Rating Advisory Mrs.Bectors Food Specialities Limited - CRISIL

13

Rating Advisory April 13, 2022 | Mumbai Mrs.Bectors Food Specialities Limited Update as on April 13, 2022 This rating advisory is provided in relation to the rating of Mrs.Bectors Food Specialities Limited The key rating sensitivity factors for the rating include: Upward factors • Substantial increase in scale of operations and rise in operating profitability to 13-15%, leading to healthy cash generation of over Rs 200 crore • Improved market share through geographical and product expansion • Build-up of cash surplus while maintaining gearing and capital structure Downward factors • Sluggish revenue and moderation in operating profitability below 10% • Weakening of capital structure due to substantially large, debt-funded capex or acquisition CRISIL Ratings has a policy of keeping its accepted ratings under constant and ongoing monitoring and review. Accordingly, it seeks regular updates from companies on business and financial performance. CRISIL Ratings is yet to receive adequate information from Mrs.Bectors Food Specialities Limited (MBFSL) to enable it to undertake a rating review. CRISIL Ratings is taking all possible efforts to get the rated entity to cooperate with its rating process for enabling it to carry out the rating review. CRISIL Ratings views information availability risk as a key factor in its assessment of credit risk. (Please refer to CRISIL Ratings’ criteria available at the following link, https://www.crisil.com/content/dam/crisil/criteria_methodology/basics-of-ratings/assessing- information-adequacy-risk.pdf) If MBFSL continues to delay the provisioning of information required by CRISIL Ratings to undertake a rating review then, in accordance with circulars SEBI/HO/MIRSD/MIRSD4/CIR/P/2016/119 dt Nov 1, 2016, SEBI/HO/MIRSD/ MIRSD4/ CIR/ P/ 2017/ 71 dt June 30, 2017 and SEBI/HO/MIRSD/CRADT/CIR/P/2020/2 dt January 3, 2020 issued by Securities and Exchange Board of India, CRISIL Ratings will carry out the review based on best available information and issue a press release. About the Company Ms Rajni Bector set up MBFSL as a joint venture (JV) with Quaker Oats, the USA (now a subsidiary of PepsiCo Inc) to supply packaged ketchup to McDonald's, in addition to buns, batter, and bread. Quaker Oats withdrew from the JV in 1999. In fiscal 2014, the company underwent a business reorganisation and demerged its food supplements (sauces, spreads, and namkeen) division. MBFSL operates in three segments: it sells biscuits under the Mrs. Bectors Cremica brand. It also sells buns and other bakery items to KFC, Burger King. It supplies bread and bakery items under its English Oven brand and English Oven brands to modern retail chains (Easy Day, Reliance Retail, Big Bazaar, More, and Spencer's) and distributors. MBFSL is the sole supplier of buns to McDonald's in India.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Rating Advisory Mrs.Bectors Food Specialities Limited - CRISIL

Rating Advisory April 13, 2022 | Mumbai

Mrs.Bectors Food Specialities Limited

Update as on April 13, 2022 This rating advisory is provided in relation to the rating of Mrs.Bectors Food Specialities Limited The key rating sensitivity factors for the rating include: Upward factors

• Substantial increase in scale of operations and rise in operating profitability to 13-15%, leading to healthy cash generation of over Rs 200 crore

• Improved market share through geographical and product expansion

• Build-up of cash surplus while maintaining gearing and capital structure

Downward factors

• Sluggish revenue and moderation in operating profitability below 10%

• Weakening of capital structure due to substantially large, debt-funded capex or acquisition

CRISIL Ratings has a policy of keeping its accepted ratings under constant and ongoing monitoring and review. Accordingly, it seeks regular updates from companies on business and financial performance. CRISIL Ratings is yet to receive adequate information from Mrs.Bectors Food Specialities Limited (MBFSL) to enable it to undertake a rating review. CRISIL Ratings is taking all possible efforts to get the rated entity to cooperate with its rating process for enabling it to carry out the rating review. CRISIL Ratings views information availability risk as a key factor in its assessment of credit risk. (Please refer to CRISIL Ratings’ criteria available at the following link, https://www.crisil.com/content/dam/crisil/criteria_methodology/basics-of-ratings/assessing-information-adequacy-risk.pdf) If MBFSL continues to delay the provisioning of information required by CRISIL Ratings to undertake a rating review then, in accordance with circulars SEBI/HO/MIRSD/MIRSD4/CIR/P/2016/119 dt Nov 1, 2016, SEBI/HO/MIRSD/ MIRSD4/ CIR/ P/ 2017/ 71 dt June 30, 2017 and SEBI/HO/MIRSD/CRADT/CIR/P/2020/2 dt January 3, 2020 issued by Securities and Exchange Board of India, CRISIL Ratings will carry out the review based on best available information and issue a press release. About the Company Ms Rajni Bector set up MBFSL as a joint venture (JV) with Quaker Oats, the USA (now a subsidiary of PepsiCo Inc) to supply packaged ketchup to McDonald's, in addition to buns, batter, and bread. Quaker Oats withdrew from the JV in 1999. In fiscal 2014, the company underwent a business reorganisation and demerged its food supplements (sauces, spreads, and namkeen) division. MBFSL operates in three segments: it sells biscuits under the Mrs. Bectors Cremica brand. It also sells buns and other bakery items to KFC, Burger King. It supplies bread and bakery items under its English Oven brand and English Oven brands to modern retail chains (Easy Day, Reliance Retail, Big Bazaar, More, and Spencer's) and distributors. MBFSL is the sole supplier of buns to McDonald's in India.

For the six months through September 2020, the company reported an EBITDA (earnings before interest, taxes, depreciation, and amortisation) of Rs 79.6 crore (Rs 40.6 crore for the same period previous fiscal) on net sales of Rs 438 crore (Rs 366 crore).

About CRISIL Ratings Limited (a subsidiary of CRISIL Limited) CRISIL Ratings pioneered the concept of credit rating in India in 1987. With a tradition of independence, analytical rigour and innovation, we set the standards in the credit rating business. We rate the entire range of debt instruments, such as bank loans, certificates of deposit, commercial paper, non-convertible/convertible/ partially convertible bonds and debentures, perpetual bonds, bank hybrid capital instruments, asset-backed and mortgage-backed securities, partial guarantees and other structured debt instruments. We have rated over 33,000 large and mid-scale corporates and financial institutions. We have also instituted several innovations in India in the rating business, including ratings for municipal bonds, partially guaranteed instruments and infrastructure investment trusts (InvITs). CRISIL Ratings Limited (‘CRISIL Ratings’) is a wholly owned subsidiary of CRISIL Limited (‘CRISIL’). CRISIL Ratings is registered in India as a credit rating agency with the Securities and Exchange Board of India (‘SEBI’). For more information, visit www.crisilratings.com About CRISIL Limited CRISIL is a global analytical company providing ratings, research, and risk and policy advisory services. We are India's leading ratings agency. We are also the foremost provider of high-end research to the world's largest banks and leading corporations. CRISIL is majority owned by S&P Global, Inc, a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets worldwide. For more information, visit www.crisil.com Connect with us: TWITTER | LINKEDIN | YOUTUBE | FACEBOOK

CRISIL Privacy Notice CRISIL respects your privacy. We may use your contact information, such as your name,

address and email id to fulfil your request and service your account and to provide you with

additional information from CRISIL. For further information on CRISIL’s privacy policy, please

visit www.crisil.com

DISCLAIMER This disclaimer is part of and applies to each credit rating report and/or credit rating rationale (‘report’) that is provided by CRISIL Ratings Limited (‘CRISIL Ratings’). To avoid doubt, the term ‘report’ includes the information, ratings and other content forming part of the report. The report is intended for the jurisdiction of India only. This report does not constitute an offer of services. Without limiting the generality of the foregoing, nothing in the report is to be construed as CRISIL Ratings providing or intending to provide any services in jurisdictions where CRISIL Ratings does not have the necessary licenses and/or registration to carry out its business activities referred to above. Access or use of this report does not create a client relationship between CRISIL Ratings and the user. We are not aware that any user intends to rely on the report or of the manner in which a user intends to use the report. In preparing our report we have not taken into consideration the objectives or particular needs of any particular user. It is made abundantly clear that the report is not intended to and does not constitute an investment advice. The report is not an offer to sell or an offer to purchase or subscribe for any investment in any securities, instruments, facilities or solicitation of any kind to enter into any deal or transaction with the entity to which the report pertains. The report should not be the sole or primary basis for any investment decision within the meaning of any law or regulation (including the laws and regulations applicable in the US). Ratings from CRISIL Ratings are statements of opinion as of the date they are expressed and not statements of fact or recommendations to purchase, hold or sell any securities/instruments or to make any investment decisions. Any opinions expressed here are in good faith, are subject to change without notice, and are only current as of the stated date of their issue. CRISIL Ratings assumes no obligation to update its opinions following publication in any form or format although CRISIL Ratings may disseminate its opinions and analysis. The rating contained in the report is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment or other business decisions. The recipients of the report should rely on their own judgment and take their own professional advice before acting on the report in any way. CRISIL Ratings or its associates may have other commercial transactions with the entity to which the report pertains. Neither CRISIL Ratings nor its affiliates, third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively, ‘CRISIL Ratings Parties’) guarantee the accuracy, completeness or adequacy of the report, and no CRISIL Ratings Party shall have any liability for any errors, omissions or interruptions therein, regardless of the cause, or for the results obtained from the use of any part of the report. EACH CRISIL RATINGS PARTY DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING BUT NOT LIMITED TO ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. In no event shall any CRISIL Ratings Party be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of any part of the report even if advised of the possibility of such damages. CRISIL Ratings may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of the instruments, facilities, securities or from obligors. Public ratings and analysis by CRISIL Ratings, as are required to be disclosed under the regulations of the Securities and Exchange Board of India (and other applicable regulations, if any), are made available on its website, www.crisilratings.com (free of charge). Reports with more detail and additional information may be available for subscription at a fee – more details about ratings by CRISIL Ratings are available here: www.crisilratings.com. CRISIL Ratings and its affiliates do not act as a fiduciary. While CRISIL Ratings has obtained information from sources it believes to be reliable, CRISIL Ratings does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives and/or relies on in its reports. CRISIL Ratings has established policies and procedures to maintain the

confidentiality of certain non-public information received in connection with each analytical process. CRISIL Ratings has in place a ratings code of conduct and policies for managing conflict of interest. For details please refer to: https://www.crisil.com/en/home/our-businesses/ratings/regulatory-disclosures/highlighted-policies.html. Rating criteria by CRISIL Ratings are generally available without charge to the public on the CRISIL Ratings public website, www.crisilratings.com. For latest rating information on any instrument of any company rated by CRISIL Ratings, you may contact the CRISIL Ratings desk at [email protected], or at (0091) 1800 267 1301. This report should not be reproduced or redistributed to any other person or in any form without prior written consent from CRISIL Ratings. All rights reserved @ CRISIL Ratings Limited. CRISIL Ratings is a wholly owned subsidiary of CRISIL Limited. CRISIL Ratings uses the prefix ‘PP-MLD’ for the ratings of principal-protected market-linked debentures (PPMLD) with effect from November 1, 2011 to comply with the SEBI circular, "Guidelines for Issue and Listing of Structured Products/Market Linked Debentures". The revision in rating symbols for PPMLDs should not be construed as a change in the rating of the subject instrument. For details on CRISIL Ratings' use of 'PP-MLD' please refer to the notes to Rating scale for Debt Instruments and Structured Finance Instruments at the following link: www.crisil.com/ratings/credit-rating-scale.html

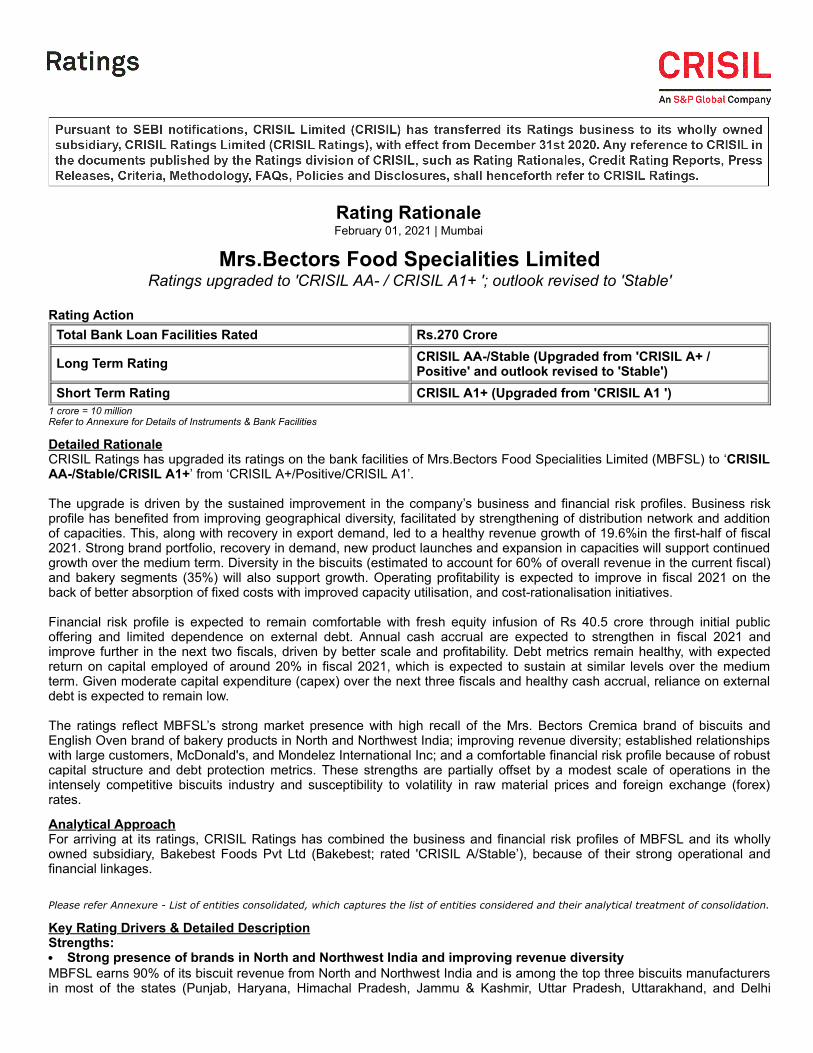

Rating RationaleFebruary 01, 2021 | Mumbai

Mrs.Bectors Food Specialities LimitedRatings upgraded to 'CRISIL AA- / CRISIL A1+ '; outlook revised to 'Stable'

Rating Action

Total Bank Loan Facilities Rated Rs.270 Crore

Long Term Rating CRISIL AA-/Stable (Upgraded from 'CRISIL A+ /Positive' and outlook revised to 'Stable')

Short Term Rating CRISIL A1+ (Upgraded from 'CRISIL A1 ')1 crore = 10 millionRefer to Annexure for Details of Instruments & Bank Facilities

Detailed RationaleCRISIL Ratings has upgraded its ratings on the bank facilities of Mrs.Bectors Food Specialities Limited (MBFSL) to ‘CRISILAA-/Stable/CRISIL A1+’ from ‘CRISIL A+/Positive/CRISIL A1’. The upgrade is driven by the sustained improvement in the company’s business and financial risk profiles. Business riskprofile has benefited from improving geographical diversity, facilitated by strengthening of distribution network and additionof capacities. This, along with recovery in export demand, led to a healthy revenue growth of 19.6%in the first-half of fiscal2021. Strong brand portfolio, recovery in demand, new product launches and expansion in capacities will support continuedgrowth over the medium term. Diversity in the biscuits (estimated to account for 60% of overall revenue in the current fiscal)and bakery segments (35%) will also support growth. Operating profitability is expected to improve in fiscal 2021 on theback of better absorption of fixed costs with improved capacity utilisation, and cost-rationalisation initiatives. Financial risk profile is expected to remain comfortable with fresh equity infusion of Rs 40.5 crore through initial publicoffering and limited dependence on external debt. Annual cash accrual are expected to strengthen in fiscal 2021 andimprove further in the next two fiscals, driven by better scale and profitability. Debt metrics remain healthy, with expectedreturn on capital employed of around 20% in fiscal 2021, which is expected to sustain at similar levels over the mediumterm. Given moderate capital expenditure (capex) over the next three fiscals and healthy cash accrual, reliance on externaldebt is expected to remain low. The ratings reflect MBFSL’s strong market presence with high recall of the Mrs. Bectors Cremica brand of biscuits andEnglish Oven brand of bakery products in North and Northwest India; improving revenue diversity; established relationshipswith large customers, McDonald's, and Mondelez International Inc; and a comfortable financial risk profile because of robustcapital structure and debt protection metrics. These strengths are partially offset by a modest scale of operations in theintensely competitive biscuits industry and susceptibility to volatility in raw material prices and foreign exchange (forex)rates.

Analytical ApproachFor arriving at its ratings, CRISIL Ratings has combined the business and financial risk profiles of MBFSL and its whollyowned subsidiary, Bakebest Foods Pvt Ltd (Bakebest; rated 'CRISIL A/Stable’), because of their strong operational andfinancial linkages. Please refer Annexure - List of entities consolidated, which captures the list of entities considered and their analytical treatment of consolidation.

Key Rating Drivers & Detailed DescriptionStrengths:

Strong presence of brands in North and Northwest India and improving revenue diversityMBFSL earns 90% of its biscuit revenue from North and Northwest India and is among the top three biscuits manufacturersin most of the states (Punjab, Haryana, Himachal Pradesh, Jammu & Kashmir, Uttar Pradesh, Uttarakhand, and Delhi

National Capital Region). The company distributes across 23 states in India through a network of 196 super stockists and748 distributors that supply to a wide range of clients through 458,000 retail outlets and 4,422 preferred outlets. Furthermore, the company has been increasing its premium product portfolio and leveraging its presence with focus onhigh-margin biscuits such as cookies, creams and crackers; and reduced dependence on low-margin glucose biscuits.Strong growth in the bakery segment is reflected in its contribution of 35-37% to the overall revenue in fiscal 2021. TheEnglish Oven is among the leading premium bakery brands in India. With addition of new lines and new products (premiumbreads, croissants, buns), the growth is likely to continue over the medium term.

Established relationships with large institutional playersThe company remains a preferred supplier of buns (for the past 15 years) to McDonald’s (Hardcastle Restaurants Pvt Ltd inWest and South, Connaught Plaza Restaurants Pvt Ltd in North and East), Burger King, and KFC (Devyani International PvtLtd). It is also targeting new quick-service restaurants, supported by continued focus on quality. Longstanding relations withlarge institutional customers have resulted in a steady source of revenue over the past few years. MBFSL also supplies toDomino's Pizza and Wendy's. Exports are expected to rebound in fiscal 2021, after a slight decline in previous fiscals due to political instability in certainAfrican countries, mainly driven by improved demand and healthy share of Indian biscuits in the exports market. Thecompany also undertakes job work manufacturing for Mondelez International Inc. Established customer relationships should continue to provide stability to operating income and profitability, given therevenue visibility and cost-plus profitability built into long-term contracts.

Strong financial risk profileFinancial risk profile continues to remain strong, with a healthy expected net-worth in fiscal 2021, low gearing of below 0.4times as on March 31, 2020, and robust debt protection metrics with cash accruals expected to be Rs 90-100 crore in thecurrent fiscal. Interest cover and NCA/TD are expected to improve further from 6.2 times and 51% in fiscal 2020respectively. Gearing has improved on a sustained basis over the last 3 fiscals from 0.5 time in 2018 to an expected 0.27time in fiscal 2021. Going forward gearing is expected to remain in range of 0.2-0.3 time over the medium term. Weaknesses:

Modest, though improving, scale of operations in an intensely competitive biscuit industryMBFSL is a relatively small player in the biscuits industry vis-à-vis other manufacturers, with estimated revenue of about Rs765 crore for fiscal 2020. Although the Cremica brand has an established presence in North and Northwest India, it haslimited presence in other parts of the country. Furthermore, the biscuit industry is intensely competitive, with large players(such as Britannia; rated ‘CRISIL AAA/Stable/CRISIL A1+’) vying for a greater market share. With the entry of ITC,Mondelez, and Unibic, the competition has intensified across product categories.

Susceptibility to changes in raw material prices and forex ratesThe biscuits segment, accounting for nearly two-thirds of the company’s total revenue, is price-sensitive with little productdifferentiation, especially in the low-end biscuits segment. Thus, players have limited ability to pass on increase in inputprices (wheat, sugar, and oil; form 50-60% of total costs) to customers. Operating profitability will likely remain exposed tosharp fluctuations in raw material prices and forex rates. Though the company undertakes forward contracts to hedgeagainst forex risk, it is able to pass on price rise to consumers only with a time lag.

Liquidity: StrongMBFSL has a strong liquidity profile on account of healthy expected cash accruals and robust debt protection metrics. Cashaccruals are expected to improve further in next 2 fiscals and will be adequate for moderate capex and debt repayments.MBFSL has also pre-paid its term loan obligations due till March 2022 in current fiscal. Current ratio stood at a healthy 1.4times as on March 31, 2020. The company also has a cash surplus of Rs 48 crore as on September 30, 2020.

Outlook: StableMBFSL is expected to achieve healthy revenue growth over the medium term on the back of improving business risk profile,established market position, better geographical diversity, and strong customer profile and brands. Financial risk profile islikely to remain comfortable.

Rating Sensitivity factorsUpward factors

Substantial increase in scale of operations and rise in operating profitability to 13-15%, leading to healthy cashgeneration of over Rs 200 croreImproved market share through geographical and product expansionBuild-up of cash surplus while maintaining gearing and capital structure

Downward factors

Sluggish revenue and moderation in operating profitability below 10%Weakening of capital structure due to substantially large, debt-funded capex or acquisition

About the CompanyMs Rajni Bector set up MBFSL as a joint venture (JV) with Quaker Oats, the USA (now a subsidiary of PepsiCo Inc) tosupply packaged ketchup to McDonald's, in addition to buns, batter, and bread. Quaker Oats withdrew from the JV in 1999.In fiscal 2014, the company underwent a business reorganisation and demerged its food supplements (sauces, spreads,and namkeen) division. MBFSL operates in three segments: it sells biscuits under the Mrs. Bectors Cremica brand. It also sells buns and otherbakery items to KFC, Burger King. It supplies bread and bakery items under its English Oven brand and English Ovenbrands to modern retail chains (Easy Day, Reliance Retail, Big Bazaar, More, and Spencer's) and distributors. MBFSL is thesole supplier of buns to McDonald's in India. For the six months through September 2020, the company reported an EBITDA (earnings before interest, taxes,depreciation, and amortisation) of Rs 79.6 crore (Rs 40.6 crore for the same period previous fiscal) on net sales of Rs 438crore (Rs 366 crore).

Key Financial Indicators Units 2020 2019Revenue Rs cr 765 786PAT Rs cr 30 33PAT margin % 4 4.2Adjusted debt/networth Times 0.41 0.48Interest coverage Times 6.17 8.33

Any other information: Not applicable

Note on complexity levels of the rated instrument:CRISIL complexity levels are assigned to various types of financial instruments. The CRISIL complexity levels are availableon www.crisil.com/complexity-levels. Users are advised to refer to the CRISIL complexity levels for instruments that theyconsider for investment. Users may also call the Customer Service Helpdesk with queries on specific instruments.

Annexure - Details of Instrument(s)ISIN Name of instrument Date of

AllotmentCouponrate (%)

Maturitydate

Issue Size(Rs. crore)

Complexitylevel

Rating assignedwith Outlook

NA Bank Guarantee NA NA NA 3.5 NA CRISIL A1+NA Letter of Credit** NA NA NA 10 NA CRISIL A1+NA Cash Credit* NA NA NA 35 NA CRISIL AA-/StableNA Overdraft Facility NA NA NA 10 NA CRISIL AA-/StableNA Term Loan NA NA Dec-24 5 NA CRISIL AA-/StableNA Term Loan NA NA Apr-25 43.95 NA CRISIL AA-/StableNA Term Loan NA NA Oct-21 16.41 NA CRISIL AA-/StableNA Term Loan NA NA Oct-21 2.43 NA CRISIL AA-/StableNA Term Loan NA NA Jun-23 7.31 NA CRISIL AA-/StableNA Term Loan NA NA May-26 9.09 NA CRISIL AA-/StableNA Term Loan NA NA Jan-25 9.52 NA CRISIL AA-/StableNA Term Loan NA NA Jan-27 45 NA CRISIL AA-/StableNA Term Loan NA NA Apr-25 12.99 NA CRISIL AA-/StableNA Term Loan NA NA Apr-26 7.21 NA CRISIL AA-/StableNA Term Loan NA NA Dec-27 27 NA CRISIL AA-/Stable

NA Working Capital TermLoan NA NA Dec-22 6.11 NA CRISIL AA-/Stable

NA Short Term BankFacility NA NA NA 10.5 NA CRISIL A1+

NA Proposed Long TermBank Loan Facility NA NA NA 3.98 NA CRISIL AA-/Stable

NA Export Packing Credit NA NA NA 5 NA CRISIL AA-/Stable*Includes Rs 20 crore of sublimit for export credit packing credit.**Includes Rs 10 crore of sublimit for bank guarantee

Annexure – List of entities consolidatedSr. No Subsidiary Companies: Subsidiary/ Joint Venture Extent of consolidation

1 Bakebest Foods Pvt Ltd Subsidiary 100%

Annexure - Rating History for last 3 Years Current 2021 (History) 2020 2019 2018 Start of

2018

Instrument Type OutstandingAmount Rating Date Rating Date Rating Date Rating Date Rating Rating

Fund BasedFacilities LT/ST 256.5

CRISILA1+ /

CRISILAA-/Stable

-- 05-03-20CRISIL

A+/Positive/ CRISIL

A131-12-19

CRISILA+/Positive

/ CRISILA1

29-09-18CRISIL

A+/Positive/ CRISIL

A1

CRISILA+/Stable/ CRISIL

A1

Non-FundBasedFacilities

ST 13.5 CRISILA1+ -- 05-03-20 CRISIL A1 31-12-19 CRISIL A1 29-09-18 CRISIL A1 CRISIL

A1

All amounts are in Rs.Cr.

Annexure - Details of various bank facilities

Current facilities Previous facilities

Facility Amount(Rs.Crore) Rating Facility Amount

(Rs.Crore) Rating

Bank Guarantee 3.5 CRISIL A1+ Bank Guarantee 3.5 CRISIL A1

Cash Credit& 35 CRISILAA-/Stable Cash Credit& 35 CRISIL

A+/Positive

Letter of Credit^ 10 CRISIL A1+ Letter of Credit^ 10 CRISIL A1

Overdraft Facility 10 CRISILAA-/Stable Overdraft Facility 10 CRISIL

A+/PositiveProposed Long Term

Bank Loan Facility 3.98 CRISILAA-/Stable

Proposed Long TermBank Loan Facility 3.98 CRISIL

A+/Positive

Short Term Bank Facility 10.5 CRISIL A1+ Short Term BankFacility 10.5 CRISIL A1

Term Loan 185.91 CRISILAA-/Stable Term Loan 185.91 CRISIL

A+/PositiveWorking Capital Term

Loan 6.11 CRISILAA-/Stable

Working Capital TermLoan 6.11 CRISIL

A+/Positive

Export Packing Credit 5 CRISILAA-/Stable Export Packing Credit 5 CRISIL

A+/PositiveTotal 270 - Total 270 -

& - Includes Rs 20 crore of sublimit for export credit packing credit.^ - Includes Rs 10 crore of sublimit for bank guarantee

Links to related criteriaCRISILs Approach to Financial RatiosCRISILs Bank Loan Ratings - process, scale and default recognitionRating criteria for manufaturing and service sector companiesRating Criteria for Fast Moving Consumer Goods IndustryCRISILs Criteria for ConsolidationCRISILs Criteria for rating short term debt

Media Relations Analytical Contacts Customer Service HelpdeskSaman KhanMedia RelationsCRISIL LimitedD: +91 22 3342 3895B: +91 22 3342 [email protected]

Naireen AhmedMedia Relations

Anuj SethiSenior DirectorCRISIL Ratings LimitedB:+91 44 6656 [email protected]

Gautam ShahiDirectorCRISIL Ratings Limited

Timings: 10.00 am to 7.00 pmToll free Number:1800 267 1301

For a copy of Rationales / Rating Reports:[email protected] For Analytical queries:[email protected]

CRISIL LimitedD: +91 22 3342 1818B: +91 22 3342 3000 [email protected]

B:+91 124 672 [email protected]

Rahul MainiRating AnalystCRISIL Ratings LimitedB:+91 22 3342 [email protected]

Note for Media:This rating rationale is transmitted to you for the sole purpose of dissemination through your newspaper / magazine / agency. The rating rationale may beused by you in full or in part without changing the meaning or context thereof but with due credit to CRISIL Ratings. However, CRISIL Ratings alone hasthe sole right of distribution (whether directly or indirectly) of its rationales for consideration or otherwise through any media including websites, portals etc.

About CRISIL Ratings Limited

CRISIL Ratings pioneered the concept of credit rating in India in 1987. With a tradition of independence, analytical rigour andinnovation, we set the standards in the credit rating business. We rate the entire range of debt instruments, such as, bank loans,certificates of deposit, commercial paper, non-convertible / convertible / partially convertible bonds and debentures, perpetualbonds, bank hybrid capital instruments, asset-backed and mortgage-backed securities, partial guarantees and other structureddebt instruments. We have rated over 33,000 large and mid-scale corporates and financial institutions. We have also institutedseveral innovations in India in the rating business, including rating municipal bonds, partially guaranteed instruments andinfrastructure investment trusts (InvITs). CRISIL Ratings Limited ("CRISIL Ratings") is a wholly-owned subsidiary of CRISIL Limited ("CRISIL"). CRISIL Ratings Limited isregistered in India as a credit rating agency with the Securities and Exchange Board of India ("SEBI"). For more information, visit www.crisil.com/ratings

About CRISIL Limited

CRISIL is a global analytical company providing ratings, research, and risk and policy advisory services. We are India's leadingratings agency. We are also the foremost provider of high-end research to the world's largest banks and leading corporations.

CRISIL is majority owned by S&P Global Inc., a leading provider of transparent and independent ratings, benchmarks, analyticsand data to the capital and commodity markets worldwide

For more information, visit www.crisil.com

Connect with us: TWITTER | LINKEDIN | YOUTUBE | FACEBOOK

CRISIL PRIVACY NOTICE CRISIL respects your privacy. We may use your contact information, such as your name, address, and email id to fulfil your request and service youraccount and to provide you with additional information from CRISIL.For further information on CRISIL’s privacy policy please visit www.crisil.com.

DISCLAIMER

This disclaimer forms part of and applies to each credit rating report and/or credit rating rationale (each a "Report") that is provided by CRISIL Ratings Limited (hereinafter referred to as "CRISIL Ratings") . For the avoidance of doubt, the term "Report" includes the information, ratings and other content forming part of theReport. The Report is intended for the jurisdiction of India only. This Report does not constitute an offer of services. Without limiting the generality of the foregoing,nothing in the Report is to be construed as CRISIL Ratings providing or intending to provide any services in jurisdictions where CRISIL Ratings does not have thenecessary licenses and/or registration to carry out its business activities referred to above. Access or use of this Report does not create a client relationship betweenCRISIL Ratings and the user.

We are not aware that any user intends to rely on the Report or of the manner in which a user intends to use the Report. In preparing our Report we have not takeninto consideration the objectives or particular needs of any particular user. It is made abundantly clear that the Report is not intended to and does not constitute aninvestment advice. The Report is not an offer to sell or an offer to purchase or subscribe for any investment in any securities, instruments, facilities or solicitation ofany kind or otherwise enter into any deal or transaction with the entity to which the Report pertains. The Report should not be the sole or primary basis for anyinvestment decision within the meaning of any law or regulation (including the laws and regulations applicable in the US).

Ratings from CRISIL Ratings are statements of opinion as of the date they are expressed and not statements of fact or recommendations to purchase, hold, or sellany securities / instruments or to make any investment decisions. Any opinions expressed here are in good faith, are subject to change without notice, and are onlycurrent as of the stated date of their issue. CRISIL Ratings assumes no obligation to update its opinions following publication in any form or format although CRISILRatings may disseminate its opinions and analysis. Rating by CRISIL Ratings contained in the Report is not a substitute for the skill, judgment and experience of theuser, its management, employees, advisors and/or clients when making investment or other business decisions. The recipients of the Report should rely on their ownjudgment and take their own professional advice before acting on the Report in any way. CRISIL Ratings or its associates may have other commercial transactionswith the company/entity.

Neither CRISIL Ratings nor its affiliates, third party providers, as well as their directors, officers, shareholders, employees or agents (collectively, "CRISIL RatingsParties") guarantee the accuracy, completeness or adequacy of the Report, and no CRISIL Ratings Party shall have any liability for any errors, omissions, orinterruptions therein, regardless of the cause, or for the results obtained from the use of any part of the Report. EACH CRISIL RATINGS' PARTY DISCLAIMS ANYAND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESSFOR A PARTICULAR PURPOSE OR USE. In no event shall any CRISIL Ratings Party be liable to any party for any direct, indirect, incidental, exemplary,compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits andopportunity costs) in connection with any use of any part of the Report even if advised of the possibility of such damages.

CRISIL Ratings may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of the instruments, facilities,securities or from obligors. CRISIL Rating's public ratings and analysis as are required to be disclosed under the regulations of the Securities and Exchange Board ofIndia (and other applicable regulations, if any) are made available on its web sites, www.crisil.com (free of charge). Reports with more detail and additionalinformation may be available for subscription at a fee - more details about ratings by CRISIL Ratings are available here: www.crisilratings.com.

CRISIL Ratings and its affiliates do not act as a fiduciary. While CRISIL Ratings has obtained information from sources it believes to be reliable, CRISIL Ratings doesnot perform an audit and undertakes no duty of due diligence or independent verification of any information it receives and / or relies in its Reports. CRISIL Ratingshas established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process. CRISILRatings has in place a ratings code of conduct and policies for analytical firewalls and for managing conflict of interest. For details please refer to:http://www.crisil.com/ratings/highlightedpolicy.html

Rating criteria by CRISIL Ratings are generally available without charge to the public on the CRISIL Ratings public web site, www.crisil.com. For latest ratinginformation on any instrument of any company rated by CRISIL Ratings you may contact CRISIL RATING DESK at [email protected], or at (0091) 1800267 1301.

This Report should not be reproduced or redistributed to any other person or in any form without a prior written consent of CRISIL Ratings.

All rights reserved @ CRISIL Ratings Limited. CRISIL Ratings Limited is a wholly owned subsidiary of CRISIL Limited.

CRISIL Ratings uses the prefix ‘PP-MLD’ for the ratings of principal-protected market-linked debentures (PPMLD) with effect from November 1, 2011 to comply withthe SEBI circular, "Guidelines for Issue and Listing of Structured Products/Market Linked Debentures". The revision in rating symbols for PPMLDs should not beconstrued as a change in the rating of the subject instrument. For details on CRISIL Ratiings' use of 'PP-MLD' please refer to the notes to Rating scale for DebtInstruments and Structured Finance Instruments at the following link: www.crisil.com/ratings/credit-rating-scale.html