RESERVE BANK O F INDIA

210

Report on Trend and Progress of Banking in India for the year ended June 30, 1997 submitted to the Central Government in terms of Section 36(2) of the Banking Regulation Act, 1949 RESERVE BANK OF INDIA REPORT ON TREND AND PROGRESS OF BANKING IN INDIA 1-6-97 (JULY-JUNE)

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of RESERVE BANK O F INDIA

Report on Trend and Progress of Banking in India f o r the year ended June 30, 1997 submitted to the Central Government in terms of Section 36(2) of the Banking Regulation Act, 1949

RESERVE BANK O F INDIA

REPORT ON TREND AND PROGRESS OF BANKING IN INDIA

1-6-97 (JULY-JUNE)

Price : In India - Rs. 85 (inclusive of postage) Abroad - US$ 35 (inclusive of Registered Air Mail Book-Post charges)

Published by K U,B. Kno for thr Reserve Bank of M i a M u m h 400 OQ1 and pnntrti by him at

Repro lndid Limited, A2, 207 S I i n t ~ h Nahar Inc3 Lstatc. Dtianrtll Mill Cnrrlp Lcrrvcr P;trcl h2tr:nlixr (lW 01 3

vdi GOVERNOR

RESERVE BANK OF INDIA CENTRAL OFFICE, SHAHEED BHAGAT SINGH ROAD, MUMBAI - 400 001. INDIA.

LETTER OF TRANSMITTAL

November 29, 1997 Agrahayana 8, 1919 (Saka)

The Secretary to the Government of India, Ministry of Finance, Department of Economic Affairs, New Delhi - 110 001.

Dear Finance Secretary,

In pursuance of the provisions of Section 36(2) of the Banking Regulation

Act, 1949, I transmit herewith two copies of the Report on Trend and

Pmgrsss af Banking in India for the year ended June 30, 1997.

Yours faithfully,

CONTENTS

S . Nos . Pnrtlculars Page Nos .

CHAmER I : BANKING DEVELOPMENTS AND POLICY PERSPECT~VES

1 . 1 introduction ............................................................................................................... 1

............................................................................................................... 1.2 Rural Credit 1

1.3 Financial Sector Reform Measures .......................................................................... 2 Interest Rate Deregulation ....................................................................................... - 2

Bank Rate ................................................................................................................... 2

Rates on Domestic Term Deposits ............................................................................. - 2

Rates on Nan-Resident Bank Deposits ...................................................................... 3

Interest Rate on Cash Balances Maintained with the Reserve Bank under CRR ....................................................................................... 3

Lending Rates ............................................................................................................ 3

Interest Rates o n Term Loans of 3 years and Above ................................................. 4

Export Credit ............................................................................................................. 4

Pre-Shipment Rupee Export Credit ............................................................................. 4

Post-Shipment Rupee Export Credit ................. ..... ............... ... . . . . 4 Interest Rate on Bank Finance to Housing Finance

......................................................... Intermediary Agencies 4

.................................... ................................ Changes in Statutory Pre-emptions ... 4

........................................................................................ Cash Reserve Requirements 4

Removal of Reserve Requirements on Inter-Bank Liabilities ....................................... 5

Reserves on Non-Resident Deposits ........................................................................... 5 . - .......................................................................................... Statutory Liquidity Ratio 5

................................................................................... Money Market Developments 6

............................................................................................. Certificate of Deposits 6 ....................................................... Routing of Transactions Through Primary Dealers 6

Investment by Money Market ~ u f u a l Funds .......................................................-...... 6

lmprovlng Credit Delhrery System .. ........................................................................... 6

Loan System for Delively of Bank Credit .................................................................... 6 Bill Finance For Settlement of Dues of 551 Suppliers 6 ...................................................

Debt Market ............................................................................................................. 6

Primary and Satellite Dealers ...................................................................................... 6 . introduction of 28-day Treasury Bills 7 .......................................................................... Introduction of Unihorm Price Auction ....................................................................... 7 Issue Amounts to be Notified in respect of all Auctions ............................................ 7 investments by Flis with 30 per cent Ceiling in Government Dated Securities .................................................................................... 7

Retailing of Government Securities by Banks ............................................................. 7 Bonds and Prlvate Debt Market ................................................................................ 7

Ready Forward Transactions in PSU Bonds and Private Debt Securities .......................................................................................... 7

.................................................................. Prudential Reguktlons and Supervision 7 ............................................................................... Prudential Accounting Standards 7

Write Back of Excess Provision Towards Depreciation on Investments ....................... 8

Banks' Access to Capital Market and Capital Adequacy ............................................. 8

Deposit Insurance ....................................................................................................... 9

........................................ .................................................................. Supervision ... 9

Restructuring of Banks .............................................................................................. 9

Revival Package For Public Sector Banks ................................................................... 9 ..................................................................... Recapitallsation of Public Sector Banks 10

Transactions in Government Dated Securities ......................................................................... by Foreign institutional Investors 1 0

Banks Allowed Freedom to Invest Foreign Currency Funds ...................................... 10

Monetary Policy Initiatives ...................................................................................... 1 1 General Refinance Facility ......................................................................................... 1 1

Bank Rate ............................................................................................................... 1 1

Financial Performance of Scheduled Commercial Banks During 1 996-97 ........... 1 1

Profitability ............................................................................................................... 1 1

Spread ................................................................................................................... I 3

Non-Performing Assets ............................................................................................ 1 3

.......................................................... Capital to Risk Weighted Assets Ratio (CRAR) 15 Payments and Settlement System ........................................................................... 1 5

Overlapping Functions of Banks and Financial institutions .................................. 1 5

Perspectives ............................................................................................................. 1 5

impact of Financial Sector Reforms .......................................................................... 1 5 Interest Rate ............................................................................................................. 1 6

Financial Soundness ......................... .... ..........,., I (j

Need for Enhancing Credit Off-take .......................................................................... I G

..................................................................................... Competition and Autonomy 17

Asset and Liability Management ............................................................................... 17

Payment and Settlement System .............................................................................. 18

TechnoloS~ U gradation ........................................................................................... 18

Rural Credit and Priority Sector Lending .................................................................. 19 Strengthening of the Supervisory System ................................................................ 19

CHAPTER I1 : DEVELOPMENTS IN COMMERCIAL BANKING

(.herview .................................................................................................................. 21

2.2 Ljabjljjl and Asset Structure of Banks .............................................................. 21

Bank Credit .............................................................................................................. -24

Investments .............................................................................................................. 29

Cash Reserves ........................................................................................................... 29

................................ ,........................ Cash Reserves on Inter-Bank Liabilities ........ 29

Export Credit ............................................................................................................ 32

Bank Credit to SicklWeak Industries ...................................................................... 32

Flow of Credit to the Small S d e Industries Sector ......................... .... ............... 32

Recommendations of t h e Abid Hussain Committee Report ...................................... 33

............................................................... 2.3 Working ResuIts of Commercial Banks 33

................................................................................... Scheduled Commercial Banks 33

................................................................................................... Public Sector Banks 34

................................................ Performance of Public Sector Banks in Stock Market 35

.................................................................................... Indian Private Sector Banks 36 ......................................................................................... New Private Sector Banks 3 8

........................................................................................................... Foreign Banks 3 9 ................................................................................... Regional Rural Banks (RRBs) 3 9

Working Results .. 3 9 ............................................................................. ......................... ...................................................................................... Deposit and Credit Growth - 3 9

.............................................................................................. Priority Sector Targets -40 ......................................................................................... Restructuring Programme 41

.................................................................................. Regional Spread of Banking -42

Money M d e t Insfrumen& ................................................ ... . ... .... .... ... .............. ... .. 45

viii

Money Market Mutual Funds (MMMFs) ................................................................... 46 ................................................................................ Government Securities Market 46

Trends in Yields in Primary and Secondary Market in ............................................................................................ Government Securities -47

Withdrawal of Refinance Against Government Securities ........................................ 4 7

.............................................................. Liquidity in Government Securities Market 47

............................................................................ Secondary Market Developments -48

Routing of Transactions Through DFHI .................................................................... 48

........................................................................................ Repos and Reverse Repos -48

.......................................................................... Treasury Bills of Varying Maturities -48

Liquidity Support to Primary Dealers (PDs) ............................................................. 48

............................................................................................... Satellite Dealers (SDs) 49

RBI Guidelines for Foreign Institutional Investors (FIls) Investment in Dated Government Securities .................................................... 49

Valuation of Investment Portfolio of Banks ........................................................... 50

Technical Advisory Committee .............................................................................. 5 0

............................................................................................................. Rural Credit 50

.......................................................... Rural lnfrastmctural Development Fund (RIDF) 52

...................................................... Priority Sector Advances by Public Sector Banks 53

................................. Priority Sector Advances by Indian Private Sector Banks (Old) 5 3

............................... Priority Sector Advances by Indian Private Sector Banks (New) 5 3

Priority Sector Advances by Foreign Banks ............................................................. 5 3

Integrated Rural Development Programme (IRDP) .................................................... 5 3

Recovery under IRDP ............................................................................................ 5 4

Lead Bank Scheme (LBS) ......................................................................................... 5 4

............................ Prime Minister's Rozgar Yojna for Educated Unemployed (PMRY) 54

......................................................... Prudential and Capftal Adequacy Measures 55

..................................................................................... Capital Adequacy Measures 55

Prudential Accounting Standards ............................................................................. 5 5

Prudential Accounting Norms ................................................................................ 5 6

Bookjng of income on Investments in Shares and Bonds ......................................... 56

Classification of Investments under 'Permanent' and 'Current' Category .................. 57

.... ...... Equity Capital and Subordinated Debt raised by Banks ........................... ,,, 57 Moratoflum. Llquldation and Amalgamation ........................................................... 57

Forejgn Banks in India ............................................................................................. gg

2*a0 lssues .......................................... ........... .......................................... 58

Network .................................................................................... 60 Shared Payment Network System (SPNS) ................................................................ 60

2.1 1 Diversification in k M n g ....................................................................................... 60 ................................................................................................. Stock-lnvest Scheme GO

Other Subsidiaries/Activities .....................................................................................GO

Scheme for Money k'larket Mutual Funds ................................................................ GO Credit card ........................................................................................................... 60

............................................................................................................ 2.12 Other I s s u e 60

Banking Ombudsmen ............................................................................................... 60

Housing Finance by Commercial Banks .................................... .... ....................... 61

Frauds and Robberies ................................................................................................ 61

Relaxations to Trade and Industry in the State of Jarnmu and Kashrnir ..................... 61

CHAPTER 111 : DEVELOPMENTS IN CO.OPERBTl VE. BANKING

.................................................................................................................. Overview 62

3.2 Progress of Credit Co-operathes ........................................................................... 6 2

..................................................................... Primary Co-operdve Banks (PCBs) 6 2

......................................................................................................... Policy Changes 6 2

....................................................................................... Interest Rate Deregulation - 6 2 .......................................................................................................... Deposit Rates - 6 3

Lending Rates ........................................................................................................... 6 3

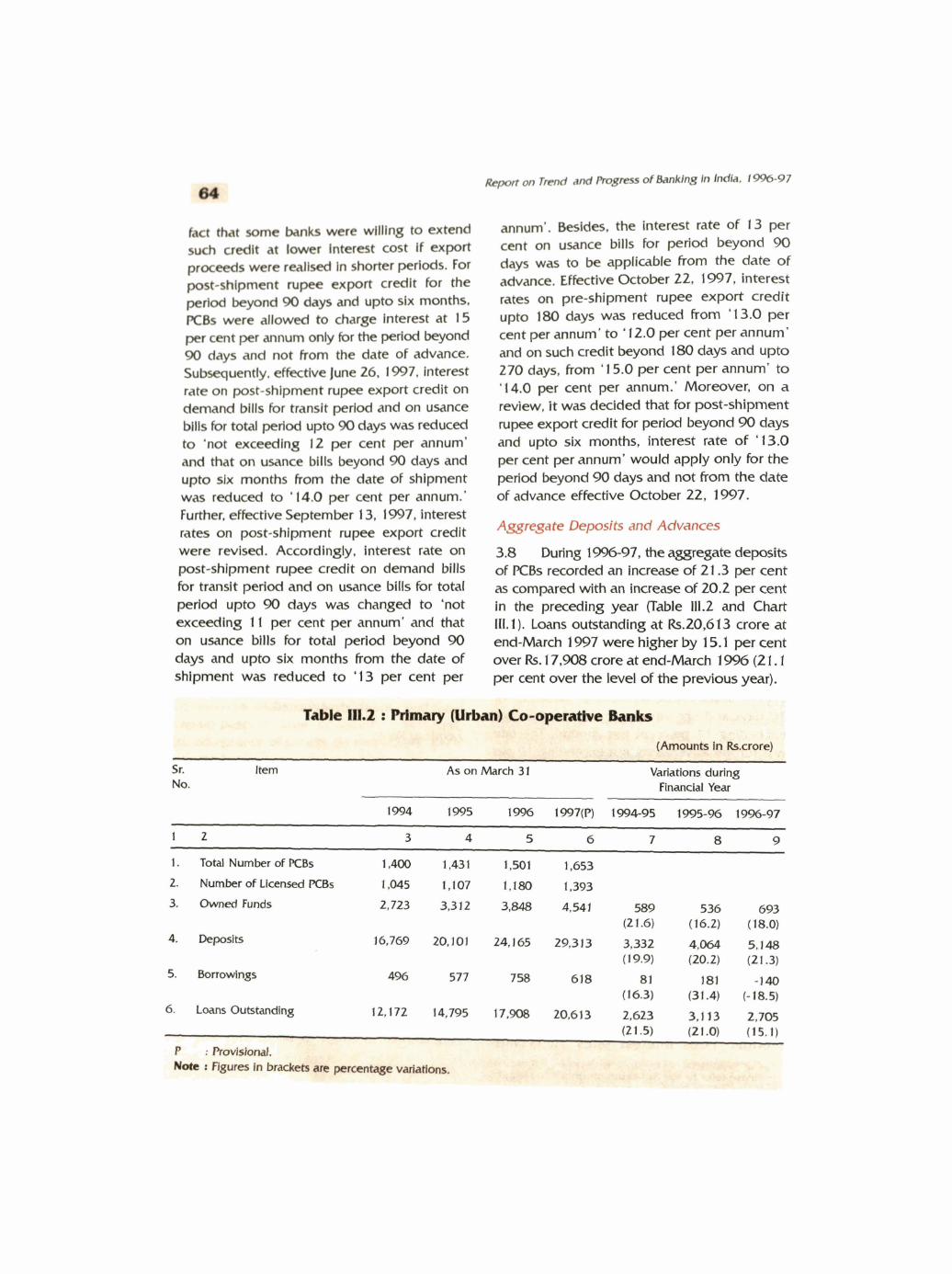

.......................................................................... Aggregate Deposits and Advances 64

.................................................................................................... kfinance Facilities 6 5

............................................................... . hofit.maklng Weak and Nonviable PCBs 6 5

............................................................................................ Non-Perlorrning Assets 6 5 .............................................................................................. Mori ty Sector Targets -65

....................................................................................... Regulation and Supervision 66 . ....................................................................................................... Branch Lfcmslng 66 .............................................................. Maximum Umlt on Single PaRy Exposures

66

..................................................................... Mmary AMculhral Credit Societies 68

.................................................................. 3.3 NABARD and the Co-operathe Sector 68 .............................................................................................. Resources of NABARD 69

......................................................................................... Refinance from NABARD 7 1

.......................................................... Rural lnfrastructural Development Fund (RIDF) 71

.......................................... Agricultural Development Finance Companies (ADFG) 72

Development Action Plans (DAPs) and Memoranda of Understandings (MoUs) ............................................................................................ 72

Policy Initiatives by NABARD .................................................................................... 73

CHAPTER IV: FINANCIAL INSTITUTIONS Overview ....................................................................................................... 76

............................................................................ 4.2 Assets of Financial Institutions 76

............................................................ 4.3 Term Lending and Investment Institutions 77

.................................................................................................. Financial Assistance 77

................................................. Pattern of Sources and Deployment of Funds of Fls 80

Prime Lending Rates of FIs ........................................................................................ 80

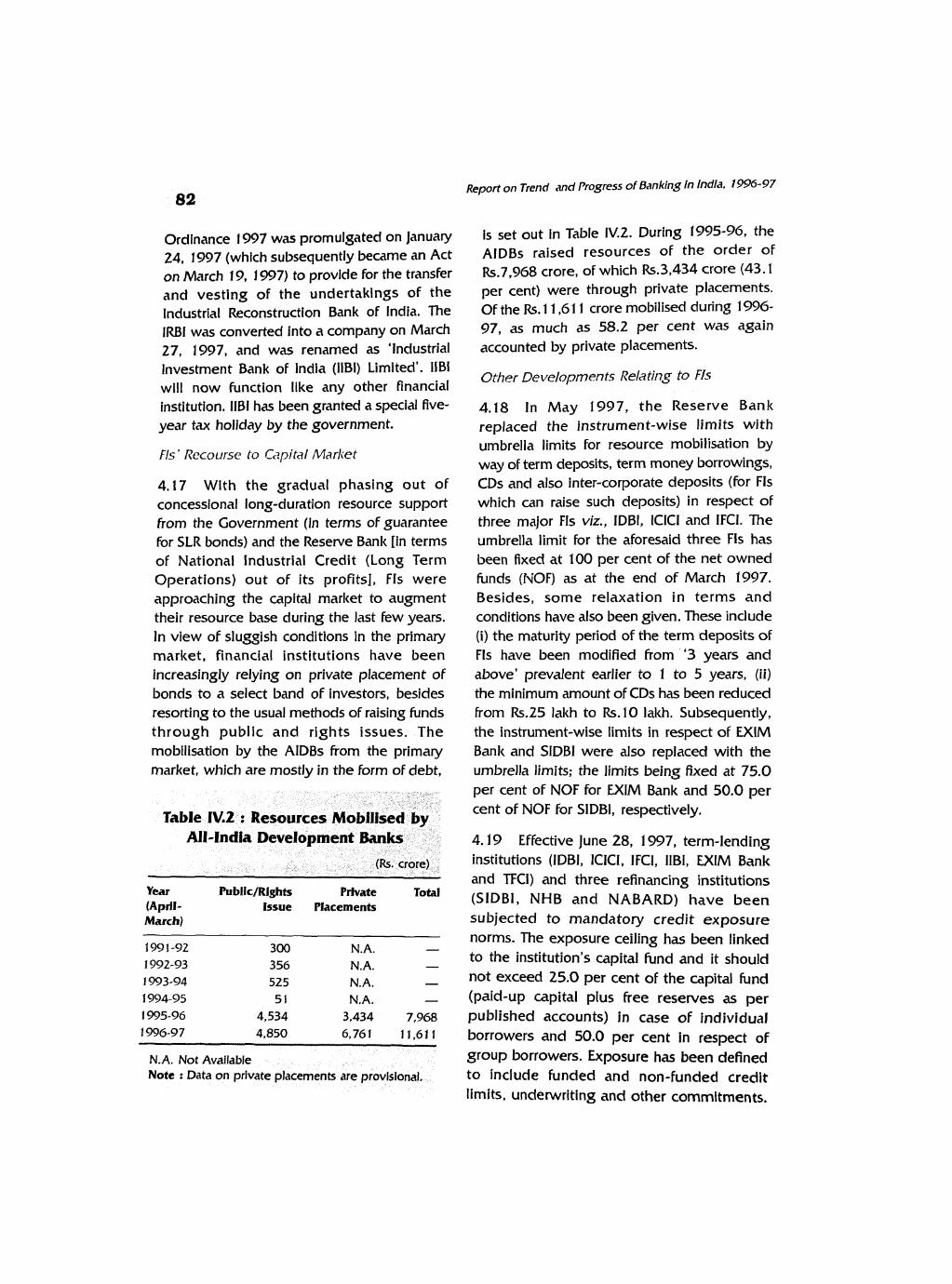

Resource Raising by Major Financial Institutions ....................................................... 81

Merger of SCICI with ICICI ........................................................................................ 8 1

................................................................................. Conversion of IRBl into IIBl Ltd 81

Rs' Recourse to Capital Market ................................................................................. 82

Other Developments Relating to FIs ...................................................................... 82

........ Prudential and Capital Adequacy Measures .................................................. 83

4.4 Reserve Bank Assfstance to Finnncinl lnstftutions ............................................... 84

4.5 Infrastructure Development Finance Company ................................................... 86

Incorporation of lDFC ............................................................................................... -86 Shareholding Pattern ................................................................................................ 8G Objectives ......................................................................................................... 8 G

......................................................................................................... 4.6 Mutual Funds 89

........................................ New Guidelines for Mutual Funds

........................................................... Types of Mutual Fund Schemes in Operation 90 New Mutual Fund Schemes ...................................................................................... 90 Asset A4anagement Committees (AMCs) by Unit Trust of India ............ ..... .......... 90

4.7 Non-Banking Financial Companies ........................................................................ 90 Regulation of NBFCs ................................................................................................. 91

Inadequacy of Legislative Framework Prior to the 1 997 Amendment .................................................................................................... 91 Recommendations of Shah Working Group ........................ ......,............. ............. 9 2

Amendments to t h e Reserve Bank of India Act. 1934 ....... : ..................................... 9 2

Amendment to NBFC (Reserve Bank) Directions. 1977 .......................................... 97

Prudential Regulation and Capital Adequacy Stipulations ......................................... 97

........................................................................................ New Guidelines for NBFCs 97

............................................................................ Supervisory Framework for NBFCs 97

Amendments to Residuary Non-Banking (Reserve Bank) Directions. 1987 ....................................................................................................... 9 8

Trends in the Growth of Deposits with Non-Banking Companies during the year ended March 31 . 1996 ................................................................... 98

Shere Working Group ............................................................................................... 9 8

List of Boxes ......................................................................................................................... xi

......................................................................................................................... List of Tables xii

Llst of Charts ....................................................................................................................... xiii

ANNEXURE I : Progress of Financial Sector Reforms : 1992-93 to 1996-97 ..................... xiv

....................................................................................................... List of Appendix Tables xvi

LIST OF BOXES

Box Nos .

....................................................................................... 11.1 Risk Management in Banks 22

.................................................................................................. 11.2 The 'Narrow Banks' 26

............................................... 11.3 Capltal Convertibility and Commercial Banks in India 27 ...................................................... 11.4 Directed Credit . Issues Relating to Rural Credit 51

Ill. 1 The Role of the Reserve Bank in Promoting Rural Development ............................. 69

............ . .................................................. IV I Speciallsed Finandal Institutions in India ; 78 ............................................................................. IV.2 Modes of Infrastructure Financing 87

1V.3 Deposit Insurance ........................ ......... .................................................................... 93 ....................................... IV.4 nmnclal frauds and Banking Instability ......... ............ 95

LIST QF TABLES

Table Nos . 1.1 Working ~esults'of Scheduled Commercial Banks .

............. . Group-wise : Some Important Financial Indicators 1995-96 and 1996-97 12

....................................... 1.2A Frequency Distribution of Net NPAs : Public Sector Banks 13

1.20 Frequency Distribution of Net NPAs : Indian Private Sector and Foreign Banks ........ 1 4

.............................................. 1.3A Frequency Distribution of CRAR : Public Sector Banks 14

. ............... 1 Y) Frequency Distribution of CRAR : indian Private Sector and Foreign Banks 14

11.1 The New Structure of Prime Lending Rate of Public Sector Banks ............................ 23

11.2 Important Banking Indicators . Scheduled Commercial Banks . .............................................................................................. 1995-96 and 1996-97 24

11.3 Sectoral Deployment of Gross Bank Credit by Major Sectors .................................. 30

...................................................... 11.4 Industry-wise Deployment of Cross Bank Credit 31

11.5 Working Results of Scheduled Commercial Banks for the years .............................................................................................. 1995-96 and 1 996-97 34

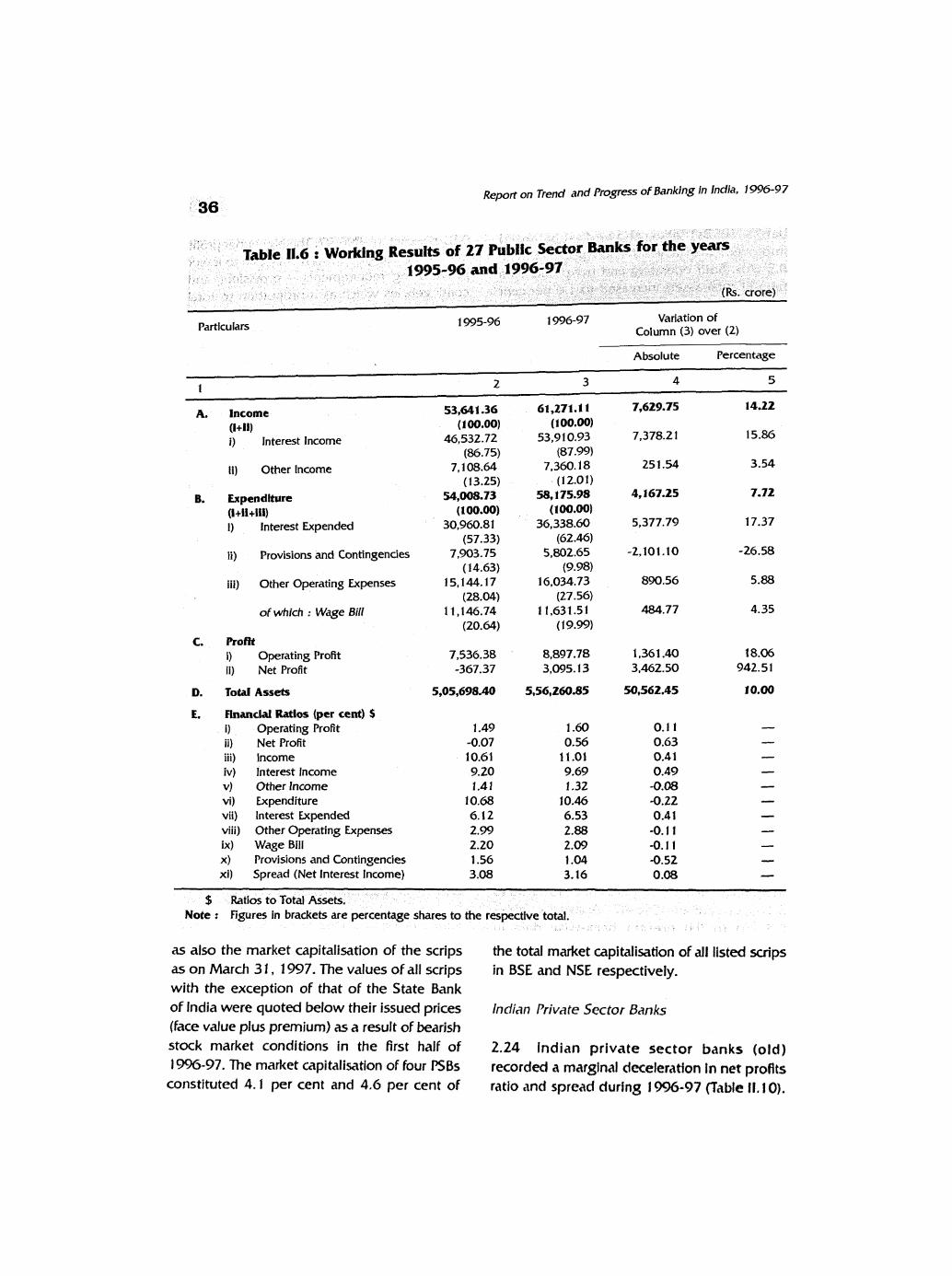

1 Working Results of 27 Public Sector Banks for the years 1 995-96 and 1 996-97 ...... 36

11.7 Working Results of State Bank of India and 7 Associates for the years 1 995-96 and 1 996-97 ............................................................................................. 3 7

....... 11.8 Working Results of 19 Nationalised Banks for the years 1995-96 and 1996-97 38

................................. 11.9 Performance of Public Sector Bank Scrips in the Stock Market 39

11.10 Working Results of 25 Old Indian Private Sector Banks for the years 1 995-96 and 1996-97 ............................................................................................. -40

11.1 1 Working Results of 9 New Indian Private Sector Banks for the years 1 995-96 and 1 996-97 .............................................................................................. 41

11.12 Working Results of 39 Foreign Banks in India for the years 1 995-96 and 1 996-97 .............................................................................................. 4 2

11.13 Working Results of RRBs : 1 994-95 and 1 995-96 .................................................... 43

............................................................. 11.14 Selected Indicators of Regional Rural Banks 44

11.15 Purpose-wise Advances of RRBs ............................................................................... 44

11.16 Yields on Government Securities in the Primary Market . 1994-95 to 1997-98 (April-October) ....................................................................... 47

11.1 7 Advances under JRDP ............................................................................................ 5 4

...................... 11.18 Annual Credit Plan of Financial Institutions under Lead Bank Scheme 55

Chart Nos .

Issue of Equity Capital by Nationalised Banks ......................................................... 57

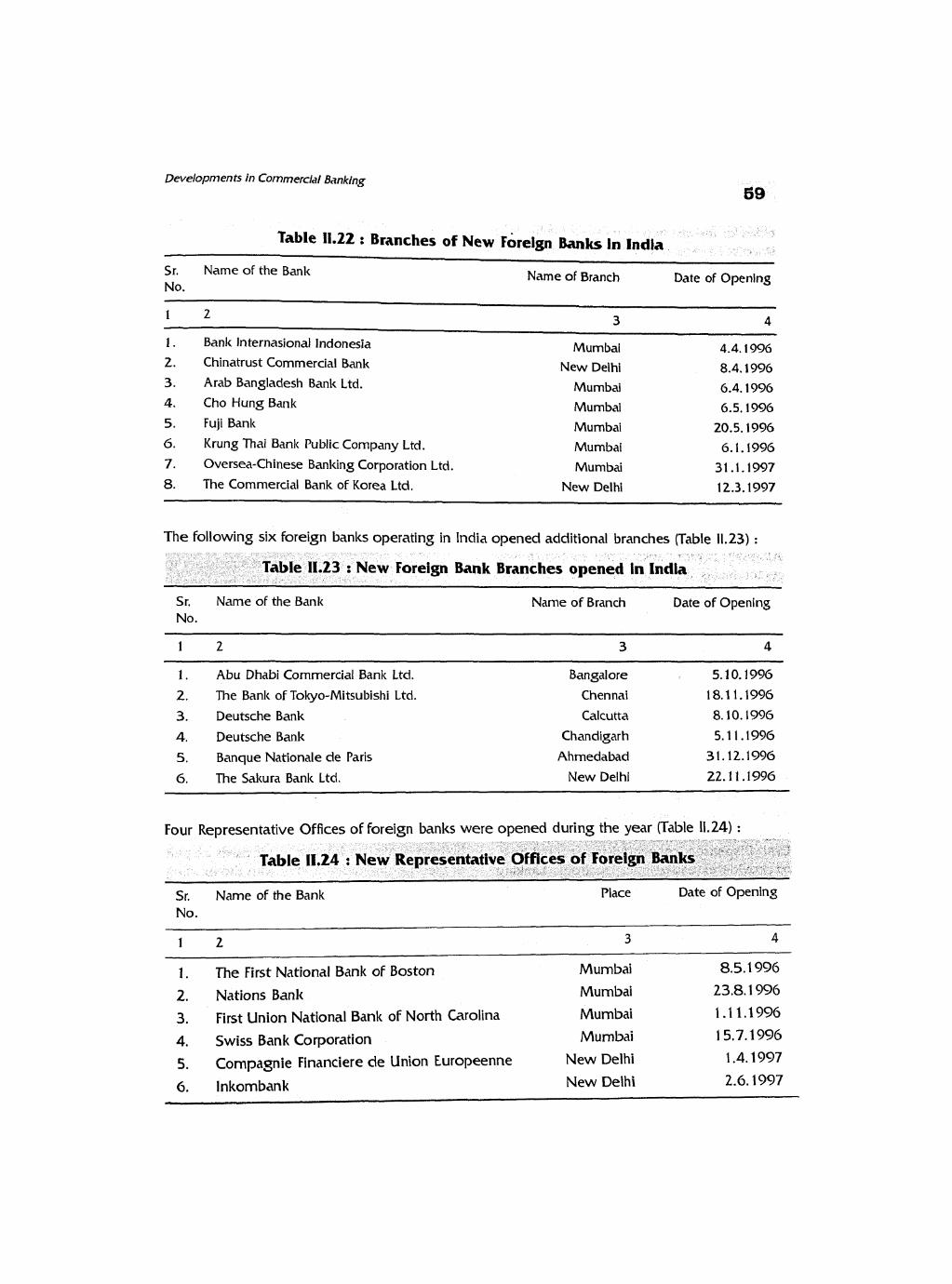

................................................................. Ehanches of New Foreign Banks in India 59

New Foreign Bank Branches opened in India ..................................................... 59

New Representative Offices of Foreign Banks .......................................................... 59

Primary Urban Co-operative Banks . Structure 63 ....................................................... Primary (Urban) Co-operative Banks .......................................................................... G 4

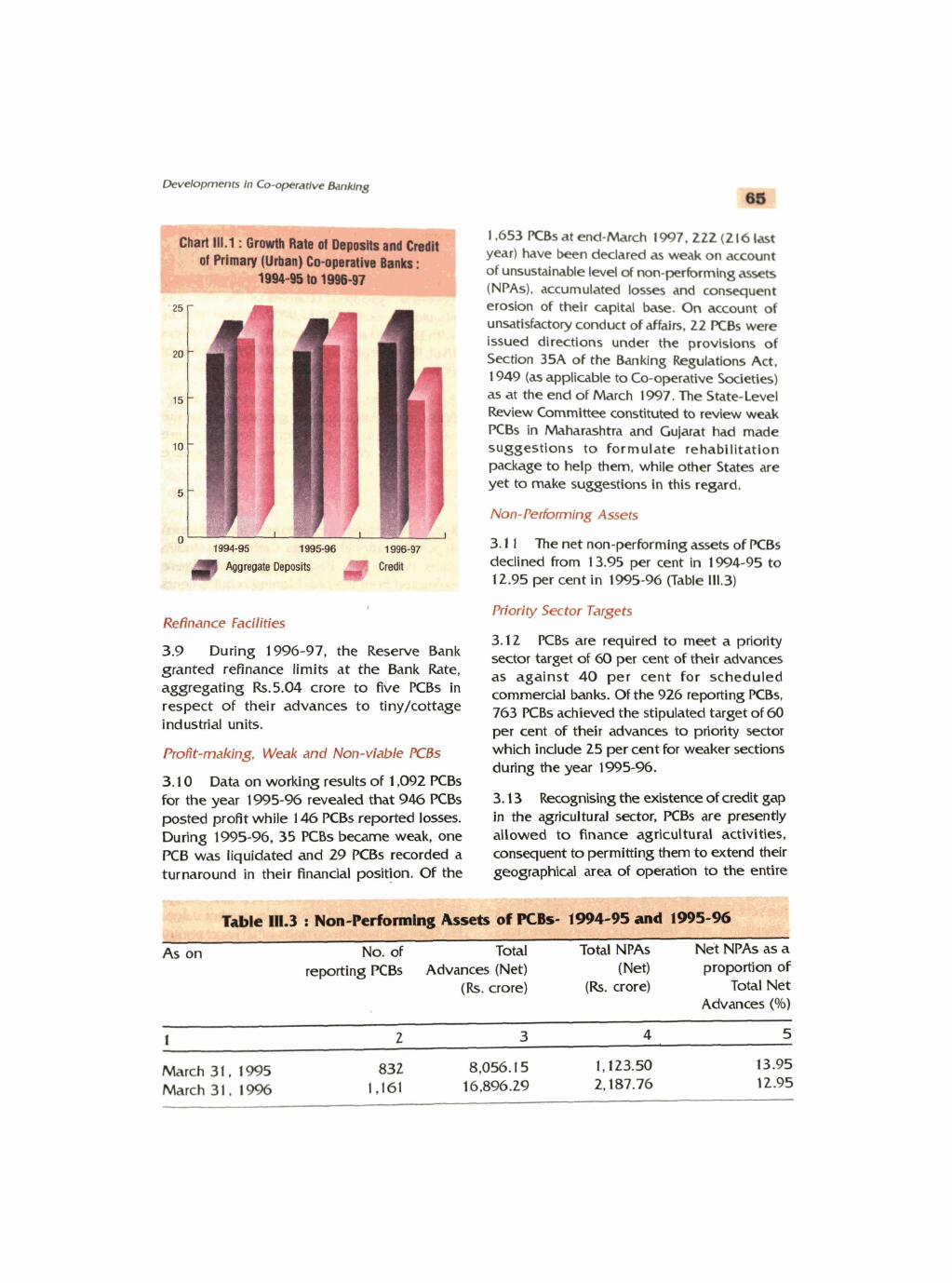

Non-Performing Assets of PCBs - 1994-95 and 1995-96 .................................. ...... 65

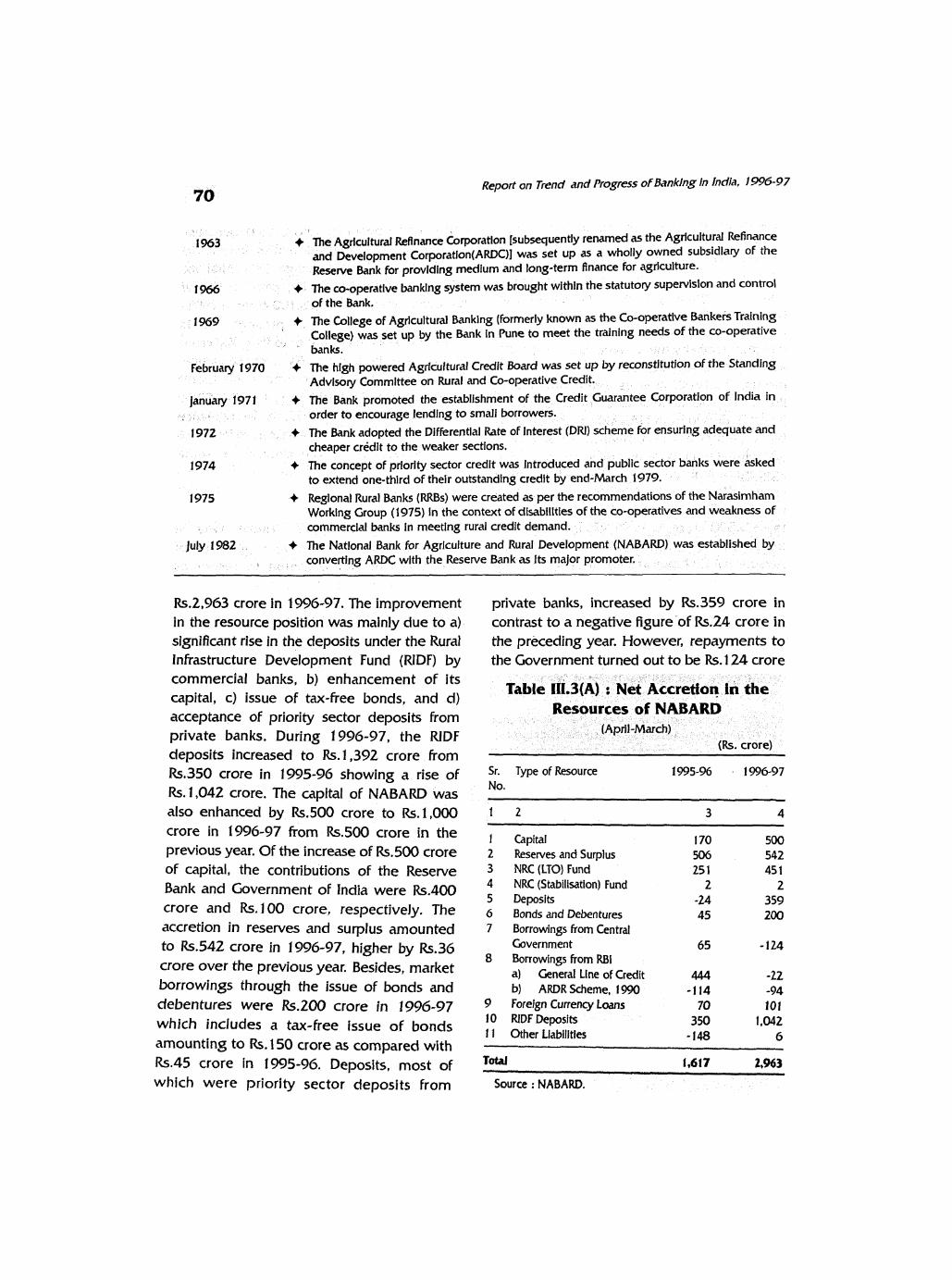

Net Accretion in the Resources of NABARD .......................................................... 70

NABARD's Credit to State Co-operative Banks and State Governments ................... 71

NABARD's Structure of Interest Rates for Term Loans .............................................. 72

Sanctions and Disbursements under RIDF.1. RIDF-11 and RIDF-Ill .............................. 73

Prime Lending Rates of Major Term-Lending Institutions ......................................... 81 Resources Mobilised by All-India Development Banks ........................................... 8 2

Prudential Regulatory Framework for Financial Institutions ...................................... 84

Capital Adequacy Ratio of Select Fls as on March 31 . 1997 .................................... 84

Asset Classification of Select Financial lnstitutions as at t h e end of .............................................................................................. March 1 996 and 1 997 85

................................ Amounts Mobilised by Mututal Funds (1 99 1-92 to 1996-97) 89

LIST OF CHARTS

Growth Rate of Bank Deposits and Non-Food Credit of Scheduled Commercial Banks in India: 1995.96. ......................................................................... 1996-97 and April.October. 1997 2 5

Investment and Reserve Deposit Ratios of Scheduled Commercial Banks in India: 1995.96. ...................................................................................... 1996-97 and October 1997 -29

Net kofits to Total Assets of Scheduled Commercial Banks . ............................................................... Bank Group-wise : 1995-96 and 1996-97 33

Snr~ad of Scheduled Commercial Banks in lndia . Bank Group-wise :

111. 1 Growth Rate of Deposlts and Credlt of Primary (Urban) ................................................................ Co-operative Banks: 1994-95 to 1 996-97 65

111.2 Growth Rate of Deposits and Credlt of State ................................................................ Co-operative Banks: 1993-94 to 1995-96 67

111.3 Growth Rate of Deposits and Credit of Central ................................................................ Co-operative Banks: 1993-94 to 1995-96 67

111.4 Growth Rate of Deposits and Credit of Primary ................................................... Agricultural Credit Societies: 1903-94 to 1995-96 68

111.5 Overdues to Demand of Co-operative Credit Institutions: ................................................................................................. 1 993-94 to 1995-96 68

IV . 1 Share of Banks and Financial lnstltutions in .............................................................................. . Financial Assets 1 994 to 1997 7 7

................... . IV.2 Financial Assistance by All-Financial Institutions 1994-95 to 1996-97 77

................................................................. IV.3 Resource Mobillsatlon by Mutual Funds 86

1'4 Share of Banks and Non-Bank Deposits in Financial Assets ................................................................................................ of Household Sector 91

ANNEXURE . PROGRESS OF FINANCIAL SECTOR REFORMS : 1992-93 TO 1996-97

* . 1 . Cash Reserve Ratio (CRR) ......................................................................................... 99

.................................................................................................... Domestic Deposits 99

...................................................................................................... External Deposits 100

2 . Statutory Liquidity Ratio (SLR) ................................................................................. 101 Domestic Deposits .................................................................................................... 101

External Deposits .................................................................................................... 102

3 . Deregulation of Interest Rates ................................................................................ 102

Lending Rates ........................................................................................................... 102

Export Credit ............................................................................................................ 104

Deposit Rates ............................................................................................................ 105

Domestic Deposits ....................................................................................... 105

External Deposits ........................................ 106

4 . Changes in the Refinance Facilities ................................................................... 107

Export Credit (Rupee) Refinance ........................................................................... 107

Export Credit Refinance - Denominated in US Dollars (PSCFC) .................................. 108

Government Securities Refinance .............................................................................. 1 0 9 General Refinance 110 ......................................................................................................

5. Bank Rate ................................................................................................................. 1 10

Term Money Market .................................................................................................. I11

Certificate Deposits (CDs) ...................................................................................... 111

~ommer=ia' Paper (CP) .............................................................................................. 111

Inter Pa*i=ipations (IBPs) ................................................................................... 112

Rediscounting Co~mercial Bills ................................................................................. 113

Money Market Mutual Funds (MMMFs) ..................................................................... 113

Internal Debt Management Policies ........................................................................ 113

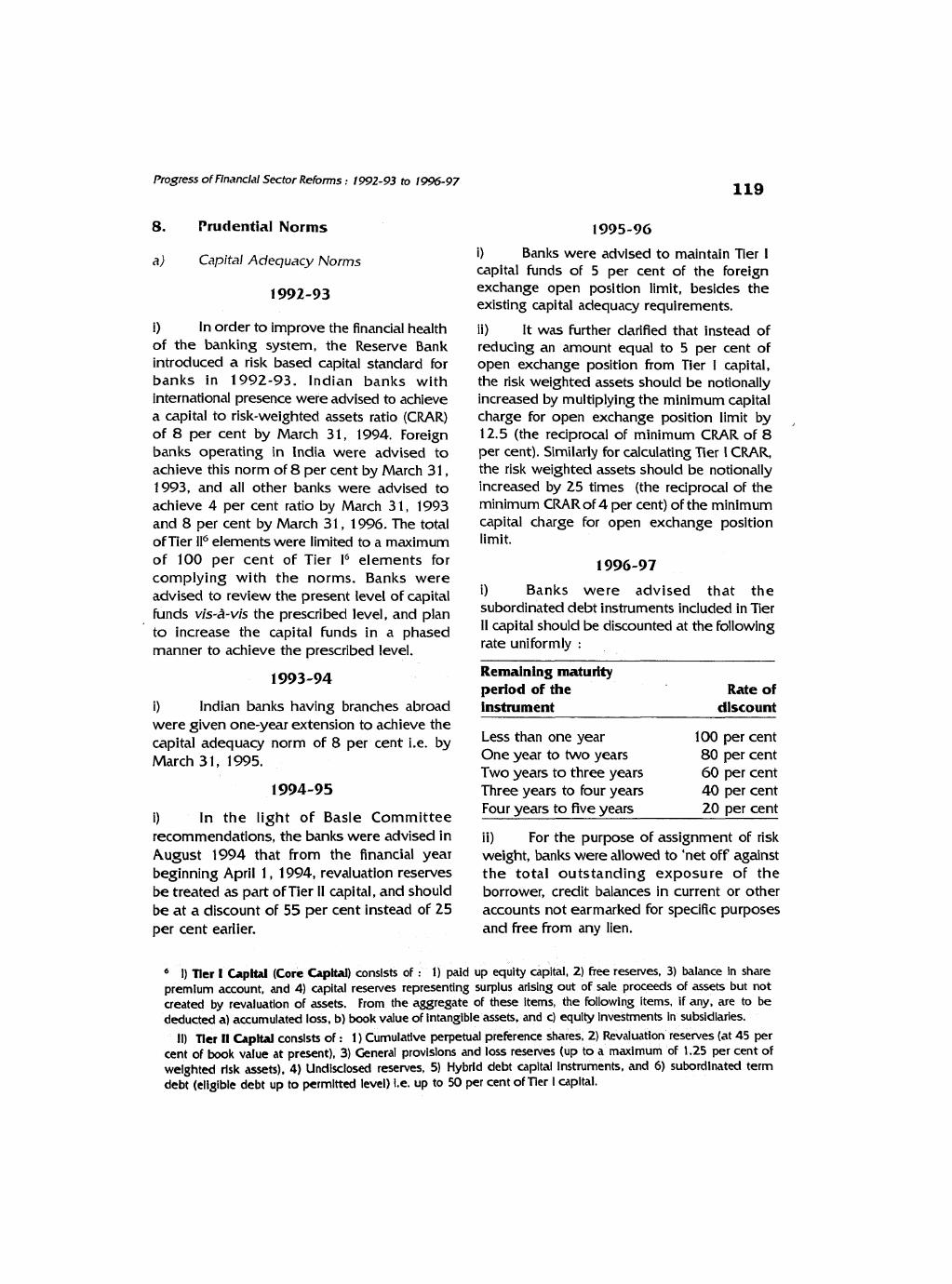

............................................................. ............................... Pmdentia1 Norms ......... 119

Capital Adequacy Norms .......................................................................................... 119

Capital Restructuring .................... ! ............................................................................. 120

lncome Recognition. Asset' Classification and Provisioning Requirements .................. 121

Credit Delivery System ........................................................................................ 124

.......................... Recovery of Bank Loans and Disclosure on Defaulting Borrowers 126

......................................... Term Lending/Bridge Loan Norms ......................... .... 127

lnvestment Norms ..................................................................................................... 128

Functional Autonomy in Nationalised Banks ............................................................ 129

Technologid Issues .............................................................................................. 129

Regulatory and Supervisory Issues ................................... .... ................................. 129 ..................................................................................................... Supervisory Issues 129

.................................................................................................. Private Sector Banks 130

Local Area Banks ................................................ ................................................... 131 ............................................................................................................ Foreign Banks 131

............................................................................................... Bank Branch Licensing 131 . ............................................................................. ................ Priority Sector Lending ; 132

..................................................................................................... Customer Services 135 .......................................................................... Preventing Frauds and Malpractices 135

Bank Restructuring ..................................................................................................... 136 ................................................................................................. Regi anal Rural Banks 136

.................................................................................. Dividend Declaration by Banks 137 ........................................................................... Reforms In Co-ope&e mklng 137

LIST OF APPENDIX TABLS

Table Nos . I . 1 (A)

1 . 1(B)

......... Net Nan-Perfirming Assets of Public Sector Banks . 1995-96 and 1 996-97 143

Net Non-Performing Assets of lndian Private Sector Banks . .............................................. ......... 195-96 and 1996-97 ................................ 144

..... . Net Non-Performing Assets of Foreign Banks in India 1995-96 and 1996-97 145

................ . Capital Adequacy Ratio of Public Sector Banks 1995-96 and 1996-97 147

.... . Capltal Adequacy Ratio of Indian Private Sector Banks 1995-96 and 1996-97 148

................................. . Capital Adequacy Ratio of Foreign Banks in India 1996-97 149 ........................................... RBI Accommodation to Scheduled Commercial Banks 150

....................................................... Viability Position of Sick/Weak Industrial Units 151

. ................................ 11.3(A) Parameters of the Working of Public Sector Banks 1996-97 152

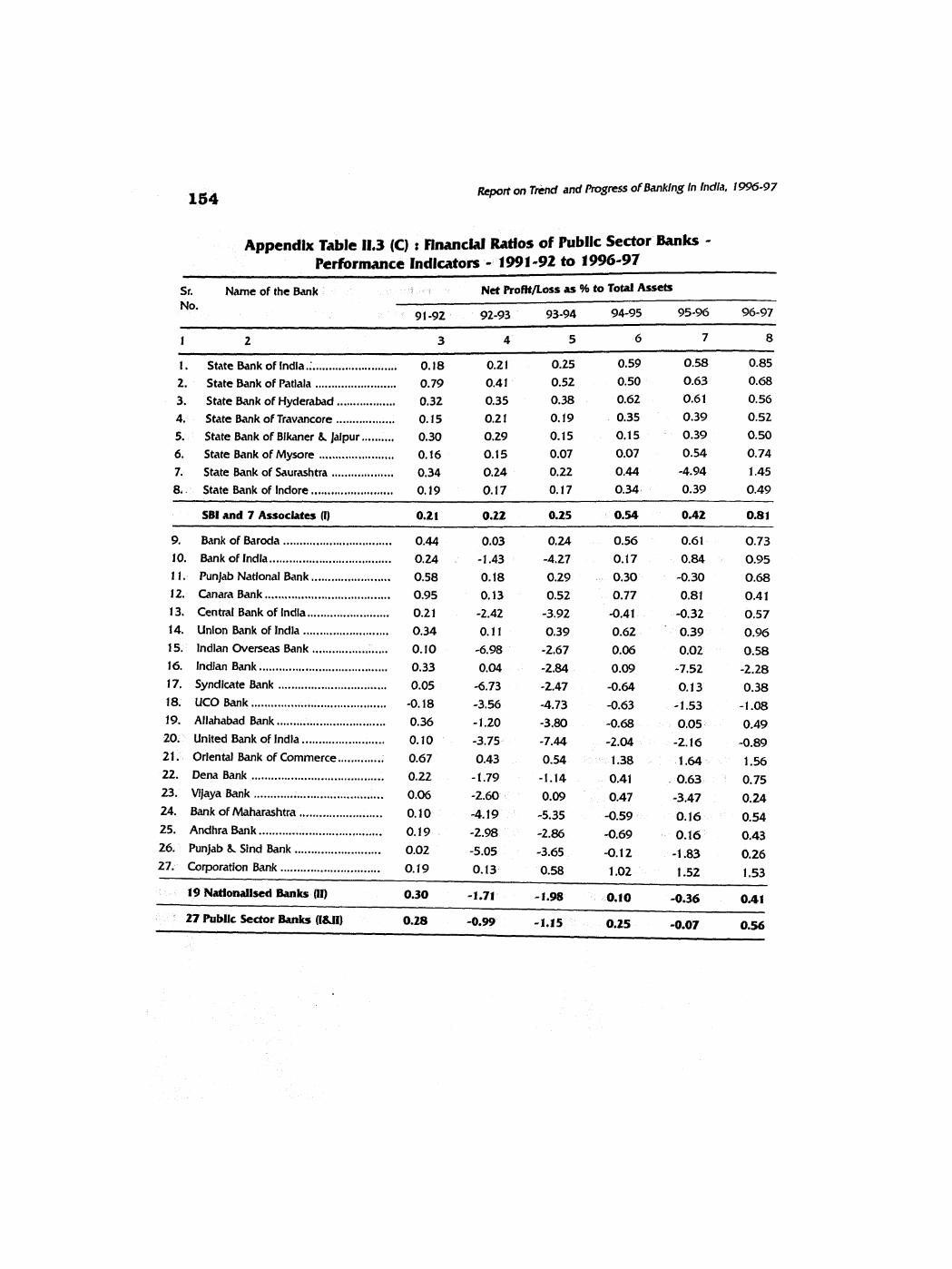

11.3(B) Financial Ratios of Public Sector Banks . Performance Indicators . ............................................................................................... 1 99 1-92 to 1996-97 153

11.3(C) Financial Ratios of Public Sector Banks . Performance Indicators . 199 1-92 to 1996-97 ............................................................................................... 1 54

11.3(D) Financial Ratios of Public Sector Banks . Performance Indicators . 199 1-92 to 1 996-97 ............................................................................................... 155

11.3(E) Financial Ratios of Public Sector Banks . Performance lndicators . 1991-92 to 1996-97 ............................................................................................... 156

11.3(F) Financial Ratios of Public Sector Banks . Performance lndicators . 1991 -92 to 1996-97 ............................................................................................... 157

11.3(G) Financial Ratios of Public Sector Banks . Performance lndicators . 1991-92 to 1996-97 ............................................................................................... 158

II.3(H) Financial Ratios of Public Sector Banks . Performance lndicators . 1991-92 to 1996-97 ............................................................................................. 159

.................... 11.4(A) Parameters of the Working of Indian Private Sector Banks . 1996-97 160

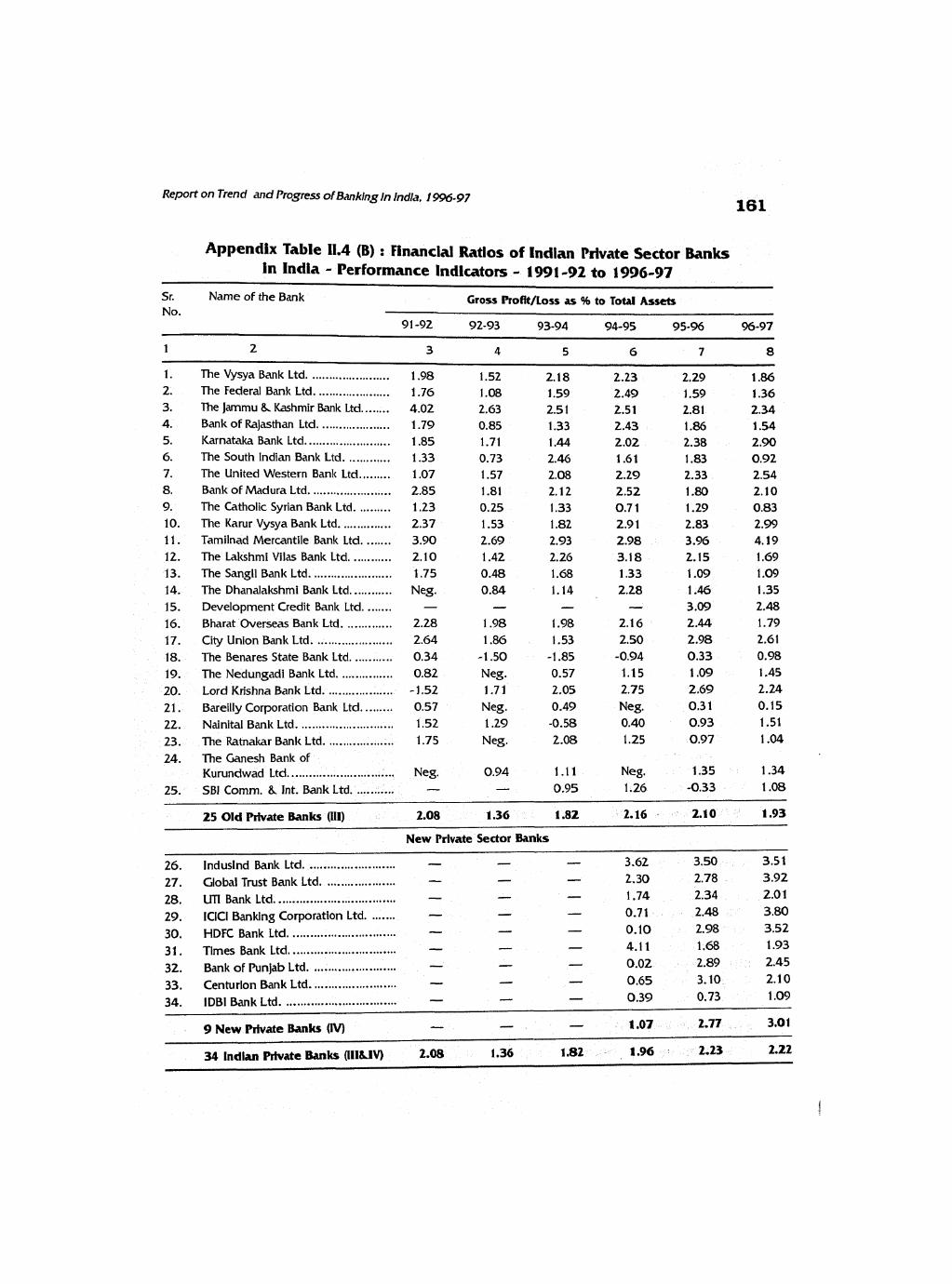

11.4(B) Financial Ratios of Indian Private Sector Banks in India . . Performance Indicators 1 99 1 -92 to 1 996-97 ..................................................... 161

4 ( C ) Financial Ratios of lndian Private Sector Banks in India . Performance Indicators . 1 99 1 -92 to 1 996-97 ...................................................... 142

11.4(D) Financial Ratios of lndian Private Sector Banks in India . Performance Indicators . 1 991 -92 to 1 996-97 ...................................................... 163

11.4(E) Financial Ratios of lndian Private Sector Banks in India . Performance Indicators . 1 991 -92 to 1996-97 ...................................................... 1 64

11.4(F) Financial Ratios of lndian Private Sector Banks in lndia . Performance Indicators . 1 99 1-92 to 1 996-97 ...................................................... 1 65

11.4(G) Financial Ratios of lndian Private Sector Banks in India . Performance Indicators . 199 I -92 to 1 996-97 ...................................................... 1 66

11.8

11.9

11.10

11.1 1

11.1 2

11.13

11.14

Ill . 1

IV . 1 (A)

IV . 1 (B)

IV.2

IV.3

Financial Ratios of lndian Private Sector Banks in India . Performance Indicators . 1 99 1-92 to 1 996-97 ...................................................... 167

Parameters of the Working of Foreign Banks in India . 1996-97 ............................ 168 Financial Ratios of Foreign Banks in lndia . Performance lndicators .

............................................................................................... 1991-92 to 1996-97 169

Financial Ratios of Foreign Banks in lndia . Performance lndicators . ............................................................................................... 1991-92 to 1996-97 170

Financial Ratios of Foreign Banks in lndia . Performance lndicators . ............................................................................................... 1991-92 to 1996-97 171

Financial Ratios of Foreign Banks in lndia . Performance Indicators . ............................................................................................... 1991-92 to 1996-97 172

Financial Ratios of Foreign Banks in lndia . Performance lndicators . ............................................................................................... 1991-92 to 1996-97 173

Financial Ratios of Foreign Banks in lndia . Performance Indicators . ............................................................................................... 1991-92 to 1996-97 174

Financial Ratios of Foreign Banks in lndia . Performance lndicators . 1 99 1 -92 to 1 99697 .......................................................................................... 175

Bank Group-wise/Population Group-wise Distribution of Commercial Bank Branches in India .................... ..... ....................................... 1 7 6

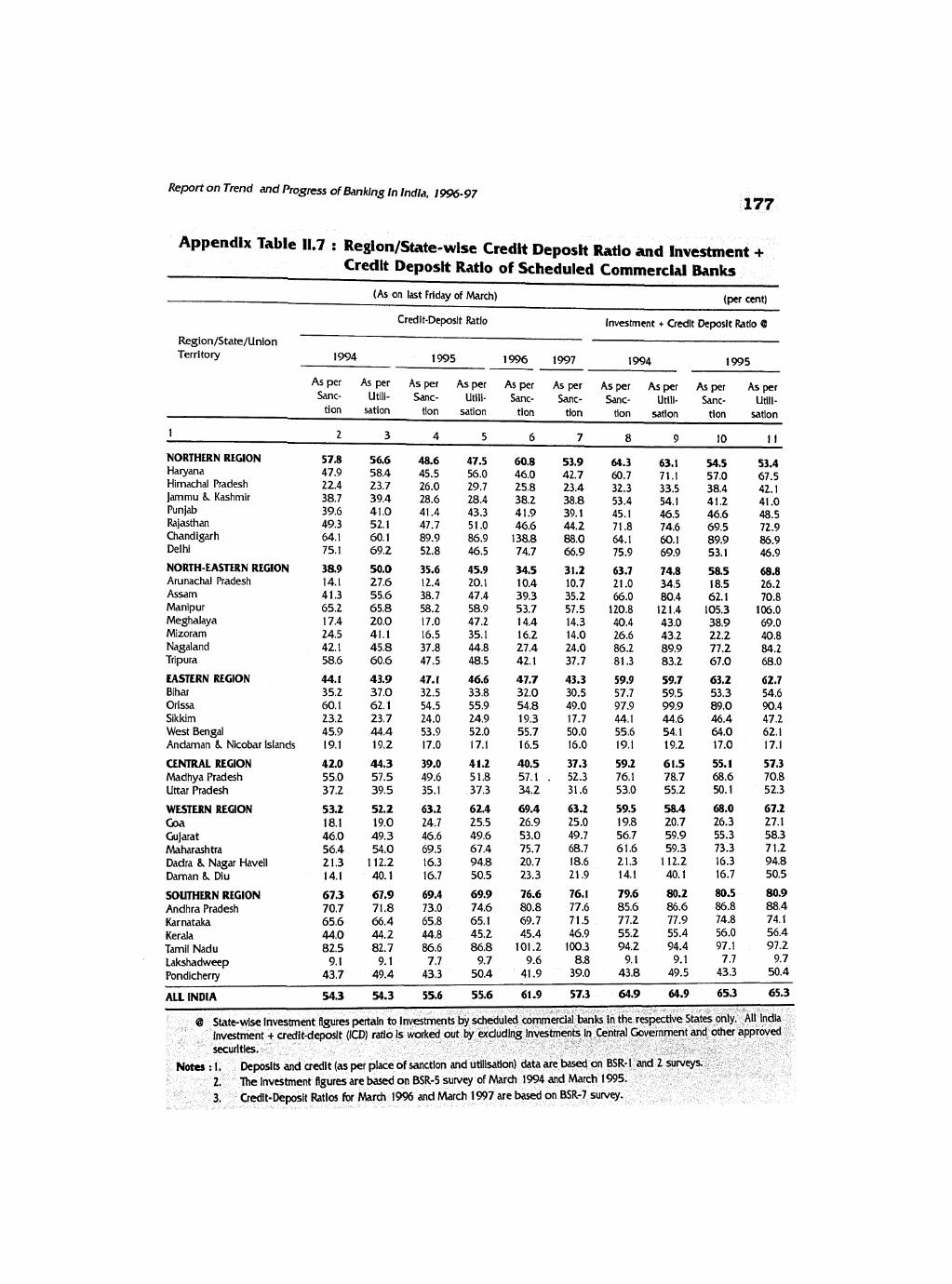

RegionIState-wise Credit Deposit Ratio and Investment t Credit Deposit Ratio of Scheduled Commercial Banks .................................................... 177

Region/State/Union Territory-wise Distribution of Commercial Bank Branches ........ 178

Issue of Certificate of Deposits by Scheduled Commercial Banks .......................... 179

.................................................................................................. Commercial Paper 180

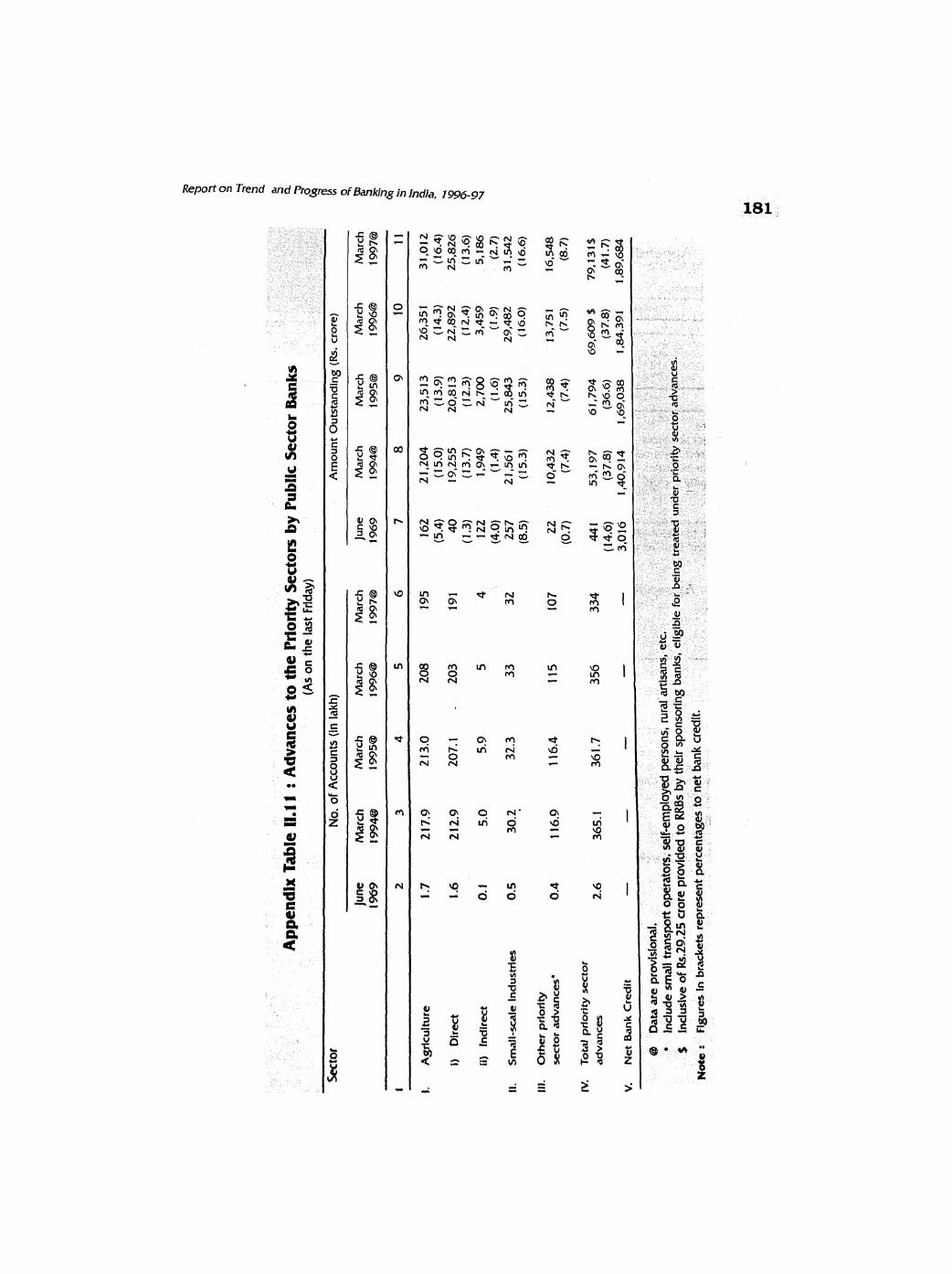

Advances to the Priority Sectors by Public Sector Banks ....................................... 181

Advances to the Priority Sectors By Indian Private Sector Banks (Old) ................... 182

................. Advances to the Priority Sectors By Indian Private Sector Banks (New) 182

................................................ Advances to the Priority Sectors By Foreign Banks 182

............................................. Progress of Co-operative Credit Movement in India 183

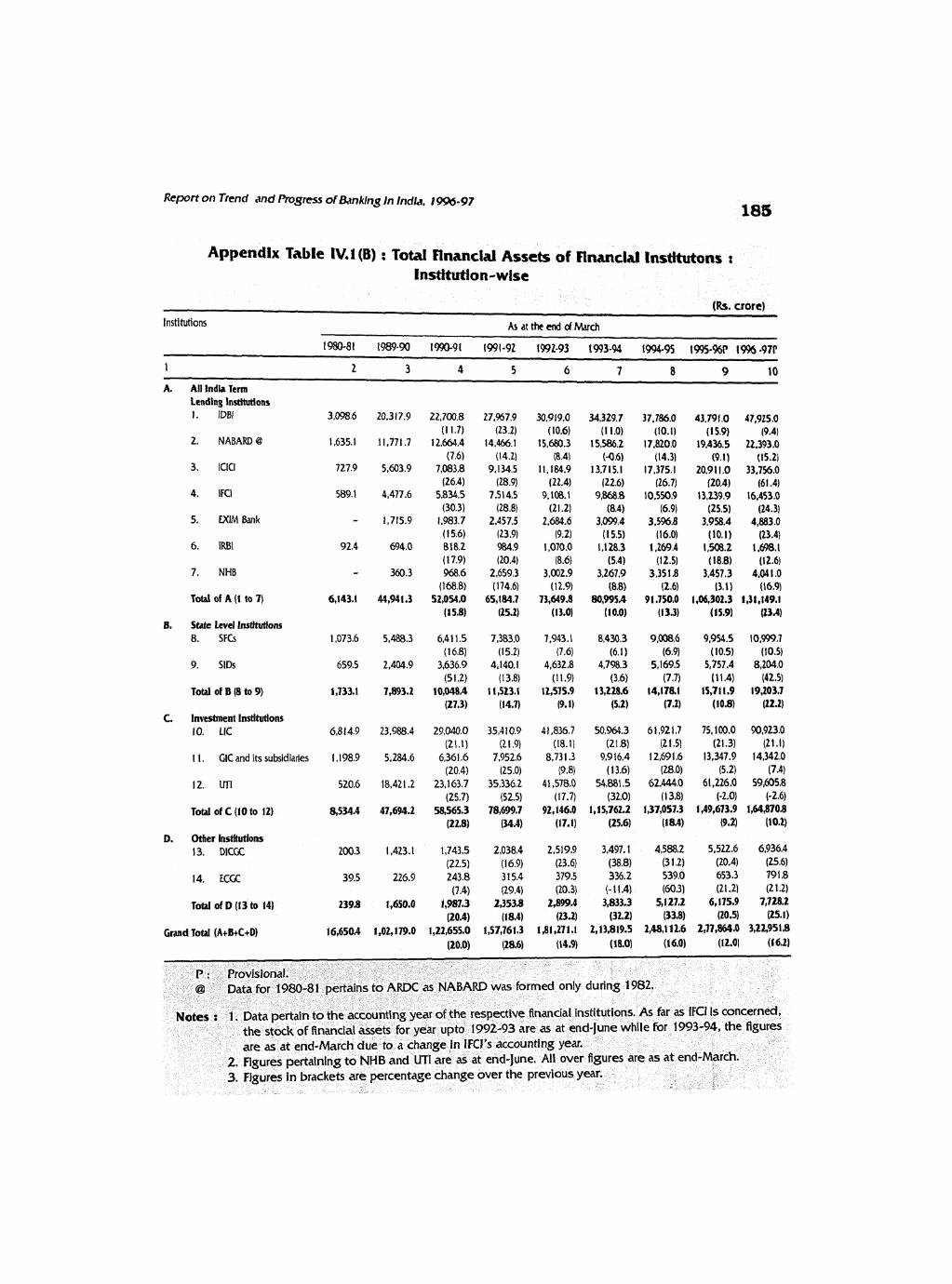

........................... ............ Financial Assets of Banks and Financial Institutions ..... 184 .............................. Total Financial Assets of Financial Institutions : Institution-wise 185

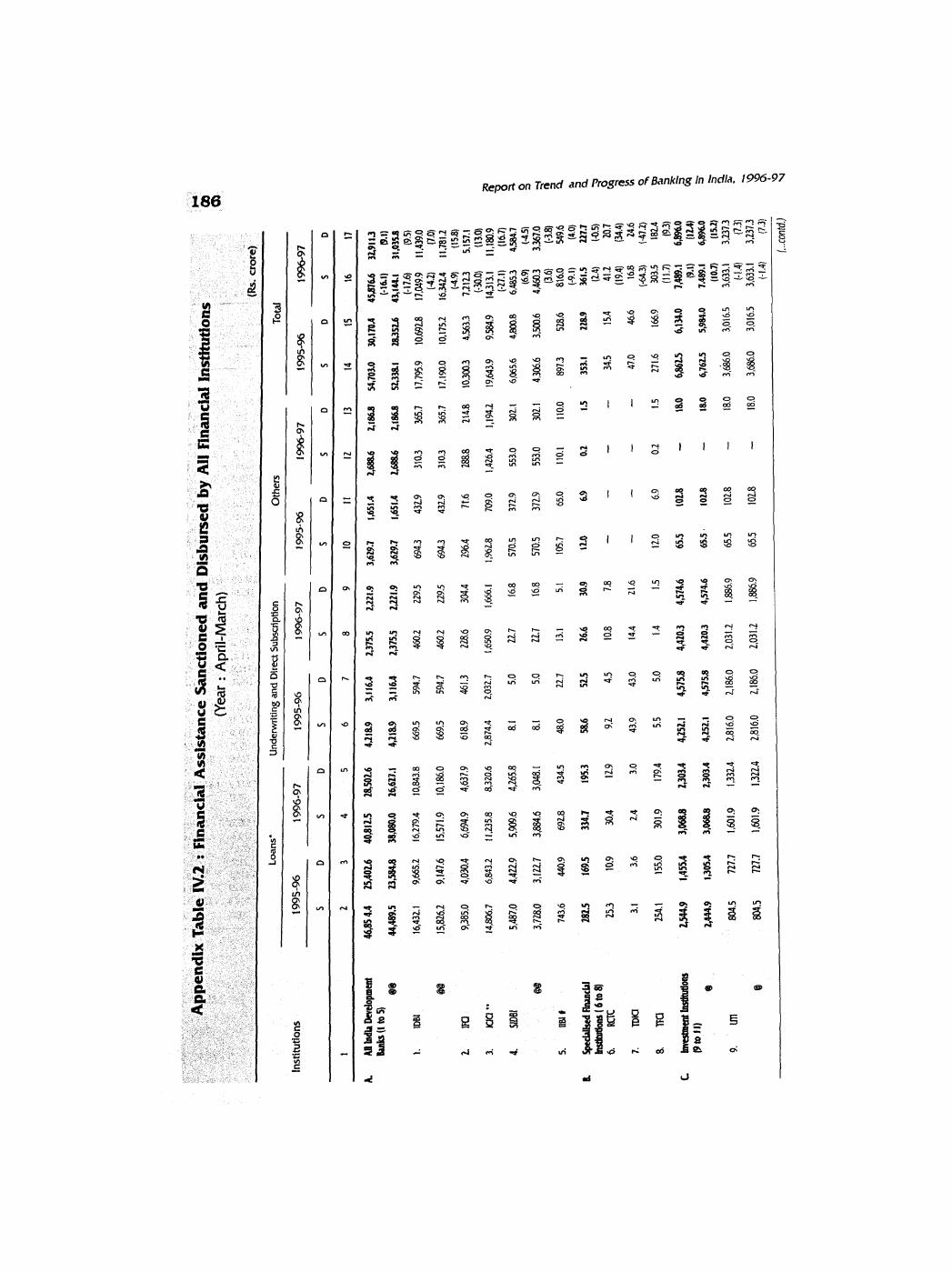

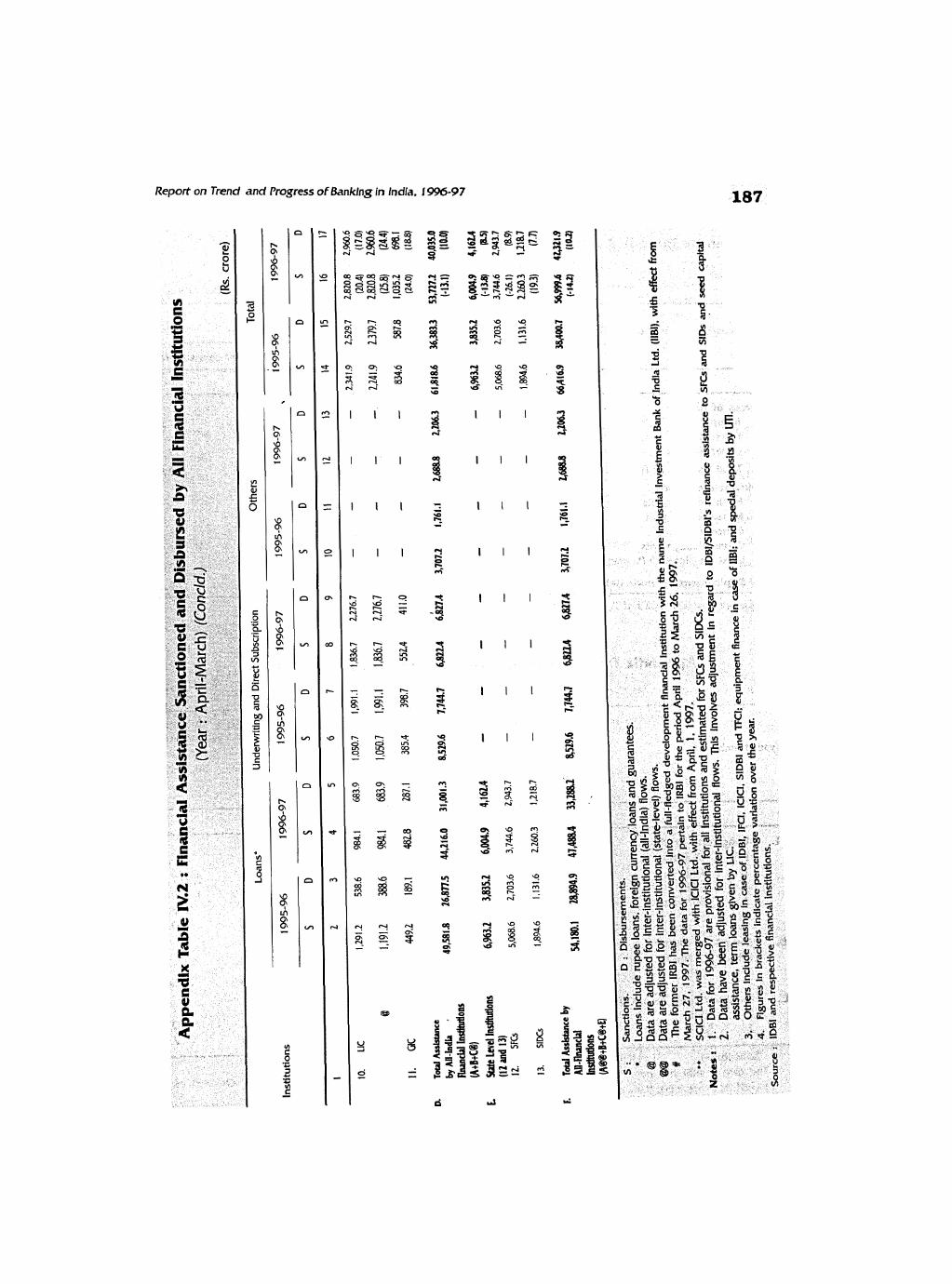

............ Financial Assistance Sanctioned and Disbursed by All Financial Institutions 186

Pattern of Sources and Deployment of Funds of Term ........................................................................... Lending Institutions . 199G-97 1 8 8 ................................................................... RBI Assistance to Financial Institutions 188

................................................................. Resource Mobilisation by Mutual Funds 189

Growth In Aggregate Deposits of Scheduled .......................... Commercial Banks and Non-Banking Companies : 1991 to 1996 190

ABBREVIATIONS

ABS - Asset Backed Securltisatlon DCA - Department of Company Affairs

ADFCS - A~rlcultural Development DCCBS - District Central Co-operative Finance Companfes Banks

AlDBs - All-lndla Development Banks DFHI - Discount and Finance House of

AMC - Asset Management Committee India Ltd. A R K - Agricultural Refinance and DFls - Development Financial

Development Corporation Institutions ARDR - Agricultural and Rural Debt DIC - Deposit Insurance Corporation Scheme Relief Scheme DlCGC - Deposit Insurance and Credit ARF - Asset Reconstruction Fund/ Guarantee Corporation

Automatic Refinance Facility DRI - Differential Rate of Interest ATM - Automated Teller Machine Scheme Scheme BCCl - Bank of Credit and Commerce DTL - Demand and Time Liabilities

International DTP - Development of Tribal BFS - Board b r Financial Supervision Programme Population Programme BGB - Bangladesh Grameen Bank ECGC - Export Credit Guarantee BOB - Bank of Baroda Corporation 501 - Bank of India ECS - Electronic Clearing Service BOLT - Build, Operate, Lease and Exim Bank - Export-Import Bank of India

Transfer FCNR(B) - Foreign Currency Non-Resident BOO - Build, Own and Operate (Banks) Accounts Scheme BOOS - Build, Own, Operate and Sale FG - Financial Guarantee BOOT - Build, Own, Operate and FIs - Financial Institutions

Transkr Flls - Foreign Institutional Investors BOT - Build, Operate and Transfer GDR - Global Depository Receipt BSE - Bombay Stock Exchange CIC - General Insurance Corporation CAC - Capital Account Convertibility GLC - General Line of Credit CAMEL - Capital Adequacy, Asset GPV - General Purpose Vehicle

quality, Management, Earnings GRF - General Refinance Facility and Liquidity HDFC - Housing DeWopment Finance

CAR - CapItal Adequacy Ratio Corporation CCBs - Central Co-operative Banks HFG - Housing Finance Companies CDs - Certificate of Deposits HPAEs - High performing Asian CD Ratio - Credit-Deposit Ratio Economies CP - Commercial Paper IBA - Indian Banks' Association CRAR - Capital to Risk-weighted Asset IBl - Industrial Bank of Japan

Ratio IBL - Inter-Bank Liabilities CRISIL - Credit Rating Information ICAl - Institute of Chartered

Services of India Ltd. Accountants of India -Cash Reserve Ratio ICD Ratio - Investment plus Credit Deposit

DAP - Development Action Plan Ratlo

1ClCl

ICS IDBl

lDCs IDFC

IDMT

IFCl

IIBl

IRBI

IRDP

KVlC

LABS LBS LIBOR LIC LTO LTPR MF MlCR

MIS

MMMF MoU MPBF

MSTLR

MTLR MTNL

MTPR NABARD

- Industrial Credit and Investment Corporation of lndia

- investor Compensation Scheme - Industrial Development Bank of

lndia - Institutional Development Cells - Infrastructure Development

Finance Company - Institute for Development and

Research in Banking Technology - Industrial Finance Corporation of

lndia - Industrial lnvestment Bank of

India - Industrial Reconstruction Bank

of lndia - Integrated Rural Development

Programme - Khadi and Village Industries

Commission - Local Area Banks - Lead Bank Scheme - London Inter-Bank Offer Rate - Life Insurance Corporation - Long-Term Operation - Long-Term Prime Rate -Mutual Fund - Magnetic Ink Character

Recognition - Management Information

System - Money Market Mutual Fund - Memorandum of Understanding

-Maximum Permissible Bank Finance

- Minimum Short Term Lending

Rate - Medium Term Lending Rate - Mahanagar Telephone Nigam

Ltd. - Medium Term Prime Rate - National Bank for Agriculture

and Rural Development

NBC - Net Bank Credit NBCs - Non-banking Companies NCC - National Clearing Centre NBDs - Non-bank Deposits NBFCs - Non-banking Financial

Companies NBNFCs - Non-banking Non-financial

Companies NDTL - Net Demand and Time

Liabilities NFA - Net Foreign Exchange Assets NGOs - Non-Governmental

Organisations NHB - National Housing Bank NHC(LT0) - National Housing Credit (Long Fund Term Operations ) Fund NOF - Net Owned Fund NPA - Non-Performing Asset NRC - National Rural Credit Stabilisation Stabilisation Fund Fund NRC (LTO) - National Rural Credit (Long- Fund Term Operations) Fund NRE - Non-Resident (External) Rupee Accounts Accounts NRNR - Non-Resident Non-Repatriable

Rupee Deposit

NSE - National Stock Exchange OTC - Over-the-counter PACS - Primary Agricultural Credit

Societies

PCBs - Primary (Urban) Co-operative Banks

PDs -'Primary Dealers PLDBs - Primary Land Development

Banks

PLR - Prime Lending Rate

PMRY - Prime Minister's Rozgar Yojana

PNB - Punjab National Bank PSBs - Public Sector Banks PSUs - Public Sector Undertakings l l L R - Prime Term Lending Rate

X X

ROC - Msk Capltal and Technology FInance Corporation Ltd.

NDF - Rural InFrastructural Development Fund

RNBCs - Residuary Non-banking Companies

RRBs -Regional Rural Banks SAO - Seasonal Agricultural

Operations SBI - State Bank of India SCARDBs - State Co-operative and

Agricultural Rural Development Banks

SGISTs - Scheduled Castes/Scheduled Tribes

SCBs - Scheduled Commercial Banks/ State Co-operative Banks

SClCl - Shipping Credit and Investment Corporation of lndia

SDs - Satellite Dealers SEBI - Securities and Exchange Board

of lndia SFCs - State Financial Corporations SF0 - Structured Financing Option SGL - Subsidiary General Ledger

SHGs - Self-Help Groups SlDBl - Small Industries Development

Bank of lndia SlDCs - State Industrial Development

Corporations SLDB - State Land Development Bank SLR - Statutory Liquidity Ratio SLRCCCDI - State Level Review and Co-

ordination Committee on Credit Delivery Innovations

SPNS - Shared Payment Network System

SPV - Special Purpose Vehicle SSI - Small Scale Industries STPLR -Short Term Prime Lending Rate TDlCl - Technology Development and

Information Company of India TDS - Tax Deduction at Source TFCI - Tourism Finance Corporation of

lndia UTI - Unit Trust of India VAR - Value-at-risk VSAT - Very Small Aperture Terminal VSNL - Videsh Sanchar Nigam Ltd. YTM - Yield to Maturity

CHAPTER 1

BANKING DEVELOPMENTS AND POLICY PLRSPLCTlVES

Introduction

The performance of the Indian banking syst6m in 1996-97 showed a distinct improvement. There was a marked relaxation of availability constraints as well as policy- based constraints on the banking system. Reductions in Cash Reserve Ratio (CRR) injected substantial liquidity, while policy initiatives such as the freedom provided to banks in regard to the application of Maximum Permissible Bank Finance (MPBF) and relaxation of the norms of consortium lending, enhanced their operational flexibility. Release of substantial liquidity through reductions in CRR and the increase in net foreign exchange assets (NFA) along with some softening of inflationary expectations led to strong deposit growth of scheduled commercial banks (SCBs), and a general softening of prime lending rates. Long-term interest rates which had exhibited downward rigidity for most part of t h e year, also tended to soften with the inflation rate coming down towards the later part of the year. All these factors, taken together, had a distinct positive impact in terms of the improvement in net profitability positions of SCBs. Furthermore, t h e r e was some improvement in the spread (i.e., net interest income).

1.2 Notwithstanding these favourable developments, credit expansion remained subdued during 1996-97. Faced with an easy liquidity situation, banks resorted to treasury operations also to improve their earnings and profitability. A substantial part of the enhanced liquidity was absorbed through Investments

in Government securities. During the first half of the current financial year i.e. 1997-98, aggregate deposits of banks continued to grow strongly. Non-food credit has shown a pickup in recent period. Besides, banks' investments in commercial paper, bonds/ debenturesfshares of Public Sector Undertal<ings (PSUs) and private corporate sector have shown a growth compared with that in the previous year. Thus, the flow of resources from banks to commercial sector has been significantly larger than in the corresponding period last year.

2. Rural Credit

1.3 Provision of adequate and timely institutional credit for rural sector continued to be a major policy concern during 1996-97. Towards t h i s end, the refinancing capacity of the National Bank for Agriculture and Rural Development (NABARD) was enhanced with t h e increase in the General Line of Credit limit from the Reserve Bank from Rs. 5,250 crore to Rs.5,500 crore during 1996-97 for short- term and seasonal agricultural operations. The limit is set to be further raised to Rs. 5,700 crore during 1997-98. Besides, the share capital of t h e NABARD was enhanced by Rs. 500 crore to Rs.1,000 crore during 1996-97 with a contribution of Rs.400 crore from the Reserve Bank and Rs. 100 crore from t h e Government of India. The Monetary and Credit Policy for the first-half of 1997-98 has unveiled a plan to raise further the share capital of the NABARD by Rs.500 crore, taking the Reserve Bank's total contribution to Rs.l,OSO crore. These steps would substantially enhance

Report on Trend and Progress of Banking in India, 1996-97

the refinancing capablllty of NABARD. In view of the imperfections in the credit market and the imperative need for funding agriculture, small-scale industry, small business and the poverty alleviation programmes, t he prescription of 40 per cent of net bank credit to the priority sector as well as the two concessional rates of interest for small loans have been retained. The priority sector target of 40 per cent of net bank credit was achieved by December 1 WG, by all banks taken together.

1.4 In recent years, a deliberate policy is being pursued to channelise any shortfall in priority sector lending by banks into rural InFrzlstructure investment through NABARD and Small Industries Development Bank of lndia (SIDBI). Accordingly, from the Rural Infrastructure Development Fund (RIDF I) instituted with NABARD, a sum of Rs. 1,183.12 crore was disbursed during 1996-97 to 18 State Governments as against a sanction of Rs.2,010.05 crore to 23 State Governments. In addition, a sanction of Rs. 2,646.88 crore was extended to 16 State Governments under the newly constituted RlDF II a t NABARD with a corpus of Rs. 2,500 crore. A sum of Rs. 291 crore was disbursed to 12 States till the end of March 1997 under this Fund. The Union Budget 1997-98 has further proposed t o launch RlDF I l l in 1997-98 with a corpus of Rs. 2,500 crore. The Reserve Bank had advised public sector banks to prepare Special Agricultural Credit Plans for the year 1996-97. The disbursements to the agriculture sector under such plans amounted to Rs12,782 crore in 1996-97 as against Rs. 10,172 crore in 1995-96. Three 'in-principle' approvals have been accorded so far by the Reserve Bank for setting up of Local Area Banks (LABS) on the lines of the guidelines established for the purpose in August 1996. The process of revamping the Regional Rural Banks (RRBs) was strengthened further during 1996-97 with fresh initiatives which included liberal branch licensing policy, rationalisation of investment guidelines, and prescription of priority sector target in place of target/non-target group approach from the

year 1997-98. Besides, with the release of budgetary provision of Rs.200 crore, 34 RRBs were taken up for capital restructuring in Phase Ill in addition to the assistance provided to 16 select RRBs during 1994-95 and 1995-96.

3. Financial Sector Reform Measures

lnterest Rate Deregulation

1.5 lnterest rate regime in lndia has undergone a rapid transformation over the years. The structure of interest rates, which was extremely complex, has now been rationalised. Banks are free t o determine interest rates on domestic term deposits of 30 days and above, effective October 22, 1997. The lending rates are also generally free except for export financing, loans upto Rs.25,000 and for loans between Rs.25,000 and Rs.2 lalth. The money market rates have been completely freed. The most significant development, however, is the reactivation of the Bank Rate as an instrument t o transmit signals of Monetary Policy and as a reference rate for influencing the direction of interest rate movement in the economy.

Bank Rate

1.6 Effective April 16, 1997, all interest rates on advances from the Reserve Bank were specifically linked to the Bank Rate. lnterest rate on term deposit of banks between 30 days to one year was also linked to Bank Rate. Following the one percentage point reduction in Bank Rate each in April, June and October 1997, there has been a corresponding reduction in deposit rates and Prime Lending Rates (PLR) of banks. Thus, the Bank Rate has served the function of signalling rate s o far. With the comfortable liquidity position of banks and the need to signal the market for further scope of reduction in interest rates, Bank Rate was further reduced (with effect from October 22, 1997) from 10 per cent per annum to 9 per cent per annum.

Rates on Domestic Term Deposits

1.7 Effective from july 2, 1996, the domain

Banking Developments and Pollcy Perspectives

of prescribed ceiling rate on deposits was made applicable only to maturities up to one year while the minimum maturity period was reduced to 30 days. With the aim of achieving a greater alignment of interest rates on term deposits with the overall interest rate structure, effective from April 16, 1997, the interest rate on domestic term deposits of maturity of 30 days and up to one year was changed from 'not exceeding 10.0 per cent per annum' (with effect from October 22, 1996) to 'not exceeding Bank Rate minus two percentage points per annum'. With the Bank Rate ruling at 11 per cent, th is implied a rate of 'not exceeding 9 per cent per annum'. Following a one percentage point cut in the Bank Rate from the close of business on June 25, 1 997, the effective ceiling rate was set at 8 per cent for term deposits of maturity upto one year from that date. With the prior approval of their respective Boards, banlts could offer different interest rates on deposits of varying maturities. For s u c h deposits with maturity up to three years, the deregulated interest rates ruled between 10.5 per cent and 1 1.5 per cent while for deposits of over three years, the rate was placed at 12.0 per cent. In order to give full fieedom to banks to determine the interest rates on term deposits, effective October 22, 1997, banks were allowed to fix their own interest rates on term deposits of 30 days and above.

R;l tes on Non-Residen t Bank Deposits

1.8 In a move to better align the interest rate and maturity structure of Non-Resident (External) Rupee (NRE) term deposits with that of domestic term deposits, t h e interest rates on NRE term deposits of over one year maturity have been freed from April 16, 1997. Besides, the interest rate offered o n NRE term deposits of G months and upto one year was prescribed at 'not exceeding Bank Rate minus 2 percentage points', i.e., in effect, 'not exceeding 9.0 per cent per annum' as against the earlier ceiling of 12.0 per cent per annum. The effective ceiling rate on NRE deposits further went down to 8.0 per cent per annum

with one percentage point reduction in the Bank Rate From June 25, 1997. Effective from September 13, 1997, interest rates on NRE deposits were completely freed for all maturities. However, the minimum maturity period of NRE deposits will continue to remain at six months.

1.9 With a view to imparting more flexibility, banks were allowed to determine interest rates on Foreign Currency Non- Resident (Banks) Accounts Scheme [FCNR (B)] deposits with effect from April 16, 1997, subject to a ceiling prescribed by the Reserve Bank from time to time. With a view to providing further flexibility to banks, effective October 22, 1997, banlts have been allowed to offer interest rates on such deposits at rates not more than the LIBOR prevailing on the last working day of the previous week for relevant maturity and currency.

lnterest Rate on Cash Balances Maintained with the Reserve Bank under CRR

1.10 The effective rate of interest on the eligible cash balances with the Reserve Bank worl<s out to 3.5 per cent under the two-tier formula first introduced in March 23, 1990. As part of rationalisation measures, with effect from October 25, 1997, banks will be paid an interest rate of 4 per cent per annum on t h e total eligible balances maintained with t h e Bank.

Lending Rates

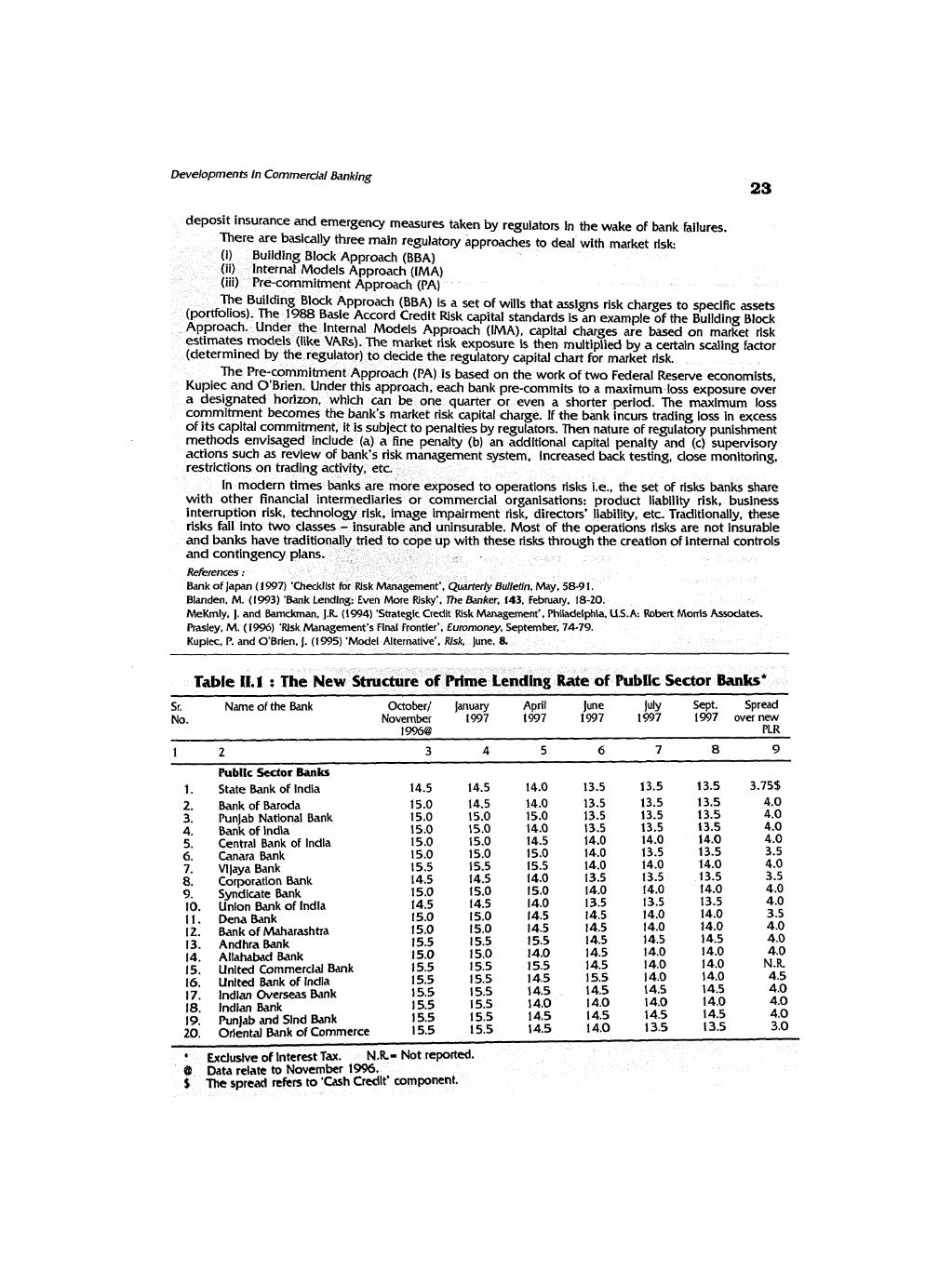

1.1 1 Despite the comfortable liquidity situation brought about by strong growth in bank deposits and substantial reduction in CRR, lending rates remained sticky downwards during t h e first half of 1996-97. In t h e second half of t h e year, however, following a sizable cut in CRR and maximum term deposit rate, prime lending rates (PLRs) of public sector banks softened to a range of 1 4.0- 1 5.5 per cent by end-March 1997 from 16.5 per cent a t end-March 1996. In order to ensure transparency and thus contain the unduly high spread over PLR, banks were directed in

Report on Trend and Progress of banking in Indla, 1996-97

October 1996 to announce the maximum spread over PLR along with the PLR for all advances other than consumer credit. Different PLRs and spreads were allowed as between cash credit and demand loans. The announced spreads over PLRs were placed within a range of 3.0-4.5 percentage points. PSBs generally have lower PLRs and spread compared with Indian private sector and foreign banks. With effect from October 22, 1997, prescription of a fixed lending rate of 1 3.5 per cent for credit limit of over Rs.25,000 and upto Rs.2 lakh has been changed to prescription of a ceiling rate of 'not exceeding 13.5 per cent'.

interest K~ tes on Term Loans of 3 years and Above

1.12 Banks were allowed freedom to fix specific rates for cash credit and loans. Effective October 22, 1997, banks have been permitted to announce, with the approval of their Boards, specific Prime Term Lending Rates (PTLR) for term loans of 3 years and above.

Export Credit

Pre-S/~ipn?en t Rupee Export Credit

1.13. Effective October 22, 1997, the interest

90 days was changed from 1 3.0 per cent per annum to 'not exceeding 13.0 per cent per annum' effective April 17, 1997. Effective September 1 2, 1997, as a measure to boost exports, the interest rate on post-shipment rupee export credit was reduced by one percentage point to 1 1 per cent (1 2 per cent earlier) and for the period beyond 90 days up to six months, the rate was reduced to 13 per cent (14 per cent earlier)'. Effective October 22, 1997, it was decided that banks should charge an interest of 13 per cent per annum only for the period beyond 90 days and not from the date of advance.

Interest Rate on Bank Finance to Housing Finance intermediary Agencies

1.1 5 As part of the process of deregulating interest rates, the stipulation that banks should extend finance to housing finance intermediary agencies for lending to ultimate beneficiaries at 1.5 percentage points below each bank's prime lending rate for credit limits of over Rs.2 lalch was withdrawn with effect from October 22, 1997.

Changes in Statutory Pre-emptions

Cash Reserve Requirements

rate on pre-shipment export credit was 1-16 Consistent with the medium-term reduced one percentage point the objective, the average Cab Reserve Ratio board: ~re-shipment rupee export credit upto (CRR) w a brought down in phases to 10.0

days reduced from per cent to per per cent by January 1997. In effective terms, cent and such credit 180 and the ratio was lower at 9.5 per cent in March

270 days from l5 per cent to l4 per 1997. The need for augmenting the lendable cent. resources of banks prompted the reduction in

Post-Shipment Rupee Export Credit

1.14 As part of a move to give general operational freedom to banks and also taking into consideration the willingness of some banks to extend post-shipment export credit at lower interest rate if export proceeds are realised in shorter periods, the interest rate on post-shipment rupee export credit up to

CRR from 14.0 per cent to 1 3.5 per cent on April 27, 1996 and further to 13.0 per cent o n May 1 1 , 1996. The C M was lowered further to 12.0 per cent with the same objective from July 6,1996. Considering the advantages of rationalisation of the CRR-export refinance trade-off, the CRR was further reduced by one percentage point in two phases of 0.5 percentage point each to 1 1.0

After September 13, 1997, the interest rates charged as a temporary measure, refer to the date of actual advance as against the earlier position when it referred to the date of shipment.

Banking Developments and Policy Pe~pectives

per cent effective from October 26, 1996 and November 9, 1996, respectively. These reductions of CRR freed cash balances and augmented the lendable resources of t h e scheduled commercial banks by about Rs. 13,575 crore during 1996-97 upto November 1 996. Finally, CRR was brought down to 10.0 per cent in two phases of 0.5 percentage point each fiom the fortnights beginning January 4 and 18, 1997, respectively. This measure released additional primary liquidity of Rs. 4,275 crore for the SCBs. Thus, in all, t h e total amount released through CRR cuts amounted to Rs. 1 7,850 crore during t h e fiscal year 1986-97. These measures have significantly strengthened the liquidity position of t h e SCBs. In accordance with t h e stance of Monetary Policy of phased reduction in statutory pre-emption of banks' resources, a 2 percentage point reduction in CRR (in eight phases) was announced on October 21, 1997 with the first reduction effective October 25, 1997. The eight-phase reduction in CRR is expected to release Rs.9,600 crore of liquidity to the banking system.

Removal of Reserve Requirements on Inter- Ban/< Liabilities

1.17 With a view t o facilitating the development of a more realistic rupee yield curve and term money market, inter-bank liabilities were exempted (except for a statutory minimum) from maintenance of CRR of 10 per cent, effective from April 26, 1997, thereby releasing lendable resources to the tune of Rs. 950 crore. As against the earlier system where positive net inter-bank liabilities were required to be part of the NDTL for the purpose of CRR, the present system exempts the inter-bank liabilities from s u c h calculation, provided a minimum CRR of three per cent is maintained on the overall NDTL inclusive of net inter-bank liabilities.

Reserves on Non-Resident Deposits

1'18 In order to bring all t h e liabilities under the scope of reserve requirements, effective kom April 26, 1997, non-resident deposits,

hitherto exempted from maintenance of CRR, were brought under the CRR prescription with a requirement of 10 per cent CRR on the incremental liabilities in respect of FCNR(B), NRE and NRNR deposit schemes over the level outstanding as on April 1 1, 1997.

Statutory Liquidity Ratio

1 . 1 9 With progressive rationalisation of the statutory pre-emption of lendable resources of banks facilitating their allocation on commercial principles, the overall effective Statutory Liquidity Ratio (SLR) came down to 26.7 per cent at t h e end of March 1997 from 28.0 per cent a year ago. The SLR requirement o n outstanding NRE deposits was reduced to 25.0 per cent from 30.0 per cent, with effect from April 13, 1996. Besides, all SCBs (excluding RRBs) were exempted from maintenance of SLR on liabilities to banking system (except for statutory minimum), effective April 26, 1997. Effective October 22, 1997, the multiple prescriptions of SLR were withdrawn in favour of a single SLR which was placed at 25 per cent.

1.20 With a view to enhancing the liquid assets at the disposal of NBFCs, increased liquidity requirement was prescribed in June 1997. Accordingly, Loan and Investment companies which are presently maintaining liquid assets at 5 per cent will be required to maintain 7.5 per cent and 10.0 per cent of their deposits in Government and other approved securities, effective January 1 and April 1 , 1998, respectively. For other NBFCs, t h e liquidity requirement is raised to 12.5 per cent and 15 per cent, respectively of their deposits, effective the above dates. The resultant increase i n liquid assets will strengthen the protection available to the depositors and ensure healthy functioning of the NBFCs. In a bid to keep these liquid assets unencumbered, the Reserve Bank directed that these securities be kept in the custody of a scheduled commercial bank designated by t h e NBFCs for th is purpose.

Report on Trend and Progress of Banking in India, 1996-97

Morley Market Developments

Certiflcc~ te of Deposits

1.21 With a view to widening the money market, the minimum size of issue of Certificate of Deposits (CDs) to a single investor was reduced From Rs. 10 lakh to Rs.5 lakh with effect from October 22, 1997. CDs above Rs.5 lakh will be in multiples of Rs. 1 lakh.

Routing of Tr<~nsactions Through Primary Dealers

1.22 The Monetary and Credit Policy announced on October 2 1 , 1997 also reduced the minimum lending limit in the call money market routed through Primary Dealers from Rs. 10 crore to Rs.5 crore.

Investment by Money Market Mutual Funds

1.23 Money Market Mutual Funds (MMMFs) are required to invest exclusively in call/notice money, Certificate of Deposits (CDs), Commercial Paper (CP), commercial bills arising out of genuine trade/commercial transactions and Treasury bills and dated Government securities having an unexpired maturity upto one year. With a view to providing flexibility for MMMF Schemes, effective October 22, 1997, MMMFs have been allowed to invest in rated corporate bonds and debentures with a residual maturity upto one year, within prescribed prudential limit.

Improving Credit Delivery System

Loan System for Delivery of Ban/< Credit

1.24 As a measure of imparting an element of discipline in the utilisation of bank credit, the percentage of 'loan component' in the working capital credit limit had been enhanced i n stages for borrowers with working capital credit limits of (a) Rs. 10 crore or above and less than Rs. 20 crore and (b) Rs. 20 crore or above. With effect from October 22, 1997, the 'loan component' level has been made uniform a t 80 per cent for the above categories

of borrowers.

Bill finance for Settlement of Dues of SSI Suppliers

1.25 With a view t o ensuring prompt settlement of dues of SSI units and also for encouraging bill culture, banks were advised to ensure that with effect from January 1, 1998, of the total inland credit purchases of the borrowers, not less than 25 per cent should be through bills drawn on them by the concerned sellers.

Bridge Loans

1.26 Banks have been permitted to sanction bridge loans to companies against expected equity flows/issues effective October 22, 1997. As a prudential measure, it has been stipulated that period of such bridge loans should not exceed one year and should be accommodated within the ceiling of 5 per cent of incremental deposits prescribed for individual bank's investment in shares.

Debt Market

Government Securities Market

Primary and Satellite Dealers

1.27 The institutional infrastructure in Government securities market has been strengthened with the system of Primary Dealers (PDs) announced in March 1995 and that of Satellite Dealers (SDs) in December 1996.

1.28 At present six PDs are in operation. With a view to providing incentives to develop t h e secondary market in Government securities, effective July 10, 1 996, the Reserve Bank introduced 'a system of payment of commission t o PDs on their purchases (including devolvement) of Government securit ies th rough subscriptions in all f loatations in t h e primary market. Subsequently, on June 2, 1997, the system of payment of commission was replaced with payment of underwriting fee on underwriting amount offered by PDs on voluntary basis,

Banking Developments and Policy Perspectives 7

through competitive bidding. In order to improve their liquidity position, PDs were allowed to tap the Commercial Paper (CP) market in September 1996. They were also permitted to participate in the call/notice/term money market, both as lenders and borrowers, so as to impart flexibility in the use of their funds. It was also announced that the norm of five per cent of total transactions in Government securities entered into by banks during a year for each of the approved broken would not be applicable to banks dealing through PDs. In April 1 991, certain institutions were given access to the calllmoney market as lenders under specified restrictions including the provision that the transactions should be routed through the Discount and Finance House of lndia (DFHI). With effect from the fortnight beginning April 26, 1997 the facility of routing such transactions was extended to all the Primary Dealers. At the same time, the minimum size of a transaction was reduced from Rs. 20 crore to Rs. 10 crore. This has been further reduced to Rs. 5 crore effective October 22, 1997.

Introduction of 28-day Treasury Bills

1 2 In order to help the cash management requirements of various segments of t h e economy, the Monetary and Credit Policy for the second half of 1997-98 announced t h e introduction of 28-day Treasury Bill on auction.

In troduction o f Uniform Price Auction

1.30 With a view to eliminating the problem of 'winners' curse' and broaden the market participation, the Monetary and Credit Policy for the second half of 1997-98 announced the introduction of uniform price auction method in respect of 91 -day Treasury Bills.

Issue Amounts to be Notified in respect of all Auctions

1.31 The amounts of issue of 91-day Treasury bills and dated securities are presently indicated, while the amounts are not notified In respect of 364-day and 14-day Treasury Bills auctions. The Monetary and Credit Policy

for the second half of 1997-98 announced the introduction of the practice of notifying amounts in the case of all the auctions, including 364-day and 14-day Treasury Bills.

Investments by FIls with 30 per cent Ceiling in Government Dated Securities

1.32 Presently, Foreign Institutional Investors (Flls) in t h e category of 100 per cent debt funds are permitted to invest in Government dated securities. The Monetary and Credit Policy for the second half of 1997-98 announced that Fils registered with SEBI and approved by t h e Reserve Bank will be allowed to invest in Government dated securities within a ceiling of 30 per cent.

Retailing of Government Securities by Banks

1.33 In order to promote the retail segment and to provide greater liquidity to retail investors, it was announced in the Monetary and Credit Policy on October 21, 1997 that banks will be allowed to freely buy and sell Government securities on an outright basis at the prevailing market prices, without any restriction on t h e period between sale and purchase.

Bonds and Private Debt Marltet

Ready Forward Transactions in PSU Bonds and Private Debt Securities

1.34 The Monetary and Credit Policy for the second half of 1997-98 announced that ready forward transactions will be allowed in PSU bonds and private corporate debt securities if they are held in dematerialised form in a depository and t h e transactions are done in recognised Stock Exchanges.

Prudential Regulations and Supervision

Pruden tial Accounting Standards