Q4 Inc. Financial Statements Q4 2021 - Mock

47

Q4 Inc. Consolidated Financial Statements December 31, 2021 and 2020 (expressed in US Dollars)

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Q4 Inc. Financial Statements Q4 2021 - Mock

Q4 Inc.Consolidated Financial StatementsDecember 31, 2021 and 2020(expressed in US Dollars)

PricewaterhouseCoopers LLP PwC Tower, 18 York Street, Suite 2600, Toronto, Ontario, Canada M5J 0B2 T: +1 416 863 1133, F: +1 416 365 8215

“PwC” refers to PricewaterhouseCoopers LLP, an Ontario limited liability partnership.

Independent auditor’s report

To the Shareholders of Q4 Inc.

Our opinion

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the financial position of Q4 Inc. and its subsidiaries (together, the Company) as at December 31, 2021 and 2020, and its financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (IFRS).

What we have audited The Company’s consolidated financial statements comprise:

the consolidated balance sheets as at December 31, 2021 and 2020;

the consolidated statements of loss and comprehensive loss for the years then ended;

the consolidated statements of changes in shareholders’ equity for the years then ended;

the consolidated statements of cash flows for the years then ended; and

the notes to the consolidated financial statements, which include significant accounting policies and other explanatory information.

Basis for opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the consolidated financial statements section of our report.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Independence We are independent of the Company in accordance with the ethical requirements that are relevant to our audit of the consolidated financial statements in Canada. We have fulfilled our other ethical responsibilities in accordance with these requirements.

Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements for the year ended December 31, 2021. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Key audit matter How our audit addressed the key audit matter

Fair value measurements of the Class A and Class B preferred share warrants using the Monte Carlo method

Refer to note 2.3(m,n) Summary of significant accounting policies, note 2.4 Significant accounting judgments, estimates and assumptions and note 10.1 Warrant liability to the consolidated financial statements.

During the year ended December 31, 2021, 513,284 Class A preferred share warrants and 98,967 Class B preferred share warrants were exercised, resulting in nil Class A and 395,869 Class B preferred share warrants as at year-end with a fair value of $1,274,695.

The Company measures its warrants at fair value on initial measurement, immediately prior to exercise of the warrants and at each balance sheet date. Fair value is the price that would be paid to transfer the liability in an orderly transaction between market participants at the measurement date. The Monte Carlo method was applied on initial measurement, immediately prior to exercise of the warrants and at each balance sheet date until the Company completed their initial public offering (IPO) on October 29, 2021. Significant assumptions used by management in the Monte Carlo method were the Company’s weighted average share price and probability of IPO. The Black-Scholes valuation model was applied to value the warrants subsequently. For the year ended December 31, 2021, management recognized a loss on derivative financial

Our approach to addressing the matter involved the following procedures, among others:

● With the assistance of professionals with specialized skill and knowledge in the field of valuation, developed an independent point estimate of the fair values of the warrants immediately prior to exercise and at each balance sheet date until the Company completed their IPO and:

Tested the underlying data used in developing the fair values using the Monte Carlo method.

Evaluated the reasonableness of the significant assumptions used by management related to the Company’s weighted average share price and the probability of IPO by considering (i) current and past performance; (ii) external market and industry data; (iii) discussions with management and those charged with governance; and (iv) evidence obtained in other areas of the audit.

● Compared the fair values of our independent point estimates to management’s fair value estimates to evaluate the reasonability of management’s estimates.

● Recalculated the loss on derivative financial instruments recorded in the consolidated statements of loss and comprehensive loss.

● Tested the disclosures made in the consolidated financial statements.

Key audit matter How our audit addressed the key audit matter

instruments of $3,418,108 in the consolidated statements of loss and comprehensive loss.

We considered this a key audit matter due to the significant judgment made by management in determining the fair values of the Class A and B preferred share warrants using the Monte Carlo method, including the use of significant assumptions. This in turn resulted in a high degree of auditor judgment, effort and subjectivity in performing procedures. Professionals with specialized skill and knowledge in the field of valuation assisted us in performing the procedures.

Other information

Management is responsible for the other information. The other information comprises the Management’s Discussion and Analysis.

Our opinion on the consolidated financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of management and those charged with governance for the consolidated financial statements

Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with IFRS, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditor’s responsibilities for the audit of the consolidated financial statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Company to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the consolidated financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

The engagement partner on the audit resulting in this independent auditor’s report is Jen Psutka.

/s/PricewaterhouseCoopers LLP

Chartered Professional Accountants, Licensed Public Accountants

Toronto, Ontario March 1, 2022

Consolidated Balance Sheets(expressed in US Dollars)

December 31,2021

December 31,2020

$ $ASSETS Current assets

Cash 63,282,777 4,575,950 Accounts receivable Note 3 9,328,431 9,724,401 Costs to obtain contracts Note 14 1,928,489 2,358,953 Contract assets Note 14 1,083,309 388,477 Prepaid expenses 2,101,704 1,729,940 Deferred financing fees — 221,956 Investment tax credits receivable Note 16 746,453 887,223

Total current assets 78,471,163 19,886,900 Non-current

Costs to obtain contracts Note 14 446,103 699,971 Contract assets Note 14 267,894 93,182 Promissory note receivable Note 17 255,596 — Intangible assets Note 4 19,510,501 22,333,661 Property and equipment Note 5 913,762 782,642 Right-of-use assets Note 6 1,675,742 2,491,993 Goodwill Note 7 7,576,311 7,576,311

Total assets 109,117,072 53,864,660

LIABILITIES AND SHAREHOLDERS' EQUITYCurrent liabilities

Accounts payable and accrued liabilities Note 8 5,456,570 5,550,832 Income taxes payable Note 16 273,139 26,048 Deferred revenue Note 14 14,205,381 12,647,647 Loans payable Note 9 — 1,701,838 Lease liability Note 6 682,904 705,195

Other liabilities Note 10 1,731,252 2,280,229 Total current liabilities 22,349,246 22,911,789 Non-current

Deferred revenue Note 14 6,510,675 5,176,514 Lease liability Note 6 1,272,941 2,067,863 Deferred tax liability Note 16 281,639 386,605

Total liabilities 30,414,501 30,542,771

SHAREHOLDERS' EQUITYShare capital Note 11 176,785,744 85,404,804 Contributed surplus 1,913,587 2,575,910 Accumulated other comprehensive income 55,864 91,028 Deficit (100,052,624) (64,749,853)

Total shareholders' equity 78,702,571 23,321,889 Total liabilities and shareholders' equity 109,117,072 53,864,660

On behalf of the Board

(Signed) Colleen Johnston Director (Signed) Darrell Heaps Director

The accompanying notes are an integral part of these consolidated financial statements

Q4 Inc.

1

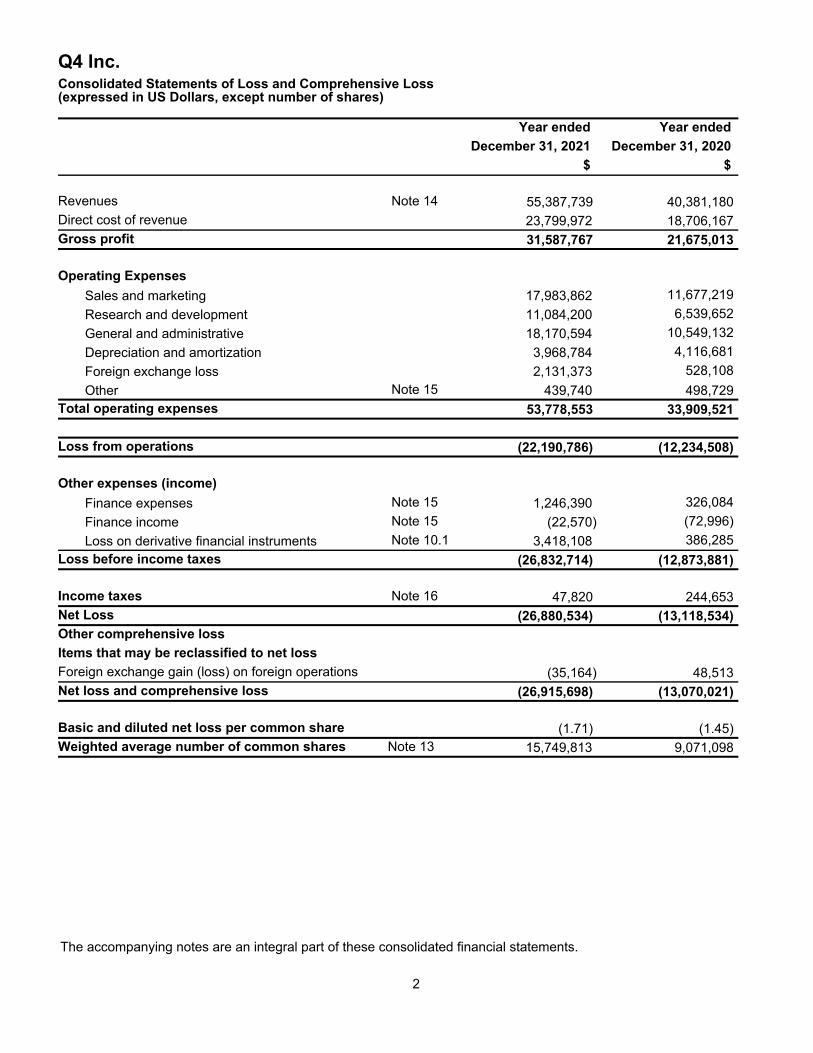

Consolidated Statements of Loss and Comprehensive Loss(expressed in US Dollars, except number of shares)

Year ended Year endedDecember 31, 2021 December 31, 2020

$ $

Revenues Note 14 55,387,739 40,381,180 Direct cost of revenue 23,799,972 18,706,167 Gross profit 31,587,767 21,675,013

Operating ExpensesSales and marketing 17,983,862 11,677,219 Research and development 11,084,200 6,539,652 General and administrative 18,170,594 10,549,132 Depreciation and amortization 3,968,784 4,116,681 Foreign exchange loss 2,131,373 528,108 Other Note 15 439,740 498,729

Total operating expenses 53,778,553 33,909,521 Loss from operations (22,190,786) (12,234,508)

Other expenses (income)Finance expenses Note 15 1,246,390 326,084 Finance income Note 15 (22,570) (72,996) Loss on derivative financial instruments Note 10.1 3,418,108 386,285

Loss before income taxes (26,832,714) (12,873,881)

Income taxes Note 16 47,820 244,653 Net Loss (26,880,534) (13,118,534) Other comprehensive lossItems that may be reclassified to net lossForeign exchange gain (loss) on foreign operations (35,164) 48,513 Net loss and comprehensive loss (26,915,698) (13,070,021)

Basic and diluted net loss per common share (1.71) (1.45) Weighted average number of common shares Note 13 15,749,813 9,071,098

The accompanying notes are an integral part of these consolidated financial statements.

Q4 Inc.

2

Consolidated Statements of Changes in Shareholders’ Equity(expressed in US Dollars)

Common Shares

Class APreferred Shares

Class BPreferred Shares

Class CPreferred Shares

Contributed surplus

Deficit Accumulated other

comprehensive

income

Total

$ $ $ $ $ $ $ $

Balance, December 31, 2019 10,662,889 985,394 20,550,635 32,850,961 2,001,899 (51,631,319) 42,515 15,462,974

Exercise of stock options Note 11 354,925 (179,987) 174,938 Share-based compensation Note 12 753,998 753,998 Net loss for the year (13,118,534) (13,118,534) Translation adjustment 48,513 48,513 Issuance of Class C Preferred

SharesNote 11 20,000,000 20,000,000

Balance, December 31, 2020 11,017,814 985,394 20,550,635 52,850,961 2,575,910 (64,749,853) 91,028 23,321,889

Exercise of stock options Note 11 3,581,868 (1,656,510) 1,925,358 Share-based compensation Note 12 994,187 994,187 Net loss for the year (26,880,534) (26,880,534) Translation adjustment (35,164) (35,164) Exercise of warrants Note 11 4,119,831 1,334,861 5,454,692 Conversion of Preferred Shares

to Common Shares 79,841,682 (5,105,225) (21,885,496) (52,850,961) —

Issuance of Common Shares upon initial public offering

Note 11 81,329,146 81,329,146

Share issuance costs Note 11 (7,407,003) (7,407,003) Stock dividend declared Note 11 8,422,237 (8,422,237) —

— Balance, December 31, 2021 176,785,744 — — — 1,913,587 (100,052,624) 55,864 78,702,571

The accompanying notes are an integral part of these consolidated financial statements.

Q4 Inc.

3

Consolidated Statements of Cash Flows(expressed in US Dollars)

Year endedDecember 31, 2021

Year endedDecember 31, 2020

$ $Operating activitiesNet loss before tax (26,832,714) (12,873,881)

Adjustments for items not affecting cash:Depreciation of property and equipment Note 5 328,929 84,770 Depreciation of right-of-use assets Note 6 816,695 957,033 Amortization of intangible assets Note 4 2,823,160 3,074,878 Unrealized foreign exchange loss 2,131,373 542,531 Loss on derivative financial instruments Note 10 3,418,108 386,285 Finance income Note 15 (22,570) (72,996) Finance expenses Note 15 1,246,390 326,084 Share-based compensation Note 12 1,169,037 753,998 Deferred tax liability Note 16 (104,966) —

Changes in non-cash working capital items:Accounts receivable 331,306 (5,819,781) Contract assets (872,813) (27,971) Prepaid expenses (372,890) (603,267) Investment tax credits receivable 140,770 9,287 Costs to obtain contracts 670,519 (864,047) Trade and other payables (182,526) 1,934,387 Other liabilities 118,556 (292,000) Deferred revenue 3,007,999 9,170,561

Income taxes paid (174,601) (201,015) Cash used in operating activities (12,360,238) (3,515,144)

Investing activitiesProceeds from short-term investment — 6,986,315 Purchase of property and equipment Note 5 (460,049) (626,139) Prepayment of right-of-use assets — (65,176) Purchase of intangible asset Note 4 — (4,000,000) Loss on short-term investment — (21,076) Interest received 19,207 72,996 Payment of contact database obligation (230,000) (230,000)

Cash provided by (used in) investing activities (670,842) 2,116,920

Financing activitiesProceeds from issuance of shares Note 11 81,154,296 — Proceeds from exercise of stock options and warrants Note 12 3,272,176 174,938 Draws on loans payable Note 9 18,560,274 7,406,475 Repayment of loan Note 9 (20,610,917) (6,249,168) Payment of principal portion of lease liability Note 6 (785,106) (883,890) Interest paid Note 15 (959,618) (134,957) Financing fees paid (81,946) (244,130) Share issuance costs Note 11 (6,928,688) —

Cash provided by financing activities 73,620,471 69,268

Net (decrease) increase in cash during the year 60,589,391 (1,328,956) Effect of foreign exchange on cash (1,882,564) 43,851 Cash, beginning of year 4,575,950 5,861,055 Cash, end of year 63,282,777 4,575,950

The accompanying notes are an integral part of these consolidated financial statements.

Q4 Inc.

4

1 Nature of business

Q4 Inc. (the Company) is a provider of a capital markets communication software platform. The Company offers a broad suite of products to publicly listed companies, investment managers and investment banks along a variety of workflows, including investor relations, corporate access, deal management and research. Our cloud-based software platform of products provides corporate customers with critical technology infrastructure and data that may be used to support their investor relations teams through our website, virtual events, CRM and analytics products. The Company delivers its services primarily over the internet on a subscription basis using the software-as-a-service (“SaaS”) model. The Company conducts business worldwide from its headquarters located in Toronto, Canada.

On October 25, 2021, the Company’s shares commenced trading on the Toronto Stock Exchange (TSX) under the symbol “QFOR”. The Company completed its initial public offering (“IPO”) on October 29, 2021. In connection with, and prior to the IPO, the Company performed a four and one-half-to-one (4.5:1) share consolidation of the Company’s issued equity instruments including common shares, options and warrants. The quantities and per unit prices presented in these audited consolidated financial statements have been retroactively adjusted to give effect to the share consolidation.

These consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries, Q4 Software Holdings ULC, Q4 US, LLC, Q4 Denmark ApS and Q4 London Limited.

The spread of COVID-19 around the world has caused significant volatility in Canadian and international markets. In response to the pandemic, the Company has modified its business practices with a focus on the health and well-being of its workforce both in Europe and North America. The Company currently employs a hybrid model allowing employees to work from home or work under strict guidelines and a capacity limit at the office. The uncertainties around the COVID-19 pandemic, continuing resurgences of COVID-19, and related restrictions to contain its spread required the use of judgments and estimates which resulted in no material accounting impacts for the year ended December 31, 2021 other than the impact on expected credit losses driven by the changes in the macroeconomic environment due to COVID-19. For information on the Company's financial instruments and risk management, refer to Note 18. The Company continues its assessment given the fluidity of COVID-19's global impact.

These consolidated financial statements of the Company and its wholly-owned subsidiaries were authorized for issue in accordance with a resolution of the directors on March 1, 2022.

2 Summary of significant accounting policies

2.1 Basis of presentation

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

The consolidated financial statements have been prepared on a historical cost basis, except for financial instrument derivatives and contingent consideration that have been measured at fair value through profit and loss. The consolidated financial statements are presented in United States dollars, unless otherwise noted. The consolidated financial statements provide comparative information in respect of the previous year.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

5

2.2 Basis of consolidation

The consolidated financial statements comprise the financial statements of the Company and its wholly-owned subsidiaries. All intercompany transactions, balances, and unrealized gains and losses are eliminated upon consolidation. Assets, liabilities, income and expenses of a subsidiary are included in the consolidated financial statements from the date the Company gains control until the date the Company ceases to control the subsidiary.

2.3 Summary of significant accounting policies

The following are the significant accounting policies applied by the Company in preparing its consolidated financial statements.

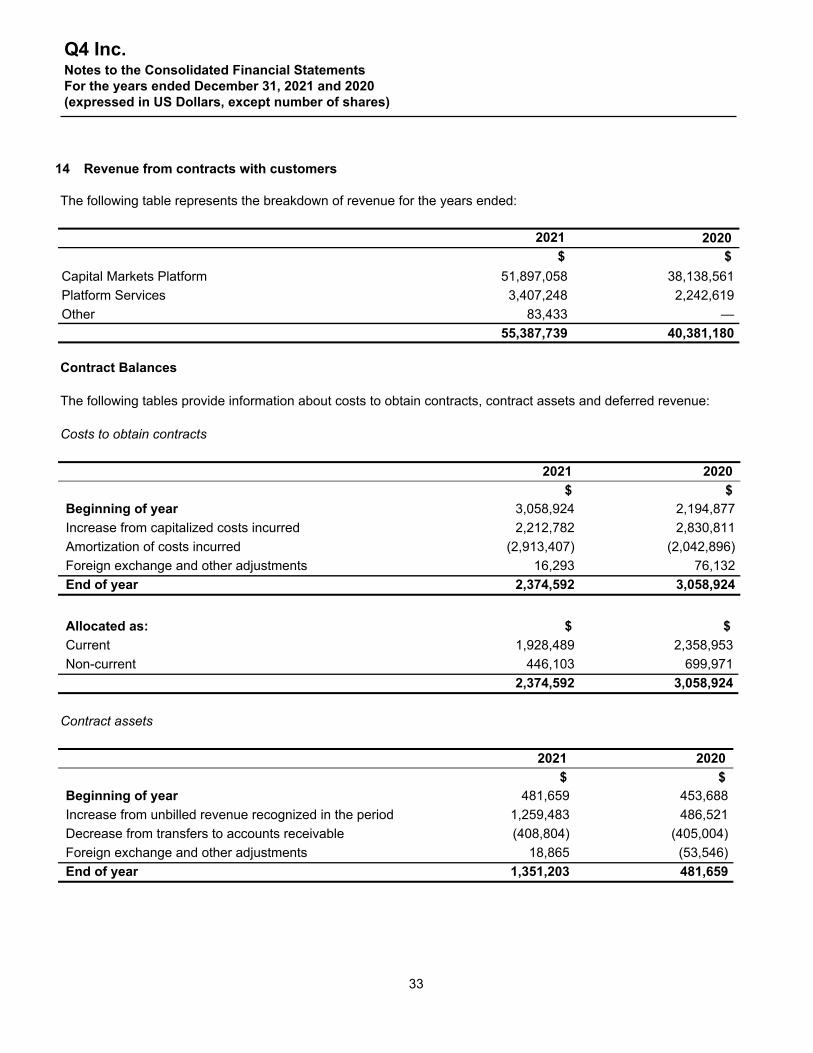

a) Revenue from contracts with customers

The Company reports revenue under two main categories being, Capital Markets Platform and Platform Services. Capital Markets Platform revenue is comprised of fees charged for website subscriptions, virtual events, CRM and analytics products. Platform Services revenue is comprised of fees charged for website and CRM implementation services. The Company accounts for a customer contract when the rights of the parties, including the payment terms, are identified, the contract has commercial substance, collection of consideration is probable, and the contract has been signed and agreed to by both parties. Revenue is recognized when, or as, performance obligations are satisfied by transferring control or economic benefit of the service to the customer in an amount that reflects the consideration the Company expects to be entitled to in exchange for its services. Revenue is reported net of any revenue-based taxes assessed by governmental authorities that are imposed on revenue producing transactions.

• Nature of products and services

Revenue from our website product, which allows customers to host their websites on Q4 software over a term, is provided on a subscription basis. Revenue from the subscription, which includes the website hosting and ongoing support services are billed and initially recorded as deferred revenue and are subsequently recognized as revenue on a ratable basis over the term of the contract once the website is launched. Initial website implementation fees do not have stand-alone value because they are only sold in conjunction with a subscription to the Company’s platform and can only be provided by the Company. The initial implementation is not a separate performance obligation and is therefore recognized on the same basis as website hosting. Revenue associated with additional design services after the initial implementation is recognized in the period performance is complete.

Revenue from our virtual events products is recognized at the time the event occurs. When annual contracts are entered into, the balances are recorded as deferred revenue and are recognized as revenue in the period in which the event takes place.

Revenue from our CRM product is provided on a subscription basis. Revenue from these subscriptions, which also include ongoing support services is billed and initially recorded as deferred revenue and is subsequently recognized as revenue on a ratable basis over the term of the contract.

Revenue from our analytics product is provided on a subscription basis. Revenue from these subscriptions, which also include ongoing support services is billed and initially recorded as deferred revenue and is subsequently recognized as revenue on a ratable basis over the term of the contract.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

6

• Contracts with multiple products or services

The Company enters into contracts that contain multiple services listed above. The Company evaluates this arrangement to determine the appropriate unit of accounting (performance obligation) for revenue recognition purposes based on whether the service is distinct from some or all of the other services in the arrangement.

Where a contract consists of more than one performance obligation, revenue is allocated to each based on their estimated stand-alone selling price (“SSP”). The SSP reflects the price the Company would charge for a specific service if it were sold separately in similar circumstances to similar customers.

• Costs to obtain contracts

Incremental costs of obtaining a contract include only those costs that would not otherwise have been incurred should the contract had not been obtained, such as sales commissions. The Company has determined certain commission programs meet the requirements to be capitalized. Commissions are typically amortized over a two-year period.

• Direct cost of revenue

The Company’s direct cost of revenue consists of costs for maintaining hosting infrastructure, third-party data fees that are integrated into the platform, other third-party costs associated with virtual events and employee expenses for the support and implementation teams.

• Contract assets and deferred revenue

The timing of revenue recognition and the contractual payment schedules often differ, resulting in contractual payments being billed before contractual products or services are delivered. When products or services have been transferred to customers and revenue has been recognized, but not billed, the Company recognizes and includes these amounts as contract assets.

Contract assets are subject to impairment assessment. Refer to accounting policies on impairment of financial assets.

Deferred revenue is recognized if a payment is received from a customer before the Company transfers the related goods or services. Deferred revenue is recognized as revenue when the Company performs under the contract (i.e., transfers control of the related goods or services to the customer).

b) Investment tax credits

Refundable research and development investment ("SR&ED") tax credits are accounted for as a reduction to research and development expenses when the Company has made the qualifying expenditures and there is reasonable assurance the credits will be realized. Upon going public, the Company will no longer meet the eligibility requirements for refundable tax credits under the SR&ED program. However, the Company expects to remain eligible for non-refundable SR&ED credits under this program, which will reduce future income taxes payable, but will have no direct impact on our research and development expenses.

c) Property and equipment

Property and equipment are recorded at cost, net of accumulated depreciation and accumulated impairment losses, if any. Such cost includes expenditures directly attributable to the acquisition of the asset. The Company provides for depreciation using rates designed to depreciate the cost of the equipment and

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

7

leasehold improvements over their estimated useful lives. The annual depreciation rates are as follows on a straight-line basis:

Furniture and fixtures 5 yearsLeasehold improvements Over the term of the lease

An item of property and equipment initially recognized is derecognized upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in profit or loss when the asset is derecognized.

The residual values, useful lives and methods of depreciation of property and equipment are reviewed at each financial year end and adjusted prospectively, if appropriate.

d) Intangible assets

Intangible assets are stated at historical cost, net of accumulated amortization and impairment losses, if any. Internally generated intangibles, excluding capitalized development costs (if any), are not capitalized and the related expenditure is reflected in profit or loss in the period in which the expenditure is incurred. Amortization is recognized on a straight-line basis over the estimated useful lives of the related assets, starting from the date they are acquired and available for use, since this most closely reflects the expected usage and pattern of consumption of the future economic benefits embodied in the asset. The annual amortization rates are as follows:

Technology 5 yearsCustomer lists 5-10 yearsContact database 5 years

An intangible asset is derecognized upon disposal (i.e., at the date the recipient obtains control) or when no future economic benefits are expected from its use or disposal. Any gain or loss arising upon derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in profit or loss.

Research and development costs

Research and development costs are generally expensed as incurred. These costs primarily consist of personnel and related expenses. No development costs have been capitalized to-date.

e) Leases

The Company assesses at contract inception whether a contract is, or contains, a lease. That is, if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

The Company applies a single recognition and measurement approach for all leases, except for short-term leases and leases of low-value assets. The Company recognizes lease liabilities representing obligations to make lease payments and right-of-use assets representing the right to use the underlying assets.

The Company has elected not to distinguish between lease and non-lease components.

Right-of-use assets

The Company recognizes right-of-use assets at the commencement date of the lease (i.e., the date the underlying asset is available for use). Right-of-use assets are measured at cost, less any accumulated

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

8

depreciation and impairment losses, and adjusted for any remeasurement of lease liabilities. The cost of right-of-use assets includes the amount of lease liabilities recognized, initial direct costs incurred, and lease payments made at or before the commencement date less any lease incentives received. Right-of-use assets are depreciated on a straight-line basis over the shorter of the lease term and the estimated useful lives of the assets, as follows:

Office space 1-10 years

If ownership of the leased asset transfers to the Company at the end of the lease term or the cost reflects the exercise of a purchase option, depreciation is calculated using the estimated useful life of the asset. The right-of-use assets are also subject to impairment. Refer to the accounting policies in section (f) Impairment of non-financial assets.

Lease liabilities

At the commencement date of the lease, the Company recognizes lease liabilities measured at the present value of lease payments to be made over the lease term. The lease payments include fixed payments (including in-substance fixed payments) less any lease incentives receivable, variable lease payments that depend on an index or a rate, and amounts expected to be paid under residual value guarantees.

The lease payments also include the exercise price of a purchase option reasonably certain to be exercised by the Company and payments of penalties for terminating the lease, if the lease term reflects the Company exercising the option to terminate. Variable lease payments that do not depend on an index or a rate are recognized as expenses in the period in which the event or condition that triggers the payment occurs.

In calculating the present value of lease payments, the Company uses its incremental borrowing rate at the lease commencement date because the interest rate implicit in the lease is not readily determinable. After the commencement date, the amount of lease liabilities is increased to reflect the accretion of interest and reduced for the lease payments made. In addition, the carrying amount of lease liabilities is remeasured if there is a modification, a change in the lease term, a change in the lease payments or a change in the assessment of an option to purchase the underlying asset.

Short-term leases and leases of low-value assets

The Company applies the short-term lease recognition exemption to its short-term leases of office space (i.e., those leases that have a lease term of 12 months or less from the commencement date and do not contain a purchase option). It also applies the lease of low-value assets recognition exemption to leases of computer equipment that are considered to be low value. Lease payments on short-term leases and leases of low-value assets are recognized as expenses on a straight-line basis over the lease term.

f) Impairment of non-financial assets

The Company assesses, at each reporting date, whether there is an indication that an asset may be impaired. If any indication exists, or when annual impairment testing for an asset is required, the Company estimates the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s (“CGU”s) fair value less costs of disposal and its value in use. The recoverable amount is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets. When the carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. A quantitative analysis was performed to determine the fair value less costs of disposal. Note 7 discusses the method and assumptions used for impairment testing.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

9

For assets excluding goodwill, an assessment is made at each reporting date to determine whether there is an indication that previously recognized impairment losses no longer exist or have decreased. If such indication exists, the Company estimates the asset’s or CGU’s recoverable amount. A previously recognized impairment loss is reversed only if there has been a change in the assumptions used to determine the asset’s recoverable amount since the last impairment loss was recognized. The reversal is limited so that the carrying amount of the asset does not exceed its recoverable amount, nor exceed the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognized for the asset in prior years.

Goodwill is tested for impairment annually as at December 31 and when circumstances indicate that the carrying value may be impaired.

Impairment is determined for goodwill by assessing the recoverable amount of the CGU to which the goodwill relates. When the recoverable amount of the CGU is less than its carrying amount, an impairment loss is recognized. Impairment losses relating to goodwill cannot be reversed in future periods.

g) Business combinations and goodwill

When the Company completes an acquisition, management is required to make judgments to determine whether the acquisition meets the definition of a business under IFRS 3 – Business Combinations. The Company determines that it has acquired a business when the acquired set of activities and assets include an input and a substantive process that together significantly contribute to the ability to create outputs. The acquired process is considered substantive if it is critical to the ability to continue producing outputs, and the inputs acquired include an organised workforce with the necessary skills, knowledge, or experience to perform that process or it significantly contributes to the ability to continue producing outputs and is considered unique or scarce or cannot be replaced without significant cost, effort, or delay in the ability to continue producing outputs.

Business combinations are accounted for using the acquisition method. The cost of an acquisition is measured as the aggregate of the consideration transferred, which is measured at acquisition date fair value, and the amount of any non-controlling interests in the acquiree. For each business combination, the Company elects whether to measure the non-controlling interests in the acquiree at fair value or at the proportionate share of the acquiree’s identifiable net assets. Acquisition-related costs are expensed as incurred and included in general and administrative expenses.

In a business combination, all identifiable assets, liabilities and contingent liabilities acquired are recorded at the date of acquisition at their respective fair values. If any intangible assets are identified, depending on the type of intangible asset and the complexity of determining its fair value, an independent external valuation expert may determine the fair value, using appropriate valuation techniques, which are generally based on a forecast of the total expected future net cash flows.

These valuations are linked closely to the assumptions made by management regarding the future performance of the assets concerned and any changes in the discount rate applied. In certain circumstances where estimates have been made, the Company may obtain third-party valuations of certain assets, which could result in further refinement of the fair-value allocation of certain purchase prices and accounting adjustments. Management is required to make judgments and estimates of the future performance of the acquired business and/or assets in order to determine the amount of contingent consideration to be recognized at acquisition and at each subsequent reporting date.

Goodwill is initially recognized at cost, which represents the excess of the purchase price over the fair value of net identifiable assets acquired. After initial recognition, goodwill is measured at cost less any accumulated impairment losses.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

10

h) Contingent consideration

Any contingent consideration to be transferred related to the acquisition of a business, property, equipment and/or intangible assets is recognized at fair value at the acquisition date. Contingent consideration classified as an asset or liability that is a financial instrument and within the scope of IFRS 3, is measured at fair value and reassessed quarterly with the changes in value recognized in profit or loss. Contingent consideration is included in other liabilities on the consolidated balance sheet.

i) Taxes

Current income tax

Current income tax assets and liabilities are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted at the reporting date in the countries where the Company operates and generates taxable income.

Current income tax relating to items recognized directly in equity is recognized in equity and not in the consolidated statement of loss and comprehensive loss. Management periodically evaluates positions taken in the tax returns with respect to situations in which applicable tax regulations are subject to interpretation and establishes provisions where appropriate.

Deferred tax

Deferred tax is provided using the liability method on temporary differences between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes at the reporting date.

Deferred tax liabilities are recognized for all taxable temporary differences.

Deferred tax assets are recognized for all deductible temporary differences, the carry forward of unused tax credits and any unused tax losses. Deferred tax assets are recognized to the extent that it is probable that taxable profit will be available against which the deductible temporary differences, and the carry forward of unused tax credits and unused tax losses can be utilised.

The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred tax asset to be utilised. Unrecognized deferred tax assets are reassessed at each reporting date and are recognized to the extent that it has become probable that future taxable profits will allow the deferred tax asset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the year when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the reporting date.

The Company offsets deferred tax assets and deferred tax liabilities if and only if it has a legally enforceable right to set off current tax assets and current tax liabilities and the deferred tax assets and deferred tax liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities which intend either to settle current tax liabilities and assets on a net basis, or to realise the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax liabilities or assets are expected to be settled or recovered.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

11

Sales tax

Expenses and assets are recognized net of the amount of sales tax, except when the sales tax incurred on a purchase of assets or services is not recoverable from the taxation authority, in which case, the sales tax is recognized as part of the cost of acquisition of the asset or as part of the expense item, as applicable.

j) Share-based compensation

The Company has multiple equity incentive plans awarded to employees (including senior executives), consultants and board members, and records all share-based payments, including grants of employee stock options, at their respective fair values. The fair value of the stock options is estimated at the grant date, using the Black-Scholes valuation model. Compensation costs are expensed over the award’s vesting period with a corresponding increase to contributed surplus. An estimate of forfeitures is applied when determining compensation expense. On exercise of the equity instrument, consideration paid by the holder together with the amount previously recognized in contributed surplus is recorded as an increase to share capital.

The cumulative expense recognized for equity-settled transactions at each reporting date until the vesting date reflects the extent to which the vesting period has expired and the Company’s best estimate of the number of equity instruments that will ultimately vest. The expense or credit in the consolidated statement of loss and comprehensive loss for a period represents the movement in cumulative expense recognized as at the beginning and end of that period.

Service and non-market performance conditions are not taken into account when determining the grant date fair value of awards, but the likelihood of the conditions being met is assessed as part of the Company’s best estimate of the number of equity instruments that will ultimately vest.

No expense is recognized for awards that do not ultimately vest because non-market performance and/or service conditions have not been met.

When the terms of an equity-settled award are modified, the minimum expense recognized is the grant date fair value of the unmodified award, provided the original vesting terms of the award are met. An additional expense, measured as at the date of modification, is recognized for any modification that increases the total fair value of the share-based compensation transaction, or is otherwise beneficial to the employee. Where an award is cancelled by the entity or by the counterparty, any remaining element of the fair value of the award is expensed immediately through profit or loss.

The fair value of performance share units ("PSUs") is determined by applying the Company's share price on the grant date to the number of PSUs granted. The PSUs are service related, and the expense is recognized in the consolidated statement of loss and comprehensive loss over the vesting period. An estimate of forfeitures is applied when determining the expense as well as estimating the probability of meeting related performance conditions where applicable.

k) Contributed surplus

The contributed surplus balance relates to the granting of stock options (collectively referred to as equity instruments) to employees, consultants and board members as part of the Company’s share-based compensation plan. Under this plan, in exchange for services rendered the employees, consultants and board members receive a certain number of equity instruments at an agreed on exercise price. The equity instruments vest in accordance with the terms of the stock option agreements.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

12

l) Foreign currency translation

Assets, liabilities and operations of foreign subsidiaries are recorded based on the functional currency of each entity. The functional currency is the currency of the primary economic environment in which the Company operates. The Company considered the following economic factors to arrive at the determination of the functional currency: cash flow indicators, sales price indicators, sales market indicators, expense indicators and financing indicators. The functional and reporting currency of the Company is the US dollar. For certain foreign operations, the functional currency is the local currency, in which case the assets, liabilities and operations are translated at current exchange rates from the local currency to the reporting currency, the US dollar. The resulting unrealized gains or losses are reported as a component of accumulated other comprehensive income.

Foreign currency transactions that are denominated in a currency other than the functional currency are recorded by applying the average exchange rate applicable for the given period. At the end of the reporting period, foreign currency-denominated monetary assets and liabilities are revalued to functional currency by applying the spot exchange rate prevailing at that date. Gains and losses arising from these foreign currency revaluations are recognized in the consolidated statement of loss and comprehensive loss. Those foreign currency-denominated transactions, which are classified as non-monetary, are remeasured using the exchange rates at the dates of the initial transactions.

m) Financial instruments

A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity.

Financial assets

Initial recognition and measurement

Financial assets are classified, at initial recognition, and subsequently measured at amortized cost, fair value through other comprehensive income ("OCI"), and fair value through profit or loss.

The classification of financial assets at initial recognition depends on the financial asset’s contractual cash flow characteristics and the Company’s business model for managing them. With the exception of trade receivables that do not contain a significant financing component or for which the Company has applied the practical expedient, the Company initially measures a financial asset at its fair value plus, in the case of a financial asset not at fair value through profit or loss, transaction costs. Trade receivables that do not contain a significant financing component or for which the Company has applied the practical expedient are measured at the transaction price determined under IFRS 15. In order for a financial asset to be classified and measured at amortized cost or fair value through OCI, it needs to give rise to cash flows that are “solely payments of principal and interest (SPPI)” on the principal amount outstanding. This assessment is referred to as the SPPI test and is performed at an instrument level. The Company’s business model for managing financial assets refers to how it manages its financial assets in order to generate cash flows. The business model determines whether cash flows will result from collecting contractual cash flows, selling the financial assets, or both. Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the market-place (regular way trades) are recognized on the trade date, i.e., the date that the Company commits to purchase or sell the asset.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

13

Subsequent measurement

For purposes of subsequent measurement, financial assets are classified in four categories:

▪ Financial assets at amortized cost (debt instruments)

▪ Financial assets at fair value through OCI with recycling of cumulative gains and losses (debt instruments)

▪ Financial assets designated at fair value through OCI with no recycling of cumulative gains and losses upon derecognition (equity instruments)

▪ Financial assets at fair value through profit or loss

Currently, the Company only has investments in financial asset debt instruments classified at amortized cost and has no financial assets within the other categories.

Financial assets at amortized cost (debt instruments)

Financial assets at amortized cost are subsequently measured using the effective interest (“EIR”) method and are subject to impairment. Gains and losses are recognized in profit or loss when the asset is derecognized, modified or impaired.

The Company’s financial assets at amortized cost include cash and accounts receivable.

Derecognition

A financial asset (or, where applicable, a part of a financial asset or part of a group of similar financial assets) is primarily derecognized (i.e., removed from the Company’s consolidated balance sheet) when the rights to receive cash flows from the asset have expired or the Company has transferred its rights to receive cash flows from the asset or has assumed an obligation to pay the received cash flows in full without material delay to a third party under a “pass-through” arrangement; and either (a) the Company has transferred substantially all the risks and rewards of the asset; or (b) the Company has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

Impairment

The Company recognizes an allowance for expected credit losses (“ECLs”) for all financial asset debt instruments not held at fair value through profit or loss. ECLs are based on the difference between the contractual cash flows due in accordance with the contract and all the cash flows that the Company expects to receive, discounted at an approximation of the original effective interest rate. The expected cash flows will include cash flows from the sale of collateral held or other credit enhancements that are integral to the contractual terms.

For trade receivables and contract assets, the Company applies a simplified approach in calculating ECLs. Therefore, the Company does not track changes in credit risk, but instead recognizes a loss allowance based on lifetime ECLs at each reporting date. The Company has established a provision matrix that is based on its historical credit loss experience, adjusted for forward-looking factors specific to the debtors and the economic environment.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

14

Financial liabilities

Initial recognition and measurement

Financial liabilities are classified, at initial recognition, as financial liabilities at fair value through profit or loss, loans and borrowings, payables, or as derivatives designated as hedging instruments in an effective hedge, as appropriate.

All financial liabilities are recognized initially at fair value and, in the case of loans and borrowings and payables, net of directly attributable transaction costs.

The fair value of the derivative liability for warrants was determined using the Monte Carlo method on initial measurement, immediately prior to exercise of the warrants and at each balance date until the date the Company completed its IPO on October 29, 2021, and the company used the Black-Scholes valuation model subsequent to IPO. Weighted average share price and probability of IPO were significant assumptions used in the Monte Carlo method. Volatility of the Company’s share price is a significant assumption in the Black-Scholes model.

The Company’s financial liabilities include accounts payable and accrued liabilities, loans payable, and other liabilities.

Subsequent measurement

For purposes of subsequent measurement, financial liabilities are classified in two categories:

▪ Financial liabilities at fair value through profit or loss

▪ Financial liabilities at amortized cost (loans and borrowings)

Financial liabilities at fair value through profit or loss

Financial liabilities at fair value through profit or loss include financial liabilities held for trading and financial liabilities designated upon initial recognition as at fair value through profit or loss.

Financial liabilities are classified as held for trading if they are incurred for the purpose of repurchasing in the near term. This category also includes derivative financial instruments, entered into by the Company that are not designated as hedging instruments in hedge relationships as defined by IFRS 9 Financial Instruments (“IFRS 9”). Separated embedded derivatives are also classified as held for trading unless they are designated as effective hedging instruments. The Company’s financial liabilities at fair value through profit or loss are limited to its derivative liabilities and contingent consideration.

Financial liabilities at amortized cost (loans and borrowings)

After initial recognition, interest-bearing loans and borrowings are subsequently measured at amortized cost using the EIR method. Gains and losses are recognized in profit or loss when the liabilities are derecognized as well as through the EIR amortization process.

Amortized cost is calculated by considering any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortization is included as finance costs in the consolidated statement of loss and comprehensive loss.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

15

Derecognition

A financial liability is derecognized when the obligation under the liability is discharged or cancelled or expires. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as the derecognition of the original liability and the recognition of a new liability. The difference in the respective carrying amounts is recognized in profit or loss.

Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount is reported in the consolidated balance sheet if there is a currently enforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, to realize the assets and settle the liabilities simultaneously.

n) Fair value measurements

The Company measures its warrants at fair value on initial measurement, at each balance sheet date and the date the warrants are exercised. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

The Company measures the fair value of its financial assets and liabilities using a fair value hierarchy. A financial instrument’s classification within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. Three levels of inputs may be used to measure fair value:

Level 1 — quoted prices in active markets for identical assets or liabilities;

Level 2 — observable inputs other than Level 1 prices such as: quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities; and

Level 3 — unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. Level 3 assets and liabilities include financial instruments whose value is determined using pricing models, discounted cash flow methodologies, or similar techniques, as well as instruments for which the determination of fair value requires significant management judgment or estimation.

o) New standards, interpretations and amendments

New accounting pronouncements are issued by the IASB or other standard-setting bodies, and they are adopted by the Company as at the specified effective date in 2021, but do not have an impact on the consolidated financial statements of the Company.

o) Standards issued but not yet effective

The Company has not early adopted any standard, interpretation or amendment that has been issued but is not yet effective. The new and amended standards and interpretations that are issued, but not yet effective, up to the date of issuance of the Company’s consolidated financial statements are disclosed below. The Company intends to adopt these new and amended standards and interpretations, if applicable, when they become effective.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

16

Amendments to IAS 1: Classification of Liabilities as Current or Non-current

In January 2020, the IASB issued amendments to paragraphs 69 to 76 of IAS 1 to specify the requirements for classifying liabilities as current or non-current. The amendments clarify:

▪ What is meant by a right to defer settlement

▪ That a right to defer must exist at the end of the reporting period

▪ That classification is unaffected by the likelihood that an entity will exercise its deferral right

▪ That only if an embedded derivative in a convertible liability is itself an equity instrument would the terms of a liability not impact its classification

The amendments are effective for annual reporting periods beginning on or after January 1, 2023 and must be applied retrospectively. The Company is currently assessing the impact the amendments will have on current practice and whether existing loan agreements may require renegotiation.

Amendments to IAS 8: Definition of Accounting Estimates

In February 2021, the IASB published "Definition of Accounting Estimates" to help entities to distinguish between accounting policies and accounting estimates. Under the new definition, accounting estimates are monetary amounts in financial statements that are subject to measurement uncertainty.

The amendments are effective for annual periods beginning on or after January 1, 2023 and changes in accounting policies and changes in accounting estimates that occur on or after the start of that period.

The amendments are not expected to have a material impact on the Company.

Amendments to IAS 12: Deferred Taxes Related to Assets and Liabilities Arising From a Single Transaction

In May 2021, the IASB issued amendments to IAS 12, to require companies to recognise deferred tax on particular transactions that, on initial recognition, give rise to equal amounts of taxable and deductible temporary differences. The proposed amendments will typically apply to transactions such as leases for the lessee and decommissioning obligations.The amendments are effective for annual reporting periods beginning on or after 1 January 2023. An entity applies the amendments to transactions that occur on or after the beginning of the earliest comparative period presented. It also, at the beginning of the earliest comparative period presented, recognises deferred tax for all temporary differences related to leases and decommissioning obligations and recognises the cumulative effect of initially applying the amendments as an adjustment to the opening balance of retained earnings at that date. The Company is currently assessing the impact the amendments will have on its leases.

Amendments to IAS 37 – Onerous Contracts: Costs of Fulfilling a Contract

In May 2020, the IASB issued amendments to IAS 37 to specify which costs an entity needs to include when assessing whether a contract is onerous or loss-making.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

17

The amendments apply a “directly related cost approach”. The costs that relate directly to a contract to provide goods or services include both incremental costs and an allocation of costs directly related to contract activities. General and administrative costs do not relate directly to a contract and are excluded unless they are explicitly chargeable to the counterparty under the contract. The amendments are effective for annual reporting periods beginning on or after January 1, 2022. The Company will apply these amendments to contracts for which it has not yet fulfilled all its obligations at the beginning of the annual reporting period in which it first applies the amendments.

Amendments to IFRS 3 – Reference to the Conceptual Framework

In May 2020, the IASB issued Amendments to IFRS 3 Business Combinations - Reference to the Conceptual Framework. The amendments are intended to replace a reference to the Framework for the Preparation and Presentation of Financial Statements, issued in 1989, with a reference to the Conceptual Framework for Financial Reporting issued in March 2018 without significantly changing its requirements. The Board also added an exception to the recognition principle of IFRS 3 to avoid the issue of potential ‘day 2’ gains or losses arising for liabilities and contingent liabilities that would be within the scope of IAS 37 or IFRIC 21 Levies, if incurred separately. At the same time, the Board decided to clarify existing guidance in IFRS 3 for contingent assets that would not be affected by replacing the reference to the Framework for the Preparation and Presentation of Financial Statements.

The amendments are effective for annual reporting periods beginning on or after January 1, 2022 and apply prospectively.

IFRS 9 Financial Instruments – Fees in the ’10 per cent’ test for derecognition of financial liabilities

As part of its 2018-2020 annual improvements to IFRS standards process the IASB issued amendment to IFRS 9. The amendment clarifies the fees that an entity includes when assessing whether the terms of a new or modified financial liability are substantially different from the terms of the original financial liability. These fees include only those paid or received between the borrower and the lender, including fees paid or received by either the borrower or lender on the other’s behalf. An entity applies the amendment to financial liabilities that are modified or exchanged on or after the beginning of the annual reporting period in which the entity first applies the amendment.

The amendment is effective for annual reporting periods beginning on or after January 1, 2022 with earlier adoption permitted. The Company will apply the amendments to financial liabilities that are modified or exchanged on or after the beginning of the annual reporting period in which the entity first applies the amendment.

The amendments are not expected to have a material impact on the Company.

Cloud computing arrangements

In March 2021, the International Financial Reporting Interpretations Committee (“IFRIC”) finalized an agenda decision which clarified the customer’s accounting for configuration and customization in a cloud computing arrangement. This decision does not have a material impact on the Company.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

18

2.4 Significant accounting judgements, estimates and assumptions

The preparation of the Company’s consolidated financial statements requires management to make judgements, estimates and assumptions that affect the reported amounts of revenues, expenses, assets and liabilities, and the accompanying disclosures, and the disclosure of contingent liabilities. Uncertainty about these assumptions and estimates could result in outcomes that require material adjustment to the carrying amount of assets or liabilities affected in future periods.

Other disclosures relating to the Company’s exposure to risks and uncertainties include:

▪ Capital management (Note 18)

▪ Financial instruments risk management and policies (Note 18)

▪ Sensitivity analyses disclosures (Note 18)

In the process of applying the Company’s accounting policies, management has made the following judgements, which have the most significant effect on the amounts recognized in the consolidated financial statements:

▪ Functional currency: The Company and its subsidiaries use the United States dollar, British pound, and Danish krone as their functional currency, based on the predominant currency of each entity’s transactions and cash flows. Management uses judgement in determining the primary economic environment in which a subsidiary operates. In assessing a subsidiary’s functional currency, management considers the currency which primarily influences the pricing of services and labour costs of the subsidiary.

▪ Valuation of derivative financial liabilities: In measuring the fair value of its derivative liabilities, the Company uses judgment to determine key assumptions used in the valuation models applied. With respect to the Monte Carlo model, the Company’s weighted average share price and probability of IPO were considered significant assumptions. In the application of the Black-Scholes model, the significant assumption is expected volatility.

Estimates and assumptions

The key assumptions concerning the future and other key sources of estimation uncertainty at the reporting date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year, are described below. The Company based its assumptions and estimates on parameters available when the consolidated financial statements were prepared. Existing circumstances and assumptions about future developments, however, may change due to market changes or circumstances arising that are beyond the control of the Company. Such changes are reflected in the assumptions when they occur.

Amortization

Amortization of intangible assets incorporate estimates of useful lives. These estimates are based on past experience and industry norms and may change as more experience is obtained or as market conditions change.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

19

Stock options

Estimating fair value for share-based compensation transactions requires the determination of the most appropriate valuation model, which depends on the terms and conditions of the grant. This estimate also requires the determination of the most appropriate inputs to the valuation model including the expected life of the stock option, volatility and dividend yield. The assumptions and models used for estimating fair value for share-based compensation transactions are disclosed in Note 12.

Valuation of warrants

The Company measures its warrants at fair value on initial measurement, at each balance sheet date and the date the warrants are exercised. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The Monte Carlo method was applied on initial measurement, immediately prior to exercise of the warrants and subsequently at each balance sheet date until the Company completed their IPO on October 29, 2021. Weighted average share price and probability of IPO were considered a significant assumption in this model. As a public company, the fair value of the derivative liability for warrants was determined using the Black-Scholes valuation model. Volatility of the Company’s share price is a significant assumption in the model.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

20

3 Accounts receivable

Accounts receivables are non-interest bearing and are generally on terms of 30 to 90 days.

2021 2020$ $

Trade accounts receivable 9,362,187 9,850,380 Provision for expected credit losses (247,930) (280,659) Tax credits receivable 214,174 154,680

9,328,431 9,724,401

The aging of accounts receivable is as follows:

2021 2020$ $

Current 6,280,984 5,253,440 1-30 days past due 1,163,990 1,293,809 31-60 days past due 867,459 1,649,270 61-90 days past due 412,208 1,074,883 Greater than 90 days past due 637,546 578,978

9,362,187 9,850,380 Less: credit loss impairment (247,930) (280,659) Add: tax credits receivable 214,174 154,680

9,328,431 9,724,401

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

21

4 Intangible assets

2021

Technology Customer Lists

Contact Database Total

$ $ $ $CostBalance, December 31, 2020 2,605,373 24,340,129 690,000 27,635,502 Additions — — — — As at December 31, 2021 2,605,373 24,340,129 690,000 27,635,502

AmortizationAs at December 31, 2020 2,371,232 2,689,109 241,500 5,301,841 Amortization 234,141 2,451,019 138,000 2,823,160 As at December 31, 2021 2,605,373 5,140,128 379,500 8,125,001

Net Book ValueAs at December 31, 2020 234,141 21,651,020 448,500 22,333,661 As at December 31, 2021 — 19,200,001 310,500 19,510,501

2020

Technology Customer Lists

Contact Database Total

$ $ $ $CostBalance, December 31, 2019 2,605,373 340,129 690,000 3,635,502 Additions — 24,000,000 — 24,000,000 As at December 31, 2020 2,605,373 24,340,129 690,000 27,635,502

AmortizationAs at December 31, 2019 1,902,379 221,084 103,500 2,226,963 Amortization 468,853 2,468,025 138,000 3,074,878 As at December 31, 2020 2,371,232 2,689,109 241,500 5,301,841

Net Book ValueAs at December 31, 2019 702,994 119,045 586,500 1,408,539 As at December 31, 2020 234,141 21,651,020 448,500 22,333,661

On January 1, 2020, the Company acquired approximately 746 clients from S&P Global Market Intelligence Inc. through an asset purchase for total consideration of $20,000,000 payable in 14,744,587 Class C-3 Preferred Shares and $4,000,000 payable in cash. As at December 31, 2021, there were 8 years remaining before the customer lists become fully amortized.

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

22

5 Property and Equipment

2021

Furniture and fixtures

Leasehold improvements Total

$ $ $CostBalance, December 31, 2020 699,795 500,749 1,200,544 Additions 444,274 15,775 460,049 As at December 31, 2021 1,144,069 516,524 1,660,593

AmortizationAs at December 31, 2020 150,037 267,865 417,902 Amortization 233,025 95,904 328,929 As at December 31, 2021 383,062 363,769 746,831

Net Book ValueAs at December 31, 2020 549,758 232,884 782,642 As at December 31, 2021 761,007 152,755 913,762

2020

Furniture and fixtures

Leasehold improvements Total

$ $ $CostBalance, December 31, 2019 122,535 451,870 574,405 Additions 577,260 48,879 626,139 As at December 31, 2020 699,795 500,749 1,200,544

AmortizationAs at December 31, 2019 73,352 259,780 333,132 Amortization 76,685 8,085 84,770 As at December 31, 2020 150,037 267,865 417,902

Net Book ValueAs at December 31, 2019 49,183 192,090 241,273 As at December 31, 2020 549,758 232,884 782,642

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

23

6 Leases

The Company has lease contracts for office space used in its operations. Leases of office space have lease terms between 1 and 10 years. The Company’s obligations under its leases are secured by the lessor’s title to the leased assets.

There are several lease contracts that include extension and termination options and variable lease payments, which are further discussed below. The Company also has certain leases of office space with lease terms of 12 months or less and leases of office equipment with low value. The Company applies the “short-term leases” and “leases of low-value assets” recognition exemptions for these leases.

Set out below are the carrying amount of right of use assets and the movements during the year:

Right of use assets

2021 2020$ $

Beginning of year 2,491,993 1,491,023 Additions — 1,981,688 Depreciation (816,695) (957,033) Exchange adjustments 444 (23,685) End of year 1,675,742 2,491,993

Lease liabilities

2021 2020$ $

Beginning of year 2,773,058 1,622,904 Additions — 1,916,512 Interest expense 110,534 131,932 Lease payments (895,640) (1,015,822) Exchange adjustments (32,107) 117,532 Ending of year 1,955,845 2,773,058

Allocated as: $ $Current 682,904 705,195 Non-current 1,272,941 2,067,863

1,955,845 2,773,058

Q4 Inc.Notes to the Consolidated Financial StatementsFor the years ended December 31, 2021 and 2020(expressed in US Dollars, except number of shares)

24

The following are the amounts recognized in profit or loss:

2021 2020$ $