Report of Financial Ratio of Malaysia Airlines System Berhad FIN 670

32

Financial Ratio of Malaysia Airlines System Berhad 1 Report of Financial Ratio of Malaysia Airlines System Berhad FIN 670 Universiti Teknologi MARA Prepared by: A’imullah bin Abd Halim 2010336497 Eva Salmee Mohd Salleh 2009713479 Mohd Khairil bin Mahmood 2010177225 Nurunnadiah binti ab Aziz 2010532647 Shaila Shermin bt Kamaluddin 2010566071 Ruzaimah Rubain 2010710629 Supervised by: Dr Jaafar Pyeman

Transcript of Report of Financial Ratio of Malaysia Airlines System Berhad FIN 670

Financial Ratio of Malaysia Airlines System Berhad 1

Report of Financial Ratio of Malaysia Airlines System Berhad

FIN 670

Universiti Teknologi MARA

Prepared by:

A’imullah bin Abd Halim 2010336497

Eva Salmee Mohd Salleh 2009713479

Mohd Khairil bin Mahmood 2010177225

Nurunnadiah binti ab Aziz

2010532647

Shaila Shermin bt Kamaluddin 2010566071

Ruzaimah Rubain 2010710629

Supervised by:

Dr Jaafar Pyeman

Financial Ratio of Malaysia Airlines System Berhad 2

Objectives

Analysis and investigation of financial ratios for MAS has

been done from five year annual report starting from 2005 to

2009. Thus the objectives are:

1. Study of liquidity of MAS from 2005 to 2009

2. Study of activity of MAS from 2005 to 2009

3. Study of profitability of MAS from 2005 to 2009

4. Study of leverage of MAS from 2005 to 2009

5. Forecast the future performance of MAS in terms of

liquidity, operating activity, profitability,

shareholders equity and leverage.

Introduction

Malaysia Airlines is listed on the stock exchange of Bursa

Malaysia under the name Malaysian Airline System Berhad (MYX:

3786). Its parent company is Penerbangan Malaysia Berhad. The

airline has suffered high losses over the years as a result of

fuel price increases and poor management. The Government of

Malaysia overhauled the operations of the airline and Idris

Jala was appointed as the new CEO in 1st December 2005. Under

his leadership, Malaysia Airlines unveiled its Business

Turnaround Plan (BTP) in February 2006 which highlighted low

yield, an inefficient network and low productivity

(overstaffing). The airline headquarters building in downtown

Financial Ratio of Malaysia Airlines System Berhad 3

Kuala Lumpur has been sold. The new corporate headquarters is

now at Sultan Abdul Aziz Shah Airport in Subang, Petaling.

The airline is owned by Penerbangan Malaysia Berhad

(PMB) (69.34%), Employees Provident Fund Board (10.72%),

Amanah Raya Nominees (Tempatan) Sdn Bhd (5.69%), State

Financial Secretary Sarawak (2.71%) and Warisan Harta Sabah

(2.4%). It has 19,546 employees (in March 2007)

In the past, MAS is believed to have over expanded its

routes and airlines fleet. It is also said to have embarked on

aggressive cost cutting, which caused negative impact on its

service quality and marketing plan. A previous restructuring

saw it disposing of aircraft assets and domestic losses to a

Khazanah Nasional Bhd owned entity.

Today, MAS fuel cost are insufficiently hedged. The

airline also struggled to come up with an effective pricing

systems which would enable it to past on the fuel cost to

customers. To make matters more challenging MAS has faced

intense competition from low cost airlines company, AirAsia,

on the domestic front, which led MAS to cut fares, a move that

had likely affect its profitability.

Therefore this study will explore the MAS financial

performance by using ratio analysis that focus on liquidity,

activity, debt and profitability ratio.

Results and discussions

Financial Ratio of Malaysia Airlines System Berhad 4

1. Liquidity ratio

Liquidity ratio is used to measure a firm ability to satisfy

its short-term obligations as they come due. In addition,

liquidity refers to solvency of the firm’s overall financing

position- the ease with which it can pay its bills. In short

it reflects to answer; can the firm pay its bills? The two

basic measures of liquidity are the current ratio and the

quick (acid-test) ratio.

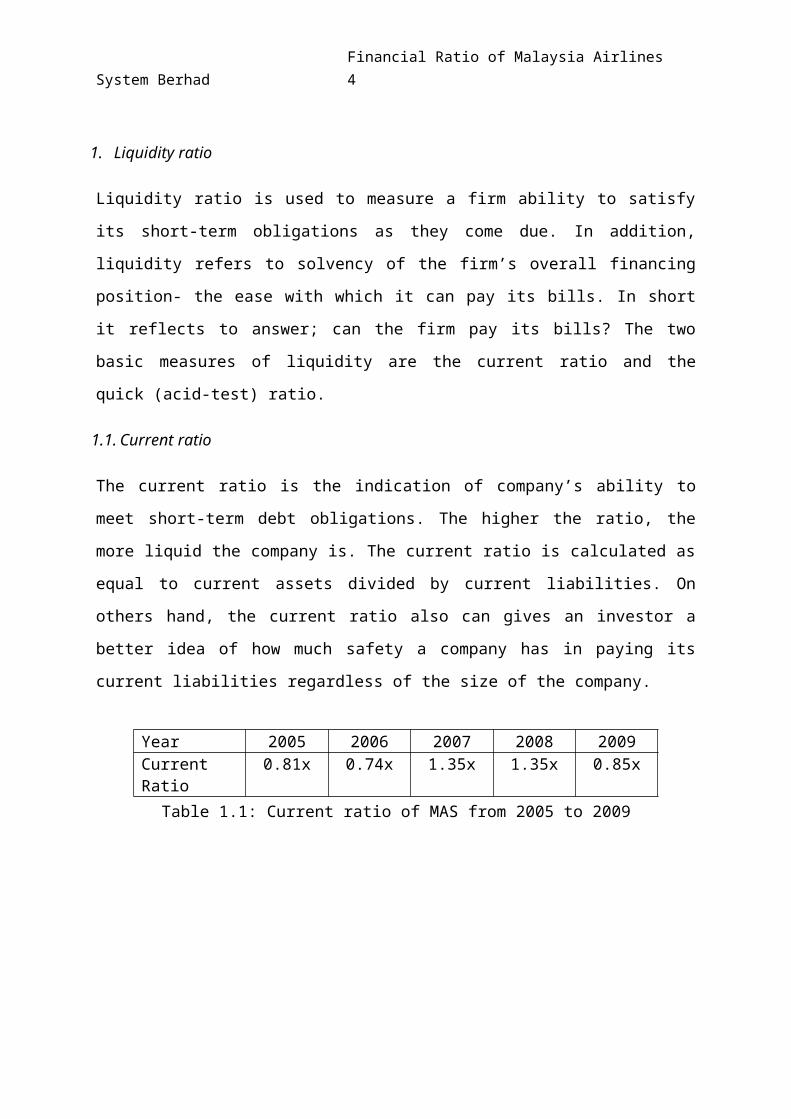

1.1. Current ratio

The current ratio is the indication of company’s ability to

meet short-term debt obligations. The higher the ratio, the

more liquid the company is. The current ratio is calculated as

equal to current assets divided by current liabilities. On

others hand, the current ratio also can gives an investor a

better idea of how much safety a company has in paying its

current liabilities regardless of the size of the company.

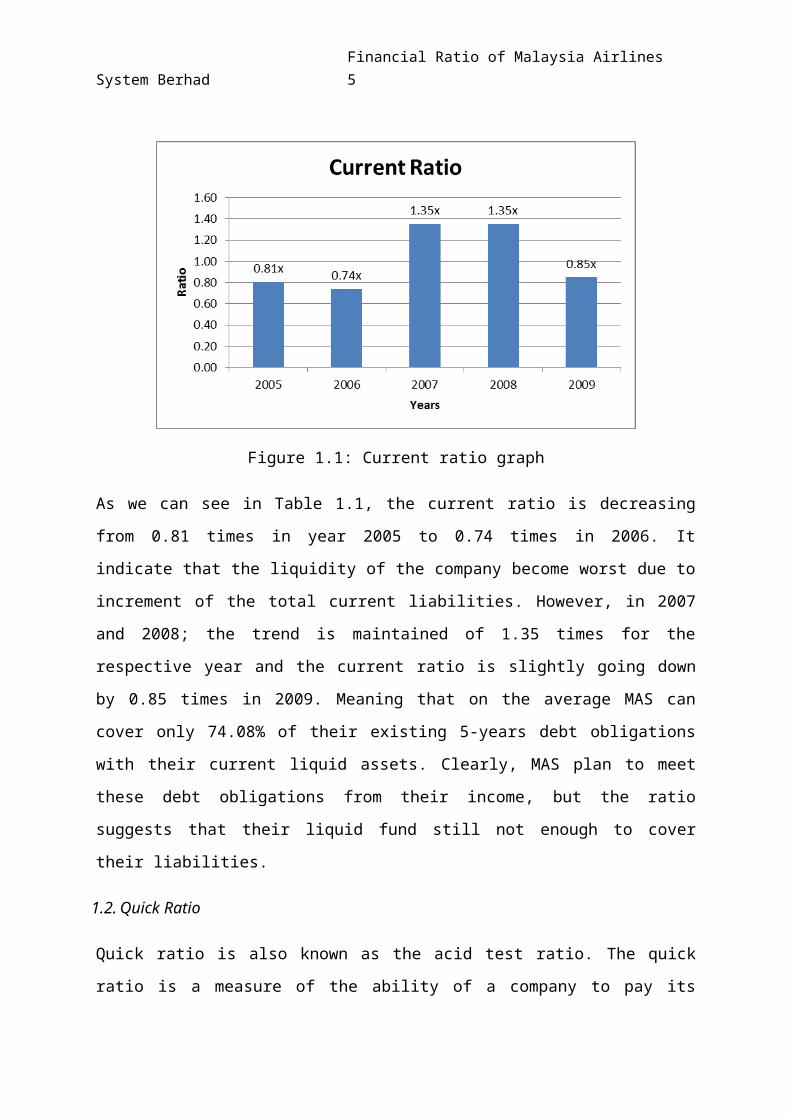

Table 1.1: Current ratio of MAS from 2005 to 2009

Year 2005 2006 2007 2008 2009Current Ratio

0.81x 0.74x 1.35x 1.35x 0.85x

Financial Ratio of Malaysia Airlines System Berhad 5

Figure 1.1: Current ratio graph

As we can see in Table 1.1, the current ratio is decreasing

from 0.81 times in year 2005 to 0.74 times in 2006. It

indicate that the liquidity of the company become worst due to

increment of the total current liabilities. However, in 2007

and 2008; the trend is maintained of 1.35 times for the

respective year and the current ratio is slightly going down

by 0.85 times in 2009. Meaning that on the average MAS can

cover only 74.08% of their existing 5-years debt obligations

with their current liquid assets. Clearly, MAS plan to meet

these debt obligations from their income, but the ratio

suggests that their liquid fund still not enough to cover

their liabilities.

1.2. Quick Ratio

Quick ratio is also known as the acid test ratio. The quick

ratio is a measure of the ability of a company to pay its

Financial Ratio of Malaysia Airlines System Berhad 6

short-term debts. As with all ratios, how high a quick ratio

should be varies among industries, but usually a quick ratio

of 1:1 or higher is considered good. In other words, a quick

ratio of 100% tells creditors that the company could pay its

immediate bills even if no inventory is converted to cash.

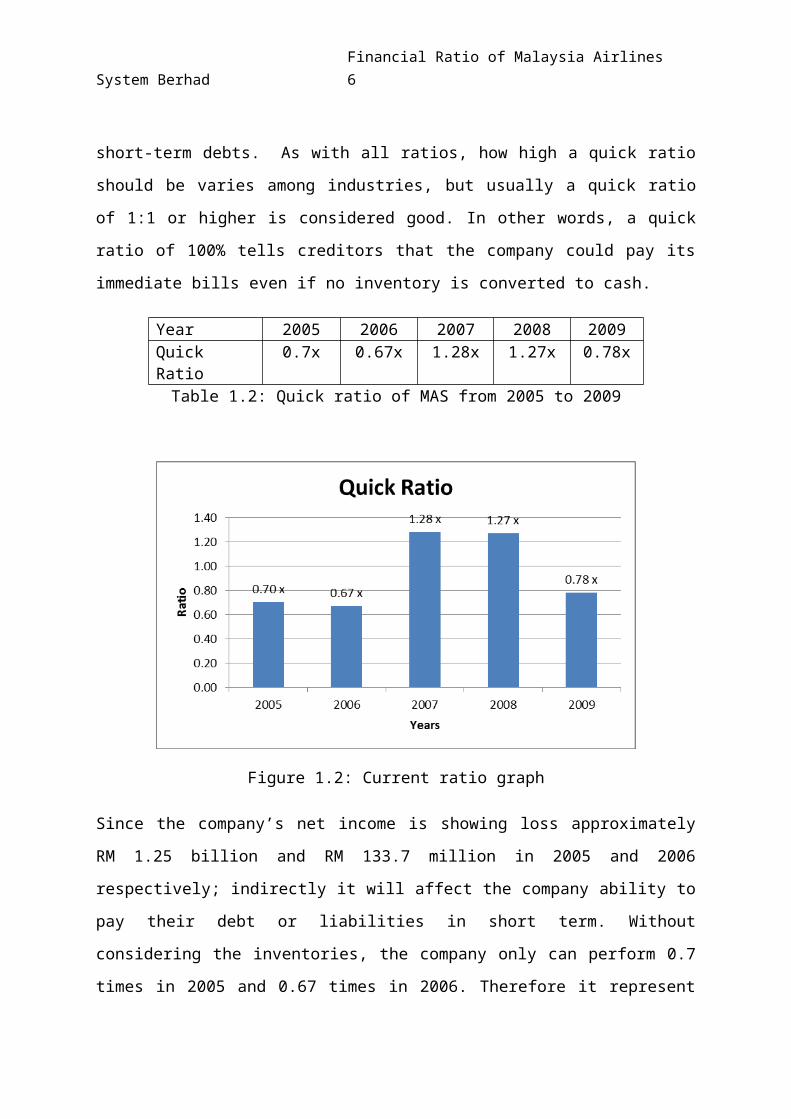

Year 2005 2006 2007 2008 2009Quick Ratio

0.7x 0.67x 1.28x 1.27x 0.78x

Table 1.2: Quick ratio of MAS from 2005 to 2009

Figure 1.2: Current ratio graph

Since the company’s net income is showing loss approximately

RM 1.25 billion and RM 133.7 million in 2005 and 2006

respectively; indirectly it will affect the company ability to

pay their debt or liabilities in short term. Without

considering the inventories, the company only can perform 0.7

times in 2005 and 0.67 times in 2006. Therefore it represent

Financial Ratio of Malaysia Airlines System Berhad 7

that MAS is doing fairly poor in managing their yield. However

in 2007 and 2008, the company liquidity is maintained at 1.28

times and 1.27 times for respective year. In 2008, the quick

ratio is higher thus the company financial performance in term

of liquidity is considered good. Moreover, due to large amount

of current liabilities; the company quick ratio is totally

drops to 0.78 times in 2009. It indicates the company had a

problem in managing their assets fund. The overall liquidity

of the firm seems to exhibit that MAS had a better improvement

in term of managing the cost or cost control. Even though the

current assets are low and being said as not efficiently

manages; MAS still be able to meet its short term obligations.

2. Activity ratio

Activity ratio defines as an accounting ratio that measure a

firm's ability to convert different accounts within their

balance sheets into cash or sales. Companies will typically

try to turn their production into cash or sales as fast as

possible because this will generally lead to higher revenues.

Such ratios are frequently used when performing fundamental

analysis on different companies. The asset turnover ratio and

inventory turnover ratio are good examples of activity ratios.

2.1. Total assets turnover

The amount of sales generated for every dollar's worth of

assets. Asset turnover measures a firm's efficiency at using

Financial Ratio of Malaysia Airlines System Berhad 8

its assets in generating sales or revenue - the higher the

number the better. It also indicates pricing strategy:

companies with low profit margins tend to have high asset

turnover, while those with high profit margins have low asset

turnover.

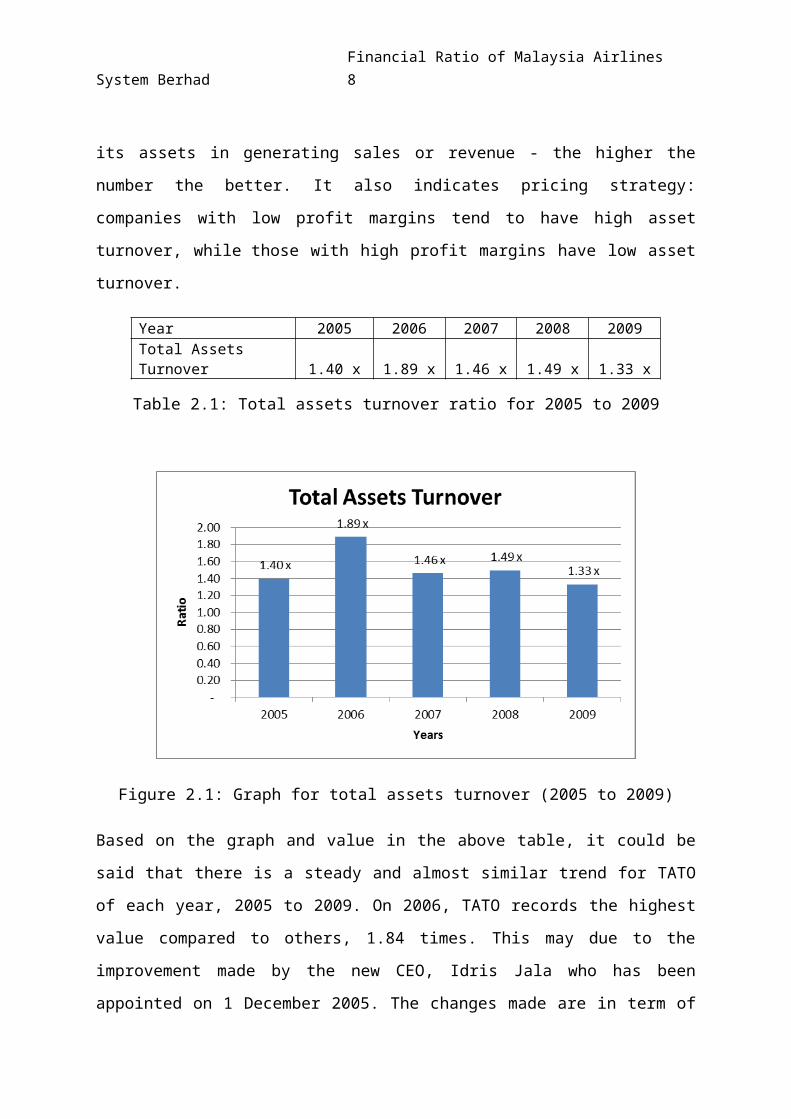

Year 2005 2006 2007 2008 2009Total Assets Turnover 1.40 x 1.89 x 1.46 x 1.49 x 1.33 x

Table 2.1: Total assets turnover ratio for 2005 to 2009

Figure 2.1: Graph for total assets turnover (2005 to 2009)

Based on the graph and value in the above table, it could be

said that there is a steady and almost similar trend for TATO

of each year, 2005 to 2009. On 2006, TATO records the highest

value compared to others, 1.84 times. This may due to the

improvement made by the new CEO, Idris Jala who has been

appointed on 1 December 2005. The changes made are in term of

Financial Ratio of Malaysia Airlines System Berhad 9

MAS’s corporate culture and in operations definitely helps to

increase TATO for year 2006. One of the most significant

things done by MAS for the year 2006 is when MAS sell their

headquarters office which later helps to increase their cash

balance. In 2009, MAS’s TATO records the lowest value ever as

the economic crisis which occurred in 2008. Almost every

industry got affected due to the recession.

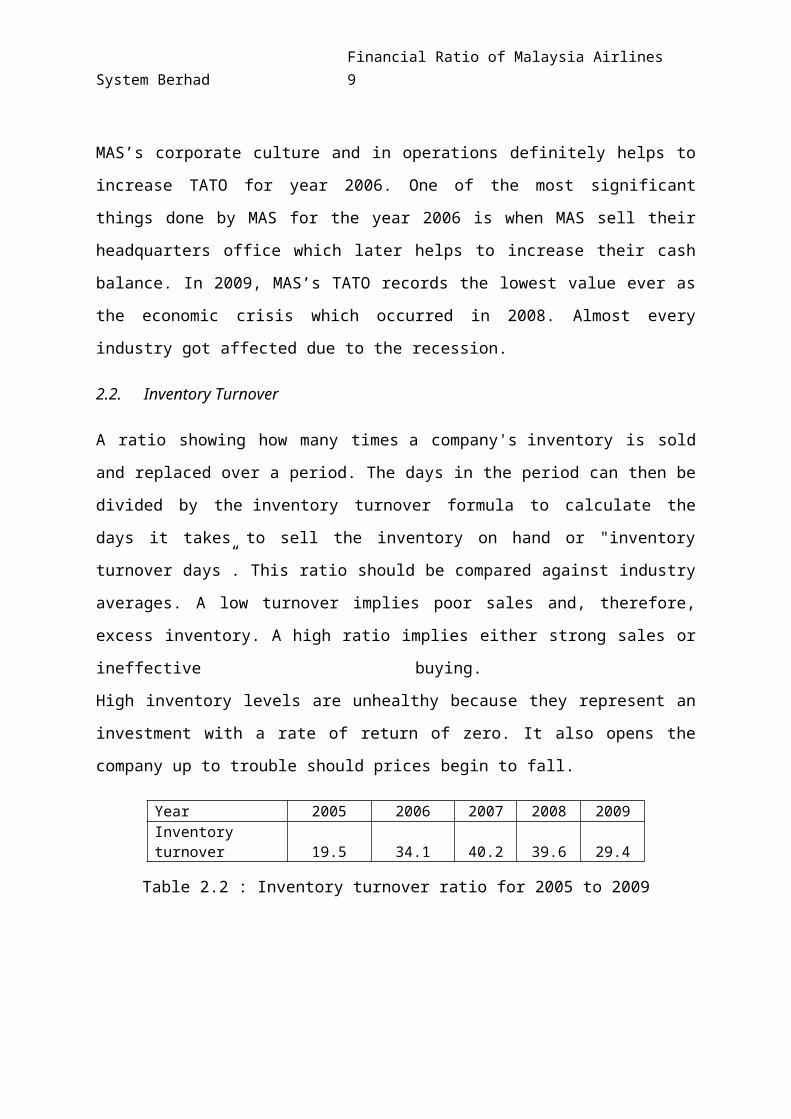

2.2. Inventory Turnover

A ratio showing how many times a company's inventory is sold

and replaced over a period. The days in the period can then be

divided by the inventory turnover formula to calculate the

days it takes to sell the inventory on hand or "inventory

turnover days”. This ratio should be compared against industry

averages. A low turnover implies poor sales and, therefore,

excess inventory. A high ratio implies either strong sales or

ineffective buying.

High inventory levels are unhealthy because they represent an

investment with a rate of return of zero. It also opens the

company up to trouble should prices begin to fall.

Year 2005 2006 2007 2008 2009Inventory turnover 19.5 34.1 40.2 39.6 29.4

Table 2.2 : Inventory turnover ratio for 2005 to 2009

Financial Ratio of Malaysia Airlines System Berhad 10

Figure 2.2 : Graph for inventories turnover (2005 to 2009)

Based on the graph above, we can see that from the year 2005

to 2008, there’s been an increment of ITO value. By referring

to year 2005, we can see that it recorded the lowest ITO value

ever as MAS are struggling with their bad financial situations

due to debts, higher costs and poor sales. It starts to

increase from year 2006 onwards and for the year 2007, ITO

value for MAS records the highest value ever compared to 5

year period (2005-2009). This is due to the changes made by

the new management team led by Dato Sri Idris Jala. Year 2007

and 2008 is slightly similar in term of ITO thanks to the good

management and business decision. For the year 2009, ITO value

for MAS declined as it was the effect of the global economic

crisis for year 2008.

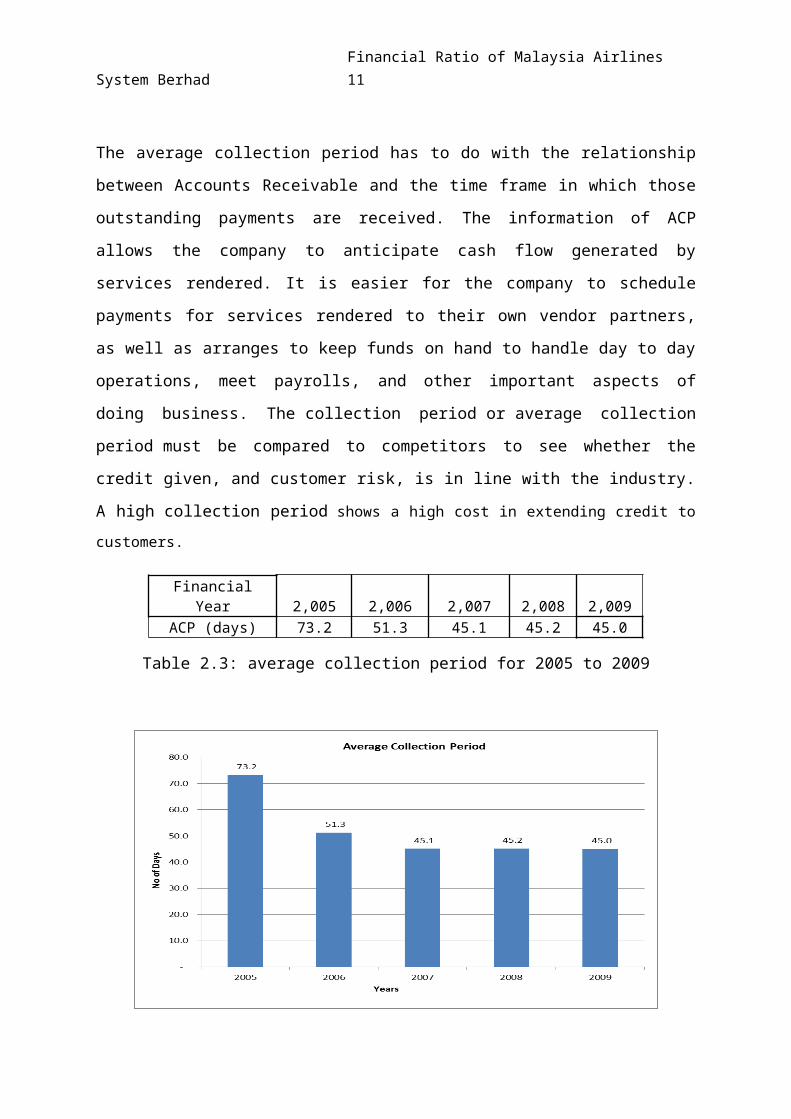

2.3. Average collection period

Financial Ratio of Malaysia Airlines System Berhad 11

The average collection period has to do with the relationship

between Accounts Receivable and the time frame in which those

outstanding payments are received. The information of ACP

allows the company to anticipate cash flow generated by

services rendered. It is easier for the company to schedule

payments for services rendered to their own vendor partners,

as well as arranges to keep funds on hand to handle day to day

operations, meet payrolls, and other important aspects of

doing business. The collection period or average collection

period must be compared to competitors to see whether the

credit given, and customer risk, is in line with the industry.

A high collection period shows a high cost in extending credit tocustomers.

FinancialYear 2,005 2,006 2,007 2,008 2,009

ACP (days) 73.2 51.3 45.1 45.2 45.0

Table 2.3: average collection period for 2005 to 2009

Financial Ratio of Malaysia Airlines System Berhad 12

Figure 2.3 : Graph for average collection period for 2005 to

2009

In the year 2005, MAS was having the highest ACP which is 73.2

days. However, it was declining to 51.3 days on 2006 as well

as year 2007 onwards which they maintain the ACP around 45

days. During this period, MAS had a lot changes in their

account policy where they had adopted of new and revised

Financial Reporting Standard (FRS). However, in year after

2006, the revision made is lesser.

3. Profitability ratio

A class of financial metrics that are used to assess a

business's ability to generate earnings as compared to its

expenses and other relevant costs incurred during a specific

period of time. For most of these ratios, having a higher

value relative to a competitor's ratio or the same ratio from

a previous period is indicative that the company is doing

well.

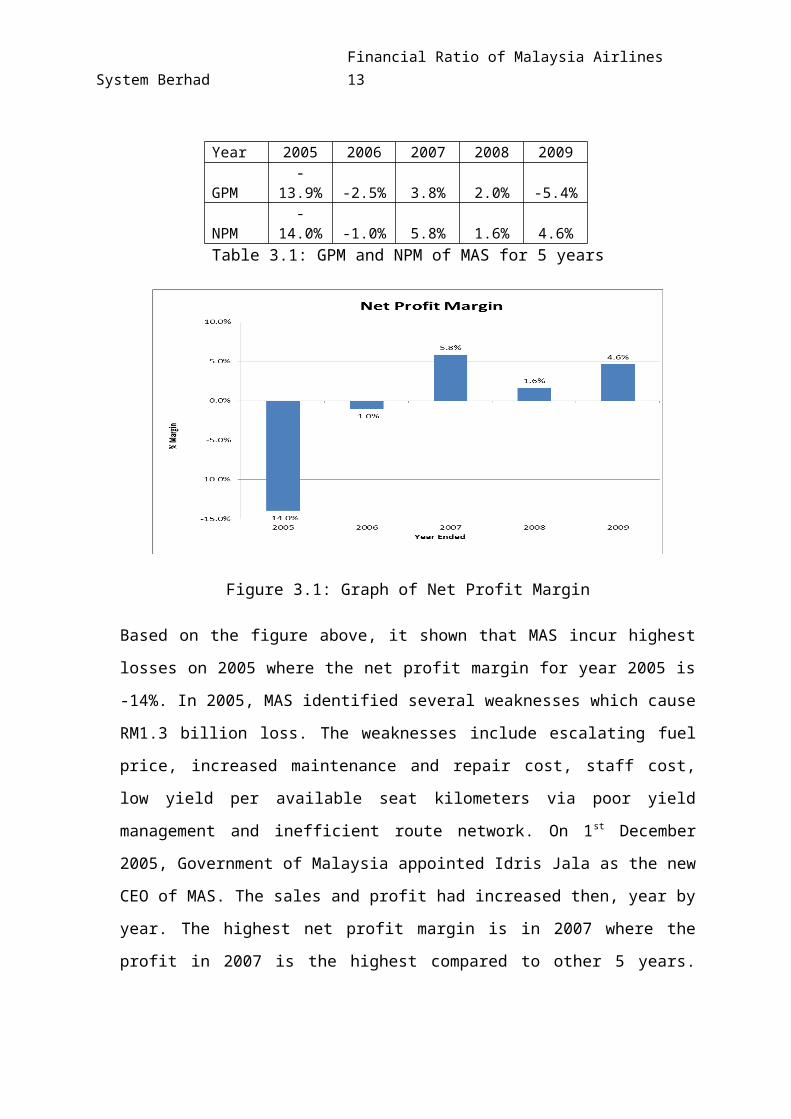

3.1. Net profit margin

Net profit margin is after-tax net income divided by net saleswhich is a measure of management's ability to carry a dollar of

sales down to the bottom line for the stockholders. In other words,

net profit margin refers to that which is left for the owners from a

dollar of sales after all expenses and taxes have been paid.

Financial Ratio of Malaysia Airlines System Berhad 13

Year 2005 2006 2007 2008 2009

GPM-

13.9% -2.5% 3.8% 2.0% -5.4%

NPM-

14.0% -1.0% 5.8% 1.6% 4.6%Table 3.1: GPM and NPM of MAS for 5 years

Figure 3.1: Graph of Net Profit Margin

Based on the figure above, it shown that MAS incur highest

losses on 2005 where the net profit margin for year 2005 is

-14%. In 2005, MAS identified several weaknesses which cause

RM1.3 billion loss. The weaknesses include escalating fuel

price, increased maintenance and repair cost, staff cost,

low yield per available seat kilometers via poor yield

management and inefficient route network. On 1st December

2005, Government of Malaysia appointed Idris Jala as the new

CEO of MAS. The sales and profit had increased then, year by

year. The highest net profit margin is in 2007 where the

profit in 2007 is the highest compared to other 5 years.

Financial Ratio of Malaysia Airlines System Berhad 14

However, in 2008 the net profit slightly decline due to the

global economic crisis and affected our country.

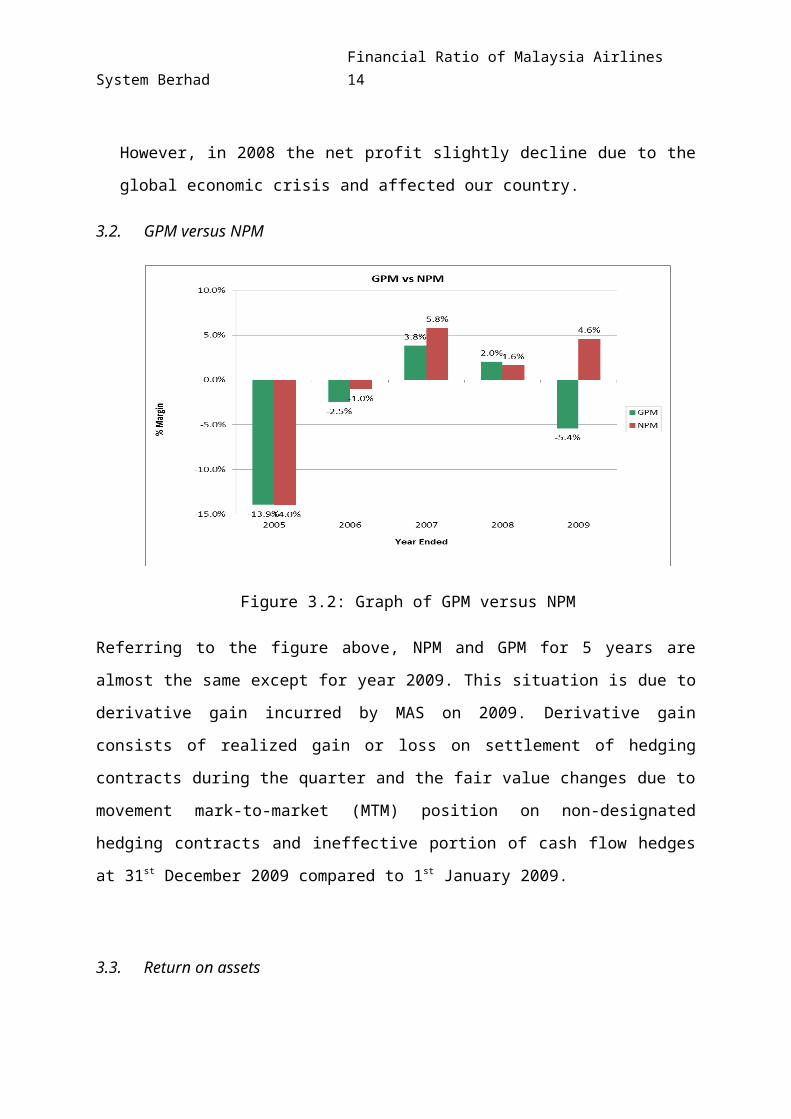

3.2. GPM versus NPM

Figure 3.2: Graph of GPM versus NPM

Referring to the figure above, NPM and GPM for 5 years are

almost the same except for year 2009. This situation is due to

derivative gain incurred by MAS on 2009. Derivative gain

consists of realized gain or loss on settlement of hedging

contracts during the quarter and the fair value changes due to

movement mark-to-market (MTM) position on non-designated

hedging contracts and ineffective portion of cash flow hedges

at 31st December 2009 compared to 1st January 2009.

3.3. Return on assets

Financial Ratio of Malaysia Airlines System Berhad 15

Return on assets (ROA) is a measure of asset intensity which

is , it will indicates how much profit a company generated for

each dollar in assets brought to the company. In other word,

it showed an effectiveness of a company in generating profits

with its available assets.

YEAR RETURN ON ASSET RETURN ON EQUITY 2005 -20.0% -62.1%2006 -1.9% -7.1%2007 8.5% 21.6%2008 2.4% 5.9%2009 5.8% 66.0%

Table 3.3 : Return on assets and return on equity of MAS for

2005 to 2009

Figure 3.3: Graph of Return on Assets

Like MAS (as an aircraft company) considered as a very asset-

intensive, meaning they required big, expensive machinery or

equipment to generate more profit. A measure of profit show

how a percentage of the capital that is handled. The lower

the profit per dollar of assets, the more asset-intensive a

Financial Ratio of Malaysia Airlines System Berhad 16

business is. High profit margin indicates good cost control,

whereas a high asset turnover ratio demonstrates efficient use

of the assets on the balance sheet. If refers to Figure 3.3,

in year of 2005 ROA of MAS is -20.0%, indicates inefficient

use of the assets in the company since the net income in that

year is the lowest compare with others 5 years. During that

year, MAS is concentrate more in escalating fuel price,

increased maintenance and repair cost, staff cost, low yield

per available seat kilometers via poor yield management and

inefficient route network instead of focusing on utilising

their assets to generate more profits. After taken over by

Idris Jala on 1st December 2005, MAS started to recover from

2005 until 2009. Year of 2007 shown huge improvement of assets

handling in MAS since in that year ROA value is the highest

(8.5%) due to very high net income generated from the wisely

utilization of assets in the company.

3.4 Return on equity

Return in equity (ROE) reveals how much profit a company

earned in comparison to the total amount of shareholder equity

found on the balance sheet. A business that has high return on

equity is more likely to be one that is capable of generating

cash internally. Companies that boost a high return on equity

with little or no debt are able to grow without large capital

expenditures, allowing the owners of the business to

withdrawal cash and reinvest in elsewhere.

Financial Ratio of Malaysia Airlines System Berhad 17

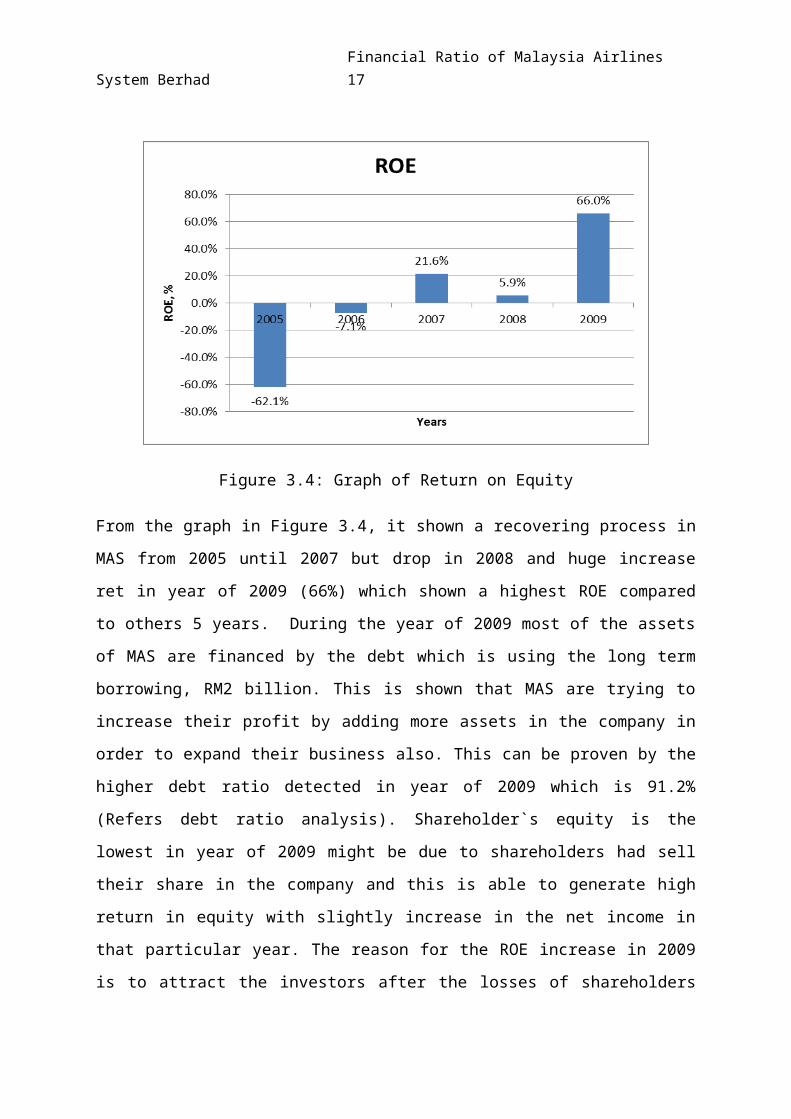

Figure 3.4: Graph of Return on Equity

From the graph in Figure 3.4, it shown a recovering process in

MAS from 2005 until 2007 but drop in 2008 and huge increase

ret in year of 2009 (66%) which shown a highest ROE compared

to others 5 years. During the year of 2009 most of the assets

of MAS are financed by the debt which is using the long term

borrowing, RM2 billion. This is shown that MAS are trying to

increase their profit by adding more assets in the company in

order to expand their business also. This can be proven by the

higher debt ratio detected in year of 2009 which is 91.2%

(Refers debt ratio analysis). Shareholder`s equity is the

lowest in year of 2009 might be due to shareholders had sell

their share in the company and this is able to generate high

return in equity with slightly increase in the net income in

that particular year. The reason for the ROE increase in 2009

is to attract the investors after the losses of shareholders

Financial Ratio of Malaysia Airlines System Berhad 18

in 2009. From the ROA and ROE calculation, it can be conclude

that MAS are trying to improve their assets management in

order to get higher returns from year to year by using

internal and external financial sources.

4. Leverage ratio

The financial leverage of a company is to get an idea of the

company's methods of financing or to measure its ability to

meet financial obligations. There are several different

ratios, but the main factors looked at include debt, equity,

assets and interest expenses.

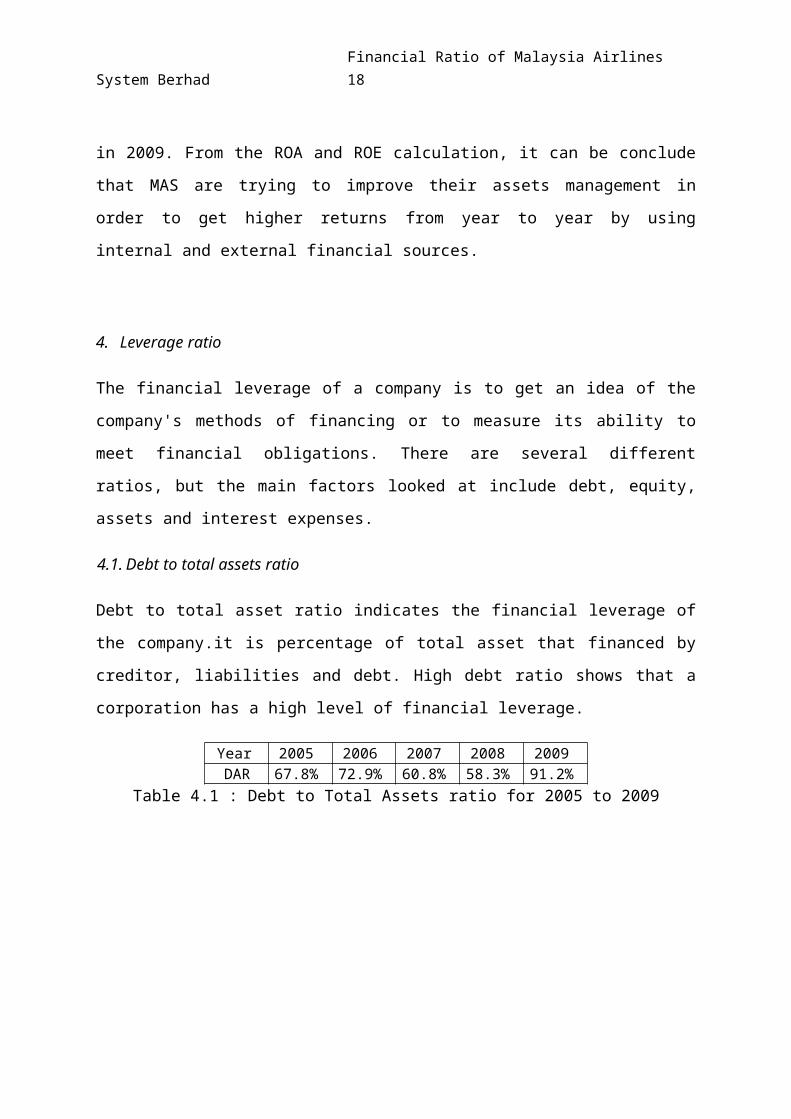

4.1. Debt to total assets ratio

Debt to total asset ratio indicates the financial leverage of

the company.it is percentage of total asset that financed by

creditor, liabilities and debt. High debt ratio shows that a

corporation has a high level of financial leverage.

Year 2005 2006 2007 2008 2009DAR 67.8% 72.9% 60.8% 58.3% 91.2%

Table 4.1 : Debt to Total Assets ratio for 2005 to 2009

Financial Ratio of Malaysia Airlines System Berhad 19

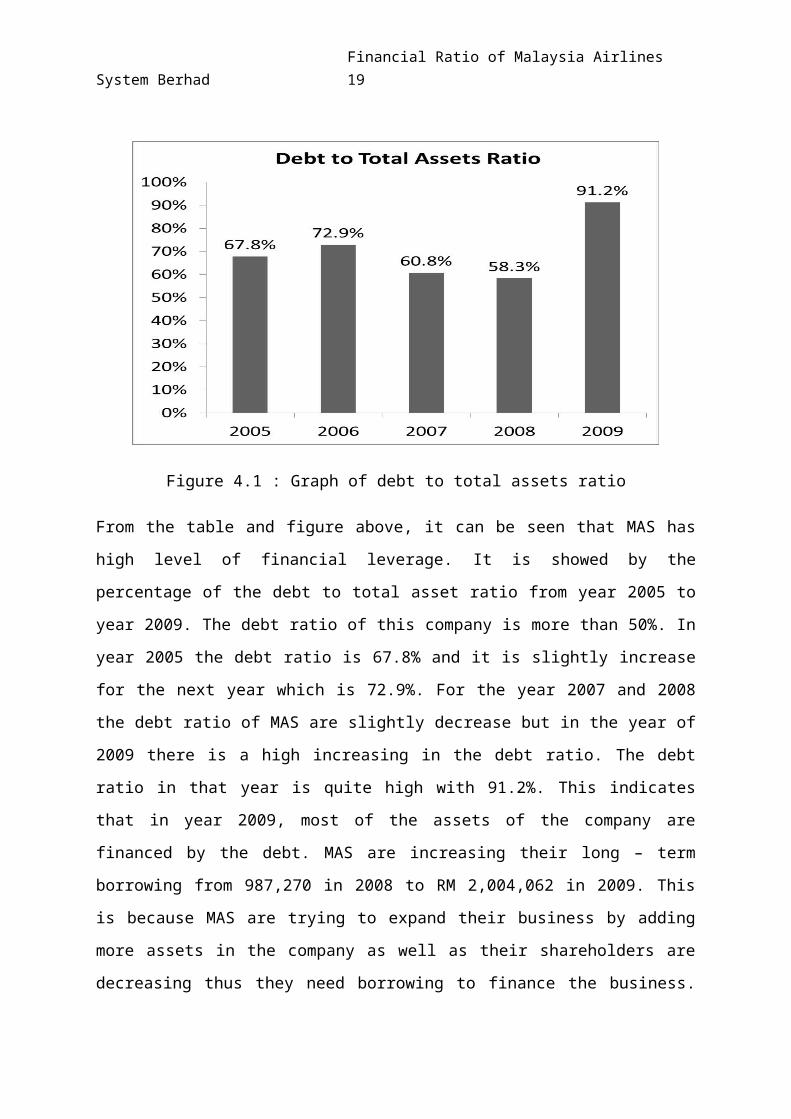

Figure 4.1 : Graph of debt to total assets ratio

From the table and figure above, it can be seen that MAS has

high level of financial leverage. It is showed by the

percentage of the debt to total asset ratio from year 2005 to

year 2009. The debt ratio of this company is more than 50%. In

year 2005 the debt ratio is 67.8% and it is slightly increase

for the next year which is 72.9%. For the year 2007 and 2008

the debt ratio of MAS are slightly decrease but in the year of

2009 there is a high increasing in the debt ratio. The debt

ratio in that year is quite high with 91.2%. This indicates

that in year 2009, most of the assets of the company are

financed by the debt. MAS are increasing their long – term

borrowing from 987,270 in 2008 to RM 2,004,062 in 2009. This

is because MAS are trying to expand their business by adding

more assets in the company as well as their shareholders are

decreasing thus they need borrowing to finance the business.

Financial Ratio of Malaysia Airlines System Berhad 20

The debt ratio in year 2009 indicates that MAS are facing the

high risk of the bankruptcy because they are depending too

much on debt in order to finance their assets.

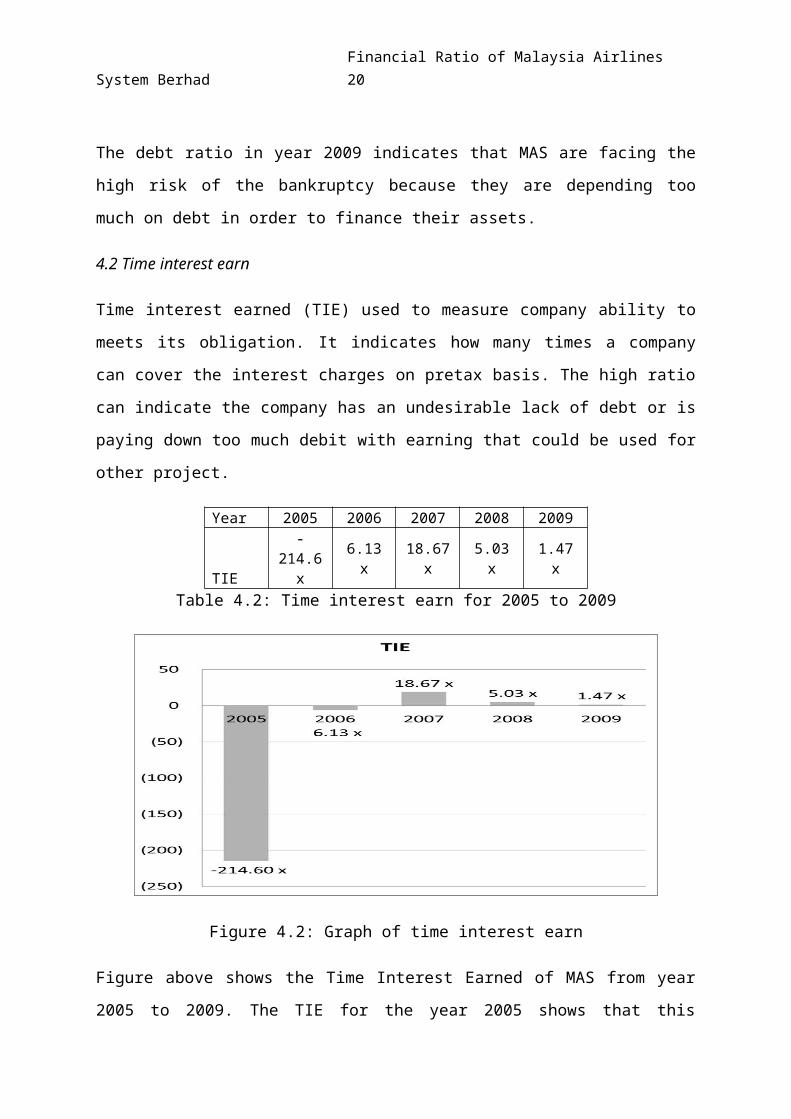

4.2 Time interest earn

Time interest earned (TIE) used to measure company ability to

meets its obligation. It indicates how many times a company

can cover the interest charges on pretax basis. The high ratio

can indicate the company has an undesirable lack of debt or is

paying down too much debit with earning that could be used for

other project.

Year 2005 2006 2007 2008 2009

TIE

-214.6x

6.13x

18.67x

5.03x

1.47x

Table 4.2: Time interest earn for 2005 to 2009

Figure 4.2: Graph of time interest earn

Figure above shows the Time Interest Earned of MAS from year

2005 to 2009. The TIE for the year 2005 shows that this

Financial Ratio of Malaysia Airlines System Berhad 21

company is making loss. The TIE for that year is -214.60 times

showing that the losses cannot cover the interest charge for

that year. In year 2006, the TIE was increase but still making

a loss. The TIE for that year is -6.13. The company is

improved but still makes a loss. The TIE for the year 2007 is

increase to 18.67 and this indicates that the company able to

pay 18.67 times the interest using their earning. For the year

2008 and 2009 the TIE slightly decrease. From the year 2005

until 2009, we can see that the company is growing and keep

making the profit since they can cover their interest using

their earned except for the earlier year 2005 and 2006.

However, in 2009 TIE is declining and it indicates the high

interest of the borrowing that they made in 2009. Thus, it

leads to the high risk of bankruptcy.

5. Forecast of ratios

There are a few factors in order to forecast the financial

ratio of MAS based on reports, expectations, strategy, annual

reports, present economic situations, share price and

etcetera. The good factors that effected the decision of

forecasting MAS are:

i. KLCI is boomed from July 2010 to December 2010 between

1300 to 1500 points respectively. Within year 2011, it

maintained at approximately slightly more than 1500. Thus,

it indicates a good economic situation and stability.

Financial Ratio of Malaysia Airlines System Berhad 22

ii. There is growth in Asia Pacific region in airlines

industry as well as other region especially Middle East

Asia showed rapid growth of airlines industry.

iii. MAS bought new aircrafts Airbus A330-300s and A330-300.

iv. “Everyday low fares” had been introduced in May 2008 in

order to increase the average capacity seated, 70%.

v. Partnership codeshare agreement with 31 Airlines companies

in July 2010.

vi. A330-300s will reduce cost 15% by 2015 as it has fewer

seats, low fuel and maintenance cost. With fewer seats it

can turn around faster, ply more routes and longer range.

vii. Newly changes in boardroom, thus it gives fresh and new

air within the company.

viii. Increased 11% passengers in India, and MAS are targeting

20% increase a year.

The bad factors that MAS has to face and might affect the

performance of the company are:

i. Jet fuel surcharges are soared at 10%.

ii. Japan tragedy of earthquakes, tsunami and nuclear in March

2011 and MAS had to stop the flight from 7 to 11 times a

week.

Financial Ratio of Malaysia Airlines System Berhad 23

iii. MAS share price fell to RM 1.84 in March 23th, 2011.

However, the trends showed that it always drop at 1st

quarter or the year and increase back in 2nd quarter and so

on.

iv. Internal Air Travel Association predicted that in 2011,

the airlines company net profit decrease 50% due to many

factors such as increasing of fuel, Japan’s disaster and

many more.

5.1 Forecast of Quick Ratio

Figure 5.1: Quick Ratio for 2011 onwards (including 2009 and

2010)

From the graph above, it can be seen the quick ratio of 2009

declined from 0.78 times to 0.65 times after being calculated

Financial Ratio of Malaysia Airlines System Berhad 24

from 4th quarter of annual report of 2010. The declining is

because of the highly debt of MAS from previous year to

finance the new investment of assets bought to the company.

However, in 2011 onwards it will keep increasing as they

manage to finance the current asset with current liability,

however due to the increase in fixed assets by increasing the

large number of airbus in 2011 as well as long-term debt to

but with maintaining the current assets, the quick ratio

decline slightly in 2013 and 2014. The quick ratio at average

0.68 times because MAS has less account payable due to the

cash transactions and operations as well as less cash in hand.

The current liability is more sensitive towards changes

because they are in period of expanding, thus including short

term borrowing that finance the assets. However, if the

forecast extended, it will increase from year to year and will

exceed more than 1 times in significant year.

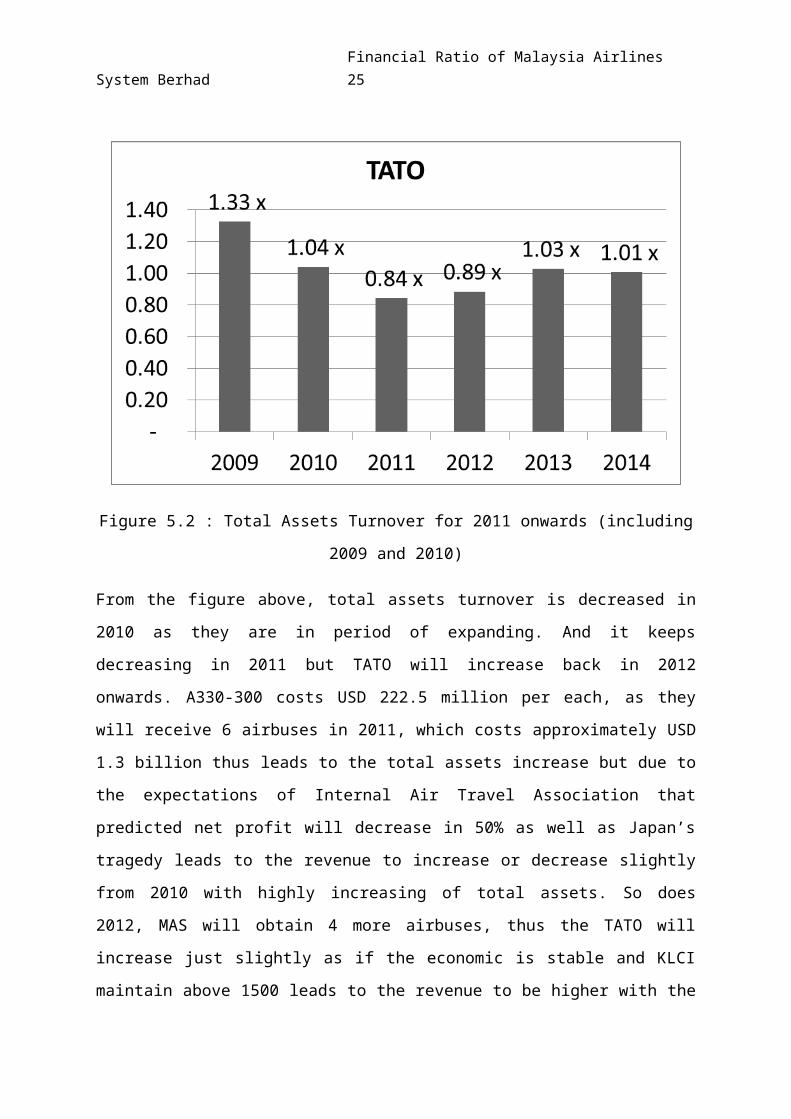

5.2 Forecast of Total Assets Turnover

Financial Ratio of Malaysia Airlines System Berhad 25

Figure 5.2 : Total Assets Turnover for 2011 onwards (including

2009 and 2010)

From the figure above, total assets turnover is decreased in

2010 as they are in period of expanding. And it keeps

decreasing in 2011 but TATO will increase back in 2012

onwards. A330-300 costs USD 222.5 million per each, as they

will receive 6 airbuses in 2011, which costs approximately USD

1.3 billion thus leads to the total assets increase but due to

the expectations of Internal Air Travel Association that

predicted net profit will decrease in 50% as well as Japan’s

tragedy leads to the revenue to increase or decrease slightly

from 2010 with highly increasing of total assets. So does

2012, MAS will obtain 4 more airbuses, thus the TATO will

increase just slightly as if the economic is stable and KLCI

maintain above 1500 leads to the revenue to be higher with the

Financial Ratio of Malaysia Airlines System Berhad 26

higher total assets in 2012. With the cost of reductions,

growth in airlines industry especially Asia Pacific, more

aircrafts that offers more potential revenue, strategy and

partnership TATO can keep increasing and will maintain at

certain level until economic situation changes.

5.3 Debt to Assets Ratio

Figure 5.3 : Debt to Assets Turnover for 2011 onwards

(including 2009 and 2010)

From Figure 5.3 above, Debt to Assets ratio is the highest in

2009 as we discussed above due to the increase in borrowing as

well as decline in shareholders. However, in 2010 it decreased

to 71.7% calculated from 4th quarter report of MAS. It will

slightly increase in 2011 as they obtain 6 new airbuses but in

2012 it will decrease significantly due to the higher assets

as 4 new airbuses obtain that year and make it as total of 10

new airbuses bought. Thus, it leads to the lower debt to

Financial Ratio of Malaysia Airlines System Berhad 27

assets turnover. It will maintain at certain level as only one

to two airbuses will be received in each year. Eventually, the

debt to assets ratio can be slightly increased if they loss

shareholders as it happened in 2009 thus, in order to finance

the incoming assets, they have to make borrowing. But if there

will be rapid increase in shareholders the debt to assets

ratio will decrease significantly.

5.4 Net profit ratio

Figure 5.4: Net Profit Margin for 2011 onwards (including 2009

and 2010)

The net profit of 2010 is declined because the expenditure is

much higher in 2010 and it has less derivative gain in 2010

compared to 2009. However, it maintain at low level of NPM in

2011 because of the expectation of Internal Air Travel

Financial Ratio of Malaysia Airlines System Berhad 28

Association (IATA), Japan’s tragedy and soar of fuel

surcharges. Those factors leads to the lower increase of

revenue and higher expenditure and results lower net profit

margin. However, from 2012 onwards it is expected for net

profit margin to be increase because by new airbuses bought,

MAS can increase the revenue as well as profit due to its less

seats and more frequent travel as it turn around faster and

increase the average sold seats above 70% per airbus. The new

airbuses also have lower fuel costs and maintenance cost, so

it reduces the expenditure as well as increase NPM.

5.5 Forecast of Return on Assets

Financial Ratio of Malaysia Airlines System Berhad 29

Figure 5.4: Return on Assets for 2011 onwards (including 2009

and 2010)

The graph above shows the return on assets from 2009 to 2011.

ROA in 2010 is declined based on 4th quarter of report. It is

predicted that in 2011 ROA will decline as well due to the new

airbuses bought and increase the total assets in MAS but with

the IATA expectations and tragedy in Japan, the net profit

will reduce 50% so it indicates that the total revenue of MAS

will probably just slight increase or decrease thus leads to

lower ROA in 2011. However, in 2012 onwards ROA will keep

rising each year. It indicates that the total revenue of those

following years will increase significantly as the assets

increase and bought into the company. With the growth of Asia

Pacific region in airline business as well as Middle East

would help MAS to increase the revenue. Furthermore, with the

Financial Ratio of Malaysia Airlines System Berhad 30

new airbuses it helps MAS to increase the frequent of

travelling; more routes and “Everyday low fares” can be

successfully done. With partnership and codeshare agreement

with 31 airlines, it also increases the revenue of MAS. It was

11% passengers increase in India as well as expected to be

increase 20% each year. There is also increase in passengers

domestically approximately around 11.1%. Thus, all these

factors help MAS to increase its revenue as well as ROA.

Conclusions

From the discussions and results, it can be seen MAS having a

problem especially in 2005 but it had redeem back the

reputation after Idris Jala being selected as a new director,

and several changes had made and MAS is improving from 2006.

However, in 2008 and 2009 it seems like a slight downfall of

MAS due to the global economic crisis and leads to loss of

shareholders in 2009. Thus, in order to finance its assets,

MAS have high leverage by borrowing the long-term debts. Even

though it indicates MAS having high leverage as well as high

risk of bankruptcy, it is actually have slight advantages

where its ROE is much higher. It happened because to attract

the investors after several losses of shareholders in 2009.

The performance of MAS is quite fluctuating, both internal and

external factors that lead to the fluctuation of MAS

Financial Ratio of Malaysia Airlines System Berhad 31

performance. When MAS change its policy and cost reduction, it

shows some improvement but external factors such as global

crisis can also affected the performance of MAS. Thus, in

order to forecast, external factors is one of the important

role as well as internal factors that can be changed anytime

due to the strategies, policies and investments. Whereas,

external factors like global crisis, natural disaster and

expectation cannot be determined accurately but with

assumptions, forecast can be done approximately accurate.

Policy and strategy need to be adjusted from time to time

depends on economic situations, competitions, opportunities,

visions, and input price that effected the expenditures and

inventories.

Now, MAS shows some positive side and potential to be

successful as they move forward and growth. From enormous

investment in 2009, they see the clearer picture of the vision

that they made and expanding it to concur the airlines

industry. With the suitable strategies and policies, perhaps,

MAS will continue to expand as well as give highly appraisable

and comfortable services

Financial Ratio of Malaysia Airlines System Berhad 32

References

Dato Sri Idris Jala & Dato' Dr Mohd Munir. (2006). Annual Report

2006. Kuala Lumpur: Malaysia Airline System Berhad.

Dato' Sri Idris Jala & Tan Sri Dr. Mohd Munir. (2008). 2008

Annual Report. Kuala Lumpur: Malaysia Airline System Berhad.

Dato' Sri Idris Jala. (2005). Annual Report 2005. Kuala Lumpur:

Malaysian Airline System Berhad.

Munir, T. D. (2010). Quartely Report on the Fourth Quarter Ended 31

December 2010. Kuala Lumpur: Malaysia Airlines.

Shahjanaz binti Kamaruddin. (2010). Investing in the Future. Kuala

Lumpur: Malaysia Airlines.

Tengku Dato' Azmil Zahiruddin & Tan Sri Dr. Mohd Munir.

(2009). 2009 Annual Report - Investing in Growth. Kuala Lumpur:

Malaysia Airlines.

Tengku Dato' Azmil Zahruddin. (2007). 2007 Annual Report. Kuala

Lumpur: Malaysia Airline System Berhad.

Wikipedia. (n.d.). Wikipedia. Retrieved April 2011, from

Malaysia Airlines:

http://en.wikipedia.org/wiki/Malaysia_Airlines