PROJECT ON mutual funds

151

INTODUCTION TO FINANCIAL MARKET: In economics, a financial market is a mechanism that allows people and entities to buy and sell (trade) financial securities (such as stocks and bonds),commodities (such as precious metals or agricultural goods), and other fungible items of value at low transaction costs and at prices that reflect supply and demand. Both general markets (where many commodities are traded) and specialized markets (where only one commodity is traded) exist. Markets work by placing many interested buyers and sellers in one "place", thus making it easier for them to find each other. An economy which relies primarily on interactions between buyers and sellers to allocate resources is known as a market economy in contrast either to a command economy or to a non-market economy such as a gift economy. In finance, financial markets facilitate: The raising of capital (in the capital markets) The transfer of risk (in the derivatives markets) The transfer of liquidity (in the money markets) International trade (in the currency markets) 1

Transcript of PROJECT ON mutual funds

INTODUCTION TO FINANCIAL MARKET:

In economics, a financial market is a mechanism that allows

people and entities to buy and sell (trade)

financial securities (such as stocks and

bonds),commodities (such as precious metals or agricultural

goods), and other fungible items of value at low transaction

costs and at prices that reflect supply and demand.

Both general markets (where many commodities are traded) and

specialized markets (where only one commodity is traded)

exist. Markets work by placing many interested buyers and

sellers in one "place", thus making it easier for them to find

each other. An economy which relies primarily on interactions

between buyers and sellers to allocate resources is known as

a market economy in contrast either to a command economy or to

a non-market economy such as a gift economy.

In finance, financial markets facilitate:

The raising of capital (in the capital markets)

The transfer of risk (in the derivatives markets)

The transfer of liquidity (in the money markets)

International trade (in the currency markets)

1

– and are used to match those who want capital to those

who have it.

Typically a borrower issues a receipt to the lender promising

to pay back the capital. These receipts are securities which

may be freely bought or sold. In return for lending money to

the borrower, the lender will expect some compensation in the

form of interest or dividends.

In mathematical finance, the concept continuous-time Brownian

motion stochastic process is sometimes used as a model.

Definition

In economics, typically, the term market means the aggregate

of possible buyers and sellers of a certain good or service

and the transactions between them.

The term "market" is sometimes used for what are more

strictly exchanges, organizations that facilitate the trade in

financial securities, e.g., a stock exchange orcommodity

exchange. This may be a physical location (like the NYSE) or

an electronic system (like NASDAQ). Much trading of stocks

takes place on an exchange; still,corporate actions (merger,

2

spinoff) are outside an exchange, while any two companies or

people, for whatever reason, may agree to sell stock from the

one to the other without using an exchange.

Trading of currencies and bonds is largely on a bilateral

basis, although some bonds trade on a stock exchange, and

people are building electronic systems for these as well,

similar to stock exchanges.

Financial markets can be domestic or they can be

international.

Types of financial markets

The financial markets can be divided into different subtypes:

Capital markets which consist of:

Stock markets, which provide financing through the

issuance of shares or common stock, and enable the

subsequent trading thereof.

Bond markets, which provide financing through the

issuance of bonds, and enable the subsequent trading

thereof.

3

Commodity markets, which facilitate the trading of

commodities.

Money markets, which provide short term debt financing and

investment.

Derivatives markets, which provide instruments for the

management of financial risk.

Futures markets, which provide standardized forward

contracts for trading products at some future date; see

also forward market.

Insurance markets, which facilitate the redistribution of

various risks.

Foreign exchange markets, which facilitate the trading

of foreign exchange.

The capital markets consist of primary markets and secondary

markets. Newly formed (issued) securities are bought or sold

in primary markets. Secondary markets allow investors to sell

securities that they hold or buy existing securities. The

transaction in primary market exist between investors and

public while secondary market its between investors.

[edit]Raising the capital

4

To understand financial markets, let us look at what they are

used for, i.e. what where firms make the capital to invest

Without financial markets, borrowers would have difficulty

finding lenders themselves. Intermediaries such as banks help

in this process. Banks take deposits from those who

have money to save. They can then lend money from this pool of

deposited money to those who seek to borrow. Banks popularly

lend money in the form of loans andmortgages.

More complex transactions than a simple bank deposit require

markets where lenders and their agents can meet borrowers and

their agents, and where existing borrowing or lending

commitments can be sold on to other parties. A good example of

a financial market is a stock exchange. A company can raise

money by selling shares to investors and its existing shares

can be bought or sold.

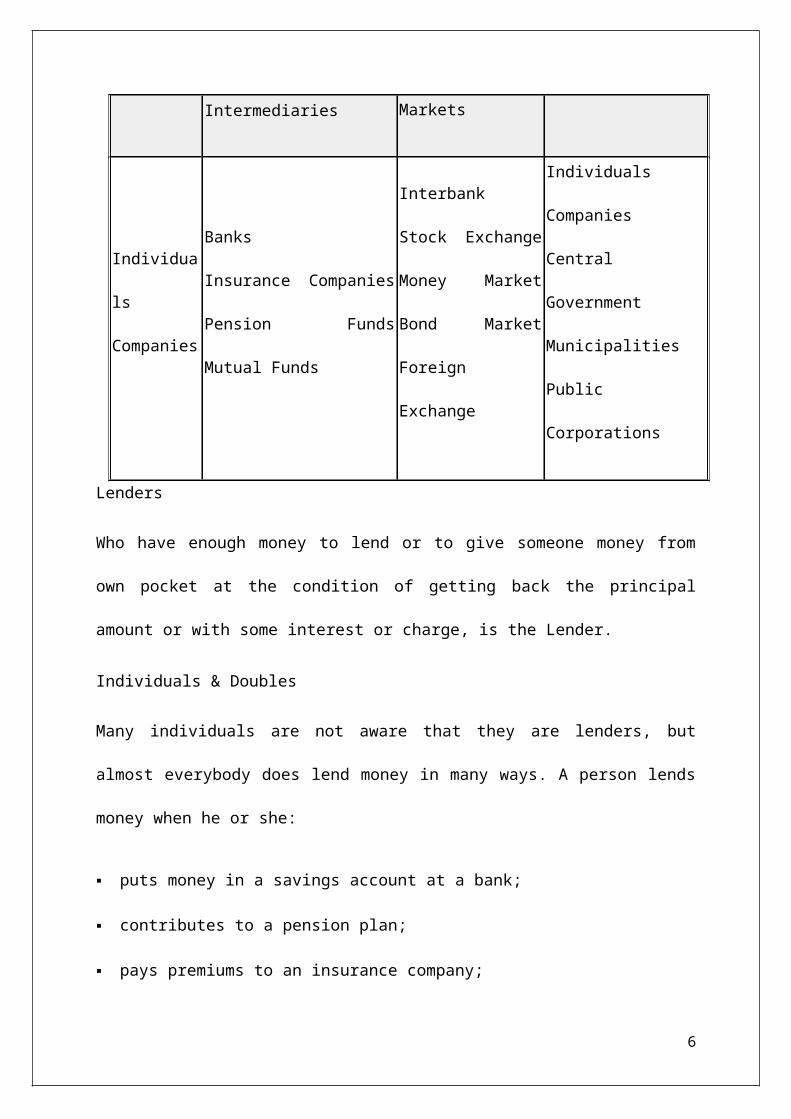

The following table illustrates where financial markets fit in

the relationship between lenders and borrowers:

Relationship between lenders and borrowers

Lenders Financial Financial Borrowers

5

Intermediaries Markets

Individua

ls

Companies

Banks

Insurance Companies

Pension Funds

Mutual Funds

Interbank

Stock Exchange

Money Market

Bond Market

Foreign

Exchange

Individuals

Companies

Central

Government

Municipalities

Public

Corporations

Lenders

Who have enough money to lend or to give someone money from

own pocket at the condition of getting back the principal

amount or with some interest or charge, is the Lender.

Individuals & Doubles

Many individuals are not aware that they are lenders, but

almost everybody does lend money in many ways. A person lends

money when he or she:

puts money in a savings account at a bank;

contributes to a pension plan;

pays premiums to an insurance company;

6

invests in government bonds; or

invests in company share

Companies

Companies tend to be borrowers of capital. When companies have

surplus cash that is not needed for a short period of time,

they may seek to make money from their cash surplus by lending

it via short term markets called money markets.

There are a few companies that have very strong cash flows.

These companies tend to be lenders rather than borrowers. Such

companies may decide to return cash to lenders (e.g. via

a share buyback.) Alternatively, they may seek to make more

money on their cash by lending it (e.g. investing in bonds and

stocks.)

[edit]Borrowers

Individuals borrow money via bankers' loans for short term

needs or longer term mortgages to help finance a house

purchase.

7

Companies borrow money to aid short term or long term cash

flows. They also borrow to fund modernisation or future

business expansion.

Governments often find their spending requirements exceed

their tax revenues. To make up this difference, they need to

borrow. Governments also borrow on behalf of nationalised

industries, municipalities, local authorities and other public

sector bodies. In the UK, the total borrowing requirement is

often referred to as the Public sector net cash

requirement (PSNCR).

Governments borrow by issuing bonds. In the UK, the government

also borrows from individuals by offering bank accounts

and Premium Bonds. Government debt seems to be permanent.

Indeed the debt seemingly expands rather than being paid off.

One strategy used by governments to reduce the value of the

debt is to influence inflation.

Municipalities and local authorities may borrow in their own

name as well as receiving funding from national governments.

In the UK, this would cover an authority like Hampshire County

Council.

8

Public Corporations typically include nationalised industries.

These may include the postal services, railway companies and

utility companies.

Many borrowers have difficulty raising money locally. They

need to borrow internationally with the aid of Foreign

exchange markets.

Borrowers having similar needs can form into a group of

borrowers. They can also take an organizational form like

Mutual Funds. They can provide mortgage on weight basis. The

main advantage is that this lowers the cost of their

borrowings.

Derivative products

During the 1980s and 1990s, a major growth sector in financial

markets is the trade in so called derivative products,

or derivatives for short.

In the financial markets, stock prices, bond prices, currency

rates, interest rates and dividends go up and down,

creating risk. Derivative products are financial products

which are used to control risk or paradoxically exploit risk.

It is also called financial economics.

9

Derivative products or instruments help the issuers to gain an

unusual profit from issuing the instruments. For using the

help of these products a contract has to be made. Derivative

contracts are mainly 3 types: 1. Future Contracts 2. Forward

Contracts 3. Option Contracts.

Currency markets

Main article: Foreign exchange market

Seemingly, the most obvious buyers and sellers of currency are

importers and exporters of goods. While this may have been

true in the distant past,[when?] when international trade created

the demand for currency markets, importers and exporters now

represent only 1/32 of foreign exchange dealing, according to

the Bank for International Settlements.[1]

The picture of foreign currency transactions today shows:

Banks/Institutions

Speculators

Government spending (for example, military bases abroad)

Importers/Exporters

Tourists

10

Analysis of financial markets

See Statistical analysis of financial

markets, statistical finance---

Much effort has gone into the study of financial markets and

how prices vary with time. Charles Dow, one of the founders

of Dow Jones & Company and The Wall Street Journal,

enunciated a set of ideas on the subject which are now

called Dow Theory. This is the basis of the so-

called technical analysis method of attempting to predict

future changes. One of the tenets of "technical analysis" is

that market trends give an indication of the future, at

least in the short term. The claims of the technical

analysts are disputed by many academics, who claim that the

evidence points rather to therandom walk hypothesis, which

states that the next change is not correlated to the last

change.

The scale of changes in price over some unit of time is

called the volatility. It was discovered by Benoît

Mandelbrot that changes in prices do not follow a Gaussian

distribution, but are rather modeled better by Lévy stable

11

distributions. The scale of change, or volatility, depends

on the length of the time unit to a power a bit more than

1/2. Large changes up or down are more likely than what one

would calculate using a Gaussian distribution with an

estimated standard deviation.

A new area of concern is the proper analysis of

international market effects. As connected as today's global

financial markets are, it is important to realize that there

are both benefits and consequences to a global financial

network. As new opportunities appear due to integration, so

do the possibilities of contagion. This presents unique

issues when attempting to analyze markets, as a problem can

ripple through the entire connected global network very

quickly. For example, a bank failure in one country can

spread quickly to others, which makes proper analysis more

difficult.

Financial market slang

Poison pill, when a company issues more shares to prevent

being bought out by another company, thereby increasing

12

the number of outstanding shares to be bought by the

hostile company making the bid to establish majority.

Quant, a quantitative analyst with a PhD (and above)

level of training in mathematics and statistical methods.

Rocket scientist, a financial consultant at the zenith of

mathematical and computer programming skill. They are

able to invent derivatives of high complexity and

construct sophisticated pricing models. They generally

handle the most advanced computing techniques adopted by

the financial markets since the early 1980s. Typically,

they are physicists and engineers by training; rocket

scientists do not necessarily build rockets for a living.

White Knight, a friendly party in a takeover bid. Used to

describe a party that buys the shares of one organization

to help prevent against a hostile takeover of that

organization by another party.

History

13

Established in 1875, the Bombay Stock Exchange is Asia's first

stock exchange.

In 12th century France the courratiers de change were

concerned with managing and regulating the debts of

agricultural communities on behalf of the banks. Because these

men also traded with debts, they could be called the

first brokers. A common misbelief is that in late 13th

century Bruges commodity traders gathered inside the house of

a man called Van der Beurze, and in 1309 they became the

"Brugse Beurse", institutionalizing what had been, until then,

an informal meeting, but actually, the family Van der Beurze

had a building in Antwerp where those gatherings occurred; the

Van der Beurze had Antwerp, as most of the merchants of that

period, as their primary place for trading. The idea quickly14

spread around Flanders and neighbouring counties and "Beurzen"

soon opened in Ghent and Amsterdam.

In the middle of the 13th century, Venetian bankers began to

trade in government securities. In 1351 the Venetian

government outlawed spreading rumours intended to lower the

price of government funds. Bankers

in Pisa, Verona, Genoa and Florence also began trading in

government securities during the 14th century. This was only

possible because these were independent city states not ruled

by a duke but a council of influential citizens. The Dutch

later started joint stock companies, which

let shareholders invest in business ventures and get a share

of their profits – or losses. In 1602, the Dutch East India

Company issued the first share on the Amsterdam Stock

Exchange. It was the first company to issue stocks and bonds.

The Amsterdam Stock Exchange (or Amsterdam Beurs) is also said

to have been the first stock exchange to introduce continuous

trade in the early 17th century. The Dutch "pioneered short

selling, option trading, debt-equity swaps, merchant banking,

unit trusts and other speculative instruments, much as we know

them". There are now stock markets in virtually every

15

developed and most developing economies, with the world's

biggest market being in the United States, United Kingdom,

Japan, India, China, Canada, Germany's (Frankfurt Stock

Exchange), France, South Korea and the Netherlands.

Importance of stock market

Function and purpose

The main trading room of the Tokyo Stock Exchange, where

trading is currently completed through computers.

The stock market is one of the most important sources

for companies to raise money. This allows businesses to be

publicly traded, or raise additional capital for expansion by

16

selling shares of ownership of the company in a public market.

The liquidity that an exchange provides affords investors the

ability to quickly and easily sell securities. This is an

attractive feature of investing in stocks, compared to other

less liquid investments such as real estate.

History has shown that the price of shares and other assets is

an important part of the dynamics of economic activity, and

can influence or be an indicator of social mood. An economy

where the stock market is on the rise is considered to be an

up-and-coming economy. In fact, the stock market is often

considered the primary indicator of a country's economic

strength and development.

Rising share prices, for instance, tend to be associated with

increased business investment and vice versa. Share prices

also affect the wealth of households and their consumption.

Therefore, central banks tend to keep an eye on the control

and behaviour of the stock market and, in general, on the

smooth operation of financial system functions. Financial

stability is the raison d'être of central banks.

Exchanges also act as the clearinghouse for each transaction,

meaning that they collect and deliver the shares, and

17

guarantee payment to the seller of a security. This eliminates

the risk to an individual buyer or seller that

the counterparty could default on the transaction.

The smooth functioning of all these activities

facilitates economic growth in that lower costs and enterprise

risks promote the production of goods and services as well as

employment. In this way the financial system contributes to

increased prosperity.

Relation of the stock market to the modern financial system

The financial system in most western countries has undergone a

remarkable transformation. One feature of this development

is disintermediation. A portion of the funds involved in

saving and financing, flows directly to the financial markets

instead of being routed via the traditional bank lending and

deposit operations. The general public's heightened interest

in investing in the stock market, either directly or

through mutual funds, has been an important component of this

process.

Statistics show that in recent decades shares have made up an

increasingly large proportion of households' financial assets

18

in many countries. In the 1970s, in Sweden, deposit

accounts and other very liquid assets with little risk made up

almost 60 percent of households' financial wealth, compared to

less than 20 percent in the 2000s. The major part of this

adjustment in financial portfolios has gone directly to shares

but a good deal now takes the form of various kinds of

institutional investment for groups of individuals, e.g.,

pension funds, mutual funds, hedge funds, insurance investment

of premiums, etc.

The trend towards forms of saving with a higher risk has been

accentuated by new rules for most funds and insurance,

permitting a higher proportion of shares to bonds. Similar

tendencies are to be found in other industrialized countries.

In all developed economic systems, such as the European Union,

the United States, Japan and other developed nations, the

trend has been the same: saving has moved away from

traditional (government insured) bank deposits to more risky

securities of one sort or another

19

The behaviour of the stock market

From experience we know that investors may 'temporarily' move

financial prices away from their long term aggregate price

'trends'. (Positive or up trends are referred to as bull

markets; negative or down trends are referred to as bear

markets.) Over-reactions may occur—so that excessive optimism

(euphoria) may drive prices unduly high or excessive pessimism

may drive prices unduly low. Economists continue to debate

whether financial markets are 'generally' efficient.

According to one interpretation of the efficient-market

hypothesis (EMH), only changes in fundamental factors, such as

the outlook for margins, profits or dividends, ought to affect

share prices beyond the short term, where random 'noise' in

the system may prevail. (But this largely theoretic academic

viewpoint—known as 'hard' EMH—also predicts that little or no

trading should take place, contrary to fact, since prices are

already at or near equilibrium, having priced in all public

knowledge.) The 'hard' efficient-market hypothesis is sorely

tested by such events as the stock market crash in 1987, when

the Dow Jones index plummeted 22.6 percent—the largest-ever

one-day fall in the United States.

20

This event demonstrated that share prices can fall

dramatically even though, to this day, it is impossible to fix

a generally agreed upon definite cause: a thorough search

failed to detect any 'reasonable' development that might have

accounted for the crash. (But note that such events are

predicted to occur strictly by chance, although very rarely.)

It seems also to be the case more generally that many price

movements (beyond that which are predicted to occur

'randomly') are not occasioned by new information; a study of

the fifty largest one-day share price movements in the United

States in the post-war period seems to confirm this.

However, a 'soft' EMH has emerged which does not require that

prices remain at or near equilibrium, but only that market

participants not be able to systematically profit from any

momentary market 'inefficiencies'. Moreover, while EMH

predicts that all price movement (in the absence of change in

fundamental information) is random (i.e., non-trending), many

studies have shown a marked tendency for the stock market to

trend over time periods of weeks or longer. Various

explanations for such large and apparently non-random price

movements have been promulgated. For instance, some research

21

has shown that changes in estimated risk, and the use of

certain strategies, such as stop-loss limits and Value at

Risk limits, theoretically could cause financial markets to

overreact. But the best explanation seems to be that the

distribution of stock market prices is non-Gaussian (in which

case EMH, in any of its current forms, would not be strictly

applicable).

Other research has shown that psychological factors may result

in exaggerated (statistically anomalous) stock price movements

(contrary to EMH which assumes such behaviors 'cancel out').

Psychological research has demonstrated that people are

predisposed to 'seeing' patterns, and often will perceive a

pattern in what is, in fact, just noise. (Something like

seeing familiar shapes in clouds or ink blots.) In the present

context this means that a succession of good news items about

a company may lead investors to overreact positively

(unjustifiably driving the price up). A period of good returns

also boosts the investor's self-confidence, reducing his

(psychological) risk threshold.

Another phenomenon—also from psychology—that works against

an objective assessment is group thinking. As social animals,

22

it is not easy to stick to an opinion that differs markedly

from that of a majority of the group. An example with which

one may be familiar is the reluctance to enter a restaurant

that is empty; people generally prefer to have their opinion

validated by those of others in the group.

In one paper the authors draw an analogy with gambling. In

normal times the market behaves like a game of roulette; the

probabilities are known and largely independent of the

investment decisions of the different players. In times of

market stress, however, the game becomes more like poker

(herding behavior takes over). The players now must give heavy

weight to the psychology of other investors and how they are

likely to react psychologically.

The stock market, as with any other business, is quite

unforgiving of amateurs. Inexperienced investors rarely get

the assistance and support they need. In the period running up

to the 1987 crash, less than 1 percent of the analyst's

recommendations had been to sell (and even during the 2000–

2002 bear market, the average did not rise above 5 %%). In the

run up to 2000, the media amplified the general euphoria, with

reports of rapidly rising share prices and the notion that

23

large sums of money could be quickly earned in the so-

called new economy stock market. (And later amplified the

gloom which descended during the 2000–2002 bear market, so

that by summer of 2002, predictions of a DOW average below

5000 were quite common.)

Irrational behaviour

Sometimes the market seems to react irrationally to economic

or financial news, even if that news is likely to have no real

effect on the fundamental value of securities itself. But this

may be more apparent than real, since often such news has been

anticipated, and a counter reaction may occur if the news is

better (or worse) than expected. Therefore, the stock market

may be swayed in either direction by press releases,

rumours, euphoria and mass panic; but generally only briefly,

as more experienced investors (especially the hedge funds)

quickly rally to take advantage of even the slightest,

momentary hysteria.

Over the short-term, stocks and other securities can be

battered or buoyed by any number of fast market-changing

24

events, making the stock market behaviour difficult to

predict. Emotions can drive prices up and down, people are

generally not as rational as they think, and the reasons for

buying and selling are generally obscure. Behaviourists argue

that investors often behave 'irrationally' when making

investment decisions thereby incorrectly pricing securities,

which causes market inefficiencies, which, in turn, are

opportunities to make money.]However, the whole notion of EMH

is that these non-rational reactions to information cancel

out, leaving the prices of stocks rationally determined.

The Dow Jones Industrial Average biggest gain in one day was

936.42 points or 11 percent, this occurred on October 13,

2008.

Crashes

25

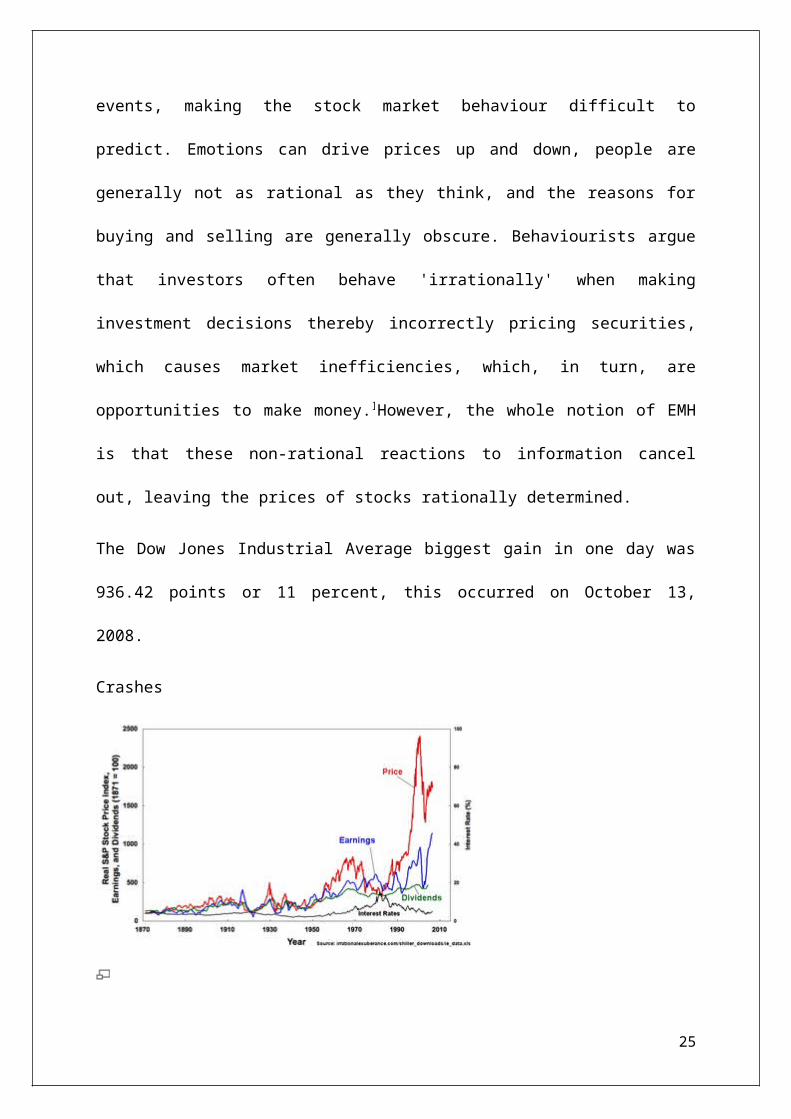

Robert Shiller's plot of the S&P Composite Real Price Index,

Earnings, Dividends, and Interest Rates, from Irrational

Exuberance, 2d ed. In the preface to this edition, Shiller

warns, "The stock market has not come down to historical

levels: the price-earnings ratio as I define it in this book

is still, at this writing [2005], in the mid-20s, far higher

than the historical average... People still place too much

confidence in the markets and have too strong a belief that

paying attention to the gyrations in their investments will

someday make them rich, and so they do not make conservative

preparations for possible bad outcomes."

Price-Earnings ratios as a predictor of twenty-year returns

based upon the plot by Robert Shiller (Figure 10.1). The

26

horizontal axis shows the real price-earnings ratio of the S&P

Composite Stock Price Index as computed in Irrational

Exuberance (inflation adjusted price divided by the prior ten-

year mean of inflation-adjusted earnings). The vertical axis

shows the geometric average real annual return on investing in

the S&P Composite Stock Price Index, reinvesting dividends,

and selling twenty years later. Data from different twenty

year periods is color-coded as shown in the key. See also ten-

year returns. Shiller states that this plot "confirms that

long-term investors—investors who commit their money to an

investment for ten full years—did do well when prices were low

relative to earnings at the beginning of the ten years. Long-

term investors would be well advised, individually, to lower

their exposure to the stock market when it is high, as it has

been recently, and get into the market when it is low."

Stock market index

The movements of the prices in a market or section of a market

are captured in price indices called stock market indices, of

which there are many, e.g., the S&P, the FTSE and

the Euronext indices. Such indices are usually market

27

capitalization weighted, with the weights reflecting the

contribution of the stock to the index. The constituents of

the index are reviewed frequently to include/exclude stocks in

order to reflect the changing business environment.

Derivative instruments

Financial innovation has brought many new financial

instruments whose pay-offs or values depend on the prices of

stocks. Some examples are exchange-traded funds (ETFs), stock

index and stock options, equity swaps, single-stock futures,

and stock index futures. These last two may be traded

on futures exchanges (which are distinct from stock exchanges—

their history traces back to commodities futures exchanges),

or traded over-the-counter. As all of these products are

only derived from stocks, they are sometimes considered to be

traded in a (hypothetical) derivatives market, rather than the

(hypothetical) stock market.

Leveraged strategies

Stock that a trader does not actually own may be traded

using short selling; margin buying may be used to purchase

stock with borrowed funds; or, derivatives may be used to

28

control large blocks of stocks for a much smaller amount of

money than would be required by outright purchase or sale.

Short selling

In short selling, the trader borrows stock (usually from his

brokerage which holds its clients' shares or its own shares on

account to lend to short sellers) then sells it on the market,

hoping for the price to fall. The trader eventually buys back

the stock, making money if the price fell in the meantime and

losing money if it rose. Exiting a short position by buying

back the stock is called "covering a short position." This

strategy may also be used by unscrupulous traders in illiquid

or thinly traded markets to artificially lower the price of a

stock. Hence most markets either prevent short selling or

place restrictions on when and how a short sale can occur. The

practice of naked shorting is illegal in most (but not all)

stock markets.

Margin buying

In margin buying, the trader borrows money (at interest) to

buy a stock and hopes for it to rise. Most industrialized

countries have regulations that require that if the borrowing

29

is based on collateral from other stocks the trader owns

outright, it can be a maximum of a certain percentage of those

other stocks' value. In the United States, the margin

requirements have been 50 %% for many years (that is, if you

want to make a $1000 investment, you need to put up $500, and

there is often a maintenance margin below the $500).

A margin call is made if the total value of the investor's

account cannot support the loss of the trade. (Upon a decline

in the value of the margined securities additional funds may

be required to maintain the account's equity, and with or

without notice the margined security or any others within the

account may be sold by the brokerage to protect its loan

position. The investor is responsible for any shortfall

following such forced sales.)

Regulation of margin requirements (by the Federal Reserve) was

implemented after the Crash of 1929. Before that, speculators

typically only needed to put up as little as 10 percent (or

even less) of the total investment represented by the stocks

purchased. Other rules may include the prohibition of free-

riding: putting in an order to buy stocks without paying

initially (there is normally a three-day grace period for

30

delivery of the stock), but then selling them (before the

three-days are up) and using part of the proceeds to make the

original payment (assuming that the value of the stocks has

not declined in the interim).

New issuance

Global issuance of equity and equity-related instruments

totaled $505 billion in 2004, a 29.8 %% increase over the

$389 billion raised in 2003. Initial public offerings (IPOs)

by US issuers increased 221 %% with 233 offerings that raised

$45 billion, and IPOs in Europe, Middle East and Africa (EMEA)

increased by 333 %%, from $ 9 billion to $39 billion.

Investment strategies

One of the many things people always want to know about the

stock market is, "How do I make money investing?" There are

many different approaches; two basic methods are classified as

either fundamental analysis or technical analysis. Fundamental

analysis refers to analyzing companies by their financial

statements found in SEC Filings, business trends, general

31

economic conditions, etc. Technical analysis studies price

actions in markets through the use of charts and quantitative

techniques to attempt to forecast price trends regardless of

the company's financial prospects. One example of a technical

strategy is the Trend following method, used by John W.

Henry and Ed Seykota, which uses price patterns, utilizes

strict money management and is also rooted in risk

control and diversification.

Additionally, many choose to invest via the index method. In

this method, one holds a weighted or unweighted portfolio

consisting of the entire stock market or some segment of the

stock market (such as the S&P 500 or Wilshire 5000). The

principal aim of this strategy is to maximize diversification,

minimize taxes from too frequent trading, and ride the general

trend of the stock market (which, in the U.S., has averaged

nearly 10 %%/year, compounded annually, since World War II).

Taxation

According to much national or state legislation, a large array

of fiscal obligations are taxed for capital gains. Taxes are

charged by the state over the transactions, dividends

32

and capital gains on the stock market, in particular in

the stock exchanges. However, these fiscal obligations may

vary from jurisdictions to jurisdictions because, among other

reasons, it could be assumed that taxation is already

incorporated into the stock price through the different taxes

companies pay to the state, or that tax free stock market

operations are useful to boost economic growth

INTRODUCTION TO MUTUAL FUNDS:

A mutual fund is a professionally managed type of collective

investment scheme that pools money from many investors to

buy stocks, bonds, short-term money market instruments, and/or

other securities.

Overview

In the United States, a mutual fund is registered with

the Securities and Exchange Commission (SEC) and is overseen

by a board of directors (if organized as a corporation)

or board of trustees (if organized as a trust). The board is

charged with ensuring that the fund is managed in the best

33

interests of the fund's investors and with hiring the fund

manager and other service providers to the fund. The fund

manager, also known as the fund sponsor or fund management

company, trades (buys and sells) the fund's investments in

accordance with the fund's investment objective. A fund

manager must be a registered investment advisor. Funds that

are managed by the same fund manager and that have the same

brand name are known as a "fund family" or "fund complex".

The Investment Company Act of 1940 (the 1940 Act) established

three types of registered investment companies or RICs in the

United States: open-end funds, unit investment trusts (UITs);

and closed-end funds. Recently, exchange-traded funds (ETFs),

which are open-end funds or unit investment trusts that trade

on an exchange, have gained in popularity. While the term

"mutual fund" may refer to all three types of registered

investment companies, it is more commonly used to refer

exclusively to the open-end type.

Hedge funds are not considered a type of mutual fund. While

they are another type of commingled investment scheme, they

are not governed by the Investment Company Act of 1940 and are

not required to register with the Securities and Exchange

34

Commission (though many hedge fund managers now must register

as investment advisors).

Mutual funds are not taxed on their income as long as they

comply with certain requirements established in the Internal

Revenue Code. Specifically, they must diversify their

investments, limit ownership of voting securities, distribute

most of their income to their investors annually, and earn

most of the income by investing in securities and currencies.

[2] Mutual funds pass taxable income on to their investors. The

type of income they earn is unchanged as it passes through to

the shareholders. For example, mutual fund distributions of

dividend income are reported as dividend income by the

investor. There is an exception: net losses incurred by a

mutual fund are not distributed or passed through to fund

investors.

Outside of the United States, mutual fund is used as a generic

term for various types of collective investment vehicles

available to the general public, such as unit trusts, open-

ended investment companies, unitized insurance

funds, Undertakings for Collective Investment in Transferable

Securities, and SICAVs.

35

Advantages of mutual funds

Mutual funds have advantages compared to direct investing in

individual securities. These include:

Increased diversification

Daily liquidity

Professional investment management

Ability to participate in investments that may be available

only to larger investors

Service and convenience

Government oversight

Ease of comparison

Disadvantages of mutual funds

Mutual funds have disadvantages as well, which include]:

Fees

Less control over timing of recognition of gains

Less predictable income

No opportunity to customize

36

History

The first mutual funds were established in Europe. One

researcher credits a Dutch merchant with creating the first

mutual fund in 1774. The first mutual fund outside the

Netherlands was the Foreign & Colonial Government Trust, which

was established in London in 1868. It is now the Foreign &

Colonial Investment Trust and trades on the London stock

exchange.

Mutual funds were introduced into the United States in the

1890s. They became popular during the 1920s. These early funds

were generally of the closed-end type with a fixed number of

shares which often traded at prices above the value of the

portfolio.

The first open-end mutual fund with redeemable shares was

established on March 21, 1924. This fund, the Massachusetts

Investors Trust, is now part of the MFS family of funds.

However, closed-end funds remained more popular than open-end

funds throughout the 1920s. By 1929, open-end funds accounted

for only 5% of the industry's $27 billion in total assets.

37

After the stock market crash of 1929, Congress passed a series

of acts regulating the securities markets in general and

mutual funds in particular. The Securities Act of

1933 requires that all investments sold to the public,

including mutual funds, be registered with the Securities and

Exchange Commission and that they provide prospective

investors with a prospectus that discloses essential facts

about the investment. The Securities and Exchange Act of

1934 requires that issuers of securities, including mutual

funds, report regularly to their investors; this act also

created the Securities and Exchange Commission, which is the

principal regulator of mutual funds. The Revenue Act of

1936 established guidelines for the taxation of mutual funds,

while the Investment Company Act of 1940 governs their

structure.

When confidence in the stock market returned in the 1950s, the

mutual fund industry began to grow again. By 1970, there were

approximately 360 funds with $48 billion in assets. The

introduction of money market funds in the high interest rate

environment of the late 1970s boosted industry growth

dramatically. The first retail index fund, First Index

38

Investment Trust, was formed in 1976 by The Vanguard Group,

headed by John Bogle; it is now called the Vanguard 500 Index

Fund and is one of the world's largest mutual funds, with more

than $100 billion in assets as of January 31, 2011.

Fund industry growth continued into the 1980s and 1990s, as a

result of three factors: a bull market for both stocks and

bonds, new product introductions (including tax-exempt bond,

sector, international and target date funds) and wider

distribution of fund shares. Among the new distribution

channels were retirement plans. Mutual funds are now the

preferred investment option in certain types of fast-growing

retirement plans, specifically in 401(k) and other defined

contribution plans and in individual retirement

accounts (IRAs), all of which surged in popularity in the

1980s. Total mutual fund assets fell in 2008 as a result of

the credit crisis of 2008.

In 2003, the mutual fund industry was involved in

a scandal involving unequal treatment of fund shareholders.

Some fund management companies allowed favored investors to

engage in late trading, which is illegal, or market timing,

which is a practice prohibited by fund policy. The scandal was

39

initially discovered by then-New York State Attorney

General Eliot Spitzer and resulted in significantly increased

regulation of the industry.

At the end of 2010, there were 7,581 mutual funds in the

United States with combined assets of $11.8 trillion,

according to the Investment Company Institute (ICI), a

national trade association of investment companies in the

United States. The ICI reports that worldwide mutual fund

assets were $24.7 trillion on the same date.

Leading mutual fund complexes

At the end of 2010, the top 10 mutual fund complexes in the

United States were:

1.Vanguard

2.Fidelity

3.American Funds (Capital Group)

4.PIMCO

5.JPMorgan Chase

6.Franklin Templeton

7.BlackRock

8.Federated

40

9.T. Rowe Price

10. BNY Mellon

Types of mutual funds

There are three basic types of registered investment companies

defined in the Investment Company Act of 1940: open-end funds,

unit investment trusts, and closed-end funds. Exchange-traded

funds are open-end funds or unit investment trusts that trade

on an exchange.

Open-end funds

Open-end mutual funds must be willing to buy back their shares

from their investors at the end of every business day at the

net asset value computed that day. Most open-end funds also

sell shares to the public every business day; these shares are

also priced at net asset value. A professional investment

manager oversees the portfolio, buying and selling securities

as appropriate. The total investment in the fund will vary

based on share purchases, share redemptions and fluctuation in

market valuation. There is no legal limit on the number of

shares that can be issued.

Closed-end funds

41

Closed-end funds generally issue shares to the public only

once, when they are created through an initial public

offering. Their shares are then listed for trading on a stock

exchange. Investors who no longer wish to invest in the fund

cannot sell their shares back to the fund (as they can with an

open-end fund). Instead, they must sell their shares to

another investor in the market; the price they receive may be

significantly different from net asset value. It may be at a

"premium" to net asset value (meaning that it is higher than

net asset value) or, more commonly, at a "discount" to net

asset value (meaning that it is lower than net asset value). A

professional investment manager oversees the portfolio, buying

and selling securities as appropriate.

Unit investment trusts

Unit investment trusts or UITs issue shares to the public only

once, when they are created. Investors can redeem shares

directly with the fund (as with an open-end fund) or they may

also be able to sell their shares in the market. Unit

investment trusts do not have a professional investment

manager. Their portfolio of securities is established at the

42

creation of the UIT and does not change. UITs generally have a

limited life span, established at creation.

Exchange-traded funds

Main article: Exchange-traded fund

A relatively recent innovation, the exchange-traded fund or

ETF is often structured as an open-end investment company,

though ETFs may also be structured as unit investment trusts,

partnerships, investments trust, grantor trusts or bonds (as

an exchange-traded note). ETFs combine characteristics of both

closed-end funds and open-end funds. Like closed-end funds,

ETFs are traded throughout the day on a stock exchange at a

price determined by the market. However, as with open-end

funds, investors normally receive a price that is close to net

asset value. To keep the market price close to net asset

value, ETFs issue and redeem large blocks of their shares with

institutional investors.

Most ETFs are index funds.

Investments and classification

Mutual funds may invest in many kinds of securities. The types

of securities that a particular fund may invest in are set

43

forth in the fund's prospectus, which describes the fund's

investment objective, investment approach and permitted

investments. The investment objective describes the type of

income that the fund seeks. For example, a "capital

appreciation" fund generally looks to earn most of its returns

from increases in the prices of the securities it holds,

rather than from dividend or interest income. The investment

approach describes the criteria that the fund manager uses to

select investments for the fund.

A mutual fund's investment portfolio is continually monitored

by the fund's portfolio manager or managers, who are employed

by the fund's manager or sponsor.

Mutual funds are classified by their principal investments.

The four largest categories of funds are money market funds,

bond or fixed income funds, stock or equity funds and hybrid

funds. Within these categories, funds may be subclassified by

investment objective, investment approach or specific focus.

The SEC requires that mutual fund names not be inconsistent

with a fund's investments. For example, the "ABC New Jersey

Tax-Exempt Bond Fund" would generally have to invest, under

normal circumstances, at least 80% of its assets in bonds that

44

are exempt from federal income tax, from the alternative

minimum tax and from taxes in the state of New Jersey.

Bond, stock and hybrid funds may be classified as either index

(passively-managed) funds or actively-managed funds.

Money market funds

Money market funds invest in money market instruments, which

are fixed income securities with a very short time to maturity

and high credit quality. Investors often use money market

funds as a substitute for bank savings accounts, though money

market funds are not government insured, unlike bank savings

accounts.

Money market funds strive to maintain a $1.00 per share net

asset value, meaning that investors earn interest income from

the fund but do not experience capital gains or losses. If a

fund fails to maintain that $1.00 per share because its

securities have declined in value, it is said to "break the

buck". Only two money market funds have ever broken the buck:

Community Banker's U.S. Government Money Market Fund in 1994

and the Reserve Primary Fund in 2008.

45

At the end of 2010, money market funds accounted for 24% of

the assets in all U.S. mutual funds.

Bond funds

Bond funds invest in fixed income securities. Bond funds can

be subclassified according to the specific types of bonds

owned (such as high-yield or junk bonds, investment-grade

corporate bonds, government bonds or municipal bonds) or by

the maturity of the bonds held (short-, intermediate- or long-

term). Bond funds may invest in primarily U.S. securities

(domestic or U.S. funds), in both U.S. and foreign securities

(global or world funds), or primarily foreign securities

(international funds).

At the end of 2010, bond funds accounted for 22% of the assets

in all U.S. mutual funds.

Stock or equity funds

Stock or equity funds invest in common stocks. Stock funds may

invest in primarily U.S. securities (domestic or U.S. funds),

in both U.S. and foreign securities (global or world funds),

or primarily foreign securities (international funds). They

may focus on a specific industry or sector.

46

A stock fund may be subclassified along two dimensions: (1)

market capitalization and (2) investment style (i.e., growth

vs. blend/core vs. value). The two dimensions are often

displayed in a grid known as a "style box."

Market capitalization or market cap is the value of a

company's stock and equals the number of shares outstanding

times the market price of the stock. Market capitalizations

are divided into the following categories:

Micro cap

Small cap

Mid cap

Large cap

While the specific definitions of each category vary with

market conditions, large cap stocks generally have market

capitalizations of at least $10 billion, small cap stocks have

market capitalizations below $2 billion, and micro cap stocks

have market capitalizations below $300 million. Funds are also

classified in these categories based on the market caps of the

stocks that it holds.

47

Stock funds are also subclassified according to their

investment style: growth, value or blend (or core). Growth

funds seek to invest in stocks of fast-growing companies.

Value funds seek to invest in stocks that appear cheaply

priced. Blend funds are not biased toward either growth or

value.

At the end of 2010, stock funds accounted for 48% of the

assets in all U.S. mutual funds.

Hybrid funds

Hybrid funds invest in both bonds and stocks or in convertible

securities. Balanced funds, asset allocation funds, target

date or target risk funds and lifecycle or lifestyle funds are

all types of hybrid funds.

Hybrid funds may be structured as funds of funds, meaning that

they invest by buying shares in other mutual funds that invest

in securities. Most fund of funds invest in affiliated funds

(meaning mutual funds managed by the same fund sponsor),

although some invest in unaffiliated funds (meaning those

managed by other fund sponsors) or in a combination of the

two.

48

At the end of 2010, hybrid funds accounted for 6% of the

assets in all U.S. mutual funds.

Index (passively-managed) versus actively-managed

Main articles: Index fund and active management

An index fund or passively-managed fund seeks to match the

performance of a market index, such as the S&P 500 index,

while an actively managed fund seeks to outperform a relevant

index through superior security selection.

Mutual fund expenses

Investors in mutual funds pay fees. These fall into four

categories: distribution charges (sales loads and 12b-1 fees),

the management fee, other fund expenses, shareholder

transaction fees and securities transaction fees. Some of

these expenses reduce the value of an investor's account;

others are paid by the fund and reduce net asset value.

Recurring expenses are included in a fund's expense ratio.

Distribution charges

Main article: Mutual fund fees and expenses

Distribution charges pay for marketing and distribution of the

fund's shares to investors.

49

Front-end load or sales charge

A front-end load or sales charge is a commission paid to

a broker by a mutual fund when shares are purchased. It is

expressed as a percentage of the total amount invested

(including the front-end load), known as the "public offering

price." The front-end load often declines as the amount

invested increases, through breakpoints. Front-end loads are

deducted from an investor's account and reduce the amount

invested.

Back-end load

Some funds have a back-end load, which is paid by the investor

when shares are redeemed depending on how long they are held.

The back-end loads may decline the longer the investor holds

shares. Back-end loads with this structure are called

contingent deferred sales charges (or CDSCs). Like front-end

loads, back-end loads are deducted from an investor's account.

12b-1 fees

A mutual fund may charge an annual fee, known as a 12b-1 fee,

for marketing and distribution services. This fee is computed

as a percentage of a fund's assets, subject to a maximum of 1%

of assets. The 12b-1 fee is included in the expense ratio.50

No-load funds

A no-load fund does not charge a front-end load under any

circumstances, does not charge a back-end load under any

circumstances and does not charge a 12b-1 fee greater than

0.25% of fund assets.

Share classes

A single mutual fund may give investors a choice of different

combinations of front-end loads, back-end loads and 12b-1

fees, by offering several different types of shares, known

as share classes. All of the shares classes invest in the same

portfolio of securities, but each has different expenses and,

therefore, a different net asset value and different

performance results. Some of these share classes may be

available only to certain types of investors.

Typical share classes for funds sold through brokers or other

intermediaries are:

Class A shares usually charge a front-end sales load

together with a small 12b-1 fee.

Class B shares don't have a front-end sales load. Instead

they, have a high contingent deferred sales charge, or CDSC

51

that declines gradually over several years, combined with a

high 12b-1 fee. Class B shares usually convert automatically

to Class A shares after they have been held for a certain

period.

Class C shares have a high 12b-1 fee and a modest contingent

deferred sales charge that is discontinued after one or two

years. Class C shares usually do not convert to another

class. They are often called "level load" shares.

Class I are subject to very high minimum investment

requirements and are, therefore, known as "institutional"

shares. They are no-load shares.

Class R are for use in retirement plans such as 401(k)

plans. They do not charge loads, but do charge a small 12b-1

fee.

No-load funds often have two classes of shares:

Class I shares do not charge a 12b-1 fee.

Class N shares charge a 12b-1 fee of no more than 0.25% of

fund assets.

Neither class of shares charges a front-end or back-end load.

Management fee

52

The management fee is paid to the fund manager or sponsor who

organizes the fund, provides the portfolio management or

investment advisory services and normally lends its brand name

to the fund. The fund manager may also provide other

administrative services. The management fee often has

breakpoints, which means that it declines as assets (in either

the specific fund or in the fund family as a whole) increase.

The management fee is paid by the fund and is included in the

expense ratio.

Other fund expenses

A mutual fund pays for other services including:

Board of directors' (or board of trustees') fees and

expenses

Custody fee: paid to a bank for holding the fund's portfolio

in safekeeping

Fund accounting fee: for computing the net asset value daily

Professional services fees: legal and accounting fees

Registration fees: when making filings with regulatory

agencies

53

Shareholder communications expenses: printing and mailing

required documents to shareholders

Transfer agent services fee: keeping shareholder records and

responding to customer inquiries

These expenses are included in the expense ratio.

Shareholder transaction fees

Shareholders may be required to pay fees for certain

transactions. For example, a fund may charge a flat fee for

maintaining an individual retirement account for an investor.

Some funds charge redemption fees when an investor sells fund

shares shortly after buying them (usually defined as within

30, 60 or 90 days of purchase); redemption fees are computed

as a percentage of the sale amount. Shareholder transaction

fees are not part of the expense ratio.

Securities transaction fees

A mutual fund pays any expenses related to buying or selling

the securities in its portfolio. These expenses may include

brokerage commissions. Securities transaction fees increase

the cost basis of the investments. They do not flow through

the income statement and are not included in the expense

54

ratio. The amount of securities transaction fees paid by a

fund is normally positively correlated with its trading volume

or "turnover".

Expense ratio

The expense ratio allows investors to compare expenses across

funds. The expense ratio equals the 12b-1 fee plus the

management fee plus the other fund expenses divided by average

net assets. The expense ratio is sometimes referred to as the

"total expense ratio" or TER.

Controversy

Critics of the fund industry argue that fund expenses are too

high. They believe that the market for mutual funds is not

competitive and that there are many hidden fees, so that it is

difficult for investors to reduce the fees that they pay.

Many researchers have suggested that the most effective way

for investors to raise the returns they earn from mutual funds

is to reduce the fees that they pay. They suggest that

investors look for no-load funds with low expense ratios.

Definitions

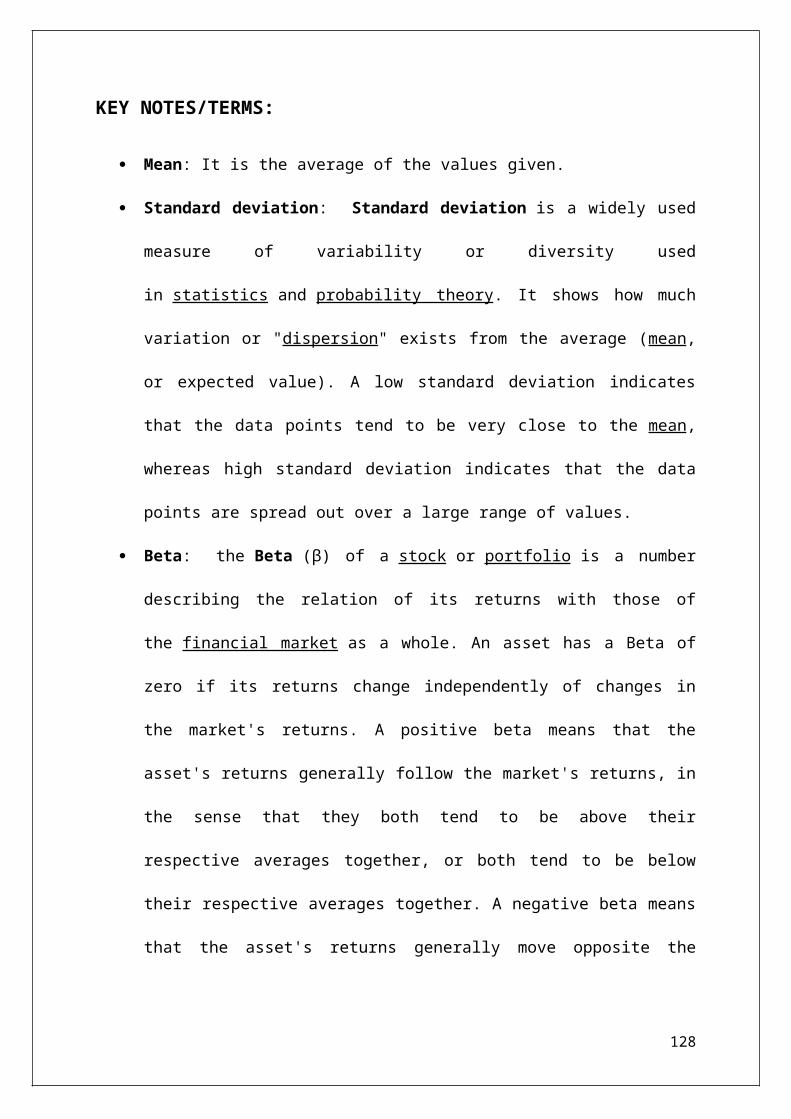

Definitions of key terms.

55

Net asset value or NAV

Main article: Net asset value

A fund's net asset value or NAV equals the current market

value of a fund's holdings minus the fund's liabilities

(sometimes referred to as "net assets"). It is usually

expressed as a per-share amount, computed by dividing by the

number of fund shares outstanding. Funds must compute their

net asset value every day the New York Stock Exchange is open.

Valuing the securities held in a fund's portfolio is often the

most difficult part of calculating net asset value. The fund's

board of directors (or board of trustees) oversees security

valuation.

Average annual total return

The SEC requires that mutual funds report the average annual

compounded rates of return for 1-year, 5-year and 10-year

periods using the following formula]

P(1+T)n = ERV

Where:

P = a hypothetical initial payment of $1,000.

T = average annual total return.

56

n = number of years.

ERV = ending redeemable value of a hypothetical

$1,000 payment made at the beginning of the 1-, 5-,

or 10-year periods at the end of the 1-, 5-, or 10-

year periods (or fractional portion).

Turnover

Turnover is a measure of the volume of a fund's

securities trading. It is expressed as a percentage

of net asset value and is normally annualized.

Turnover equals the lesser of a fund's purchases or

sales during a given period (of no more than a year)

divided by average net assets. If the period is less

than a year, the turnover figure is annualized.

MUTUAL FUNDS IN INDIA:

The first introduction of a mutual fund in India occurred in

1963, when the Government of India launched Unit Trust of

India (UTI). Until 1987, UTI enjoyed a monopoly in the Indian

mutual fund market. Then a host of other government-controlled

Indian financial companies came up with their own funds. These

57

included State Bank of India, Canara Bank, and Punjab National

Bank. This market was made open to private players in 1993, as

a result of the historic constitutional amendments brought

forward by the then Congress-led government under the existing

regime

of Liberalization, Privatizationand Globalization (LPG). The

first private sector fund to operate in India was Kothari

Pioneer, which later merged with Franklin Templeton.

Current Scenario

The major fund houses which have operated in India include:

Fortis

Birla Sunlife

Bank of Baroda

HDFC

ING Vysya

ICICI Prudential

SBI Mutual Fund

Tata

Kotak Mahindra

Unit Trust of India

Reliance

58

IDFC

Franklin Templeton

Sundaram Mutual Fund

Religare Mutual Fund

Principal Mutual Fund

Mutual funds are an under tapped market in India

Despite being available in the market for over two decades now

with assets under management equaling Rs 7,81,71,152 Lakhs (as

of 28 February 2010) (Source: Association of Mutual Funds,

India), less than 10% of Indian households have invested in

mutual funds. A recent report on Mutual Fund Investments in

India published by research and analytics firm, Boston

Analytics, suggests investorsare holding back from putting

their money into mutual funds due to their perceived high risk

and a lack of information on how mutual funds work. This

report is based on a survey of approximately 10,000

respondents in 15 Indian cities and towns as of March 2010.

There are 43 Mutual Funds recently.

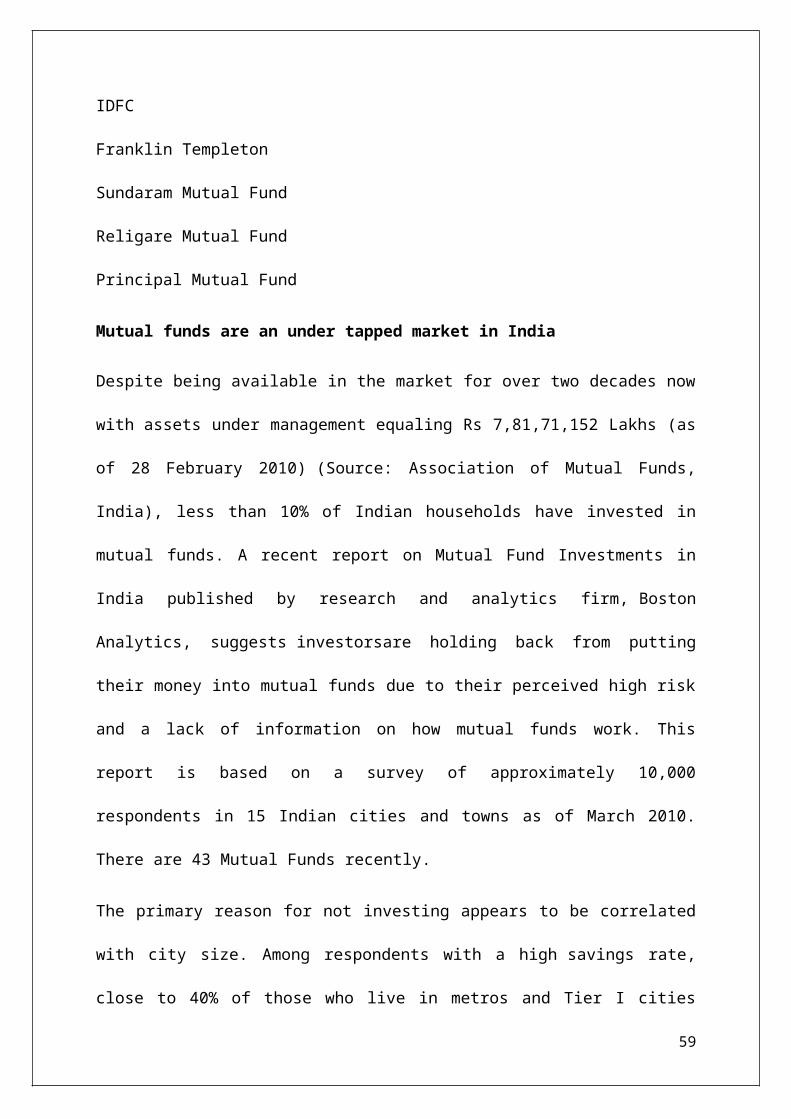

The primary reason for not investing appears to be correlated

with city size. Among respondents with a high savings rate,

close to 40% of those who live in metros and Tier I cities

59

considered such investments to be very risky, whereas 33% of

those in Tier II cities said they did not how or where to

invest in such assets.

Reasons for not investing in mutual funds in India

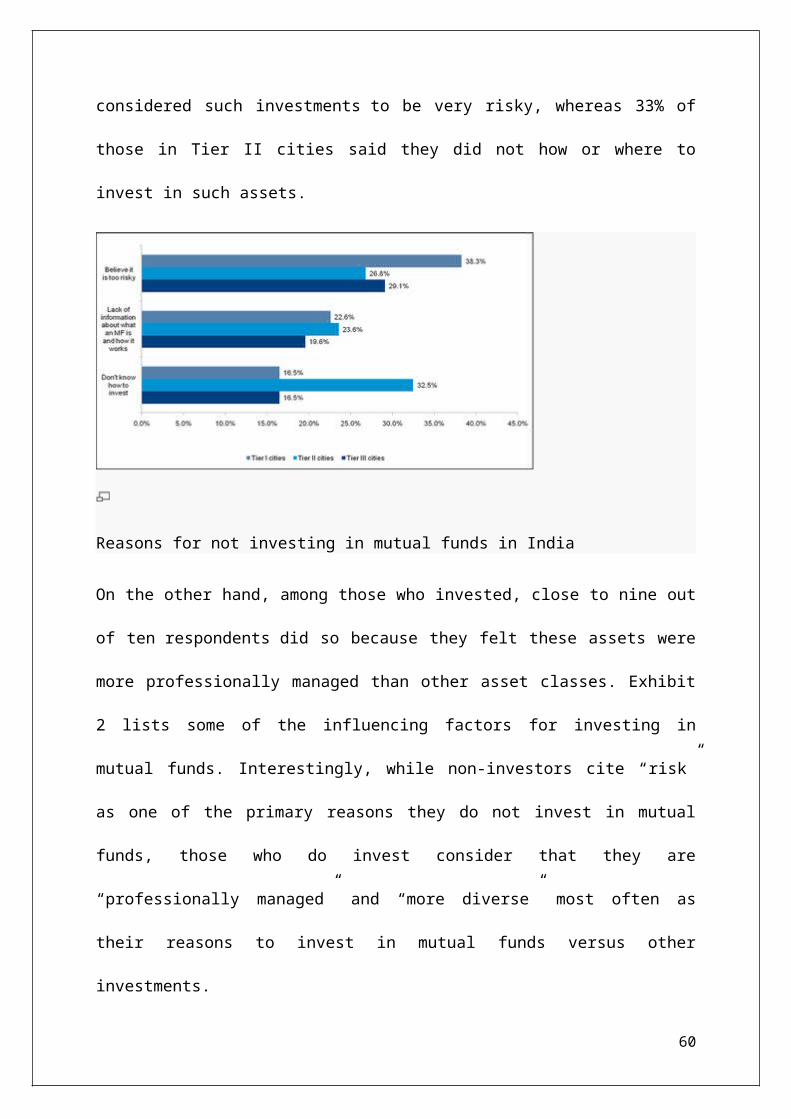

On the other hand, among those who invested, close to nine out

of ten respondents did so because they felt these assets were

more professionally managed than other asset classes. Exhibit

2 lists some of the influencing factors for investing in

mutual funds. Interestingly, while non-investors cite “risk”

as one of the primary reasons they do not invest in mutual

funds, those who do invest consider that they are

“professionally managed” and “more diverse” most often as

their reasons to invest in mutual funds versus other

investments.

60

MUTUAL FUND MARKET TREND:

A lone UTI with just one scheme in 1964, now competes with as many as 400 odd

products and 34 players in the market. In spite of the stiff competition and

losing market share, UTI still remains a formidable force to reckon with.

Last six years have been the most turbulent as well as exiting ones for the

industry. New players have come in, while others have decided to close shop by

either selling off or merging with others. Product innovation is now passé

with thegame shifting to performance delivery in fund management as well as

service. Those directly associated with the fund management industry like

distributors, registrars and transfer agents, and even the regulators have

61

become more mature and responsible.

The industry is also having a profound impact on financial markets. While UTI

has always been a dominant player on the bourses as well as the debt markets,

the new generation of private funds which have gained substantial mass are now

seen flexing their muscles. Fund managers, by their selection criteria for

stocks have forced corporate governance on the industry. By rewarding honest

and transparent management with higher valuations, a system of risk-reward has

been created where the corporate sector is more transparent then before.

Funds have shifted their focus to the recession free sectors like

pharmaceuticals, FMCG and technology sector. Funds performances are improving.

Funds collection, which averaged at less than Rs.100bn per annum over five-year

period spanning 1993-98 doubled to Rs.210bn in 1998-99. In the current year

mobilization till now have exceeded Rs.300bn. Total collection for the current

financial year ending March 2000 is expected to reach Rs.450bn.

What is particularly noteworthy is that bulk of the mobilization has been by

the private sector mutual funds rather than public sector mutual funds. Indeed

private MFs saw a net inflow of Rs.7819.34 crore during the first nine months

of the year as against a net inflow of Rs.604.40 crore in the case of public

62

sector funds.

Mutual funds are now also competing with commercial banks in the race for

retail investor’s savings and corporate float money. The power shift towards

mutual funds has become obvious. The coming few years will show that the

traditional saving avenues are losing out in the current scenario. Many

investors are realizing that investments in savings accounts are as good as

locking up their deposits in a closet. The fund mobilization trend by mutual

funds in the current year indicates that money is going to mutual funds in a

big way. The collection in the first half of the financial year 1999-2000

matches the whole of 1998-99.

India is at the first stage of a revolution that has already peaked in the

U.S. The U.S. boasts of an Asset base that is much higher than its bank

deposits. In India, mutual fund assets are not even 10% of the bank deposits,

but this trend is beginning to change. Recent figures indicate that in the

first quarter of the current fiscal year mutual fund assets went up by 115%

whereas bank deposits rose by only 17%. (Source: Thinktank, The Financial

Express September, 99) This is forcing a large number of banks to adopt the

concept of narrow banking wherein the deposits are kept in Gilts and some other

assets which improves liquidity and reduces risk. The basic fact lies that

63

banks cannot be ignored and they will not close down completely. Their role as

intermediaries cannot be ignored. It is just that Mutual Funds are going to

change the way banks do business in the future.

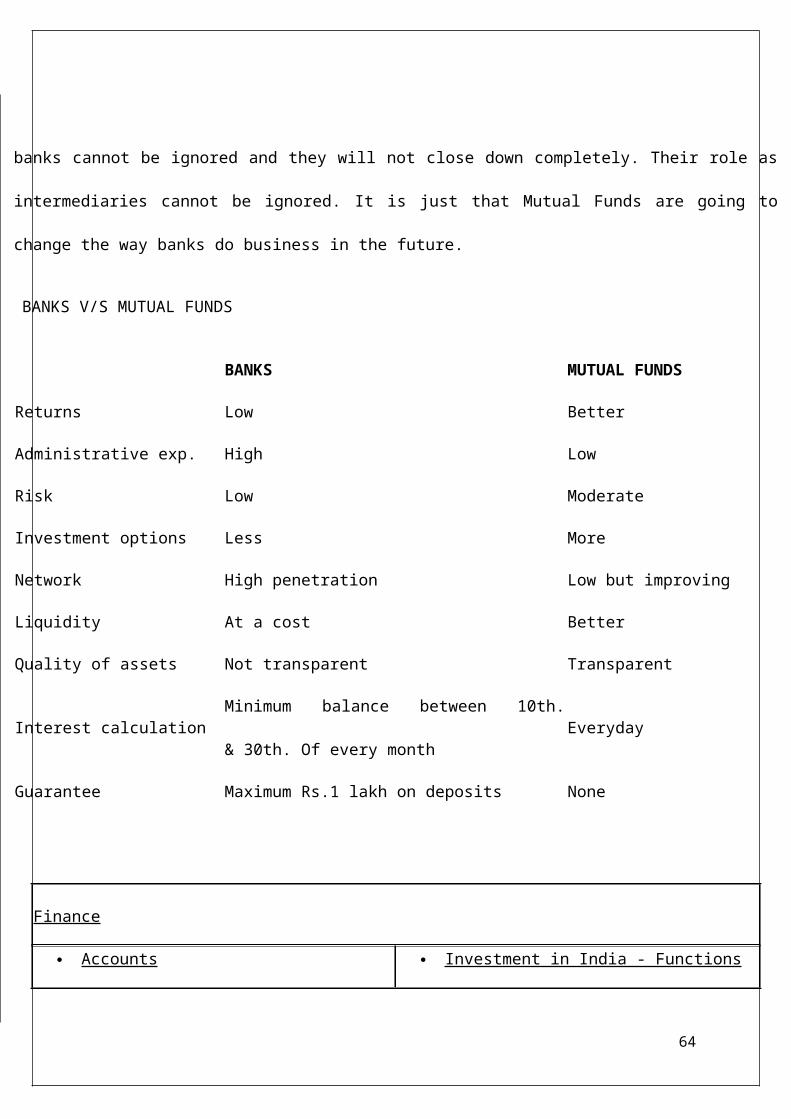

BANKS V/S MUTUAL FUNDS

BANKS MUTUAL FUNDS

Returns Low Better

Administrative exp. High Low

Risk Low Moderate

Investment options Less More

Network High penetration Low but improving

Liquidity At a cost Better

Quality of assets Not transparent Transparent

Interest calculationMinimum balance between 10th.

& 30th. Of every monthEveryday

Guarantee Maximum Rs.1 lakh on deposits None

Finance

Accounts Investment in India - Functions

64

ATM - Automatic Teller Machine

Banks of India

Company Shares / Debentures

Credit card - Costs

Credit Card - Glossary

Credit Card - Hard Facts

Credit Cards - Eligibility

Criteria

Credit Cards

Direct Investment with

Repatriation Benefits

Electronic Banking

Euro Issues by Indian Companies

Financial sector and Banking

Financial Sector Reforms in

India

Credit Card - Find the one that

suits your needs

Fixed Deposits

FIPB - Foreign Investment

Investment in Government

Securities

Investments by Non-Residents

Mutual Funds - Frequently Asked

Questions

Regulatory Aspects Of Mutual

Fund

Benefits Of Investing In Mutual

Funds

Mutual Funds - Glossary

Mutual Funds - History

Types of Mutual Fund

Mutual Funds

Mutualfund - Market Trends

Mutualfunds - Global Scenario

Mutual Funds - Net Asset Value

(NAV)

NRI - FAQ

NRI Investments - Company

65

Promotion Board

IDBI - Industrial Development

Bank of India

Internet Banking

Investing in india

Investment by Foreign Companies

Investment in India - Approval

by FIPB

Investment in India -

Composition

Deposits

NRI Investments - Government

Securities/Units

Overdraft

Portfolio Investment Scheme

Portfolio Investment in

Shares/Debentures

Private Banking

R B I - Reserve Bank of India

Sale / Transfer of Shares /

Securities

Purchase of Shares and

Securities by Non-Residents

Transfer of Shares/Securities by

Non-Residents to Residents

66

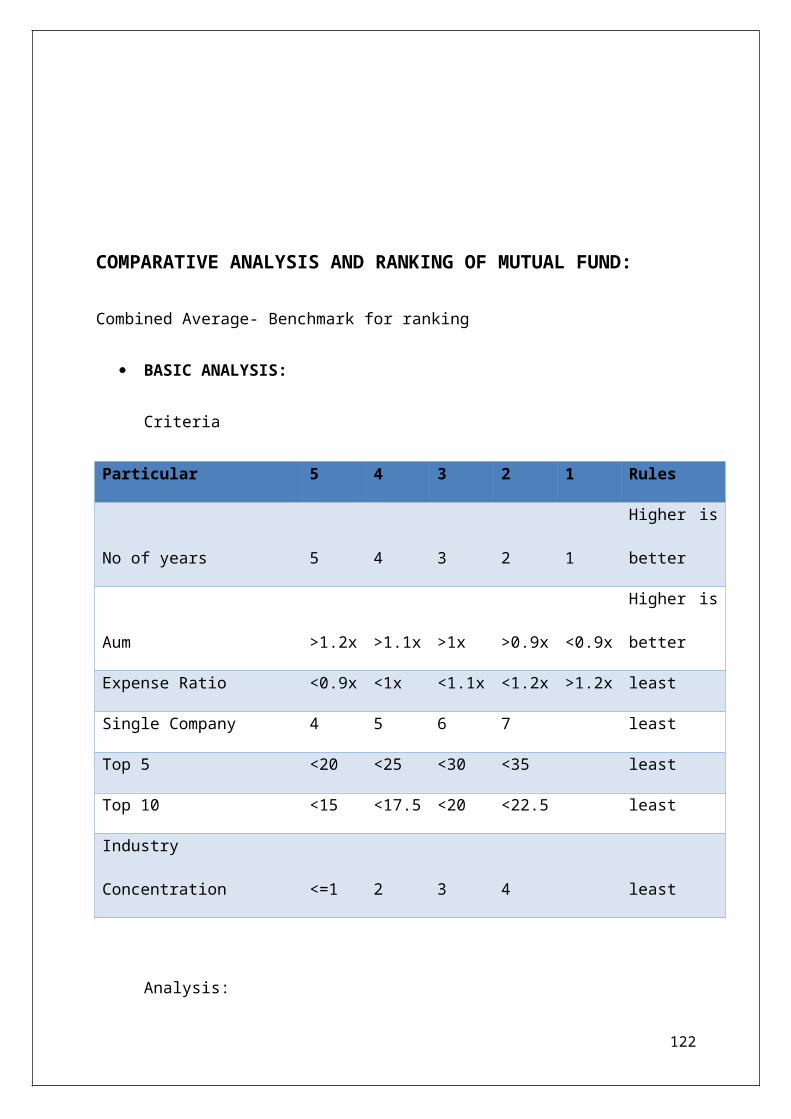

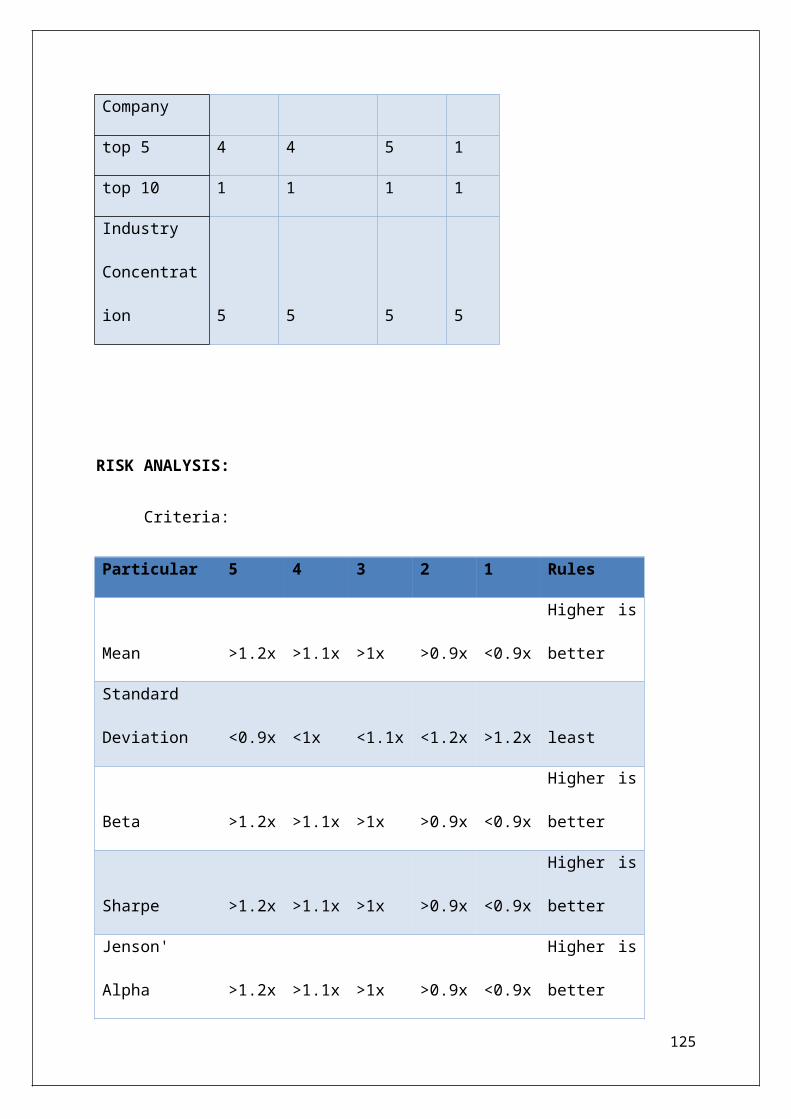

RANKING OF MUTUAL FUND:

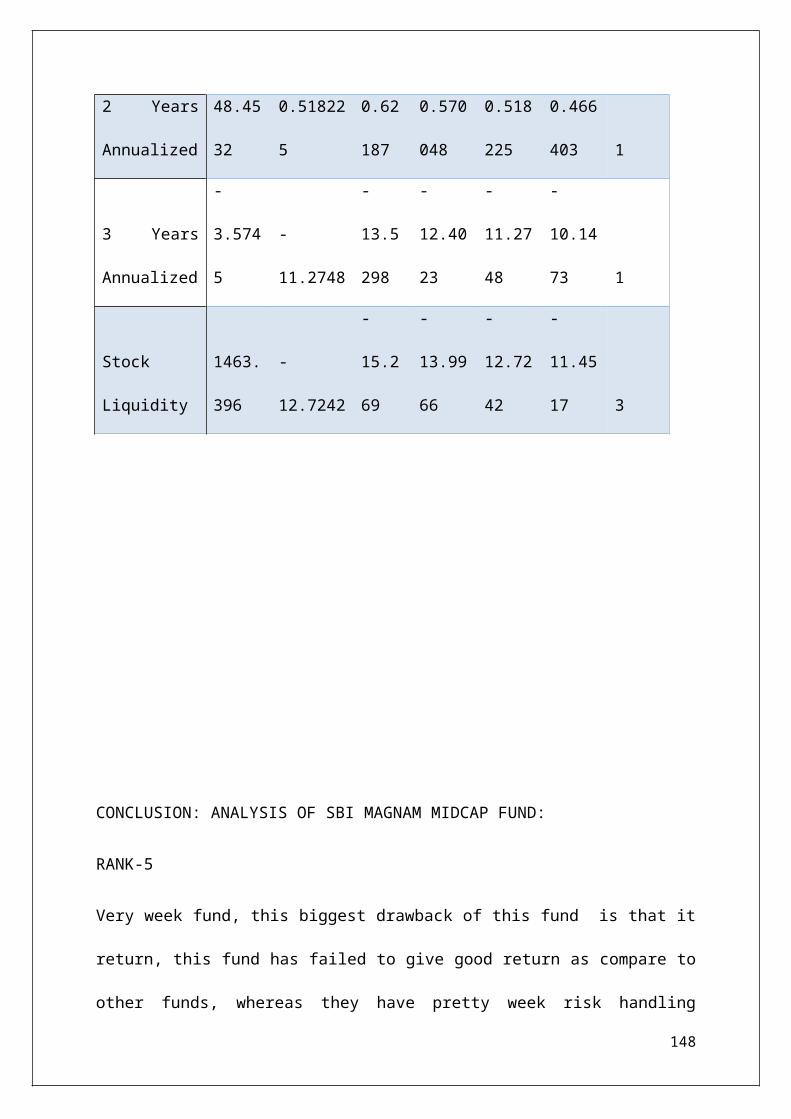

Mutual funds have become a very common mode to enter into

financial market. Simpler way to enter the market but it can

go all wrong if an investor fails to select the right fund.

The big question is how to select the best mutual fund to

invest? An investor would probably go with the fund which is

the best ranked, one with a good NAV, having a good nav does

not mean the fund is good, it is one the criteria’s to rank a

mutual fund.

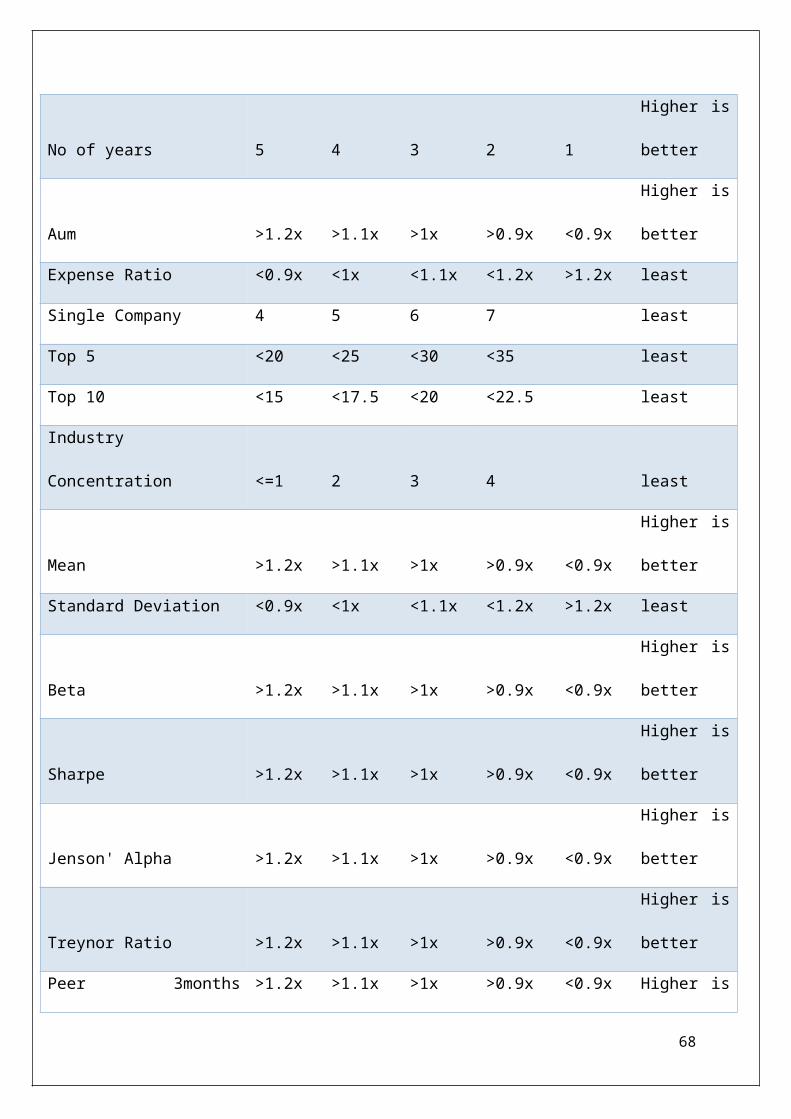

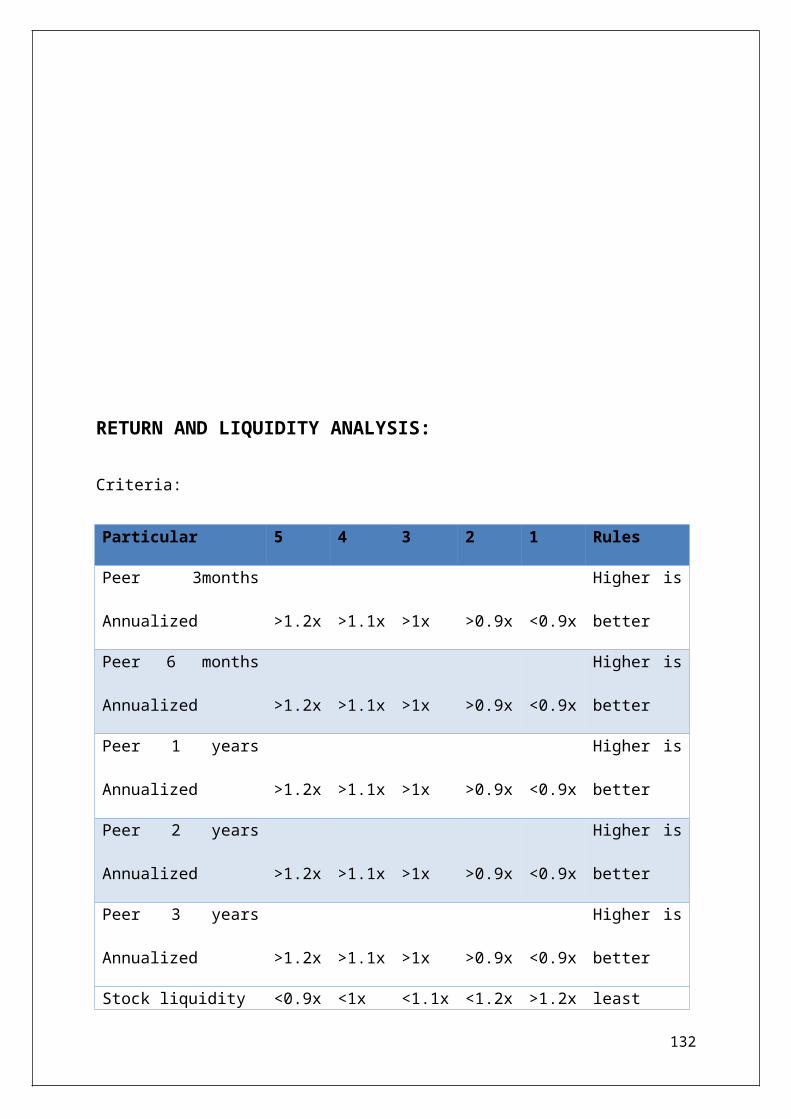

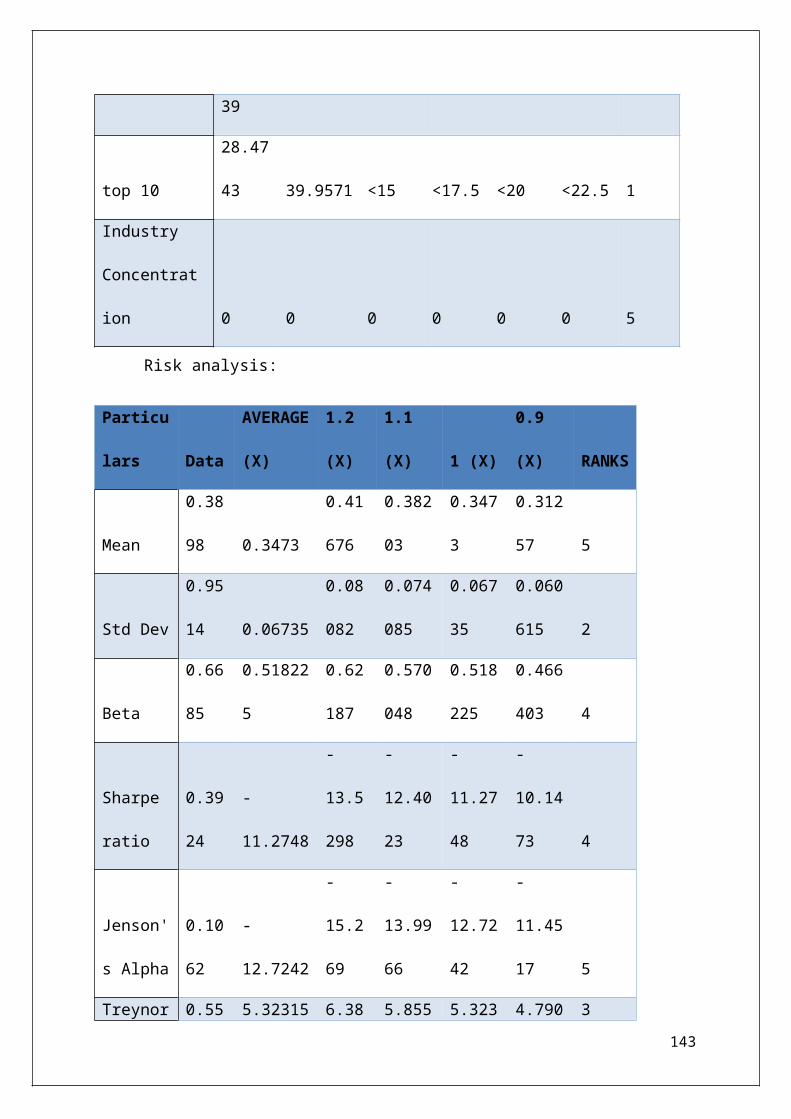

Ranking criteria’s:

Scores

Particular 5 4 3 2 1 Rules

67

No of years 5 4 3 2 1

Higher is

better

Aum >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Expense Ratio <0.9x <1x <1.1x <1.2x >1.2x least

Single Company 4 5 6 7 least

Top 5 <20 <25 <30 <35 least

Top 10 <15 <17.5 <20 <22.5 least

Industry

Concentration <=1 2 3 4 least

Mean >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Standard Deviation <0.9x <1x <1.1x <1.2x >1.2x least

Beta >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Sharpe >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Jenson' Alpha >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Treynor Ratio >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Peer 3months >1.2x >1.1x >1x >0.9x <0.9x Higher is

68

Annualized better

Peer 6 months

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Peer 1 years

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Peer 2 years

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Peer 3 years

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Benchmark 3 month

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Benchmark 6 month

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Benchmark 1 year

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Benchmark 2 years

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Benchmark 3 years

Annualized >1.2x >1.1x >1x >0.9x <0.9x

Higher is

better

Stock liquidity <0.9x <1x <1.1x <1.2x >1.2x least

69

Weightage:

Note: ‘X’ is referred to the peer

group, it is nothing but the

average the peer group funds.

70

Parameters

Weightag

e (%)

Basic 5

Company

concentration 7

Industry

concentration 8

Risk Analysis 15

Performance 60

Liquidity 5

Total 100

COMPANY

PROFILE:

71

CANARA ROBECO:

Robeco is a Dutch asset management firm founded in 1929 as

the Rotterdamsch Beleggings Consortium (Rotterdam Investment

Consortium). By year end 2009, the company had over € 130

billion of assets under management.It was acquired in 2001 by

the Rabobank Groep.

Robeco offers assets management services to

both institutional and private investors. The funds for

private investors are available through Robeco itself and

other financial institutions, a number of these funds are also

listed on major European stock exchanges. Since 1981 the

company also offers savings accounts through its own savings

bank Roparco.

Canara Robeco Asset Management Company Limited (CRAMC), the

investment managers of Canara Robeco Mutual Fund, is a joint

venture between Canara Bank andRobeco of the Netherlands, a

72

global asset management company that manages about US$180

Billion worldwide. The joint venture brings together Canara

Bank's experience in the Indian market and Robeco's global

experience in asset management.

Canara Robeco Mutual Fund is the oldest Mutual Fund in India,

established in December 1987 as Canbank Mutual Fund.

Subsequently, in 2007, Canara Bank partnered Robeco and the

mutual fund was renamed as Canara Robeco Mutual Fund. Since

then, it has consistently been one of the fastest growing

mutual funds in India in terms of AuM, having grown 94% year-

on-year from March 2009 to March 2010. Our solutions offer a

range of investment options, including diversified and

thematic equity schemes, hybrid and monthly income funds and a

wide range of debt and treasury products.

Canara Robeco AMC manages the assets of Canara Robeco Mutual

Fund by virtue of an investment management agreement dated

16th June 1993 (as amended from time to time). As of 31

December 2010, the AMC has Rs. 7,392 crores of average assets

73

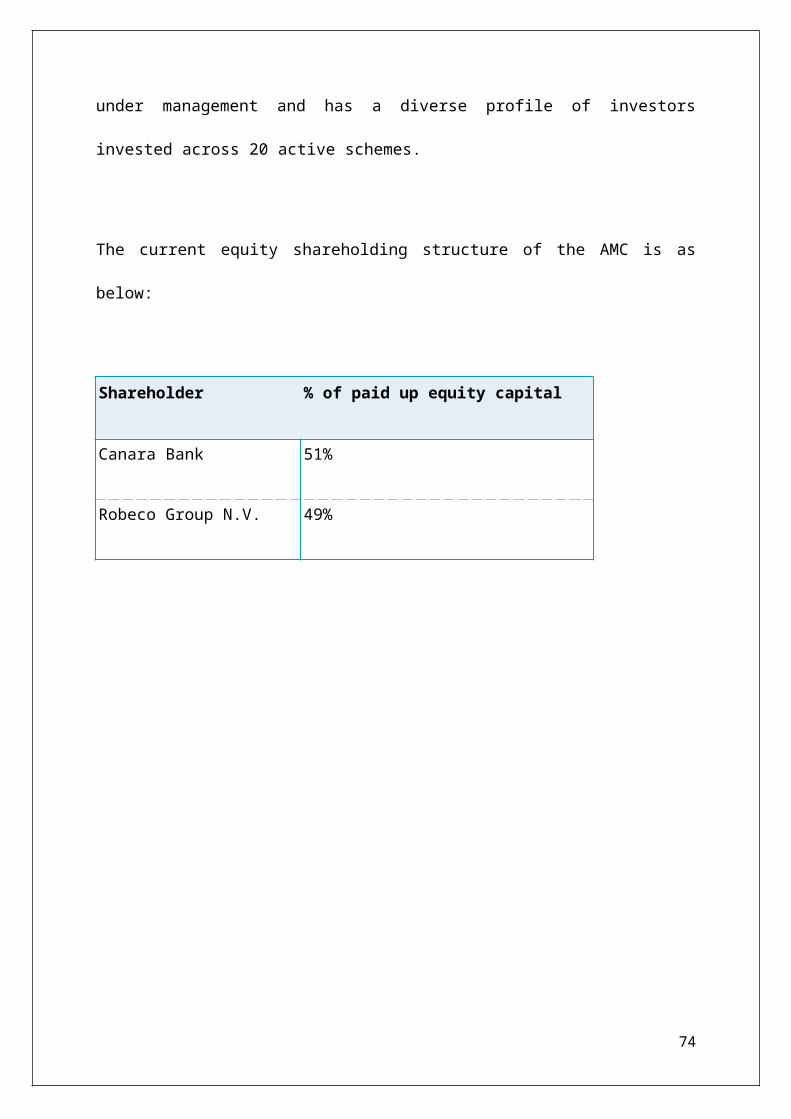

under management and has a diverse profile of investors

invested across 20 active schemes.

The current equity shareholding structure of the AMC is as

below:

Shareholder % of paid up equity capital

Canara Bank 51%

Robeco Group N.V. 49%

74

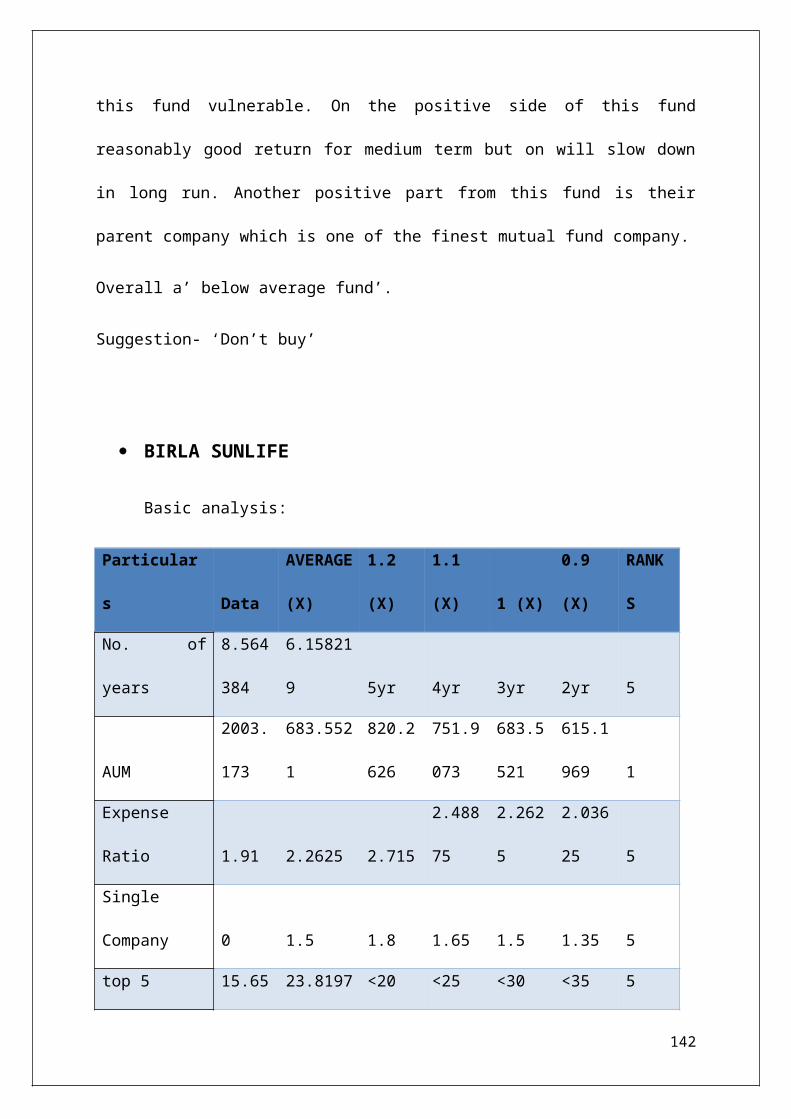

DSP BLACKROCK:

DSP BlackRock Investment Managers is one of the premier asset

management companies in India. It is a joint venture between

the DSP Group and BlackRock. Currently the firm manages and

advises assets worth INR 41,484 cr (as on Jul 29, 2011).

The DSP Group, headed by Mr. Hemendra Kothari, is one of the

oldest financial services firms in India. It has a track

record of over 145 years and was one of the founding members

of the Bombay Stock Exchange.

BlackRock is the largest listed asset management company in

the world. It is a premier provider of investment solutions

through a variety of product structures, including individual

and institutional separate accounts, mutual funds and other

pooled investment vehicles, and the industry-leading iShares®

ETFs to investors around the world. Currently the firm manages