This concept was described to the authors by Mr. Jagadish Krishnaswamy of Wipro Technologies

2446

Aligning Supplier Integration Practices with Time-Based Performance: A Conceptual Framework

Ru-Jen Lin, [email protected]

Lunghwa University of Science and Technology, Taiwan Shih-Chia Chang, [email protected]

Li-Hua Huang, [email protected] National Taipei College of Business, Taiwan

Abstract In view of the market demand variations and technological revolution have triggered manufacturers to implement the practices of supplier integration. Supplier involvement and collaboration is considered as an imperative strategy to sustain competitive advantage. The works of manufacturing strategy have verifies the truth that the degree of supplier integration facilitate the buying firms to effectively enhance time-based capability. The present study offers a framework for conceptualizing the relationship between supplier integration practices and time-based capability (e.g., delivery promptness, new product development time, delivery reliability/dependability, and manufacturing cycle time). Some hypotheses referring to those two elements are provided based on previous literature. Moreover, several supplier integration practices are discussed such as the degree of supplier involvement, the design of component responsibility, supplier commitment, information sharing, and supplier base reduction. Our study not only serves as a guideline for firms to implement different supplier integration practices for promoting specific kinds of time-based performance, but also makes a theoretical contribution towards further empirical research. Keywords: supplier integration practices; time-based capabilities Introduction

In last decade, the shorter product life cycle, intensive technology innovation, and dynamic global competition, the time-based capability in terms of the rapid delivery, quick new product development (NPD), and reduced manufacturing cycle time have become market advantage creation and sustaining weapons (Jayaram et al., 1999). Obtaining the time-based capability is to strengthen the critical supplier integration relationship in the supply chain (Ragatz et al., 1997). The supplier integration practices include limiting the supplier to play a simple role of purchasing product design consulter transforming into an active participator in the NPD, even more delegating responsibility in the design in the supplier outsourcing parts and constructing the information sharing mechanism among suppliers. Based on the effective execution of the supplier integration practices, the time-based performance in terms of the rapid NPD and delivery would be improved (Ragatz et al., 2002).

The past studies related to the supplier integration practices and time-based capability only limited to the early involvement degree of the supplier in terms of purchasing NPD. They focus on the supplier integration practices to the effects in the NPD performance or business performance (Carr and Pearson, 2002; Ragatz et al., 2002; Petersen et al., 2003; Ragatz et al., 1997). The supplier integration practices and time-based capability both have multi-dimensional characteristics nature. There are five dimensions of the supplier integration practices including the degree of supplier involvement, the design of component responsibility, supplier commitment, information sharing, and supplier base reduction (Chen and Paulraj, 2004; McIvor and Humphreys, 2004). The measures of the time-based capability comprise of the delivery promptness, new product development time, delivery reliability/dependability, and manufacturing cycle time (Droge et al., 2004). If we only focus on one single or aggregate dimension to conduct research, we would forgo the clarification and identification of each supplier integration practice to different time-based capability. The managerial application and the scope of the related studies would be restricted. We thus integrate the supplier integration practices and time-based performance to construct their own conceptual framework of the one-to-one relationships.

2447

Practices of Supplier Integration

The supplier integration practices are various practices for the manufacturers and suppliers to maintain long-term reciprocal highly cooperation (Droge et al., 2004). In order to respond to the international operating competitive demands and global supply chain function, in the issue of the supplier relationship management, many manufacturing strategy scholars have turned the traditional short-term profit orientation into the long-term cooperation strategy partnership. The operating flexibility and fast responsiveness to the market changes would be thus strengthened. The conventional supplier management selection was based on the price rather than the quality. Therefore, under the mutual short-term profit superseding base, there was few interaction between the supplier and purchasing manufacturer (Liker et al., 1998). Since Toyota and most Japanese manufacturers aggressively establish the long-term partnership with their suppliers and effectively improve the manufacturing advantages including the product quality level, rapid delivery, and fast new product development. How to maintain the highly collaboration relationship between the manufacturer and the supplier has become one of the imperative study issue of the contemporary supply chain management.

Clark (1989) and Clark and Fujimoto (1991) examine the case studies of Japanese manufacturers. They find the supplier adopting the early participation in the NPD, aggressively involving various quality improvement management programs, and maintaining the bona fine cooperation relationship. Funk (1993), Newman (1989), and Hartely et al. (1997a; 1997b) suggest the manufacturer delegating higher responsibility in terms of the outsourcing parts and adopting supplier base reduction strategy both construct the closer trust relationship with the suppliers. Derocher and Kilpatrick (2000) and Evans and Wurster (1997) indicate that the purchasing manufacturer and the suppliers utilize the information sharing mechanism established by the network technology. They apply the necessary information communication and maintain appropriate mutual trust. Lee and Billington (1992) and Kumar (1996) define the supplier commitment is the willingness to conduct critical investment in accordance with the purchasing manufacturer strategic development intention. They also advocate the supplier highly commitment is one of unavoidable important dimension of the supplier integration practices. We summarize the above mentioned scholars and conclude five dimensions of the supplier integration practices including: the degree of supplier involvement; supplier responsibility of the component design; supplier base reduction; information sharing, and supplier commitment. Degree of Supplier Involvement The degree of supplier involvement indicates the aggregate participation level in terms of the new product development (product concept development, prototype design, pilot test, or production) and various quality improvement programs. Several studies advocate the early supplier aggressive participation in the purchasing manufacturer new product development would contribute positive shortening in the new product development cycle time (Takeishi, 2001; Swink, 1999). The aggressive involvement in various quality improvement programs would strengthen the time-based capability of the order manufacturing cycle (Liker et al., 1998). Narasimhan et al. (2004) suggest that the supplier involvement incorporating the early participation in the new product development procedure, various product development committees (such as design for manufacturability (DFM) or design for assembly (DFA)), and various quality management program. Design of Component Responsibility Asanuma (1989) and Helper (1991) suggest that there are four kinds of parts productions including: in-house design and production, in-house design/supplier production, design and production with suppliers, or fully delegation of the supplier design and production. Traditionally, the outsourcing parts were designed in-house and transformed the part specifications to supplier for production. But recent a lot of manufacturing management literatures support that the Japanese automobile manufacturers have delegated their suppliers in terms of outsourcing design responsibility. The overall supply chain in the automobile industry quality level and competition have been improved. Based on the supplier professional competency and the reciprocal trust establishment, the delegation of the design of component responsibility to the supplier has become a common strategy approach in terms of supplier integration practice.

2448

Supplier Base Reduction In the past due to the price competition and risk diversification, the manufacturer applied the multiple supplier strategy for purchasing parts (Newman, 1989; Shin et al., 2000). In recent practices, most manufacturers have turned from the traditional multiple supplier strategy into supplier base reduction. The major reason is the cost higher than the price benefit derived from the multiple supplier management. More importantly, the multiple supplier strategy won’t establish the long-term cooperation and trust with the suppliers (Gadde and Hakarsson, 1994). Besides the supplier base quantity reduction, the immediate tier reduction of the supply chain is an imperative task of the supplier base reduction. That is the manufacturer as possible as to purchase the assembled system rather than the individual parts in order to reduce the supply chain supplying levels. In this kind of practice, the first tier supplier should directly provide products to the purchasing manufacturer. Compared to the second or third tier suppliers, the first tier supplier has closer relationship with the purchasing manufacturer. The mutual partnership is easier to establish. Supplier Commitment The supplier commitment is the willingness and intention for the suppliers to match the operating strategy of downstream manufacturer. The suppliers devote their input resources continuously and maintain reciprocal long-term cooperation relationship (Dion et al., 1992). Lee and Billington (1992) find the effects derived from the overall supply chain performance or the operating advantage of the supply chain members most based on the highly trust and commitment. Several studies advocate that the purchasing manufacturer and their suppliers keep better reliability and commitment would construct the concrete supply chain integration practices (Heide and John, 1990; Handfield and Bechtel, 2002). Canon and Perreault (1999) measure the commitment based on the reciprocal technology investment level among the supply chain members. Prahinski and Benton (2004) apply the mutual trust, length of the long-term cooperation, and the willingness to solve the problems mutually to measure. Information Sharing The information sharing is defined as the mutual degree in terms of critical, core, or professional information to exchange and sharing between the purchasing manufacturer and supplier (Towill, 1997). Recent supply chain management advocate that if the upstream and downstream members could establish a sound information communication and sharing mechanism, the rapid responsiveness capability to the market demand would be improved (Sahin and Robinson, 2002). In respect of the information sharing content, Mentzer et al. (2000) indicate the mutual information contents include: strategic information (business strategy plan and product development plan); activity information (production schedule plan and quality management information); market and customer demand information, and distribution information. Prahinski and Benton (2004) and Ward and Zhou (2006) adopt the information sharing channel perspective and suggest that the manufacturer and supplier enable to share reciprocal information through multiple approaches in terms of face-to-face communication, telephone, fax, or internet information technology.

Time-Based Performance

As the highly dynamic customer demand change and shorter product life cycle, most manufacturers ponder how to apply time-based capability to improve their competitive advantage in the global or regional market (Stalk and Hout, 1990; Handfield and Pannesi, 1995). The Boston Consulting Group initially conceptualizes the time-based strategy and applies in the business practices. The strategy management of the time-based competition (TBC) is one of imperative issue for practitioners and academics. Several well-known case studies adopting the time-based capability strategy practices and result impressed performance. Jayaram et al. (1999) find 3M applying time-based strategy approach and shortened the new product development time from two years into two month. The time-based strategy application in Fuji Xeron has successfully reduced the R&D cycle time of the copier machine from four years into two years. Various time-based competition-oriented practices utilizing in Toyota have decreased the new car model R&D time to two years. Toyota has preceded the Big Three automobile manufacturers (GM, Ford, and Chrysler) in the new product development cycle time. Several successful business cases have substantially reduced the new product development time over 75 % (Trygg, 1993). Carter et al. (1995), Tunc and Gupta (1993), and Handfield (1993) find the well-know cellular phone maker- Motorola, the manufacturing cycle has dramatically

2449

reduced to four hours instead of previous several weeks. For Toyota to manufacture an automobile, it only takes two days, compared to their North American counterparts in less than three days. For Johnson and Johnson, their popular Acuvue only takes less than three days to deliver the order and 99.9% prompt delivery rate. This kind of prompt delivery capability results their leading position in the contact lens market.

Carter et al. (1995) and Tersine and Hummingbird (1995) demonstrate the time-based capability showing the multi-dimensional characteristics. Various manufacturing management programs result distinct time-based capability performance. Roth and Miller (1990) explore the relationship between the manufacturing strategy and business performance, they measure the time-based capability by the delivery promptness, delivery reliability/ dependability; and new product development time. Vickery et al. (1995) examine the determinants of business performance and suggest the manufacturers enabling to strengthen the time-based capability in terms of the new product development cycle time, the quantity of the new product introduction, manufacturing cycle time, and delivery time. Besides the delivery promptness, delivery reliability, delivery dependability, and new product development time to market, Roth and Maruchek (1993) and Safizadeh et al. (1995) also advocate that the responsiveness capability to the customer need or complaint should be included in the measures of the time-based capability. Therefore, the sound customer relationship would be maintained. When Jayaram et al. (1999) investigate the empirical study of the time-based capability in North American Automobile industry, they suggest that the manufacturing cycle time should be one of important indicator. The promptness of the manufacturing department upon receipt of order till the order completion should be honored. Droge et al. (2004) discuss the time-based capability to attribute the business performance in terms of the new product time to market, manufacturing time to product, and rapid responsiveness as measuring dimensions. The rapid responsiveness capability focuses on the strategy or approach to respond to the customer needs. We summarize the above mentioned scholars aspects and category the following time-based capabilities. (1) New Product Development Time: the capability which the manufacturer can quickly modify current product quality or develop a new product (Vickery et al. 1995). We measure the numbers of new product introductions or the time required for the new product development. (2) Manufacturing Cycle Time: the capability which the manufacturer can shorten the time upon receipt of customer’s order, placing the production request to the manufacturing department, and the order production completion (Handfield and Pannesi, 1995). This is to measure the promptness of manufacturing department. (3) Delivery Promptness: the capability which the manufacturer can shorten the time effectively in the receipt of customer order till the product delivery to the customer (Handfield, 1992; Droge et al. 2004). (4) Delivery Reliability/ Dependability: the capability which the manufacturer can follow the customer delivery time request and deliver the products to the customers punctually and correctly (Handfield and Pannesi, 1995; Roth and Miller, 1990). The delivery dependability indicates the manufacturer can satisfy the order request in terms of the product quantity, type, and specification. Proposition

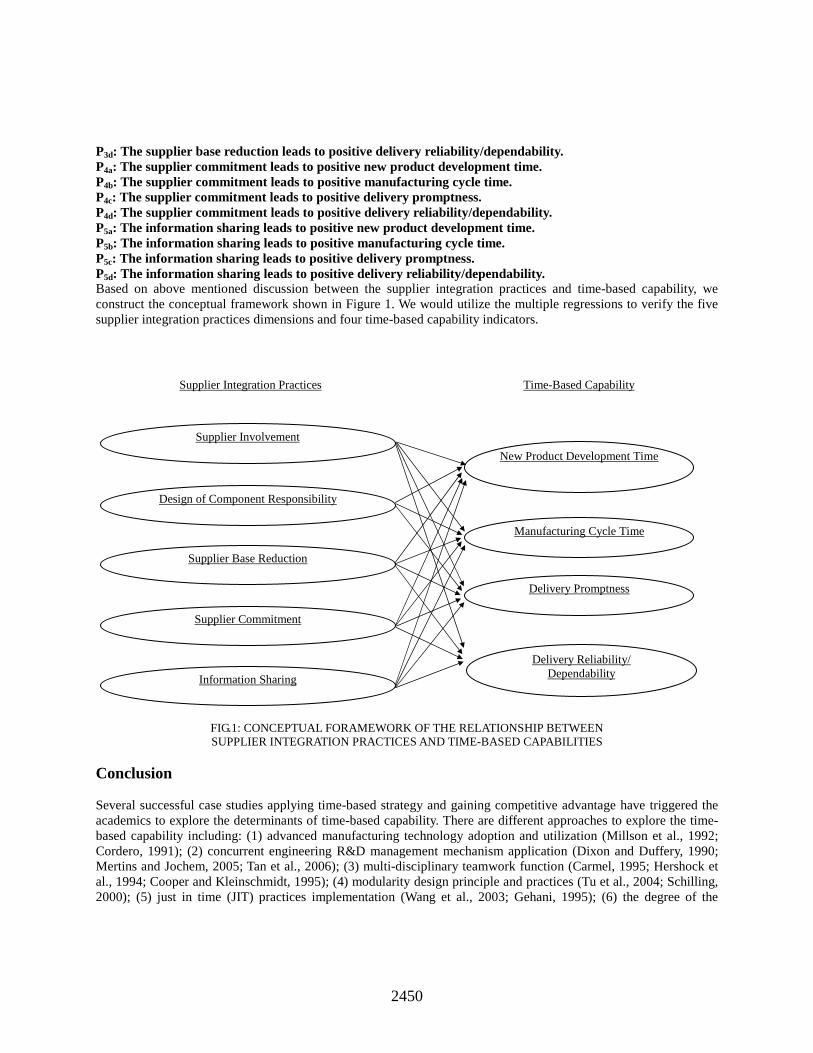

Applied the related research of the supplier integration practices and time-based capability, we demonstrate the following research propositions. P1a: The degree of supplier involvement leads to positive new product development time. P1b: The degree of supplier involvement leads to positive manufacturing cycle time. P1c: The degree of supplier involvement leads to positive delivery promptness. P1d: The degree of supplier involvement leads to positive delivery reliability/dependability. P2a: The supplier design component responsibility leads to positive new product development time. P2b: The supplier design component responsibility leads to positive manufacturing cycle time. P2c: The supplier design component responsibility leads to positive delivery promptness. P3a: The supplier base reduction leads to positive new product development time. P3b: The supplier base reduction leads to positive manufacturing cycle time. P3c: The supplier base reduction leads to positive delivery promptness.

2450

P3d: The supplier base reduction leads to positive delivery reliability/dependability. P4a: The supplier commitment leads to positive new product development time. P4b: The supplier commitment leads to positive manufacturing cycle time. P4c: The supplier commitment leads to positive delivery promptness. P4d: The supplier commitment leads to positive delivery reliability/dependability. P5a: The information sharing leads to positive new product development time. P5b: The information sharing leads to positive manufacturing cycle time. P5c: The information sharing leads to positive delivery promptness. P5d: The information sharing leads to positive delivery reliability/dependability. Based on above mentioned discussion between the supplier integration practices and time-based capability, we construct the conceptual framework shown in Figure 1. We would utilize the multiple regressions to verify the five supplier integration practices dimensions and four time-based capability indicators.

FIG.1: CONCEPTUAL FORAMEWORK OF THE RELATIONSHIP BETWEEN SUPPLIER INTEGRATION PRACTICES AND TIME-BASED CAPABILITIES

Conclusion

Several successful case studies applying time-based strategy and gaining competitive advantage have triggered the academics to explore the determinants of time-based capability. There are different approaches to explore the time-based capability including: (1) advanced manufacturing technology adoption and utilization (Millson et al., 1992; Cordero, 1991); (2) concurrent engineering R&D management mechanism application (Dixon and Duffery, 1990; Mertins and Jochem, 2005; Tan et al., 2006); (3) multi-disciplinary teamwork function (Carmel, 1995; Hershock et al., 1994; Cooper and Kleinschmidt, 1995); (4) modularity design principle and practices (Tu et al., 2004; Schilling, 2000); (5) just in time (JIT) practices implementation (Wang et al., 2003; Gehani, 1995); (6) the degree of the

Supplier Involvement

Design of Component Responsibility

Supplier Base Reduction

Supplier Commitment

Information Sharing

Supplier Integration Practices Time-Based Capability

New Product Development Time

Manufacturing Cycle Time

Delivery Promptness

Delivery Reliability/ Dependability

2451

supplier involvement in the new product development (Ragatz et al., 2002; Petersen et al., 2003). Therefore, the past literature focuses on the process technology, R&D management, cross-functional teamwork, modularity design, and JIT production practices perspectives to explore on how to improve the time-based capability. Therefore, our study proposes five dimensions of the supplier integration practices to affect four time-based capabilities. Our research has innovation and uniqueness compared to previous perspectives.

There were abundant studies regarding the supplier integration practices and time-based capability, but they only limited to the early involvement in the new product development, the effects to the new product development performance, or the business performance. There were scant studies related to the five supplier integration practices influence to the business performance. Obviously, the past research is not rigorous yet. Pertaining to the time-based capability determinants, most studies referring from the aspects of process technology, R&D management, cross-functional teamwork, modularity design, and JIT production practices on how to improve the time-based capability. There were few issues based on the supplier integration practices to conduct the influence to the time-based capability. In other words, we integrate the supplier integration practices and time-based capability to investigate their influential relationship exhibiting innovative and unique presentation.

There are multi-dimensional natures of the supplier integration practices and time-based capability. The past one single or aggregate indicator is not sufficient to delineate or discuss their insightful cause-and-effect relationship. In our study, we identify one-to-one perspectives from the five supplier integration practices to four time-based capabilities. We present a conceptual framework can serve a managerial decision direction. The manager can choose appropriate supplier integration practices for anticipated time-based capability improvement. Our study would be conducted in further investigation for related research.

References

[1] Asanuma, B. (1989). Manufacturer-supplier relationships in Japan and the concept of relation-specific skill. Journal of the Japanese and International Economies, 3, 1-30.

[2] Cannon, J.P., & Perreault, Jr. W.D. (1999). Buyer-seller relationships in business markets. Journal of Marketing Research, 36, 439-460.

[3] Carmel, E. (1995). Cycle time in packaged software firms. Journal of Product Innovation Management, 12, 110-123.

[4] Carr, A.S. & Pearson, J.N. (1999). Strategically managed buyer-supplier relationships and performance outcomes. Journal of Operations Management, 17, 497-519.

[5] Carr, A.S. & Pearson, J.N. (2002). The impact of purchasing and supplier involvement on strategic purchasing and its impact on firms’ performance. International Journal of Operations and Production Management, 22(9/10), 1032-1053.

[6] Carter, P. L., Melnyk, S.A., & Handfield, R.B. (1995). Identifying the basic process strategies for time-based competition. Production and Inventory Management Journal, 36(1), 65-70.

[7] Chen, I.J., & Paulraj, A. (2004). Understanding supply chain management: critical research and a theoretical framework. International Journal of Production Research, 42(1), 131-163.

[8] Clark, K.B. (1989). Project scope and project performance: the effect of parts strategy and supplier involvement on product development. Management Science, 35, 1247-1263.

[9] Clark, K.B. & Fujimoto, T. (1991). Product Development Performance: Strategy Organization and Management in the World Auto Industry, Harvard Business School Press, Boston, MA.

[10] Cooper, R.G. & Kleinschmidt, E.J. (1995). Benchmarking the firm’s critical success factors in new product development. Journal of Product Innovation Management, 12(5), 374-391.

[11] Cordero, R. (1991). Managing for speed to avoid product obsolescence: a survey of techniques. Journal of Product Innovation Management, 8(4), 283-294.

[12] Derocher, R.P. & Kilpatrick, J. (2000). Six supply chain lessons for the new millennium. Supply Chain Management Review, 3(4), 34-41.

2452

[13] Dion, J.R., Banting, P., Picard, S., & Blenkhorn, D. (1992). JIT implementation: a growth opportunity for purchasing. International Journal of Purchasing and Materials Management, 28, 33-.

[14] Dixon, D. & Duffey, M.R. (1999). The neglect of engineering design. California Management Review, Winter, 9-23.

[15] Droge, C., Jayaram, J., & Vickery, S.K. (2004). The effects of internal versus external integration practices on time-based performance and overall firm performance. Journal of Operations Management, 22, 557-573.

2453

Clusters and Cluster Performance Management

Drahomira Pavelkova, [email protected] Adriana Knapkova, [email protected]

Eva Jircikova, [email protected] Tomas Bata University in Zlin, Czech Republic

Abstract This contribution deals with some critical issues of cluster performance management. The first topic discussed is the use of clusters as a tool for increasing the performance of companies and regions in the conditions of globalization, followed by governmental and local policies and their impact on the development of clusters. Finally, some important factors of cluster performance management based on results obtained from surveys and structured interviews of managers of selected clusters are identified. Introduction There are a number of definitions of clusters in the literature. Cortright [3] concludes that one fixed definition of clusters cannot be made. It is necessary to modify one’s definition depending on the purpose of the given study. For the purpose of this paper we will use the definition proposed by Porter. Porter [8] defines a cluster as “a geographic concentration of mutually interconnected companies, specialized suppliers, providers of services, companies in similar fields and associated institutions, such as universities, agencies and associations of different orientations, which compete, but also cooperate.”

Clusters may represent forms of vertical as well as horizontal integration of companies. Debate is ongoing as to whether globalization will make clusters more or less important, with the literature

leaning towards greater regional importance. Some economists argue that regional specialization and clustering of related activities are becoming more important features of the world economy as a result of globalization. Clusters as a Tool for Increasing the Performance of Companies and Regions The development of clusters seems to promise an answer to the challenges created by increased international competition and the growing importance of innovation in the knowledge economy. Clusters of interrelated firms can be an important source of competitive advantage and active membership of cluster can lead to increased performance of individual firms. Let’s try to answer question what could be the reasons for that.

At the beginning, we have to identify possibilities for cooperation among members of cluster. There are several fields for cooperation, particularly:

� networking � human resource management � research and development, innovation processes � marketing, public relations � investments � lobbying, etc.

Networking represents the creation of conditions for formal and informal flow of information and knowledge within the cluster. It increases the availability and rate of transfer of information and technologies due to the proximity of the companies, strong ties between them and the highly competitive nature of the cluster. It can have the form of short meetings of representatives of individual cluster members, information support by common web site, newspaper, setup information center etc. The management of a cluster may arrange contacts not only among the members of the cluster, but also with suppliers, customers, providers of financial capital, with

2454

educational, research and other institutions, which are not members of the cluster. However, the creation of networks must not be an end in itself, it has to be useful for the companies and move them forward.

Human resources, their availability to the companies and the improvement of their qualifications, represent an important field for the cooperation within the clusters. This can be a common vocational guidance and education of employees by organizing courses, common seminars and conferences, by creation of educational centers. A cluster usually organizes these activities in cooperation with educational institutions; it can finance them from its own resources or can use financing from different supporting projects. Cooperation of the cluster with secondary schools, colleges and universities can be significant in creating cooperative networks, helpful in formulation of demands on graduates of these schools according to the needs of industrial practice (orientation of programs of studies, modification of curricula etc.). The presence of a strong cluster in a region may also attract talents from elsewhere.

The experience from the existence of clusters shows that for a dynamic growth of the cluster and of the companies in the cluster it is essential to pay attention to the sphere of research and innovation. Innovations maintain the viability and prosperity of companies in the marketplace; research and development create the condition for future growth. The support of innovation is directed towards the development of new products or the improvement of their properties or towards the process improvements. The support of research brings new know-how. These processes are interrelated even if they represent different activities of the cluster. The cooperation of the companies within the cluster may have the form of sharing information and ideas, mutual research projects, support of formation and expansion of spin-off companies etc. Companies may develop a mutual research infrastructure together or cooperate with research institutions (research institutes or universities), which have the necessary materials, technical facilities and equipments as well as properly trained personnel and which are often initiators and operators of „incubators“ and scientific and technical parks. Universities and research institutes can also greatly benefit from the cooperation with clusters - they can better move the results of their research into implementation in practice and commercialization. Skokan [9] shows in his publication that innovation processes are not perceived today as being linear, but as interactive, linked up, integrated and acting on a feedback. It is therefore absolutely essential to create a network environment for the cooperating subjects within the regional infrastructure, which allows the transfer of technologies and know-how to the environment of entrepreneurial subjects.

The field of business cooperation and promotion includes activities as joint purchasing and a possibility of a higher pressure on the quality of delivered goods and their pricing, or shared production. There is a possibility to fill large orders or possibility of greater specialization; a cluster may combine companies from different links of the value chain. This enables smaller companies to specialize and compete with larger, vertically linked companies. Additional benefits of cooperation are more effective logistic management; shared expenses for marketing research of trends and markets; joint participation in trade fairs; joint catalogue of products and services for the member of clusters; the possibility to utilize joint logo, trademark, advertisement etc.

Obtaining sources for financing of investment projects are very important for the strategic development of a cluster. Attracting investors with advantageous conditions of financing or joint financing can be a significant resource for reducing capital costs and risk. An access to financing can be easier for a cluster than for an individual company. Investors (often venture capital) may be attracted into the region due to positive image created by the presence of a strong cluster. Financing of necessary investment projects creates conditions for a further growth of the cluster.

Another no less important field useful for the growth of a cluster and its members is lobbing on behalf of building a necessary infrastructure, improvement of legislature, grant policy etc. A cluster magnifies the power and voice of smaller companies. They can urge the government or regional representation to make investments in specialized infrastructure. Thanks to the visibility of a cluster, cost effectiveness and higher return on investment represented by a cluster, its additional possible investments are more easily justifiable.

For the growth of a cluster, other supporting activities that the cluster management can offer to its members can be important. These activities can secure an effective collaboration in above-mentioned areas, such as help with preparation and management of projects; securing service in the form of accounting a legislative consulting; banking services; insurance; benchmarking etc.

2455

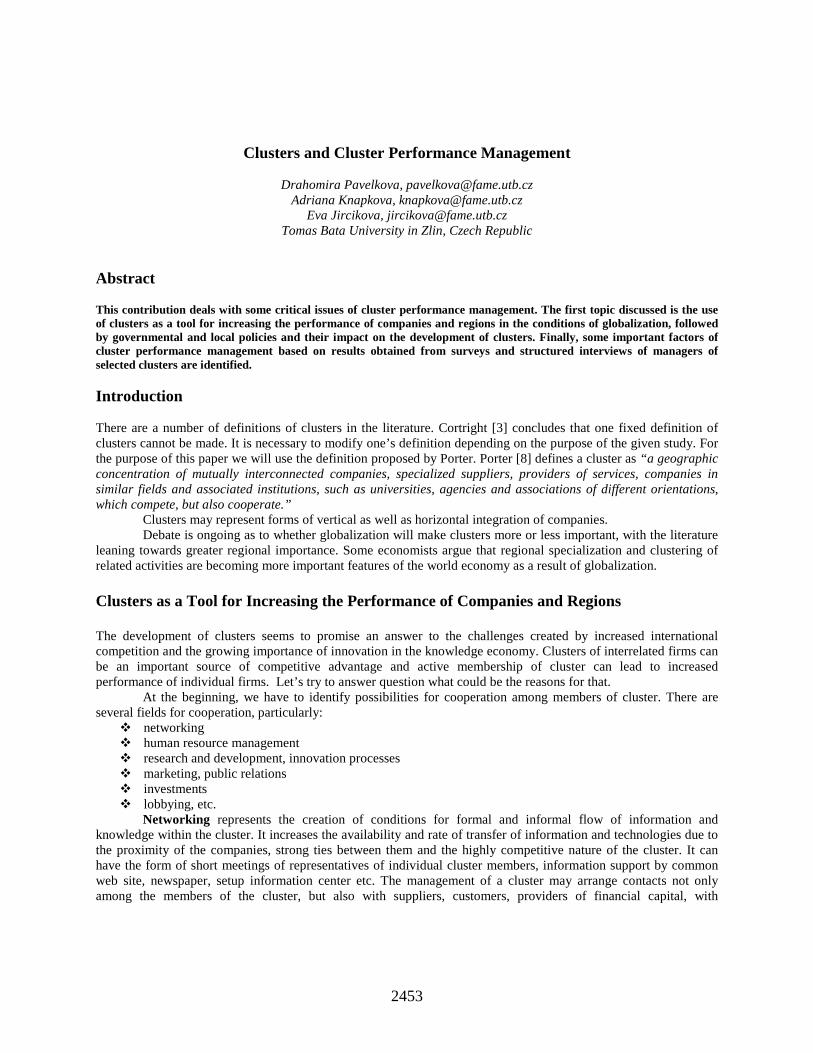

From the above it follows that there are many activities that can be implemented within the cluster, which can contribute to the increase of efficiency of individual companies.

Preliminary results from the authors´ own survey carried out by interviews of cluster managers in different countries are presented on Figures 1-6. This survey is continuing; in this phase; 20 cluster managers have taken part in this research.

Figures demonstrate shares of joint activities, which: (1) clusters currently offer to their members, (2) clusters currently do not offer , but plan doing so in few years, (3) clusters currently do not offer, but in case of need cluster managements are able to arrange, (4) clusters neither offer nor plan doing so.

0% 20% 40% 60% 80% 100%

Information support

Common w orkshops, meetings

Arranging contacts among cluster members

Arranging contacts w ith vendors or customers

Area of Networking

1 2 3 4

FIG. 1: ACTIVITIES OF CLUSTERS IN THE AREA OF NETWORKING

Almost all clusters involved in the survey offer information support in the form of joint website,

newspaper, information center; common workshops and meetings; and management of clusters arrange contacts between the cluster members. More than a half of clusters arranges contacts with vendors or customers; others are planning to do so or cluster managers are able to arrange them if necessary.

2456

0% 20% 40% 60% 80% 100%

Organization of joint seminars and conferences

Training of employees

Cooperation with educational institutions

Area of Human Resources

1 2 3 4

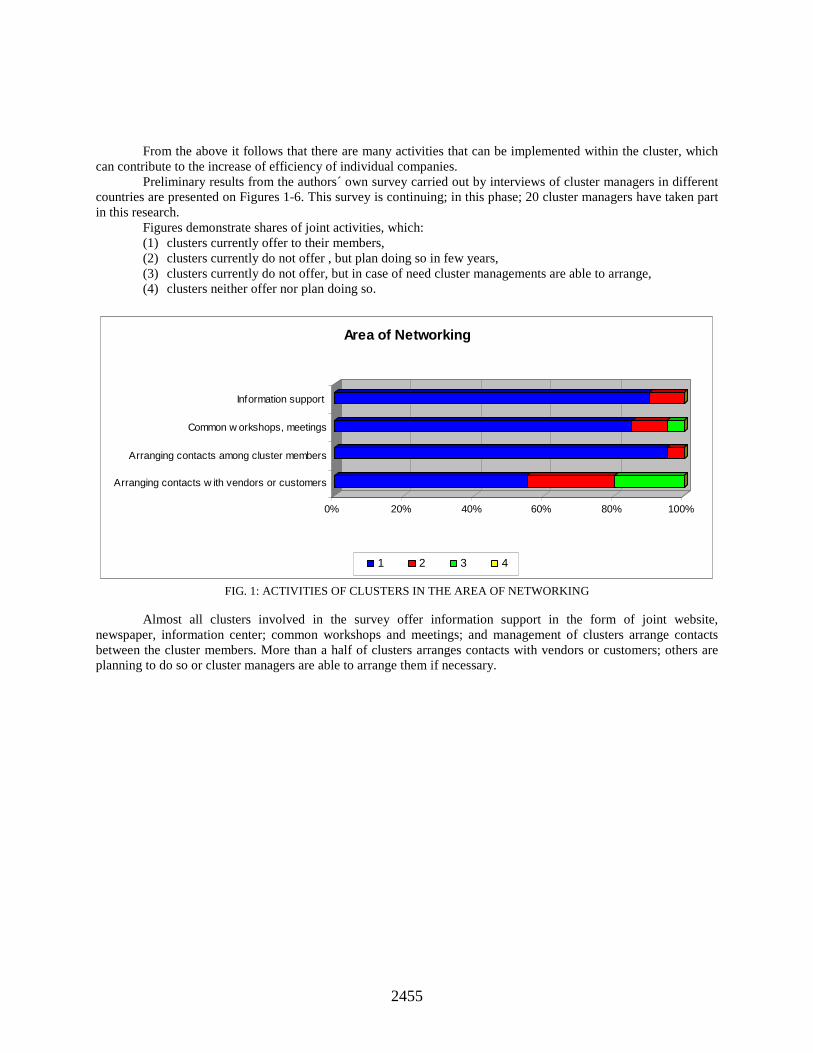

FIG. 2: ACTIVITIES OF CLUSTERS IN THE AREA OF HUMAN RESOURCES

All clusters involved in the survey organize (or could organize, if necessary) joint seminars and

conferences, or plan doing so. Half of them offer common training of employees. Almost all of clusters providing these activities cooperate with educational institutions.

0% 20% 40% 60% 80% 100%

Joint research and development

Cooperation w ith research institutions

Innovations of products and processes

Support of spin-offs creation

Incubator services

Area of Research and Innovations

1 2 3 4

FIG. 3: ACTIVITIES OF CLUSTERS IN THE AREA OF RESEARCH AND INNOVATIONS

A good deal of the clusters involved in the survey carry out joint research, innovations of products and

processes, and cooperate with research institutions. Almost half of them support spin-offs; further one third of clusters plan doing so in future. Incubator services are offered quite rarely, but additional clusters are able to offer them if necessary or plan them in future.

2457

0% 20% 40% 60% 80% 100%

Joint purchasing

Logistic management

Joint participation in trade fairs

Joint logo, trade name

Electronic marketplace

Area of Business Cooperation and Promotion

1 2 3 4

FIG. 4: ACTIVITIES OF CLUSTERS IN THE AREA OF BUSINESS COOPERATION AND PROMOTION

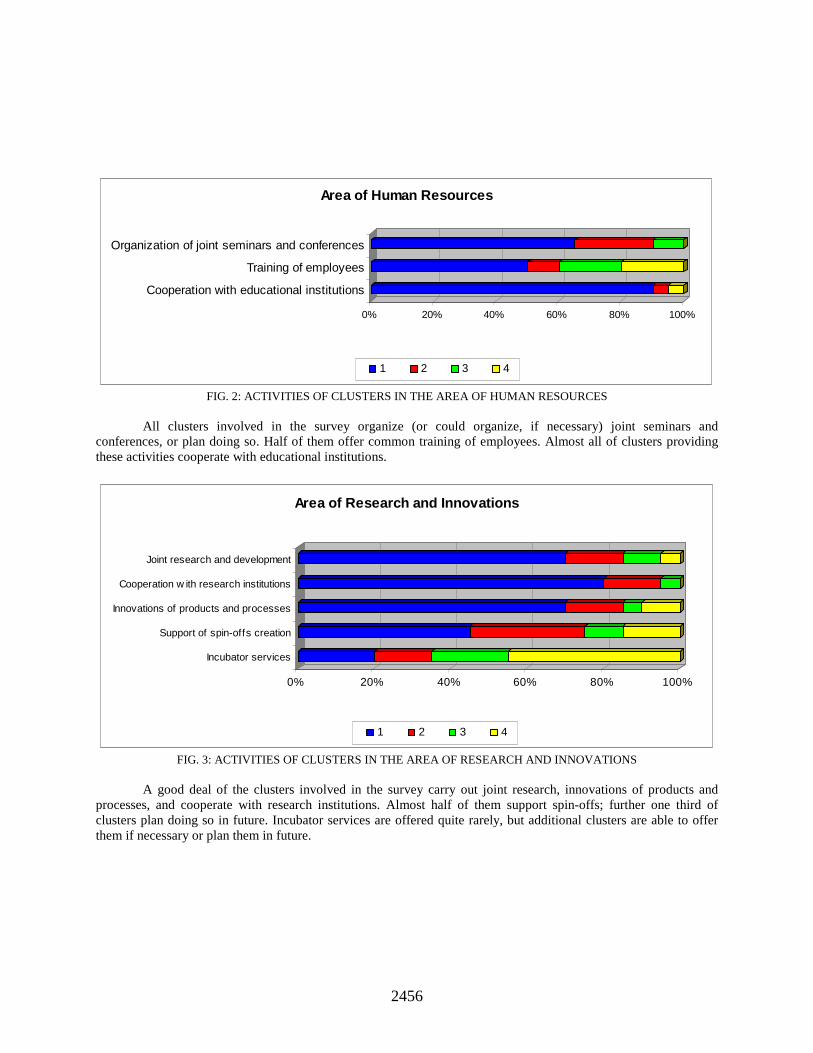

Most common activities in area of promotion are joint participation in trade fairs, marketing, research of

trends and markets and joint logo, trade name or advertisement. Business cooperation in the form of logistic management, joint purchase or shared production are quite rare activities in the clusters, but in case of interest, clusters are able to ensure them in many cases.

0% 20% 40% 60% 80% 100%

Help in preparation and management of projects

Benchmarking

Support service

Area of Support Activities

1 2 3 4

FIG. 5: ACTIVITIES OF CLUSTERS IN THE AREA OF SUPPORT ACTIVITIES

The most widespread support activity is a help in preparation and/or management of projects. Support

services in a form of banking services/insurance/legal, accounting and tax consultancy and etc. are not provided commonly. Benchmarking is quite popular; almost all clusters use it or are going to use it in close future.

2458

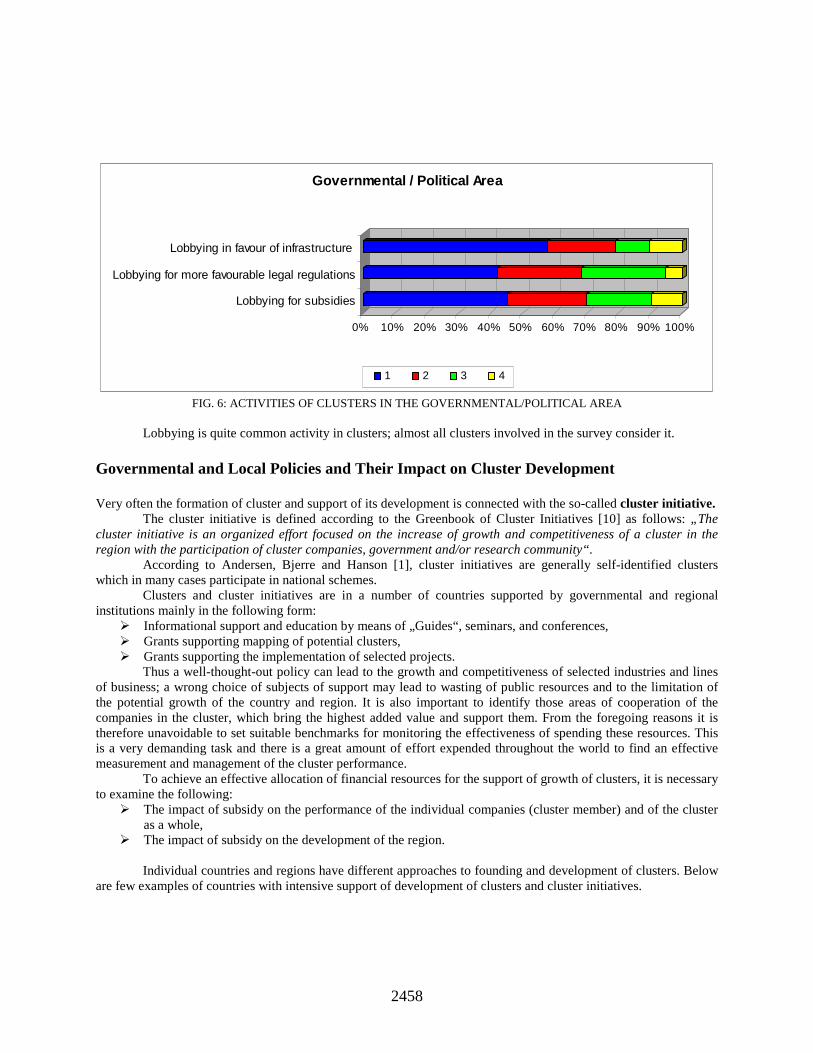

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Lobbying in favour of infrastructure

Lobbying for more favourable legal regulations

Lobbying for subsidies

Governmental / Political Area

1 2 3 4

FIG. 6: ACTIVITIES OF CLUSTERS IN THE GOVERNMENTAL/POLITICAL AREA

Lobbying is quite common activity in clusters; almost all clusters involved in the survey consider it.

Governmental and Local Policies and Their Impact on Cluster Development Very often the formation of cluster and support of its development is connected with the so-called cluster initiative.

The cluster initiative is defined according to the Greenbook of Cluster Initiatives [10] as follows: „The cluster initiative is an organized effort focused on the increase of growth and competitiveness of a cluster in the region with the participation of cluster companies, government and/or research community“.

According to Andersen, Bjerre and Hanson [1], cluster initiatives are generally self-identified clusters which in many cases participate in national schemes.

Clusters and cluster initiatives are in a number of countries supported by governmental and regional institutions mainly in the following form:

� Informational support and education by means of „Guides“, seminars, and conferences, � Grants supporting mapping of potential clusters, � Grants supporting the implementation of selected projects.

Thus a well-thought-out policy can lead to the growth and competitiveness of selected industries and lines of business; a wrong choice of subjects of support may lead to wasting of public resources and to the limitation of the potential growth of the country and region. It is also important to identify those areas of cooperation of the companies in the cluster, which bring the highest added value and support them. From the foregoing reasons it is therefore unavoidable to set suitable benchmarks for monitoring the effectiveness of spending these resources. This is a very demanding task and there is a great amount of effort expended throughout the world to find an effective measurement and management of the cluster performance.

To achieve an effective allocation of financial resources for the support of growth of clusters, it is necessary to examine the following:

� The impact of subsidy on the performance of the individual companies (cluster member) and of the cluster as a whole,

� The impact of subsidy on the development of the region.

Individual countries and regions have different approaches to founding and development of clusters. Below are few examples of countries with intensive support of development of clusters and cluster initiatives.

2459

Through the National Research Council of Canada (NRC), the Government of Canada has made a series of investments in clusters as a part of National Innovation Strategy. NRC is composed of 20 institutes located across Canada. Canada, given its vast geography, relatively small and dispersed population, and the predominance of SMEs, has taken a collaborative approach in building community innovation over the past decade. Increasingly, innovation has taken the form of community-based "technology clusters", a term that describes the growth of a significant concentration of innovative companies around a nucleus of R&D facilities. NRC cluster initiatives have focused on building science and technology-based innovation capacity in areas of local and regional strengths to foster economic growth and improve quality of life. The process involves: bringing the leadership needed to gather stakeholders together to define a collective vision; building trust within a cluster by fostering networking and collaborative R&D between firms engaging in community consultation; providing specialized research infrastructure and highly qualified personnel; supporting the creation, growth, and attraction of firms; facilitating the development of external linkages; and supporting the clusters in attracting new resources. Up to now, 11 cluster initiatives have been established and NRC has received over 300 million CAD in four rounds of funding to establish and reinforce cluster initiatives across the country.

FIG. 7: MODEL OF THE NRC´ CLUSTER POLICY [11]

In Austria, clusters have been supported from the early 1990s. Each cluster can count on public support in terms of cluster management and cluster funding. Cluster development in Austria operates at different levels: regional clusters, nationwide clusters, and industry-research linking competence centers. Regions are entitled to set their own innovation and technology policies. They take over the active part of building clusters, i.e., cluster management and co-operation platforms. However, national institutions provide a general framework for regional cluster policy: financial support; technology transfer programs; training plans; and R&D policies [6].

Since 1998, the Regional Government of Upper Austria has pursued a cluster-oriented economic and technology policy on the basis of the “Upper Austria 2000+” Strategic Program. The aim is to achieve a sustained improvement in the competitiveness of the location. TMG, the regional institution for the promotion of technology and marketing (owned by the Regional Government of Upper Austria) was given responsibility for cluster management. For period 2005-2010, new Strategic Program “Innovative Upper Austria 2010” was prepared. The focal point of the program is formed by a concentration of capacity on five main areas comprised by: R&D, networks, EU-networking, Upper Austria as an economic and technology location, and professional qualification. Upper Austria is the European leader with regard to economic networking. No other region has such a well-

2460

established climate of cooperation. At present, approximately 1,200 companies, R&D bodies, and educational institutes are partners in the inter-branch network Clusterland Upper Austria, Ltd., as following: Automotive-Cluster, Health-Cluster, Plastics-Cluster, Furniture/Timber-Construction-Cluster, and Mechatronics-Cluster. Clusterland supports cluster and network initiatives. The Clusterland partners employ more than 219,000 people and have total annual sales of € 39.02 billion. The Clusterland sustained more than 220 co-operation projects and more than 500 training events.

Lower Austria’s cluster policy has become an important part of regional innovation and technology policy as well. The trend in Lower Austria has turned around from step by step increasing independency for cluster initiatives (as planned in 2001 when the first initiatives started) to a clear mandate for the Regional Development Agency (RDA) to run cluster initiatives as an economic policy instrument to strengthen SMEs. The regional government provides the main part of financial resources to operate the cluster managements for a limited short period of time (5 - 10 years). Companies’ financial participation in clusters should be generated from moderate membership fees, fees for workshops or events and sponsoring. Fees foster involvement of companies, but also a service orientation of the cluster team. The regional development agency Ecoplus explores and maps cluster potentials, implements cluster initiatives, provides the financial and information support and employs cluster managers. Ecoplus combines different economic instruments for a better cluster development like technology services, business location development, business parks, and support for start-ups, etc. Ecoplus has already established cluster initiatives in six next-generation sectors: timber, automotive, green building, wellbeing, plastics and food industry. 475 companies with more than 58,000 employees are already participating as partners in these clusters. Around 100 cooperation projects have already been completed, with more than 400 companies participating.

Cluster initiatives in the Czech Republic have been supported by the program “KLASTRY”, which began in 2004 and has enabled identification and support of new sectors and sub-sectors with potential to improve competitiveness through collaboration and innovation. The program focuses on the financial support to regions demonstrating commitment to innovative clusters. The KLASTRY program is managed by the CzechInvest, an agency of the Ministry of Industry and Trade. The total budget for the program over the years 2004-2006 was approximately 12 million EUR (average of 4 million EUR per year). The budget per cluster may reach up to € 33,000 for activities connected with the creation of a cluster, not to exceed 75% of eligible costs. Eligible costs include items such as studies, meetings, or workshops and associated materials. The budget for the development of the cluster may range from approx. € 100,000 to 1.6 million for management and development of clusters (for the total program period of up to three years). Reimbursement cannot exceed 50% of the total project cost based on the following schedule (maximum of 75% of eligible costs in year 1, 50% in year 2, and 25% in year 3). Eligible costs may include cluster staff, tangible and intangible assets for the cluster initiative, consulting services, benchmark studies, cluster promotion, evaluation of economic impact, and research (market, competition, and innovation). Supported clusters must be in the Czech Republic (but not in Prague), include at least 15 firms (min. 60% of members are SMEs), include at least one university or research institute. [5, 12]. Per CzechInvest, there are 51 different clusters or potential clusters across Czech regions. Prior to launching the program, CzechInvest offered a training and cluster awareness sessions to cluster facilitators, academics and regional government and private sector representatives. Periodic training sessions as well as the Annual National Cluster Conference are organized. CzechInvest also plans to develop a formal accreditation process for specific cluster facilitation skills. New program for supporting clusters, pole of excellence and networks – “Cooperation” (financed by EU funds) will be launched in the second half of the year 2007. Cluster Performance Management What can contribute greatly to the progress of clusters and to the support of their performance? Since cluster performance is not a single-dimensional concept, it is necessary to look at a range of factors influencing this performance.

2461

Generally, in order for a business to grow, it must be able to access the necessary external resources and operate within a supportive business environment. The macroeconomic framework for the growth of enterprise is the widest dimension influencing the performance of subjects acting here. Much innovation support focuses on individual or groups of companies, helping them address and improve internal competences, e.g. technology, skills, funding. Even if companies have addressed all their internal issues, but they cannot readily access finance to grow, or if there is a lack of suitably skilled staff available, this will limit their development.

National or regional policies can to a high degree contribute to the formation of clusters (mapping of potential grouping) and their growth, as has been mentioned and demonstrated in selected countries. However, clusters can be formed and developed even without a special set-up cluster policy of a government or region.

An organization of cluster activities and mutual communication between the members of clusters can be done by the professional management or by representatives of individual cluster members. The efficiency of cluster management may play a significant role in the development of a cluster and its members, as well as of cooperating institutions.

According to Breschi and Malerba [2], the key feature of successful clusters is related to the high level of embeddedness of local firms in a very thick network of knowledge sharing, which is supported by close social interactions and by institution building trust and encouraging informal relations among actors. The possibility for individual firms to tap into the body of localized knowledge and capabilities depends on the fundamental way on the ability to establish and maintain effective social links and lines of communication. Besides offering an industrial atmosphere favorable to innovation and entrepreneurship, and a social capital supporting trust and a cooperative relationships, the additional key feature of technology-intensive clusters is related to the availability of a common set of resources, some endogenously given, like universities and public research centers, and some others endogenous to the cluster development, like a pool of specialized and skilled labor.

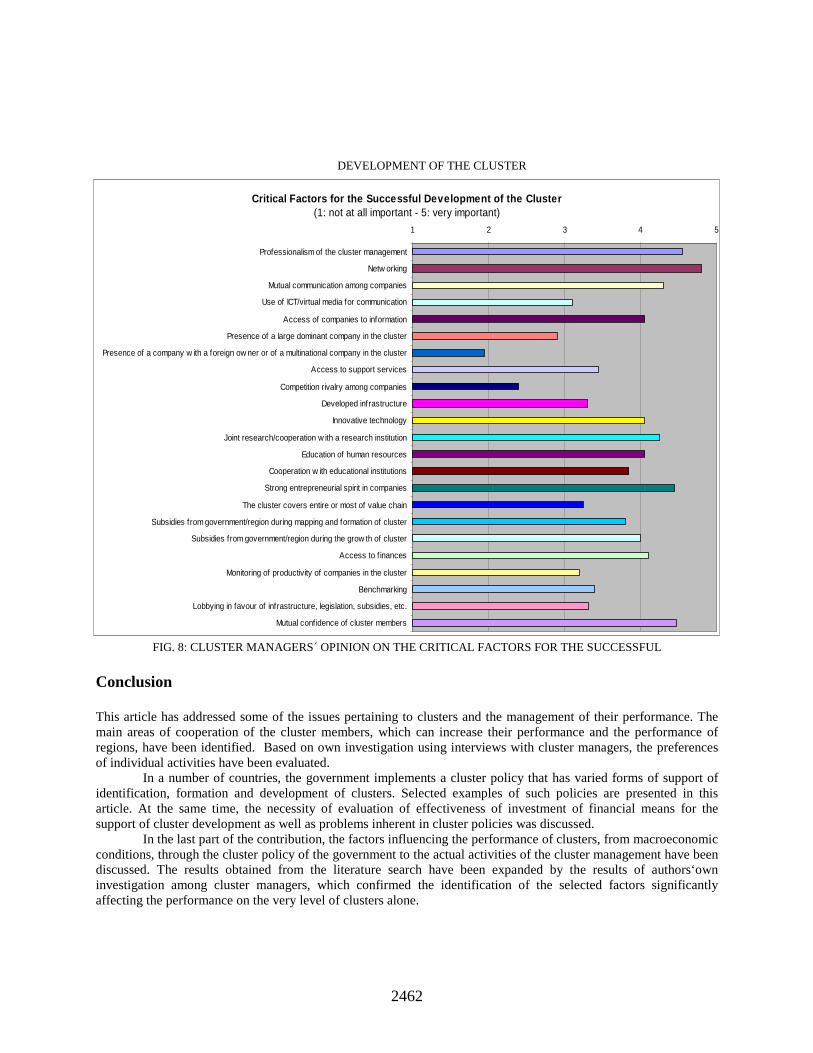

These propositions have been preliminary confirmed by authors´ own survey carried out by interviews of cluster managers in different countries (as mentioned above). The following aspects were identified as being essential for the cluster development and cluster performance management:

� Networking and mutual communication among cluster members; � Professionalism of the cluster management; � Mutual confidence and communication among cluster members; � Strong entrepreneurial spirit in companies; � Joint research or cooperation with a research institutions; � Access to finances; � Access of companies to information; � Cooperation with educational institutions; � Education of human resources; � Innovative technologies, � Subsidies from government/region during the growth of cluster.

Cluster managers do not consider a presence of a company with a foreign owner or of a multinational company and competition rivalry among companies in the cluster as very important factors for cluster development.

More detailed results of survey of cluster managers opinions can be seen in Fig. 8.

2462

DEVELOPMENT OF THE CLUSTER

FIG. 8: CLUSTER MANAGERS´ OPINION ON THE CRITICAL FACTORS FOR THE SUCCESSFUL

Conclusion This article has addressed some of the issues pertaining to clusters and the management of their performance. The main areas of cooperation of the cluster members, which can increase their performance and the performance of regions, have been identified. Based on own investigation using interviews with cluster managers, the preferences of individual activities have been evaluated.

In a number of countries, the government implements a cluster policy that has varied forms of support of identification, formation and development of clusters. Selected examples of such policies are presented in this article. At the same time, the necessity of evaluation of effectiveness of investment of financial means for the support of cluster development as well as problems inherent in cluster policies was discussed.

In the last part of the contribution, the factors influencing the performance of clusters, from macroeconomic conditions, through the cluster policy of the government to the actual activities of the cluster management have been discussed. The results obtained from the literature search have been expanded by the results of authors‘own investigation among cluster managers, which confirmed the identification of the selected factors significantly affecting the performance on the very level of clusters alone.