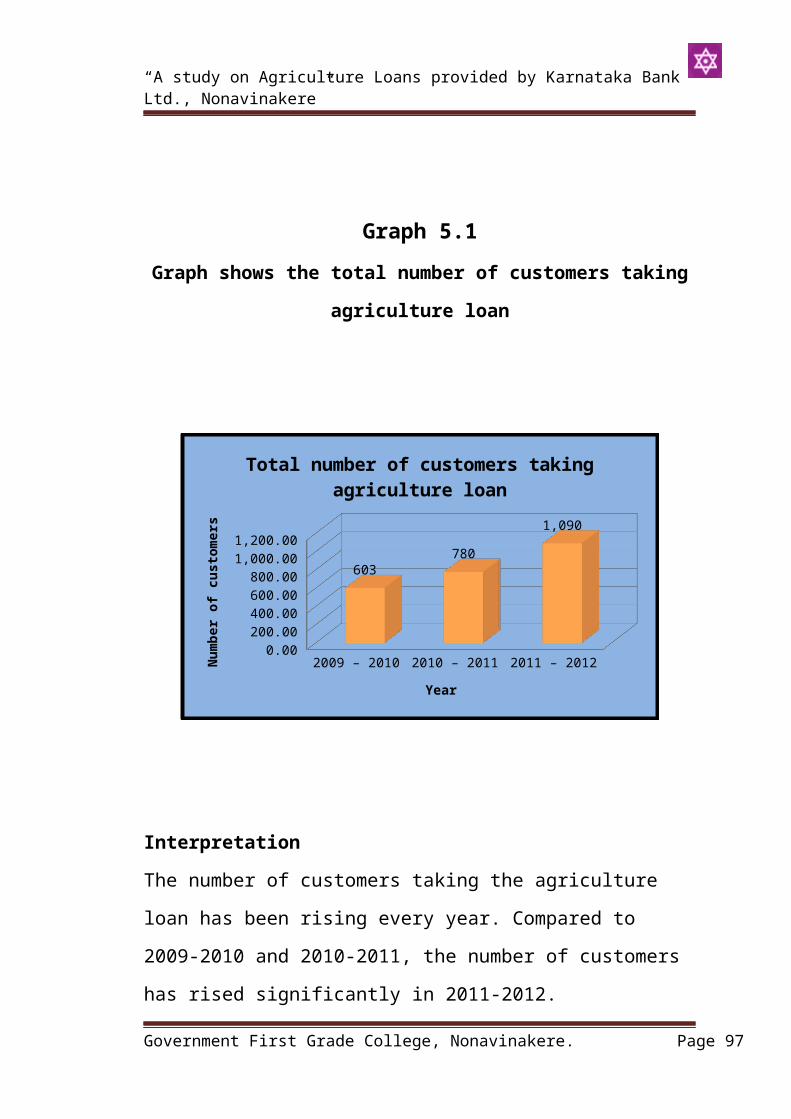

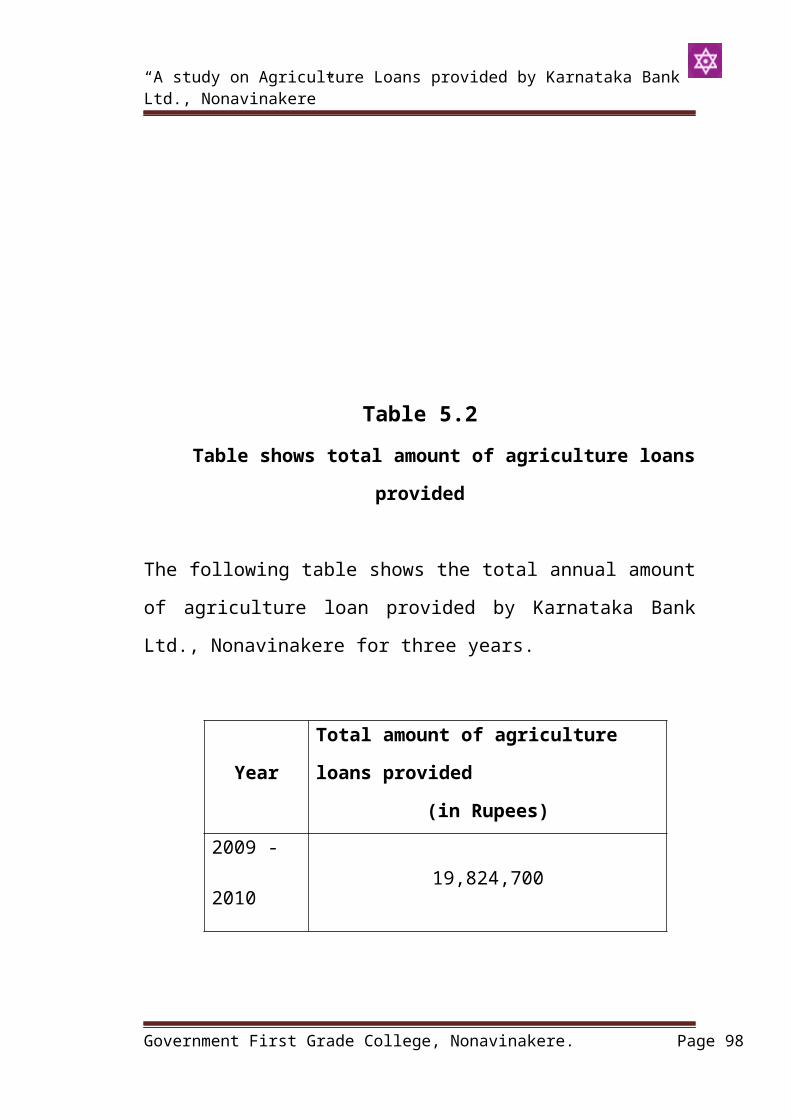

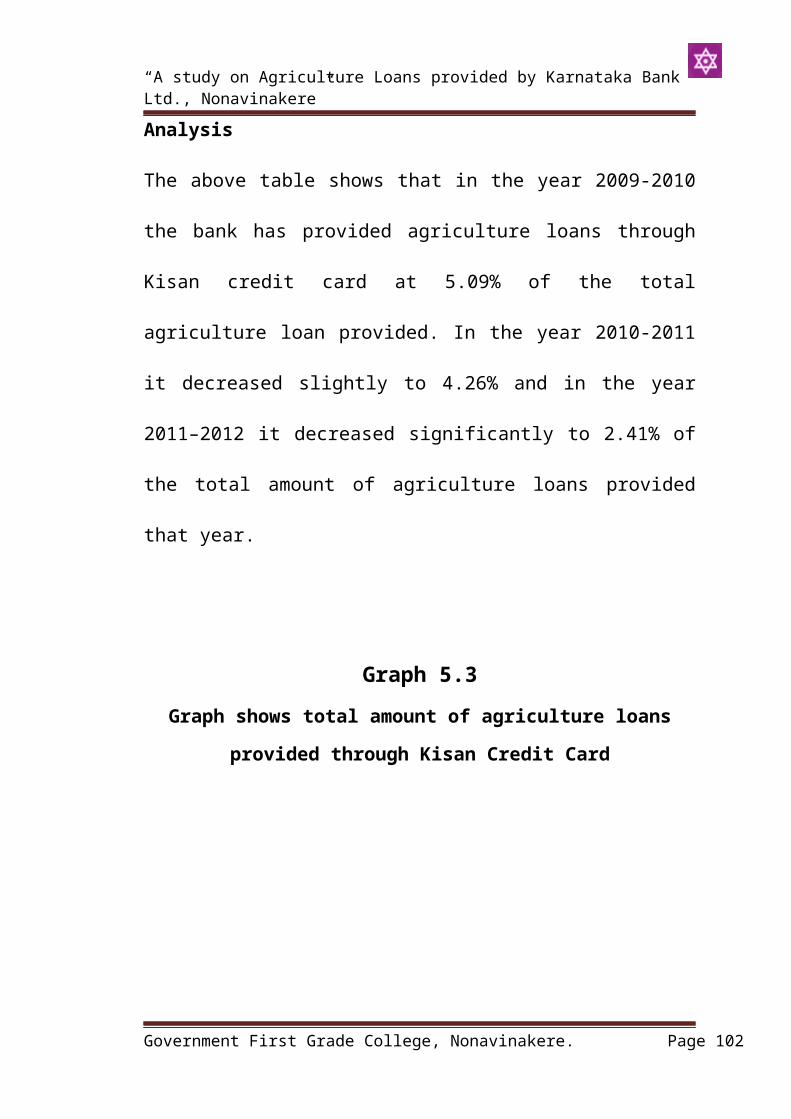

Agri Loans by KBL

123

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” CHAPTER-1 INTRODUCTION Finance In our present day economy, finance is defined as the provision of money at the time when it is required. Every enterprise, whether big, medium or small, needs finance to carry on its operations and to achieve its targets. In fact, finance is so indispensable today that is rightly said that finance is the life blood of an enterprise. Without adequate finance, no enterprise can possibly accomplish its objectives. Meaning Finance is the branch of Economics concerned with resource allocation as well as resource management, acquisition and investment. Simply, finance deals with matters related to money and the markets. Definition Government First Grade College, Nonavinakere. Page 1

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Agri Loans by KBL

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

CHAPTER-1

INTRODUCTION

Finance

In our present day economy, finance is defined as

the provision of money at the time when it is

required. Every enterprise, whether big, medium

or small, needs finance to carry on its

operations and to achieve its targets. In fact,

finance is so indispensable today that is rightly

said that finance is the life blood of an

enterprise. Without adequate finance, no

enterprise can possibly accomplish its

objectives.

Meaning

Finance is the branch of Economics concerned with

resource allocation as well as resource

management, acquisition and investment. Simply,

finance deals with matters related to money and

the markets.

Definition

Government First Grade College, Nonavinakere. Page 1

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Paul. G. Hastings has defined finance as “the

management of the monitory affairs of the

company. It includes determining what has to be

paid for and when, raising the money on the best

terms available and devoting the available funds

to the best uses”.

Definition of Financial Management

According to S.C Kuchhal, “Financial Management

deals with procurement of funds and their

effective utilization in the business”.

Objectives of Financial Management

1.Profit Maximization

In the economic theory, the behavior of a firm is

analyzed in terms of profit maximization. Profit

maximization implies that a firm either produces

maximum output for a given amount of input, or

uses minimum input for producing a given output.

The underlying logic of profit maximization is

efficiency. It is assumed that profit

maximization causes the efficient allocation of

Government First Grade College, Nonavinakere. Page 2

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” resources under the competitive market

conditions, and profit is considered as the most

appropriate measure of a firm’s performance.

2.Shareholder Wealth Maximization

Shareholder Wealth Maximization means maximizing

the net present value of a course of action to

shareholders. Net present value (NPV) or wealth

of a course of action is the difference between

the present value of its benefits and the present

value of its costs. A financial action that has a

positive NPV creates wealth for shareholders and,

therefore, is desirable. A financial action

resulting in negative NPV should be rejected

since it would destroy shareholders’ wealth.

Therefore, the wealth will be maximized if NPV

criterion is followed in making financial

decisions.

From the shareholders’ point of view, the wealth

created by a company through its actions is

reflected in the market value of the company’s

shares. The value of the company’s shares is

represented by their market price which in turn,

Government First Grade College, Nonavinakere. Page 3

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” is a reflection of shareholders’ perception about

quality of the firm’s financial decisions. The

market price serves as the firm’s performance

indicator.

Finance Function

Finance function is the most important of all

business functions. It remains a focus of all

activities. It is not possible to substitute or

eliminate this function because the business will

close down in the absence of finance. The need

for money is continuous. It starts with the

setting up of an enterprise and remains at all

times. The development and expansion of business

rather needs more commitment for funds. The funds

will have to be raised from various sources. The

sources will be selected in relation to the

implications attached with them. The receiving of

money is not enough, its utilization is more

important. The money once received will have to

be returned also. If its use is proper then its

return will be easy; otherwise it will create

Government First Grade College, Nonavinakere. Page 4

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” difficulties for repayment. The management should

have an idea of using the money profitably. It

may be easy to raise funds but it may be

difficult to repay them. The inflows and outflows

of funds should be properly matched.

Approaches to Finance Function

1.The Traditional Approach

The traditional approach to the finance function

relates to the initial stages of its evolution

during 1920s and 1930s when the term ‘corporation

finance’ was used to describe what is known in

the academic world today as the ‘financial

management’. According to this approach, the

scope of finance function was confined to only

procurement of funds needed by a business on most

suitable terms. The utilization of funds was

considered beyond the purview of finance

function. It was felt that decisions regarding

the application of funds are taken somewhere else

in the organization. However, institutions and

instruments for raising funds were considered to

be a part of finance function.

Government First Grade College, Nonavinakere. Page 5

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

2.The Modern Approach

The modern approach views finance function in

broader sense. It includes both raising of funds

as well as their effective utilization under the

purview of finance. The finance function does not

stop only by finding out sources of raising

enough funds; their proper utilization is also to

be considered. The cost of raising funds and the

returns from their use should be compared. The

funds raised should be able to give more returns

than the costs involved in procuring them. The

utilization of funds requires decision making.

Finance has to be considered as an integral part

of overall management. So finance function,

according to this approach, covers financial

planning, raising of funds, allocation of funds,

financial control etc.

Aims or goals of finance function

1.Acquiring sufficient funds

The main aim of finance function is to assess the

financial needs of an enterprise and then finding

out suitable sources for raising them. If funds

Government First Grade College, Nonavinakere. Page 6

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” are needed for longer periods then long-term

sources like share capital, debentures, term

loans may be explored. A concern with longer

gestation period should rely more on owner’s

funds instead of interest-bearing securities

because profits may not be there for some years.

On the other hand, if funds are needed for small

periods, short-term sources like retained

earnings, portion of profits may be explored.

2.Proper utilization of funds

Though raising of funds is important but their

effective utilization is more important. The

funds should be used in such a way that maximum

benefit is derived from them. The returns from

their use should be more than their cost. It

should be ensured that funds do not remain idle

at any point of time.

3.Increasing profitability

The planning and control of finance function aims

at increasing profitability of concern. It isGovernment First Grade College, Nonavinakere. Page 7

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” true that money generates money. To increase

profitability, sufficient will have to be

invested. Finance function should be so planned

that the concern neither suffers from inadequacy

of funds nor wastes more funds than required.

4.Maximizing firm’s value

Finance function also aims at maximizing the

value of the firm. It is generally said that a

concern’s value is linked with its profitability.

Even though profitability influences a firm’s

value but it is not at all. Besides profits, the

type of sources used for raising funds, the cost

of funds, the condition of money market, the

demand for products are some other considerations

which also influence a firm’s value.

Scope of Finance Function/Financial

Management

1.Estimation of Financial Requirements

The first task of a financial manager is to

estimate short-term and long-term financial

requirements of his business. For this purpose,

Government First Grade College, Nonavinakere. Page 8

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” he will prepare a financial plan for present as

well as for future. The amount required for

purchasing fixed assets as well as needs of funds

for working capital will have to be ascertained.

The estimations should be based on sound

financial principles so that neither there are

inadequate nor excess funds with the concern.

2.Deciding Capital Structure

The capital structure refers to the kind and

proportion of different securities for rasing

funds. After deciding about the quantum of funds

required it should be decided which type of

securities should be raised. It may be wise to

finance fixed assets through long-term debts.

Even here if gestation period is longer, then

share capital may be most suitable. Long-term

funds should be employed to finance working

capital also, if not wholly then partially.

Entirely depending upon overdrafts and cash

credits for meeting working capital needs may not

be suitable.

3.Selecting a Source of Finance

Government First Grade College, Nonavinakere. Page 9

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” After preparing a capital structure, an

appropriate source of finance is selected.

Various sources from which finance may be raised

include: share capital, debentures, financial

institutions, commercial banks, public deposits

etc. If finances are needed for short term

periods then banks, public deposits and financial

institutions may be appropriate; On the other

hand, if long-term finances are required then

share capital and debentures may be used.

4.Selecting a Pattern of investment

When funds have been procured then a decision

about investment pattern is to be taken. The

selection of an investment pattern is related to

the use of funds. A decision will have to be

taken as to which assets are to be purchased? The

funds will have to be spent first on fixed assets

and then an appropriate portion will be retained

for working capital.

5.Proper Cash Management

Cash management is also an important task of

finance manager. He has to assess various cash

Government First Grade College, Nonavinakere. Page 10

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” needs at different times and then make

arrangements for arranging cash.

Cash may be required to:

a)Purchase raw materials

b)Make payments to creditors

c)Meet wage bills

d)Meet day-to-day expenses

The usual sources of cash may be:

a)Cash sales

b)Collection of debts

c)Short-term arrangements with banks etc.

The cash management should be such that neither

there is a shortage of it and nor it is idle.

6.Implementing Financial Controls

An efficient system of financial management

necessitates the use of various control devices.

Financial control devices generally used are:

a)Return on investment

b)Budgetary control

c)Break even analysis

Government First Grade College, Nonavinakere. Page 11

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

d)Cost and Internal audit

7.Proper Use of Surpluses

The utilization of profits or surpluses is also

an important factor in financial management. A

judicious use of surpluses is essential for

expansion and diversification plans and also in

protecting the interests of shareholders.

A finance manager should consider the influence

of various factors, such as:

a)Trend of earnings of the enterprise

b)Expected earnings in future

c)Market value of shares

d)Need for funds for financing, expansion etc.

A judicious policy for distributing surpluses

will be essential for maintaining proper growth

of the unit.

Government First Grade College, Nonavinakere. Page 12

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

LOAN

In finance, a loan is a debt evidenced by a note

which specifies, among other things, the

principal amount, interest rate, and date of

repayment. A loan entails the reallocation of the

subject asset(s) for a period of time, between

the lender and the borrower.

In a loan, the borrower initially receives or

borrows an amount of money, called the principal,

from the lender, and is obligated to pay back or

repay an equal amount of money to the lender at a

later time. Typically, the money is paid back in

regular installments, or partial repayments; in

an annuity, each installment is the same amount.

Government First Grade College, Nonavinakere. Page 13

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” The loan is generally provided at a cost,

referred to as interest on the debt, which

provides an incentive for the lender to engage in

the loan. In a legal loan, each of these

obligations and restrictions is enforced by

contract, which can also place the borrower under

additional restrictions known as loan covenants.

Acting as a provider of loans is one of the

principal tasks for financial institutions. For

other institutions, issuing of debt contracts

such as bonds is a typical source of funding.

Types of loans

1.Secured

A secured loan is a loan in which the borrower

pledges some asset (e.g. a car or property) as

collateral.

A mortgage loan is a very common type of debt

instrument, used by many individuals to purchase

housing. In this arrangement, the money is used

to purchase the property. The financial

institution, however, is given security - a lien

Government First Grade College, Nonavinakere. Page 14

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” on the title to the house - until the mortgage is

paid off in full. If the borrower defaults on the

loan, the bank would have the legal right to

repossess the house and sell it, to recover sums

owing to it.

2.Unsecured

Unsecured loans are monetary loans that are not

secured against the borrower's assets. These may

be available from financial institutions under

many different guises or marketing packages:

a)credit card debt

b)personal loans

c)bank overdrafts

d)credit facilities or lines of credit

e)corporate bonds (may be secured or unsecured)

Interest rates on unsecured loans are nearly

always higher than for secured loans, because an

unsecured lender's options for recourse against

the borrower in the event of default are severely

limited. An unsecured lender must sue the

borrower, obtain a money judgment for breach of

contract, and then pursue execution of the

Government First Grade College, Nonavinakere. Page 15

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” judgment against the borrower's unencumbered

assets (that is, the ones not already pledged to

secured lenders). In insolvency proceedings,

secured lenders traditionally have priority over

unsecured lenders when a court divides up the

borrower's assets. Thus, a higher interest rate

reflects the additional risk that in the event of

insolvency, the debt may be uncollectible.

3.Demand

Demand loans are short term loans that are

atypical in that they do not have fixed dates for

repayment and carry a floating interest rate

which varies according to the prime rate. They

can be "called" for repayment by the lending

institution at any time. Demand loans may be

unsecured or secured.

4.Subsidized

A subsidized loan is a loan on which the interest

is reduced by an explicit or hidden subsidy

Government First Grade College, Nonavinakere. Page 16

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

5.Unsubsidized

An unsubsidized loan is a loan that gains

interest at a market rate from the date of

disbursement.

Loan payment

The most typical loan payment type is the fully

amortizing payment in which each monthly rate has

the same value over time.

The fixed monthly payment P for a loan of L for

n months and a monthly interest rate c is:

Introduction to Agriculture

Meaning

Government First Grade College, Nonavinakere. Page 17

P= c(1+c) n (1+c)1

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” The word agriculture indicates plowing a field,

planting seed, harvesting of crop and feeding

livestock.

Agriculture is a critical sector of the Indian

economy. Though its contribution to the overall

Gross Domestic Product (GDP) of the country has

fallen from about 30% in 1990-91 to less than 15%

in 2011-12, a trend that is expected in the

development process of any economy, agriculture

yet forms the backbone of development. An average

Indian still spends almost half of his/her total

expenditure on food, while roughly half of

India’s work force is still engaged in

agriculture for its livelihood. Being both a

source of livelihood and food security for a vast

majority of low income, poor and vulnerable

sections of society, its performance assumes

greater significance in view of the proposed

National Food Security Bill and the ongoing

Mahatma Gandhi National Rural Employment

Guarantee Act (MGNREGA) scheme. The experience

from BRICS countries indicates that a one

percentage growth in agriculture is at least two

Government First Grade College, Nonavinakere. Page 18

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” to three times more effective in reducing poverty

than the same growth emanating from non-

agriculture sectors. Given that India is still

home to the largest number of poor and

malnourished people in the world, a higher

priority to agriculture will achieve the goals of

reducing poverty and malnutrition as well as of

inclusive growth. Since agriculture forms the

resource base for a number of agro-based

industries and agro-services, it would be more

meaningful to view agriculture not as farming

alone but as a holistic value chain, which

includes farming, wholesaling, warehousing

(including logistics), processing, and retailing.

Further, it may be noted that in the last two

Five Year Plans, it is clearly mentioned that for

the economy to grow at 9%, it is important that

agriculture should grow at least by 4% per annum.

Achieving an 8-9 % rate of growth in overall GDP

may not deliver much in terms of poverty

reduction unless agricultural growth accelerates.

At the same time ‘growth with inclusiveness’ can

be achieved only when agriculture growth

Government First Grade College, Nonavinakere. Page 19

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” accelerates and is also widely shared amongst

people and regions of the country. All these

factors point to just one thing: that agriculture

has to be kept at the centre of any reform agenda

or planning process, in order to make a

significant dent on poverty and malnutrition, and

to ensure long-term food security for the people.

At the time of independence, the revenue from the

agricultural sector was quite low compared to

what it is today. The main reason for the

increase in revenue is the increase in

agricultural production that was brought about by

the Green Revolution.

The Green Revolution of the 70's was responsible

for bringing additional area under cultivation,

extending irrigation facilities, providing better

quality seeds, improving techniques of farming

and plant protection.

Over the years, agriculture has emerged as one of

the top priorities of the Central and State

Governments. Keeping this in mind, various

schemes have been launched to improve farm

Government First Grade College, Nonavinakere. Page 20

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” productivity and the standard of living of

millions of farmers who work to feed the nation.

In 2000, the government announced the first-ever

National Agriculture Policy.

The main aims of this policy are to:

1.Actualize the vast untapped growth potential

of Indian agriculture

2.Strengthen rural infrastructure to support

faster agricultural development

3.Promote value addition, accelerate the growth

of agro business

4.Create employment in rural areas

5.Secure a fair standard of living for all

agriculturalists

6.Discourage migration to urban areas and face

the challenges arising out of economic

liberalization and globalization.

Agriculture loan

Government First Grade College, Nonavinakere. Page 21

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Agriculture loan is also called as farm loan.

Agriculture loan is a type of secured loan.

Agriculture loans are secured by real estate

property, poultry stored in warehouse and other

agricultural collaterals such as crops, livestock

and work animals. Agriculture loan's primary

purpose is to finance the processes involved in

farming that needs vast amount of investment;

planting, harvesting, gathering and other common

processes. This loan is provided to farmers and

other individuals who engage in agriculture

business to help them uplift their lives as well

as the nation by producing food.

Agriculture loan may be used for financing a land

purchase, farm machines and equipments, supplies

like fertilizers and seeds, poultry, livestock,

even work animals and other similar items.

Agriculture loan is catered mostly and primarily

to tillers, farmers, owners, co-operatives,

compact farms, and to settle their agricultural

losses. However, corporations, single

proprietorship that engage in agricultural

industries may also avail an agriculture loan.

Government First Grade College, Nonavinakere. Page 22

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Types of Agriculture Loans

Agricultural production loans to individual

borrowers can be provided for different purposes

and different lending terms. The most important

loan types are:

1.Seasonal Loans for Working Capital

These loans are used to buy working capital for

agricultural production such as seeds,

fertilizer, and tools, as well as for financing

operating costs such as wages for hired farm

labour. These loans are usually given according

to the seasonal nature of agricultural

production.

2.Harvest Loans

These are short-term loans to finance hired

labour or machine rent for harvesting the crops.

These loans can also be addressed at the time of

financing marketing measures.

3.Improvement Loans

Government First Grade College, Nonavinakere. Page 23

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” These loans are invested in durable improvement

measures to increase farm productivity, such as a

water pump for irrigation.

4.Investment Loans

These loans are used for purchasing real estate

or heavy machinery for long-term use, such as

tractors.

In livestock activities, buying animals can also

be classified as an investment loan. In addition,

investment loans are also used for financing the

plantation of perennial crops such as coffee or

lemon trees that will require several years

before generating returns.

Agriculture loans may be categorized as short-

term, intermediate-term and long-term, depending

on their maturity.

1.Short-term loans

These are often used for operating expenses. Loan

maturity usually matches the length of the

agricultural production cycle (6 to 18 months).

2.Intermediate-term loans

Government First Grade College, Nonavinakere. Page 24

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” These are used to finance depreciable assets such

as machinery, equipment, breeding livestock and

improvements. These loans usually range from 18

to 36 months.

3.Long-term loans

These are used to acquire, construct and develop

land and buildings, and usually are amortized

over periods longer than 36 months.

Government First Grade College, Nonavinakere. Page 25

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

CHAPTER-2

RESEARCH DESIGN

2.1 Title of the Study

“A study on Agriculture Loans provided by

Karnataka Bank Ltd., Nonavinakere”

2.2 Statement of problem

Agriculture loans are available for a multitude

farming purposes. Farmers may apply for loans to

buy inputs for the cultivation of food grain,

crops as well as for horticulture, aquaculture,

animal husbandry, floriculture and sericulture

business.

Banks play a vital role in providing agriculture

loans to farmers.

This study is related to agriculture loans

provided at Karnataka Bank Ltd., Nonavinakere.

2.3 Objectives of the study

1.To study the agriculture loans provided by

Karnataka Bank Ltd.

Government First Grade College, Nonavinakere. Page 26

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

2.To study the different schemes of agriculture

loans provided by Karnataka Bank Ltd.

3.To study the loan provided in different

sectors of agriculture.

4.To study on the effectiveness of agriculture

loans.

2.4 Scope of the study

This study reveals information on agriculture

loan provided by the Karnataka Bank Ltd.,

Nonavinakere. Since agriculture is the base for

the development in Indian economy, today’s

banking sector is providing loans for the

development and growth of farmers and crops.

This study is to analyse various schemes provided

by Karnataka Bank Ltd. to farmers and how their

utilization by farmers is done.

2.5 Research Methodology

Research methodology is a way to systematically

solve the research problem. It is a science of

studying how research is done scientifically.

Government First Grade College, Nonavinakere. Page 27

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Methodology

Personal interview was adopted for collecting

data from Karnataka Bank Ltd., Nonavinakere

regarding agriculture loans.

Tools and techniques of data

Analysis and interpretation of data is based on

the primary and secondary data

Primary Data

Primary data are those which are collected afresh

and for the first time and thus happen to be

original in character.

Primary data was collected through personal

interview method.

Secondary Data

Secondary data are those which have already been

collected by someone else and which have already

been passed through statistical process.

Government First Grade College, Nonavinakere. Page 28

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Secondary data was obtained from Text books,

Annual reports and official website of the bank.

2.6 Limitations of the study

1.This study on agriculture loans is provided

for 3 years only.

2.Time factor is another major limitation of

this study.

3.This study is restricted to the available

information from the financial statement and

records.

Government First Grade College, Nonavinakere. Page 29

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Chapter Scheme

Chapter 1: Introduction

This chapter deals with the subject background.

Chapter 2: Research Design

This chapter tells about title of the study,

statement of the problem, scope of the study,

objectives and limitations of the study,

methodology adopted and the chapter scheme.

Chapter 3: Industry Profile

This chapter explains history of Banking as an

Industry and its profile.

Chapter 4: Company Profile

This chapter gives the profile of Karnataka Bank

Ltd.

Chapter 5: Data Analysis and Interpretation

Government First Grade College, Nonavinakere. Page 30

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” This chapter deals with analysis of data. In this

chapter various inferences are drawn from the

results of analysis.

Chapter 6: Findings, Suggestions and

Conclusion

This chapter includes findings of the study,

suggestions and conclusions.

Bibliography

Annexure

Government First Grade College, Nonavinakere. Page 31

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

CHAPTER-3

INDUSTRY PROFILE

Origin of the term Bank

Authorities on banking are divided in their

opinions regarding the origin of the term

“bank”.

According to some the English Word “bank” is

derived from the Italian word “bancus” and the

French word “banque” which mean a bench. They are

of the opinion that the medieval European bankers

(i.e. money changers and money lenders)

transacted their banking activities, viz. money

changing (i.e. exchanging one currency for

another) and money lending, by displaying coins

of different countries, and of different

denominations in big heaps on the benches in the

market places. As such the word “bank” should be

associated with the Italian word “banco”.

According to others, the term “bank” is derived

from the German word “banck”, which means a joint

Government First Grade College, Nonavinakere. Page 32

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” stock fund or a common fund (i.e. a heap of

money) raised from a large number of members of

the public for the purpose of financing the

needy. As banks deal in common fund or heap of

money raised from the public the term “bank”

should be traced to the German word “banck”.

Of these two views, the latter view seems to be

more convincing, because the word bank is

generally associated with an institution dealing

in money raised from the public.

Definition of Bank

It is very difficult to define the term bank

or banker precisely. Even the best authorities

on banking have failed to provide a precise

and satisfactory definition of this term. This

is because a modern bank performs numerous

activities and it is really difficult to

include all the activities of a modern bank in

a simple and satisfactory definition.

Government First Grade College, Nonavinakere. Page 33

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Meaning of Bank

A bank is a financial institution that accepts

deposits and channels those deposits into

lending activities.

Characteristics of Bank

Acceptance of deposits from the public on

current, fixed and saving bank a/c.

Allowing of withdrawals of those deposits by

cheques, drafts, orders or otherwise.

Utilization of deposits in hand for the

purpose of lending or investment in

securities.

Performance of other activities called

subsidiary services in addition to the

principle activities of receiving of deposits

and lending of funds.

Performance of banking biz as the main biz.

Using the term ‘bank’, banker or banking

company as part of the name.

Government First Grade College, Nonavinakere. Page 34

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Functions of Bank or Banker

Accepting deposit according to demanding of

customers.

Lending and investment.

Buying and selling of Bulletin exchange.

Bank negotiating of loans and advances.

Collecting and transmitting of money and

security.

The providing of safe deposit vaults.

The granting and issuing if letters of

credit, travellers cheques and circular

notes.

The buying and selling of Foreign exchange

including foreign bank notes.

The acquiring holding, issuing on

commissions, underwriting and dealing in

stocks, funds, shares debentures, debenture

stock, bonds, obligations.

Government First Grade College, Nonavinakere. Page 35

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Needs and Importance of Banking or Bank

Banks play vital role in shaping economic dieting

of a nation. They collect the scattered Savings

of the community & make them available for

socially desirable and economically beneficial

purposes. They contribute, to the growth

stability of economy by providing finance to

industrial and importance of banks can be stated

as follows:

Mobilization of Sailings: Banks mobilize the

small and scattered saving of the people and

make them available for the socially

desirable sectors. Thus, they contribute

capital formation.

Government First Grade College, Nonavinakere. Page 36

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Financing industry: Banks provide finance to

the industrial sector, thus provide short

term, medium and long term to industry.

Financing Trade: The commercial banks provide

finance both for Internal & external trade.

They provide loans to retailers, wholesalers,

importers & exporters for meeting their

various financial requirements.

Development to capital market: Commercial

banks and write the shares & debentures of

public limited companies. They have also gone

in for mutual fund.

Financing agriculture: Commercial banks

provide finance to agriculture. They provide

loans to traders to trade in agricultural

commodities

Advantages of Bank Account

Government First Grade College, Nonavinakere. Page 37

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Customer is surplus money is kept safe in the

bank

The banker allows interest on the amount

deposited.

The customer can make payment easily.

In time of difficulty the customer can obtain

advance from the Bank.

The banker will undertake to collect changes

drafts, dependents, pension etc. on behalf of

the customers

Funds can be easily transferred from one to

another by

Credit information can be obtained from the

bank.

Valuables like gold, securities, etc. can be

kept with the bank Safety

Traders can get letters of credit which are a

grant use in trade.

The banker will assist it customers filing

income trade Returns.

Government First Grade College, Nonavinakere. Page 38

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

History of Banking in India

With a sound effective banking system in India it

cannot have a healthy economy. The banking system

of India should not only be hassle free but it

should be able to meet new challenges posed by

the technology and any other external and

internal factors.

For the past three decades India’s banking system

several outstanding achievements to its credit.

The most striking is its extensive reach. It is

no longer confined to only metropolitans or

cosmopolitans in India. In fact, Indian banking

system has reached even to the remote corners of

the country. This is one of the main reasons of

India’s growth process.

Government First Grade College, Nonavinakere. Page 39

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” The government’s regular policy for Indian Bank

since 1969 has paid rich dividends with the

nationalization of 14 major private banks of

India.

Not long ago, an account holder had to wait for

hours at the bank counter for getting a draft or

for withdrawing his own money. Today, he has a

choice. Gone are days when the most efficient

bank transferred money from one branch to other

in two days. Now it is simple as instant

messaging or dial a pizza. Money has become the

order of the day.

The first bank in India, though conservative, was

established in 1786. From 1786 till today, the

journey of Indian Banking System can be

segregated into three distinct phases. They are

as mentioned below:

Early phase from 1786 to 1969 of Indian Banks

Nationalization of Indian Banks and up to

1991 prior to Indian banking sector Reforms.

Government First Grade College, Nonavinakere. Page 40

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

New phase of Indian Banking System with the

advent of Indian Financial and banking Sector

Reforms after 1991.

To make this write-up more explanatory, I

prefix the scenario as phase I, phase II and

phase III.

Phase I (Pre-Independence)

The general Bank of India was set up in the

year 1786. Next came Bank of Hindustan and

Bengal Bank. The East India Company

established Bank of Bengal (1809), Bank of

Bombay (1840) and Bank of Madras (1843) as

independent units and called it Presidency

Banks. These three banks were amalgamated in

1920 and Imperial bank of India was

established which started as private

shareholders banks, mostly Europeans

shareholders.

In 1865 Allahabad Bank was established and

first time exclusively by Indians, Punjab

National Bank Ltd. was set up in 1894 with

headquarters at Lahore. Between 1906 and 1913,

Government First Grade College, Nonavinakere. Page 41

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Bank of India, Central Bank of India, Bank of

Baroda, Canara Bank, Indian Bank, and Bank of

Mysore were set up. Reserve Bank of India came

in 1935.

During the first phase the growth was very

slow and banks also experienced periodic

failures between 1913 and 1948. There were

approximately 1100 banks, mostly small. To

stream line the functioning and activities of

commercial banks, the government of India came

up with The Banking companies Act of 1965

( act NO.23 of 1965). Reserve Bank of India

was vested with extensive powers for the

supervision of banking in India as the Central

Banking Authority.

During those days public had lesser confidence

in the banks. As an aftermath deposit

mobilization was slow. Abreast of it the

savings bank facility provided by the Postal

department was comparatively safer. Moreover,

funds were largely given to traders.

Phase II (Post-Independence)

Government First Grade College, Nonavinakere. Page 42

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Government took major steps in this Indian

Banking Sector Reform after Independence. In

1955, it nationalized Imperial Bank of India with

extensive banking facilities on a large scale

especially in rural semi-urban areas. It formed

State Bank of India to act as the principal agent

of RBI and to handle banking transactions of the

Union and state Governments all over the country.

Seven banks forming subsidiary of State Bank of

India was nationalized in 1960 on 19th July,

1969, major process of nationalization was

carried out. It was the effort of the then Prime

Minister of India, Mrs Indira Gandhi. 14 major

commercial banks in the country were

nationalized.

Second phase of nationalization Indian Banking

Sector Reform was carried out in 1980 with seven

more banks. This step brought 80% of the banking

segment in India under Government ownership.

The following are the steps taken by the

Government of India to regulate banking

Institutions in the country:

Government First Grade College, Nonavinakere. Page 43

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

1949: Enactment of Banking Regulation Act.

1955: Nationalization of State Bank of India.

1959: Nationalization of SBI subsidiaries.

1961: Insurance cover extended to deposits.

1969: Nationalization of 14 major Banks.

1971: Creation of credit guarantee

corporation.

1975: Creation of regional rural banks.

1980: Nationalization of seven Banks with

deposits over 200 crore.

After the nationalization of banks, the branches

of the public sector bank India rose to

approximately 800% in deposits and advances took

a huge jump by 11,000%. Banking in the sunshine

of Government ownership gave the public implicit

faith and immense confidence about the

sustainability of these institutions.

Phase III (After 1990)

Government First Grade College, Nonavinakere. Page 44

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” This phase has introduced many more products and

facilities in the banking sector in its reforms

measure. In 1991, under the chairmanship of M

Narasimhan, a committee was set up by his name

which worked for the liberalization of banking

practices.

The country is flooded with foreign banks and

their ATM stations. Efforts are being put to give

a satisfactory service to customers. Phone

banking and net banking is introduced. The entire

system became more convenient and swift. Time is

given more importance than money.

The financial system of India has shown great

deal of resilience. It is sheltered from any

crisis triggered by any external macroeconomics

shock as other East Asian Countries suffered.

This is all due to be flexible exchange rate

regime, the foreign reserves are high, the

capital account is not yet fully convertible, and

banks and their customers have limited foreign

exchange exposure.

Government First Grade College, Nonavinakere. Page 45

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Types of Banks

On the basis of their functions, banks are

classified into 5 categories. They are:

1. Commercial Banks/ Deposit Banks

2. Industrial banks/ Investment banks

3. Agricultural banks

4. Exchange banks

5. Savings banks

Commercial Banks

Commercial banks are banks which accept deposits

from the public and lend them mainly to commerce

for short periods. As they finance mainly

commerce, they are called commercial banks.

Industrial Banks

Industrial banks are banks which provide blocks

or fixed capital (i.e. long term and medium-term

finance) to industries. As they finance

industries, they are called industrial Banks.

Agricultural banksGovernment First Grade College, Nonavinakere. Page 46

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Agricultural Banks are banks which provide

finance to agriculture. As they provide finance

to agriculture, they are called agricultural

banks.

Exchange Banks

Exchange banks are banks which finance mainly the

foreign exchange business (i.e. the export and

import trade) of a country. As they finance

mainly the foreign exchange business of a country

they called exchange banks.

Savings Banks

Savings banks are special which specialize in the

mobilization of the small savings of the middle

and low income groups. As they are concerned with

the mobilization of the small savings of the

people, they are called savings banks.

Some other types of bank

Central BankGovernment First Grade College, Nonavinakere. Page 47

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” The Reserve bank of India is central Bank that is

fully owned by the government. It is governed by

a central bank (headed by a governor) appointed

by the central government. It issues guidelines

for the functioning of all banks operating within

the country.

Public Sector Banks

State bank of India and its associate banks

called the State bank group.

20 Nationalized banks

Regional rural banks mainly sponsored by

public sector banks.

Private Sector Banks

Old generation private banks

New generation private banks

Foreign banks operating in India

Scheduled co-operative banks

Non-Scheduled banksGovernment First Grade College, Nonavinakere. Page 48

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Co-operative Sector Banks

The co-operative sector is very much useful for

rural people. The co-operative banking sector is

divided into the following categories.

State co-operative banks

Central co-operative banks

Primary Agriculture credit societies.

Nationalized Banks in India

Nationalized banks dominate the banking system in

India. The history of nationalized banks in India

dates back to mid-20th century, when Imperial

banks of India was nationalized (under the SBI

act of 1955) and re-christened as state bank of

India (SBI) in July 1955. Then on 19th July 1960,

its seven subsidiaries were also nationalized

with deposits over 200 crores. These subsidiaries

of SBI were State Bank of Bikaner and Jaipur

(SBBI), State Bank of Hyderabad (SBH), State Bank

of Indore (SBIR), State Bank of Mysore (SBM),

State Bank of Patiala (SBP), State Bank of

Government First Grade College, Nonavinakere. Page 49

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Saurashtra (SBS) and State Bank of Travacore

(SBT).

However the major nationalization of banks

happened in 1969 by the then- Prime Minister

Indira Gandhi. The major objective behind

nationalization was to spread banking

infrastructure in rural areas and make cheap

finance available to Indian farmers. The

nationalized 14 major commercial banks were

Allahabad Bank, Andhra Bank, Bank of Baroda, Bank

of India, Bank of Maharastra, Canara Bank,

Central bank of India, Corporation bank, Dena

bank, Indian bank, Indian overseas bank, oriental

bank of commerce ( OBC),Punjab and sind bank,

Punjab National bank (PNB), Syndicate bank of

India ( UBI) and Vijaya bank.

In the year of 1980 the second phase of

Nationalization of Indian Banks took place, in

which 7 more banks were nationalized with

deposits over 200 corers. With this, the

government of India held a central over 91% of

the banking industry in India. After the

nationalization of banks there was a huge jump in

Government First Grade College, Nonavinakere. Page 50

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” the deposits and advances with the banks. At

present, the State Bank of India is the largest

commercial bank of India and is ranked one of the

top five banks worldwide. It serves 90 million

customers through a network of 9000 branches.

Government First Grade College, Nonavinakere. Page 51

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

CHPTER-4

COMPANY PROFILE

HISTORY OF KARNATAKA BANK AND OTHER

CORPORATE MATTERS

Karnataka Bank Ltd, a premier private sector

bank, is a leading 'A' Class Scheduled Commercial

Bank in India. It was incorporated on February

18, 1924 as ‘The Karnataka Bank Limited’ at

Mangalore in Karnataka state to cater to the

banking needs of the South Kanara Region. The

certificate to commence business was obtained on

May 23, 1924. Karnataka Bank was promoted by Late

Shri B.R. Vysarayachar and other leading members

of the South Kanara Region. Under the guidance of

Shri K.S.N. Adiga, the second Chairman of the

Bank who held the post for a period of 21 years,

Karnataka Bank made significant progress thereby

providing a strong foundation and as a result

grew in stature in terms of number of branches,

deposits, advances etc. Over the years bank grew

with the merger of Sringeri Sharada Bank Limited,

Government First Grade College, Nonavinakere. Page 52

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Chitladurg Bank Limited and Bank of Karnataka. At

present Karnataka Bank provides wide gamut of

financial services to cater to the needs of

trade, industry, commerce and agriculture. With

over 88 years of experience at the forefront of

providing professional banking services and

quality customer service, the Bank now has a

national presence with a network of 544 branches

spread across 20 states and 2 Union Territories.

Managed by a dedicated & professional management

team, we have over 6,084 employees, 105,099

shareholders and over 6.7 million customers (As

on 31-3-2013). Today, Karnataka Bank has emerged

as a leading financial service institution in

India.

Mission statement: "Our mission is to be a

technology savvy, customer centric progressive

bank with a national presence, driven by the

highest standards of corporate governance and

guided by sound ethical values."

Logo:

Government First Grade College, Nonavinakere. Page 53

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

The Logo of Karnataka Bank was adapted in 1977.

It is a holy sign of Ganesha, who enjoys premier

position among the Hindu gods for worship as he

is believed to be “Vighna nivaraka”.

The logo represents growth with the safety,

security and inducing success for all beings. The

sign also signifies the family concept of father,

mother and their progeny, symbolizing their

security.

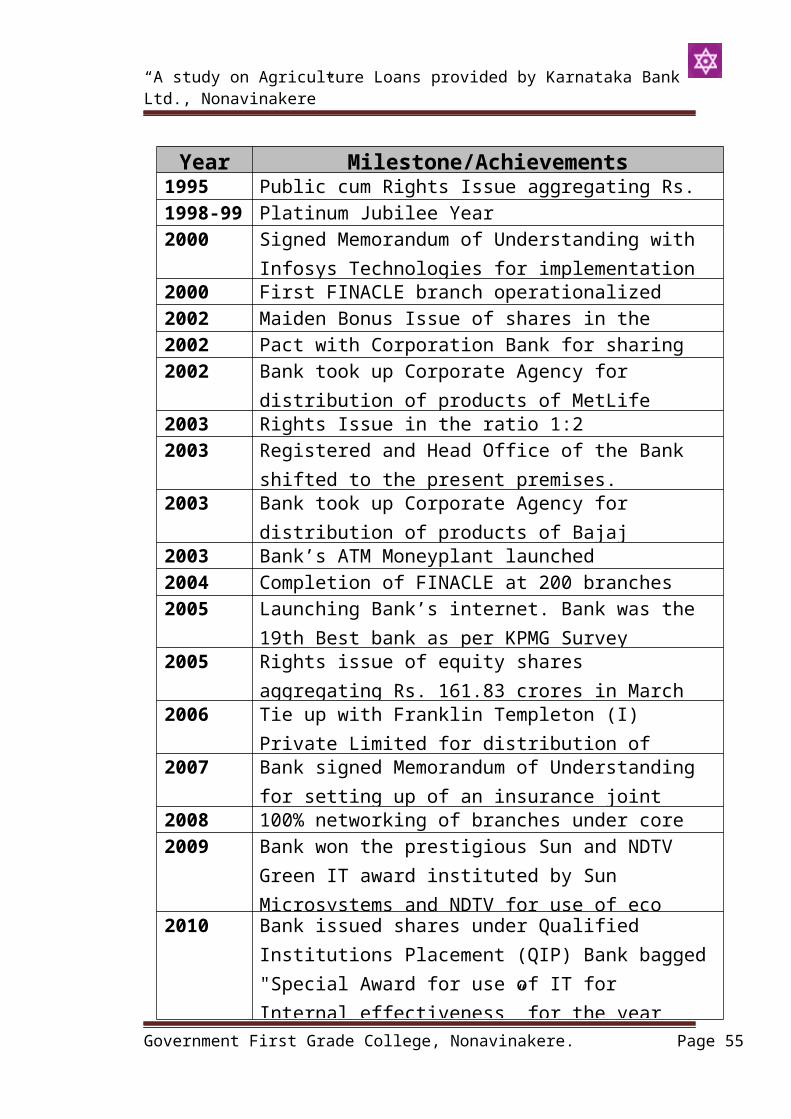

Key Milestones of Karnataka Bank

Government First Grade College, Nonavinakere. Page 54

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Government First Grade College, Nonavinakere. Page 55

Year Milestone/Achievements1995 Public cum Rights Issue aggregating Rs.

81 crores1998-99 Platinum Jubilee Year2000 Signed Memorandum of Understanding with

Infosys Technologies for implementation 2000 First FINACLE branch operationalized2002 Maiden Bonus Issue of shares in the

ratio 1:12002 Pact with Corporation Bank for sharing ATM’s2002 Bank took up Corporate Agency for distribution of products of MetLife

2003 Rights Issue in the ratio 1:2 aggregating Rs. 33.72 crores2003 Registered and Head Office of the Bank shifted to the present premises.

2003 Bank took up Corporate Agency for distribution of products of Bajaj

2003 Bank’s ATM Moneyplant launched2004 Completion of FINACLE at 200 branches2005 Launching Bank’s internet. Bank was the

19th Best bank as per KPMG Survey2005 Rights issue of equity shares

aggregating Rs. 161.83 crores in March 2006 Tie up with Franklin Templeton (I)

Private Limited for distribution of 2007 Bank signed Memorandum of Understanding

for setting up of an insurance joint 2008 100% networking of branches under core

banking platform.2009 Bank won the prestigious Sun and NDTV Green IT award instituted by Sun Microsystems and NDTV for use of eco

2010 Bank issued shares under Qualified Institutions Placement (QIP) Bank bagged"Special Award for use of IT for Internal effectiveness” for the year

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Main Objects of Karnataka Bank

The main objects of Karnataka Bank as per its

Memorandum of Association are as under:

To establish and carry on the business of the

Bank, where of the Head office or place of

business shall be in Mangalore with such

branches or agencies as may from time to time

be determined upon.

To carry on the business of banking in all

its branches and departments including the

borrowing or raising or taking up of money,

the discounting, buying and selling of and

dealing in Government securities, bills of

exchange, hundies, promissory notes and other

negotiable and transferable instruments and

securities, the granting and issuing of

letters of credit and circular notes, buying

and selling of the and dealings in bullion

and specie, such as gold, silver etc., the

negotiating of loans and advances, the

receiving of money and valuables on deposit,

or for safe custody or otherwise the lending

or advancing of money on promotes, on theGovernment First Grade College, Nonavinakere. Page 56

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

security of jewels, Government Securities,

Port Trust Bonds, Municipal debentures,

shares or debentures of any other companies,

insurance policies, or other valuable

securities, or merchandise or any other

movable property and also on the security of

immovable property, by deposit of title deeds

or otherwise the collecting and transmitting

of money and securities and the transacting

of all kinds of agency business, commonly

transacted by Bankers.

To take or acquire the whole or any part of

any business similar to that of the Bank or

any business which the Bank is authorized to

carry on and such other business which is

capable of being conducted to the benefit

directly or indirectly of the Bank.

To purchase or otherwise acquire any sites

with or without building thereon, erect or

construct buildings and repair and improve

them for the purpose of investment or

otherwise as may be determined upon.

Government First Grade College, Nonavinakere. Page 57

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Generally to purchase, take on lease or in

Exchange, hire or otherwise acquire any

immovable or movable property and any rights

or privileges which the Bank may think

necessary or convenient with reference to any

of the objects, for which is established or

acquisition of which may seem calculated to

facilitate to the realization of any

securities held by the Bank or to prevent or

diminish any apprehended loss or liability.

To take shares or otherwise acquire shares in

Banking Companies or in other joint stock

business companies or guaranteed corporations

at the discretion of the Directors.

To encourage, assist and finance any and

every description of financial, commercial,

mercantile, industrial, manufacturing and

agency business undertakings, and operations

at the discretion of the Directors.

To take or concur in the taking up of all

such steps and proceedings as may seem best

calculated to uphold and support the credit

of the Bank. To establish and support or aid

in the establishment and support ofGovernment First Grade College, Nonavinakere. Page 58

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

associations, institutions, funds, trusts,

and conveniences calculated to benefit

employees or ex-employees of the Bank, or the

dependents or connections of such persons, to

grant pensions and allowances and to make

payments towards insurance and to set apart

and appropriate from the annual net profits,

towards the general, mental, moral and

physical advancement of the members of the

Dravida Brahmin Community, such sums as may

be deemed fit.

To sell and dispose of the entire undertaking

of the Bank but not part of it only for such

consideration as the Bank may think fit

either for cash or shares, debentures, or

securities of any other company having

objects all together or in part similar to

those of the Bank.

To sell, manage, develop, exchange, lease,

mortgage, dispose of, turn to account, or

otherwise deal with all or any part of the

property and rights of the bank.

To do all or any of the above things as

principals, agents, contractors, trustees orGovernment First Grade College, Nonavinakere. Page 59

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

otherwise and by or through trustees, agents

or otherwise.

To do all such other things as are incidental

or conducive to the attainments of the above

objects.

To engage in all or any one or more of the

forms of business enumerated in Section 6 (1)

of the Banking Regulation Act, 1949.

To open, establish, maintain and operate

currency chests and small coins depots on

such terms and conditions as may be required

by the Reserve Bank of India established

under the Reserve Bank of India Act, 1934,

and enter into all administrative or other

arrangements for undertaking such functions

with the Reserve Bank of India.

The main object clause of the Memorandum of

Association of the Bank enables it to undertake

the activities for which the funds are being

raised and the activities which it has been

carrying on till date. There have been no

changes in object clause since the previous

rights issue of bank in the year 2005.

Government First Grade College, Nonavinakere. Page 60

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

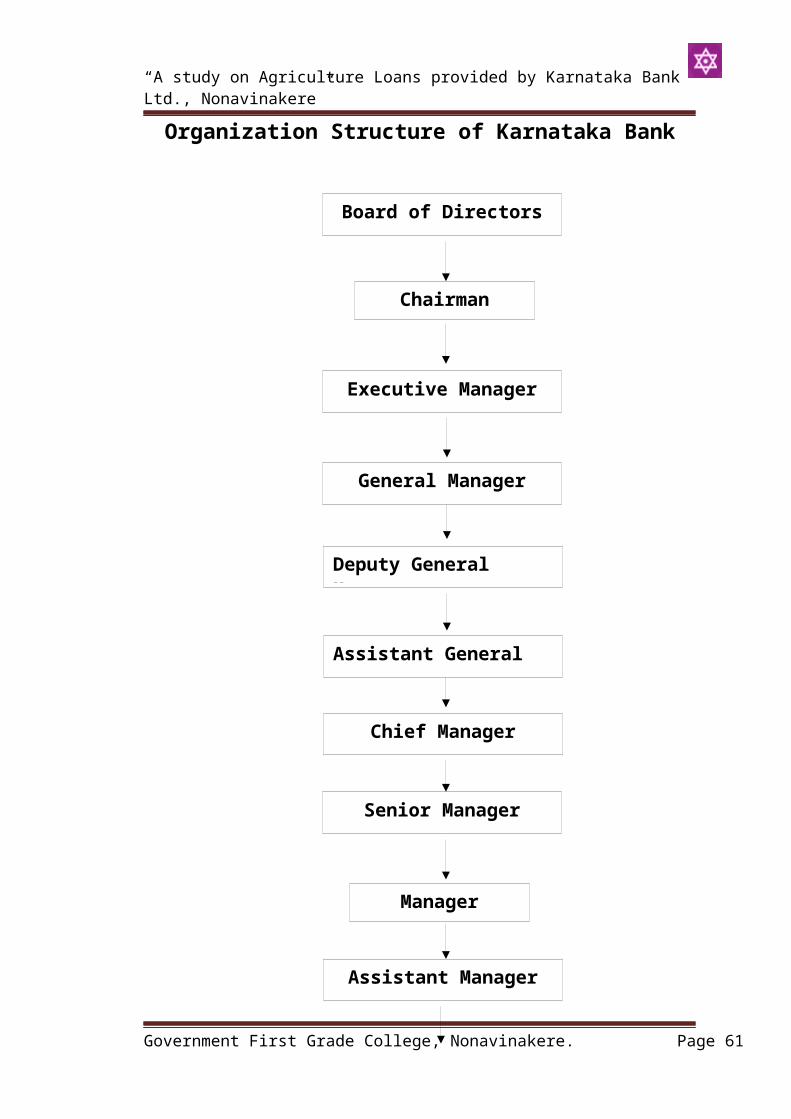

Organization Structure of Karnataka Bank

Government First Grade College, Nonavinakere. Page 61

Board of Directors

Chairman

Executive Manager

General Manager

Senior Manager

Deputy General Manager

Assistant General Manager

Chief Manager

Manager

Assistant Manager

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Types of Loans

1.GOLD LOAN

It is fully secured short-term advance made by

the banker to his customer by pledging gold as

security for the advance made.

The banker will advance both for member and non-

member of the bank. Period of loan is one year.

Penal interest at 2% will be charged on the

balance due after the expiry of loan period,

until its collection.

Amount of loan sanction

The bank’s appraisers will appraise the gold

which is going to be pledge with the bank. The

bank receives the appraiser’s certificate and

will advance 75 % of the appraisal value of the

gold to the borrower.

Conditions that are required to be fulfilled by

the barrower

Government First Grade College, Nonavinakere. Page 62

Staff

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

The borrower has to submit duly filled

application to the bank in the form

prescribed by the bank itself.

Bank will verify the application to make sure

that the applicant has furnished all the

required details and agreed for all the rules

of the bank regarding the loan.

The bank appraises the gold from its

appraiser and will receive appraiser’s

certificate to fix the amount of loan to be

advanced.

Bank will pledge the gold with it as the

security for the advance which it is going to

make.

Bank will sanction 75% of the appraisal value

as advance, if it is satisfied with

information furnished by the borrower.

Mode of repayment

The borrower can repay the principle loan amount

after the full completion of loan period. But

compulsorily he has to pay interest amount in

monthly or quarterly installments. He is required

Government First Grade College, Nonavinakere. Page 63

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” to pay 2% penal interest on the due installments

of interest if any.

Recovery of loan from the default borrower

The bank will send the quarterly notice to

the default borrower after 3 months from the

expiry of the loan period requesting for the

repayment of dues from him.

If there is no response from the borrower the

bank will send the cautionary notice to the

borrower. The same procedure will be

continued till the 3rd quarter.

If there is no response from the borrower

even after the 4th quarter also, the bank will

sell the pledged gold through auction,

without taking any permission from the

borrower.

The bank will repay the extra amount if any

even after the full settlement of all the

dues of the borrower, otherwise, will take

legal action for further collection of

remaining dues.

2.DEPOSIT LOAN

Government First Grade College, Nonavinakere. Page 64

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

It is fully secured short term advance made by

the banker from the deposits with the bank.

Members and non-members of the bank can take

the deposit loans. Period of loan is unlimited.

Rate of interest charged on this loan is 2%

more than the interest allowed by the bank for

the particular deposit.

Amount of loan sanctioned is 75% to 90% of the

amount of deposit, which was taken as security.

Conditions required to be fulfilled by the

borrower

The borrower should apply for the loan in the

form of written application because the bank

is not maintaining any prescribed forms of

application for this type of loan.

The barrower should clearly mention which

deposit is to be taken as security to the

loan amount. He should pledge the deposit

bond with the bank.

Recovery of balance due from the default

barrower

If the barrower fails to repay the principle

amount after its maturity for the fullGovernment First Grade College, Nonavinakere. Page 65

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

settlement of all the dues from him, the bank

will repay the surplus of deposits to the

barrower if any even after the full settlement

of his dues to the bank.

3.CASH CREDITS

Cash credit is a financial arrangement under

which a borrower is allowed an advance under a

separate account called cash credit account up to

a specific limit. The borrower can withdraw the

amount in installments as and when he needs.

Cash credits are generally granted against

collateral securities and the interest is charged

only on the amount actually utilized and the

interest will be calculated at the end of each

month on the basis of daily debit balances and is

charged to the account.

Usually the cash credit will be given for a short

period, say 6 months or a year. The rate of

interest charged on this loan is 13.75% which is

payable in quarterly intervals on the daily debit

balance for the actual period of utilization.

Government First Grade College, Nonavinakere. Page 66

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” The cash credit arrangement is the most popular

method of borrowing. The popularity of the cash

credit is due to the reason that the borrower is

required to pay interest not on the amount of

cash credit sanctioned but only on the amount

actually withdrawn by him. Other reason is that

the borrower is not required to pledge the stock

with it; just it is enough to hypothecate it.

4.OVERDRAFTS

An overdraft is a popular type of advance made

by the bank. It is a financial arrangement

under which a current account holder is

permitted by the bank to overdraw his account

i.e. to draw more than the amount standing to

his credit up to an agreed limit. Period of

loan is 6 months or a year. Rate of interest

charged on the deposit pledge overdraft is 2%

over and above the rate of interest allowed to

the bank on the deposit. This is going to

pledge by the customers.

Mode of repayment

Government First Grade College, Nonavinakere. Page 67

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

The borrower can repay the loan amount on the

last day of the loan period. But he has to pay

the interest on the quarterly installment.

Conditions required to be fulfilled by the

borrower while taking overdraft by the bank

He has to apply for the overdraft in the form

prescribed by the bank.

He has to furnish all the required

information in the application.

He has to mention clearly the purpose and

amount of overdraft required and he has to

pledge the amount in the credit of his other

deposit account as security for the overdraft

loan.

He has to clearly mention his total income

from all the sources.

He has to obey and agree to follow all the

rules and conditions laid down by the bank

regarding the loan from time to time.

Procedures followed by the bank while giving

overdraft facility to a customer

Government First Grade College, Nonavinakere. Page 68

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

The bank will receive the duly filled

application for the overdraft loan from the

borrower in prescribed form.

It will check the application to confirm

whether the borrower has furnished all the

required details or not.

It will check the type of security he is

giving.

If the bank is satisfied with all the details

and security provided by the borrower, it

will provide him overdraft facility with a

limit not exceeding the maximum limit as

decided in the board meeting on the current

accounts.

Recovery of the balance due from the default

borrower

The bank will send a quarterly notice after 3

months from the last date of loan period.

If there is no response from the borrower,

the same process will continue till the 4th

quarter.

Government First Grade College, Nonavinakere. Page 69

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

If there is no response from the borrower

even for the 4th cautionary notice also, the

bank will follow legal actions to collect the

loan amount due from the borrower. It will

set-off the deposit amount against the

balance due or auction the stock held at the

go down.

It will set-off the dues from the amount

realized in the auction of the stock, and

will repay to the customer any extra amount,

if any, even after the full settlement of the

dues.

5. Installment Loan

Installment is a fully secured medium term

advance granted by the bank to its customers to

meet their financial requirement of housing

repairs, or to carry on business, or to

industries for construction of industrial

building or to meet the day-to-day working

capital requirements or to purchase the

machineries.

Government First Grade College, Nonavinakere. Page 70

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Amount of Loan is sanctioned

The minimum amount of installment loan is 10,000

rupees. The maximum amount of loan to be

sanctioned will depend upon the repayment

capacity of the borrower or Rs. 1 crore whichever

is less.

While deciding the loan amount to be sanctioned

the board of directors of the bank will consider

the tangible security provided by the borrower

along with the repayment capacity of the

borrower.

Period of Loan sanctioned

Usually the period for the repayment of loan is

34 months and sometimes 120 months are also

allowed if the party makes any request.

The bank will grant loan even for the period less

than 60 months if the borrower wishes to take.

Rate of Interest

Government First Grade College, Nonavinakere. Page 71

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Rate of interest charged on installment loan is

13% and 2% penal interest will be charged on the

due amount of installment (i.e. Principal +

interest).

Conditions required to be fulfilled by the

borrower

Borrower should apply for the loan in the

form prescribed by the bank by fulfilling all

the required details asked in the

application.

He should clearly mention the purpose of loan

in the application form.

He should provide necessary documents

required by the bank and obey the regulations

laid down by the bank from time to time

during the loan period, about the repayment

procedures and rate of interest etc.

Procedures followed by the bank while granting

the installment loan

The bank will receive duly filled application

for the loan from the borrower.

Government First Grade College, Nonavinakere. Page 72

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

The bank will check the purpose for which the

loan will be used and will receive a source

of income certificate to fix the amount of

monthly installment.

The bank will receive the adequate security

in the form of collateral tangible assets for

the loan amount granted and will pledge them

with it.

Finally the bank will grant the loan if it is

satisfied with all the information and

securities provided by the borrower.

Different documents required to be provided by

the borrower while applying for the installment

loan for different purposes

1.Original title deeds

2.Previous original title deeds

3.Municipal Khatha Endorsement

4.Demand register extract of loan and building

5.Asst. list of loan with building liable to

taxation

6.Encumbrance certificate for 13 years in form

15

Government First Grade College, Nonavinakere. Page 73

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

7.Up to date tax payment receipt

8.Approved plan

9.License for construction

10. Detailed estimates of construction of

building

11. Conversion copy with approved layout

plans copy

12. Genealogical tree

13. Project report

14. Suitable shareholder’s security

15. Sources of income certificates

16. Recent salary certificate

17. Five recent passport size photos

18. KST and CST certificate

19. Partnership deed copy

20. Form-3 and Form-4, along with 3 years

balance sheet

21. Telephone numbers, etc.

Government First Grade College, Nonavinakere. Page 74

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Mode of Repayment

Borrower is required to pay interest only on

the due amount of principle amount of loan

repayable in each installment.

Total amount of loan sanctionedNumber of months allocated Interest on

due amount of principle for the repayment of

In case of default, borrower should be liable

to pay 2% penal interest in the repayment

period that will start from 1 month after the

date of sanction of the loan.

Recovery of due amounts from the default

borrowers

The bank will send a quarterly notice after 3

months from the date of the loan period,

requesting for the repayment of the dues to the

bank.

The bank, up to 1 year will follow the same

procedure if there is no reply from the

borrower.

Government First Grade College, Nonavinakere. Page 75

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere”

Even if there is no response for the 4th

quarterly notice also, the legal actions will

be taken by the bank to collect the balance due

from him.

The bank will take action to sell the

securities, which it accepted from the borrower

and will make use of the amount realized for

the settlement of dues of default borrower.

6. KBL VIDYANIDHI (Education Loan Scheme)

Eligibility for Student

Any student, representing himself / herself if

major, or a minor student represented by parent

or guardian, of Indian nationality, who has

secured admission to a professional / technical /

other course, in India or abroad.

Courses eligible for finance

Government First Grade College, Nonavinakere. Page 76

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” Studies in India: Graduate Courses - B.A., B.Sc.,

B.Com., B.C.A., B.B.M., Diploma in Engineering,

Post Graduate Courses - Masters and Ph.D;

Professional Courses - Engineering, Medical,

Agriculture, Nursing, Veterinary, Law, Dental,

Management, Computer, Pharmacy, Physiotherapy,

Hotel Management, ICWA, CA, CFA; Courses

conducted by IIM, IIT, XLRI, NIFT; Courses

offered in India by reputed foreign universities;

Evening Courses of approved Institutes; Other

Courses leading to Diploma / Degree conducted by

Colleges / Universities approved by UGC / GOVT. /

AICTE / AIBMS / ICMR; Courses offered by National

Institutes and other reputed private

Institutions.

Studies Abroad: Graduation - Only for job

oriented professional / technical courses offered

by the reputed Universities; Post Graduation -

MCA, MBA, MS; Courses conducted by CIMA-London,

CPA in USA etc.

Amount of loan available

For studies in India - a maximum of Rs. 10 lakh.

Government First Grade College, Nonavinakere. Page 77

“A study on Agriculture Loans provided by Karnataka Bank Ltd., Nonavinakere” For studies abroad - a maximum of Rs.20 lakh.

Types of expenses covered by the loan