PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT: INDUSTRY AND FIRM-LEVEL EVIDENCE FOR EUROPE AND THE US

28

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT: INDUSTRY AND FIRM-LEVEL EVIDENCE FOR EUROPE AND THE US Nicola Matteucci n , Mary O’Mahony nn , Catherine Robinson nn and Thomas Zwick nnn Abstract This paper considers the contribution of information and communications technology (ICT), to international productivity performance. It first uses an international industry data set and a growth accounting framework, to show that ICT has typically had a lower impact on productivity in Europe than in the US, although there is considerable variation within Europe. The paper also analyses the European situation in greater depth by examining micro-economic data from Germany, Italy and the UK. While direct comparisons between the national findings are difficult, the results suggest that the UK experience with ICT has been closer to the US than other European countries. I Introduction An important indicator of workplace performance is productivity defined as the amount of output produced for inputs used. International comparisons of productivity offer an important point of reference for our economic and political performance, compared with our major trading partners and competitors. Such comparisons also offer insight into where different nationalities’ strengths lie, and in particular, highlight best-practice methods of combining inputs and incorporating new technologies and practices. International comparisons set the scene for more detailed analyses of the underlying causes of productivity differences. The purpose of this paper is to analyse the use of information and communications technology (ICT) as a driver of productivity differences between the US and Europe. In so doing, this paper highlights the complementary nature of industry and firm-level analyses in identifying the reasons for cross-country differences in workplace performance. n Universita` Politecnica delle Marche, Ancona, Italy nn National Institute of Economic and Social Research, London, UK nnn Centre for European Economic Research (ZEW), Mannheim, Germany kdlkdlkdooeopeoi Scottish Journal of Political Economy, Vol. 52, No. 3, July 2005 r Scottish Economic Society 2005, Published by Blackwell Publishing, 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA 359

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT: INDUSTRY AND FIRM-LEVEL EVIDENCE FOR EUROPE AND THE US

PRODUCT I V I TY , WORKPLACEP ERFORMANCE AND I C T : I NDU S TRY

AND F I RM - L EVEL EV IDENCE FOREUROPE AND THE U S

Nicola Matteuccin, Mary O’Mahonynn, Catherine Robinsonnn and

Thomas Zwicknnn

Abstract

This paper considers the contribution of information and communications

technology (ICT), to international productivity performance. It first uses an

international industry data set and a growth accounting framework, to show that

ICT has typically had a lower impact on productivity in Europe than in the US,

although there is considerable variation within Europe. The paper also analyses the

European situation in greater depth by examining micro-economic data from

Germany, Italy and the UK. While direct comparisons between the national

findings are difficult, the results suggest that the UK experience with ICT has been

closer to the US than other European countries.

I Introduction

An important indicator of workplace performance is productivity defined as the

amount of output produced for inputs used. International comparisons of

productivity offer an important point of reference for our economic and political

performance, compared with our major trading partners and competitors. Such

comparisons also offer insight into where different nationalities’ strengths lie,

and in particular, highlight best-practice methods of combining inputs and

incorporating new technologies and practices. International comparisons set the

scene for more detailed analyses of the underlying causes of productivity

differences. The purpose of this paper is to analyse the use of information and

communications technology (ICT) as a driver of productivity differences

between the US and Europe. In so doing, this paper highlights the

complementary nature of industry and firm-level analyses in identifying the

reasons for cross-country differences in workplace performance.

nUniversita Politecnica delle Marche, Ancona, ItalynnNational Institute of Economic and Social Research, London, UKnnnCentre for European Economic Research (ZEW), Mannheim, Germany

kdlkdlkdooeopeoi

Scottish Journal of Political Economy, Vol. 52, No. 3, July 2005r Scottish Economic Society 2005, Published by Blackwell Publishing, 9600 Garsington Road, Oxford OX4 2DQ, UKand 350 Main Street, Malden, MA 02148, USA

359

ICT is considered to have both a direct and an indirect impact on productivity.

The direct impact may be measured by ICT capital investment over time, a capital

deepening effect; however, indirect impacts are the more subtle changes that result

as ICT capital changes the nature of production processes (Atrostic and Nguyen,

2004). These processes are generally described as workplace organisational

changes (Black and Lynch, 2001). In addition, these might also include external

benefits or spillovers from investing in ICT (Rincon and Vecchi, 2004).

Empirically, at both the industry level and the firm level, considerable evidence

now exists to suggest a strong positive impact of ICT on workplace productivity

in the US, with increasing evidence also emerging for other countries (OECD,

2004). This paper briefly reviews this evidence and then presents some new results.

Using the recently constructed industry-level international data set under-

lying O’Mahony and Van Ark (2003), this paper first compares labour and total

factor productivity (TFP) across countries, and examines the extent to which

these trends are associated with investment in ICT capital. This section of the

paper relies on the use of growth accounting methods.

Micro-studies, with their emphasis on econometric techniques, have

traditionally found a bigger impact of ICT than industry-level studies

(Brynjolfsson and Hitt, 1996; Lehr and Lichtenberg, 1999; Brynjolfsson and

Hitt, 2000). Some new research findings using micro-data for UK, Germany and

Italy are presented in the second part of the paper. Taken together these results

suggest that ICT is an important driver of productivity change.

The following section of the paper begins with an overview of the growth

accounting method. It then combines this with the international industry data

set to highlight some of the major trends and differences among European

countries in comparison with the US. The section concentrates on the extent of

ICT investment and is suggestive that this is an important influence on recent

divergences in productivity growth among these countries. Section III goes on to

elaborate on the nature of these relationships, analysed at the micro-level in a

handful of European countries, referring both to existing literature and

presenting new results that attempt to explain the precise nature of the impact

of new technology at the firm level. Section IV draws together both the macro-

and the micro-economic evidence and highlights the importance of micro-

economic analyses in explaining aggregate trends.

II Research Methods and Data

Growth accounting methods

The growth accounting approach to TFP estimation has been extensively

employed to estimate the impact of ICT capital deepening on output and

productivity growth (see e.g. Jorgenson and Stiroh, 2000; Oliner and Sichel,

2000; for the US, Oulton, 2002; for the UK). It is useful in that it allows for the

decomposition of output or labour productivity growth into contributions from

factor inputs and underlying productivity growth or TFP. This method is

employed in the industry analysis in section III.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK360

r Scottish Economic Society 2005

Assume the production function of an industry in country ( j) may be

written as

Qjt ¼ Aj

t fjðLj

t;Kjt Þ; ð1Þ

where Q is real output (here measured as real value added (VA)), K and L are

capital and labour inputs, respectively, and A is an index of technical progress or

TFP. Under assumptions of perfectly functioning markets and constant returns

to scale, differentiating (1) with respect to time, yields an index of TFP growth

known as the Divisia index. This index is a valid measure of TFP growth in

continuous time, regardless of the functional form of the production function. In

practice, as changes are not observed continuously, an approximation is

required. Assuming a Translog production function, the Tornqvist index is the

appropriate approximation of the Divisia index (Jorgenson et al., 1987), and

output growth may then be decomposed into its various components in the

following way:

lnQ

jt

Qjt�1

!¼ ajðt; t� 1Þ ln L

jt

Ljt�1

!þ ð1� ajðt; t� 1ÞÞ ln K

jt

Kjt�1

!

þ lnA

jt

Ajt�1

!; ð2Þ

where a(t, t� 1) is the share of labour in VA averaged over the two time periods.

Incorporating quality adjustments to inputs stems originally from Jorgenson

and Griliches (1967). In studies relating to the impact of ICT on productivity,

this has involved quality adjustment of capital, accounting for substitution

between new technology and traditional capital. This approach is also adopted

here but in addition this analysis includes a labour quality adjustment, which is a

refinement to many of the earlier studies on the impact of ICT.

To incorporate quality adjustments to inputs, the growth in aggregate labour

and aggregate capital can be estimated as Tornqvist indexes of their

components. Suppose there are l types of labour and k types of capital. Then

these indexes are given by

lnLjt

Ljt�1

!¼Xl

a jl ðt; t� 1Þ ln

Ljl;t

Ljl;t�1

!; ð3aÞ

lnK

jt

Kjt�1

!¼Xk

akjðt; t� 1Þ lnK

jk;t

Kjk;t�1

!; ð3bÞ

where a jl ðt; t� 1Þ is the share of type l labour in the total wage bill and a j

k

ðt; t� 1Þ is the share of type k capital in the value of capital. Thus if the

employment of (highly paid) skilled labour is growing faster than unskilled

types, weighting by wage bill shares leads to faster growth in labour input than a

simple count of hours worked.

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 361

r Scottish Economic Society 2005

Econometric Analysis

In the sections reporting results based on firm-level data, regression analysis is

employed to estimate augmented production functions. All three studies use a

standard Cobb–Douglas framework, where output is related to a time-variant

index of technical progress (Hicks neutral, common to all firms) and to j

productive inputs (Xj) and variables that measure the use of ICT (I ) plus other

control variables. In its general form this relation can be log-linearised, in a form

amenable to direct estimation:

ln Yit ¼ ln Aþ Sjaj ln Xijt þ Sjbj ln Iijt þ Sjgj ln Zijt þ Zit: ð4Þ

The variables included and details of the econometric methods employed are

discussed in each subsection.

Data

The industry analysis employs the data set underlying O’Mahony and Van Ark

(2003). Output is real gross VA and the volume of labour input is measured by

hours worked. The growth accounting analysis was carried out for 26 individual

industries in the US, France, Germany and the UK. Capital is measured as

consisting of six asset types of which three are ICT, defined as computing

equipment, software and communications equipment. In the estimates below,

contributions of ICT and non-ICT capital are shown separately, thus delineating

the main capital quality components. Oliner and Sichel (2000) highlight the fact

that in the growth accounting framework, the productive stock is the variable of

interest (i.e. how much assets produce each period) and not the wealth stock

(their market value). To take account of this, user costs rather than acquisition

prices are employed in constructing weights for each type of asset. In addition

the special nature of ICT capital stock requires adjustment to the standard

approach to deflation. Deflators based on the US hedonic price index, adjusted

for international price or exchange rate movements, have been employed in

many international or individual country studies of the impact of ICT capital on

growth, (e.g. Colecchia and Schreyer, 2002; Oulton, 2002; Van Ark et al., 2002

to name but a few). This is primarily because a viable alternative is generally not

available outside the US, given time series requirements for the analysis

considered here. This is also the approach adopted in this analysis.

Investment series at constant prices are converted into estimates of

productive capital stocks using the perpetual inventory method with geometric

depreciation rates. US depreciation rates are employed for all four countries but

these are allowed to vary by asset type and hence by industry.1 In addition to

incorporating a quality adjustment for capital, the data set also includes quality

adjustments for labour force skills. This is achieved by disaggregating hours

1Further details on capital services estimation are provided in O’Mahony and Van Ark(2003) and its practical application in the data set employed in this paper is extensivelyconsidered in Inklaar et al. (2003). In addition, output series for the ICT producing sectoremploy deflators based on the US hedonic price indexes for these industries.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK362

r Scottish Economic Society 2005

worked by skill type and weighting each by its share in the total wage bill, as in

equation (3a). The skill divisions are allowed to vary across country. The

difference between the growth in this index and one which simply adds together

hours is the labour quality index shown in the tables.

The data employed in each of the micro-economic studies reported below

vary by country and so are described in each subsection. In general, although

they consist of surveys of firms or establishments that contain data on the use of

information technology.

III Inter-Country Comparisons of Industry Performance

Labour productivity levels

This section considers the industry evidence on comparative productivity

performance since 1979 using the data set underlying O’Mahony and Van Ark

(2003). It compares productivity growth rates in four countries during this time

period, the US, the UK, France and Germany, focusing on the industry

distribution of productivity growth differences between the US, on the one

hand, and the three EU countries on the other. The analysis considers the extent

to which investment in ICT is associated with these cross industry differences,

and is confined to market sectors, as non-market services (health, education and

public administration) are not accurately measured in the underlying national

accounts data.

Before considering growth rates it is useful to place these in the context of

relative productivity levels. Table 1 shows output per hour worked relative to

levels in the US in the three EU countries in the market economy and a broad

three way division of this total into agriculture, production industries and

market services. Over the two decades covered here, the European countries

have narrowed their labour productivity gap with the US in the market

economy, continuing the process of postwar convergence. However, the mid-

1990s represented a break in this process with the US moving further ahead, and

significantly so relative to France and Germany. The broad industry breakdown

in Table 1 shows that this break was largely driven by trends in market services.

Note that the numbers for the aggregate economy reflect not only the US going

ahead in market services but also the increasing share of economic activity

represented by that sector in all four countries.

An extensive literature has developed in recent years linking this change in

the relative fortunes of the US to that country’s earlier adoption of ICT. Thus,

Jorgenson and Stiroh (2000) and Oliner and Sichel (2000, 2002) have shown a

significant and growing impact of ICT capital deepening on labour productivity

growth in the US. Recently evidence has suggested that there may also be a

payoff from investment in ICT equipment on TFP growth (Stiroh, 2002;

O’Mahony and Vecchi, 2005). In much of the US literature the importance of

service sectors in driving these changes has been identified (see e.g. Triplett and

Bosworth, 2003).

O’Mahony and Van Ark (2003) and Inklaar et al. (2003) have extensively

analysed the importance of increased investment in ICT comparing aggregates

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 363

r Scottish Economic Society 2005

across European Union member states with the US. This section focuses on the

three European countries mentioned above and on the varying experiences in

manufacturing and market service sectors.

Growth accounting results

Growth accounting estimates of input growth and TFP were calculated for 25

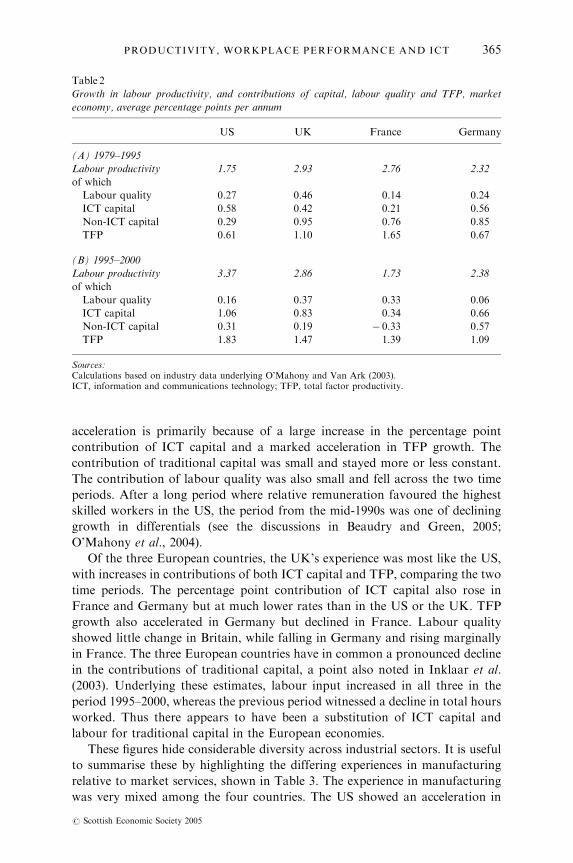

market sectors annually for the period 1979–2000.2 Table 2 summarises the main

findings from the growth accounting approach for the market economy,

employing labour productivity decompositions derived by dividing both sides of

equation (2) by hours worked. The sample is split into two time periods, from

1979 to 1995 and thereafter. The year 1995 is generally considered the break

point in trend US labour productivity growth (see the discussion in Inklaar and

McGuckin, 2003).

The first striking feature of Table 2 is the pronounced acceleration in US

labour productivity growth in the second period relative to the first. In contrast

rates in the UK and Germany were largely unchanged while France shows a

decline. In the US, the decomposition of the sources of growth show that the

Table 1

Comparative labour productivity levels by sector: output per hour worked (US5 100)

1979 1990 1995 2001

United Kingdom

Market economya 62 67 75 73

Agriculture 95 63 73 53

Industryb 56 66 75 77

Market servicesc 64 67 73 72

France

Market economy 84 99 99 91

Agriculture 44 39 52 42

Industry 85 89 91 93

Market services 98 118 112 95

Germany

Market economy 85 91 93 89

Agriculture 27 24 29 25

Industry 86 83 79 80

Market services 88 97 104 94

Notes:aTotal economy excluding, health, education, public administration and real estate.bMining, manufacturing, utilities and construction.cTransport, communications, distribution, hotels and catering, financial and business services and personalservices.Source:Updates of estimates in O’Mahony and DeBoer (2002).

2 Tables by detailed industry and country are printed in O’Mahony and Van Ark (2003); theunderlying data are downloadable from www.niesr.ac.uk/epke/

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK364

r Scottish Economic Society 2005

acceleration is primarily because of a large increase in the percentage point

contribution of ICT capital and a marked acceleration in TFP growth. The

contribution of traditional capital was small and stayed more or less constant.

The contribution of labour quality was also small and fell across the two time

periods. After a long period where relative remuneration favoured the highest

skilled workers in the US, the period from the mid-1990s was one of declining

growth in differentials (see the discussions in Beaudry and Green, 2005;

O’Mahony et al., 2004).

Of the three European countries, the UK’s experience was most like the US,

with increases in contributions of both ICT capital and TFP, comparing the two

time periods. The percentage point contribution of ICT capital also rose in

France and Germany but at much lower rates than in the US or the UK. TFP

growth also accelerated in Germany but declined in France. Labour quality

showed little change in Britain, while falling in Germany and rising marginally

in France. The three European countries have in common a pronounced decline

in the contributions of traditional capital, a point also noted in Inklaar et al.

(2003). Underlying these estimates, labour input increased in all three in the

period 1995–2000, whereas the previous period witnessed a decline in total hours

worked. Thus there appears to have been a substitution of ICT capital and

labour for traditional capital in the European economies.

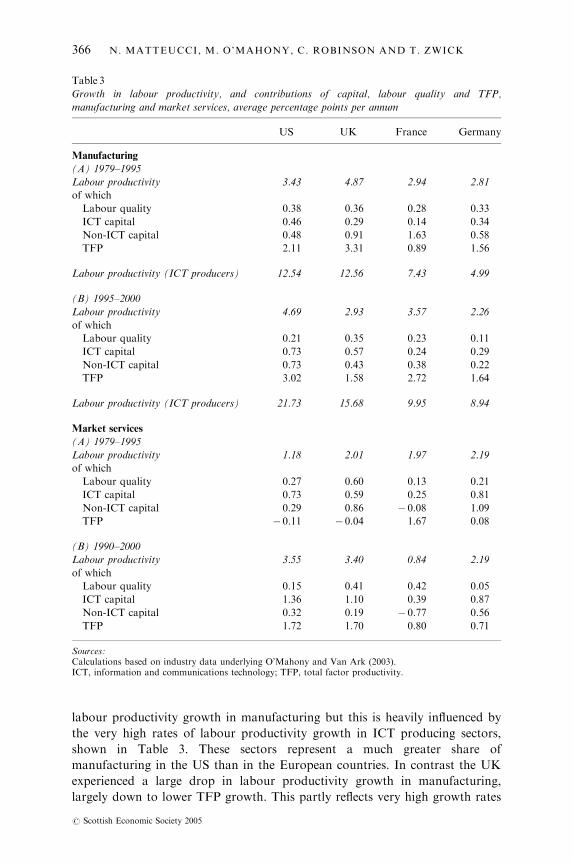

These figures hide considerable diversity across industrial sectors. It is useful

to summarise these by highlighting the differing experiences in manufacturing

relative to market services, shown in Table 3. The experience in manufacturing

was very mixed among the four countries. The US showed an acceleration in

Table 2

Growth in labour productivity, and contributions of capital, labour quality and TFP, market

economy, average percentage points per annum

US UK France Germany

(A) 1979–1995

Labour productivity 1.75 2.93 2.76 2.32

of which

Labour quality 0.27 0.46 0.14 0.24

ICT capital 0.58 0.42 0.21 0.56

Non-ICT capital 0.29 0.95 0.76 0.85

TFP 0.61 1.10 1.65 0.67

(B) 1995–2000

Labour productivity 3.37 2.86 1.73 2.38

of which

Labour quality 0.16 0.37 0.33 0.06

ICT capital 1.06 0.83 0.34 0.66

Non-ICT capital 0.31 0.19 � 0.33 0.57

TFP 1.83 1.47 1.39 1.09

Sources:Calculations based on industry data underlying O’Mahony and Van Ark (2003).ICT, information and communications technology; TFP, total factor productivity.

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 365

r Scottish Economic Society 2005

labour productivity growth in manufacturing but this is heavily influenced by

the very high rates of labour productivity growth in ICT producing sectors,

shown in Table 3. These sectors represent a much greater share of

manufacturing in the US than in the European countries. In contrast the UK

experienced a large drop in labour productivity growth in manufacturing,

largely down to lower TFP growth. This partly reflects very high growth rates

Table 3

Growth in labour productivity, and contributions of capital, labour quality and TFP,

manufacturing and market services, average percentage points per annum

US UK France Germany

Manufacturing

(A) 1979–1995

Labour productivity 3.43 4.87 2.94 2.81

of which

Labour quality 0.38 0.36 0.28 0.33

ICT capital 0.46 0.29 0.14 0.34

Non-ICT capital 0.48 0.91 1.63 0.58

TFP 2.11 3.31 0.89 1.56

Labour productivity (ICT producers) 12.54 12.56 7.43 4.99

(B) 1995–2000

Labour productivity 4.69 2.93 3.57 2.26

of which

Labour quality 0.21 0.35 0.23 0.11

ICT capital 0.73 0.57 0.24 0.29

Non-ICT capital 0.73 0.43 0.38 0.22

TFP 3.02 1.58 2.72 1.64

Labour productivity (ICT producers) 21.73 15.68 9.95 8.94

Market services

(A) 1979–1995

Labour productivity 1.18 2.01 1.97 2.19

of which

Labour quality 0.27 0.60 0.13 0.21

ICT capital 0.73 0.59 0.25 0.81

Non-ICT capital 0.29 0.86 � 0.08 1.09

TFP � 0.11 � 0.04 1.67 0.08

(B) 1990–2000

Labour productivity 3.55 3.40 0.84 2.19

of which

Labour quality 0.15 0.41 0.42 0.05

ICT capital 1.36 1.10 0.39 0.87

Non-ICT capital 0.32 0.19 � 0.77 0.56

TFP 1.72 1.70 0.80 0.71

Sources:Calculations based on industry data underlying O’Mahony and Van Ark (2003).ICT, information and communications technology; TFP, total factor productivity.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK366

r Scottish Economic Society 2005

relative to other countries in the 1980s (the Thatcher effect) and very poor

performance in the mid- to late-1990s. Note however that despite this relatively

poor performance, UK manufacturing continued to invest heavily in ICT

capital. As with the market economy, traditional capital intensity declined in

UK manufacturing. France showed patterns in manufacturing closer to the US,

with a large increase in TFP while the German experience was a (muted) version

of that experienced by Britain, i.e. a slowdown in labour productivity growth

and non-ICT capital intensity but in Germany’s case TFP growth did not fall.

Underlying these trends were accelerations in labour productivity growth (and

TFP) in ICT producing manufacturing sectors in all three countries, similar to

that experienced in the US, but at much lower rates.

Turning to market services, there is a clear division between the US and the

UK on the one hand, and the remaining two European countries, on the other.

In the US and the UK, comparing the two time periods, there was an

acceleration in both labour productivity and TFP growth in market services,

with the UK performance dampened again by a fall in the contribution of non-

ICT capital. In both countries, the contributions of ICT capital have become

very large, accounting for about one-third of labour productivity growth. In

contrast France showed declining growth rates in both labour productivity and

TFP growth and very low contributions from ICT investment. Germany

performs better than France with no change in labour productivity growth and

an acceleration in TFP growth but at nothing like the rates experienced in the

US and UK. Neither France nor Germany shows a large increase in the

contribution of ICT capital.

Therefore looking beneath the aggregate figures suggests that comparisons

between the US and UK yield a different picture than those comparing the US

and Continental European countries. Britain performs relatively badly in

manufacturing but looks better in market services. However this conclusion

should be tempered with a note of caution as the relative levels estimates in

Table 1 show Britain a long way behind both France and Germany in market

services. Nevertheless it is possible that Britain may make up some of this

deficiency by its earlier adoption and more extensive use of ICT, and thus there

is some cause for cautious optimism in the case of the UK.

The results above show that ICT capital has had a significant impact in

raising labour productivity growth through the capital deepening channel.

However there may be external effects from investing in this type of capital

which also raise underlying TFP growth. Or it may be the case that omitted

variables such as organisational changes associated with adoption of ICT raises

TFP growth. Some suggestion of a positive impact of ICT on TFP can be seen

from dividing market services into a number of subdivisions. Table 4 shows TFP

growth rates and the percentage point contribution of ICT capital for one such

division. In all four countries TFP growth in the Communications sector showed

accelerating TFP growth simultaneously with increased contributions of ICT

capital. In the US and the UK, TFP growth rates appear to accelerate in sectors

where the ICT contributions were greatest but such a pattern is not so readily

observable for France and Germany.

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 367

r Scottish Economic Society 2005

Turning to the whole sample of 25 industries, it is useful to consider the

correlation between TFP growth and ICT capital’s contribution to labour

productivity growth. A positive and significant correlation suggests that there

may be an impact of ICT capital on TFP growth that is not captured by the

growth accounting method. Table 5 shows such an effect is apparent in the US

and the UK in the post-1995 period, but not earlier. In contrast, the correlation

is negative in France and Germany during the later period.

The results in Tables 4 and 5 are suggestive that the increased investment in

ICT may be an important driver of TFP growth since the mid-1990s, at least in

the US and the UK. The growth accounting method is not capable of measuring

spillover effects because by definition it assumes no divergence between private

Table 4

TFP growth and labour productivity contributions of ICT capital: market services

US UK France Germany

TFP growth

1979–1995

Communications � 0.28 2.46 4.93 1.99

Distributiona 0.98 0.41 2.63 1.39

Financial services � 3.24 � 1.79 2.77 0.26

Business services 0.11 � 1.08 2.00 � 2.05

Other servicesb � 0.04 0.63 � 0.78 0.38

1995–2000

Communications 3.00 5.87 7.63 13.10

Distribution 5.12 1.89 0.30 0.63

Financial services 0.82 2.63 � 1.21 2.36

Business services � 0.72 0.82 1.47 � 1.56

Other services � 0.65 1.10 0.33 0.19

Contribution ICT capital to labour productivity growth

1979–1995

Communications 0.90 0.74 0.40 1.61

Distribution 0.84 0.74 0.13 0.29

Financial services 1.67 1.12 1.03 1.40

Business services 0.51 0.63 0.10 1.51

Other services 0.21 0.07 0.14 0.11

1995–2000

Communications 1.89 3.00 0.55 1.91

Distribution 1.28 1.56 0.28 0.66

Financial services 3.06 1.05 1.59 1.59

Business services 0.73 1.30 0.18 1.12

Other services 0.57 0.14 0.25 0.22

Notes:Percentage points per annum.aWholesale plus retail trade.bTransport, hotels and catering, personal services.Sources:Calculations based on industry data underlying O’Mahony and Van Ark (2003).ICT, information and communications technology.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK368

r Scottish Economic Society 2005

and social returns. An alternative method would be to use econometric methods

using the industry panel data. This is complicated as it requires paying attention

to the time series properties of the data, see the discussion in O’Mahony and

Vecchi (2005). This latter paper suggests greater than market returns for ICT

capital in the US, over the long run, but with little evidence for such an effect in

the UK. However the correlations in Table 5 suggest some such effect may be

becoming apparent for the UK for recent years.

The disadvantage of industry data is their aggregated nature which hides the

variation that aids in pinpointing associations between variables in econometric

analysis. Therefore, rather than pursuing this line of inquiry further the next

section considers evidence using firm-level data, for three countries, Germany,

the UK and Italy. Data availability considerations at the time the data were

constructed meant that Italy could not be included in the growth accounting

results shown above. However it is worth considering Italy’s productivity

position based on available data to put this country’s performance in

perspective. Therefore Table 6 compares growth in output per hour worked in

Italy in the two periods considered in earlier tables, in the market economy,

industry and market services. This shows a pronounced deceleration in the

market economy, attributed entirely to a collapse of labour productivity growth

in industry. In fact market services show a small increase.

Venturini (2004) considers growth accounts for Italy, discussing where the

Italian productivity story has diverged from the EU pattern. He suggests that

overall, ICT capital deepening in Italy has been close to the lower end of the

distribution in EU countries. Estimates of the contribution of ICT capital

deepening to labour productivity growth are shown in italics in Table 6, as they

are not strictly comparable with those for the other European countries.3

Nevertheless they confirm that small contributions in both industry and services,

and show little growth in the latter. However Venturini (2004) suggests that the

decline in TFP is found to play a more important role in the deceleration of

Italian labour productivity growth. The results for Italy show the increased

weakness of traditional manufacturing sectors. These are the bulk of Italian

economy, where it has enjoyed its main comparative advantage in international

trade but is more vulnerable to Asian competitors.

Table 5

Correlation between TFP growth and ICT capital contribution

1979–1995 1995–2000

US � 0.14 0.25

UK � 0.10 0.51

France 0.08 � 0.09

Germany � 0.45 � 0.05

ICT, information and communications technology; TFP, total factor productivity.

3 In particular these estimates do not employ a hedonic price deflator for computingequipment.

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 369

r Scottish Economic Society 2005

IV The Impact of ICT on Firm-Level Performance

Micro-economic data are generally more detailed and enable more specific

estimation of the mechanisms through which productivity changes travel. One of

the fundamental problems with micro-economic analyses has been the sheer data

requirements. This has been compounded by an inability to compare survey

results from one country to another, usually because of a lack of coordination in

surveys. In addition, institutional differences might sometimes make compar-

isons less than meaningful. In this section, firm-level evidence from three

European countries (Germany, Italy and the UK) is considered, to see if

together these provide further evidence of productivity impacts from the use of

information technology.

ICT and workplace performance in Germany

In recent years, several authors investigated the impact of ICT investments on

establishment or firm productivity in Germany. Zwick (2003) finds substantial

effects of ICT investments on establishment productivity. In contrast to the bulk

of the literature, establishments without ICT capital are also included and

lagged effects of ICT investments are analysed. In addition, a broad range of

establishment and employee characteristics are taken into account in order to

avoid omitted variable bias. It is shown that taking into account unobserved

heterogeneity of the establishments using a fixed effects panel estimation

increases the estimated lagged productivity impact of ICT investments. Also the

endogeneity of ICT investments is corrected by introducing an instrumental

variables estimator with external instruments. This correction increases the

estimated productivity impact of ICT.

Hempell (2005) also finds a very high net-rate of return to ICT investments

on the basis of the Mannheim Innovation Panel in Services. He uses a translog

production function including non-ICT capital, ICT capital and labour, and

Table 6

Labour productivity growth for Italy, 1979–2000

1979–1995 1995–2000

Labour

productivity

growth

Contribution of

ICT capital

Labour

productivity

growth

Contribution

of ICT capital

Market economy 2.30 0.26 1.18 0.31

Industry 2.90 0.23 0.96 0.27

Market services 0.62 0.37 0.84 0.40

Sources:Calculations based on industry data underlying O’Mahony and Van Ark (2003), GGDC Total EconomyGrowth Accounting database of Timmer et al. (2003) and, for ICT capital, Bassenetti et al. (2004).ICT, information and communications technology.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK370

r Scottish Economic Society 2005

corrects the endogeneity of ICT intensity and unobserved heterogeneity by using

system GMM estimations. Controlling for unobserved heterogeneity reduces the

coefficient of ICT capital and it is no longer significant. When endogeneity is

also taken into account, the measured productivity effect, however, increases

again. Also on the basis of the Mannheim Innovation Panel, Licht and Moch

(1999) find a very high impact of personal computers on productivity, while the

impact of ICT investments on productivity is smaller. Bertschek and Kaiser

(2004) find similarly high impacts of ICT investments on productivity in a

comparable econometric setting using the German ‘Service Sector Business

Survey’.

These papers do not distinguish between the potentially different impact ICT

investments have on productivity in the manufacturing and service sector in

Germany. The estimation presented here therefore first tests if the impact differs

between both sectors and then estimates the different productivity effects. It uses

the two-step estimation procedure developed by Black and Lynch (2001) and

implemented by Zwick (2003). The estimation is based on the representative

German IAB establishment panel, waves 1997–2001. A definition of all variables

as well as their average values can be found in Table A1 in Zwick (2003).

This study estimates the impact of ICT investment in 1996/1997 on average

productivity in 1997–2000. In order to account for unobserved time-invariant

heterogeneity, the parameters of the time-variant input factors capital and

labour from equation (4) are determined by a simple fixed effects Cobb–Douglas

production function on the basis of panel data from 1997 to 2000 in the first

step. The effects of the (almost) time-invariant determinants including ICT

investments are regressed on the fixed effects from the panel analysis in the

second step. The fixed effects estimation in the first step is

lnYt ¼ a lnKt þ b lnLt þ uþ et with t ¼ 1997�2000; ð5Þ

where Y is VA (sales minus input costs), K is capital which is calculated by the

perpetual inventory method from replacement investments (Black and Lynch,

2001; Hempell, 2005),4 L is the number of employees, u is the unobserved time-

invariant establishment-specific fixed effect, and et the idiosyncratic component

of the error term. The results of this estimation step are identical to those by

Zwick (2003, Table A8).5

On the basis of estimating equation (5), the fixed effect u for every

establishment can be calculated. The fixed effect is the average establishment-

specific difference to productivity predicted on the basis of the variable inputs or

in other words TFP. It serves as the dependent variable for the second

estimation step. The vector of explanatory variables in the second step contains

all (almost) time-invariant establishment characteristics that might have an

4Depreciation is assumed to be linear while the average depreciation rate is assumed to equal10%. The average growth rate of investments is assumed to equal 5% (Hempell, 2005). Changesin these assumptions did not influence the results from the productivity estimations.

5Note that the first step total factor productivity estimations suffer from omitted variablebias and measurement error – labour and capital coefficients therefore may be too low (Harrisand Drinkwater, 2000).

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 371

r Scottish Economic Society 2005

impact on establishment productivity from equation (4): ICT investments

(ICT ), training investments, the share of qualified employees, work organisa-

tion, the presence of works councils or if an establishment is bound by collective

bargaining, five establishment size dummies, 16 dummies for sector, dummies

for East or West German establishments, exporters and four legal forms. It

includes three dummy variables indicating if an establishment introduced re-

organisations (introduction of team work, reduction of hierarchies, and

introduction of autonomous workgroups) that are closely correlated (Wolf

and Zwick, 2002). This means that there may be multi-collinearity if they are

estimated separately. Therefore, the observed three re-organisations are

aggregated to one independent ‘re-organisations’ factor R by a factor analysis.

All variables (besides the dummy for works councils) are in values for 1997 and

collected in vector X.6

u ¼ g ICTþ d0X þ e: ð6Þ

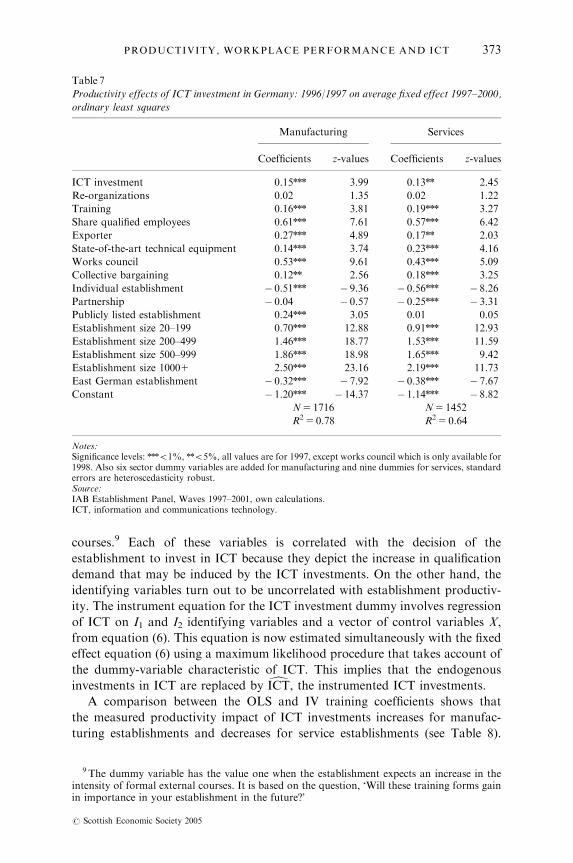

In order to test if the manufacturing and services sectors differ significantly in

their productivity determinants, a Chow-test is performed. It shows that

equation (6) should be estimated separately for both sectors.7 The estimation

results of equation (6) are shown in Table 7. ICT investments have a significant

positive impact on the establishment-specific fixed effects in the manufacturing

and the services sector. Both coefficients do not differ, however. The control

variables all have the expected effects on the productivity of the enterprises. The

productivity gap between East and West Germany is still persistent, individual

establishments and partnerships are on average less productive than limited

liability companies and publicly listed establishments, and the sector dummies

are jointly significant (see also Wolf and Zwick, 2002). The larger the enterprise

the higher is its productivity. We find that works councils and collective

bargaining have a positive impact on productivity (see also Hubler and Jirjahn,

2003; Zwick, 2004). Re-organisations that increase employee participation do

not have a positive impact on productivity which may be a consequence of

endogeneity bias (Wolf and Zwick, 2002). Establishments that train the

workforce and have a high share of qualified employees are more efficient

(Black and Lynch, 2001; Zwick, 2005). The main difference between service and

manufacturing sector is that publicly listed establishments are not more

productive than limited liability establishments in the service sector while

partnerships are not less productive in the manufacturing sector.

Final statements on the effects of ICT investments on productivity can only

be made, however, if we control for training endogeneity. Two suitable exclusion

restrictions can be identified: an expected increase in demand for qualification

and training8 and an expected increase in the incidence of formal training

6Details of the construction of R are given in Zwick (2003) as are descriptive statistics for X(Table A1).

7 The test statistic is: w2(17)5 51.07, Prob o0.01.8 The dummy variable has the value one when the establishment expects an increase in the

demand for qualification and training. It is based on the question, ‘Which personnel problemsdo you expect in the following two years?’

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK372

r Scottish Economic Society 2005

courses.9 Each of these variables is correlated with the decision of the

establishment to invest in ICT because they depict the increase in qualification

demand that may be induced by the ICT investments. On the other hand, the

identifying variables turn out to be uncorrelated with establishment productiv-

ity. The instrument equation for the ICT investment dummy involves regression

of ICT on I1 and I2 identifying variables and a vector of control variables X,

from equation (6). This equation is now estimated simultaneously with the fixed

effect equation (6) using a maximum likelihood procedure that takes account of

the dummy-variable characteristic of ICT. This implies that the endogenous

investments in ICT are replaced by dICT, the instrumented ICT investments.

A comparison between the OLS and IV training coefficients shows that

the measured productivity impact of ICT investments increases for manufac-

turing establishments and decreases for service establishments (see Table 8).

Table 7

Productivity effects of ICT investment in Germany: 1996/1997 on average fixed effect 1997–2000,

ordinary least squares

Manufacturing Services

Coefficients z-values Coefficients z-values

ICT investment 0.15nnn 3.99 0.13nn 2.45

Re-organizations 0.02 1.35 0.02 1.22

Training 0.16nnn 3.81 0.19nnn 3.27

Share qualified employees 0.61nnn 7.61 0.57nnn 6.42

Exporter 0.27nnn 4.89 0.17nn 2.03

State-of-the-art technical equipment 0.14nnn 3.74 0.23nnn 4.16

Works council 0.53nnn 9.61 0.43nnn 5.09

Collective bargaining 0.12nn 2.56 0.18nnn 3.25

Individual establishment � 0.51nnn � 9.36 � 0.56nnn � 8.26

Partnership � 0.04 � 0.57 � 0.25nnn � 3.31

Publicly listed establishment 0.24nnn 3.05 0.01 0.05

Establishment size 20–199 0.70nnn 12.88 0.91nnn 12.93

Establishment size 200–499 1.46nnn 18.77 1.53nnn 11.59

Establishment size 500–999 1.86nnn 18.98 1.65nnn 9.42

Establishment size 10001 2.50nnn 23.16 2.19nnn 11.73

East German establishment � 0.32nnn � 7.92 � 0.38nnn � 7.67

Constant � 1.20nnn � 14.37 � 1.14nnn � 8.82

N5 1716 N5 1452

R2 5 0.78 R2 5 0.64

Notes:Significance levels: nnno1%, nno5%, all values are for 1997, except works council which is only available for1998. Also six sector dummy variables are added for manufacturing and nine dummies for services, standarderrors are heteroscedasticity robust.Source:IAB Establishment Panel, Waves 1997–2001, own calculations.ICT, information and communications technology.

9 The dummy variable has the value one when the establishment expects an increase in theintensity of formal external courses. It is based on the question, ‘Will these training forms gainin importance in your establishment in the future?’

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 373

r Scottish Economic Society 2005

Investments in ICT in 1996/1997 increase the average productivity of

manufacturing establishments in 1997–2000 by 36% while they do not have

an impact on productivity of service establishments. Obviously the selection

mechanism is different in both sectors: while in the manufacturing sector it is the

establishments with a productivity deficit that invest in ICT, this does not seem

to be the case for the services sector. The other covariates are very similar in

both regressions.

The results of the instrumental equation that explains the decision of the

establishments to invest in ICT or not can be found in Table 9. According to the

theoretical considerations, expected higher demand for training and qualifica-

tions and an increase of the importance of formal internal training courses have

a positive impact on the probability that an establishment invests in ICT.

International competitive pressure has a positive impact on the propensity of

establishments to invest in ICT because strong international competition drives

establishments to innovation and rapid technology adoption (Osterman, 1994).

Table 8

Productivity effects of ICT investment in Germany: 1996/1997 on average fixed effect 1997–2000,

instrumental variables regression

Manufacturing Services

Coefficients z-values Coefficients z-values

ICT investment 0.36nnn 3.28 0.08 0.33

Re-organizations 0.08 0.54 0.03 1.55

Training 0.15nnn 3.43 0.21nnn 3.37

Share qualified employees 0.58nnn 7.01 0.57nnn 6.52

Exporter 0.24nnn 4.24 0.19nn 2.21

State-of-the-art technical equipment 0.13nnn 3.42 0.25nnn 4.25

Works council 0.50nnn 8.68 0.45nnn 5.12

Collective bargaining 0.12nn 2.57 0.18nnn 3.27

Individual establishment � 0.50nnn � 9.08 � 0.57nnn � 8.27

Partnership � 0.04 � 0.64 � 0.26nnn � 3.32

Publicly listed establishment 0.23nnn 3.04 � 0.00 � 0.00

Establishment size 20–199 0.69nnn 12.61 0.93nnn 12.97

Establishment size 200–499 1.44nnn 18.34 1.55nnn 11.61

Establishment size 500–999 1.86nnn 19.15 1.67nnn 9.44

Establishment size 10001 2.48nnn 22.89 2.24nnn 12.16

East German establishment � 0.32nnn � 7.88 � 0.38nnn � 7.72

Constant � 1.24nnn � 14.50 � 1.09nnn � 7.59

N5 1716 N5 1452

Wald test of

independent equations,

Prob4w2 5 0.04

Wald test of

independent equations,

Prob4w2 5 0.37

Notes:Significance levels: nnno1%, nno5%, all values are for 1997, except works council which is only available for1998. Also six sector dummy variables are added for manufacturing and nine dummies for services, standarderrors are heteroscedasticity robust.Source:IAB Establishment Panel, Waves 1997–2001, own calculations.ICT, information and communications technology.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK374

r Scottish Economic Society 2005

It is also found that the adoption of ICT is positively influenced by the adoption

or presence of organisational forms that increase the participation of employees

(Bresnahan et al., 2002). In addition, the qualification level of the employees and

training investments have a positive impact on the inclination of the establish-

ment to invest in ICT (Zwick, 2003). The enterprises need well-educated

employees in order to effectively implement new ICT and the complementary

new organisational forms that require greater levels of cognitive skill, flexibility,

and autonomy. Works councils also have a positive impact on ICT investments.

Larger establishments do not seem to invest more frequently in ICT.

ICT and workplace performance in Italy

For Italy, micro-data sets providing data on ICT investment are still in short

supply. The Survey on Firms Accounts (see ISTAT, 2001) provides a truly

longitudinal firm-level data set, but its micro-data are not released to external

researchers. Using these data, Milana and Zeli (2004) analyse the TFP

determinants in a sample of 2248 Italian non-agricultural firms, focusing on

ICT. The authors build a Malmqvist-like index of TFP growth for each firm,

and then estimate, separately for each industry, a firm-level regression for TFP

Table 9

Instrumental variable regression for Germany, endogeneous variable: ICT investments 1996/1997

Variables

Manufacturing Services

Coefficient z-value Coefficient z-value

Re-organizations 0.14nnn 5.78 0.18nnn 6.50

Training 0.16n 1.94 0.18nn 2.06

Share qualified employees 0.51nnn 3.55 0.14 1.10

Exporter 0.35nnn 3.56 0.26nn 2.08

State-of-the-art technical equipment 0.15nn 2.07 0.21nn 2.52

Works council 0.40nnn 3.94 0.29nn 2.31

Individual establishment � 0.16 � 1.62 � 0.19n 1.93

Partnership 0.09 0.71 � 0.01 � 0.06

Publicly listed establishment 0.12 0.66 � 0.23 � 0.99

Establishment size 20–199 0.11 1.18 0.12 1.22

Establishment size 200–499 0.26 1.59 0.32 1.58

Establishment size 500–999 0.01 0.03 0.32 1.16

Establishment size 10001 0.27 1.22 0.91nn 2.46

Expected large demand for training and

qualification (instrument)

0.15n 1.64 0.20n 1.87

Expected increase in formal internal

courses (instrument)

� 0.09 � 0.77 0.37n 1.74

Constant � 1.01nnn � 6.85 � 0.75nnn � 4.19

Notes:Significance levels: nnno1%, nno5%. All variables take the values of year 1997 (except works councils thatare only available for 1998). Also six sector dummy variables are added for manufacturing and nine dummiesfor services, standard errors are heteroscedasticity robust.Source:IAB Establishment Panel, Waves 1997 and 1998, own calculations.ICT, information and communications technology.

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 375

r Scottish Economic Society 2005

changes, expressed as long differences over the period 1996–1999. The latter are

regressed on the intensities of R&D and ICT capital stock on total capital,

together with the wage share of skilled workers on total labour costs; moreover,

controls for size, location and other firm characteristics are used. Among their

results, the coefficient on ICT capital intensity is positive and significant for

most industries, the skill factor is of smaller significance (and only for a few

industries), while the R&D intensity is never significant.

This paper uses the Capitalia data set, representative of manufacturing. It is

based on a rotating panel and gives both a larger sample (ALL), fixed for a

3-year period (there are two waves, 1995–1997 and 1998–2000) and a

longitudinal smaller one (LONG), composed of those firms which are present

across the two waves. The LONG sample will be the reference sample: besides

the econometric reasons explained later, it is also more representative of

manufacturing.

For the regression analysis, aimed at measuring the ICT impact on TFP, a

standard Cobb–Douglas framework is employed as outlined above, but where

ICT capital is separated from other forms of capital:

ln Yit ¼ ln Aþ ltþ a ln Lit þ b ln Kit þ g ln KICTit þ Zit: ð7Þ

In this framework, the TFP addendum should measure the residual growth of

output (exogenous disembodied technical progress), left after accounting for the

growth of all the productive inputs. In practice, a series of factors can still

influence TFP – particularly in a growth accounting framework, where the input

coefficients are set to their nominal input shares. TFP will also pick up any

returns to scale, resource reallocation and ‘omitted variables’ bias. This paper

focuses on the first and the third element. As employed recently by a few

scholars,10 one way to control for the presence of increasing (or ‘excess’, with

respect to the single input) returns – particularly those attributable to the ICT

capital – is that of calculating first the usual index of TFP, and then to use it as

the dependent variable in the Cobb–Douglas estimation.11 This solution also has

the advantage of avoiding other biases, such as measurement errors involved in

the direct estimation of the ICT elasticity parameter with the production

function in differences.12 However, this strategy is not immune from the

‘omitted variable’ bias; in fact, a positive and significant ‘excess’ output elasticity

coefficient found for ICT capital could partly capture the impact of other

unmeasured inputs. As recently explored by the literature (see Brynjolfsson and

Hitt, 2000; Bresnahan et al., 2002; Brynjolfsson and Hitt, 2003), ICT investment

10 See Brynjolfsson and Hitt (2003). A different procedure for detecting excess return ischosen by Lehr and Lichtenberg (1999), who go to estimate the excess return directly, withoutcalculating the TFP index.

11 The theoretical framework underlying this procedure is presented in Brynjolfsson and Hitt(2003). A different procedure for detecting excess returns on IT capital is chosen by Lehr andLichtenberg (1999), who estimate the excess returns directly, without calculating the TFP index.

12 In a production function estimated in differences, labour adjusts faster than the otherquasi-fixed factors like capital (be it normal or ICT). Because of the small share of ICT capital,its real contribution to productivity is more likely to be overwhelmed by measurement errors(Brynjolfsson and Hitt, 2003).

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK376

r Scottish Economic Society 2005

is typically accompanied by other complementary (mostly intangible) assets, like

innovations in business methods and organisation; moreover, productivity gains

should show up with a delay (see also David, 1990). Most of these

complementary assets are difficult to measure, and cannot easily be proxied

by qualitative variables or simple dummies. Hence this paper borrows from the

previous literature (as surveyed in e.g. Griliches, 1995; Bartelsman and Doms,

2000; Mairesse and Monhen, 2003), taking the firms’ own R&D capital as a

proxy for most of these immeasurable phenomena.

Having calculated the TFP index, and taking time differences, the TFP index

is regressed on the ICT and R&D capital, to test the ‘excess elasticity’

assumption. However, in many micro-data sets (including the one employed

here) ICT and R&D inputs are not segregated out of the traditional inputs (total

labour and capital), so that applying the above procedure suffers a double

counting problem. The solution traditionally found in the literature is that of

considering the ‘normal’ output elasticities of the ICT and R&D capital as

already incorporated in those of the traditional inputs (which in this case

represent a mix of heterogeneous inputs), imputed during the calculation of the

TFP index; consequently, those elasticities being estimated can, if significant, be

interpreted as the ‘excess’ ‘above average’ elasticities of the ICT and R&D

capital.13

The same logic applies when the data set does not allow the construction of

the R&D and ICT capital stocks, but offers data on R&D and ICT investment,

at least for 1 year (like ours). In this case, the production function can be

expressed in terms of ‘excess’ rate of return, and the ICT and R&D investment

are taken as proxies for their respective capital variations.14 Therefore our

estimating equation becomes

Dln TFP98�00 ¼ lþ rðICT=VAÞ98 þ sðR&D=VAÞ98þz ln EMPL98

þwSPINOFFSþ fM&Aþ SjjjINDUSTRYj þ e;

ð8Þ

with the ICT and R&D investment intensity coefficients representing excess rates

of return, both for ICT (r5 @VA/@KICT) and R&D (s5 @VA/@KR&D).

Looking at the left-hand side of equation (8), the TFP index is computed as

VA minus labour and capital inputs (all in logs), multiplied by their respective

shares on VA. These shares (averaged over 1998–2000) do not refer to single

firms, but are computed for each industry. This is equivalent to assuming that

there are as many perfectly competitive markets as industries, each of them with

a different capital/labour ratio (Baily et al., 1992). All monetary variables have

13This procedure is quite common in the ‘R&D productivity’ literature. An early descriptioncan be found in Griliches and Lichtenberg (1984, sect. 5). Other data sets, instead, allow thedouble counting correction: an illustrative exercise is presented in Hall and Mairesse (1995).

14 This implies assuming a negligible depreciation rate for the R&D capital stock, close tozero (on this point, see also Griliches and Lichtenberg, 1984). Further details on the theoreticalframework underlying the ‘rate of return’ specification can be found in Mairesse and Sassenou(1991); more recent empirical evidence is presented in Hall and Mairesse (1995) and Harhoff(1998).

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 377

r Scottish Economic Society 2005

been deflated and labour input is measured by the number of total workers.15

Finally, the change in TFP is computed as a 2-year log difference between the

initial and final year of the last wave of the Capitalia survey (1998–2000). In

principle, the analysis could have started by using the previous wave of the

survey (1995–1997). However, for the reasons that shall be explained later, both

the use of longer differences and panel data estimation with first differences were

not feasible solutions.

Moving to the right-hand side of equation (8), the R&D investment intensity

refers to the initial year of the survey wave: in this way, R&D intensity is pre-

determined with respect to the TFP variation. However, contrary to R&D

expenditures, the survey does not provide annual data on ICT investments: firms

are asked to report only their cumulative expenditures on ICT items over the

previous 3 years. As a consequence, that referring to the initial year (1998) is not

the ‘true’ ICT intensity, but represents one-third of the total investment in ICT

during 1998–2000. Because of this imputation, the ICT intensity variable is not

truly pre-determined with respect to TFP changes, and this aggravates the

problem of endogeneity. To alleviate the latter, the previous wave of the

Capitalia survey (1995–1997) was employed from which a lagged variable for

ICT intensity was obtained, referring to the year 1997. The lack of annual data

for ICT investment prevented implementation of panel data estimation in first

differences or performing an estimation of equation (8) based on differences

longer than 2 years: in effect, the only way to get a truly lagged ICT variable it to

compute an index of TFP change over the last wave of the survey and to regress

it on the ICT intensity resulting from the previous wave. Obviously, to do it is

not possible to use the entire (ALL) sample of the last wave, but instead results

are based on the (LONG) sample of firms that took part in both waves (reducing

dramatically the number of observations from 3918 to 1119). Finally, the ICT

intensity is expressed at constant (1995) prices, and the deflation procedure takes

into account its internal composition by item.

The other explanatory variables included in equation (4) are used as controls.

The natural log of total workers (ln EMPL) should capture the possible effect of

firm size on TFP growth. As the TFP index could have been affected by

discontinuous changes in the size of firms, two other dummy variables are

inserted in the regression: one for the spin-offs or the selling of plants or lines of

business (SPINOFFS) and another for mergers and acquisitions (M&A) that

occurred during the period 1998–2000. Finally, 16 industry dummies are

included (not shown in the tables).

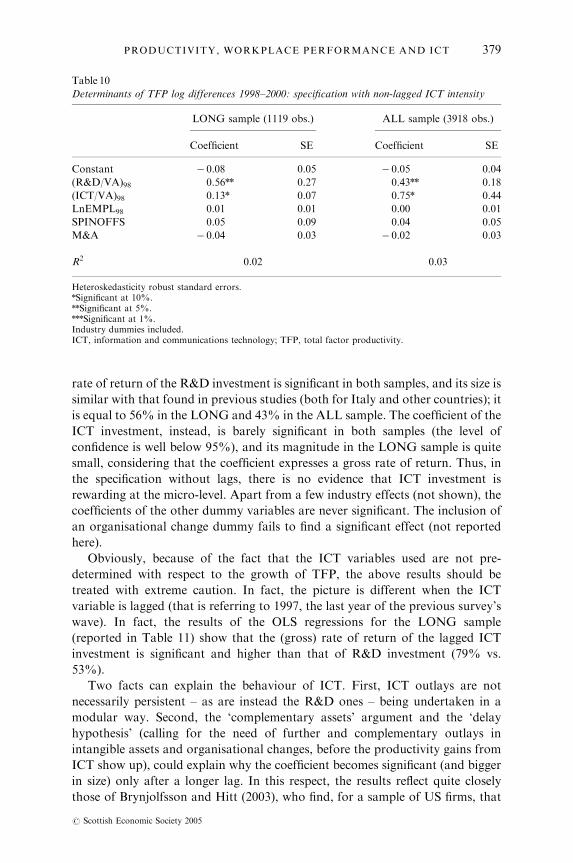

Table 10 presents the results of two OLS regressions carried out for equation

(8) without lagging ICT intensities: the main advantage of doing so is the

possibility of comparing the results arising from the LONG and the ALL

sample, with the latter having a very large number of observations. First of all,

the findings are quite consistent between the two samples. The estimated (gross)

15 Further details on deflation and econometric methodology are provided in Matteucci andSterlacchini (2004), who also present some sample descriptive statistics. Here it is sufficient tonote that the ICT deflator used builds on US hedonic prices.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK378

r Scottish Economic Society 2005

rate of return of the R&D investment is significant in both samples, and its size is

similar with that found in previous studies (both for Italy and other countries); it

is equal to 56% in the LONG and 43% in the ALL sample. The coefficient of the

ICT investment, instead, is barely significant in both samples (the level of

confidence is well below 95%), and its magnitude in the LONG sample is quite

small, considering that the coefficient expresses a gross rate of return. Thus, in

the specification without lags, there is no evidence that ICT investment is

rewarding at the micro-level. Apart from a few industry effects (not shown), the

coefficients of the other dummy variables are never significant. The inclusion of

an organisational change dummy fails to find a significant effect (not reported

here).

Obviously, because of the fact that the ICT variables used are not pre-

determined with respect to the growth of TFP, the above results should be

treated with extreme caution. In fact, the picture is different when the ICT

variable is lagged (that is referring to 1997, the last year of the previous survey’s

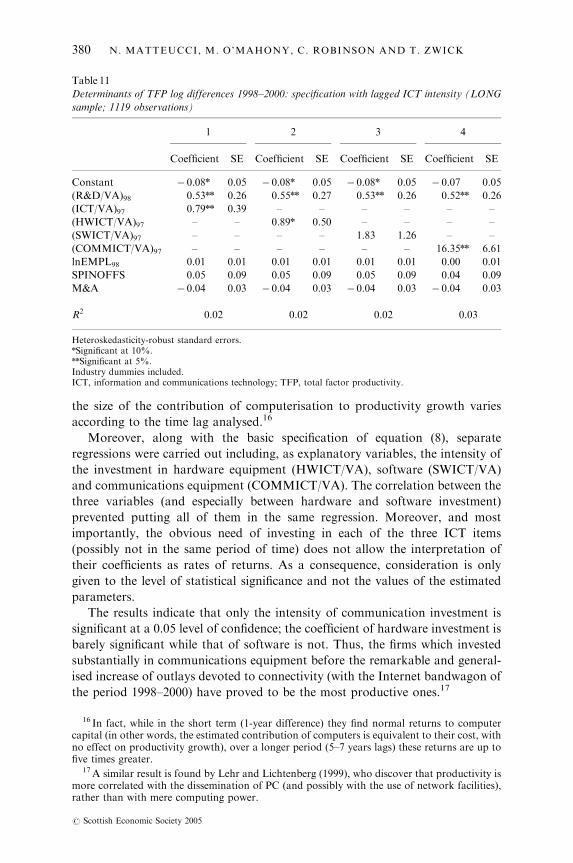

wave). In fact, the results of the OLS regressions for the LONG sample

(reported in Table 11) show that the (gross) rate of return of the lagged ICT

investment is significant and higher than that of R&D investment (79% vs.

53%).

Two facts can explain the behaviour of ICT. First, ICT outlays are not

necessarily persistent – as are instead the R&D ones – being undertaken in a

modular way. Second, the ‘complementary assets’ argument and the ‘delay

hypothesis’ (calling for the need of further and complementary outlays in

intangible assets and organisational changes, before the productivity gains from

ICT show up), could explain why the coefficient becomes significant (and bigger

in size) only after a longer lag. In this respect, the results reflect quite closely

those of Brynjolfsson and Hitt (2003), who find, for a sample of US firms, that

Table 10

Determinants of TFP log differences 1998–2000: specification with non-lagged ICT intensity

LONG sample (1119 obs.) ALL sample (3918 obs.)

Coefficient SE Coefficient SE

Constant � 0.08 0.05 � 0.05 0.04

(R&D/VA)98 0.56nn 0.27 0.43nn 0.18

(ICT/VA)98 0.13n 0.07 0.75n 0.44

LnEMPL98 0.01 0.01 0.00 0.01

SPINOFFS 0.05 0.09 0.04 0.05

M&A � 0.04 0.03 � 0.02 0.03

R2 0.02 0.03

Heteroskedasticity robust standard errors.nSignificant at 10%.nnSignificant at 5%.nnnSignificant at 1%.Industry dummies included.ICT, information and communications technology; TFP, total factor productivity.

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 379

r Scottish Economic Society 2005

the size of the contribution of computerisation to productivity growth varies

according to the time lag analysed.16

Moreover, along with the basic specification of equation (8), separate

regressions were carried out including, as explanatory variables, the intensity of

the investment in hardware equipment (HWICT/VA), software (SWICT/VA)

and communications equipment (COMMICT/VA). The correlation between the

three variables (and especially between hardware and software investment)

prevented putting all of them in the same regression. Moreover, and most

importantly, the obvious need of investing in each of the three ICT items

(possibly not in the same period of time) does not allow the interpretation of

their coefficients as rates of returns. As a consequence, consideration is only

given to the level of statistical significance and not the values of the estimated

parameters.

The results indicate that only the intensity of communication investment is

significant at a 0.05 level of confidence; the coefficient of hardware investment is

barely significant while that of software is not. Thus, the firms which invested

substantially in communications equipment before the remarkable and general-

ised increase of outlays devoted to connectivity (with the Internet bandwagon of

the period 1998–2000) have proved to be the most productive ones.17

Table 11

Determinants of TFP log differences 1998–2000: specification with lagged ICT intensity (LONG

sample; 1119 observations)

1 2 3 4

Coefficient SE Coefficient SE Coefficient SE Coefficient SE

Constant � 0.08n 0.05 � 0.08n 0.05 � 0.08n 0.05 � 0.07 0.05

(R&D/VA)98 0.53nn 0.26 0.55nn 0.27 0.53nn 0.26 0.52nn 0.26

(ICT/VA)97 0.79nn 0.39 – – – – – –

(HWICT/VA)97 – – 0.89n 0.50 – – – –

(SWICT/VA)97 – – – – 1.83 1.26 – –

(COMMICT/VA)97 – – – – – – 16.35nn 6.61

lnEMPL98 0.01 0.01 0.01 0.01 0.01 0.01 0.00 0.01

SPINOFFS 0.05 0.09 0.05 0.09 0.05 0.09 0.04 0.09

M&A � 0.04 0.03 � 0.04 0.03 � 0.04 0.03 � 0.04 0.03

R2 0.02 0.02 0.02 0.03

Heteroskedasticity-robust standard errors.nSignificant at 10%.nnSignificant at 5%.Industry dummies included.ICT, information and communications technology; TFP, total factor productivity.

16 In fact, while in the short term (1-year difference) they find normal returns to computercapital (in other words, the estimated contribution of computers is equivalent to their cost, withno effect on productivity growth), over a longer period (5–7 years lags) these returns are up tofive times greater.

17A similar result is found by Lehr and Lichtenberg (1999), who discover that productivity ismore correlated with the dissemination of PC (and possibly with the use of network facilities),rather than with mere computing power.

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK380

r Scottish Economic Society 2005

To summarise, the predetermination of the ICT variable suggests that the

second specification (with the lagged ICT intensity) is the most suitable one to

analyse the TFP growth. With this specification, a significant relation between

ICT investment and TFP emerges, similar to that found recently for other

countries. Finally, we are aware of the limits of our test, given that it does not

address completely the possible endogeneity of the ICT and R&D variables.

ICT and workplace performance UKn

Micro-work for the UK on the use and impact of ICT has been limited to a

handful of studies, primarily commissioned by the UK National Statistics Office

(Clayton et al., 2003; Clayton and Waldron, 2003; Criscuolo and Waldron,

2003). The focus of these studies has been the measurement of the impact of

computer network use on labour and TFP. Criscuolo and Waldron (2003)

limited their study to UK manufacturing, following the work of Atrostic and

Nguyen (2002) for the US. While the questions available from the survey do not

allow an exact comparison of findings with the US study, they consider e-buying

and e-selling separately and find productivity impacts differing in sign. In

particular, they do not find a positive impact from e-selling, which they partly

attribute to negative pricing effects, because of improved price transparency.

The authors also highlight the fact that any impact detected is likely to be an

underestimation of the productivity effect of ICT because presently there are no

ICT capital stock series available at the micro-level.18

Clayton and Criscuolo (2002) argue that e-commerce has had a significantly

positive impact on the way business to business transactions are conducted,

improving information flows between suppliers and consumers, and speeding up

market access. However, only around 2% of business sales are thought to

transmit through e-commerce, which makes it difficult to identify these sorts of

effects at the industry level, as in section II. Also, ICT activity as a whole

accounted for less than 10% of UK VA (Clayton and Criscuolo, 2002) which

highlights the importance of growth in ICT use rather than absolute levels, even

at the micro-level of analysis.

Enterprise panels linking ICT investment and productivity performance

similar to those employed in Germany and Italy are not yet readily available for

the UK, although there is on-going research facilitated by the Office for

National Statistics linking of survey data to financial information from the

annual business inquiry (ABI). Instead in this section preliminary results from

linking a survey of e-commerce for 2001 to financial information from the ABI

are presented. This covers both production industries and service sectors.

Combining data sets is an extremely useful way of increasing the potential of

micro-data. The merged data set for the UK consists of a single cross-section for

2001 which includes variables on the nature of e-commerce activity and financial

variables from the ABI.

18Although ONS are currently engaged on matching business investment surveys to financialdata.

PRODUCTIVITY, WORKPLACE PERFORMANCE AND ICT 381

r Scottish Economic Society 2005

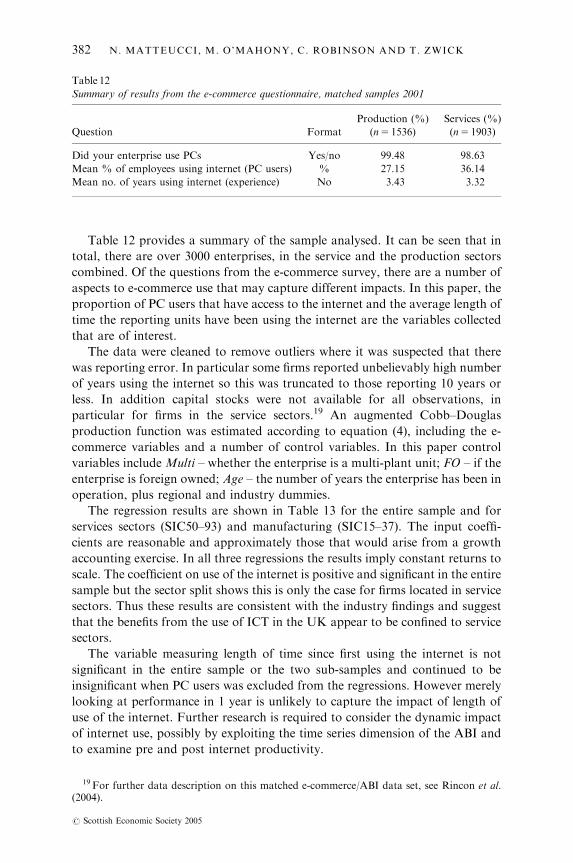

Table 12 provides a summary of the sample analysed. It can be seen that in

total, there are over 3000 enterprises, in the service and the production sectors

combined. Of the questions from the e-commerce survey, there are a number of

aspects to e-commerce use that may capture different impacts. In this paper, the

proportion of PC users that have access to the internet and the average length of

time the reporting units have been using the internet are the variables collected

that are of interest.

The data were cleaned to remove outliers where it was suspected that there

was reporting error. In particular some firms reported unbelievably high number

of years using the internet so this was truncated to those reporting 10 years or

less. In addition capital stocks were not available for all observations, in

particular for firms in the service sectors.19 An augmented Cobb–Douglas

production function was estimated according to equation (4), including the e-

commerce variables and a number of control variables. In this paper control

variables include Multi – whether the enterprise is a multi-plant unit; FO – if the

enterprise is foreign owned; Age – the number of years the enterprise has been in

operation, plus regional and industry dummies.

The regression results are shown in Table 13 for the entire sample and for

services sectors (SIC50–93) and manufacturing (SIC15–37). The input coeffi-

cients are reasonable and approximately those that would arise from a growth

accounting exercise. In all three regressions the results imply constant returns to

scale. The coefficient on use of the internet is positive and significant in the entire

sample but the sector split shows this is only the case for firms located in service

sectors. Thus these results are consistent with the industry findings and suggest

that the benefits from the use of ICT in the UK appear to be confined to service

sectors.

The variable measuring length of time since first using the internet is not

significant in the entire sample or the two sub-samples and continued to be

insignificant when PC users was excluded from the regressions. However merely

looking at performance in 1 year is unlikely to capture the impact of length of

use of the internet. Further research is required to consider the dynamic impact

of internet use, possibly by exploiting the time series dimension of the ABI and

to examine pre and post internet productivity.

Table 12

Summary of results from the e-commerce questionnaire, matched samples 2001

Question Format

Production (%)

(n5 1536)

Services (%)

(n5 1903)

Did your enterprise use PCs Yes/no 99.48 98.63

Mean % of employees using internet (PC users) % 27.15 36.14

Mean no. of years using internet (experience) No 3.43 3.32

19 For further data description on this matched e-commerce/ABI data set, see Rincon et al.(2004).

N. MATTEUCCI, M. O’MAHONY, C. ROBINSON AND T. ZWICK382

r Scottish Economic Society 2005

V Conclusions ^ ICTand productivity

This paper considered the impact of ICT on productivity in European countries,

using both industry and firm-level data. Both sources of information suggest

that there appear to be some productivity impacts from investment in ICT in all

three countries, but there is little evidence to suggest that these impacts are as yet

close to those found for the US. Of the European countries studied, the UK

experience is closest to the US, with both the industry- and firm-level evidence

pointing to a greater impact in services than in manufacturing. In contrast the

evidence presented suggests little evidence of a significant impact from ICT on

service sectors in the Continental European countries.

It is too early to tell if the lack of a US style payoff to ICT investment in

Europe is because of lagged adjustments given the earlier adoption of this

technology in the US or if the answer lies in the institutional framework facing

firms in Europe. The European country that appears to be performing best is the

UK which is generally regarded as one of the least regulated of the larger EU

countries. But there may also be other explanations, such as the rapid expansion

in higher education in the UK in the 1990s. In addition it should be recalled that

the UK productivity levels remain well below those in countries like France and

Germany so that the UK has had more scope for catch-up growth.

In Germany, ICT investments lead to a significant productivity increase for

several years in manufacturing, while the available evidence suggests service

establishments have not yet increased their VA by investing in ICT.

Acknowledgements

The authors gratefully acknowledge the financial contribution of the European

Commission (Research contract HPSE-CT-2001, Employment Prospects in the

Knowledge Economy-EPKE). We would like to thank our EPKE consortium

Table 13

Regression results, all firms, services and manufacturing, 2001

Services Manufacturing

Constant 1.427n (0.084) 1.351n (0.257) 1.385n (0.102)

Emp 0.263n (0.011) 0.290n (0.016) 0.229n (0.018)

Kap 0.116n (0.012) 0.147n (0.021) 0.093n (0.015)

Inter 0.633n (0.012) 0.582n (0.019) 0.678n (0.016)

Experience 0.003 (0.004) 0.002 (0.008) 0.005 (0.005)