Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1 ...

15

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1) June 16, 2021 Preliminary Rating Class Preliminary rating(i) Balance (mil. $) Anticipated repayment date Legal maturity (years) A-2 BBB (sf) 180 June 2028 30 Note: This presale report is based on information as of June 16, 2021. The ratings shown are preliminary. Subsequent information may result in the assignment of final ratings that differ from the preliminary ratings. Accordingly, the preliminary ratings should not be construed as evidence of final ratings. This report does not constitute a recommendation to buy, hold, or sell securities. (i)The rating does not address post-ARD contingent interest. ARD--Anticipated repayment date. Executive Summary Hardee's Funding LLC/Carl's Jr. Funding LLC's series 2021-1 issuance is a $180 million corporate securitization of CKE Restaurants Holdings Inc.'s (CKE) business. CKE will use the proceeds for general corporate purposes as well as transaction fees and expenses. The series 2021-1 class A-2 fixed-rate notes will be collateralized by existing and future domestic and international franchise royalties and fees, contributed company restaurants and related assets, and owned real property and intellectual property. The new notes have a seven-year anticipated repayment date and a 30-year legal maturity. The note issuance will result in a leverage (total debt/run-rated covenant-adjusted EBITDA) of approximately 7.2x as of the series 2021-1 close. Key credit features of the transaction include: - The brands' long operating history of over 60 years: Carl's Jr. was established in 1956, and Hardee's was established in 1960. - The large and diverse franchise base, with a 93% franchised system, results in a less volatile cash flow stream. In addition, 61% of CKE's 335 franchisees operate five or fewer restaurants, with the largest franchisee representing 8% of franchised restaurants. - The stable historical systemwide sales with positive growth in nine out of the last 10 years and a cumulative average annual growth rate of 3.0% since 2010. - The stable domestic performance during the COVID-19 pandemic. The last three servicer reports indicate positive domestic SSS over the last three quarters. Additionally, international SSS have recently turned positive. However, because these metrics compare the current Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1) June 16, 2021 PRIMARY CREDIT ANALYST Christine Dalton New York + 1 (212) 438 1136 christine.dalton @spglobal.com SECONDARY CONTACT Jacob Dabrowski New York jacob.dabrowski @spglobal.com ANALYTICAL MANAGER Ildiko Szilank New York (1) 212-438-2614 ildiko.szilank @spglobal.com www.standardandpoors.com June 16, 2021 1 © S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer on the last page. 2668124

-

Upload

khangminh22 -

Category

Documents

-

view

9 -

download

0

Transcript of Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1 ...

Presale:

Hardee's Funding LLC/Carl's Jr. Funding LLC (Series2021-1)June 16, 2021

Preliminary Rating

Class Preliminary rating(i) Balance (mil. $) Anticipated repayment date Legal maturity (years)

A-2 BBB (sf) 180 June 2028 30

Note: This presale report is based on information as of June 16, 2021. The ratings shown are preliminary. Subsequent information may result inthe assignment of final ratings that differ from the preliminary ratings. Accordingly, the preliminary ratings should not be construed asevidence of final ratings. This report does not constitute a recommendation to buy, hold, or sell securities. (i)The rating does not addresspost-ARD contingent interest. ARD--Anticipated repayment date.

Executive Summary

Hardee's Funding LLC/Carl's Jr. Funding LLC's series 2021-1 issuance is a $180 million corporatesecuritization of CKE Restaurants Holdings Inc.'s (CKE) business. CKE will use the proceeds forgeneral corporate purposes as well as transaction fees and expenses. The series 2021-1 class A-2fixed-rate notes will be collateralized by existing and future domestic and international franchiseroyalties and fees, contributed company restaurants and related assets, and owned real propertyand intellectual property. The new notes have a seven-year anticipated repayment date and a30-year legal maturity. The note issuance will result in a leverage (total debt/run-ratedcovenant-adjusted EBITDA) of approximately 7.2x as of the series 2021-1 close.

Key credit features of the transaction include:

- The brands' long operating history of over 60 years: Carl's Jr. was established in 1956, andHardee's was established in 1960.

- The large and diverse franchise base, with a 93% franchised system, results in a less volatilecash flow stream. In addition, 61% of CKE's 335 franchisees operate five or fewer restaurants,with the largest franchisee representing 8% of franchised restaurants.

- The stable historical systemwide sales with positive growth in nine out of the last 10 years anda cumulative average annual growth rate of 3.0% since 2010.

- The stable domestic performance during the COVID-19 pandemic. The last three servicerreports indicate positive domestic SSS over the last three quarters. Additionally, internationalSSS have recently turned positive. However, because these metrics compare the current

Presale:

Hardee's Funding LLC/Carl's Jr. Funding LLC (Series2021-1)June 16, 2021

PRIMARY CREDIT ANALYST

Christine Dalton

New York

+ 1 (212) 438 1136

SECONDARY CONTACT

Jacob Dabrowski

New York

ANALYTICAL MANAGER

Ildiko Szilank

New York

(1) 212-438-2614

www.standardandpoors.com June 16, 2021 1

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

system performance to the trough quarters of the pandemic, they are not indicative ofsustainable SSS.

- The moderate increase in royalty payments as stores recovered from the pandemic, moderateinternational growth in both store count and average unit volume, and higher royalty rates (fromnew international units and refranchised stores).

- The domestic geographic concentration: the three largest U.S. states accounted for 34% ofsystemwide sales as of Jan. 25, 2021.

- Foreign exchange risk: international revenue isn't hedged for foreign exchange fluctuation,which leaves cash flows vulnerable to potential swings in exchange rates.

S&P Global Ratings believes there remains high, albeit moderating, uncertainty about theevolution of the coronavirus pandemic and its economic effects. Vaccine production is ramping upand rollouts are gathering pace around the world. Widespread immunization, which will help pavethe way for a return to more normal levels of social and economic activity, looks to be achievableby most developed economies by the end of the third quarter. However, some emerging marketsmay only be able to achieve widespread immunization by year-end or later. We use theseassumptions about vaccine timing in assessing the economic and credit implications associatedwith the pandemic (see our research here: www.spglobal.com/ratings). As the situation evolves,we will update our assumptions and estimates accordingly.

The class A-1 notes contain stated interest at LIBOR plus a fixed margin. While the originaldeadline for LIBOR cessation was December 2021, the phase-out date is now expected after June2023 for most U.S. dollar LIBOR maturities, such as the one- and three-month maturities. In 2019,the Federal Reserve's Alternative Reference Rates Committee published recommended guidelinesfor fallback language in new securitizations, and the language in this transaction is generallyconsistent with its key principles: trigger events, a list of alternative rates, and a spreadadjustment. We will continue to monitor reference rate reform and consider changes specific tothis transaction when appropriate.

Transaction Timeline/Participants

Transaction Timeline

Expected closing date June 24, 2021.

First interest payment date September 2021.

Class A-2 ARD June 2028.

Legal maturity date June 2051.

Note payment frequency Quarterly, beginning September 2021.

ARD--Anticipated repayment date.

Participants

Sole structuringadviser

Barclays Capital Inc.

Co-issuers Hardee's Funding LLC and Carl's Jr. Funding LLC.

Guarantors Hardee's SPV Guarantor LLC, Carl's Jr. SPV GuarantorLLC, Hardee's Restaurants LLC, and Carl's Jr.Restaurants LLC.

Trustee Citibank N.A.

Servicer Midland Loan Services (a division of PNC Bank N.A.).

Manager CKE Restaurants Holdings Inc.

Backup manager FTI Consulting Inc.

www.standardandpoors.com June 16, 2021 2

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Rating Rationale

The preliminary 'BBB (sf)' rating assigned to Hardee's Funding LLC/Carl's Jr. Funding LLC's seniorsecured A-2 notes series 2021-1 reflect our assessment of the transaction's:

- Brand strength. This includes the strength of the CKE brands, the likelihood for the brands tosurvive through a CKE bankruptcy, and the brands' capacity to continue generating sufficientcash flows from business operations, provided that adequate servicing remains in place.

- Replaceable manager. The manager's responsibilities are generally limited to sales, general,and administrative (SG&A) functions, which we believe increase the likelihood of successfulreplacement following a termination of the current manager. In addition, the transaction'sbackup manager, FTI Consulting Inc. (established at the transaction's closing), reviewed thebusiness' cost structure relative to the sizing of the management fee and believes it isadequate should the backup manager need to step in.

- Legal isolation of the assets. The securitization issuer owns most of the business'cash-generating assets. They have been sold through a true sale to the issuer and guarantors,which are bankruptcy-remote entities. This should decrease the likelihood that existing CKEcreditors could disrupt cash flow to the securitization following a manager bankruptcy. Legalopinions related to true sale and nonconsolidation have been, or will be, provided at or beforethe transaction closes.

- Asset performance not fully correlated with manager performance. A system of franchisedrestaurants will likely continue to generate cash flow following the manager's bankruptcybecause individual franchisees generally operate independently from the manager (aside fromSG&A functions, which we believe can be transferred to a backup).

- Cash flow coverage. Given the brand's strength, the replaceable nature of the manager, and thelegal isolation of the assets from the manager, our analysis include long-term cash flowprojections. Our analysis incorporates cash flow haircuts to stress the business' assets inpotential adverse economic conditions. Under these conditions, our analysis shows the cashflows generated by the business are sufficient to meet all debt service obligations of the ratednotes.

- Liquidity. An interest reserve account is in place to cover three months of interest on the series2018-1, 2020-1, and 2021-1 notes.

Environmental, Social, And Governance (ESG)

Our rating analysis considered the potential exposure of the transaction to ESG credit factors. Wehave not identified any material ESG credit factors in our analysis. Therefore, ESG credit factorsdo not influence our assessment of the transaction's credit quality.

Key Credit Metrics And Peer Comparisons

www.standardandpoors.com June 16, 2021 3

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Table 1

Key Credit Metrics And Peer Comparisons

Brands Series

S&PGlobalRatings'creditrating(i)

Storecount

(no.)

AUV(mil.

$)Franchised

(%)(ii)International

(%)(ii)

Operatinghistory(fromfounding)

Concepttype

Leverage(total

debt/adjustedEBITDA)(iii)

S&PGlobal

Ratings'min.

base-caseDSCR(iv)

S&PGlobal

Ratings'min.

downsideDSCR(iv)

Hardee's/Carl'sJr.

2021-1 BBB (sf) 3,834 93 94 26 Over 30years

QSR 7.2 1.8 1.4

Wendy's(v) 2021-1 BBB (sf) 6,838 1.78 95 14 Over 30years

QSR 6.9 1.76 1.45

Domino's 2021-1 BBB+(sf)

17,644 0.9 98 63.98 Over 30years

QSR 6.4 1.8 1.4

SERVPRO 2021-1 BBB-(sf)(ii)

1,860 1.5 100 0 Over 30years

Restorationservices

8.1 1.7 1.4

ServiceMasterBrands

2020-1 BBB-(sf)

2,392 1.1 99 31 Over 30years

R/R 7.1 1.7 1.3

Hardee's/Carl'sJr.

2020-1 BBB (sf) 3,840 1.2 93 25 Over 30years

QSR 6.8 1.8 1.5

Driven Brands 2020-2 BBB-(sf)

3,229 1 84 19 Over 30years

Autoservices

6.7 1.9 1.6

Sonic 2020-1 BBB (sf) 3,583 1.3 94 0 Over 30years

QSR 5.9 1.8 1.6

Jersey Mike's 2019-1 BBB (sf) 1,615 0.8 99 0.3 Over 30years

QSR 6.4 2.2 1.7

Planet Fitness 2019-1 BBB-(sf)

1,899 2.1 96 2.7 29 years Fitness 6.5 1.7 1.3

Wendy's 2019-1 BBB (sf) 6,710 1.6 95 8 Over 30years

QSR 6.6 1.7 1.4

Jack in the Box 2019-1 BBB (sf) 2,240 1.5 94 0 Over 30years

QSR 4.9 1.9 1.6

Applebee's/IHOP 2019-1 BBB (sf) 3,652 2.2 98 7 Over 30years

CDR 6 1.7 1.4

Dunkin' Brands 2019-1 BBB (sf) 20,912 0.8 100 43 Over 30years

QSR 6.2 1.6 1.4

Taco Bell 2018-1 BBB (sf) 6,505 1.6 91 6 Over 30years

QSR 5.3 1.6 1.5

Jimmy John's 2017-1 BBB (sf) 2,690 0.8 98 0 Over 30years

QSR 5.2 1.8 1.7

Cajun Global 2017-1 BBB-(sf)

1,588 0.7 85 32 Over 30years

QSR 5.2 1.8 1.4

Five Guys 2017-1 BBB-(sf)

1,437 1.2 69 5 Over 30years

QSR 6.7 1.6 1.5

TGIF 2017-1 B (sf) 903 2.7 94 48 Over 30years

CDR 5.6 1.3 1

www.standardandpoors.com June 16, 2021 4

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Table 1

Key Credit Metrics And Peer Comparisons (cont.)

Brands Series

S&PGlobalRatings'creditrating(i)

Storecount

(no.)

AUV(mil.

$)Franchised

(%)(ii)International

(%)(ii)

Operatinghistory(fromfounding)

Concepttype

Leverage(total

debt/adjustedEBITDA)(iii)

S&PGlobal

Ratings'min.

base-caseDSCR(iv)

S&PGlobal

Ratings'min.

downsideDSCR(iv)

Arby's 2015-1 BBB-(sf)

3,335 1 72 1 Over 30years

QSR 5.3 1.6 1.2

(i)Ratings for the senior-most securitization notes issued (closed transactions). (ii)Percentage of total store count. (iii)As reported. (iv)As of each series' closing date unlessotherwise noted. (v)Preliminary. AUV--Average unit volume. DSCR--Debt service coverage ratio. QSR--Quick-service restaurant. CDR--Casual dining restaurant.R/R--Remediation/reconstruction. Hardee's/Carl's Jr.--Hardee's Funding LLC/Carl's Jr. Funding LLC. Driven Brands--Driven Brands Funding LLC (Maaco, Meineke, andothers). Sonic--Sonic Capital LLC. Jersey Mike's--Jersey Mike's Funding LLC. Planet Fitness--Planet Fitness Master Issuer LLC. Domino's--Domino's Pizza Master IssuerLLC. ServPro--ServPro Master Issuer LLC. Wendy's--Wendy's Funding LLC. Jack in the Box--Jack in the Box Funding LLC. Applebee's/IHOP--Applebee's Funding LLC/IHOPFunding LLC (Dine Brands Global). Dunkin' Brands--DB Master Finance LLC (AUV represents domestic for both brands, leverage assumes no variable-funding note). TacoBell--Taco Bell Funding LLC. Jimmy John's--Jimmy John's Funding LLC. Cajun Global--Cajun Global LLC (Church's Chicken). Five Guys--Five Guys Funding LLC. TGIF--TGIFFunding LLC. Arby's--Arby's Funding LLC.

Industry Outlook

The restaurant industry is highly competitive in price and product offerings. Many operators focuson altering the menu mix and new products toward value offerings to drive guest traffic. Leadinginto 2020, the sector's performance was mixed due to tepid economic conditions and meaningfulweakness at certain restaurant operators. Amid the COVID-19 pandemic, there was a large shifttoward delivery options as consumers obeyed stay-at-home orders. This led to a pick-up indelivery orders and ticket sizes due to the influx of people working from home.

However, with the rollout of several vaccines globally and the easing of lockdown, we expect thisshift to delivery to slow in 2021. In addition, many independently owned businesses closed duringthe pandemic-induced lockdowns, creating opportunities for larger players to increase theirmarket share. However, this trend likely won't continue as restrictions ease.

Quick-service restaurants (QSRs) have been performing well overall, while casual diningrestaurants continue to face challenges. We expect limited domestic growth and believerestaurants' ability to take market share will drive revenue and profit growth. We also expect sloweconomic growth to continue to limit guest traffic gains, and any cost inflation would pressureoperating margins over the near term because it likely will not be fully passed along to customers.And while labor inflation would affect store profits, the impact may not be meaningful for thehighly franchised models. Companies with an international presence have expansionopportunities in various markets.

Summary Of The Business

CKE's restaurants operate primarily under the Carl's Jr. and Hardee's brands, both of which dateback over 60 years. Domestic Carl's Jr. restaurants are located in Western U.S., whereas theinternational Carl's Jr. restaurants are located primarily in Mexico and Latin America, with agrowing presence in Europe and Asia. Domestic Hardee's restaurants are located predominantlyin the Southeastern and Midwestern U.S., with a strong international footprint outside of the U.S.

As of Jan. 25, 2021, CKE operates 3,834 restaurants systemwide. Ninety-nine percent of thedomestic units have drive-through windows, and over 90% of the domestic sales are from

www.standardandpoors.com June 16, 2021 5

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

off-premise channels. Approximately 99% of CKE's domestic restaurants remained openthroughout the COVID-19 crisis because of the prevalence of drive-through, delivery, and take-outservices. Ninety-one percent of Carl's Jr. and 71% of Hardee's restaurants have active deliverycoverage. The international impact varied by market, and restaurants located in travel centers andmalls temporarily closed.

Since 2014, CKE has transitioned its franchise mix to 93% from 73% through a series ofrefranchising transactions and an emphasis on development from new franchise openings.

Charts 1-4 show the characteristics of the collateral backing the transaction.

Chart 1

www.standardandpoors.com June 16, 2021 6

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Chart 2 Chart 3

Chart 4

www.standardandpoors.com June 16, 2021 7

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

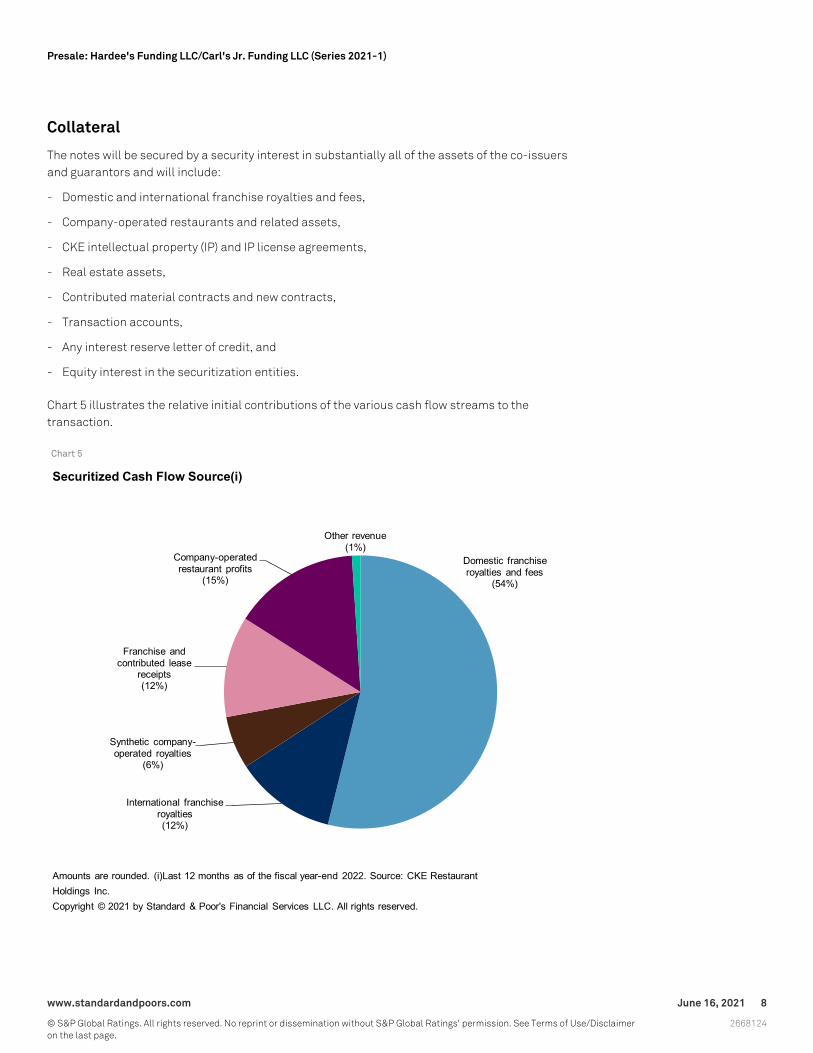

Collateral

The notes will be secured by a security interest in substantially all of the assets of the co-issuersand guarantors and will include:

- Domestic and international franchise royalties and fees,

- Company-operated restaurants and related assets,

- CKE intellectual property (IP) and IP license agreements,

- Real estate assets,

- Contributed material contracts and new contracts,

- Transaction accounts,

- Any interest reserve letter of credit, and

- Equity interest in the securitization entities.

Chart 5 illustrates the relative initial contributions of the various cash flow streams to thetransaction.

Chart 5

www.standardandpoors.com June 16, 2021 8

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Our base-case scenario assumes that the system experiences zero growth from its currentperformance as of the 12 months ended May 17, 2021--a timeframe that doesn't include theinitial COVID-19-related shutdowns. We do not believe that CKE's performance during thepandemic is reflective of what we should expect in a base case cash flow scenario.

(See the table 4 below for more details on each category of securitization collections.)

Key Credit Considerations

Table 2

Key Credit Considerations

Long operating history The first CKE restaurant (a Hardee's location) opened in 1956, and, since then, the CKE brandhas survived multiple economic downturns and has built a loyal customer base. This supportsthe likelihood that brand loyalty (and thus sales) will continue even if CKE is replaced as themanager.

High franchisedpercentage

As of Jan. 25, 2021, franchisees operated 93% of CKE's 3,834 systemwide stores. We believe ahigh franchised percentage provides the transaction with better cash flow stability andindependence from the manager than transactions with lower percentages of franchised stores.

Unhedged revenue frominternational operations

While all payments are made in U.S. dollars, the payment amount is based on revenues in localdollars and the amount is then exchanged at a spot rate. The revenues from internationaloperations are not hedged for foreign exchange fluctuation, leaving cash flows vulnerable topotential swings in exchange rates.

Concentration in producttype

Although the transaction is backed by two different brands, there is low diversification becauseburgers are the leading product at both restaurants.

Large domesticgeographicconcentrations

Geographic concentration in the three largest states accounts for more than 34% of thecompany's U.S. store count.

CKE--CKE Restaurants Holdings Inc.

Credit Rating Methodology

Table 3 shows our specific conclusions for each of the five analytical steps in our ratings process.

Table 3

Credit Rating Step

Step Result Comment

Step 1

Eligibilityanalysis

Pass We believe that the system of franchised restaurants would likely continue to generatecash flow following a bankruptcy by the manager because the individual franchiseesgenerally operate independently from the manager (aside from their reliance on themanager's SG&A functions, which we believe can be transferred to a backup manager).As long as a brand has sufficient customer loyalty, royalty revenues can remainavailable to service securitization debt, assuming the assets have been isolated via atrue sale to a bankruptcy-remote special-purpose entity. Because we do not believethat substantially all cash flow from the system will be at risk following a managerbankruptcy, our subsequent analysis quantifies the impact of the correlated cash flowdecline from the CKE system and compares that to ongoing required interest andprincipal payments to the rated debt.

www.standardandpoors.com June 16, 2021 9

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Table 3

Credit Rating Step (cont.)

Step Result Comment

Step 2

Businessvolatility score(BVS)

4(i) CKE's business risk profile (BRP) is fair, which maps to an unadjusted BVS of '4'(i). Weadjusted that BVS one notch to '3' because the cash flows are revenue-based, and thesystem has demonstrated stability for more than 30 years.

Cash flowassumptions

See table 4below

Min. base DSCR 1.77x Principal and interest are paid in full in this scenario.

Anchor bbb- Determined based on table 1 of our corporate securitization criteria, "GlobalMethodology And Assumptions For Corporate Securitizations," published June 22,2017.

Min. downsiderun DSCR

1.39x Principal and interest are paid in full in this scenario.

Step 3

Resiliency score Satisfactory Determined based on table 3 of the Corporate Securitization criteria.

Resiliencyadjusted anchor

bbb Determined based on table 4 of the Corporate Securitization criteria.

Step 4

Modifier analysis No adjustment Though leverage has increased since the series 2020-1 closing date, we do not considerit an outlier relative to that of similar transactions at the 'BBB' category. Should itbecome an outlier, we may choose to make a downward modifier adjustment to therating. The anticipated repayment dates and the liquidity and deleveraging triggers areall comparable to those of other rated QSR transactions.

Step 5

Comparablerating analysis

No adjustment CKE's overall profile, including its system size, AUV, royalty rates, franchisedpercentage, and recent performance, are typical of its peer group. Therefore, we do notbelieve any upward or downward notching is necessary. Given that we did not make anyadjustments in step four or step five, our preliminary rating is 'BBB (sf)'.

(i)The mappings from BRP to BVS are: excellent=1, strong=2, satisfactory=3, fair=4, weak=5, and vulnerable=6. SG&A--Sales, general, andadministrative. DSCR--Debt service coverage ratio. CKE--CKE Restaurants Holdings Inc. AUV--Average unit volume. QSR--Quick-servicerestaurants.

Table 4 shows our cash flow assumptions.

Table 4

Cash Flow Assumptions

Cumulative decline (%)

Asset cash flowcategory

Basecase

Downsidecase(i) Description

Royalty revenue and fees 0 15 Franchise and company-owned store royalties, which representmost of the overall projected cash flow, are a function of storecount, AUV, and royalty rates.

All other securitizationcollections

0 30 All other securitization collections.

(i)For the downside case, we applied periodic stresses to non-U.S. store revenue to address the risk of foreign exchange rate volatility andassumed foreign currency depreciation rates consistent with our criteria, "Foreign Exchange Risk In Structured Finance--Methodology AndAssumptions," published April 21, 2017. AUV--Average unit volume.

www.standardandpoors.com June 16, 2021 10

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

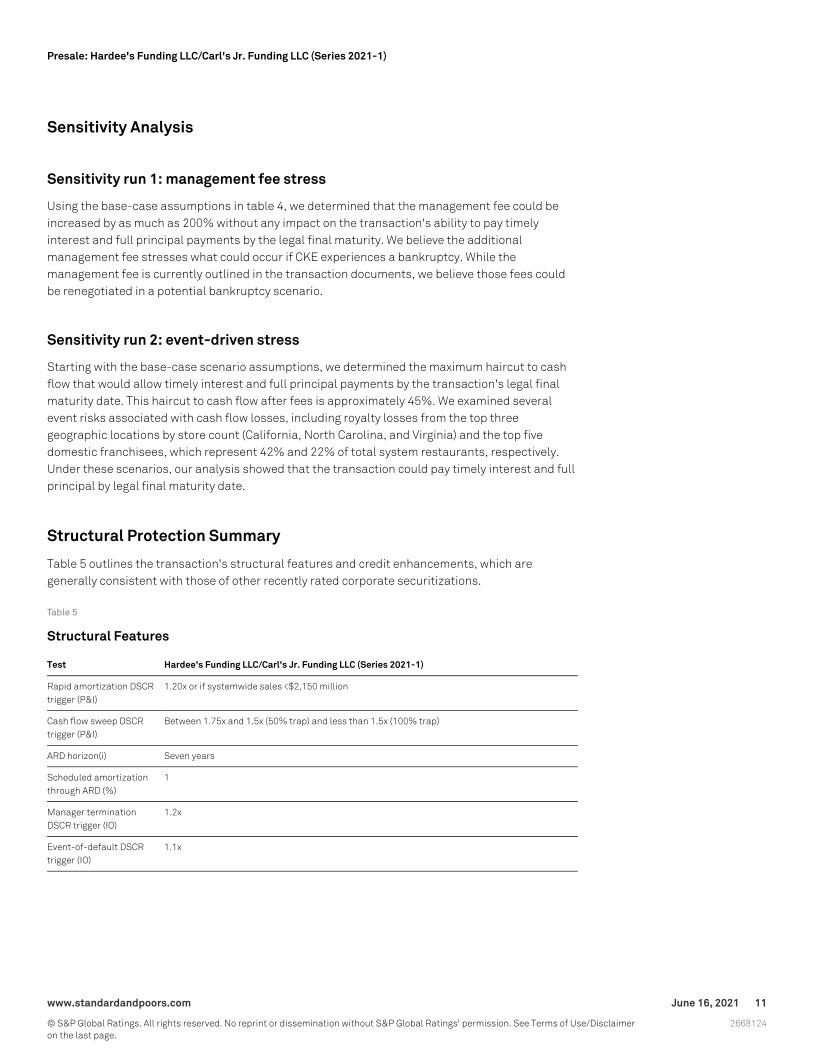

Sensitivity Analysis

Sensitivity run 1: management fee stress

Using the base-case assumptions in table 4, we determined that the management fee could beincreased by as much as 200% without any impact on the transaction's ability to pay timelyinterest and full principal payments by the legal final maturity. We believe the additionalmanagement fee stresses what could occur if CKE experiences a bankruptcy. While themanagement fee is currently outlined in the transaction documents, we believe those fees couldbe renegotiated in a potential bankruptcy scenario.

Sensitivity run 2: event-driven stress

Starting with the base-case scenario assumptions, we determined the maximum haircut to cashflow that would allow timely interest and full principal payments by the transaction's legal finalmaturity date. This haircut to cash flow after fees is approximately 45%. We examined severalevent risks associated with cash flow losses, including royalty losses from the top threegeographic locations by store count (California, North Carolina, and Virginia) and the top fivedomestic franchisees, which represent 42% and 22% of total system restaurants, respectively.Under these scenarios, our analysis showed that the transaction could pay timely interest and fullprincipal by legal final maturity date.

Structural Protection Summary

Table 5 outlines the transaction's structural features and credit enhancements, which aregenerally consistent with those of other recently rated corporate securitizations.

Table 5

Structural Features

Test Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Rapid amortization DSCRtrigger (P&I)

1.20x or if systemwide sales <$2,150 million

Cash flow sweep DSCRtrigger (P&I)

Between 1.75x and 1.5x (50% trap) and less than 1.5x (100% trap)

ARD horizon(i) Seven years

Scheduled amortizationthrough ARD (%)

1

Manager terminationDSCR trigger (IO)

1.2x

Event-of-default DSCRtrigger (IO)

1.1x

www.standardandpoors.com June 16, 2021 11

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Table 5

Structural Features (cont.)

Test Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Management fee The management fee, which includes both fixed and variable components, is a function ofretained collections. According to the transaction documents, the fixed component is assumedto be $15 million annually, and the variable component is assumed to be $13,730 per every$100,000 of retained collections. The management fee is also subject to a 2% annual increase ofthe fixed component if the increased amount does not exceed 35% of retained collections in thepreceding four quarterly collection periods.

(i)Failure to pay the note in full by the ARD constitutes a rapid amortization event, but not an event of default. DSCR--Debt service coverageratio. P&I--Principal and interest. ARD--Anticipated repayment date. IO--Interest only.

Payment Priority

The series 2021-1 issuance includes one class of notes that will pay interest and principalquarterly of each March, June, September, and December, with payments commencingSeptember 2021. If a rapid amortization event occurs, the series 2018-1 class A-1variable-funding notes (VFN) will be paid before any principal payments to the series 2018-1 classA-2 notes, series 2020-1 class A-2 notes, and series 2021-1 class A-2 notes. Following an event ofdefault, the series 2018-1 class A-1 VFN notes will rank pari passu with each series 2021 classA-2 term notes (see table 6).

Table 6

Payment Priority

Priority Payment

1 Solely, with respect to indemnification, asset disposition, and insurance/condemnation payment amounts: to thetrustee and then the servicer for unreimbursed advances; to the manager for any unreimbursed advances; and topay the class A-1 notes, pro rata, on or after any class A-1 notes' renewal date. If a rapid amortization event hasoccurred and is continuing, to pay the class A-1 notes, pro rata; and to pay all senior notes other than the classA-1 notes, pro rata in alphanumerical order of designation. If all prepayments are made to the previoussubclauses, to pay the subordinated notes, pro rata in alphanumerical order of designation, if any.(ii)

2 To the trustee, then the servicer, then the backup manager, then the manager for unreimbursed advances, andthen to the servicer for servicer fees, liquidation fees, and workout fees.

3 The successor manager transition expenses, if any.

4 To the manager, weekly management fees.

5 Capped securitization operating expense amount if no event of default has occurred; the post-default cappedtrustee expense amount to the trustee; and after a mortgage recording event, all mortgage recording fees to thetrustee.

6 Interest payments on the senior notes, pro rata, by amounts due within each series; the class A-1 notecommitment fee amounts; and hedge payments, if any, excluding any termination payable to a hedgecounterparty.(ii)

7 The capped class A-1 note administrative expense amount.

8 Interest on the senior subordinated notes, pro rata, by amounts due within each class, if any.

9 The senior note interest reserve account deficit amount and then the senior subordinated note interest reserveaccount deficit amount, if any.

10 The senior notes scheduled principal payment amount and then the senior notes scheduled principal paymentdeficiency amount, if any.(ii)

11 The supplemental management fee, if any.

www.standardandpoors.com June 16, 2021 12

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

Table 6

Payment Priority (cont.)

Priority Payment

12 On and after any class A-1 notes' renewal date, to the class A-1 notes' principal.

13 If no rapid amortization has occurred, any cash-trapping amount to the cash-trap reserve account.

14 If a rapid amortization event has occurred, all remaining amounts to pay down the class A notes and then allremaining amounts to pay down the senior subordinated notes.

15 If no rapid amortization event has occurred, the senior subordinated notes' scheduled principal payment amountand then the senior subordinated notes' scheduled principal payment deficiency amount, if any.

16 Interest on the subordinated notes, if any.

17 If no rapid amortization event has occurred, the subordinated notes' scheduled principal payment amount andthen the subordinated notes' scheduled principal payment deficiency amount, if any.

18 If a rapid amortization event has occurred, all remaining amounts to pay down the subordinated notes.

19 Any excess securitization operating expenses.

20 The excess class A-1 note administrative expense amounts, if any.

21 Other class A-1 note amounts.

22 After the anticipated repayment date, pay contingent interest on the senior notes(i)(ii).

23 After the anticipated repayment date, pay contingent interest on the senior subordinated notes(i)(ii).

24 After the anticipated repayment date, pay contingent interest on the subordinated notes(i).

25 Hedge termination payments and other unpaid hedge payments.

26 Any unpaid premiums and make-whole prepayment premiums on the notes.

27 Any remaining funds to or at the direction of the co-issuers.

(i)Ratings do not address the likelihood of receiving post-ARD interest. (ii)All notes that are part of a class with an alphanumerical designationthat contain the letter "A"" (such as 2018-1 class A-1 notes, 2018-1 class A-2 notes, 2020-1 class A2 notes, and 2021-1 class A-2 notes),together with any subclasses or tranches thereof (such as 2018-1 class A-2-II notes and 2018-1 class A-2-III notes), will be classified as "class Anotes" or "senior notes."

Surveillance

We will maintain active surveillance on the rated notes until the notes mature or are retired. Thepurpose of surveillance is to assess whether the notes are performing within the initialparameters and assumptions applied to each rating category. The transaction terms require theissuer to supply periodic reports and notices to S&P Global Ratings for maintaining continuoussurveillance on the rated notes.

We view CKE performance as an important part of analyzing and monitoring the performance andrisks associated with the transaction. While company's performance will likely have an effect onthe transaction, other factors, such as cash flow, debt reduction, and legal framework, alsocontribute to our overall analysis.

Related Criteria

- Criteria | Structured Finance | General: Global Framework For Payment Structure And CashFlow Analysis Of Structured Finance Securities, Dec. 22, 2020

www.standardandpoors.com June 16, 2021 13

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

- Criteria | Structured Finance | Legal: U.S. Structured Finance Asset Isolation AndSpecial-Purpose Entity Criteria, May 15, 2019

- Criteria | Structured Finance | General: Counterparty Risk Framework: Methodology AndAssumptions, March 8, 2019

- Criteria | Structured Finance | General: Incorporating Sovereign Risk In Rating StructuredFinance Securities: Methodology And Assumptions, Jan. 30, 2019

- Criteria | Structured Finance | ABS: Global Methodology And Assumptions For CorporateSecuritizations, June 22, 2017

- Criteria | Structured Finance | General: Foreign Exchange Risk In StructuredFinance--Methodology And Assumptions, April 21, 2017

- Criteria | Structured Finance | General: Global Framework For Assessing Operational Risk InStructured Finance Transactions, Oct. 9, 2014

- General Criteria: Global Investment Criteria For Temporary Investments In TransactionAccounts, May 31, 2012

- General Criteria: Principles Of Credit Ratings, Feb. 16, 2011

Related Research

- Restaurant Securitizations Are Structured To Survive A Big Bite, Sept. 7, 2017

- Why Social Media Should Be A #trendingtopic In Corporate Securitization Analysis, June 9,2017

- Global Structured Finance Scenario And Sensitivity Analysis 2016: The Effects Of The Top FiveMacroeconomic Factors, Dec. 16, 2016

www.standardandpoors.com June 16, 2021 14

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors.S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributedthrough other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available atwww.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respectiveactivities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has establishedpolicies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed andnot statements of fact. S&P's opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase,hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation toupdate the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment andexperience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not actas a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable,S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-relatedpublications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limitedto, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certainregulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Partiesdisclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damagealleged to have been suffered on account thereof.

Copyright © 2021 Standard & Poor's Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any partthereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrievalsystem, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not beused for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees oragents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are notresponsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or forthe security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESSOR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE ORUSE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THECONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct,indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, withoutlimitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advisedof the possibility of such damages.

Standard & Poor’s | Research | June 16, 2021 15

2668124

Presale: Hardee's Funding LLC/Carl's Jr. Funding LLC (Series 2021-1)