Rose−Hudgins: Bank Management and Financial Services, Seventh Edition II. Financial Statements and...

42

Rose-Hudgins: Bank Management and Financial Services, Seventh Edition II. Financial Statements and Financial Firm Performance 6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors © The McGraw-Hill Companies, 2008 CHAPTER SIX Measuring and Evaluating the Performance of Banks and Their Principal Competitors Key Topics in This Chapter • Stock Values and Profitability Ratios • Measuring Credit, Liquidity, and Other Risks • Measuring Operating Efficiency • Performance of Competing Financial Firms • Size and Location Effects • The UBPR and Comparing Performance 6–1 Introduction Humorist and poet Ogden Nash once wrote, “Bankers are just like anybody else, except richer.” It turns out that statement may or may not be true; a lot depends upon how suc- cessful bankers and other financial-service managers are as performers in the financial marketplace. Indeed, in today’s world, bankers and their competitors are under great pres- sure to perform well all the time. What do we mean by the word perform when it comes to financial firms? In this case performance refers to how adequately a financial firm meets the needs of its stockholders (owners), employees, depositors and other creditors, and borrowing customers. At the same time, financial firms must find a way to keep government regulators satisfied that their operating policies, loans, and investments are sound, protecting the public interest. The success or lack of success of these institutions in meeting the expectations of others is usually revealed by a careful study of their financial statements. Why are financial statements under such heavy scrutiny today? One key reason is that banks and other financial institutions now depend heavily upon the open market to raise the funds they need, selling stocks, bonds, and short-term IOUs (including deposits). Entry into the open market to raise money means that a financial firm’s financial statements will 163

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Rose−Hudgins: Bank Management and Financial Services, Seventh Edition II. Financial Statements and...

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

C H A P T E R S I X

Measuring andEvaluating thePerformance of Banksand Their PrincipalCompetitorsKey Topics in This Chapter

• Stock Values and Profitability Ratios

• Measuring Credit, Liquidity, and Other Risks

• Measuring Operating Efficiency

• Performance of Competing Financial Firms

• Size and Location Effects

• The UBPR and Comparing Performance

6–1 IntroductionHumorist and poet Ogden Nash once wrote, “Bankers are just like anybody else, exceptricher.” It turns out that statement may or may not be true; a lot depends upon how suc-cessful bankers and other financial-service managers are as performers in the financialmarketplace. Indeed, in today’s world, bankers and their competitors are under great pres-sure to perform well all the time.

What do we mean by the word perform when it comes to financial firms? In this caseperformance refers to how adequately a financial firm meets the needs of its stockholders(owners), employees, depositors and other creditors, and borrowing customers. At thesame time, financial firms must find a way to keep government regulators satisfied thattheir operating policies, loans, and investments are sound, protecting the public interest.The success or lack of success of these institutions in meeting the expectations of others isusually revealed by a careful study of their financial statements.

Why are financial statements under such heavy scrutiny today? One key reason is thatbanks and other financial institutions now depend heavily upon the open market to raisethe funds they need, selling stocks, bonds, and short-term IOUs (including deposits). Entryinto the open market to raise money means that a financial firm’s financial statements will

163

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

be gone over “with a fine tooth comb” by stock and bond market investors, credit ratingagencies (such as Moody’s and Standard & Poor’s), regulators, and scores of other peopleand institutions.

This development has placed the management of banks and many of their competitorsunder great pressure to set and meet the institution’s performance goals or suffer seriousfinancial and reputational losses. In 2002 J. P. Morgan Chase, the second largest bankingcompany in the United States, became a prominent example. The firm’s credit ratingcame under review and, for a time, it faced rising borrowing costs as major depositors andother creditors reacted negatively to the bank’s potential loan losses and the adverse pub-licity from its alleged involvement with Enron Corporation and other troubled companies.Subsequently, J. P. Morgan Chase’s position strengthened and improved.

At the same time, as we saw in Chapters 1–4, competition for traditional loan and depositcustomers has increased dramatically. Credit unions, money market funds, insurance com-panies, brokerage firms and security dealers, and even chain stores are fighting for a biggerslice of nearly every credit or deposit market. Bankers have been called upon to continuallyreevaluate their loan and deposit policies, review their plans for growth and expansion, andassess their returns and risk exposure in light of this new competitive environment.

In this chapter we take a detailed look at the most widely used indicators of the quality andquantity of bank performance and at some performance indicators used to measure banking’sprincipal competitors. The chapter centers on the most important dimensions of perfor-mance—profitability and risk. After all, financial institutions are simply businesses organized tomaximize the value of the shareholders’ wealth invested in the firm at an acceptable level ofrisk. The objectives of maximum (or at least satisfactory) profitability with a level of riskacceptable to the institution’s owners is not easy to achieve, as recent institutional failuresaround the globe suggest. Aggressive pursuit of such an objective requires a financial firm tobe continually on the lookout for new opportunities for revenue growth, greater efficiency,and more effective planning and control. The pages that follow examine the most importantmeasures of return and risk for banks and some of their toughest competitors.

6–2 Evaluating PerformanceHow can we use financial statements, particularly the Report of Condition (balance sheet)and Report of Income (income statement), to evaluate how well a financial firm is per-forming? What do we look at to help decide if a financial institution is facing serious prob-lems that its management should deal with?

Determining Long-Range ObjectivesThe first step in analyzing financial statements is to decide what objectives the bank orother financial firm is seeking. Performance must be directed toward specific objectives. Afair evaluation of any financial firm’s performance should start by evaluating whether ithas been able to achieve the objectives its management and stockholders have chosen.

Certainly many financial institutions have their own unique objectives. Some wish togrow faster and achieve some long-range growth objective. Others seem to prefer the quietlife, minimizing risk and conveying the image of a sound institution, but with modestrewards for their shareholders.

Maximizing the Value of the Firm: A Key Objective for Nearly All Financial-Service InstitutionsWhile all of the foregoing goals have something to recommend them, increasingly finan-cial-service corporations are finding they must pay close attention to the value of their

164 Part Two Financial Statements and Financial Firm Performance

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

stock. Indeed, the basic principles of financial management, as that science is practicedtoday, suggest strongly that attempting to maximize a corporation’s stock value is the keyobjective that should have priority over all others. If the stock fails to rise in value com-mensurate with stockholder expectations, current investors may seek to unload theirshares and the financial institution will have difficulty raising new capital to support itsfuture growth. Clearly, then, management should pursue the objective of maximizing thevalue of the financial firm’s stock.

What will cause a financial firm’s stock to rise in value? Each institution’s stock price isa function of the

(6–1)

where E(Dt) represents stockholder dividends expected to be paid in future periods, dis-counted by a minimum acceptable rate of return (r) tied to the financial firm’s perceivedlevel of risk. The minimum acceptable rate of return, r, is sometimes referred to as an insti-tution’s cost of capital and has two main components: (1) the risk-free rate of interest (oftenproxied by the current yield on government bonds) and (2) the equity risk premium(which is designed to compensate an investor for accepting the risk of investing in a finan-cial firm’s stock rather than in risk-free securities).

The value of the financial firm’s stock will tend to rise in any of the following situations:

1. The value of the stream of future stockholder dividends is expected to increase, due per-haps to recent growth in some of the markets served or perhaps because of profitableacquisitions the organization has made.

2. The financial organization’s perceived level of risk falls, due perhaps to an increase inequity capital, a decrease in its loan losses, or the perception of investors that the institu-tion is less risky overall (perhaps because it has further diversified its service offerings andexpanded the number of markets it serves) and, therefore, has a lower equity risk premium.

3. Market interest rates decrease, reducing shareholders’ acceptable rates of return via therisk-free rate of interest component of all market interest rates.

4. Expected dividend increases are combined with declining risk, as perceived by investors.Research evidence over the years has found the stock values of financial institutions to

be especially sensitive to changes in market interest rates, currency exchange rates, andthe strength or weakness of the economy that each serves. Clearly, management can workto achieve policies that increase future earnings, reduce risk, or pursue a combination ofboth actions in order to raise its company’s stock price.

The formula for the determinants of a financial firm’s stock price presented in Equation(6–1) assumes that the stock may pay dividends of varying amounts over time. However, ifthe dividends paid to stockholders are expected to grow at a constant rate over time, perhapsreflecting steady growth in earnings, the stock price equation can be greatly simplified intothe form

Po � D1/(r � g) (6–2)

where D1 is the expected dividend on stock in period 1, r is the rate of discountreflecting the perceived level of risk attached to investing in the stock, g is the

Value ofstock1Po 2

�

Expected stream of futurestockholder dividends

Discount factor 1based onthe minimum required marketrate of return on equity capital

given each financial firm'sperceived level of risk 2

� aq

t�0

E1Dt 211 � r 2 t

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 165

Key URLsThe mostcomprehensive sites onthe World Wide Webfor the financialstatements of individualbanks and for theindustry as a whole arewww2.fdic.gov/sdiand www.ffiec.gov/nicpubweb/nicweb/nichome.aspx.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

expected constant growth rate at which stock dividends will grow each year, and rmust be greater than g.

For example, suppose that a bank is expected to pay a dividend of $5 per share in period 1,dividends are expected to grow 6 percent a year thereafter, and the appropriate discount rateto reflect shareholder risk is 10 percent. Then the bank’s stock price must be valued at

Po � $5/(0.10 � 0.06) � $125 per share

The two stock-price formulas discussed above assume the financial firm will pay div-idends indefinitely into the future. Most capital-market investors have a limited timehorizon, however, and plan to sell the stock at the end of their planned investmenthorizon. In this case the current value of a financial corporation’s stock is determinedfrom

(6–3)

where we assume the investor will hold the stock for n periods, receiving the stream of div-idends D1 D2, ..., Dn, and sell the stock for price Pn at the end of the planned investmenthorizon. For example, suppose investors expect a bank to pay a $5 dividend at the end ofperiod 1, $10 at the end of period 2, and then plan to sell the stock for a price of $150 pershare. If the relevant discount rate to capture risk is 10 percent, the current value of thebank’s stock should approach:

Po �$5

11 � 0.10 2 1 �$10

11 � 0.10 2 2 �$150

11 � 0.10 2 2 � $136.78 per share1

Po �D1

11 � r 2 1 �D2

11 � r 2 2 � p �Dn

11 � r 2n �Pn

11 � r 2n

166 Part Two Financial Statements and Financial Firm Performance

1A financial calculator can be used to help solve the above equation for stock price per share where N = 2, I/Y = 10, PV = (?),Pmt = 5, FV = 155.

Profitability Ratios: A Surrogate for Stock ValuesWhile the behavior of a stock’s price is, in theory, the best indicator of a financial firm’sperformance because it reflects the market’s evaluation of that firm, this indicator is oftennot available for smaller banks and other relatively small financial-service corporationsbecause the stock issued by smaller institutions is frequently not actively traded in inter-national or national markets. This fact forces the financial analyst to fall back on surro-gates for market-value indicators in the form of various profitability ratios.

Concept Check

6–1. Why should banks and other corporate financialfirms be concerned about their level of profitabilityand exposure to risk?

6–2. What individuals or groups are likely to be interestedin these dimensions of performance for a financialinstitution?

6–3. What factors influence the stock price of a financial-service corporation?

6–4. Suppose that a bank is expected to pay an annualdividend of $4 per share on its stock in the currentperiod and dividends are expected to grow 5 percenta year every year, and the minimum required returnto equity capital based on the bank’s perceived levelof risk is 10 percent. Can you estimate the currentvalue of the bank’s stock?

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Key Profitability RatiosAmong the most important ratio measures of profitability used today are the following:

(6–4)

(6–5)

(6–6)

(6–7)

(6–8)

(6–9)

Like all financial ratios, each of these profitability measures often varies substantially overtime and from market to market.

Interpreting Profitability RatiosEach of the foregoing ratios looks at a slightly different aspect of profitability. Thus, returnon assets (ROA) is primarily an indicator of managerial efficiency; it indicates how capablemanagement has been in converting assets into net earnings. Return on equity (ROE), onthe other hand, is a measure of the rate of return flowing to shareholders. It approximates the

Earnings per shareof stock 1EPS 2 �

Net incomeCommon equity shares outstanding

Net operating margin �

a Total operating revenues� Total operating expenses

bTotal assets

Net noninterestmargin

�

a Noninterest revenues� Noninterest expenses

bTotal assets2

Net interest margin �

a Interest income� Interest expense

bTotal assets2

Return on assets1ROA 2 �

Net incomeTotal assets

Return on equity capital1ROE 2 �Net income

Total equity capital

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 167

FINANCIAL FIRMS IMPROVE PERFORMANCE BY OUTSOURCINGFinancial firms utilize information handled by computers fornearly every service they offer. As electronic data processingof financial information becomes more and more integral to thefunctions of financial-service firms, their managers can realizecost advantages from outsourcing—transferring tasks frominside the financial firm itself to outside firms specializing ininformation technology, known as vendors. Often the vendorsare centered in distant locations, such as China, India, andCosta Rica.

Institutions like Wachovia Bank, Bank of America, and Germany’s Deutsche Bank have become leaders in the adoptionof outsourcing designed to reduce the cost of operations. By out-sourcing computer facilities and people, these leading financial-service firms hope to save money and time while improvingoverall accuracy. Savings on personnel and equipment are obvi-ous benefits, but outsourcing also improves efficiency by elimi-nating “dead time” when a financial firm’s computer equipmentand staff are not being fully utilized. Through outsourcing, finan-cial institutions are basically “renting” the facilities and employ-ees of the vendor on an “as needed” basis.

E - B A N K I N G A N D E - C O M M E R C E

FactoidContrary to popularopinion, the largestbanks in the industryare not always the mostprofitable. The same istrue for the smallestbanks. The highestROAs and ROEs oftenlie among medium-sizeinstitutions.

2Many authorities prefer to use total earning assets in the denominator of the net interest margin and noninterest margin.Earning assets are those generating interest or fee income, principally loans and security investments. The reasoning is thatnet interest income as well as net noninterest income should be compared, not to all assets, but rather to those assets thataccount for the majority of all income.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

net benefit that the stockholders have received from investing their capital in the finan-cial firm (i.e., placing their funds at risk in the hope of earning a suitable profit).

The net operating margin, net interest margin, and net noninterest margin are efficiencymeasures as well as profitability measures, indicating how well management and staff havebeen able to keep the growth of revenues (which come primarily from loans, investments,and service fees) ahead of rising costs (principally the interest on deposits and other borrow-ings and employee salaries and benefits). The net interest margin measures how large aspread between interest revenues and interest costs management has been able to achieve byclose control over earning assets and pursuit of the cheapest sources of funding. The net non-interest margin, in contrast, measures the amount of noninterest revenues stemming fromservice fees the financial firm has been able to collect relative to the amount of noninterestcosts incurred (including salaries and wages, repair and maintenance of facilities, and loan-loss expenses). Typically, the net noninterest margin is negative: Noninterest costs generallyoutstrip fee income, though fee income has been rising rapidly in recent years as a percent-age of all revenues.

Another traditional measure of earnings efficiency is the earnings spread, or simply thespread, calculated as follows:

(6–10)

The spread measures the effectiveness of a financial firm’s intermediation function in bor-rowing and lending money and also the intensity of competition in the firm’s marketarea. Greater competition tends to squeeze the difference between average asset yieldsand average liability costs. If other factors are held constant, the spread will decline ascompetition increases, forcing management to try to find other ways (such as generatingfee income from new services) to make up for an eroding earnings spread.

Earningsspread

�Total interest incomeTotal earning assets

�Total interest expenseTotal interest-bearing

liabilities

168 Part Two Financial Statements and Financial Firm Performance

Concept Check

6–5. What is return on equity capital and what aspectof performance is it supposed to measure? Canyou see how this performance measure might beuseful to the managers of financial firms?

6–6. Suppose a bank reports that its net income for thecurrent year is $51 million, its assets total $1,144million, and its liabilities amount to $926 million.What is its return on equity capital? Is the ROE youhave calculated good or bad? What information doyou need to answer this last question?

6–7. What is the return on assets (ROA), and why is itimportant? Might the ROA measure be important tobanking’s key competitors?

6–8. A bank estimates that its total revenues will amountto $155 million and its total expenses (includingtaxes) will equal $107 million this year. Its liabilitiestotal $4,960 million while its equity capital amounts

to $52 million. What is the bank’s return on assets?Is this ROA high or low? How could you find out?

6–9. Why do the managers of financial firms often payclose attention today to the net interest margin andnoninterest margin? To the earnings spread?

6–10. Suppose a banker tells you that his bank in the yearjust completed had total interest expenses on allborrowings of $12 million and noninterest expensesof $5 million, while interest income from earningassets totaled $16 million and noninterest revenuestotaled $2 million. Suppose further that assetsamounted to $480 million, of which earning assetsrepresented 85 percent of that total while totalinterest-bearing liabilities amounted to 75 percent oftotal assets. See if you can determine this bank’s netinterest and noninterest margins and its earningsbase and earnings spread for the most recent year.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Useful Profitability Formulas for Banks and Other Financial-Service CompaniesIn analyzing how well any given financial-service firm is performing, it is often useful tobreak down some of these profitability ratios into their key components. For example, it iseasy to see that ROE and ROA, two of the most popular profitability measures in usetoday, are closely related. Both use the same numerator: net income. Therefore, these twoprofit indicators can be linked directly:

(6–11)

Or, in other words:

(6–12)

But we note that net income is equal to total revenues minus operating expenses and taxes.Therefore,

(6–13)

The relationships in Equations (6–12) and (6–13) remind us that the return to a financialfirm’s shareholders is highly sensitive to how its assets are financed—whether more debtor more owners’ capital is used. Even a financial institution with a low ROA can achievea relatively high ROE through heavy use of debt (leverage) and minimal use of owners’capital.

In fact, the ROE–ROA relationship illustrates quite clearly the fundamental trade-offthe managers of financial-service firms face between risk and return. For example, a bankwhose ROA is projected to be 1 percent this year will need $10 in assets for each $1 incapital to achieve a 10 percent ROE. That is, following Equation (6–11):

If, however, the bank’s ROA is expected to fall to 0.5 percent, a 10 percent ROE is attain-able only if each $1 of capital supports $20 in assets. In other words:

Indeed, we could construct a risk-return trade-off table like the one following that willtell us how much leverage (debt relative to equity) must be used to achieve a financialinstitution’s desired rate of return to its stockholders. For example, the trade-off table onpage 170 indicates that a financial firm with a 5-to-1 assets-to-capital ratio can expect (a) a2.5 percent ROE if ROA is 0.5 percent and (b) a 10 percent ROE if ROA is 2 percent. Incontrast, with a 20 to 1 assets-to-capital ratio a financial firm can achieve a 10 percentROE simply by earning a modest 0.5 percent ROA.

Clearly, as earnings efficiency represented by ROA declines, the firm must take onmore risk in the form of higher leverage to have any chance of achieving its desired rate ofreturn to its shareholders (ROE).

ROE �0.005 � $20 � 100

$1� 10 percent

�0.01 � $10 � 100

$1� 10 percent

ROE � ROA �Total assets

Total equity capital

ROE �

Total revenues � Total operatingexpenses � Taxes

Total assets�

Total assetsTotal equity capital

Net incomeTotal equity capital

�Net incomeTotal assets

�Total assets

Total equity capital

ROE � ROA �Total assets

Total equity capital

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 169

FactoidWho must declare thata bank operating in theUnited States hasfailed? Who usually sellsor liquidates the failedinstitution? Answer: Afailure declaration mustcome from the agencyissuing the bank’scharter; the seller orliquidator is normallythe FDIC.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Breaking Down Equity Returns for Closer AnalysisAnother highly useful profitability formula focusing upon ROE is this one:

(6–14)

or

ROE � Net profit margin � Asset utilization ratio � Equity multiplier

where:

(6–15)

(6–16)

(6–17)

Each component of this simple equation is a telltale indicator of a different aspect of afinancial firm’s operations. (See Exhibit 6–1.)

For example:

The net profit margin effectiveness of expensemanagement (cost control) andservice pricing policies.

The degree of asset portfolio management policies, utilization (AU) especially the mix and yield on

assets.The equity multiplier leverage or financing policies: the

sources chosen to fund the (EM)financial institution (debt or equity).

If any of these ratios begins to decline, management needs to pay close attention and assessthe reasons behind that change. For example, of these three financial ratios the equity multi-plier (EM), or assets to equity ratio, is normally the largest, averaging about 15X or larger formost banks. Bigger banks often operate with multipliers of 20X or more. The multiplier is a

reflects›

reflects›

reflects›

The equitymultiplier 1EM 2 �

Total assetsTotal equity capital

The degree ofasset utilization 1AU 2 �

Total operating revenuesTotal assets

The netprofit margin 1NPM 2 �

Net incomeTotal operating revenues

�Total assets

Total equity capital

ROE �Net income

Total operating revenue�

Total operating revenueTotal assets

170 Part Two Financial Statements and Financial Firm Performance

ROE with an ROA of:

Ratio of Total Assets to Total Equity Capital Accounts 0.5% 1.0% 1.5% 2.0%

5:1 2.5% 5.0% 7.5% 10.0%10:1 5.0 10.0 15.0 20.015:1 7.5 15.0 22.5 30.020:1 10.0 20.0 30.0 40.0

Risk-Return Trade-Offs for Return on Assets (ROA) and Return on Equity (ROE)

(NPM)

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

direct measure of financial leverage—how many dollars of assets must be supported by eachdollar of equity (owners’) capital and how much of the financial firm’s resources, therefore,must rest on debt. Because equity must absorb losses on assets, the larger the multiplier, themore exposed to failure risk the financial institution is. However, the larger the multiplier, thegreater the potential for high returns for the stockholders.

The net profit margin (NPM), or the ratio of net income to total revenues, is also sub-ject to some degree of management control and direction. It reminds us that financial-service corporations can increase their earnings and the returns to their stockholders bysuccessfully controlling expenses and maximizing revenues. Similarly, by carefully allo-cating assets to the highest-yielding loans and investments while avoiding excessive risk,management can raise the average yield on assets (AU, or asset utilization).

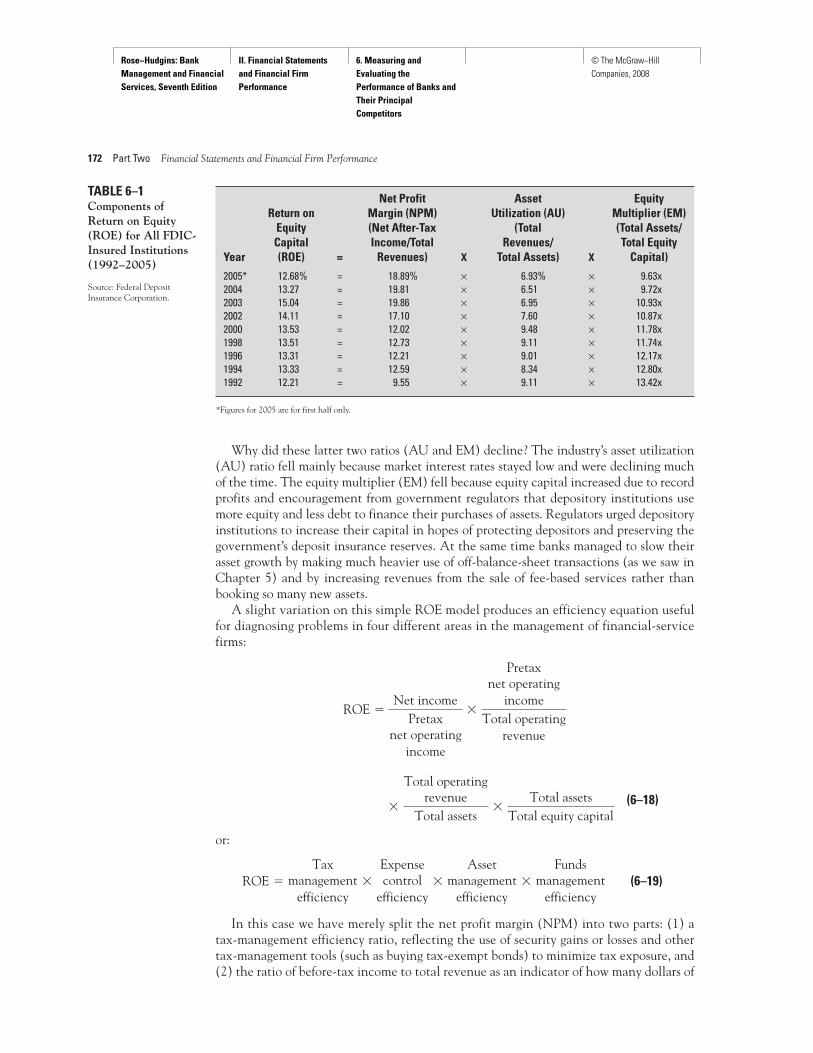

An interesting case in point is the recent track record of average ROE for all FDIC-insured depository institutions between 1992 and 2005, shown in Table 6–1. Carefulperusal of the figures in this table reveals very attractive ROEs for FDIC-insured deposi-tory institutions covering more than a decade. The lowest earnings over this period fordepository institutions, as measured by ROE, were a very acceptable 12.21 percent in1992. The average ROE for the industry gradually increased over the years, reaching 15.04percent in 2003 before falling back slightly.

What created such healthy ROEs between 1992 and 2005? Table 6–1 shows clearly thatthe primary cause was the industry’s net profit margin (NPM), which surged upward (par-ticularly noninterest revenues or fee income). Operating revenues expanded significantlyfaster than operating expenses. The industry’s expanding net profit margin more than off-set decreases in its asset utilization (AU) ratio and equity multiplier (EM).

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 171

Rate of returnearned on thestockholders’investment(ROE or net

income/equitycapital)

Equity multiplier (EM)or the employment offinancial leverage to

raise net earningsfor the stockholders

(total assets/equity capital)

Return on assets(ROA) as a measureof overall operating

efficiency (ROAor net

income/total assets)

Net profitmargin (net

income/operatingrevenues)

(NPM)

Management decisionsregarding capital structure:

What sources offunding shouldbe used?

What dividendsshould be paidto stockholders?

Management decisionsregarding:

The mix of fundsraised and invested

How big the institutionshould be

Control of operatingexpenses

The pricing ofservices

How to minimize thefinancial firm’s tax liability

Assetutilization(AU) as ameasureof asset

managementefficiency(operating

revenue/totalassets)

EXHIBIT 6–1 Elements that Determine the Rate of Return Earned on the Stockholders’ Investment (ROE) in a Financial Firm

FactoidIn the years since WorldWar II the number ofU.S. banks failingannually has averagedless than 1 or 2 percentof the industrypopulation.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Why did these latter two ratios (AU and EM) decline? The industry’s asset utilization(AU) ratio fell mainly because market interest rates stayed low and were declining muchof the time. The equity multiplier (EM) fell because equity capital increased due to recordprofits and encouragement from government regulators that depository institutions usemore equity and less debt to finance their purchases of assets. Regulators urged depositoryinstitutions to increase their capital in hopes of protecting depositors and preserving thegovernment’s deposit insurance reserves. At the same time banks managed to slow theirasset growth by making much heavier use of off-balance-sheet transactions (as we saw inChapter 5) and by increasing revenues from the sale of fee-based services rather thanbooking so many new assets.

A slight variation on this simple ROE model produces an efficiency equation usefulfor diagnosing problems in four different areas in the management of financial-servicefirms:

(6–18)

or:

(6–19)

In this case we have merely split the net profit margin (NPM) into two parts: (1) atax-management efficiency ratio, reflecting the use of security gains or losses and othertax-management tools (such as buying tax-exempt bonds) to minimize tax exposure, and(2) the ratio of before-tax income to total revenue as an indicator of how many dollars of

ROE �

Taxmanagement

efficiency�

Expensecontrol

efficiency�

Assetmanagement

efficiency�

Fundsmanagement

efficiency

�

Total operatingrevenue

Total assets�

Total assetsTotal equity capital

ROE �Net income

Pretaxnet operating

income

�

Pretaxnet operating

incomeTotal operating

revenue

172 Part Two Financial Statements and Financial Firm Performance

Net Profit Asset Equity Return on Margin (NPM) Utilization (AU) Multiplier (EM)

Equity (Net After-Tax (Total (Total Assets/Capital Income/Total Revenues/ Total Equity

Year (ROE) = Revenues) X Total Assets) X Capital)

2005* 12.68% = 18.89% × 6.93% × 9.63x2004 13.27 = 19.81 × 6.51 × 9.72x2003 15.04 = 19.86 × 6.95 × 10.93x2002 14.11 = 17.10 × 7.60 × 10.87x2000 13.53 = 12.02 × 9.48 × 11.78x1998 13.51 = 12.73 × 9.11 × 11.74x1996 13.31 = 12.21 × 9.01 × 12.17x1994 13.33 = 12.59 × 8.34 × 12.80x1992 12.21 = 9.55 × 9.11 × 13.42x

TABLE 6–1Components ofReturn on Equity(ROE) for All FDIC-Insured Institutions(1992–2005)

Source: Federal DepositInsurance Corporation.

*Figures for 2005 are for first half only.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

revenue survive after operating expenses are removed—a measure of operating efficiencyand expense control. For example, suppose a bank’s Report of Condition and Report ofIncome show the following figures:

Net income � $1.0 million

Pretax net operating income � $1.3 million

Total operating revenue � $39.3 million

Total assets � $122.0 million

Total equity capital � $7.3 million

Its ROE must be

Clearly, when any one of these four ratios begins to drop, management needs toreevaluate the financial firm’s efficiency in that area. In the banking example shownabove, if the ratio of net income to pretax net operating income falls from 0.769 to0.610 next year, management will want to look closely at how well the bank’s tax expo-sure is being monitored and controlled. If pretax net operating income to operatingrevenue drops from 0.033 to 0.025 in the coming year, the bank’s effectiveness in con-trolling operating expenses needs to be reviewed. And if the ratio of operating revenuesto assets plummets from 0.322 to 0.270, a careful reexamination of asset portfolio poli-cies is warranted to see if the decline in asset yields is due to factors within manage-ment’s control.

ROE � 0.769 � 0.033 � 0.322 � 16.71 � 0.137, or 13.7 percent

ROE �$1.0 mil$1.3 mil

�$1.3 mil$39.3 mil

�$39.3 mil$122.0 mil

�$122.0 mil$7.3 mil

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 173

QUESTIONABLE ACCOUNTING PRACTICES CANTURN BANK PERFORMANCE SOURIn 2001 Superior Bank of Chicago—a federal savings bank—failed and was taken over by the Federal Deposit InsuranceCorporation (FDIC). This failed banking firm provides a classicexample of how misleading accounting practices that inflateasset values and revenues and deflate liabilities and expensescan hurt a financial institution’s performance and ultimatelybring it down.

In 2002 the FDIC, acting as receiver and liquidator, filed suitagainst the public accounting firm of Ernst and Young LLP,claiming that the firm’s auditors detected flawed accountingpractices at Superior Bank, but did not report their findingsuntil months later. Allegedly, this delay on the part of the out-side auditors prevented regulators from acting quickly to min-imize losses to the government’s insurance fund.

Ernst and Young allegedly had both an auditor–client and aconsultant–client relationship with Superior. The FDIC charged

that this dual relationship compromised the auditors’ judgmentand discouraged them from “blowing the whistle” on thebank’s accounting problems. The delay in reporting overvalua-tion of the bank’s mortgage-related assets allegedly causedthe FDIC’s loss to eventually balloon to about three-quarters ofa billion dollars. The Sarbanes-Oxley Accounting StandardsAct of 2002 now restricts combined auditing and consultingrelationships in order to promote auditor objectivity and inde-pendence. However, that law was passed after the SuperiorBank failure occurred.

In short, strong performance on the part of financial-ser-vice providers depends on honest reporting that fairly valuescurrent and expected revenues, operating costs, assets, andliabilities so that both insiders and outsiders get a clear pictureof how well a financial firm is performing and where it seemsto be headed.

Source: Federal Deposit Insurance Corporation.

E T H I C S I N B A N K I N G A N DF I N A N C I A L S E R V I C E S

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Breakdown Analysis of the Return on AssetsWe can also divide a financial firm’s return on assets (ROA) into its component parts, asshown in Table 6–2. Actually, ROA is based on three simple component ratios:

Components of ROA

(6–20)

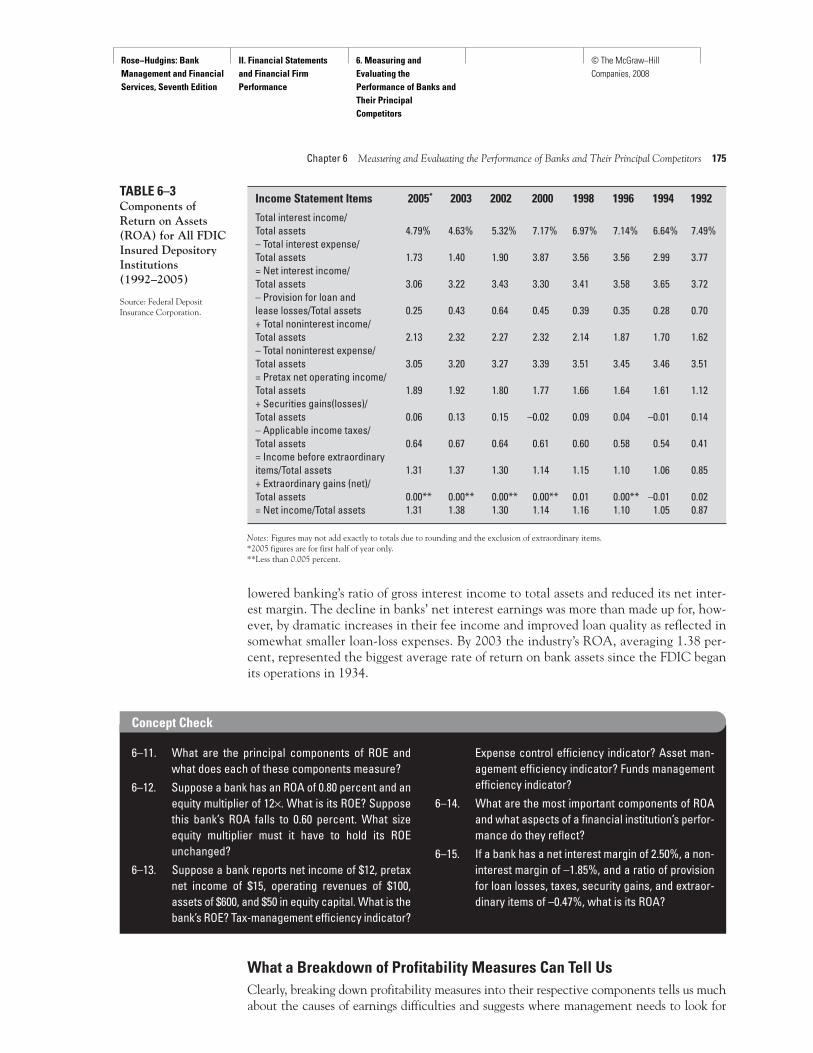

Such a breakdown of the components of return on assets (ROA) can be very helpful inexplaining some of the recent changes that financial-service providers have experiencedin their financial position. For example, as shown in Table 6–3, the average ROA for allFDIC-insured institutions between 1992 and 2005 rose from 0.87 percent in 1992 to ahigh of 1.38 percent in 2003 before leveling out in 2004 and 2005.

Why did ROA for 1992–2003 keep getting better and better? Better control overexpenses, led by advances in automation and mergers that eliminated many overlappingfacilities, along with an expanding economy, which propelled upward the public’sdemand for financial services, resulted in a rapid expansion of fee (noninterest) incomeand loan revenues. All this occurred in the face of falling market interest rates, which

Return on assets 1ROA, 2or the ability of

management to generate incomefrom assets 2

�

EQUALSNet incomeTotal assets

Special transactionsaffecting its net

income�

LESSProvision for loan losses; securities gains 1or losses 2

� taxes � extraordinary net gains

Total assets

Net noninterest margin �

PLUS1Noninterest income 2

� Noninterest expense 2Total assets

Net interest margin �1Interest income � Interest expense 2

Total assets

174 Part Two Financial Statements and Financial Firm Performance

Gross interest income ÷ Total assets Income from holding assets– Interest expense ÷ Total assets Supply cost of funds for holding assets= Net interest margin ÷ Total assets Return earned because the lending

institution’s credit quality is better than itscustomers’ credit quality

+ Noninterest income ÷ Total assets Income from handling customer transactions– Noninterest expenses ÷ Total assets Cost of operations– Provision for loan losses ÷ Total assets Accrual expense= Pretax net operating income ÷ Total assets Return on assets before taxes– Income taxes ÷ Total assets* The financial firm’s share of the cost of

government services= Income before extraordinary items ÷ Total assets Net income from recurring sources of revenue+ Extraordinary net gains ÷ Total assets Nonrecurring sources of income or loss= Net income ÷ Total assets (or ROA) Earnings left over for the stockholders after

all costs are metddd

ddddd

dddTABLE 6–2

Calculation Returnon Assets (ROA)

*Both income and taxes applicable to income need to be adjusted for any tax-exempt earnings received. One can restate such income on afully tax-equivalent basis by multiplying the amount of tax-exempt income by the expression 1 ÷ (1 – t) where t is the firm’s tax bracket rate.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

lowered banking’s ratio of gross interest income to total assets and reduced its net inter-est margin. The decline in banks’ net interest earnings was more than made up for, how-ever, by dramatic increases in their fee income and improved loan quality as reflected insomewhat smaller loan-loss expenses. By 2003 the industry’s ROA, averaging 1.38 per-cent, represented the biggest average rate of return on bank assets since the FDIC beganits operations in 1934.

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 175

Income Statement Items 2005* 2003 2002 2000 1998 1996 1994 1992

Total interest income/Total assets 4.79% 4.63% 5.32% 7.17% 6.97% 7.14% 6.64% 7.49%– Total interest expense/Total assets 1.73 1.40 1.90 3.87 3.56 3.56 2.99 3.77= Net interest income/ Total assets 3.06 3.22 3.43 3.30 3.41 3.58 3.65 3.72– Provision for loan and lease losses/Total assets 0.25 0.43 0.64 0.45 0.39 0.35 0.28 0.70+ Total noninterest income/Total assets 2.13 2.32 2.27 2.32 2.14 1.87 1.70 1.62– Total noninterest expense/Total assets 3.05 3.20 3.27 3.39 3.51 3.45 3.46 3.51= Pretax net operating income/Total assets 1.89 1.92 1.80 1.77 1.66 1.64 1.61 1.12+ Securities gains(losses)/Total assets 0.06 0.13 0.15 –0.02 0.09 0.04 –0.01 0.14– Applicable income taxes/Total assets 0.64 0.67 0.64 0.61 0.60 0.58 0.54 0.41= Income before extraordinaryitems/Total assets 1.31 1.37 1.30 1.14 1.15 1.10 1.06 0.85+ Extraordinary gains (net)/Total assets 0.00** 0.00** 0.00** 0.00** 0.01 0.00** –0.01 0.02= Net income/Total assets 1.31 1.38 1.30 1.14 1.16 1.10 1.05 0.87

TABLE 6–3Components ofReturn on Assets(ROA) for All FDICInsured DepositoryInstitutions(1992–2005)

Source: Federal DepositInsurance Corporation.

Concept Check

6–11. What are the principal components of ROE andwhat does each of these components measure?

6–12. Suppose a bank has an ROA of 0.80 percent and anequity multiplier of 12×. What is its ROE? Supposethis bank’s ROA falls to 0.60 percent. What sizeequity multiplier must it have to hold its ROEunchanged?

6–13. Suppose a bank reports net income of $12, pretaxnet income of $15, operating revenues of $100,assets of $600, and $50 in equity capital. What is thebank’s ROE? Tax-management efficiency indicator?

Expense control efficiency indicator? Asset man-agement efficiency indicator? Funds managementefficiency indicator?

6–14. What are the most important components of ROAand what aspects of a financial institution’s perfor-mance do they reflect?

6–15. If a bank has a net interest margin of 2.50%, a non-interest margin of –1.85%, and a ratio of provisionfor loan losses, taxes, security gains, and extraor-dinary items of –0.47%, what is its ROA?

Notes: Figures may not add exactly to totals due to rounding and the exclusion of extraordinary items.*2005 figures are for first half of year only.**Less than 0.005 percent.

What a Breakdown of Profitability Measures Can Tell UsClearly, breaking down profitability measures into their respective components tells us muchabout the causes of earnings difficulties and suggests where management needs to look for

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

possible cures for any earnings problems that surface. The foregoing analysis reminds us thatachieving superior profitability for a financial institution depends upon several crucial factors:

1. Careful use of financial leverage (or the proportion of assets financed by debt asopposed to equity capital).

2. Careful use of operating leverage from fixed assets (or the proportion of fixed-costinputs used to boost operating earnings as output grows).

3. Careful control of operating expenses so that more dollars of sales revenue become netincome.

4. Careful management of the asset portfolio to meet liquidity needs while seeking thehighest returns from any assets acquired.

5. Careful control of exposure to risk so that losses don’t overwhelm income and equitycapital.

Measuring Risk in Banking and Financial Services3

Risk to the manager of a financial institution or to a regulator supervising a financial institu-tion means the perceived uncertainty associated with a particular event. For example, willthe customer renew his or her loan? Will deposits and other sources of funds grow nextmonth? Will the financial firm’s stock price rise and its earnings increase? Are interest ratesgoing to rise or fall next week, and will a financial institution lose income or value if they do?

Bankers, for example are usually interested in achieving high stock values and highprofitability, but none can fail to pay attention to the risks they are accepting to achievethese goals. Earnings may decline unexpectedly due to factors inside or outside the finan-cial firm, such as changes in economic conditions, competition, or laws and regulations.For example, recent increases in competition have tended to narrow the spread betweenearnings on assets and the cost of raising funds. Thus, stockholders always face the possi-bility of a decline in their earnings per share of stock, which could cause the bank’s stockprice to fall, eroding its resources for future growth.

Among the more popular measures of overall risk for a financial firm are the following:

• Standard deviation (σ) or variance (σ 2) of stock prices.• Standard deviation or variance of net income.• Standard deviation or variance of return on equity (ROE) and return on assets (ROA).

The higher the standard deviation or variance of the above measures, the greater theoverall risk. Risk can be broken down into a number of components and even referencedusing different terms as illustrated by the different risk matrices used currently by U.S. fed-eral regulatory agencies and summarized below.

176 Part Two Financial Statements and Financial Firm Performance

FactoidWhich banks in theindustry tend to havethe biggest net interestmargins between theirinterest income fromloans and securities andthe interest cost ofborrowed funds?Answer: The smallestbanks usually do.

National Credit Federal Reserve System Comptroller of the Currency Union Administration

Credit Credit CreditLiquidity Liquidity LiquidityMarket Interest Rate Interest RateOperational Transaction TransactionalLegal Compliance ComplianceReputation Reputation Reputation

Strategic Strategic

Risk Matrices Used by Selected U.S. Regulatory Agencies

3This section is based, in part, on Peter S. Rose’s article in the Canadian Banker [3] and is used with permission.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Each of these forms of risk can threaten a financial firm’s day-to-day performance andits solvency and long-run survival. Let’s examine now several of the most important typesof risk encountered daily by financial institutions.

Credit RiskThe probability that some of a financial institution’s assets, especially its loans, will declinein value and perhaps become worthless is known as credit risk. Because financial firmstend to hold little owners’ capital relative to the aggregate value of their assets, only asmall percentage of total loans needs to turn bad to push them to the brink of failure. Thefollowing are four of the most widely used indicators of credit risk:

• The ratio of nonperforming assets to total loans and leases.• The ratio of net charge-offs of loans to total loans and leases.• The ratio of the annual provision for loan losses to total loans and leases or to equity

capital.• The ratio of allowance for loan losses to total loans and leases or to equity capital.• The ratio of nonperforming assets to equity capital.

Nonperforming assets are income-generating assets, including loans, that are past due for90 days or more. Charge-offs, on the other hand, are loans that have been declared worth-less and written off the lender’s books. If some of these loans ultimately generate income,the amounts recovered are deducted from gross charge-offs to yield net charge-offs. Asthese ratios rise, exposure to credit risk grows, and failure of a lending institution may be

Insights and Issues

HOW TOP-EARNING BANKS GET THAT WAYA number of research studies have examined top-earning firms inthe banking industry in an effort to answer a simple question:What distinguishes a bank with above-average profitability frombanks that are only average performers? How did top-earningbanks get that way?

Bank size is clearly one factor. The top-earning banks in theindustry, at least as measured by their ROA and ROE, are oftenmedium-size or larger institutions that seem to benefit from loweroverall operating costs and greater operating efficiency.

Expense control stands out as the most important discrimina-tor between top performers and the also-rans. For example, high-profit banks manage their operating expenses better, generallyposting lower average interest costs, and especially lower per-sonnel expenses and overhead. Their ratios of operating expensesto operating revenues tend to be significantly below the expense-to-revenue ratios of low-profit institutions.

The deposit structure also appears to influence profit perfor-mance. Top-earning banks often hold more demand deposits thanother banks; these checkable deposits pay little or no interest andcarry customer service fees that bring in more revenues. Relat-edly, many highly profitable banks hold a large volume of coredeposits—smaller denomination deposits from individuals andsmall businesses that pay low interest rates and are more loyal tothe bank than larger deposit accounts.

Employee productivity tends to be higher among top earners.For example, banks with the best profits seem to generate andmanage more assets and income per employee and pay theirmore productive employees higher salaries.

Leverage (lower equity capital and greater use of debt) alsoemerges as a profit motivator. Top-earning banks, for example,generally economize on using high-cost owners’ capital and relyon the earnings-leveraging effects of cheaper debt.

The expansion of fee income has become a key element instrategies to increase profits in recent years. Government deregula-tion has put added pressure on financial institutions to charge feesfor many formerly “free” services and develop new fee-generatingservices.

Growth in assets, deposits, and loans seems to play a rolebecause top-earning banks seem to grow faster than average, pos-sibly reflecting the presence of more aggressive management orgreater customer acceptance of their services. However, growthshould not become a substitute for profits. Top-earning banks seemto recognize that growth can be overdone, resulting in uncontrolledexpansion that increases operating expenses faster than revenues.Moderate growth is usually a better route to high profits.

For further information on the characteristics of high-profitbanks see especially Elizabeth C. Klee and Fabio M. Natalucci,“Profits and Balance Sheet Developments at U.S. CommercialBanks in 2004,” Federal Reserve Bulletin, Spring 2005, pp. 143–74.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

just around the corner. The final two credit risk indicator ratios reveal the extent towhich a lender is preparing for loan losses by building up its loan-loss reserves (theallowance for loan losses) through annual charges against current income (the provisionfor loan losses).

Another popular and long-standing credit risk measure is:

• The ratio of total loans to total deposits.

As this ratio grows, examiners representing the regulatory community may become moreconcerned because loans are usually among the riskiest of all assets for depository institu-tions, and, therefore, deposits must be carefully protected. A rise in bad loans or decliningmarket values of otherwise good loans relative to the amount of deposits creates greaterdepositor risk.

Liquidity RiskFinancial-service managers are also concerned about the danger of not having sufficientcash and borrowing capacity to meet customer withdrawals, loan demand, and other cashneeds. Faced with liquidity risk a financial institution may be forced to borrow emergencyfunds at excessive cost to cover its immediate cash needs, reducing its earnings. Very fewfinancial firms ever actually run out of cash because of the ease with which liquid fundscan be borrowed from other institutions. In fact, so rare is such an event that when a smallMontana bank in the early 1980s had to refuse to cash checks for a few hours due to a tem-porary “cash-out,” there was a federal investigation of the incident!

Somewhat more common is a shortage of liquidity due to unexpectedly heavy depositwithdrawals, which forces a depository institution to borrow funds at an elevated interestrate, higher than the interest rates other institutions are paying for similar borrowings. Forexample, significant decline in its liquidity position often forces a bank to pay higher inter-est rates to attract negotiable money market CDs, which are sold in million-dollar unitsand therefore are largely unprotected by deposit insurance. One useful measure of liquid-ity risk exposure is the ratio of

• Purchased funds (including Eurodollars, federal funds, security RPs, large CDs, andcommercial paper) to total assets.

Heavier use of purchased funds increases the chances of a liquidity crunch in the eventdeposit withdrawals rise or loan quality declines. Other indicators of exposure to liquidityrisk include the ratios of

• Cash and due from balances held at other depository institutions to total assets.• Cash assets and government securities to total assets.

Cash assets include vault cash held on the financial firm’s premises, deposits held withthe central bank in the region, deposits held with other depository institutions to com-pensate them for clearing checks and other interbank services, and cash items in theprocess of collection (mainly uncollected checks). Standard remedies for reducing a finan-cial institution’s exposure to liquidity risk include increasing the proportion of funds com-mitted to cash and readily marketable assets, such as government securities, or usinglonger-term liabilities to fund the institution’s operations.

Market RiskIn market-oriented economies, where most of the world’s leading financial institutionsoffer their services today, the market values of assets, liabilities, and net worth of financial-service providers are constantly in a state of flux due to uncertainties concerning marketrates or prices. Market risk is composed of both price risk and interest rate risk.

178 Part Two Financial Statements and Financial Firm Performance

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Price RiskEspecially sensitive to these market-value movements are bond portfolios and stockhold-ers’ equity (net worth), which can dive suddenly as market prices move against a finan-cial firm. Among the most important indicators of price risk in financial institutions’management are

• The ratio of book-value assets to the estimated market value of those same assets.• The ratio of book-value equity capital to the market value of equity capital.• The market value of bonds and other fixed-income assets held relative to their value as

recorded on a financial institution’s books.• The market value of common and preferred stock per share, reflecting investor per-

ceptions of a financial institution’s risk exposure and earnings potential.

Interest Rate RiskMovements in market interest rates can also have potent effects on the margin of revenuesover costs for both banks and their competitors. For example, rising interest rates canlower the margin of profit if the structure of a financial institution’s assets and liabilities issuch that interest expenses on borrowed money increase more rapidly than interest rev-enues on loans and security investments.

The impact of changing interest rates on a financial institution’s margin of profit iscalled interest rate risk. Among the most widely used measures of interest-rate risk expo-sure are these:

• The ratio of interest-sensitive assets to interest-sensitive liabilities: when interest-sensi-tive assets exceed interest-sensitive liabilities in a particular maturity range, a financialfirm is vulnerable to losses from falling interest rates. In contrast, when rate-sensitiveliabilities exceed rate-sensitive assets, losses are likely to be incurred if market interestrates rise.

• For a depository institution, the ratio of uninsured deposits to total deposits, whereuninsured deposits are usually government and corporate deposits that exceed theamount covered by insurance and are usually so highly sensitive to changing interestrates that they will be withdrawn if yields offered by competitors rise even slightlyhigher.

With more volatile market interest rates in recent years, bankers and their competitorshave developed several new ways to defend their earnings margins against interest-ratechanges, including interest-rate swaps, options, and financial futures contracts. We willexamine these and other risk-management tools in Chapters 7, 8, and 9.

Operational (Transactional) RiskOperational risk refers to uncertainty regarding a financial firm’s earnings due to failures incomputer systems, errors, misconduct by employees, floods, lightning strikes, and similarevents. The broad group of actions included in this risk definition often decrease earningsdue to unexpected operating expenses. Some analysts say that operational risk is the risk ofloss due to anything other than credit or market risk. Others say it includes legal and com-pliance risk, but not reputation or strategic risk. The consolidation and convergence of finan-cial firms and the complexity of today’s financial-services technology has made operationalrisk a broad risk category that needs to be addressed by both managers of financial firmsand government regulators.

As technology has improved, computer hardware and software systems have becomeessential to the daily operations of most financial firms. If computer systems involve apatchwork of old programs, requiring employee intervention to reconcile and create

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 179

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

reports, then operational risk may be high. While the failure of a new computer systemmay be less likely, heavy reliance by the institution’s personnel and customers on such sys-tems creates vulnerability for any financial firm.

Today, acts of terrorism such as 9/11 and natural disasters such as hurricanes, earth-quakes, and tsunamis can lead to great loss for any financial firm. These natural and not-so-natural disasters may close financial institutions for extended periods and interrupttheir service to customers. Foregone income from such disasters is unpredictable, resultingin unexpected operating expenses and greater variability in earnings.

Financial fraud provides the plots for great movies, such as Rogue Trader, The Bank, andBoiler Room, and the basis for many “60 Minutes” episodes. It’s about money, stealing, andthe ultimate failure of some at-risk institutions. A financial firm’s owners, employees, cus-tomers, or outsiders may violate the law and perpetrate fraud, forgery, theft, misrepresenta-tion, or other illegal acts, sometimes leading to devastating losses to otherwise well-managedfinancial institutions.

Legal and Compliance RisksLegal risk creates variability in earnings resulting from actions taken by our legal system.Unenforceable contracts, lawsuits, or adverse judgments may reduce a financial firm’s rev-enues and increase its expenses. Lawyers are never cheap and fines can be expensive! In abroader sense compliance risk reaches beyond violations of the legal system and includesviolations of rules and regulations. For example, if a depository institution fails to holdadequate capital, costly corrective actions must be taken to avoid its closure. These cor-rective actions are laid out in capital adequacy regulations and are examined in moredetail in Chapter 15.

Reputation RiskNegative publicity, whether true or not, can affect a financial firm’s earnings by dissuadingcustomers from using the services of the institution, just as positive publicity may serve topromote a financial firm’s services and products. Reputation risk is the uncertainty associ-ated with public opinion. The very nature of a financial firm’s business requires maintain-ing the confidence of its customers and creditors.

Strategic RiskVariations in earnings due to adverse business decisions, improper implementation of deci-sions, or lack of responsiveness to industry changes are parts of what is called strategicrisk. This risk category can be characterized as the human element in making bad long-range management decisions that reflect poor timing, lack of foresight, lack of persistence,and lack of determination to be successful.

Capital RiskThe impact of all the risks examined above can affect a financial firm’s long-run survival,often referred to as its capital risk. Because variability in capital stems from other types ofrisk it is often not considered separately by government regulatory agencies. However, risksto the capital that underlies every financial firm captures the all-important risk of insol-vency or ultimate failure.

For example, if a bank takes on an excessive number of bad loans or if a large portion ofits security portfolio declines in market value, generating serious capital losses when sold,then its equity capital account, which is designed to absorb such losses, may be over-whelmed. If investors and depositors become aware of the problem and begin to withdrawtheir funds, regulators may have no choice but to declare the institution insolvent andclose its doors.

180 Part Two Financial Statements and Financial Firm Performance

Key URLsMany of the types ofrisk discussed in thissection have beendeveloped and refinedby the Bank forInternationalSettlements atwww.bis.org and by arelated entity, the BaselCommittee onInternational CapitalStandards, atwww.bis.org/publ/bcbs/107.htm, which isexplored in detail inChapter 15.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

The failure of a financial-service corporation may leave its stockholders with none ofthe capital they committed to the institution. Moreover, in the case of depository institu-tions, depositors not covered by insurance also risk losing a substantial portion of theirfunds. For this reason, the prices and yields on capital stock and on large uninsureddeposits can serve as an early warning sign of solvency problems. When investors believethat a financial firm has an increased chance of failing, the market value of its capital stockusually begins to fall and it must post higher interest rates on its borrowings in order toattract needed funds. Economists call this phenomenon market discipline: interest rates andsecurity prices in the financial marketplace move against the troubled firm, forcing it tomake crucial adjustments in policies and performance in order to calm investors’ worstfears. This suggests that capital risk can be measured approximately by such factors as

• The interest rate spread between market yields on debt issues (such as capital notes andCDs issued by depository institutions) and the market yields on government securities ofthe same maturity. An increase in that spread indicates that investors in the market ex-pect increased risk of loss from purchasing and holding a financial institution’s debt.

• The ratio of stock price per share to annual earnings per share. This ratio often falls ifinvestors come to believe that a financial firm is undercapitalized relative to the risks ithas taken on.

• The ratio of equity capital (net worth) to total assets, where a decline in equity fundingrelative to assets may indicate increased risk exposure for shareholders and debtholders.

• The ratio of purchased funds to total liabilities. Purchased funds usually include unin-sured deposits and borrowings in the money market from banks, nonbank corporations,and governmental units that fall due within one year.

• The ratio of equity capital to risk assets, reflecting how well the current level of a fi-nancial institution’s capital covers potential losses from those assets most likely to de-cline in value.

Risk assets consist mainly of loans and securities and exclude cash, plant and equipment,and miscellaneous assets. Some authorities also exclude holdings of short-term governmentsecurities from risk assets because the market values of these securities tend to be stable andthere is always a ready resale market for them. Concern in the regulatory community over therisk exposure of depository institutions has resulted in heavy pressure on their management toincrease capital. As we saw earlier in this chapter, capital, at least in the banking industry, hasmoved significantly higher relative to the industry’s assets and liabilities in recent years.

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 181

FilmtoidWhat 2000 film starsPaul Newman as anincarcerated bankrobber who had stolenmillions from the banksto which he sold andinstalled securitysystems and thenreturned to rob them?Answer: Where theMoney Is.

Concept Check

6–16. To what different kinds of risk are banks and theirfinancial-service competitors subjected today?

6–17. What items on a bank’s balance sheet and incomestatement can be used to measure its risk expo-sure? To what other financial institutions do theserisk measures seem to apply?

6–18. A bank reports that the total amount of its netloans and leases outstanding is $936 million, itsassets total $1,324 million, its equity capitalamounts to $110 million, and it holds $1,150 millionin deposits, all expressed in book value. The esti-

mated market values of the bank’s total assets andequity capital are $1,443 million and $130 million,respectively. The bank’s stock is currently valuedat $60 per share with annual per-share earnings of$2.50. Uninsured deposits amount to $243 millionand money-market borrowings total $132 million,while nonperforming loans currently amount to $43million and the bank just charged off $21 million inloans. Calculate as many of the risk measures asyou can from the foregoing data.

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

Other Goals in Banking and Financial-Services ManagementIn an effort to maximize profitability and the value of the shareholders’ investment in a finan-cial institution, many financial firms recognize the need for greater efficiency in their opera-tions. This usually means reducing operating expenses and increasing the productivity of theiremployees through the use of automated equipment and improved employee training. Thegovernment deregulation movement has forced depository institutions, for example, to payhigher interest costs for their funds and encouraged management to reduce noninterest costs,especially employee salaries and benefits and overhead costs. Among the most revealing mea-sures of operating efficiency and employee productivity for a financial institution are its

(6–21)

Not all financial firms pursue high profitability, maximum stock values, increasedgrowth, or greater efficiency as key goals, however. There is considerable evidence thatsome institutions prefer greater market power in the markets they serve, not only because itgives them increased control over prices and customer relationships, but also because afinancial-service provider with greater market influence can enjoy a more “quiet life,” orface less risk of losing earnings or market share. Several recent studies have found, for exam-ple, that some banks in this situation display expense preference behavior: They spendmore on salaries and wages of management and staff, enjoy more fringe benefits, or buildlarger and more sumptuous offices. Unfortunately for the stockholders of these institutions,a preference for expenses sacrifices profits and limits potential gains in stock values.

6–3 Performance Indicators among Banking’s Key CompetitorsMany of the performance indicators discussed in the foregoing sections apply equally wellfor measuring the performance of both banks and their nonbank competitors. This is espe-cially true of those nonbank financial institutions that are private, profit-making corpora-tions, including stockholder-owned thrift institutions, insurance companies, finance andcredit-card companies, security broker and dealer firms, and mutual funds.

Among the key bank performance indicators that often are equally applicable to pri-vately owned, profit-making nonbank financial firms are these:

Prices on common and preferred stock Return on equity capital (ROE)Return on assets (ROA) Net operating marginNet interest margin Equity multiplierAsset utilization ratio Cash accounts to total assetsNonperforming assets to equity capital ratio Interest-sensitive assets to interest-

sensitive liabilitiesBook-value assets to market-value assets Interest-rate spread between yields onEquity capital to risk-exposed assets the financial firm’s debt and market Earnings per share of stock yields on government securities

Some performance indicators are unique to each nonbank financial-service industry. Forexample, among insurance companies, key performance measures include the growth of netpremiums written (a measure of total sales) and the size of life and pension reserves (their

Employee productivity ratio �Net operating income

Number of full-time-equivalent employees

Operating efficiency ratio �Total operating expensesTotal operating revenues

182 Part Two Financial Statements and Financial Firm Performance

Key URLsPerformance data onbanking’s closestcompetitors—nonbankdepositoryinstitutions—can mosteasily be found at suchWeb sites aswww.ots.treas.gov,www.fdic.gov, andwww.ncua.gov.

FactoidWhich banks tend to bemost efficient incontrolling costs andrevenues? Answer:Usually medium-sizeand larger institutions(over $100 million inassets).

FactoidIn recent years FDIC-insured savingsassociations (savingsand loans and savingsbanks) have had lowerassets and equity returnsthan insuredcommercial banks, butnot by much. Forexample, for all of 2004commercial banksreported an averageROA of 1.31 percentversus 1.17 percent forsavings associations andan average ROE of13.80 percent versus10.87 percent forsavings associations.Why do you think thesedifferences exist?

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008

chief liabilities) relative to total assets. Insurers also pay close attention to an efficiencymeasure—the combined ratio of claims paid out plus operating expenses relative to premi-ums earned from policyholders.

Among mutual funds, key performance markers include the growth of net sales (i.e.,gross sales of shares less share redemptions by the public), service fees relative to aver-age assets, and the rate of return on funds invested. In contrast, finance and credit-cardcompanies often pay close attention to the growth of their outstanding debt and theirgross receivables (a measure of total loans extended to customers). Finally, among com-peting depository institutions, such as credit unions and mutual savings associations,key performance measures include total loans to members relative to capital reserves (a measure of risk), home mortgage loans to total assets (a rapidly growing credit ser-vice), and the number of actual members (customers) relative to potential members(customers).

No financial institution can safely ignore its level of performance today relative to itspast performance and relative to its competitors. Even if some financial-service institu-tions don’t seem to care about their performance, both the public and the regulatory com-munity clearly do.

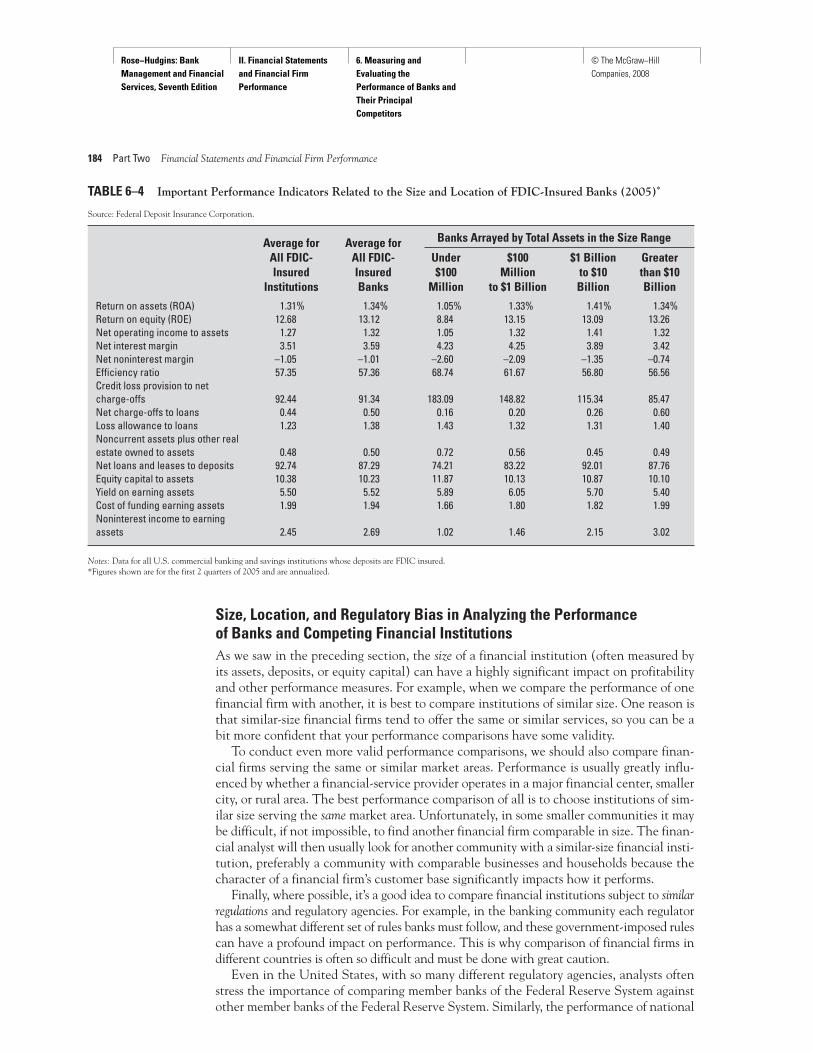

6–4 The Impact of Size on PerformanceWhen the performance of one financial firm is compared to that of another, size—oftenmeasured by total assets or, in the case of a depository institution, total deposits—becomesa critical factor. Most of the performance ratios presented in this chapter are highly sensi-tive to the size group in which a financial institution finds itself.

Thus, “size bias” is especially evident in the banking industry. For example, as Table 6–4shows, key earnings and risk measures change dramatically as we move from the smallestbanks (those in the table with assets of less than $100 million) to the largest banking firms(with assets exceeding $10 billion). For example, the most profitable banks in terms ofROA were banks with more than $1 billion in assets and less than $10 billion in assets,while the largest equity returns (ROE) were obtained by the very largest banks with morethan $10 billion in assets in 2005.

On the other hand, middle-size and large banks with assets ranging from $100 mil-lion to $10 billion in total assets often display the most favorable net operating marginsand the best operating efficiency (often with the lowest operating-expense-to-revenueratio). Similarly, the largest banks generally report the highest (least negative) nonin-terest margins because they charge fees for so many of their services. Smaller and medium-size banks frequently display larger net interest margins and, therefore,greater spreads between interest revenue and interest costs because most of theirdeposits are small-denomination accounts with lower average interest costs. Moreover,a larger proportion of small and medium-size banks’ loans tend to be higher-interestconsumer loans.

In terms of balance-sheet ratios, many of which reflect the various kinds of risk expo-sure banks face, the smallest banks usually report higher ratios of equity capital to assets.Some bank analysts argue that larger banks can get by with lower capital-to-asset cushionsbecause they are more diversified across many different markets and have more risk-hedg-ing tools at their disposal. Smaller banks appear to be more liquid, as reflected in theirlower ratios of net loans to deposits, because loans are often among a bank’s least liquidassets. The biggest banks also appear to carry greater credit risk as revealed by their higherloan-loss (net charge-offs to total loans and leases) ratios.

Chapter 6 Measuring and Evaluating the Performance of Banks and Their Principal Competitors 183

Rose−Hudgins: Bank Management and Financial Services, Seventh Edition

II. Financial Statements and Financial Firm Performance

6. Measuring and Evaluating the Performance of Banks and Their Principal Competitors

© The McGraw−Hill Companies, 2008