Research Report_EFD_April 2016- Edited.pdf - Business ...

46

Research Report on Introduction and Adoption of Electronic Fiscal Devices (EFDs) by the Business Community in Tanzania: Lessons Learned, Opportunities and Challenges for Dialogue Process Submitted to: The Centre for Policy Research & Advocacy (CPRA) University of Dar es Salaam Business School (UDBS) By: Dr. Siasa Issa Mzenzi 1 , Dr. Mariam Nchimbi, Dr. Deogratius Mahangila, Mr. Said Suluo, and Mr. Simon Edward Department of Accounting University of Dar es Salaam Business School (UDBS) Dar es Salaam, TANZANIA April 2016 1 Contacting researcher: [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Research Report_EFD_April 2016- Edited.pdf - Business ...

Research Report on

Introduction and Adoption of Electronic Fiscal Devices (EFDs) by the Business

Community in Tanzania: Lessons Learned, Opportunities and Challenges for

Dialogue Process

Submitted to:

The Centre for Policy Research & Advocacy (CPRA)

University of Dar es Salaam Business School (UDBS)

By:

Dr. Siasa Issa Mzenzi1, Dr. Mariam Nchimbi, Dr. Deogratius Mahangila, Mr.

Said Suluo, and Mr. Simon Edward

Department of Accounting

University of Dar es Salaam Business School (UDBS)

Dar es Salaam, TANZANIA

April 2016

1 Contacting researcher: [email protected]

i

Acknowledgement

This study was funded by BEST-Dialogue through the Centre for Policy Research &

Advocacy (CPRA) of the University of Dar es Salaam Business School. The authors

are very grateful to these institutions. We also thank our respondents who spent their

valuable time answering our questions. Furthermore, we are grateful to the University

of Dar es Salaam for giving us research clearance. However, the views expressed in

this research should not be attributed to these institutions.

ii

Executive Summary

Objective - This study was aimed at obtaining an in-depth understanding of the

adoption and implementation of EFDs by the business community in Tanzania. In

particular, this research aimed to achieve the following objectives: (1) To analyse the

mechanisms and/or processes used to adopt EFDs and assess their impact and/or

influence on the level of compliance by the business community in Tanzania (2) To

analyse the challenges of using EFDs and the methods used by the business

community to channel their concerns; and (3) To identify opportunities and

challenges of the dialogue process.

Methodology – This research was conducted using mainly qualitative inquiry. Three

main sources of data were used, namely, documentary sources, in-depth interviews

and observation. The collected data was analysed using the qualitative approach

recommended by Strauss & Corbin (1998).

Findings –The findings generally show that the mechanisms used to adopt and

implement EFDs were inappropriate. This was mainly attributed to the failure of the

responsible officials to actively involve all major stakeholders in the process. As a

result, the adoption and implementation EFDs in both phases faced a number of

challenges, including (1) the high cost of EFDs (2) network problems (3) poor quality

of paper rolls (4) the location of approved EFD suppliers (5) poor quality of EFDs and

weak batteries (6) the lack of provision of an after-sales service (7) compatibility

issues (8) limited technical functions and lack of technicians (9) the reluctance of

traders to use EFDs (10) limited implementation and coverage of EFDs and (11) weak

enforcement of EFD-related laws and regulations. Since appropriate platforms for

dialogue were unavailable, in most cases, traders used protests to communicate these

challenges. In this regard, the adoption and implementation of EFDs created the

following opportunities for the dialogue process: (1) debate on the appropriate public

finance and taxation policies (2) appropriateness of EFD-related laws and regulations

(3) debate on how the noted challenges can be addressed (4) the role of the media in

influencing the usage of EFDs (5) debate on the appropriate platforms for discussing

matters relating to EFDs and (6) debate on the roles and responsibilities of the various

stakeholders. However, these opportunities may face the following challenges: (1) the

absence of reliable dialogue platforms (2) the possibility of attracting a low number of

participants (3) difficulty in reaching a consensus on major contentious issues (4)

failure of the responsible parties to implement the agreed resolution and (5) the

possibility that the dialogue may consume too much time and money. Thus, it is

important to institute reliable dialogue mechanisms to address the noted challenges.

Practical Implications – The findings indicate that EFDs could potentially increase

tax revenue collection when implementation challenges are adequately addressed.

Originality/value – Most studies on EFDs have focused on developed countries; this

is one of the few qualitative studies which focused on an emerging economy

(Tanzania). Also, unlike the previous study by TCCIA&PAMOMA (2012), which

focused on VAT-registered traders only, this study involved both VAT and non-VAT-

registered traders.

Keywords: EFDs, tax compliance, tax administration

iii

Table of Contents

Acknowledgement .......................................................................................................... i

Executive Summary ....................................................................................................... ii

Table of Contents ......................................................................................................... iii

List of Tables ................................................................................................................. v

List of Figures ................................................................................................................ v

Acronyms ...................................................................................................................... vi

1.0 Introduction ......................................................................................................... 1

1.1 Background Information ........................................................................................... 1

1.2 Research Objectives .................................................................................................. 2

2.0 Research Methodology ....................................................................................... 2

2.1 Methodological Approach ......................................................................................... 2

2.2 Data Collection and Analysis .................................................................................... 3

3.0 Findings............................................................................................................... 4

3.1 Adoption and Implementation of EFDs in Tanzania ................................................. 4

3.1.1 Historical Background of EFDs in Tanzania ..................................................... 4

3.1.2 Technical Preparation of EFDs.......................................................................... 5

3.1.3 Types of EFD Applicable in Tanzania .............................................................. 7

3.1.4 EFDs Phase I ..................................................................................................... 8

3.1.5 EFDs Phase II .................................................................................................. 10

3.2 Challenges of Implementing EFDs ......................................................................... 14

3.2.1 Cost of EFDs ................................................................................................... 14

3.2.2 Network Problems ........................................................................................... 15

3.2.3 Poor Quality of Paper Rolls ............................................................................. 16

3.2.4 The Location of Approved Suppliers .............................................................. 17

3.2.5 Poor Quality of EFDs and Weak Batteries ...................................................... 18

3.2.6 The lack of Provision of an After-Sales Service ............................................. 19

3.2.7 Compatibility Issues ........................................................................................ 20

3.2.8 Limited Technical Functions and Lack of Technicians ................................... 20

3.2.9 Reluctance of Traders to Use EFDs ................................................................ 21

3.2.10 Limited Coverage and Implementation of EFDs ............................................. 23

3.2.11 Weak Enforcement of the Laws and Regulations............................................ 24

3.3 Lessons Learnt from the Adoption and Implementation of EFDs ........................... 24

3.3.1 Importance of the Participatory Approach: ..................................................... 25

3.3.2 Change Management Requires Investment ..................................................... 25

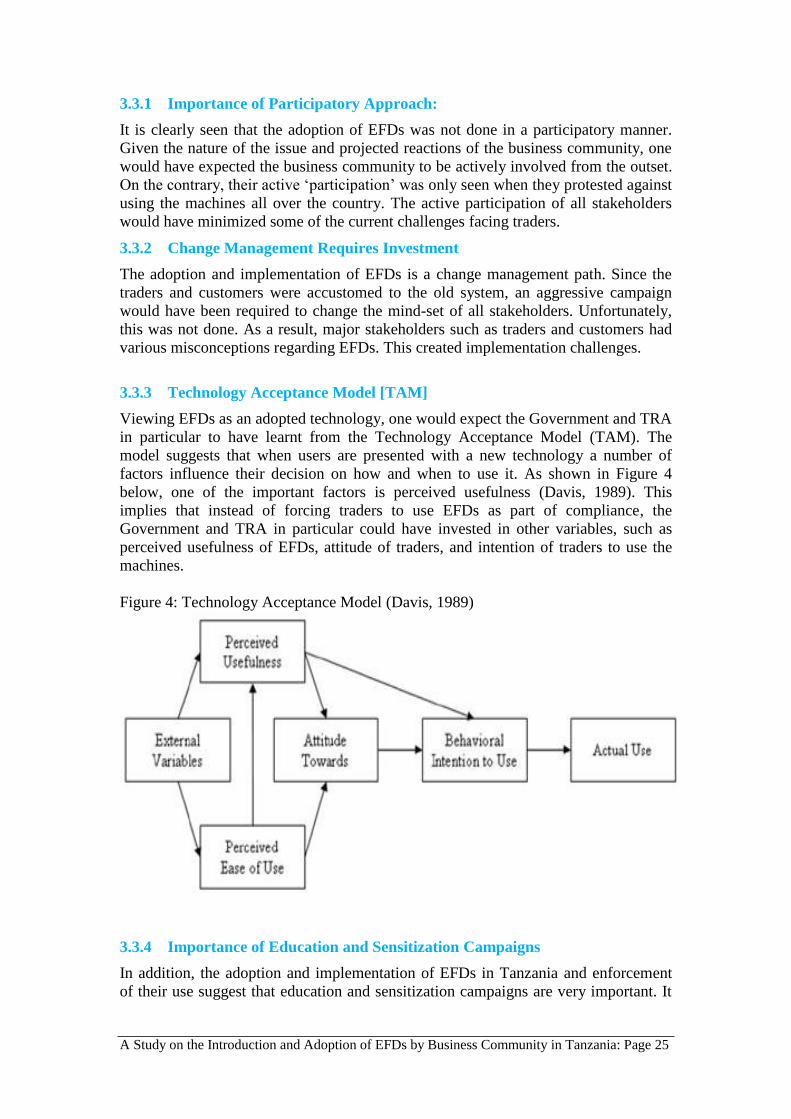

3.3.3 Technology Acceptance Model [TAM] .......................................................... 25

iv

3.3.4 Importance of Education and Sensitization Campaigns .................................. 25

3.3.5 Importance of Appropriate Platforms .............................................................. 26

3.3.6 Tax is Burdesome to Taxpayers ...................................................................... 26

3.3.7 Importance of Investing in Human Resources ................................................ 26

3.3.8 Having a Clear Understanding of the Implementation Phases ........................ 26

3.3.9 Importance of the Media ................................................................................. 27

3.3.10 Unique Role of Customers .............................................................................. 27

3.4 Opportunities and Challenges for the Dialogue Process ......................................... 27

3.4.1 Opportunities for the Dialogue Process ........................................................... 27

3.4.2 Challenges of the Dialogue Process ................................................................ 28

4.0 Conclusion and Recommendations ................................................................... 29

4.1 Conclusion ............................................................................................................... 29

4.2 Recommendations ................................................................................................... 30

4.2.1 Recommendations for the Government ........................................................... 30

4.2.2 Recommendations for TRA ............................................................................. 31

4.2.3 Recommendations for the Approved EFDs Suppliers ..................................... 32

4.2.4 Recommendations for the Approved EFDs Manufacturers ............................. 33

4.2.5 Recommendations for the Network Providers-Vodacom and Airtel ............... 33

4.2.6 Recommendations for the Traders [EFD Users] ............................................. 34

4.2.7 Recommendations for the Customers .............................................................. 34

4.2.8 Recommendations for the Media ..................................................................... 35

Appendices ................................................................................................................... 36

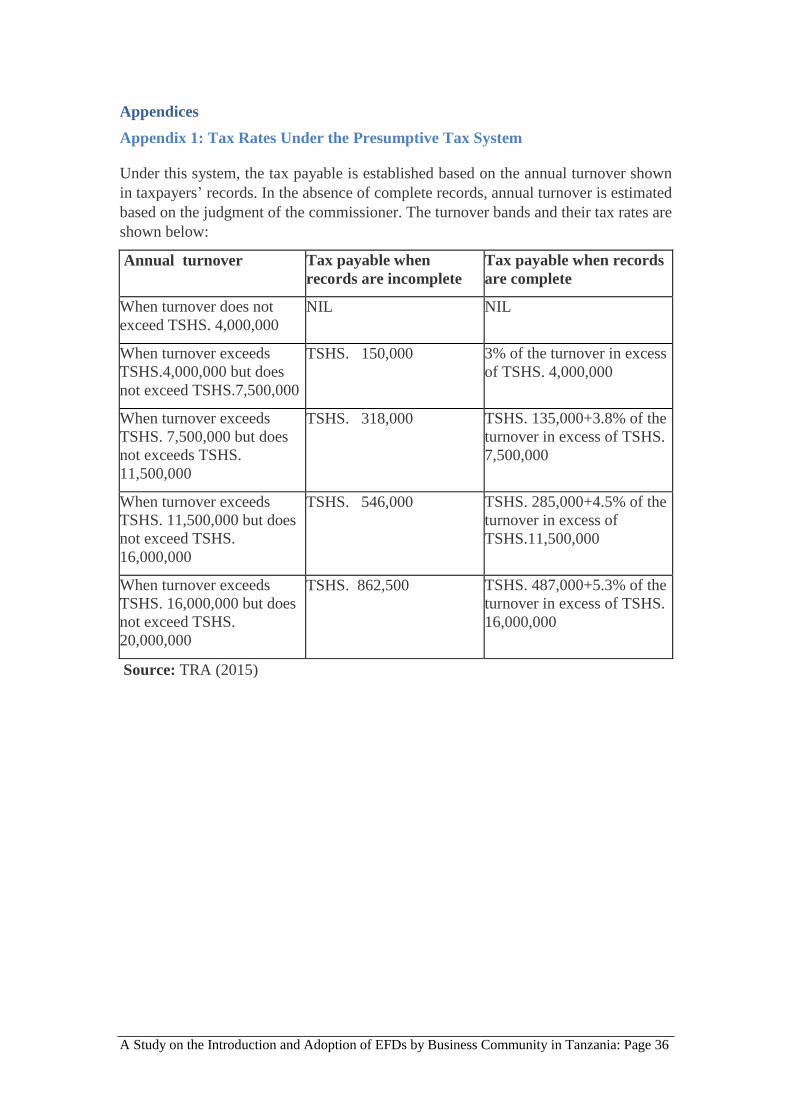

Appendix 1: Tax Rates Under the Presumptive Tax System .............................................. 36

Appendix 2: Arrest of the Chairman of the Traders’ Association ....................................... 37

Appendix 3: Picture of EFDs [Sample] ............................................................................... 37

References .................................................................................................................... 39

v

List of Tables

Table 1: Reviewed Documents [Selected] ..................................................................... 3

Table 2: Profile of Respondents ..................................................................................... 4

Table 3: List of the Approved EFD Models Distributed in Tanzania ............................ 5

Table 4: List of the Approved Manufacturers of EFDs in Tanzania ............................. 6

Table 5: List of the Approved Suppliers of EFDs in Tanzania ...................................... 6

List of Figures

Figure 1: Domestic VAT Collection in Mainland Tanzania ........................................ 10

Figure 2: Some Traders Protesting against Usage of EFDs ......................................... 11

Figure 3: Traders Protesting against Usage of EFDs ................................................... 13

Figure 4: Technology Acceptance Model (Davis, 1989) ............................................. 25

Figure 5: Potential EFD Stakeholders to participate in the Dialogue Process ............. 28

vi

Acronyms

CPRA Centre for Policy Research & Advocacy

EFDs Electronic Fiscal Devices

IT Information Technology

SMEs Small and Medium Enterprises

TAM Technology Acceptance Model

TAPSOA Tanzania Petrol Stations Operators Association

TAS Tanzanian Shillings

TCCIA Tanzania Chamber of Commerce, Industry and Agriculture

TRA Tanzania Revenue Authority

TTA Tanzania Trade Association

VAT Value Added Tax

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 1

1.0 Introduction

1.1 Background Information

The primary concern of any tax administration is how to increase tax compliance

without causing economic distortion in the economy. Taxes are “the compulsory,

unrequited payments to the general government sectors” (Messere, & Owens, 1987,

p.37). Tax compliance includes four issues: registration of the taxpayer, filling in tax

returns to declare tax liability, paying taxes on time, and submission of complete

information to the tax authority (Kirchler et al. 2007; Casey & Castro, 2015). To

increase tax compliance, tax administrations have increasingly been using information

technology (IT) as a key enabler in controlling tax evasion (Casey & Castro, 2015).

Tax evasion is the tendency of people to reduce their tax liability illegally (Allingham

and Sandmo,1972). One of the ways taxpayers use to evade tax is to manipulate their

records or not provide sales receipts, resulting in the under-declaration of taxable

revenue. Consequently, the Tanzania Revenue Authority (TRA) adopted the

Electronic Fiscal Device (EFD) to “combat non-compliance, particularly concerning

sales and value added tax (VAT) payable on sales” (Casey & Castro, 2015, p. 7). An

EFD is a machine designed for use in business for efficient management control in

areas of sales analysis and stock control which conform to the requirements specified

in the Valued Added Tax (Electronic Fiscal Devices) regulations), 2010 and the

Income Tax (Electronic Fiscal Devices) Regulation, 2012). Using the machine, the

TRA can monitor business transactions in real time as they are recorded via the

internet. Thus, effective use of EFDs enhances two components of tax compliance:

submission of complete information on time, and declaration of accurate tax returns

when the tax is charged on sales as in the case of VAT.

Despite the above seemingly good promise of EFDs, most businesses in Mainland

Tanzania perceive their introduction to be burdensome. This is attributed to the

challenges faced by traders during adoption and implementation of EFDs in the

country. In particular, the deployment of EFDs faced a number of challenges,

including battery problems, the lack of a Swahili EFD version, inadequate training in

how to use them, network and printer failure, the issuing of inferior receipts, and slow

repairs of EFDs (TCCIA& PAMOMA, 2012; Weru at al., 2013; Ikasu, 2014).

Similarly, immediately after their introduction in 2011, most EFDs had network

problems, which limited submission of important reports to TRA, and many failed to

do so (TCCIA & PAMOMA, 2012). Also, as a result of inadequate knowledge and

the skills needed for using EFDs, many businesses made wrong entries, resulting in

the declaration of higher revenue than intended, in which case sometimes the

additional tax paid was not rectified by the TRA. Furthermore, many businesses

reported the absence of maintenance services at their business premises as most

suppliers are located in major cities and towns such as Dar es Salaam, Mwanza,

Arusha and Mbeya.

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 2

Therefore, some businesses have been reluctant to use EFDs, leading to a

confrontation between taxpayers (traders) and TRA. Despite numerous attempts by

TRA to resolve these misunderstandings through negotiation, confrontation has

continued, which has caused traders to strike in many parts of the country.

Unfortunately, strikes and shop closures cost the government an estimated loss of tax

of Tshs 3 billion a day (Malanga, 2015), and denied customers much-needed goods.

In an attempt to address the matter, in early 2015, the Government filed a case against

some business leaders for allegedly mobilising their counterparts to boycott the

implementation of EFDs. As of now, the business community still has concerns about

the usage of EFDs.

Despite this, rigorous research on the adoption and implementation of EFDs is

lacking. What research there is has tended to focus on the challenges of EFDs

(TCCIA & PAMOMA, 2012; Ikasu, 2010) and their impact on VAT compliance

(Sagas, Nelimalyani, and Kosgeikimaiyo, 2015; Casey and Castro, 2015). As a result,

evaluation of EFDs from adoption to implementation is lacking. Also, little is known

about how the responsible parties such as TRA and the business community engage

with each other to address the noted challenges of EFDs. Similarly, the manner in

which each party addresses the claimed challenges and their impact on the level of

compliance is not known. Therefore, this study traces the adoption and

implementation of EFDs in Tanzania and provides recommendations for improving

the level of compliance. This study focused on both VAT and non-VAT-registered

traders who are required to use EFDs and therefore extends the previous study done

by TCCIA& PAMOMA (2012) which focused on VAT-registered traders only.

1.2 Research Objectives

This study was aimed at obtaining an in-depth understanding of the pertinent issues

which characterized the introduction and adoption of EFDs by the business

community in Tanzania so as to identify the opportunities and challenges of the

dialogue process. It explored relevant issues from the different groups, namely, the

business community and their associations, tax officials and other stakeholders. In

particular, this research aimed to achieve the following objectives: (1) To analyse the

mechanisms and/or processes used to adopt EFDs and assess their impact and/or

influence on the level of compliance by the business community in Tanzania (2) To

analyse the challenges of using the EFDs and the methods used by the business

community to voice their concerns; and (3) To identify the opportunities and

challenges of the dialogue process.

2.0 Research Methodology

2.1 Methodological Approach

This research was undertaken using mainly qualitative inquiry. The approach is

deemed appropriate when studying events which have multiple realities (Burrell and

Morgan, 1977; Strauss and Corbin, 1998). In fact, stakeholders have different views

on the introduction and implementation of EFDs in Tanzania. This warrants the use of

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 3

qualitative inquiry which ensures that multiple realities are captured (Parker, 2008). In

general, a study of this kind should include all stakeholders involved in the entire

process of adopting and implementing EFDs in Tanzania. These include TRA

officials, business associations, responsible ministries, individual traders, and EFD

manufacturers and suppliers. However, given the duration of this study some potential

respondents/stakeholders were not involved. For instance, all EFD manufacturers are

located outside the country and therefore were not included in the study. Similarly,

the bureaucratic nature of government offices made it difficult to interview some

important officials from the two ministries of Planning and Finance and Trade and

Industry. However, the views of those stakeholders were sought from those

interviewed. For instance, the concerns of EFD manufacturers were partly captured

through the interviews conducted with TRA officials, EFD suppliers and individual

traders.

2.2 Data Collection and Analysis

Three main data collection approaches were employed in this study, namely, review

of the relevant documentary sources, in-depth interviews with the relevant

stakeholders and observation. The review concentrated on those documents deemed

relevant for understanding the adoption and implementation of EFDs in Tanzania.

They excluded those which were consulted as part of the literature review. In

particular, the review included tax laws (statutes), policies and other relevant reports.

A list of the reviewed documents is shown in Table 1.

Table 1: Reviewed Documents [Selected]

S/N Name of the Document Source

1. The Value Added Tax Act, Cap 148 TRA

2. The Value Added Tax (Electronic Fiscal Devices)

Regulations, 2010 TRA

3. The Income Tax Act, Cap 332

4. The Income Tax (Electronic Fiscal Devices) Regulations,

2012

5. Taxes and Duties at Glance 2014/2015 TRA

6. A Guide to the Electronic Fiscal Devices (EFDs) for Non-

VAT Traders TRA

7. Regulatory Constraints on the Competitiveness of the

Tourism Sector in Tanzania: Platform for Advocacy by Zaki

Raheem and Alex Mkindi

The Tourism

Confederation of

Tanzania (TCT)

8. Challenges facing VAT-Registered Businesses in Operating

EFDs in Tanzania: A Pilot Study of Morogoro, Iringa and

Njombe Regions and a Small Part of Dar es Salaam Region

TCCIA,

Morogoro

The texts were read and relevant issues relating to the adoption and implementation of

EFDs in Tanzania were noted. To complement the issues raised in the reviewed

documents, the mode of operations in the visited approved suppliers was observed.

Then, 32 interviews with key informants from TRA, EFD suppliers, trade

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 4

associations, individual traders and members of business dialogue/advocacy platforms

were conducted. To get a complete picture of EFD implementation, customers were

also interviewed. Within each of these groups, we chose those (representatives) who

were directly involved in the adoption and implementation of EFDs in the country.

For instance, in the case of traders, the study interviewed those who are using EFDs

and those who might use them in future. To obtain a detailed understanding of the

complexities involved in each of the two phases of implementing EFDs, traders using

them in both phases were also involved. In particular, hotels, supermarkets, bureaux

de change, retail outlets, petrol stations and merchandising entities were included in

the interviews. TRA officials concerned with the management and operationalization

of EFDs were involved. In the case of trade associations, interviews were conducted

with members who were directly involved in negotiating with tax officials concerning

the application of EFDs. The following table shows the profile of the respondents.

Table 2: Profile of Respondents

Interviewees Number

TRA Officials 4

Approved EFD Suppliers 3

Customers 5

Members of Trade Associations 3

Traders [Supermarkets, petrol stations, Bureaux de Change, Retail, etc.] 15

Members of Advocacy/Dialogue Initiatives 2

Total 32

On average, the interviews took 70 minutes and focused on issues relating to the

adoption and implementation of EFDs in Tanzania. In particular, the interviewees

were asked to provide clarification on the background and rationale for the

introduction of EFDs, their implementation challenges and the mechanisms used to

engage the business community. For instance, during the interviews, questions such as

‘why did TRA decide to introduce EFDs’, ‘what would be regarded as challenges

hindering the implementation of EFDs’ and ‘was the business community effectively

engaged in the introduction and implementation of EFDs’ were asked. All interviews

were hand-written and analysed using the qualitative approach recommended by

Strauss &Corbin (1998).

3.0 Findings

3.1 Adoption and Implementation of EFDs in Tanzania

3.1.1 Historical Background of EFDs in Tanzania

The idea behind EFDs started many years ago when the Government of the United

Republic of Tanzania intended to enhance businesses’ record keeping for various

purposes including taxation. In 2000, the Government through the Ministry of

Finance and TRA introduced the Electronic Cash Register. This decision was made

after the Government learnt that the same system was introduced in Zambia, which

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 5

increased its revenue by 20 percent. Electronic Cash Registers, which were introduced

to VAT-registered traders only, were very successful initially. They were used mainly

by supermarkets and other large businesses for both internal and external purposes.

Internally, they were used as part of record keeping and an internal accountability

check. The same register was used externally for audit and tax purposes. However,

after some time, the usage rate became very low. Most traders abandoned the system

completely and lack of enforcement was regarded as the major reason for the failure.

As one TRA official noted, ‘we did not put in place effective enforcement mechanisms

to ensure that traders comply with the introduced Electronic Cash Register’.

After the failure of the Electronic Cash Register and following major restructuring of

the then Tax Department to become the current TRA, the Government embarked on a

project which would enhance domestic tax revenue collection. In the course of

implementing this, the Government and TRA learned that other countries were using

EFDs. As part of their learning, some TRA staff were sent to Kenya, Italy and

Ethiopia, which were using EFDs and were deemed appropriate for providing lessons

for Tanzania. Together with learning, the Government, and TRA in particular, started

undertaking various internal arrangements for successful implementation of EFDs,

including education and sensitization programmes for the traders.

3.1.2 Technical Preparation of EFDs

Since EFDs are fixed machines which cannot be used for any other purpose, and as

part of technical preparation, the Government decided to design the machine’s

specifications. The models included in the following Table have passed the Technical

Specifications Compliance Test and approved to be distributed in Tanzania:

Table 3: List of the Approved EFD Models Distributed in Tanzania

S/N Model Name of the Manufacturer Country of Origin

1. expert SX Daisy Technology Bulgaria

2. DP 25 Datecs Limited Bulgaria

3. TREMOLS Tremol Limited Bulgaria

4. JSMART Custom Engineering SPA Italy

5. PRIMA HCP d.o.o Serbia

6. DP 05 Datecs Limited Bulgaria

7. FUEL POS 500 Datecs Limited Bulgaria

8. DP 35 Datecs Limited Bulgaria

9. TREMOLM Tremol Limited Bulgaria

Source: TRA (2013)

Based on the approved EFD models to be distributed in Tanzania, a tender was

floated to the potential manufacturers of the machines to apply. In the first phase, four

(4) approved manufacturers were selected to produce the EFDs based on the

developed specifications. It is worth noting that all manufacturers were obtained from

outside Tanzania. A Memorandum of Understanding (MoU) between TRA and the

manufacturers was drawn up spelling out the rights and obligations of both parties.

Later, and especially after the introduction of EFDs Phase II, it was decided to

increase the number of manufacturers in order to cope with the increased demand for

EFDs. In this regard, four (4) additional manufacturers were added. Therefore, in

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 6

total, there are eight (8) TRA-approved manufacturers of EFDs. The rights and

obligations of the approved manufacturers of EFDs are spelt out in Regulation 8 of

the Value Added Tax (Electronic Fiscal Devices) Regulations, 2010 and in Regulation

7 of the Income Tax (Electronic Fiscal Devices) Regulations, 2012. A list of the

approved manufacturers of EFDs in Tanzania is shown in the Table below:

Table 4: List of the Approved Manufacturers of EFDs in Tanzania

S/N Name of the Manufacturer Country of Origin

1. Custom Engineering SPA Italy

2. RCH SPA Italy

3. Dates Limited Bulgaria

4. Incotex Bulgaria

5. Archlik A.S. Turkey

6. Daisy Technologies Bulgaria

7. HCP d.o.o Serbia

8. Tremol Limited Bulgaria

Source: TRA (2013)

The same process was used to select suppliers of EFDs and six (6) were selected as

approved suppliers in the first phase of implementation. Later, and especially after the

introduction of EFDs Phase II, it was decided to increase the number of suppliers to

cope with the increased demand for EFDs and their related services. In this regard,

five (5) additional suppliers were included. Therefore, in total, there are eleven (11)

approved suppliers of EFDs in the country. As regards manufacturers, the rights and

obligations of EFD suppliers are described in Regulation 7 of the Value Added Tax

(Electronic Fiscal Devices) Regulations, 2010 and Regulation 7 of the Income Tax

(Electronic Fiscal Devices) Regulations, 2012. A list of the approved suppliers of

EFDs in Tanzania is shown in the Table below:

Table 5: List of the Approved Suppliers of EFDs in Tanzania

S/N Name of the Supplier Head Office in the Country

1. Advatech Office Supplies Limited Dar es Salaam, Tanzania

2. Bolsto Solutions Limited Dar es Salaam, Tanzania

3. Business Machines Tanzania Limited [BMTL] Dar es Salaam, Tanzania

4. Checknocrats Tanzania Limited Dar es Salaam, Tanzania

5. Compulynx Tanzania Limited Dar es Salaam, Tanzania

6. Maxcom Africa Limited Dar es Salaam, Tanzania

7. Pergamon Group Limited Dar es Salaam, Tanzania

8. Power Computers Telecommunication Limited Dar es Salaam, Tanzania

9. SoftNet Technologies Limited Dar es Salaam, Tanzania

10. Total Fiscal Solutions Limited Dar es Salaam, Tanzania

11. Web Technologies Tanzania Limited Dar es Salaam, Tanzania

Source: TRA (2013)

It is important to note that in the previous study conducted by TCCIA and PAMOMA

(2012), three suppliers not in the list were found to be supplying EFDs to traders.

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 7

These were Altech, Nameet/Namit and Planet 2000. As the study recommended, it is

important for TRA to establish the legality of these three suppliers and take

appropriate action.

At the operational level, suppliers are required to purchase the approved EFDs from

approved manufacturers and to sell and distribute them to traders in Mainland

Tanzania. In this regard, TRA is responsible for connecting the two. Regulation 7 (1)

(c) of the Value Added Tax (Electronic Fiscal Devices) Regulations, 2010 and

Regulation 7 (1) (c) of the Income Tax (Electronic Fiscal Devices) Regulations, 2012

require approved EFD suppliers to submit to the Commissioner General relevant

evidence of EFD sales to users. The required details have to include information on

sales, invoices, job card, users’ particulars, including Taxpayers Identification

Number and, where relevant, the VAT Registration Number. In addition, an approved

EFD supplier must prepare a monthly inventory of the machines, indicating the

number of machines in existence at the beginning of the month, number of machines

purchased from approved manufacturers, number of machines sold to traders,

particulars of the traders, and the machines remaining in the store. To track EFDs,

their details are submitted to the Commissioner General on a monthly basis. As part

of the MoU, the approved suppliers are also required to provide an after-sales service,

such as (1) issuing an instruction manual (2) distributing EFDs to the users (3)

installing, configuring and activating the supplied EFD at users’ premises (4) keeping

a stock of spare parts and accessories for users for a period of not less than five years

from the time when the last batch was supplied (5) training users in the efficient use

of EFDs (6) supporting and maintaining the supplied EFDs at users’ premises to

ensure their smooth running. The following sections discuss the extent to which this

after-sales services is provided.

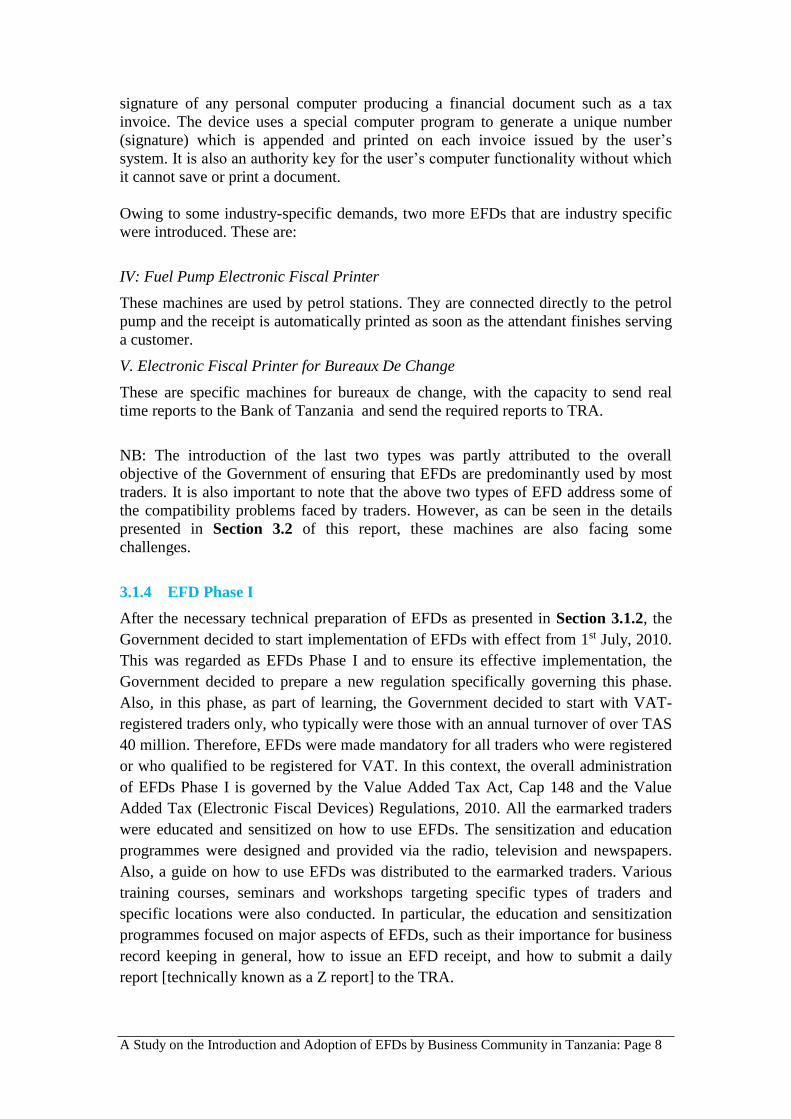

3.1.3 Types of Electronic Fiscal Devices (EFDs) Applicable in Tanzania

There are various types of EFDs in use [See Appendix 3], depending on the type of

business. However, in the context of Tanzania, the following EFDs were initially

introduced:

I: Electronic Tax Register

This device is appropriate and commonly used by retail businesses that issue receipts

manually, also known as the Electronic Fiscal Cash Register. It may be used as a

stand-alone device as it keeps totals in a fiscal memory and prints receipts on an in-

built printer.

II: Electronic Fiscal Printer

This device is commonly used by computerised retail outlets. It is connected to a

computer network that stores every sale in its fiscal memory as the user issues receipts

to customers. It is similar to printers that are currently used in supermarkets, except

for the fiscal memory. Users of this kind of device include supermarkets, petrol

stations and ticketing.

III: Electronic Signature Device

This device is used by computerised businesses that issue receipts or invoices via

special accounting software such as Tally. The device is designed to authenticate the

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 8

signature of any personal computer producing a financial document such as a tax

invoice. The device uses a special computer program to generate a unique number

(signature) which is appended and printed on each invoice issued by the user’s

system. It is also an authority key for the user’s computer functionality without which

it cannot save or print a document.

Owing to some industry-specific demands, two more EFDs that are industry specific

were introduced. These are:

IV: Fuel Pump Electronic Fiscal Printer

These machines are used by petrol stations. They are connected directly to the petrol

pump and the receipt is automatically printed as soon as the attendant finishes serving

a customer.

V. Electronic Fiscal Printer for Bureaux De Change

These are specific machines for bureaux de change, with the capacity to send real

time reports to the Bank of Tanzania and send the required reports to TRA.

NB: The introduction of the last two types was partly attributed to the overall

objective of the Government of ensuring that EFDs are predominantly used by most

traders. It is also important to note that the above two types of EFD address some of

the compatibility problems faced by traders. However, as can be seen in the details

presented in Section 3.2 of this report, these machines are also facing some

challenges.

3.1.4 EFD Phase I

After the necessary technical preparation of EFDs as presented in Section 3.1.2, the

Government decided to start implementation of EFDs with effect from 1st July, 2010.

This was regarded as EFDs Phase I and to ensure its effective implementation, the

Government decided to prepare a new regulation specifically governing this phase.

Also, in this phase, as part of learning, the Government decided to start with VAT-

registered traders only, who typically were those with an annual turnover of over TAS

40 million. Therefore, EFDs were made mandatory for all traders who were registered

or who qualified to be registered for VAT. In this context, the overall administration

of EFDs Phase I is governed by the Value Added Tax Act, Cap 148 and the Value

Added Tax (Electronic Fiscal Devices) Regulations, 2010. All the earmarked traders

were educated and sensitized on how to use EFDs. The sensitization and education

programmes were designed and provided via the radio, television and newspapers.

Also, a guide on how to use EFDs was distributed to the earmarked traders. Various

training courses, seminars and workshops targeting specific types of traders and

specific locations were also conducted. In particular, the education and sensitization

programmes focused on major aspects of EFDs, such as their importance for business

record keeping in general, how to issue an EFD receipt, and how to submit a daily

report [technically known as a Z report] to the TRA.

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 9

Anecdotal evidence suggests that EFD Phase I was generally successful in various

ways. Firstly, there were no major complaints from the business community on the

usage of the machines. As illustrated in the following quote, even TRA officials had

the same feeling:

“…It [Phase I] was a very successful phase. We had no major problems. Except for a

few technical challenges, we had no major complaints from users of EFDs … [TRA

Official] [Emphasis added]

This might be attributed to the fact that few traders were required to use EFDs in this

phase and they were relatively large traders. In fact, only VAT-registered traders

(with an annual turnover exceeding TAS 40 million) were required to use EFDs in

Phase I. Because the cost of EFDs was fully met through a VAT refund, there were no

major complaints regarding their cost. It could be argued that large traders (VAT

registered) already had the experience of dealing with tax machines and most of them

had electronic tax registers in place. Secondly, the use of EFDs in this phase

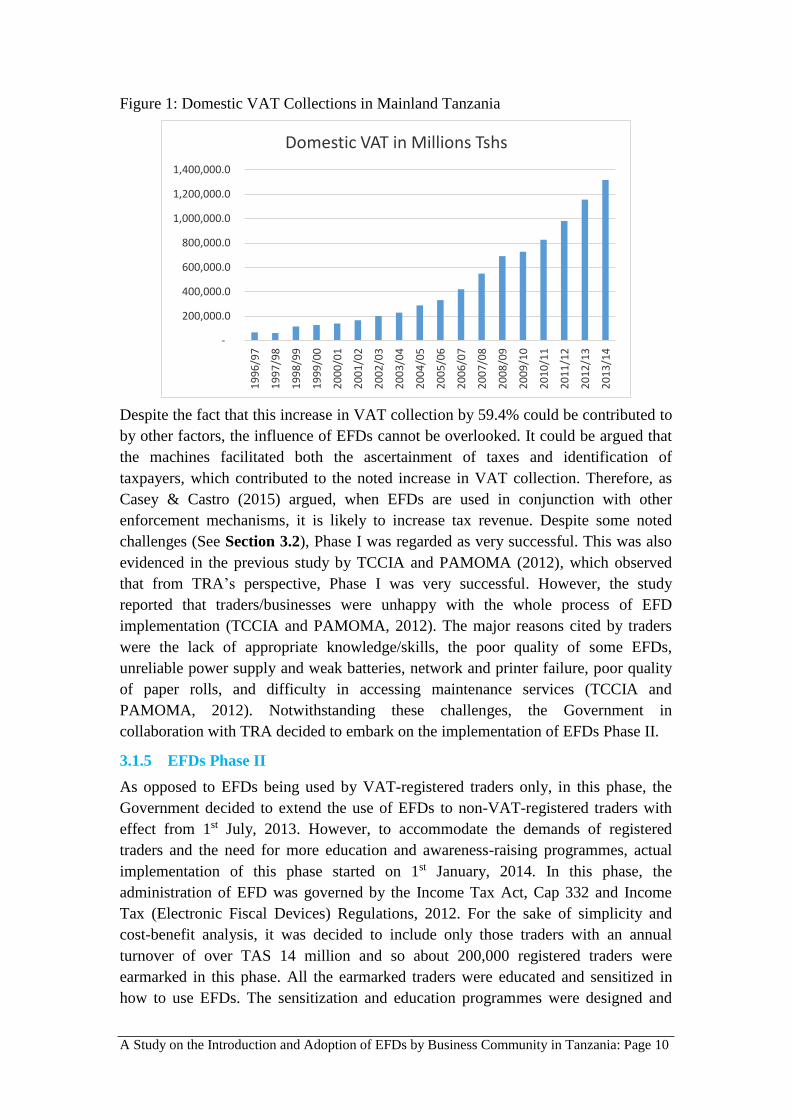

contributed to increased VAT collections. In fact, as Figure 1 below shows, there was

a nominal increase in domestic VAT in Mainland Tanzania from TAS 825,853.3

million in the Financial Year 2010/2011 to TAS 1,316,820.7 million in 2013/2014.

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 10

Figure 1: Domestic VAT Collections in Mainland Tanzania

-

200,000.0

400,000.0

600,000.0

800,000.0

1,000,000.0

1,200,000.0

1,400,000.0

19

96

/97

19

97

/98

19

98

/99

19

99

/00

20

00

/01

20

01

/02

20

02

/03

20

03

/04

20

04

/05

20

05

/06

20

06

/07

20

07

/08

20

08

/09

20

09

/10

20

10

/11

20

11

/12

20

12

/13

20

13

/14

Domestic VAT in Millions Tshs

Despite the fact that this increase in VAT collection by 59.4% could be contributed to

by other factors, the influence of EFDs cannot be overlooked. It could be argued that

the machines facilitated both the ascertainment of taxes and identification of

taxpayers, which contributed to the noted increase in VAT collection. Therefore, as

Casey & Castro (2015) argued, when EFDs are used in conjunction with other

enforcement mechanisms, it is likely to increase tax revenue. Despite some noted

challenges (See Section 3.2), Phase I was regarded as very successful. This was also

evidenced in the previous study by TCCIA and PAMOMA (2012), which observed

that from TRA’s perspective, Phase I was very successful. However, the study

reported that traders/businesses were unhappy with the whole process of EFD

implementation (TCCIA and PAMOMA, 2012). The major reasons cited by traders

were the lack of appropriate knowledge/skills, the poor quality of some EFDs,

unreliable power supply and weak batteries, network and printer failure, poor quality

of paper rolls, and difficulty in accessing maintenance services (TCCIA and

PAMOMA, 2012). Notwithstanding these challenges, the Government in

collaboration with TRA decided to embark on the implementation of EFDs Phase II.

3.1.5 EFDs Phase II

As opposed to EFDs being used by VAT-registered traders only, in this phase, the

Government decided to extend the use of EFDs to non-VAT-registered traders with

effect from 1st July, 2013. However, to accommodate the demands of registered

traders and the need for more education and awareness-raising programmes, actual

implementation of this phase started on 1st January, 2014. In this phase, the

administration of EFD was governed by the Income Tax Act, Cap 332 and Income

Tax (Electronic Fiscal Devices) Regulations, 2012. For the sake of simplicity and

cost-benefit analysis, it was decided to include only those traders with an annual

turnover of over TAS 14 million and so about 200,000 registered traders were

earmarked in this phase. All the earmarked traders were educated and sensitized in

how to use EFDs. The sensitization and education programmes were designed and

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 11

provided via the radio, television and newspapers. Also, a guide on how to use EFDs

was distributed to the earmarked traders. Various training courses, seminars and

workshops targeting specific types of traders and specific locations were also

conducted. In particular, the education and sensitization programmes focused on

major aspects of EFDs, such as their importance for business record keeping in

general, how to issue an EFD receipt, and how to submit a daily report [technically

known as a Z report] to TRA. Most registered traders in this phase are regarded as

small and medium enterprises (SMEs) and given the low level of financial literacy,

some had problems understanding how to use EFDs appropriately:

“Most of these traders lack knowledge on how to use the machines [EFDs]. We train

them many times but some don’t know even how to issue a receipt [Fiscal Receipt]. It

is very challenging… [Approved EFDs Supplier] [Emphasis Added].

Unlike in Phase I, most of the registered traders earmarked to be supplied with EFDs

in this phase lacked financial capacity. Therefore, the introduction of an EFD was

regarded by them as an additional burden. As a result, within the first three months of

introducing EFDs in this phase (January-March, 2014), the country witnessed a major

protest by the registered traders. This involved, among others, go-slows, shut-downs

and strikes, which took place in major parts of the country including Dar es Salaam,

Mwanza, Morogoro, Mbeya and Kagera regions. As the following picture shows, the

protesting registered traders gave a very clear message to the Government, and TRA

in particular, “we don’t need machines (EFDs)”.

Figure 2: Some Traders Protesting against the Usage of EFDs

Source: https://www.google.co.tz/search?q=EFDs+strikes+in+Tanzania+in+Picture

During and after the protest, mixed statements were made by the Government

(represented mainly by TRA) and the traders. On the one hand, the Government

insisted that the machines were not a problem:

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 12

“…Traders across the country have been misled by false and inaccurate information

on the use of EFDs and that is why they remain reluctant to use them despite the

government’s repeated orders to do so…To reverse and correct the misconception

[…] TRA is to conduct an awareness-raising campaign across the country…Traders

have been misled by self-interested individuals who are disrupting the economic

development of the nation for personal gain… As an authority we are aware that the

traders have been misled and so we are conducting this campaign to educate them on

the use and value of EFDs……” [Richard Kayombo, Director for Taxpayer Services

and Education, TRA, quoted in the Guardian Newspaper, 2nd April, 2014] [Emphasis

Added].

The quoted Director specifically stated that:

“…[T]he reasons the traders give as to why they are unwilling to use EFDs are all

evidence of their misconception…”[Richard Kayombo, Director for Taxpayer

Services and Education, TRA, quoted in the Guardian Newspaper, 2nd April, 2014]

In contrast, the registered traders maintained that the machines had some technical

and operational problems which made their implementation difficult. This is

illustrated in the following quote:

“…Unlike TRA’s misconception, the traders are not against paying taxes but they

want an improvement in the tax collection system… The EFDs are not user

friendly…they only record sales but not purchases…so what good is that for the

trader?…” [Johnson Minja, Chairman of the Business Community of Kariakoo, Dar

es Salaam, quoted in the Guardian Newspaper, 2nd April, 2014].

Despite the various initiatives to address the matter, an antagonistic relationship

between TRA and registered traders continued. As a testimony to the problem and the

importance of using EFDs, the then President of the United Republic of Tanzania,

Hon. Jakaya Mrisho Kikwete, was once quoted saying:

“…I know there are a lot of issues raised concerning the machines [EFDs]. But my

advice is that you discuss the problems and find solutions. If the problem is price, it

should be resolved. We need this system for efficient collection of tax...” [Emphasis

Added]

As a response to the President’s directives, TRA started a massive sensitization

campaign to educate traders on the importance of EFDs and clear up what were

regarded by Government officials as outspoken misconceptions. As indicated in the

box below, the door for discussion was opened for the traders to raise their concerns

relating to the implementation of EFDs.

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 13

Box 1: Opening a Room for Negotiation between TRA and Traders

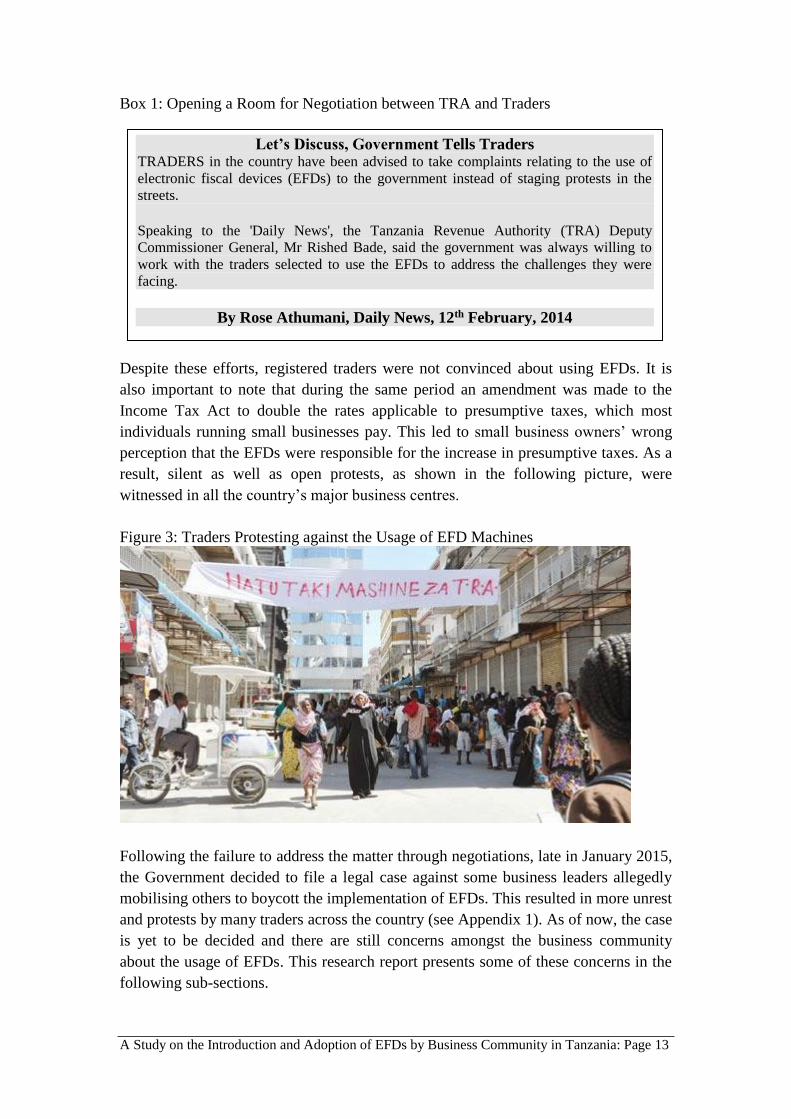

Despite these efforts, registered traders were not convinced about using EFDs. It is

also important to note that during the same period an amendment was made to the

Income Tax Act to double the rates applicable to presumptive taxes, which most

individuals running small businesses pay. This led to small business owners’ wrong

perception that the EFDs were responsible for the increase in presumptive taxes. As a

result, silent as well as open protests, as shown in the following picture, were

witnessed in all the country’s major business centres.

Figure 3: Traders Protesting against the Usage of EFD Machines

Following the failure to address the matter through negotiations, late in January 2015,

the Government decided to file a legal case against some business leaders allegedly

mobilising others to boycott the implementation of EFDs. This resulted in more unrest

and protests by many traders across the country (see Appendix 1). As of now, the case

is yet to be decided and there are still concerns amongst the business community

about the usage of EFDs. This research report presents some of these concerns in the

following sub-sections.

Let’s Discuss, Government Tells Traders TRADERS in the country have been advised to take complaints relating to the use of

electronic fiscal devices (EFDs) to the government instead of staging protests in the

streets.

Speaking to the 'Daily News', the Tanzania Revenue Authority (TRA) Deputy

Commissioner General, Mr Rished Bade, said the government was always willing to

work with the traders selected to use the EFDs to address the challenges they were

facing.

By Rose Athumani, Daily News, 12th February, 2014

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 14

3.2 Challenges of the Implementation of EFDs

3.2.1 Cost of the EFDs

There have been concerns amongst the business community that the machines are

very expensive. In this regard, it is important to note that these concerns were raised

during Phase II. This is partly attributed to the fact that those involved in Phase I were

VAT-registered traders who can claim the whole cost of EFDs from VAT.

Nevertheless, depending on the type and envisaged functions of the machine, the price

ranges from TAS 2,000,000 to TAS 6,000,000. It was noted during fieldwork that the

machine with the lowest price was the Electronic Tax Register, which is used mainly

by retail business that issue receipts manually and the highest price was for the

Electronic Fiscal Printer, especially those used at petrol stations, as one trader

claimed:

“These machines [EFDs] are very expensive. It is difficult to buy them. In a business

like this [small business], it is very challenging to maintain the machine…” [Trader]

[Emphasis Added].

Similar claims were made by another trader who was also Chairman of the Tanzania

Taxpayers Association:

“This move will drive many small-scale businesses out of business because the

burden of paying for the EFD is unbearable… Many small-scale businesses have an

annual turnover of 14m/-, which if we take into consideration a 30 percent profit

recognized by the Income Tax Act, we get 9.8m/-, which translates into 816,000/- as

start-up capital and this is what the EFD costs… [T]he minimum threshold should be

pegged at [TAS] 20m/- turnover per annum…[Otieno Igogo, Chairman of the

Tanzania Taxpayers Association, quoted in All Africa, 6th January, 2014][Emphasis

Added].

It is worth noting that even large businesses had similar concerns. This is reflected in

the following quote:

“As for us, each pump needs to be fitted with its own EFD which costs 2,500 to 3,000

US dollars. In petrol stations you have four to six pumps with machines, and so this

issue needs to be looked at critically…EFD manufacturers need to come up with

gadgets which can be connected to two fuel pumps…” [Farough Barghoza, Chairman

of the Tanzania Petrol Stations Operators Association (TAPSOA), quoted in the

Daily News, 15th February, 2016].

On the other hand, the Government and TRA officials in particular insisted that the

claims are baseless as the full cost of EFDs is recovered through tax deductions: “The

claim that EFDs are expensive does not hold water. We all know that the trader can recover

the entire cost of the machines through tax deductions…” [TRA Official].

However, looking at the respective tax laws (the VAT Act and the Income Tax Act)

the only traders who can recover the whole cost of the EFDs are those who are VAT

registered, who can claim the whole cost of EFDs as a tax credit/tax deduction under

the VAT Act. As regards the non-VAT-registered traders, those submitting income

tax returns (turnover from TZS 20 million and above) are eligible to claim the full

cost of the machine as a class 8 depreciable asset (this being a deduction by

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 15

calculating taxable income, thus receiving a saving of only up to a 30% of the tax

payable). Despite the fact that non-VAT traders can claim the cost as a deduction

under Class 8 [Depreciable Assets] under the Income Tax Act, in practice it is

difficult to claim the entire cost in the year of purchase. In the meantime, the

Government is planning to issue EFDs freely to earmarked traders. During a

conversation with the Chairman of the Business Community of Kariakoo, the

President of the United Republic of Tanzania, Hon. John Pombe Magufuli, reiterated

the need to supply EFDs freely to the earmarked traders. On this, he said:

“…If it had been up to me, I would have given you the devices [EFDs] free of charge

and see how much I collect in revenue, simple…”[President John Pombe Magufuli,

quoted in the Guardian, 8th December, 2015[Emphasis Added].

However, some interviewed approved EFD suppliers were concerned about the

proposed decision of the Government on the grounds that traders who are given the

gadgets freely may not be committed to using them. In this regard, one approved EFD

supplier argued, ‘if they don’t use and take care for the ones they purchased, I don’t

think they will appropriately and consistently use and take care of those which will be

provided freely’. It is also important to note that the Government is planning to buy

EFDs directly from the approved manufacturers and let the approved suppliers

distribute them to the earmarked traders. This move is highly contested by the

approved suppliers. Whilst it is encouraging that the Government is now involved

in addressing the challenges relating to the cost of acquiring EFDs, care is

needed to ensure that the intervention is appropriate and good results are

produced for all the parties involved.

3.2.2 Network Problems

Our research respondents generally cited network connectivity as a major problem of

the EFDs. Interestingly, even the interviewed TRA officials and approved suppliers

raised the same concern. Registered traders are required to send a daily report,

technically known as a Z report, to the TRA. The gadget is empowered with a chip

[SIM card] which communicates with the TRA server. The service providers of the

network are Vodacom and Airtel and all the chips are maintained and secured by

TRA. It is worth noting that network problems was also prevalent in Phase I of EFD

implementation (TCCIA and PAMOMA, 2012). This is further illustrated by the

trader who installed the machine during EFD Phase I:

“…The machine is good but the network is the major problem. It is very difficult to

issue a receipt and send a Z report to TRA. It takes too long to send the report and

sometimes it is not sent at all. It is very frustrating…” [Trader]

Initially, the machine was configured to send a Z report daily and if a trader failed to

submit it within 24 hours, the machine was automatically locked. The interviewed

TRA officials were of the view that this was necessary to ensure that all the daily

sales of EFD traders are stored in the TRA server to facilitate the administration of

taxes. However, following repeated claims by the business community of problems

with the network, TRA decided to lengthen the time for submitting the Z report from

24 hours (1day) to 72 hours (3 days). Rationalising this decision, one TRA official

stated:

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 16

“…We assume that within 3 days the network breakdown should be over and the

trader should be able to submit the Z report…” [TRA Official]

However, our findings suggest differently. Some of our interviewed traders

experienced network problems beyond the allowed 3 days, and in some cases, the

problem lasted for about 7 days. This is partly attributed to the increased number of

users of EFDs. Unfortunately, most traders tend to communicate with the approved

suppliers of EFDs concerning a network problem, but they can do nothing:

“[…] Traders normally call us to resolve their network problem. They think we will

be able to help them. In fact, we cannot. We normally advise them to wait for the

network to be restored….” [Approved EFD Supplier].

As a testimony to the magnitude of the network problem, we interviewed a trader who

spent about 9 hours moving around with his EFD to get help with submitting his Z

report to TRA. Therefore, it is high time for the Government and TRA in

particular to address the network problem. This could be partly addressed by

allowing other service providers, which may enhance competition. Similarly, it is

important to have a platform where service providers can communicate with

other EFD stakeholders, including traders. While there was a lot of interaction

between traders and approved EFD suppliers, our study did not find the

evidence of this between traders and network service providers. Another

intervention would be to enhance the TRA server so that it can handle the heavy

traffic of EFD Z reports that come in daily, as the queue in the server could be

the main reason for the delay and the failure of some traders to submit their

reports. This is attributed to the fact that the network service providers have

quite a high level of reliability and there are no serious network problems in

other services.

3.2.3 Poor Quality of Paper Rolls

The quality of paper rolls used in the EFDs has also been a subject of discussion

because the EFD receipts issued do not last long before fading due to the poor quality

of the paper rolls. The previous study by TCCIA and PAMOMA (2012) also observed

this. In particular, the study found that the fiscal receipts issued were of poor quality

and did not last long, which was confirmed by traders and customers who complained

of the poor quality as one trader claimed:

“The receipts [fiscal receipts] fade within a very short period of time after being

issued. They are totally unreadable, while TRA wants the receipt to be stored for a

period of 5 years…I have a copy of Z reports of the last few months and they are

completely unreadable …” [Trader][Emphasis Added].

Our interview with one of the approved EFDs suppliers suggests that even the

technical problems experienced by some machines were attributed to the poor quality

of the paper rolls. This is illustrated in the following quote:

“…We have a certain customer who is always complaining about his EFD. I sent all

my technicians, but the problem was still there. I decided to go myself. Then I asked

him to give me his machine. After opening it, I realized that the paper rolls used were

of poor quality and affected the path of the machine which slides the papers. Then, I

asked one of my technicians to go and buy a quality paper roll and I put it in the

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 17

trader’s machine. Since then, the machine has been operating smoothly…”

[Approved EFDs Supplier].

In an attempt to address this anomaly, TRA has emphasized that the paper used for

printing EFDs receipts must be thermal paper, which is expected to last for about five

(5) years without losing its character. To ensure the usage of quality paper and

minimise public outcry, in Phase II, TRA selected suppliers of fiscal paper rolls who

would supply them to other suppliers. These approved suppliers are (1) Checknocrats

Tanzania Limited, (2) Advantech Office Supplies (3) Total Fiscal Solutions Tanzania

Limited, and (4) Business Machines Tanzania Limited. Despite these efforts, poor

quality paper rolls are still available in the market and a solution is being sought to

remove them. One approved supplier claimed that most traders prefer poor quality

paper rolls because they are cheaper. This claim is substantiated by the fact that the

average price of quality paper rolls from approved suppliers is TAS 3500, while those

available from unapproved suppliers stood at TAS 2000. Therefore, to ensure

sustainability of fiscal receipts for record keeping and appropriate usage of the

EFDs, it is recommended that TRA take immediate measures to ensure that only

paper rolls from approved suppliers are used by traders.

3.2.4 Location of the Approved Suppliers

It was noted during this study that approved EFD suppliers did not exist in many parts

of the country. As part of the agreement between the approved EFD suppliers and the

Government, the former has to establish and operate service centres in every region in

the United Republic of Tanzania. In fact, the approved suppliers must have offices in

all business centres to effectively serve EFD users, and they are required to offer

support and maintain the supplied EFDs at the users’ premises. However, this was not

observed. Instead, all the suppliers are concentrated in major cities and towns such as

Dar es Salaam, Mwanza, Arusha, and Mbeya. Rationalising this, one approved EFD

supplier claimed that:

“This country is huge. It is very difficult to serve the entire country. We are trying to

have offices in major business cities and towns but it is very difficult to serve the

entire country. It is not practicable….” [Approved EFD Supplier]

Similar comments were made by another approved EFD supplier:

“…Yah, we are supposed to operate in the entire country. Yes, we are trying, but it is

difficult. You know the geographical locations of this country, it is difficult. Even

TRA has no offices in all business centres…” [Approved EFDs Supplier][Emphasis

Added].

As a result, we found traders travelling from different parts of the country to the

offices of the approved suppliers for support and maintenance. In some cases, traders

are forced to send EFDs to the suppliers for this. In this context, it is difficult to

suggest that the approved suppliers deal with malfunctions within forty eight (48)

hours from the reporting time as required by EFD regulations. Surprisingly, the same

problem was noted four (4) years ago by the study conducted on VAT-registered

traders by TCCIA and PAMOMA (2012). This indicates that the situation is yet to be

rectified. Therefore, whilst it seems impracticable for the approved suppliers to

establish an office in each business centre, appropriate arrangements could be

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 18

made to ensure availability of the service close to EFD users. In particular, TRA

could work with local government authorities located in parts not easily covered

by the approved EFD suppliers and find appropriate mechanisms for serving

EFD users located in their jurisdiction.

3.2.5 Poor Quality of EFDs and Weak Batteries

“Poor functioning of the EFDs, including the system being very slow, was reported to cause a

lot of inconvenience, especially when they attended to many customers. Unnecessary delays

were experienced which again caused unnecessary stress and put pressure on both the

customers and sellers. The VAT-registered traders from the survey areas reported to have

experienced damaged/failed devices many times” (TCCIA & PAMOMA, 2012, p.27).

Our study also noted the problems mentioned above. In particular, traders claimed

that the quality of EFDs and their batteries was poor and they need to be phased out:

“I am pretty sure that these machines are of poor quality. These are not genuine

machines. They cannot operate smoothly without frequent repairs and maintenance.

To be honest, these are fake machines…” [Trader].

However, the above claims were refuted by both TRA and the approved EFD

suppliers. Interestingly, the interviewed TRA officials and the approved suppliers had

the same observation that traders are avoiding using the machines and their poor

quality has been cited as an excuse. This is reflected in the following quote:

“…My friend, these machines are genuine. They passed all the international tests.

And you cannot say that these machines are of poor quality. You know these traders

are very intelligent. If you go to their business premises, everything is working except

EFDs. You may find the car is working, the computer is working…everything is

working except EFDs ….” [Approved EFDs Supplier].

Despite the above claims, traders were still of the view that some supplied EFDs are

of poor quality. Notwithstanding the fact that this could be used by dishonest

traders as an excuse for not using EFDs, it is important that TRA and the

approved EFD suppliers enhance the quality control mechanisms of the supplied

machines. This is further substantiated by the fact that fake EFDs are being supplied

by dishonest and unapproved suppliers in the country2.

Some traders also claimed that the batteries used in the machines are substandard.

This, coupled with the unreliability of the power supply which recharges them, led to

the implementation challenge. In response, the interviewed suppliers were of the view

that most traders do not know how to properly use the machines:

“You know, these machines are like computers. You can charge them while you have

power and then you may continue to use them even if there is no power. Instead, most

of our traders tend to use the machines without being connected to the power supply.

Therefore, after some time, the battery goes flat. Others, especially those who use the

2 “On August13, during a government crackdown by the police, they nabbed several businessmen with

fake EFD, reportedly stolen from Mwanza. Fasad Nasoro, the owner and director of CI Group was

arrested during an operation led by Deputy Minister of Finance, Mwigulu Mchemba with officials from

TRA. When arrested he was in possession of a machine with serial numbers 031TZ 54000053…”

[Reported by Nelso Kessy, Guardian on Sunday, 17th August, 2014].

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 19

machines occasionally, such as construction companies, we normally advise them to

put the machine on and charge it frequently. In my view, if you follow the

instructions on how to use these machines, you will not experience any problems…”

[Approved EFDs Supplier]

In fact, in the previous study by TCCIA & PAMOMA (2012) batteries were observed

to be the major problem followed by network failure. Therefore, there is a need for

the Tanzania Bureau of Standards to examine and certify the quality of the

manufactured EFDs and their batteries before being supplied to the registered

traders.

3.2.6 Inappropriate Provision of After-Sales Service

The MoU between TRA and approved EFD suppliers requires the latter to enter into a

written after-sales service agreement with the user to ensure that EFDs are

maintained. This is also in accordance with Reg. 7(1) (m) of the Value Added Tax

(Electronic Fiscal Devices) Regulations, 2010 and Reg. 7(1) (m) of the Income Tax

(Electronic Fiscal Devices) Regulations, 2012. The envisaged after-sales service

includes repairs and maintenance, training, education and other support. As discussed

in the previous section, these services are required to be provided at the users’

premises. However, it was observed during fieldwork that most traders have to go to

the approved suppliers for maintenance and other support services. This was also

noted in the previous study by TCCIA &PAMOMA (2012), indicating that this

anomaly has not been addressed.

Also, it is important to note that each approved supplier has its own arrangements for

dealing with after-sales service once the time of one year has elapsed. Other suppliers

offer a free service for the first three months and additional costs are applicable after

that. The traders then sign a service agreement whereby they need to pay the agreed

fee to the approved EFD supplier. Given the fact that the machines are claimed to be

of poor quality, most of the interviewed traders were concerned about the increased

maintenance costs:

“…In case of a problem, I have to go to my supplier and pay for service. We have a

service agreement with them and we pay an annual fee of TAS 200,000. Therefore, in

the case of any problem, we go there and our machine gets serviced…” [Trader]

Despite the concerns of the traders, it is fair to note that Reg. 20(5) of the Income Tax

(Electronic Fiscal Devices) Regulations, 2012 and Reg. 19(5) of the Value Added Tax

(Electronic Fiscal Devices) Regulations, 2010 state clearly that the expenses for

periodic maintenance of the Electronic Fiscal Devices shall be covered by each user

of the serviced device. However, to ensure the fair treatment of traders, TRA

should indicate the cost of servicing different types of EFDs. Similarly, it is

recommended that TRA conducts a survey on traders to assess whether the

delivery of the after-sales service provided by the approved EFD suppliers is

efficient. This survey would inform the TRA on the extent to which the approved

EFD suppliers provide an after-sales service as agreed in the MoU. Furthermore,

as the Government intends to supply EFDs freely to the earmarked traders, the

issue of maintenance needs to be discussed by all stakeholders. For instance, it is

not known whether the cost will be borne by the Government, suppliers or the

traders themselves and what would be the implications in terms of compliance.

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 20

3.2.7 Compatibility Issues

Some traders claimed that EFDs are not compatible with some of the systems already

in place in their businesses. As a result, it created difficulties in integrating the

systems in order to have accurate information, as one trader stated:

“You know, I have this EFD here and as a supermarket, I have my own computerised

system. But this machine [EFD] is not compatible with my system. I think they

supplied me with an old version which cannot read the system. This is very

problematic indeed. I think their machines are very outdated…” [Trader].

Similar claims have been made in petrol stations:

“…We are not against the usage of EFDs but most of them do not relate to the pumps at

our petrol stations…We will seek an audience with TRA officials and the EFD

manufacturers to see how best they can provide […] machines that can be connected to

our pumps…” [Farough Baghozah, Chairman of the Tanzania Petrol Stations Operators

Association (TAPSOA), quoted in the Daily News, 15th February, 2016] [Emphasis

Added].

As highlighted in the above quotes, a dialogue between EFD stakeholders,

including TRA, approved EFD suppliers, approved EFD manufacturers,

network providers and individual traders, could address these concerns. In this

regard, it is fair to acknowledge the efforts made by TRA to connect the business

community and the approved EFD suppliers. Therefore, the same could be done

with respect to the approved EFD manufacturers and other important

stakeholders.

3.2.8 Limited Technical Functions and Lack of Technicians

Traders were concerned about EFDs having limited functions. Their argument is that

since the machine is used for tax purposes, it should provide full details of all the

expenditure of the trader and not their sales only. It is important to note that this was

one of the major reasons behind the country-wide protest to using EFDs, which

occurred in 2014 and 2015. This is illustrated in the following quote:

“…The EFDs are not user friendly,…they only record sales made and not purchases

for example…so what good is that for the trader?….” [Johnson Minja, Chairman of

the Business Community of Kariakoo, quoted in the Guardian, 2nd April, 2014]

Since most of the traders involved in Phase II come under presumptive taxes3, they

were concerned that TRA could use their sales information to increase the amount of

estimated taxes to be paid. This also contributed to the widespread boycotting of

EFDs.

Furthermore, some EFDs, especially those installed at petrol stations, were claimed to

have recurring technical problems:

3 Presumptive tax is the system of estimating taxes applicable to sole proprietors with an annual

turnover not exceeding Tshs 20 million (Income Tax Act, 2004).

A Study on the Introduction and Adoption of EFDs by Business Community in Tanzania: Page 21

“…When the computing machines are stuck, we cannot conduct any sales since the

system does not allow it. TRA should have enough experts that are capable of sorting

out the machines as quickly as possible…” [Victoria Luande, Managing Director,

Puma Petrol Station Sea View, quoted in the Guardian, 18th March, 2015].

It was noted during fieldwork that whenever EFDs had a problem, the manager-cum-

operator disconnected them from the pumps and continued to sell fuel without issuing

EFD receipts. This was also noted in other businesses such as bureaux de change,

supermarkets and other merchandising entities. It is important to note that Reg. 18(1)

of the Income Tax (Electronic Fiscal Device) Regulations, 2012 allows users to

temporarily use an alternative means of transacting business by issuing manual

receipts or invoices where (a) the Electronic Fiscal Device is undergoing inspection;

(b) the Electronic Fiscal Device has been seized for investigation; (c) the Electronic

Fiscal Device is undergoing maintenance; and (d) the user has reported to the

Commissioner that the device has failed to operate for any reason acceptable to the

Commissioner. Even when these conditions are met, the user is still required to key

into the Electronic Fiscal Device all the information contained in the manually issued

receipts and invoices at the start of the operation of an Electronic Fiscal Device (Reg.

18(2) of the Income Tax (Electronic Fiscal Device) Regulations, 2012). This was not

observed during fieldwork. Instead, users continued to issue EFD receipts once the

machine is restored, without dealing with the transactions for which manual receipts

were issued. On this, one trader stated clearly that ‘we don’t go back and trace

manually issued receipts. It is time consuming. Once the machine is ready, we

proceed’. As most of these traders are non-VAT registered, they did not have the

incentive to make sure that all the sales are recorded in the EFDs. Surprisingly, this

practice was also noted in the study conducted on relatively large businesses (VAT

registered) by TCCIA&PAMOMA (2012), and they associated this tendency with the

time factor and the voluminous amount of transactions.

Since it is an offence for registered traders to operate a business in the country

without using an Electronic Fiscal Device (Reg. 10(2) of the Income Tax

(Electronic Fiscal Device) Regulations, 2012 and Reg. 10(2) of the Value Added

Tax (Electronic Fiscal Device) Regulations, 2010), TRA should put in place

appropriate mechanisms to ensure that technical problems relating to EFDs are

addressed promptly. Also, TRA should enhance investigation and follow up to

ensure that the previously manually issued receipts or invoices are entered into

the EFDs. Similarly, the Government and TRA in particular should consider

raising the level of awareness of breaking the law to deter purposeful acts aimed

at making EFDs dysfunctional.