MOCK TEST - MKG CA EDUCATION

32

MOCK TEST 21.04.2014 MAY-2014 Intermediate-IPC (With solution) Total No. of Question – 7 Total No. of Printed Pages –32 Time Allowed – 3 Hour Maximum Marks – 100 Answers to questions are to be given only in English except in the case of candidates who have opted for Hindi medium. If a candidate who has not opted for Hindi medium, answers in Hindi, his answers in Hindi will not be valued. Questions No.1 is compulsory. Attempt any five questions from the remaining six questions Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made and stated clearly by way of note. Question 1(a): Marks 5 Mr. X has started rendering services w.e.f. 01/04/2013 and it is not covered in the Negative List and also not covered in Mega Exemption. He has submitted particulars as given below: 1. Rendered services on 01/05/2013 and issued bill on 10/06/2013 for ` 6 lakhs and payment was received on 10/12/2013. 2. Rendered services on 07/06/2013 and issued bill on 30/06/2013 for ` 15 lakhs and payment was received on 07/03/2014. 3. Rendered services on 12/07/2013 and issued bill on 31/08/2013 for ` 30 lakhs and payment was received on 07/01/2014. 4. Rendered services on 22/11/2013 and issued bill on 28/12/2013 for ` 60 lakhs and payment was received on 10/02/2014. All the above amounts are exclusive of Service Tax and Service Tax has been charged separately, wherever applicable. Compute the Service Tax Payable for each quarter and also last date upto which Service Tax should be paid. If there was delay of 10 days on each payment, compute interest payable under section 75. Solution:1(a) First bill issued is of ` 6 lakhs and it is exempt from Service Tax because Service Provider is eligible for SSP exemption.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of MOCK TEST - MKG CA EDUCATION

MOCK TEST 21.04.2014

MAY-2014 Intermediate-IPC

(With solution)

Total No. of Question – 7 Total No. of Printed Pages –32

Time Allowed – 3 Hour Maximum Marks – 100

Answers to questions are to be given only in English except in the case of candidates

who have opted for Hindi medium. If a candidate who has not opted for Hindi

medium, answers in Hindi, his answers in Hindi will not be valued.

Questions No.1 is compulsory.

Attempt any five questions from the remaining six questions

Working notes should form part of the answer.

Wherever necessary, suitable assumptions may be made and stated clearly by way of note.

Question 1(a): Marks 5

Mr. X has started rendering services w.e.f. 01/04/2013 and it is not covered in the Negative List and also not

covered in Mega Exemption. He has submitted particulars as given below:

1. Rendered services on 01/05/2013 and issued bill on 10/06/2013 for ` 6 lakhs and payment was received on

10/12/2013.

2. Rendered services on 07/06/2013 and issued bill on 30/06/2013 for ` 15 lakhs and payment was received on

07/03/2014.

3. Rendered services on 12/07/2013 and issued bill on 31/08/2013 for ` 30 lakhs and payment was received on

07/01/2014.

4. Rendered services on 22/11/2013 and issued bill on 28/12/2013 for ` 60 lakhs and payment was received on

10/02/2014.

All the above amounts are exclusive of Service Tax and Service Tax has been charged separately, wherever

applicable.

Compute the Service Tax Payable for each quarter and also last date upto which Service Tax should be paid.

If there was delay of 10 days on each payment, compute interest payable under section 75.

Solution:1(a)

First bill issued is of ` 6 lakhs and it is exempt from Service Tax because Service Provider is eligible for

SSP exemption.

2

Second bill issued is of ` 15 lakhs, out of which ` 4 lakhs is not taxable because Service Provider is eligible

for SSP exemption and balance of ` 11 lakhs shall be taxable on actual receipt basis in the 4th

quarter.

Third bill issued is of ` 30 lakhs and is taxable on actual receipt basis in the 4th

quarter.

Fourth bill issued is of ` 60 lakhs, out of which ` 9 lakhs (50-11-30) is taxable on actual receipt basis in the

4th

quarter and balance of ` 51 lakhs shall be taxable on the basis of Rule 3 of Point of Taxation Rules, 2011

and Point of Taxation shall be 22/11/2013 and taxable in third quarter.

`

Quarter 1: NIL

Quarter 2: NIL

Quarter 3:

Value of Services 51,00,000

Service Tax @12% 6,12,000

Add: Education Cess @2% 12,240

Add: SHEC @1% 6,120

Total Service Tax 6,30,360

This should be paid up to 05/01/2014.

Interest u/s 75:

6,30,360x15%x10/365 2,591

Quarter 4:

Value of Services (11,00,000+30,00,000+9,00,000) 50,00,000

Service Tax @12% 6,00,000

Add: Education Cess @2% 12,000

Add: SHEC @1% 6,000

Total Service Tax 6,18,000

This should be paid up to 31/03/2014.

Interest u/s 75:

6,18,000x15%x10/365 2,540

Question 1(b): Marks 5

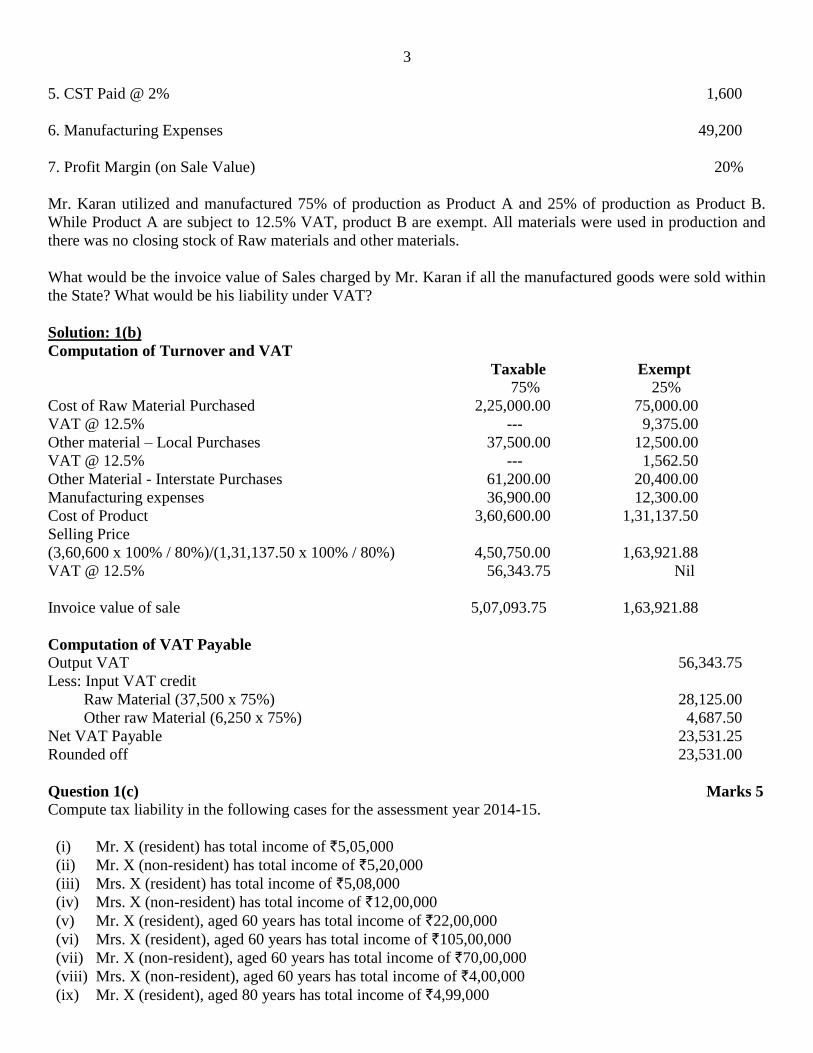

The following particulars are provided by Mr. Karan of Calcutta, who has purchased Raw materials for

manufacturing product A and Product B from Mr. Piyush. The State VAT for Raw Materials and other

materials was 12.5%.

` 1. Cost of Raw materials purchased 3,00,000

2. VAT paid to Mr. Piyush 37,500

3. Cost of other materials

- Local Purchases 50,000

- Interstate Purchases 80,000

4. VAT paid on Local Materials Purchased-12.5% 6,250

3

5. CST Paid @ 2% 1,600

6. Manufacturing Expenses 49,200

7. Profit Margin (on Sale Value) 20%

Mr. Karan utilized and manufactured 75% of production as Product A and 25% of production as Product B.

While Product A are subject to 12.5% VAT, product B are exempt. All materials were used in production and

there was no closing stock of Raw materials and other materials.

What would be the invoice value of Sales charged by Mr. Karan if all the manufactured goods were sold within

the State? What would be his liability under VAT?

Solution: 1(b)

Computation of Turnover and VAT

Taxable Exempt

75% 25%

Cost of Raw Material Purchased 2,25,000.00 75,000.00

VAT @ 12.5% --- 9,375.00

Other material – Local Purchases 37,500.00 12,500.00

VAT @ 12.5% --- 1,562.50

Other Material - Interstate Purchases 61,200.00 20,400.00

Manufacturing expenses 36,900.00 12,300.00

Cost of Product 3,60,600.00 1,31,137.50

Selling Price

(3,60,600 x 100% / 80%)/(1,31,137.50 x 100% / 80%) 4,50,750.00 1,63,921.88

VAT @ 12.5% 56,343.75 Nil

Invoice value of sale 5,07,093.75 1,63,921.88

Computation of VAT Payable

Output VAT 56,343.75

Less: Input VAT credit

Raw Material (37,500 x 75%) 28,125.00

Other raw Material (6,250 x 75%) 4,687.50

Net VAT Payable 23,531.25

Rounded off 23,531.00

Question 1(c) Marks 5

Compute tax liability in the following cases for the assessment year 2014-15.

(i) Mr. X (resident) has total income of `5,05,000

(ii) Mr. X (non-resident) has total income of `5,20,000

(iii) Mrs. X (resident) has total income of `5,08,000

(iv) Mrs. X (non-resident) has total income of `12,00,000

(v) Mr. X (resident), aged 60 years has total income of `22,00,000

(vi) Mrs. X (resident), aged 60 years has total income of `105,00,000

(vii) Mr. X (non-resident), aged 60 years has total income of `70,00,000

(viii) Mrs. X (non-resident), aged 60 years has total income of `4,00,000

(ix) Mr. X (resident), aged 80 years has total income of `4,99,000

4

(x) Mrs. X (resident), aged 80 years has total income of `103,00,000

Solution 1(c):

Solution: `

(i) Computation of Tax Liability

Total Income 5,05,000

Tax on `5,05,000 at slab rate 31,000

Add: Education cess @ 2% 620

Add: SHEC @ 1% 310

Tax Liability 31,930

(ii) Computation of Tax Liability Total Income 5,20,000

Tax on `5,20,000 at slab rate 34,000

Add: Education cess @ 2% 680

Add: SHEC @ 1% 340

Tax Liability 35,020

(iii) Computation of Tax Liability Total Income 5,08,000

Tax on `5,08,000 at slab rate 31,600

Add: Education cess @ 2% 632

Add: SHEC @ 1% 316

Tax Liability 32,548

Rounded off u/s 288B 32,550

(iv) Computation of Tax Liability

Total Income 12,00,000

Tax on `12,00,000 at slab rate 1,90,000

Add: Education cess @ 2% 3,800

Add: SHEC @ 1% 1,900

Tax Liability 1,95,700

(v) Computation of Tax Liability

Total Income 22,00,000

Tax on `22,00,000 at slab rate 4,85,000

Add: Education cess @ 2% 9,700

Add: SHEC @ 1% 4,850

Tax Liability 4,99,550

(vi) Computation of Tax Liability

Total Income 105,00,000

Tax on `105,00,000 at slab rate 29,75,000

Add: Surcharge @ 10% 2,97,500

Tax before education cess 32,72,500

Add: Education cess @ 2% 65,450

Add: SHEC @ 1% 32,725

Tax Liability 33,70,675

Rounded off u/s 288B 33,70,680

5

(vii) Computation of Tax Liability

Total Income 70,00,000

Tax on `70,00,000 at slab rate 19,30,000

Add: Education cess @ 2% 38,600

Add: SHEC @ 1% 19,300

Tax Liability 19,87,900

(viii) Computation of Tax Liability

Total Income 4,00,000

Tax on `4,00,000 at slab rate 20,000

Add: Education cess @ 2% 400

Add: SHEC @ 1% 200

Tax Liability 20,600

Note: Rebate under section 87A is not allowed for non-resident.

(ix) Computation of Tax Liability

Total Income 4,99,000

Tax on `4,99,000 at slab rate Nil

Add: Education cess @ 2% Nil

Add: SHEC @ 1% Nil

Tax Liability Nil

(x) Computation of Tax Liability

Total Income 103,00,000

Tax on `103,00,000 at slab rate 28,90,000

Add: Surcharge @ 10% 2,89,000

Tax before education cess 31,79,000

Increase in income `3,00,000 over `100,00,000 and increase in tax in comparison to income

of `100,00,000,`3,79,000 (31,79,000 – 28,00,000), but increase in tax cannot be more than

increase in income hence marginal relief shall be `3,79,000 – `3,00,000 79,000

Tax after marginal relief 31,00,000

Add: Education cess @ 2% 62,000

Add: SHEC @ 1% 31,000

Tax Liability 31,93,000

Question 1(d) Marks 5

Mr. Rakesh and Mr. Anish are brothers and they earned the following incomes during the financial year 2013-

14. Mr. Rakesh settled in U.K. in the year 1975 and Mr. Anish settled in Surat. Compute the gross total income

for the Assessment Year 2014-15.

Sr. No. Particulars Mr. Rakesh Mr. Anish

1. Interest on U.K. development bonds, 50% of interest received in

India

25,000 20,000

2. Dividend from British Company received in London

8,000 10,000

3. Profit from a business in Mumbai, but managed directly from 10,000 12,000

6

London

4. Profit on sale of shares of an Indian company received in India

50,000 80,000

5. Income from a business in Delhi

20,000 20,000

6. Fees for technical services rendered in India, but received in

London

1,00,000 -

7. Interest on fixed deposit in SBI, Bangalore

5,000 15,000

8. Agricultural income from a land situated in Rajasthan

25,000 25,000

9. Income under the head House Property at Bangalore

50,400 33,600

Solution 1(d):

Computation of Total Income of Mr. Rakesh and Mr. Anish for the A.Y. 2014-15

Sl.

No.

Particulars Mr. Rakesh

Non-Resident

Mr. Anish

ROR

1. Interest on U.K. Development Bonds

12,500 20,000

2. Dividend from British Company received in London

- 10,000

3. Profit from a business in Mumbai but managed directly from London

10,000 12,000

4. Profit on sale of shares of an Indian company received in India

50,000 80,000

5. Income from a business in Delhi

20,000 20,000

6. Fees for technical services rendered in India but received in London

1,00,000 -

7. Interest on fixed Deposit in SBI Bangalore

5,000 15,000

8. Agricultural income from a land in Rajasthan [(Exempt u/s.10(1)]

- -

9. Income under the head House property at Bangalore

50,400 33,600

Gross Total Income 2,47,900 1,90,600

Notes:

1. Dividend received from British company in London, by a non-resident assessee is not taxable income, while

the same received by an ROR assessee is taxable and is not exempt under section 10(34) of Income Tax Act,

1961.

2. Agricultural income from a land situated in the State of Rajasthan, is exempted under section 10(1) of Income

tax Act, 1961 in case of both non-resident and resident assessee.

7

Question 2(a) Marks 5

Mr. X has let out one house property @ `70000 per month and there is unrealised Rent of 2 months and there is

vacancy of 3 month. Fair rent `60,000 per month, municipal valuation `55,000 per month and standard rent

`80,000 per month. Municipal tax paid `62,000. Interest on loan for construction of the house property is

`75,000.The assessee has unrealised Rent of `2,00,000 in P.Y. 2010-11 and he has recovered `1,50,000 in P.Y.

2013-14 and interest of `18,000 and he has incurred `11,000 as legal expense.

He is registered under DVAT/CST and he has purchased goods for `20,00,000 from Punjab and paid CST @

2% and goods were sold in Delhi at a profit of 30% on sale price and DVAT is charged @ 12.5%.

Compute his tax liability for assessment year 2014-15 and show the treatment for VAT. (ignore provisions of

section 44AD)

Solution 2(a)

Income under the head House Property

Gross annual value 7,20,000.00

Working Note: `

(a) Fair rent (60,000 x 12) 7,20,000

(b) Municipal valuation (55,000 x 12) 6,60,000

(c) Higher of (a) or (b) 7,20,000

(d) Standard Rent (80,000 x 12) 9,60,000

(e) Expected Rent {Lower of (c) or (d)} 7,20,000

(f) Rent Received (70,000 x 7) 4,90,000

If there was no vacancy , then Rent Receivable shall be 70,000 x 10 =

7,00,000, which is lower than the expected rent , hence the GAV shall be

7,20,000

Less: Municipal taxes paid 62,000.00

Net Annual Value 6,58,000.00

Less: 30% of NAV u/s 24(a) 1,97,400.00

Less: Interest on capital borrowed u/s 24(b) 75,000.00

3,85,600.00

Unrealised rent recovered of 2009-10 section 25AA 1,50,000.00

5,35,600.00

Income under the head Business and Profession

Sales (20,40,000 / 70%) 29,14,286.00

Purchases (20,00,000 + 40,000) 20,40,000.00

Profit 8,74,286.00

Income under the head House Property 5,35,600.00

Income under the head Business/Profession 8,74,286.00

Income from other sources 18,000.00

Gross Total Income 14,27,886.00

Less: Deduction u/s 80C to 80U NIL

Total Income 14,27,886.00

Rounded off u/s 288A 14,27,890.00

Computation of Tax Liability

Tax on `14,27,890 at slab rate 2,58,367.00

Add: EC @ 2% 5,167.34

8

Add: SHEC @ 1% 2,583.67

Tax Liability 2,66,118.01

Rounded off u/s 288B 2,66,120.00

Treatment of DVAT

Output VAT (29,14,286 x 12.5%) 3,64,285.75

Input tax credit Nil

VAT Payable 3,64,285.75

Rounded off 3,64,286.00

Question 2(b) Marks 4

(i) Siddhi Ltd. exported some goods to Samson Inc. of USA. It received US $ 9,000 as consideration for the

same and sold it @ ` 44 per US dollar. Compute the value of taxable service under rule 2B of the Service Tax

(Determination of Value) Rules, 2006 in the following cases:-

(a) RBI reference rate for US dollar at that time is ` 45 per US dollar.

(b) RBI reference rate for US dollars is not available.

(ii) What would be the value of taxable service if US $ 9,000 are converted into UK £ 4,500. RBI reference rate

at that time for US $ is ` 46 per US dollar and for UK £ is ` 88 per UK Pound.

Solution 2(b):

(i) (a) For a currency, when exchanged from, or to, Indian Rupees (INR), the value shall be equal to the

difference in the buying rate or the selling rate, as the case may be, and the Reserve Bank of India (RBI)

reference rate for that currency at that time, multiplied by the total units of currency.

Hence, in the given case, value of taxable service would be as follows:-

(RBI reference rate for $ – Selling rate for $) × Total units of US $

= ` (45-44) × 9,000

= ` 9,000

(b) If the RBI reference rate for a currency is not available, the value shall be 1% of the gross amount of Indian

Rupees provided or received, by the person changing the money .

Hence, in the given case, value of taxable service would be as follows:-

1% of ` (44 × 9,000)

=` 3,960

(ii) Where neither of the currencies exchanged is Indian Rupee, the value shall be equal to 1% of the lesser of

the two amounts the person changing the money would have received by converting any of the two currencies

into Indian Rupee on that day at the reference rate provided by RBI.

Hence, in the given case, value of taxable service would be 1% of the lower of the following:-

(a) US dollar converted into Indian rupees = $ 9,000 × ` 46

= ` 4,14,000

(b) UK pound converted into Indian rupees = £ 4,500× ` 88

= ` 3,96,000

Value of taxable service = 1% of ` 3,96,000

= ` 3,960

Question 2(c) Marks 4

Manufacturer A of Jaipur extracted raw produce X and raw produce Y from mines at `30,000 and `40,000

respectively and sold the same at 150% margin to Manufacturer B of Jaipur (VAT rate is 4% on produce X and

12.5% on produce Y).

Manufacturer B of Jaipur used X and Y as raw material; added 100% of cost of raw material towards

manufacturing expenses and profits and sold the resultant product to wholesaler C of Delhi (CST rate is 2%).

9

Wholesaler C of Delhi sold the same to Retailer D of Delhi at 20% above cost (VAT rate is 4%).

The Retailer D sold the same to a consumer at 20% above cost (VAT rate is 4%).

Show, by way of invoice method, the amount of VAT payable by each person.

Solution 2(c):

`

Manufacturer A

Cost of raw material X 30,000

Add: Profit @ 150% of `30,000 45,000

Total 75,000

Add: VAT @ 4% 3,000

Total Selling Price 78,000

Cost of raw material Y 40,000

Add: Profit @ 150% of `40,000 60,000

Total 1,00,000

Add: VAT @ 12.5% 12,500

Total Selling Price 1,12,500

Manufacturer B

Cost of Manufacturer B (`75,000 + `1,00,000) 1,75,000

Add: Profit @ 100% of cost 1,75,000

Total 3,50,000

Add: CST @ 2% 7,000

Total Selling Price 3,57,000

Balance in the VAT receivable account (3,000 + 12,500) – 7,000 8,500

Wholesaler C

Cost of Wholesale C 3,57,000

Add: Profit @ 20% 71,400

Total 4,28,400

Add: VAT @ 4% 17,136

Total Selling Price 4,45,536

Retailer D

Cost of Retailer D 4,28,400

(VAT credit shall be allowed for `17,136)

Add: Profit @ 20% 85,680

Total 5,14,080

Add: VAT @ 4% 20,563

Total Selling Price 5,34,643

Net tax payable shall be (20,563 – 17,136) 3,427

Question 2(d) Marks 3

Mr. Vaibhav owns five houses at Cochin. Compute the gross annual value of each house from the information

given below:

`

10

House-I House-II House-III House-IV House –V

Municipal value 1,20,000 2,40,000 1,10,000 90,000 75,000

Fair rent 1,50,000 2,40,000 1,14,000 84,000 80,000

Standard rent 1,08,000 N.A. 1,44,000 N.A. 78,000

Actual rent received/

receivable

1,80,000 2,10,000 1,20,000 1,08,000 72,000

Solution 2(c):

House I `

Computation of Gross Annual Value

(a) Fair Rent 1,50,000

(b) Municipal Valuation 1,20,000

(c) Higher of (a) or (b) 1,50,000

(d) Standard Rent 1,08,000

(e) Expected Rent {Lower of (c) or (d)} 1,08,000

(f) Rent Received/Receivable 1,80,000

(g) Higher of (e) or (f) shall be GAV 1,80,000

House II `

Computation of Gross Annual Value

(a) Fair Rent 2,40,000

(b) Municipal Valuation 2,40,000

(c) Higher of (a) or (b) 2,40,000

(d) Standard Rent N.A

(e) Expected Rent {Lower of (c) or (d)} 2,40,000

(f) Rent Received/Receivable 2,10,000

(g) Higher of (e) or (f) shall be GAV 2,40,000

House III `

Computation of Gross Annual Value

(a) Fair Rent 1,14,000

(b) Municipal Valuation 1,10,000

(c) Higher of (a) or (b) 1,14,000

(d) Standard Rent 1,44,000

(e) Expected Rent {Lower of (c) or (d)} 1,14,000

(f) Rent Received/Receivable 1,20,000

(g) Higher of (e) or (f) shall be GAV 1,20,000

House IV `

Computation of Gross Annual Value

(a) Fair Rent 84,000

(b) Municipal Valuation 90,000

(c) Higher of (a) or (b) 90,000

(d) Standard Rent N.A

(e) Expected Rent {Lower of (c) or (d)} 90,000

(f) Rent Received/Receivable 1,08,000

(g) Higher of (e) or (f) shall be GAV 1,08,000

11

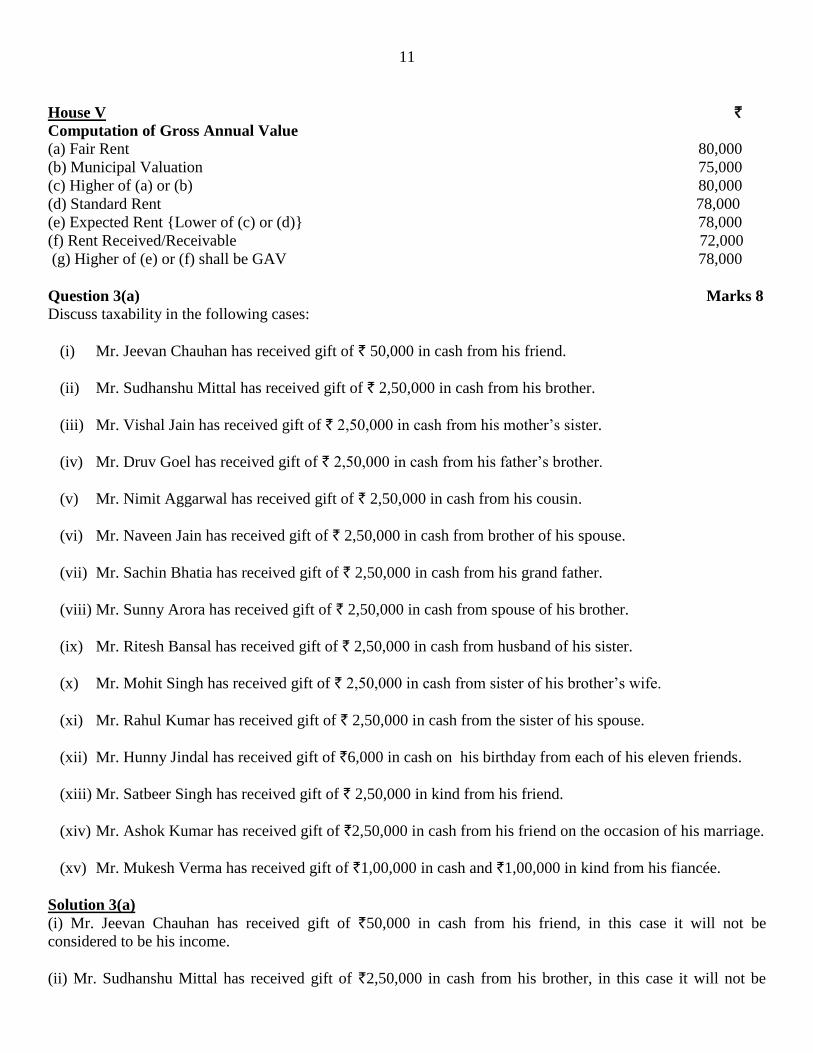

House V `

Computation of Gross Annual Value

(a) Fair Rent 80,000

(b) Municipal Valuation 75,000

(c) Higher of (a) or (b) 80,000

(d) Standard Rent 78,000

(e) Expected Rent {Lower of (c) or (d)} 78,000

(f) Rent Received/Receivable 72,000

(g) Higher of (e) or (f) shall be GAV 78,000

Question 3(a) Marks 8

Discuss taxability in the following cases:

(i) Mr. Jeevan Chauhan has received gift of ` 50,000 in cash from his friend.

(ii) Mr. Sudhanshu Mittal has received gift of ` 2,50,000 in cash from his brother.

(iii) Mr. Vishal Jain has received gift of ` 2,50,000 in cash from his mother’s sister.

(iv) Mr. Druv Goel has received gift of ` 2,50,000 in cash from his father’s brother.

(v) Mr. Nimit Aggarwal has received gift of ` 2,50,000 in cash from his cousin.

(vi) Mr. Naveen Jain has received gift of ` 2,50,000 in cash from brother of his spouse.

(vii) Mr. Sachin Bhatia has received gift of ` 2,50,000 in cash from his grand father.

(viii) Mr. Sunny Arora has received gift of ` 2,50,000 in cash from spouse of his brother.

(ix) Mr. Ritesh Bansal has received gift of ` 2,50,000 in cash from husband of his sister.

(x) Mr. Mohit Singh has received gift of ` 2,50,000 in cash from sister of his brother’s wife.

(xi) Mr. Rahul Kumar has received gift of ` 2,50,000 in cash from the sister of his spouse.

(xii) Mr. Hunny Jindal has received gift of `6,000 in cash on his birthday from each of his eleven friends.

(xiii) Mr. Satbeer Singh has received gift of ` 2,50,000 in kind from his friend.

(xiv) Mr. Ashok Kumar has received gift of `2,50,000 in cash from his friend on the occasion of his marriage.

(xv) Mr. Mukesh Verma has received gift of `1,00,000 in cash and `1,00,000 in kind from his fiancée.

Solution 3(a)

(i) Mr. Jeevan Chauhan has received gift of `50,000 in cash from his friend, in this case it will not be

considered to be his income.

(ii) Mr. Sudhanshu Mittal has received gift of `2,50,000 in cash from his brother, in this case it will not be

12

considered to be his income.

(iii) Mr. Vishal Jain has received gift of ` 2,50,000 in cash from his mother’s sister, in this case it will not be

considered to be his income.

(iv) Mr. Druv Goel has received gift of `2,50,000 in cash from his father’s brother, in this case it will not be

considered to be his income.

(v) Mr. Nimit Aggarwal has received gift of `2,50,000 in cash from his cousin, in this case it will be chargeable

to tax.

(vi) Mr. Naveen Jain has received gift of `2,50,000 in cash from brother of his spouse, in this case it will not be

considered to be his income.

(vii) Mr. Sachin Bhatia has received gift of `2,50,000 in cash from his grand father, in this case it will not be

considered to be his income.

(viii) Mr. Sunny Arora has received gift of `2,50,000 in cash from spouse of his brother, in this case it will not

be considered to be his income.

(ix) Mr. Ritesh Bansal has received gift of `2,50,000 in cash from husband of his sister, in this case it will not

be considered to be his income.

(x) Mr. Mohit Singh has received gift of `2,50,000 in cash from sister of his brother’s wife, in this case it will

be considered to be his income.

(xi) Mr. Rahul Kumar has received gift of `2,50,000 in cash from the sister of his spouse, in this case it will not

be considered to be his income.

(xii) Mr. Hunny Jindal has received gift of `6,000 in cash on his birthday from each of his eleven friends, in

this case it will be considered to be his income because the total amount is exceeding `50,000.

(xiii) Mr. Satbeer Singh has received gift of `2,50,000 in kind from his friend, in this case it will be considered

to be his income.

(xiv) Mr. Ashok Kumar has received gift of `2,50,000 in cash from his friend on the occasion of his marriage,

in this case it will not be considered to be his income.

(xv) Mr. Mukesh Verma has received gift of `1,00,000 in cash and `1,00,000 in kind from his fiancee, in this

case gift in cash will be considered to be his income and the gift in kind shall also be considered to be his

income.

Question 3(b) Marks 4

Sambahv Private Limited is engaged in providing the services liable to service tax. Compute the service tax

payable by it in the month of October, 2013 from the information furnished below:-

Particulars Amount

(`)

Services rendered to poor people free of cost (Value of the services computed on comparative 40,000

13

basis)

Advances received in October, 2013 from clients for which no service has been rendered so far 50,000

Renting of agro machinery for agricultural purpose 5,00,000

Amount received for the services rendered in July, 2013 (Bills for the same were issued on July

29, 2013)

60,000

Note: The aforesaid amounts are exclusive of service tax. Sambahv Private Limited is not eligible for small

service providers’ exemption in the financial year 2013-14.

Solution: 3(b)

Computation of Service Tax Payable by Sambhav Private Limited in the month of October, 2013:-

Particulars Amount(`)

Services rendered to poor people free of cost (Note-1) Nil

Advances received in October, 2013 from clients (Note-2) 50,000

Renting of agro machinery for agricultural purpose (Note-3) Nil

Amount received for the services rendered in July, 2013 ( Note-4) Nil

Value of taxable services 50,000

Service tax @ 12% = `50,000 × 12% 6,000

Education cess @ 2% = ` 6,000 × 2% 120

Secondary and higher education cess @ 1% = ` 6,000 × 1% 60

Service Tax Payable 6,180

Notes:

1. Service tax is chargeable on the value of service. Thus, service tax is not payable in case of free services

as there is no consideration in such case.

2. Advances received in October, 2013 shall be taxable in the month of receipt of advance only.

[Explanation to rule 3 of the Point of Taxation Rules, 2011].

3. Services relating to renting of agro machinery for agricultural purpose is included in the negative list of

service. Hence, it is not taxable.

4. Point of taxation in respect of the services rendered in July, 2013 is July 29, 2013. Hence, receipts of `

60,000 is not chargeable to service tax in October, 2013 [Rule 3(a) of the Point of Taxation Rules, 2011].

Question 3(c) Marks 4

Bhim, a registered dealer under DVAT /CST Act submits the following information for the month of February,

2014.

Particulars Amount

`

Rate of

VAT

Details of purchase

Raw material purchased from another State (CST @ 2%).

Raw material X purchased within the State

Raw material Y imported from Singapore (includes custom duty paid @ 10%)

Raw material Z purchased within the State.

12,00,000

18,00,000

13,00,000

8,00,000

1%

12.5%

Details of sales

Sale of goods produced from raw material X.

Sale of goods produced from inter-State purchase and imported raw materials.

Sale of goods produced from raw material Z.

30,00,000

34,00,000

12,00,000

4%

1%

12.5%

Note: The purchase and sales figures given above do not include VAT/CST.

14

Assume that there was no opening or closing inventory. Compute the amount of Value Added Tax (VAT)

payable by Bhim for the month of February, 2014.

Solution:3(c)

`

Computation of VAT payable by Bhim for the month of February’ 2014

Raw material purchased from another State

Purchase Price 12,00,000

Add: CST @ 2% 24,000

Total purchase price 12,24,000

Raw material X purchased within the State

Purchase Price 18,00,000

Add: VAT @ 1% 18,000

Raw material Y imported from Singapore

Purchase Price 13,00,000

Raw material Z purchased within the State

Purchase Price 8,00,000

Add: VAT @ 12.5% 1,00,000

Sale of goods produced from raw material X.

Sale Price 30,00,000

Add: VAT @ 4% 1,20,000

Sale of goods produced from inter-State purchase and imported raw materials.

Sale Price 34,00,000

Add: VAT @ 1% 34,000

Sale of goods produced from raw material Z.

Sale Price 12,00,000

Add: VAT @ 12.5% 1,50,000

Net Tax payable

Output tax (1,20,000 + 34,000 + 1,50,000) 3,04,000

Less: Tax credit (18,000 + 1,00,000) 1,18,000

Net tax payable 1,86,000

Question 4(a) Marks 4

Check the taxability of the following gifts received by Mrs. Rashmi during the previous year 2013-14 and

compute the taxable income from gifts for Assessment Year 2014-15:

(i) On the occasion of her marriage on 14.08.2013, she has received `90,000 as gift out of which `70,000 are

from relatives and balance from friends.

(ii) On 12.09.2013, she has received gift of `18,000 from cousin of her mother.

(iii) A cell phone of `21,000 is gifted by her employer on 15.08.2013.

15

(iv) She gets a gift of `25,000 from the elder brother of her husband's grandfather on 25.10.2013.

(v) She has received a gift of `2,000 from her friend on 14.04.2013.

Solution 4(a)

Computation of taxable income of Mrs. Rashmi from gifts for A.Y. 2014-15

Particulars Taxable amount Reason for taxability or

` otherwise of each gift

Relatives and friends Nil Gifts received on the occasion of

marriage are not taxable.

Cousin of Mrs. Rashmi’s mother 18,000 Cousin of Mrs. Rashmi’s mother is

not a relative. Hence, the gift is taxable.

Elder brother of husband’s grandfather 25,000 Brother of husband’s grandfather is

not a relative. Hence, the gift is taxable.

Friend 2,000 Gift from friend is taxable.

Aggregate value of gifts 45,000

Since the aggregate value of gifts received by Mrs. Rashmi during the previous year 2013-14 does not exceed

`50,000, the same is not chargeable to tax under section 56 of the Income-Tax Act, 1961.

Gift received from the employer in kind upto `5,000 is exempt from income tax but excess over it is taxable

hence in this case taxable amount of gift shall be `16,000 (21,000 – 5,000) and it will be taxable under the head

Salary.

Question 4(b) Marks 4

Mr. X has paid advance tax as given below:

Upto September 15, 2013 `45,000

Upto December 15, 2013 `95,000

He has not estimated any capital gain but he had long term capital gains of `3,00,000 on 01.01.2014. He has

paid advance tax upto 15th

March 2014 `1,70,000.

His actual income other than capital gains was found to be `11,00,000.

He has filed return of income on 10.12.2014 and has paid difference of the tax on 10.12.2014.

Last date for filing of return is 31.07.2014.

Compute interest payable under section 234A, 234B and 234C.

Solution 4(b)

Computation of Tax Liability

16

` Normal Income 11,00,000

Long term capital gains 3,00,000

Total Income 14,00,000

Tax on `11,00,000 at slab rate 1,60,000

Tax on `3,00,000 @ 20% 60,000

Add: Education cess @ 2% 4,400

Add: SHEC @ 1% 2,200

Tax Liability 2,26,600

(Tax liability excluding capital gains `11,00,000 at slab rate + EC @ 3% 1,64,800)

Computation of Interest under section 234C

Since capital gains arises on 1st January 2014, installments for 15

th September and 15

th December shall be

checked without including tax on capital gain and shall be as given below:

Amount payable

as advance tax

Amount actually paid

by way of advance tax

Shortfall Interest

` ` ` ` Upto September 15, 2013

(1,64,800 x 30%)

49,440 45,000 4,440

(4,400 x 1% x 3)

132

Upto December 15, 2013

(1,64,800 x 60%)

98,880 95,000 3,880

(3,800 x 1% x 3)

114

Installment for 15th

March shall be including tax on capital gains and is as given below:

Amount payable

as advance tax

Amount actually paid

by way of advance tax

Shortfall Interest

` ` ` ` Upto March 15, 2014

(2,26,600 x 100%)

2,26,600 1,70,000 56,600

(56,600 x 1% x 1)

566

Interest payable under section 234C ` 812

Interest under section 234B

56,600 x 1% x 9 `5,094

Interest under section 234A

56,600 x 1% x 5 `2,830

Question 4(c) Marks 4

Define the term “Negative List”. Specify all the services which have been included in Negative List of

Services.

Solution: 4(c)

According to Section 65B (34) of Finance Act, 1994 “negative list” means the services which have been listed

in section 66D. Following Seventeen services have been listed in Section 66D.

S. No. Description

1. Services by Government or a local authority excluding the following services to the extent

they are not covered elsewhere—

17

(i) services by the Department of Posts by way of speed post, express parcel post, life

insurance and agency services provided to a person other than Government;

(ii) services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an

airport;

(iii) transport of goods or passengers; or

(iv) support services, other than services covered under clauses (i) to (iii) above, provided to

business entities;

2. services by the Reserve Bank of India;

3. services by a foreign diplomatic mission located in India;

4. services relating to agriculture or agricultural produce by way of—

(i) agricultural operations directly related to production of any agricultural produce including

cultivation, harvesting, threshing, plant protection or testing;

(ii) supply of farm labour;

(iii) processes carried out at an agricultural farm including tending, pruning, cutting,

harvesting, drying, cleaning, trimming, sun drying, fumigating, curing, sorting, grading,

cooling or bulk packaging and such like operations which do not alter the essential

characteristics of agricultural produce but make it only marketable for the primary market;

(iv) renting or leasing of agro machinery or vacant land with or without a structure

incidental to its use;

(v) loading, unloading, packing, storage or warehousing of agricultural produce;

(vi) agricultural extension services;

(vii) services by any Agricultural Produce Marketing Committee or Board or services

provided by a commission agent for sale or purchase of agricultural produce;

5. trading of goods;

6. any process amounting to manufacture or production of goods;

7. selling of space or time slots for advertisements other than advertisements broadcast by radio or

television;

8. service by way of access to a road or a bridge on payment of toll charges;

9. betting, gambling or lottery;

10. admission to entertainment events or access to amusement facilities;

11. transmission or distribution of electricity by an electricity transmission or distribution utility;

12. services by way of—

(i) pre-school education and education up to higher secondary school or equivalent;

(ii) education as a part of a curriculum for obtaining a qualification recognised by any law

for the time being in force;

(iii) education as a part of an approved vocational education course;

13. services by way of renting of residential dwelling for use as residence;

14. services by way of—

(i) extending deposits, loans or advances in so far as the consideration is represented

by way of interest or discount;

(ii) inter se sale or purchase of foreign currency amongst banks or authorised dealers of

foreign exchange or amongst banks and such dealers;

15. service of transportation of passengers, with or without accompanied belongings, by—

(i) a stage carriage;

(ii) railways in a class other than—

(A) first class; or

(B) an air-conditioned coach;

(iii) metro, monorail or tramway;

(iv) inland waterways;

18

(v) public transport, other than predominantly for tourism purpose, in a vessel between

places located in India and

(vi) metered cabs, radio taxis or auto rickshaws.

16. services by way of transportation of goods—

(i) By road except the services of -

(A) a goods transportation agency; or

(B) a courier agency;

(ii) by an aircraft or a vessel from a place outside India upto the customs station of clearance

in India; or

(iii) by inland waterways;

17. Funeral, burial, crematorium or mortuary services including transportation of the deceased.

Question 4(d) Marks 4

Mention the purchases which are not eligible for input tax credit (any eight items) under Value Added Tax.

Solution:4(d) The following purchases are not eligible for input tax credit:

(i) purchases from unregistered dealer;

(ii) purchases from a registered dealer who opts for composition scheme;

(iii) purchases of goods as may be notified by the State Government;

(iv) purchases of goods where the purchase invoice is not available with the claimant;

(v) purchases of goods where invoice does not show the amount of tax separately;

(vi) purchases of goods which are being utilized in the manufacture of exempted goods;

(vii) purchases of goods used for personal use or provided free of charge as gifts;

(viii) imports from outside the territory of India;

(ix) imports from other States;

goods in stock, which have suffered tax under an earlier Act, but under the VAT Act they are covered under

exempted items. (Note: Any eight points may be given.)

Question 5(a) Marks 8 Determine the taxability of the following incomes in the hands of a resident and ordinarily resident, resident but

not ordinarily resident, and non-resident for the A.Y. 2014-15 –

Particulars Amount (` )

(1) Interest on UK Development Bonds, 50% of interest received in India 10,000

(2) Income from a business in Chennai (50% is received in India) 20,000

(3) Profits on sale of shares of an Indian company received in London 20,000

(4) Dividend from British company received in London 5,000

(5) Profits on sale of plant at Germany 50% of profits are received in India 40,000

19

(6) Income earned from business in Germany which is controlled from Delhi (`40,000 is

received in India)

70,000

(7) Profits from a business in Delhi but managed entirely from London 15,000

(8) Income from property in London deposited in a Indian Bank at London, brought to

India

50,000

(9) Interest for debentures in an Indian company received in London. 12,000

(10) Fees for technical services rendered in India but received in London 8,000

(11) Profits from a business in Bombay managed from London 26,000

(12) Pension for services rendered in India but received in Burma 4,000

(13) Income from property situated in Pakistan received there 16,000

(14) Past foreign untaxed income brought to India during the previous year 5,000

(15) Income from agricultural land in Nepal received there and then brought to India 18,000

(16) Income from profession in Kenya which was set up in India, received there but spent

in India

5,000

(17) Gift received on the occasion of his wedding 20,000

(18) Interest on savings bank deposit in State Bank of India 10,000

(19) Income from a business in Russia, controlled from Russia 20,000

(20) Dividend from Reliance Petroleum Limited, an Indian Company 5,000

(21) Agricultural income from a land in Rajasthan 15,000

Solution: 5(a)

Computation of Gross Total Income for the A.Y.2014-15

Particulars Resident and

ordinarily resident

`

Resident but not

ordinarily resident

`

Non

resident

`

(1) Interest on UK Development Bonds, 50% of

interest received in India

10,000 5,000 5,000

(2) Income from a business in Chennai (50% is

received in India)

20,000 20,000 20,000

(3) Profits on sale of shares of an Indian company

received in London

20,000 20,000 20,000

(4) Dividend from British company received in

London

5,000 - -

(5) Profits on sale of plant at Germany 50% of

profits are received in India

40,000 20,000 20,000

(6) Income earned from business in Germany

which is controlled from Delhi, out of which

`40,000 is received in India

70,000 70,000 40,000

(7) Profits from a business in Delhi but managed

entirely from London

15,000 15,000 15,000

(8) Income from property in London deposited in

a Bank at London, later on remitted to India

50,000 - -

(9) Interest for debentures in an Indian company

received in London.

12,000 12,000 12,000

(10) Fees for technical services rendered in India

but received in London

8,000 8,000 8,000

(11) Profits from a business in Bombay managed

from London

26,000 26,000 26,000

(12) Pension for services rendered in India but

received in Burma

4,000 4,000 4,000

20

(13) Income from property situated in Pakistan

received there

16,000 - -

(14) Past foreign untaxed income brought to India

during the previous year

- - -

(15) Income from agricultural land in Nepal

received there and then brought to India

18,000 - -

(16) Income from profession in Kenya which was

set up in India, received there but spent in India

5,000 5,000 -

(17) Gift received on the occasion of his wedding

[not an income]

- - -

(18) Interest on savings bank deposit in State

Bank of India

10,000 10,000 10,000

(19) Income from a business in Russia, controlled

from Russia

20,000 - -

(20) Dividend from Reliance Petroleum Limited,

an Indian Company [it is exempt u/s 10(34)]

- - -

(21) Agricultural income from a land in Rajasthan

[it is exempt u/s 10(1)]

- - -

Gross Total Income 3,49,000 2,15,000 1,80,000

Question 5(b) Marks 4

Lakhanpur Post Office provided the following services to persons other than Government during the quarter

ending 31.03.2014:-

Services rendered Amount (`)

Basic mail services 1,00,000

Transfer of money through money orders 5,00,000

Operation of saving accounts 1,50,000

Rural postal life insurance services 2,00,000

Distribution of mutual funds, bonds and passport applications 5,00,000

Issuance of postal orders 3,00,000

Collection of telephone and electricity bills 1,00,000

Pension payment services 50,000

Speed post services 5,00,000

Express parcel post services 2,00,000

Compute the service tax liability of Lakhanpur Post Office for the quarter ending 31.03.2014.

Notes:

1. Point of taxation for all the aforesaid cases fall during the quarter ending 31.03.2014.

2. All the service charges stated above are exclusive of service tax.

3. Small Service Providers’ exemption need not be taken into account while solving the aforesaid question.

Solution 5(b)

Services provided by the Government or a local authority are not chargeable to service tax as they are included

in the negative list. However, following services provided to a person other than Government, by the

Department of Posts are excluded from the negative list:-

(i) Speed post

(ii) Express parcel post

(iii) Rural postal Life Insurance

(iii) Agency services which include distribution of mutual funds, bonds, passport applications, collection of

telephone and electricity bills, etc.

Hence, the aforesaid services are taxable.

21

Thus, the amount of service tax payable by Lakhanpur Post Office for the quarter ending 31.03.2014 would be

as follows:-

Particulars Amount(`)

Basic mail services Nil

Transfer of money through money orders Nil

Operation of saving accounts Nil

Rural postal life insurance services 2,00,000

Distribution of mutual funds, bonds and passport applications 5,00,000

Issue of postal orders Nil

Collection of telephone and electricity bills 1,00,000

Pension payments Nil

Speed post services 5,00,000

Express parcel post 2,00,000

Value of taxable service 15,00,000

Service tax @ 12% [15,00,000×12%] 1,80,000

Education cess @ 2% [1,80,000×2%] 3,600

Secondary and higher education cess @ 1% [1,80,000×1%] 1,800

Service tax liability 1,85,400

Question 5 (c) Marks 4

The following are details of purchases, sales, etc. effected by Vasudha & Co., a registered dealer, for the year

ended 31.03.2014:

Particulars Amount

(`)

Purchase of raw materials within State, 1000 units, inclusive of VAT levy at 6% 5,30,000

Inter-State purchase of raw materials, inclusive of CST at 2% 2,04,000

Import of raw materials, inclusive of basic customs duty plus education cess of `36,050 4,35,000

Capital goods purchased on 01.05.2013, inclusive of VAT levy at 10% 3,30,000

(input credit to be spread over 2 financial years)

Other manufacturing expenses 1,50,000

Sale of taxable goods within State, inclusive of VAT levy at 4% 7,28,000

Sale of goods within State, exempt from levy of VAT 1,20,000

(Goods were manufactured from the Inter-State purchase of raw materials)

Closing stock as on 31.03.2014 was 100 units of raw materials purchased within the State

Input credit is allowed only on raw material used in manufacture of the taxable goods. Compute the VAT

liability of the dealer for the year ended 31.03.2014.

Solution:5(c)

Computation of VAT liability of Vasudha & Co. for the year ended 31.03.2014:-

Particulars Amount

22

(`) Input tax credit:

Intra-State purchases of 1000 units of raw materials

106

6000,30,5 30,000

Inter-State purchases of raw materials --

Import of raw materials --

Purchase of Capital Goods

2110

10000,30,3 15,000

Other manufacturing expenses --

Total input tax credit available : 45,000

Output VAT payable:

Sale of taxable goods within State [(7,28,000 x 4)/104] 28,000

Sale of exempted goods within State [Refer Note 2] --

VAT credit to be carried forward (28,000 – 45,000) (17000)

Notes:- 1. VAT paid on purchase of capital goods is eligible for input tax credit. However, the same has to be

spread over a period of two years.

2. VAT system allows credit in respect of purchases made during a period to be set-off against the taxable

sales during that period, irrespective of when the supplies/inputs purchased are utilized/sold. Therefore,

input tax credit in respect of closing stock of raw materials need not be reduced from total input tax

credit available.

Note: The statement in the question, “Input credit is allowed only on raw materials used in manufacture of the

taxable goods”, implies that the same is not allowable in respect of sale of goods within the State which are

exempt from levy of VAT.

Question 6(a) Marks 8

Determine residential status of Mr. Naresh Jindal for the assessment year 2014-15, who stays in India during

various financial years asunder:

Previous

Years

1 2 3 4 5 6 7 8

2013-14 65 183 181 69 300 70 72 95

2012-13 91 90 87 110 97 99 94 92

2011-12 190 78 98 91 103 104 101 100

2010-11 89 120 189 196 110 98 97 96

2009-10 87 91 92 93 94 95 94 93

2008-09 86 99 92 95 99 100 101 100

2007-08 84 66 93 94 366 210 209 208

2006-07 105 210 91 93 — 0 91 92

2005-06 110 110 92 92 362 300 200 100

2004-05 112 94 93 91 10 99 88 77

2003-04 100 96 91 90 310 100 99 92

2002-03 91 199 90 89 210 92 94 96

23

2001-02 94 81 89 8 92 80 70 60

2000-01 97 82 88 87 88 55 65 75

1999-00 99 83 87 86 84 40 50 60

Solution:6(a)

CASE 1:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Non-Resident

2009-10 Resident

2008-09 Resident

2007-08 Resident

2006-07 Resident

2005-06 Resident

2004-05 Resident

2003-04 Resident

Total stay in 7 years preceding the relevant previous year is 732 days.

Since the assessee is not able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be ROR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

CASE 2:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Resident

2009-10 Resident

2008-09 Resident

2007-08 Resident

2006-07 Resident

2005-06 Resident

2004-05 Resident

2003-04 Resident

Total stay in 7 years preceding the relevant previous year is 754 days.

Since the assessee is not able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be ROR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

24

CASE 3:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Resident

2009-10 Resident

2008-09 Resident

2007-08 Resident

2006-07 Resident

2005-06 Non-Resident

2004-05 Non-Resident

2003-04 Non-Resident

Total stay in 7 years preceding the relevant previous year is 742 days.

Since the assessee is not able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be ROR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

CASE 4:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Resident

2009-10 Resident

2008-09 Resident

2007-08 Resident

2006-07 Non-Resident

2005-06 Non-Resident

2004-05 Non-Resident

2003-04 Non-Resident

Total stay in 7 years preceding the relevant previous year is 772 days.

Since the assessee is not able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be ROR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

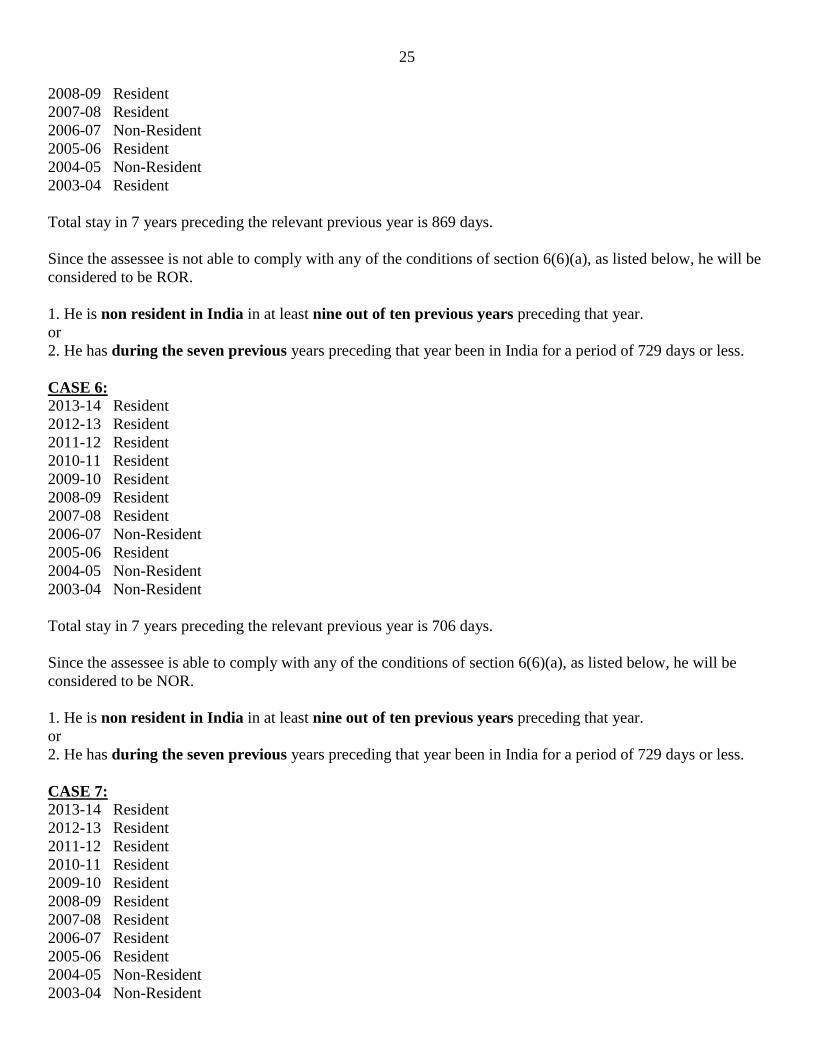

CASE 5:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Resident

2009-10 Resident

25

2008-09 Resident

2007-08 Resident

2006-07 Non-Resident

2005-06 Resident

2004-05 Non-Resident

2003-04 Resident

Total stay in 7 years preceding the relevant previous year is 869 days.

Since the assessee is not able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be ROR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

CASE 6:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Resident

2009-10 Resident

2008-09 Resident

2007-08 Resident

2006-07 Non-Resident

2005-06 Resident

2004-05 Non-Resident

2003-04 Non-Resident

Total stay in 7 years preceding the relevant previous year is 706 days.

Since the assessee is able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be NOR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

CASE 7:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Resident

2009-10 Resident

2008-09 Resident

2007-08 Resident

2006-07 Resident

2005-06 Resident

2004-05 Non-Resident

2003-04 Non-Resident

26

Total stay in 7 years preceding the relevant previous year is 787 days.

Since the assessee is not able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be ROR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

CASE 8:

2013-14 Resident

2012-13 Resident

2011-12 Resident

2010-11 Resident

2009-10 Resident

2008-09 Resident

2007-08 Resident

2006-07 Resident

2005-06 Non-Resident

2004-05 Non-Resident

2003-04 Non-Resident

Total stay in 7 years preceding the relevant previous year is 781 days.

Since the assessee is not able to comply with any of the conditions of section 6(6)(a), as listed below, he will be

considered to be ROR.

1. He is non resident in India in at least nine out of ten previous years preceding that year.

or

2. He has during the seven previous years preceding that year been in India for a period of 729 days or less.

Question 6(b) Marks 8

Briefly answer the following questions:-

(i) Does a service provider have an option to pay service tax at a rate different from the general rate

applicable on gross value of taxable services, in the case of purchase or sale of foreign currency?

(ii) What is EASIEST scheme and state the benefits in the context of service tax ?

(iii) Vibha Ltd. is engaged in providing management consultancy services. It was liable to pay the service

tax amounting to ` 10,000, electronically, for the month of August 2013. However, due to some

unavoidable circumstances, it could not pay the said amount on due date and paid the service tax on 30th

November, 2013. You are required to compute the interest payable by Vibha Ltd. on delayed payment of

service tax. (Assume that value of taxable services is above `60 lakh in preceding financial year.)

(iv) State the due dates for filing of service tax returns. Will the delayed filing of service tax return result in

payment of any late fee? If so, how much?

Solution:6(b)

27

(i) Yes, the person liable to pay service tax in relation to purchase or sale of foreign currency, including

money changing, has an option to pay an amount at the following rates instead of paying service tax at the rate

of 12%:-

S. No. For an amount Service tax shall be calculated at the rate of

1. Upto ` 100,000 0.12 % of the gross amount of currency exchanged

or

` 30

whichever is higher

2. Exceeding ` 1,00,000 and upto

`10,00,000

` 120 + 0.06 % of the gross amount of currency

exchanged – `1 lakh)

3. Exceeding ` 10,00,000 ` 660 + 0.012 % of the gross amount of currency

exchanged – `10 lakh)

or

` 6,000

whichever is lower

However, the person providing the service shall exercise such option for a financial year and such option shall

not be withdrawn during the remaining part of that financial year.

(ii) EASIEST stands for Electronic Accounting System in Excise and Service Tax. It makes tax payment

easy. This facility is available with 28 banks.

The benefits of EASIEST to the taxpayer are as follows:-

(a) Only one copy of the challan is to be filled instead of four copies as required earlier.

(b) EASIEST facilitates online verification of the status of tax payment using Challan Identification

Number.

(iii) Computation of interest payable on delayed payment of service tax by Vibha Ltd.:-

Due date of payment of service tax 06.09.2013

Actual date of payment 30.11.2013

No. of days of delay (24+31+30) 85

Amount of service tax ` 10,000/-

Calculation of interest under section 75 @ 18% per annum* 10,000 x 365

85x

100

18

Amount of interest payable ` 419/-

(iv) The service tax return (in Form ST-3) should be filed on half yearly basis by the 25th of the month

following the particular half-year. The due dates on this basis are as under:

Half year Due date

1st April to 30th September 25th October

1st October to 31st March 25th April

In case the due date of filing of return falls on a public holiday, the assessee can file the return on the

immediately succeeding working day.

Yes, late fee will be levied for delay in furnishing of the service tax return. The prescribes late is given

hereunder:

S. No.

Period of delay Late fee

Particulars `

(a)

(b)

(c)

15 days from the date prescribed for submission of the return

Beyond 15 days but not later than 30 days from the date

prescribed for submission of the return.

Beyond 30 days from the date prescribed for submission of the

500

1,000

An amount of ` 1,000 plus `100

28

return for every day from the 31st day

till the date of furnishing the

said return

However, the total late fee for delayed submission should not exceed ` 20,000

Question 7(a) Marks 4

(i) Compute the eligible deduction under section 80C for A.Y.2014-15 in respect of life insurance premium

paid by Mr. Himesh during the P.Y.2013-14, the details of which are given hereunder –

Date of issue

of Policy

Person insured Actual capital

Sum assured

(`)

Insurance

premium paid

during 2013-14

(`)

(i) 1/6/2011 Mr. Himesh 2,00,000 75,000

(ii) 1/5/2012 Mrs. Himani, his wife 2,00,000 25,000

(iii) 1/7/2013 Ms. Shweta, his handicapped

daughter (section 80U disability)

3,00,000 60,000

(iv) 1/7/2013 Mr. Siddhartha, his son 4,00,000 25,000

Total Premium paid 1,85,000

(ii) Mr. Aayush purchased a residential house property for self-occupation at a cost of ` 28 lakh on 1.5.2013, in respect of

which he took a housing loan of ` 20 lakh from the State Bank of India (SBI) @12% p.a. on the same date. The SBI had

sanctioned housing loan of ` 22 lakhs on 29th April, 2013. Compute the eligible deduction in respect of interest on

housing loan for A.Y.2014-15 under the provisions of the Income-tax Act, 1961, assuming that the entire loan was

outstanding as on 31.3.2014 and he does not own any other house property.(assume assessee satisfy all the condition for

claiming higher deduction under section 24(b))

Solution:7(a)

(i) Computation of eligible deduction under section 80C for A.Y. 2014-15

(in respect of life insurance premium paid by Mr. Himesh)

Date of issue

of policy

Person insured Actual capital

sum assured

Insurance

premium

paid during

2013-14

Restricted

to % of

sum assured)

Deduction

u/s 80C for

A.Y.2014-

15

(i) 1/6/2011 Mr. Himesh 2,00,000 75,000 20% 40,000

(ii) 1/5/2012 Mrs. Himani 2,00,000 25,000 10% 20,000

(iii) 1/7/2013 Handicapped

daughter

3,00,000 60,000 15% 45,000

(iv) 1/7/2013 Son 4,00,000 25,000 10% 25,000

Total 1,30,000

Maximum deduction u/s 80C restricted to 1,00,000

Note:

In respect of policies issued Maximum deduction u/s 80C

(% of actual capital sum assured)

between 01-04-2003 and 31-03-2012 20%

between 01-04-2012 and 31-03-2013 10%

29

on or after 01-04-2013

- Insurance on life of person with disability u/s 80U

- Others

15%

10%

(ii)

Computation of eligible deduction in respect of interest on housing loan for A.Y. 2014-15

Particulars ` Deduction under section 24(b) [See Note 1]

` 2,20,000 [` 20,00,000 × 12% × 11/12]

Restricted to 1,50,000

Deduction under section 80EE (` 2,20,000 – `1,50,000) [See Note 2] 70,000

Note:

(1) Mr. Aayush is entitled to deduction under section 24(b) in respect of interest on loan taken for purchase of

self-occupied property, subject to a maximum of ` 1,50,000.

(2) Mr. Aayush is also entitled to deduction under section 80EE under Chapter VIA (i.e. deductions from gross

total income), in addition to deduction under section 24(b) since –

(1) the loan is sanctioned by State Bank of India, being a financial institution, during the period between

1.4.2013 and 31.3.2014;

(2) the loan amount sanctioned is less than ` 25 lakh;

(3) the value of the house property is less than ` 40 lakh;

(4) he does not own any other residential house property.

Note: The maximum deduction under section 80EE is ` 1,00,000. Since Mr. Aayush has availed only `70,000

in the P.Y. 2013-14, he can avail the balance ` 30,000 as deduction under section 80EE in the P.Y.2014-15

(A.Y. 2015-16) in addition to deduction of ` 1,50,000 under section 24 for that year.

Question 7(b) Marks 4

Bhupesh owns a residential house property. It has two identical units—unit I and unit II. Unit I is self–occupied

by Bhupesh and his family members, unit II is let out (rent being `7,500 per month, this unit remained vacant

for one month during which it was self-occupied). Municipal value of the property is `1,30,000. Standard rent is

`1,40,000 and fair rent is `1,53,000. Municipal taxes is imposed @ 12% (on municipal value) which is paid by

Bhupesh. Other expenses for the previous year 2013-14 being repairs `5,100 and insurance `6,300.

Bhupesh borrowed `9,00,000 on 01.07.2010 from LIC @ 12% p.a. to construct the property. Construction of

the house was completed on 30.06.2012. The entire loan is still unpaid.

Compute the total income and tax liability of Mr. Bhupesh for the assessment year 2014-15 on the assumption

that income of Bhupesh from other sources is `2,90,000.

Solution:7(b) `

Computation of income of Unit-I

Since the unit is self-occupied throughout the year. Hence its income shall be computed under section 23(2),

accordingly there will be loss `30,000.

Computation of income of Unit-II

It will be considered to be partially self-occupied and partially let out and income shall be computed under

section 23(3) in the manner given below:

30

` Gross Annual Value 82,500.00

Working Note: `

(a) Fair Rental Value 76,500

(b) Municipal Valuation 65,000

(c) Higher of (a) or (b) 76,500

(d) Standard Rent 70,000

Expected Rent {Lower of (c) or (d) 70,000

(e) Expected Rent 70,000

(f) Rent Received/Receivable (7,500 x 11) 82,500

GAV = Higher of (e) or (f) 82,500

Less: Municipal taxes 7,800.00

Net Annual Value 74,700.00

Less: 30% of NAV u/s 24(a) 22,410.00

Less: Interest on capital borrowed u/s 24(b) 72,900.00

Working note:

Current period interest

From 01.04.2013 to 31.03.2014

= 9,00,000 x 12% = `1,08,000

Prior period interest

From 01.07.2010 to 31.03.2012

= 9,00,000 x 12% x 21 / 12 =1,89,000

Installment = 1,89,000 / 5 = 37,800

Total interest= 1,08,000 + 37,800 = 1,45,800

Interest allowed for one unit = 1,45,800 / 2 = `72,900

Loss from house property (20,610.00)

Loss under the head House Property is

(`20,610) + (`30,000) (50,610.00)

Income under the head Other Sources 2,90,000.00

Gross Total Income 2,39,390.00

Less: Deductions u/s 80C to 80U Nil

Total Income 2,39,390.00

Computation of Tax Liability

Tax on `2,39,390 at slab rate 3,939.00

Less: Rebate u/s 87A (3,939 or 2,000 whichever is less) 2,000.00

Tax before education cess 1,939.00

Add: Education cess @ 2% 38.78

Add: SHEC @ 1% 19.39

Tax Liability 1,997.17

Rounded off u/s 288B 2,000.00

Note: Since condition regarding certificate has not been complied with hence interest has been allowed

maximum to the extent of `30,000.

Question 7(d) Marks 4

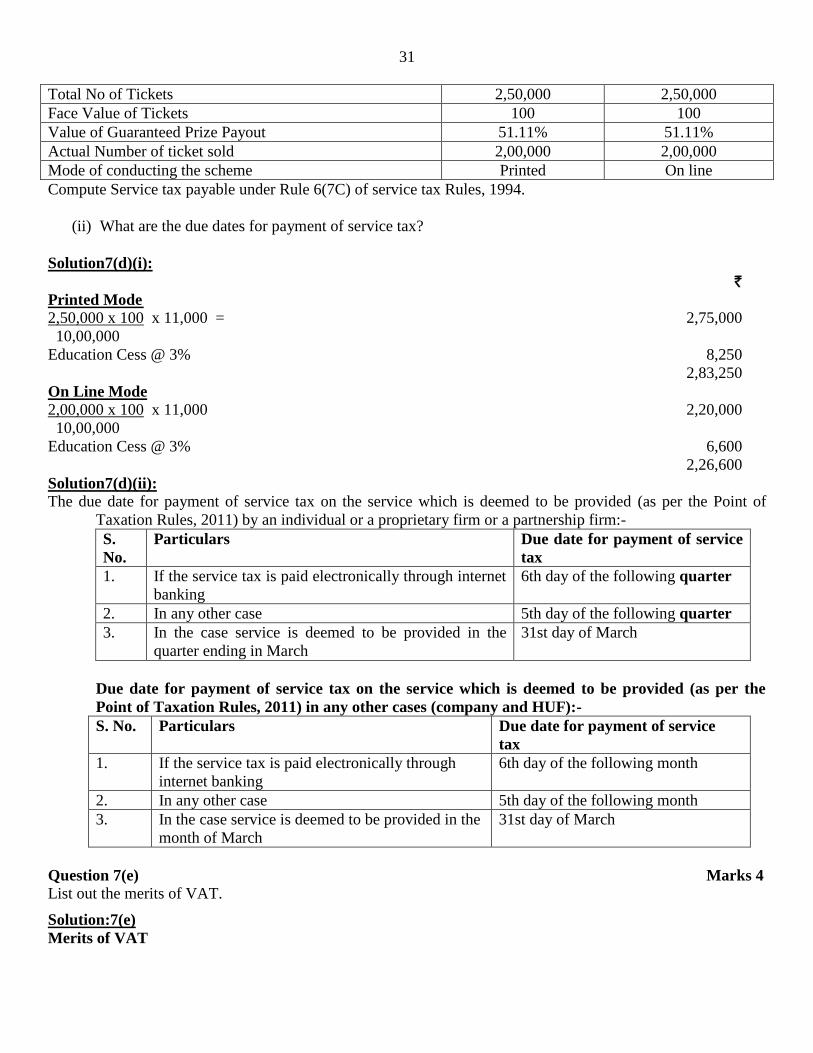

(i) M/s Future Gaming Solutions India Private Limited is a distributor of lottery organized by State of

Sikkim provides following information:

Particulars Diwali Bumper Diwali Dhamaka

31

Total No of Tickets 2,50,000 2,50,000

Face Value of Tickets 100 100

Value of Guaranteed Prize Payout 51.11% 51.11%

Actual Number of ticket sold 2,00,000 2,00,000

Mode of conducting the scheme Printed On line

Compute Service tax payable under Rule 6(7C) of service tax Rules, 1994.

(ii) What are the due dates for payment of service tax?

Solution7(d)(i):

`

Printed Mode

2,50,000 x 100 x 11,000 = 2,75,000

10,00,000

Education Cess @ 3% 8,250

2,83,250

On Line Mode

2,00,000 x 100 x 11,000 2,20,000

10,00,000

Education Cess @ 3% 6,600

2,26,600

Solution7(d)(ii):

The due date for payment of service tax on the service which is deemed to be provided (as per the Point of

Taxation Rules, 2011) by an individual or a proprietary firm or a partnership firm:-

S.

No.

Particulars Due date for payment of service

tax

1. If the service tax is paid electronically through internet

banking

6th day of the following quarter

2. In any other case 5th day of the following quarter

3. In the case service is deemed to be provided in the

quarter ending in March

31st day of March

Due date for payment of service tax on the service which is deemed to be provided (as per the

Point of Taxation Rules, 2011) in any other cases (company and HUF):-

S. No. Particulars Due date for payment of service

tax

1. If the service tax is paid electronically through

internet banking

6th day of the following month

2. In any other case 5th day of the following month

3. In the case service is deemed to be provided in the

month of March

31st day of March

Question 7(e) Marks 4

List out the merits of VAT.

Solution:7(e)

Merits of VAT

32

1. No tax evasion is possible as the credit of duty paid is allowed against the liability on the final product

manufactured or sold. Under VAT, unless proper records are kept in respect of various inputs, it is not possible

to claim credit. A perfect system of VAT is a perfect chain where tax evasion is difficult.

2. Neutrality is the greatest advantage of VAT. VAT does not interfere in the choice of decision for purchases

because it has anti-cascading effect. The system is neutral with regard to choice of production technique, as well

as business organisation. All other things remaining the same, the issue of tax liability does not vary the

decision about the source of purchase.

3. It has a certainty as it is based simply on transactions. There is no need to go through complicated definitions

like sales, sales price, turnover of purchases and turnover of sales. The tax is also broad-based and applicable to

all sales in business leaving little room for different interpretations.

4. Transparency is ensured as the buyer knows, out of the total amount paid for purchases of material, what is

the amount paid towards VAT. This transparency enables the State Governments to know as to what is the exact

amount of tax coming at each stage. Thus, it is a great aid to the Government while taking decisions with regard

to rate of tax etc.

5. For Government, better revenue collection and stability is achieved as the tax credit will be given only if the

proof of tax paid at an earlier stage is produced. This means that if the tax is evaded at one stage, full tax will be

recoverable from the person at the subsequent stage or from a person unable to produce proof of such tax

payment.

6. Since the tax paid on an earlier stage is to be received back, the system promotes better accounting systems.

Note: Any four points may be given.