PROJECT REPORT On A STUDY OF LOANS AND ADVANCES ...

97

PROJECT REPORT On A STUDY OF LOANS AND ADVANCES OFFERED IN BAJAJ FINANCE LIMITED BY GANGIREDDIGARI JYOTHIREDDY 1NH18MBA23 Submitted to DEPARTMENT OF MANAGEMENT STUDIES NEW HORIZON COLLEGE OF ENGINEERING, OUTER RING ROAD, MARATHALLI, BENGALURU In partial fulfilment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under the guidance of A.SHESHU Sr. Asst. Professor 2018 - 2020

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of PROJECT REPORT On A STUDY OF LOANS AND ADVANCES ...

PROJECT REPORT

On

A STUDY OF LOANS AND ADVANCES OFFERED IN

BAJAJ FINANCE LIMITED

BY

GANGIREDDIGARI JYOTHIREDDY

1NH18MBA23

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BENGALURU

In partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

A.SHESHU

Sr. Asst. Professor

2018 - 2020

CERTIFICATE

This is to certify that GANGIREDDIGARI JYOTHIREDDY bearing

USN 1NH18MBA23, is a bonafide student of Master of Business

Administration course of the Institute 2018-20 , autonomous program,

affiliated to Visvesvaraya Technological University, Belgaum. Project

report on “A STUDY OF LOANS AND ADVANCES OFFERED IN

BAJAJ FINANCE LIMITED” is prepared by him/her under the

guidance of A.SHESHU in partial fulfilment of requirements for the

award of the degree of Master of Business Administration of Visvesvaraya

Technological University, Belgaum Karnataka. Signature of Internal Guide Signature of HOD Principal

Name of the Examiners with affiliation Signature with date 1. External Examiner 2. Internal Examiner

DECLARATION

I, GANGIREDDIGARI JYOTHIREDDY hereby declare that the project report on “A

STUDY OF LOANS AND ADVANCES OFFERED IN BAJAJ FINANCE LIMITED”

with reference to “BAJAJ FINANCE LIMITED” prepared by me under the guidance of

A.SHESHU, faculty of M.B.A Department, New Horizon College of Engineering.

I also declare that this project report is towards the partial fulfilment of the university

regulations for the award of the degree of Master of Business Administration by

Visvesvaraya Technological University, Belgaum.

I have undergone an industry project for a period of Eight weeks. I further declare that this

report is based on the original study undertaken by me and has not been submitted for the

award of a degree/diploma from any other University / Institution.

Signature of Student

Place:

Date:

ACKNOWLEDGEMENT

The successful completion of the project would not have been possible without

the guidance and support of many people. I express my sincere gratitude to

LAKSHMI NARAYANA TC, MANAGER- CREDIT OPERATIONS, BAJAJ

FINANCE LIMITED, Bangalore), for allowing to do my project at BAJAJ

FINANCE LIMITED.

I thank the staff of BAJAJ FINANCE LIMITED Bangalore for their support

and guidance and helping me in completion of the report.

I am thankful to my internal guide A.SHESHU, for his constant support and

inspiration throughout the project and invaluable suggestions, guidance and also

for providing valuable information.

Finally, I express my gratitude towards my parents and family for their

continuous support during the study.

GANGIREDDIGARI JYOTHIREDDY

1NH18MBA23

TABLE OF CONTENTS

SL. NUMBER CONTENTS PAGE NUMBERS

1 Executive Summary 1

2 Theoretical Background Of The Study 2-28

3 Industry Profile &Company Profile 29-56

4 Application Of Theoretical Framework 57-62

5 Analysis And Interpretation Of Financial

Statements And Reports 63-80

6 Learning Experience- Findings,

Suggestions And Conclusion 81-85

7 Bibliography 86

1 | P a g e

EXECUTIVE SUMMARY

I have taken Finance as a specialization with the title of “A STUDY OF LOANS AND

ADVANCES OFFERED IN BAJAJ FINANCE LIMITED “The objective behind this project was to

primarily focus on loans advances offered in Bajaj Finance for the consumers. This required a firsthand

experience in understanding end to end process flow for loans processing to payment disbursement.

Also I discuss about the Bajaj EMI loans, the Bajaj Finserv Lending Company which is one of the

lending company they also make available EMI Loan option for the loan. I have collected the

Secondary data from Books, Company Annual Report & internet Articles etc. Bajaj Finance Ltd is one

of the leading loans issuing company in the India.

I also focused on the surrogates required for loan approval, which documents are necessary for

approval of loan. SWOT analysis of Company. I have also tried to explain the loan procedure Through

this project, I learn how to given a loan on consumer durable product and how to solve customer

difficulties about the documentation. I was dealing with proper customer, provided them loans by

completing their files and getting the approval online form Bajaj Finance Limited website. This

process helped me to better understand the Loan procedure of Loans and Advances at Bajaj Finserv

Lending.

The major part of my project includes the loans issue process, Eligibility criteria, Interest rates, and

processing charges. Financial statements and Loans lending statement analysis in different sectors.

Different analytical tools used to analyze and the calculation of EMI etc.

2 | P a g e

CHAPTER - I

THEORETICAL BACKGROUNG OF THE STUDY

INTRODUCTION:-

Money is an essential element for any business, because it fulfills the short term and long term

requirement of funds. It is not possible for the owner to bring all the money himself, so he/she take

recourse to loans and advances. Loans refer to a debt provided by a financial institution for a particular

period while Advances are the funds provided by the banks to the business to fulfill working capital

requirement which are to be payable within one year. The loan amount is required to be repaid along

with the interest, either in lump sum or in suitable installments. It can be a term loan (payable after 3

years) or demand loan (payable within 3 years). In the same way, advances also requirement

repayment along with the interest within one year. These two terms are always uttered in the same

breath, but there are a number of differences between loans and advances.

Meaning of Loans and Advances:-

The term ‘loan’ refers to the amount borrowed by one person from another. The amount is in

the nature of loan and refers to the sum paid to the borrower. Thus From the view point of borrower, it

is ‘borrowing’ and from the view point of bank, it is ‘lending’. Loan may be regarded as ‘credit’

granted where the money is disbursed and its recovery is made on a later date. It is a debt for the

borrower. While granting loans, credit is given for a definite purpose and for a predetermined period.

Interest is charged on the loan at agreed rate and intervals of payment. ‘Advance’ on the other hand, is

a ‘credit facility’ granted by the bank. Banks grant advances largely for short-term purposes, such as

purchase of goods traded in and meeting other short-term trading liabilities. There is a sense of debt in

loan, whereas an advance is a facility being availed of by the borrower. However, like loans, advances

are also to be repaid. Thus a credit facility- repayable in installments over a period is termed as loan

while a credit facility repayable within one year may be known as advances.

3 | P a g e

Meaning of Loan:-

The amount lent by the lender to the borrower for a specific purpose like the construction of the

building, capital requirements and purchase of machinery and so on, for a particular period of time is

known as Loan. In general, loans are granted by the banks and financial institutions. It is an obligation

which needs to be repaid back after the expiry of the stipulated period.

The loan carries an interest rate on the debt advanced. Before advancing loans, the lending

institution checks the credit report of the customer, to know about his credibility, financial position and

capacity to pay.

Definition:-

According to Thembi Palane “a loan is a financial transaction in which one party (the lender)

agrees to give another party (the borrower) a certain amount of money with the total expectation of

repayment agreed upon by both parties. Usually there’s a predetermined time for repaying a loan with

conditions attached to it”

According to oxford dictionary “Money that someone borrow from a bank or other financial

organization for a period of time during which they pay interest”

Loan is classified in the following categories:-

On the basis of Security:

o Secured Loan: The loan which is backed by securities is Secured Loan.

o Unsecured Loan: The loan on which no asset is pledged as security is Unsecured Loan.

4 | P a g e

On the basis of Repayment:

o Demand Loan: The loan which is repaid on demand of the lender is Demand Loan.

o Time Loan: Loan, which is repaid in full at a future specified date, is Time Loan.

o Installment Loan: Loans which are to be repaid in evenly distributed monthly installments is

Installment Loan.

On the basis of Purpose:

o Home Loan

o Car Loan

o Education Loan

o Commercial Loan

o Industrial Loan

Definition of Advances:-

Advances are the source of finance, which is provided by the banks to the companies to meet the

short-term financial requirement. It is a credit facility which should be repaid within one year as per

the terms, conditions and norms issued by Reserve Bank of India for lending and also by the schemes

of the concerned bank.

Definition:-

According to the oxford dictionary Advance means “an amount of money paid before it is due

or for work only partly completed”

5 | P a g e

They are granted against securities which are as under:

Primary Security: Hypothecation of Debtors, Stock Pro-notes, etc.

Collateral Security: Mortgage of land and buildings, machinery, etc.

Guarantees: Guarantees given by partners, directors or promoters, etc.

The following are the forms of Advances:-

Short term loans: Advance in which the entire amount is provided to the borrower at one

time.

Overdraft: A facility provided by the bank in which the customer can overdraw money from

his account up to a specified limit.

Cash Credit: A facility granted by the bank in which the customer can advance money up to

a certain limit against the asset pledged.

Bills Purchased: An advance facility provided by the bank against the security of bills.

The Advantages and Disadvantages of Loan:-

Loan is a form of debt, often with interest. There are several reasons why people apply for loans.

Usually they borrow money to purchase a house, buy a car, or start a business. Often, applying for a

loan is necessary because most do not have available financial resources they need to make a purchase.

Other forms of loans, like the student loans have helped a lot of students get through school. Those

who use student loan debt consolidation clearly have multiple student loans. They do this to manage

their obligations better.

Since loan is borrowed, the lender expects to receive payment with the interest specified. In

addition, borrowers should make the payments at the specified due date for a certain period. This is

where most people have problems. Most problems start when people cannot make the monthly

payments required due to different circumstance. Some finds it difficult to pay their loan because of

6 | P a g e

the many other debts they have. Some encounter additional problems such as medical emergencies and

job loss.

Since getting a loan is a commitment, you have to be very careful with your decisions. Choose

the right lender. There is more to picking a lender than just looking for one with the least interest. Keep

in mind that those with low interest require longer period. Remember, when choosing a lender, check

its stability, its flexibility, repayment schemes, and interest rates.

Before you decide to get a loan, it is only right that you review its advantages and disadvantages.

Advantages:-

Below are the advantages of getting a loan. These are also the reasons why many apply for it:

There is a loan for just about anything. If you are in need of money to purchase a house, you can

apply for a housing loan. If you need a car, you can apply for a car loan. With all the loans

available, you will be able to purchase everything you need.

It helps a person afford an expensive purchase. All of us wish to acquire a property. However, we

do not have the amount of money to make the purchase. Loans allow us to do this. They lend us

the money so that we can finally afford our desired property.

Payment is staggered, which makes it affordable. This enables the person to pay off the loan

gradually. If a person has chosen a good deal, he should be able to finish paying off the loan in the

time specified.

One gets the funding he needs. If a person wants to start a business, he can do so by applying for a

business loan. He does not have to wait for his savings to build up before he can start his own

business. They can also use the amount they loan for investment purposes.

Getting a loan is very helpful to start building your dream. However, you have to be very careful

with your decisions. This is because of the problems you will possibly encounter if you

mismanage your loans and other debts. If you have multiple loans, make sure to manage it well.

Use a debt consolidation loan calculator and check if it is better to consolidate all your loans.

7 | P a g e

Make sure that you manage your loans from the start. Keep in mind that loans have disadvantages

too.

Disadvantages:-

Here are some of the disadvantages of having loans:

is a long-term debt. This means that you have to deal with it for a specified period, which means

that you have to commit yourself to making monthly payments specified in your agreement for the

period indicated to repay the loans.

If you miss payments, you will face serious consequences. You can face foreclosure or

repossession of the property. In addition, you could also face penalties and legal issues. It will also

reflect in your credit rating, which can lead to a low credit scores.

You may not be able to make early loan repayment. Few lenders give option for early repayment.

Although there are some who will allow you to do this, they will charge you with early repayment

fees.

Loans are very helpful. However, you have to manage them well because you can get into a lot of

trouble if you fail to make the expected payments.

Advantages and disadvantages of Cash Advances:-

At some time or another you will have to use some sort of cash advance system, especially if you don’t

have any credit cards or know someone you can borrow money from. While it may be alright to use

cash advances every so often, becoming dependant on them to help you pay bills every month is not.

Cash advances can be extremely expensive because you are charged a fee in addition to the money you

are borrowing. Overtime, these monthly fees could be used to make a down payment on a house or car.

This is why it is important to learn the proper ways to use this type of loan service and to educate you

about the advantages and disadvantages of cash advances.

Advantages of Cash Advances:-

Pay bills on time and avoid disruption of services. Some people consider having running water,

and/or electricity more of a priority than being charged a service fee for obtaining a cash advance.

8 | P a g e

Avoid late fees or penalties. Oftentimes, cash advance fees are less expensive than the late fees or

penalties put into effect by the credit card companies or other lenders.

Most businesses that offer cash advance services do not require an in depth credit check; therefore

people with bad credit are more likely to get approved for cash advances.

You are charged a onetime fee for borrowing the money. And you have a specific amount of time

to pay back the cash advance, otherwise additional fees will apply.

Disadvantages of Cash Advances:-

You are charged a fee based on the amount of money you borrow or based on the percentage of

money you borrow.

Overtime, cash advance fees can add up to quite a bit of money. If you take out a cash advance

every single month for a year and the fee is $15 each month; that is $180 that you are throwing

away. So you may want to see if there is any way you can save a little bit at a time to pay your

bills every month.

If you don’t have the money in your account to pay back the cash advance, you will be charged an

additional fee by the lender.

If you don’t have sufficient funds in your checking account, you will have to pay the fee

associated with insufficient funds put into effect by your financial institution when your check

bounces.

As you can see there are many advantages and disadvantages of cash advances. To find out if a

cash advance is the right solution for your current financial situation, you should first weigh the

pros and cons before you sign on the dotted line. While cash advances may be one of the easiest

ways to obtain cash when you have bad credit or no credit history, they should be used sparingly

and with caution. Make sure to read all the rules and stipulations associated with the cash advance

loan before making an agreement to pay it back. By following these cash advance tips, you will

know when you should use this type of loan and when you should consider other available

options.

9 | P a g e

Note:- Cash advances are not entirely bad and not entirely good. However, they do make it possible

for some people to make ends meet when times are tough. Learn some of the advantages and

disadvantages of using cash advances and when you should consider using them to help pay bills.

Utility of Loans and Advances:-

Loans and advances granted by banks and other financial institutions are highly beneficial to

individuals, firms, companies and industrial concerns. The growth and diversification of business

activities are effected to a large extent through bank financing. Loans and advances granted by banks

help in meeting short-term and long term financial needs of business enterprises. We can discuss the

role played by banks in the business world by way of loans and advances as follows:-

Loans and advances can be arranged from banks in keeping with the flexibility in business

operations. Traders may borrow money for day to day financial needs availing of the facility of

cash credit, bank overdraft and discounting of bills. The amount raised as loan may be repaid

within a short period to suit the convenience of the borrower. Thus business may be run efficiently

with borrowed funds from banks for financing its working capital requirements.

Loans and advances are utilized for making payment of current liabilities, wage and salaries of

employees, and also the tax liability of business.

Loans and advances from banks are found to be ‘economical’ for traders and businessmen,

because banks charge a reasonable rate of interest on such loans/advances. For loans from money

lenders, the rate of interest charged is very high. The interest charged by commercial banks is

regulated by the Reserve Bank of India.

Banks generally do not interfere with the use, management and control of the borrowed money.

But it takes care to ensure that the money lent is used only for business purposes.

Bank loans and advances are found to be convenient as far as its repayment is concerned. This

facilitates planning for future and timely repayment of loans. Otherwise business activities would

have come to a halt.

Loans and advances by banks generally carry element of secrecy with it. Banks are duty-bound to

maintain secrecy of their transactions with the customers. This enhances people’s faith in the

banking system.

10 | P a g e

Objectives of Loans and Advances:-

General Objective:

The general objective of the study is to figure out the Loan and Advances of Bajaj Finance limited.

Specific objectives are:

1. To have idea regarding various types of Loan and Advances of Bajaj Finance Limited.

2. To identify the loan sanction procedure in different sectors in last some years.

3. To identify the credit approval, their securities and monitoring process of Bajaj Finance Limited

4. To know the loan and advances activities of Bajaj Finance Limited.

5. To identify the recovery rates of the loans in different sectors in last some years and have a

comparison among them.

6. To identify the problems regarding loan and advances and give some recommendations for

improving the effectiveness and efficiency of Loan and Advances services.

Types of loans:-

11 | P a g e

Highlights

Loans can be classified basis collateral requirements and usage

Secured loans vary based on the asset used as collateral

Personal loans are the most popular form of unsecured loans

Avail instant financing with pre-approved loan offers

A loan is essentially money borrowed with a promise of return within a specific time period/tenor. The

lender decides a fixed rate of interest that you must pay on the money you borrow, along with the

principal amount borrowed. Let us take a look at the different types of loans that are available in India.

There are various types of loans available in India, and they are classified based on two factors:

- Whether they require collateral

- The purpose they are used for

Based on whether they require collateral, loans are classified into secured loans and unsecured loans.

Let’s take a look at each type.

I. Secured loans:-

These are loans that do require collateral, i.e., you have to provide an asset to the lender as

security for the money you are borrowing. That way, if you are unable to repay the loan, the lender still

has some means to get back their money. The rate of interest of secured loans tends to be lower as

compared to those for loans without collateral.

Types of secured loans:-

1. Home loan

Home loans are a secured mode of finance, that give you the funds to buy or build the home of your

choice. The following are the type of home loans available in India:

Land purchase loan: Purchase land for your new home

Home construction loan: Build a new home

Home loan balance transfer: Transfer the balance of your existing home loan at a lower interest rate

12 | P a g e

Top up loan: Can be used to renovate an existing home or have the latest interiors for your new home

Note that while buying a new property/home, the lender requires you make a down payment of at least

10-20% of the property’s value. The rest is financed. The loan amount disbursed depends on your

income, its stability and current liabilities among others.

2. Loan against property (LAP)

Loan against property is one of the most common forms of a secured loan where you can pledge any

residential, commercial or industrial property for availing the funds required. The loan amount

disbursed is equivalent to a certain percentage of the property’s value and varies across lenders.

While some lenders may offer an amount equivalent to 50-60% of the property’s value, others may

offer an amount close to 80%. A loan against property helps you unlock the dormant value of your

asset and can be used to satiate personal life goals such as higher education of children or marriage.

Businesses use a loan against property for business expansion, R&D and product development among

others.

3. Loans against insurance policies

Yes, you can also avail loans against your insurance policy. However, note that all insurance policies

don’t qualify for this. Only policies, such as endowment and money-back policies, which have a

maturity value can be used to avail loans.

Thus, you can’t avail a loan against a term insurance plan as it doesn’t have any maturity benefits.

Also, loans can’t be availed against unit-linked plans as the returns aren’t fixed and depends on the

performance of the market. It’s essential to note that you can opt for a loan against endowment and

money back policies only after they’ve acquired a surrender value. These policies acquire a surrender

value only after paying regular premiums continuously for 3 years.

4. Gold loans

For the longest time, gold has been one of the most favored asset classes. The organized Indian gold

loan industry is expected to touch Rs.3,101 billion by 2019-20, according to a KPMG report, thanks to

flexible interest rates offered by financial institutions.

13 | P a g e

A gold loan requires you to pledge gold jeweler or coins as collateral. The loan amount sanctioned is a

certain percentage of the gold’s value pledged. Gold loans are generally used for short-term needs and

have a short repayment tenor compared to home loans and loan against property.

5. Loans against mutual funds and shares

An ideal vehicle for long-term wealth creation, mutual funds can also be pledged as collateral for a

loan. You can pledge equity or hybrid funds to the financial institution for availing a loan. For doing

so, you need to write to your financier and execute a loan agreement.

Your financier then will write to the mutual fund registrar and a lien on the certain number of units to

be pledged is marked. Typically, you can get 60-70% of the value of units pledged as a loan.

Similarly, with shares, financial institutions create a lien against shares against which the loan is taken

and the loan value is equivalent to a percentage of the value of the shares.

6. Loans against fixed deposits

The humble fixed deposit not only offers assured returns but can also come handy when you need a

loan. The amount of loan can vary between 70-90% of the FD’s value and varies across lenders.

However, it’s essential to note that the loan tenor can’t be more than the FD’s tenor.

II. Unsecured loans

These are loans that do not require collateral. The lender lends you the money based on past

associations, and your credit score and history. Thus, you have to have a good credit history to avail

these loans. Unsecured loans usually come at a higher rate of interest due to the lack of collateral.

Types of unsecured loan:-

14 | P a g e

1. Personal loan

Offering an instant flush of liquidity, a personal loan is one of the most popular types of unsecured

loans. However, since a personal loan is an unsecured mode of finance, the interest rates are higher

compared to secured loans. A good credit score along with high and stable income ensures you can

avail this loan at a competitive rate of interest. Personal loans can be used for the following purposes-

- Manage all expenses of a family wedding

- Pay for a vacation or an international trip

- Finance your home renovation project

- Fund the cost of your child’s higher education

- Consolidate all your debts into a single loan

- Meet unexpected/ unplanned/ urgent expenses

2. Short-term business loans

Another type of unsecured loans, a short-term business loan can be used to meet their expansion and

daily expenses by various entities and organizations.

- Working capital loans

- Machinery loans and equipment finance

- Small business loans for MSMEs

- Loans for women entrepreneurs

- Loans for traders

- Loans for manufacturers

- Loans for service enterprises

Flexi Loans

A facility whereby you can avail funds from your approved limit and as when required and pay interest

only on the amount used. You can withdraw on your loan limit, any number of times and prepay when

you have extra cash, at no extra cost. Such a unique facility gives you the freedom to be in full control

of your finances unlike rigid term loans and offers you savings on your EMIs by up to 45%. Here, you

also have the option to pay only interest as EMIs, with the principal payable at the end of the tenor.

15 | P a g e

Based on what they are used for, loans are classified mainly into:

1. Education loans

Aspiration for higher education from reputed institutions have bolstered the demand for education

loans in the country. This loan covers the basic fees of the course along with allied expenses such as

the accommodation, exam fee, etc. In this loan, the student is the main borrower while parents, siblings

and spouse are co-applicants.

An education loan can be taken for a full-time, part-time or vocational course along with graduation

and post-graduation course in the fields of management, engineering and medicine, among others. The

loan must repaid by the student once the course is complete.

A unique feature of an education loan is the moratorium period, wherein the student has the option of

not paying the EMIs until after 12 months of completing the course or 6 months after he/she starts

working, whichever is earlier.

2. Vehicle loans

A vehicle loan is extended in the form of a two or four-wheeler loan which helps you to buy your

dream vehicle. Vehicle loans are offered either on purchase of a new vehicle or a used one. Your credit

score, ratio of debt to income, loan tenor, etc., play a crucial role in determining the loan amount.

With Bajaj Finserv you can get pre-approved offers on all the above-mentioned loans and there are no

queues, forms or details needed. Here, your loan offer is already approved, so you can avail instant

financing. All you need to do is simply provide some basic details and get your pre-approved offer.

16 | P a g e

Documents required for the loan approval:-

Personal Loan:-

One of the options to get money from reputed banks for all needs is through personal loan. And, to

apply successfully for a personal loan an applicant needs to provide certain set of documents.

These documents helps lender (be it a Bank or a NBFC) to know and understand the financial stability

of the borrower and analyze the credit risk. Apart from that it helps a lender know and verify all the

details about the applicant such as age, income, address, employer and employment. It is on the basis

of this a lender decides whether to lend or not to the applicant.

As personal loans are unsecured loans, the lender does not takes anything as collateral for the lending

amount, hence there is always a potential risk of borrower defaulting or absconding on the loan. Hence

to be double triple sure a lender asks for a certain set of documents so that it can learn and analyse the

applicant and then decide.

The documents required for personal loan help a lender to know and understand the following about

the applicant:

1. Identity

2. Age

3. Income

4. Address

5. Existing Loans

17 | P a g e

6. Repayment History (if any)

Once a lender has these details, they can know and understand the applicant better. And, using the

information provided, they can come up with the best loan offer for the applicant.

As such, providing the required documents while applying for a personal loan, helps the applicant to

get the best offer.

Above is the checklist of all the required documents for a personal loan.

Home loan:-

Here is a checklist of the documents required to apply for a home loan.

1. Passport Size Photographs

2. Identity Proof: Passport / Driving License / Voter ID / PAN Card / Aadhaar Card.

3. Address Proof: Driving License / Registered Rent Agreement / Electricity Bill (up to 3 months

old) / Passport.

4. Employment Appointment Letter: Required if the current employment is less than 1-year old.

5. Financial Documents:

Last3monthssalaryslip

6monthbankstatement

2 year Form 16

18 | P a g e

6. Property Documents: Sale deed, Khata, transfer of ownership.

7. Advance Processing Cheque: A cancelled cheque for validation of bank account.

8. Financial Documents:

For Salaried Individual: 3 month salary slip, Form 16 and bank statement

For Self-Employed Individual: IT returns for last 2 years along with computation of income tax

for past 2 years certified by a Chartered accountant

For Self-Employed Non- Professionals: IT returns for last 3 years along with computation of

income tax for past 2 years certified by a Chartered accountant

9. Complete Home Loan Application form duly filled

Vehicle Loan:-

Here is the checklist of the documents required to apply for a car loan:

Proof of age

Identification proof

Application form

Passport size photograph

Proof of residence

Income proof

19 | P a g e

Bank statement

Signature verification proof

Pro-forma Invoice or Rate List

Reasonable interest rates, affordable EMIs, simplistic paperwork, and quick disbursement are a few

reasons why car loans have become such a comfortable option for today’s common man. Now the

dream of owning a car is no longer far-fetched- a few documents are all you need.

Predominantly, the lender banks look for proof that you are a good credit risk and are in a position to

repay the car loan. This information, along with your credit report and score, will directly impact the

interest rates that you are charged.

Since your credit rating will be assessed while applying, it is worth cleaning up any existing debts

before you lodge your initial application. This is sure to improve your chances of approval. If you have

a bad credit history, the lender bank will also want to see your credit card statements, mortgage details

and verification of other loans that you hold.

Educational Loan:-

Documents required for an Educational Loan:

For students seeking a loan for studies within the country, they can provide the following documents.

Duly-filled application form.

20 | P a g e

2 passport size photographs.

Graduation, Secondary School Certificate, or High School Certificate or mark sheets

KYC documents that include ID, address, and age proof.

Signature Proof

Income Proof of parents or guardian

If collateral is required, documentation for Immovable property, FDs, etc.

For students interested in a loan to study abroad, they will need to provide the documents below.

Duly-filled application form.

2 passport size photographs.

KYC Documents that include ID, residence and age proof.

A copy of statement of marks or certificates of last examination passed.

Proof of admission to the university and the course

Schedule of course expenses

If you have received a scholarship, a copy of the scholarship letter is needed.

Copy of Foreign Exchange permit if you have it.

Bank account statement for last six months of the borrower, parents or guardian.

Last 2 years’ Income Tax assessment of the borrower, parents or guardian.

For loans with collateral, the details of security offered must be furnished. You might also be

required to provide an advocate’s search and report about its marketability, mortgage ability, etc.

Proof of the source of margin is required.

Educational loans are a sector which is promoted as it gives students the opportunity to study further. It

enhances the growth and development of the citizens and the country. Educational loans are an

investment into the future, so it is important to do your research and take your time. Government and

banks also offer subsidies and lower interest rates to promote education for all.

21 | P a g e

Gold loan:-

Two passport size photograph

ID Proof such as Driving License / PAN Card / Form 60/61 / Passport Copy / Voter ID Card /

Aadhaar Card / Ration Card. Any one document needs to be submitted

Address Proof such as Driving License / Voter ID Card / Ration Card / Aadhaar Card / Passport

Copy / registered lease agreement with not older than 3 months utility bills in the name of landlord

(any one)

Proof of land holding in case of agriculture loan of more than Rs. 1 lakh

Terms and conditions of loan agreement:-

22 | P a g e

What is a Loan Agreement?

Few people sail through life without borrowing. With few exceptions, almost everyone takes a

loan to buy a car, finance a home purchase, pay for a college education or cover a medical

emergency. Loans are nearly ubiquitous and so are the agreements that guarantee their repayment.

Loan agreements are binding contracts between two or more parties to formalize a loan process.

There are many types of loan agreements, ranging from simple promissory notes between friends

and family members to more detailed contracts like mortgages, auto loans, credit card and short-

or long-term payday advance loans.

Simple loan agreements can be little more than short letters spelling out how long a borrower has

to pay back money and what interest might be added to the principal. Others, like mortgages, are

elaborate documents that are filed as public records and allow lenders to repossess the borrower’s

property if the loan isn’t repaid as agreed.

Each type of loan agreement and its conditions for repayment are governed by both state and

federal guidelines designed to prevent illegal or excessive interest rate on repayment.

Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate

terms and the duration over which it must be repaid. Default terms should be clearly detailed to

avoid confusion or potential legal court action. In case of default, terms of collection of the

outstanding debt should clearly specify the costs involved in collecting the debt. This also applies

to parties using promissory notes as well.

Purpose of a Loan Agreement:-

The main purpose of a loan contract is to define what the parties involved are agreeing to, what

responsibilities each party has and for how long the agreement will last. A loan agreement should be in

compliance with state and federal regulations, which will protect both lender and borrower should

either side fail to honor the agreement. Terms of the loan contract and which state or federal laws

govern the performance obligations required by both parties, will differ depending upon the loan type.

Most loan contracts define clearly how the proceeds will be used. There is no distinction made in law

as to the type of loan made for a new home, a car, how to pay off new or old debt, or how binding the

terms are. The signed loan contract is proof that the borrower and the lender have a commitment that

funds will be used for a specified purpose, how the loan will be paid back and at what amortization

23 | P a g e

rate. If the money is not used for the specified purpose, it should be paid back to the lender

immediately.

Other Reasons for Using Loan Agreements:-

Borrowing money is a huge financial commitment, which is why a formal process is in place to

produce positive results on both sides.

Most of the terms and conditions are standard fare – amount of money borrowed, interest charged,

repayment plan, collateral, late fees, penalties for default – but there are other reasons that loan

agreements are useful.

A loan agreement is proof that the money involved was a loan, not a gift. That could become an

issue with the IRS.

Loan agreements are especially useful when borrowing or loaning to a family member or friend.

They prevent arguments over terms and conditions.

A loan agreement protects both sides if the matter goes to a court. It allows the court to determine

whether the conditions and terms are being met.

If the loan includes interest, one side may want to include an amortization table, which spells out

how the loan will be paid off over time and how much interest is involved in each payment.

Loan agreements can spell out the exact monthly payment due on a loan.

It is safe to say that anytime you borrow or lend money, a legal loan agreement should be part of

the process.

On Demand vs. Fixed Repayment Loans:-

Loans use two sorts of repayment: on demand and fixed payment.

Demand notes are usually used for short-term borrowing and are often used when people borrow

from friends or family members. Sometimes banks will offer demand loans to customers with whom

they have an established relationship. These loans typically don’t require collateral and are for small

amounts.

Their key feature is how they are repaid. Unlike longer term loans, repayment can be required

whenever the lender desires, as long as sufficient notification is given. The notification requirement is

usually spelled out in the loan agreement. Demand loans with friends and family member might be a

24 | P a g e

written agreement, but it might not be legally enforceable. Banks demand loans are legally

enforceable. A check overdraft facility is one example of a bank demand loan – if you don’t have the

money in your account to cover a check, the bank will loan you the money and pay the check, but you

are expected to repay the bank quickly, usually with a penalty fee.

Fixed term loans are commonly used for large purchases and lenders often demand that the item

purchased, perhaps a house or a car, serve as collateral if the borrower defaults. Repayment is on a

fixed schedule, with terms established at the time the loan is signed. The loan has with a maturity date

when it must be fully repaid. In some cases, the loan can be paid off early without penalty. In others,

early repayment comes with a penalty.

Legal Terms to Consider:-

All loan agreements must specify general terms that define the legal obligations of each party. For

instance, the terms regarding repayment schedule, default or contract breach, interest rate, loan

security, as well as collateral offered must be clearly outlined.

There are some standard legal terms involved in loan agreements that all sides should be aware of,

regardless of whether the contract is between family and friends or between lending institutions and

customers.

Here are four key terms you should know before signing a loan agreement:

Choice of Law: This term refers to the difference between laws in two or more jurisdictions. For

example, the laws governing a specific part of a loan agreement in one state may differ from the same

law in another state. It is important to identify which state (or jurisdiction’s) laws will apply. This term

is also known as a “Conflict of Law.”

Involved Parties: This refers to personal information about the borrower and lender that should be

clearly stated in the loan agreement. That information should include the names, addresses, social

security numbers and phone numbers for both sides.

Severability Clause: This term states that terms of a contract are independent of each other. Thus, if

one condition of the contract is deemed unenforceable by a court, that doesn’t mean all conditions are

unenforceable.

25 | P a g e

Entire Agreement Clause: This term defines what the final agreement will be and supersedes any

agreements previously made in negotiations, whether written or oral. In other words, this is the final

say and anything that was said (or written) before, no longer applies.

Interest Rate Determination:-

Many borrowers in their first experience securing a loan for a new home, automobile or credit

card are unfamiliar with loan interest rates and how they are determined. The interest rate depends on

the type of loan, the borrower’s credit score and if the loan is secured or unsecured.

In some cases, a lender will request that the loan interest be tied to material assets like a car

title or property deed. State and federal consumer protection laws set legal limits regarding the amount

of interest a lender can legally set without it being considered an illegal and excessive usury amount.

If the loan includes interest payments, as most do, the terms will be spelled out in the loan’s terms and

conditions. Interest is either fixed fee or floating fee.

A fixed fee, or fixed rate, loan establishes an interest rates that remains unchanged during the

repayment of the loans. If you borrow money with a 4% annual rate, you will pay the lender 4% a year

on the balance due until the loan is paid off. The amount of interest you pay will decrease over time as

the balance is paid down and the principal payment will increase. If you borrow $200,000 to buy a

house, the monthly payment will remain constant, but the portion of the payment that goes to interest

and principal will change each month as the loan is balance is reduced.

Floating fee interest rates, also called variable rate loans, carry interest rates that change over

time. The amount of interest based on a benchmark rate, usually a widely followed index like the

LIBOR those changes regularly. Floating fee rates are adjusted periodically and generally are only

used in complex loans like adjustable-rate home mortgages.

Contract Length & Amortization:-

The length of a loan contract is determined by a lender’s reliance upon an amortization schedule.

Once the lender and the borrower have determined the amount of money needed, the lender will use

the amortization table to calculate what the monthly payment will be by dividing the number of

payments to be made and adding the interest onto the monthly payment.

26 | P a g e

Unless there are certain loan conditions that penalize the borrower for early loan payment, it is in

the best interest of the borrower to pay back the loan as quickly as possible. The faster the loan debt is

retired the less money it costs the borrower.

Pre-Payment Fees and Penalties

While the goal to pay back a loan quickly is a financially sound practice, there are certain loans

that penalize the borrower with pre-paid fees and penalties for doing so. Prepayment penalties are

typically found in automobile loans or in mortgage subprime loans. They also can occur when

borrowers choose to refinance a home or auto loan.

Pre-payment penalties are applied to protect the lender, who expects a certain return on his loan

over a certain amount of time. For example, if the borrower repays a 5-year loan in three years, the

lender would be out the interest he expected the last two years of the loan.

Prepayment penalties usually are 2% of the amount due on the loan or six months of interest

payments. It can have a dramatic effect on the cost of refinancing a loan. Many sub-prime loans

include prepayment penalties, which opponents say target the poor, who usually are the ones with

subprime loans.

On the other side are homes financed through government-backed FHA loans. Federal law

specifically forbids prepayment penalties on FHA loans. The exception is if the borrower has a

mortgage that contains a due-on-sale clause and the clause has been allowed as part of the mortgage.

Breach or Default

If a loan contract is paid off late, the loan is considered in default. The borrower can be liable for

a myriad of potential legal damages to compensate the lender for any losses suffered.

The breached or defaulted lender can pursue litigation and have a court hold the borrower liable for

legal costs, liquidated damages and even have assets and property attached or sold for repayment of the

debt. In addition, a breach or default of court judgment can be placed on the borrower’s credit record.

Mandatory Arbitration:-

Mandatory arbitration is an increasingly popular provision in loan agreements that requires parties

to resolve disputes through an arbitrator, rather than the court system.

27 | P a g e

More than 50% of lending institutions include mandatory arbitration as part of their loan contracts

because it is supposed to be faster and cheaper than going to court. Arbitration puts the final decision

in the hands of one person, who likely is more experienced and sophisticated about the law than six

jurors in a courtroom.

In most cases, mandatory arbitration clearly favors the lenders, who have legal counsel that

specialize in this area of law on their side. The borrower often has no lawyer or inadequate

representation because lawyers are not guaranteed payment in arbitration cases.

The borrower is at an even bigger disadvantage if the arbitration is binding, meaning there can be

no appeal. The rules in the Fair Credit Reporting Act and the Truth in Lending Act have no bearing in

arbitration cases, which also favors the lender.

Members of the military are especially vulnerable to loan agreements that include mandatory

arbitration. A solider serving out of the country may not be able to attend or have competent

representation at an arbitrary hearing and because of that, lose possession of a car or other asset. The

arbitrator’s decision can’t be appealed, so there is no recourse if the decision goes against the soldier.

Before you sign a loan agreement, read it closely and if it includes a mandatory arbitration clause,

decide whether you are comfortable with that as a means of settling disputes.

Usury and Predatory Protections

Several federal and state consumer protection laws protect consumers against predatory and usury

loan tactics used by lenders. The Truth In Lending Act, Real Estate Settlement Act and the Home

Owners Protection Act federally protect borrowers against predatory lenders.

Many states enacted companion consumer predatory and usury protection acts to protect borrowers.

Both parties benefit because lenders make reasonable interest repayment rates and borrowers receive a

much-needed loan.

Several federal and state consumer protection laws protect consumers against predatory and usury

loan tactics used by lenders.

Promissory Notes:-

Promissory notes resemble loan agreements but lack complexity. Often, they are little more

than commitment-to-pay letters like IOUs or simple payment on demand notes. Usually the borrower

28 | P a g e

writes a letter specifying how much money he or she is borrowing and the terms under which it will be

repaid. They are almost always used for small loans between people who know one another well.

Promissory notes are signed and dated and can be legally binding. Promissory notes can be secured or

unsecured. Secured loans offer the lender collateral is the loan isn’t repaid, while unsecured loans

don’t use collateral. They can contain terms about installment payments and interest, though they

might not.

Unlike loan agreements, which can contain complex payment terms, promissory notes are more

like paper trails that document that one person has lent money and that the borrower agrees to repay

the money within a certain amount of time, either in a lump sum or in installments. It’s used primarily

to avoid financial misunderstandings and shouldn’t be confused with a loan agreement, which contains

an assortment of legally enforceable terms and remedies.

29 | P a g e

CHAPTER-II

INDUSTRY PROFILE & COMPANY PROFILE

NBFC IN INDIA

NBFC - INDUSTRY OVERVIEW:-

A Non-Banking Financial Company (NBFC) is a company registered under the

Companies Act, 1956 engaged in the business of loans and advances, acquisition of

shares/stocks/bonds/debentures/securities issued by Government or local authority or other marketable

securities of a like nature, leasing, hire-purchase, insurance business, chit business but does not include

any institution whose principal business is that of agriculture activity, industrial activity, purchase or

sale of any goods (other than securities) or providing any services and sale/purchase/construction of

immovable property. The NBFC sector is an important part of the Indian financial sector. They have

shown dynamism in delivering innovation and in assisting financial inclusion.

NBFCs typically have several advantages over banks due to their focus on niche segment,

expertise in the specific asset classes, and deeper penetration in the rural and unbanked markets.

However, on the flip side, they depend to a large extent on bank borrowings, leading to high cost of

borrowings and face competition from banks which have lower cost of funds.

The growing asset size of the NBFC sector has increased the need for risk management in the

sector due to growing interconnectedness of NBFCs with other financial sector intermediaries. The

Reserve Bank of India (RBI) has been in the recent past trying to strengthen the risk management

framework in the sector, simplify the regulations and plug regulatory gaps so as to prevent regulatory

arbitrage between banks and NBFCs.

The Reserve Bank of India released the ‘Revised Regulatory Framework for NBFCs’ on

November 10, 2014 which broadly focuses on strengthening the structural profile of NBFC sector,

wherein focus is more on safeguarding of the depositors money and regulating NBFCs which have

increased their asset-size over time and gained systemic importance.

30 | P a g e

Due to subdued economic growth, last two years, have been challenging period for the

NBFCs with moderation in rate of asset growth, rising delinquencies resulting in higher provisioning

thereby impacting profitability. However, comfortable capitalization levels and conservative liquidity

management, continues to provide comfort to the credit profile of NBFCs in spite of impact on

profitability.

The Associated Chambers of Commerce and Industry of India (ASSOCHAM):-

Non-banking finance companies (NBFCs) form an integral part of the Indian financial system.

They play an important role in nation building and financial inclusion by complementing the banking

sector in reaching out credit to the unbanked segments of society, especially to the micro, small and

medium enterprises (MSMEs), which form the cradle of entrepreneurship and innovation. NBFCs’

ground-level understanding of their customers’ profile and their credit needs gives them an edge, as

does their ability to innovate and customize products as per their clients’ needs. This makes them the

perfect conduit for delivering credit to MSMEs.

However, NBFCs operate under certain regulatory constraints, which put them at a disadvantage

vis-à-vis banks. While there has been a regulatory convergence between banks and NBFCs on the asset

side, on the liability side, NBFCs still do not enjoy a level playing field. This needs to be addressed to

help NBFCs realize their full potential and thereby perform their duties with greater efficiency.

Moreover, with the banking system clearly constrained in terms of expanding their lending

activities, the role of NBFCs becomes even more important now, especially when the government has

a strong focus on promoting entrepreneurship so that India can emerge as a country of job creators

instead of being one of job seekers. Innovation and diversification are the important contributors to

achieve the desired objectives.

31 | P a g e

IMF (International Monetary Fund) cuts India’s growth rate to 4.8% citing slowdown in local

demand, stress in NBFC sector

8 per cent for the current fiscal year which is expected to rise to 5.8 per cent in 2020?

The IMF attributed the slash in growth rate to the slowdown in demand in the domestic market

and stress in the nonbank financial sector.

“India’s growth is estimated at 4.8 percent in 2019, projected to improve to 5.8 percent in 2020

and 6.5 percent in 2021,” said IMF in a statement.

The 5.8 per cent estimate in 2020 is down by 0.9 per cent from the previous estimate.

The steep cut in India’s growth rate has affected the IMF’s projection on the world economy,

which is now expected to expand 2.9 per cent in 2019 as compared with the previous forecast at

3.0 per cent.

In its World Economic Outlook Report, IMF stated that the growth markdown largely reflects a

downward revision to India’s projection, where domestic demand has slowed more sharply than

expected amid stress in nonbank financial sector and a decline in credit growth.

According to IMF, the global economy is expected to accelerate to 3.3 per cent in 2020 from 2.9

per cent in 2019. Further, it is expected to rise to 3.4 per cent in 2021.

However, the IMF has in its latest estimates trimmed the global growth rate by 0.1 per cent each

for 2019 and 2020 and by 0.2 percentage for 2021.

Earlier in December, IMF chief economist Gita Gopinath had estimated a likely cutdown in

India’s growth estimate during the January review.

United Nations had also cut down India’s growth estimate for Financial Year 2020 to 5 per cent

from 5.7 per cent. World Bank had also cut its estimate to 5 per cent from its earlier prediction of

6 per cent

NBFC crisis:-

The continuing liquidity crunch facing non- banking financial companies is likely to result in creasing bad loans risks for banks both from these shadow banks as well as from companies relying on such lenders for funding, warns a report.

The spillover of stress among NBFCs to borrowers, and ultimately to banks, will hinder improvements in banks' asset quality, profitability and capital, which is credit negative.

32 | P a g e

Owing to liquidity crisis, NBFCs are forced to reduce lending, leading to funding constraints for

borrowers relying on non-bank lenders.

This increases the risk of loan losses for NBFCs, and as a result, they will continue to have difficulty in obtaining funding.

Also, as NBFC customers' financials weaken, banks will reduce lending to them, which in turn

will further worsen their funding stress and can lead to more bad loans from these companies for

banks, it warned.

A type of NBFC credit to controlling shareholders, or promoters, of large listed companies across

various industries is also emerging as a source of asset risk for banks.

Corporate promoters use their company shares as collateral to borrow, mostly from NBFCs or

mutual funds, typically for the purpose of making investments, including in external businesses

"The risk for banks is that promoters with weak governance can use company resources to repay

their debt, causing financial damage to their businesses, which as a consequence, can default on

their own loans from banks, the report said.

Refinancing can be difficult for promoters of companies as investments they make using

Loans are often illiquid, a problem made worse by tighter availability of credit from NBFCs.

The report further said the non-bank lenders collectively have a large market share in retail and

SME loans, a segment that has grown rapidly in recent years and now is susceptible to asset

quality deterioration as the economy slows.

"A curtailing of lending by NBFCs will add to risks from retail loans for banks by reducing the

availability of credit that individuals can use for refinancing and by contributing to the slowdown,"

the agency said.

The report also said real estate companies are under significant stress, and tighter funding will

further increase stress in the sector. It could lead to more NPLs for banks because they have large

exposures to NBFCs active in real estate lending.

Banks also have direct exposures to real estate companies, and the growing stress in the NBFC

sector will result in more impairment of bank loans to these borrowers.

33 | P a g e

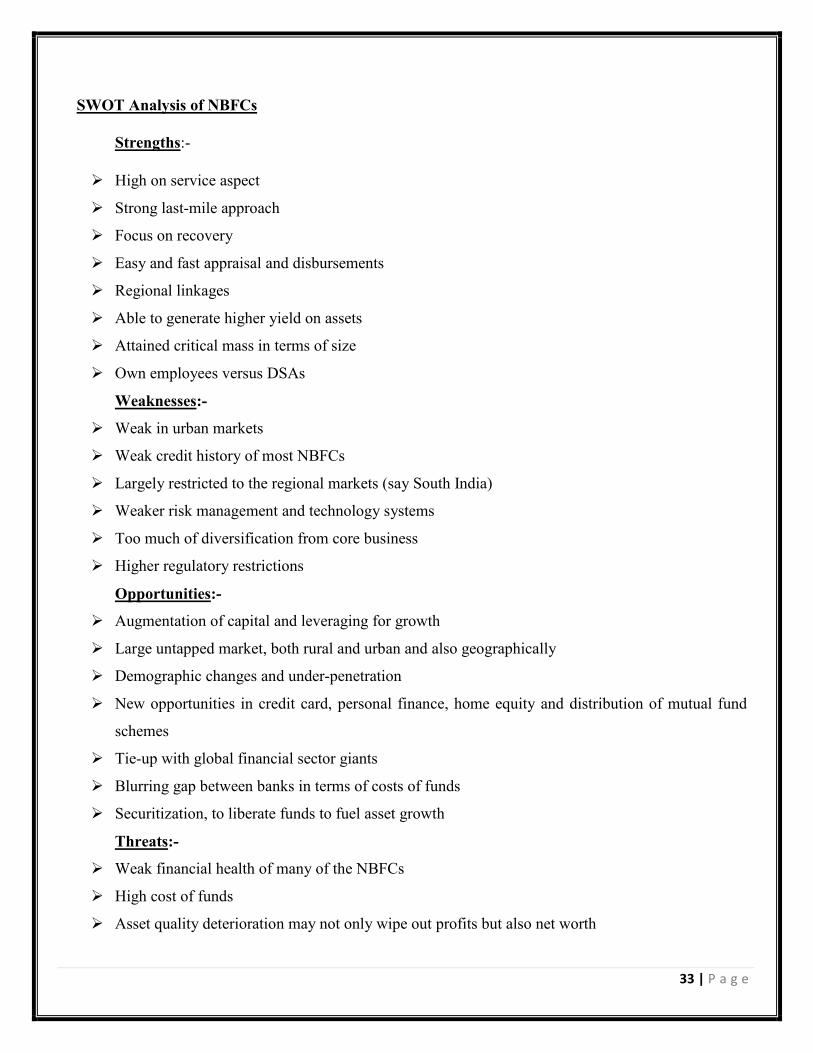

SWOT Analysis of NBFCs

Strengths:-

High on service aspect

Strong last-mile approach

Focus on recovery

Easy and fast appraisal and disbursements

Regional linkages

Able to generate higher yield on assets

Attained critical mass in terms of size

Own employees versus DSAs

Weaknesses:-

Weak in urban markets

Weak credit history of most NBFCs

Largely restricted to the regional markets (say South India)

Weaker risk management and technology systems

Too much of diversification from core business

Higher regulatory restrictions

Opportunities:-

Augmentation of capital and leveraging for growth

Large untapped market, both rural and urban and also geographically

Demographic changes and under-penetration

New opportunities in credit card, personal finance, home equity and distribution of mutual fund

schemes

Tie-up with global financial sector giants

Blurring gap between banks in terms of costs of funds

Securitization, to liberate funds to fuel asset growth

Threats:-

Weak financial health of many of the NBFCs

High cost of funds

Asset quality deterioration may not only wipe out profits but also net worth

34 | P a g e

Entry of foreign players in post-2009 scenario

Growing retail thrust within banks

CRISIL NBFC REPORT:-

"However, increases in banks' real estate NPLs will be marginal as their direct exposures to real estate companies remain small, growing more slowly than NBFC loans to the sector," it said

After witnessing healthy growth over the past few years, non-bank credit growth slowed down in the second half of fiscal 2019 due to the tight liquidity conditions that engulfed the sector. Consequently, Non Bank Financial Companies (NBFCs) which were gaining market share from banks across major asset classes in the past could not do so in fiscal 2019.

Going forward, NBFCs will need to recalibrate their strategies in order to deal with the changing business dynamics. How would this impact the credit growth of the sector? When is the liquidity situation going to improve? Can NBFCs achieve pre-2018 growth in the medium term or will the growth remain anemic?

What are the key factors that will drive their growth? Will their earnings growth trajectory be lower? What will be the capital that they will need over the next 1-2 years? What will separate the winners from the losers? Where are the opportunities for growth?

CRISIL Research's NBFC Report, 2019 delves deep into the fast-changing industry landscape to come up with the answers. The report contains CRISIL Research's perspective on growth prospects, competitive scenario and the attractiveness of the 11 segments in which NBFCs operate and also gives a perspective on the emerging fintech market.

The coverage also includes:

Outlook on growth and delinquencies, credit costs by segment

Segment-wise profitability outlook, considering business growth, resource profile and asset

quality

Detailed assessment of competitive scenario with banks and market share of NBFCs in various

segments

Perspective on regulatory direction in each segment

Financial and operational benchmarks across various segments

35 | P a g e

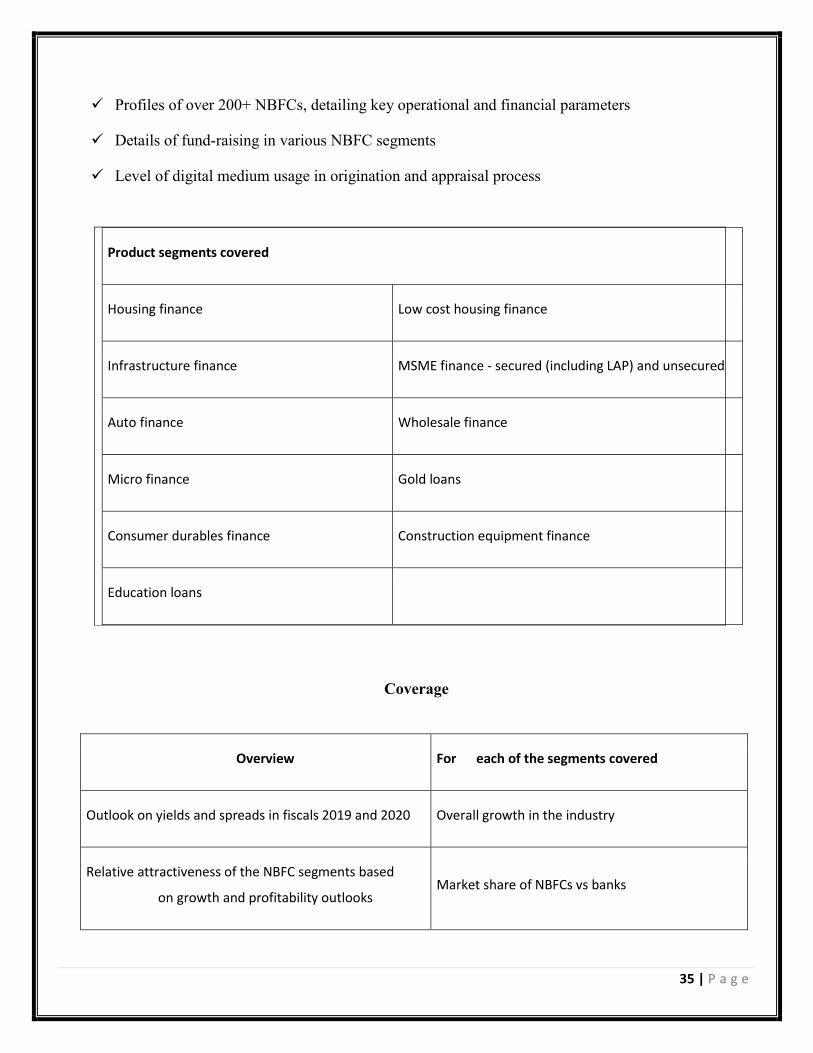

Profiles of over 200+ NBFCs, detailing key operational and financial parameters

Details of fund-raising in various NBFC segments

Level of digital medium usage in origination and appraisal process

Product segments covered

Housing finance Low cost housing finance

Infrastructure finance MSME finance - secured (including LAP) and unsecured

Auto finance Wholesale finance

Micro finance Gold loans

Consumer durables finance Construction equipment finance

Education loans

Coverage

Overview For each of the segments covered

Outlook on yields and spreads in fiscals 2019 and 2020 Overall growth in the industry

Relative attractiveness of the NBFC segments based

on growth and profitability outlooks Market share of NBFCs vs banks

36 | P a g e

Competitive positioning of NBFCs across key segments Growth outlook for NBFCs

Outlook on asset quality in the NBFC industry Profitability of NBFCs: Review & outlook

View on the borrowing mix of NBFCs Asset quality: Review & outlook

Capital-raising requirement in the medium term Key growth drivers and challenges

Growth in NBFC:-

The challenges faced by non-banks in access to funding following the credit cliff event in

September 2018 and recent defaults by some large non-banks has only increased the risk aversion

of lenders and investors.

A clear differentiation is visible between groups of non-banks. At an overall level, players with a

strong parentage are still getting funds, while those without any parentage continue to face

challenges.

Bifurcating this further, wholesale NBFCs without strong parentage are the worst hit. Home loan-

and retail- focused non-banks are relatively better off.

With all of this, growth in the second half of fiscal 2019 was around half of what was seen in the

first half. But given the strong growth in the first half, growth in overall non-bank credit in fiscal

2019 was still at ~15%, with assets under management reaching Rs 23.7 lakh crore.

Growth is expected to be remain subdued at least in the first half of fiscal 2020, with overall assets

under management growth for the year estimated at 12-13%. With securitization expected to

sustain as a preferred funding mode, the on-balance growth of non-banks is expected to be lower.

37 | P a g e

COMPANY PROFILE:-

BAJAJ GROUP:-

Bajaj Group is an Indian conglomerate founded by Jamnalal Bajaj in 1926, Mumbai. Bajaj Group is one of the oldest & largest conglomerates based in Mumbai, Maharashtra. The group comprises 34 companies & its flagship company Bajaj Auto is ranked as the world's fourth largest two- and three-wheeler manufacturer. some of the notable companies are Bajaj Electricals, Mukand Ltd & Bajaj Hindustan Ltd. Involvement in various industries that include automobiles (2- and 3-wheelers), home appliances, lighting, iron and steel, insurance, travel and finance. The Group is headed by Rahul Bajaj.

38 | P a g e

BAJAJ GROUP OF COMPANIES:-

Bachhraj & Company Pvt. Ltd.

Bachhraj Factories Pvt. Ltd.

Bajaj Allianz General Insurance Company Ltd.

Bajaj Allianz Life Insurance Company Ltd.

Bajaj Auto Finance Ltd.

Bajaj Auto Holdings Ltd.

Bajaj Auto Ltd.

Bajaj Electricals Ltd.

Bajaj Finserv Ltd.

Bajaj Holdings & Investment Ltd.

Bajaj International Pvt. Ltd.

Bajaj Sevashram Pvt. Ltd.

Bajaj Ventures Ltd.

Baroda Industries Pvt. Ltd.

Hercules Hoists Ltd.

Hind Lamps Ltd.

Hind Musafir Agency Ltd.

Jamnalal Sons Pvt. Ltd.

Jeevan Ltd.

Maharashtra Scooters Ltd.

Mukand Engineers Ltd.

39 | P a g e

Mukand Global Finance Ltd.

Mukand International Ltd.

Mukand Ltd.

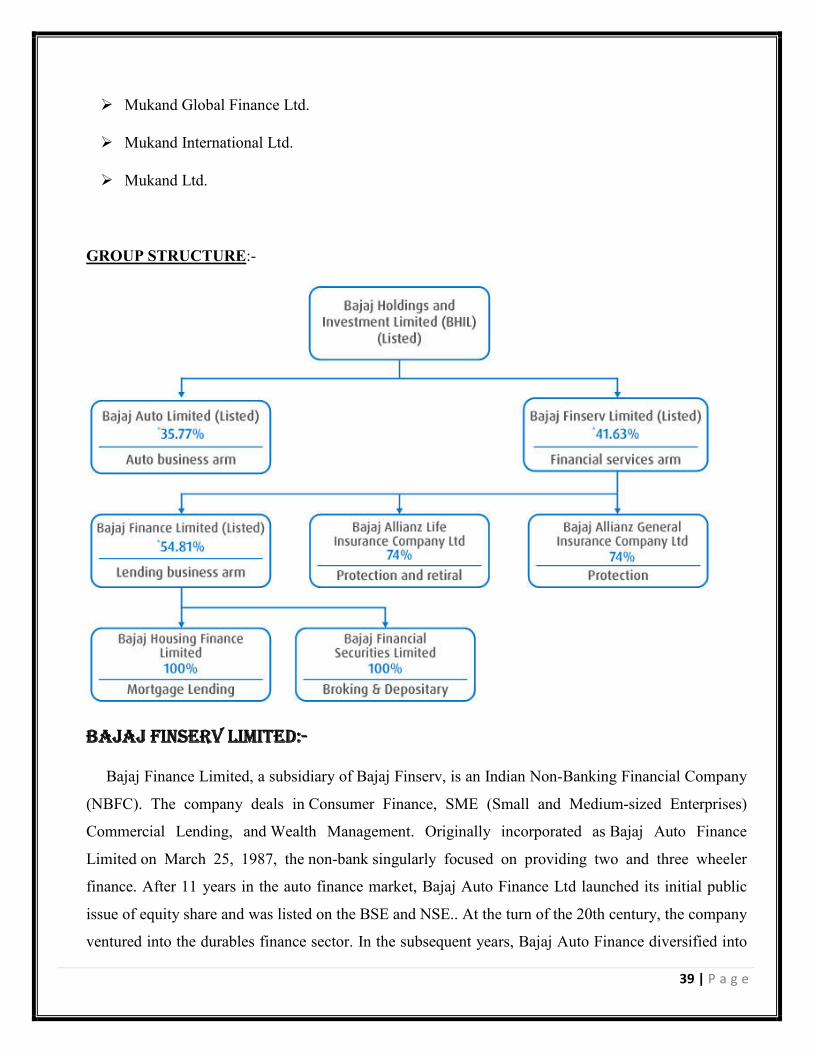

GROUP STRUCTURE:-

BAJAJ FINSERV LIMITED:-

Bajaj Finance Limited, a subsidiary of Bajaj Finserv, is an Indian Non-Banking Financial Company

(NBFC). The company deals in Consumer Finance, SME (Small and Medium-sized Enterprises)

Commercial Lending, and Wealth Management. Originally incorporated as Bajaj Auto Finance

Limited on March 25, 1987, the non-bank singularly focused on providing two and three wheeler

finance. After 11 years in the auto finance market, Bajaj Auto Finance Ltd launched its initial public

issue of equity share and was listed on the BSE and NSE.. At the turn of the 20th century, the company

ventured into the durables finance sector. In the subsequent years, Bajaj Auto Finance diversified into

40 | P a g e

business and property loans as wellhttps://en.wikipedia.org/wiki/Bajaj_Finance - cite_note-3. In the year

2006, the company’s assets under management hit the Rs.1,000 crore mark and is currently at

Rs.52,332 crore. 2010 saw the company’s registered name change from Bajaj Auto Finance Limited to

Bajaj Finance Limited.

Bajaj Finserv was formed in April 2007 as a result of its demerger from Bajaj Auto Limited as a

separate entity to focus purely on the financial services business of the group. The process of

demerger was completed in Feb 2008.

This demerger was not only to unlock the value in the high growth business areas of Auto,

Insurance, Finance sectors and Wind Power but to also to independently run these core businesses

and strengthen their competencies.

The wind power project, the stakes in the life and general insurance companies and consumer

finance along with their respective assets and liabilities got vested in Bajaj Finserv Limited. In

addition to that, cash and cash equivalent of INR 8,000 million (then market value) was also

transferred to the company.

The demerger has enabled investors to hold separate focused stocks and also facilitated transparent

benchmarking of the companies to their peers in their respective industries.

The constantly changing demographics and dynamics of the Indian economy, has led to creation

of various needs of the customer.

The Indian customer now demands proper avenues of channelizing their savings, financial

protection and is also desirous of spending more on valuable goods and services.

All these wants need to be met by dynamic players in the financial services space. Bajaj Finserv

was formed specifically to cater to these needs.

The company was also formed to touch and improve the lives of a growing number of people in

the country, and in doing so, deliver superior corporate values to its shareholders.

41 | P a g e

He operating companies carry with them the Bajaj brand, which carries with it decades of

commitment to business ethics, integrity and highest standards of fiduciary responsibility.

Vision and Mission of the Organization:-

Vision:

Bajaj Finserv has a vision to become a full-fledged financial services company and be the financial

partner to the Indian consumer and help him across his financial needs, whether for finance, for

investment management, for protection or for post-retirement support, throughout his lifecycle.

Mission:

Bajaj Finserv aims to be the most useful, reliable and efficient provider of Financial Services. It is our

continuous endeavor to be a trustworthy advisor to our clients, helping them achieve their financial

goals.

Area of operation:

Consumer Durable Finance

Two and Three Wheeler Finance

Lifestyle product finance

Vendor finance

Construction Equipment Finance

Objective of the Organization:

Our main objects as contained in our Memorandum of Association include:

1. To Finance industrial by way advance ,deposit or lend money, securities and propertied or with any

Company, Body corporate, trust, firm, person or association whether falling under the same

management or otherwise, with or without security and on such terms as may be determined from

time to time, and to carry on and undertake the business of finance and investment and to provide

venture capital, seed capital, loan capital and to participate in equity preference share capital or to

give guarantees on behalf of the company in the matter and to promote companies engaged in

industrial and trading business and to act as Financial Consultants, Management Consultants,

Brokers, Dealers, Agents and to carry on the business of share broking, money broking ,exchange

42 | P a g e

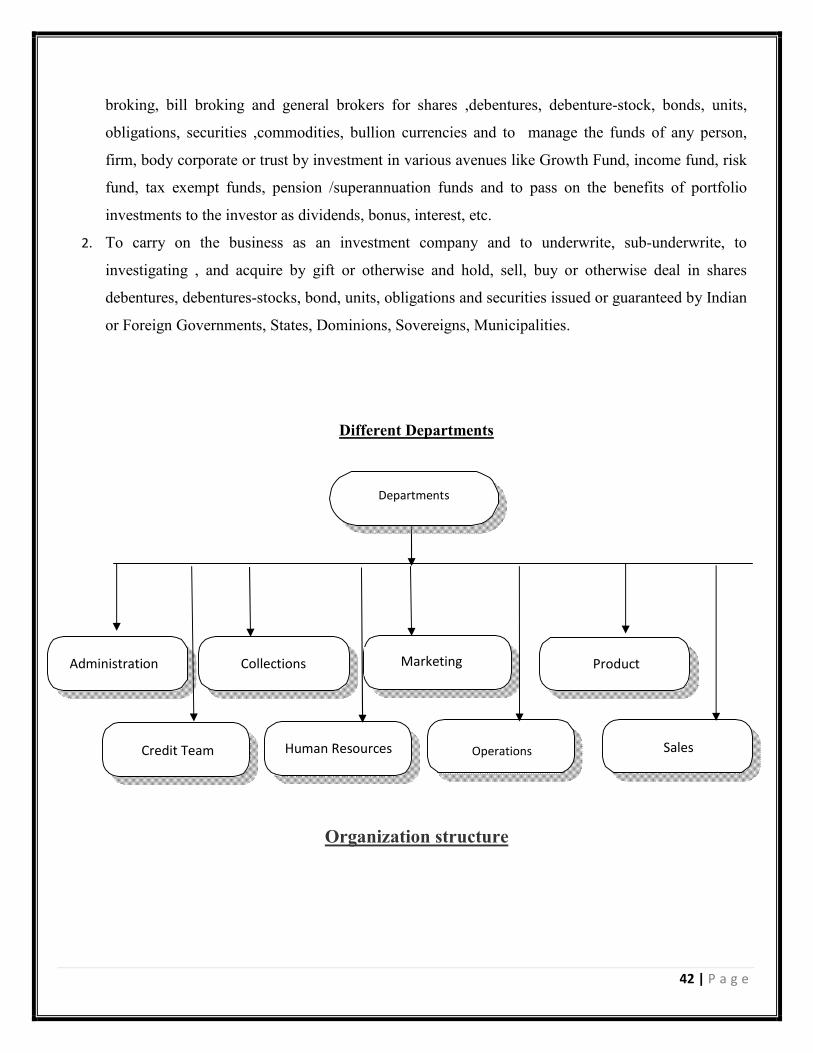

Departments

Administration Collections Marketing Product

Credit Team Human Resources Operations Sales

broking, bill broking and general brokers for shares ,debentures, debenture-stock, bonds, units,

obligations, securities ,commodities, bullion currencies and to manage the funds of any person,

firm, body corporate or trust by investment in various avenues like Growth Fund, income fund, risk

fund, tax exempt funds, pension /superannuation funds and to pass on the benefits of portfolio

investments to the investor as dividends, bonus, interest, etc.

2. To carry on the business as an investment company and to underwrite, sub-underwrite, to

investigating , and acquire by gift or otherwise and hold, sell, buy or otherwise deal in shares

debentures, debentures-stocks, bond, units, obligations and securities issued or guaranteed by Indian

or Foreign Governments, States, Dominions, Sovereigns, Municipalities.

Different Departments

Organization structure

43 | P a g e

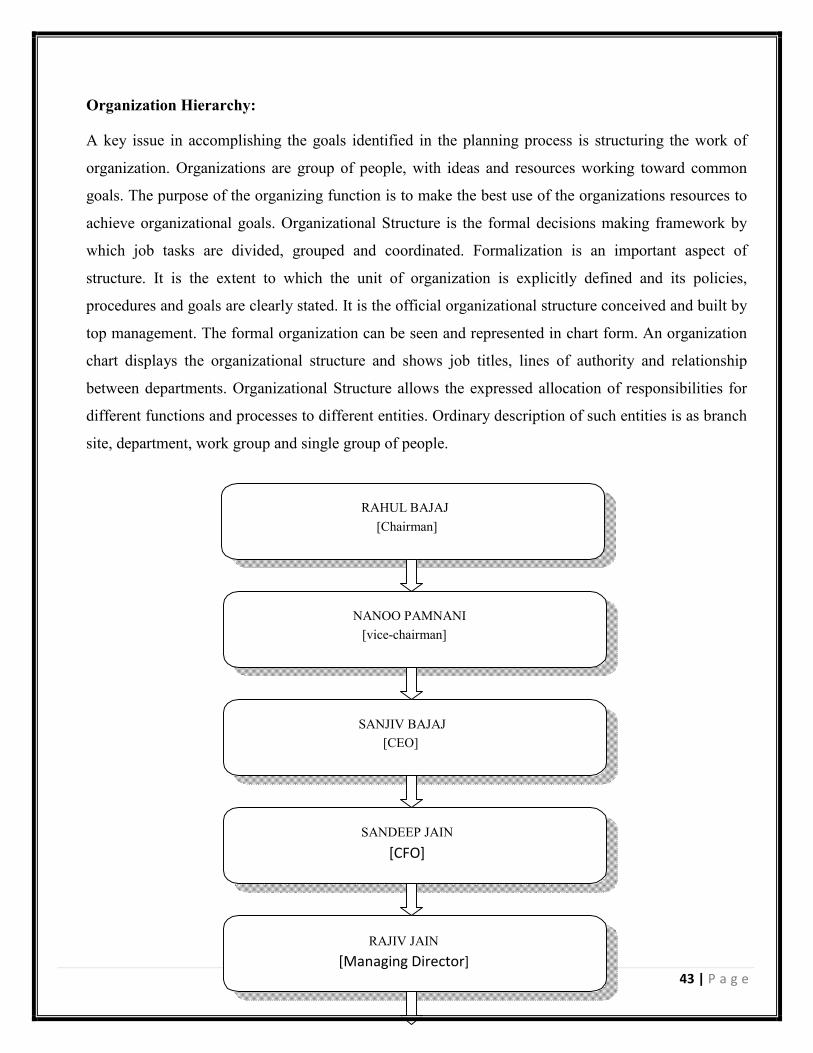

RAHUL BAJAJ

[Chairman]

NANOO PAMNANI

[vice-chairman]

SANJIV BAJAJ

[CEO]

SANDEEP JAIN

[CFO]

RAJIV JAIN

[Managing Director]

Organization Hierarchy:

A key issue in accomplishing the goals identified in the planning process is structuring the work of

organization. Organizations are group of people, with ideas and resources working toward common

goals. The purpose of the organizing function is to make the best use of the organizations resources to

achieve organizational goals. Organizational Structure is the formal decisions making framework by

which job tasks are divided, grouped and coordinated. Formalization is an important aspect of

structure. It is the extent to which the unit of organization is explicitly defined and its policies,

procedures and goals are clearly stated. It is the official organizational structure conceived and built by

top management. The formal organization can be seen and represented in chart form. An organization

chart displays the organizational structure and shows job titles, lines of authority and relationship

between departments. Organizational Structure allows the expressed allocation of responsibilities for

different functions and processes to different entities. Ordinary description of such entities is as branch

site, department, work group and single group of people.

44 | P a g e

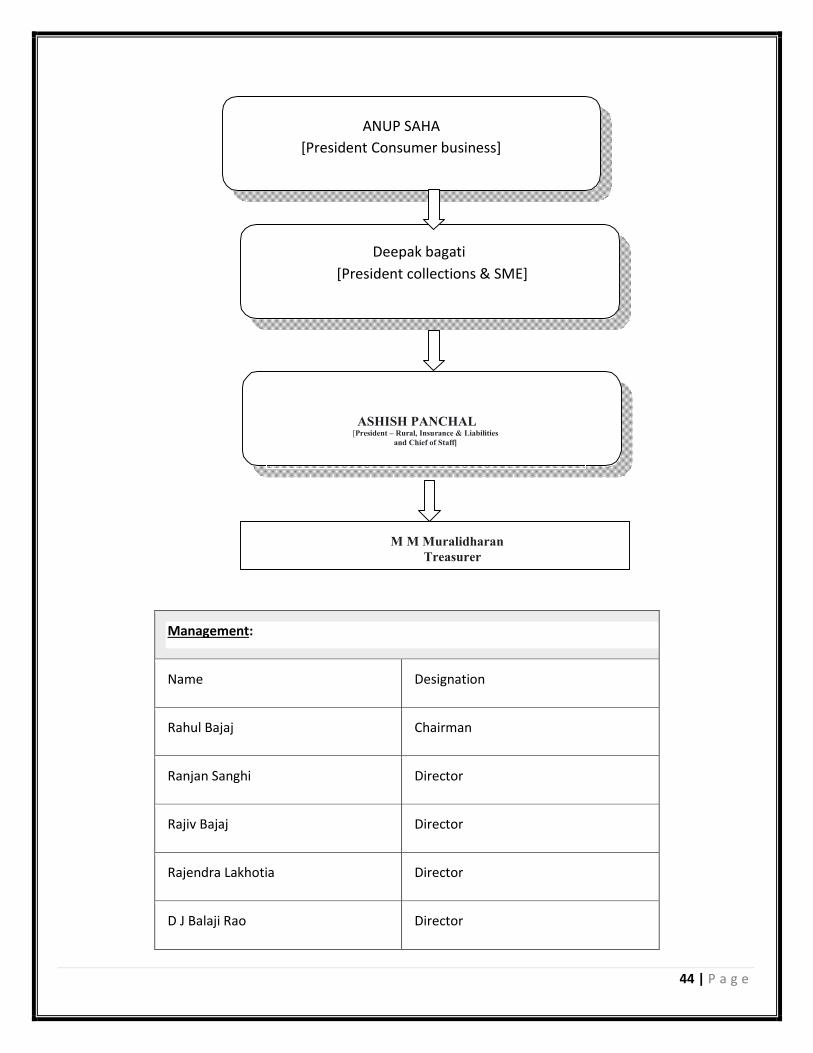

Management:

Name Designation

Rahul Bajaj Chairman

Ranjan Sanghi Director

Rajiv Bajaj Director

Rajendra Lakhotia Director

D J Balaji Rao Director

ANUP SAHA

[President Consumer business]

Deepak bagati

[ [President collections & SME]

ASHISH PANCHAL [President – Rural, Insurance & Liabilities

and Chief of Staff]

M M Muralidharan Treasurer

45 | P a g e

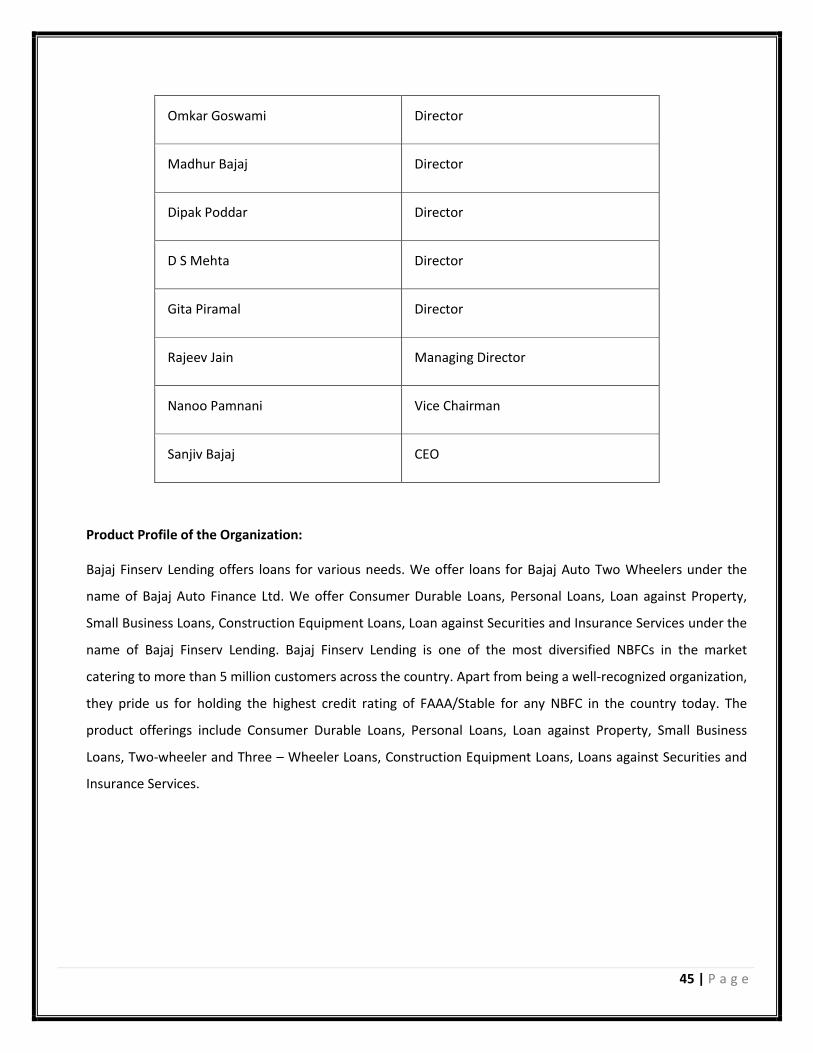

Omkar Goswami Director

Madhur Bajaj Director

Dipak Poddar Director

D S Mehta Director

Gita Piramal Director

Rajeev Jain Managing Director

Nanoo Pamnani Vice Chairman

Sanjiv Bajaj CEO

Product Profile of the Organization:

Bajaj Finserv Lending offers loans for various needs. We offer loans for Bajaj Auto Two Wheelers under the

name of Bajaj Auto Finance Ltd. We offer Consumer Durable Loans, Personal Loans, Loan against Property,

Small Business Loans, Construction Equipment Loans, Loan against Securities and Insurance Services under the

name of Bajaj Finserv Lending. Bajaj Finserv Lending is one of the most diversified NBFCs in the market

catering to more than 5 million customers across the country. Apart from being a well-recognized organization,

they pride us for holding the highest credit rating of FAAA/Stable for any NBFC in the country today. The

product offerings include Consumer Durable Loans, Personal Loans, Loan against Property, Small Business

Loans, Two-wheeler and Three – Wheeler Loans, Construction Equipment Loans, Loans against Securities and

Insurance Services.

46 | P a g e

Home Loan

Construction

Equipment Loan

Consumer

Durable Loan

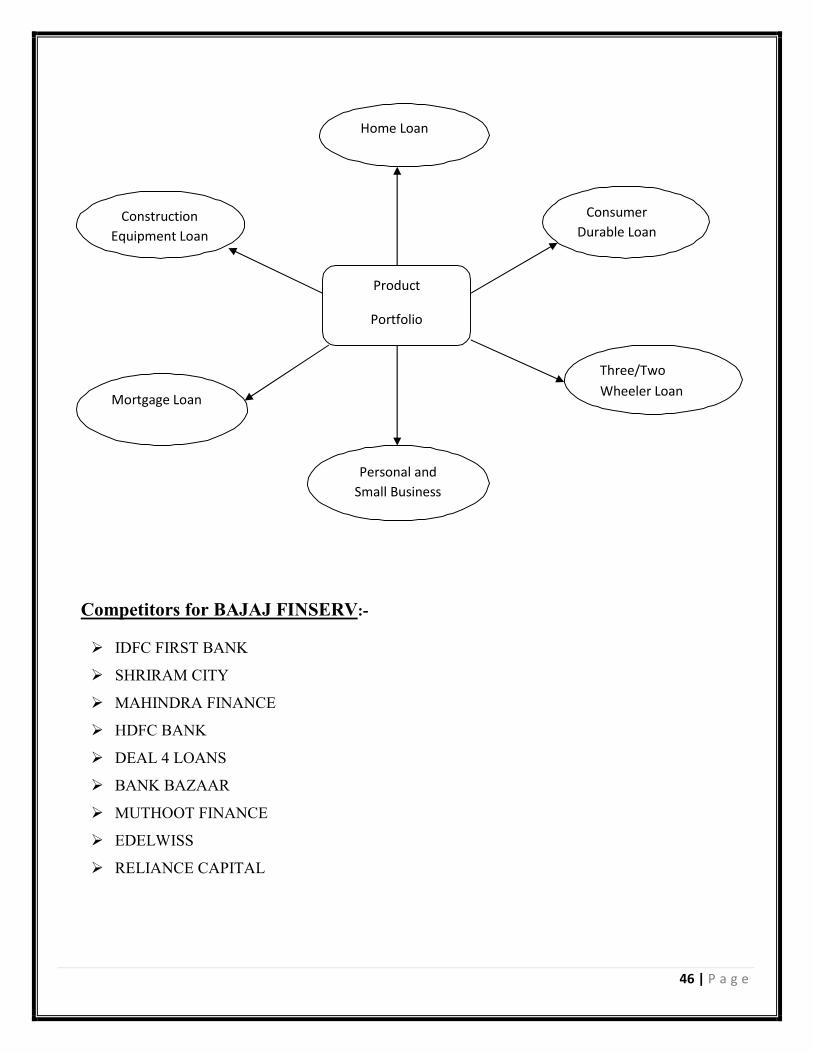

Product

Portfolio

Three/Two

Mortgage Loan Wheeler Loan

Personal and

Small Business

Competitors for BAJAJ FINSERV:-

IDFC FIRST BANK

SHRIRAM CITY

MAHINDRA FINANCE

HDFC BANK

DEAL 4 LOANS

BANK BAZAAR

MUTHOOT FINANCE

EDELWISS

RELIANCE CAPITAL

47 | P a g e

Consumer Finance

Durable Finance

Lifestyle Finance

Digital Product Finance

EMI Card

2 & 3 Wheeler Finance

Personal Loan

Loan against FD

Extended warranty

Gold Loan

Home Loan

Retail EMI

Retailer Finance