R E S E A R C H P A P E R S in Retailing - CiteSeerX

63

R E S E A R C H P A P E R S in Retailing

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of R E S E A R C H P A P E R S in Retailing - CiteSeerX

R E S E A R C H

P A P E R S

in

Retailing

Not for quotation or reproduction without ISSN 0265 9778the express permission of the author

Dr Keri Davies is a lecturer at the Institute for Retail Studies, Department of Marketing,University of Stirling, Stirling, Scotland, U.K. FK9 4LA

Working Paper 9301

The Lure of One Billion NewCustomers: Foreign Investment inthe Retail Sector of the People's

Republic of China

Keri Davies

Disclaimer

The opinions expressed in this working paper are the responsibility of the author alone.

Institute for Retail Studies. All rights reserved.

1

Institute for Retail Studies. All rights reserved.

2

1. INTRODUCTION

Since 1978 the government of the People's Republic of China has pursued a policy of

economic liberalisation - moving away from a high degree of state control towards a

competitive market. The initial reforms were concentrated on the manufacturing sector; more

recently, the central government has looked to loosen the degree of state control over

retailing, most particularly allowing foreign companies to invest in the sector. To outside

companies, the lure of over one billion new customers (Xu, 1990) has been quite intoxicating,

even if they have been a bit more difficult to find in practice.

Whilst some of these changes represent a wish by the government to move to a more market-

orientated economy, they also represent the reaction to a ground swell of discontent with the

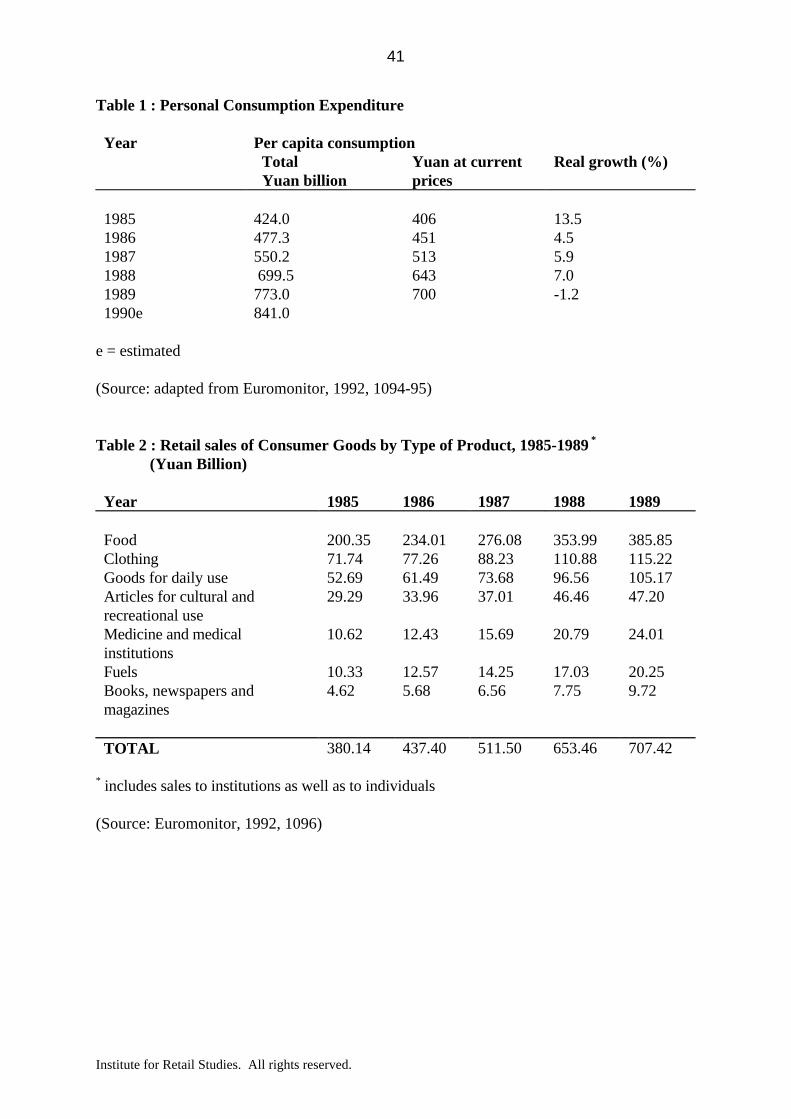

existing system amongst consumers. Per capita consumption expenditure nearly doubled

during the period 1985-1990 (Table 1) and this was reflected in the increase in the level of

retail sales of consumer goods over the same period (Table 2). As their disposable income has

risen, consumers have been unhappy with the quality of the products available through the

state-run stores, preferring foreign brands, including those manufactured in China by foreign-

local joint ventures.

The implementation of the changes to the rules and regulations and their effects have been

mixed however. China is the world's largest developing country and it is still seen as being

essentially rural in character. The spatial distribution of population is unbalanced, with

concentrations in the coastal provinces and in the Changjiang (Yangtze) Basin and North

China Plain. As a result of historical circumstances and geographical conditions, the level of

economic development varies greatly between different regions. Furthermore, just twenty-one

per cent of the population was classified as "urban" in 1988 - but this represented 230 million

people, almost as many as the population of the whole of the United States of America (Tang

and Jenkins, 1990, 203). As a result of these spatial imbalances, there are tensions between

the central State Council and the governments of the provinces and the largest municipalities

(Figure 1) over the form of the legislation governing foreign companies and the speed at which

it should be implemented. All of these issues will affect foreign companies wishing to invest in

the retail sector in China.

Institute for Retail Studies. All rights reserved.

3

This paper will set out the basic changes which have taken place in the administration of

retailing in the People's Republic of China and show the type and pattern of investment which

has been undertaken by foreign companies since the rules were relaxed. It will then look at

some of the problems and challenges facing foreign investors and examine the prospects for

the sector in the near future.

2. EVOLUTION OF THE POLICY FRAMEWORK

2.1 Changes in the period 1950 - 1990

Free market retailing, much of which was related to the marketing of agricultural produce,

continued to exist in China, with certain periods of interruption, long after the Chinese

Communists' victory in 1949. It was outlawed at the beginning of the Cultural Revolution in

1966 (Reeder, 1983, 74) and, whilst illegal or "black market" sales were not eliminated,

virtually all retail distribution was carried out through state-owned stores. Merchandise was

manufactured by state-owned factories and food was grown on state-owned communes; a

system of stated-owned middlemen distributed all goods and prices were set by the

government (Vernon-Wortzel and Wortzel, 1987, 60).

One of the aims of this high level of state control during the period 1952 - 1977 was to allow

China to try to establish retail price stability. In this aim it was partially successful.

'The 1950s saw steady but moderate retail price increases so that the general retailprice index in 1958 stood at 121.6 (1950=100) or 8.8% higher than in 1952. Theearly 1960s saw an explosion in the retail price level when it rose 20.6% from 1960to 1962 before it was reduced to an index of 133.2 in 1967. Thereupon therecommenced a period of aggregate price stability that lasted throughout the ten yearsof chaos of the cultural revolution...In 1977 a 2% increase in the general retail priceindex heralded the end of ten years of stable prices and by 1982 the general retailprice index was 13.6% higher than in 1977"

(Peebles, 1986, 478)

In 1978 China initiated its Four Modernizations programme which aimed to modernize

agriculture, industry, national defence, and science and technology. This carried with it the

Institute for Retail Studies. All rights reserved.

4

need to achieve a fundamental reorganisation of the production of all goods and services in the

country. Accordingly, in December 1978, the Third Plenary Session of the Eleventh Central

Committee of the Communist Party announced the restoration of both private farming plots,

allowing individuals to grow food, and "free markets", where they could sell some of their

produce (Reeder, op cit). The articles by Reeder (1983), Vernon-Wortzel and Wortzel

(1987), Qiang and Harris (1990) and Watson (1992) document the effect that these changes

have had on the "free markets" and the retailing of, primarily, agricultural products.

Central control of retail prices in an attempt to achieve stability ended at the same time

because of these policies and the outside influences on the Chinese economy. (See also the

debate between Wang (1988) and Peebles (1989) regarding the actual success or otherwise of

the policies to achieve stable retail prices.) Guo (1992, 26) suggests that the purpose of the

price reforms which followed was, in broad terms, to ensure the success of the post-1979

economic reform programme. Henceforward, prices were to be used mainly to signal relative

costs, needs and scarcities to enterprises and households; to guide production and improve

quality; and to guide expenditure in investment decisions.

In the early 1980s, the Chinese government also began the process of decentralising much of

its authority, allowing provincial governments, fourteen port cities and five Special Economic

Zones (SEZs)(Shenzen, Zhuhai and Shantou in Guangdong Province, Xiamen in Fujian

province and Hainan - see Figure 2) the right to manage their own economic affairs within

broad policy guidelines (Price, 1988, 35; Luo, 1992). Each of the SEZs, and particularly

Shenzen in Guangdong Province which adjoins Hong Kong, has attracted foreign investment

in manufacturing activities and greatly expanded and diversified the level of its foreign trade

(Reardon, 1991). Almost ninety per cent of cumulative foreign investment has gone to the

ports and coastal SEZs, with Guangdong Province taking around forty per cent of the national

total (Goldstein, 1992b).

Whilst progress was slow at first, the economic growth consequent upon these changes was

substantial and was reflected in a growing level of consumer affluence, particularly in the

SEZs. As incomes have grown, so Chinese consumers have wanted better products and better

service for their money. Their awareness of what is available has been raised by more contact

with Hong Kong itself or with those who have been to Hong Kong. The greater penetration

Institute for Retail Studies. All rights reserved.

5

of foreign consumer goods, despite the existing distribution problems, and the greatly

increased level of advertising of such products (Xu, 1990) have also helped.

The ban on foreign investment in the retail trades continued to be enforced however, even

including the SEZs. The only sizable loophole seems to have been the provision for the

establishment of dedicated sales counters in Chinese department stores selling products

manufactured in China by foreign companies, including those run by companies such as

Goldlion (see below). Imports of consumer goods into China were controlled by the state

trading companies in each province and had to be sold in a state store. The state's desire to

control imports was reinforced by a dual currency system. This system consists of the local

currency, the yuan (¥), which is available as Renminbi (or "People's Money") or the Foreign

Exchange Certificate (FEC). (In 1991 the £ : ¥ exchange rate was approximately 1 : 10)

Renminbi cannot be exchanged (legally) outside China and thus can be used to buy locally

produced products only, whilst the FEC is issued to foreign visitors and companies in

exchange for hard currency. The encouragement of free market retailing in the early 1980s did

not extend to permission for foreign retailers to enter the market but it did open up new

channels of distribution. In particular, free market retailers acted with Hong Kong middlemen

to use FECs to get more imported goods into China and the middlemen would then use yuan

to purchase local products which they exported to the rest of South-East Asia (Vernon-

Wortzel and Wortzel, 1987).

Free market retailing has remained small in terms of the percentage which it comprises of

China's total retail sales but the changes introduced in 1978 were responsible for an explosive

growth in store numbers. In 1978 there were just over one million retail stores in China; by

1985 this number had risen nearly eight-fold and the figure topped nine million in 1988 before

falling back slightly to just under eight-and-a-half million in 1989 (Table 3). The bulk of the

stores in 1989, around seven million, were licensed stores run by individuals. Of the

remainder, where chains are common, the food, department store and general store sectors

Institute for Retail Studies. All rights reserved.

6

were the most significant, although the latter is the only sector to have declined in every year

since 1985.

The trend is even more obvious if we look at the average number of persons served by each

outlet (Figure 3). Following the victory of the Communist forces in the late 1940s, the

number of people served by each shop grew for a full fifteen year period, quadrupling from

200 in the early 1950s to 800 by 1965. It then stabilised during the period of the Cultural

Revolution. The rate of decline after 1978, marking the creation of new retail enterprises, was

even more dramatic than its rise, although there was a slight increase in the figures in 1989.

The pattern for food stores is similar to that for all stores, beginning and ending at around 800

persons per store but reaching 9,000 persons per store in 1978.

These changes have been more marked in some regions than in others; for example, Price

(1988) reported that free market retailing was best established in Guangzhou, where retailers

were acting as importers/ exporters and wholesalers, and weakest in the Chinese hinterland,

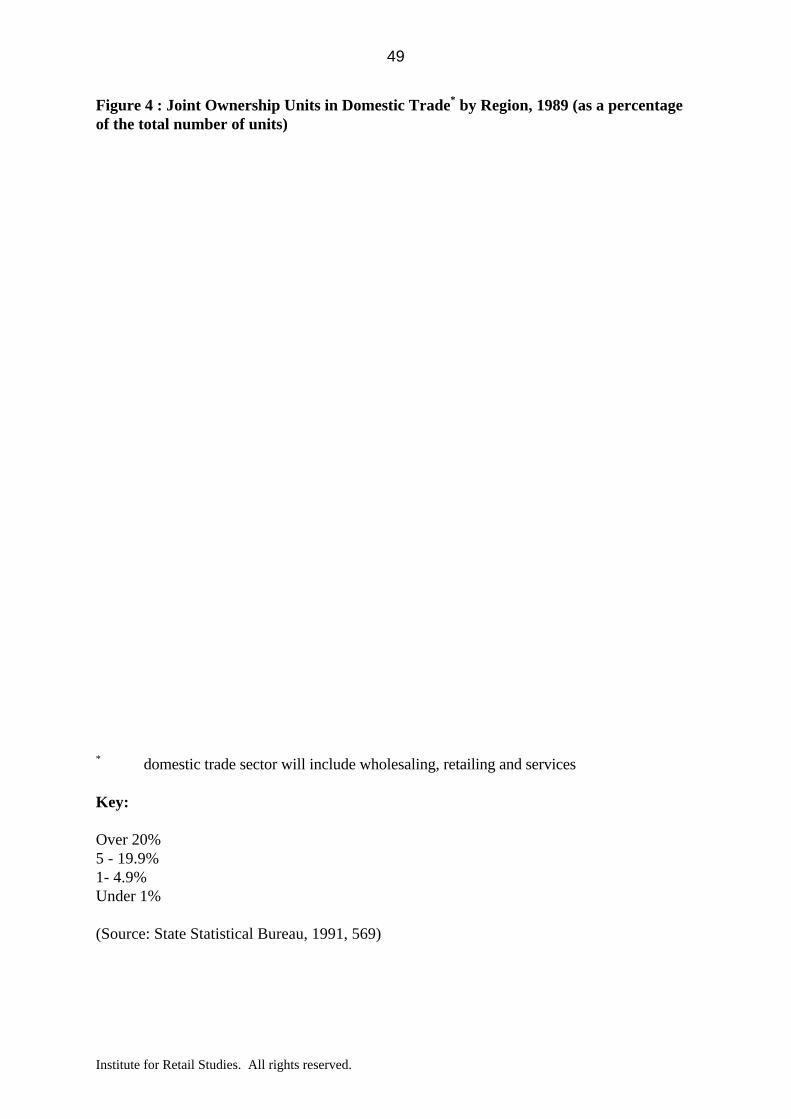

in areas like Chengdu in Sichuan province. Joint ownership units in the "domestic trade"

category (which includes wholesaling, retailing and services) are those most likely to involve

foreign retailers or to be linked to foreign retailers. In 1989 there were 2,742 such units in

the country (State Statistical Bureau, 1991, 569). However, Figure 4 shows that these units

were concentrated in Guangzhou (28%), Shanghai (23%) and the coastal province of Fujian

(11%), with significant numbers also in Beijing (5.5%) and the inland city of Xi'an in Shaanxi

province (6%). These concentrations were much higher than can be attributed to the existing

southern and coastal bias to the distribution of all stores.

Whilst the number of stores run by individuals increased rapidly (Table 3), the large retail

groups remained state-owned during the 1980s and their numbers changed little. A survey

published by the Hong Kong Trade Development Council in 1992 shows that the state-run

department stores are still the largest retail groups in the country by far (Table 4). (The bulk

of the enterprises on the original list were agricultural wholesalers.) Beijing, Shanghai,

Guangzhou and Tianjin dominate the list reflecting their economic positions in the country.

Institute for Retail Studies. All rights reserved.

7

Despite their size, however, efforts by the state-run stores to modernise have not met with too

much success. Price reported that 16 out of the 32 self-service supermarkets opened in

Beijing between 1982 and 1988 were running at a loss because of their higher operating costs

than ordinary stores, the heavy costs of purchasing equipment such as refrigerators, and the

level of bureaucracy (Price, 1988, 36-37; see also the comments in Blois (1987) and Blois

(1988)). Effective competition was precluded because access to the retail markets was still

restricted and foreign companies were not allowed to establish retail outlets in China. Foreign

consumer goods were normally imported by Chinese foreign trade companies and were subject

to stiff tariff rates and licensing requirements. Foreign investment enterprises, such as joint

ventures, were required to export their products to earn foreign exchange. If they wanted to

sell in China, they would have to go through Chinese wholesalers to get their goods

distributed (Dennis, 1993).

2.2 Changes since 1990 in the general policy framework

There has been a gradual change in this position. As time has gone by, so the pressures have

grown on the government to redistribute the benefits of economic growth more widely and to

allow the reforms in the manufacturing sector to spread into the service sector. This tension

was highlighted by the visit of Deng Xiaoping to the southern coastal provinces in January

1992 during which he held the Shenzen Economic Zone up to the nation as a model for future

growth.

During 1992 a number of general changes were made to the legislative framework, some of

which will affect retailing indirectly:

• In June 1992 Peking authorised 21 additional cities to offer additional incentives,

such as tax breaks, to foreign investors. The bulk of these were along the Yangtze

River Valley plus several in the north east of the country. At the same time, Peking

clamped down on areas offering unauthorised tax breaks or other incentives to

foreign investors (Goldstein, 1992b).

Institute for Retail Studies. All rights reserved.

8

• Local governments have been allowed to sell "land use rights" to both domestic and

foreign buyers. The State Council first legalised the practice in 1989 but under

severely limited circumstances (Potter, 1991). Since then city governments have been

expanding the limits, generating revenues in the process. The effect has been to allow

relatively clear 50-year leases on property. Goldstein (1992a) notes that this provides

a familiar environment for investors from Hong Kong, where all land is owned by the

Crown but is "sold" to private users for 99-year leaseholds - although under the

current agreement between the U.K. and China no Hong Kong leaseholds may be

extended beyond 2047 either (Cottrell, 1993).

• Restrictions have been relaxed on domestic sales of locally made items ranging from

electrical appliances to soap powders that formerly had to be exported (Goldstein,

1992b).

• The monopoly of the state-supply bureaux is being broken up. Foreign companies

are now allowed to establish their own warehouses and to hire sales teams to get their

goods into local stores (Goldstein, 1992b). However, imported goods are still

subject to high tariff levels and the state-imposed licensing requirements.

• The Chinese acceded in 1992 to the pressures being placed on them regarding their

use of Trade Related Investment Measures (TRIMs) (see Greenaway, 1991; K.

Davies, 1993) to block foreign investment in the country. In 1991 the United States

government's launched a Section 301 investigation of China's trade practices

following complaints from American firms that they were unlawful and unfair (Barale,

1991). As a consequence of the negotiations which ensued, a Memorandum of

Understanding (MOU) on market access was signed between the U.S.A. and China in

October 1992 providing a binding commitment to honour a bilateral trade agreement.

Commitment to this relationship should also help to open up the Chinese market to

companies from other countries besides the U.S.A..

Massey (1992) reported that the Section 301 market access negotiations covered four basic

areas: transparency of trade-related rules and regulations; import bans and quotas; the import

licensing system; and, technical barriers to trade. The MOU's most fundamental achievement,

Institute for Retail Studies. All rights reserved.

9

and the most significant one for retailing currently, came in the area of trade related rules and

regulations. China has a system of internal (neibu) regulations which cover many aspects of

business and govern what a company may or may not do. Foreigners were not permitted to

see these neibu regulations. Following the MOU, the Chinese have committed themselves to

publishing all neibu regulations by the end of October 1993 and, thereafter, only published

(and readily available) regulations will be enforceable. This provision is in accordance with

General Agreement on Tariffs and Trade (GATT) requirements and provides a means for

foreign businesspeople to act on the same levels of information as Chinese companies. An

underlying aim of the American government is that once all neibu regulations are published it

will be possible also to push for a reduction in the number of restrictive regulations and rules

governing companies in China.

2.3 Changes since 1990 in the policy framework governing retailing

At the same time as all of these general changes, the State Council has bowed to the pressures

to allow foreign investment in the ailing retail sector. In 1992 the 14th Congress of the

Chinese Communist Party, in addition to giving its endorsement to the economic policies

formulated in 1978, approved the further development of the tertiary industry (including

retailing) (Leung, 1992c). The upshot is that there now a number of different routes into the

retail sector in China.

2.3.1 Prestigious import-export enterprises

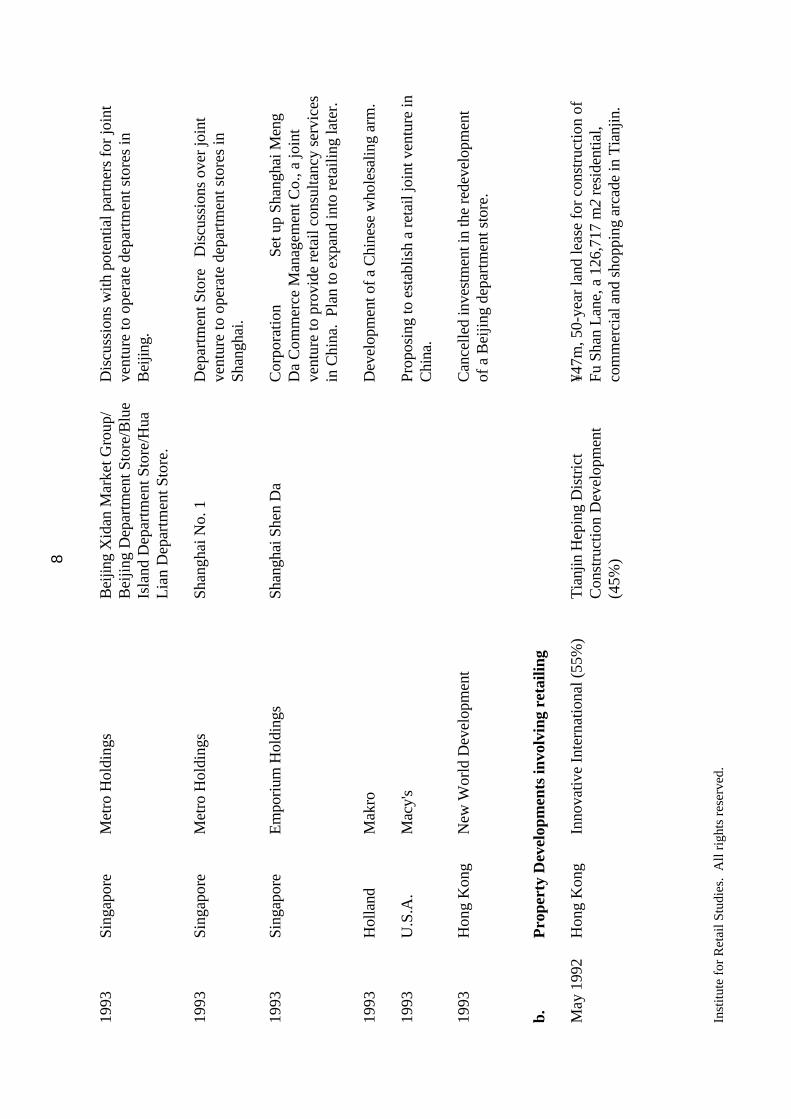

In 1992 the State Council established a scheme to allow foreign retailers to open joint ventures

in Beijing, Tianjin, Shanghai, Guangzhou, Dalian, Qingdao, and the five SEZs. Two large

Sino-foreign joint venture department stores will be allowed to be set up in each of these

locations (Anon, 1993b) - a maximum of just twenty-two developments! The companies

involved in this experiment will enjoy special privileges, particularly in regard to the rules

surrounding imported products.

Institute for Retail Studies. All rights reserved.

10

The provisions set out by the State Council outline the form and scope of business limits of

import and export authorities and the tax treatment of foreign investment enterprises (f.i.e.)

engaged in retail business in China. According to Dennis (1993), the provisions, which are

neibu (and, hence, would not have been published and available to foreigners in the past),

stipulate that:

1. F.i.e. may take the form of equity joint ventures or cooperative joint ventures but

wholly foreign-owned enterprises will not be permitted.

2. The details of the proposed f.i.e. shall be submitted by the regional governments to

the State Council for approval. The qualifications of the parties to the joint venture

shall be examined and approved by the newly-formed Ministry of Internal Trade.

3. The business scope of the enterprise is limited to the retailing of general merchandise

and the commercial business of import and export. It is not permitted for the

enterprise to engage in wholesale business or to act as an import and export agency

for another company.

4. Commodities that may be imported by the enterprise are limited to general

merchandise. The amount of merchandise imported throughout the year must not

exceed thirty per cent of the turnover that year. Approved formalities for the

importation of domestic electrical appliances, cosmetics, cigarettes, wine and

beverages shall be completed in accordance with the approved provisions of the

State.

5. Tax treatment shall be implemented in accordance with the State's policy in the areas

where the business is located. Income tax will normally, therefore, be at 33% with no

tax-free period, as retail will not be regarded as a production enterprise.

6. The enterprise shall have autonomy to purchase commodities for sale and fix their

selling prices unless the State or local administrators of commodity prices stipulate

Institute for Retail Studies. All rights reserved.

11

otherwise. After obtaining the approval of the relevant department of foreign

exchange control, the imported commodities can be sold in foreign exchange

certificates.

The framing of the regulations implies that the State Council will be very selective in awarding

these prestigious projects; small and medium firms are unlikely to be considered. The Yaohan

joint venture with the Shanghai No. 1 Department Store and the Yansha Friendship Shopping

City in Beijing (see below) were the first two projects to be approved by the State Council

under this scheme.

2.3.2 Other joint venture retail enterprises

The State Council's decision to create a new category of large projects is not meant to deter

investment by smaller firms. Foreign-funded enterprises currently operating in China are

allowed to sell a certain portion (usually 30%) of the products that they manufacture. Some

small and medium-sized firms, mainly from Hong Kong, are already investing in the retail

sector through their existing manufacturing joint ventures. Indeed, local authorises have

indicated recently that foreign-funded enterprises could enjoy even larger domestic sales ratios

as long as they can balance their foreign exchange accounts. (Domestic sales restrictions are

set to be scrapped when the renminbi becomes fully convertible.) Domestic sales ratios of

50% are being quoted by many officials, whilst an official from Shenyang in Liaoning province

is said to have suggested that a 100% ratio may be possible provided that firms continue to

balance their foreign exchange accounts (Anon, 1993b).

Such joint ventures are said to be popular with Chinese consumers because the products

manufactured by the joint venture in China are generally of a higher quality than those from

State factories, whilst the prices are much lower than those for comparable imported products

(ibid). Foreign funded manufacturers can sell their products to a domestic wholesale

distributor; they can set up their own sales counters; or, they can enter into joint ventures with

Chinese companies to open and run stores. This is the route that companies such as Giordano,

Goldlion, Pacific Concord, Benetton and Stefanel have followed with some success.

Institute for Retail Studies. All rights reserved.

12

2.3.3 Wholly-owned foreign retail enterprises

Foreign companies may also apply to run their own retail shops, provided that they do not

require any import-export rights. These projects can be approved by municipal and provincial

governments and there is no strict limit on the number of such companies. In practice,

foreign-funded retailers without import-export rights can still import goods either through

state-owned import and export corporations or through importers located in the SEZs.

However, such products will generally be more expensive than those brought in by retailers

with import-export rights (Anon, 1993b).

2.3.4 Property development

The final route into the retail sector is through property development projects. Appendix A,

section (b), provides a sample of some of the schemes which have been proposed for the

development of commercial property in urban centres. (As in all booming economies, the

number of proposals far exceeds the number of developments which will actually be

undertaken.) Property companies may apply for a business licence to operate retail shops

when the project nears completion (Anon, 1993b).

2.4 Local initiatives

State control over retail development and, to a degree, property development including

retailing has been weakened by these reforms. One of the problems for the government is that

its experiments in the retail field have been taken up by the named provinces and are being

pushed to their limit. For example:

• Fujian province has invited foreign companies to develop shopping centres in Fuzhou,

Quanzhou and Liangzhou cities. The minimum investment in these projects will be

¥50m (£5m) and the minimum size per development must be 20,000 m2 (The China-

Britain Trade Review, July 1992).

Institute for Retail Studies. All rights reserved.

13

• Guangzhou has announced a fifteen-year development plan which permits foreign

businesses to run retail businesses and to develop shopping centres and large-scale

tourist projects in the city (The China-Britain Trade Review, October 1992).

• Beijing has invited foreign investment in the retail sector, with the publication of a list

of projects involving food processing, garment manufacturing and the construction of

shopping centres and warehouses (The China-Britain Trade Review, October 1992).

• In 1992 the Shanghai Municipal Government was negotiating with a number of Hong

Kong and Taiwanese companies in advance of the deliberations of the central

government (Leung, 1992a). Whilst the central government has to approve major

shopping centres or projects, such as the retail development by Yaohan, the

Municipal Government has the power to grant approval for cooperative projects

involving the setting up of smaller department stores in Paxi with no import and

export capabilities or preferential tax treatment. The Municipal Government has been

encouraging foreign joint ventures to operate retail businesses on a trial basis in the

Pudong and Paxi districts and implementing more flexible policies allowing foreign-

invested enterprises to open retail outlets selling not only their own products but also

related items manufactured by mainland enterprises.

The decision by the State Council to extend special treatment to retail enterprises in the SEZs

and major cities makes perfect sense for a limited experiment. These are the areas which also

have the highest levels of per capita income and, hence, the levels of demand to support

foreign enterprises and the importing of foreign goods. However, pressures are building up in

the retail sector because many of the other municipal and provincial governments see their

areas being doubly disadvantaged by this policy, receiving little or no foreign investment in

either manufacturing or the service sector. They are wishing to see the current experiment

extended to cover more of the country and may, in certain circumstances, be prepared to bend

the existing rules. For example, the No.1 Commercial Bureau of Chongqing, not yet on the

Institute for Retail Studies. All rights reserved.

14

approved list of areas, has submitted an application to the central government for approval to

set up joint venture department stores. It is believed that approval will be granted in 1993

(Leung, 1993a).

This is the policy framework within which retail development in China must take place

currently. We now turn to look at the type and level of foreign investment which these

measures have attracted to China.

3. FOREIGN INVESTMENT IN THE RETAIL SECTOR

The lack of accurate and up-to-date government statistics on foreign investment in the retail

sector (which is often amalgamated with wholesaling or other services) makes it difficult to

judge the full extent of the flows taking place. In addition, many of the reports on the retail

sector have concentrated on high profile projects, such as the State Council approved joint

venture department stores, or on the activities of retailers from specific countries, such as the

various reports by the Hong Kong Trade Development Council.

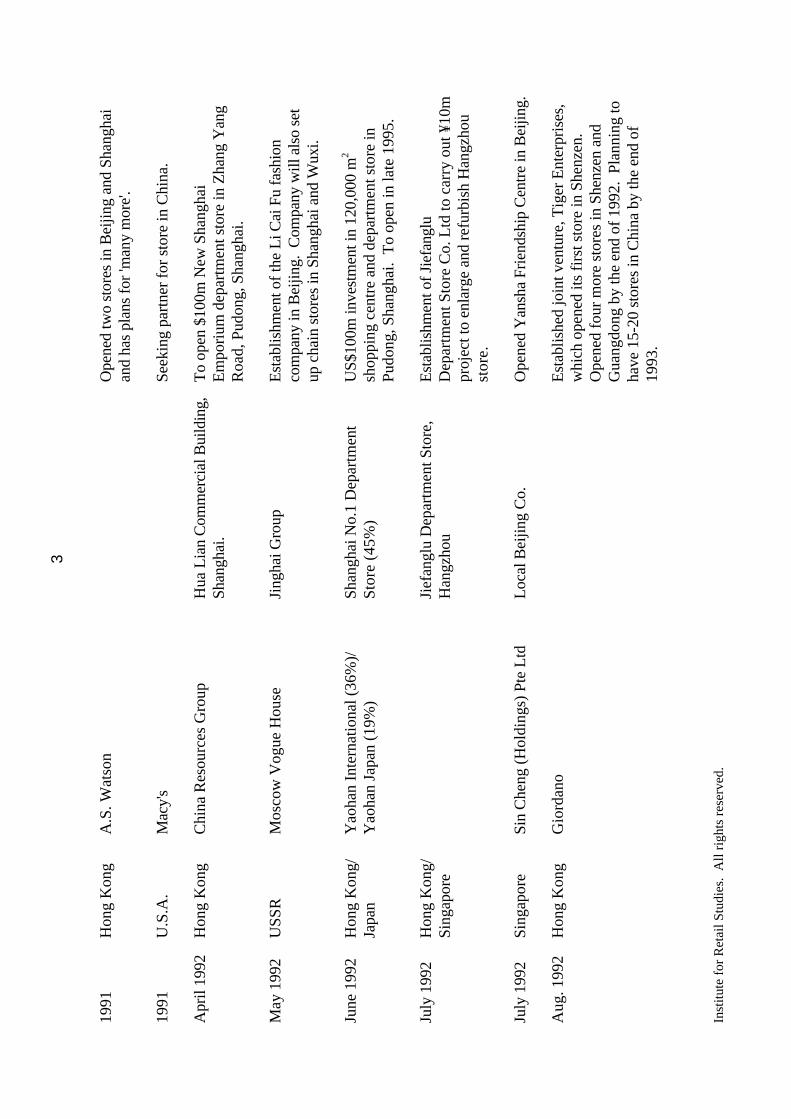

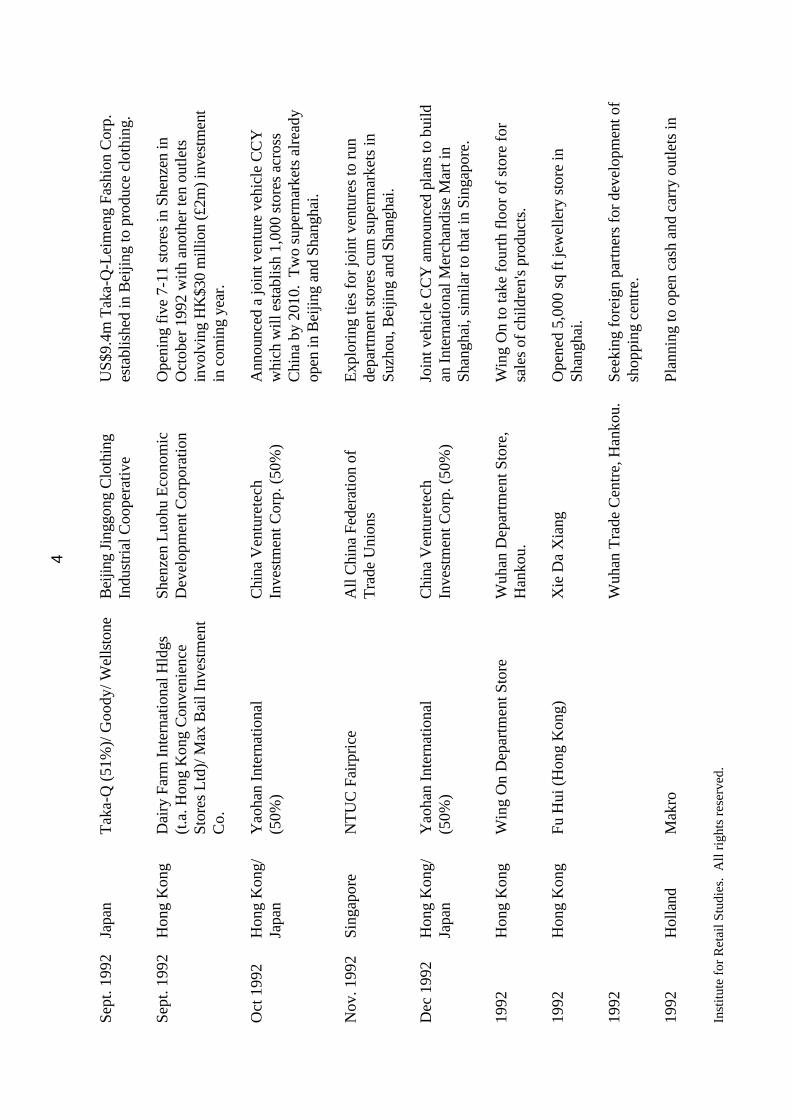

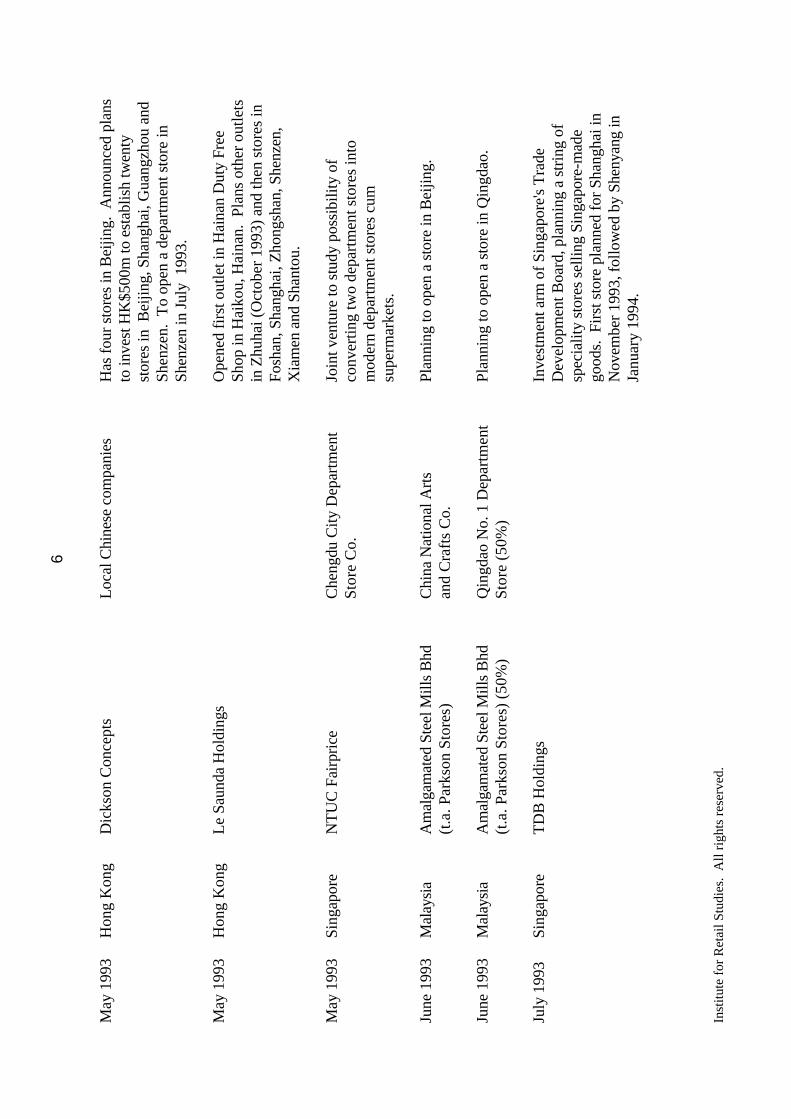

Accordingly, this study includes a compilation of the known investments in the sector by

foreign retailers and by foreign property developers (Appendix A). As such it should be

treated as a sample which can only reflect the concerns of the sources from which it has been

drawn. (The dates provided relate mainly to when the activity took place, but may, in some

cases, refer to when the activity was reported if no specific date is specified for the activity.)

However, it is believed to be the most complete published list currently available. From this

list, we can, first, draw out some general comments about the methods of entry, the origins

and destinations of investment and the sectors involved. Secondly, some specific examples are

presented to show how the policy framework has been interpreted differently by different

companies and different municipalities and provincial governments.

Institute for Retail Studies. All rights reserved.

15

3.1 General Comments on the Pattern of Foreign Investment in the Retail Sector

3.1.1 Method of Entry into the Retail Sector

Table 5 shows the different entry methods used by retail companies (drawn from Appendix A,

section a, only) and the rough dates of when they took place. This table refers to the initial

entry by a company and not to the subsequent reinforcement of that entry by, for example,

further store openings. Table 6 shows the entry methods used, by the country of origin of the

retailer involved. By cross-referencing between the two tables and Appendix A we can see

that the early entrants into the Chinese market were the Japanese department stores. Several

of these companies opened Representative Offices in Beijing and Shanghai immediately

following the relaxation of controls in 1978. The Representative Offices acted, primarily, as

buying offices for the Japanese market, sourcing clothes and other goods. Management

agreements were also entered into between Japanese retailers and some Chinese department

stores. The Japanese companies brought retail expertise which could be harnessed in the

running of the Chinese stores; the Chinese companies brought their knowledge of the Chinese

distribution system and links to domestic manufacturers. Whilst the Japanese companies have,

no doubt, learnt much about the Chinese market through these tie-ups, their prime purpose

was to service the demand for Chinese goods at home.

During the 1980s a number of companies began the move into the retail sector through sales

counters in department stores and through joint venture stores. Such an early entry into the

Chinese market represented a reasonable degree of faith that the economic reforms would

continue and that consumers' disposable income would begin to reach the levels at which they

could afford the products offered. Developments like the supermarkets attached to hotel

facilities which were run by Wellcome and Park N Shop can be seen to be targeted at tourists

and expatriates. The sales counters and stores developed by companies such as Goldlion and

Pacific Concord were the offshoot of the manufacturing concerns already being run by Hong

Kong companies. As such these companies were already committed to China and entering

retail sales was one way of hedging their bets against currency fluctuations and recession in

other markets.

Institute for Retail Studies. All rights reserved.

16

New entries dropped away in 1990, partly because of the economic slowdown in China and

partly because of the political uncertainties following the clampdown on the student

demonstrations in Tiananmen Square, Beijing in 1989. The return to growth since 1991 and

the avowed desire of the government to keep the barriers to trade down has seen an increase

in the number of ventures reported in each of the past three years, as well as those companies

said to be expressing interest in the market (S. Davies, 1993). The easing of controls has

meant that all of the reported activities have involved some form of store development,

generally in a joint venture with a Chinese company. The spread of countries is also much

greater now, with Singapore registering the largest number of links after Hong Kong and

Japan. The known developments by companies from the U.S.A., Italy, France and Germany,

as well as the Japanese entry from Taka-Q, all represent some form of spin-off from a

manufacturing enterprise.

The dominant presence of companies based in Hong Kong can be explained in a number of

ways. First, some foreign companies (for example, Yaohan) have established operations in

Hong Kong especially to allow them to expand into China when the trading environment is

judged to be right. Secondly, Hong Kong's domestic companies now have a strong interest in

establishing a strong presence in China in advance of 1997. They will not enjoy domestic

status under the Chinese foreign trade regulations before that date, but some companies wish

to get a feel for the market and to establish alliances and partnerships well in advance of that

time. Finally, one of the features of the early 1990s, and something which accounts for some

of the level of interest by Asian companies in particular, has been the inclusion of retail

companies in trade missions to China. The Hong Kong Trade Development Council has been

marketing the Chinese retail sector to Hong Kong companies for several years and has even

arranged to set up its own sales counters in Chinese department stores to showcase products

and to show what can be done. (Similarly, recent trade visits by the Retail Associations from

Singapore and Malaysia have boosted awareness and links with these countries, which has

been reflected in the recent entry of NTUC Fairprice, Metro, QAF and Parkson into China.)

It is interesting to note that the Japanese department stores have made little effort to expand

upon their early interest in China to date. If one excludes the involvement of Yaohan Japan in

the Shanghai project (see below), Isetan is the only Japanese department store chain to have

actually opened a store in China. There are a number of possible explanations for this trend.

Institute for Retail Studies. All rights reserved.

17

First, the 1990s so far have not been a good period for these companies. Economic recession

at home and in some of their larger overseas markets, changing consumer tastes and the

current willingness of the Japanese to patronise discount chains has caused the level of their

domestic sales to fall for almost eighteen months. A reticence to enter a major, untried market

such as China under these circumstances can be understood. Secondly, only Yaohan (which

has moved its international headquarters to Hong Kong) has shown itself to be prepared to

make a long-term commitment to China. As business connections (guanxi) are an important

part of the environment of Chinese retailing (as shown by Appendix A), this is an activity the

influence of which should not be underestimated.

3.1.2 Sector of Entry

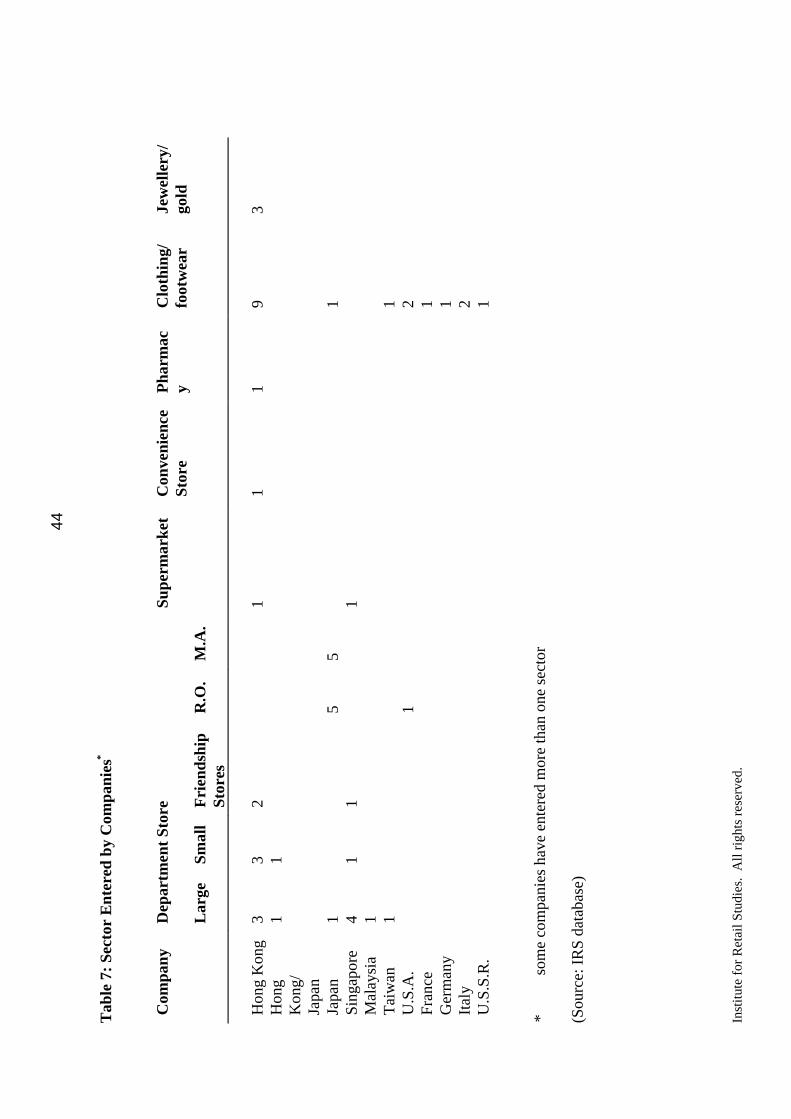

Table 7 shows the sectors which have been entered by the retail companies represented in

Appendix A. Two sectors are very clearly important: department stores and the clothing/

footwear sector. The department store sector was an obvious one for foreign retailers to

choose. As Table 4 showed, this sector is the strongest and most organised in China; it also

offers a natural fit to the department store groups from Japan, Hong Kong, Singapore and

Malaysia which occupy similar strong positions domestically. Almost all of the recent joint

ventures set up to develop department stores seem to involve some form of import-export

enterprise. However, the most recent plans from Yaohan and Sincere (see below) appear to

be built on a form of operation more akin to them being recognised as essentially Chinese

companies with only limited capabilities to import products.

The second strong sector has been clothing and footwear. As was noted above, this has come

about because of the transference of manufacturing capacity in this sector to China over the

past decade. Once foreign companies are involved in a joint venture manufacturing clothing in

China, it is an easy step for them to seek to sell some of their output on the domestic market.

There are fewer reasons why companies operating in other sectors, and especially those which

are not already based in Hong Kong, should wish to enter China. Indeed, the sole exception

listed in the sample was NTUC Fairprice, the retailing arm of the Singaporean trade union

movement, which is aiming to export its expertise throughout Asia.

Institute for Retail Studies. All rights reserved.

18

3.2 EXAMPLES OF RETAIL DEVELOPMENTS AND ENTRY MECHANISMS

3.2.1 Joint ventures: Yaohan

The development of Yaohan into potentially a major force in Chinese retailing has taken

several years and falls into several separate and distinct phases.

• In 1989/ 90 Yaohan Departmentstore of Japan announced that it was to move the

head office of its international operations to Hong Kong. In terms of the ratio

between domestic and overseas outlets and the sales which they generate, Yaohan is

probably the most international of the Japanese department store groups. The move

to Hong Kong was designed to be symbolic, symbolising the company's commitment

to becoming a major force in Chinese retailing - this part of the company will become

a Chinese company from 1997 (Wada, 1992). As will be seen below, this move has

opened a number of doors in Hong Kong and in China for the company's

management and it has certainly speeded the rate at which it has been allowed to

develop within China.

• Yaohan International opened its first store in China in Sha Tau Kok in Shenzen in

September 1991. A total HK$10m was invested, to which Yaohan contributed 49%,

paying HK$%m in cash; the Chinese partner, Sha Tau Kok Pte Ltd, put up the other

51% in land. Sales already exceed those of the Yaohan store in Sha Tin in Hong

Kong - and as ninety per cent of sales are made in Hong Kong dollars, there is no

problem repatriating the profits. It is said that Yaohan's Hong Kong base did make it

easier to gain entry to the market (Leung, 1993b, 5).

• A joint venture between Yaohan International (36%), Yaohan Japan (19%) and the

Shanghai No. 1 Department Store (45%) was the first store to be approved by the

government following its relaxation of the rules on foreign investment in 1991-1992.

The No. 1 Department Store made sales of ¥13m (£12.5m) in January 1992, an all-

time record in China. The shop, which has 30,000 varieties of products on sale,

receives 300,000 visitors a day. As a comparison, Selfridges had approximately

100,000 visitors a day during its January sales in 1992 (The China-Britain Trade

Institute for Retail Studies. All rights reserved.

19

Review, March 1992). The funds for the No. 1 Department Store will come from

shares to the value of ¥120m which it is to issue following its move to a limited

liability company basis (The China-Britain Trade Review, July 1992).

Over US$100m will be invested in the proposed new store on Zhang Yang Road in

Pudong, Shanghai. It will cover 20,000 m2 and have a total floor area of 80,000 m2.

Construction was due to start at the end of 1992 and the store is due to open at the

end of 1995.

The Board of Directors will consist of nine members, five from the Japanese side and

four from the Chinese side. The Chairman of the Board will be a representative of

the Chinese side while the General Manager will be a member of the Japanese side.

However, the method for passing resolutions still remains to be agreed. It has also

been granted the right to import up to thirty per cent of the goods sold in the store

(Leung, 1992a). At the same time, to take advantage of Yaohan's extensive

international distribution network, the joint venture can also conduct export business

in order to achieve a balance of foreign exchange and export surplus. In the first five

years of operation, the joint venture will enjoy a reduced income tax rate of fifteen

per cent, as opposed to the regular thirty per cent set by the state (Leung, op cit).

• Yaohan International has entered into a joint venture agreement with the state run

China Venturetech Investment Corporation. (It is unlikely that such a prestigious

joint venture would have been available to Yaohan without the positive signals about

its faith in China that Yaohan's move to Hong Kong had been sending to the State

Council.) The joint venture vehicle, CCY (owned 50/50 by Yaohan and CVIC),

already has two department stores cum supermarkets in Beijing and Shanghai. In

October 1992 CCY announced plans to establish 1,000 stores across China by the

year 2010 and in December 1992 further plans were forthcoming for an International

Merchandise Mart in Shanghai, similar to that already operating in Singapore. CCY

is also to build production facilities in several Chinese cities for its own brand of

shoes, cosmetics, ham and biscuits (The China-Britain Trade Review, July 1992).

Institute for Retail Studies. All rights reserved.

20

3.2.2Joint ventures: Sincere

The Sincere Department Store Co. of Hong Kong has signed a deal with Chinese partners to

demolish an existing building in the Nanjing Dong Lu, Huangpu District of Shanghai and to

build a 7,000 m2, US$12.8m department store (Goldstein, 1992a; Leung, 1992a). The

company which runs the store has been incorporated in China as the Sincere Shanghai

Department Store. This will allow it to bypass the procedures required by foreign joint

ventures for approval to operate other retail businesses. The company has already announced

plans to cooperate with local enterprises in setting up outlets in Sichuan Province (Anon,

1993b).

3.2.3 Joint venture: Giordano

Giordano, the Hong Kong clothing retailer, runs its Chinese operations through a holding

company, Tiger Enterprises. It opened its first Chinese store in Shenzen in August 1992. A

further four stores followed in Shenzen and Guangdong by the end of 1992 and the company

plans to have between fifteen and twenty stores by the end of 1993. Whilst Giordano's stores

in Hong Kong are a compact 1,000 - 2,000 sq ft each (and extremely numerous), its outlets in

China are as large as 15,000 sq ft to accommodate the greater variety of styles demanded

by the Chinese consumers. In Hong Kong the company stocks eighty basic styles while in

China it has 230, nearly three times as many (Clifford, 1993).

Clifford also notes the need for more focused, product based advertising in China. He quotes

Paul Kua, chief executive of Tiger Enterprises, as saying that advertising in the hinterland has

to be very direct. 'In Chengdu, you have to say "I'm selling cotton polo shirts"'. In one test an

informal group of Chinese consumers thought that a Giordano advertisement featuring

Brazilian carnival dancers was meant to sell film or paint.

3.2.4 Joint venture: QAF

QAF Ltd of Singapore is planning to invest ¥78 million (S$23.9 million) in a joint venture with

Chengdu Department Emporium (CDE). Under the terms of the agreement it will operate

CDE's supermarket cum department store and participate in the construction of an extension

Institute for Retail Studies. All rights reserved.

21

to the six-storey store which will expand the total area of CDE to 100,000 m2. The joint

venture vehicle will be Chengdu Department Emporium Co. Ltd. CDE will transfer its land

use rights to the joint venture company for ¥5.3 million when the annexe building is

completed. QAF will also guarantee a yearly pre-tax profit of ¥7.5 million to CDE until the

completion of the annexe but QAF will get any profits in excess of this amount. Upon

completion of the annexe, any profits will be shared equally between the partners.

3.2.5 Manufacturer sales counters: Goldlion

Goldlion, a Hong Kong-based manufacturer and retailer of upmarket men's accessories, began

advertising in China in 1983-84, well in advance of its entry into the market in 1986. The

company sells through exclusive Goldlion counters in department stores selected because of

their willingness to cooperate and because of the size of their customer flows. Instead of

paying rent for the counter, Goldlion sells its merchandise to the stores with a twenty per cent

discount built into the agreement. There are now 460 Goldlion counters in major cities and

urban areas such as Guangzhou, Tianjin, Shanghai, Beijing, Xian and Shenzen.

A large part of Goldlion's success has been based on its use of advertising and promotion.

Since 1983 it has done many things, from sponsoring football tournaments to advertising on

buses. In addition, patriotism is used as part of the marketing effort, despite the company's

origins in Hong Kong. As Chairman Tsang Hin Chi puts it: 'We let our customers know that

this is a Chinese brand and they are proud of it.' (Clifford, 1993). Tsang is one of the few

overseas delegates to the National People's Congress in China and he is currently backing

China's bid for the Year 2000 Olympic Games with a campaign to collect 10 million signatures

from shoppers. In the past he has generated publicity from his charitable activities; he has

donated more than twenty buildings worth some HK$200 million (US$26 million) to schools,

universities and government organisations. Tsang's success shows the vital role that guanxi

and the creation of links (through gift-giving) can play in business development in China.

Institute for Retail Studies. All rights reserved.

22

Goldlion's sales in China have nearly doubled in each year since 1988, reaching HK$260

million in 1992 and with sales forecast to reach HK$400 million in 1993. Over sixty per cent

of Goldlion's sales now come from China. Its tactics have now been followed by other Hong

Kong companies such as Crocodile and Silver Eagle, both of which have set up counters in

Beijing and Shanghai. In recent years the Hong Kong Trade Development Council has also

looked to set up special counters in selected department stores to act as promotional centres

for Hong Kong's products.

3.2.6 Manufacturer turned retailer: Pacific Concord Holdings

Pacific Concord of Hong Kong operates over 12,000 sales outlets throughout China, set up to

promote its own products, whilst its wholesale operation includes product design and material

sourcing for Chinese retailers. Much of the company's success has come from the rights which

it was granted as a manufacturing enterprise to sell the products of its joint venture within

China. It opened its first department store in Xiamen, Fujian province in 1984 (Soo, 1992)

and its second store opened in Beijing in December 1991. This store represented an

investment of HK$150m (£12m) over fifteen years (The China-Britain Trade Review, April

1990). The company plans to open a further ten stores in major Chinese cities by 1995.

Although twenty-five per cent of the merchandise sold in its two department stores comes

from Pacific Concord's own joint venture companies and includes goods such as electronics,

leather products, watches, garments, toys and cosmetics, one-third of sales are of imported

goods and products of other joint ventures.

3.2.7 Friendship Stores: Yansha Friendship Shopping City

Friendship Stores originally stocked goods either imported from the West or in short supply in

the ordinary stores. Access was restricted to foreigners and to the Chinese elite with access to

foreign currency. However, they were not very friendly and staff exhibited a surly fuwa taidu,

or service attitude, and made no real attempt at displaying the products (Walker, 1993a).

Faced by competition from companies such as Yaohan, Benetton and Stefanel, the Friendship

Stores in the larger cities are having to change their ways. One such project resulted in the

creation of the Yansha Friendship Shopping City in Beijing which opened in July 1992. It has

Institute for Retail Studies. All rights reserved.

23

six floors, a total sales area of 23,000 m2, sells over 300,000 kinds of goods and has 2,000

staff (95% of whom are said to have at least one foreign language). More than forty special

tourist groups visit the store each day, making up thirty per cent of all shoppers. The store

expects to handle 50,000 customers each weekday, with around 100,000 visits being made on

Saturdays. Daily sales average ¥1.5 million or ¥47 million per month.

The Shopping City is located in the Lufthansa Centre (a Sino-German commercial and hotel

complex) near Beijing airport. It is a joint venture between a local Beijing company and Sin

Cheng (Holdings) Pte Ltd of Singapore who contributed fifty per cent each of the ¥60 million

(US$5 million) investment. It was the second retail joint venture (after the Yaohan store in

Shanghai) to be approved when controls were relaxed by the State Council.

4. PROSPECTS AND PROBLEMS FOR THE FUTURE

The general prospects for foreign investment in China's retail sector appear mixed. Investment

is going to favour the SEZs and the major cities because that is where the

consumer demand is strongest and the infrastructure is most modern. Moving beyond these

areas, Yaohan's plans notwithstanding, is going to take time and may have to wait for further

state investment in distribution and other infrastructure facilities. Companies will continue to

cultivate their contacts and to keep a keen watch for political change, particularly if there

comes a point at which the huge ranks of China's small shopkeepers are mobilised to complain

about the level of retail change (cf the role being played by such retailers in Japan, Thailand

and Singapore). Currently, we can identify four areas which are causing concern to foreign

retailers in China: consumer demand; retail price inflation and currency movements;

regionalism and economic and political fragmentation; and, smuggling.

4.1 Consumer demand

It has not take long for businessmen and other analysts to recognise that the promise of one

billion new consumers in China for foreign companies is well off the mark because of the low

levels of disposable income of most consumers and the poor distribution system. (Marks &

Spencer are reported to have said that they will not expand their Hong Kong operation over

the border until there is a greater movement upmarket by Chinese consumers.) Nonetheless, a

Institute for Retail Studies. All rights reserved.

24

recent study by McKinsey (reported by Holberton (1992)), argues that there are currently 60

million Chinese consumers currently earning at least US$1,000 (£657) a year. This would be

as large as the consumer markets in the Republic of China (Taiwan) and the Republic of Korea

combined. It would also mean that consumers in the more affluent areas of China may well be

as rich, or richer, than the average Malaysian, Thai or Indonesian consumer. The study further

forecasts that by the end of the decade the number of affluent consumers could have risen to

200 million, making it larger than most of the east and south-east Asian markets today.

The Chinese consumer market has seen major changes in recent years. The economic reforms

since 1978 have increased consumer incomes. In 1991 the total value of retail sales reached

¥939.8 billion, averaging ¥811.6 per person, at a time when the market was still depressed

after a two-year recession (Cheung, 1991). More importantly, that period of recession had

masked some major changes in demand and consumption behaviour. Jian (1992), Hong Kong

Trade Development Council (1992) and Barnes (1992) have noted the following changes:

• demand for food has changed from large quantities to higher quality;

• clothing has seen a considerable increase in consumption (it has been estimated that

ready made clothing will make up half of the clothes owned by Chinese consumers

within ten years), and there has been a considerable shift towards fashionable styles,

designs and fabrics among urban consumers;

• durables are showing a shift from basic goods such as bicycles towards sophisticated

electronic items;

Institute for Retail Studies. All rights reserved.

25

• changing employment patterns, particularly in the SEZs, are providing workers with

more free time, leading to a surge in demand fr sporting goods, photographic film and

supplies, videos, books, and music cassettes and compact discs;

• infant and child-oriented products are also big sellers. (In Guangdong, the

combination of China's single child policy and the relatively high discretionary

incomes is creating a phenomenon known as the "little emperor" syndrome. In most

homes in the province, no expense is spared in meeting the needs of the family's one

child and the market for disposable nappies, baby food, fashionable clothes, and toys

is growing rapidly.)

Consumers, and particularly those in the big cities, have become more interested in buying

foreign and imported manufactured goods. Some of this is due to the increase in living

standards (aided by advertising), but it can also be attributed to the rejection by consumers of

the outdated and shoddy products being manufactured by state enterprises (Anon, 1991).

Chief among the unwanted items are textiles and clothes, black-and-white TVs, refrigerators

and bicycles. Instead, consumers are switching their priorities to colour TVs, video recorders,

air conditioning, vacuum cleaners and home furnishings (Cheung, 1991).

'The foreign brands that attract most Guangdong consumers tend to be the same onesthat are across the border in Hong Kong. Virtually every household in the PearlRiver Delta has erected a towering TV antenna to tune into the latest trends - andadvertisements - from Hong Kong. If Guangdong consumers seem to think anything"foreign" is good, they appear to view anything "American" as even better. Thisbelief is evident from the growing popularity of American symbols in Guangdongpackaging and marketing efforts.'

(Barnes, 1992, 29)

The immediate effect would seem to favour foreign joint ventures and foreign products. At

the same time, however, it is provoking the local retailers to do more to fight back. For

example, in April 1991, the government approved a three-month nationwide sale by state-run

department stores and collectives of industrial and consumer good worth ¥20 billion.

Institute for Retail Studies. All rights reserved.

26

Unfortunately for the local stores, even discounts of up to 30% failed in their aim of clearing

out inventories - some of the products were deemed virtually unsaleable because of their poor

quality or obsolescence (Cheung, 1991).

Where is the money coming from for these purchases?

• A major source is those workers who have jobs in the foreign enterprises in the SEZs

and coastal cities. In 1990 and 1991, the fastest growth was in coastal cities such as

Shenzen, Zhuhai, Xiamen, Guangzhou, Shanghai, Beijing, Hangzhou and Dalian,

where per capita GDP is up to 10 times the average nationwide urban per capita GDP

of ¥2,701 (Hong Kong Trade Development Council, 1992). In addition to this high

level of current income, many families have built up substantial levels of personal

savings over the past ten or fifteen years. These savings have had few outlets and

have either been kept as cash or converted into bank deposits or gold.

• Private businessmen (dubbed da kua, or "big money") who have entered into the

manufacturing and service sectors, either on their own or in partnership with foreign,

usually Hong Kong-based, companies. Some of the money spent by da kua is also

believed to come from smuggling (see below).

• Ordinary Chinese who do not work for themselves or for foreign companies have had

to counter by taking second jobs or relying on bonuses from their existing jobs.

The economic motor, therefore, for much of the expansion of consumer spending, particularly

in southern China, is the relaxation of controls over companies and the encouragement of

foreign investment and joint venture companies in China.

Institute for Retail Studies. All rights reserved.

27

4.2 Retail Price Inflation and Currency Movements

4.2.1 Retail Price inflation

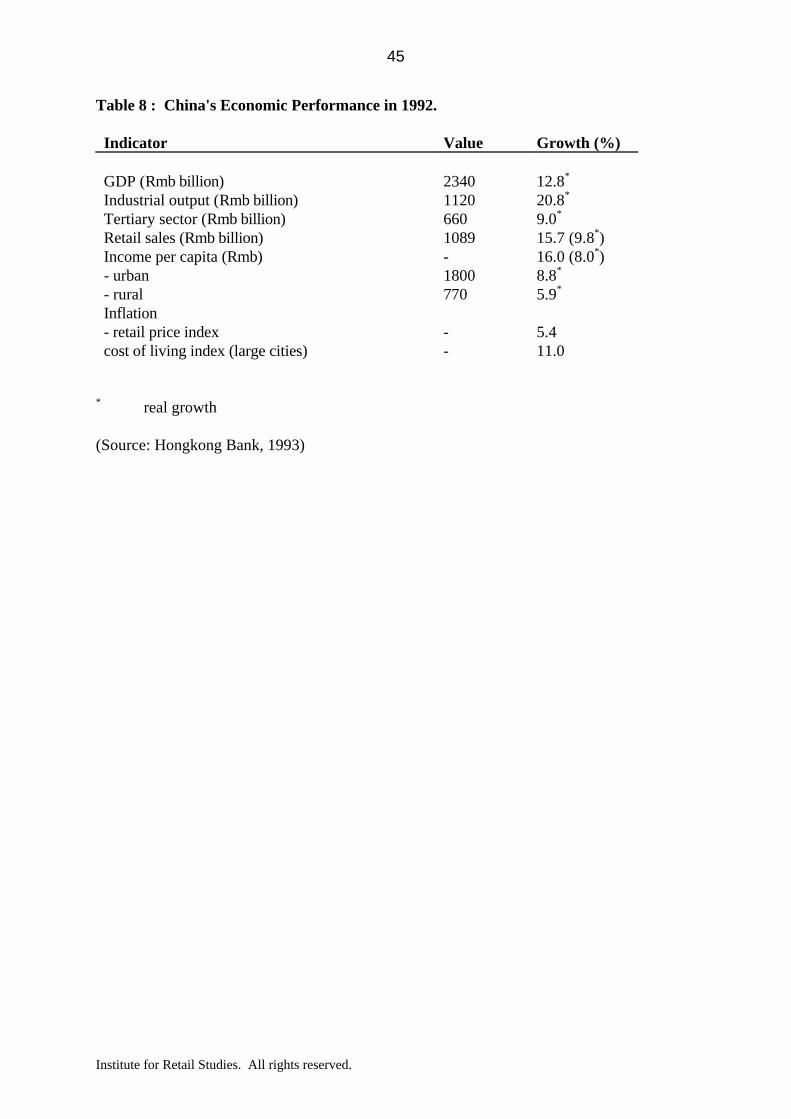

According to the review of the year by the Hongkong Bank (1993), the Chinese economy

strengthened substantially in 1992 (Table 8). Retail sales however saw growth of under 10%,

slower than the growth in investment and industrial output. This is partly because people have

been diverting funds to provide for housing, medical and other needs (as other reforms are

reducing state welfare coverage) and to invest in securities. Price levels in retail sales (mainly

of consumer goods) remained steady throughout the year, and up to 70% of retail inflation is

believed to have come from government price adjustments and not from demand pull.

The Hongkong Bank has commented that the economic boom in 1992 was mainly investment-

led with a marked disparity between the growth of investment and consumption demands.

This was different from the overheating of 1988 and the subsequent austerity when investment

and consumption moved together in either expansion or contraction.

'As a result, the economy is now characterised by rapid growth in investment andrelatively slow retail sales, higher growth for heavy than for light industries, and highdemand for many capital goods (leading to inventory depletion, shortages, high priceincreases and high import growth) but inadequate demand for many consumer goods(leading to stockpiling and stable prices). Nevertheless, the relatively slow retail salesof consumer goods at present is in fact healthy and normal; China should avoid takingmeasures to stimulate the level of consumption artificially, as this would only increasestate subsidies and fuel inflation.'

(Hongkong Bank, 1993, 2)

Not everyone sees the position as being quite so healthy. The annualized rate of inflation in

China's 35 largest cities reached 17% in April 1993 (Kaye, 1993). As a result, the level of

private bank savings fell during the first part of 1993 (for the first time since 1988) and

consumer spending increased to ¥4.5 billion in March 1993. The government's response was

to appoint a high-ranking official, Mr Zhu Rongji, senior vice-premier, to the role of governor

of the Bank of China. He has acted to curb bank lending by raising interest rates on bank

deposits in mid-May and again on July 11 1993 (O'Donnell, 1993). This step sought to

increase bank deposits (and banks were said to be running short of cash in early 1993) by

Institute for Retail Studies. All rights reserved.

28

encouraging companies to repatriate hard currency and by mopping up some of the cash

savings of the population which was being converted into goods and gold (Kaye, 1993;

Sender, 1993a). The government has also been trying to rein in the high levels of investment

being undertaken by municipal and provincial governments (see below).

The government's efforts are targeted at easing some of the pressure caused by an over-

heating economy, particularly in the south and among the coastal provinces. The danger is

that either because of economic miscalculation or political in-fighting, the government will fail

in its objectives. Neither the continuation of high levels of inflation from the economic boom

nor the dangers of an economic slump will be good for consumer confidence. A move away

from the current, relatively open economic policies would be likely to damage the credibility of

the investment regime which is attracting foreign investment in retailing, despite the size of the

potential market.

4.2.2 Currency movements

A major problem for foreign retailers is being caused by the rapid devaluation of the renminbi.

The currency has been devalued officially several times in recent years: 21.2% in December

1989, 9.57% in November 1990 and dozens of minor adjustments since 1991 (Anon, 1993a).

However, these devaluations were reflecting the fact that the official exchange rate had moved

out of line with the swap market rate and they had little effect on foreign investors. In recent

months the renminbi has fallen further on the swap and black markets, losing more than 20%

of its value between November 1992 and March 1993 (Blass, 1993a), leaving a discrepancy of

more than 30% between the official and swap rates again (Anon, 1993a). When the

government finally removed its cap on the quasi-official swap markets on June 1 1993, the

renminbi promptly fell 25% against the US dollar, from 8.14 to 10.17 per dollar and then

down to ¥11 (Sender, 1993b). Likewise, Foreign Exchange Certificates (FEC) now command

a premium of more than two-thirds over the value of the renminbi.

The sharp fall in the value of the renminbi in the first half of the year is partly attributable to

inflationary pressures in China in recent years and to demand for foreign currency as more

Chinese businessmen and tourists travel abroad (Anon, 1993a). Many commentators however

also see links to China's hopes for imminent reentry into GATT and the need for a fully

Institute for Retail Studies. All rights reserved.

29

convertible currency. (Convertibility will also mean the demise of the FEC; probably sooner

rather than later (Kaye, 1993).) The pressures to devalue can only increase as GATT entry

gets closer, so analysts believe that at least some of the recent downward movement has been

deliberate government policy to do things early rather than later (Sender, 1993b).

Unfortunately, the downward spiral is then intensified by the desire of many Chinese to

exchange their renminbi for foreign currency before the rate falls further (Anon, 1993a).

Renminbi devaluation can be advantageous for foreign companies manufacturing in China for

export because the cost of their goods has fallen in recent months. This contrasts with

investments in domestic services such as retailing and restaurants which have been hard hit by

devaluation. Companies such Goldlion, Giordano, Pacific Concord, Cafe de Coral and

Fairwood have seen their profits eroded as their generated incomes in the mainland are largely

in renminbi (Anon, 1993a). There is a variety of ways to minimise these effects: first, some

companies, particularly those which also attract tourists and expatriates, may be able to

generate foreign currency which can be repatriated without losses. The Yaohan store in

Shenzen, for example, displays all its prices in HK$ and, with only 10% of sales in renminbi, it

has no difficulties in repatriating its profits (Soo, 1992). (Indeed, a substantial proportion of

the whole stock of issued HK$ is believed to be circulating in southern China at any one time

where it is treated as hard currency.) Secondly, companies such as Sincere are reinvesting

their renminbi earnings in their Chinese operations, thus hiding some of the effects of

devaluation. Thirdly, joint venture companies can make greater use of products manufactured

in China, keeping currency transfers down to a minimum. Finally, companies can raise prices

but higher prices are unlikely to be accepted by the market unless the goods are very

competitive or difficult to substitute (ibid).

As Sender (1993b) notes, however; it is not necessarily the changes in exchange rates which

are worrying companies, as much as the volatility of the situation. Blass (1993a) quotes Paul

Kua, president of Tiger Enterprises, the China division of Giordano, as saying: 'In other

markets you can buy [currency] futures. But in China the only thing we can do to hedge is

raise prices.' But, like many newcomers to China, Giordano believes it must keep prices low

to establish a foothold. For most of its casual clothing line, prices are set months in advance,

with profit margins around 30-40%. 'We had a game plan going in', says Kua, 'but we didn't

anticipate a depreciation of this magnitude.'

Institute for Retail Studies. All rights reserved.

30

If the currency is stabilised, then accurate predictions of future income streams can be made.

But, in tandem with its recent efforts to control inflation, the government has been supporting

its currency again in the financial markets. Between the first of June and mid-July 1993, the

yuan rose against the US$ from ¥11 to ¥8.65 (O'Donnell, 1993). What are companies to

make of such contradictory expressions of policy?

4.3 Regionalism and Political and Economic Fragmentation

The legislation and reforms pursued by the central government have been seen as

revolutionary and wide-ranging. The review of the economy by the Hongkong Bank (1993)

shows that the recent rapid decentralisation of economic autonomy to enterprises and regions

has not only reversed the partial recentralisation applied during the late 1980s and early 1990s

but has also exceeded the extent of decentralisation in 1988. But this now means that the

government has lost even more control over prices and over the actions of localities and

enterprises (Kaye, 1993).

One of the problems with this decentralisation of power has been competition for investment

and funds. Government investment in fixed assets was up 70% in the first quarter of 1993 and

first quarter investment pledges by local officials jumped to US$25 billion, up 347% from a

year earlier, though only US$3 billion was actually disbursed (Koan and Kaye, 1993). As part

of its efforts to get inflation under control, the government has also been seeking to rein in this

investment. The number of economic development zones grew from 117 officially approved

zones at the end of 1991 to at least 2,000 by the end of 1992. These economic zones enjoy

special privileges, such as tax breaks and the demand for building materials which they have

fuelled has added to the increases in price inflation in 1992.

Matters have been aggravated further by the manner in which the majority of foreign

investment is being drawn to the southern coastal provinces, particularly Guangdong, leading

to higher wages and living standards, inflationary pressures and political stresses. The

McKinsey study reported by Holberton (1992) found that affluent consumers are concentrated

in southern China (particularly Shenzen, Guangzhou and Shanghai) and around Beijing and

Tianjin in the north.

Institute for Retail Studies. All rights reserved.

31

Past government policy has encouraged provincial governments to aim for self-sufficiency.

One of the goals of China's current economic reforms is to achieve a unified domestic market

by improving internal distribution. However, government efforts to restrain the coastal

provinces and to promote the north and interior have caused their own problems. The

economic squeeze designed to stop inflationary pressures in 1988-89 has been described as a

"crude method of slowing the economy by slamming its efficient parts into a brick wall"

(Anon, 1993e).

In more recent years provincial governments have been more aggressive in their efforts to

protect their local economies. Thus, when in 1992 Guangdong refused to pay high

government prices for its oil supplies and it was threatened with an oil squeeze which would

have brought its business sector to a halt, the provincial government chartered an oil tanker

from Kuwait to import oil bought on the international spot market (Anon, 1993d).

This "economic warlordism" is to be seen in the conflict which is beginning to appear in the

retail sector too. The controls over retailing are, along with many other sectors of the

economy, showing the strains being placed on China by the differences between the rich and

poor provinces. China appears to be returning to the position of several years ago, when Price

(1988) commented on the different approaches being taken by the various provincial

governments and regional arms of the central bureaucracy and their effect on forward

planning, saying:

'The law is applied across the country with consistent inconsistency. Furthermore,the Chinese have an unsettling habit of moving the goalposts in the middle of thegame. Rules are constantly being revised and this makes it extremely difficult toestablish costs and benefits in advance.'

Institute for Retail Studies. All rights reserved.

32

4.4 Smuggling and Counterfeiting

Every year since 1990, at least US$1 billion worth of durable foods - from Sony Walkmans to

Honda motorcycles - are believed to have been smuggled into China from Hong Kong alone

(Blass, 1993b). Towns in the Pearl River delta, such as Xintang, thrive on smuggling, drawing

customers from Shanghai and economically-backward Sichuan province alike to buy high

technology consumer goods which are either not yet available in China or which may be

subject to tariffs of up to 100% if imported legally. By one official estimate, more than 90%

of the VCRs sold in China are smuggled into the country (ibid).

'Smuggling has become so pervasive, in fact, that some economists and businessleaders say that it has unwittingly introduced market forces into South China. Competition from illicit traders, who offer everything from Sanyo air conditioners toToshiba refrigerators, has pushed mainland manufacturers to develop moresophisticated products. "If they gave a medal for market progressiveness inGuangdon province", says a foreign economist based in Canton, "smugglers wouldget the gold hands down."'

(op cit, 35)

Not all goods enter by such illegal channels. For instance, some goods arrive legitimately

through duty-free channels and then "leak" into the general market (Barnes, 1992, 34).

Indeed, Curry (1993) reports that obtaining accurate market surveys has become more difficult

because many enterprises are acquiring goods through unofficial means (including smuggling)

outside the central distribution network. As a result the compilation of official statistics about

the breakdown of market share can be inaccurate. For example, a large demand for

photocopiers has led to smuggling and a much greater market for these machines than official

data indicate.

5. CONCLUSION

What are the future prospects for foreign investment in the retail sector in China? In terms of

the general economic situation, de Keijzer (1993) argues that China is likely to remain a

good investment in the near future. He believes that economic growth will continue, aided by

domestic reforms and an open foreign trade system. He sees Hong Kong as already so well

integrated into the economy of the Pearl River Delta that, in economic terms, there will be no

Institute for Retail Studies. All rights reserved.

33

big change when 1997 comes around. It is also likely that the increasing levels of economic

integration between the People's Republic of China and the Republic of China (Taiwan) will

create an even larger and more powerful economic zone. All of these changes, it is believed,

can only be good for China and, hence, for the retail sector too.

'Economists hold that foreign businessmen's influx into China's consumer goodsmarkets will bring both advantages and disadvantages to China. Anyhow, the formerwill exceed the latter. If China seizes this chance, it will not only be able to attractmore foreign investment to its retail commerce but will also help improve thecommodity quality, sales service and management skills of its commercial businesses. This is also beneficial to the modernization of China's commerce and the gradualmixing of China's consumer goods market and the international market.'

(Jian, 1992, 6)

There are a number of imponderables in these statements however. First, in the short term,

the economic slow-down being engineered by Zhu Rongji is causing problems for retailers,

although these are not thought to be insuperable. The austerity plans are an attempt to

channel existing financial resources from property speculation into more productive activities.

Some companies will almost certainly pull out of China because of the current difficulties. S.

Davies (1993) quotes a merchant banker in Hong Kong as saying: 'Retailers were paying a

fraction of the labour and land costs of Hong Kong, but charging double the prices for the

product. It could never last.'

Nonetheless, a number of Hong Kong companies (and some Hong Kong-based foreign

companies) are committed to China in the long run, partly because of the size of the market

and partly because of their desire to establish themselves in the market in advance of 1997.

For example, according to S. Davies, the decisions by Mr Robert Kuok and New World

Development to pull out of commercial developments in Beijing result from disagreements

with the joint venture partners rather than concerns over the state of the market. Other Hong

Kong companies are considering taking over these projects currently.

Secondly, the pace of change, particularly in the south of the country, is having substantial,

and sometimes unwanted side effects, on Chinese society. Siu (1993) argues that Guangdong

is being detached from the rest of China by the powerful draw, via Hong Kong, of Western

capitalist enterprises and the attendant consumer culture. For those with access to sufficient

Institute for Retail Studies. All rights reserved.

34

money and the right contacts, this can manifest itself in conspicuous consumption.

'The Chinese themselves appear shocked by such displays of wealth. The largestcrowds in Yaohan's store [in Beijing]...gather at the windows of the gold-fish bowlstyle swimming pool. There, parents sip cocktails while their children splash aroundin the pool below. But the frivolity does not come without its critics. A circumspectPeople's Daily commentary in December, focused on people standing outside high-class stores, loath to enter and be labelled a "coward" for not buying anything. Thenewspaper said officials fiddling expense accounts, newly-weds and criminals hadjoined the da kua to form China's "consumer aristocracy"'.

(Hendry, 1993)

As is hinted at in this quote, for those outside the new consumer culture confusion, and even

alienation, is increasingly in evidence. High rates of drug addiction, gambling and violent