Management of Loans & Advances

16

Term Paper of FIN-4209: Management of Financial Institutions

Transcript of Management of Loans & Advances

Term Paper of FIN-4209: Management of Financial Institutions

Term Paper On

Man

agem

ent o

f Loan

& A

dva

nces

Md. Omar Faruque

Assistant Professor

Department of Finance

Faculty of Business Studies

Jagannath University, Dhaka

Sultan Ahmed Khan

Representative of the group

Epimetheus

BBA 3rd Batch

Department of Finance

Faculty of Business Studies

Jagannath University, Dhaka.

Submitted by

Submitted to

Group Name: Epimetheus

Name of the members of the group:

Serial No: Name of the members of the group Roll Number

01 Sultan Ahmed Khan 091597

02 Md. Mynul Islam 091633

03 Md. Anik Mahmud 091636

04 Sharjil Ahmed 091623

05 Protiva Talukder 091602

06 Md. Mehedi Hassan 091590

07 Mohammad Didarul Islam Khan 091613

08 Mohammad Mahmudul Hasan 091534

09 Sakhawat Hosain 091574

Group Representative: Sultan Ahmed Khan.

Group Coordinator : Md. Mynul Islam.

Contact : [email protected]

Web : epimetheus.yolasite.com

NAME Page no

Vita

Acknowledgement

Abstract

Introduction

Loan & Advances and Difference between

both of this

01

Classification of Loan & Advances 02

Factor determining growth mix of loan 04

Step in lending process 05

Literature Review

Regulations in terms of Bangladesh 07

Classification of Supervision system 16

Regarded Department 18

Principle of Sound Lending 21

Objectives &

Hypothesis

Objectives 23

Recommendation 23

Research Methodology

Responsibility of Management 24

Factors affecting sound lending 25

CAMELS 27

Liquidity rating 28

Loan Proposal form 29

Data Analysis

Restriction of lending to Directors 50

Standard Bank Analysis 53

Premier Bank Analysis 66

Bank Asia Analysis 70

BRAC Bank Analysis 76

Southeast Bank Analysis 81

Conclusion

Summary of the findings 92

Suggestion 94

Bibliography Bibliography 95

Index 96

March 05, 2013

The Course Instructor

Md. Omar Faruque

Assistant Professor

Department of Finance

Jagannath University, Dhaka.

Sub: Thanks giving letter to the respective faculty member.

Sir,

We are the student of Department of Finance (3rd batch) of Jagannath University, Dhaka &

also from the group named “Epimetheus”. We are very much enthusiastic about our

presentation. We are really happy to have such a presentation of challenging and interesting

like this presentation & also thanks to you for making us worthy for corporate. Our topic is

“Management of Loans & Advances”. We have learned many things from this topic which

will help us in future to conduct as a finance official. There were some obstacles we have

faced at the time of collecting data about our topic. But we have overcome all the obstacles

by the endeavor effort by each member of our group and tried our best to give an overview of

our topic.

We the group “Epimetheus” tried our best to make this term paper impeccable, interesting,

informative and enjoyable by the help of electronic and print media in association with our

honorable teacher, mentor, counselor, instructor and advocate “Md. Omar Faruque”. We are

really grateful to him. We had limitations at the time preparing presentation. So mistakes may

occur in our demonstration of our presentation. We hope that, you will exempt our mistakes.

Thanking in anticipation,

Yours Fidel,

Sultan Ahmed Khan

Group Representative,

Group-“Epimetheus”

BBA 3rd Batch

Department of Finance

Jagannath University,Dhaka.

Name of the Researcher Roll Number Date of

Birth

Place of

Birth

Degree

Sultan Ahmed Khan 091597 26/12/91 Barisal BBA(Finance)

8th Semester

Md. Mynul Islam 091633 07/11/90 Barisal BBA(Finance)

8th Semester

Md. Anik Mahmud 091636 1/1/90 Natore BBA(Finance)

8th Semester

Sharjil Ahmed 091623 11/11/90 Rajbari BBA(Finance)

8th Semester

Protiva Talukder 091602 20/10/90 Sylhet BBA(Finance)

8th Semester

Md. Mehedi Hassan 091590 16/3/90 Barisal BBA(Finance)

8th Semester

Sakhawat Hosain 091574 4/5/90 Chittagong BBA(Finance)

8th Semester

Mohammad Didarul Islam

Khan

091613 16/5/90 Tangail BBA(Finance)

8th Semester

Mohammad Mahmudul

Hasan

091534 6/12/90 Dhaka BBA(Finance)

8th Semester

Publications: All the publications are available at https:// epimetheus.yolasite.com

First of all we would like to thank the Almighty for giving us the strength, and the aptitude to

complete this report within due time. We are deeply indebted to our course teacher, mentor,

and counselor, Md. Omar Faruque for assigning us such an interesting topic named

“Management of Loans & Advances”. We also express the depth of my appreciation to our

honorable course teacher for his suggestion and guidelines, which helped us in completing

this term paper.

We are also grateful to the following person who has helped us a lot

Senior Officer (in Charge)

Banking Regulation & Policy Department

Bangladesh Bank

Head Office

Dhaka

Customer Relation Executives

Standard Bank Limited

Customer Relation Executives

Premier Bank Limited

Customer Relation Executives

Bank Asia Limited

Customer Relation Executives

Southeast Bank Limited

Customer Relation Executives

BRAC Bank Limited

In finance, a loan is a debt evidenced by a note which specifies, among other things, the

principal amount, interest rate, and date of repayment. A loan entails the reallocation of the

subject asset(s) for a period of time, between the lender and the borrower. In a loan, the

borrower initially receives or borrows an amount of money, called the principal, from the

lender, and is obligated to pay back or repay an equal amount of money to the lender at a later

time. Typically, the money is paid back in regular installments, or partial repayments; in an

annuity, each installment is the same amount. Principle amount available when a borrower

draws from a line of credit, takes a cash advance against a bank credit card, or disburses a

loan at specific periodic stages. Advances may be secured or unsecured.

Lending institutions are among the most closely regulated of all financial services

institutions. Not surprisingly, the mix, quality and yield of the loan portfolio are heavily

influenced by the character and depth of the regulations. In order to strengthen credit

discipline and improve the recovery position of loans and advances by the banks, Bangladesh

Bank vide BCD Circular No. 34/1989 introduced a new system covering loan classification,

the suspension of interest due, and the making of provisions against potential loan loss.

Bangladesh Bank has already introduced 'Special Mention Account' vide BRPD Circular No.

02/2005 and09/2005 for the banks to raise early warning signals for accounts showing first

signs of weakness and making appropriate provisioning therein.

Supervision is the on-going monitoring of credit union’s financial and operational condition.

Examiners monitor their assigned credit unions as needed through on-site supervision,

supervisory contacts and off-site through submitted regulatory reports and financial

statements and periodic trend analysis of selected ratios. In credit union with more serious

financial problems, supervision may also include follow up examination and monthly

monitoring financial trends and ratios. There are two supervision system of Bangladesh Bank

such as: On-side & Off-side supervision.

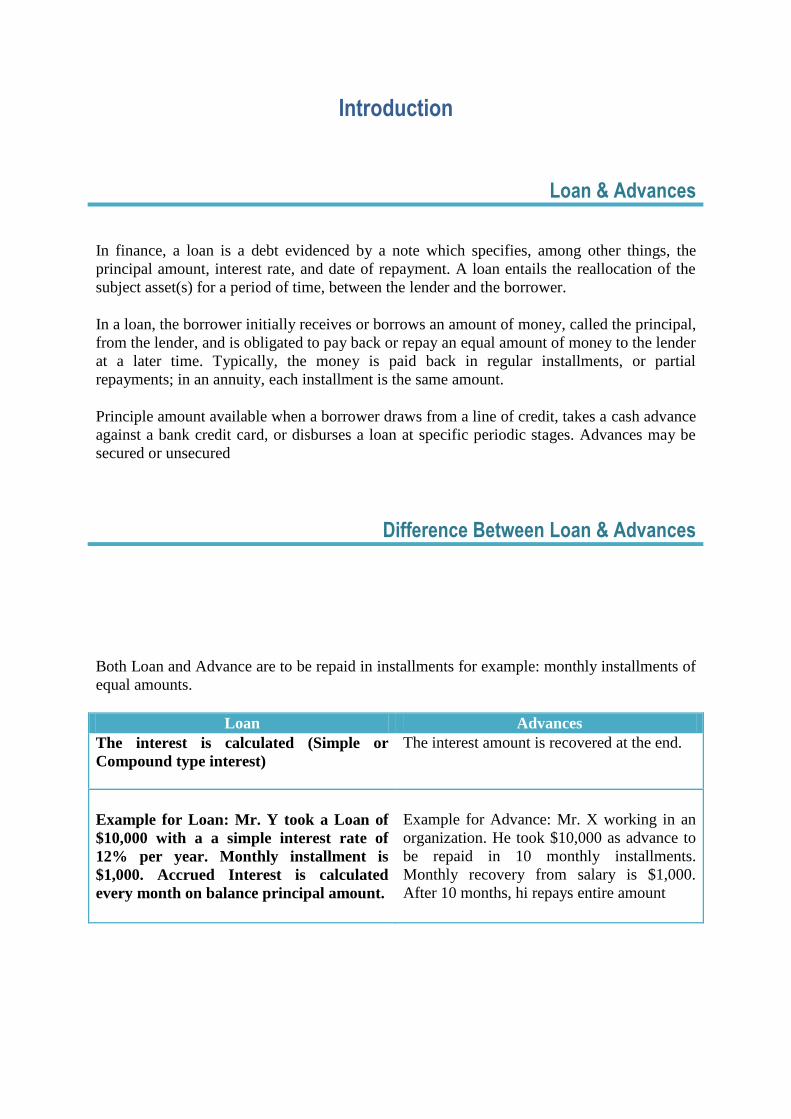

Introduction

Loan & Advances

In finance, a loan is a debt evidenced by a note which specifies, among other things, the

principal amount, interest rate, and date of repayment. A loan entails the reallocation of the

subject asset(s) for a period of time, between the lender and the borrower.

In a loan, the borrower initially receives or borrows an amount of money, called the principal,

from the lender, and is obligated to pay back or repay an equal amount of money to the lender

at a later time. Typically, the money is paid back in regular installments, or partial

repayments; in an annuity, each installment is the same amount.

Principle amount available when a borrower draws from a line of credit, takes a cash advance

against a bank credit card, or disburses a loan at specific periodic stages. Advances may be

secured or unsecured

Difference Between Loan & Advances

Both Loan and Advance are to be repaid in installments for example: monthly installments of

equal amounts.

Loan Advances

The interest is calculated (Simple or

Compound type interest)

The interest amount is recovered at the end.

Example for Loan: Mr. Y took a Loan of

$10,000 with a a simple interest rate of

12% per year. Monthly installment is

$1,000. Accrued Interest is calculated

every month on balance principal amount.

Example for Advance: Mr. X working in an

organization. He took $10,000 as advance to

be repaid in 10 monthly installments.

Monthly recovery from salary is $1,000.

After 10 months, hi repays entire amount

Classification of Loan & Advances

Source: Bank Management & Financial Services (7th Ed.) Part 16-2

Lease

Financing

Receivable

Individual /

To Individual

Commerce &

Industry

Agriculture

Financial

Institution

Real Estate

Loan

Real Estate Loan

Real estate loan is secured by real estate property. It includes short-term loan for

constructions & long-term loan to finance the purchase of farmland & other properties.

Financial Institution Loan

Financial institutional loan include credit to bank, insurance companies & other financial

institution.

Agriculture Loan

Agriculture loan are extended to farms and ranches to assist in planting & harvesting crops

and supporting the feeding and care of livestock.

Commercial & Industrial Loan

Commercial & industrial loan are granted to business to cover purchasing inventories, paying

taxes & meeting payrolls.

Loans to Individuals

It includes credit to finance the purchase of automobiles, mobile homes, appliances & other

retails goods, to repair & modernized homes, & to cover the cost of medical care & other

personal expenses, & are either extended directly to individuals or indirectly through retails

dealers.

Miscellaneous Loan

It includes all loans not listed above, including securities loans.

Lease Financing Receivables

Where the lender buys equipment or vehicles and leases them to its customers.

Of the loan categories shown, the largest in dollar volume is real estate loans, accounting for

just over half of total bank loans. The next largest category is commercial & industrial loans,

representing about one-fifth of the total followed by the loans to individuals & families,

accounting for about one-sixth of all loans federally insured banks make.

Factor deterring the growth & mix of loans

Different kind of loans mix usually defers form institutions to institutions. One of the key

factors in shaping an individual lenders loan portfolio is the profile of characteristics of the

market area itself. It means each lender must respond to the demand.

Other factors are given below:

Dependent on the Local Areas

Lenders are not totally depended on the local areas they served for all the loans they acquire.

They can purchase whole loans or peace of loan credit derivatives to offset the economic

volatility.

Lender Size

Larger banks are often wholesale lenders to large denomination loans to business firms. On

the other hands smaller banks tend to emphasis retails credit. Actually the volume of capital

held to determine its “legal lending limit”.

The Experience & Expertise of Management

To prohibit loan officers from making certain kind of loans this make different types of loans

which composite the loan portfolio as the loan policy.

Expected Yield Rate

Finally loan mixes rely on the expected yield. Each loan offers relatively higher yield all

other asset the lender could acquire after all expenses & risks are taken into account.

Net Yield Rate

Actually the lender size gives a significant influence on the net yield. Both the smaller and

larger bank has their benefit. Of course customer size can affect relative loan yield.

Most Efficient Producer

Larger lender generally bears the lowest cost on credit loans. On the other hand smaller

lenders appear to have few cost advantages. But these smaller lenders are frequently among

the most effective at controlling loan losses.

Step in Lending Process

Finding Prospective Loan Customer

Most loans to individuals arises from a direct request from a customer who approaches a

member of lender’s staff and ask to fill out a loan application. The lending game is becoming

a sales position. Sometimes loan officer will call on the same customers for month before the

customer finally agrees to give the lending institutions a try by filling out a loan application.

Evaluating a prospective Customer character & sincerity of purposes

Once a customer decides to request a loan, an interview with a loan officer usually follows,

giving the customer the opportunity to explain his or her credit needs. That interview is

particularly important because it provides an opportunity for the loan officers to assess the

customer character & sincerity of purposes.

Making site visits and evaluating a prospective customer credit record

If a business or mortgage loan is applied for, a loan officer makes a site visit to assess the

customer location and the condition of the property and to ask clarifying the question. The

loan officer may contact with other officer to assess any information regarding the customer.

For total file browse

http://adf.ly/6b2AP skip the ad then E-Learning Papers and Acts> Papers.

It’s free!!!!! free!!!!! free!!!!!