RISK CAPITAL FINANCING AND THE SEPARATION OF OWNERSHIP AND CONTROL IN BUSINESS GROUPS

26

Journal of Banking and Finance 13 (1989) 747-772. North-Holland RISK CAPITAL FINANCING AND THE SEPARATION OF OWNERSHIP AND CONTROL IN BUSINESS GROUPS* Francesco BRIOSCHI and Luigi BUZZACCHI Politecnico di Milano, 20133 Milano, Italy Massimo G. COLOMBO CTS - Consiglio Nazionale delle Ricerche, Milano, Italy Received March 1988, final version received April 1989 This paper analyses business groups, composed of legally independent firms connected through a network of cross-shareholdings. A model which allows to calculate the value of the firms of a group and the integrated ownership shares held by an outside stockholder, is described. A taxonomy for the collection of risk capital generalizing the one which applies for a single firm is proposed; the connection between the process of raising risk capital and the separation of ownership from control in business groups is demonstrated and given a formal mathematical description. Empirical evidence relating to the amount of risk capital collected by Italian business groups in the ’80s and to the extent of the divorce between ownership and control is also provided. 1. Introduction Business groups composed of legally independent firms, connected through equity linkages, constitute a form of organizing economic activity widely diffused in Japan and Europe, and specifically in Italy. The transactional literature [see, for instance, Williamson (1973, Daems (1980), Goto (1982)] has pointed out that business groups may be considered as ‘intermediate’ economic institutions between markets and hierarchies. According to such literature and referring mainly to the Japanese case (to which most of the attention has so far been devoted), business groups enjoy information, monitoring and control advantages similar to the very well known ones, of the multi-divisional (M-Form) corporations typical of the American economic system. However, thanks to the fact that the various activities are organized through legally independent units, they allow more *Financial support for this paper was provided by the CNR research project ‘Servizi e strutture per l’internazionalizzazione delle imprese’, research contract no. 86.02815.54. A preliminary version of this paper was presented at the 14th Annual E.F.A. Meeting, Madrid, 1987. 03784246/89/$3.50 0 1989, Elsevier Science Publishers B.V. (North-Holland)

Transcript of RISK CAPITAL FINANCING AND THE SEPARATION OF OWNERSHIP AND CONTROL IN BUSINESS GROUPS

Journal of Banking and Finance 13 (1989) 747-772. North-Holland

RISK CAPITAL FINANCING AND THE SEPARATION OF OWNERSHIP AND CONTROL IN BUSINESS GROUPS*

Francesco BRIOSCHI and Luigi BUZZACCHI

Politecnico di Milano, 20133 Milano, Italy

Massimo G. COLOMBO

CTS - Consiglio Nazionale delle Ricerche, Milano, Italy

Received March 1988, final version received April 1989

This paper analyses business groups, composed of legally independent firms connected through a network of cross-shareholdings.

A model which allows to calculate the value of the firms of a group and the integrated ownership shares held by an outside stockholder, is described. A taxonomy for the collection of risk capital generalizing the one which applies for a single firm is proposed; the connection between the process of raising risk capital and the separation of ownership from control in business groups is demonstrated and given a formal mathematical description.

Empirical evidence relating to the amount of risk capital collected by Italian business groups in the ’80s and to the extent of the divorce between ownership and control is also provided.

1. Introduction

Business groups composed of legally independent firms, connected through equity linkages, constitute a form of organizing economic activity widely diffused in Japan and Europe, and specifically in Italy.

The transactional literature [see, for instance, Williamson (1973, Daems (1980), Goto (1982)] has pointed out that business groups may be considered as ‘intermediate’ economic institutions between markets and hierarchies. According to such literature and referring mainly to the Japanese case (to which most of the attention has so far been devoted), business groups enjoy information, monitoring and control advantages similar to the very well known ones, of the multi-divisional (M-Form) corporations typical of the American economic system. However, thanks to the fact that the various activities are organized through legally independent units, they allow more

*Financial support for this paper was provided by the CNR research project ‘Servizi e strutture per l’internazionalizzazione delle imprese’, research contract no. 86.02815.54. A preliminary version of this paper was presented at the 14th Annual E.F.A. Meeting, Madrid, 1987.

03784246/89/$3.50 0 1989, Elsevier Science Publishers B.V. (North-Holland)

748 F. Brioschi et al., Risk capital$nancing

flexibility and managerial autonomy than the M-Form corporation. Even though such arguments are certainly relevant, it is the authors’ opinion that they fail to explain satisfactorily the extension of the phenomenon and its determinants, which are, to a large extent, of financial nature and in particular are connected to the ownership and control issue.

A business group differs, in fact, from an M-form corporation in one essential aspect: admitting the participation of outside stockholders in various firms of the group, it allows one to separate control over the firms of which the group is composed from their ownership, by means of mechanisms which go beyond those involving the abstention from voting on the part of minority shareholders. The notion of ownership itself needs to be modified in the case of a firm which belongs to a group: in fact it must include, in addition to the share of firm’s equity capital held directly by a shareholder, the share owned indirectly through the network of equity linkages which connect member firms to each other.

By modifying the connection between the ownership of a firm’s equity capital and the degree of control, corporate grouping plays a central role when, in order to finance firms’ operations, the need for an equity capital increase arises. If the controlling stockholder of a given firm is not able and/or willing to commit to the firm the required amount of capital in proportion to its ownership share, he must face an unpleasant alternative. Either he may look for new stockholders, accepting the risk of losing control should his ownership share fall below the threshold given by the majority of the voting stock, or he may take the decision to give up the increase of equity capital, bearing all the consequences that such a decision may imply. By resorting to group structure, the controlling stockholder is no more subject to an alternative of that sort. Namely, he can look for minority stockholders in the various firms constituting the group (either already existing or created expressly for this purpose), while ensuring certain control over all activities of the group.

It is interesting to point out that the group structure widens the typology of the collection of risk capital. In addition to the issue of new securities, the sale of intra-group shareholdings so as to maintain control over all activities within the group must be regarded as a mechanism for raising risk capital. This distinction (issue of new shares/sale of previously issued shares) can be coupled with the traditional one relating to the way in which collecting operations are carried out (offered to existing stockholders, who are provided with preemptive rights/offered to the public or third parties), obtaining a new taxonomy for describing the collection of risk capital in business groups.

In this paper, the two sets of variables - namely, the integrated ownership shares held by an outside stockholder in the firms of a group and the collection of risk capital in its various forms - which, as said, are deeply connected, are given a formal mathematical description allowing a precise

F. Brioschi et al., Risk capitalfinancing 749

measure. For this purpose, a Leontief-type, input-output model is presented; given the equity linkages among all firms of a group, it allows to calculate for all firms: (a) the global value, given their value excluding intra-group shareholdings; (b) the integrated ownership shares (defined as the sum of direct and indirect ownership shares) held by an outside stockholder, given his direct ownership shares, and: (c) the collection of risk capital in accord with the taxonomy described above.

The model [specifically, points (b) and (c)] is subsequently applied to the study of a relevant portion of the Italian industrial system, comprising the I&Fiat, the Orlando and the Pirelli groups, in the period 1980-1986. In particular, the amount of risk capital collected by each group in the different forms is determined; the value of the integrated ownership shares held by the controlling stockholders in the various member firms is measured, and its trend during the period under examination is analysed. The ownership data are also compared with the degree of control exercised by the controlling stockholders.

The empirical results are quite impressive. In the first place, they illustrate the growing separation in Italian major firms of ownership, which tends to become widely diffused, from control, which instead firmly remains with a subset of stockholders (in general, members of the founder’s family), thus preserving the characteristics of family capitalism of the Italian economic system. Secondly, evidence is provided showing the large amount of risk capital raised by Italian groups in the ’80s. Finally, the linkages between the collection of risk capital and the mechanisms engendering the divorce between ownership and control are also discussed. More generally, the study sheds light on the determinants of the evolution of the structure of Italian business groups during the ’80s.

The paper is organized as follows. Section 2 contains the definition of business groups employed in this work and some remarks on the general characteristics of these organizations. In section 3, the business groups system in Italy is briefly described. Section 4 is devoted to the exposition of the value and ownership models; the description of the taxonomy for the collection of risk capital in business groups and of the mathematics involved follows in section 5. In section 6, the empirical results of the research are illustrated. Some concluding remarks relating also to policy aspects are set forth in section 7.

2. Business groups: Definitions and general remarks

As anticipated in the introduction, the term ‘business group’ will denote in the sequel a set of N legally independent firms, the ‘member firms’, connected through equity linkages which, jointly, guarantee a common control over all the activities of the group.

JBF-K

750 F. Brioschi et al., Risk capital financing

According to the definition given above, a member firm has, in general, shareholdings in other firms which belong to the same group, while shares of its own equity capital are held by other member firms. The aforementioned being the general case, two specific situations can be pointed out. Firstly, some firms within a business group may actually hold no shareholdings in other member firms; these are the operating companies. Secondly, cases may be given when the equity capital of a member firm is possessed by no other firms within the same group; the firm is then referred to as the group’s parent holding company.

These definitions are helpful in order to obtain a taxonomy of the structure of business groups. A distinction is usually made in literature between ‘A-type’ and ‘B-type’ groups [Goto (1982)]. The former are com- posed of a number of firms, basically equal in power, connected through a network of mutual equity linkages; no parent holding company exists within the group. Coordination of activities is secured, in most cases, through informal exchanges and tacit agreements. The latter instead do center around a single holding company (more rarely around a few holding companies), and are essentially characterized by a pyramidal structure; monitoring and decision-making activities are hierarchically organized. A-type groups are typical of the Japanese economic system, while B-type groups largly predo- minate in Europe.’

In B-type groups and, to some lesser extent, in A-type groups too, the relevant decision entity, in particular with respect to strategic issues, is the group and not the single firms which belong to it. Nevertheless, in many countries, including Italy, groups have no legal relevance. As a consequence, no regulatory framework is available for settling the various conflicts of interest among the different ‘stakeholders’ of the firms of a group (outside majority and minority stockholders, financial institutions, employees, sup- pliers, customers, central government) which derive from the centralization of the decision process.

It is important to recall at this point that, in come cases, defining the boundaries of different business groups (that is to say, determining which firms belong to which business group) may be a matter of subjective judgement.’ In some economic systems (this is the case of Japan, and, as we

‘Several data, recently published in the economic literature, illustrate the diffusion of business groups in Japan and in Europe. In 1977, in Japan, 64 of the top 100 manufacturing firms were members of one of the 6 most important groups (Mitsubishi, Mitsui, Sumimoto, Fuji, Sanwa and Daiichi-Kangin). Such groups represented, jointly, 16.1% of the assets and 14.3% of the sales of all Japanese companies [see Cable and Yasuki (1985)]. In France, as pointed out by Encaoua and Jacquemin (1982), in 1974, firms belonging to 319 groups accounted for 40% of the employees, 50% of the value added and 60”/, of the fixed assets in the manufacturing sector.

sSuch difftculties depend upon the difficulty to identify the control coalition of a firm, particularly in the case of ‘factual control’ (that is, when control is based on the ownership of a share of equity capital lower than 50’/,). These topics have been widely discussed since the publishing of ‘The Modern Corporation and Private Property’ [Berle and Means (1932)]; see, for example, Nyman and Silberstone (1978), Cubbin and Leech (1983), Leech (1987).

F. Brioschi et al., Risk capitalfinancing 751

will show later, of Italy too) a thick network of equity linkages connects a very large portion of the existing large firms. A careful examination of the behaviour of each firm and a deep understanding of the nature of the relationships among firms are needed in order to distinguish between: (i) intra-group equity linkages, and: (ii) other equity linkages (normally of minor quantitative relevance), which can be neglected for the purpose of defining business groups’ boundaries. It must however be noted that linkages connecting firms of different business groups are important for understanding the overall conduct of the system of groups and, consequently, to some extent, of the entire economy.

As said, in general, the equity capital of a firm which belongs to a business group is not entirely possessed by firms of the same group. Any stockholder of the member firms other than the member firms themselves, will be referred to in the following paragraphs as an ‘outside stockholder’. An outside stockholder may be a private stockholder, a group of private stockholders or even a firm not belonging to the business group.

3. Business groups in Italy

In Italy, a vast part of the economic activity is performed by a limited number of business groups, each one consisting of a very large number of legally autonomous firms, domestic and foreign, which depend directly or indirectly upon a single holding company.

Restricting the attention to quoted firms, the weight of the group phenomenon clearly increases. At the end of 1986, as many as 76 out of the 202 firms quoted on Italian stock exchanges (jointly representing 74.3% of the whole capitalization)3 belonged to only five groups, namely the &Fiat group, controlled by the Agnelli family, the state-controlled IRI group, the Generali group, the Montedison group and the Cofide-Olivetti group, controlled by Carlo De Benedetti.

Italian business groups are essentially structured as pyramids of fums with several layers (B-type groups). Cross-shareholdings and, more generally, loops of shareholdings do exist within groups, but their extent is fairly limited.

A phenomenon of growing relevance in the Italian economy is the presence of i~~er-~o~~ equity linkages (i.e., equity linkages among firms belonging to different groups). While each inter-group linkage is usually of limited importance, the share of the equity capital of a firm of a given

“We refer here to gross capitalization values given by the sum of the capitalizatron values of all Ftrms composing a particular group. Due to equity linkages among firms, such measure overstates groups’ capitalization.

4At group level, loops of shareholdings can be viewed as an extension of the ownership on the part of a single firm of its own stock. However, according to the Italian law, they incur very weak restrictions regarding voting rights.

152 F. Brioschi et al., Risk capital financing

business group jointly owned by companies belonging to other groups may, in some specific cases, be sizeable and, above all, play a strategic role for the purpose of control. In general, inter-group equity linkages are a non- negligible, though not primary, component for the control of Italian groups. The situation differs markedly for the different groups: some groups are substantially autonomous from the point of view of control, while the others rely heavily on the voting stock held by other groups.

Finally, it is interesting to remark that the Italian situation is, in a way, dual to the Japanese one. The main Japanese business groups are A-type groups, while member firms usually form their own B-type groups, composed of themselves together with their subsidiaries. Italian groups belong, on the contrary, to the B category: considering each group as a single unit and taking into account inter-group equity linkages, the portion of the economic system in which groups operate may be regarded as a unique A-type macro- group. It is also interesting to note that, while in Japan groups’ final control is managerial, in Italy groups are either state-controlled or controlled by a single family (often the founder’s family).

4. Value and ownership in business groups

The aim of this paragraph is to describe a mathematical model [developed in Brioschi and Colombo (1986a, b)] for determining: (a) the value of the firms members of a business group, given the value of their net assets with the exception of intra-group shareholdings, and: (b) the integrated ownership share (defined as the sum of direct and indirect ownership shares) of an outside stockholder in all the firms of the group.

The model is based on the following simplifying assumptions relating to the capital structure of member firms: (i) only one class of equity capital is issued, and: (ii) no convertible securities are issued.5

For the formulation of the model some definitions are needed. Let aij represent the share of member firm’s j equity capital held by member firm i and A= [aij] be the (N *N) cross-shareholdings matrix, describing the intra-group equity linkages. Clearly:

05aij51 i=l ,..., N; j=l,..., N, and

Ciaij 5 1 j=l,...,N.

In addition, the coefficients aij must be such as not to allow any subset

‘As will be pointed out afterwards (see section 6), the model can also be applied to financial systems, such as the Italian one, where those hypotheses do not hold. For this purpose, it suffices to neglect the differences among the various classes of stock and to introduce suitable assumptions regarding convertible securities.

F. Brioschi et al., Risk capital financing 753

composed of k member firms (k = 1,. . . , IV) to be entirely possessed by the k firms themselves, a condition which has no economic significance. If such condition and conditions (1) and (2) are met, it is possible to show [see Brioschi et al. (1988b)] that the largest eigenvalue (in absolute value) of matrix A, A(A) (the Frobenius root) is such as:

A(A) < 1. (3)

Furthermore, let wi denote the value of member firm i excluding intra- group shareholdings and w = [wr . . . w,]‘. Let also xi denote the share of the equity capital of member firm i held directly by an outside stockholder and X=[$...x,].

4.1. The model of value

The calculation of the value of member firms relies on the ‘additivity principle’ [see, for instance, Brealey and Myers (1984)]. According to it, a firm’s value is simply given by the sum of the values of its assets. This implies that no value is created by diversifying risk. Furthermore, eventual synergic effects deriving from interdependencies among member firms are assumed to be already captured by the values Wi, i= 1,. . . , N.

When no loops of corporate shareholdings exist within a business group, determining the value of member firms is trivial. For instance, consider a group composed of only two firms, A and B, and suppose that firm A holds a 50% share of the equity capital of firm B. Then, the value of tit-m A is obviously given by w,+OSw,. However, when loops of shareholdings are present, things are different.

Let Vi represent the (unknown) value of member lit-m i and v=[u, . ..+I’. The value of member firm i, vi, can be thought of as the sum of two terms: the first term is the value of firm i intra-group shareholdings, while the second term corresponds to the (known) value of the other assets of firm i, net of debts. Moreover, the first term will be equal to the sum of the (still unknown) values of all member firms weighted by the shares of their equity capital possessed by firm i, provided that the parameters wi are such as to ensure that all Ui be non-negative. 6 A sufficient condition for that is w,zO, i=l >...> N.7

Then:

‘If this were not the case, that is to say if the value of a firm j were allowed to be negative, the value of firm i shareholding m firm j would be null; this results from the condition of limited liability.

‘The condition is not necessary. In order for all elements of vector v to be non-negative, vector w is only required to be comprised within the hypercone mdividuated by the columns of matrix (I-A), a condition which is consistent with some elements of vector w being negative.

154 F. Brioschi et al., Risk capitalfinancing

Vi = ZjaijVj + Wi i=l N. ,***> (4)

This expression can be written in matrix form as: v = Av + W. Thus:*

v=(Z-A)yw. (5)

It is worth noting that, A being a non-negative matrix and v a non- negative vector, it results: Vim Wi, i= 1,. . . , N. In particular, when firm i is an operating company: vi = wi.

4.2. The model of ownership

This model permits to calculate the integrated ownership shares held by an outside stockholder in the firms of a group, given direct ownership shares and the cross-shareholdings matrix. The notion of integrated ownership, defined earlier, can perhaps be clarified by means of a simple example. Consider a group composed of only two firms, A and B. Suppose that a 20% share of the equity capital of firm A is held by an outside stockholder and that firm A holds a 50% share of the equity capital of firm B. Even though the stockholder directly owns no shareholdings in firm B, it sounds reasonable to consider him as the indirect owner of a 10% share of firm B. Owing to the presence of loops of corporate shareholdings within a business group, the problems of evaluating integrated ownership is in general not straightforward.

Let yi represent the stockholder’s (unknown) share of integrated ownership in member firm i and y = [yi . . . ~~1’. In order to derive an expression for y, let us focus on a particular member firm i. As mentioned earlier, the stockholder’s integrated ownership share can be obtained by adding to the share he owns directly the one he owns through his shareholdings in other member firms, the latter share being unknown. If the integrated ownership shares in every member firm were known, the stockholder’s share of indirect ownership would be given by the sum of the shares directly held by the remaining members of the group weighted by the integrated ownership shares the stockholder holds in each of them. Contingent on the above, we derive for integrated ownership the following expression:

Yi=~jajiYj+Xi i=l N. ,...> (6)

Expression (6) can be written in matrix form as: y= A’y+x, thus obtaining:9

8Thanks to conditions (l), (2) and (3), matrix (I--A) has a non-negative inverse matrix [see Nikaido (1970, p. 11 S)].

‘Also matrix (I--A’) has a non-negative mverse matrix [see again Nikaido (1970, p. 118)].

F. Brioschi et al., Risk capitalfinancing 155

y = (I - A’) - lx. (7)

Since matrix A’ and vector x are non-negative, it results: y, 2 xi, i = 1,. . . , N. In particular, the relation yi=xi, holds for a holding company.

4.3. The duality relation between value and ownership

As the previous analysis has shown, the value of the firms of a group and the integrated ownership shares held by an outside stockholder are dual to each other, like quantities and prices in a linear economic system. Hence, from the duality relation of linear economic analysis [see, for instance, Nikaido (1979, p. 195)], we get:”

X’Y =y’w. (8)

The duality relation allows the following interesting interpretation. Consider the value P of a stockholder’s portfolio deriving from his stock- holdings in the member firms of a group. P will obviously equal the sum of the value ui of each firm weighted by the direct ownership share xi. Hence: P=x’v. From the duality relation it follows that: P=x’v=y’w. The value of the stockholder’s portfolio can then be interpreted as the sum of the ‘own’ net value Wi of each member firm (obtained by excluding from the value of its assets that. of intra-group shareholdings) weighted by the corresponding share yi of integrated ownership.

5. The collection of risk capital in business groups

5.1. The collection of risk capital in business groups: A taxonomy

The term ‘collection of risk capital of a business group’ refers here to all financing operations which allow a business group to raise risk capital from external sources, while maintaining unchanged the set of activities controlled.

For an independent firm, the problem of raising risk capital consists in the evaluation of alternative methods for issuing new securities.” On the contrary, a wider set of options is available to a business group. Namely, each member firm can resort to an additional collection mechanism, consisting in the sale of previously issued securities. More specifically, it is the authors’ opinion that the sale of intra-group shareholdings such as to

“The expression can also be derived from expressions (5) and (7). “This topic is widely discussed in the financial literature. See, for instance, Smith (1977) and

Smith (1986).

756 F. Brioschi et al., Risk capital financing

maintain within the group the control of all existing firms is to be regarded as a risk capital raising 0peration.l’

In fact by means of a series of two operations (a spin-off and a merger), a sale of previously issued securities can be shown to be equivalent to a ‘traditional’ increase of equity capital. To this aim, let us examine the following example. Consider a firm A, the equity capital of which is 100% held by an outside stockholder X. The net value of the assets of the firm (which can be thought of as the value of its equity capital) amounts to wA + wg, wg being the value of the division B of firm A and wA referring to its other assets. Let us now analyse two alternative ways for raising risk capital. In case I, firm A initially spins off its division B, which becomes a legally autonomous firm, 100% owned by firm A, and subsequently, sells to a third party Y a 25% share of the equity capital of firm B, collecting an amount of funds equal to 0.25w,, while maintaining the control of firm B. Finally, firm A takes the decision to merge with firm B: to this end, an increase of firm A’s equity capital equal to 0.25~~ reserved to Y is carried on. By this operation no additional funds are raised. The net value of firm A’s assets finally amounts to w,+ 1.25~~; the share of its equity capital held by Y is given by 0.25w,J(wA+ 1.25~~). Alternatively, firm A can increase its equity capital of an amount equal to 0.25w,, the operation being reserved to a third pary (in our case to Y). The outcome in terms of the amount of risk capital raised as well as of the ownership pattern turns out to be identical in the two cases.

In order to identify the different forms of risk capital collection available to firms members of a business group, the distinction pointed out above concerning the nature of the financial instrument (issue of new securities versus sale of previously issued securities) must be coupled with the traditional one relating to the method of the operation (rights method versus offerings to the public or to a third party). In such a way, four different operations are identified thanks to which it is possible for a firm belonging to a group to collect risk capital. These are:

(1) capital increase (i.e., issue of new securities) through a rights issue: the offerings of the new issue is restricted to existing stockholders, who are provided with preemptive rights;

(II) capital increase through an issue offered to investors at large (general cash offer) or placed directly with third parties (private placement);

(III) sale of intra-group shareholdings (i.e., of previously issued securities) such as to maintain unvaried the set of firms composing the group, offered to existing stockholders through the rights method;

(IV) sale of intra-group shareholdings such as to maintain unvaried the set of firms comprising the group, offered to the public or to third parties.

At group level, however, the collection of risk capital deriving from an

‘*The same does not hold true for sales implying transfer of control.

F. Brioschi et al., Risk capital financing 757

operation belonging to one of the four categories illustrated above, does not coincide, in general, with the amount of cash raised by the firm which carries out the operation. Namely, in order to obtain the amount of risk capital collected by the group, all the cash inflows of the remaining firms associated with the operation under scrutiny are to be taken into account. Those cash flows depend upon the behaviour of all firms of the group relating to the purchse of the securities issued or sold and to the sale/purchase of rights. The firms of the group may exercise their preemptive rights and subscribe the new issue or the sale of intra-group shareholdings; this originates a cash outflow, which corresponds to a negative collection. Alternatively, they may sell the rights and by this way raise new funds (positive collection), or they may subscribe the securities offered to the public. The set of all cash flows deriving from a specific collecting operation carried out by a single firm of the group will be denominated risk capital collecting operation at group level.

Without loss of generality, we can assume that the firms of a group adopt a ‘passive behaviour’: namely, they fully exercise their preemptive rights and do not subscribe operations offered to the public. Under this assumption, every operation fully specifies, in addition to the cash inflow of the firm which performs the operation, the cash outflows of the remaining firms of the group. In this case, the four operations considered can be called elementary risk capital raising mechanisms. Namely, it is easy to show that every actual collecting operation at group level either coincides with one elementary mechanism or with a suitable sequence of elementary mechanisms. The following example clarifies the point. Suppose that firm A, holding a given share of the equity capital of firm B, member of the same group, decides not to subscribe to a new issue offered by firm B to its existing stockholders, and instead to sell the rights. Such operation can be described by a sequence of: (i) an increase of the capital of firm B subscribed by its existing stockholders including firm A (mechanism I); and: (ii) a sale to the public on the part of firm A of the stock of firm B subscribed (mechanism IV).

The four elementary collecting mechanisms can conveniently be associated in pairs. Namely, mechanisms I and II imply an increase of the value of the firm which carries out the operation of an amount equal to the capital increase. By contrast, mechanisms III and IV imply no variation in firm value, but a rebalancing of firms’ assets, a decrease of intra-group share- holdings corresponding to an increase of firms’ liquidity. Moreover, mechan- isms I and III allow a business group’s outside stockholders to maintain constant their integrated ownership shares in member firms (specifically, in the company which is increasing its capital in the first case, and in the company of which a share of capital is on sale in the second case). By contrast, through mechanisms II and IV the collection of risk capital is obtained at the expense of a decrease in integrated ownership shares. Note finally that mechanisms I and III imply a difference between the gross and

J.B F -L

758 F. Brioschi et al., Risk capital financing

the net collection of risk capital for the group as a whole, the difference being due to the cash outflows that the firms have to pay for acquisition of securities according to the rights method. The net collection and the gross collection coincide for mechanisms III and IV.

5.2. The collection of risk capital in business groups: An analytical model

This section has the aim of deriving a model for determining the net amount of the risk capital collection of all firms comprising a group when each one raises risk capital through the same collecting mechanism.

For this purpose, some definitions are needed. Let Awi, AVi and Aq be, respectively, the amount of risk capital to be collected, the increase of the value and the increase of the equity capital of firm i, and: Av=

(Av~,Avz,..., Au,), Az=(Az,, AZ, ,..., AZ,), Aw=Aw,, Aw, ,..., Aw,). Barring market imperfections, an increase AZi of the equity capital of firm i (corresponding either to mechanism I or mechanism II) implies a variation Aoi of firm i’s value of an amount equal to the one of the capital increase: Avi=Azi, i=l,..., N. Furthermore, let Aa,j be the variation of the share of the equity capital of firm j directly held by firm i and: AA=[AaJ, i=l,... ,N, j=l,..., N.

Expression (4) namely: wi=ui-Zjaipj, i= 1,. . . , N, defines the value of firm i excluding intra-group shareholdings as a function of the values of all firms of the group and of coefficients aij. In correspondence to variations Avi of the value vi of the firms due to capital increases AZi and to variations Aaii of coefficient aij, term Awi has the meaning of a itet collection of risk capital. Its expression is the following:

Awi=Azi-Cj[aijAzj+Aaij(~~+Azj)] i=l,...,N.

Case I. Collection of risk capital when all firms employ collection mech- anism I.

Risk capital raising through collection mechanism I implies that, in correspondence to a capital increase Azi of firm i, all the firms of the group subscribe the newly issued shares in such a way as to maintain constant their proportionate direct ownership (d+=O). Then, from expression (9) we obtain: Awi = AZ,- Cjaij AZj, i = 1,. . . , N, or in matrix form:

Aw=Az-Adz. (10)

Expression (10) shows that the net amount of funds raised by a firm which belongs to the group equals the difference between the volume of its own capital increase and the amount of funds needed to subscribe the equity capital increases of all member firms.

F. Brioschi et al., Risk capital financing 759

Case II. Collection of risk capital when all firms employ collection mech- anism II.

In this case, the amount of funds dwi raised by firm i is simply given by the amount of its capital increase dz,, as no cash outflow for subscribing increases of the equity capital of the other firms of the group occurs. This result also follows from expression (9). Since the capital increase Azj of firm j is not subscribed, by definition, by any firm of the group, the direct ownership shares aij held in firm j by all the firms of the group will decrease, of an amount Aaij equal to:

da,= -aijAzj/(vj+Azj) i=l,... ,N, j=l,..., N. (11)

Substituting (11) in (9), we derive: Awi = Azi, i = 1,. . . , N, or, in matrix form:

Aw=Az. (12)

Case III. Collection of risk capital when all firms employ collection mechanism III.

Collection mechanism III allows firm i to raise risk capital by selling to its existing shareholders through the rights method a share of the equity capital of other firms of the group. As said, firms of the group having shareholdings in firm i fully exercise their rights. Let Aa:j (Aa$<O) be the variation in the direct ownership share held by firm i in firm j, and AA* = [da;], i = 1,. . . , N, j=l,..., N. If firm i sells to its existing shareholders a portion of firm j, it may perform the sale at any value lower than or equal to the ‘true value’ Vj of firm j. Without loss of generality,r3 we can make the assumption that the sale is carried out at the true value vj. Hence, the cash inflow of firm i deriving from the sale of shareholdings in all firms of the group is:

(13)

However, if firm i holds a share of the equity capital of firm k, k = 1,. . . , N, (aik >O), the sale on the part of firm k of shareholdings in other firms of the group involves, according to collection mechanism III, a cash outflow for firm i given by:

Aw; = ,Zkai,Cj( - Aa$)vj. (14)

The net value of the risk capital collection is hence given by the difference between terms (13) and (14): Awi = Zj( - Aa$)vj - Zkai,Jj( - Aa,*i)vj, i=l , . . . , N, or in matrix form:

13A sale at a price lower than the market price can be interpreted as the combination of a sale at the market price and of a stock dividend.

760 F. Brioschi et al., Risk capital financing

dw=(-AA*u)-A(-AA*u)= -(AA*--ALlA*)v. (15)

Expression (15) is formally identical to expression (lo), regarding collecting mechanism I, if term AZ is substituted by term (-AA*v). Similarly to that expression, it indicates that the net amount of funds raised by a member firm by means of collecting mechanism III equals the difference between the volume of its sales of intra-group shareholdings and the amount of funds needed for exercising its subscription rights relating to the sales of intra- group shareholdings on the part of all member firms.

Case II/: Collection of risk capital when all firms employ collection mechanism IV.

Also in this case it results AZi= AUi=O, i= 1,. . . , N. Therefore, we can specify expression (9) as : Awi = - Cj Aaijvj, i = 1,. . . , N, or in matrix form:

Aw= - AAv. (16)

The amount of funds raised by member firms equals the net difference betweeen sales and purchases of intra-group shareholdings.

Finally, we will show that, as discussed in section 5.1, variations Ayi, i=l , . . . , N, associated with collection mechanisms I and III are null. Taking account of expression (6), variations Ayi, i= 1,. . . , N, of the integrated ownership shares held by an outside stockholder will be given by: Ayi= Axi + Ej[aji Ay, + Aaji(yi + Ay,)], i = 1,. . . , N, or in matrix form:

Ay = Ax + A’ Ay + A A’O, + Ay). (17)

From (7) and (17) we obtain:14

Ay=(Z-A’-AA’)-l[Ax+AA’(Z-A’)-‘x]. (18)

As for collection mechanism I, since Ax and AA’ are null, we obtain from expression (18): Ay = 0.

In the case of collection mechanism III, the variation of the direct ownership shares held in all member firms by an outside stockholder are given by: Axi = Cj( - Aa$)xj, i = 1,. . . , N. In matrix form: Ax = ( - AA*‘)x.

From expression (15) we derive: AA’ = AA*‘- AA*‘A’ = AA*‘(Z - A’). There- fore: Ay=(Z-A’-AA*‘+AA*‘A’)-‘[-AA*‘+AA*’(Z-A’)(Z-A’)-‘]x=O.

“%nce conditions (l), (2) and (3) apply also to matrix (A’ + AA’), matrix (I-A’ - A A’) has a non-negative inverse [see again Nikaido (1970, p. 118)].

F. Brioschi et al., Risk capital financing 761

6. The empirical analysis

In this section we shall present an empirical contribution pointing out the characteristics of the risk capital collecting process of Italian business groups and showing the extent of the separation between ownership and control. The analysis refers to the 1980-1986 period and concerns a sample composed of three groups, the I&Fiat, the Orlando and the Pirelli groups.

The section is divided into two parts. Section 6.1 provides some general information about the three groups considered. In section 6.2, the empirical results are set forward. They address the following points:

(a) risk capital collection of each single group, following the taxonomy proposed in section 5.1;

(b) financial flows connected to operations carried out by the firms of a group and referring to the risk capital of firms controlled by the other two groups of the sample. Such flows would be included in the risk capital collection of the macro-group if the set of groups were considered as a single macro-group;

(c) integrated ownership shares held by the controlling stockholders in the various firms of the groups. Such shares are successively compared with the shares of voting stock available to the controlling stockholders.

Finally, it is worth noting that the definition of risk capital employed in the empirical analysis comprises all types of stock (voting and non-voting stock) and also convertible securities.l’

6.1. The sample

The sample examined in this paper comprises the Hi-Fiat, the Orlando and the Pirelli groups, which, at the end of 1986, jointly accounted for 25.3% of the capitalization of all firms quoted on Italian stock exchanges.

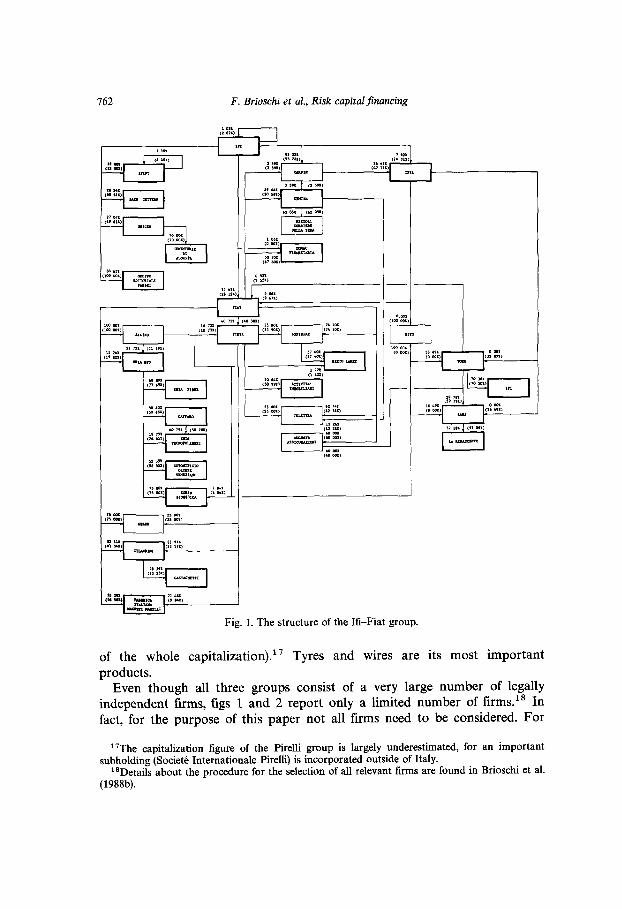

The I&Fiat group is the main Italian private group (23.5% of the whole capitalization). As shown in fig. 1, l6 its structure is essentially pyramidal with several hierarchical layers. Though its activities are mainly in the motor vehicles and motor vehicle equipment sector, the I&Fiat group is widely diversified. The Orlando group operates essentially in the copper industry. It includes a series of firms, three of which are quoted on the Milan Stock Exchange (0.37% of the whole capitalization). With respect to quoted firms (see fig. 2), its structure is a ‘pure’ pyramid with three hierarchical levels. The Pirelli group (see fig. 2) is the main Italian truly multinational group (1.44%

“The reason IS that, though technically convertible securities are not equity capital, in essence they are ‘delayed stock’. Furthermore, during the period under examination rights to convert have almost always been exercised. For more details see Brioschi et al. (1988a).

16For simplicity, equity linkages representing less than 1% of a firm’s capital have been neglected in the figure. The same applies to fig. 3.

162 F. Brioschi et al., Risk capital jhancing

--

<LO

r

J

Fig. 1. The structure of the &Fiat group.

of the whole capitalization). ” T res y and wires are its most important products.

Even though all three groups consist of a very large number of legally independent firms, figs 1 and 2 report only a limited number of firms.‘* In fact, for the purpose of this paper not all firms need to be considered. For

“The capitalization figure of the Pirelli group is largely underestimated, for an important subholding (Societi: Internationale Pirelli) is incorporated outside of Italy.

“Details about the procedure for the selection of all relevant firms are found in Brioschi et al. (1988b).

F. Brioschi et al., Risk capital financing 163

GIN I PIRELLI 6 C I 26.21% (35.95%)

I I

12.72% (14.22%)

PIRELLI SPA

10.95% (18.10%)

SIP

48.60% 51.40% (48.60%) (51.40%)

I

Fig. 2. The structure of the Orlando and Pirelli groups.

example, an operating company totally owned by another firm of the same group can be viewed, both from the point of view of ownership and of the collection of risk capital, as a division of the latter. This is, for instance, the case of Fiat Auto, a wholly owned subsidiary of Fiat which approximately accounts for 35% of sales of the entire group. In addition, member firms almost entirely owned by another firm of the group and firms of limited size have been neglected.

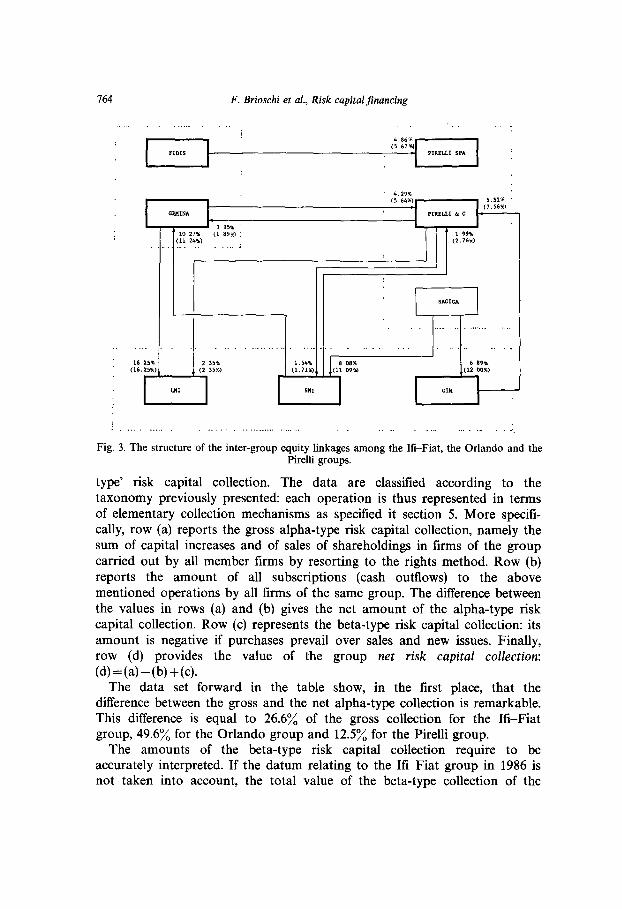

Fig. 3 illustrates the main inter-group equity linkages. In general, they are quite relevant. In particular, it is worth noting that the equity linkages between the firms of the groups Pirelli and Orlando (Gim is the main single shareholder of Pirelli & Co. with a 7.7% share of its voting stock, while Sagica, a company of the Pirelli group, is the second shareholder of Gim and Smi) are extremely relevant for their control.

6.2. The empirical results

6.2.1. The collection of risk capital

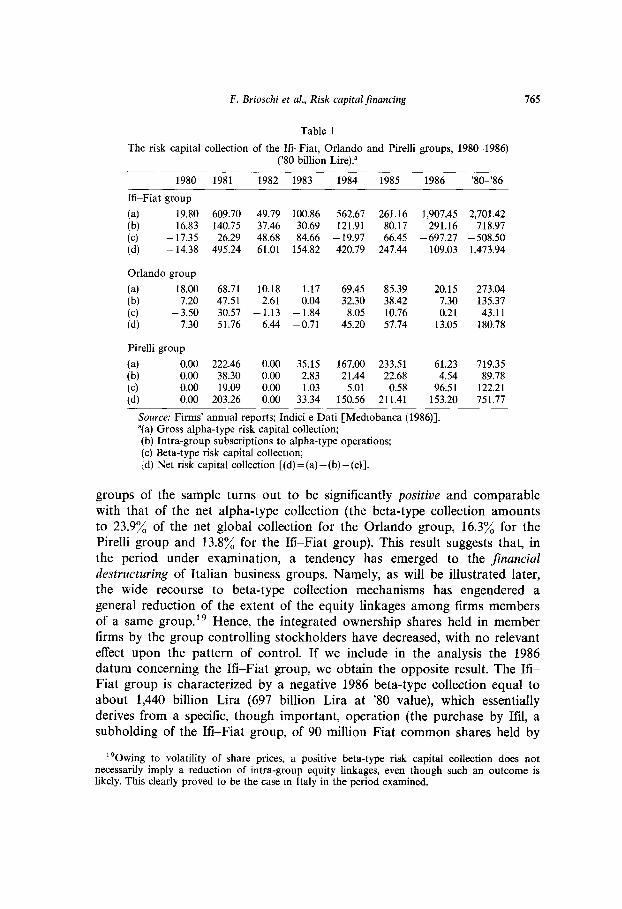

Yearly data of the amount of risk capital collected by each group of the sample in the period 1980-1986 (expressed in ‘80 billion Lira) are set forth in table 1. For simplicity, the amount of risk capital collected through mechanisms I and III will be called, in what follows, ‘alpha-type’ risk capital collection and the amount collected through mechanisms II and IV ‘beta-

164 F. Brioschi et al., Risk capital Jinancing

Fig. 3. The structure of the inter-group equity linkages among the S-Fiat, the Orlando and the Pirelli groups.

type’ risk capital collection. The data are classified according to the taxonomy previously presented: each operation is thus represented in terms of elementary collection mechanisms as specified it section 5. More specifi- cally, row (a) reports the gross alpha-type risk capital collection, namely the sum of capital increases and of sales of shareholdings in firms of the group carried out by all member firms by resorting to the rights method. Row (b) reports the amount of all subscriptions (cash outflows) to the above mentioned operations by all firms of the same group. The difference between the values in rows (a) and (b) gives the net amount of the alpha-type risk capital collection. Row (c) represents the beta-type risk capital collection: its amount is negative if purchases prevail over sales and new issues. Finally, row (d) provides the value of the group net risk capital collection:

(d)=(a)-(b)+(c). The data set forward in the table show, in the first place, that the

difference between the gross and the net alpha-type collection is remarkable. This difference is equal to 26.6% of the gross collection for the I&Fiat group, 49.6% for the Orlando group and 12.5% for the Pirelli group.

The amounts of the beta-type risk capital collection require to be accurately interpreted. If the datum relating to the H-Fiat group in 1986 is not taken into account, the total value of the beta-type collection of the

F. Brioschi et al., Risk capital financing 165

Table 1

The risk capital collection of the Hi-Fiat, Orlando and Pirelli groups, 1980-1986) (‘80 billion Lire).

1980 1981 1982 1983 1984 1985 1986 ‘80’86

K-Fiat group

I:; 19.80 16.83 609.70 140.75 49.19 37.46 100.86 30.69 562.67 121.91 261.16 80.17 1,907.45 291.16 2,701.42 718.97 I: - --14.38 17.35 495.24 26.29 48.68 61.01 154.82 84.66 -19.97 420.79 247.44 66.45 -697.27 109.03 - 1,473.94 508.50

Orlando group

ii; 18.00 7.20 47.51 68.71 10.18 2.61 0.04 1.17 69.45 32.30 85.39 38.42 20.15 7.30 273.04 135.37 i?) -3.50 7.30 30.57 51.76 -1.13 6.44 -0.71 -1.84 45.20 8.05 51.14 10.76 13.05 0.21 180.78 43.11

Pirelli group

I$ 0.00 0.00 222.46 38.30 0.00 0.00 35.15 2.83 167.00 21.44 233.51 22.68 61.23 4.54 719.35 89.78 t; 0.00 0.00 203.26 19.09 0.00 0.00 33.34 1.03 150.56 5.01 211.41 0.58 153.20 96.51 751.77 122.21

Source: Firms’ annual reports; Indici e Dati [Mediobanca (1986)]. “(a) Gross alpha-type risk capital collection; (b) Intra-group subscriptions to alpha-type operations; (c) Beta-type risk capital collection; :d) Net risk capital collection [(d) =(a)-(b) + (c)l.

groups of the sample turns out to be significantly positive and comparable with that of the net alpha-type collection (the beta-type collection amounts to 23.9% of the net global collection for the Orlando group, 16.3% for the Pirelli group and 13.8% for the U-Fiat group). This result suggests that, in the period under examination, a tendency has emerged to the financial destructuring of Italian business groups. Namely, as will be illustrated later, the wide recourse to beta-type collection mechanisms has engendered a general reduction of the extent of the equity linkages among firms members of a same group.rg Hence, the integrated ownership shares held in member firms by the group controlling stockholders have decreased, with no relevant effect upon the pattern of control. If we include in the analysis the 1986 datum concerning the hi--Fiat group, we obtain the opposite result. The Ifi- Fiat group is characterized by a negative 1986 beta-type collection equal to about 1,440 billion Lira (697 billion Lira at ‘80 value), which essentially derives from a specific, though important, operation (the purchase by Ifil, a subholding of the It&Fiat group, of 90 million Fiat common shares held by

“Owing to volatility of share prices, a positive beta-type risk capital collection does not necessarily imply a reduction of intra-group equity linkages, even though such an outcome is likely. This clearly proved to be the case m Italy in the period examined.

166 F. Brioschi et al., Risk capita/financing

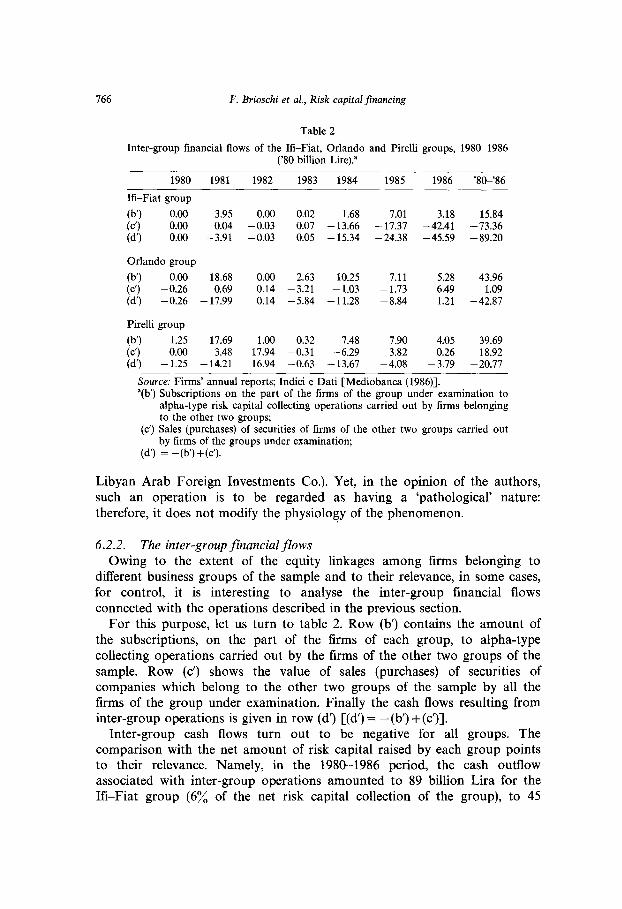

Table 2

Inter-group financial flows of the H-Fiat, Orlando and Pirelli groups, 1980-1986 (‘80 billion Lire).”

1980 1981 1982 1983 1984 1985 1986 ‘80-‘86

I&Fiat group

(b’) 0.00

Orlando group

(b’) 0.00 -0.26 -0.26

Pirelli group

(b’) 1.25 0.00

- 1.25

18.68 0.00 2.63 10.25 7.11 0.69 0.14 -3.21 - 1.03 - 1.73

- 17.99 0.14 -5.84 -11.28 - 8.84

17.69 1.00 0.32 7.48 7.90 4.05 39.69 3.48 17.94 -0.31 - 6.29 3.82 0.26 18.92

- 14.21 16.94 -0.63 -13.67 - 4.08 - 3.79 - 20.77

0.00 0.02 1.68 7.01 3.18 15.84 -0.03 0.07 - 13.66 - 17.37 -42.41 -73.36 -0.03 0.05 - 15.34 - 24.38 - 45.59 - 89.20

5.28 43.96 6.49 1.09 1.21 - 42.87

Source: Firms’ annual reports; Indici e Dati [Mediobanca (1986)]. “(b’) Subscriptions on the part of the firms of the group under examination to

alpha-type risk capital collecting operations carried out by firms belonging to the other two groups;

(c’) Sales (purchases) of securities of firms of the other two groups carried out by firms of the groups under examination;

(d’) = -(b’)+(c’).

Libyan Arab Foreign Investments Co.). Yet, in the opinion of the authors, such an operation is to be regarded as having a ‘pathological’ nature: therefore, it does not modify the physiology of the phenomenon.

6.2.2. The inter-group financial flows Owing to the extent of the equity linkages among firms belonging to

different business groups of the sample and to their relevance, in some cases, for control, it is interesting to analyse the inter-group financial flows connected with the operations described in the previous section.

For this purpose, let us turn to table 2. Row (b’) contains the amount of the subscriptions, on the part of the firms of each group, to alpha-type collecting operations carried out by the firms of the other two groups of the sample. Row (c’) shows the value of sales (purchases) of securities of companies which belong to the other two groups of the sample by all the firms of the group under examination. Finally the cash flows resulting from inter-group operations is given in row (d’) [(d’) = -(b’) + (c’)].

Inter-group cash flows turn out to be negative for all groups. The comparison with the net amount of risk capital raised by each group points to their relevance. Namely, in the 1980-1986 period, the cash outflow associated with inter-group operations amounted to 89 billion Lira for the E-Fiat group (6% of the net risk capital collection of the group), to 45

F. Brioschi et al., Risk capitalfinancing 167

billion Lira for the Orlando group (25% of the net collection) and to 58 billion for the Pirelli group (8% of the net collection). Furthermore, while for the Pirelli group sales of shareholdings in firms members of the other sample groups prevail over purchases, for the Orlando group sales balance purchases and for the I&Fiat group purchases largely predominate.

The data reported suggest that while intra-group equity linkages have normally been decreased in the ’80s within the Italian economic system, inter-group equity linkages have, in general, been maintained and in some cases strengthened.

6.2.3. The pattern of ownership and the separation of ownership from control

in Italian business groups This section has the aim of providing empirical evidence concerning the

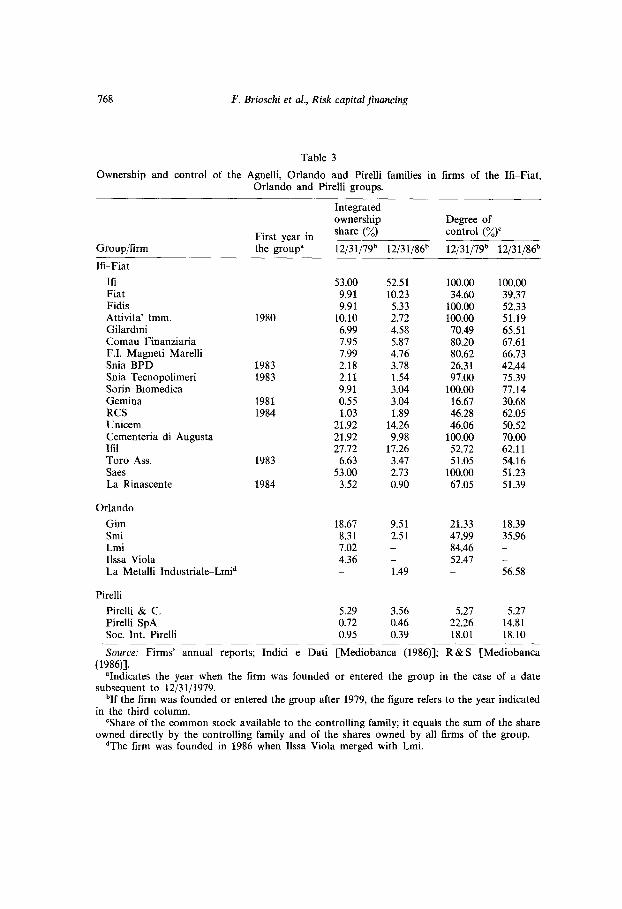

level of ownership of the controlling stockholders in the various firms of the three groups taken into consideration. The data allow the evaluation of the extension of the separation between ownership and control in Italian business groups, and illustrate also its trend in the ’80s. In particular, table 3 shows at the beginning and at the end of the period considered:

(a) the share of integrated ownership held in the firms of each group by the controlling shareholders2’ (namely, the Agnelli family for the &Fiat group, the Orlando family for the Orlando group and Fin.P., a financial company owned by the Pirelli family, for the Pirelli group);

(b) the percentage share of the common stock of the firms of each group available to the groups’ controlling stockholders; it equals the sum of the share of common stock held directly and of the shares held by all the firms which belong to the same group.

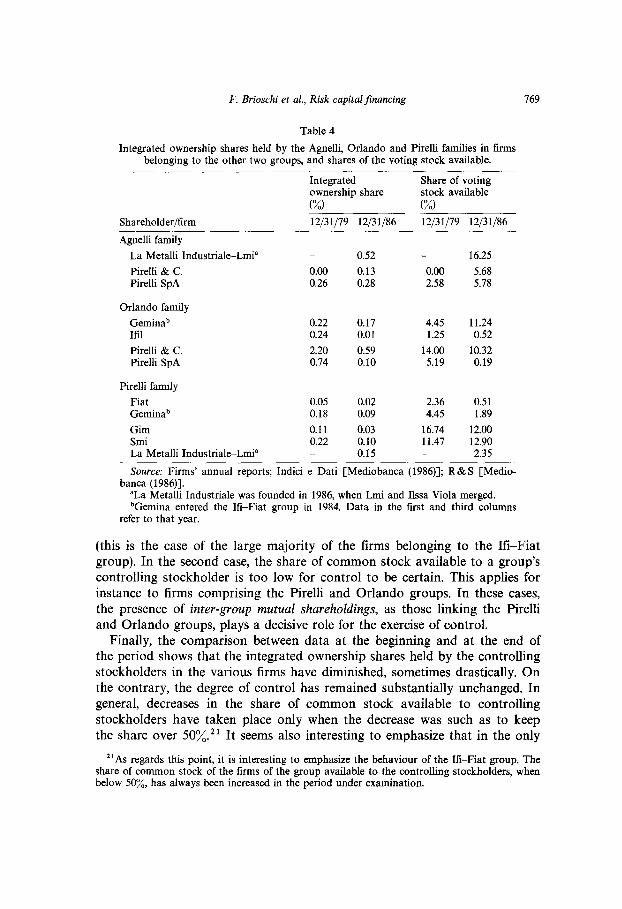

Finally, table 4 sets forward the integrated ownership shares held by the controlling stockholders of each group in some firms members of the other two groups of the sample, and also the percentage amount of votes available to them.

Integrated ownership data clearly point out that ownership of the firms comprising the sample groups is widely diffused: the phenomenon is particu- larly remarkable for operating companies. For instance, whereas the inte- grated ownership share held by the Agnelli family in Ifi, at the end of 1986, accounts for 52.5% of the whole equity capital, it decreases to about 10% in Fiat, an industrial subholding company and to 1.5% in Snia Tecnopolimeri, an operating company.

As for control, it is possible to identify two different patterns. In the first case, the voting power of the majority shareholders exceeds or is near to 50%

“‘Data relating to direct ownership shares of controlling stockholders are often not available. Therefore, the (very likely) assumption has been made that majority stockholders have direct shareholdings only in the parent holding company of the group they control.

768 F. Brioschi et al., Risk capital financing

Table 3

Ownership and control of the Agnelli, Orlando and Pirelli families in firms of the I&Fiat, Orlando and Pirelli groups.

Group/firm

b-Fiat

First year in the group”

share (%/,j control (%)

12/31/79b 12/31/86” 12/31/79” 12/31/86b

Ili 53.00 52.51 100.00 100.00 Fiat 9.91 10.23 34.60 39.37 Fidis 9.91 5.33 100.00 52.33 Attivita’ Imm. 1980 10.10 2.72 100.00 51.19 Gilardmi 6.99 4.58 70.49 65.51 Comau Finanziaria 7.95 5.87 80.20 67.61 F.I. Magneti Marelli 7.99 4.76 80.62 66.73 Snia BPD 1983 2.18 3.78 26.31 42.44 Snia Tecnopolimeri 1983 2.11 1.54 97.00 75.39 Sorin Btomedica 9.91 3.04 100.00 77.14 Gemina 1981 0.55 3.04 16.67 30.68 RCS 1984 1.03 1.89 46.28 62.05 Unicem 21.92 14.26 46.06 50.52 Cementeria di Augusta 21.92 9.98 100.00 70.00 Iti1 27.72 17.26 52.72 62.11 Toro Ass. 1983 6.63 3.47 51.05 54.16 Saes 53.00 2.73 100.00 51.23 La Rinascente 1984 3.52 0.90 67.05 51.39

Orlando

Gim 18.67 9.51 21.33 Smi 8.31 2.51 47.99 Lmi 7.02 _ 84.46 Ilssa Viola 4.36 _ 52.47 La Metalli Industrials-Lmid _ 1.49 _

18.39 35.96 _

56.58

Pirelli

Pirelli & C. Pirelli SpA Sot. Int. Pirelli

5.29 3.56 5.27 5.27 0.72 0.46 22.26 14.81 0.95 0.39 18.01 18.10

Integrated ownership Degree of

Source: Firms’ annual reports; Indici e Dati [Mediobanca (1986)]; R&S [Mediobanca (1986)].

“Indicates the year when the firm was founded or entered the group in the case of a date subsequent to 12/31/1979.

“If the firm was founded or entered the group after 1979, the figure refers to the year indicated in the third column.

“Share of the common stock available to the controlling family; it equals the sum of the share owned directly by the controlling family and of the shares owned by all fnms of the group.

dThe firm was founded in 1986 when Ilssa Viola merged with Lmi.

F. Brioschi et al., Risk capitalfinancing 769

Table 4

Integrated ownership shares held by the Agnelli, Orlando and Pirelli families in firms belonging to the other two groups, and shares of the voting stock available.

Shareholder/firm

Integrated ownership share

(%)

12131179 12131186

Share of voting stock available

(%)

12131179 12/31/86

Agnelli family

La Metalli Industriale-Lmi”

Pirelli & C. Pirelli SpA

Orlando family

Geminab Itil

Pirelli & C. Pirelli SpA

Pirelli family

Fiat Geminab

Gim Smi La Metalli Industrials-Lmi”

_ 0.52 - 16.25

0.00 0.13 0.00 5.68 0.26 0.28 2.58 5.78

0.22 0.17 4.45 11.24 0.24 0.01 1.25 0.52

2.20 0.59 14.00 10.32 0.74 0.10 5.19 0.19

0.05 0.02 2.36 0.51 0.18 0.09 4.45 1.89

0.11 0.03 16.74 12.00 0.22 0.10 11.47 12.90 _ 0.15 _ 2.35

Source: Firms’ annual reports; Indici e Dati [Mediobanca (1986)]; R&S [Medio- banca (1986)].

“La Metalli Industriale was founded in 1986, when Lmi and Ilssa Viola merged. “Gemina entered the R-Fiat group in 1984. Data in the first and third columns

refer to that year.

(this is the case of the large majority of the firms belonging to the Hi-Fiat group). In the second case, the share of common stock available to a group’s controlling stockholder is too low for control to be certain. This applies for instance to firms comprising the Pirelli and Orlando groups. In these cases, the presence of inter-group mutual shareholdings, as those linking the Pirelli and Orlando groups, plays a decisive role for the exercise of control.

Finally, the comparison between data at the beginning and at the end of the period shows that the integrated ownership shares held by the controlling stockholders in the various firms have diminished, sometimes drastically. On the contrary, the degree of control has remained substantially unchanged. In general, decreases in the share of common stock available to controlling stockholders have taken place only when the decrease was such as to keep the share over 50%. ‘l It seems also interesting to emphasize that in the only

‘iAs regards this point, it is interesting to emphasize the behaviour of the I&Fiat group. The share of common stock of the firms of the group available to the controlling stockholders, when below SO%, has always been increased in the period under examination.

110 F. Brioschi et al., Risk capital financing

case in which the aforementioned share has been subject to a significant reduction (in Pirelli SpA, from 22% to 15%), such reduction has been balanced by a similar increase in inter-group linkages.

7. Concluding remarks

In this paper, a formal description of a business group, composed of a set of legally autonomous firms connected through a network of cross- shareholdings, has been presented. In particular, it has been shown that the value of the firms of a group and the ownership share of an outside stockholder can be described by two linear, Leontief-type systems dual to each other. The determination of an expression for the ownership share held by a controlling stockholder allows a quantitatve measure of the divorce of ownership from control. Furthermore, a new taxonomy for the collection of risk capital which generalizes the traditional one holding for an independent firm, has been proposed. It relies on the recognition that the sale on the part of the firms of a group of shareholdings in other firms of the same group such as to maintain within the group control over all firms must be regarded as a risk capital collecting operation. An analytical expression for the collection of risk capital is obtained from a suitable differentiation of the equation of value. The possibility of raising risk capital without losing control, which is to be regarded as one of the main determinants of the diffusion of business groups, establishes a strong connection between the ownership/control issue and the process of raising risk capital.

The model described in the first part of the paper has subsequently been applied to the analysis of an important portion of the Italian economic system, including the &Fiat, the Orlando and the Pirelli groups. The analysis has documented that the structure of Italian groups is essentially pyramidal, with some loops of intra-group shareholdings generally of minor importance. By contrast, mutual equity linkages among different groups have proved to be widely diffused in Italy. The paper has provided clear evidence that in the period examined (1980-1986):

(a) the level of ownership of the controlling stockholders in the various firms of the groups considered is low, and rapidly decreasing. As a conse- quence, the separation of ownership and control is wide, and rapidly growing. The role played by inter-group equity linkages for the control of different groups has also been documented;

(b) the amount of risk capital raised by Italian groups is remarkable. A non- negligible share of that amount corresponds to operations which imply no disbursement from the controlling stockholders and, consequently, a reduction in their integrated ownership share. Such reduction has had no consequence on the pattern of control.

More in general, in our opinion at least, the paper has shown that it is

F. Brioschi et al., Risk capital financing 171

reasonable to claim that the business group system is to be regarded as new, to a large extent unexplored, mode of functioning of the capitalistic system, characterized by a number of important peculiarities [see Brioschi (1988)]. In the first place the divorce between ownership and control allowed by the business group system makes hostile take-overs impossible and deprives the capital market of its traditional function of efficient capital allocator. Thus large enterprizes are allowed to pursue long-term strategies neglecting short- term profitability constraints. The growth of the large enterprizes is also made easier by the augmented possibilities of raising risk capital. The influence of the banking sector on the industrial system through credit rationing is also reduced. Consequently, an increase of overall concentration in the product market and possibly of collusion is a likely outcome of the existence of the business group phenomenon. Mutual inter-group equity linkages may foster collusive behaviour. Furthermore, the presence of a network of corporate shareholdings linking firms to each other reduces transparency and increases information asymmetries. Stock market imperfec- tions and sources of insider trading are multiplied. Finally, as widely recognized (see for instance the proposed 9th EEC Directive), the group system multiplies the conflicts of interest among the different stockholders of the various firms constituting a group (for instance, between the controlling stockholders and the minority stockholders of the operating companies).

The discussion of the problems which have been briefly raised goes well beyond the scope of the present paper. Yet, it clearly constitutes an essential premise for setting up a regulatory framework, which is missing in most countries where business groups are largely diffused.

References

Berle, A.A. and G.C. Means, 1932, The modern corporation and private property (Macmillan, New York).

Brealey, R. and S. Myers, 1984, Principles of corporate finance (McGraw-Hill, Singapore). Brioschr. F., 1988, Struttura proprietaria e comportamento concorrenziale de1 sistema industriale

itahano, in: P. Bianchi, ed., Estensione de1 mercato e politica della concorrenza (11 Mulino, Bologna).

Brroschi, F. and M.G. Colombo, 1986a, Evaluating stockholders’ ‘global’ ownership in a business group’s member firms, 13th Annual EARIE Meeting (Berlinc

Brioschi, F. and M.G. Colombo. 1986b. Possesso, controllo e raccolta di canitali de rischio nei gruppi industriali, in: Nomisma-Laboratorio di Politica Industriale, eds.,-Riaggiustamento e crescita esterna dei gruppi e delle imprese in Italia (Bologna).

Brioschi, F., L. Buzzacchi and M.G. Colombo, 1988a, La raccolta di capitale di rischio nei gruppi industriali itahani e la separazione fra possesso e controllo, in: IRS, eds., Rapport0 sul mercato azionario. Progress0 e crisr della Borsa italtana: Le ragioni e i problemi aperti (Le Edizioni de1 Sole-24 Ore, Milano).

Brioschi, F., L. Buzzacchi and M.G. Colombo, 1988b, Risk capital financing and the separation of ownership and control in business groups, Mimeo. 88-009 (Politecnico di Milano, Dipartimento di Elettronica, Milano).

Cable, J. and H. Yasuki, 1985, Internal organisation, business groups and corporate perfor- mance, International Journal of Industrial Organization 3, 401-420.

772 F. Brioschi et al., Risk capital financing

Cubbin, J.L. and D. Leech, 1983, The effect of shareholding dispersion on the degree of control in British companies: Theory and measurement, Economic Journal 93, 351-369.

Daems, H., 1980, The determinants of the hierarchical organization of industry, EIASM Working Paper no. 80-12.

Encaoua, D. and A. Jacquemin, 1982, Organisational efftciency and monopoly power. The case of French mdustrial groups, European Economic Review 19, 25-51.

Goto, A., 1982, Business groups in a market economy, European Economic Review 19, 53-70. Leech, D., 1987, Ownership concentration and the theory of the firm: A simple-game-theoretic

approach, Journal of Industrial Economics 3, 225-240. Nikaido, H., 1979, Introduction to sets and mappings in modern economics (North-Holland,

Amsterdam). Nyman, S. and A. Silberstone, 1978, The ownership and control of industry, Oxford Economic

Papers 30, 74-101. Smith, C., 1977, Alternative methods for raising capital, Journal of Financial Economics 5,

273-307. Smith, C., 1986, Investment banking and the capital acquisition process, Journal of Financial

Economics 15,3-29. Wiliamson, O.E., 1975, Market and hierarchies: Analysis and antitrust implications (Free Press,

New York).