Coursework short term loans

33

Coursework “Short-term loans” Contents Introduction................................................... 3 1. Essence and types of short-term loans.......................4 2. Essence of credit policy of a commercial bank...............9 3. Issue and redemption conditions............................12 4. Financial position of consumers who use short term credit. .14 Income Levels................................................14 Lack of access to alternative sources of credit..............16 5. Consumer needs met through use of short term credit........17 6. Stages of the credit process...............................19 Conclusion.................................................... 22 Bibliography.................................................. 24

-

Upload

independent -

Category

Documents

-

view

5 -

download

0

Transcript of Coursework short term loans

Coursework“Short-term loans”

Contents

Introduction...................................................31. Essence and types of short-term loans.......................42. Essence of credit policy of a commercial bank...............93. Issue and redemption conditions............................124. Financial position of consumers who use short term credit. .14Income Levels................................................14Lack of access to alternative sources of credit..............16

5. Consumer needs met through use of short term credit........176. Stages of the credit process...............................19Conclusion....................................................22Bibliography..................................................24

Introduction

To begin with, I have chosen this theme for my coursework because of the relevance of short-term loans for commercial and for bank sectors, especially in Russia. While the rise of the Russian production is considerably connected with implementationof potential credit relations, and practice confirms that the overwhelming part of the credits are provided by the credit organizations, the choice of a subject of course work dropped out on studying of the short-term credit policies used by banks.

In the whole world practice placement of money in the form of the credit is the main active transaction performed by banks. Itis connected, first of all, with high profitability of such transactions. At the same time, crediting is connected with the significant risk which is showing in possible losses and losses for banks in case of a non-return of the credits and default on interest payment on them. Thus, the effective organization of credit relations of bank with borrowers therefore meet the main objectives of banking activity - profit earning in case of minimization of credit risks. Owing to above stated the subject of the coursework is very relevant in nowadays situation in economics.

Bank loan - very convenient and in many cases an irreplaceable form of financial services which allow to consider flexibly needs of each borrower and to adapt to their conditions of receipt of the loan. For example, development of credit relations of the population with bank is a question not only economic, but also political and social. In addition to necessary economic and political stabilization, it requires further upgrade of forms and credit methods, enhancement of percentage policy and conditions of provision and settlement of the credits, use of experience of foreign countries with market economy.

The main priority of credit policy of commercial banks is the increase in amount of a credit portfolio by building-up of amounts of crediting of real production sector, socially significant programs of regions, expansions of services in crediting of enterprise customers, crediting growths in volumes with simultaneous improvement of its quality.

Changes in system of the economic relations, occurred in the Russian Federation, were considerably reflected in the organization of a bank system and products of its activities.

For the last decade the credit granting system in Russia did a considerable way of development.

The occurred changes not only in banking philosophies, but also in technology of credit operations.

The purpose of this work is in studying of methods of short-termlending in Russia

For achievement of the specified purpose the following tasks areset:

to classify types of short-term loans;

to study conditions of issue and settlement of types of short-term loans;

to create the main conclusions based on results achieved during the development of the course paper.

1.Essence and types of short-term loans

Short-term lending is intended for providing of the client with short-term financing. Short-term loans are utilized for financing gaps in the paying balance of trade and production enterprises, in case of a lack of means on the settlement account, short-term transactions, acceleration of turnover of assets of the entities as an insurance in case of a payment delay of suppliers and for other purposes.

Short-term financing can be used over a period of up to a year to help corporations increase inventory orders, payrolls and daily supplies. Short-term financing includes the following financial instruments:

Commercial Paper

This is an unsecured promissory note with a fixed maturity of 1 to 364 days in the global money market. It is issued by large corporations to get financing to meet short-term debt obligations. It is only backed by an issuing bank or corporation's promise to pay the face amount on the maturity date specified on the note. Since it is not backed by collateral, only firms with excellent credit ratings from a recognized rating agency will be able to sell their commercial paper at a reasonable price.

Asset-backed commercial paper (ABCP) is a form of commercial paper that is collateralized by other financial assets. ABCP is typically a short-term instrument that matures between 1 and 180days from issuance and is typically issued by a bank or other financial institution.

Promissory Note

This is a negotiable instrument, wherein one party (the maker orissuer) makes an unconditional promise in writing to pay a determinate sum of money to the other (the payee), either at a fixed or determinable future time or on demand of the payee, under specific terms.

Asset-based Loan

This type of loan, often short term, is secured by a company's assets. Real estate, accounts receivable (A/R), inventory and equipment are typical assets used to back the loan. The loan maybe backed by a single category of assets or a combination of assets (for instance, a combination of A/R and equipment).

Repurchase Agreements

These are short-term loans (normally for less than two weeks andfrequently for just one day) arranged by selling securities to an investor with an agreement to repurchase them at a fixed price on a fixed date.

Letter of Credit

This is a document that a financial institution or similar partyissues to a seller of goods or services which provides that the issuer will pay the seller for goods or services the seller delivers to a third-party buyer. The issuer then seeks reimbursement from the buyer or from the buyer's bank. The document serves essentially as a guarantee to the seller that itwill be paid by the issuer of the letter of credit, regardless of whether the buyer ultimately fails to pay.

Short-term loans can be, as a rule, granted for a period of up to 30 days on the following purposes:

- replenishment of current assets (purchase of goods, accessories, consumable materials);

- financing of short-term gaps in payments.

Short-term credit products can represent the greatest interest for the following groups:

- the entities of wholesale and retail trade for increase in turnover;

- the production enterprises making products for the final consumer for increase in turnover;

- production enterprises as a whole, for the purpose of salary payment, taxes or covering of the deficit arising in case of stabely functioning of the entity owing to structure of a cash flow;

- distributors;

- importers and others;

Benefits of short-term commercial credits:

- flexibility of use of credit resources on terms. The credits are issued for a period of 1 till 30 days, so there is an opportunity for more rational manage of amount of loan resources;

- flexibility of use of credit resources depending on the amount. The credits are issued within a limit, depending on the size of need of the client in resources at the moment, that is to be spent less funds for servicing of the credits;

- the rate on the credit is more attractive, than on the standard credits, so the servicing of the credit is cheaper;

- flexibility of use of credit resources on providing. The bank credits for short term the core business of the entity rather the cash flow arriving on the settlement account of the entity

in bank the creditor thereof tough need for liquid pledge is absent.

Short-term loans divide on:

- current account credits;

- accounting credits;

- oval credits;

- administrative credits;

- acceptance credits.

The current account credit serves to finance the current transactions of the entities (firms) and to avoid problems with liquidity. Therefore within the case of credits to firms it has special value.

The current account credit is the open account credit limited on amount which the bank provides to the client. The bank opens to the client for a certain term a credit line on which the maximum amount of the credit is determined. Within this credit line the client can flexibly act, without approving its use withcredit institute. The borrower can utilize this current account credit in full amout, partially or not at all. Time and amount, and also the purpose of use of the credit amounts are determinedby the client. If the borrower did not completely utilized the current account credit, there is a free reserve of liquidity. Oncurrent account payment receipts and effected payments of the client, as a rule, are to be register. On the same account calculation of the current account credit is being made.

To determine used credit amount, the current account is balanced in case of each turnover (record on credit or the account debit), i.e. payment receipts and payments are compared and counted. The corresponding extent of balance is a basis for charge of percent. In connection with this method the current account credit is called an open account credit.

It is necessary to distinguish the "close" of the current account which is being made mostly quarterly. Thus a client billis made out for the established percent, commission charges and charges. All individual clauses (records into the debit and theaccounts) of the closed period (quarter) pass then as speak, in new balance. Now only this balance is discussed if there are disagreements. Essential sign of the current account credit is the changing amount of its use. The credit amount changes with each posting on the current account.

The current account credit — is the instrument of short-term financing. In case of purposeful application used credit amountsreturn and are replaced with use in the new sphere. Usually current account is constantly in movement, i.e. the credit constantly is wrapped. If economic conditions of the client during validity period are not worsen and current account is kept according to the arrangement, the bank constantly prolongs the current account credit. It can be done silently or through the signaturing of the agreement.

As a result of credit prolongation formally short-term current account loan becomes medium-term or even long-term.

The current account credits in principle can be terminated in a short period of time. However, in this regard it is necessary tospecify that short-term termination of the credit from bank happens, for example, because of obvious deterioration of an economic situation of the client that at the majority of borrowers conducts to considerable difficulties with liquidity. Thereof freedom of the client of dealing with money on hand is becoming limited. Liabilities of suppliers, for example, can't be paid in complete amount or can't be paid at all. It is necessary to expect negative impact on business activity of the client.

It is necessary to recognize that also business relations with bank will worsen. There is a danger of not returning of the

current account credit. For the called reasons termination of the current account credit becomes problematic.

The current account credits represent the instrument of short-term and flexible financing which approaches to production and goods turnover financing. By means of this credit it is possibleto avoid short-term difficulties with liquidity.

Depending on a specific purpose of application, the current account credits are provided as:

- credit for replenishment of current assets;

- seasonal loan;

- overdraft;

- the credit for interim financing for overcoming of temporary shortage of liquid means.

Credit for replenishment of current assets. This credit serves for financing of processes of productive activity. At the expense of this credit goods and raw materials are purchased. Thus the entity can use price discounts of the supplier due to direct payment (a discount in case of a cash payment or ahead ofschedule). Thanks to the production credit time of shortage of financing between goods receipt, production and its sale is being overcomen. Loan repayment is being made due to the income account from turnover.

Seasonal loan. Seasonal loans serve for demand which arises regularly, in certain periods, for example, annually, in the period of the increased demand for the equity which is required for financing of procurement and sale of products. Thus, the seasonal loan is a special form of the production credit. Seasonal loans take the entities which production processes are exposed to seasonal fluctuations. It belongs, for example, to

sector of agricultural industry or production of toys, or confectionery goods, or to trade (Christmas trade).

Overdraft. For physical persons about provision of the overdraftspeak in that case when the borrower exceeds the account on the approved crediting limit. Though, as a rule, the credit is utilized without special coordination with bank, however it allows the use of the credit in a certain framework. By means ofthe overdraft one-time, temporary and foreseeable shortages of liquid means are to be overcome. Such shortages of liquid means can arise, for example, as a result of unexpected additional taxpayments or unplanned events. The client shall pay the increasedpercent for credit excess.

For legal entities the overdraft is the credit provided on the current account of the client with a good financial state to a certain limit and for a certain period of time for financing theeconomic activity. The borrower uses the overdraft in that case when his financial liabilities exceed the size of means on his account. Money transfer reduces the size of debt of the borroweron the current account.

The size of the overdraft is approved in the credit agreement towhich precedes the process of carrying out regular credit analysis. In addition to the amount of percent on the size of the used overdraft, bank can demand from the client commission charges for the liability on the amount of the unused overdraft

2.Essence of credit policy of a commercial bank

Before characterizing credit policy of bank, it is necessary to give credit determination in general which characterizes the initial relations of appropriate subjects. There are various determinations of this category. In the western economic literature the term credit is usually characterised as "... trust which the person that has assumed the liability of future payment has, from the person having the right for this sum, - that is trust which the creditor renders to the debtor" [20, page 24]. This determination is given at the beginning of the XXcentury by the known German economist V. Leksis.

Later in works of Y.E. Shengera, V. I. Rybina, O. I. Lavrushina,I.V. Lavchuka and other authors credit relations were researchedin more detail view, the understanding of the credit as economiccategory was created.

All historically developed concepts should be considered in caseof modern understanding and determination of this economic category. Thus, we will understand the credit as a set of the relations connected with returnable provision of resources and settlement of liabilities arising. The bank loan as one of its

types represents set of the relations arising in the course of forming by bank of resources and their placement on the terms ofrecoverability, urgency and the paid nature.

The principle of recoverability reflects need of timely return of the received financial resources after completion of their use by the borrower. The principle of urgency means that the credit shall be not simply returned, and is returned in strictlycertain time. Violation of the specified condition is for a creditor good cause for application to the borrower with economic sanctions.

Recoverability and urgency of crediting is caused by that creditresources of bank are temporarily free money of the entities, organizations and the population.

The principle of the payments assumes not only direct return by the borrower of the credit resources received from bank, but also payment of the right for their temporary use. The economic essence of a payment for the credit (percent) is expressed in the actual distribution of profit in addition got at the expenseof its use between the borrower and the creditor.

The paid nature of the credit stimulates the borrower to use it more productively, and provides a bank - creditor with the covering of the costs connected with interest payment for funds raised in deposits, costs on device content, and also provides profit earning.

The additional principles of crediting are security of the credit, its target and differentiated nature.

Banking credit operations are subdivided into two big groups: passive, when the bank acts as the borrower, raising funds of

clients; active when the bank acts as the creditor, representingmeans to clients. Active credit operations also are object of studying and research in this work.

So, having given general determination of the credit, we will dwell upon such category, as credit policy.

Credit policy — is the policy connected with movement of the credit.

Really in practice banks carry out monetary, credit, percentage,monetarist policies. That is bank policy as generalizing concept, represents set of elements: deposit policy; credit policy; policy in the field of the organization of settlement and cash customer service; percentage policy; monetarist policy;policy on carrying out separate banking activities (consulting, trust, share, electronic and other).

Thus, being an indivisible element of bank policy as a whole, credit policy of commercial bank shall be considered not separately, and taking into account influence, interconditionality of all elements of the bank policy.

In modern economic literature in parallel there are two line items concerning content of credit policy of commercial bank. First, credit policy at macroeconomic level usually is understood as bank policy. Secondly, credit policy at a microeconomic level is considered, as a rule, as policy of specific bank in the field of management of credit process (in confined sense). Credit policy in confined sense also will be engaged in the analysis further.

Credit policy at the level of specific bank is expressed in the form of its strategy and tactics in the field of the

organization and implementation of credit operations and services for the purpose of ensuring reliability, profitability and liquidity of its functioning. As strategy of credit policy of bank most often is understood the general direction and a method of use of credit resources for achievement of the purposes set by bank.

Tactics of credit policy of bank, as a rule, reflects the set ofspecific means, acceptances and goal achievement methods, a conduct or a line of conduct. Strategy and tactics are closely interconnected. The last acts as specific means of goal achievement of the first. Therefore, the combination of strategic and tactical planning in the field of crediting is content of credit policy and allows banks to avoid failures in the activities.

3.Issue and redemption conditions

At legislative level the essence of credit relations is determined by paragraph 2 of the Civil code Russian Federation "Credit". According to Art. 819 "Credit agreement" the credit agreement of the bank or other credit organization (creditor) undertake to provide money (credit) to the borrower in the amount of and on the conditions provided by the agreement, and the borrower undertakes to return the received sum of money and to pay percent on it.

The relations in the credit agreement are coordinated by the rules provided by paragraph 1 of chapter 42 "A loan and the credit" according to which to the loan agreement one party (lessor) transfers to the possession to other party (borrower) money or other things determined by patrimonial signs are applied, and the borrower undertakes to return to the lessor thesame amount of money (loan amount) or equal quantity of other things of the same sort and quality received by it. The loan

agreement is considered concluded after the date of transmissionof money or other things.

Condition of development of credit relations is the trust of thecreditor to the borrower which is possible in case of observanceof the following principles:

recoverability - need of repayment of the loan; urgency - need of repayment of the loan in time determined

by terms of the contract; the paid nature - the indicator of this principle is the

loan interest representing the price of the loan granted intemporary use;

security of protection of valuable interests of bank and incase of possible violation by the borrower of assumed liabilities on return of the money received on the basis ofthe credit;

special-purpose character of the credit, meaning that the loan is issued on certain and known to bank the purpose or the activities of the borrower approved by it.

The credit line is the legally arranged liability of bank to theborrower to provide it during the certain period of time the credits within the approved limit. The credit line has benefits before the one-time agreement for both parties: for the borroweris more certain prospect of a business activity, economy of overheads and time, inevitably connected with negotiating and the conclusion of each free standing credit agreement. Same is for the creditor. However conditions of the agreement on a credit line can be reviewed by both participants of the transaction. So, the bank can refuse loan granting before the termination of the stipulated term if, for example, the financial position of the borrower significantly worsens and it won't satisfy other conditions of the agreement of the parties. The borrower owing to these reasons can not use a credit line fully or partially. The agreement is often accompanied by a condition about storage by the client of a compensating balance

on the current account in creditor bank in the amount of at least 20% of the amount of a credit line.

If the creditor aims to present at the market of the borrower for many years, he sometimes goes for provision of a credit linefor long term.

4.Financial position of consumers who use short term credit

Income Levels

Studies of short term credit have consistently found that borrowers on very low incomes constitute a significant percentage of the people who use short term loans:

• Dean Wilson's 2002 study found that 43% of payday borrowers earned less than $20,852 per annum and 85% of borrowers earned below $31,304 per annum. Overall 44% of payday consumers had dependent children and 80% lived in rental accommodation.

• In the recent Marston and Shevellar pilot study of the Queensland short term lending market borrowers in Queensland, the authors state that “the overwhelming majority of the borrowers we spoke with were living below widely accepted measures of poverty. A quarter of the borrowers we spoke with were routinely accessing emergency relief for food vouchers". Ofthe 44 borrowers interviewed, only six had full-time employment.

• The 2010 Consumer Action Legal Centre Report found that 28.1% of respondents were in part-time or casual employment and 21.9% unemployed. For those consumers who were employed, 72.8% had income levels below the average wage. 23.4% had incomes of less than $20,000.

• Policis reports that half of the payday customers it surveyed for its Australian paper “The Dynamics of Low Income Credit Use”had household incomes of below $35,000.

• Data provided by Cash Stop (quoting uncited research of over 122 lending outlets and 4000 borrowers by Smiles Turner for the NFSF in 2006) found that 50.1% of applicants received social security payments (including where this was their only income).

• The Wesley Community Legal Service noted in its 2010 Green Paper Submission that in its experience short term loans are used by vulnerable classes of consumers, including indigenous people, people with disabilities, people with gambling problems,and those with little education and very low financial literacy.National Legal Aid stated that the majority of consumers who came to legal aid in relation to these loans were Centrelink recipients or low income workers.

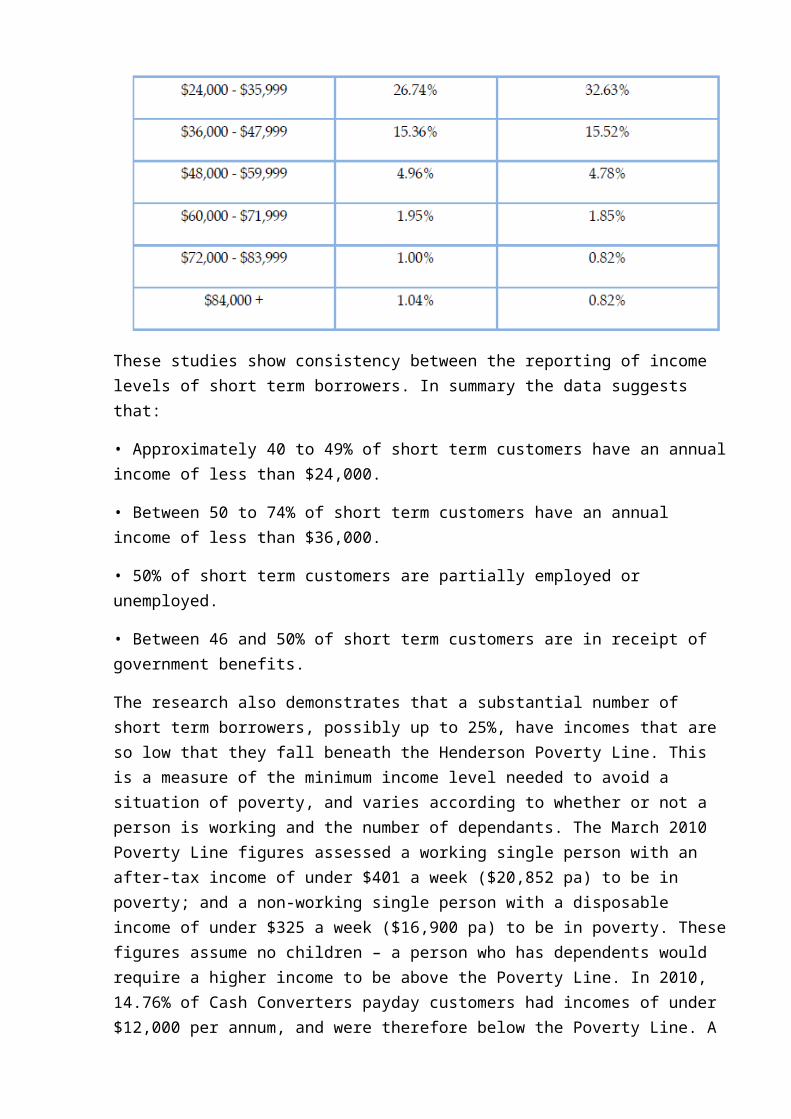

• 2010 Cash Converters data shows that 46.15% of borrowers of loans of less than $1000 and of one month duration (Cash AdvanceLoans) received government benefits (although they may also be in receipt of other income). The figure was 43.93% for borrowersof their other main product (a Personal Loan), a loan over $1000with a duration of 6 – 12 months. Table 3 below sets out the income level of borrowers for each type of loan, and shows that for Cash Advance loans, 75.69% of customers have an income of under $36,000 and just under half had an income of under $24,000.

These studies show consistency between the reporting of income levels of short term borrowers. In summary the data suggests that:

• Approximately 40 to 49% of short term customers have an annualincome of less than $24,000.

• Between 50 to 74% of short term customers have an annual income of less than $36,000.

• 50% of short term customers are partially employed or unemployed.

• Between 46 and 50% of short term customers are in receipt of government benefits.

The research also demonstrates that a substantial number of short term borrowers, possibly up to 25%, have incomes that are so low that they fall beneath the Henderson Poverty Line. This is a measure of the minimum income level needed to avoid a situation of poverty, and varies according to whether or not a person is working and the number of dependants. The March 2010 Poverty Line figures assessed a working single person with an after-tax income of under $401 a week ($20,852 pa) to be in poverty; and a non-working single person with a disposable income of under $325 a week ($16,900 pa) to be in poverty. Thesefigures assume no children – a person who has dependents would require a higher income to be above the Poverty Line. In 2010, 14.76% of Cash Converters payday customers had incomes of under $12,000 per annum, and were therefore below the Poverty Line. A

further 34.19% of their customers had incomes of between $12,000and $24,000, a portion of whom would also fall below the PovertyLine. These figures are consistent with those in Wilson's 2002 study, which found that 43% of payday borrowers earned less than$20,852 per annum and 38% were below the Henderson Poverty Line.25 The 2010 CALC report showed 23.4% of surveyed consumers had incomes of less than $20,000 and were therefore just on or below the Poverty Line.

These figures are consistent with the US experience of short term lending (notwithstanding differences in product structure in that country that mean the poorest consumers tend to be excluded from the short term credit market). The American Federal Reserve Board undertakes a tri-annual Survey of ConsumerFinances. In 2007 the mean income of families who took out a payday loan was $32,614 (the median was $30,892), contrasted to a mean income of $85,473 (median was $48,397) for those who did not use a payday loan. Families who had borrowed from payday lenders had a mean net worth of $22,616 (and, remarkably, had a median net worth of $0). Those who did not use payday lenders had a mean net worth more than 20 times that – $469,374 (median $80,510). 41% of families borrowing from a payday lender were headed by single women, and 40% were headed by married couples.

Lack of access to alternative sources of credit

The Australian research demonstrates that many consumers use small amount lenders because they are unable to access alternative forms of credit:

• In its submission Cash Stop quotes research undertaken by Smiles Turner for the NFSF of 3408 consumers across Australia. Cash Stop states that the research demonstrated that a large proportion of consumers reported that they had no access to other forms of credit – 71.6% (QLD), 72.1% (SA), 76.7% (NSW); 81.6% WA.

• The submission by the Financiers Association of Australia and Minit-Software to the Green Paper lists poor credit history as one of the reasons consumers access short term loans.

• Cash Converters report that 3 in 10 of their clients cannot get credit from other types of lenders.

• Consumers surveyed in the Marston and Shevellar Pilot Study also reported that they felt they had little choice but to access high cost credit.

There is qualitative evidence that the inability to access alternative credit, and the consequent need to obtain a short term loan, is perceived by some borrowers as a personal failure because of an inability to manage their finances.36 Analysis of qualitative interviews indicates that some borrowers felt that their need to use these types of loans was shameful or embarrassing, and as something that would be concealed from friends and family.

5. Consumer needs met through use of short term credit

The data below demonstrates, across a range of sources, that approximately 70% of loans are used by consumers to meet recurrent or basic living expenses:

• The 2010 CALC paper reported that 71.3% of surveyed consumers used short term loans to pay for basic expenses: utility bills (21%), food (17.6%) and rent (10.7%).37 22% of the loans were used to pay for car repairs or registration.

• The 2002 Wilson paper reported that respondents had taken out short term loans to pay for bills (32%), day to day living expenses (26%), car repairs or registration (10%), and rent or

mortgage (10%). In total 78% of borrowers were borrowing for non-discretionary spending.

• Research by the Policis research consultancy found that credit, particularly small sum credit, is used by low income households primarily for essentials and to ensure the effective functioning of household finances. Policis described 28% of borrowing as “distress borrowing” to deal with cash shortfalls; 29% was used to meet unexpected bills and expenses; and 9% was used to meet regular bills and expenses. Credit was used to finance spending on discretionary items in only 10% of cases.

• Data provided by Cash Converters in a 2008 submission to Treasury is consistent with these findings, showing that nearly 6 in 10 of their clients with incomes less than $35,000 per annum would be unable to manage a cash emergency without borrowing and 55% would be unable to renew or repair essential equipment. This suggests that its clients are borrowing to meet emergencies of this type.

• Data provided by Cash Stop, quoting Smiles Turner research, found that the top uses for credit were for basic expenses and bills (29.8%), personal (32.9%), car expenses (8.1%) and groceries (5.6%). A similar SA study undertaken by Smiles Turnerin 2007 of 533 South Australian consumers had similar findings: bills (25.3%); groceries and food (22%); shopping (undefined) (16.1%); living costs (11.2%); and car repairs / maintenance (10%).

In summary, between 50 and 70% of short term borrowers primarilyuse short term credit to meet basic living expenses, presumably because of their low incomes.

In addition to the above uses, Australian data also suggests that short term loans are used by problem gamblers when they have exhausted other alternative sources of funds (for example, accessing available money in transaction or home loan accounts, or on a credit card). The extent of this use has not been quantified, although the South Australian Centre for Economic Studies in a 2010 paper quoted data suggested that 8% of problemgamblers had obtained funds from short term lenders. The

Honourable Ann Bressington, Member of the South Australian Legislative Council referred to this issue during her reading speech for the Consumer Credit (South Australia)(Pay Day Lending) Amendment Bill. She said: “there are about 20 payday lenders operating in Adelaide, and just about all of them are located in lower socioeconomic areas in the north and south. Many are located within close proximity to gambling facilities, and social welfare groups have advised my office that they have heard many reports of people using these loans to gamble or buy drugs and alcohol.”

Again, the Australian research as to the use of funds provided by short term lenders is consistent with that undertaken in the United Kingdom and the United States.

In the United Kingdom research by Paul Jones from the Universityof Liverpool found that over 90% of participants needed to obtain credit to make ends meet. The interviews and focus groupsidentified how people regularly borrowed to pay bills, to buy clothes and school uniforms, and for birthdays, holidays and Christmas. Berthoud and Kempson found that “poorer families, on the whole, use credit to ease financial difficulties and those who are better-off take on credit commitments to finance a consumer life-style”.

The American Survey of Consumer Finances found that 29% of borrowers gave their reason for borrowing as an emergency, 21% cited a basic consumption need, 8% stated that it was the only option available to them, while 34% borrowed for convenience.

6.Stages of the credit process.

As a whole, any bank divides credit process on the following stages:

1) the consulting:

consultation and carrying out primary interview with the Client for the purpose of determination of needs of the Client in this or that credit banking product, consultation and assistance in case of a choice of an optimum form and type of loan;

informing of the Client about Partners of Bank according to credit programs;

explanation to the Client of requirements of Bank concerning thesolvency of the Borrower, the Guarantor, ensuring credit recovery (pledge of personal/real estate, the guarantee, other),the list of the documents necessary for confirmation of

information provided by the Client and an order of use of this information by Bank, an assessment of mortgage property, its legal status and a physical condition, insurance (mortgage property, life and working ability of the Borrower, the propertyright to real estate, etc.);

explanation of orders and imprisonment terms of credit and security agreements, provisions and loan repayments, including an order of making of all actions connected with obligatory state registration of transactions on pledge of real estate, statement of vehicles on accounting in traffic police, need of the notarial certificate of separate documents, receipts of necessary soglasiya and permissions (bodies of guardianship and guardianship, the spouse (and));

informing on the rights and Bank and Borrower obligations.

2) preparatory (forming of documents according to the credit request);

receipt of the credit request (the fact of receipt of the creditrequest is reflected in the journal of registration of credit requests. The journal of registration of credit requests is keptin electronic form or on paper in credit divisions of Bank;

3) analytical (carrying out underwriting of the Client, guarantors);

the analysis of the packet of documents provided by the Client;

assessment of solvency and creditworthiness of the Client;

the analysis of the scheme of crediting proceeding from specifics of the Standard credit program or credit conditions, other than Standard credit programs;

the conclusion on absence of the negative information about the Client, his guarantors, Partners of Bank;

4) decision making about loan granting (preparation of the expert opinion, the credit memorandum, decision making by the officials according to the procedure approved by Credit committee);

transfer of the expert opinion to the head of UKFL/SPF, on statement to the official having according to the decision of Credit committee a personal limit of decision making in the corresponding amount on Standard programs a crediting/sublimit on decision making after non-standard credit conditions; in all other cases - transfer of the credit memorandum to the secretaryof Credit committee for consideration at meeting of Credit committee according to the order established in Bank.

5) registration and signing of credit documents;

preparation of a packet of credit documents according to the made decision: the credit agreement, security agreements (the pledge agreement, the guarantee agreement), the statement for write-off of means without acceptance in loan repayment and other documents in compliance with conditions of Standard programs of crediting / on non-standard (non-standard) credit conditions in the presence of the positive decision of the Credit committee/official within a personal limit;

registration of the statement of the Client based on which moneyis transferred on purpose (to the settlement account of a motor show, trade organization, travel agency, educational institution, into the account of the seller of the apartment, etc.); statements of the Client on implementation of converting of money (if necessary);

obtaining from the Client all necessary documents provided by the Standard program of crediting / on non-standard (non-standard) credit conditions in the presence of the positive

decision of the Credit committee/official within a personal limit.

6) loan granting;

Provision of borrowing facilities in currency of the Russian Federation can be performed by cash through cash desk of Bank orin a non-cash order by transfer of money on a personal account of an on-demand deposit of the Borrower, provision of borrowing facilities in foreign currency - in a non-cash order by transferof money on a personal account of an on-demand deposit of the Borrower.

7) credit monitoring;

the current control of execution by the Borrower of liabilities according to the credit agreement: settlement of a current debt (principal debt and interests on credit) and overdue debt;

check of target use of borrowing facilities;

carrying out solvency analysis and creditworthiness of the Client (if necessary - it is determined by the head of UKFL/SPF);

as required (it is determined by the head of UKFL/SPF) carrying out checks of a condition of the pledge provided by the Borrowerwith signing of acts following the results of checks;

monitoring of activity of the Borrower on other transactions in Bank (deposits, bank cards, etc.);

control of accomplishment by the Borrower of conditions of credit and security agreements (provision of necessary documents, conclusion of agreements of pledge, insurance, etc.).

8) credit servicing.

Loan repayment and interest for using borrowing facilities is performed by the Borrower according to the debt repayment schedule containing in the credit agreement / based on the written application of the Borrower. The credit debt and debt onpercent is settled by write-off from a personal account of the Borrower on the on-demand deposit, opened in Bank, based on the written application of the Borrower. By cash deposit of money inBank cash desk, without transfer of money into the account of anon-demand deposit of the Borrower, the debt in Russian rubles can be settled only.

Conclusion

In modern Russian economy banks, which being, in fact, commercial enterprises, impose commercial nature on all system of their credit activity. First of all, proceeding from the principle of profitability of bank economy, bank loans are

profiting. But matter not only in it. Banks as trade enterprisestrade with, first of all, the resources, placing them in credit operations. For this reason in normal (crisis-free) economy for the banks which are acting, first of all as large credit institutes, the income from credit activities is fundamental.

The size of a credit product of bank depends not only on amount of its own means, but also on the attracted resources. In modernmarket system it is possible to trade large volume of means onlywhen the bank in addition raised funds from the clients. As the bank attracts resources not for itself, but for others, it appears that the amount of a credit product becomes higher whilemore weight is accumulated by it on the basis of recoverability of money.

The modern economy is inconceivable without credit relations. The credit in many respects is a condition and the prerequisite of development of the modern economy, an indivisible element of economic growth. Both large enterprises and associations, and small production, agricultural and trade enterprises use it. It is used both by the states and the governments, and certain citizens. Only due to the credit in a national economy the meansreleased in the course of activities of the entities, and also savings of the population and resources of banks are used effectively.

The problem of credit relations and credit system is very actualnow. The Russian economy is only on a formation way, isn't arranged properly also a credit system. Nevertheless, the creditsystem is vital to economy. Without it there can't be real a process of a modulation of one industries in others of the equity, it is necessary for maintenance of a continuity of a circulation of funds of operating plants, servicing of implementation process of manufactured goods that is especially important at a stage of formation of the market relations.

Thus, transition of Russia to the market relations, overcoming of crisis and renewal of economic growth, increase of efficiencyof functioning of economy, creation of necessary infrastructure

it is impossible to provide without use and further development of credit relations.

Specifics of modern practice of crediting prove that the Russianbanks in some cases don't possess the single methodical and regulatory base of the organization of credit process. The old bank instructions regulating credit operations and oriented on distribution system, are unacceptable for market conditions.

In practice of provision to clients of loans the various methodsare applied. It is necessary to understand issue and loan repayment methods as methods of crediting according to the principles of crediting.

Now the methods of issue and settlement of the credits by commercial banks are determined by the Provision of the Central Bank of the Russian Federation "About an order of provision (placement) by the credit organizations of money and their return (settlement)" of August 31, 1998 No. 54-P. In particular,it is provided the placement of money to clients of bank by the following main methods: one-time transfer of money on the bank account; opening of a credit line; overdraft; participation of bank in provision of placement of money to the client of bank ona syndicated basis.

The credit methods recommended by the Central Bank of the Russian Federation to domestic commercial banks, actually rely on the vast experience of the foreign banks which has been savedup for many years of work with a market economy.

In foreign banking practice two methods of crediting are used. The essence of the first method is that an issue of loan provision to the borrower in case of the request for it in bank each time is resolved in an individual order. In case of the second method loans are granted in the amount of predefined by bank amount to the borrower for a certain term, which is based on the credit agreement in process of emergence of requirement for additional resources for productive activity within the stipulated term and without additional negotiations with bank

and any documentary registrations. In such order borrowers are credited according to the overdraft, by opening of a so-called credit line and according to the current account.

The experience of the western banks which has been saved up in the field of establishment of credit lines and modes of their functioning represents, thus, huge potential for enhancement of services of the Russian banks.

Bibliography

1. Intermediate Financial Management; Cengage Learning, 2009;Authors: Eugene F. Brigham,Phillip R. Daves

2. The Future of Business: The Essentials; Cengage Learning, 2008; Authors: Lawrence J. Gitman,Carl McDaniel

3. Financial Management; Principles and Practice; Freeload Press, Inc., 1968; Authors: Gallagher and Andrew

4. Financial Management; Jae K. Shim, Joel G. Siegel; Barron'sEducational Series, 2000

5. https://www.boundless.com/finance/capital-budgeting/ introduction-to-capital-budgeting/long-term-vs-short-term-financing/

6. http://online.wsj.com/news/articles/ SB10001424052702304520704579125233281961504