Safex Options and the Greeks 101

10

JSE Limited Registration Number: 2005/022939/06 One Exchange Square, Gwen Lane, Sandown, South Africa. Private Bag X991174, Sandton, 2146, South Africa. Telephone: +27 11 520 7000, Facsimile: +27 11 520 8584, www.jse.co.za Member of the World Federation of Exchanges Executive Directors: RM Loubser (CEO), NF Newton-King, F Evans (CFO), JH Burke, LV Parsons Non-Executive Directors: HJ Borkum (Chairman), AD Botha, ZL Combi, MR Johnston, DM Lawrence, W Luhabe, A Mazwai, NS Nematswerani, N Nyembezi-Heita, N Payne, G Serobe Alternate Director: J Berman Company Secretary: GC Clarke Safex Options and the Greeks 101 Dr A. A. Kotzé 1 November 2010 If you have traded a few options but are relatively new to trading them, you are probably battling to understand why some of your trades aren’t profitable. You start to realise that trying to predict what will happen to the price of a single option or a position involving multiple options as the market changes can be a difficult undertaking. You experience the forces of the market and see that an option price does not always appear to move in conjunction with the price of the underlying asset or share. If you want to trade in any financial instrument, it is important to understand what factors contribute to the movement in the price of that instrument, and what effect they have. In previous lessons you did learn about option pricing and the Black-Scholes equation used to value options. In these lessons you learnt that an option price is influenced by the following parameters Value of the underlying futures contract The strike price The time till expiration or close-out date The volatility of the underlying futures contract If you’ve done some wider reading you should have picked up that we left out two parameters: interest rates and dividends or a dividend yield. The reason being that Safex’s options are options on futures contracts and the futures level take these two parameters into account implicitly; we thus do not have to worry about them. Gaining an understanding of some the abovementioned variables that influence options pricing can help you become a more successful trader – it is a must for any investor who would like to invest in options. When we talk about these variables in relation to option pricing, we call them the Greeks. You might have heard terms such as Delta or Vega and you immediately thought option trading is too difficult or risky. However, what you will learn in this lesson is that learning things the 'Greek' way is like knowing the baby steps towards potential gains. While many traders focus on stock prices and trends, options pricing and its unpredictability seems to be a bigger problem. For one, the value of options is so uncertain that sometimes trends and factors provide no help at all. If you know about 1 Consultant from Financial Chaos Theory. For more details surf to www.quantonline.co.za V

-

Upload

johannesburg -

Category

Documents

-

view

4 -

download

0

Transcript of Safex Options and the Greeks 101

JSE Limited Registration Number: 2005/022939/06

One Exchange Square, Gwen Lane, Sandown, South Africa.

Private Bag X991174, Sandton, 2146, South Africa. Telephone:

+27 11 520 7000, Facsimile: +27 11 520 8584, www.jse.co.za

Member of the World Federation of Exchanges

Executive Directors: RM Loubser (CEO), NF Newton-King, F

Evans (CFO), JH Burke, LV Parsons Non-Executive Directors:

HJ Borkum (Chairman), AD Botha, ZL Combi, MR Johnston, DM

Lawrence, W Luhabe, A Mazwai, NS Nematswerani, N

Nyembezi-Heita, N Payne, G Serobe Alternate Director: J

Berman

Company Secretary: GC Clarke

Safex Options and the Greeks 101 Dr A. A. Kotzé1 November 2010

If you have traded a few options but are relatively new to trading them, you are probably battling to understand why some of your trades aren’t profitable. You start to realise that trying to predict what will happen to the price of a single option or a position involving multiple options as the market changes can be a difficult undertaking. You experience the forces of the market and see that an option price does not always appear to move in conjunction with the price of the underlying asset or share. If you want to trade in any financial instrument, it is important to understand what factors contribute to the movement in the price of that instrument, and what effect they have. In previous lessons you did learn about option pricing and the Black-Scholes equation used to value options. In these lessons you learnt that an option price is influenced by the following parameters

Value of the underlying futures contract The strike price The time till expiration or close-out date The volatility of the underlying futures contract

If you’ve done some wider reading you should have picked up that we left out two parameters: interest rates and dividends or a dividend yield. The reason being that Safex’s options are options on futures contracts and the futures level take these two parameters into account implicitly; we thus do not have to worry about them. Gaining an understanding of some the abovementioned variables that influence options pricing can help you become a more successful trader – it is a must for any investor who would like to invest in options. When we talk about these variables in relation to option pricing, we call them the Greeks. You might have heard terms such as Delta or Vega and you immediately thought option trading is too difficult or risky. However, what you will learn in this lesson is that learning things the 'Greek' way is like knowing the baby steps towards potential gains. While many traders focus on stock prices and trends, options pricing and its unpredictability seems to be a bigger problem. For one, the value of options is so uncertain that sometimes trends and factors provide no help at all. If you know about

1 Consultant from Financial Chaos Theory. For more details surf to www.quantonline.co.za

V

Page 2 of 10

technical analysis of shares, try some of those analyses on option values. You will quickly realise that momentum or stochastics are of no use at all. Further to the above, we pile on the fact that the Greeks cannot simply be looked up in your everyday option tables nor will you see them on screen where you see the option bids and offers. They need to be calculated which means you will need access to a computer or electronic calculator that calculates them for you. I am sure that you are thinking: why bother in trading options? Trading just the futures seems much simpler and easier. However, please bear with me. Simply put, understanding option Greeks provides a corresponding remedy, as it introduces options pricing in a much more comprehensible manner. We will also look at some easy ways in calculating them. In this lesson we will investigate the following Greeks: the Delta, the Gamma, the Theta and the Vega. Let’s start with the Delta.

Delta – The Bang for Your Buck

SYMBOL: Delta is the measure of how an option’s value (or premium) changes given a unit change in the underlying futures price. Basically, it describes the relationship between the future’s price movement and the gain or loss on your option. This statement can be interpreted in 3 different ways. First If we use the Alsi future as an example, the Delta of an option on the Alsi future tells us how much the value of an Alsi option will change based upon a 1 point change in the futures market. The delta value for a call option ranges between zero and one, often expressed as a percentage of zero to 100 percent. A put would have negative delta values, ranging from 0 to -100 percent. A zero delta would have little movement, while an option with a 99 or 100 delta would experience large price swings. For example, let’s look at the March 2011 Alsi futures contract. Today, 11 November 2010 the future’s MtM was 28436 and the ATM volatility is 19.75%. If we calculate the delta for an ATM option (strike 28450) we get a delta of 52%. What does this mean? It means that the option value changes by R5.20 if the futures level changes by 1 point to 28437. If you are long this call option, you will gain R5.20. How did we get the R5.20? We do the following Change in option value = Delta (as percentage) X 100 divided by 10 = 52% X 100 / 10 = 5.20 How did we calculate the Delta? We first calculate the option value with an Alsi level of 28436 and this is R13,037.61. Keep everything the same but increase the Alsi level by 1 point to 28437 and calculate the value. This comes to R13,042.82. The difference, divided by 10 is the Delta Delta = (Black-Scholes value (Alsi: 28437) – Black-Scholes value (Alsi: 28436))/10 = (13,042.82 – 13,037.61 )/10 = 52%

Page 3 of 10

Why do we divide by 10? Remember, the Alsi future has a R10 per point value – called the multiplier. It means that for every one point gain in the index, you either make or loose R10. The same method can be used to find the Delta for an option on a Single Stock Future. Let’s look at MTN. The March 2011 future is trading at R131.00 per contract. As an example, we assume we want to buy a put to hedge a long futures position. To make the option a little less expensive, we are looking at a R125 strike price. The volatility is 27.5% and we then have Delta = (Black-Scholes value (MTN: 131.01) – Black-Scholes value (MTN: 131.00)) = (545.59 – 545.94 ) = -35.4% We thus increased the MTN price by 1 cent. We do not have to divide by 10 because a 1 cent gain on MTN is exactly a 1 cent gain – there is no multiplier. Second Now, the usefulness of the Delta does not end here. Its real use comes into play if you see it as a hedging parameter or a hedge ratio. Delta used in this way is sometimes called the “Position Delta” and the trading strategy is called “Delta Neutral Trading”. Delta is in effect a hedge ratio because it tells us how many option contracts are needed to hedge a long or short position in the underlying. It is a very easy concept to grasp. If you bought 100 of the abovementioned Alsi calls and future gains 1 point, your gain in option value is

100 X R5.20 = R520. However, if the Alsi future loses 1 point, you will lose R520! Please remember that the Delta is symmetrical around the strike price. If you cannot get out of your position, what will you do? You need to hedge. You will hedge your long call position by selling futures. The question is how many futures? You need to sell so many futures such that your gain on your short position is R520. This means you need to sell 52 futures! Please remember the R10 per point value of an Alsi futures contract. We can thus summarise this as Number of futures to sell = Delta as percentage X 100 Third The Delta of an option has a sign: a long call is positive while a long put’s Delta is negative. We use the sign in telling us whether to buy or sell the underlying future when we want to hedge. A positive Delta tells us to SELL and a negative Delta tells us to BUY! In out first example the long Alsi call had a Delta of 52%. This means you have to SELL 52 Alsi future contracts to hedge yourself. In our MTN example, the long put, the Delta was -35%. If you want to hedge this put, BUY 35 MTN futures contracts! Some More Notes Please also note further: I mentioned that the Delta is influenced by the strike price. If we look at the abovementioned Alsi call, but change the strike to 25,000, the Delta changes to 83%. If the strike is set at 31,000, the Delta changes to 20%. In general, please note the following:

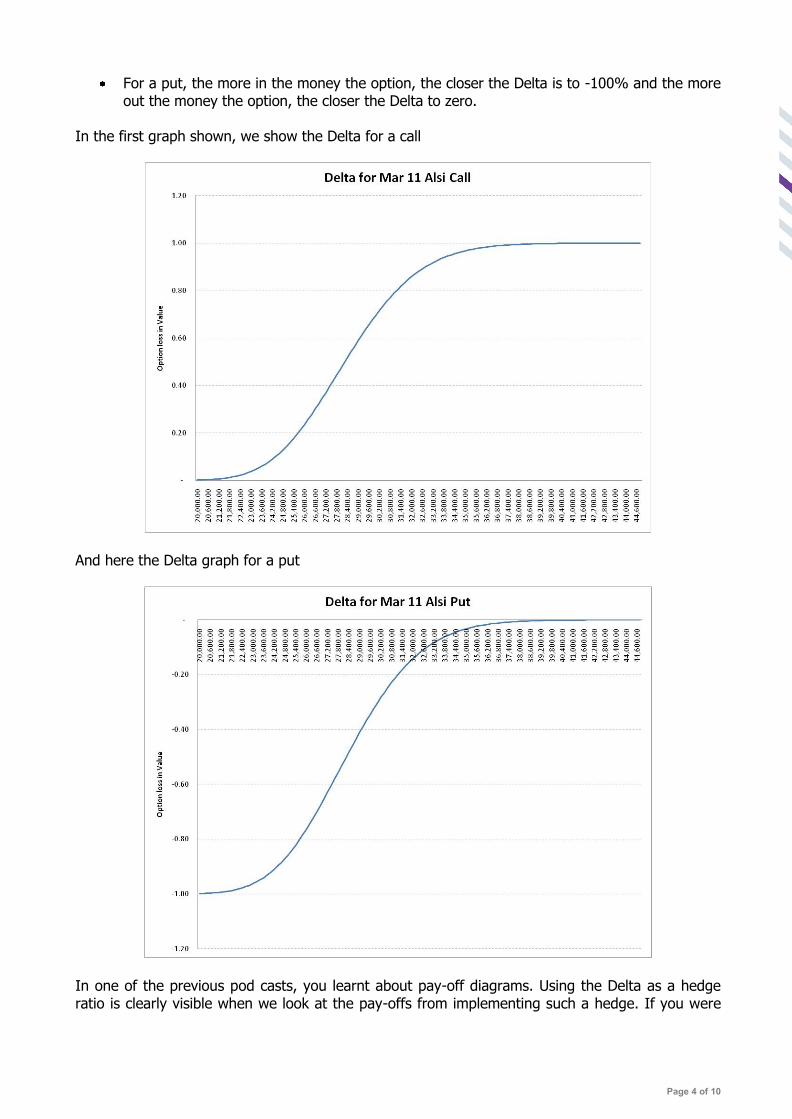

For a call, the more in the money the option, the closer the Delta is to 100% and the more out the money the option, the closer the Delta to zero.

Page 4 of 10

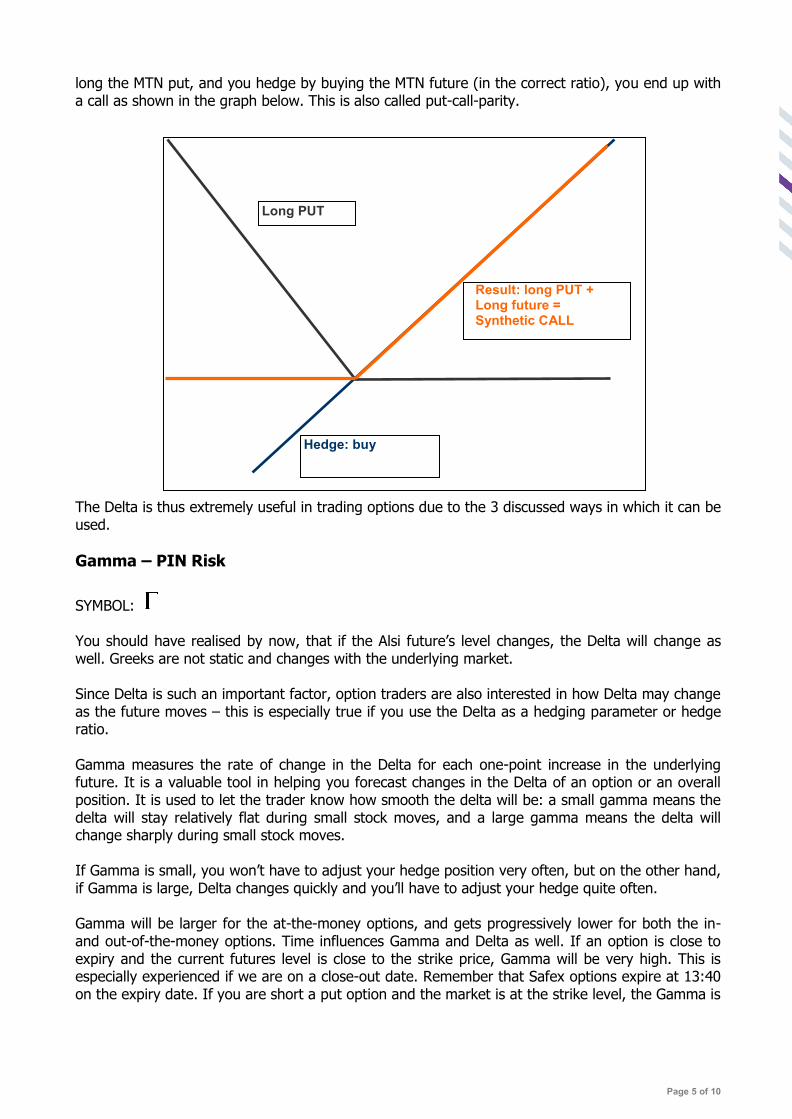

For a put, the more in the money the option, the closer the Delta is to -100% and the more out the money the option, the closer the Delta to zero.

In the first graph shown, we show the Delta for a call

And here the Delta graph for a put

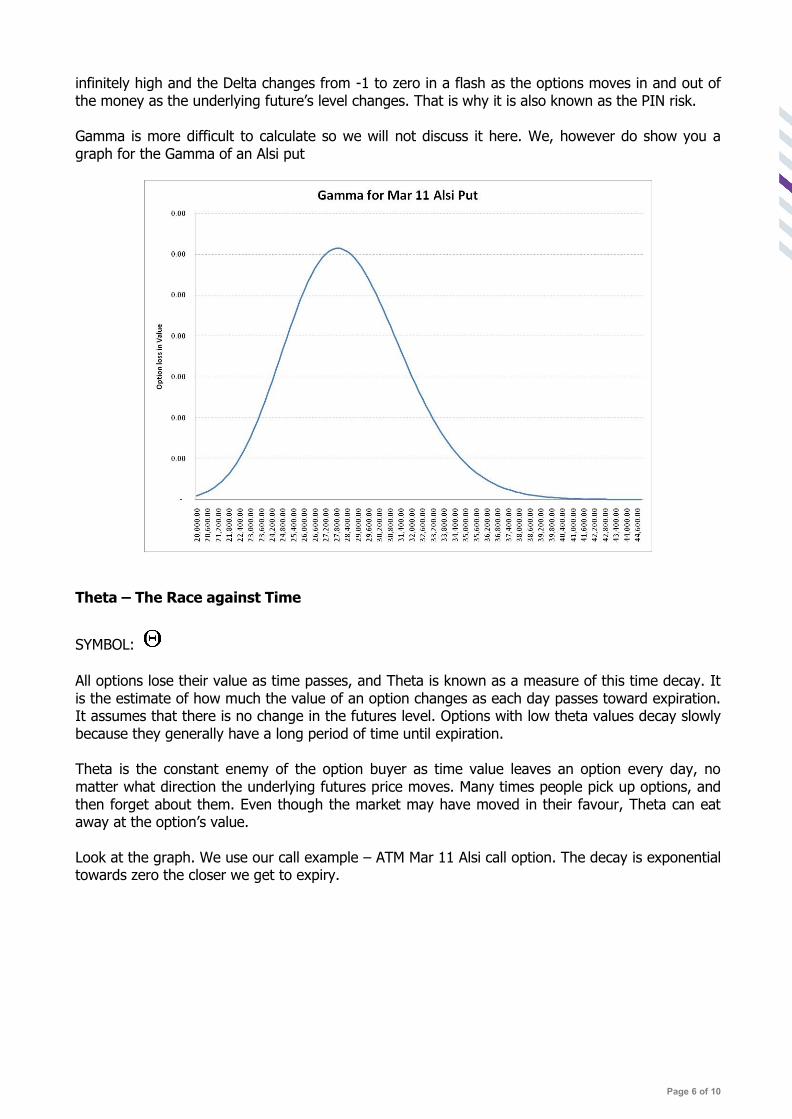

In one of the previous pod casts, you learnt about pay-off diagrams. Using the Delta as a hedge ratio is clearly visible when we look at the pay-offs from implementing such a hedge. If you were

Page 5 of 10

long the MTN put, and you hedge by buying the MTN future (in the correct ratio), you end up with a call as shown in the graph below. This is also called put-call-parity. The Delta is thus extremely useful in trading options due to the 3 discussed ways in which it can be used.

Gamma – PIN Risk

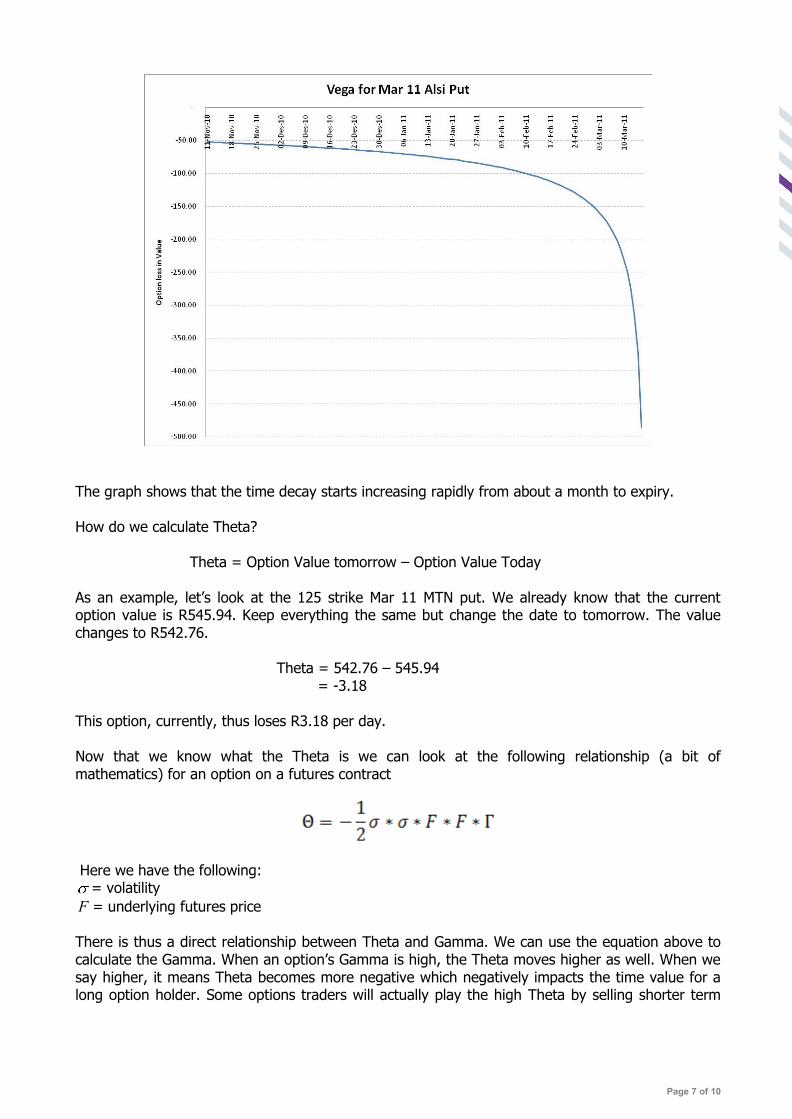

SYMBOL: You should have realised by now, that if the Alsi future’s level changes, the Delta will change as well. Greeks are not static and changes with the underlying market. Since Delta is such an important factor, option traders are also interested in how Delta may change as the future moves – this is especially true if you use the Delta as a hedging parameter or hedge ratio. Gamma measures the rate of change in the Delta for each one-point increase in the underlying future. It is a valuable tool in helping you forecast changes in the Delta of an option or an overall position. It is used to let the trader know how smooth the delta will be: a small gamma means the delta will stay relatively flat during small stock moves, and a large gamma means the delta will change sharply during small stock moves. If Gamma is small, you won’t have to adjust your hedge position very often, but on the other hand, if Gamma is large, Delta changes quickly and you’ll have to adjust your hedge quite often. Gamma will be larger for the at-the-money options, and gets progressively lower for both the in- and out-of-the-money options. Time influences Gamma and Delta as well. If an option is close to expiry and the current futures level is close to the strike price, Gamma will be very high. This is especially experienced if we are on a close-out date. Remember that Safex options expire at 13:40 on the expiry date. If you are short a put option and the market is at the strike level, the Gamma is

Long PUT

Hedge: buy

Result: long PUT + Long future = Synthetic CALL

Page 6 of 10

infinitely high and the Delta changes from -1 to zero in a flash as the options moves in and out of the money as the underlying future’s level changes. That is why it is also known as the PIN risk. Gamma is more difficult to calculate so we will not discuss it here. We, however do show you a graph for the Gamma of an Alsi put

Theta – The Race against Time

SYMBOL:

All options lose their value as time passes, and Theta is known as a measure of this time decay. It is the estimate of how much the value of an option changes as each day passes toward expiration. It assumes that there is no change in the futures level. Options with low theta values decay slowly because they generally have a long period of time until expiration. Theta is the constant enemy of the option buyer as time value leaves an option every day, no matter what direction the underlying futures price moves. Many times people pick up options, and then forget about them. Even though the market may have moved in their favour, Theta can eat away at the option’s value. Look at the graph. We use our call example – ATM Mar 11 Alsi call option. The decay is exponential towards zero the closer we get to expiry.

Page 7 of 10

The graph shows that the time decay starts increasing rapidly from about a month to expiry. How do we calculate Theta? Theta = Option Value tomorrow – Option Value Today As an example, let’s look at the 125 strike Mar 11 MTN put. We already know that the current option value is R545.94. Keep everything the same but change the date to tomorrow. The value changes to R542.76. Theta = 542.76 – 545.94 = -3.18 This option, currently, thus loses R3.18 per day. Now that we know what the Theta is we can look at the following relationship (a bit of mathematics) for an option on a futures contract

Here we have the following:

= volatility

F = underlying futures price There is thus a direct relationship between Theta and Gamma. We can use the equation above to calculate the Gamma. When an option’s Gamma is high, the Theta moves higher as well. When we say higher, it means Theta becomes more negative which negatively impacts the time value for a long option holder. Some options traders will actually play the high Theta by selling shorter term

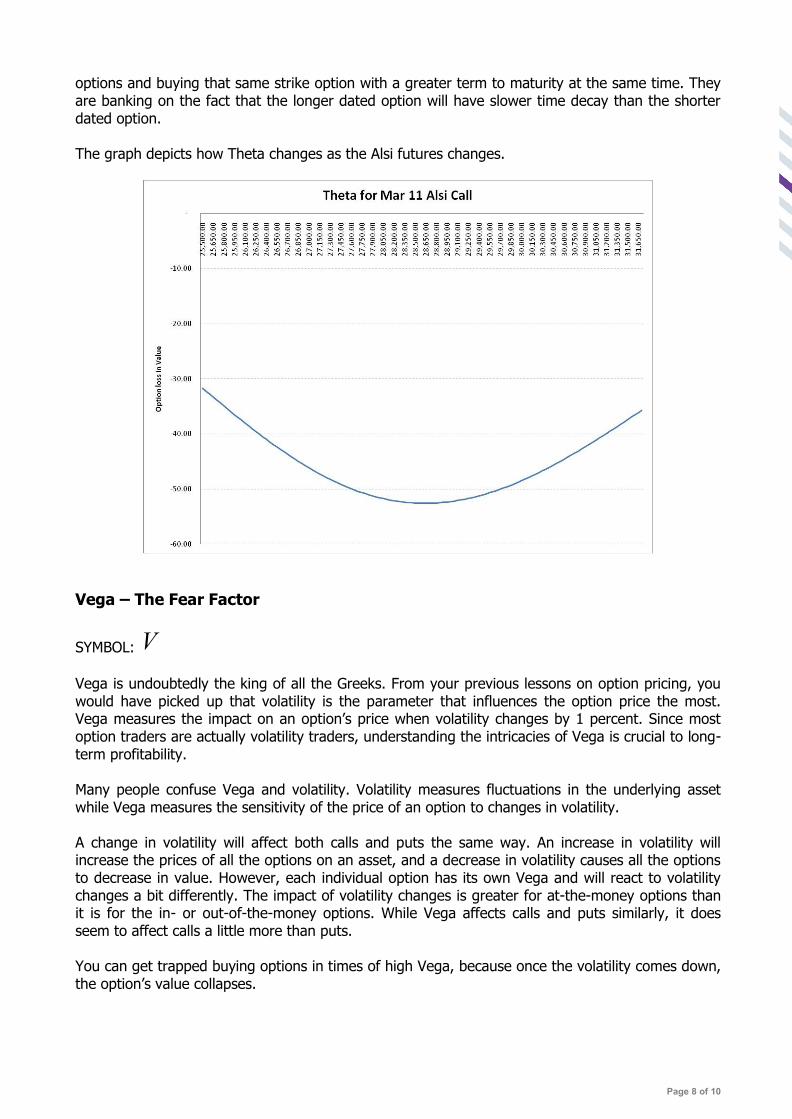

Page 8 of 10

options and buying that same strike option with a greater term to maturity at the same time. They are banking on the fact that the longer dated option will have slower time decay than the shorter dated option. The graph depicts how Theta changes as the Alsi futures changes.

Vega – The Fear Factor

SYMBOL: V

Vega is undoubtedly the king of all the Greeks. From your previous lessons on option pricing, you would have picked up that volatility is the parameter that influences the option price the most. Vega measures the impact on an option’s price when volatility changes by 1 percent. Since most option traders are actually volatility traders, understanding the intricacies of Vega is crucial to long-term profitability. Many people confuse Vega and volatility. Volatility measures fluctuations in the underlying asset while Vega measures the sensitivity of the price of an option to changes in volatility. A change in volatility will affect both calls and puts the same way. An increase in volatility will increase the prices of all the options on an asset, and a decrease in volatility causes all the options to decrease in value. However, each individual option has its own Vega and will react to volatility changes a bit differently. The impact of volatility changes is greater for at-the-money options than it is for the in- or out-of-the-money options. While Vega affects calls and puts similarly, it does seem to affect calls a little more than puts. You can get trapped buying options in times of high Vega, because once the volatility comes down, the option’s value collapses.

Page 9 of 10

How do we calculate Vega? Vega = Option Value with volatility + 1% - Option Value with current volatility As an example, let’s look at the MTN put. The current value is R545.94. If we increase the volatility from 27.5% to 28.5% the option value becomes R574.15. We then have

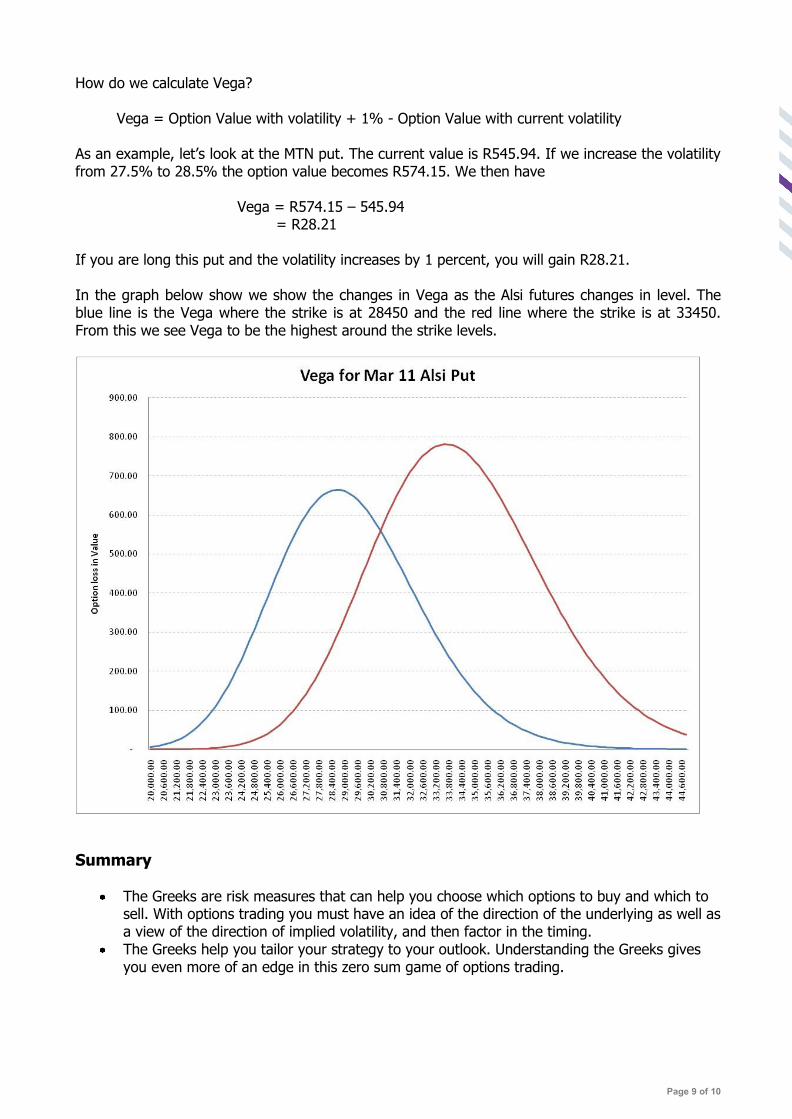

Vega = R574.15 – 545.94 = R28.21 If you are long this put and the volatility increases by 1 percent, you will gain R28.21. In the graph below show we show the changes in Vega as the Alsi futures changes in level. The blue line is the Vega where the strike is at 28450 and the red line where the strike is at 33450. From this we see Vega to be the highest around the strike levels.

Summary

The Greeks are risk measures that can help you choose which options to buy and which to sell. With options trading you must have an idea of the direction of the underlying as well as a view of the direction of implied volatility, and then factor in the timing.

The Greeks help you tailor your strategy to your outlook. Understanding the Greeks gives you even more of an edge in this zero sum game of options trading.

Page 10 of 10

References These notes were complied from various resources. Here are a few good references for further reading: A. A. Kotzé, Equity Derivatives: effective and practical techniques for mastering and trading equity derivatives, Workshop proceedings (2002) A. A. Kotzé, Stock Price Volatility: a primer, The South African Financial Markets Journal, 1 (April 2005) A. A. Kotzé, Derivatives on Equities and Equity Futures in the South African Market, Working Paper (July 2001) J. Hull, Options, Futures, and other Derivatives, Prentice-Hall (1997) – newer editions are available The following web resources are excellent http://www.letstalkfutures.com/2010/02/24/options-greeks-101/ http://en.wikipedia.org/wiki/Greeks_(finance) http://ezinearticles.com/?Understanding-Option-Greeks-That-Make-Sense&id=2568405 http://www.investopedia.com/articles/optioninvestor/04/121604.asp http://www.optiontradingpedia.com/free_option_greeks.htm http://www.tradingmarkets.com/.site/options/how_to/articles/-77087.cfm

![[5365]-11 MBA 101](https://static.fdokumen.com/doc/165x107/6322631aae0f5e819105deed/5365-11-mba-101.jpg)

![[3937]-101 P553](https://static.fdokumen.com/doc/165x107/63338430a6138719eb0aa5bc/3937-101-p553.jpg)

![[5437]-101 M.Sc ENVIRONMENTAL SCIENCE EVSC 101](https://static.fdokumen.com/doc/165x107/631d8020ec7900c0c80d1eb7/5437-101-msc-environmental-science-evsc-101.jpg)