Solutions of Multivariate Polynomial Systems using Macaulay Resultant Expressions

Upload

independentCategory

view

4download

0

Page 1 of 23

RAJASTHAN ELECTRICITY REGULATORY COMMISSION, JAIPUR

Suo-Motu

In the matter of Determination of Benchmark Capital Cost for Solar PV

and Solar Thermal Power Projects and resultant Generic Levellised Tariff.

Coram :

Shri D.C. Samant, Chairman

Shri S.K. Mittal, Member

Shri S. Dhawan, Member

Date of hearing: 13.03.2012

Date of Order: 30.05.2012

ORDER

BACKGROUND

1. In accordance with the provisions of Electricity Act, 2003 and

National Tariff Policy notified by Govt. of India (GoI), the

Commission under its RERC (Terms and Conditions for

Determination of Tariff) Regulations, 2009 had incorporated the

enabling provisions for determination of tariff of solar power

projects.

2. Commission has issued the last tariff order on 25.05.2010 after

taking into account the comments received from the stakeholders

on the draft tariff order dt. 10.03.2010 wherein the Commission has

determined generic tariff for solar power. This tariff was applicable

for solar plants (SPV) to be commissioned by 31.03.2012 and solar

thermal plants to be commissioned by 31.03.2013 wherein PPAs

have been signed by 31.03.2011. The commission as per its order

dt 29.09.2010 has amended the tariff order dt 25.5.2010 to extend

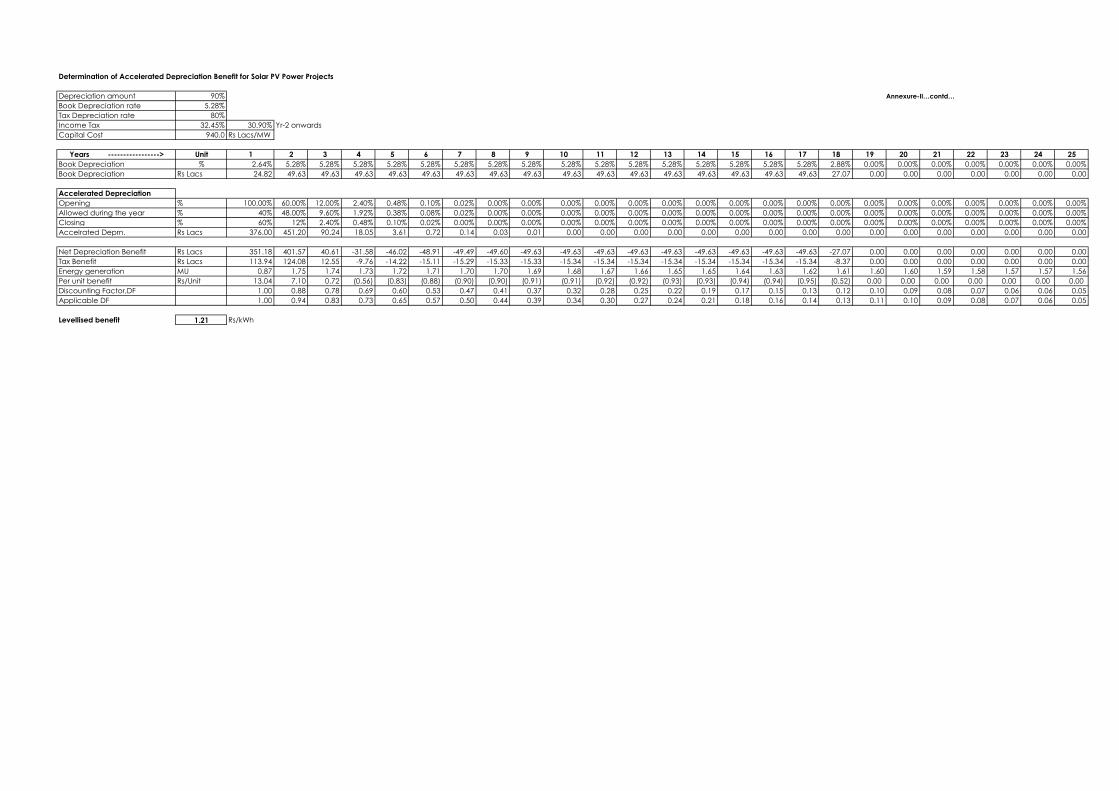

the tariff as applicable for MW scale solar thermal plants to small

solar thermal plants covered under GoI’s subsidy scheme. The

tariffs as per the orders dt 25.05.2010 and 29.09.2010 are given in

the following Table-1.

Page 2 of 23

Table-1: Solar Tariffs in Rajasthan as per orders dt. 25.05.2010 and

29.09.2010

3. CERC had issued tariff order dt 26.04.2010, applicable for projects

where the PPAs were to get signed by 31.03.2011 and

commissioned by 31.03.2012 for SPV projects and by 31.03.2013 for

solar thermal projects and the levellised tariff for solar PV was

`17.91 per kWh and for solar thermal it was `15.31 per kWh.

4. There has been a steady decline in the tariffs due to lower cost of

solar modules and components and the emerging competitive

scenario in the country. This is best exemplified by the reverse

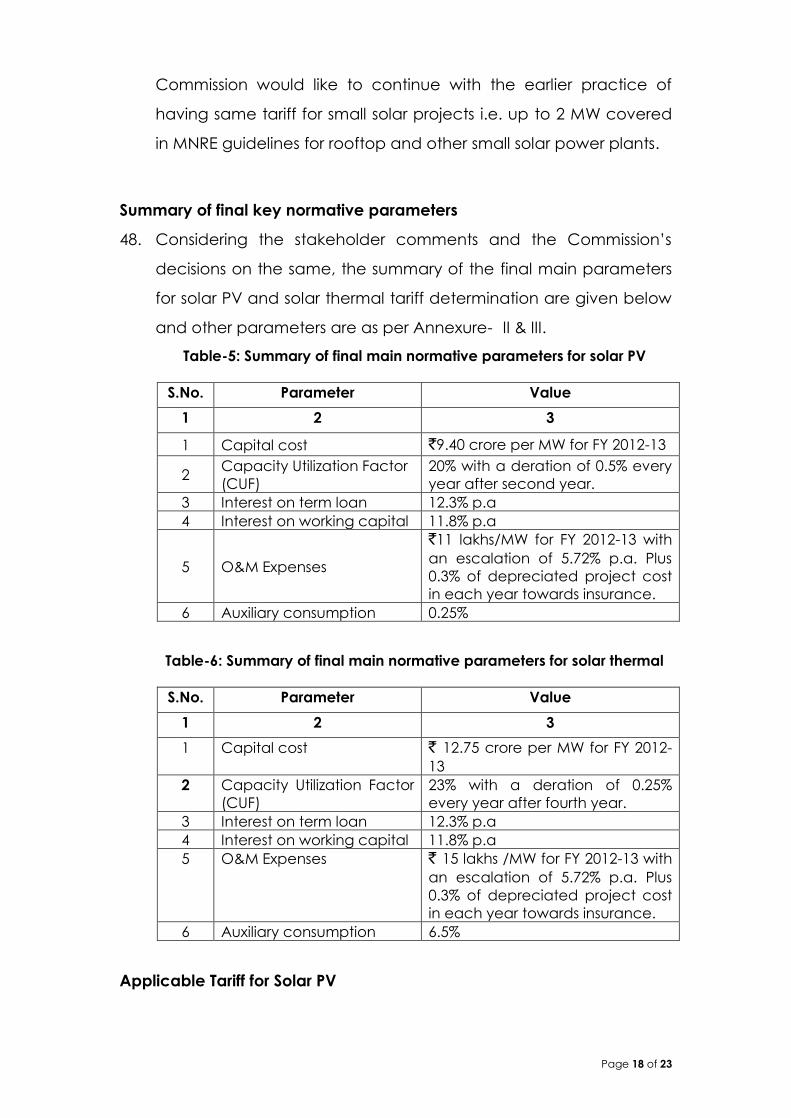

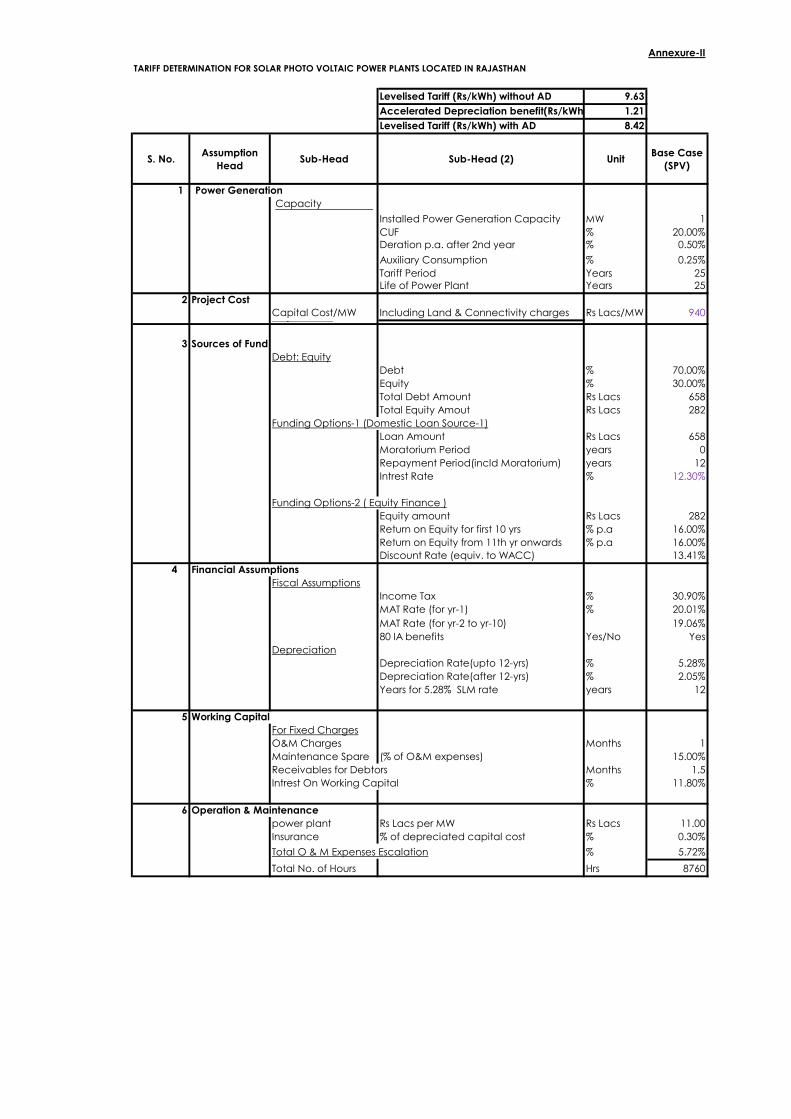

bidding process that was adopted for allotment of projects in the

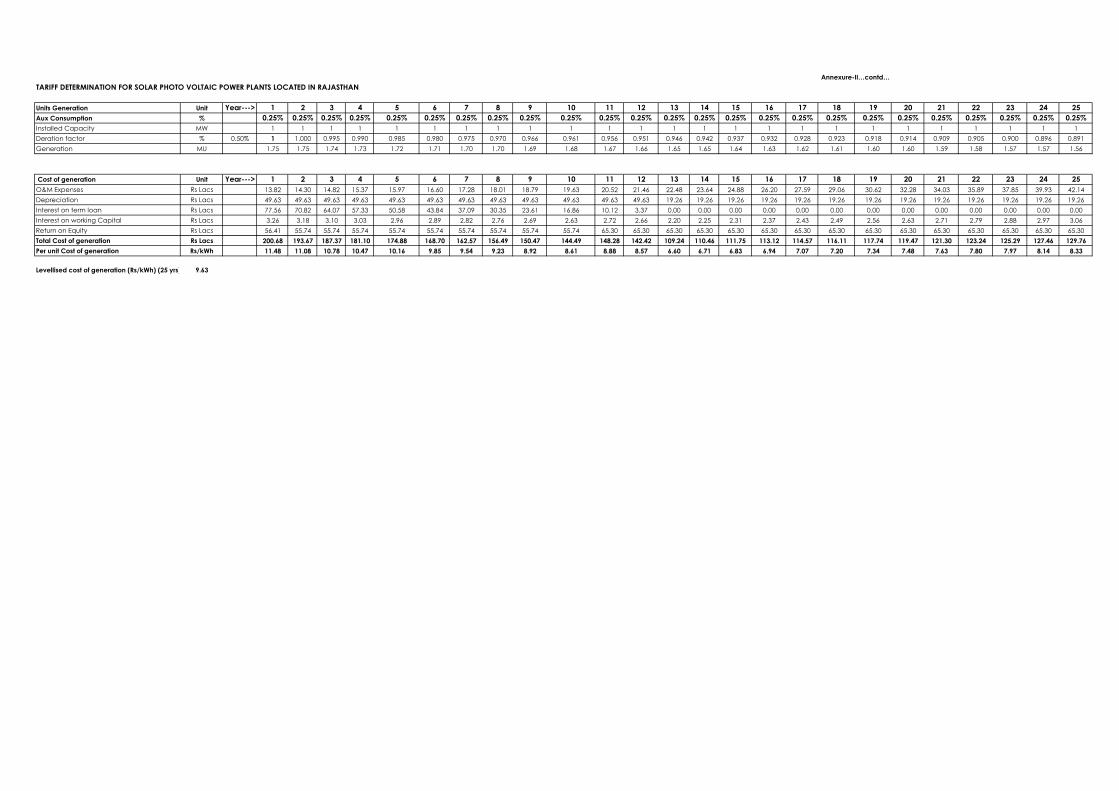

1st Batch of Phase 1 of JNNSM, by NTPC Vidyut Vyapar Nigam Ltd

(NVVN), the nodal agency under JNNSM Phase-1 for purchase of

solar power, which has resulted in substantial discounts on the

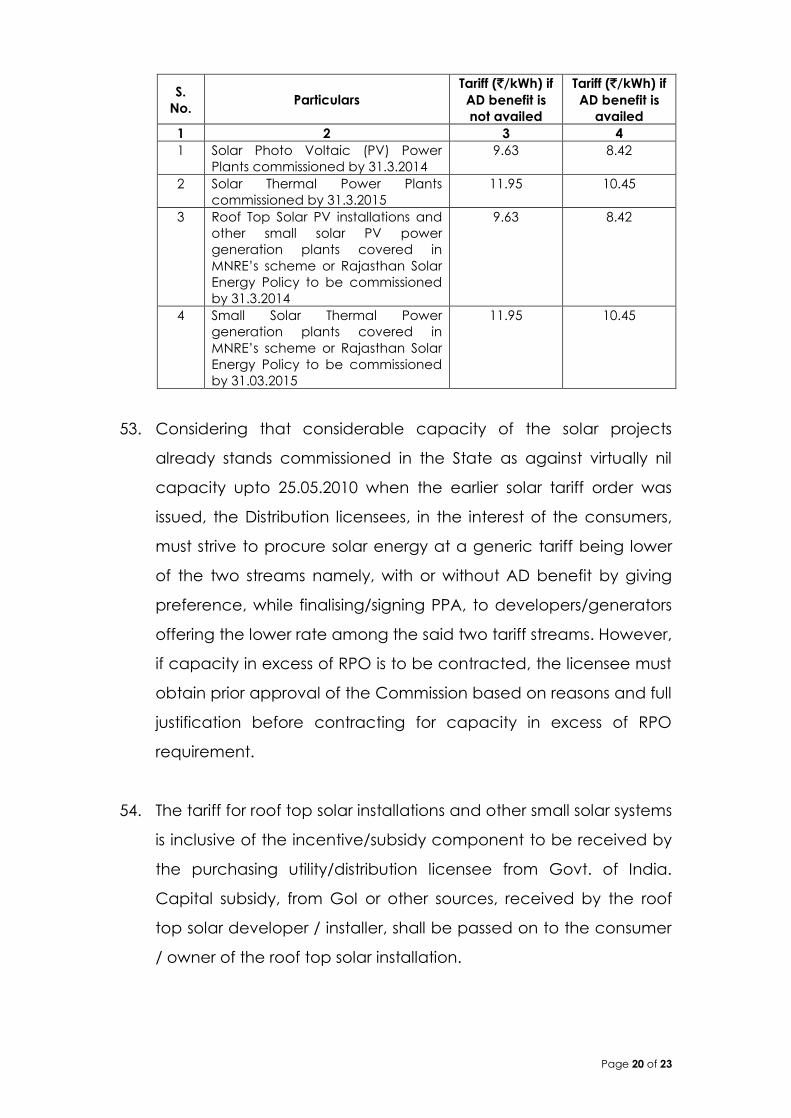

benchmark tariffs, given in para 3 above, that were determined

by CERC.

5. CERC has, subsequently, issued order dt. 09.11.2010 (255/2010 suo-

motu) for Determination of benchmark capital cost norms for Solar

PV power projects and Solar Thermal power projects applicable

S.No. Particulars

Tariff (in `/kWh)

without AD

benefit

Tariff (in `/kWh)

if AD benefit is

availed

1 2 3 4

1 Solar Thermal Power Plants

commissioned by 31.3.2013

12.58 10.99

2 Solar Photo Voltaic (PV)

Power Plants commissioned

by 31.3.2012

15.32 13.19

3 Roof Top Solar PV Installations

and other small solar power

generation plants covered in

GoI’s subsidy scheme

commissioned by 31.3.2012

15.32 13.19

4 Small Solar Thermal Power

generation plants covered in

GoI’s subsidy scheme

commissioned by 31.03.2013

12.58 10.99

Page 3 of 23

during FY 2011-12. The revised benchmark capital cost for solar PV

was determined as `14.42cr per MW and `15cr per MW for solar

thermal projects for the FY 2011-12. Further, CERC has issued final

order dt 09.11.2010 (256/2010 suo-motu) for determination of

generic levellised generation tariff. The generic tariff was

determined as `15.39 per kWh for Solar PV and `15.04 per kWh for

Solar Thermal and would be applicable for projects wherein the

PPAs would be signed by 31.03.2012 and the plants would get

commissioned by 31.03.2013 in case of solar PV and by 31.03.2014

in case of solar thermal.

6. The final tariffs that resulted in selection of solar PV projects for the

2nd Batch of Phase-1 of JNNSM in December, 2011 through

bidding, were again substantially lower than the benchmark CERC

tariff i.e. `15.39 per kWh consequent to lower capital costs on

account of sharp drop in solar PV module prices.

7. Government of Rajasthan has issued Rajasthan Solar Energy Policy,

2011 vide Notification No. F. 20 (6) Energy /2010 dated 19.04.2011

for promoting solar energy in Rajasthan. Some of the key

objectives of the policy are

Developing a global hub of solar power of 10000-12000 MW

capacity in next 10 to 12 years to meet energy requirements of

Rajasthan and India.

Contributing to long term energy security of Rajasthan as well

as ecological security by reduction of carbon emissions and

dependence on fossil fuel resources.

Productive use of abundant wastelands, thereby utilizing the

non-industrialized desert area for creation of an industrial hub.

Creating conditions favourable to solar manufacturing

capabilities by providing fiscal incentives. Generating large

direct and indirect employment opportunities in solar and

allied industries

Page 4 of 23

To achieve the grid parity in next 7 to 8 years, the State will

encourage the Solar Power Developers to establish their

manufacturing plants in Rajasthan.

8. Commission vide its earlier order dated 2.04.2008 has prescribed

an obligation on the distribution licensees to buy 50 MW of solar

power and the same was increased to 100MW vide the

Commission’s order dt 25.05.2010. RERC notification No.

RERC/Secy./Regulation-85 dtd. 24th May, 2011, gives the

Renewable Purchase Obligation in respect of various sources

expressed as percentage of energy consumption1 and in respect

of solar, the obligation for FY 2011-12, FY 2012-13 & FY 2013-14

being 0.5%, 0.75% and 1.00% respectively.

9. CERC vide notification No. L-1/94/CERC/2011 dt 06.02.2012 has

determined the benchmark capital cost for solar PV projects at

`10.00 crores/MW with the CUF of 19% ( deration of modules has

been considered as nil and auxiliary consumption as nil) and

`13.00 crores/MW for solar thermal projects with a CUF of 23% (

deration has been considered as nil and auxiliary consumption as

10%). The interest rate for term loan was taken as 300 basis points

over the average of the Base Rate of SBI for the first six months of

the previous year and for working capital the interest rate was

considered as 350 basis points over the average of the Base Rate

of SBI for the first six months of the previous year.

10. CERC has issued final order on 27.03.2012 (Petition No. 35/2012

(Suo-Motu) in respect of the above and has determined a generic

tariff of `10.39 per unit (`9.35 per unit if AD benefit is availed) in

respect of solar PV projects and has determined a generic tariff of

1 energy consumption shall mean ‘consumption of obligated entity’ as defined in regulation 3(g) of RERC

(Renewable Energy Certificate and Renewable Purchase Obligation Compliance Framework) Regulations,

2010.

Page 5 of 23

`12.46 per unit (`11.22 per unit if AD benefit is availed) for solar

thermal projects whose PPAs would be signed by 31.03.2013 and

to be commissioned by 31.03.2014 in the case of solar PV projects

and by 31.03.2015 in the case of solar thermal projects.

11. The RERC tariff orders for solar plants dated 25.5.2010 and dated

29.9.2010 were applicable for the projects that have signed PPA

by 31.03.2011 and to be commissioned by 31.03.2012 the case of

solar PV and by 31.03.2013 in the case of solar thermal.

Draft Tariff Order

12. The Commission undertook an exercise to determine Benchmark

Capital Costs for Solar PV and Solar Thermal Power Projects and

resultant Generic Levellised Tariff for the MW scale solar plants

where PPAs would be signed by 31.03.2013 and to be

commissioned by 31.03.2014 in the case of solar PV plants and to

be commissioned by 31.03.2015 in the case of solar thermal plants.

13. In the draft tariff order issued on 23.01.2012, Commission

considered it appropriate to retain the financial norms, as

stipulated in Part – III of RERC Tariff Regulations, 2009 i.e. debt :

equity ratio, RoE, O&M escalation etc, that are applicable for the

tariff determination of other RE sources like wind/bio-mass and

were used for tariff order dt 25.05.2010 for solar projects. All the

parameters, for both solar PV and solar thermal projects, were

retained as per the tariff order dt 25.05.2010 except for capital

cost, CUF, interest rate and O&M expenses. The summary of Norms

and Parameters considered in the draft order are as under:

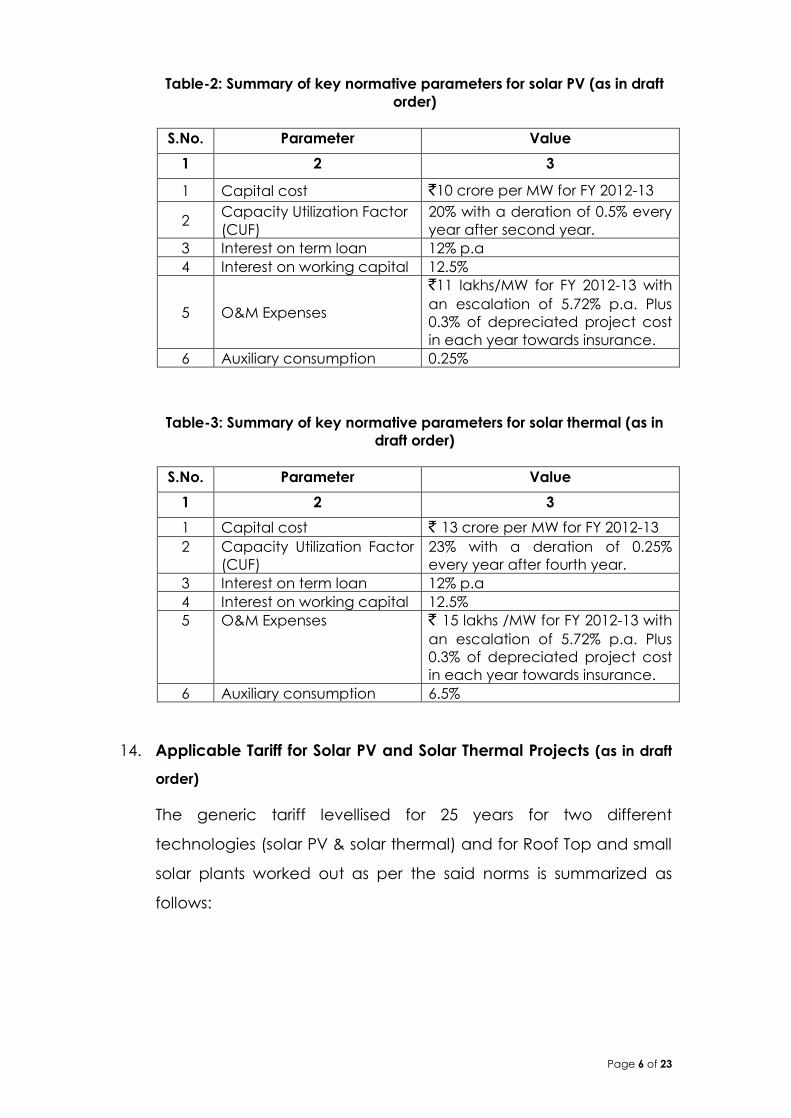

Page 6 of 23

Table-2: Summary of key normative parameters for solar PV (as in draft

order)

S.No. Parameter Value

1 2 3

1 Capital cost `10 crore per MW for FY 2012-13

2 Capacity Utilization Factor

(CUF)

20% with a deration of 0.5% every

year after second year.

3 Interest on term loan 12% p.a

4 Interest on working capital 12.5%

5 O&M Expenses

`11 lakhs/MW for FY 2012-13 with

an escalation of 5.72% p.a. Plus

0.3% of depreciated project cost

in each year towards insurance.

6 Auxiliary consumption 0.25%

Table-3: Summary of key normative parameters for solar thermal (as in

draft order)

S.No. Parameter Value

1 2 3

1 Capital cost ` 13 crore per MW for FY 2012-13

2 Capacity Utilization Factor

(CUF)

23% with a deration of 0.25%

every year after fourth year.

3 Interest on term loan 12% p.a

4 Interest on working capital 12.5%

5 O&M Expenses ` 15 lakhs /MW for FY 2012-13 with

an escalation of 5.72% p.a. Plus

0.3% of depreciated project cost

in each year towards insurance.

6 Auxiliary consumption 6.5%

14. Applicable Tariff for Solar PV and Solar Thermal Projects (as in draft

order)

The generic tariff levellised for 25 years for two different

technologies (solar PV & solar thermal) and for Roof Top and small

solar plants worked out as per the said norms is summarized as

follows:

Page 7 of 23

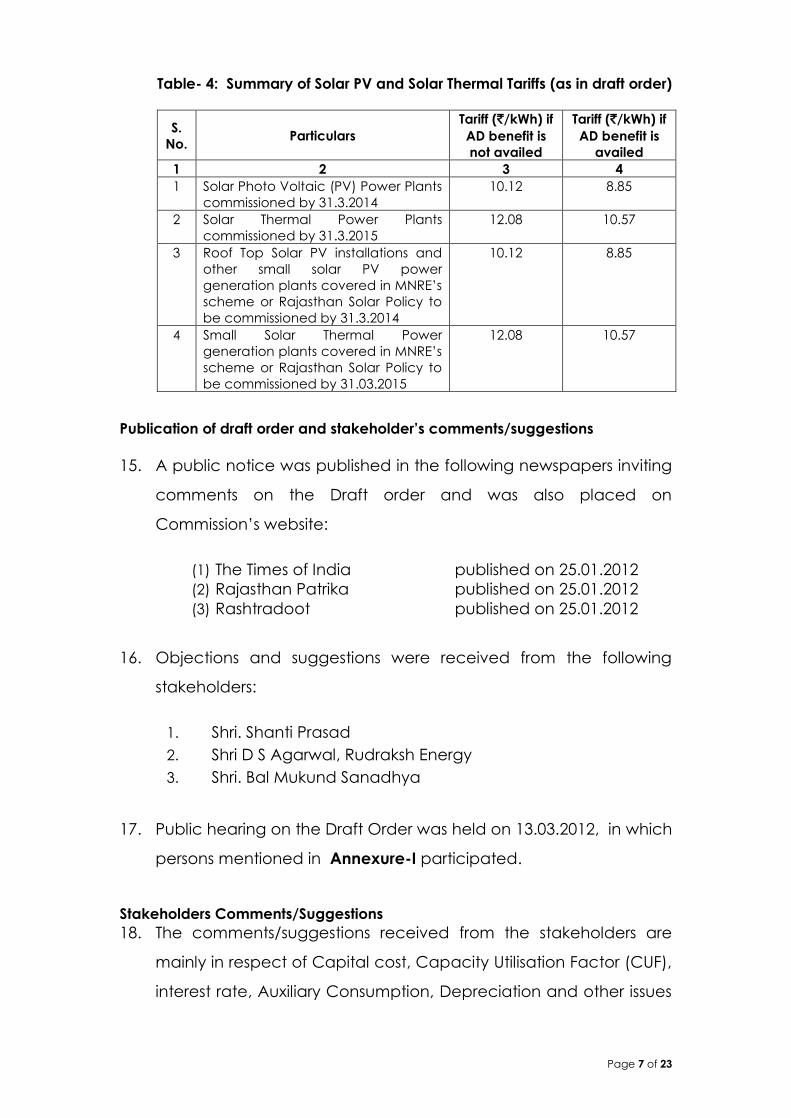

Table- 4: Summary of Solar PV and Solar Thermal Tariffs (as in draft order)

S.

No. Particulars

Tariff (`/kWh) if

AD benefit is

not availed

Tariff (`/kWh) if

AD benefit is

availed

1 2 3 4

1 Solar Photo Voltaic (PV) Power Plants

commissioned by 31.3.2014

10.12 8.85

2 Solar Thermal Power Plants

commissioned by 31.3.2015

12.08 10.57

3 Roof Top Solar PV installations and

other small solar PV power

generation plants covered in MNRE’s

scheme or Rajasthan Solar Policy to

be commissioned by 31.3.2014

10.12 8.85

4 Small Solar Thermal Power

generation plants covered in MNRE’s

scheme or Rajasthan Solar Policy to

be commissioned by 31.03.2015

12.08 10.57

Publication of draft order and stakeholder’s comments/suggestions

15. A public notice was published in the following newspapers inviting

comments on the Draft order and was also placed on

Commission’s website:

(1) The Times of India published on 25.01.2012

(2) Rajasthan Patrika published on 25.01.2012

(3) Rashtradoot published on 25.01.2012

16. Objections and suggestions were received from the following

stakeholders:

1. Shri. Shanti Prasad

2. Shri D S Agarwal, Rudraksh Energy

3. Shri. Bal Mukund Sanadhya

17. Public hearing on the Draft Order was held on 13.03.2012, in which

persons mentioned in Annexure-I participated.

Stakeholders Comments/Suggestions

18. The comments/suggestions received from the stakeholders are

mainly in respect of Capital cost, Capacity Utilisation Factor (CUF),

interest rate, Auxiliary Consumption, Depreciation and other issues

Page 8 of 23

relating to approval of bid documents, power evacuation

arrangement and public awareness. These comments have been

dealt with in the following paras.

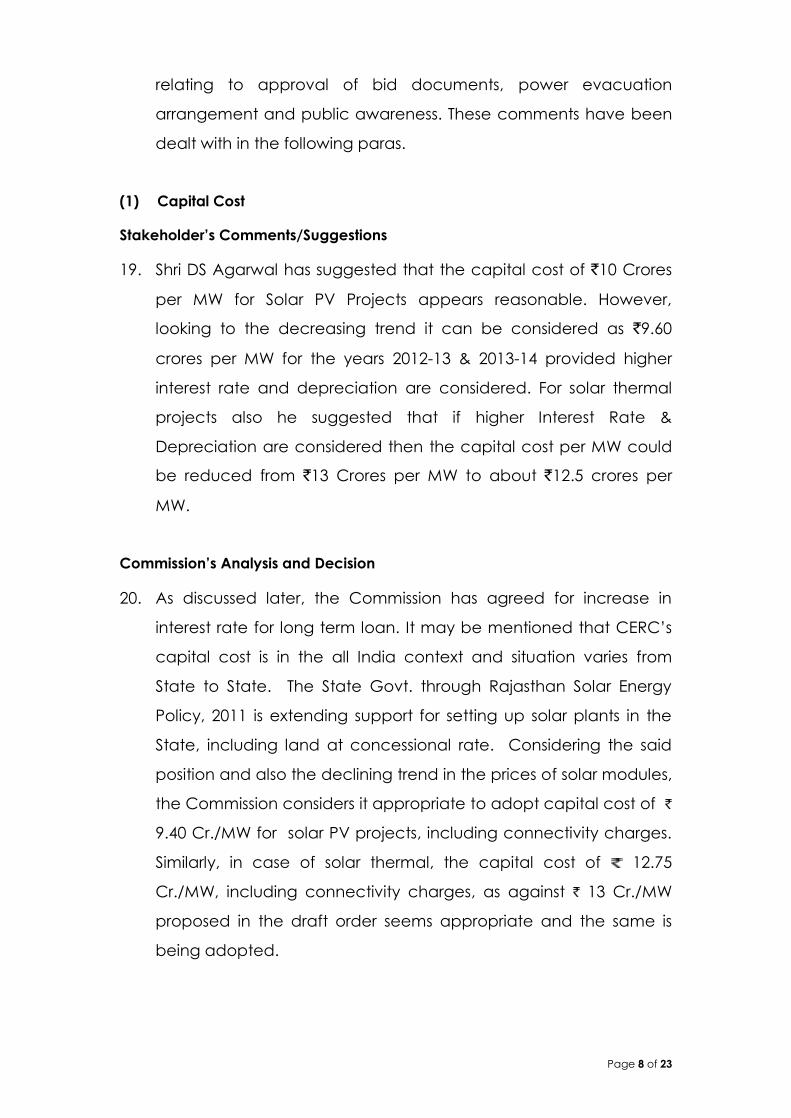

(1) Capital Cost

Stakeholder’s Comments/Suggestions

19. Shri DS Agarwal has suggested that the capital cost of `10 Crores

per MW for Solar PV Projects appears reasonable. However,

looking to the decreasing trend it can be considered as `9.60

crores per MW for the years 2012-13 & 2013-14 provided higher

interest rate and depreciation are considered. For solar thermal

projects also he suggested that if higher Interest Rate &

Depreciation are considered then the capital cost per MW could

be reduced from `13 Crores per MW to about `12.5 crores per

MW.

Commission’s Analysis and Decision

20. As discussed later, the Commission has agreed for increase in

interest rate for long term loan. It may be mentioned that CERC’s

capital cost is in the all India context and situation varies from

State to State. The State Govt. through Rajasthan Solar Energy

Policy, 2011 is extending support for setting up solar plants in the

State, including land at concessional rate. Considering the said

position and also the declining trend in the prices of solar modules,

the Commission considers it appropriate to adopt capital cost of

9.40 Cr./MW for solar PV projects, including connectivity charges.

Similarly, in case of solar thermal, the capital cost of 12.75

Cr./MW, including connectivity charges, as against 13 Cr./MW

proposed in the draft order seems appropriate and the same is

being adopted.

Page 9 of 23

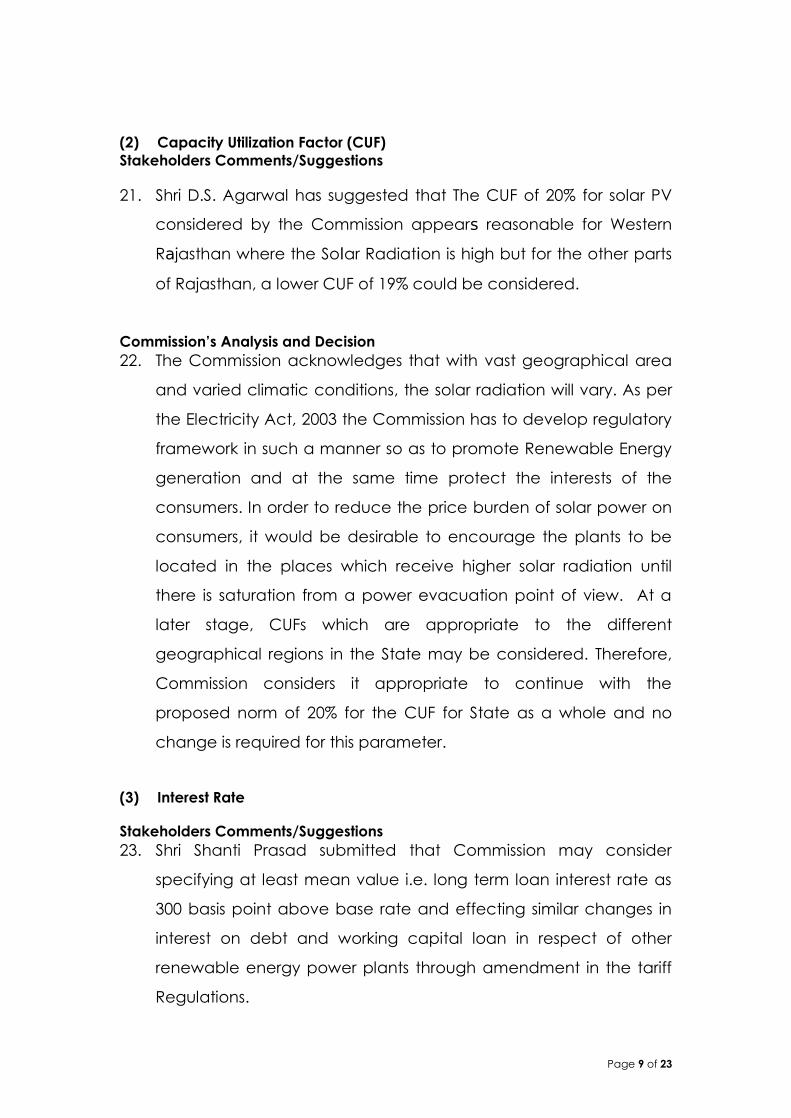

(2) Capacity Utilization Factor (CUF)

Stakeholders Comments/Suggestions

21. Shri D.S. Agarwal has suggested that The CUF of 20% for solar PV

considered by the Commission appears reasonable for Western

Rajasthan where the Solar Radiation is high but for the other parts

of Rajasthan, a lower CUF of 19% could be considered.

Commission’s Analysis and Decision

22. The Commission acknowledges that with vast geographical area

and varied climatic conditions, the solar radiation will vary. As per

the Electricity Act, 2003 the Commission has to develop regulatory

framework in such a manner so as to promote Renewable Energy

generation and at the same time protect the interests of the

consumers. In order to reduce the price burden of solar power on

consumers, it would be desirable to encourage the plants to be

located in the places which receive higher solar radiation until

there is saturation from a power evacuation point of view. At a

later stage, CUFs which are appropriate to the different

geographical regions in the State may be considered. Therefore,

Commission considers it appropriate to continue with the

proposed norm of 20% for the CUF for State as a whole and no

change is required for this parameter.

(3) Interest Rate

Stakeholders Comments/Suggestions

23. Shri Shanti Prasad submitted that Commission may consider

specifying at least mean value i.e. long term loan interest rate as

300 basis point above base rate and effecting similar changes in

interest on debt and working capital loan in respect of other

renewable energy power plants through amendment in the tariff

Regulations.

Page 10 of 23

24. Shri D.S. Agarwal of Rudrakash Energy submitted that Interest Rate

on term loans adopted as SBI Base Rate + 200 basis points appears

to be on lower side and suggested that it should be SBI Base Rate

+ 300 basis points. Similarly, the interest rate on short term loan

should be SBI Base Rate + 300 basis points.

Commission’s Analysis and Decision

25. It may be mentioned that Commission, in the draft Order , has

proposed to consider the SBI base rate as on 31st January,2012 plus

200 basis points for long term loans and SBI base rate as on 31st

January 2012 plus 250 basis points for interest on working capital

loans. However, recently Commission has finalised the fourth

amendment in RERC Tariff Regulations, 2009 where Commission

has considered average of SBI base rate for first six months of

previous financial year as the benchmark for interest rate as the

same period has been considered by CERC. In view of this

Commission considers it appropriate to take average SBI base rate

for first six months of previous financial year as bench mark for the

purpose of interest rate.

26. The Commission has taken note of the interest rate charged by

IREDA and PFC for various renewable energy projects and Interest

rate norm adopted by CERC for Solar projects as well as

suggestions of stakeholders to increase interest rate and considers

it appropriate to adopt the interest rate on long term loans as SBI

base rate (average of the base rate of the first six months of the

previous year) + 300 basis points as against 200 basis points above

the SBI Base Rate on 31st January, 2012.

27. As regards interest rate on working capital, since the loan

requirement is for shorter duration with lower associated risk, the

Page 11 of 23

interest rate would normally be lower than that of long term loan.

Commission, therefore, considers it appropriate to adopt interest

rate norm of average SBI base rate for first six months of previous

financial year plus 250 bps for working capital requirement, being

50 base points lower than that of long-term loan.

(4) Auxiliary Consumption

Stakeholders Comments/Suggestions

28. Shri D.S. Agarwal has suggested that for solar thermal plants

auxilliary consumption @ 6.5% appears to be on lower side.

Commission’s Analysis and Decision

29. Commission is of the view that the Auxiliary Consumption norm for

solar thermal projects was arrived at after detailed deliberations.

Further, the practical experience relating to solar thermal projects

so far is limited. It would, therefore, be inappropriate to change

the auxiliary consumption norm. The proposed auxiliary

consumption norm of 6.50% for solar thermal projects is, therefore ,

being retained.

(5) Depreciation

Stakeholders Comments/Suggestions

30. Shri Shanti Prasad has commented that in the calculations of tariff,

Depreciation has been considered at the rate of 5.28% p.a. for 12

years and 2.05% thereafter. RERC Tariff Regulations, 2009 specifies

depreciation to be calculated for renewable power plants as per

Regulation 23 and Appendix-1. Different rates of depreciation as

per asset categories (e.g. land, office buildings, power plant, self

propelled vehicles, communication equipments , IT equipments /

softwares, etc) have been specified at Appendix-1 of the

Regulations. Commission may clearly specify whether

depreciation will be determined category wise as per Appendix-1

or at flat rate(s) as per assumptions in the calculations of tariff and

Page 12 of 23

may, if required, accordingly amend the regulations. Similarly,

Written Down Value (WDV) method does not consider salvage

value (vide CERC ‘s calculations on RE power plant tariffs) and on

this account there is conflict between WDV method and

regulation 23.

31. Shri D.S. Agarwal has suggested that the rate of depreciation

should be 5.83% instead of 5.28% considered by the Commission.

Commission’s Analysis and Decision

32. In generic tariff determination, the Regulations have specified

lump sum capital-cost without assets-wise break-up. In view of this,

while item-wise depreciation rate can be applied for project

specific tariff, wherein different items of the project cost are

approved based on prudent check; the same is not applicable for

RE projects under generic tariff due to the lumpsum project cost

adopted. CERC also, as far as RE projects are concerned, has

been applying depreciation at a uniform rate on the adopted

project cost. The said position has been suitably incorporated in

Appendix-I of regulation 23 vide Fourth Amendment finalized

recently.

33. As regards the suggestion of conflict between WDV method and

regulation 23, it is stated that the issue raised, prima facie, seems

to relate with methodology of calculation of Accelerated

Depreciation benefit. The methodology has been revisited and AD

benefit has been reworked by following the method adopted by

CERC in applying depreciation on notional basis to calculate the

gain in Income Tax on Availing Accelerated Depreciation.

Depreciation of 5.28% as per straight line method (Book

depreciation as per Companies Act,1956) has been compared

with depreciation allowable as per Income Tax Act 1962 i.e. 80% of

written down value. For the purpose of calculations, it has been

Page 13 of 23

considered that the project would capitalized during second half

of the relevant Financial Year (i.e. Project getting commissioned

after 180 days of the Financial Year), as is being followed by CERC.

As per Income Tax Act, the depreciation rate applicable for the

first year would be 40% (50% of 80%). The income tax benefit, likely

to be so availed , has been worked out considering income tax

rate of 32.445% (=30% Income Tax Rate + 5% Surcharge+ 3%

Education Cess) for first year and 30.90%(=30% Income Tax Rate +

3% Education Cess) for subsequent years on the net depreciation

benefit. The per unit levelised AD benefit has been computed by

discounting the net depreciation benefit considering weighted

average cost of capital (WACC) as the discount factor i.e. 13.41%

(= 0.7x12.30% + 0.3 x16%).

34. In addition to above, Commission would like to clarify that

presently parameters for determination of tariff for sale of power

from solar power projects are not governed by the existing RERC

Tariff Regulations, 2009. For the purpose of determination of

generic tariff, depreciation is being applied at the general rate of

5.28% for first 12 years and remaining depreciable value spread

over the balance useful life based on norms adopted in this order.

(6) Other Comments

(a) Regulatory Approval for the Bid Documents under Competitive Bidding

Process

Stakeholders Comments/Suggestions

35. Shri Shanti Prasad has commented that Para 42 of draft order

specifies competitive tariff bidding in respect of new renewable

energy generating stations to be commissioned during Control

Period. Reg. 87 of RERC Tariff regulations specifies that the

Commission shall adopt the tariff for RE power projects as

envisaged under Section 63 of the Act and for the purpose of

competitive bidding process, until the Central Government notifies

Page 14 of 23

the competitive bidding guidelines including the Standard Bid

Documents as applicable for RE projects, the Commission shall

approve the bid documents or deviations applicable for

conventional power plant under case-2 for each type of RE

sources separately. However, for competitive bidding by Discoms

or by any agency on their behalf, the procedures need regulatory

scrutiny under section 63 and aforesaid reg. 87. The Guidelines for

Determination of Tariff by Bidding Process for Procurement of

Power by Distribution Licensees issued by the Govt. of India vide

notification of 19.1.2005, provides vide para 5.15 that the bidder

who has quoted lowest levellised tariff as per evaluation

procedure, shall be considered for the award. Thus these

guidelines do not provide for selection of bidders other than lowest

tariff. Award(s) on L1, L2, L3, etc offers till capacity requirement is

fulfilled, as has been done by NVVNL, is a major deviation requiring

regulatory commission’s approval. Commission , while considering

such deviation, may consider strictly following Govt. of India’s

guidelines with rebidding for balance quantity or following

NVVNL’s methodology or not considering different rates for the

same bidder or restricting selection within a percentage range

above L1 offer and rebidding for balance capacity or to modify

penalty and BG requirement so that it may lead to further lower

tariff or to adopt both competitive bidding as well as generic tariff

route with weighted average competitive bid price plus margin

(as determined by overall success rate) as one of the guiding

factor to determine generic tariff.

36. Shri D S Agarwal has commented on Clauses 41 & 42 that for the

projects to be selected through Competitive Bidding, the bidder

should offer discount on the Bench Mark tariff proposed at para 39

i.e, `10.12 for Solar PV & ` 12.08 for Solar thermal instead of final

tariff to be determined by the commission, so as to avoid delay.

Page 15 of 23

Commission’s Analysis and Decision

37. Commission has taken note of the suggestion /comments.

Commission would like to state that the existing competitive

bidding guidelines issued by Ministry of Power (MoP) under Section

63 of the Electricity Act 2003 do not cover the procurement of

power from RE sources and a committee has recently been

constituted to, inter-alia, evolve guidelines for competitive bidding

for procurement of power from such sources.

38. The Commission has recently examined the question of specifying

Regulations/ guidelines for introduction of competitive bidding in

the State. In the draft 4th amendment in RERC (Terms and

Conditions for determination of Tariff) Regulation, 2012 placed in

public domain and which was subsequently dropped vide order

dated 10.5.2011, the Commission came to the following

conclusion, as given in para 13 of the said order:

“In the light of the fact that Hon’ble Supreme Court has stayed

the directions of Hon’ble Tribunal in respect of issue of

guidelines by KERC to introduce competitive bidding process

and considering the stand taken by the Central Government in

the Delhi High Court, it emerges that the Commission through

Regulation or otherwise cannot frame guidelines for

transparent bidding under Sec. 63 or any other provision of the

Electricity Act and Sec. 62 is the only available option for tariff

determination in the circumstances prevailing as on date. “

39. Accordingly, the competitive bidding stipulated in draft order

would not be applicable and instead generic tariff under Section

62 of the Electricity Act 2003 is being determined through this

order.

(b) Other Comments – Power Evacuation Arrangement

Stakeholders Comments/Suggestions

40. Shri Shanti Prasad has commented that with number of solar

projects coming in and around the same substation, RVPN/

Page 16 of 23

Discoms will find it difficult to allocate one bay for each project

due to space constraints or to create additional substations due to

resources constraints. It would be appropriate that regulatory

commission considers creation of such substations and their

locations, approved by RVPN/Discoms (after considering, interalia,

no interference with Right of Way of future transmission /

Distribution system) by the private sector so that there is common

transmission line for number of power stations created by

developer of solar park or transmission licensee. It is suggested

that Commission may cover such cases by specifying that in such

cases losses and wheeling charges will be separately determined

from generating station to pooling station and for common

transmission system at pooling station and from pooling station to

substation of RVPN/Discoms on actual cost or benchmark cost

whichever is less.

Commission’s Analysis and Decision

41. Commission is of the view that the scope of present regulatory

exercise is limited to the determination tariff for sale of power from

solar power projects to the Discoms of the State and therefore,

issues relating to transmission of such power fall outside the

purview of the present order.

(c) Other Comments - General

Stakeholders Comments/Suggestions

42. Shri Bal Mukund Sanadhya has given various general comments

pertaining to public awareness of the regulatory process,

determination of tariff parameters, need for discussions on the

draft order at various state and national level fora etc.,

Page 17 of 23

Commission’s Analysis and Decision

43. The Commission is following the Electricity (Procedure for Previous

Publication) Rules, 2005 as provided under the Electricity Act, 2003

which is fair and adequate.

Roof top and small solar PV and thermal systems: Applicable Tariff (as

in Draft Order)

44. The Commission is of the considered view that the generic tariff as

applicable for MW scale solar plants be extended to roof top and

small solar power generation systems covered under MNRE /

JNNSM schemes and Rajasthan Solar Energy Policy, 2011.

Stakeholders Comments/Suggestions

45. Shri D.S. Agarwal has commented that Tariff for Roof Top & Small

Solar PV & Thermal Systems should be higher than that of MW

scale plants, since there will be a higher Capital cost per MW &

higher O & M charges for small projects.

Commission’s Analysis and Decision

46. Commission would like to state that setting up of a MW scale

power plant a set of preliminary works are required to be done

which also include land acquisition and development etc. For a

typical green field grid connected solar PV MW scale project, the

cost component towards land, civil and general works, preliminary

and preoperative expenses comes in the vicinity of 17-19% . For

Roof Top Solar PV systems such expenses would be lower.

However, CUF for roof top PV systems would be lower as such

systems may be located predominantly in the areas having lesser

solar radiation when compared with western Rajasthan which has

better solar radiation potential and also due to impact of shading

of trees/adjoining buildings.

47. Considering the above position, Commission at present finds no

merit in specifying different tariff for such systems. Similarly,

Page 18 of 23

Commission would like to continue with the earlier practice of

having same tariff for small solar projects i.e. up to 2 MW covered

in MNRE guidelines for rooftop and other small solar power plants.

Summary of final key normative parameters

48. Considering the stakeholder comments and the Commission’s

decisions on the same, the summary of the final main parameters

for solar PV and solar thermal tariff determination are given below

and other parameters are as per Annexure- II & III.

Table-5: Summary of final main normative parameters for solar PV

S.No. Parameter Value

1 2 3

1 Capital cost `9.40 crore per MW for FY 2012-13

2 Capacity Utilization Factor

(CUF)

20% with a deration of 0.5% every

year after second year.

3 Interest on term loan 12.3% p.a

4 Interest on working capital 11.8% p.a

5 O&M Expenses

`11 lakhs/MW for FY 2012-13 with

an escalation of 5.72% p.a. Plus

0.3% of depreciated project cost

in each year towards insurance.

6 Auxiliary consumption 0.25%

Table-6: Summary of final main normative parameters for solar thermal

S.No. Parameter Value

1 2 3

1 Capital cost ` 12.75 crore per MW for FY 2012-

13

2 Capacity Utilization Factor

(CUF)

23% with a deration of 0.25%

every year after fourth year.

3 Interest on term loan 12.3% p.a

4 Interest on working capital 11.8% p.a

5 O&M Expenses ` 15 lakhs /MW for FY 2012-13 with

an escalation of 5.72% p.a. Plus

0.3% of depreciated project cost

in each year towards insurance.

6 Auxiliary consumption 6.5%

Applicable Tariff for Solar PV

Page 19 of 23

49. Considering the parameters discussed above, the generic tariff for

the solar PV plants is being determined as ` 9.63/kWh, as per

calculation sheet placed at Annnexure-II. This tariff is levellised

tariff for 25 years and applicable for plants commissioned without

availing benefit of Accelerated Depreciation. With AD benefit, the

tariff would be lower by `1.21/kWh i.e. ` 8.42/kWh. This tariff would

be applicable for solar PV plants where PPA is signed on or before

31.03.2013 and which get commissioned on or before 31.03.2014.

Applicable Tariff for Solar Thermal

50. Considering the parameters discussed above, the generic tariff for

the solar thermal power plants is being determined as `11.95/kWh,

as per calculation sheet given in Annexure-III. This tariff is levellised

tariff for 25 years and applicable for plants commissioned without

availing benefit of Accelerated Depreciation. The tariff would be

lower by ` 1.50/kWh if accelerated depreciation is availed i.e. the

tariff would be `10.45/kWh. This tariff would be applicable for solar

thermal plants where PPA is signed on or before 31.03.2013 and

which get commissioned on or before 31.03.2015.

Guidelines for Metering, Billing and other Requirements

51. The guidelines laid down as per order dt 25.05.2010 as regards (i)

Metering and Billing arrangement; (ii) Technical requirements; and

(iii) General Terms and Conditions are being retained and would

be suitably incorporated in the PPA.

Conclusion

52. The generic tariff levellised for 25 years for two different

technologies (solar PV & solar thermal) and for Roof Top and small

solar plants is summarized as under:

Table- 7: Summary of Solar PV and Solar Thermal Tariffs

Page 20 of 23

S.

No. Particulars

Tariff (`/kWh) if

AD benefit is

not availed

Tariff (`/kWh) if

AD benefit is

availed

1 2 3 4

1 Solar Photo Voltaic (PV) Power

Plants commissioned by 31.3.2014

9.63 8.42

2 Solar Thermal Power Plants

commissioned by 31.3.2015

11.95 10.45

3 Roof Top Solar PV installations and

other small solar PV power

generation plants covered in

MNRE’s scheme or Rajasthan Solar

Energy Policy to be commissioned

by 31.3.2014

9.63 8.42

4 Small Solar Thermal Power

generation plants covered in

MNRE’s scheme or Rajasthan Solar

Energy Policy to be commissioned

by 31.03.2015

11.95 10.45

53. Considering that considerable capacity of the solar projects

already stands commissioned in the State as against virtually nil

capacity upto 25.05.2010 when the earlier solar tariff order was

issued, the Distribution licensees, in the interest of the consumers,

must strive to procure solar energy at a generic tariff being lower

of the two streams namely, with or without AD benefit by giving

preference, while finalising/signing PPA, to developers/generators

offering the lower rate among the said two tariff streams. However,

if capacity in excess of RPO is to be contracted, the licensee must

obtain prior approval of the Commission based on reasons and full

justification before contracting for capacity in excess of RPO

requirement.

54. The tariff for roof top solar installations and other small solar systems

is inclusive of the incentive/subsidy component to be received by

the purchasing utility/distribution licensee from Govt. of India.

Capital subsidy, from GoI or other sources, received by the roof

top solar developer / installer, shall be passed on to the consumer

/ owner of the roof top solar installation.

Page 21 of 23

55. A generator claiming the higher tariff worked out for projects

without AD benefit would have to furnish an undertaking in

advance to the buyer regarding AD benefit not being availed

and this would have to be followed for each financial year by a

certificate of the Chief Executive or the person responsible for filing

Income Tax return of the generating unit to the effect that AD

benefit has not been claimed/availed in that financial year.

56. The benefit availed by the solar project developer under the clean

development mechanism shall be shared between the distribution

licensee and project developer in the ratio of 25:75 as provided

under the regulation 42 of RERC Tariff Regulations, 2009.

57. This is also to clarify that the project developer to the extent of

capacity contracted by signing PPA with distribution licensee

would not be availing benefit of REC and such an undertaking

would be incorporated in PPA.

58. As regards grid connectivity charges, this is to state that charges

would be governed as per Regulation 89(2) of current MYT

Regulations. Connectivity charges for capacity exceeding 50 MW

are payable @ 2.00 lac/MW whereas no charges are payable

upto 50 MW. Since the Regulations are valid upto FY 13-14, any

separate order for this period is neither required nor would be

effective to the extent of its variance with the Regulations. When

the earlier order dated 25.5.2010 was issued, not a single MW scale

project had been commissioned in the State. However, the

situation has undergone sea change in past two years after

success of bidding conducted by NVVN under National Solar

Mission. The observation of the Commission in the earlier order

dated 25.5.2010 comes in conflict with the said Regulation once

total installed capacity in the State exceeds 50 MW and

Page 22 of 23

connectivity charges as per Regulation are payable for capacity

getting commissioned beyond the said limit of 50 MW.

59. The metering shall be at the generator premises as provided in

CEA Metering Regulations. However, in case where the injection of

power to the grid is agreed to be at the premises/ (substation) of

the licensee, then tariff shall be calculated after considering losses

and wheeling charges in line with Regulation 83(6)(b) of RERC

Tariff Regulations, 2009.

60. Copy of this order be sent to the State Government, Central

Electricity Authority (CEA), MNRE , RREC, Distribution Licensees,

stakeholders and be also placed on the Commission’s website

(S. Dhawan)

Member

(S.K. Mittal)

Member

(D.C. Samant)

Chairman

Page 23 of 23

List of Participants in the Public Hearing on 13.03.2012

S. No Name Designation Organisation

1 D.S. Agarwal Consultant Rudraksh Energy

2 V K Gupta Consultant Rudraksh Energy

3 J K Agarwal Consultant SSAEL

4 Aditya Jandhyala Consultant SSAEL

5 Anil Patni Project Manager RREC

6 K K Purohit SE(Commercial) JVVNL

Annexure-I

TARIFF DETERMINATION FOR SOLAR PHOTO VOLTAIC POWER PLANTS LOCATED IN RAJASTHAN

Levelised Tariff (Rs/kWh) without AD 9.63

Accelerated Depreciation benefit(Rs/kWh) 1.21

Levelised Tariff (Rs/kWh) with AD 8.42

S. No.Assumption

HeadSub-Head Sub-Head (2) Unit

Base Case

(SPV)

1 Power Generation

Capacity

Installed Power Generation Capacity MW 1

CUF % 20.00%

Deration p.a. after 2nd year % 0.50%

Auxiliary Consumption % 0.25%

Tariff Period Years 25

Life of Power Plant Years 25

2 Project Cost

Capital Cost/MW Including Land & Connectivity charges Rs Lacs/MW 940Project Cost Power Plant Cost Rs Lacs 940

3 Sources of Fund

Debt: Equity

Debt % 70.00%

Equity % 30.00%

Total Debt Amount Rs Lacs 658

Total Equity Amout Rs Lacs 282

Funding Options-1 (Domestic Loan Source-1)

Loan Amount Rs Lacs 658

Moratorium Period years 0

Repayment Period(incld Moratorium) years 12

Intrest Rate % 12.30%

Funding Options-2 ( Equity Finance )

Equity amount Rs Lacs 282

Return on Equity for first 10 yrs % p.a 16.00%

Return on Equity from 11th yr onwards % p.a 16.00%

Discount Rate (equiv. to WACC) 13.41%

4 Financial Assumptions

Fiscal Assumptions

Income Tax % 30.90%

MAT Rate (for yr-1) % 20.01%MAT Rate (for yr-2 ) % 19.06%

MAT Rate (for yr-2 to yr-10) 19.06%

80 IA benefits Yes/No Yes

Depreciation

Depreciation Rate(upto 12-yrs) % 5.28%

Depreciation Rate(after 12-yrs) % 2.05%

Years for 5.28% SLM rate years 12

5 Working Capital

For Fixed Charges

O&M Charges Months 1

Maintenance Spare (% of O&M expenses) 15.00%

Receivables for Debtors Months 1.5

Intrest On Working Capital % 11.80%

6 Operation & Maintenance

power plant Rs Lacs per MW Rs Lacs 11.00

Insurance % of depreciated capital cost % 0.30%

Total O & M Expenses Escalation % 5.72%No. of Days Days 365

Total No. of Hours Hrs 8760

Annexure-II

TARIFF DETERMINATION FOR SOLAR PHOTO VOLTAIC POWER PLANTS LOCATED IN RAJASTHAN

Units Generation Unit Year---> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Aux Consumption % 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25%

Installed Capacity MW 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Deration factor % 0.50% 1 1.000 0.995 0.990 0.985 0.980 0.975 0.970 0.966 0.961 0.956 0.951 0.946 0.942 0.937 0.932 0.928 0.923 0.918 0.914 0.909 0.905 0.900 0.896 0.891

Generation MU 1.75 1.75 1.74 1.73 1.72 1.71 1.70 1.70 1.69 1.68 1.67 1.66 1.65 1.65 1.64 1.63 1.62 1.61 1.60 1.60 1.59 1.58 1.57 1.57 1.56

Cost of generation Unit Year---> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

O&M Expenses Rs Lacs 13.82 14.30 14.82 15.37 15.97 16.60 17.28 18.01 18.79 19.63 20.52 21.46 22.48 23.64 24.88 26.20 27.59 29.06 30.62 32.28 34.03 35.89 37.85 39.93 42.14

Depreciation Rs Lacs 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 19.26 19.26 19.26 19.26 19.26 19.26 19.26 19.26 19.26 19.26 19.26 19.26 19.26

Interest on term loan Rs Lacs 77.56 70.82 64.07 57.33 50.58 43.84 37.09 30.35 23.61 16.86 10.12 3.37 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Interest on working Capital Rs Lacs 3.26 3.18 3.10 3.03 2.96 2.89 2.82 2.76 2.69 2.63 2.72 2.66 2.20 2.25 2.31 2.37 2.43 2.49 2.56 2.63 2.71 2.79 2.88 2.97 3.06

Return on Equity Rs Lacs 56.41 55.74 55.74 55.74 55.74 55.74 55.74 55.74 55.74 55.74 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30 65.30

Total Cost of generation Rs Lacs 200.68 193.67 187.37 181.10 174.88 168.70 162.57 156.49 150.47 144.49 148.28 142.42 109.24 110.46 111.75 113.12 114.57 116.11 117.74 119.47 121.30 123.24 125.29 127.46 129.76

Per unit Cost of generation Rs/kWh 11.48 11.08 10.78 10.47 10.16 9.85 9.54 9.23 8.92 8.61 8.88 8.57 6.60 6.71 6.83 6.94 7.07 7.20 7.34 7.48 7.63 7.80 7.97 8.14 8.33

200.68 193.67 187.37 181.10 174.88 168.70 162.57 156.49 150.47 144.49 148.28 142.42 109.24 110.46 111.75 113.12 114.57 116.11 117.74 119.47 121.30 123.24 125.29 127.46 129.76

Levellised cost of generation (Rs/kWh) (25 yrs) 9.63

Annexure-II…contd…

Determination of Accelerated Depreciation Benefit for Solar PV Power Projects

Depreciation amount 90%

Book Depreciation rate 5.28%

Tax Depreciation rate 80%

Income Tax 32.45% 30.90% Yr-2 onwards

Capital Cost 940.0 Rs Lacs/MW

Years -----------------> Unit 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Book Depreciation % 2.64% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 2.88% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Book Depreciation Rs Lacs 24.82 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 49.63 27.07 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Accelerated Depreciation

Opening % 100.00% 60.00% 12.00% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Allowed during the year % 40% 48.00% 9.60% 1.92% 0.38% 0.08% 0.02% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Closing % 60% 12% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Accelrated Deprn. Rs Lacs 376.00 451.20 90.24 18.05 3.61 0.72 0.14 0.03 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Net Depreciation Benefit Rs Lacs 351.18 401.57 40.61 -31.58 -46.02 -48.91 -49.49 -49.60 -49.63 -49.63 -49.63 -49.63 -49.63 -49.63 -49.63 -49.63 -49.63 -27.07 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Tax Benefit Rs Lacs 113.94 124.08 12.55 -9.76 -14.22 -15.11 -15.29 -15.33 -15.33 -15.34 -15.34 -15.34 -15.34 -15.34 -15.34 -15.34 -15.34 -8.37 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Energy generation MU 0.87 1.75 1.74 1.73 1.72 1.71 1.70 1.70 1.69 1.68 1.67 1.66 1.65 1.65 1.64 1.63 1.62 1.61 1.60 1.60 1.59 1.58 1.57 1.57 1.56

Per unit benefit Rs/Unit 13.04 7.10 0.72 (0.56) (0.83) (0.88) (0.90) (0.90) (0.91) (0.91) (0.92) (0.92) (0.93) (0.93) (0.94) (0.94) (0.95) (0.52) 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Discounting Factor,DF 1.00 0.88 0.78 0.69 0.60 0.53 0.47 0.41 0.37 0.32 0.28 0.25 0.22 0.19 0.17 0.15 0.13 0.12 0.10 0.09 0.08 0.07 0.06 0.06 0.05

Applicable DF 1.00 0.94 0.83 0.73 0.65 0.57 0.50 0.44 0.39 0.34 0.30 0.27 0.24 0.21 0.18 0.16 0.14 0.13 0.11 0.10 0.09 0.08 0.07 0.06 0.05

Levellised benefit 1.21 Rs/kWh

Annexure-II…contd…

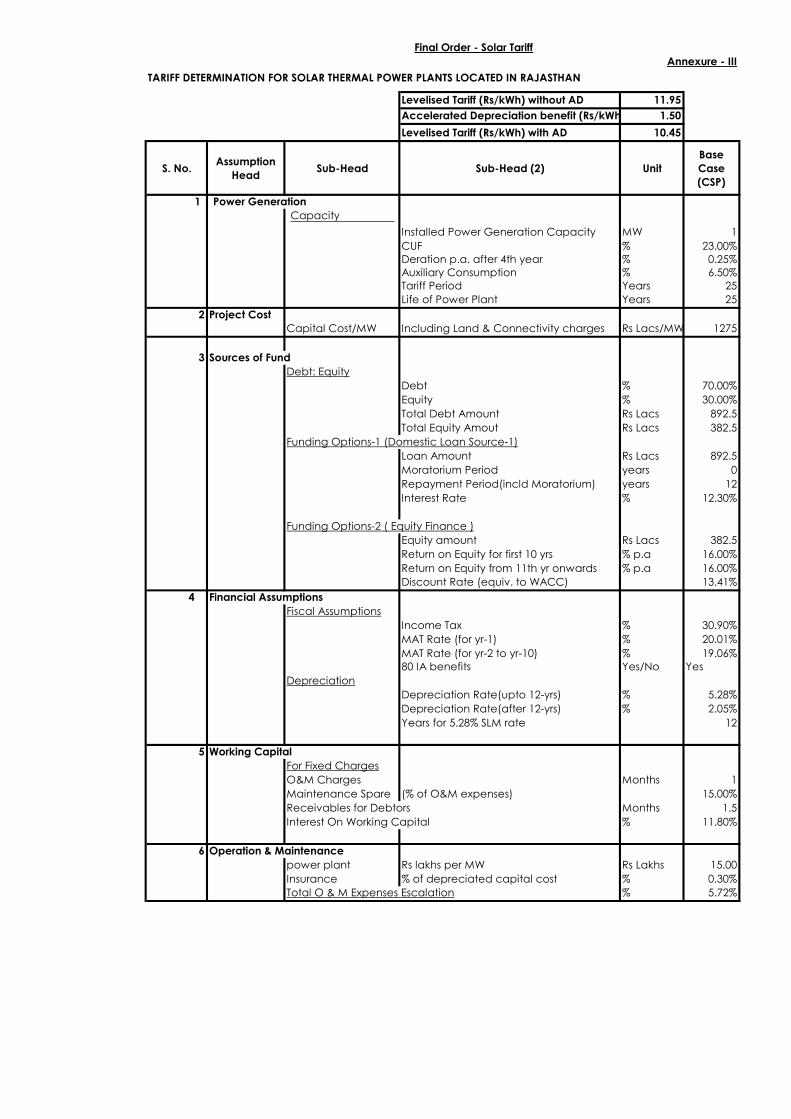

TARIFF DETERMINATION FOR SOLAR THERMAL POWER PLANTS LOCATED IN RAJASTHAN

Levelised Tariff (Rs/kWh) without AD 11.95

Accelerated Depreciation benefit (Rs/kWh) 1.50

Levelised Tariff (Rs/kWh) with AD 10.45

S. No.Assumption

HeadSub-Head Sub-Head (2) Unit

Base

Case

(CSP)

1 Power Generation

Capacity

Installed Power Generation Capacity MW 1

CUF % 23.00%

Deration p.a. after 4th year % 0.25%

Auxiliary Consumption % 6.50%

Tariff Period Years 25

Life of Power Plant Years 25

2 Project Cost

Capital Cost/MW Including Land & Connectivity charges Rs Lacs/MW 1275

3 Sources of Fund

Debt: Equity

Debt % 70.00%

Equity % 30.00%

Total Debt Amount Rs Lacs 892.5

Total Equity Amout Rs Lacs 382.5

Funding Options-1 (Domestic Loan Source-1)

Loan Amount Rs Lacs 892.5

Moratorium Period years 0

Repayment Period(incld Moratorium) years 12

Interest Rate % 12.30%

Funding Options-2 ( Equity Finance )

Equity amount Rs Lacs 382.5

Return on Equity for first 10 yrs % p.a 16.00%

Return on Equity from 11th yr onwards % p.a 16.00%

Discount Rate (equiv. to WACC) 13.41%

4 Financial Assumptions

Fiscal Assumptions

Income Tax % 30.90%

MAT Rate (for yr-1) % 20.01%

MAT Rate (for yr-2 to yr-10) % 19.06%

80 IA benefits Yes/No Yes

Depreciation

Depreciation Rate(upto 12-yrs) % 5.28%

Depreciation Rate(after 12-yrs) % 2.05%

Years for 5.28% SLM rate 12

5 Working Capital

For Fixed Charges

O&M Charges Months 1

Maintenance Spare (% of O&M expenses) 15.00%

Receivables for Debtors Months 1.5

Interest On Working Capital % 11.80%

6 Operation & Maintenance

power plant Rs lakhs per MW Rs Lakhs 15.00

Insurance % of depreciated capital cost % 0.30%

Total O & M Expenses Escalation % 5.72%

Final Order - Solar Tariff

Annexure - III

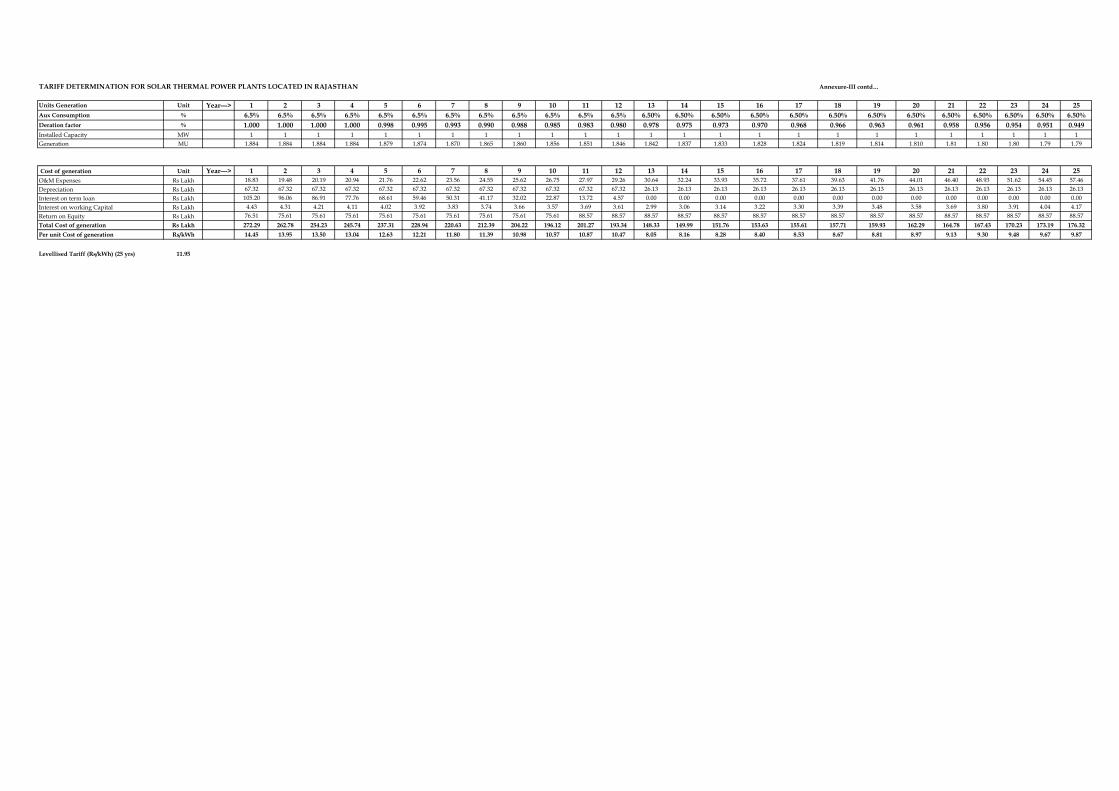

TARIFF DETERMINATION FOR SOLAR THERMAL POWER PLANTS LOCATED IN RAJASTHAN Annexure-III contd…

Units Generation Unit Year---> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Aux Consumption % 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50% 6.50%

Deration factor % 1.000 1.000 1.000 1.000 0.998 0.995 0.993 0.990 0.988 0.985 0.983 0.980 0.978 0.975 0.973 0.970 0.968 0.966 0.963 0.961 0.958 0.956 0.954 0.951 0.949

Installed Capacity MW 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Generation MU 1.884 1.884 1.884 1.884 1.879 1.874 1.870 1.865 1.860 1.856 1.851 1.846 1.842 1.837 1.833 1.828 1.824 1.819 1.814 1.810 1.81 1.80 1.80 1.79 1.79

Cost of generation Unit Year---> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

O&M Expenses Rs Lakh 18.83 19.48 20.19 20.94 21.76 22.62 23.56 24.55 25.62 26.75 27.97 29.26 30.64 32.24 33.93 35.72 37.61 39.63 41.76 44.01 46.40 48.93 51.62 54.45 57.46

Depreciation Rs Lakh 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 26.13 26.13 26.13 26.13 26.13 26.13 26.13 26.13 26.13 26.13 26.13 26.13 26.13

Interest on term loan Rs Lakh 105.20 96.06 86.91 77.76 68.61 59.46 50.31 41.17 32.02 22.87 13.72 4.57 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Interest on working Capital Rs Lakh 4.43 4.31 4.21 4.11 4.02 3.92 3.83 3.74 3.66 3.57 3.69 3.61 2.99 3.06 3.14 3.22 3.30 3.39 3.48 3.58 3.69 3.80 3.91 4.04 4.17

Return on Equity Rs Lakh 76.51 75.61 75.61 75.61 75.61 75.61 75.61 75.61 75.61 75.61 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57 88.57

Total Cost of generation Rs Lakh 272.29 262.78 254.23 245.74 237.31 228.94 220.63 212.39 204.22 196.12 201.27 193.34 148.33 149.99 151.76 153.63 155.61 157.71 159.93 162.29 164.78 167.43 170.23 173.19 176.32

Per unit Cost of generation Rs/kWh 14.45 13.95 13.50 13.04 12.63 12.21 11.80 11.39 10.98 10.57 10.87 10.47 8.05 8.16 8.28 8.40 8.53 8.67 8.81 8.97 9.13 9.30 9.48 9.67 9.87

Levellised Tariff (Rs/kWh) (25 yrs) 11.95

Determination of Accelerated Depreciation Benefit for Solar Thermal Power Projects

Depreciation amount 90% Annexure-III contd…

Book Depreciation rate 5.28%

Tax Depreciation rate 80%

Income Tax 32.45% 30.90%

Capital Cost 1275.0 Rs Lacs/MW

Years -----------------> Unit 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Book Depreciation % 2.64% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 5.28% 2.88% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Book Depreciation Rs Lacs 33.66 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 67.32 36.72 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Accelerated Depreciation

Opening % 100.00% 60.00% 12.00% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Allowed during the year % 40% 48.00% 9.60% 1.92% 0.38% 0.08% 0.02% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Closing % 60% 12% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Accelrated Deprn. Rs Lacs 510.00 612.00 122.40 24.48 4.90 0.98 0.20 0.04 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Net Depreciation Benefit Rs Lacs 476.34 544.68 55.08 -42.84 -62.42 -66.34 -67.12 -67.28 -67.31 -67.32 -67.32 -67.32 -67.32 -67.32 -67.32 -67.32 -67.32 -36.72 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Tax Benefit Rs Lacs 154.55 168.31 17.02 -13.24 -19.29 -20.50 -20.74 -20.79 -20.80 -20.80 -20.80 -20.80 -20.80 -20.80 -20.80 -20.80 -20.80 -11.35 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Energy generation MU 0.94 1.88 1.88 1.88 1.88 1.87 1.87 1.87 1.86 1.86 1.85 1.85 1.84 1.84 1.83 1.83 1.82 1.82 1.81 1.81 1.81 1.80 1.80 1.79 1.79

Per unit benefit Rs/Unit 16.41 8.93 0.90 (0.70) (1.03) (1.09) (1.11) (1.11) (1.12) (1.12) (1.12) (1.13) (1.13) (1.13) (1.14) (1.14) (1.14) (0.62) 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Discounting Factor,DF 1.00 0.88 0.78 0.69 0.60 0.53 0.47 0.41 0.37 0.32 0.28 0.25 0.22 0.19 0.17 0.15 0.13 0.12 0.10 0.09 0.08 0.07 0.06 0.06 0.05

Applicable DF 1.00 0.94 0.83 0.73 0.65 0.57 0.50 0.44 0.39 0.34 0.30 0.27 0.24 0.21 0.18 0.16 0.14 0.13 0.11 0.10 0.09 0.08 0.07 0.06 0.05

Levellised benefit 1.50 Rs/kWh

Copyright © 2022 FDOKUMEN