Revenge of the Nerds - Empire Justice Center

160

Revenge of the Nerds Making the Most of Technical Defenses in Foreclosure Cases February 22, 2017 Slides ................................................................................................................................................1 Relevant Statutes............................................................................................................................30 RPAPL § 1303 ...................................................................................................................30 RPAPL § 1304 ...................................................................................................................33 RPAPL § 1306 ...................................................................................................................38 CPLR R. 4518 ....................................................................................................................40 Case Example: Bank of America v. Thompson .............................................................................43 Case Example: US Bank v. Crick ..................................................................................................86 Various Pro Se Papers ..................................................................................................................115

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Revenge of the Nerds - Empire Justice Center

Revenge of the Nerds Making the Most of Technical Defenses in Foreclosure Cases

February 22, 2017

Slides ................................................................................................................................................1

Relevant Statutes ............................................................................................................................30

RPAPL § 1303 ...................................................................................................................30

RPAPL § 1304 ...................................................................................................................33

RPAPL § 1306 ...................................................................................................................38

CPLR R. 4518 ....................................................................................................................40

Case Example: Bank of America v. Thompson .............................................................................43

Case Example: US Bank v. Crick ..................................................................................................86

Various Pro Se Papers ..................................................................................................................115

Reven

ge of th

e Nerd

sM

aking th

e Mo

st of Tech

nical D

efenses in

Foreclo

sure C

ases

Cath

erin

e Iso

be

Bro

oklyn

Legal Se

rvices

Jose

ph

Re

be

llaM

FY Le

gal Service

s, Inc.

Febru

ary 22

, 20

17

1

1

Ou

tline

I.In

trod

uctio

n

II.P

roced

ural Po

sture in

the Fo

reclosu

re Case

III.Th

e Defen

ses

IV.

Co

nclu

sion

and

Qu

estion

s

2

2

Proced

ural Po

sture: A

nsw

er

•First o

pp

ortu

nity to

assert defen

ses

•O

bvio

usly, every p

ossib

le defen

se is still on

the tab

le

•B

e sure to

assert waivab

led

efenses (stan

din

g!) that are likely to

arise

•R

ecent ch

anges to

CP

LR R

. 34

08

–rem

emb

er the exten

ded

timelin

e to

answ

er after the first settlem

ent co

nferen

ce

3

3

Proced

ural Po

sture:

Post-C

on

ference, Pre-M

otio

n, A

nsw

er In•

If there’s b

een an

answ

er, you

can m

ove to

amen

d to

assert any d

efenses th

at were n

ot raised

in

the A

nsw

er. You

do

no

t need

to su

pp

ly an excu

se for th

e failure to

raise it.

•“Leave sh

all be freely given

up

on

such

terms as m

ay be ju

st”. CP

LR R

. 30

25

(b). Leave to

amen

d is

app

rop

riate “pro

vided

the am

end

men

t is no

t palp

ably in

sufficien

t, do

es no

t preju

dice o

r surp

rise th

e op

po

sing p

arty, and

is no

t paten

tly devo

id o

f merit”. R

eyes v. Brin

ks Glo

b. Servs. U

SA, In

c., 11

2

A.D

.3d

80

5, 8

06

, 97

8 N

.Y.S.2d

63

, 64

(Ap

p. D

iv. 2d

De

p’t 2

01

3); Po

stiglio

ne

v. Ca

stro, 1

19

A.D

.3d

9

20

, 92

2, 9

90

N.Y.S.2

d 2

57

, 25

9 (A

pp

. Div. 2

d D

ep’t 2

01

4).

•P

rejud

ice to th

e op

po

sing p

arty relates on

ly to “p

rejud

ice or su

rprise resu

lting d

irectly from

the

delay in

seeking leave.” Tirp

ack

v. 12

5 N

. 10

, LLC, 1

30

A.D

.3d

91

7, 9

19

, 14

N.Y.S.3

d 1

10

, 11

3 (A

pp

. D

iv. 2d

De

p’t 2

01

5); see a

lso Lu

cido

v. Ma

ncu

so, 4

9 A

.D.3

d 2

20

, 22

9, 8

51

N.Y.S.2

d 2

38

, 24

5 (A

pp

. D

iv. 2d

De

p’t 2

00

8) (co

urt m

ust m

easure w

heth

er or n

ot “d

elay in seekin

g the am

end

men

t wo

uld

cau

se preju

dice o

r surp

rise”).

•A

pp

lies to d

efenses w

aived u

nd

er CP

LR 3

21

1(e). A

uro

ra Lo

an

Servs., LLC v. D

imu

ra, 1

04

A.D

.3d

7

96

, 79

7, 9

62

N.Y.S.2

d 3

04

, 30

6 (A

pp

. Div. 2

d D

ep’t 2

01

3) (h

old

ing th

at “defen

ses waived

un

der

CP

LR 3

21

1(e) can

neverth

eless be in

terpo

sed b

y leave of co

urt p

ursu

ant to

CP

LR 3

02

5(b

) so lo

ng

as the am

end

men

t do

es no

t cause th

e oth

er party p

rejud

ice or su

rprise resu

lting d

irectly from

th

e delay”).

4

4

Proced

ural Po

sture:

Post-C

on

ference, Pre-M

otio

n, N

o A

nsw

er•

Will n

eed to

file a mo

tion

to co

mp

el acceptan

ce of an

un

timely

answ

er. CP

LR §

30

12

(d).

•C

ou

rts have ro

utin

ely perm

itted service o

f a late answ

er wh

ere (1)

there is a reaso

nab

le excuse, (2

) the d

efend

ant h

as merito

riou

s d

efenses an

d (3

) service of th

e answ

er do

es n

ot u

nfairly p

rejud

ice the

plain

tiff. See, e.g., N

ickell v. Pa

thm

ark Sto

res, Inc., 4

4 A

.D.3

d 6

31

, 6

32

, 84

3 N

.Y.S.2d

17

7, 1

78

(Ap

p. D

iv. 2d

Dep

’t 20

07

); Jolko

vskyv.

Legem

an

, 32

A.D

.3d

41

8, 4

19

, 81

9 N

.Y.S.2d

56

1, 5

62

(Ap

p D

iv. 2d

D

ep’t 2

00

6); W

atso

n v. Po

llacch

i, 32

A.D

.3d

56

5, 5

65

-66

, 81

9 N

.Y.S.2d

6

12

, 61

3 (A

pp

. Div. 3

d D

ep’t 2

00

6); N

aso

nv. Fish

er, 30

9 A

.D.2

d 5

26

, 5

26

, 76

5 N

.Y.S.2d

32

, 33

(Ap

p. D

iv. 1st D

ep’t 2

00

3).

5

5

Proced

ural Po

sture:

Facing M

otio

n fo

r Sum

mary Ju

dgm

ent

•P

laintiff m

ust m

ake prim

a facie case and

refute asserted

defen

ses.

•If yo

u h

ave an u

np

led d

efense, yo

u m

ay be ab

le to raise it (R

og

off

v. Sa

n Ju

an

Ra

cing

Ass'n

, Inc., 5

4 N

.Y.2d

88

3, 8

85

, 42

9 N

.E.2d

41

8, 4

19

(1

98

1)) b

ut th

e cou

rt cou

ld also

find

that it h

as been

waived

. Do

n’t

try to b

ring u

p stan

din

g or statu

te of lim

itation

s for th

e first time.

•N

ot a d

efense, b

ut alw

ays loo

k for evid

entiary issu

es, especially

hearsay th

at do

esn’t m

eet the b

usin

ess record

s exceptio

n

requ

iremen

ts.

6

6

Bu

siness R

ecord

s Ru

le

Fou

nd

ation

requ

iremen

ts for ad

missio

n o

f a bu

siness reco

rd (o

r testim

on

y based

on

review o

f a bu

siness reco

rd:

1. Th

e record

mu

st be m

ade in

the o

rdin

ary cou

rse of b

usin

ess reflectin

g a rou

tine, regu

larly con

du

cted b

usin

ess activity need

ed an

d

relied o

n in

the p

erform

ance o

f the fu

nctio

n o

f the b

usin

ess;

2. It m

ust b

e the regu

lar cou

rse of th

e bu

siness to

make th

e record

;

3. Th

e record

mu

st have b

een m

ade at th

e time o

f the act,

transactio

n, o

ccurren

ce or even

t, or w

ithin

a reason

able tim

e th

ereafter, assurin

g the reco

llection

is fairly accurate an

d th

e entries

rou

tinely m

ade (See C

PLR

§4

51

8(a)).

7

7

Bu

siness R

ecord

s Ru

le

A p

rop

er fou

nd

ation

for th

e adm

ission

of th

e bu

siness reco

rd [o

r the

testimo

ny] m

ust b

e pro

vided

by so

meo

ne w

ith p

erson

al kno

wled

ge of

the m

aker’s bu

siness p

ractices and

pro

cedu

res. Seba

tino

v. Turf H

ou

se, 7

6 A

.D.2

d 9

45

, 94

6 (3

d D

ep’t 1

98

0). See also

, HSB

C M

ortg

ag

e Services, In

c. v. Ro

yal, 14

2 A

.D.3

d 9

52

(2d

Dep

’t 20

16

).

Wh

olesale ad

missio

n o

f files is un

acceptab

le; a fou

nd

ation

mu

st be

laid fo

r each reco

rd. V

ermo

nt C

om

missio

ner o

f Ba

nkin

g a

nd

Insu

ran

ce v. W

elbilt

Co

rp., 1

33

A.D

.2d

39

6 (2

d D

ep’t 1

98

7).

8

8

Bu

siness R

ecord

s Ru

le

•M

ost co

mm

on

plain

tiff misstep

is an in

app

rop

riate reliance o

n b

usin

ess reco

rds o

f oth

er entities. Th

is hap

pen

s in n

early every case in w

hich

servicin

g transfers after th

e case is b

rou

ght. Lo

ok at n

otices, stan

din

g, etc.

•Servicer actin

g as attorn

ey in fact fo

r plain

tiff cann

ot sw

ear to facts n

ot

with

in its o

wn

perso

nal kn

ow

ledge. Pero

siv. LiGreci, 9

8 A

.D.3

d 2

30

(2d

D

ep’t 2

01

2); C

ymb

olv. C

ymb

ol, 1

22

A.D

.2d

77

1 (2

d D

ep’t 1

98

6).

•Likew

ise, a servicer cann

ot sw

ear to even

ts pre-d

ating its servicin

g of th

e lo

an w

here kn

ow

ledge is b

ased o

n th

e bu

siness reco

rds o

f ano

ther en

tity. W

ells Farg

o B

an

k, N.A

. v. Jon

es, 13

9 A

.D.3

d 5

20

, 52

1-5

22

(1st

Dep

’t May

17

, 20

16

). C.f. Peo

ple v. C

ratsley, 8

6 N

.Y. 2d

81

, 90

(19

95

).

9

9

Examp

le of Im

perm

issible B

usin

ess Reco

rds

Lod

ato

v. Greyh

aw

k, 39

A.D

.3d

49

4, 4

95

, 83

4 N

.Y.S.2d

23

9, 2

40

(Ap

p. D

iv. 2d

Dep

't 20

07

) ("the m

ere filing o

f p

apers received

from

oth

er entities, even

if they are retain

ed in

the regu

lar cou

rse o

f bu

sine

ss, is insu

fficient

to q

ualify th

e do

cum

en

ts as bu

siness reco

rds b

ecau

se such

pap

ers simp

ly are no

t mad

e in th

e regu

lar cou

rse

of b

usin

ess o

f the

recipien

t").

“It is self-eviden

t, that w

ith th

e adven

t of

com

pu

ters and

electron

ic record

keep

ing, M

r. B

en

nett h

ad access to

all of th

e reco

rds related

to

the su

bje

ct loan

, inclu

din

g tho

se reco

rds

from

the p

rior servicers . . . th

at were

inco

rpo

rated w

ith, an

d in

to, th

e record

s of

Ru

shm

ore”.

10

10

Proced

ural Po

sture:

Facing M

otio

n fo

r Defau

lt Jud

gmen

t•

If there’s b

een d

elay pre-filin

g, you

can raise ab

and

on

men

t -C

PLR

3

21

5(c) –

and

seek dism

issal.

•A

ny ju

risdictio

nal ch

allenges, su

ch as im

pro

per service o

f pro

cess, can

be raised

in a cro

ss mo

tion

to d

ismiss.

•If th

e case h

asn’t b

een ab

and

on

ed an

d th

ere is no

jurisd

iction

al basis

to d

ismiss th

e action

, you

will p

rob

ably n

eed to

cross-m

ove to

com

pel

acceptan

ce of a late an

swer. G

enerally, th

is requ

ires a merito

riou

s d

efense an

d a reaso

nab

le excuse fo

r the d

elay –C

PLR

§3

01

2(d

).

11

11

Proced

ural Po

sture:

Facing M

otio

n fo

r Jud

gmen

t of Fo

reclosu

re & Sale

•A

t this p

oin

t, sum

mary ju

dgm

ent o

r defau

lt jud

gmen

t has b

een gran

ted.

Argu

men

t is goin

g to b

e limited

to issu

es with

the referee’s rep

ort itself.

•O

f cou

rse, jurisd

iction

al challen

ges (service of p

rocess, su

it bro

ugh

t against

a dead

perso

n) rem

ain.

•If th

e un

derlyin

g ord

er was d

ecided

on

defau

lt, you

may b

e able to

cross

mo

ve to vacate th

e un

derlyin

g ord

er if you

have a m

eritorio

us d

efense an

d

a reason

able excu

se for th

e defau

lt. CP

LR §

50

15

.

•A

dd

ition

ally, you

can raise an

y pro

cedu

ral pro

blem

s with

ob

tainin

g the

un

derlyin

g ord

er and

referral, such

as imp

rop

er service of th

e MSJ o

r b

ringin

g a mo

tion

for d

efault ju

dgm

ent ex p

arte w

hen

parties h

ave ap

peared

.

12

12

Defen

ses: Previou

s Cases

•Pen

din

g foreclo

sure su

it: RPA

PL §

13

01

(3) p

revents a m

ortgagee fro

m

brin

ging sim

ultan

eou

s suits w

itho

ut leave fro

m co

urt. Lo

ok o

ut fo

r it w

hen

the p

reviou

s suit h

as been

aban

do

ned

or th

e Plain

tiff has lo

st o

n M

SJ and

is overeager to

file a new

suit. U

nlike C

PLR

32

11

(a)(4), th

e o

perative fact is th

e mo

rtgage deb

t, no

t the p

arties.

•If th

ere have b

een m

ultip

le disco

ntin

uan

ces, see if CP

LR R

. 32

17

(c) ap

plies –

“a disco

ntin

uan

ce by m

eans o

f no

tice op

erates as an

adju

dicatio

n o

n th

e merits if th

e party h

as on

ce befo

re disco

ntin

ued

b

y any m

etho

d an

action

based

on

or in

clud

ing th

e same cau

se of

action

”

13

13

Defen

ses: RPA

PL §

13

03

•Fo

reclosin

g party b

ears the b

urd

en o

f sho

win

g strict com

plian

ce with

th

e statute. First N

at. B

an

k of C

hica

go

v. Silver,73

A.D

.3d

16

2, 1

70

, 8

99

N.Y.S.2

d 2

56

, 26

2 (A

pp

. Div. 2

d D

ep’t 2

01

0);P

ritcha

rd v. C

urtis,

10

1 A

.D.3

d 1

50

2, 1

50

4, 9

57

N.Y.S.2

d 4

40

, 44

3 (A

pp

. Div. 3

d D

ep’t

20

12

).

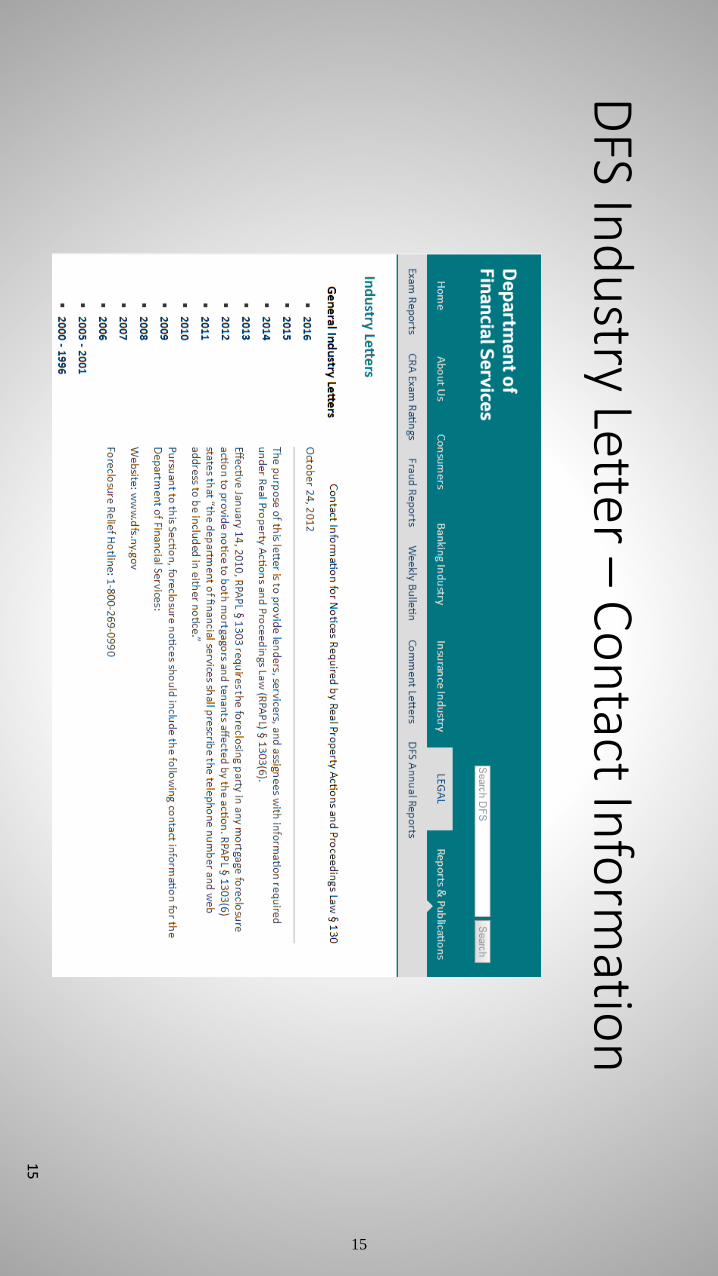

•See D

FS Ind

ustry Letter d

ated O

ctob

er 24

, 20

12

prescrib

ing

teleph

on

e con

tact for D

FS to b

e inclu

ded

in R

PAP

L §1

30

3 N

otice:

http

://ww

w.d

fs.ny.go

v/legal/ind

ustry/il1

21

02

4.h

tm

•In

recently b

rou

ght case

s, be su

re that th

e plain

tiff is usin

g the

up

dated

langu

age abo

ut th

e ho

meo

wn

er’s right to

remain

in th

e h

om

e wh

ile the fo

reclosu

re is pen

din

g.

14

14

DFS In

du

stry Letter –C

on

tact Info

rmatio

n

15

15

Defen

ses: R

PAP

L §1

30

3

•C

heck fo

nts: title o

f the n

otice m

ust b

e in b

old

, 20

po

int typ

e; bo

dy o

f th

e no

tice mu

st be in

bo

ld, 1

4 p

oin

t type. P

rocess servers o

ften

redu

ce pap

ers by 1

0%

wh

en co

pyin

g or serve a co

py w

hich

is so fain

t th

at it cann

ot b

e con

sidered

in “b

old

” prin

t.

•Fo

nt size is d

efined

in G

eneral C

on

structio

n Law

§6

2.

•Is th

e no

tice prin

ted o

n co

lored

pap

er?

•D

id th

e defen

dan

t receive service of p

rocess b

ut w

aive his/h

er right

to co

ntest p

erson

al jurisd

iction

? If no

tice no

t received b

y defen

dan

t, can

still raise no

n-service o

f the R

PAP

L §13

03

No

tice as a defen

se.

16

16

Defen

ses: RPA

PL §

13

04

•N

otice th

at mu

st be sen

t at least 90

days b

efore th

e foreclo

sure is filed

•M

ust in

clud

e:

•List o

f Ho

usin

g Co

un

selors

•R

einstatem

ent A

mo

un

t

•R

einstatem

ent D

ate

•Statu

torily M

and

ated Lan

guage

•R

PAP

L §1

30

4 req

uires strict co

mp

liance. See, e.g

., Hu

dso

n C

ity Sav. B

an

k v. D

ePa

squ

ale, 1

13

A.D

.3d

59

5, 5

96

, 97

7 N

.Y.S.2d

89

5 (A

pp

. Div. 2

d D

ep’t

20

14

); Au

rora

Loa

n Servs., LLC

v. Weisb

lum

, 85

A.D

.3d

95

, 10

3, 9

23

N.Y.S.2

d

60

9, 6

14

(Ap

p. D

iv. 2d

Dep

’t 20

11). So

loo

k ou

t for an

ythin

g wro

ng w

ith th

e n

otice.

17

17

Prob

lems w

ith 1

30

4 N

otices

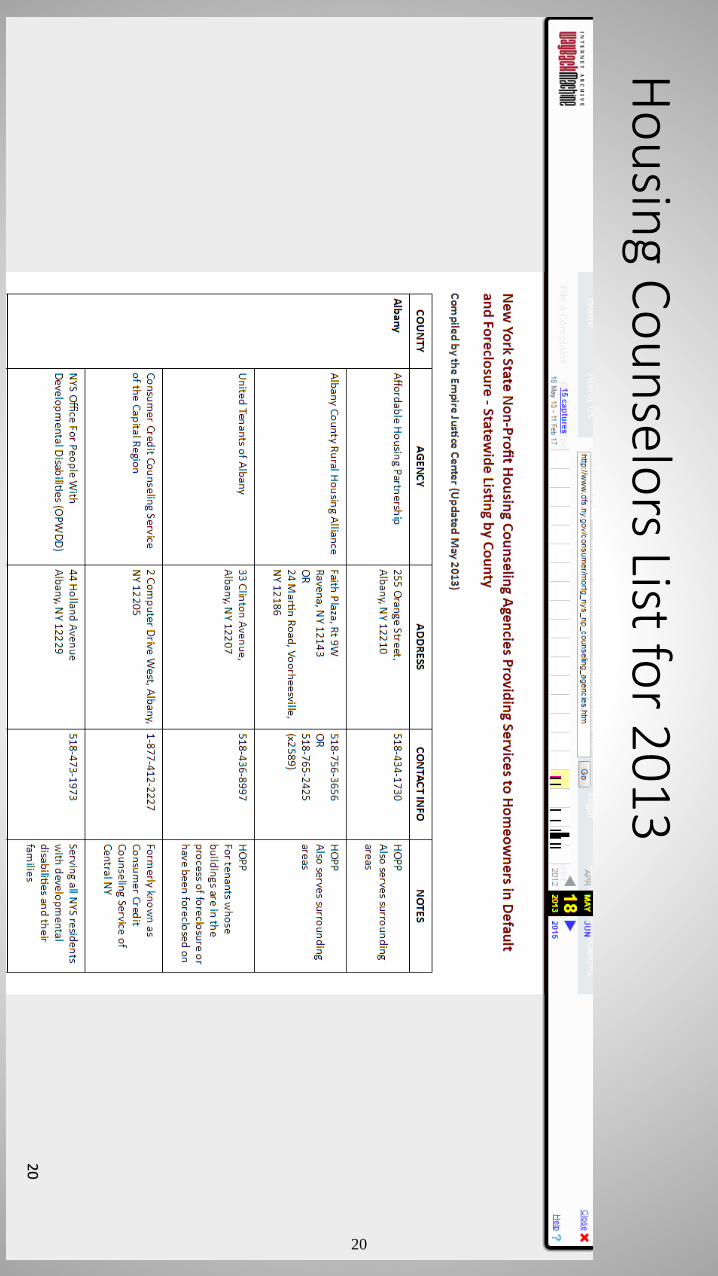

•List o

f Ho

usin

g Co

un

selo

rs is ou

tdated

or o

therw

ise inaccu

rate. See w

ayback

mach

ine

for earlie

r version

s of th

e cou

nse

lor list. Fo

r examp

le, A

CO

RN

, defu

nct

since 2

00

9, is still so

metim

es in

clud

ed

on

the

list. Co

mp

are the

curren

t list at: h

ttp://w

ww

.dfs.n

y.gov/co

nsu

me

r/mo

rtg_n

ys_np

_co

un

selin

g_agen

cies.htm

to th

e archived

version

s and

check fo

r errors su

ch as w

ron

g cou

nty.

•D

efault d

ate and

amo

un

t du

e d

o n

ot m

atch th

e d

escriptio

n o

f defau

lt in P

laintiff’s

affirmatio

n. Fo

r examp

le, th

e 1

30

4 n

otice w

as sent in

De

cem

be

r 20

14

, bu

t the

affid

avits state that d

efend

ant “failed

to co

mp

ly with

the term

s, coven

ants an

d

con

ditio

ns o

f said n

otes, m

ortgages an

d Fin

al Loan

Mo

dificatio

n b

y failing an

d

om

itting to

pay, to

the

plain

tiff, paym

ents d

ue

on

March

1, 2

01

5”.

•N

otice

no

t mailed

on

the

date stated

–ch

eck th

e certified m

ail tracking

info

rmatio

n if th

e n

otice w

as sent in

the

last two

years and

also ch

eck P

laintiff’s

wh

ich w

ill som

etime

s just state a d

ifferent d

ay.

18

18

Ho

usin

g Co

un

selors To

day

19

19

Ho

usin

g Co

un

selors List fo

r 20

13

20

20

Defen

ses: RPA

PL §

13

06

•A

fter send

ing th

e RPA

PL §

13

04

no

tice, the P

laintiff m

ust file w

ith th

e D

epartm

ent o

f Finan

cial Services with

in th

ree bu

siness d

ays.

•Th

e filing itself is a p

recon

ditio

n to

foreclo

sure.

•Th

is com

es up

in tw

o situ

ation

s:•

First, wh

ere the 1

30

4 N

otice

is defective d

ue to

an in

correct d

ate, you

sho

uld

also

argue th

at the 1

30

6 Filin

g is defective as w

ell becau

se it con

tains false

info

rmatio

n an

d/o

r wasn

’t mad

e with

in th

e pro

per tim

e perio

d.

•Seco

nd

, som

etimes th

e servicer will fin

d a d

efect in th

e 13

04

No

tice an

d sen

d

ano

ther o

ne to

correct th

e defect. I’ve n

ever seen th

e servicer file a secon

d

time w

ith D

FS.

21

21

Defen

ses: Co

ntractu

al No

tice of D

efault

•Th

e GSE Fo

rm M

ortgage in

clud

es in Paragrap

h 2

2 a p

rovisio

n

requ

iring th

at the m

ortgagee p

rovid

e a no

tice of d

efault givin

g at least 3

0 d

ays to rein

state the m

ortgage.

•N

Y Co

urts h

ave held

that it is a co

ntractu

al con

ditio

n p

receden

t to

foreclo

sure. See G

MA

C M

ortg

ag

e, LLC v. B

ell, 12

8 A

.D.3

d 7

72

, 11

N

.Y.S.3d

73

(Ap

p. D

iv. 2d

Dep

’t 20

15

); Wells Fa

rgo

Ba

nk, N

.A. v Eisler,

11

8 A

.D.3

d 9

82

, 98

8 N

.Y.S.2d

68

2 (A

pp

. Div. 2

d D

ep’t 2

01

4);

HSB

C

Mo

rtg. C

orp

. (USA

) v. Gerb

er, 10

0 A

.D.3

d 9

66

, 95

5 N

.Y.S.2d

13

1 (A

pp

. D

iv. 2d

Dep

’t 20

12

).

•In

FHA

mo

rtgages, the n

otice is o

nly ad

dressed

in th

e regulatio

ns.

(We’ll talk ab

ou

t this later in

the p

resentatio

n.)

22

22

Defen

ses: Co

ntractu

al No

tice of D

efault

•Lo

ok fo

r similar p

rob

lems to

tho

se that arise in

the 1

30

4 N

otice –

inco

nsisten

cy with

the 1

30

4 N

otice, in

con

sistency w

ith th

e Plain

tiff’s affid

avits/com

plain

t, etc.

•N

ote th

at wh

ile RPA

PL §

13

04

do

es no

t requ

ire that th

e defau

lt be re

-n

otice in

the even

t of a rein

statemen

t and

re-defau

lt with

in o

ne year,

the m

ortgage h

as no

such

pro

vision

.

•A

lso b

e sure th

at it was sen

t to th

e pro

per p

erson

. (Paragraph

15

of

GSE Fo

rm M

ortgage)

23

23

Defen

ses: FHA

& R

ESPA

•B

oth

HU

D (fo

r FHA

mo

rtgages) and

RESPA

(for all fed

erally related

mo

rtgages) pro

vide regu

lation

s limitin

g the ab

ility of servicers to

fo

reclose.

•H

UD

’s mo

rtgage servicing regu

lation

s –2

4 C

FR §

20

3.5

00

-61

6 –

lack an

y direct, p

rivate right o

f enfo

rcemen

t. Regu

lation

X –

12

CFR

§1

02

4 –

wh

ich im

plem

ents R

ESPA, o

nly p

rovid

es mo

netary d

amages.

•H

ow

ever, bo

th are (w

ith so

me excep

tion

s) inco

rpo

rated d

irectly into

th

e langu

age of th

e mo

rtgage con

tract, so yo

u sh

ou

ld rely o

n th

e co

ntractu

al ho

ok in

the m

ortgage rath

er than

the regu

lation

directly.

24

24

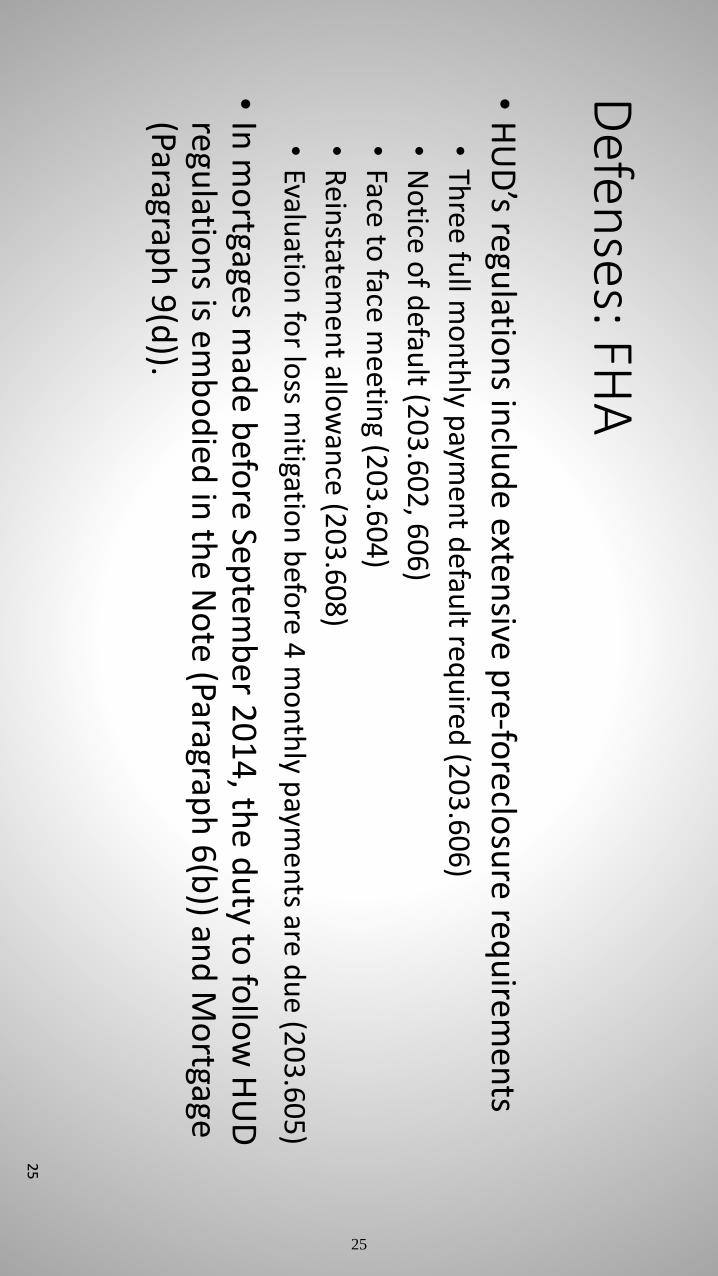

Defen

ses: FHA

•H

UD

’s regulatio

ns in

clud

e extensive p

re-foreclo

sure req

uirem

ents

•Th

ree fu

ll mo

nth

ly paym

en

t defau

lt requ

ired (2

03

.60

6)

•N

otice

of d

efault (2

03

.60

2, 6

06

)

•Face

to face

meetin

g (20

3.6

04

)

•R

einstatem

en

t allow

ance (2

03

.60

8)

•Evalu

ation

for lo

ss mitigatio

n b

efore 4

mo

nth

ly paym

en

ts are du

e (20

3.6

05

)

•In

mo

rtgages mad

e befo

re Septem

ber 2

01

4, th

e du

ty to fo

llow

HU

D

regulatio

ns is em

bo

died

in th

e No

te (Paragraph

6(b

)) and

Mo

rtgage (Paragrap

h 9

(d)).

25

25

Defen

ses: FHA

•N

Y Co

urts h

ave generally fo

un

d th

at the regu

lation

s can b

e used

to p

rovid

e a d

efense to

a foreclo

sure actio

n. See, e.g

., Green

Pla

net Servicin

g, LLC

v. M

artin

, 14

1 A

.D.3

d 8

92

, 89

3, 3

4 N

.Y.S.3d

91

1 (A

pp

. Div. 3

d D

ep’t 2

01

6);

HSB

C B

an

k USA

, N.A

. v. Teed, 4

8 M

isc. 3d

19

4, 1

97

, 4 N

.Y.S.3d

82

6, 8

28

(Steu

ben

Cty. C

t. 20

14

); Fed. N

at. M

ortg

. Ass'n

v. Ricks, 8

3 M

isc. 2d

81

4,

82

5, 3

72

N.Y.S.2

d 4

85

, 49

7 (K

ings C

ty. Sup

. Ct. 1

97

5).

•B

ut th

e langu

age inco

rpo

rating th

e regulatio

ns b

y reference w

as remo

ved

with

ou

t no

tice in Se

ptem

ber 2

01

4. In

Janu

ary, HU

D m

ade a p

relimin

ary d

ecision

to ad

d th

e langu

age back an

d accep

ted p

ub

lic com

men

ts on

it. W

e’ll see wh

at hap

pen

s!

26

26

Defen

ses: RESPA

•Likew

ise, RESPA

/Regu

lation

X is in

corp

orated

by referen

ce into

the G

SE Fo

rm M

ortgage.

•Paragrap

h 1

6 states “A

ll rights an

d o

bligatio

ns co

ntain

ed in

this Secu

rity In

strum

ent are su

bject to

any req

uirem

ents an

d lim

itation

s of A

pp

licable

Law.”

•A

pp

licable

Law is d

efined

in Paragrap

h I as “A

ll con

trollin

g app

licable

federal, state an

d lo

cal statutes, regu

lation

s, ord

inan

ces and

adm

inistrative

rules an

d o

rders (th

at have th

e effect of law

) as well as all ap

plicab

le final,

no

n-ap

pealab

le, jud

icial op

inio

ns”.

•So

, wh

ere Regu

lation

X lim

its the ab

ility of a servicer to

initiate fo

reclosu

re (1

2 C

.F.R. §

10

24

.41

), that lim

itation

sup

ersedes th

e right o

f the

mo

rtagageeto

brin

g suit u

po

n d

efault (Paragrap

h 2

2 o

f the m

ortgage).

27

27

Defen

ses: RESPA

•P

rior to

Janu

ary 10

, 20

14

, RESPA

did

no

t have an

y pro

vision

s that

limited

the righ

t of a servicer to

brin

g a foreclo

sure.

•A

s a result, th

e case law

on

usin

g RESPA

via the m

ortgage co

ntract is

basically n

on

existent, an

d th

ere is a lot o

f case law statin

g that R

ESPA

do

es no

t preven

t a foreclo

sure (b

ecause at th

e time, R

ESPA’s servicin

g ru

les were ab

ou

t QW

Rs –

with

no

limit o

n fo

reclosu

re wh

ile the Q

WR

w

as pen

din

g –an

d m

ainten

ance o

f escrow

accou

nts).

•Fo

cus o

n R

egulatio

n X

, wh

ich is n

ew, an

d th

e mo

rtgage con

tract to

differen

tiate you

rself from

old

case law

.

28

28

Co

nclu

sion

•Th

ank yo

u everyb

od

y.

•Th

ere are samp

le pap

ers in th

e materials.

•If yo

u h

ave any q

uestio

ns later, yo

u can

con

tact us at

jrebella@

mfy.o

rgan

d ciso

be@

lsnyc.o

rg.

29

29

§ 1303. Foreclosures; required notices, NY RP ACT & PRO § 1303

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 1

McKinney's Consolidated Laws of New York AnnotatedReal Property Actions and Proceedings Law (Refs & Annos)

Chapter 81. Of the Consolidated Laws (Refs & Annos)Article 13. Action to Foreclose a Mortgage (Refs & Annos)

McKinney's RPAPL § 1303

§ 1303. Foreclosures; required notices

Effective: December 20, 2016Currentness

1. The foreclosing party in a mortgage foreclosure action, involving residential real property shall provide notice to:

(a) any mortgagor if the action relates to an owner-occupied one-to-four family dwelling; and

(b) any tenant of a dwelling unit in accordance with the provisions of this section.

2. The notice to any mortgagor required by paragraph (a) of subdivision one of this section shall be delivered with thesummons and complaint. Such notice shall be in bold, fourteen-point type and shall be printed on colored paper thatis other than the color of the summons and complaint, and the title of the notice shall be in bold, twenty-point type.The notice shall be on its own page.

3. The notice to any mortgagor required by paragraph (a) of subdivision one of this section shall appear as follows:

Help for Homeowners in Foreclosure

New York State Law requires that we send you this notice about the foreclosure process. Please read it carefully.

Summons and Complaint

You are in danger of losing your home. If you fail to respond to the summons and complaint in this foreclosure action,you may lose your home. Please read the summons and complaint carefully. You should immediately contact an attorneyor your local legal aid office to obtain advice on how to protect yourself.

Sources of Information and Assistance

The State encourages you to become informed about your options in foreclosure. In addition to seeking assistance froman attorney or legal aid office, there are government agencies and non-profit organizations that you may contact forinformation about possible options, including trying to work with your lender during this process.

To locate an entity near you, you may call the toll-free helpline maintained by the New York State Department ofFinancial Services at (enter number) or visit the Department's website at (enter web address).

Rights and Obligations

30

§ 1303. Foreclosures; required notices, NY RP ACT & PRO § 1303

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 2

YOU ARE NOT REQUIRED TO LEAVE YOUR HOME AT THIS TIME. You have the right to stay in your homeduring the foreclosure process. You are not required to leave your home unless and until your property is sold at auctionpursuant to a judgment of foreclosure and sale.

Regardless of whether you choose to remain in your home, YOU ARE REQUIRED TO TAKE CARE OF YOURPROPERTY and pay property taxes in accordance with state and local law.

Foreclosure rescue scams

Be careful of people who approach you with offers to “save” your home. There are individuals who watch for notices offoreclosure actions in order to unfairly profit from a homeowner's distress. You should be extremely careful about anysuch promises and any suggestions that you pay them a fee or sign over your deed. State law requires anyone offeringsuch services for profit to enter into a contract which fully describes the services they will perform and fees they willcharge, and which prohibits them from taking any money from you until they have completed all such promised services.

3-a. No later than sixty days after the effective date of this subdivision, the department of financial services shall publisha Consumer Bill Of Rights, in consultation with all stakeholders, which shall detail the rights and responsibilities ofthe plaintiff and defendant in a foreclosure proceeding. Such Bill of Rights shall be updated on an annual basis and asappropriate.

4. The notice to any tenant required by paragraph (b) of subdivision one of this section shall be delivered within tendays of the service of the summons and complaint. Such notice shall be in bold, fourteen-point type, and the paragraphof the notice beginning with the words “ALL RENT-STABILIZED” and ending with the words “FULL HEARINGIN COURT” shall be printed entirely in capital letters and underlined. The foreclosing party shall provide its name,address and telephone number on the notice. The notice shall be printed on colored paper that is other than the colorof the summons and complaint, and the title of the notice shall be in bold, twenty-point type. The notice shall be onits own page. For buildings with fewer than five dwelling units, the notice shall be delivered to the tenant, by certifiedmail, return receipt requested, and by first-class mail to the tenant's address at the property if the identity of the tenantis known to the plaintiff, and by first-class mail delivered to “occupant” if the identity of the tenant is not known to theplaintiff. For buildings with five or more dwelling units, a legible copy of the notice shall be posted on the outside ofeach entrance and exit of the building.

5. The notice required by paragraph (b) of subdivision one of this section shall appear as follows:

Notice to Tenants of Buildings in Foreclosure

New York State Law requires that we provide you this notice about the foreclosure process. Please read it carefully.

We, (name of foreclosing party), are the foreclosing party and are located at (foreclosing party's address). We can bereached at (foreclosing party's telephone number).

The dwelling where your apartment is located is the subject of a foreclosure proceeding. If you have a lease, are not theowner of the residence, and the lease requires payment of rent that at the time it was entered into was not substantiallyless than the fair market rent for the property, you may be entitled to remain in occupancy for the remainder of your leaseterm. If you do not have a lease, you will be entitled to remain in your home until ninety days after any person or entitywho acquires title to the property provides you with a notice as required by section 1305 of the Real Property Actions and

31

§ 1303. Foreclosures; required notices, NY RP ACT & PRO § 1303

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 3

Proceedings Law. The notice shall provide information regarding the name and address of the new owner and your rightsto remain in your home. These rights are in addition to any others you may have if you are a subsidized tenant underfederal, state or local law or if you are a tenant subject to rent control, rent stabilization or a federal statutory scheme.

ALL RENT-STABILIZED TENANTS AND RENT-CONTROLLED TENANTS ARE PROTECTED UNDERTHE RENT REGULATIONS WITH RESPECT TO EVICTION AND LEASE RENEWALS. THESE RIGHTSARE UNAFFECTED BY A BUILDING ENTERING FORECLOSURE STATUS. THE TENANTS IN RENT-STABILIZED AND RENT-CONTROLLED BUILDINGS CONTINUE TO BE AFFORDED THE SAME LEVELOF PROTECTION EVEN THOUGH THE BUILDING IS THE SUBJECT OF FORECLOSURE. EVICTIONSCAN ONLY OCCUR IN NEW YORK STATE PURSUANT TO A COURT ORDER AND AFTER A FULLHEARING IN COURT.

If you need further information, please call the New York State Department of Financial Services' toll-free helpline at(enter number) or visit the Department's website at (enter web address).

6. The department of financial services shall prescribe the telephone number and web address to be included in eithernotice.

7. The department of financial services shall post on its website or otherwise make readily available the name and contactinformation of government agencies or non-profit organizations that may be contacted by mortgagors for informationabout the foreclosure process, including maintaining a toll-free helpline to disseminate the information required by thissection.

Credits(Added L.2006, c. 308, § 4, eff. Feb. 1, 2007. Amended L.2007, c. 154, § 13, eff. July 3, 2007; L.2008, c. 472, § 1, eff. Aug.5, 2008; L.2009, c. 507, § 1, eff. Jan. 14, 2010; L.2010, c. 358, § 1, eff. Sept. 12, 2010; L.2011, c. 62, pt. A, § 104, eff. Oct.3, 2011; L.2012, c. 155, § 83, eff. July 18, 2012; L.2016, c. 73, pt. Q, § 5, eff. Dec. 20, 2016.)

McKinney's R. P. A. P. L. § 1303, NY RP ACT & PRO § 1303Current through L.2017, chapters 1 to 6.

End of Document © 2017 Thomson Reuters. No claim to original U.S. Government Works.

32

§ 1304. Required prior notices, NY RP ACT & PRO § 1304

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 1

McKinney's Consolidated Laws of New York AnnotatedReal Property Actions and Proceedings Law (Refs & Annos)

Chapter 81. Of the Consolidated Laws (Refs & Annos)Article 13. Action to Foreclose a Mortgage (Refs & Annos)

McKinney's RPAPL § 1304

§ 1304. Required prior notices

Effective: December 20, 2016Currentness

1. [Eff. until Jan. 14, 2020, pursuant to L.2009, c. 507, § 25, subd. a; L.2016, c.73, pt. Q, § 11. See, also, subd. 1 below.]Notwithstanding any other provision of law, with regard to a home loan, at least ninety days before a lender, an assigneeor a mortgage loan servicer commences legal action against the borrower, or borrowers at the property address and anyother address of record, including mortgage foreclosure, such lender, assignee or mortgage loan servicer shall give noticeto the borrower in at least fourteen-point type which shall include the following:

“YOU MAY BE AT RISK OF

FORECLOSURE. PLEASE READ THE FOLLOWING NOTICE CAREFULLY”

“As of ___, your home loan is ___ days and ___ dollars in default. Under New York State Law, we are required to sendyou this notice to inform you that you are at risk of losing your home.

Attached to this notice is a list of government approved housing counseling agencies in your area which provide freecounseling. You can also call the NYS Office of the Attorney General's Homeowner Protection Program (HOPP)toll-free consumer hotline to be connected to free housing counseling services in your area at 1-855-HOME-456(1-855-466-3456), or visit their website at http://www.aghomehelp.com/. A statewide listing by county is also available athttp://www.dfs.ny.gov/consumer/mortg nys np counseling agencies.htm. Qualified free help is available; watch out forcompanies or people who charge a fee for these services.

Housing counselors from New York-based agencies listed on the website above are trained to help homeowners who arehaving problems making their mortgage payments and can help you find the best option for your situation. If you wish,you may also contact us directly at _________ and ask to discuss possible options.

While we cannot assure that a mutually agreeable resolution is possible, we encourage you to take immediate steps totry to achieve a resolution. The longer you wait, the fewer options you may have.

If you have not taken any actions to resolve this matter within 90 days from the date this notice was mailed, we maycommence legal action against you (or sooner if you cease to live in the dwelling as your primary residence.)

If you need further information, please call the New York State Department of Financial Services' toll-free helpline at(show number) or visit the Department's website at (show web address).

IMPORTANT: You have the right to remain in your home until you receive a court order telling you to leave theproperty. If a foreclosure action is filed against you in court, you still have the right to remain in the home until a courtorders you to leave. You legally remain the owner of and are responsible for the property until the property is sold by

33

§ 1304. Required prior notices, NY RP ACT & PRO § 1304

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 2

you or by order of the court at the conclusion of any foreclosure proceedings. This notice is not an eviction notice, and

a foreclosure action has not yet been commenced against you. 1

1. [Eff. Jan. 14, 2020, pursuant to L.2009, c. 507, § 25, subd. a; L.2016, c.73, pt. Q, § 11. See, also, subd. 1 above.]Notwithstanding any other provision of law, with regard to a high-cost home loan, as such term is defined in sectionsix-l of the banking law, a subprime home loan or a non-traditional home loan, at least ninety days before a lender ora mortgage loan servicer commences legal action against the borrower, including mortgage foreclosure, the lender ormortgage loan servicer shall give notice to the borrower(s) at the property address and any other address of record inat least fourteen-point type which shall include the following:

“YOU MAY BE AT RISK OF

FORECLOSURE. PLEASE READTHE FOLLOWING NOTICE CAREFULLY”

“As of ___, your home loan is ___ days and _______ dollars in default. Under New York State Law, we are requiredto send you this notice to inform you that you are at risk of losing your home. There may be options available to youto keep your home. This may include applying for a loan modification of your mortgage, or reinstating your loan bymaking the payment.

Attached to this notice is a list of government approved housing counseling agencies in your area which provide free orvery low-cost counseling. You can also call the NYS Office of the Attorney General's Homeowner Protection Program(HOPP) toll-free consumer hotline to be connected to free housing counseling services in your area at 1-855-HOME-456(1-855-466-3456), or visit their website at http://www.aghomehelp.com/. A statewide listing by county is also available athttp://www.dfs.ny.gov/consumer/mortg nys np counseling agencies.htm. Qualified free help is available; watch out forcompanies or people who charge a fee for these services.

Housing counselors from New York-based agencies listed on the website above are trained to help homeowners who arehaving problems making their mortgage payments and can help you find the best option for your situation. If you wish,you may also contact us directly at __________ and ask to discuss possible options.

While we cannot assure that a mutually agreeable resolution is possible, we encourage you to take immediate steps totry to achieve a resolution. The longer you wait, the fewer options you may have.

If you have not taken any actions to resolve this matter within 90 days from the date this notice was mailed, we maycommence legal action against you (or sooner if you cease to live in the dwelling as your primary residence.)

If you need further information, please call the New York State Department of Financial Services' toll-free helpline at

(show number) or visit the Department's website at (show web address)”. 2

IMPORTANT: You have the right to remain in your home until you receive a court order telling you to leave theproperty. If a foreclosure action is filed against you in court, you still have the right to remain in the home until a courtorders you to leave. You legally remain the owner of and are responsible for the property until the property is sold byyou or by order of the court at the conclusion of any foreclosure proceedings. This notice is not an eviction notice, and

a foreclosure action has not yet been commenced against you. 3

34

§ 1304. Required prior notices, NY RP ACT & PRO § 1304

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 3

2. [Eff. until Jan. 14, 2020, pursuant to L.2009, c. 507, § 25, subd. a; L.2016, c.73, pt. Q, § 11. See, also, subd. 2 below.] Suchnotice shall be sent by such lender, assignee (including purchasing investor) or mortgage loan servicer to the borrower,by registered or certified mail and also by first-class mail to the last known address of the borrower, and to the residencethat is the subject of the mortgage. Such notice shall be sent by the lender, assignee or mortgage loan servicer in a separateenvelope from any other mailing or notice. Notice is considered given as of the date it is mailed. The notice shall containa current list of at least five housing counseling agencies serving the county where the property is located from the mostrecent listing available from department of financial services. The list shall include the counseling agencies' last knownaddresses and telephone numbers. The department of financial services shall make available on its websites a listing, bycounty, of such agencies. The lender, assignee or mortgage loan servicer shall use such lists to meet the requirementsof this section.

2. [Eff. Jan. 14, 2020, pursuant to L.2009, c. 507, § 25, subd. a; L.2016, c.73, pt. Q, § 11. See, also, subd. 2 above.] Suchnotice shall be sent by the lender or mortgage loan servicer to the borrower, by registered or certified mail and also byfirst-class mail to the last known address of the borrower, and to the residence which is the subject of the mortgage.Notice is considered given as of the date it is mailed. The notice shall contain a current list of United States departmentof housing and urban development approved housing counseling agencies, or other housing counseling agencies servingthe county where the property is located from the most recent listing available from the department of financial services.The list shall include the counseling agencies' last known addresses and telephone numbers. The department of financialservices shall make available a listing, by county, of such agencies which the lender or mortgage loan servicer may useto meet the requirements of this section.

3. The ninety day period specified in the notice contained in subdivision one of this section shall not apply, or shall ceaseto apply, if the borrower has filed for bankruptcy protection under federal law, or if the borrower no longer occupiesthe residence as the borrower's principal dwelling. Nothing herein shall relieve the lender, assignee or mortgage loanservicer of the obligation to send such notice, which notice shall be a condition precedent to commencing a foreclosureproceeding.

4. The notice and the ninety day period required by subdivision one of this section need only be provided once in a twelvemonth period to the same borrower in connection with the same loan and same delinquency. Should a borrower cure adelinquency but re-default in the same twelve month period, the lender shall provide a new notice pursuant to this section.

5. For any borrower known to have limited English proficiency, the notice required by subdivision one of this sectionshall be in the borrower's native language (or a language in which the borrower is proficient), provided that the languageis one of the six most common non-English languages spoken by individuals with limited English proficiency in the stateof New York, based on United States census data. The department of financial services shall post the notice required bysubdivision one of this section on its website in the six most common non-English languages spoken by individuals withlimited English proficiency in the state of New York, based on the United States census data.

6. [Eff. until Jan. 14, 2020, pursuant to L.2009, c. 507, § 25, subd. a; L.2016, c.73, pt. Q, § 11. See, also, subd. 6 below.](a) “Home loan” means a loan, including an open-end credit plan, other than a reverse mortgage transaction, in which:

(i) The borrower is a natural person;

35

§ 1304. Required prior notices, NY RP ACT & PRO § 1304

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 4

(ii) The debt is incurred by the borrower primarily for personal, family, or household purposes;

(iii) The loan is secured by a mortgage or deed of trust on real estate improved by a one to four family dwelling, or acondominium unit, in either case, used or occupied, or intended to be used or occupied wholly or partly, as the home orresidence of one or more persons and which is or will be occupied by the borrower as the borrower's principal dwelling;and

(iv) The property is located in this state.

(b) “Lender” means a mortgage banker as defined in paragraph (f) of subdivision one of section five hundred ninetyof the banking law or an exempt organization as defined in paragraph (e) of subdivision one of section five hundredninety of the banking law.

6. [Eff. Jan. 14, 2020, pursuant to L.2009, c. 507, § 25, subd. a. See, also, subd. 6 above.] (a) “Annual percentage rate”means the annual percentage rate for the loan calculated according to the provisions of the Federal Truth-in-LendingAct (15 U.S.C. § 1601, et seq.), and the regulations promulgated thereunder by the federal reserve board (as said act andregulations are amended from time to time).

(b) “Home loan” means a home loan, including an open-end credit plan, other than a reverse mortgage transaction,in which:

(i) The principal amount of the loan at origination did not exceed the conforming loan size that was in existence at thetime of origination for a comparable dwelling as established by the federal national mortgage association;

(ii) The borrower is a natural person;

(iii) The debt is incurred by the borrower primarily for personal, family, or household purposes;

(iv) The loan is secured by a mortgage or deed of trust on real estate upon which there is located or there is to be locateda structure or structures intended principally for occupancy of from one to four families which is or will be occupied bythe borrower as the borrower's principal dwelling; and

(v) The property is located in this state.

(c) “Subprime home loan” for the purposes of this section, means a home loan consummated between January first, twothousand three and September first, two thousand eight in which the terms of the loan exceed the threshold as definedin paragraph (d) of this subdivision. A subprime home loan excludes a transaction to finance the initial construction ofa dwelling, a temporary or “bridge” loan with a term of twelve months or less, such as a loan to purchase a new dwellingwhere the borrower plans to sell a current dwelling within twelve months, or a home equity line of credit.

36

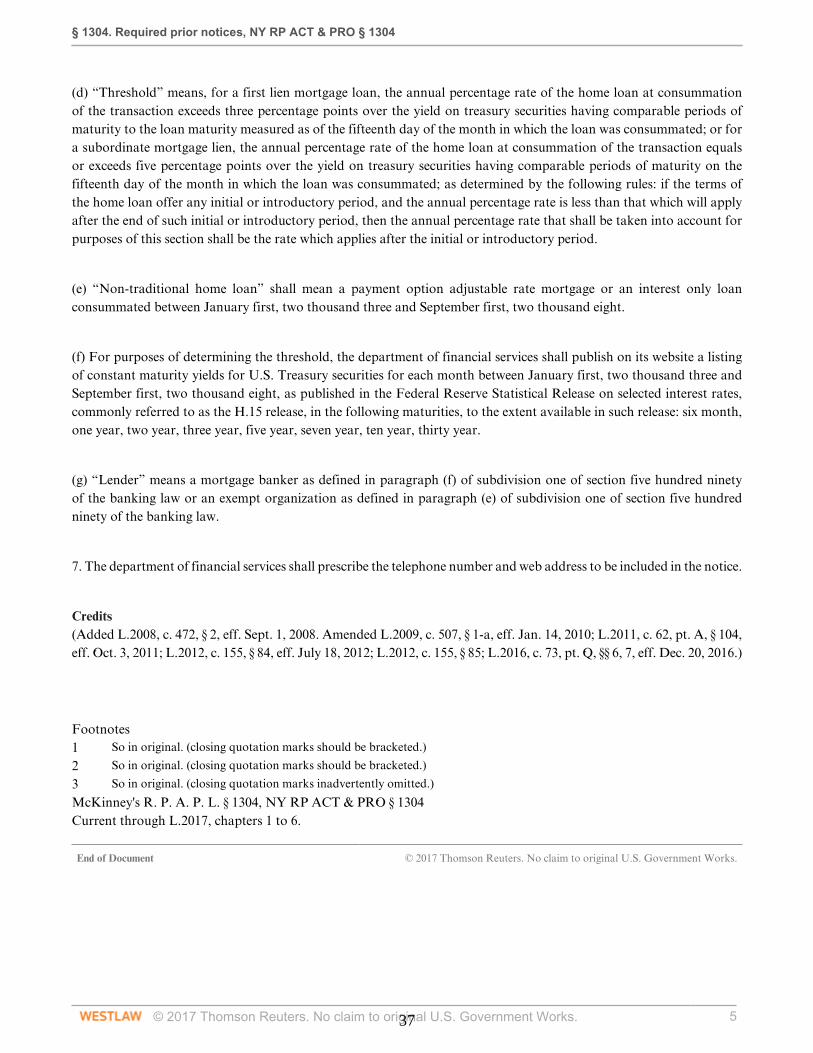

§ 1304. Required prior notices, NY RP ACT & PRO § 1304

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 5

(d) “Threshold” means, for a first lien mortgage loan, the annual percentage rate of the home loan at consummationof the transaction exceeds three percentage points over the yield on treasury securities having comparable periods ofmaturity to the loan maturity measured as of the fifteenth day of the month in which the loan was consummated; or fora subordinate mortgage lien, the annual percentage rate of the home loan at consummation of the transaction equalsor exceeds five percentage points over the yield on treasury securities having comparable periods of maturity on thefifteenth day of the month in which the loan was consummated; as determined by the following rules: if the terms ofthe home loan offer any initial or introductory period, and the annual percentage rate is less than that which will applyafter the end of such initial or introductory period, then the annual percentage rate that shall be taken into account forpurposes of this section shall be the rate which applies after the initial or introductory period.

(e) “Non-traditional home loan” shall mean a payment option adjustable rate mortgage or an interest only loanconsummated between January first, two thousand three and September first, two thousand eight.

(f) For purposes of determining the threshold, the department of financial services shall publish on its website a listingof constant maturity yields for U.S. Treasury securities for each month between January first, two thousand three andSeptember first, two thousand eight, as published in the Federal Reserve Statistical Release on selected interest rates,commonly referred to as the H.15 release, in the following maturities, to the extent available in such release: six month,one year, two year, three year, five year, seven year, ten year, thirty year.

(g) “Lender” means a mortgage banker as defined in paragraph (f) of subdivision one of section five hundred ninetyof the banking law or an exempt organization as defined in paragraph (e) of subdivision one of section five hundredninety of the banking law.

7. The department of financial services shall prescribe the telephone number and web address to be included in the notice.

Credits(Added L.2008, c. 472, § 2, eff. Sept. 1, 2008. Amended L.2009, c. 507, § 1-a, eff. Jan. 14, 2010; L.2011, c. 62, pt. A, § 104,eff. Oct. 3, 2011; L.2012, c. 155, § 84, eff. July 18, 2012; L.2012, c. 155, § 85; L.2016, c. 73, pt. Q, §§ 6, 7, eff. Dec. 20, 2016.)

Footnotes1 So in original. (closing quotation marks should be bracketed.)

2 So in original. (closing quotation marks should be bracketed.)

3 So in original. (closing quotation marks inadvertently omitted.)

McKinney's R. P. A. P. L. § 1304, NY RP ACT & PRO § 1304Current through L.2017, chapters 1 to 6.

End of Document © 2017 Thomson Reuters. No claim to original U.S. Government Works.

37

§ 1306. Filing with superintendent, NY RP ACT & PRO § 1306

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 1

McKinney's Consolidated Laws of New York AnnotatedReal Property Actions and Proceedings Law (Refs & Annos)

Chapter 81. Of the Consolidated Laws (Refs & Annos)Article 13. Action to Foreclose a Mortgage (Refs & Annos)

McKinney's RPAPL § 1306

§ 1306. Filing with superintendent

Effective: October 3, 2011Currentness

1. Each lender, assignee or mortgage loan servicer shall file with the superintendent of financial services (superintendent)within three business days of the mailing of the notice required by subdivision one of section thirteen hundred four ofthis article or subsection (f) of section 9-611 of the uniform commercial code the information required by subdivisiontwo of this section. Notwithstanding any other provision of the laws of this state, this filing shall be made electronicallyas provided for in subdivision three of this section. Any complaint served in a proceeding initiated pursuant to this articleshall contain, as a condition precedent to such proceeding, an affirmative allegation that at the time the proceeding iscommenced, the plaintiff has complied with the provisions of this section.

2. Each filing delivered to the superintendent shall be on such form as the superintendent shall prescribe, and shall includeat a minimum, the name, address, last known telephone number of the borrower, and the amount claimed as due andowing on the mortgage, and such other information as will enable the superintendent to ascertain the type of loan atissue. The superintendent may subsequently request such readily available information as may be reasonably necessaryto facilitate a review of whether the borrower might benefit from counseling or other foreclosure prevention services.

3. Within one hundred eighty days of the effective date of this section, or such later time as the superintendent maydetermine, the superintendent shall develop with the assistance of the commissioner of the division of housing andcommunity renewal, an electronic database that shall be capable of receiving all filings required by this section.

4. The information provided to the superintendent pursuant to this section shall not be subject to article six of thepublic officers law or paragraphs (a), (c) and (d) of subdivision one or subdivision six of section ninety-four of thepublic officers law. All such information shall be used by the superintendent exclusively for the purposes of monitoringon a statewide basis the extent of foreclosure filings within this state, to perform an analysis of loan types which werethe subject of a pre-foreclosure notice and directing as appropriate available public and private foreclosure preventionand counseling services to borrowers at risk of foreclosure. The superintendent may share information contained in thedatabase with housing counseling agencies designated by the division of housing and community renewal as well as withother state agencies with jurisdiction over housing, for the purpose of coordinating or securing help for borrowers atrisk of foreclosure.

5. The superintendent is hereby authorized to promulgate such rules and regulations as shall be necessary to implementthe purposes of this section.

38

§ 1306. Filing with superintendent, NY RP ACT & PRO § 1306

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 2

Credits(Added L.2009, c. 507, § 5, eff. Feb. 13, 2010. Amended L.2011, c. 62, pt. A, § 104, eff. Oct. 3, 2011; L.2011, c. 182, §9, eff. July 20, 2011.)

McKinney's R. P. A. P. L. § 1306, NY RP ACT & PRO § 1306Current through L.2017, chapters 1 to 6.

End of Document © 2017 Thomson Reuters. No claim to original U.S. Government Works.

39

Rule 4518. Business records, NY CPLR Rule 4518

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 1

McKinney's Consolidated Laws of New York AnnotatedCivil Practice Law and Rules (Refs & Annos)

Chapter Eight. Of the Consolidated LawsArticle 45. Evidence (Refs & Annos)

McKinney's CPLR Rule 4518

Rule 4518. Business records

Effective: August 15, 2007Currentness

(a) Generally. Any writing or record, whether in the form of an entry in a book or otherwise, made as a memorandumor record of any act, transaction, occurrence or event, shall be admissible in evidence in proof of that act, transaction,occurrence or event, if the judge finds that it was made in the regular course of any business and that it was the regularcourse of such business to make it, at the time of the act, transaction, occurrence or event, or within a reasonable timethereafter. An electronic record, as defined in section three hundred two of the state technology law, used or stored assuch a memorandum or record, shall be admissible in a tangible exhibit that is a true and accurate representation of suchelectronic record. The court may consider the method or manner by which the electronic record was stored, maintainedor retrieved in determining whether the exhibit is a true and accurate representation of such electronic record. All othercircumstances of the making of the memorandum or record, including lack of personal knowledge by the maker, may beproved to affect its weight, but they shall not affect its admissibility. The term business includes a business, profession,occupation and calling of every kind.

(b) Hospital bills. A hospital bill is admissible in evidence under this rule and is prima facie evidence of the facts contained,provided it bears a certification by the head of the hospital or by a responsible employee in the controller's or accountingoffice that the bill is correct, that each of the items was necessarily supplied and that the amount charged is reasonable.This subdivision shall not apply to any proceeding in a surrogate's court nor in any action instituted by or on behalf ofa hospital to recover payment for accommodations or supplies furnished or for services rendered by or in such hospital,except that in a proceeding pursuant to section one hundred eighty-nine of the lien law to determine the validity andextent of the lien of a hospital, such certified hospital bills are prima facie evidence of the fact of services and of thereasonableness of any charges which do not exceed the comparable charges made by the hospital in the care of workmen'scompensation patients.

(c) Other records. All records, writings and other things referred to in sections 2306 and 2307 are admissible in evidenceunder this rule and are prima facie evidence of the facts contained, provided they bear a certification or authentication bythe head of the hospital, laboratory, department or bureau of a municipal corporation or of the state, or by an employeedelegated for that purpose or by a qualified physician. Where a hospital record is in the custody of a warehouse, or“warehouseman” as that term is defined by paragraph (h) of subdivision one of section 7-102 of the uniform commercialcode, pursuant to a plan approved in writing by the state commissioner of health, admissibility under this subdivisionmay be established by a certification made by the manager of the warehouse that sets forth (i) the authority by whichthe record is held, including but not limited to a court order, order of the commissioner, or order or resolution of thegoverning body or official of the hospital, and (ii) that the record has been in the exclusive custody of such warehouseor warehousemen since its receipt from the hospital or, if another has had access to it, the name and address of suchperson and the date on which and the circumstances under which such access was had. Any warehouseman providinga certification as required by this subdivision shall have no liability for acts or omissions relating thereto, except for

40

Rule 4518. Business records, NY CPLR Rule 4518

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 2

intentional misconduct, and the warehouseman is authorized to assess and collect a reasonable charge for providing thecertification described by this subdivision.

(d) Any records or reports relating to the administration and analysis of a genetic marker or DNA test, including recordsor reports of the costs of such tests, administered pursuant to sections four hundred eighteen and five hundred thirty-two of the family court act or section one hundred eleven-k of the social services law are admissible in evidence underthis rule and are prima facie evidence of the facts contained therein provided they bear a certification or authenticationby the head of the hospital, laboratory, department or bureau of a municipal corporation or the state or by an employeedelegated for that purpose, or by a qualified physician. If such record or report relating to the administration and analysisof a genetic marker test or DNA test or tests administered pursuant to sections four hundred eighteen and five hundredthirty-two of the family court act or section one hundred eleven-k of the social services law indicates at least a ninety-five percent probability of paternity, the admission of such record or report shall create a rebuttable presumption ofpaternity, and shall, if unrebutted, establish the paternity of and liability for the support of a child pursuant to articlesfour and five of the family court act.

(e) Notwithstanding any other provision of law, a record or report relating to the administration and analysis of a geneticmarker test or DNA test certified in accordance with subdivision (d) of this rule and administered pursuant to sectionsfour hundred eighteen and five hundred thirty-two of the family court act or section one hundred eleven-k of the socialservices law is admissible in evidence under this rule without the need for foundation testimony or further proof ofauthenticity or accuracy unless objections to the record or report are made in writing no later than twenty days beforea hearing at which the record or report may be introduced into evidence or thirty days after receipt of the test results,whichever is earlier.

(f) Notwithstanding any other provision of law, records or reports of support payments and disbursements maintainedpursuant to title six-A of article three of the social services law by the office of temporary and disability assistance orthe fiscal agent under contract to the office for the provision of centralized collection and disbursement functions areadmissible in evidence under this rule, provided that they bear a certification by an official of a social services districtattesting to the accuracy of the content of the record or report of support payments and that in attesting to the accuracyof the record or report such official has received confirmation from the office of temporary and disability assistanceor the fiscal agent under contract to the office for the provision of centralized collection and disbursement functionspursuant to section one hundred eleven-h of the social services law that the record or report of support payments reflectsthe processing of all support payments in the possession of the office or the fiscal agent as of a specified date, and thatthe document is a record or report of support payments maintained pursuant to title six-A of article three of the socialservices law. If so certified, such record or report shall be admitted into evidence under this rule without the need foradditional foundation testimony. Such records shall be the basis for a permissive inference of the facts contained thereinunless the trier of fact finds good cause not to draw such inference.

(g) Pregnancy and childbirth costs. Any hospital bills or records relating to the costs of pregnancy or birth of a childfor whom proceedings to establish paternity, pursuant to sections four hundred eighteen and five hundred thirty-two ofthe family court act or section one hundred eleven-k of the social services law have been or are being undertaken, areadmissible in evidence under this rule and are prima facie evidence of the facts contained therein, provided they bear acertification or authentication by the head of the hospital, laboratory, department or bureau of a municipal corporationor the state or by an employee designated for that purpose, or by a qualified physician.

41

Rule 4518. Business records, NY CPLR Rule 4518

© 2017 Thomson Reuters. No claim to original U.S. Government Works. 3

Credits(L.1962, c. 308. Amended Jud.Conf.1970 Proposal No. 2; L.1982, c. 695, § 3; L.1983, c. 311, § 1; L.1984, c. 792, § 3;L.1992, c. 381, § 1; L.1994, c. 170, § 350; L.1995, c. 81, § 236; L.1997, c. 398, §§ 87 to 89, eff. Nov. 11, 1997; L.2002, c.136, § 1, eff. July 23, 2002; L.2005, c. 741, § 1, eff. Oct. 18, 2005; L.2007, c. 601, § 10, eff. Aug. 15, 2007.)

McKinney's CPLR Rule 4518, NY CPLR Rule 4518Current through L.2017, chapters 1 to 6.

End of Document © 2017 Thomson Reuters. No claim to original U.S. Government Works.

42

SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF KINGS: FORECLOSURE RESOLUTION PART 1 ----------------------------------------------------------------------------X BANK OF AMERICA, NATIONAL ASSOCIATION,

Plaintiff,

-against-

BRENDA V. THOMPSON; MORTGAGE ELECTRONIC REGISTRATION SYSTEMS, INC.; LENOX HILL MEDICAL ANESTHESIOLOGY; MUNICIPAL CREDIT UNION; CONSOLIDATED DEVELOPMENT OF CANARSIE; NEW YORK STATE DEPARTMENT OF TAXATION AND FINANCE; EMPIRE PORTFOLIOS INC, “JOHN DOE #1” through “JOHN DOE #12,” the last twelve names being fictitious and unknown to the plaintiff, the persons or parties intended being the tenants, occupants, persons or corporations, if any, having or claiming an interest in or lien upon the premises, described in the complaint,

Defendants.

----------------------------------------------------------------------------X

Index No. 505850/2014 Hon. Noach Dear

DEFENDANT’S MEMORANDUM OF LAW IN OPPOSITION TO PLAINTIFF’S MOTION FOR SUMMARY JUDGMENT AND IN SUPPORT OF HER CROSS-

MOTION FOR SUMMARY JUDGMENT DISMISSING THE COMPLAINT

BROOKLYN LEGAL SERVICES

Catherine P. Isobe, Of Counsel 1360 Fulton Street, Suite 301 Brooklyn, New York 11216

(718) 233-6434 (voice) (718) 398-6414 (fax)

Attorneys for Defendant Brenda V. Thompson

43

TABLE OF CONTENTS PRELIMINARY STATEMENT ................................................................................................................... 1 STATEMENT OF FACTS ............................................................................................................................ 1 ARGUMENT ................................................................................................................................................ 5 I. Should the Court Decline to Dismiss this Action, Plaintiff’s Motion for Summary