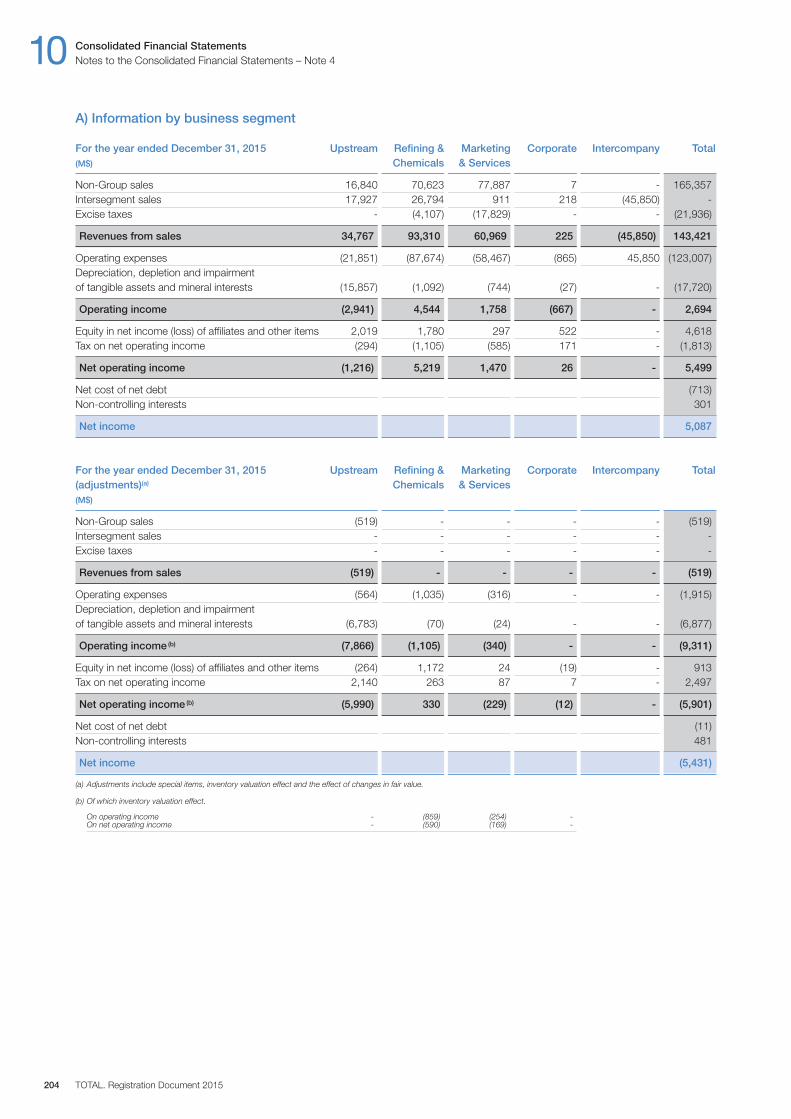

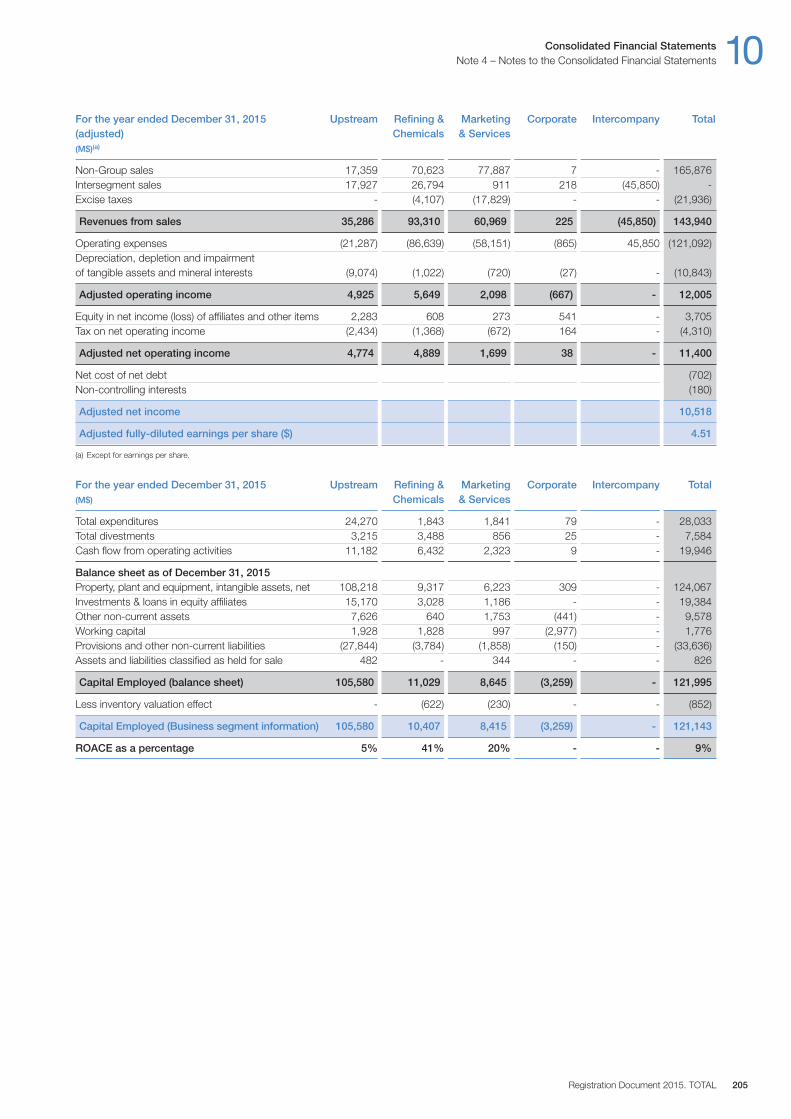

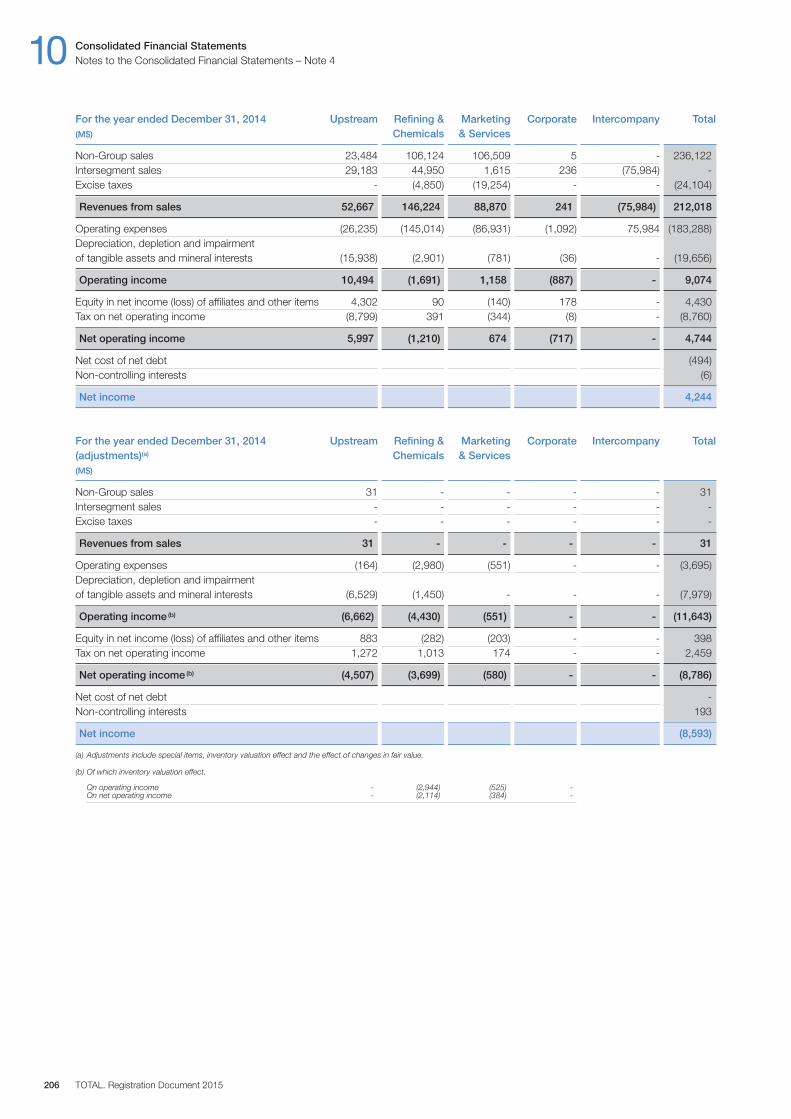

registration document - Total Energies

366

registration document 2015 EDITION

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of registration document - Total Energies

registrationdocument

2015 EDITION

couvertures_210*297 14/03/2016 15:44 Page2

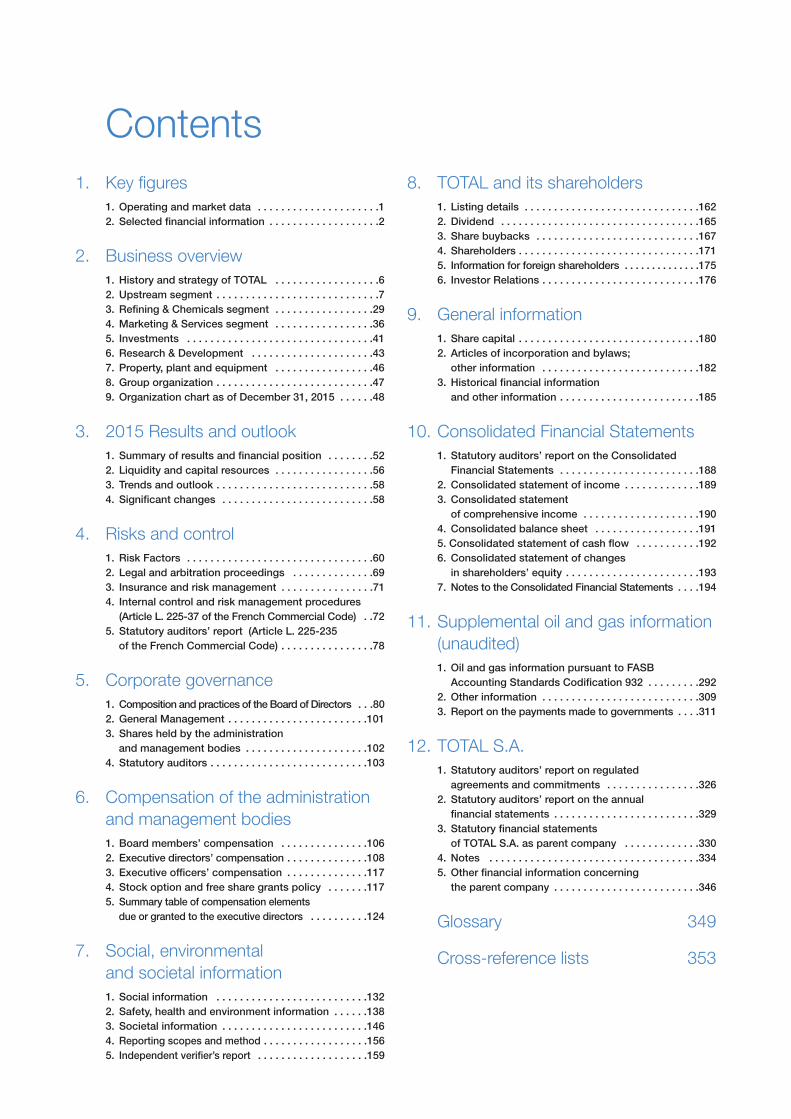

Contents1. Key figures

1. Operating and market data . . . . . . . . . . . . . . . . . . . . .12. Selected financial information . . . . . . . . . . . . . . . . . . .2

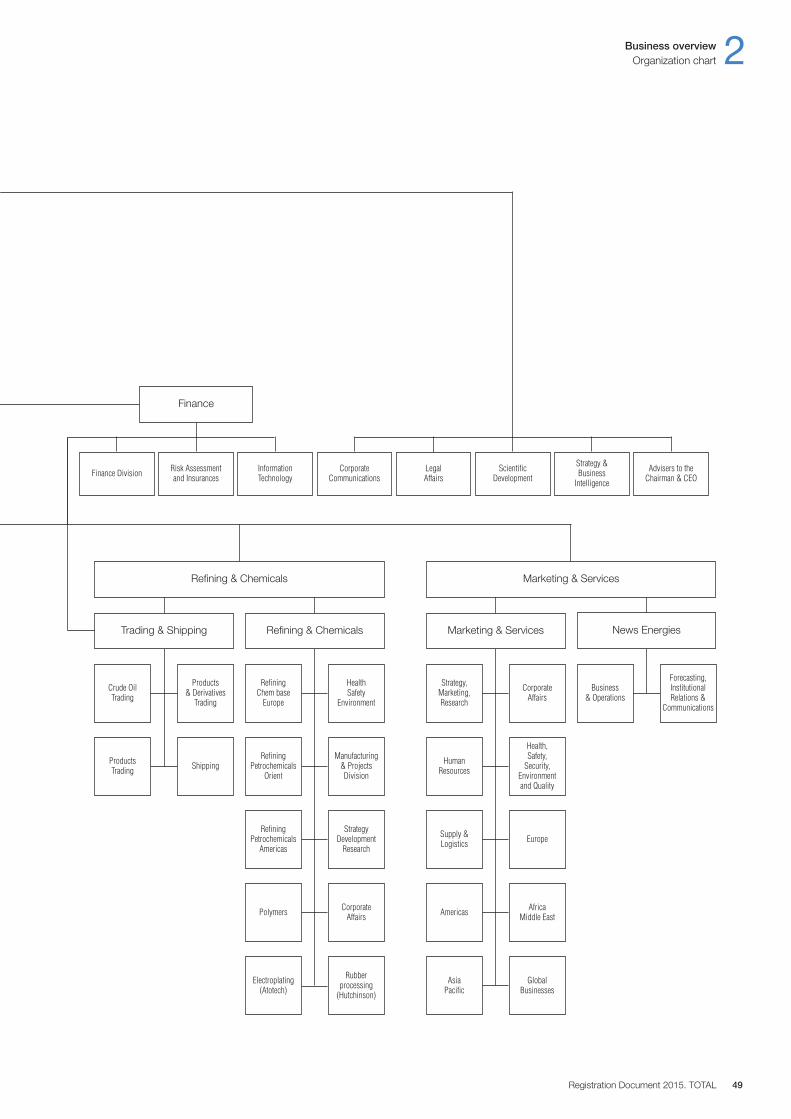

2. Business overview1. History and strategy of TOTAL . . . . . . . . . . . . . . . . . .62. Upstream segment . . . . . . . . . . . . . . . . . . . . . . . . . . . .73. Refining & Chemicals segment . . . . . . . . . . . . . . . . .294. Marketing & Services segment . . . . . . . . . . . . . . . . .365. Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .416. Research & Development . . . . . . . . . . . . . . . . . . . . .437. Property, plant and equipment . . . . . . . . . . . . . . . . .468. Group organization . . . . . . . . . . . . . . . . . . . . . . . . . . .479. Organization chart as of December 31, 2015 . . . . . .48

3. 2015 Results and outlook1. Summary of results and financial position . . . . . . . .522. Liquidity and capital resources . . . . . . . . . . . . . . . . .563. Trends and outlook . . . . . . . . . . . . . . . . . . . . . . . . . . .584. Significant changes . . . . . . . . . . . . . . . . . . . . . . . . . .58

4. Risks and control1. Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .602. Legal and arbitration proceedings . . . . . . . . . . . . . .693. Insurance and risk management . . . . . . . . . . . . . . . .714. Internal control and risk management procedures

(Article L. 225-37 of the French Commercial Code) . .725. Statutory auditors’ report (Article L. 225-235

of the French Commercial Code) . . . . . . . . . . . . . . . .78

5. Corporate governance1. Composition and practices of the Board of Directors . . .802. General Management . . . . . . . . . . . . . . . . . . . . . . . .1013. Shares held by the administration

and management bodies . . . . . . . . . . . . . . . . . . . . .1024. Statutory auditors . . . . . . . . . . . . . . . . . . . . . . . . . . .103

6. Compensation of the administrationand management bodies1. Board members’ compensation . . . . . . . . . . . . . . .1062. Executive directors’ compensation . . . . . . . . . . . . . .1083. Executive officers’ compensation . . . . . . . . . . . . . .1174. Stock option and free share grants policy . . . . . . .1175. Summary table of compensation elements

due or granted to the executive directors . . . . . . . . . .124

7. Social, environmental and societal information1. Social information . . . . . . . . . . . . . . . . . . . . . . . . . .1322. Safety, health and environment information . . . . . .1383. Societal information . . . . . . . . . . . . . . . . . . . . . . . . .1464. Reporting scopes and method . . . . . . . . . . . . . . . . . .1565. Independent verifier’s report . . . . . . . . . . . . . . . . . . .159

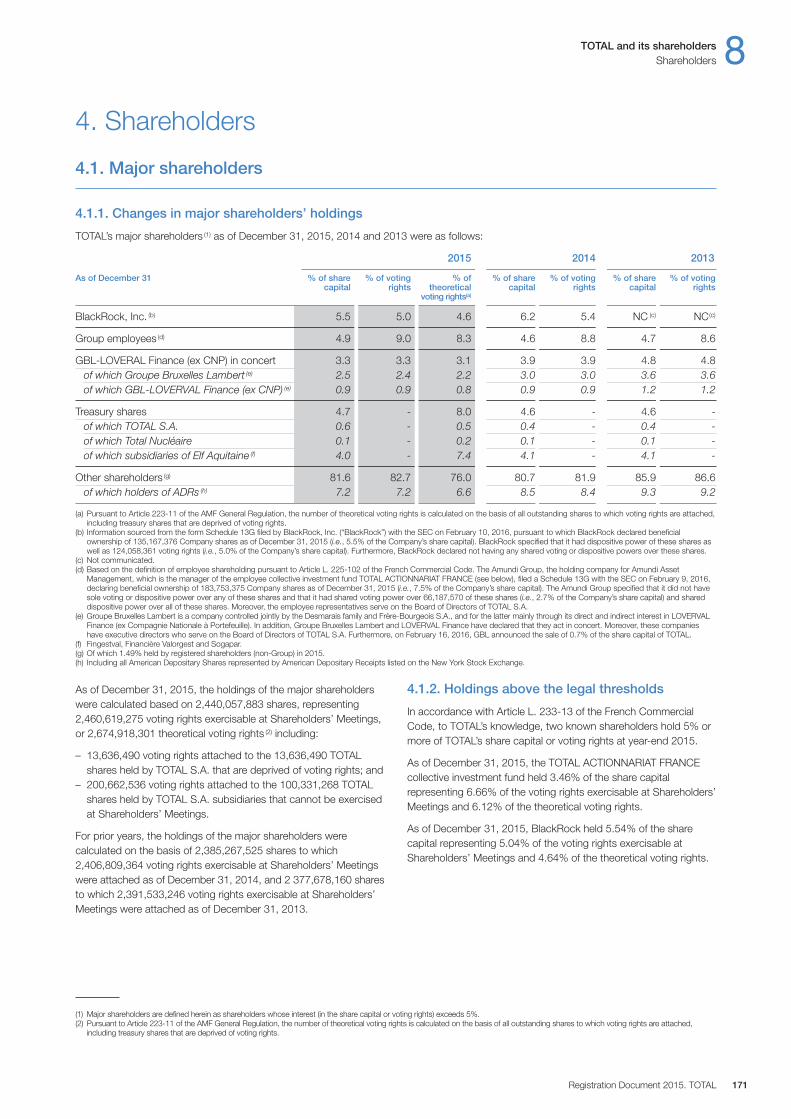

8. TOTAL and its shareholders1. Listing details . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1622. Dividend . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1653. Share buybacks . . . . . . . . . . . . . . . . . . . . . . . . . . . .1674. Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1715. Information for foreign shareholders . . . . . . . . . . . . . .1756. Investor Relations . . . . . . . . . . . . . . . . . . . . . . . . . . .176

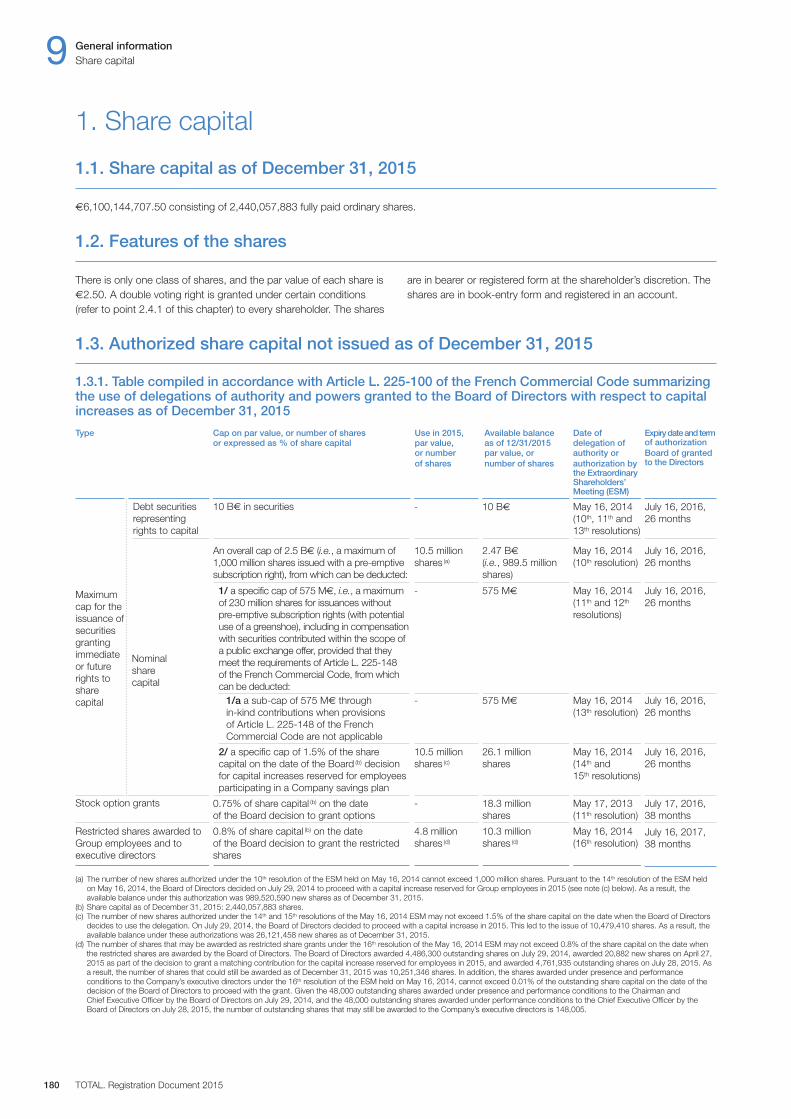

9. General information1. Share capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1802. Articles of incorporation and bylaws;

other information . . . . . . . . . . . . . . . . . . . . . . . . . . .1823. Historical financial information

and other information . . . . . . . . . . . . . . . . . . . . . . . .185

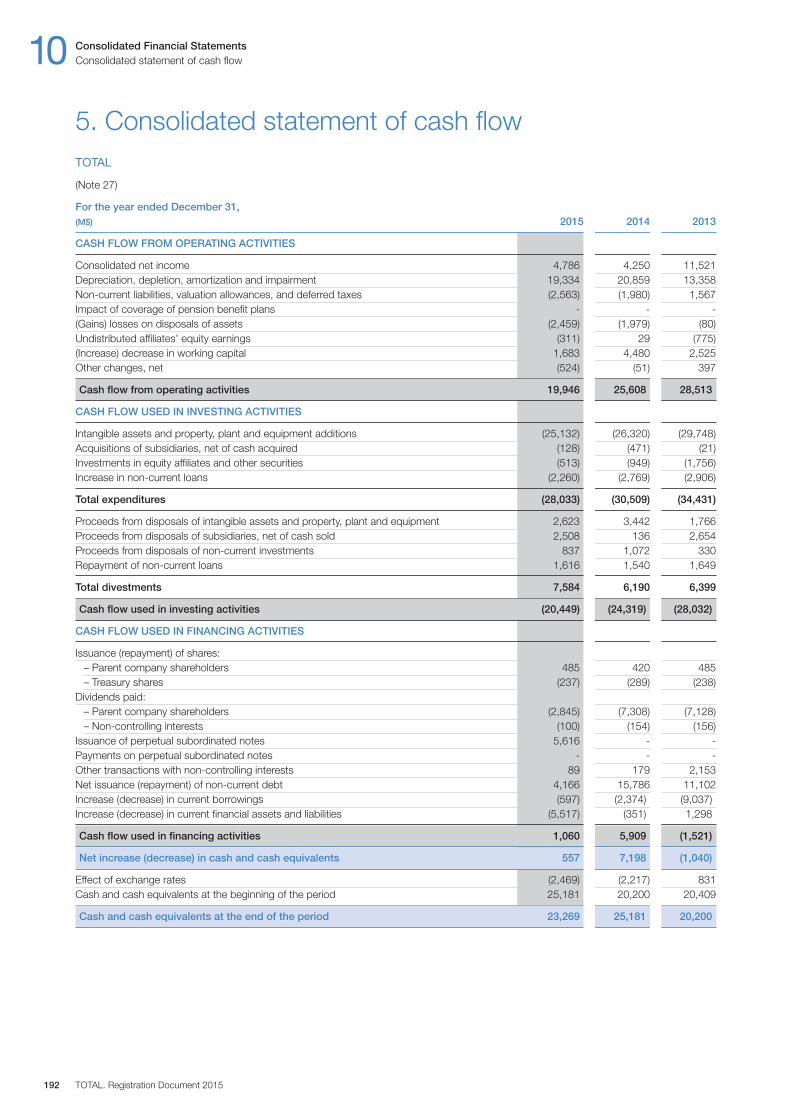

10. Consolidated Financial Statements1. Statutory auditors’ report on the Consolidated

Financial Statements . . . . . . . . . . . . . . . . . . . . . . . .1882. Consolidated statement of income . . . . . . . . . . . . .1893. Consolidated statement

of comprehensive income . . . . . . . . . . . . . . . . . . . .1904. Consolidated balance sheet . . . . . . . . . . . . . . . . . .1915. Consolidated statement of cash flow . . . . . . . . . . .1926. Consolidated statement of changes

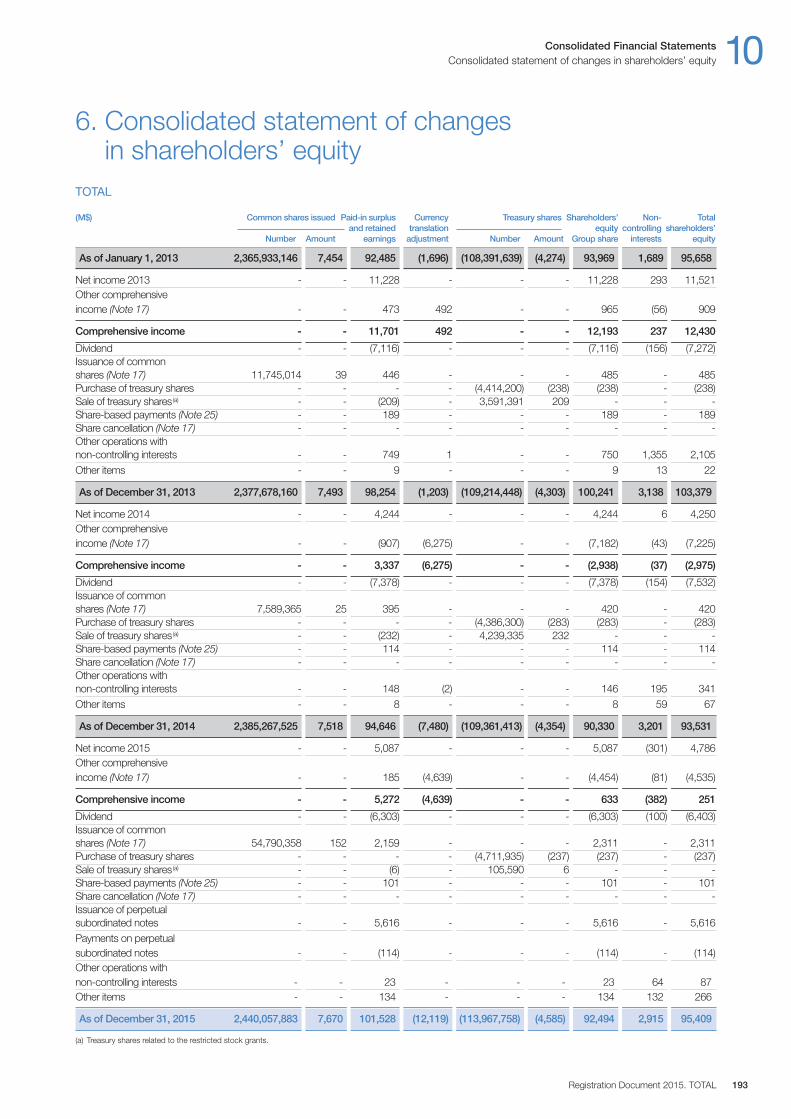

in shareholders’ equity . . . . . . . . . . . . . . . . . . . . . . .1937. Notes to the Consolidated Financial Statements . . . .194

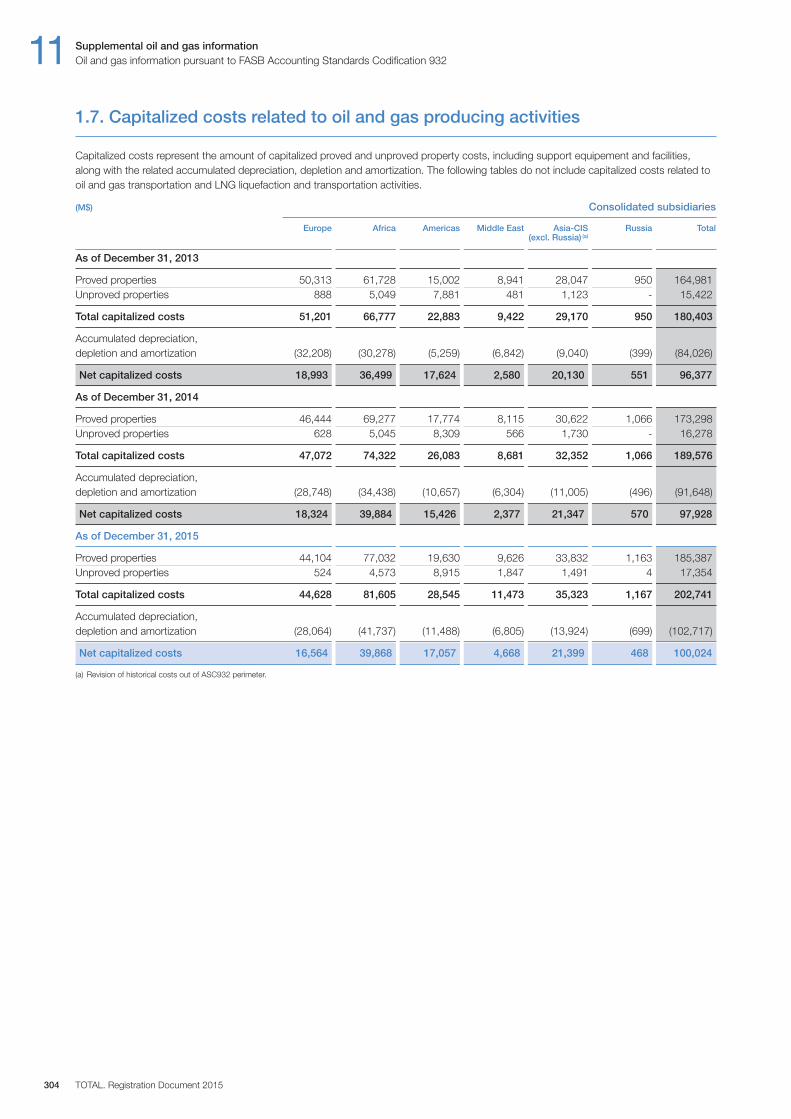

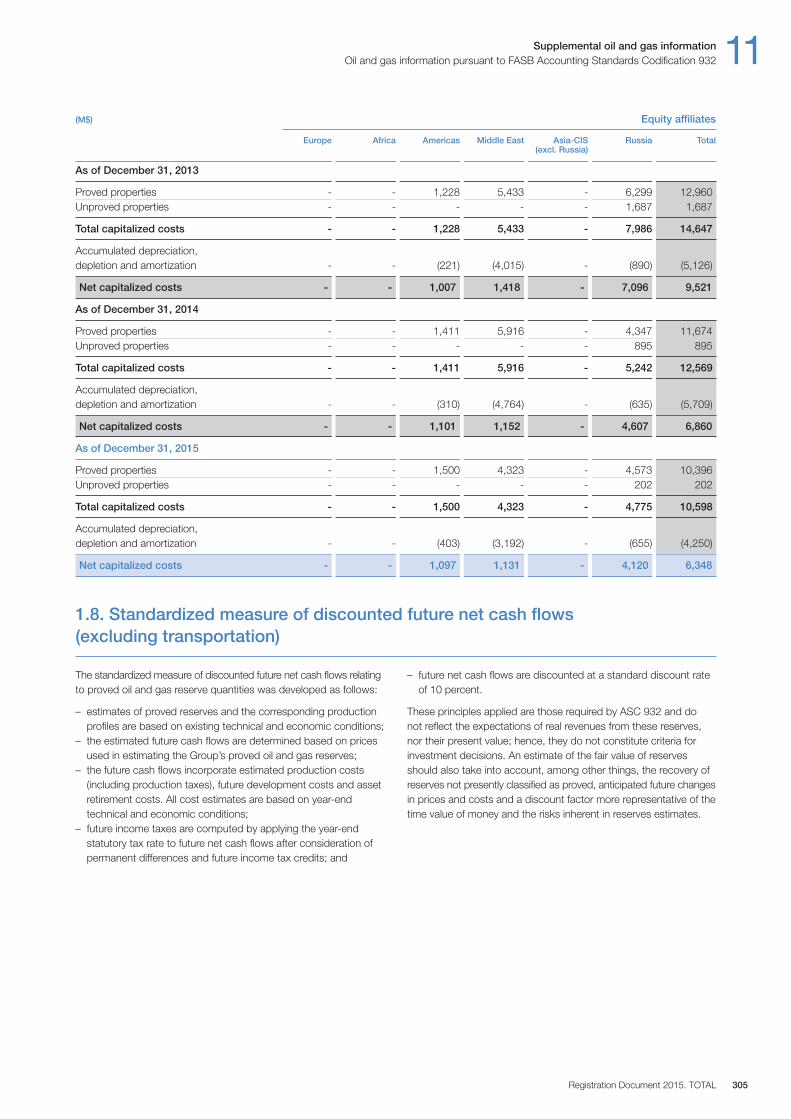

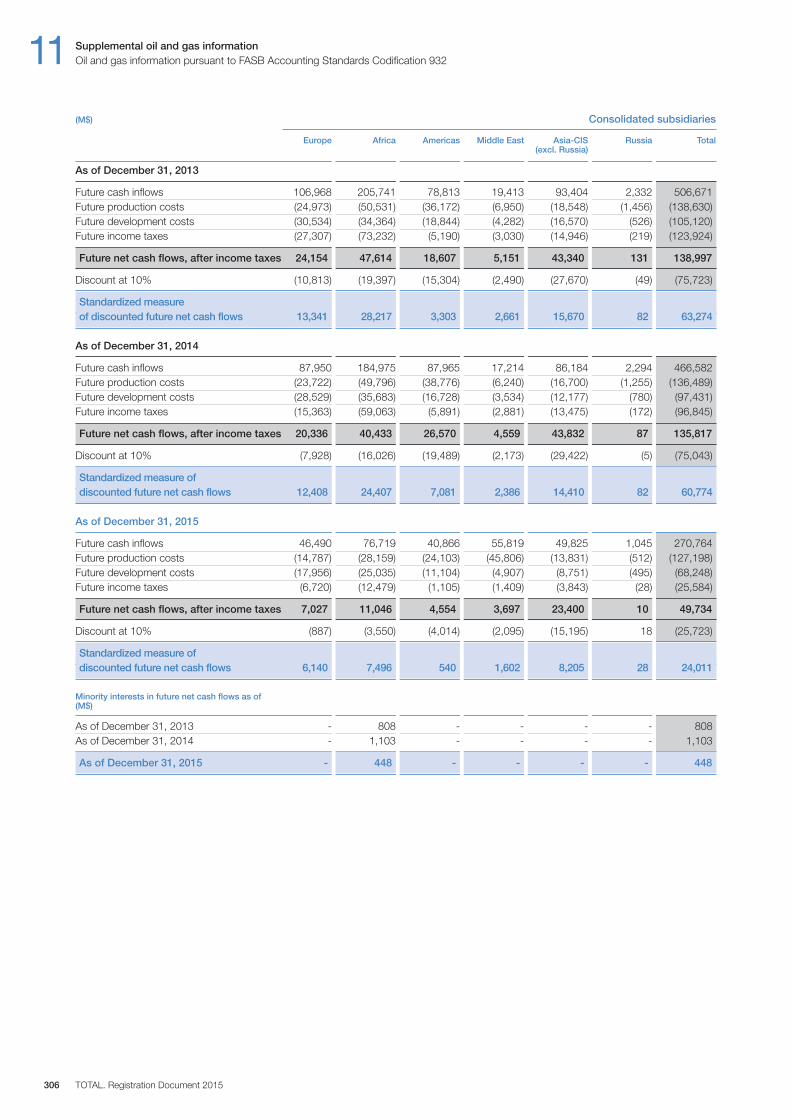

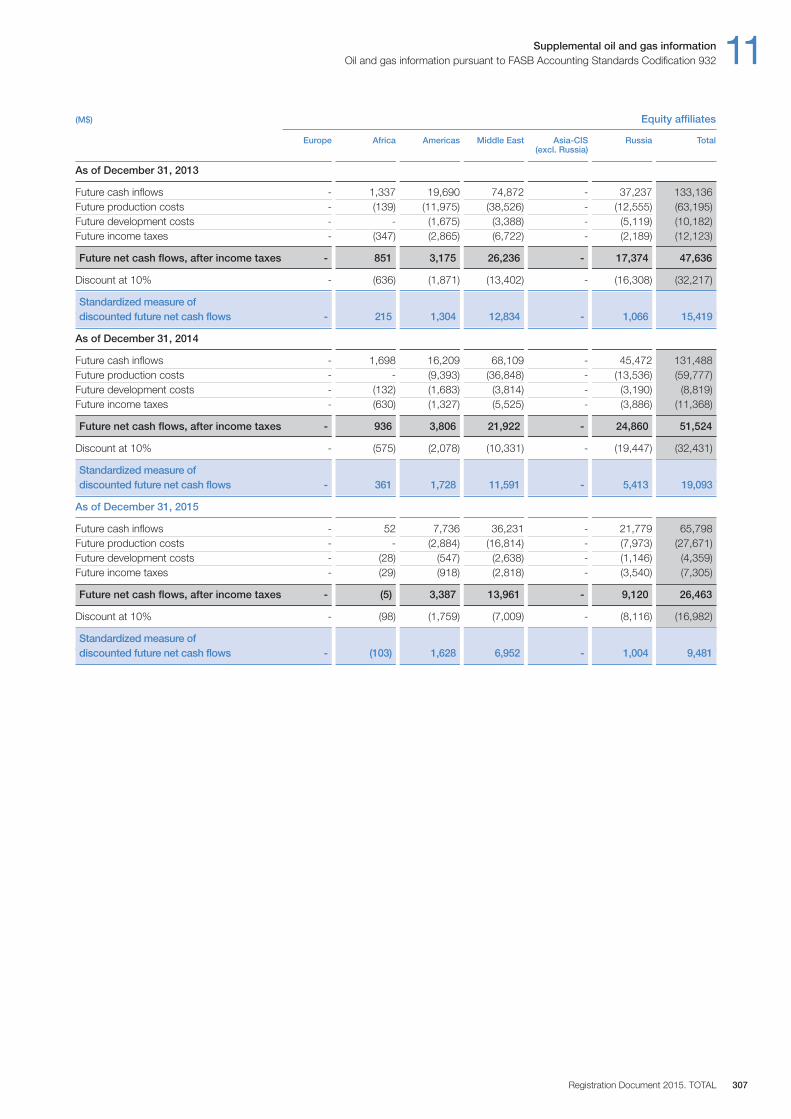

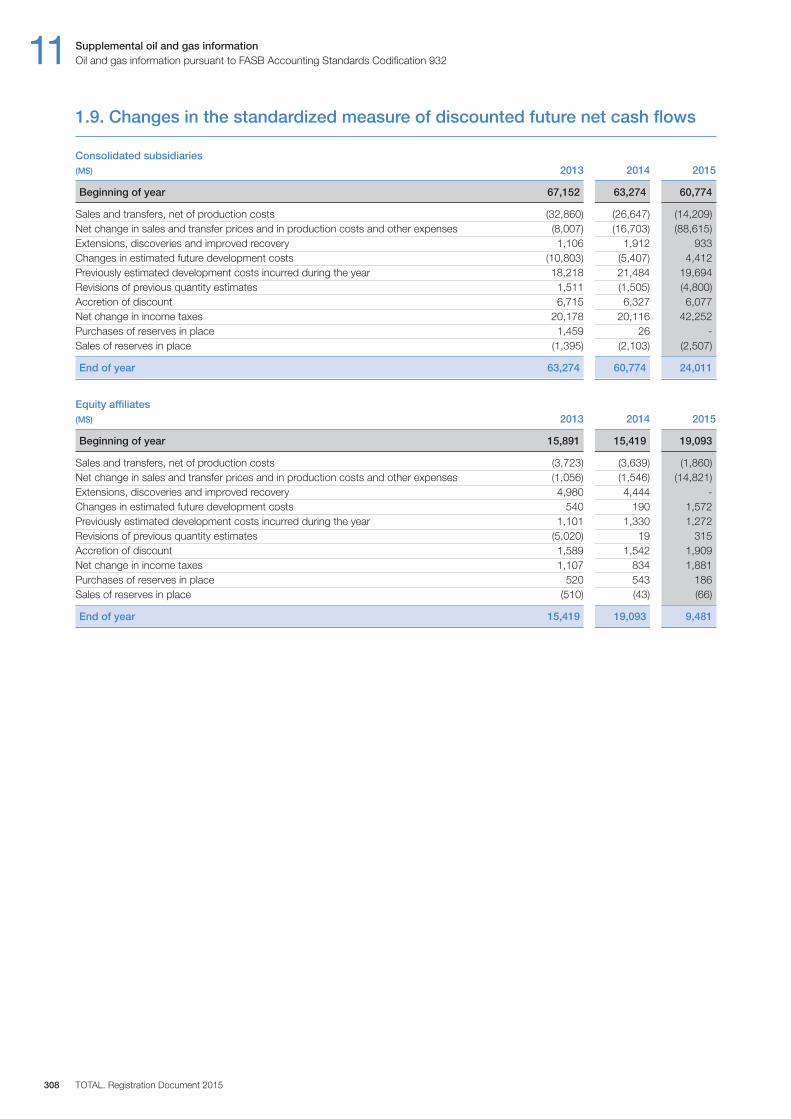

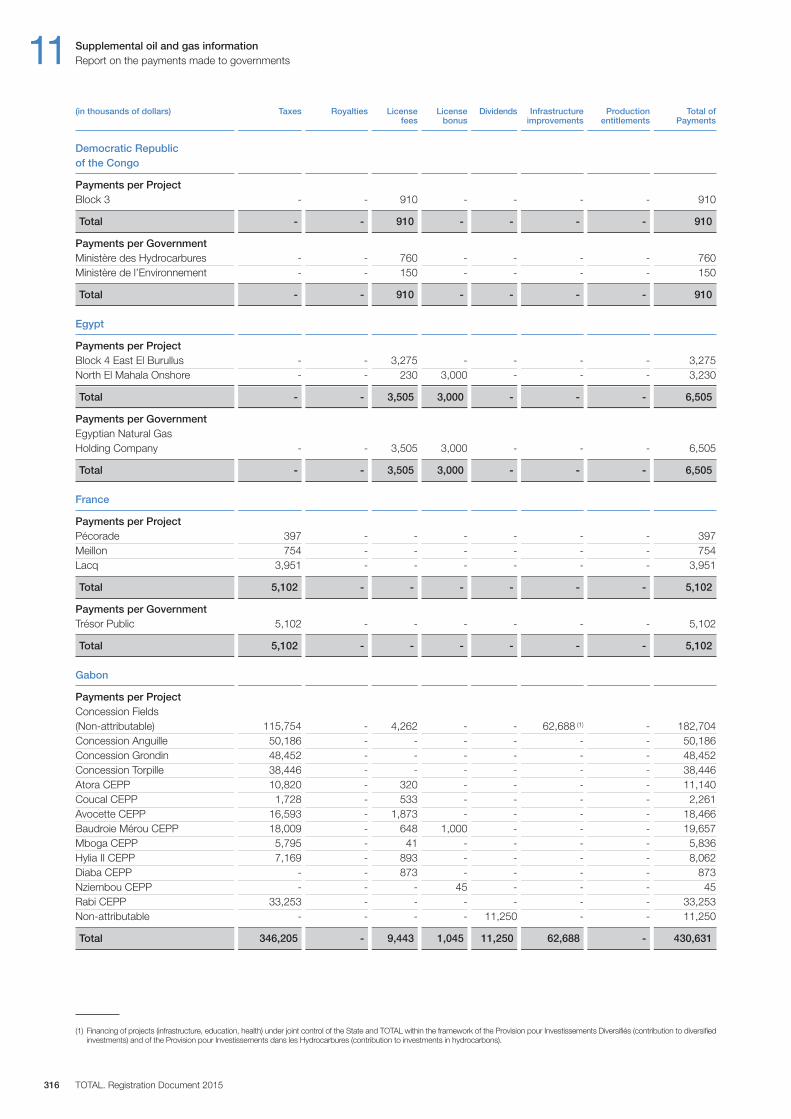

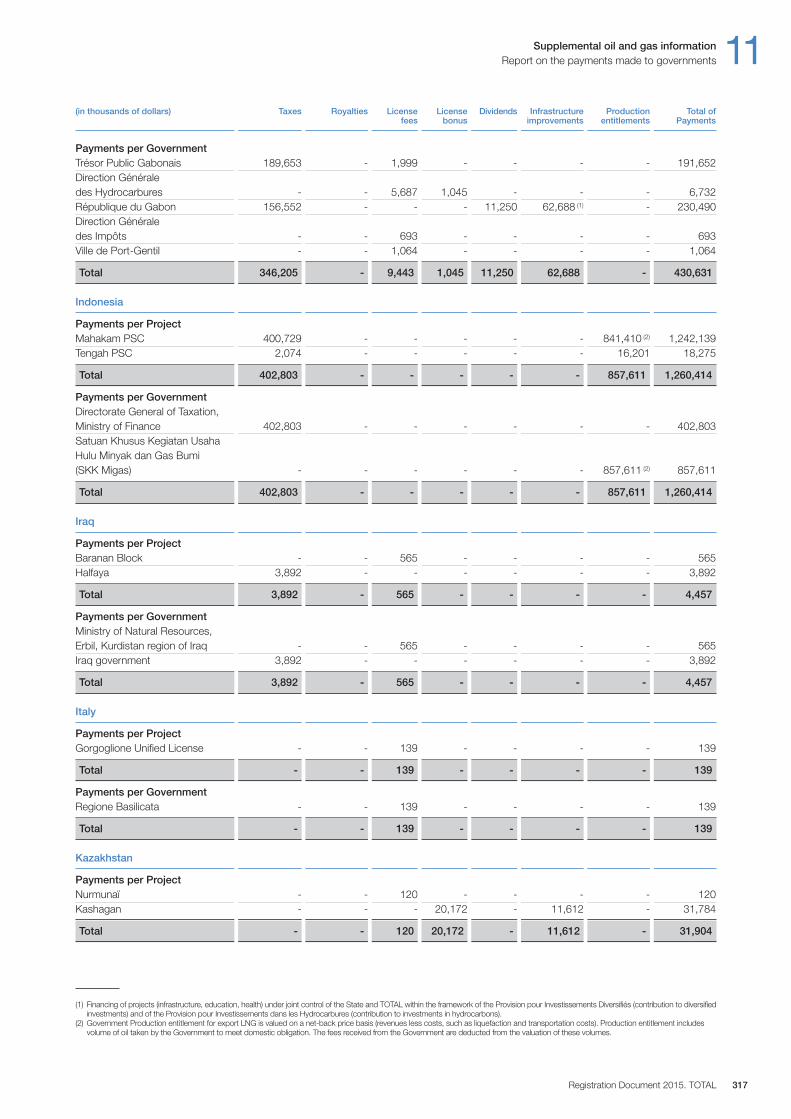

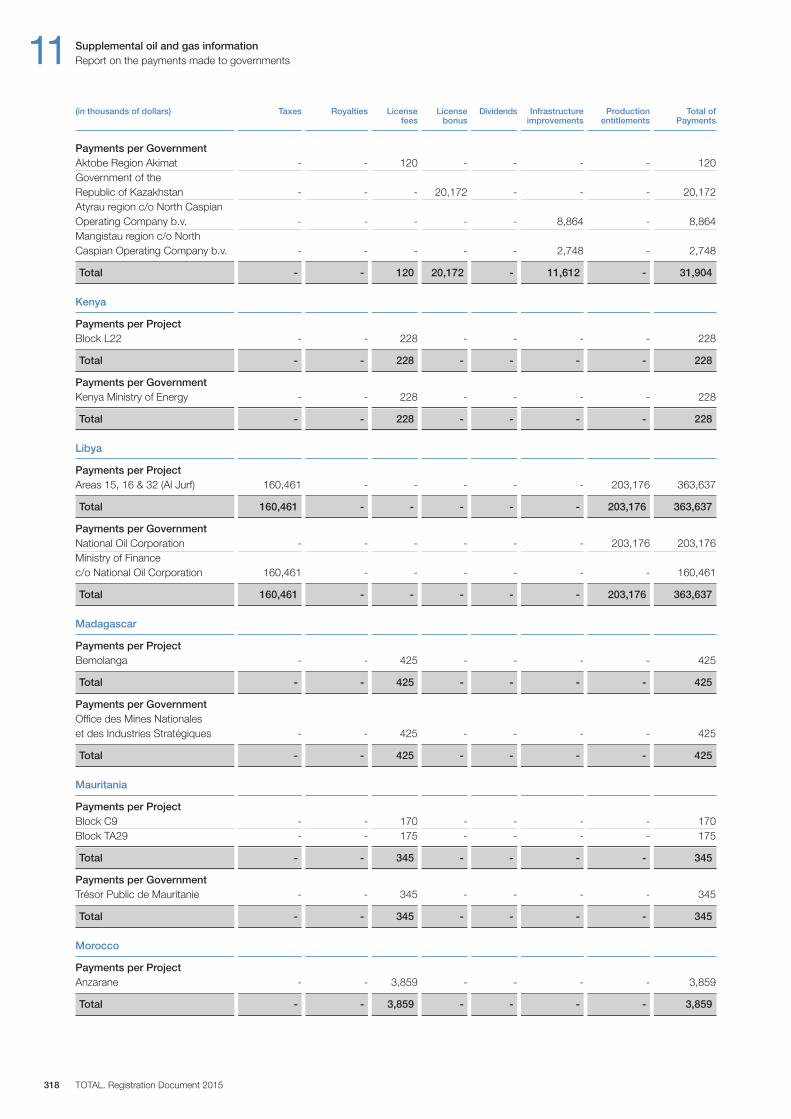

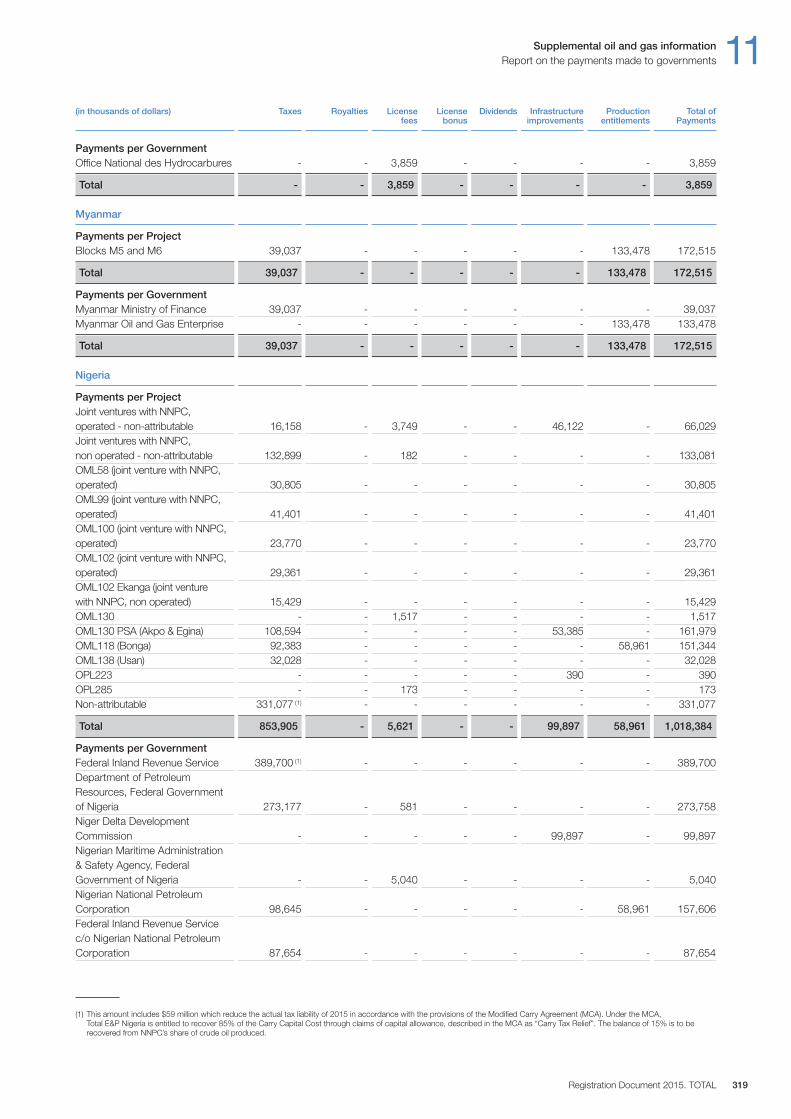

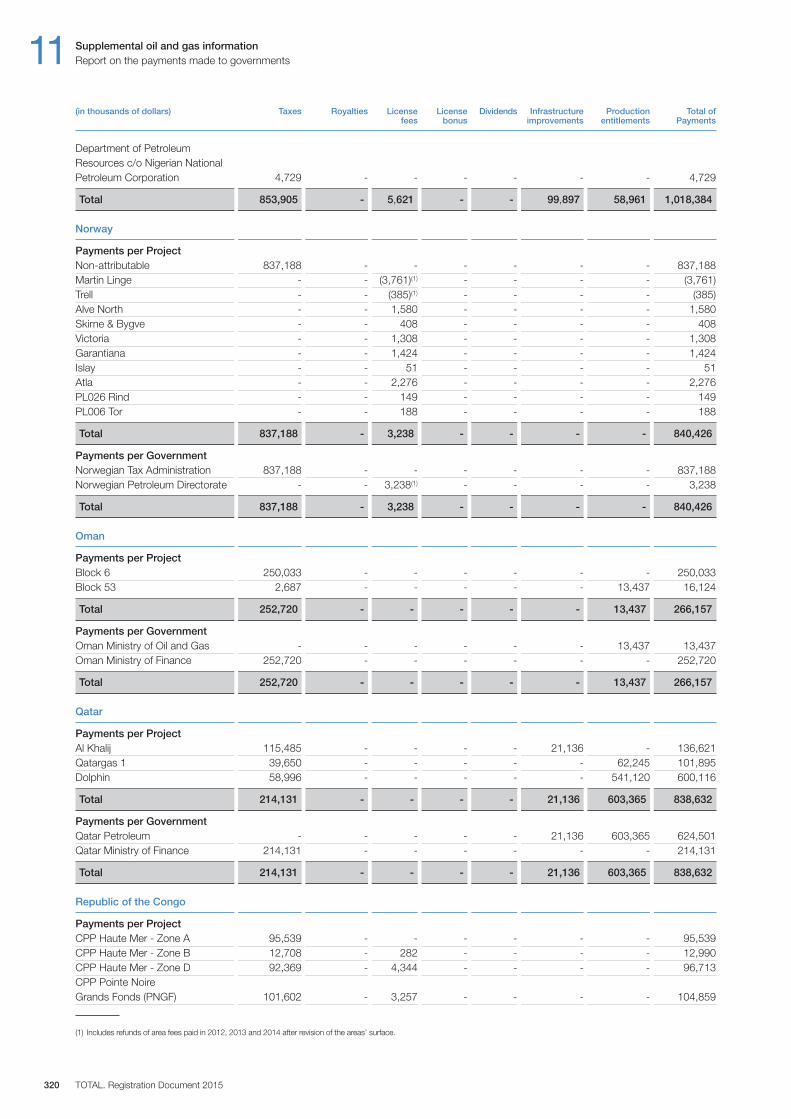

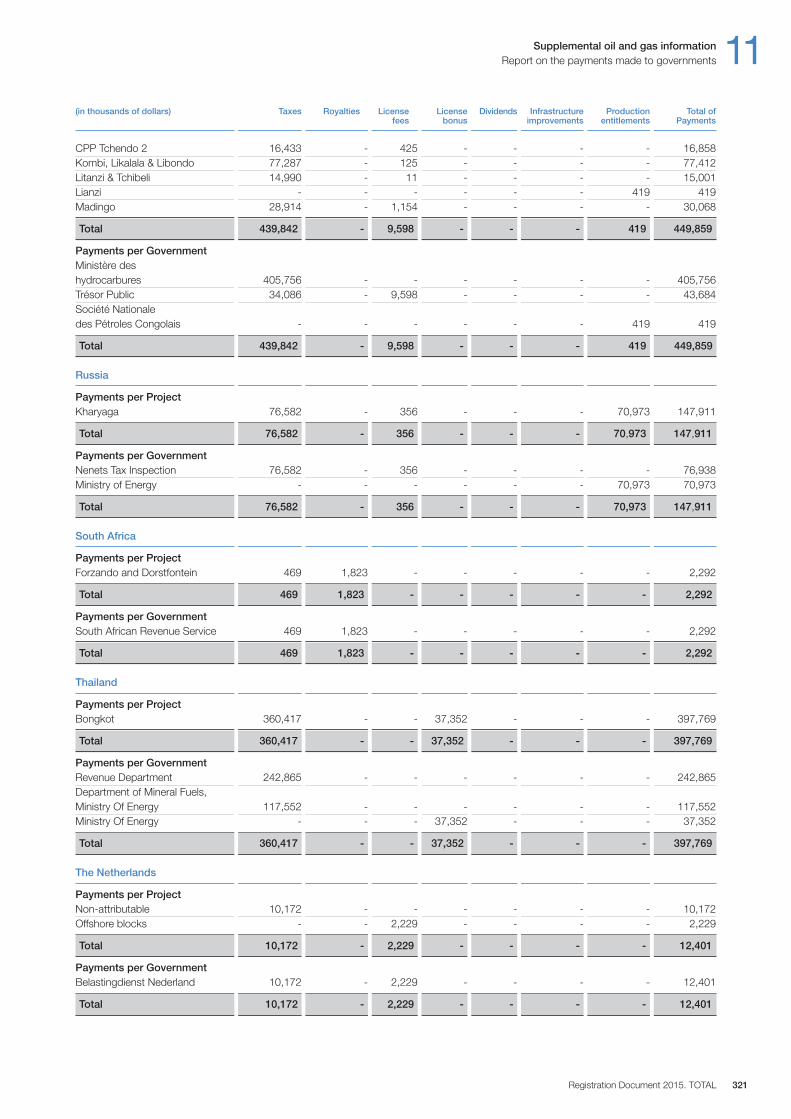

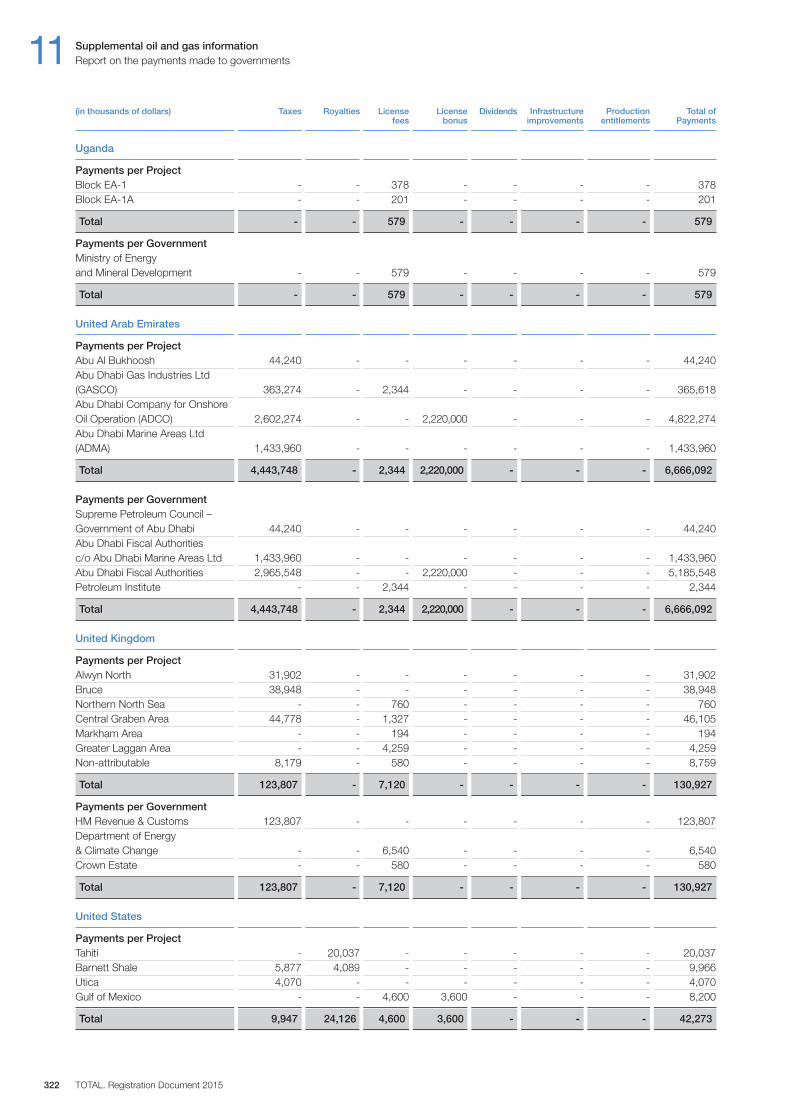

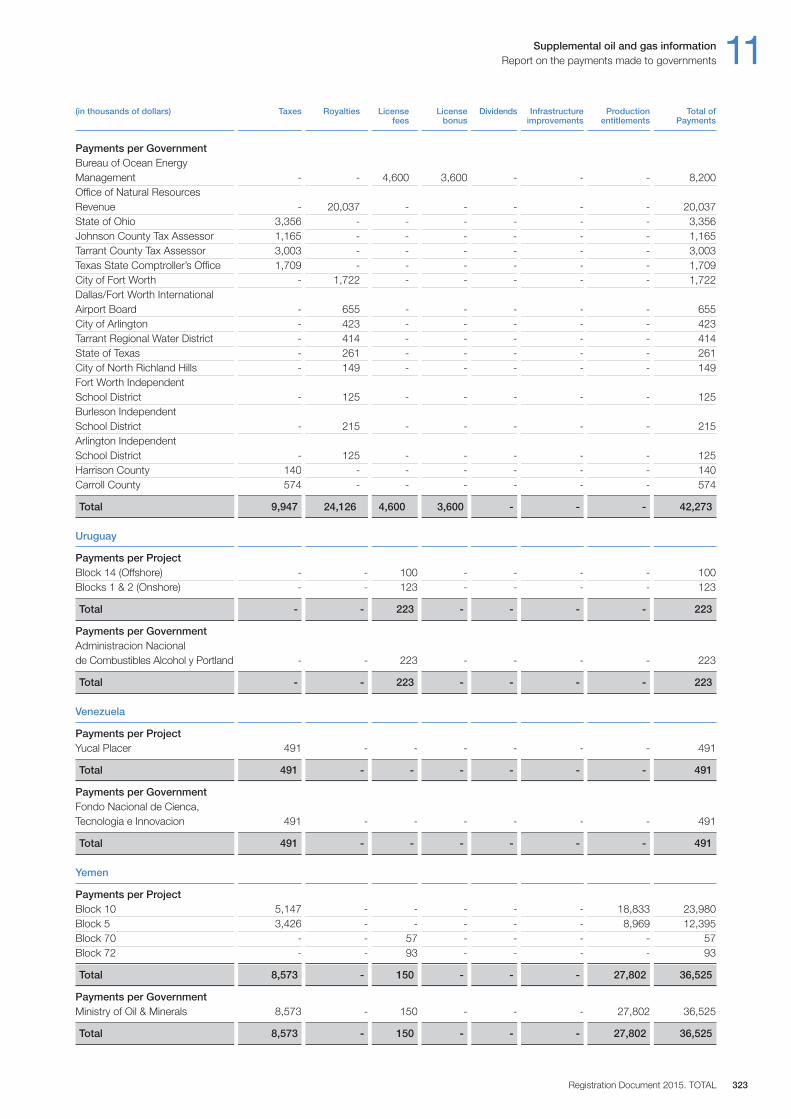

11. Supplemental oil and gas information(unaudited)1. Oil and gas information pursuant to FASB

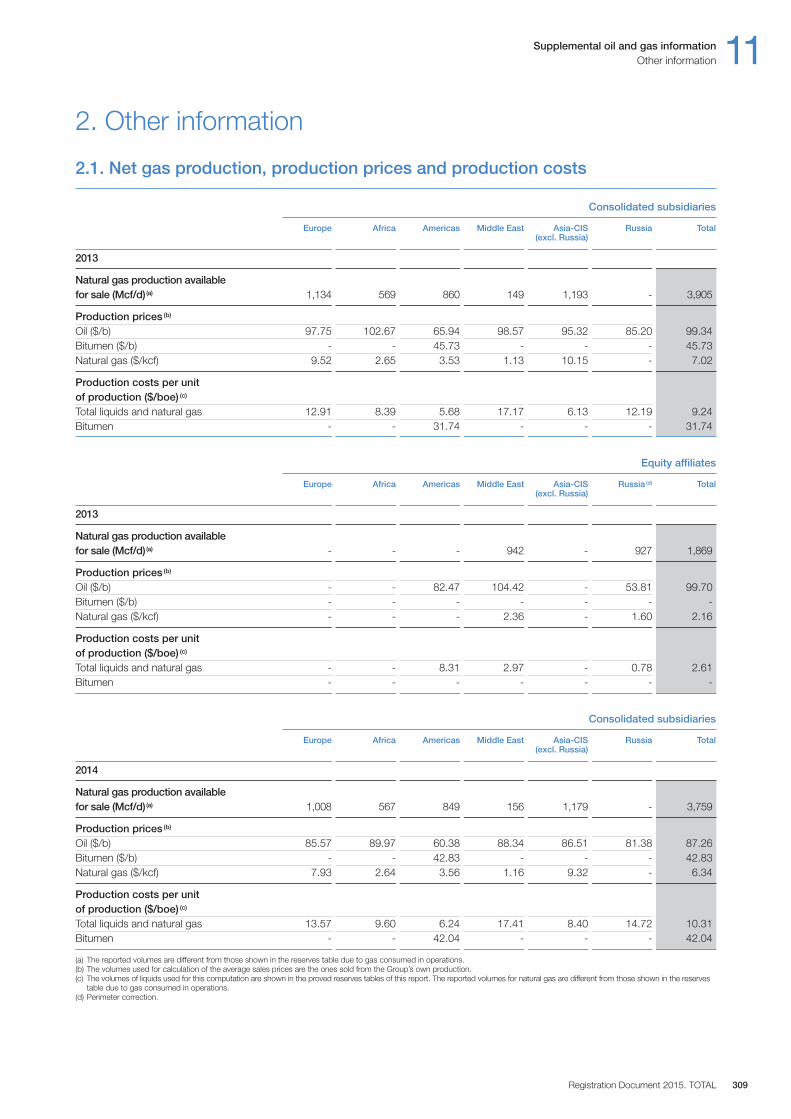

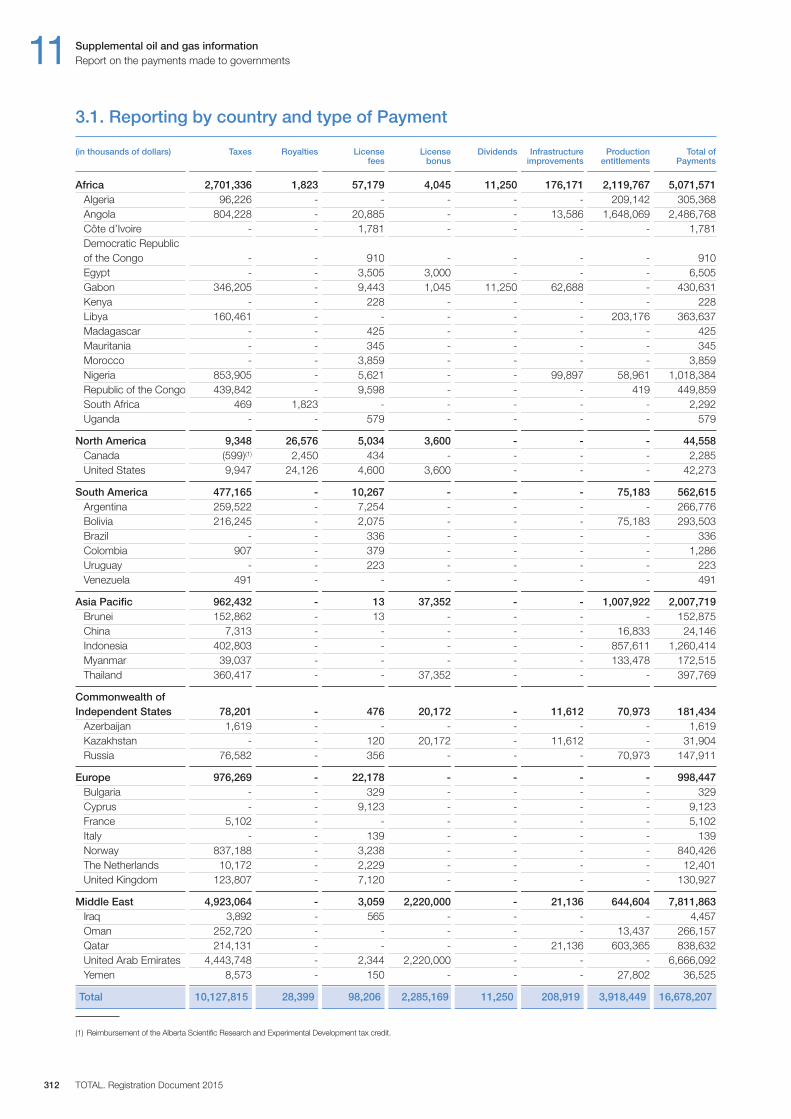

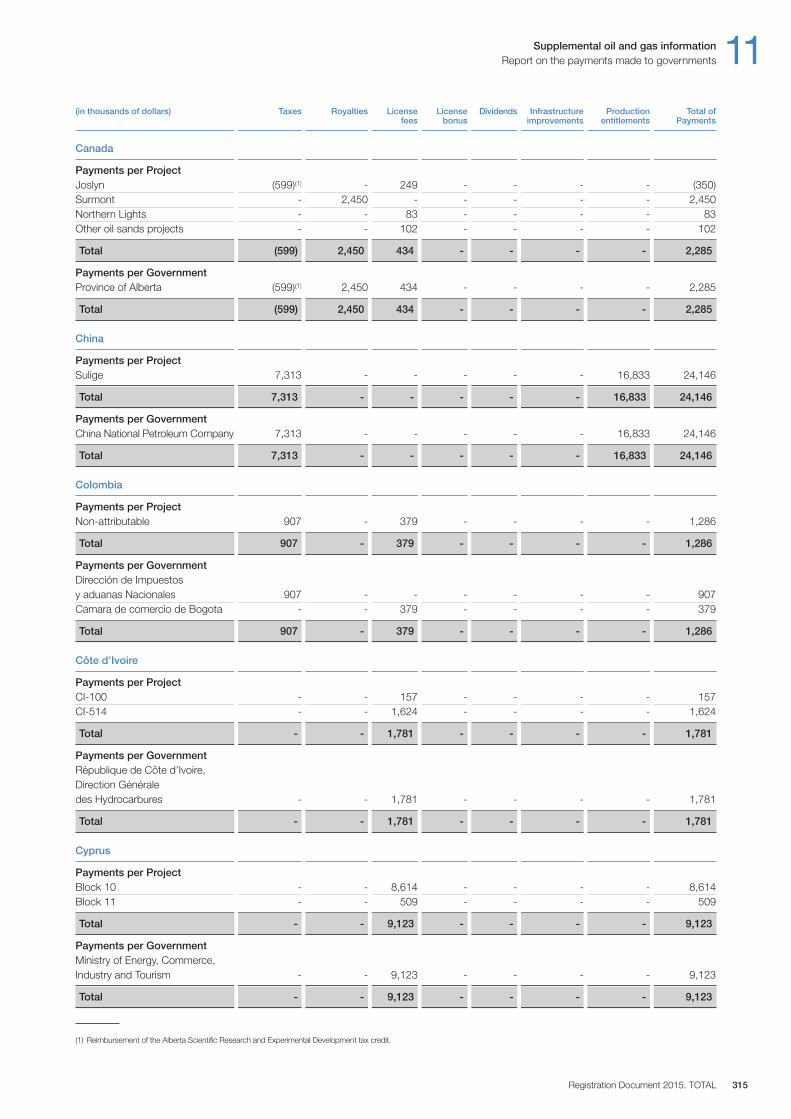

Accounting Standards Codification 932 . . . . . . . . .2922. Other information . . . . . . . . . . . . . . . . . . . . . . . . . . .3093. Report on the payments made to governments . . . .311

12. TOTAL S.A.1. Statutory auditors’ report on regulated

agreements and commitments . . . . . . . . . . . . . . . .3262. Statutory auditors’ report on the annual

financial statements . . . . . . . . . . . . . . . . . . . . . . . . .3293. Statutory financial statements

of TOTAL S.A. as parent company . . . . . . . . . . . . .3304. Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3345. Other financial information concerning

the parent company . . . . . . . . . . . . . . . . . . . . . . . . .346

Glossary 349

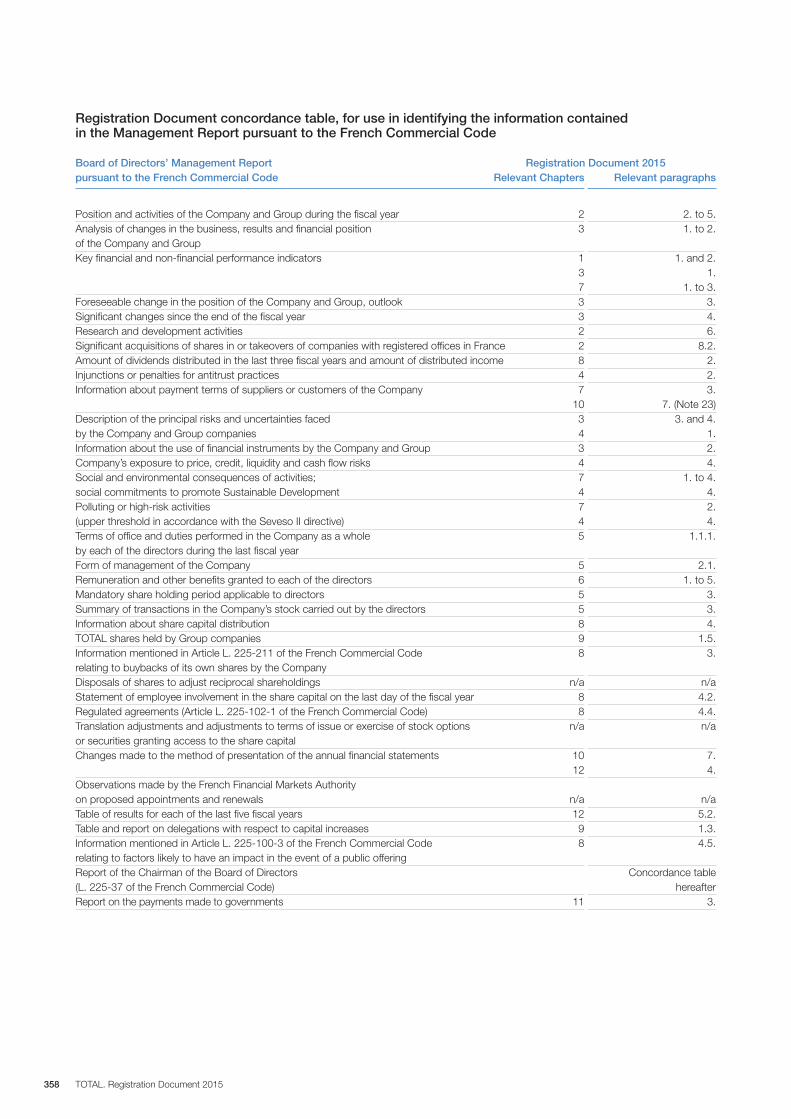

Cross-reference lists 353

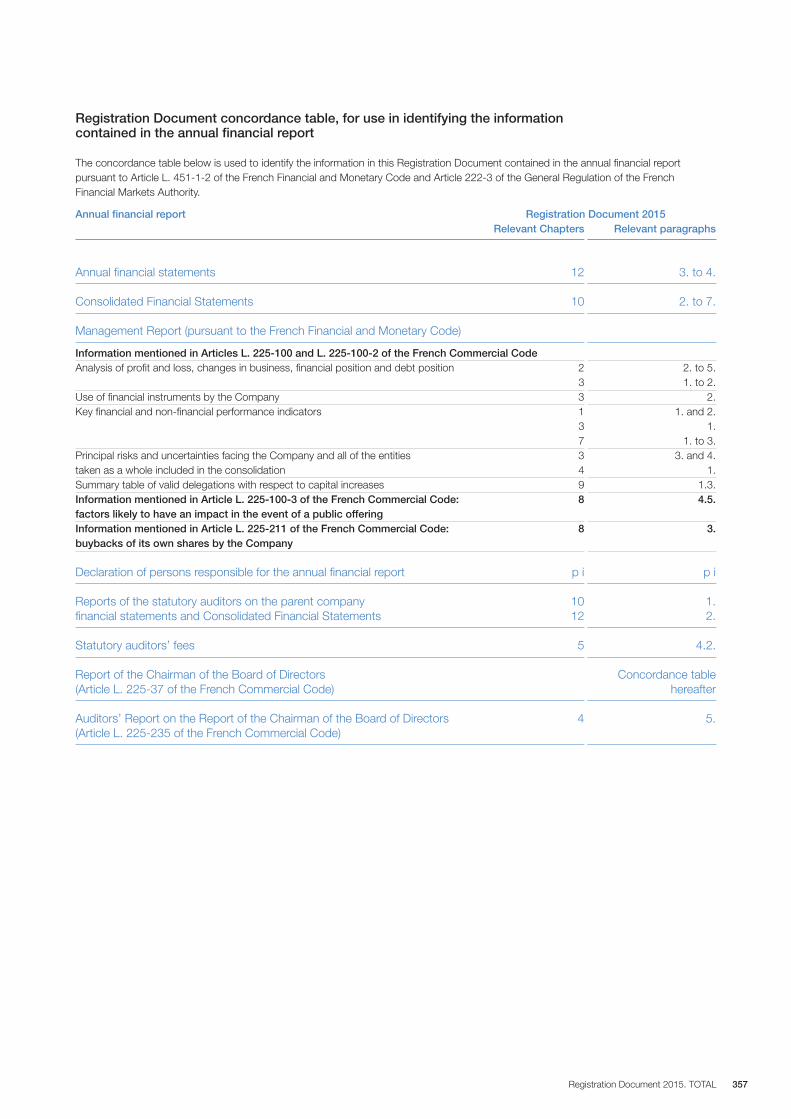

Registration Document 2015including the annual financial report

This translation is a non binding translation into English of the Chairman and Chief Executive Officer’s certification issued in French and isprovided solely for the convenience of English-speaking readers.

“I certify, after having taken all reasonable measures to this purpose and to the best of my knowledge, that the information contained in thisDocument de référence (Registration Document) is in accordance with the facts and makes no omission likely to affect its import.

I certify, to the best of my knowledge, that the statutory and Consolidated Financial Statements of TOTAL S.A. (the Company) have beenprepared in accordance with applicable accounting standards and give a fair view of the assets, liabilities, financial position and results of theCompany and of all the entities included in the consolidation, and that the rapport de gestion (Management Report) of the Board of Directorsas referenced in the cross reference list included on page 357 of this Document de référence (Registration Document) presents a fair view ofthe development and performance of the business and financial position of the Company and of all the entities included in the consolidation,as well as a description of the main risks and uncertainties they are exposed to.

I have received a completion letter from the statutory auditors in which they state that they have audited the information related to the financialsituation and the financial statements included in this Document de référence (Registration Document), as well as read this Document deréférence (Registration Document) in its entirety.

The statutory auditors have reviewed the historical financial information contained in this Document de référence (Registration Document).The statutory auditors’ report on the Consolidated Financial Statements for the year ended December 31, 2015, is included on page 188 of this Document de référence (Registration Document). The statutory auditors’ report on the Consolidated Financial Statements for the yearended December 31, 2014, included on page 242 of the Registration Document 2014 filed on March 26, 2015, with the French FinancialMarkets Authority (AMF), contains a remark on the matter set out in the “Introduction” Note to the Consolidated Financial Statements whichsets out a change in accounting methods related to the change in the presentation currency of the Consolidated Financial Statements fromthe euro to the U.S. dollar.”

On March 15, 2016

Patrick PouyannéChairman and Chief Executive Officer

Registration Document 2015. TOTAL i

The French language version of this Document de référence (Registration Document) was filed with the French Financial Markets Authority(Autorité des marchés financiers) on March 16, 2016 pursuant to Article 212-13 of its general regulations. It may be used to support afinancial operation only if supplemented by a transaction note approved by the French Financial Markets Authority. This document wasprepared by the issuer and is binding for its signatories.

TOTAL. Registration Document 2015ii

Abbreviations

b: barrelcf: cubic feet / d: per day / y: per year€: euro$ and / or dollar: U.S. dollart: metric tonboe: barrel of oil equivalentkboe / d: thousand boe / dkb / d: thousand barrel / dBtu: British thermal unitM: millionB: billionMW: megawattMWp: megawatt peak (direct current)TWh: terawatt hourAMF: French Financial Markets AuthorityAPI: American Petroleum InstituteERMI: European Refining Margin Indicator. ERMI is an indicator intended to

represent the margin after variable costs for a hypothetical complexrefinery located around Rotterdam in Northern Europe. The indicatormargin may not be representative of the actual margins achieved byTOTAL in any period because of TOTAL’s particular refinery configurations,product mix effects or other company-specific operating conditions.

FEED: Front-End Engineering and DesignFPSO: Floating Production Storage and OffloadingIEA: International Energy AgencyIFRS: International Financial Reporting StandardsLNG: liquefied natural gasLPG: liquefied petroleum gasROE Return on EquityROACE: Return on Average Capital EmployedSAGD: Steam Assisted Gravity DrainageSEC: United States Securities and Exchange Commission

Conversion table

1 boe = 1 barrel of crude oil = approx. 5,390 cf of gas* in 2015.1 b / d = approx. 50 t / y1 t = approx. 7.5 b (for a gravity of 37° API)1 Bm³ / y = approx. 0.1 Bcf / d1 m³ = approx. 35.3 cf1 t of LNG = approx. 48 kcf of gas1 Mt / y of LNG = approx. 131 Mcf / d

* This ratio is calculated based on the actual average equivalent energy content of TOTAL’s natural gas reserves and is subject to change.

Définitions

The terms “TOTAL” and “Group” as used in this Registration Document refer toTOTAL S.A. collectively with all of its direct and indirect consolidated subsidiaries located in, or outside of France. The terms “Company” or “issues” as used in thisRegistration Document only refer to TOTAL S.A., parent company of the Group.

© TOTAL S.A. March 2016

Key figures

1. Operating and market data

2015 2014 2013

Brent ($ / b) 52.4 99.0 108.7Exchange rate (€-$) 1.11 1.33 1.33European Refining Margin Indicator (ERMI) ($ / t) 48.5 18.7 17.9

Hydrocarbon production (kboe / d) 2,347 2,146 2,299Liquids (kb / d) 1,237 1,034 1,167Gas (Mcf / d) 6,054 6,063 6,184

Refinery throughput (kb / d) 1,938 1,775 1,719Petroleum product sales (a) (kb / d) 4,005 3,769 3,521

(a) Including Trading.

Effective January 1, 2014, TOTAL changed the presentation currency of the Group’s Consolidated Financial Statements from the euro to the U.S. dollar. Comparative 2013 information has been restated.

Registration Document 2015. TOTAL 1

Key figures 1

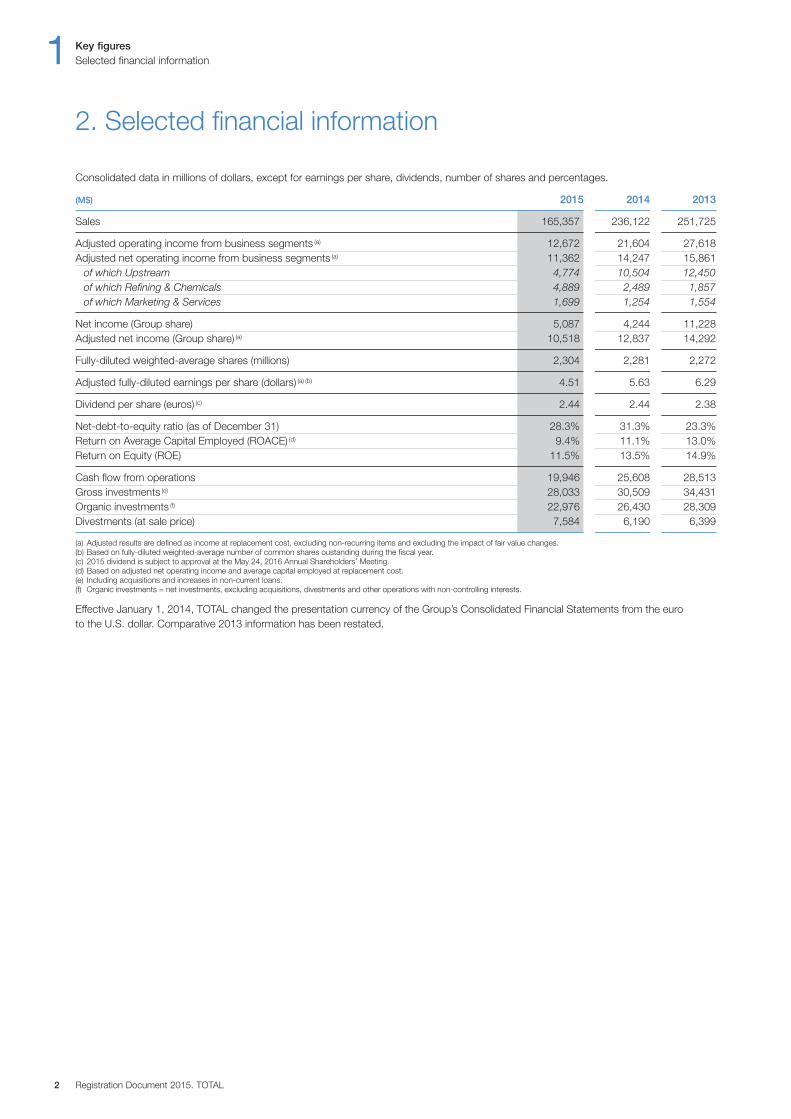

2. Selected financial information

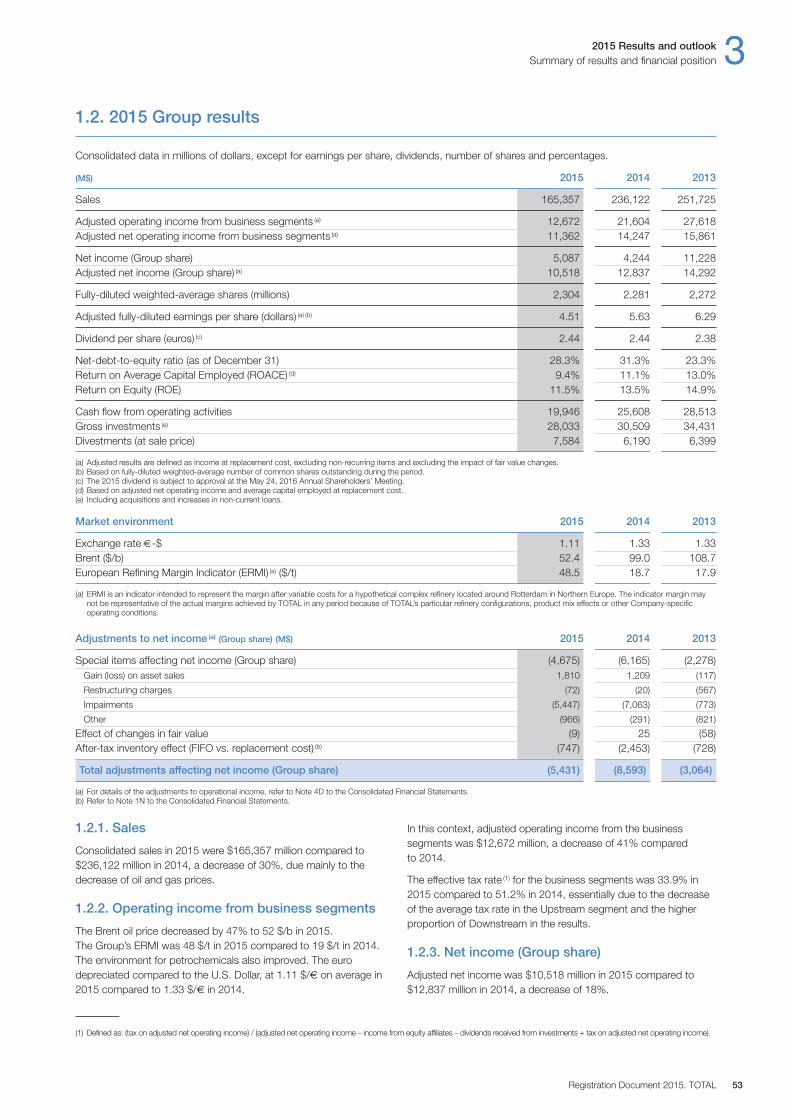

Consolidated data in millions of dollars, except for earnings per share, dividends, number of shares and percentages.

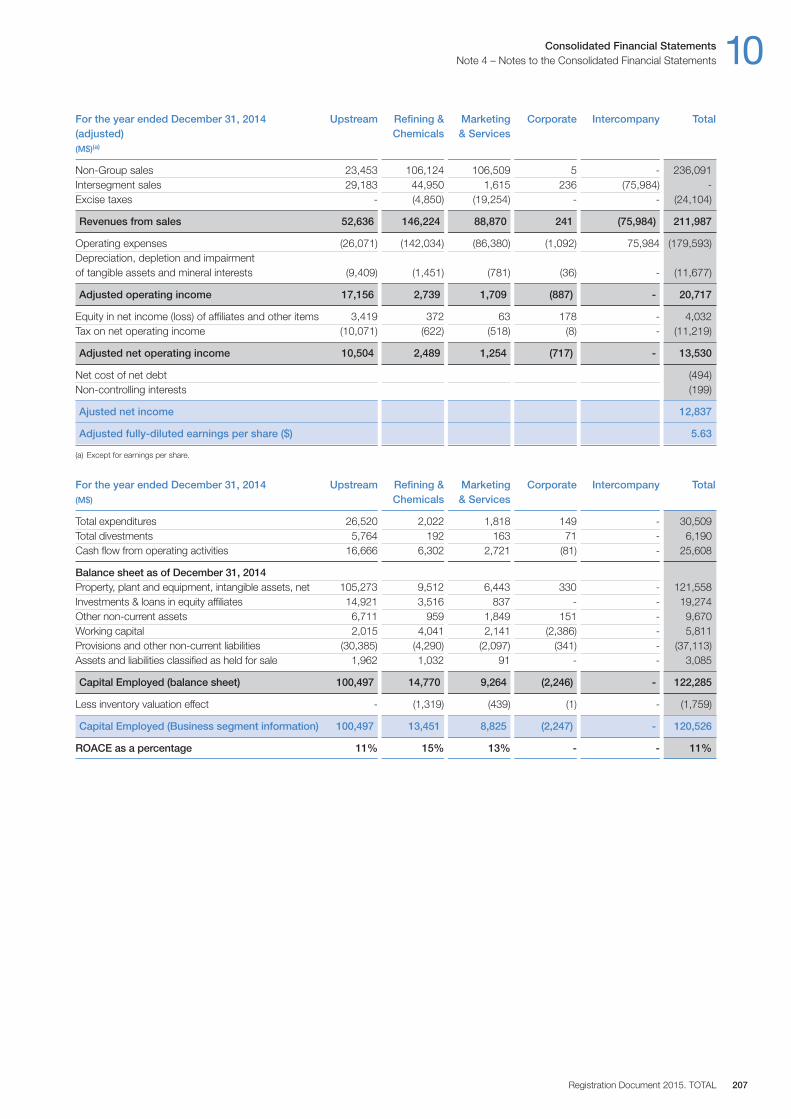

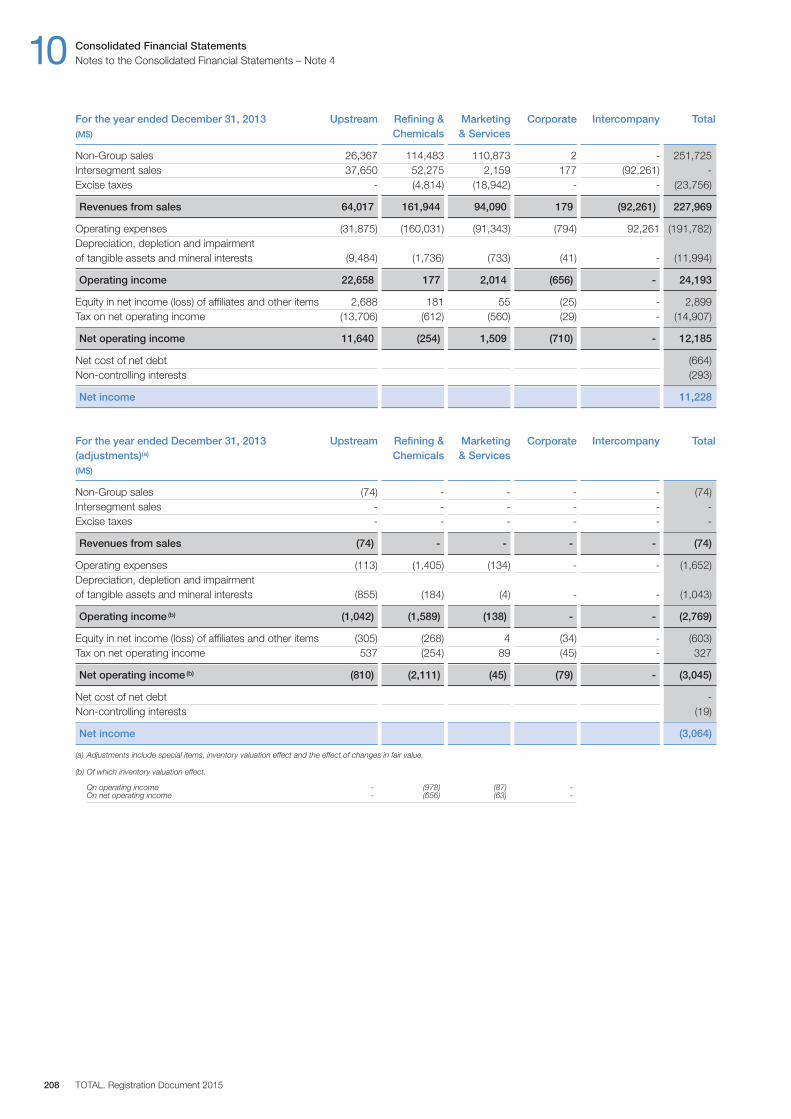

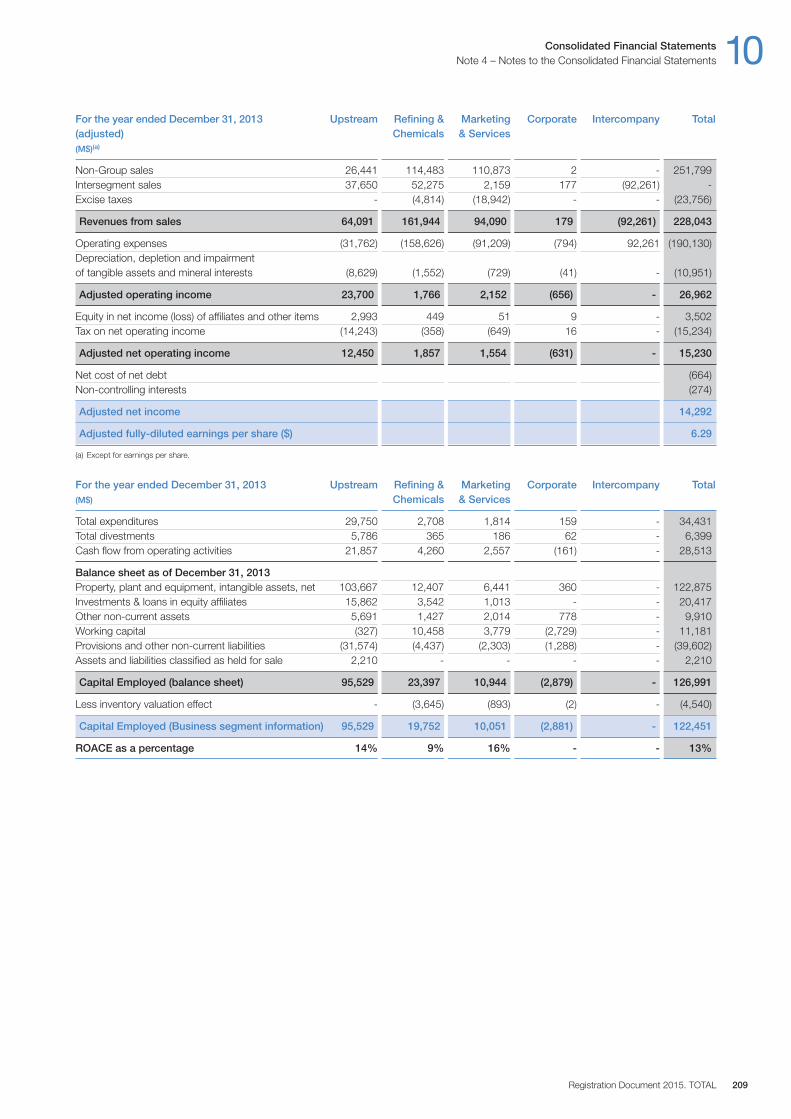

(M$) 2015 2014 2013

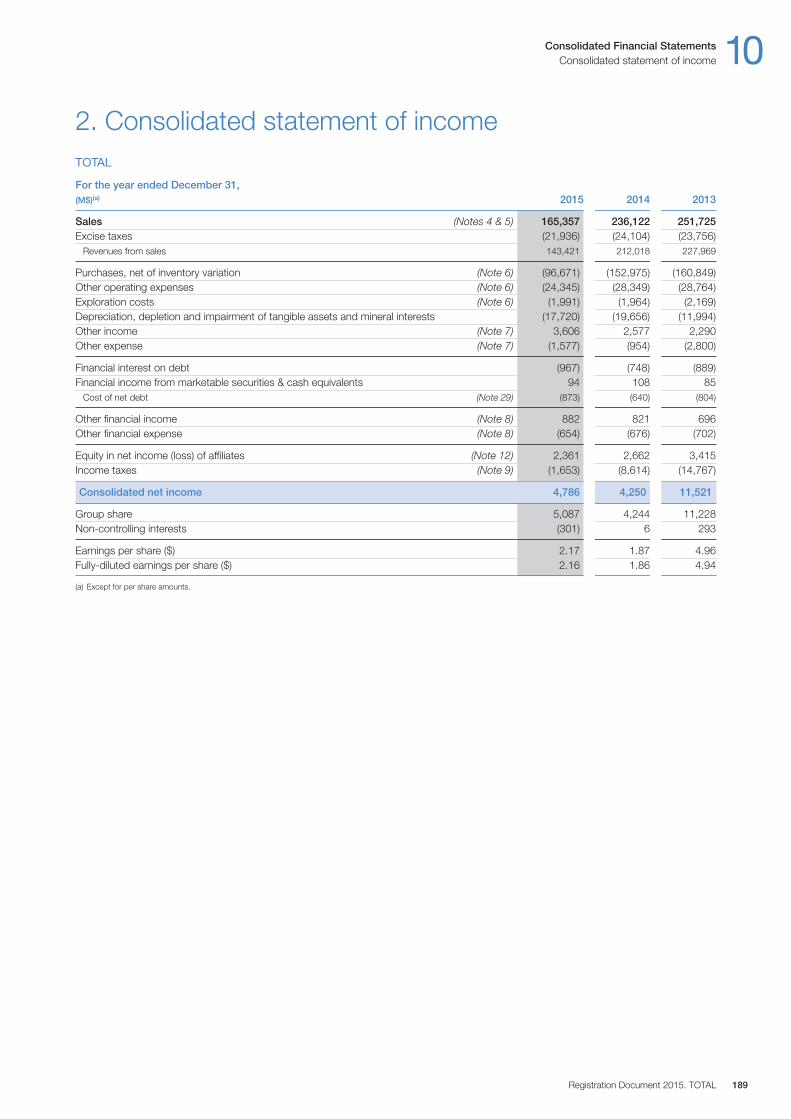

Sales 165,357 236,122 251,725

Adjusted operating income from business segments (a) 12,672 21,604 27,618Adjusted net operating income from business segments (a) 11,362 14,247 15,861

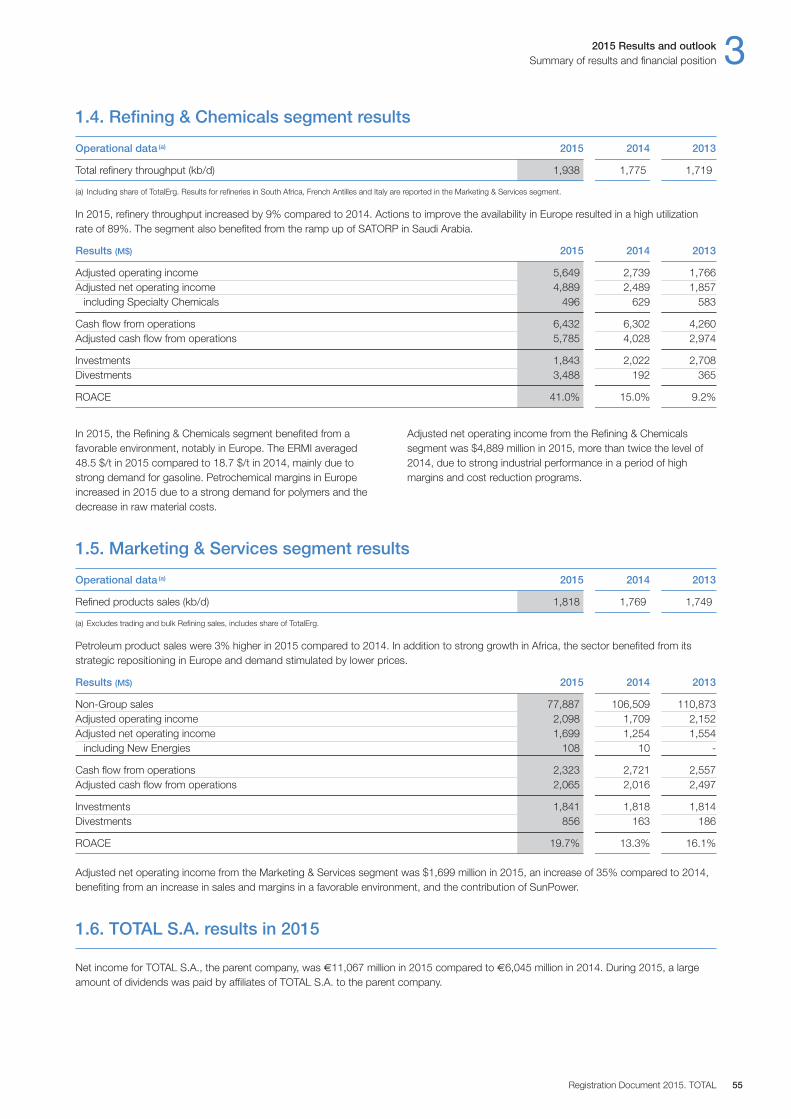

of which Upstream 4,774 10,504 12,450of which Refining & Chemicals 4,889 2,489 1,857of which Marketing & Services 1,699 1,254 1,554

Net income (Group share) 5,087 4,244 11,228Adjusted net income (Group share) (a) 10,518 12,837 14,292

Fully-diluted weighted-average shares (millions) 2,304 2,281 2,272

Adjusted fully-diluted earnings per share (dollars) (a) (b) 4.51 5.63 6.29

Dividend per share (euros) (c) 2.44 2.44 2.38

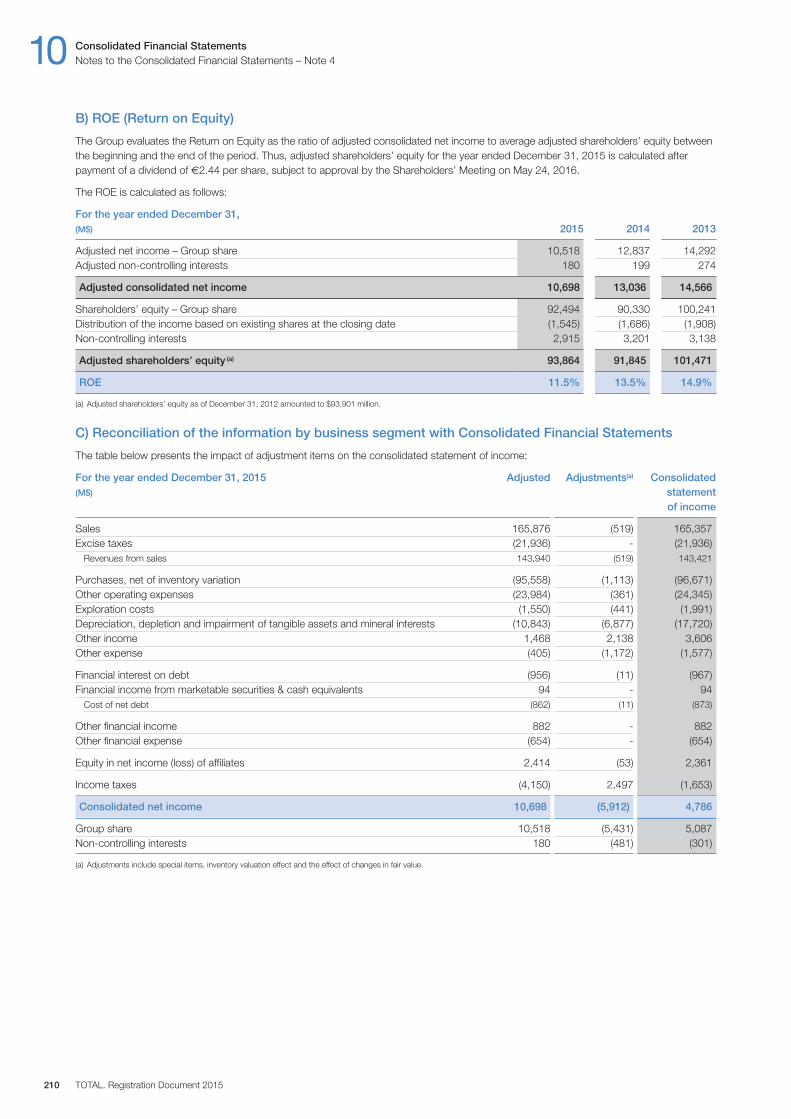

Net-debt-to-equity ratio (as of December 31) 28.3% 31.3% 23.3%Return on Average Capital Employed (ROACE) (d) 9.4% 11.1% 13.0%Return on Equity (ROE) 11.5% 13.5% 14.9%

Cash flow from operations 19,946 25,608 28,513Gross investments (e) 28,033 30,509 34,431Organic investments (f) 22,976 26,430 28,309Divestments (at sale price) 7,584 6,190 6,399

(a) Adjusted results are defined as income at replacement cost, excluding non-recurring items and excluding the impact of fair value changes.(b) Based on fully-diluted weighted-average number of common shares oustanding during the fiscal year.(c) 2015 dividend is subject to approval at the May 24, 2016 Annual Shareholders’ Meeting.(d) Based on adjusted net operating income and average capital employed at replacement cost.(e) Including acquisitions and increases in non-current loans.(f) Organic investments = net investments, excluding acquisitions, divestments and other operations with non-controlling interests.

Effective January 1, 2014, TOTAL changed the presentation currency of the Group’s Consolidated Financial Statements from the euro to the U.S. dollar. Comparative 2013 information has been restated.

Registration Document 2015. TOTAL2

1 Key figuresSelected financial information

Registration Document 2015. TOTAL 3

Key figures 1Selected financial information

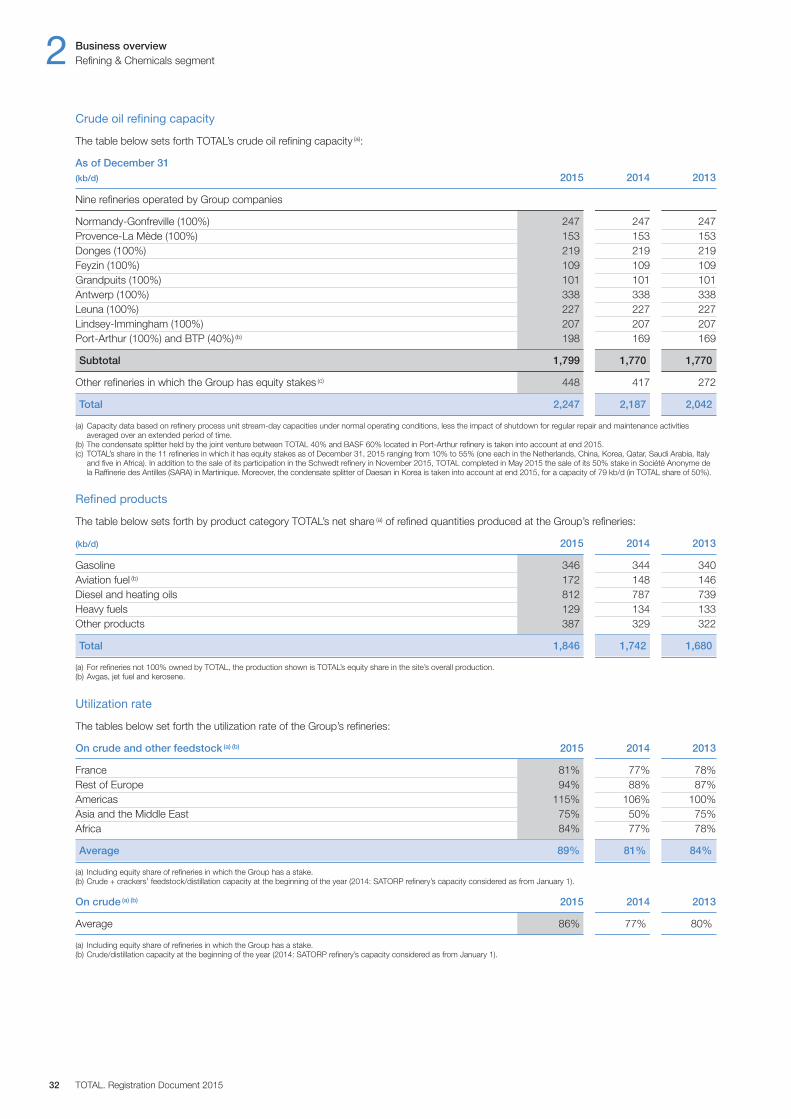

Refining capacity as of December 31, 2015

Liquids and gas reserves

Petroleum product salesincluding Trading

Oil and gas production

Petrochemicals production capacity by geographic area as of December 31, 2015

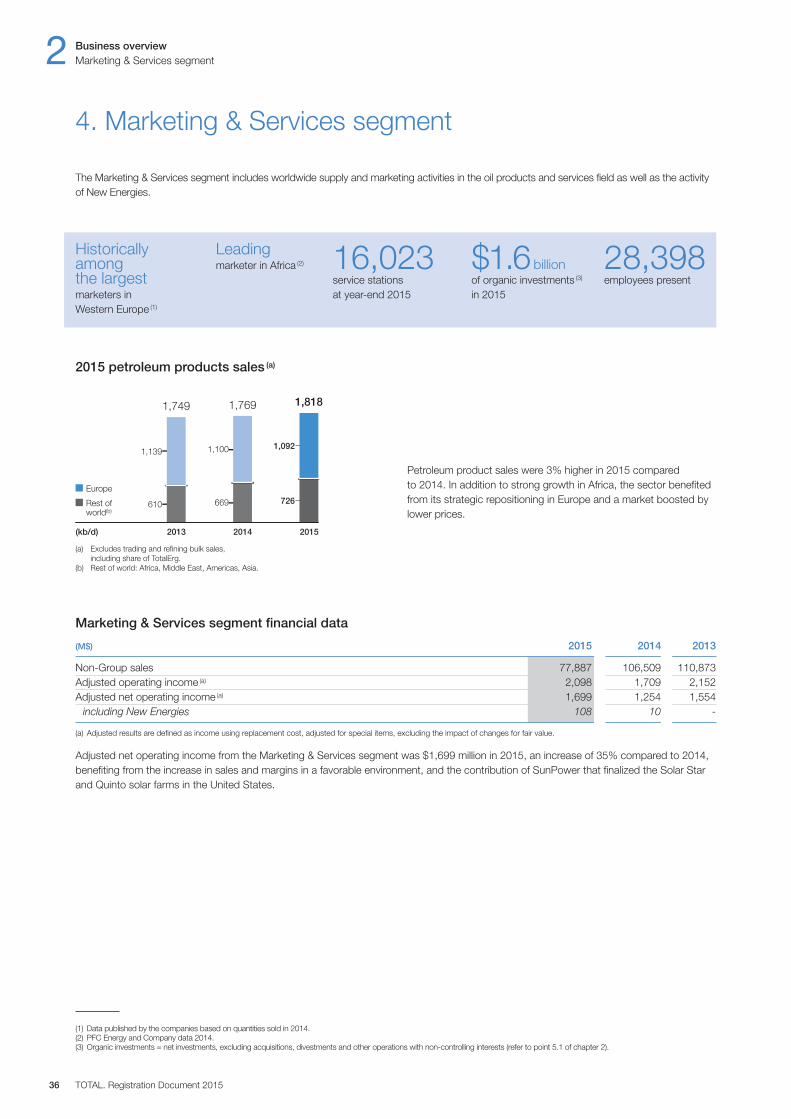

Marketing & Services petroleumproduct sales by geographicarea in 2015

Upstream

Refining & Chemicals and Marketing & Services

Asia and CIS

Middle East

Americas

Africa

Europe

2013(kboe/d) 2014 2015

374

678

255

492

548

364

657

247

391

487

392

670

239

536

462

2,2992,146

2,347

Rest ofworld

Europe

2013(kb/d) 2014 2015

2,078

1,443

2,184

1,821

2,047

1,722

3,5213,769

4,005

Rest ofworld

Europe

2013(kb/d) 2014 2015

1,736

306

1,699

548

1,736

451

2,0422,187 2,247

21,312 kt

Europe10,394 kt

Rest of world10,918 kt

(kt) 2015

Europe1,092 kb/d

Rest of world726 kb/d

1,818 kb/d

(kb/d) 2015

Gas

Liquids

2013(Mboe) 2014 2015

5,605

5,975

5,303

6,2206,113

5,413

11,58011,526 11,523

Registration Document 2015. TOTAL4

1 Key figuresSelected financial information

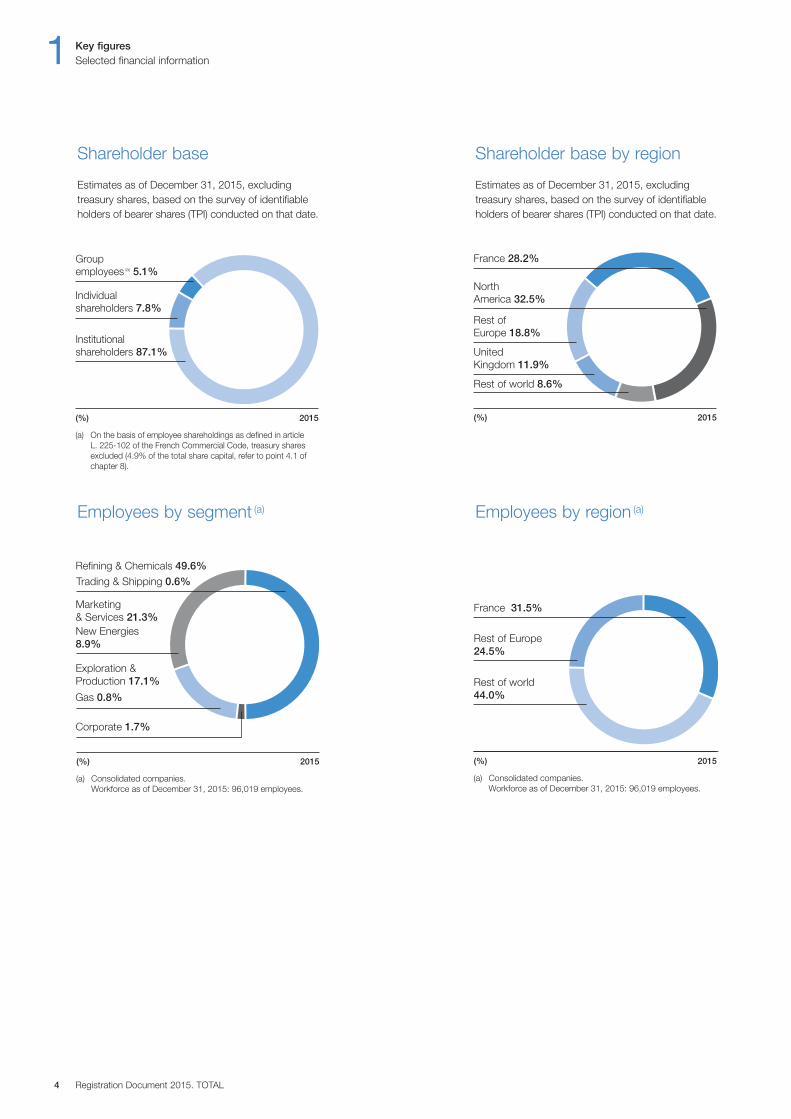

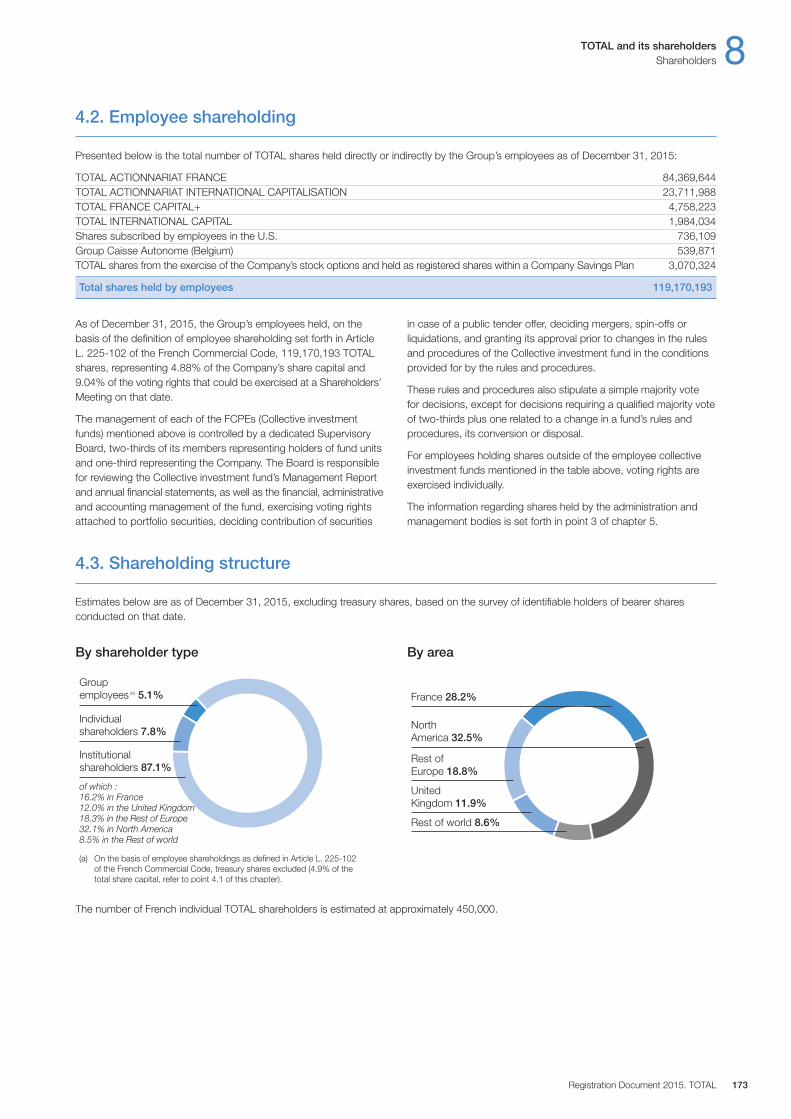

Shareholder base

Estimates as of December 31, 2015, excludingtreasury shares, based on the survey of identifiableholders of bearer shares (TPI) conducted on that date.

Shareholder base by region

Estimates as of December 31, 2015, excludingtreasury shares, based on the survey of identifiableholders of bearer shares (TPI) conducted on that date.

Employees by segment (a)

Refining & Chemicals 49.6%

Exploration &Production 17.1%

Gas 0.8%

Corporate 1.7%

Marketing& Services 21.3%

Trading & Shipping 0.6%

New Energies8.9%

(%) 2015

(a) Consolidated companies.Workforce as of December 31, 2015: 96,019 employees.

Employees by region (a)

Rest of Europe 24.5%

France 31.5%

Rest of world44.0%

(%) 2015

(a) Consolidated companies.Workforce as of December 31, 2015: 96,019 employees.

(%) 2015

Individual shareholders 7.8%

Group employees (a) 5.1%

Institutionalshareholders 87.1%

(a) On the basis of employee shareholdings as defined in article L. 225-102 of the French Commercial Code, treasury shares excluded (4.9% of the total share capital, refer to point 4.1 of chapter 8).

Rest of Europe 18.8%

United Kingdom 11.9%

France 28.2%

North America 32.5%

Rest of world 8.6%

(%) 2015

1. History and strategy of TOTAL 61.1. History and development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61.2. Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

2. Upstream segment 72.1. Exploration & Production . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .92.2. Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

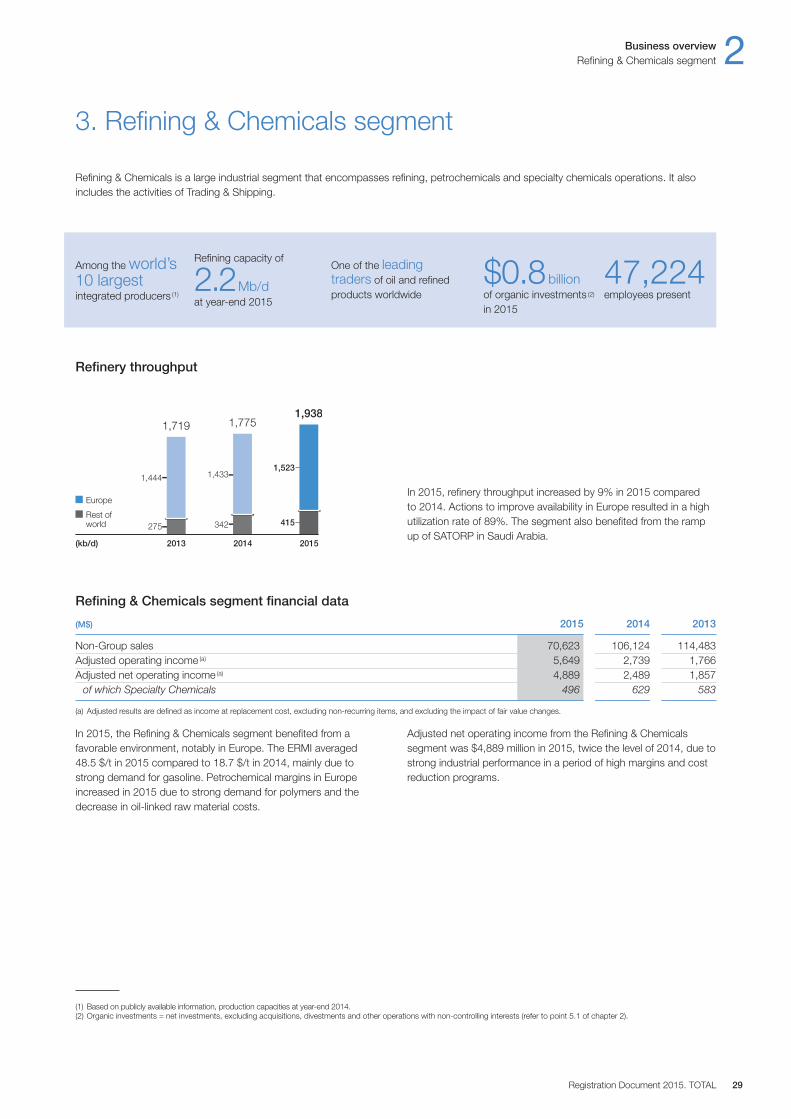

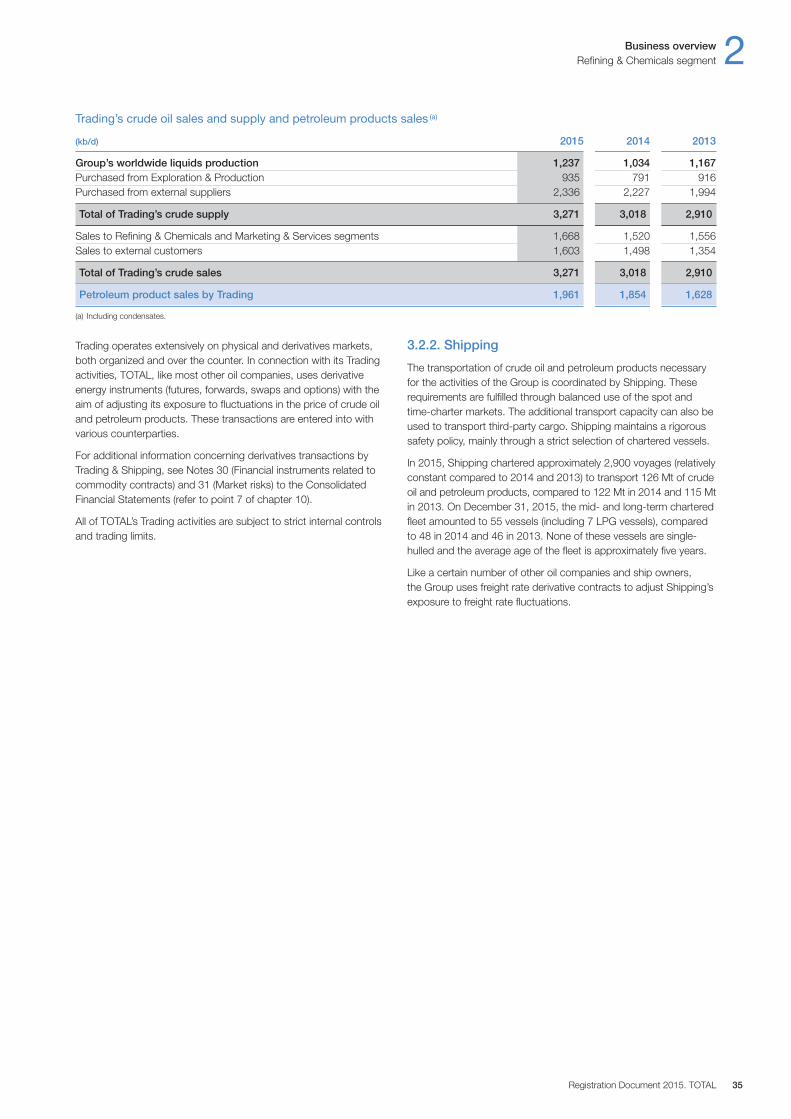

3. Refining & Chemicals segment 293.1. Refining & Chemicals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .303.2. Trading & Shipping . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34

4. Marketing & Services segment 364.1. Marketing & Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .374.2. New Energies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40

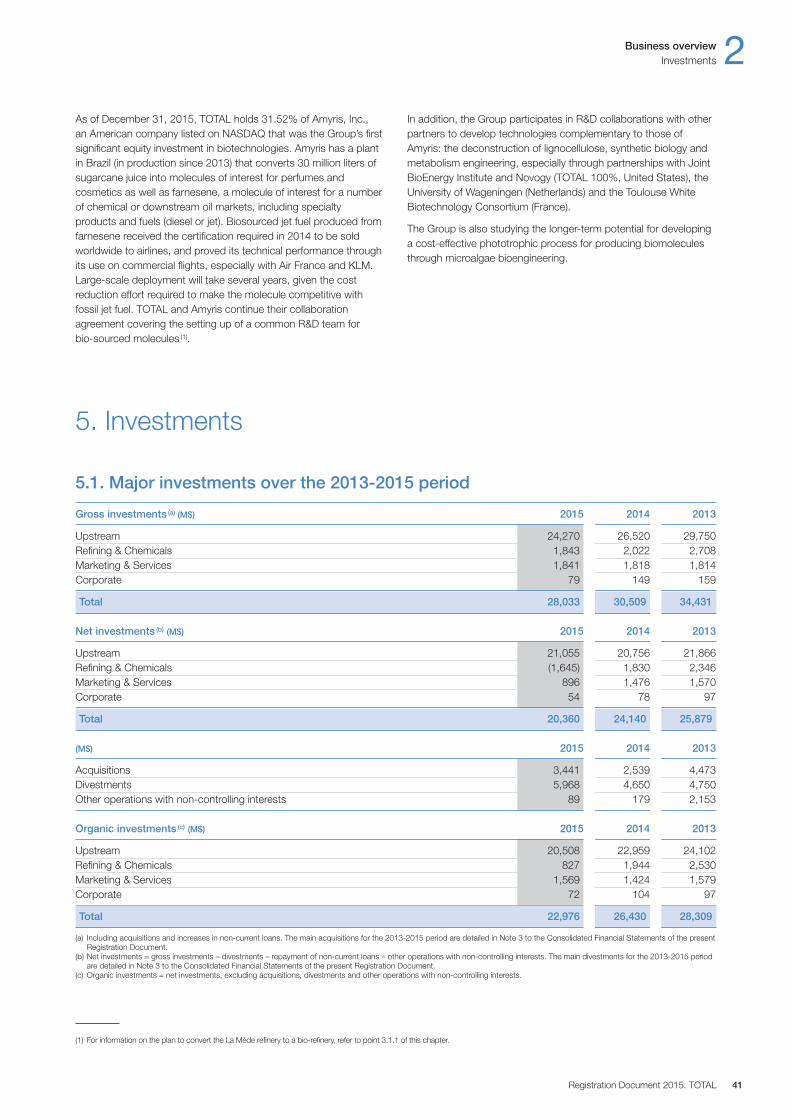

5. Investments 415.1. Major investments over the 2013-2015 period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .415.2. Major planned investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42

6. Research & Development 436.1. Upstream . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .436.2. Refining & Chemicals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .446.3. Marketing & Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .446.4. Environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .456.5. R&D organization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .46

7. Property, plant and equipment 46

8. Group organization 478.1. Position of the Company within the Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .478.2. Company subsidiaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .478.3. Group interests in publicly-traded companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47

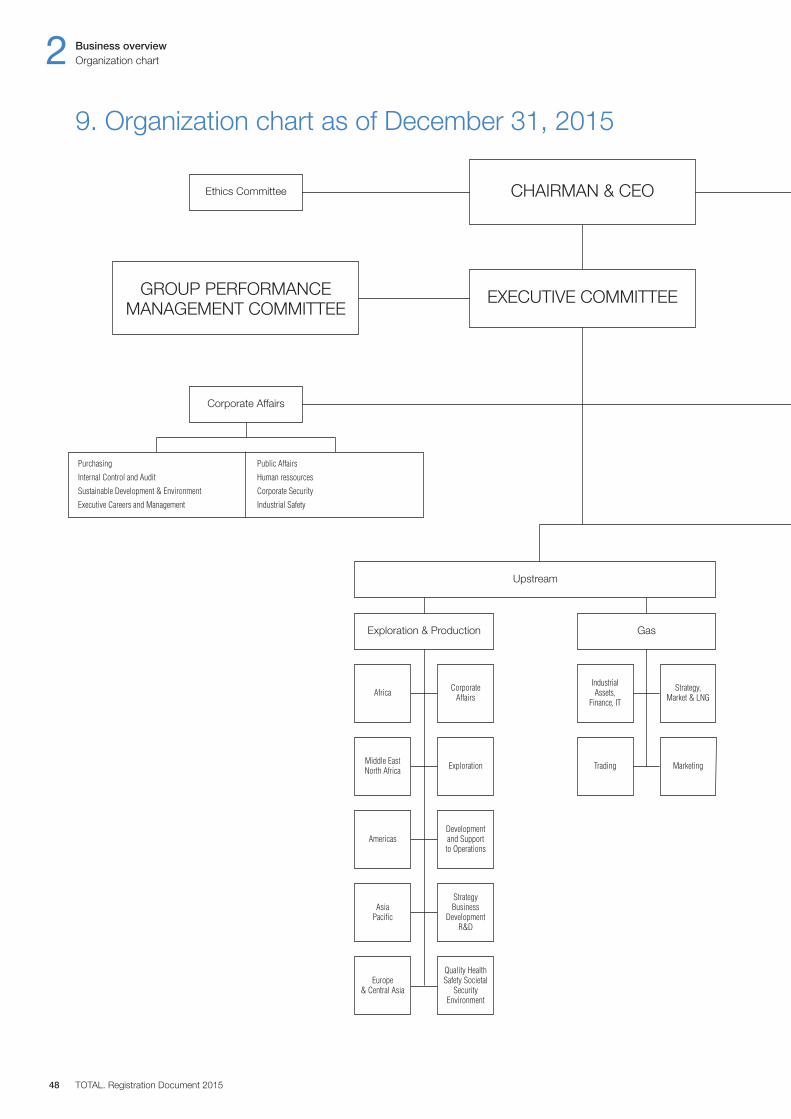

9. Organization chart as of December 31, 2015 48

Business overview

Registration Document 2015. TOTAL 5

Business overview2.Présentation des activités 2

The Group’s goal is to be a global energy company. TOTAL is aleading international oil and gas company, and is active in newenergy sources, such as solar energy and biomass. To achieve thisgoal, TOTAL leverages its integrated business model, which enablesit to capture synergies between the different business segments ofthe Group. TOTAL stands out due to its operational excellence, itstechnological expertise and its capacity to manage complexprojects. The Group’s strategy is based on four main priorities:

– driving profitable, sustainable growth in Exploration & Production’shydrocarbon activities;

– developing competitive, top-tier refining and petrochemicalcomplexes;

– responding to its customer needs by delivering innovativesolutions and services that go beyond the supply of petroleumproducts; and

– consolidating its leadership in solar energy and continuing todevelop biomass in order to offer the most appropriate energysolutions.

This strategy incorporates the challenges of climate change, usingthe International Energy Agency 2°C scenario (450 ppm) as a pointof reference. TOTAL’s challenge is to contribute to satisfying thedemand for energy of the world’s growing population, while providingconcrete solutions to limit the effects of climate change. To do so,the Group focuses its actions around several key points, includingthe development of gas and renewable energies.

At the core of TOTAL’s strategy is a strong belief that energy is vital,drives progress and must be made available to everyone. Energy isa precious resource that must be used wisely. The Group is helpingto produce the energy that people around the planet need to liveand thrive, while ensuring that its operations deliver economic,societal and environmental benefits. TOTAL is meeting thischallenge with and for its employees, its stakeholders and localcommunities.

Beyond safety, the values of respect, responsibility and exemplaryconduct underpin TOTAL’s Code of Conduct and accompany prioritybusiness principles in the realms of safety / security / health / theenvironment, integrity (preventing corruption, fraud and anti-competitivepractices) and human rights. It is through strict adherence to thesevalues and principles that TOTAL will be able to build strong andsustainable growth for the Group and its stakeholders and fulfill itsmotto: committed to better energy.

1.2. Strategy

TOTAL S.A., a French société anonyme (limited company)incorporated on March 28, 1924 is, together with its subsidiariesand affiliates, the world’s fourth largest publicly-traded integrated oiland gas company (1).

With operations in more than 130 countries, TOTAL is engaged inevery sector of the oil industry, including upstream (hydrocarbonexploration, development and production) and downstream (refining,petrochemicals, specialty chemicals, trading and shipping of crudeoil and petroleum products and marketing). TOTAL also operates inthe renewable energies and power generation sectors.

TOTAL began its Upstream operations in the Middle East in 1924.Since then, the Company has grown and expanded its operationsworldwide. In early 1999, the Company acquired control ofPetroFina S.A. and in early 2000 it acquired control of Elf Aquitaine.Since the repeal in 2002 of the decree of December 13, 1993 thatestablished a golden share of Elf Aquitaine held by the Frenchgovernment, there are no longer any agreements or regulatoryprovisions governing shareholding relationships between TOTALand the French government. Information on TOTAL S.A.’sshareholding structure is presented in point 4.1 of chapter 8.

1. History and strategy of TOTAL

1.1. History and development

2 Business overviewHistory and strategy of TOTAL

TOTAL. Registration Document 20156

(1) Based on market capitalization (in dollars) as of December 31, 2015.

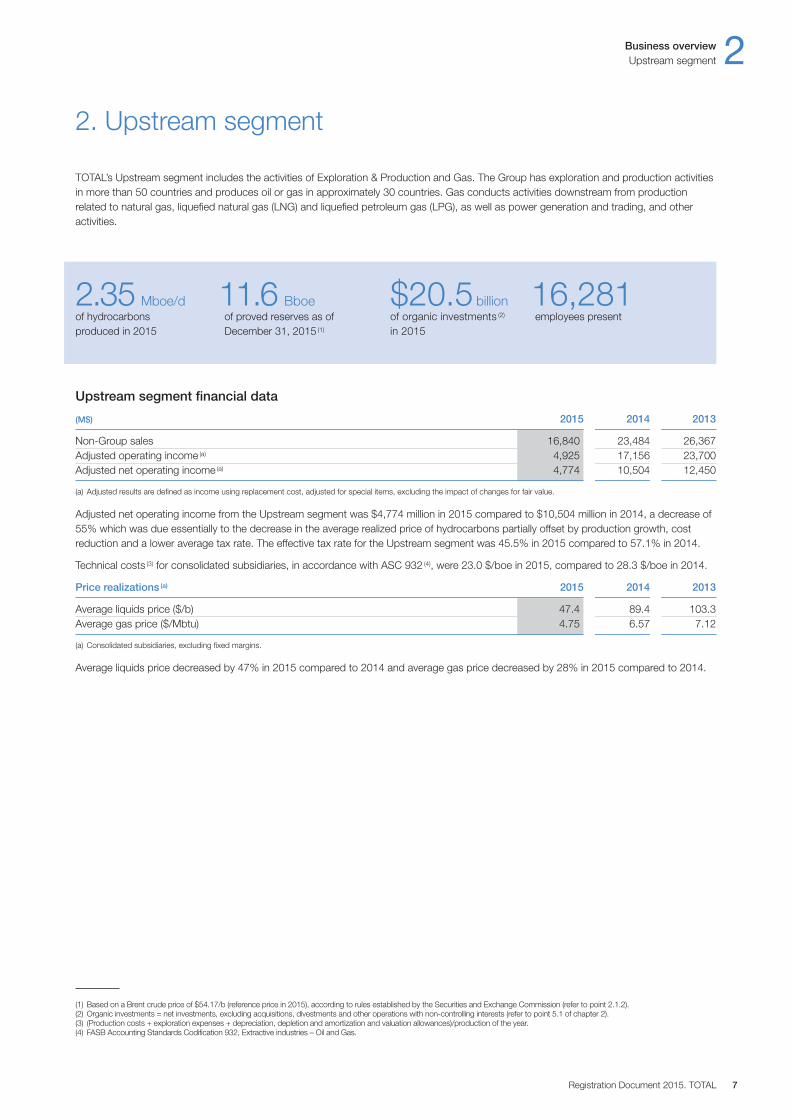

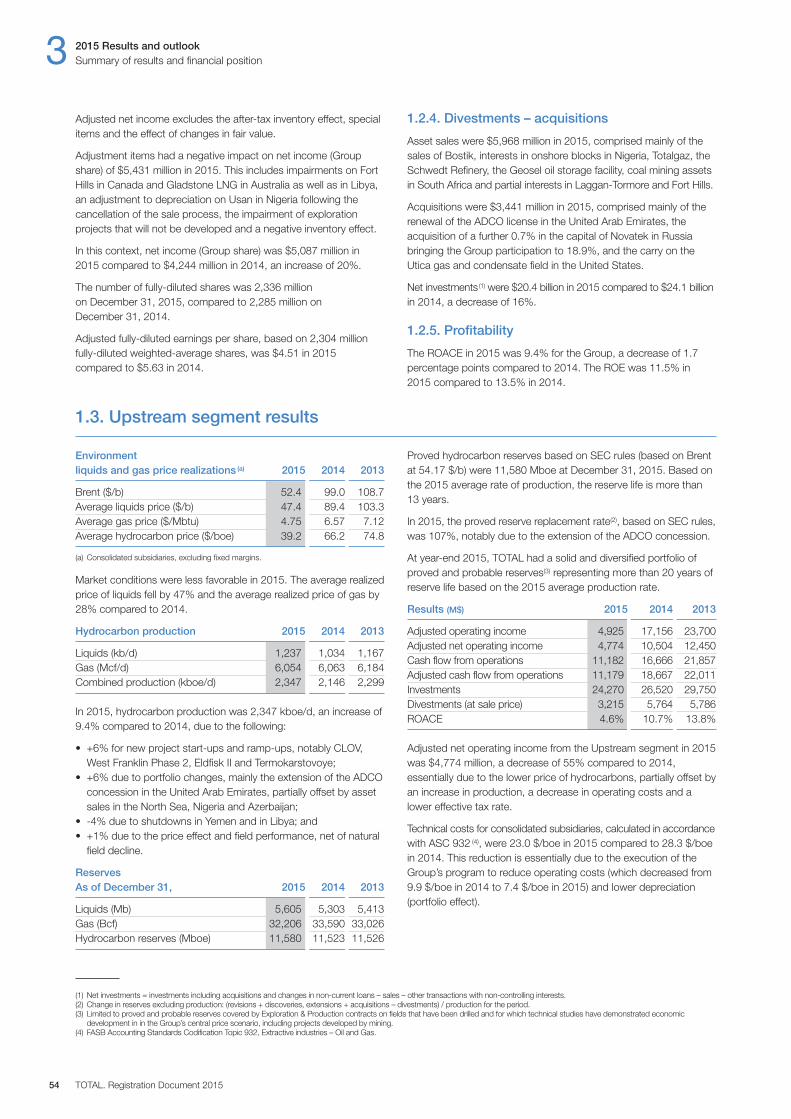

Upstream segment financial data

(M$) 2015 2014 2013

Non-Group sales 16,840 23,484 26,367Adjusted operating income (a) 4,925 17,156 23,700Adjusted net operating income (a) 4,774 10,504 12,450

(a) Adjusted results are defined as income using replacement cost, adjusted for special items, excluding the impact of changes for fair value.

Adjusted net operating income from the Upstream segment was $4,774 million in 2015 compared to $10,504 million in 2014, a decrease of55% which was due essentially to the decrease in the average realized price of hydrocarbons partially offset by production growth, costreduction and a lower average tax rate. The effective tax rate for the Upstream segment was 45.5% in 2015 compared to 57.1% in 2014.

Technical costs (3) for consolidated subsidiaries, in accordance with ASC 932 (4), were 23.0 $ / boe in 2015, compared to 28.3 $ / boe in 2014.

Price realizations (a) 2015 2014 2013

Average liquids price ($ / b) 47.4 89.4 103.3Average gas price ($ / Mbtu) 4.75 6.57 7.12

(a) Consolidated subsidiaries, excluding fixed margins.

Average liquids price decreased by 47% in 2015 compared to 2014 and average gas price decreased by 28% in 2015 compared to 2014.

2. Upstream segment

TOTAL’s Upstream segment includes the activities of Exploration & Production and Gas. The Group has exploration and production activitiesin more than 50 countries and produces oil or gas in approximately 30 countries. Gas conducts activities downstream from productionrelated to natural gas, liquefied natural gas (LNG) and liquefied petroleum gas (LPG), as well as power generation and trading, and otheractivities.

Business overview 2Upstream segment

Registration Document 2015. TOTAL 7

11.6 Bboeof proved reserves as ofDecember 31, 2015 (1)

2.35 Mboe / dof hydrocarbonsproduced in 2015

$20.5billionof organic investments (2)

in 2015

16,281employees present

(1) Based on a Brent crude price of $54.17/b (reference price in 2015), according to rules established by the Securities and Exchange Commission (refer to point 2.1.2).(2) Organic investments = net investments, excluding acquisitions, divestments and other operations with non-controlling interests (refer to point 5.1 of chapter 2).(3) (Production costs + exploration expenses + depreciation, depletion and amortization and valuation allowances)/production of the year.(4) FASB Accounting Standards Codification 932, Extractive industries – Oil and Gas.

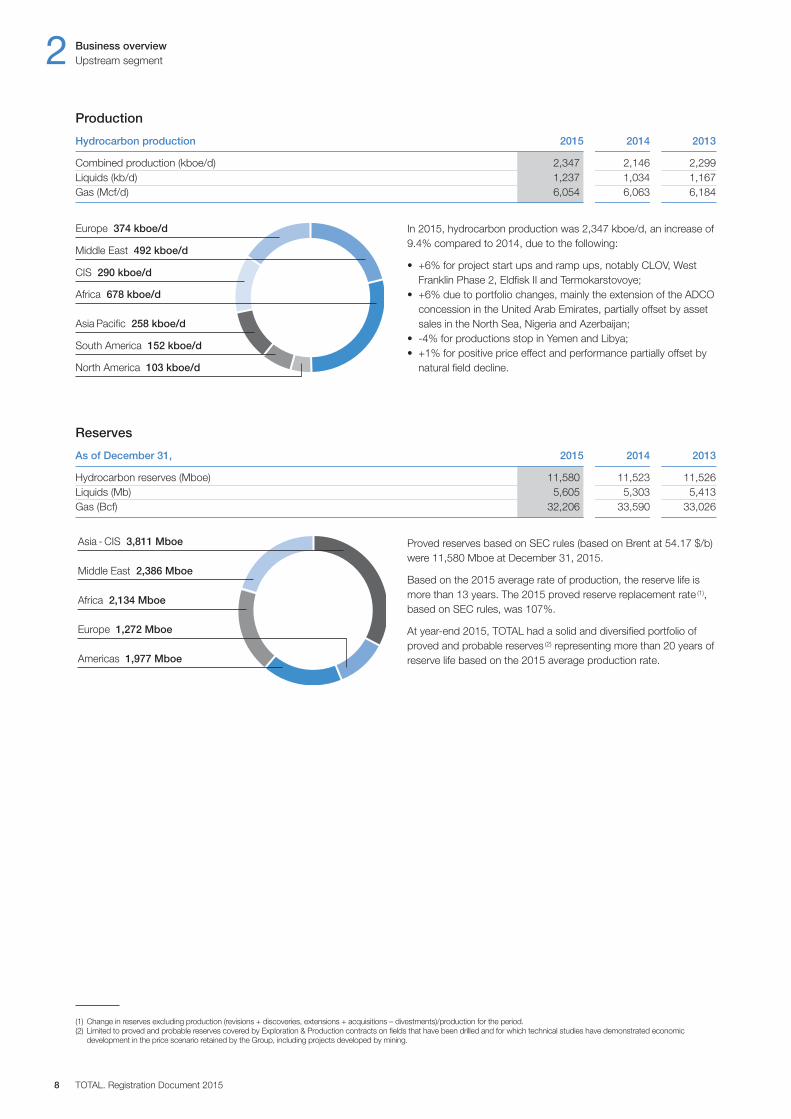

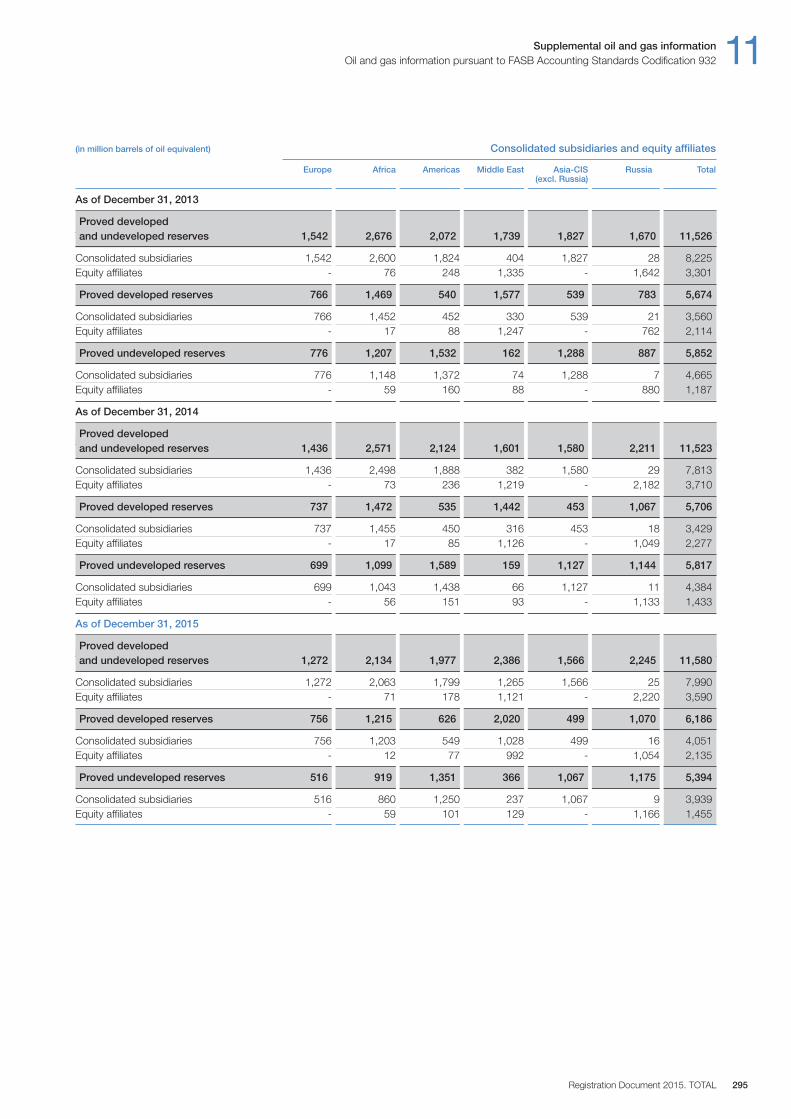

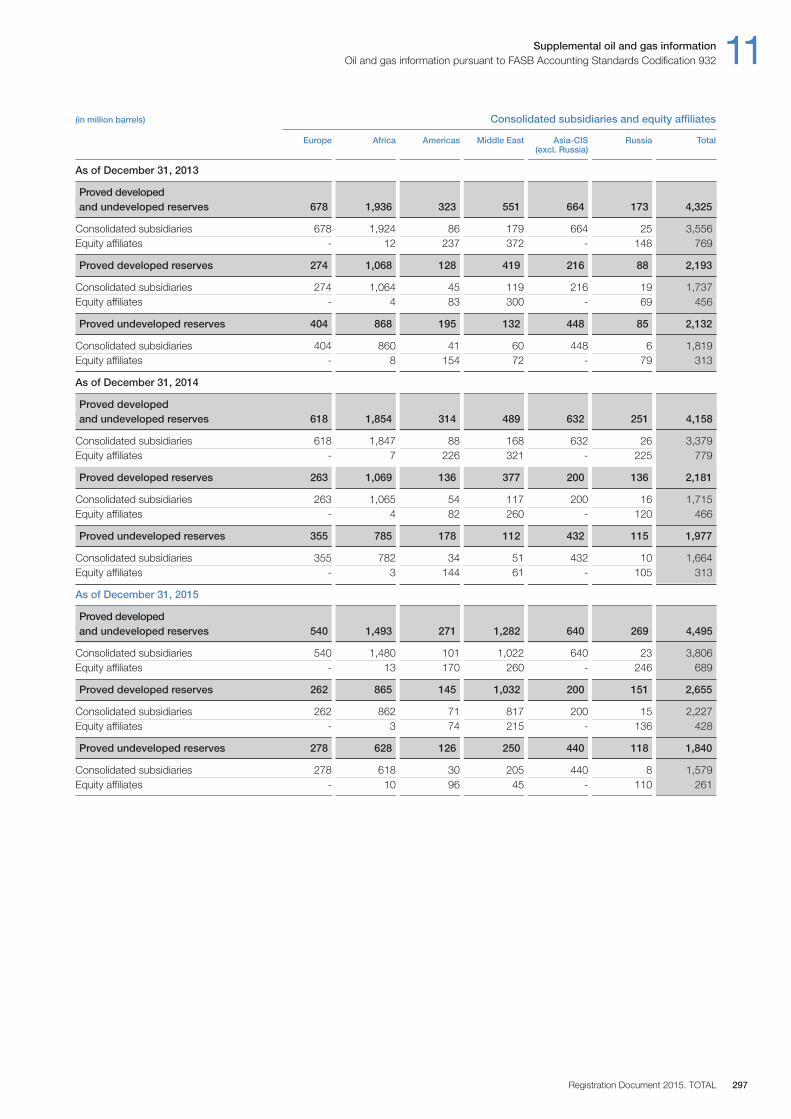

Proved reserves based on SEC rules (based on Brent at 54.17 $ / b)were 11,580 Mboe at December 31, 2015.

Based on the 2015 average rate of production, the reserve life ismore than 13 years. The 2015 proved reserve replacement rate (1),based on SEC rules, was 107%.

At year-end 2015, TOTAL had a solid and diversified portfolio ofproved and probable reserves (2) representing more than 20 years ofreserve life based on the 2015 average production rate.

Reserves

As of December 31, 2015 2014 2013

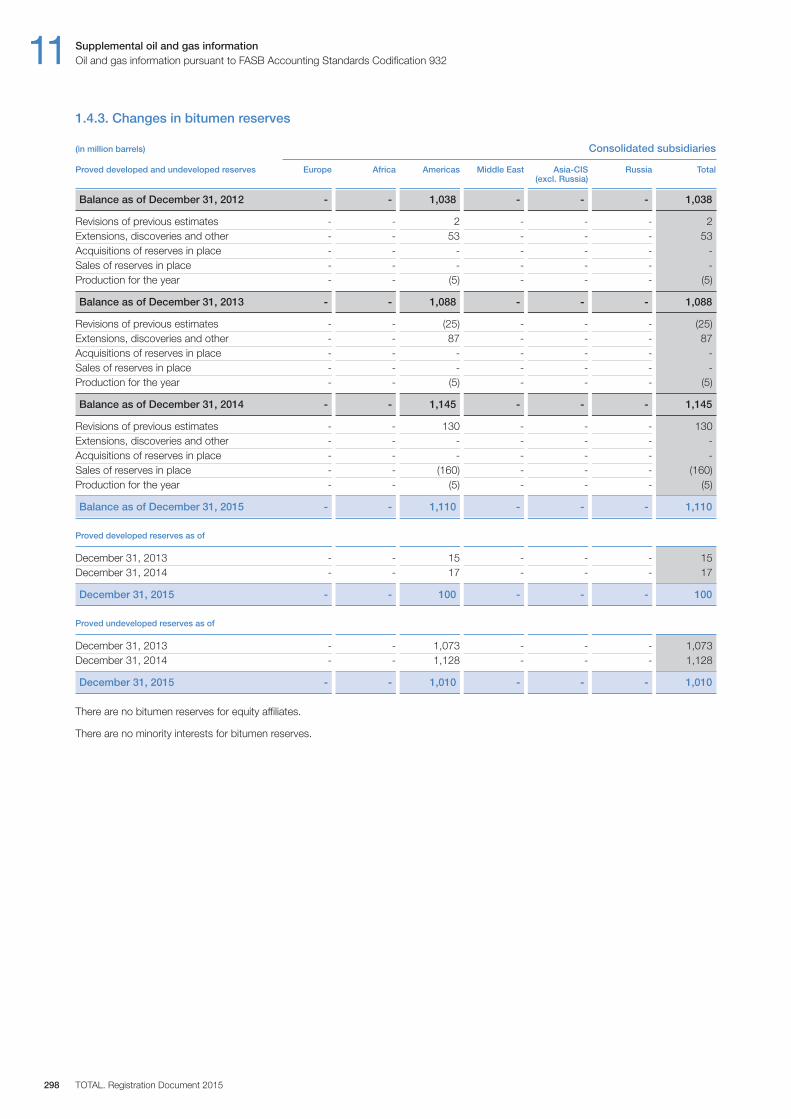

Hydrocarbon reserves (Mboe) 11,580 11,523 11,526Liquids (Mb) 5,605 5,303 5,413Gas (Bcf) 32,206 33,590 33,026

In 2015, hydrocarbon production was 2,347 kboe / d, an increase of9.4% compared to 2014, due to the following:

• +6% for project start ups and ramp ups, notably CLOV, WestFranklin Phase 2, Eldfisk II and Termokarstovoye;

• +6% due to portfolio changes, mainly the extension of the ADCOconcession in the United Arab Emirates, partially offset by assetsales in the North Sea, Nigeria and Azerbaijan;

• -4% for productions stop in Yemen and Libya;• +1% for positive price effect and performance partially offset by

natural field decline.

Production

Hydrocarbon production 2015 2014 2013

Combined production (kboe / d) 2,347 2,146 2,299Liquids (kb / d) 1,237 1,034 1,167Gas (Mcf / d) 6,054 6,063 6,184

2 Business overviewUpstream segment

TOTAL. Registration Document 20158

Europe 1,272 Mboe

Americas 1,977 Mboe

Asia - CIS 3,811 Mboe

Africa 2,134 Mboe

Middle East 2,386 Mboe

Africa 678 kboe/d

North America 103 kboe/d

Asia Pacific 258 kboe/d

South America 152 kboe/d

Europe 374 kboe/d

CIS 290 kboe/d

Middle East 492 kboe/d

(1) Change in reserves excluding production (revisions + discoveries, extensions + acquisitions – divestments)/production for the period.(2) Limited to proved and probable reserves covered by Exploration & Production contracts on fields that have been drilled and for which technical studies have demonstrated economic

development in the price scenario retained by the Group, including projects developed by mining.

Exploration & Production’s mission is to discover and develop oiland gas fields in order to meet growing energy demand. Safety is acore value for that mission.

In an environment marked by the significant drop in hydrocarbonprices, Exploration & Production’s strategy is based on:

– developing its operational excellence (reduction of operatingcosts and development costs, and operational efficiencyimprovement) by drawing on its technological expertise and on innovation;

– maintaining a leading position in the Group’s technical areas of excellence, such as deep offshore and LNG;

– renewing reserves through exploration and access to alreadydiscovered but undeveloped resources.

This strategy aims at developing an oil and gas production modelthat is resilient (i.e., which can withstand a long period of lowhydrocarbon prices), profitable and sustainable.

Additionally, Exploration & Production thrives to minimize theenvironmental impact of its activities.

In 2015, the Group’s production grew 9.4% compared to 2014.Exploration & Production is exiting a heavy investments phase,which peaked in 2013, and which is expected to lead to a productionincrease of 5% per year over the period of 2014-2019. The maingrowth levers include, on the one hand, the start-up of 20 majorprojects between 2015 and 2019 and, on the other hand, theimprovement of the operational efficiency of the facilities. In 2015,nine projects were started up. After 2020, TOTAL’s objective for organic production growth of 1 to 2% is in line with worldwidegrowth in demand for hydrocarbons.

2.1.1. Exploration and development

TOTAL evaluates exploration opportunities based on a variety ofgeological, technical, political, economic (including taxes and licenseterms) environmental and societal factors.

The exploration strategy deployed since 2015 aims to prioritizedrilling that creates value and resources. The Group expects morebalanced exploration investments:

– 50% for core and emerging basins, where the presence ofhydrocarbons is already proven;

– 25% for near-field exploration around operated assets; and– 25% for high-potential frontier basins.

In April 2015, a new organization for the Group’s explorationactivities, adapted to the new strategy, was implemented with anew senior exploration management team. The organizationalchanges are focused notably on strengthening regional basinmastery and technical excellence.

In 2015, exploration expenditure from all Exploration & Productionsubsidiaries stood at $1.9 billion (excluding exploration bonuses),which were made mainly in the United States, Iraq, Norway, Brazil,Papua New Guinea, Nigeria and the United Kingdom, compared to$2.6 billion in 2014 and $2.9 billion in 2013. The 2016 explorationbudget is $1.5 billion.

Organic investments(1) from all Exploration & Production subsidiariesstood at $20.5 billion in 2015, compared to $23 billion in 2014

and $24 billion in 2013, and were mainly made in Angola, Nigeria,the Republic of the Congo, Norway, Canada, Australia, the UnitedKingdom, Russia, Kazakhstan, Indonesia, the United States and Argentina.

2.1.2. Reserves

The definitions used for proved, proved developed and provedundeveloped oil and gas reserves are in accordance with the UnitedStates Securities & Exchange Commission (SEC) Rule 4-10 ofRegulation S-X as amended by the SEC Modernization of Oil andGas Reporting release issued on December 31, 2008. Provedreserves are estimated using geological and engineering data todetermine with reasonable certainty whether the crude oil or naturalgas in known reservoirs is recoverable under existing regulatory,economic and operating conditions.

TOTAL’s oil and gas reserves are consolidated annually, taking into account, among other factors, levels of production, fieldreassessments, additional reserves from discoveries andacquisitions, disposal of reserves and other economic factors.

Unless otherwise indicated, any reference to TOTAL’s proved reserves,proved developed reserves, proved undeveloped reserves andproduction reflects the Group’s entire share of such reserves orsuch production. TOTAL’s worldwide proved reserves include theproved reserves of its consolidated subsidiaries as well as itsproportionate share of the proved reserves of equity affiliates. Thereserves estimation process involves making subjective judgments.Consequently, estimates of reserves are not exact measurementsand are subject to revision under well-established control procedures.

The reserves booking process requires, among other things:

– internal peer review of technical evaluations to ensure that theSEC definitions and guidance are followed; and

– that management makes significant funding commitmentstowards the development of the reserves prior to booking.

For further information concerning the reserves and their evaluationprocess, see points 1 and 2 of chapter 11.

Proved reserves for 2015, 2014 and 2013

In accordance with the amended Rule 4-10 of Regulation S-X,proved reserves at December 31 are calculated using a 12-monthaverage price determined as the unweighted arithmetic average ofthe first-day-of-the-month price for each month of the relevant yearunless prices are defined by contractual arrangements, excludingescalations based upon future conditions. The reference prices for2015, 2014 and 2013 were, respectively, $54.17 / b, $101.27 / b and$108.02 / b for Brent crude.

As of December 31, 2015, TOTAL’s combined proved reserves ofoil and gas were 11,580 Mboe (53% of which were proved developedreserves). Liquids (crude oil, condensates, natural gas liquids andbitumen) represented approximately 48% of these reserves andnatural gas the remaining 52%. These reserves were located inEurope (mainly in Norway and the United Kingdom), Africa (mainly inAngola, Gabon, Nigeria and the Republic of the Congo), the Americas(mainly in Canada, Argentina, the United States and Venezuela), theMiddle East (mainly in Qatar, the United Arab Emirates and Yemen),and Asia-Pacific (mainly in Australia) and in Kazakhstan and Russia.

2.1. Exploration & Production

Business overview 2Upstream segment

Registration Document 2015. TOTAL 9

(1) For Exploration & Production, organic investments include exploration investments, net development investments and net financial investments.

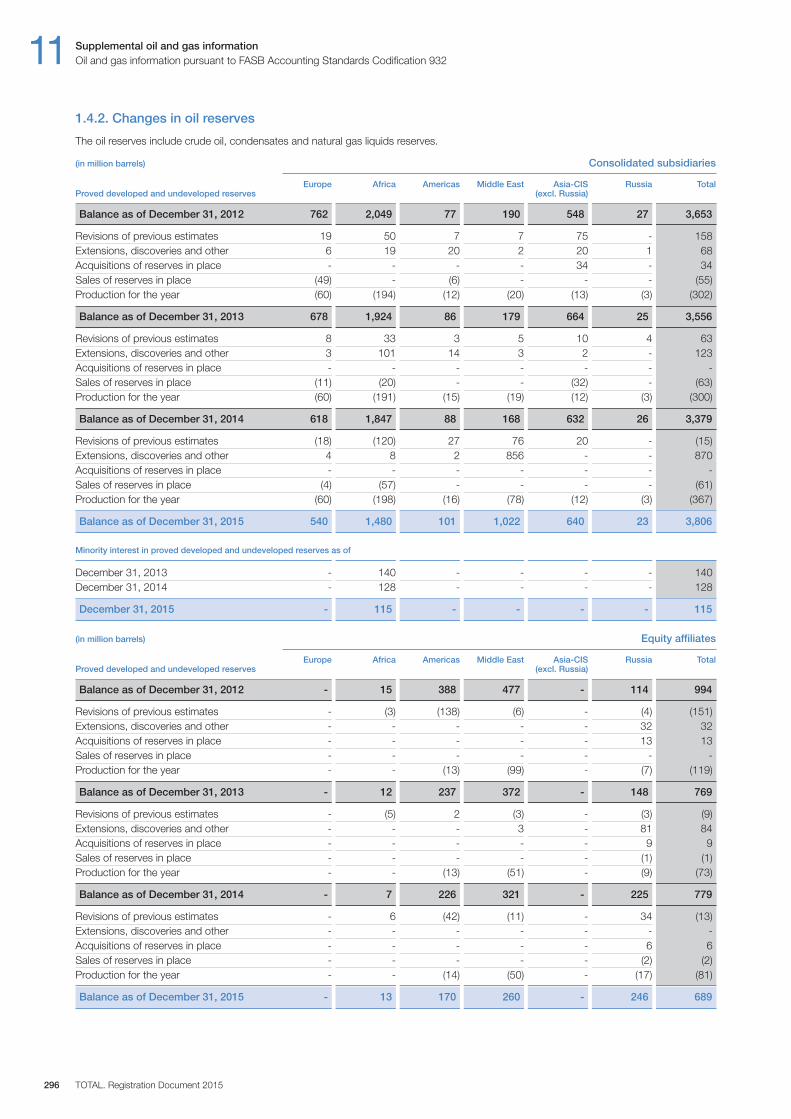

Discoveries of new fields and extensions of existing fields broughtan additional 2,762 Mboe to the Upstream segment’s proved reservesduring the 3-year period ended December 31, 2015 (beforededucting production and sales of reserves in place and adding anyacquisitions of reserves in place during this period). The net level ofreserve revisions during this 3-year period is +244 Mboe, whichwas due to the overall positive revisions in field behaviors, a scopechange in two projects in 2013, the impairment of two assets inLibya in 2015 due to the degradation of the security situation and to the positive impact of the decrease in hydrocarbon prices in 2015that led to a reserves increase on fields with production sharing orservice contracts and on Canadian bitumen fields (royalty effect),which was partially offset by the reserves decrease resulting from thesuspension or cancellation due to economic reasons of capitalexpenditures associated with, or from shorter producing life of,certain producing fields.

As of December 31, 2014, TOTAL’s combined proved reserves ofoil and gas were 11,523 Mboe (50% of which were proved developedreserves) compared to 11,526 Mboe (49% of which were proveddeveloped reserves) as of December 31, 2013. Liquids (crude oil,condensates, natural gas liquids and bitumen) at year-end 2014represented approximately 46% of these reserves and natural gasthe remaining 54% and, at year-end 2013, approximately 47% of these reserves and natural gas the remaining 53%.

Sensitivity to oil and gas prices

Changes in the price used as a reference for the proved reservesestimation result in non-proportionate inverse changes in provedreserves associated with production sharing and risked servicecontracts (which together represent approximately 20% of TOTAL’sreserves as of December 31, 2015). Under such contracts, TOTALis entitled to a portion of the production, the sale of which is meantto cover expenses incurred by the Group. As oil prices decrease,more barrels are necessary to cover the same amount of expenses.Moreover, the number of barrels recoverable under these contractsmay vary according to criteria such as cumulative production, therate of return on investment or the income-cumulative expensesratio. This increase is partly offset by a reduction of the duration overwhich fields can be produced economically. However, the decreasein reserves due to this reduction is generally less than the increasein reserves under production sharing or risked service contractsdue to such lower prices. As a result, lower prices usually lead to anincrease in TOTAL’s reserves. In Canada, a decrease in the referenceprice per barrel used as a reference for estimating proved reservesleads to a decrease in the volume of royalties and, therefore, anincrease of the proved reserves, and vice versa.

Lastly, for any type of contract, a significant decrease in thereference price of petroleum products that negatively impactsprojects profitability may lead to a reduction of proved reserves.

2.1.3. Production

The average daily production of liquids and natural gas was 2,347 kboe / d in 2015 compared to 2,146 kboe / d in 2014 and2,299 kboe / d in 2013. Liquids represented approximately 53% and natural gas approximately 47% of TOTAL’s overall production in 2015.

The tables on the following pages set forth TOTAL’s annual andaverage daily production of liquids and natural gas by geographicarea and for each of the last three fiscal years.

Consistent with industry practice, TOTAL often holds a percentageinterest in its fields rather than a 100% interest, with the balance beingheld by joint venture partners (which may include other internationaloil companies, state-owned oil companies or government entities).The Group’s entities may frequently act as operator (the partyresponsible for technical production) on acreage in which it holdsan interest. Refer to the table “Presentation of production activitiesby region” on the following pages for a presentation of the Group’sproducing assets.

As in 2014 and 2013, substantially all of the liquids production fromTOTAL’s Upstream segment in 2015 was marketed by the Trading &Shipping division of TOTAL’s Refining & Chemicals segment (refer totable “Trading’s crude oil sales and supply and petroleum productssales” in point 3.2.1 of this chapter).

2.1.4. Delivery commitments

The majority of TOTAL’s natural gas production is sold under long-term contracts. However, its North American production, and partof its production from the United Kingdom, the Netherlands andNorway, is sold on the spot market. The long-term contracts underwhich TOTAL sells its natural gas usually provide for a price relatedto, among other factors, average crude oil and other petroleumproduct prices, as well as, in some cases, a cost-of-living index.Though the price of natural gas tends to fluctuate in line with crudeoil prices, a slight delay may occur before changes in crude oilprices are reflected in long-term natural gas prices.

Some of TOTAL’s long-term contracts, notably in Bolivia, Indonesia,Nigeria, Norway, Thailand and Qatar, specify the delivery of quantitiesof natural gas that may or may not be fixed and determinable. Suchdelivery commitments vary substantially, both in duration and scope,from contract to contract throughout the world. For example, insome cases, contracts require delivery of natural gas on an as-needed basis, and, in other cases, contracts call for the delivery ofvaried amounts of natural gas over different periods of time.Nevertheless, TOTAL estimates the fixed and determinable quantityof gas to be delivered over the period 2016-2018 to be 3,591 Bcf.The Group expects to satisfy most of these obligations through theproduction of its proved reserves of natural gas, with, if needed,additional sourcing from spot market purchases (refer to points 1and 2 of chapter 11).

2.1.5. Contractual framework of activities

Licenses, permits and contracts governing the Group’s ownershipof oil and gas interests have terms that vary from country to countryand are generally granted by or entered into with a governmententity or a state-owned company and are sometimes entered intowith private owners. These agreements usually take the form ofconcessions or production sharing contracts.

In the framework of oil concession agreements, the oil company ownsthe assets and the facilities and is entitled to the entire production.In exchange, the operating risks, costs and investments are the oilcompany’s responsibility and it agrees to remit to the relevant hostcountry, usually the owner of the subsoil resources, a production-based royalty, income tax, and possibly other taxes that may applyunder local tax legislation.

The production sharing contract (“PSC”) involves a more complexlegal framework than the concession agreement: it defines the termsand conditions of production sharing and sets the rules governing

2 Business overviewUpstream segment

TOTAL. Registration Document 201510

the cooperation between the company or consortium in possessionof the license and the host country, which is generally representedby a state-owned company. The latter can thus be involved inoperating decisions, cost accounting and production allocation.The consortium agrees to undertake and finance all exploration,development and production activities at its own risk. In exchange,it is entitled to a portion of the production, known as “cost oil”, thesale of which is intended to cover its incurred expenses (capital andoperating costs). The balance of production, known as “profit oil”, is thenshared in varying proportions, between the company or consortium,on the one hand, and the host country or state-owned company,on the other hand.

Today, concession agreements and PSCs can coexist, sometimesin the same country or even on the same block. Even though thereare other contractual models, TOTAL’s license portfolio iscomprised mainly of concession agreements.

On most licenses, the partners and authorities of the host country,often assisted by international accounting firms, perform jointventure and PSC cost audits and ensure the observance ofcontractual obligations.

In some countries, TOTAL has also signed contracts called “riskedservice contracts”, which are similar to PSCs. However, the profit oilis replaced by a defined cash monetary remuneration, agreed bycontract, which depends notably on field performance parameterssuch as the amount of barrels produced.

Oil and gas exploration and production activities are subject toauthorization granted by public authorities (licenses), which aregranted for specific and limited periods of time and include anobligation to relinquish a large portion, or the entire portion in case of failure, of the area covered by the license at the end of the exploration period.

TOTAL pays taxes on income generated from its oil and gasproduction and sales activities under its concessions, PSCs andrisked service contracts, as provided for by local regulations. Inaddition, depending on the country, TOTAL’s production and salesactivities may be subject to a number of other taxes, fees andwithholdings, including special petroleum taxes and fees. The taxesimposed on oil and gas production and sales activities are generallysubstantially higher than those imposed on other industrial orcommercial businesses.

Business overview 2Upstream segment

Registration Document 2015. TOTAL 11

2 Business overviewUpstream segment

TOTAL. Registration Document 201512

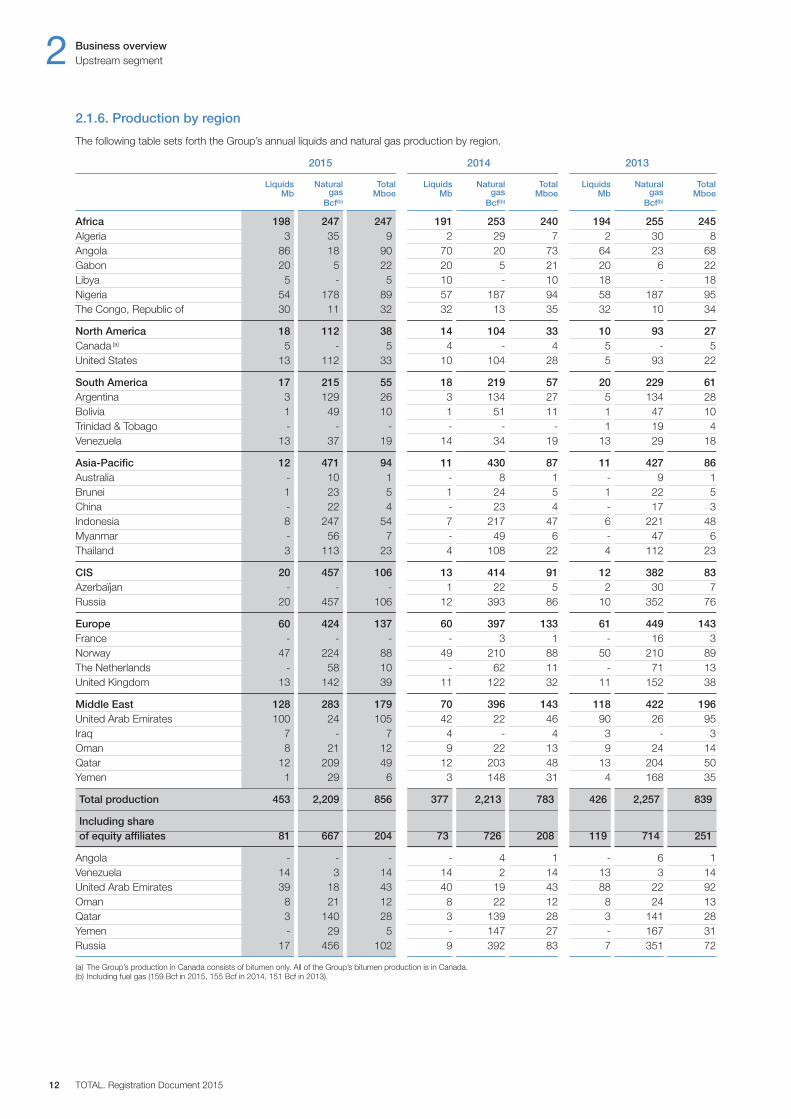

2.1.6. Production by region

The following table sets forth the Group’s annual liquids and natural gas production by region.

2015 2014 2013

Liquids Natural Total Liquids Natural Total Liquids Natural Total Mb gas Mboe Mb gas Mboe Mb gas Mboe Bcf(b) Bcf(b) Bcf(b)

Africa 198 247 247 191 253 240 194 255 245Algeria 3 35 9 2 29 7 2 30 8Angola 86 18 90 70 20 73 64 23 68Gabon 20 5 22 20 5 21 20 6 22Libya 5 - 5 10 - 10 18 - 18Nigeria 54 178 89 57 187 94 58 187 95The Congo, Republic of 30 11 32 32 13 35 32 10 34

North America 18 112 38 14 104 33 10 93 27Canada (a) 5 - 5 4 - 4 5 - 5United States 13 112 33 10 104 28 5 93 22

South America 17 215 55 18 219 57 20 229 61Argentina 3 129 26 3 134 27 5 134 28Bolivia 1 49 10 1 51 11 1 47 10Trinidad & Tobago - - - - - - 1 19 4Venezuela 13 37 19 14 34 19 13 29 18

Asia-Pacific 12 471 94 11 430 87 11 427 86Australia - 10 1 - 8 1 - 9 1Brunei 1 23 5 1 24 5 1 22 5China - 22 4 - 23 4 - 17 3Indonesia 8 247 54 7 217 47 6 221 48Myanmar - 56 7 - 49 6 - 47 6Thailand 3 113 23 4 108 22 4 112 23

CIS 20 457 106 13 414 91 12 382 83Azerbaïjan - - - 1 22 5 2 30 7Russia 20 457 106 12 393 86 10 352 76

Europe 60 424 137 60 397 133 61 449 143France - - - - 3 1 - 16 3Norway 47 224 88 49 210 88 50 210 89The Netherlands - 58 10 - 62 11 - 71 13United Kingdom 13 142 39 11 122 32 11 152 38

Middle East 128 283 179 70 396 143 118 422 196United Arab Emirates 100 24 105 42 22 46 90 26 95Iraq 7 - 7 4 - 4 3 - 3Oman 8 21 12 9 22 13 9 24 14Qatar 12 209 49 12 203 48 13 204 50Yemen 1 29 6 3 148 31 4 168 35

Total production 453 2,209 856 377 2,213 783 426 2,257 839

Including shareof equity affiliates 81 667 204 73 726 208 119 714 251

Angola - - - - 4 1 - 6 1Venezuela 14 3 14 14 2 14 13 3 14United Arab Emirates 39 18 43 40 19 43 88 22 92Oman 8 21 12 8 22 12 8 24 13Qatar 3 140 28 3 139 28 3 141 28Yemen - 29 5 - 147 27 - 167 31Russia 17 456 102 9 392 83 7 351 72

(a) The Group’s production in Canada consists of bitumen only. All of the Group’s bitumen production is in Canada.(b) Including fuel gas (159 Bcf in 2015, 155 Bcf in 2014, 151 Bcf in 2013).

Business overview 2Upstream segment

Registration Document 2015. TOTAL 13

The following table sets forth the Group’s average daily liquids and natural gas production by region.

2015 2014 2013

Liquids Natural Total Liquids Natural Total Liquids Natural Total kb/d gas kboe/d kb/d gas kboe/d kb/d gas kboe/d Mcf/d(b) Mcf/d(b) Mcf/d(b)

Africa 542 677 678 522 693 657 531 699 670Algeria 7 96 25 5 79 20 5 82 21Angola 238 49 248 191 54 200 175 62 186Gabon 55 15 59 55 14 58 55 16 59Libya 14 - 14 27 - 27 50 - 50Nigeria 147 487 245 156 511 257 158 511 261The Congo, Republic of 81 30 87 88 35 95 88 28 93

North America 48 308 103 39 285 90 28 256 73Canada (a) 14 - 14 12 - 12 13 - 13United States 34 308 89 27 285 78 15 256 60

South America 47 588 152 50 599 157 54 627 166Argentina 8 354 72 9 367 75 13 366 78Bolivia 3 133 28 4 139 30 4 129 28Trinidad & Tobago - - - - - - 2 52 12Venezuela 36 101 52 37 93 52 35 80 48

Asia-Pacific 34 1,290 258 30 1,178 238 30 1,170 235Australia - 28 4 - 23 4 - 25 4Brunei 3 62 15 2 66 15 2 59 13China - 59 11 - 63 12 - 46 8Indonesia 22 676 147 18 594 130 17 605 131Myanmar - 153 19 - 135 17 - 129 16Thailand 9 312 62 10 297 60 11 306 63

CIS 54 1,252 290 36 1,135 249 32 1,046 227Azerbaijan - - - 3 59 14 5 82 20Russia 54 1,252 290 33 1,076 235 27 964 207

Europe 161 1,161 374 165 1,089 364 168 1,231 392France - - - - 9 2 1 45 9Norway 125 614 239 135 576 242 136 575 243The Netherlands 1 158 28 1 171 31 1 195 35United Kingdom 35 389 107 29 333 89 30 416 105

Middle East 351 778 492 192 1,084 391 324 1,155 536United Arab Emirates 274 66 287 115 61 127 247 71 260Iraq 18 1 18 12 1 12 7 1 7Oman 25 58 36 24 61 36 24 66 37Qatar 32 573 134 32 555 132 36 558 137Yemen 2 80 17 9 406 84 10 459 95

Total production 1,237 6,054 2,347 1,034 6,063 2,146 1,167 6,184 2,299

Including share of equity affiliates 219 1,828 559 200 1,988 571 325 1,955 687

Angola - - - - 10 2 - 16 3Venezuela 36 7 37 37 6 38 35 7 37United Arab Emirates 107 50 116 109 51 118 240 61 253Oman 24 58 34 23 61 34 23 66 35Qatar 7 383 77 7 381 77 8 385 78Yemen - 80 15 - 404 75 - 458 84Russia 45 1,250 280 24 1,075 227 19 962 197

(a) The Group’s production in Canada consists of bitumen only. All of the Group’s bitumen production is in Canada.(b) Including fuel gas (435 Mcf / d in 2015, 426 Mcf / d in 2014, 415 Mcf / d in 2013).

2 Business overviewUpstream segment

TOTAL. Registration Document 201514

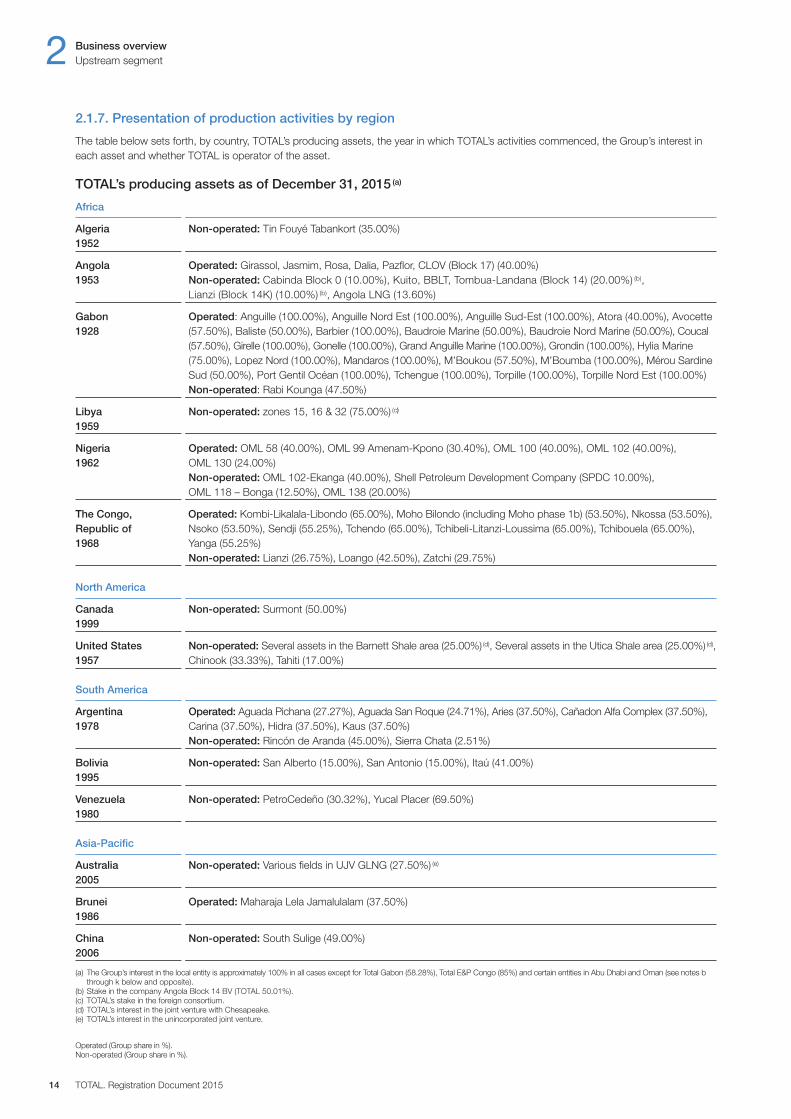

2.1.7. Presentation of production activities by region

The table below sets forth, by country, TOTAL’s producing assets, the year in which TOTAL’s activities commenced, the Group’s interest ineach asset and whether TOTAL is operator of the asset.

TOTAL’s producing assets as of December 31, 2015 (a)

Africa

Algeria Non-operated: Tin Fouyé Tabankort (35.00%)1952

Angola Operated: Girassol, Jasmim, Rosa, Dalia, Pazflor, CLOV (Block 17) (40.00%)1953 Non-operated: Cabinda Block 0 (10.00%), Kuito, BBLT, Tombua-Landana (Block 14) (20.00%) (b),

Lianzi (Block 14K) (10.00%) (b), Angola LNG (13.60%)

Gabon Operated: Anguille (100.00%), Anguille Nord Est (100.00%), Anguille Sud-Est (100.00%), Atora (40.00%), Avocette1928 (57.50%), Baliste (50.00%), Barbier (100.00%), Baudroie Marine (50.00%), Baudroie Nord Marine (50.00%), Coucal

(57.50%), Girelle (100.00%), Gonelle (100.00%), Grand Anguille Marine (100.00%), Grondin (100.00%), Hylia Marine(75.00%), Lopez Nord (100.00%), Mandaros (100.00%), M’Boukou (57.50%), M’Boumba (100.00%), Mérou SardineSud (50.00%), Port Gentil Océan (100.00%), Tchengue (100.00%), Torpille (100.00%), Torpille Nord Est (100.00%)Non-operated: Rabi Kounga (47.50%)

Libya Non-operated: zones 15, 16 & 32 (75.00%) (c)

1959

Nigeria Operated: OML 58 (40.00%), OML 99 Amenam-Kpono (30.40%), OML 100 (40.00%), OML 102 (40.00%), 1962 OML 130 (24.00%)

Non-operated: OML 102-Ekanga (40.00%), Shell Petroleum Development Company (SPDC 10.00%), OML 118 – Bonga (12.50%), OML 138 (20.00%)

The Congo, Operated: Kombi-Likalala-Libondo (65.00%), Moho Bilondo (including Moho phase 1b) (53.50%), Nkossa (53.50%), Republic of Nsoko (53.50%), Sendji (55.25%), Tchendo (65.00%), Tchibeli-Litanzi-Loussima (65.00%), Tchibouela (65.00%), 1968 Yanga (55.25%)

Non-operated: Lianzi (26.75%), Loango (42.50%), Zatchi (29.75%)

North America

Canada Non-operated: Surmont (50.00%)1999

United States Non-operated: Several assets in the Barnett Shale area (25.00%) (d), Several assets in the Utica Shale area (25.00%) (d),1957 Chinook (33.33%), Tahiti (17.00%)

South America

Argentina Operated: Aguada Pichana (27.27%), Aguada San Roque (24.71%), Aries (37.50%), Cañadon Alfa Complex (37.50%),1978 Carina (37.50%), Hidra (37.50%), Kaus (37.50%)

Non-operated: Rincón de Aranda (45.00%), Sierra Chata (2.51%)

Bolivia Non-operated: San Alberto (15.00%), San Antonio (15.00%), Itaú (41.00%)1995

Venezuela Non-operated: PetroCedeño (30.32%), Yucal Placer (69.50%)1980

Asia-Pacific

Australia Non-operated: Various fields in UJV GLNG (27.50%) (e)

2005

Brunei Operated: Maharaja Lela Jamalulalam (37.50%)1986

China Non-operated: South Sulige (49.00%)2006

(a) The Group’s interest in the local entity is approximately 100% in all cases except for Total Gabon (58.28%), Total E&P Congo (85%) and certain entities in Abu Dhabi and Oman (see notes bthrough k below and opposite).

(b) Stake in the company Angola Block 14 BV (TOTAL 50.01%).(c) TOTAL’s stake in the foreign consortium.(d) TOTAL’s interest in the joint venture with Chesapeake.(e) TOTAL’s interest in the unincorporated joint venture.

Operated (Group share in %).Non-operated (Group share in %).

Business overview 2Upstream segment

Registration Document 2015. TOTAL 15

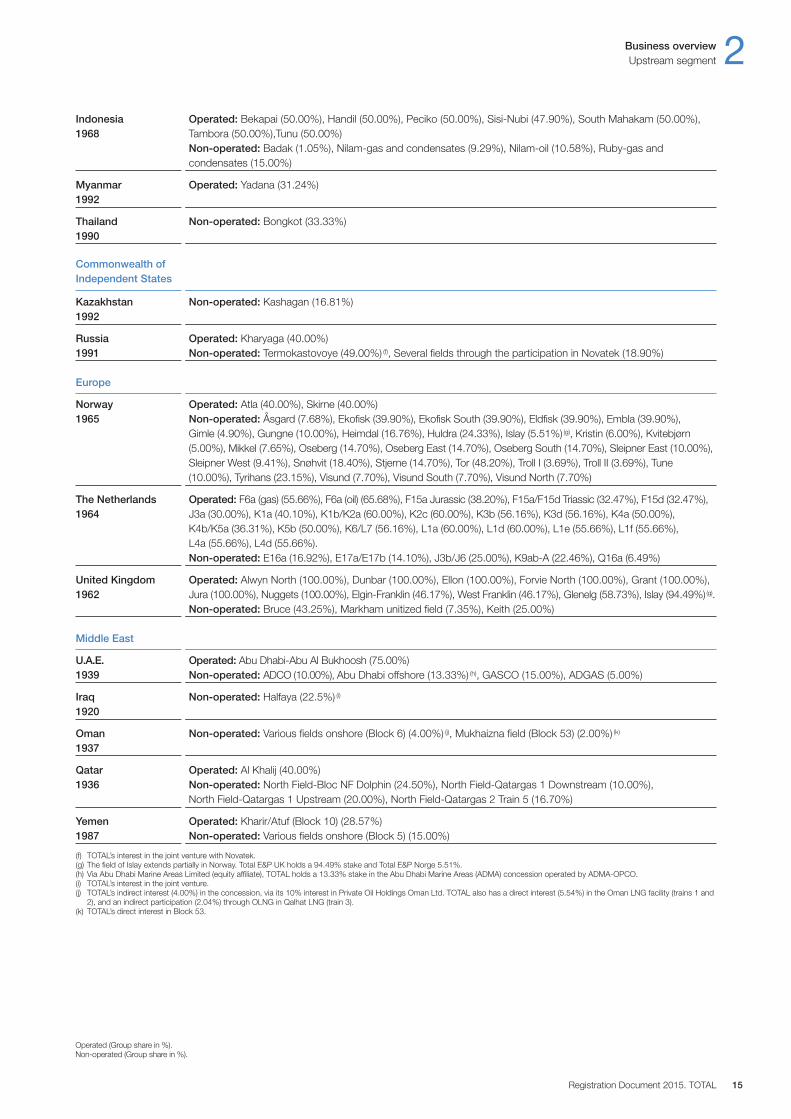

Indonesia Operated: Bekapai (50.00%), Handil (50.00%), Peciko (50.00%), Sisi-Nubi (47.90%), South Mahakam (50.00%), 1968 Tambora (50.00%),Tunu (50.00%)

Non-operated: Badak (1.05%), Nilam-gas and condensates (9.29%), Nilam-oil (10.58%), Ruby-gas and condensates (15.00%)

Myanmar Operated: Yadana (31.24%)1992

Thailand Non-operated: Bongkot (33.33%)1990

Commonwealth of Independent States

Kazakhstan Non-operated: Kashagan (16.81%)1992

Russia Operated: Kharyaga (40.00%)1991 Non-operated: Termokastovoye (49.00%) (f), Several fields through the participation in Novatek (18.90%)

Europe

Norway Operated: Atla (40.00%), Skirne (40.00%)1965 Non-operated: Åsgard (7.68%), Ekofisk (39.90%), Ekofisk South (39.90%), Eldfisk (39.90%), Embla (39.90%),

Gimle (4.90%), Gungne (10.00%), Heimdal (16.76%), Huldra (24.33%), Islay (5.51%) (g), Kristin (6.00%), Kvitebjørn(5.00%), Mikkel (7.65%), Oseberg (14.70%), Oseberg East (14.70%), Oseberg South (14.70%), Sleipner East (10.00%),Sleipner West (9.41%), Snøhvit (18.40%), Stjerne (14.70%), Tor (48.20%), Troll I (3.69%), Troll II (3.69%), Tune(10.00%), Tyrihans (23.15%), Visund (7.70%), Visund South (7.70%), Visund North (7.70%)

The Netherlands Operated: F6a (gas) (55.66%), F6a (oil) (65.68%), F15a Jurassic (38.20%), F15a / F15d Triassic (32.47%), F15d (32.47%),1964 J3a (30.00%), K1a (40.10%), K1b / K2a (60.00%), K2c (60.00%), K3b (56.16%), K3d (56.16%), K4a (50.00%),

K4b / K5a (36.31%), K5b (50.00%), K6 / L7 (56.16%), L1a (60.00%), L1d (60.00%), L1e (55.66%), L1f (55.66%),L4a (55.66%), L4d (55.66%).Non-operated: E16a (16.92%), E17a / E17b (14.10%), J3b / J6 (25.00%), K9ab-A (22.46%), Q16a (6.49%)

United Kingdom Operated: Alwyn North (100.00%), Dunbar (100.00%), Ellon (100.00%), Forvie North (100.00%), Grant (100.00%),1962 Jura (100.00%), Nuggets (100.00%), Elgin-Franklin (46.17%), West Franklin (46.17%), Glenelg (58.73%), Islay (94.49%)(g).

Non-operated: Bruce (43.25%), Markham unitized field (7.35%), Keith (25.00%)

Middle East

U.A.E. Operated: Abu Dhabi-Abu Al Bukhoosh (75.00%) 1939 Non-operated: ADCO (10.00%), Abu Dhabi offshore (13.33%) (h), GASCO (15.00%), ADGAS (5.00%)

Iraq Non-operated: Halfaya (22.5%) (i)

1920

Oman Non-operated: Various fields onshore (Block 6) (4.00%) (j), Mukhaizna field (Block 53) (2.00%) (k)

1937

Qatar Operated: Al Khalij (40.00%)1936 Non-operated: North Field-Bloc NF Dolphin (24.50%), North Field-Qatargas 1 Downstream (10.00%),

North Field-Qatargas 1 Upstream (20.00%), North Field-Qatargas 2 Train 5 (16.70%)

Yemen Operated: Kharir / Atuf (Block 10) (28.57%)1987 Non-operated: Various fields onshore (Block 5) (15.00%)

(f) TOTAL’s interest in the joint venture with Novatek.(g) The field of Islay extends partially in Norway. Total E&P UK holds a 94.49% stake and Total E&P Norge 5.51%.(h) Via Abu Dhabi Marine Areas Limited (equity affiliate), TOTAL holds a 13.33% stake in the Abu Dhabi Marine Areas (ADMA) concession operated by ADMA-OPCO.(i) TOTAL’s interest in the joint venture.(j) TOTAL’s indirect interest (4.00%) in the concession, via its 10% interest in Private Oil Holdings Oman Ltd. TOTAL also has a direct interest (5.54%) in the Oman LNG facility (trains 1 and

2), and an indirect participation (2.04%) through OLNG in Qalhat LNG (train 3).(k) TOTAL’s direct interest in Block 53.

Operated (Group share in %).Non-operated (Group share in %).

2 Business overviewUpstream segment

TOTAL. Registration Document 201516

2.1.8. Main activities by geographic area

The information presented below describes the Group’s mainexploration and production activities by geographic area, withoutdetailing all of the assets held by TOTAL. The mentioned capacitiesare expressed in 100%.

Africa

In 2015, TOTAL’s production in Africa was 678 kboe / d,representing 29% of the Group’s overall production, comparedto 657 kboe / d in 2014 and 670 kboe / d in 2013. The two mainproducing countries in Africa in 2015 were Angola and Nigeria.

In Algeria, TOTAL’s production was 25 kboe / d during 2015,compared to 20 kboe / d in 2014 and 21 kboe / d in 2013. All of theGroup’s production in Algeria comes from the Tin Fouyé Tabankort(TFT) field (35%). TOTAL also has a 37.75% stake in the Timimoungas development project.

The development of the Timimoun field continued in 2015 withengineering activities, the start of plant construction and drillingpreparation.

In Angola, where TOTAL is the leading oil operator in the country(1),the Group’s production was 248 kboe / d in 2015 compared to 200kboe / d in 2014 and 186 kboe / d in 2013. This production comesfrom blocks 17,14 and 0.

– Deep offshore Block 17 (40%, operator) is TOTAL’s main asset inAngola. It is composed of four major producing hubs: Girassol,Dalia, Pazflor and CLOV. The latest greenfield project, CLOV,started production in June 2014 and, since September 2014, its production plateau of 160 kboe / d has been maintained. InJuly 2015, Dalia Phase 1A, a new development in the Dalia field,started production.

– On the ultra-deep offshore Block 32 (30%, operator), theKaombo project was launched in April 2014 to develop thediscoveries in the southeast part of the block via two FPSOs(Floating Production Storage and Offloading facilities) with acapacity of 115 kb / d each. The drilling campaign of 59 wellsbegan in October 2015 and production start-up is planned for2017. The exploration and delineation of the center and northparts of the block (outside Kaombo) is ongoing.

– On Block 14 (20%)(2), production comes from the Tombua-Landana and Kuito fields as well as the BBLT project, comprisingthe Benguela, Belize, Lobito and Tomboco fields.

– Block 14K (36.75%) is the offshore unitization zone betweenAngola (Block 14) and the Republic of the Congo (Haute Merlicense). The Lianzi field, which was connected to the existingBBLT platform (Block 14), started production at the end ofOctober 2015. The project is expected to reach a productionplateau of 40 kb / d. TOTAL’s interest in the unitized zone is held10% through Angola Block 14 BV and 26.75% through TotalE&P Congo.

– On Block 0 (10%), the development of Mafumeira Sul wasapproved by the partners and authorities in 2012. This projectconstitutes the second development phase of the Mafumeirafield and is expected to start production by the end of 2016.

– In April 2014, TOTAL sold its entire stake in Block 15 / 06 (15%).

In the Bas-Congo basin, TOTAL is the operator of exploration Block17 / 06 (30%). The Group relinquished Block 33 (58.67%, operator)in November 2014.

In the Kwanza basin, deep offshore, TOTAL is also operator ofBlocks 25 (35%), 40 (40%) and 39 (7.5% following the finalization ofthe sale of half of its stake in March 2015). TOTAL is alsodeveloping its LNG activities through the Angola LNG project(13.6%), which includes a gas liquefaction plant near Soyo suppliedby gas associated with production from blocks 0, 14, 15, 17 and18. LNG production started in June 2013, but various technicalincidents required the extended shutdown of the plant. LNGproduction is expected to resume in 2016.

In Gabon, the Group’s production in 2015 was 59 kboe / dcompared to 58 kboe / d in 2014 and 59 kboe / d in 2013. TheGroup’s exploration and production activities in Gabon wereprimarily carried out by Total Gabon(3).

– On the Anguille field (100%, operator), production of phase 3 of the redevelopment project (production capacity estimated at20 kboe / d) from the AGM Nord platform started in 2013 and 18 wells are operational today.

– On the Torpille field (100%, operator), the data acquired duringthe 3D seismic survey performed in 2014 is now beingprocessed.

– On the deep-offshore Diaba license (42.5%, operator), anexploration well (Diaman-1B), drilled in 2013, showed anaccumulation of gas and condensates. Additional seismic dataacquired at the end of 2014 on the western part of the license isbeing processed and is expected to generate a full inventory ofthe license’s prospectivity.

– On the Nzeimbou (20%) license, the Igongo-1X well (which revealeda multilayer accumulation of oil and gas) was commissioned byconnecting to the facilities of the Echira field in June 2015.

In Libya, where the security context remains unstable, the Group’sproduction was 14 kb / d in 2015 compared to 27 kb / d in 2014 and50 kb / d in 2013. This production comes from blocks located onoffshore areas 15, 16 and 32 (Al Jurf, 75%(4)), which have not beenaffected by the security issues. Since the fourth quarter of 2014,production as well as exploration activities have been stopped onMabruk – onshore areas 70 and 87 (75%(4)) – and on El Sharara – onshore areas 129, 130 (30%(4)), and 130 and 131 (24%(4)). In thisenvironment of uncertainty, an impairment on the onshore assetswas booked in the 2015 Consolidated Financial Statements.

In Morocco, the 3D seismic processing and interpretation studiesacquired in 2013 in the south of the block continued in the scope ofthe reconnaissance authorization of Anzarane offshore, which coversan ocean region of 100,000 km² and was allocated in December 2011to TOTAL by the ONHYM (National Office of Hydrocarbons andMines). The results of geological studies having not been encouraging,the reconnaissance authorization, which had been extended untilDecember 2015, was not transformed into an exploration license.

In Nigeria, the Group’s production, primarily offshore, was 245 kboe / din 2015, compared to 257 kboe / d in 2014 and 261 kboe / d in 2013.This decrease is explained mainly by the sale of interests in certainlicenses of the Shell Petroleum Development Company (SPDC) jointventure as well as by an upsurge of oil bunkering activities since 2013.This has negatively affected onshore production and has had an

(1) Company data.(2) Stake held by the company Angola Block 14 BV (TOTAL 50.01%).(3) Total Gabon is a company under Gabonese law listed on Euronext Paris. TOTAL holds 58.28%, the Republic of Gabon holds 25% and the public float is 16.72%.(4) TOTAL’s stake in the foreign consortium.

Business overview 2Upstream segment

Registration Document 2015. TOTAL 17

impact on the integrity of the SPDC joint venture facilities as well ason the local environment.

TOTAL operates 5 of the 31 oil mining leases (OML) in which it hasinterests and also holds interests in 4 oil prospecting licenses (OPL).

Regarding the principal variations in TOTAL’s permits since 2013:

– TOTAL was granted approval by the authorities in 2013 to increaseits stake in OPL 285 from 26.67% to 60% and it drilled theEkpeyi-1 exploration well in 2015;

– In 2013, TOTAL was granted approval by the authorities for therenewal of OMLs 99, 100 and 102 for a period of 20 years;

– On OML 138 (20%), the production of the offshore field Usanreached 130 kboe / d in 2013. In 2014, two exploration wells,Ukot South-2B and Ukot South-3, and an exploration well in 2015,Ukot South-4, led to three oil discoveries. The sale process,launched in November 2012, could not be closed. This asset isno longer accounted under “assets classified as held for sale”(refer to Note 4D Additional Information on adjustments andimpairments point 7 of chapter 10). TOTAL has ceased to be theoperator of OML 138 since February 2014;

– TOTAL sold its 10% interest in OMLs 18 and 29 (in 2015) andOML 24 (in 2014), operated via the SPDC joint venture. Inaddition, the sale process is underway for OML 25.

TOTAL continues to develop its operated assets, in particular:

– OML 58 (40%, operator, onshore): in the scope of its jointventure with the Nigerian National Petroleum Corporation(NNPC), TOTAL has finalized the increase of gas productioncapacity from 370 Mcf / d to 550 Mcf / d;

– OML 102 (40%, operator): in December 2014, TOTAL stoppedroutine flaring on the Ofon field (Ofon phase 2 project). The gasassociated with the production of oil is now compressed andevacuated to shore and monetized via the Nigeria LNG plant;

– OML 130 (24%, operator): the development of the Egina field(200 kboe / d capacity) launched in 2013 is underway. The drillingcampaign for 44 wells started at the end of 2014;

– OML 99 (40%, operator): additional studies are underway for the development of the Ikike field.

TOTAL is also developing LNG activities with a 15% stake in theNigeria LNG Ltd company, which owns a liquefaction plant with a 22 Mt / year total capacity. Assessments are underway for theinstallation of an additional capacity of approximately 8.5 Mt / year.In an effort to focus its activities, TOTAL is currently re-evaluating its participation in the Brass LNG project, in which it holds a20.48% interest.

The Group’s non-operated production in Nigeria comes mostly fromthe SPDC joint venture in which TOTAL holds a 10% stake. TOTALalso holds an interest in deep offshore OML 118 (12.5%). On thislease in 2015, the Bonga field contributed 19 kboe / d to the Group’sproduction. A unitization agreement for the Bonga SouthWest / Aparo discovery (10%) was submitted to the authorities in 2015.

In Uganda, a growth area for the Group and where TOTAL hasbeen present in the upstream since 2012, the Group has a 33.33%stake in the EA-1, EA-1A and EA-2 licenses and 28.33% in the EA-3license located in the region of Lake Albert. TOTAL is the operatorof licenses EA-1 and EA-1A and partner on the other licenses.

– On the EA-1 license, a drilling campaign, production tests and3D seismic acquisition survey were carried out between 2012and mid-2014. As of the end of 2014, five development planshad been submitted to the authorities. In 2015, discussions for the obtaining of production licenses continued, anddevelopment optimization studies were conducted in order to start the project phase.

– The EA-1A license expired in 2013 at the end of a drillingcampaign that resulted in one discovery (Lyec). With theexception of the area relating to this discovery, the license wasrelinquished to the authorities.

– On the EA-2 license, the drilling campaign and production testsstarted in 2012 were completed in 2014. Two development planswere submitted to the authorities in 2013. In 2015, discussionscontinued for the obtaining of production licenses.

– The development plan for Kingfisher field, located on the EA-3production license, was approved by the authorities in 2013 and the work to develop the field continues.

– In 2015, discussions were continued with the authorities of Uganda in order to assess the best option for the layout for the crude oil export pipeline to the Indian Ocean.

In the Republic of the Congo, the Group’s production was 87 kboe / din 2015 compared to 95 kboe / d in 2014 and 93 kboe / d in 2013. In December 2013, Qatar Petroleum International Upstream (QPI)purchased a 15% stake in the capital of Total E&P Congo, via ashare capital increase of the subsidiary.

– On the offshore field Moho Bilondo (53.5%, operator), phase 1bproject (estimated capacity: 40 kboe / d) started production inDecember 2015. Production of the Moho Nord project (estimatedcapacity: 100 kboe / d) is expected to start by the first half of 2017.

– Block 14K (36.75%) corresponds to the offshore unitization areabetween the Republic of the Congo (Haute Mer license) andAngola (Block 14 located in Angola). The production of the Lianzifield started at the end of October 2015. TOTAL’s interests in theunitization area are held 26.75% by Total E&P Congo and 10%by Angola Block 14 BV.

– Since 2013, as part of the renewal of licenses, the stake held bythe Group has been 42.5% on the Loango license and 29.75%on the Zatchi license.

– Total E&P Congo is operator of Djéno (63%) the sole oil terminalin the country.

Rest of AfricaTOTAL also holds interests in exploration licenses in South Africa,Côte d’Ivoire, Egypt, Kenya, Madagascar, Mauritania, Mozambiqueand the Democratic Republic of the Congo, and is negotiating withthe authorities with the view to resume exploration activities in theRepublic of South Sudan.

North America

In 2015, TOTAL’s production in North America was 103 kboe / d,representing 4% of the Group’s total production, compared to90 kboe / d in 2014 and 73 kboe / d in 2013.

In Canada, the Group’s production was 14 kboe / d in 2015 comparedto 12 kboe / d in 2014 and 13 kboe / d in 2013. This production comesentirely from TOTAL’s 50% stake in the Surmont project developed bySAGD(1). Phase 2 of the project was commissioned in September 2015and at the end of the ramp-up in 2017, the project is expected to havea total capacity of approximately 150 kb / d (75 kb / d in Group share).

(1) Steam Assisted Gravity Drainage, production by injection of recycled water vapor.

2 Business overviewUpstream segment

TOTAL. Registration Document 201518

Construction of the second oil sands project in which TOTAL has a stake, the Fort Hills mining project, has progressed on time andwithin budget. At a more than 50% completion rate as at the end of 2015, production from Fort Hills is expected to start toward theend of 2017. As a result of a full comparative analysis of its globalasset portfolio in the context of lower oil prices, the Group decided in 2015 to reduce its exposure to Canadian oil sands. In November 2015,TOTAL sold 10% of its 39.2% stake in the FortHills project to the operator, reducing its interest to 29.2%.Following this divestment, an impairment on the part of the assetsold was booked in the 2015 Consolidated Financial Statements.

On the Joslyn (38.25%, operator) and Northern Lights (50% operator)oil sands licenses, the projects were suspended and works havebeen strictly limited to legal and contractual obligations, andmaintaining safety.

The Group booked an impairment of $2.2 billion on its oil sandsassets in its 2014 Consolidated Financial Statements.

In the United States, the Group’s production was 89 kboe / d in2015 compared to 78 kboe / d in 2014 and 60 kboe / d in 2013.

– In the Gulf of Mexico, TOTAL holds interests in the deep offshorefields Tahiti (17%) and Chinook (33.33%).In 2015, the TOTAL (40%) – Cobalt (60%, operator) alliance,formed in 2009 for exploration in the Gulf of Mexico, carried outfurther drilling to evaluate the size of the North Platte discovery.

– TOTAL is also present in shale gas production in the United Statesthrough its 25% stake in two joint ventures operated by Chesapeakein the Barnett (Texas) and Utica (Ohio) basins. Drilling activity inthese basins was greatly reduced in 2015 due to the decrease in the price of gas and related liquids. In Barnett, four wells weredrilled in 2015 compared to 40 in 2014 and approximately 60 in2013. In Utica, the number of drilling rigs employed has beenreduced from nine to one in 2015 and TOTAL participated ineight wells with Chesapeake. In 2014, approximately 170 wellswere drilled by the joint venture and over 200 were drilled in 2013.Following successive decreases in gas prices in the UnitedStates, impairments on shale gas assets were booked in the2013, 2014 and 2015 Consolidated Financial Statements.

The R&D stage oil shale projects (in situ and ex situ productiontechnology) in which the Group holds a stake (through AmericanShale Oil LLC, 55.7%, and the 50 / 50 joint venture with thecompany Red Leaf Resources) including the development of theRed Leaf pilot, have been deferred.

South America

In 2015, TOTAL’s production in South America was 152 kboe / d,representing 7% of the Group’s total production, compared to 157 kboe / d in 2014 and 166 kboe / d in 2013. The two mainproducing countries in South America in 2015 were Argentinaand Venezuela.

In Argentina, TOTAL operated approximately 30%(1) of thecountry’s gas production in 2015. The Group’s production was 72 kboe / d in 2015 compared to 75 kboe / d in 2014 and 78 kboe / din 2013. From 2012, the Argentinean government concluded gasprice agreements with various producers under which the governmentguarantees the price of gas for quantities above a fixed productionlevel in exchange for compliance with defined production targetsand applicable penalties (i.e., “deliver or pay”). In 2013, TOTAL

signed an agreement of this type for a period of five years withretroactive effect from December 1, 2012.

– In Tierra del Fuego, the Group operates the Carina and Ariesoffshore fields (37.5%). A drilling campaign for two additionalwells off the existing platform was completed in 2015. The VegaPleyade field (37.5%, operator), where development work waslaunched in 2013 (with a production capacity of 350 Mcf / d),started production in February 2016.

– In the Neuquén basin, two pilot projects were launched followingpositive initial results of the drilling campaign on its mininglicenses in order to assess its gas and shale oil potential: one onthe Aguada Pichana Block (27.3%, operator) where productionstarted mid-2015, and the other on the Rincón la Ceniza Block(42.5%, operator).

In Bolivia, the Group’s production, mainly gas, was 28 kboe / d in2015 compared to 30 kboe / d in 2014 and 28 kboe / d in 2013.TOTAL is active on seven licenses: three production licenses at SanAlberto (15%), San Antonio (15%) and Block XX Tarija Oeste (41%);two licenses in development phase, Aquio and Ipati (60%,operator); and two exploration phase licenses, Rio Hondo (50%)and Azero (50%, operator of the exploration phase).

– Following the discovery of the Incahuasi gas field, located in theIpati Block, TOTAL was granted approval by the authorities tolaunch the first development phase of the project, including theconnection of three wells already drilled in a 6.5 Mm³ / d capacityprocessing plant. The project is expected to start productionmid-2016. In mid-2014, TOTAL reduced its stake in Aquio andIpati from 80% to 60%.

– In 2013, TOTAL acquired a 50% stake in the Azero explorationlicense located in the Andean foothills, which extends over anarea of 7,800 km². The exploration period began in June 2014.

In Brazil, a growth area for the Group, TOTAL acquired in 2013 a20% stake in the Libra field, located in the Santos basin. The field islocated in the ultra-deep offshore (2,000 m) approximately 170 kmoff the coast of Rio de Janeiro and covers an area of 1,550 km². In 2014, a 50 kb / d capacity boat was reserved for long durationproduction testing. In 2015, the drilling of two wells was completedand one of two others started in the northwest and center of the field.

The Group also holds stakes in 18 exploration licenses, followingthe 2015 acquisition of a 50% stake in Blocks P-M 1269, 1271,1351 and 1353 in the Pelotas basin.

In Venezuela, where TOTAL has been active since 1980, the Group’sproduction was 52 kboe / d in 2015 as in 2014 and compared to 48 kboe / d in 2013. TOTAL has stakes in PetroCedeño (30.3%) and Yucal Placer (69.5%) as well as the offshore exploration Block 4of Plataforma Deltana (49%).

Development of the extra heavy oil field of PetroCedeño continuesin the southern area as in the main area (47 production wells weredrilled in 2015 compared to 86 in 2014 and 43 in 2013), as well asthe debottlenecking project for the water separation and treatmentfacilities.

In the Yucal Placer field, following the signature of an amendment tothe gas sale contract, a new development phase was launched in 2012.In April 2014, the field’s production increased following thecommissioning of new clusters and the debottlenecking of the existinggas processing train (production capacity of 150 Mcf / d in 2015).

(1) Source: Department of Federal Planning, Public Investment and Services, Energy Secretariat.

Business overview 2Upstream segment

Registration Document 2015. TOTAL 19

Rest of South AmericaTOTAL also holds interests in exploration licenses in Aruba,Colombia, French Guiana and Uruguay.

Asia-Pacific

In 2015, TOTAL’s production in Asia-Pacific was 258 kboe / d,representing 11% of the Group’s overall production, comparedto 238 kboe / d in 2014 and 235 kboe / d in 2013. The two mainproducing countries in Asia-Pacific in 2015 were Indonesia and Thailand.

In Australia, where TOTAL has had mining rights since 2005, theGroup’s production was 4 kboe / d in 2015, 2014 and 2013.

– The Ichthys project (30%) involves the development of a gas andcondensate field located in the Browse Basin. This development willinclude a floating platform designed for the production (CPF, CentralProcessing Facility), processing and exploration of gas, an FPSO(with condensate processing capacity of 100 kb / d) to stabilize andexport the condensate, an 889 km gas pipeline and an onshoreliquefaction plant (with 8.9 Mt / y LNG and 1.6 Mt / y LPG capacities) at Darwin. The LNG has already been sold mainly to Asian buyersunder long-term contracts. Production is expected to start in 2017.

– Gladstone LNG (GLNG) (27.5%) is an integrated gas production,transportation and liquefaction project of 7.2 Mt / y based on thedevelopment of coal seam gas from the Fairview, Roma, Scotiaand Arcadia fields. The development of a first upstream phasewas completed with the start of production of Fairview 3 and 4and Roma 2. Train 1 (3.6 Mt / y capacity) started production inSeptember 2015 and the first LNG cargo left GLNG for SouthKorea in October 2015. The development of the liquefactionplant continues with the construction of train 2, which isexpected to start production in 2016. An asset impairment ofapproximately $1.4 billion was booked in TOTAL’s 2015Consolidated Financial Statements.

– The WA-492 and WA-493 licenses, located in the Carnarvonbasin, were awarded to TOTAL (100%, operator) in 2013. A 2Dseismic regional campaign began in January 2015.

– In 2012, TOTAL signed an agreement to enter into three shalegas exploration licenses located in the South Georgina basin inthe center of the country. In 2013, a 2D seismic survey wasacquired on three licenses and a drilling campaign began in 2014with two wells. Technical studies are ongoing.

In Brunei, TOTAL operates the offshore Maharaja Lela Jamalulalamgas and condensate field located on Block B (37.5%). The Group’sproduction was 15 kboe / d in 2015 as in 2014 and compared to 13 kboe / d in 2013. The gas is delivered to the Brunei LNG liquefaction plant.