Pulp and Paper Advisory Group for Latin America

234

C H I E POTENTIAL PULP AND PAP E R EXPORTER Pulp and Paper Advisory Group for Latin America (Economic Commission For Latin America, Food and Agriculture Organization, and Technical Assistance Administration) UNITED NATIONS Santiago, Chile, 1957

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Pulp and Paper Advisory Group for Latin America

C H I E P O T E N T I A L P U L P A N D

P A P E R E X P O R T E R

Pulp and Paper Advisory

Group for Latin America

(Economic Commission For Latin America, Food and Agriculture Organization, and Technical Assistance Administration)

UNITED NATIONS Sant iago, Ch i le ,

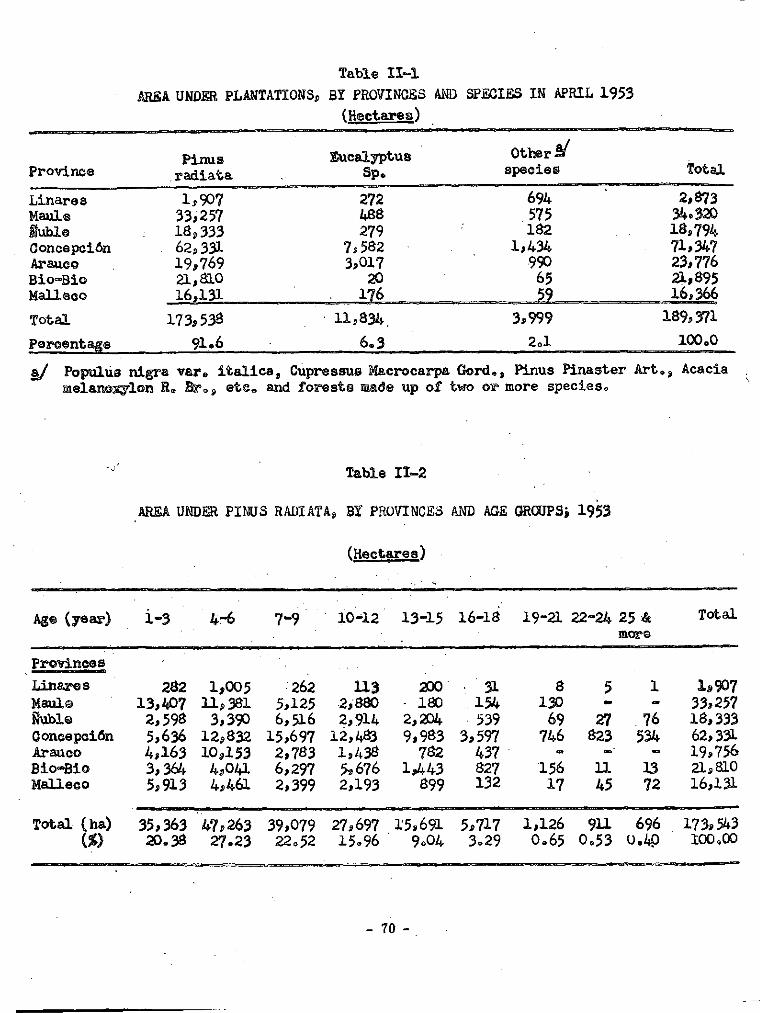

1 9 5 7

f

,1,

I!

^ 1,

I

P O T E N T I A L ' PULP A N D

P A P E R . E X.1 P O R T E R

Pulp and Paper Advisory

Group For Latin America

(Economic Commission for Latin Amarica, Food and Agricidluro. Organization, and Tii ch nical A ssistun ca A dm in ist ru lion)

E / C N . 1 2 / 4 2 4 / R e v . 1 FAO/ETAP N° 5 6 0 / R e v . 1

T A A / C H I / 3 / R e v . l

August 1957

INTBOHJCTION AND ACKNOWLEDGMENTS

The following study deals with the, technical and economic p o s s i b i l i t i e s for the establishment of a pulp and paper export industry in Chile as one of the l inks in a regional development plan to secure future ¡supplies of paper products for Latin America. I t was undertaken a t ¡the request o f the Government of Chile and the Corporación de Fomento d e , l a Producción.

In the preparation of the supporting background material , contained in the Appendices to the report, great ass is tance was rendered by the Corporación de Fomento. The Advisory Group wishes to express i t s s incere g r a t i t u d e f o r t h e i r invaluable help and c o - o p e r a t i o n to t h i s Organization and i t s s t a f f in general , and in p a r t i c u l a r t o :

Mr. Luis Adduard, General Manager, and Mr. P a t r i c i o Asenjo, Industr ial ' Division, who

c o l l a b o r a t e d in the g r e a t e r par t of the study.

Since the general conclusion reached i s that conditions in Chile are favourable to the creat ion o f an export industry which would be of great benefit t o the country, i t i s hoped that the report , which i s hereby respectful ly submitted, may be useful in planning future development.

Arne Sundelin Chief, Pulp and Paper Advisory

Group to Latin Vnerica

NOTE

Throughout the report an exchange ra te of 500 Chilean pesos to 1 US dollar i s used. Nevertheless, at the time of going to press, the purchasing power of the peso i s equivalent

exchange r a t e of 700. The c a l c u l a t i o n s are not mater ia l ly a f fec ted by t h i s , since the increase i exchange r a t e corresponds approximately t o the r i s e in the domestic c o s t s during this period ( infl r a t e June 1956 to June 1957 has been approximately 37 per c e n t ) .

Ton always r e f e r s to metric tons, unless otherwise s t a t e d .

- l i

TAPLE OF CONTENTS • » Page

Preface t o Second Edition 1

Aim and Scope of the Study ; '5

Giapter I : The International Pulp and Paper Market . . . . . . . . . • ^

1. North America ; . . . . . . . . 2. Europe ? 3 . Latin .America ® 4. Chile 8

5. The other d e f i c i t regions 9 6. Conclusions : • • 9

Chapter I I : Pinus Radiata - Pulp-mood Supply and Cost . . . . . 10

1. Location : . ' . , . . . , . . . . . . . . , r . • • • j • • IP 2. Area and yield ,. I . s . 1 • M • ; • 1 ; • - • • > • • • • 1 0

3. Stumpape value . . . i . . . : . ! I . . i , J • • • • ; - * ,• ; • • f ; • • * * ^ 4. Cost at mill s i t e ^

5. Management and future yields H

Chapter I I I : Other Paw materials and Problems 12

1. Chemicals and fuels 12 2. E l e c t r i c energy 12

3 . Fresh water supply and eff luent disposal 13

Chapter IV: The Transport Problem 14

1. Pulpwood Transport • 14 2. Transport of finished products 14

3. The port s i tua t ion 15

Chapter V; Investment and Production Costs 16

1. Investments and c a p i t a l requirements 16 2. Pulp mills 16 3. Integrated mills 18 4. Newsprint mil ls 18 5. Production c o s t s 18

Chapter VI: Economic Evaluation of the Projects and an Over-All Assessment 20

1. Evaluation on p r o f i t and deferred payment basis - the investors ' viewpoint 20 2. Limitations in wood supply 21 3. Assessment of foreign exchange earning capacity - the national viewpoint 22

4. Over-all assessment of the economic prospects 22

Chapter VII: Recommendations * * *. 24

1. General recommendations 24 2. Specif ic recommendations . . . 25 3. Final recommendation 26

^ - Hi -

9

Page Annex I : The Market situation for Pulp and Paper 27

A. Structure of the International Market 27

1. Short-term fluctuations in prices and balance of supply and demand 27 % The problem of supply over the long term 29

B. A Forecast of Future Demand and the Situation in Different Regions of the World . . . . 31

1. Methods used in forecasting dan and 3l 2. The si tuation in North America 35 3. The situation in Europe 4. Latin America • 50 5. The other d e f i c i t regions 60

C. Conclusions 62

Appendix I-A: Exports of Newsprint from North America and Europe 63 AppemHx I-B: North America and Europe: Exports of Wood Pulp (All grades) 64 Appendix I-C: Latin .%nerica: Production, import and apparent consumption of newsprint. . 65 Appendix I-D: Production, Import and Apparent Consmiption of All Papers and Boards

Except Newsprint in Latin America 66 Appendix I -E : Europe and North America: Reports of Chemical and Mechanical Pulp to Latin

AnKrx03 1937*54 • • • • • • • • • • • • • • • p 67 Appendix I - F : Chile: Projection of Demand for Newsprint and other Papers and Boards in

1960 and 1965 . . . . . . . . . . . . . . . . . . . . 68

Annex I I : Forestry Aspects .... , 69

A. Plantations of Pinus Radiata in the Southern Area of Central Chile 69

1. Forested areas and s o i l s 69 2 . Volume in plantation of pinus radiata (1953) . . . . . . . . . . 72 3 . Growth and yields of pinus radiata plantations 72 4. Forest ownership 73 5. Production and consumption of pinus radiata wood 75 6 . Damages 75

B. Cost of Pulpwood from Pinus Radiata 76

1. Value of standing timber 76 2 . Cost of fell ing and transport to roadside 81 3. Cost of transport from roadside to mill s i t e 81 4. Administration and supervision 84 5. Siflimary of pinus radiata pulpwood costs 85

C. Future Yields from Pinus Radiata Plantations in Chile . . . . . 86

Appendix II-A: Cost of Housing for Transport Personnel 89 Appendix I I - B : Forest Department: Administration and Supervisory Personnel and Cost . . 90 Appendix II-C: Forest Department: Cost of Housing for Administrative Personnel 90

- iv -

Annex I I I : Marketing Possibilities for Pinus Radiata Sawnteood . . . 91

1. Introduction . . . . . . 91 2. Production, exports and apparent consumption of Pinus Radiata in Chile, 1946-55 . . . 91 3 . Estimate of potential supply and demand for 1960 and 1965 94 4. Conclusions •

Appendix III-A: Problems Affecting Exports of Pinus Radiata Lumber . . 98

Appendix I I I - B : Saw Timber Stumpage Price and \verage Diameter of Standing Trees . . . . . 99

Annex IV: Availability and Cost of Oieaicals and Fuels 100

Annex V: Electric Energy Situation 103 Appendix V-A: Let ter from the General Manager of Endesa to the Vice-President of Corfo . . 104 Appendix V-B: Let ter from the General Manager of Endesa t o a Private Firm 109

Annex VI: The Transport Problem H I

1. The road network I l l 2. Railways 113 3. Ports 113 4. Floating of pulpwood 113

Appendix VI-A: Recommendations by the Ministry of Public Works and Corrmunicat ions Concerning limitations in Truck Loading Capacity 114

Appendix VI-B: Cost of Transporting Finished Products from Plant to Port 116 Appendix VI-C: Cost of Road-Building 120 Appendix VI-D: Railway Freight [fetes by Carloads 121 Appendix VI-E: Prices of Railway Freight Cars and Cost of Building Sidings . . . 126 Appendix VI-F: Embarkation and Maritime Freight Charges . 126

Annex VII: Investaents and Capital Requirements 128

1. Basis for estimates of investments . . . . . . . . 128 2. Community costs for workers and employees 136

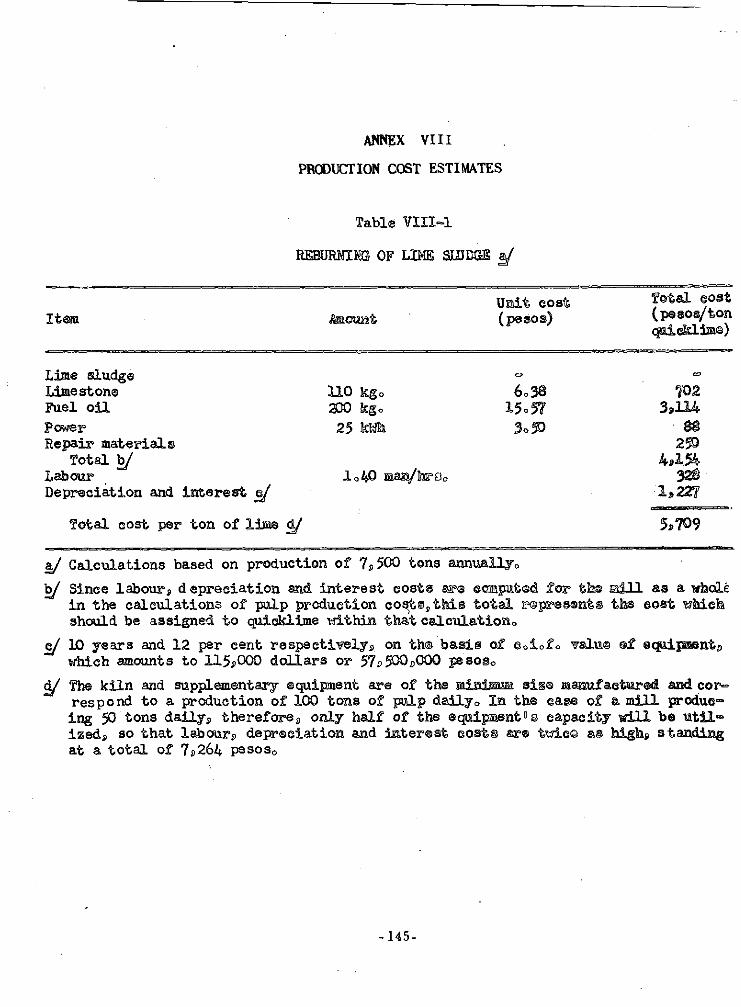

Annex VIII : Production Cost Estimates „ „ 145

Annex: IX: Econoaic Evaluation of the Projects 170

1. Calculation of minimum acceptable profi t 170 2. Venture profit 171 3. Assessment on prof i t basis - the investors point of view 173 4. Evaluation on the basis of foreign exchange earning capacity - the national viewpoint . 175 5. Summary • 177

.Appendix IX-A: Estimate of pulp and paper sales values from mills in Chile 178 Appendix IX-B: Venture prof i ts in industrial operations 179 Appendix IX-C: Foreign exchange earnings . . . 180 Appendix IX-D: Repayments periods for foreign exchange investment 1.81 Appendix IX-E: Amortization 182 Appendix IX-F: Taxes 182

Annex X: Prices in June 1957 related to a specific project 183

1. Cost of wood and other raw materials 183 2 . Building materials and fuel costs . . . " 184 3. Salaries and wages 185

- v -

INDEX OF TABLES Page

Table 1 -1 Production and Consumption of paper and Board by Regions, 1954 27 Table 1-2 Production and Consumption of Woodpulp by Regions, 1954 28 Table 1 - 3 Estimated Increase in Demand for Paper and Board, 1950-52 to 1960-62, by Region and

by Category 30 Table 1 - 4 Estimated Pulp Requirements in 1960-62 31 Table 1-5 Variation of E l a s t i c i t y Coeff ic ients for Paper Consumption with Gross National

Product per Capita 33 Table 1 - 6 Newsprint Production, Consumption and Export A v a i l a b i l i t y in North America 1948-55 . 35 Table 1 -7 Export and Import of Newsprint in North America, 1937-55 36 Table 1-8 United S t a t e s : Comparison of Demand Forecasts for Newsprint 37 Table 1 - 9 Canada: Comparison of Demand Forecasts for .Newsprint 37 Table 1 - 1 0 North America: Estimate of Newsprint Demand, 1955-65 38 Table I - 1 1 North America: Estimate of Newsprint Capacity and Production, 1955-58 38 Table 1 -12 North .America: Production, Consumption and Export Avai labi l i ty of All Papers and » .

Hoards Except Newsprint, 1948-55 39 Table 1 -13 North America: Export and Import of Papers and Hoards others than Newsprint, 1948-55 40 Table 1 -14 North America: Comparative Forecasts of Demand for a l l Papers and Boards, Except

Newsprint, 1955-65 '. . . 41 Table 1 -15 United S t a t e s : Production Capacity for Papers and Hoards, 1955-58 41 Table 1 - 1 6 Canada: balance of Trade in Paper and Board, except Newsprint, 1948-54 42 Table 1-17 North .America: Balance of Supply and Demand for Other Papers and Boards,

1955 and 1958 43 Table 1-18 North America: Production, Consumption and Export Avai labi l i ty of a l l Grades of

Woodpulp 1948-55 . 44 Table 1 - 1 9 North .America: Production, Consumption and Export A v a i l a b i l i t y of Dissolving Grade

Woodpulp, 1948-55 45 Table 1 - 2 0 Europe: Newsprint Production, Consumption and Export Avai labi l i ty 1948-55 46 Table 1 -21 Europe: Newsprint Demand Forecasts 1055-65 47 Table 1 -22 Europe: Production, Consumption and Export A v a i l a b i l i t y of a l l Papers and Boards

Except Newsprint, 1948-54 48 Table 1 -23 Europe: Forecast of Demand for a l l Papers and Boards, Except Newsprint, 1955-65 . . 48 Table 1 - 2 4 Europe: Export of Woodpulp in 1937 and 1948-54 49 Table 1-25 Europe: Change in Net Evjjort of Pulp and Paper, 1937 to 1954 '50 Table 1 -26 Latin America: Consumption, lVahiction and Import Itequirement of Newsprint 1948-55 . 51 Table 1-27 Latin America: Forecast of Newsprint Demand 1955 to 1965 . . . 52 Table 1 - 2 8 Latin America: Comparison of Newsprint Demand Forecas ts 52 Table 1 -29 Latin America: Consumption, Production and Import Requirement o f Papers and Boards,

Except Newsprint, 1948-54 ! 53 Table 1 - 3 0 Latin America: Estimate of Future Demand for Paner and Boards, Except Newsprint,

1955-65. . . . . . . . . 54 Table 1-31 Latin America: Comparison of Demand Forecasts f o r Papers and Boards Other than

Newsprint, 1955-65 . . .' 55 Table 1-32 Exports of All Grades of Pulp From North America and Europe to Latin America,

1937 and 1948-54 56 Table 1-33 Distribution of Pulp Exports from North America and Europe t o Défic i t fegions . 57 Table 1 - 3 4 Lat in America: Estimate of future Demand of Rilp for Regional Paper and Board

Production 57 Table 1-35 Chile: Paper and Board Production, Imports and Apparent Consumption, 1948-54 . . . . 58 Table 1 -36 Chile: Demand Forecast for Papers and Boards, 1956-65 59 Table 1-37 Future Supply and Demand Si tuat ion for Papers and Boards in Other Def ic i t Regions . 61

Table I I - l Area Under Planta t ions , by Provinces and Species in April 1953 . . 70 Table I I - 2 Area Under Pinus Radiata, by Provinces and Age Groups, 1953 70 Table I I - 3 Plantat ions of Pinus Radiata, Relationship Between S i t e Indices and Classes . . . . 71

- vi -

Page

Table I I - 4 Pirius Radiata: Area of Plantations by S i t e Class, in April 1953 : 71 Table I I - 5 Actual Cubic Volumes (1953) in Plantations of Pinus Radiata, by Use 72 Table I I - 6 Average Maximum Annual Growth in Plantat ions of Pinus Radiata 73 Table II -7 Pinus Radiata Plantat ions : Future Yields 73 Table I I - 8 Pinus Radiata Plantat ions : Ownership Distribution - • 74 Table I I - 9 Distribution of the Area Lhder Pinus Radiata, by Size of lb 1 dings 74 Table 11-10 Production, Export and Apparent Domestic Consumption of Pinus Radiata Sawntimber . . 75 Table 11-11 Average Cost of Establishing and Maintaining Pinus Radiata Plantations 77 Table 11-12 Stumpage Value of Pinus Radiata According t o Year and Si te . 79 Table 11-13 Minimum Stumpage Value and Age of Maximum Economic Yield for Pinus Radiata

Plantations on Different S i t e s . . . . . . . 79 Taole 11-14 Area Distribution and f i e l d s from Pinus Radiata Plantations According to S i te . . . 80 Table 11-15 Pulpwood Extract ion Costs in Pinus Radiata Plantations 81 Table 11-16 Travel Distance and Transport Capacity of Trucks per \ear • 82 Table 11-17 Transport Costs for Pulpwood 83 Table 11-18 Forest Administration and Supervision by Size of Operation 84 Table 11-19 Estimated Average Transport Distances for Different Supply Quantities of Rilpwood

in the Huepi 1 Area . 85 fable 11-20 Pulpwood Cost as a Function of fAilp Mill Size 86 Table 11-21 Future Annual Yields By Si te Classes . . . . . 87 Table 11-22 Future Annual Yields , . . . , 88

Table I I I - 1 Chile: Production, Export and Consumption of Sawnwood in General and of Conifers . . 92 Table I I I -2 Chile : Production, Export and \p¡>ii rent Consumption of Pinus Radiata Sawnwood . . . . 93 Table I I I - 3 Chile: Estimate of Danestic Consumption ami Export \ v a i l a b i l i t i e s of Pinus Radiata,

1960 and 1965 94 Table I I I - 4 Argentina: Consumption of Sawnwood from Conifers and Gross Investment . . . . . . . 95 Table I I I - 5 Argentina: Project ion of Apparent Consumption o f Sawnwood from Conifers . . . . ' . . 95 Table I I I - 6 Argentina: Project ion of Imports of Conifer and Pinus Radiata Sawnwood from Q i i l e . 96 Table I I I - 7 Chile: Project ion of Export \vai labi litie.s of Pinus Radiata . . . . . 96

Table IV-1 Pr ices of Chemicals and Fuels 100 Table IV-2 Raw Materials : Estimated Cost at Mil! . 101 Table IV-3 Water Requirements in Pulp and Paper M i l l s 102 Table IV-4 Minimum Stream Flow Requirements - 102

Table A Comparative Progress of the E l e c t r i f i c a t i o n Plan lYepared by the Corporación de Fomento and ENDESA, 1942-56 106

Table B Estimate of Probable, Rejected or Postponed Consumption ; 107

Table VI-1 Materials to be Transported at Sulphate Pulp Mills With a Daily Capacity of 250 tons . I l l

Table VI-2 Ministry ox Public Works and Cbnmunications: Road Plan 1954-58 112 Table VI-P-1 Distance of Trips and Transport Capacity of Trucks, Annually . . . . . . . 117 Table VI-B-2 Transport Costs for Finished Products, Including Loading and Unloading 118 Table VI-B-3 Transport Costs for Finished Products, Including Loading and Unloading 119 Table VI-P-4 Housing Costs . . . . . . . . . . • • • 119

Table VII-1 Investments: Pulp Mills . . . . . . ' . . 130 Table VII-2 Investment: Integrated Mills . . 1 3 1 Table VII-3 Investments: Newsprint Mills . . . . . i 132 Table VII-4 Building Volumes: Pulpmills . . 133 Table VII-5 Building Volumes: Integrated Mills . . 134 Ta^le VTI-6 Estimate of Building Volumes: Newsprint Mills ];-S5 Table VII-7 Costs of Community Services and Housing for Employees and Workers in l\ilp Mills . . 137 Table VII-8 Cost of Community Services and-Housing for Workers and Rrtployees in Integrated Mills 13(l Table VII-9 Estimate of Working Capital Requirements 140 Table VII-10 Forest Investment I l l Table VTI-11 Capital Requirements Pulpmills 142

- vu -

Page

Table VII-12 Capital Requirements: Integrated ¡¿ills 143 Table VII-13 Capital Requirements: Newsprint Mills 144

Table VIII-1 Reburning of Lime Sludge 145 Table VIII-2 Heat and Power Balance 146 Table VIII-3 Heat and Rawer Balance, Newsprint Mills 147 Table VIII-4 Heat Consumption and Pbsser Generated in Steam Turbine Operation 148 Table VIII-5 Labour Force in Pulp Mills 149 Table VIII-6 Labour Force: Integrated Mills 150 Table VIII-7 Labour Force: Newsprint Mills . . . 151 Table VIII-8 Labour Cost: Pulpnills 152 Table VIII-9 Labour Cost: Integrated Mills 153 Table VIII-10 Labour Cost: Newsprint Mills . . . . . 154 Table VIII-11 Administration and Supervision: Pulpmills 155 Table VIII-12 Adninistration and Supervision: Integrated Mills 156 Table VIII-13 Administration and Supervision: Nswsprint Mills 157 Table VIII-14 Annual Community Maintenance Costs in ftilp Mills 158 Table VIII-15 Annual Coimiunifcy Maintenance Costs in Integrated Pulp and Paper Mills 158 Table VIII-16 Capital Costs: Pulpnills 159 Table VIII-17 Capital Costs: Integrated Mills 160 Table VIII-18 Capital Costs: Newsprint Mills 161 Table VIII-19 Production Cost Estimate: Unbleached FWp 162 Table VIII-20 Production Cost: Estimate; Bleached iHilp 164 Table VIII-21 Production Cost Estimate; Unbleached Kraft Papers 166 Table VIII-22 ft-oduction Cost Estimate; Bleached Kraft Papers 167 Table VIII-23 Production Cost Estimate: Newsprint 168

Table IX-1 Annual Venture Profits Obtained From a Mill Investment of 25 Million Dollars . . . . 173 Table IX-2 Mill Investment Required to Obtain an Annual Venture Profit of 10 Per Cent on

Capital 174 Table IX-3 Venture Profit Per Cubic Metre of Wood at an Annual Supply Level of 400,000

Cubic Metres 175 Table DC-4 Capital Recovery Tine for a Foreign Exchange Part of Mill Investment of 17.5

Million Dollars . . . . . 176 Table IX-5 Foreign Exchange Earnings per Cubic Metre of Wood at an Annual Supply Level of

400,000 Cubic Metres 176 Table IX-6 Order of Econcsaic Attractiveness for Different Pulp and Paper Projects 177

Between INDEX OF FIGURES pages:

Map I Southern ftrt of Central Chile: Pinus Radiata Plantations . . 10 and 11

Map Fresh Water Supply Sources in the Pinus Radiata Zone 12 ' 13

Figure I - I Correlation Between Industrial Production and Paper Consumption in Figure 62 ' 63

Figure I - I I Annual Changes in Price of Newsprint and Kraft FVilp Imported to Chile . . 62 ' 63 Figure I - I I I Relationship Between Elast ic i ty Coefficient for Newsprint and Gross

National Product per Capita 62 ' 63 Figure I - IV Variation of Elas t i c i ty Coefficient for All Papers and Boards, Except

Newsprint, with Per Capita Income 62 ' 63 Figure I - V Relationship Between Newsprint Consumption and Gross National Product

Per Capita 62 ' 63 Figure I - VI Consumption of All Papers and Boards, Except Newsprint, as a Function of

62 ' 63 Figure I - VII Correlation Between Per Capita Gross Product and Paper and Beard Figure

Consumption per Head and Year in All Latin American Countries Except 62 ' 63

- viii -

Detweea pages :

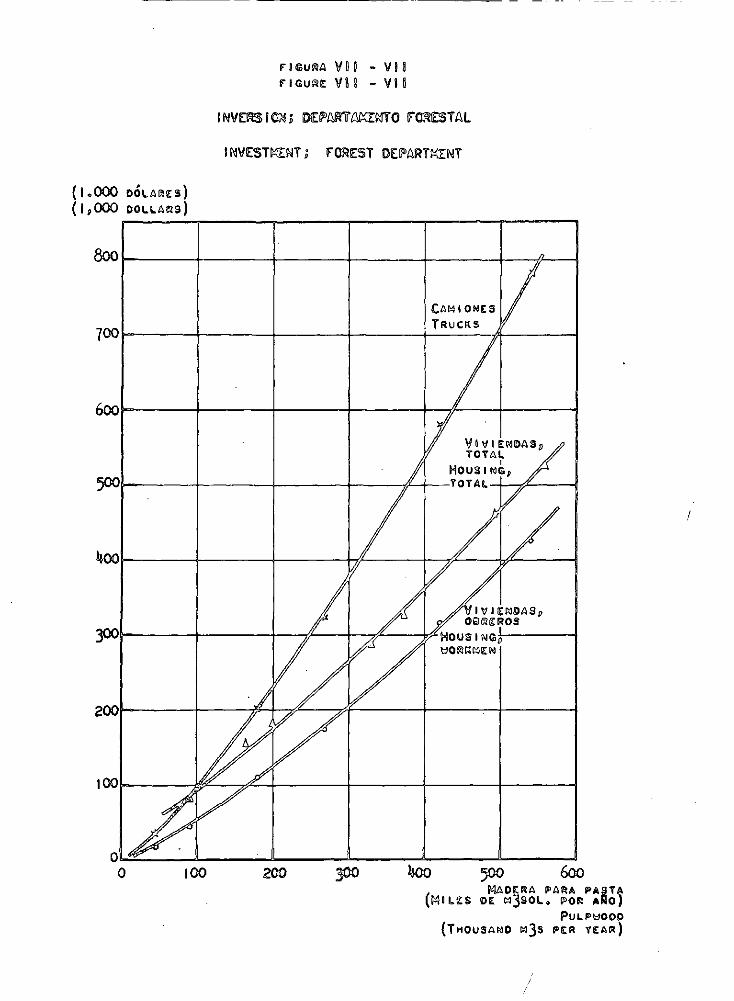

figure II - I Stumpage Value of Pinus Radiata 88 ' 89 Figure II - II Pu 1 pwood Transport Capacity and Travel Distance per Truck and Year . . . 38 ' 89 Figure II - III Transport Cost for Pülpwood 88 ' 89 Figure II - IV Atininistration Cost: Forest Department . . . 88 ' 89 Figure II - V Transport Distance and Pulpwood Cost as Function of Supply Quantities . . 88 89 Figure II - VI Future Yields of Pinus Radiala PUlpwood from Existing Plantations . . . . 88 ' 89

Figure VII - I Investment as Function of Mill Size IVib leached i\ilp 144 ' 145 Figure VII - II Investment as Function of Mill Size pleached F\slp 144 ' 145 Figure VII - III Investment as Function of Mill Size Unble.ached Papers 144 ' 145 Figure VÌI - IV Investment as Function of Mill Size Bleached Papers . 144 ' 145 Figure VII - V Investment as Function of Mill Size Newsprint 144 ' 145 Figure VII - VI I busi ne and Conmunity Investment and Operating Cost as Function of

Number of Workmen and Employees » 144 ' 145 Figure VII - VII Investment; Forest Department 144 ' 145 Figure VII - VIII Capital Requirements During Construction Period 144 ' 145 Figure VII - IX Project Investment as Function of Wood Supply 144 ' 145 Figure- VII - X Project Investment as Function of Wood Supply 144 ' 145

Figure VIII - I Production Cost as Function of Mill Size Unbleached Pulp 169 ' 170 Figure, VIII - II Production Cost as Function.of Mill Size Bleached Pulp 169 ' 170 Figure VIII - I II Production Cost as Function of Mill Size Unbleached Kraft Papers . . . . 169 ' 170 Figure VIII - IV Production Cost as Function* of Mill Size Bleached Kraft Papers . . . . . 169 ' 170 Figure VIII - V Production Cost as Function of Mill Sige Newsprint . . . . . . . . . . . 169 ' 170

Figure DC - I Venture Profit After Taxation in Industrial Operations 182 ' 183 Figure IX - * II Venture ft-ofit \fter Taxation in Combined Industrial ami Forest Qperatìms 182 ' 183 Figure IX - III Venture Profi t After Taxation T " . ' . 182 ' 183 Figure IX - IV Foreign Exchange Earnings . 182 ' 183 Figure IX - V Foreign Exchange Earnings 182 183 Figure IX - VI Inpayment Fferiods for Foreign Exchange Investment by Gross Annual FVofits 182 ' 183

/

- ¿a

PREFACE TO SECOND EDITION

The present t e x t o f the report "Chile - P o t e n t i a l Pulp and Paper E x p o r t e r " i s a p r a c t i c a l l y un-changed version of the f i r s t edition published i a Asigast 1956. Apart i t m the correc t ion of e r r o r s , only minor changes have been made in tbs t e x t .

In view of the suggestions and s r i t i c i s a r e c e i v e d a f t e r p u b l i c a t i o n o f the f i r s t e d i t i o n end the changes in condit ions which have occurred i a t h e past y e a r , i t was considered n e c e s s a r y t o make some additional c l a r i f i c a t i o n s and comments in order t o bring the report up t o d a t e . In sosfc c a s e s time has p.ot permitted changes to be made in the main t e a t and the various aspects a r e therefore é t a i t with below in the order in which they appear in the report i t s e l f .

The international pulp and paper mrkst (Chapter T)

In the past year demand has continued t o rise, a t approximately eh® r a t e iadicsfeed i a 61» report, •Jhe rapid expansion of production capaci ty» o a i n i y in North America b a t a l s o in Northern Europe, has gradually brought about a s i t u a t i o n with a s l i g h t excess of production over consuaiptiisi. f a r t h e r e d a c i -t y increases « . i l l be rea l ized at the end of the current year and i s 1958 and i t i s sgcpected t h a t produc-t ion wi l l continue t o o u t s t r i p denaxid for » a m time t o come. This s i t u a t i o n wi l l pxwbably be temporary, provided that no major r e c e s s i s the current eco&oeic de-relopaesifc takes p l a c e , and a r e a© i n d i c -ations that the long-tens trend with increasing sugpiy d i f f i c u l t i e s f o r the d e f i c i t £«gicn$, as outlined in the report , will change.

The r e p o r t ' s conclusion that the r a t s of i n c r e a s e its regi<«ai c a p a c i t y does not keep pace with the r i s ing demand is confirmed. In the case o f nesrspri&t the est imated addi t ional c a p a c i t y o f 180 ,000 t e a s in 1958 w i l l not be reached as t h e l a t e s t i n f o s m t i o n i n d i c a t e s a Bet gain of ©aiy 145 ,000 tons , d is -t r i b u t e d as follows:

Chile 55 ,008 tons Colombia 30,000 " Cuba 30,000 " Mexico 30 ,000 "

145,000 tons ' * ^

The Argentine project with a. capaci ty of 3 0 , 0 0 0 tons w i l l be delayed because o f tike lack of foreign exchange and one of the p r o j e c t s in Mexico { 3 0 , 0 0 0 tons) wi l l not go into production u n t i l 19S9- Ch the other hand, i t has been announced that a 30 ,000 ten mill in Cuba w i l l be ready for operation in 1958. As a resul t i t i s estimated t h a t the r e g i o n ' s import requirements s i l l remain unchanged i n 1953 but w i l l then increase by some 100 ,000 tons in I960 a m 485 ,000 tons in 1965; t h i s means that they w i l l reach a t o t a l of more than 900 ,000 tons in the l a s t year , unless fur ther expansion of the industry i s r e a l i s e d .

A lag in the development r a t e for the production o f o t h e r papers and boards s i m i l a r t o t h a t f o r newsprint i s l i k e l y t o o c c u r as a r e s u l t o f t h e f o r e i g n exchange s i t u a t i o n i n A r g e n t i n a . T h i s i s especial ly true for the period up fco I960 , in which year t h e r e g i o n s import requirements w i l l i n c r e a s e from the present f igure of about 200 ,000 t o an est imated 4 5 0 , 0 0 0 t o n s . There i a thus ample confirmation of the heed for determined e f f o r t s t o expand production f a c i l i t i e s , e s p e c i a l l y i a Argent ina , which accounts f o r about o n e - t h i r d o f t h e r e g i o n ' s consumption.

.As regards the s i t u a t i o n i n Chile t h e r e w i l l a l s o be a delay in t h e development prograsme. The newsprint mill at San Pedro did not s t a r t operations unt i l the second quarter of the current year and the pulp m i l l at Laj a ( p r o j e c t 2 ) is not expected t o be f inished u n t i l the middle o f 1958- The projec t o f Empresa Naeional de Celulosa S,A. (projec t 3) i s a l s o delayed and cannot be taken i n t o consideration as a supply source b e f o r e I960 , The plans a f C e l u l o s a s C h i l e S .A. ( p r o j e c t 4 } a r e , however, to -day more d e f i n i t e with a projec t f o r a pulp m i l l o f some 200-250 tons per day which may be completed i a 1960 /61 . As a r e s u l t , the export surplus of sane 100 ,000 tons of pulp envisaged f o r the y e a r 1958 w i l l not be r e a l i z e d u n t i l 1960 or 1961.

- 1 -

World market pr ices of pulp and paper have regained f a i r l y s table in the past year with a slight increase for newsprint, o ther papers and bleached pulp, whereas in the case of unbleached sulphite a s l ight downward trend has been noted in the second quarter of 1957 as a r e s u l t o f the current surplus s i tuat ion . There are no signs indicating that major changes wi l l take place in the near future and the slow r ise in the price level recorded since the second half of 1953, as a result of increasing production costs , will probably continue at about the same rate .

Pinus radiata - pulpwood supply and cost (Chapter II)

The comments which were received dealt e s s e n t i a l l y with three aspects - p o t e n t i a l y ie lds from the exis t ing plantat ions, wood transport costs and marketing p o s s i b i l i t i e s for lumber.

As t o the question of yie lds i t has been pointed out tha t , ( a ) the s i t e c lass system used by GQPK) in the i r inventory i s unfortunate since less than 2 per cent

of the plantation area f a l l s into c l a s s e s I and I I and 98 per cent in the three remaining c l a s s e s . A c lass system similar to that currently used in New Zealand with only three c lasses and a more even dis-t r ibut ion between the c l a s s e s would have been more adequate and f a c i l i t a t e d the comparison of yields in the two countries;

(b) some areas of very poor s o i l and growth near Canteras are included in the inventory. They are not typical and should not have been planted;

( c ) in calculat ing actual volumes, only the t r e e s with a diameter of more than 5 inches at breast height were included.

The c l a s s i f i c a t i o n system used and the fact that unsuitable areas are included in the inventory do not a f f e c t the yields from ex is t ing plantations but may give a misleading pic ture of the future poten-t i a l . On the other hand, the exclusion of small s ize t r e e s , r e s u l t s in a conservative estimate of the yields, which thus are somewhat higher than indicated in the report .

The calculations of economic yields from the plantations suggested that in the case of plantations belonging t o s i t e c l a s s e s IV and V a policy should be adopted with short r o t a t i o n periods and clear cutting at the age of maximum economic return. As a resul t , i t was recommended that those areas should be set aside for the production of pulp-wood only and that no thinning or pruning o f these stands should be undertaken. I t has been pointed out that such a policy may increase the damage from i n s e c t s , fungi and f i r e . Obviously, the recommendation should t h e r e f o r e be p r o v i s i o n a l , i . e . such sylvicultural measures should be undertaken as to reduce those r isks but not with a view to producing sawtimber since the stumpage value of the t r e e s which are allowed t o grow into sawtimber dimensions in these s i t e classes w i l l be much too high.

Regarding transport costs for pulpwood i t seems likely that the calculations in the report are some-what opt imist ic for two reasons; under present road conditions the assumed average driving speed of 30 kms per hour i s probably too high and the estimated cost of road building may be on the low side. I t has been suggested that an average trucking speed with load of 20 kms per hour would be a more r e a l i s t i c figure. Ch the other hand, the time allowance for loading and unloading is ample, provided modern equip-ment and methods are used.' The combined effect of these factors may result in transport costs which are somewhat higher than estimated but the increase would not be large enough to have any s i g n i f i c a n t in-fluence on the price o f wood delivered at the fac tory . In t h i s context i t should also be kept in mind that the stumpage values indicated in the report , are on the high side as they are calculated with a 10 per cent prof i t on plantation investments. This i s demonstrated by the fact that the current price for pulpwood i s 1,400 pesos per m at roadside which gives an estimated net stumpage value of about 600 pesos as compared with a calculated weighted average of 900 pesos in the report.

The most controvers ia l point in the report i s the estimate o f potent ial markets for Insignis pine lumber which is generally considered too pessimistic. Available data on local consumption and the export trends do not support a more optimist ic view at present. I t has been claimed, however, that the market and demand for this lumber could be considerably expanded by an improvement of the quality through better grading, s o r t i n g , et cetera. Further measures which may r a i s e the domestic consumption include the eventual adoption of a housing development programme in the country based on an increased ut i l iza t ion of wood.

None of these measures i s , however, l i k e l y to have any s i g n i f i c a n t influence on the market in the period before I960 as a q u a l i t y improvement of the lumber, such as would be required by the export

market, would also depend on sylvicultural measures which could only have a long-range e f f e c t . In 1965, the sawtimber avai labi l i ty will outstrip, by three times, the demand as estimated in the report - a margin which must be considered large enough to cover the possible increases in requirements. The conclusion is therefore that the c a l c u l a t e d potent ia l a v a i l a b i l i t y of pulpwood in the year 1965 -about 135 million cubic feet - i s not l ikely t o be affec ted by an increase in the demand for sawtimber. I t i s expected, however, that this question will be further analysed at the end of t h i s year by a special study of a F&) expert on the marketing of lumber.

Other rm» materials and problems (Chatter III)

No additional information has been received as regards supply of chemicals and fuels. Pr ices have increased during the year - f o r fuel o i l as a r e s u l t o f the Suez c r i s i s and for coal and domestically produced chemicals because of the general inflat ion in the country. (See also chapter V, Investment and production c o s t s ) .

The prospects for an improvement in the e l e c t r i c energy supply s i tuat ion are today b e t t e r than las t year as a result of the recent ly authorized increase o f the r a t e s . I t may thus be expected that the i n s t a l l a t i o n of new generating capacity wi l l be encouraged. Also, Guile has recently received a loan from the International Rank for the development of h y d r o - e l e c t r i c r e s o u r c e s . These changes im the situation over that of last year have been introduced in awnex V, which has been modified accordingly. The need for additional measures t o secure a s a t i s f a c t o r y development should, however, be stressed - i n part icular , an amendment of the law governing the rates and which would allow a larger re-investment of profi ts .

The fresh water supply and effluent disposal problems -both deciding factors in the locating of new mills- have not been fur ther invest igated and the need for r e l i a b l e information about those problems should again be s t ressed .

The trmsport problea (Guspter IV)

i t has not been poss ible to obtain addit ional infoffaQtiora abofflfc developments in the t ranspor t sec tor . As pointed out in the report , asi improvement in the exis t ing ccaditiosts i s necessary to secure a rapid expansion o f the industry. An analysis of the transport problems inside the plantation area and for the shipment of finished products i s therefore required in order to assess the industrial development prospects.

The transport s i tua t ion , together with the problems of water supply aad contend nation -apart from wood avai labi l i ty - are the main factors to be considered in selecting potential a i l l s i t e s . To help the Government in assessing these locat ions ! problems, both for immediate and future developments, FAQ has assigned to the country an expert in this f ie ld , who i s at present working in close collaboration with the Corporación de Fomento. His study will be finished at the end of this year and wi l l no doubt be of great value as a follow-up of the present report .

Investment cmd production costs (Chapter V)

In the year s ince the publication of the f i r s t edi t ion o f t h i s report the cost o f pulp and paper machinery has increased by some 10 t o 15 per cent , depending on the country o f or igin . During the same period construction c o s t s in l o c a l currency have increased by 25 t o 30 per cent ; nevertheless as the d o l l a r exchange r a t e has meanwhile increased by about 30 per cent the construct ion cost in terms of dollars has in fac t remained unchanged over the year. As the foreign exchange part accounts for same 70 per cent of the t o t a l investment i t may thus be estimated that the c a p i t a l requirements indicated in the study will have increased by scone 7 to 10 per cent as of today.

I t has been pointed out that some of the investment figures indicated for the separate mill sections are out of l ine and should be c o r r e c t e d . This r e f e r s p a r t i c u l a r l y t o the c o s t s for the e l e c t r o l y t i c plants and the steam and power s t a t i o n s , which a r e both estimated on the low side f o r the small mil l

- 3 -

units but are too high for the larger plants . I f c6r rec ted , these f igures would tend to increase the price d i f f e r e n c e s between m i l l s of d i f f e r e n t c a p a c i t i e s , but would not be la rge enough t o have any significant influence on the production costs as calculated in the report. Undoubtedly, the estimates of investments in o t h e r m i l l s e c t i o n s should a l s o in some cases be c o r r e c t e d , but i t i s nevertheless believed that the aggregate capi ta l requirements, with the proper price adjustments indicated above, are accurate, enough for the purpose of estimating production cos ts .

Raw material costs have increased over the year but the pr ice movements have not been consistent; thus, while the p r i c e s of coal and fuel o i l have been approximately doubled the cost of sa l tcake has remained v i r t u a l l y unchanged. I t may be estimated that the net e f f e c t of the pr ice adjustments i s a 30 per cent r i s e in t h e c o s t of raw m a t e r i a l s c a l c u l a t e d in l o c a l currency , i . e . the p r i c e level has remained approximately unchanged in terms of d o l l a r s . The same a l s o applies t o operating cos ts and overheads; labour wages and s a l a r i e s have increased by some 30 t o 32 per cent ( l o c a l currency) while repair materials and plant supplies may have increased by 10 t o 15 per cent (in d o l l a r s ) .

Up-to-date information on prices of various raw materials , wages, e t ce tera , has been obtained from one of the groups currently engaged in projecting a new pulp m i l l . I t has been considered of interest that this information from an independent source should be made available t o readers and i t is therefore, included as an additional annex to the report (see annex X).

Since capi ta l charges account for approximately 40 t o 50 per cent of the t o t a l production costs i t may be estimated that these will have increased by some 3 to 5 per cent as a resul t of the 7 t o 10 per cent r i s e in c a p i t a l requirements.

The combined e f f e c t of the price movements over the year on production costs has been estimated at approximately 5 per c e n t . In medium-sized mil l s t h i s increase corresponds t o about 4 dol la rs for un-bleached pulp, 5 dol lars for bleached pulp and newsprint and some 8 to 10 dollars for papers - a r ise in production costs which corresponds approximately to the i n c r e a s e s over the year in the international, prices of these products.

Economic evaluation of the projects and an over-all assessment (Chapter VI)

In the year that has passed since the publication of the f i r s t edition of this report no significant changes have taken place which warrant a re-assessment o f the development p o s s i b i l i t i e s for a pulp and paper industry based on the wood from the Insignis pine plantat ions nor of the economic prospects for this industry. On the other hand, only limited progress has been made towards the implementation of a development programme. The various recommendations made in the report with a view t o encouraging indus-t r i a l development should t h e r e f o r e once again be s t r e s s e d , in p a r t i c u l a r those which r e f e r to the a t t r a c t i o n of foreign c a p i t a l , without which a rapid expansion cannot be achieved.

AIM AND SCOPE OF THE STUDY

The aim of the following report i s to establish, in general terms, the technical and economic possi-b i l i t i e s for the development of a pulp and paper export industry in Chile. I t must be emphasized that the study i s of a general c h a r a c t e r , and cannot be used for the f inal appraisal of s p e c i f i c mil l pro-j e c t s , which must be evaluated according to their individual merits . Such evaluation i s a long and cost -ly process, requiring detai led invest igat ion of a l t e r n a t i v e mill s i t e s , e t c . . and i s thus outside the scope of the present report .

As regards development, prospects, i t must f i r s t be asked whether a market for pulp and paper pro-duced in Chile already e x i s t s or whether i t could be developed in the near future and what i t s s ize i s likely to be. To answer this question, a special analysis has been piade of developments in the different regions of the world during the post-war period (1943-55) . I t includes forecasts of future demand, based par t ly on previous estimates from different sources, which have, however, been revised in the l ight ox l a t e r developments, and p a r t l y on a new technique which s l i g h t l y deviates from standard methods. The market study i s included in annex I to the report and i s b r i e f l y summarised in chapter I o f the main t e x t .

I t was c l e a r even at a preliminary s tage that of the c o u n t r y ' s p o t e n t i a l f ibrous resources the plantations of Pinus radiata in the southern part of Central Qiiie offered by far the best prospects, not only for technological reasons -the prevalence of a s ingle species wifcli long f i b r e s - but a lso from an economic point of view. Furthermore, the amount of wood which these p l a n t a t i o n s wil l produce in the future i s large enough to support a greater industrial capacity than i s l ikely to be established in Chile within the next 10 years . Discussion has therefore been confined to pulp and paper production based on this raw material , and does not take into account the potential resources of the natural f o r e s t s in the south of the country.

The fibrous raw material s i t u a t i o n i s analysed in d e t a i l in annex I I , ehich i s divided i n t o three p a r t s , dealing r e s p e c t i v e l y with the f o r e s t inventory, the probable cost of pulpwood and prospect ive future y ie lds . This annex i s sunsnarized in chapter I I .

Since the a v a i l a b i l i t y of pulpwood depends on what percentage of the t o t a l y i e l d from the planta-tions will be diverted t o the production of sawn goods, annex I I I contains a short review of the market-ing p o s s i b i l i t i e s for lumber from Pinus radia ta .

Chapter I I I , which deals mainly with the a v a i l a b i l i t y and cos t of chemicals and fuels , includes a paragraph on the problem of fresh water supply, since, in many cases, t h i s i s l ikely to present d i f f i c u l -t i e s and limit the choice o f a l ternat ive mill s i t e s .

The greatest obstacle t o a l a r g e - s c a l e development of the pulp and paper industry i s the country 's t ransport s i t u a t i o n , t o which some general considerat ion has been given in chapter IV and annex VI. N'eedless to say, t h i s report cannot indicate ways or means of solving the problem, a task which must be undertaken in a broadest context; i t merely serves to indicate the magnitude of the problem and to add the warning that detailed investigations are necessary for each project and mill s i t e .

Chapter V summarises the ca lcula t ions o f investment and production c o s t s for s ixteen mill p r o j e c t s of d i f f e r e n t c a p a c i t y , and producing d i f f e r e n t q u a l i t i e s o f pulp and paper. Hie es t imates have been made for the following purposes:

( a ) to determine the minimum economic mill unit for each product; (b) to indicate the capital requirements for a new project ; and ( c ) to serve as a basis for the economic evaluation of individual projec ts , as well as for the over-

a l l assessment o f development prospects and t h e i r economic implications, contained %n chapter VI, which evaluates such p o s s i b i l i t i e s , both from the pr iva te investors ' and from the national viewpoint.

In order to preserve a logica l sequence in the main t e x t , i t has been kept in tent ional ly short , and side issues have as a rule been avoided. In few c a s e s only has reference been made t o d e t a i l s in the annexes, which should be considered as separate , and, in most ca se s , enlarged chapters, containing the supporting data.

• 5 -

CHAPTER I

'HIE INTERNATIONAL PULP AND PAPER MARKET

1. During the l a s t decades, the world market for pulp and paper has perhaps experienced more violent and frequent f l u c t u a t i o n s , both in the balance of supply and demand and in the pr ice l e v e l , than any other. [here are two main reasons for this i n s t a b i l i t y . F i r s t , the consumption of paper and board i s a sensitive indicator of a country's cultural , economic and industrial a c t i v i t i e s ; and, secondly, while in-ternational trade in these commodities is but marginal in relation to tota l production said consumption in Europe and North America, these marginal quantities account for a large share of consumption in the defi-c i t regions. As a result , snail variations in the domestic markets of Europe and North America have fax-reaching consequences on the international paper trade. 2. Two other factors further aggravate the short-term price fluctuations; when the world economy is ex-panding and marginal export a v a i l a b i l i t i e s are small, ocean freight t a r i f f s tend to increase; and, at the same time, importer countries, for fear of supply d i f f i c u l t i e s and further pr ice increases , often make soeculative stock purchases, which give additional momentum to the pr ice movement. 3. Far more dangerous and disquieting for such importer countries than the short-term price fluctuations on the world pulp and paper market i s the uncertainty o f supply over the long-term. This problem has in recent years commanded increasing attention from both national and international bodies, especial ly the United Nations and i t s specialized agencies, which have emphasized in several studies the threat inherent in the long-term supply question. 4. Ihe present study amply confirms the seriousness of this problem. In fact , the estimates of future demand, revised in the l ight of recent developments on the international market, indicate that consump-tion will probably r i s e f a s t e r than was predicted in e a r l i e r f o r e c a s t s . More energet ic e f f o r t s must therefore be made to develop regional resources in the d e f i c i t areas with a view to avoiding a depressed paper consumption, incommensurate with cultural and economic standards. The s i tuat ion in the different regions, as predicted in annex I , is br ief ly reviewed below.

i. North Anerica

5. During the period 1948-55, newsprint consumption increased by a l i t t l e less than 1 . 3 million tons -from below 5 million tons in 1948 to over 6 .2 million in 1955- which represented an annual increment of

s l i g h t l y under 3 per cent . In the seme period production expanded by almost 2 million tons and export a v a i l a b i l i t i e s from 50 thousand tons to 750 thousand tons per y e a r . In 1955-65 demand i s expected to grow more slowly than in 1948-54, at a ra te of 2 . 7 per cent as against the h i s t o r i c a l r a t e o f 3 . 3 per cent annually. Total consimption i s estimated at 6 . 8 , 7 . 1 and 8 . 1 mi 11 ion tons for the years 1958, 19®) and 1965, respectively. Dy 1958, current plans for the expansion of the industry will have raised annual production by more than 1 million tons, which means that the exportable surplus may amount t o some 1.2 million tons in the same year . 6 . Production and consumption o f paper and board other than newsprint has f luctuated considerably i a the post-war per iod, bearing out the contention t h a t paper consumption i s a s e n s i t i v e index o f a country's economic s i tuat ion. From 1948 t o 1955, the volume o f year ly demand rose by almost 5 . 5 million tons, or an annual increment of about 3 . 6 per cent, reaching 25.4 million tons. Production has ^proxim-ately balanced consumption, leaving a net export ava i labi l i ty of some 225 thousand tons as an average for the year 1948-54 . Hie demand f o r e c a s t indica tes that consumption wi l l increase by so&te 3 . 5 per cent annually, a t t a i n i n g 2 7 . 7 5 , 2 9 . 9 and 3 6 million tons in the y e a r s 19§8, 1 9 ® and 1965» r e s p s c t i v e l y . Existing plans for the development of the industry will not meet the expected expansion o f demand, and the present net export a v a i l a b i l i t y wil l probably disappear in 1958. 7. Before the war North America imported a net quantity of more than 1 million tona of woodpulp equal -ly i r o n Europe. In the period 1 9 4 8 - 5 0 t h i s dependence on imports was reduced t o an average o f 450 thousand tons, and by 1955 i t had been converted into an exportable surplus of some 750 thousand. Un-fortunately , no data on future expansion plans were avai lable , but i t seoms l ikely that North America

- 6 .

will maintain or even increase i t s present net exports during the next few years . On the other hand, the long-term trend will undoubtedly take the form of a decline in export a v a i l a b i l i t i e s , mainly as a resul t of inadequate wood supplies, but a l so because the North American industry wi l l probably be re luctant t o make substantial additions t o i t s production capaci ty for the sake o f exports t o d e f i c i t regions where from time to time d o l l a r shortages may cause changes in the import pol icy . 8. The si tuation in North America may be summarized as folIowas a) i t i s l ikely that the export avai la-b i l i t y of newsprint in the region w i l l expand considerably in the next few y e a r s and approximately balance the glowing d e f i c i t s in the other regions; b ) production o f other papers and boards w i l l cover the internal demand but net exports w i l l probably disappear; c ) the present export a v a i l a b i l i t y o f wood pulp i s likely to be maintained. The long-term trend, however, indicates that North America -as the only surplus region- will not be in a position to cover the increasing d e f i c i t s in the other regions.

Europe ^

9. As a result o f the changes in Europe's economy during and immediately a f t e r the war, production and consumption of newsprint declined sharply from the pre-war l e v e l -production 2 . 6 and consumption 2 . 4 million tons- and not unti l the year 1954 did the market regain i t s 1937 tonnages. Since the population has increased by some 10 per c®it as from t h i s year , i t follows that per capi ta consumption i s s t i l l de-pressed, and i s l i k e l y to r i s e at a f a s t e r r a t e than would normally be expected from the increase in per capita income. The demand forecast sho^a an annual increment in t o t a l consumption of 6 per cent for the period 1955-1965 as against a h i s t o r i c a l r a t e of 11 per cent in the years 1948-55. Consumption i s thus estimated t o r i se from 2 . 6 4 mill ion tons in 1955 t o 3 . 4 5 in 1958 3 . 8 5 in 1960 and 4 . 7 mil l ion tons in 1965. Present expansion plans, as quoted in different sources, indicate that by the year 1958 production will increase by some 550 thousand teas per annum as camp&psd t© an estimated consumption increase of 810 thousand tons. The 1955 export surplus of 170 thousand tons i s thus l ikely t o become a net import r e -quirement of seme 100 thousand tons, an est imate which for several reasons may be on the low side . 10. Production and consumption of papers and boards, other than newsprint, have more than doubled in the* 7-year period 1948-54. Production increased from 4 . 8 4 to 10 .64 and consumption from 4 . 3 5 t o 9 .80 million tons, while the export a v a i l a b i l i t y increased during the same period from about hal f a million tons to a l i t t l e more than 800 thousand. Demand i s estimated t o r i s e by 55 per cent between 1955 and 1965 which corresponds to an annual increment of 4 . 5 per cent as compared t o more- than 12 per cent in the y e a r s 1948-54; thus a considerable slow-down in the consumption i n c r e a s e r a t e i s foreseen. I t i s , neverthe-less , higher than previous forecas ts made by the United Nations and other bodies which -as demonstrated by developments in the 1950-55 period- underestimated the increase in consumption. As a r e s u l t , a more pessimistic view must be taken than previously expressed on Europe's p o s s i b i l i t i e s of s a t i s f y i n g her own demand and at the same time maintaining the present export level . No r e l i a b l e data are available on the i n d u s t r i a l expansion, but es t imates i n d i c a t e that the f o r e s t increment i n Scandinavia may support an addit ional pulping capac i ty of some 1 .5 mil l ion tons. Assuming t h a t an addi t ional quanti ty of h a l f a mil l ion tons could be produced in the r e s t o f Europe, the t o t a l i n c r e a s e of 2 m i l l i o n tons would be suff ic ient to produce about 600 thousand tons of newsprint and some. 2 mil l ion tons of other papers and boards. I f this capacity increase actual ly takes place within the next five years, by 1960 Europe's pre-sent export surplus of about 800 thousand tons of papers and boards (except newsprint) would s t i l l become" a net import requirement in excess of h a l f a million tons, an estimate which presupposes that the net ex-port of pulp i s maintained a t the 1954 level o f 200 thousand tons per year . 11. Annual exports of woodpulp from Europe decreased by more than 1 mill ion tons from 1937 to 1948, ¡aid in the post-war years the amount has remained r e l a t i v e l y s table a t some 700 t o 900 thousand tons, while imports from North America have increased by more than 300 thousand tons. Net exports have, as a r e s u l t , decreased from a pre-war l e v e l of more than 1 . 6 m i l l i o n tons t o only 200 thousand tons in 1955. An interest ing aspect of Europe's pulp and paper exports i s the change in proportion which has taken place between the two items; thus, while pulp accounted for almost 65 per cent o£ the net exports in 1937-1938, i t had decreased t o only 20 per c e n t in 1954. There i s every reason t o b e l i e v e t h a t the tendency towards integrat ion of pulp with paper production, which i s the background f o r t h i s change in expor ts , will continue, and the export surplus o f pulp wil l gradually disappear.

1/ All figures exclude Eastern Europe and the If.S.S.R.

- 7 -

12. To sum up the European supply and demand s i tuat ion; i t seems l ikely that , by 1960, the present net export surplus o£ 170 thousand tons of newsprint w i l l change t o a net import requirement of some 100 thousand tons, the surplus of other papers and boards, 800 thousand tons, will disappear and Europe will depend on imports from North America for half a mill ion tons of her supply i f pulp exports are to be maintained a t the present leve l . Developments a f t e r 1960 are d i f f i c u l t t o assess but there i s l i t t l e doubt that Europe may have serious d i f f i c u l t i e s in sa t is fying a demand for paper products commensurate with the economic and c u l t u r a l level in the region.

3. Latin Merica

13. Annual consunption of a l l papers and boards in the region i s today s l i g h t l y over 1 . 5 million tons, o f which newsprint accounts for a l i t t l e over 500 thousand. Some 450 thousand tons of newsprint and about 200 thousand tons of other papers and boards are imported, corresponding to 43 per cent o f the t o t a l consumption. In addition, import requirements o f pulp amount to approximately half a million tons per year -more than 50 per cent o f the t o t a l requirements of the local industry. Demand i s expected to r i s e sharply; newsprint consumption i s estimated at 775 thousand tons in 1960 and 1 .5 million tons in 1965, o ther papers and boards at 1 . 6 3 and 2 . 2 4 mil l ion tons , r e s p e c t i v e l y , i . e . a combined annual increment of 8 per cent as compared to about 3 per cent in the period. 1948-54. This increase in consump-t ion r a t e i s mainly accounted for by an expected r i s e in demand in Argentina where consumption has been highly depressed. 14= Additional capacity, plaruted and likely to be constructed before 1960, does not exceed 500 thousand tons per annum, which means that the present d e f i c i t in domestic supply o f some 650 thousand tons will increase to 850 thousand in 1960 and not l e s s than 1 .8 million tons in 1965, of which newsprint will account for 550 and 930 thousand tons respectively. Since i t i s unlikely that these additional quanti-t i e s will be available from North America and Europe, or that Lat in America can afford to spend foreign exchange on paper imports, mainly in d o l l a r s , amounting to some 330 mill ion d o l l a r s (1955 p r i c e s ) per year by 1965, the unavoidable conclusion i s drawn that unless the regional capacity i s expanded at a much f a s t e r r a t e than i s a t present envisaged, Lat in America will s u f f e r a high degree o f deferred consump-tion, detrimental to both economic and cul tural development. 15. Assuming that iiqports of pulp and paper could be maintained a t the present level and that local paper production i s expanded to s a t i s f y the balance in demand, the requirements of pulp, mechanical and chemical, could increase over the 1955 level by 560 thousand and 1 .5 million tons in the years I960 and 1965, respect ively -approximately h a l f of each quality. Aggregate expansion plans for the industry in 1954 comprised 190 and 580 thousand tons of mechanical and chemical pulp, including general objectives which had not yet been studied as to f e a s i b i l i t y . Should these plans be inplemented to t h e i r ful l ex-tent , Latin America would by 1960 have reduced the import dependency to some 200 thousand tons, a quanti-ty which -due to the expected r i s e in demand between 1960 and 1965- would again increase t o an aggregate of more than 1 million tons in the l a t t e r year . As i t i s unlikely that a l l the projec ts wil l be rea l -ized, the d e f i c i t s quoted here are probably on the low s i d e . In addition t o the supply d i f f i c u l t i e s which t h i s quantity i s l i k e l y to impose, Lat in Americ a ' s heavy dependency on the marginal markets of Europe and North America (before the war one t h i r d of the combined e x p o r t s t o d e f i c i t regions, two t h i r d s in the post-war years ) obviously places t h i s region in a precarious s i tuat ion during periods of scarce supply, and strong e f f o r t s should be made to reduce the r i s k by developing local production faci-l i t i e s *

4. Chile

16. Since the present report deals with the development prospects in Chile, s p e c i a l mention should be made of the consumption trends and expansion plans in t h i s country. In the post-war period consumption of newsprint as well as of other papers and boards has remained p r a c t i c a l l y unchanged, except for year to year var ia t ions . Che of the explanations of this fac t probably res ides in foreign exchange r e s t r i c t i o n s applied t o these items and', as a r e s u l t , the country has today a depressed consumption in re la t ion to per c a p i t a income. Consumption o f newsprint i s s l i g h t l y over 2 0 thousand tons, and o ther papers and boards 40 thousand, which correspond to a per c a p i t a consumption o f 3 . 7 and 6 . 2 kilogrammes per year. Future demand i s estimated t o r i s e to 39 and~50~thousand tons of newsprint in 1960 and 1965 respectively,

- 8 -

and to 61 and 77 thousand tons respectively of other papers and boards. Except for a quantity of some 10 thousand tons of imported newsprint the supply i s met by local production, which, however, depends on imports of chemical pulp. Expansion plans for the industry include three mi l l s , at present under cons-truction, a newsprint mill with a rated capacity of about 50 thousand tons, a k r a f t pulp mill with an annual capacity of some 70 thousand tons and a small sulphate pulp mill with an estimated annual produc-tion of some 7 thousand tons. In addition there is a project under serious consideration for a pulp mill with an annual capacity of some 70 to 90 thousand tons. Taking those p r o j e c t s into consideration, by 1960 Chile will have an export surplus of about 10 thousand tons of newsprint and some 95 thousand tons of chemical pulp, an estimate which presupposes that the e x i s t i n g production capacity for newsprint i s converted to the production of other papers. As will be seen la ter in the report , however, the potential prospects are far in excess of the development plans.

5. The other deficit regions

17. No special study of the s i tuat ion in the other d e f i c i t regions has been made for t h i s report , and the demand forecast below is takers from a report on the world situation prepared by the liiited Nations in 1953 %J• According to this report the t o t a l average consumption in the years 1950-52 was close to 1 .8 million tons of papers and boards of which about 480 thousand tons were newsprint; these figures exclude Japan and Mainland China. Hie t a c i t assumption was that these two countries will be able to meet t h e i r own rising needs. Of the t o t a l consumption some 1.2 million tons i . e . about two thi rds were imported. Demand was expected to increase in the period 1950-52 to 1960-62 by 68 per cent for newsprint and 59 per cent for other papers and boards, to 800 thousand tons and 2 . 1 million tons, respect ively . Development plans f e l l short of expected consumption increase by a l i t t l e over 100 thousand tons o f newsprint and some 225 thousand tons of other papers and boards. Subsequent development in the region suggests that the assessment made above has been too opt imis t i c ; in 1954 production of newsprint had r i s e n by only 30 thousand and of other papers and boards by 100 thousand tons. I t i s therefore likely that the competing claims from these regions on the export a v a i l a b i l i t i e s from North .America and Europe wil l be stronger than indicated above.

6. Conclusions

18. The following main conclusions regarding the future world market in pulp and paper are drawn from the regional assessments in the preceeding paragraphs and from annex I ; a. I t seems probable that the supply and demand of newsprint in the next three years w i l l be approxim-ately balanced. Beginning in 1958 or 59, a gradual tightening of the market wi l l take place unless the present rate of production increase in the d e f i c i t regions i s acce lera ted considerably. The s i tuat ion will be further aggravated in the 1960-65 period, and i f determined e f f o r t s are not made to secure regional supplies, consumption i s l i k e l y to be highly depressed in the, d e f i c i t a reas . b. The supply and demand si tuation for other papers and boards i s more disturbing since there are indic-ations that a world d e f i c i t s i tuation may develop already within the next few years , again provided that regional capacity i s not greatly increased. Tentatively i t i s estimated that there will be a world defi-c i t of close to 1 million tons per year in 1958-59. c . The pulp market is l ikely to experience more or less the same development as i s the case for papers and boards other than newsprint; i . e . a d e f i c i t s i t u a t i o n w i l l a r i s e during the next few years unless regional resources are created. d. Europe will in a r e l a t i v e l y short time change from a net exporter to d e f i c i t area, and North America alone remain as the net exporter to other regions. Consequently i t may be expected t h a t an increasing share of imports to the d e f i c i t regions will have to be liquidated in dollars, as a s i tuation where Europe has to purchase pulp and paper from North America in order to maintain her exports to d e f i c i t areas i s unlikely to continue permanently. e. Summing up for the purpose of this report: a prospective market for pulp and papar produced in Chile already e x i s t s and i s l ikely to expand rapidly in the coming decade.

2J Oorld Pulp and Paper Resources and Prospects. (World Survey) UN/FAO publication. Woa York 19S<3.'

- 9 -

CHAPTER 11

PINUS RADI ATA - PULPTOOD SUPPLY .AND COST

Jo Location

19. The main s tands o f Piraus r a d i a t a p l a n t a t i o n s are found in the seven provinces o f Maule, Linares, ¡Nuble, Bío-Bío, Concepción, Arauco and Malleco in the southern area o f central Chile (see map I ) . These provinces l i e in a c e n t r a l v a l l e y which runs north and south and i s flanked by the Andes on one side and the C o r d i l l e r a de l a Costa on the o t h e r . I t i s on t h e l a t t e r , which only in a few p l a c e s r i s e s above 1 ,000 metres and which was once covered by nat ive f o r e s t s , that most o f the plantat ions have been established. Other important stands are found on some a l l u v i a l t e r r a c e s in the c e n t r a l val ley .

2. Area end yield

20. The forest inventory prepared by Corporación de Fomento in 1953 shows that the area under plantation in that year {¡mounted t o shout 175 thousand h e c t a r e s , of which more than one third i s in the province of Concepcibn. Ctmsiderable plantation work has been carr ied out in the following years and i t i s estimated t h a t in 1956 the t o t a l area well exceeds 200 thousand h e c t a r e s . - 11 f igures and c a l c u l a t i o n s of future y ie lds given beloss and in the appendices r e f e r , however, t o t h e p l a n t a t i o n s e x i s t i n g in 1953 and are t h e r e f o r e oa t h e c o n s e r v a t i v e s i d e . F u r t h e r , in c a l c u l a t i n g t h e volumes of wood only t r e e s with a diameter a t b r e a s t h e i g h t of 6 inches with bark a r e included. 21. The volume of standing timber, calculated according t o these c r i t e r i a , was 9 . 8 million cubic metres without bark. (All f igures of volumes End yields are given in sol id cubic metres without bark). Of this t o t a l volume alrecst two t h i r d s a r e contained in p l a n t a t i o n s o f 10-15 years o f age, and more than one thi rd in the age group of 13-15 years . This i s important to bear in mind s i n c e , as wi l l be seen la ter , the age of minimum c o s t for the wood varies from 16 to 20 years and i s 16 years for most of the planta-t ions . Consequently, the main part of the plantations is rapidly approaching the age of maximum economic re turn , a f t e r which age the stumpags value of the wood will increase . 22. In the Forest Inventory the plantat ions have been grouped in f ive di f ferent c a t e g o r i e s ( s i t e c lass-e s ) , the c la&si f i ca t iom being based on the average height at 20 "years of the dominant and co-dominant t r e e s of the stand, i . e . on the growth rate which, in turn, depends on s o i l conditions, climate, e tc . J J . The growth ra te var ies considerably between the s i t e c l a s s e s ; from a maximum average annual increment of 9 cubic metres per hec tare for S i t e V to more than 60 cubic metres for S i te I . From the percentage dis-t r i b u t i o n of the s i t e c l a s s e s -about 80 per cent of s i t e s IV and V and l e s s than 5 per cent of s i t e s I and ' II - the average growth ( to the year of maximum yie ld) for a l l plantat ions has been determined at 18.2 cubic metres per h e c t a r e and year,, almost 8 times as high as in the coniferous f o r e s t s of Scandinavia, (annex I I , s e c t i o n A).

' . • • • • 3. Stumpage value

23. To e s t a b l i s h the probable cos t o f pulpwood, a "ca lcula t ion has been made of the stumpage values of Pinus r a d i a t a in ^he d i f f e r e n t s i t e c l a s s e s and a t var ious ages. The est imate i s based on the present p l a n t a t i o n and maintenance c o s t s and assumes t h a t t h e f o r e s t owner w i l l r e c e i v e 10 per cent compound i n t e r e s t on h i s c a p i t a l investment. Since the c a p i t a l grows at an increasing r a t e each year, whereas the increment in wood volume decl ines a f t e r a c e r t a i n age, i t follows t h a t the value of standing timber will resach a minimum point . (See f i g u r e I I - l ) . The age when t h i s point i s reached i s determined for each s i t e . c l a s s by the increment curve and the r a t e of i n t e r e s t . With 10 per cent i n t e r e s t , a s used in the present study, the age of minimum c o s t i s considerably lower than the age of maximum annual y i e l d ; for

I/ For a c o a p a r i s o n with the classi-Sieatioa u s e d f o r t i e P i n u s radiata plantations in New Zealand see 'Preface t o 2nd edition'.

- 10 -

CENTRO-SUR DE CHILE: PLANTACIONES DE PINUS RADIATA -SOUTHERN PART OF CENTRAL CHILE: PINUS RADIATA PLANTATIONS

(1953)

MAPA 1 MAP. I

instance in the case of s i t e c l a s s V, which accounts for more than 40 per cent of the t o t a l plantation are«, the minimum cost will be obtained at 16 years against a final cutting at 22 years to reach maximum yield,. The weighted average yield from a l l s i t e c l a s s e s , determined at the ages of minimum c o s t , i s 15 cubic metres per hectare and year, against 10 when calcula ted at the age of maximum yield , 24. The stunpage value estimated on the basis outlined in the preceding paragraph, var ies from 1 dollar per cubic metre"for the combined s i t e c lass 1 and I I to 3 dol lars for s i t e V, with a weighted average of 1 . 7 9 d o l l a r s ; t h i s value i s about o n e - f i f t h t o o n e - s i x t h of the stumpage p r i c e o f spruce and pine in Scandinavia in 1955. This low value of the standing timber, which i s due to the very high growth rate of Pinus radiata in Chile, cons t i tu tes the main reason why, (as will be seen l a t e r in the report ) , pulp and paper can be produced in the country at pr ices which are competitive on the international market.

4. Cost at mil stte

The aggregate c o s t of puljwood delivered t o a mill s i t e comprises, apart from the stumpage price , the c o s t of e x t r a c t i o n to road aide, t ranspor t t o the m i l l , and the overheads. Hie e x t r a c t i o n c o s t , which has been est imated on the b a s i s o f a c t u a l opera t ions , i s approximately 1 . 6 0 d o l l a r s per cubic metre. Transport cost and overheads natural ly vary with the s ize of operations and the location of the mil l in re la t ion to the plantations; for a hypothetical mill in the province of Nuble producing 250 tons of pulp per day they have been estimated at 1 . 6 0 d o l l a r s . Thus the t o t a l c o s t o f pulpwood del ivered mill s i t e wil l be approximately 5 dol lars per cubic metre, which i s approximately one thi rd of the cos t in Scandinavia.

Management and future yields

2 5 . An analysis of loca l consumption trends and export a v a i l a b i l i t i e s for sawnwoods from Pinus radia ta (annex I I I ) indicates that only a small f rac t ion of the t o t a l a v a i l a b i l i t y of sawtimber, as determined in the Forest Inventory, could be marketed. In most ca se s thinning and pruning operations which are undertaken in order t o produce more or b e t t e r sawtimber i s a waste of money, and i t i s t h e r e f o r e r e -commended t h a t , as a general pol icy , plantations belonging to s i t e c l a s s e s IV and V should be reserved mainly for the production of pulpwood and c l e a r c u t a t the ages of minimum stumpage value. As a con-sequence, i t i s a l s o recoasnended t h a t the planned t ra ining programme and c r e d i t f a c i l i t i e s for b e t t e r s y l v i c u l t u r a l management of the plantat ions should be revised i 26 . ^ I f the plantations are managed in the way described in the previous paragraph, the annual yield of pulpKocd will gradually increase from about J . 3 million cubic metres in 1956 t o more than 3 .7 million in 1965.L In addit ion, t h e r e i s today an accumulated quantity of some 3 . 4 mil l ion cubic metres a v a i l a b l e from planta t ions which have already passed the age of minimum c o s t . The average quantity produced by plantation^ e x i s t i n g in 1953 i s ca lculated at a minimum of 2 . 8 mill ion cubic metres per year during the period.1956-69 ( see f igure I I - V I ) - a quantity which i s s u f f i c i e n t for a production of some 600 thousand tons of pulp or 850 thousand of newsprint per year. There i s therefore 110 doubt that , judged by the raw m a t e r i a l supply, ;a•considerable expansion o f the industry over and above the present plans can take place, and should taJce place in the near future before the planta t ions pass the age of minimum stumpage value. In f a c t , an expansion o f the pulp and paper industry seems to be the only solution by which the value of the plantat ions -estimated at some 60 million d o l l a r s a t the present cos t of planting- could be saved.

CHAPTER I I I

OTHER RAW MATERIAS AND PRTLEMS

1= Chemicals and fuels (annex IV)

27. In the production of pulp and paper and for ancil lary processes (steam and power generation, produc-tion of caustic soda and chlorine, e t c e t e r a ) , various chemicals and fuels are required, the a v a i l a b i l i -ty of which as to quality and volume should be ensured within reasonable price l imits . The base chem-i c a l s for the pulping operation are :

in the sulphate process; sa l t cake (sodium sulphate) or cormion sa l t and sulphur and lime-stone, and

in the sulphite process; sulphur (or pyrites) and limestone. These chemicals are available in Chile in s u f f i c i e n t quanti t ies and with the requisi tes mentioned

above. They are, however, not available in the pine plantation area and the regular supply does there-fore involve a t ransport problem which must be c a r e f u l l y studied for each p a r t i c u l a r mill s i t e . (See chapter IV). 28. Chile has indigenous resources of coal and the production capacity is in excess of current demand. The mines are trainly located in the coastal zone, the two most important being Lota and Coronel about 30 kilometres from the town of Conception, and thus in the vic ini ty of the plantation centre . The quality is infer ior , but acceptable for industrial use. Oily minor quantities of oi l are produced in the country and requirements are mainly imported. 29. A mill producing unbleached sulphate pulp is pract ical ly self-supporting in energy which is produced in s u f f i c i e n t quantity in the chemical recovery system by burning the organic mater ia l in the waste l iquor. In the case of bleached pulp, various grades of paper and newsprint, however, energy must be supplied from outside, e i t h e r as fuel , or e l e c t r i c energy or both. I f fuel only is supplied, i . e . the mill produces i t s own e l e c t r i c energy, the required quantities are considerable for some of the products. Thus, about 650 kilogrammes of coal are required per ton of product in a mill producing bleached kraft papers and supplying i t s own needs of caust ic soda and chlorine, i . e . an annual quantity of some 45,000 tons for a 200 tons per day mill u n i t . Here again, a v a i l a b i l i t y and pr ice do not pose any problems, whereas the transport s i t u a t i o n at present may cause d i f f i c u l t i e s for a large sca le development of the industry.

2. Electric energy. (annex V)

30. The s i tuat ion as regards e l e c t r i c energy supply in the country today i s far from s a t i s f a c t o r y and demand is greatly in excess of exis t ing supply possibi l i t ies ; the estimated def ic i t in 1955 was more than 200 thousand kilowatts. The reason for the lag in capacity increase is two-fold; the law regulating the t a r i f f s at a level of insuff ic ient return on investments, and the s c a r c i t y of c a p i t a l . Indications are that the s i t u a t i o n w i l l be considerably eased in the next few years as the t a r i f f laws have recently been amended by Congress and c a p i t a l could now possibly be obtained from the funds established through the Agricul tural Surplus Agreement with the United S t a t e s or by loans from the International Rank for Reconstruction and Development. Apart from the development planned by ENTESA (Empresa Nacional de Elec-t r i c i d a d S .A , ) which c a l l s f o r an increase in generating capac i ty of 579 thousand kilowatts by 1964, further expansion i s l i k e l y t o take place in the pr ivate sector, mainly through the a c t i v i t i e s of the Compañía Chilena de E l e c t r i c i d a d (subsidiary of the American and Foreign Power Company), who recently announced their decision to build a thermo-electr ic plant with a capaci ty of 120 thousand kilowatts , to be finished in 1959. 31 . Since a pulp and paper m i l l , and p a r t i c u l a r l y a newsprint m i l l , i s a large consumer of e l e c t r i c energy - f o r instance, a newsprint mil l with a daily capacity of 300 tons needs an e l e c t r i c a l input of

- 1 2 -

RJEfclTES DE AGUA DULCE EN LA 2CMA QIL PI MUS

rRESH WATER SUPPLY SQUBCES IN THE PI RIß R/S9tÄTA 2TOE

LA S U P E R F I C I E FORESTAL EN 1953» HECTARES , se INOICA CO« C I F R A S ¡ENTRE

P A R É N T E S I S ; (IÖ.500) A FÁBRICAS EM CONSTRUCCION EN 1 : " TO« POR OÍa, PAPEL OC OIARtO

A G - 2 0 0 TO« POR o f A , PASTA SULFATO

+ E S T I M A C I Ó N A BASE DE UNA SOLA OBSERVACIÓN

MAXIMUM FLOW, M^/SEC , IND ICATED BY UNDERL INED F I G U R E ; 2 0

MINIMUM FLOW, M^/SEC , IND ICATED BY P L A I N F I 6 U R E J 7

F O R E S T AREA IN 1953, HECTARES , I N D I C A T E D BY F IGURE IN B R A C K E T S ; (18.500) A M I L L E UNDER CONSTRUCTION 1 9 5 6 : A F - 1 6 0 TOW PER DAY NEWSPRINT

A G - 2 0 0 TOM PER DAY SULFATE P U L P

+ E S T I M A T E D FROM "ONE S INGLE OBSERVAT ION

t

ì

some 23 thousand kilowatts- the investment in a thermo-electric plant is considerable but, on the other hand, the scale of operation is large enough to ensure a reasonable c o s t .

In view of the uncertainty of future supplies from outside, i t therefore seems prudent that new mill projects should as far as possible take into consideration the development o f t h e i r own e l e c t r i c i t y supply sources. In a l l the hypothetical projects calculated in t h i s study provisions have thus been made for self-sufficiency in e l e c t r i c energy.