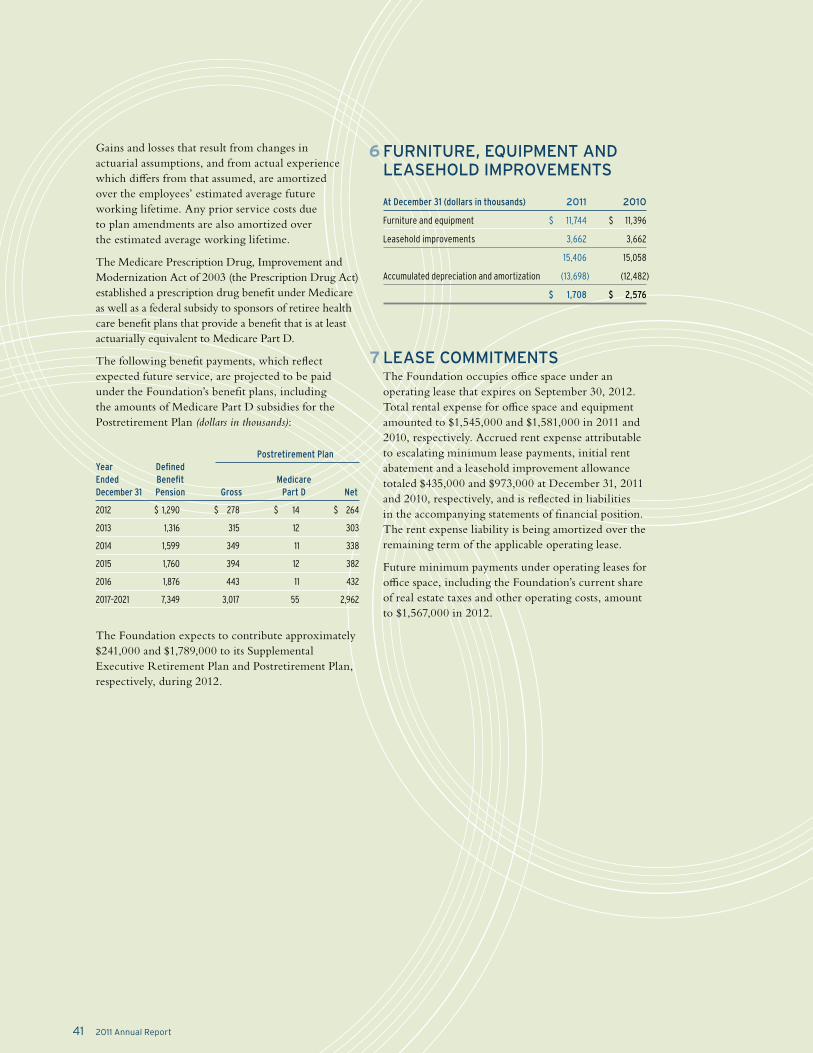

RELIABLE RELEVANT COMPARABLE CONSISTENT - FASB

48

RELIABLE RELEVANT COMPARABLE CONSISTENT Annual Report Financial Accounting Foundation 2011

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of RELIABLE RELEVANT COMPARABLE CONSISTENT - FASB

RELIABLE

RELEVANT

COMPARABLE

CONSISTENT

Annual Report

Financial Accounting Foundation

20

11

2011 A Year in Review 2

Outreach 4

FAF Highlights 6

A Note from FAF 7

GASB Highlights 8

A Note from GASB 9

FASB Highlights 10

A Note from FASB 13

Trustees & Board Members 16

FAF Officers & Committees 19

GASB & FASB Advisory Groups 20

Financial Highlights 25

2011 Annual Report1

RELIABLE. RELEVANT. COMPARABLE. CONSISTENT.Those characteristics define high-quality financial

reporting. High-quality financial reporting, in turn, is

dependent on high-quality financial accounting standards.

Financial information that is reliable, relevant, comparable,

and consistent enables investors to make better informed

decisions about how to allocate their limited capital,

improving the efficiency of U.S. capital markets and

enabling the economy to grow. In the world of state and

local governments, standards that drive high-quality

financial reporting enable taxpayers to better understand

how their elected officials are spending their tax dollars,

and make more informed decisions about the future

of their communities.

Reliable. Relevant. Comparable. Consistent. Those are

the benchmarks that guide the work of the Financial

Accounting Standards Board and the Governmental

Accounting Standards Board, the standard-setting

bodies of the Financial Accounting Foundation.

Financial Accounting Foundation 2

JAN

UA

RY

2011 A YEAR IN REVIEW

FEB

RU

AR

Y

MA

RC

H

AP

RIL

MA

Y

JU

NE

FAF• FAF appoints

Daryl E. Buck and R. Harold Schroeder to the FASB

• Blue-Ribbon Panel addressing standards for private companies submits report of recommendations to FAF

FASB• Susan M. Cosper

named technical director of the FASB

FAF• FAF reappoints

Thomas J. Linsmeier to a second term on the FASB

• 2011 nongovern-mental U.S. GAAP Financial Reporting Taxonomy adopted and supported by SEC effective February 28, 2011

GASB• GASB proposes

guidance for applying termination of hedge accounting provisions

FAF• FAF forms Trustee

Working Group, outlines plans to address standard setting for nonpublic entities

• FAF announces new video webcasting of FASB education sessions

GASB• GASB issues

research brief that examines timeliness of state and local financial reporting in comparison with user needs

GASB• GASB adds project

on financial guarantees to its technical agenda

FASB• FASB issues

Accounting Standards Update to improve financial reporting about troubled debt restructurings

• FASB and IASB report substantial progress toward completion of convergence program

• FASB issues Accounting Standards Update to improve financial reporting of repurchase agreements

FAF• FAF selects FIN

48 for Post-Implementation Review “pilot test”

• FAF commissions study examining role of GASB standards in assessing accountability of reporting governments

FASB• FASB and IASB

issue common fair value measurement and disclosure requirements

FASB• FASB launches IN

FOCUS educational webcast series with CPE credit

• FASB launches new Taxonomy online review and comment system

• FASB issues Accounting Standards Update to improve presentation of comprehensive income

• FASB launches website portal for private companies and not-for-profit organizations

2011 Annual Report3

DEC

EM

BE

R

JU

LY

AU

GU

ST

SEP

TEM

BER

OC

TOB

ER

NO

VE

MB

ER

GASB• GASB proposes

major improvements for pension reporting

• GASB issues Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position

• GASB issues Statement No. 64, Derivative Instruments: Application of Hedge Accounting Termination Provisions (an amendment of GASB Statement No. 53)

• GASB issues Preliminary Views on recognition and measurement of elements of financial statements

FASB• FASB staff submits

report identifying six factors that differentiate private company financial reporting from public company financial reporting

• FASB and IASB announce intention to re-expose leasing proposals

GASB• GASB proposes

recognition of specific items as deferred outflows and deferred inflows of resources

FASB• FASB reports

progress on work to create a differential standard-setting framework for private companies

FASB• FASB issues

Accounting Standards Update to simplify testing goodwill for impairment

• FASB issues Accounting Standards Update to improve employer disclosures for multiemployer pension plans

FAF• FAF seeks comments

on plan to create a private company council

GASB• GASB proposes

technical corrections necessary to resolve conflicting guidance

• GASB extends comment period for pensions proposals

FASB• FASB hosts

private company roundtables

FAF• FAF Board of

Trustees submits comment letter on SEC Staff Paper on “Condorsement,” Exploring a Possible Method of Incorporation

• FAF reappoints Russell G. Golden and Lawrence W. Smith to second terms on the FASB

• FAF reappoints Jan I. Sylvis to a second term on the GASB

• FAF appoints three new Trustees: Paul G. Camell, W. Daniel Ebersole, and Michelle R. Seitz

• FAF appoints five new members to the Governmental Accounting Standards Advisory Council

• FAF appoints 13 new members to the Financial Accounting Standards Advisory Council

FASB• FASB adds two

agenda projects to improve financial reporting by not-for-profit organizations

• FASB and IASB publish revised proposal for revenue recognition

• FASB adds an agenda project on fair value measurement disclosures for private companies and not-for-profit organizations

FAF• FAF names Charles

H. Noski as chairman of the Financial Accounting Standards Advisory Council

GASB• GASB proposes

financial projections for assessing economic condition of governments

FASB• FASB and IASB

issue common offsetting disclosure requirements

• FASB defers certain aspects of comprehensive income Accounting Standards Update

4Financial Accounting Foundation

OUTREACH

GASB

FASB

FAF ENSURING A ROBUST, INCLUSIVE, AND TRANSPARENT STANDARD-SETTING PROCESS

PROMOTING GREATER UNDERSTANDING OF STATE AND LOCAL FINANCIAL REPORTING

BALANCING CONSTITUENT PERSPECTIVES

Extensive outreach is fundamental to the standard-setting

process. It provides the FAF, GASB, and FASB with a broad

spectrum of views from a wide range of constituents, enabling

better informed decisions. Here’s a sample of the outreach

efforts undertaken by the FAF, GASB, and FASB.

2011 Annual Report5

• Informed state CPA societies and state boards of accountancy of current developments in standard setting, including private company and convergence issues and the post-implementation review process; delivered speeches and served on panels to discuss current developments of interest to users, preparers, and practitioners.

• Briefed members of Congress and federal and state regulatory officials on critical issues affecting the standard-setting Boards; discussed issues of importance to the standard-setting process with state and local government financial reporting organizations; discussed GASB funding issues with a range of constituents.

• Solicited input from private company stakeholders on FAF plan to improve private company financial reporting through small group meetings, comment letters, and at four roundtables — in Atlanta, Dallas-Ft. Worth, Palo Alto, and Boston; hosted webcast and podcast on the private company issue.

• Launched “From the President’s Desk,” an interactive online column to enhance stakeholder communication; hosted webcast on Post-Implementation Review process.

• Hosted three public hearings, three user forums, four podcasts, and two webinars on GASB public pensions project.

• Delivered approximately 100 speeches to state and local government preparers, users, and others with an interest in high-quality financial reporting.

• Responded to more than 1,800 technical inquiries from constituents; earned high marks from more than 95 percent of those constituents surveyed, who expressed satisfaction with the promptness, helpfulness, and understandability of responses.

• Launched expanded and updated GASB user guide series with What You Should Know about Your Local Government’s Finances: A Guide to Financial Statements, 2ND edition.

• Launched GASB educational webinar series offering CPE credit, available free of charge to participants.

• Conducted roundtables, small group meetings, industry-specific focus groups, conference calls, and other interactive communications events designed to elicit targeted stakeholder input on proposals and projects undertaken by the FASB, as well as more general topics, including convergence and private company issues.

• Utilized a variety of interactive tools, including IN FOCUS CPE webcasts, speeches, podcasts, FASB in Focus project overviews, and www.fasb.org to educate a broad range of stakeholders on project-specific activities and broad issues in standard-setting.

• Participated in more than 100 speaking events and panels, providing financial reporting professionals, investors, and others the opportunity to hear firsthand FASB updates on projects and initiatives.

• Participated with the SEC and PCAOB on the SEC Financial Reporting Series to ensure consistency among agencies in developing high-quality financial reporting standards for U.S. publicly traded companies.

• Presented testimony before Congress on issues of importance to the U.S. financial system, and met with Congressional members and staff on issues of specific interest to their constituents.

• Engaged in ongoing meetings and dialogue with advisory and resource groups — including FASAC, PCFRC, SBAC, ITAC, EITF, the Valuation Resource Group, and the recently formed Not-for-Profit Advisory Committee (NAC) and Not-for-Profit Resource Group — to hear perspectives on issues of importance to high-quality financial reporting standards.

Financial Accounting Foundation 6

FAF

HIG

HLI

GH

TSPROPOSAL TO CREATE A PRIVATE COMPANY COUNCILThe FAF took major steps toward improvements in the standard-setting structure for private companies. Early in the year, the FAF/AICPA/NASBA-sponsored “Blue-Ribbon Panel” issued its recommended improvements. In response, the FAF formed a Trustee Working Group to study this input and other feedback received as part of its “big picture” view of the issue. As a result of the Working Group’s findings, in October 2011, the FAF Board of Trustees issued for public comment its “Plan to Create the Private Company Standards Improvement Council (PCSIC).” As proposed, the PCSIC would have the authority to identify, propose and vote on specific improvements to U.S. accounting standards for private companies,

to then be submitted to the FASB for ratification. Stakeholder input received in comment letters and four roundtables hosted across the country will be considered as the Trustees

redeliberate the proposal. A final decision is expected

during the first half of 2012.

POST-IMPLEMENTATION REVIEW PROCESSIn May of 2011, FAF announced it would launch a “pilot test” of its Post-Implementation Review (PIR) process to assess whether standards set by both the FASB and the GASB are meeting their intended financial reporting objectives. The first standard to be reviewed: FASB Interpretation (FIN) No. 48, Accounting for Uncertainty in Income Taxes. FIN 48 was chosen because it was considered complex, had elicited concerns among some stakeholders, was not currently under review by the FASB, and was not one of the standards on the FASB’s joint “Memorandum of Understanding” projects with the International Accounting Standards Board. The PIR team concluded its pilot test late in the year, and issued its final report on FIN 48 in January 2012.

FAF SUBMITS COMMENT LETTER ON SEC PLAN FOR “CONDORSEMENT”On November 15, 2011, the FAF Board of Trustees submitted its comment letter on the SEC Staff Paper on “Condorsement,” Exploring a Possible Method of Incorporation. In the letter, the FAF expressed conditional support of the SEC’s proposed “condorsement” model. As a policy matter, the Trustees said that the United States should agree to, over time, incorporate into U.S. GAAP those International Financial Reporting Standards that improve or maintain the quality of U.S. GAAP and that increase the global comparability of accounting standards. Among other recommendations, the FAF said the FASB should retain its authority as the independent standard setter for capital markets in the United States, and that the FASB should incorporate into U.S. GAAP major new international standards that improve the quality of U.S. GAAP. Incorporation would be based on criteria consistent with those that have guided the standard-setting activities of the FASB throughout its history.

141,167,000Individual tax returns filed in 20101

93.3 MILLIONU.S. retail investors2

[ ACCOUNTING BY THE NUMBERS ]

In October 2011, the FAF Board of Trustees issued for public comment its “Plan to Create the Private Company Standards Improvement Council (PCSIC).”

FAF

2011 Annual Report7

54State CPA Societies5

93.3 MILLION

Teresa S. Polley President & Chief Executive Officer FAF

John J. Brennan Chairman

FAF Board of Trustees

A NOTE FROM FAF

Number of accountants and auditors in 20083 CPAs in the U.S.41,290,600 656,650

FAF in 2011: Looking to the FutureHigh-quality financial reporting is critical to the efficient operation of U.S. capital markets and the growth of the U.S. economy — and to the ability of taxpayers to assess how well their elected officials are spending their tax dollars.

But high-quality financial reporting doesn’t just happen. It is built on a foundation of high-quality accounting standards that result in reliable, relevant, comparable, and consistent financial information. High-quality standards meet the needs of investors and taxpayers, as well as those who prepare and audit the financial statements of public and private companies, not-for-profits, and state and local governments.

Ensuring that our U.S. standard-setting Boards — the Financial Accounting Standards Board (FASB) and the Governmental Accounting Standards Board (GASB) — have the ways and means, the people, and the independence they need to consistently create high-quality standards is the job of the Financial Accounting Foundation (FAF).

In 2011, the Foundation continued to build a strong foundation for the future of fair and independent standard setting in the United States. Foundation initiatives included sharing its vision for developing more comparable global accounting standards; addressing the process for considering the accounting concerns of private companies; reviewing the operation and effectiveness of standards once they are in place; and examining the appropriate scope of governmental accounting standard setting.

More comparable global accounting standardsThe Foundation in November shared its views on the move to create more comparable global accounting standards in a letter to the Securities and Exchange Commission (SEC). The letter, which commented on an SEC staff paper, expressed our support for the incorporation of International Financial Reporting Standards (IFRS) into U.S. Generally Accepted Accounting Principles (U.S. GAAP). We also included several recommendations that we believe would significantly improve the incorporation framework as outlined in the staff paper.

The Foundation’s recommended approach emphasizes improving financial reporting while also meeting U.S. investors’ needs and advancing global comparability. In our comment letter, we noted the importance of establishing criteria to evaluate standards for incorporation and suggested that they be based on the criteria that historically have guided the FASB’s standard setting — among them, the importance of the investor perspective and an independent, robust due process.

Our recommendations envision active U.S. involvement in setting new international standards and a continuation of U.S. sovereignty over accounting standards to be used in the U.S. capital markets. Adopting that approach would protect the interests of U.S. investors and other constituents and ensure that any new standard would meet the needs of U.S. capital markets.

FAF plan to create a private company councilPrivate companies were a major focus for the Foundation in 2011. In October, the Trustees asked for public comment on a proposal to create a new body that, in effect, would set the agenda for determining whether exceptions or modifications to U.S. GAAP are warranted for private companies. As proposed, the new private company council would submit its recommendations to the FASB for ratification.

The Foundation followed up with extensive constituent outreach, including a series of roundtables in Massachusetts, Georgia, Texas, and California; meetings with the FASB’s advisory groups; briefings and listening sessions with state CPA societies; and meetings with financial executives and other interested parties. A final decision on the plan is expected in mid-2012.

Post-Implementation Review processIn 2011, the Foundation initiated its first Post-Implementation Review (PIR) as part of its responsibility for overseeing the standard-setting processes of the FASB and GASB. We decided to “pilot test” the PIR process with a review of FASB Interpretation (FIN) No. 48, Accounting for Uncertainty in Income Taxes. For much of 2011, a PIR team of experienced staff members conducted research and outreach that led to the release of a final report in January 2012. The report concluded that FIN 48 had generally met its objectives, but suggested several process improvements to the FASB. Reviews of two more FASB standards and one GASB standard are planned for 2012.

Examining the purposes of state and local government financial reportingIn May 2011, the Foundation’s Board of Trustees announced that it had commissioned an independent academic study to examine the purposes of financial accounting and reporting for state and local governments. When completed, the data collected in the study is expected to serve as a tool to aid the Foundation’s Board of Trustees in its ongoing oversight of the GASB, its further assessment of the scope of the GASB mission, and in its determination of how the GASB can best serve stakeholders within the context of its mission.

Looking ahead to 2012In 2012, the Foundation will keep its eye on the future and continue to build on the progress we made in 2011. The Foundation will continue to monitor global standard-setting issues and hold discussions with a variety of constituents about how the U.S. might incorporate IFRS into U.S. GAAP.

With a decision on the private company plan expected in the first half of the year, we anticipate focusing on the implementation of that plan during the second half of 2012.

The PIR process will continue with the second phase of standards, including our first GASB standard, GASB Statement No. 3, Deposits with Financial Institutions, Investments (including Repurchase Agreements), and Reverse Repurchase Agreements. We also will review FASB Statements No. 141R, Business Combinations, and No. 131, Disclosures about Segments of an Enterprise and Related Information. The Trustees will review and analyze the findings of the academic study, with an eye toward considering the appropriate scope and nature of the GASB’s standard-setting activities. That work may include asking for additional feedback from stakeholders.

In closing, we’d like to thank our colleagues at the FASB, GASB, and FAF for their outstanding work this year. We’d also like to thank you, our stakeholders, for your participation and input into the standard-setting process. You are at the heart of what we do every day, and you keep us accountable for developing the highest quality financial reporting standards possible.

Financial Accounting Foundation 8

HIG

HLI

GH

TSPROPOSALS TO IMPROVE ACCOUNTING AND FINANCIAL REPORTING FOR STATE AND LOCAL GOVERNMENT PENSION BENEFITSIn July, the GASB issued two Exposure Drafts, Accounting and Financial Reporting for Pensions and Financial Reporting for Pension Plans, which proposed important changes to how governments account for and report on the pension benefits they promise to their employees.

The proposals would, among other things, require:

• Recognizinganetpensionliability equal to the difference between a government’s total pension liability and the value of assets set aside in a qualifying trust to pay benefits

• Recognizingpensionexpensesover a period more consistent with the time during which employees are working and earning pension benefits

• Usingasinglecostallocationmethod, which would result in more comparable information across governments, and

• Presentingmoreinformativenote disclosures and required supplementary information.

PROPOSAL ON FINANCIAL PROJECTIONS FOR ASSESSING THE ECONOMIC CONDITION OF GOVERNMENTSIn December, the GASB issued a Preliminary Views, Economic Condition Reporting: Financial Projections. The Preliminary Views presents the Board’s initial thinking on the key issues related to reporting financial projections to assist users with assessing a government’s fiscal sustainability and overall economic condition.

It envisions a presentation of at least five years of projections of cash inflows and outflows, and of financial obligations on an accrual basis, as well as a narrative description of intergovernmental service interdependencies as required supplementary information.

This kind of forward-looking information would help users

to assess a government’s ability and willingness to generate inflows of resources necessary to honor current service commitments and to meet

its financial obligations as they come due, without

transferring financial obligations to future periods that do not result in commensurate benefits. Such information would help users discern whether a government is on a financially sustainable path.

GASB STANDARDS ISSUED IN 2011In 2011, the GASB issued two final Statements of Governmental Accounting Standards:

60,000$3.7TRILLIONState and local municipal bond issuers7In holdings of U.S. municipal securities

by taxpayers, bond funds, money market funds, banks and insurance companies6

GASB Statement No. 64Derivative Instruments: Application of Hedge Accounting Termination Provisions, amends existing standards to respond to concerns of governments whose derivatives had become ineffective from a financial reporting perspective through no fault of their own. Statement No. 64 enables those governments in certain circumstances to continue to use hedge accounting when their swap counterparty, or counterparty’s credit support provider, is replaced, but the remainder of the swap agreement terms is effectively unchanged.

GASB Statement No. 63Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position clarifies where deferred amounts should appear in a new statement of net position. The GASB’s Statements on derivative instruments and service concession arrangements may require the recognition of deferred outflows of resources and deferred inflows of resources but do not specify where and how they should be reported in financial statements. Statement No. 63 helps constituents apply those Statements and future standards that might require reporting of deferrals.

[ ACCOUNTING BY THE NUMBERS ]

GA

SB

63

64

2011 Annual Report9

500,000U.S. Elected government officials as of 20099State and local municipal bond issuers7 Local governments in the U.S., including municipal,

county, township and borough as of 20078

89,527

A NOTE FROM GASB

Robert H. Attmore Chairman GASB

During 2011, the Governmental Accounting Standards Board (GASB) and its staff worked diligently to provide assistance to our constituents — the preparers, auditors, and users of state and local government financial statements. Serving the needs of constituents is at the heart of everything that we do. Whether setting new standards, improving on existing ones, or helping constituents to implement and understand those standards, our aim is to promote greater transparency, to support well-informed decision making, and to help users assess a government’s financial accountability. We made significant progress toward those ends in 2011.

Final Statements The GASB issued two final statements in 2011 that solved important practice issues facing our constituents.

Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position, clarifies where deferred amounts should appear in a new statement of net position.

Statement No. 64, Derivative Instruments: Application of Hedge Accounting Termination Provisions, amends existing standards to respond to concerns of governments whose derivatives had become ineffective from a financial reporting perspective through no fault of their own.

Due Process DocumentsIssuing a pronouncement is not the end of the standard-setting process. It is vital that our constituents receive the assistance they need to understand and implement our standards and that over time those standards continue to function properly and result in decision-useful information for financial report users. Toward that end, the Board and staff devoted significant time and attention to the review and improvement of our current pension accounting and financial reporting standards.

Last summer, the GASB issued two Exposure Drafts, Accounting and Financial Reporting for Pensions and Financial Reporting for Pension Plans, which proposed important changes to how governments account for and report on the pension benefits they promise to their employees.

The Board also continued its work on other projects. In December, we issued a Preliminary Views, Economic Condition Reporting: Financial Projections. It presents the Board’s initial thinking on the key issues related to reporting financial projections to assist users with assessing a government’s fiscal sustainability and overall economic condition.

Last summer, the GASB issued a Preliminary Views of a Concepts Statement, Recognition of Elements of Financial Statements and Measurement Approaches. It addresses how and when an item should be reported in financial statements and how to measure the amount of the item reported. This project is expected to yield one of the fundamental building blocks of the GASB’s conceptual framework, which promotes conceptual consistency in our standard-setting activities and helps to guide the Board in its work.

Two additional Exposure Drafts issued in 2011 led to final Statements issued in March 2012. One addressed items previously reported as assets and liabilities that should henceforth be reported as deferred outflows of resources, deferred inflows of resources, or current-period outflows or inflows. This is closely related to Statement No. 63 that was mentioned earlier; the result should be the reporting of more comparable and accurate information. The other Exposure Draft proposed technical corrections to eliminate conflicting guidance that arose due to the issuance of two recent Statements.

Serving Our ConstituentsWhile the majority of our time is devoted to developing accounting and financial reporting standards, GASB staff spends a significant amount of time helping constituents understand and implement standards by providing them direct assistance addressing their specific facts and circumstances. In 2011, we responded to nearly 1,800 technical inquiries that required a specific response about the application and implementation of our standards. Each year, we receive and answer thousands of additional, more general questions about our standards and current projects. More than 95 percent of constituents who submitted technical inquiries were satisfied with the promptness, helpfulness, and understandability of our responses. The GASB has achieved this high degree of constituent satisfaction every year since we began surveying constituents in 2006.In addition, we made approximately 100 presentations at events across the country, and published educational materials designed to enhance the understandability of our work, including plain-language articles, podcasts, a monthly newsletter, and a user-oriented electronic newsletter. In 2011, we offered our first webinars — at no charge. Also, we published the annual updated Comprehensive Implementation Guide, which answers nearly 2,000 questions on governmental accounting topics.The GASB staff made significant progress in updating and expanding the GASB’s series of user guides, which are written for a nontechnical audience using plain language and are intended to serve as a primer to understanding governmental financial reports. The first revised guide, which addresses local government finances, was issued late last year. Updated or entirely new guides addressing school districts, business-type activities, and information for financial analysts will be published in 2012.

Looking AheadIn 2012, the GASB will continue its focus on improving financial reporting through its work on a host of projects. The GASB expects to issue two final pension Statements in the summer of 2012. Once those standards have been issued, deliberations on the companion project on other postemployment benefits are scheduled to restart.Board deliberations are due to resume on the financial projections project after public hearings have been held in March and April. The Board will review the comments received from constituents and consider whether, or in what form, a further due process document might be issued for this project. The GASB’s project on recognition and measurement approaches as well as projects on financial guarantees, government combinations, and fair value measurement will all be considered on the Board’s 2012 current agenda. In closing, I would like to express my appreciation to my fellow Board members, the FAF Trustees, members of the GASB and FAF staff, the GASAC members, and those who volunteer their time and expertise to serve on GASB task forces and advisory committees for their dedication and outstanding contributions in 2011.I also would like to thank all those who read and responded to our due process documents providing thoughtful feedback. The input you provide us is essential to the process of improving accounting and financial reporting and is greatly appreciated.

Financial Accounting Foundation 10

HIG

HLI

GH

TSIMPROVING U.S. GAAPSimplification, consistency, and transparency in financial reporting guided the FASB’s efforts to improve U.S. GAAP. Troubled Debt Restructuring created consistency in how GAAP is applied for various types of debt restructurings. Repurchase Agreements created greater transparency by requiring substantial new disclosures, including disclosures about a transferring company’s continued involvement with transferred assets. Presentation of Other Comprehensive Income increased the prominence of other comprehensive income in financial statements. Testing Goodwill for Impairment simplified how a company performs this test. Finally, Multiemployer Pension Plans provided more information about an employer’s potential obligations to multiemployer

pension plans.

INTERNATIONAL CONVERGENCEThe FASB and the IASB made substantial progress toward completion of their priority agenda projects covering revenue recognition, leases, and accounting for financial instruments, as well as their joint project to improve insurance accounting standards. Citing the need for further stakeholder outreach and input, the Boards agreed to extend the timetable for three priority agenda projects beyond June 2011 and decided to re-expose two of the proposals. The Boards issued a new standard on fair value measurement and disclosure requirements, which improved and converged guidance on how fair value should be applied where its use is already required or permitted by other standards within IFRS or U.S. GAAP. In December, the Boards issued new disclosure requirements on offsetting, intended to allow investors to better compare financial statements prepared in accordance with IFRS or U.S. GAAP.

PRIVATE COMPANIESIn 2011, the Board took major steps to address private company stakeholder concerns about the complexity, cost, and relevance of U.S. GAAP. A project was undertaken to develop a decision-making framework for whether and when modifications for private companies are appropriate. FASB staff members were assigned to each project team as private company liaisons. Webcasts, roundtables, meetings, and other vehicles also were employed to improve communication with private companies. The results of these efforts included increased participation in the standard- setting process by private company stakeholders, delayed effective dates for private companies on key FASB standards, and issuance of the testing goodwill for impairment standard that simplified this test for private and public companies alike.

Private companies in the U.S., including S corporations and sole proprietorships as of 20078

29,000,000

In 2011, the Board took major steps to address private company stakeholder concerns about the complexity, cost, and relevance of U.S. GAAP.

[ ACCOUNTING BY THE NUMBERS ]

FAS

B

2011 Annual Report11

U.S. GAAP FINANCIAL REPORTING TAXONOMYXBRL, or eXtensible Business Reporting Language, is a standard for tagging business and financial reports to increase the transparency and accessibility of business information by using a uniform format. The U.S. GAAP Financial Reporting Taxonomy is a list of computer-readable tags in XBRL that allows companies to label precisely the thousands of pieces of financial data that are included in typical long-form financial statements and related footnote disclosures. The tags allow computers to automatically search for and assemble data so those data can be readily accessed and analyzed by investors, analysts, journalists, and the SEC staff. The FASB’s development of the Taxonomy is investor-focused and its use has increased substantially over the past few years. As a result, the FASB is continually striving to understand how the information is used by investors and other users. It created the FASB Taxonomy Advisory Group (made up of analysts, data aggregators, accounting firms, service providers, and preparers) to advise it on these matters. The FASB also launched an online review and comment system to make it easier for stakeholders to submit comments on the U.S. GAAP Financial Reporting Taxonomy.

IN FOCUS WEBCASTSIn June, the FASB launched IN FOCUS, an educational webcast series offering CPE credit to those participating in live broadcasts. The FASB hosted a total of six IN FOCUS webcasts in 2011, focusing on private company issues, revenue recognition, XBRL, and the Board’s proposals on investment companies, investment property entities, and consolidations. Live video webcasts of the Board’s education sessions were also launched in 2011.

NOT-FOR-PROFITSCreated in late 2009, the Not-for-Profit Advisory Committee (NAC) submitted recommendations to the FASB on how to refresh the current not-for-profit reporting model. While NAC members expressed overall satisfaction with the current model, they offered a number of suggestions for improving the information not-for-profit financial statements provide to donors and other users.

The FASB responded by adding both a standard-setting and a research project to the Board’s agenda. The standard-setting project seeks to improve the current net asset classification scheme and information provided in financial statements and notes about an organization’s liquidity, financial performance, and cash flows. The research project will study other means of communication that not-for-profit organizations can use to tell their financial story.

15,188U.S. publicly traded companies as of 2011 (on exchanges and OTC)11U.S. not-for-profit organizations as of 201010

1,643,306

FASB launched IN FOCUS, an educational webcast series that offers continuing professional education (CPE) credit to those participating in its live broadcasts.Created in late 2009,

the Not-for-Profit Advisory Committee (NAC) submitted its recommendations to the FASB on how to refresh the current not-for-profit reporting model.

Financial Accounting Foundation 12

UPDATE No. 2011-01Receivables (Topic 310): Deferral of the Effective Date of Disclosures about Troubled Debt Restructurings in Accounting Standards Update No. 2010-20

UPDATE No. 2011-04Fair Value Measurement (Topic 820): Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRS

UPDATE No. 2011-07Health Care Entities (Topic 954): Presentation and Disclosure of Patient Service Revenue, Provision for Bad Debts, and the Allowance for Doubtful Accounts for Certain Health Care Entities (a consensus of the FASB Emerging Issues Task Force)

UPDATE No. 2011-10Property, Plant, and Equipment (Topic 360): Derecognition of in Substance Real Estate — a Scope Clarification (a consensus of the FASB Emerging Issues Task Force)

UPDATE No. 2011-02Receivables (Topic 310): A Creditor’s Determination of Whether a Restructuring is a Troubled Debt Restructuring

UPDATE No. 2011-05Comprehensive Income (Topic 220): Presentation of Comprehensive Income

UPDATE No. 2011-08Intangibles — Goodwill and Others (Topic 350): Testing Goodwill for Impairment

UPDATE No. 2011-11Balance Sheet (Topic 210): Disclosure about Offsetting Assets and Liabilities

UPDATE No. 2011-03Transfers and Servicing (Topic 860): Reconsideration of Effective Control for Repurchase Agreements

UPDATE No. 2011-06Other Expenses (Topic 720): Fees Paid to Federal Government by Health Insurers (a consensus of the FASB Emerging Issues Task Force)

UPDATE No. 2011-09Compensation — Retirement Benefits — Multiemployer Plans (Subtopic 715-80): Disclosures about an Employer’s Participation in a Multiemployer Plan

UPDATE No. 2011-12Comprehensive Income (Topic 220): Deferral of the Effective Date for Amendments to the Presentation of Reclassifications of Items Out of Accumulated Other Comprehensive Income in Accounting Standards Update No. 2011-05

01

05

09

11

FASB ACCOUNTING STANDARDS ISSUED IN 2011

Credit rating agencies in the U.S. as of 201013

8132,122Accounting firms in the U.S. as of 201112

HIG

HLI

GH

TSFA

SB

[ ACCOUNTING BY THE NUMBERS ]

A NOTE FROM FASB

State Boards of Accountancy: including boards in Guam, Puerto Rico, D.C., Virgin Islands and Commonwealth of the Northern Mariana Islands4

U.S. financial analysts as of May 201014

55220,810

2011 Annual Report13

Leslie F. Seidman Chairman FASB

2011: A Year of ListeningIf I were to describe the year 2011 with only one word, that word would be “listening.” We listened to our private company stakeholders, whose suggestions on making the standard-setting process more accessible resulted in improvements to the way we interact with and respond to all of our stakeholders. We listened to our public company stakeholders, whose desire for improved, converged standards led us to simplify our proposals and allow more time for comment on our key projects with the International Accounting Standards Board (IASB). And we listened to our not-for-profit stakeholders by adding projects to refresh the nonprofit financial reporting model.

Private Companies and Not-for-ProfitsDeveloping financial reporting standards that produce relevant information at a reasonable cost requires listening to and balancing the perspectives of a wide range of interested parties. With less time and fewer resources to devote to following FASB projects and initiatives, private companies and their auditors have expressed concerns that the standard-setting process has not been meeting their needs. In 2011, the Board took significant steps to better understand and respond to the issues of private companies.

First, we undertook a project to develop a collective, common understanding of how private companies are different from public companies. We currently are developing a decision-making framework for deciding whether and when to adjust the requirements for recognition, measurement, presentation, disclosure, effective dates, and transition methods for the standards that apply to private companies. We expect to issue that framework for public comment in 2012 but will wait to finalize it until any new private company council set up by the Financial Accounting Foundation has the opportunity to share their views and agree to the new framework.

In 2011, we assigned a private company liaison, a staff member whose role is to solicit and share private company input, to every FASB project team. We also hosted private company roundtables in various cities to hear concerns and suggestions from these constituents. Other initiatives included hosting private company roundtables on key projects; scheduling semiannual webcasts focused on our proposals and how they could affect private companies; and creating a private company resource group to provide additional input on Board activities.

These efforts already have generated some important results. Private company concerns about the complexity of the goodwill impairment test led the Board to issue an Accounting Standards Update on testing goodwill for impairment. Both private and public companies told us that the new standard significantly reduced the complexity of goodwill testing. The Board also delayed the implementation dates for several standards. Finally, at the close of 2011, the Board decided to revisit the disclosures about fair value for private companies and not-for-profits.

Not-for-profit organizations also were the focus of the FASB’s “active listening.” In late 2011, the Not-for-Profit Advisory Committee (NAC) submitted recommendations on how to refresh the current not-for-profit reporting model. In response to these recommendations, we added to our agenda a standard-setting project that will address

the effect of restrictions on the presentation of net assets and improve information about an organization’s liquidity, financial performance, and cash flows. We also added a research project to study other means of communication that not-for-profit organizations can use to better tell their financial story.

Joint Agenda with the IASBActive listening drove progress on the FASB’s joint agenda with the IASB. We listened when U.S. stakeholders told us that it was more important to get these important standards right than to meet a particular deadline. We listened carefully to their suggestions for improving the Boards’ proposals on revenue recognition, leases, accounting for financial instruments, and insurance. In the interest of “getting it right,” the Boards agreed to extend the timetables for our remaining priority convergence projects beyond June 2011 to analyze stakeholder input.

In the fourth quarter of 2011, we issued a revised Exposure Draft (ED) on Revenue Recognition that incorporated feedback from more than 1,000 comment letters received on the 2010 ED. The revised proposal maintains the original principle, but reduces complexity and clarifies some application guidance. Depending on the nature of the feedback we receive and how long it takes us to work through it, the Boards expect to finalize a converged new standard in 2012.

The FASB undertook the Leases project primarily to address investor concerns that significant lease obligations were not being reported on the balance sheet. Our joint, 2010 ED with the IASB proposed that the rights and obligations related to leases belong on the balance sheet. While the Boards remain committed to this principle, we have simplified the proposal in many respects and are still addressing some concerns about the income statement effects resulting from the proposed right-of-use model. In 2011, the Boards announced that we will issue a revised ED on Leases, which we expect to issue in 2012.

Our stakeholders urged the Boards to reduce differences in our respective models for Accounting for Financial Instruments. In November of 2011, the IASB decided to make limited modifications to IFRS 9. In early 2012, the Boards announced that we would work together to align our respective financial instruments models, which improves our prospects for a converged solution on financial instruments. We also are making good progress on an expected loss approach for impairment of financial assets, which we plan to issue for comment later this year.

Finally, in 2011, the Boards reaffirmed our desire for a converged standard on Insurance Contracts. We are developing a model that would reflect current estimates of the amount necessary to fulfill an insurance obligation. While we have struggled to reach consistent conclusions about several elements of the model, we are working to identify potential opportunities to resolve our differences.

Listening is essential to improving our processes and product. I’d like to thank the many stakeholders and organizations that shared their views and insights about our standard-setting projects. Your time, resources, and good ideas are invaluable to our ability to continually improve our process and our standards.

Financial Accounting Foundation 14

High-quality financial reporting increases investor confidence.

Increased investor confidence leads to better capital allocation

decisions and, by extension, a stronger economy.

FAF STATEMENT OF CORE VALUES

2011 Annual Report15

Financial Accounting Foundation 16

FAF BOARD OF TRUSTEES

GASB MEMBERS

FASB MEMBERS

1

1

1

2

2

2

3

3

3

4

4

4

5

5

5

6

6

6

7

7

7

8

9 10 11 12 13 14 15 16

17

FAF1 John J. Brennan

Chairman Emeritus Vanguard Group Inc.

2 Frank H. Brod Corporate Vice President — Finance & Administration & Chief Accounting Officer Microsoft Corporation

3 Paul G. Camell Executive Vice President — Mergers & Acquisitions & Chief Accounting Officer CDM Smith

4 Carol Anthony (John) Davidson Senior Vice President, Controller, & Chief Accounting Officer Tyco International

5 Jeffrey J. Diermeier Retired President & Chief Executive Officer CFA Institute

6 W. Daniel Ebersole Retired Georgia State Treasurer

7 Cynthia P. Eisenhauer Government Financial Management Consultant

8 Edward M. Harrington General Manager San Francisco Public Utilities Commission

9 Stephen R. Howe, Jr. Americas Managing Partner Ernst & Young

10 Dennis M. Kass Chairman & Chief Executive Officer Jennison Associates LLC

11 W. M. (Mack) Lawhon Chairman Weaver, LLP

12 Edward E. Nusbaum Chief Executive Officer & Executive Partner Grant Thornton International

13 John J. Perrell Retired Vice President — Global Policies American Express Company

14 Michelle R. Seitz Head of Investment Management William Blair & Company

15 Mary S. Stone Director & Hugh Culverhouse Endowed Chair of Accountancy Culverhouse College of Commerce & Business Administration at the University of Alabama

16 Luis M. Viceira George E. Bates Professor Harvard Business School

FASB1 Leslie F. Seidman Chairman

2 Daryl E. Buck

3 Russell G. Golden

4 Thomas J. Linsmeier

5 R. Harold Schroeder

6 Marc A. Siegel

7 Lawrence W. Smith

GASB1 Robert H. Attmore Chairman

2 William W. Fish

3 Michael H. Granof

4 David E. Sundstrom

5 Jan I. Sylvis

6 Marcia L. Taylor

7 James M. Williams

2011 Annual Report

18Financial Accounting Foundation

19

OFFICERSJohn J. Brennan Chairman

Teresa S. Polley President & Chief Executive Officer

Dennis M. Kass Vice Chairman

Frank H. Brod Secretary & Treasurer

Ronald P. Guerrette Vice President

Jodi P. Dottori Vice President, Chief of Staff, & Assistant Secretary

BOARD OF TRUSTEESJohn J. Brennan Chairman Emeritus Vanguard Group Inc.

Frank H. Brod Corporate Vice President — Finance & Administration & Chief Accounting Officer Microsoft Corporation

Paul G. Camell Executive Vice President — Mergers & Acquisitions & Chief Accounting Officer CDM Smith

Carol Anthony (John) Davidson Senior Vice President, Controller & Chief Accounting Officer Tyco International

Jeffrey J. Diermeier Retired President & Chief Executive Officer CFA Institute

W. Daniel Ebersole Retired Georgia State Treasurer

Cynthia P. Eisenhauer Government Financial Management Consultant

Edward M. Harrington General Manager San Francisco Public Utilities Commission

Stephen R. Howe, Jr. Americas Managing Partner Ernst & Young

Dennis M. Kass Chairman & Chief Executive Officer Jennison Associates LLC

W. M. (Mack) Lawhon Chairman Weaver, LLP

Edward E. Nusbaum Chief Executive Officer Grant Thornton International

John J. Perrell Retired Vice President — Global Policies American Express Company

Michelle R. Seitz Head of Investment Management William Blair & Company

Mary S. Stone Director & Hugh Culverhouse Endowed Chair of Accountancy Culverhouse College of Commerce & Business Administration at the University of Alabama

Luis M. Viceira George E. Bates Professor Harvard Business School

Completed Service in 2011Robert T. Blakely (Former Vice Chairman, FAF Board of Trustees) Retired Executive Vice President & Chief Financial Officer Fannie Mae

Ellyn L. Brown President Brown & Associates

Douglas A. Donahue, Jr. Managing Partner Brown Brothers Harriman

John J. Radford Retired State Controller Oregon

TRUSTEE COMMITTEES

ExecutiveJohn J. Brennan, Chair

John Davidson

Jeffrey J. Diermeier

Edward M. Harrington

Dennis M. Kass

John J. Perrell

Appointments and EvaluationsJohn J. Perrell, Chair

Paul G. Camell

Jeffrey J. Diermeier

Edward M. Harrington

W. M. (Mack) Lawhon

Edward E. Nusbaum

Mary S. Stone

Audit and ComplianceJohn Davidson, Chair

W. Daniel Ebersole

Stephen R. Howe

Edward E. Nusbaum

Finance and CompensationDennis M. Kass, Chair

Frank H. Brod

W. Daniel Ebersole

Cynthia P. Eisenhauer

Michelle R. Seitz

Luis M. Viceira

Standard-Setting Process OversightJeffrey J. Diermeier, Co-Chair

Edward M. Harrington, Co-Chair

John Davidson

Cynthia P. Eisenhauer

John J. Perrell

Luis M. Viceira

FAF

2011 Annual Report

Financial Accounting Foundation 20

Completed Service in 2011Jane C. Driskell U.S. Conference of Mayors

Eric Lupher (Former GASAC Vice Chairman) Governmental Research Association

Sue Menditto National Association of College & University Business Officers

Mark D. Robbins Association for Budgeting & Financial Management

G. Robert Smith, Jr. American Accounting Association

Official ObserverGene L. Dodaro Government Accountability Office

MembersLisa Blumerman U.S. Census Bureau

Shirley Broz Association of School Business Officials International

Ryan G. Claw Native American Finance Officers Association

Dominic Colafati National Association of State Budget Officers

Cline Comer Healthcare Financial Management Association

Mary Kay Cooney National Federation of Municipal Analysts

Vance Holloman Member at-Large

Karl Jacob Bond Rater

Terrill Menzel American Institute of CPAs

Amanda Noble Association of Local Government Auditors

John Overdorff National Association of Bond Lawyers

Cathy Provencher Council of State Governments

Jim Reardon National Governors Association

Jacqueline L. Reck* American Accounting Association

Randy H. Riggs National League of Cities

Pat Robertson National Association of State Retirement Administrators

Anne G. Ross Securities Industry & Financial Markets Association

Robert W. Scott Government Finance Officers Association

Odd Stalebrink* Association for Budgeting & Financial Management

Joseph Stefko* Governmental Research Association

Charles A. Tegen* National Association of College & University Business Officers

Steven T. Thompson International City/County Management Association

Gary VanLandingham National Conference of State Legislatures

Thomas J. Weyl Investment Company Institute

Glen Whitley* National Association of Counties

Mindy Willis American Public Power Association

Michael W. Zaroogian Insurance Industry Investors

GASAC (GOVERNMENTAL ACCOUNTING STANDARDS ADVISORY COUNCIL)

GASAC ChairmanMartin J. Benison National Association of State Auditors, Comptrollers & Treasurers

GASAC Vice ChairmanEric S. Berman Association of Government Accountants

* New members in 2012

21 2011 Annual Report

FASAC ChairmanCharles H. Noski

Executive Director FASB Advisory GroupsAlicia A. Posta

* New members in 2012

MembersJohn (Arch) Archambault Senior Partner — Professional Standards & Global Public Policy Grant Thornton LLP

Carmen L. Bailey Partner in Charge — SEC & Practice Advisory KPMG LLP

Prat Bhatt Vice President & Corporate Controller — Principal Accounting Officer Cisco Systems

Kay Booth* Managing Director Golden Seeds Fund

Neri Bukspan Executive Managing Director & Chief Quality Officer Standard & Poor’s

Peter M. Carlson* Executive Vice President & Chief Accounting Officer Met Life

William G. Clark Senior Vice President & Chief Investment Officer Federal Reserve Employee Benefits System

Susan S. Coffey* Senior Vice President, Public Practice & Global Alliances American Institute of CPAs

Kenneth Daly* President & Chief Executive Officer National Association of Corporate Directors (NACD)

Marc A. Delametter Vice President — Accounting/Controller QuikTrip Corporation

Anthony J. Dowd* Chief of Staff Office of Paul A. Volcker

Cynthia M. Fornelli* Executive Director Center for Audit Quality

John C. Gerspach Chief Financial Officer Citigroup Inc. (Citi)

Gail L. Hanson Senior Vice President & Chief Financial Officer Aurora Health Care, Inc.

Jan Hauser* Partner PricewaterhouseCoopers LLC

Marie N. Hollein President & Chief Executive Officer Financial Executives International

Patrick E. Hopkins* Professor of Accounting Deloitte Foundation Accounting Faculty Fellow Kelley School of Business Indiana University

Adam G. Hurwich* Portfolio Manager Ulysses Management LLC

Samuel J. Levenson Senior Vice President of Investor Relations Las Vegas Sands Corp.

Joseph Longino* Principal Sandler O’Neill + Partners, LP

Kenneth D. Marshall Partner, Americas Financial Accounting Advisory Services Ernst & Young, LLP

Alan M. Meder Senior Vice President Duff & Phelps Investment Management Co.

Jamie S. Miller Vice President, Controller & Chief Accounting Officer General Electric Company

Patrick T. Mulva* Vice President & Controller Exxon Mobil Corporation

George Muñoz Principal Muñoz Investment Banking Group

Jeremy Perler Forensic Accountant Coatue Management

Ann Marie Petach Managing Director & Chief Financial Officer BlackRock, Inc.

Sandra J. Peters, CFA Head, Policy Financial Reporting Group CFA Institute

Kathy Petroni Deloitte/Michael Licata Professor of Accounting Eli Broad College of Business Michigan State University

Lawrence K. Probus Chief Financial Officer & Senior Vice President World Vision U.S.

Allen Puwalski Senior Vice President Paulson & Company

James R. Taylor* Assurance Partner Hogan Taylor LLP

Shannon S. Warren Managing Director & Deputy Controller JP Morgan Chase

John W. White* Partner Cravath, Swaine & Moore LLP

Completed Service in 2011Joan L. Amble Executive Vice President & Corporate Comptroller American Express Company

Charles K. Bobrinskoy Vice Chairman — Director of Research Ariel Investments

James L. Bothwell Founder & President Financial Market Strategies LLC

Carolyn M. Callahan KPMG Distinguished Professor of Accounting & Director of the School of Accountancy The University of Memphis

Dennis H. Chookaszian (Former FASAC Chairman) Retired

Jerry M. de St. Paer Executive Chairman GNAIE — Group of North American Insurance Enterprises

Lewis A. Dulitz Formerly of Covidien

Gary R. Kabureck Vice President & Chief Accounting Officer Xerox Corporation

Mark H. Lang Thomas W. Hudson, Jr./Deloitte & Touche LLP Distinguished Professor Kenan-Flagler Business School University of North Carolina

Feilong Li Executive Vice President & Chief Financial Officer China Oilfield Service Limited

Joel S. Osnoss Partner — Global IFRS & Offerings Services Deloitte & Touche LLP

Richard N. Ramsden Managing Director Goldman Sachs & Co., Inc

Arleen R. Thomas Senior Vice President, Member Competency & Development AICPA

William F. Widdowson Head — Group Accounting Policy UBS AG

Jed Wrigley Fund Manager & Director — Accounting & Valuation Fidelity International Ltd

FASAC (FINANCIAL ACCOUNTING STANDARDS ADVISORY COUNCIL)

Financial Accounting Foundation 22

Deborah Adkins Chief Financial Officer & Partner NPerspective, LLC

James Beck Managing Director & Chief Operating Officer Mayfield Fund

P. Glenn Bradley Partner Mountjoy Chilton Medley LLC

Gary M. Cademartori Managing Partner Prism Consulting, LLP

Robert A. Dyson Director — Professional Practices Group Marks Paneth & Shron LLP

Mark Ellis Chief Financial Officer PetCare Rx

Richard E. Forrestel, Jr. Treasurer Cold Spring Construction Company, Inc.

Richard H. Gesseck Partner J.H. Cohn LLP

Dennis R. Hein, CPA Partner Seim Johnson, LLP

Robert E. Hoffman Chief Financial Officer Arena Pharmaceuticals

W. Stephen Holmes General Partner InterWest Partners

C. Michael Jacobi Owner Stable House 1, LLC

R. Michael S. Menzies, Sr. President & Chief Executive Officer Easton Bank & Trust

Albert G. Pastino Managing Director Kildare Capital

Patricia P. Piteo Partner Cohen & Company Ltd.

Leonard Steinberg Principal Steinberg Enterprises, LLC

Peter B. Stickler Senior Vice President & Chief Financial Officer Inland Bancorp, Inc.

Scott M. Waite Senior Vice President & Chief Financial Officer Patelco Credit Union

Russell D. Wasson Director — Tax, Finance & Accounting Policy National Rural Electric Cooperative Association

Deborah A. Wilson Chief Financial Officer CAC Management Ltd.

Lawrence S. Wizel Director American Oriental Bioengineering, Inc.

Candace Wright Audit Director Postlethwaite & Netterville

Completed Service in 2011Samuel E. Wilson, CPA Formerly of Bonneville International Corporation

Gary Buesser Director Lazard Asset Management, LLC

Adam D. Compton Sector Analyst & Fund Manager GMT Capital Corporation

Gregory Jonas Managing Director Morgan Stanley, Research

Joyce Joseph Managing Director Standard & Poor’s

Mark C. LaMonte Managing Director & Chief Credit Officer — Financial Institutions Group Moody’s Investors Service

Dina M. Maher, CPA Examining Officer — Accounting Policy Financial Institution Supervision Group Federal Reserve Bank of New York

Elizabeth F. Mooney Accounting Analyst The Capital Group Companies

Dane Mott, CFA, CPA U.S. Equity Research — U.S. Accounting & Valuation J.P. Morgan Securities Inc.

Mark R. Newsome Director ING Capital LLC

Rita J. Spitz Principal William Blair & Company, LLC

Joseph A. Stieven Chief Executive Officer Stieven Capital Advisors, LP

Completed Service in 2011Neri Bukspan Executive Managing Director & Chief Quality Officer Standard & Poor’s

Jack Ciesielski President R.G. Associates, Inc.

Michael A. Moran Vice President — Global Markets Institute Goldman, Sachs & Co.

Mary Hartman Morris Investment Officer — Corporate Governance — Global Equities California Public Employees Retirement System.

Janet L. Pegg Managing Director & Accounting Analyst — UBS Strategy & Valuation UBS AG

FASB ADVISORY GROUPS

SMALL BUSINESS ADVISORY COMMITTEE

INVESTORS TECHNICAL ADVISORY COMMITTEE

23

Committee ChairmanJeffrey D. Mechanick Assistant Director — Nonpublic Entities Financial Accounting Standards Board

Committee MembersShari Berenbach Director — Office of Microenterprise Development US Agency for International Development

Gregory Capin Partner Capin Crouse LLP

Gordon Edwards Chief Financial Officer Gundersen Lutheran Health System

Kenneth Euwema Vice President — Membership Accountability United Way Worldwide

Stephen Golding Vice President of Finance & Treasurer University of Pennsylvania

Roger Goodman Partner The Yuba Group LLC

Teresa Gordon Professor Emeritus University of Idaho

Gail Harrity President & Chief Operating Officer Philadelphia Museum of Art

Melanie Herman Executive Director Nonprofit Risk Management Center

John Mattie Partner-in-Charge, Higher Education & Not-for-Profit Industry Practice PricewaterhouseCoopers LLP

Clara Miller President F. B. Heron Foundation

Cynthia Pierce Partner-in-Charge, Higher Education & Not-for-Profit Industry Practice Crowe Horwath LLP

Laura Roos Partner Moss Adams LLP

Michael Tarnoff Executive Vice President & Chief Financial Officer Jewish Federation of Metropolitan Chicago

Bill Titera Partner Ernst & Young LLP

Bennett Weiner Chief Operating Officer Better Business Bureau Wise Giving Alliance

William Weldon Chief Financial Officer Roman Catholic Diocese of Charlotte

Participating ObserversChristopher Cole AICPA

Dena Markowitz Pennsylvania Bureau of Charitable Organizations (representing National Association of State Charity Officials)

Larry Probus World Vision US (representing FASAC)

2011 Annual Report

Judith H. O’Dell, Chair President O’Dell Valuation Consulting, LLC

George W. Beckwith Controller National Gypsum Company

Stephen W. Bodine Principal LarsonAllen LLP

John R. Burzenski President Burzenski & Company, PC

Michael Cain Senior Executive Vice President Frost Bank

Thomas J. Groskopf Director Barnes Dennig

MaryAnn Lawrence Senior Vice President Key Corporation

David Lomax Assistant Vice President Liberty Mutual Surety

Steven D. Lords Chief Financial Officer CF Jordan Construction LLC

Chris A. Rogers Vice President of Finance & Administration Infragistics, Inc.

Steven A. Shelton President Way, Ray, Shelton & Company, P.C.

James K. Smith Vice President & Chief Financial Officer Phonon Corporation

James Stevenson Chief Financial Officer ABS Capital Partners

NOT-FOR-PROFIT ADVISORY COMMITTEE

PRIVATE COMPANY FINANCIAL REPORTING COMMITTEE

Paul Barnes Managing Director, Global Leader — Valuation Advisory Services Duff & Phelps, LLC

Muneera Carr Controller & Chief Accounting Officer Comerica Bank

Donald L. Charles America’s Leader — Capital Transformation Transaction Advisory Services Ernst & Young LLP

Frank A. Ciccotto, Jr. Senior Vice President — Global Head of Valuations S&P Capital IQ

Michael B. DeLuke Director Houlihan Lokey Financial Advisors, Inc.

Wallace Enman Vice President — Senior Credit Officer Moody’s Investors Service

Gregory Forsythe Director Deloitte Financial Advisory Services LLP

Carla G. Glass Managing Director HSSK Group

Gordon Goodman Vice President — Planning & Control Occidental Energy Marketing, Inc.

Yassir Karam Chief Advisory Services Officer CliftonLarsonAllen LLP

David L. Larsen Managing Director — Portfolio Valuation Duff & Phelps, LLC

Gerald Mehm Senior Vice President & Senior Managing Director American Appraisal

Andreas Ohl Partner PricewaterhouseCoopers LLP

Amy Ripepi Managing Director Financial Reporting Advisors, LLC

Richard Stuart Partner — National Professional Standards Group McGladrey & Pullen LLP

Chris Thorne Technical Director International Valuation Standards Council

Gina Weaver Vice President & Assistant Controller Pfizer Inc.

Brenna Wist Partner KPMG LLP

FASB ADVISORY GROUPS

VALUATION RESOURCE GROUP

24Financial Accounting Foundation

Task Force ChairmanSusan M. Cosper Technical Director Financial Accounting Standards Board

EITF Fellow CoordinatorMichael P. Breen Practice Fellow Financial Accounting Standards Board

Task Force MembersMark M. Bielstein Partner KPMG LLP

James G. Campbell Vice President — Finance & Enterprise Services & Corporate Controller Intel Corporation

Stuart H. Harden Partner Hemming Morse, LLP

Carl Kampel Director — Professional Standards Ellin & Tucker, Chartered

Mark LaMonte Vice President & Senior Credit Officer Accounting Specialist Team Moody’s Investors Service

Carlo D. Pippolo Partner — Assurance Services Ernst & Young LLP

Matthew L. Schroeder Managing Director — Accounting Policy Goldman Sachs Group, Inc.

Ashwinpaul C. Sondhi President A.C. Sondhi & Associates, LLC

Robert Uhl Partner Deloitte & Touche LLP

Lawrence E. Weinstock Vice President — Finance & Chief Financial Officer Mana Products, Inc.

Participating ObserversPaul A. Beswick Deputy Chief Accountant — Accounting Office of the Chief Accountant U.S. Securities & Exchange Commission

Judith H. O’Dell (PCFRC) President O’Dell Valuation Consulting, LLC

Richard C. Paul AICPA Financial Reporting Executive Committee Partner — Deloitte & Touche LLP

Completed Service in 2011Mitchell A. Danaher Deputy Comptroller General Electric Company

Jan R. Hauser Partner PricewaterhouseCoopers LLP

EMERGING ISSUES TASK FORCE

2011 Annual Report25

Management’s Discussion & Analysis 26

Statements of Activities 31

Statements of Financial Position 32

Statements of Cash Flows 33

Notes to Financial Statements 34

Management’s Report on Financial Responsibility & Internal Controls 42

Independent Auditor’s Report 44FIN

AN

CIA

L H

IGH

LIG

HTS

Financial Accounting Foundation 26

MANAGEMENT’S DISCUSSION & ANALYSIS

2011 SUMMARYThe mission of the Financial Accounting Foundation (Foundation) and its standard-setting Boards, the Financial Accounting Standards Board (FASB) and the Governmental Accounting Standards Board (GASB), is to establish and improve standards of financial accounting and reporting for public and private companies, not-for-profit organizations, and state and local governments. Financial accounting and reporting standards help foster and protect investor confidence, facilitate efficient operation of capital markets and enable citizens to assess the stewardship of public resources by their state and local governments. The Foundation is committed to the development of high-quality financial accounting and reporting standards through an independent and open process that results in useful financial information, considers all stakeholder views and ensures public accountability.

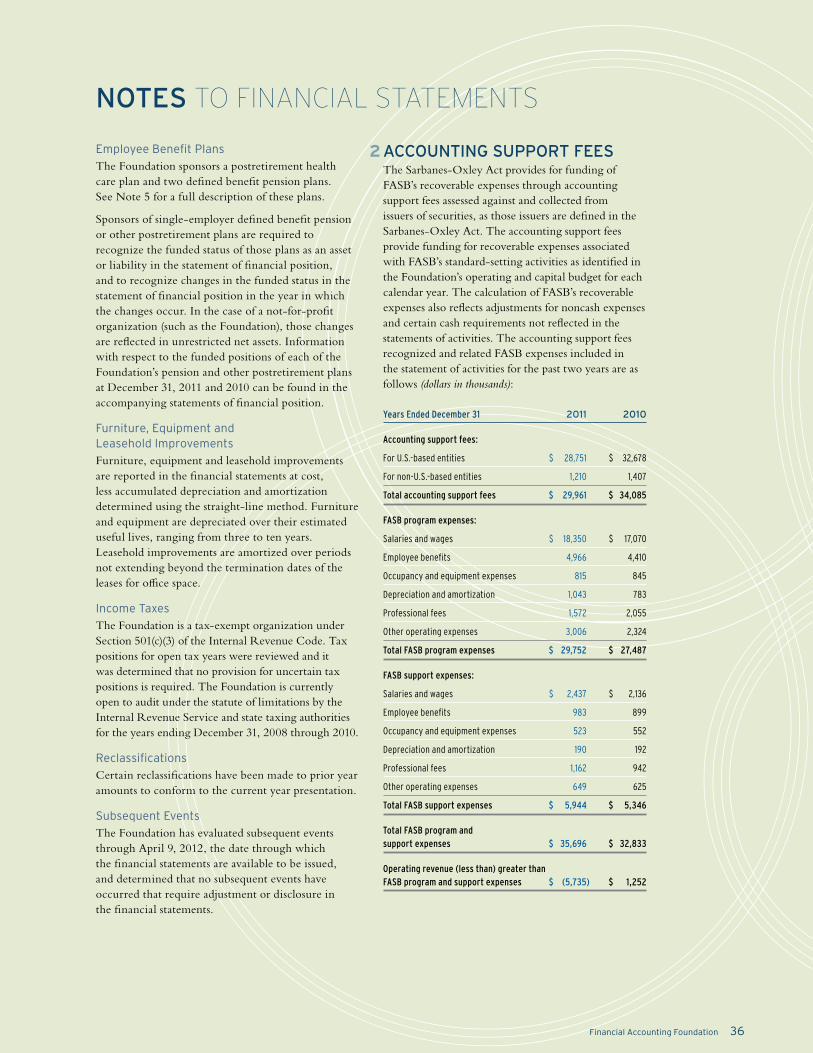

The Foundation is responsible for the oversight, administration and finances of the FASB, the GASB, and their advisory councils, the Financial Accounting Standards Advisory Council (FASAC) and the Governmental Accounting Standards Advisory Council (GASAC). The Foundation presently obtains its funding from: (1) accounting support fees that finance FASB’s operating and capital expenses pursuant to Section 109 of the Sarbanes-Oxley Act of 2002, as amended (Sarbanes-Oxley Act); (2) the sale and licensing of FASB- and GASB-related materials; and (3) voluntary cash contributions in support of the GASB. (In February 2012, pursuant to rules promulgated under Section 978 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 [“Dodd-Frank”], the United States Securities and Exchange Commission [“SEC”] approved a rule establishing an accounting support fee to fund the annual budget of the GASB. The Foundation expects that accounting support fees for the GASB will be assessed beginning in the first quarter of 2012.)

In 2011, program and support expenses totaled $44 million, a $3.1 million increase from 2010, reflecting several new and ongoing important initiatives. First, the FAF Board of Trustees increased FASB Board membership from five to seven members beginning in February 2011 (the FASB had operated with seven Board members from its inception in 1973 until 2008). Second, the FAF and the FASB continued its second year of work on the maintenance of the U.S. GAAP Financial Reporting Taxonomy (Taxonomy)

for eXtensible Business Reporting Language (XBRL) applicable to public issuers registered with the SEC.

Third, the Foundation in late 2010 established a process for conducting post-implementation reviews (PIR) of financial accounting and reporting standards issued by the FASB and the GASB. The purpose of the PIR process is to assess whether the intended financial reporting objectives underlying those standards are being met.

In addition, 2011 results reflect the FASB’s commitment to fostering convergence of nongovernmental GAAP and International Financial Reporting Standards (IFRS) and several proposals and projects to improve financial reporting by U.S. companies and not-for-profit organizations. The results also reflect the Foundation’s evaluation of the accounting standards-setting process as it relates to nonpublic, nongovernmental entities. In connection with this evaluation, in October 2011, the Foundation issued for public comment a plan to establish the Private Company Standards Improvement Council (PCSIC). The Foundation expects to finalize its plan following completion of its consideration of input received.

FINANCIAL RESULTSThe Foundation’s financial statements are presented in accordance with U.S. GAAP and reflect the specific reporting requirements of not-for-profit organizations. The following is a discussion of the key highlights of the activities and financial position of the Foundation as presented in the accompanying audited financial statements.

OVERVIEW

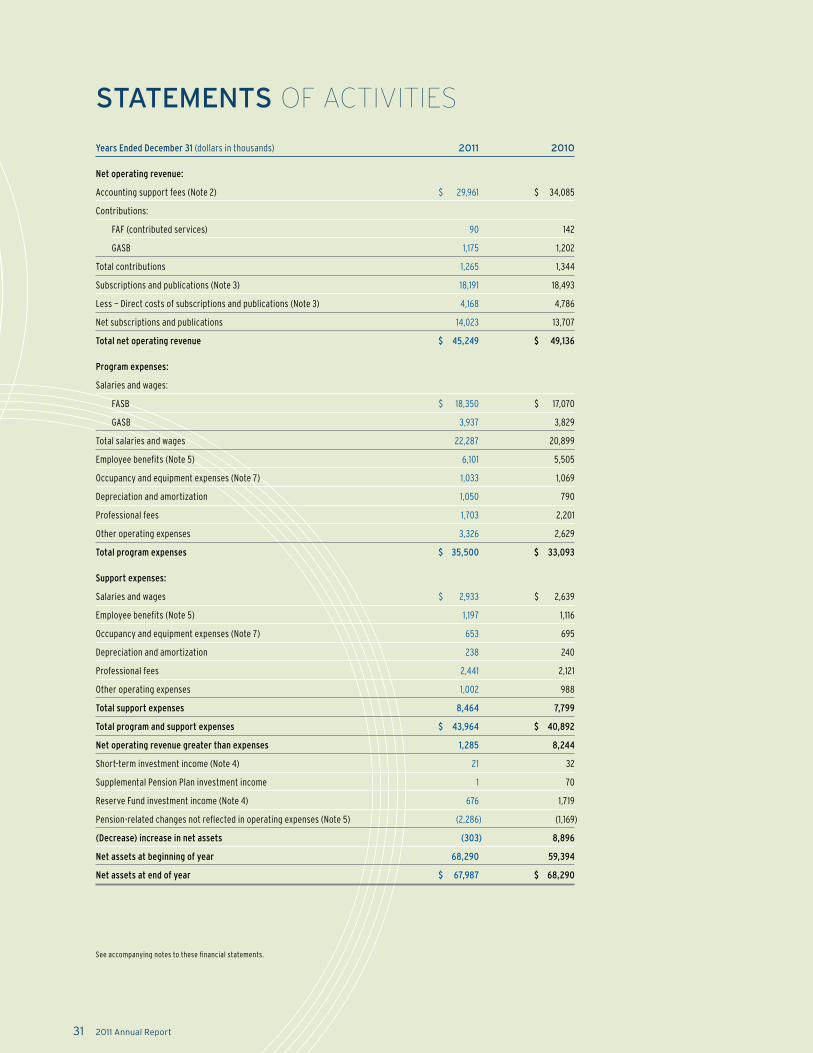

• TheFoundationendedtheyearwithnetoperatingrevenues exceeding expenses by $1.3 million in 2011, compared to $8.2 million in 2010.

• Netoperatingrevenuedecreasedto$45.2millionin 2011 from $49.1 million in 2010, reflecting a $4.1 million decrease in accounting support fees. The Foundation offsets FASB recoverable expenses with excess Reserve Funds (funded primarily from subscription and publication revenues) when calculating the accounting support fees. The Foundation was able to provide a significantly higher amount of excess Reserve Funds in 2011 resulting in a reduction in the amount of accounting support fees assessed.

2011 Annual Report27

• Totalprogramandsupportexpensesincreased$3.1 million to $44.0 million. Program expenses represent approximately 81 percent of total expenses in both 2011 and 2010.

• Netassetsdecreasedto$68.0millionin2011 from $68.3 million, reflecting an operating surplus of $1.3 million offset by $1.6 million in other nonoperating changes in net assets (investment return and pension-related changes).

STATEMENTS OF ACTIVITIES

The following charts display the sources of operating revenues and program and support expenses for 2011 and 2010:

Accounting Support Fees

The Foundation’s most significant source of revenue consists of accounting support fees assessed against issuers of securities, as such issuers are defined in the Sarbanes-Oxley Act. Accounting support fees under the Sarbanes-Oxley Act fund the expenses and other cash requirements for the FASB’s standard-setting activities that are included in the Foundation’s operating and capital budget for each year—the recoverable expenses. Accounting support fees for 2011 and 2010 totaled $30.0 million and $34.1 million, respectively. The decrease in accounting support fees in 2011 is primarily due to an increase in the amount of excess Reserve Funds that the Foundation used to offset FASB recoverable expenses when calculating the accounting support fees for 2011.

Equity issuers with an average market capitalization of over $25 million, and investment company issuers with an average market capitalization or net asset value over $250 million, are assessed a share of the accounting support fees. The Foundation has designated the Public Company Accounting Oversight Board (the PCAOB) as its agent for invoicing and collection of FASB accounting support fees. The Foundation paid the PCAOB approximately $209,000 for this service in both years.

GASB Contributions

Contributions for GASB amounted to approximately $1.3 million in both 2011 and 2010. State governments, which contributed $1 million in both 2011 and 2010, are the largest source of contributions. Local governments and other sources contributed $176,000 and $202,000 in 2011 and 2010, respectively.

2011 Sources of Operating Revenue

Accounting Support Fees 66%

Net Subscriptions & Publications 31%

Contributions 3%

2010 Sources of Operating Revenue

Accounting Support Fees 69%

Net Subscriptions & Publications 28%

Contributions 3%

2011 & 2010 Expenses

Program — Standard Setting 81%

Support 19%

Financial Accounting Foundation 28

MANAGEMENT’S DISCUSSION & ANALYSIS

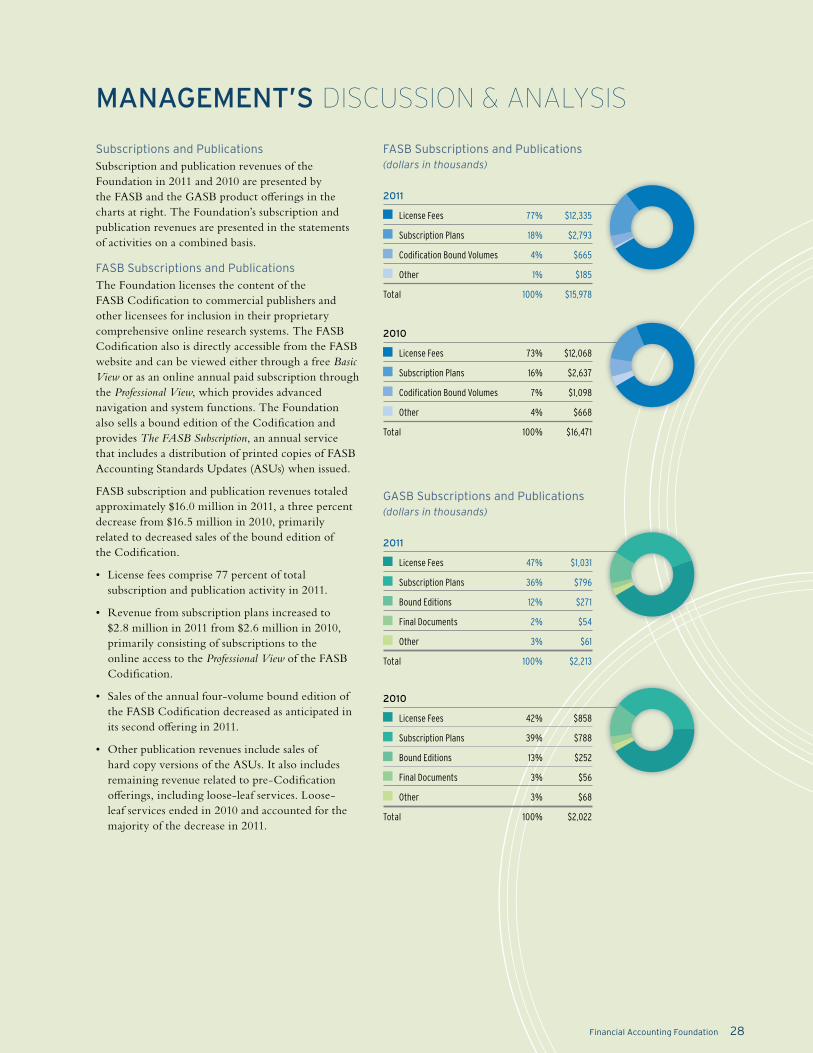

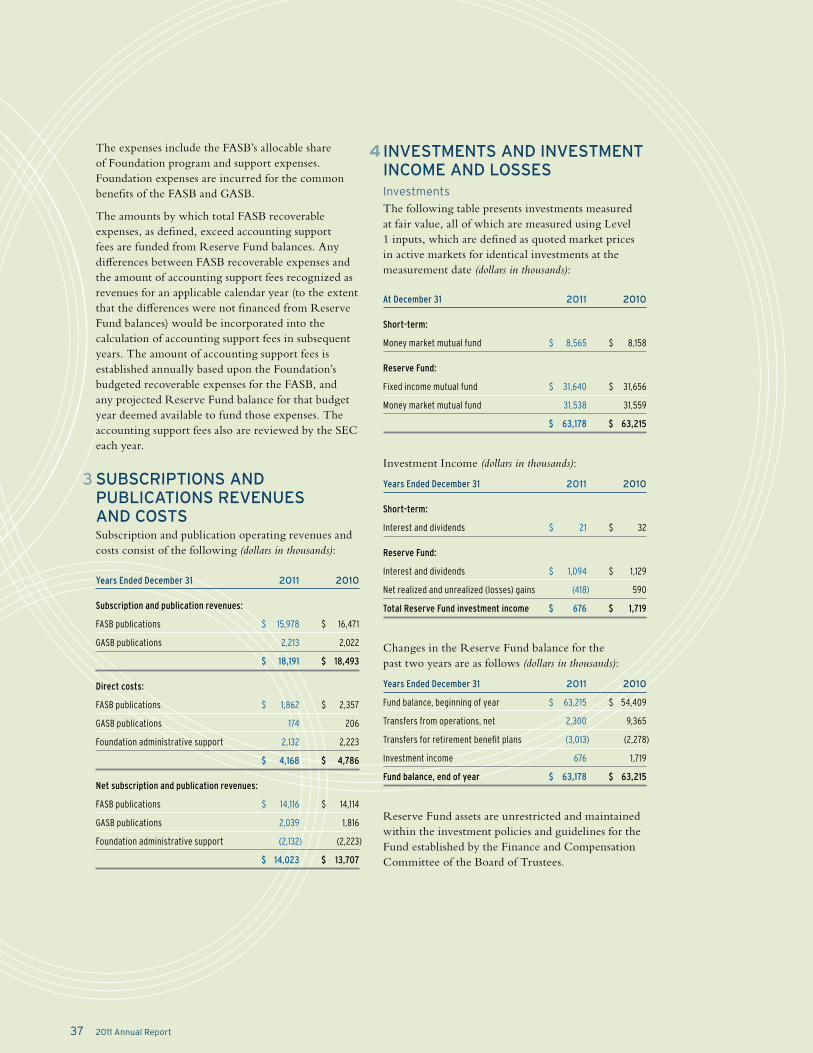

Subscriptions and Publications

Subscription and publication revenues of the Foundation in 2011 and 2010 are presented by the FASB and the GASB product offerings in the charts at right. The Foundation’s subscription and publication revenues are presented in the statements of activities on a combined basis.

FASB Subscriptions and Publications

The Foundation licenses the content of the FASB Codification to commercial publishers and other licensees for inclusion in their proprietary comprehensive online research systems. The FASB Codification also is directly accessible from the FASB website and can be viewed either through a free Basic View or as an online annual paid subscription through the Professional View, which provides advanced navigation and system functions. The Foundation also sells a bound edition of the Codification and provides The FASB Subscription, an annual service that includes a distribution of printed copies of FASB Accounting Standards Updates (ASUs) when issued.

FASB subscription and publication revenues totaled approximately $16.0 million in 2011, a three percent decrease from $16.5 million in 2010, primarily related to decreased sales of the bound edition of the Codification.

• Licensefeescomprise77percentoftotalsubscription and publication activity in 2011.

• Revenuefromsubscriptionplansincreasedto$2.8 million in 2011 from $2.6 million in 2010, primarily consisting of subscriptions to the online access to the Professional View of the FASB Codification.

• Salesoftheannualfour-volumeboundeditionofthe FASB Codification decreased as anticipated in its second offering in 2011.

• Otherpublicationrevenuesincludesalesofhard copy versions of the ASUs. It also includes remaining revenue related to pre-Codification offerings, including loose-leaf services. Loose-leaf services ended in 2010 and accounted for the majority of the decrease in 2011.

FASB Subscriptions and Publications (dollars in thousands)

GASB Subscriptions and Publications (dollars in thousands)

2011

License Fees 47% $1,031

Subscription Plans 36% $796

Bound Editions 12% $271

Final Documents 2% $54

Other 3% $61

Total 100% $2,213

2010

License Fees 42% $858

Subscription Plans 39% $788

Bound Editions 13% $252

Final Documents 3% $56

Other 3% $68

Total 100% $2,022

2011

License Fees 77% $12,335

Subscription Plans 18% $2,793

Codification Bound Volumes 4% $665

Other 1% $185

Total 100% $15,978

2010

License Fees 73% $12,068

Subscription Plans 16% $2,637

Codification Bound Volumes 7% $1,098

Other 4% $668

Total 100% $16,471

2011 Annual Report29

GASB Subscriptions and Publications

The Foundation licenses GASB materials to commercial publishers and other licensees for inclusion on their proprietary comprehensive online research systems. GASB materials are also available through various subscription plans sold directly by the Foundation including The GASB Subscription (consisting of final documents as issued and The GASB Report newsletter), GASB Board Packages, and the CD-ROM-based Governmental Accounting Research System (GARS). In addition, the Foundation sells bound editions of the GASB Codification, GASB Original Pronouncements, and the GASB Comprehensive Implementation Guide as well as hard copies of other pronouncements, research reports and other documents. In 2011, GASB subscription and publication revenues increased to $2.2 million from $2 million in 2010, primarily due to increased license fees of $173,000.

Direct Costs Of Subscriptions and Publications