RiskandReward - Premia Research LLC

43

© Metal Bulletin plc 2001. All rights reserved. No part of this publication (text, data, or graphics) may be reproduced, stored in a data retrieval system, or transmitted, in any form whatsoever or by any means (electronic, mechanical, photocopying, recording or otherwise) without obtaining Metal Bulletin plc’s prior written consent. Unauthorised and/or unlicensed copying of any part of this publication is in violation of copyright law. Violators may be subject to legal proceedings and liable for substantial monetary damages per infringement as well as costs and legal fees. For information about copyright licences please contact Rhoda Embling, COPYWATCH in the UK on +44 (020) 7827 9977. Brief extracts may be used for the purposes of publishing commentary or review only provided that the source is acknowledged. Published jointly by FOW and MAR/Hedge The reports on investment managers in this publication are based solely on information and data supplied by the respective investment manager. The accuracy and completeness of such information and data have not been verified by the publisher, and therefore we do not and cannot guarantee the accuracy or completeness of such information. Further, any statement non-factual in nature and any statements of opinion constitute only current opinions of the authors, which are subject to change and not necessarily the opinions of the publisher. No information in this newsletter constitutes or should be interpreted as a solicitation for investment in any of the investments reported on. A prospective client should independently investigate an investment manager before engaging the services of that manager, and should consult with independent qualified sources of investment advice and other legal and tax professionals before using the services of an investment manager. Due to, among other things, the volatile nature of the markets in which the investments and investment managers reported in this publication are involved, the investments written about in this newsletter may only be suitable for certain qualified investors, and may be subject to other requirements and/or restrictions enacted and/or enforced by national and/or local regulatory agencies. Past performance records as reported should not be considered indicative of future results. © 2001 by Managed Accounts Reports Inc. All rights reserved. Reproduction in any form whatsoever forbidden without permission. Risk and Reward strategic thinking in alternative assets September 2001 Aussie rules 16 Australia has just established a chapter of Aima and is experiencing substantial growth in alternative investments. We look at the providers and investors and future directions. Simon Segal. Stock tactics 21 The stock market turbulence is serving only to sharpen up provision of equity options analytics, particularly online. We review the products and the trends. Andy Webb. New manager profile: Nothing ails (y)a 26 Yes, it’s a contrived headline, alright, but with the backgrounds and niche these guys have, you’d be hard pressed to find reasons why Ailsa Capital wouldn’t succeed. Kim Hunter Stress testing 29 We thought it was about time we looked at what makes us tick as human beings, so in the first article in a personal and professional development series, we take a good hard look at the stress monster. Florence Lombard & Sue Liburd. Two heads are better than one 34 ‘Artificial intelligence’ might have slipped into the lexicon, but what does it actually mean? And how do you build a system that can help make investment decisions? Our real-life rocket scientist tells us how. Vlade Milanovich. Life at Sharpe’s end 39 We all know the Sharpe Ratio is not the last word in performance measurement, but here we assess its probable complete misapplication to hedge fund strategies containing written optionality. Hilary Till. Features Regulars Contributors 4 The low-down on R&R’s experts Editorial comment 5 A letter from R&R’s consultant editor First movers 6 Innovations in fund structures and services People moves 10 Who’s gone where and why New fund launches 14 A digest of recent and upcoming launches Legal review 44 Pumping and dumping, the hedge fund way (and what the regulars are going to do about it) Zurich Capital Markets data 47 Performance-related statistics and commentary Survey 50 Cap Gemini Ernst & Young’s asset management systems survey 2001 Contents

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of RiskandReward - Premia Research LLC

© Metal Bulletin plc 2001. All rights reserved. No part of this publication (text, data, or graphics) may be reproduced, stored in a data retrieval system, or transmitted, in any form whatsoever or by any means(electronic, mechanical, photocopying, recording or otherwise) without obtaining Metal Bulletin plc’s prior written consent. Unauthorised and/or unlicensed copying of any part of this publication is in violation ofcopyright law. Violators may be subject to legal proceedings and liable for substantial monetary damages per infringement as well as costs and legal fees. For information about copyright licences please contact RhodaEmbling, COPYWATCH in the UK on +44 (020) 7827 9977. Brief extracts may be used for the purposes of publishing commentary or review only provided that the source is acknowledged.

Published jointly by FOW and MAR/Hedge

The reports on investment managers in this publication are based solely on information and data supplied by the respective investment manager. The accuracy and completeness of such information and data have not beenverified by the publisher, and therefore we do not and cannot guarantee the accuracy or completeness of such information. Further, any statement non-factual in nature and any statements of opinion constitute only currentopinions of the authors, which are subject to change and not necessarily the opinions of the publisher. No information in this newsletter constitutes or should be interpreted as a solicitation for investment in any of theinvestments reported on. A prospective client should independently investigate an investment manager before engaging the services of that manager, and should consult with independent qualified sources of investmentadvice and other legal and tax professionals before using the services of an investment manager. Due to, among other things, the volatile nature of the markets in which the investments and investment managers reportedin this publication are involved, the investments written about in this newsletter may only be suitable for certain qualified investors, and may be subject to other requirements and/or restrictions enacted and/or enforced bynational and/or local regulatory agencies. Past performance records as reported should not be considered indicative of future results.© 2001 by Managed Accounts Reports Inc. All rights reserved. Reproduction in any form whatsoever forbidden without permission.

Risk and Rewardstrategic thinking in alternative assets

September 2001

Aussie rules 16Australia has just established a chapter ofAima and is experiencing substantialgrowth in alternative investments. We look at theproviders and investors and future directions. SimonSegal.

Stock tactics 21The stock market turbulence is serving onlyto sharpen up provision of equity optionsanalytics, particularly online. We review theproducts and the trends. Andy Webb.

New manager profile: Nothing ails (y)a 26Yes, it’s a contrived headline, alright, butwith the backgrounds and niche these guys have,you’d be hard pressed to find reasons why AilsaCapital wouldn’t succeed. Kim Hunter

Stress testing 29We thought it was about time we looked atwhat makes us tick as human beings, so inthe first article in a personal and professionaldevelopment series, we take a good hard look at thestress monster. Florence Lombard & Sue Liburd.

Two heads are better than one 34‘Artificial intelligence’ might have slippedinto the lexicon, but what does it actuallymean? And how do you build a system that canhelp make investment decisions? Our real-life rocketscientist tells us how. Vlade Milanovich.

Life at Sharpe’s end 39We all know the Sharpe Ratio is not the lastword in performance measurement, but herewe assess its probable complete misapplication tohedge fund strategies containing written optionality.Hilary Till.

Features

RegularsContributors 4The low-down on R&R’s experts

Editorial comment 5A letter from R&R’s consultant editor

First movers 6Innovations in fund structures and services

People moves 10Who’s gone where and why

New fund launches 14A digest of recent and upcoming launches

Legal review 44Pumping and dumping, the hedge fund way(and what the regulars are going to do about it)

Zurich Capital Markets data 47Performance-related statistics andcommentary

Survey 50Cap Gemini Ernst & Young’s assetmanagement systems survey 2001

Contents

4 SEPTEMBER 2001 RISK & REWARD

Simon Segal, freelance writerSimon Segal is a freelance financial journalist based in Sydney. He has recently relocated from South Africa where forseventeen years he was involved in researching, writing and commenting on a broad range of issues relating to financialmarkets, macroeconomics, investment, corporate profiles, industrial relations, agriculture and socio-economicdevelopment. He has an MBA degree, is the recipient of a number of prestigious awards for financial journalism andconsulted to high profile organisations involved in the dissemination of information that includes South Africa’s Truth andReconciliation Commission, public broadcaster SABC and media trainers Institute for the Advancement of Journalism.

Florence Lombard, executive director, Alternative Investment Management Association,London As executive director of AIMA since January 1993, Florence is responsible for its day-to-day management, as well asthe development and implementation of projects in the areas of research, regulation and education. She is also incharge of the development of the Association in Asia and the Middle East. During the last five years, she has studieddifferent areas of personal development including neuro-linguistics and coaching. She leads weekend workshops invarious European countries and qualified this year as an NLP Coach.

Vlade Milanovic, Nomura InternationalVlade is a computer programmer, who has for the last five years worked for investment banks in London; currently heis with Nomura International. Since the early 1990s Vlade has been developing forecasting and trading models using artificial intelligence tools.Currently he is completing a PhD at Brunel University on the application of advanced technologies for trading financialmarkets, including neural networks, genetic algorithms and natural language processing systems.Vlade studied at the Technical Military Academy in Yugoslavia, where he specialised in rocket engineering for surface-to-surface missile systems. After graduating he worked at the Orao Aircrafts works, where he was responsible fortesting flights systems for MIG fighter jets.

Dick Frase, Decherts Dick Frase has specialised in the legal and regulatory aspects of financial services since the 1980s. He has worked in-houseat the Securities & Futures Authority and as general counsel for MeesPierson ICS in London; and was featured by LegalBusiness in their ‘highly recommended’ listing of lawyers in the managed futures area. From 1994 to 1998 he was head oflitigation at the Personal Investment Authority, joining Dechert’s London practice in late 1998. He specialises in regulation,investment management, broker-dealing and retail investment products. He has contributed chapters to books on futurestrading and hedge funds, and is currently editing a new book for Sweet & Maxwell on the law and regulation of investmentexchanges. Decherts‘ London practice focuses on multinationals, hedge funds and alternative investments.

Contributors

Hilary Till, principal, Premia Capital ManagementHilary has been involved in the commodity derivatives markets since 1990, when she developed the pricing and riskmanagement system for Chicago-based Continental Bank's commodity derivatives desk. In 1992-3, she set up HarvardManagement Company's commodity investment programme. From 1994-8, she was Boston-based Putnam Investment'scommodity portfolio manager for institutional clients, and its chief of derivatives strategies from 1995 to 1998. From 1998to the present, she has been a principal at Premia Capital Management, LLC, a firm which has developed systematic, total-return futures products.Hilary holds a BA (Hons) in statistics from the University of Chicago and an MSc in statistics from the London School ofEconomics (LSE).

Sue Liburd, managing director Sage BlueSue Liburd, md of Sage Blue and non-executive director of a number of small companies, is an experienced HR managementand employee development professional, workshop facilitator, creative management consultant and personal effectivenesscoach. She works internationally in multinationals as well as small businesses, across a range of industry sectors.Her practice is centred on looking beyond the traditional to achieve realistic workable solutions to real problems and needs.Sue is an experienced stress debriefer, subscribing to the view that stress is not bad in itself, but ‘just a funky message’ – aninvitation to make a change for the better. If you don't want the message to get louder, she says, all you have to do is listen.

Andy Webb, freelance finance writerAndy Webb is a freelance finance and technology writer with 18 years' experience, most recently specialising inderivatives, technology and trading methodologies. He has written regularly for a wide range of journals including TheSunday Times, Sunday Business, Futures & Options World, Treasury & Risk Management, Global Finance, DerivativesStrategy and Wall Street & Technology.

DDeeaarr FFrriieennddss,,

Well, summer’s over. It’s time to put away frivolous things and get back to serioussubjects again. If we don’t, the regulators will do it for us.

In this issue’s legal and regulatory review (p. 44) Dick Frase details the SEC’s firstaction against portfolio pumping and dumping in a hedge fund context. Whichbrings us, in an almost straight line, to pricing in general.

Read the results of CMRA’s fair pricing/NAV survey on p. 6, whose most horrifyingconclusion probably comes courtesy of those who didn’t take part. When principalLeslie Rahl asked them why not, many managers told her that somebody else –often external to the fund manager – was responsible for that kind of thing.

Which makes you wonder who was responsible for valuation at MJ Select, which as R&R was going to press wasin the midst of disclosing losses that seem to have grown almost weekly since its figures were first reported in earlyJuly. By late August the initial 0.5% return for June and translated into a 4.4% loss. According to a letter to investorsfrom Oceanic Bank & Trust, administrators for two of the ultimate investment funds invested in by MJ Select Global,were having difficulties in valuing the funds’ assets.

While we are querying valuations this month, one of our authors has also had a go at that hallowed hedge fundperformance measurement tool, the Sharpe ratio. In the first in a pair of articles on performance measurement,Hilary Till uncovers hedge fund strategies whose return comes not from alpha but from buying economic risks otherfinancial institutions do not want to own. Such strategies’ implicit short optionality makes them unsuitable formeasurement by the Sharpe ratio, she concludes (p. 39).

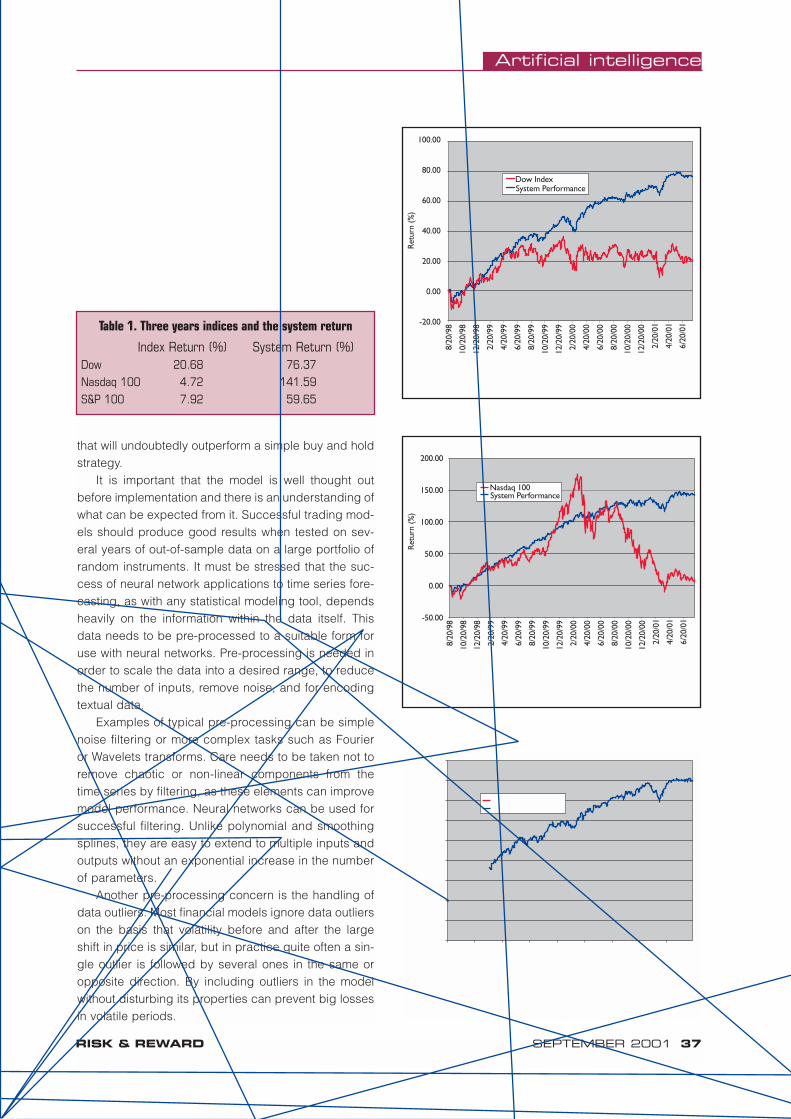

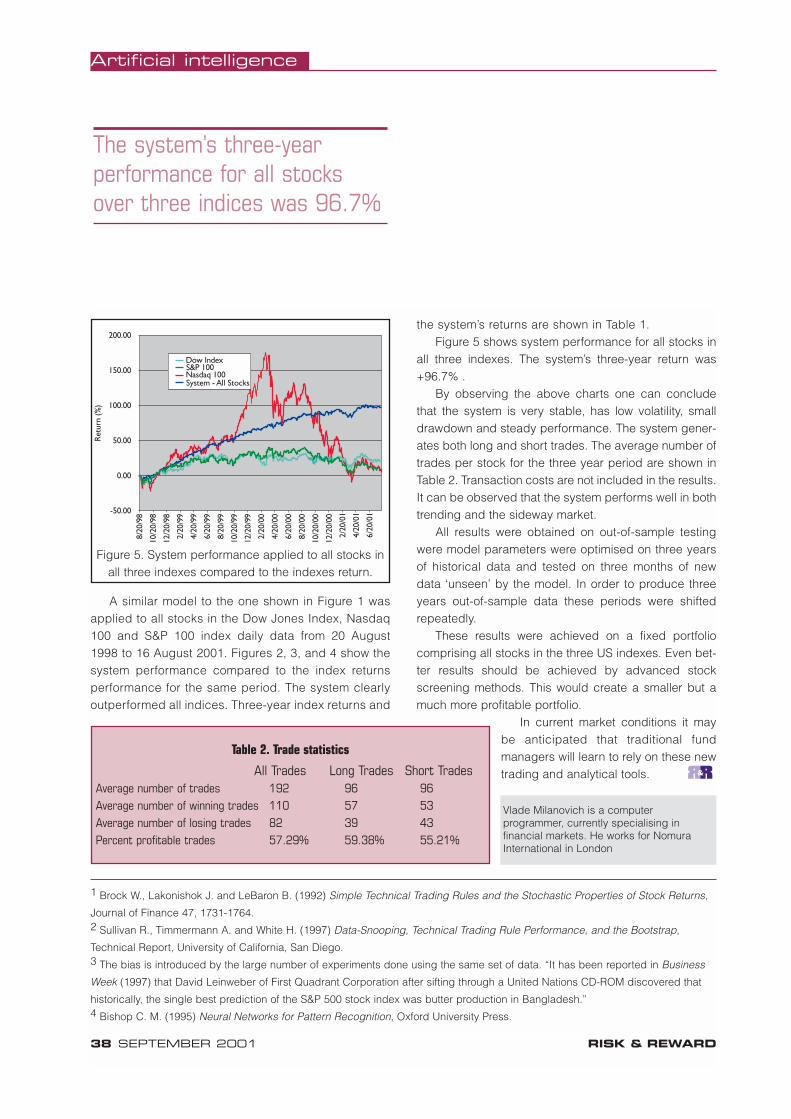

But let’s not be too serious. It’s bad for your health. Or so say Florence Lombard and Sue Liburd on their article onstress busting on p.29. According to Florence, potential investors will pick up on a stressed out organisation; it’s timeto do something about it. And for quality smile-time you could do worse in the first instance than read VladeMilanovich’s article on artificial intelligence. This former rocket scientist has just run tests on his own AI system andcome up with returns that beat the S&P 100 by 50 percentage points over three years. That’s what I call a good read.

With best wishes,

Kim HunterConsultant editor

RISK & REWARD SEPTEMBER 2001 5

Letter from the editor

consultant editorKim Hunter+44 (0)20 7827 6407email: [email protected]

editor, MAR/HedgeMichael Ocrant+1 212 213 6202email: [email protected]

editorial productionJennifer White

editorial director FOW LtdEmma Davey

president, MAR LLCGreg Newton

managing director, FOW LtdDavid Setters

group businessdevelopment manager John-Owen Waller+44 (0)20 7827 5254email: [email protected]

advertisement sales executive Nancy Fournier+44 (0) 20 7827 6456email: [email protected]

advertisement productionMaria Pennington

marketing manager - productsMichelle Hemstedt

subscriptions managerJohn Fea

advertising sales & editorial office16 Lower Marsh,London SE1 7RJ.+44 (0)20 7827 9977Fax +44 (0)20 7827 6413

http://www.fow.com

advertising productionand accountsPark House, 3 Park Terrace,Worcester Park,Surrey KT4 7HY, UKTel +44 (0)20 7827 9977Fax +44 (0)20 7827 8943http://www.fow.com

MAR/Hedge head offfice220 Fifth Avenue, 19th floorNew York, NY 10001-7781Tel +1 212 213 6202Fax +1 212 213 1870http://www.marhedge.com

Printed by Stephens and George

metal bulletindirectorsG M. Clarke, T Hempenstall (Chief Executive), R J Kidson, B MMoritz, M Thomas, L Reed

© FOW Ltd & Managed AccountReports Inc

6 SEPTEMBER 2001 RISK & REWARD

First movers

What with the pricing problems atManhattan Investment Fund andHeartland Advisors, and the first SECaction against ‘pumping and dump-ing’ (see legal review, p44), it is notsurprising that pricing issues areattracting widespread attention.

The Investor Risk Committee, thecommittee of the InternationalAssociation of Financial Engineerscharged with developing risk man-agement standards, has just issuedits second report, and Capital MarketRisk Advisors has undertaken its ownsurvey into NAV/fair value practices.

Tanya Beder, md of CaxtonAssociates and IRC chairman, says,“The IRC approach is that an indus-try standard approach should betaken to perform calculations such asVaR. This therefore requires stan-dards pricing of the risk factors at aminimum.”

While over 200 individuals fromhedge funds and institutionalinvestors have reached consensuson IRC findings, Beder says it is tooearly to predict that IRC’s work willbecome industry standard. However,IRC members have set an ambitiousagenda for the next phase of theirwork. As well as expanding the detailand content of current studies intopricing policy, the committee hasearmarked a redefinition of fund cat-egories such as long/short andglobal macro. This, says, Beder willenable fund and investors to betterbenchmark their activities againsttheir peers. All eventual standardswill remain voluntary.

Lights, CMRA, action?CMRA’s study focused highly regu-lated institutions, though didcomprise 26.7% hedge fund respon-dents. Principal Leslie Rahl believesthe mutual fund world is becomingattuned to and grouping around pric-ing issues, and that once theirguidance is tangible, hedge fundswill also adopt a set of standards.

The biggest issue is the difficultyin making NAV comparisons in a fieldwith so much variation in attributedvalue. For example, among thewidest variations come, not surpris-

ingly, in collateralised mortgageobligations. CMRA reviewed thedealer prices provided for a mort-gage hedge fund on a single dayand found differences between theprices provided by five CMO dealersranging from 6% to 44%. “With thesetypes of price differences the differ-ent methodologies for incorporatingdealer quotes can create significantlydifferent results,” says her report. Forexample, using the average of thedealer quotes created up to a four-point differences in valuation versususing the ‘drop the high and low,then average’ method.

The study also found that 22.2%of convertible bond funds makeadjustments to NAV of varying sizes,while the rest make no adjustments.“Which convertible bond funds arereally outperforming?” she asks.

Among the response set, repre-senting around $2 trillion in assets,only 13% made adjustments of somekind to the prices they receive fromtheir valuation sources. While mostrespondents indicated that adjust-ments represented less than 2% ofNAV, in some cases that figure roseto 30%. No respondents adjustedfor US government bonds. Rahlcomments, “One only has to remem-ber back to the illiquidity ofoff-the-run treasury in the fall of 1998to question whether a 1x1 market foran off-the-run issue is the appropri-ate mark for a $1bn position.”

The study also concludes that tra-ditional managers are more likelythan hedge fund or mutual funds torely on a single dealer quote. Neither,as already hinted, is there a consis-tent market practice governing howdealer quotes are incorporated intovaluations.

Rahl heads up all this detail onvariation among respondents with a stern word for non-respondents.While 93% of respondents docu-mented their pricing policies andexceptions, a “troubling number” of non-respondents claimed thatpricing issues were not theirresponsibility, but that of theircustodian, administrator, or third-party pricing services.

Price perfect“One only has to remember

back to the illiquidity of

off-the-run treasury in the fall

of 1998 to question whether

a 1x1 market for an off-the-

run issue is the appropriate

mark for a $1bn position.”

– Leslie Rahl, CMRA

8 SEPTEMBER 2001 RISK & REWARD

First movers

“We believe the joint

ownership creates the basis

for a longer relationship than

an advisory relationship does”

– Christopher Fawcett

Fauchier Partners and BNP ParibasAsset Management have teamed upto create a joint venture company tomanage BNP’s hedge fund FOFs.BNP Paribas Fauchier Partners Ltdplans to launch new productssometime this autumn.

Christopher Fawcett, Fauchier’sfinance director says this is the firstspecialist/institutional tie-in that hasgone the full joint venture route. “Webelieve the joint ownership createsthe basis for a longer relationshipthan an advisory relationshipdoes,” he says. He believes otherbanks will probably take a similarapproach, since building an in-house department with existing staffleads either to poor results or tostaff becoming frustrated at not hav-ing an equity stake and leaving.“The risk is infinitely lower with anindependent structure,” he says.

The new company has seniormanagement in place (thoughFawcett will not say who), and isbusy building its own team on the

floor below Fauchier Partners’London offices.

Responsibility between the twopartners will be divided so thatdemand is provided by the assetmanagement arm of the hugeParibas banking group. In thissense, for Fauchier Partners it is likehaving a huge client (BNP PAM has$150bn under management) a flightof stairs away.

Fauchier will construct and moni-tor the hedge fund portfolios.Product design will be based on theneeds of Paribas clients. (BNP has acouple of small FOFs already, whichwill form the basis of the new range.)

Fauchier has already done guar-anteed notes with the group.Fawcett comments, “Structuredproducts are an important part ofthe product range. Financial engi-neering is becoming more and moreimportant.” Fawcett expects suchstructures to be an important part ofthe work undertaken for BNP PAM’slargely institutional client base.

All tied up

Portfolio construction the 21stcentury

Standard Life’s risk managementteam has pooled the results of itsportfolio construction research in asoft-backed book of the samename. Portfolio construction – anintegrated approach focuses on thegeneral shape a portfolio shouldtake in order to meet predefinedrisk parameters, rather thanapproaching the issue from thestandard fund manager parametersof competition and aggression.

Investment risk director JulianCoutts takes a more objectiveframework for designing funds, frombenchmark setting to position taking.This framework leads to what Coutts(in common with test pilot assess-ments of safety regimes for aircraft)calls a ‘flight envelop’ for the fund. Inorder to ‘explode’ the fund risk intohow it can be forecast from otherparameters, the team has madeapproximations to cut to the main

decisions made by fund managers.The exploration begins with the

overall market a fund has to com-pete in and cuts into increasinglevels of detail. How should abenchmark be set? How much riskshould be taken at the asset alloca-tion level? How much risk should bedelegate to stock selectors? For agiven level of risk within an assetclass, how many stocks should bein the portfolio? If returns are pre-dicted, how heavily should theseviews be supported.

These are questions pertinent to the alternative and mainstreamsalike.

Investing in the 21st century, paper 2:Portfolio construction: an integratedapproach by Julian Coutts. Edinburgh:Standard Life Investments. 2001. Pricedetails unavailable. [email protected].

Fund managers write specs

for funds by considering the

competition and use their

combined years of wisdom to

set how aggressive a portfolio

should be – Julian Coutts

RISK & REWARD SEPTEMBER 2001 9

First movers

If you have an innovation infund, structure, or service,email [email protected]

Next month New York Board ofTrade will launch futures andoptions on the CMI index, the first ina series of products which, accord-ing to developers AssetSight, willimprove a hedge fund portfolio’sability to adequately protect a tradi-tional stock/bond portfolio.

The CMI Index takes both longand short positions in markets suchas commodities, currencies, and soon, in order to reflect the full rangeof hedge activity driving returns incommercial markets. Positions aredetermined according to predefinednon-forecasting rules to govern apassive, systematic, trend-followingtrading process. In so doing, CMIseeks to provide investors with ameans of ‘owning’ the price volatilitythat hedgers seek to offload.

As a result, while the long-volatil-ity CMI index is not correlated witheither hedge funds or with broadindices such as the S&P 500, it iscorrelated with actively managedfutures, with a higher risk-adjustedperformance. (Several academicstudies have shown that adding amanaged futures component to ahedge funds portfolio contributes tooverall diversification.)

According to research by

AssetSight, many hedge funds’returns are based on arbitrage-typestrategies with short volatility expo-sure. This weakness, saysAssetSight, is clearly demonstratedin the high correlations between theHedge Fund Research CompositeIndex and the CSFB Tremont Indexand traditional markets such as USequities.

Conversely, in periods of nega-tive three-month rolling returns forthe S&P 500 (between March 1999and December 2000) the CMIreturned an average 2.48%. In peri-ods of positive return over the sametime-frame the CMI returned anaverage 1.99%. A portfolio com-posed of 80% hedge funds and20% CMI reduced the downsideperformance to near zero andreturned 4.62% when the marketwas strong.

AssetSight intimated that theindex would fulfil all the criteria for afuture exchange-traded fund listing.

Separately, Chicago Board ofTrade has said that it will launch anexchange-traded managed futuresfund. It was tight-lipped on thedetails, however, claiming that certain“novel features” in the plan may besubject to patent protection.

Total protection

While the long-volatility CMI

index is not correlated with

either hedge funds or with

broad indices such as the S&P

500, it is correlated with

actively managed futures, with

a higher risk-adjusted

performance

Client Objective Value Contact Effective Adviser

CSS/PSS (Australian Unknown A$100m Chief investment Unknown Total Risk Managementsuperannuation fund) (of A$15bn fund) officer Andre Morony (Aus) for tender

programme, with Wilshire as alternative assets conusltant

Canadian Pension Plan Core/satellite approach $1.8bn (10% of fund) Unknown Over next five UnknownInvestment board, with Canadaian and foreign yearsToronto index fund core and private

equity satellites

Retail Superannuation Allocation to single hedge A$75m (US$38m) Michael Lillicrap, Completed UnknownTrust, Australia fund Holowesko Global REST general

Fund marks Australia's managerbiggest allocation to date. Further allocations dependent on results

Searches and mandates

Source: Compiled from MAR Hedge

10 SEPTEMBER 2001 RISK & REWARD

Andrew Malloy Planning to build hedge fund outfit from scratch TAG Associates

Andrew Ross Cazenove Group CE HSBC Asset Management

Anne Yobage Axa Investment Managers Member high-yield bond team Co-founder Cardinal Capital Management

Barry Steinhart HBV Capital Analyst Enron Capital & TradeManagement UK Ltd

Brant Nehr Parker Global Strategies Senior associate strategic initiatives Kenmar

Brian Kilgannon Trade propietary capital in Sells his share of Aus advisordiscretionary style Reef Capital to co-founder

Nick Radge

Caroline Hoysted GLC, London CE, resp day-to-day running of UK, GNI Fund Managementand opening of Aus, office

Chris Crawford RG Niederhoffer Capital Director operations Offshore administrator, Management Vanguard Group

Clare Dobie Global Asset Management Md marketing BGI, London, head of risk management

Clayton Cheek Ivy Asset Management Vp client development, Sage Capital ManagementCorp resp new institutional business

Daniel Harley HBV Capital New office formed to act asManagement UK Ltd subadvisdor

Egidio Robertiello Blackstone Alternative Md manager selection team Summit Fiduciary ServicesAsset Management

Elliot Arnold HBV Capital Trader Vp, ING BaringsManagement UK Ltd

Frank Savage Africa Millenium Fund Heads up firm, which is intended to Alliance Capital ManagementManagement develop into global financial Holding

services firm

Gary Knapp Hedge Fund Research Part of HFR’s effort to move from Ex-executive General Motorsconsulting to FOF management? Investment Management

Corporation

Gary Shugrue Ascendant Capital CIO COO, Double Agent Partners, Berwyn PA

Hannah Strasser Axa Investment Managers Member high-yield bond team Co-founder Cardinal Capital Management

Who Joins In order to… From

People moves

RISK & REWARD SEPTEMBER 2001 11

People moves

James Hague Millburn Corp Senior portfolio manager, resp Glenwood Capitalguiding hedge fund business strategy

James Marler Investor Select Advisors, Md European clients E-Trade, MdLondon office

Jean-Philippe ING Furman Selz Asset Md alternative investments West Broadway Partners,Carriol Management resp risk and convertible

arbitrage

Jim Kottler Royal Bank Private Equity Investment Manager Bank Austria Private Equity, (new opportunities)

Jin Park Carlye Asset Management World Bank alternative investments manager

John Carlisle ABN AMRO Prime Md, Dallas office Vp Deutsche Banc Alex BrownBrokerage

John Kelly Man Investment Products Director, US sales Internal move

John O'Hara ‘Will resurface after Md Goldman Sachs hedge gardening leave’ fund strategies group

John Rohal EGM Capital Vc board of directors Global research director Robertson Stephens

Jonathan Mosely Global Asset Md European clients Merrill Lynch InternationalManagement private client group

Kenzo Tanaka Man Investment Products Senior marketing exec HSBC Securities, Tokyo

Laurent Chevalier Millburn Corp Allocation and due diligence for FOF Head of research Weston Capital Management

Lilian Wong Bank of Bermuda, Md/country head of global fund Internal promotionHong Kong services

Marc Malek Self-started firm, Launch Conquest Global Macro/CTA, Enterprise Asset Management,Conquest Capital, using following split from former partner which closesEnterprise Asset Nigol Koulajian, who is also reportedManagement systems to be preparing new product

Margaret Towle Northern Trust Global Chief investment officer Puget Sound Asset Advisors, Stamford, Ct Management

Matthew Dubicq HBV Capital Analyst ABC ArbitrageManagement UK Ltd

Who Joins In order to… From

12 SEPTEMBER 2001 RISK & REWARD

People moves

Michael Fields Lighthouse Partners, Head up new New York office Tiedemann Investment GroupJupiter, Fl

Michio Jibiki AIMA Japan chapter Chairman Remains head of alternative investments at Asahi Life Asset Management

Peter Adamson Eli Broad family office First external cio Lee Bass family office

Peter Grunblatt Bank Leu, Zurich Head of alternative investments Bank Julius Baer

Ralph Sinsheimer Neuberger Berman SVP Trust Companies Wealth Officer at Offitbank, wealthManagement Group management unit of Wachovia

Ricardo Cortez Torrey Associates President private client services Product manager Goldman Sachs

Rich Ewan Man Investment Products Will report to John Kelly Internal move

Richard Campagna Shaker Investments Md research Manning & Napier Advisors, senior analyst, co-manager

Richard Johnson Lucerne Partners Md, responsible for developing ING Baringsinstitutional relationships

Robin Apps Beaumont Capital Partner, to be involved in Deputy CIO, UBS AssetManagement management of funds Management

Ross Jones GNI Fund Management CE Move from parent group

Stephen Brent Neuberger Berman COO, Trust Companies Wealth Officer at Offitbank, wealthWells Management Group management unit of Wachovia

Stephen Pearson Jupiter International Set up European long/short fund Director Sloane Robinson

Steve Bossi Deutsche Asset Director, FOF team AI International, family officeManagement

Tetsuya Tanaka Man Investment Products Senior marketing exec Morgan Garanty Trust, global custody

Thomas Spak Weston Capital COO Vp institutional client servicesManagement Morgan Stanley IM

Thomas Taylor Alpha Investment CEO: rumoured dressing up firm BBT PartnersManagement for possible sale

Tom Northcote Fall River Capital Vp marketing and sales Lindner Asset Management, St Louis

Who Joins In order to… From

People moves is compiled from MAR/Hedge weekly reports, July/August 2001

14 SEPTEMBER 2001 RISK & REWARD

Fund launches

Fund manager Fund name Style

Africa Millenium Fund Management Africa Millenium Fund Infrastructure fund

Altis Capital Management Global Futures Portfolio Diversified quantitative fund

Asset Alliance Emerging Manager Fund Seed fund with variety of strategies

AXA Global Structured Products New Horizons Absolute Return Fund FOF

Bank of Bermuda Kangaroo Fund Incubator

Bank of Bermuda All Points Alternative Opportunity Class FOF

Bank of Ireland Private Banking Hedge Certs Five-year principal-protected structured deposit linked to portfolio of Group's Asset Alliance HF mans

Barclays Global Investors Diversified Alpha Fund FOF

Broyhill Asset Management, Variable Universal Life Private Placement Allocated to Broyhill All Weather FOFNorth Carolina

Choice Investment Management, Denver Adams Select Fund Offshore Long/short

Commerzbank Securities Comas Plus FOF

Creedon Capital Management Alta Partners Discount Convertible Convertible ArbitrageArbitrage Fund

Deutsche Asset Management Deutsche Absolute Spectrum Global Equity 21 such managersLong/Short Fund

Ephesus Capital Partners GDO Equity Arbitrage Master Fund Long/short

GNI Fund Management Global Strategies Fund Multi-manager capital guaranteed fund

Harris Associates Pleiades Offshore fund FOF

Highland Capital Management, Australia Highland Growth Fund

ING Furman Salez Asset Management Windridge Partners International; Anvers Real estate and related securities; healthcare products and servicesHealthcare Investors Int

Invesclub, Milan Pleiades 1 FOF

Investor Select Advisors ISA Partners FOF

Jupiter International Group Europa (not confirmed) Long/short European equity

K@talyst Ventures, Cambridge UK K@talyst Hydrogen Fund Long/short equity with long bias

Kenmar International [Unconfirmed] Span managed futures and hedge funds

Key Asset Management Key Recovery Fund Multi-manager fund: Distressed and restructured debt, mainly US

Kyte Fund Management Kyte Mirador Fund Merger arb/event trades/corporate restructurings

Lansdown Partners Lansdown UK Equity Fund Long/short equity

Man Investment Products Man-IP 220 Plus Seies 4 Multi-strategy FOF

Martin James Capital Management Market Neutral Options Arbitrage Fund LP Option arbitrage

New Star Asset Management New Star European Hedge Fund Long/short European equity

Okumus Capital, NY Okumus Market Neutral fund Market neutral

Polar Capital Partners Polar Capital Technology Absolute Return Fund Long/short global technology

Prescient Capital Prescient Investment Partners LP Growth and technology

Ram Sen, Singapore LowRiskProfits Capital Management Trend-following, multi-market system

Rampart Investment Management Rampart Statistical Arbitrage/Rampart Statistical arbitrage/long-shortLong/Short

Strome Investment Management Strome Arbitrage Partners Risk arbitrage

Systeia Capital Management [Unconfirmed] Range of funds, including event-driven, equity statistical arbitrage, convertible arbitrage, catastrophe bonds and weather derivatives

T Young & Co [Blended fund of two trading managers]

Talisman Capital Talon fund Relative value/capital structure arbitrage

Talorcan (Abbey National subsidiary) Talorcan Equity Pairs Plus

Talorcan (Abbey National subsidiary) Talorcan Forex Fund

Talorcan (Abbey National subsidiary) Talorcan Global Fund

Watch Hill Investment Partners Watch Hill Strategic International Fund Market neutral mortgage-backed

RISK & REWARD SEPTEMBER 2001 15

Fund launches

Launch date Fee structure Minimum Other details

To be announced

Raising capital now 2/20 plus expenses $100,000

By year end Flat 1% $10 million Aimed at institutions wanting to ensure capacity

1% Target 20-40 funds; single fund max 7.5%; single strategy max 15%

For Aus managers seeking to raise assets offshore

Fund managers with under 12-months track record

17 July $56,000 Target returns 10-12% pa

September 1/10 (beyond libor) Three broad strategies

Manager is part of Broyhill family office

Before end September 1/20 $250,000 Offshore version of Adams Select

1.5/10 (high watermark) €25,000 Combination absolute return and net directional strateiges. Monthly liquidity

1 July 2/20 Seeks undervalued convertible positions

1.1/15 US$2,550 To meet retail demand

September 2/20 $1 million

17 September 2% man/5% incentive/ $50,000 Multi-strategy. Aimed at retail1% risk man/0.3% admin/2% offering

2 July 1/20 Invests in relative value arb managers

A$500,000 30% of investments allocated to external funds/trading advisors

1/20 $250,000 Follow onshore versions of same fund

9 July 1.5/15 €100,000

1 August 1/5 $500,000 Long/short, convertible arb, short-biased and event-driven managers

October 1.5/20 $100,000

1 August 1.5/20 Specialist companies dealing with production and consumption of energy

To be announced

2 July 1.5/5 $500,000

1 October 1/20 $1 million

1 August 1.5/20 (high water mark) $250,000

Under offer period 3/20 $50,000 Capital guaranteed

Mid-June 2/20 $1 million

September $150,000

1 August 1/20 $500,000 Short index positions to maintain market neutrality

9 July 1.25/20 (with high watermark) $100,000 Managed by ex-Henderson staffer Brian Ashford-Russell

1/20 $500,000

Trading liquid currency, interest rate, commodity and equity markets

August-September 1/20 $500,000 Focus on recapitalisation events and merger subjects

Staggered launches up to Seed capital from Crédit Lyonnaisnew year 2002

$50,000 Meyer Capital Management/Beuthe Crabel Trading

1 July 1.5/20 45% European/45% US/balance in Asian securities

27 June 1.5/20 €125,000

18 July 1.5/20 €250,000

1 August 1.5/20 €250,000

1July 1/20 $1 million Higher leverage than onshore version

Country profile: Australia

16 SEPTEMBER 2001 RISK & REWARD

If the key participants are right, Australia is on theverge of a significant breakthrough in both its whole-sale and retail alternative investment market. Butthere are substantial hurdles that include Australia’s

regulatory environment, track record and market depth.In other words, the big players are yet to make theirappearance.

Angus Grinham, director at Grinham ManagedFunds, Australia’s largest alternative hedge fund man-ager with A$700 million in funds under management,says that over the past year the Australian alternativeinvestment market has moved “from the educationalstage to the early growth stage. We are starting to seereal momentum.”

Deon Joubert, managing director at AbsoluteCapital, which claims to be Australia’s largest allocatorof capital to the domestic hedge fund sector with A$200million under management, is convinced the next yearwill be significant. He says, “The A$2.5bn market can

increase tenfold without blinking. The massive attentionon Australian alternative investments will soon bematched by dollars changing hands. Suddenly, a lot offund managers are hiring staff and setting up depart-ments. The superannuation (pension) funds are sendingasset consultants to look at hedge funds as the trusteesprepare to make decisions.”

Other Australian managers are similarly convincedthe enquiries will soon start translating into real dealsand large mandates, mirroring the worldwide trend.Managing director of Merrill Lynch InvestmentManagers’ alternative strategies section, FabioSavoldelli, says local trustees have crossed the ‘what isthis?’ bridge. Many have crossed the ‘do these assetsbelong in my fund?’ bridge, and some are even askingthose vital final questions, ‘how much?’ and ‘to whom?’

A wave of superannuation funds have indicated theyare looking to invest in hedge funds as part of their alter-native investments strategy. The first major commitment

Aussie rules

Australia could very well be the next place to witness the massive uptake inalternative investments that has occurred in the US and parts of Europe,

says Simon Segal

Country profile: Australia

RISK & REWARD SEPTEMBER 2001 17

has been made by CSS/PSS (the scheme for public ser-vants), Australia’s second-largest superannuation fund.It is expected to allocate A$100 million to hedge funds,making it the largest institutional hedge fund investor inAustralia. Beyond hedge funds themselves, the fundhas committed to invest 10 per cent of its entire portfo-lio in alternative assets.

In July this year, in an effort to boost returns, theRetail Employees Superannuation Trust allocated A$75million to the US-based Holowesko Fund.

These market moves have been matched on theinfrastructure side with the launch earlier this year of alocal chapter of the UK-based Alternative InvestmentManagement Association. The body, which has 23founding members, including most of Australia’s hedgefunds and three of its major broking houses (MerrillLynch, Morgan Stanley Dean Witter and GoldmanSachs) intends to fulfil an educational brief. Equallyimportant perhaps it is the first effort to bind the smallhedge fund community in Australia.

Local AIMA deputy chairman Kim Ivey saysAustralian managers make up the industry’s small sizewith a sophisticated approach. “Hedge fund managersare very conscious of risk management,” he says. Ivey,too, forecasts a doubling of assets under managementin the near term, with most money coming from the insti-tutional market. “Pension fund trustees have been on asteep learning curve,” he says.

Ivey notes that Australian pension funds, now worthA$600 billion, are growing at 10 to 12 per cent a year.He also expects money to start flowing into Australianhedge funds from abroad. “The Australian stock market,Asia’s second largest after Japan, offers ample liquidity,and investors will appreciate the steady 3-4 per centannual growth that the Australian economy has postedover the past five years,” he says.

However, hedge fund managers are as likely to gainfrom weak financial markets as from general economicgrowth. Here as elsewhere, the most conservative oftrustees are having to listen to predictions of a new eraof lower overall returns. In such a scenario, even the

most conservative of trustees will be pressured to con-sider alternative assets. “Expectations around returnshave been raised by the phenomenal performances offinancial markets. As markets now face a down period,the pressure mounts on fund managers to seek newtools such as alternative investments in their armoury,”says Grinham.

Debbie Alliston, Rothschild director and head ofportfolio management, believes that in 10 years’ time theaverage portfolio could have perhaps 20 to 30 per centin alternative investments, with the intent both ofincreasing overall returns and diversifying portfoliosaway from market risk.

Alliance Capital senior manager of institutional mar-keting Brad Karp finds that the decision for investors totake the first step into hedge funds is being made eas-ier as more and more managers introduce credibleproducts into the Australian market. “Our experience isthat investors will probably make an initial allocation to awell-diversified fund of global hedge funds,” he says.

There are, however, factors tempering the optimism.Lack of liquidity and skilled managers in Australia hin-ders growth. The limited capacity of products – there areonly six funds of funds at the moment – controls theamount of money that flows into the sector. All agree thatthe interest in hedge funds has not yet been matched byinflows.

Rothschild associate director of alternative invest-ments Richard Keary believes the strength of productdevelopment teams and the global ability to researchinternational hedge fund managers will become increas-ingly important. “It will be hard for an Australian FOFmanager with a couple of people in the product devel-opment team to actively compete when the standardsare lifted,” he says.

However, Rowan Menzies, head of investmentresearch at Absolute Capital, is convinced that theAustralian alternative investment industry is globallycompetitive. “It is as sophisticated in terms of peopleskills and systems. It is lacking in capital inflows,” hesays. Frank Russell Australia managing director

“The superannuation (pension)funds are sending asset

consultants to look at hedgefunds as the trustees prepare

to make decisions” — DeonJoubert, md Absolute Capital

Country profile: Australia

RISK & REWARD SEPTEMBER 2001 19

A potted history The bulk of Australia’s alternative investments are in private equity. Hedge funds estimated by Absolute Capital mdDeon Joubert to be worth A$2.5 billion, invested among some 50 hedge fund managers.Funds of funds are the most popular vehicles.

Deutsche Asset Management and Rothschild Australia Asset Management were the first mainstream names tointroduce fund-of-fund hedge fund products into Australia. According to Deutsche, Australia’s first locally-devel-oped and registered multi-manager hedge fund was its Strategic Value Fund launched in December 1999. It nowhas over A$100 million in assets under management from both retail and institutional investors.

In November 2000, Macquarie Bank launched its first hedge fund, trading equities, interest rates, commodities andcurrencies. Based in Bermuda, the fund will have $100 million, including $60 million invested by the bank.

In the mid-1990s, Grinham and Platinum Capital became the first hedge funds in Australia to operate outside of amajor banking group.

In the past few months financial institutions that include global players Frank Russell, Schroders, Colonial First State,and Credit Suisse have announced plans to set-up multi-manager global hedge funds for Australian investors.

Grinham Managed Funds claims to be Australia’s largest hedge fund manager with A$700 million in funds undermanagement, while Absolute Capital lays claim to be Australia’s largest hedge fund and fund-of-funds managerwith A$200 million under management onshore and in domestic products. Deutsche contends it is Australia’slargest hedge fund manager in terms of its A$800 million in assets under management. Of this it says around halfis invested in domestic products. Absolute, which allocates 60% of its assets to locally based managers, has struc-tured its Absolute Return Fund into five sub-funds, allocating 36% to global strategies, 29% to yield strategies, 13%of assets to equity long/short equities, 12% to arbitrage strategies and 10% to relative value.

Absolute operates on three levels. It allocates to funds of funds in Europe and the United States, it allocates tohedge funds directly in Australia and abroad, and it manages assets itself.

This year has seen a string of developments:

• Credit Suisse Asset Management (CSAM) plans to launch two multi-manager international hedge funds intoAustralia this year. The fund of funds are managed out of CSAM’s New York office

• Rothschilds, in addition to its domestic hedge fund product for the wholesale market, launched a global hedgefund of funds in partnership with the Grosvenor Group of Chicago.

• Frank Russell launched its Alternative Strategies Fund, a multi-manager global hedge fund that provides super-annuation funds with an investment list of 15 leading hedge fund managers, mostly in the US

• New York-based AXA Global Structured Products (AXA GSP) launched a global fund of hedge funds into theAustralian wholesale market. The fund is marketed and distributed in Australia by Alliance Capital

• Schroder Investment Management has said it is considering launching a series of international hedge funds intothe Australian market to capitalise on growing demand from super funds for alternative investments

• Deutsche launched its second Australian multi-manager fund, the Absolute Spectrum Global Equity Long/ShortFund. The firm is marketing the fund to retail and institutional investors as an innovative way of investing in inter-national equities with a lower volatility than traditional equities

• Colonial First State Australia forged a sub-advisory agreement with Harcourt Investment Consulting AG to man-age the six different funds of funds Colonial plans to launch. For Harcourt, based in Zurich, Switzerland, this isan opportunity to break into the Australian hedge fund market without establishing an office on the continent

• Lazard formed a new arm in the US to expand its alternative investment business and created a new hedge fund-of-funds product. Lazard already offers a its Global Opportunities Hedge Fund – a long/short equity fund – toAustralian institutions

• Hedge Funds of Australia, which has one fund in the market, expects to bring a second product to market thisyear and a third next year. HFA claims to be the only hedge fund in Australia available to individuals.

Country profile: Australia

20 SEPTEMBER 2001 RISK & REWARD

Alan Schoenheimer adds that, “the uptake of new ideasis a lot quicker than in most other markets,” though FrankRussell will not offer an equivalent multi-manager stylefor hedge funds domiciled in Australia. “The alternativeasset classes are a global game and our strategy is tobring clients access to the best hedge fund managersregardless of where they are located,” he says.

Retail movesIn the end, hedge funds will only become truly main-stream if they are taken up by retail clients. GlennPoswell, vice president at Deutsche AssetManagement’s Strategic Investment Group, believes thisdevelopment will occur through wraps and masterfunds, though other observers, such as Rothschild’sKeary, emphasise retail investors’ frustration at the lackof funds available.

Keary emphasises that it is still early days for hedgefunds in Australia. “The other problem,” says Keary, “isthat investors are being confronted with an unfamiliarnumber of brand names as hedge funds might be soldunder their overseas manager’s name more prominentlyin the future.” And while he is on the subject of thwartedambition, he cites the lack of ratings and surveys for thesector as a handicap, though he believes they willbecome more common as products build a track record.

A report released in January by local ratings houseInTech highlights issues of liquidity, risk and diversifica-tion that need to be carefully considered by trusteesbefore changing a fund’s portfolio to incorporate what itdeems a ‘generally high risk/high return asset class’.The mere existence of the report stands testament tothe flush of interest in hedge funds, but the report’soverall tone is cautionary. In contrast to optimistic mar-ket participants, author Dennis Sams finds, “Trusteesare questioning whether they should be gettinginvolved.” He goes on to advise trustees not to bespurred on simply by the pressure to secure ever-higherreturns. “There is a natural tendency to seek out highgrowth investments that may give a boost to perform-ance. The trade-off, naturally, is higher risk,” he says,

adding that the local industry still lacks a lot of history inareas like the volatility of alternative asset classes andtheir correlation.

According to local AIMA chairman and ColonialAbsolute Return Fund head Damien Hatfield, “Australianinvestors want to look closely at the managers within afund-of-funds product that they invest in. Relative lengthof track record, leverage and overall process are keyfactors.”

Savoldelli argues that hedge funds are probablyhandled better by the big investment houses, andbelieves that asset consultants are still coming to termswith how to handle, advise and monitor hedge funds.

Though the Australian market may have its ownfoibles and drawbacks, it is at least some way fromexperiencing the capacity constraints of the interna-tional industry. According to Hatfield, the structure of theoverall industry – 50 per cent of which is invested inlong/short directional equity strategies – means capac-ity problems are a long way off.

Another major hurdle — being lobbied against byAIMA — are restrictive tax regulations that penalise off-shore investors in Australian hedge funds. Many of theunderlying managers in the Australian hedge fund prod-ucts are domiciled offshore, which introduces ForeignInvestment Fund (FIF) tax implications that see investorstaxed each year on an accruals basis. “Government canmake it easier for hedge funds to develop their businesswith offshore investors. We’ve all had to set up offshorevehicles,” says Ivey.

On the regulatory front Keary is optimistic. “It is sen-sible and benign, certainly not an impediment.” Liquidityand institutional interest are clearly bigger obstacles.The early participants are ready and expecting things tohappen at a rapid pace from now on.

Simon Segal is a freelance financial journalist livingand working in New South Wales

“It will be hard for anAustralian FOF manager with acouple of people in the productdevelopment team to activelycompete when the standardsare lifted” – Richard Keary

Kim Ivey

Technology focus

RISK & REWARD SEPTEMBER 2001 21

One might assume that with global equity mar-kets in what can (at best) be described as anuncertain state, equity option technologywould be in a similar condition. But appar-

ently not. Perhaps vendors dissemble well, but to judgeby the range of new products being launched, it wouldappear that activity has done anything but collapse.Demand from the hedge fund community appears to beplaying something of a role in this unexpectedresilience, with several independent factors at work.

At the simplest level, a number of equity funds withmandates that allow the use of options have started totake advantage of the fact. As it becomes harder to gen-erate alpha on their long positions, these funds are usinga number of strategies (everything from simple coveredcall writing to relative value plays) in an attempt garnerexcess return. Though these strategies may not neces-sarily occupy the cutting edge of financial engineering,they are at least keeping the market for shrink-wrappedproduct ticking along.

At the other end of the spectrum, there has beenincreasing demand for products that can handle thecomplex equity derivative products created by combin-ing simpler structures. With markets in less than ebullientmood, managers are increasingly looking for tools capa-ble of highlighting arbitrage opportunities where suchcombined products are mispriced. In addition, therehave been several funds trying to get a new angle onpreviously profitable strategies, such as dispersiontrades, that have recently run out of steam. The other bigwinners have been convertibles, where demand from amixture of convertible arbitrage funds and more conven-tional players has also been buoyant. In addition, a moregeneral theme has been the move by several vendors tooffer their analytics online in an ASP format.

Some might question many hedge fund managers’devotion to the discipline per se, but demand for riskmanagement-related functionality also remains strong.This may not necessarily take the form of more esotericrisk analytics, but some basic reporting, or at least thefacility to export position information or a VaR number, isbecoming de rigeur.

Then there is the continued demand, particularly fromthe more specialised hedge funds, for increased model-ling flexibility. At the sharpest end of OTC equity deriva-tives the concept of a market standard model doesn’treally exist. Managers who see their financial engineeringskills as their competitive edge are no longer prepared tojust accept out-of-the box models. Instead, they want theability to tweak the existing model mathematics or eveninsert complete models of their own.

Though quite a few vendors have offered this facilityfor a while, it has to be said than in at least some casesthe functionality has been cumbersome, and in othersseverely overstated. The main difficulty is trying to strikea balance between adequate flexibility and performanceon the one hand and ease of use on the other. While it isperfectly possible to use fourth generation languagessuch as Python for such tasks, there is usually a sub-stantial run time performance penalty when comparedwith languages such as C or C++.

“In the past, this sort of functionality has been verymuch a case of ‘square peg, round hole’,” says the headof trading floor technology at one US hedge fund. “Whileit might have been theoretically possible, it often provedsomething of a challenge in practice. Another issue hasbeen the aggravation of having to take down a produc-tion system and restart it every time even a minor tweakhas been made to a model’s maths.”

One vendor that has been making something of aflexibility push is SciComp. The company’s ASPEN(Algorithm SPEcification Notation) scripting languageallows non-programmers to create or tweak complexmodels and then automatically generates the appropri-ate C code. (Those who prefer can edit their own C codedirectly.) SciComp provides two core products – SciPDE

Equity markets may be experiencinguncertainty, but that only fuels theanalytics development process,discovers Andy Webb

Stock tactics

Technology focus

22 SEPTEMBER 2001 RISK & REWARD

(which uses finite difference methods to price partial dif-ferential equations), and SciMC (a Monte Carlo engine)both of which can be customised using ASPEN.(SciComp’s source code is included in the license fee.)Quick evaluation of any modelling can be performed inExcel by using SciXL, which automatically generatesExcel add-ins based on the code. SciComp, which hastraditionally targeted the broker-dealer market, is nowstarting to turn its sights on the hedge fund communitywith annual license fees starting at $25K.

Some, while acknowledging the importance of modelflexibility, have seen increasing emphasis being laid byhedge funds on the ability to value a combination ofexisting instruments as a single structure. “While hedgefunds obviously want to be able to tweak the models,we’ve seen more demand of late for flexibility when itcomes to combining valuation routines, such as in a multiasset Monte Carlo model,” says Mamdouh Barakat, man-aging director of derivatives vendor MBRM. “They needto be able to do scenario modelling for shifts in variouscurves and the underlying assets on hybrid instruments,such as quanto Asian basket options, or Asian forwardstarting baskets. They are pushing to extremes withthese more esoteric structures in order to try and dis-

cover where the market may not be accurately pricedand there are arbitrage opportunities.”

In common with a number of other vendors, MBRMhas also seen increasing demand from hedge funds forASP versions of its equity option analytics. Those man-agers who don’t relish the prospect of in-house applica-tion maintenance can now run the MBRM pricing mod-els online, and (if they wish to avoid re-keying data) canstore their portfolios there as well.

Sophis, Imagine Software, FinancialCad, andSavvysoft are also among the increasing number of ana-lytics vendors that have launched ASP versions of theirproducts. Imagine has taken the derivatives functional-ity of its Imagine Trading System and made it availableonline at Derivatives.com. The service includes real-timedata for a range of markets, and is accessed via light-weight Java client. FinancialCad’s FinCad.net service ispowered by the same library of 550 modelling functionsprovided in its original offline products. Users can opt toaccess Fincad.net in several ways – directly through aconventional web browser or via the company’s FincadXL or Fincad Developer applications. Secure data stor-age and tools for developing custom pricing routinesare also provided. Savvysoft has recently launched

Technology focus

24 SEPTEMBER 2001 RISK & REWARD

Analytics4Rent.com, which is the first product to allowusers to run derivatives analytics on the Internet fromwithin an Excel spreadsheet. The pricing routines that liebehind Analytics4Rent.com are Savvysoft’s establishedTOPS 2000 models.

Savvysoft’s founder, Rich Tanenbaum, has a slightlydifferent slant on the importance of flexibility to hedgefunds. “I think the concept of tweaking models in order toexploit mispricing is something more common in the bro-ker dealer community,” he says. “In our experience,hedge funds are happy enough to buy in pricing expert-ise. They see their competitive advantage lies more inhow they use those analytics to best effect – such as tak-ing a position and then devising the best way of hedgingit to obtain an acceptable risk/return ratio. However, theyare keen on technological flexibility – so we find that beingable to provide equity option pricing routines via a num-ber of routes (such as Excel, DLLs, ASP etc) is essential.”

Tanenbaum has also noted some particular require-ments among the hedge fund community when it comesto risk management. “The majority of funds that we talk to aren’t particularly interested in risk management as an abstract science,” he says. “However, they increas-

ingly need to beable to satisfy therequirements ofbanks/dealers whomight provide themwith funding andpotential investors.The funds obvi-ously don’t want to provide actual position information, sothey are looking for something to provide a proxy for this,such as delta equivalents and some VaR numbers.”

That’s also the view of Ravi Jain, ceo of EgarTechnology. “Investors are becoming far more demandingand actually want to see the risk management and report-ing systems in place before they part with any capital,” hesays. “They are no longer prepared to take this on trust oron the basis of the manager’s reputation, nor are theyprepared to accept the basic risk analysis traditionallyprovided by hedge fund administrators. Even if an equityoption trading system doesn’t provide that functionalityitself, it must as a minimum be capable of making infor-mation to support that process easily available.”

Egar itself provides risk reporting through its estab-lished Focus product, which in addition to providingextensive derivatives coverage (including listed andOTC equity products) also includes a middle and backoffice infrastructure suitable for a smaller regional bankor hedge fund. EGAR has also recently launched twoproducts more specifically targeted at equity options.ETS (Equity Trading System) is an open rapid develop-ment platform that allows Egar to create client-specificsolutions. That said, ETS is nevertheless fully functionalstraight out of the box, and in that guise should cover thebulk of the requirements of most equity option traders,including quotes views, risk views, risk matrices, marketstructure, real-time feeds, trade entry and position man-agement blotters, and reporting.

Egar’s most recent product release is EGARDispersion, which is designed to cater for a type ofequity option trade that has become hugely popularover the past two years, but has somewhat run aground

”We’ve seen more demand forflexibility in combiningvaluation routines, such as ina multi-asset Monte Carlomodel” – Mamdouh Barakat

Mamdouh Barakat

Rich Tanenbaum

Technology focus

RISK & REWARD SEPTEMBER 2001 25

in the last six months. Dispersion trades typically consistof short selling options on a stock index while simulta-neously buying options on a basket of constituentstocks. The objective is that the individual underlyingstocks will move in different directions, which will havethe effect of reducing overall movement in the relatedindex. The net result is a relative volatility trade, which ifsuccessful, profits from the volatility discrepancybetween the basket of stocks and the parent index.

“For a some time this was a beautiful trade, particu-larly in tech indices such as the Nasdaq and MorganStanley Tech Index, but with a one-way market the basicstrategy has collapsed,” says Jain. “However, a numberof hedge funds are now looking for tools that will helpthem to put together more sophisticated dispersionstrategies. These tools need to be able to perform indepth analysis of the volatility relationship betweenstocks and the parent index, such as the volatility con-tribution of individual stocks.”

The snag is that this requires access to a substantialamount of high quality historical implied volatility data,which apart from the proprietary service offered by per-haps one investment bank to selected clients, is not read-ily available. However, Egar has addressed this challengethrough its Ivolatility.com service, which provides much ofthis necessary data, together with simple analytics, forfree. (A more sophisticated set of online modelling toolsand data is also available on a subscription basis.)

The convertible market has been particularly busy.Apart from the traditional convertible arbitrage players,bond traders looking for an equity kicker and equitytraders seeking the reassurance of a bond floor havealso boosted activity. This boom in convertible activity

(and that more generally in equity option products) cer-tainly doesn’t appear to be doing vendor MONIS anyharm. “The convertible arbitrage hedge fund sector hadan excellent 2000 and has also been strong so far thisyear,” says Paul Compton, VP for global education atMONIS. “We’ve also seen increasing interest from a var-ious other types of hedge fund.”

MONIS’ convertible analytics are available in threeways – Convertibles Analyzer, Convertibles XL, andConvertibles LIB. Convertibles Analyzer is a completetrading and portfolio management solution,Convertibles XL is the Excel based version, whileConvertibles LIB is a callable convertible functionslibrary. In addition, several other derivative vendorshave also established formal partnerships with Monisthat make it possible to use its convertible models fromwithin their own products. For example, Front CapitalSystems and Monis announced an agreement early thisyear to provide Front clients with access to Monis mod-els within Front Arena. Like Egar, Monis has also spottedthe need for clean data and provides a data service forboth convertible prices as well as terms and conditions.

Looking ahead, it seems likely that the trend towardsgreater flexibility will continue and possibly accelerate.That is certainly the view of Xenomorph, which hasrecently launched its PerfectVine trading and risk man-agement solution for hedge funds. As standard,PerfectVine can access equity option and convertiblemodels from MBRM and Monis, and it can also beconnected to proprietary models as well as those fromvendors Derivative Solutions, FinancialCad, and FEA.

“We’ve also designed PerfectVine so that usersaren’t obliged to use our presentation layer,” says NiallMcIntyre, head of marketing at Xenomorph. “That’s alsobeen driven by the feedback we’ve been getting fromhedge fund clients, who increasingly wish to be able touse their own GUIs as well as picking and customisingthe analytics that underlie them.”

Andy Webb is a freelance financial and technologyjournalist

“A number of hedge funds arenow looking for tools that will

help them to put togethermore sophisticated dispersion

strategies” – Ravi Jain

Ravi Jain

Profile

26 SEPTEMBER 2001 RISK & REWARD

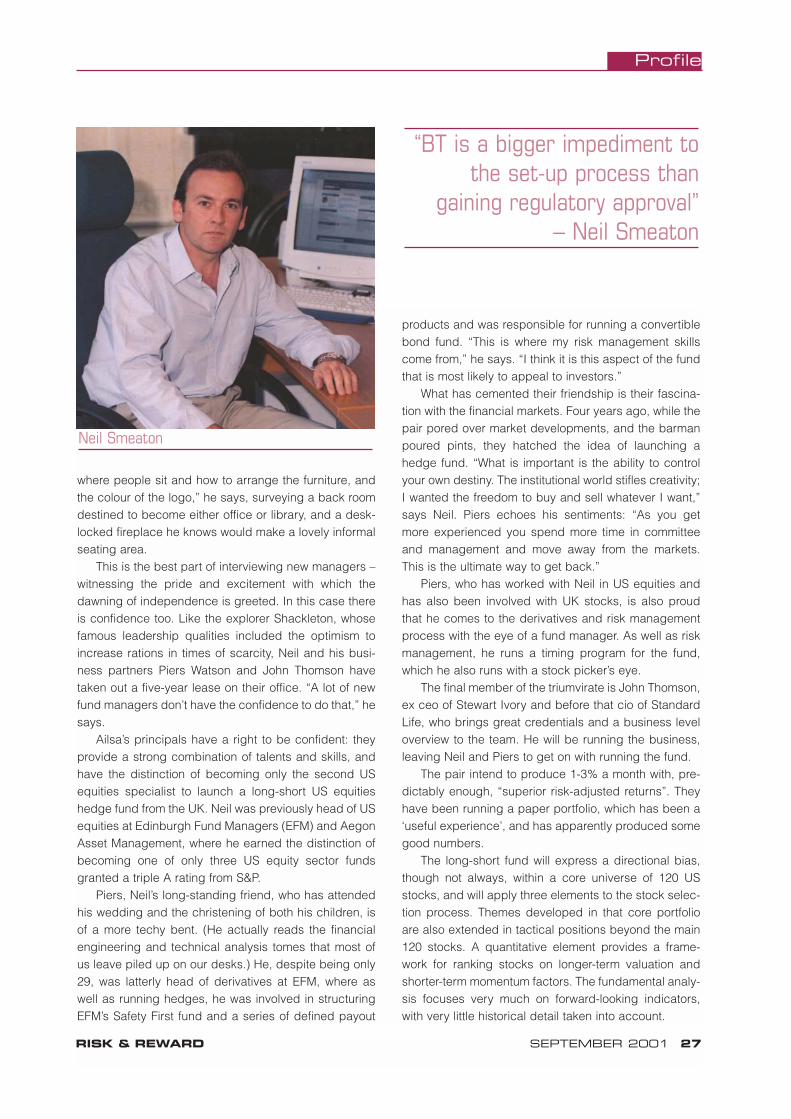

Nothing ails (y)a

Kim Hunter finds out why Neil Smeaton and Piers Watson believe they havedeveloped a winning formula with Edinburgh-based start-up Ailsa Capital

Somehow, my bungling attempts to get toEdinburgh (one flight missed; another delayed)to interview new fund manager Neil Smeatonwere successful in the end. And as I sat oppo-

site him in his Georgian offices it became clear that hadI failed, only myself and British Telecom would have heldup the unfolding of the Ailsa Capital master plan.

But I would have had to work hard at incompetenceto match BT, who, according to Neil, is “a bigger imped-iment to the set-up process than gaining regulatory

approval”. In fact, IMRO were fabulous, he says: theIMRO licence can be obtained in four months; it took halfthat for BT to install a high-speed modem line. Telecomsincompetence notwithstanding, with the IMRO licencejust granted, and roughly $15m seed capital locked infor two years, the Ailsa US Equity fund is bang on targetfor its 1 October launch.

Neil has been surprised that housekeeping detailshave attained such prominence in the set-up process.“The biggest discussions we have had have been about

Profile

RISK & REWARD SEPTEMBER 2001 27

where people sit and how to arrange the furniture, andthe colour of the logo,” he says, surveying a back roomdestined to become either office or library, and a desk-locked fireplace he knows would make a lovely informalseating area.

This is the best part of interviewing new managers –witnessing the pride and excitement with which thedawning of independence is greeted. In this case thereis confidence too. Like the explorer Shackleton, whosefamous leadership qualities included the optimism toincrease rations in times of scarcity, Neil and his busi-ness partners Piers Watson and John Thomson havetaken out a five-year lease on their office. “A lot of newfund managers don’t have the confidence to do that,” hesays.

Ailsa’s principals have a right to be confident: theyprovide a strong combination of talents and skills, andhave the distinction of becoming only the second USequities specialist to launch a long-short US equitieshedge fund from the UK. Neil was previously head of USequities at Edinburgh Fund Managers (EFM) and AegonAsset Management, where he earned the distinction ofbecoming one of only three US equity sector fundsgranted a triple A rating from S&P.

Piers, Neil’s long-standing friend, who has attendedhis wedding and the christening of both his children, isof a more techy bent. (He actually reads the financialengineering and technical analysis tomes that most ofus leave piled up on our desks.) He, despite being only29, was latterly head of derivatives at EFM, where aswell as running hedges, he was involved in structuringEFM’s Safety First fund and a series of defined payout

products and was responsible for running a convertiblebond fund. “This is where my risk management skillscome from,” he says. “I think it is this aspect of the fundthat is most likely to appeal to investors.”

What has cemented their friendship is their fascina-tion with the financial markets. Four years ago, while thepair pored over market developments, and the barmanpoured pints, they hatched the idea of launching ahedge fund. “What is important is the ability to controlyour own destiny. The institutional world stifles creativity;I wanted the freedom to buy and sell whatever I want,”says Neil. Piers echoes his sentiments: “As you getmore experienced you spend more time in committeeand management and move away from the markets.This is the ultimate way to get back.”

Piers, who has worked with Neil in US equities andhas also been involved with UK stocks, is also proudthat he comes to the derivatives and risk managementprocess with the eye of a fund manager. As well as riskmanagement, he runs a timing program for the fund,which he also runs with a stock picker’s eye.

The final member of the triumvirate is John Thomson,ex ceo of Stewart Ivory and before that cio of StandardLife, who brings great credentials and a business leveloverview to the team. He will be running the business,leaving Neil and Piers to get on with running the fund.

The pair intend to produce 1-3% a month with, pre-dictably enough, “superior risk-adjusted returns”. Theyhave been running a paper portfolio, which has been a‘useful experience’, and has apparently produced somegood numbers.

The long-short fund will express a directional bias,though not always, within a core universe of 120 USstocks, and will apply three elements to the stock selec-tion process. Themes developed in that core portfolioare also extended in tactical positions beyond the main120 stocks. A quantitative element provides a frame-work for ranking stocks on longer-term valuation andshorter-term momentum factors. The fundamental analy-sis focuses very much on forward-looking indicators,with very little historical detail taken into account.

“BT is a bigger impediment tothe set-up process than

gaining regulatory approval” – Neil Smeaton

Neil Smeaton

Neil says he doesn’t miss working with a largeresearch team. His aim is to have a high level of knowl-edge of the stocks in his universe, and most of what heand Piers do is based on years of experience in deter-mining what make the best investment criteria. “We arealways looking for the catalyst that will expose deterio-rating fundamentals,” says Neil.

The third element is the timing model, which is onlyused as an execution aid once a stock has beendeemed attractive or otherwise.

Neil and Piers make short work of the accusation thatmainstream-turned-hedge-fund managers shouldn’t beallowed top proactive shorting stocks with investors’money. “There’d be no hedge fund managers,” saysNeil. “Half the equity long/short managers in Europecome from long-only backgrounds. When people sit andlisten, they will understand what makes us likely to besuccessful.”

What may cause some confusion in the investmentcommunity is the idea of a US equity specialist so farfrom the domestic market. “People will ask how you can

run a pure US fund from the UK. But people will eitherhave that bias or they won’t. Those with an open mindwill be interested in our process,” says Neil. At Aegonhis fund was generally known for out-performing in allmarket conditions.

With the set-up process still fresh in their minds it isworth asking for a little bit of advice for others followingin their wake. Ailsa has gone the quality route, spendinga little more (at $500,000 in the first year including run-ning costs) than the average start up. Neil and Piershave chosen Goldman Sachs as a prime broker (andwere very impressed with Morgan Stanley) and have allthe systems functionality they had in their institutionaldays. As administrators they chose IFS in Dublin.Crucially, says Neil, waving a fat bundle of legal agree-ments under my nose, you have to know what you wantto get out of these relationships; you get let down a lot.Timetables get shuttled back, but [London-based legalfirm] Simmons & Simmons have really looked after us.”

Honing that further, he says, “The big secret [anddetails have not been released] is seed capital. Qualitymoney – people who will support the business – isabsolutely crucial.”

Piers adds that though it is easy to get bogged downin detail, you also have to remember that everything youdo during the set-up process has to stand up furtherdown the line. “Don’t,” for example, “have a logo you’renot happy with.”

But through these details the grand plan remainsintact. And it is a very simple one. “I am most looking for-ward to sitting in a room with a colleague I know and likeand trust, and doing what I love to do,” says one. “That’swhy we’re doing it,” says the other. Aw.

Profile

28 SEPTEMBER 2001 RISK & REWARD

“The risk management aspectof the fund that is most likelyto appeal to investors” –Piers Watson

John Thomson

Piers Watson

Personal & professional development

RISK & REWARD SEPTEMBER 2001 29

StresstestingAs well as being executive director ofAIMA Florence Lombard is also aneuro-linguistic programming masterpractitioner. Here she teams up withlife coach Sue Liburd to explain how todetermine your stress levels and whatto do about it

Personal & professional development

30 SEPTEMBER 2001 RISK & REWARD

Stress is one of those words that raises bothinterest and anxiety. More often than not mostof us prefer to ignore stress; its sources andconsequences. I was amused to see, however,

that in the June issue of Risk & Reward, business-related stress was mentioned twice. “Listen to hisstresses as he tries to beat the market, keep his wifehappy, keep his investors happy and keep to his dietaryregime,” (page 8) about sums it up.